Embed Size (px)

Citation preview

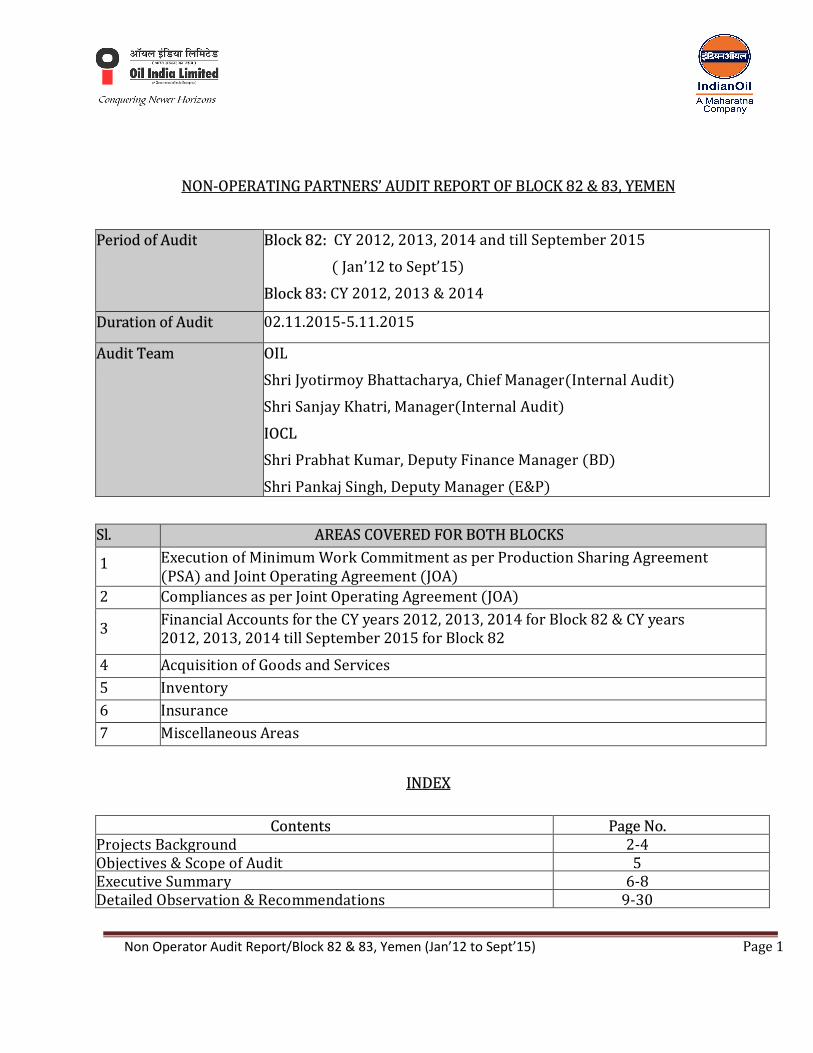

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 1

NON-OPERATING PARTNERS’ AUDIT REPORT OF BLOCK 82 & 83, YEMEN

Period of Audit Block 82: CY 2012, 2013, 2014 and till September 2015

( Jan’12 to Sept’15)

Block 83: CY 2012, 2013 & 2014

Duration of Audit 02.11.2015-5.11.2015

Audit Team OIL

Shri Jyotirmoy Bhattacharya, Chief Manager(Internal Audit)

Shri Sanjay Khatri, Manager(Internal Audit)

IOCL

Shri Prabhat Kumar, Deputy Finance Manager (BD)

Shri Pankaj Singh, Deputy Manager (E&P)

Sl.No.

AREAS COVERED FOR BOTH BLOCKS

1 Execution of Minimum Work Commitment as per Production Sharing Agreement (PSA) and Joint Operating Agreement (JOA)

2 Compliances as per Joint Operating Agreement (JOA)

3 Financial Accounts for the CY years 2012, 2013, 2014 for Block 82 & CY years 2012, 2013, 2014 till September 2015 for Block 82

4 Acquisition of Goods and Services

5 Inventory

6 Insurance

7 Miscellaneous Areas

INDEX

Contents Page No. Projects Background 2-4 Objectives & Scope of Audit 5 Executive Summary 6-8 Detailed Observation & Recommendations 9-30

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 2

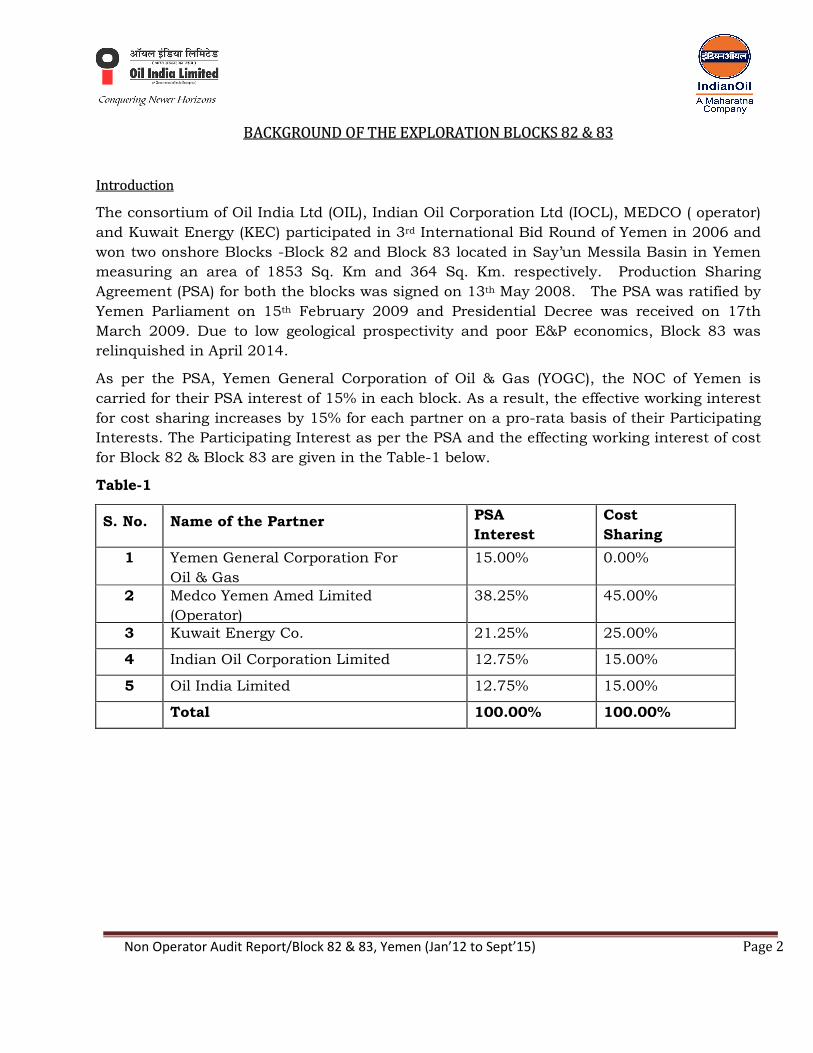

BACKGROUND OF THE EXPLORATION BLOCKS 82 & 83

Introduction

The consortium of Oil India Ltd (OIL), Indian Oil Corporation Ltd (IOCL), MEDCO ( operator)

and Kuwait Energy (KEC) participated in 3rd International Bid Round of Yemen in 2006 and

won two onshore Blocks -Block 82 and Block 83 located in Say’un Messila Basin in Yemen

measuring an area of 1853 Sq. Km and 364 Sq. Km. respectively. Production Sharing

Agreement (PSA) for both the blocks was signed on 13th May 2008. The PSA was ratified by

Yemen Parliament on 15th February 2009 and Presidential Decree was received on 17th

March 2009. Due to low geological prospectivity and poor E&P economics, Block 83 was

relinquished in April 2014.

As per the PSA, Yemen General Corporation of Oil & Gas (YOGC), the NOC of Yemen is

carried for their PSA interest of 15% in each block. As a result, the effective working interest

for cost sharing increases by 15% for each partner on a pro-rata basis of their Participating

Interests. The Participating Interest as per the PSA and the effecting working interest of cost

for Block 82 & Block 83 are given in the Table-1 below.

Table-1

S. No. Name of the Partner PSA

Interest

Cost

Sharing

1 Yemen General Corporation For

Oil & Gas

15.00% 0.00%

2 Medco Yemen Amed Limited

(Operator)

38.25% 45.00%

3 Kuwait Energy Co. 21.25% 25.00%

4 Indian Oil Corporation Limited 12.75% 15.00%

5 Oil India Limited 12.75% 15.00%

Total 100.00% 100.00%

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 3

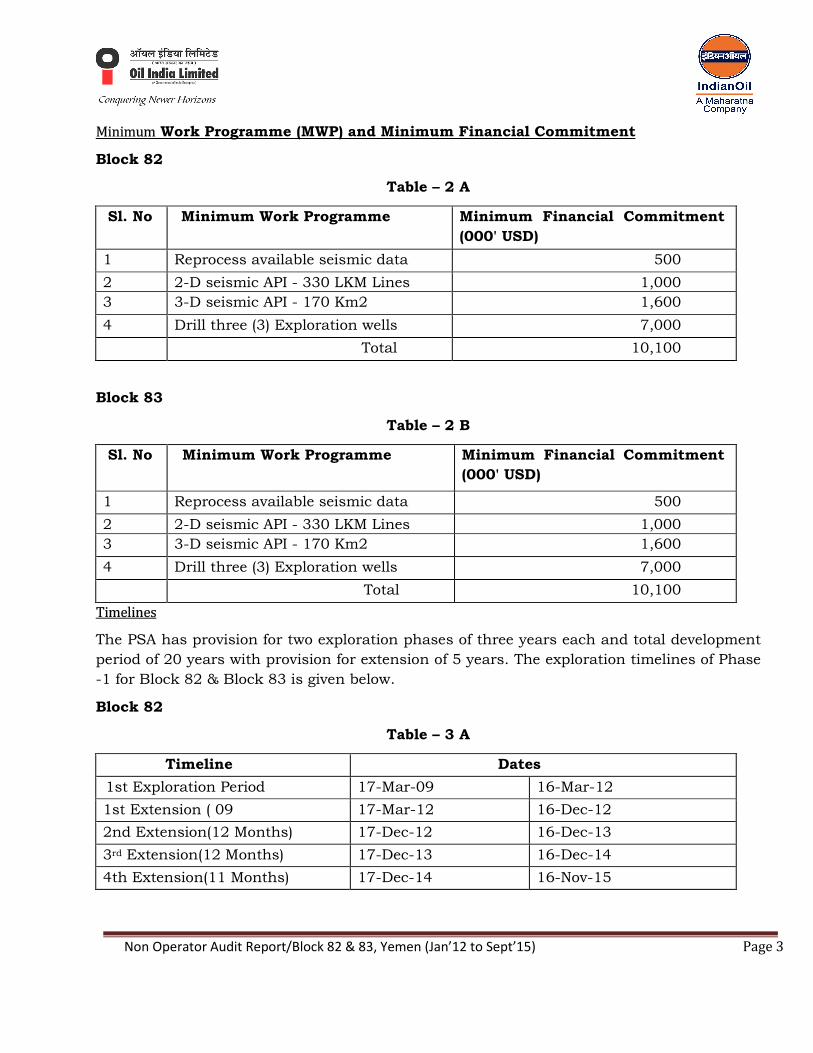

Minimum Work Programme (MWP) and Minimum Financial Commitment

Block 82

Table – 2 A

Sl. No Minimum Work Programme Minimum Financial Commitment

(000' USD)

1 Reprocess available seismic data 500

2 2-D seismic API - 330 LKM Lines 1,000

3 3-D seismic API - 170 Km2 1,600

4 Drill three (3) Exploration wells 7,000

Total 10,100

Block 83

Table – 2 B

Sl. No Minimum Work Programme Minimum Financial Commitment

(000' USD)

1 Reprocess available seismic data 500

2 2-D seismic API - 330 LKM Lines 1,000

3 3-D seismic API - 170 Km2 1,600

4 Drill three (3) Exploration wells 7,000

Total 10,100

Timelines

The PSA has provision for two exploration phases of three years each and total development

period of 20 years with provision for extension of 5 years. The exploration timelines of Phase

-1 for Block 82 & Block 83 is given below.

