Embed Size (px)

Citation preview

Prepared by: C. Douglas Cloud Professor Emeritus of AccountingPepperdine University

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Fixed Assets and Intangible Assets

Chapter 9

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Learning Objectives

1. Define, classify, and account for the cost of fixed assets.

2. Compute depreciation, using the following methods: straight-line method, units-of-production method, and double-declining-balance method.

3. Journalize entries for the disposal of fixed assets.

4. Compute depletion and journalize the entry for depletion.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Learning Objectives

5. Describe the accounting for intangible assets, such as patents, copyrights, and goodwill.

6. Describe how depreciation expense is reported in an income statement and prepare a balance sheet that includes fixed assets and intangible assets.

7. Describe and illustrate the fixed asset turnover ratio to assess the efficiency of a company’s use of its fixed assets.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Learning Objective 1

Define, classify, and account for the cost of

fixed assets.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Nature of Fixed Assets

Fixed assets are long-term or relatively permanent assets, such as equipment, machinery, buildings, and land. Other descriptive titles for fixed assets are plant assets or property, plant, and equipment.

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Nature of Fixed Assets

Fixed assets have the following characteristics: They exist physically and, thus, are tangible

assets. They are owned and used by the company

in its normal operations. They are not offered for sale as part of

normal operations.

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

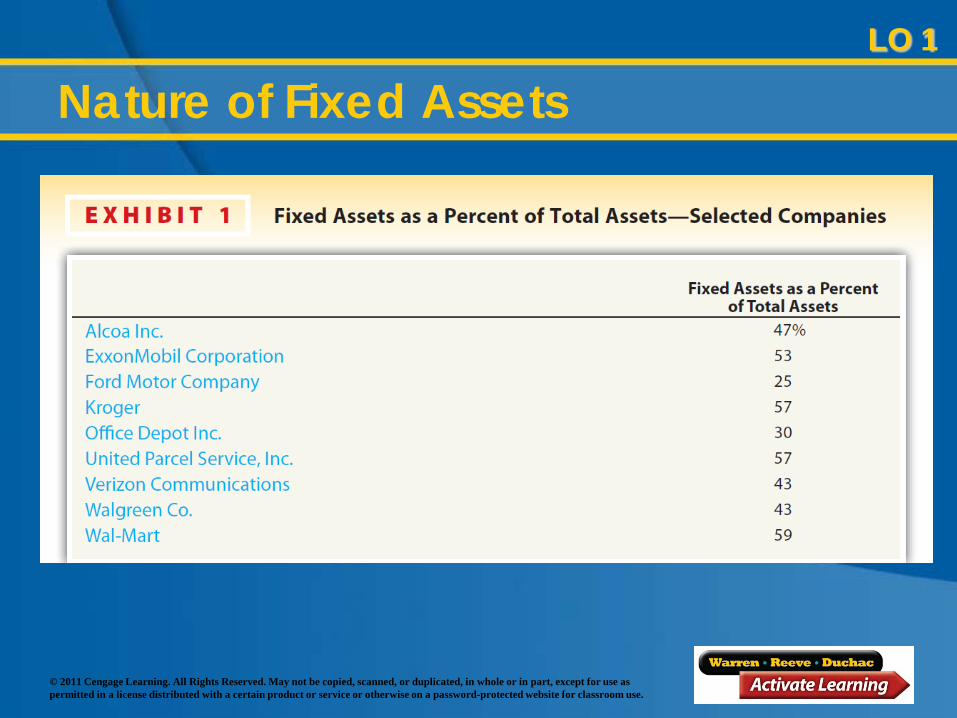

Nature of Fixed AssetsLO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

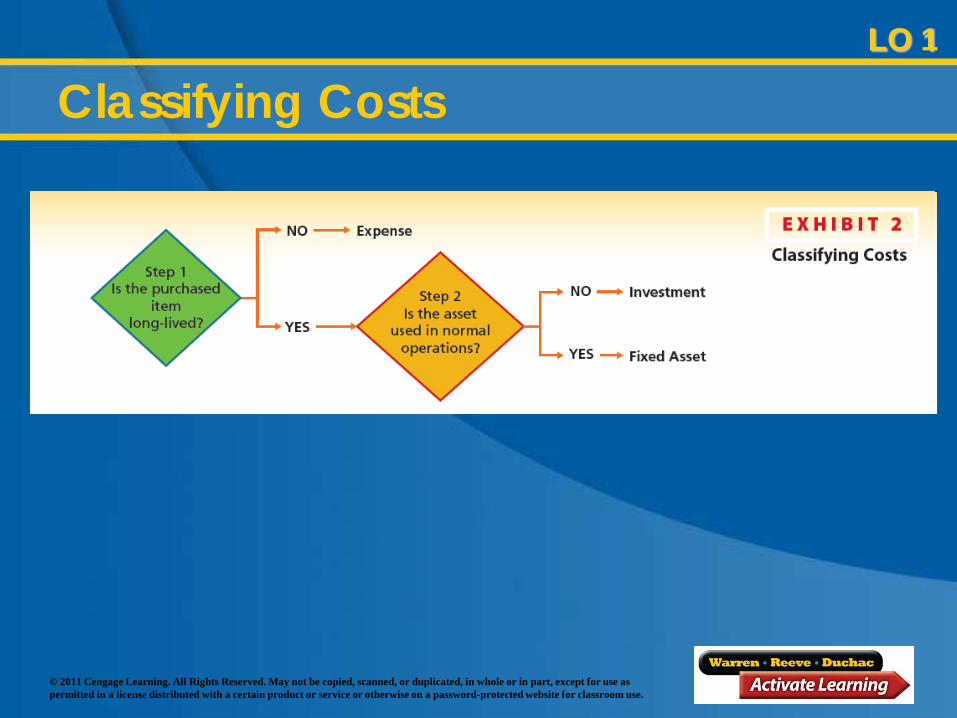

Classifying CostsLO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

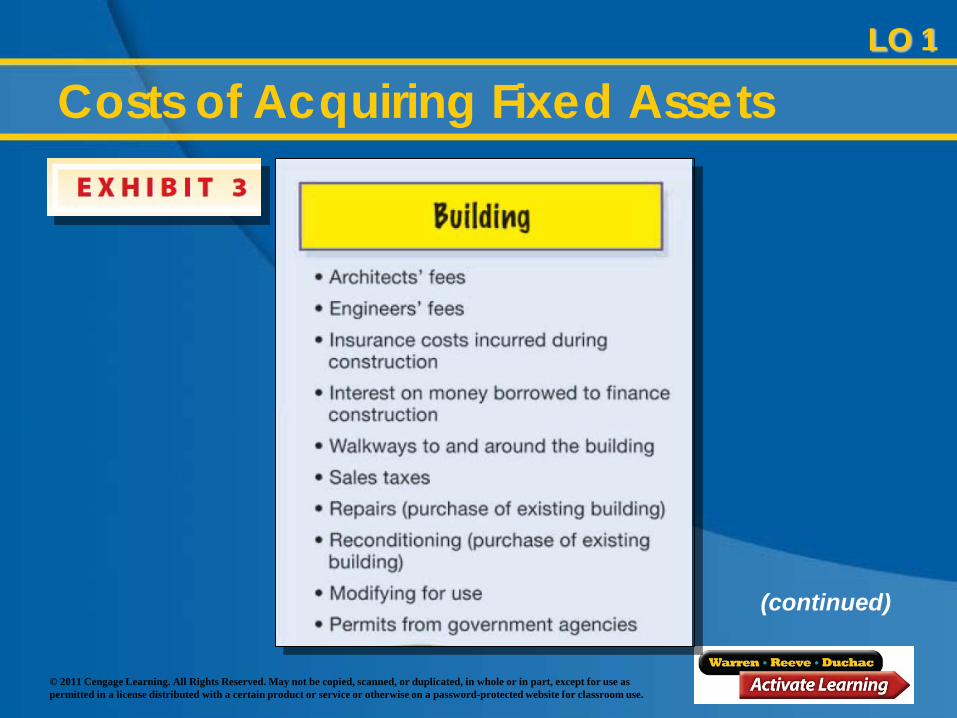

LO 1

Costs of Acquiring Fixed Assets

(continued)

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

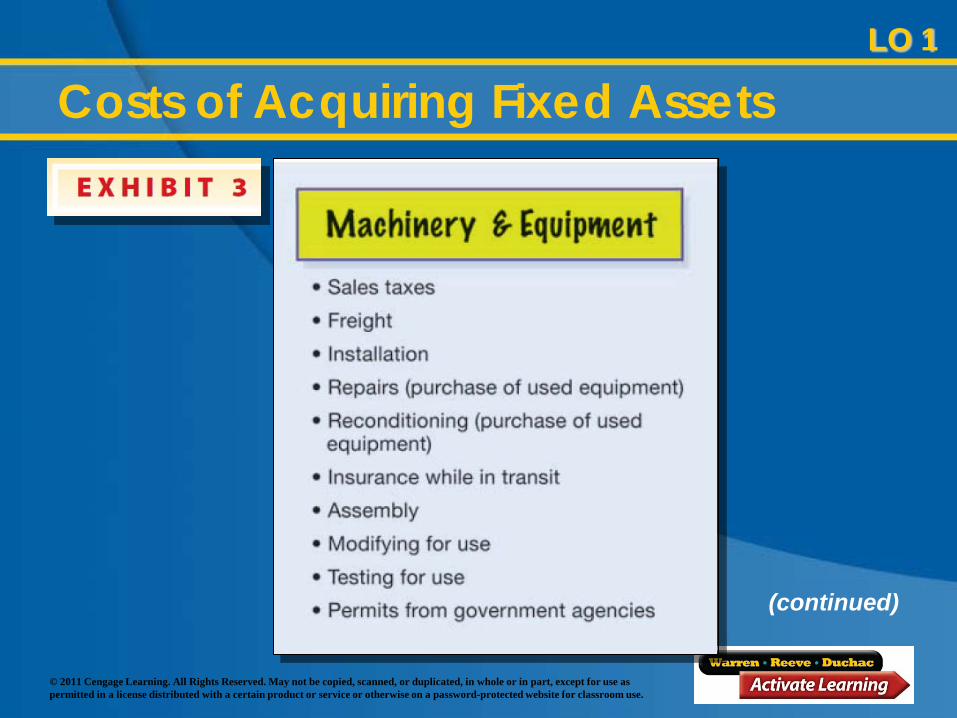

LO 1

(continued)

Costs of Acquiring Fixed Assets

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

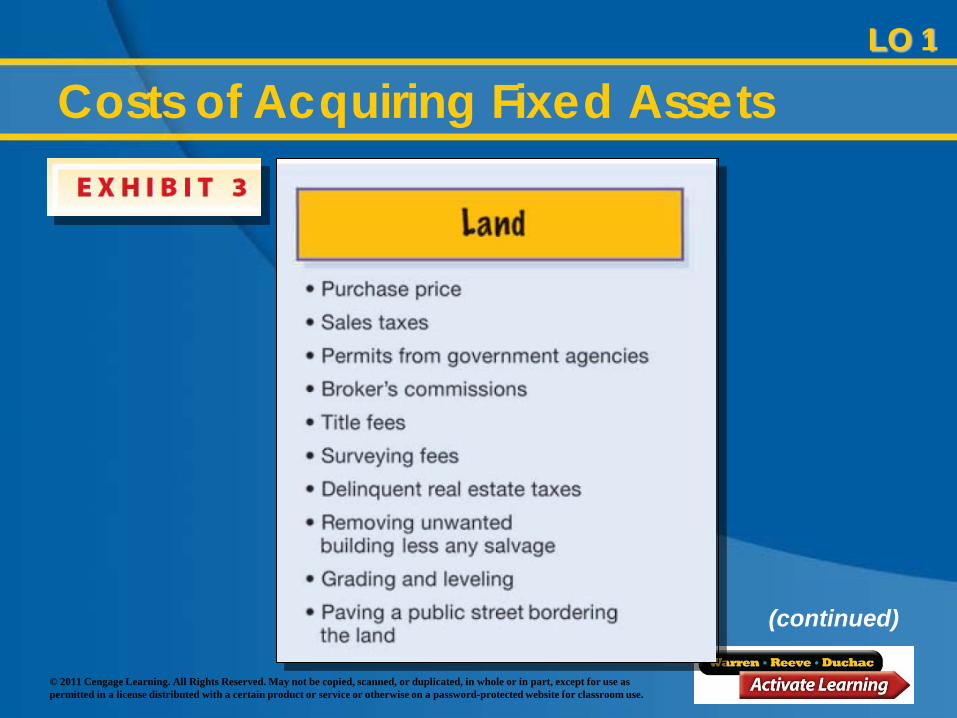

LO 1

(continued)

Costs of Acquiring Fixed Assets

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

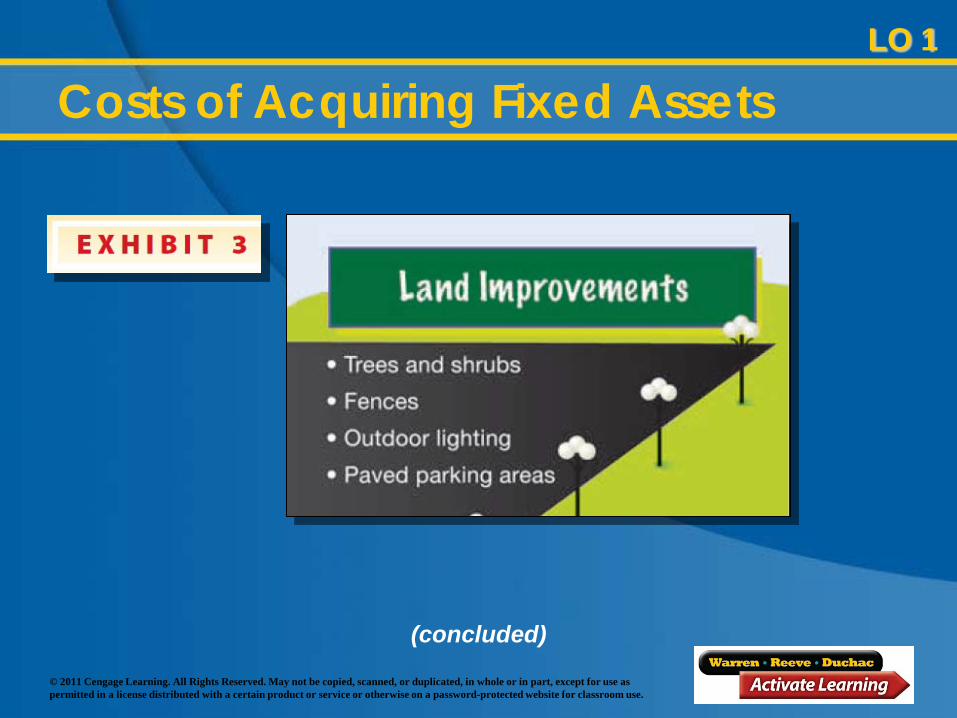

LO 1

(concluded)

Costs of Acquiring Fixed Assets

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Costs of Acquiring Fixed Assets

Unnecessary costs that do not increase the asset’s usefulness are recorded as an expense. Vandalism Mistakes in installation Uninsured theft Damage during unpacking and installing Fines for not obtaining proper permits from

government agencies

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

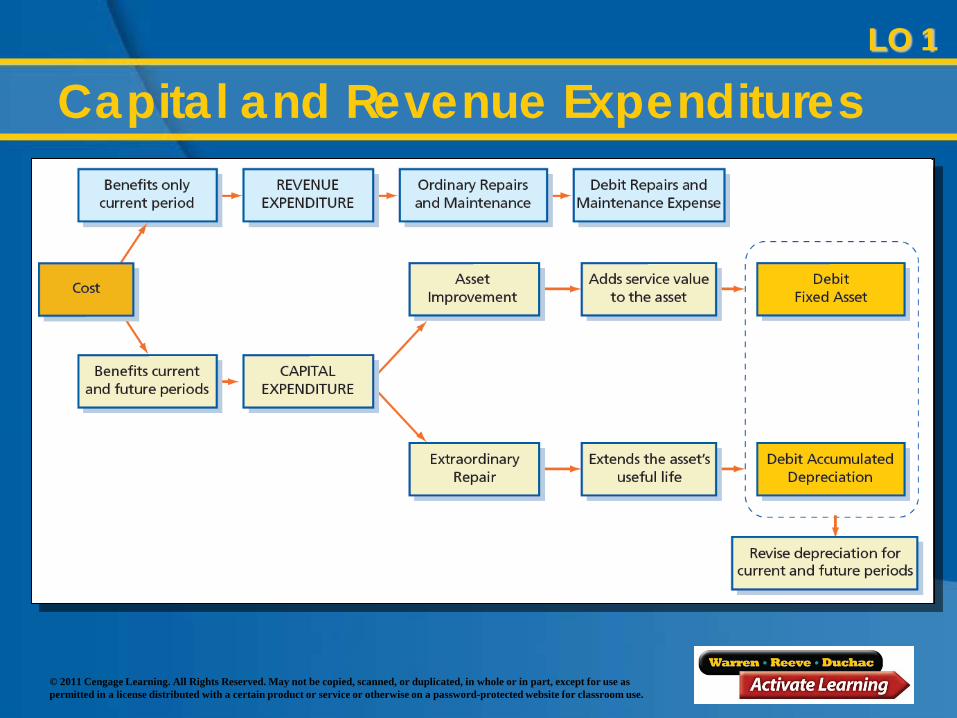

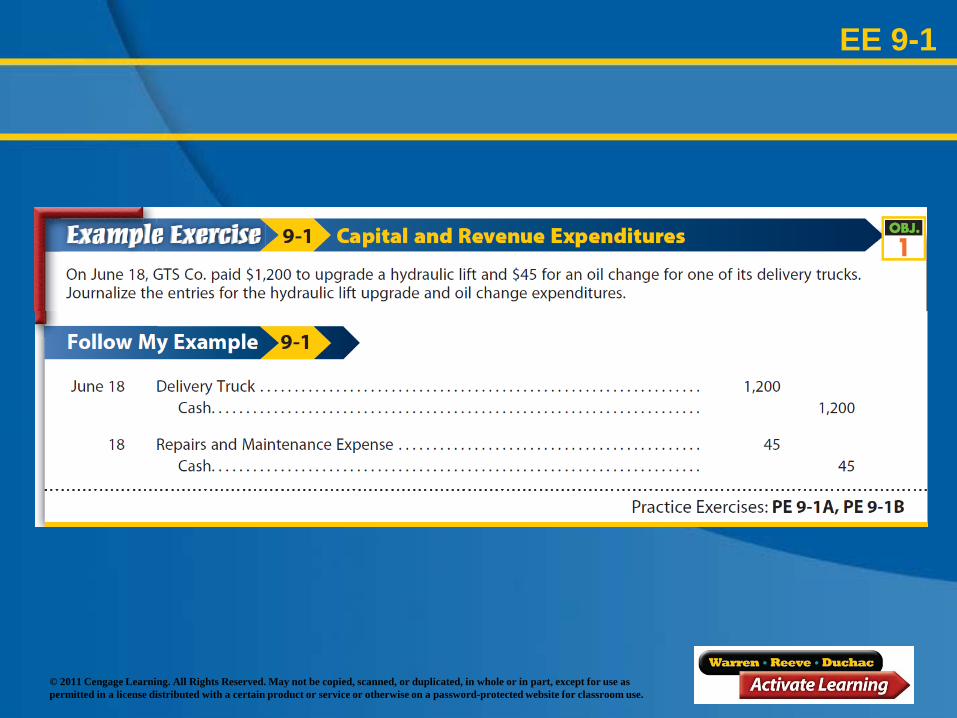

Capital and Revenue Expenditures

Expenditures that benefit only the current period are called revenue expenditures.

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Capital and Revenue Expenditures

Expenditures that improve the asset or extend its useful life are capital expenditures.

