Embed Size (px)

Citation preview

February 8, 2016

MRAA/Baird Marine Retailer Pulse Report January 2016

Craig Kennison, CFA [email protected] 414.765.3870

Matt Gruhn President, MRAA 763.333.2421

PLEASE REFER TO APPENDIX – IMPORTANT DISCLOSURES AND ANALYST CERTIFICATION AT END OF DOCUMENT

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

This page intentionally left blank.

2

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

Overview

Robert W. Baird, in partnership with Marine Retailers Association of the Americas (MRAA), is pleased to present the January 2016 Marine Retailer Pulse Report.

We recently surveyed 80 marine retailers to assess recent trends in North America.

Thank you to each of the retailers who participated in this survey.

If you have any questions or comments that you would like to direct to MRAA, please contact Matt Gruhn, President of MRAA at 763.333.2421.

If you have any questions or comments, would like additional research on the marine industry, or are a retailer and would like to participate in our next survey, please email Senior Analyst Craig Kennison [[email protected]].

Note: This is not a scientific survey, rather it is meant to give investors an indication of current industry trends. Some quotes have been edited to protect the anonymity of respondents.

3

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

Table of Contents

Marine Retailer Pulse Report

Retailer Profile 5

Retailer Sentiment 6

Retail Trends 7 – 9

Comments 10 – 11

Inventory 12

Financing 13

Inventory Restocking Plans 14

Comments 15 – 16

Additional Comments 17

Key Statistics

Macro Overview 18 – 20

U.S. Powerboat Retail 21 – 23

U.S. Retail By Category 24 – 26

Brokerage Trends 27

Stock Seasonality 28

Disclosures 29 – 34

4

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

Retailer Profile

5

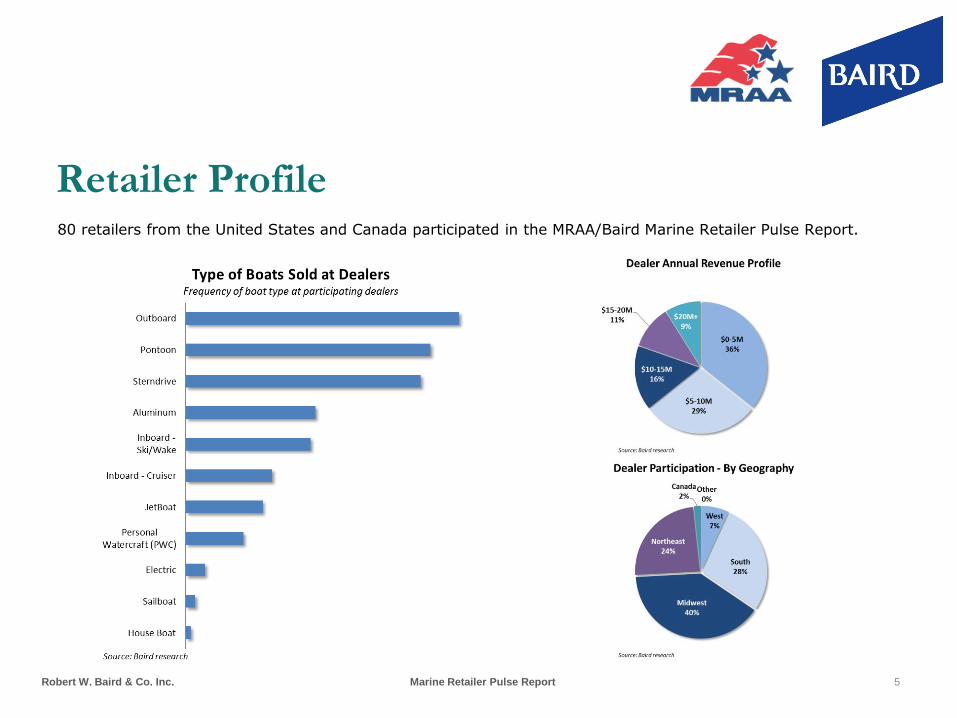

80 retailers from the United States and Canada participated in the MRAA/Baird Marine Retailer Pulse Report.

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

Retailer Sentiment

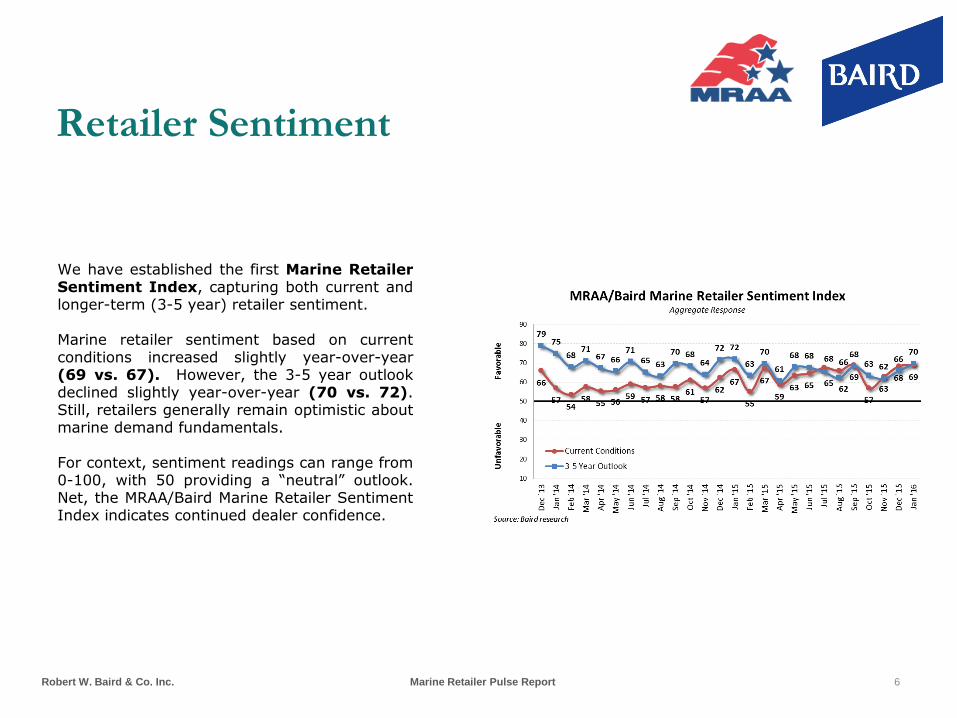

We have established the first Marine Retailer Sentiment Index, capturing both current and longer-term (3-5 year) retailer sentiment. Marine retailer sentiment based on current conditions increased slightly year-over-year (69 vs. 67). However, the 3-5 year outlook declined slightly year-over-year (70 vs. 72). Still, retailers generally remain optimistic about marine demand fundamentals. For context, sentiment readings can range from 0-100, with 50 providing a “neutral” outlook. Net, the MRAA/Baird Marine Retailer Sentiment Index indicates continued dealer confidence.

6

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

Retail Results January Retail Growth Estimates

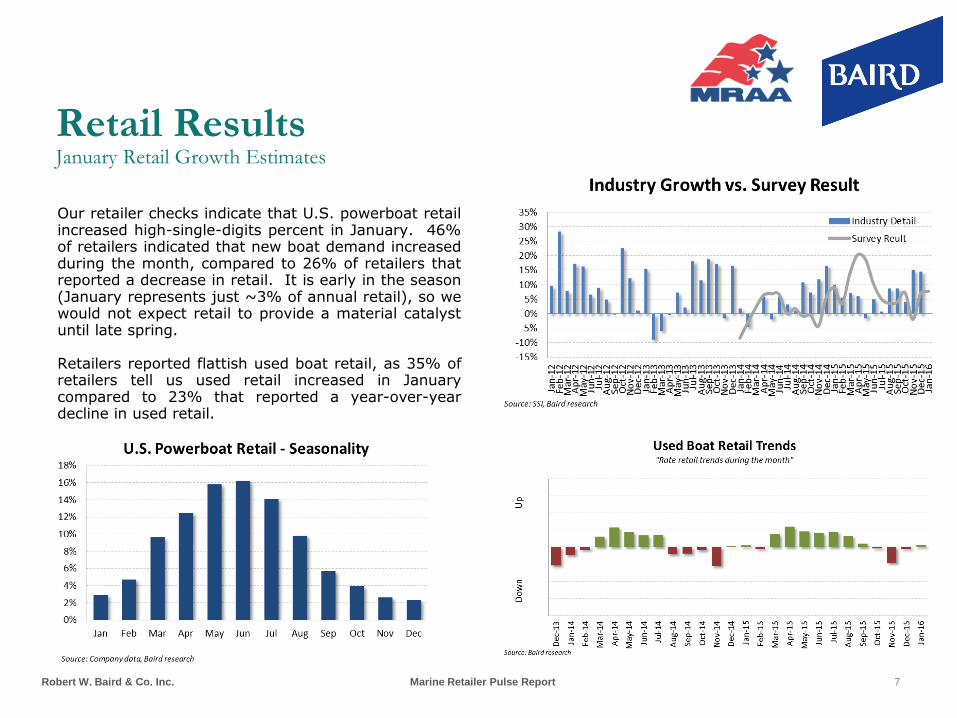

Our retailer checks indicate that U.S. powerboat retail increased high-single-digits percent in January. 46% of retailers indicated that new boat demand increased during the month, compared to 26% of retailers that reported a decrease in retail. It is early in the season (January represents just ~3% of annual retail), so we would not expect retail to provide a material catalyst until late spring. Retailers reported flattish used boat retail, as 35% of retailers tell us used retail increased in January compared to 23% that reported a year-over-year decline in used retail.

