Embed Size (px)

Citation preview

1

Challenges and Opportunitiesfor the NAFTA Steel Industry

and Governments

North American Steel Trade Committee (NASTC) MeetingOttawa, Canada − May 20, 2004

2

The inaugural NASTC meeting set the stage for promoting further openness in the North American steel

market, and addressing more effectively the common challenges facing the NAFTA steel industry.

Areas of mutual interest include:

• Understanding market developments through trade/market data exchange

• Identifying intra-NAFTA competitiveness problems and solutions/synergies

• Identifying common external trade concerns and developing collective NAFTA responses

• Cooperating on trade policy in multilateral fora (OECD, FTAA, WTO)

• Further exploring, consistent with antitrust regulations, the integration of the North American steel market through appropriate government policies

• Promoting the health and financial stability of the North American steel sector through appropriate government policies

3

The NAFTA steel industry has identified key steel industry fundamentals and proposes

several NASTC opportunities.

•Non-NAFTA imports are diverse, and characterized by a propensity to injure.

StrategicIndustry

NAFTA FinancialSustainability

Trade Flows

NAFTA Steel Strategies

• The steel industry is a strategic and progressive force.

•The NAFTA has resulted in greater openness of the N.A. steel market and has drawn the three industries and governments together for common purposes.

•Recent tight market conditions must be put into the context of long-term industry trends.

•The NAFTA steel industry proposes several NASTC opportunities.

4

The steel industry is a strategic and progressive force in the NAFTA region.

•Strategic industry

•Economic/social contribution

•Market/productivity growth

•Labor efficiency

•Investment/innovation

•Environmental management

StrategicIndustry

NAFTA FinancialSustainability

Trade Flows

NAFTA Steel Strategies

5

Steel is a strategic material for North American manufacturing.

• It is a critical input in all major industrial activities.

─ Construction• Infrastructure• Commercial/Industrial• Residential

─ Automobile and auto parts─ Shipbuilding─ Electrical equipment─ Heavy machinery─ Appliance─ Oil and gas

• It is also vital to national defense and homeland security including the steel that goes into our energy, transportation security and health and public safety infrastructures and our commercial, industrial and institutional complexes.

6

• It directly employs 200,000 people.• It indirectly employs over 1 million people.• It provides a healthy, safe and environmentally

responsible workplace. • It provides highly skilled jobs with above average pay. • It is a significant consumer of natural gas and electricity,

and has demonstrated a commitment to energy conservation.

• It is a strategic link to any successful effort to preserve and strengthen the manufacturing base, and directly impacts many other economic sectors, including the railroad/transportation industries.

The NAFTA steel industry is significant to the three domestic economies in North America – and a strong

steel industry is critical to a strong manufacturing base.

7

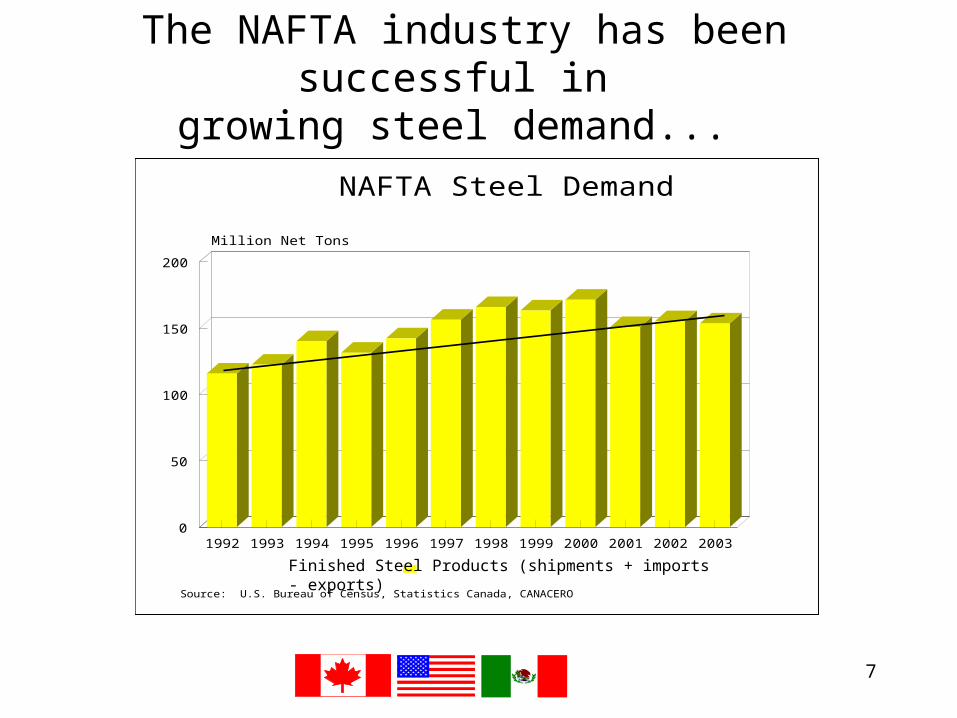

The NAFTA industry has been successful in growing steel demand...

NAFTA Steel Demand

Source: U.S. Bureau of Census, Statistics Canada, CANACERO

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 20030

50

100

150

200

Million Net Tons

Series 1Finished Steel Products (shipments + imports - exports)

8

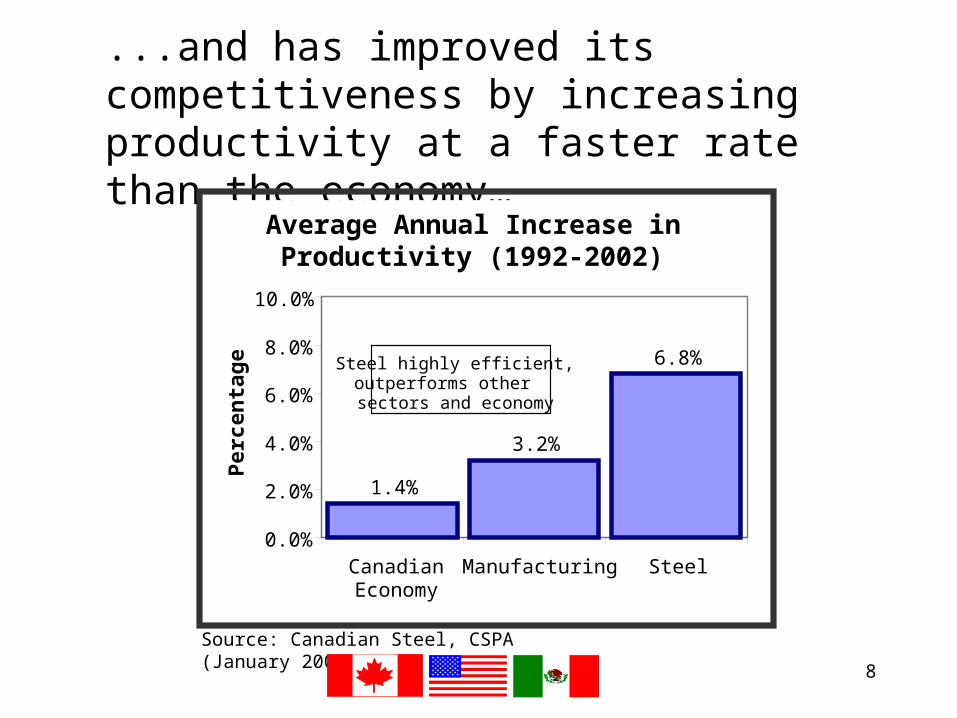

...and has improved its competitiveness by increasing productivity at a faster rate than the economy…

Average Annual Increase in Productivity (1992-2002)

1.4%

3.2%

6.8%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

CanadianEconomy

Manufacturing Steel

Per

cen

tag

e Steel highly efficient, outperforms other sectors and economy

Source: Canadian Steel, CSPA (January 2004)