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

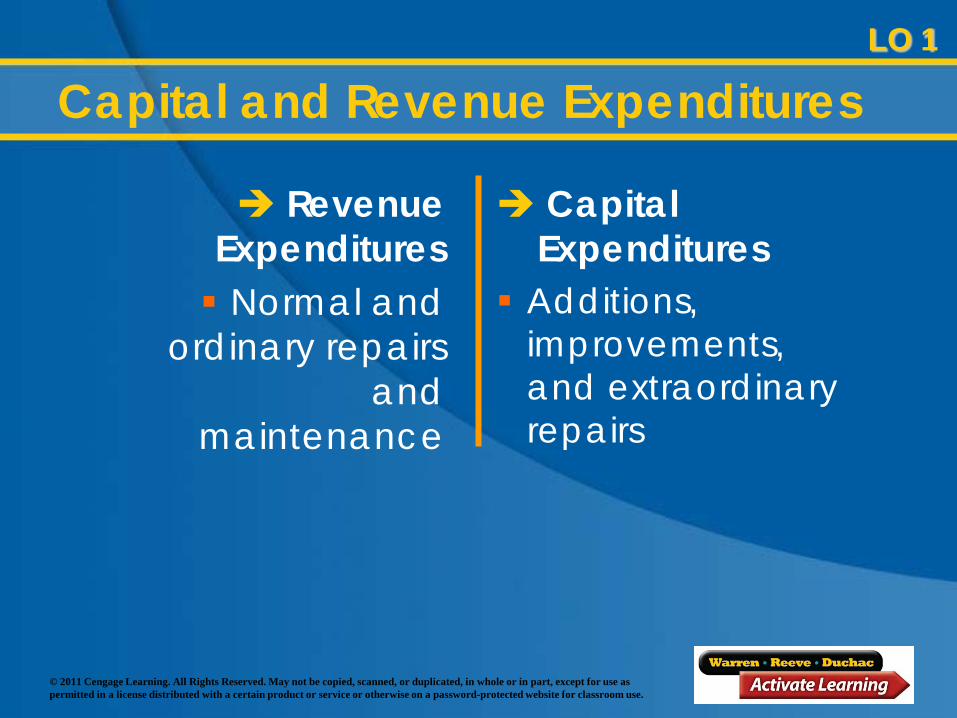

Capital and Revenue Expenditures

Revenue Expenditures Normal and

ordinary repairs and

maintenance

Capital Expenditures

Additions, improvements, and extraordinary repairs

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

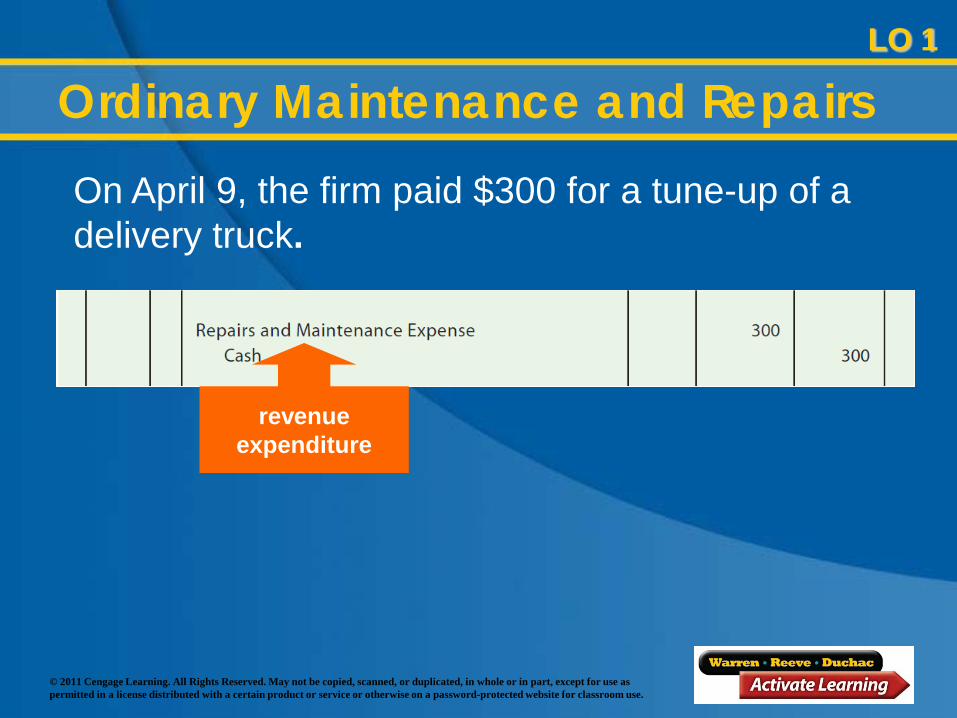

Ordinary Maintenance and RepairsLO 1

revenue expenditure

On April 9, the firm paid $300 for a tune-up of a delivery truck.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

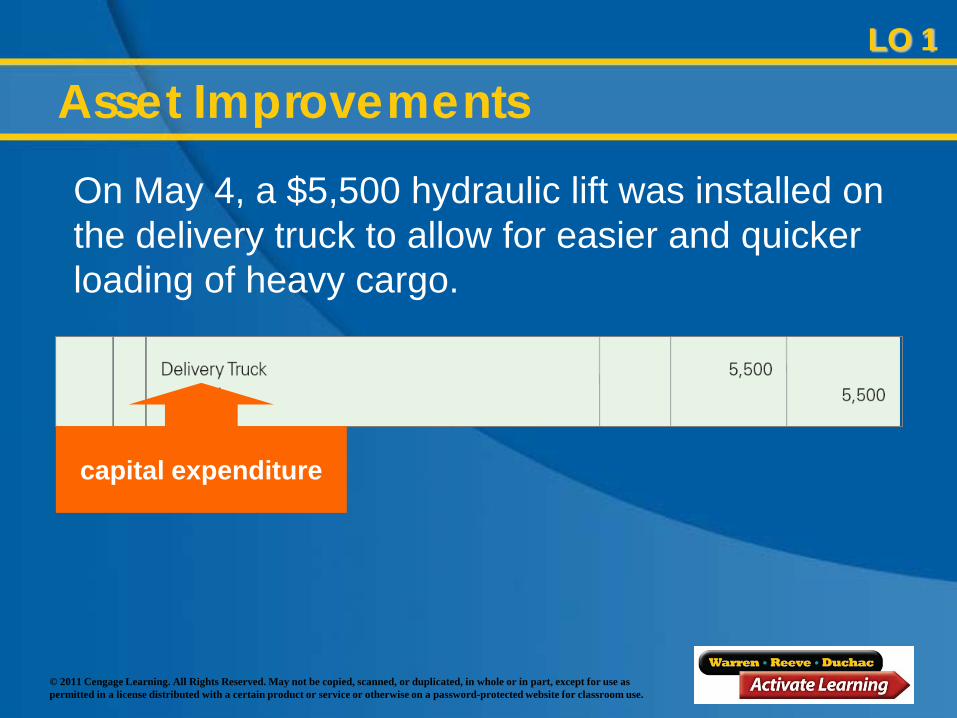

Asset ImprovementsOn May 4, a $5,500 hydraulic lift was installed on the delivery truck to allow for easier and quicker loading of heavy cargo.

LO 1

capital expenditure

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

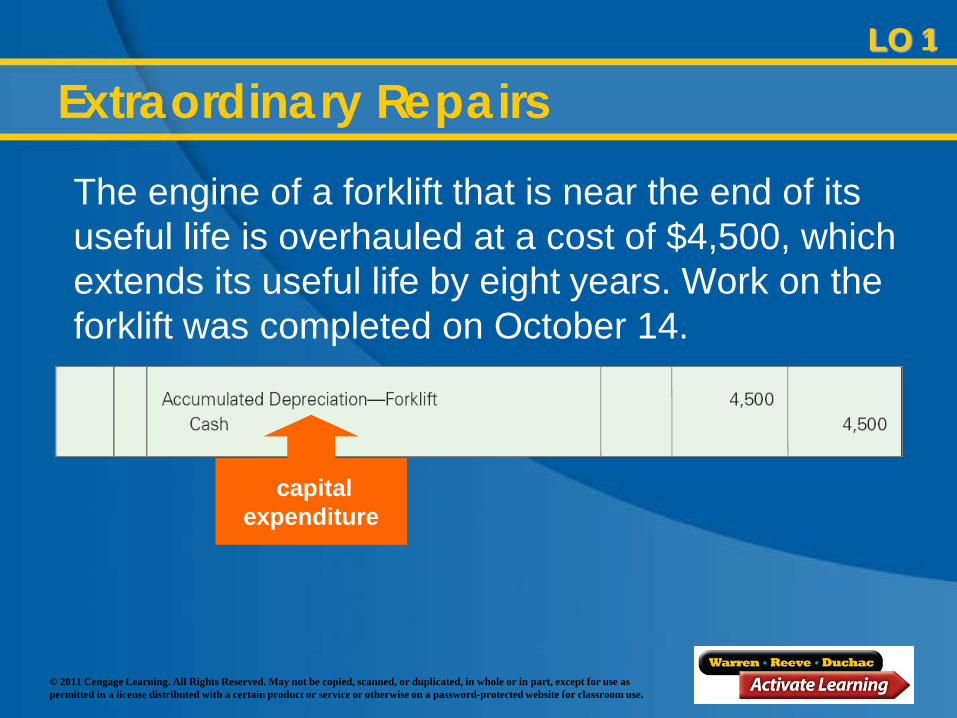

capital expenditure

Extraordinary Repairs

The engine of a forklift that is near the end of its useful life is overhauled at a cost of $4,500, which extends its useful life by eight years. Work on the forklift was completed on October 14.

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Capital and Revenue ExpendituresLO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EE 9-1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Leasing Fixed Assets The two parties to a lease contract: The lessor is the party who owns the asset. The lessee is the party to whom the rights to

use the asset are granted by the lessor.

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Leasing Fixed Assets

A capital lease is accounted for as if the lessee has, in fact, purchased the asset. The asset is then amortized (written off as an expense) over the life of the capital lease.

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Leasing Fixed Assets

A lease that is not classified as a capital lease for accounting purposes is classified as an operating lease. An operating lease is treated as an expense, because the lessee is renting the asset for the lease term.

LO 1

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Learning Objective 2

Compute depreciation, using the following methods: straight-line

method, units-of-production method, and double-declining-

balance method.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Depreciation

Over time, most fixed assets (equipment, buildings, and land improvements) lose their ability to provide services. The periodic recording of the cost of fixed assets as an expense is called depreciation.

LO 2

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Accounting for Depreciation

Depreciation can be caused by physical or functional factors. Physical depreciation factors include wear

and tear during use or from exposure to the weather.

Functional depreciation factors include obsolescence and changes in customer needs that cause the asset to no longer provide services for which it was intended.

LO 2

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Accounting for Depreciation

Two common misunderstandings that exist about depreciation as used in accounting include:1. Depreciation does not measure a decline

in the market value of a fixed asset.2. Depreciation does not provide cash to

replace fixed assets as they wear out.

LO 2

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 2

Factors in Computing Depreciation

Three factors determine the depreciation expense for a fixed asset:1. The asset’s initial cost2. The asset’s expected useful life3. The asset’s estimated residual value

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Factors in Computing Depreciation

The expected useful life of a fixed asset is estimated at the time the asset is placed into service. The residual value of a fixed asset at the end of its useful life is also estimated at the time the asset is placed into service.

LO 2

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

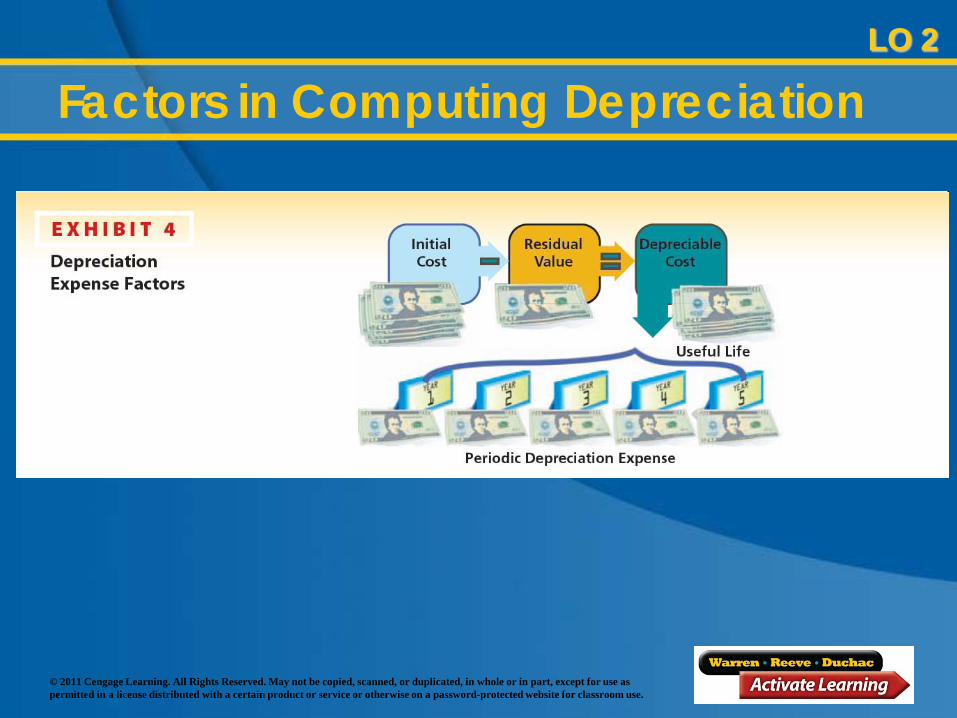

LO 2

Factors in Computing Depreciation

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

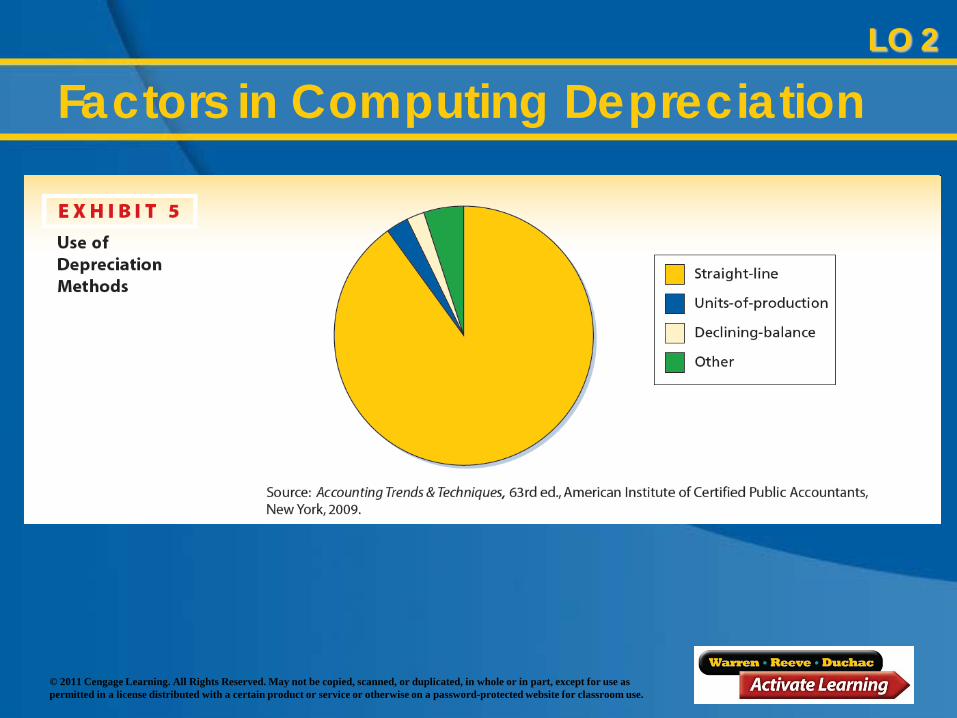

LO 2

Factors in Computing Depreciation

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

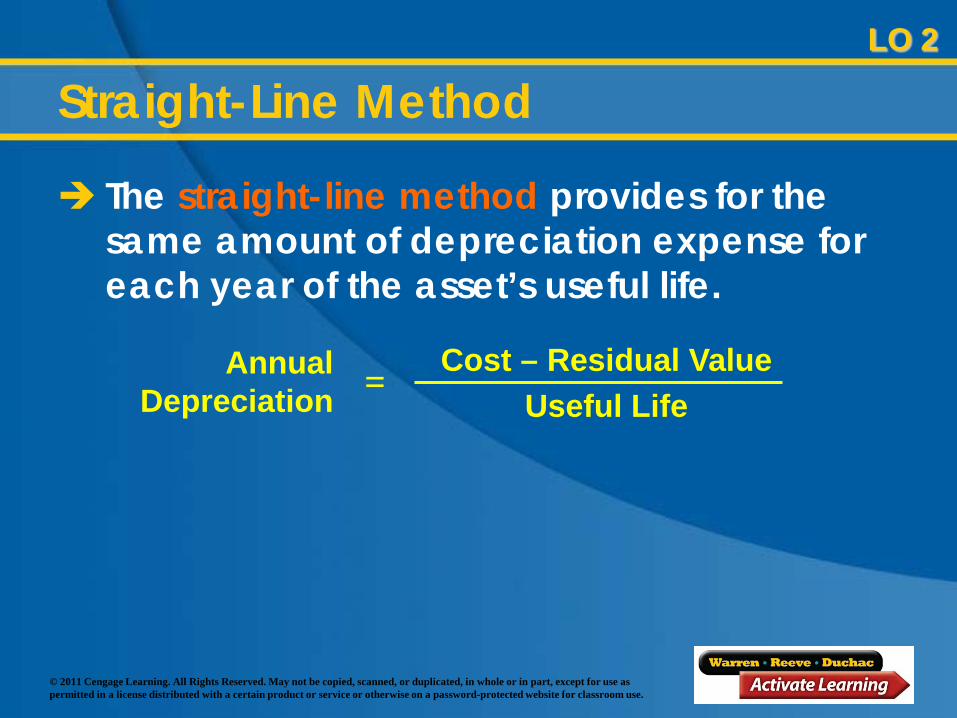

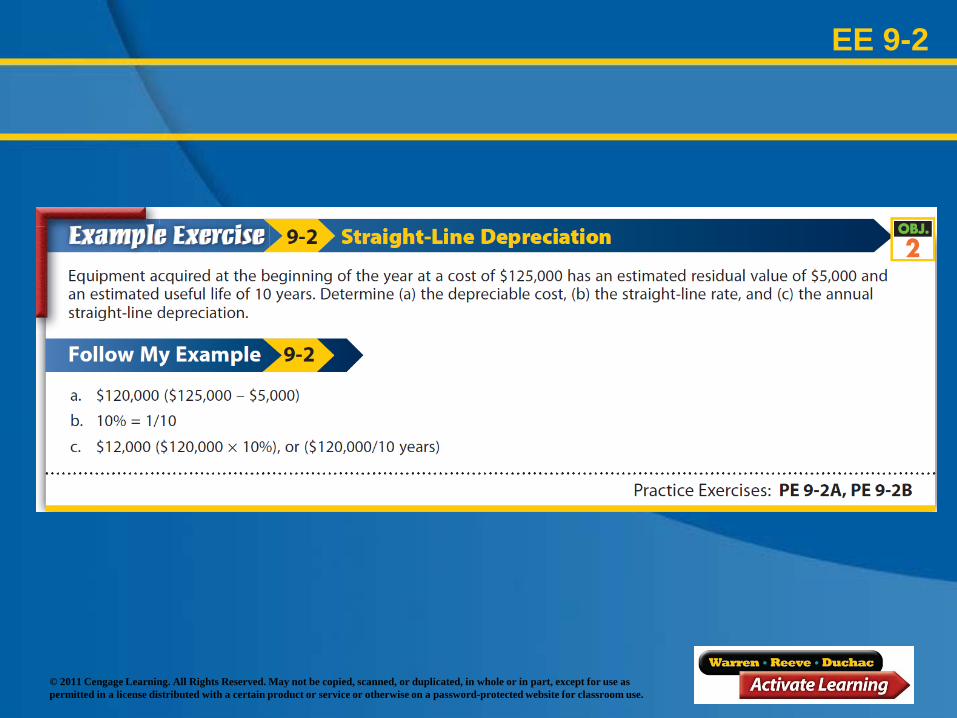

Straight-Line Method

The straight-line method provides for the same amount of depreciation expense for each year of the asset’s useful life.

