Embed Size (px)

Citation preview

Multiplex retailers versus

wholesalers

581

Multiplex retailers versuswholesalers

A test of the total valueof purchasing model

Robert F. LuschMichael F. Price College of Business Administration,

University of Oklahoma, Norman, Oklahoma, USA, andStephen L. Vargo

California Polytechnic State University, California, USA

IntroductionAlternate distribution channels for supplying the business or commercialcustomer in the US have become more common over the last two decades.Increasingly office supplies and equipment are being distributed to the businesscustomer through office supply superstores such as Office Depot, Office Max, andStaples which sell approximately 80 per cent of their merchandise tobusiness/commercial accounts. Building materials and related products are beingpurchased by general and specialty contractors and other business/commercialaccounts from warehouse home centers such as Home Depot, Home Base, HomeQuarters, and Builders Square which sell approximately 20-30 per cent of theirvolume to these customers. And everything from food supplies, to office suppliesand industrial supplies and equipment is finding its way to the business customervia membership warehouse clubs such as Sams and Price/Costco which sell about50-70 per cent of their merchandise to business/commercial accounts.

Importantly, within the last five years membership warehouse clubs from theUSA have entered Canada, Mexico, South America, Europe, and Asia (Chanil,1994; Ferguson, 1997; Thornton, 1994). Furthermore the US office supplysuperstore chains have also entered these markets. Coupled with this expansionis the power of the Internet and the ability to market globally. For instanceWal*Mart has established Sam’s Club Exports which offers a wide assortmentof consumer merchandise available from one source in name brand and privatelabel non-perishable food, and hard-line products. This division of Wal*Mart isin the business to sell small- and medium-sized businesses at a lower coststructure than other types of distribution, allowing for cost savings and thusgreater value. Orders must consist of a single item in full container quantitiesfrom one manufacturer. If full container quantities are not preferred, a $10,000USD minimum per item is required.

Because these new forms of power retailing are restructuring distributionchannels and because of the breadth of their impact, a research study was

International Journal of PhysicalDistribution & Logistics

Management, Vol. 28 No. 8, 1998,pp. 581-598. © MCB University

Press, 0960-0035

Received August 1997Revised April 1998

IJPDLM28,8

582

conducted to help answer the question of why businesses are purchasing frommultiplex retailers. In this study we compare traditional wholesale sources ofsupply with these new multiplex retailer supply sources. To shed light on ourfundamental question we use a “total value of purchasing” model as atheoretical framework. Implicit in this model is the assumption that businessesselect suppliers in order to maximize their perceived total value of purchasingand suppliers offer them services to help them accomplish this goal. This modelis not new; rather, it is distilled from a number of overlapping models from theorganizational buyer behavior and marketing channels literature. What isunique to this study, unlike previous tests of the related models, is the use ofdata representing actual perceptions and behavioral intentions. Additionally,the study represents the only investigation of buyer choice involving thequickly growing alternative channel for wholesale distribution of multiplexretailers. The theoretical rationale for this model is presented and then it is usedto assess the determinants of patronizing traditional wholesale supply sourcesversus multiplex retailer supply sources. Before we proceed, however, a briefreview of multiplex retailing is provided because this largely US phenomenonhas global potential for explosive growth which would disrupt many traditionalmarketing channels around the world.

Multiplex retailingA multiplex retailer is one that targets both the traditional household market aswell as the business or commercial market. Thus with one distribution formatthese firms attempt to appeal to two distinct market segments by performing bothwholesaling and retailing functions. Although it is true that multiplex retailing isnot new; for example, hardware stores have historically sold to contractors and thelocal grocery store would frequently sell to restaurants short on supplies;multiplex retailing is gaining momentum because of the number and variety ofpower retailers pursuing the multiplex retail strategy (Lusch and Zizzo, 1995).

Multiplex retailing coupled with power retailing is sending a clear signal toall channel members in virtually all industries: stop and consider the future ofthis distribution format. This is because power retailers have such a highdegree of relative power that suppliers (either manufacturers or wholesaler-distributors) are unable to counteract this power without a substantialinvestment of time, effort, and financial resources. In effect, the retailer becomesthe “captain” of the marketing channel. For some companies, power retailing isa strategic advantage that provides prolonged competitive strength in both themarketplace for consumer and business purchasing.

To gain a better insight into the history and growth of multiplex power retailingwe briefly review the two lines of trade studied in this research: warehouse homecenters (pioneered in 1979) and office supply superstores (pioneered in 1986).

Warehouse home centersIn 1979, Bernard Marcus and Arthur Blank opened in Atlanta, Georgia threeHome Depot stores of approximately 65,000 square feet in size and handling

Multiplex retailers versus

wholesalers

583

18,000 SKUs. In 1981 Home Depot became a publicly held company and twoyears later operated 19 stores. That year, 1983, was a key year for the industrybecause it witnessed the spread of this concept to other parts of the country:Builders Square in Texas; HomeClub in California; and Home QuartersWarehouse in Virginia. Currently, about a dozen companies operate the “big box”warehouse home center format stores across the country. One of the latecomers tothe warehouse retailing format has been Lowe’s. In the 1970s, Lowe’s was apioneer in the do-it-yourself market with a chain of small, showroom-type stores,and, in fact, was the industry leader in terms of sales. In the late 1980s, however,sales gains began to slow, and by 1990, Home Depot had overtaken Lowe’s as thelargest home improvement chain. Finally, in the early 1990s, Lowe’s announced amajor repositioning strategy to enter the warehouse home center industry. Today,warehouse home centers operate in most major metropolitan areas and havebegun entering smaller markets as well. Warehouses usually average 100,000square feet, primarily selling space, with an additional 10,000 to 15,000 squarefeet outside devoted to lawn and garden. These warehouses typically stock 30,000SKUs but some of the larger stores stock up to 50,000 SKUs. Indeed warehousehome centers, serving both the professional customer and household customer,have become a formidable competitive force in US distribution. Meanwhile HomeDepot has entered Canada and is considering future international expansion.

Office supply superstoresThe office supply superstore traces its roots to both membership warehouseclubs and warehouse home centers. In 1986, two companies independentlyopened the first stores in this format. Staples opened in Massachusetts in May,and Office Depot launched its first store in Florida in October. Staples’ co-founders Leo Kahn and Thomas Stemberg were from supermarket retailingbackgrounds and had observed the success membership warehouse clubs werehaving with office supplies. The three founding partners of Office Depot wantedto apply Home Depot’s techniques – large, well-stocked, no-frills stores – to theoffice supply industry. In fact, Office Depot copied so well, right down to thename, that they had to state there was no affiliation with Home Depot for sixmonths and give that company $25,000 worth of office supplies to keep HomeDepot’s legal department at bay. These companies were dedicated to shorteningthe channel of distribution for office supplies. Staples and Office Depot, bypurchasing direct from the manufacturer, were able to sell office supplies andproducts for 20 to 70 percent less than other retailers.