9

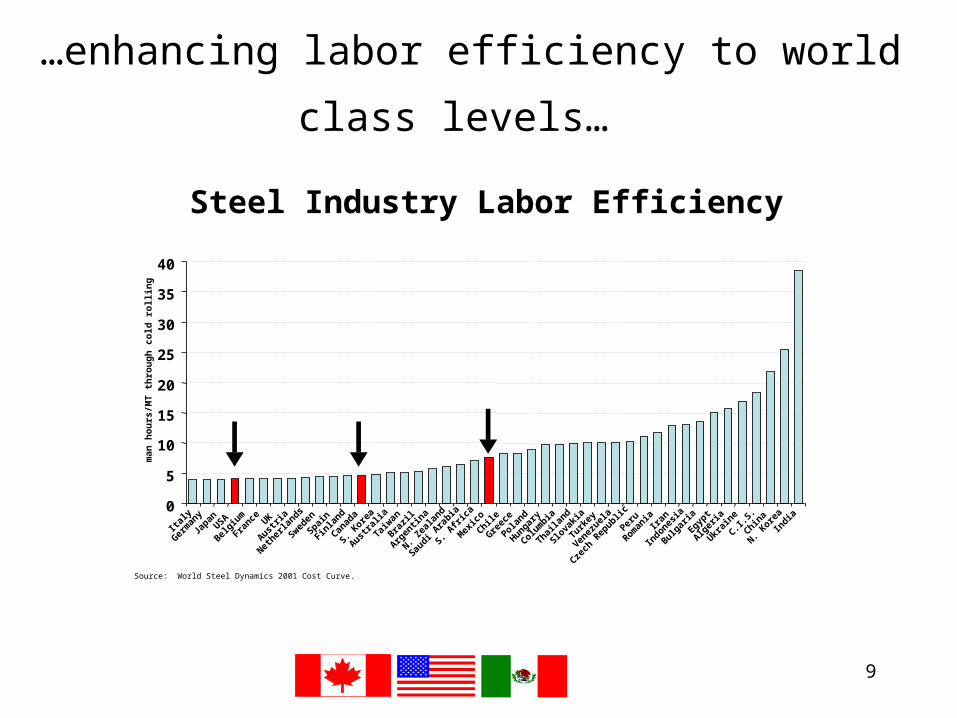

…enhancing labor efficiency to world class levels…

Steel Industry Labor Efficiency

0

5

10

15

20

25

30

35

40

Italy

Germ

any

Japan

USA

Belgiu

m

France UK

Austria

Nether

lands

Sweden

Spain

Finlan

d

Canad

a

S. Kor

ea

Australi

a

Taiwan

Brazil

Argen

tina

N. Zea

land

Saudi A

rabia

S. A

frica

Mex

icoChile

Greec

e

Poland

Hungary

Colum

bia

Thailan

d

Slovak

ia

Turkey

Venez

uela

Czech

Rep

ublicPer

u

Roman

iaIr

an

Indon

esia

Bulgaria

Egypt

Algeria

Ukrain

eC.I.

S.

China

N. Kor

eaIn

dia

man

hou

rs/M

T t

hrou

gh c

old

rolli

ng

Source: World Steel Dynamics 2001 Cost Curve.

10

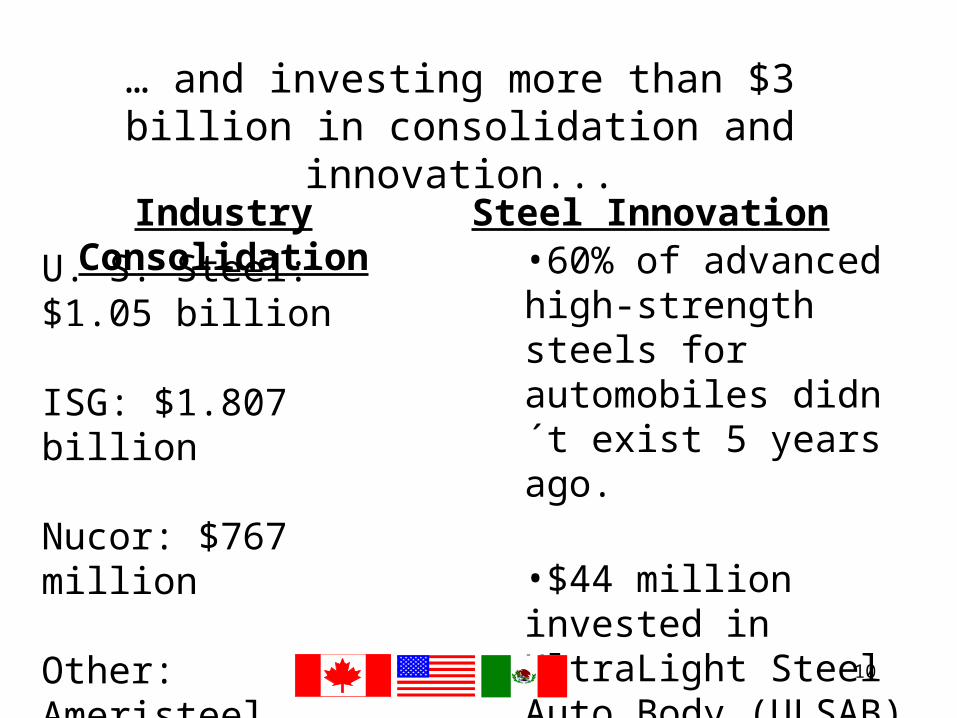

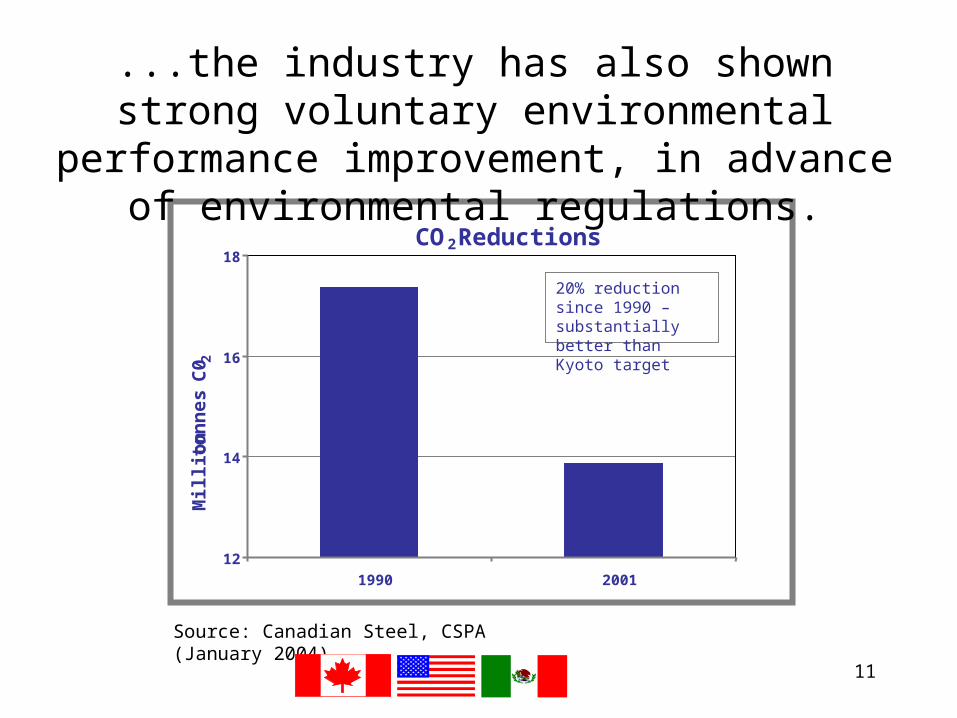

… and investing more than $3 billion in consolidation and innovation...

U. S. Steel: $1.05 billion

ISG: $1.807 billion

Nucor: $767 million

Other: Ameristeel, Delaware Steel Capital

Industry Consolidation•60% of advanced high-strength steels for automobiles didn´t exist 5 years ago.

•$44 million invested in UltraLight Steel Auto Body (ULSAB) initiatives.

Steel Innovation

11

12

14

16

18

1990 2001

20% reduction since 1990 – substantially better than Kyoto target

CO2 Reductions

Mil

lion

ton

nes

C

0 2

...the industry has also shown strong voluntary environmental performance improvement, in advance

of environmental regulations.

Source: Canadian Steel, CSPA (January 2004)

12

The steel industry is a strategic and progressive force in the NAFTA region.

•The industry has, and continues to develop, strong economic/social fundamentals.

•The industry is succeeding in maintaining steel as the material of choice for North American manufacturers.

•The industry remains critical to a strong NAFTA manufacturing base – including the automotive, construction and energy sectors.

13

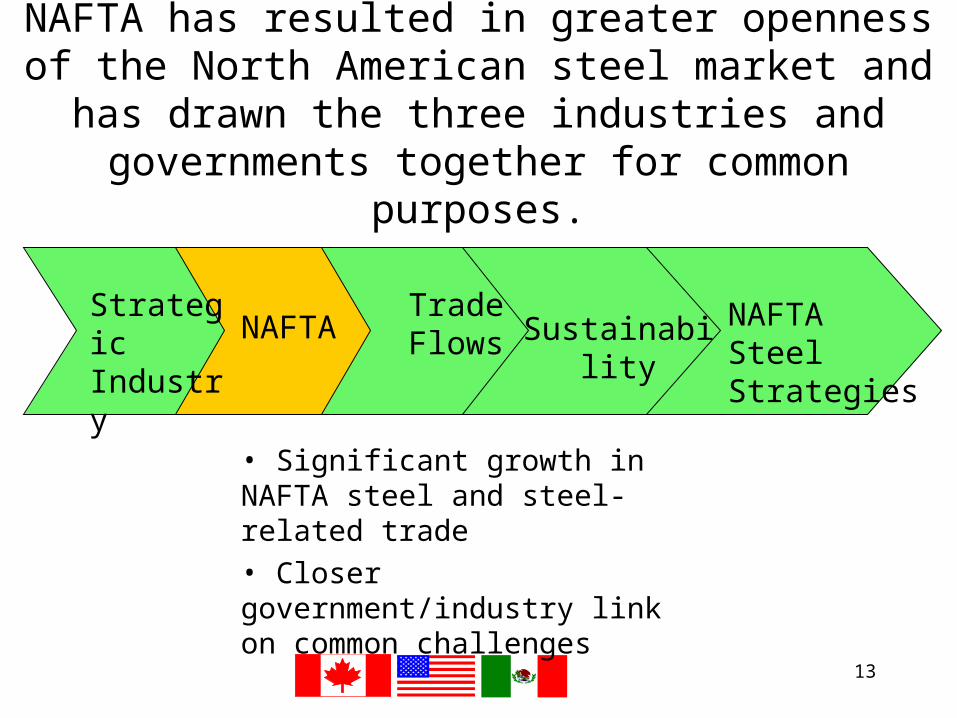

NAFTA has resulted in greater openness of the North American steel market and has drawn the three industries

and governments together for common purposes.

