Embed Size (px)

Citation preview

NATIONAL STRATEGY STUDY

FOR IMPLEMENTATION OF

THE CDM IN COLOMBIA

FINAL REPORT

(ENGLISH VERSION)

SANTAFÉ DE BOGOTÁ, AUGUST 2000

PROGRAM OF NATIONAL CDM/JI STRATEGY STUDIESNSS PROGRAM

Acknowledgements

The authors of this study would like to acknowledge the financial and technicalassistance of the World Bank, as well as the Swiss Government and member ofSteering Committee.

Peter Kalas World Bank – NSS Program Walter Vergara World Bank Martin Enderlin Swiss Goverment Anne Arquit Swiss Goverment Elsa Lozano F Colombian Association of Reforesters - ACOFORE Rodrigo Cid Colombian Association of Reforesters - ACOFORE Daniel Vergara Colombian Association of Petroleum Producers– ACP Angela Gómez National Association of Colombian Industries – ANDI Carlos Herrera National Association of Colombian Industries – ANDI María Emilia Correa Sustainable Development National Cauncil– CECODES Ricardo León Márquez National Center of Clean Production Juan Pablo Bonilla FUNDESARROLLO Alexandra Hernández Colombian Insitute of Cement Producers – ICPC Oscar Suarez Colombian Institute of Metheorology, Hidrology and

Envierontal Studies - IDEAM María Teresa Palacios Ministry of Agriculture Nelson Lozano Ministry of Agriculture Eduardo Salas Ministry of Economic Development Felipe Ramos Ministry of Economic Development Hernando Trujillo Ministry of Justice Mauricio Amaya Ministry of Justice Javier Camargo Ministry of the Environment Felipe García Administration Unit of National Natural Park System -

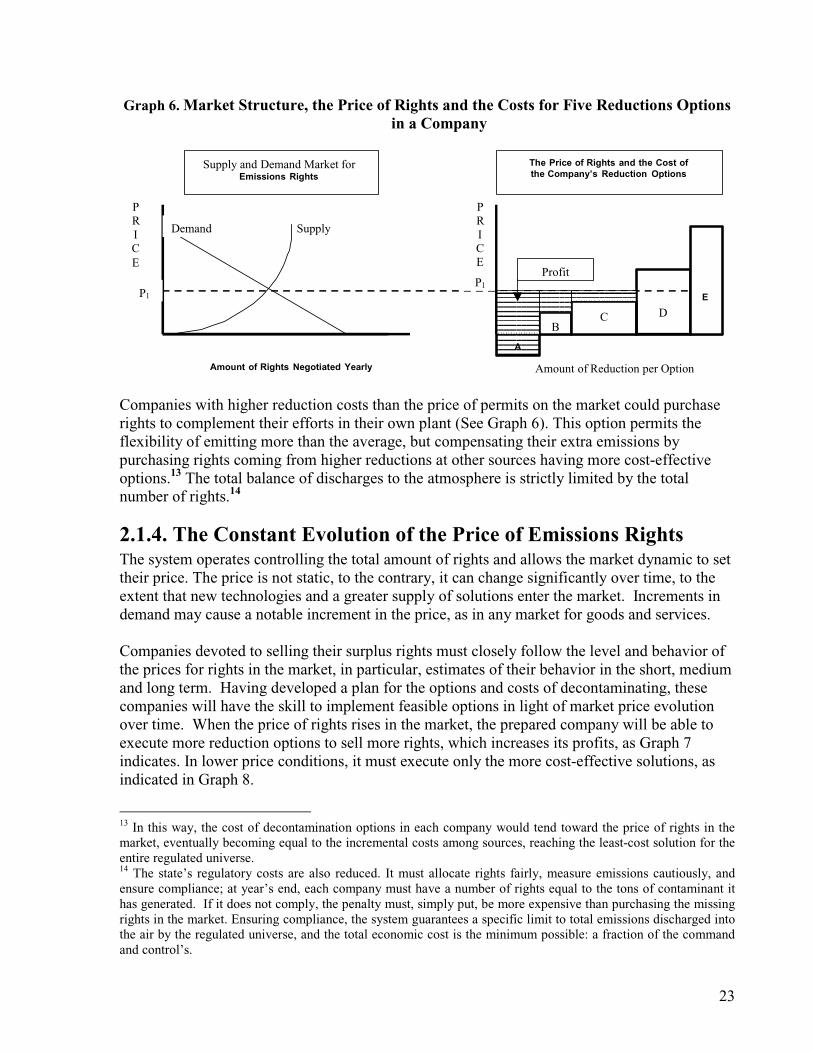

UAESPNN Gilberto Jaimes Planing Unit of Mining and Energy - UPME Marcela Bonilla Ministry of the Environment

iii

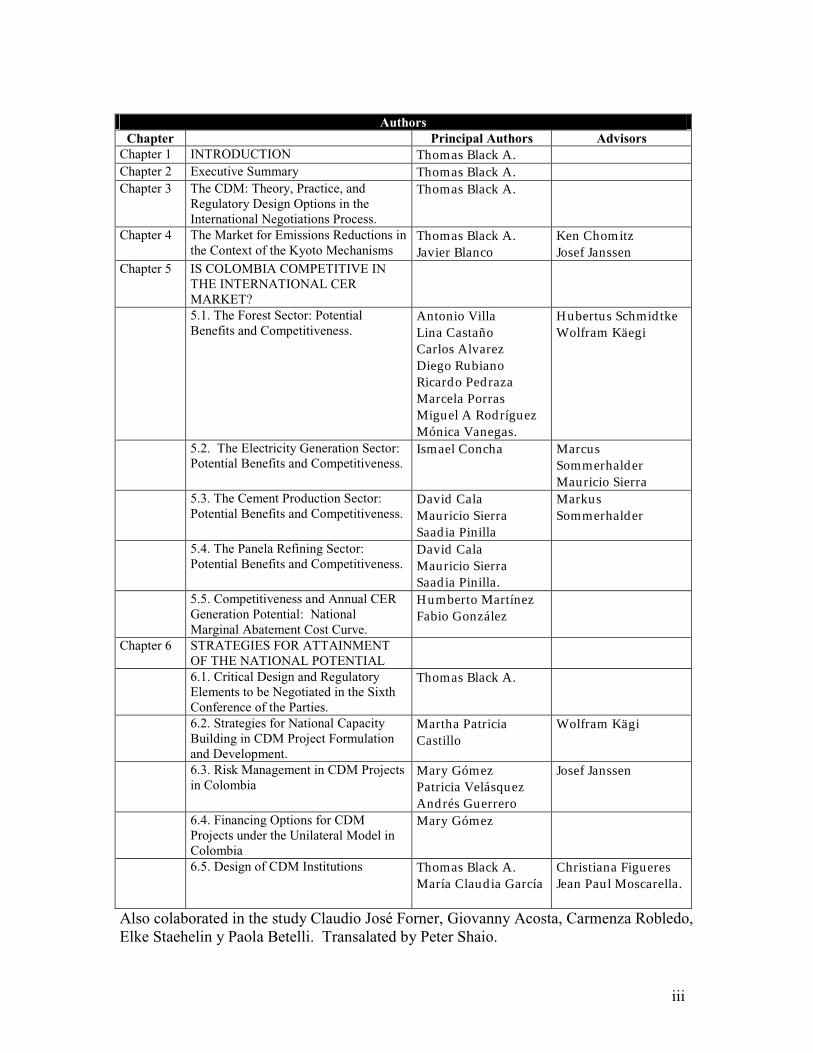

AuthorsChapter Principal Authors AdvisorsChapter 1 INTRODUCTION Thomas Black A.Chapter 2 Executive Summary Thomas Black A.Chapter 3 The CDM: Theory, Practice, and

Regulatory Design Options in theInternational Negotiations Process.

Thomas Black A.

Chapter 4 The Market for Emissions Reductions inthe Context of the Kyoto Mechanisms

Thomas Black A.Javier Blanco

Ken ChomitzJosef Janssen

Chapter 5 IS COLOMBIA COMPETITIVE INTHE INTERNATIONAL CERMARKET?5.1. The Forest Sector: PotentialBenefits and Competitiveness.

Antonio VillaLina CastañoCarlos AlvarezDiego RubianoRicardo PedrazaMarcela PorrasMiguel A RodríguezMónica Vanegas.

Hubertus SchmidtkeWolfram Käegi

5.2. The Electricity Generation Sector:Potential Benefits and Competitiveness.

Ismael Concha MarcusSommerhalderMauricio Sierra

5.3. The Cement Production Sector:Potential Benefits and Competitiveness.

David CalaMauricio SierraSaadia Pinilla

MarkusSommerhalder

5.4. The Panela Refining Sector:Potential Benefits and Competitiveness.

David CalaMauricio SierraSaadia Pinilla.

5.5. Competitiveness and Annual CERGeneration Potential: NationalMarginal Abatement Cost Curve.

Humberto MartínezFabio González

Chapter 6 STRATEGIES FOR ATTAINMENTOF THE NATIONAL POTENTIAL6.1. Critical Design and RegulatoryElements to be Negotiated in the SixthConference of the Parties.

Thomas Black A.

6.2. Strategies for National CapacityBuilding in CDM Project Formulationand Development.

Martha PatriciaCastillo

Wolfram Kägi

6.3. Risk Management in CDM Projectsin Colombia

Mary GómezPatricia VelásquezAndrés Guerrero

Josef Janssen

6.4. Financing Options for CDMProjects under the Unilateral Model inColombia

Mary Gómez

6.5. Design of CDM Institutions Thomas Black A.María Claudia García

Christiana FigueresJean Paul Moscarella.

Also colaborated in the study Claudio José Forner, Giovanny Acosta, Carmenza Robledo,Elke Staehelin y Paola Betelli. Transalated by Peter Shaio.

iv

Contents

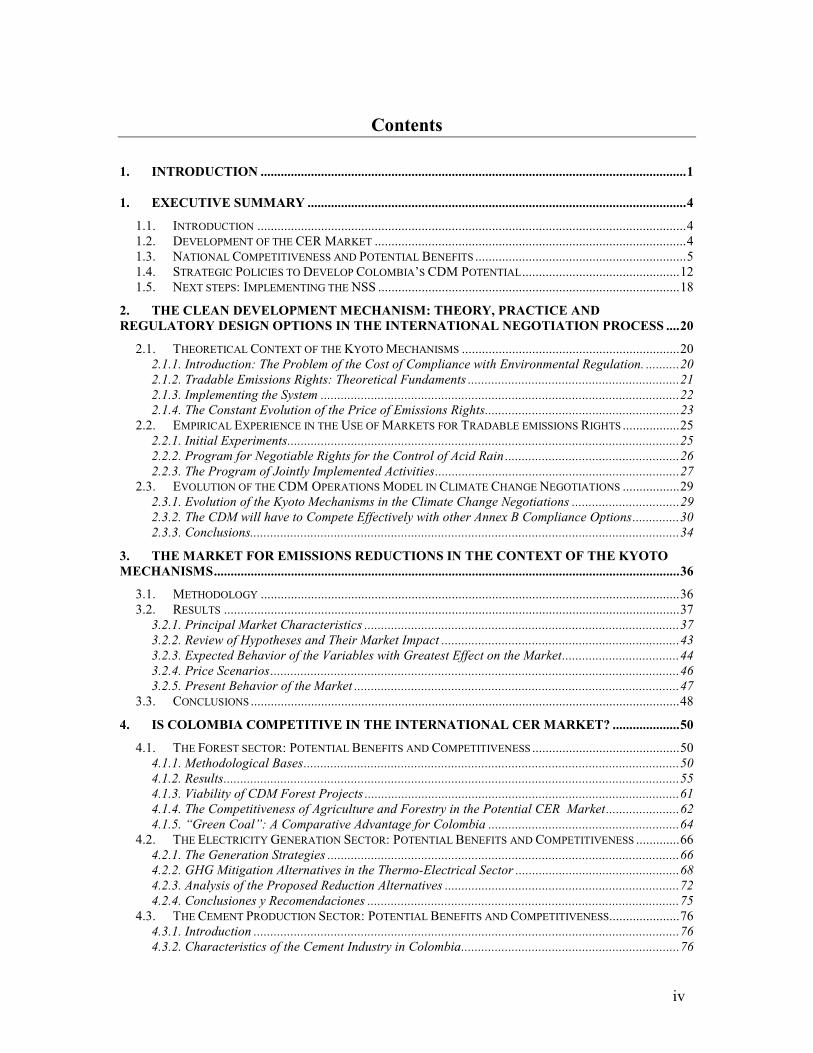

1. INTRODUCTION ...............................................................................................................................1

1. EXECUTIVE SUMMARY .................................................................................................................4

1.1. INTRODUCTION ................................................................................................................................41.2. DEVELOPMENT OF THE CER MARKET .............................................................................................41.3. NATIONAL COMPETITIVENESS AND POTENTIAL BENEFITS ...............................................................51.4. STRATEGIC POLICIES TO DEVELOP COLOMBIA’S CDM POTENTIAL...............................................121.5. NEXT STEPS: IMPLEMENTING THE NSS ..........................................................................................18

2. THE CLEAN DEVELOPMENT MECHANISM: THEORY, PRACTICE ANDREGULATORY DESIGN OPTIONS IN THE INTERNATIONAL NEGOTIATION PROCESS ....20

2.1. THEORETICAL CONTEXT OF THE KYOTOMECHANISMS .................................................................202.1.1. Introduction: The Problem of the Cost of Compliance with Environmental Regulation. ..........202.1.2. Tradable Emissions Rights: Theoretical Fundaments ...............................................................212.1.3. Implementing the System ...........................................................................................................222.1.4. The Constant Evolution of the Price of Emissions Rights..........................................................23

2.2. EMPIRICAL EXPERIENCE IN THE USE OFMARKETS FOR TRADABLE EMISSIONS RIGHTS .................252.2.1. Initial Experiments.....................................................................................................................252.2.2. Program for Negotiable Rights for the Control of Acid Rain ....................................................262.2.3. The Program of Jointly Implemented Activities.........................................................................27

2.3. EVOLUTION OF THE CDM OPERATIONSMODEL IN CLIMATE CHANGE NEGOTIATIONS .................292.3.1. Evolution of the Kyoto Mechanisms in the Climate Change Negotiations ................................292.3.2. The CDM will have to Compete Effectively with other Annex B Compliance Options..............302.3.3. Conclusions................................................................................................................................34

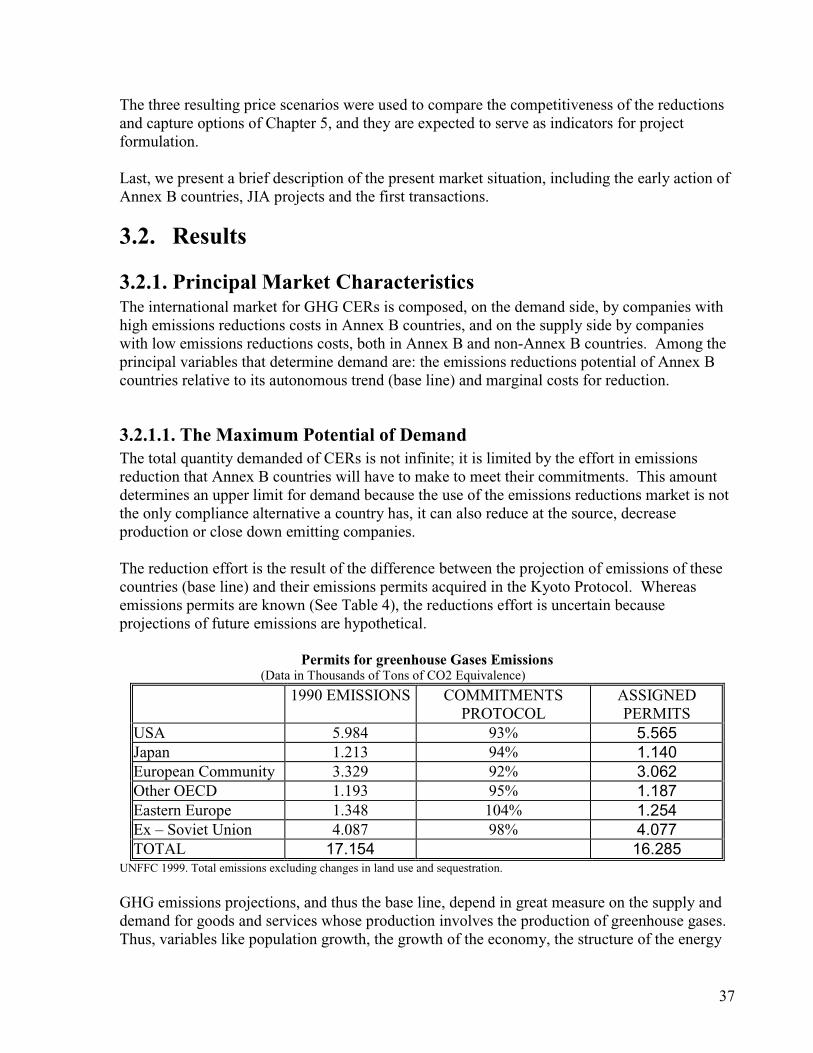

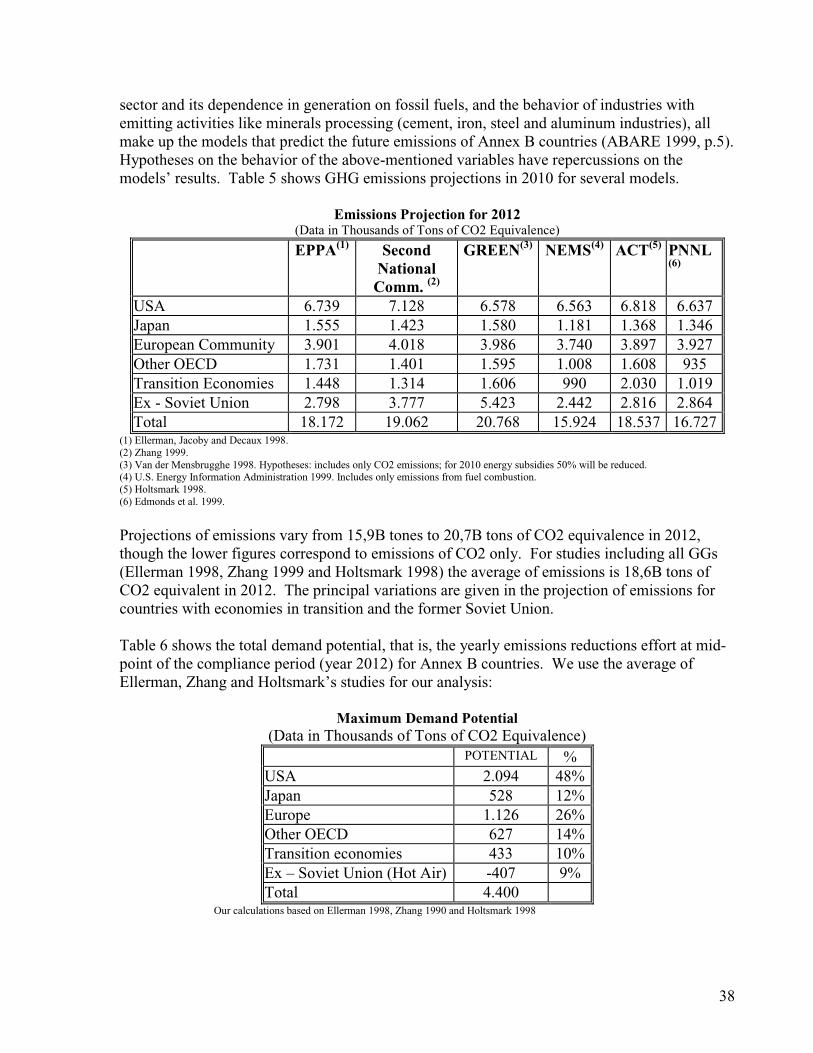

3. THE MARKET FOR EMISSIONS REDUCTIONS IN THE CONTEXT OF THE KYOTOMECHANISMS...........................................................................................................................................36

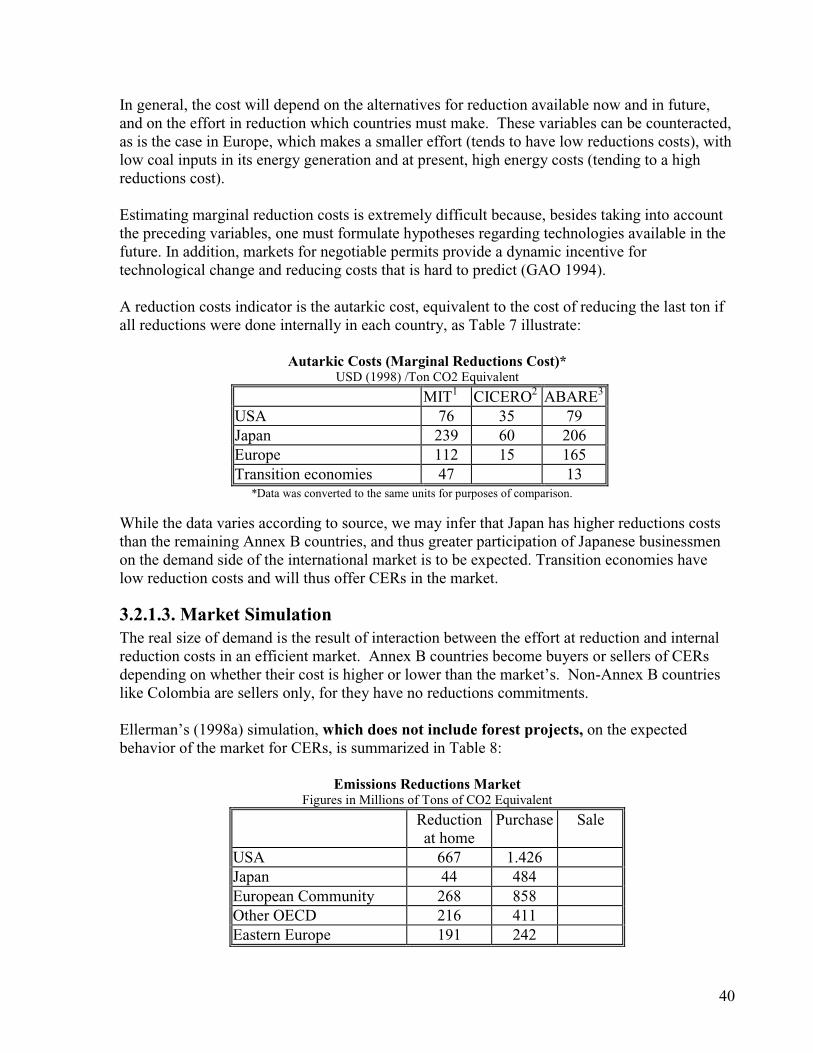

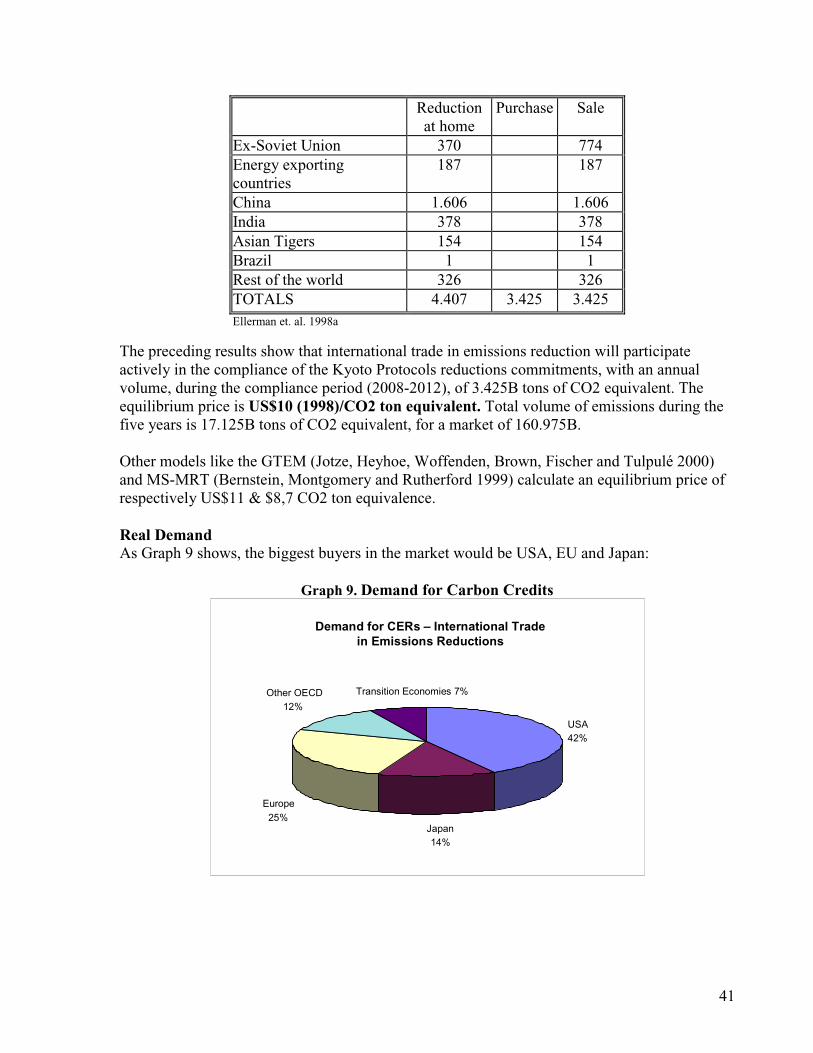

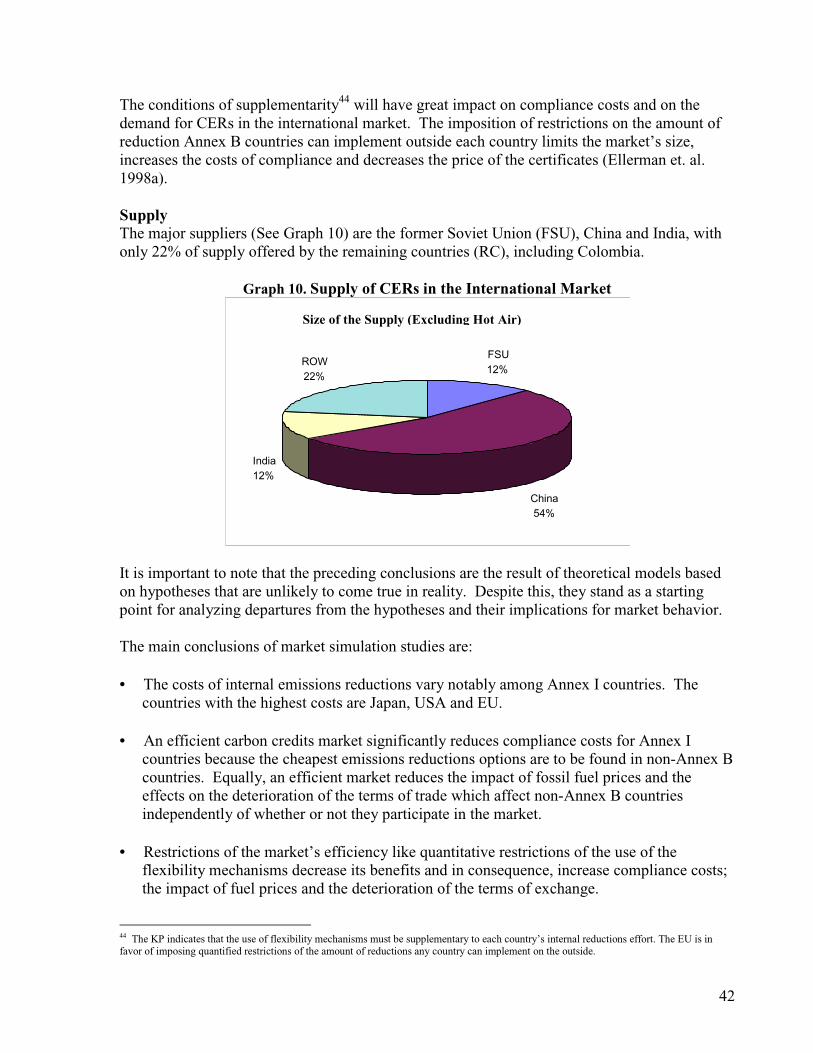

3.1. METHODOLOGY .............................................................................................................................363.2. RESULTS ........................................................................................................................................373.2.1. Principal Market Characteristics ..............................................................................................373.2.2. Review of Hypotheses and Their Market Impact .......................................................................433.2.3. Expected Behavior of the Variables with Greatest Effect on the Market...................................443.2.4. Price Scenarios..........................................................................................................................463.2.5. Present Behavior of the Market .................................................................................................47

3.3. CONCLUSIONS ................................................................................................................................48

4. IS COLOMBIA COMPETITIVE IN THE INTERNATIONAL CER MARKET? ....................50

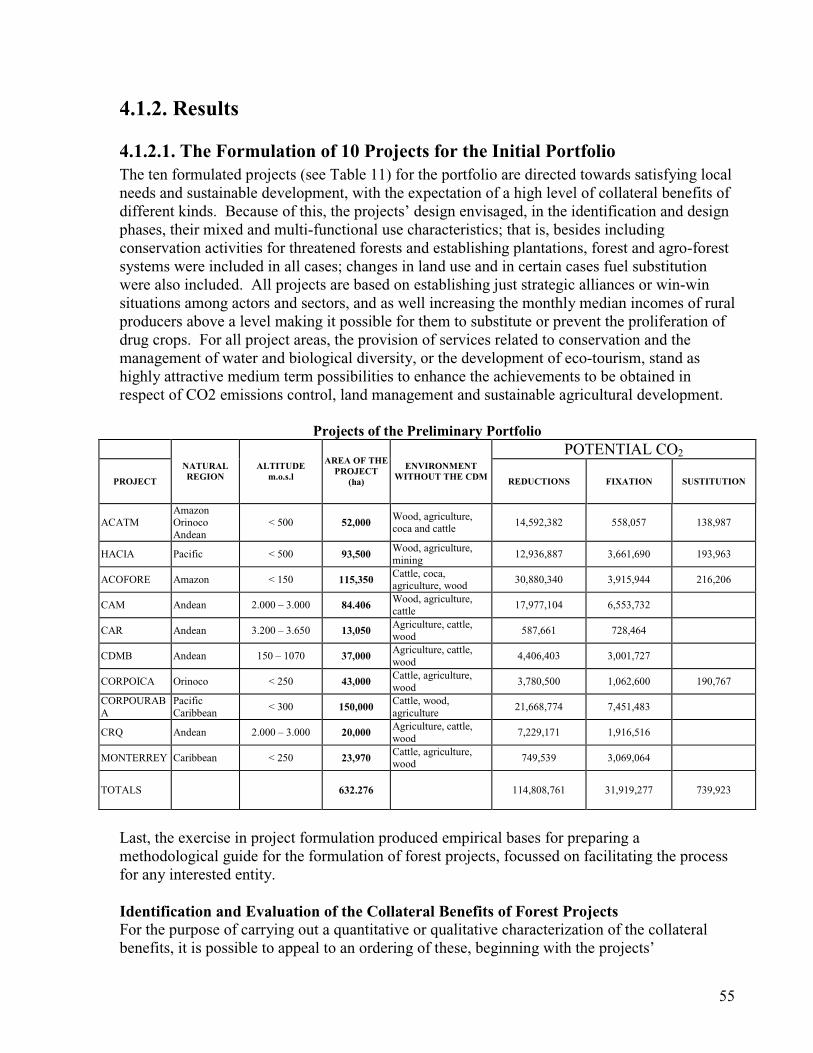

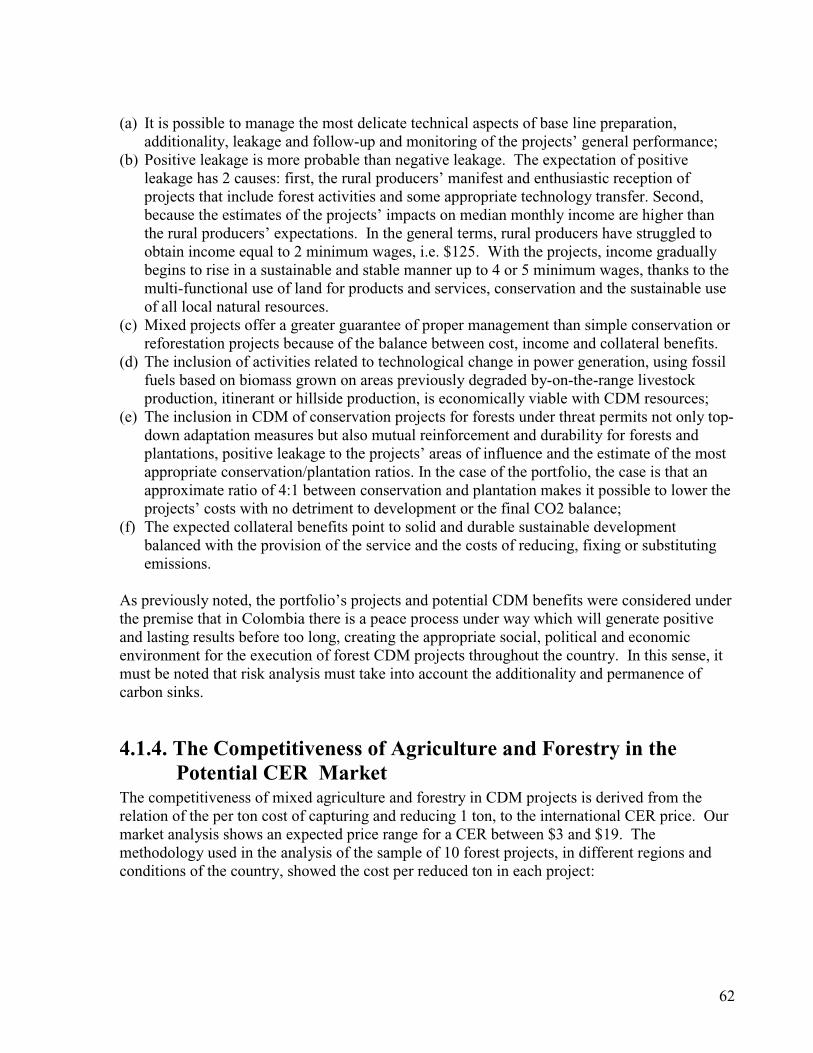

4.1. THE FOREST SECTOR: POTENTIAL BENEFITS AND COMPETITIVENESS ............................................504.1.1. Methodological Bases................................................................................................................504.1.2. Results........................................................................................................................................554.1.3. Viability of CDM Forest Projects ..............................................................................................614.1.4. The Competitiveness of Agriculture and Forestry in the Potential CER Market......................624.1.5. “Green Coal”: A Comparative Advantage for Colombia .........................................................64