Since its inception 12 years ago, the office supply superstore industry hasalready experienced the rapid growth and consolidation phases of its life cycle.Many similar companies were started and expanded rapidly before their numberspeaked in 1989 at 19 chains. Consolidation was just as rapid and fierce over thenext few years, until today the industry is dominated by three companies: OfficeDepot, Office Max, and Staples. Today, most of these stores are in the 18,000 to25,000 square foot range and stock 5,000 to 6,000 SKUs covering a broad range ofoffice supplies and equipment. This type of method for distributing office supplies

IJPDLM28,8

584

and products can also be expected to experience global growth. For instance,Office Depot went international in 1992 when it acquired the Great CanadianOffice Supplies Warehouse chain and converted the five stores into Office Depotsand began opening stores throughout Canada. Next in 1993, an internationallicensing agreement was signed which resulted in Office Depot stores in Columbiaand Israel. Shortly after that, in 1995, a joint venture agreement with GrupoGigante led to stores opening in Guadalajara, Mexico. Also in this year the firststore in Poland was opened and in 1996 two stores in France opened under a jointventure with Carrefour. In 1997 two stores were opened in Thailand in cooperationwith Central Department Stores. A joint venture with Daiichi Corporation shouldresult in the first Office Depot in Japan in 1998.

The total value of purchasing modelIn a search for why these firms may have succeeded, we sought an explanationfor why businesses, which have traditionally purchased office supplies andhardware supplies from wholesale-distributors, may be purchasing from officesupply superstores and warehouse home centers. In this search we were able todistill a model of the total value of purchasing. This model considers the totalperceived value of purchasing and how business buyers attempt to minimizecost and maximize value of services obtained.

Whether purchasing components to be used in production, or capital goods andconsumables to be used in the production process, commercial purchases are madewith the intention of profit realization. Defined in terms of maintaining costs at alevel below revenue, profit is a rather straight-forward concept. However, theidentification of the relevant “costs” of a particular product is not always a simplematter. For example, two alternative components to a production process mayhave the same purchase price but different overall costs due to quality differences;or they may have the same purchase price and quality but different overall costsdue to differences in supplier reliability in delivery, credit terms, technical support,problem recovery, etc. That is, total product costs comprise not only purchaseprice, but also costs associated with the full range of supplier services provided (ornot provided). It is from this total value (a function of perceived total costs)perspective that we explore how business firms make supplier choices between atraditional wholesale-distributor and the new emerging multiplex retailers –specifically, office supply super-centers and warehouse home centers.

This total value of purchasing model is not entirely new. However, the presentstudy differs from previous studies in several important regards. First, previousstudies have tended to focus on suppliers which manufactured and supplied asingle (or limited range of) product(s). Consequently, product quality and othersupplier services were inextricably intertwined. In the present study, however, bothwholesale distributors and multiplex retailers offer a wide variety and often thesame or similar products, though possibly different assortments (a service issue).Second, since most previous studies have focused on different suppliers supplyingspecific products, product/supplier selection analyses have usually been limited tothe comparison of attribute importance weights rather than actual supplier

Multiplex retailers versus

wholesalers

585

selection intentions. The present study offers a relatively unique opportunity toanalyze supplier selection intentions as a function of the total value of the servicespurchased, under conditions in which “product quality” is relatively controlled.

Supplier analysisTwo general approaches to evaluating alternative suppliers are found in theorganizational buying literature. The first is a normative approach concernedwith the development of optimal models for comparative analysis of alternativeproducts or suppliers. Related literature is usually conceptual but may bederived from or offer case study analysis for support. The second approach ismore positively oriented and consists of empirical investigation of relativeattribute importance employed in different buying situations. What is missingin this literature is the empirical investigation of actual perceptions of decisioncriteria in relation to intended behavior.

Normative modelsNormative models are typically extensions of one of three supplier evaluationmodels that are purported to be commonly employed in industry (Giuniperoand Brewer, 1993; Timmerman, 1986). These three models are the “categoricalapproach,” the “weighted-point plan”, and the “cost-ratio approach,” and aresummarized in Table I.

Several of the normative approaches (e.g. Gregory, 1986; Timmerman, 1987)simply recommend methods for standardization and the “objective” evaluation ofcriteria. Others propose more extensive modifications. For example, Thompson(1990) proposes a modified weighted-point model that replaces single-pointsupplier evaluations with ranges for each evaluative criterion. Graphicalrepresentation of these ranges can be used to compare potential suppliers.

Some normative models recommend multiple-step approaches to supplierselection (see Table I). These models (e.g. Giunipero and Brewer, 1993; Smytkaand Clemens, 1993) typically involve subjective evaluation of relationshipsfollowed by more objective evaluation of preselected alternative suppliers. Ellram

Model type Approach

Categorical Qualitative rating (e.g. satisfactory, neutral, unsatisfactory) ofsuppliers based on a priori evaluative categories (e.g. costdelivery, etc.)

Weighted-point plan Sum of quantitative ratings of a priori dimensions weighted bythe relative importance of the dimension

Cost-ratio plan Quantitative adjustment to selling price based on weighted(performance-based) derived “costs” (from internal analysis)associated with standardized evaluative criteria

Multi-step Pre-qualification based on qualitative evaluation of relationshipwith suppliers followed by quantitative evaluation (e.g. usingweighted-point or cost ratio approach) of qualified suppliers

Table I.Normative models of

supplier selection

IJPDLM28,8

586

and Siferd (1993) (see also Ellram, 1994) group all of these approaches under therubric “Total cost of ownership” (TOC), and Ellram (1995, pp. 12-13) distinguishesbetween two approaches to TOC: a “dollar-based” approach, based on actualcosts; and “value-based” approaches, which “combine dollar/cost data with otherperformance data which are difficult to ‘dollarize’.” The trend in these prescriptivestudies is clearly in the direction of the incorporation of performance, improvedquality, relationship, and other service factors that affect total value, in addition tothe more traditional and narrow concerns for selling price.

Positive analysesThis trend in purchasing management toward an emphasis on quality andservice, in addition to selling price, is partially supported by empirical studiesintended to assess evaluation criteria actually employed by organizationalpurchasers. However, relative attribute importance has been noted to varyacross buying situations and product categories. For example, Lehmann andO’Shaughnessy (1974) found that relative importance weights assigned toattributes by purchasing agents varied considerably across product types.Reliability of delivery was ranked as important across all product types.However, price was more highly ranked for products that were routinely orderedand for products where there was interdepartmental disagreement about theevaluation on other criteria; service attributes such as technical support weremore highly ranked for products which required training and behavioral change.In a follow-up study, Lehmann and O’Shaughnessy (1982) found economiccriteria (e.g. price) to be most important for standard products of simple make-up, standard application, and low dollar value, while performance criteria weremost important for products of complex make-up and/or novel application.

