Embed Size (px)

Citation preview

Newbuildings & Yards20 June 2018

Marine Money Week |New York

Prepared by Angelica Kemene |Head of Market Analysis & Intelligence

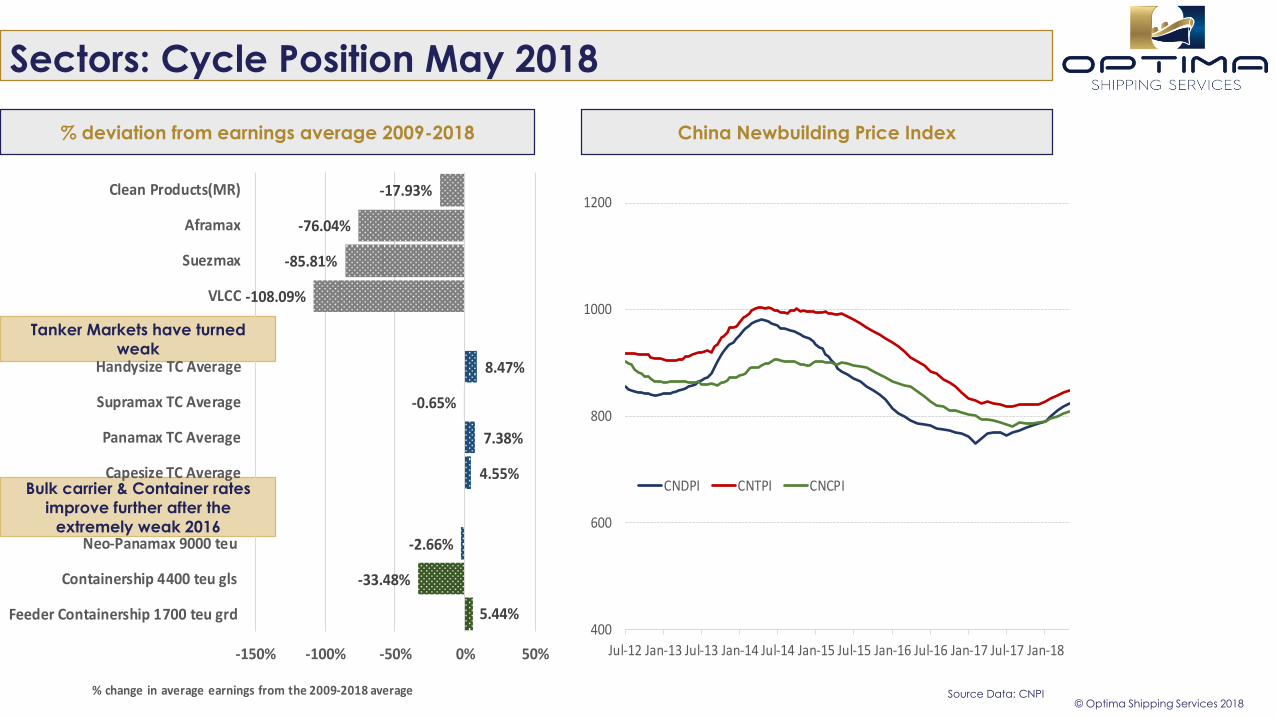

Sectors: Cycle Position May 2018

% deviation from earnings average 2009-2018

© Optima Shipping Services 2018

Tanker Markets have turned

weak

Bulk carrier & Container rates

improve further after the

extremely weak 2016

5.44%

-33.48%

-2.66%

4.55%

7.38%

-0.65%

8.47%

-108.09%

-85.81%

-76.04%

-17.93%

-150% -100% -50% 0% 50%

Feeder Containership 1700 teu grd

Containership 4400 teu gls

Neo-Panamax 9000 teu

Capesize TC Average

Panamax TC Average

Supramax TC Average

Handysize TC Average

VLCC

Suezmax

Aframax

Clean Products(MR)

