Embed Size (px)

Citation preview

8/8/2019 Mortgage Market Trend Outlook 2011

http://slidepdf.com/reader/full/mortgage-market-trend-outlook-2011 1/13

8/8/2019 Mortgage Market Trend Outlook 2011

http://slidepdf.com/reader/full/mortgage-market-trend-outlook-2011 2/13

Queries to [email protected] or 01 6339243

Mortgage Market Trend Outlook 2011.

Contents:

1. Introduction

2. Headline findings3. This years forecast4. How last years forecast (for 2010) turned out.

Introduction

In short, 2011 is likely to be a washout in the Irish mortgage market, lending will berestricted and only done at higher margins. We thought that most of the correction couldhappen in 2010 but political pressure, EU/IMF and State support as well as Regulatory intervention stopped the market from making many of the adjustments that perhaps

should have occurred.

These changes cannot be put off indefinitely and for that reason we find many of them inour 2011 outlook.

Lending is down 87% from peak in terms of euro figures and down 85% from peak in thenumber of mortgages drawn, in the meantime €70 billion euro has left our banks and thereis somewhere between 70,000 and 100,0001 mortgages of the 790,000 we have that are introuble in some shape or form. Unemployment is 13.5%2 and the flow of arrears is notshowing signs of ‘curing’ but rather of worsening3.

This is creating a perfect storm for Irish banks and banks operating in Ireland. The flight of deposits is crushing funding, the reduced repayments are also hurting a key aspect of funding (banks use repayments to create credit and fund operating costs), our banks arenot trusted and that makes raising money expensive, at the same time, our nation has beensaved by Europe and the IMF and our bond yields seem to be showing a lower rangeresistance at levels in excess of 8%.

Bearing these things in mind, our report isn’t particularly downbeat, rather it is a reflectionon the circumstances we find ourselves in. It is also important to remember that Irelandsfuture is not contingent upon the mortgage market, this may be a barometer of many of our national ills but recovery will come eventually as it always does, the trajectory towards

the bottom has been painful, for many people in this country the last three years will be atime they never forget for all the wrong reasons, but it is a necessary path that we must

walk in order to move onwards and upwards once again.

Karl DeeterOperations ManagerIrish Mortgage BrokersJanuary 6th 2011

1http://www.mortgagebrokers.ie/blog/index.php/2010/11/17/what-are-the-real-arrears-figures/

2 http://www.rte.ie/news/business/economy/unemployment.html 3

http://www.independent.ie/business/irish/mortgage-crisis-gets-worse-with-36500-now-in-arrears-2321340.html

8/8/2019 Mortgage Market Trend Outlook 2011

http://slidepdf.com/reader/full/mortgage-market-trend-outlook-2011 3/13

Queries to [email protected] or 01 6339243

Our forecast this year, headline findings:

• Banks will push up interest rates by another 100bps or 1% (independent of any move by the ECB) costing the average borrower (loan of €200k over 25yrs) anadditional €1,280 p.a. Rate hikes may start as early as this month.

• Variable interest rates will generally start to rest at or north of 5% by 2012. The statecontrolled banks in particular will be forced to make some painful decisions oninterest rates they charge to customers.

• Fixed rates may be temporarily removed from the market, offered on a limited basisor priced out of the market.

• Property prices will continue to decline.

• Segmentation of the property market.

• Total credit not likely to pass €6bn in 2011, with tranche management being a key consideration, there may be funding gaps in Irish banks during the year which causedelays in draw-downs.

• Rental prices.

• Large increases in repossessions.

• Distressed property sales to begin

• Banks shedding staff and closing branches.• Failure of our mortgage rescue scheme (Deferred Interest Scheme)

• Further funding issues in Irish banks

• Loan to Value trends

• Several ‘maybe’ trends that could start in 2011

Interest rates

We envisage 100 basis points (or 1%) by year end with first moves likely as early as thismonth, some banks gave an undertaking to make no more hikes until the new year (2011)so from this point on all bets are off. In general we think the moves will come inincrements with the first 50 bps raised in the first half of the year and the second half of them brought in during H2.

Variable rates in non-government owned banks will be near or at 5% by year end. This willleave some lenders with little to do (e.g. PTsb) and others with significant ground forcatching up (AIB/BOI – who must follow suit eventually). Foreign banks will also respond,

the likes of NIB are only a small portion of Danske but responsible for about 30% of thegroup bank losses and for that reason they will not hold back as the general price levelincreases. How this, along with rising commodity prices will read into our economy experiencing inflation is yet to be determined.

You would also have to question the rational of lending to a person at 3.5% when you canget a coupon of 9% ‘risk free’4. In 2011 we are certain that rates are going to continue their

bank lead movement upwards.

4 ‘Risk Free’ meaning a Sovereign Bond which is far from risk free but is still considered a benchmark for low risk lending.

