Embed Size (px)

Citation preview

I n t e g r i t y - S e r v i c e - E x c e l l e n c e

Headquarters U.S. Air Force

Natural Infrastructure Asset Valuation for Financial Managers

Ms. Michele IndermarkSAF/IEE

Richard PinkhamBooz Allen Hamilton

Joint Services Environmental Management Conference

May 24, 2007

2I n t e g r i t y - S e r v i c e - E x c e l l e n c e

Topics

BackgroundUses of natural infrastructure (NI) asset valuesOverview of concepts and terminology

Types of NI assets and valuesValuation techniques

Accounting for NI asset values in the asset management processManagerial accountingFinancial accounting

Concluding remarks

3I n t e g r i t y - S e r v i c e - E x c e l l e n c e

Background

Government, academia, conservation organizations and other NGOs are increasingly recognizing the need to account for the services and products that ecosystems provide to human beingsValuation approaches and accounting concepts have been evolving

These include monetary and non-monetary approachesFASAB and FASB reports and statements, National Research Council report, EPA working group, etc.

New types of assets are emergingEmission reduction credits, habitat conservation credits, carbon credits, etc.

Lots of relevant concepts and distinctions existMarket and non-market values, ecosystem goods and services, natural and statutory assets, costs and benefits, financial and managerial accounting, environmental equity, leveraging asset value, etc.

DoD is developing “natural infrastructure asset valuation” as part of an overarching asset management framework

NI asset valuation is a tool for leveraging NI assets to support and sustain the military mission

4I n t e g r i t y - S e r v i c e - E x c e l l e n c e

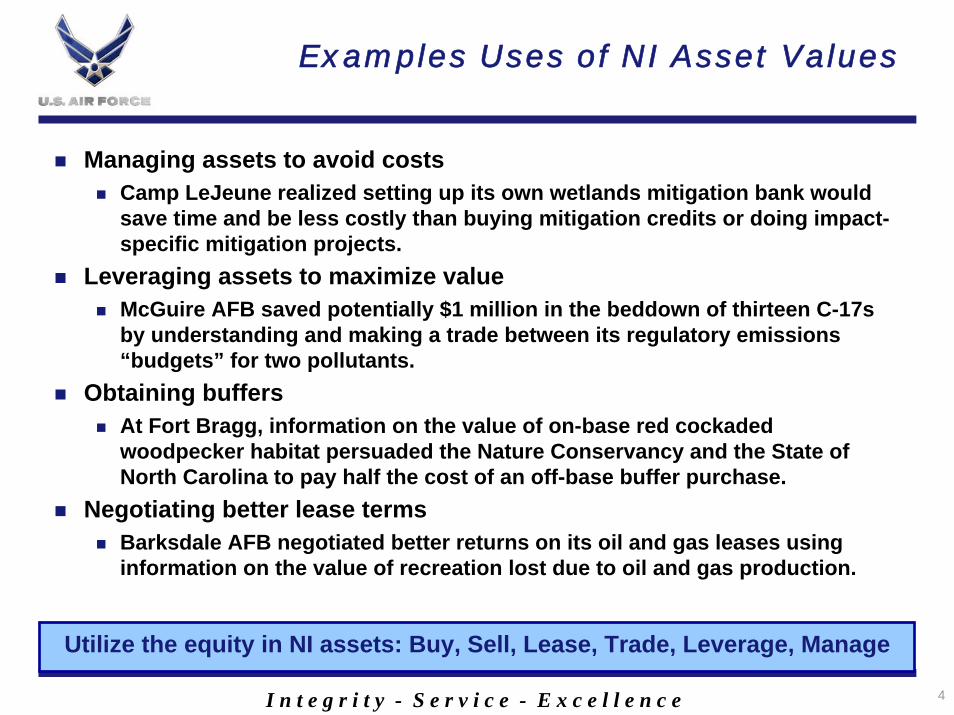

Examples Uses of NI Asset Values

Managing assets to avoid costsCamp LeJeune realized setting up its own wetlands mitigation bank would save time and be less costly than buying mitigation credits or doing impact-specific mitigation projects.

Leveraging assets to maximize valueMcGuire AFB saved potentially $1 million in the beddown of thirteen C-17s by understanding and making a trade between its regulatory emissions “budgets” for two pollutants.

Obtaining buffersAt Fort Bragg, information on the value of on-base red cockaded woodpecker habitat persuaded the Nature Conservancy and the State of North Carolina to pay half the cost of an off-base buffer purchase.

Negotiating better lease termsBarksdale AFB negotiated better returns on its oil and gas leases using information on the value of recreation lost due to oil and gas production.

