Embed Size (px)

Citation preview

MOODYS.COM

19 DECEMBER 2013

NEWS & ANALYSIS Corporates 2

» 3M’s Plans to Boost Shareholder Returns Are Credit Negative » Hong Kong Electric’s Proposed Spinoff Is Credit Positive for

Hutchison Whampoa » Bumi Plc-Bakrie Separation Is Credit Positive for Berau and

Bumi Resources

Infrastructure 6

» Mexico’s Energy Reform Is Credit Positive for the Electricity Sector

» Norway’s Equity Injection into Grid Operator Statnett Is Credit Positive

Banks 9

» Basel Committee’s Final Standard on Equity Investments in Funds Is Credit Positive for Banks

» Zions’ Charge on Trust Preferred CDOs Is Credit Negative » Norway Sets Countercyclical Capital Buffer for Banks, a Credit

Positive » Alpha Bank’s Warrants Exercise Is Credit Positive » China’s Regulation for Financial Leasing Companies Is

Credit Positive » Japanese Lenders’ Additional Exposure to TEPCO Is

Credit Negative

Insurers 18 » AIG’s Sale of ILFC to AerCap Is Negative for ILFC, Positive

for AIG » Spain’s Pension Reform Will Likely Increase Life Insurers’ Sales

Sovereigns 22

» Mexico Approves Energy Reform, a Credit Positive

Sub-sovereigns 24

» Mexican State of Sonora’s Elimination of Vehicle Tax Is Credit Negative

Securitization 26 » Amendments to Italian Law Are Credit Positive for

Securitizations and Covered Bonds

CREDIT IN DEPTH US Public Finance 28

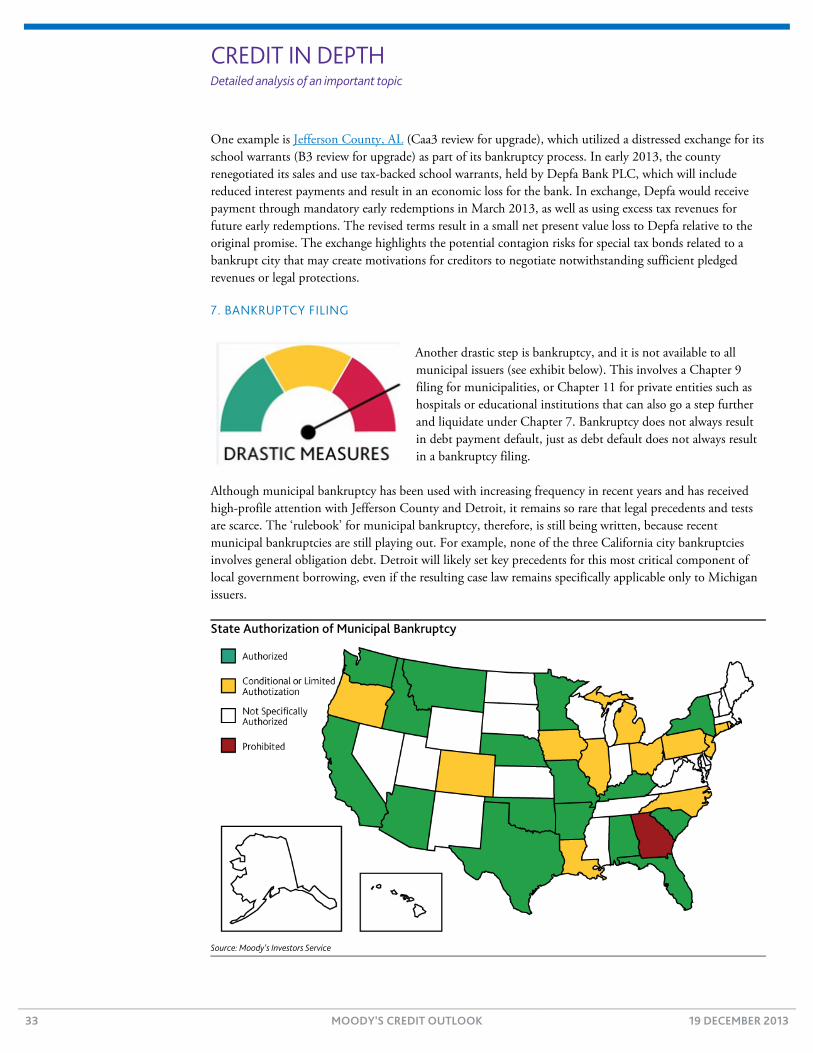

We describe the steps we have observed local US governments take to address credit stress. The measures taken depend on the level of financial stress local governments face and we discuss them in order of the credit risk they pose to municipal bond investors: adjust fiscal policies and operating costs, defer tough decisions, request state oversight and support, merger or dissolution, selective default, distressed exchange and bankruptcy filing.

RECENTLY IN CREDIT OUTLOOK

» Articles in Last Monday’s Credit Outlook 35 » Go to Last Monday’s Credit Outlook

This is the last issue of Moody’s Credit Outlook in 2013. Our next issue will be Thursday 9 January.

We wish you happy holidays and a credit positive 2014.

NEWS & ANALYSIS Credit implications of current events

2 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Corporates

3M’s Plans to Boost Shareholder Returns Are Credit Negative On Tuesday, 3M Company (Aa2 stable) disclosed that its five-year strategic plan will include a 35% increase in its dividend starting in the first quarter of 2014, and sharply higher share repurchases through 2017. We view the announcement as credit negative because it indicates that 3M is shifting to a more leveraged capital structure.

The company said it plans to repurchase shares valued at $17-$22 billion through 2017 (excluding proceeds from options exercised by employees), up from its previously projected range of $7.5-$15.0 billion in buybacks. The 35% dividend increase would add $600 million a year in payments, leading to a total dividend outflow of roughly $2.3 billion a year. The company also reaffirmed that it expects to invest $5-$10 billion in acquisitions through 2017, in line with its previous guidance of $1-$2 billion a year. This contrasts with the company’s free cash flow of $2.9 billion for the 12 months ended 30 September.

Acquisitions would contribute incremental revenues, earnings and cash flows, tempering the effect on financial metrics. But accelerated share repurchases would increase indebtedness and have a more detrimental effect on 3M’s credit quality.

By orienting its capital structure to achieve a lower total cost of capital versus a lower cost of debt, 3M would edge toward a capital structure closer to other highly rated diversified manufacturers, most of which have senior unsecured ratings that are three notches lower. They include Emerson Electric Company (A2 stable), Danaher Corporation (A2 stable), United Technologies Corporation (A2 negative), Honeywell International Inc. (A2 stable) and Illinois Tool Works Inc. (A2 stable). General Electric Company (Aa3 stable) is the exception at one notch below 3M.

At the end of September, 3M’s debt/EBITDA was roughly 1.2x and its EBIT/interest was 20x (both as adjusted by us), versus 2012 cross-industry medians for the A2 category of 2.3x and 8.0x, respectively. 3M’s metrics are likely to strengthen by year-end owing to an anticipated improvement in the funded position of its pension plans and modest earnings growth in the fourth quarter. With the company expecting to take on $2-$4 billion in additional debt in 2014, we expect debt/EBITDA leverage to climb to 1.4x-1.7x, excluding the effect of the company’s expectation of a pension adjustment and fourth-quarter earnings growth.

As the distinctions between 3M and its lower-rated peers start to blur, it is more likely that the company’s ratings will gravitate toward the lower-rated peer group, but not necessarily through a single, multi-notch downgrade. If such a scenario were to develop, only long-term ratings would likely be affected because 3M appears to have no intention to take leverage to a level that would threaten its short-term rating.

3M retains substantial scale, diversification and meaningfully higher margins than most of its peers. Moreover, its liquidity remains excellent, with cash and short-term investments totaling $4.9 billion as of 30 September, compared with total funded debt of $5.9 billion.

The pace at which 3M incurs additional debt and how strong it maintains liquidity now that it has resumed commercial paper borrowings will determine the timing and magnitude of any rating action.

Edwin Wiest Vice President - Senior Credit Officer +1.212.553.1461 [email protected]

NEWS & ANALYSIS Credit implications of current events

3 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Hong Kong Electric’s Proposed Spinoff Is Credit Positive for Hutchison Whampoa On 15 December, a Hutchison Whampoa Limited (HWL, A3 stable) subsidiary announced plans to spin off 50.1%-70.0% of Hong Kong Electric Company Ltd (HEC, unrated), one of the two regulated electric utilities in Hong Kong. The plan is credit positive for HWL because it is likely to enhance the value of its interests in the 78%-owned subsidiary Cheung Kong Infrastructure (CKI, unrated), which owns 38.87% of Power Assets Holding Ltd. (PAH, unrated), which in turn owns 100% of HEC.