Block 82

Table – 3 A

Timeline Dates

1st Exploration Period 17-Mar-09 16-Mar-12

1st Extension ( 09

Months)

17-Mar-12 16-Dec-12

2nd Extension(12 Months) 17-Dec-12 16-Dec-13

3rd Extension(12 Months) 17-Dec-13 16-Dec-14

4th Extension(11 Months) 17-Dec-14 16-Nov-15

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 4

Block 83

Table – 3 B

Timeline Dates

1st Exploration Period 17-Mar-09 16-Mar-12

1st Extension (09 Months) 17-Mar-12 16-Dec-12

2nd Extension(12 Months) 17-Dec-12 16-Dec-13

3rd Extension till 31st March’ 14 17-Dec-13 31-March-14

MWP v/s Achievements

Block 82

Table – 4 A

Sl. No Minimum Work

Programme

Achievements

1 Reprocess available

seismic data

Not reprocessed due to non-availability of existing

data

2 2-D seismic API -

330 LKM

61 LKM Completed. Another 280.11 km of New 2D

API program is being carried out with higher

nominal fold, topography survey for which has been

completed.

3 3-D seismic API - 170

Km2

236.54 Km2

4 Drill three (3)

Exploration wells

NIL

Block 83

Table – 4 B

Sl. No Minimum Work Programme

Achievements

1 Reprocess available seismic

data

575 LKM Completed.

2 2-D seismic API - 330 LKM 371 LKM Completed.

3 3-D seismic API - 170 Km2 Completed 235 Km2

4 Drill three (3) Exploration wells NIL

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 5

OBJECTIVES & SCOPE OF AUDIT

The objective of our Audit is to assess whether control procedures are in place and operating

effectively and to ascertain whether there is compliance with Joint Operating Agreement and

Production Sharing Contract with the Government of India.

Our audit comprised of discussion with Operator’s personnel, an evaluation of control and

operating procedures, observations of ongoing operations and examination of records and

supporting documents.

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 6

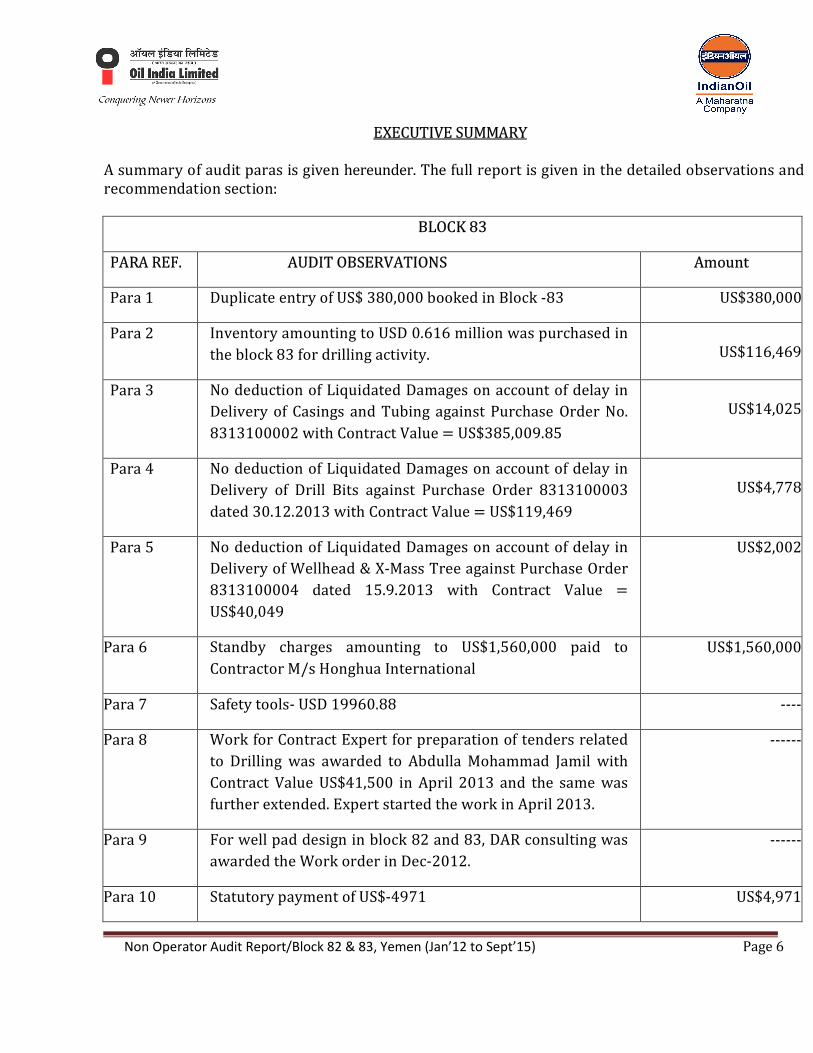

EXECUTIVE SUMMARY

A summary of audit paras is given hereunder. The full report is given in the detailed observations and recommendation section:

BLOCK 83

PARA REF. AUDIT OBSERVATIONS Amount

Para 1 Duplicate entry of US$ 380,000 booked in Block -83 US$380,000

Para 2 Inventory amounting to USD 0.616 million was purchased in

the block 83 for drilling activity. US$116,469

Para 3 No deduction of Liquidated Damages on account of delay in

Delivery of Casings and Tubing against Purchase Order No.

8313100002 with Contract Value = US$385,009.85

US$14,025

Para 4 No deduction of Liquidated Damages on account of delay in

Delivery of Drill Bits against Purchase Order 8313100003

dated 30.12.2013 with Contract Value = US$119,469

US$4,778

Para 5 No deduction of Liquidated Damages on account of delay in

Delivery of Wellhead & X-Mass Tree against Purchase Order

8313100004 dated 15.9.2013 with Contract Value =

US$40,049

US$2,002

Para 6 Standby charges amounting to US$1,560,000 paid to

Contractor M/s Honghua International

US$1,560,000

Para 7 Safety tools- USD 19960.88 ----

Para 8 Work for Contract Expert for preparation of tenders related

to Drilling was awarded to Abdulla Mohammad Jamil with

Contract Value US$41,500 in April 2013 and the same was

further extended. Expert started the work in April 2013.

------

Para 9 For well pad design in block 82 and 83, DAR consulting was

awarded the Work order in Dec-2012.

------

Para 10 Statutory payment of US$-4971 US$4,971

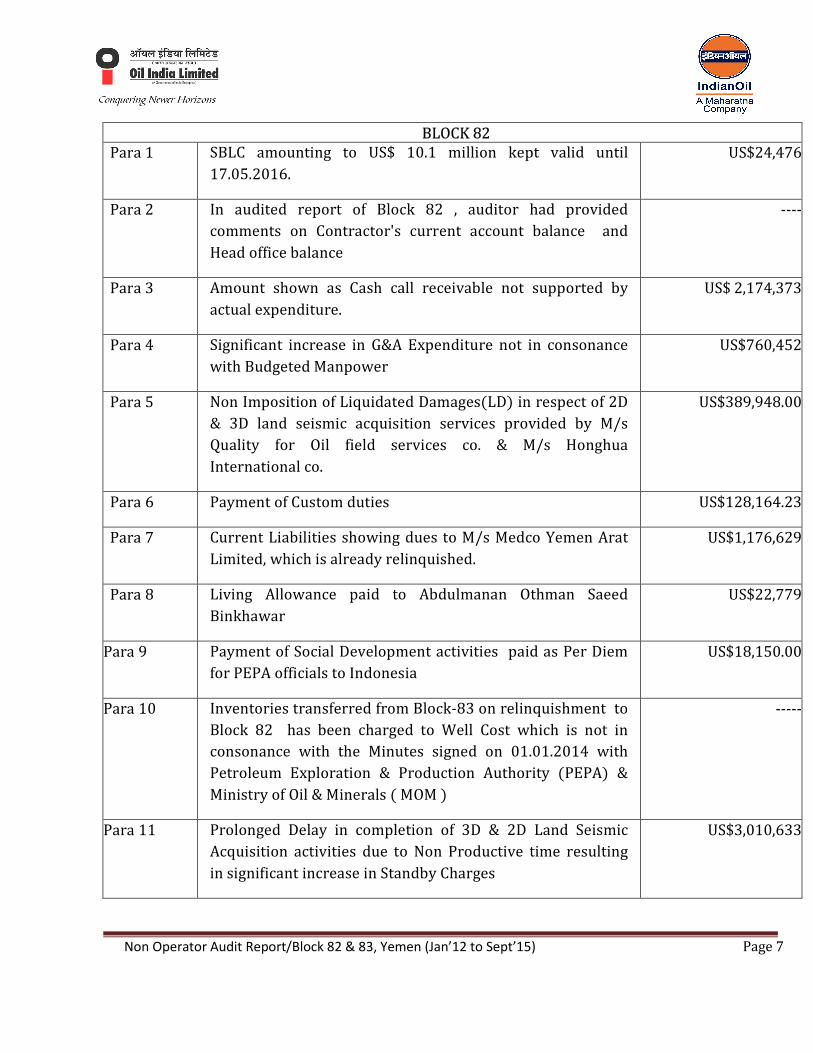

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 7

BLOCK 82 Para 1 SBLC amounting to US$ 10.1 million kept valid until

17.05.2016.

US$24,476

Para 2 In audited report of Block 82 , auditor had provided

comments on Contractor's current account balance and

Head office balance

----

Para 3 Amount shown as Cash call receivable not supported by

actual expenditure.