• Significant growth in NAFTA steel and steel-related trade

• Closer government/industry link on common challenges

StrategicIndustry NAFTA Sustainability

Trade Flows

NAFTA Steel Strategies

14

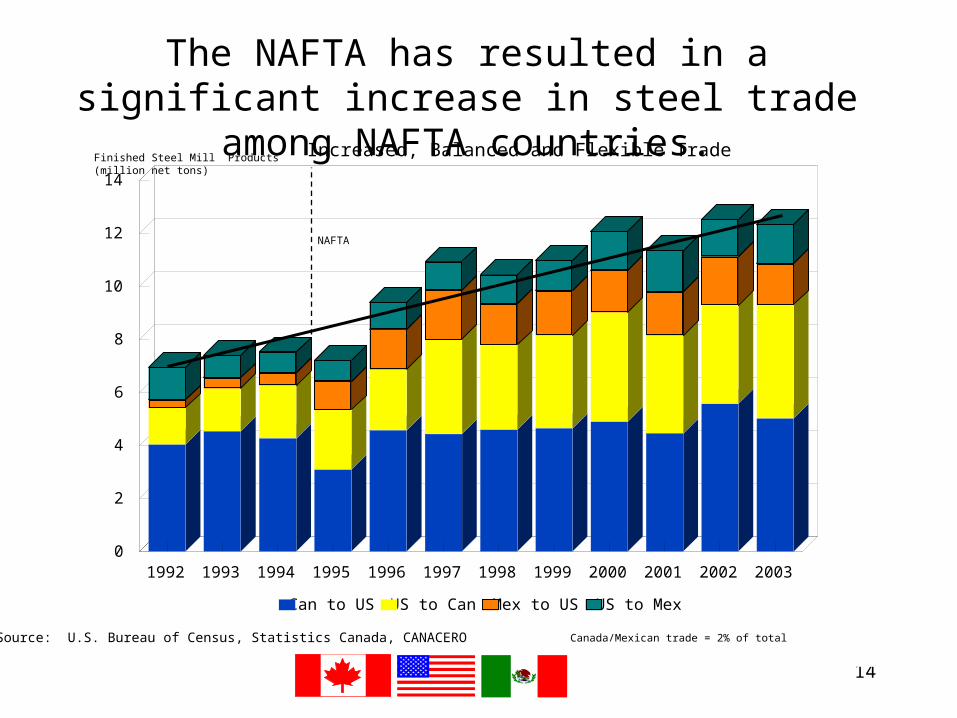

Increased, Balanced and Flexible Trade

Source: U.S. Bureau of Census, Statistics Canada, CANACERO Canada/Mexican trade = 2% of total

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 20030

2

4

6

8

10

12

14

Million Net Tons (Thousands)

Can to US US to Can Mex to US US to Mex

Finished Steel Mill Products (million net tons)

The NAFTA has resulted in a significant increase in steel trade among NAFTA countries.

NAFTA

15

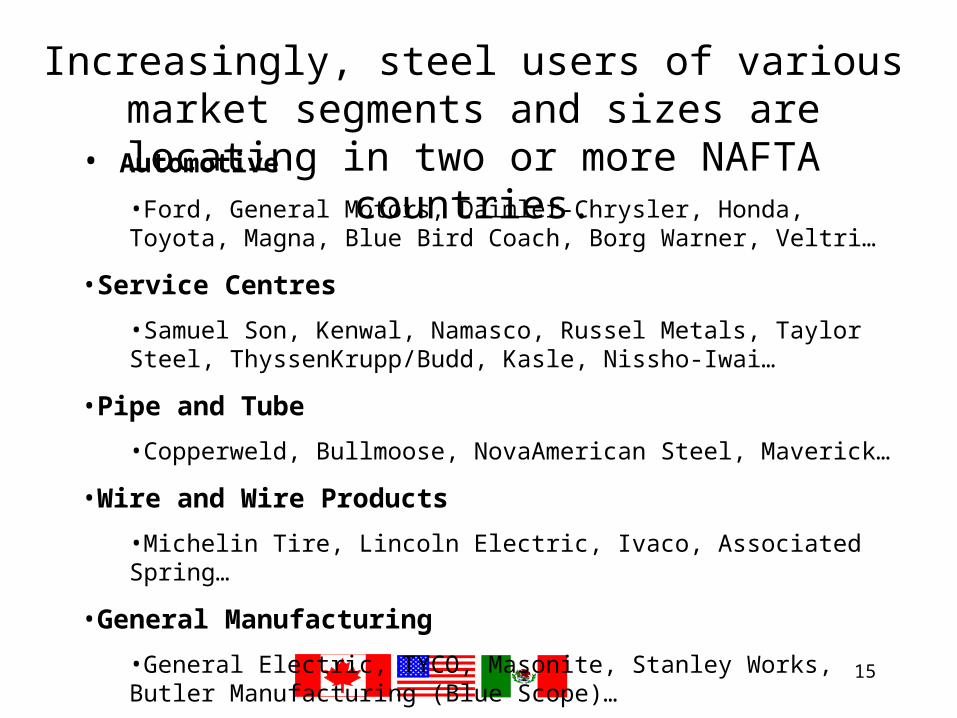

Increasingly, steel users of various market segments and sizes are locating in two or more NAFTA countries.

• Automotive

•Ford, General Motors, Daimler-Chrysler, Honda, Toyota, Magna, Blue Bird Coach, Borg Warner, Veltri…

•Service Centres

•Samuel Son, Kenwal, Namasco, Russel Metals, Taylor Steel, ThyssenKrupp/Budd, Kasle, Nissho-Iwai…

•Pipe and Tube

•Copperweld, Bullmoose, NovaAmerican Steel, Maverick…

•Wire and Wire Products

•Michelin Tire, Lincoln Electric, Ivaco, Associated Spring…

•General Manufacturing

•General Electric, TYCO, Masonite, Stanley Works, Butler Manufacturing (Blue Scope)…

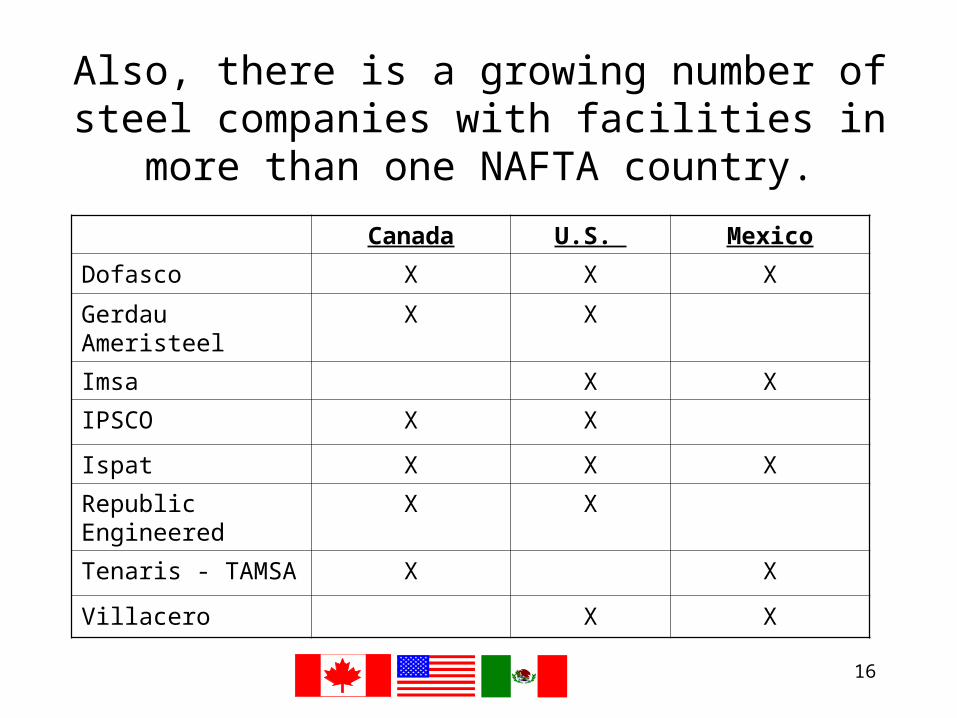

16

Also, there is a growing number of steel companies with facilities in more than one NAFTA country.

Canada U.S. Mexico

Dofasco X X X

Gerdau Ameristeel X X

Imsa X X

IPSCO X X

Ispat X X X

Republic Engineered X X

Tenaris - TAMSA X X

Villacero X X

17

The NAFTA reinforces common challenges and opportunities.

•Both industry and governments have recognized the benefits of close consultation and cooperative approaches.