Doyle et al. (1979) found that delivery, price, and payment-terms were mostimportant in straight-rebuy situations, while price, product performance, delivery,and guarantee were most important in first-time buying and modified-rebuysituations. However, they also found that post-purchase evaluation and search forpotential suppliers was very limited in most industrial rebuy situations. Puto et al.(1985) found evidence of a “loyalty barrier” in industrial buying. Specifically, theyfound that in a modified-rebuy situation, the current supplier was more likely tobe selected even when an alternative supplier offered less risk (e.g. a guarantee).That is, supplier loyalty seemed to mediate risk taking.

Several researchers have noted differential relative attribute importance as afunction of product purpose. For example, Kauffman (1994) found evidence thatfor products purchased for use in the “production process” (components), allindividual attributes (“physical”, “non-physical”, “price”, and “distribution”) wereimportant, while for “capital equipment” products and “administrative” productsphysical and distribution attributes were more important. The implication seemsto be that while service, economic, and physical attributes are important forproduction products, service is more important for the other product classes.

Wilson (1994) in comparing a review of past studies concerning relativeproduct and supplier attributes with a current survey of buying center members,

Multiplex retailers versus

wholesalers

587

suggests that there has been a general shift in relative attribute importance overthe past 20 years. Specifically, she notes a shift away from price and delivery andtoward “service” (service-call response time) and quality (durability). She(Wilson, 1994, p. 36) sees this shift stemming, in part, from globalization andincreasing competitiveness and contends: “the relationship of the quality andservice factors to total product cost is an important element in this equation. Apurchased product’s total cost is made up of initial price, various direct andindirect costs associated with product quality, and a similar array of costsassociated with the service required to support acquisition and use of theproduct. It is not surprising that purchasers who strive to minimize total costplace greater emphasis on quality and service and less emphasis on price.”

Most of the empirical studies reviewed have several common characteristics.First they typically involve the sampling of purchasing managers of relativelylarge firms, and less often include the selection criteria of internal users. Second,they are usually based on the selection of suppliers offering a single product orlimited range of products, and therefore supplier analysis is inextricablyintertwined with product analysis. Third, most are based on relative importanceweights, but do not investigate the perceived performance attributes of thosesuppliers actually selected. Fourth, most rely on single-measure indices of themodeled attributes of total cost. Finally, with some exception (e.g. Doyle et al., 1979;Puto et al., 1985), most do not explore the role of supplier loyalty, buyer inertia, andbuyer-seller relationship in the purchasing decision. Of particular interest may bethe role that these variables may play in “overriding” other attribute weights.

Present studyMiddlemen, either wholesalers or retailers, can attract customers by providingvalue-added services, such as directly lowering costs or providing otherperceived cost-reduction services. By adopting this perspective we view allactivities performed by middlemen as services (cf. Stern et al., 1996). That is,whether classified as a wholesale-distributor or a retailer, the functions ofentities that supply products to other entities are, by definition, services.Services that are not performed by manufacturers or middlemen must be borneby the purchaser. Therefore fewer value-added services represents a potentialcost to the purchaser because they must perform the service for themselves thatmiddlemen do not perform.

From this perspective, total value can be seen as a combination of the price andthe indirect perceived costs that the purchaser incurs due to inadequate or fewervalue-added services being provided by the middleman. These value-addedservices, include providing credit, product acquisition services, and product useservices. We call the components of this four component total-value model: price,credit services, acquisition services, and purchase-risk reduction servicesrespectively. This classification is similar to Lehmann and O’Shaughnessy’s(1982) “economic”, “integrative”, and “adaptive” criteria classification. However,unlike the Lehmann and O’Shaughnessy classification, we see productperformance, or more appropriately the quality of the product assortment offered,

IJPDLM28,8

588

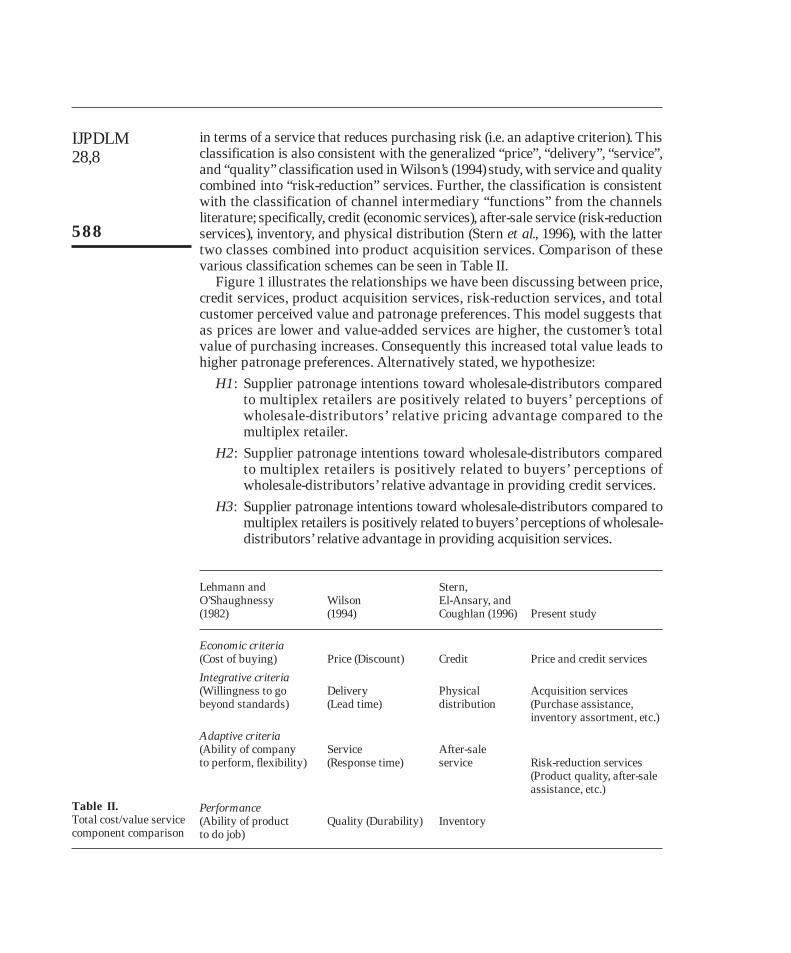

in terms of a service that reduces purchasing risk (i.e. an adaptive criterion). Thisclassification is also consistent with the generalized “price”, “delivery”, “service”,and “quality” classification used in Wilson’s (1994) study, with service and qualitycombined into “risk-reduction” services. Further, the classification is consistentwith the classification of channel intermediary “functions” from the channelsliterature; specifically, credit (economic services), after-sale service (risk-reductionservices), inventory, and physical distribution (Stern et al., 1996), with the lattertwo classes combined into product acquisition services. Comparison of thesevarious classification schemes can be seen in Table II.

