Embed Size (px)

Citation preview

For professional investors only. This material is not suitable for retail clients

Schroders fixed incomeNiagara Institutional DialogueJune 2015

Alan Cauberghs, CFA Senior Investment Director, Fixed Income

� Quantitative easing (“QE”) – the right response?

� Structural market changes – liquidity gap

� Unintended consequences – a brave new world

� Outlook – what to expect going forward

2

Source: Schroders.

IntroductionA brave new world – did we think this through?

Quantitative easing

Quantitative easingStimulating real economy?

4

Source: BBC, The Telegraph, The Guardian

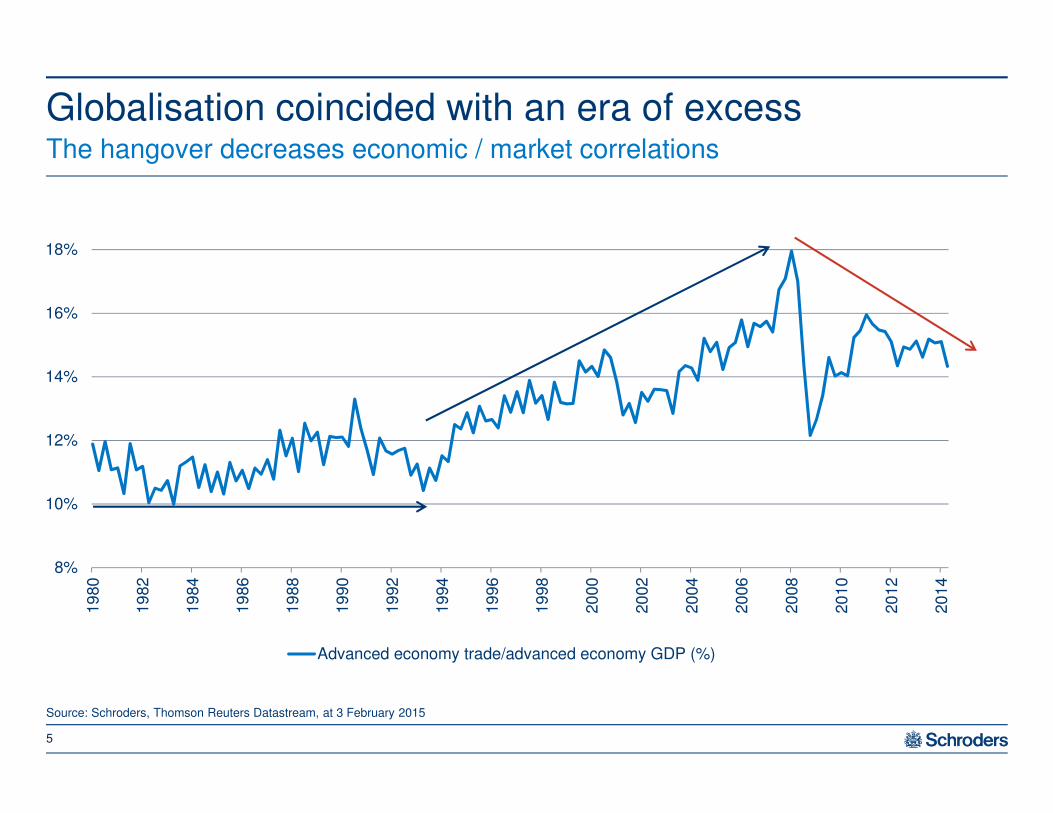

Globalisation coincided with an era of excessThe hangover decreases economic / market correlations

5

Source: Schroders, Thomson Reuters Datastream, at 3 February 2015

8%

10%

12%

14%

16%

18%

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

Advanced economy trade/advanced economy GDP (%)

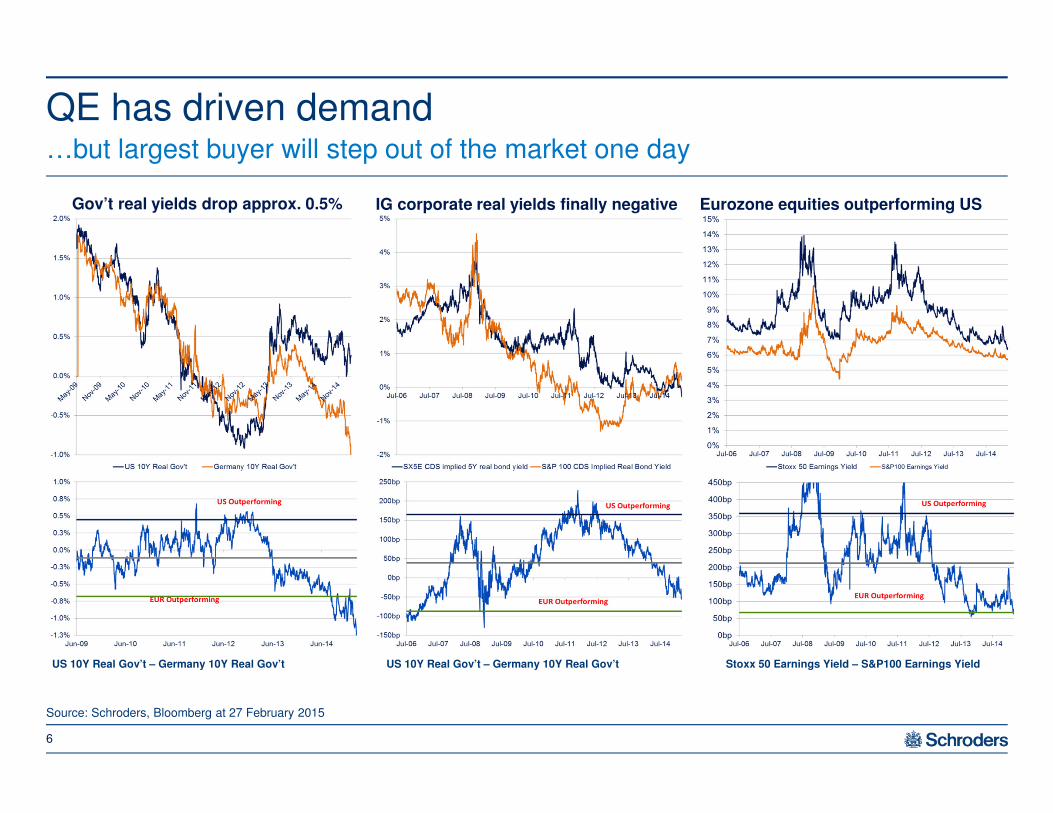

QE has driven demand…but largest buyer will step out of the market one day

Source: Schroders, Bloomberg at 27 February 2015

6

11/06/2015 12:30:48

Gov’t real yields drop approx. 0.5% IG corporate real yields finally negative Eurozone equities outperforming US