US$ 2,174,373

Para 4 Significant increase in G&A Expenditure not in consonance

with Budgeted Manpower

US$760,452

Para 5 Non Imposition of Liquidated Damages(LD) in respect of 2D

& 3D land seismic acquisition services provided by M/s

Quality for Oil field services co. & M/s Honghua

International co.

US$389,948.00

Para 6 Payment of Custom duties US$128,164.23

Para 7 Current Liabilities showing dues to M/s Medco Yemen Arat

Limited, which is already relinquished.

US$1,176,629

Para 8 Living Allowance paid to Abdulmanan Othman Saeed

Binkhawar

US$22,779

Para 9 Payment of Social Development activities paid as Per Diem

for PEPA officials to Indonesia

US$18,150.00

Para 10 Inventories transferred from Block-83 on relinquishment to

Block 82 has been charged to Well Cost which is not in

consonance with the Minutes signed on 01.01.2014 with

Petroleum Exploration & Production Authority (PEPA) &

Ministry of Oil & Minerals ( MOM )

-----

Para 11 Prolonged Delay in completion of 3D & 2D Land Seismic

Acquisition activities due to Non Productive time resulting

in significant increase in Standby Charges

US$3,010,633

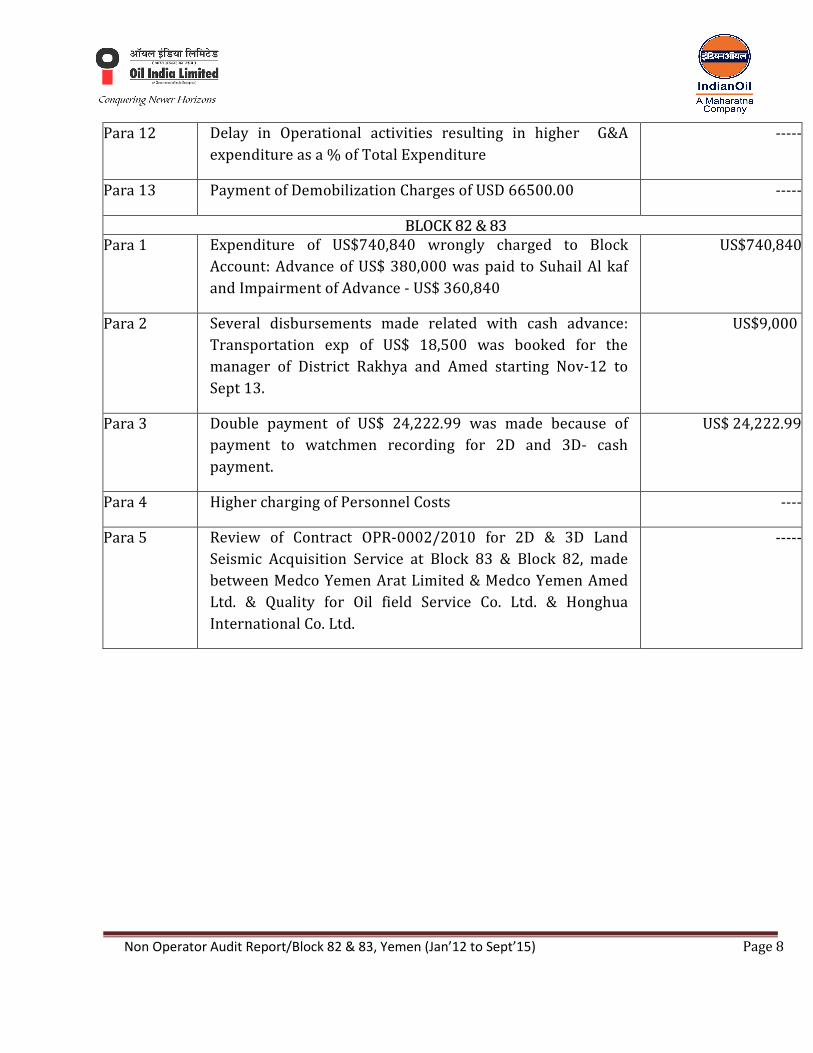

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 8

Para 12 Delay in Operational activities resulting in higher G&A

expenditure as a % of Total Expenditure

-----

Para 13 Payment of Demobilization Charges of USD 66500.00 -----

BLOCK 82 & 83 Para 1 Expenditure of US$740,840 wrongly charged to Block

Account: Advance of US$ 380,000 was paid to Suhail Al kaf

and Impairment of Advance - US$ 360,840

US$740,840

Para 2 Several disbursements made related with cash advance:

Transportation exp of US$ 18,500 was booked for the

manager of District Rakhya and Amed starting Nov-12 to

Sept 13.

US$9,000

Para 3 Double payment of US$ 24,222.99 was made because of

payment to watchmen recording for 2D and 3D- cash

payment.

US$ 24,222.99

Para 4 Higher charging of Personnel Costs ----

Para 5 Review of Contract OPR-0002/2010 for 2D & 3D Land

Seismic Acquisition Service at Block 83 & Block 82, made

between Medco Yemen Arat Limited & Medco Yemen Amed

Ltd. & Quality for Oil field Service Co. Ltd. & Honghua

International Co. Ltd.

-----

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 9

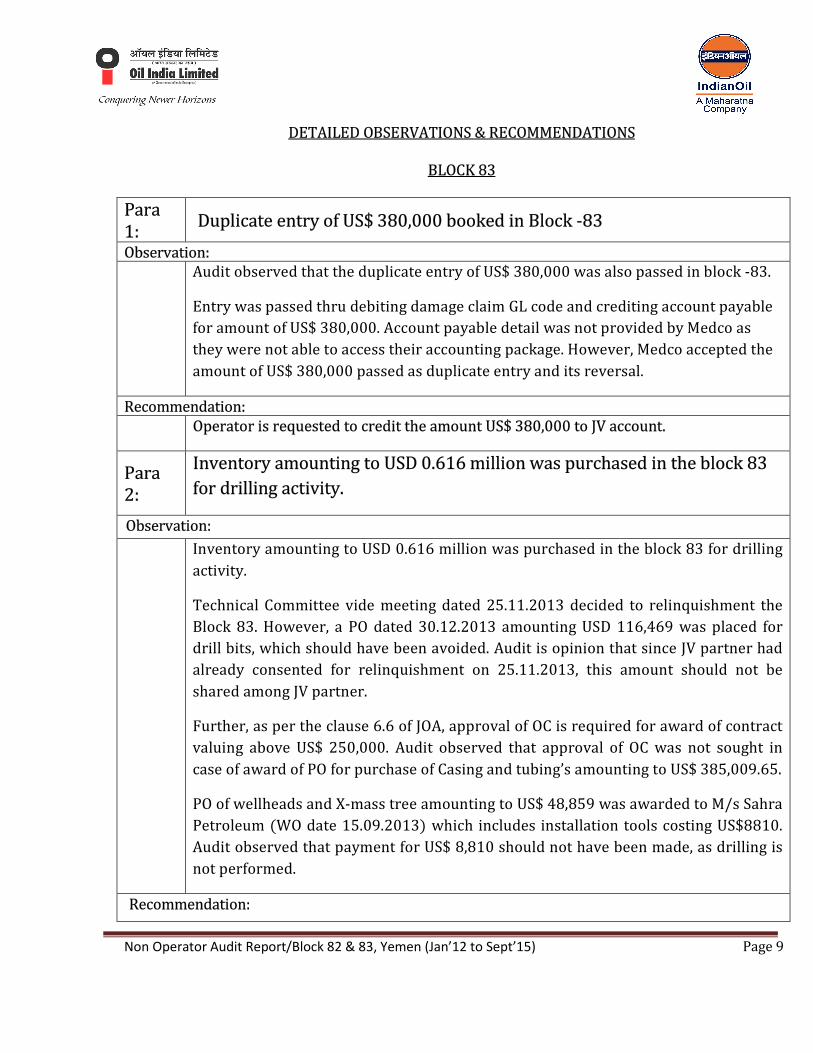

DETAILED OBSERVATIONS & RECOMMENDATIONS

BLOCK 83

Para 1:

Duplicate entry of US$ 380,000 booked in Block -83

Observation: Audit observed that the duplicate entry of US$ 380,000 was also passed in block -83.

Entry was passed thru debiting damage claim GL code and crediting account payable

for amount of US$ 380,000. Account payable detail was not provided by Medco as

they were not able to access their accounting package. However, Medco accepted the

amount of US$ 380,000 passed as duplicate entry and its reversal.

Recommendation:

Operator is requested to credit the amount US$ 380,000 to JV account.

Para 2:

Inventory amounting to USD 0.616 million was purchased in the block 83

for drilling activity.

Observation:

Inventory amounting to USD 0.616 million was purchased in the block 83 for drilling

activity.

Technical Committee vide meeting dated 25.11.2013 decided to relinquishment the

Block 83. However, a PO dated 30.12.2013 amounting USD 116,469 was placed for

drill bits, which should have been avoided. Audit is opinion that since JV partner had

already consented for relinquishment on 25.11.2013, this amount should not be

shared among JV partner.

Further, as per the clause 6.6 of JOA, approval of OC is required for award of contract

valuing above US$ 250,000. Audit observed that approval of OC was not sought in

case of award of PO for purchase of Casing and tubing’s amounting to US$ 385,009.65.

PO of wellheads and X-mass tree amounting to US$ 48,859 was awarded to M/s Sahra

Petroleum (WO date 15.09.2013) which includes installation tools costing US$8810.

Audit observed that payment for US$ 8,810 should not have been made, as drilling is

not performed.

Recommendation:

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 10

Operator is therefore requested to credit the amount of US$116,469 to Joint venture account towards drill bits purchased for Block 83.

Para 3:

No deduction of Liquidated Damages on account of delay in Delivery of

Casings and Tubing against Purchase Order No. 8313100002 with Contract

Value = US$385,009.85.

Observation:

PO for Casing was placed on 29.8.2013 with delivery period of 4 months for Tubing &

3 months for Casing. Casings got shipped from China in three lots with 1st lot on 16th

Feb 2014. By shipment, consignment got delayed by more than ten weeks. As per PO

there is LD clause of 1% per day of delay with no limitation. However, as per the

quote of Tianjin, LD of 0.5% shall be levied for per week of delay subject to max of 5%

of undelivered value. Accordingly, LD should have been levied on delay which

amounts to US$14,025. Audit observed that LD amounting to US$ 14,025 was not

deducted from vendor's bill payment.

Recommendation:

Operator is requested to recover the said amount from vendor either from

encashment of BG or any pending payment and the same may be credited to JV

account.