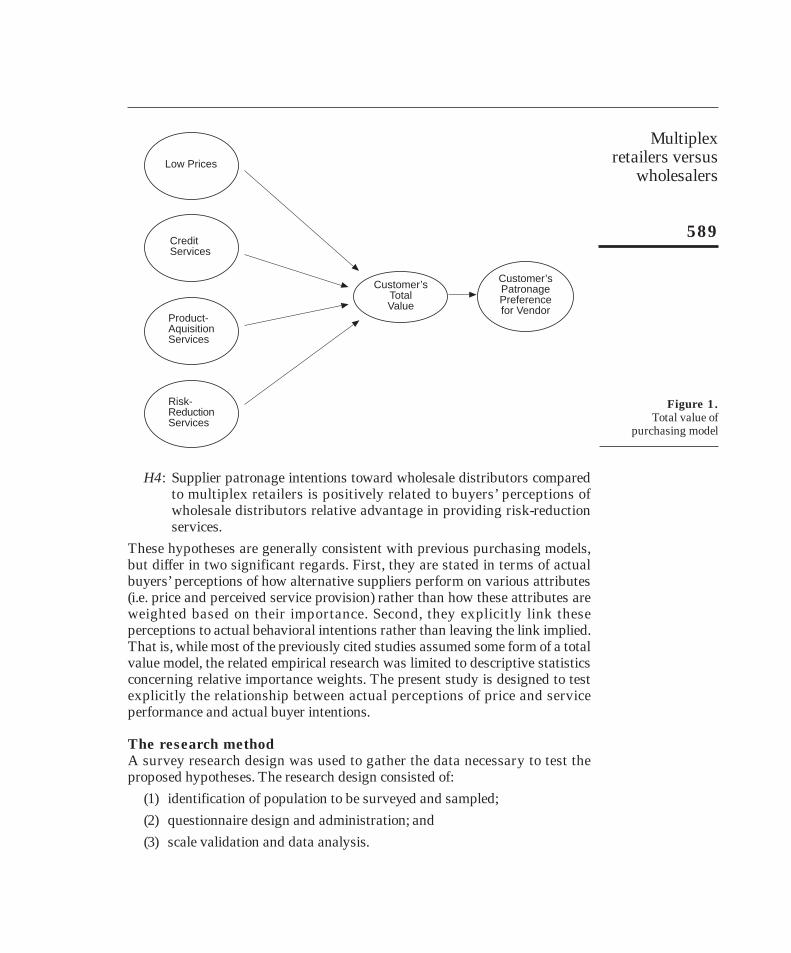

Figure 1 illustrates the relationships we have been discussing between price,credit services, product acquisition services, risk-reduction services, and totalcustomer perceived value and patronage preferences. This model suggests thatas prices are lower and value-added services are higher, the customer’s totalvalue of purchasing increases. Consequently this increased total value leads tohigher patronage preferences. Alternatively stated, we hypothesize:

H1: Supplier patronage intentions toward wholesale-distributors comparedto multiplex retailers are positively related to buyers’ perceptions ofwholesale-distributors’ relative pricing advantage compared to themultiplex retailer.

H2: Supplier patronage intentions toward wholesale-distributors comparedto multiplex retailers is positively related to buyers’ perceptions ofwholesale-distributors’ relative advantage in providing credit services.

H3: Supplier patronage intentions toward wholesale-distributors compared tomultiplex retailers is positively related to buyers’ perceptions of wholesale-distributors’ relative advantage in providing acquisition services.

Lehmann and Stern,O’Shaughnessy Wilson El-Ansary, and (1982) (1994) Coughlan (1996) Present study

Economic criteria(Cost of buying) Price (Discount) Credit Price and credit services

Integrative criteria(Willingness to go Delivery Physical Acquisition servicesbeyond standards) (Lead time) distribution (Purchase assistance,

inventory assortment, etc.)

Adaptive criteria(Ability of company Service After-saleto perform, flexibility) (Response time) service Risk-reduction services

(Product quality, after-sale assistance, etc.)

Performance(Ability of product Quality (Durability) Inventoryto do job)

Table II.Total cost/value servicecomponent comparison

Multiplex retailers versus

wholesalers

589

H4: Supplier patronage intentions toward wholesale distributors comparedto multiplex retailers is positively related to buyers’ perceptions ofwholesale distributors relative advantage in providing risk-reductionservices.

These hypotheses are generally consistent with previous purchasing models,but differ in two significant regards. First, they are stated in terms of actualbuyers’ perceptions of how alternative suppliers perform on various attributes(i.e. price and perceived service provision) rather than how these attributes areweighted based on their importance. Second, they explicitly link theseperceptions to actual behavioral intentions rather than leaving the link implied.That is, while most of the previously cited studies assumed some form of a totalvalue model, the related empirical research was limited to descriptive statisticsconcerning relative importance weights. The present study is designed to testexplicitly the relationship between actual perceptions of price and serviceperformance and actual buyer intentions.

The research methodA survey research design was used to gather the data necessary to test theproposed hypotheses. The research design consisted of:

(1) identification of population to be surveyed and sampled;

(2) questionnaire design and administration; and

(3) scale validation and data analysis.

Figure 1.Total value of

purchasing model

Low Prices

CreditServices

Product-AquisitionServices

Risk-ReductionServices

Customer’sTotalValue

Customer’sPatronagePreferencefor Vendor

IJPDLM28,8

590

Population selection and samplingThe population was businesses that regularly purchased from wholesaler-distributors as well as from multiplex retailers. The multiplex retailers we wereinterested in studying were warehouse home centers and office supplysuperstores. Consequently, for each we identified, through exploratoryresearch, a list of representative businesses that would be likely to purchasefrom the line of multiplex retailing under study. For warehouse home centers,businesses in 13 SIC codes representing the building and contractor trades andsome lines of retail trade were selected. For office supply superstores,businesses in eight SIC codes representing service firms were chosen.

As regards the survey of geographic markets, two options were to surveybusiness customers throughout the entire USA (in the SIC codes selected) oronly in selected markets. Since warehouse home centers and office supplysuperstores currently operate in nearly every major metropolitan market in thecountry, a sample of medium and large cities was selected. The selection waseventually narrowed to six markets: two large markets and four medium-sizedmarkets. The two large markets chosen were Dallas/Fort Worth, Texas, and LosAngeles, California. These two cities were, respectively, the 2nd and 7th largestwholesale markets in the USA. The four medium-sized cities selected were:Fresno, California; Grand Rapids, Michigan; Tulsa, Oklahoma; and Wichita,Kansas. All markets are among the largest 75 cities in the USA. In addition,multiplex retailers of both types were present in each market, and the level ofcompetition ranged from moderate to high in each of these cities.

