Embed Size (px)

Citation preview

New Charter School Audit Requirementsfor all Indiana Charter Schools

August 2012

1

Contents

• Summary of New Audit Requirements

• Statutory Authority and US DOE Requirement

• New Audit Requirements

• Frequently Asked Questions

• Contacts and Resources

2

Summary of New Audit Requirements for all Indiana Charter Schools

• Effective immediately, the State Board of Accounts (“SBOA”) will no longer conduct biennial audits of Indiana charter schools.

• Instead, all charter schools must contract with a Private Examiner to conduct a financial, compliance and (if applicable) federal OMB Circular A-133 audit that complies with the SBOA’s new guidelines for charter school audits.

• Per US DOE requirements for states that receive the federal Public Charter School Program (“PCSP”) grant, charter school audits must be conducted on an annual basis.

• Contracts with Private Examiners must be approved by the SBOA prior to commencement of the audit.

• Audits may be prepared using either the accrual or cash basis of accounting. The method of preparation will be established by each charter school’s authorizer.

3

Contents

• Summary of New Audit Requirements

• Statutory Authority and US DOE Requirement

• New Audit Requirements

• Frequently Asked Questions

• Contacts and Resources

4

Statutory Authority

• Indiana Code 5-11-1-9 gives the State Board of Accounts (“SBOA”) the responsibility for examining all accounts and all financial affairs (i.e., performing an audit) of every unit of government, including charter schools.

• Under Indiana Code 5-11-1-7, the SBOA may allow Private Examiners to perform this audit, in accordance with the guidelines established by the SBOA for charter schools.

• Until July 2012, the SBOA has conducted biennial audits of all Indiana charter schools.

• Effective immediately, the SBOA will no longer conduct charter school audits.

• Instead, the SBOA now requires charter schools to contract with Private Examiners to conduct an audit in accordance with the guidelines established by the SBOA for charter schools.

• As has always been the case, the cost of audits that comply with SBOA requirements are the responsibility of the charter school.

5

US DOE Requirements

• This change in state auditing procedures for Indiana charter schools is required by the US DOE for states, such as Indiana, that receive and administer the federal Public Charter School Program (“PCSP”) planning and implementation grant for charter schools.

• Specifically, the US DOE requires that all charter schools undergo annual, independent audits. In 2012, the US DOE determined that the biennial audit conducted by the SBOA did not meet either requirement.

• Therefore, the SBOA adopted new audit guidelines for charter schools as outlined in this PowerPoint document, and explained in detail in the “Guidelines for the Audits of Charter Schools Performed by Private Examiners” manual posted on the SBOA’s website: http://www.in.gov/sboa/

6

Contents

• Summary of New Audit Requirements

• Statutory Authority and US DOE Requirement

• New Audit Requirements

• Frequently Asked Questions

• Contacts and Resources

7

New Audit Requirements - 1

• The new Charter Schools Manual is located on the SBOA’s website at the following address: http://www.in.gov/sboa/3872.htm

• The new audit requirements are effective immediately.• Audits musts be conducted on an annual basis.• Charter schools must contract with a Private Examiner to

conduct an audit that complies with the audit guidelines for charter schools established by the SBOA.

• For audit periods ending June 30, 2012, notification must be sent to the SBOA by September 15, 2012, of the intent to contract for audit by Private Examiner.

• Note that all contracts must first be approved by the SBOA, as depicted on the flow chart on Slide 12 of this PowerPoint document.

8

New Audit Requirements - 2

• Schools that were scheduled for the SBOA to conduct a biennial audit this year will NOT be audited by the SBOA. Instead, these schools must now contract with a Private Examiner to conduct an audit covering the 2010-2011 and 2011-2012 fiscal years.

• Audits must be performed on a July 1-June 30 fiscal year basis at the individual school level. – Currently, an organizer with multiple schools may not submit a consolidated

audit with segmented school-level financial information.

• Audits may be prepared using either the accrual or cash basis of accounting. A school’s authorizer will establish guidelines regarding whether audits should be prepared using the accrual vs. cash basis of accounting.

9

New Audit Requirements - 3

• Audits performed by Private Examiners are to be completed and all required reports issued within 180 days after the close of the audit period (i.e., by the end of December)

• A school’s financial statements must utilize the Chart of Accounts established by the SBOA. – Note that a school need only use those accounts that apply to the school.

The full Chart of Accounts in its entirety need not be utilized.

• All charter schools are required to utilize prescribed forms as set forth by the SBOA. – Note that replicas of these prescribed forms may be used, but these

replicas must first be approved by the SBOA.