•North American Steel Council (NASC)/North American Steel Industry Coalition (NASIC)

•NASTC

•OECD

•WTO

•FTAA

18

Non-NAFTA imports are diverse, and characterized by a propensity to injure.

• Imports

•Trade Cases

StrategicIndustry NAFTA

Trade Flows

NAFTA Steel Strategies

FinancialSustainability

19

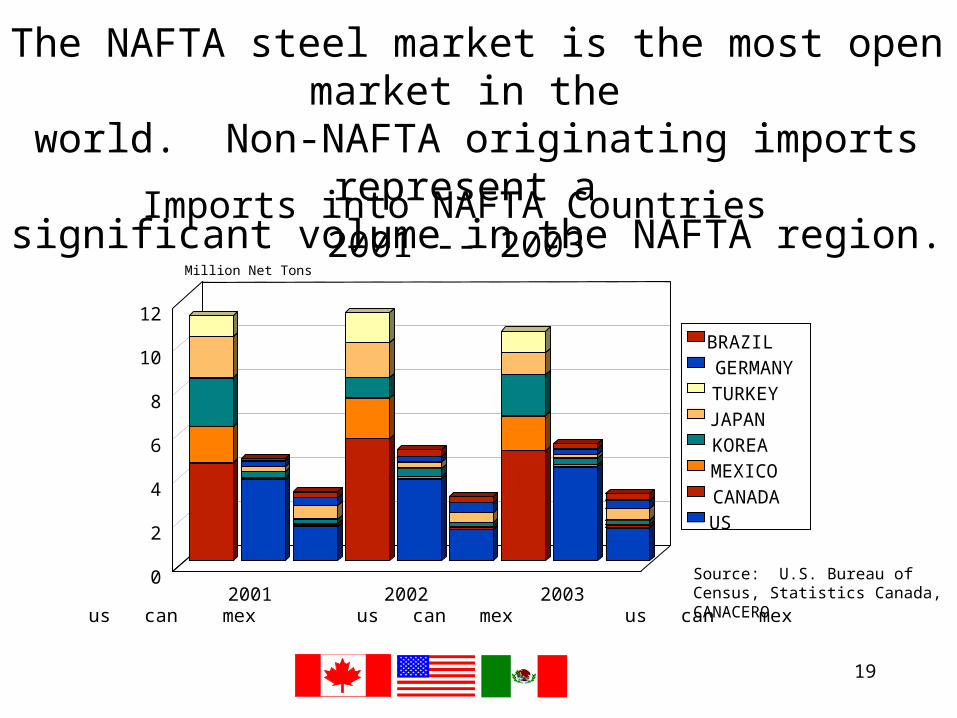

The NAFTA steel market is the most open market in the world. Non-NAFTA originating imports represent a

significant volume in the NAFTA region.

Imports into NAFTA Countries

2001 -- 2003

2001 2002 2003 0

2

4

6

8

10

12

Million Net Tons

US CANADA MEXICO KOREA JAPAN TURKEY GERMANY BRAZIL

us can mex us can mex us can mex

Source: U.S. Bureau of Census, Statistics Canada, CANACERO

20

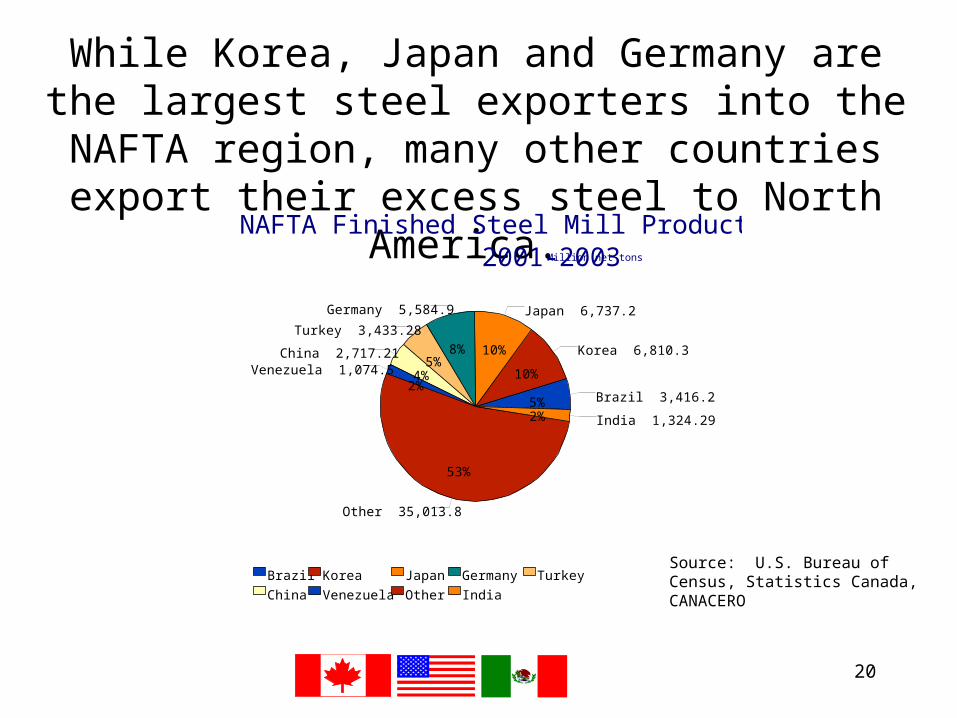

While Korea, Japan and Germany are the largest steel exporters into the NAFTA region, many other countries

export their excess steel to North America.

NAFTA Finished Steel Mill Product Imports 2001-2003 Million net tons

Brazil 3,416.2

Korea 6,810.3

Japan 6,737.2Germany 5,584.9

Turkey 3,433.28

China 2,717.21Venezuela 1,074.5

Other 35,013.8

India 1,324.295%

10%

10%8%5%

4%2%

53%

2%

Brazil Korea Japan Germany Turkey

China Venezuela Other India

Source: U.S. Bureau of Census, Statistics Canada, CANACERO

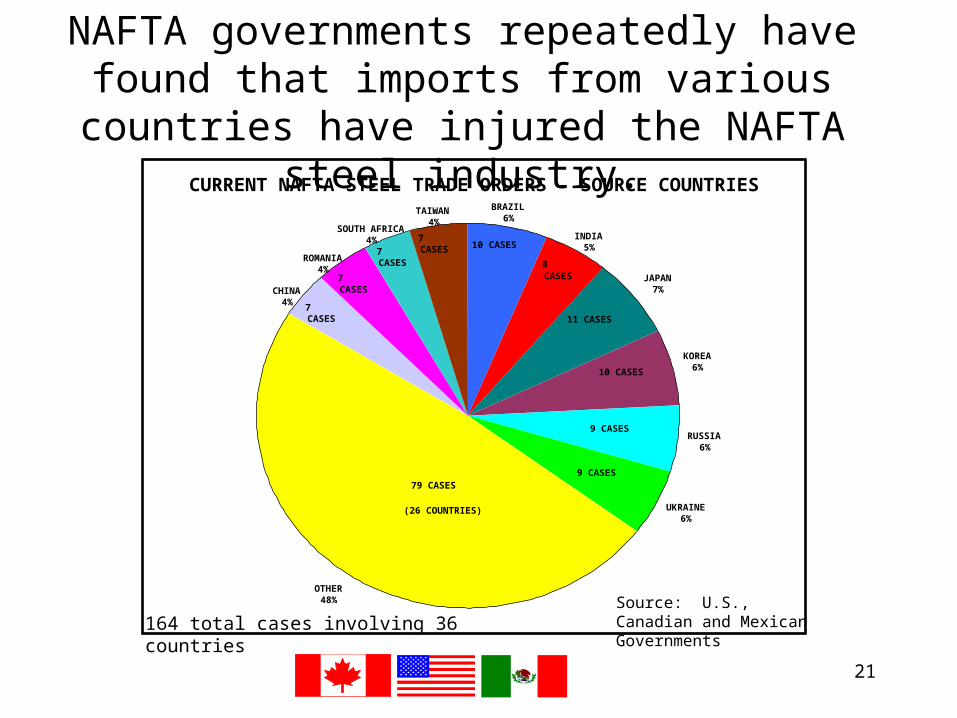

21

CURRENT NAFTA STEEL TRADE ORDERS - SOURCE COUNTRIES

JAPAN7%

KOREA6%

RUSSIA6%

UKRAINE6%

OTHER48%

CHINA4%

INDIA5%

ROMANIA4%

SOUTH AFRICA4%

TAIWAN4%

BRAZIL6%

10 CASES

79 CASES

10 CASES

8CASES

11 CASES

9 CASES

9 CASES

(26 COUNTRIES)

7CASES

7CASES

7CASES

7CASES

NAFTA governments repeatedly have found that imports from various countries have injured the

NAFTA steel industry.

164 total cases involving 36 countriesSource: U.S., Canadian and Mexican Governments

22

Non-NAFTA imports are diverse, and characterized by a propensity to injure.

• The NAFTA steel industry supports fairly traded imports.

• However, offshore dumped and subsidized imports lead to downward price movements and injury to the NAFTA market.

• This injury negatively impacts access to capital for customer-driven investments and innovation.