A total of 3,410 questionnaires were mailed during May 1994: 2,090 topotential customers of warehouse home centers and 1,320 to potentialcustomers of office supply superstores. The smaller sample size for the officesupply study was determined by the sponsor of the research who wasinterested in both types of multiplex retailers but felt that the warehouse homecenters posed more of a competitive threat to a wider number of wholesaler-distributors. In the two larger cities we sent 525 questionnaires to potentialcustomers of warehouse home centers and 330 to potential customers of officesupply superstores. In the four smaller cities we sent 260 questionnaires topotential customers of warehouse home centers and 165 to potential customersof office supply superstores.

Questionnaire design and administrationThe primary goal of the questionnaire, as it relates to this study, was to identifythe services a wholesaler-distributor or multiplex retailer could offer businessesand how each of these alternative supply sources was rated on performance, asperceived by the business customer. Also collected were patronage data and avariety of demographic and descriptive data of the responding firms. Separate,but largely similar, questionnaires were developed for potential customers ofthe two survey groups. The questionnaires were refined and pretested onapproximately 15 businesses in a major metropolitan area in the Southwestern,US.

Multiplex retailers versus

wholesalers

591

The two questionnaires were mailed to 3,410 businesses as described earlier.Several things were done to increase the response rate: a personalized coverletter with a hand-written self-sticking note to the respondent urging theirparticipation; a one dollar bill was included as a tangible symbol ofappreciation for the respondent’s time; first class mailing, with return postage-paid envelope enclosed; and a follow-up reminder postcard sent within five toseven days of the original mailing. The random sample of company names andaddresses for businesses in the selected SIC codes were provided by AmericanBusiness Lists of Omaha, Nebraska. Although this firm is a well-respectedprovider of mailing lists, about 6.7 per cent of the addresses were non-deliverable, due to businesses being terminated, sold, or relocated. Therefore, ofthe 3,181 questionnaires actually delivered, 1,211 were returned for a responserate of 38.1 per cent. Of those returned, 425 were usable for this study. Thereduction in size was because we only analyzed those responses where thebusinesses purchased both at a wholesaler-distributor and a multiplex retailer(office supply superstore or warehouse home center) within the last year.

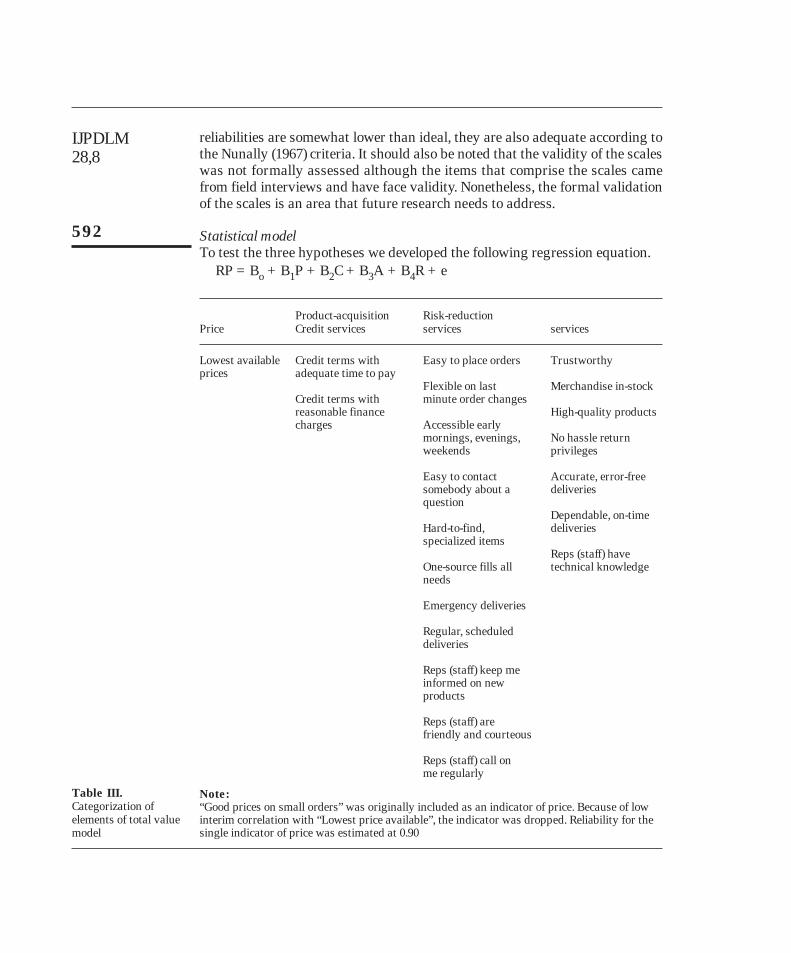

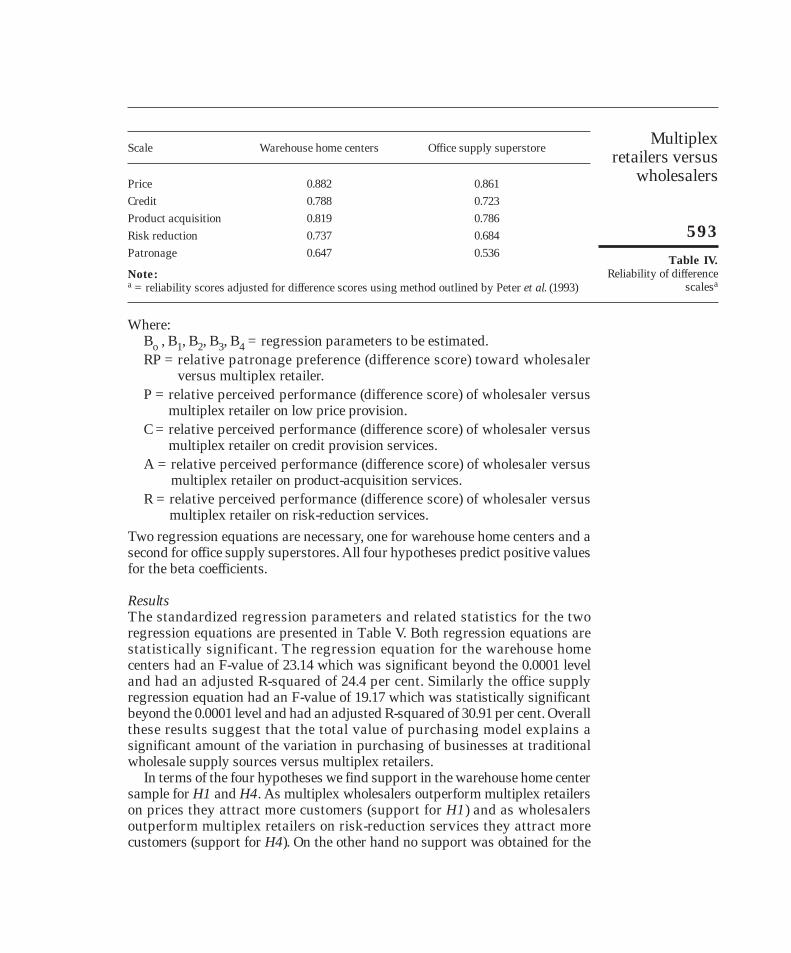

Scale validationAs suggested in the four hypotheses that were developed, we needed tomeasure buyers’ perceptions of supplier performance on price, credit services,product-acquisition services, and risk-reduction services and patronageintentions toward suppliers. Table III shows the four service categories for the21 specific service attributes used in the study.

