Embed Size (px)

Citation preview

BENPOSIUM 2016

NGL EXPORTS AND GLOBAL PETROCHEMICAL FEEDSTOCK COMPETITION

Kendall Puig Senior Analyst, NGLs and LPG Platts Analytics, Bentek products

Copyright © 2016 by S&P Global. All rights reserved.

RESTRICTIONS ON USE: YOU MAY USE THE PRICES, INDEXES, ASSESSMENTS AND OTHER RELATED INFORMATION (COLLECTIVELY, “DATA”) IN THIS PRESENTATION ONLY FOR YOUR PERSONAL USE. YOU MAY NOT PUBLISH, REPRODUCE, DISTRIBUTE, RETRANSMIT, RESELL, CREATE ANY DERIVATIVE WORK FROM AND/OR OTHERWISE PROVIDE ACCESS TO DATA OR ANY PORTION THEREOF TO ANY PERSON (EITHER WITHIN OR OUTSIDE YOUR COMPANY INCLUDING, BUT NOT LIMITED TO, VIA OR AS PART OF ANY INTERNAL ELECTRONIC SYSTEM OR INTERNET SITE), FIRM OR ENTITY. DISCLAIMER: PLATTS, ITS AFFILIATES AND ALL OF THEIR THIRD-PARTY LICENSORS DISCLAIM ANY AND ALL REPRESENTATIONS AND WARRANTIES, EXPRESS OR IMPLIED, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE AS TO THE DATA, OR THE RESULTS OBTAINED BY ITS USE OR AS TO THE PERFORMANCE THEREOF. LIMITATION OF LIABILITY: IN NO EVENT WHATSOEVER SHALL PLATTS, ITS AFFILIATES OR THEIR THIRD-PARTY LICENSORS BE LIABLE FOR ANY INDIRECT, SPECIAL, INCIDENTAL, PUNITIVE OR CONSEQUENTIAL DAMAGES, INCLUDING BUT NOT LIMITED TO LOSS OF PROFITS, TRADING LOSSES, OR LOST TIME OR GOODWILL, EVEN IF THEY HAVE BEEN ADVISED OF THE POSSIBILITY OF SUCH DAMAGES, WHETHER IN CONTRACT, TORT, STRICT LIABILITY OR OTHERWISE. THE DATA IS PROVIDED ON AN “AS IS” BASIS AND YOUR USE OF THE DATA IS AT YOUR OWN RISK. COPYRIGHT © 2016 BY PLATTS, MCGRAW HILL FINANCIAL, INC. ALL RIGHTS RESERVED. NO PORTION OF THIS PUBLICATION MAY BE PHOTOCOPIED, REPRODUCED, RETRANSMITTED, PUT INTO A COMPUTER SYSTEM OR OTHERWISE REDISTRIBUTED WITHOUT PRIOR AUTHORIZATION FROM PLATTS. PLATTS IS A TRADEMARK OF MCGRAW HILL FINANCIAL.

Source: Lisa Frank

3 BENPOSIUM 2016

Key Takeaways

• A large spread between gas and liquids prices in the US led to rapid NGL production growth over the past five years. Exports have served as a “relief value” for much of the resulting oversupply.

• Midstream and shipping companies pursued investment projects expecting continued production growth, leading to an infrastructure overbuild.

• US NGLs have found new markets overseas, largely from petrochemical producers looking to move lower on the cost curve, but this demand is not limitless.

• Going forward, the outlook for US NGL exports will vary by product, region, and even individual terminal.

• Gas indexed pricing could make Marcus Hook ethane exports more competitive than USGC Mont Belvieu indexed barrels.

• LPG exports will be flat to declining in the short term and there may be greater competition between terminals for export volumes.

BENPOSIUM 2016

HOW DID WE GET HERE? EXPORTS DRIVEN BY SUPPLY PUSH

5 BENPOSIUM 2016

Large spread between gas and liquids incentivized NGL production growth

5

0

5

10

15

20

25

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

$/M

MB

tu

WTI Henry Hub Mont Belvieu NGLs Brent

Source: Platts, Bentek

Large “Value Gap” incentivizes: • Increased drilling for

liquids • NGL demand/export

projects

6 BENPOSIUM 2016

A tighter spread makes many US petrochemical and export projects less attractive

6

0

5

10

15

20

25

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

$/M

MB

tu

WTI Henry Hub Mont Belvieu NGLs Brent

Source: Platts, Bentek

Smaller “Value Gap” leads to: • Decreased drilling activity • Less attractive economics