% change in average earnings from the 2009-2018 average

China Newbuilding Price Index

400

600

800

1000

1200

Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18

CNDPI CNTPI CNCPI

Source Data: CNPI

Newbuilding Prices out of the bottom - Bulkers

© Optima Shipping Services 2018

81K DWT Panamax Bulkcarrier NB Prices 61-64K DWT Supramax NB Prices

0

10

20

30

40

50

60

70

80

90

1976 1982 1988 1994 2000 2006 2012 2018

$ Mln

Nominal

Inflation adjusted

0

10

20

30

40

50

60

1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 2015 2018

$ Mln

Nominal

Inflation adjusted

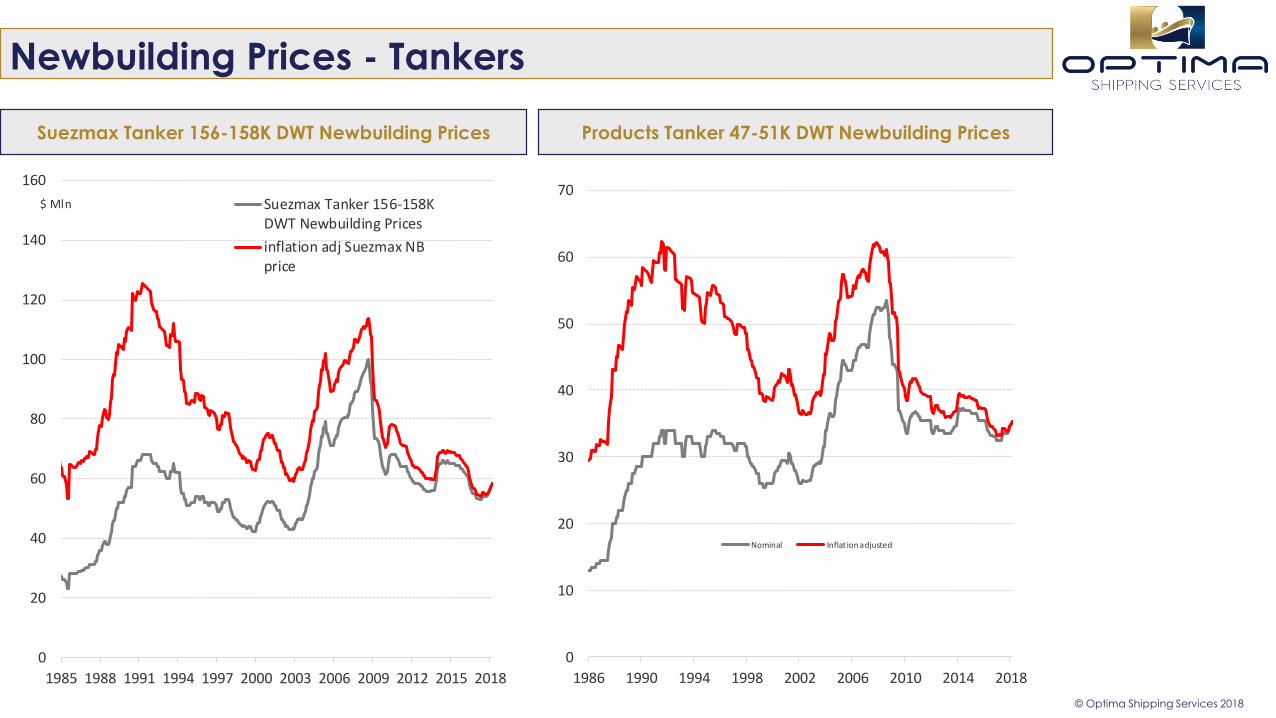

Newbuilding Prices - Tankers

© Optima Shipping Services 2018

Suezmax Tanker 156-158K DWT Newbuilding Prices Products Tanker 47-51K DWT Newbuilding Prices

0

20

40

60

80

100

120

140

160

1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 2015 2018

$ Mln Suezmax Tanker 156-158KDWT Newbuilding Prices

inflation adj Suezmax NBprice

0

10

20

30

40

50

60

70

1986 1990 1994 1998 2002 2006 2010 2014 2018

Nominal Inflat ion adjusted

Newbuilding Prices - Containers

© Optima Shipping Services 2018

Containers 1700 TEU Newbuilding Prices Containers 8800 TEU Newbuilding Prices

Base Payment Terms | What about options placement?