7

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

Retail Results January Retail Growth Estimates

8

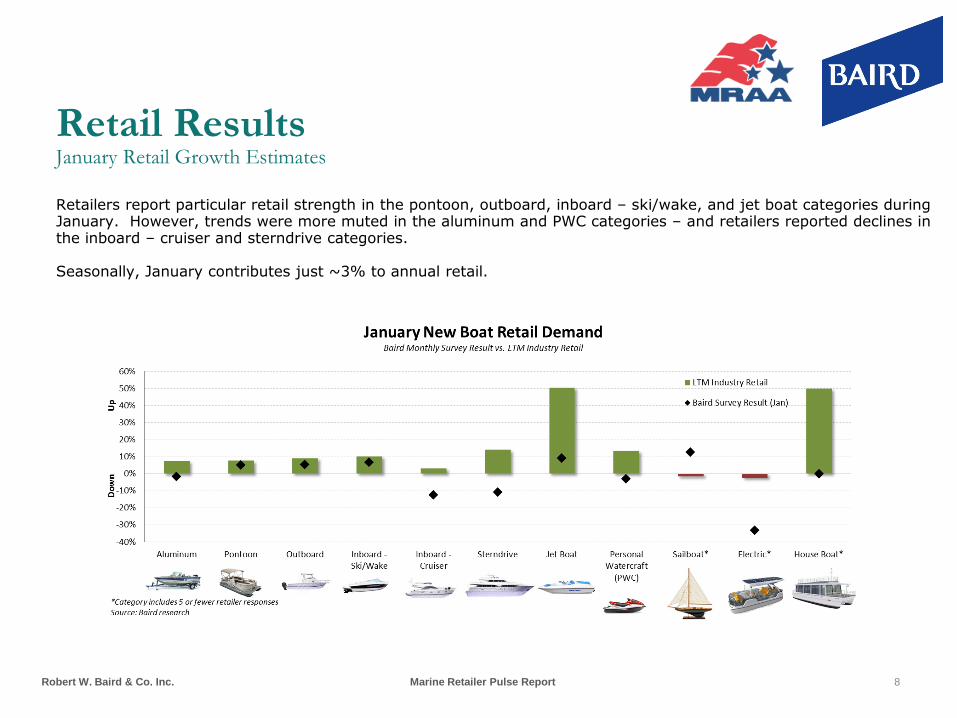

Retailers report particular retail strength in the pontoon, outboard, inboard – ski/wake, and jet boat categories during January. However, trends were more muted in the aluminum and PWC categories – and retailers reported declines in the inboard – cruiser and sterndrive categories. Seasonally, January contributes just ~3% to annual retail.

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

Retail Demand Factors January Retail Growth Estimates

9

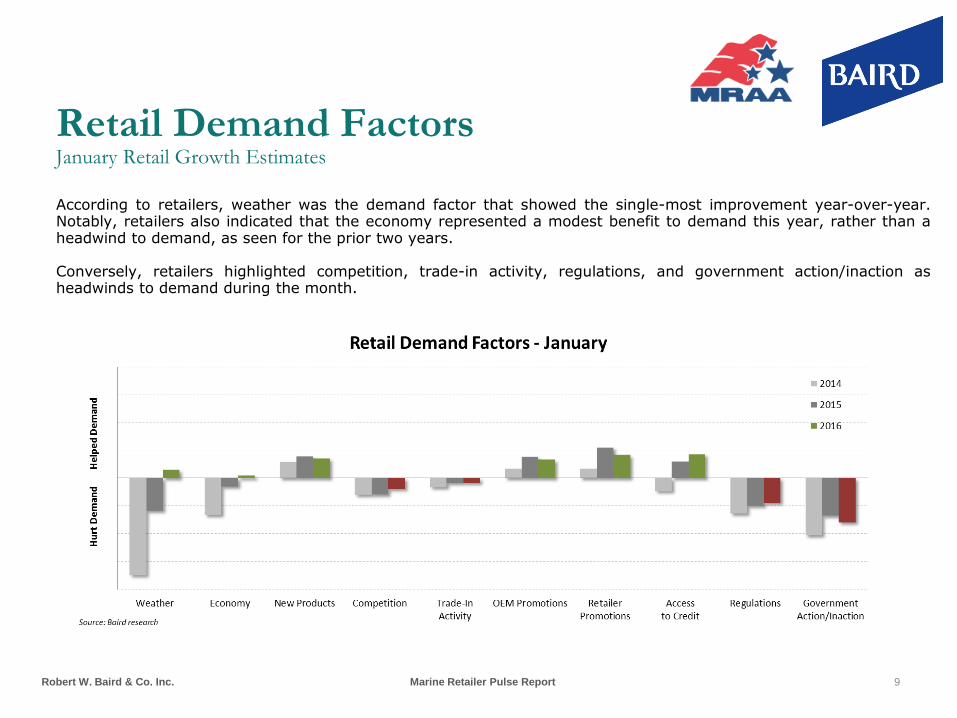

According to retailers, weather was the demand factor that showed the single-most improvement year-over-year. Notably, retailers also indicated that the economy represented a modest benefit to demand this year, rather than a headwind to demand, as seen for the prior two years. Conversely, retailers highlighted competition, trade-in activity, regulations, and government action/inaction as headwinds to demand during the month.

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

What’s Working Comments

“ Bryant Boats’ new WT1 [is] certainly turning heads at the boat show with a price tag of $40,000 for an inboard with wakesurf and board. Overstaffing was good with the amount of traffic at shows this year.”

“ Surf capable boats. Fishing boats. New Electronics.”

“ Big premium dual consoles and tritoons.”

“ Boat show was very successful for us this year. Traffic was up as well as sales.”

“ Boat shows good so far. We had an earlier than usual one for us, which proved to be better than expected. Milder than usual January weather was a bonus as well.”

“ Loose flat-bottoms and portable outboards.”

“ New models [and] dealer promotions.”

“ New, innovative products.”

“ No positive effect in January.”

“ Not much. Whatever you stock, they want a different color or model.”

“ OEM incentives. Provide customer/prospect a very positive interaction, whether they purchase or not. Quality of product and service is key for success.”

“ Rain/snow.”

“ Robalo "reel deals" [and] internet marketing.”

“ E-blasts.”

“ Hard to answer most of these questions, as we are a seasonal business and are closed for the month of January. Very little business done in January.”

10

√

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

X What’s Not Working Comments

“ Had lots of snow then lots of rain. No boat shows in January. Economy was slow as well in our region.”

“ I would like to see more grow boating campaigns to non-boaters.”

“ I/O's are soft for us at the moment.”

“ New boat packages.”

“ Parts and accessories are in serious decline. People with money are buying new boats, not fixing the old ones. People who buy those older boats fix them themselves and purchase parts online, not at a traditional dealership.”

“ Poor quality products coming from mfg.”

“ Sterndrive fiberglass.”

“ Still not selling sport boats or cruisers.”

“ The stock market affects our sales and the current market is not helping much!”

“ Weak builder promotions [and] longtime unchanged models.”

“ Commission sales.”

“ Government on all levels.”

“ Press and politicians.”