Para 4:

No deduction of Liquidated Damages on account of delay in Delivery of

Drill Bits against Purchase Order 8313100003 dated 30.12.2013 with

Contract Value = US$119,469

Observation:

As per the PO, MI Overseas to deliver the Wellhead & X-mas Tree with in one month

from date of PO. However, drill bit got delivered in month of April 2014 with a delay

of more than 8 weeks. As per the PO, LD shall be levied 0.5% per week delay with max

of 5% which amounts to 4% for 8 weeks i.e. US$4,778. Audit observed that LD

amounting to US$ 4,778 was not deducted from vendor's bill payment.

Recommendation:

Operator is requested to recover the said amount from vendor either from

encashment of BG or any pending payment and the same may be credited to JV

account.

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 11

Para 5:

No deduction of Liquidated Damages on account of delay in Delivery of

Wellhead & X-Mass Tree against Purchase Order 8313100004 dated

15.9.2013 with Contract Value = US$40,049

Observation:

As per the PO, Sahra Petroleum to deliver the drill bits within 90 days from date of

PO. However, Wellhead & X-mas Tree got delayed by 130 days i.e. delivered on

14.4.2014. AS per the PO, LD shall be levied 1% per week delay with max of 5% which

amounts to max 5% i.e. US$2,002.

Audit observed that LD amounting to US$ 2,002 was not deducted from vendor's bill

payment.

Recommendation:

Operator is requested to recover the said amount from vendor either from

encashment of BG or any pending payment and the same may be credited to JV

account.

Para 6:

Standby charges amounting to 1,560,000 paid to Contractor M/s Honghua

International

Observation:

Audit observed that Standby Charges amounting to US$1.56 million were paid to

HongHua without proper supporting document.

Recommendation:

Para 7:

Statutory payment of US$4971

Observation:

Audit observed that amount US$4971 kept as account payable from March-13. A detail of this statutory liability is not available with operator.

Recommendation:

Operator is requested to reverse the liability.

Para 8:

Well pad design in block 82 and 83.

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 12

Observation:

Before finalizing location and drilling plan, Audit observed that work was awarded to

DAR consulting in Dec-2012 for designing of well pad and water well amounting to

USD19,200.

Recommendation:

Operator is suggested to start the preparatory work for drilling only after finalization

and approval of at least one drilling location by JV.

Para 9:

Work for Contract Expert for preparation of tenders related to Drilling was

awarded to Abdulla Mohammad Jamil with Contract Value US$41,500 in

April 2013 and the same was further extended. Expert started the work in

April 2013.

Observation:

Audit observed that well location was decided during TCM on 18.06-20.06.13.

However, work for contract expert for preparation of tender documents was awarded

in April-2013 before OC approval for drilling a well. Subsequently, Expert started the

work in April 2013 and payments were made to the expert.

Recommendation:

Operator is suggested to start the preparatory work for drilling only after finalization

and approval of at least one drilling location by JV.

Para 10:

Safety tools amounting to US$19,960.88

Observation:

Audit observed that the Safety Tools pertaining to drilling activities had been booked

under safety expenses. However, these items are new unused items and must be kept

in fixed assets list so that necessary disposal may be arranged.

Recommendation:

Operator is suggested to keep the unused and new safety tools in fixed asset list.

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 13

BLOCK 82,

Para 11:

SBLC amounting to US$ 10.1 million is kept valid until 17.05.2016.

Observation:

Audit observed that SBLC amounting to US$ 10.1 million had been kept valid until

17.05.2016. However, the counter guarantee of US$10.1 million is valid up to

20.12.2015. As it is already agreed between the partners to relinquish the block, it is

advised to keep SBLC valid until 20.12.2015.

Recommendation:

It is suggested that the Operator may keep the SBLC valid until 20.12.2015 only.

Para 12:

In audited report of Block 82 , auditor had provided comments on

Contractor's current account balance and Head office balance

Observation:

The Independent auditors of the Block 82, had qualified their audit report as under:

“We have not been provided with reconciliations of the US$ 3.3 million difference

between the balance of Medco Head office account presented under Contractor's

current account and the confirmation received from Medco Head Office".

Please furnish the details of US$ 3.3 Million as mentioned above. Whether any transaction is

taking place from Medco Head Office account for this block and if so, the details may be

furnished to audit. Incidentally, there is no such qualification in the Audited Accounts of Block

83.

Whether the reconciliation as mentioned above has been done for the same amount and if so,

the detail can be provided to Non Operator’s Audit for review. The Medco Yemen Amed

Limited Head Office Account balance is shown for US$ 4782 only under related party

disclosure in the Audited accounts of 2014. Reasons for above-mentioned amount of USD 3.3

Million not shown under Related Party Disclosure may be furnished to audit.

Recommendation:

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 14

Operator is requested to provide the details as requested above.

Para 13:

Amount shown as Cash call receivable not supported by actual

expenditure.

Observation:

Current Assets include Prepayments & other receivables comprising of Cash Calls

without expenditure details in the Audited Accounts for the year ended 31st

December 2014:

An amount of USD 2,174,373 is shown as Cash Calls receivable representing the

excess of total expenditures over cash call received from Partners. The same is not

reflected in the Statement of Cash Flows for the year ended 31st December 2014

neither in Operating activities nor under Investing or Financing activities. Hence,

Excess of expenditure over Cash Calls received cannot be established. The Operator

has done manual adjustment in the Balance sheet instead of passing necessary entries

in the books of account. Because of the same, it is not appearing in the Trial Balance

as a Partner’s Contribution. Operator in its reply given on 19th November 2015

provided the break-up of Cash call and mentioned that this amount should be

reversed in 2015.

Audit Comments :

i. Detailed reconciliation of such actual excess expenditure vis-à-vis Cash Call to

be provided immediately to Audit for verification and review.

ii. Details of non-cash transactions in respect of Inter-related parties – M/s

Medco Yemen Arat Ltd. to be checked & necessary adjustment entries, be

passed in the books of accounts and action taken in this regard be confirmed to

audit for review.

Recommendation:

Operator is requested to provide the details as requested above.

Para 14:

Significant increase in G&A Expenditure not in consonance with Budgeted

Manpower.

Observation:

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 15

As per the Payroll Information of Approved Work Plan & Budget by PEPA for

exploration affairs on 16.01.2014: Total Strength of employees Resident & Rotational

for 2014 considered 52 vis a vis 48 (2013). However, there is significant increase in

G&A expenditure in 2014 as compared to 2013, although the number of employees

has been marginally increased from 48 to 52 as per WP&B approved by PEPA.

Further, no major activities were carried out in 2014 on account of seismic activities

of acquisition. Following table shows the abnormal increase in G&A Expenditure

during 2014 vis-à-vis the same of 2013.

General Administrative Expenses 2013 2014 Abs.Var Var %

(USD) (USD) (USD)

Salaries & Wages 538748 993497 454749 84%

Rent Exp. 124479 232166 107687 87%

Travel & Accommodation 60388 123519 63131 105%

Utilities 31585 74498 42913 136%

Insurance 14478 61901 47423 328%

Office Stationery 18366 40434 22068 120%

Miscellaneous 87472 109953 22481 26%

Total 875516 1635968 760452 87%

Audit Comments :

Reasons for the above-mentioned increase and justification for the same may be

furnished to audit.

Recommendation:

Operator is requested to provide the details as requested above.

Para 15:

Non Imposition of Liquidated Damages(LD) in respect of 2D & 3D land

seismic acquisition services provided by M/s Quality for Oil field services

co. & M/s Honghua International co.

Observation:

As per GCC clause 10 of Contract no. OPR-0002/2010 awarded to M/s Quality for Oil

field services co. & M/s Honghua International co.(Contractor) for 2D & 3D land

Seismic Acquisition services:

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 16

“Except for Force Majeure & Standby not charged to the Operator, if the contractor

fails to meet the block wise delivery schedule within the respective scheduled

completion period fixed for that part of the work or at any time repudiates part of the

contract before completion of work , the operator may recover from the contractor

LD not as penalty as per table given in the Contract.”

Clarification is sought whether LD was imposed in respect of delay in completion of

work by Contractor in this contract. Incidentally the Operator has admitted damage

claims towards standby charges of US$ 3051198.44 as at 31st Dec, 2014 which is

shown as Exploration & Evaluation Assets - Intangibles under “Geological &

Geophysical” under Note 6 to the Financial Statements.

Financial Impact: 5% of Contract Price (Block-wise) i.e for Block 82 – 5% of

USD7798968.00 =USD 389948.00.

Audit Comments :

Reasons for no recovery of Liquidated Damages (LD) as per contractual terms for USD 389,948 in Block 82 may please be provided to Audit for review.

Recommendation:

Operator is requested to provide the details as requested above.

Para 16:

Payment of Custom duties

Observation:

An amount of US$128,164.23 is paid during 2014 towards Taxes & custom duty and shown under GL 170438-DRIL , the same needs to be clarified whether it is exempted or not ? The detail may be provided to audit. Operator was unable to provide the details of Expenditure incurred towards Taxes & Custom duty at the time of audit. However vide their e-mail dated 19th November, 2015, it was mentioned that these charges should be booked under transportation expense for drilling materials. Transport cost of materials from Aden warehouse to Wade Doan( Block 82) warehouse by Vendor , Wadi Al-Kheir. Audit Comments : Normally Taxes are exempt for drilling equipment. The same needs to be rechecked /confirmed as per PSA provision. Operator is requested to provide the complete

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 17

details with tax provisions of the country in this regard to audit for review. The reason for booking the amount of US$128,164.23 under Taxes and customs duty may please be furnished to audit. Also clarify, whether the same amount is exempted or not with detail supporting.

Recommendation:

Operator is requested to provide the details as requested above.

Para 17:

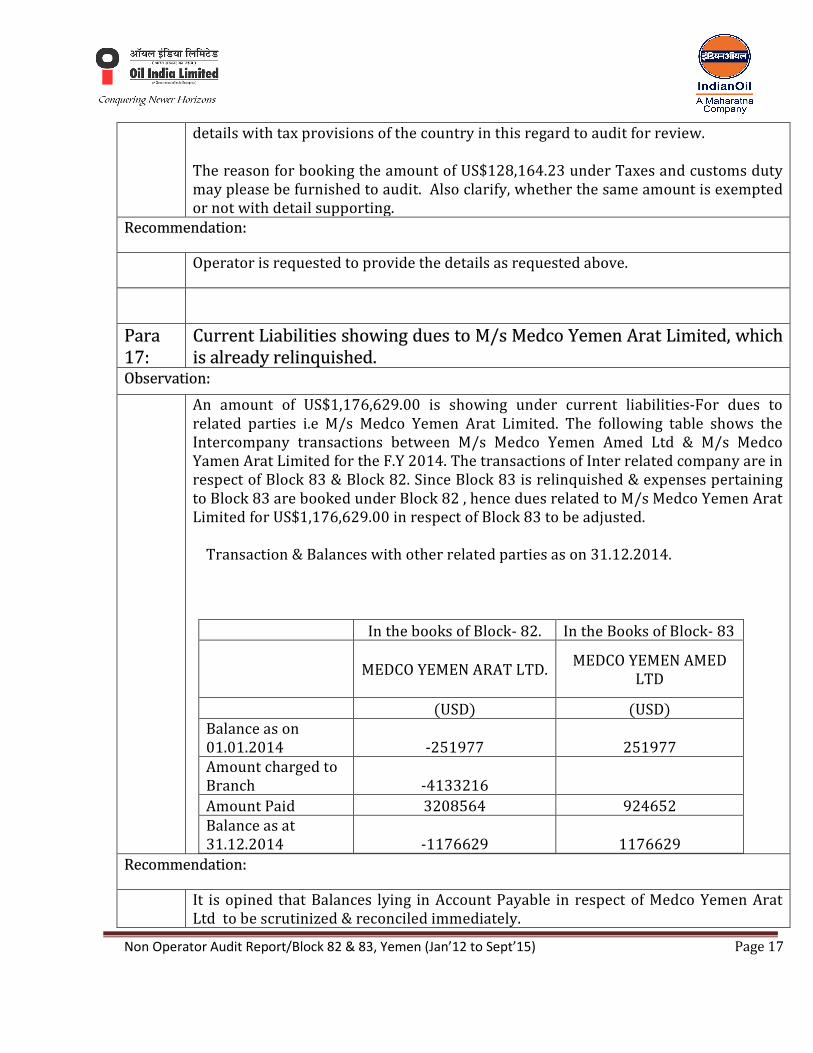

Current Liabilities showing dues to M/s Medco Yemen Arat Limited, which is already relinquished.

