Embed Size (px)

Citation preview

Company Presentation

August 2017

Navios South American Logistics Inc.

2

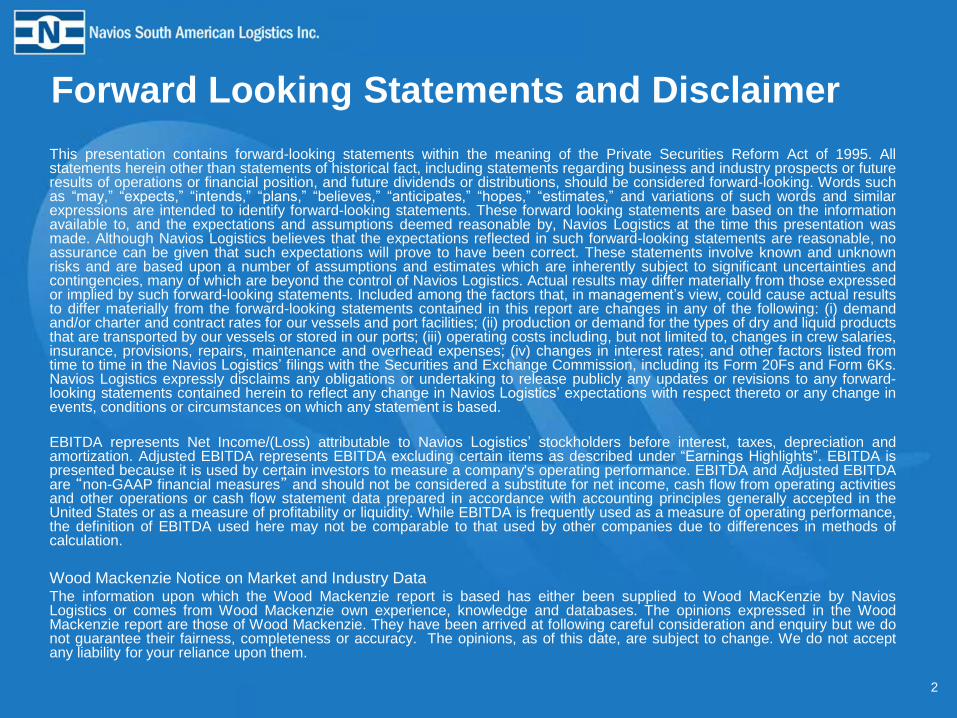

This presentation contains forward-looking statements within the meaning of the Private Securities Reform Act of 1995. All statements herein other than statements of historical fact, including statements regarding business and industry prospects or future results of operations or financial position, and future dividends or distributions, should be considered forward-looking. Words such as “may,” “expects,” “intends,” “plans,” “believes,” “anticipates,” “hopes,” “estimates,” and variations of such words and similar expressions are intended to identify forward-looking statements. These forward looking statements are based on the information available to, and the expectations and assumptions deemed reasonable by, Navios Logistics at the time this presentation was made. Although Navios Logistics believes that the expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. These statements involve known and unknown risks and are based upon a number of assumptions and estimates which are inherently subject to significant uncertainties and contingencies, many of which are beyond the control of Navios Logistics. Actual results may differ materially from those expressed or implied by such forward-looking statements. Included among the factors that, in management’s view, could cause actual results to differ materially from the forward-looking statements contained in this report are changes in any of the following: (i) demand and/or charter and contract rates for our vessels and port facilities; (ii) production or demand for the types of dry and liquid products that are transported by our vessels or stored in our ports; (iii) operating costs including, but not limited to, changes in crew salaries, insurance, provisions, repairs, maintenance and overhead expenses; (iv) changes in interest rates; and other factors listed from time to time in the Navios Logistics’ filings with the Securities and Exchange Commission, including its Form 20Fs and Form 6Ks. Navios Logistics expressly disclaims any obligations or undertaking to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in Navios Logistics’ expectations with respect thereto or any change in events, conditions or circumstances on which any statement is based.

EBITDA represents Net Income/(Loss) attributable to Navios Logistics’ stockholders before interest, taxes, depreciation and amortization. Adjusted EBITDA represents EBITDA excluding certain items as described under “Earnings Highlights”. EBITDA is presented because it is used by certain investors to measure a company's operating performance. EBITDA and Adjusted EBITDA are “non-GAAP financial measures” and should not be considered a substitute for net income, cash flow from operating activities and other operations or cash flow statement data prepared in accordance with accounting principles generally accepted in the United States or as a measure of profitability or liquidity. While EBITDA is frequently used as a measure of operating performance, the definition of EBITDA used here may not be comparable to that used by other companies due to differences in methods of calculation.

Wood Mackenzie Notice on Market and Industry Data The information upon which the Wood Mackenzie report is based has either been supplied to Wood MacKenzie by Navios Logistics or comes from Wood Mackenzie own experience, knowledge and databases. The opinions expressed in the Wood Mackenzie report are those of Wood Mackenzie. They have been arrived at following careful consideration and enquiry but we do not guarantee their fairness, completeness or accuracy. The opinions, as of this date, are subject to change. We do not accept any liability for your reliance upon them.

Forward Looking Statements and Disclaimer

3

Navios South American Logistics

www.navioslogistics.com

Price(1) Yield(1) Amount

7.250% Unsecured Bonds Due 2022

CUSIP 63938NAE4

$97.586 7.865% $375M

Navios Logistics Bond

(1) As of market close 7/31/2017

4

Navios Logistics Overview

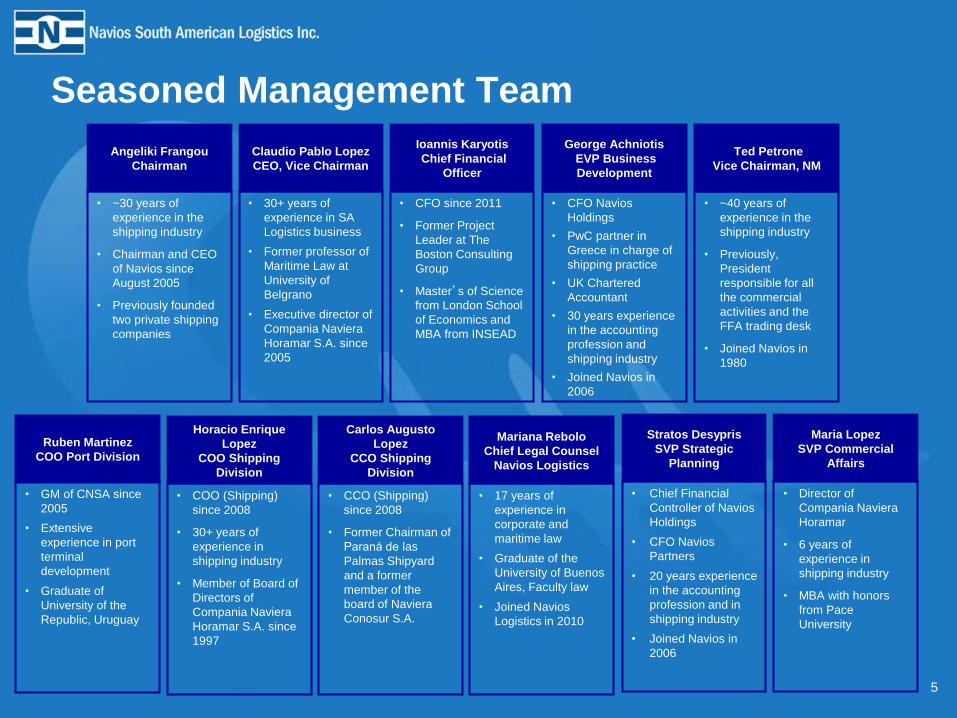

Seasoned Management Team

5

• CCO (Shipping)

since 2008

• Former Chairman of

Paraná de las

Palmas Shipyard

and a former

member of the

board of Naviera

Conosur S.A.

Carlos Augusto

Lopez

CCO Shipping

Division

• ~30 years of

experience in the

shipping industry

• Chairman and CEO

of Navios since

August 2005

• Previously founded

two private shipping

companies

Angeliki Frangou

Chairman

• GM of CNSA since

2005

• Extensive

experience in port

terminal

development

• Graduate of

University of the

Republic, Uruguay

Ruben Martinez

COO Port Division

• 30+ years of

experience in SA

Logistics business

• Former professor of

Maritime Law at

University of

Belgrano

• Executive director of

Compania Naviera

Horamar S.A. since

2005

Claudio Pablo Lopez

CEO, Vice Chairman

• CFO since 2011

• Former Project

Leader at The

Boston Consulting

Group

• Master’s of Science

from London School

of Economics and

MBA from INSEAD

Ioannis Karyotis

Chief Financial

Officer

• CFO Navios

Holdings

• PwC partner in

Greece in charge of

shipping practice

• UK Chartered

Accountant

• 30 years experience

in the accounting

profession and

shipping industry

• Joined Navios in

2006

George Achniotis

EVP Business

Development

• Director of

Compania Naviera

Horamar

• 6 years of

experience in

shipping industry

• MBA with honors

from Pace

University

Maria Lopez

SVP Commercial

Affairs

• COO (Shipping)