Utilize the equity in NI assets: Buy, Sell, Lease, Trade, Leverage, Manage

5I n t e g r i t y - S e r v i c e - E x c e l l e n c e

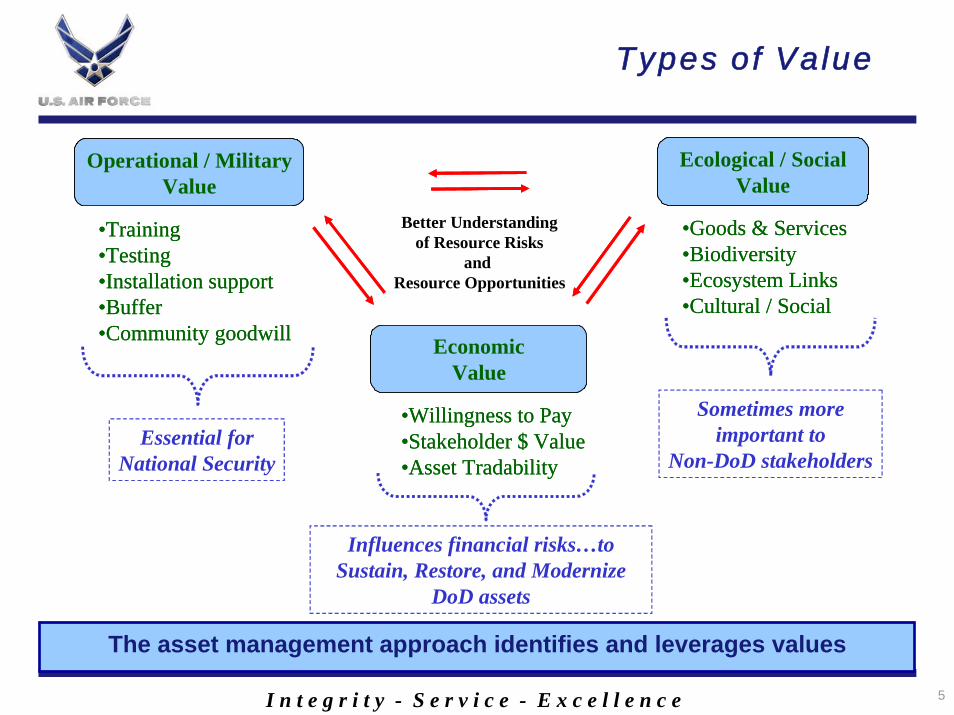

Types of Value

Ecological / SocialValue

•Goods & Services•Biodiversity•Ecosystem Links•Cultural / Social

Ecological / SocialValue

•Goods & Services•Biodiversity•Ecosystem Links•Cultural / Social

EconomicValue

•Willingness to Pay•Stakeholder $ Value•Asset Tradability

EconomicValue

•Willingness to Pay•Stakeholder $ Value•Asset Tradability

Operational / MilitaryValue

•Training•Testing•Installation support•Buffer•Community goodwill

Operational / MilitaryValue

•Training•Testing•Installation support•Buffer•Community goodwill

Essential forNational Security

Sometimes moreimportant to

Non-DoD stakeholders

Influences financial risks…to Sustain, Restore, and Modernize

DoD assets

Better Understandingof Resource Risks

and Resource Opportunities

The asset management approach identifies and leverages values

6I n t e g r i t y - S e r v i c e - E x c e l l e n c e

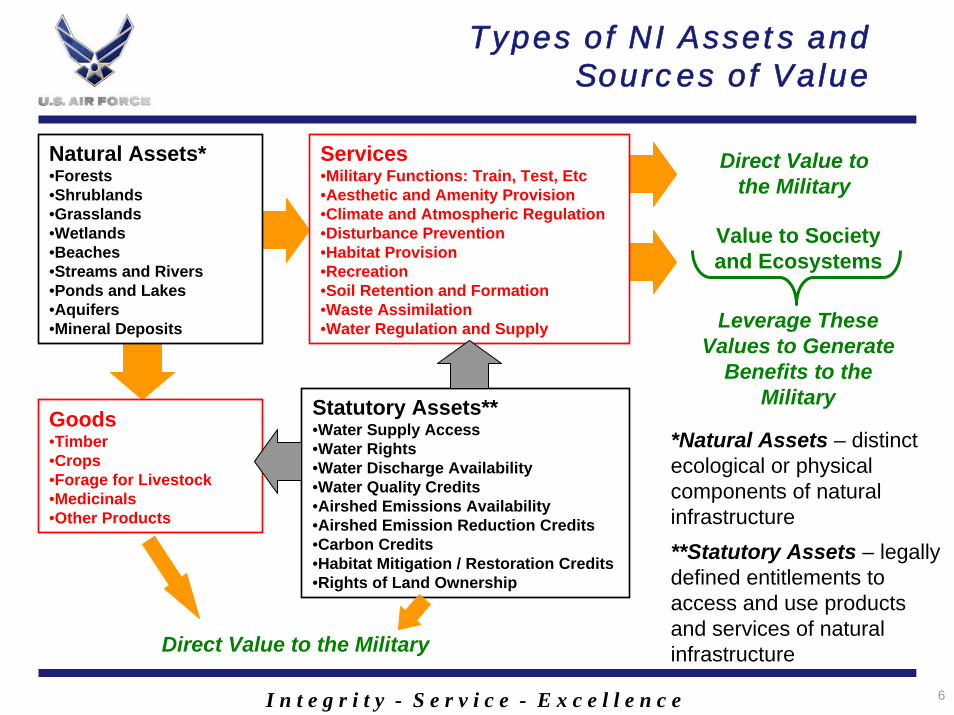

Types of NI Assets and Sources of Value

Natural Assets*•Forests•Shrublands•Grasslands•Wetlands•Beaches•Streams and Rivers•Ponds and Lakes•Aquifers•Mineral Deposits

Statutory Assets**•Water Supply Access•Water Rights•Water Discharge Availability•Water Quality Credits•Airshed Emissions Availability•Airshed Emission Reduction Credits•Carbon Credits•Habitat Mitigation / Restoration Credits•Rights of Land Ownership

