Embed Size (px)

Citation preview

MOODYS.COM

20 APRIL 2015

NEWS & ANALYSIS Corporates 2 » Raytheon’s $2 Billion Patriot Defense System Order Is

Credit Positive

» Emirates Engine Order Is Positive for Rolls-Royce, Negative for GE and United Technologies

» Grainger’s $3 Billion Share Repurchase Program Is Credit Negative

» Builders FirstSource’s $1.63 Billion ProBuild Purchase Is Credit Negative

» Colt Defense’s Proposed Debt Restructuring Is Credit Negative

» Smurfit Kappa Group’s Acquisition of Inspirepac Is Credit Positive

Infrastructure 8 » Empresas ICA Will Gain Nearly $200 Million from New Toll-

Road Joint Venture

» Strong Performance of Transurban’s US and Australia Toll Roads Bodes Well for NorthConnex Project

» Perth Airport’s Decline in Passenger Traffic Is Credit Negative

Banks 14 » Russian Central Bank Continues to Shut Down Problematic

Small Banks, a Credit Positive

» China Merchants Bank’s Employee Stock Incentive Plan Is Credit Positive

» China's Relaxation on Brokerage Account Rules Is Credit Negative for Securities Companies

» Taiwan Targets Banks’ Exposure to China, a Credit Positive

Insurers 22 » EXOR’s Bid for PartnerRe Is Credit Negative for PartnerRe and

AXIS Capital

» Spain’s Motor Insurers’ Claims Will Increase with Third-Party Bodily Injury Reforms

Money Market Funds 27 » First Multi-Billion Euro Money Market Fund Survives Outflow

from Negative Yield

Sub-sovereigns 29 » New Transparency Law is Credit Positive for Mexican Sub-

sovereign Governments

» Legislative Changes Boost Istanbul’s and Izmir’s Tax Revenues, a Credit Positive

