Embed Size (px)

Citation preview

Ninth Report of Duff & PhelpsCanada Restructuring Inc. asCourt-Appointed Receiver ofPriszm Income Fund, PriszmCanadian Operating Trust,Priszm Inc., KIT Finance Inc. andPriszm LP

June 26, 2014

Duff & Phelps Canada Restructuring Inc. Page i of i

ContentsPage

1.0 Introduction..........................................................................................................1

1.1 Purposes of this Report............................................................................2

1.2 Currency ..................................................................................................3

1.3 Restrictions ..............................................................................................3

2.0 Background .........................................................................................................3

3.0 Sysco Dispute......................................................................................................4

4.0 Denial of Coverage of the Sysco Claim................................................................5

5.0 Distributions and Holdbacks ................................................................................6

5.1 Cash Position...........................................................................................6

5.2 Security Opinion and Distributions to Date ...............................................6

5.3 Proposed Distribution...............................................................................7

5.4 Supplier Charge Holdback .......................................................................7

5.5 Receiver’s Charge Holdback....................................................................8

5.6 HST Holdback..........................................................................................8

5.7 Holdback for Sysco D&O Claim and the Reduction of D&O Charge.........9

5.8 Holdback for Reserve with Respect to KEYreit.........................................9

5.9 Holdback for Non-assigned Leases re: HFFI Transaction ......................10

5.10 Contingency ...........................................................................................10

5.11 Conclusion .............................................................................................10

6.0 Overview of the Receiver’s Activities .................................................................10

7.0 Conclusion and Recommendation .....................................................................12

Appendices

Receivership Order ........................................................................................................ A

Receiver’s Third Report to Court (without appendices)................................................... B

Reserve Agreement ....................................................................................................... C

Duff & Phelps Canada Restructuring Inc. Page 1

Court File No.: CV-11-9375-00CL

ONTARIOSUPERIOR COURT OF JUSTICE

IN BANKRUPTCY AND INSOLVENCY(COMMERCIAL LIST)

THE PRUDENTIAL INSURANCE COMPANY OF AMERICA, PRUCO LIFE INSURANCECOMPANY AND PRUDENTIAL RETIREMENT INSURANCE AND ANNUITY COMPANY

-and-

PRISZM INCOME FUND, PRISZM CANADIAN OPERATING TRUST, PRISZM INC.,KIT FINANCE INC. AND PRISZM LP

NINTH REPORT OF DUFF & PHELPS CANADA RESTRUCTURING INC.IN ITS CAPACITY AS COURT-APPOINTED RECEIVER

June 26, 2014

1.0 Introduction

1. Pursuant to an order of the Ontario Superior Court of Justice (Commercial List)(“Court”) made on March 31, 2011 (“Filing Date”), as amended and restatedpursuant to an order of the Court made on April 29, 2011 (“CCAA Order”),Priszm Income Fund, Priszm Canadian Operating Trust, Priszm Inc., KitFinance Inc. and Priszm LP (collectively, “Company”) commencedproceedings (“CCAA Proceedings”) under the Companies’ CreditorsArrangement Act, R.S.C. 1985, c. C-36, as amended (“CCAA”). FTIConsulting Canada Inc. was appointed as the monitor (“Monitor”) in the CCAAProceedings.

2. Pursuant to an application of The Prudential Insurance Company of America,Pruco Life Insurance Company and Prudential Retirement Insurance andAnnuity Company (collectively, “Prudential”), the Court made an order onSeptember 14, 2011 (“Receivership Order”) which provided that following theclosing of the FMI Transaction (as defined below), RSM Richter Inc. (“Richter”)was to be appointed as receiver (“Receiver”) of the assets, undertakings andproperties of the Company.

3. The termination of the CCAA Proceedings and the commencement of thereceivership proceedings became effective on September 21, 2011. A copy ofthe Receivership Order is attached as Appendix “A” to this report.

Duff & Phelps Canada Restructuring Inc. Page 2

4. Pursuant to a Court order made on December 12, 2011 (“Substitution Order”),Duff & Phelps Canada Restructuring Inc. (“D&P”) was substituted in place ofRichter as Receiver as a result of D&P’s acquisition of the Torontorestructuring practice of Richter1.

1.1 Purposes of this Report

1. The purposes of this report (“Report”) are to:

a) Provide background information about the Company and theseproceedings;

b) Provide an update regarding a claim made by Sysco Canada Inc.(“Sysco”) against the Company and its Directors and Officers (“D&Os”)in respect of payments made to it by the Company immediately prior tothe commencement of the CCAA proceedings, which payments did notclear the Company’s bank account because of the commencement ofthe CCAA proceedings;