since 2008

• 30+ years of

experience in

shipping industry

• Member of Board of

Directors of

Compania Naviera

Horamar S.A. since

1997

Horacio Enrique

Lopez

COO Shipping

Division

• 17 years of

experience in

corporate and

maritime law

• Graduate of the

University of Buenos

Aires, Faculty law

• Joined Navios

Logistics in 2010

Mariana Rebolo

Chief Legal Counsel

Navios Logistics

• Chief Financial

Controller of Navios

Holdings

• CFO Navios

Partners

• 20 years experience

in the accounting

profession and in

shipping industry

• Joined Navios in

2006

Stratos Desypris

SVP Strategic

Planning

• ~40 years of

experience in the

shipping industry

• Previously,

President

responsible for all

the commercial

activities and the

FFA trading desk

• Joined Navios in

1980

Ted Petrone

Vice Chairman, NM

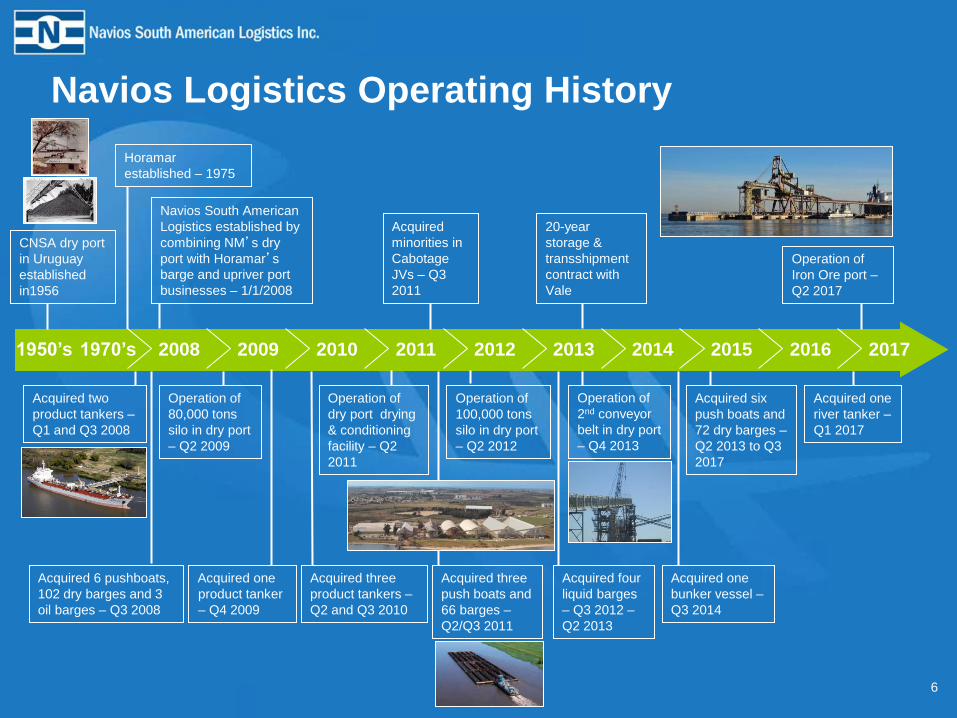

Navios Logistics Operating History

6

2008

Operation of

80,000 tons

silo in dry port

– Q2 2009

Acquired two

product tankers –

Q1 and Q3 2008

Acquired one

product tanker

– Q4 2009

Acquired three

product tankers –

Q2 and Q3 2010

Operation of

dry port drying

& conditioning

facility – Q2

2011

Navios South American

Logistics established by

combining NM’s dry

port with Horamar’s

barge and upriver port

businesses – 1/1/2008

Acquired 6 pushboats,

102 dry barges and 3

oil barges – Q3 2008

1950’s 1970’s

CNSA dry port

in Uruguay

established

in1956

Horamar

established – 1975

Acquired three

push boats and

66 barges –

Q2/Q3 2011

Acquired

minorities in

Cabotage

JVs – Q3

2011

Operation of

100,000 tons

silo in dry port

– Q2 2012

Acquired four

liquid barges

– Q3 2012 –

Q2 2013

Operation of

2nd conveyor

belt in dry port

– Q4 2013

2009 2010 2011 2012 2013

Acquired six

push boats and

72 dry barges –

Q2 2013 to Q3

2017

2014

Acquired one

bunker vessel –

Q3 2014

2015

20-year

storage &

transshipment

contract with

Vale

2016 2017

Operation of

Iron Ore port –

Q2 2017

Acquired one

river tanker –

Q1 2017

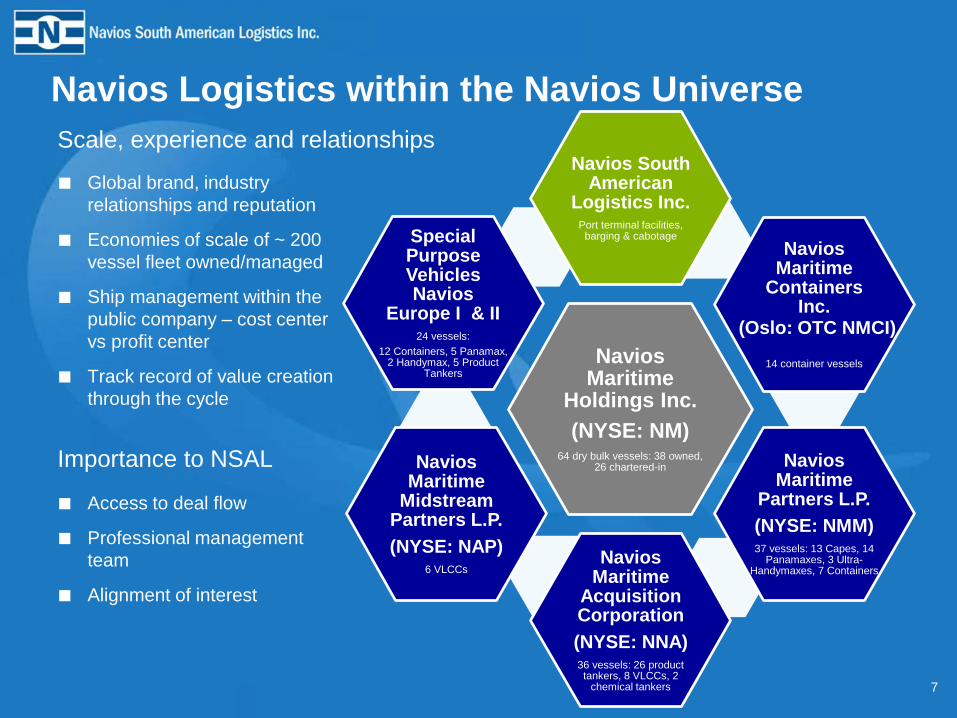

Navios Logistics within the Navios Universe

7

Navios Maritime

Holdings Inc.

(NYSE: NM) 64 dry bulk vessels: 38 owned,

26 chartered-in

Navios South American

Logistics Inc. Port terminal facilities,

barging & cabotage

Navios Maritime

Containers Inc.

14 container vessels

Navios Maritime

Partners L.P.

(NYSE: NMM) 37 vessels: 13 Capes, 14

Panamaxes, 3 Ultra-Handymaxes, 7 Containers

Navios Maritime

Acquisition Corporation

(NYSE: NNA) 36 vessels: 26 product tankers, 8 VLCCs, 2

chemical tankers

Navios Maritime

Midstream Partners L.P.

(NYSE: NAP) 6 VLCCs

Special Purpose Vehicles Navios

Europe I & II 24 vessels:

12 Containers, 5 Panamax, 2 Handymax, 5 Product

Tankers

Scale, experience and relationships

■ Global brand, industry

relationships and reputation

■ Economies of scale of ~ 200

vessel fleet owned/managed

■ Ship management within the

public company – cost center

vs profit center

■ Track record of value creation

through the cycle

■ Access to deal flow

■ Professional management

team

■ Alignment of interest

Importance to NSAL

(Oslo: OTC NMCI)

8

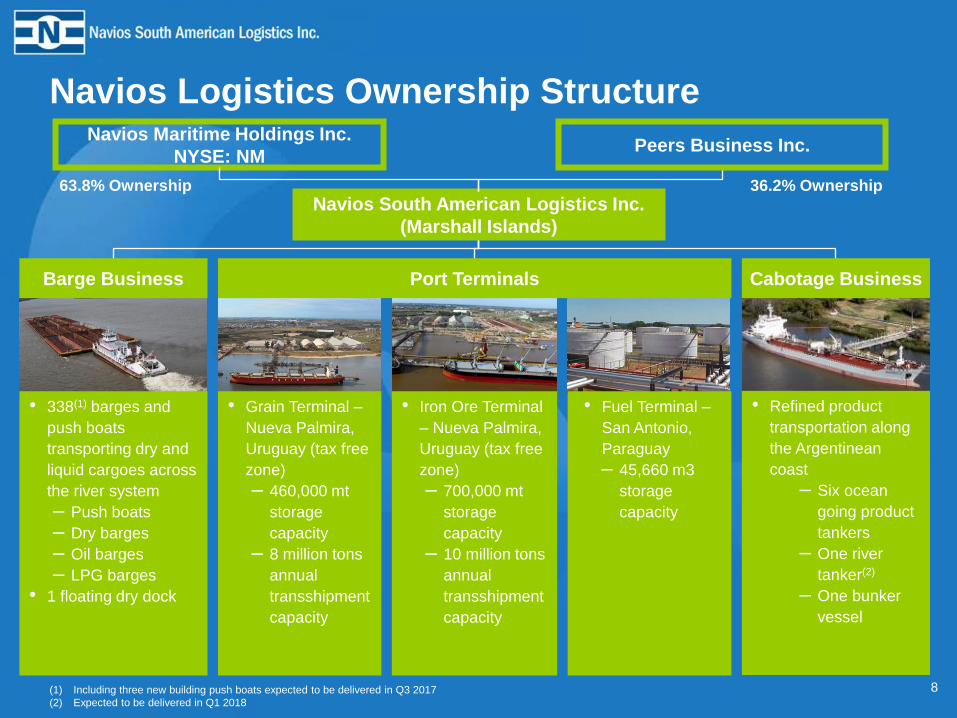

Navios Logistics Ownership Structure

Port Terminals

• 338(1) barges and

push boats

transporting dry and

liquid cargoes across

the river system

– Push boats

– Dry barges

– Oil barges

– LPG barges

• 1 floating dry dock

Cabotage Business

Navios South American Logistics Inc.

(Marshall Islands)

(1) Including three new building push boats expected to be delivered in Q3 2017

(2) Expected to be delivered in Q1 2018

Navios Maritime Holdings Inc.

NYSE: NM

63.8% Ownership 36.2% Ownership

Peers Business Inc.

Barge Business

• Grain Terminal –

Nueva Palmira,

Uruguay (tax free

zone)

– 460,000 mt

storage

capacity

– 8 million tons

annual

transshipment

capacity

• Iron Ore Terminal

– Nueva Palmira,

Uruguay (tax free

zone)

– 700,000 mt

storage

capacity

– 10 million tons

annual

transshipment

capacity

• Fuel Terminal –

San Antonio,

Paraguay

– 45,660 m3

storage

capacity

• Refined product

transportation along

the Argentinean

coast

– Six ocean

going product

tankers

– One river

tanker(2)

– One bunker

vessel

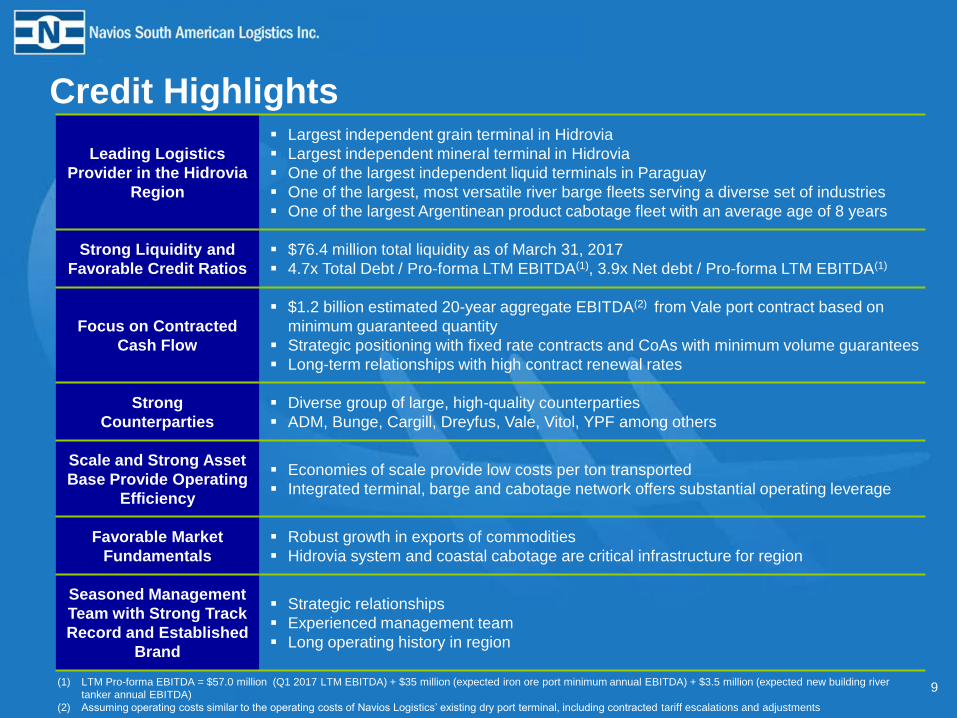

Credit Highlights

9

Leading Logistics

Provider in the Hidrovia

Region

Largest independent grain terminal in Hidrovia

Largest independent mineral terminal in Hidrovia

One of the largest independent liquid terminals in Paraguay

One of the largest, most versatile river barge fleets serving a diverse set of industries