11

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

Inventory

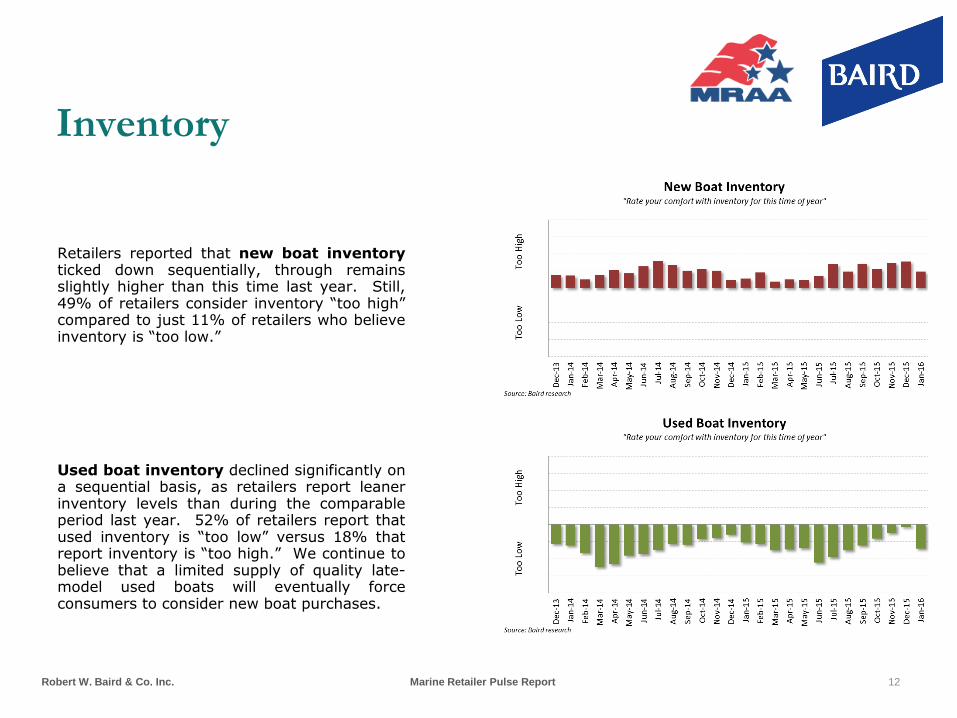

Retailers reported that new boat inventory ticked down sequentially, through remains slightly higher than this time last year. Still, 49% of retailers consider inventory “too high” compared to just 11% of retailers who believe inventory is “too low.” Used boat inventory declined significantly on a sequential basis, as retailers report leaner inventory levels than during the comparable period last year. 52% of retailers report that used inventory is “too low” versus 18% that report inventory is “too high.” We continue to believe that a limited supply of quality late-model used boats will eventually force consumers to consider new boat purchases.

12

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

Financing

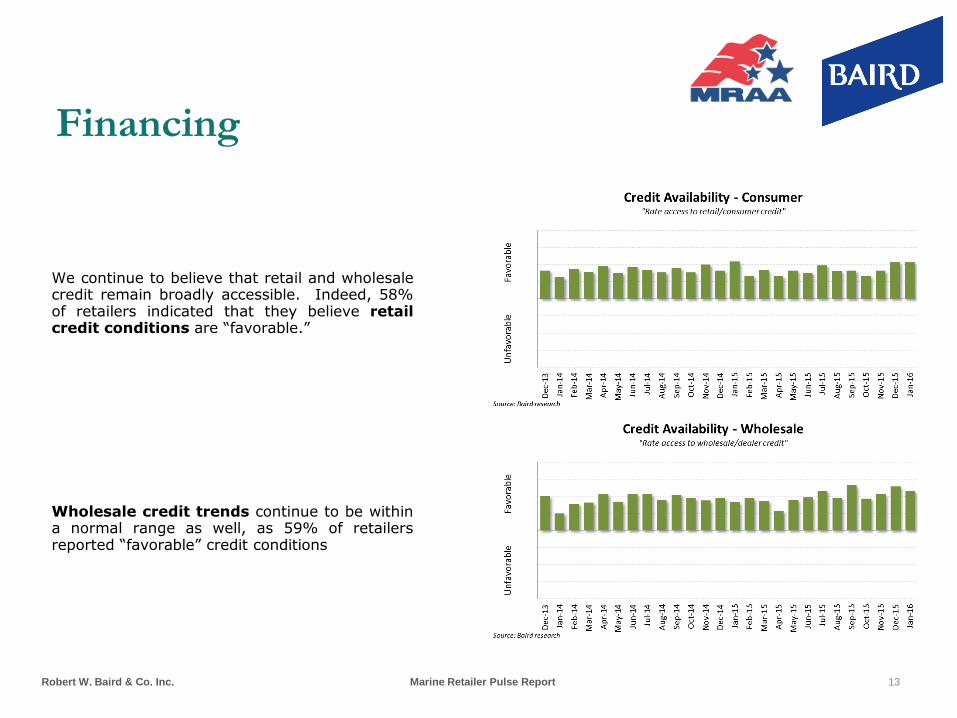

We continue to believe that retail and wholesale credit remain broadly accessible. Indeed, 58% of retailers indicated that they believe retail credit conditions are “favorable.” Wholesale credit trends continue to be within a normal range as well, as 59% of retailers reported “favorable” credit conditions

13

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

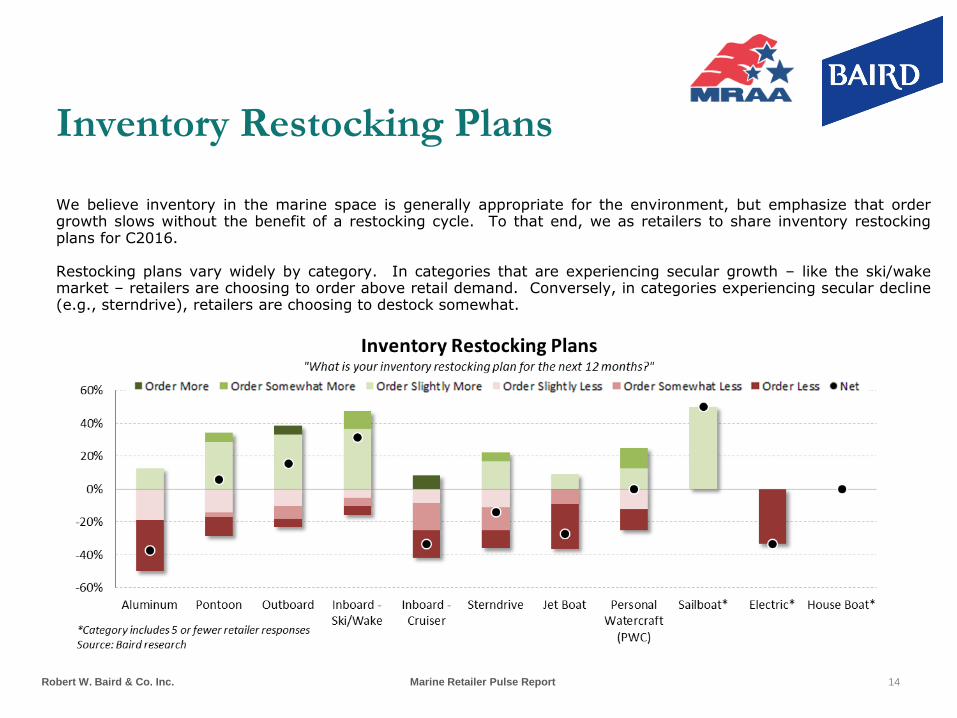

Inventory Restocking Plans

14

We believe inventory in the marine space is generally appropriate for the environment, but emphasize that order growth slows without the benefit of a restocking cycle. To that end, we as retailers to share inventory restocking plans for C2016. Restocking plans vary widely by category. In categories that are experiencing secular growth – like the ski/wake market – retailers are choosing to order above retail demand. Conversely, in categories experiencing secular decline (e.g., sterndrive), retailers are choosing to destock somewhat.

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

Inventory Restocking Plans Comments

“ Deplete inventory as fast as possible before floorplan interest chews up what little profit we make and then not re-stock until the boat manufacturers kick-off their 2017 interest assist programs.”

“ Use caution – watch days on hand closely, despite what manufacturers tell you.”

“ We think we are going to hang low on inventory for I/O powered boats. That is a rough area on LI. Concentrate on our Sea Pro line.”

“ We will be cautious. Dealers don't go broke for not enough inventory, but go broke for having too much inventory. Err on the side of caution.”

“ Due to sluggish economy in our region we have ordered less inventory.”

