Embed Size (px)

Citation preview

Bombay Chartered Accountants’ Society

CA Bhavesh Vora – 04/08/2016

NBFC Prudential Norms &

Compliances – Important Aspects

Coverage

04/08/2016BCAS - CA Bhavesh Vora2

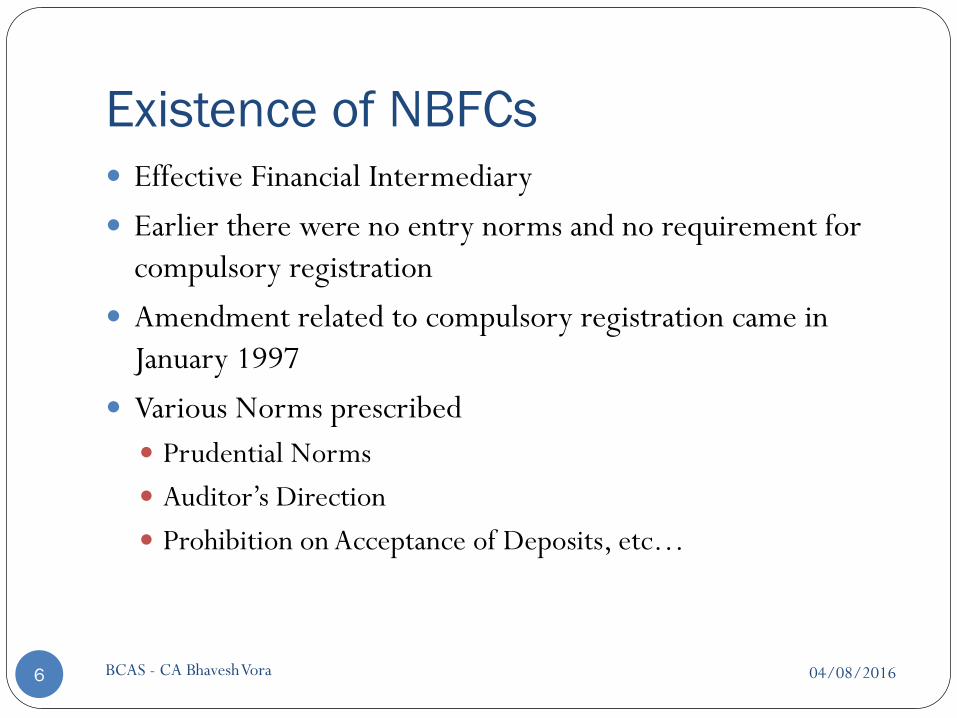

Existence of NBFCs

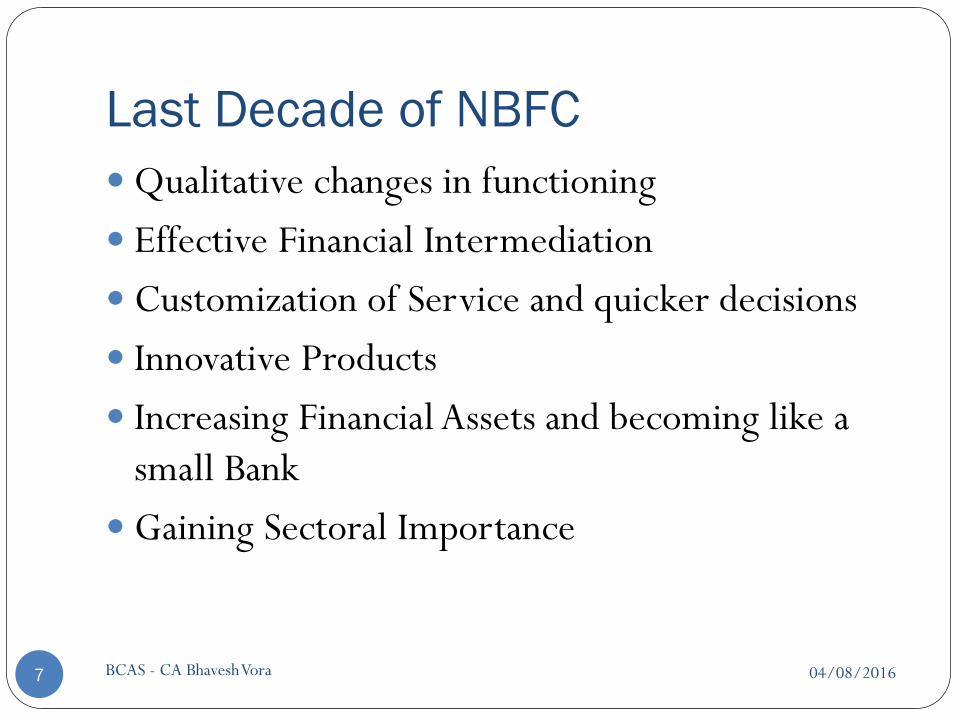

Last Decade of NBFC

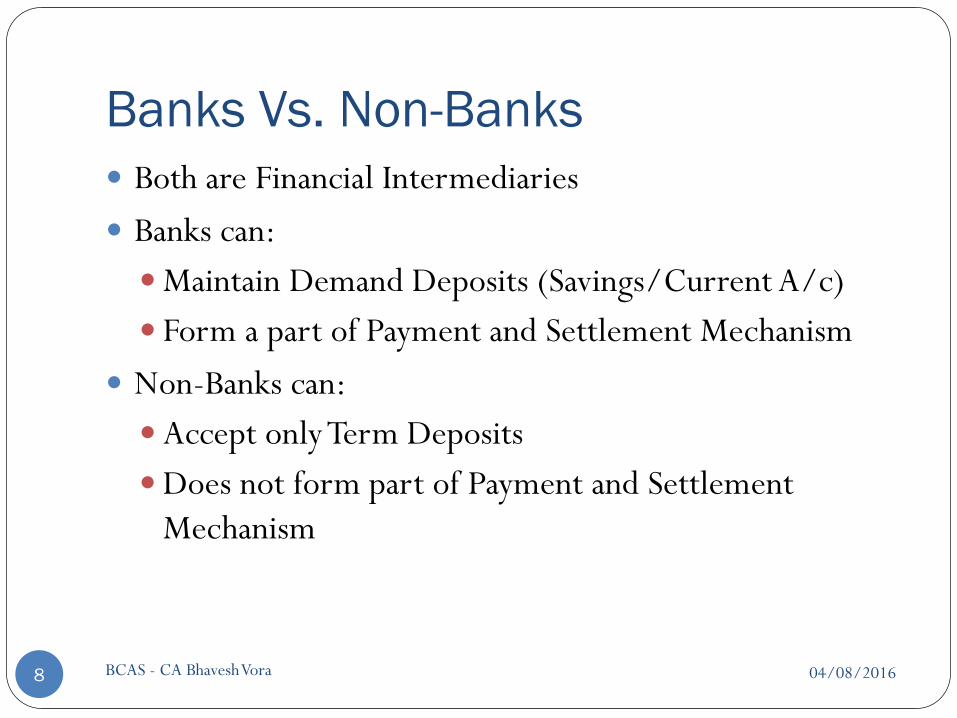

Banks Vs. Non-Banks

Meaning of NBFCs

Major Changes in 2007-08

Recent Developments

Applicability and Issues

Public Funds Vs. Public Deposits

Income Recognition

Accounting as per Prudential Norms

Asset Classification and Provisioning

Capital Adequacy

Leverage Ratio

Coverage (Contd.)