US Public Finance 34 » Limited Federal Disaster Aid Is Credit Negative for

Massachusetts Local Governments

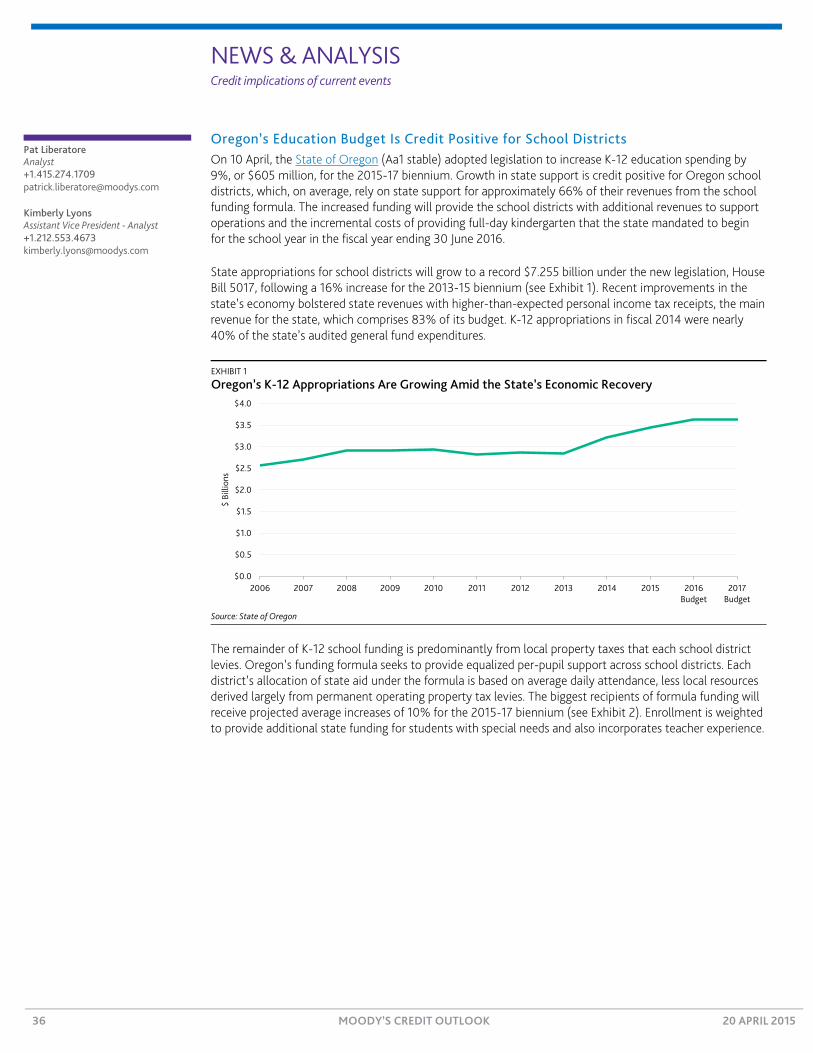

» Oregon’s Education Budget Is Credit Positive for School Districts

RATINGS & RESEARCH Rating Changes 38

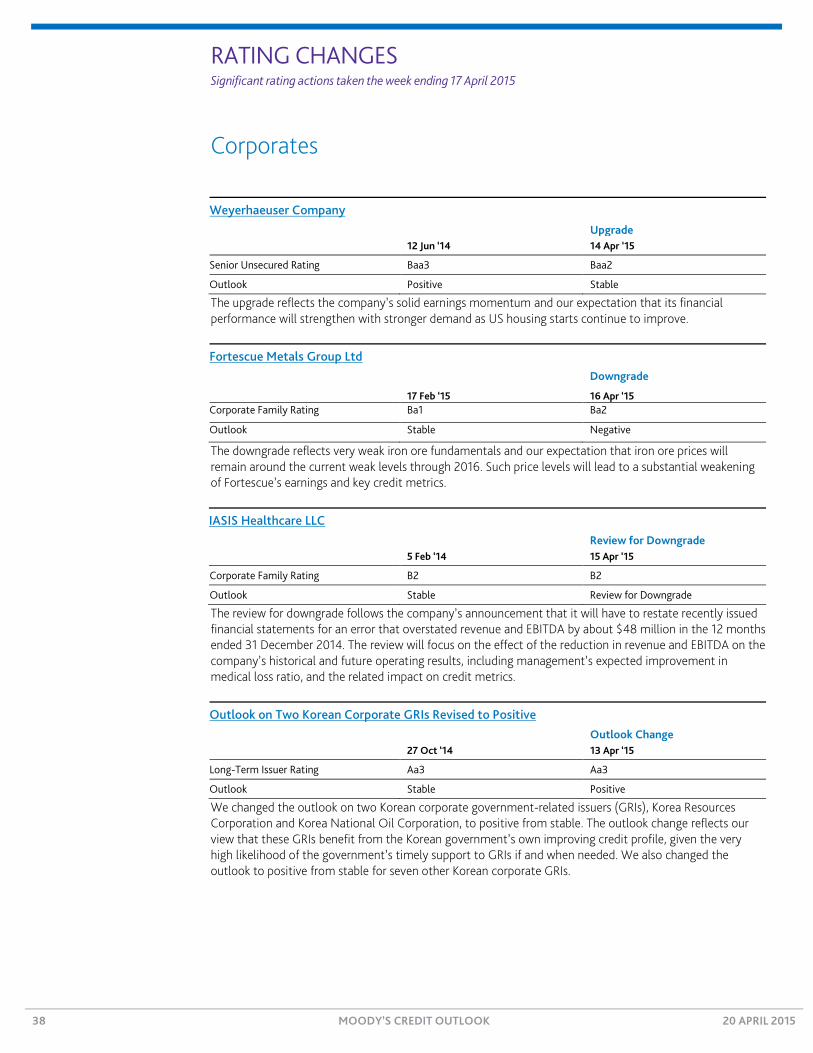

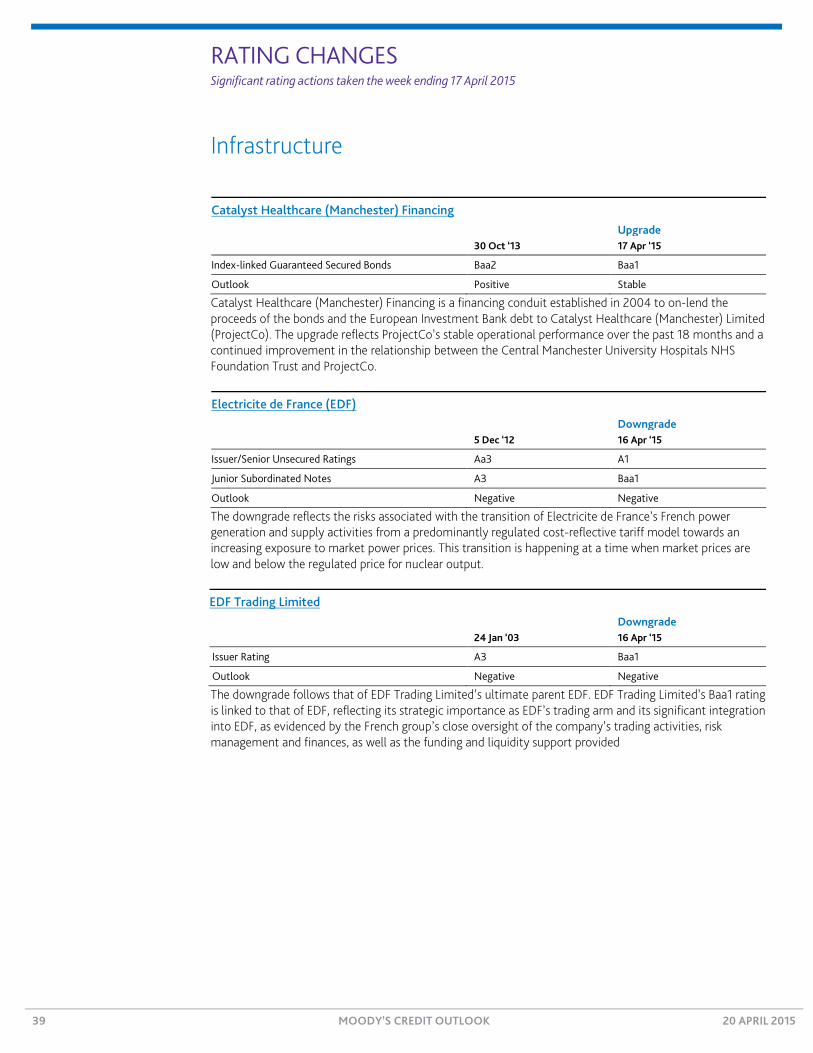

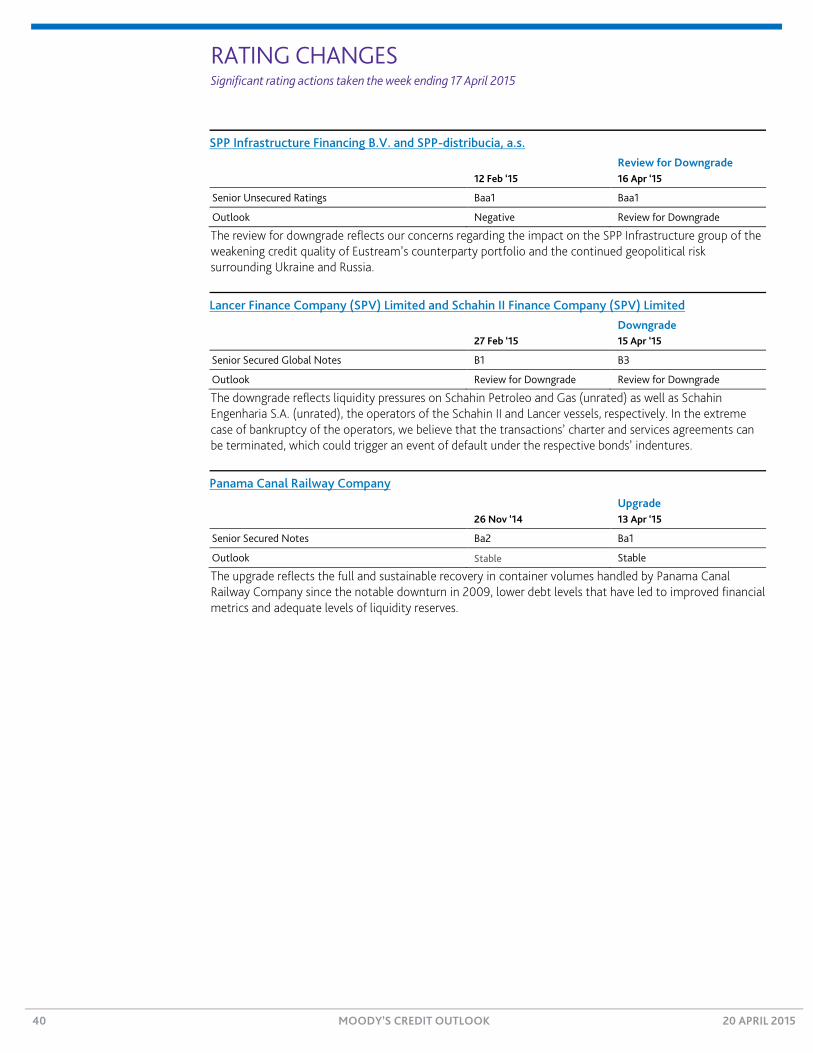

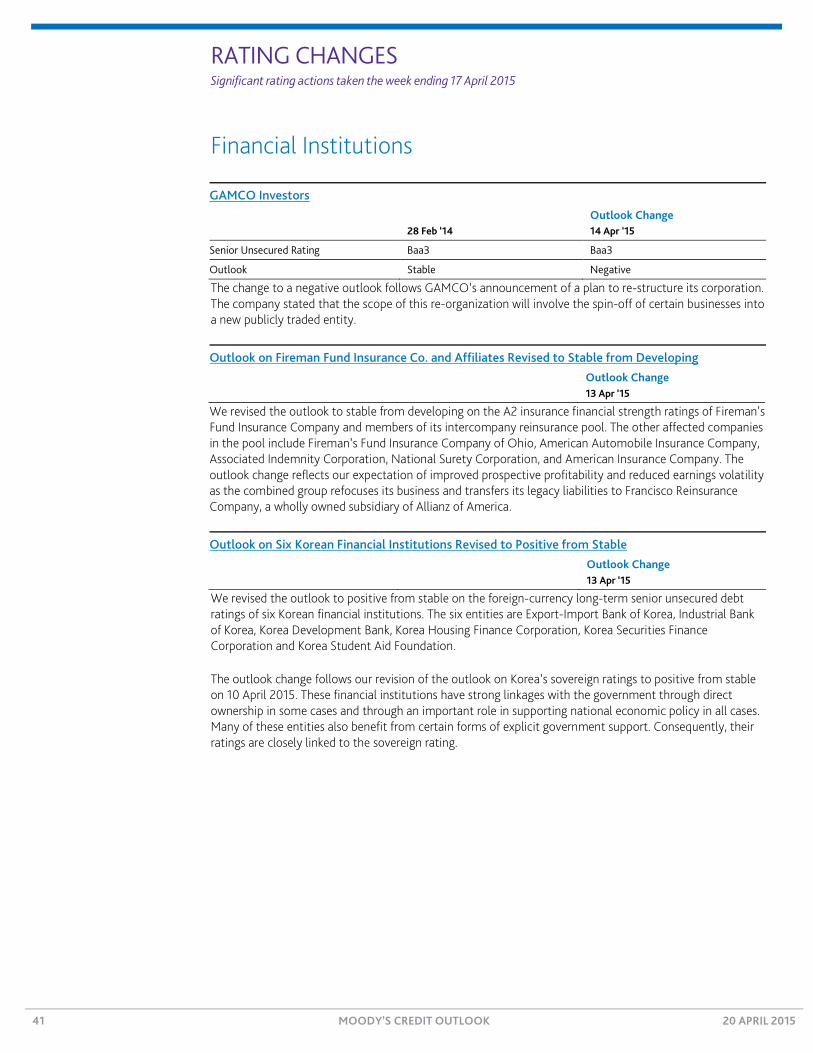

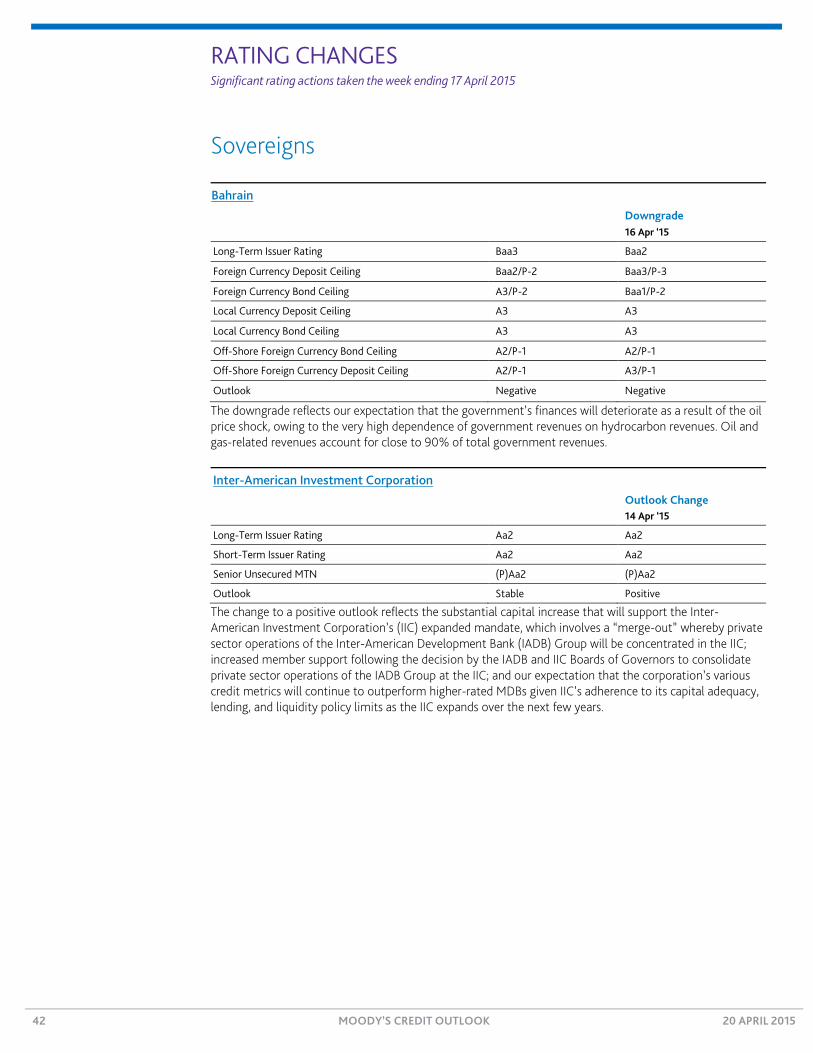

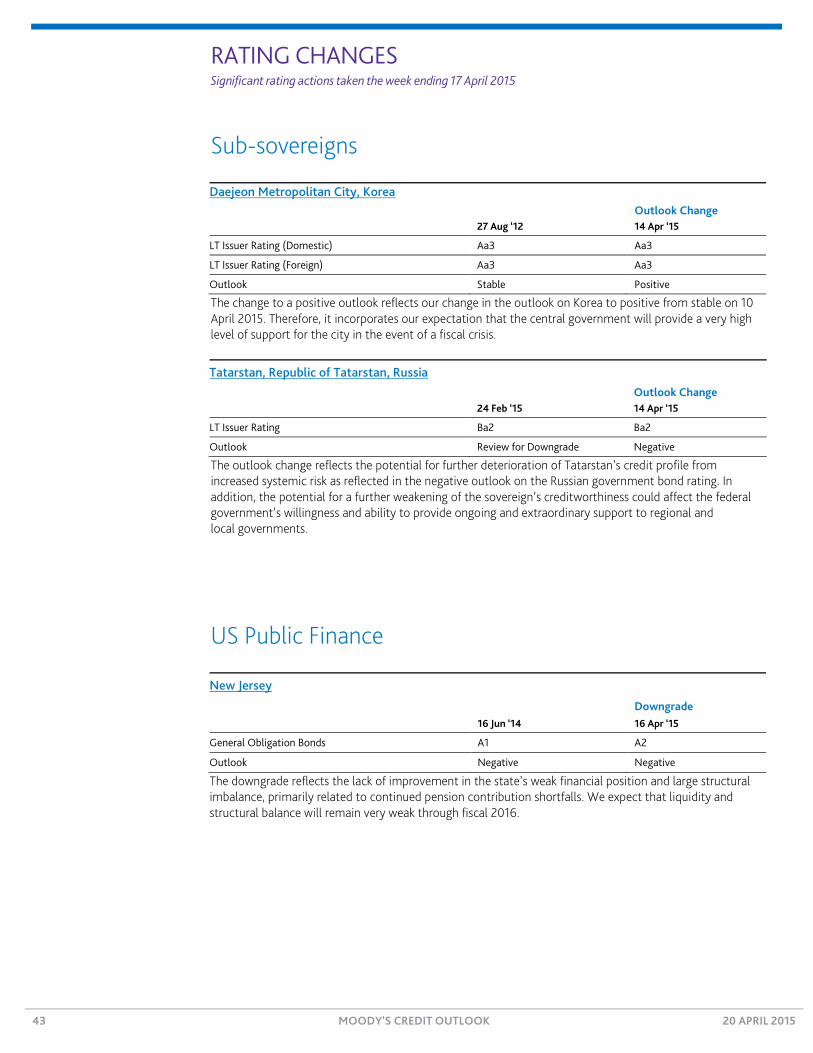

Last week we downgraded Fortescue Metals, Electricite de France, EDF Trading, Lancer Finance Company, Schahin II Finance Company, Bahrain and New Jersey, and upgraded Weyerhaeuser, Catalyst Healthcare (Manchester) Financing and Panama Canal Railway, among other rating actions.

Research Highlights 44

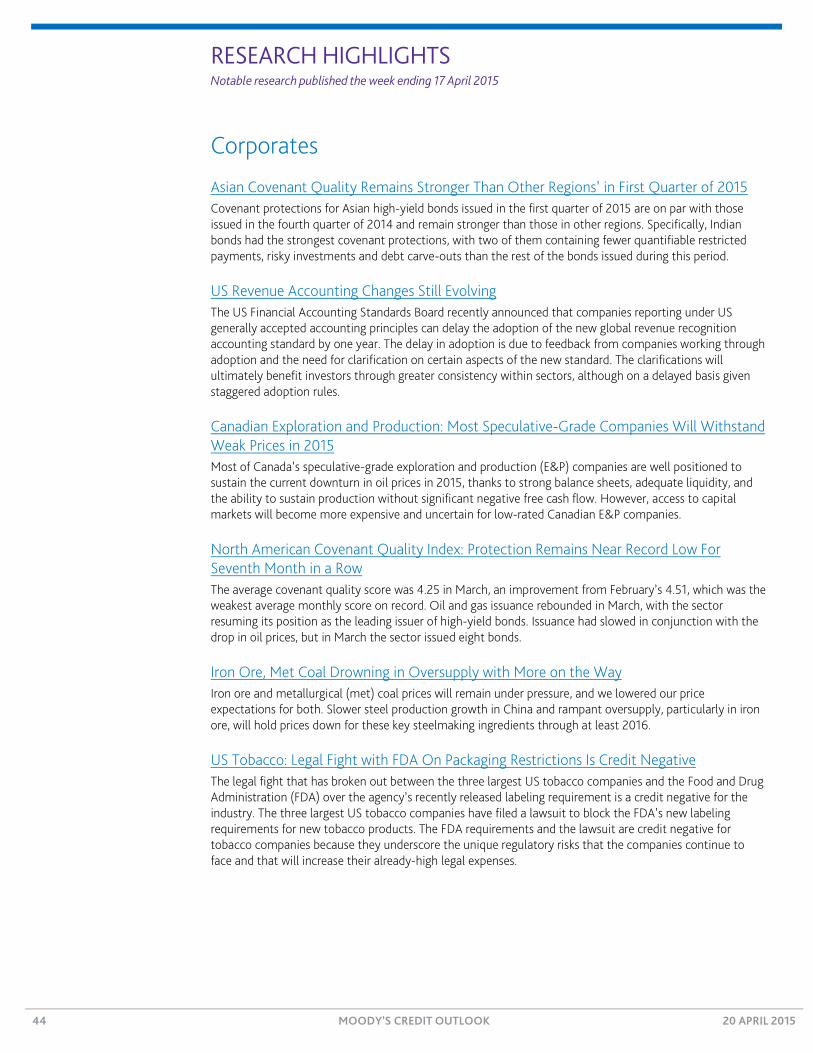

Last week we published on Asian corporate covenants, US accounting rules, Canadian exploration and production, North American covenants, global iron ore and metallurgical coal, US tobacco industry, China pharmaceuticals, European hotels, global home prices, Latin American corporates, China capital markets, EMEA beer makers, US gaming, Chinese property developers, US consumer durables, US packaging companies, UK hospitals, French toll roads, UK water, EMEA infrastructure, global insurers, global banks, Korea, Ukraine, Fondo Latinoamericano de Reservas, Australia, European quantitative easing, US universities, US highway infrastructure, European RMBS and ABS, French covered bonds, US subprime auto ABS, global CLOs, US student loans, US ABS, Canadian ABCP, EMEA ABCP and Korean structured finance, among other reports.

RECENTLY IN CREDIT OUTLOOK

» Articles in Last Thursday’s Credit Outlook 53 » Go to Last Thursday’s Credit Outlook

NEWS & ANALYSIS Credit implications of current events

2 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

Corporates

Raytheon’s $2 Billion Patriot Defense System Order Is Credit Positive On Friday, Raytheon Company (A3 stable) announced that it had received an award valued at more than $2 billion to provide the Patriot Air and Missile Defense System to an undisclosed international customer that we believe is in the Middle East. This order is credit positive, adding both incremental backlog and international sales exposure, while also mitigating revenue pressure at the company’s Integrated Defense Systems (IDS) segment, of which the Patriot Air and Missile Defense System is a core product.

The order follows a $2 billion Patriot order in December 2014 from Qatar and both underscore a credit-positive trend for global defense contractors with significant Middle East exposure, including Thales (A2 negative), General Dynamics Corporation (A2 stable), Lockheed Martin Corporation (Baa1 positive) and BAE Systems plc (Baa2 stable). The brisk order activity over the past six months supports our view that increasing geopolitical risk has and will continue to offset the dilutive effect of lower oil prices on oil-exporting nations’ willingness to invest in defense.

This order will materially increase Raytheon’s backlog and international sales, while stemming the tide of declining Patriot-related sales at Raytheon’s IDS segment. A $2 billion order equals about 6% of the company’s 2014 year-end total backlog of $33.6 billion and about 30% of the IDS segment’s backlog. Notably, the IDS segment’s backlog declined more than 6% in 2014 from 2013, but would have declined more without Qatar’s Patriot order announced at the end of 2014. Revenue and margin trends are similar, with 2014 sales declining $404 million, or approximately 6%, to about $6.1 billion and segment margins falling 120 basis points to 16%. A $441 million reduction in Patriot-related revenue, driven by the completion of previously awarded production contracts for international customers, was the primary factor for the revenue and margin declines. We expect that Friday’s $2 billion order, along with the Qatar order and a $770 million Patriot order in March 2015 from South Korea, will offset these declines.

These orders will bolster Raytheon’s international growth and considerably enhance the company’s competitive position for a number of large, near-term international awards. Raytheon’s international sales base of 30% of 2014 consolidated sales compares favorably with industry peers, and we expect Raytheon’s international sales as a percent of total sales to grow further this year given that last year’s international backlog constituted around 40% of total backlog and this year’s notable orders are from overseas.

Moreover, Raytheon’s international missile defense sales improve the company’s competitive position on future bids because of interoperability considerations. Potential customers such as Poland, which we expect to award a $3-$4 billion contract to Raytheon or MBDA Inc. in the second half of this year, seek missile defense integration with their security partner nations. In that context, use of the Patriot system by the US, five NATO members and seven other nations is a key competitive consideration.

More broadly, this order confirms the notion that low oil prices and related budgetary pressure will not severely constrain (and may only mildly temper) purchasing activity in the context of heightened geopolitical risk and regional security deterioration. As a result, we expect that defense contractors will continue to solicit and receive large international orders, which will moderate the effect of still-weak defense outlays in other developed economies. However, we expect that competition and increasingly burdensome offset requirements (whereby the contractor agrees to use a local industrial partner or offer goods and/or services as part of an attempt to win a given contract) will reduce the heretofore more favorable margin and cash flow profiles typically associated with international contracts.

Russell Solomon Senior Vice President +1.212.553.4301 [email protected]

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page on www.moodys.com for the most updated credit rating action information and rating history.

NEWS & ANALYSIS Credit implications of current events

3 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

Emirates Engine Order Is Positive for Rolls-Royce, Negative for GE and United Technologies Last Friday, Rolls-Royce plc (A3 stable) announced that it had received the largest order ever of Trent 900 engines and maintenance services from Dubai’s Emirates airline. The order for 200 engines and service is valued at £6.1 billion ($9.2 billion) in aggregate and is credit positive for Rolls-Royce because of its large size and strategic importance in the context of supporting the Airbus A380 widebody program’s biggest and most important customer.

Because this is the first order of Rolls-Royce engines from Emirates for its super-jumbo fleet, and a rare customer defection from current A380 engine supplier Engine Alliance (EA), it is credit negative for EA’s two joint-venture partners, General Electric Company (A1 stable) and United Technologies Corporation’s (A2 stable) Pratt & Whitney subsidiary. It also suggests that Rolls-Royce would likely be the sole engine provider if A380 manufacturer Airbus Group N.V. (A2 stable) undertakes an A380neo (new engine option) program.

The engines will power 50 A380s that are scheduled to enter service beginning in 2016. With this order, Rolls-Royce has now captured more than 50% market share for engines used on A380s. The Trent 900 engine has received favorable reviews and is touted as delivering the lowest lifetime fuel burn and emissions for the four-engine A380 airplane (compared with EA’s GP7200 engine), important attributes for an aircraft engine program at a time of increased fuel efficiency demands and regulatory standards. A380s have had their own challenges, with no new orders placed since 2013. Moreover, Airbus is only this year expecting break-even profitability on a unit cost basis for the first time since the A380’s introduction in 2007. Although no additional orders have been placed for the A380, Friday’s announcement suggests that future orders would likely be a source of incremental business for Rolls-Royce’s Trent 900 engine.

The order supports our expectation that Rolls-Royce will continue to see revenue growth increasingly derived from the more stable civil aerospace businesses. Engines for the commercial aircraft and corporate jet markets account for almost half of Rolls-Royce’s revenue, constituting approximately £6.8 billion of sales on a combined basis in 2014. More than 80% of the company’s £73.7 billion backlog at year-end 2014 comprised orders for engines and services for commercial aircraft.

The large order follows a challenging 2014 for Rolls-Royce, with lower volumes. Constrained government defense expenditures and pricing pressure in the land and sea segment caused a more than 5% decline in sales to about £13.9 billion in 2014 from £14.6 billion in 2013. The company was also adversely affected by the substantial decline in oil prices and foreign exchange headwinds. In particular, deferred and cancelled orders owing to challenging market conditions caused a 3% decline in the marine order book in 2014.

Partly in response to the recent, more difficult market conditions, Rolls-Royce has put multiple programs in place to reduce its global footprint and lower supply chain costs. These programs, coupled with higher research and development spending and working capital growth in support of ramping engine programs, have diluted margins and constrained the company’s free cash flow generating capability. However, we believe these programs will increase margins and build a foundation of longer-term growth beginning in 2016-17. The latest order for the Trent 900 provides additional earnings for Rolls-Royce and further contributes to an already high level of revenue predictability and relative stability.

Russell Solomon Senior Vice President +1.212.553.4301 [email protected]

NEWS & ANALYSIS Credit implications of current events

4 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

Grainger’s $3 Billion Share Repurchase Program Is Credit Negative Last Thursday, W.W. Grainger Inc. (short-term rating P-1) announced that its board had approved the repurchase of $3 billion of its common stock over the next three years. The planned buyback is credit negative because its marks a fundamental shift to a more aggressive financial policy that will result in higher leverage.

Grainger plans to fund the share repurchase with operating cash flow and new long-term debt. Internally generated cash will fund buybacks of $400 million a year through 2017, which the company will supplement with debt-financed share repurchases of $1 billion in 2015 and $400 million in both 2016 and 2017.