LO 2

Annual Depreciation

Cost – Residual ValueUseful Life

=

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

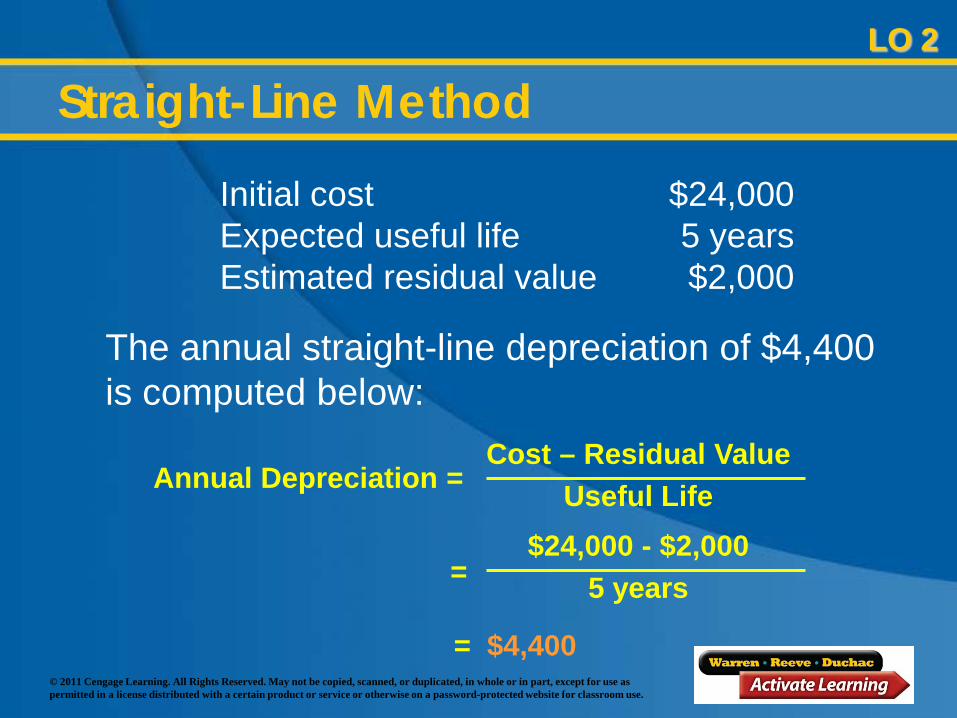

Straight-Line MethodLO 2

Initial cost $24,000Expected useful life 5 yearsEstimated residual value $2,000

The annual straight-line depreciation of $4,400 is computed below:

Annual Depreciation =Cost – Residual Value

Useful Life$24,000 - $2,000

5 years=

= $4,400

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

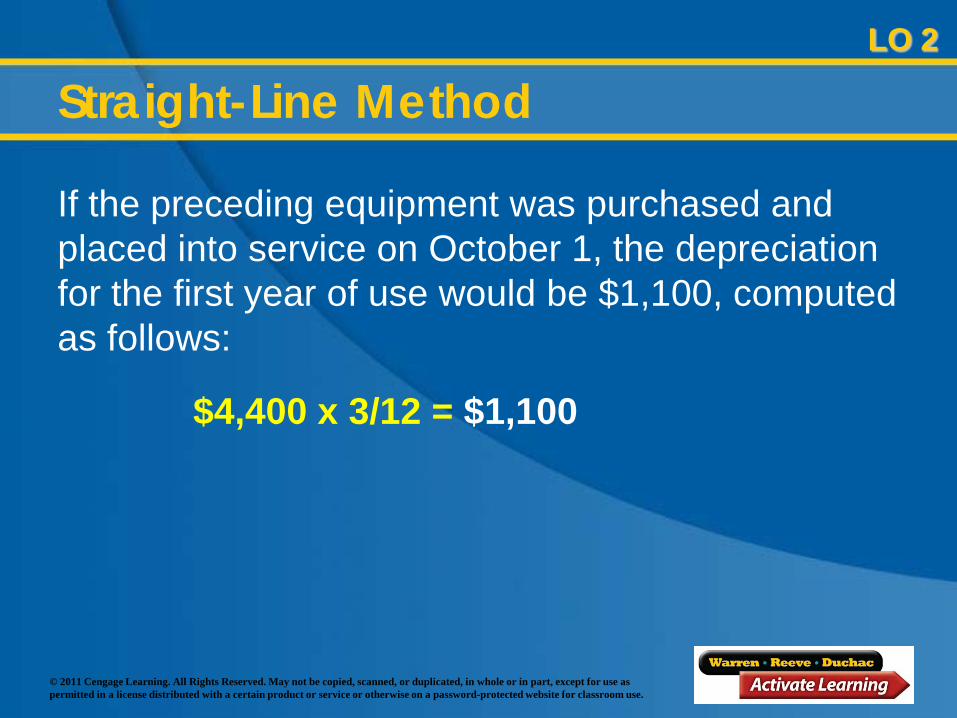

Straight-Line MethodLO 2

If the preceding equipment was purchased and placed into service on October 1, the depreciation for the first year of use would be $1,100, computed as follows:

$4,400 x 3/12 = $1,100

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

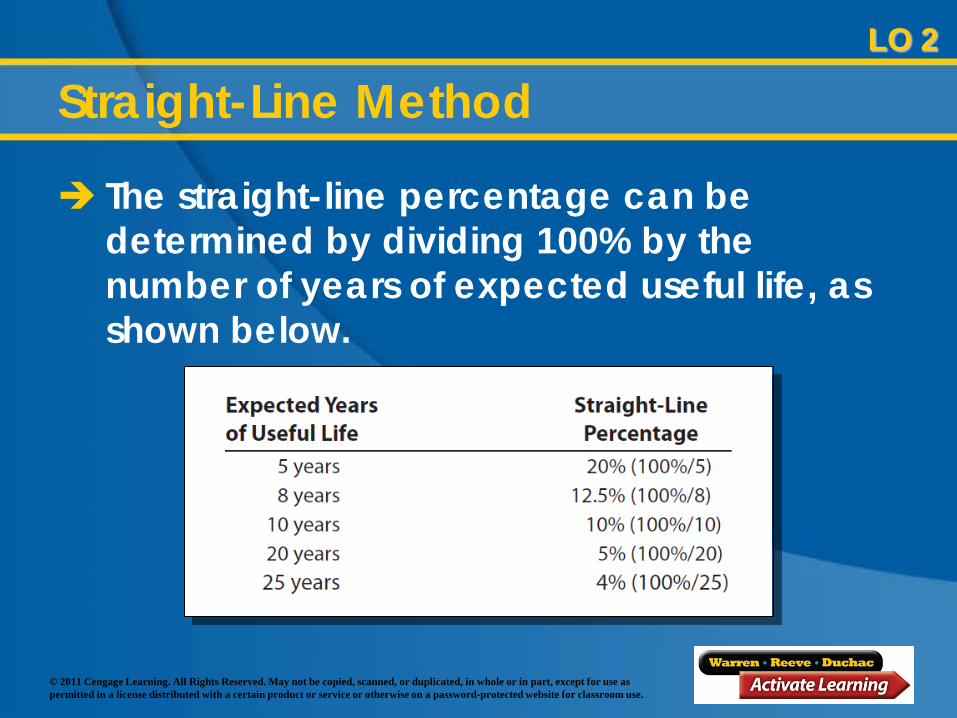

Straight-Line Method

The straight-line percentage can be determined by dividing 100% by the number of years of expected useful life, as shown below.

LO 2

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EE 9-2

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 2

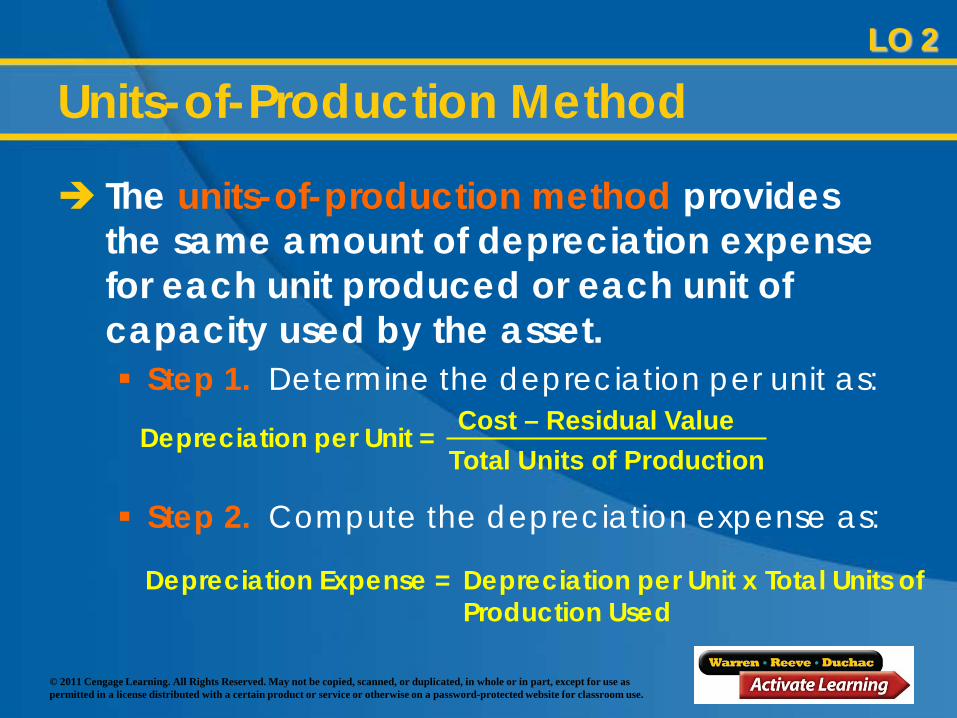

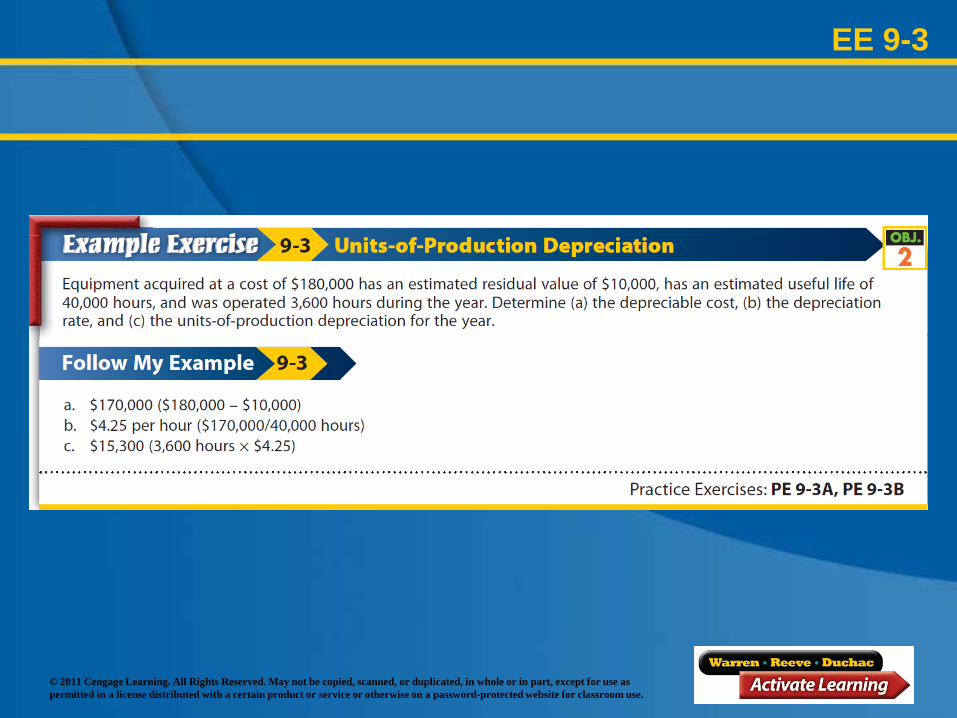

Units-of-Production Method

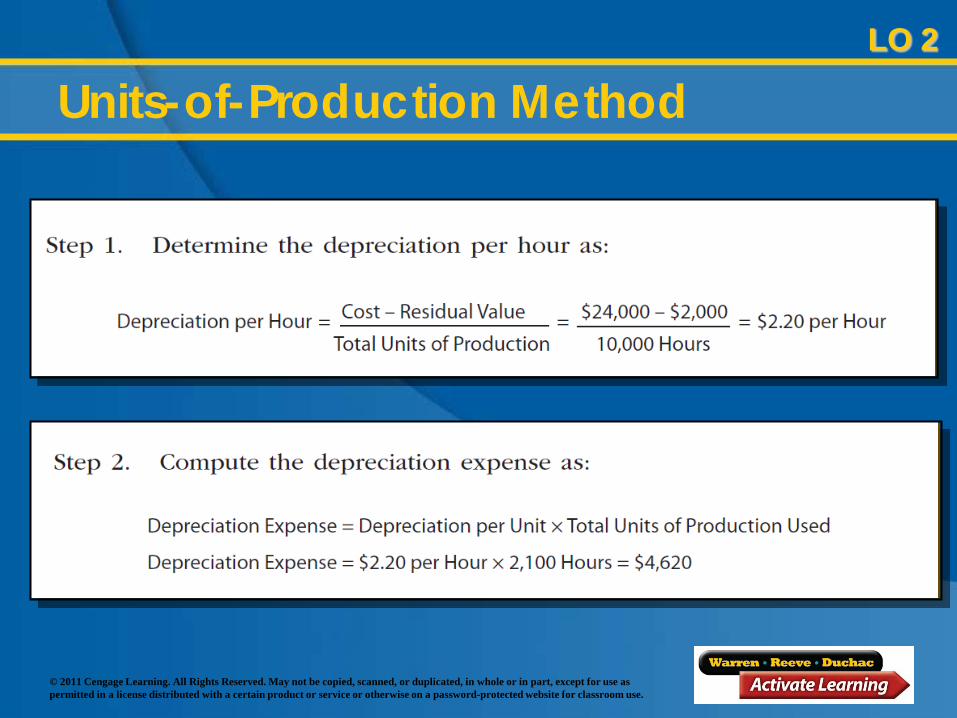

The units-of-production method provides the same amount of depreciation expense for each unit produced or each unit of capacity used by the asset. Step 1. Determine the depreciation per unit as:

Step 2. Compute the depreciation expense as:

Depreciation Expense = Depreciation per Unit x Total Units of Production Used

Depreciation per Unit = Cost – Residual ValueTotal Units of Production

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

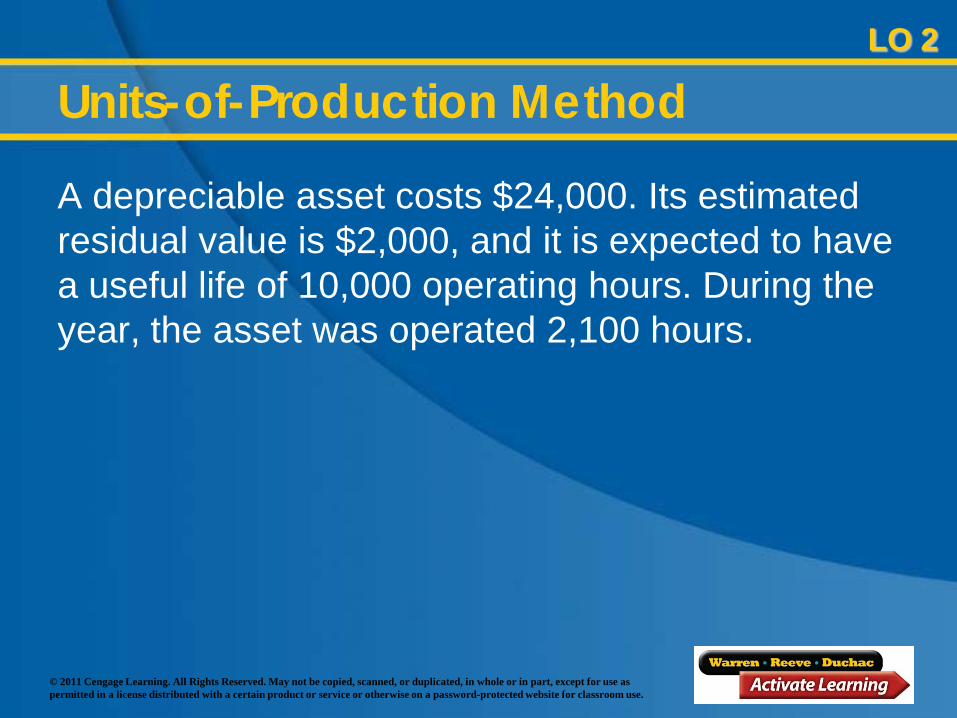

Units-of-Production Method

A depreciable asset costs $24,000. Its estimated residual value is $2,000, and it is expected to have a useful life of 10,000 operating hours. During the year, the asset was operated 2,100 hours.

LO 2

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Units-of-Production MethodLO 2

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EE 9-3

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Double-Declining-Balance Method

The double-declining-balance methodprovides for a declining periodic expense over the expected useful life of the asset.

LO 2

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Double-Declining-Balance Method

The double-declining-balance method is applied in three steps: Step 1. Determine the straight-line

percentage using the expected useful life.

Step 2. Determine the double-declining-balance rate by multiplying the straight-line rate from Step 1 by 2.

LO 2

(continued)

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Double-Declining-Balance Method

Step 3. Compute the depreciation expense by multiplying the double-declining-balance rate from Step 2 times the book value of the asset.

LO 2

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

The double-declining-balance rate is determined by doubling the straight-line rate.

A shortcut to determining the straight-line rate is to divide one by the number of years (for example, 1 ÷ 5 = 0.20).

Using the double-declining-balance method, a five-year life results in a 40 percent rate (0.20 × 2).

LO 2

Double-Declining-Balance Method

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Double-Declining-Balance Method

For the first year, the book value of the equipment is its initial cost of $24,000.

After the first year, the book value (cost minus accumulated depreciation) declines and, thus, the depreciation also declines.

LO 2

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

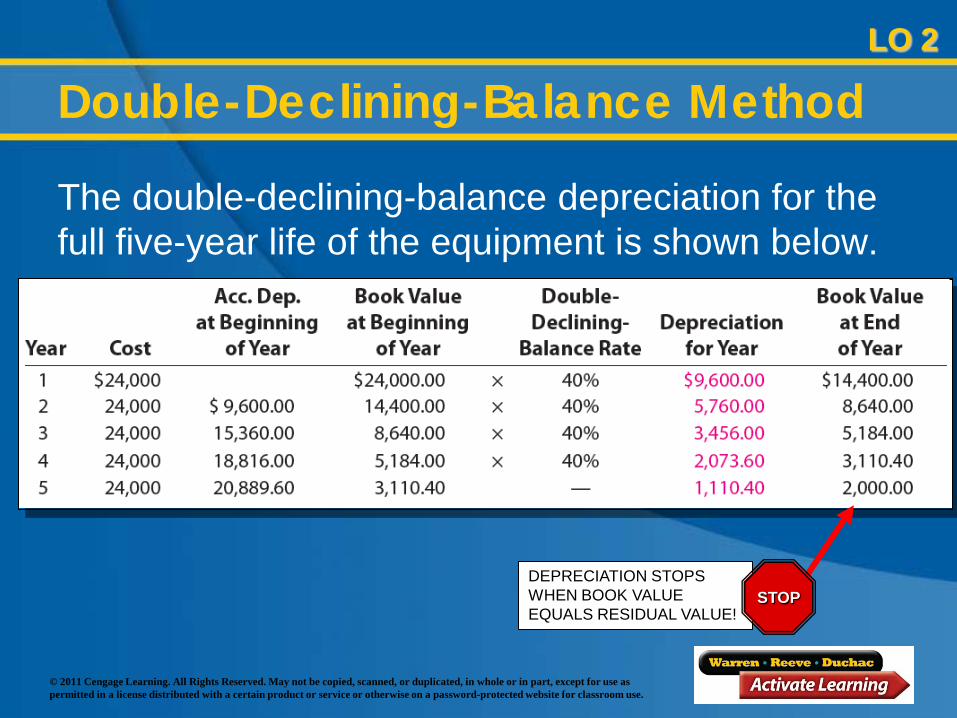

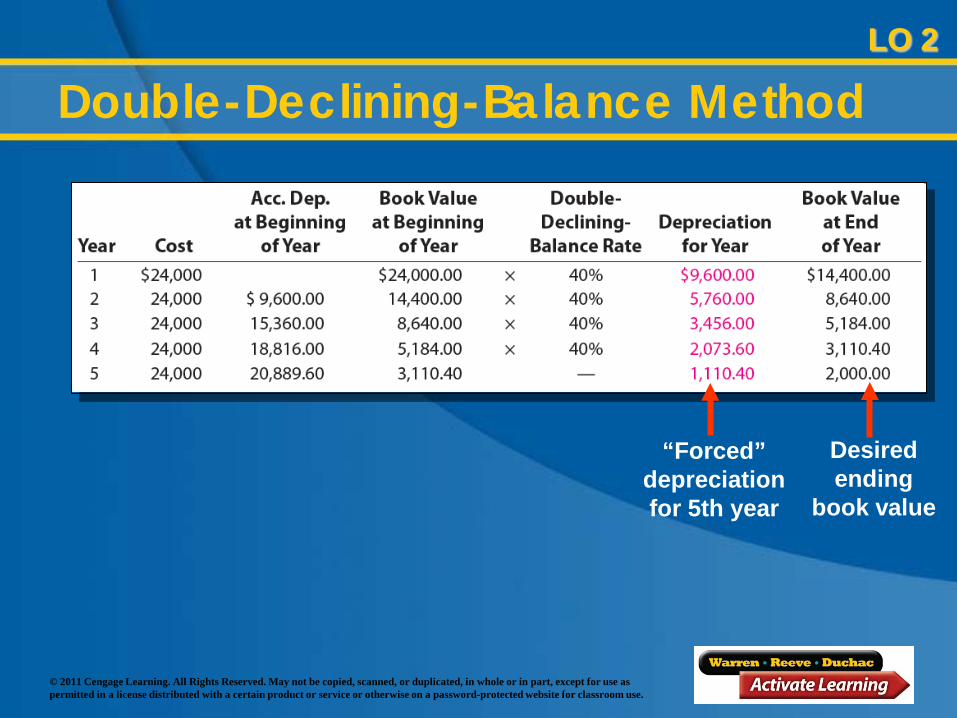

Double-Declining-Balance Method

The double-declining-balance depreciation for the full five-year life of the equipment is shown below.