04/08/2016BCAS - CA Bhavesh Vora3

Loan against Shares

Credit Concentration Norms

Restructuring of Advances

Disclosures to be made

Submissions to RBI

Policies and Committees

Corporate Governance

Restrictions on Investments

Prohibitions

Change in Control

Penal Provisions

Miscellaneous Compliances

Future of NBFC Sector

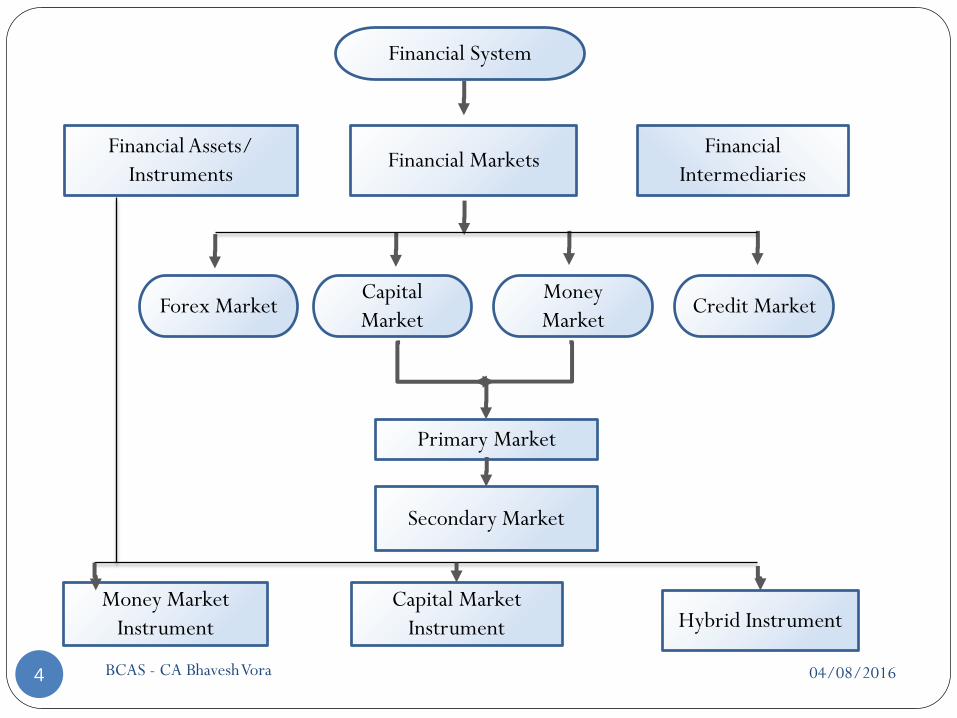

Financial System

Financial Assets/

InstrumentsFinancial Markets

Financial

Intermediaries

Capital

Market

Money

MarketCredit Market

Primary Market

Secondary Market

Money Market

Instrument

Capital Market

Instrument Hybrid Instrument

Forex Market

BCAS - CA Bhavesh Vora4 04/08/2016

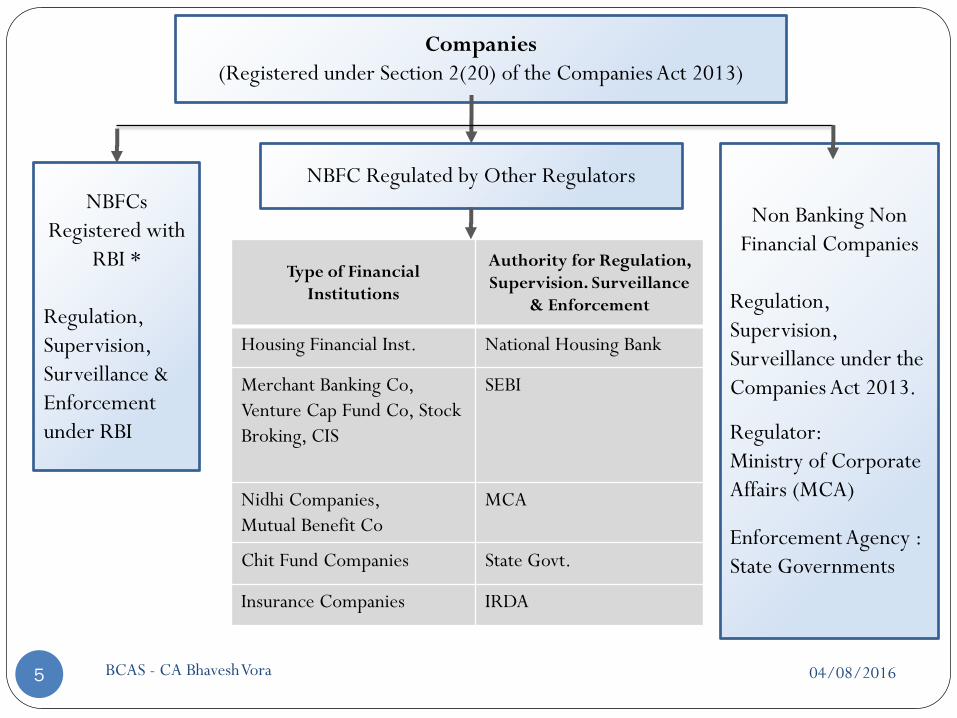

Companies

(Registered under Section 2(20) of the Companies Act 2013)

NBFC Regulated by Other Regulators

Non Banking Non

Financial Companies

Regulation,

Supervision,

Surveillance under the

Companies Act 2013.

Regulator:

Ministry of Corporate

Affairs (MCA)

Enforcement Agency :

State Governments

NBFCs

Registered with

RBI *

Regulation,

Supervision,

Surveillance &

Enforcement

under RBI

Type of Financial

Institutions

Authority for Regulation,

Supervision. Surveillance

& Enforcement

Housing Financial Inst. National Housing Bank

Merchant Banking Co,

Venture Cap Fund Co, Stock

Broking, CIS

SEBI

Nidhi Companies,

Mutual Benefit Co

MCA

Chit Fund Companies State Govt.

Insurance Companies IRDA

04/08/2016BCAS - CA Bhavesh Vora5

Existence of NBFCs

04/08/2016BCAS - CA Bhavesh Vora6

Effective Financial Intermediary

Earlier there were no entry norms and no requirement for

compulsory registration

Amendment related to compulsory registration came in

January 1997

Various Norms prescribed

Prudential Norms

Auditor’s Direction

Prohibition on Acceptance of Deposits, etc…

Last Decade of NBFC

04/08/2016BCAS - CA Bhavesh Vora7

Qualitative changes in functioning

Effective Financial Intermediation

Customization of Service and quicker decisions

Innovative Products

Increasing Financial Assets and becoming like a

small Bank

Gaining Sectoral Importance

Banks Vs. Non-Banks

04/08/2016BCAS - CA Bhavesh Vora8

Both are Financial Intermediaries

Banks can:

Maintain Demand Deposits (Savings/Current A/c)

Form a part of Payment and Settlement Mechanism

Non-Banks can:

Accept only Term Deposits

Does not form part of Payment and Settlement

Mechanism

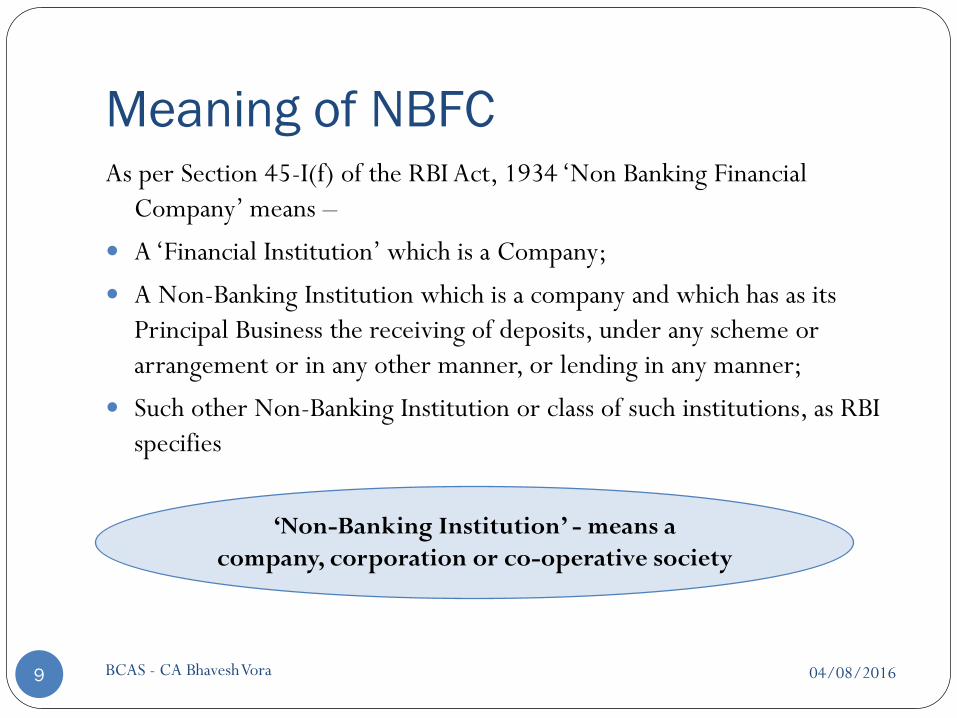

Meaning of NBFC

04/08/2016BCAS - CA Bhavesh Vora9

As per Section 45-I(f) of the RBI Act, 1934 ‘Non Banking Financial

Company’ means –

A ‘Financial Institution’ which is a Company;

A Non-Banking Institution which is a company and which has as its

Principal Business the receiving of deposits, under any scheme or

arrangement or in any other manner, or lending in any manner;

Such other Non-Banking Institution or class of such institutions, as RBI

specifies

.

‘Non-Banking Institution’ - means a

company, corporation or co-operative society

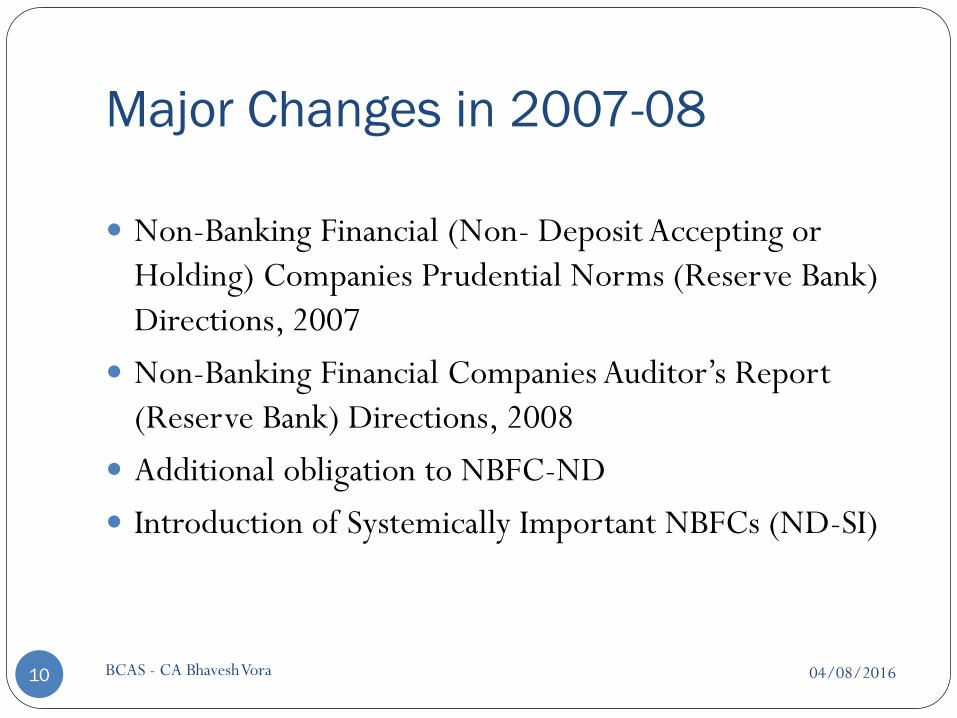

Major Changes in 2007-08

04/08/2016BCAS - CA Bhavesh Vora10

Non-Banking Financial (Non- Deposit Accepting or

Holding) Companies Prudential Norms (Reserve Bank)

Directions, 2007

Non-Banking Financial Companies Auditor’s Report

(Reserve Bank) Directions, 2008

Additional obligation to NBFC-ND

Introduction of Systemically Important NBFCs (ND-SI)

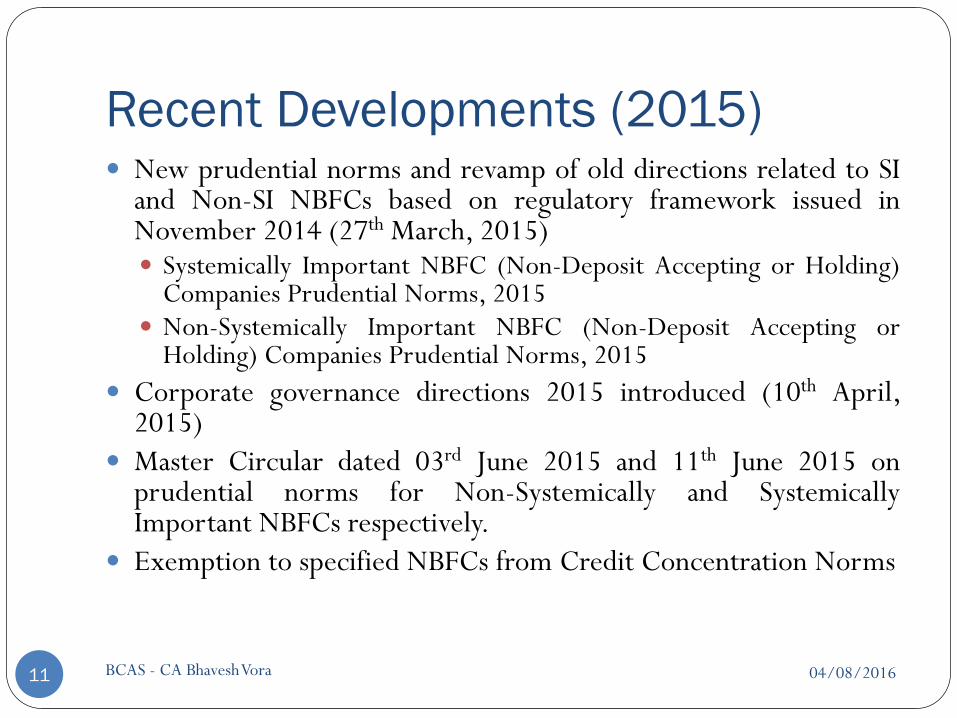

Recent Developments (2015)

04/08/2016BCAS - CA Bhavesh Vora11

New prudential norms and revamp of old directions related to SIand Non-SI NBFCs based on regulatory framework issued inNovember 2014 (27th March, 2015) Systemically Important NBFC (Non-Deposit Accepting or Holding)

Companies Prudential Norms, 2015 Non-Systemically Important NBFC (Non-Deposit Accepting or

Holding) Companies Prudential Norms, 2015

Corporate governance directions 2015 introduced (10th April,2015)

Master Circular dated 03rd June 2015 and 11th June 2015 onprudential norms for Non-Systemically and SystemicallyImportant NBFCs respectively.