One of the largest Argentinean product cabotage fleet with an average age of 8 years

Strong Liquidity and

Favorable Credit Ratios

$76.4 million total liquidity as of March 31, 2017

4.7x Total Debt / Pro-forma LTM EBITDA(1), 3.9x Net debt / Pro-forma LTM EBITDA(1)

Focus on Contracted

Cash Flow

$1.2 billion estimated 20-year aggregate EBITDA(2) from Vale port contract based on

minimum guaranteed quantity

Strategic positioning with fixed rate contracts and CoAs with minimum volume guarantees

Long-term relationships with high contract renewal rates

Strong

Counterparties

Diverse group of large, high-quality counterparties

ADM, Bunge, Cargill, Dreyfus, Vale, Vitol, YPF among others

Scale and Strong Asset

Base Provide Operating

Efficiency

Economies of scale provide low costs per ton transported

Integrated terminal, barge and cabotage network offers substantial operating leverage

Favorable Market

Fundamentals

Robust growth in exports of commodities

Hidrovia system and coastal cabotage are critical infrastructure for region

Seasoned Management

Team with Strong Track

Record and Established

Brand

Strategic relationships

Experienced management team

Long operating history in region

(1) LTM Pro-forma EBITDA = $57.0 million (Q1 2017 LTM EBITDA) + $35 million (expected iron ore port minimum annual EBITDA) + $3.5 million (expected new building river

tanker annual EBITDA)

(2) Assuming operating costs similar to the operating costs of Navios Logistics’ existing dry port terminal, including contracted tariff escalations and adjustments

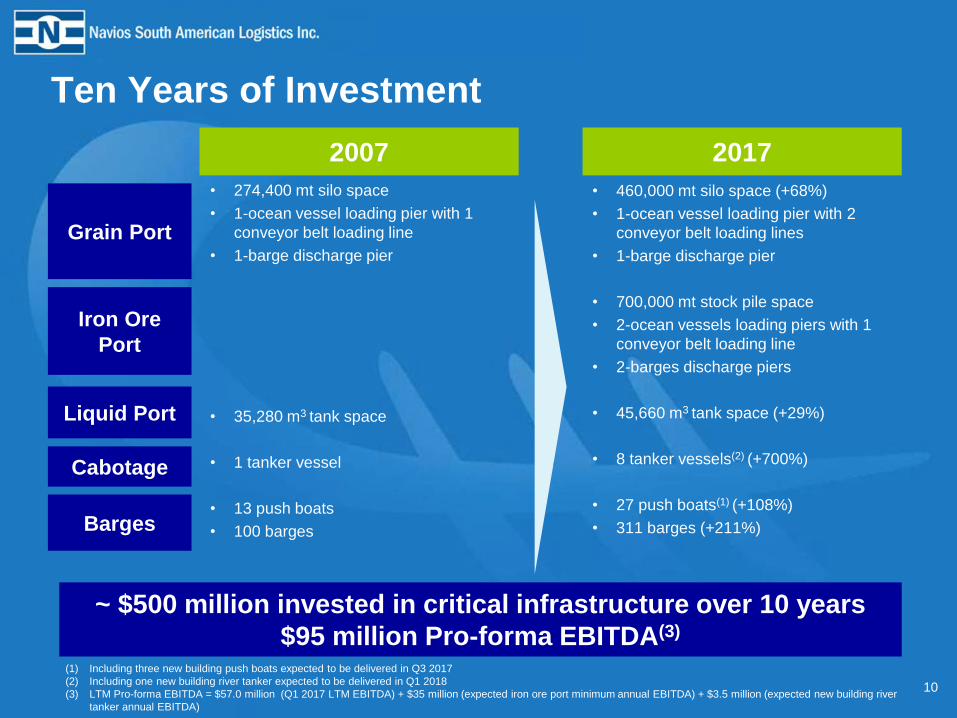

Ten Years of Investment

10

2007 2017

Grain Port

Liquid Port

Barges

Cabotage

• 274,400 mt silo space

• 1-ocean vessel loading pier with 1

conveyor belt loading line

• 1-barge discharge pier

• 35,280 m3 tank space

• 1 tanker vessel

• 13 push boats

• 100 barges

• 460,000 mt silo space (+68%)

• 1-ocean vessel loading pier with 2

conveyor belt loading lines

• 1-barge discharge pier

• 700,000 mt stock pile space

• 2-ocean vessels loading piers with 1

conveyor belt loading line

• 2-barges discharge piers

• 45,660 m3 tank space (+29%)

• 8 tanker vessels(2) (+700%)

• 27 push boats(1) (+108%)

• 311 barges (+211%)

(1) Including three new building push boats expected to be delivered in Q3 2017

(2) Including one new building river tanker expected to be delivered in Q1 2018

(3) LTM Pro-forma EBITDA = $57.0 million (Q1 2017 LTM EBITDA) + $35 million (expected iron ore port minimum annual EBITDA) + $3.5 million (expected new building river

tanker annual EBITDA)

~ $500 million invested in critical infrastructure over 10 years

$95 million Pro-forma EBITDA(3)

Iron Ore

Port

Barges

Reduced demand for iron ore

transportation in 2015/2016

Adverse weather conditions in 2016

impacted regional trade

Renewed demand for long-term barge

transportation contracts

Increased push boat capacity to move

grain, ore and liquid cargoes

+4.5 convoys from 2016 (new

deliveries and excess capacity) 11

Significant Capacity for Growth

Dynamics Opportunity

Iron Ore

Port

Corumba produces high grade lump ore

Corumba lump ore commands

significant premium over the standard

62% Fe Sinter Fines benchmark

2016 regional production reflected a

historical low in iron ore prices

Capitalize on 6 million tons of available

capacity at new port for Vale and other

industry participants

10 million tons p.a. total

Port expansion into available land

Grain

Port

Hidrovia countries = ~ 55% of global

soybean production

6% 17–year CAGR in exports

Navios terminal throughput up from 2.2

to 4.7 million tons in 10 years

Adverse weather impact in 2016

Addition of 2nd conveyor belt loading line

has increased grain port capacity

Capitalize on 3 million tons of available

capacity

8 million tons p.a. total

Port expansion into available land

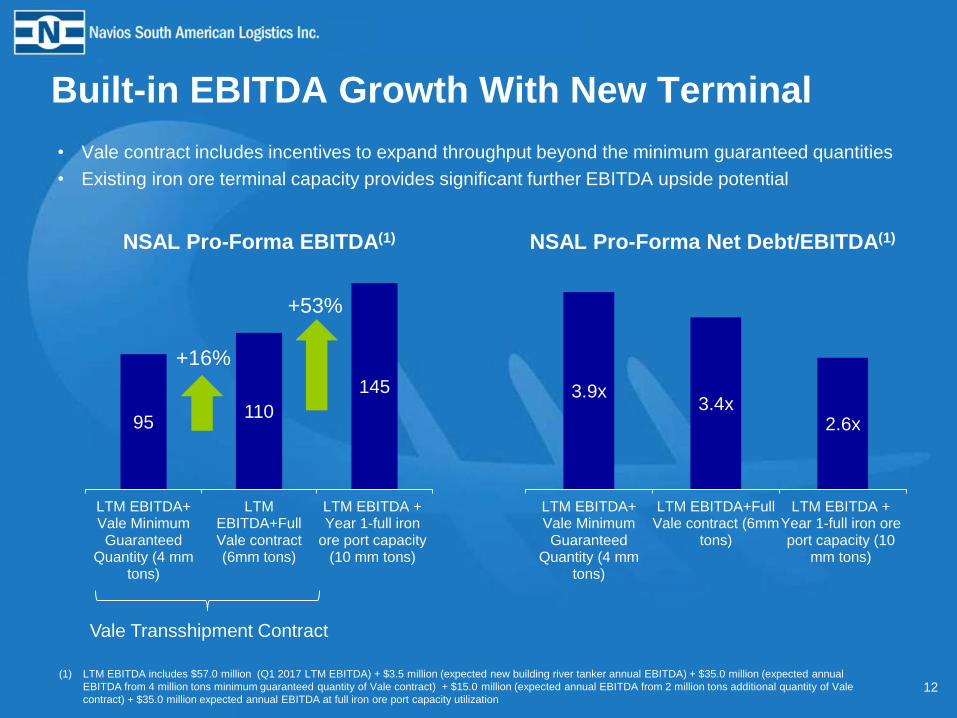

Built-in EBITDA Growth With New Terminal

• Vale contract includes incentives to expand throughput beyond the minimum guaranteed quantities

• Existing iron ore terminal capacity provides significant further EBITDA upside potential

12

3.9x 3.4x

2.6x

LTM EBITDA+Vale MinimumGuaranteed

Quantity (4 mmtons)

LTM EBITDA+FullVale contract (6mm

tons)

LTM EBITDA +Year 1-full iron oreport capacity (10

mm tons)

(1) LTM EBITDA includes $57.0 million (Q1 2017 LTM EBITDA) + $3.5 million (expected new building river tanker annual EBITDA) + $35.0 million (expected annual

EBITDA from 4 million tons minimum guaranteed quantity of Vale contract) + $15.0 million (expected annual EBITDA from 2 million tons additional quantity of Vale

contract) + $35.0 million expected annual EBITDA at full iron ore port capacity utilization

95 110

145

LTM EBITDA+Vale MinimumGuaranteed

Quantity (4 mmtons)

LTMEBITDA+FullVale contract(6mm tons)

LTM EBITDA +Year 1-full iron

ore port capacity(10 mm tons)

+16%

+53%

NSAL Pro-Forma EBITDA(1) NSAL Pro-Forma Net Debt/EBITDA(1)