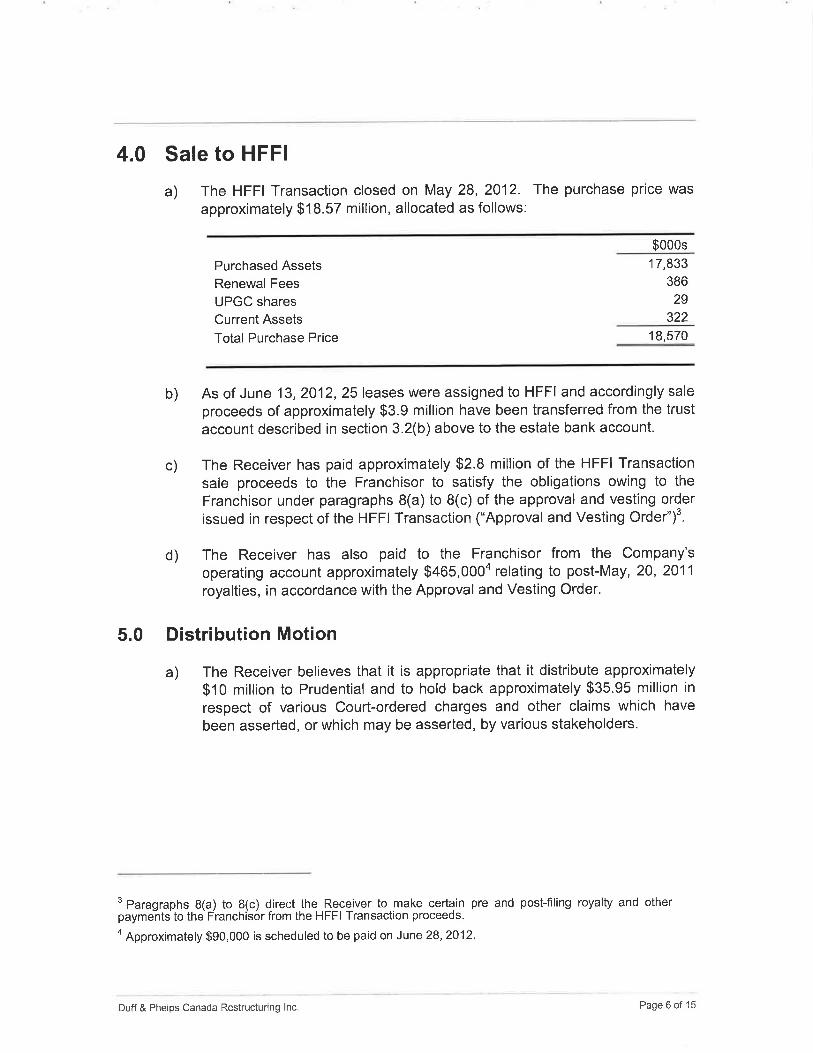

c) Detail a proposed distribution to Prudential in the amount of $2.174million (the “Proposed Distribution”) and provide the rationale for theProposed Distribution;

d) Detail the reasons that the Receiver is recommending that theDirectors and Officers Charge (“D&O Charge”) be eliminated and that arelated holdback for the legal costs of the Company’s D&Os bereduced from its present balance to $75,000; and

e) Recommend that this Honourable Court make an order:

Directing the Receiver to make the Proposed Distribution;

Eliminating the D&O Charge and reducing the holdbackestablished to fund the costs of the D&Os legal counsel from itspresent balance to $75,000; and

Approving the Receiver’s activities as set out in this Report.

1On December 9, 2011, the assets used by Richter in its Toronto restructuring practice were acquired by

D&P. Pursuant to the Substitution Order, D&P was substituted in place of Richter in certain ongoingmandates, including acting as Receiver in these proceedings. The licensed trustees/restructuringprofessionals overseeing this mandate prior to December 9, 2011, remain unchanged.

Duff & Phelps Canada Restructuring Inc. Page 3

1.2 Currency

1. Unless otherwise noted, all currency references in this Report are to Canadiandollars.

1.3 Restrictions

1. In preparing this Report, the Receiver has relied upon the Company’s booksand records. The Receiver has not performed an audit or other verification ofsuch information.

2. Future oriented financial information relied upon in this Report is based onassumptions regarding future events; actual results achieved may vary fromthis information and these variations may be material.

2.0 Background

1. The Company was a franchisee of Yum! Restaurants International (Canada)LP.

2. At the time the CCAA Order was made, the Company was the largest operatorof KFC franchises in Canada.

3. In addition to operating KFC franchises, the Company operated a limitednumber of multi-branded restaurants that included a KFC restaurant and eithera Taco Bell or Pizza Hut restaurant.

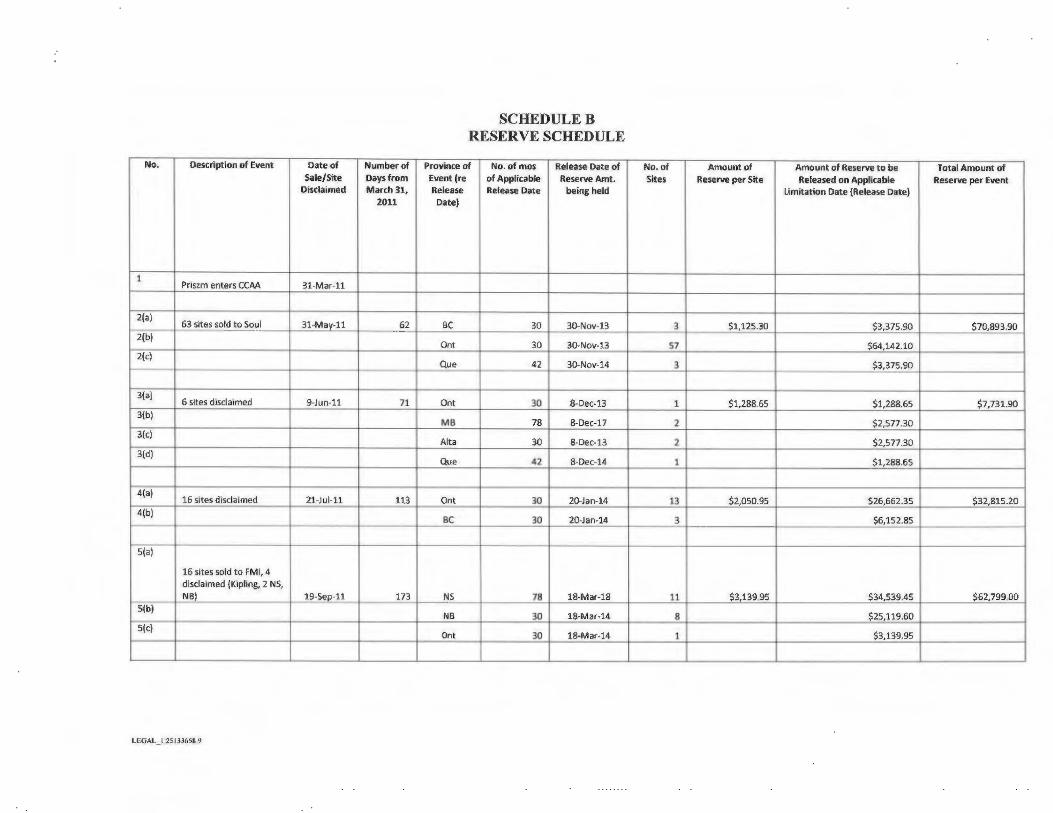

4. During the CCAA Proceedings, the Company completed the followingtransactions:

the sale of the majority of its locations in British Columbia and Ontarioto Soul Foods Canada Inc. (“Soul Transaction”). Stores in BritishColumbia and Ontario that were excluded from the Soul Transactionhave been closed; and

the sale of the majority of its locations in Nova Scotia and NewBrunswick to FMI Atlantic Inc. (“FMI Transaction”). Stores in NovaScotia and New Brunswick that were excluded from the FMITransaction have been closed.