Services•Military Functions: Train, Test, Etc•Aesthetic and Amenity Provision•Climate and Atmospheric Regulation•Disturbance Prevention•Habitat Provision•Recreation•Soil Retention and Formation•Waste Assimilation•Water Regulation and Supply

Goods•Timber•Crops•Forage for Livestock•Medicinals•Other Products

Value to Society and Ecosystems

Direct Value to the Military

Leverage These Values to Generate

Benefits to the Military

*Natural Assets – distinct ecological or physical components of natural infrastructure**Statutory Assets – legally defined entitlements to access and use products and services of natural infrastructure

Direct Value to the Military

7I n t e g r i t y - S e r v i c e - E x c e l l e n c e

Valuation of NI Assets, Goods, and Services

Market Appraisal Techniques: Comparable Sales, Income Streams, Replacement Costs

Advanced Economic Techniques:• Contingent Valuation• Hedonic Pricing• Etc

Benefits Transfer

Non-Monetary Valuation Techniques

Descriptive (Qualitative) Valuation

Commodity Valuation

Natural Assets*•Forests•Shrublands•Grasslands•Wetlands•Beaches•Streams and Rivers•Ponds and Lakes•Aquifers•Mineral Deposits

Statutory Assets**•Water Supply Access•Water Rights•Water Discharge Availability•Water Quality Credits•Airshed Emissions Availability•Airshed Emission Reduction Credits•Carbon Credits•Habitat Mitigation / Restoration Credits•Rights of Land Ownership

Services•Military Functions: Train, Test, Etc•Aesthetic and Amenity Provision•Climate and Atmospheric Regulation•Disturbance Prevention•Habitat Provision•Recreation•Soil Retention and Formation•Waste Assimilation•Water Regulation and Supply

Goods•Timber•Crops•Forage for Livestock•Medicinals•Other Products

8I n t e g r i t y - S e r v i c e - E x c e l l e n c e

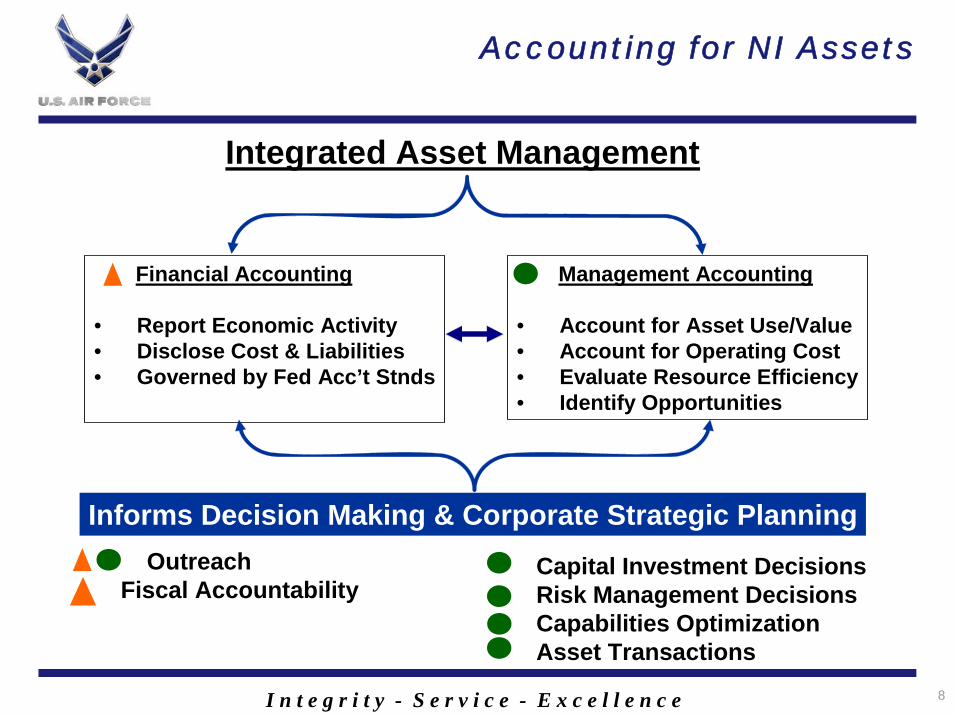

Accounting for NI Assets

Integrated Asset Management

Financial Accounting

• Report Economic Activity• Disclose Cost & Liabilities• Governed by Fed Acc’t Stnds

Management Accounting

• Account for Asset Use/Value• Account for Operating Cost• Evaluate Resource Efficiency• Identify Opportunities

• Outreach• Fiscal Accountability

Informs Decision Making & Corporate Strategic Planning

• Capital Investment Decisions• Risk Management Decisions• Capabilities Optimization • Asset Transactions

9I n t e g r i t y - S e r v i c e - E x c e l l e n c e

UsesAnalytical Process OutputsInputs

InventoryAssets

andDeficiencies

Gather Existing

Data

Classifyand

CharacterizeAssets andDeficiencies

IdentifyNI Strategic

Opportunities(Potential

NI Management

Actions)

AnalyzeAsset Valuesand Action

Benefits andCosts

UtilizeInformationIn DecisionMaking andBusiness

Processes

General Framework for NI Asset Valuation in the Asset Management Process

10I n t e g r i t y - S e r v i c e - E x c e l l e n c e

Identify… Analyze… Utilize…

Detailed Asset Management Framework w/ Financial and Managerial Accounting

Bookable AssetAppraisals

Manageable Asset& Service Valuations• Monetary, non-monetary

• Pre-action, post-action

Benefits

• Benefit/CostAnalysis

• Cost EffectivenessAnalysis

Costs

Book Assetsto Balance

Sheet

Make NIManagementDecisions• Buy• Trade• Lease• Sell• Partner• Site• Restore• Enhance• Etc.