US 10Y Real Gov’t – Germany 10Y Real Gov’t US 10Y Real Gov’t – Germany 10Y Real Gov’t Stoxx 50 Earnings Yield – S&P100 Earnings Yield

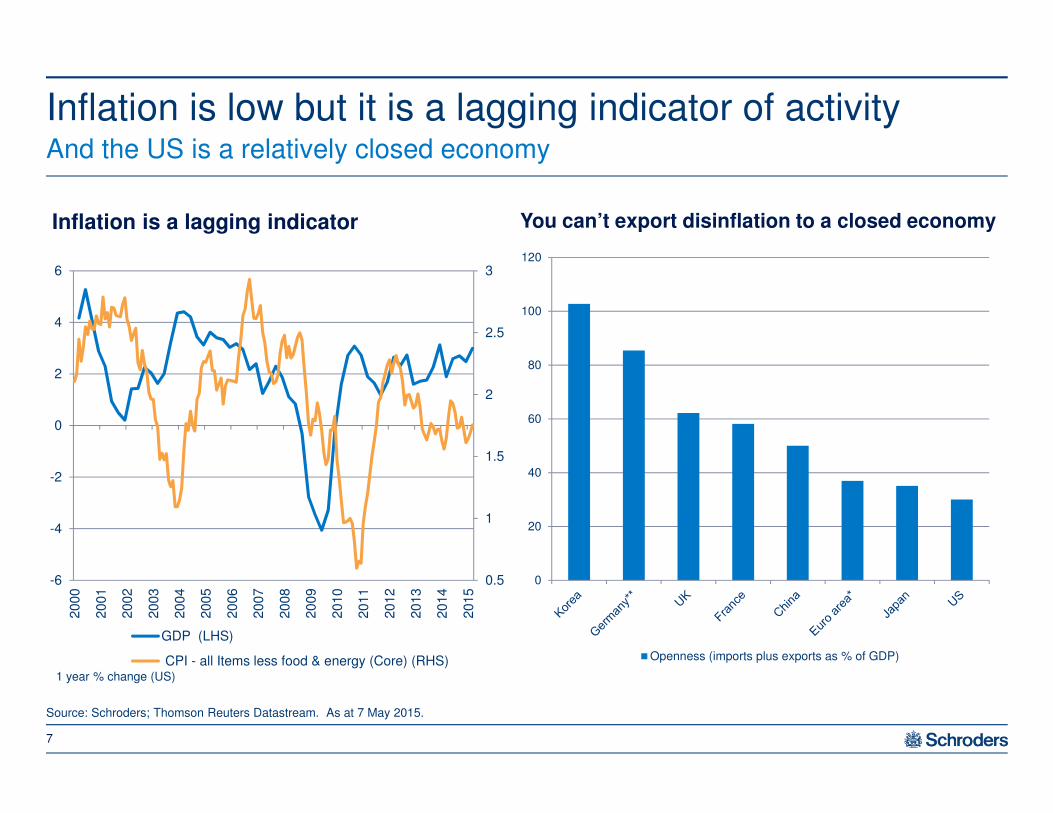

Inflation is low but it is a lagging indicator of activityAnd the US is a relatively closed economy

7

0.5

1

1.5

2

2.5

3

-6

-4

-2

0

2

4

6

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

1 year % change (US)

GDP (LHS)

CPI - all Items less food & energy (Core) (RHS)

Inflation is a lagging indicator You can’t export disinflation to a closed economy

0

20

40

60

80

100

120

Openness (imports plus exports as % of GDP)

Source: Schroders; Thomson Reuters Datastream. As at 7 May 2015.

8

Some 10 year government bond yields at all time lows

“Safe haven” assets are no longer safeFuture returns being brought forward – tomorrow’s lunch has been eaten

Source: Schroders; Thomson Reuters Datastream. As at 3 February 2015.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