for NGL demand and export projects

7 BENPOSIUM 2016

Growth of NGL production from gas plants expected to level off

0.0

1.0

2.0

3.0

4.0

5.0

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Mb/

d

US NGL Supply from Gas Plants Prior to ethane rejection

Ethane Propane Normal Butane Isobutane Natural Gasoline

Liquids premium leads to 75% growth

in 5 years…

…but is expected to drop to 14% due to

lower prices

Source: Bentek Market Call: North American NGLs 2Q2016

8 BENPOSIUM 2016

Recent NGL oversupply balanced mainly by increased exports and ethane rejection

0%5%10%15%20%25%30%35%40%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

MM

b/d

Domestic Demand vs. Oversupply

Ethane Rejection Exports

Domestic Demand % Oversupply (Exports + Rejection)

Source: Bentek Market Call: North American NGLs 2Q2016

BENPOSIUM 2016

ALLEVIATING CONSTRAINTS

10 BENPOSIUM 2016

Rejection balanced the ethane market, pushed prices to the gas floor

10

0

2

4

6

8

10

12

14

$/M

Mbt

u

Ethane Prices vs. Natural Gas

Henry Hub Natural GasMont Belvieu Ethane

0200400600800

1,0001,2001,4001,6001,8002,000

Mb/

d

Ethane Gas Production From Gas Plants (prior to rejection) vs. Petchem Demand

Gas Plants Petchem

11 BENPOSIUM 2016

Canadian petchem producers are able to take advantage of low-cost US ethane by pipeline

Benposium 2015 11

0

20

40

60

80

100

Mb/

d

US Ethane/Ethylene Exports

Source: Bentek, EIA

12 BENPOSIUM 2016

Enterprise Morgan’s

Point

Waterborne ethane exports require new terminal infrastructure

12

Owner Project Name Location Ethane Capacity (Mb/d)

In-Service Date Region

Sunoco Logistics Marcus Hook Delaware, PA ~40 March 2016 Northeast Enterprise Morgan’s Point Houston Ship Channel, TX 200 3Q2016 US Gulf Coast

Sunoco Marcus Hook

Source: Platts cFlow Source: Platts cFlow

13 BENPOSIUM 2016

Shipping capacity buildout will support waterborne export volumes

13

Ship owner Name/End User Number of ships

Unit capacity (cubic meters)

Est. Unit Capacity (Mb) In-Service Date

Delivered Evergas JS INEOS Insight 27,500 260 2015 Evergas JS INEOS Intrepid 27,500 260 2015 Evergas JS INEOS Ingenuity 27,500 260 2015 Evergas JS INEOS Inspiration 27,500 260 2016 Orderbook Evergas INEOS 4 27,500 260 2015-2016 Evergas INEOS 4 (2) 32,000 301 2018 Reliance/ Mitsui Reliance 6 87,000 835 2016-2017 Navigator Gas Borealis 1 35,000 325 2016 Navigator Gas TBD 3 35,000 301 2016 Ocean Yield SABIC 3 36,000 310 2016 Hartmann Schiffahrts Oriental Energy 5 85,000 802 2017-2018

Source: Bentek, Wartsila, Reliance

14 BENPOSIUM 2016

Propane and butane oversupply pushed US from net importer to a net exporter

14

-800

-600

-400

-200

0

200

400

Mb/

d

US LPG Net Imports

Total Propane Imports Total Normal Butane ImportsTotal Isobutane Imports Total Propane ExportsTotal Normal Butane Exports Total Isobutane ExportsNet Imports

Source: EIA, Bentek

15 BENPOSIUM 2016

Global LPG price spreads have also narrowed as US supply floods market

15

Source: Platts, Bentek

0

50

100

150

200

250

300

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

Cent

s/ga

l

Global Propane Prices

Mt. Belvieu Northwest Europe Japan FOB Saudi Arabia CP

Large spread between US and Asia/Europe demand markets incentivizes terminal buildout

Lower arbitrage opportunity with tight spread

16 BENPOSIUM 2016

US LPG export volumes no longer constrained by terminal capacity

Source: Bentek Market Call: North American NGLs 2Q2016, NGL Facilities Databank

Company Project Name State Capacity (Mb/d) ISD

Existing LPG Export Terminals 1045 Enterprise Enterprise TX 130 NA Enterprise Enterprise Expansion I TX 120 2013 Enterprise Enterprise Expansion II TX 50 2015 Enterprise Enterprise Expansion III TX 233 2015 Targa Galena Park TX 50 NA Targa Galena Park Expansion I TX 83 2013 Targa Galena Park Expansion II TX 84 2014 Sunoco Logistics Marcus Hook PA 17 NA Sunoco Logistics Marcus Hook Expansion I PA 40 2015 DCP Midstream Chesapeake VA 8 2015 Petrogas Ferndale WA 30 NA Sunoco Logistics Mariner South TX 200 2015