PAH’s leverage will decline after the spinoff and its liquidity will increase. CKI will continue to receive the same level of dividends from PAH because PAH intends to pay the same level of dividends this year and next as it did in 2012.

Although PAH will receive less in dividends from HEC after the partial disposal, the proceeds from the transaction and earnings from other overseas investments will support dividend payouts at the same level or greater than the 2012 level of HKD5.2 billion ($667 million). As a result, the dividend flow to PAH’s immediate parent CKI and ultimate parent HWL will remain stable.

PAH said that it expects the spinoff to generate proceeds of HKD52.6-HKD61.9 billion ($6.8-$8.0 billion), comprising the spinoff proceeds of HKD31.7-HKD41.0 billion ($4.1-$5.3 billion) and HEC’s HKD20.9 billion ($2.7 billion) repayment of intercompany loans. PAH will therefore record a pro forma gain of HKD53.0-HKD53.3 billion ($6.8-$6.9 billion).

We expect that PAH will take some time to deploy the cash it receives in new investments and that it will make investments in a way that does not materially raise its leverage beyond its current level.

The HEC spinoff involves the use of a business trust structure that will be listed on the Hong Kong Stock Exchange. As part of this structure, an entity called HK Electric Investments will acquire HEC in exchange for an issue of share-stapled units, proceeds from the global offering and proceeds from a loan facility. The spinoff would involve a recapitalization, with HEC raising HKD28.3 billion ($3.7 billion) in debt.

A shareholder meeting to vote on the transaction is scheduled for 6 January. CKI will be able to vote its shares as part of the transaction. Hence, shareholder approval seems assured. Even with shareholder approval, the transaction will not proceed unless the spun-off entity achieves a minimum market capitalization of HKD48 billion ($6.2 billion).

HWL is one of the largest Hong Kong-based conglomerates with a large presence in Asia and Europe. Its six core businesses are ports and related services, property and hotels, retail, telecommunications, energy and infrastructure. Its 2012 revenues, excluding its share of associates and joint ventures, were HKD243 billion ($31.2 billion). HEC had 2012 revenues of HKD10.4 billion ($1.3 billion).

Joe Morrison Vice President - Senior Analyst +852. 3758. 1376 [email protected]

NEWS & ANALYSIS Credit implications of current events

4 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Bumi Plc-Bakrie Separation Is Credit Positive for Berau and Bumi Resources On 17 December, Bumi Plc’s (unrated) shareholders voted to sell the company’s minority stake in Bumi Resources Tbk (P.T.) (Ca stable) to the Bakrie Group (unrated) for $501 million. In turn, the Bakrie Group will sell its 23.8% stake in Bumi Plc to affiliated companies of Bumi Plc Chairman Samin Tan for $223 million. The transactions are credit positive for Bumi Plc’s remaining operating subsidiary, Berau Coal Energy Tbk (P.T.) (BCE, B1 negative), and Bumi Resources.

The Bumi Plc-Bakrie Group separation is credit positive for BCE because Bumi Plc has committed to review BCE’s capital structure with the aim of reducing its interest cost. However, Bumi Plc’s longer-term financial policies regarding distributions from BCE are unclear. A distribution of cash to Bumi Plc from BCE would be credit negative for BCE.

Bumi Plc will return roughly $400 million of the deal proceeds to shareholders and use the remainder, or roughly $101 million, for debt reduction or other corporate purposes. We believe Bumi Plc will use part or all of the remaining proceeds to refinance BCE’s $450 million 12.5% notes due July 2015. The call premium on these notes drops to 103.125% in July 2014.

Bumi Plc owns 84.7% of BCE, which will remain its sole operating asset post-separation, and 29.2% of Bumi Resources. The Bakrie Group, through a relationship agreement, had the right to nominate the chairman, CEO and CFO of Bumi Plc, which gave it significant control over the company before it had agreed to sell its stake in Bumi Plc.

If Bumi Plc reduces BCE’s debt with the full $101 million of retained cash, we expect BCE’s adjusted debt/EBITDA for 2014 to decline toward the 3.7x-4.2x range from our earlier projection of 4.0x-4.5x.

We also expect the separation to improve corporate governance and accountability at BCE since no single shareholder will have a controlling interest in Bumi Plc. An independent review in 2013 revealed accounting irregularities, weaknesses in accounting practices, and $201 million of expenses with no clear business purpose. BCE began addressing these issues by bringing in a new CEO, CFO and chief mining officer. As part of the Bumi Plc-Bakrie Group separation, Bumi Plc agreed to add an independent chairman and allow certain shareholders to nominate independent directors to its board, which will be managed in accordance with the UK Corporate Governance Code.

For Bumi Resources, there will be no immediate effect other than leaving the Bumi Plc family. However, the transaction is credit positive in that it simplifies the shareholder structure and allows management to focus on a balance-sheet restructuring.

News of the separation follows the 12 December announcement that Bumi Resources had completed its consent solicitation from bondholders to execute the previously announced debt-for-equity exchange with China Investment Company (CIC, unrated).

Bumi Resources will hold a board meeting on 20 December to vote on the CIC deal, which, if approved, should allow for the transaction to close in January now that most of the necessary consents have been obtained. The completion of the exchange is Bumi Resources’ first meaningful step in addressing an untenable capital structure, which includes more than $800 million in maturities next year, in addition to the debt included in the CIC transaction.

Brian Grieser Vice President - Senior Analyst +65.6398.3713 [email protected]

Rachel Chua Associate Analyst +65.6398.8313 [email protected]

NEWS & ANALYSIS Credit implications of current events

5 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Bumi Plc expects to complete the Bumi Plc-Bakrie Group separation in January. Post-separation, Bumi Plc (to be renamed Asia Resources Minerals Plc) will continue to own 84.7% of BCE and will no longer be affiliated to the Bakrie Group, as shown in the exhibit below. Under its new shareholder structure, Samin Tan-controlled affiliates Borneo Bumi (unrated) and RACL (unrated) will own 48% of Bumi Plc, while the remaining 52% will be publicly held.

Pre- and Post-transaction Structure of Bumi Plc

Source: Bumi Plc presentation, 7 November 2013

NEWS & ANALYSIS Credit implications of current events

6 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Infrastructure

Mexico’s Energy Reform Is Credit Positive for the Electricity Sector Last Monday, a majority of Mexico’s (Baa1 stable) state legislators approved the country’s energy reform bill, which followed the Mexican Congress’ approval. The states’ approval was the last hurdle to a long-anticipated constitutional reform that ends Comision Federal de Electricidad’s (CFE, Baa1/Aaa.mx stable) monopoly in electric power generation and commercialization. Passage of the law is credit positive for private electricity companies because it will increase their business. It is also credit positive for the state-owned electricity company CFE because it will lower its production costs and investment needs.

The reform will increase electricity generation capacity with cleaner technologies through private investment, boost efficiency via more private participation and reduce electricity costs. The Mexican government will maintain control of the national electricity system and exclusively transmit and distribute energy, but now CFE can contract other companies to provide these services.

Today, private generation is limited to self supply, cogeneration and an independent power producers scheme, under which producers must sell their energy to CFE. Currently, private generation accounts for 44% of Mexico’s total capacity (see exhibit). To meet demand in 2026, CFE and independent power producer capacity must grow by 60% to 86 gigawatts from 53 gigawatts currently. The reform bill will create important business opportunities for energy generation private companies such as Infraestructura Energética Nova, S.A. de C.V. (Baa1/Aaa.mx stable), a subsidiary of Sempra Energy (Baa1 stable), and the Mexican subsidiaries of Gas Natural SDG, S.A. (Baa2 stable) and Iberdrola S.A. (Baa1 negative). The bill also creates a market to trade energy production with companies other than the CFE to further increase the sector’s efficiencies.

Mexico’s 61,570 Megawatt Installed Capacity at 2011 by Producer

*Includes the now-defunct Luz y Fuerza del Centro **Private generation that must be sold to CFE Source: Mexico Secretaría de Energia, Prospectiva del Sector Eléctrico 2012-26

The comprehensive reform will lower CFE’s production costs by making natural gas more available and allowing the company to switch from fuel oil. It may also improve CFE’s leverage by lowering the sizable funding requirements for its ambitious capital investment program, which has increased its debt in recent years. CFE recorded indebtedness of MXN302.4 billion as of September 2013, versus MXN92.2 billion at year-end 2007.

Comision Federal de Electricidad*66%

Independent Energy Producers**19%

Private15%

Adrián Javier Garza Assistant Vice President - Analyst +52.55.1253.5709 [email protected]

NEWS & ANALYSIS Credit implications of current events

7 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

The reform strengthens the current electricity regulator and creates a new decentralized body that will take operative control of the national electric system and the wholesale power market. This body will also ensure that there is open access to the transmission and distribution grids.