SZ GE SW NL FR AT BE JP FI

% of debt outstanding with negative yield

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

10 Year Govt YTM (%)

Unprecedented % of outstanding government bonds have negative yields

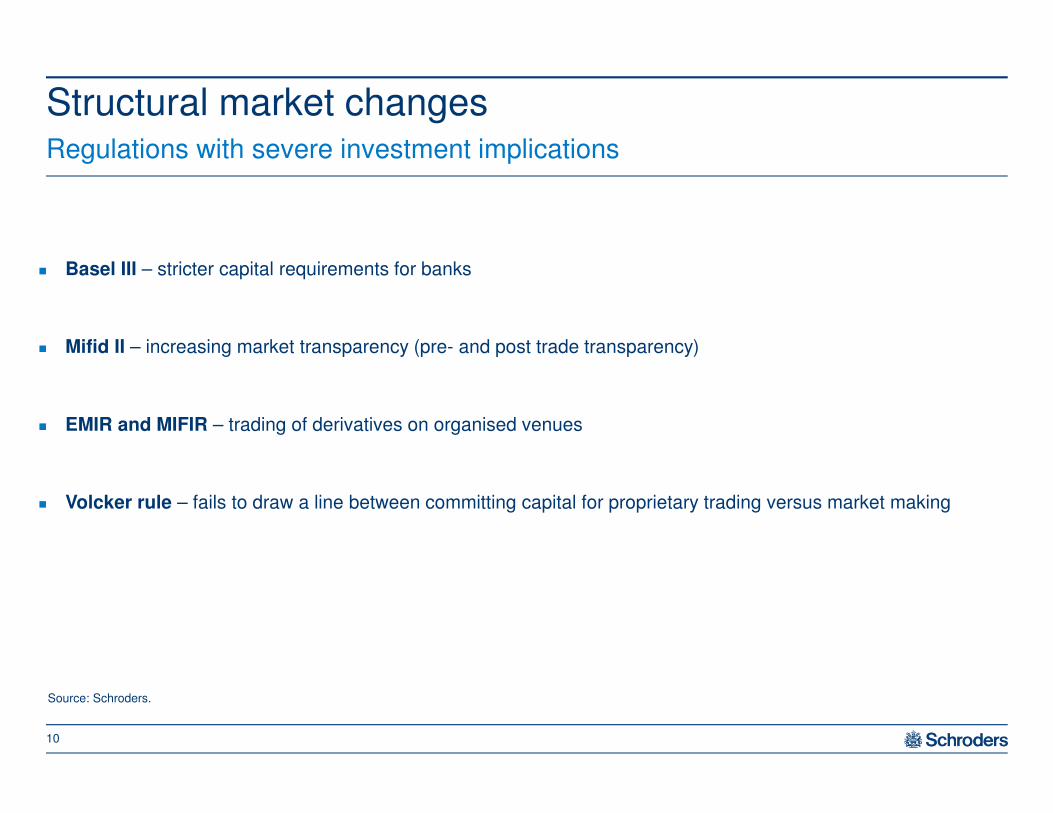

Structural market changes

� Basel III – stricter capital requirements for banks

� Mifid II – increasing market transparency (pre- and post trade transparency)

� EMIR and MIFIR – trading of derivatives on organised venues

� Volcker rule – fails to draw a line between committing capital for proprietary trading versus market making

10

Source: Schroders.

Structural market changesRegulations with severe investment implications

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

IG

HY

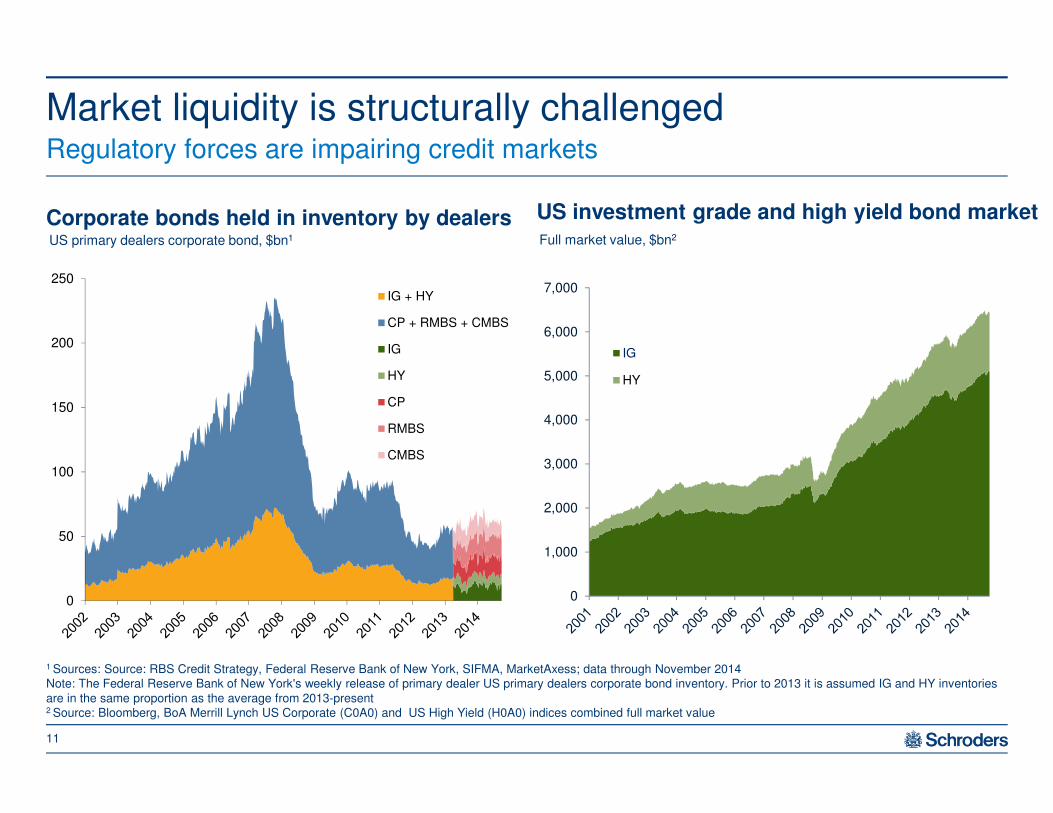

Corporate bonds held in inventory by dealers US investment grade and high yield bond market

Market liquidity is structurally challengedRegulatory forces are impairing credit markets

11

1 Sources: Source: RBS Credit Strategy, Federal Reserve Bank of New York, SIFMA, MarketAxess; data through November 2014Note: The Federal Reserve Bank of New York's weekly release of primary dealer US primary dealers corporate bond inventory. Prior to 2013 it is assumed IG and HY inventories are in the same proportion as the average from 2013-present2 Source: Bloomberg, BoA Merrill Lynch US Corporate (C0A0) and US High Yield (H0A0) indices combined full market value