Vale Transshipment Contract

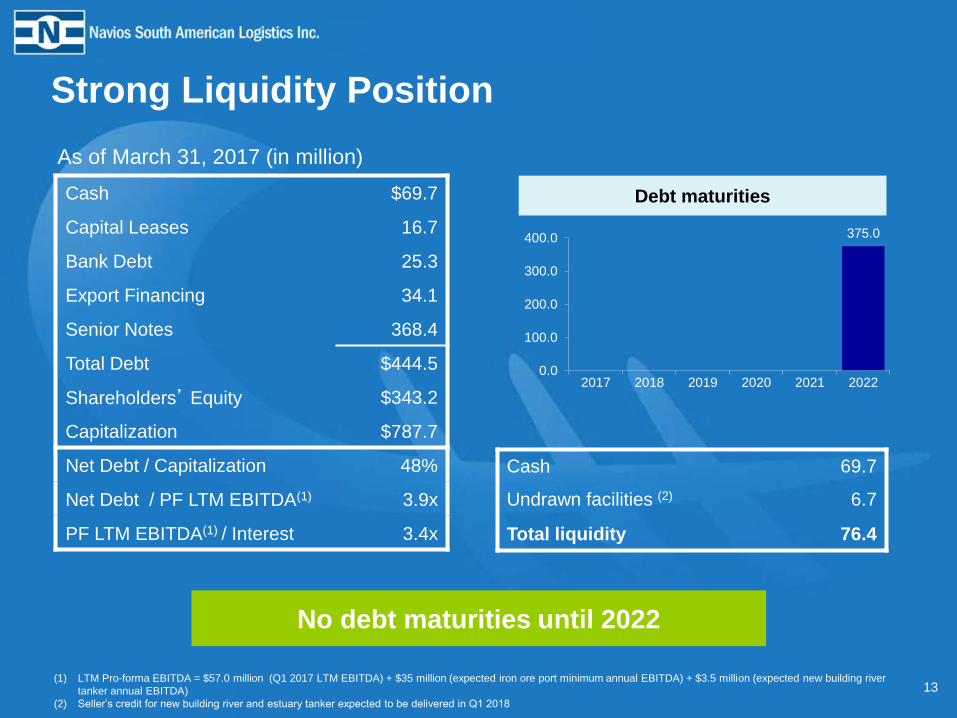

Strong Liquidity Position

13

375.0

0.0

100.0

200.0

300.0

400.0

2017 2018 2019 2020 2021 2022

Debt maturities Cash $69.7

Capital Leases 16.7

Bank Debt 25.3

Export Financing 34.1

Senior Notes 368.4

Total Debt $444.5

Shareholders’ Equity $343.2

Capitalization $787.7

Net Debt / Capitalization 48%

Net Debt / PF LTM EBITDA(1) 3.9x

PF LTM EBITDA(1) / Interest 3.4x

As of March 31, 2017 (in million)

Cash 69.7

Undrawn facilities (2) 6.7

Total liquidity 76.4

No debt maturities until 2022

(1) LTM Pro-forma EBITDA = $57.0 million (Q1 2017 LTM EBITDA) + $35 million (expected iron ore port minimum annual EBITDA) + $3.5 million (expected new building river

tanker annual EBITDA)

(2) Seller’s credit for new building river and estuary tanker expected to be delivered in Q1 2018

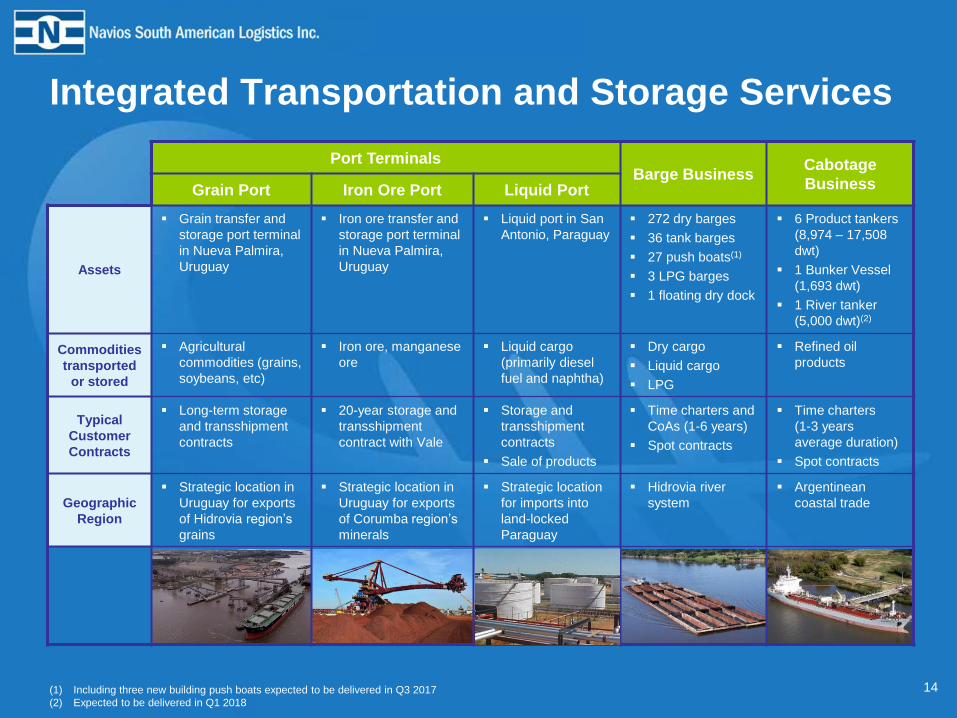

Integrated Transportation and Storage Services

Port Terminals Barge Business

Cabotage

Business Grain Port Iron Ore Port Liquid Port

Assets

Grain transfer and

storage port terminal

in Nueva Palmira,

Uruguay

Iron ore transfer and

storage port terminal

in Nueva Palmira,

Uruguay

Liquid port in San

Antonio, Paraguay

272 dry barges

36 tank barges

27 push boats(1)

3 LPG barges

1 floating dry dock

6 Product tankers

(8,974 – 17,508

dwt)

1 Bunker Vessel

(1,693 dwt)

1 River tanker

(5,000 dwt)(2)

Commodities

transported

or stored

Agricultural

commodities (grains,

soybeans, etc)

Iron ore, manganese

ore

Liquid cargo

(primarily diesel

fuel and naphtha)

Dry cargo

Liquid cargo

LPG

Refined oil

products

Typical

Customer

Contracts

Long-term storage

and transshipment

contracts

20-year storage and

transshipment

contract with Vale

Storage and

transshipment

contracts

Sale of products

Time charters and

CoAs (1-6 years)

Spot contracts

Time charters

(1-3 years

average duration)

Spot contracts

Geographic

Region

Strategic location in

Uruguay for exports

of Hidrovia region’s

grains

Strategic location in

Uruguay for exports

of Corumba region’s

minerals

Strategic location

for imports into

land-locked

Paraguay

Hidrovia river

system

Argentinean

coastal trade

14 (1) Including three new building push boats expected to be delivered in Q3 2017

(2) Expected to be delivered in Q1 2018

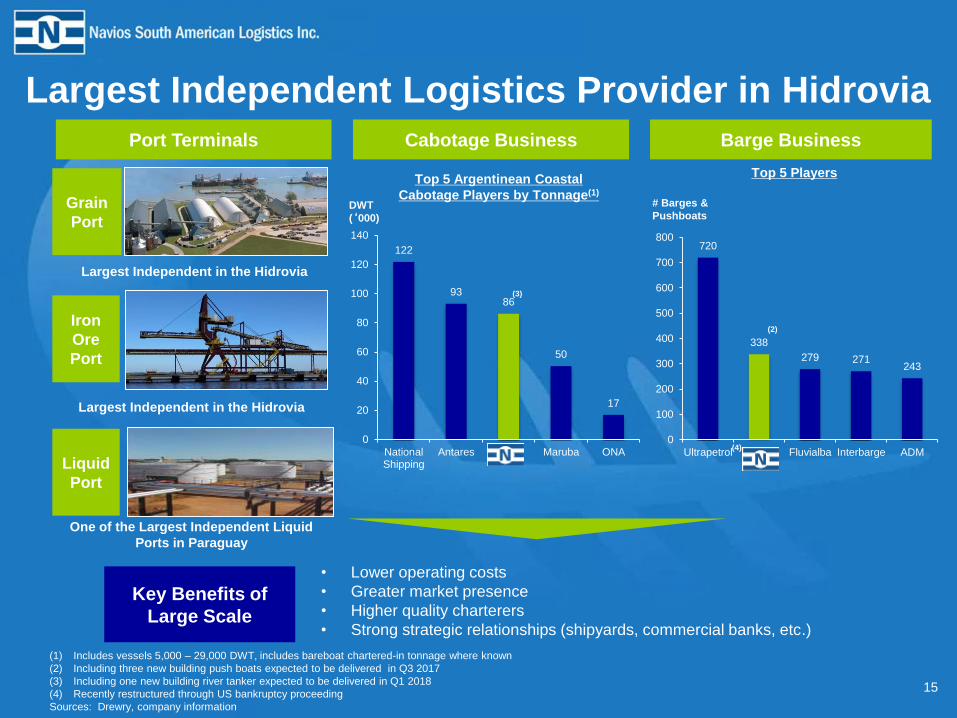

# Barges &

Pushboats

Largest Independent in the Hidrovia

One of the Largest Independent Liquid

Ports in Paraguay

• Lower operating costs

• Greater market presence

• Higher quality charterers

• Strong strategic relationships (shipyards, commercial banks, etc.)

DWT

(‘000)

Top 5 Players Top 5 Argentinean Coastal

Cabotage Players by Tonnage(1)

Largest Independent Logistics Provider in Hidrovia

15

720

338

279 271 243

0

100

200

300

400

500

600

700

800

Ultrapetrol NSAL Fluvialba Interbarge ADM

(2)

Port Terminals Barge Business Cabotage Business

Key Benefits of

Large Scale

122

93 86

50

17

0

20

40

60

80

100

120

140

NationalShipping

Antares NSAL Maruba ONA

(3)

(1) Includes vessels 5,000 – 29,000 DWT, includes bareboat chartered-in tonnage where known

(2) Including three new building push boats expected to be delivered in Q3 2017

(3) Including one new building river tanker expected to be delivered in Q1 2018

(4) Recently restructured through US bankruptcy proceeding

Sources: Drewry, company information

Largest Independent in the Hidrovia

(4)

Grain

Port

Iron

Ore

Port

Liquid

Port

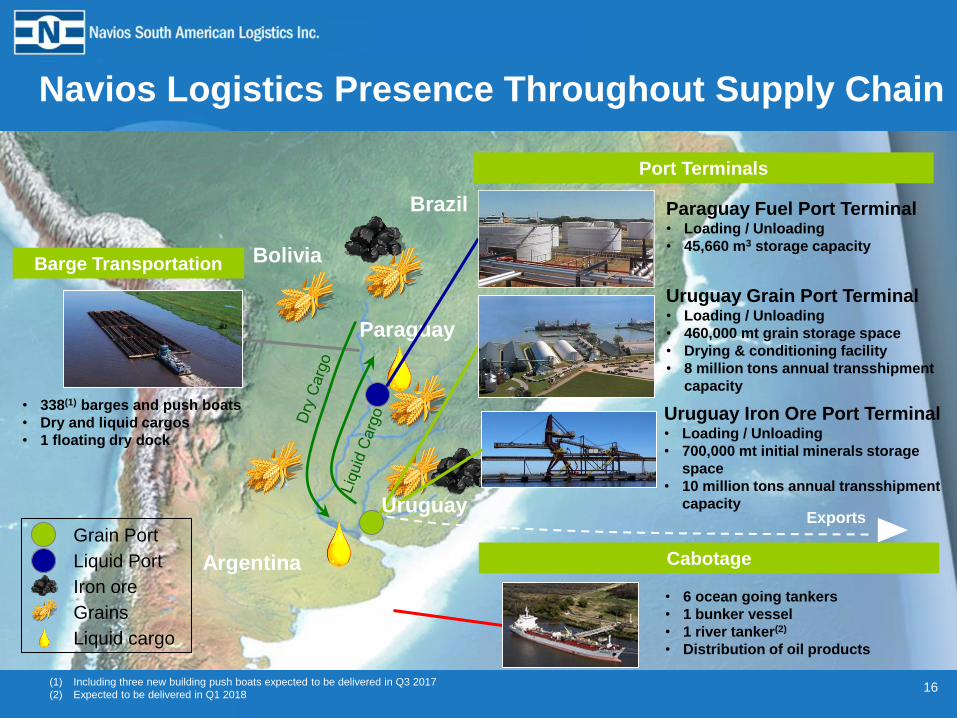

Navios Logistics Presence Throughout Supply Chain

16

Argentina

Paraguay

Brazil

Bolivia

Iron ore

Grains

Liquid cargo

Grain Port

Liquid Port

Paraguay Fuel Port Terminal • Loading / Unloading

• 45,660 m3 storage capacity

Uruguay Grain Port Terminal • Loading / Unloading

• 460,000 mt grain storage space

• Drying & conditioning facility

• 8 million tons annual transshipment

capacity

• 6 ocean going tankers

• 1 bunker vessel

• 1 river tanker(2)