NEWS & ANALYSIS Credit implications of current events

8 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Norway’s Equity Injection into Grid Operator Statnett Is Credit Positive On Tuesday, the Government of Norway (Aaa stable) approved a capital injection of NOK3.25 billion (€400 million) into 100% state-owned Norwegian high-voltage electricity grid owner and operator, Statnett SF (A2 stable). The equity injection is credit positive because it reduces the amount of debt that Statnett will need to raise to fund a significant upgrade of Norway’s transmission capacity over the next four years.

The equity injection supports the company’s plans to invest NOK40 billion (€4.75 billion) between 2013 and 2017. Despite the injection, we still expect Statnett’s net debt to rise by around 50% to approximately NOK30 billion (€3.55 billion) by December 2016. However, we expect Statnett’s financial ratios to remain stable, with the ratio of funds from operations to net debt around 8% and the ratio of retained cash flow to net debt about 7%, well within the range we indicate for the rating.

The Norwegian government will more than double Statnett’s equity capital to NOK5.95 billion (€700 million) from NOK2.7 billion. In addition to the equity injection, the government has agreed to other credit-positive measures for Statnett, including no dividend declaration in the 2013 financial year and halving its dividend policy to 25% of profit after tax for the 2014-16 financial years.

The equity injection demonstrates the Norwegian government’s willingness to support new infrastructure projects that it expects will benefit Norway’s economy through its ability to develop and export its natural resources and maximise GDP. The Norwegian electricity regulator, the NVE, also increased Statnett’s allowed return on assets at the beginning of 2013, which will underpin revenue growth as new assets are commissioned. The investment in the grid reflects similar levels of investment across Europe to reduce congestion and increase the connection of ongoing high levels of renewable energy commissioning.

Statnett is undertaking grid upgrade work that will reduce the congestion on the network when hydro-based electricity output is high and reduce system losses by upgrading lines to a higher voltage. In addition, Statnett is supporting Norway’s economic growth through the connection of new oil and gas fields, connecting new wind and hydro capacity and supporting the construction of three new interconnectors to Germany, Denmark and the UK to facilitate the export of electricity to traditionally higher-priced electricity markets.

Statnett’s A2 stable ratings incorporate three notches of uplift over its baseline credit assessment of baa2, reflecting the high level of support from the Norwegian government and the company’s dependence on the Norwegian economy.

Paul Lund Vice President - Senior Credit Officer +44.20.7772.1955 [email protected]

NEWS & ANALYSIS Credit implications of current events

9 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Banks

Basel Committee’s Final Standard on Equity Investments in Funds Is Credit Positive for Banks On 13 December, the Basel Committee on Banking Supervision released its final standard revising the prudential requirements for banks’ equity investments in funds (including hedge funds, investment funds and managed funds) set out in the Basel II risk-based capital framework. The final standard is credit positive for banks because it strengthens the existing Basel framework by incorporating a fund’s leverage in setting a bank’s capital requirements for an equity investment in the fund. This ensures that a bank’s risk-weighted assets calculation takes into account off-balance-sheet leverage.

The standard will apply to all banks regardless of whether they use the standardized or internal ratings-based (IRB) approaches for credit risk, although national supervisors have the discretion to exempt investments in funds that meet certain conditions set out in the Basel II framework. The final standard takes effect 1 January 2017 and applies to banks’ equity investments in all funds that are held in the banking book.

Before the global financial crisis, the full extent of banks’ leverage was often under-reported because their activities were conducted by funds structured as certain types of off-balance-sheet vehicles such as conduits and structured investment vehicles in which the banks had an equity stake. These exposures were not fully captured by the Basel II framework, within which banks risk weight these equity investments using the standardized approach, or look through to the fund’s underlying assets as separate and distinct investments using the IRB approach.

The revised standard also benefits bank credit quality because it encourages due diligence and more transparent reporting of investments in funds by clarifying and augmenting the approaches for setting capital requirements for equity investments in funds.

Banks will use three approaches in a hierarchy that starts with the look-through approach (LTA), whereby the underlying exposures of a fund are risk-weighted as if they were held directly by the bank. If LTA conditions do not apply, banks will use the mandate-based approach (MBA) and calculate regulatory capital using information in a fund’s mandate or in national regulations governing these funds. Although both approaches were previously part of the Basel II capital framework, the revised standard clarifies the conditions for their use and how they should be applied. If banks cannot use either the LTA or MBA, they will need to use the fall-back approach, which applies a punitive 1,250% risk weight to a bank’s equity investment in a fund and aims to encourage banks to use one of the other two approaches.

Fuller coverage of the risks in a fund’s underlying investments will materially increase some banks’ required regulatory capital. In some cases, banks may decide that certain types of fund investments no longer give sufficiently attractive risk-adjusted returns and they may therefore reduce their holdings in such funds.

Following comments on the Basel Committee’s July 2013 consultative document on the standard, the Basel Committee simplified the three approaches, and if certain conditions are met, banks will be allowed to use them in combination in setting the capital requirements for an equity investment in an individual fund.

Other requirements in the revised standard will improve how banks report their exposure to equity investments in funds. They also ensure that risk weights will reflect more appropriately the risk of a fund’s underlying investments by imposing higher capital charges in cases where a fund’s holdings are not sufficiently transparent.

Matthew Maxwell Vice President - Senior Analyst +852.3758.1539 [email protected]

NEWS & ANALYSIS Credit implications of current events

10 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Zions’ Charge on Trust Preferred CDOs Is Credit Negative On Monday, Zions Bancorporation ((P)Ba1 stable) announced that it will mark its $1.8 billion (amortized cost) portfolio of trust preferred CDOs to fair value through an other-than-temporary-impairment (OTTI) non-cash charge to earnings in the fourth quarter of this year. The charge is credit negative because it will result in a large net loss in the fourth quarter, and leave the company essentially breakeven for 2013, negatively affecting its capital position.

The charge is in response to the final rules implementing the Volcker Rule provision of the Dodd-Frank Wall Street Reform and Consumer Protection Act, which disallows banks to hold these types of investment securities because they fall within the definition of covered funds. Banks have until 21 July 2015 to divest the securities unless they receive an extension to 21 July 2017. Zions estimated that if it took the OTTI charge as of 30 September 2013, it would have been $629 million pre-tax and $387 million after-tax.

Zions holds these securities in both its held-to-maturity and available-for-sale (AFS) accounts. All securities will be reclassified as AFS and marked to fair value as required by accounting rules. Zions has long had a sizable unrealized loss against the AFS investments, which will now flow through earnings as an OTTI charge. Based on the company’s preliminary estimate, its 30 September common equity Tier 1 ratio would have fallen 73 basis points to 9.74%, which is just below its year-end 2012 level, reversing the increases recorded this year.

This charge also comes as Zions participates in the Federal Reserve’s Comprehensive Capital Analysis and Review (CCAR) for the first time. We do not think the charge will materially hinder Zions’ ability to pass CCAR because Zions will still have high capital ratios. However, it could affect its ability to increase its shareholder distributions.

In addition, Zions will remain exposed to market risk until it sells these securities. The company has indicated that it is evaluating a number of ways, separately and in combination, to comply with the Volcker Rule requirements, not all of which may involve a sale. If its compliance does not involve a sale, we will evaluate the level and extent of risk transfer that Zions achieves.

Although the fourth-quarter charge is credit negative, Zions’ exit from these securities will reduce a substantial concentration risk, which we view as highly correlated with its commercial real estate lending. Selling the securities also eliminates a historical source of earnings volatility. We have long viewed this concentration negatively and incorporated a high level of losses from these investments in our analysis of Zions’ capital adequacy.

Rita R. Sahu, CFA Vice President - Senior Analyst +1.212.553.1648 [email protected]

NEWS & ANALYSIS Credit implications of current events

11 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Norway Sets Countercyclical Capital Buffer for Banks, a Credit Positive Last Thursday, Norway’s Ministry of Finance announced that it will require banks to establish a countercyclical capital buffer of 1% of risk-weighted assets as part of their capital requirements, effective July 2015. The announcement is credit positive for Norwegian banks because it increases their capital requirements and ensures capital retention.

The level of countercyclical buffer is in line with a recommendation from Norges Bank, Norway’s central bank, following consultation with Norway’s Financial Supervisory Authority. Norges Bank’s recommendation was based mainly on four indicators that provide early warning signals of vulnerabilities and financial imbalances: the ratio of total credit to mainland GDP, the ratio of house prices to household disposable income, commercial property prices and the wholesale funding ratio of Norwegian credit institutions.