We expect the share repurchases to raise Grainger’s debt/EBITDA, as adjusted by us, to 1.2x by 2017 from its current level of about 0.6x. Despite this higher leverage, the company’s end market diversity, strong liquidity profile and leading position in the maintenance, repair and operations market will continue to provide solid support for the P-1 rating.

Furthermore, we expect Grainger to continue to generate free cash flow of at least $350 million annually, allowing for continued investment in infrastructure, supply chain and growth.

Eoin Roche Vice President - Senior Analyst +1.212.553.2868 [email protected]

NEWS & ANALYSIS Credit implications of current events

5 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

Builders FirstSource’s $1.63 Billion ProBuild Purchase Is Credit Negative Last Monday, Builders FirstSource, Inc. (B3 review for downgrade) announced that it planned to acquire building materials supplier ProBuild Holdings LLC (unrated) for approximately $1.63 billion. The deal, which the companies expect to close in the second half of the year, is credit negative for Builders FirstSource because the company plans to finance the all-cash purchase with as much as $1.6 billion of new debt. Following the announcement, we placed Builders FirstSource’s ratings on review for downgrade.

ProBuild is one of the largest building materials suppliers, with about $4.5 billion in revenue in 2014, and the combined entity would have about $6.1 billion in annualized revenue. The companies said the transaction offers diversification and scale, the chance to sell more higher-margin products, cost savings of $100-$120 million a year, and sufficient cash flow to reduce the pro forma $2.1 billion of debt the combined business had at the end of 2014. The new company would be in a good position to take advantage of the ongoing recovery in the residential real estate market, according to the deal announcement.

Although we recognize the rationale for the deal and the strength of repair and remodeling activity and new housing construction – the main revenue drivers for the combined entity – the large amount of debt being used for the acquisition is a risk. Also, the integration of the combined entities could pose challenges, delaying expected cost synergies.

Cash for the transaction will come from up to $1.6 billion of new debt, $100 million from a marketed follow-on public offering and the assumption of $300 million of lease finance obligations. Balance sheet debt will balloon by about $1.9 billion to approximately $2.3 billion.

The ratings review, which could affect about $350 million of debt, will focus on integration plans and expected cost synergies. We will also examine the combined entity’s ability to expand operating margins and reduce balance sheet debt from free cash flow since fixed-charge payments, including interest payments and term loan amortization, are likely to approach $150 million per year.

Builders FirstSource makes and supplies structural and related building products for residential new construction and repair and remodeling, including prefabricated components, windows and doors, lumber and millwork products. JLL Partners and Warburg Pincus own approximately 50% of the company. ProBuild operates lumberyards, component facilities, millwork shops, gypsum yards and retail stores across 40 states.

Peter Doyle Vice President - Senior Analyst +1.212.553.4475 [email protected]

NEWS & ANALYSIS Credit implications of current events

6 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

Colt Defense’s Proposed Debt Restructuring Is Credit Negative Last Tuesday, Colt Defense LLC (Caa3 negative) announced that it had launched an exchange offer for its $250 million 8.75% senior notes due in 2017. The company also said that it had asked noteholders to approve a prepackaged Chapter 11 reorganization plan that the company would enter into if it fails to complete the exchange offer or determines that it would be more advantageous to the company to choose the prepackaged reorganization plan. The announcement is credit negative because we would consider the completion of either the exchange offer or the prepackaged bankruptcy plan to be a default.

If Colt completes the exchange offer, which would require 98% tender approval by noteholders, we will likely view the transaction as a distressed exchange and append a limited default designation to Colt’s probability of default rating. Alternatively, if the company enters into a prepackaged plan of bankruptcy, which would require approval of two thirds of voting noteholders by par amount and a majority by number of those voting, we would lower the company’s ratings to reflect the default.

As part of the proposed exchange offer, Colt would exchange its existing notes for an amount meaningfully below par constituting a distressed exchange per our definition of a default. Colt’s existing $250 million unsecured notes due in 2017 would be exchanged at a rate of $300 for every $1,000 of par amount, plus accrued and unpaid interest. In addition, holders of existing notes that tender their notes and approve the company’s proposed amendments and vote to accept the prepackaged plan will receive a consent payment of $50 in principal amount of the proposed new notes per $1,000 principal amount of existing notes, according to the company’s public filings.

We expect the proposed new notes to be secured by certain junior liens on substantially all of Colt’s assets. We expect interest on the proposed notes to accrue at a rate of 10% per year in cash, compared with the company’s existing 8.75% notes.

Concurrently with the launch of the exchange offer, Colt is soliciting holders of the existing notes to approve a prepackaged plan bankruptcy plan as an alternative to the exchange offer. If the restructuring is accomplished through the prepackaged plan, 100% of the existing notes, plus accrued and unpaid interest, will be cancelled and holders of the existing notes will receive their pro rata share of the new notes.

The exchange offer and the consent solicitation will expire on 11 May 2015. Colt said that the exchange offer and issuance of the new notes would reduce the overall amount of Colt’s debt, which is currently slightly more than $350 million, reduce total cash interest payments and extend the company’s maturity profile. Absent the proposed restructuring transactions, we believe the company will not be able to meet these maturities and therefore, its likelihood of remaining a going concern would be uncertain.

Gigi Adamo Assistant Vice President - Analyst +1.212.553.2977 [email protected]

NEWS & ANALYSIS Credit implications of current events

7 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

Smurfit Kappa Group’s Acquisition of Inspirepac Is Credit Positive Last Wednesday, Smurfit Kappa Group plc (SKG, Ba1 stable), a leading manufacturer of containerboard and corrugated containers in Europe and Latin America, said that it had agreed to acquire Inspirepac (unrated), a UK-based non-integrated corrugated container producer, from the Logson Group for €60 million, or 6x EBITDA, including synergies. Although the transaction will not affect SKG in terms of its size and financial metrics, the acquisition is credit positive because it complements SKG’s leading position in the UK market and expands its existing capabilities in the high-quality-print and point-of-sale markets.

The deal is SKG’s third since March, and is in line with the company’s strategy to expand through organic growth and accretive acquisitions in Europe and Latin America, the company’s higher growth markets. SKG’s credit quality improves when it builds long-term value through acquisitions funded from operating cash flow, rather than pursue more shareholder friendly financial policies. Both SKG’s geographic diversity and its integrated model have contributed to more robust earnings.

SKG recently increased its dividend by 30% and reiterated that in the absence of accretive acquisition opportunities it would evaluate alternative uses of capital, including returning surplus capital to shareholders, while remaining committed to its Ba1 credit rating.

However, the flurry of recent deal announcements suggests that finding potential targets may not be an issue. In addition to Inspirepac, SKG has agreed to purchase Grupo CYBSA, which operates in El Salvador and Costa Rica, and Hexacomb, which has operations in Europe and Mexico. Combined with the Inspirepac deal, SKG has spent €175 million on acquisitions since March. By comparison, SKG spent €160 million on four acquisitions during all of 2014.

SKG has a track record of reducing financial leverage, having lowered its Moody’s-adjusted debt/EBITDA to 3.9x as of December 2014 from 6.2x in December 2009, through a mix of debt repayments and improvements in operating profitability.

Matthias Volkmer Vice President - Senior Analyst +49.69.70730.758 [email protected]

Dirk Steinicke Associate Analyst +49.69.70730.949 [email protected]

NEWS & ANALYSIS Credit implications of current events

8 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

Infrastructure

Empresas ICA Will Gain Nearly $200 Million from New Toll-Road Joint Venture Last Tuesday, Empresas ICA, S.A.B. de C.V. (ICA, B2 stable), a Mexican engineering and construction company, announced that it had reached a MXN3 billion ($196 million) deal with Caisse De Dépôt Et Placement Du Québec (CDPQ, unrated) that gives the Canadian investment management firm a 49% stake in a new joint venture that will house ICA’s toll-road projects in a single entity. The joint venture would include ICA’s four toll roads at the outset.

The transaction is credit positive for ICA, which will use most of the proceeds to continue deleveraging. Since ICA has said it plans to generate MXN5 billion in cash proceeds from asset sales this year, the joint-venture agreement places the company well on its way to meet its target. The remaining MXN2 billion in asset-sale proceeds would help ICA achieve a reported debt/EBITDA ratio of 7.4x-8.6x by the end of this year, despite its macroeconomic and foreign-exchange disadvantages.

ICA’s leverage is highly sensitive to further depreciation of the weak Mexican peso. The company had about MXN5.7 billion in cash at the end of 2014, when the peso traded at 14.8 to the US dollar. Since then, the peso has weakened to 15.3, and about half of ICA’s debt is dollar-denominated, compared with just 30% of its EBITDA.

Although the transaction is credit positive for ICA, we do not expect immediate upward ratings pressure, mainly because a positive rating action would require that ICA maintain its consolidated Moody’s-adjusted leverage below 6.5x. Using the company’s outlook for this year, which includes revenue growth of 10%-12%, EBITDA margins of 14%-16% and assuming the full MXN5 billion asset sales and a foreign exchange rate between MXN15-MXN16 per US dollar, we estimate that ICA’s adjusted gross leverage would be 6.6x-7.5x.

ICA’s concessions portfolio today contains six operational highways, five of which ICA fully owns and controls. The joint venture with CDPQ contains four of them, which ICA will continue maintaining. We consider the sale credit neutral for the debt of the toll-roads, including Consorcio del Mayab, S.A. de C.V. (Mayab, Baa3/Aa3.mx stable) because the projects’ operation and maintenance will remain with ICA.

Moreover, since ICA will continue to consolidate these projects, the EBITDA that they generate will continue to lower ICA’s leverage (see exhibit). Mayab holds the concession for the Kantunil (Merida) - Cancun road and the extensions currently under construction for the Tintal - El Cedral and Tintal - Playa del Carmen roads, a rapidly growing international tourist destination in the Mayan Riviera. In 2014, Mayab contributed 44% of the total adjusted EBITDA of the portfolio. The concession expires in December 2050.

Sandra Beltran Analyst +52.55.1253.5718 [email protected]

Adrián Garza Assistant Vice President - Analyst +52.55.1253.5709 [email protected]

NEWS & ANALYSIS Credit implications of current events

9 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

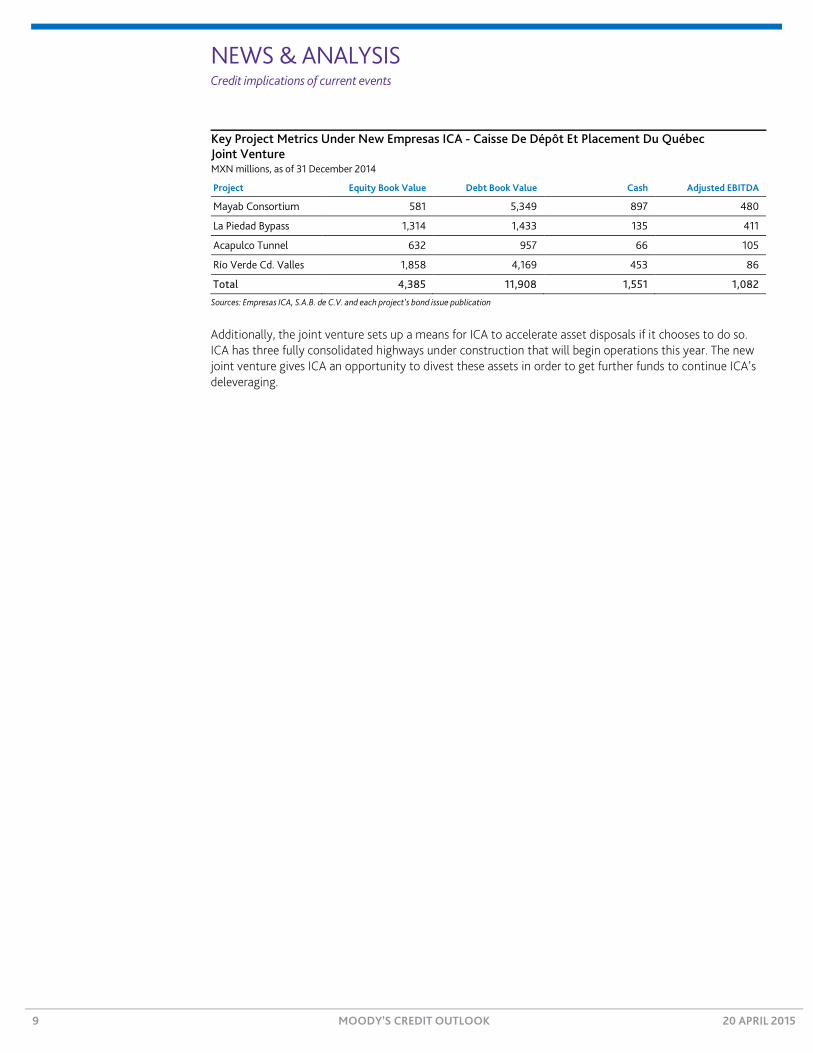

Key Project Metrics Under New Empresas ICA - Caisse De Dépôt Et Placement Du Québec Joint Venture MXN millions, as of 31 December 2014

Project Equity Book Value Debt Book Value Cash Adjusted EBITDA

Mayab Consortium 581 5,349 897 480

La Piedad Bypass 1,314 1,433 135 411

Acapulco Tunnel 632 957 66 105

Río Verde Cd. Valles 1,858 4,169 453 86

Total 4,385 11,908 1,551 1,082

Sources: Empresas ICA, S.A.B. de C.V. and each project’s bond issue publication

Additionally, the joint venture sets up a means for ICA to accelerate asset disposals if it chooses to do so. ICA has three fully consolidated highways under construction that will begin operations this year. The new joint venture gives ICA an opportunity to divest these assets in order to get further funds to continue ICA’s deleveraging.

NEWS & ANALYSIS Credit implications of current events

10 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

Strong Performance of Transurban’s US and Australia Toll Roads Bodes Well for NorthConnex Project Last Tuesday, Transurban Group, Australia’s largest toll road operator and for which Transurban Finance Company Pty Ltd. (Baa1 stable) is the finance company, reported a strong ramp-up in traffic volumes on two key capital expansion programmes. The projects are the construction of the Interstate 95 express lanes in Northern Virginia in the US, of which Transurban owns a 77.5% stake, and the M5 South West Motorway expansion in Sydney, Australia. Transurban owns a 50% interest in Interlink Roads Pty Ltd. (A2 stable), the M5 concessionaire.

The strong performance of these roads is credit positive for Transurban because it increases the company’s financial cushion against challenges arising at the complex AUD3.2 billion NorthConnex project in Sydney, Australia, of which Transurban owns a 50% interest. The project includes construction of two nine-kilometre tunnels in an urban area.

Transurban completed both the M5 and I-95 projects within time and budgets constraints in late 2014, and the roads are achieving traffic growth rates that exceed our base-case expectations. The M5 reported annual average daily traffic volumes of around 133,000 vehicles for the March 2015 quarter, which exceeds our base-case expectation by around 10%. Meanwhile, the toll-based express lanes of I-95, which connect with Transurban’s Interstate 495 express lanes project, reported average daily toll revenue in excess of $100,000 for the March quarter, a figure that materially exceeds I-495’s run rate for its first full quarter of operations in 2013 (see Exhibit 1). If sustained, the I-95 project’s revenue performance will avoid missing expectations like the I-495 project did in its early days.