DEPRECIATION STOPS WHEN BOOK VALUE EQUALS RESIDUAL VALUE!

STOP

LO 2

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Desired ending

book value

“Forced” depreciation for 5th year

LO 2

Double-Declining-Balance Method

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

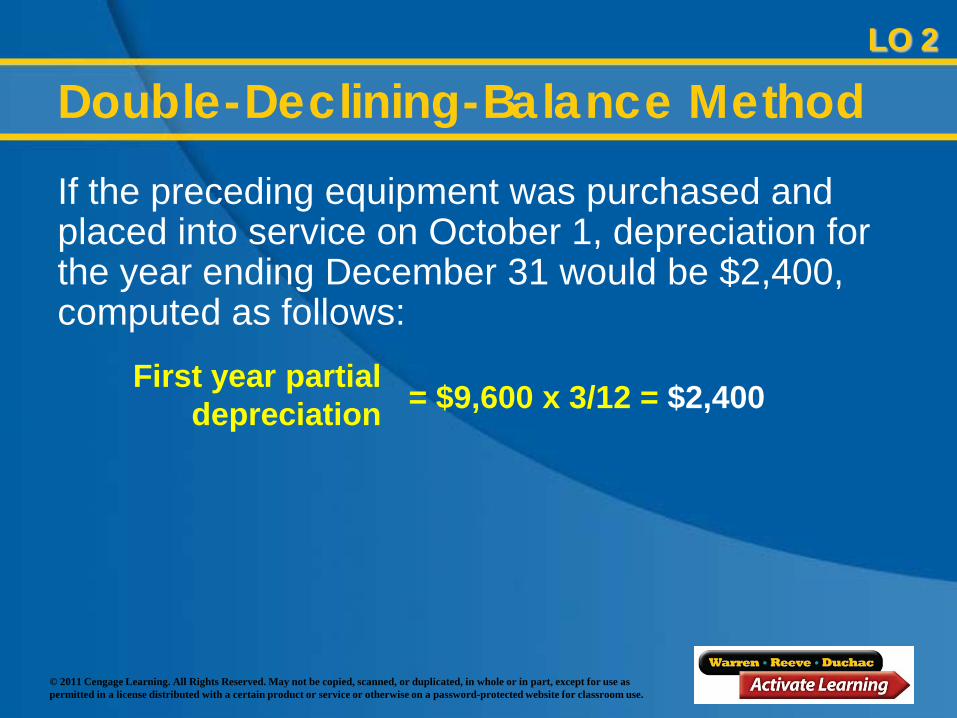

Double-Declining-Balance Method

If the preceding equipment was purchased and placed into service on October 1, depreciation for the year ending December 31 would be $2,400, computed as follows:

LO 2

= $9,600 x 3/12 = $2,400First year partial depreciation

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

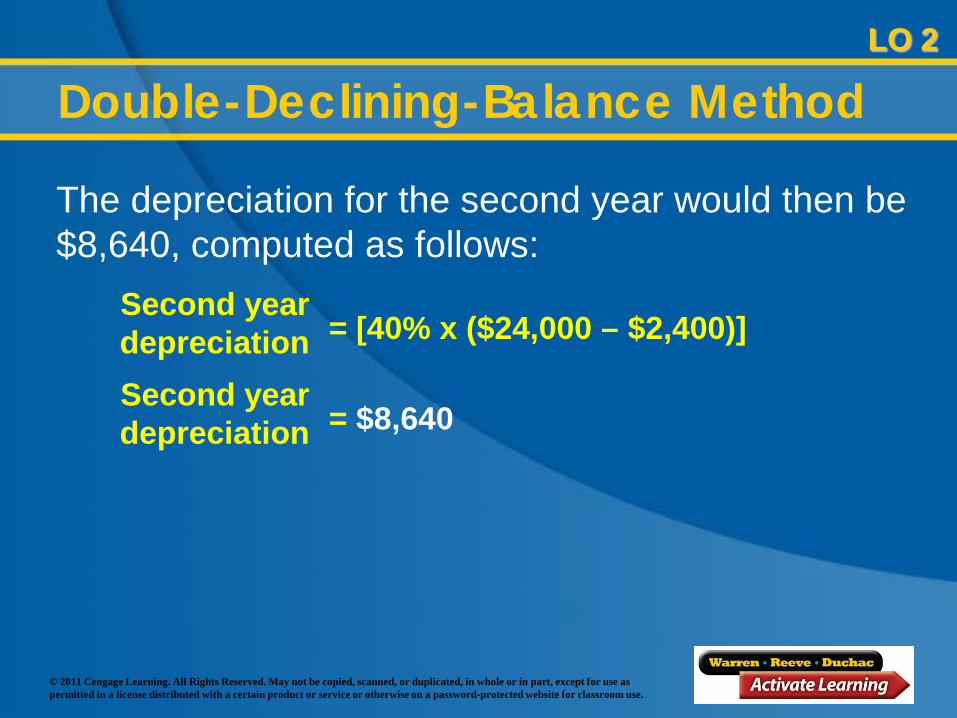

The depreciation for the second year would then be $8,640, computed as follows:

Double-Declining-Balance MethodLO 2

= [40% x ($24,000 – $2,400)]Second year depreciation

= $8,640Second year depreciation

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

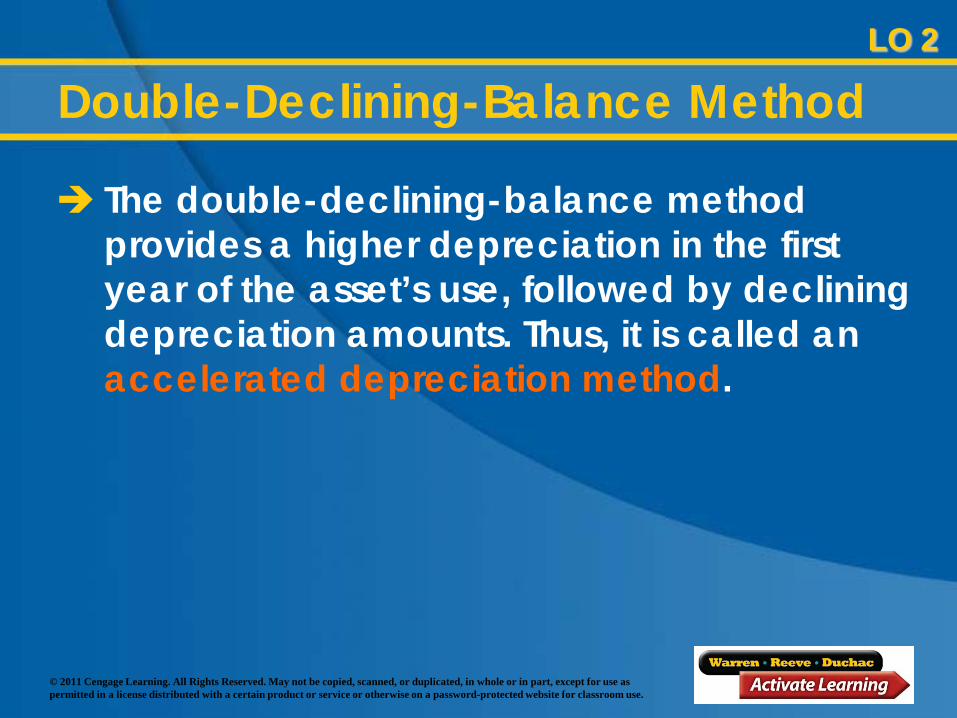

The double-declining-balance method provides a higher depreciation in the first year of the asset’s use, followed by declining depreciation amounts. Thus, it is called an accelerated depreciation method.

Double-Declining-Balance MethodLO 2

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EE 9-4

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 2

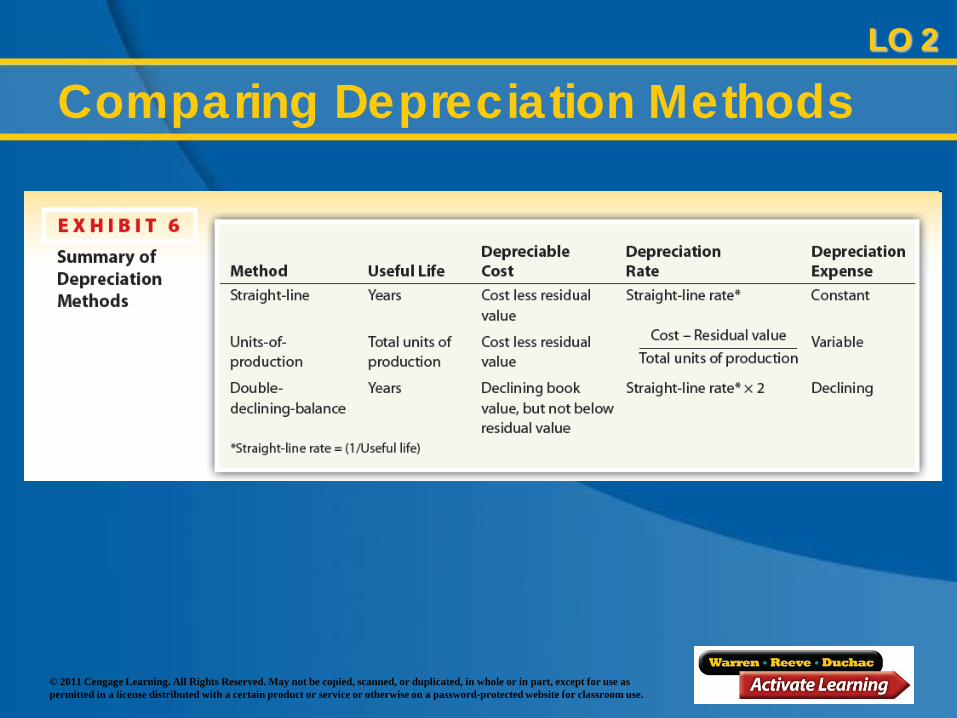

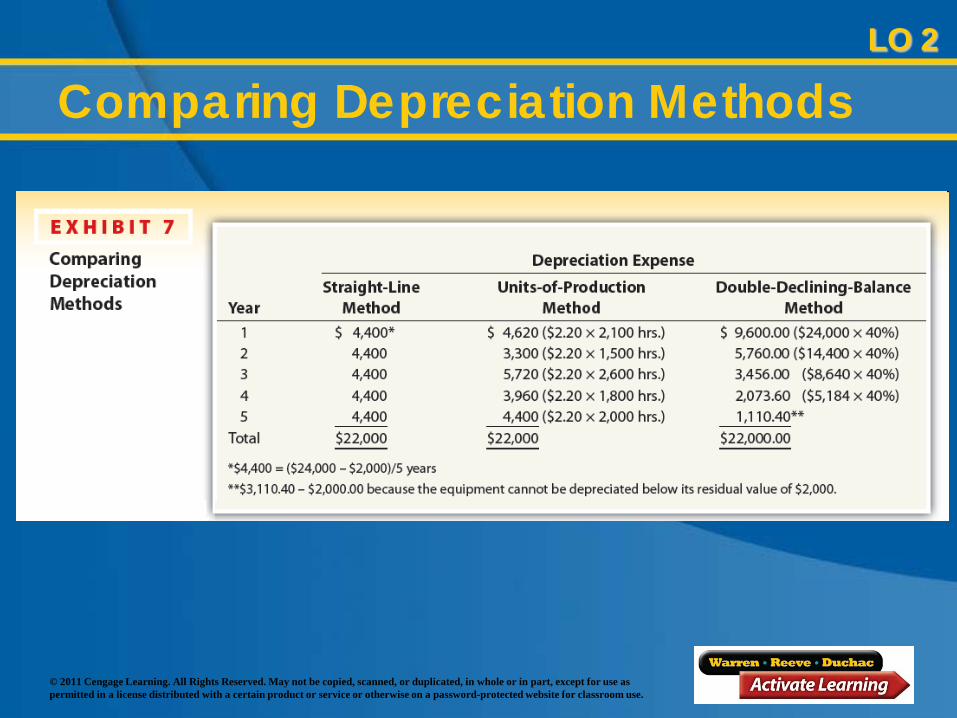

Comparing Depreciation Methods

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 2

Comparing Depreciation Methods

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

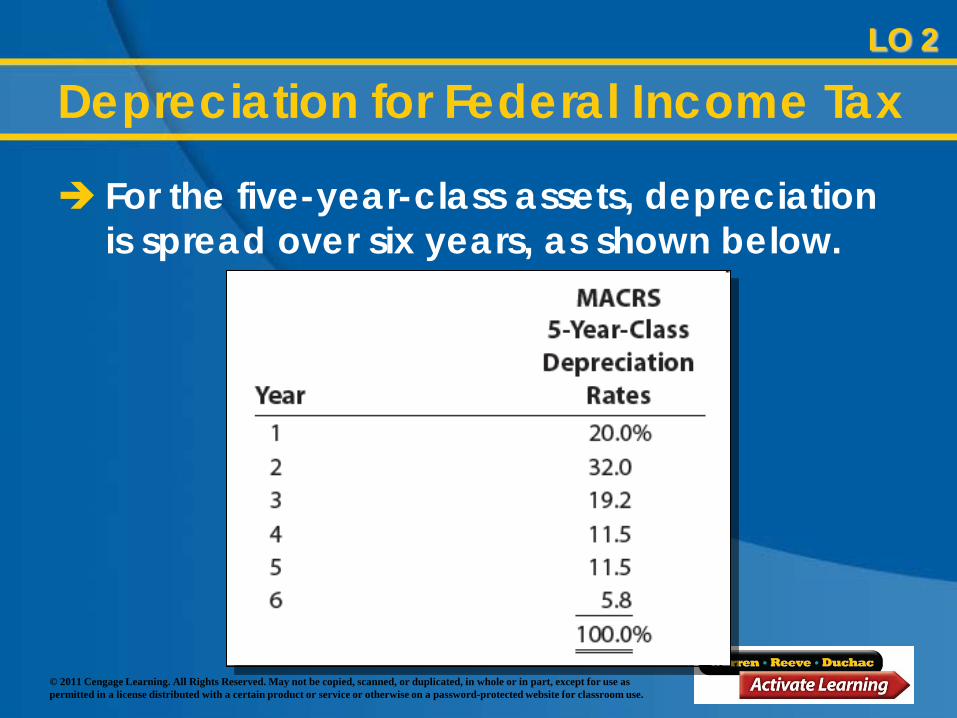

Depreciation for Federal Income Tax

The Internal Revenue Code specifies the Modified Accelerated Cost RecoverySystem (MACRS) for use by businesses in computing depreciation for tax purposes.

LO 2

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Depreciation for Federal Income Tax

MACRS specifies eight classes of useful life and depreciation rates for each of the eight classes.

The two most common classes are the five-year class (includes automobiles and light-duty trucks) and the seven-year class (includes most machinery and equipment).

LO 2

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Depreciation for Federal Income Tax

For the five-year-class assets, depreciation is spread over six years, as shown below.