Observation:

An amount of US$1,176,629.00 is showing under current liabilities-For dues to related parties i.e M/s Medco Yemen Arat Limited. The following table shows the Intercompany transactions between M/s Medco Yemen Amed Ltd & M/s Medco Yamen Arat Limited for the F.Y 2014. The transactions of Inter related company are in respect of Block 83 & Block 82. Since Block 83 is relinquished & expenses pertaining to Block 83 are booked under Block 82 , hence dues related to M/s Medco Yemen Arat Limited for US$1,176,629.00 in respect of Block 83 to be adjusted.

Transaction & Balances with other related parties as on 31.12.2014.

In the books of Block- 82. In the Books of Block- 83

MEDCO YEMEN ARAT LTD.

MEDCO YEMEN AMED LTD

(USD) (USD)

Balance as on 01.01.2014 -251977 251977

Amount charged to Branch -4133216

Amount Paid 3208564 924652

Balance as at 31.12.2014 -1176629 1176629

Recommendation:

It is opined that Balances lying in Account Payable in respect of Medco Yemen Arat Ltd to be scrutinized & reconciled immediately.

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 18

The dues in the books of Medco Yemen Amed Ltd includes inventory & other Assets for which Cash Calls have already been raised in the Books of Block 83, hence the reconciliation & adjustment of Inter Related Party transactions to be done immediately.

Para 18:

Review of living allowance paid to Abdulmanan Othman Saeed Binkhawar

Observation:

In the month of November 2013 , the following Living allowance were paid :

Batch No. &

Date

Name of the

Person

Amount

(USD)

Cheque No. &

Date

Month

642

dt.28.11.201

3

Abdulmanan

Othman Saeed

Binkhawar

22779.00 000596 dated

17.11.2013

Living allowance for the

month of Nov;2013

Akram Ameen

Mohammed Ali

Kasim

16804.00 000600 dated

19.11.2013

Living allowance for the

month of Nov;2013

Abdulmanan

Othman Saeed

Binkhawar

23603.00 000620 dated

24.11.2013

Living allowance for the

month of Nov;2013

Aseel

Mohammed

Ahmed AlTashi

8540.00 000621 dated

24.11.2013

Living allowance for the

month of November

‘2013

It is to be noted that Abdulmanan Othman Saeed Binkhawar has been paid twice Living

allowance for the month of November 2013.

Recommendation:

It is opined that details of expenditure in respect of Living allowances paid to

employees for whole year along with related employees to be furnished by operator.

Para 19:

Review of payment of Social Development activities paid as “ Per Diem”

for PEPA officials to Indonesia

Observation:

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 19

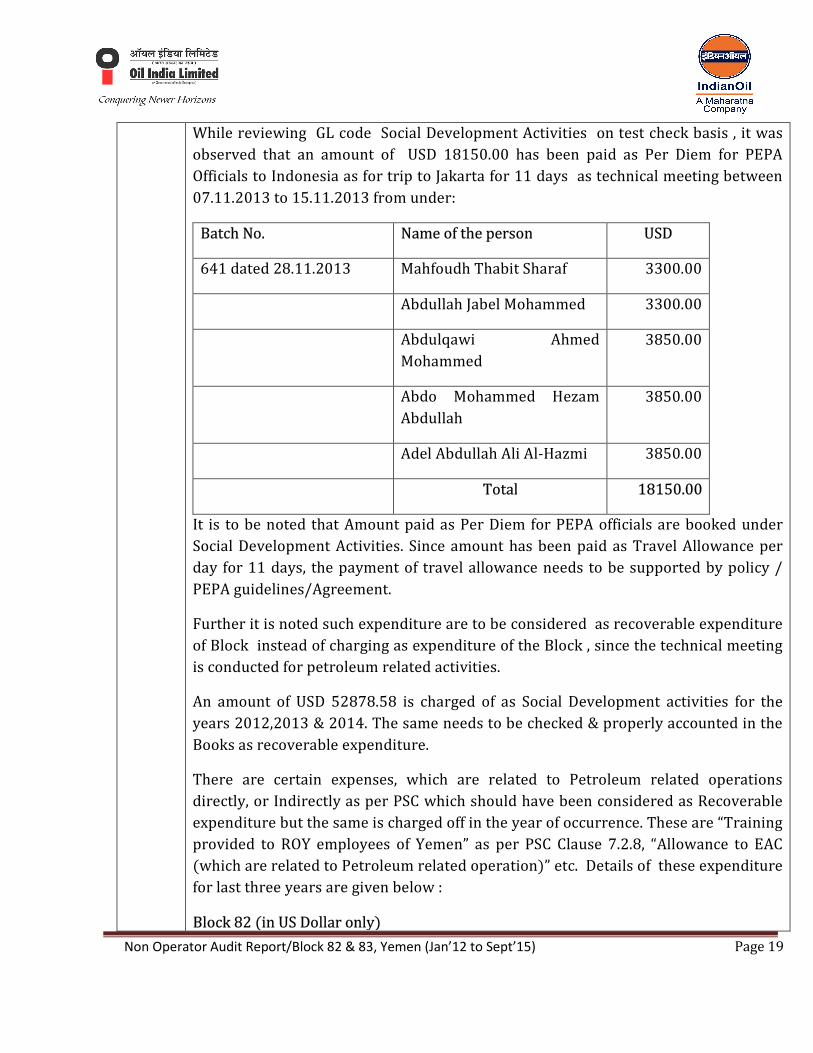

While reviewing GL code Social Development Activities on test check basis , it was

observed that an amount of USD 18150.00 has been paid as Per Diem for PEPA

Officials to Indonesia as for trip to Jakarta for 11 days as technical meeting between

07.11.2013 to 15.11.2013 from under:

Batch No. Name of the person USD

641 dated 28.11.2013 Mahfoudh Thabit Sharaf 3300.00

Abdullah Jabel Mohammed 3300.00

Abdulqawi Ahmed

Mohammed

3850.00

Abdo Mohammed Hezam

Abdullah

3850.00

Adel Abdullah Ali Al-Hazmi 3850.00

Total 18150.00

It is to be noted that Amount paid as Per Diem for PEPA officials are booked under

Social Development Activities. Since amount has been paid as Travel Allowance per

day for 11 days, the payment of travel allowance needs to be supported by policy /

PEPA guidelines/Agreement.

Further it is noted such expenditure are to be considered as recoverable expenditure

of Block instead of charging as expenditure of the Block , since the technical meeting

is conducted for petroleum related activities.

An amount of USD 52878.58 is charged of as Social Development activities for the

years 2012,2013 & 2014. The same needs to be checked & properly accounted in the

Books as recoverable expenditure.

There are certain expenses, which are related to Petroleum related operations

directly, or Indirectly as per PSC which should have been considered as Recoverable

expenditure but the same is charged off in the year of occurrence. These are “Training

provided to ROY employees of Yemen” as per PSC Clause 7.2.8, “Allowance to EAC

(which are related to Petroleum related operation)” etc. Details of these expenditure

for last three years are given below :

Block 82 (in US Dollar only)

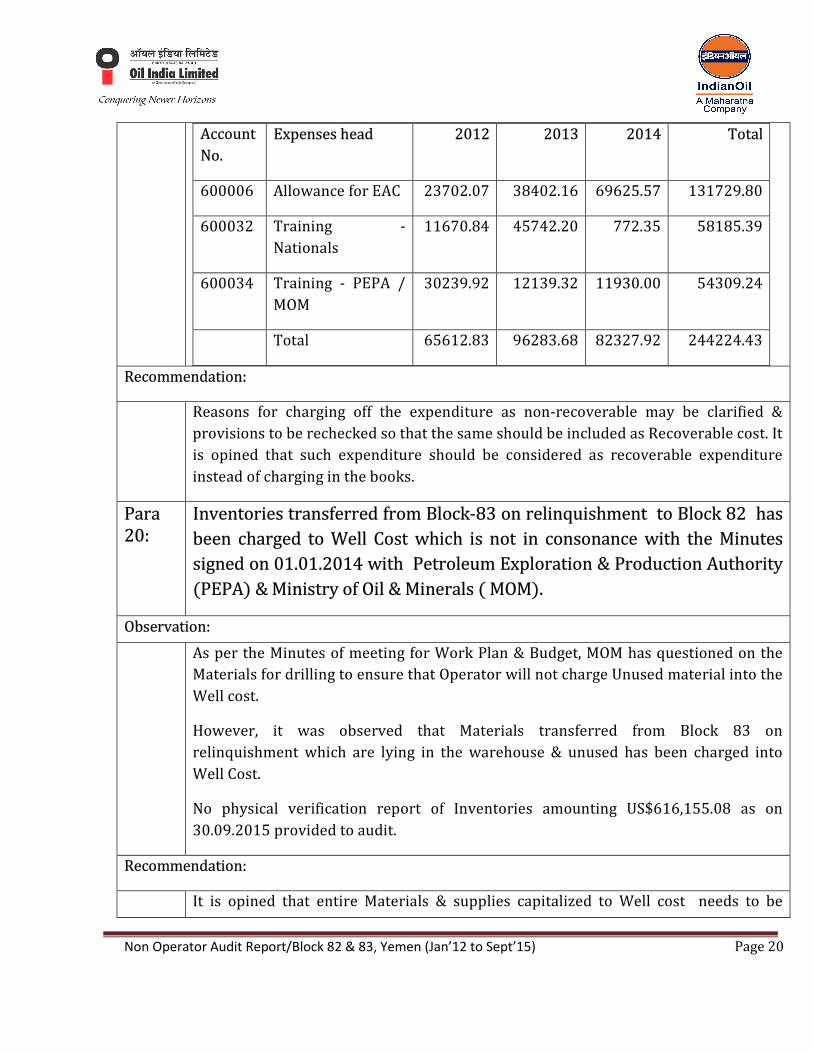

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 20

Account

No.