Exemption to specified NBFCs from Credit Concentration Norms

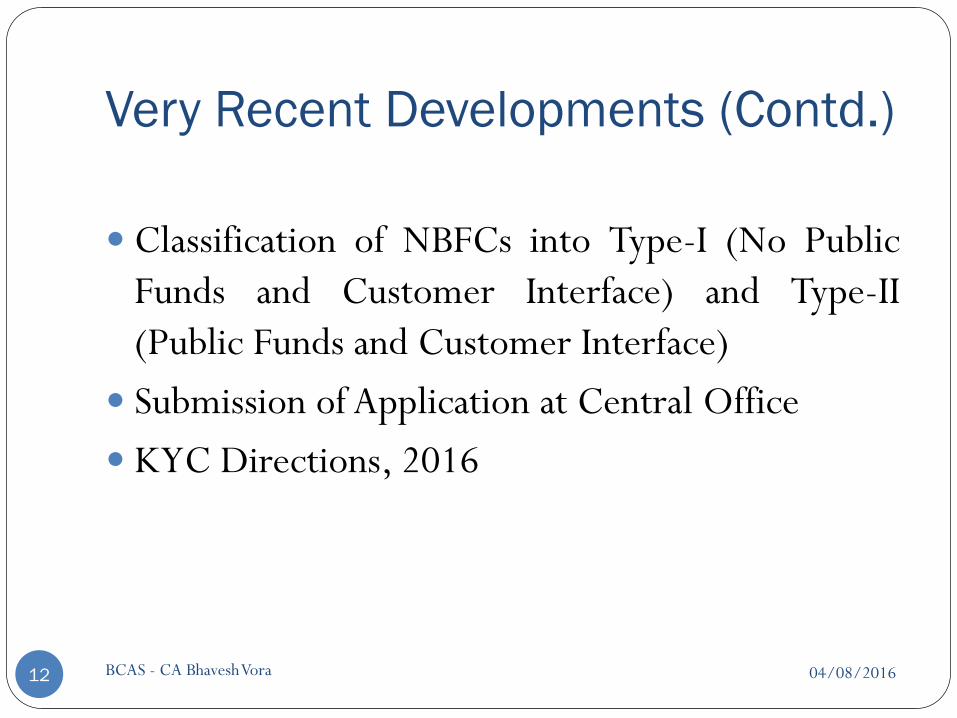

Very Recent Developments (Contd.)

04/08/2016BCAS - CA Bhavesh Vora12

Classification of NBFCs into Type-I (No Public

Funds and Customer Interface) and Type-II

(Public Funds and Customer Interface)

Submission of Application at Central Office

KYC Directions, 2016

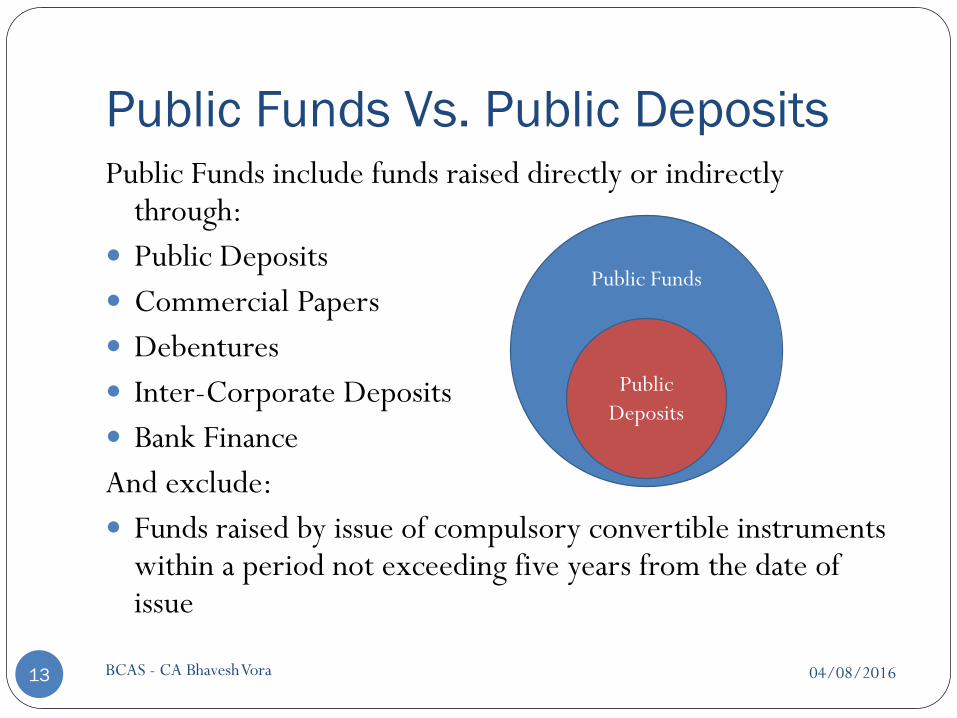

Public Funds Vs. Public Deposits

04/08/2016BCAS - CA Bhavesh Vora13

Public Funds include funds raised directly or indirectly through:

Public Deposits

Commercial Papers

Debentures

Inter-Corporate Deposits

Bank Finance

And exclude:

Funds raised by issue of compulsory convertible instruments within a period not exceeding five years from the date of issue

Public Funds

Public

Deposits

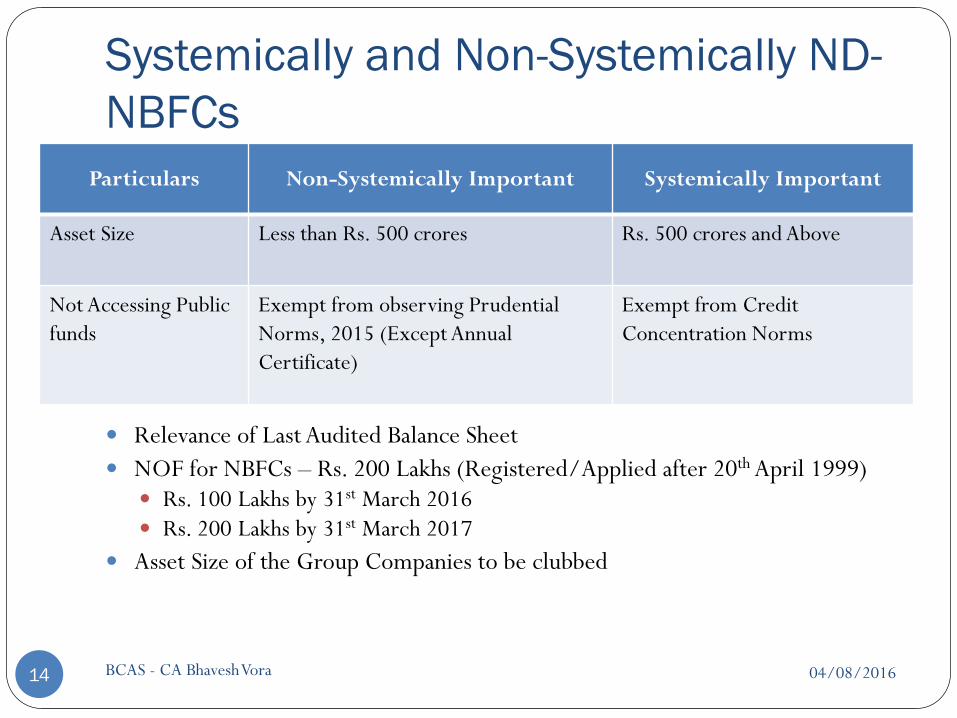

Systemically and Non-Systemically ND-

NBFCs

04/08/2016BCAS - CA Bhavesh Vora14

Relevance of Last Audited Balance Sheet

NOF for NBFCs – Rs. 200 Lakhs (Registered/Applied after 20th April 1999) Rs. 100 Lakhs by 31st March 2016

Rs. 200 Lakhs by 31st March 2017

Asset Size of the Group Companies to be clubbed

Particulars Non-Systemically Important Systemically Important

Asset Size Less than Rs. 500 crores Rs. 500 crores and Above

Not Accessing Public

funds

Exempt from observing Prudential

Norms, 2015 (Except Annual

Certificate)

Exempt from Credit

Concentration Norms

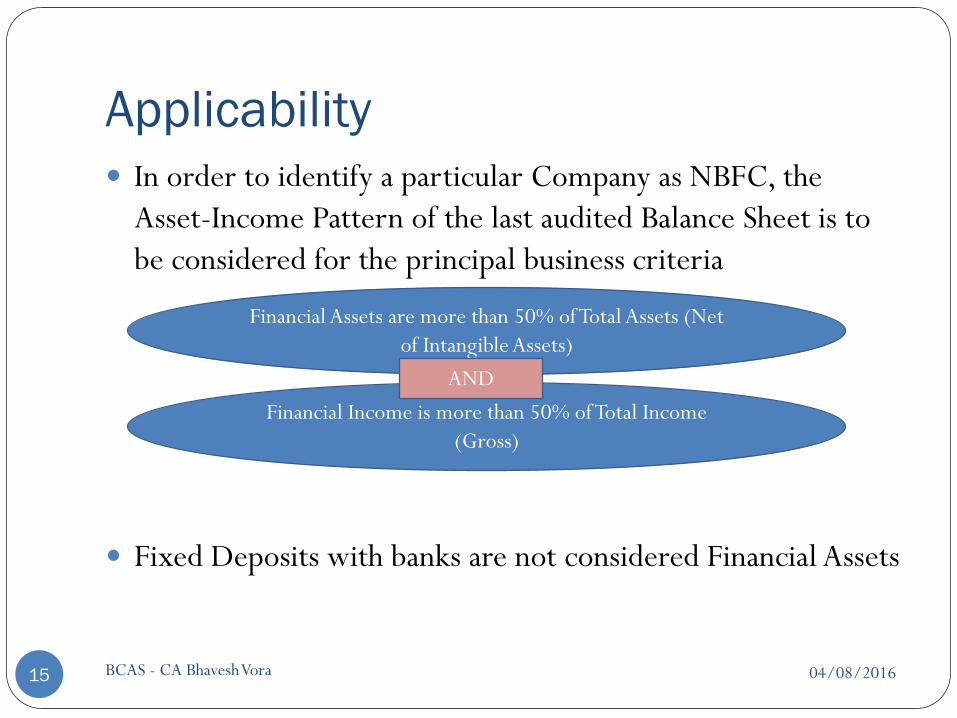

Applicability

04/08/2016BCAS - CA Bhavesh Vora15

In order to identify a particular Company as NBFC, the

Asset-Income Pattern of the last audited Balance Sheet is to

be considered for the principal business criteria

Fixed Deposits with banks are not considered Financial Assets

Financial Assets are more than 50% of Total Assets (Net

of Intangible Assets)

