Embed Size (px)

Citation preview

The Intersection of FamilyOffice and Philanthropy

By Eric L. Johnson and Kristina A. Rasmussen

Reprinted from Tax Notes, July 25, 2016, p. 537

taxnotes®

Volume 152, Number 4 July 25, 2016

(C)

TaxA

nalysts2016.A

llrightsreserved.

TaxA

nalystsdoes

notclaim

copyrightin

anypublic

domain

orthird

partycontent.

The Intersection of FamilyOffice and Philanthropy

by Eric L. Johnson and Kristina A. Rasmussen

Table of Contents

I. Brief Overview of Selected Excise TaxRules . . . . . . . . . . . . . . . . . . . . . . . . . . . . 538A. Self-Dealing . . . . . . . . . . . . . . . . . . . . . 538B. Excess Business Holdings . . . . . . . . . . . 539

II. Personal Services Arrangements . . . . . . . . 540A. Case Study: The Miller Family . . . . . . . 540B. The Provision of Personal Services . . . . . 540C. Compensation That Is Not Excessive . . . 541

III. Co-Investment Opportunities . . . . . . . . . . 541A. Case Study: Family Fund Structure . . . . 541B. Is the Investment a Self-Dealing

Violation? . . . . . . . . . . . . . . . . . . . . . . 542C. Tangible Benefits From Co-Investment . . 542D. Profits Allocations and Incentive Fees . . 543

E. Excess Business Holdings . . . . . . . . . . . 543F. Jeopardizing Investments . . . . . . . . . . . . 544G. UBTI . . . . . . . . . . . . . . . . . . . . . . . . . . 544H. Co-Investment Planning

Considerations . . . . . . . . . . . . . . . . . . . 545IV. Cohabitation Situations . . . . . . . . . . . . . . 545

A. Case Study: Sharing Space andPersonnel . . . . . . . . . . . . . . . . . . . . . . 545

B. Sharing Office Space . . . . . . . . . . . . . . . 546C. Sharing Supplies and Equipment . . . . . . 546D. Sharing Personnel . . . . . . . . . . . . . . . . 547

V. Conclusion . . . . . . . . . . . . . . . . . . . . . . . 547

A growing number of wealthy families are mak-ing significant charitable and philanthropic com-mitments. Those families will certainly be a catalystfor positive change in the years to come, whetherthrough the highly publicized Giving Pledge,1 so-cially responsible investing and venture philan-thropy, or the establishment of family-fundedprivate foundations with missions to solve some ofthe world’s most pressing problems.

These wealthy families often use a family officeto centralize the management of and control overfamily assets and decisions, as well as to plan forfamily succession. Separately, many wealthy fami-lies form private foundations to further the family’sphilanthropic mission.2 The family office can beintimately involved with family philanthropy, oftenproviding significant services and support to theprivate foundation and its activities.

To ensure that its charitable purposes arefulfilled, private foundations are held accountableto a strict set of rules and regulations and can incurcostly tax penalties for noncompliance with thoserules. Unfortunately, some interactions between thefamily office and the family’s private foundationmay inadvertently breach some of those rules.Continued failure to comply with the rules couldultimately result in revocation of the privatefoundation’s tax-exempt status.

1Available at http://givingpledge.org.2The term ‘‘private foundation’’ throughout this report is

used to cover both private operating and nonoperating founda-tions legally structured as corporations or trusts, as well ascharitable split-interest trusts that are required to follow specificexcise tax rules, such as charitable lead trusts and charitableremainder trusts.

Kristina A. Rasmussen

Eric L. Johnson

Eric L. Johnson is a partnerin Deloitte Tax LLP’s Chicagooffice and serves as the nationalcompetency leader for Delo-itte’s estate, gift, trust, andcharitable competency group.Kristina A. Rasmussen is a di-rector in Deloitte’s Minneapolisoffice and exclusively servestax-exempt organizations.

Through a case studyapproach, Johnson and Ras-mussen highlight common in-teractions between the familyoffice and family private foun-dation and offer planning con-siderations to reduce exposureto potential excise taxes andpenalties.

This report does not constitute tax, legal, or otheradvice from Deloitte, which assumes no responsi-bility regarding assessing or advising the readerabout tax, legal, or other consequences arising fromthe reader’s particular situation.

Copyright 2016 Deloitte Development LLC.All rights reserved.

tax notes™

SPECIAL REPORT

TAX NOTES, July 25, 2016 537

(C) T

ax Analysts 2016. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

For more Tax Notes content, please visit www.taxnotes.com.

This report examines some common situations inwhich the family office intersects with the family’sprivate foundation activities. They include (1) per-sonal services arrangements between the familyoffice and the private foundation; (2) private foun-dation co-investment with the family office andother family members or family entities; and (3)cohabitation arrangements — that is, the sharing ofspace, equipment and supplies, and personnel be-tween the family office and the private foundation.

To properly set the stage for these case studies,we first review two of the more relevant excise taxesthat apply in these situations: the section 4941excise tax on self-dealing and the section 4945 excisetax on excess business holdings. Other excise taxesand issues will be addressed throughout the casestudies.

I. Brief Overview of Selected Excise Tax Rules

A. Self-DealingSelf-dealing is a transaction between a private

foundation and a disqualified person. The defini-tion of self-dealing covers a wide range of directand indirect transactions that are prohibited eventhough they may benefit the private foundation andnot benefit the disqualified person.