Source Data: Optima Shipping Services, CNPI

© Optima Shipping Services 2018

Bulk Carriers

Payment Term 10% 10% 10% 10% 60%

Key Point Contract Signing Steel Cutting Keel Laying Launching Delivery

Months Before Delivery 24 12 6 3 0

Oil Tankers

Payment Term 10% 10% 10% 10% 60%

Key Point Contract Signing Steel Cutting Keel Laying Launching Delivery

Months Before Delivery 24 14 8 4 0

Containers

Payment Term 10% 10% 10% 10% 60%

Key Point Contract Signing Steel Cutting Keel Laying Launching Delivery

Months Before Delivery 24 12 7 4 0

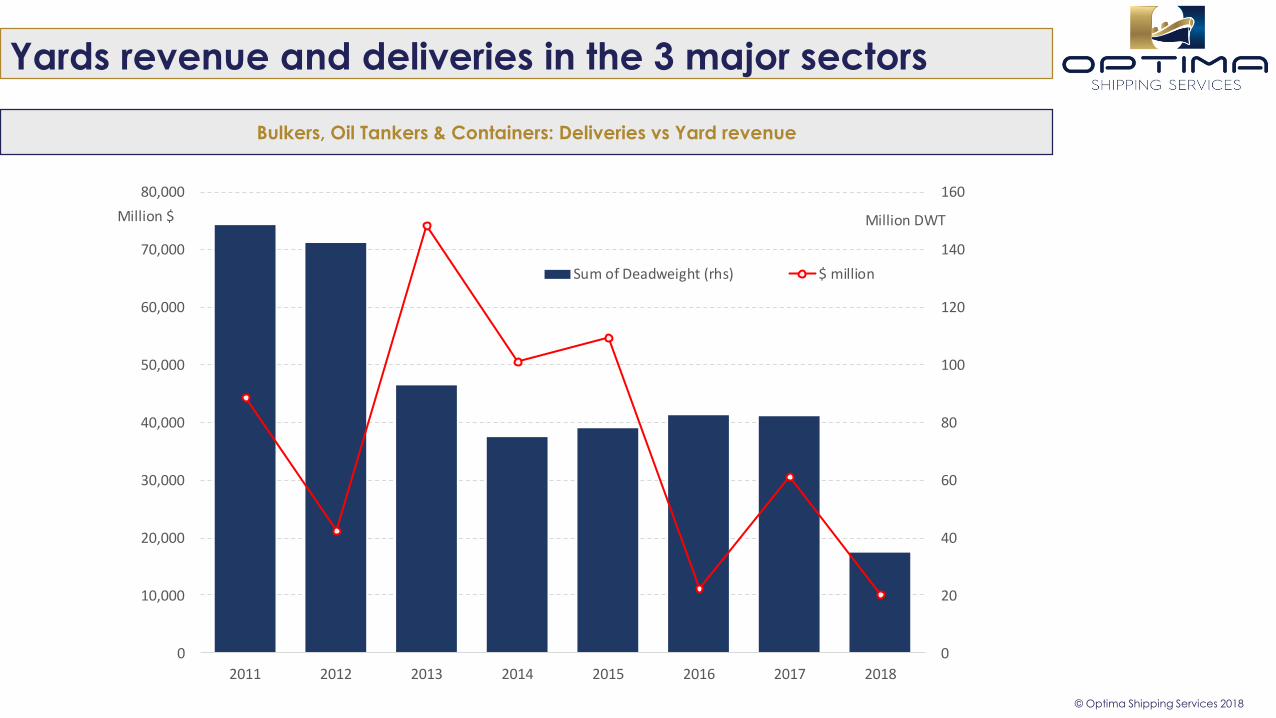

Yards revenue and deliveries in the 3 major sectors

© Optima Shipping Services 2018

Bulkers, Oil Tankers & Containers: Deliveries vs Yard revenue

0

20

40

60

80

100

120

140

160

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2011 2012 2013 2014 2015 2016 2017 2018

Million DWTMillion $

Sum of Deadweight (rhs) $ million

A shift towards Chinese Ship Yards

Major Shipbuilding Countries Current Orderbook %

© Optima Shipping Services 2018

0% 20% 40% 60% 80% 100%

Bulk Carrier

Container

Crude Oil Tanker

Products Tanker

China, People's Republic Of Korea, South Japan Others

For the 3 major sectors there are currently 188active yards – of which 35% is expected todeliver their final order this year, whilst 78% ofthem will deliver their final order until the endof 2019.

In 2007 285 yards received more than 1 order,while in 2017 91 yards received more than 1order – A decrease of 68%.