LO 2

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

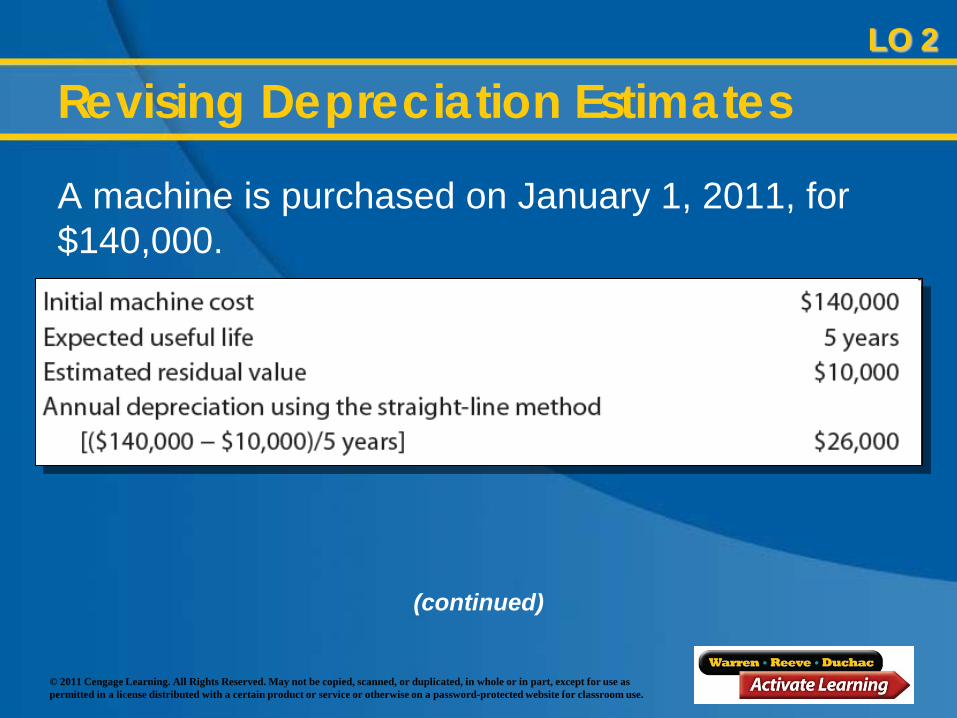

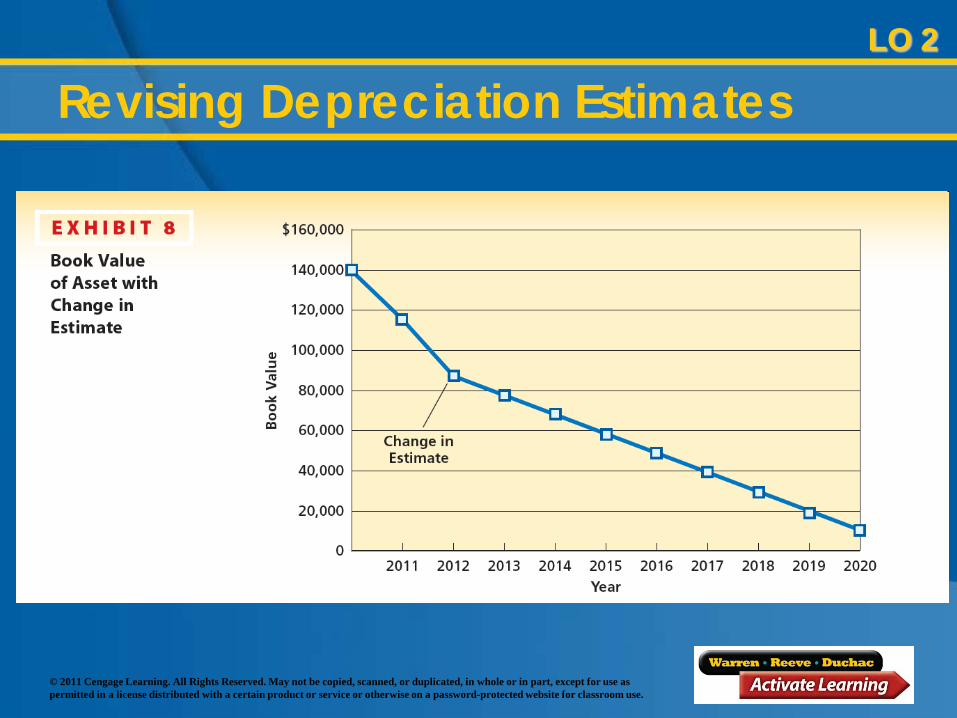

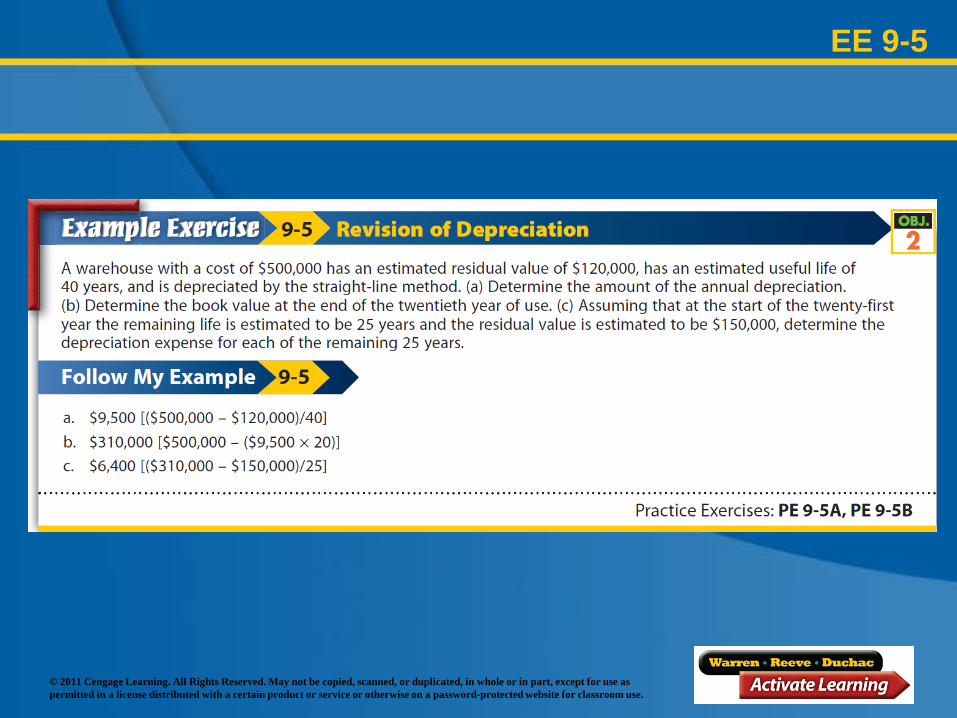

Revising Depreciation Estimates

A machine is purchased on January 1, 2011, for $140,000.

LO 2

(continued)

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

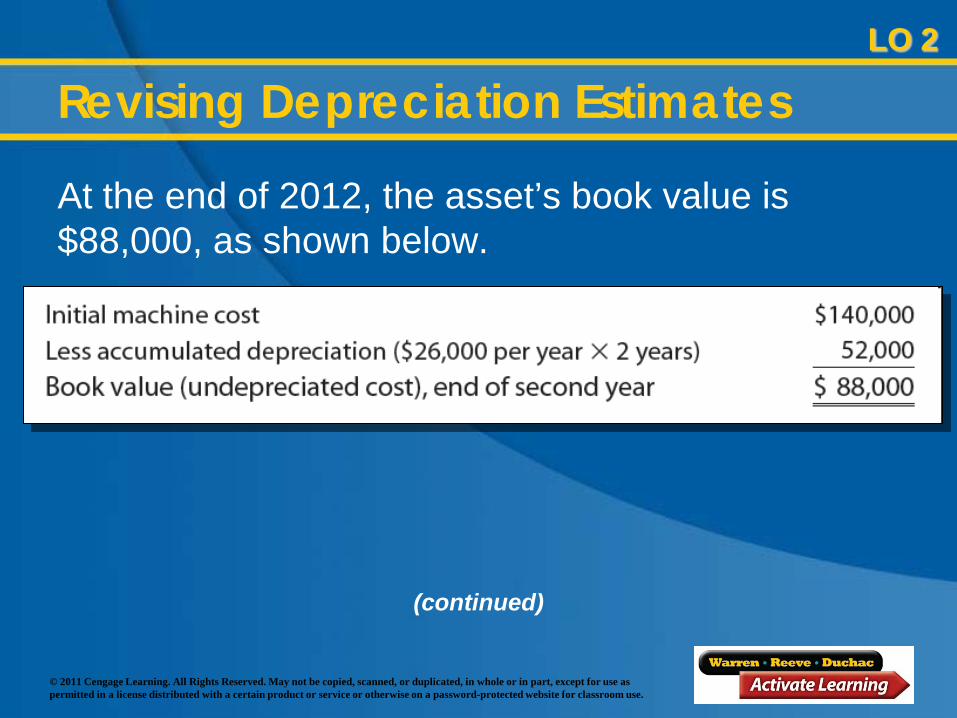

Revising Depreciation Estimates

At the end of 2012, the asset’s book value is $88,000, as shown below.

(continued)

LO 2

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

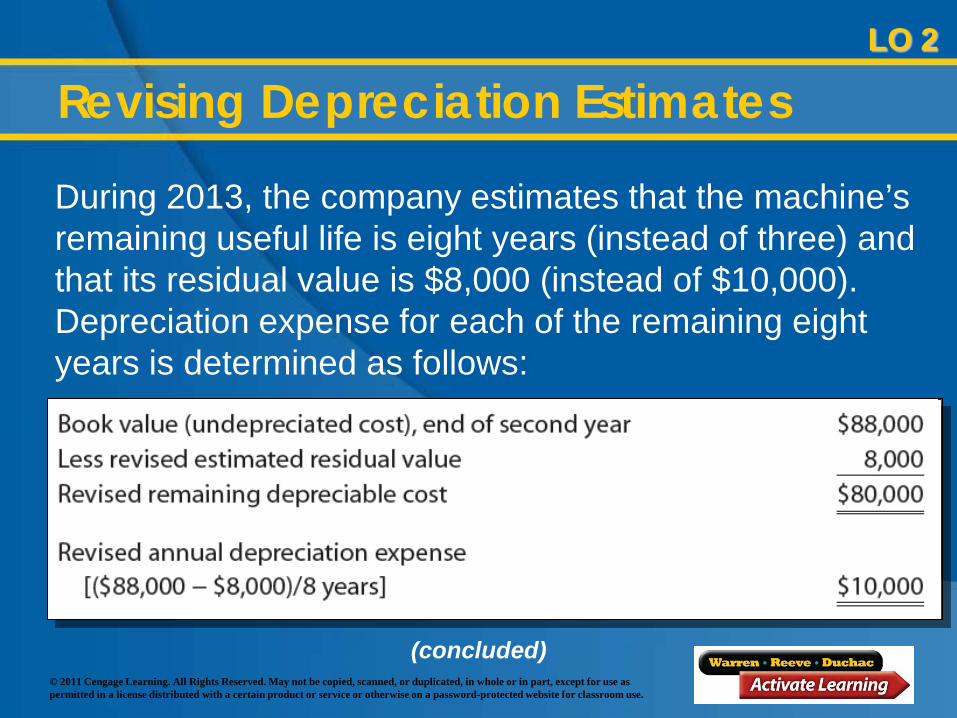

Revising Depreciation Estimates

During 2013, the company estimates that the machine’s remaining useful life is eight years (instead of three) and that its residual value is $8,000 (instead of $10,000). Depreciation expense for each of the remaining eight years is determined as follows:

LO 2

(concluded)

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 2

Revising Depreciation Estimates

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EE 9-5

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Learning Objective 3

Journalize entries for the disposal of

fixed assets.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

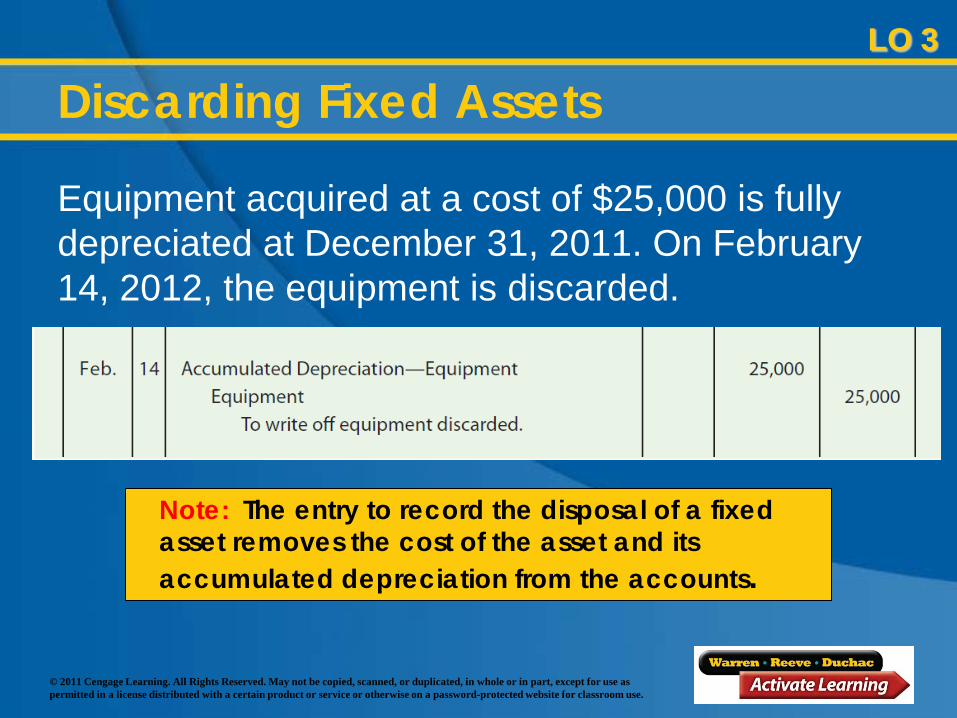

Discarding Fixed Assets

Equipment acquired at a cost of $25,000 is fully depreciated at December 31, 2011. On February 14, 2012, the equipment is discarded.

LO 3

Note: The entry to record the disposal of a fixed asset removes the cost of the asset and its accumulated depreciation from the accounts.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

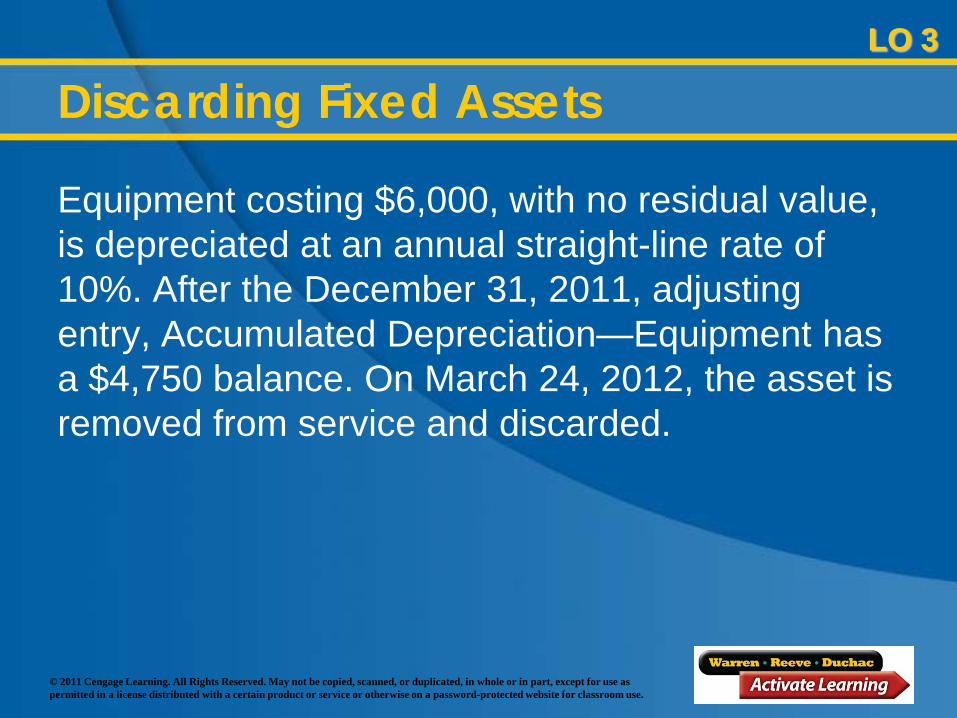

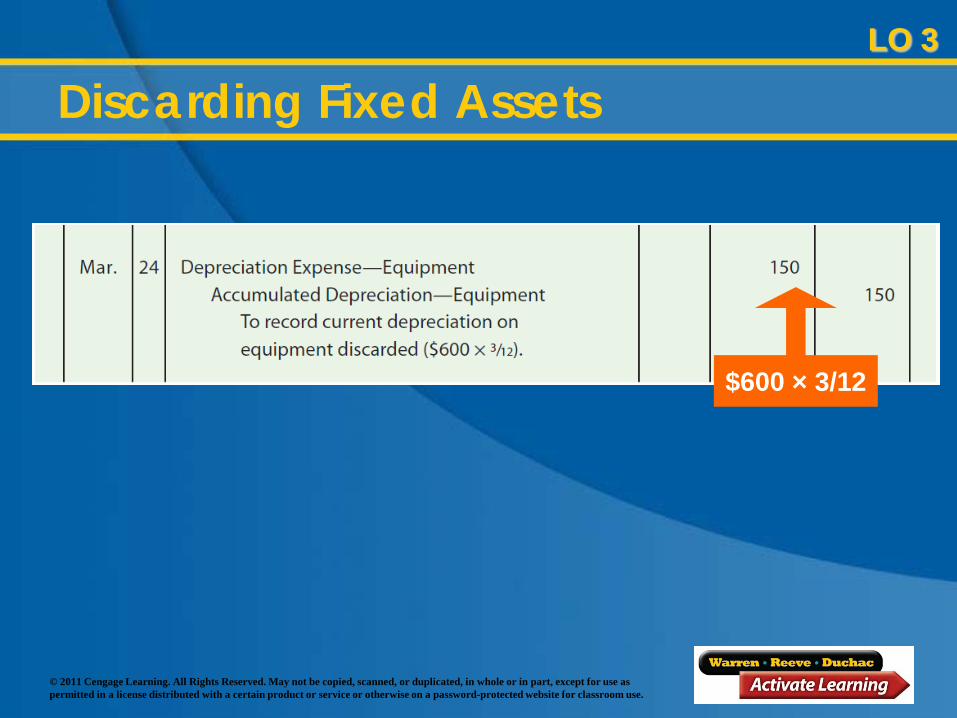

Discarding Fixed Assets

Equipment costing $6,000, with no residual value, is depreciated at an annual straight-line rate of 10%. After the December 31, 2011, adjusting entry, Accumulated Depreciation—Equipment has a $4,750 balance. On March 24, 2012, the asset is removed from service and discarded.

LO 3

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Discarding Fixed AssetsLO 3

$600 × 3/12

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

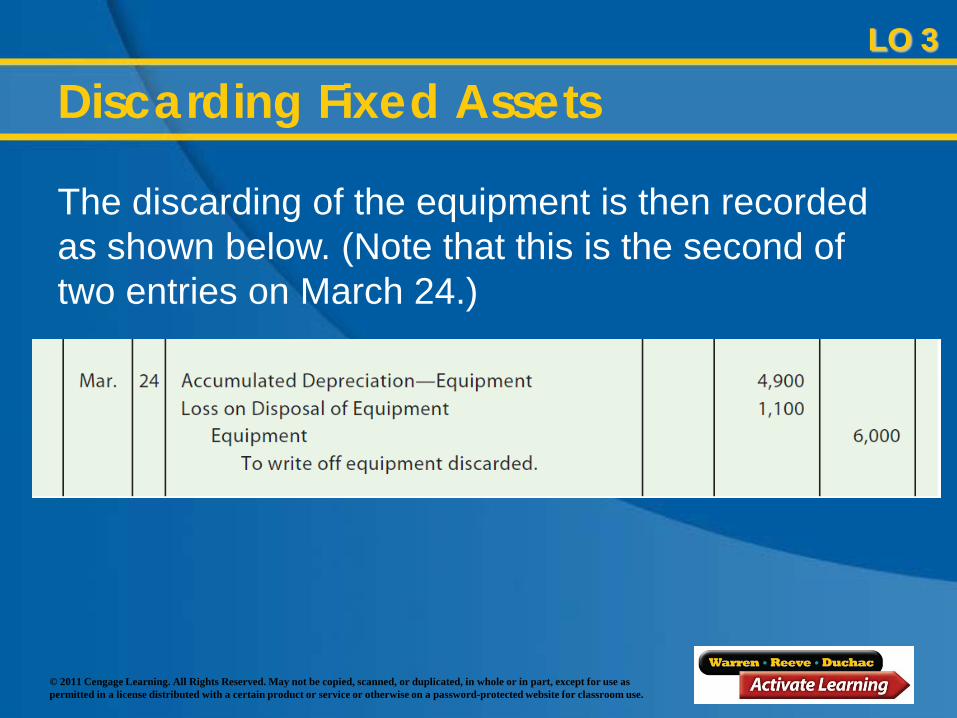

The discarding of the equipment is then recorded as shown below. (Note that this is the second of two entries on March 24.)