When reviewing a transaction to evaluatewhether it constitutes an act of self-dealing, it isimportant to understand which individuals andentities could be considered disqualified persons.The statutory list of individuals and entities definedas disqualified persons reflects a vast array ofrelationships and ownership, including:

1. substantial contributors (both individualsand entities);

2. foundation managers (officers, directors,trustees, and people with similar powers);

3. individuals who are more than 20 percentowners of substantial contributors;

4. family members of an individual describedin 1, 2, or 3, including spouses, ancestors,children, grandchildren, great grandchildren,and spouses thereof (note that family mem-bers do not include siblings);

5. entities owned more than 35 percent by aperson described in 1, 2, 3, or 4 (throughvoting power in a corporation, profits interestin a partnership, or beneficial interest in a trustor estate); and

6. government officials.3

Decades ago, when the self-dealing rules wereput in place, Congress was concerned that donors toprivate foundations were unduly benefiting fromtransactions with the foundations, such as sales ofstock and payment for services rendered. As aresult, it specified acts that would be banned be-tween a private foundation and disqualified per-sons. Section 4941 identifies the following types of(direct or indirect) activities as prohibited self-dealing:

• the sale, exchange, or leasing of property be-tween a private foundation and a disqualifiedperson;

• the lending of money or other extension ofcredit between a private foundation and adisqualified person;

• the furnishing of goods, services, or facilitiesbetween a private foundation and a disquali-fied person;

• the payment of compensation (or payment orreimbursement of expenses) by a private foun-dation to a disqualified person;

• the transfer of the income or assets of a privatefoundation to a disqualified person, or the useof the foundation’s income or assets by or forthe benefit of a disqualified person; and

• the agreement by a private foundation to makeany payment of money or other property to agovernment official (as defined in section4946(c)), other than an agreement to employthat individual for any period after the termi-nation of his government service if he is termi-nating his government service within a 90-dayperiod.4

There are also several exceptions and specialrules, including the following:

• the transfer of real or personal property by adisqualified person to a private foundationwill be treated as a sale or exchange if theproperty is subject to a mortgage or similar lienthat the private foundation assumes, or if it issubject to a mortgage or similar lien that thedisqualified person placed on the propertywithin the 10-year period ending on the date ofthe transfer;

• the lending of money by a disqualified personto a private foundation will not be an act ofself-dealing if the loan is without interest orother charge and if the proceeds of the loan areused exclusively for purposes specified in sec-tion 501(c)(3);

• the furnishing of goods, services, or facilitiesby a disqualified person to a private founda-tion will not be an act of self-dealing if it is

3Section 4946(a). 4Section 4941(d)(1).

COMMENTARY / SPECIAL REPORT

538 TAX NOTES, July 25, 2016

(C) T

ax Analysts 2016. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

For more Tax Notes content, please visit www.taxnotes.com.

done without charge and if the goods, services,or facilities are used exclusively for purposesspecified in section 501(c)(3);

• the furnishing of goods, services, or facilitiesby a private foundation to a disqualified per-son will not be an act of self-dealing if it is ona basis no more favorable than that on whichthose goods, services, or facilities are madeavailable to the general public;

• except for a government official, the paymentof compensation (and the payment or reim-bursement of expenses) by a private founda-tion to a disqualified person for personalservices that are reasonable and necessary tocarrying out the foundation’s exempt purposewill not be an act of self-dealing if the compen-sation (or payment or reimbursement) is notexcessive; and

• any transaction between a private foundationand a corporate disqualified person under aliquidation, merger, redemption, recapitaliza-tion, or other corporate adjustment, organiza-tion, or reorganization will not be an act ofself-dealing if all the securities of the sameclass as that held by the private foundation aresubject to the same terms and if those termsprovide for the private foundation’s receipt ofno less than fair market value.5

To deter self-dealing, a tax equal to 10 percent ofthe amount involved in the act of self-dealing isassessed.6 This tax applies for each year in the taxperiod, is imposed on the disqualified person, andis not abatable, even if there is reasonable cause.7Further, a tax of 5 percent is imposed on a founda-tion manager who knowingly and willingly partici-pates in an act of self-dealing.8 Correcting the act ofself-dealing (that is, undoing the transaction) is alsorequired, and the private foundation must be left inno worse a position than it would have been in hadthe transaction not occurred.9 If the self-dealing isnot corrected, a 200 percent tax may be imposed.10

B. Excess Business HoldingsA foundation must also limit its ownership of

businesses. Private foundations may not control asubstantial interest in a business enterprise, such asa corporation or partnership. Here, the definition ofa business enterprise is crucial. A business enter-prise is the active conduct of a trade or business,including any activity carried on for the production

of income from the sale of goods or the performanceof services, that constitutes an unrelated trade orbusiness.11 Bond holdings do not constitute a hold-ing in a business enterprise unless they are consid-ered an interest in the business. Further, a leaseholdinterest in real property is not an interest in abusiness enterprise, even if the rent is based on theincome or profits of the property, unless the lease-hold interest is an interest in the income or profits ofan unrelated trade or business as defined in section513.12 If a foundation is investing in a business tofurther an exempt purpose such as a program-related investment, that investment is not consid-ered a business enterprise for purposes of the excessbusiness holdings rules.

The most commonly used exception to the term‘‘business enterprise’’ is a business in which at least95 percent of the gross income is derived frompassive sources, including dividends, interest, an-nuities, royalties, rental income from real property,and gains or losses from the disposition of prop-erty.13 The 95 percent test is calculated each year, oran average of the previous 10 years may be used.

In general, a private foundation can hold aninvestment of up to 2 percent in any business (the 2percent de minimis threshold).14 However, a privatefoundation will be deemed to have excess businessholdings when it, together with all disqualifiedpersons, owns more than 20 percent of the votingcontrol of a business enterprise.15 Under some cir-cumstances, the 20 percent amount can be increasedto 35 percent.16

In many instances, an investment partnershipthat holds passive investment assets would not beconsidered a business enterprise and thereforecould give a private foundation and other disquali-fied persons the ability to collectively invest. Becareful, however, to look through to the underlyingholdings of a partnership. For example, if a privatefoundation owns 30 percent of Partnership A andA’s assets consist of 100 percent of the stock of acorporation (a business enterprise), the privatefoundation would be deemed to own 30 percent ofthe corporation. In this example, the private foun-dation would be deemed to have excess businessholdings unless the 35 percent limitation applied.

Excess business holdings are subject to a 10percent excise tax on the value of the excess hold-ings.17 This tax applies for each year in the tax

5Section 4941(d)(2).6Section 4941(a).7Section 4962(b).8Section 4941(a)(2).9Section 4941(e)(3).10Section 4941(b).