Inability to secure orders at a profit. Issue: Yard Consolidation China: “Plans on structural reform 2016-2020 in

shipbuilding industry” China’s top 10 state-

owned shipbuilders will be responsible for 70%of the country’s new tonnage by 2020.

Japan follows the trend (capacity cuts &mergers), but S. Korea remains skeptical.

Cost increase: steel prices, labor cost,exchange rates.

The extra cost can be balanced if builderscharge higher.

Asset Play with Newbuildings |Older years vs 2018

© Optima Shipping Services 2018

Asset play was always on thetable, but times havechanged.

Market dynamics havealtered: financing, newregulations, shorter cycles, AI

Need for access to capital,buy fleets instead of a ship,flexibility for financialstructuring

The “asset play” innewbuildings is a differentgame now.

Sectors: Fleet Age Profile

Bulk Carriers: Existing Fleet Age Profile Tankers: Existing Fleet Age Profile

© Optima Shipping Services 2018

133

431

56

175

108

165

163

528

147

325

184

263

214

457

190

296

117

144

111

144

39

126

80

122

78

100

7

50

23

16

0% 20% 40% 60% 80% 100%

Handysize

MR1/MR2

Panamax/LR1

Aframax/LR2

Suezmax/LR3

VLCC/ULCC

0-4 yrs 5-9 yrs 10-14 yrs 15-19 yrs 20 yrs & over

Sectors: Fleet Age Profile

Containers: Existing Fleet Age Profile

© Optima Shipping Services 2018

287

78

9

198

86

88

390

337

84

196

135

7

940

414

100

188

1

8

473

183

67

19

0

0

817

76

10

6

0

0

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Feeder

3,000-5,999 TEUs

6,000-7,999 TEUs

8,000-11,999 TEUs

12,000-14,999 TEUs

15,000 + TEUs

0-4 yrs 5-9 yrs 10-14 yrs 15-19 yrs 20 yrs & over

0

200

400

600

800

1000

1200

1400

1600

1800

2012 2013 2014 2015 2016 2017 2018

Bulk Carrier Containers Crude Oil Tanker Products Tanker

Contracting Pace in major sectors No of Contracts

No expectation to

return to firm levels

though

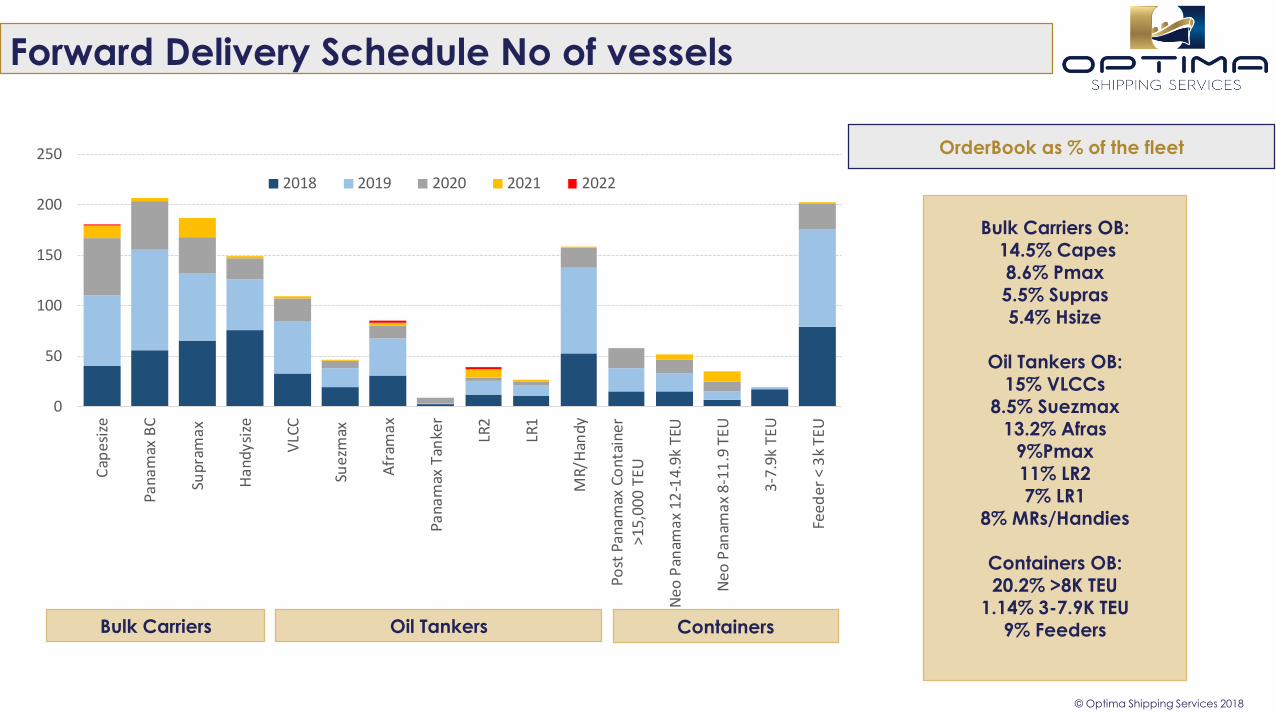

Forward Delivery Schedule No of vessels

© Optima Shipping Services 2018

Bulk Carriers OB:14.5% Capes8.6% Pmax5.5% Supras5.4% Hsize

Oil Tankers OB:15% VLCCs

8.5% Suezmax13.2% Afras

9%Pmax11% LR27% LR1

8% MRs/Handies

Containers OB:20.2% >8K TEU

1.14% 3-7.9K TEU9% Feeders

0

50

100

150

200

250

Cap

esiz

e

Pana

max

BC

Sup

ram

ax

Han

dysi

ze

VLC

C

Suez

max

Afr

amax

Pan

amax

Tan

ker

LR2

LR1

MR

/Han

dy

Post

Pan

amax

Co

ntai

ner

>15,

000

TEU

Neo

Pan

amax

12

-14.