• Note that the biannual financial report (Form 9) required by the Indiana Department of Education must be prepared using the cash basis of accounting. This is separate from the audit report.

10

Process for Contracting with Private Examiner

• The process for contracting with a Private Examiner to conduct a financial and compliance (and, if applicable, federal OMB Circular A-133) audit is described in the “Guidelines for the Audits of Charter Schools Performed by Private Examiners” manual posted on the SBOA’s website: http://www.in.gov/sboa/2415.htm

• At the end of this manual are two flowcharts that depict the following processes (please refer to pages E-1 and E-2 in the manual):– How to select and enter into a contract with a Private Examiner, in

compliance with SBOA review and approval requirements.– How to work with the SBOA to obtain the necessary review and approval of

the draft audit report prepared by the Private Examiner.

• The flowchart depicting the Private Examiner contracting process is replicated on the next slide (Slide 10).

11

Process for Contracting with Private Examiner

12

Charter School creates a Request for Proposal (“RFP”) for the annual financial, compliance and, if applicable, federal OMB Circular A-133 audit.

Charter School sends RFP to State Board of Accounts (“SBOA”) for approval. RFPs should be

emailed to: [email protected].

SBOA reviews RFP.

SBOA approves RFP and sends back to Charter School.

SBOA recommends changes to RFP or denies the RFP and sends back to Charter School.

Charter School publishes RFP, receives proposals and selects a Private Examiner to conduct the audit.

Charter School and Private Examiner negotiate terms of contract for SBOA review.

Charter School sends contract to SBOA for final approval. Contracts should be emailed to:

SBOA reviews contract.

SBOA recommends changes to the contract or denies the contract and sends back to

Charter School.

SBOA approves contract and sends back to Charter

School.

Charter School and Private Examiner each sign contract.

Audit commences

Contents

• Summary of New Audit Requirements

• Statutory Authority and US DOE Requirement

• New Audit Requirements

• Frequently Asked Questions

• Contacts and Resources

13

Frequently Asked Questions

The Questions and Answers on the following slides are excerpted from the Q&A session that took place during the August 24, 2012, WebEx led by Paul Joyce, Deputy Examiner for the State Board of Accounts and facilitated by the Indiana Department of Education and the Indiana

Charter School Board.

14

Frequently Asked Questions

Q: When are the new charter school audit requirements effective?

A: These requirements are effective immediately, for the Fiscal Year ending June 30, 2012.

Q: How can the SBOA require this of us when we are not due for an SBOA audit until 2014?

A: The SBOA has the statutory authority to establish audit requirements for all units of government, including charter schools. Until this year, the SBOA conducted biennial audits covering a two-year period, using its own staff. Because of US DOE requirements for states that receive the federal Public Charter School Program (“PCSP”) grant, Indiana charter schools must now receive annual, independent audits. Therefore, the SBOA will no longer conduct audits directly, but instead requires charter schools to contract with a Private Examiner to conduct an annual audit.

15

Frequently Asked QuestionsQ: Why not start this next year and give charter schools the courtesy of a year to plan?

A: The US DOE required the Indiana Department of Education to submit an assurance that an annual, independent audit will be conducted for all Indiana charter schools, effective immediately. In order to ensure the continuation of PCSP funding for Indiana charter schools, the state must comply with this annual audit requirement.

Q: What communication is being sent out to schools about the new requirement?

A: The SBOA conducted a WebEx on August 24, which will be posted on the IDOE’s Charter Schools webpage. In addition, the SBOA is meeting with all Indiana authorizers on September 7 to discuss its requirements in more detail. Each authorizer will be responsible for ensuring the schools it oversees is aware of the new audit requirements. Finally, notification of the new audit requirements will be distributed through SAMS.

16

Frequently Asked QuestionsQ: For the 2011-2012 school year, can schools continue with the audit they already have scheduled?

A: No. Before the auditor commences the audit, the school must first ensure the scope of services with the auditor complies with the SBOA’s new charter school audit guidelines. Please send the contract ASAP to: [email protected].

Q: We have a financial audit completed every year. Can we use our existing auditor to perform both audits at the same time, as long as the RFP is approved?

A: In the past, the SBOA conducted biennial financial and compliance audits of charter schools using its own staff. Some authorizers, like Ball State, also required charter schools to conduct an annual financial audit on the “off” year. Effective immediately, the SBOA will no longer conduct audits with its own staff. Therefore, only one financial and compliance audit will be conducted on an annual basis by a Private Examiner.

17

Frequently Asked QuestionsQ: If an authorizer has already contracted with a Private Examiner for all of its schools, does each school still need to submit an RFP?