11Reg. section 53.4943-10(a)(1).12Id.13Reg. section 53.4943-10(c)(1).14Section 4943(c)(2)(C).15Section 4943(c)(2)(A).16Section 4943(c)(2)(B).17Section 4943(a)(1).

COMMENTARY / SPECIAL REPORT

TAX NOTES, July 25, 2016 539

(C) T

ax Analysts 2016. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

For more Tax Notes content, please visit www.taxnotes.com.

period and is imposed on the private foundation,but it may be abated if the foundation can demon-strate reasonable cause. Correcting the excess busi-ness holding (that is, undoing the transaction) isalso required, such that no interest in the businessenterprise held by the foundation is classified as anexcess business holding.18 If the excess holdings arenot corrected, a 200 percent tax may be imposed.19

If a transaction by a disqualified person createsan excess business holding for a private foundation,the foundation has 90 days from the date it knowsof the holding to dispose of it and avoid the 10percent excise tax.20 The determination of when theprivate foundation is deemed to know of the hold-ing is based on the facts and circumstances. In allinstances, a private foundation that knowingly en-ters into a transaction that creates an excess busi-ness holding must immediately divest of theinvestment and pay the excise tax. A private foun-dation that receives a holding in a business enter-prise by gift, bequest, etc. (other than a purchase)has five years to divest of the excess businessholding and avoid the excise tax.21 An additionalfive-year period can be requested.22

Given the complexity surrounding the self-dealing and excess business holdings rules, it isimportant to consider these elements before a pri-vate foundation makes an investment with a dis-qualified person. It is equally important to monitorthe investment throughout its duration. For ex-ample, a capital call may swing a private founda-tion’s ownership significantly and present excessbusiness holdings problems.

With a base level of understanding about self-dealing and excess business holdings, we can nowturn to the case studies.

II. Personal Services Arrangements

A. Case Study: The Miller Family

The Miller Family Office (MFO) is a full-servicefamily office that serves the various extended mem-bers, trusts, and related entities of the Miller family.MFO was founded by its patriarch, John Miller, butownership has transitioned to his two sons, Henryand Arthur. Among other services, MFO providesaccounting, tax return preparation, and investment

consulting services to the extended family andtrusts in exchange for a market-based fee.23

John also formed the Miller Family Foundation(MFF), a private nonoperating foundation that sup-ports education causes. MFF maintains its ownwell-diversified investment portfolio.

The MFF manager is interested in having MFOprovide these same services to MFF. You have beenasked to provide advice on this potential relation-ship.

The self-dealing limitation casts a wide net andincludes the payment of compensation from a pri-vate foundation to a disqualified person. MFO isclearly a disqualified person because MFF waswholly funded by John and MFO is wholly ownedby his two sons.24

Fortunately, there is an often-used exception thatpermits a private foundation to avoid an act ofself-dealing if (1) the compensation is for personalservices, (2) the objective of the services is to carryout the tax-exempt purpose of the foundation, and(3) the total amount of compensation is not exces-sive.25

B. The Provision of Personal ServicesSeveral examples in the regulations clarify the

definition of personal services, even though theterm is not specifically defined.26 According to theexamples, personal services include the services ofattorneys and investment advisers. In fact, one ofthe examples is similar to a family office arrange-ment:

C, a manager of private foundation X, owns aninvestment counseling business. Acting in hiscapacity as an investment counselor, C man-ages X’s investment portfolio for which hereceives an amount which is determined to notbe excessive. The payment of such compensa-tion to C shall not constitute an act of self-dealing.27

Also, private letter rulings expand on the conceptof personal services. Although those rulings maynot be cited or relied on as precedent, they can beinstructive. One letter ruling concluded that anewly formed family office’s provision of tax ser-vices, administrative services, and management ser-vices was personal services.28 Another letter rulingconcluded that the provision of asset management

18Reg. section 53.4943-9(c).19Section 4943(b).20Reg. section 53.4943-2(a)(1)(ii).21Section 4943(c)(6).22Section 4943(c)(7).

23Although irrelevant to this case study, we’ll assume thatMFO qualifies under the SEC family office rule and is exemptfrom investment adviser registration.

24As defined in section 4940(d)(3)(i) and (iii).25Section 4941(d)(2)(E).26Reg. section 53.4941(d)-3(c)(1).27Reg. section 53.4941(d)-3(c), Example 2.28LTR 9238027.

COMMENTARY / SPECIAL REPORT

540 TAX NOTES, July 25, 2016

(C) T

ax Analysts 2016. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

For more Tax Notes content, please visit www.taxnotes.com.

services, coordination of tax matters, and otherfinancial services was personal services.29 Note,however, that not all services are necessarily con-sidered personal services. In one decision, the TaxCourt noted that the services must be ‘‘professionaland managerial in nature,’’ and it distinguishedthose services from maintenance, janitorial, andsecurity services.30

Turning back to our case study, it would appearthat the accounting, tax return preparation, andinvesting consulting services that MFO proposes toprovide to MFF should clearly fall under the per-sonal services exception.

C. Compensation That Is Not ExcessiveTo determine whether compensation for the pro-

vision of personal services is not excessive, theself-dealing regulations direct us to the income taxregulations.31 The income tax regulations do notprovide any bright-line tests, but they indicate thatthe compensation must be reasonable and in anamount ‘‘as would ordinarily be paid for like ser-vices by like enterprises under like circum-stances.’’32

Further, keep in mind that the term ‘‘not exces-sive’’ (and the personal services exception gener-ally) should be considered side by side with theprivate inurement doctrine. That doctrine requiresthat no part of the net earnings of tax-exemptcharitable organizations,33 including private foun-dations, inure to the benefit of persons in theirprivate capacity.34 Thus, the concept of privateinurement includes excessive or unreasonable com-pensation, and a private foundation must be able tosupport the position that the compensation pro-vided to a disqualified person is reasonable and notexcessive.