According to Norges Bank’s analysis, these four ratios are at historically high levels and exceed long-term trend estimates, suggesting that there has been a build-up of financial imbalances. This imbalance led to the 1% recommendation, although this level is at the lower end of the Basel III range of 0.0%-2.5%. The banks have 18 months to comply with the new requirements, giving them more time than the 12 months originally envisaged.

As shown in the exhibit below, Norwegian banks’ current common equity Tier 1 (CET1) requirement is 9% and increases to 10% in July 2014 once the systemic risk buffer is fully phased in. In July 2015, following the introduction of the countercyclical buffer, the CET1 requirement rises to 12% for Norway’s eight systemically important financial institutions (SIFIs)1 and to 11% for non-SIFI banks. Norges Bank and the Ministry of Finance also warned that if the financial imbalances build up further, the buffer may increase.

Norwegian Banks’ Common Equity Tier 1 Requirements, 2013-15

Source: Norges Bank

The requirement applies to banks, financial institutions and parent companies of financial non-insurance groups. The regulation will also apply to banks’ activities in other countries, unless that country’s authorities have set their own buffer requirements.

1 See SIFI proposal Is Credit Positive for Eight Norwegian Banks, 11 November 2013.

4.5% 4.5% 4.5% 4.5%

2.5% 2.5% 2.5% 2.5%

2.0%3.0% 3.0% 3.0%

1.0%1.0%

0%

2%

4%

6%

8%

10%

12%

1 July 2013 1 July 2014 1 January 2015 1 July 2015

Minimum Requirement Conservation BufferSystemic Risk Buffer Countercyclical BufferBuffer for Systematically Important Banks

Julia Dulneva Associate Analyst +44.20.7772.1954 [email protected]

Blake Foster Assistant Vice President - Analyst +44.20.7772.1579 [email protected]

NEWS & ANALYSIS Credit implications of current events

12 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

For foreign branches in Norway, the requirement will apply starting in 2016, but will be implemented gradually, thereby creating a temporary situation in which branches of foreign banks in Norway will have lower regulatory requirements than domestic banks. For example, unless Sweden introduces a buffer before July 2015, Swedish banks’ Norwegian branches would attract the current Swedish CET1 requirement for non-SIFI banks of 7%, versus Norwegian banks’ requirement of 11%. As a result, Swedish branches in Norway would have a competitive advantage because the lower capital requirements would allow them to charge lower loan rates.

We believe that most Norwegian banks are already well on their way to meeting these requirements, and therefore we do not expect significant capital raising among banks. However, we view the regulation as credit positive because it will discourage banks from releasing capital over the next 18 months for such things as dividend increases.

NEWS & ANALYSIS Credit implications of current events

13 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Alpha Bank’s Warrants Exercise Is Credit Positive On Tuesday, Alpha Bank AE (Caa1 stable, E/caa2 stable)2 announced the exercise of 28.8 million warrants owned by its private shareholders, who paid a total consideration of around €95.8 million to the state-owned Hellenic Financial Stability Fund (HFSF). Following this exercise, private shareholders’ interest in the bank rose to 18.3% from 16.3%.

This development is credit positive for Alpha Bank because it indicates that private shareholders are willing to eventually regain ownership in the bank, which we believe will eliminate any constraints on its strategic direction arising from the HFSF owning most of the bank’s shares. Nonetheless, we recognise that Alpha Bank and other Greek banks still face significant asset quality challenges that will continue to exert pressure on their earnings over the next 12-18 months.

Alpha Bank was recapitalised in June 2013, with the HFSF investing around €4 billion for an 83.7% stake in the bank, and private shareholders investing approximately €550 million for a 16.3% stake. Based on local regulation, Alpha Bank needed to raise at least 10% of its total capital needs of €4.6 billion from private investors to avoid a full-fledged nationalisation. The private shareholders also obtained around 1.2 billion warrants, which they can exercise in six-month intervals between December 2013 and December 2017 and which provides them the opportunity to gradually regain control of the bank.

The current warrants exercise indicates that private shareholders are willing to gradually obtain a majority stake in the bank from the HFSF, which now has an 81.7% interest. Although private investors exercised only around 2.3% of the total warrants available in this first round, we believe that it is a good indication that private investors will eventually reduce the HFSF’s stake in the bank to less than 50%. The fact that all relevant strike prices are already in the money (first strike price of €0.4488, compared with a share price of €0.61 at the exercise date of 10 December 2013) also provides an incentive for private shareholders to continue exercising the balance of their warrants on the future eligible dates.

The gradual reduction of the HFSF’s interest in Alpha Bank is positive for creditors because the bank’s strategic direction and decision-making will no longer be constrained, and because a return to a normal private ownership will allow the bank to attract more capital. We note that the HFSF currently has a veto power over any strategic decision the bank makes. A larger private shareholder base is also a positive indication of investors’ perception of the potential volatility in the bank’s future performance, which partially limits the downside risks for creditors.

However, we recognise that Alpha Bank’s credit challenges are still quite significant and will keep its earnings under pressure over the next 12-18 months. Nonperforming loans increased to 32.9% in September from 28.6% at the beginning of the year, while its elevated loan-loss provisions resulted in a pre-tax operating loss of €725 million in the first nine months of this year, excluding the one-off negative goodwill gain of €2.6 billion from the acquisition last February of Emporiki Bank of Greece S.A. (unrated) from Credit Agricole S.A. (A2 stable, D/ba2 stable).

2 The bank ratings shown in this report are the bank’s deposit rating, its standalone bank financial strength rating/baseline credit

assessment and the corresponding rating outlooks.

Nondas Nicolaides Vice President - Senior Analyst +357.25.586.586 [email protected]

NEWS & ANALYSIS Credit implications of current events

14 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

China’s Regulation for Financial Leasing Companies Is Credit Positive On Monday, the China Banking Regulatory Commission (CBRC) issued a request for comment on a proposed revision of regulations for financial leasing companies. The proposed revisions would provide these companies with new funding tools, allow them to set up branches and subsidiaries, tighten the rules on risk management and require parental support of liquidity and capital, all credit positives.

A key benefit is the broadening of funding sources. Under the current rules in effect since 2007, China’s leasing companies have relied on banks for a large part of their funding (see exhibit). Although in principle they can issue debt, regulatory approval has been on a case-by-case basis and in practice has been difficult to obtain.

Chinese Financial Leasing Companies Funding Sources

Notes: Data is as of the end of 2012. Long-term and short-term borrowings are mainly from banks. CMB = China Merchants Bank, BoCom = Bank of Communications. Because there is limited disclosure on the leasing industry by both the companies and regulators, the information in this exhibit is from issuers’ prospectuses and thus reflects only those with debt in the market. Source: Company statements and prospectuses

Together with the revised regulation, the CBRC will introduce a system that will categorize leasing companies based on the effectiveness of their risk management and their operational efficiency. Those that rank high will be given more regular access to debt capital markets through financial bond issuance and securitization programs, benefitting stronger players such as ICBC Financial Leasing Limited (A3 stable). The new regulation also opens the door for financial leasing companies to borrow in renminbis from overseas markets upon regulatory approval. In addition, they will be able to take deposits with tenors of three months or more from non-bank shareholders. Currently, the minimum tenor is one year.

A second benefit of the revision is increased flexibility in liquidity management and asset allocation. Financial leasing companies will be allowed to invest in fixed-income securities, which will help them better match their assets and liabilities and thus improve liquidity management. The new regulation also allows entities other than commercial banks to buy leasing companies’ accounts receivable.

A third benefit is the impetus to business development by allowing branches and subsidiaries. This will particularly benefit companies such as Bangxin Financial Leasing (unrated) that are affiliated with non-bank financial institutions or smaller banks and thus constrained by their parent companies’ limited distribution channels and business referral. We believe the expansion of distribution through new branches and subsidiaries will help increase leasing penetration in China.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Huarong Financial Leasing CMB Financial Leasing BoCom Financial Leasing Jiangsu Financial Leasing

Short-Term Borrowings Long-Term Borrowings Deposits & Placements Repurchase Agreements Bonds Payable Others

Bin Hu Vice President - Senior Analyst +852.3758.1503 [email protected]

NEWS & ANALYSIS Credit implications of current events

15 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Another benefit of the revised regulation is that it mandates explicit parental support of financial leasing companies. It requires shareholders to state in the corporate articles that the parent companies will provide liquidity support if the financial leasing company has difficulty meeting its payment obligations and that the parent will inject capital when the leasing company’s capital base is eroded by losses.

The revision also contains rules that should improve leasing companies’ risk management, including rules on concentration, related-party transactions and residual value management.

Although the revision is mostly credit positive for leasing companies, it will also lower the barriers to entry for new investors in the leasing industry and could lead to more intense competition. However, we believe that the CBRC will approve leasing licenses in an orderly fashion, and that the negative effect from increased competition will be more than offset by the proposed revision’s benefits.