For each of the 21 attributes in Table III, we asked the respondent to rate boththe wholesale-distributor’s and the multiplex retailer’s performance on a scaleranging from “1” poor performance to a “9” outstanding performance. Therelative measure of performance was thus computed as the score the wholesalerreceived minus the score the retailer received. It was these difference scores forwhich we computed reliability scores. These reliability statistics are reported inTable III. Peter et al. (1993) report that difference scores can be less reliable thantheir component parts. Consequently we use procedures these authorsrecommend to determine the true reliability of these difference scores. For thefour measures used as independent variables (price, credit, acquisition, andrisk) the reliability measures were between 0.68 and 0.88. According to Nunally(1967) reliabilities in the 0.50 to 0.70 range are adequate.

Patronage was measured with two questions. One question had therespondent indicate on a “1” to “5” scale the likelihood of their buying at thesupply source (either wholesaler or multiplex retailer) in the future. The secondquestion had the respondent reply on a “1” to “5” rating if they planned to buymore from the supply source in the future. These items were summed to obtaina total score and then the score the multiplex retailer received was subtractedfrom the score the wholesale-distributor received. Table IV shows the reliabilityfor these difference scores. The reliability for the relative patronage preferencefor office supply superstores versus office supply wholesalers was 0.54 and thatfor warehouse home centers versus hardware wholesalers was 0.65. While these

IJPDLM28,8

592

reliabilities are somewhat lower than ideal, they are also adequate according tothe Nunally (1967) criteria. It should also be noted that the validity of the scaleswas not formally assessed although the items that comprise the scales camefrom field interviews and have face validity. Nonetheless, the formal validationof the scales is an area that future research needs to address.

Statistical modelTo test the three hypotheses we developed the following regression equation.

RP = Bo + B1P + B2C + B3A + B4R + e

Product-acquisition Risk-reductionPrice Credit services services services

Lowest available Credit terms with Easy to place orders Trustworthyprices adequate time to pay

Flexible on last Merchandise in-stockCredit terms with minute order changesreasonable finance High-quality productscharges Accessible early

mornings, evenings, No hassle returnweekends privileges

Easy to contact Accurate, error-freesomebody about a deliveriesquestion

Dependable, on-timeHard-to-find, deliveriesspecialized items

Reps (staff) haveOne-source fills all technical knowledgeneeds

Emergency deliveries

Regular, scheduleddeliveries

Reps (staff) keep meinformed on newproducts

Reps (staff) arefriendly and courteous

Reps (staff) call onme regularly

Note:“Good prices on small orders” was originally included as an indicator of price. Because of lowinterim correlation with “Lowest price available”, the indicator was dropped. Reliability for thesingle indicator of price was estimated at 0.90

Table III.Categorization of elements of total value model

Multiplex retailers versus

wholesalers

593

Where:Bo , B1, B2, B3, B4 = regression parameters to be estimated.RP = relative patronage preference (difference score) toward wholesaler

versus multiplex retailer.P = relative perceived performance (difference score) of wholesaler versus

multiplex retailer on low price provision.C = relative perceived performance (difference score) of wholesaler versus

multiplex retailer on credit provision services.A = relative perceived performance (difference score) of wholesaler versus

multiplex retailer on product-acquisition services.R = relative perceived performance (difference score) of wholesaler versus

multiplex retailer on risk-reduction services.Two regression equations are necessary, one for warehouse home centers and asecond for office supply superstores. All four hypotheses predict positive valuesfor the beta coefficients.

ResultsThe standardized regression parameters and related statistics for the tworegression equations are presented in Table V. Both regression equations arestatistically significant. The regression equation for the warehouse homecenters had an F-value of 23.14 which was significant beyond the 0.0001 leveland had an adjusted R-squared of 24.4 per cent. Similarly the office supplyregression equation had an F-value of 19.17 which was statistically significantbeyond the 0.0001 level and had an adjusted R-squared of 30.91 per cent. Overallthese results suggest that the total value of purchasing model explains asignificant amount of the variation in purchasing of businesses at traditionalwholesale supply sources versus multiplex retailers.

In terms of the four hypotheses we find support in the warehouse home centersample for H1 and H4. As multiplex wholesalers outperform multiplex retailerson prices they attract more customers (support for H1) and as wholesalersoutperform multiplex retailers on risk-reduction services they attract morecustomers (support for H4). On the other hand no support was obtained for the

Scale Warehouse home centers Office supply superstore

Price 0.882 0.861Credit 0.788 0.723Product acquisition 0.819 0.786Risk reduction 0.737 0.684Patronage 0.647 0.536

Note:a = reliability scores adjusted for difference scores using method outlined by Peter et al. (1993)

Table IV.Reliability of difference

scalesa

IJPDLM28,8

594

role of credit services (H2) and product-acquisition services (H3). This suggeststhat the business or commercial purchaser of hardware and building supplies ismost driven by price and risk-reduction services. Especially in the building andremodeling trades, risk-reduction services are critical because errors in deliveries,stock-outs, unknowledgeable personnel, and so on, can create substantial costs tothe builder or remodeler. This customer has a crew and equipment scheduled todo a job and a mistake made by the supplier (either wholesale-distributor orwarehouse home center) can cost more than the product itself. A sense for thetradeoffs commercial customers are willing to make between price and riskreduction services can be obtained by examining the standardized regressionparameters which are 0.17 for price and 0.31 for risk. If a warehouse home centerperforms poorly on risk reduction services than it can compensate for this onlyby a more than proportionate gain in price performance (i.e. lower prices).Alternatively wholesalers that perform well on risk-reduction services comparedto warehouse home centers do not need to be as price competitive.

The results from the office supply superstore regression equation were evenmore strongly supportive of the total cost of purchasing model. In this situationall but the credit services (H2) were positively related to relative patronagepreferences. Importantly all three of the standardized regression parameters hadapproximately the same value with the value on risk a bit higher. This suggeststhat a higher price can be traded off with improved product acquisition servicesand better risk reduction services. On the other hand if a multiplex retailer failsto do a comparable job to wholesale-distributors on product-acquisition servicesand/or risk-reduction services it will need to proportionately lower its prices toattract customers.