So what should MFF do to demonstrate that theproposed compensation charged by MFO is notexcessive? First, an objective compensation methodshould be established. This can be accomplished bydetermining that the compensation provided toMFO is similar to others in comparable positions orby using compensation studies by an independentparty.35 Second, the compensation method shouldbe applied regularly and continuously, and careshould be taken that the other MFO family clientsare not directly or indirectly benefiting from the

arrangement (that is, a private inurement issue).Finally, the compensation method should be memo-rialized through contemporaneous documentation,such as a services agreement between MFO andMFF.36

Accordingly, assuming MFO takes the necessarysteps outlined above, its provision of personal ser-vices to MFF should not be considered an act ofself-dealing.

III. Co-Investment Opportunities

A. Case Study: Family Fund StructureThe Miller family had previously formed an

investment partnership37 (Marketable LP) thatholds marketable, exchange-traded assets investedwith separate account managers. The family iscontemplating a second partnership (Illiquid LP) toserve as a fund of funds, holding various hedgefund and other illiquid investments.

MFO is the general partner for Marketable LP,and it is expected to be the general partner forIlliquid LP. The limited partners are John’s variousdescendants and the trusts established for theirbenefit. As the general partner, MFO intends tocharge a management fee to each partnership forthe investment consulting services it provides. Ex-hibit 1 illustrates the family fund structure.

Through its foundation manager, MFF has ex-pressed an interest in becoming a limited partner inMarketable LP as well as in Illiquid LP. MFO is

29LTR 9703031.30Madden v. Commissioner, T.C. Memo. 1997-395.31Reg. section 53.4941(d)-3(c)(1) references reg. section 1.162-

7.32Reg. section 1.162-7(b)(3).33Under section 501(c)(3).34Reg. section 1.501(c)(3)-1(c)(2).35Reg. section 53.4958-6(c)(2)(i).

36For a more in-depth discussion on leading practices forstructuring those compensation arrangements, see Eric L. John-son and Ryan E. Thomas, ‘‘Family Office Management ofPrivate Foundation Funds,’’ 150 Trusts & Estates 33 (Oct. 2011).

37Our references to ‘‘partnership’’ throughout this report areused to cover limited partnerships, limited liability partner-ships, limited liability companies, Delaware business trusts, andother arrangements taxed as partnerships for federal tax pur-poses. Accordingly, the term ‘‘partner’’ is used to cover bothpartners and members of these entities.

Figure 1. Co-InvestmentExample Proposed MFF Investment Into the

Miller Family Investment Structure

MillerFamily

Foundation

Trusts

Non-ManagingMembers

ProposedInvestment

MgmtFee Managing

Member

Miller FamilyInvestment

PartnershipsMarketable LLP Illiquid LP

MillerFamilyOffice

COMMENTARY / SPECIAL REPORT

TAX NOTES, July 25, 2016 541

(C) T

ax Analysts 2016. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

For more Tax Notes content, please visit www.taxnotes.com.

excited about this prospect because the additionalfunds contributed by MFF will significantly in-crease assets under management. MFF’s participa-tion in Marketable LP will allow MFO to negotiatelower fees with the partnership’s separate accountmanagers and to pursue investment opportunitieswith funds that require higher investment mini-mums.

Why would MFF want to invest in these partner-ships in the first place? There may be severaldifferent reasons. Participation in one or more ofthese partnerships may help MFF access differentasset classes and thus diversify its investment port-folio. MFF might also gain access to investmentswith higher minimum investment requirements,investments that would otherwise be unavailable toMFF in maintaining its own portfolio. Moreover,MFF might benefit from economies of scale andresulting cost savings by negotiating lower invest-ment management fees from these arrangements.These are all valid reasons for MFF to invest withthe family’s partnerships, but this arrangementraises potential excise tax considerations.

B. Is the Investment a Self-Dealing Violation?Would MFF’s investment in Marketable LP or

Illiquid LP be self-dealing? As noted earlier, a saleor exchange between a private foundation and adisqualified person is an act of self-dealing. So wemust first determine whether Marketable LP orIlliquid LP is a disqualified person.

Marketable LP is by definition a disqualifiedperson because more than 35 percent of its profitsinterests are owned by the Miller family membersand related trusts. Is Illiquid LP a disqualifiedperson? Self-dealing presupposes a transaction be-tween a private foundation and a disqualified per-son. However, self-dealing does not include atransaction between a private foundation and adisqualified person if the disqualified person statusarises only as a result of that transaction. This isknown in philanthropic circles as the ‘‘first bite’’rule.38 So in our case study, Illiquid LP is not adisqualified person, assuming MFF’s initial invest-ment is simultaneous with those of the Millerfamily members and trusts to initially form IlliquidLP. However, the first bite rule does not apply toany later transaction between the private founda-tion and the disqualified person once disqualifiedperson status has been established.

So Marketable LP is a disqualified person, andIlliquid LP may soon become one if there aresubsequent partner capital changes. Accordingly,the next question is whether specific transactions

between MFF and the partnerships (contributionsand redemptions) would be considered a sale orexchange under the excise tax rules. If they are,those transactions would be deemed impermissibleacts of self-dealing.

The excise tax rules do not define a sale orexchange for purposes of self-dealing. And al-though the partnership rules use the term ‘‘ex-change’’ when providing for nonrecognition of gainor loss on contribution,39 the IRS seems to havedisregarded that definition in defining sale or ex-change for excise tax purposes.

Two lines of letter rulings appear to permit aprivate foundation to invest in a family-ownedpartnership that is deemed to be a disqualifiedperson. One line seems to conclude that because thetaxpayer has represented that the private founda-tion’s investment in the partnership is not consid-ered a sale or exchange under ‘‘applicable statelaw,’’ there is no sale or exchange for purposes ofthe excise tax rules and thus no act of self-dealing.40

Unfortunately, these letter rulings provide no analy-sis regarding that position, and the factual redac-tions make it impossible to determine thetaxpayer’s applicable state. The second line of rul-ings concludes that the private foundation’s invest-ment in the partnership, including contributions toand withdrawals from it, is simply a co-investmentarrangement and not a sale or exchange for pur-poses of the excise tax rules.41 However, theserulings, too, provide limited analysis regarding thatposition.