We note that the revision only applies to the approximately two dozen financial leasing companies that the CBRC regulates and thus its credit-positive effects would only pertain to these companies. Although the CBRC regulates the largest Chinese leasing companies by assets and capital, there are numerous smaller leasing companies, such as those affiliated with manufacturers.

NEWS & ANALYSIS Credit implications of current events

16 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Japanese Lenders’ Additional Exposure to TEPCO Is Credit Negative On Wednesday, the Nikkei newspaper reported that 11 Japanese financial institutions plan to disburse loans totaling ¥500 billion on 26 December to Tokyo Electric Power Company, Incorporated (TEPCO, Ba3 negative), operator of the accident-stricken Fukushima Daiichi nuclear power station. These loans are credit negative for the lenders.

The loans include existing loan refinancings of ¥200 billion and new loans totaling ¥300 billion. The lenders include three Japanese mega banks – Sumitomo Mitsui Banking Corporation (Aa3 stable, C/a3 stable3), Mizuho Bank, Ltd. (A1 stable, C-/baa1 stable) and Bank of Tokyo-Mitsubishi UFJ, Ltd. (Aa3 stable, C/a3 stable) – and the Development Bank of Japan Inc. (Aa3 stable).

The exhibit below lists the banks involved in the financing and the loans they are making to TEPCO.

Distribution of Japanese Bank Loans to TEPCO

Rating New Loans, ¥ Billions Total Loans, ¥ Billions

Development Bank of Japan Inc. Aa3 stable ¥150 ¥300

Sumitomo Mitsui Banking Corporation Aa3 stable, C/a3 stable ¥40 ¥54

Mizuho Bank, Ltd. A1 stable, C-/baa1 stable ¥21 ¥28

Nippon Life Insurance Company Aa3 stable ¥19 ¥25

Dai-ichi Life Insurance Company, Ltd. A1 stable ¥17 ¥23

The Bank of Tokyo-Mitsubishi UFJ, Ltd. Aa3 stable, C/a3 stable ¥14 ¥19

Sumitomo Mitsui Trust Bank, Ltd. A1 stable, C/a3 stable ¥14 ¥19

Meiji Yasuda Life Insurance Company A1 stable ¥10 ¥13

Mitsubishi UFJ Trust and Banking Corporation Aa3 stable, C/a3 stable ¥9 ¥12

Sumitomo Life Insurance Company A2 stable ¥4 ¥5

Mizuho Trust & Banking Co., Ltd. A1 stable, C-/baa1 stable ¥2 ¥3

Total -- ¥300 ¥500

Source: Nikkei newspaper and Moody’s Investors Service

The loans will worsen the banks’ credit concentration, although each bank’s exposure to TEPCO will remain within the legal lending limit of up to 25% of capital. Japanese banks historically have high corporate credit concentration, reflecting the primacy of bank lending in financing Japanese corporations. We factor such a high credit concentration into our standalone bank financial strength ratings of Japanese banks, but it is unusual for lenders to underwrite this size of additional credit commitment to an entity in a troubled situation.

We believe the banks’ unusual decision is based on TEPCO’s indispensible role as an electric utility and the bankers’ strong expectation that it will receive financial support from the government. Also, we expect that the decision to lend to TEPCO on this scale must have been well coordinated with relevant government and regulatory bodies.

3 The bank ratings shown in this report are the banks’ deposit ratings, their standalone bank financial strength ratings/baseline credit

assessments and the corresponding rating outlooks.

Tetsuya Yamamoto Vice President - Senior Analyst +81.3.5408.4053 [email protected]

Kazusada Hirose Vice President - Senior Credit Officer +81.3.5408.4175 [email protected]

NEWS & ANALYSIS Credit implications of current events

17 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

The largest portion of the new loans will come from DBJ, a government-related institution, under the Crisis Response Operations framework established by the government. However, the three mega banks, all private institutions, are also participating in the lending.

We believe that the bank lenders already have significant outstanding loans to TEPCO. According to numerous media reports in 2011, they furnished emergency loans worth around ¥1.9 trillion to TEPCO after the earthquake and tsunami in March of that year. The emergency loans roughly doubled their exposure to TEPCO, according to reports.

The credit profile for TEPCO has somewhat stabilized since it received a ¥1 trillion public capital injection in July 2012, and it has become a government-related issuer according to our definition. However, the utility sector remains a source of uncertainty for Japanese banks’ asset quality. Japan’s national energy policy continues to lack clarity on the future role of nuclear power generation and the potential separation of generation and transmission of electricity. It is also unclear how any changes in these areas will affect sector profitability.

NEWS & ANALYSIS Credit implications of current events

18 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Insurers

AIG’s Sale of ILFC to AerCap Is Negative for ILFC, Positive for AIG On Monday, American International Group, Inc. (AIG, Baa1 stable) agreed to sell aircraft lessor International Lease Finance Corporation (ILFC, Ba3 negative) to Netherlands-based AerCap Holdings N.V. (unrated) for a total consideration of $5.4 billion, including $3.0 billion of cash and $2.4 billion of AerCap common stock (based on the closing share price of 13 December).

The transaction is credit negative for ILFC because of merger-integration risk, given that ILFC’s aircraft portfolio is approximately four times the size of AerCap’s, and because of incremental debt being issued to help fund the purchase. Following the sale announcement, we changed the ILFC rating outlook to negative from stable. The transaction is credit positive for AIG, which begins to monetize a non-core asset that relies heavily on wholesale funding and has a weaker credit profile than AIG’s core insurance operations.

The proposed transaction exposes ILFC’s creditors to integration risk as AerCap absorbs ILFC’s much larger aircraft fleet and transitions key personnel and management systems onto AerCap’s business platform. Moreover, acquisition-related debt, along with purchase accounting adjustments, will result in far higher leverage at the combined company than at ILFC or AerCap separately. We estimate that the combined entity will have a debt/equity ratio of 5.9x at closing, versus ILFC’s 3.0x and AerCap’s 2.6x as of 30 September. Following the acquisition, we expect AerCap to reduce leverage toward its target of 3x (on a net debt basis) through cash flow from incremental revenues and cost savings. However, given its large order book and strong market demand, the company will likely keep leverage above historical levels.

Positive aspects of the transaction for ILFC include increased clarity regarding ownership and strategy. The combination of AerCap and ILFC will create a market leader in commercial aircraft leasing with a combined fleet of more than 1,100 owned aircraft and an order book of 383 new aircraft, including desirable delivery slots for new technology aircraft from Boeing and Airbus. Strong demand for the new aircraft will strengthen lease yields, profits and cash flow, assuming AerCap preserves ILFC’s strong customer relationships and marketing capabilities.

AerCap will have an opportunity to improve ILFC’s historical performance by reducing operating redundancies, improving fleet mix through selective aircraft sales and realizing tax efficiencies. Under Section 338(h)(10) of the US Internal Revenue Code, AerCap will step up the tax basis in ILFC’s assets, resulting in tax savings and higher cash flow. The firm will generate additional tax savings by relocating ILFC’s US-domiciled aircraft to Ireland, which has a lower corporate tax rate.

AerCap plans to fund its $3 billion payment to AIG with a combination of cash on hand and proceeds from senior unsecured bonds. As a funding contingency, AerCap obtained a $2.75 billion unsecured bridge facility from UBS and Citibank. AIG will also provide a $1 billion, five-year unsecured line of credit. Longer-term liquidity concerns relate to financing the combined entity’s $25 billion of new aircraft and other equipment orders and refinancing existing debt.

For AIG, the proposed sale marks the last major divestiture in a broad restructuring program following the financial crisis of 2008-09. With this transaction, AIG will have divested more than 30 businesses for aggregate proceeds exceeding $70 billion. ILFC, with more than $20 billion of debt outstanding and a steady reliance on wholesale funding, has a weaker credit profile than AIG’s core insurance operations. AIG’s net cash proceeds at closing will total $2.4 billion after settlement of intercompany loans. AIG will

Mark Wasden Vice President - Senior Credit Officer +1.212.553.4866 [email protected]

Bruce Ballentine Vice President - Senior Credit Officer +1.212.553.7212 [email protected]

NEWS & ANALYSIS Credit implications of current events

19 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

also own 46% of AerCap’s common shares, subject to a holding period whereby it may sell up to one third of its stake after nine months, up to two thirds after 12 months and the entire stake after 15 months. We expect AIG to sell its AerCap shares over time as business and market conditions permit, subject to the constraints of the holding period.

NEWS & ANALYSIS Credit implications of current events

20 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Spain’s Pension Reform Will Likely Increase Life Insurers’ Sales On 13 December, Spain’s Senate approved a pension reform bill that included a number of important changes, such as linking pensions to both life expectancies and the financial health of the pension system, and ending the indexation of pensions to the annual inflation rate. These changes will lead to a significant reduction in state pension payments, an improvement in the country’s public finances4 and higher pension sale volumes for Spanish life insurers, all credit positives.