Financial Income is more than 50% of Total Income

(Gross)

AND

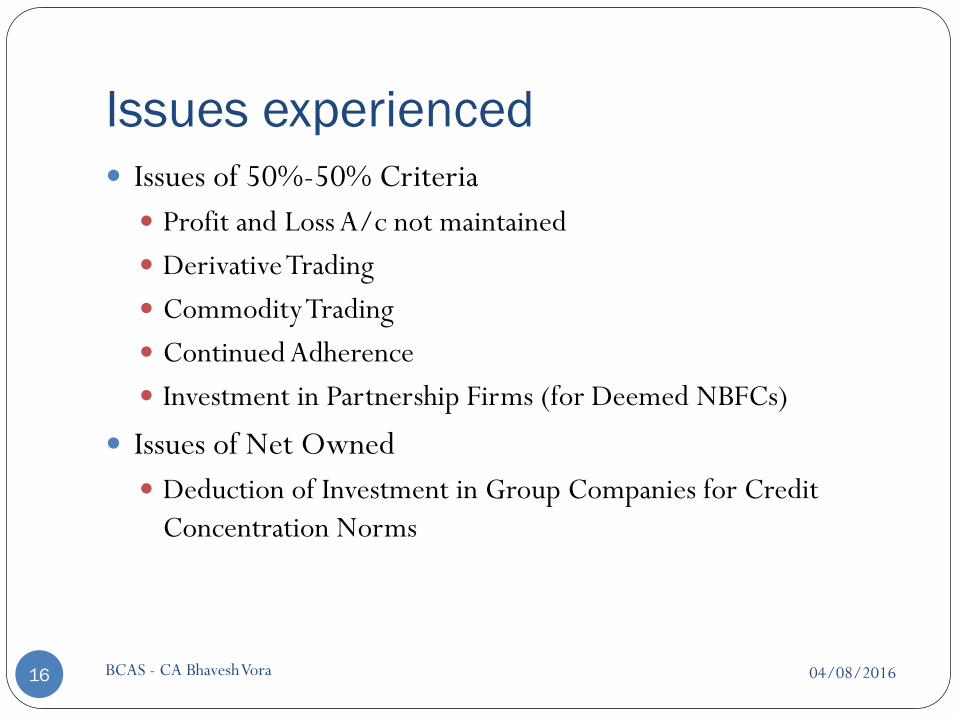

Issues experienced

04/08/2016BCAS - CA Bhavesh Vora16

Issues of 50%-50% Criteria

Profit and Loss A/c not maintained

Derivative Trading

Commodity Trading

Continued Adherence

Investment in Partnership Firms (for Deemed NBFCs)

Issues of Net Owned

Deduction of Investment in Group Companies for Credit

Concentration Norms

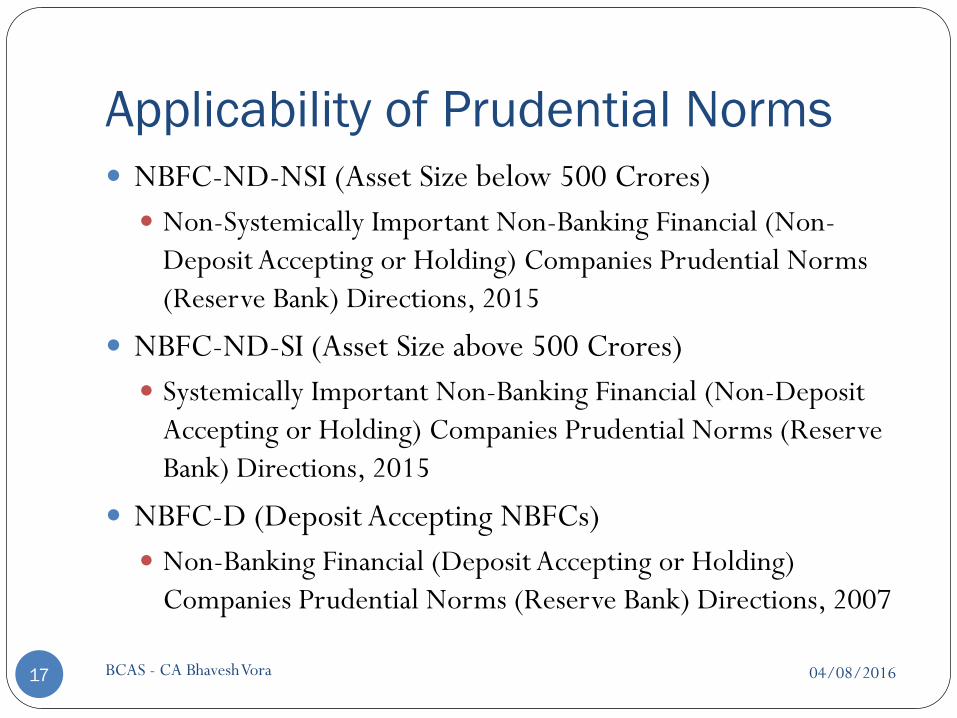

Applicability of Prudential Norms

04/08/2016BCAS - CA Bhavesh Vora17

NBFC-ND-NSI (Asset Size below 500 Crores)

Non-Systemically Important Non-Banking Financial (Non-

Deposit Accepting or Holding) Companies Prudential Norms

(Reserve Bank) Directions, 2015

NBFC-ND-SI (Asset Size above 500 Crores)

Systemically Important Non-Banking Financial (Non-Deposit

Accepting or Holding) Companies Prudential Norms (Reserve

Bank) Directions, 2015

NBFC-D (Deposit Accepting NBFCs)

Non-Banking Financial (Deposit Accepting or Holding)