A: The scope of audit services must comply with the SBOA’s new requirements for charter school audits. The authorizer in question must send the contract to the SBOA for approval prior to the commencement of any audit services. It is possible the contract may need to be amended.

Q: We have an audit scheduled with the SBOA for both 2010-2011 and 2011-2012. Are the SBOA auditors still coming or do we need to contact a Private Examiner to conduct this two-year audit?

A: The new charter school audit requirements are effective immediately. Therefore, SBOA staff will not be conducting the previously scheduled biennial audit, and the school must contract with a Private Examiner.

Q: Can the audit be prepared using the accrual method of accounting, or must it be prepared using the cash basis of accounting?

A: The audit may be prepared using either method. The required method of accounting will be established by each charter school’s authorizer.

18

Frequently Asked QuestionsQ: What is the deadline for submitting a draft contract to the SBOA for review and approval?

A: The deadline is September 15, 2012. However, the SBOA will work with schools to adjust this deadline if needed, given that these are new guidelines for charter schools.

Q: Our Board must select the auditor. Our next Board Meeting is not scheduled until September 18. How are we able to send you a contract prior to Board selection of the auditor?

A: Please contact the SBOA at [email protected]. We will work with you to provide necessary input on the contract and modify the deadline if needed.

Q: Will the SBOA approve a two-year contract with a Private Examiner as long as the contract is approved in Year One?

A: The duration of the contract can be for whatever length of time the charter school and Private Examiner agree is appropriate. The only requirements are that the scope of audit services comply with SBOA requirements, and that the contract is approved by the SBOA.

19

Frequently Asked Questions

Q: If the SBOA denies the contract, do you give specific feedback about how to change it?

A: Yes. The SBOA will work with the school and the Private Examiner to ensure the contract meets SBOA requirements.

Q: Does the Private Examiner need to be licensed in Indiana?

A: Yes. The CPA or auditing firm must be licensed to perform audits in Indiana.

Q: Can you provide an estimate of fees for an annual audit? What about the cost of an audit covering the last two fiscal years (2010-2011 and 2011-2012)?

A: Audit costs will range depending upon the size of the school. Typically, the additional cost to audit two years is about 15%-20% more than the cost to audit one year.

20

Frequently Asked QuestionsQ: Can you provide an example of an RFP that schools can use?

A: Indiana authorizers are meeting the week of August 27 and will work to create a sample RFP that all charter schools can use. Note that the RFP may have to be modified by each school to reflect the scope of services that are relevant to their specific circumstances.

Q: If we are opening our school in 2013, do we conduct an audit after the first year of operation? Or will an audit be conducted for the pre-operational year?

A: The first audit required by the SBOA and the US DOE is following the school’s first year of operation. At its discretion, a school may choose to have a pre-operational year audit conducted.

Q: Do we have to use Komputrol as accounting software?

A: No. Komputrol is just one of many software options. The SBOA requires that forms used by the school comply with SBOA guidelines. A school may create its own forms, as long as the forms contain the required information and are first approved by the SBOA. See the SBOA Charter Schools Manual for additional information.

21

Contents

• Summary of New Audit Requirements

• Statutory Authority and US DOE Requirement

• New Audit Requirements

• Frequently Asked Questions

• Contacts and Resources

22

SBOA Website: www.in.gov/sboa/

23

Charter School Manual on SBOA Website

24

On the left-hand side menu bar on the SBOA’s Home Page, click on “Manuals.” All SBOA Manuals, including the new Charter Schools Manual, are posted here.

Guidelines for Private Examiners on SBOA Website

25

On the left-hand side menu bar on the SBOA’s Home Page, click on “Guidelines for Independent Auditors.” It will take you to the webpage where the Charter School Audit guidelines are posted.

SBOA Contact Information – Deputy Examiner

26

On the left-hand side menu bar on the SBOA’s Home Page, click on “Contact Us.” You will find contact information for all SBOA staff, including Paul Joyce, Deputy Examiner. Mr. Joyce oversaw the creation of the new Charter School Audit Guidelines.