Full market value, $bn2US primary dealers corporate bond, $bn1

0

50

100

150

200

250

IG + HY

CP + RMBS + CMBS

IG

HY

CP

RMBS

CMBS

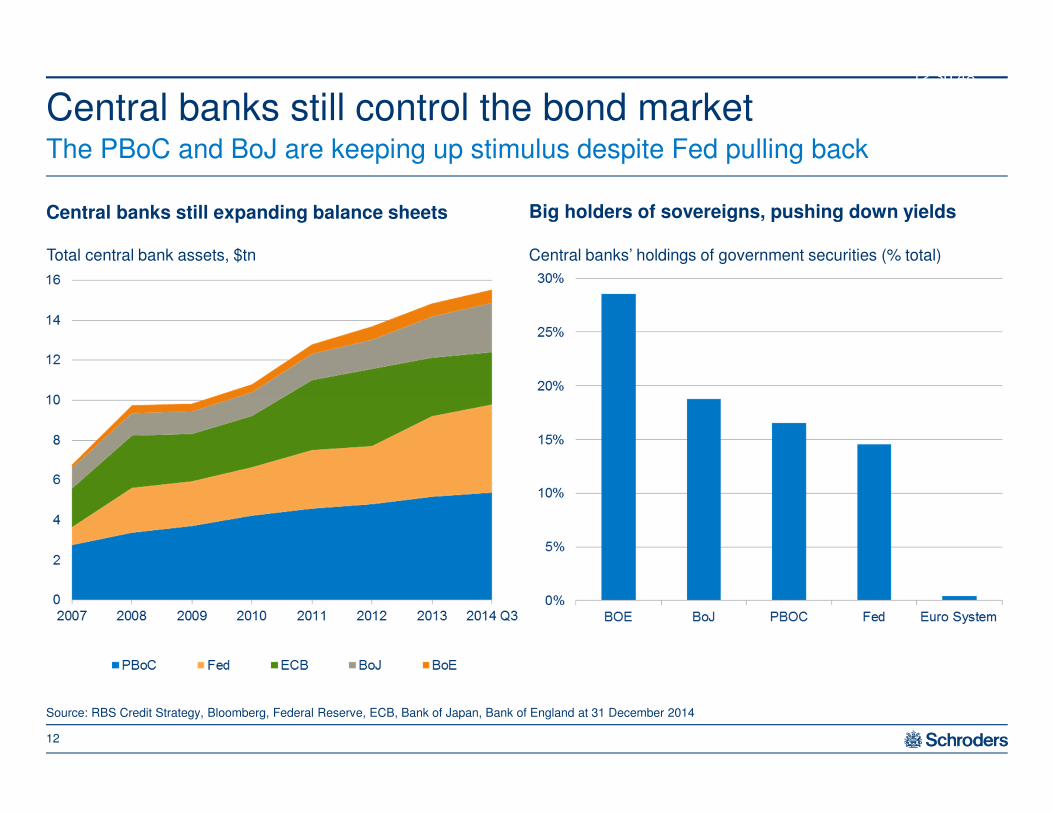

Central banks still control the bond marketThe PBoC and BoJ are keeping up stimulus despite Fed pulling back

12

Source: RBS Credit Strategy, Bloomberg, Federal Reserve, ECB, Bank of Japan, Bank of England at 31 December 2014

Central banks still expanding balance sheets Big holders of sovereigns, pushing down yields

11/06/2015 12:30:48

Total central bank assets, $tn Central banks’ holdings of government securities (% total)

Unintended consequences

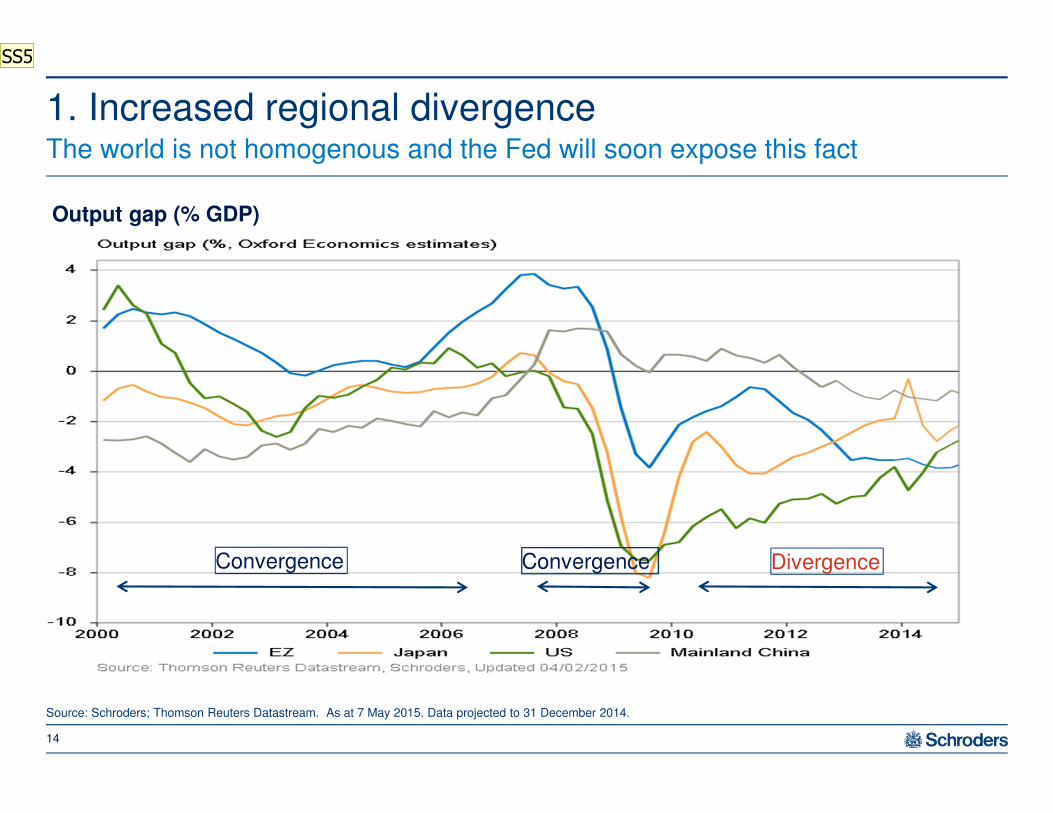

1. Increased regional divergenceThe world is not homogenous and the Fed will soon expose this fact

14

Source: Schroders; Thomson Reuters Datastream. As at 7 May 2015. Data projected to 31 December 2014.

Output gap (% GDP)

Convergence Convergence Divergence

SS5

Slide 14

SS5 suggested edit - in header consider changing 'will' to 'may' given recent events?