The pension bill is subject to the Spanish Congress’ final approval, although market participants do not expect any material amendments to the bill. The law is set to take effect on 1 January.

The current pension bill is the second reform in the past three years and aims to address the important structural issues arising in the public pension system because of an increasingly elderly population, rising life expectancy and Spain’s weak economy, in which unemployment is likely to remain high and growth subdued. In addition, Spain has had one of the most generous state pension systems in Europe as measured by gross replacement ratios, which are effectively state pension payments as a proportion of final salary pre-retirement. Spain’s gross replacement ratio has been around 74% of final earnings, on average, versus an average of 57.9% for members of the Organisation for Economic Co-operation and Development (see Exhibit 1).

EXHIBIT 1

Comparison of Spain’s 2012 Gross Replacement Ratio with Other Countries

Note: Gross replacement ratio is the ratio of gross pension entitlement upon retirement and gross pre-retirement earnings Source: Organisation for Economic Co-operation and Development

The proposed reduction in Spain’s state pension will likely lead to strong growth in insured pensions as an alternative long-term savings solution. Indeed, Spanish life insurers have reported higher insured pension volumes as a result of the political discussions about pension reform. The industry’s insured pension provisions consistently grew by more than 20% over the past three years to €16 billion in the first nine months of this year, nearly double 2010 levels (Exhibit 2).

4 See Spain’s Pension Proposals Are Credit Positive for the Sovereign, 13 June 2013.

0%

10%

20%

30%

40%

50%

60%

70%

80%

Spain Italy France OECD 34 Portugal Germany UK

Laura Perez Martinez, CFA Analyst +44.20.7772.1602 [email protected]

NEWS & ANALYSIS Credit implications of current events

21 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

EXHIBIT 2

Growth of Spanish Insurers’ Pension Provisions

Note: Insured pensions are defined as the sum of Planes de Prevision Asegurados and Planes Individuales de Ahorro Sistematico Source: Association of Spanish Insurers (ICEA) and Moody’s calculations

Despite life insurers’ significant growth in recent years, insurance penetration in Spain is low, with Spanish households investing a significantly lower proportion of their financial investments in life insurance and pensions. The average household in Spain invested only 15% of their financial assets in life insurance and pensions plans, compared with 37% for Europe overall (Exhibit 3). This likely reflects Spain’s historically generous pension system. Although pension reform will also benefit other financial institutions such as banks and asset managers, we believe that life insurers remain well placed to benefit from continued strong private pension flows, driven by the differentiating insured pension features with long-term minimum guarantees that are typically attractive to less risk-adverse individuals.

EXHIBIT 3

Comparison of Spanish Households’ Investment in Insurance and Pension Plans versus the European Union

Source: VidaCaixa and Inverco

The government has also publicly announced further incentives for the private pension system through tax incentives and a reduction in maximum commissions, although details on both remain scarce. A reduction in maximum commissions would reduce the margin on these products, but overall we expect the increased flows to be credit positive for insurers.

€0

€2

€4

€6

€8

€10

€12

€14

€16

€18

2010 2011 2012 9m 2013

€Bi

llion

s

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Spain 2012 European Union 2011

Other Fixed Income Life Insurance and Pension Plans Investment Funds Deposits

NEWS & ANALYSIS Credit implications of current events

22 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Sovereigns

Mexico Approves Energy Reform, a Credit Positive On Monday, a majority of Mexico’s (Baa1 stable) state legislatures had approved a comprehensive reform of the energy sector, the last legislative step needed to complete a constitutional reform previously passed by Mexico’s Congress. We expect this legislation to have a significant effect on Petroleos Mexicanos (PEMEX, Baa1stable) and the oil industry, attracting investment and enhancing Mexico’s growth prospects over the next three to five years, all credit positives for the sovereign.

The approved reform was more wide-ranging and far-reaching than we had expected, providing conditions that will be broadly similar to those offered by countries that have successfully attracted private investment to their oil sector. The government’s initial proposal contemplated only profit-sharing contracts, a feature that the government modified in the final draft that Congress approved.

The reform effectively eliminates the monopoly status of PEMEX, the state oil company, allowing private-sector participation in oil exploration and exploitation. And although the government will retain ownership of hydrocarbon reserves, participating companies will be able to register the economic interest of their contracts in line with US Securities and Exchange Commission rules.

The reform incorporates a wider range of options for the type of contracts private companies can enter into with the government, including profit- and production-sharing agreements and concession-like licenses. The government, through the National Hydrocarbons Commission, will assign the contracts and determine the applicable compensation mechanism. Private-sector involvement in downstream activities will be broad enough to allow for participation in refining, transportation, storing and distribution.

The reform seeks to improve PEMEX’s governance, eliminating five seats on the company’s board of directors that the workers’ union controlled. Although PEMEX can choose which oil fields it will exploit before the private players do, the company will have to become a “productive enterprise of the state” within two years, meaning it will have to revamp itself to compete on equal footing with private-sector competitors.

Given that about one third of the Mexican government’s revenues are oil-related, future changes in PEMEX’s tax regime that allow it to keep a higher share of its revenues and which will reduce its contributions to the government could negatively affect government finances. But, increased oil production should partially compensate for this.

Congress will have 120 days next year to issue secondary laws that provide details about how the reform will operate. These laws will include how an oil stabilization fund created to manage the oil rent will operate and how much of that fund will be transferred to the federal government for budgetary purposes.

Although prospects appear encouraging, implementation risks will pose major challenges to the reform. In addition, attempts to mobilize public opinion by the left-of-center PRD party and other groups opposed to the reform and a call for a constitutional referendum pose further risks.

The extent to which the reform is successful will depend on how effective it is in promoting increased private investment and oil production. If the reform proves effective in this respect, we expect it to lift

Ariane Ortiz Marrufo Associate Analyst +1.212.553.4872 [email protected]

Mauro Leos Vice President - Senior Credit Officer/Manager +1.212.553.1947 [email protected]

NEWS & ANALYSIS Credit implications of current events

23 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Mexico’s potential growth to 3%-4% from its current 2%-3%, although the effect will become evident during 2016-19, the second half of President Enrique Peña Nieto’s administration.

The energy reform was the last element of the government’s reform agenda. Together with other structural reforms that the Congress has already passed – including those related to labor, telecommunications, fiscal, financial, and education – Mexico’s sovereign credit profile should strengthen.

NEWS & ANALYSIS Credit implications of current events

24 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Sub-sovereigns

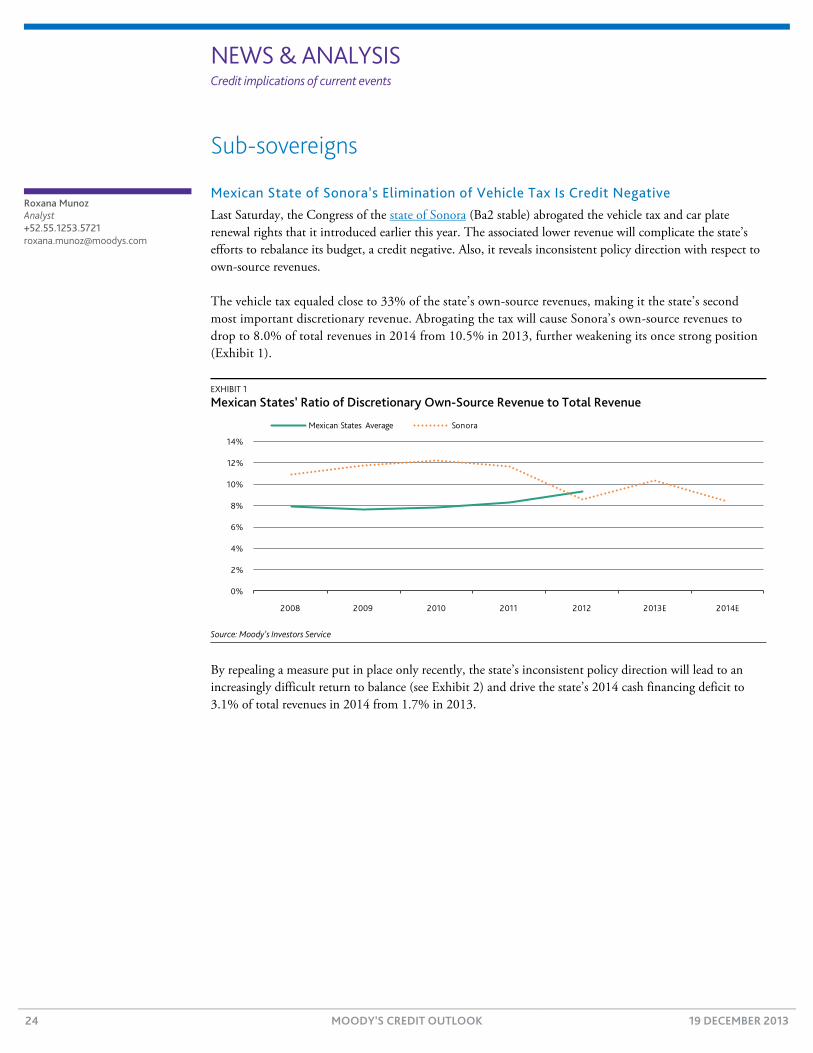

Mexican State of Sonora’s Elimination of Vehicle Tax Is Credit Negative Last Saturday, the Congress of the state of Sonora (Ba2 stable) abrogated the vehicle tax and car plate renewal rights that it introduced earlier this year. The associated lower revenue will complicate the state’s efforts to rebalance its budget, a credit negative. Also, it reveals inconsistent policy direction with respect to own-source revenues.