Expenses head 2012 2013 2014 Total

600006 Allowance for EAC 23702.07 38402.16 69625.57 131729.80

600032 Training -

Nationals

11670.84 45742.20 772.35 58185.39

600034 Training - PEPA /

MOM

30239.92 12139.32 11930.00 54309.24

Total 65612.83 96283.68 82327.92 244224.43

Recommendation:

Reasons for charging off the expenditure as non-recoverable may be clarified &

provisions to be rechecked so that the same should be included as Recoverable cost. It

is opined that such expenditure should be considered as recoverable expenditure

instead of charging in the books.

Para 20:

Inventories transferred from Block-83 on relinquishment to Block 82 has

been charged to Well Cost which is not in consonance with the Minutes

signed on 01.01.2014 with Petroleum Exploration & Production Authority

(PEPA) & Ministry of Oil & Minerals ( MOM).

Observation:

As per the Minutes of meeting for Work Plan & Budget, MOM has questioned on the

Materials for drilling to ensure that Operator will not charge Unused material into the

Well cost.

However, it was observed that Materials transferred from Block 83 on

relinquishment which are lying in the warehouse & unused has been charged into

Well Cost.

No physical verification report of Inventories amounting US$616,155.08 as on

30.09.2015 provided to audit.

Recommendation:

It is opined that entire Materials & supplies capitalized to Well cost needs to be

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 21

physically verified & status of the Materials & Supplies to be evaluated & report on

the same to be furnished for review.

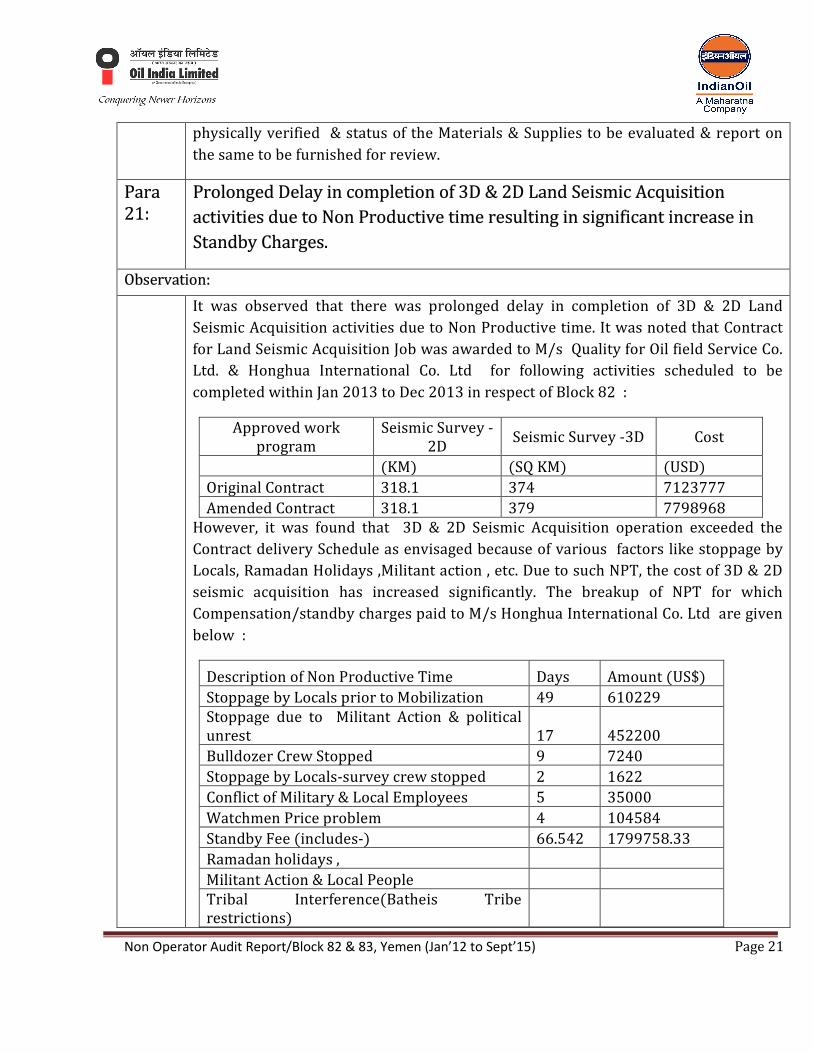

Para 21:

Prolonged Delay in completion of 3D & 2D Land Seismic Acquisition

activities due to Non Productive time resulting in significant increase in

Standby Charges.

Observation:

It was observed that there was prolonged delay in completion of 3D & 2D Land

Seismic Acquisition activities due to Non Productive time. It was noted that Contract

for Land Seismic Acquisition Job was awarded to M/s Quality for Oil field Service Co.

Ltd. & Honghua International Co. Ltd for following activities scheduled to be

completed within Jan 2013 to Dec 2013 in respect of Block 82 :

Approved work program

Seismic Survey - 2D

Seismic Survey -3D Cost

(KM) (SQ KM) (USD)

Original Contract 318.1 374 7123777

Amended Contract 318.1 379 7798968 However, it was found that 3D & 2D Seismic Acquisition operation exceeded the

Contract delivery Schedule as envisaged because of various factors like stoppage by

Locals, Ramadan Holidays ,Militant action , etc. Due to such NPT, the cost of 3D & 2D

seismic acquisition has increased significantly. The breakup of NPT for which

Compensation/standby charges paid to M/s Honghua International Co. Ltd are given

below :

Description of Non Productive Time Days Amount (US$)

Stoppage by Locals prior to Mobilization 49 610229

Stoppage due to Militant Action & political unrest 17 452200

Bulldozer Crew Stopped 9 7240

Stoppage by Locals-survey crew stopped 2 1622

Conflict of Military & Local Employees 5 35000

Watchmen Price problem 4 104584

Standby Fee (includes-) 66.542 1799758.33

Ramadan holidays ,

Militant Action & Local People

Tribal Interference(Batheis Tribe restrictions)

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 22

Total 152.54 3,010,633.33

It is pertinent to note that no major activities were performed after July’2013 until

Dec’2013 in respect of the Seismic acquisition & consequently contractual period

extended.

Recommendation:

The reason for payment of such higher amount towards Non Productive activities

may please be clarified to audit with proper justification for review.

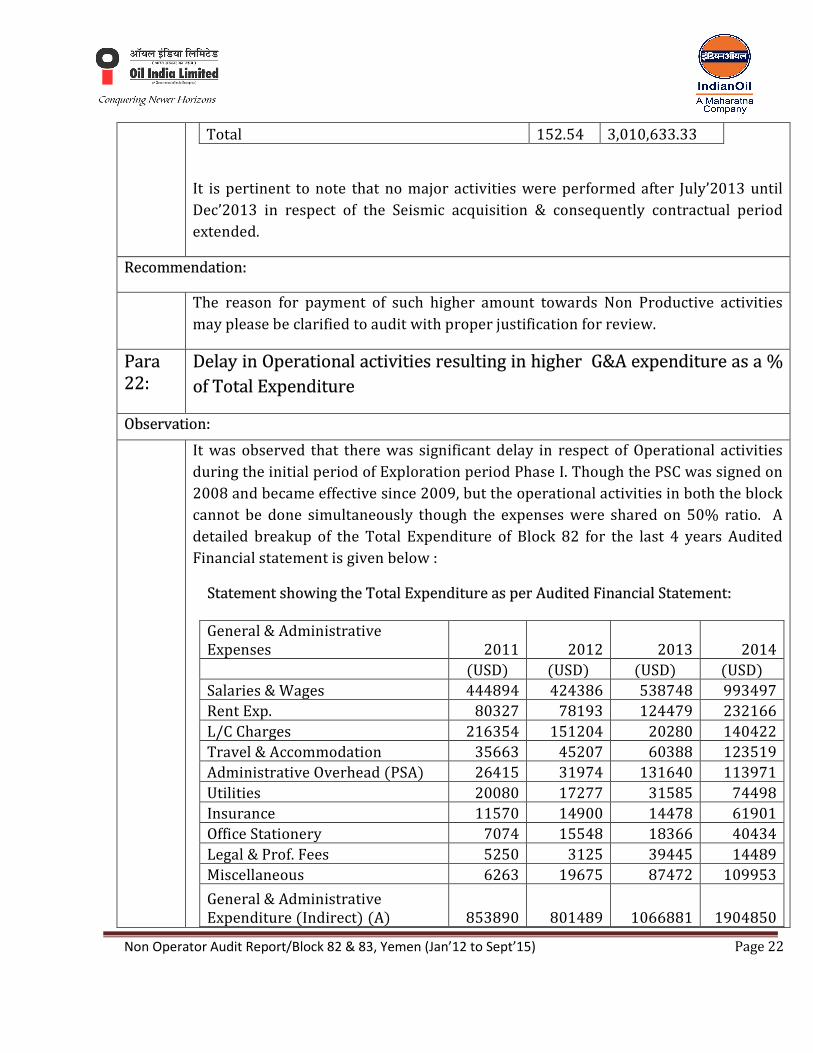

Para 22:

Delay in Operational activities resulting in higher G&A expenditure as a %

of Total Expenditure

Observation:

It was observed that there was significant delay in respect of Operational activities

during the initial period of Exploration period Phase I. Though the PSC was signed on

2008 and became effective since 2009, but the operational activities in both the block

cannot be done simultaneously though the expenses were shared on 50% ratio. A

detailed breakup of the Total Expenditure of Block 82 for the last 4 years Audited

Financial statement is given below :

Statement showing the Total Expenditure as per Audited Financial Statement: General & Administrative Expenses 2011 2012 2013 2014

(USD) (USD) (USD) (USD)

Salaries & Wages 444894 424386 538748 993497

Rent Exp. 80327 78193 124479 232166

L/C Charges 216354 151204 20280 140422

Travel & Accommodation 35663 45207 60388 123519

Administrative Overhead (PSA) 26415 31974 131640 113971

Utilities 20080 17277 31585 74498

Insurance 11570 14900 14478 61901

Office Stationery 7074 15548 18366 40434

Legal & Prof. Fees 5250 3125 39445 14489

Miscellaneous 6263 19675 87472 109953

General & Administrative Expenditure (Indirect) (A) 853890 801489 1066881 1904850

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 23

Exploration & Evaluation Assets

Seismic Survey 5350

Up Hole Test 163020

Mobilization & Demobilization 80750 66500 Seismic Acquisition thru Vibroseis 3D 3299899 500000

Seismic Acquisition thru Vibroseis 2D 353187 725987

Seismic Processing 3D 152086

Damage claims (L) 0 0 2907956 143243

Bits ,Casing Equipment & Cementing ,Well Head 62826.23 368328

Geological & Geophysical exp (B) 0 5350 6867638 1956144 General & Administrative Expenditure (Direct) (c) 258077 434876 1318425 2794194

Tangible Assets (Furniture, Computer Office Equipment) 10374 7070 59618 196823

PSA Bonus & Contribution (D) 1100000 1100000 1100000 1100000

PSA 3% Fixed Tax 27208 32933 279477 201362

Total Expenditure (E) 2249549 2381718 10692039 8153373 G&A (Direct & Indirect) % of Total Expenditure {(A+C)/E} 49% 52% 22% 58%

PSA Bonus & Contribution % of Total Expenditure (D/E) 49% 46% 10% 13% Geological & Geophysical expenses (including Damage Claims) % of Total Expenditure (B/E) 0% 0% 64% 24%

Damage Claims % Total Expenditure (L/E) 0% 27% 2%

Recommendation:

Para 23:

Payment of Demobilization Charges of USD 66500.00

Observation:

It was observed that an amount of US$66,500.00 was paid as Extra Demobilization

Fee for Block A vide Bill ref no. 75/hh/opr-0002/2010/20141126 dated 26.11.2014.