EXHIBIT 1

Comparison of Average Daily Revenue Generated by Express Lanes in First Quarter of Operations

Sources: Transurban Group and Moody’s Investors Service

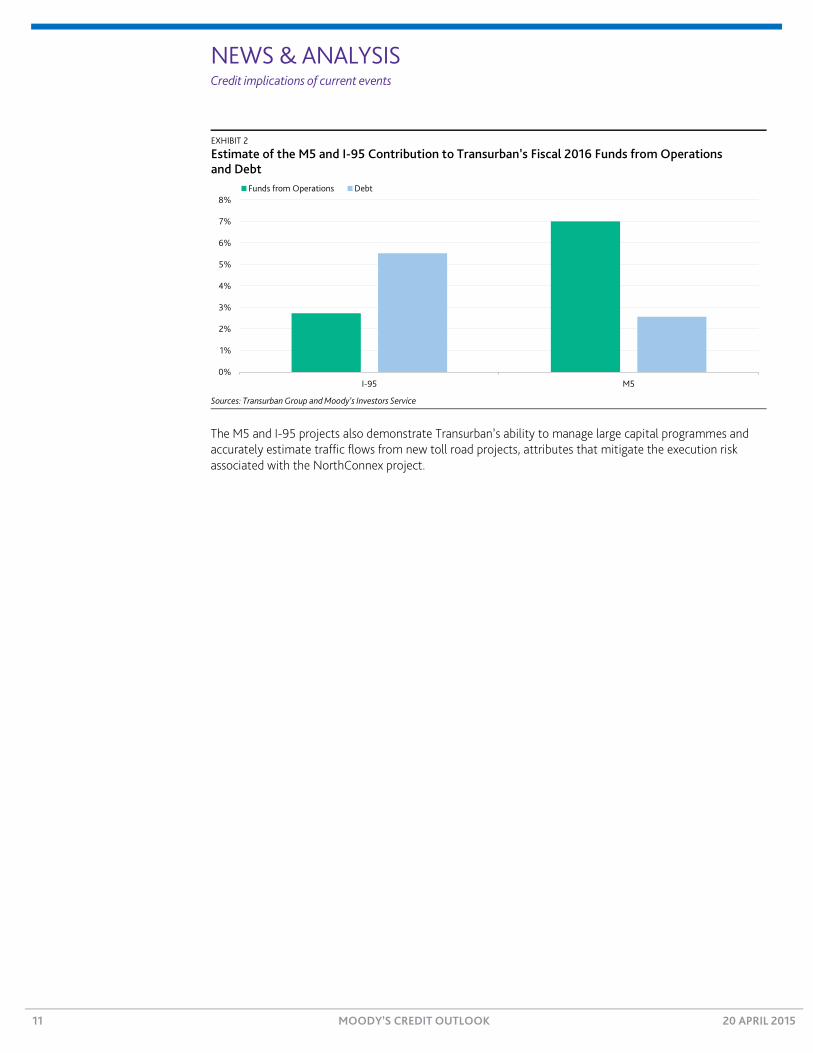

Exhibit 2 shows our expectation of the material contribution that the I-95 and M5 projects will make to Transurban’s consolidated funds from operations (FFO) and debt for the fiscal year ending 30 June 2016. Because the I-95 project is in early ramp-up, we expect its contribution to FFO to grow to more than 7% over the next three years. We estimate that the outperformance of these two roads will improve Transurban’s fiscal 2016 financial leverage, as measured by FFO to debt, by 20-30 basis points over our previous expectation of 6.5%.

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

I-495 March 2013 Quarter I-95 -March 2015 Quarter

$ Th

ousa

nds

Arnon Musiker Vice President - Senior Credit Officer +61.2.9270.8161 [email protected]

NEWS & ANALYSIS Credit implications of current events

11 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

EXHIBIT 2

Estimate of the M5 and I-95 Contribution to Transurban’s Fiscal 2016 Funds from Operations and Debt

Sources: Transurban Group and Moody’s Investors Service

The M5 and I-95 projects also demonstrate Transurban’s ability to manage large capital programmes and accurately estimate traffic flows from new toll road projects, attributes that mitigate the execution risk associated with the NorthConnex project.

0%

1%

2%

3%

4%

5%

6%

7%

8%

I-95 M5

Funds from Operations Debt

NEWS & ANALYSIS Credit implications of current events

12 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

Perth Airport’s Decline in Passenger Traffic Is Credit Negative Last Tuesday, Perth Airport Pty Ltd. (Baa2 stable) reported its first decline in quarterly passenger numbers since June 2002. The drop was mainly the result of lower domestic passenger traffic, which comprises around two thirds of total passenger numbers, driven by a slowdown in mining activity in Western Australia. We believe the decline is an inflection point for Perth Airport and indicates the end of high growth for the airport.

Declining revenue growth is credit negative for Perth Airport, particularly at a time when it will take on additional debt to complete the final stages of its capital expansion program this year, which will increase its outstanding debt to around AUD1.7 billion from AUD1.3 billion as of July 2013.

The decline in passenger volumes will flow directly into revenue, given that more than 80% of Perth Airport’s revenue is linked to passenger volumes. This includes charges it levies on the airlines for passenger use of its terminal facilities and income from the rental of retail facilities and car parks. Over the three months ended March 2015, the number of passengers who travelled through the airport fell 1% from 2014 levels (see Exhibit 1).

EXHIBIT 1

Quarter-over-Quarter Change in Perth Airport’s Quarterly Passenger Traffic

Source: Perth Airport

In addition to slower mining activity affecting domestic passenger volume, the airlines cut capacity on unprofitable routes, particularly those serving remote mining hubs in the state, and reduced airfare discounts to increase yield on a per-passenger basis.

Although these changes have also led to moderating domestic passenger traffic in other Australian airports, Perth has been more adversely affected given its greater exposure to mining-related activities in the state’s resource-dominated economy. Perth Airport was the fastest-growing airport in Australia in 2011 and 2012, benefiting from double-digit increases in domestic passenger traffic each year as a result of mining developments that required workers to travel to and from remote sites on a regular basis.

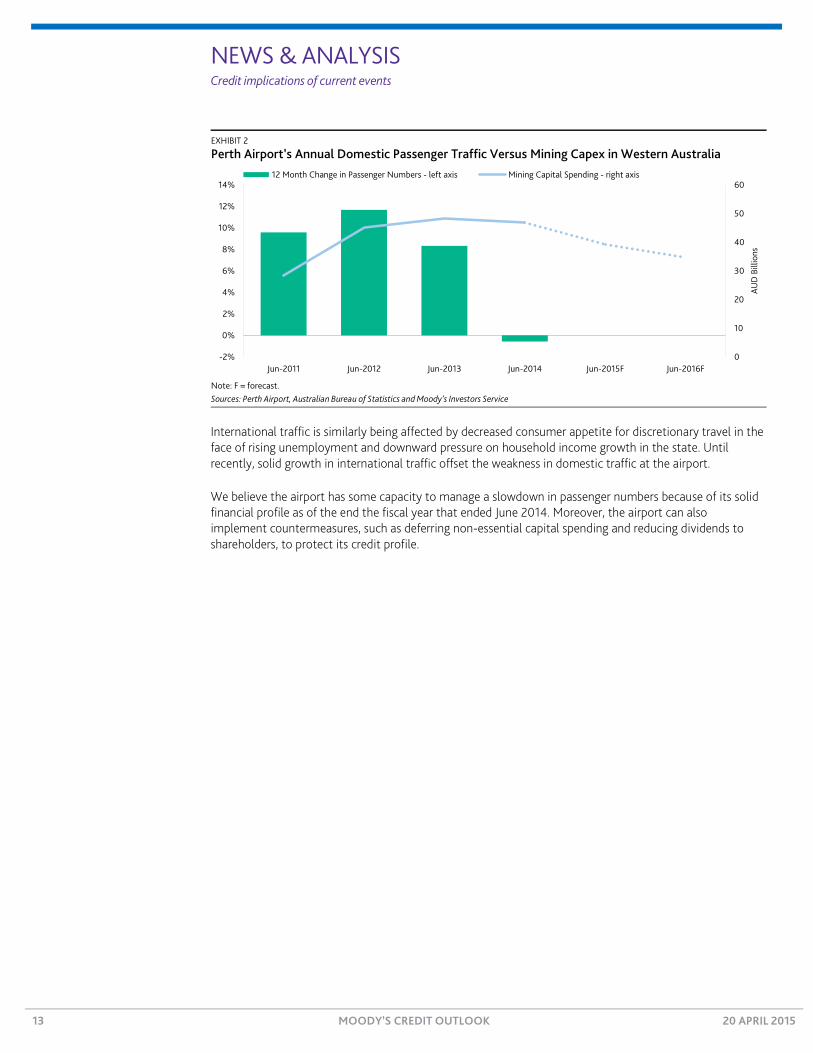

As capital spending in mining has slowed, the rate of growth in passenger numbers has correspondingly declined, as shown in Exhibit 2. Given the softness in commodity prices and miners’ focus on cost cutting, including reduced exploration activity and staffing, we believe mining-related traffic is unlikely to increase soon.

-2%

0%

2%

4%

6%

8%

10%

12%

Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15

Domestic International Total

Spencer Ng Vice President - Senior Analyst +61.2.9270.8191 [email protected]

NEWS & ANALYSIS Credit implications of current events

13 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

EXHIBIT 2

Perth Airport’s Annual Domestic Passenger Traffic Versus Mining Capex in Western Australia

Note: F = forecast. Sources: Perth Airport, Australian Bureau of Statistics and Moody’s Investors Service

International traffic is similarly being affected by decreased consumer appetite for discretionary travel in the face of rising unemployment and downward pressure on household income growth in the state. Until recently, solid growth in international traffic offset the weakness in domestic traffic at the airport.

We believe the airport has some capacity to manage a slowdown in passenger numbers because of its solid financial profile as of the end the fiscal year that ended June 2014. Moreover, the airport can also implement countermeasures, such as deferring non-essential capital spending and reducing dividends to shareholders, to protect its credit profile.

0

10

20

30

40

50

60

-2%

0%

2%

4%

6%

8%

10%

12%

14%

Jun-2011 Jun-2012 Jun-2013 Jun-2014 Jun-2015F Jun-2016F

AUD

Bill

ions

12 Month Change in Passenger Numbers - left axis Mining Capital Spending - right axis

NEWS & ANALYSIS Credit implications of current events

14 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

Banks

Russian Central Bank Continues to Shut Down Problematic Small Banks, a Credit Positive Last Monday, the Central Bank of Russia (CBR) said that it had revoked the licenses of Tikhookeanskiy Vneshtorgbank (unrated), a small private lender operating in Russia’s Far East, and Moscow-based private banks IpoTek (unrated) and Transnational (unrated). The license withdrawals are credit positive because they remove weak banks with governance and other problems from the banking system, promote industry consolidation and reduce industry overcapacity. The withdrawals are fresh examples of the CBR’s effort to clean up the Russian banking sector under Elvira Nabiullina, who became head of the central bank in mid-2013.

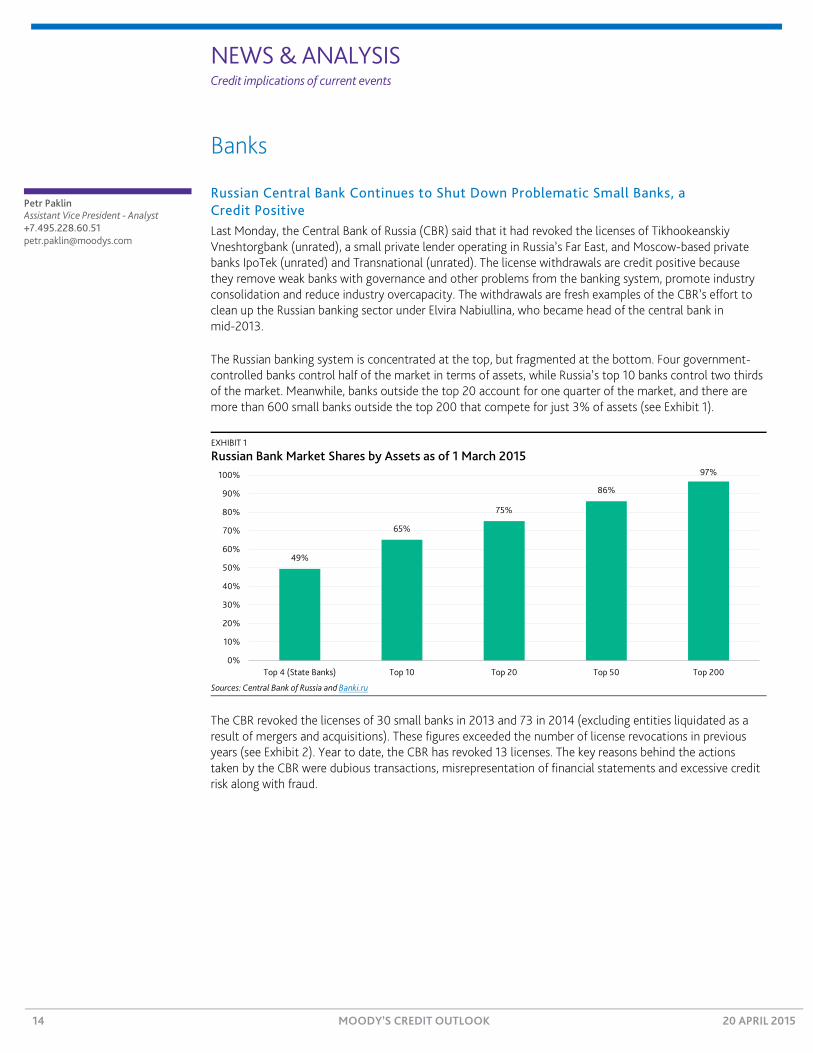

The Russian banking system is concentrated at the top, but fragmented at the bottom. Four government-controlled banks control half of the market in terms of assets, while Russia’s top 10 banks control two thirds of the market. Meanwhile, banks outside the top 20 account for one quarter of the market, and there are more than 600 small banks outside the top 200 that compete for just 3% of assets (see Exhibit 1).

EXHIBIT 1

Russian Bank Market Shares by Assets as of 1 March 2015

Sources: Central Bank of Russia and Banki.ru

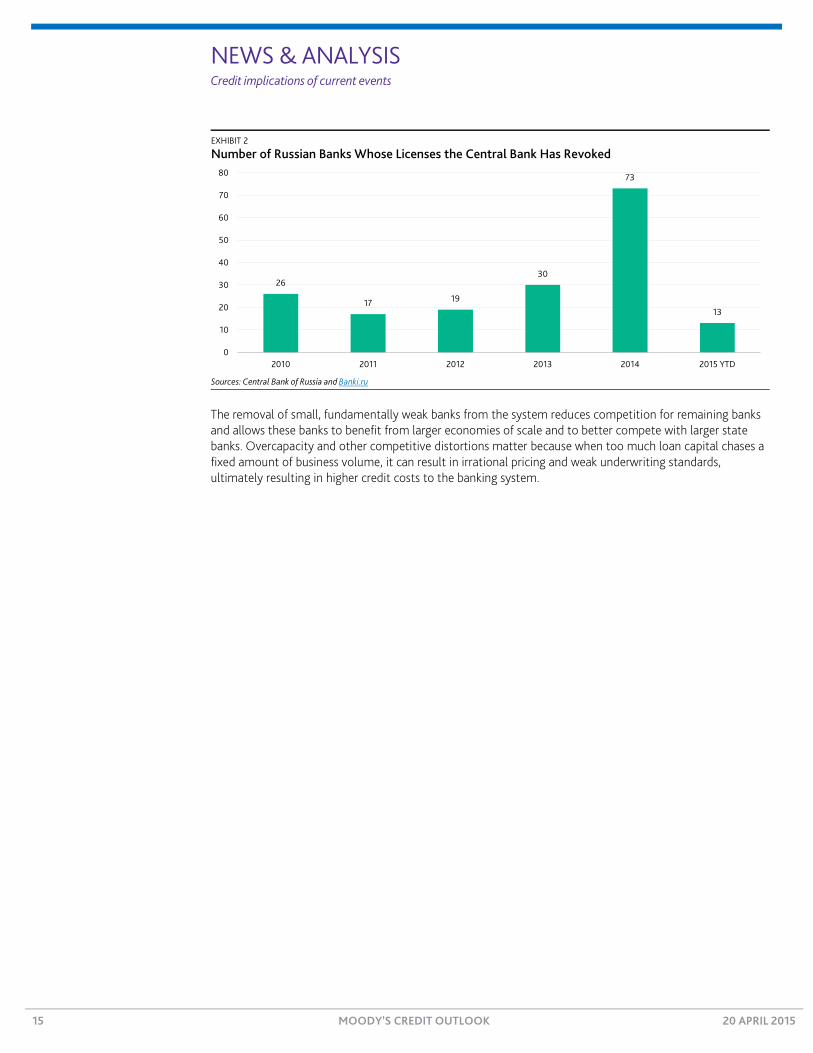

The CBR revoked the licenses of 30 small banks in 2013 and 73 in 2014 (excluding entities liquidated as a result of mergers and acquisitions). These figures exceeded the number of license revocations in previous years (see Exhibit 2). Year to date, the CBR has revoked 13 licenses. The key reasons behind the actions taken by the CBR were dubious transactions, misrepresentation of financial statements and excessive credit risk along with fraud.