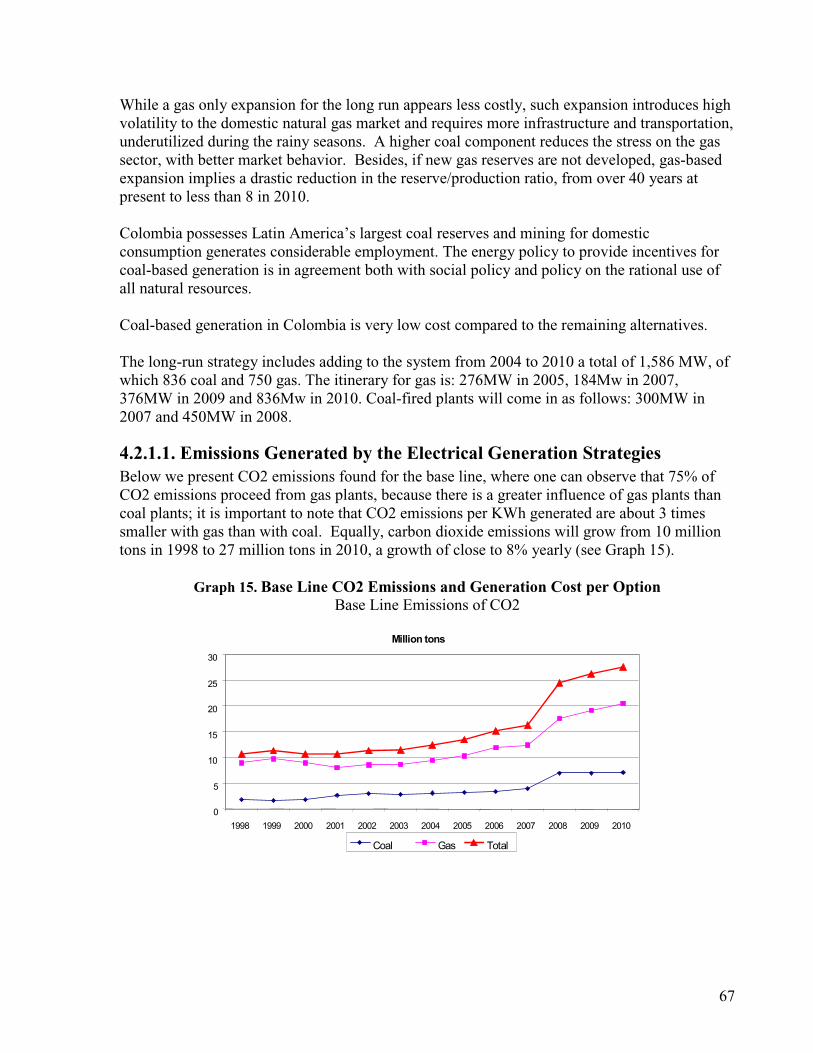

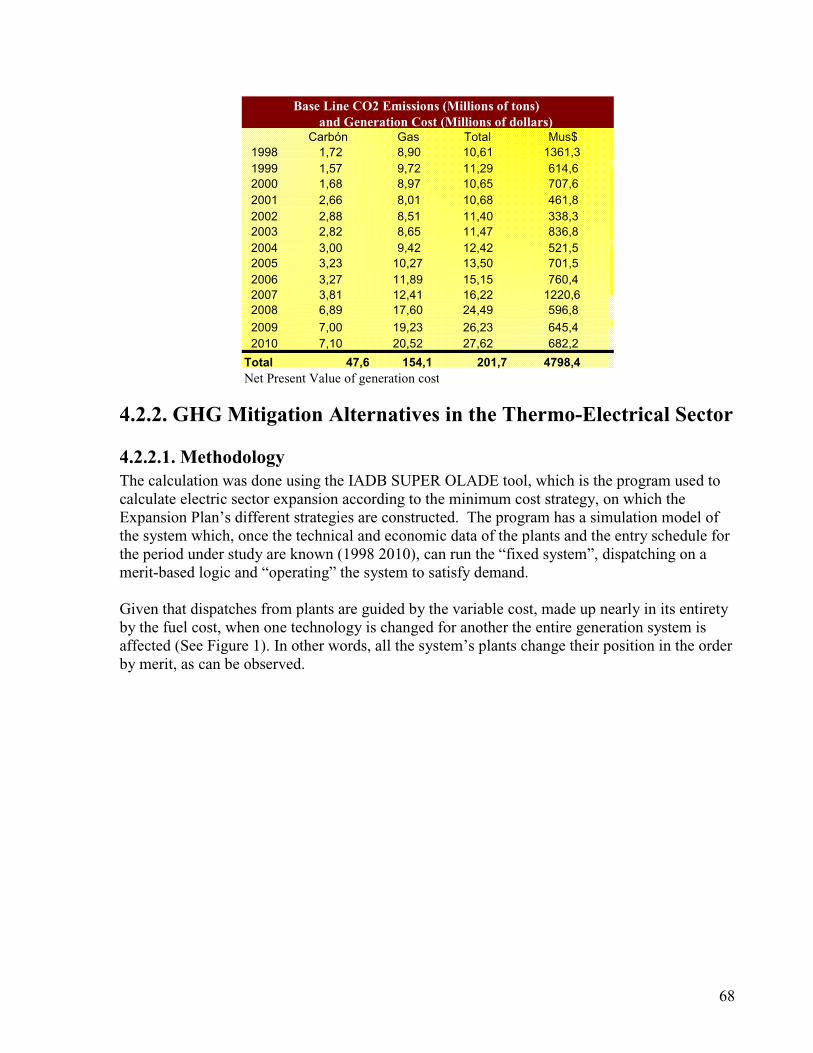

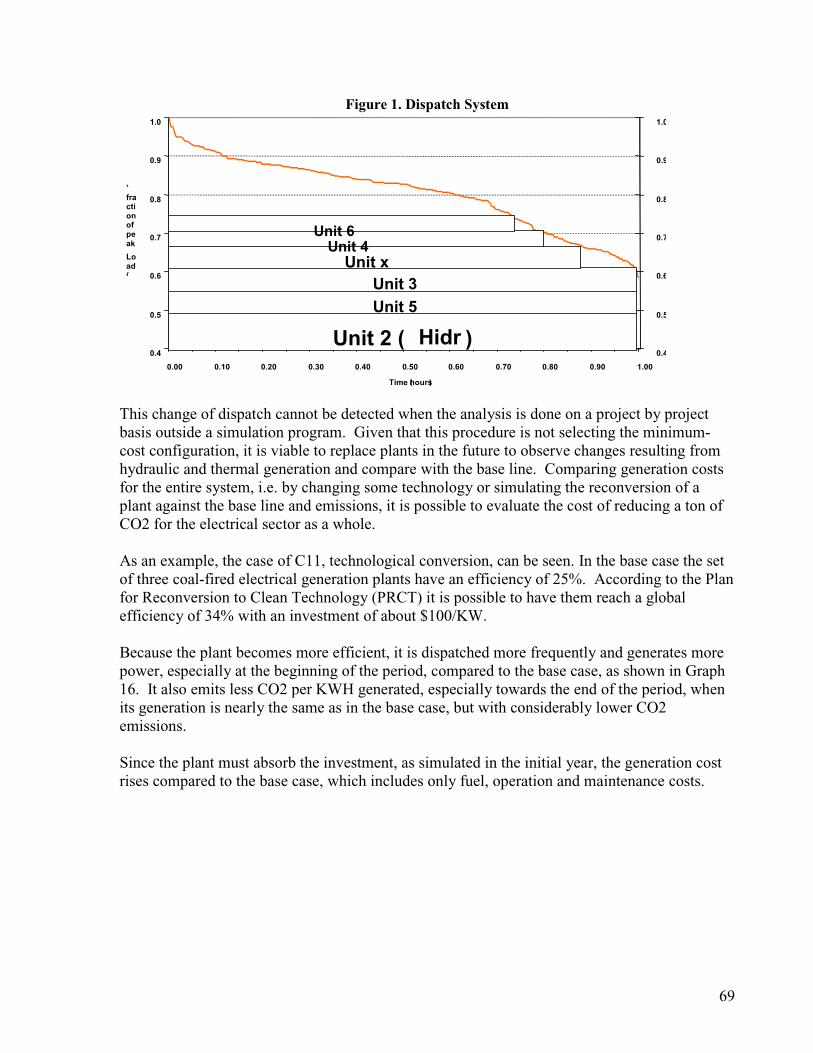

4.2. THE ELECTRICITY GENERATION SECTOR: POTENTIAL BENEFITS AND COMPETITIVENESS .............664.2.1. The Generation Strategies .........................................................................................................664.2.2. GHG Mitigation Alternatives in the Thermo-Electrical Sector .................................................684.2.3. Analysis of the Proposed Reduction Alternatives ......................................................................724.2.4. Conclusiones y Recomendaciones .............................................................................................75

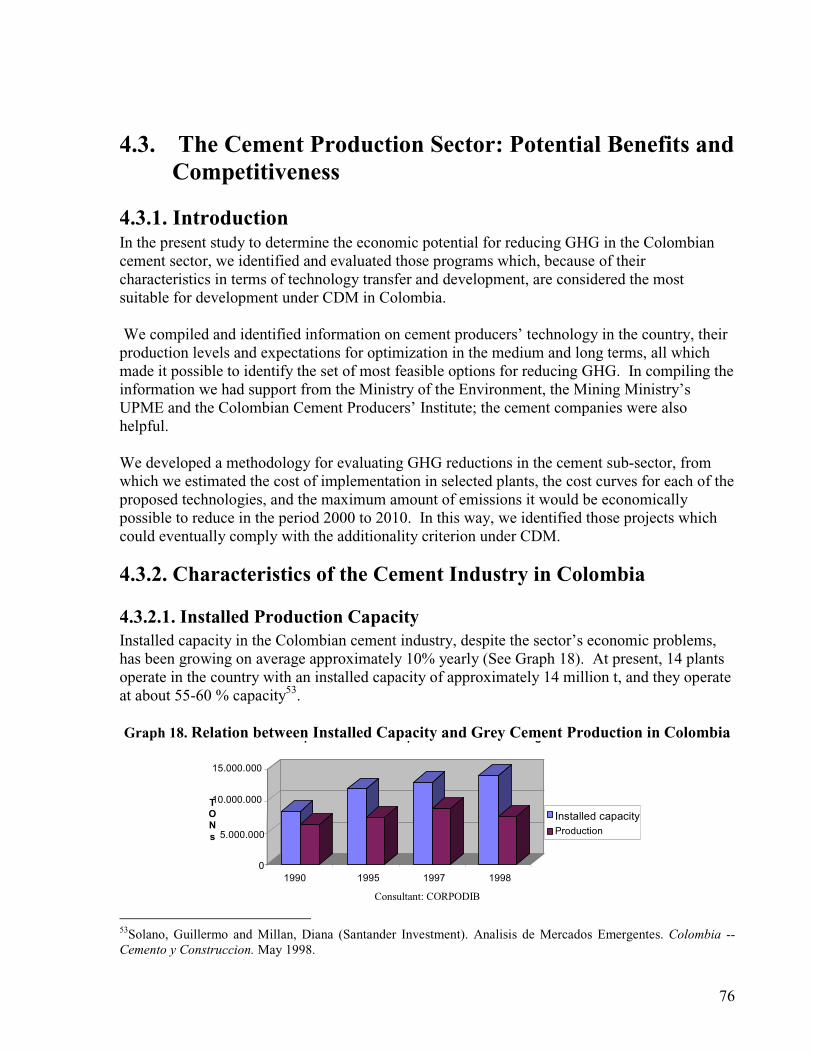

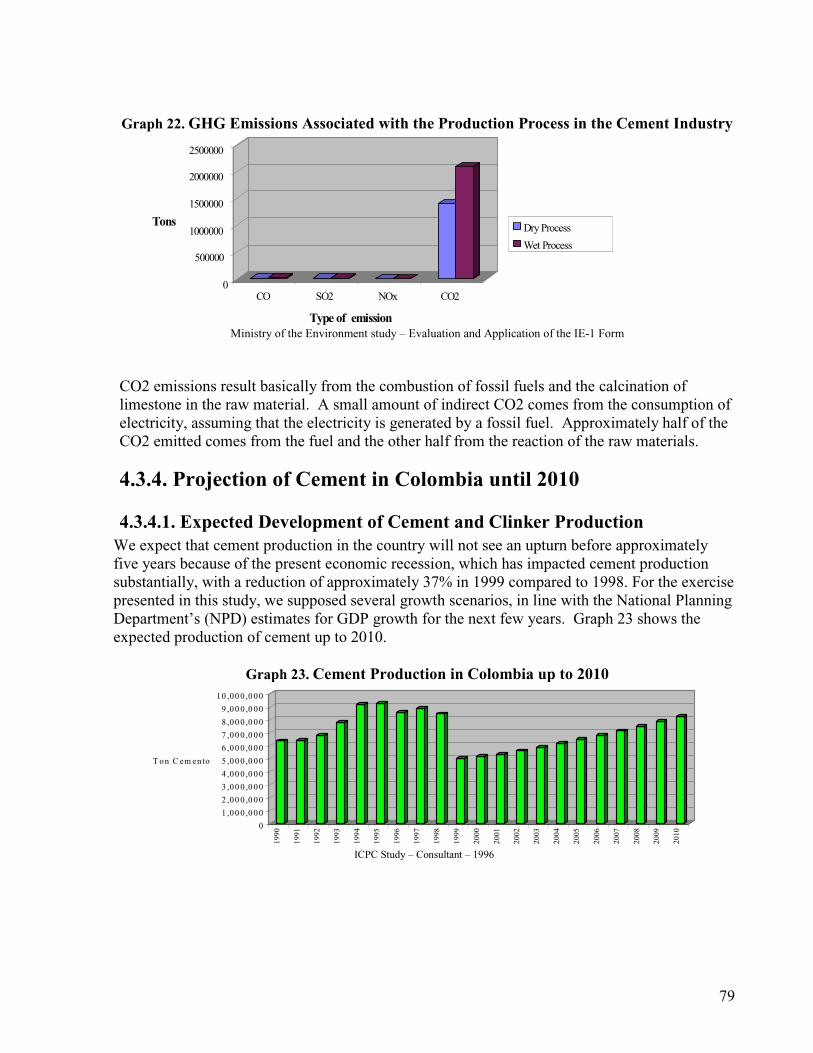

4.3. THE CEMENT PRODUCTION SECTOR: POTENTIAL BENEFITS AND COMPETITIVENESS.....................764.3.1. Introduction ...............................................................................................................................764.3.2. Characteristics of the Cement Industry in Colombia.................................................................76

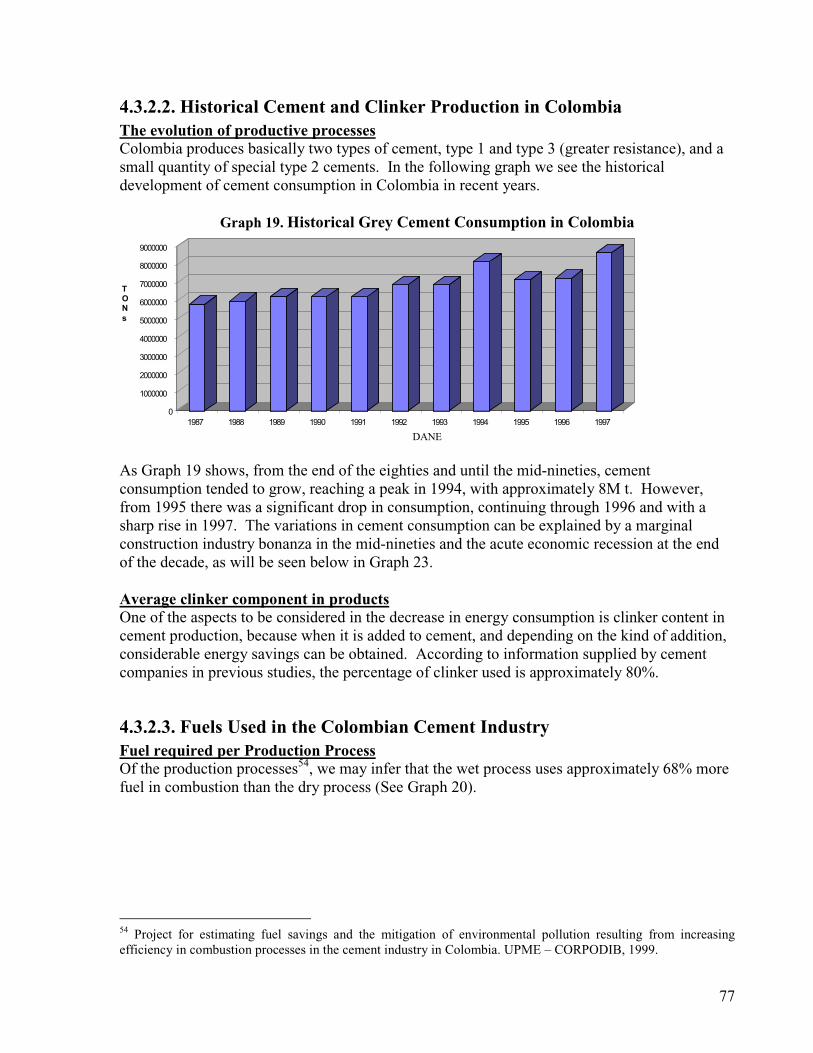

v

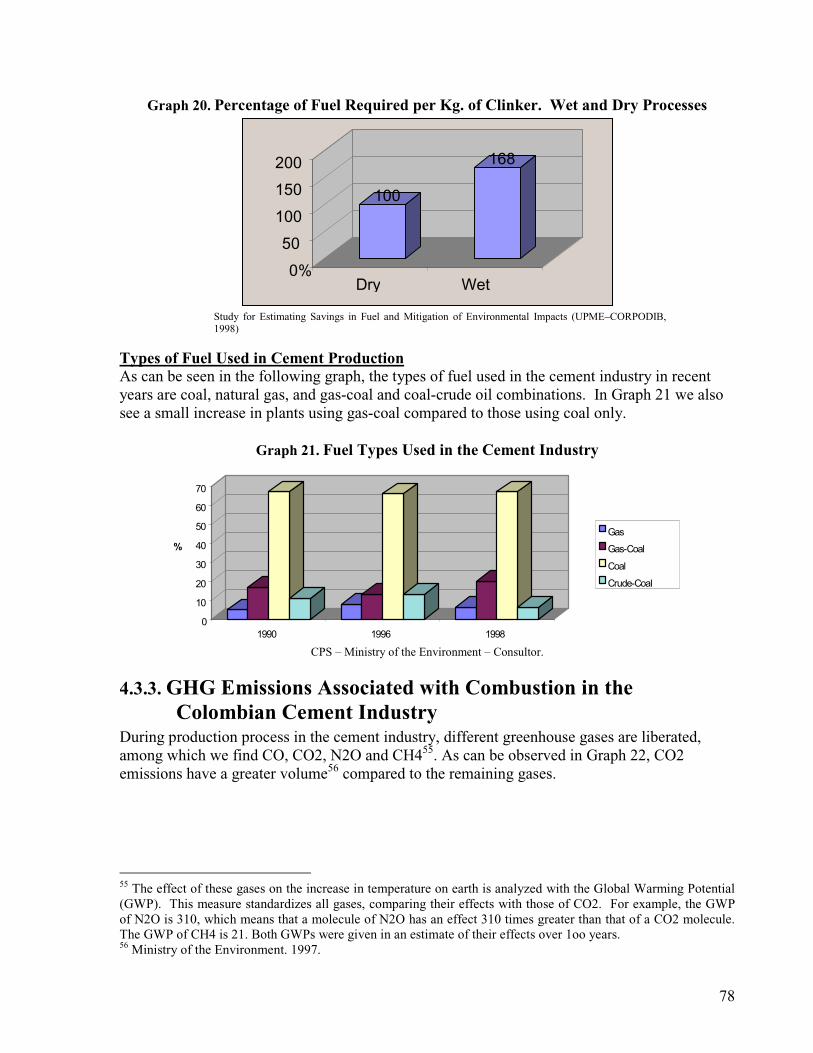

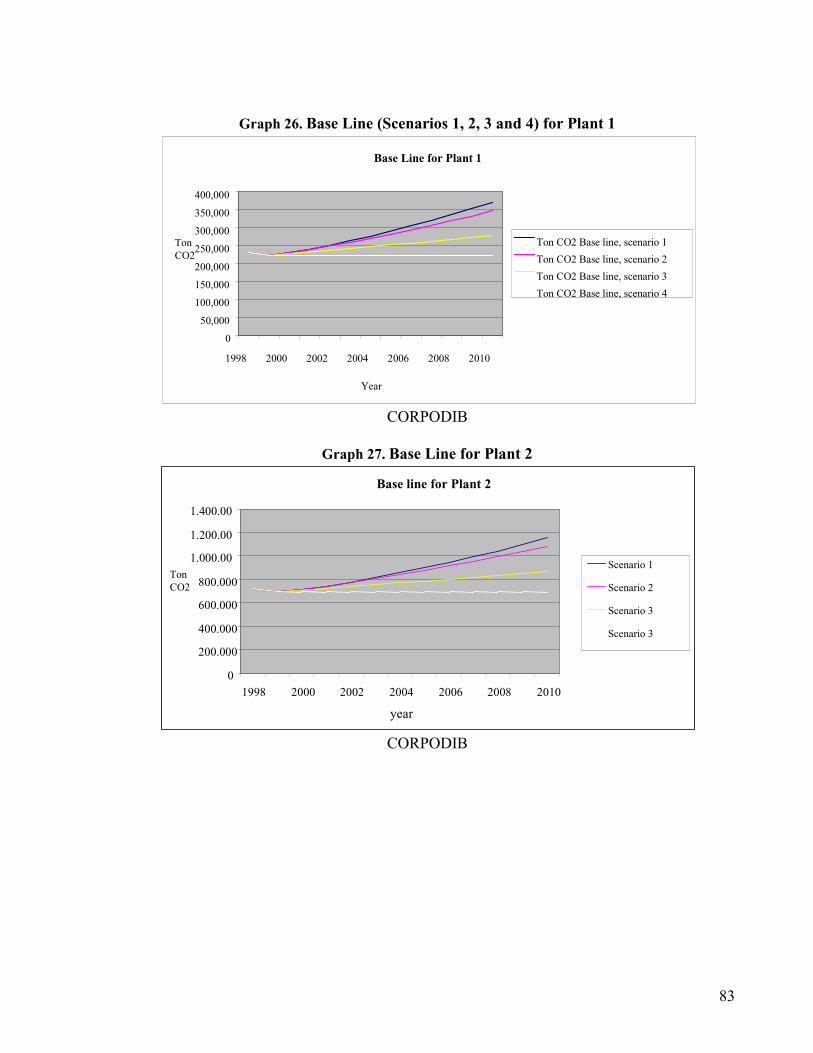

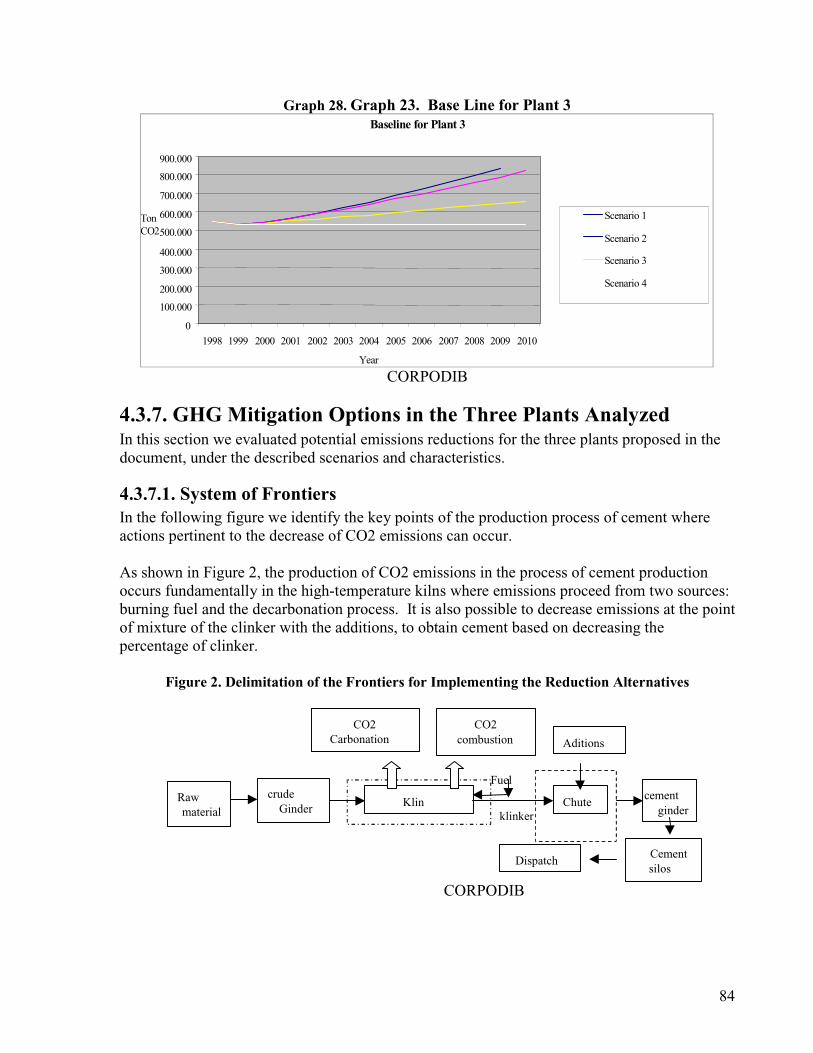

4.3.3. GHG Emissions Associated with Combustion in the Colombian Cement Industry ..................784.3.4. Projection of Cement in Colombia until 2010 ...........................................................................794.3.5. Technology and Installed Capacity in the Cement Sector in Colombia.....................................804.3.6. Base Line of GHG Emissions in the Cement Sector ..................................................................804.3.7. GHG Mitigation Options in the Three Plants Analyzed ............................................................844.3.8. Analysis of Proposed Reduction Alternatives ............................................................................924.3.9. Conclusions and Recommendations ..........................................................................................93