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 24

As per Annexure exhibit D of Contract clause 5.6 “ No Demobilisation charges are

Payable for the movement of the equipment /Personnel between the two work areas

under this contract or under any other contract within Yemen region.”

Further Clause 5.7 provides “In the event , the work under the contract is not

completed for any reason no Demobilisation charges shall be payable to the

Contractor”. The Operator vide their mail on 19.11.2015 has confirmed for holding

the payment of Demobilisation.

It was noted that in Minutes of Coordination meeting for Termination dated

14.03.2015 , made between Operator & Contractor –M/s Honghua International ,it

was agreed that “Demobilisation Fee –USD 66500.00 shall be paid (refer Minutes

point-(h)).

Recommendation:

Reasons for accounting for of Demobilization fee – twice may be clarified by the

Operator.

BLOCK 82 & 83

Para 1:

Review of Contract OPR-0002/2010 for 2D & 3D Land Seismic Acquisition

Service at Block 83 & Block 82, made between Medco Yemen Arat Limited

& Medco Yemen Amed Ltd. & Quality for Oil field Service Co. Ltd. &

Honghua International Co. Ltd.

Observation:

The Contract was entered on 21.12.2010 at an Estimated Contract Price of USD

5,701,223.00 for Block -83 & USD 6,906,970.00 for Block -82 .The timeline scheduled

was 7 months for Block 83 i.e. from Jan 2011 to July 2011 & 8 months for Block 82 i.e.

from May 2011 to Dec 2011.

However, the Seismic Survey was started only from March 2012 due to many

stoppage by local people & travel ban by Chinese Govt. to their citizen to visit Yemen

which affected the movement of Contractors’ employees & hence completion period

for Seismic acquisition for Block 83 was scheduled up to Nov 2012. Similarly Contract

period for Seismic Survey in Block 82 was amended on Dec 21 2012 for 12 months

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 25

from Jan 2013 to Dec 2013.

1. The above timeline as originally fixed had been changed from 7 months for

Block 83 to 9 months & similarly 12 months for Block 82. The amendment in

the Contract period was made on Dec 19, 2012 but the approval from PEPA

was on 23.12.2012. This is a serious violation of PSC & JOA.

Amendment in the Contract Price & additional clause in definition for “Standby” :

The Third amendment in the Contract was made on Feb 2 ,2013 incorporating change

in Estimated Contract Price for Block 82 for US$7,798,968 from US$6,906,970 i.e.

Increase in Estimated Contract Price by US$891,998.00 with specific Increase in the

Basic Unit Price for Vibroseis 3D from US$381 to US$478.

2. Though the Contract was amended with Contractor M/s on Feb 2 2013, but

approval from PEPA was given on 11.03.2013 . Amendment in the contract

was not approved by PEPA on the date of Amendment of Contract. This is a

serious violation of PSC.

It was further noted that “Standby” definition in Clause 7.1 of Annexure D of Contract

was amended to include7.1.4 “Any stoppage by Local People reported by Contractors

permitting supervisor & acknowledge by Contractor’s party chief. The determination

of the stoppage by local must follow the Operators’ Standard Operating Procedure.

The standby rate will be paid if such report has been verified & approved by the

Operator.

3. Based on the above amendment in the Contract definition for “Standby “ ,

Operator has approved the standby charge for stoppage by locals for the

period of 14 days @ USD 15408 amounting to USD 215708.00 in respect of

period from January 12 , 2013 to Jan 27 2013.

The observation is serious in nature since the approval for amendment in definition

of “Standby” would have been effective from Feb, 2013 & any approval for standby

charges prior to Feb, 2013 is contradicting the Contractual agreement resulting a

Financial Impact of USD 215708.00.

Payment of Standby Charges before Mobilization period not in consonance with

Clause 7.1 of Annexure D of Contract.

4. Clause 7.1 of annexure D of Contract provides for “Standby rates will be

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 26

payable only if the Equipment(s) & all the Equipments are in the Operational

Condition”.

It was noted that the Contractor has completed the Mobilization in the month of May, 2013 which is evident from their Bill No. 25/HH/OPR-0002/2010/20130524. Hence till May, 2013 , all the equipments prior to Mobilization were not in operational condition as envisaged in the definition of Standby rates . Therefore, the payment of US$898,675 towards Standby Charges prior to Mobilization is not in consonance with the definition of Standby. The related Invoices are as under :

Invoice No. Amount (USD)

19/HH/OPR-0002/2010/20130331 199,320.00 23/HH/OPR-0002/2010/20130502 215,708.00 24/HH/OPR-0002/2010/20130504 184,556.00

26/hh/opr-0002/2010/20130525 175,000.00 27/hh/opr-0002/2010/20130531 124,091.00

Total 898,675.00

Reasons for the same may be provided to audit for review.

5. No Statement of Account with the Contractor was available as on 31.12.2013 &

31.12.2014, It was further noted that Contractor has submitted 41/HH/OPR-

0002/2010/20131118 on 18.11.2013 as a consolidated bill for standby

charges for the 01.06.2013 to 31.10.2013 for USD 2872800 in addition to

separate bills for Standby charges on monthly basis.

The reconciliation statement in respect of Bills raised & payment made against such

bills are not available on the date of audit.

6. No Standard rates defined in respect of Compensation paid to M/s Honghua

International for Stoppage by Local people before Mobilisation.

It was observed that compensation for USD 1,062,429.00 was paid to Contractor in respect of stoppage by Local People. Out of above amount, for USD 610,229.00 there was no standard rate fixed for such compensation, which was paid as per rates charged by M/s Honghua International.

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 27

As per Annexure 3 Exhibit –A –Scope of work , clause 6 which provides for Staged

Operations – Services to be performed in two stages – Advance Party & Basic Party.

“Advance Party “includes activities setting up & implementing Socialization (Public relation) program with all Government, Village & religious leaders. “Basic Party” includes all operational activities after the Advance Party activities are completed. The contractor’s obligation in respect of “Advance Party ” requires development of Public relation which was a part of scope of work & hence contractor shall be liable for proper coordination with the Local people , Village leaders.

Payment of compensation to Contractor before mobilization in respect of failure to

fulfill “Advance Party “Obligation is not tenable.

Recommendation:

Operator is requested to provide the details as requested above.

Para 2:

Higher charging of Personnel Costs

Observation:

Audit has done a sample review of Manpower cost charged by the Operator. It has

been observed that as per SOE as of 31-03-2013 the detail of Personnel cost are given

as under :- IN US DOLLAR

Cost element January 2013 February 2013 March 2013

G&A 43811.54 49037.74 39606.62

G&G 24136.82 85288.75 92989.56

TOTAL 67948.36 134326.49 132596.18

Against the above expenditure shown under SOE, the detail manpower positioning

(no. of personnel) and their cost booked are tabled as under :-

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 28

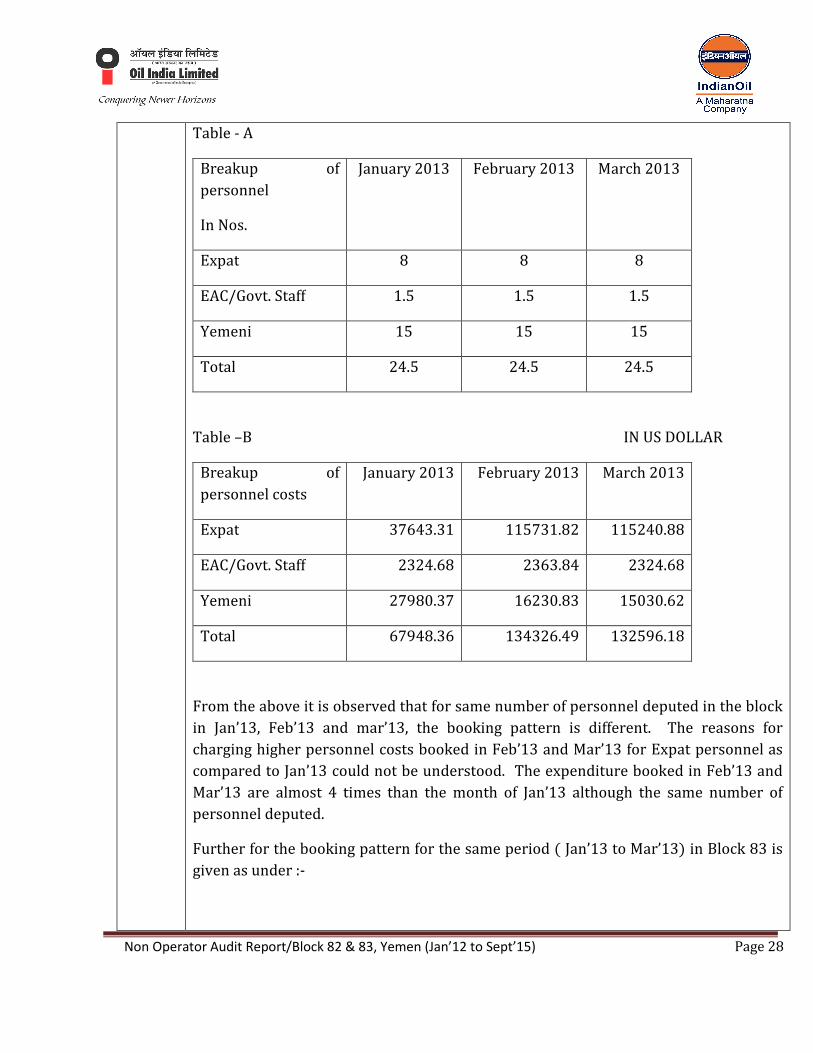

Table - A

Breakup of

personnel

In Nos.