49%

65%

75%

86%

97%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Top 4 (State Banks) Top 10 Top 20 Top 50 Top 200

Petr Paklin Assistant Vice President - Analyst +7.495.228.60.51 [email protected]

NEWS & ANALYSIS Credit implications of current events

15 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

EXHIBIT 2

Number of Russian Banks Whose Licenses the Central Bank Has Revoked

Sources: Central Bank of Russia and Banki.ru

The removal of small, fundamentally weak banks from the system reduces competition for remaining banks and allows these banks to benefit from larger economies of scale and to better compete with larger state banks. Overcapacity and other competitive distortions matter because when too much loan capital chases a fixed amount of business volume, it can result in irrational pricing and weak underwriting standards, ultimately resulting in higher credit costs to the banking system.

26

17 19

30

73

13

0

10

20

30

40

50

60

70

80

2010 2011 2012 2013 2014 2015 YTD

NEWS & ANALYSIS Credit implications of current events

16 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

China Merchants Bank’s Employee Stock Incentive Plan Is Credit Positive On 11 April, China Merchants Bank Co., Ltd. (CMB, Baa1 stable, baa31) announced that it would issue common stock to its employees at a 12% discount to its closing stock price on 2 April before the stock halted trading the following week because of the plan. The plan, which is part of CMB’s new employee incentive program, is credit positive because it will improve CMB’s capital. The plan is also likely to prompt other banks to execute similar schemes.

If fully subscribed, the plan would increase CMB’s Tier 1 capital ratio by about 20 basis points based on the bank’s risk-weighted assets at the end of 2014. The capital increase would partially offset weakening in the bank’s ability to generate capital internally if profitability is negatively affected by rising credit costs and China’s interest rate liberalization. CMB’s nonperforming loan ratio increased to 1.11% at the end of 2014 from 0.83% at the end of 2013, while its return on average assets decreased to 1.28% in 2014 from 1.39% in 2013, and its return on average equity decreased to 19.28% from 22.22%.

The plan, which CMB’s board has approved, awaits sign-off from shareholders and regulators. Up to 8,500 of CMB employees will be eligible to participate, and the plan will raise as much as RMB6 billion this year.

CMB is the first Chinese bank with a state-owned enterprise as a major shareholder to introduce an employee stock scheme of this scale, and other Chinese banks are likely to emulate it because these schemes improve banks’ ability to maintain key employees and adds flexibility to banks’ staff cost structure, which is a positive. These schemes allow banks to decrease the percentage of fixed labor costs and to link total costs more with profitability. They are also likely to help the industry attract and retain talent to meet the higher operation and risk management standards arising from banking reforms.

Although all banks have a similar need to bolster their performance benchmarks, mid-tier banks will benefit more from innovative and flexible compensation arrangements because of their higher staff costs. As the exhibit below shows, joint-stock commercial banks have higher staff costs per employee than state-owned banks. Some joint-stock commercial banks, such as Shanghai Pudong Development Bank Co. Ltd. (Baa1 stable, ba1), have begun to reduce their staff costs amid a more challenging environment.

Rated Chinese Banks’ Yearly Salary, Bonus, Allowance and Subsidy per Employee

Note: ICBC = Industrial & Commercial Bank of China Limited; CCB = China Construction Bank Corporation; BOC = Bank of China Limited; ABC = Agricultural Bank of China Limited; CMB = China Merchants Bank; CITIC = China CITIC Bank; SPDB = Shanghai Pudong Development Bank Co. Ltd.; CEB = China Everbright Bank; PAB = Ping An Bank. Source: The banks

1 The ratings shown are the bank’s deposit rating and baseline credit assessment.

0

50

100

150

200

250

300

350

400

450

ICBC CCB BOC ABC CMB CITIC SPDB CEB PAB

RMB

Thou

sand

s

2013 2014

Yulia Wan Assistant Vice President - Analyst +86.21.2057.4017 [email protected]

NEWS & ANALYSIS Credit implications of current events

17 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

There is a risk that these employee stock incentive plans will create a stronger alignment between the interests of employees and shareholders, which could lead to more risk-taking that benefits the banks’ growth, profits and returns on equity in the short term, but threatens their asset quality or capitalization in the long run. However, in CMB’s case, this risk is somewhat mitigated by a three-year lock-up period, which evaluates the bank’s performance over a longer period.

NEWS & ANALYSIS Credit implications of current events

18 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

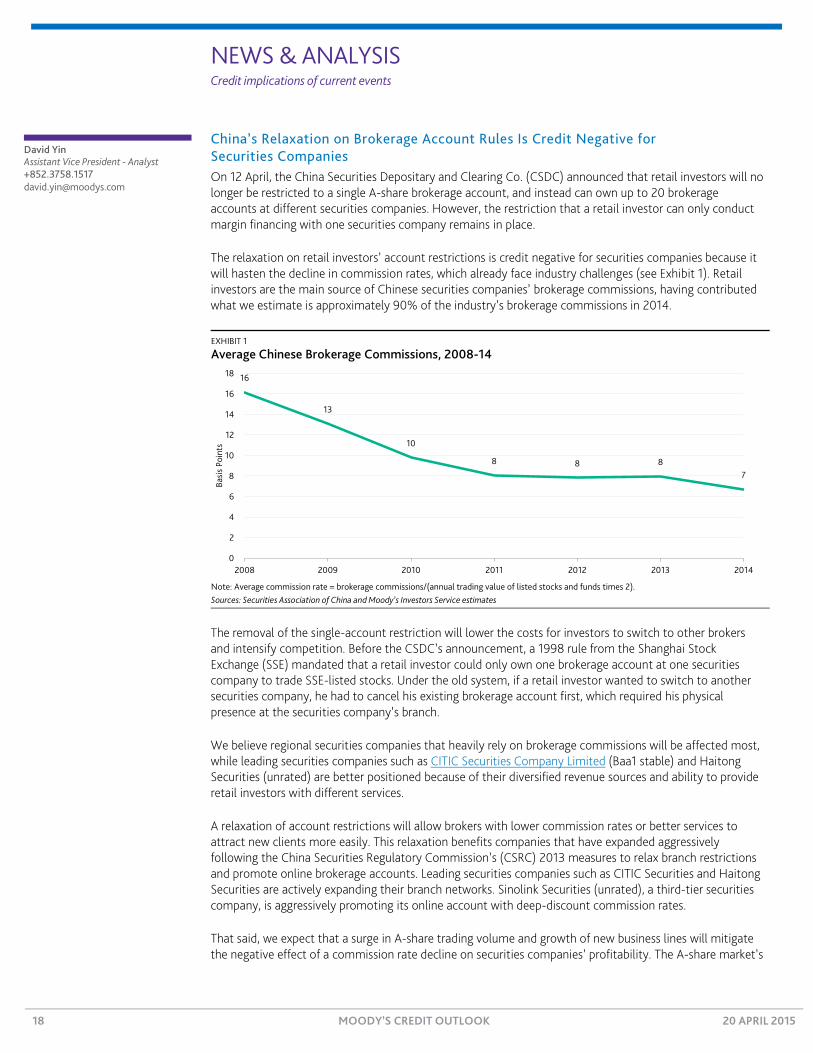

China’s Relaxation on Brokerage Account Rules Is Credit Negative for Securities Companies On 12 April, the China Securities Depositary and Clearing Co. (CSDC) announced that retail investors will no longer be restricted to a single A-share brokerage account, and instead can own up to 20 brokerage accounts at different securities companies. However, the restriction that a retail investor can only conduct margin financing with one securities company remains in place.

The relaxation on retail investors’ account restrictions is credit negative for securities companies because it will hasten the decline in commission rates, which already face industry challenges (see Exhibit 1). Retail investors are the main source of Chinese securities companies’ brokerage commissions, having contributed what we estimate is approximately 90% of the industry’s brokerage commissions in 2014.

EXHIBIT 1

Average Chinese Brokerage Commissions, 2008-14

Note: Average commission rate = brokerage commissions/(annual trading value of listed stocks and funds times 2). Sources: Securities Association of China and Moody’s Investors Service estimates

The removal of the single-account restriction will lower the costs for investors to switch to other brokers and intensify competition. Before the CSDC’s announcement, a 1998 rule from the Shanghai Stock Exchange (SSE) mandated that a retail investor could only own one brokerage account at one securities company to trade SSE-listed stocks. Under the old system, if a retail investor wanted to switch to another securities company, he had to cancel his existing brokerage account first, which required his physical presence at the securities company’s branch.

We believe regional securities companies that heavily rely on brokerage commissions will be affected most, while leading securities companies such as CITIC Securities Company Limited (Baa1 stable) and Haitong Securities (unrated) are better positioned because of their diversified revenue sources and ability to provide retail investors with different services.

A relaxation of account restrictions will allow brokers with lower commission rates or better services to attract new clients more easily. This relaxation benefits companies that have expanded aggressively following the China Securities Regulatory Commission’s (CSRC) 2013 measures to relax branch restrictions and promote online brokerage accounts. Leading securities companies such as CITIC Securities and Haitong Securities are actively expanding their branch networks. Sinolink Securities (unrated), a third-tier securities company, is aggressively promoting its online account with deep-discount commission rates.

That said, we expect that a surge in A-share trading volume and growth of new business lines will mitigate the negative effect of a commission rate decline on securities companies’ profitability. The A-share market’s

16

13

10

8 8 8 7

0

2

4

6

8

10

12

14

16

18

2008 2009 2010 2011 2012 2013 2014

Basi

s Po

ints

David Yin Assistant Vice President - Analyst +852.3758.1517 [email protected]

NEWS & ANALYSIS Credit implications of current events

19 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

average daily trading value jumped to RMB722 billion in the first quarter of 2015 from RMB 197 billion in 2013 (see Exhibit 2). In addition, leading securities companies have reduced their reliance on brokerage commissions owing to the rapid development of new business lines such as margin financing. In 2014, brokerage commissions only accounted for 29% of Haitong Securities’ total revenue and 30% of CITIC Securities’ total revenue (see Exhibit 3).

EXHIBIT 2

Chinese A-Share Average Daily Trading Volume

Sources: China Securities Regulatory Commission

EXHIBIT 3

Chinese Securities Companies’ Brokerage Commission as a Percent of Total Revenue

Sources: Company reports

38

190

109

220 225 173

129

197

304

722

0

100

200

300

400

500

600

700

800

2006 2007 2008 2009 2010 2011 2012 2013 2014 1Q15

RMB

Billi

ons

38%35%

44%49%

53%58%

29% 30%

38% 40% 41%46%

0%

10%

20%

30%

40%

50%

60%

Haitong Securities CITIC Securities Guangfa Securities China MerchantsSecurities

Huatai Securities Evebright Securities

2013 2014

NEWS & ANALYSIS Credit implications of current events

20 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

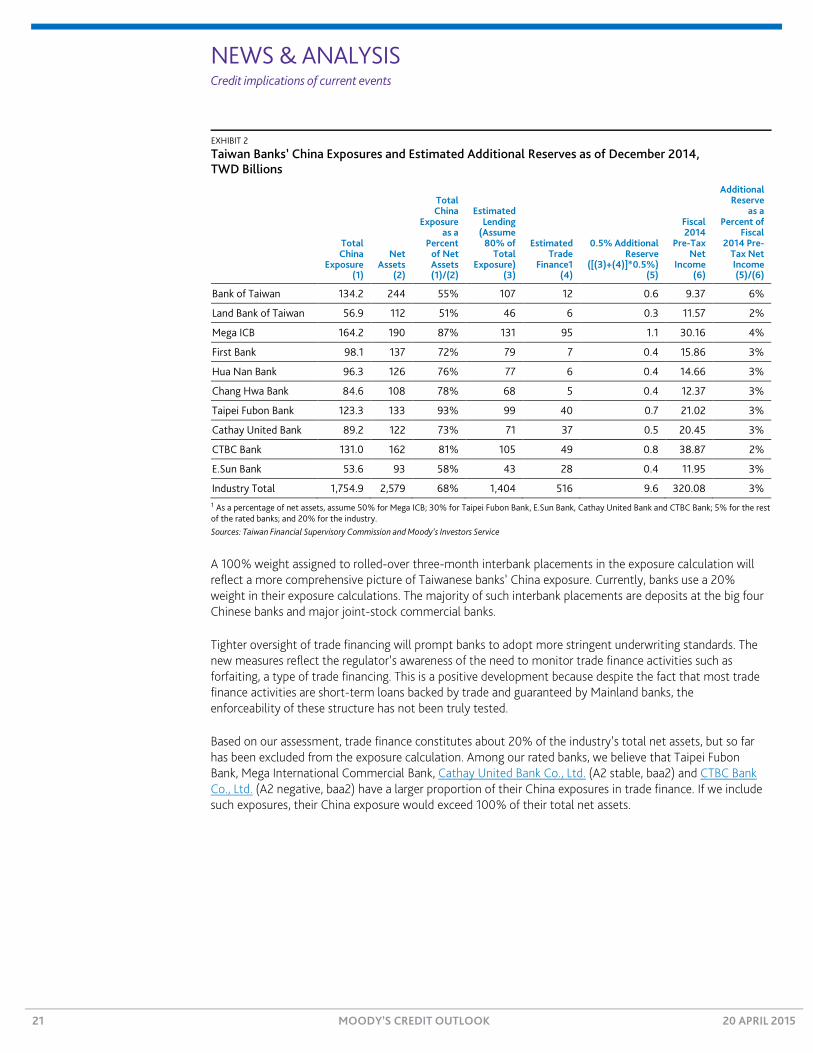

Taiwan Targets Banks’ Exposure to China, a Credit Positive Last Monday, Taiwan’s Financial Supervisory Commission (FSC) announced several measures targeting banks’ business in Mainland China. Key measures include an increase of the general provision on China-related lending to at least 1.5% from the current 1.0% level by the end of 2015; a 100% weight for rolled-over three-month interbank placements in exposure calculations, versus 20% currently; and increased oversight of banks’ short-term trade financing business. These measures are credit positive because they will add to banks’ loss-absorption capability in their China exposures, which have experienced high growth in recent years following more formalized relations with Mainland China. Additionally, the FSC’s call for higher provisioning will likely prompt banks to improve their risk-based pricing.

According to the FSC, Taiwanese banks’ China exposure, including loans, interbank placements, and investments, hit a high of TWD1.755 trillion (about $55.3 billion) at the end of 2014, and constituted 68% of the system’s net assets, up from 49% at the end of 2013 (see Exhibit 1). Increasing mainland risk exposures subject Taiwanese banks to asset risk arising from China’s slowing economy.

EXHIBIT 1

Select Taiwanese Bank’s Exposure to Mainland China as a Percent of Net Assets

Note: SCSB = The Shanghai Commercial Savings Bank. Source: Taiwan Financial Supervisory Commission

The latest measures will benefit the credit quality of banks with the largest Mainland exposures relative to their net assets. These include Taipei Fubon Commercial Bank Co., Ltd. (A2 stable, baa22), Mega International Commercial Bank (A1 stable, baa2), Bank Sinopac Company Limited (unrated) and The Shanghai Commercial Savings Bank, Ltd. (unrated), all of which at the end of 2014 had the highest level of China exposure among Taiwan’s 39 local banks at more than 85%3 of their net assets.

Under the new measures, banks will add reserves to strengthen their loss-absorption ability against downturns. We estimate that most of our rated banks will need to reserve an additional TWD300 million to TWD1.1 billion, or 2%-6% of 2014 full-year pre-tax net income, to comply with the new rules (see Exhibit 2).