Plan

Budget

Program

DERP Siteinventories

Non-DERP siteinventories

INRMPSNEPA document

Resource management

plansGeneral plans

Other documents

Geospatial data

NIMSE results

NIVAAsset

s&

Services

Inventory

NIVADeficiencies

& WorkaroundsInventory

Bookable/Manageable Assets

Manageable Assets

Manageable EcosystemServices

TractableDeficiencies& Workarounds

IntractableDeficiencies& Workarounds

Identify NIStrategic Opportunities

• To Maximize Returns on Assets

• To Resolve Deficiencies& Workarounds

• To ReduceRisks

Manage & Leverage Assets

PossibleNI Actions• Buy• Trade• Lease• Sell• Partner• Site• Restore• Enhance• Etc

Meet Fin. Accountability

Stds.

Cost Analysis• Of deficiencies

& workarounds• Of NI actions• Monetary, non-monetary

11I n t e g r i t y - S e r v i c e - E x c e l l e n c e

Financial Accounting: DoD and Component Balance Sheets

NI liabilities are recognized…Under Note 14, “Environmental Liabilities”

NI assets not so much…Land is included under Note 10, “General Property, Plant, and Equipment”Tangible natural resources such as timber and water are notably absentAs are statutory assets

12I n t e g r i t y - S e r v i c e - E x c e l l e n c e

FASAB Task Force Report, June 2000

Federal Accounting Standards Advisory Board convened a Natural Resources Task ForceFinal report, “Accounting for the Natural Resources of the Federal Government,” issued June 2000

Only addressed “traditional” natural resources such as timber, oil and gas, forage (grazing), and mineralsConcluded these should not be reported on the balance sheet, but rather should be included in Notes to the Financial Statements (e.g., Financial Footnote Disclosures) and as stewardship information

Stewardship reporting is relatively new and still under developmentWould allow for more information than footnote disclosuresBut does not provide data in the principle financial statements, thereby not providing those statements with a complete picture of DoD’s financial position

In summary, these recommendations fall short of what practitioners of NI asset valuation believe is valid and useful

13I n t e g r i t y - S e r v i c e - E x c e l l e n c e

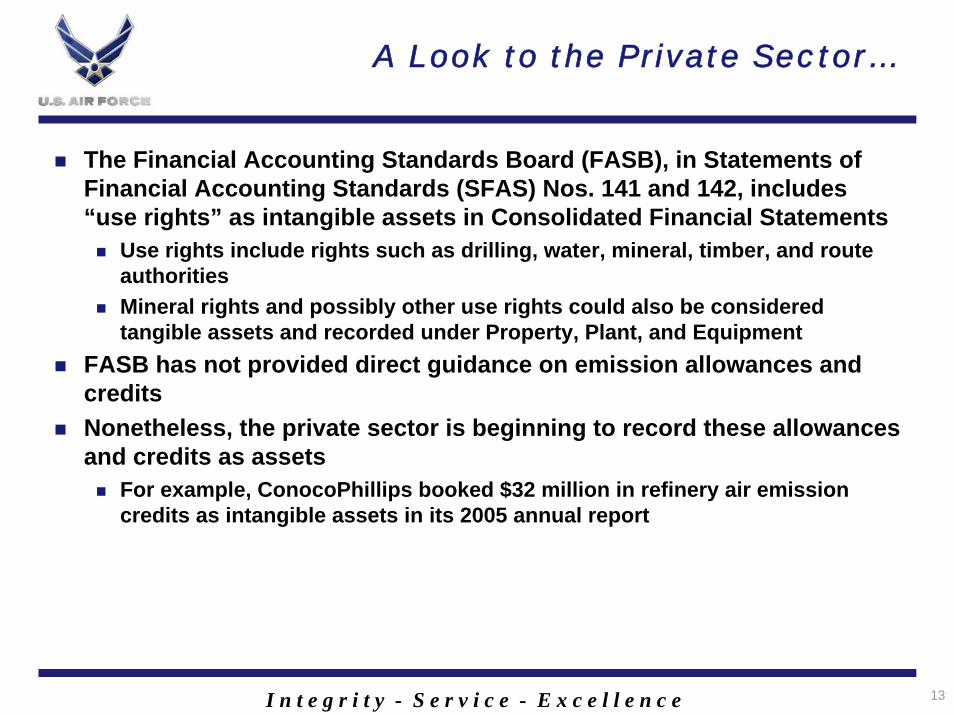

A Look to the Private Sector…

The Financial Accounting Standards Board (FASB), in Statements of Financial Accounting Standards (SFAS) Nos. 141 and 142, includes“use rights” as intangible assets in Consolidated Financial Statements

Use rights include rights such as drilling, water, mineral, timber, and route authoritiesMineral rights and possibly other use rights could also be considered tangible assets and recorded under Property, Plant, and Equipment