9k T

EU

Neo

Pan

amax

8-1

1.9

TEU

3-7

.9k

TE

U

Feed

er <

3k

TEU

2018 2019 2020 2021 2022

Bulk Carriers Oil Tankers Containers

OrderBook as % of the fleet

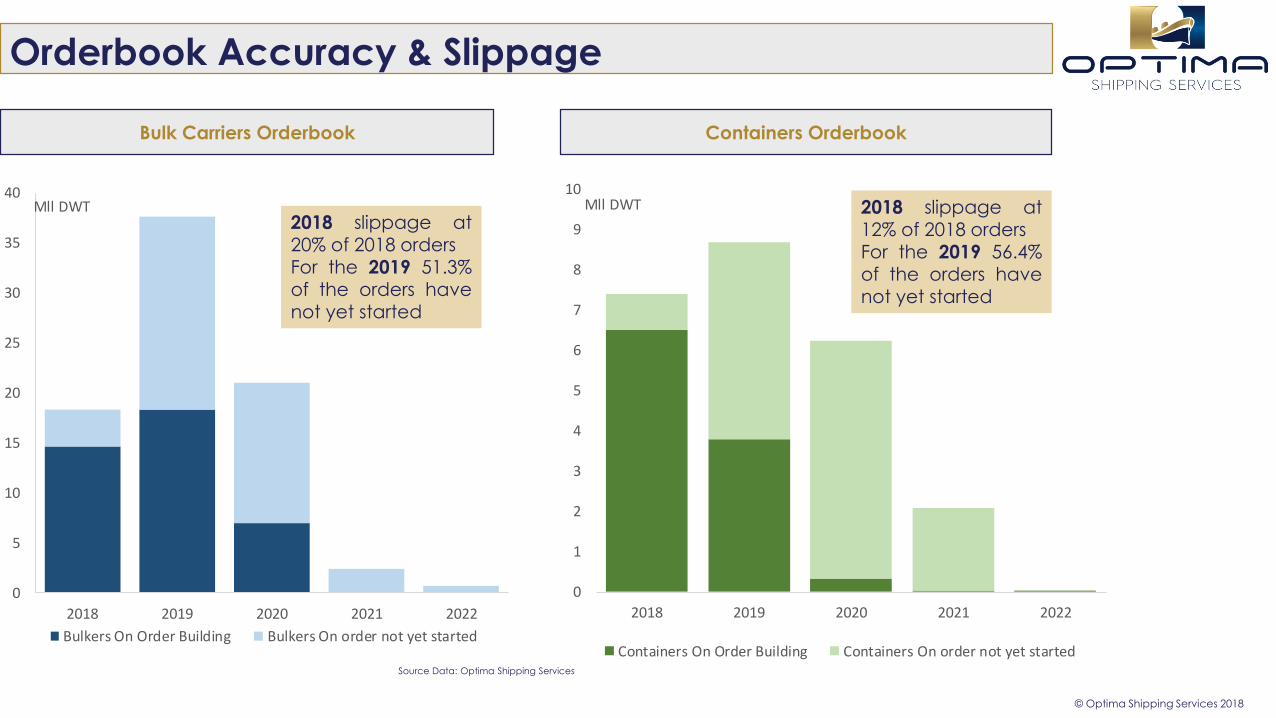

Orderbook Accuracy & Slippage

© Optima Shipping Services 2018

Bulk Carriers Orderbook Containers Orderbook

0

5

10

15

20

25

30

35

40

2018 2019 2020 2021 2022

Mll DWT

Bulkers On Order Building Bulkers On order not yet started

0

1

2

3

4

5

6

7

8

9

10

2018 2019 2020 2021 2022

Mll DWT

Containers On Order Building Containers On order not yet started

2018 slippage at

20% of 2018 ordersFor the 2019 51.3%of the orders havenot yet started