Duff & Phelps Canada Restructuring Inc. Page 4

5. During the receivership proceedings, the Receiver completed transactions for:

the sale of the majority of the Company’s locations in Alberta andManitoba to Hi-Flyer Food (Canada) Inc. (“HFFI”) (“HFFI Transaction”).Stores in these provinces that were excluded from the HFFITransaction have been closed; and

the sale of the majority of the Company’s locations in Quebec toOlympus Food (Canada) Inc. (“Olympus Transaction”). Stores inQuebec that were excluded from the Olympus Transaction have beenclosed.

6. Additional information concerning the Company and these proceedings isprovided in the application materials filed in the Receivership Proceedings andin the CCAA Proceedings, including:

the affidavit of Paul Procyk, a Vice-President of Prudential InvestmentManagement, Inc., sworn September 9, 2011, filed in the context of thereceivership application;

the Receiver’s reports to Court, which are available on the Receiver’swebsite at www.duffandphelps.com/restructuringcases; and

motion materials and reports filed by the Monitor in the CCAAProceedings, which are available on the Monitor’s website athttp://cfcanada.fticonsulting.com/priszm/.

3.0 Sysco Dispute

1. In the days preceding the commencement of the CCAA proceedings (March 14to March 28, 2011), the Company issued eleven cheques totallingapproximately $1.386 million to Sysco (“Sysco Cheques”). The SyscoCheques were not honoured as a result of the commencement of the CCAAproceedings.

2. Sysco asserted that the D&Os issued the Sysco Cheques notwithstanding theyknew that the cheques would not be honoured and therefore Sysco submitteda D&O Claim for $1.4 million (the “Initial Sysco Claim”) in the processestablished to solicit claims against the Company’s D&Os pursuant to a Courtorder dated June 29, 2011 (the “D&O Claims Solicitation Procedure”).

3. In anticipation of making a distribution to Prudential, as of the date of theReceiver’s third report to Court dated June 28, 2012 (“Third Report”) and asnoted therein, the Receiver, counsel to Sysco and counsel to the D&Os agreedto a holdback in the amount of $1.4 million pending resolution of the Syscoissue (the “Sysco Holdback”).

Duff & Phelps Canada Restructuring Inc. Page 5

4. As detailed in the Receiver’s sixth report to Court dated April 18, 2013 (“SixthReport”), on December 20, 2012, after discussions with counsel to Sysco whoexpressed concern about the impending expiry of the limitation period, theReceiver wrote to counsel to Sysco to advise that the Receiver did not intend toseek an adjudication process to deal with the Initial Sysco Claim andsuggested that Sysco file a statement of claim with respect to the matter.

5. On February 28, 2013, Sysco served materials in respect of a motion seekingan order lifting the stay of proceedings so that Sysco could issue its statementof claim to preserve its rights given the limitation period to advance a claim wasapproaching.

6. The draft statement of claim of Sysco included the Initial Sysco Claim in theamount of approximately $1.4 million, plus a further punitive damages claim for$5 million (the “Damages Claim”).

7. On November 29, 2014, the Court granted an Order withdrawing andabandoning the Damages Claim and the Damages Claim was barred pursuantto the terms of the D&O Claims Solicitation Procedure Order dated June 29,2011.

8. On April 22, 2014, the Receiver and Sysco finalized a settlement of the SyscoDispute by executing minutes of settlement and release (“Minutes ofSettlement”) in respect of the Initial Sysco Claim.

9. Pursuant to the Minutes of Settlement, a payment of $200,000 was made toSysco in consideration of, among other things: (i) the release and discharge ofthe Sysco Holdback in the amount of $1.4 million in respect of the Initial SyscoClaim; and (ii) acceptance by the Receiver of $2.6 million as an unsecuredclaim of Sysco in the receivership2. The Receiver sought and obtained theapproval of the D&Os to enter into the Minutes of Settlement.

4.0 Denial of Coverage of the Sysco Claim

1. As detailed in the Receiver’s eighth report to Court dated February 4, 2014(“Eighth Report”), Great American Insurance Company (“Insurer”) deniedcoverage on behalf of the D&Os for the Sysco Claim on the basis that,pursuant to an endorsement to the policy, the Insurer is not liable to makepayment for loss in connection with any claim arising out of, directly orindirectly, the franchise operations of the Priszm Entities.

2No distributions to unsecured creditors are expected.

Duff & Phelps Canada Restructuring Inc. Page 6

2. The Insurer took the position that since all of the restaurant locations operatedby the Priszm Entities were franchise locations and that the Priszm Entitiesoperated no “homegrown” restaurants, the cheques that are the subject of theSysco Claims were issued in purported payment to Sysco for the supply ofgoods to franchise restaurant locations, and therefore “involve the franchiseoperations of the Company”. The Receiver objected to the Insurer’s position.

3. Since the date of the Eighth Report, the Receiver has reached an agreementwith the Insurer whereby the Insurer will pay the Receiver $125,000, and inconsideration, the Receiver and each of the D&Os will release and dischargethe Insurer from any and all actions, causes of action, claims and demands ofevery nature or kind.

4. The D&Os have executed minutes of settlement and release formalizing termsreached with the Insurer.

5.0 Distributions and Holdbacks

5.1 Cash Position

1. As at June 24, 2014, the estate cash balance totalled approximately $4.14million, including monies invested in short-term GICs and net of $38,000 ofknown accrued post-filing liabilities.

5.2 Security Opinion and Distributions to Date

1. As detailed in the Third Report, the Monitor obtained Opinions (as defined inthe Third Report) providing that, subject to the assumptions, qualifications andlimitations contained therein, the security granted by the Company toComputershare Trust Company of Canada, as agent for Prudential, is validand that, except for the collateral charges in respect of certain leaseholdinterests described in the Third Report, the necessary registrations have beenmade in the relevant jurisdictions in order to perfect or evidence such security.As noted in the Third Report, the Receiver obtained opinion reliance lettersfrom each of the firms that provided the Opinions confirming that the Receivermay rely on the Opinions as of the date upon which the Opinions were issued.A copy of the Third Report is attached (without appendices) as Appendix “B” tothis Report.

2. Pursuant to the terms of three Distribution Orders previously made in theseproceedings, approximately $51.104 million has been distributed to Prudential.