“ First two quarters will determine order intake for next model year.”

“ Have our inventory for the spring in stock.”

“ Higher stocking levels required by Boston Whaler.”

“ If economy tanks my orders will become next to zero.”

“ If you are committed to growth, you must ‘order more than sold.’ ”

“ Intend to maintain balance.”

“ It’s an election year. We will be more conservative moving forward. Would like to see an increase in inventory turns.”

“ Like most Marine Retailers in the Northeast, we build inventory in March and April and let it tail off for the rest of the year!”

“ Sell one then buy one.”

“ So far so good - but it is not yet crunch time. We will see if the manufacturers actually have what we need, when we need it!”

“ Very concerning. Low traffic count, walk-in, internet and phone.”

“ Watching it very closely.”

“ We see smaller boats moving faster than anticipated; we will run short if we can’t get inventory soon.”

“ Wish I never had to order another sterndrive.”

15

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

Inventory Restocking Plans Comments

“ Trying to sell the non-currents before we bring in any ‘17s.

“ Added new line for 2016.”

“ As boats sell, I will re-order.”

“ Be very careful!!”

16

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

Additional Comments Comments

“ High wholesale floorplan interest rates are too high for the margins that manufacturers force us dealers to sell by. Mass advertised boats at 15% margins and then [our lender] hits us with 7.25-9.20% rates. No point in stocking any boats outside of interest assisted programs. I would like to see manufacturers work on such low margins!”

“ Too many little dirt lot dealers popping up again in this time of prosperity. This industry just recreates its mistakes every business cycle. Low barriers to entry create weak competitors that take business away from the dealers that have invested money in facilities and training to excel, as builders requested.”

“ Consumer attitude seems fragmented.”

“ Economy seems to have buyers on edge. Weather is helping.”

“ Hope to see improvement as weather improves.”

“ Interested as to which states collect no sales tax on private party transactions, but charge full state and city sales tax if a dealer sells the same used boat? This is a big disadvantage to dealers, over 8% in Arizona and Nevada.”

“ Need less big box stores [dealers].”

“ The uncertainty of the national election could do great harm to our economy. Folks might become fearful and postpone big-ticket purchases.”

“ U.S. government needs to get it together.”

“ We were closed for first half of January which has skewed our report.”