2 The bank ratings shown in this report are the bank’s deposit rating and baseline credit assessment. 3 The regulatory cap is 100%.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

TaipeiFubonBank

Mega ICB BankSinoPac

SCSB CTBCBank

ChangHwaBank

Hua NanBank

CathayUnitedBank

First Bank E.SunBank

Bank ofTaiwan

LandBank

Industry RatedBanks

4Q 2013 2Q 2014 4Q 2014

Ginger Kao Analyst +852.3758.1317 [email protected]

NEWS & ANALYSIS Credit implications of current events

21 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

EXHIBIT 2

Taiwan Banks’ China Exposures and Estimated Additional Reserves as of December 2014, TWD Billions

Total China

Exposure (1)

Net Assets

(2)

Total China

Exposure as a

Percent of Net Assets (1)/(2)

Estimated Lending

(Assume 80% of

Total Exposure)

(3)

Estimated Trade

Finance1 (4)

0.5% Additional Reserve

([(3)+(4)]*0.5%) (5)

Fiscal 2014

Pre-Tax Net

Income (6)

Additional Reserve

as a Percent of

Fiscal 2014 Pre-

Tax Net Income (5)/(6)

Bank of Taiwan 134.2 244 55% 107 12 0.6 9.37 6%

Land Bank of Taiwan 56.9 112 51% 46 6 0.3 11.57 2%

Mega ICB 164.2 190 87% 131 95 1.1 30.16 4%

First Bank 98.1 137 72% 79 7 0.4 15.86 3%

Hua Nan Bank 96.3 126 76% 77 6 0.4 14.66 3%

Chang Hwa Bank 84.6 108 78% 68 5 0.4 12.37 3%

Taipei Fubon Bank 123.3 133 93% 99 40 0.7 21.02 3%

Cathay United Bank 89.2 122 73% 71 37 0.5 20.45 3%

CTBC Bank 131.0 162 81% 105 49 0.8 38.87 2%

E.Sun Bank 53.6 93 58% 43 28 0.4 11.95 3%

Industry Total 1,754.9 2,579 68% 1,404 516 9.6 320.08 3% 1 As a percentage of net assets, assume 50% for Mega ICB; 30% for Taipei Fubon Bank, E.Sun Bank, Cathay United Bank and CTBC Bank; 5% for the rest of the rated banks; and 20% for the industry. Sources: Taiwan Financial Supervisory Commission and Moody’s Investors Service

A 100% weight assigned to rolled-over three-month interbank placements in the exposure calculation will reflect a more comprehensive picture of Taiwanese banks’ China exposure. Currently, banks use a 20% weight in their exposure calculations. The majority of such interbank placements are deposits at the big four Chinese banks and major joint-stock commercial banks.

Tighter oversight of trade financing will prompt banks to adopt more stringent underwriting standards. The new measures reflect the regulator’s awareness of the need to monitor trade finance activities such as forfaiting, a type of trade financing. This is a positive development because despite the fact that most trade finance activities are short-term loans backed by trade and guaranteed by Mainland banks, the enforceability of these structure has not been truly tested.

Based on our assessment, trade finance constitutes about 20% of the industry’s total net assets, but so far has been excluded from the exposure calculation. Among our rated banks, we believe that Taipei Fubon Bank, Mega International Commercial Bank, Cathay United Bank Co., Ltd. (A2 stable, baa2) and CTBC Bank Co., Ltd. (A2 negative, baa2) have a larger proportion of their China exposures in trade finance. If we include such exposures, their China exposure would exceed 100% of their total net assets.

NEWS & ANALYSIS Credit implications of current events

22 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

Insurers

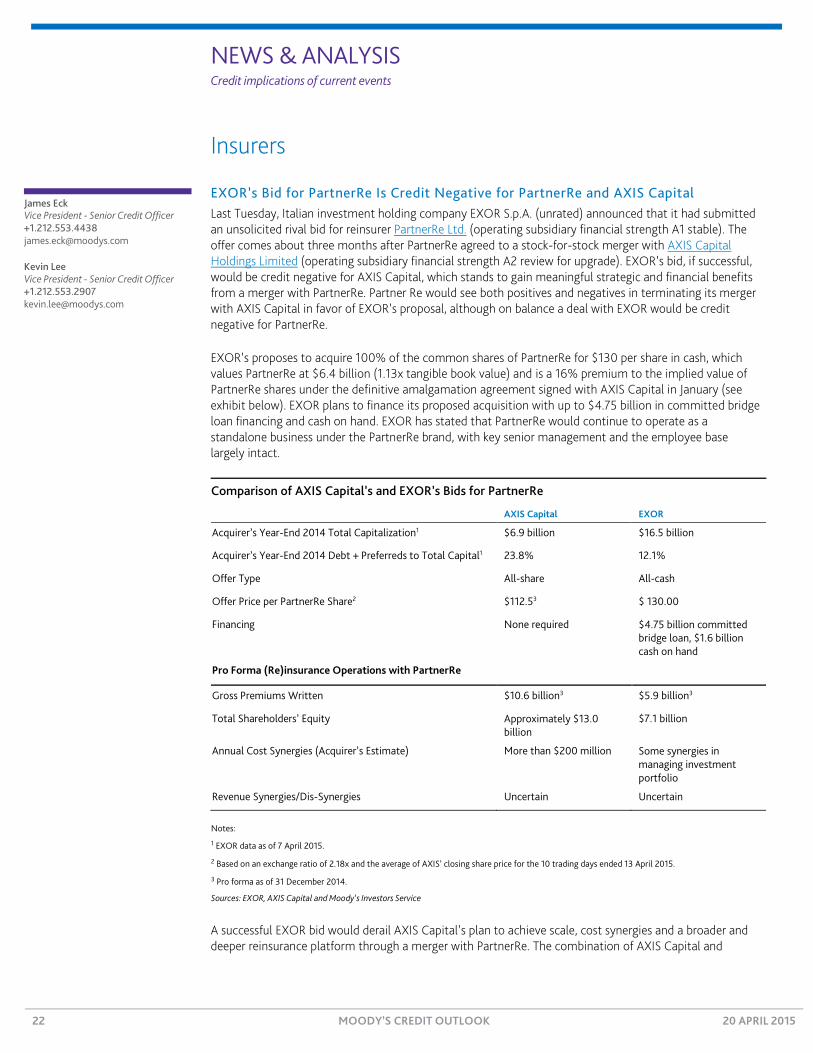

EXOR’s Bid for PartnerRe Is Credit Negative for PartnerRe and AXIS Capital Last Tuesday, Italian investment holding company EXOR S.p.A. (unrated) announced that it had submitted an unsolicited rival bid for reinsurer PartnerRe Ltd. (operating subsidiary financial strength A1 stable). The offer comes about three months after PartnerRe agreed to a stock-for-stock merger with AXIS Capital Holdings Limited (operating subsidiary financial strength A2 review for upgrade). EXOR’s bid, if successful, would be credit negative for AXIS Capital, which stands to gain meaningful strategic and financial benefits from a merger with PartnerRe. Partner Re would see both positives and negatives in terminating its merger with AXIS Capital in favor of EXOR’s proposal, although on balance a deal with EXOR would be credit negative for PartnerRe.

EXOR’s proposes to acquire 100% of the common shares of PartnerRe for $130 per share in cash, which values PartnerRe at $6.4 billion (1.13x tangible book value) and is a 16% premium to the implied value of PartnerRe shares under the definitive amalgamation agreement signed with AXIS Capital in January (see exhibit below). EXOR plans to finance its proposed acquisition with up to $4.75 billion in committed bridge loan financing and cash on hand. EXOR has stated that PartnerRe would continue to operate as a standalone business under the PartnerRe brand, with key senior management and the employee base largely intact.

Comparison of AXIS Capital’s and EXOR’s Bids for PartnerRe

AXIS Capital EXOR

Acquirer’s Year-End 2014 Total Capitalization1 $6.9 billion $16.5 billion

Acquirer’s Year-End 2014 Debt + Preferreds to Total Capital1 23.8% 12.1%

Offer Type All-share All-cash

Offer Price per PartnerRe Share2 $112.53 $ 130.00

Financing None required $4.75 billion committed bridge loan, $1.6 billion cash on hand

Pro Forma (Re)insurance Operations with PartnerRe

Gross Premiums Written $10.6 billion3 $5.9 billion3

Total Shareholders’ Equity Approximately $13.0 billion

$7.1 billion

Annual Cost Synergies (Acquirer’s Estimate) More than $200 million Some synergies in managing investment portfolio

Revenue Synergies/Dis-Synergies Uncertain Uncertain

Notes:

1 EXOR data as of 7 April 2015.

2 Based on an exchange ratio of 2.18x and the average of AXIS’ closing share price for the 10 trading days ended 13 April 2015.

3 Pro forma as of 31 December 2014.

Sources: EXOR, AXIS Capital and Moody’s Investors Service

A successful EXOR bid would derail AXIS Capital’s plan to achieve scale, cost synergies and a broader and deeper reinsurance platform through a merger with PartnerRe. The combination of AXIS Capital and

James Eck Vice President - Senior Credit Officer +1.212.553.4438 [email protected]

Kevin Lee Vice President - Senior Credit Officer +1.212.553.2907 [email protected]

NEWS & ANALYSIS Credit implications of current events

23 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

PartnerRe would create the fifth-largest property and casualty reinsurer by premiums, the largest exclusive broker-market reinsurer and one of the 10 largest life and health reinsurers. Moreover, a stock-for-stock merger with PartnerRe would likely improve AXIS Capital’s capital adequacy and financial leverage.

Absent a merger, we expect AXIS Capital to carry on as before with the same credit profile. As a silver lining, AXIS Capital would receive a breakup fee of $250 million, equal to approximately 30% of its 2014 earnings, if PartnerRe were to choose EXOR or another suitor.

For PartnerRe, the credit implications of a successful EXOR bid are more nuanced. On balance, we see it as credit negative since PartnerRe would miss out on an opportunity to strengthen its market position and improve its product diversification by gaining access to AXIS Capital’s profitable specialty primary insurance platform. In an increasingly competitive and tiered reinsurance marketplace, a PartnerRe-AXIS Capital combination would provide the scale and breadth of product offerings that are highly valued by brokers and clients.

On the positive side, however, an acquisition by EXOR would not significantly alter PartnerRe’s current business or financial profile, since the company would operate as a separate business unit within the EXOR group. PartnerRe’s policyholders and creditors could benefit from the company’s private status within a larger organization with a long-term investment focus. Under EXOR’s ownership, PartnerRe could better withstand the current challenging reinsurance market conditions by remaining focused on longer-term goals and through access to the group’s resources should large catastrophe losses create a need for capital.

One critical wildcard related to EXOR’s bid for PartnerRe is how EXOR’s capital structure would evolve post-acquisition. EXOR’s debt would significantly increase through the use of up to $4.75 billion in bridge loans to finance the deal, and the consolidation of PartnerRe’s debt. However, EXOR could deleverage through the planned divestment of its 81% ownership interest in real estate firm Cushman & Wakefield (unrated) and other possible asset sales, as well as by retaining earnings. That said, to the extent that EXOR decided to significantly increase its financial leverage on a long-term basis following an acquisition of PartnerRe, it would weaken PartnerRe’s credit profile.

NEWS & ANALYSIS Credit implications of current events

24 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

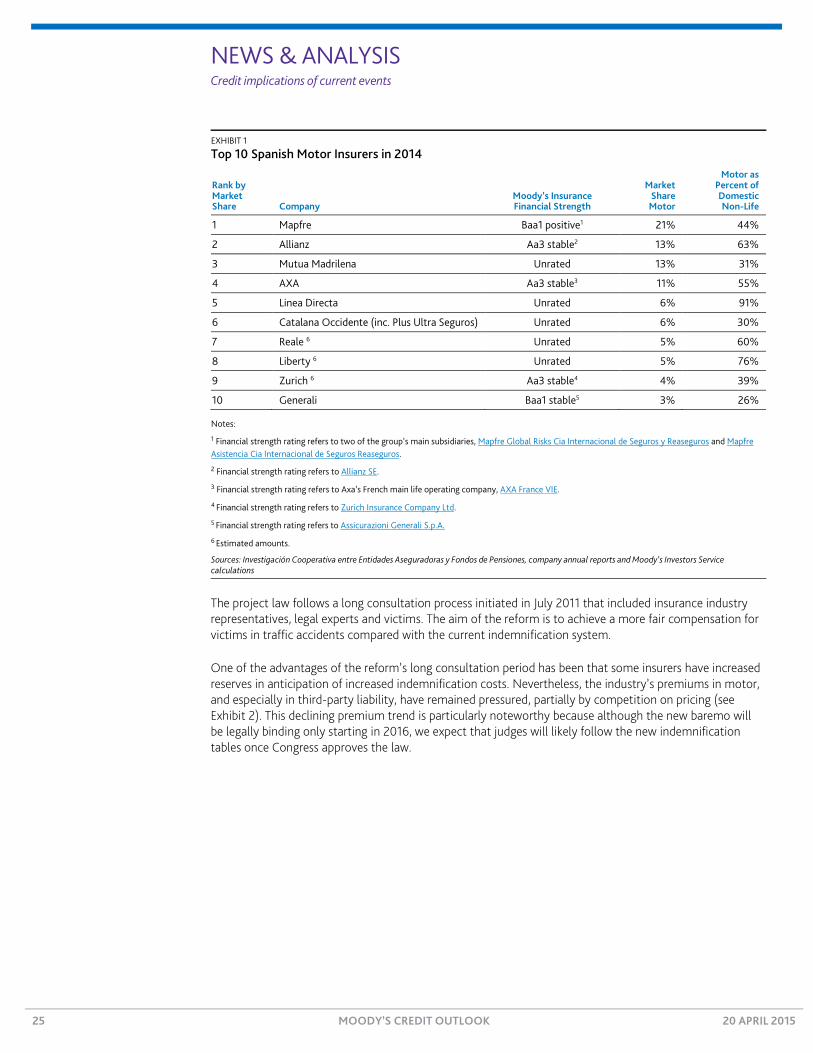

Spain’s Motor Insurers’ Claims Will Increase with Third-Party Bodily Injury Reforms Last Monday, Spain’s Ministry of Justice published its project law reforming third-party (i.e., parties other than the driver) body injury motor insurance, also known as baremo. If Spanish lawmakers approve the law in its current form, the reforms will increase the cost of third-party liability claims by an average of 16%, or around €400 million, according to industry estimates, a credit negative for motor insurers’ profitability. The law next goes to Congress, where it will likely gain approval by summer, and the new baremo will likely be implemented in 2016.

The baremo reform will weigh on the already-weak profitability of the industry’s third-party liability motor insurance, which has experienced underwriting losses in recent years. Third-party liability motor combined ratios (i.e., the total cost of insurance claims divided by premiums) have exceeded 100% as a result of price competition, indicating that the insurers have underwriting losses. We estimate that the industry’s combined ratio for third-party motor liability will increase by an average of eight percentage points and total motor insurance (including comprehensive cover with greater insurance covers) will rise by four percentage points, based on past accident experience.

Claims for the most severe accidents will increase the most, by an average of 50%, according to industry’s estimates, although the ultimate cost for insurers will likely be partially mitigated by the use of reinsurance for larger claims, which is quite common in this business line. Less severe but higher frequency claims, such as for whiplash, will likely see costs decline from current levels. The overall effect for the industry will be meaningful since third-party liability insurance is one of the largest non-life lines in Spain, constituting around 50% of Spain’s total motor premiums and 16% of the industry’s non-life premiums in 2014.

Small insurers with the greatest exposure to motor relative to their premiums and with weaker pricing power to raise prices will likely be the most affected by this reform. Exhibit 1 shows the 10 largest motor insurance writers. Conversely, insurers that have had stronger combined ratios in motor with greater pricing power, or are less exposed to motor, such as Mapfre S.A. (unrated) or Grupo Catalana Occidente (unrated), owner of Atradius NV (operating subsidiary financial strength A3 stable), will be less affected and have the potential to gain market share.

Laura Perez-Martinez, CFA Assistant Vice President - Analyst +44.20.7772.1602 [email protected]

NEWS & ANALYSIS Credit implications of current events

25 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

EXHIBIT 1

Top 10 Spanish Motor Insurers in 2014

Rank by Market Share Company

Moody’s Insurance Financial Strength

Market Share

Motor

Motor as Percent of Domestic Non-Life

1 Mapfre Baa1 positive1 21% 44%

2 Allianz Aa3 stable2 13% 63%

3 Mutua Madrilena Unrated 13% 31%

4 AXA Aa3 stable3 11% 55%

5 Linea Directa Unrated 6% 91%

6 Catalana Occidente (inc. Plus Ultra Seguros) Unrated 6% 30%

7 Reale 6 Unrated 5% 60%

8 Liberty 6 Unrated 5% 76%

9 Zurich 6 Aa3 stable4 4% 39%

10 Generali Baa1 stable5 3% 26%

Notes:

1 Financial strength rating refers to two of the group’s main subsidiaries, Mapfre Global Risks Cia Internacional de Seguros y Reaseguros and Mapfre Asistencia Cia Internacional de Seguros Reaseguros.