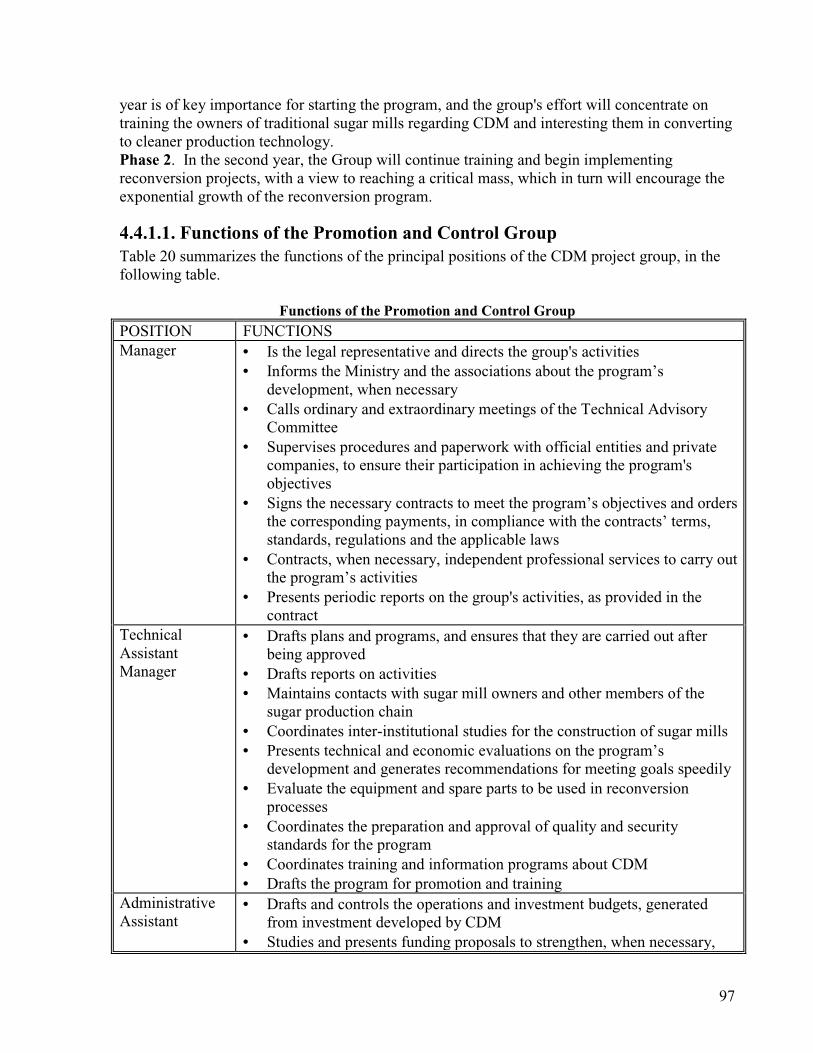

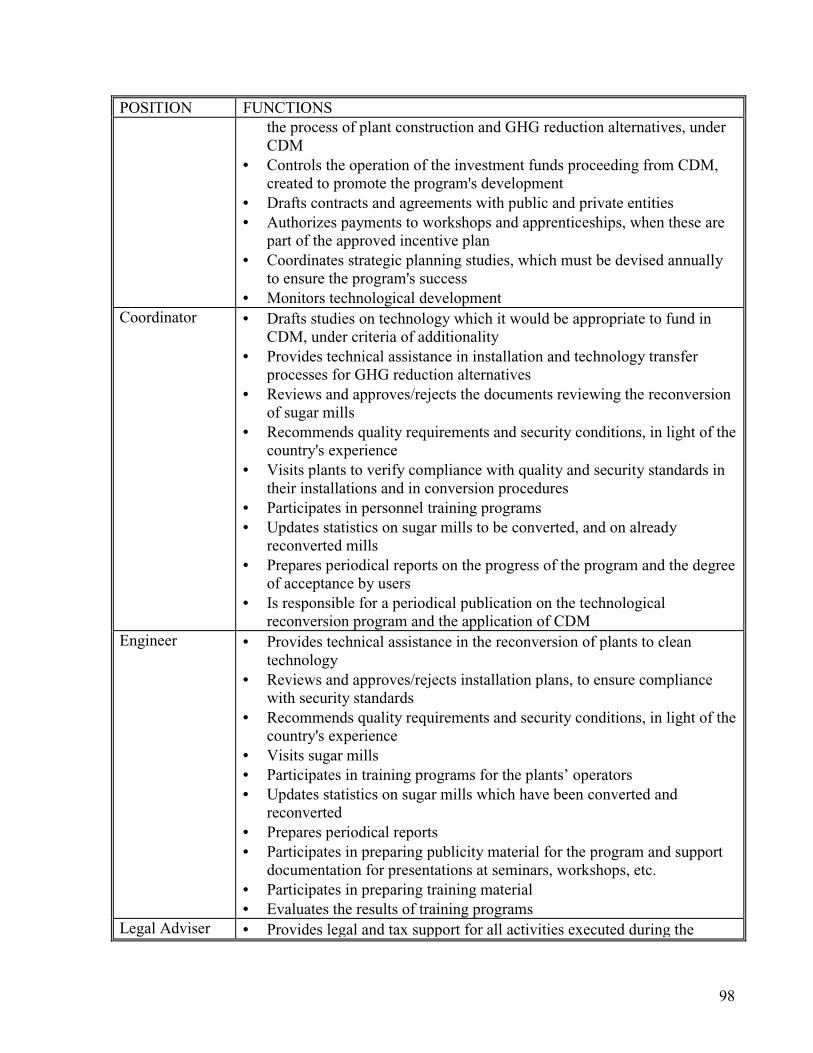

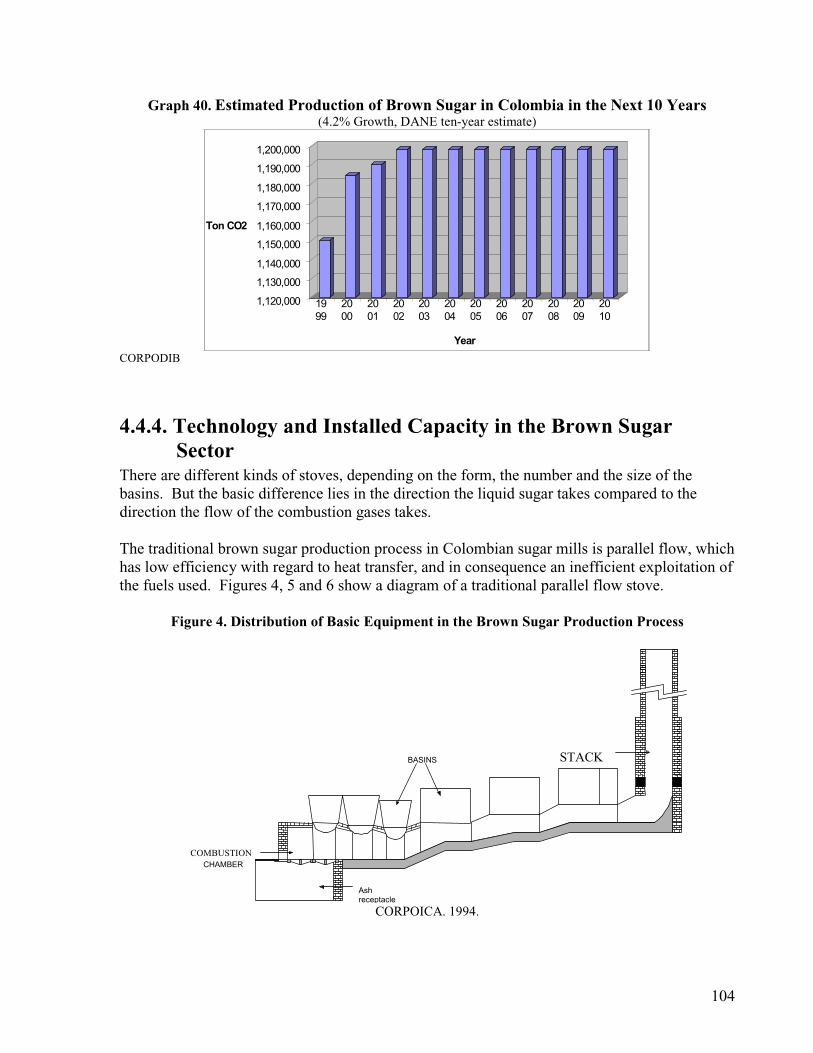

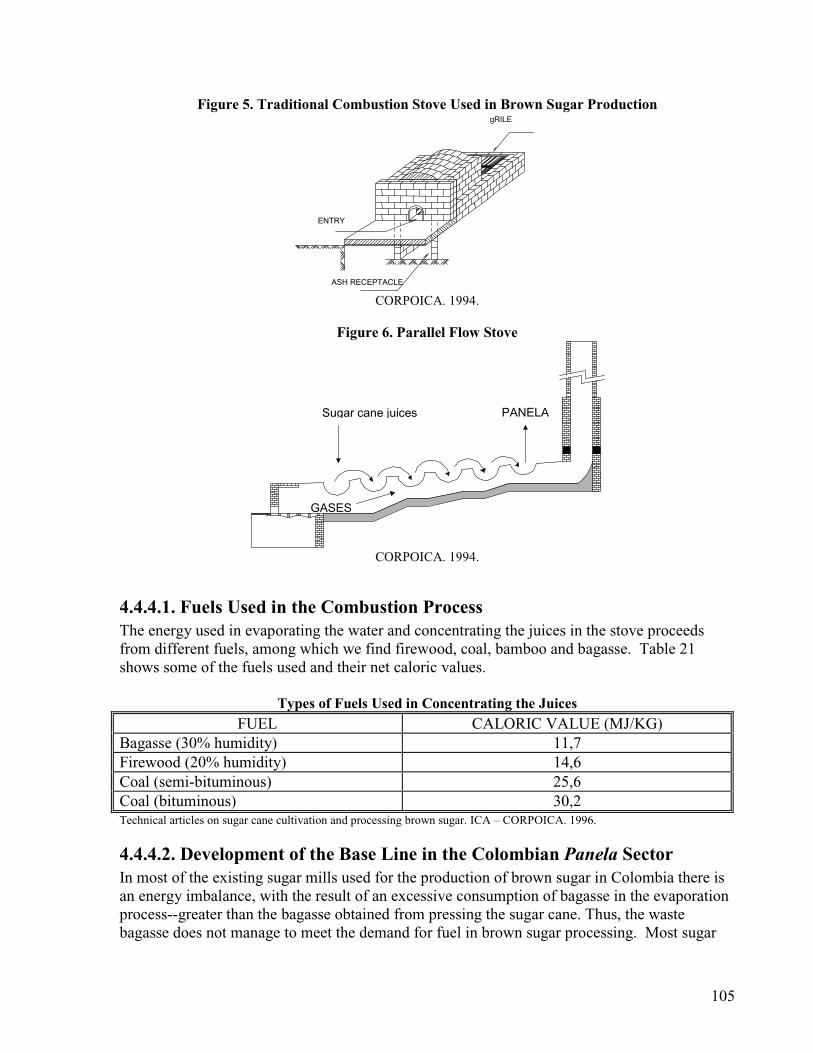

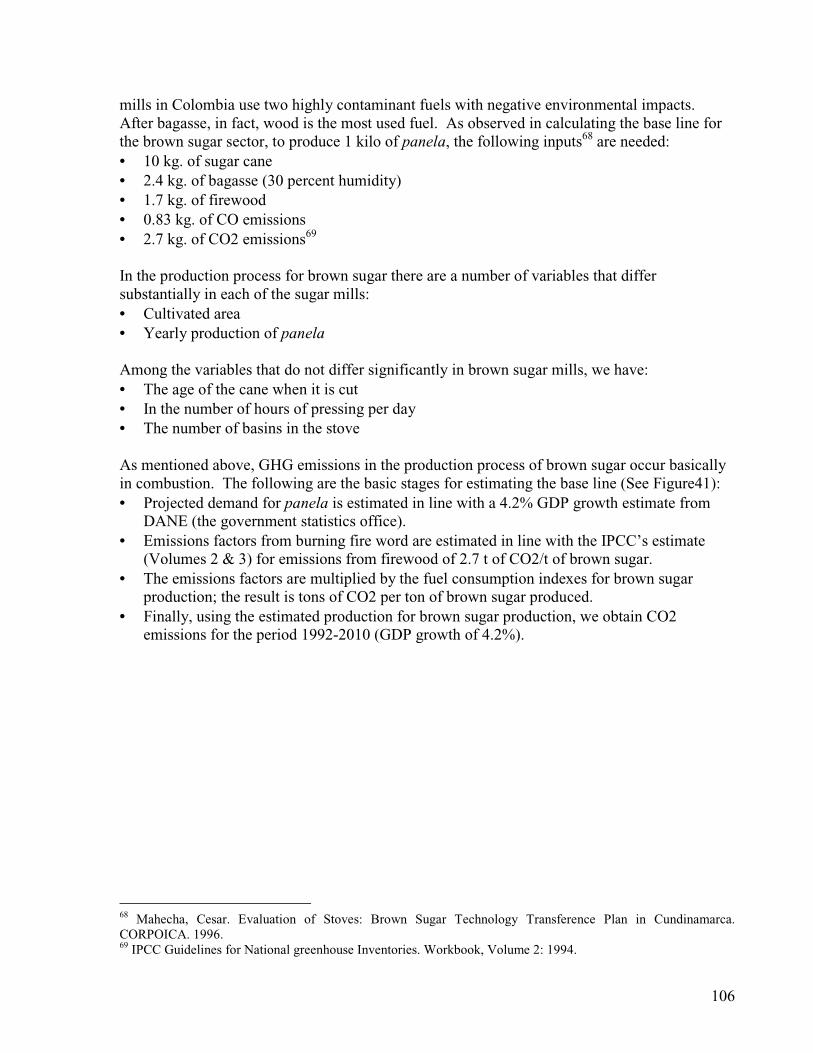

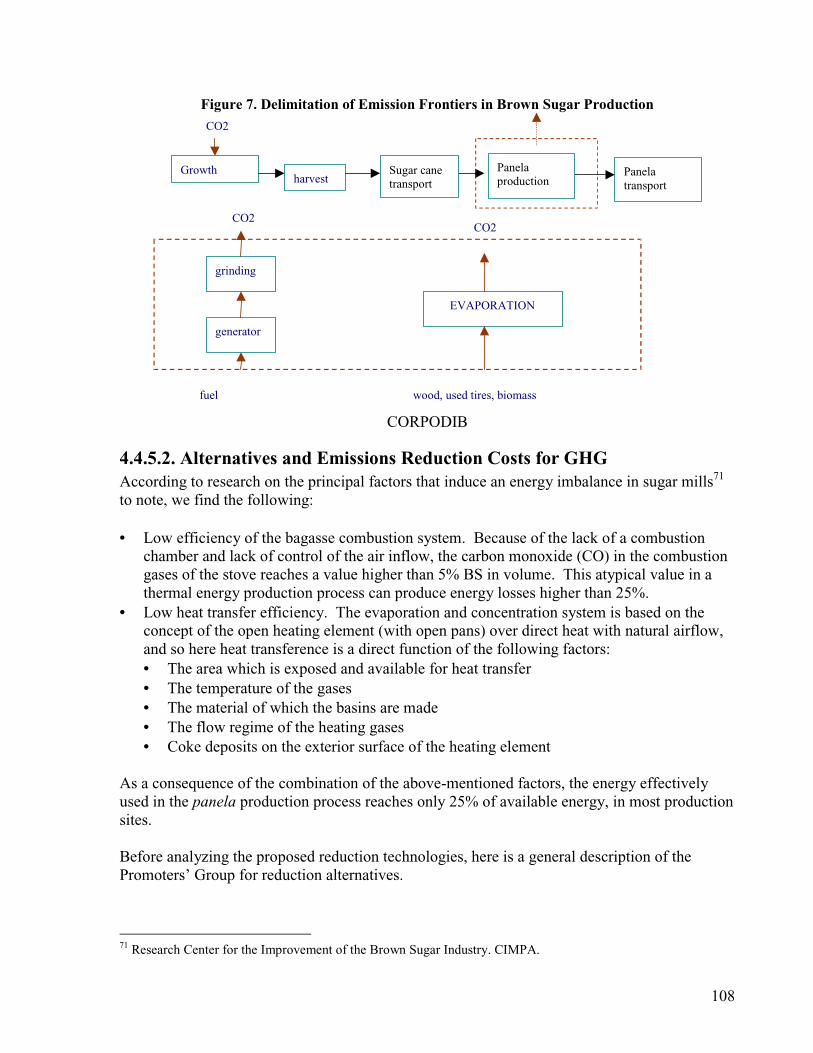

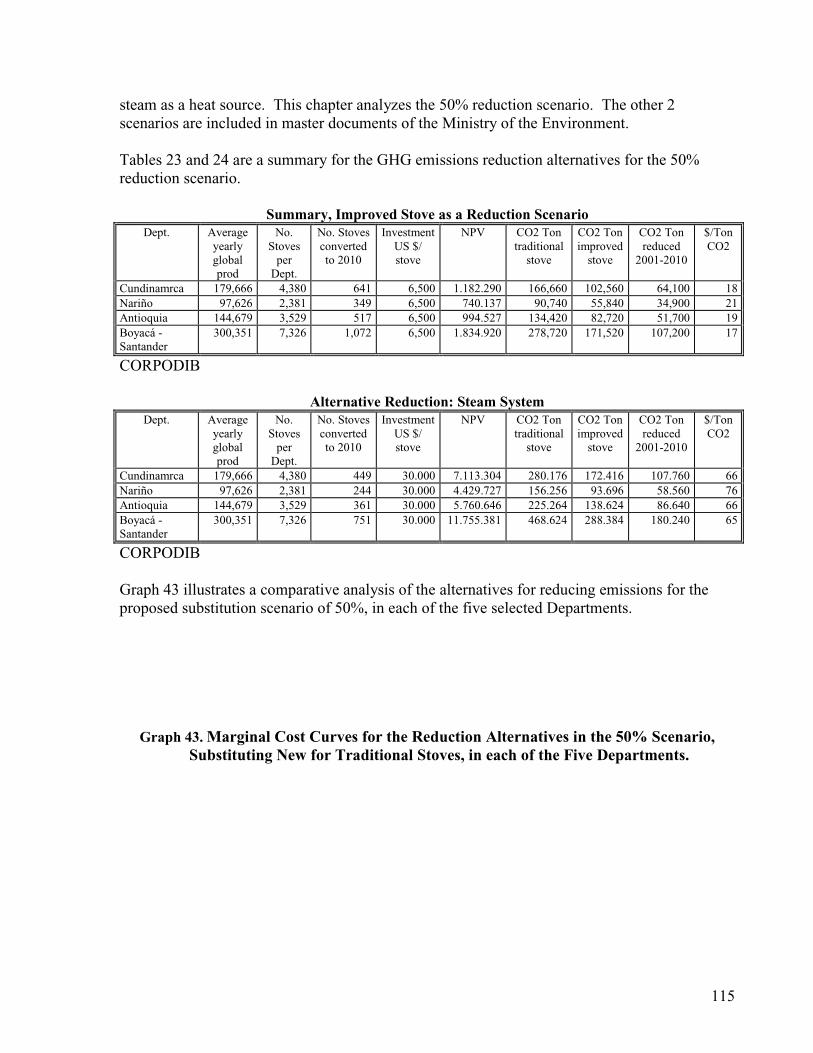

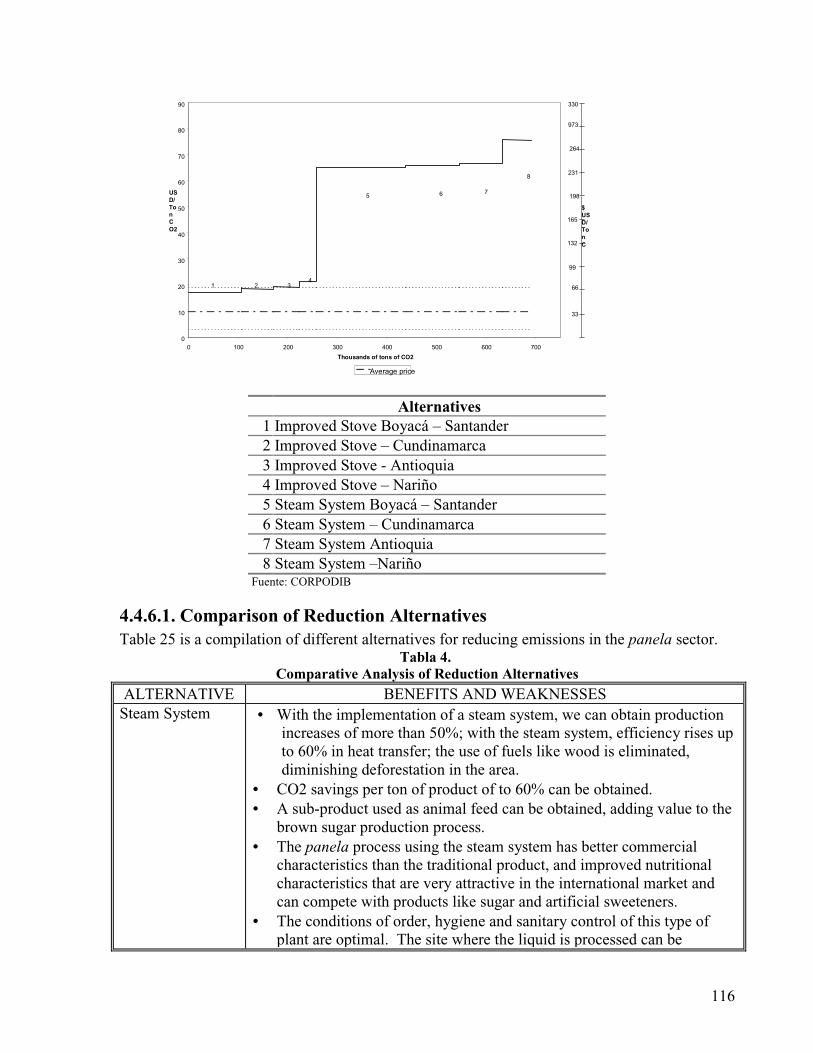

4.4. THE PANELA REFINING SECTOR: POTENTIAL BENEFITS AND COMPETITIVENESS...........................954.4.1. Promoters’ Group for Connecting the Sector with CDM ..........................................................964.4.2. Present Situation of Brown Sugar Production in Colombia ....................................................1004.4.3. Expected Development and Evolution of the Brown Sugar Sector until 2010 .........................1034.4.4. Technology and Installed Capacity in the Brown Sugar Sector ..............................................1044.4.5. GHG Mitigation Options .........................................................................................................1074.4.6. Analysis of the Proposed Reduction Alternatives ....................................................................1144.4.7. Conclusions and Recommendations ........................................................................................117

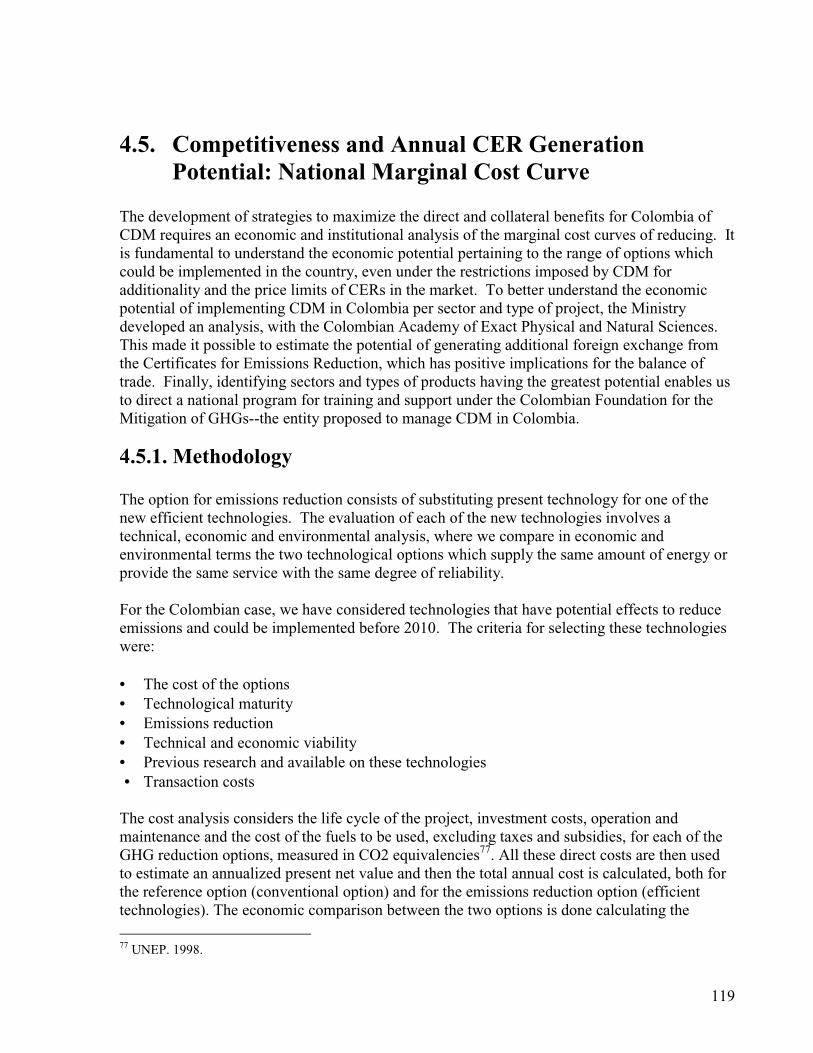

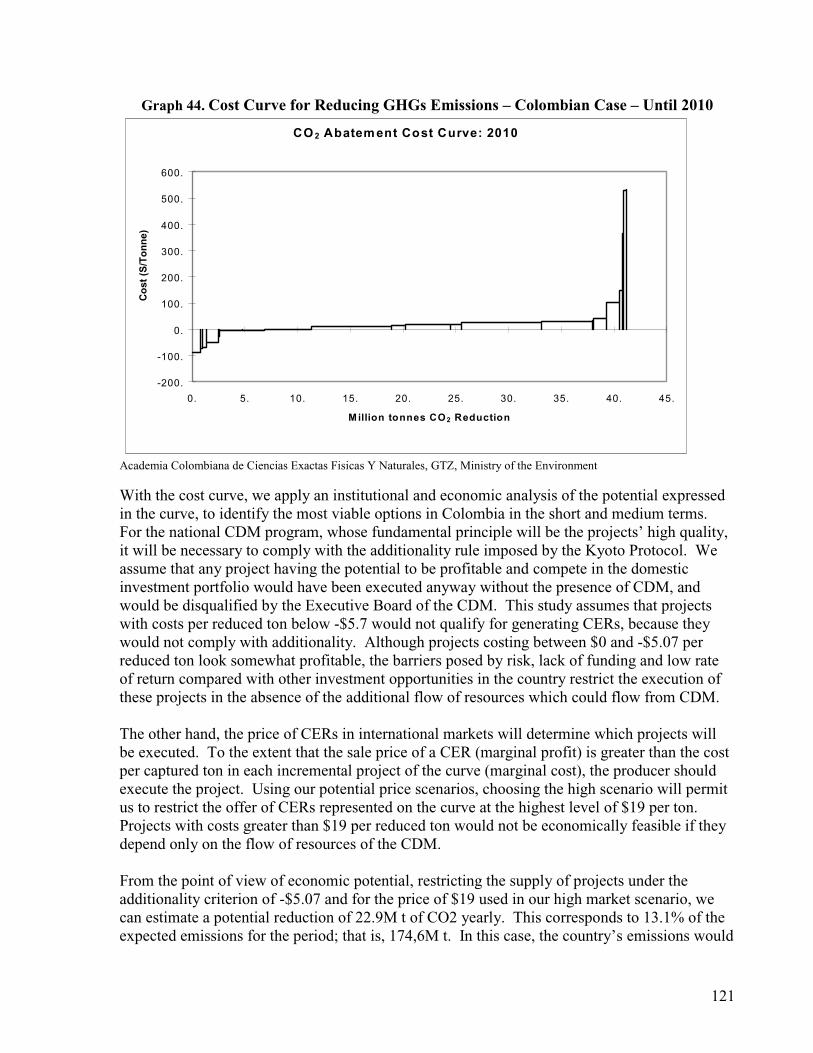

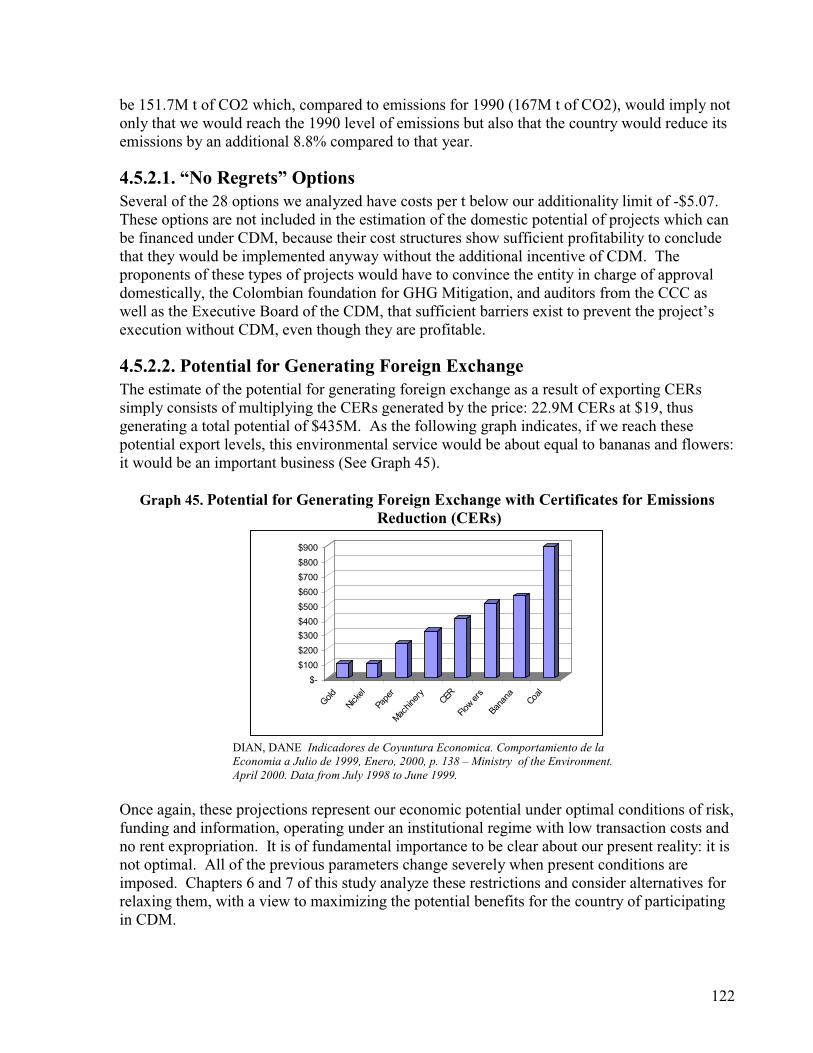

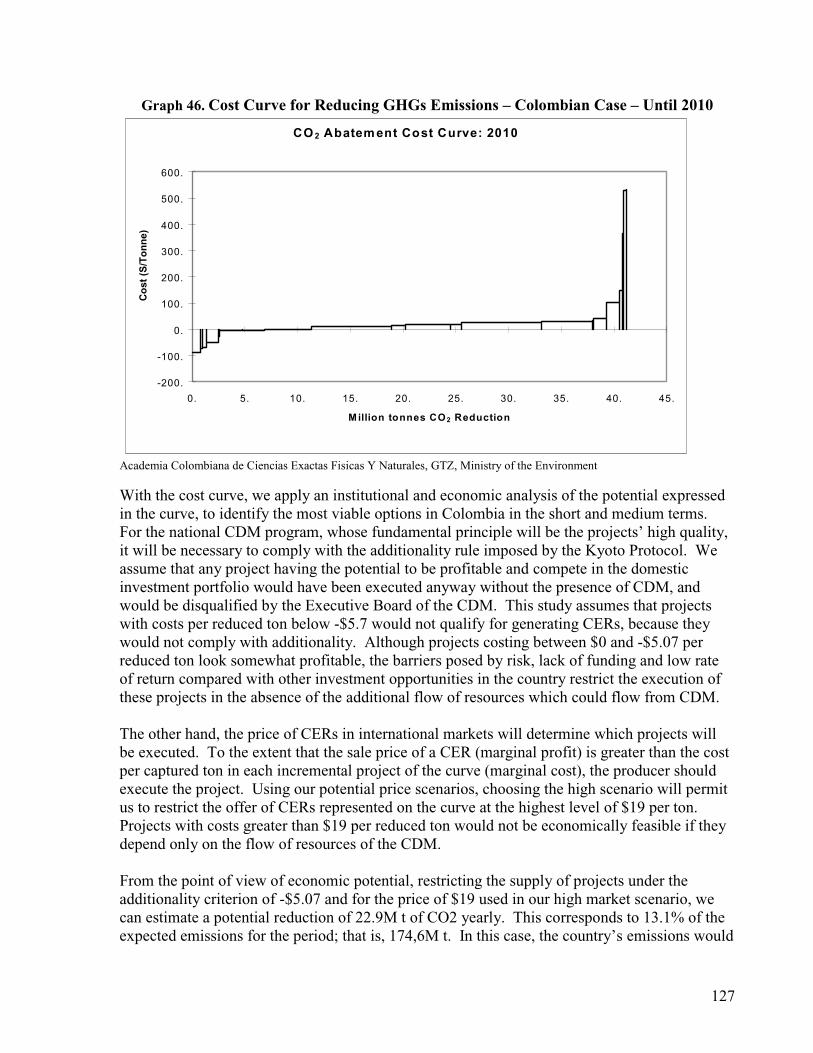

4.5. COMPETITIVENESS AND ANNUAL CER GENERATION POTENTIAL: NATIONALMARGINAL COSTCURVE.....................................................................................................................................................1194.5.1. Methodology ............................................................................................................................1194.5.2. Results......................................................................................................................................1204.5.3. CER Export as a Way of Compensating the Effect of Reducing on Fossil Fuel Exports.........123

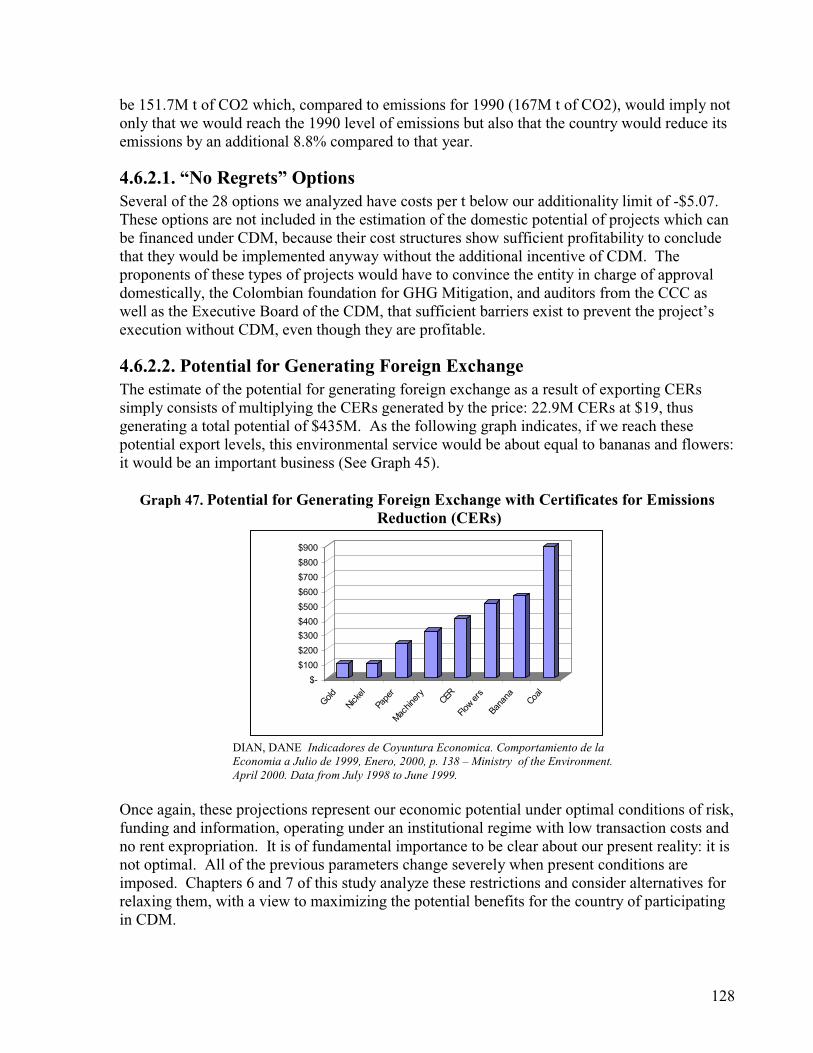

4.6. COMPETITIVENESS AND ANNUAL CER GENERATION POTENTIAL: NATIONALMARGINAL COSTCURVE.....................................................................................................................................................1254.6.1. Methodology ............................................................................................................................1254.6.2. Results......................................................................................................................................1264.6.3. CER Export as a Way of Compensating the Effect of Reducing on Fossil Fuel Exports.........129

5. STRATEGIES FOR ATTAINMENT OF THE NATIONAL POTENTIAL .............................131

5.1. CRITICALDESIGN AND REGULATORY ELEMENTS TO BE NEGOTIATED IN THE SIXTH CONFERENCEOF THE PARTIES.......................................................................................................................................1315.1.1. Ensuring CDM Implementation from January 2000 ...............................................................1325.1.2. Minimizing International Transaction costs, Risks and Barriers ............................................1325.1.3. Managing Base Lines and Additionality..................................................................................1335.1.4. Equal Treatment for the Three Flexibility Mechanisms ..........................................................1345.1.5. The Inclusion of Sinks ..............................................................................................................1345.1.6. The Unilateral Model for Project Formulation Must be Approved to Maximize Participation ofColombian Projects and Those from Other High-Risk Countries .....................................................1355.1.7. Free Trading of CERs in Financial Exchanges and Secondary Markets Should not beRestricted ...........................................................................................................................................1365.1.8. Limits Stemming from Supplementarity Should be Voluntary for Each Annex B Country ......1375.1.9. The Sustainable Development Criterion must be a National Criterion ...................................1375.1.10. Promoting Financial Support for the Creation of a National Capacity ................................138

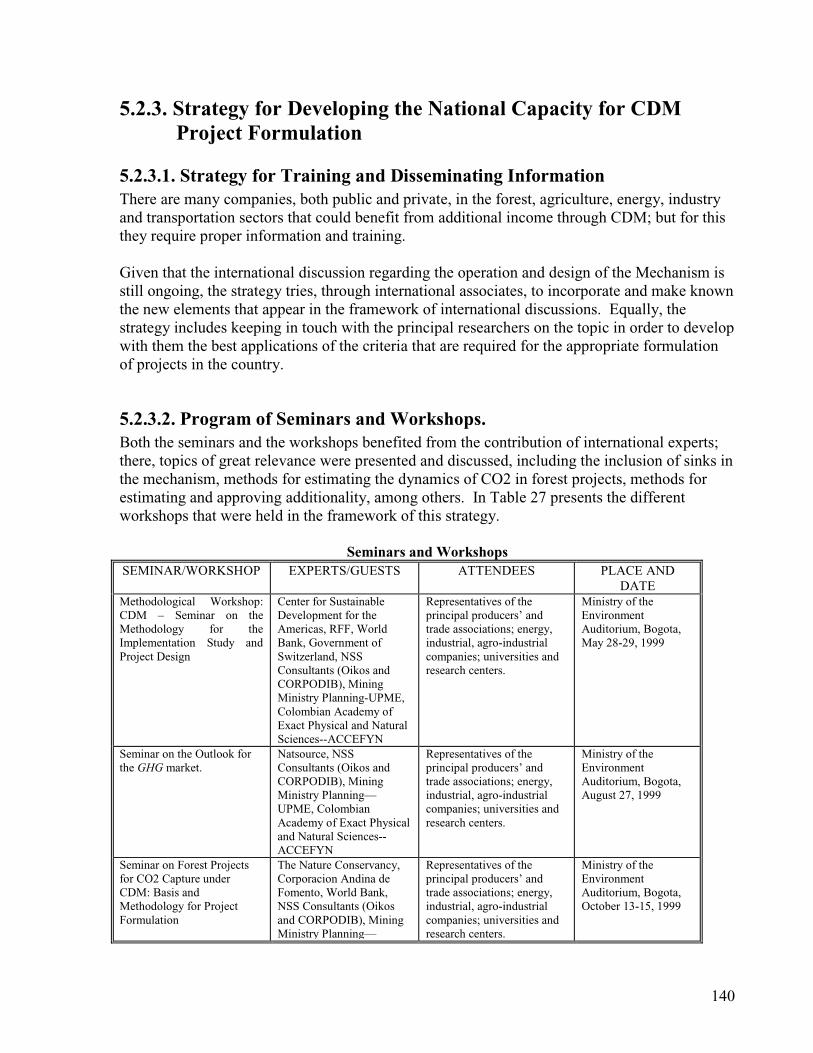

5.2. STRATEGIES FOR NATIONAL CAPACITY BUILDING IN THE CDM PROJECT FORMULATION ANDDEVELOPMENT........................................................................................................................................1385.2.1. Introduction .............................................................................................................................1385.2.2. Methodology ............................................................................................................................1395.2.3. Strategy for Developing the National Capacity for CDM Project Formulation......................1405.2.4. Requirements for Training and Support to Maximize the Potential Benefits of CDM inColombia ...........................................................................................................................................1415.2.5. Conclusions..............................................................................................................................146