Duff & Phelps Canada Restructuring Inc. Page 7

5.3 Proposed Distribution

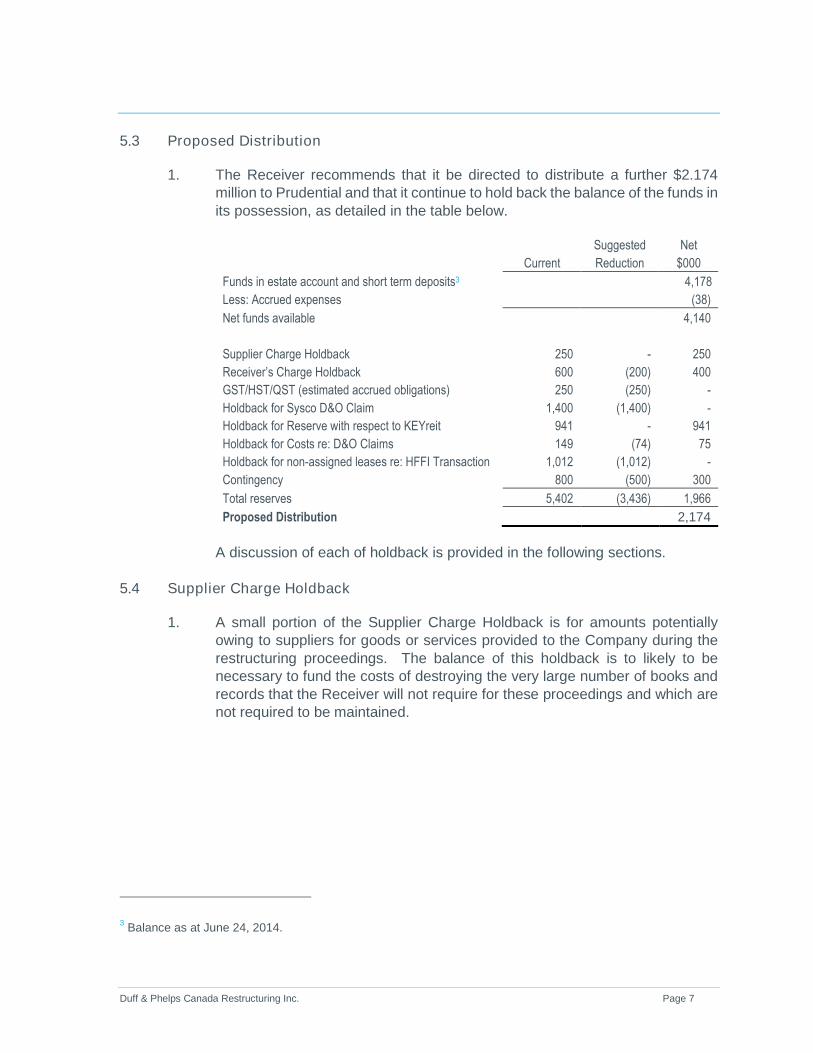

1. The Receiver recommends that it be directed to distribute a further $2.174million to Prudential and that it continue to hold back the balance of the funds inits possession, as detailed in the table below.

Current

Suggested

Reduction

Net

$000

Funds in estate account and short term deposits3 4,178

Less: Accrued expenses (38)

Net funds available 4,140

Supplier Charge Holdback 250 - 250

Receiver’s Charge Holdback 600 (200) 400

GST/HST/QST (estimated accrued obligations) 250 (250) -

Holdback for Sysco D&O Claim 1,400 (1,400) -

Holdback for Reserve with respect to KEYreit 941 - 941

Holdback for Costs re: D&O Claims 149 (74) 75

Holdback for non-assigned leases re: HFFI Transaction 1,012 (1,012) -

Contingency 800 (500) 300

Total reserves 5,402 (3,436) 1,966

Proposed Distribution 2,174

A discussion of each of holdback is provided in the following sections.

5.4 Supplier Charge Holdback

1. A small portion of the Supplier Charge Holdback is for amounts potentiallyowing to suppliers for goods or services provided to the Company during therestructuring proceedings. The balance of this holdback is to likely to benecessary to fund the costs of destroying the very large number of books andrecords that the Receiver will not require for these proceedings and which arenot required to be maintained.

3Balance as at June 24, 2014.