• Distribution of oil products

• 338(1) barges and push boats

• Dry and liquid cargos

• 1 floating dry dock

Exports

(1) Including three new building push boats expected to be delivered in Q3 2017

(2) Expected to be delivered in Q1 2018

Uruguay Iron Ore Port Terminal • Loading / Unloading

• 700,000 mt initial minerals storage

space

• 10 million tons annual transshipment

capacity Uruguay

Port Terminals

Cabotage

Barge Transportation

17

The New Iron Ore Terminal

18

Network of Large, Independent Port Terminals

Grain Terminal

Storage and Transshipment

• Located in Nueva Palmira,

Uruguay (tax free zone)

• 460,000 mt grain storage

capacity

• Drying and conditioning

facility

• 8 million tons annual

transshipment capacity

Iron Ore Terminal Liquid Terminal

Storage, transshipment, sale

of oil products

• Located in San Antonio,

Paraguay

• 45,660 m3 storage capacity

Port Terminals

Storage and Transshipment

• Located in Nueva Palmira,

Uruguay (tax free zone)

• 700,000 mt minerals storage

capacity

• 10 million tons annual

transshipment capacity

20-year contract with Vale for

port services – expected $35

million annual minimum

EBITDA

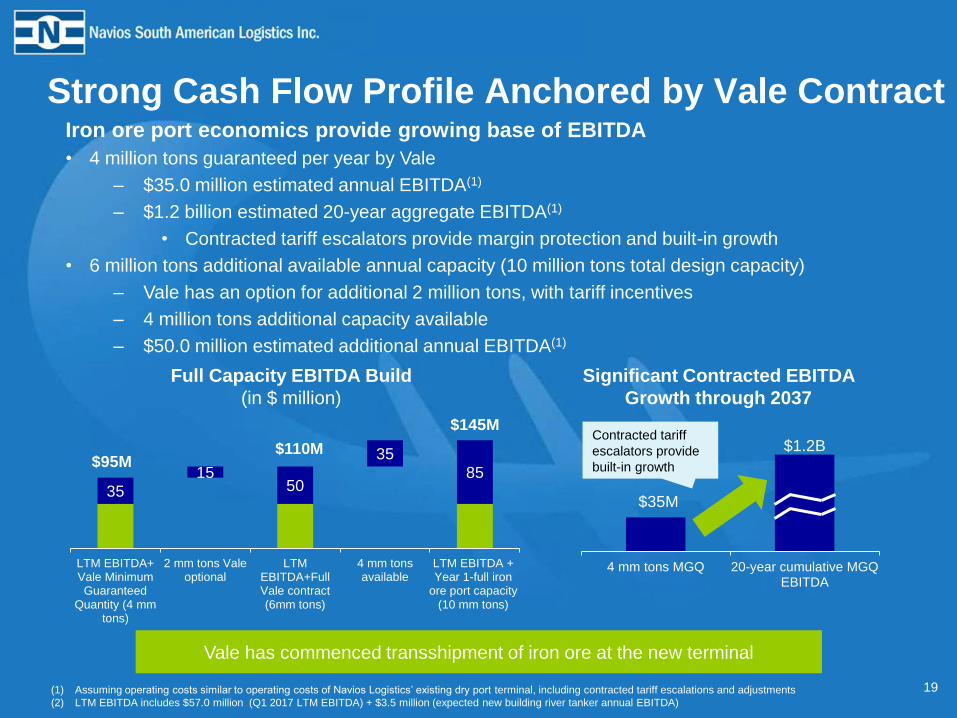

Strong Cash Flow Profile Anchored by Vale Contract Iron ore port economics provide growing base of EBITDA

• 4 million tons guaranteed per year by Vale

– $35.0 million estimated annual EBITDA(1)

– $1.2 billion estimated 20-year aggregate EBITDA(1)

• Contracted tariff escalators provide margin protection and built-in growth

• 6 million tons additional available annual capacity (10 million tons total design capacity)

– Vale has an option for additional 2 million tons, with tariff incentives

– 4 million tons additional capacity available

– $50.0 million estimated additional annual EBITDA(1)

(1) Assuming operating costs similar to operating costs of Navios Logistics’ existing dry port terminal, including contracted tariff escalations and adjustments

(2) LTM EBITDA includes $57.0 million (Q1 2017 LTM EBITDA) + $3.5 million (expected new building river tanker annual EBITDA)

19

35 15

50

35 85

LTM EBITDA+Vale MinimumGuaranteed

Quantity (4 mmtons)

2 mm tons Valeoptional

LTMEBITDA+FullVale contract(6mm tons)

4 mm tonsavailable

LTM EBITDA +Year 1-full iron

ore port capacity(10 mm tons)

4 mm tons MGQ 20-year cumulative MGQEBITDA

$35M

$1.2B

Full Capacity EBITDA Build

(in $ million)

Significant Contracted EBITDA

Growth through 2037

Contracted tariff

escalators provide

built-in growth

Vale has commenced transshipment of iron ore at the new terminal

$95M

$145M

$110M

20

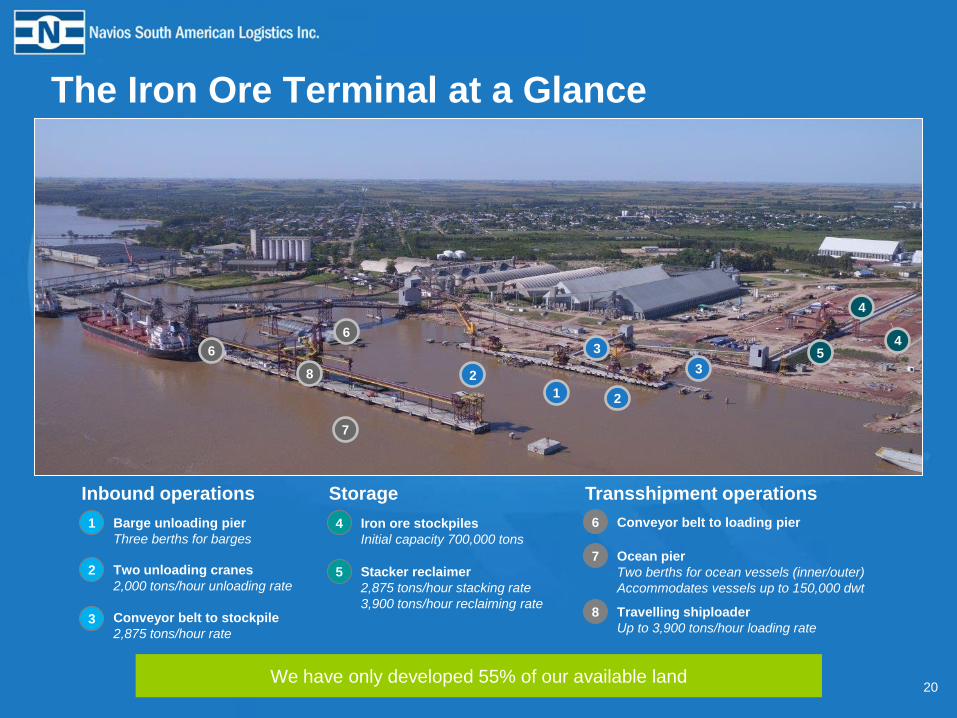

The Iron Ore Terminal at a Glance

1 Barge unloading pier

Three berths for barges

Inbound operations

2 Two unloading cranes

2,000 tons/hour unloading rate

3 Conveyor belt to stockpile

2,875 tons/hour rate

4 Iron ore stockpiles

Initial capacity 700,000 tons

Storage

5 Stacker reclaimer

2,875 tons/hour stacking rate

3,900 tons/hour reclaiming rate

6 Conveyor belt to loading pier

Transshipment operations

7 Ocean pier

Two berths for ocean vessels (inner/outer)