23

Recent tight market conditions must be put into the

context of long-term industry trends.

StrategicIndustry

NAFTATrade Flows

NAFTA Steel Strategies

•Declining prices/return on equity (ROE)

•Overcapacity and trade-distorting practices

•China concerns

FinancialSustainability

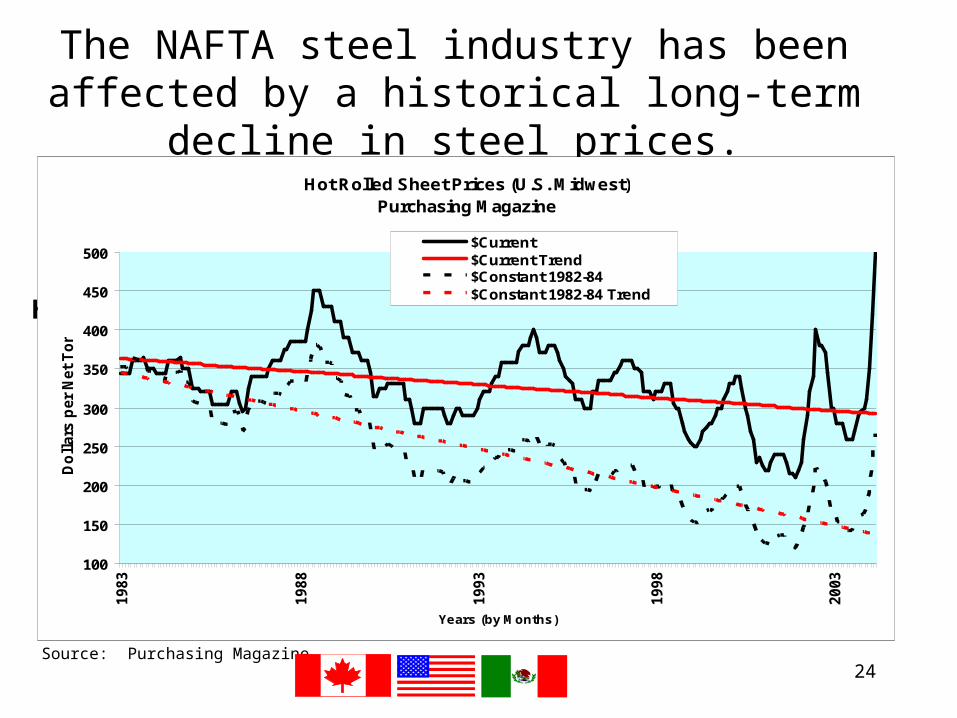

24Source: Purchasing Magazine

Historic Volatility of Spot Prices for Ht-Rolled Steel

The NAFTA steel industry has been affected by a historical long-term decline in steel prices.

Hot Rolled Sheet Prices (U.S. Midwest)Purchasing Magazine

100

150

200

250

300

350

400

450

500

1983

1988

1993

1998

2003

Years (by Months)

Do

llars

per

Net

To

n

$Current$Current Trend$Constant 1982-84$Constant 1982-84 Trend

25

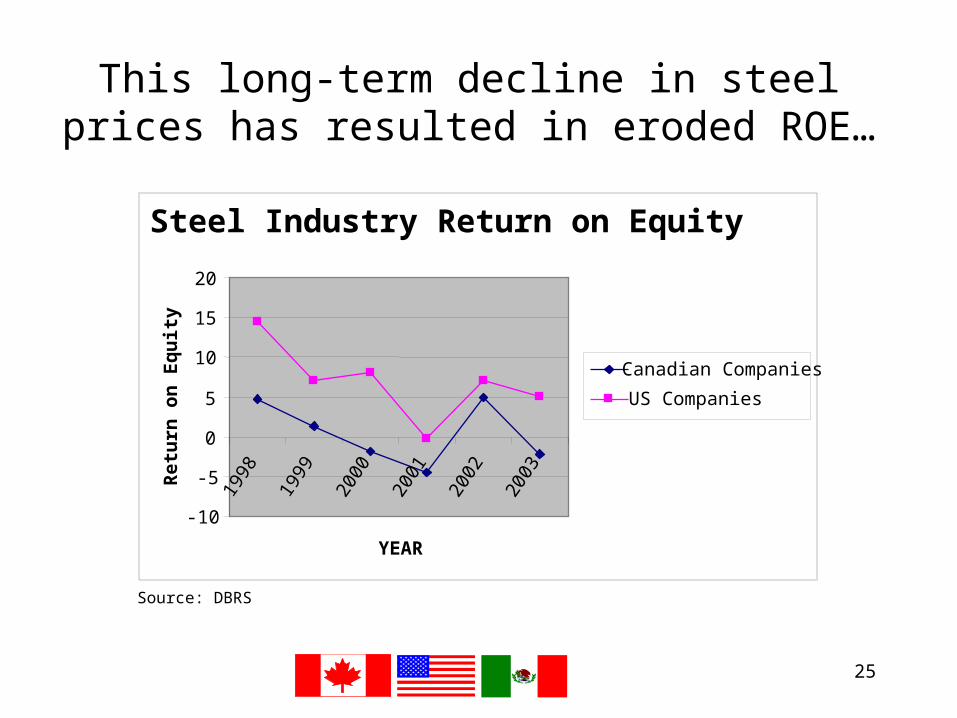

This long-term decline in steel prices has resulted in eroded ROE…

Steel Industry Return on Equity

-10

-5

0

5

10

15

20

1998

1999

2000

2001

2002

2003

YEAR

Ret

urn

on

Eq

uit

y

Canadian Companies

US Companies

Source: DBRS

26

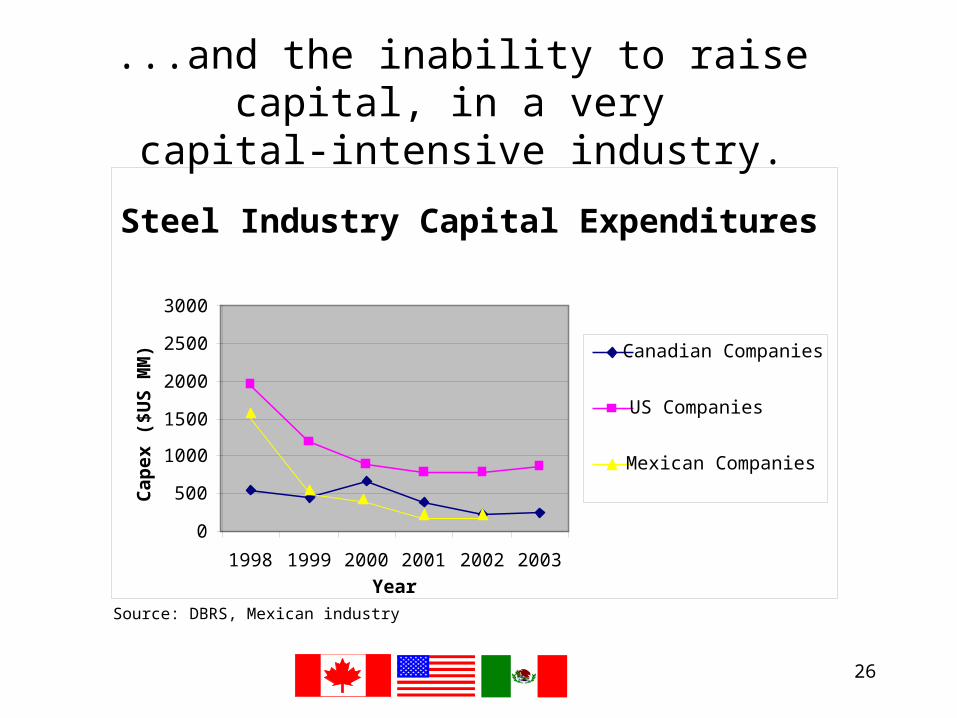

...and the inability to raise capital, in a very capital-intensive industry.