The vehicle tax equaled close to 33% of the state’s own-source revenues, making it the state’s second most important discretionary revenue. Abrogating the tax will cause Sonora’s own-source revenues to drop to 8.0% of total revenues in 2014 from 10.5% in 2013, further weakening its once strong position (Exhibit 1).

EXHIBIT 1

Mexican States’ Ratio of Discretionary Own-Source Revenue to Total Revenue

Source: Moody’s Investors Service

By repealing a measure put in place only recently, the state’s inconsistent policy direction will lead to an increasingly difficult return to balance (see Exhibit 2) and drive the state’s 2014 cash financing deficit to 3.1% of total revenues in 2014 from 1.7% in 2013.

0%

2%

4%

6%

8%

10%

12%

14%

2008 2009 2010 2011 2012 2013E 2014E

Mexican States Average Sonora

Roxana Munoz Analyst +52.55.1253.5721 [email protected]

NEWS & ANALYSIS Credit implications of current events

25 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

EXHIBIT 2

Sonora, Mexico’s Cash Financing Deficit to Total Revenues

Source: Moody’s Investors Service

Taxes and rights in Mexico are two of the few types of discretionary revenues that states use to fund operating expenditures. By international standards, and as a result of the fiscal arrangements between the federal and state governments, Mexican states have low collection powers.

The vehicle tax is one of the few sources of direct revenue at the state’s disposal. Originally designed as a federal tax, it was transferred to the states in 2011, giving them full discretion on its management starting in 2012. The majority of the rated Mexican states had either decided not to implement it or to partially collect it. In 2013, Sonora implemented the vehicle tax as a key component of its plan to regain its fiscal balance.

-10%

-8%

-6%

-4%

-2%

0%

2%

2008 2009 2010 2011 2012 2013E 2014E

NEWS & ANALYSIS Credit implications of current events

26 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Securitization

Amendments to Italian Law Are Credit Positive for Securitizations and Covered Bonds Last Friday, the Italian government approved amendments to Law 130/1999 in Law-Decree Destinazione Italia5 that improve the segregation of transaction funds and, in case of debtors’ default, limit potential claw backs of prepayments. These measures are credit positive for Italian securitizations and covered bond programmes because they will reduce certain risks associated with servicer and debtor defaults.

The proposed amendments clarify the circumstances under which collections and other cash deposits relating to securitizations and covered bond programmes can be effectively segregated in case of servicer insolvency, and spell out the consequences of such segregation. As a result, the amendments will mitigate legal risks associated with servicer default at both the special-purpose vehicle (SPV) and servicer levels.

SPVs used in securitization structures or covered bond programmes6 can open segregated accounts with the servicer for the receipt of both collections arising from securitized receivables and funds relating to the securitization (i.e., cash reserves). Should the servicer default, the credit balance of such an account would not become part of the servicer’s estate and as a consequence an equivalent amount would be paid by the insolvency administrator to the SPV, without any stay of payment.

For servicers, any collections channeled through a bank account opened by a servicer or a delegated servicer will be segregated for the benefit of securitization creditors or covered bondholders and excluded from the insolvency estate of the servicer. However, we note that the amendment does not address the consequences of a default of a third-party account bank. Consequently, loss because of a servicer default could be partially mitigated by segregation. But the issuer may eventually not be able to make timely payments to the bondholders if there is some delay because of insolvency rules.

Despite these benefits, it is unclear if and how the legal segregation mechanism would work if collections are paid into a servicer’s general account that receives other payments unrelated to the securitization or covered bonds. Another question is whether the new provisions will apply to existing transactions in the absence of a formal amendment to transaction documents. Currently, commingling and account bank risk are usually partially mitigated through contractual rating triggers to change the account bank or servicer, or provide cash reserves.

The new provisions also remove the ability to claw back prepayments made by commercial borrowers under any type of securitized claim or cover pool asset. The amendments will benefit Italian transactions whose collateral includes financings to non-individual borrowers, such as small and midsize enterprise loan securitizations or covered bond programmes of commercial mortgage pools.7 SPVs will no longer risk

5 The law-decree will be effective immediately upon publication in the Italian official gazette and will have to be converted into law

within 60 days from publication. 6 In Italian securitization structures, the issuer of the bonds is typically an SPV and purchases receivables from their originator,

whereas with Italian covered bonds the issuer is typically the originator and transfers the cover pool assets to an SPV acting as guarantor for the benefit of the covered bondholders.

7 We understand that the amended provision does not apply to public-sector covered bond programmes because public entities are subject to a specific insolvency regime.

Valentina Varola Vice President - Senior Analyst +39.02.9148.1122 [email protected]

Pier Paolo Vaschetti Vice President - Senior Analyst +39.02.9148.1139 [email protected]

Monica Bianchi Associate Analyst +44.20.7772.8745 [email protected]

Elise Lucotte Vice President - Senior Analyst +33.1.53.30.10.22 [email protected]

NEWS & ANALYSIS Credit implications of current events

27 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

having to return collections from prepayments in case of debtors’ bankruptcy8 and there will be no need for prepayment reserves or other measures to mitigate claw back risk.

8 Under Italian law, if a borrower of certain types of debt makes a prepayment and the initial maturity of the debt occurs after the

debtor is declared bankrupt, that prepayment can be clawed back if the debtor is declared bankrupt within two years after the prepayment date. The amendment neutralizes this rule with respect of claims to commercial borrowers in securitization and covered bond transactions.

CREDIT IN DEPTH Detailed analysis of an important topic

28 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Break in Case of Municipal Emergency: Tools Available to Stressed Government Issuers and What They Mean for Bondholders This report describes steps we have observed local governments take to address credit stress. The measures taken depend on the level of financial stress local governments face and we will discuss them in order of the credit risk they pose to municipal bond investors:

» Adjust fiscal policies and operating costs

» Defer tough decisions

» Request state oversight and support

» Merger or dissolution

» Selective default

» Distressed exchange

» Bankruptcy filing

The overwhelming majority of local governments weathered the financial crisis without significant credit deterioration. Only a handful of cities and other municipal issuers defaulted in the last five years; less than 2% of Moody’s rated entities even descended into speculative grade ratings. Most governments successfully rebalanced operations by making the tough decisions needed to preserve their fundamental credit strengths. These methods included:

» cutting or delaying spending

» finding ways to boost revenues

» judiciously using reserves to buy time and soften the blows

» reducing or deferring borrowing for capital improvement projects

» borrowing to fund operating deficits and quickly repaying that debt

But what happens when these actions are not enough and credit stress threatens to overwhelm the local government? Stressed issuers typically pursue various and fairly predictable measures to remain financially viable. As discussed below, some measures are fairly routine, widely utilized and pose little risk to muni investors (represented in green). Others measures are more aggressive and involve more risk to investors (yellow). At the extreme, distressed issuers may resort to drastic measures which may elevate the risk of default and cause losses for creditors (red).

Anne Van Praagh Managing Director +1.212.553.3744 [email protected]

Alfred Medioli Vice President - Senior Credit Officer +1.212.553.4173 [email protected]

CREDIT IN DEPTH Detailed analysis of an important topic

29 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

1. ADJUST FISCAL POLICIES AND OPERATING COSTS

Once credit pressures emerge, a government can take sharp and decisive action to adjust tax revenues and user fees, cut operating costs through staffing and service reductions, or employ a combination of both. The critical goal here is to rebalance the budget to meet current and long-term obligations to bondholders and other creditors. Municipalities try to avoid overreacting if the revenue crisis is likely to be short-term because trimming staff and services, or raising taxes and fees, are painful to some

constituents. This option may have its limits – economic, political and legal – depending on the ability to extract additional tax revenues from a tax base and the political appetite and legal ability to change existing union contracts or work rules. Most Moody’s-rated government issuers have made sufficient adjustments to emerge from the recession with their credit profile intact.