2 Financial strength rating refers to Allianz SE.

3 Financial strength rating refers to Axa’s French main life operating company, AXA France VIE.

4 Financial strength rating refers to Zurich Insurance Company Ltd.

5 Financial strength rating refers to Assicurazioni Generali S.p.A.

6 Estimated amounts.

Sources: Investigación Cooperativa entre Entidades Aseguradoras y Fondos de Pensiones, company annual reports and Moody’s Investors Service calculations

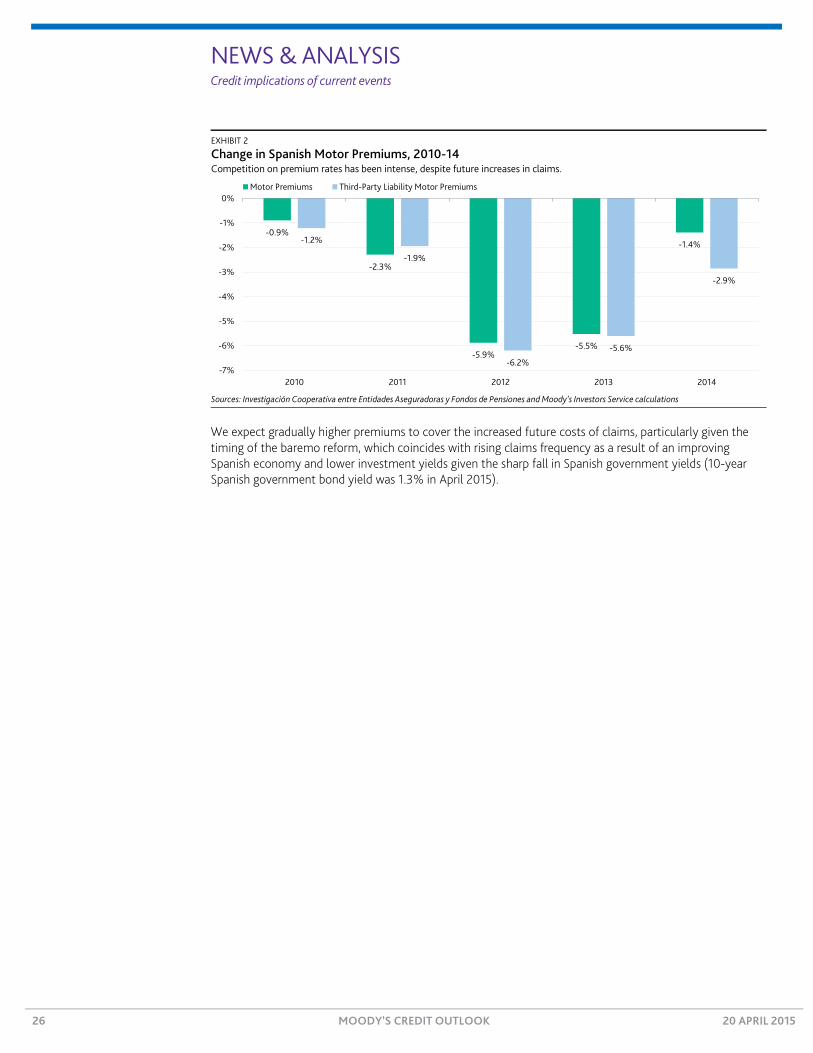

The project law follows a long consultation process initiated in July 2011 that included insurance industry representatives, legal experts and victims. The aim of the reform is to achieve a more fair compensation for victims in traffic accidents compared with the current indemnification system.

One of the advantages of the reform’s long consultation period has been that some insurers have increased reserves in anticipation of increased indemnification costs. Nevertheless, the industry’s premiums in motor, and especially in third-party liability, have remained pressured, partially by competition on pricing (see Exhibit 2). This declining premium trend is particularly noteworthy because although the new baremo will be legally binding only starting in 2016, we expect that judges will likely follow the new indemnification tables once Congress approves the law.

NEWS & ANALYSIS Credit implications of current events

26 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

EXHIBIT 2

Change in Spanish Motor Premiums, 2010-14 Competition on premium rates has been intense, despite future increases in claims.

Sources: Investigación Cooperativa entre Entidades Aseguradoras y Fondos de Pensiones and Moody’s Investors Service calculations

We expect gradually higher premiums to cover the increased future costs of claims, particularly given the timing of the baremo reform, which coincides with rising claims frequency as a result of an improving Spanish economy and lower investment yields given the sharp fall in Spanish government yields (10-year Spanish government bond yield was 1.3% in April 2015).

-0.9%

-2.3%

-5.9%-5.5%

-1.4%-1.2%

-1.9%

-6.2%

-5.6%

-2.9%

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

2010 2011 2012 2013 2014

Motor Premiums Third-Party Liability Motor Premiums

NEWS & ANALYSIS Credit implications of current events

27 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

Money Market Funds

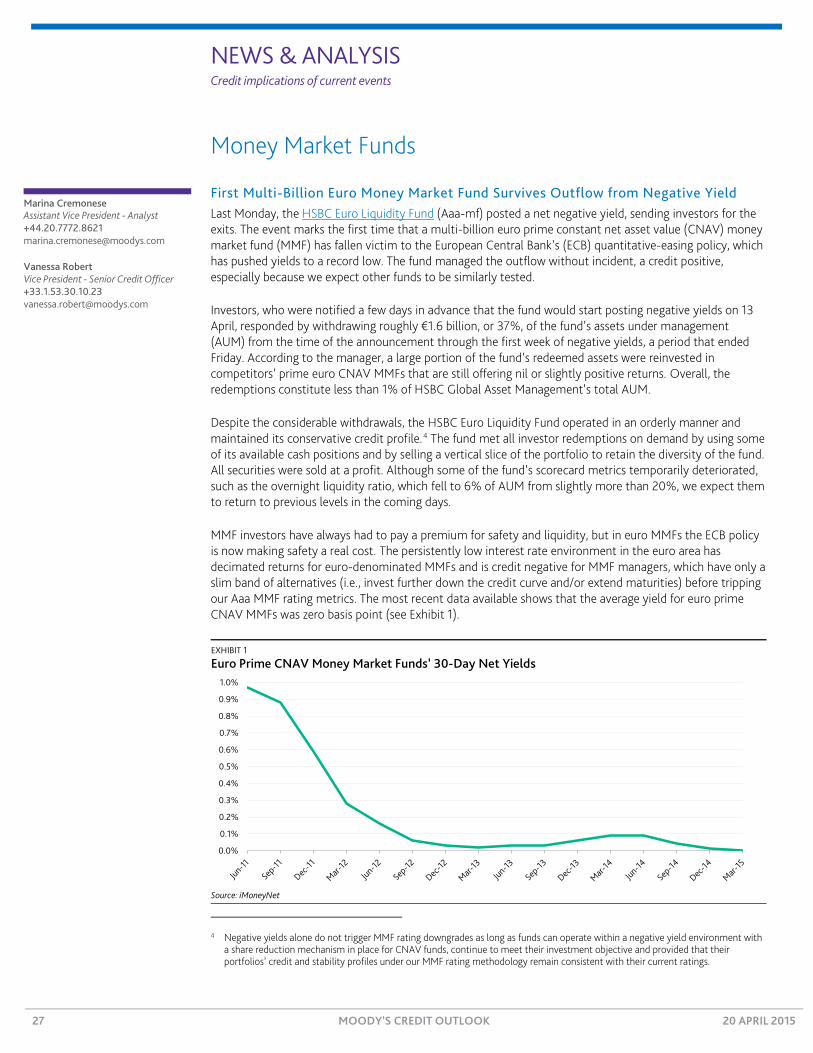

First Multi-Billion Euro Money Market Fund Survives Outflow from Negative Yield Last Monday, the HSBC Euro Liquidity Fund (Aaa-mf) posted a net negative yield, sending investors for the exits. The event marks the first time that a multi-billion euro prime constant net asset value (CNAV) money market fund (MMF) has fallen victim to the European Central Bank’s (ECB) quantitative-easing policy, which has pushed yields to a record low. The fund managed the outflow without incident, a credit positive, especially because we expect other funds to be similarly tested.

Investors, who were notified a few days in advance that the fund would start posting negative yields on 13 April, responded by withdrawing roughly €1.6 billion, or 37%, of the fund’s assets under management (AUM) from the time of the announcement through the first week of negative yields, a period that ended Friday. According to the manager, a large portion of the fund’s redeemed assets were reinvested in competitors’ prime euro CNAV MMFs that are still offering nil or slightly positive returns. Overall, the redemptions constitute less than 1% of HSBC Global Asset Management’s total AUM.

Despite the considerable withdrawals, the HSBC Euro Liquidity Fund operated in an orderly manner and maintained its conservative credit profile.4 The fund met all investor redemptions on demand by using some of its available cash positions and by selling a vertical slice of the portfolio to retain the diversity of the fund. All securities were sold at a profit. Although some of the fund’s scorecard metrics temporarily deteriorated, such as the overnight liquidity ratio, which fell to 6% of AUM from slightly more than 20%, we expect them to return to previous levels in the coming days.

MMF investors have always had to pay a premium for safety and liquidity, but in euro MMFs the ECB policy is now making safety a real cost. The persistently low interest rate environment in the euro area has decimated returns for euro-denominated MMFs and is credit negative for MMF managers, which have only a slim band of alternatives (i.e., invest further down the credit curve and/or extend maturities) before tripping our Aaa MMF rating metrics. The most recent data available shows that the average yield for euro prime CNAV MMFs was zero basis point (see Exhibit 1).

EXHIBIT 1

Euro Prime CNAV Money Market Funds’ 30-Day Net Yields

Source: iMoneyNet

4 Negative yields alone do not trigger MMF rating downgrades as long as funds can operate within a negative yield environment with

a share reduction mechanism in place for CNAV funds, continue to meet their investment objective and provided that their portfolios’ credit and stability profiles under our MMF rating methodology remain consistent with their current ratings.

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

0.8%

0.9%

1.0%

Marina Cremonese Assistant Vice President - Analyst +44.20.7772.8621 [email protected]

Vanessa Robert Vice President - Senior Credit Officer +33.1.53.30.10.23 [email protected]

NEWS & ANALYSIS Credit implications of current events

28 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

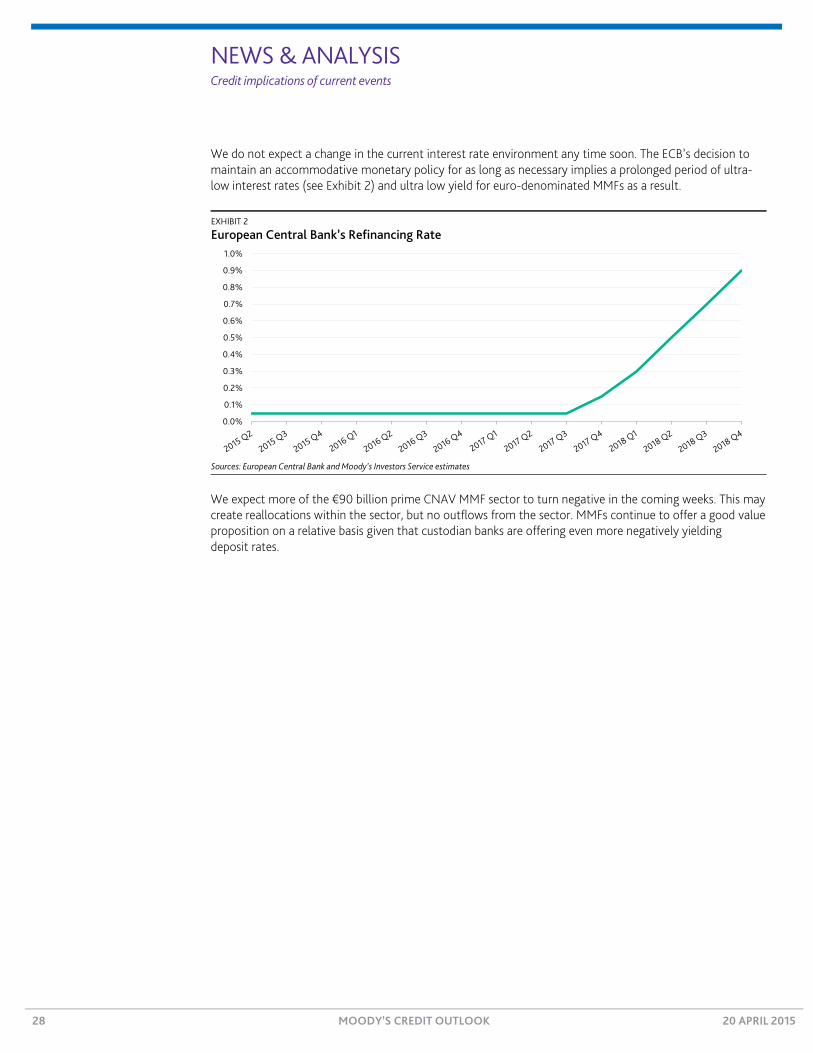

We do not expect a change in the current interest rate environment any time soon. The ECB’s decision to maintain an accommodative monetary policy for as long as necessary implies a prolonged period of ultra-low interest rates (see Exhibit 2) and ultra low yield for euro-denominated MMFs as a result.

EXHIBIT 2

European Central Bank’s Refinancing Rate

Sources: European Central Bank and Moody’s Investors Service estimates

We expect more of the €90 billion prime CNAV MMF sector to turn negative in the coming weeks. This may create reallocations within the sector, but no outflows from the sector. MMFs continue to offer a good value proposition on a relative basis given that custodian banks are offering even more negatively yielding deposit rates.

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

0.8%

0.9%

1.0%

NEWS & ANALYSIS Credit implications of current events

29 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

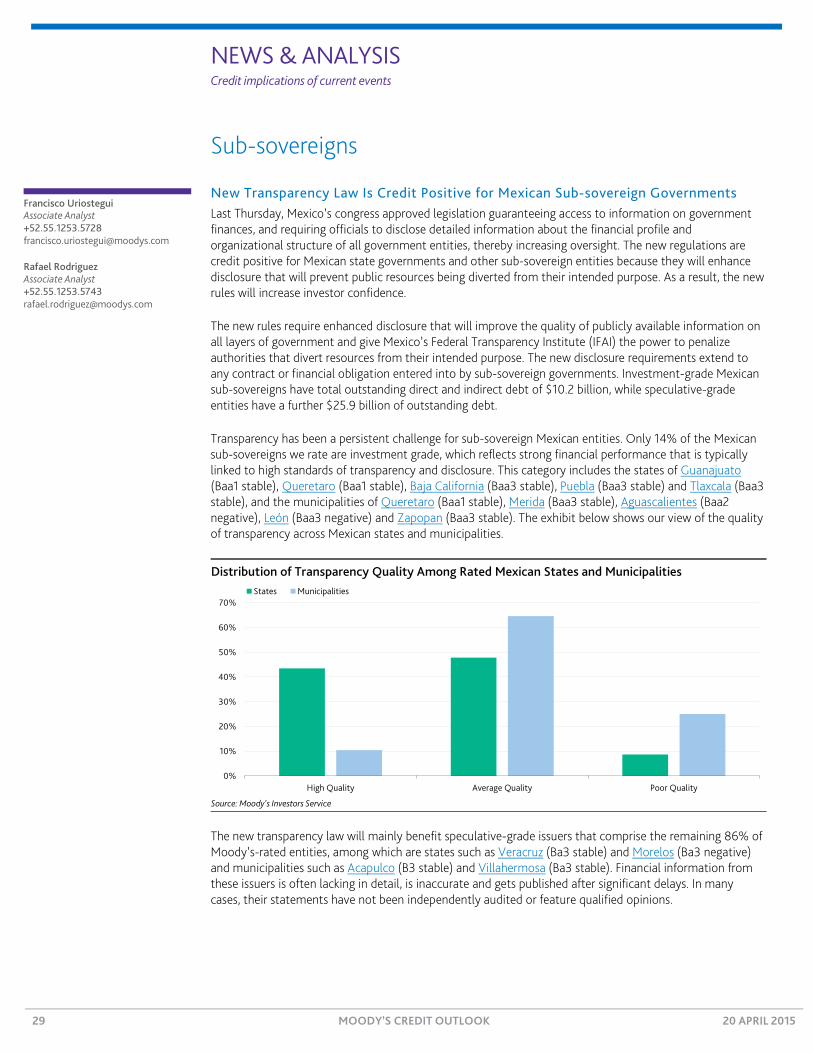

Sub-sovereigns

New Transparency Law Is Credit Positive for Mexican Sub-sovereign Governments Last Thursday, Mexico’s congress approved legislation guaranteeing access to information on government finances, and requiring officials to disclose detailed information about the financial profile and organizational structure of all government entities, thereby increasing oversight. The new regulations are credit positive for Mexican state governments and other sub-sovereign entities because they will enhance disclosure that will prevent public resources being diverted from their intended purpose. As a result, the new rules will increase investor confidence.