Source: DBRS, Mexican industry

Steel Industry Capital Expenditures

0

500

1000

1500

2000

2500

3000

1998 1999 2000 2001 2002 2003

Year

Cap

ex

($U

S M

M) Canadian Companies

US Companies

Mexican Companies

27

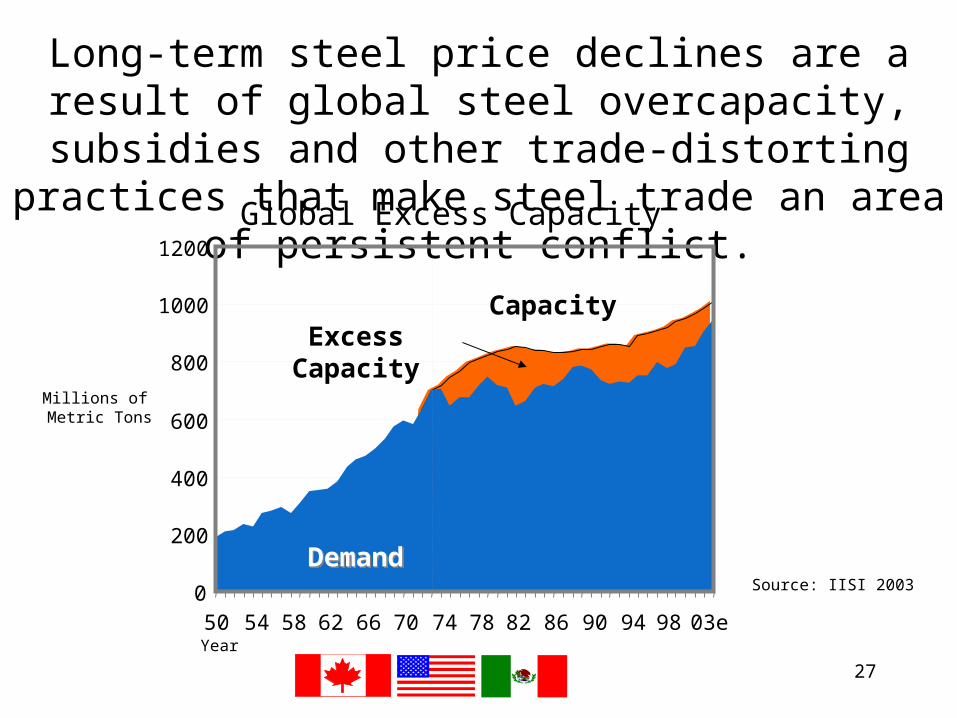

Long-term steel price declines are a result of global steel overcapacity, subsidies and other trade-distorting practices

that make steel trade an area of persistent conflict.

Global Excess Capacity

Source: IISI 2003

200

400

600

800

1000

1200

03e050 54 58 62 66 70 74 78 82 86 90 94 98

DemandDemand

Capacity

Millions of Metric Tons

Year

Excess Capacity

28

The root causes of the last steel crisis have not been resolved; enormous foreign steel capacity

additions are planned or underway.•Large steel-producing and exporting countries outside the NAFTA region are currently engaged in significant steel capacity expansions, much of this with foreign government support.

–China will increase capacity 62% in 2005 vs. 2002, climbing from 193 MT to 312 MT/year; capacity is expected to reach 385 MT by 2010

–India plans to produce 100 MT/year by 2020 (vs. current 34 MT)

–Russia plans to build 10 new mini-mills over the next decade – they will produce at least 20 MT/year; two 1 MT/year plants will be online by the end of 2004

–Brazil plans to increase capacity by 30% by the end of 2008

–Indonesia is building a new hot strip mill to produce 2.2-2.4 MT/year

–Korea is building new galvanizing lines, which will produce 1 MT/year

•Along with subsidized steel capacity expansions abroad, subsidized foreign capacity growth in steel-containing goods contributes to the “disappearing North American customer.”

29

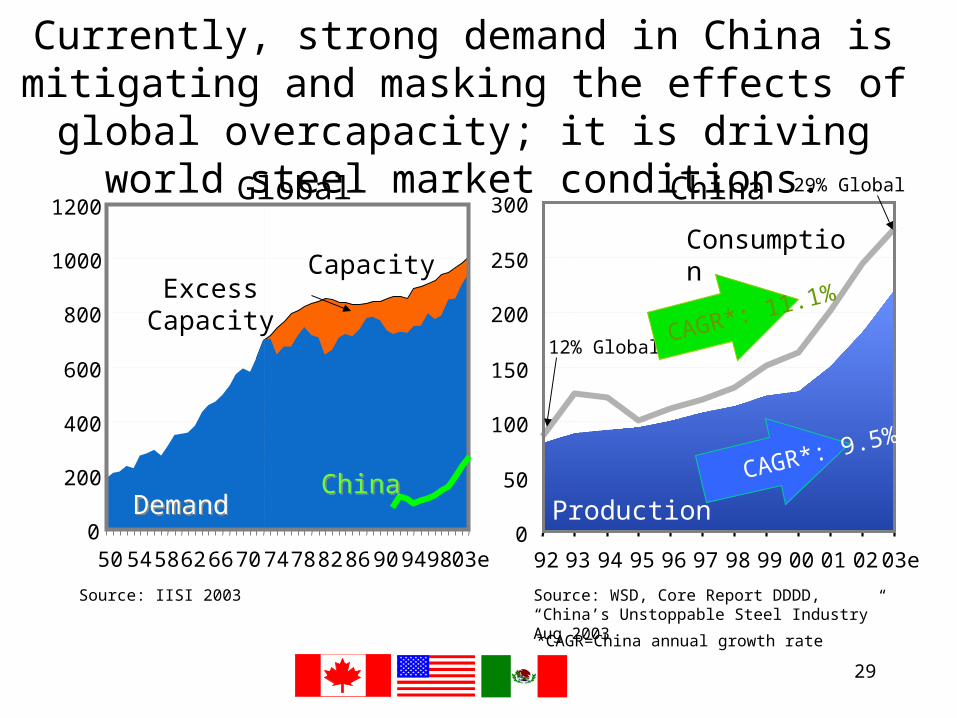

Currently, strong demand in China is mitigating and masking the effects of global overcapacity; it is driving

world steel market conditions.Global

Source: IISI 2003

200

400

600

800

1000

1200

03e050 54 5862 66 70 74 78 82 86 90 9498

DemandDemand

Capacity

0

50

100

150

200

250

300

92 93 94 95 96 97 98 99 00 01 02 03e

Production

Consumption

29% Global

12% Global CAGR*: 11.1%

CAGR*: 9.5%

ChinaChina

Source: WSD, Core Report DDDD, “China’s Unstoppable Steel Industry” Aug 2003

China

Excess Capacity

*CAGR=China annual growth rate

30

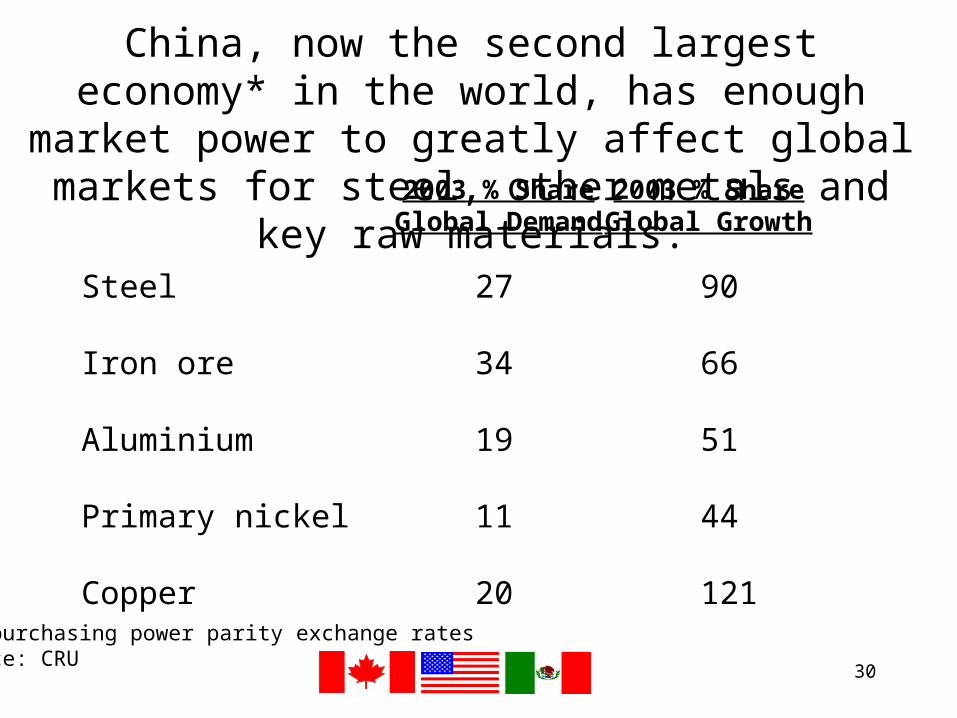

China, now the second largest economy* in the world, has enough market power to greatly affect global

markets for steel, other metals and key raw materials.