More extreme examples of cost cutting measures include the city of Pontiac, MI (Caa1 developing), which has downsized itself to bare-bones operations (from a peak of 650 full-time workers to about 25) through outsourcing and privatization. Another example is the city of Camden, NJ (unrated), which outsourced its police department in an effort to reduce fixed costs.

Among the successful examples in this category are a range of Arizona cities including Phoenix (Aa1 stable), Mesa (Aa2 stable), Glendale (A3 negative) and Tempe (Aa1 stable). When faced with double-digit losses in tax base and sale tax revenues, these cities responded with aggressive cuts in operations, including sizeable workforce reductions. In some cases, city residents approved tax increases and city management implemented timely budget actions; most maintained their credit quality. Glendale, however, was burdened by an obligation to support a professional hockey stadium, which weakened financial operations and led to a downgrade despite a 25% cut in city-wide operating staff.

Making fiscal and operating adjustments in response to shifting demographic trends can be a bit trickier. This is the case in Michigan where school choice allows children to attend neighboring K-12 public or charter schools. When a student moves to a competing school, their state funding follows them, leaving their previous school with less funding. This element of competition is exacerbated by ongoing population declines in some regions, such as southeast Michigan, that pre-date the recession. Some districts have sustained their financial and credit standing by successfully attracting new students. Others, including Clintondale Community Schools (Ba3 negative), Mount Clemens Community School District (Ba3 negative) and Ypsilanti School District (Ba3) have been unable to stem enrolment losses and balance the associated downsizing against the accompanying loss of revenue.

CREDIT IN DEPTH Detailed analysis of an important topic

30 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

2. DEFER TOUGH DECISIONS

Another frequent tactic involves delaying fiscal adjustment. This strategy may actually work well if a crisis proves to be short-term and an entity has enough reserves to lean on. But if the crisis lasts longer, the strategic imbalance will just continue to build. The tactic will then have shifted from “riding out the storm” to “kicking the can down the road,” which often results in higher unaffordable debt levels. Without some combination of economic growth or fiscal adjustment, these debt levels may prove unsustainable. This tactic is

often tempting because it is politically expedient – it avoids the backlash that come with cutting staff or services. “Kicking the can” will appear to keep a government’s general fund operations positive or balanced in the near term, only to show the strain in the future.

Recent examples of delaying the inevitable include:

» reduced or skipped annual pension contributions (Chicago, A3 negative)

» deferred maintenance on infrastructure (Detroit, Caa3 negative)

» deficit financing (Puerto Rico (Baa3) and Detroit)

» pension obligation bond issuance, which is another form of deficit financing (Woonsocket, RI (B3 negative))

3. REQUEST STATE OVERSIGHT AND SUPPORT

Another tool used by local governments is to request state oversight or intervention, when it is available. This is often invoked if a municipality is politically deadlocked or otherwise unable to take the steps necessary to restore fiscal and financial balance.

The amount and type of oversight will vary significantly depending on the state. California (A1 stable), for example, offers no oversight or intervention for cities or counties, though it does provide

significant oversight and support of school districts. By contrast, in North Carolina (Aaa stable), the state closely monitors local government financial operations and debt management so that intervention is rarely needed.

Across all the states, however, oversight or intervention typically does not include direct financial assistance. In states with strong oversight programs, the types of tools may include state appointment of a financial receiver or other oversight body with broad management powers that include:

» close control or maintenance of operations

» setting of tax rates

» cancellation of contracts

» other key decision making powers

CREDIT IN DEPTH Detailed analysis of an important topic

31 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Back in the 1970s, New York City (Aa2 stable) and Cleveland, OH (A1 stable) benefited from timely and extensive state oversight that ameliorated their serious financial crises. State intervention enabled these entities to make fiscal and operational adjustments sufficient enough to restore debt affordability and financial stability.

But even in those states that have a long tradition of strong state oversight, this alone may not be enough to prevent debt payment default or bankruptcy, two more drastic measures described below. For example, Michigan and Pennsylvania have well established systems for intervention to help distressed local governments restore financial health, but the challenges of Detroit and Harrisburg, PA (not rated) were too daunting for these programs to prevent bond defaults.9 Some local governments currently under state oversight are under so much fiscal strain that they have low ratings in the B or Caa range, despite the fiscal benefits that generally accrue from such oversight.

While state oversight can be effective, it can also lead to long-term dependence and a kind of municipal limbo. Ecorse, MI (not rated), Scranton, PA (not rated) and Newburgh, NY (Ba1 positive) are all cities that have been under oversight for decades without significant improvement in credit quality, although they have avoided default.

4. MERGER OR DISSOLUTION

Merger and dissolution are more aggressive tactics, but are less commonly used by governments and more often employed by stressed enterprises such as hospitals and universities. Merger or dissolution can avert failure over the long term or may be used as a tactic to finally resolve bondholder recovery. Local governments when under more severe credit pressure on occasion will merge with other governments, spin off certain functions to other governments, or dissolve with their debt assumed by the surviving entity.

Merger is common in the corporate world, and enterprises in the public sector use similar tactics when in stress. West Penn Allegheny Health System (Caa2 developing) has twice undergone a merger with another hospital system.

Asset disposition is another alternative among public sector enterprises, like Boston Biomedical Research Institute (unrated). The single-facility scientific enterprise fell into speculative grade in 2010 following poor investment returns and a critical weakening of it main grant and research contract revenues. The Institute’s credit situation continued to weaken until it was forced to close its doors in late 2012. The Institute was able to sell off its single real estate asset in mid-2013 at a price sufficient to make bondholders whole.

Local governments also employ variations of this approach. Municipalities can consolidate or contract out operations, or they can sell off non-core operations or assets. Pontiac, MI (Caa1 developing), for example, sold off the Detroit Lions football stadium, as well as its sewer treatment system. It then went on to radically privatize nearly all other operations as noted earlier. In the different example of Harrisburg, PA the city is in the process of trying to sell off the incinerator project that has been the source of significant financial problems to a county solid waste authority.

9 For more information on municipal defaults, please refer to our default study.

CREDIT IN DEPTH Detailed analysis of an important topic

32 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013

Two Michigan public school districts, Muskegon Heights (not rated) and Highland Park (not rated), have taken even more aggressive steps. By converting their public school operations to charter school status, they substantially reduced salaries and fixed costs relating to pensions and other post-employment liabilities. In each of these cases, the municipal issuer has essentially gone out of business, though the debt service levy remains in place to make full and timely payment on outstanding bonds.

5. SELECTIVE DEFAULT

In a more extreme action, a city or municipal issuer may choose to selectively default on some debt as a way of easing financial or fiscal stress. This option is most often used if the debt relates to a non-core facility or speculative enterprise that the city had helped underwrite in some form. Local governments can get themselves involved in supporting projects of this type either through cronyism or the perhaps better intentioned efforts to promote economic development. But if the risk is contingent on general government

support, it can end badly.

There are several examples of municipal issuers that chose not to pay a lease obligation related to a non-essential asset because of the legal ability to not appropriate and terminate the lease. Contrary to some issuers’ expectations, non-appropriation is a payment default by Moody’s definition and in the eyes of the larger bond market. This tactic, in its own way, reflects quick and decisive action, but the issuer may also avoid making hard decisions about fundamental budget imbalances, which continue as usual. Generally, the price of the mistake is borne by the bondholders. Some examples include Cicero, NY (A2), which defaulted on a lease obligation for a skating rink in 2003, and Vadnais Heights, MN (Ba1 stable), which similarly defaulted on a lease for a sports center in 2012.

Another example is Harrisburg, PA which defaulted on general obligation debt (not rated), both direct and guaranteed, but continued to pay water revenue bonds (not rated) and parking revenue bonds (Ba3 developing) with a dedicated revenue source.

Selective default on revenue or lease bonds can work in providing near-term financial relief, but at some damage to market credibility. In each of the above examples, the city’s GO rating was downgraded reflecting managerial weakness.

6. DISTRESSED EXCHANGE

Another option is a distressed exchange whereby: 1) an obligor offers creditors a new or restructured debt, or a new package of securities, cash or assets that amount to a diminished financial obligation relative to the original obligation and 2) the exchange has the effect of allowing the obligor to avoid a bankruptcy or payment default in the future.

A distressed exchange may be deemed a default by Moody’s definition. More commonly used by distressed non-financial corporate and sovereigns, this tactic has been used by only a handful of municipal issuers.

CREDIT IN DEPTH Detailed analysis of an important topic

33 MOODY’S CREDIT OUTLOOK 19 DECEMBER 2013