Discarding Fixed AssetsLO 3

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

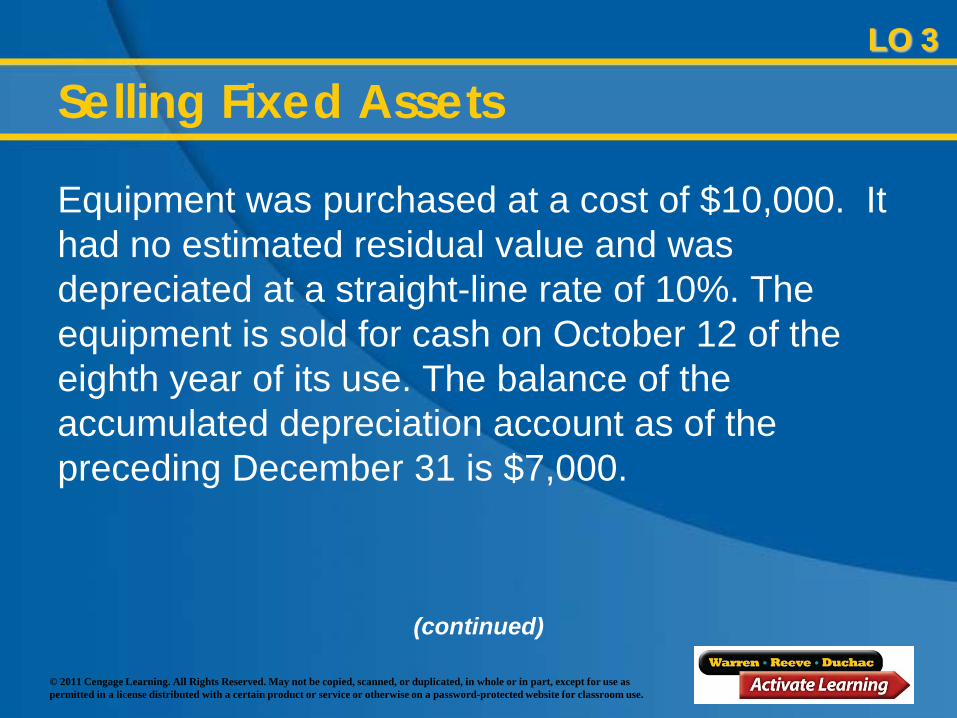

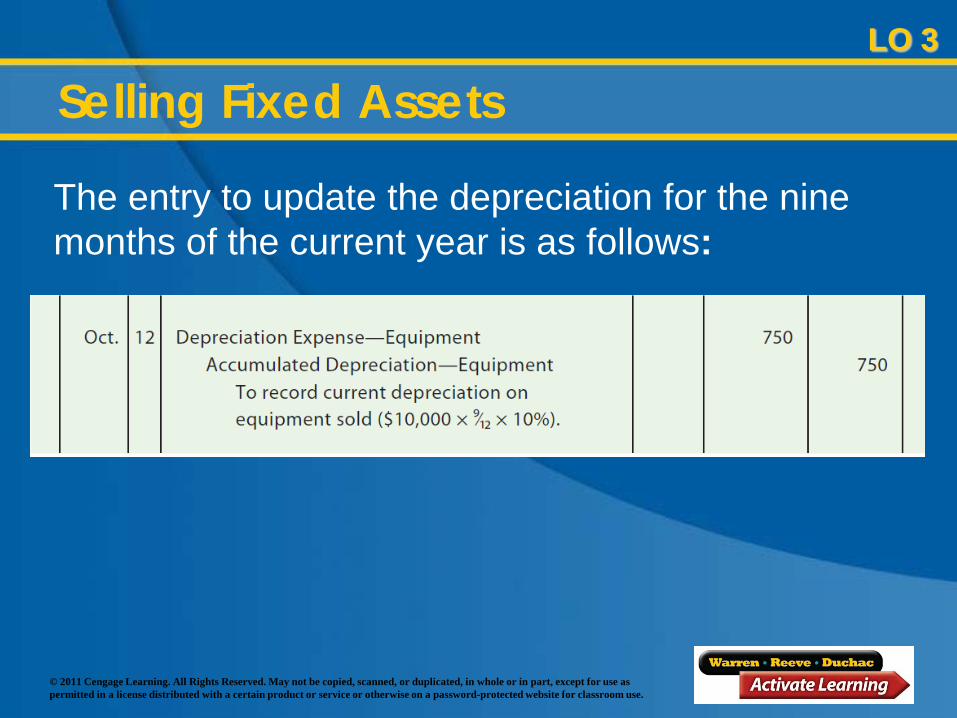

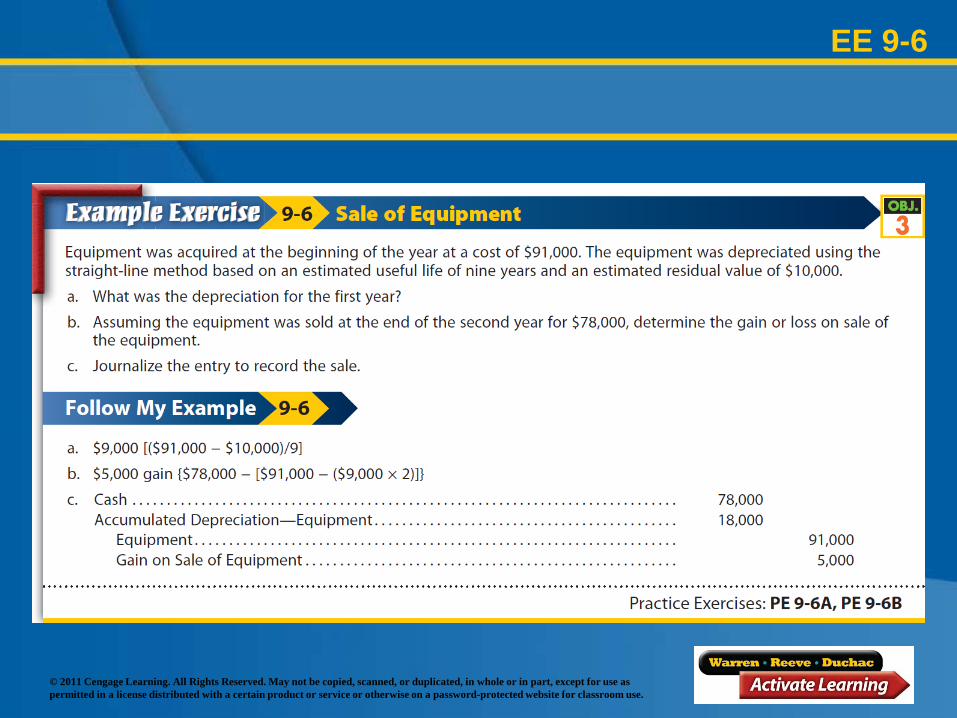

Selling Fixed Assets

Equipment was purchased at a cost of $10,000. It had no estimated residual value and was depreciated at a straight-line rate of 10%. The equipment is sold for cash on October 12 of the eighth year of its use. The balance of the accumulated depreciation account as of the preceding December 31 is $7,000.

LO 3

(continued)

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Selling Fixed AssetsLO 3

The entry to update the depreciation for the nine months of the current year is as follows:

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

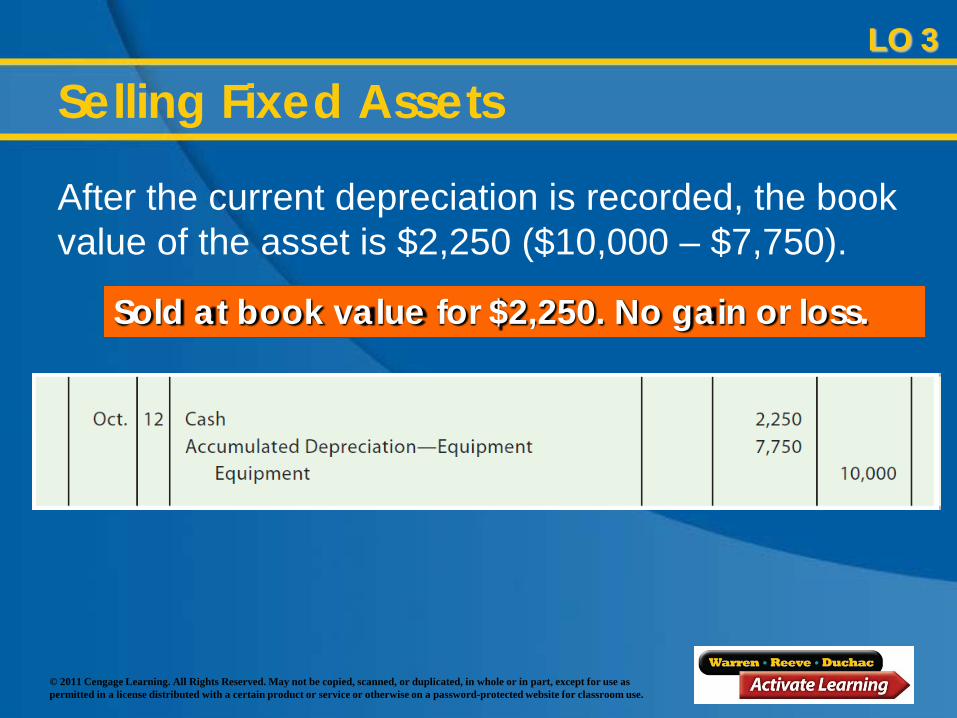

Selling Fixed Assets

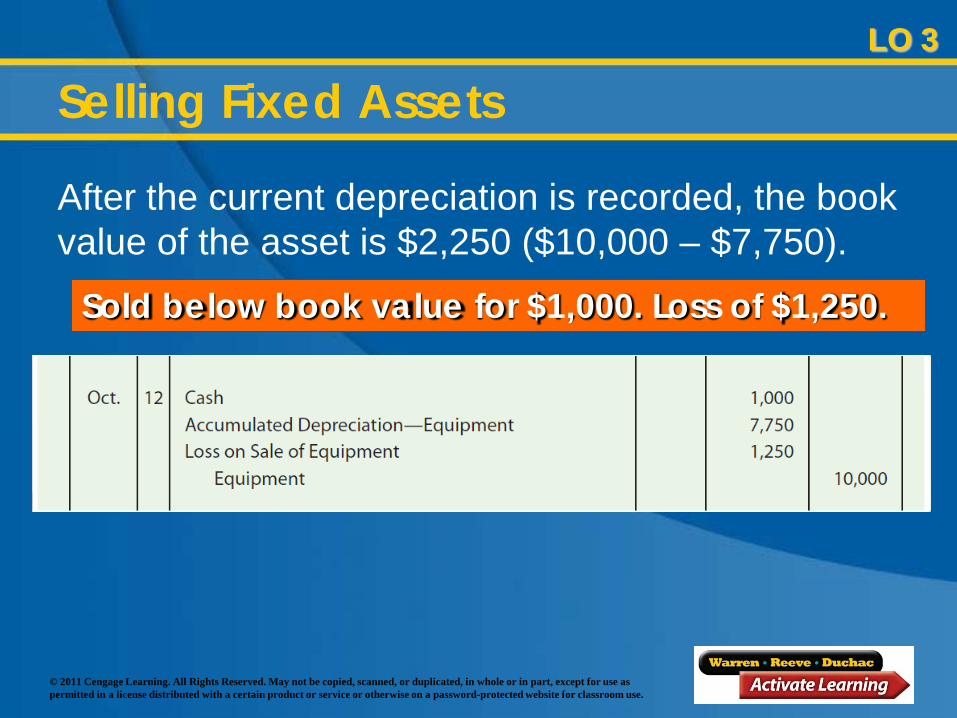

After the current depreciation is recorded, the book value of the asset is $2,250 ($10,000 – $7,750).

LO 3

Sold at book value for $2,250. No gain or loss.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Selling Fixed AssetsLO 3

Sold below book value for $1,000. Loss of $1,250.

After the current depreciation is recorded, the book value of the asset is $2,250 ($10,000 – $7,750).

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Selling Fixed AssetsLO 3

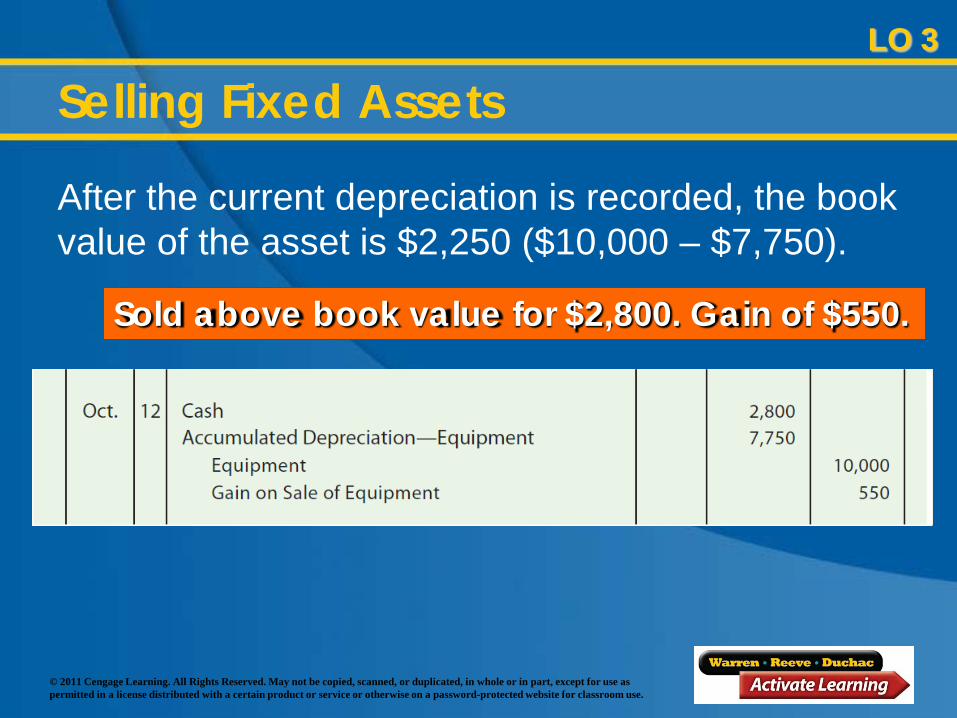

Sold above book value for $2,800. Gain of $550.

After the current depreciation is recorded, the book value of the asset is $2,250 ($10,000 – $7,750).

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EE 9-6

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Learning Objective 4

Compute depletion and journalize the entry for depletion.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

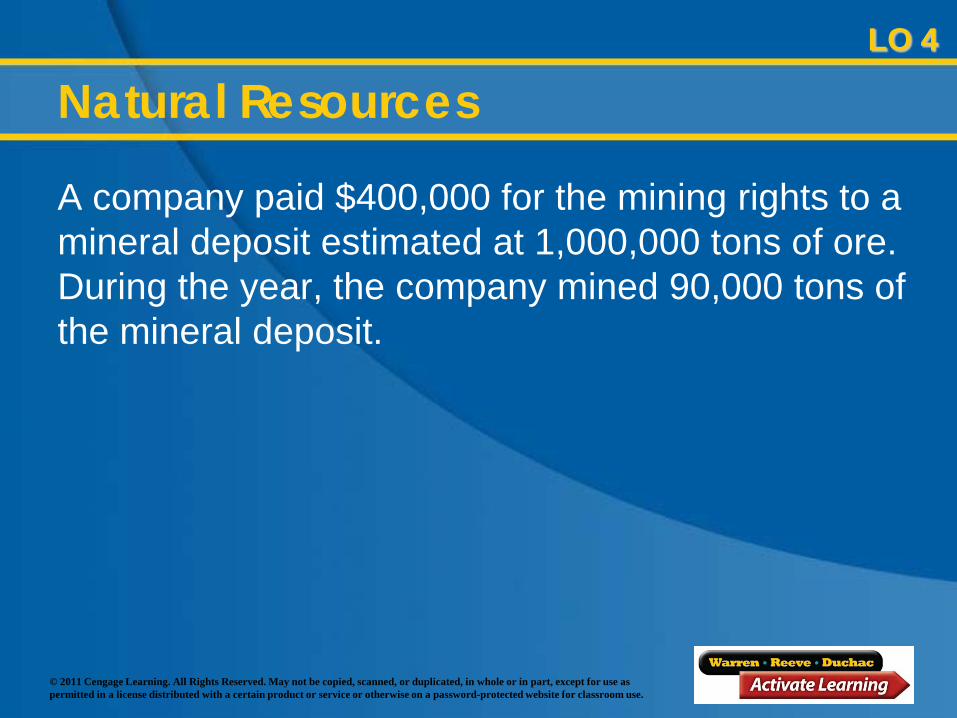

Natural Resources

The process of transferring the cost of natural resources to an expense account is called depletion.

LO 4

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

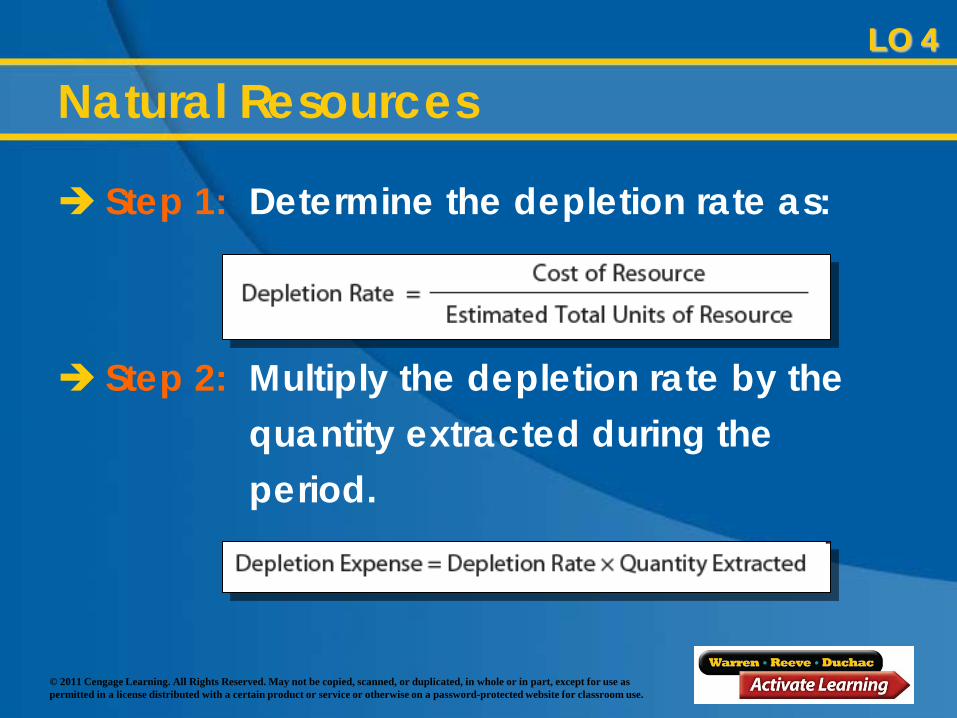

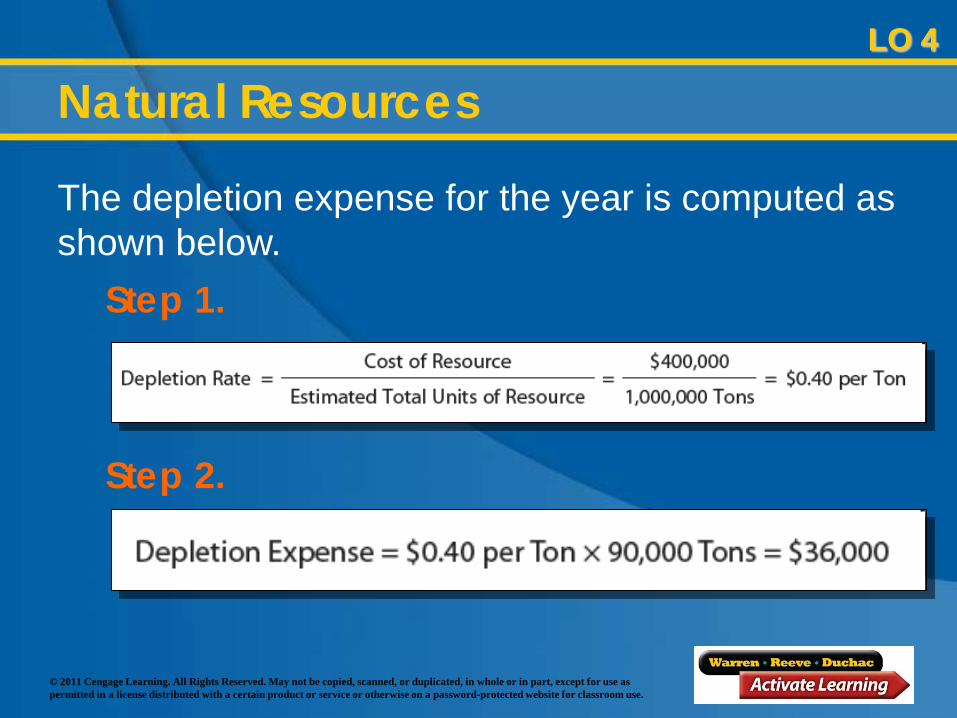

Natural Resources

Step 1: Determine the depletion rate as:

Step 2: Multiply the depletion rate by the quantity extracted during the period.

LO 4

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Natural Resources

A company paid $400,000 for the mining rights to a mineral deposit estimated at 1,000,000 tons of ore. During the year, the company mined 90,000 tons of the mineral deposit.

LO 4

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Natural Resources

The depletion expense for the year is computed as shown below.

LO 4

Step 1.

Step 2.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

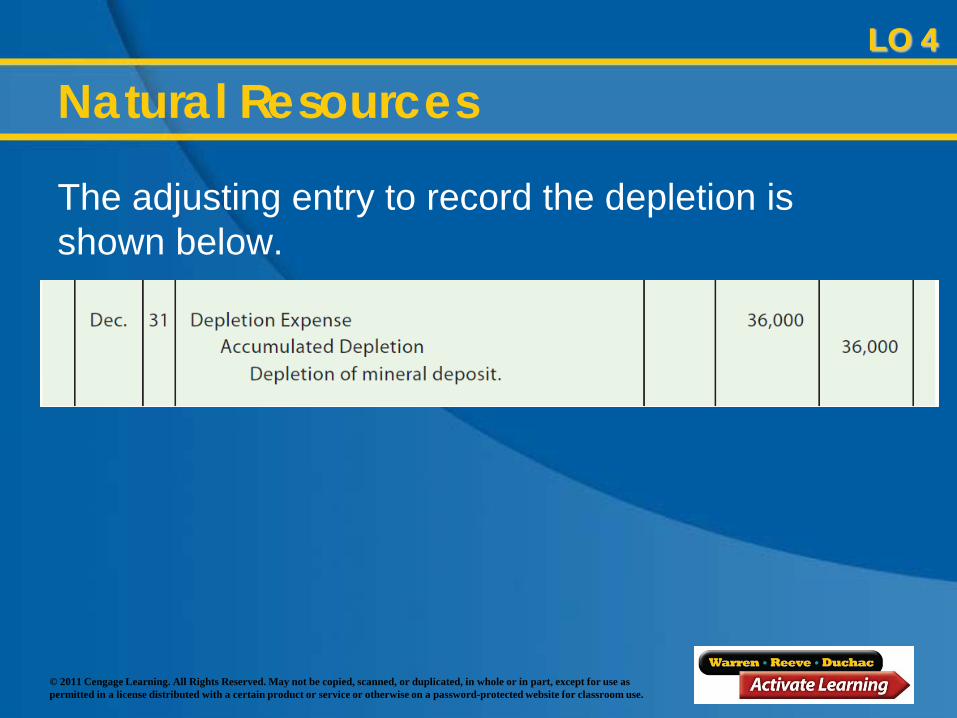

Natural Resources

The adjusting entry to record the depletion is shown below.