FASB has not provided direct guidance on emission allowances andcreditsNonetheless, the private sector is beginning to record these allowances and credits as assets

For example, ConocoPhillips booked $32 million in refinery air emission credits as intangible assets in its 2005 annual report

14I n t e g r i t y - S e r v i c e - E x c e l l e n c e

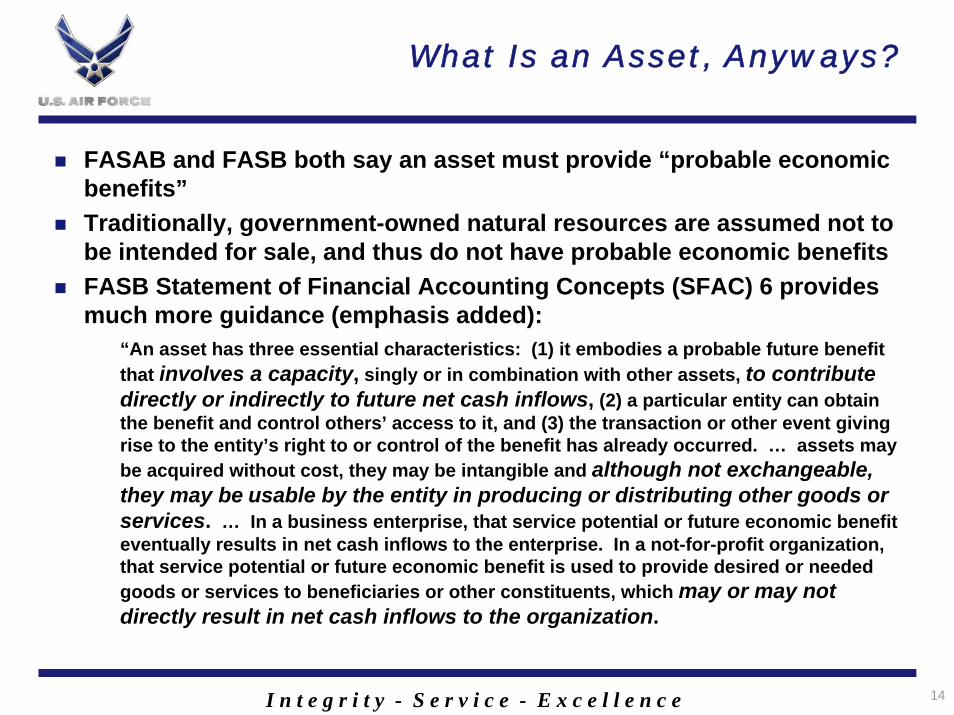

What Is an Asset, Anyways?

FASAB and FASB both say an asset must provide “probable economicbenefits”Traditionally, government-owned natural resources are assumed not to be intended for sale, and thus do not have probable economic benefitsFASB Statement of Financial Accounting Concepts (SFAC) 6 provides much more guidance (emphasis added):

“An asset has three essential characteristics: (1) it embodies a probable future benefit that involves a capacity, singly or in combination with other assets, to contribute directly or indirectly to future net cash inflows, (2) a particular entity can obtain the benefit and control others’ access to it, and (3) the transaction or other event giving rise to the entity’s right to or control of the benefit has already occurred. … assets may be acquired without cost, they may be intangible and although not exchangeable, they may be usable by the entity in producing or distributing other goods orservices. … In a business enterprise, that service potential or future economic benefit eventually results in net cash inflows to the enterprise. In a not-for-profit organization, that service potential or future economic benefit is used to provide desired or needed goods or services to beneficiaries or other constituents, which may or may not directly result in net cash inflows to the organization.