Companies Prudential Norms (Reserve Bank) Directions, 2007

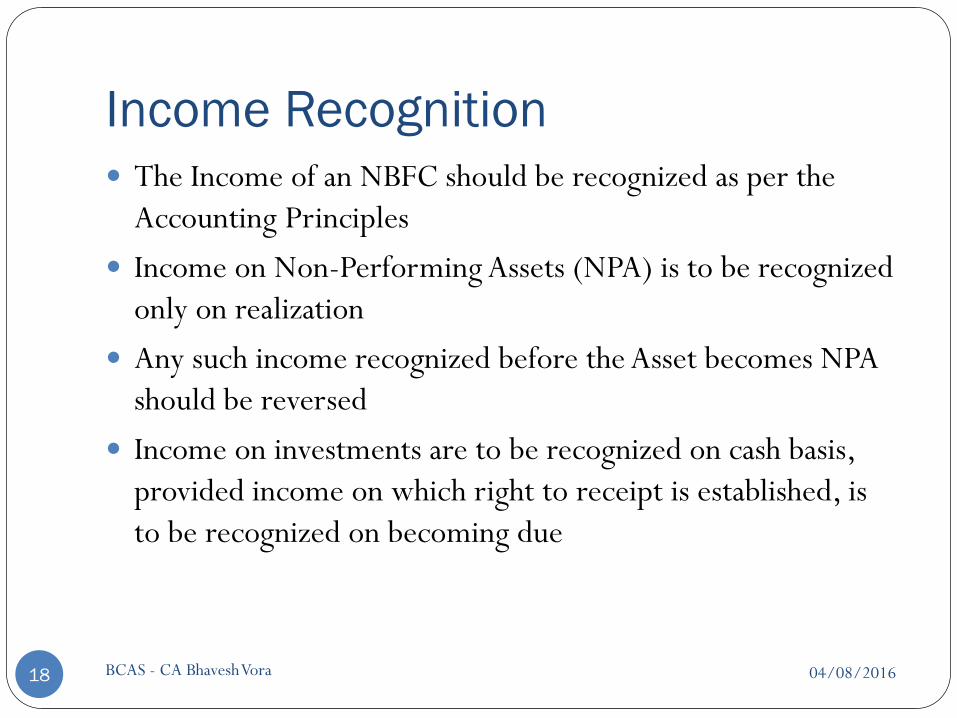

Income Recognition

04/08/2016BCAS - CA Bhavesh Vora18

The Income of an NBFC should be recognized as per the

Accounting Principles

Income on Non-Performing Assets (NPA) is to be recognized

only on realization

Any such income recognized before the Asset becomes NPA

should be reversed

Income on investments are to be recognized on cash basis,

provided income on which right to receipt is established, is

to be recognized on becoming due

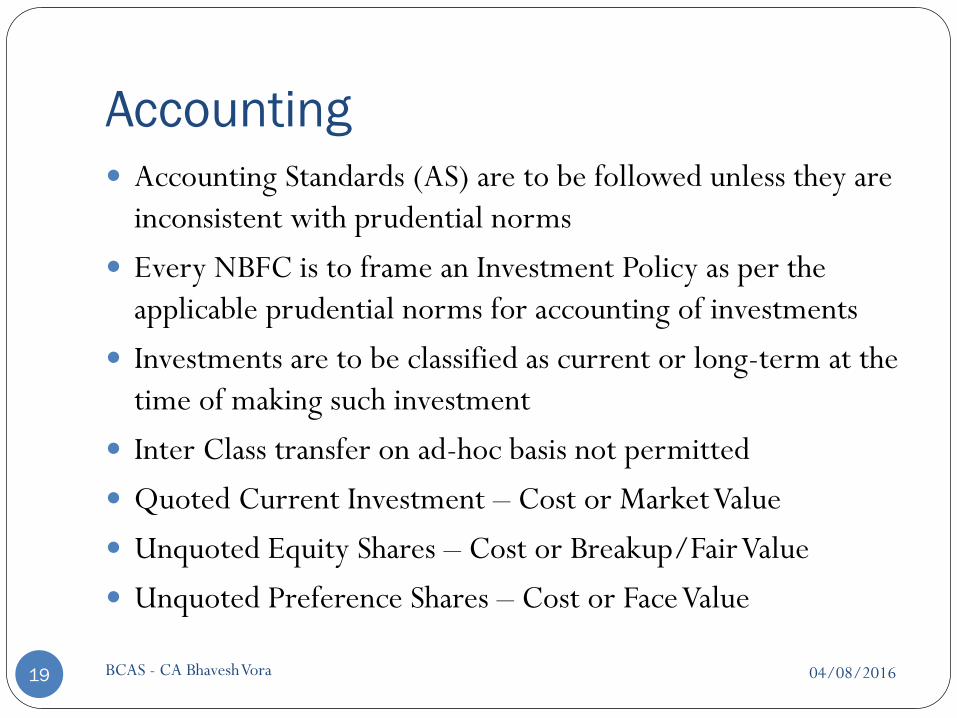

Accounting

04/08/2016BCAS - CA Bhavesh Vora19

Accounting Standards (AS) are to be followed unless they are

inconsistent with prudential norms

Every NBFC is to frame an Investment Policy as per the

applicable prudential norms for accounting of investments

Investments are to be classified as current or long-term at the

time of making such investment

Inter Class transfer on ad-hoc basis not permitted

Quoted Current Investment – Cost or Market Value

Unquoted Equity Shares – Cost or Breakup/Fair Value

Unquoted Preference Shares – Cost or Face Value

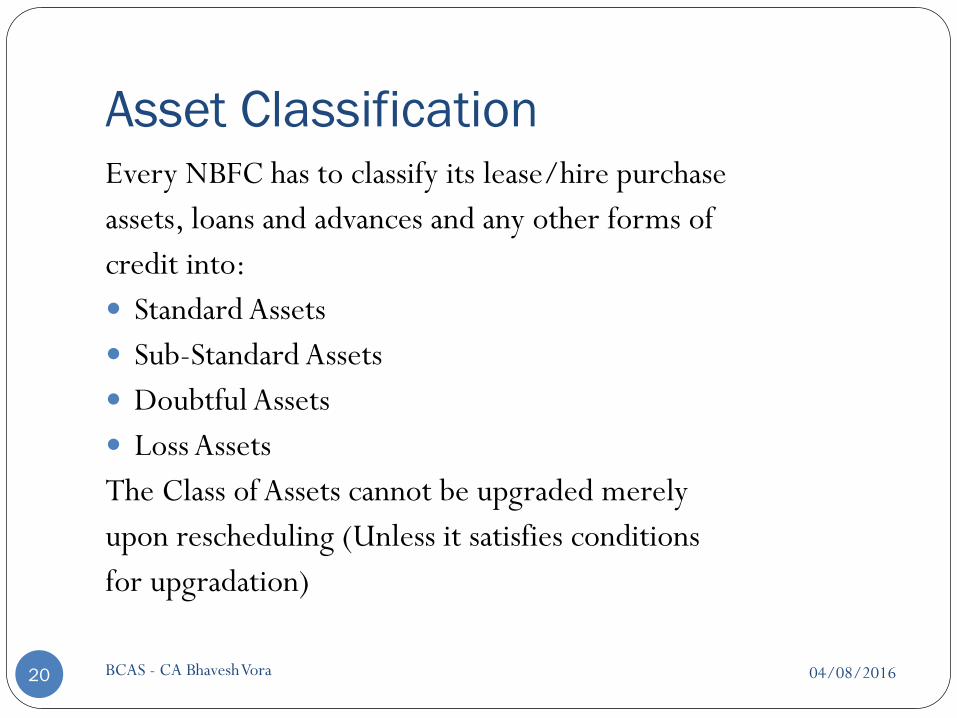

Asset Classification

04/08/2016BCAS - CA Bhavesh Vora20

Every NBFC has to classify its lease/hire purchase

assets, loans and advances and any other forms of

credit into:

Standard Assets

Sub-Standard Assets

Doubtful Assets

Loss Assets

The Class of Assets cannot be upgraded merely

upon rescheduling (Unless it satisfies conditions

for upgradation)

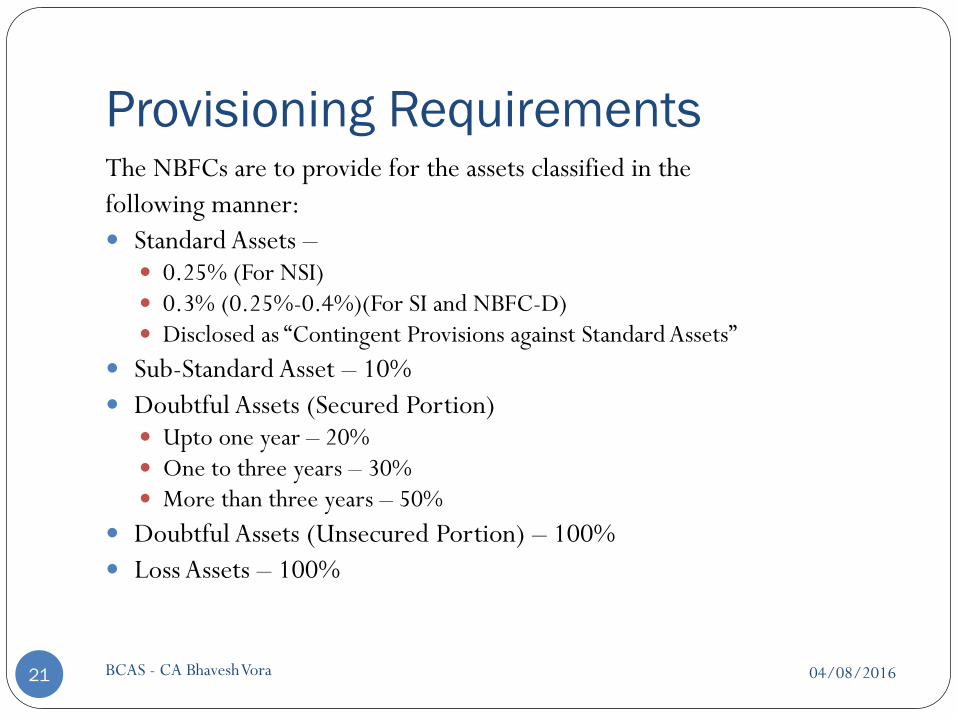

Provisioning Requirements

04/08/2016BCAS - CA Bhavesh Vora21

The NBFCs are to provide for the assets classified in the

following manner:

Standard Assets – 0.25% (For NSI) 0.3% (0.25%-0.4%)(For SI and NBFC-D) Disclosed as “Contingent Provisions against Standard Assets”

Sub-Standard Asset – 10%

Doubtful Assets (Secured Portion) Upto one year – 20% One to three years – 30% More than three years – 50%

Doubtful Assets (Unsecured Portion) – 100%

Loss Assets – 100%

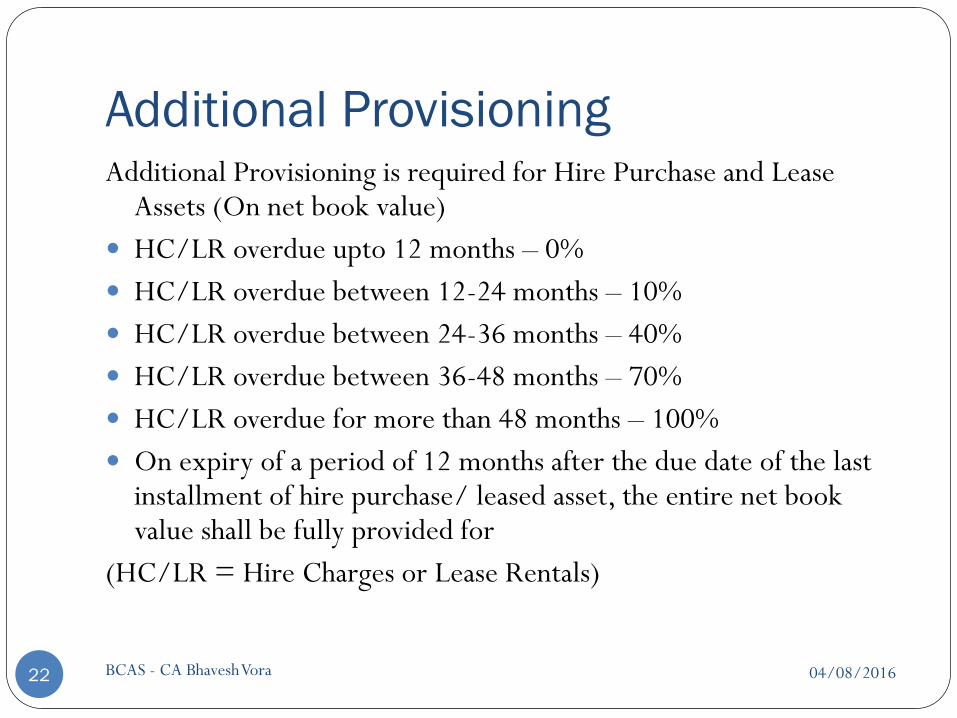

Additional Provisioning

04/08/2016BCAS - CA Bhavesh Vora22

Additional Provisioning is required for Hire Purchase and Lease Assets (On net book value)

HC/LR overdue upto 12 months – 0%

HC/LR overdue between 12-24 months – 10%

HC/LR overdue between 24-36 months – 40%

HC/LR overdue between 36-48 months – 70%

HC/LR overdue for more than 48 months – 100%

On expiry of a period of 12 months after the due date of the last installment of hire purchase/ leased asset, the entire net book value shall be fully provided for

(HC/LR = Hire Charges or Lease Rentals)