StandardizedVariable parameter t-value p-value

Warehouse home centersIntercept n/a n/a n/aPrice 0.1701 2.85 0.0047Credit –0.297 –0.49 0.6247Product acquisition 0.1180 1.23 0.2189Risk reduction 0.3117 3.21 0.0015

Note: a F-value = 23.14; p = 0.0001; adjusted R-squared = 0.2436

Office supply superstoresIntercept n/a n/a n/aPrice 0.2022 2.92 0.0041Credit –0.0632 –0.83 0.4097Product acquisition 0.2661 2.35 0.0199Risk reduction 0.3117 2.31 0.0224

Note: a F-value = 19.17; p = 0.0001; adjusted R-squared = 0.3091Table V.Regression resultsa

Multiplex retailers versus

wholesalers

595

DiscussionA relatively simple total value model of supplier selection by businesspurchasers was able to explain from 24-31 per cent of patronage behavior. Themodel postulates that businesses purchasers decide between alternativesuppliers based on the relative performance of these suppliers on price, creditservices, product-acquisition services, and risk-reduction services. Its empiricalsupport confirms previous research of organizational buyer behavior that hasnot previously been tested directly. As a supplier is able to offer lower prices andcredit terms the purchaser’s direct cost of purchase declines. At the same timeas the supplier is able to offer more product-acquisition services and risk-reduction services the perceived indirect costs of purchasing decline for thepurchaser and thus patronage toward this higher performing supplier rises.

Generally this model was supported, with the exception that credit serviceswere not shown to be a significant predictor of supplier selection. Perhaps creditmarkets are highly efficient and business purchasers of office supplies andhardware recognize that they are paying the market rate for credit terms that areoffered by suppliers. They may recognize that it is better to not take trade creditand instead finance purchases and inventory with other sources of working capital.The nonsupport for credit services in these two organizational buying settings isalso consistent with Lehmann and O’Shaughnessy’s (1982) conclusion that totalcost is differentially determined as a function of product type and application.

The fact that this relatively simple model performed so well is a bit surprisingwhen one compares it to retail patronage models of household purchasing. Thesemodels tend to be more complex and at the same time explain relatively littlevariation in retail patronage behavior (Darden and Lusch, 1983). Perhaps thepurchasing of businesses is inherently more predictable or explainable than that ofhouseholds. Of course, one possibility is that the models of retail patronagebehavior of households may be misspecified. One might question if the total valueof purchasing model might also be a good framework for explaining householdretail patronage preferences. Do households choose between alternative retailersbased on price, credit, product-acquisition services, and risk-reduction services?Can their behavior also be explained in terms of a simple total value model? Thiscould be a fruitful area for future research. Competitive strategy implications canalso be derived from the total value of purchasing model. Currently, wholesale-distributors feel threatened by multiplex retailers as these firms make moreinroads into their markets (Lusch and Zizzo, 1995). These wholesalers often feelthey cannot meet the prices of the multiplex power retailers. Our results suggestthat they should not attempt to enter into price competition but instead concentrateon developing their product-acquisition services and risk-reduction services, thusenhancing the total value of the relationship (cf. Maltz and Ellram, 1997). These areservices that traditional full-service wholesalers have excelled on and for whichthey can defend themselves against the power retailers. Offering these servicesincreases the cost of business of the wholesaler and at the same time lowers thecosts of its customer and thus increases the value it receives in the businessrelationship. However, only if the wholesaler can obtain a price that is sufficient tooffset the cost of these services will this strategy be profitable. If this can be done

IJPDLM28,8

596

we believe the strategy is a good one especially considering it is a strategy whichis hard to copy quickly. A multiplex retailer could easily duplicate a pricingstrategy but service related strategies are more hidden and thus harder to identifyand replicate. In this regard distributors (both retailers and wholesalers) may findthat they cannot meet global price competition, however, if they can provide value-added services more cost effectively and/or at a higher quality then they may havethe means to remain competitive. The sophisticated business purchaser is lookingat more than price but total value obtained in the business relationship.

ConclusionIntertype competition has increased in retailing as retailers from different lines oftrade have pursued scrambled merchandising and thus have found themselvescompeting with each other. More recently a new type of competition has evolvedand is beginning to diffuse globally. This is where a new type middleman, whichwe call a multiplex retailer, caters to both the traditional customer of thewholesaler as well as to the household market the traditional retailer hashistorically pursued. As these multiplex retailers develop alternate distributionchannels, retailers and wholesalers will find themselves increasingly competingwith each other. Not only will retailers sell more to businesses but wholesalerswill begin to pursue the household market. Given this development it is importantthat distribution educators and executives begin to better understand what willdetermine patronage preferences at these new multiplex business formats. Thisresearch has made a first attempt at this goal and it is hoped will stimulateadditional research and discussion on this topic around the world. A sample of theresearch questions that might be addressed include:

• How do business purchasers view the total value of purchasing modelwhen they source products via mail order or the Internet?

• How will the membership warehouse clubs, hardware home centers, andoffice supply superstores make inroads into rapidly developing countriessuch as China?

• If power retailers can change how business sources products what doesthis mean for channel leadership? Can powerful multiplex retailers offermore value by offering private brands? In this regard will global privatebrands develop? If so how do conventional manufacturer’s brandscompete and survive?

• Can manufacturers, using the total value of purchasing model, developstrategies to sell direct to business users and households? In short, whichdistribution intermediaries can be eliminated from the distribution systemwhile at the same time increasing total value to the end user?

All of these issues are more than local in nature; they apply to more than theUSA and Europe where mega-stores and power retailers have a good foothold.The challenge is global because new-wave distribution formats will continue todiffuse rapidly around the world as electronic commerce and world capitalmarkets pursue innovations in distribution that offer competitive advantage.

Multiplex retailers versus

wholesalers

597

ReferencesChanil, D. (1994), “Wholesale clubs: a new era?”, Discount Merchandiser, Vol. 34 No. 11, pp. 38-51.Darden, W. and Lusch, R. (1983), Patronage Behavior and Retail Management, North-Holland,

New York, NY.Doyle, P., Woodside, A.G. and Michell, P. (1979), “Organizations buying in new task and rebuy

situations”, Industrial Marketing Management, Vol. 8 No. 1, pp. 7-11.Ellram, L.M. (1994), “A taxonomy of total cost of ownership models”, Journal of Business

Logistics, Vol. 15 No. 1, pp. 171-91.Ellram, L.M. (1995), “Total cost of ownership: an analysis for purchasing”, International Journal

of Physical Distribution and Logistics Management, Vol. 25 No. 8, pp. 5-23.Ellram, L.M. and Siferd, S.P. (1993), “Purchasing: the cornerstone of the total cost of ownership

concept”, Journal of Business Logistics, Vol. 14 No. 1, pp. 163-84.Ferguson, T.W. (1997), “A revolution that has a long way to go”, Forbes, Vol. 160 No. 3, pp. 106-12.Giunipero, L.C. and Brewer, D.J. (1993), “Performance based evaluation systems under total quality

management”, International Journal of Purchasing and Materials Management, Vol. 29 No. 1,pp. 35-41.