LO 4

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

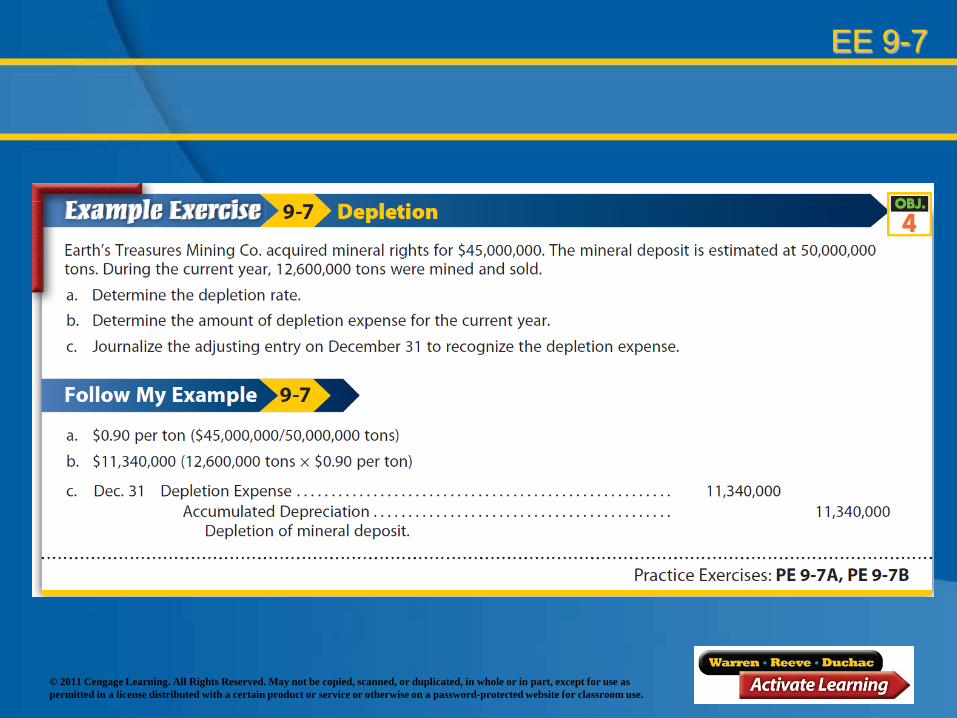

EE 9-7

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Learning Objective 5

Describe the accounting for

intangible assets, such as patents, copyrights,

and goodwill.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Intangible Assets

Patents, copyrights, trademarks, and goodwill are long-lived assets that are used in the operations of a business and not held for sale. These assets are called intangible assets because they do not exist physically.

LO 5

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Intangible Assets

The accounting for intangible assets is similar to that for fixed assets. The major issues are: Determining the initial cost. Determining the amortization, which is the

amount of cost to transfer to expense.

LO 5

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Patents

The exclusive right granted by the federal government to produce and sell goods with one or more unique features is called a patent. These rights continue in effect for 20 years.

LO 5

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

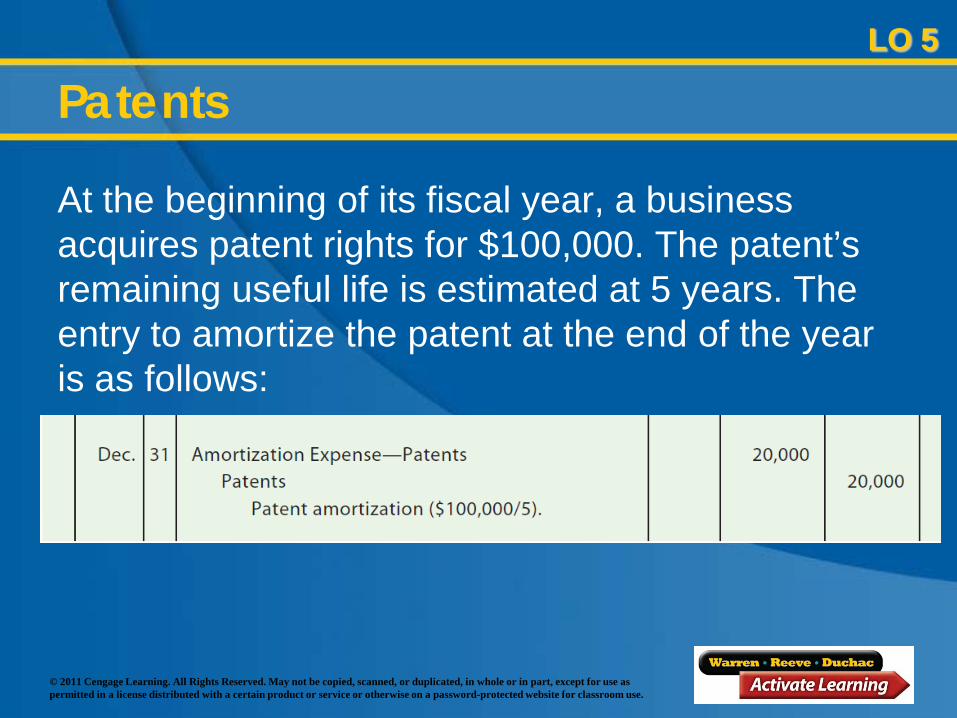

Patents

At the beginning of its fiscal year, a business acquires patent rights for $100,000. The patent’s remaining useful life is estimated at 5 years. The entry to amortize the patent at the end of the year is as follows:

LO 5

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Patents

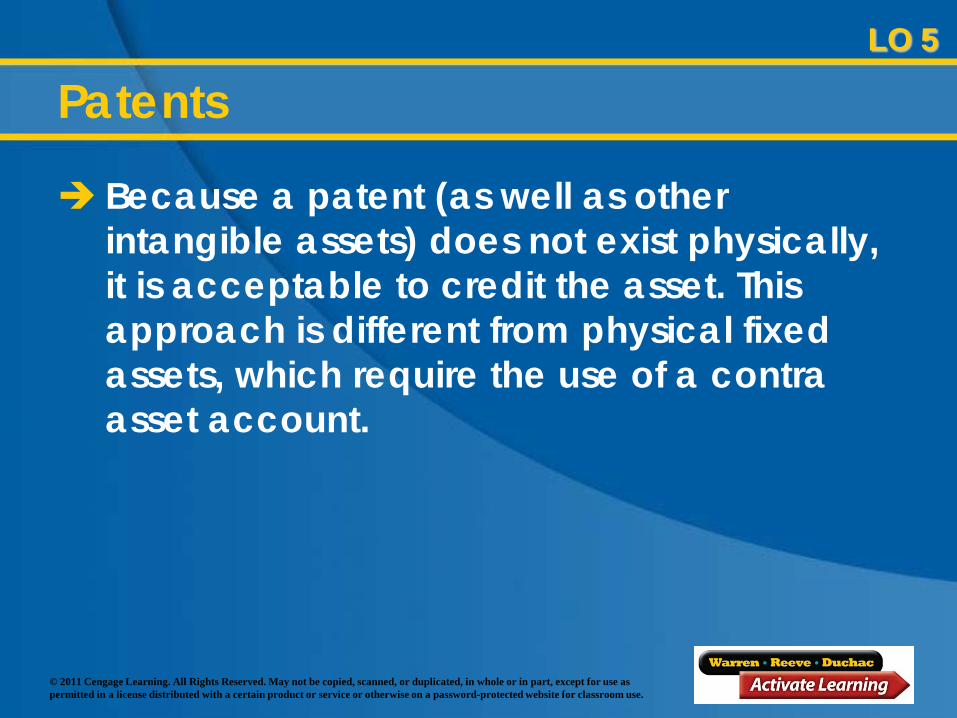

Because a patent (as well as other intangible assets) does not exist physically, it is acceptable to credit the asset. This approach is different from physical fixed assets, which require the use of a contra asset account.

LO 5

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Copyrights and Trademarks

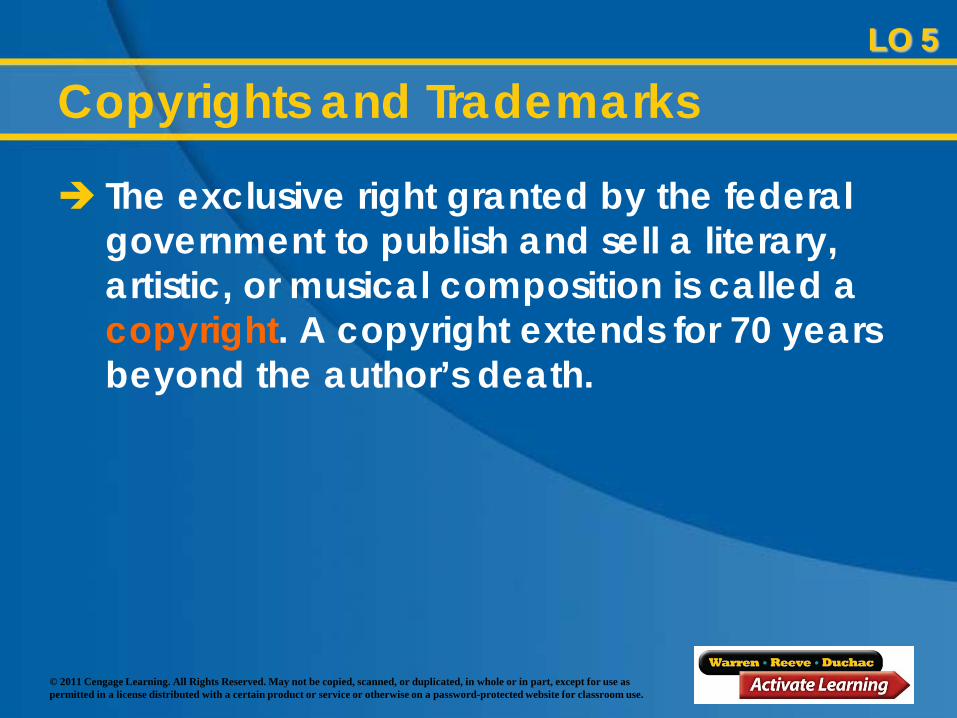

The exclusive right granted by the federal government to publish and sell a literary, artistic, or musical composition is called a copyright. A copyright extends for 70 years beyond the author’s death.

LO 5

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Copyrights and Trademarks

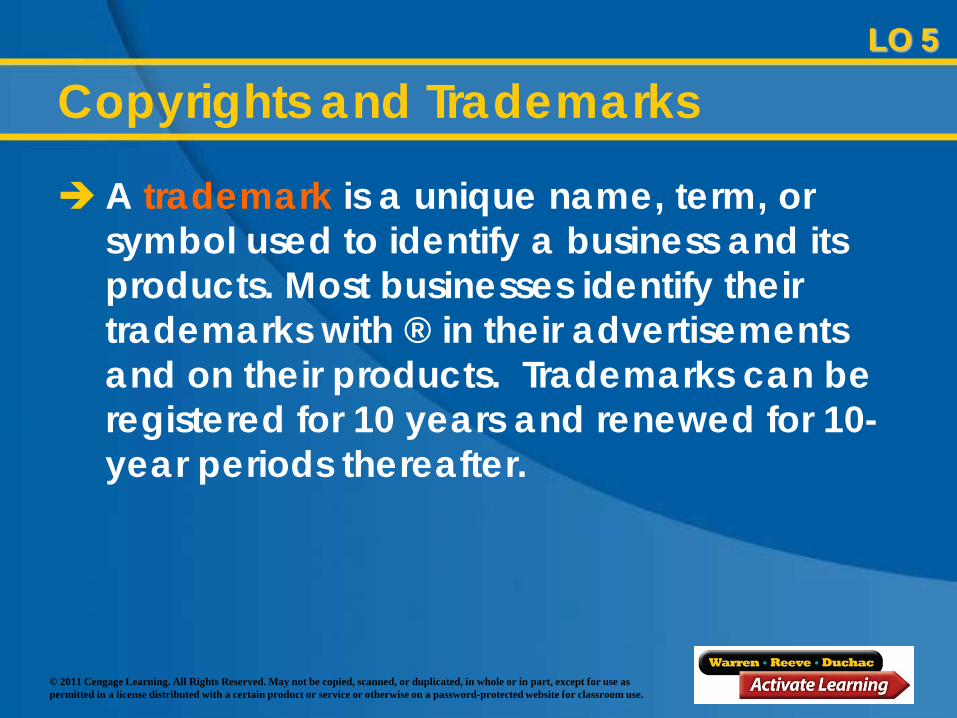

A trademark is a unique name, term, or symbol used to identify a business and its products. Most businesses identify their trademarks with ® in their advertisements and on their products. Trademarks can be registered for 10 years and renewed for 10-year periods thereafter.

LO 5

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Goodwill

In business, goodwill refers to an intangible asset of a business that is created from such favorable factors as location, product quality, reputation, and managerial skill.

LO 5

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Goodwill

Generally accepted accounting principles (GAAP) permit goodwill to be recorded in the accounts only if it is objectively determined by a transaction.

LO 5

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

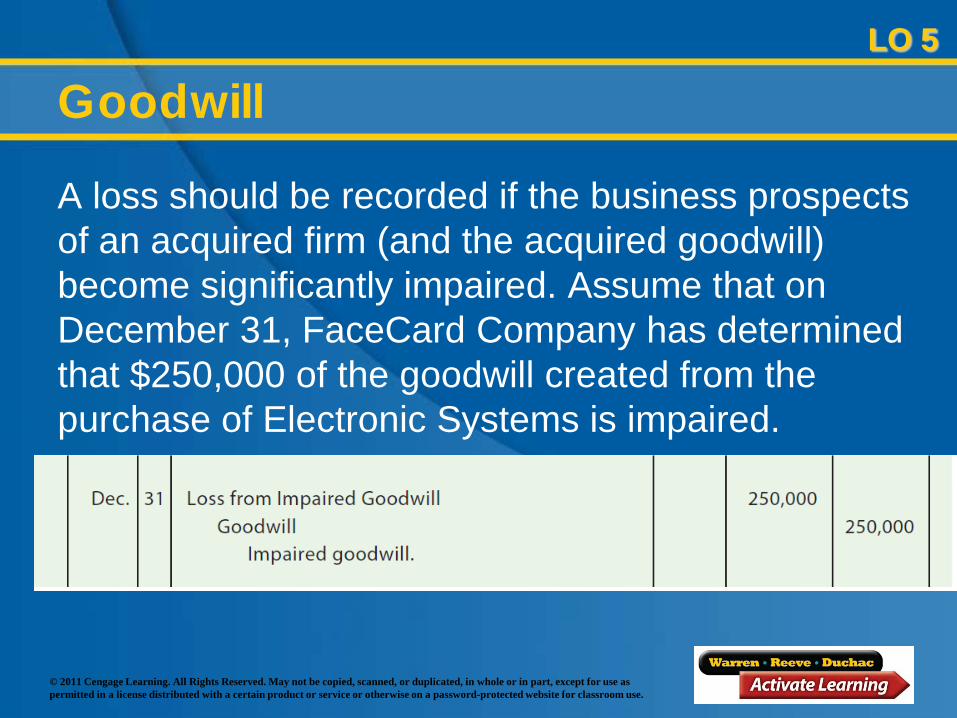

Goodwill

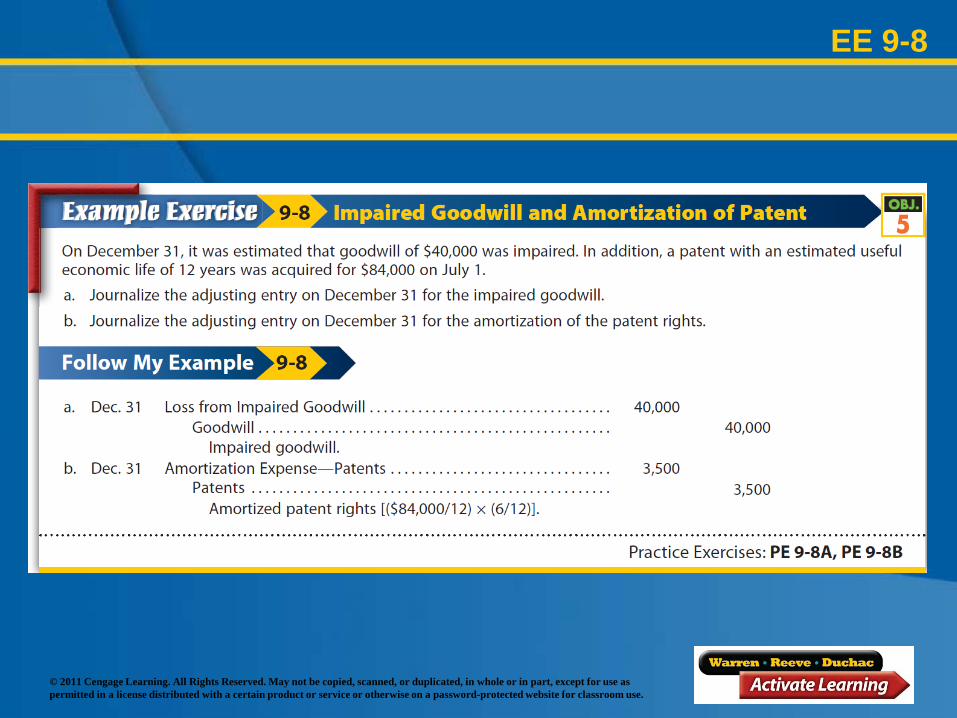

A loss should be recorded if the business prospects of an acquired firm (and the acquired goodwill) become significantly impaired. Assume that on December 31, FaceCard Company has determined that $250,000 of the goodwill created from the purchase of Electronic Systems is impaired.