Duff & Phelps Canada Restructuring Inc. Page 8

5.5 Receiver’s Charge Holdback

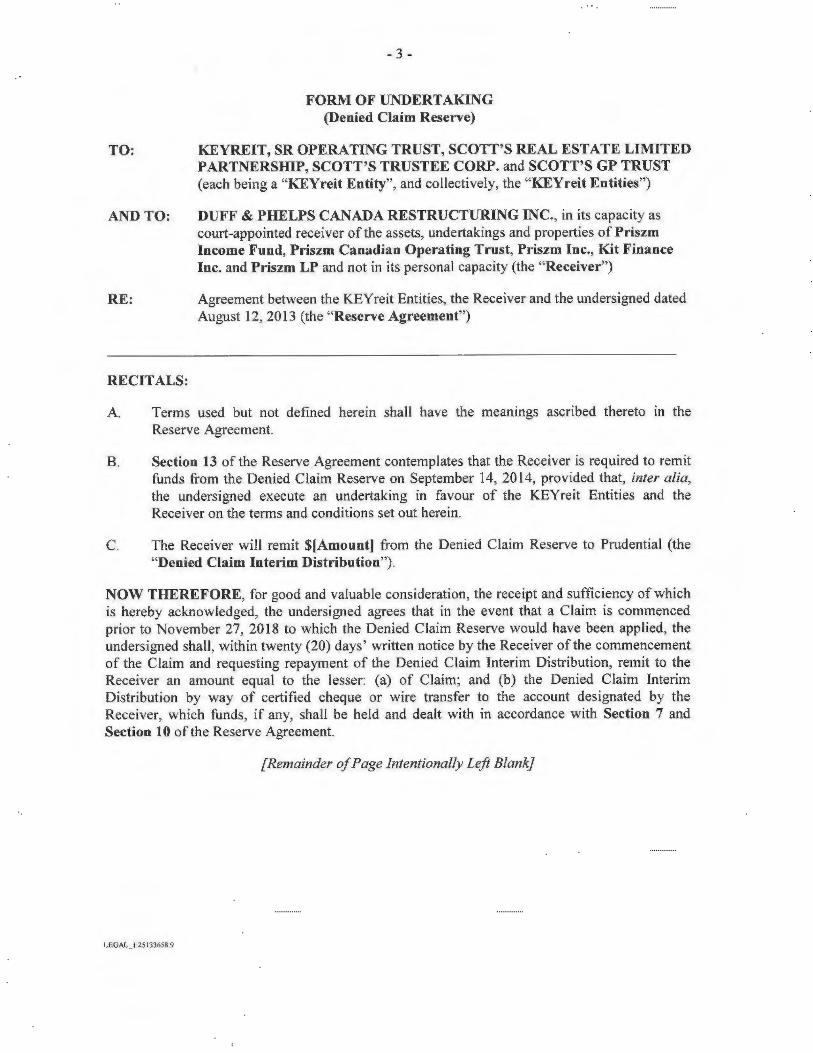

1. The Receiver’s Charge Holdback (for the Receiver and its counsel) has beenreduced from $600,000 to $400,000. Several issues remain outstanding inthese proceedings, including administration of an agreement entered intoamong the Receiver, KEYreit (formerly Scott’s Real Estate Investment Trust),Scott’s Real Estate Limited Partnership, Scott’s Trustee Corp. and Scott’s GPTrust (each being a “KEYreit Entity”, and collectively, the “KEYreit Entities”)and Prudential in respect of post-filing insurance claims arising at the KEYreitEntities’ locations during the receivership period (the “Reserve Agreement”).The KEYreit Entities were formerly the Company’s largest landlord.

5.6 HST Holdback

1. The Company is current in respect of its Goods and Services(“GST”)/Harmonized Sales Tax (“HST”), and provincial sales tax (forManitoba and Quebec) remittances and filings.

2. During the receivership proceedings, Company representatives advised theReceiver that a Quebec Sales Tax (“QST”) audit was completed for the yearended December 31, 2009 and that they believe an Ontario Retail Sales Taxaudit was also completed through that date.

3. The Company requested that new sales tax audits be performed by therespective government agencies. Manitoba Finance responded to therequest with a letter dated October 1, 2012 stating that the Company’s taxaccount had been closed. Revenu Quebec and Canada Revenue Agency(“CRA”) did not respond to the request.

4. On April 1, 2013, the Receiver left follow-up voicemail messages with RevenuQuebec and CRA. As of the date of this Report, the Receiver has notreceived a response from Revenu Quebec or CRA. This issue was previouslyraised in the Third Report, the Sixth Report and the Receiver’s seventh reportto Court dated November 22, 2013 (“Seventh Report”). The Seventh Reportnoted the Receiver’s intention to seek an order at the next distribution motionpermitting it to distribute the balance being held back for this purpose($250,000). CRA and Revenu Quebec were both served the Third Report,Sixth Report and Seventh Report and as at the date of this Report, neither hasadvised the Receiver of a claim for HST/QST. Accordingly, the Receiver isseeking an order permitting it to distribute the balance of these monies.

5. It should be noted that the other provinces in which the Company previouslyoperated had provincial taxes administered by CRA.

Duff & Phelps Canada Restructuring Inc. Page 9

5.7 Holdback for Sysco D&O Claim, Holdback for Costs re: D&O Claims andReduction of D&O Charge

1. The Sysco Claim has been resolved, as detailed in Section 3 above.Accordingly, the Receiver recommends that the amounts previously heldbackin respect of the Sysco Claim, being $1.4 million, be made available fordistribution to creditors in accordance with their priorities, meaning that themonies available for distribution would be paid to Prudential.

2. In addition to the previous $1.4 million holdback, a reserve of $175,0004 wasestablished to fund the legal costs of the parties covered by the D&O Charge.Since that reserve was established, a total of $97,692 has been paid to MindenGross LLP (“Minden Gross”), counsel to the Company’s Chief RestructuringOfficers. The Receiver is in receipt of one additional invoice from MindenGross in the amount of $5,350 and one invoice from Blake, Cassels & GraydonLLP, counsel to the Company’s independent directors, in the amount of$66,106. These invoices will be paid imminently.

3. As a result of the settlement of the Sysco Claim, the Receiver proposes toeliminate the D&O Charge and reduce the Holdback for Costs re D&O Claimsfrom its present balance of $149,000 to $75,000, with this amount being usedto fund the legal costs noted in paragraph 2 above.