The new rules require enhanced disclosure that will improve the quality of publicly available information on all layers of government and give Mexico’s Federal Transparency Institute (IFAI) the power to penalize authorities that divert resources from their intended purpose. The new disclosure requirements extend to any contract or financial obligation entered into by sub-sovereign governments. Investment-grade Mexican sub-sovereigns have total outstanding direct and indirect debt of $10.2 billion, while speculative-grade entities have a further $25.9 billion of outstanding debt.

Transparency has been a persistent challenge for sub-sovereign Mexican entities. Only 14% of the Mexican sub-sovereigns we rate are investment grade, which reflects strong financial performance that is typically linked to high standards of transparency and disclosure. This category includes the states of Guanajuato (Baa1 stable), Queretaro (Baa1 stable), Baja California (Baa3 stable), Puebla (Baa3 stable) and Tlaxcala (Baa3 stable), and the municipalities of Queretaro (Baa1 stable), Merida (Baa3 stable), Aguascalientes (Baa2 negative), León (Baa3 negative) and Zapopan (Baa3 stable). The exhibit below shows our view of the quality of transparency across Mexican states and municipalities.

Distribution of Transparency Quality Among Rated Mexican States and Municipalities

Source: Moody’s Investors Service

The new transparency law will mainly benefit speculative-grade issuers that comprise the remaining 86% of Moody’s-rated entities, among which are states such as Veracruz (Ba3 stable) and Morelos (Ba3 negative) and municipalities such as Acapulco (B3 stable) and Villahermosa (Ba3 stable). Financial information from these issuers is often lacking in detail, is inaccurate and gets published after significant delays. In many cases, their statements have not been independently audited or feature qualified opinions.

0%

10%

20%

30%

40%

50%

60%

70%

High Quality Average Quality Poor Quality

States Municipalities

Francisco Uriostegui Associate Analyst +52.55.1253.5728 [email protected]

Rafael Rodriguez Associate Analyst +52.55.1253.5743 [email protected]

NEWS & ANALYSIS Credit implications of current events

30 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

In the past, inadequate financial disclosure and a lack of oversight led to abrupt financial deterioration among Mexican sub-sovereigns. We expect the new law to gradually narrow the gap in terms of quality and timeliness of financial disclosure within the sector, reducing the scope for future unexpected financial problems.

NEWS & ANALYSIS Credit implications of current events

31 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

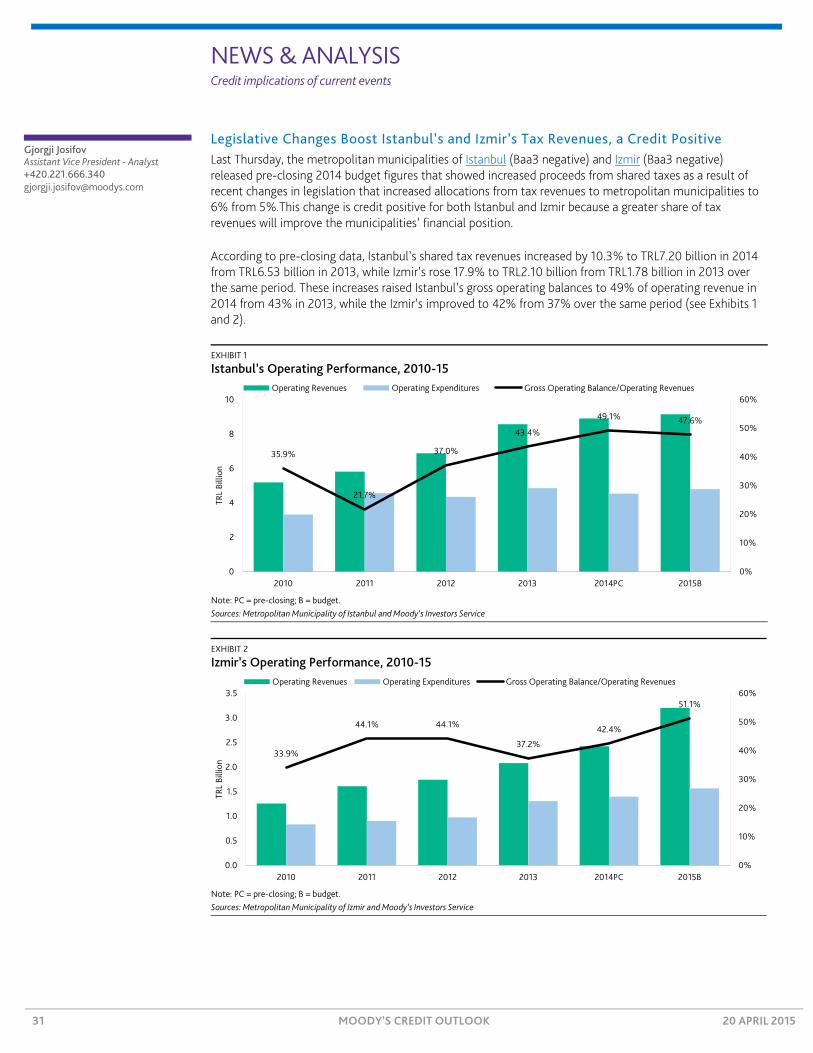

Legislative Changes Boost Istanbul’s and Izmir’s Tax Revenues, a Credit Positive Last Thursday, the metropolitan municipalities of Istanbul (Baa3 negative) and Izmir (Baa3 negative) released pre-closing 2014 budget figures that showed increased proceeds from shared taxes as a result of recent changes in legislation that increased allocations from tax revenues to metropolitan municipalities to 6% from 5%.This change is credit positive for both Istanbul and Izmir because a greater share of tax revenues will improve the municipalities’ financial position.

According to pre-closing data, Istanbul’s shared tax revenues increased by 10.3% to TRL7.20 billion in 2014 from TRL6.53 billion in 2013, while Izmir’s rose 17.9% to TRL2.10 billion from TRL1.78 billion in 2013 over the same period. These increases raised Istanbul’s gross operating balances to 49% of operating revenue in 2014 from 43% in 2013, while the Izmir’s improved to 42% from 37% over the same period (see Exhibits 1 and 2).

EXHIBIT 1

Istanbul’s Operating Performance, 2010-15

Note: PC = pre-closing; B = budget. Sources: Metropolitan Municipality of Istanbul and Moody’s Investors Service

EXHIBIT 2

Izmir’s Operating Performance, 2010-15

Note: PC = pre-closing; B = budget. Sources: Metropolitan Municipality of Izmir and Moody’s Investors Service

35.9%

21.7%

37.0%

43.4%

49.1% 47.6%

0%

10%

20%

30%

40%

50%

60%

0

2

4

6

8

10

2010 2011 2012 2013 2014PC 2015B

TRL

Billi

on

Operating Revenues Operating Expenditures Gross Operating Balance/Operating Revenues

33.9%

44.1% 44.1%

37.2%

42.4%

51.1%

0%

10%

20%

30%

40%

50%

60%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2010 2011 2012 2013 2014PC 2015B

TRL

Billi

on

Operating Revenues Operating Expenditures Gross Operating Balance/Operating Revenues

Gjorgji Josifov Assistant Vice President - Analyst +420.221.666.340 [email protected]

NEWS & ANALYSIS Credit implications of current events

32 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

Because the reform on metropolitan municipalities and corresponding changes in the law on allocations from tax revenues went into effect in April 2014, the legislative changes will take full effect this year. Therefore, we expect shared tax revenues to continue growing and the financial performance of Istanbul and Izmir to remain robust. Turkish metropolitan municipalities largely depend on shared tax revenue growth because share taxes comprise, on average, more than 80% of their budgets. Around 81% of Istanbul’s operating revenues are derived from shared tax revenues, while in Izmir shared taxes account for 86% of operating revenues.

Both municipalities have had strong financial performance in recent years, which has led to their each having comfortable liquidity positions. Their accumulated cash reserves averaged 15% of operating revenue in 2014, creating a solid financial cushion against potential budgetary pressures and supporting capex funding over the next two years. We expect cash reserves to gradually increase toward 20% of their operating revenue in 2015-16 following the increase in proceeds from the shared taxes. Exhibits 3 and 4 show how the composition of Istanbul’s and Izmir’s operating revenues have evolved over the years.

EXHIBIT 3

Composition of Istanbul’s Operating Revenues, 2010-15

Note: PC = pre-closing; B = budget. Sources: Metropolitan Municipality of Istanbul and Moody’s Investors Service

EXHIBIT 4

Composition of Izmir’s Operating Revenues, 2010-15

Note: PC = pre-closing; B = budget. Sources: Metropolitan Municipality of Izmir and Moody’s Investors Service

81.6% 83.8% 81.3% 76.3% 81.0% 81.9%

8.8% 7.1% 5.9%4.1%

4.1% 2.4%

9.6% 9.1% 12.7%19.6% 14.9% 15.7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014PC 2015B

Shared Taxes Local Taxes Other Own-Source Revenues

86.4%79.8%

86.4% 85.6% 86.6% 86.4%

8.7%8.5%

8.2% 9.8% 6.3% 5.8%

4.9%11.7% 5.4% 4.6% 7.0% 7.9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014PC 2015B

Shared Taxes Local Taxes and Fees Other Own-Source Revenues

NEWS & ANALYSIS Credit implications of current events

33 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

Following a decline in debt issuance, which lowered Istanbul’s and Izmir’s debt levels, we expect that the increase in tax revenues and the associated improvement in financial performance will reduce the municipalities’ appetite for debt-financed investments. The decline in Istanbul’s debt stock over the past three years has resulted in a drop in debt servicing costs to 11% of operating revenue in 2014 from 15% in 2012-13, and we expect it to decline to less than 10% in 2015-16. These positive factors mitigate Istanbul’s exposure to growing debt-servicing costs arising from a depreciating Turkish lira, given that 94% of its direct debt stock is issued in foreign currency.

Rising operating surpluses will also support Izmir’s debt-servicing capacity, although with 53% of its direct debt denominated in foreign currency, Izmir is less vulnerable to exchange-rate fluctuations than Istanbul.

NEWS & ANALYSIS Credit implications of current events

34 MOODY’S CREDIT OUTLOOK 20 APRIL 2015

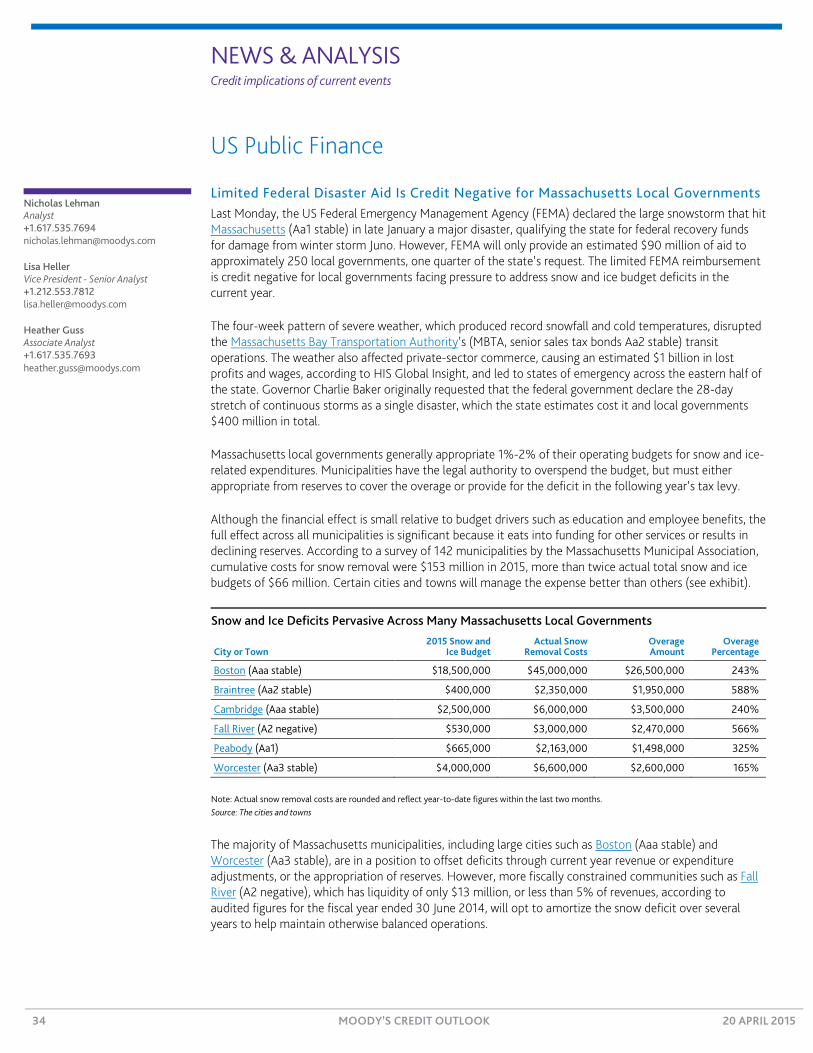

US Public Finance

Limited Federal Disaster Aid Is Credit Negative for Massachusetts Local Governments Last Monday, the US Federal Emergency Management Agency (FEMA) declared the large snowstorm that hit Massachusetts (Aa1 stable) in late January a major disaster, qualifying the state for federal recovery funds for damage from winter storm Juno. However, FEMA will only provide an estimated $90 million of aid to approximately 250 local governments, one quarter of the state’s request. The limited FEMA reimbursement is credit negative for local governments facing pressure to address snow and ice budget deficits in the current year.

The four-week pattern of severe weather, which produced record snowfall and cold temperatures, disrupted the Massachusetts Bay Transportation Authority’s (MBTA, senior sales tax bonds Aa2 stable) transit operations. The weather also affected private-sector commerce, causing an estimated $1 billion in lost profits and wages, according to HIS Global Insight, and led to states of emergency across the eastern half of the state. Governor Charlie Baker originally requested that the federal government declare the 28-day stretch of continuous storms as a single disaster, which the state estimates cost it and local governments $400 million in total.

Massachusetts local governments generally appropriate 1%-2% of their operating budgets for snow and ice-related expenditures. Municipalities have the legal authority to overspend the budget, but must either appropriate from reserves to cover the overage or provide for the deficit in the following year’s tax levy.

Although the financial effect is small relative to budget drivers such as education and employee benefits, the full effect across all municipalities is significant because it eats into funding for other services or results in declining reserves. According to a survey of 142 municipalities by the Massachusetts Municipal Association, cumulative costs for snow removal were $153 million in 2015, more than twice actual total snow and ice budgets of $66 million. Certain cities and towns will manage the expense better than others (see exhibit).

Snow and Ice Deficits Pervasive Across Many Massachusetts Local Governments

City or Town 2015 Snow and

Ice Budget Actual Snow

Removal Costs Overage Amount

Overage Percentage

Boston (Aaa stable) $18,500,000 $45,000,000 $26,500,000 243%

Braintree (Aa2 stable) $400,000 $2,350,000 $1,950,000 588%

Cambridge (Aaa stable) $2,500,000 $6,000,000 $3,500,000 240%

Fall River (A2 negative) $530,000 $3,000,000 $2,470,000 566%

Peabody (Aa1) $665,000 $2,163,000 $1,498,000 325%

Worcester (Aa3 stable) $4,000,000 $6,600,000 $2,600,000 165%

Note: Actual snow removal costs are rounded and reflect year-to-date figures within the last two months. Source: The cities and towns

The majority of Massachusetts municipalities, including large cities such as Boston (Aaa stable) and Worcester (Aa3 stable), are in a position to offset deficits through current year revenue or expenditure adjustments, or the appropriation of reserves. However, more fiscally constrained communities such as Fall River (A2 negative), which has liquidity of only $13 million, or less than 5% of revenues, according to audited figures for the fiscal year ended 30 June 2014, will opt to amortize the snow deficit over several years to help maintain otherwise balanced operations.

Nicholas Lehman Analyst +1.617.535.7694 [email protected]