Steel 27 90

Iron ore 34 66

Aluminium 19 51

Primary nickel 11 44

Copper 20 121

2003 % ShareGlobal Growth

2003 % ShareGlobal Demand

*At purchasing power parity exchange ratesSource: CRU

31

CRU: Export FOB Brazil

Slab(dlls/ton)

WSD: China – USA

Ocean Freight(dlls/ton)

00 01 02 03 0499WSD: Export FOB China WSD: FOB Brazil

Pig Iron(dlls/ton)

Coke(dlls/ton)

Tex Report: CVRD FOB Brazil

Iron Ore(dlls/ton)

HM#1 USA(dlls/ton)

American Metal Market

0

50

100

150

200

250

00 01 02 03 0499

00 01 02 03 049928

30

32

34

36

38

40

42

100

140

180

220

260

300

99 00 01 02 03 0450

100

150

200

250

300

350

400

25

30

35

40

45

50

55

60

00 01 02 03 0499120

160

200

240

280

320

360

400

440

480

00 01 02 03 0499

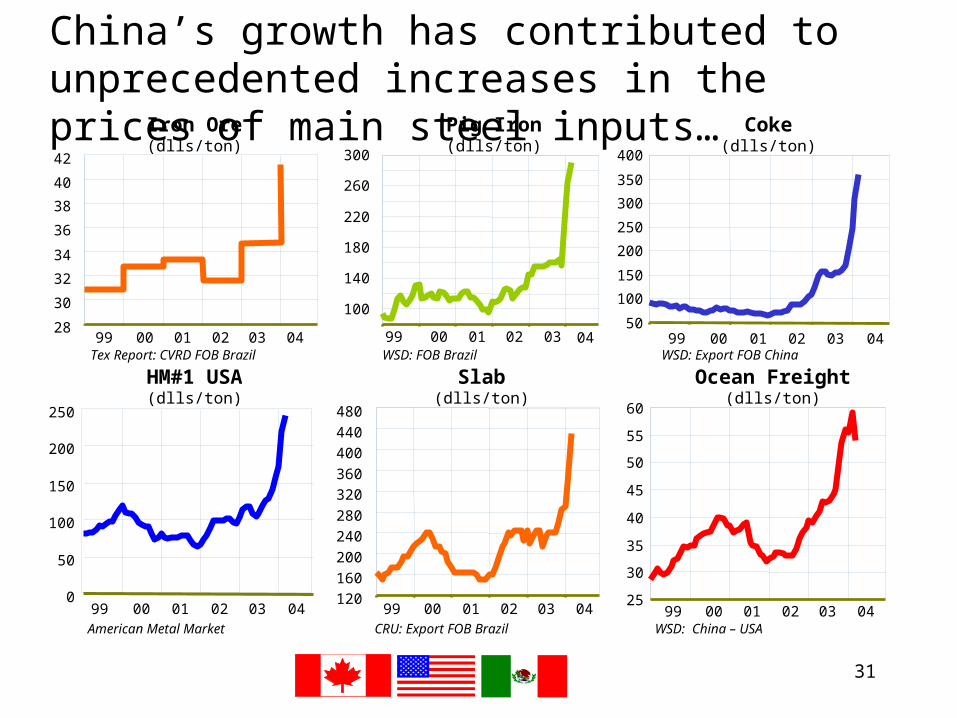

China’s growth has contributed to unprecedented increases in the prices of main steel inputs…

32

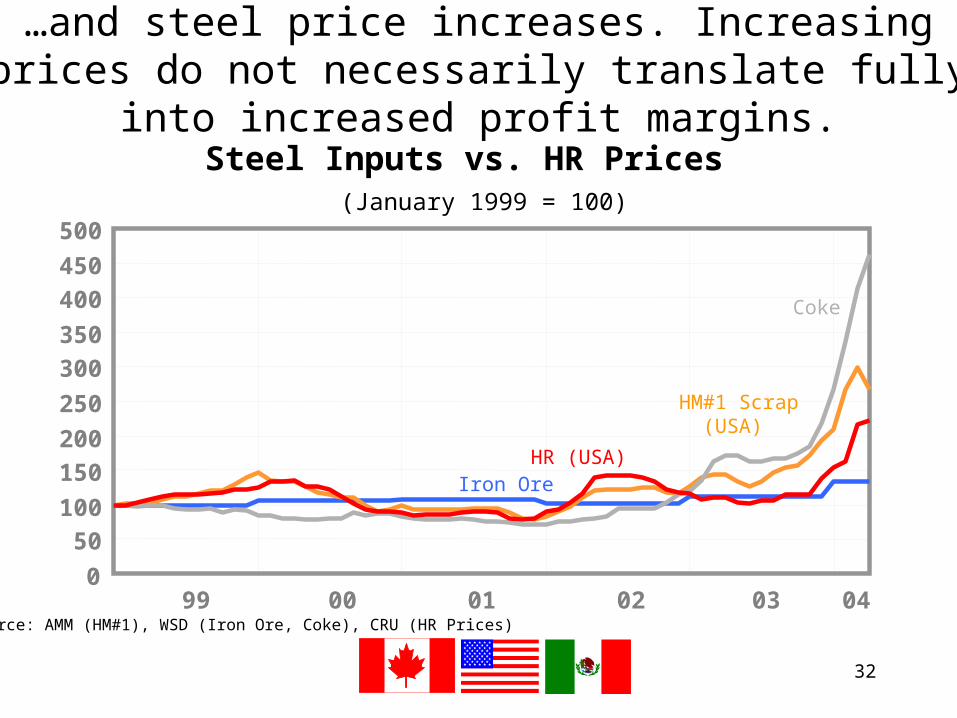

…and steel price increases. Increasing prices do not necessarily translate fully into increased profit margins.

Steel Inputs vs. HR Prices (January 1999 = 100)

0

50

100

150

200

250

300

350

400

450

500

Coke

HM#1 Scrap(USA)

HR (USA)Iron Ore

99 00 01 02 03 04Source: AMM (HM#1), WSD (Iron Ore, Coke), CRU (HR Prices)

33

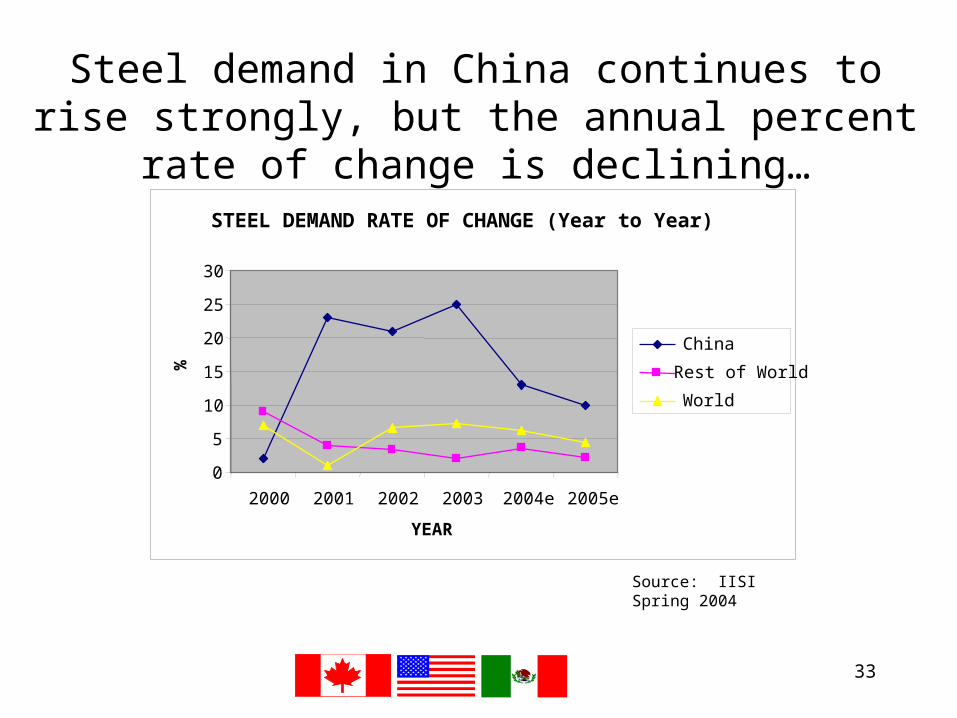

Steel demand in China continues to rise strongly, but the annual percent rate of change is declining…

STEEL DEMAND RATE OF CHANGE (Year to Year)

0

5

10

15

20

25

30

2000 2001 2002 2003 2004e 2005e

YEAR

%

China

Rest of World

World

Source: IISI Spring 2004

34

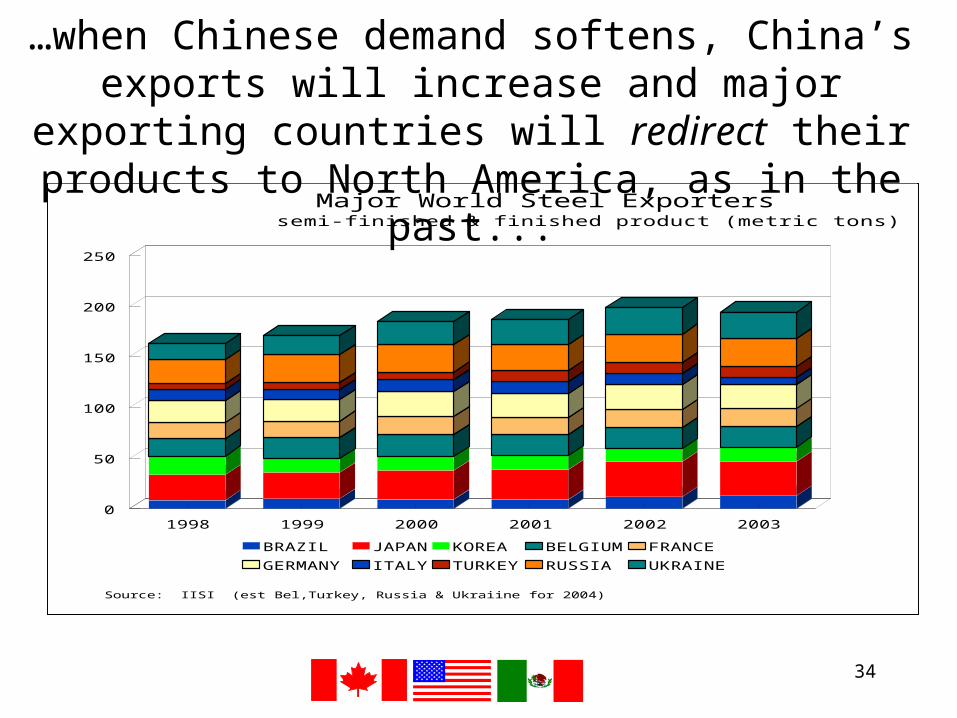

Major World Steel Exporterssemi-finished & finished product (metric tons)

Source: IISI (est Bel,Turkey, Russia & Ukraiine for 2004)

1998 1999 2000 2001 2002 20030

50

100

150

200

250

BRAZIL JAPAN KOREA BELGIUM FRANCE

GERMANY ITALY TURKEY RUSSIA UKRAINE

…when Chinese demand softens, China’s exports will increase and major exporting countries will redirect their

products to North America, as in the past...