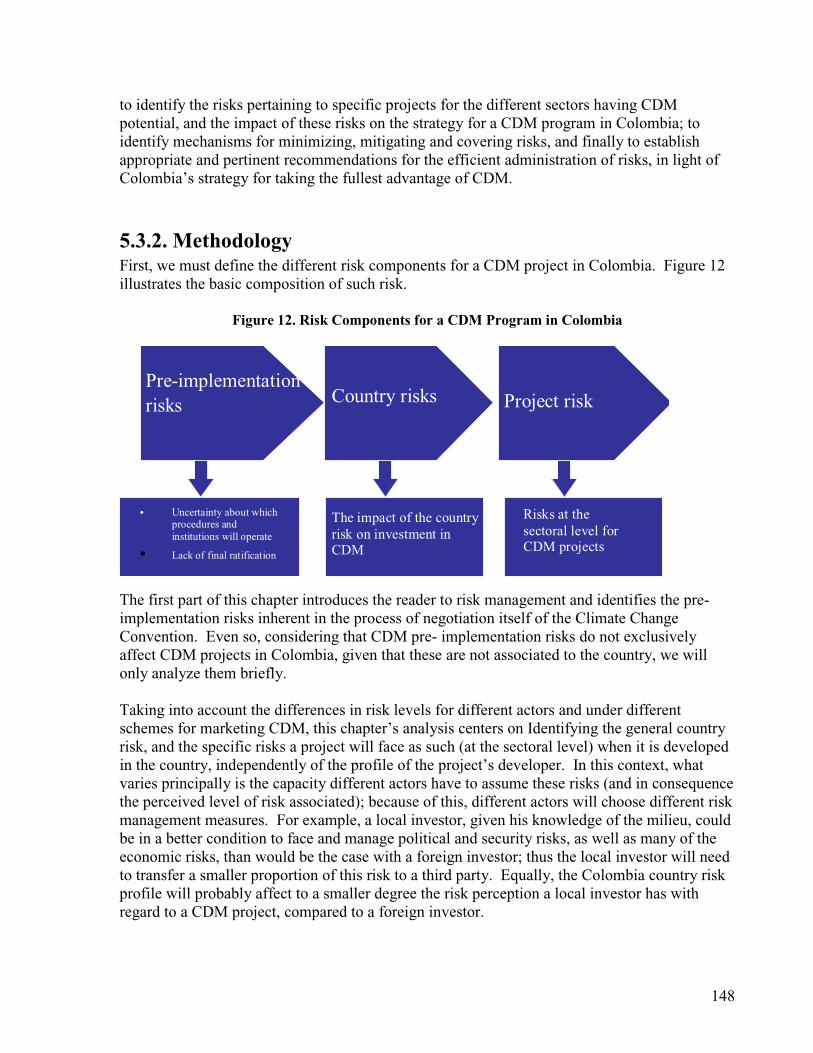

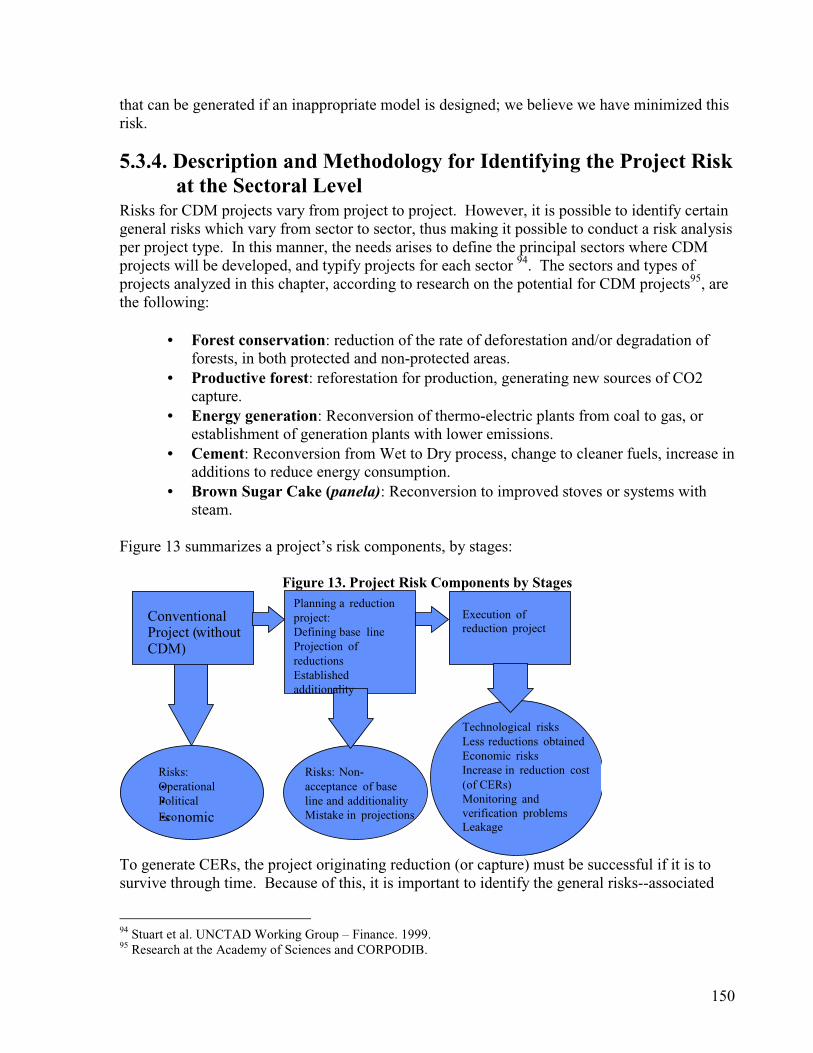

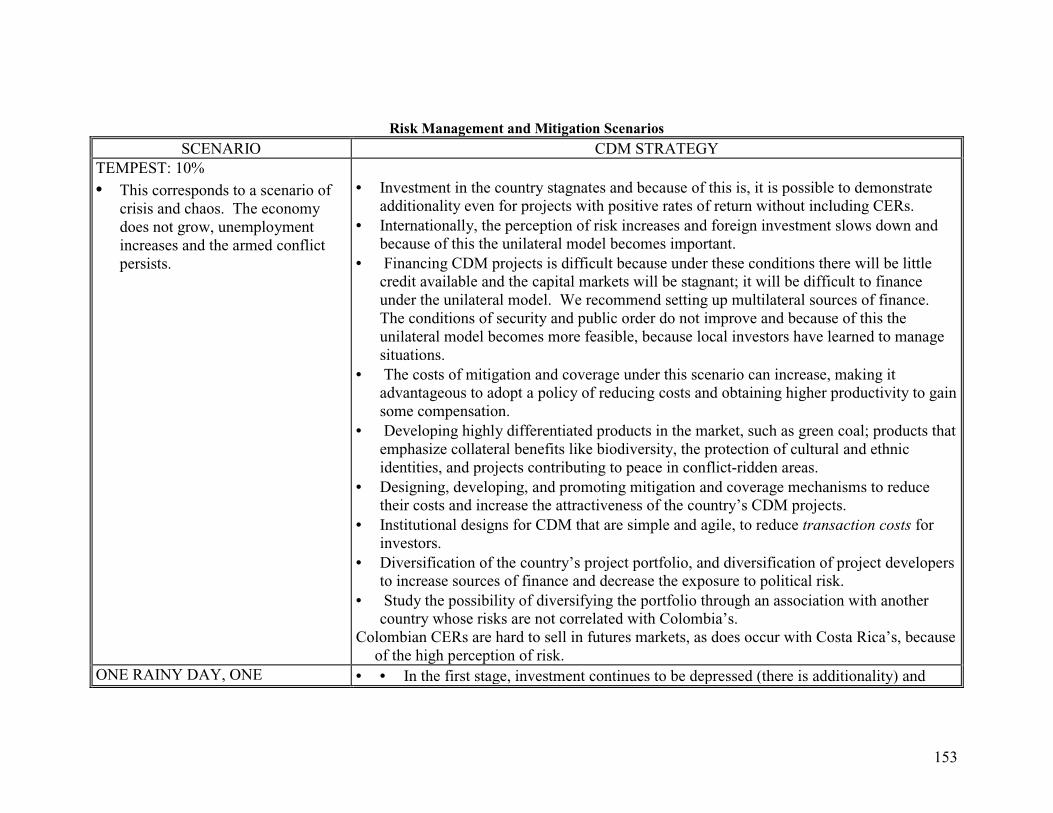

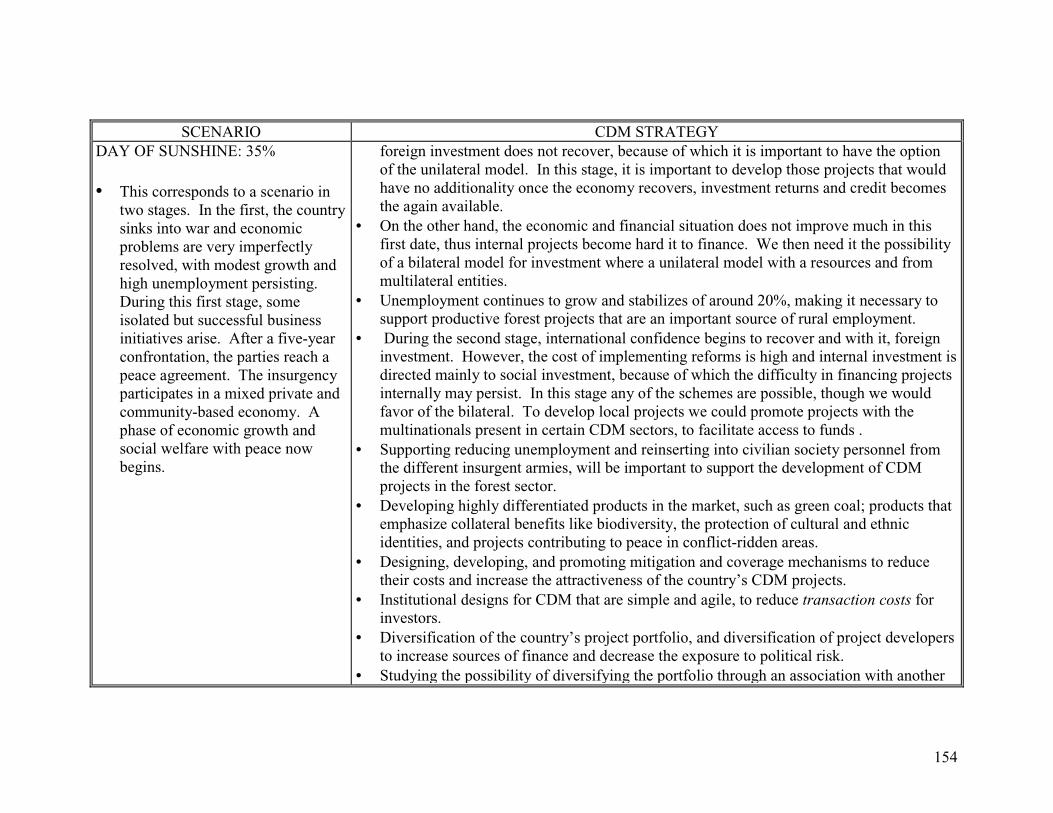

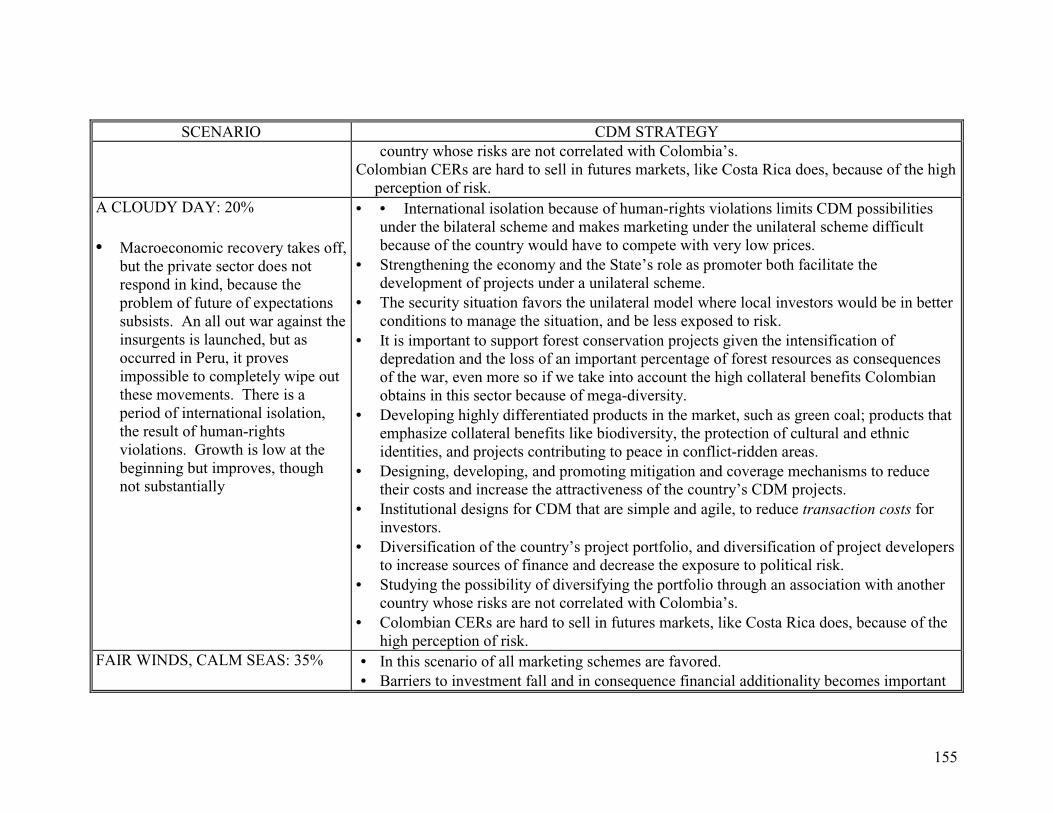

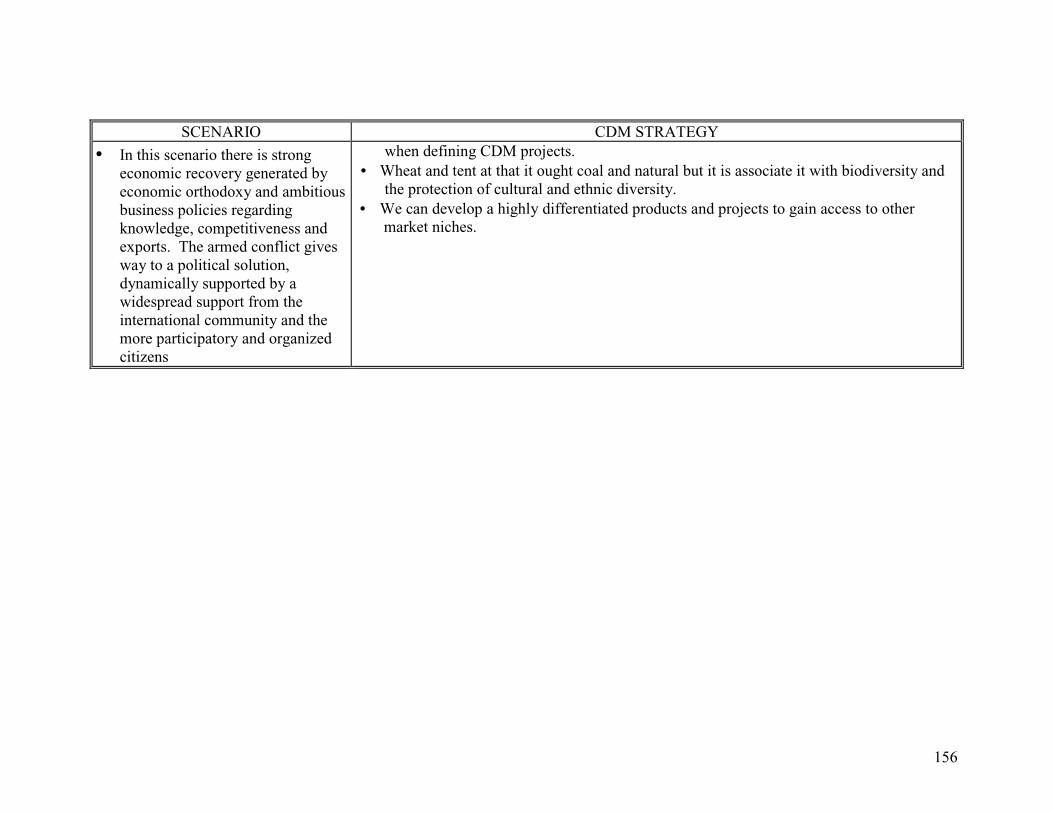

5.3. RISKMANAGEMENT IN CDM PROJECTS IN COLOMBIA................................................................1475.3.1. General and Specific Objectives..............................................................................................1475.3.2. Methodology ............................................................................................................................1485.3.3. Description and Methodology for Drafting the Country Risk Profile......................................1495.3.4. Description and Methodology for Identifying the Project Risk at the Sectoral Level..............1505.3.5. Identification of Mitigation and Coverage Mechanisms..........................................................1515.3.6. Principal Conclusions and Recommendations ........................................................................152

vi

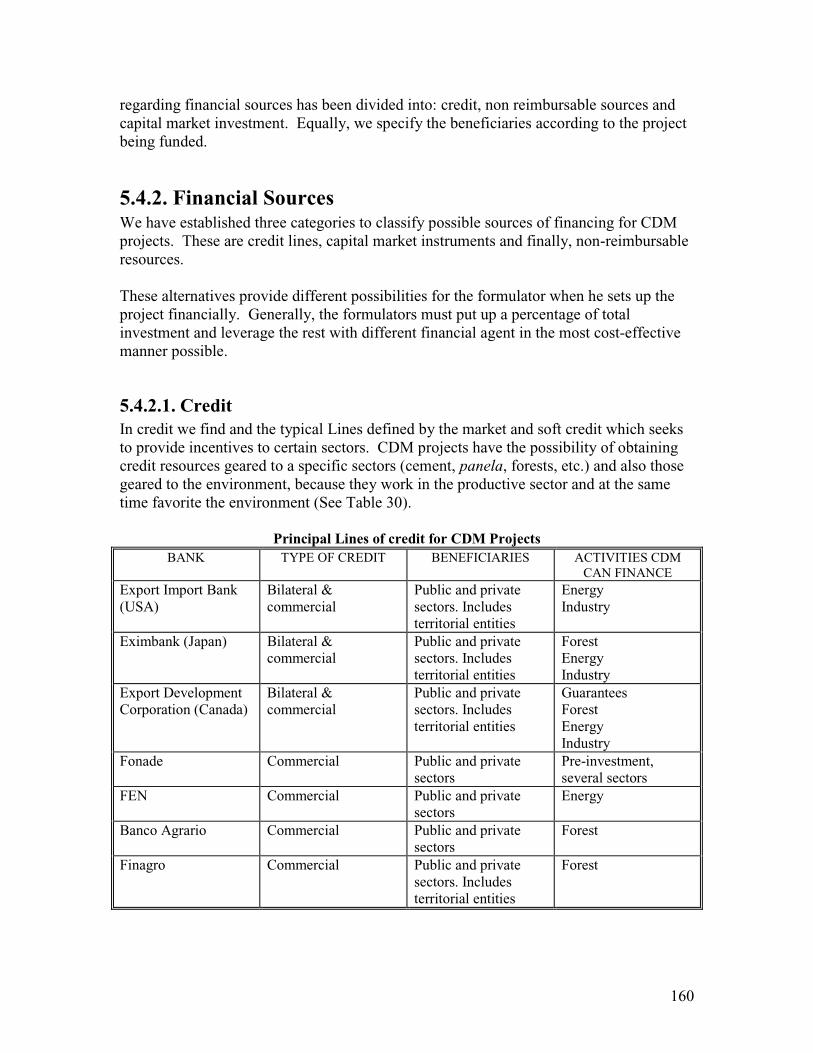

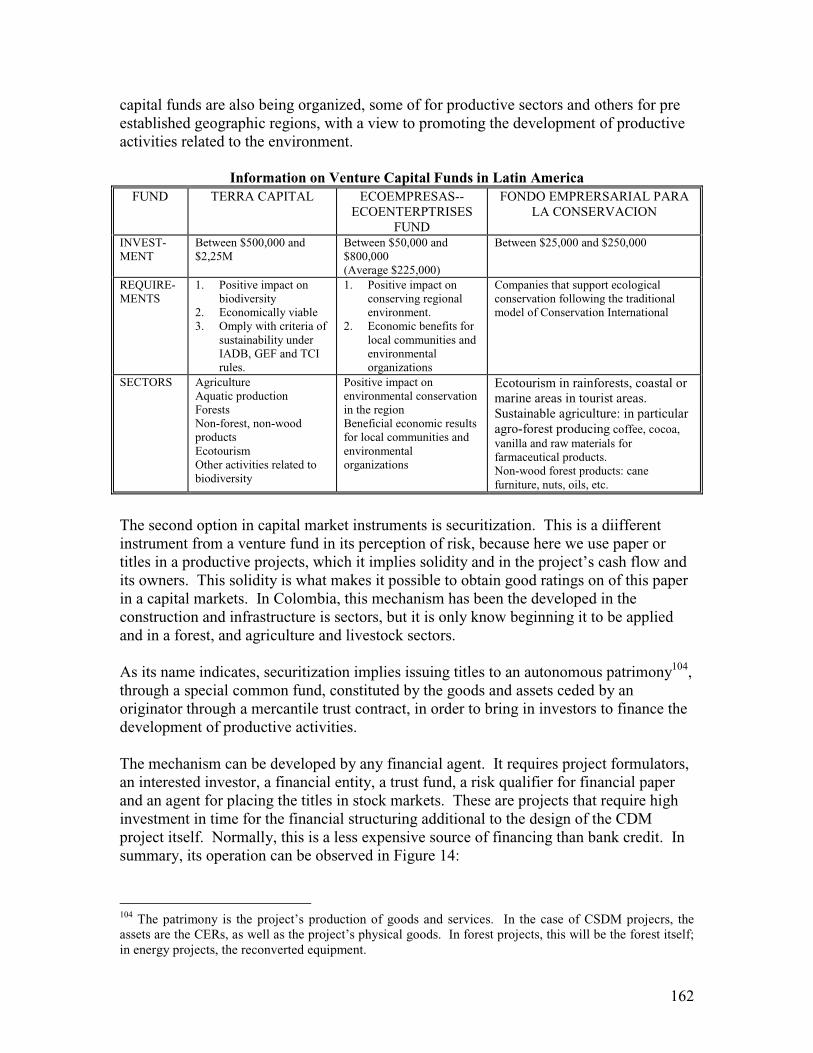

5.4. FINANCINGOPTIONS FOR CDM PROJECTS UNDER OF THE UNILATERALMODEL IN COLOMBIA ..1585.4.1. General Considerations...........................................................................................................1585.4.2. Financial Sources ....................................................................................................................1605.4.3. Conclusions..............................................................................................................................164

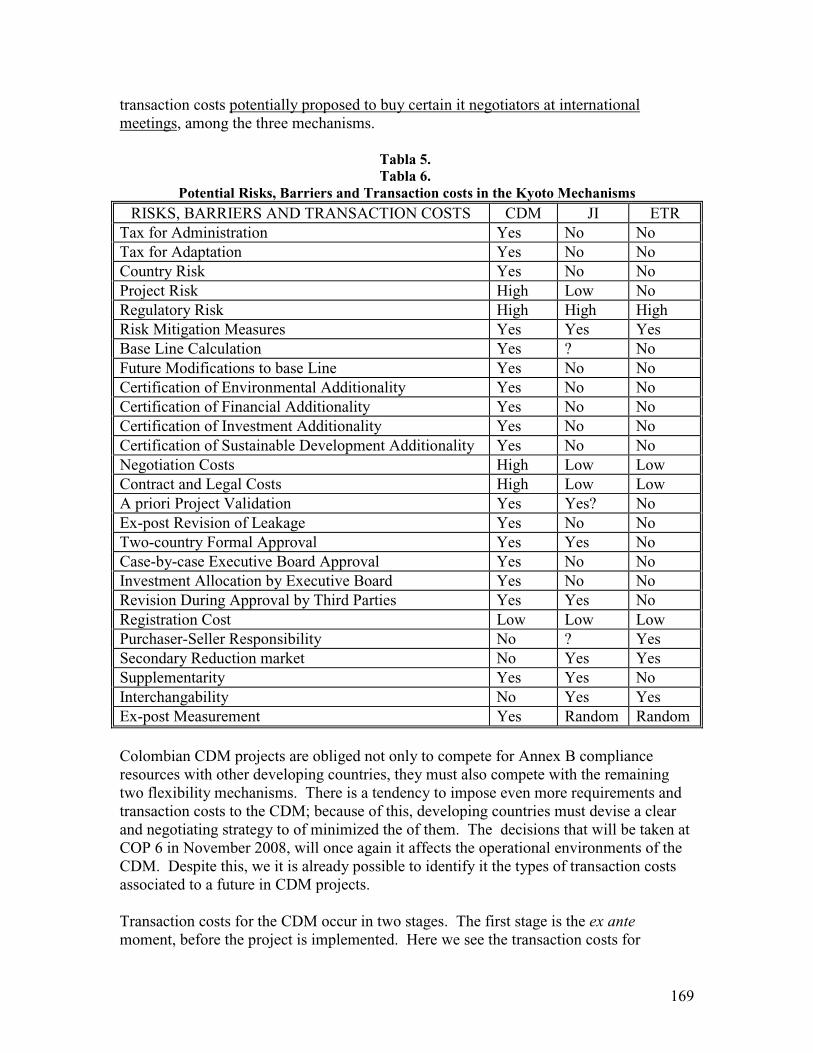

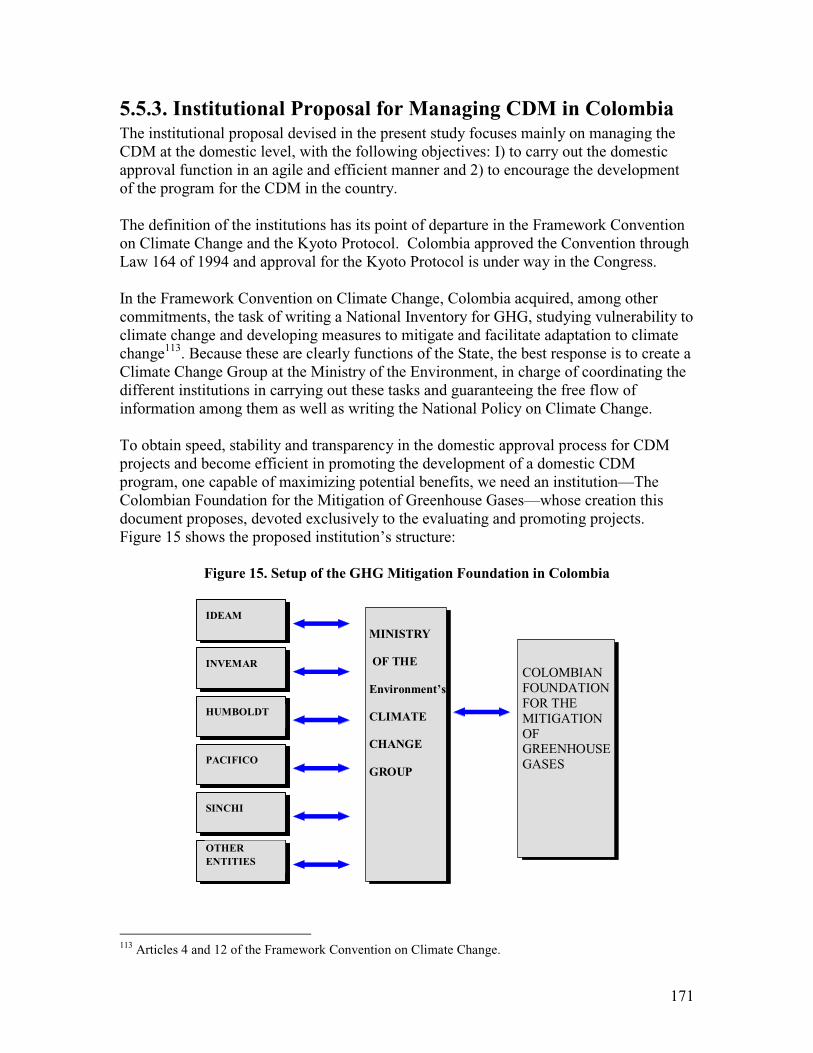

5.5. DESIGN OF CDM INSTITUTIONS ...................................................................................................1645.5.1. Rent Seeking.............................................................................................................................1665.5.2. Transaction costs .....................................................................................................................1675.5.3. Institutional Proposal for Managing CDM in Colombia.........................................................171

5.6. CONCLUSIONS AND RECOMMENDATIONS.....................................................................................174

6. NEXT STEPS: ACTION PLAN TO IMPLEMENT CDM IN COLOMBIA.............................177

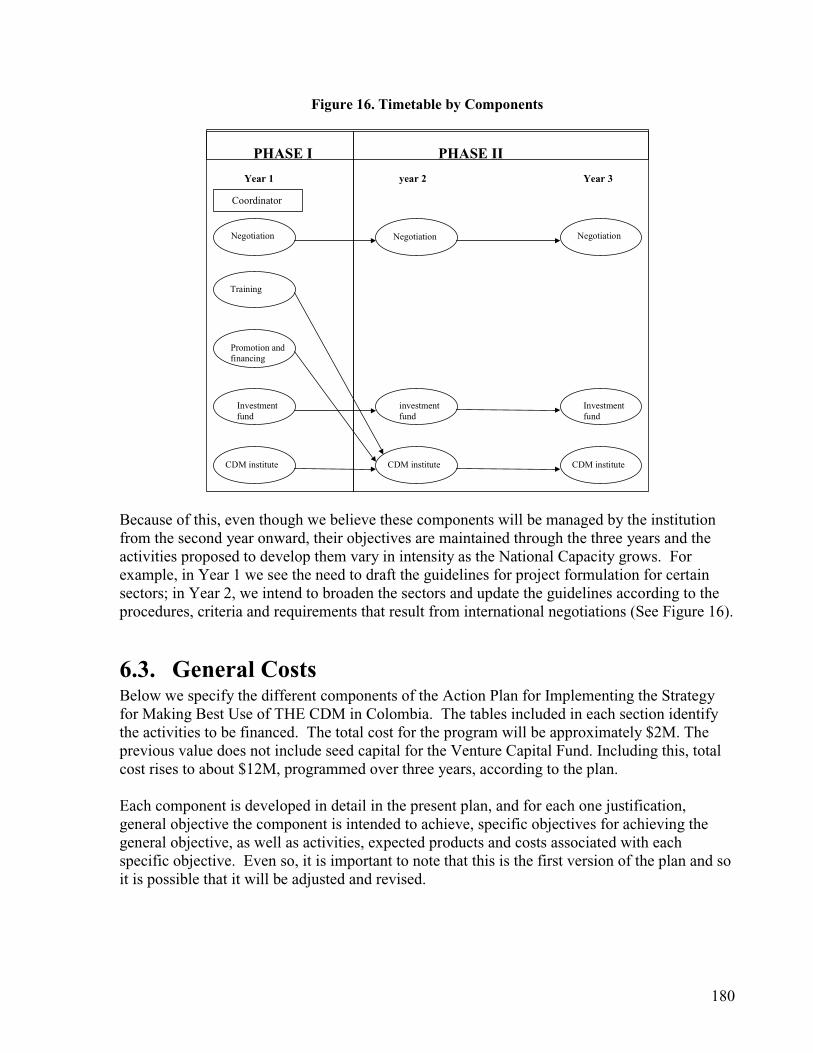

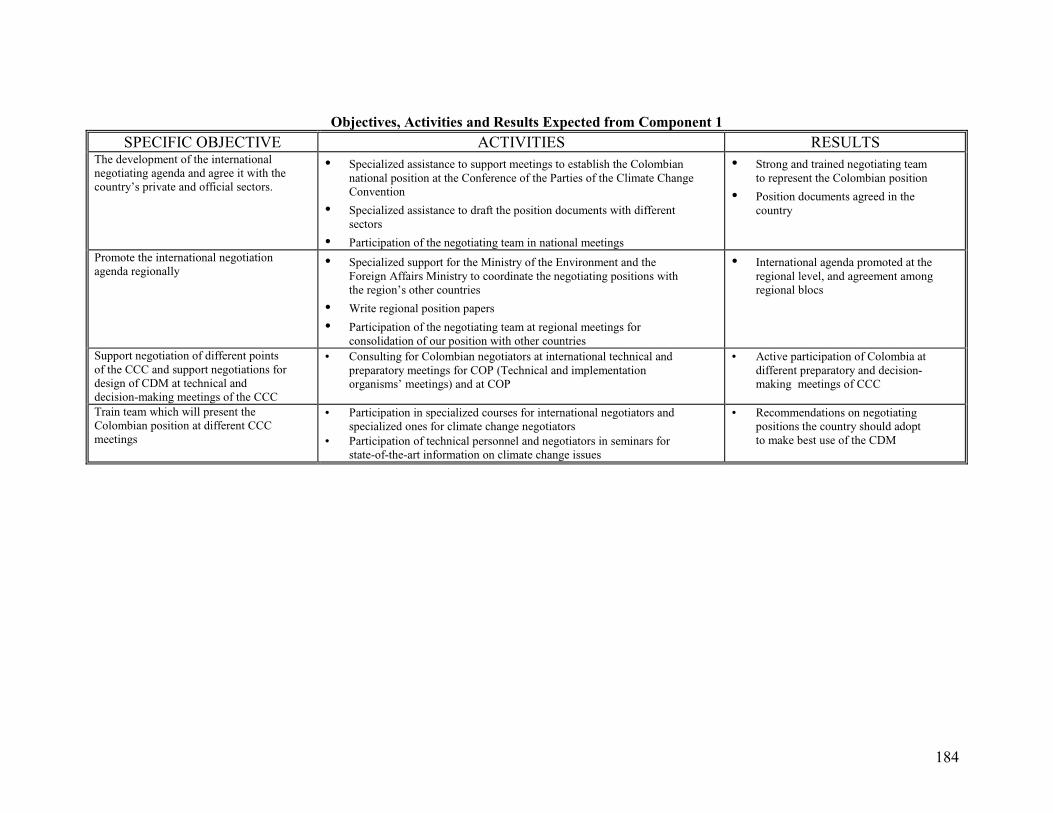

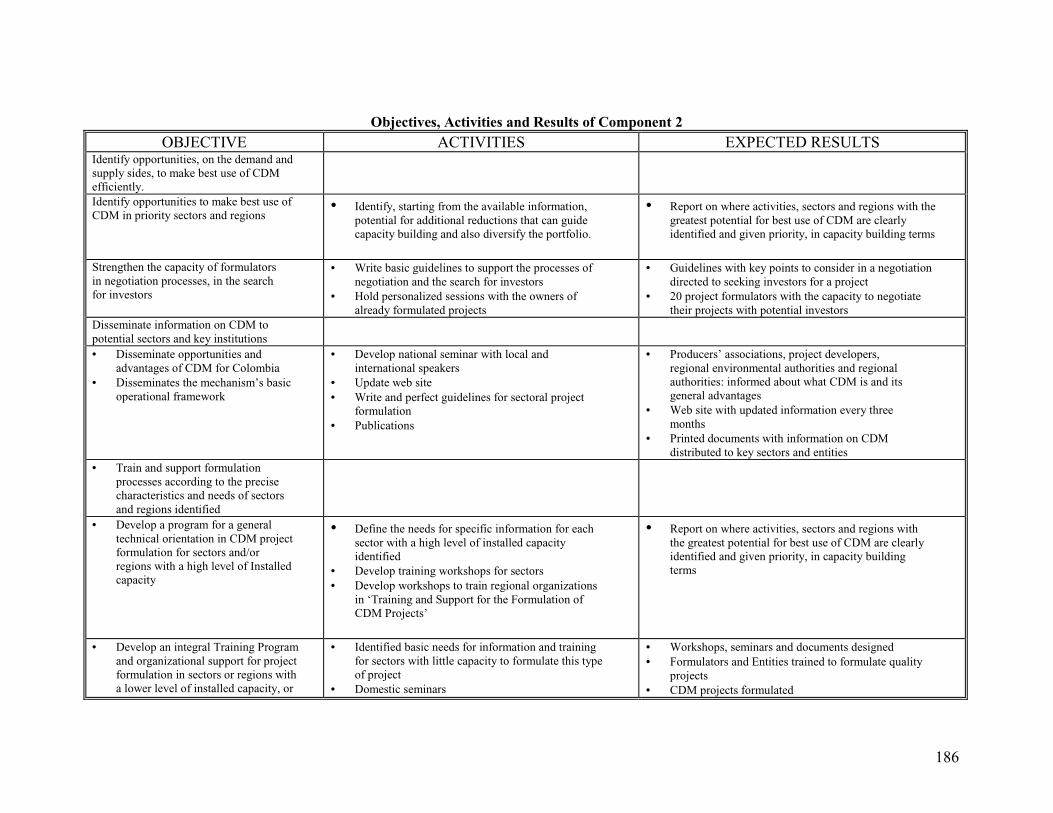

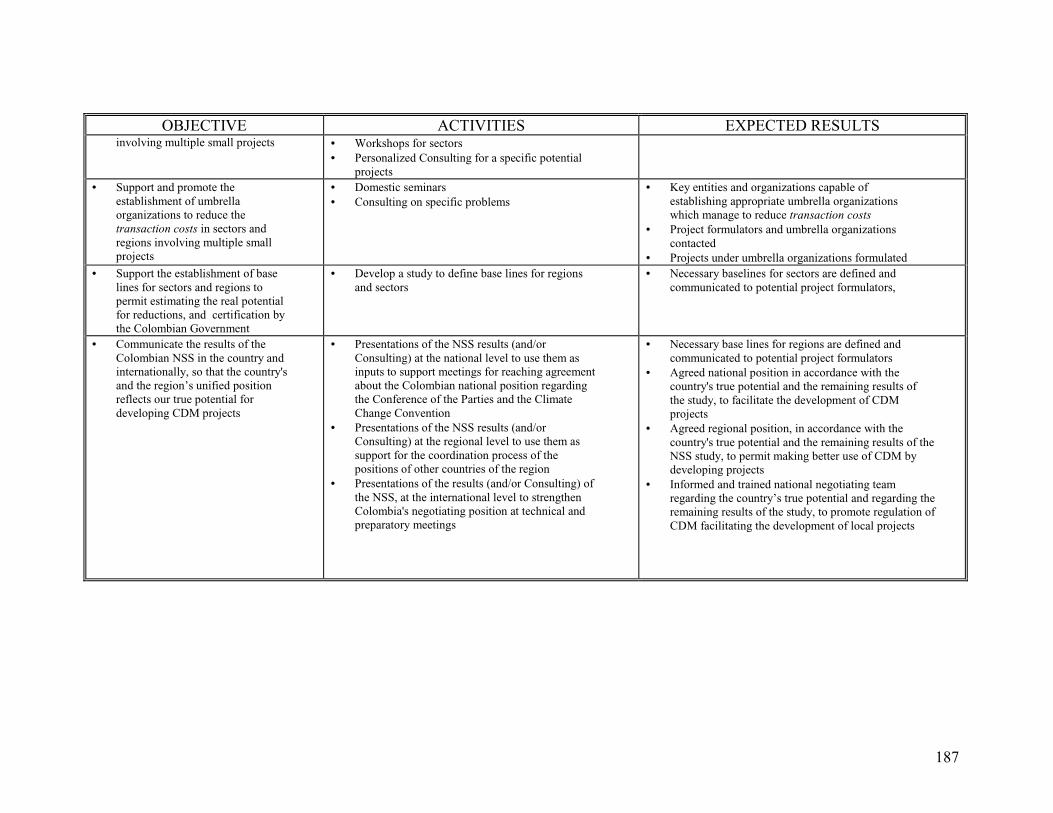

6.1. OBJECTIVE ...................................................................................................................................1776.2. STRUCTURE OF THE PROGRAM AND COMPONENTS ......................................................................1776.3. GENERAL COSTS ..........................................................................................................................1806.4. COMPONENT 1: STRENGTHENINGNEGOTIATING CAPACITY ........................................................1816.5. COMPONENT 2: STRENGTHENINGNATIONAL CAPACITY FOR DEVELOPING CDM PROJECTS.......1856.6. COMPONENT 3: SUPPORT FOR FINANCING ANDMARKETING THE CDM PROJECTS PORTFOLIO ...1886.7. COMPONENT 4: SUPPORT FOR DEVELOPING AVENTURE CAPITAL FUND FOR FINANCING CDMPROJECTS ................................................................................................................................................1916.8. COMPONENT 5: CREATION AND CONSOLIDATION OF INSTITUTIONAL CAPACITY TOMANAGE CDMIN COLOMBIA ..........................................................................................................................................1936.9. CONSOLIDATING INSTITUTIONAL CAPACITY FORMANAGING CDM IN COLOMBIA .....................195