2018 slippage at12% of 2018 ordersFor the 2019 56.4%of the orders havenot yet started

Source Data: Optima Shipping Services

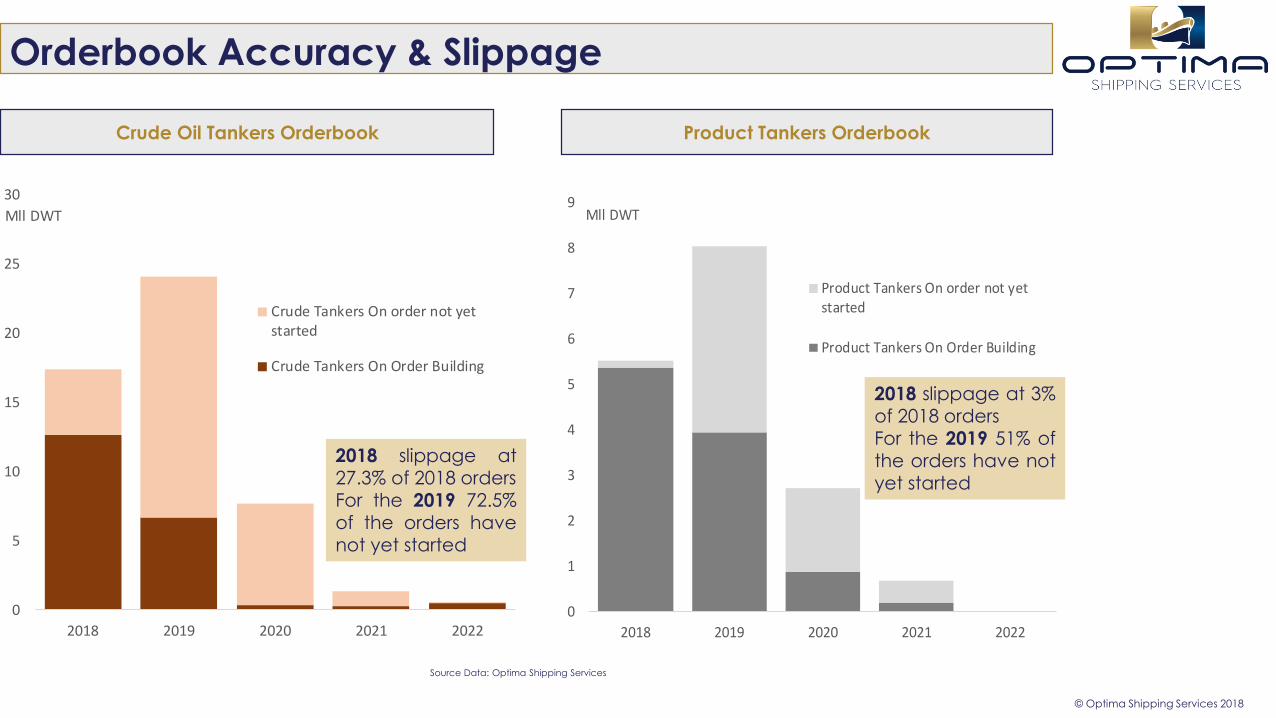

Orderbook Accuracy & Slippage

© Optima Shipping Services 2018

Crude Oil Tankers Orderbook Product Tankers Orderbook

0

5

10

15

20

25

30

2018 2019 2020 2021 2022

Mll DWT

Crude Tankers On order not yetstarted

Crude Tankers On Order Building

0

1

2

3

4

5

6

7

8

9

2018 2019 2020 2021 2022

Mll DWT

Product Tankers On order not yetstarted

Product Tankers On Order Building

2018 slippage at27.3% of 2018 ordersFor the 2019 72.5%of the orders havenot yet started