Gregory, R.E. (1986), “Source selection: a matrix approach”, Journal of Purchasing and MaterialsManagement, Vol. 22 No. 2, pp. 24-9.

Kauffman, R.G. (1994), “Influences on industrial buyer’s choice of products: effects of productapplication, product type, and buying environment”, International Journal of Purchasing andMaterials Management, Vol. 30 No. 2, pp. 29-38.

Lehman, D.L. and O’Shaughnessy, J. (1974), “Difference in attribute importance for differentindustrial products”, Journal of Marketing, Vol. 38 No. 1, pp. 36-42.

Lehman, D.L. and O’Shaughnessy, J. (1982), “Decision criteria used in buying different categoriesof products”, Journal of Purchasing and Materials Management, Vol. 18 No. 1, pp. 9-14.

Lusch, R.F. and Zizzo, D. (1995), Competing for Customers: How Wholesaler-Distributors Can Meetthe Power Retailer Challenge, Distribution Research & Education Foundation, Washington, DC.

Maltz, A.B. and Ellram, L.M. (1997), “Total cost of relationship: an analytical framework for thelogistics outsourcing decision”, Journal of Business Logistics, Vol. 18 No. 1, pp. 45-66.

Nunnally, J.C. (1967), Psychometric Theory, McGraw-Hill, New York, NY.Peter, P.J., Churchill Jr, G.A. and Brown, T.J. (1993), “Caution in the use of difference scores in

consumer research”, Journal of Consumer Research, Vol. 19 No. 1, pp. 655-62.Puto, C.P., Patton, W.E. and King, R.K. (1985), “Risk handling strategies in industrial vendor

selection decisions”, Journal of Marketing, Vol. 49 No. 1, pp 89-98.Smytka, D.L. and Clemens, M.W. (1993), “Total cost supplier selection model: a case study”,

International Journal of Purchasing and Materials Management, Vol. 29 No. 1, pp. 12-49.Stern, L.W., El-Ansary, A.I. and Coughlan, A.T. (1996), Marketing Channels, Prentice Hall, Upper

Saddle River, NJ.Timmerman, E. (1986), “An approach to vendor performance evaluation”, Journal of Purchasing

and Materials Management, Vol. 22 No. 4, pp. 2-8.Thompson, K.N. (1990), “Vendor profile analysis”, Journal of Purchasing and Materials

Management, Vol. 26 No. 1, pp. 11-18.Thornton, E. (1994), “Revolution in Japanese retailing”, Fortune, Vol. 129 No. 3, pp. 52-6.Wilson, E.J. (1994), “The relative importance of supplier selection criteria: a review and update”,

International Journal of Purchasing and Materials Management, Vol. 30 No. 3, pp. 34-41.

Further readingAnderson, E., Chu, W. and Weitz, B. (1987), “Industrial purchasing: an empirical exploration of

buyclass framework”, Journal of Marketing, Vol. 51 No. 3, pp. 71-86.

IJPDLM28,8

598

Bellizzi, J.A. and McVey, P. (1983), “How valid is the buygrid model?”, Industrial MarketingManagement, Vol. 12 No. 1, pp. 57-62.

Bonoma, T.V., Zaltman, G. and Johnston, W.J. (1978), Industrial Buying Behavior, MarketingScience Institute, Cambridge, MA.

Chao, C., Scheuing, E.E. and Ruch, W.A. (1993), “Purchasing performance evaluation: aninvestigation of different perspectives”, International Journal of Purchasing and MaterialsManagement, Vol. 29 No. 3, pp. 33-9.

Choffray, J. and Lilien, G. (1978), “Assessing response to industrial marketing strategy”, Journal ofMarketing, Vol. 42 No. 1, pp. 20-31.

Ferguson, W. (1979), “An evaluation of the BUYGRID framework”, Industrial MarketingManagement, Vol. 8 No. 1, pp. 40-4.

Jackson, D.W., Keith, J.E. and Burdick, R.K. (1984), “Purchasing agents’ perceptions of industrialbuying center influence”, Journal of Marketing, Vol. 48 No. 4, pp. 75-83.

Johnston, W.J. (1994), “Organizational buyer behavior – 25 years of knowledge and research”,Journal of Business and Industrial Marketing, Vol. 9 No. 3, pp. 4-5.

Kohli, A. (1989), “Determinants of influence in organizational buying: a contingency approach”,Journal of Marketing, Vol. 53 No. 3, pp. 50-65.

Mayer, W.U. (1983), “Situational variables and industrial buying”, Journal of Purchasing andMaterials Management, Vol. 19 No. 3, pp. 21-5.

McQuiston, D.H. (1989), “Novelty, complexity, and importance as causal determinants ofindustrial buyer behavior”, Journal of Marketing, Vol. 53 No. 1, pp. 66-79.

Moriarty, R.T. (1983), Industrial Buying Behavior, Lexington Books, Lexington, MA.Moriarty, R.T. and Galper, M. (1978), Organizational Buying Behavior: A-State-of-the-Art Review

and Conceptualization, Marketing Science Institute, Cambridge, MA.Nauman, E., Lincoln, D.J. and McWilliams, R.D. (1984), “The purchase of components: functional

areas of influence”, Industrial Marketing Management, Vol. 13 No. 1, pp. 113-22.Pingy, J.R. (1974), “The engineer and purchasing agent compared”, Journal of Purchasing, Vol. 10

No. 4, pp. 33-45.Qualls, W.J. and Puto, C.P. (1989), “Organizational climate and decision framing: an integrated

approach to analyzing industrial buying decisions”, Journal of Marketing Research, Vol. 26No. 2, pp. 179-92.

Robinson, P.J., Faris, C.W. and Wind, Y. (1967), Industrial Buying and Creative Marketing, Allyn &Bacon, Boston, MA.

Ronchetto, J.R., Hutt, M.D. and Reigen, P.H. (1989), “Embedded influence patterns inorganizational buying systems”, Journal of Marketing, Vol. 53 No. 4, pp. 51-62.

Sheth, J.N. (1973), “A model of industrial buyer behavior”, Journal of Marketing, Vol. 37 No. 4, pp. 50-6.

Sweeney, T.W., Mathews, H.L. and Wilson, D.T. (1973), “An analysis of industrial buyer’s riskreduction behaviors: some personality correlates”, in American Marketing AssociationProceedings, American Marketing Association, Chicago, IL, pp. 217-21.

Webster, F.E. (1991), Industrial Marketing Strategy, John Wiley, New York, NY.Webster, F.E. and Wind, Y. (1972), “A general model for understanding organizational buying

behavior”, Journal of Marketing, Vol. 36 No. 2, pp. 12-19.