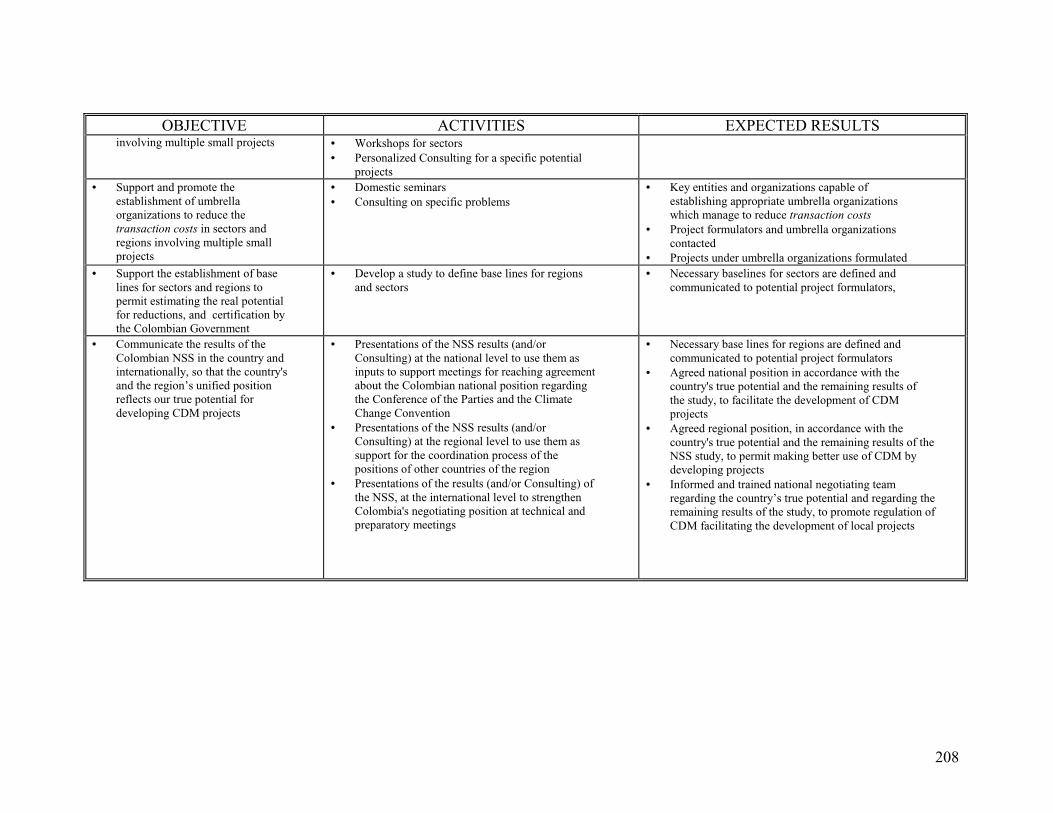

7. NEXT STEPS: ACTION PLAN TO IMPLEMENT CDM IN COLOMBIA.............................198

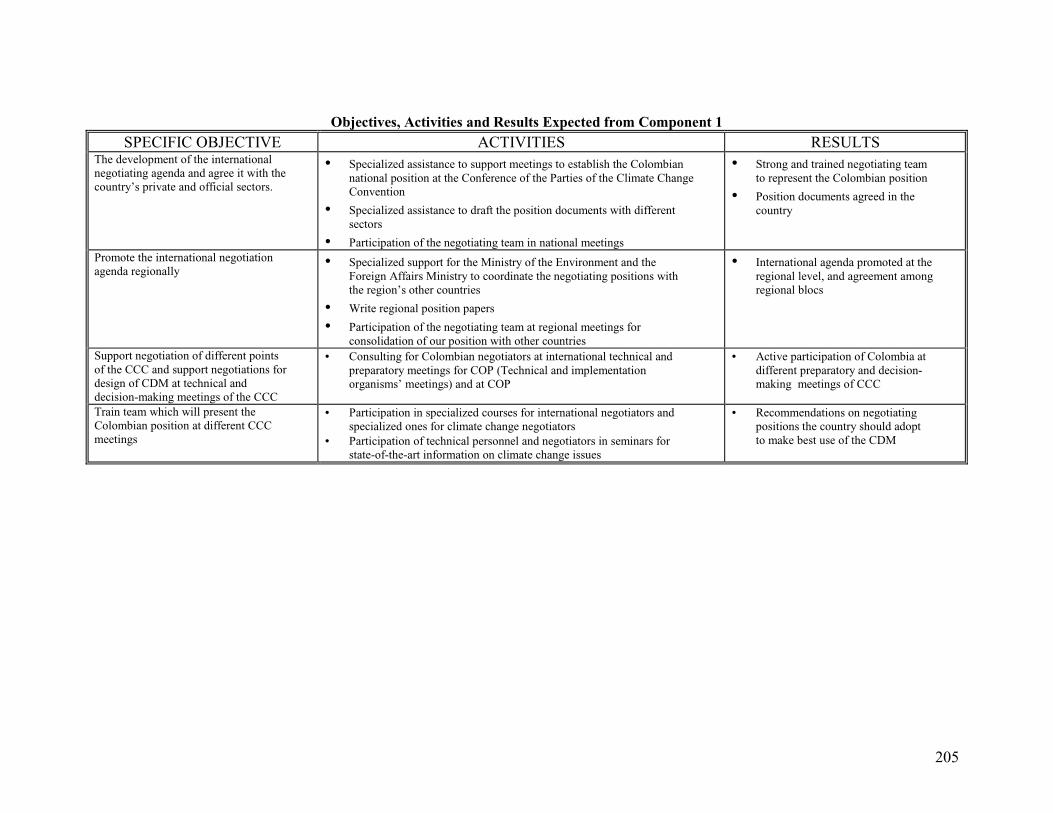

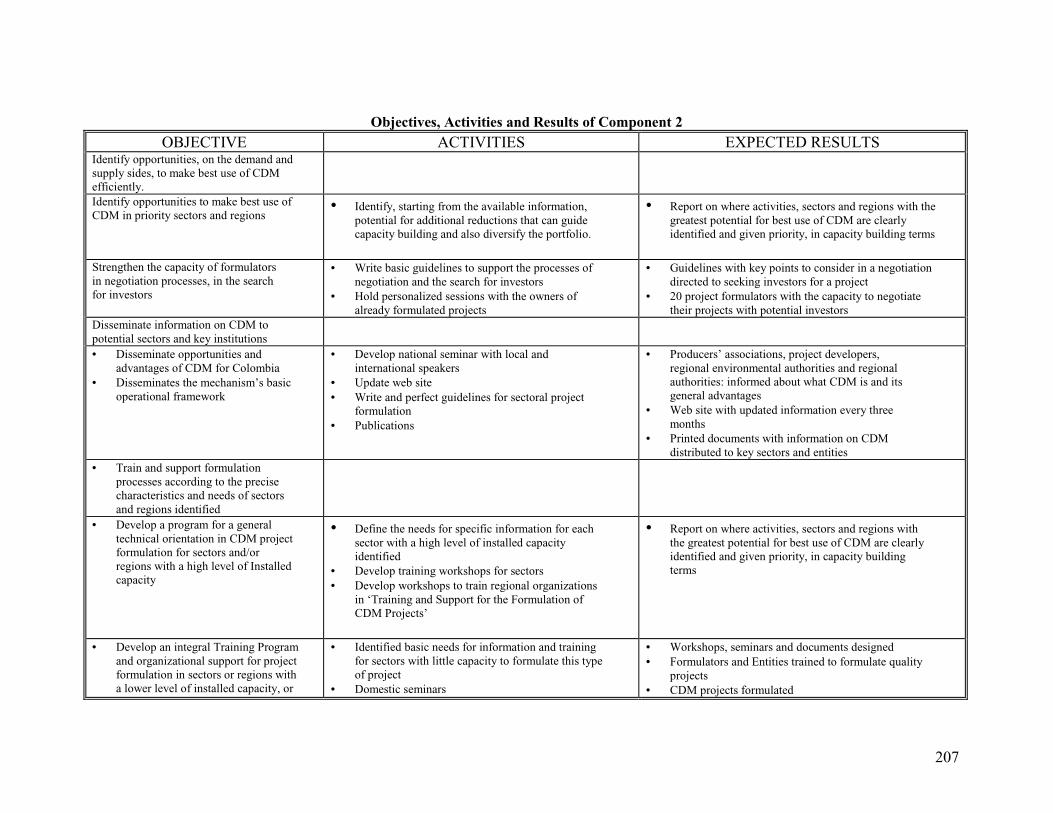

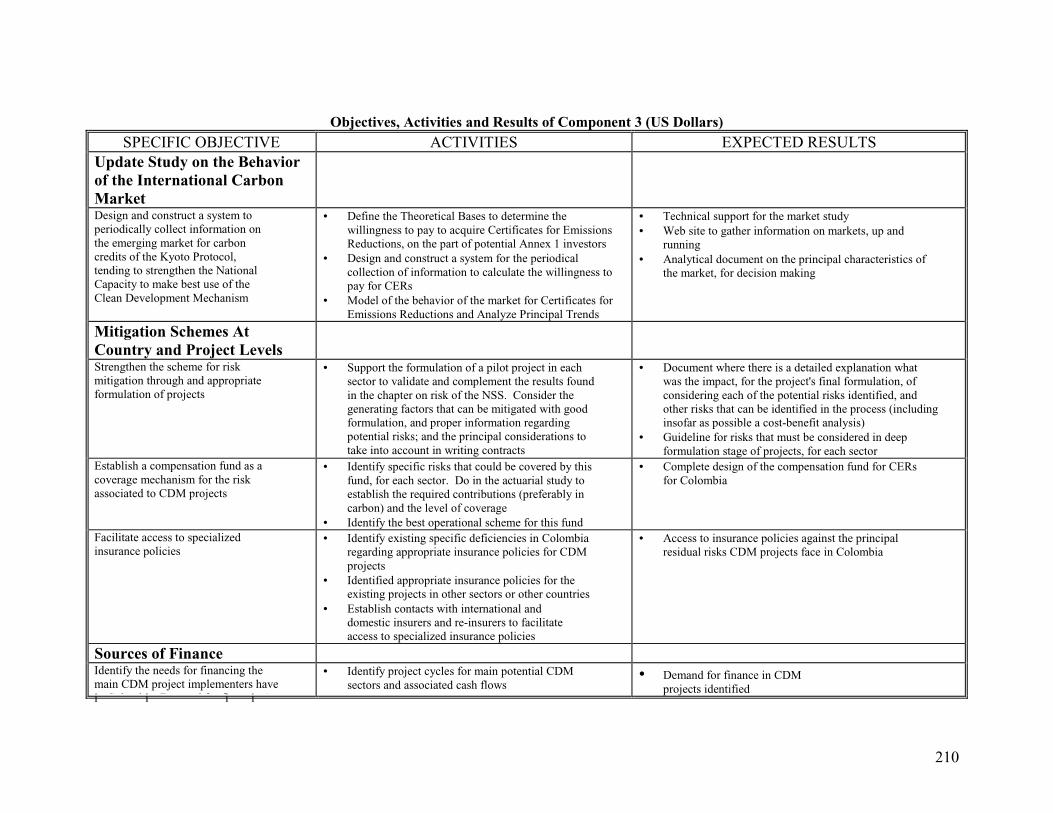

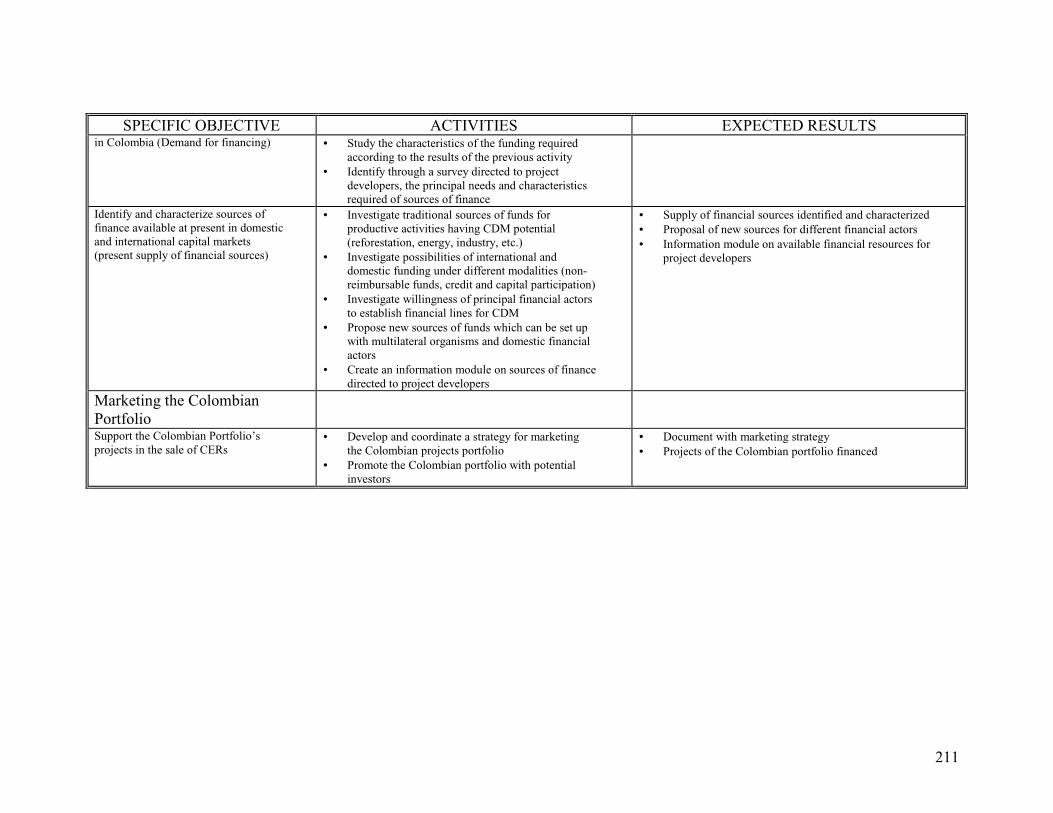

7.1. OBJECTIVE ...................................................................................................................................1987.2. STRUCTURE OF THE PROGRAM AND COMPONENTS ......................................................................1987.3. GENERAL COSTS ..........................................................................................................................2017.4. COMPONENT 1: STRENGTHENINGNEGOTIATING CAPACITY ........................................................2027.5. COMPONENT 2: STRENGTHENINGNATIONAL CAPACITY FOR DEVELOPING CDM PROJECTS.......2067.6. COMPONENT 3: SUPPORT FOR FINANCING ANDMARKETING THE CDM PROJECTS PORTFOLIO ...2097.7. COMPONENT 4: SUPPORT FOR DEVELOPING AVENTURE CAPITAL FUND FOR FINANCING CDMPROJECTS ................................................................................................................................................2127.8. COMPONENT 5: CREATION AND CONSOLIDATION OF INSTITUTIONAL CAPACITY TOMANAGE CDMIN COLOMBIA ..........................................................................................................................................2147.9. CONSOLIDATING INSTITUTIONAL CAPACITY FORMANAGING CDM IN COLOMBIA .....................216

8. EXECUTIVE SUMMARIES OF THE PROJECT PORTFOLIO..............................................219

8.1. CONSERVATION OF NATURAL FORESTS UNDER THREAT IN THETINIGUA PARK AND LAMACARENA219

8.2. CONSERVATION AND RESTORATION OF FORESTS IN THEMID ATRATO, IN THE COLOMBIAN PACIFIC220

8.3. MANAGEMENT OF FORESTS, FOREST SYSTEMS, AGRO-FORESTS AND TREE-DRIVEN ENERGY FORECONOMIC, SOCIAL AND ENVIRONMENTALOPTIMIZATION OF LAND USE IN CALAMAR, COLOMBIANAMAZON .................................................................................................................................................2238.4. CONSERVATION, RESTORATION ANDMANAGEMENT OF THE BIOLOGICAL CORRIDOR ‘PURACENATIONAL PARK’ AND ‘CUEVA DE LOS GUACHAROS’NATIONAL PARK, IN SOUTHERN HUILA DEPARTMENT

2248.5. CONTRIBUTION TOMITIGATING CLIMATE CHANGE THROUGH FOREST DEVELOPMENT IN THEREGION OF THE PARAMO DE GUERRERO, BY THE CAR ............................................................................2258.6. ESTABLISHING, RESTORING AND CONSERVING RAINFOREST AND ANDEAN FORESTS TO CAPTUREGG ON THEMESETA DE BUCARAMANGA, CDMB JURISDICTION ..............................................................2278.7. CONVERSION OF LAND USED FOR ON-THE-RANGE CATTLE AND ITINERANT AGRICULTURE TOFORESTS, AGRICULTURE AND FOREST, AND FOREST AND PASTURE SYSTEMS FOR RURAL PRODUCTIONAND POWER GENERATION IN PUERTO CARREÑO, COLOMBIAN ORINOCO...............................................2298.8. RECOVERY AND INTEGRATEDMANAGEMENT OF ECOSYSTEMS TO CONSERVE BIODIVERSITY ANDIMPLEMENT THE CLEAN DEVELOPMENTMECHANISM IN URABA............................................................230

vii

8.9. CONSERVATION AND EXPANSION OF FOREST COVERING TO REGULATEWATER RESOURCES ANDMANAGE GG EMISSIONS AS A SUSTAINABLE DEVELOPMENT OPTION IN QUINDIO DEPARTMENT..........2328.10. ECONOMIC AND SOCIALDEVELOPMENT OF RURAL COMMUNITIES IN COLOMBIA’S CARIBBEANPLAIN BASED ON.....................................................................................................................................2328.10. THE SUSTAINABLEMANAGEMENT OF NATURAL FORESTS AND FOREST PLANTATIONS ...........2338.11. WIND ENERGY DEVELOPMENT IN UPPER GUAJIRA ..................................................................234

2. BIBLIOGRAPHY............................................................................................................................237

viii

Table Index

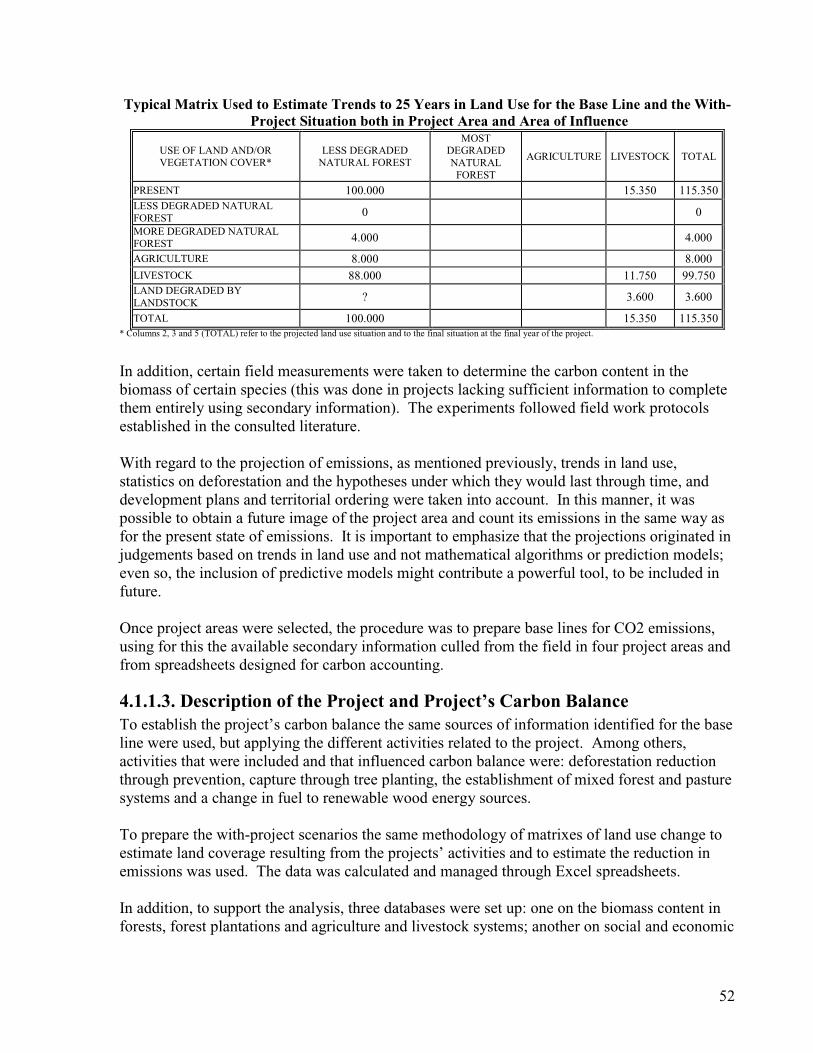

Market Survey of International CDM Experts.................................................................... 4Impacts on fossil fuels exports and potential revenues from CDM.................................. 11Criteria for Capacity Building by Sector .......................................................................... 14Permits for greenhouse Gases Emissions ......................................................................... 37Emissions Projection for 2012.......................................................................................... 38Maximum Demand Potential ............................................................................................ 38Autarkic Costs (Marginal Reductions Cost)* ................................................................... 40Emissions Reductions Market........................................................................................... 40Grouping of the levels of variables that affect the market’s Operation............................ 46Typical Matrix Used to Estimate Trends to 25 Years in Land Use for the Base Line and

the With-Project Situation both in Project Area and Area of Influence ................... 52Projects of the Preliminary Portfolio ................................................................................ 55Land Use and Social Products of Three Agricultural and Livestock Activities in

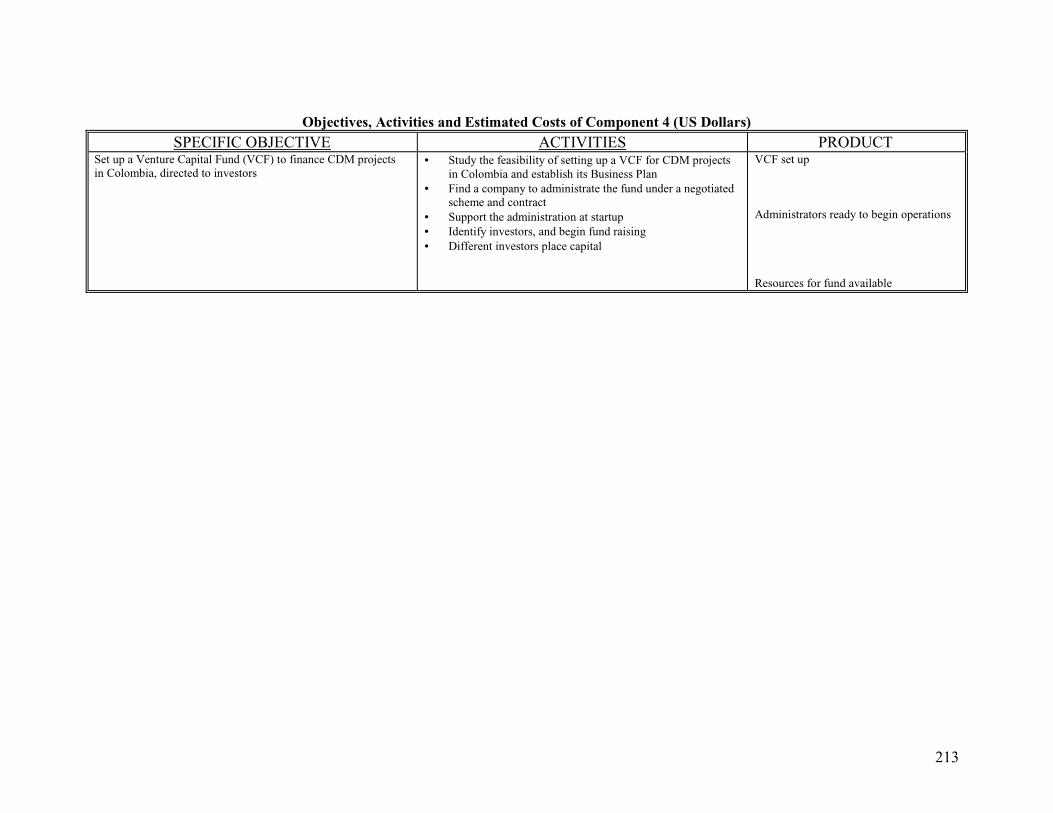

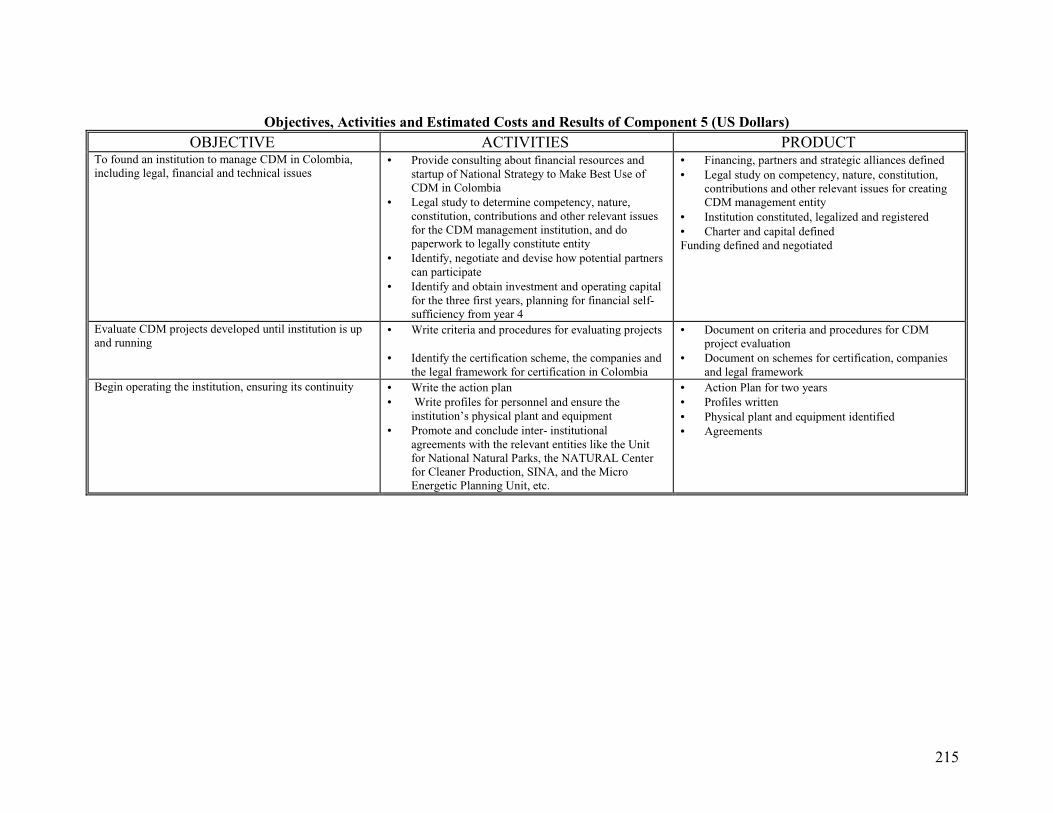

Colombia................................................................................................................... 57The Dimension of Erosion in Colombia ........................................................................... 57Technology Transfer in the Colombian Portfolio’s Forest Projects. ................................ 61Summary of Benefits and Weaknesses of the Alternatives .............................................. 85Values of the Fuel and Electrical Power Data .................................................................. 86Percentage of Clinker and Type of Addition .................................................................... 86Type of Addition and Energy Decrease Percentage ......................................................... 87Alternatives Analyzed in a GDP Growth Scenario of 4.2%............................................. 92Functions of the Promotion and Control Group ............................................................... 97Types of Fuels Used in Concentrating the Juices ........................................................... 105Values of Fuel and Electricity......................................................................................... 110Summary, Improved Stove as a Reduction Scenario...................................................... 115Alternative Reduction: Steam System ............................................................................ 115Comparative Analysis of Reduction Alternatives........................................................... 116Impacts on Fossil Fuels Exports and Potential Income from CDM ............................... 124Impacts on Fossil Fuels Exports and Potential Income from CDM ............................... 130Seminars and Workshops................................................................................................ 140Bases for a National Training Program .......................................................................... 142Risk Management and Mitigation Scenarios .................................................................. 153Principal Lines of credit for CDM Projects .................................................................... 160Information on Venture Capital Funds in Latin America............................................... 162Potential Risks, Barriers and Transaction costs in the Kyoto Mechanisms.................... 169Objectives, Activities and Results Expected from Component 1 ................................... 184Objectives, Activities and Results of Component 2 ....................................................... 186Objectives, Activities and Results of Component 3 (US Dollars).................................. 189Objectives, Activities and Estimated Costs of Component 4 (US Dollars).................... 192Objectives, Activities and Estimated Costs and Results of Component 5 (US Dollars) 194Objectives, Activities, Expected Results (US Dollar) .................................................... 196Objectives, Activities and Results Expected from Component 1 ................................... 205Objectives, Activities and Results of Component 2 ....................................................... 207Objectives, Activities and Results of Component 3 (US Dollars).................................. 210

ix

Objectives, Activities and Estimated Costs of Component 4 (US Dollars).................... 213Objectives, Activities and Estimated Costs and Results of Component 5 (US Dollars) 215Objectives, Activities, Expected Results (US Dollar) .................................................... 217

Graph Index

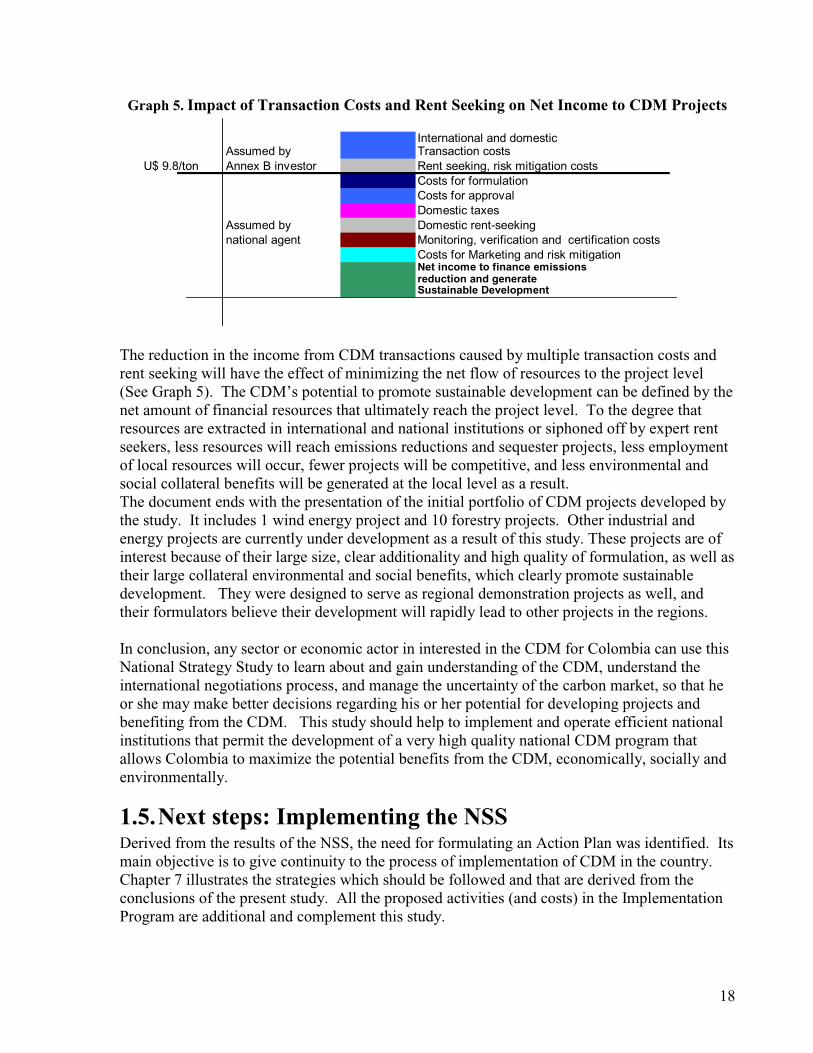

Graph 1. Marginal Costs of CO2 Capture in 10 Large Forestry Projects........................... 7Graph 2. Marginal Costs of CO2 Abatement in the National Energy Generation Grid ..... 8Graph 3. Estimation of Annual Aggregated GHG Mitigation Potential........................... 10Graph 4. Gross Potential of Annual CER Exports from Colombia (excluding oil). ........ 10Graph 5. Impact of Transaction Costs and Rent Seeking on Net Income to CDM Projects

................................................................................................................................... 18Graph 6. Market Structure, the Price of Rights and the Costs for Five Reductions Options

in a Company ............................................................................................................ 23Graph 7. Increment in the Price of Rights Resulting from a Significant Rise in Demand

under Inelastic Supply............................................................................................... 24Graph 8. Price Reduction Resulting from Low Demand and High Supply of Rights in the

Market ....................................................................................................................... 24Graph 9. Demand for Carbon Credits ............................................................................... 41Graph 10. Supply of CERs in the International Market.................................................... 42Graph 11. Entrance into Force of the Kyoto Protocol (Year and Probability). ................ 45Graph 12. Expectations Regarding Forest Projects .......................................................... 45Graph 13. Average Income from Different Rural Activities ............................................ 59Graph 14. Marginal Cost Curve for Reduction in the Forest Sector per Project .............. 63Graph 15. Base Line CO2 Emissions and Generation Cost per Option ........................... 67Graph 16. Comparison of Emissions and Generating Cost. Case 11................................ 70Graph 17. Marginal Costs Curve: Thermo-electrical Sector. ........................................... 73Graph 18. Relation between Installed Capacity and Grey Cement Production in Colombia

................................................................................................................................... 76Graph 19. Historical Grey Cement Consumption in Colombia........................................ 77Graph 20. Percentage of Fuel Required per Kg. of Clinker. Wet and Dry Processes ..... 78Graph 21. Fuel Types Used in the Cement Industry......................................................... 78Graph 22. GHG Emissions Associated with the Production Process in the Cement

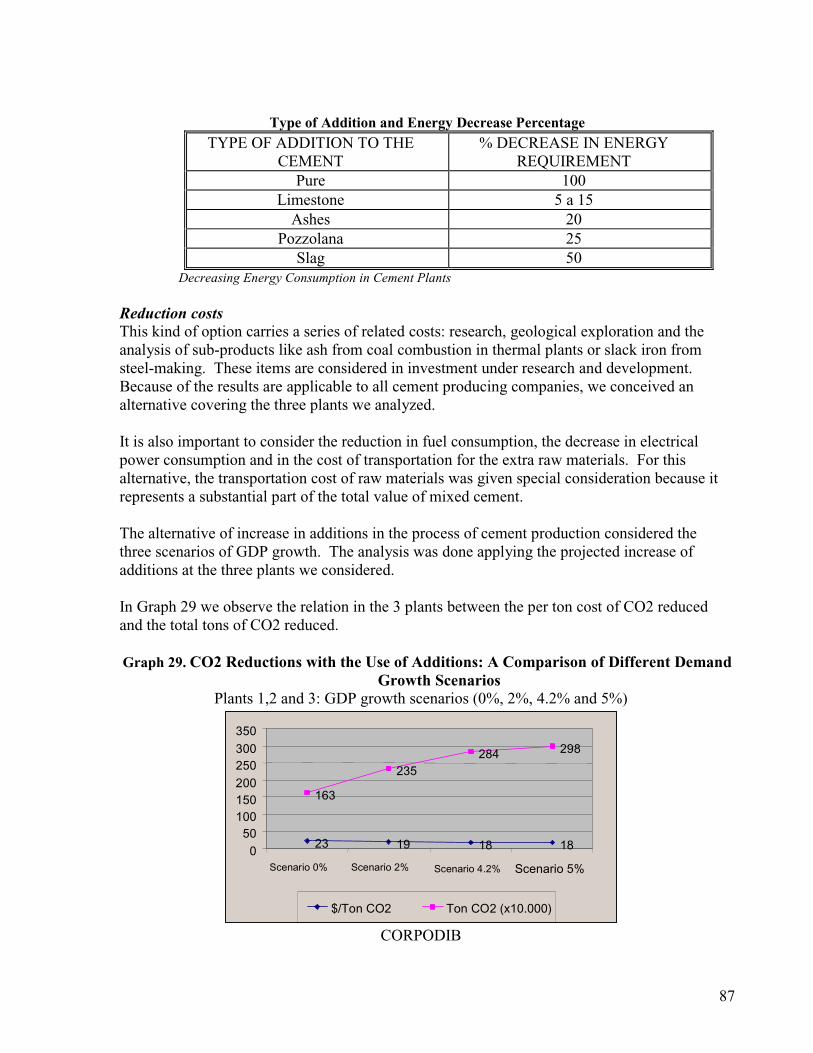

Industry ..................................................................................................................... 79Graph 23. Cement Production in Colombia up to 2010.................................................... 79Graph 24. Technological Evolution in the Colombian Cement Sector ............................ 80Graph 25. Global CO2 Emissions by the Colombian Cement Industry ........................... 80Graph 26. Base Line (Scenarios 1, 2, 3 and 4) for Plant 1................................................ 83Graph 27. Base Line for Plant 2........................................................................................ 83Graph 28. Graph 23. Base Line for Plant 3...................................................................... 84Graph 29. CO2 Reductions with the Use of Additions: A Comparison of Different

Demand Growth Scenarios ....................................................................................... 87Graph 30. Base Line and Reduction Alternative by the Use of Addititives (GDP growth

at 4.2%) ..................................................................................................................... 88

x

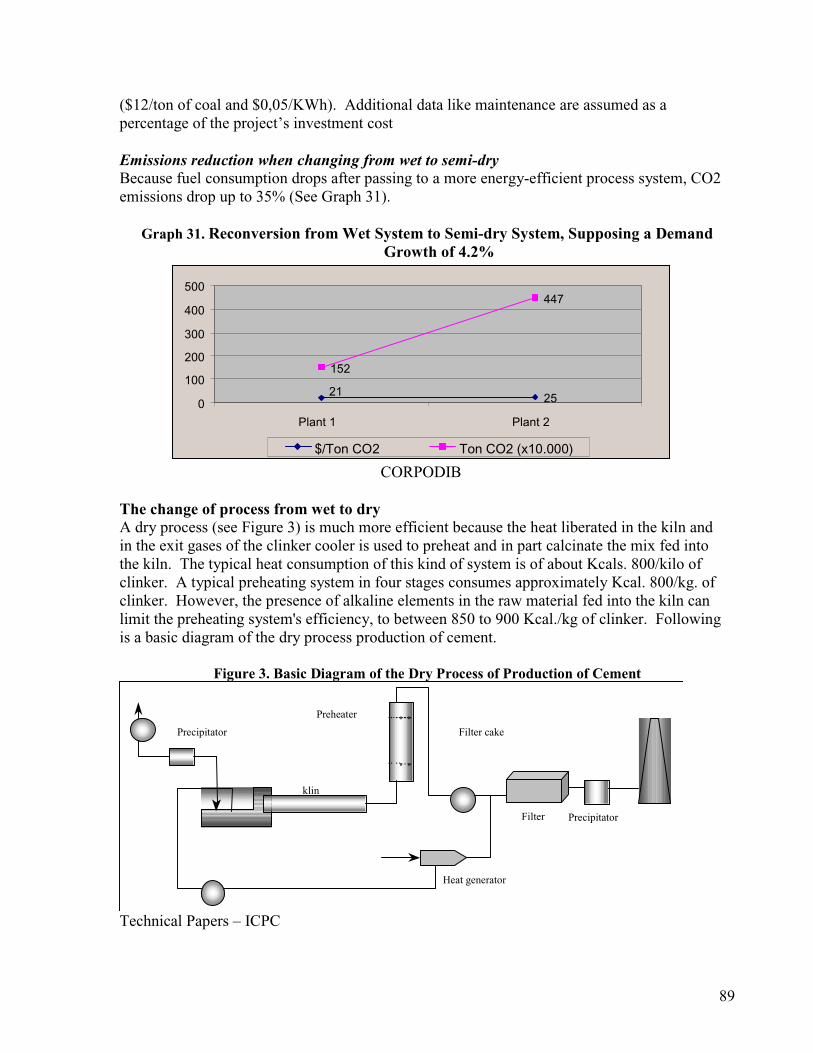

Graph 31. Reconversion from Wet System to Semi-dry System, Supposing a DemandGrowth of 4.2%......................................................................................................... 89