Accordingly, because letter rulings cannot berelied on by other taxpayers, it seems prudent forMFF to consider requesting its own ruling beforemaking any investment in Marketable LP or IlliquidLP. It appears that the IRS will eventually providefurther guidance on this matter.42 However, beforeMFF makes any investment in the partnerships, itshould consider a few more issues, discussed be-low.

C. Tangible Benefits From Co-Investment

MFO indicated that the inclusion of MFF in thefund structure and the corresponding increase inassets under management would allow MFO tonegotiate lower investment management fees in

38Reg. section 53.4941(d)-1(a).

39Section 721.40LTR 200043047; and LTR 200423029.41LTR 200318069; LTR 200420029; and LTR 200551025.42See Treasury and the IRS, ‘‘2015-2016 Priority Guidance

Plan,’’ at 10 (Feb. 5, 2016) (listing the following as an exemptorganizations project: ‘‘guidance under section 4941 regarding aprivate foundation’s investment in a partnership in whichdisqualified persons are also partners’’).

COMMENTARY / SPECIAL REPORT

542 TAX NOTES, July 25, 2016

(C) T

ax Analysts 2016. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

For more Tax Notes content, please visit www.taxnotes.com.

Marketable LP and pursue investment opportuni-ties with higher investment minimums in IlliquidLP. If a disqualified person would benefit from theprivate foundation’s co-investment, this may resultin private inurement, another form of self-dealing.

Private inurement, although not specifically de-fined in the regulations, results in any transactionbetween a charity and a private individual (forexample, a disqualified person) when the indi-vidual appears to receive a disproportionate shareof the benefits of the transaction relative to thecharity. There are two potential private inurementissues.

The first is the potential benefit that the disquali-fied person may receive from reduced asset man-agement fees in Marketable LP. A possible solutionmight be to include in the partnership operatingagreement a provision indicating that if the partner-ship achieves any cost savings as a result of theprivate foundation’s investment and if those sav-ings could not be achieved if the private foundationwas not an investor, all the savings will inure to theprivate foundation. It would be important to ensurethat the partnership’s economic and tax allocationsto the private foundation and other partners re-flected that provision.

The second problem is the potential benefit thatthe disqualified person might receive from gainingaccess to more exclusive funds in Illiquid LP. Onepossible solution would be to conclude that thisbenefit is ‘‘incidental and tenuous’’ and thereforequalifies for an exception from self-dealing.43 Al-though the Treasury regulations do not define themeaning of incidental and tenuous, the IRS con-cluded that in a similar arrangement, any benefitsthat the investment partnership and other membersderived from the private foundation’s participationwas incidental and tenuous under the regulation.44

D. Profits Allocations and Incentive FeesRecall that MFO intends to charge a management

fee to each partnership for the investment consult-ing services it provides. In the earlier case study, weconcluded that the provision of personal services byMFO to MFF qualified for an exception to theself-dealing rules. That same analysis holds true inthis case study as well, with MFO providing ser-vices to partnerships in which MFF is a partner.

But what if MFO is compensated through a moresophisticated compensation arrangement, such as a‘‘1 and 10 carry’’ (that is, a 1 percent managementfee and a 10 percent profits interest — a commonarrangement in the financial services industry)? Is a

profits allocation reasonable compensation for pur-poses of the personal services exception to theself-dealing rules? There appears to be no directguidance on this matter. Interestingly, the previ-ously mentioned example in the regulations doesnot specify the form of the compensation; it simplyindicates that the investment counselor receives an‘‘amount’’ that is determined to be not excessive.45

One letter ruling cited earlier included a fact patternwith a profits allocation, but the taxpayer carefullystructured the arrangement so the profits allocationwas not taken from (nor received by) the privatefoundation.46 In another letter ruling, the managercharged the partnership a performance fee forachieving returns exceeding a specified threshold,but the manager waived that fee for the privatefoundation partner.47 Given the lack of direct guid-ance, taxpayers should proceed with extreme cau-tion in these situations.

E. Excess Business HoldingsCould MFF’s investment in Marketable LP or

Illiquid LP be considered excess business holdings?Recall that in general, a private foundation and alldisqualified persons, in aggregate, may not ownmore than 20 percent of a partnership’s profitsinterest.48 Because our facts indicate that MFF’sinvestments in the partnerships will meet that testand certainly exceed the 2 percent de minimisthreshold, those investments must be tested.

For Marketable LP, it’s clear that one of thecommon exceptions applies: A business enterprisethat earns at least 95 percent of its gross incomefrom passive sources is not subject to the excessbusiness holdings rule.49 Because Marketable LP’sportfolio consists of exchange-traded securities in-vested with separate account managers, MFF’s in-vestment in Marketable LP will not result in excessbusiness holdings.

What about Illiquid LP? In one letter ruling, theIRS concluded that a partnership’s only activityconsisted of investments in private businesses,mainly as a limited partner in limited partnerships,and that because the partnership would not bemanaging the businesses of the limited partner-ships, the limited partnerships represented passiveinvestments comparable to stock and securities.50

43Reg. section 53.4941(d)-2(f)(2).44LTR 200551025.

45Reg. section 53.4941(d)-3(c)(2), Example 2.46LTR 200318069. In this ruling, the private foundation was

only a co-investor in the management company that receivedthe profit allocation, and the profits allocation was speciallyallocated to other partners of the management company.

47LTR 200551025.48Section 4943(c)(3).49Section 4943(d)(3)(B).50LTR 199939046.

COMMENTARY / SPECIAL REPORT

TAX NOTES, July 25, 2016 543

(C) T

ax Analysts 2016. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

For more Tax Notes content, please visit www.taxnotes.com.

The partnership’s investments were therefore pas-sive investments, and the partnership was not abusiness enterprise for purposes of the excess busi-ness holdings rule. Assuming Illiquid LP remains afund of funds partnership, it would appear thatHedge LP itself should not be construed as abusiness enterprise under that test.