Accommodates vessels up to 150,000 dwt

8 Travelling shiploader

Up to 3,900 tons/hour loading rate

1

3

2

2

3

4

5

6

6

7

8

4

We have only developed 55% of our available land

21

Critical Infrastructure Asset Improves Logistics

Advantageous Location

• Ideally located at the mouth of

the river, where the confluence

of the Parana and Uruguay

Rivers meets the Atlantic

• Strategic location set as early as

1956 when US Steel first

established the port

• Further upstream requires

expensive pilots and tugs

and poses size restrictions

for oceangoing vessels

• Further downstream open

water is unsuitable for river

barges to navigate

Operational Efficiency

• Facility specialized for iron ore

transshipment, built to meet Vale

specifications

• State-of-the-art unloading

equipment with 2 cranes and

conveyor belt system

• Stacker-Reclaimer able to

handle cargo without trucks or

payloaders decreasing cost

• Travelling Shiploader loads

3,900 tons/hour translating into

<2 day turnaround for baby

Capesize vessels

• Environmentally friendly facility

Unique Ability to Stockpile

• Only port in the region with

ability to stockpile 700,000 tons

storage capacity with room for

future expansion into adjacent

land

• Stockpile ensures iron ore

availability year-round, avoiding

loading downtime while waiting

for cargo – a serious operational

challenge for other regional ports

• Mitigates potential seasonal

volatility

22

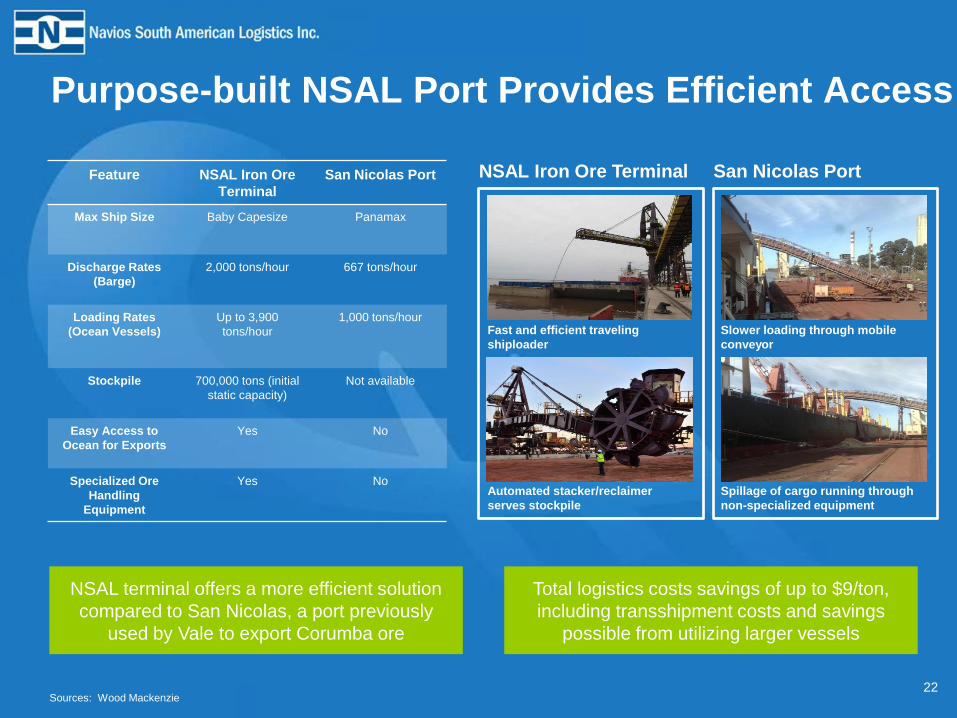

Purpose-built NSAL Port Provides Efficient Access

NSAL Iron Ore Terminal San Nicolas Port

Fast and efficient traveling

shiploader

Slower loading through mobile

conveyor

Automated stacker/reclaimer

serves stockpile

Spillage of cargo running through

non-specialized equipment

Feature NSAL Iron Ore

Terminal

San Nicolas Port

Max Ship Size Baby Capesize Panamax

Discharge Rates

(Barge)

2,000 tons/hour 667 tons/hour

Loading Rates

(Ocean Vessels)

Up to 3,900

tons/hour

1,000 tons/hour

Stockpile 700,000 tons (initial

static capacity)

Not available

Easy Access to

Ocean for Exports

Yes No

Specialized Ore

Handling

Equipment

Yes No

NSAL terminal offers a more efficient solution

compared to San Nicolas, a port previously

used by Vale to export Corumba ore

Total logistics costs savings of up to $9/ton,

including transshipment costs and savings

possible from utilizing larger vessels

Sources: Wood Mackenzie

23

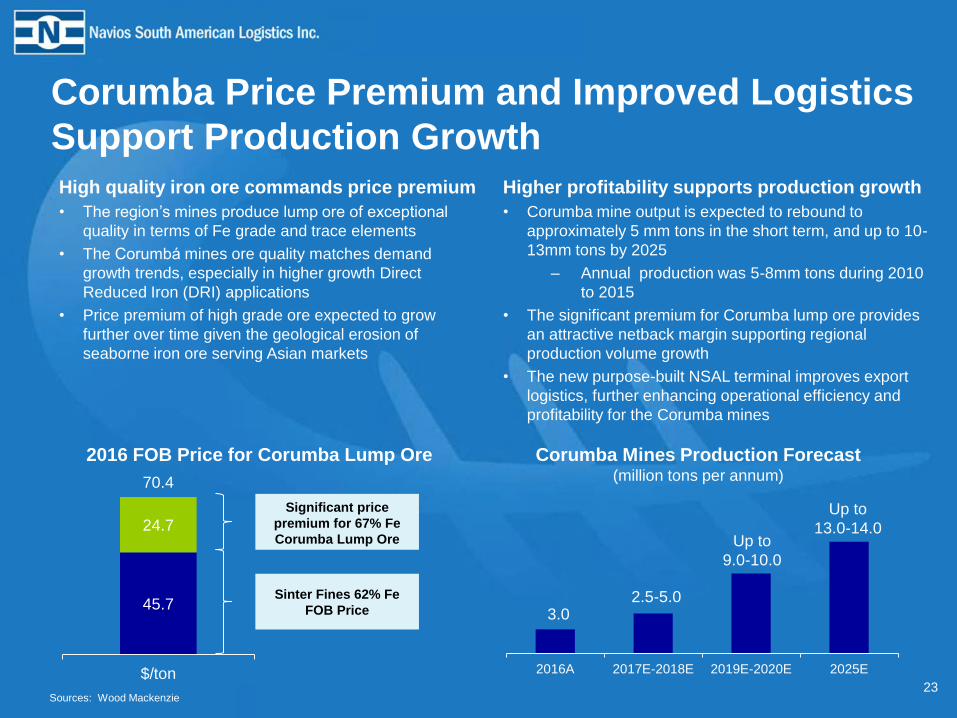

Corumba Price Premium and Improved Logistics

Support Production Growth

High quality iron ore commands price premium

• The region’s mines produce lump ore of exceptional

quality in terms of Fe grade and trace elements

• The Corumbá mines ore quality matches demand

growth trends, especially in higher growth Direct

Reduced Iron (DRI) applications

• Price premium of high grade ore expected to grow

further over time given the geological erosion of

seaborne iron ore serving Asian markets

45.7

24.7

70.4

$/ton

Significant price

premium for 67% Fe

Corumba Lump Ore

Sinter Fines 62% Fe

FOB Price

Higher profitability supports production growth

• Corumba mine output is expected to rebound to

approximately 5 mm tons in the short term, and up to 10-

13mm tons by 2025

– Annual production was 5-8mm tons during 2010

to 2015

• The significant premium for Corumba lump ore provides

an attractive netback margin supporting regional

production volume growth

• The new purpose-built NSAL terminal improves export

logistics, further enhancing operational efficiency and

profitability for the Corumba mines

2016 FOB Price for Corumba Lump Ore

2016A 2017E-2018E 2019E-2020E 2025E

Corumba Mines Production Forecast (million tons per annum)

3.0 2.5-5.0

Up to

9.0-10.0

Up to

13.0-14.0

Sources: Wood Mackenzie

24

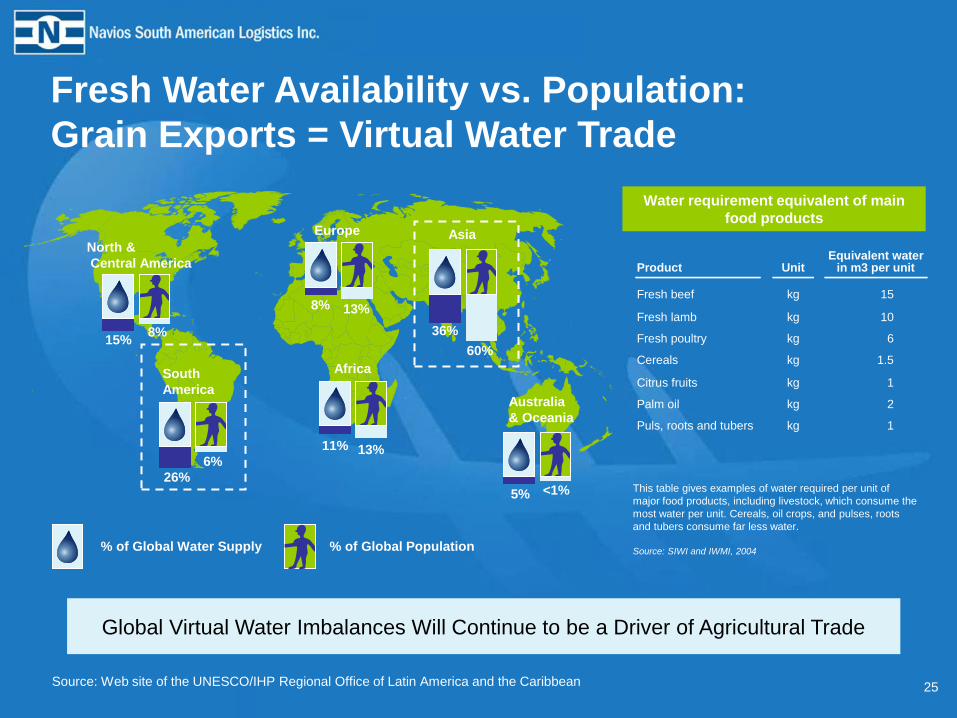

Market Overview

Source: Web site of the UNESCO/IHP Regional Office of Latin America and the Caribbean

Water requirement equivalent of main

food products

This table gives examples of water required per unit of

major food products, including livestock, which consume the

most water per unit. Cereals, oil crops, and pulses, roots

and tubers consume far less water.

Source: SIWI and IWMI, 2004

Product Unit Equivalent water

in m3 per unit

Fresh beef kg 15

Fresh lamb kg 10

Fresh poultry kg 6

Cereals kg 1.5

Citrus fruits kg 1

Palm oil kg 2

Puls, roots and tubers kg 1

North &

Central America

Africa

Asia

South

America

Europe

15% 8%

26%

6%

11% 13%

8% 13%

36%

60%

5% <1%

Australia

& Oceania

% of Global Water Supply % of Global Population

Fresh Water Availability vs. Population:

Grain Exports = Virtual Water Trade

25

Global Virtual Water Imbalances Will Continue to be a Driver of Agricultural Trade

26

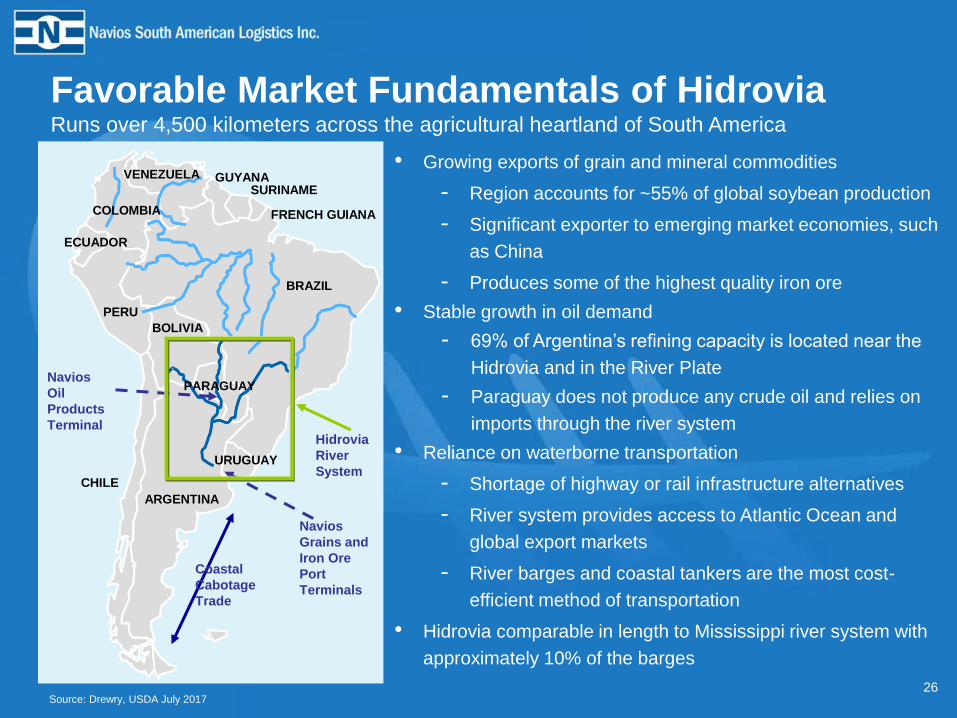

Favorable Market Fundamentals of Hidrovia Runs over 4,500 kilometers across the agricultural heartland of South America