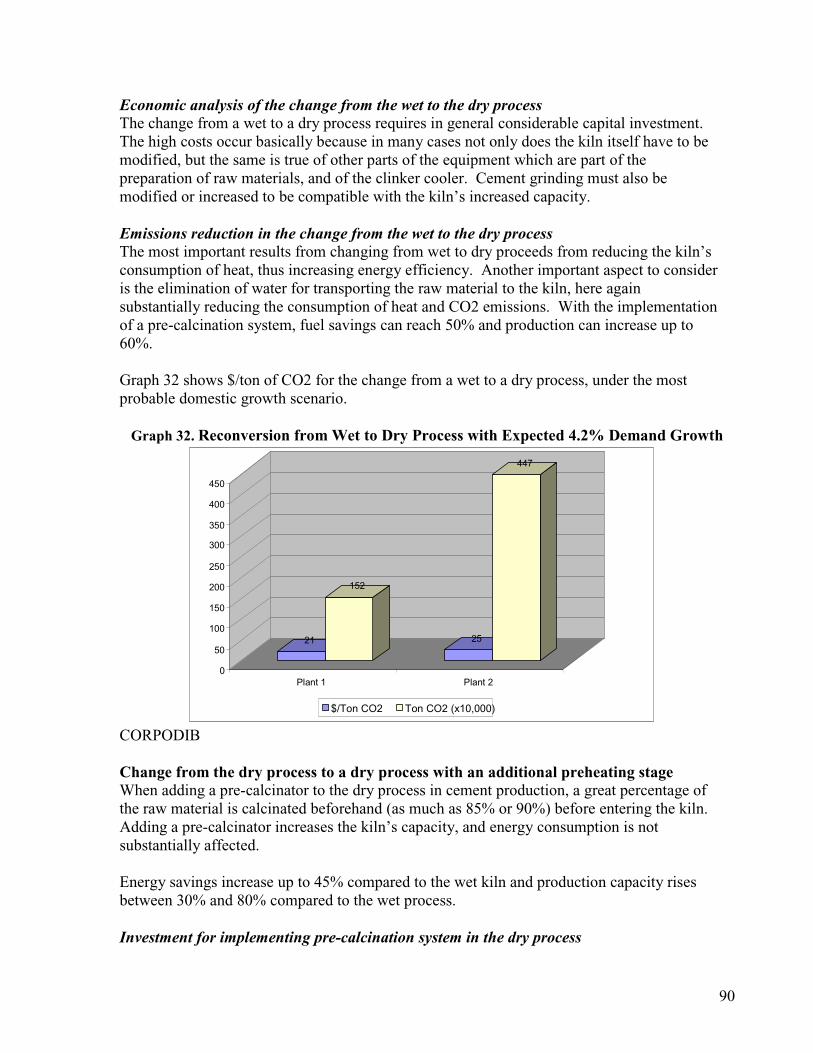

Graph 32. Reconversion from Wet to Dry Process with Expected 4.2% Demand Growth................................................................................................................................... 90

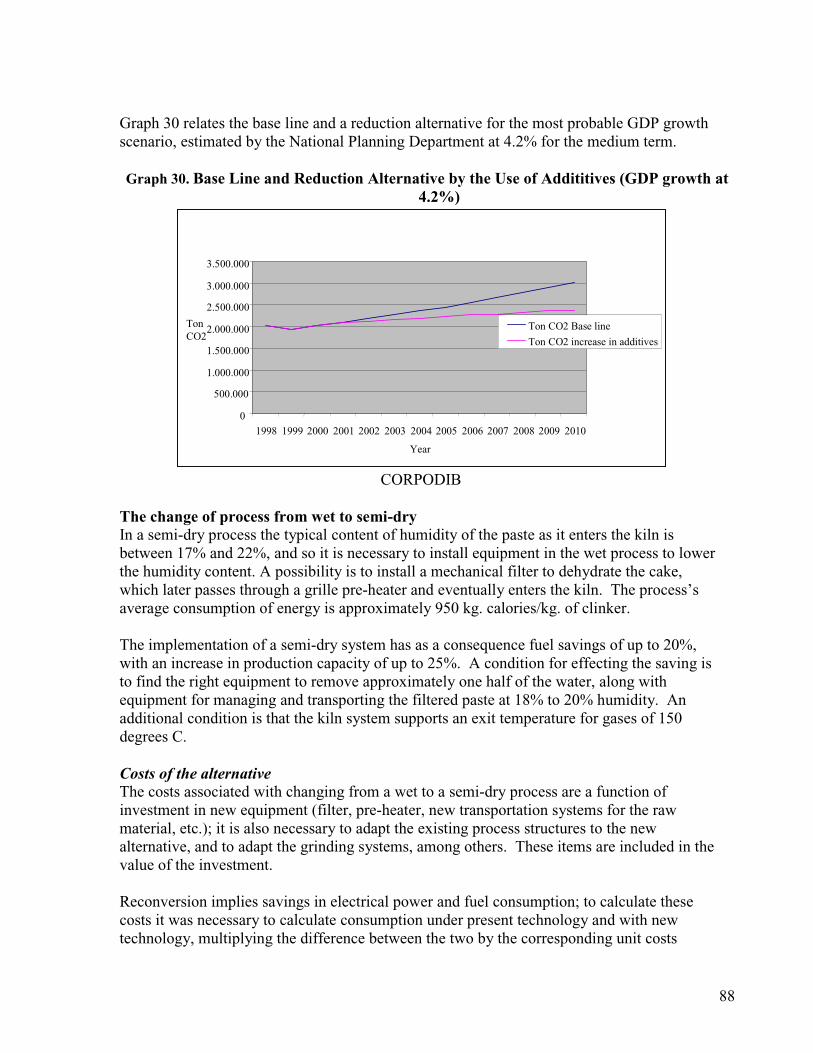

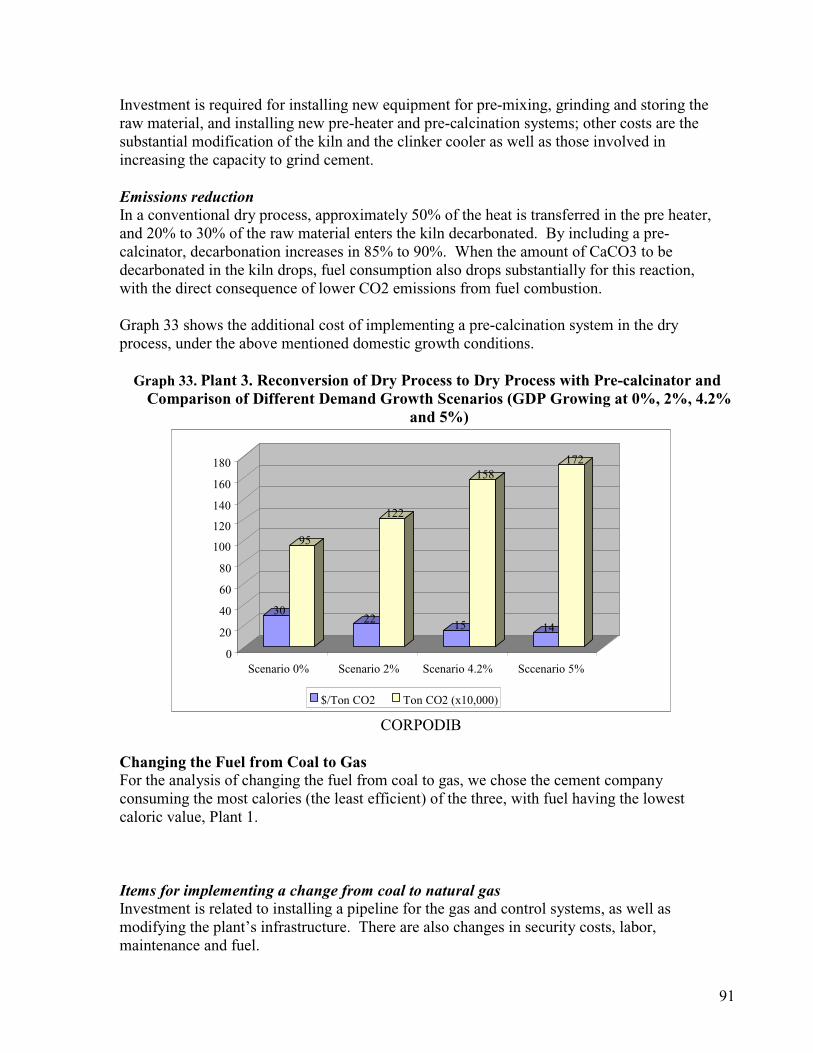

Graph 33. Plant 3. Reconversion of Dry Process to Dry Process with Pre-calcinator andComparison of Different Demand Growth Scenarios (GDP Growing at 0%, 2%,4.2% and 5%)............................................................................................................ 91

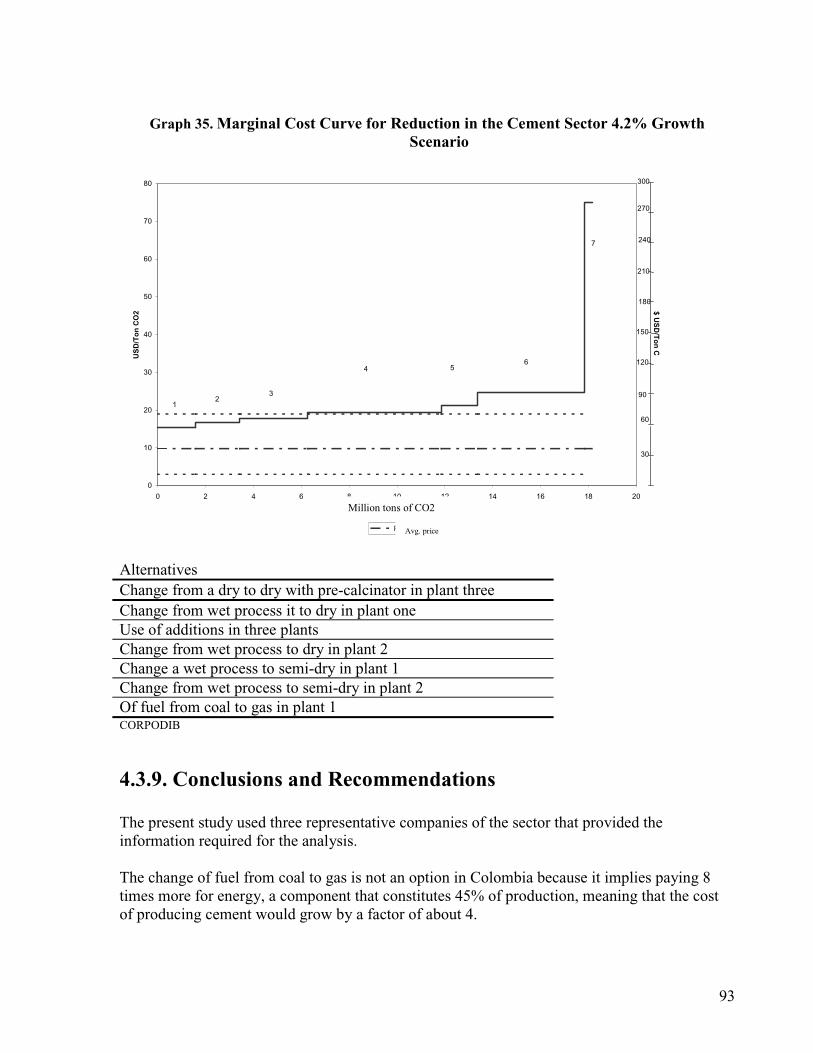

Graph 34. Change in Fuel from Coal to Natural Gas in Plant 1. ...................................... 92Graph 35. Marginal Cost Curve for Reduction in the Cement Sector 4.2% Growth

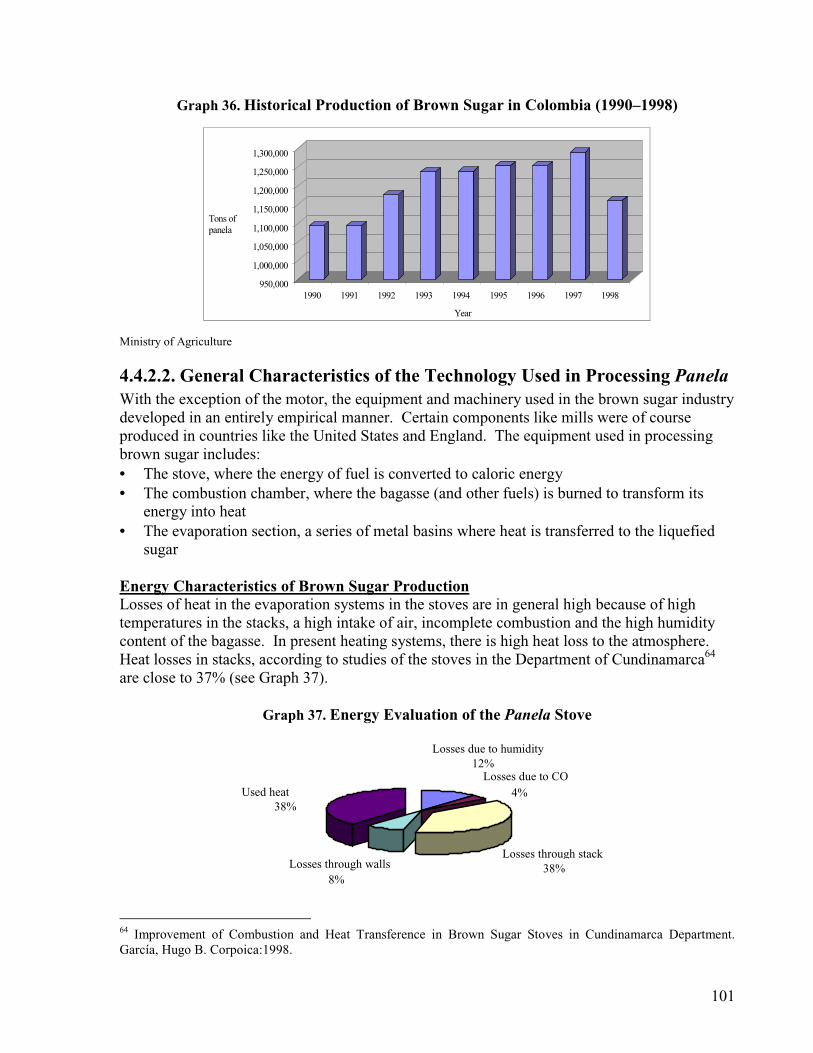

Scenario..................................................................................................................... 93Graph 36. Historical Production of Brown Sugar in Colombia (1990–1998) ................ 101Graph 37. Energy Evaluation of the Panela Stove ......................................................... 101Graph 38. Historical Consumption of Firewood as a Fuel in the Production of Brown

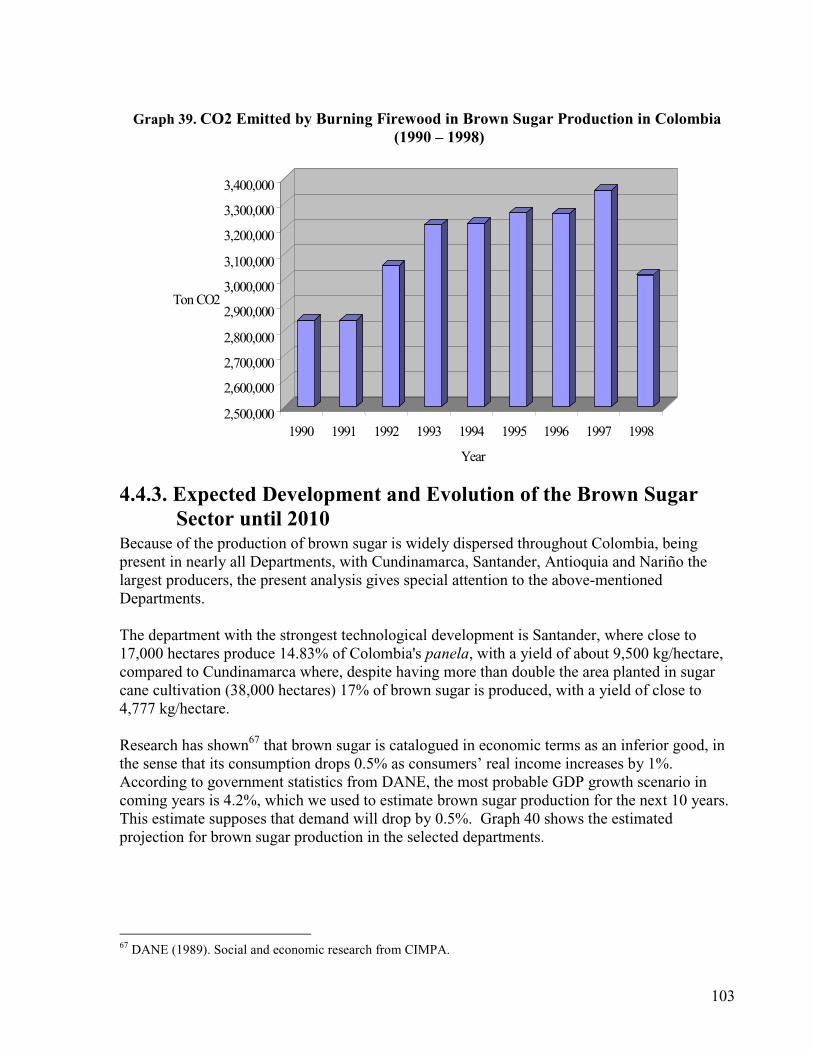

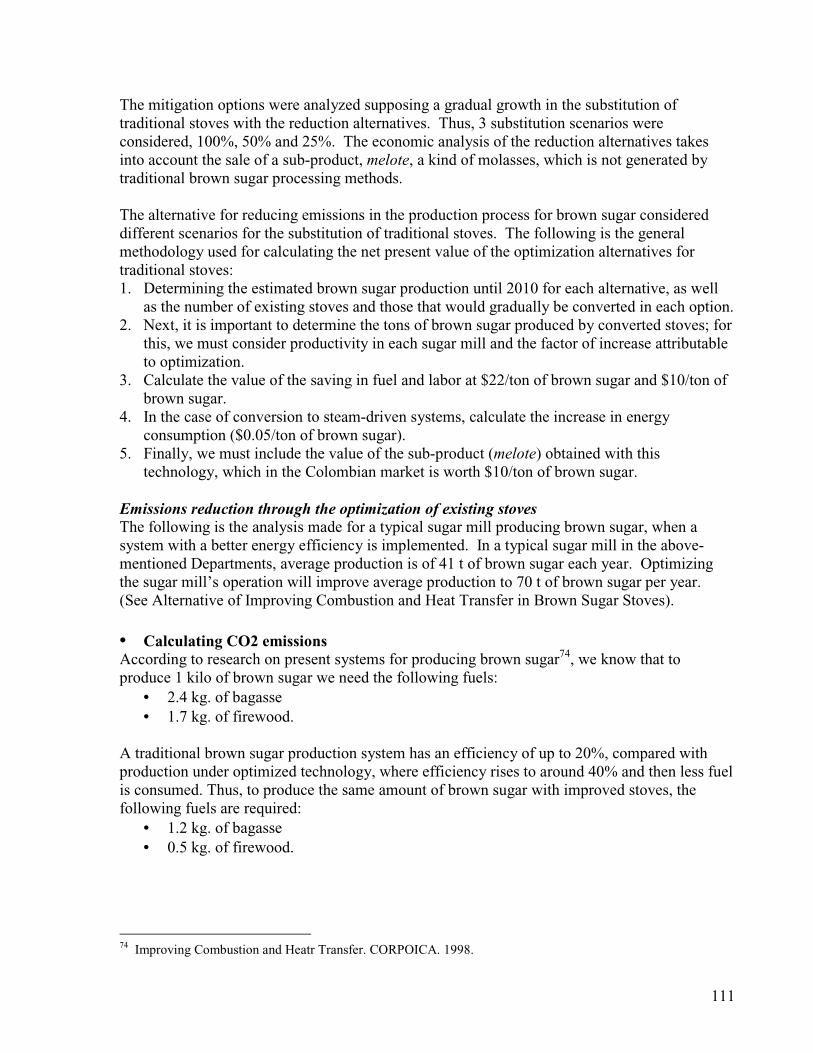

Sugar in Colombia .................................................................................................. 102Graph 39. CO2 Emitted by Burning Firewood in Brown Sugar Production in Colombia

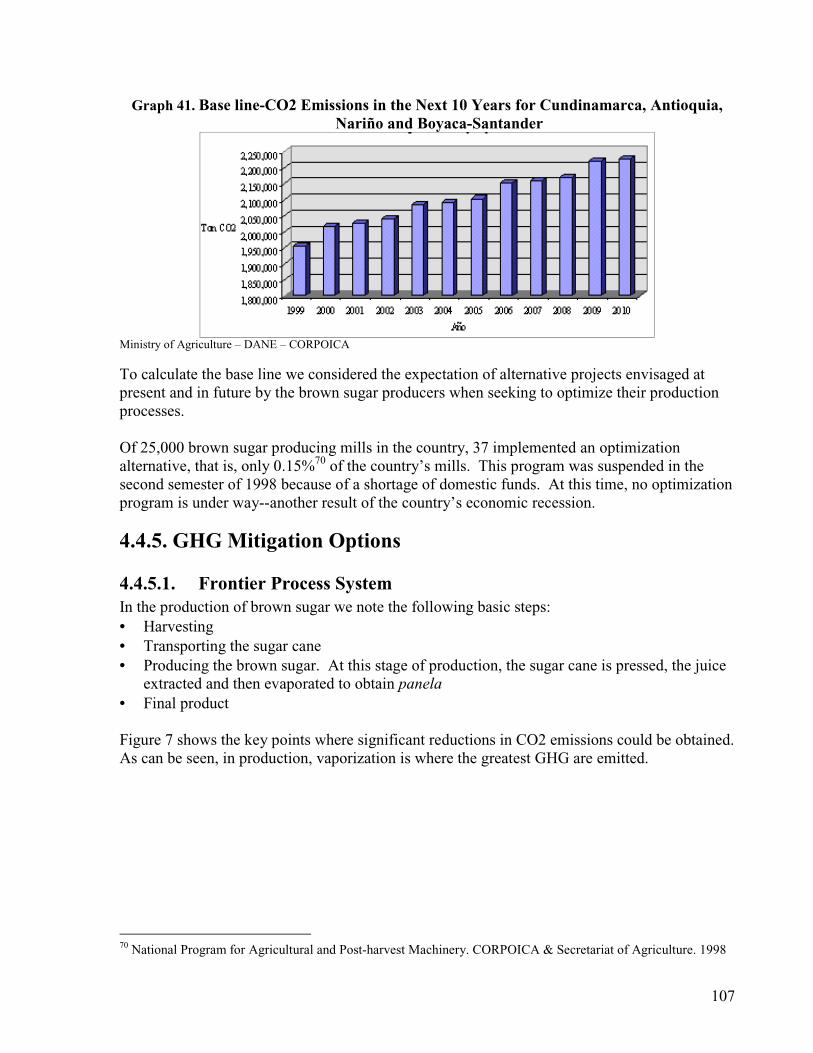

(1990 – 1998).......................................................................................................... 103Graph 40. Estimated Production of Brown Sugar in Colombia in the Next 10 Years ... 104Graph 41. Base line-CO2 Emissions in the Next 10 Years for Cundinamarca, Antioquia,

Nariño and Boyaca-Santander ................................................................................ 107Graph 42. Base Line for a Traditional Sugar Mill and the Reduction Alternative......... 112Graph 43. Marginal Cost Curves for the Reduction Alternatives in the 50% Scenario,

Substituting New for Traditional Stoves, in each of the Five Departments. .......... 115Graph 44. Cost Curve for Reducing GHGs Emissions – Colombian Case – Until 2010121Graph 45. Potential for Generating Foreign Exchange with Certificates for Emissions

Reduction (CERs) ................................................................................................... 122Graph 46. Cost Curve for Reducing GHGs Emissions – Colombian Case – Until 2010127Graph 47. Potential for Generating Foreign Exchange with Certificates for Emissions

Reduction (CERs) ................................................................................................... 128Graph 48. With and Without Project Scenarios in the Forest Sector.............................. 145Graph 49. With and Without-Project Scenario in the Industrial and Energy Sectors..... 145Graph 50. Effects of Transaction costs and Rent-Seeking Behavior on Net Income from

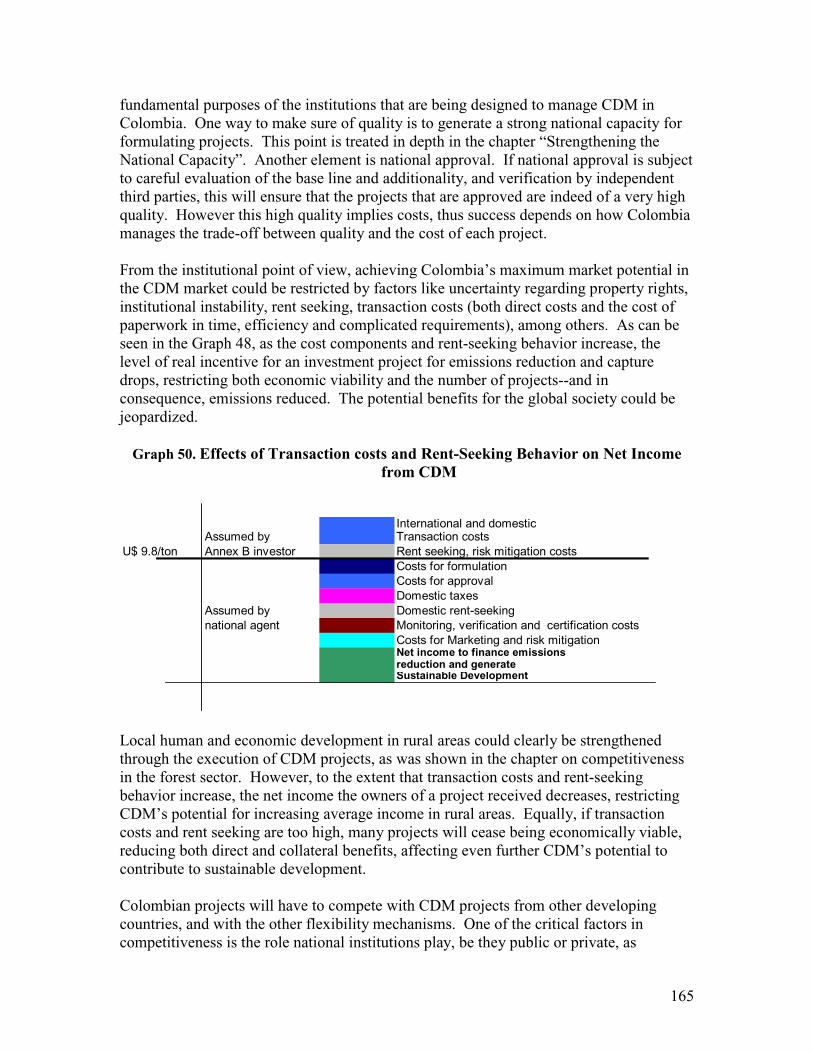

CDM ....................................................................................................................... 165

Figure Index

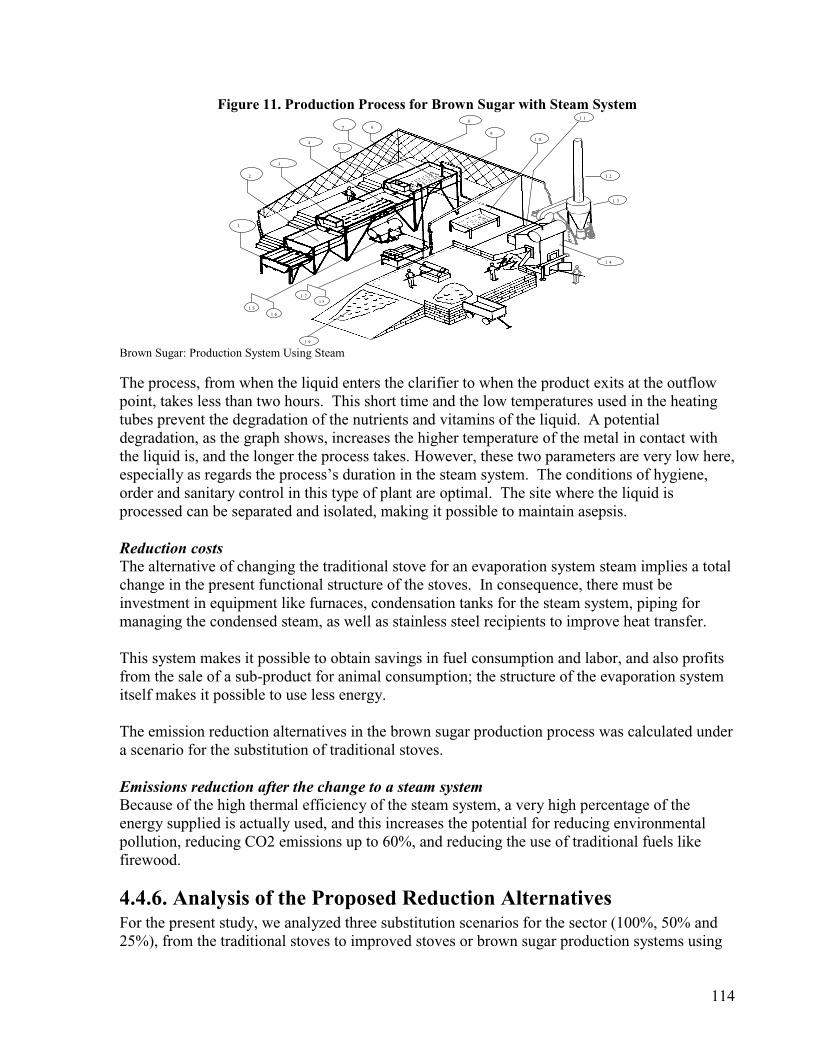

Figure 1. Dispatch System ................................................................................................ 69Figure 2. Delimitation of the Frontiers for Implementing the Reduction Alternatives .... 84Figure 3. Basic Diagram of the Dry Process of Production of Cement............................ 89Figure 4. Distribution of Basic Equipment in the Brown Sugar Production Process ..... 104Figure 5. Traditional Combustion Stove Used in Brown Sugar Production................... 105Figure 6. Parallel Flow Stove.......................................................................................... 105Figure 7. Delimitation of Emission Frontiers in Brown Sugar Production .................... 108Figure 8. Panela Production Optimization Alternative.................................................. 109Figure 9. Grille in Pig Iron.............................................................................................. 109Figure 10. Recipients Used in Panela Production .......................................................... 110Figure 11. Production Process for Brown Sugar with Steam System............................. 114

xi

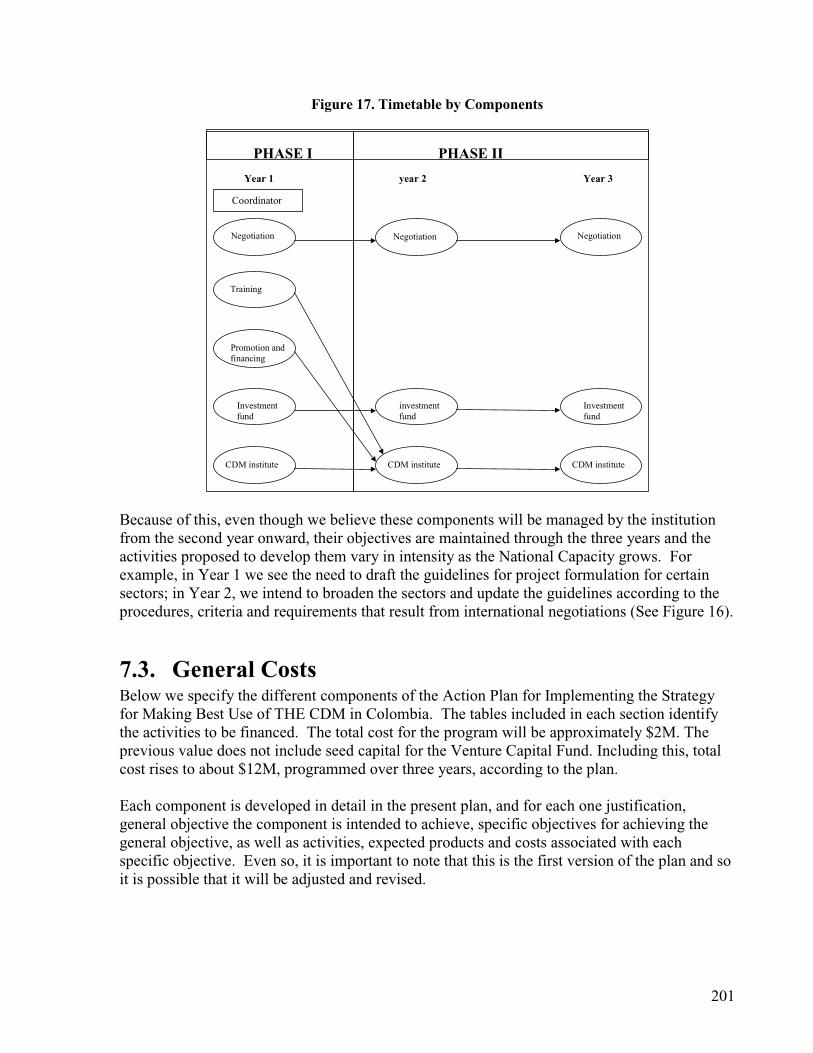

Figure 12. Risk Components for a CDM Program in Colombia .................................... 148Figure 13. Project Risk Components by Stages.............................................................. 150Figure 14. Operation of Securitization............................................................................ 163Figure 15. Setup of the GHG Mitigation Foundation in Colombia ................................ 171Figure 16. Timetable by Components............................................................................. 180Figure 17. Timetable by Components............................................................................. 201

1

1. IntroductionAs a response to global warming, the Climate Change Convention and the Kyoto Protocolestablished the bases of a market for emissions reductions of Greenhouse Gases (GG). Theycreated the Clean Development Mechanism (CDM) to reduce the cost of compliance with thegoals for emissions reductions assumed by Annex B countries (industrialized countries) andpromote sustainable development in developing countries. Because the effect of a reduction ofGG on the climate is the same whether it is effected in Bogota or London, CDM permits large-scale emitters in Annex B to invest a part of their compliance resources in cost-effectiveprojects in developing countries. Experts and multilateral entities committed to this topicestimate that CDM has the potential top generate investment in developing countries of 7.5Bannually, if the Parties ratify the Protocol.

Given the potential represented by CDM for developing countries, this document has threeobjectives: First, to evaluate Colombia’s potential in the new market regarding potentialbenefits and competitiveness. Second, to identify restrictions that could limit the developmentof this potential and, third, to develop strategic lines to overcome these restrictions andmaximize CDM’s potential benefits for the country.