15I n t e g r i t y - S e r v i c e - E x c e l l e n c e

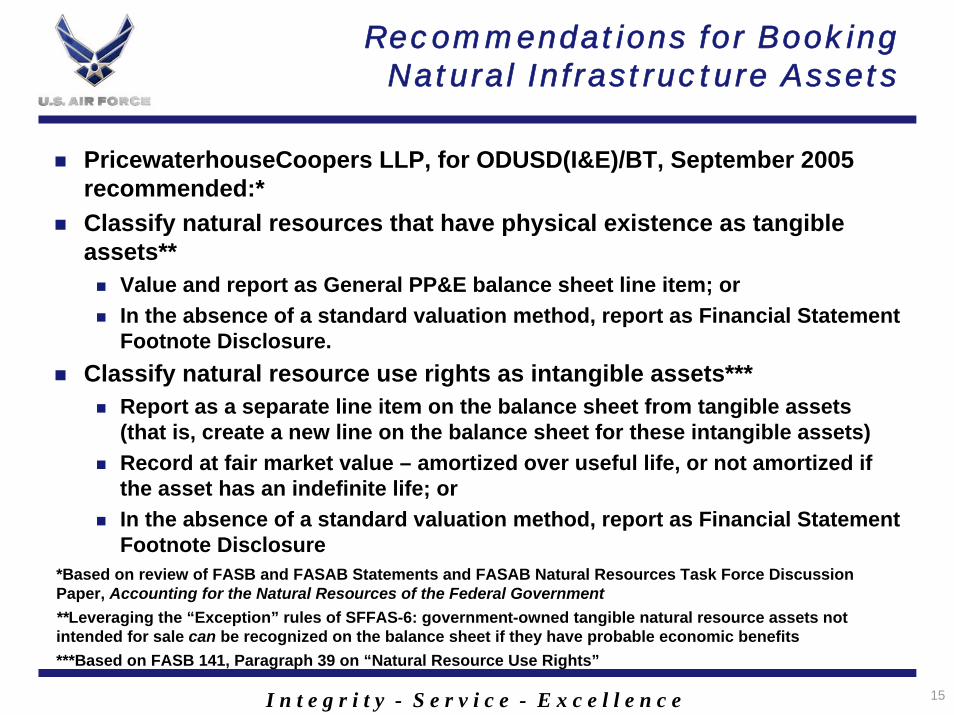

Recommendations for Booking Natural Infrastructure Assets

PricewaterhouseCoopers LLP, for ODUSD(I&E)/BT, September 2005 recommended:*Classify natural resources that have physical existence as tangible assets**

Value and report as General PP&E balance sheet line item; or In the absence of a standard valuation method, report as Financial Statement Footnote Disclosure.

Classify natural resource use rights as intangible assets*** Report as a separate line item on the balance sheet from tangible assets (that is, create a new line on the balance sheet for these intangible assets)Record at fair market value – amortized over useful life, or not amortized if the asset has an indefinite life; orIn the absence of a standard valuation method, report as Financial Statement Footnote Disclosure

*Based on review of FASB and FASAB Statements and FASAB Natural Resources Task Force Discussion Paper, Accounting for the Natural Resources of the Federal Government**Leveraging the “Exception” rules of SFFAS-6: government-owned tangible natural resource assets not intended for sale can be recognized on the balance sheet if they have probable economic benefits***Based on FASB 141, Paragraph 39 on “Natural Resource Use Rights”

16I n t e g r i t y - S e r v i c e - E x c e l l e n c e

Concluding Remarks

Utility of NI asset valuation for supporting and sustaining the missionAd hoc examples and lessons from NI asset valuation pilot and application studies show the usefulness of increased attention to NI asset values

Coming soon, underway…Air Force NI Asset Valuation Guidance Manual

Under development by SAF/IEE, in coordination with SAF/FM and A7Integration of data on credits and other NI assets into the Air Force NIM data tool

And stay tuned for… Continued consideration of NI asset valuation at the OSD level (NICWG)Incorporation of NI asset valuation concepts into DoD and Component directives, instructions, and other policiesEvolving financial accounting standards for NI assets

17I n t e g r i t y - S e r v i c e - E x c e l l e n c e

Questions?