However, to complete our analysis, we must alsoexamine the underlying holdings of Illiquid LP toconfirm that the 20 percent test will not be met on alook-through basis. Further, if Illiquid LP decides tomake significant, direct investments in private eq-uity deals or involves itself in the management ofthose businesses, those holdings could be problem-atic. So MFF’s investment in Illiquid LP will need tobe carefully monitored, and MFO, as investmentmanager, will need to be aware of these limitationswhen considering subsequent investments in theportfolio.

F. Jeopardizing InvestmentsThe rules regarding jeopardizing investments

were put in place to safeguard the private founda-tion’s ability to carry out its exempt purpose.51 Inother words, private foundations cannot invest in away that would show lack of good business judg-ment. The determination of whether an investmentis considered jeopardizing is done at the time of theinvestment. It considers the portfolio as a wholeand is not affected by future income or losses fromthe investment.

To further deter and prevent foundation manag-ers (for example, board members, trustees, or thosewith similar influence) from making jeopardizinginvestments, a tax equal to 10 percent of the amountinvolved in the jeopardizing action is assesseddirectly on the foundation manager.52 The tax isabatable if there is reasonable cause.53 If the foun-dation manager knowingly and willingly made theinvestment, an additional 10 percent tax is im-posed.54 Further, if the asset is not removed fromjeopardy, a 25 percent tax may be imposed on theprivate foundation.55

Could an investment by MFF in Illiquid Fund LPbe deemed a jeopardizing investment? Unlikely.Although no category of investment is treated as aper se violation, there are some practical guidelines.The Treasury regulations provide that trading insecurities on margin; trading in commodity futures;investments in working oil and gas wells; purchasesof puts, calls, and straddles; purchases of warrants;

and selling short will be ‘‘closely scrutinized.’’56

However, this list was developed over 30 years ago,and modern portfolio theory would suggest thatthese investments, as part of an overall diversifiedportfolio, arguably provide low or negative corre-lation with other investments and thus may miti-gate overall portfolio risk. Moreover, at least oneletter ruling determined that a private foundation’sinvestment in a hedge fund was not a jeopardizinginvestment.57

G. UBTI

The concept of unrelated business taxable incomehas been around for decades. Before 1950 a chari-table organization could conduct commercial-typeactivities that did not relate to its exempt purposeand shield any net income from that activity fromincome tax. The rules at that time looked at the useof the funds generated rather than the activity itselfwhen determining whether the income was subjectto taxation. As a result, many tax-exempt organiza-tions were engaging in all sorts of activities thatwere not related to their exempt purpose anddirectly competed with for-profit business enter-prises. After much scrutiny and debate, Congressincluded in the Revenue Act of 1950 provisions thatsubjected income from an activity that was notrelated to an organization’s overall tax-exempt pur-pose to income tax at the corporate or trust incometax rates. Those rules still apply.

All tax-exempt organizations, including privatefoundations, may be subject to income tax onUBTI.58 UBTI can be generated through activities inwhich the private foundation directly engaged orthrough its investment in a passthrough entity, suchas a partnership or S corporation.59 For partnershipentities, the private foundation would look throughto the activities of the entity and evaluate whetherthey were tax exempt in nature. For most operatingentities, the activities conducted are consideredUBTI by a private foundation investor. Generallyspeaking, however, UBTI does not include passivetypes of income such as dividends, interest, rents,and royalties,60 unless the asset generating that

51Section 4944.52Section 4944(a)(1).53Section 4962(a).54Section 4944(a)(2).55Section 4944(b)(1).

56Reg. section 53.4944-1(a)(2)(i).57LTR 200318069. Although the investment was made

through the hedge fund’s general partner, the IRS viewed it asan indirect investment in the hedge fund’s underlying invest-ments. Even though the private foundation’s investment in-volved most of the foundation’s assets, the IRS determined thatthe hedge fund was sufficiently diversified and accordingly wasnot a jeopardizing investment.

58Section 511.59Under section 512(e), 100 percent of an exempt organiza-

tion’s share of S corporation income is treated as UBTI.60Section 512(b).

COMMENTARY / SPECIAL REPORT

544 TAX NOTES, July 25, 2016

(C) T

ax Analysts 2016. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

For more Tax Notes content, please visit www.taxnotes.com.

income is debt-financed.61 Therefore, careful analy-sis of the Schedule K-1 received from a passthroughentity is required to evaluate potential UBTI impact.

UBTI from all sources is totaled and reported onForm 990-T, ‘‘Exempt Organization Business In-come Tax Return.’’ Keep in mind that in addition tofederal UBTI, most states also impose a tax andrequire filings concerning state-sourced UBTI. Ac-cordingly, although Marketable LP will likely gen-erate the passive types of income previouslymentioned, Illiquid Fund LP will likely generaterevenue from operations that would be consideredUBTI. Therefore, before investing in Illiquid FundLP, MFF should carefully analyze the tax impact ofpotential federal and state UBTI.

H. Co-Investment Planning ConsiderationsAssuming MFF continues to pursue an invest-

ment within Illiquid Fund LP, it appears that spe-cific provisions could be included in the partnershipagreement to limit the exposure from the aboveconcerns. Several of the favorable letter rulings onthis topic have provided a nonexclusive list of thesepotential provisions.

For example, the partnership agreement in LTR199939046 prohibited the partnership from:

• making any investments that would result inexcess business holdings for the private foun-dation’s partners and its disqualified persons;

• holding a more than 20 percent interest in anylimited partnership;

• directly engaging in an operating business;• making any jeopardizing investments that

would subject any of the private foundationpartners to tax;

• engaging in property or credit transactionswith any disqualified persons of the privatefoundation partners that would constitute self-dealing; and

• purchasing or selling investments in an at-tempt to provide an advantage to a disquali-fied person.