The study has been organized to operate as a training document for sectors and institutionsinterested in developing CDM’s potential. These include, among others, industry executives,communities, domestic and international investors, environmental experts and legislators. Afterreading the study, the interested professional should understand the market dynamics forCertificates for Emissions reduction (CERs), the basics of developing a project for reducing orcapturing emissions and the requisite institutional framework to make this new exportopportunity operate with efficiency and effectiveness. The document contains clear indicationson the country’s sectors and types of projects having the potential to compete in internationalmarkets and clarity regarding the management of the associated risks, and pointers on lining upfinancial resources.

Colombia is endowed with great potential in the CDM market. In optimal conditions ofinformation, risks, and with perfect institutions in the domestic and international spheres, theColombian economy could reduce competitively up to 22.9M t of CO2 yearly, generatingforeign exchange comparable to that produced by bananas and flowers. Internationalinvestment could transfer modern technology for cleaner production and the critical know howto increase productivity and quality in the sectors involved.

In optimal conditions, the collateral benefits could be as important as the direct ones, both inagro-forestry and in energy. If net income accruing to the producer of a CER is high enough,the CO2 capture in forest, mixed agriculture and forest and forest and pasture programs couldincrease producers’ incomes to levels competitive with the present model of on-the-range cattleoperations, unsustainable exploitation of natural forests and drug crops. The sale of CERs forthe capture of CO2 through natural regeneration and reforestation in river basins—nowdeforested—could co-finance the restoration of water sources and conserve them in the longrun, equally controlling critical processes of erosion. This would have a positive impact on

2

preserving biodiversity and the Andean and Tropical ecosystems, at present dramaticallythreatened, offering us the possibility of protecting and studying the genetic resources that willbe so important for the Planet’s future.

Society could also receive collateral benefits from converting industry and energy production tocleaner technology, to reduce CO2. Reconverting industrial boilers and generators will reduceparticulate emissions, sulfur dioxide, and nitrogen oxides, at present the causes of severpollution, smog and public health problems in Colombian cities. Similar effects might beexpected from reconverting transportation to natural gas or “green diesel”, with added benefitsstemming from less congestion and noise.

Even so, there are factors—international and domestic—severely restricting the country’scapacity to achieve it potential in the Clean Development Mechanism’s market. Like otherdeveloping countries, Colombia is subject to a variety of factors limiting the execution of agreat part of its CDM potential. Only to the extent that developing countries can dealeffectively with these restrictions, will they be able to begin exporting significant values ofCERs and enjoy the collateral benefits.

On the international scene, several factors will affect Colombia’s model and level ofparticipation. Negotiations at the next Conference of the Parties (COP) of the CCC willestablish CDM design and modus operandi, and certain proposals on the table might severelyaffect developing countries’ potential, especially Colombia’s. For example:• Countries like Germany and China have manifested their position about excluding sinksfrom CDM

• The EU proposes imposing “supplementarity”, a severe limit to the use of CDM comparedto other compliance options.

• India and China insist on a rigid bilateral investment model, where Colombia would besubject to Annex B countries choosing it as a foreign investment. This imposes high costson projects for searching, negotiation, contracts and administration. Given the perceivedrisk of investing in Colombia, this bilateral model would place the country at a cleardisadvantage.

These international proposals could be devastating for CDM in Colombia. Besides, it ispossible that large international bureaucracies will be created, with high transactions andapproval costs for projects and other appropriations of the value of CDM transactions byinternational institutions that the COP is about to create. These factors could significantlyreduce net income to the country’s project formulators, reducing the economic incentivenotably, and the number and profitability of CDM projects in the country, and finally potentialincome for the country’s rural and industrial producers. These design distortions and rent-seeking impulses must be restrained during international negotiations, to maximize thecountry’s potential benefits.

The decision on where to invest emissions reduction resources is a matter for Annex B emittersto decide on an individual basis. Besides CDM, they will have several options: to reduce intheir own plants, comply through domestic options, purchase emissions rights from Annex B

3

countries through Emissions Rights Trading (ERT) or invest in Joint Implementation (JI)projects in Annex B.

On the domestic scene, several factors exist which could restrict CDM development and theenjoyment of potential benefits, including:

Risks: The risks of investing in Colombia are perceived to be high: because it is a marketdependant on mid and long-term foreign investment, international perception on the risk ofworking and investing in Colombia places the country at a clear disadvantage compared todozens of countries like Costa Rica, Chile and Brazil, that compete for the same resources.

Information: Scarcity of information on the CDM program, the market and the rules forformulating projects: most communities, companies and farmers that could benefit from CDMare not knowledgeable about its mode of operation. The formulators cannot design projects ornegotiate with investors without knowing the market dynamics, especially the expected saleprices of CERs in the future.

Financing: Lack of funds for feasibility studies, project formulation and the execution ofprojects proper.

Institutional factors: Similar programs in some foreign countries have shown that officialorganisms have imposed high transaction, approval and contracting costs. These costs dodiminish even more the net revenue to the CDM rural or industrial investor; they also imposeadditional conditions to potential foreign investors. On the other hand, Colombia will not beallowed to benefit from the CDM if the National Congress does not approve the ratification ofthe protocol. Moreover, Colombia needs the implementation and operation of a CDM office forapproval and fomentation of CDM projects, which can work efficiently, transparently andactively in the process.

4

1. Executive Summary

1.1.Introduction

1.2.Development of the CER MarketChapter IV reviews the current state of the market for Certificates of Emission Reduction,reflecting the uncertainties, the structure of demand and supply, and expectations regarding itsfuture development. The negotiation of efficient regulations for operation of the Kyotomechanisms could consolidate a robust market for emission reduction credits. The studyevaluated various models that have been used to simulate market potential, with particularinterest in their price projection methodology.

The major sources of potential demand for emission rights are the United States, WesternEurope and Japan. Effective demand will depend on each Annex B country’s ability to regulateinternal measures to control GHG emissions and each country’s inclusion of the CDM as acompliance alternative. Major sources of potential supply are China, India and the SovietUnion. Potentially, these nations could supply up to 80% of market demand; however, effectivesupply will probably be much less due to CDM’s complexity, transactions costs, informationproblems and institutional constraints in those countries.

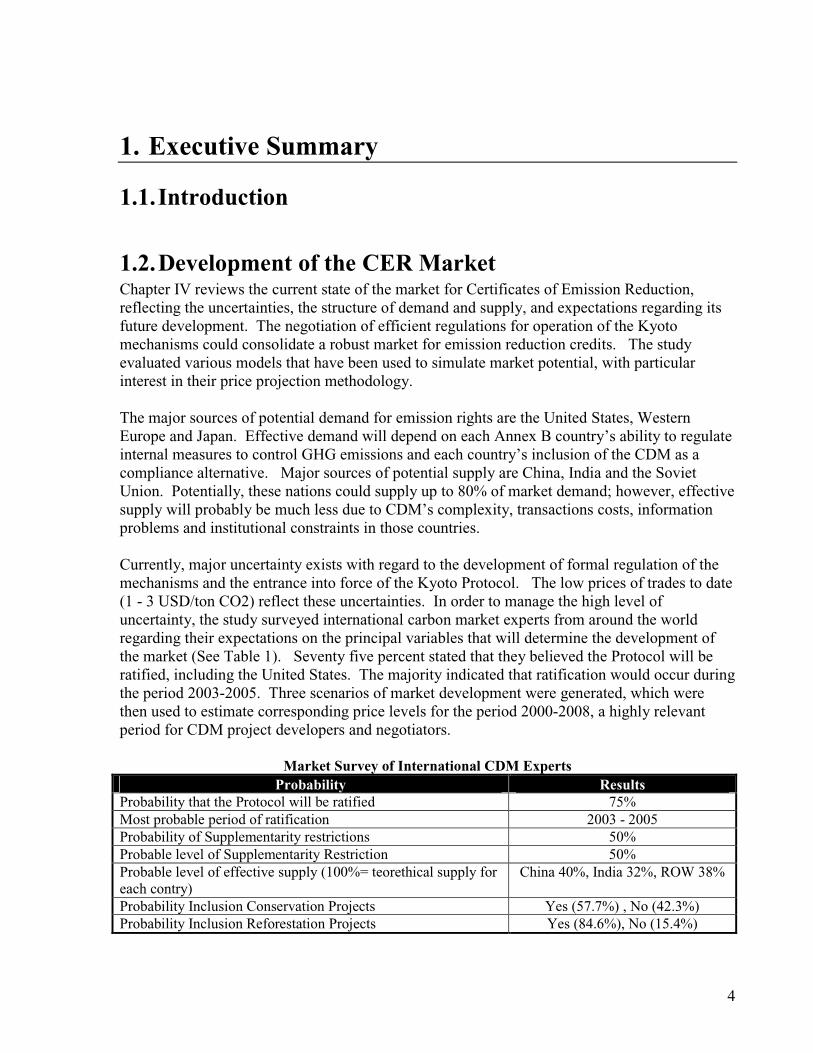

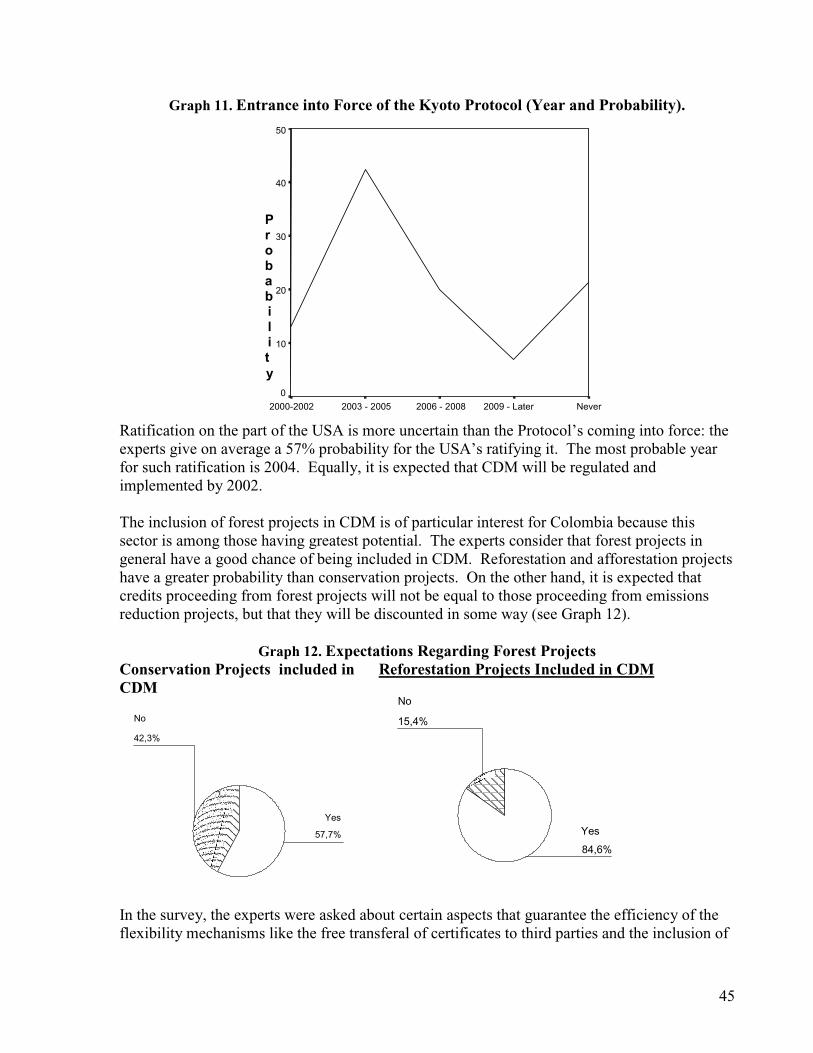

Currently, major uncertainty exists with regard to the development of formal regulation of themechanisms and the entrance into force of the Kyoto Protocol. The low prices of trades to date(1 - 3 USD/ton CO2) reflect these uncertainties. In order to manage the high level ofuncertainty, the study surveyed international carbon market experts from around the worldregarding their expectations on the principal variables that will determine the development ofthe market (See Table 1). Seventy five percent stated that they believed the Protocol will beratified, including the United States. The majority indicated that ratification would occur duringthe period 2003-2005. Three scenarios of market development were generated, which werethen used to estimate corresponding price levels for the period 2000-2008, a highly relevantperiod for CDM project developers and negotiators.

Market Survey of International CDM ExpertsProbability Results

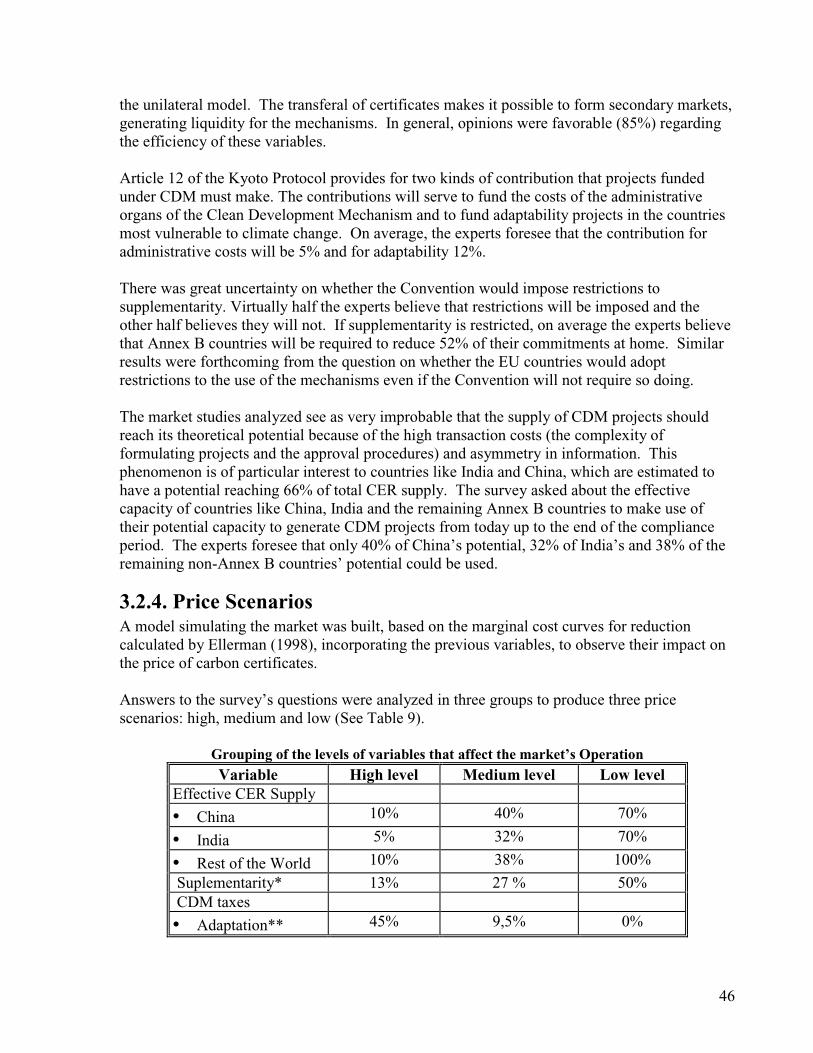

Probability that the Protocol will be ratified 75%Most probable period of ratification 2003 - 2005Probability of Supplementarity restrictions 50%Probable level of Supplementarity Restriction 50%Probable level of effective supply (100%= teorethical supply foreach contry)

China 40%, India 32%, ROW 38%

Probability Inclusion Conservation Projects Yes (57.7%) , No (42.3%)Probability Inclusion Reforestation Projects Yes (84.6%), No (15.4%)

5

The modeling results generate an upper bound of CER price of $19 USD/Ton CO2, $9.8/TonCO2 for the most probable scenario and $3/Ton CO2 for the weak market scenario. This rangeof prices was used throughout the study to evaluate the competitiveness of Colombia’s economyin the generation of Certificates of Emission Reduction.

The analysis indicates that the market could develop even without ratification of the KyotoProtocol, given recent developments. Major multinational energy firms such as BritishPetroleum and Shell Oil have implemented internal emissions reductions programs. In Japan,Tokyo Electric Power Company has begun investing in overseas forestry projects to offset itsemissions from burning of coal. In London, Aurthur Andersen has formed a new fund to investin emissions trading. In Australia, the Sydney Carbon Exchange was recently established tosupport market development, which includes forestry projects. The World Bank PrototypeCarbon Fund will invest US$150 million in CDM projects in Asia, Eastern Europe, LatinAmerica and Africa.

Similarly, several industrialized nations are preparing implementation of domestic regulatoryprograms to reduce greenhouse gas emissions. The European Union aims to implement aregional emissions trading program by 2005. England, Australia, France, Denmark,Switzerland and Norway have either imposed or are preparing to impose pollution charges ordomestic emissions trading programs to control CO2 emissions. The US government ispreparing a national program of renewable energy with similar objectives.

1.3.National Competitiveness and Potential BenefitsChapter V estimates potential benefits from Colombia’s participation in the CDM and evaluatesthe competitiveness of the economy with respect to the emerging new market. Four sectors areevaluated: cement production, electricity generation, panela (raw sugar) processing and forestry.In addition, 28 promising project types throughout the economy are evaluated.

The analysis evaluates the abatement options in each sector, estimating the cost per ton CO2reduced and potential tonnage reductions for each option1. Marginal abatement cost curveswere produced for each sector and aggregated with promising project types to produce an initialmarginal abatement cost curve for the national economy. Finally, the cost curves werejuxtaposed onto the relevant range of CER market prices developed in the market study toestimate the level of competitiveness by project type, economic sector and for the economy ingeneral.

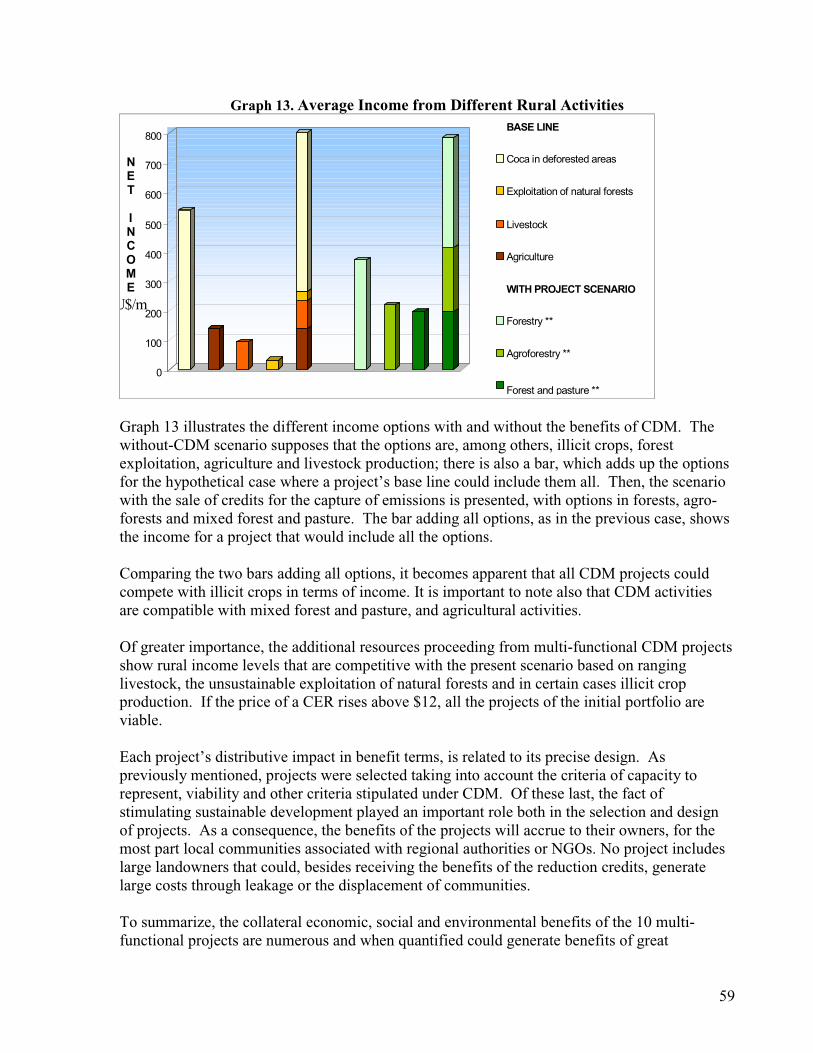

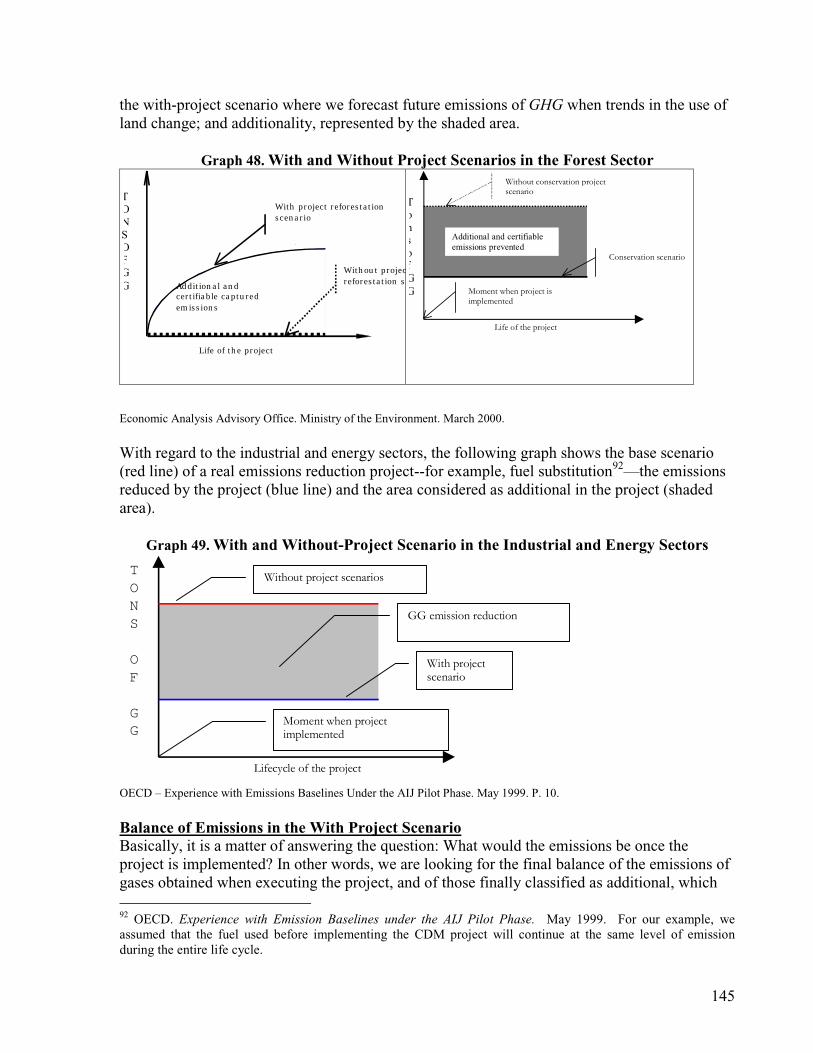

The Forestry Sector.To undertake the analysis of the forestry sector, the study developed 10 CDM projects indiffering conditions and regions of the country encompassing 632 thousand hectares. Fieldmeasurements indicate an excellent capacity for CO2 sequestration at competitive costs. Highlevels of social and environmental benefits were identified in the course of project development,including an increase in the average income per hectare that could provide viable alternatives to

1 Although many analyses use Carbon, we use CO2 because it is the unit required by UNFCCC for reporting. Topromote clarity, our abatement cost graphics include both Carbon and CO2 axes.

6

the current unsustainable activities of illicit crop production, extensive cattle ranching anddestructive exploitation of the natural forest. The study concludes that a functioning CERmarket with prices at or above $9.80 per ton reduced could make a significant contribution tothe peace process through greater employment, incomes and related benefits. However, thiswould require a massive capacity building program to cover major rural areas and target groups.

Projects must be carefully formulated with local social and economic groups in order to developprojects that control leakage, ensure additionality, provide permanent CO2 storage, andgenerate high levels of social and environmental benefits. The formulation methodologies andtheir results satisfactorily address many of the uncertainties related to sinks in the CDMcurrently being debated at the international level. The chapter identifies each of the elementscurrently under debate and provides empirical responses to each from the 10 projectsformulated in Colombia.

The focus on maximization of social and environmental benefits in project formulation wouldsupport improved livelihoods of rural workers and a more environmentally sustainable model ofproduction. Results indicate that positive leakage may be more probable than negative leakage,given the enthusiastic embrace of the CDM opportunity by the groups associated with projectdesign and development. Of great importance, the increase in the average wages supported bythe projects exceeds the stated salary needs of rural workers. The project-specific cash flowanalyses indicate that wages begin to increase gradually over time and attain levels four to fivetimes greater than current minimum wages, due to the multifunctional nature of the projects, theadded income from CO2 capture, and the sustainable uses of the local natural resources base.

The multiple-use focus of the projects offers a better probability of sustainable and productiveuse of the land than projects that only focus on one element of the CDM (conservation orreforestation alone), because of the ability to optimize among the elements of cost, income, andcollateral benefits for the social groups involved.

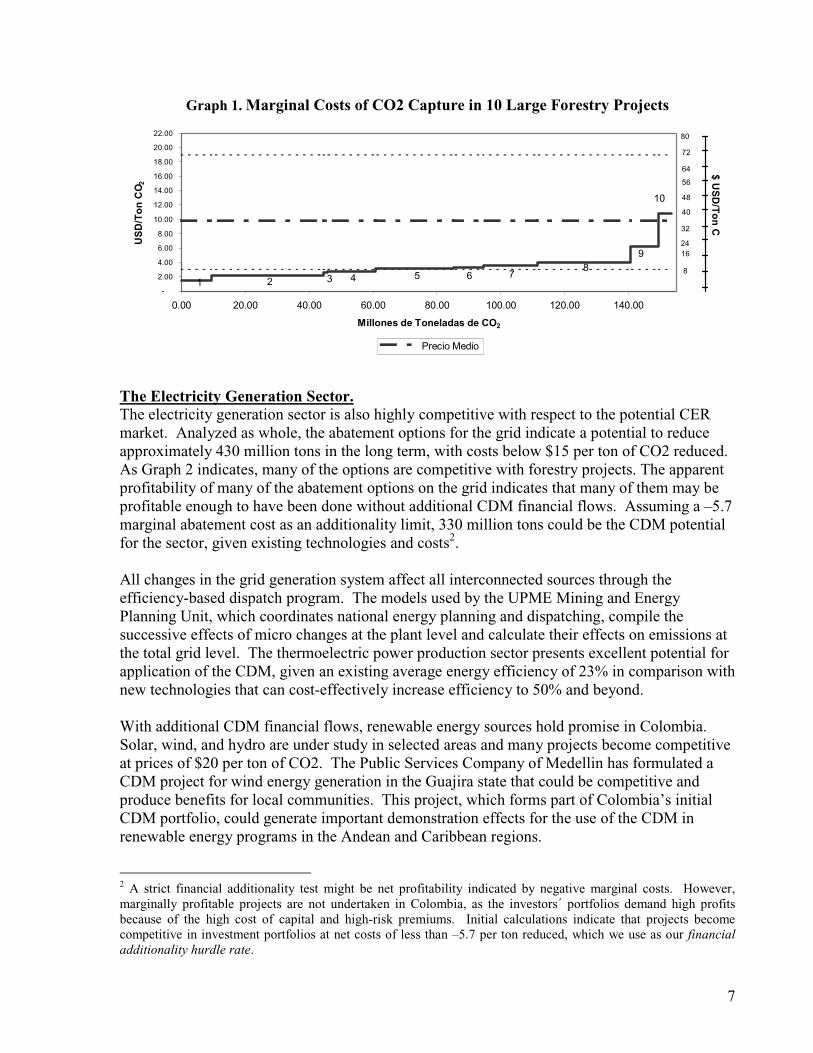

The economic analysis of the forestry projects (Graph 1) demonstrates that the generation ofCERs to offer Green Coal is an economically efficient option for Colombia’s exporters of low-sulfur coal. 90% of the projects generate CERs at a low cost per ton. Geographically,Colombia is closer to North American energy markets than other major competitors that couldoffer green coal, allowing lower transport costs. Because local coal producers already managelocal project risks, operate effectively in existing institutional frameworks and have access tofinance sources, they could efficiently diversify into tropical forestry production to generate theCERs for bundling with their coal exports. Colombia’s exporters could ameliorate the impactof the Kyoto Protocol on their exports in this fashion while contributing important social andenvironmental benefits to rural communities in their regions.

7

Graph 1. Marginal Costs of CO2 Capture in 10 Large Forestry Projects

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

22.00

0.00 20.00 40.00 60.00 80.00 100.00 120.00 140.00

Millones de Toneladas de CO2

USD/TonCO2

Precio Medio

1 2 3 4 5 6 78

9

10

$USD/TonC32

40

48

56

64

72

16

8

24

80

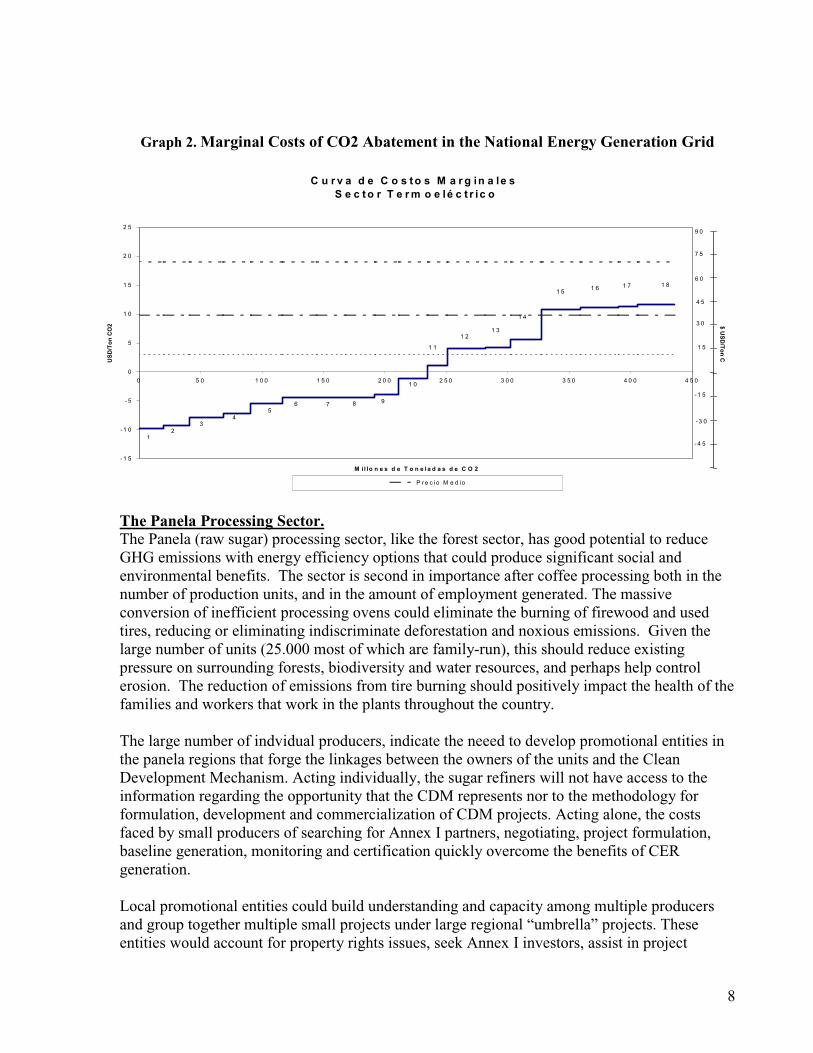

The Electricity Generation Sector.The electricity generation sector is also highly competitive with respect to the potential CERmarket. Analyzed as whole, the abatement options for the grid indicate a potential to reduceapproximately 430 million tons in the long term, with costs below $15 per ton of CO2 reduced.As Graph 2 indicates, many of the options are competitive with forestry projects. The apparentprofitability of many of the abatement options on the grid indicates that many of them may beprofitable enough to have been done without additional CDM financial flows. Assuming a –5.7marginal abatement cost as an additionality limit, 330 million tons could be the CDM potentialfor the sector, given existing technologies and costs2.

All changes in the grid generation system affect all interconnected sources through theefficiency-based dispatch program. The models used by the UPME Mining and EnergyPlanning Unit, which coordinates national energy planning and dispatching, compile thesuccessive effects of micro changes at the plant level and calculate their effects on emissions atthe total grid level. The thermoelectric power production sector presents excellent potential forapplication of the CDM, given an existing average energy efficiency of 23% in comparison withnew technologies that can cost-effectively increase efficiency to 50% and beyond.

With additional CDM financial flows, renewable energy sources hold promise in Colombia.Solar, wind, and hydro are under study in selected areas and many projects become competitiveat prices of $20 per ton of CO2. The Public Services Company of Medellin has formulated aCDM project for wind energy generation in the Guajira state that could be competitive andproduce benefits for local communities. This project, which forms part of Colombia’s initialCDM portfolio, could generate important demonstration effects for the use of the CDM inrenewable energy programs in the Andean and Caribbean regions.

2 A strict financial additionality test might be net profitability indicated by negative marginal costs. However,marginally profitable projects are not undertaken in Colombia, as the investors´ portfolios demand high profitsbecause of the high cost of capital and high-risk premiums. Initial calculations indicate that projects becomecompetitive in investment portfolios at net costs of less than –5.7 per ton reduced, which we use as our financialadditionality hurdle rate.

8

Graph 2. Marginal Costs of CO2 Abatement in the National Energy Generation Grid

The Panela Processing Sector.The Panela (raw sugar) processing sector, like the forest sector, has good potential to reduceGHG emissions with energy efficiency options that could produce significant social andenvironmental benefits. The sector is second in importance after coffee processing both in thenumber of production units, and in the amount of employment generated. The massiveconversion of inefficient processing ovens could eliminate the burning of firewood and usedtires, reducing or eliminating indiscriminate deforestation and noxious emissions. Given thelarge number of units (25.000 most of which are family-run), this should reduce existingpressure on surrounding forests, biodiversity and water resources, and perhaps help controlerosion. The reduction of emissions from tire burning should positively impact the health of thefamilies and workers that work in the plants throughout the country.

The large number of indvidual producers, indicate the neeed to develop promotional entities inthe panela regions that forge the linkages between the owners of the units and the CleanDevelopment Mechanism. Acting individually, the sugar refiners will not have access to theinformation regarding the opportunity that the CDM represents nor to the methodology forformulation, development and commercialization of CDM projects. Acting alone, the costsfaced by small producers of searching for Annex I partners, negotiating, project formulation,baseline generation, monitoring and certification quickly overcome the benefits of CERgeneration.

Local promotional entities could build understanding and capacity among multiple producersand group together multiple small projects under large regional “umbrella” projects. Theseentities would account for property rights issues, seek Annex I investors, assist in project

C u r v a d e C o s to s M a rg in a le sS e c to r T e rm o e lé c t r ic o

- 1 5

- 1 0

- 5

0

5

1 0

1 5

2 0

2 5

0 5 0 1 0 0 1 5 0 2 0 0 2 5 0 3 0 0 3 5 0 4 0 0 4 5 0

M il lo n e s d e T o n e l a d a s d e C O 2

USD/TonCO2

P re c io M e d io

12

34

56 7 8 9

1 0

1 1

1 21 3

1 4

1 51 6

1 5

3 0

4 5

6 0

7 5

9 0

-1 5

-3 0

- 4 5

$USD/TonC

1 7 1 8

9

formulation, carry out an accounting of projects undertaken successfully, and transfer the CERsappropriately among producers and investors. Helping to assure quality and additionality of thelarge umbrella projects, these entities would also manage complex national and internationalapproval processes, search for Annex B investors, and coordinate the execution and monitoringof the projects. This organizational model was developed in detail working with the PanelaProducers Association, and could be adapted to other sectors such as forestry and transport,which present similar conditions and transactions costs.