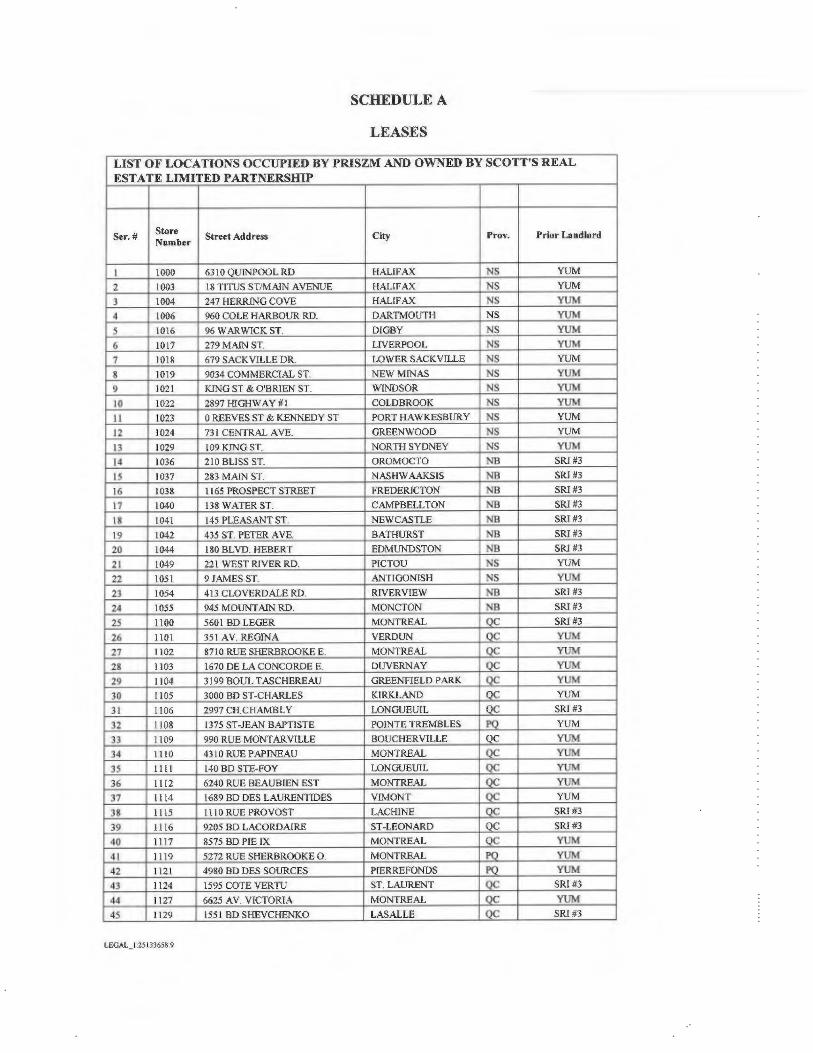

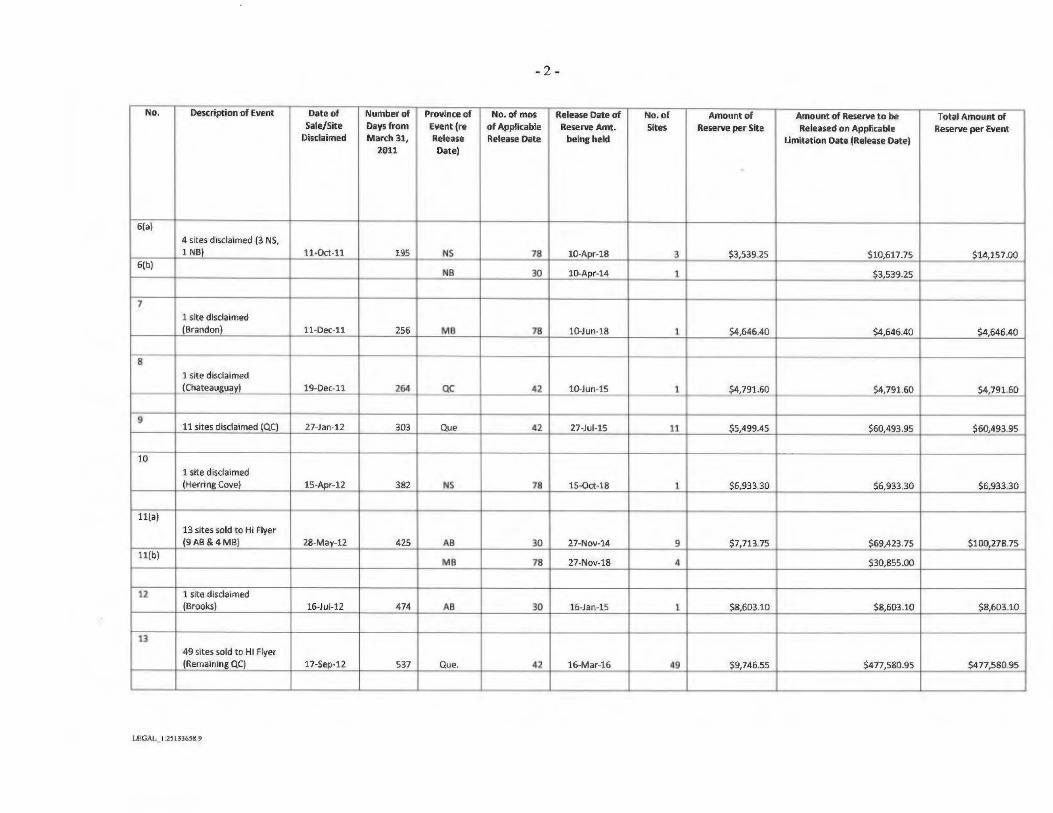

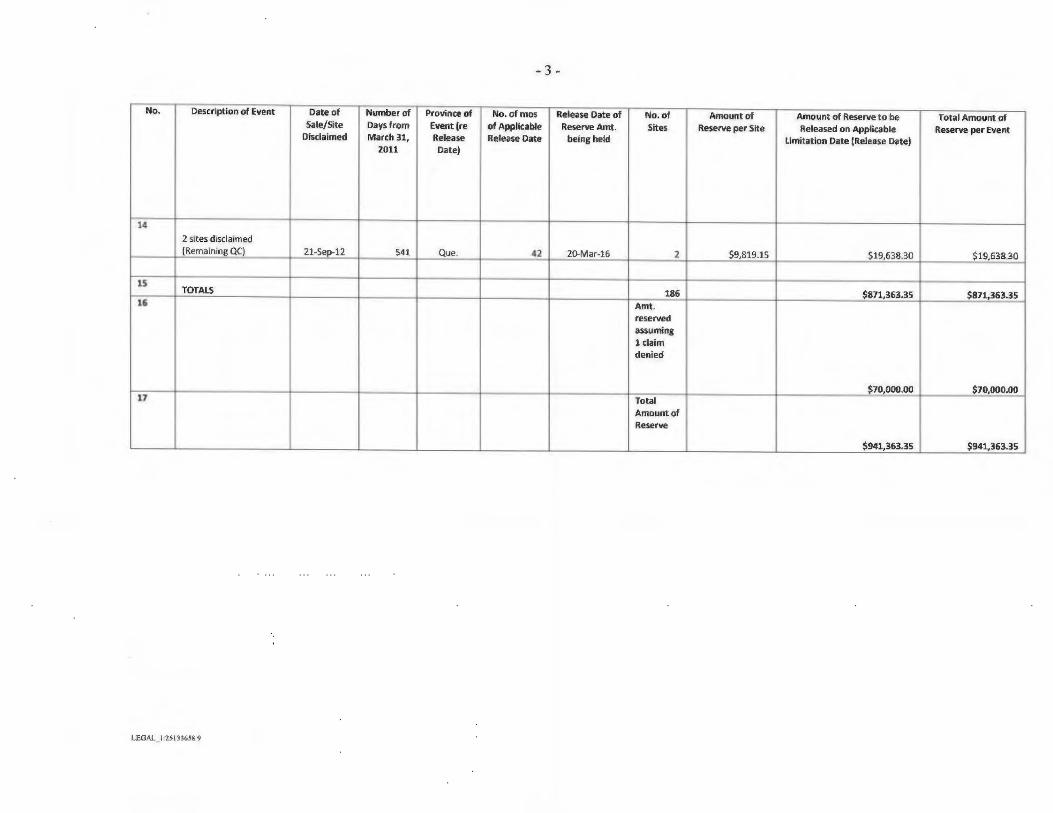

5.8 Holdback for Reserve with Respect to KEYreit

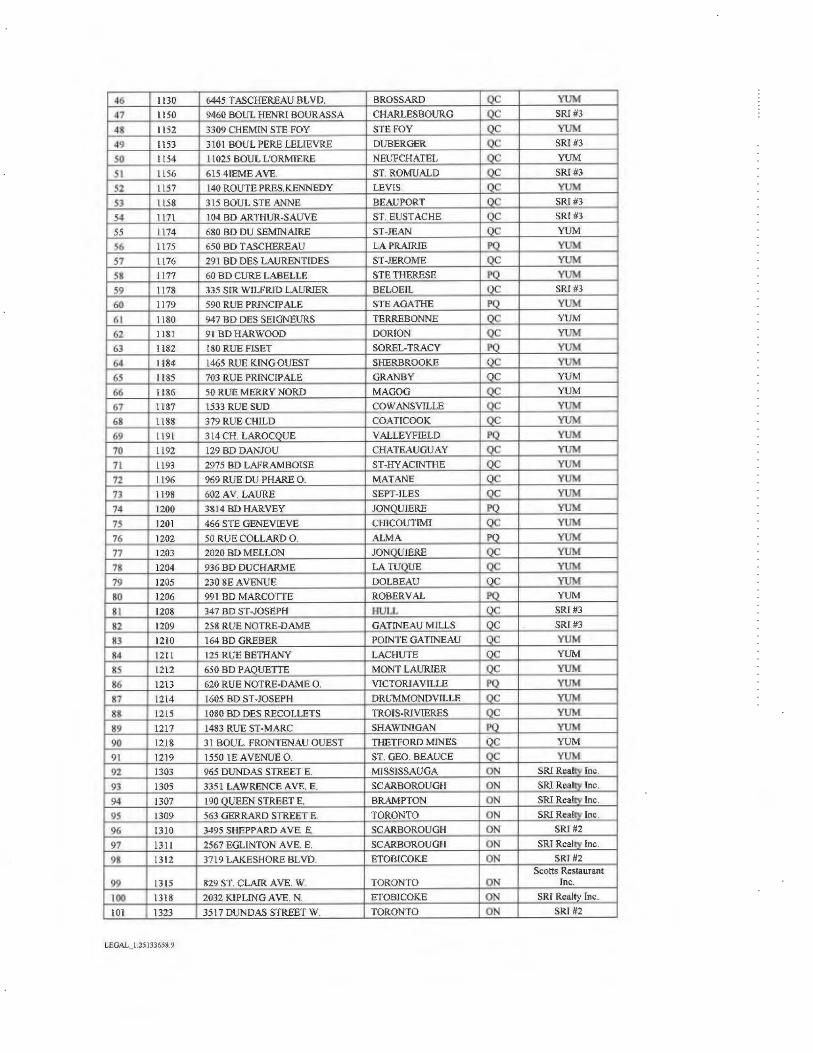

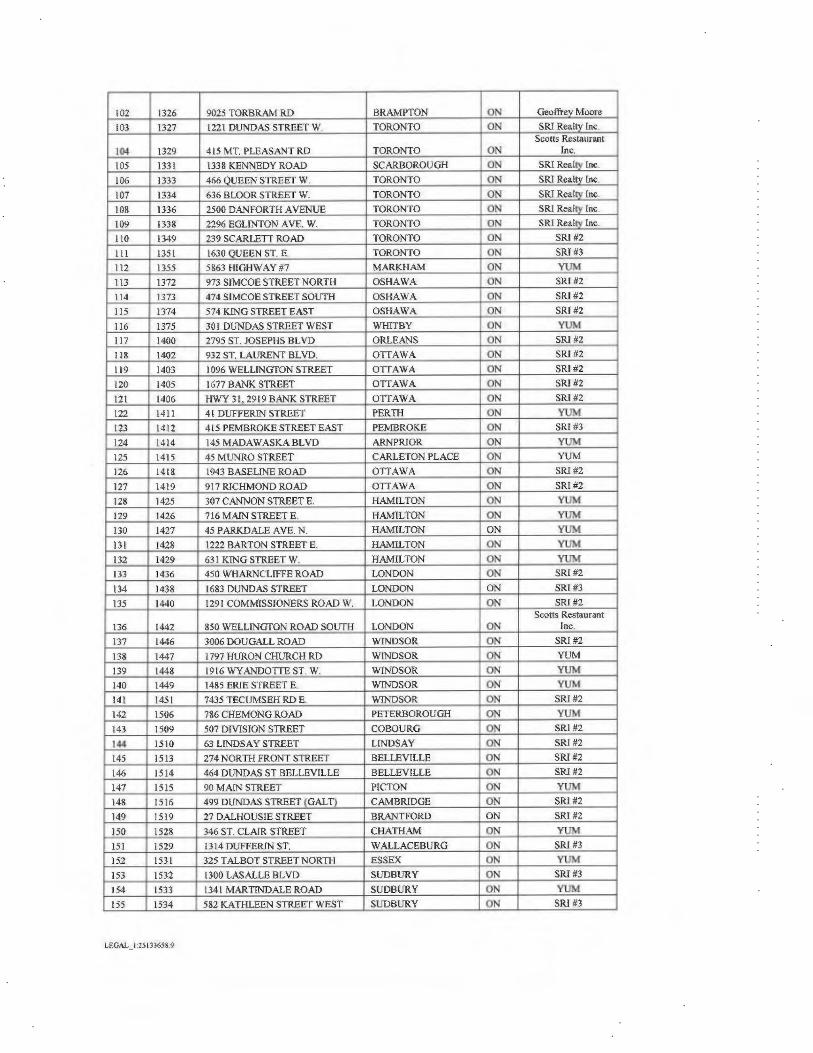

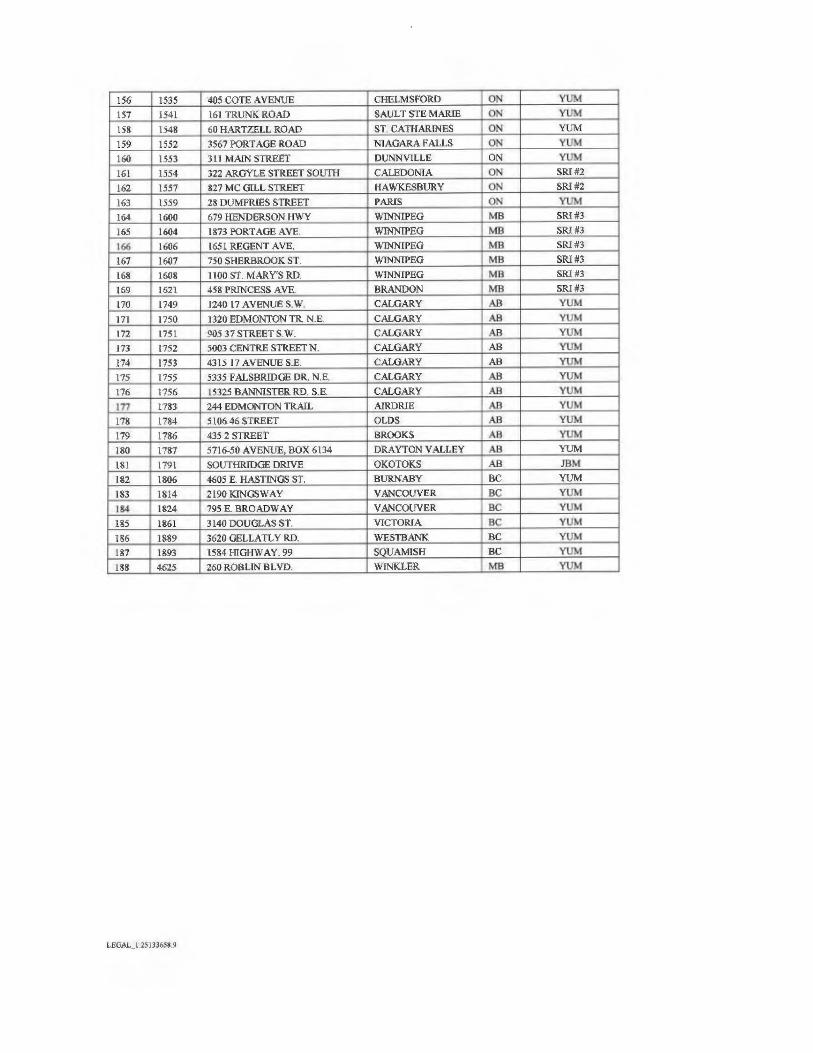

1. The Company operated 188 stores across Canada where KEYreit was thelandlord (the “Locations”).

2. To address the possibility that KEYreit may have insurance claims forpost-filing operations of the Company in the Locations, the Receiver andKEYreit negotiated the Reserve Agreement. A copy of the Reserve Agreementis attached as Appendix “C” to this Report.

3. The Reserve Agreement establishes a mechanism to deal with insuranceclaims that may be asserted against the Company and/or the KEYreit Entitiesin respect of the Company’s post-filing operations at the Locations (the“Claims”). It also provides that the Receiver will hold $941,363 (the “ReserveAmount”) to satisfy deductibles owing in respect of Claims that are covered byinsurance and that relate to the post-filing operations of the Company at theLocations.

4See line item in the table in Section 5.3 entitled “Holdback for Costs re: D&O Claims”. This line item was

originally $175,000 but was reduced to $149,000.

Duff & Phelps Canada Restructuring Inc. Page 10

4. As at the date of this Report, no distributions have been made pursuant to theterms of the Reserve Agreement and the Receiver continues to hold theReserve Amount. It should be noted, however, that in accordance with theterms of the Reserve Agreement, the Receiver intends to distribute toPrudential approximately $146,000 forthwith and the Reserve will then beadjusted accordingly.