Brownfield Expansions 275 Sunoco Logistics Marcus Hook Expansion II PA 275 2017

Greenfield New Builds 287 AltaGas Prince Rupert BC 40 2018 Occidental Chemical Ingleside TX 100 TBD Phillips 66 Freeport LPG TX 147 2016 Cancelled 112 Waterside Energy WA Storage & Transfer WA 75 TBD Pembina West Coast Terminal OR 37 TBD

6%

91%

3%

Current Waterborne Export Capacity

East CoastUSGCWest Coast

22%

73%

5% 2018 Waterborne Export Capacity

East CoastUSGCWest Coast

17 BENPOSIUM 2016

VLGC spot rates on the decline as more ships enter the market

17

Source: Platts, BW LPG

0

10

20

30

40

50

60

70

80

Cen

ts/g

al

VLGC Spot Freight Rates

VLGC Freight Houston-Northwest EuropeVLGC Freight Houston-JapanVLGC Freight Persian Gulf-Japan

• VLGC capacity was not enough to facilitate increased flows from the US to Asia, leading to high freight rates.

• The current fleet of VLGCs is about 221 vessels with 53 ships on order.

• New ship deliveries have driven down rates. The Panama Canal expansion could lead to further decreases.

18 BENPOSIUM 2016

Propane and butane exports reached a record 962 Mb/d in January 2016 per EIA data

18

-

200

400

600

800

1,000

1,200

Mb/

d

Propane and Butane Exports

Propane Exports Normal Butane Exports Isobutane Exports

2014 Avg: 497 Mb/d

Record high: 962 Mb/d

2012 Avg: 197 Mb/d

Source: EIA, Bentek

BENPOSIUM 2016

FINDING OVERSEAS DEMAND

20 BENPOSIUM 2016

0

100

200

300

400

500

600

700

800

900

1000

0 20,000 40,000 60,000 80,000 100,000 120,000 140,000

$/MT

Cumulative Capacity ('000 MT)

Global Ethylene Cost Curve

Saudi Ethane

Iran Ethane US Ethane

US E/P Mix

WE Naphtha

SE Asia Naphtha NE Asia Naphtha

ME Ethane

CTO/MTO

Ethylene production cost curve highlights US advantage from shale gas ethane

Source: Platts Analytics

21 BENPOSIUM 2016

US cracker feedslate lighter; Europe, Asia remain naphtha dominated

0%

50%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

US Steam Cracker Feedslate

Ethane Propane Butane Naphtha

0%

50%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

European Steam Cracker Feedslate

Ethane Propane Butane Naphtha GasoilSource: Jacobs Consultancy’s Hodson Report

22 BENPOSIUM 2016

European steam crackers were the first to receive US waterborne ethane shipments

22

Company Location Country

Ethylene Capacity

(MMlbs/yr) Max Ethane

Demand (Mb/d)*

INEOS Rafnes Norway 1,213 32

INEOS Grangemouth UK 1,610 42

ExxonMobil Mossmorran UK 1,830 48

Borealis Stenungsund Sweden 1,378 36

SABIC Wilton UK 1,900 50

Source: Bentek Market Call: North American NGLs, 2Q2016 *Assumes a 95% utilization rate and 100% ethane feedslate

23 BENPOSIUM 2016

Reliance and Braskem have also announced contracts to import US ethane

Benposium 2015 23

Reliance contracted 72.5 Mb/d from Enterprise for 3

crackers

Ethane Propane Naphtha

Ethanol

Braskem purchased ethane from Enterprise

for Camcari cracker

24 BENPOSIUM 2016

Asia is now largest destination for US LPG exports

24

0100200300400500600700800900

1,000

Mb/

d

US LPG Exports to Region

North America South America Central America CaribbeanEurope Asia Africa

Source: EIA data through March 2016 , Bentek. Note: North America includes Canada and Mexico

16%

11%

5% 7%

14%

47%

0%

Export % to Region 2016 YTD

25 BENPOSIUM 2016

US LPG Exports to Asia and Europe Growing

25

0

20

40

60

80

100

Mb/d Western Europe

Netherlands France UK Portugal Spain

- 50

100 150 200 250 300 350 400 450Mb/d Asia

China Japan South Korea Singapore

0

50

100

150

200

250

300

2000 2002 2004 2006 2008 2010 2012 2014 1/1/2016YTD

Mb/d Latin America

Venezuela Panama Honduras Dominican Republic Chile Brazil Mexico

Source: EIA data through March 2016 , Bentek.