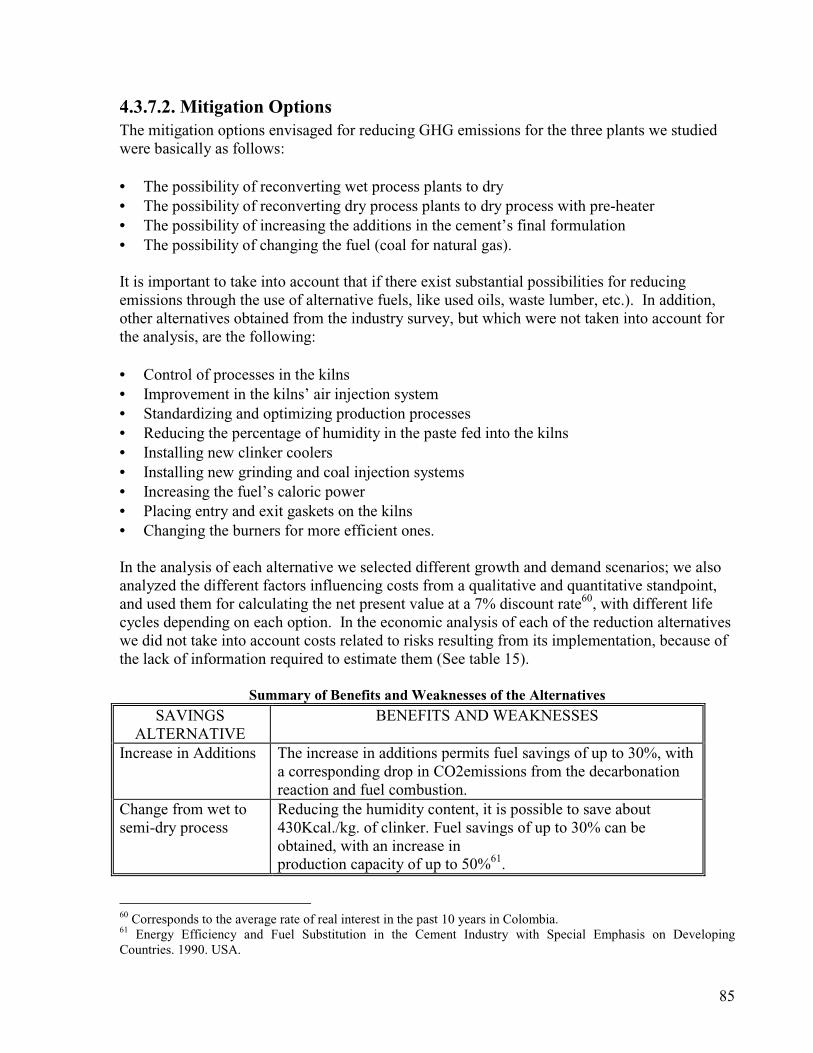

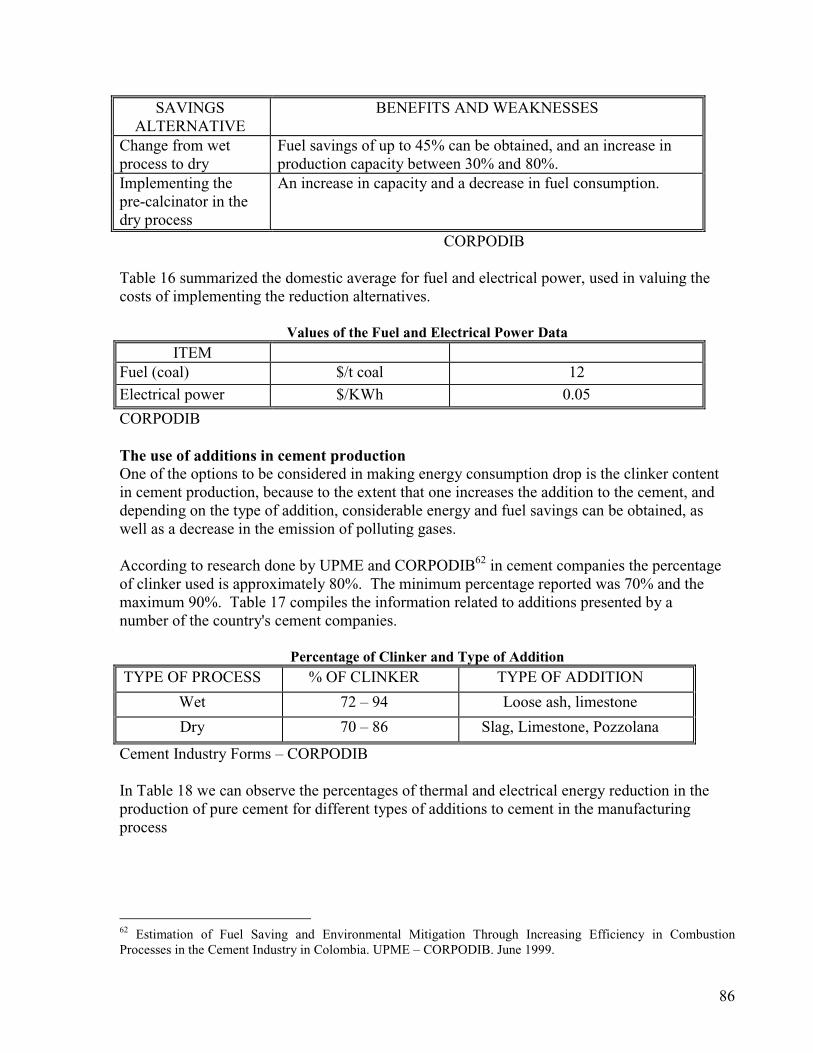

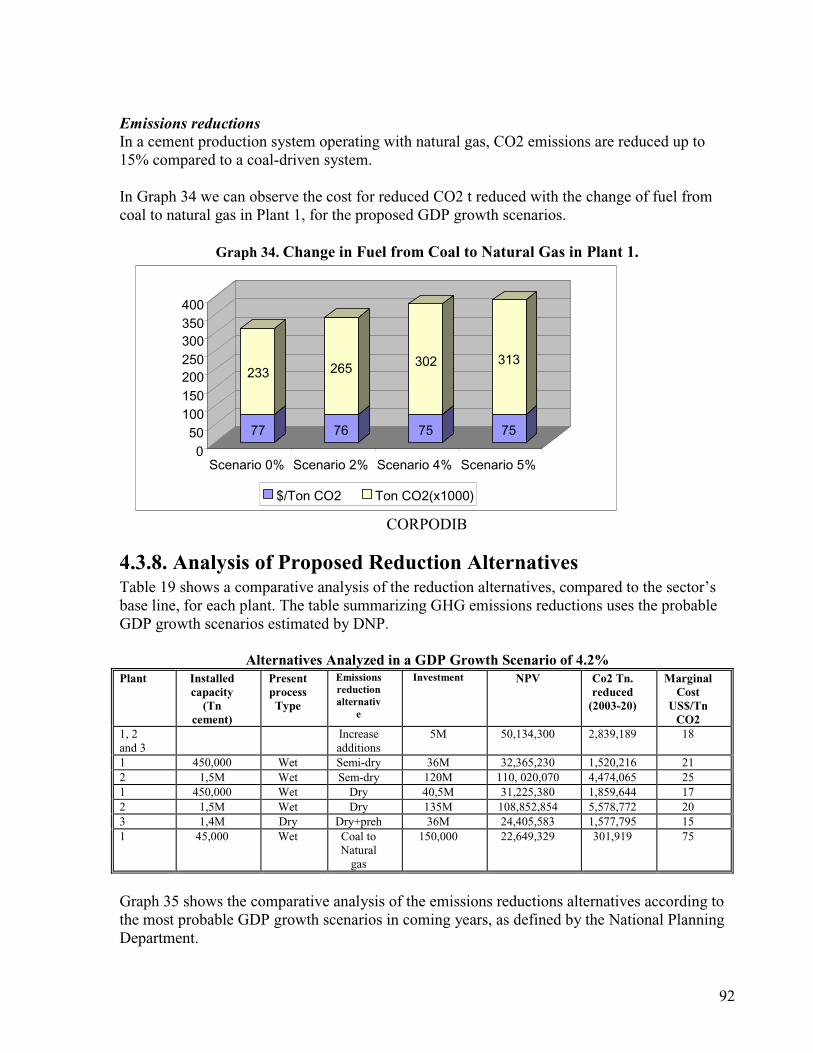

The Cement Production Sector.Case studies in three large plants were used to analyze options in the Cement sector. Incomparison with the other 3 sectors analyzed, abatement costs are relatively high relative to theestimated CER price range. Changing from local coal to natural gas is not a feasible option inmost cases because of the very low cost of the coal and long distance to gas pipelines. In oneplant, changing from coal to natural gas implied increasing the energy budget eight-fold, whichrepresented a 45% increase in operating costs. Assuming the high CER price scenario ofUS$19, three alternatives appear viable via the CDM: preheating the dry process, changing theproduction system from wet to dry, and the use of additives in combustion. The results indicatethat the most cost-effective alternative is the first. The use of additives could be competitive butrequires more research and development.

Although the additional options have costs per ton reduced, higher than the estimated pricerange, the CDM could finance a significant share of conversion costs. Seen in this light, theCDM represents financing option for improvement of productivity and competitiveness in thesector. For example, the study evaluated the potential for conversion from wet to dry process ina plant with installed capacity to produce 1’500.000 tons of cement annually. This investmentcould reduce upwards of 5.6 million tons of GHG during the life of the project at a cost of $135million dollars. The sale of CERs at 9.80, our median price estimate, would generate 54.6million dollars for the investment. If the technological conversion is interesting for additionalreasons, the CER flow could leverage the investment.

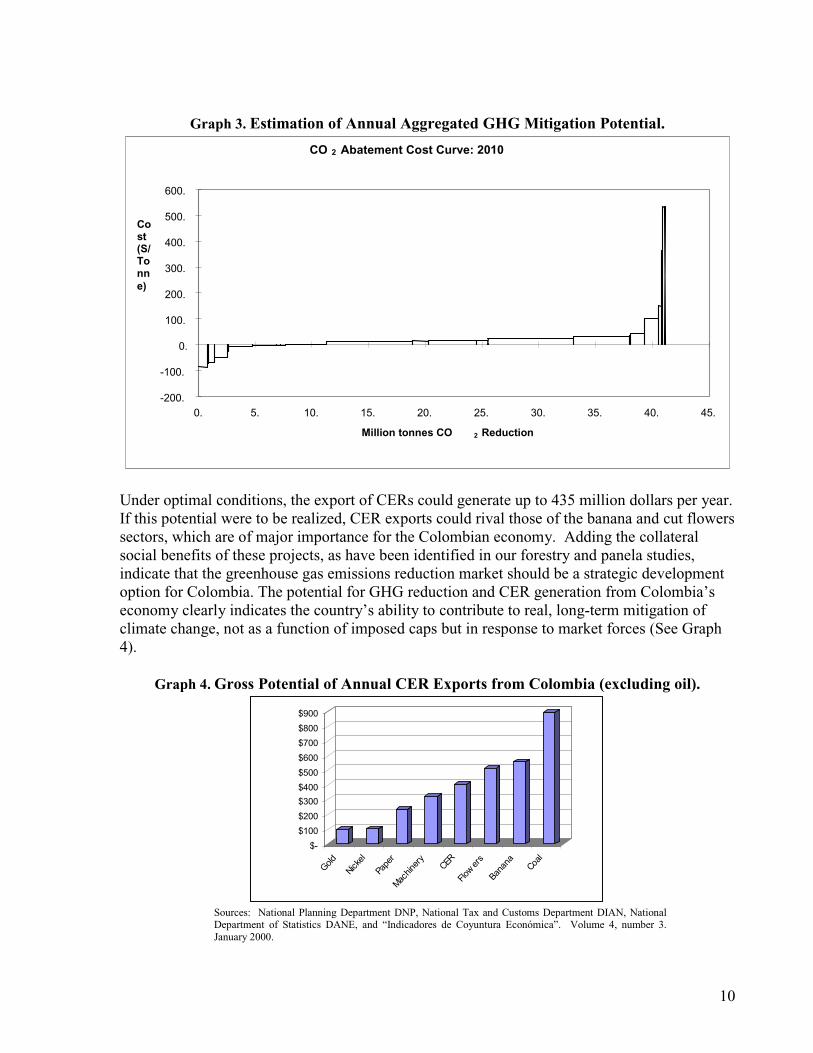

Potential benefits of Colombia´s participation in the CDMTo estimate the economic potential of implementing the CDM in the Colombian economy on anannual basis, the Ministry team worked with the National Academy of Sciences to evaluate thepotential opportunities for GHG reductions in 28 promising project types, including the projectsidentified in the 4 sectoral analyses. The analysis estimates the annualized costs per tonreduced and the yearly tonnage reduction potential for each option. Assuming optimalconditions (perfect information, low risk, efficient capital markets and institutions), theseoptions could reduce up to 42 million tons of CO2 equivalent per year. Technogically, this ispossible. However, when CDM additionality criteria and market price constraints are imposed,the potential is estimated at 22.9 million tons. Assuming that projects with costs of less than –$5.7 per ton will be profitable enough to be carried out without CDM, environmentaladditionality is promoted. Projects with costs above our high CER price scenario of $19 willprobably not be undertaken as a result of the CDM (See Graph 3).

10

Graph 3. Estimation of Annual Aggregated GHGMitigation Potential.

CO 2 Abatement Cost Curve: 2010

-200.

-100.

0.

100.

200.

300.

400.

500.

600.

0. 5. 10. 15. 20. 25. 30. 35. 40. 45.

Million tonnes CO 2 Reduction

Cost(S/Tonne)

Under optimal conditions, the export of CERs could generate up to 435 million dollars per year.If this potential were to be realized, CER exports could rival those of the banana and cut flowerssectors, which are of major importance for the Colombian economy. Adding the collateralsocial benefits of these projects, as have been identified in our forestry and panela studies,indicate that the greenhouse gas emissions reduction market should be a strategic developmentoption for Colombia. The potential for GHG reduction and CER generation from Colombia’seconomy clearly indicates the country’s ability to contribute to real, long-term mitigation ofclimate change, not as a function of imposed caps but in response to market forces (See Graph4).

Graph 4. Gross Potential of Annual CER Exports from Colombia (excluding oil).

$-

$100

$200

$300

$400

$500

$600

$700

$800

$900

Gold

Nickel

Paper

Machinery

CER

Flowers

Banana Coal

Sources: National Planning Department DNP, National Tax and Customs Department DIAN, NationalDepartment of Statistics DANE, and “Indicadores de Coyuntura Económica”. Volume 4, number 3.January 2000.

11

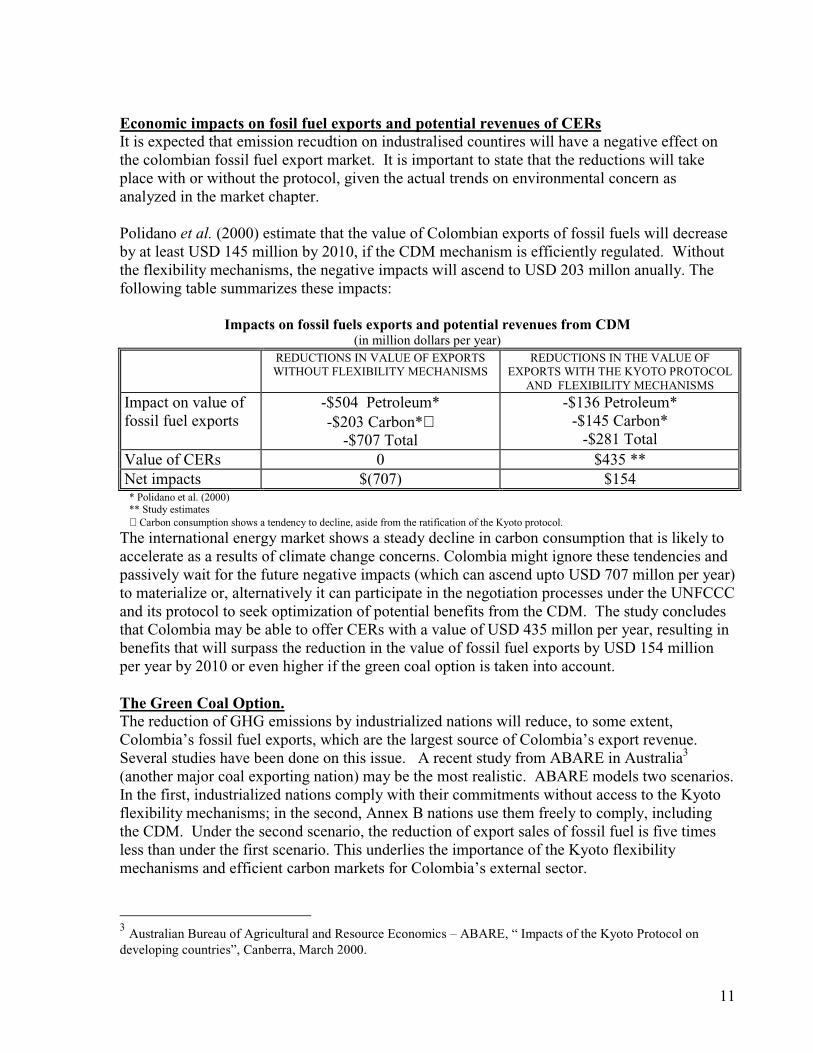

Economic impacts on fosil fuel exports and potential revenues of CERsIt is expected that emission recudtion on industralised countires will have a negative effect onthe colombian fossil fuel export market. It is important to state that the reductions will takeplace with or without the protocol, given the actual trends on environmental concern asanalyzed in the market chapter.

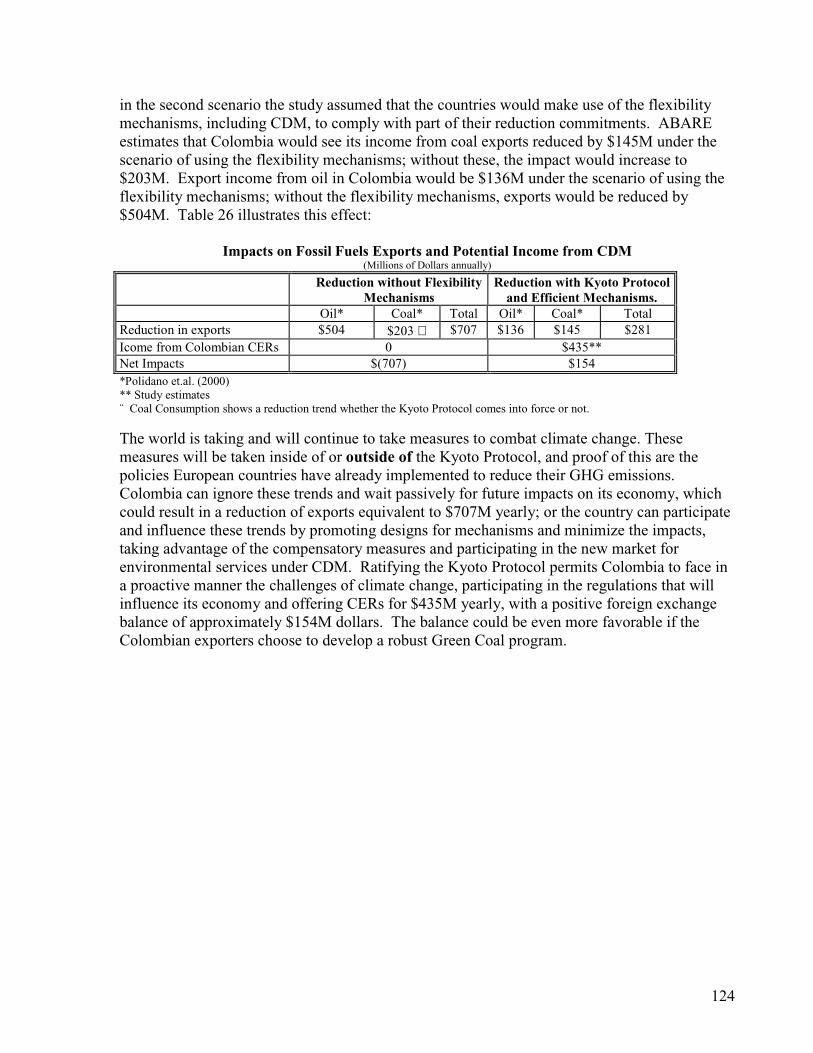

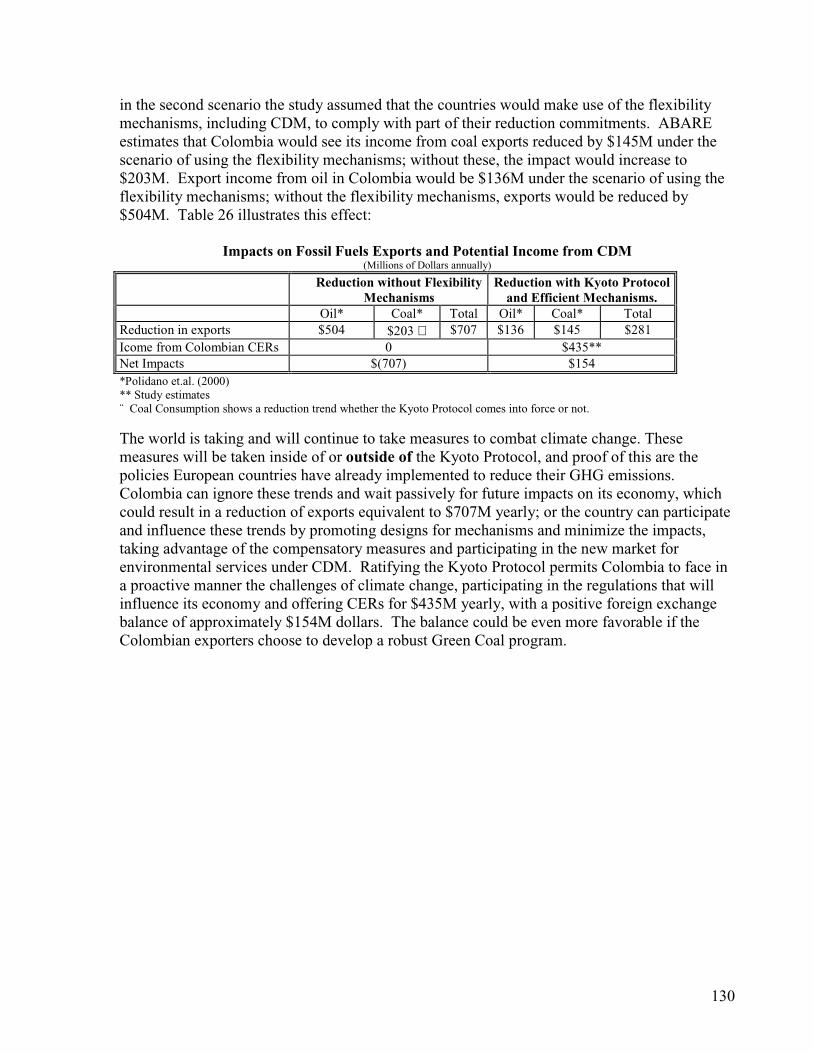

Polidano et al. (2000) estimate that the value of Colombian exports of fossil fuels will decreaseby at least USD 145 million by 2010, if the CDM mechanism is efficiently regulated. Withoutthe flexibility mechanisms, the negative impacts will ascend to USD 203 millon anually. Thefollowing table summarizes these impacts:

Impacts on fossil fuels exports and potential revenues from CDM(in million dollars per year)

REDUCTIONS IN VALUE OF EXPORTSWITHOUT FLEXIBILITY MECHANISMS

REDUCTIONS IN THE VALUE OFEXPORTS WITH THE KYOTO PROTOCOLAND FLEXIBILITY MECHANISMS

Impact on value offossil fuel exports

-$504 Petroleum*-$203 Carbon*∇-$707 Total

-$136 Petroleum*-$145 Carbon*-$281 Total

Value of CERs 0 $435 **Net impacts $(707) $154* Polidano et al. (2000)** Study estimates∇ Carbon consumption shows a tendency to decline, aside from the ratification of the Kyoto protocol.The international energy market shows a steady decline in carbon consumption that is likely toaccelerate as a results of climate change concerns. Colombia might ignore these tendencies andpassively wait for the future negative impacts (which can ascend upto USD 707 millon per year)to materialize or, alternatively it can participate in the negotiation processes under the UNFCCCand its protocol to seek optimization of potential benefits from the CDM. The study concludesthat Colombia may be able to offer CERs with a value of USD 435 millon per year, resulting inbenefits that will surpass the reduction in the value of fossil fuel exports by USD 154 millionper year by 2010 or even higher if the green coal option is taken into account.

The Green Coal Option.The reduction of GHG emissions by industrialized nations will reduce, to some extent,Colombia’s fossil fuel exports, which are the largest source of Colombia’s export revenue.Several studies have been done on this issue. A recent study from ABARE in Australia3

(another major coal exporting nation) may be the most realistic. ABARE models two scenarios.In the first, industrialized nations comply with their commitments without access to the Kyotoflexibility mechanisms; in the second, Annex B nations use them freely to comply, includingthe CDM. Under the second scenario, the reduction of export sales of fossil fuel is five timesless than under the first scenario. This underlies the importance of the Kyoto flexibilitymechanisms and efficient carbon markets for Colombia’s external sector.

3 Australian Bureau of Agricultural and Resource Economics – ABARE, “ Impacts of the Kyoto Protocol ondeveloping countries”, Canberra, March 2000.

12

In an international environment that is moving toward “decarbonization” with or without theKyoto Protocol, Colombia can maintain its export competitiveness by bundling CERs generatedfrom our competitive forest projects with coal and oil to export Greenhouse Gas CompensatedCoal, or “Green Coal”. In interviews with individual coal exporters, many expressed theirbelief that Colombia could become the major provider of Green Coal for the United States andCanada, based on three factors: low CER generation costs, low transportation costs based onColombia’s geographic proximity, and the high BTU rating and low sulfur content ofColombian coal.

These simulations represent Colombia’s potential for GHG mitigation and CER export underoptimal conditions. However, conditions for CDM market development are far from perfect inColombia. In practice under the status quo, only a small fraction of this potential will berealized without efficient and effective policies to promote the CDM and relax existingconstraints.

Technology transfer needsAn important outcome from the analysis of the different projects and sectors was to identify thelack of technology and know how. In this respect, the success and viability of the differentMDL projects will surely depend on providing a solution for these lacks at the regional andlocal levels. Furthermore, capacity building was also an important component which has to beaddressed in order to promote the transition to the scenario brought by the project.

In the forestry sector, the main findings were related to sustainable use of forests andmainentace of planted areas. The cement sector was found that the lack with respect totechnology was due to economic factors. As the sector represents industries from a well-defined portion of the economy, their situation with respect to know-how is said to becustomary. The results revealed by the Panela producing sector showed that there is a need forthe individual producers to gather into greater groups, which can canalize all informatiuonneeded for the formulation of MDL projects.

As a general requirement, the know-how of CDM project formulation should be a primary stepfor implementing the strategy.To strenghen their opportunities in the CDM market, there is aneed for implementing a technology transfer and capacity building programmes, focused onlatest and cleaner technologies and on CDM project formulation (mainly baseline andaditionality).

1.4.Strategic Policies to Develop Colombia’s CDM PotentialChapter VI develops alternatives to remove the international and national constraints that canlimit the development of the CDM potential identified in this study. In the international arena,inefficient regulations may distort the operation of the CDM, severely limiting its potential toallocate resources towards cost-effective emissions reduction projects in developing countries.At the national level, factors such as information constraints, high risk to foreign investors, lackof finance for prefeasibility studies, inefficient institutions and high transaction costs could limitthe development of Colombia’s potential. To the degree that these and related issues areadequately addressed by sound policy and programs, the CDM could produce real benefits forColombia’s sustainable development.

13

Design of the CDM.As discussed in the introduction, a number of issues/barriers could severely constrain the CDM.Key issues could be negotiated and regulated in ways that favor market efficiency andmaximize investments in the developing world, or they could do the opposite. Many of thesewill be negotiated and rules written at the sixth Conference of the Parties in November 2000.The study identifies key areas where regulations should be oriented towards economicefficiency and environmental effectiveness so that the model can usefully address the objectivesof the Kyoto Protocol while maximizing the potential benefits in Colombia and otherdeveloping nations. The study also proposes the key elements of a negotiation position beforethe COP.

Regulations should promote the inclusion of the widest range of projects that can effectivelymitigate greenhouse gas concentrations. Assuming strict additionality rules and effectivemonitoring, Annex I emitters should be free to invest their compliance dollars in the most costeffective options they find anywhere on the planet and be encouraged to begin emissionsreductions as soon as possible. GHG concentrations will be lowered at the greatest speed byincluding both emissions reductions and sequester projects. In order to promote sustainabledevelopment, the CDM should channel investment flows towards all sectors: energy, transport,industry and forests. Colombia, like most developing nations, has strong interests in theemployment, income and environmental benefits that may be derived from new major forestryprojects in the rural sector.

Negotiation position before the COPIn order to promote the objectives of the Kyoto Protocol and maximize the potential benefits ofthe CDM for Colombia, the national negotiating position for COP6 is based on the followingprinciples, resulting from the study, where they are described in detail:

§ Ensure CDM eligibility for all projects formulated after January 1st, 2000. Ensure thatqualifying CDM projects are creditable from January 1 of 2000 onward. This will enable awindow of opportunity for participating countries to inmediately formulate and developeligible projects and therefore inmediately ensure benefits from these investments.

§ Minimize international transaction costs, risks and barriers. Minimize all internationaltransaction costs and potential barriers to the use of the CDM, including search, negotiation,legal, approval, monitoring and certification costs, both at the international and domesticlevels.

§ Define baselines and ensure additionality of CDM projects. Support methods foremissions baseline formulation which ensure additionality of all CDM projects whilelowering formulation costs.

§ Promote equal treatment among the 3 Kyoto flexibility mechanisms, including the useof equivalent rules for all mechanisms and the adoption of equivalent administrative andadaptation charges.

§ Promote the inclusion of carbon sinks in the CDM. The study demonstrates that carbonsink projects in Colombia are cost effective, have the potential for substantial sequestrationof Carbon, hence contributing to the objective of the UNFCCC and could providesignificant co-benefits.

14

§ Include the unilateral model of project formulation in order to reduce the risk barrier thatwould be imposed by the bilateral model.

§ Tradability and fungibility of CERs should not be constrained. Annex B nations shouldbe free to seek and invest in the most cost effective emissions mitigation projects throughoutthe world, in order to meet the objectives of Article 12. This will enable the efficient use ofthe unilateral model and prevent the slowing down of the market.

§ Supplementarity limits to the use of the CDM should be voluntary and reflect eachAnnex B nation’s internal policy. The market analysis demonstrates that supplementaritylimits reduce the international market for CERs and therefore may constraint the flow offunds for sustainable development in non Annex B nations.

§ Sustainable development criteria for approval of CDM projects must be defined byeach developing nation. Each country has different priorities and conditions forsustainable development and these should not be defined externally.

Information ConstraintsOn the domestic front, information constraints will be the principal obstacle to overcome inorder to be able to approach the national potential. The great majority of individuals and firmsin the sectors with the economic and technological potential to benefit from CDM investmentflows have no knowledge of what the CDM is or how it functions. Given its access toinformation on the development of the framework of this regulatory-driven market, oneimportant role of the state is to transfer regulatory information to the sectors with potential andbuild their capacity to participate effectively in the market. Project developers, such as smallindustrial managers, farming communities, energy producers and transport coalitions, all requireconstant flows of high quality information and useful capacity building in order to make thebest decisions on the CDM for their particular conditions.

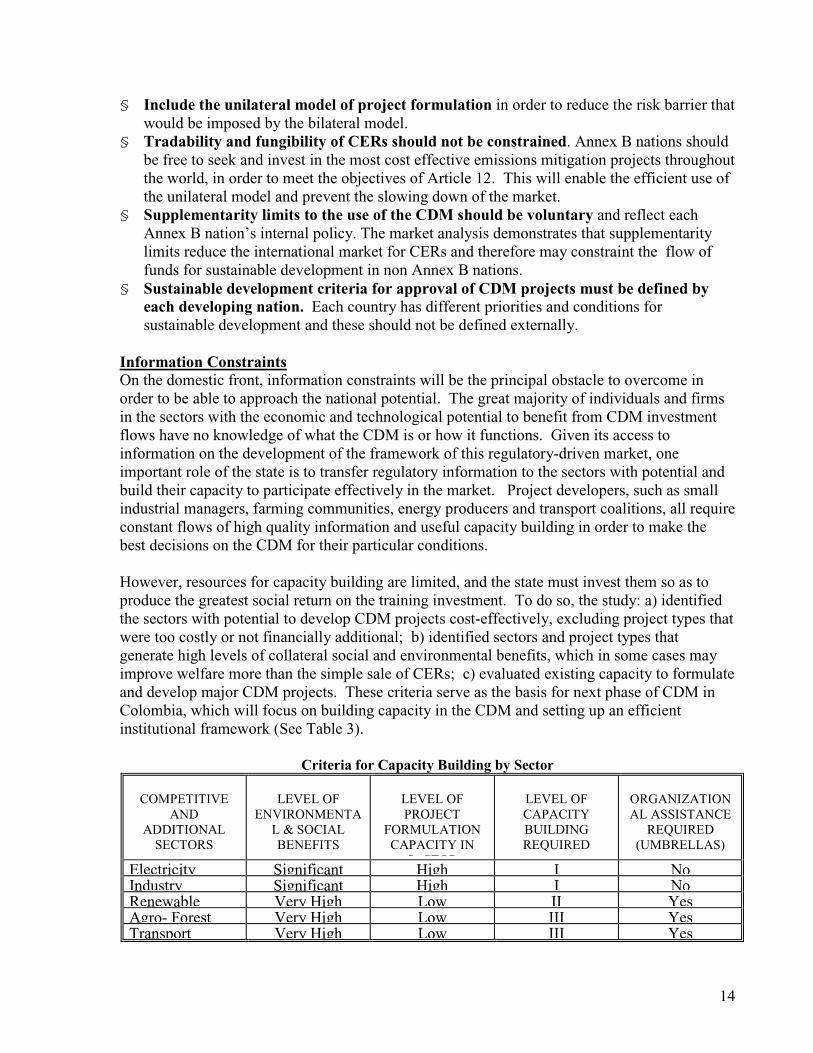

However, resources for capacity building are limited, and the state must invest them so as toproduce the greatest social return on the training investment. To do so, the study: a) identifiedthe sectors with potential to develop CDM projects cost-effectively, excluding project types thatwere too costly or not financially additional; b) identified sectors and project types thatgenerate high levels of collateral social and environmental benefits, which in some cases mayimprove welfare more than the simple sale of CERs; c) evaluated existing capacity to formulateand develop major CDM projects. These criteria serve as the basis for next phase of CDM inColombia, which will focus on building capacity in the CDM and setting up an efficientinstitutional framework (See Table 3).

Criteria for Capacity Building by Sector

COMPETITIVEAND

ADDITIONALSECTORS

LEVEL OFENVIRONMENTAL & SOCIALBENEFITS

LEVEL OFPROJECT

FORMULATIONCAPACITY INS CTOR

LEVEL OFCAPACITYBUILDINGREQUIRED

ORGANIZATIONAL ASSISTANCEREQUIRED

(UMBRELLAS)

Electricity Significant High I NoIndustry Significant High I NoRenewable Very High Low II YesAgro- Forest Very High Low III YesTransport Very High Low III Yes

15

In order to assure high quality, strict additionality, methodological consistency andminimization of transactions costs, the study developed step-by-step CDM project formulationmanuals for the forestry and energy sectors. These are also being published as independentdocuments. These guides were produced using the results of the study and the experiencegained in the formulation of the project portfolio. They will be revised annually to reflect theevolution of the regulatory framework.

Capacity building and manuals must be complemented by organizational assistance in sectorswhere transactions costs and information scarcity limit the execution of the thousands small anddispersed projects. Acting individually, property rights owners in the transport, forest and smallenergy sectors probably will not be able to benefit from the CDM, as they have little knowledgeabout what CDM or how to design a project. Worse, the costs of the CDM project cycle willovercome the potential price benefits of participating in the CDM. For a bus owner, a smallfarmer or a small community, the costs of searching for an Annex I partner, negotiating aninvestment and formulating a baseline are very costly relative to the sale of a few CERs yearly.The national capacity building program must promote organizational models that enablemultiple small projects to be summed, offered and managed as single, large umbrella projects.4

The Panela case study proposes an organizational model based on an existing cooperative runby the Panela Producers Association, but other models may be developed with NGO orcommunity groups. These models are especially critical in sectors where the collateral socialand environmental benefits are high, such as the forest sector. If Colombia seeks to maximizethe benefits from CDM, focused capacity building and organizations models are paramount.

Risk ManagementUnder the bilateral CDM formulation model, Annex B entities hold the initiative to select theirdeveloping nation partners. High-risk countries must compete with dozens of low risk countriesfor CDM investments. Given the high perceived risk of investing in Colombia, cost-effectiverisk management options must be developed. If not, risk could be the principal barrier to CDMinvestment in Colombia.