18I n t e g r i t y - S e r v i c e - E x c e l l e n c e

BACK-UP SLIDES

19I n t e g r i t y - S e r v i c e - E x c e l l e n c e

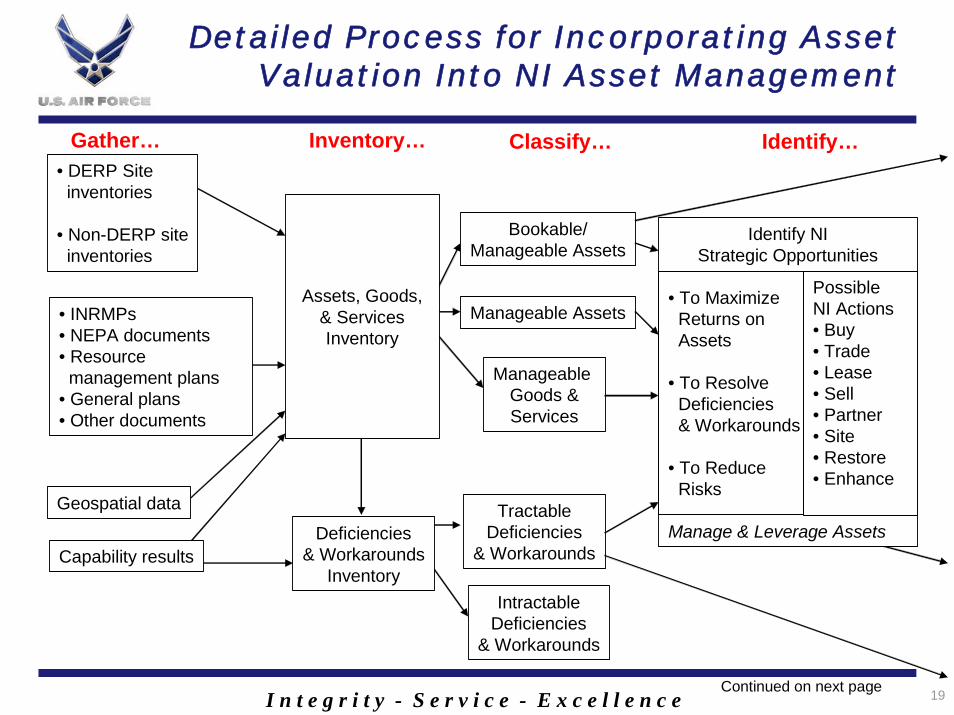

Gather… Inventory… Classify… Identify…

Detailed Process for Incorporating Asset Valuation Into NI Asset Management

Identify NIStrategic Opportunities

• To Maximize Returns on Assets

• To Resolve Deficiencies& Workarounds

• To ReduceRisks

Manage & Leverage Assets

• DERP Siteinventories

• Non-DERP siteinventories

• INRMPs• NEPA documents• Resource management plans

• General plans• Other documents

Geospatial data

Capability results

Assets, Goods,& ServicesInventory

Deficiencies& Workarounds

Inventory

Bookable/Manageable Assets

Manageable Assets

Manageable Goods &Services

TractableDeficiencies

& Workarounds

IntractableDeficiencies

& Workarounds

Continued on next page

PossibleNI Actions• Buy• Trade• Lease• Sell• Partner• Site• Restore• Enhance

20I n t e g r i t y - S e r v i c e - E x c e l l e n c e

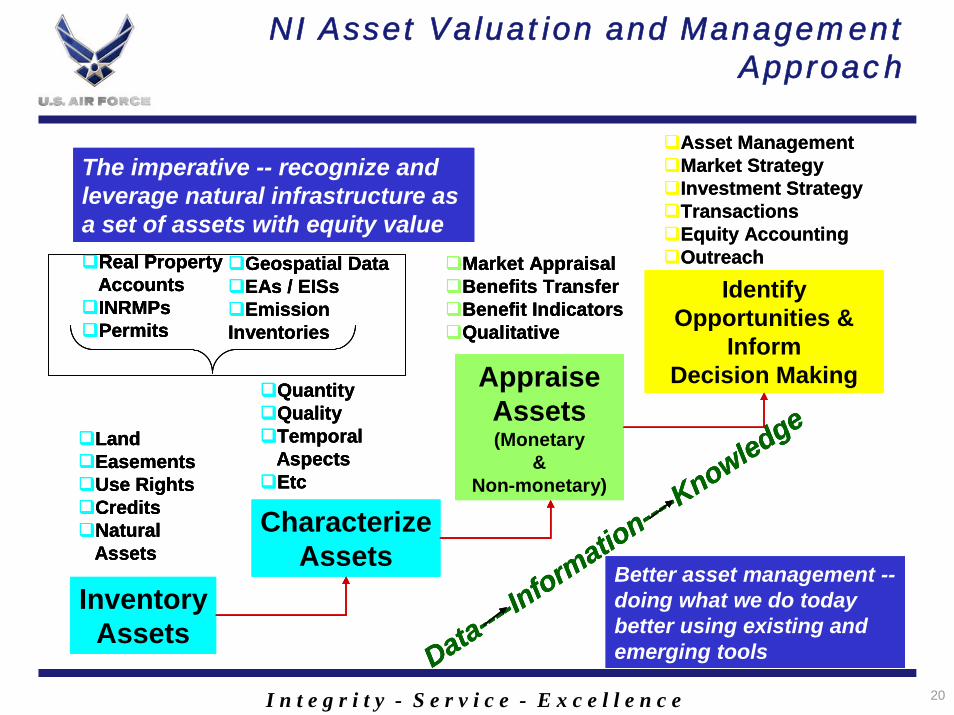

NI Asset Valuation and Management Approach

Asset ManagementMarket StrategyInvestment StrategyTransactionsEquity AccountingOutreach

Data----Inform

ation----Knowledge

InventoryAssets

CharacterizeAssets

AppraiseAssets(Monetary

&Non-monetary)

Identify Opportunities &

InformDecision Making

Real Property AccountsINRMPsPermits

Market AppraisalBenefits TransferBenefit IndicatorsQualitative

The imperative -- recognize and leverage natural infrastructure as a set of assets with equity value

Better asset management --doing what we do today better using existing and emerging tools

LandEasementsUse RightsCreditsNatural Assets

QuantityQualityTemporal AspectsEtc

Geospatial DataEAs / EISsEmission

Inventories

Asset ManagementMarket StrategyInvestment StrategyTransactionsEquity AccountingOutreach

Data----Inform

ation----Knowledge

Data----Inform

ation----Knowledge

InventoryAssets

CharacterizeAssets

AppraiseAssets(Monetary

&Non-monetary)

Identify Opportunities &

InformDecision Making

Real Property AccountsINRMPsPermits

Market AppraisalBenefits TransferBenefit IndicatorsQualitative

The imperative -- recognize and leverage natural infrastructure as a set of assets with equity value

Better asset management --doing what we do today better using existing and emerging tools

LandEasementsUse RightsCreditsNatural Assets

QuantityQualityTemporal AspectsEtc

Geospatial DataEAs / EISsEmission

Inventories

InventoryAssets

CharacterizeAssets

AppraiseAssets(Monetary

&Non-monetary)

Identify Opportunities &

InformDecision Making

Real Property AccountsINRMPsPermits

Market AppraisalBenefits TransferBenefit IndicatorsQualitative

The imperative -- recognize and leverage natural infrastructure as a set of assets with equity value

Better asset management --doing what we do today better using existing and emerging tools