Defer to speaker/team on this. Scheffer, Scott, 6/04/15

1. Increased regional divergence

15

0

2

4

6

8

10

12

14

Jan-0

6

Jul-06

Jan-0

7

Jul-07

Jan-0

8

Jul-08

Jan-0

9

Jul-09

Jan-1

0

Jul-10

Jan-1

1

Jul-11

Jan-1

2

Jul-12

Jan-1

3

Jul-13

Jan-1

4

Jul-14

Jan-1

5

Unemployment rates %

US UK Eurozone Japan

-1

0

1

2

3

4

5

6

2011 2012 2013 2014 2015 2016

Consensus forecasts consumer prices (%YoY, mean)

US Eurozone Japan China

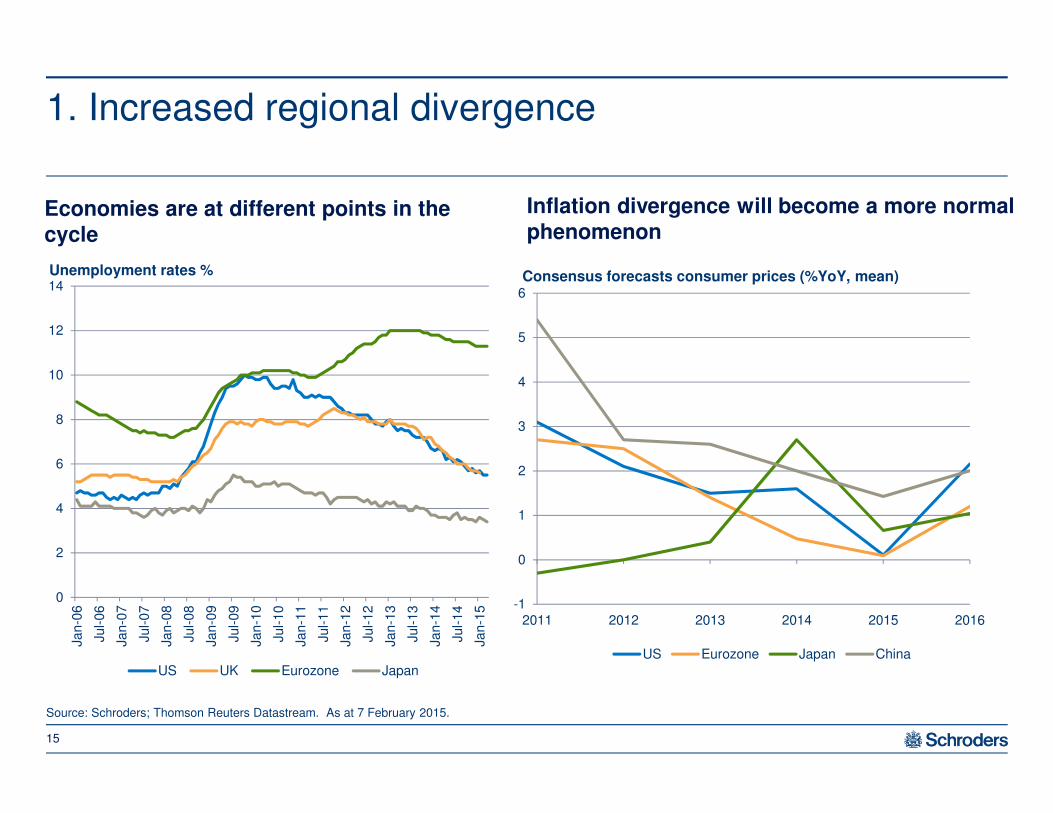

Economies are at different points in the

cycle

Inflation divergence will become a more normal

phenomenon

Source: Schroders; Thomson Reuters Datastream. As at 7 February 2015.

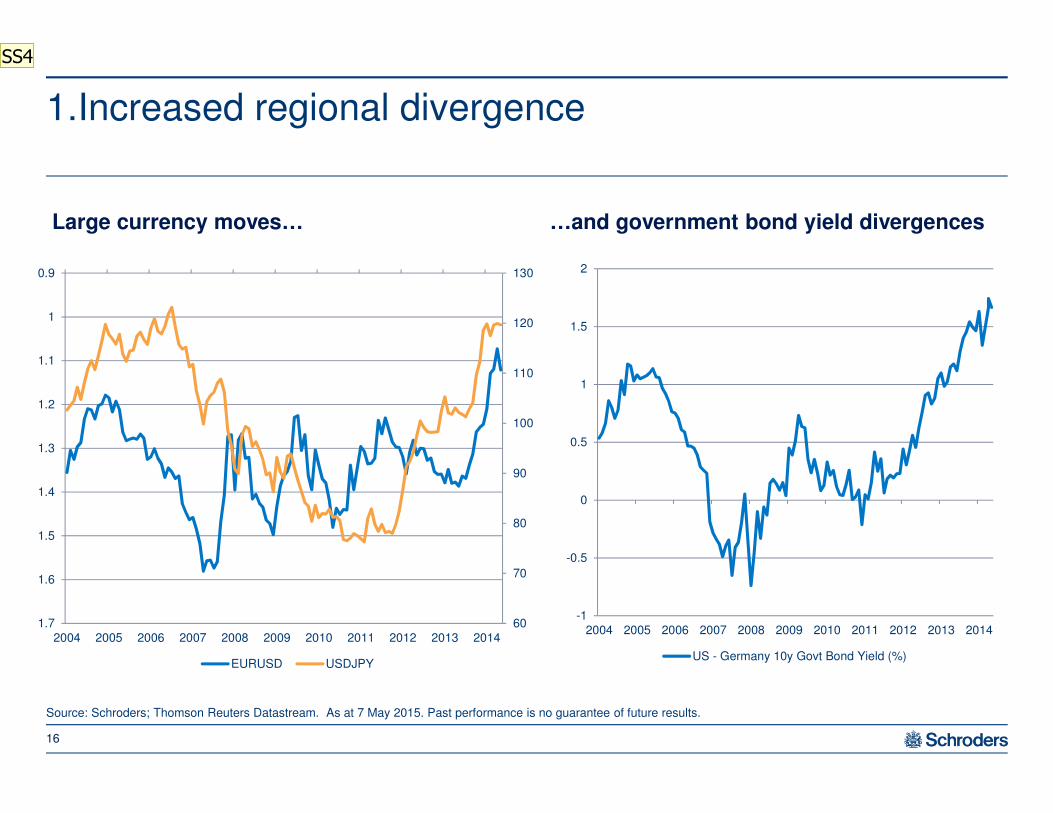

1.Increased regional divergence

16

Source: Schroders; Thomson Reuters Datastream. As at 7 May 2015. Past performance is no guarantee of future results.