LO 5

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 5

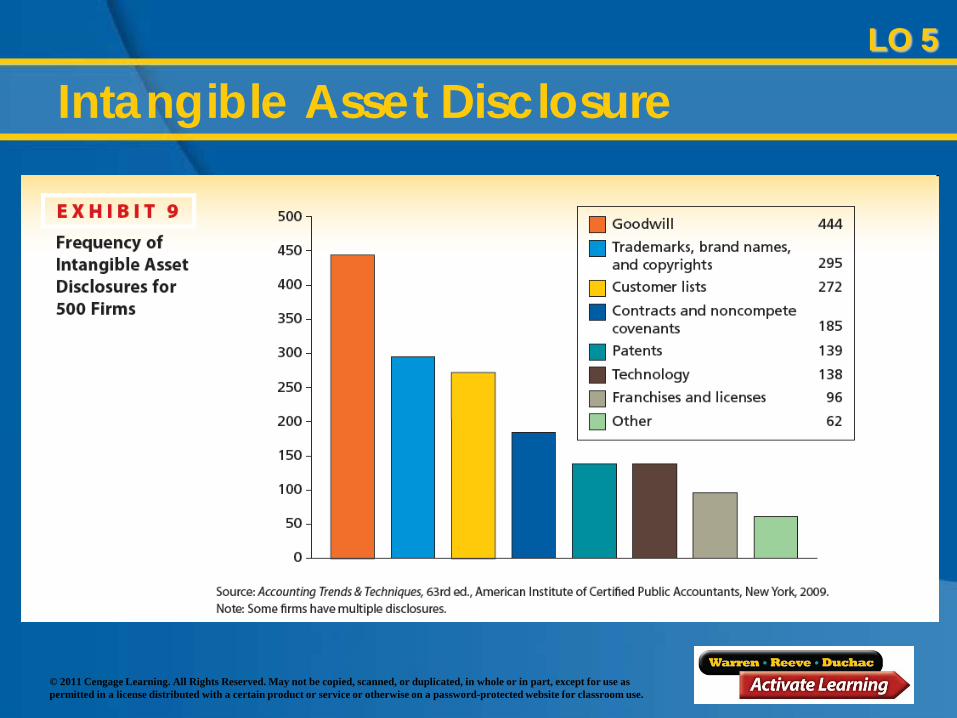

Intangible Asset Disclosure

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

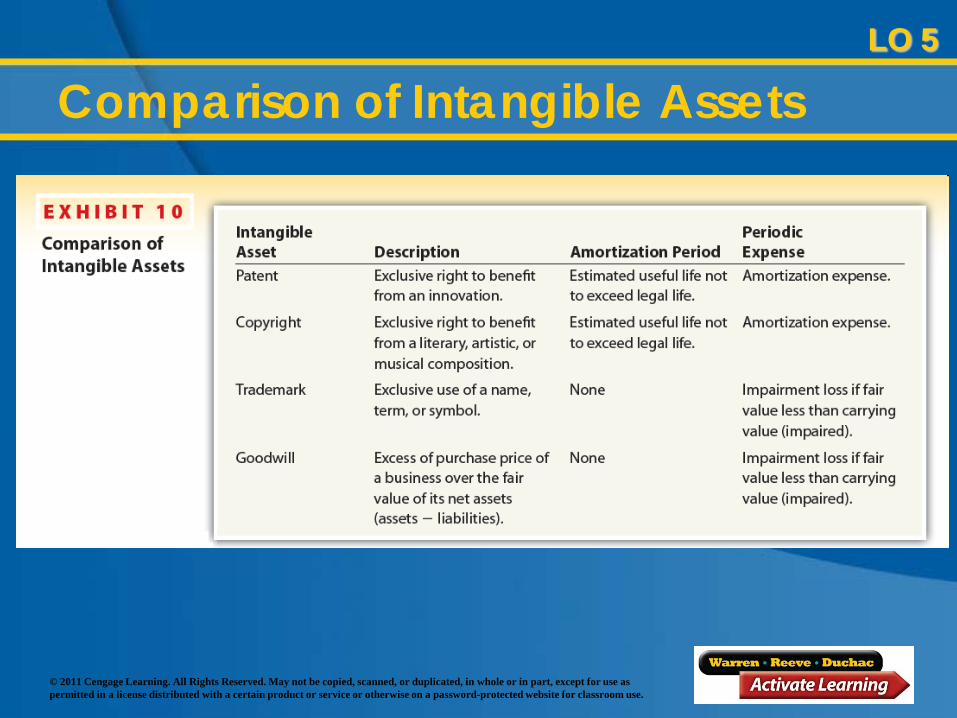

LO 5

Comparison of Intangible Assets

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

EE 9-8

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Learning Objective 6

Describe how depreciation expense is reported in an income

statement and prepare a balance sheet that

includes fixed assets and intangible assets.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

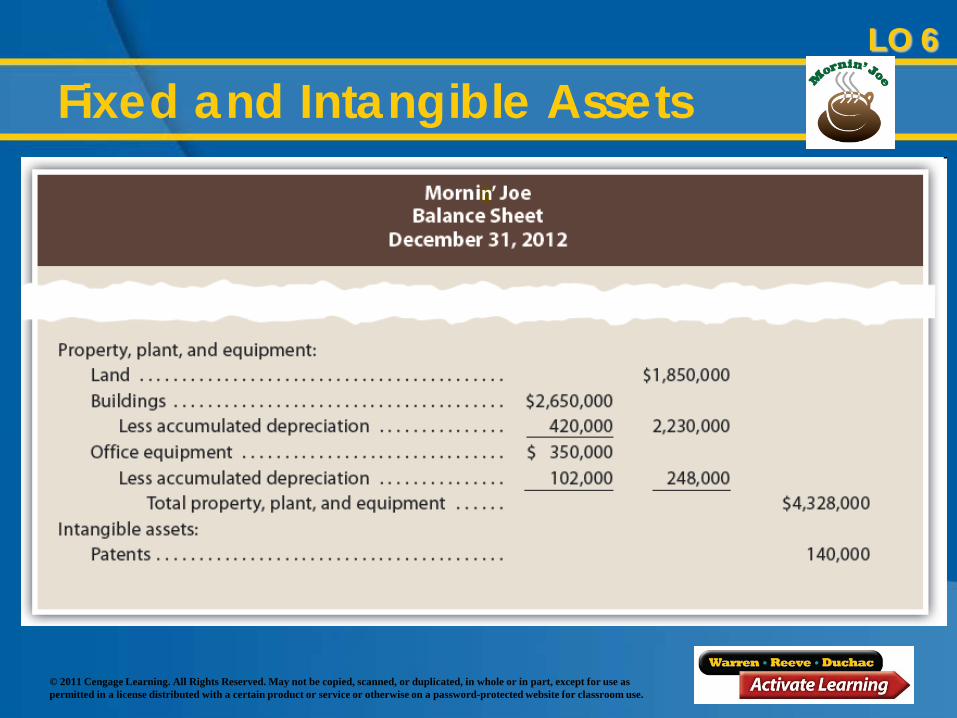

Fixed and Intangible AssetsLO 6

n

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

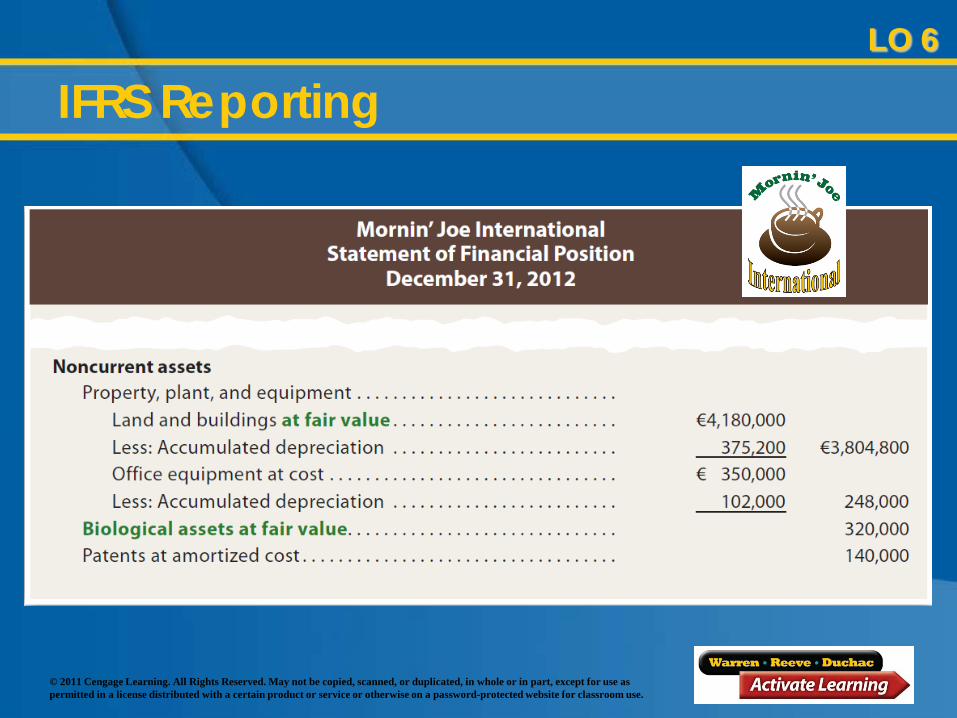

IFRS ReportingLO 6

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

LO 6

Fixed and Intangible Assets

Intangible assets are usually reported in the balance sheet in a separate section following fixed assets.

The balance of each class of intangible assets should be disclosed net of any amortization.

The cost and related accumulated depletion of mineral rights are normally shown as part of the Fixed Assets section of the balance sheet.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Learning Objective 7

Describe and illustrate the fixed asset turnover ratio to

assess the efficiency of a company’s use of

its fixed assets.

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

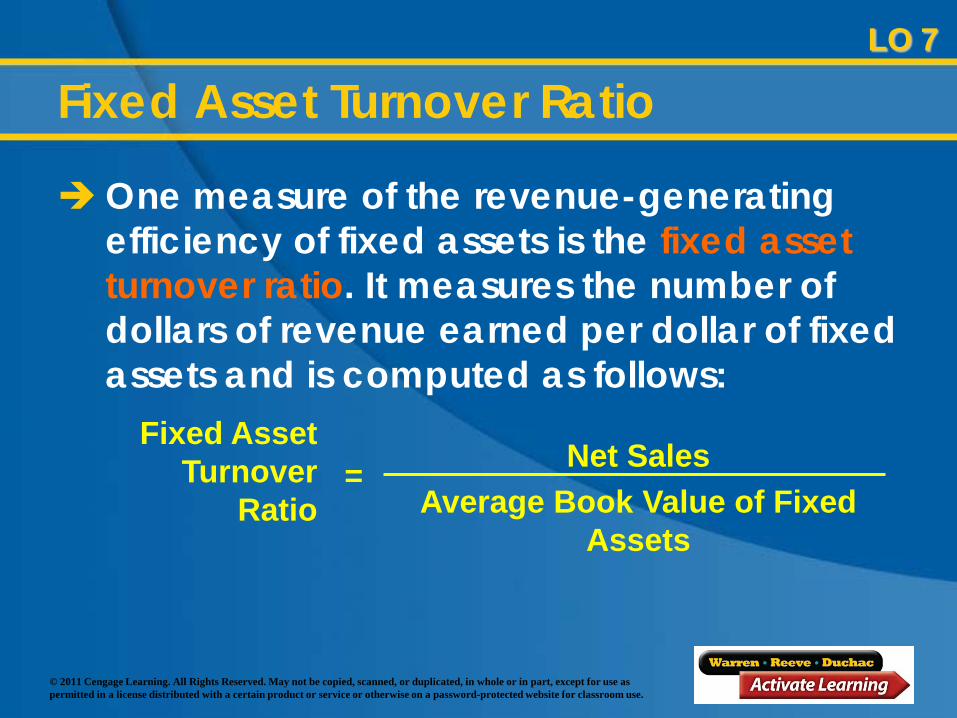

Fixed Asset Turnover Ratio

One measure of the revenue-generating efficiency of fixed assets is the fixed assetturnover ratio. It measures the number of dollars of revenue earned per dollar of fixed assets and is computed as follows:

Fixed Asset Turnover

RatioNet Sales

Average Book Value of Fixed Assets

=

LO 7

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

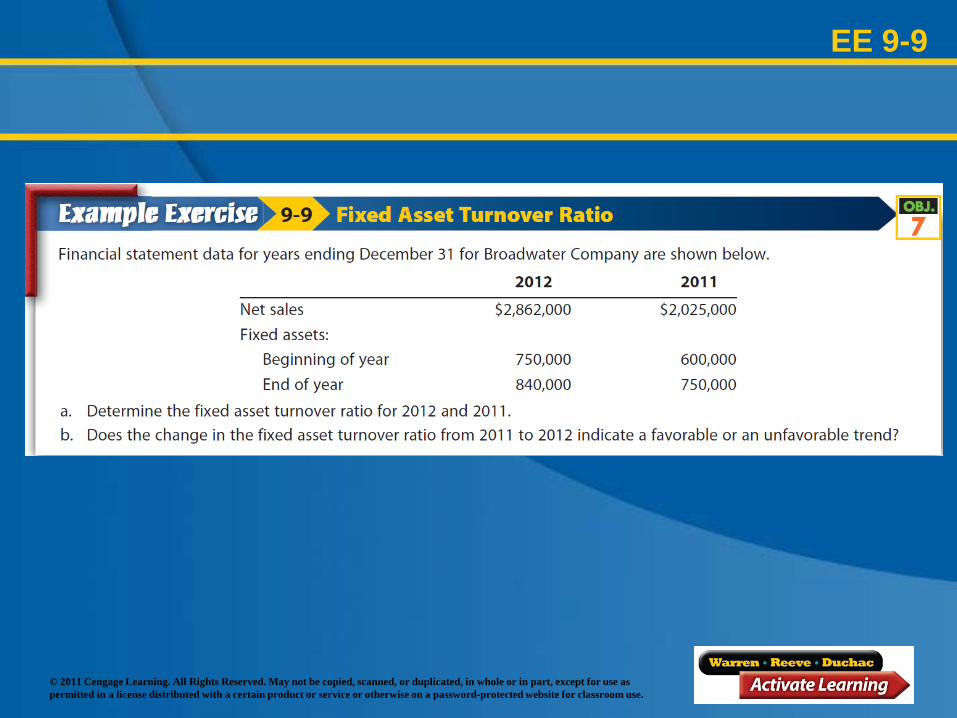

EE 9-9

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

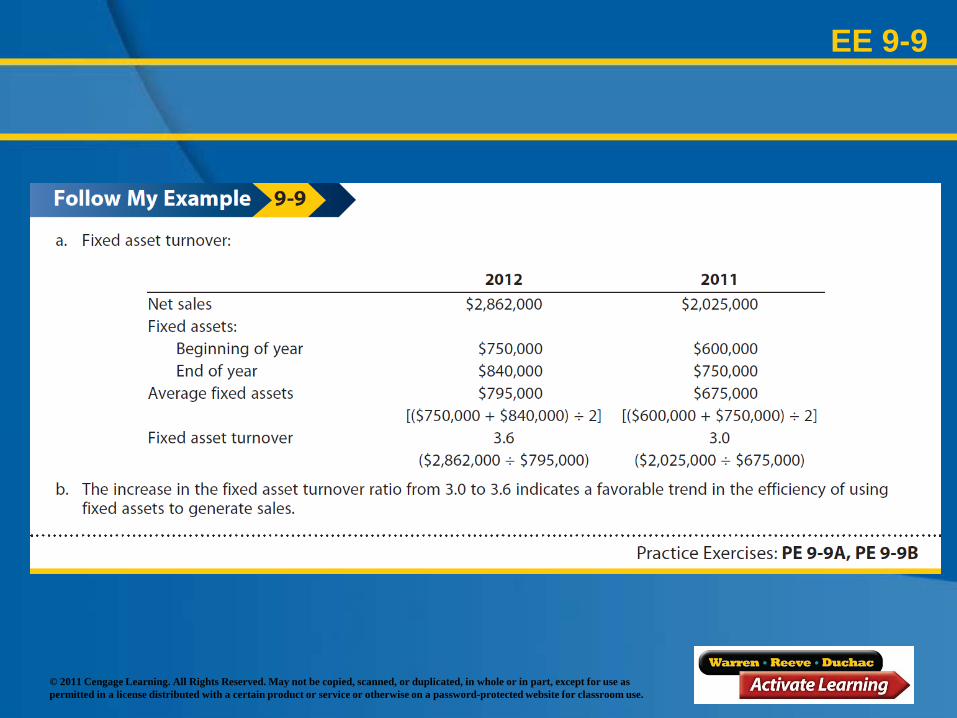

EE 9-9

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Appendix

Exchanging Similar

Fixed Assets

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Exchanging Similar Fixed Assets

Old equipment is often traded for new equipment having a similar use. In such cases, the seller allows the buyer a trade-in allowance for the old equipment traded in.

The remaining balance—the amount owed—is either paid in cash or recorded as a liability. It is normally called boot.

Appendix

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

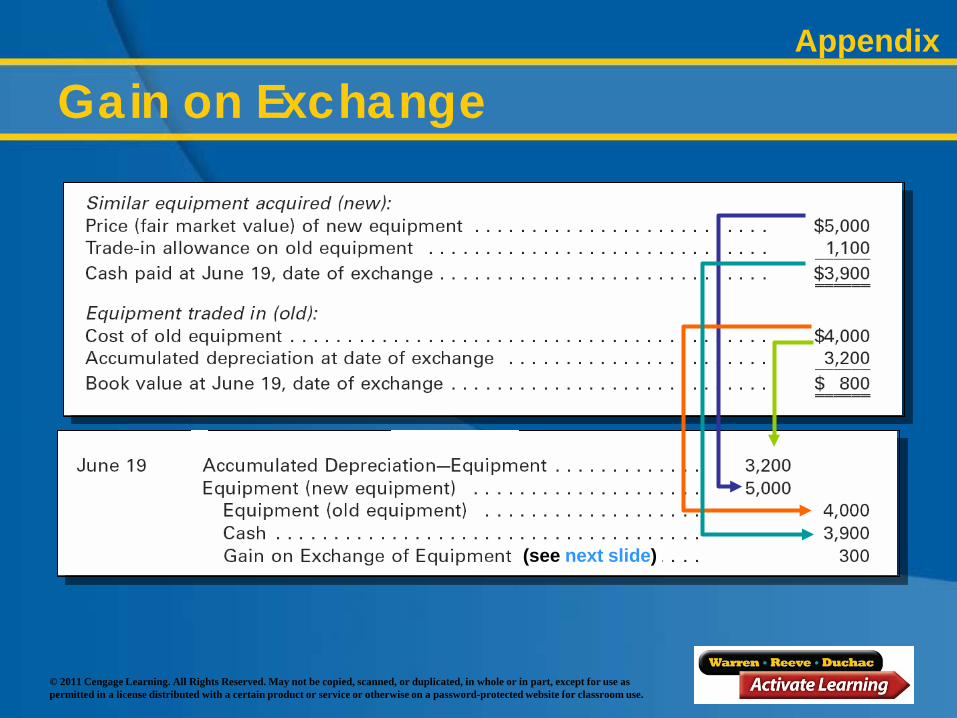

(see next slide)

Gain on ExchangeAppendix

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Gain on Exchange

Price (fair market value) of newequipment $5,000

Less assets given up in exchange:Book value of old equipment

($4,000 – $3,200) $ 800Cash paid on the exchange 3,900 4,700

Gain on exchange of assets $ 300

Appendix

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Loss on Exchange

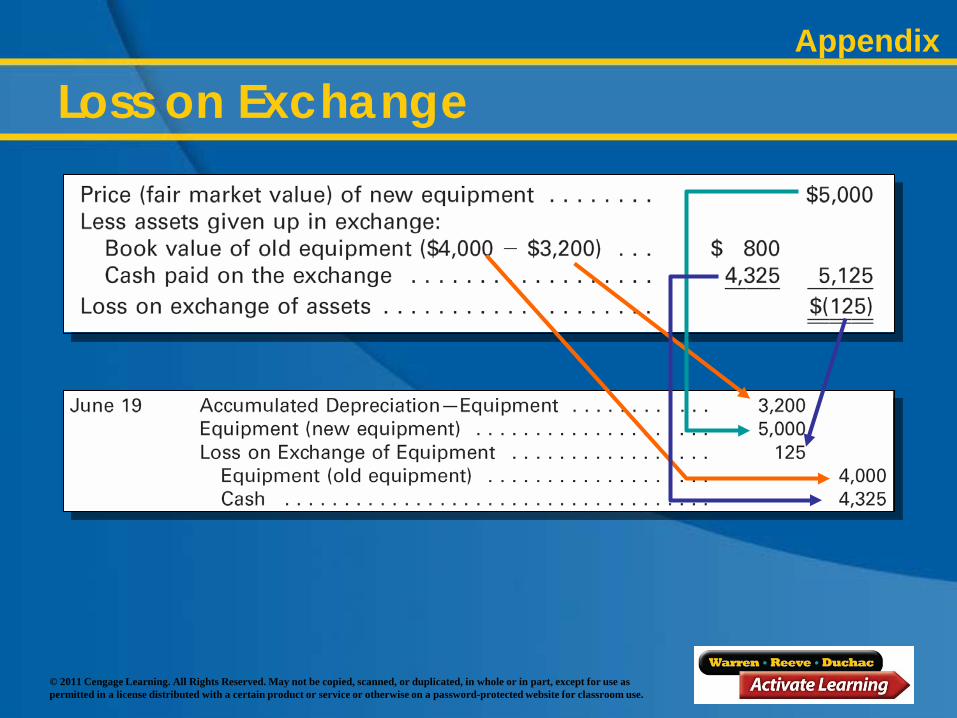

This time assume that only a $675 trade-in allowance was allowed toward the purchase of the new equipment. Because the market value of the new equipment is $5,000, the cash paid on the exchange is $4,325.

Appendix

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Loss on ExchangeAppendix

Prepared by: C. Douglas Cloud Professor Emeritus of AccountingPepperdine University

© 2011 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Fixed Assets and Intangible Assets

The End