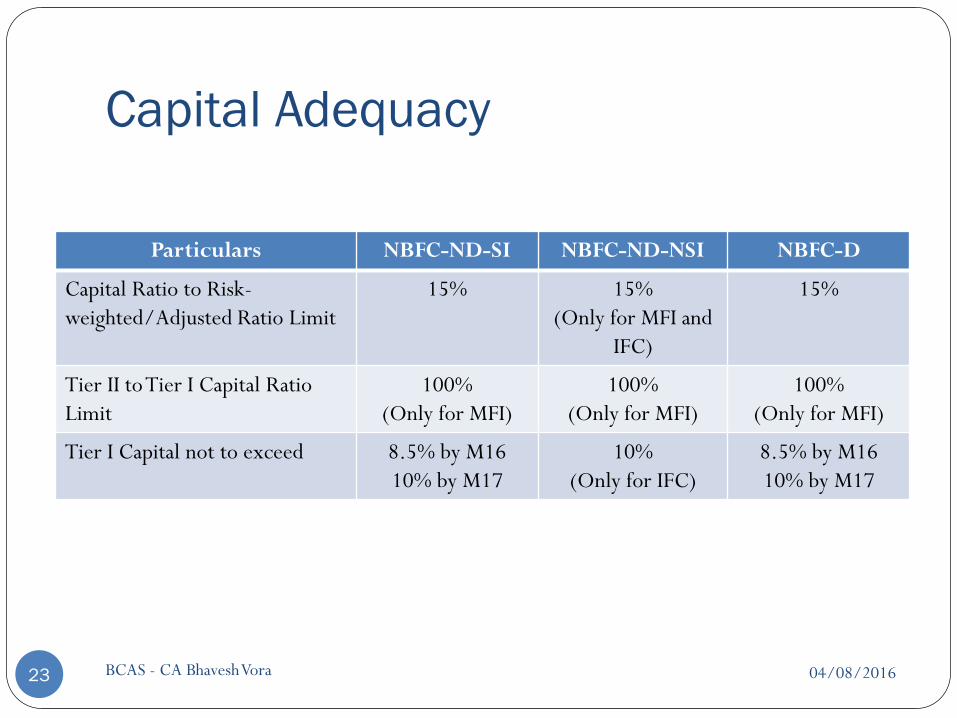

Capital Adequacy

04/08/2016BCAS - CA Bhavesh Vora23

Particulars NBFC-ND-SI NBFC-ND-NSI NBFC-D

Capital Ratio to Risk-

weighted/Adjusted Ratio Limit

15% 15%

(Only for MFI and

IFC)

15%

Tier II to Tier I Capital Ratio

Limit

100%

(Only for MFI)

100%

(Only for MFI)

100%

(Only for MFI)

Tier I Capital not to exceed 8.5% by M16

10% by M17

10%

(Only for IFC)

8.5% by M16

10% by M17

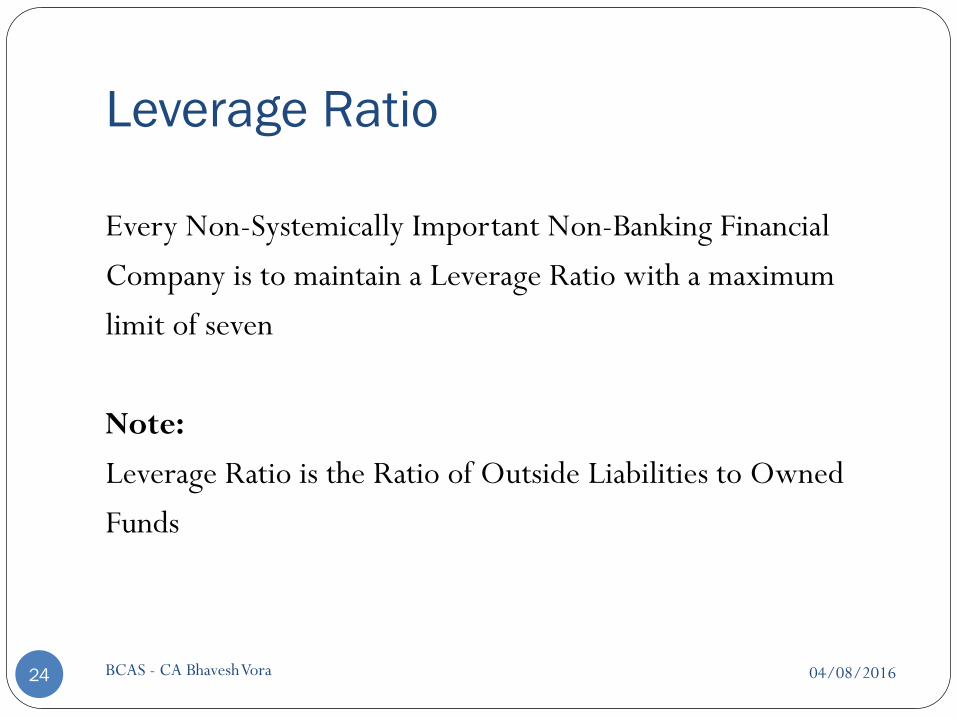

Leverage Ratio

04/08/2016BCAS - CA Bhavesh Vora24

Every Non-Systemically Important Non-Banking Financial

Company is to maintain a Leverage Ratio with a maximum

limit of seven

Note:

Leverage Ratio is the Ratio of Outside Liabilities to Owned

Funds

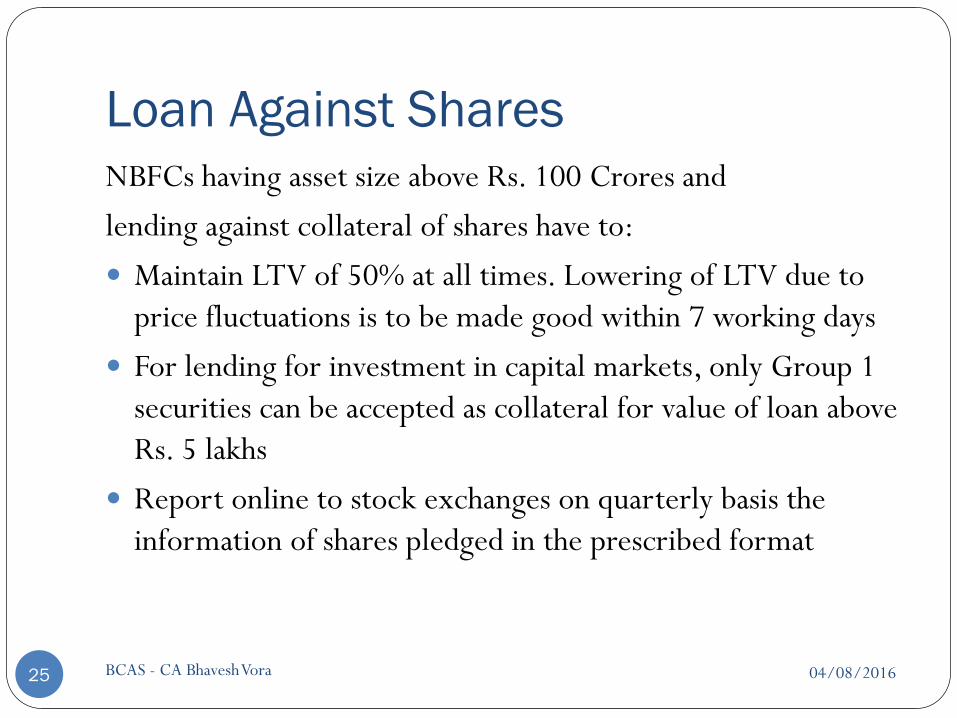

Loan Against Shares

04/08/2016BCAS - CA Bhavesh Vora25

NBFCs having asset size above Rs. 100 Crores and

lending against collateral of shares have to:

Maintain LTV of 50% at all times. Lowering of LTV due to

price fluctuations is to be made good within 7 working days

For lending for investment in capital markets, only Group 1

securities can be accepted as collateral for value of loan above

Rs. 5 lakhs

Report online to stock exchanges on quarterly basis the

information of shares pledged in the prescribed format

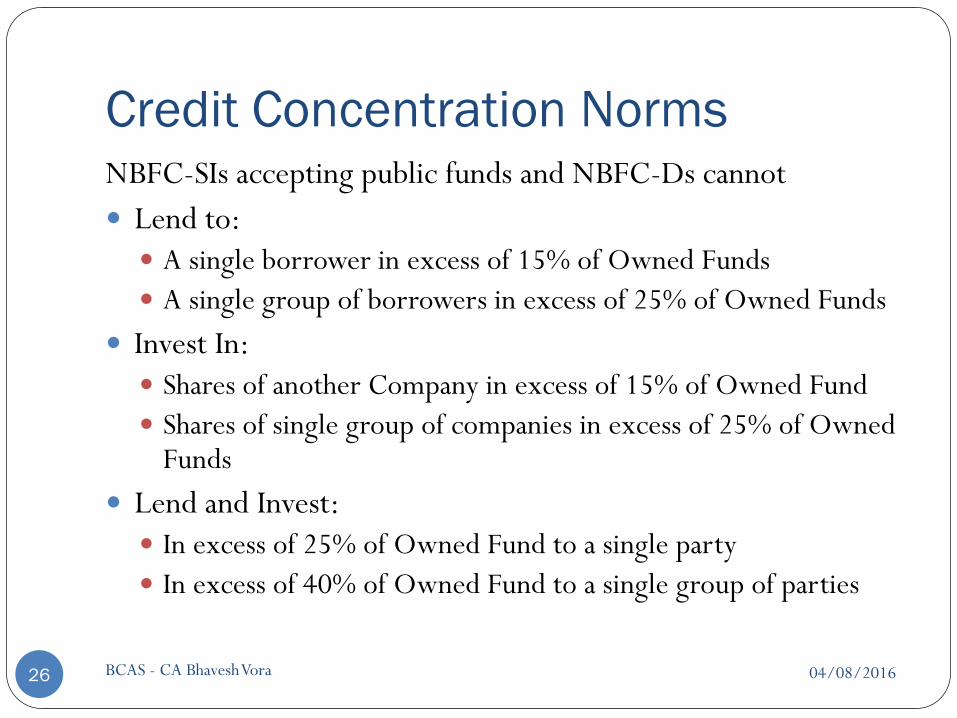

Credit Concentration Norms

04/08/2016BCAS - CA Bhavesh Vora26

NBFC-SIs accepting public funds and NBFC-Ds cannot

Lend to:

A single borrower in excess of 15% of Owned Funds

A single group of borrowers in excess of 25% of Owned Funds

Invest In:

Shares of another Company in excess of 15% of Owned Fund

Shares of single group of companies in excess of 25% of Owned Funds

Lend and Invest:

In excess of 25% of Owned Fund to a single party

In excess of 40% of Owned Fund to a single group of parties

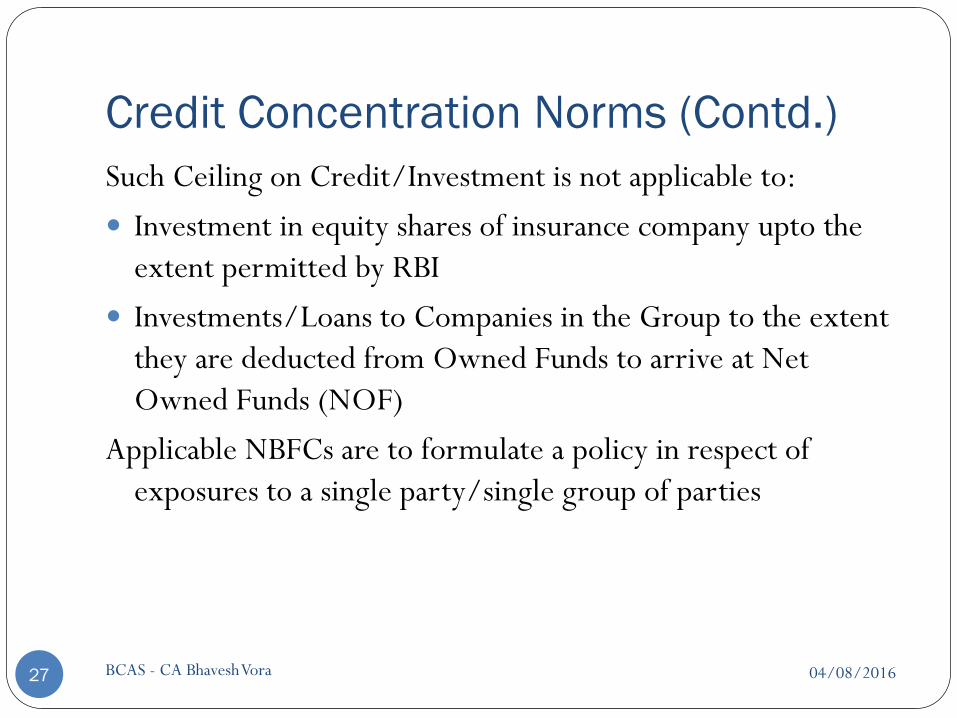

Credit Concentration Norms (Contd.)