60

70

80

90

100

110

120

1300.9

1

1.1

1.2

1.3

1.4

1.5

1.6

1.72004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

EURUSD USDJPY

Large currency moves…

-1

-0.5

0

0.5

1

1.5

2

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

US - Germany 10y Govt Bond Yield (%)

…and government bond yield divergences

SS4

Slide 16

SS4 add FN in redScheffer, Scott, 6/04/15

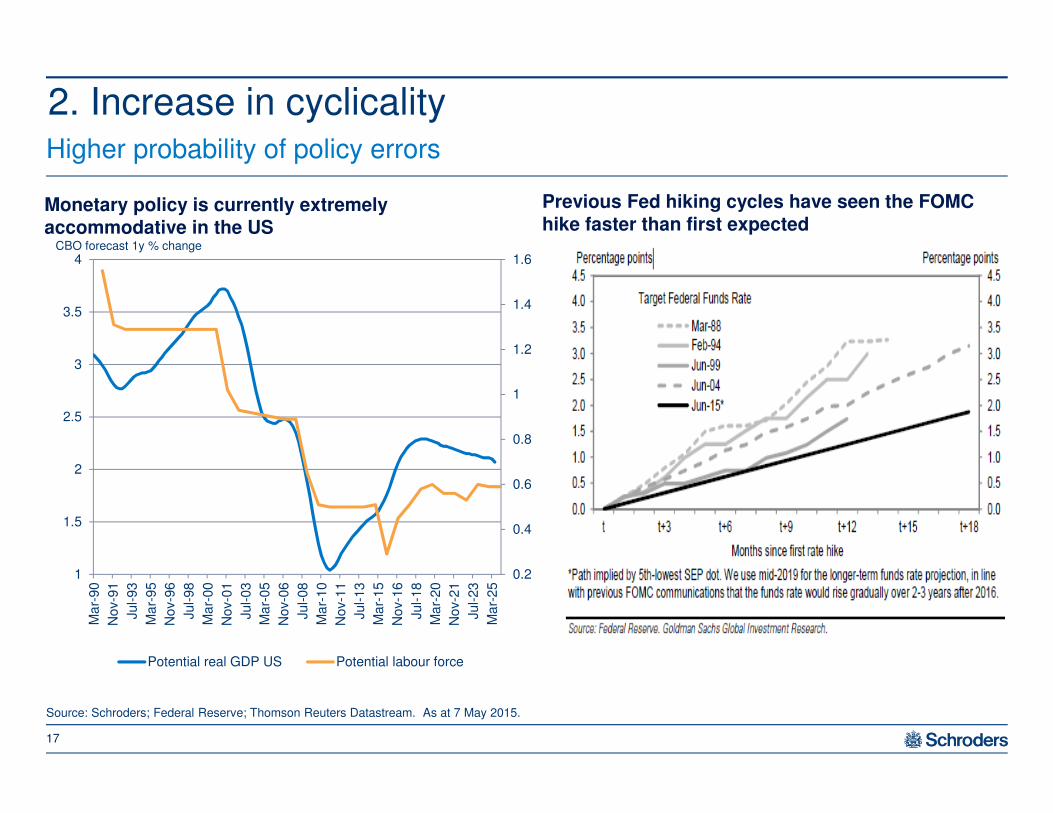

2. Increase in cyclicalityHigher probability of policy errors

17

Source: Schroders; Federal Reserve; Thomson Reuters Datastream. As at 7 May 2015.