5.9 Holdback for Non-assigned Leases re: HFFI Transaction

1. As at the date of this Report, the Receiver has obtained lease assignments forall locations subject to the HFFI Transaction. These monies have beendistributed to Prudential in accordance with an order of the Court dated July 31,2012. Accordingly, no further holdback with respect to the HFFI Transaction isrequired.

5.10 Contingency

1. The contingency reserve has been reduced from $800,000 to $300,000. Thisreserve is recommended to cover off any items not contemplated above.

5.11 Conclusion

1. The Receiver is seeking an order of the Court to make the ProposedDistribution to Prudential. The Receiver is of the view that there are sufficientholdbacks to address potential claims that may need to be funded, and that anorder should be issued directing it to pay forthwith $2.174 million to Prudential.

2. Due to the resolution of the Sysco Claim, the Receiver is also seeking an orderof the Court eliminating the D&O Charge and reducing to $75,000 theHoldback for Costs re the D&O Claim.

3. The Receiver is of the view that any monies which become available fordistribution resulting from a reduction in the holdbacks detailed in Section 5 ofthis Report, or any further recoveries (if any), should be distributed by theReceiver to Prudential without further order of the Court.

6.0 Overview of the Receiver’s Activities

1. In addition to the activities detailed above and related thereto, since February4, 2014, the date of the Eighth Report, the Receiver’s activities have included:

Monitoring and reviewing all receipts and disbursements and signing allcheques and wire transfers;

Reviewing monthly bank statements;

Duff & Phelps Canada Restructuring Inc. Page 11