04/08/2016BCAS - CA Bhavesh Vora27

Such Ceiling on Credit/Investment is not applicable to:

Investment in equity shares of insurance company upto the

extent permitted by RBI

Investments/Loans to Companies in the Group to the extent

they are deducted from Owned Funds to arrive at Net

Owned Funds (NOF)

Applicable NBFCs are to formulate a policy in respect of

exposures to a single party/single group of parties

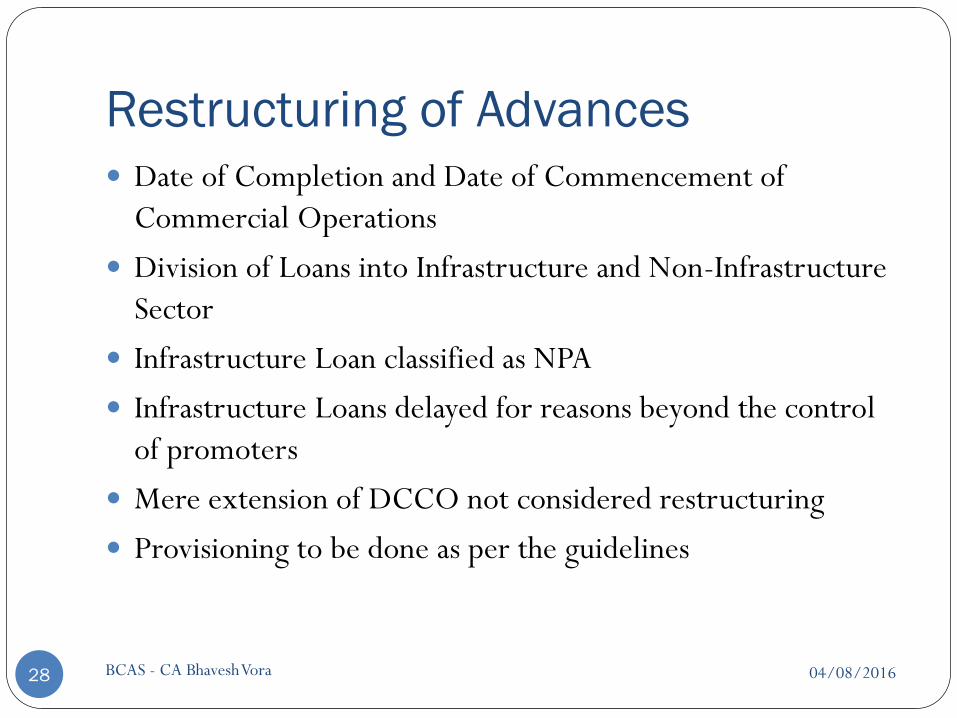

Restructuring of Advances

04/08/2016BCAS - CA Bhavesh Vora28

Date of Completion and Date of Commencement of

Commercial Operations

Division of Loans into Infrastructure and Non-Infrastructure

Sector

Infrastructure Loan classified as NPA

Infrastructure Loans delayed for reasons beyond the control

of promoters

Mere extension of DCCO not considered restructuring

Provisioning to be done as per the guidelines

Disclosures

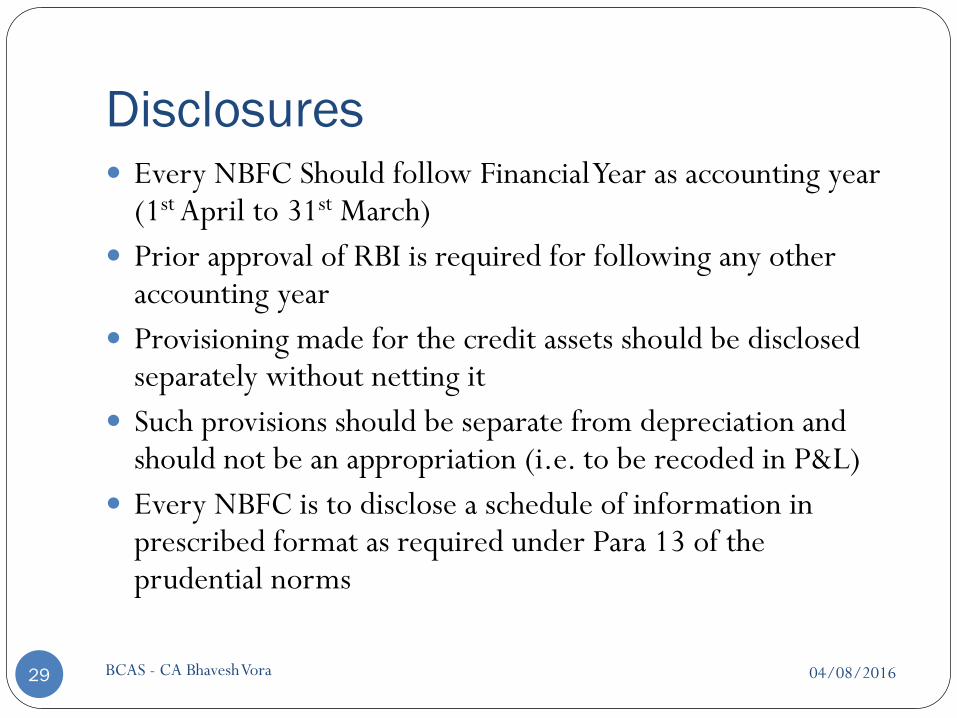

04/08/2016BCAS - CA Bhavesh Vora29

Every NBFC Should follow Financial Year as accounting year (1st April to 31st March)

Prior approval of RBI is required for following any other accounting year

Provisioning made for the credit assets should be disclosed separately without netting it

Such provisions should be separate from depreciation and should not be an appropriation (i.e. to be recoded in P&L)

Every NBFC is to disclose a schedule of information in prescribed format as required under Para 13 of the prudential norms

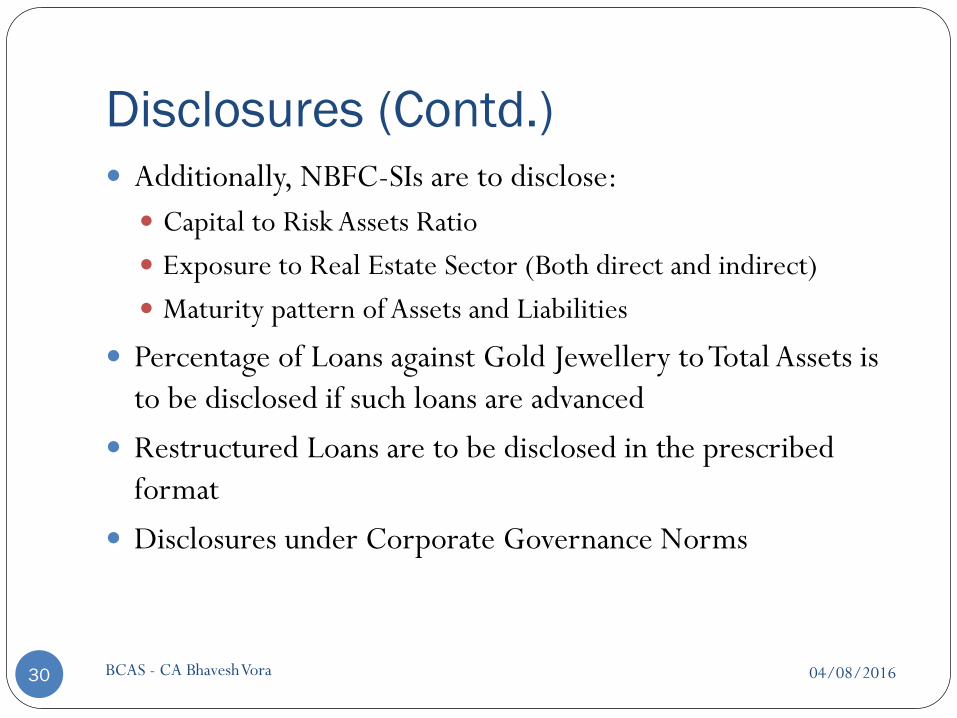

Disclosures (Contd.)