35

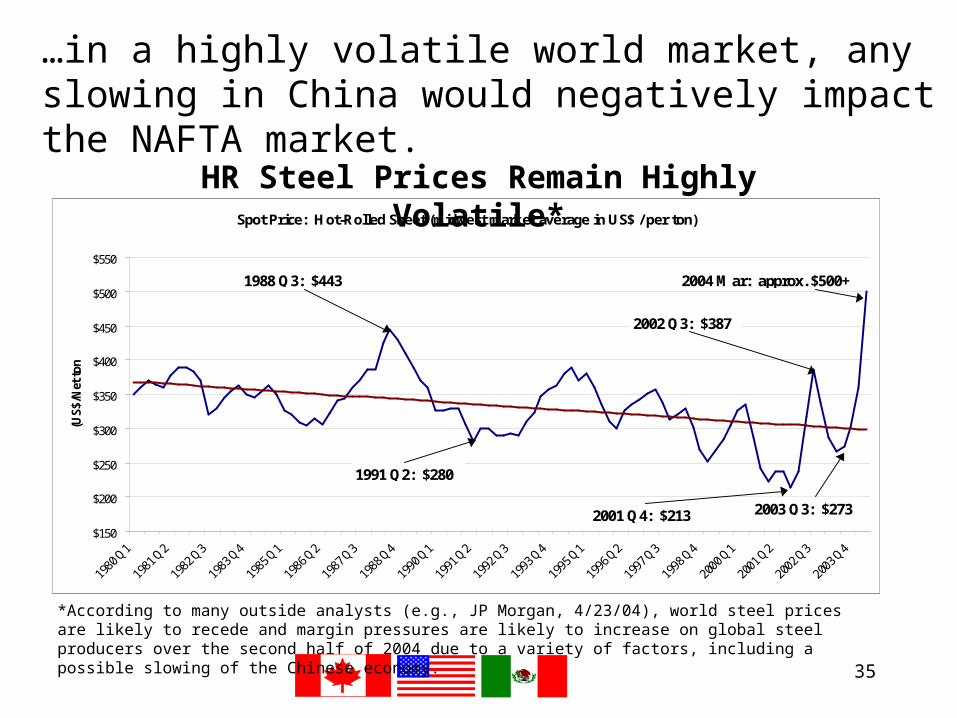

…in a highly volatile world market, any slowing in China would negatively impact the NAFTA market.

Spot Price: Hot-Rolled Sheet (midwest market average in US$ / per ton)

$150

$200

$250

$300

$350

$400

$450

$500

$550

(US

$/N

et t

on

)

2002 Q3: $387

2001 Q4: $213

1991 Q2: $280

1988 Q3: $443 2004 Mar: approx. $500+

2003 Q3: $273

HR Steel Prices Remain Highly Volatile*

*According to many outside analysts (e.g., JP Morgan, 4/23/04), world steel prices are likely to recede and margin pressures are likely to increase on global steel producers over the second half of 2004 due to a variety of factors, including a possible slowing of the Chinese economy.

36

Recent tight market conditions must be put into the context of long-term industry trends.

• NAFTA and world steel markets remain highly volatile.• Global steel industry structural imbalances and

worldwide steel trade-distorting practices persist.• No one knows for certain what will happen and when,

but negative impacts from China’s unstable financial system, provincial/central government frictions and irrational commercial behavior – coupled with its size – are a cause of serious concern.

37

The NAFTA steel industry proposes several NASTC opportunities.

•Intra-NAFTA

•External trade

•Multilateral fora

•Competitiveness

StrategicIndustry

NAFTA Trade Flows

NAFTA Steel Strategies

FinancialSustainability

38

Intra-NAFTA trade opportunities

• Streamline import permits– Currently import permits must be taken out on each

individual shipment (20 tons/permit) vs. offshore boatloads (15,000 tons/permit).

– Recommend that governments implement a WTO-consistent weekly summary permit for NAFTA partners.

– Benefits:• Reduction in trade administrative costs for NAFTA industry

and governments.

39

Intra-NAFTA trade opportunities (cont’d)

• Explore Harmonized System (HS) code consistency– Currently all countries have same HS codes at 6-digit level, but

differ at 7-10 digit level.– Recommend that governments explore extending the common

codes to at least the 8-digit level, assuming we can maintain the historical continuity of worldwide data and the integrity of bilateral and regional trade agreements that rely on certain 8-digit numbers for specific rules of origin.

– Benefits: • Consistent NAFTA statistics.

– Same import/export categories– Facilitation of NAFTA-wide import reporting

• Reduced administration costs of intra-company shipments across NAFTA borders.

40

• Load limit improvements– Currently there are differing maximum load limits from

country to country and state to state; this requires loads to be split during delivery, adding costs

– Recommend standardized higher load limits

– Benefits• Reduced transportation and administrative costs.

Intra-NAFTA trade opportunities (cont’d)

41

External trade opportunities

• Develop common and transparent, web-based NAFTA-wide reporting on imports, including import prices (using import permits/data).

• Consult with foreign governments to address trade-distorting practices at an early stage.

• Work together to prevent injurious trade diversion into the NAFTA market from other countries’ restrictive steel trade agreements.

• Oppose foreign government intervention in raw material markets.

42

External trade opportunities (cont’d)

• Oppose government financing of projects that increase world steel overcapacity.– NAFTA governments, non-NAFTA governments and

quasi-government agencies (e.g., IMF) should not be lending money for new steel capacity

43

One common NAFTA approach to international trade negotiations

• OECD– Coordinate positions to (1) ensure positive result from steel

subsidies agreement (SSA) negotiation and (2) maintain OECD Steel Committee after SSA negotiation ends.

• WTO– Oppose strongly trade law weakening and support

fundamental reform of dispute settlement (e.g., include trade counsel in proceedings).

• FTAA– Oppose strongly trade law weakening.

44

One common NAFTA approach to international trade negotiations (cont’d)

• China– Ensure that China is subject to WTO-consistent trade laws.

– Encourage China to revalue and adopt a floating currency.

– Engage industry in a cooperative assessment of the steel industry in China and ensure that Chinese market-distorting practices are eliminated before according “market economy” status to China in AD cases.

– Work with industry to monitor, anticipate and mitigate the negative impacts from an economic slowdown in China.

45

The NAFTA steel industry wants to work together with NAFTA governments to develop pro-competitive policies to promote the health and financial stability of

the North American steel sector.• Manufacturing

– Implement and coordinate policies, where appropriate, to preserve and strengthen the manufacturing base.

• Energy– Ensure reliable and cost-competitive energy supplies.

• Raw Materials– Ensure a free flow of raw materials.

• Access to capital– Promote policies to improve access.

• Customs– Explore opportunities to enhance customs enforcement cooperation.

46

The NAFTA steel industry looks forward working with NAFTA governments in developing an “opportunities-

oriented” action plan.

StrategicIndustry

NAFTATrade Flows

NAFTA Steel Strategies

•Non-NAFTA imports are diverse, and characterized by a propensity to injure.

• The steel industry is a strategic and progressive force.

•The NAFTA has resulted in greater openness of the N.A. steel market and has drawn the three industries and governments together for common purposes.

•Recent tight market conditions must be put into the context of long-term industry trends.

•The NAFTA steel industry proposes several NASTC opportunities.

FinancialSustainability

47

NAFTA Steel StrategiesAn Industry-Government Partnership to Achieve a Healthy and

Financially Stable NAFTA Steel-Producing Industry

Promoting Distortion-Free Markets:•Ensure positive OECD result.•Maintain strong, effective trade laws.•Develop an effective NAFTA-wide import monitoring, permitting and reporting system, including joint analysis/identification of distortions.•Use joint NAFTA government “jaw-boning” at first sign of import surges.•Prevent injurious diversion from interventions by non-NAFTA governments.•Support market forces – no currency manipulation, no subsidies, no export controls.

Facilitating NAFTASteel Trade:•Streamline import permits.•Explore HS code consistency.•Identify/define “integration” goals.

Improving Competitiveness and Creating Strong Fundamentals:•Access to capital.•Energy.•Consolidation and restructuring.•R&D – innovation.•Market development.•Customer base -- manufacturing.

Close Consultation and Common NAFTA Approach to Multilateral Trade Negotiations, Where Possible — OECD, WTO, FTAA