The partnership agreement in LTR 200420029contained the following provisions:

• the right for the private foundation to with-draw from the partnership, in whole or in part,as of the end of any period (perhaps drafted asa put right);

• the right for the private foundation to receivean in-kind distribution of its interest (that is, apro rata share) if it elects to withdraw;

• a veto right provided to the private foundationfor specifically defined decisions;

• a special provision indicating that if any cost,fee, or expense is incurred by the partnershipand is based on a percentage of the partnershipassets, the private foundation will pay thelowest possible percentage of fees and theother investors will bear the burden of and paythe remainder of those fees (for example, in-vestment manager fees);

• a special provision indicating that if the part-nership achieves any savings on costs, fees, orexpenses because the amount of the invest-ment exceeds the minimum asset amountthresholds, and if those savings could not beachieved if the private foundation was not aninvestor, all the savings will inure to the pri-vate foundation; and

• a provision that the manager or managers ofthe partnership may receive a manager’s feenot in excess of the usual and customarymoney management fees assessed by profes-sional fiduciaries of the community.

The real challenge with any co-investment ar-rangement is not in establishing the arrangementbut in the necessary monitoring of partner capitalchanges, partnership investment selection, feescharged by the manager or outside providers, andpotential transactions between partners. Absent theestablishment of formal procedures to continuallymonitor these arrangements, even good intentionscan lead to unintended consequences. In our casestudy, the better route may be to have MFF notco-invest in the partnerships but rather maintain aseparate investment portfolio. MFO could manageMFF’s investment portfolio under an administra-tive services agreement structured to meet the per-sonal services exception.

IV. Cohabitation Situations

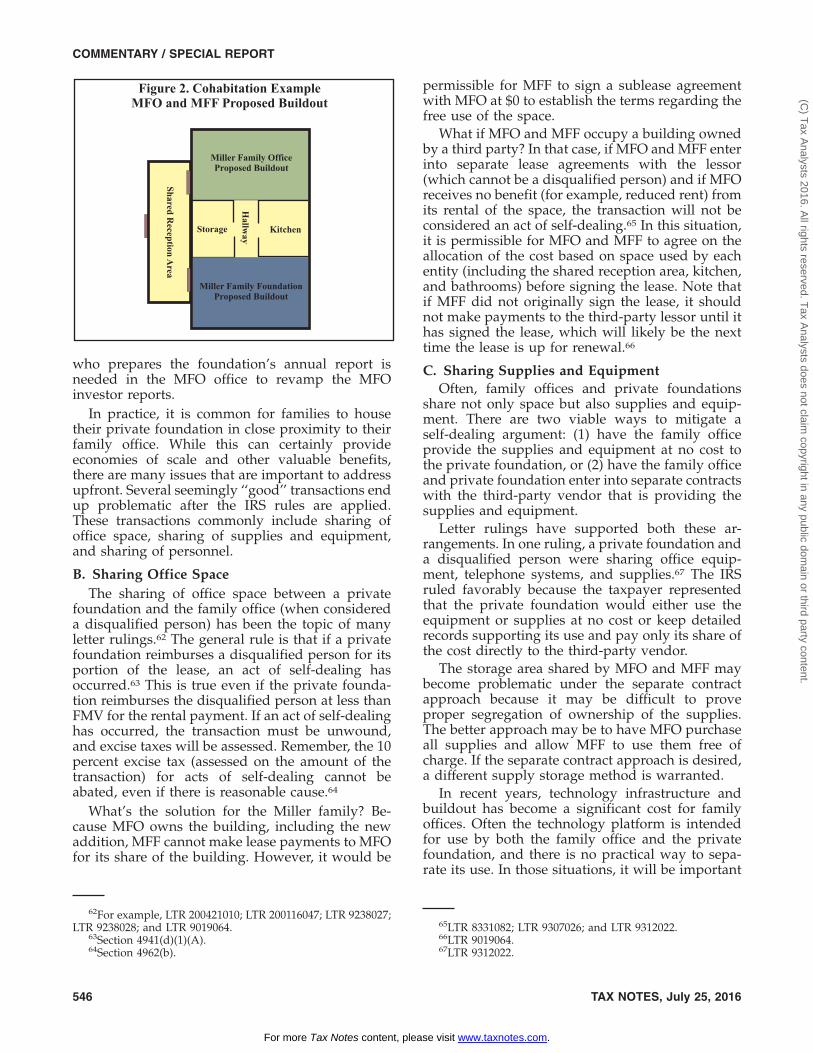

A. Case Study: Sharing Space and PersonnelMFO has built out new office space to accommo-

date the increasing technology needs of the office.The space is excellent, and the MFF board hasdecided to move its operations there also. Thefamily is excited about this opportunity becausehaving both MFO and MFF in the same locationshould increase efficiency and provide economiesof scale through the sharing of personnel, technol-ogy, vendors, and supplies.

As Exhibit 2 illustrates, the buildout will have ashared reception area but separate office space forMFO and MFF. The offices are connected by ahallway, and MFO and MFF will share a storagearea and kitchen.

Also, although MFO and MFF maintain separatepayrolls, there is an agreement to share specificemployees: An administrative assistant will servicethe shared reception area, and an MFF employee61Section 514.

COMMENTARY / SPECIAL REPORT

TAX NOTES, July 25, 2016 545

(C) T

ax Analysts 2016. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

For more Tax Notes content, please visit www.taxnotes.com.

who prepares the foundation’s annual report isneeded in the MFO office to revamp the MFOinvestor reports.

In practice, it is common for families to housetheir private foundation in close proximity to theirfamily office. While this can certainly provideeconomies of scale and other valuable benefits,there are many issues that are important to addressupfront. Several seemingly ‘‘good’’ transactions endup problematic after the IRS rules are applied.These transactions commonly include sharing ofoffice space, sharing of supplies and equipment,and sharing of personnel.

B. Sharing Office SpaceThe sharing of office space between a private

foundation and the family office (when considereda disqualified person) has been the topic of manyletter rulings.62 The general rule is that if a privatefoundation reimburses a disqualified person for itsportion of the lease, an act of self-dealing hasoccurred.63 This is true even if the private founda-tion reimburses the disqualified person at less thanFMV for the rental payment. If an act of self-dealinghas occurred, the transaction must be unwound,and excise taxes will be assessed. Remember, the 10percent excise tax (assessed on the amount of thetransaction) for acts of self-dealing cannot beabated, even if there is reasonable cause.64

What’s the solution for the Miller family? Be-cause MFO owns the building, including the newaddition, MFF cannot make lease payments to MFOfor its share of the building. However, it would be

permissible for MFF to sign a sublease agreementwith MFO at $0 to establish the terms regarding thefree use of the space.