04/08/2016BCAS - CA Bhavesh Vora30

Additionally, NBFC-SIs are to disclose:

Capital to Risk Assets Ratio

Exposure to Real Estate Sector (Both direct and indirect)

Maturity pattern of Assets and Liabilities

Percentage of Loans against Gold Jewellery to Total Assets is

to be disclosed if such loans are advanced

Restructured Loans are to be disclosed in the prescribed

format

Disclosures under Corporate Governance Norms

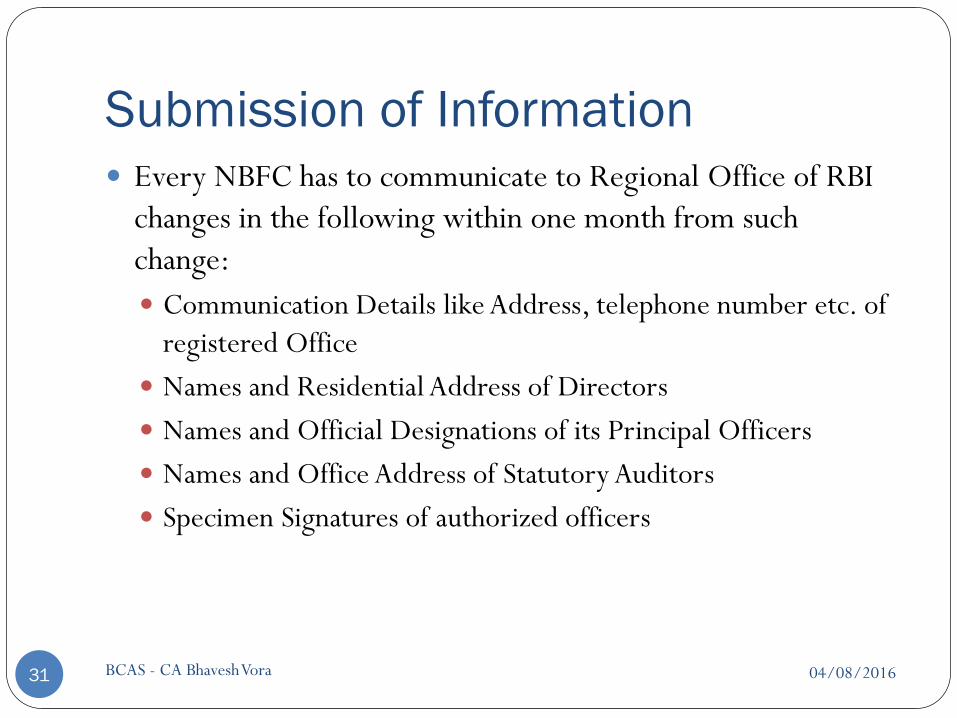

Submission of Information

04/08/2016BCAS - CA Bhavesh Vora31

Every NBFC has to communicate to Regional Office of RBI

changes in the following within one month from such

change:

Communication Details like Address, telephone number etc. of

registered Office

Names and Residential Address of Directors

Names and Official Designations of its Principal Officers

Names and Office Address of Statutory Auditors

Specimen Signatures of authorized officers

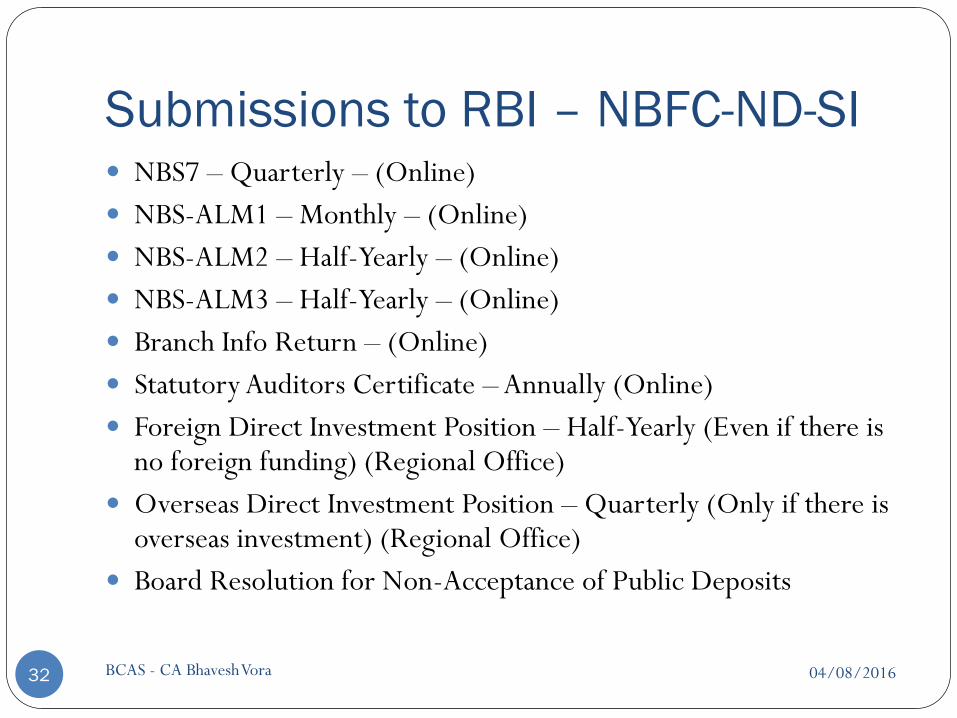

Submissions to RBI – NBFC-ND-SI

04/08/2016BCAS - CA Bhavesh Vora32

NBS7 – Quarterly – (Online)

NBS-ALM1 – Monthly – (Online)

NBS-ALM2 – Half-Yearly – (Online)

NBS-ALM3 – Half-Yearly – (Online)

Branch Info Return – (Online)

Statutory Auditors Certificate – Annually (Online)

Foreign Direct Investment Position – Half-Yearly (Even if there is no foreign funding) (Regional Office)

Overseas Direct Investment Position – Quarterly (Only if there is overseas investment) (Regional Office)

Board Resolution for Non-Acceptance of Public Deposits

Submissions to RBI – NBFC-ND-NSI

04/08/2016BCAS - CA Bhavesh Vora33

NBS8 –Yearly (For NBFC ND having asset size between 100

to 500 crores) (Online)

NBS9 –Yearly (For NBFC ND having asset size below 100

crores) (Online)

Branch Info Return – (Online)

Statutory Auditors Certificate – Annually (Online)

Board Resolution for Non-Acceptance of Public Deposits

Policy on Demand/Call Loans

04/08/2016BCAS - CA Bhavesh Vora34

Every NBFC intending to grant demand/call loans should

frame a policy and implement it

The Policy should include:

Cut-Off date

Rate of Interest

Interest – Payable at monthly or quarterly rests

Cut-Off date for performance review of loans (Not exceeding

six months from date of sanction)

Fair Practices Code

04/08/2016BCAS - CA Bhavesh Vora35

Loan Documentation

Application and Processing

Loan Appraisal and Terms and Conditions

Language of Documentation / Communication

Recovery of Loans

System of not charging excessive interest

Grievance Redressal Officer

Committees

04/08/2016BCAS - CA Bhavesh Vora36

Every NBFC-ND-SI and NBFC-D are to formulate

the following committees:

Audit Committee

Nomination Committee

Risk Management Committee

Corporate Governance Norms

04/08/2016BCAS - CA Bhavesh Vora37

Every NBFC-ND-SI and NBFC-D shall:

Frame internal guidelines on corporate governance

Frame a Fit and Proper Policy

Rotate partners of CA Firm every 3 years and ensure the

retiring partner completes the cooling off period of 3

years before re-appointment

Prohibitions

04/08/2016BCAS - CA Bhavesh Vora38

NBFCs are prohibited from:

Lending against its own shares

NBFC-D is prohibited to make investments or give loans if it

has defaulted in repayment of any deposit and for as long as

such default exists

All NBFCs are prohibited from becoming partners in

Partnership Firms

Further NBFCs require prior approval from RBI

For opening branches in excess of 1000 in number

Change in Control

04/08/2016BCAS - CA Bhavesh Vora39

Prior Approval from RBI

Takeover/Acquisition/Mergers/Amalgamation

Before approaching the court

Resulting in acquisition/transfer of shareholding of 26% or

more

Resulting in change of management of 30% or more

Progressive change over time

Public Notice of one month

Intimation of all the changes are to be communicated

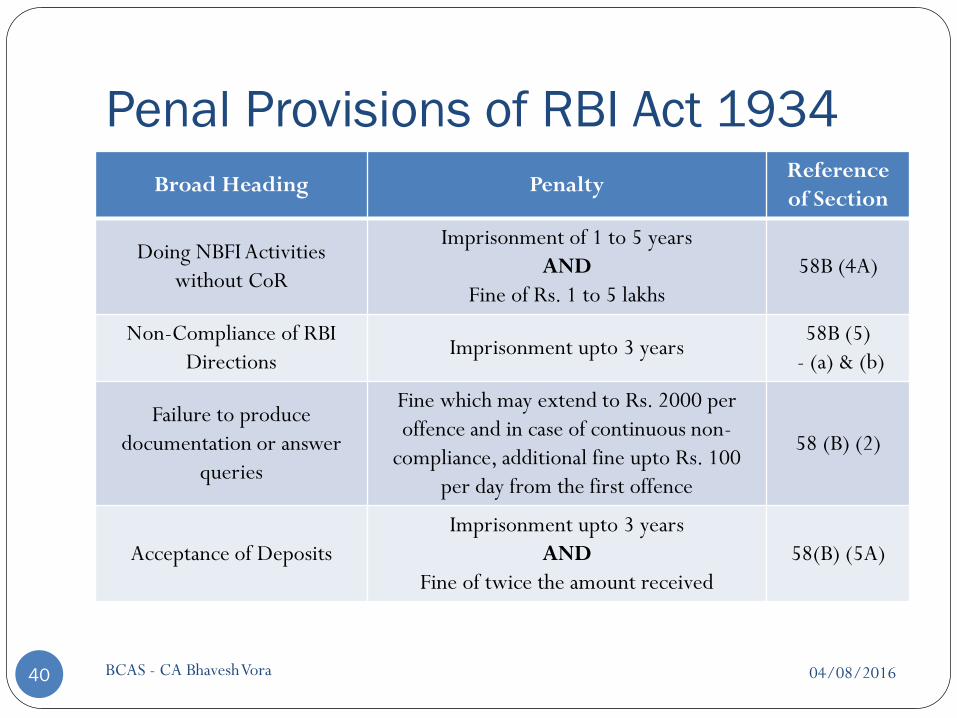

Penal Provisions of RBI Act 1934

04/08/2016BCAS - CA Bhavesh Vora40

Broad Heading PenaltyReference

of Section

Doing NBFI Activities

without CoR

Imprisonment of 1 to 5 years

AND

Fine of Rs. 1 to 5 lakhs

58B (4A)

Non-Compliance of RBI

DirectionsImprisonment upto 3 years

58B (5)

- (a) & (b)

Failure to produce

documentation or answer

queries

Fine which may extend to Rs. 2000 per

offence and in case of continuous non-

compliance, additional fine upto Rs. 100

per day from the first offence

58 (B) (2)

Acceptance of Deposits

Imprisonment upto 3 years

AND

Fine of twice the amount received

58(B) (5A)

Miscellaneous Compliances

04/08/2016BCAS - CA Bhavesh Vora41

Membership of all Credit Information Companies

Core Investment Companies’ submission of

annual auditor’s certificate under CIC Directions

2011

Transfer to Statutory Reserve U/s 45-IC

Future of NBFC Sector

04/08/2016BCAS - CA Bhavesh Vora42

Peer to Peer Lending Crowd Funding Operational Business Models KYC Issues

Account Aggregator Only NBFC – AA Exemption to Regulated entities Prohibition form conducting any other business Cannot support transactions in financial assets

On Tap Licensing of Universal Banks Eligible Promoters Fit and Proper Criteria Minimum Capital Requirement Corporate Governance, Prudential and Exposure Norms

Bombay Chartered Accountants’ Society

CA Bhavesh Vora – 04/08/2016

NBFC Prudential Norms &

Compliances – Important Aspects