17

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

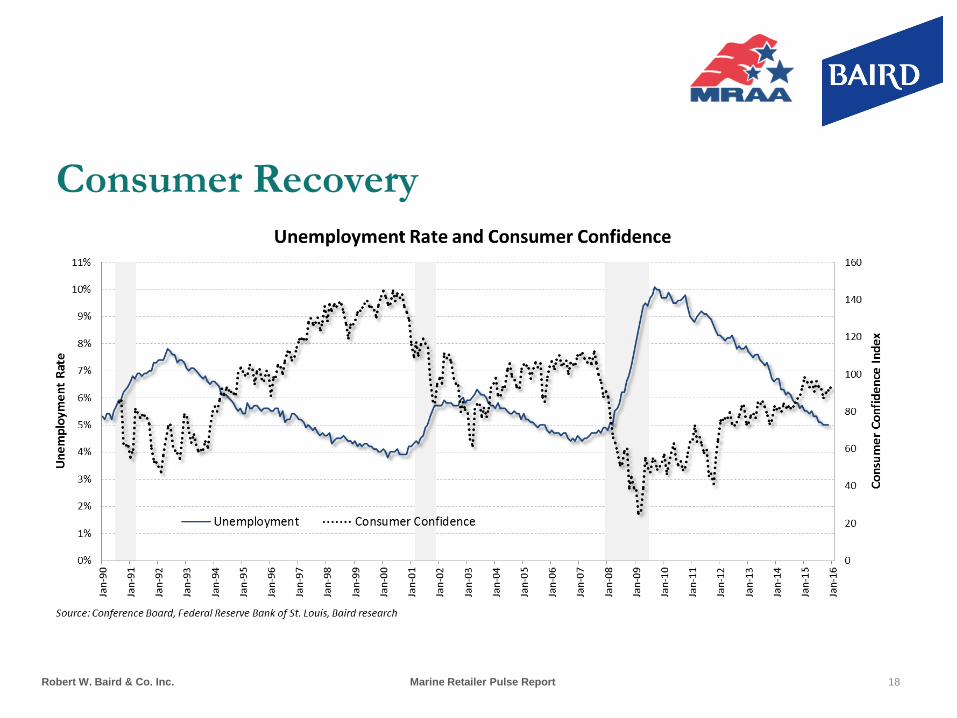

Consumer Recovery

18

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

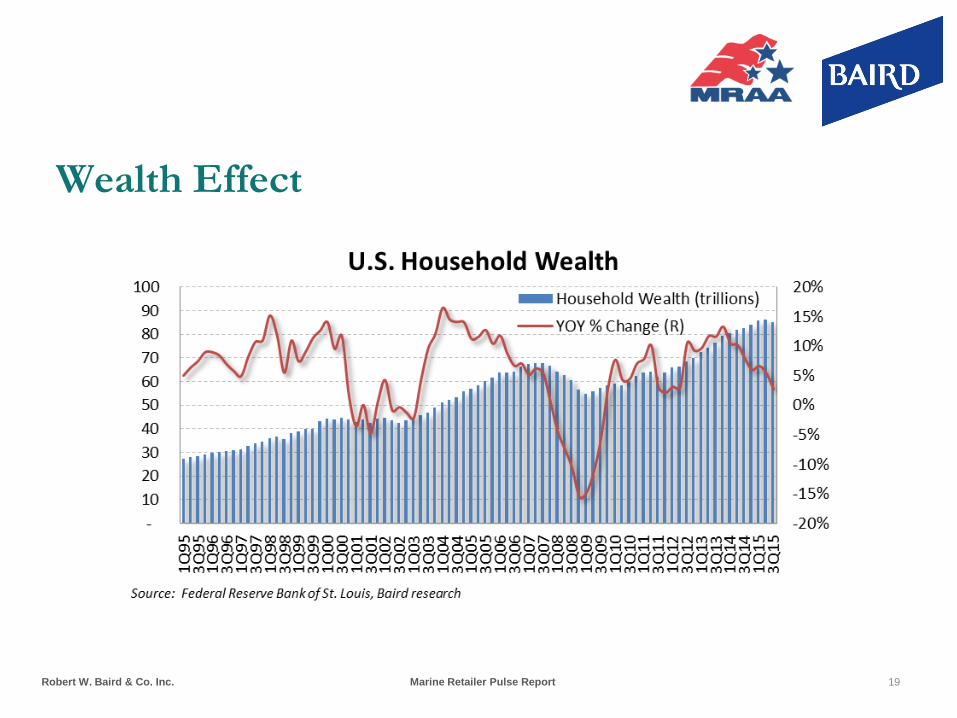

Wealth Effect

19

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

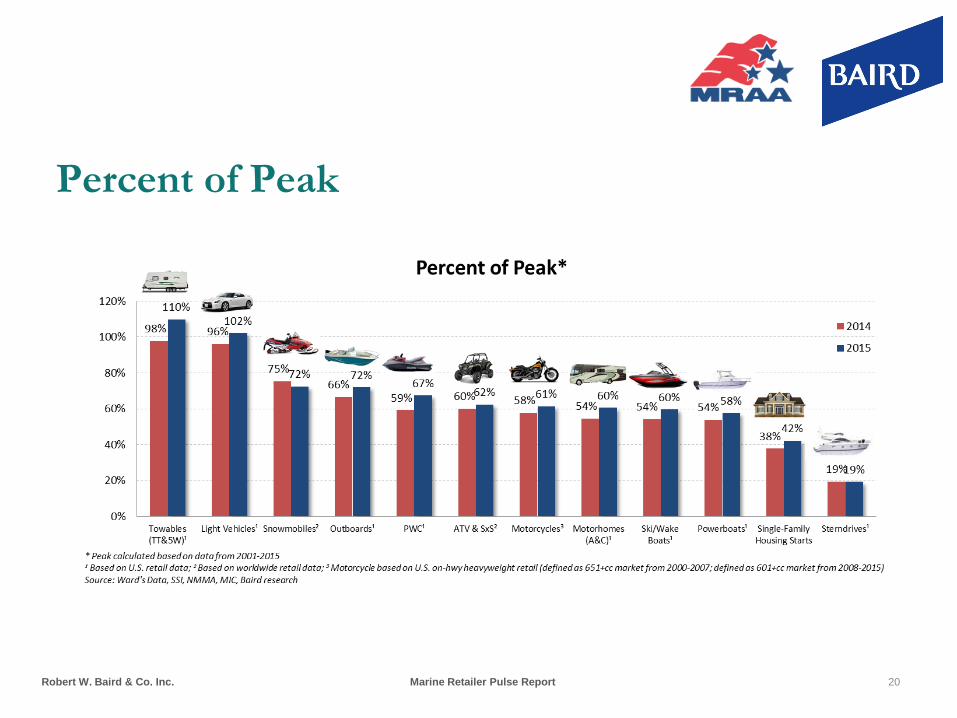

Percent of Peak

20

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

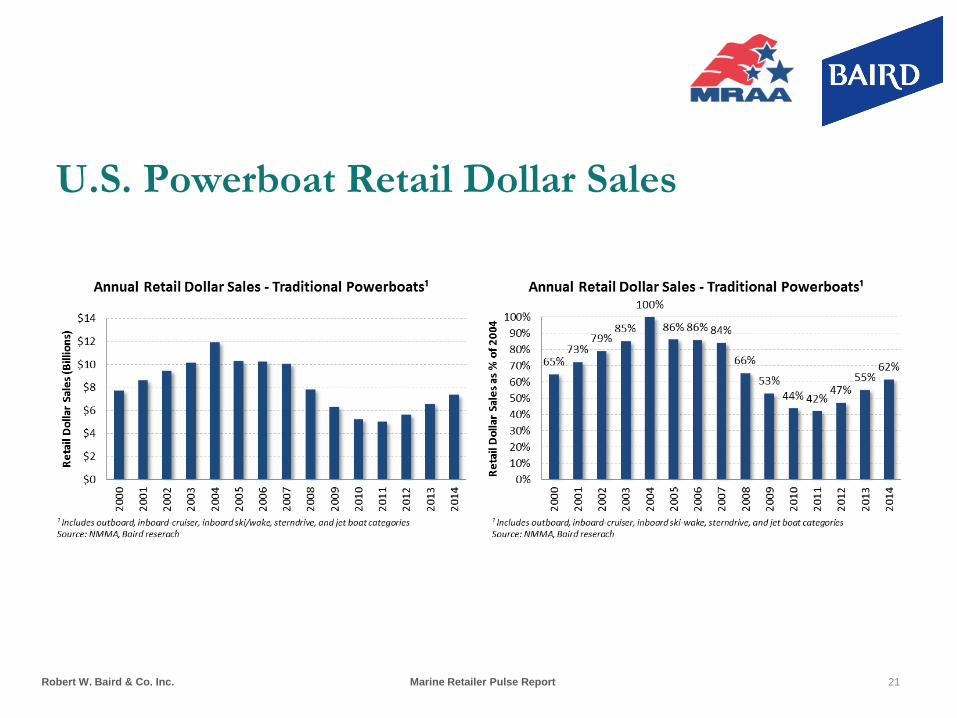

U.S. Powerboat Retail Dollar Sales

21

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

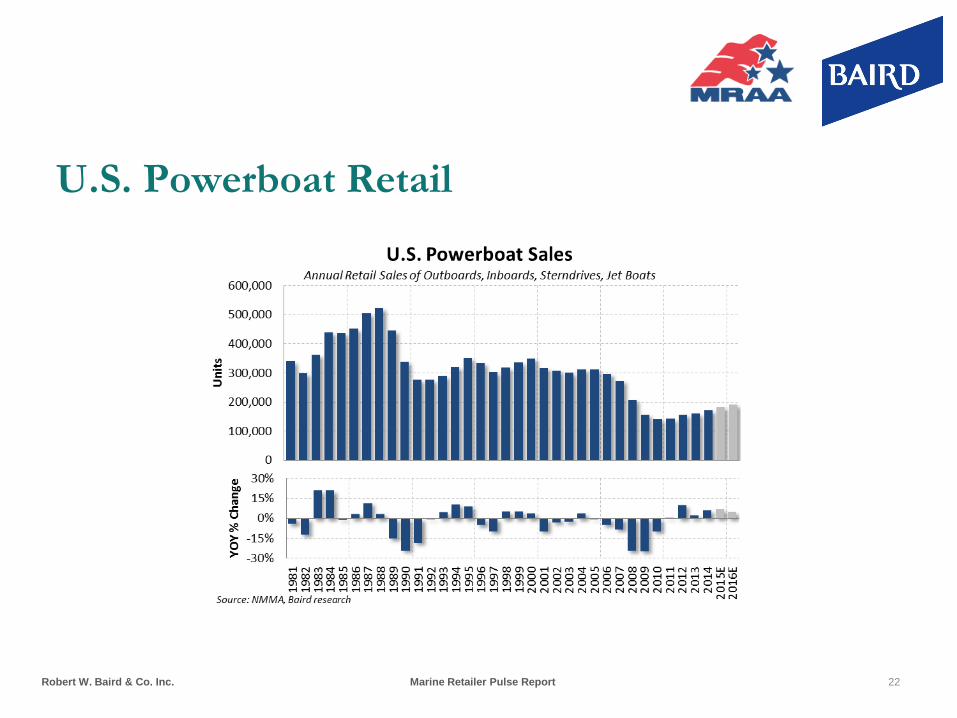

U.S. Powerboat Retail

22

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

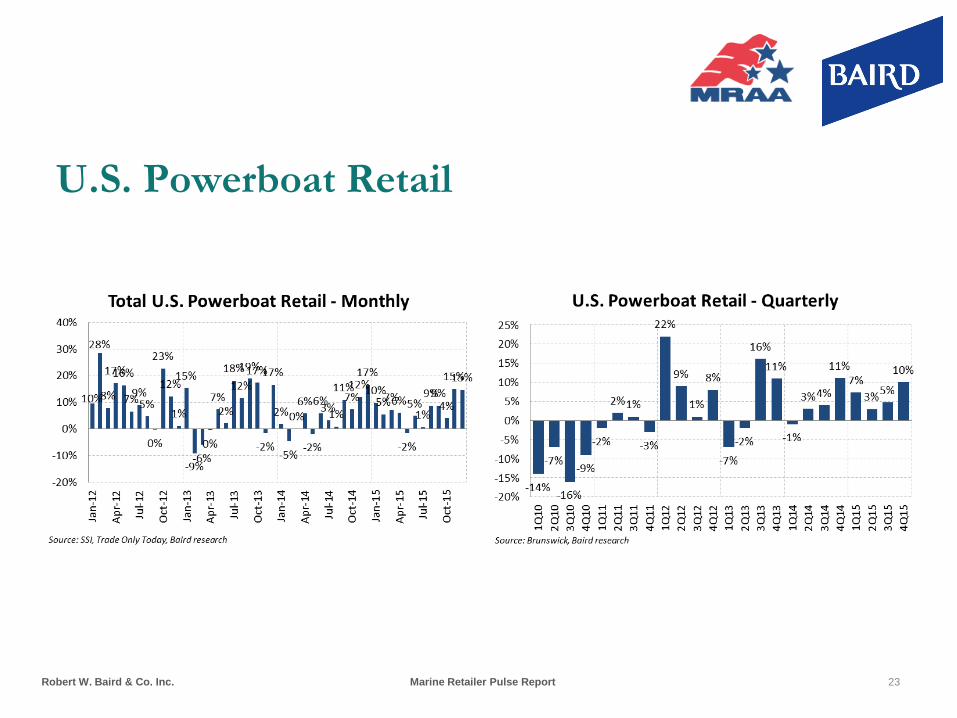

U.S. Powerboat Retail

23

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

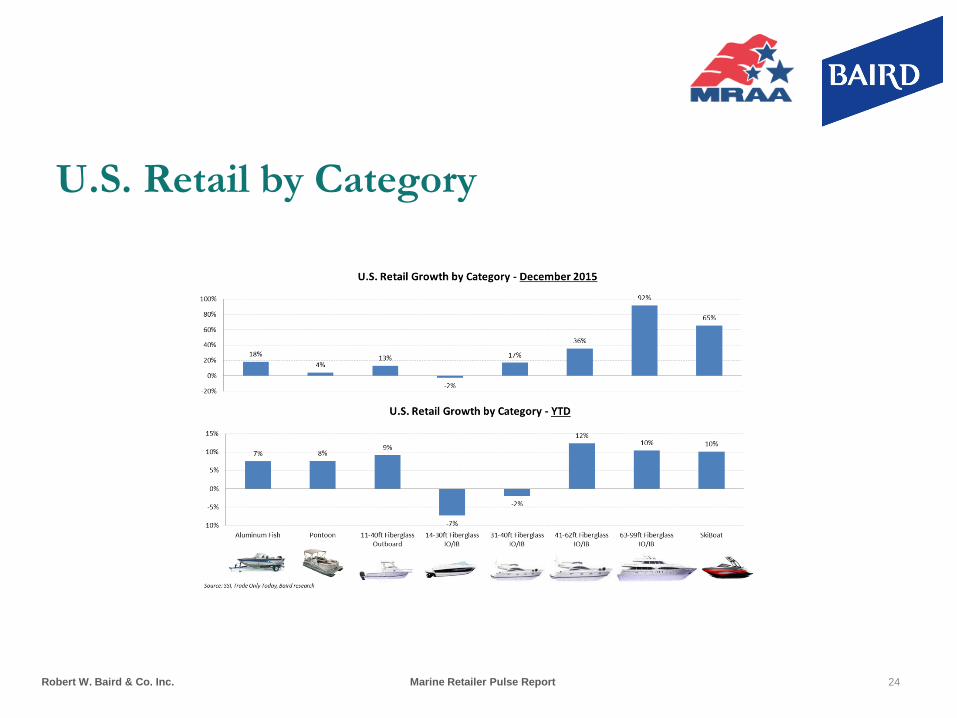

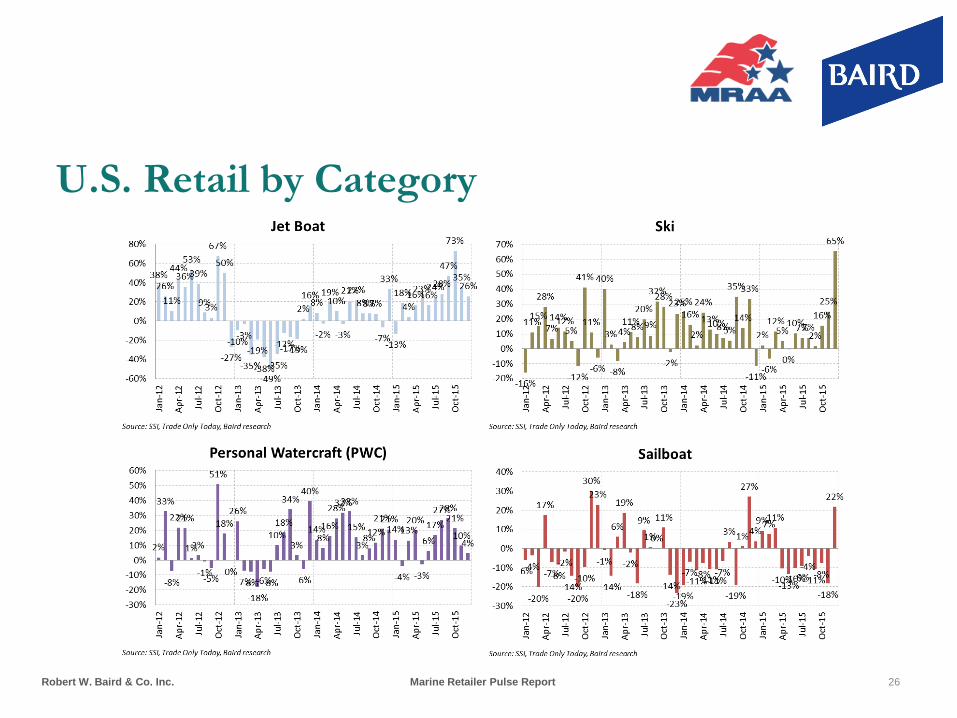

U.S. Retail by Category