Corresponding with the Company’s insurance brokers and insuranceadjusters regarding post-filing insurance claims arising at theLocations;

Corresponding with KEYreit, the insurance adjuster, Osler, Hoskin &Harcourt LLP (“Osler”), the Receiver’s counsel, and Miller ThompsonLLP, counsel to KEYreit, regarding the Reserve Agreement;

Reviewing and executing extensions to occupation agreementsbetween the Receiver and HFFI and corresponding with counsel toHFFI regarding same;

Reviewing and executing lease assignments in respect of the HFFITransaction;

Corresponding with Osler, HFFI, and Dickinson Wright LLP, counsel toOlympus and HFFI, regarding lease assignments;

Preparing schedules of monthly occupancy costs to be paid by theReceiver on behalf of HFFI and providing same to HFFI forreimbursement;

Accessing information from the Company’s IT equipment and systemsrequired for the administration of the estate, including responding toemployee information requests in the context of records of employmentand T4 slips;

Corresponding with Osler and Sysco Canada regarding the claim filedby Sysco Canada in the D&O Claims Solicitation Procedure;

Reviewing various iterations of the Minutes of Settlement anddiscussing same with Osler;

Reviewing the Company’s books and records as they pertain to theSysco pre-filing claim;

Corresponding with Lenczner Slaght Royce Smith Griffin LLP, Oslerand Minden Gross regarding the Minutes of Settlement;

Preparing, in the context of the Sysco settlement, a summary ofprofessional fees paid to counsel to the former directors and officers ofthe Company;

Reviewing on a daily basis the Company’s mail; the mail has beenredirected to the Receiver’s office;

Appendix “A”

Appendix “B”

Appendix “C”