Monetary policy is currently extremely

accommodative in the US

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1

1.5

2

2.5

3

3.5

4

Ma

r-90

Nov-9

1

Jul-93

Ma

r-95

Nov-9

6

Jul-98

Ma

r-00

Nov-0

1

Jul-03

Ma

r-05

Nov-0

6

Jul-08

Ma

r-10

Nov-1

1

Jul-13

Ma

r-15

Nov-1

6

Jul-18

Ma

r-20

Nov-2

1

Jul-23

Ma

r-25

CBO forecast 1y % change

Potential real GDP US Potential labour force

Previous Fed hiking cycles have seen the FOMC

hike faster than first expected

UK nominal GDP vs. base rate US nominal GDP vs. Fed funds

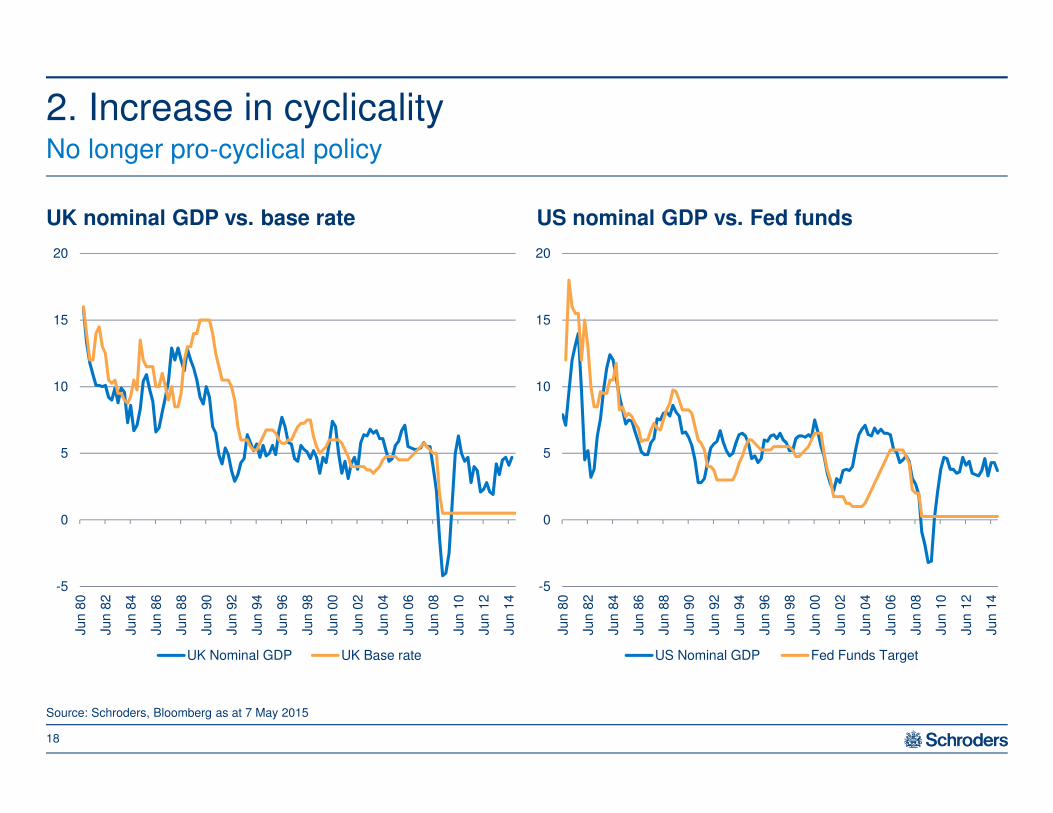

2. Increase in cyclicality

18

Source: Schroders, Bloomberg as at 7 May 2015

-5

0

5

10

15

20

Jun 8

0

Jun 8

2

Jun 8

4

Jun 8

6

Jun 8

8

Jun 9

0

Jun 9

2

Jun 9

4

Jun 9

6

Jun 9

8

Jun 0

0

Jun 0

2

Jun 0

4

Jun 0

6

Jun 0

8

Jun 1

0

Jun 1

2

Jun 1

4

UK Nominal GDP UK Base rate

-5

0

5

10

15

20

Jun 8

0

Jun 8

2

Jun 8

4

Jun 8

6

Jun 8

8

Jun 9

0

Jun 9

2

Jun 9

4

Jun 9

6

Jun 9

8

Jun 0

0

Jun 0

2

Jun 0

4

Jun 0

6

Jun 0

8

Jun 1

0

Jun 1

2

Jun 1

4

US Nominal GDP Fed Funds Target

No longer pro-cyclical policy

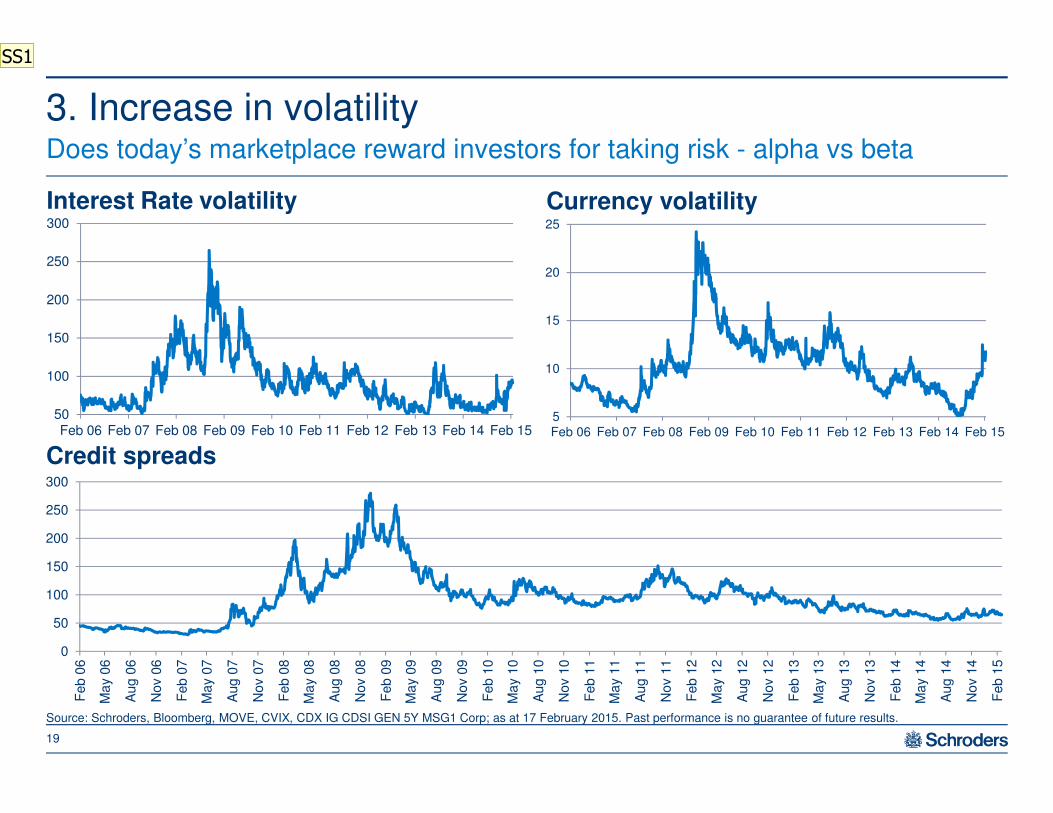

3. Increase in volatilityDoes today’s marketplace reward investors for taking risk - alpha vs beta

19

Source: Schroders, Bloomberg, MOVE, CVIX, CDX IG CDSI GEN 5Y MSG1 Corp; as at 17 February 2015. Past performance is no guarantee of future results.