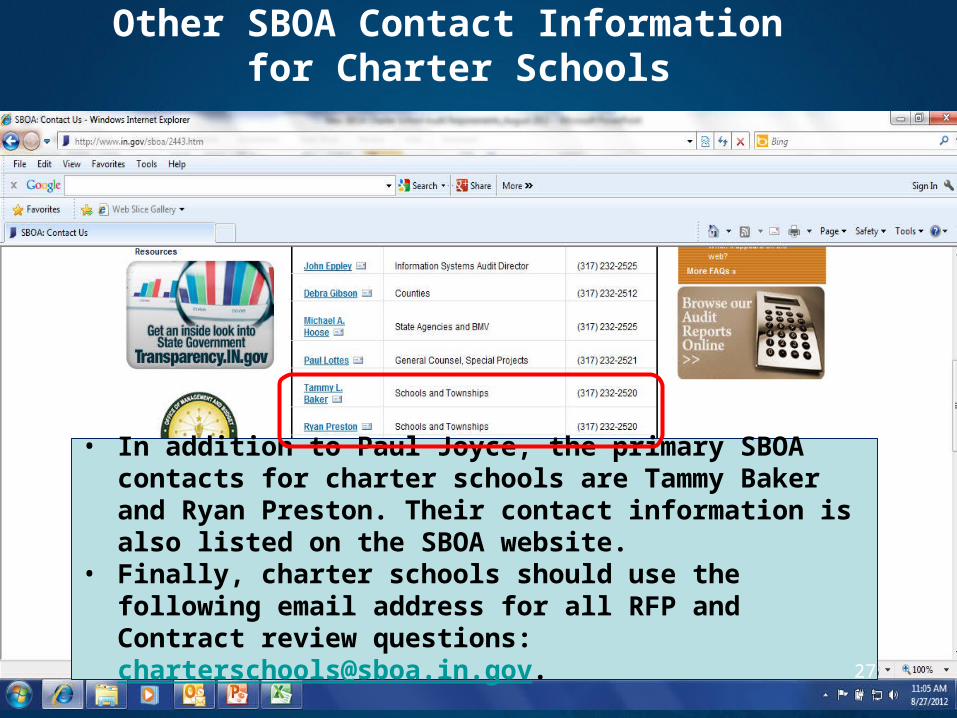

Other SBOA Contact Information for Charter Schools

• In addition to Paul Joyce, the primary SBOA contacts for charter schools are Tammy Baker and Ryan Preston. Their contact information is also listed on the SBOA website.

• Finally, charter schools should use the following email address for all RFP and Contract review questions: [email protected].

27

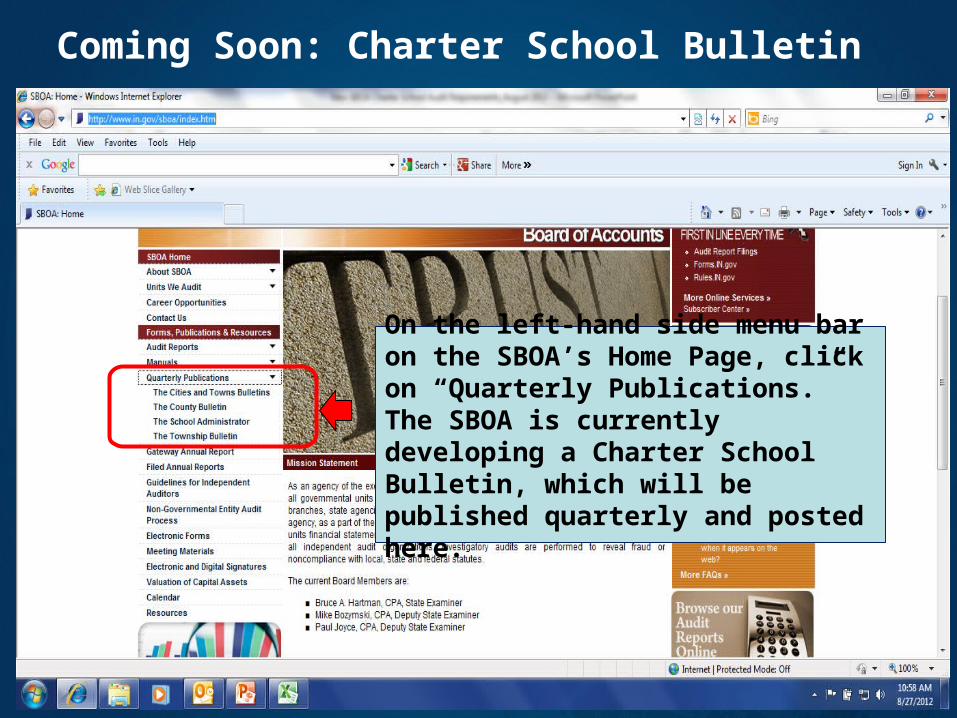

Coming Soon: Charter School Bulletin

28

On the left-hand side menu bar on the SBOA’s Home Page, click on “Quarterly Publications.” The SBOA is currently developing a Charter School Bulletin, which will be published quarterly and posted here.