VENEZUELA

BOLIVIA

ARGENTINA

BRAZIL

FRENCH GUIANA

SURINAMEGUYANA

COLOMBIA

ECUADOR

PERU

PARAGUAY

URUGUAY

CHILE

VENEZUELA

BOLIVIA

ARGENTINA

BRAZIL

FRENCH GUIANA

SURINAMEGUYANA

COLOMBIA

ECUADOR

PERU

PARAGUAY

URUGUAY

CHILE

• Growing exports of grain and mineral commodities

- Region accounts for ~55% of global soybean production

- Significant exporter to emerging market economies, such

as China

- Produces some of the highest quality iron ore

• Stable growth in oil demand

- 69% of Argentina’s refining capacity is located near the

Hidrovia and in the River Plate

- Paraguay does not produce any crude oil and relies on

imports through the river system

• Reliance on waterborne transportation

- Shortage of highway or rail infrastructure alternatives

- River system provides access to Atlantic Ocean and

global export markets

- River barges and coastal tankers are the most cost-

efficient method of transportation

• Hidrovia comparable in length to Mississippi river system with

approximately 10% of the barges

Coastal

Cabotage

Trade

Navios

Oil

Products

Terminal

Navios

Grains and

Iron Ore

Port

Terminals

Hidrovia

River

System

Source: Drewry, USDA July 2017

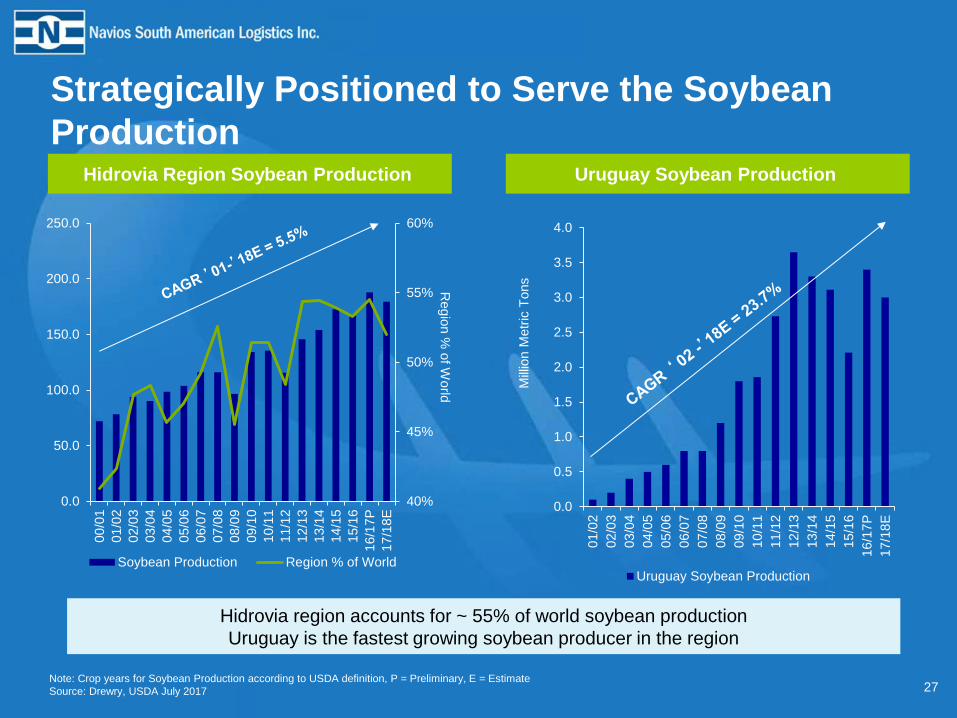

Strategically Positioned to Serve the Soybean

Production

27 Note: Crop years for Soybean Production according to USDA definition, P = Preliminary, E = Estimate

Source: Drewry, USDA July 2017

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

01

/02

02

/03

03

/04

04

/05

05

/06

06

/07

07

/08

08

/09

09

/10

10

/11

11

/12

12

/13

13

/14

14

/15

15

/16

16

/17

P

17

/18

E

Uruguay Soybean Production

Mill

ion M

etr

ic T

ons

Regio

n %

of W

orld

40%

45%

50%

55%

60%

0.0

50.0

100.0

150.0

200.0

250.0

00

/01

01

/02

02

/03

03

/04

04

/05

05

/06

06

/07

07

/08

08

/09

09

/10

10

/11

11

/12

12

/13

13

/14

14

/15

15

/16

16

/17

P

17

/18

E

Soybean Production Region % of World

Hidrovia Region Soybean Production Uruguay Soybean Production

Hidrovia region accounts for ~ 55% of world soybean production

Uruguay is the fastest growing soybean producer in the region

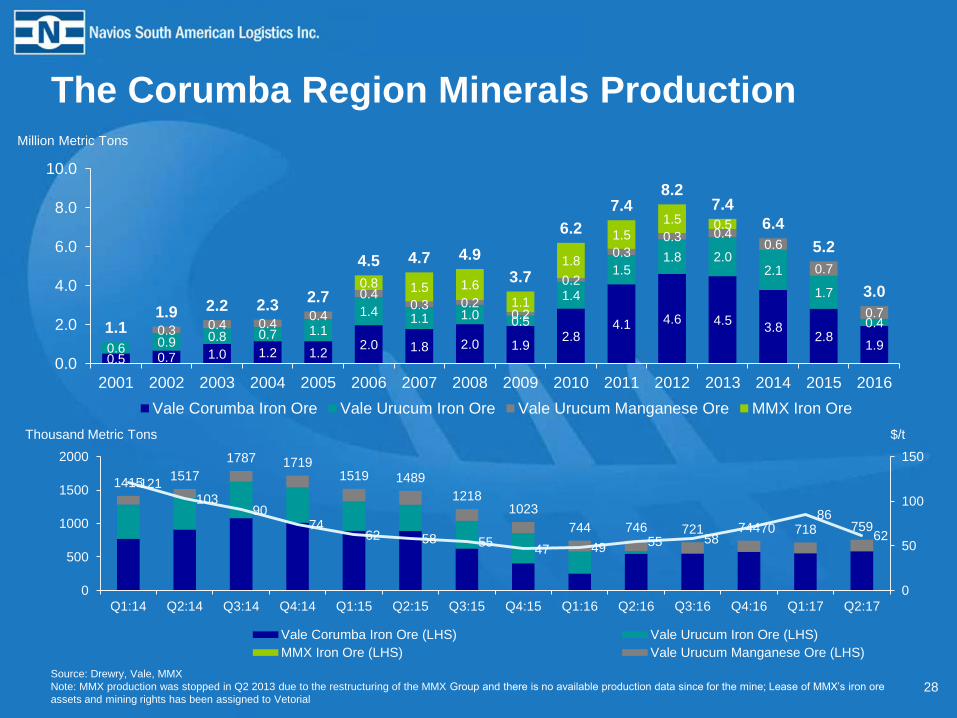

The Corumba Region Minerals Production

28

1415 1517

1787 1719 1519 1489

1218 1023

744 746 721 744 718 759

121

103 90

74 62 58 55

47 49 55 58 70

86

62

0

50

100

150

0

500

1000

1500

2000

Q1:14 Q2:14 Q3:14 Q4:14 Q1:15 Q2:15 Q3:15 Q4:15 Q1:16 Q2:16 Q3:16 Q4:16 Q1:17 Q2:17

Vale Corumba Iron Ore (LHS) Vale Urucum Iron Ore (LHS)

MMX Iron Ore (LHS) Vale Urucum Manganese Ore (LHS)

Million Metric Tons

Thousand Metric Tons

0.5 0.7 1.0 1.2 1.2 2.0 1.8 2.0 1.9

2.8 4.1 4.6 4.5

3.8 2.8

1.9 0.6 0.9 0.8 0.7 1.1

1.4 1.1 1.0

0.5

1.4

1.5 1.8 2.0

2.1

1.7

0.4 0.3 0.4 0.4

0.4

0.4 0.3 0.2

0.2

0.2

0.3

0.3 0.4 0.6

0.7

0.7

0.8 1.5 1.6

1.1

1.8

1.5

1.5 0.5

1.1 1.9 2.2 2.3

2.7

4.5 4.7 4.9

3.7

6.2

7.4 8.2

7.4

6.4

5.2

3.0

0.0

2.0

4.0

6.0

8.0

10.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Vale Corumba Iron Ore Vale Urucum Iron Ore Vale Urucum Manganese Ore MMX Iron Ore

$/t

Source: Drewry, Vale, MMX

Note: MMX production was stopped in Q2 2013 due to the restructuring of the MMX Group and there is no available production data since for the mine; Lease of MMX’s iron ore

assets and mining rights has been assigned to Vetorial

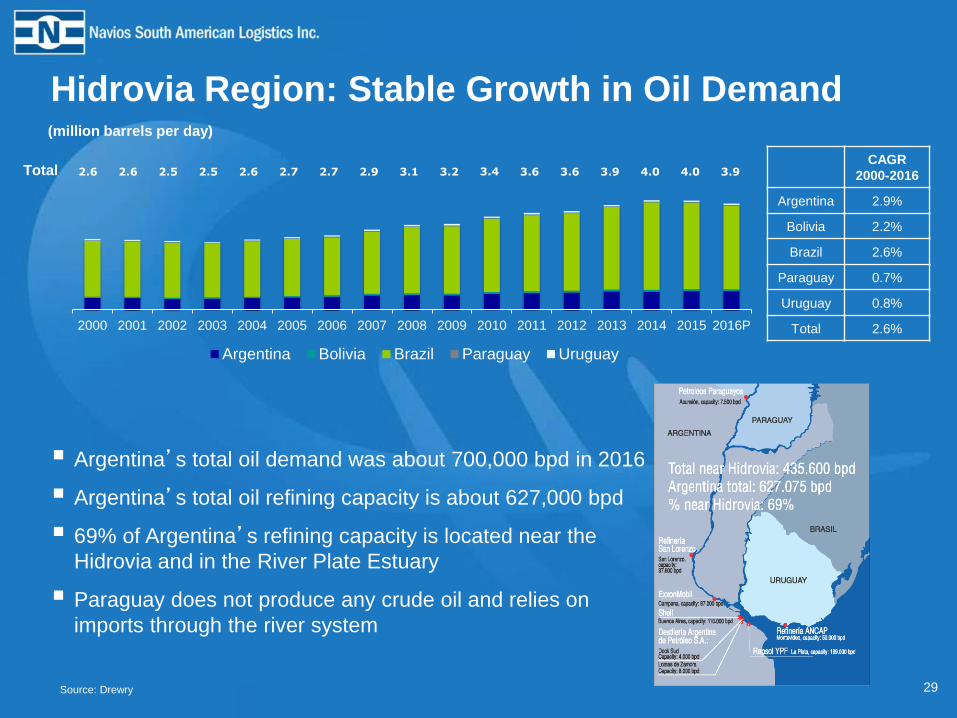

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016P

Argentina Bolivia Brazil Paraguay Uruguay

29

(million barrels per day)