26 BENPOSIUM 2016

China is now the largest destination for US LPG, mainly due to new PDH units

Chinese PDH units

Plant Propylene Output (mt/yr)

Est. Propane Demand (Mb/d)

ISD

Tianjin Bohai Chemical 600,000 23.2 Oct 2013

Zhejiang Ningbo Haiyue 600,000 23.2 July 2014

Zhejiang Satellite Petchem 450,000 17.5 Aug 2014

Shaoxing Sanyuan Petchem 450,000 17.5 Sept 2014

Ningbo Oriental Energy I 660,000 29.1 May 2015

Yantai Wanhua 750,000 25.6 Aug 2015

Zhongjing Petrochemical 800,000 35.3 2016

Ningbo Oriental Energy II 660,000 29.1 2016

Hebei Haiwei Group 500,000 22.0 2016

Fujian Meide Petrochemical 660,000 29.1 2017

TOTAL 6,130,000 251.6

Source: Bentek

The US exported 111 Mb/d of LPG to China in 2015. This has increased to 168 Mb/d in 2016 YTD.

27 BENPOSIUM 2016

0200400600800

10001200140016001800

$/M

T

China Propane - Propylene Margin

Propane - Propylene Margin Propane China Propylene China

Development of additional Chinese PDH challenged by lower margins

Source: Platts, Bentek

Low margins decrease utilization of existing

units

28 BENPOSIUM 2016

Asian and European crackers take more LPG when it is at a discount to naphtha

28

Source: Bentek

-300

-200

-100

0

100

200

300

200

300

400

500

600

700

800

Jan-15 May-15 Sep-15 Jan-16 May-16

$/m

t

$/m

t

Japan C3 vs Naphtha

DifferencePlatts Propane Refrigerated CFR Japan 30-45 daysPlatts Naphtha MOPJ strip 45-75 Days

-300

-200

-100

0

100

200

300

0

100

200

300

400

500

600

700

800

$/m

t

$/m

t

Northwest Europe C3 to Naphtha Spread

Difference

Platts Propane CIF NWE 7kt+

Platts Naphtha CIF NWE Cargo

Source: Platts, Bentek

BENPOSIUM 2016

WHAT HAPPENS NEXT?