24

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

U.S. Retail by Category

25

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

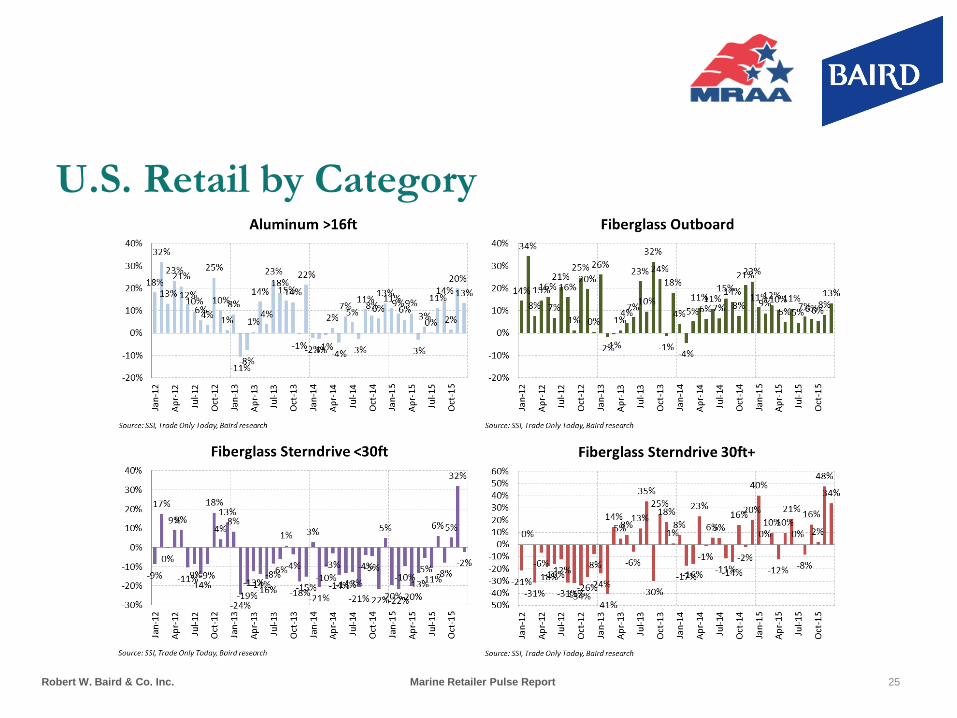

U.S. Retail by Category

26

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

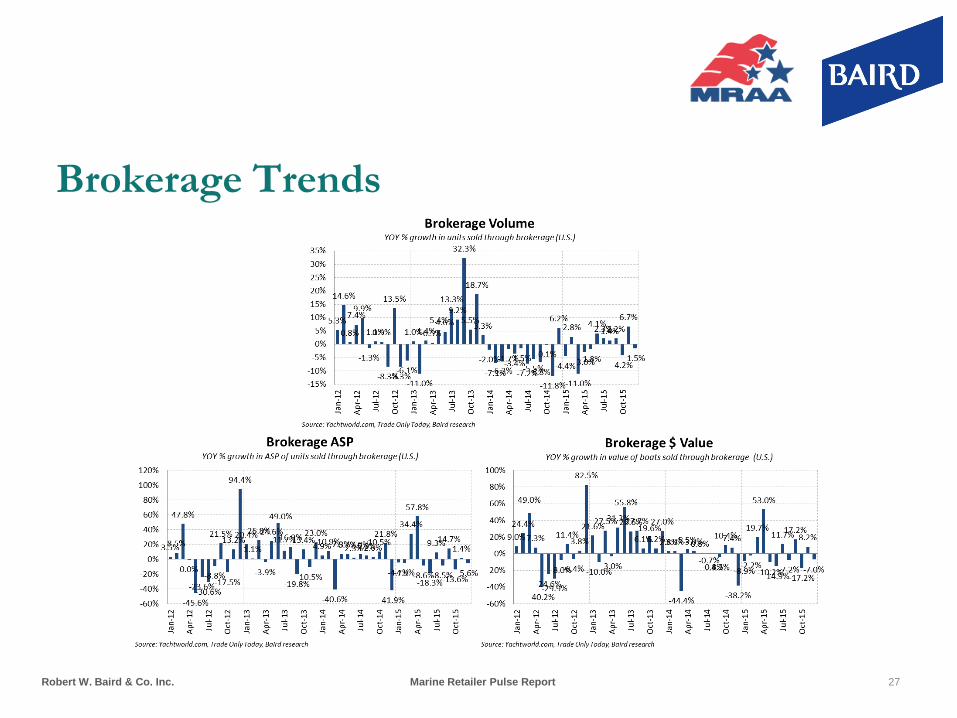

Brokerage Trends

27

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

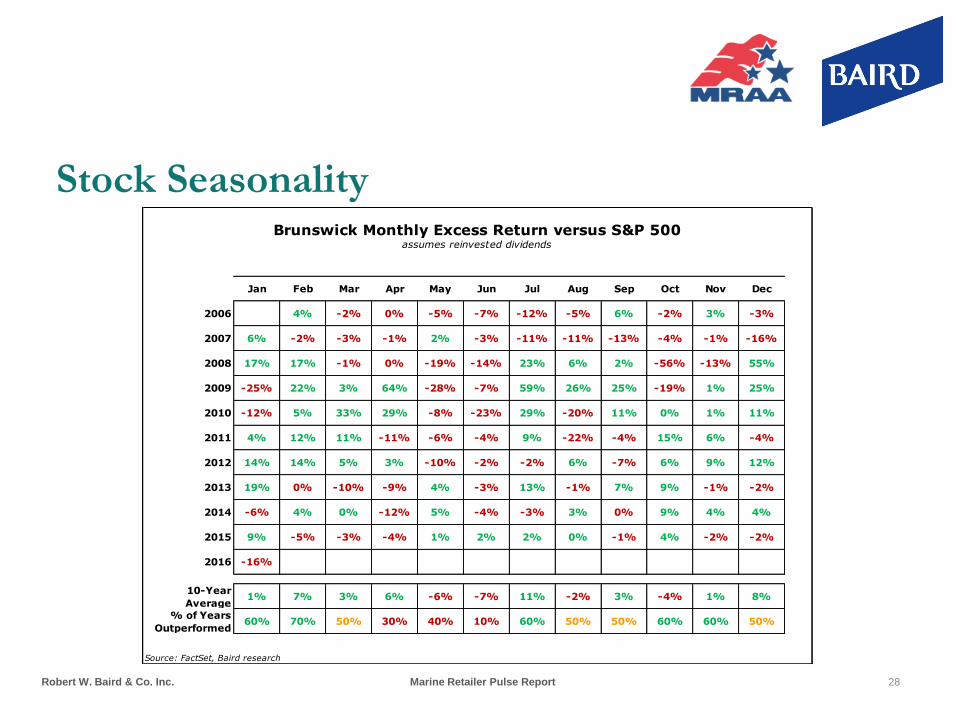

Brunswick Monthly Excess Return versus S&P 500

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2006 4% -2% 0% -5% -7% -12% -5% 6% -2% 3% -3%

2007 6% -2% -3% -1% 2% -3% -11% -11% -13% -4% -1% -16%

2008 17% 17% -1% 0% -19% -14% 23% 6% 2% -56% -13% 55%

2009 -25% 22% 3% 64% -28% -7% 59% 26% 25% -19% 1% 25%

2010 -12% 5% 33% 29% -8% -23% 29% -20% 11% 0% 1% 11%

2011 4% 12% 11% -11% -6% -4% 9% -22% -4% 15% 6% -4%

2012 14% 14% 5% 3% -10% -2% -2% 6% -7% 6% 9% 12%