Argentina’s total oil demand was about 700,000 bpd in 2016

Argentina’s total oil refining capacity is about 627,000 bpd

69% of Argentina’s refining capacity is located near the

Hidrovia and in the River Plate Estuary

Paraguay does not produce any crude oil and relies on

imports through the river system

2.6 2.6 2.5 2.5 2.6 2.7 2.7 2.9 3.1 3.2

CAGR

2000-2016

Argentina 2.9%

Bolivia 2.2%

Brazil 2.6%

Paraguay 0.7%

Uruguay 0.8%

Total 2.6%

Total

Hidrovia Region: Stable Growth in Oil Demand

3.6

Source: Drewry

3.6 3.4 3.9 4.0 4.0 3.9

30

Q1 2017 Financial Highlights

31

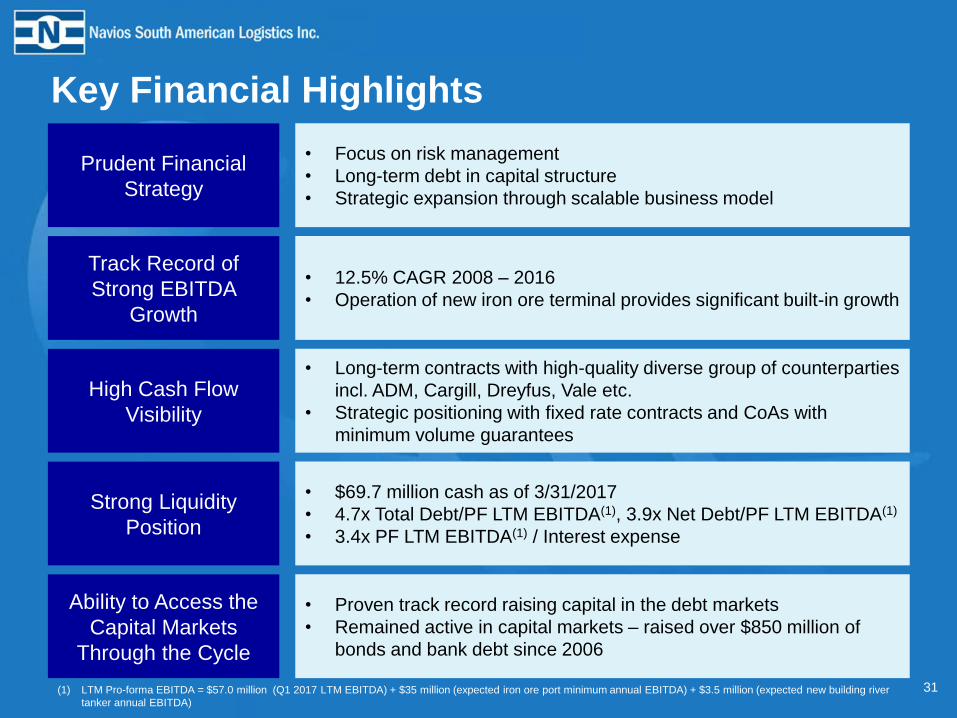

Key Financial Highlights

Prudent Financial

Strategy

Track Record of

Strong EBITDA

Growth

High Cash Flow

Visibility

Strong Liquidity

Position

Ability to Access the

Capital Markets

Through the Cycle

• Focus on risk management

• Long-term debt in capital structure

• Strategic expansion through scalable business model

• 12.5% CAGR 2008 – 2016

• Operation of new iron ore terminal provides significant built-in growth

• Long-term contracts with high-quality diverse group of counterparties

incl. ADM, Cargill, Dreyfus, Vale etc.

• Strategic positioning with fixed rate contracts and CoAs with

minimum volume guarantees

• $69.7 million cash as of 3/31/2017

• 4.7x Total Debt/PF LTM EBITDA(1), 3.9x Net Debt/PF LTM EBITDA(1)

• 3.4x PF LTM EBITDA(1) / Interest expense

• Proven track record raising capital in the debt markets

• Remained active in capital markets – raised over $850 million of

bonds and bank debt since 2006

(1) LTM Pro-forma EBITDA = $57.0 million (Q1 2017 LTM EBITDA) + $35 million (expected iron ore port minimum annual EBITDA) + $3.5 million (expected new building river

tanker annual EBITDA)

32

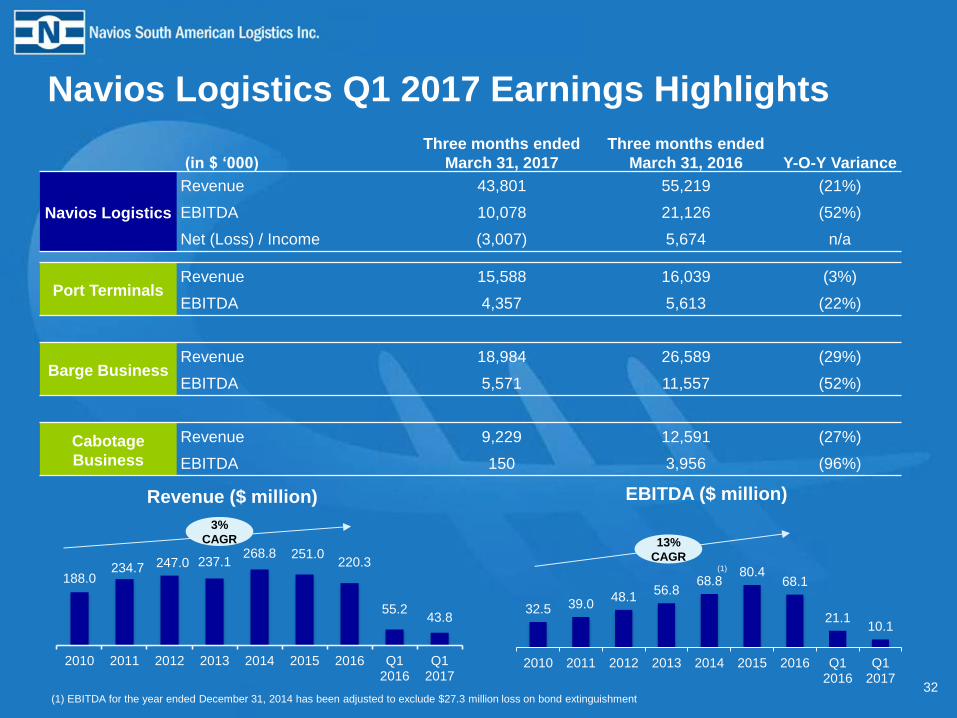

Navios Logistics Q1 2017 Earnings Highlights

(in $ ‘000)

Three months ended

March 31, 2017

Three months ended

March 31, 2016 Y-O-Y Variance

Navios Logistics

Revenue 43,801 55,219 (21%)

EBITDA 10,078 21,126 (52%)

Net (Loss) / Income (3,007) 5,674 n/a

Port Terminals Revenue 15,588 16,039 (3%)

EBITDA 4,357 5,613 (22%)

Barge Business Revenue 18,984 26,589 (29%)

EBITDA 5,571 11,557 (52%)

Cabotage

Business

Revenue 9,229 12,591 (27%)

EBITDA 150 3,956 (96%)

188.0 234.7 247.0 237.1

268.8 251.0 220.3

55.2 43.8

2010 2011 2012 2013 2014 2015 2016 Q12016

Q12017

32.5 39.0 48.1

56.8 68.8

80.4 68.1

21.1 10.1

2010 2011 2012 2013 2014 2015 2016 Q12016

Q12017

3%

CAGR 13%

CAGR

EBITDA ($ million) Revenue ($ million)

(1) EBITDA for the year ended December 31, 2014 has been adjusted to exclude $27.3 million loss on bond extinguishment

(1)

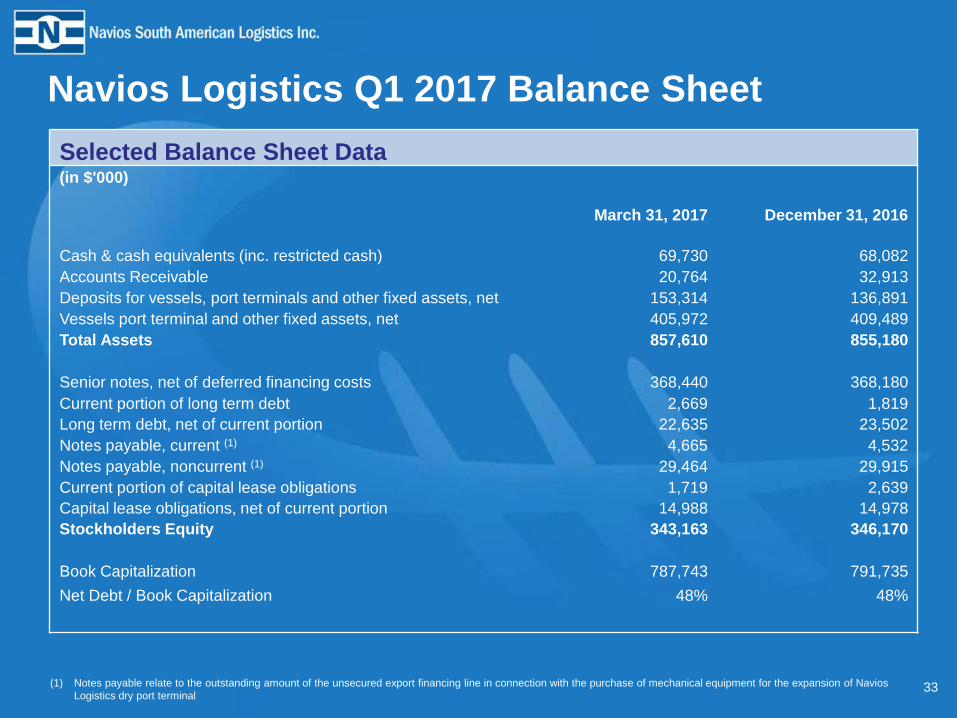

Navios Logistics Q1 2017 Balance Sheet

Selected Balance Sheet Data (in $'000)

March 31, 2017 December 31, 2016

Cash & cash equivalents (inc. restricted cash) 69,730 68,082

Accounts Receivable 20,764 32,913

Deposits for vessels, port terminals and other fixed assets, net 153,314 136,891

Vessels port terminal and other fixed assets, net 405,972 409,489

Total Assets 857,610 855,180

Senior notes, net of deferred financing costs 368,440 368,180

Current portion of long term debt 2,669 1,819

Long term debt, net of current portion 22,635 23,502

Notes payable, current (1) 4,665 4,532

Notes payable, noncurrent (1) 29,464 29,915

Current portion of capital lease obligations 1,719 2,639

Capital lease obligations, net of current portion 14,988 14,978

Stockholders Equity 343,163 346,170

Book Capitalization 787,743 791,735

Net Debt / Book Capitalization 48% 48%

(1) Notes payable relate to the outstanding amount of the unsecured export financing line in connection with the purchase of mechanical equipment for the expansion of Navios

Logistics dry port terminal

33

www.navioslogistics.com