Interest Rate volatility Currency volatility

Credit spreads

50

100

150

200

250

300

Feb 06 Feb 07 Feb 08 Feb 09 Feb 10 Feb 11 Feb 12 Feb 13 Feb 14 Feb 15

0

50

100

150

200

250

300

Feb 0

6

Ma

y 0

6

Aug

06

Nov 0

6

Feb 0

7

Ma

y 0

7

Aug

07

Nov 0

7

Feb 0

8

Ma

y 0

8

Aug

08

Nov 0

8

Feb 0

9

Ma

y 0

9

Aug

09

Nov 0

9

Feb 1

0

Ma

y 1

0

Aug

10

Nov 1

0

Feb 1

1

Ma

y 1

1

Aug

11

Nov 1

1

Feb 1

2

Ma

y 1

2

Aug

12

Nov 1

2

Feb 1

3

Ma

y 1

3

Aug

13

Nov 1

3

Feb 1

4

Ma

y 1

4

Aug

14

Nov 1

4

Feb 1

5

5

10

15

20

25

Feb 06 Feb 07 Feb 08 Feb 09 Feb 10 Feb 11 Feb 12 Feb 13 Feb 14 Feb 15

SS1

Slide 19

SS1 should sub-head end with a ? mark

also add FN noted in redScheffer, Scott, 6/04/15

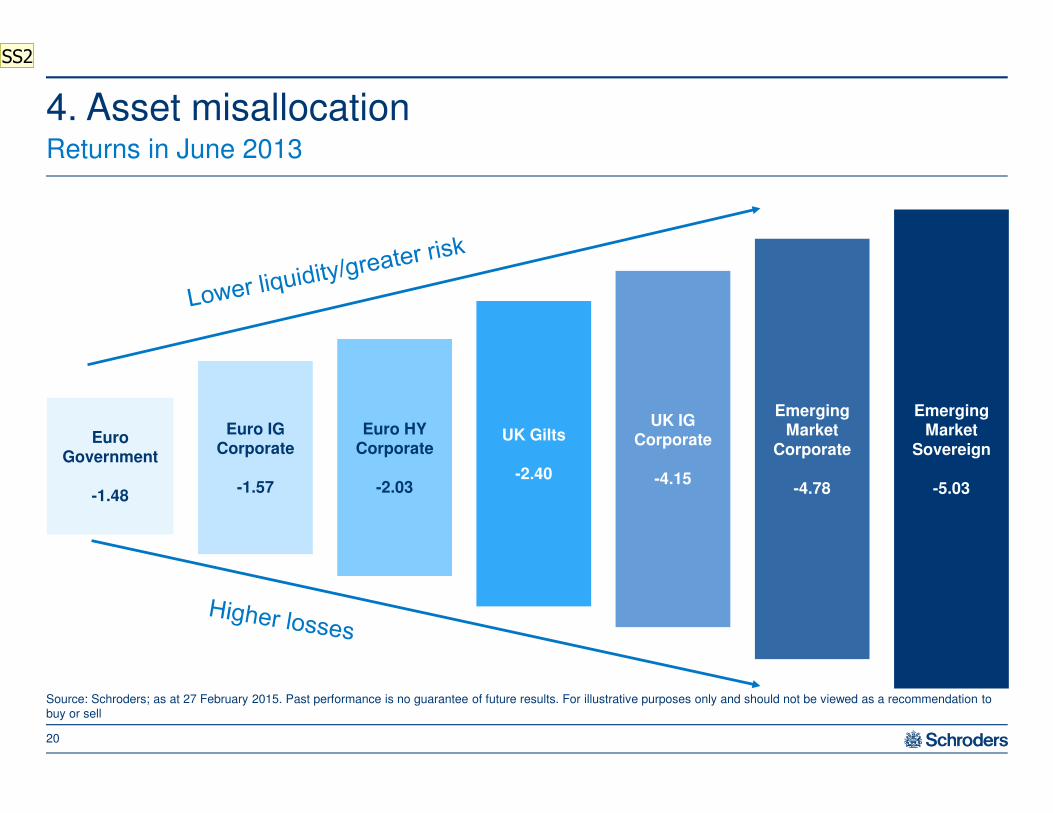

4. Asset misallocationReturns in June 2013

20

Source: Schroders; as at 27 February 2015. Past performance is no guarantee of future results. For illustrative purposes only and should not be viewed as a recommendation to buy or sell

11/06/2015 12:30:48

Euro IG Corporate

-1.57

Euro HY Corporate

-2.03

UK Gilts

-2.40

UK IG Corporate

-4.15

Emerging Market

Corporate

-4.78

Emerging Market

Sovereign

-5.03

Euro Government

-1.48

SS2

Slide 20

SS2 add FN noted in redScheffer, Scott, 6/04/15

Outlook

� Lower asset returns

� Higher cyclicality

� Regional divergence

� Lower terminal rate

22

Source: Schroders. Views current as at date of this material and is subject to change over time.

Wrong policy, unintended consequencesWhat next?

SS3

Slide 22

SS3 add views FN, in redScheffer, Scott, 6/04/15

Schroder Investment Management North America Inc. is an indirect wholly owned subsidiary of Schroders plc and an SEC registered investment adviser registered in Canada in the capacity of Portfolio Manager with the securities regulatory authorities in the Provinces of Alberta, British Columbia, Manitoba, Nova Scotia, Ontario, Quebec and Saskatchewan, and provides asset management products and services to clients in those jurisdictions. This document does not purport to provide investment advice and the information contained in this document is for general informational purposes only. It does not constitute or form part of any offer for sale or solicitation of any offer to buy or subscribe for any securities. It does not purport to describe the business or affairs of any issuer and is not being provided for delivery to or review by any prospective purchaser so as to assist the prospective purchaser to make an investment decision in respect of any securities, and is not otherwise provided in furtherance of a trade in securities. This document is delivered to certain qualified recipients only and may not be communicated, disclosed or quoted from except as specifically approved by Schroder Investment Management North America Inc.

Schroder Fund Advisors, LLC is a wholly-owned subsidiary of Schroder Investment Management North America Inc. and is a FINRA registered limited purpose Broker/Dealer and is registered in Canada in the capacity of Exempt Market Dealer with the Securities Commissions of Alberta, British Columbia, Manitoba, New Brunswick, Nova Scotia, Ontario, Quebec, and Saskatchewan.

Schroders investment products are only available to Permitted Clients as that term is defined by Canadian securities laws. This document does not constitute an offer to sell securities. Qualified investors will receive material documentation containing important information about their investments prior to investing.

Past performance is not guarantee of future results. The value of an investment can go down as well as up and is not guaranteed.

Schroder Investment Management North America Inc.875 Third Avenue, New York, NY 10022-6225(212) 641-3800www.schroders.com/canada

Important information

23