2013 19% 0% -10% -9% 4% -3% 13% -1% 7% 9% -1% -2%

2014 -6% 4% 0% -12% 5% -4% -3% 3% 0% 9% 4% 4%

2015 9% -5% -3% -4% 1% 2% 2% 0% -1% 4% -2% -2%

2016 -16%

10-Year

Average1% 7% 3% 6% -6% -7% 11% -2% 3% -4% 1% 8%

% of Years

Outperformed60% 70% 50% 30% 40% 10% 60% 50% 50% 60% 60% 50%

Source: FactSet, Baird research

assumes reinvested dividends

Stock Seasonality

28

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

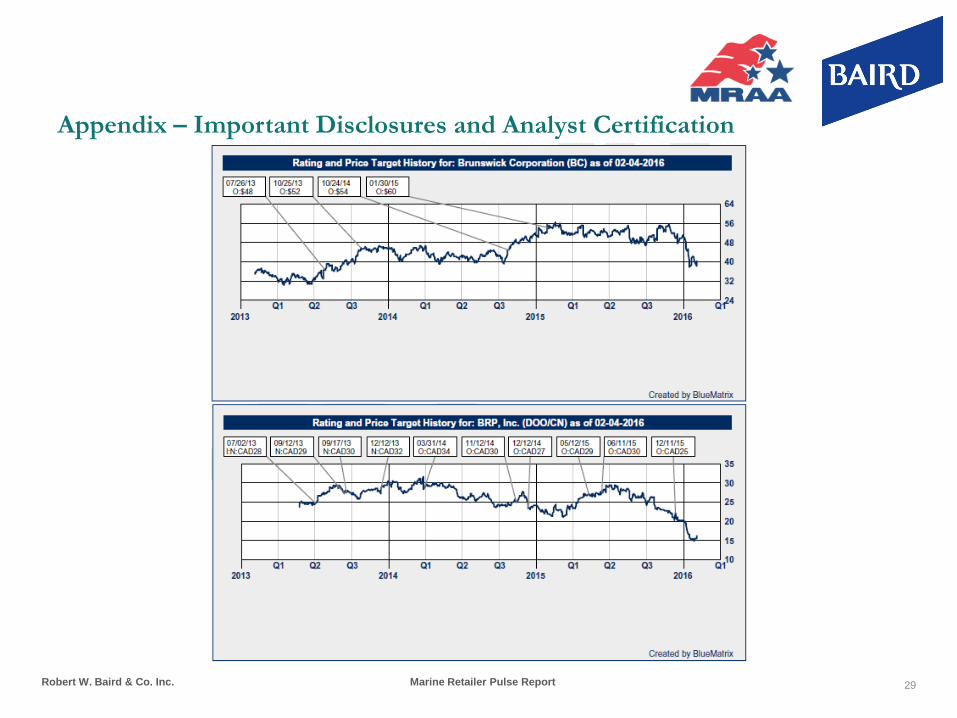

Appendix – Important Disclosures and Analyst Certification

29

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

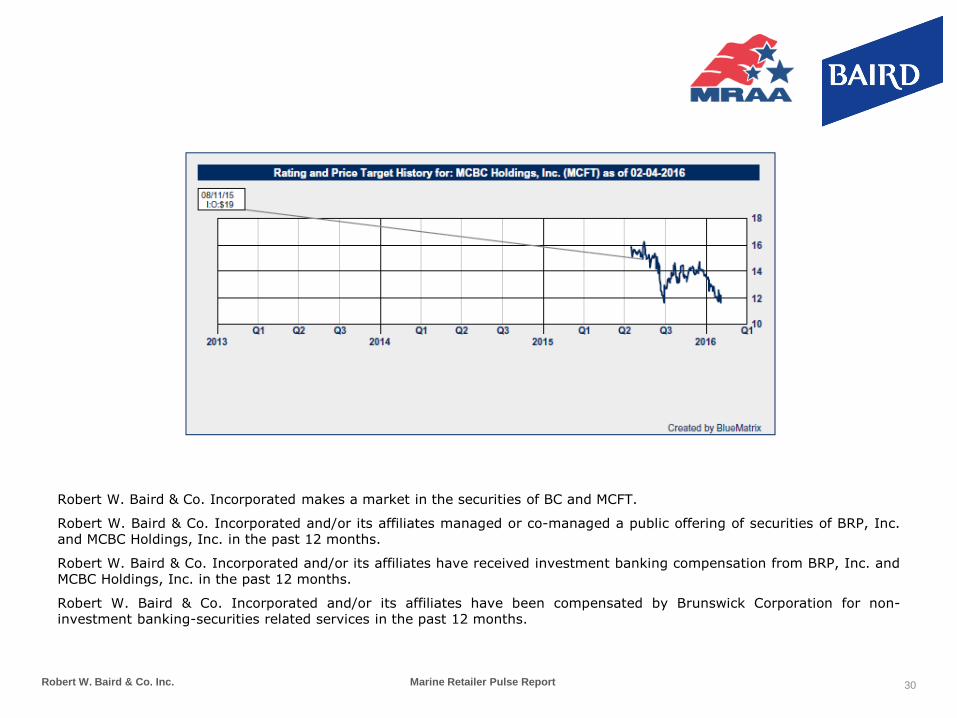

Robert W. Baird & Co. Incorporated makes a market in the securities of BC and MCFT.

Robert W. Baird & Co. Incorporated and/or its affiliates managed or co-managed a public offering of securities of BRP, Inc. and MCBC Holdings, Inc. in the past 12 months.