2018 slippage at 3%of 2018 ordersFor the 2019 51% ofthe orders have notyet started

Source Data: Optima Shipping Services

Orderbook Replacement Tonnage in Mll DWT |SOx

© Optima Shipping Services 2018

0

10

20

30

40

50

60

70

80

90

Crude Tankers Product Tankers Bulkers Containers

age above 20 yrs old Orderbook

0

20

40

60

80

100

120

140

Crude Tankers Product Tankers Bulkers Containers

age above 15 yrs old Orderbook

Orderbook vs Vessels age above 20 years old Orderbook vs Vessels age above 15 years old

Source Data: Optima Shipping Services

Orderbook Replacement Tonnage in Mll DWT |SOx

© Optima Shipping Services 2018

SOxcompliance

Tier 2

Delivery 2019|2020

Retrofit like 2nd hand market

Scrubber Ready

marginally the majority

of the orderbook

Scrubber Fitted

“Wait and see”

attitude

THANK YOU !

© Optima Shipping Services 2018

This report has been prepared by Optima Shipbrokers and is addressed to Optima Shipbrokers customers only and is for distribution only under such circumstances as may be permitted by applicable law. This information has no regard to specific investment objectives, financial situation or particular needs of any specific recipient. It is published solely for informational purposes and this information is not, and should not be construed as, an offer or solicitation to sell or buy any product, investment, security or any other financial instrument. Optima Shipbrokers does not make any representation or warranty, express or implied, as to the accuracy, completeness or correctness of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in the report. Neither Optima Shipbrokers , nor any of its directors, employees or agents, accepts any liability for any loss or damage, howsoever caused, arising from any reliance on any information or views contained in this report. While this report, and any opinions expressed in it, have been derived from sources believed to be reliable and in good faith they are not to be relied upon as authoritative or taken in substitution for the exercise of your own commercial judgment. Any opinions expressed in this report are subject to change without notice. Optima Shipbrokers is under no obligation to update or keep current the information contained herein. This report may not be reproduced or redistributed, in whole or in part, without the written permission of Optima Shipbrokers accepts no liability whatsoever for the action of third parties in the respect. This information is the intellectual property of Optima Shipbrokers . Optima Shipbrokers logo is the trademark of the company. All rights reserved.