LandEasementsUse RightsCreditsNatural Assets

QuantityQualityTemporal AspectsEtc

Geospatial DataEAs / EISsEmission

Inventories

21I n t e g r i t y - S e r v i c e - E x c e l l e n c e

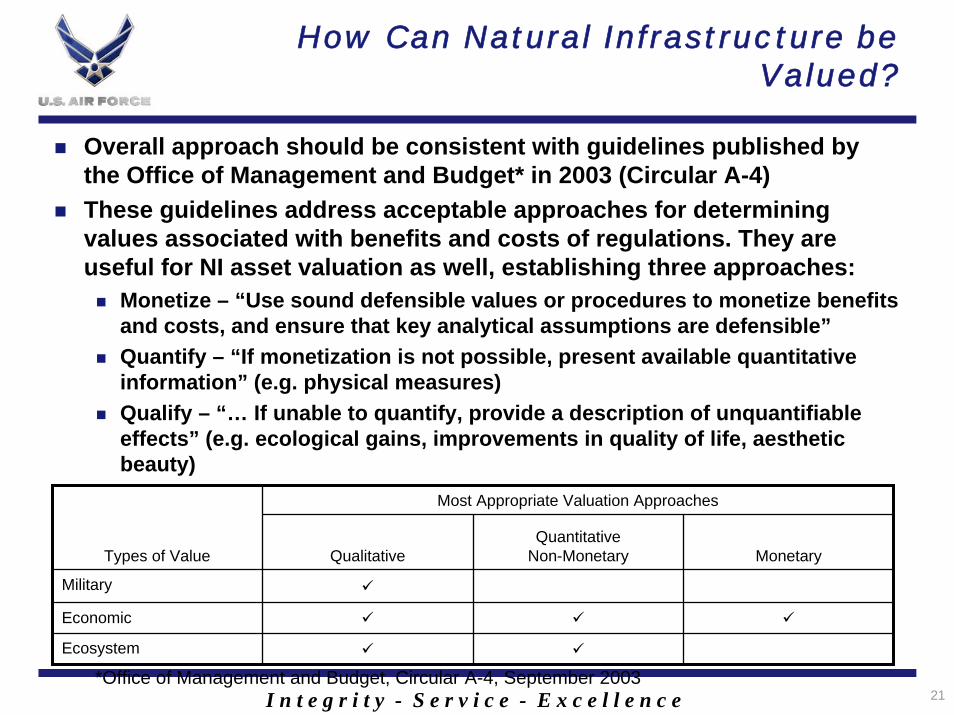

How Can Natural Infrastructure be Valued?

Overall approach should be consistent with guidelines published by the Office of Management and Budget* in 2003 (Circular A-4)These guidelines address acceptable approaches for determining values associated with benefits and costs of regulations. They are useful for NI asset valuation as well, establishing three approaches:

Monetize – “Use sound defensible values or procedures to monetize benefitsand costs, and ensure that key analytical assumptions are defensible” Quantify – “If monetization is not possible, present available quantitative information” (e.g. physical measures)Qualify – “… If unable to quantify, provide a description of unquantifiable effects” (e.g. ecological gains, improvements in quality of life, aesthetic beauty)

*Office of Management and Budget, Circular A-4, September 2003

Most Appropriate Valuation Approaches

Types of Value QualitativeQuantitative

Non-Monetary Monetary

Military

Economic

Ecosystem

22I n t e g r i t y - S e r v i c e - E x c e l l e n c e

Methodology

Summarize monetary and non-monetary values of natural infrastructure assets and servicesCreate ‘roll-up’ tables of monetary, quantitative, and descriptive values

Summarize monetary and non-monetary values of natural infrastructure assets and servicesCreate ‘roll-up’ tables of monetary, quantitative, and descriptive values

Natural AssetsNatural Assets

Environmental Benefit Indicators,

Habitat Equivalency Analysis, etc.

Environmental Benefit Indicators,

Habitat Equivalency Analysis, etc.

Step1:Inventory & characterize NI

Step 2: Identify valuations to perform

Step 3: Describe NI values

Step 4:Summarize values

Step 4: Quantify selected values

Step 5: Monetize selected values

MarketAppraisal,Benefits Transfer

MarketAppraisal,Benefits Transfer

Resource CharacteristicsNatural Assets: size, location, species, seasonal variations, other biophysical measures

Statutory Assets: permit conditions, quantified discharges, credits, etc.Services provided by natural assets

Resource CharacteristicsNatural Assets: size, location, species, seasonal variations, other biophysical measures

Statutory Assets: permit conditions, quantified discharges, credits, etc.Services provided by natural assets

Statutory AssetsStatutory Assets Services to MonetizeServices to Monetize Other Services Other Services SpeciesSpecies

Forests, Wetlands, Croplands, Streams,

etc.

Forests, Wetlands, Croplands, Streams,

etc.

Permits, Rights, Credits, etc.

Permits, Rights, Credits, etc.

Farming, Grazing, Timbering,

Recreation, etc.

Farming, Grazing, Timbering,

Recreation, etc.

Habitat Provision,Water Regulation, Waste Assimilation,

etc.

Habitat Provision,Water Regulation, Waste Assimilation,

etc.

Area, Quality, etc.

Area, Quality, etc.

Volumes, TemporalAspects, etc.

Volumes, TemporalAspects, etc.

Lease Conditions,Visitor Days, etc.

Lease Conditions,Visitor Days, etc.

Threatened andEndangered

Species, Other Valued Spices

Threatened andEndangered

Species, Other Valued Spices

Market Appraisal, Substitute Costs

Benefits Transfer, etc.

Market Appraisal, Substitute Costs

Benefits Transfer, etc.

Market Appraisal: Comparable Sales,

Income Stream,Replacement Cost,

etc.

Market Appraisal: Comparable Sales,

Income Stream,Replacement Cost,

etc.