Robert W. Baird & Co. Incorporated and/or its affiliates have received investment banking compensation from BRP, Inc. and MCBC Holdings, Inc. in the past 12 months.

Robert W. Baird & Co. Incorporated and/or its affiliates have been compensated by Brunswick Corporation for non-investment banking-securities related services in the past 12 months.

30

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

Robert W. Baird & Co. Incorporated and/or its affiliates expect to receive or intend to seek investment-banking related compensation from the company or companies mentioned in this report within the next three months.

Robert W. Baird & Co. Incorporated may not be licensed to execute transactions in all foreign listed securities directly. Transactions in foreign listed securities may be prohibited for residents of the United States. Please contact a Baird representative for more information.

Investment Ratings: Outperform (O) - Expected to outperform on a total return, risk-adjusted basis the broader U.S. equity market over the next 12 months. Neutral (N) - Expected to perform in line with the broader U.S. equity market over the next 12 months. Underperform (U) - Expected to underperform on a total return, risk-adjusted basis the broader U.S. equity market over the next 12 months.

Risk Ratings: L - Lower Risk - Higher-quality companies for investors seeking capital appreciation or income with an emphasis on safety. Company characteristics may include: stable earnings, conservative balance sheets, and an established history of revenue and earnings. A - Average Risk - Growth situations for investors seeking capital appreciation with an emphasis on safety. Company characteristics may include: moderate volatility, modest balance-sheet leverage, and stable patterns of revenue and earnings. H - Higher Risk - Higher-growth situations appropriate for investors seeking capital appreciation with the acceptance of risk. Company characteristics may include: higher balance-sheet leverage, dynamic business environments, and higher levels of earnings and price volatility. S - Speculative Risk - High-growth situations appropriate only for investors willing to accept a high degree of volatility and risk. Company characteristics may include: unpredictable earnings, small capitalization, aggressive growth strategies, rapidly changing market dynamics, high leverage, extreme price volatility and unknown competitive challenges.

Valuation, Ratings and Risks. The recommendation and price target contained within this report are based on a time horizon of 12 months but there is no guarantee the objective will be achieved within the specified time horizon. Price targets are determined by a subjective review of fundamental and/or quantitative factors of the issuer, its industry, and the security type. A variety of methods may be used to determine the value of a security including, but not limited to, discounted cash flow, earnings multiples, peer group comparisons, and sum of the parts. Overall market risk, interest rate risk, and general economic risks impact all securities. Specific information regarding the price target and recommendation is provided in the text of our most recent research report.

Distribution of Investment Ratings. As of January 29, 2016, Baird U.S. Equity Research covered 714 companies, with 52% rated Outperform/Buy, 47% rated Neutral/Hold and 1% rated Underperform/Sell. Within these rating categories, 14% of Outperform/Buy-rated and 5% of Neutral/Hold-rated companies have compensated Baird for investment banking services in the past 12 months and/or Baird managed or co-managed a public offering of securities for these companies in the past 12 months.

31

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

Analyst Compensation. Analyst compensation is based on: 1) the correlation between the analyst's recommendations and stock price performance; 2) ratings and direct feedback from our investing clients, our institutional and retail sales force (as applicable) and from independent rating services; 3) the analyst's productivity, including the quality of the analyst's research and the analyst's contribution to the growth and development of our overall research effort and 4) compliance with all of Robert W. Baird’s internal policies and procedures. This compensation criteria and actual compensation is reviewed and approved on an annual basis by Baird's Research Oversight Committee.

Analyst compensation is derived from all revenue sources of the firm, including revenues from investment banking. Baird does not compensate research analysts based on specific investment banking transactions.

A complete listing of all companies covered by Baird U.S. Equity Research and applicable research disclosures can be accessed at http://www.rwbaird.com/research-insights/research/coverage/research-disclosure.aspx. You can also call 1-800-792-2473 or write: Robert W. Baird & Co., Equity Research, 777 E. Wisconsin Avenue, Milwaukee, WI 53202.

Analyst Certification

The senior research analyst(s) certifies that the views expressed in this research report and/or financial model accurately reflect such senior analyst's personal views about the subject securities or issuers and that no part of his or her compensation was, is, or will be directly or indirectly related to the specific recommendations or views contained in the research report.

Disclaimers

Baird prohibits analysts from owning stock in companies they cover.

This is not a complete analysis of every material fact regarding any company, industry or security. The opinions expressed here reflect our judgment at this date and are subject to change. The information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy.

ADDITIONAL INFORMATION ON COMPANIES MENTIONED HEREIN IS AVAILABLE UPON REQUEST The Dow Jones Industrial Average, S&P 500, S&P 400 and Russell 2000 are unmanaged common stock indices used to measure and report performance of various sectors of the stock market; direct investment in indices is not available.

Baird is exempt from the requirement to hold an Australian financial services license. Baird is regulated by the United States Securities and Exchange Commission, FINRA, and various other self-regulatory organizations and those laws and regulations may differ from Australian laws. This report has been prepared in accordance with the laws and regulations governing United States broker-dealers and not Australian laws.

32

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

Copyright 2016 Robert W. Baird & Co. Incorporated

Other Disclosures

The information and rating included in this report represent the Analyst’s long-term (12 month) view as described above. The research analyst(s) named in this report may at times, discuss, at the request of our clients, including Robert W. Baird & Co. salespersons and traders, or may have discussed in this report, certain trading strategies based on catalysts or events that may have a near-term impact on the market price of the equity securities discussed in this report. These trading strategies may differ from the analysts’ published price target or rating for such securities. Any such trading strategies are distinct from and do not affect the analysts’ fundamental long-term (12 month) rating for such securities, as described above. In addition, Robert W. Baird & Co. Incorporated and/or its affiliates (Baird) may provide to certain clients additional or research supplemental products or services, such as outlooks, commentaries and other detailed analyses, which focus on covered stocks, companies, industries or sectors. Not all clients who receive our standard company-specific research reports are eligible to receive these additional or supplemental products or services. Baird determines in its sole discretion the clients who will receive additional or supplemental products or services, in light of various factors including the size and scope of the client relationships. These additional or supplemental products or services may feature different analytical or research techniques and information than are contained in Baird’s standard research reports. Any ratings and recommendations contained in such additional or research supplemental products are consistent with the Analyst’s long-term ratings and recommendations contained in more broadly disseminated standard research reports.

United Kingdom (“UK”) disclosure requirements for the purpose of distributing this research into the UK and other countries for which Robert W. Baird Limited (“RWBL”) holds a MiFID passport.

This material is distributed in the UK and the European Economic Area (“EEA”) by RWBL, which has an office at Finsbury Circus House, 15 Finsbury Circus, London EC2M 7EB and is authorized and regulated by the Financial Conduct Authority (“FCA”).

For the purposes of the FCA requirements, this investment research report is classified as investment research and is objective.

This material is only directed at and is only made available to persons in the EEA who would satisfy the criteria of being "Professional" investors under MiFID and to persons in the UK falling within articles 19, 38, 47, and 49 of the Financial Services and Markets Act of 2000 (Financial Promotion) Order 2005 (all such persons being referred to as “relevant persons”). Accordingly, this document is intended only for persons regarded as investment professionals (or equivalent) and is not to be distributed to or passed onto any other person (such as persons who would be classified as Retail clients under MiFID).

Robert W. Baird & Co. Incorporated and RWBL have in place organizational and administrative arrangements for the disclosure and avoidance of conflicts of interest with respect to research recommendations.

33

Robert W. Baird & Co. Inc. Marine Retailer Pulse Report

This material is not intended for persons in jurisdictions where the distribution or publication of this research report is not permitted under the applicable laws or regulations of such jurisdiction.

Investment involves risk. The price of securities may fluctuate and past performance is not indicative of future results. Any recommendation contained in the research report does not have regard to the specific investment objectives, financial situation and the particular needs of any individuals. You are advised to exercise caution in relation to the research report. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

RWBL is exempt from the requirement to hold an Australian financial services license. RWBL is regulated by the FCA under UK laws, which may differ from Australian laws. This document has been prepared in accordance with FCA requirements and not Australian laws.

Dividend Yield. As used in this report, the term “dividend yield” refers, on a percentage basis, to the historical distributions made by the issuer relative to its current market price. Such distributions are not guaranteed, may be modified at the issuer’s discretion, may exceed operating cash flow, subsidized by borrowed funds or include a return of investment principal.

34