Produced by Optima Shipbrokers Research

10, Ouranou Str166 71Kavouri VouliagmenisGreeceTel: +30 210 8922000

Email: [email protected] www.optimashipbrokers.com

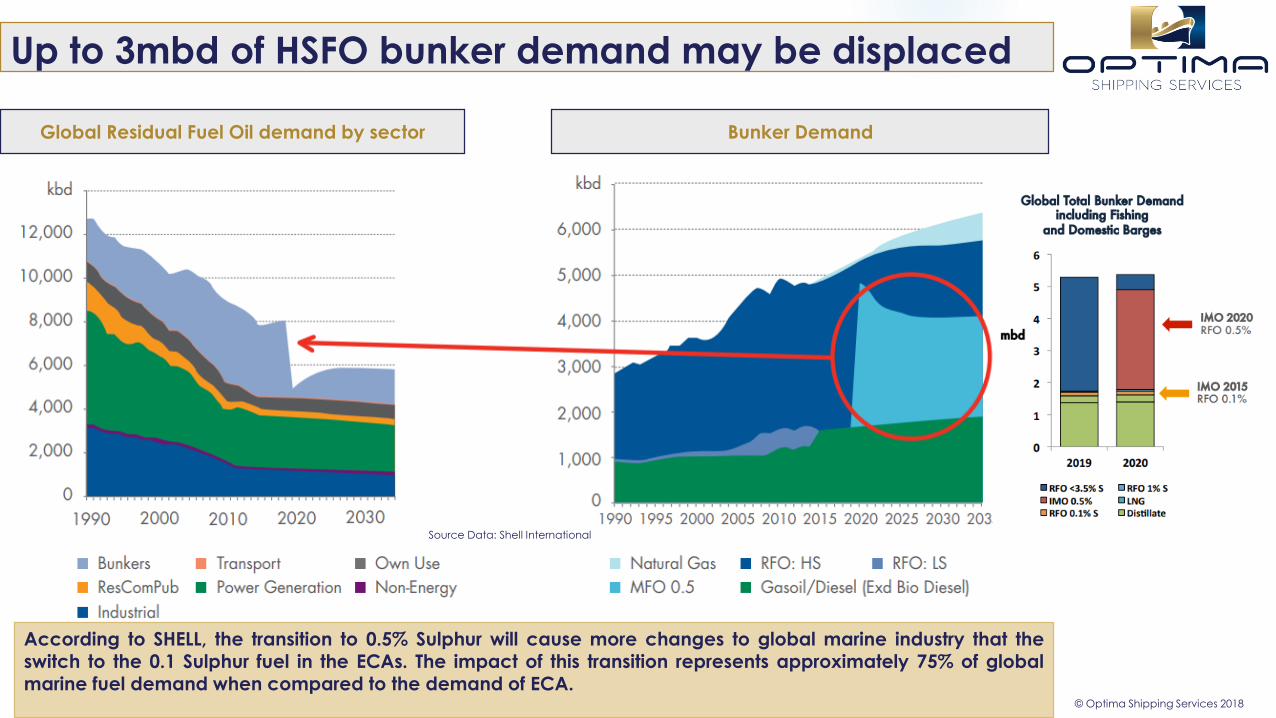

Up to 3mbd of HSFO bunker demand may be displaced

© Optima Shipping Services 2018

Global Residual Fuel Oil demand by sector Bunker Demand

According to SHELL, the transition to 0.5% Sulphur will cause more changes to global marine industry that theswitch to the 0.1 Sulphur fuel in the ECAs. The impact of this transition represents approximately 75% of globalmarine fuel demand when compared to the demand of ECA.

Source Data: Shell International

Who will convert, finally?

© Optima Shipping Services 2018

Alternative fuels are likely to be a more viable option for smaller vessels, while scrubbers are more suitable for larger vessels – due to their increased fuel consumption and benefits of economies of scale.

Each vessel is different, so specific studies on each should be made. An additional hidden cost is the approximately 2% additional energy needed to run a scrubber. Cheap Fuel Oil in 2020 will not guarantee cheap HSFO bunkers:

Logistic Margin: maintaining HSFO infrastructure will become a lot more expensive.Inelastic Demand: a number of suppliers have already advised owners and operators looking to use

scrubbers in 2020 to lock up their volume now so they can ensure future supply. Blended fuels will be considered a very attractive option and may be cheaper than MGO. The price of MDO today might be the best indicator for foreseeing the complying diesel oil price in 2020. Some oil majors have indicated that the price for low Sulphur HFO would be somewhere between the current

HFO and MDO prices. Naturally, nobody knows what the actual prices at that time will be. “Doing nothing is not an option” – IMO, BIMCO, INTERTANKO, ICS are all united and the flag states are on board

for the end results, although the means to get there are not clear.

Source Data: Eikon Reuters

Is there a real impact in vessel earnings?

© Optima Shipping Services 2018

Bunker Prices vs Vessel Earnings

Source Data: Shell International

0

200

400

600

800

1000

1200

1400

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

Jan-00 Jan-02 Jan-04 Jan-06 Jan-08 Jan-10 Jan-12 Jan-14 Jan-16 Jan-18

$/t

n$/D

ay

TC Rate Pmax TC Rate Afra MDO Spore IFO 380 Spore

Limited evidence fuel costs impact vessel earnings

However, they do impact voyage costs We would expect some extra 1knot speed

(slow steaming) reduction to appear if fuel costs soar to high levels.

Expectations are that since the 2H 2019 the shipping and the refining market will start seeing changes in fuel demand, supply and prices.

Currently, swap curves for middle distillates and fuel oil are in backwardation implying that the IMO2020 has not yet invaded into the oil market. But it will soon do! – No move yet into longer term supply contracts.

Source Data: Eikon Reuters

Fuel Oil Forward curve, $/tonne