What if MFO and MFF occupy a building ownedby a third party? In that case, if MFO and MFF enterinto separate lease agreements with the lessor(which cannot be a disqualified person) and if MFOreceives no benefit (for example, reduced rent) fromits rental of the space, the transaction will not beconsidered an act of self-dealing.65 In this situation,it is permissible for MFO and MFF to agree on theallocation of the cost based on space used by eachentity (including the shared reception area, kitchen,and bathrooms) before signing the lease. Note thatif MFF did not originally sign the lease, it shouldnot make payments to the third-party lessor until ithas signed the lease, which will likely be the nexttime the lease is up for renewal.66

C. Sharing Supplies and EquipmentOften, family offices and private foundations

share not only space but also supplies and equip-ment. There are two viable ways to mitigate aself-dealing argument: (1) have the family officeprovide the supplies and equipment at no cost tothe private foundation, or (2) have the family officeand private foundation enter into separate contractswith the third-party vendor that is providing thesupplies and equipment.

Letter rulings have supported both these ar-rangements. In one ruling, a private foundation anda disqualified person were sharing office equip-ment, telephone systems, and supplies.67 The IRSruled favorably because the taxpayer representedthat the private foundation would either use theequipment or supplies at no cost or keep detailedrecords supporting its use and pay only its share ofthe cost directly to the third-party vendor.

The storage area shared by MFO and MFF maybecome problematic under the separate contractapproach because it may be difficult to proveproper segregation of ownership of the supplies.The better approach may be to have MFO purchaseall supplies and allow MFF to use them free ofcharge. If the separate contract approach is desired,a different supply storage method is warranted.

In recent years, technology infrastructure andbuildout has become a significant cost for familyoffices. Often the technology platform is intendedfor use by both the family office and the privatefoundation, and there is no practical way to sepa-rate its use. In those situations, it will be important

62For example, LTR 200421010; LTR 200116047; LTR 9238027;LTR 9238028; and LTR 9019064.

63Section 4941(d)(1)(A).64Section 4962(b).

65LTR 8331082; LTR 9307026; and LTR 9312022.66LTR 9019064.67LTR 9312022.

Figure 2. Cohabitation ExampleMFO and MFF Proposed Buildout

Miller Family OfficeProposed Buildout

Storage Kitchen

Miller Family FoundationProposed Buildout

Sh

ared

Recep

tion

Area

Hallw

ay

COMMENTARY / SPECIAL REPORT

546 TAX NOTES, July 25, 2016

(C) T

ax Analysts 2016. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

For more Tax Notes content, please visit www.taxnotes.com.

to have the family office own the technology andallow the private foundation to use it at no charge.

D. Sharing PersonnelIt is entirely possible for the family office and the

private foundation to share employees, but thedevil is in the details — that is, the form of thearrangement is important to reduce self-dealingconcerns. In our case study, MFO and MFF main-tain separate payroll, but there is a formal agree-ment to share two specific employees. We will lookseparately at the administrative assistant, who willmanage the shared reception area, and the MFFemployee, who is needed in the MFO office torevamp the MFO investor reports.

As discussed earlier, the provision of personalservices does not constitute an act of self-dealing.Are secretarial services considered personal ser-vices? The answer was complicated by the TaxCourt’s decision in Madden.68 In that case, the courtconcluded that personal services should be con-strued narrowly, and it defined them as servicesthat are ‘‘essentially professional and managerial innature.’’ Following Madden, some letter ruling re-quests appear to have curtailed the range of pro-posed services, explicitly excluding secretarialservices.69 Accordingly, it would be prudent for theadministrative assistant to be an employee of MFO,with any allocable share of services provided toMFF performed at no cost.

The arrangement regarding the MFF employeewho is needed to revamp the MFO investor reportsis clearly problematic. MFF employees cannot pro-vide services to disqualified persons (that is, MFO).What is the likely solution? MFO should hire thisemployee separately. That is, the employee wouldbe formally employed by both MFO and MFF,receive wages separately from both organizations,and receive separate Forms W-2.

Finally, although our case study indicates thatMFO and MFF have separate payrolls, many fami-lies like to use a master payroll for all employees,whether they serve in the family office or privatefoundation. To reduce self-dealing concerns when asingle payroll is desired, it is important for thefamily office to employ all those professionals andcharge the private foundation an amount thatwould be deemed not excessive. A reimbursementat cost designed as an hourly charge might beappropriate.

V. ConclusionCareful planning is required when family office

activities intersect with the family’s philanthropicendeavors. This report covered three of the mostcommon intersections: (1) the provision of personalservices by the family office to the private founda-tion; (2) co-investment opportunities between thefamily office, family members, and the privatefoundation; and (3) cohabitation arrangements be-tween the family office and private foundation. Atfirst blush, it may seem that the private foundationrules were put into place to prevent those familyinteractions, but that is not the case. The rulescontemplate that these interactions will occur, andthey attempt to provide a framework for structur-ing the arrangements in a manner to protect theinterests of the private foundation.

Unfortunately, many of these rules were enactedover 30 years ago, and although well-intended, theydo not adequately cover common arrangements intoday’s world, particularly in the co-investmentarea. Subsequent guidance provided in letter rul-ings has generally trended positive and been in-structive, but it cannot be relied on by othertaxpayers. Further guidance, particularly on co-investment, is welcome and appears to be forth-coming from the IRS. All three of the intersectionscovered in the report can be successfully navigated,but good intentions, thoughtful foresight, and anappreciation of the private foundation rules arenecessary to secure a desirable outcome.

68T.C. Memo. 1997-395.69E.g., LTR 200217056; and LTR 200238053.

COMMENTARY / SPECIAL REPORT

TAX NOTES, July 25, 2016 547

(C) T

ax Analysts 2016. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

For more Tax Notes content, please visit www.taxnotes.com.