30 BENPOSIUM 2016

Ethane exports will continue to move, but not all terminals are created equal

Enterprise Morgan’s Point Mont Belvieu index ethane

contracts

Sunoco Marcus Hook Natural gas or naphtha-index ethane contracts

- 50

100 150 200 250 300 350

Mb/

d

US Ethane Exports

Pipeline to Canada Marcus HookEnterprise

Source: Bentek Market Call: North American NGLs, 2Q2016

- 2 4 6 8

10 12 14

$/M

MB

tu

Ethane vs Gas Price Forecast

Henry Hub Mont Belvieu Ethane

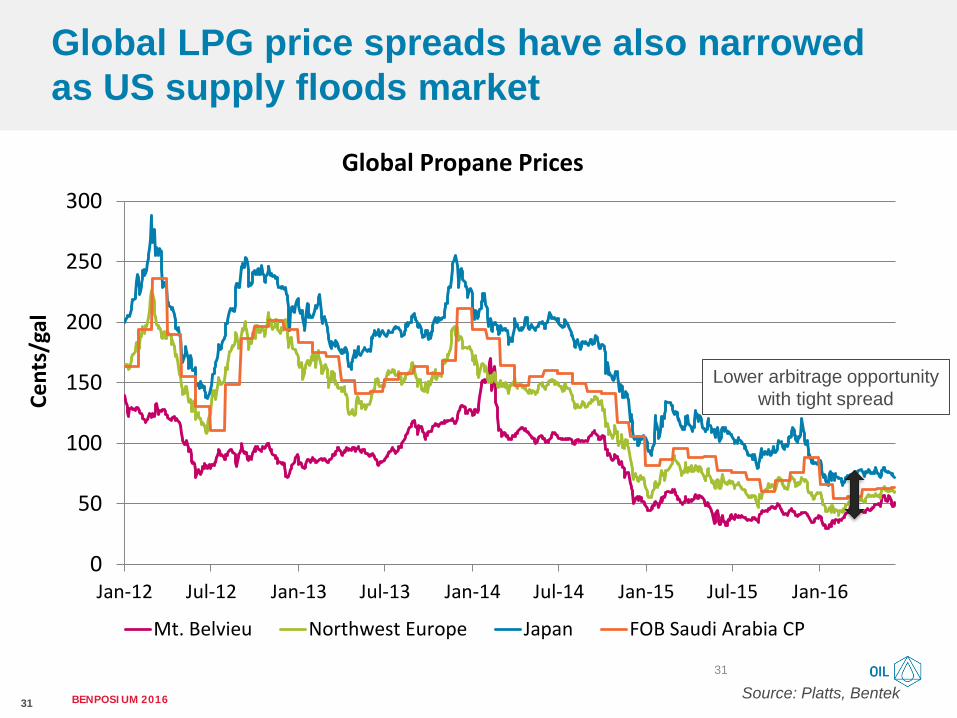

31 BENPOSIUM 2016

Global LPG price spreads have also narrowed as US supply floods market

31

Source: Platts, Bentek

0

50

100

150

200

250

300

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

Cent

s/ga

l

Global Propane Prices

Mt. Belvieu Northwest Europe Japan FOB Saudi Arabia CP

Lower arbitrage opportunity with tight spread

32 BENPOSIUM 2016

Record LPG exports are not sustainable as stocks are lower and global price spreads have narrowed

32

Source: Platts, Bentek

Source: EIA weekly estimates

0

20

40

60

80

100

120

MM

bbl

US Propane/Propylene Stocks

5-year range 5-year average2015 2016

0

200

400

600

800

1000

1200

Mb/

d

US LPG Exports

CapacityBentek's Waterborne LPG ModelEIA

Stocks drawn 40% MB prices rose 22%

33 BENPOSIUM 2016

-40

-20

0

20

40

60

80

100

120

Oct-13 Apr-14 Oct-14 Apr-15 Oct-15 Apr-16

Cen

ts/g

al

USGC Propane Export Value

Houston - NW Europe Houston - NE Asia

Relative value of terminal capacity has fallen

Export Value = Destination Price - Freight - Mont Belvieu

Source: Platts, Bentek

Constrained terminal capacity

High freight Fewer constraints, lower spreads

34 BENPOSIUM 2016

High terminal and cancellation fees distorting export economics in the short term

-50

0

50

100

150

200

250

cent

s/ga

l

Propane Firm Contract Economics

Difference Arab Gulf + Freight + US Cancellation Mont Belvieu + Fee + Frieght

Assumes 13 cents/gal terminal

fee and 7 cents/gal cancellation fee

Source: Platts, Bentek

Contract renegotiations?

35 BENPOSIUM 2016

LPG terminal utilization rates to decline from previous highs

Source: Bentek Market Call: North American NGLs, NGL Facilities Databank

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Mb/

d

LPG Exports vs Terminal Capacity

LPG Exports Forecast - 2Q2015

LPG Export Forecast - 2Q2016

Total US LPG Export Capacity

36 BENPOSIUM 2016

USGC will face increased competition from Northeast when Mariner East 2 comes online

36

West Coast

Gulf Coast

Northeast

Source: Bentek Market Call: North American NGLs 2Q2016

-

200

400

600

800

1,000

2015 2016 2017 2018 2019 2020 2021

Mb/

d

LPG Exports by Region

PADD 3 PADD 1 PADD 5

37 BENPOSIUM 2016

A lower supply curve and domestic feedstock competition has changed the exports story

37

0200400600800

1,0001,2001,4001,6001,8002,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Mb/

d

Total US NGL Exports Forecast Comparison

2Q2015 2Q2016

Source: Bentek Market Call: North American NGLs

38 BENPOSIUM 2016

Key Takeaways

• A large spread between gas and liquids prices in the US led to rapid NGL production growth over the past five years. Exports have served as a “relief value” for much of the resulting oversupply.

• Midstream and shipping companies pursued investment projects expecting continued production growth, leading to an infrastructure overbuild.

• US NGLs have found new markets overseas, largely from petrochemical producers looking to move lower on the cost curve, but this demand is not limitless.

• Going forward, the outlook for US NGL exports will vary by product, region, and even individual terminal.

• Gas indexed pricing could make Marcus Hook ethane exports more competitive than USGC Mont Belvieu indexed barrels.

• LPG exports will be flat to declining in the short term and there may be greater competition between terminals for export volumes.

BENPOSIUM 2016

THANK YOU!

Kendall Puig Senior Analyst, NGLs and LPG T: 720.264.6709 [email protected]