January 2013 February 2013 March 2013

Expat 8 8 8

EAC/Govt. Staff 1.5 1.5 1.5

Yemeni 15 15 15

Total 24.5 24.5 24.5

Table –B IN US DOLLAR

Breakup of

personnel costs

January 2013 February 2013 March 2013

Expat 37643.31 115731.82 115240.88

EAC/Govt. Staff 2324.68 2363.84 2324.68

Yemeni 27980.37 16230.83 15030.62

Total 67948.36 134326.49 132596.18

From the above it is observed that for same number of personnel deputed in the block

in Jan’13, Feb’13 and mar’13, the booking pattern is different. The reasons for

charging higher personnel costs booked in Feb’13 and Mar’13 for Expat personnel as

compared to Jan’13 could not be understood. The expenditure booked in Feb’13 and

Mar’13 are almost 4 times than the month of Jan’13 although the same number of

personnel deputed.

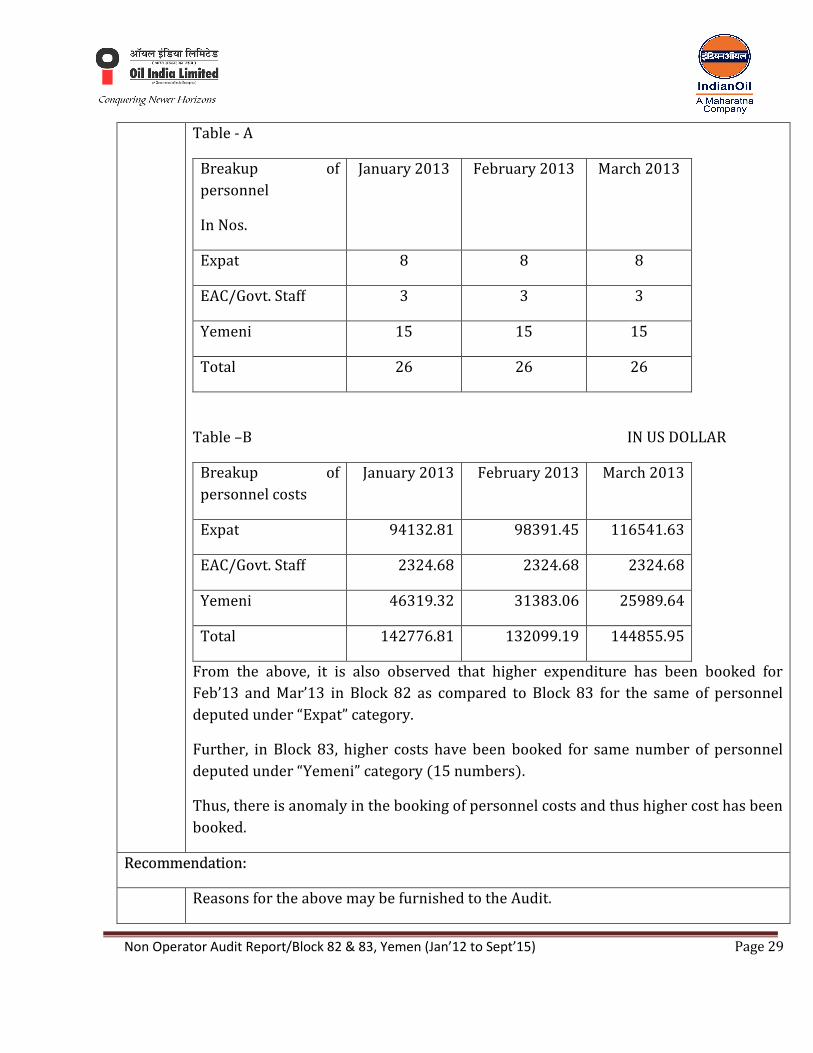

Further for the booking pattern for the same period ( Jan’13 to Mar’13) in Block 83 is

given as under :-

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 29

Table - A

Breakup of

personnel

In Nos.

January 2013 February 2013 March 2013

Expat 8 8 8

EAC/Govt. Staff 3 3 3

Yemeni 15 15 15

Total 26 26 26

Table –B IN US DOLLAR

Breakup of

personnel costs

January 2013 February 2013 March 2013

Expat 94132.81 98391.45 116541.63

EAC/Govt. Staff 2324.68 2324.68 2324.68

Yemeni 46319.32 31383.06 25989.64

Total 142776.81 132099.19 144855.95

From the above, it is also observed that higher expenditure has been booked for

Feb’13 and Mar’13 in Block 82 as compared to Block 83 for the same of personnel

deputed under “Expat” category.

Further, in Block 83, higher costs have been booked for same number of personnel

deputed under “Yemeni” category (15 numbers).

Thus, there is anomaly in the booking of personnel costs and thus higher cost has been

booked.

Recommendation:

Reasons for the above may be furnished to the Audit.

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 30

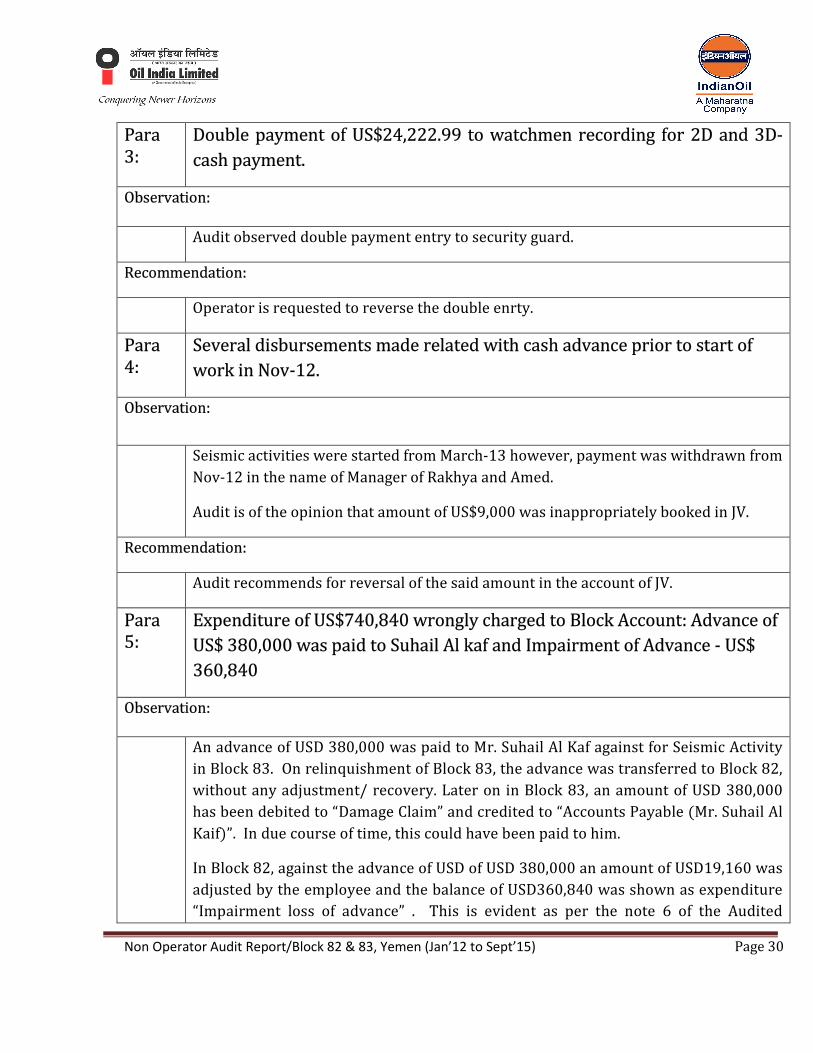

Para 3:

Double payment of US$24,222.99 to watchmen recording for 2D and 3D-

cash payment.

Observation:

Audit observed double payment entry to security guard.

Recommendation:

Operator is requested to reverse the double enrty.

Para 4:

Several disbursements made related with cash advance prior to start of

work in Nov-12.

Observation:

Seismic activities were started from March-13 however, payment was withdrawn from

Nov-12 in the name of Manager of Rakhya and Amed.

Audit is of the opinion that amount of US$9,000 was inappropriately booked in JV.

Recommendation:

Audit recommends for reversal of the said amount in the account of JV.

Para 5:

Expenditure of US$740,840 wrongly charged to Block Account: Advance of

US$ 380,000 was paid to Suhail Al kaf and Impairment of Advance - US$

360,840

Observation:

An advance of USD 380,000 was paid to Mr. Suhail Al Kaf against for Seismic Activity

in Block 83. On relinquishment of Block 83, the advance was transferred to Block 82,

without any adjustment/ recovery. Later on in Block 83, an amount of USD 380,000

has been debited to “Damage Claim” and credited to “Accounts Payable (Mr. Suhail Al

Kaif)”. In due course of time, this could have been paid to him.

In Block 82, against the advance of USD of USD 380,000 an amount of USD19,160 was

adjusted by the employee and the balance of USD360,840 was shown as expenditure

“Impairment loss of advance” . This is evident as per the note 6 of the Audited

Non Operator Audit Report/Block 82 & 83, Yemen (Jan’12 to Sept’15) Page 31

accounts (ref : Prepayments and Other Receivables) of MEDCO YEMEN AMED

LIMITED for the year ended 31st December 2014 in respect of Block 82.

The above treatment of advance and related transaction has resulted into the

following:-

i. The Expenditure of USD 380,000 in Block 83 and USD 360,840 in Block

82 have been debited to partners account which is not tenable.

ii. Any expenditure for joint account incurred in excess of USD 250000

should have been duly approved by the non-operating partners through

AFE. In the given instance, the reason for charging the amount of USD

380,000 in Block 83 and USD 360,840 in Block 82 separately as

expenses is higher than the ceiling mentioned for AFE in Clause 6.7.

The reasons for such deviation may be provided to Audit for review.

iii. There is likely to be a duplicate payment of USD380,000 to employee,

Mr Suhail Al Kaf since it is lying as “Accounts Payable” instead of

adjusting the same against Advance.

Recommendation:

Therefore Audit is of the view that the expenditure of USD 380,000 shown as Damage

Claim in Block 83 and USD 360,840 shown as Impairment loss in Block 82 be

reversed and be credited to Partners Account as per their Participating Interest. Due

to such Inter related Transactions (Between Block 82 & 83) there is likely chances of

Raising Cash Call twice. Hence, reconciliation of Cash Call & Expenditure as per

audited accounts should be made immediately. Secondly, Block 83 accounts [Assets &

Liabilities in respect of Inter related transactions with Medco Amed (Block 82)] to be

immediately reconciled since the block is relinquished.

(Prabhat Kumar) (Pankaj Singh) (Sanjay Khatri) (Jyotirmoy Bhattacharya) DFM (BD) DM (E&P) Manager(Internal Audit) Ch. Manager(Internal Audit) IOCL IOCL OIL OIL