8/8/2019 Mortgage Market Trend Outlook 2011

http://slidepdf.com/reader/full/mortgage-market-trend-outlook-2011 4/13

Queries to [email protected] or 01 6339243

Fixed Rates

Last year we determined that Standard Variables may cease to exist in favour of TVR's.This year the product change that we are contemplating is that Fixed Rates may beeffectively discontinued. By year end it is highly likely that some banks will cease to offer

fixed rates (this will be temporary as opposed to permanent), or any that are on offer will be at maximum premiums. It could also appear as restrictions although we are not sure if they will restrict new business or existing clients.

Irish bank swap rates are ranging from 7% (2yr) to 11% (5yr) and at those prices offering afixed rate below that is nonsensical, in particular when it creates a transfer from taxpayersto the borrower via a non commercial rate in a tax payer owned institution. This is onedriver behind the demise of fixed rates in 2011, the other is a reduction in the amounts

being kept in current accounts. As well as the fact that if you want to utilize the funds that banks actually use for fixed rates then why not purchase a sovereign bond with it?

Property prices

Will continue a downward trajectory, however, there is a genuine issue with financing costs which may negate any benefit to buyers who continue to hold out. This is not a call to buy now, or ever for that matter , merely an observation about financing costs, if interest ratesgo the direction we believe they will then much of the gain to the buyer will be captured.

As an example, a buyer who purchased a property for €400,000 in 2007 with an ECB+1%tracker is paying about €1,479 per month and their mortgage balance is €370,000 and

we’ll say that they are in negative equity of €70,000. The cost of credit over the life of the

loan is going to be €132,000 and the total repaid will be €532,000.

Then you have the person who held out and bought at today’s price of €300,000 but theirrate is 4% (with no price promise), their monthly payment is €1,432 finance costs will be€215,000 and the total repaid is €516,000 so the savings is nowhere near the perceiveddifference in price. The difference in financing costs (€16,000) also needs to be offset forthe three years rent paid from 07-10 because at the back end of the loan in year 27 (for thesecond person), the one who bought in 07’ is living mortgage free.

Banks are going to capture any gains in price by negating the gain from a cost perspective.Cash buyers are probably best advised to hold out for another year and then see where the

market is at that point for now the trend is still downwards but not accelerating5.

The total number of properties for sale is slowly coming down and the oversupply of 120,0006 will take some time to work through (not confusing ‘empties’ with ‘oversupply’),

but properties are selling at the right price and that is important to remember.

Residential Property Tax is also something to remain aware of, much of this hinges upon whoever is in power after the coming election, it may be unpopular at the polls but arecurring property tax is likely to be introduced from 2012 with an announcement later inthe year. Site Value Tax is the fairest but implementation is difficult, however, we suspectthat the new postcodes and well run property cadastre will tie into this and both of these

are already in the making.

5 http://www.daft.ie/report/Daft-House-Price-Report-Q3-2010.pdf 6 http://www.irishtimes.com/newspaper/property/2010/1202/1224284552711.html

8/8/2019 Mortgage Market Trend Outlook 2011

http://slidepdf.com/reader/full/mortgage-market-trend-outlook-2011 5/13

Queries to [email protected] or 01 6339243

Segmentation of the property market (residential)

An increased acceptance of a two tier property market (apts vs. houses) is likely to beconfirmed in 2011. From our experience buyers are just not that interested in apartments,this will present problems for apartment sellers as the only way to attract them will be viaprice drops, having said that, a 2 bed apartment for three times the average industrial wage

is a good thing, it is only bad for many of the sellers.

Getting there will take time however as so much supply is now in state hands. The market will further segregate into cities/towns and hinterlands in each county with each furtherdisplaying their own dynamic and market clearing prices. Our ongoing view is that themarket will be active in certain price ranges and certain neighbourhoods (up to €500k non-apartment second hand homes in cities) with little activity elsewhere.

Total Credit

The figure of €5bn in lending for 2010 is part forecast on our part as the Irish BankingFederation figures have not yet been released. However, we believe that an estimation of €4.75 to €5 billion is reasonable; it is based on the quarter on quarter figures for the yearto date. In 2011 we do think that we will see a higher level of lending in the region of €5-6bn (which we calculated by correlating our brokerage figures against the wider marketand then looking at the existing pipeline and expected drawdown’s).

This is a weak basis for a forecast call but it’s the best we have to work with at present, andthe adjustments in the property market as many people’s positions are liquidated willlikely ensure that there are good deals available and they will be bought. Lending tohouseholds has been trending down since 2007 and has been negative since Q3 of 2009

2010 is likely to have been our low point from a mortgage credit perspective.

8/8/2019 Mortgage Market Trend Outlook 2011

http://slidepdf.com/reader/full/mortgage-market-trend-outlook-2011 6/13

Queries to [email protected] or 01 6339243

Taking all of these considerations we are confident in our call of €5-6bn which meansanother year in the trenches for people in the Mortgage business, but a likely upwardsturning point in 2012, the number of loans will increase (as the size of individual loansdecreases) with 30-45,000 draw downs in 2011.

8/8/2019 Mortgage Market Trend Outlook 2011

http://slidepdf.com/reader/full/mortgage-market-trend-outlook-2011 7/13

Queries to [email protected] or 01 6339243

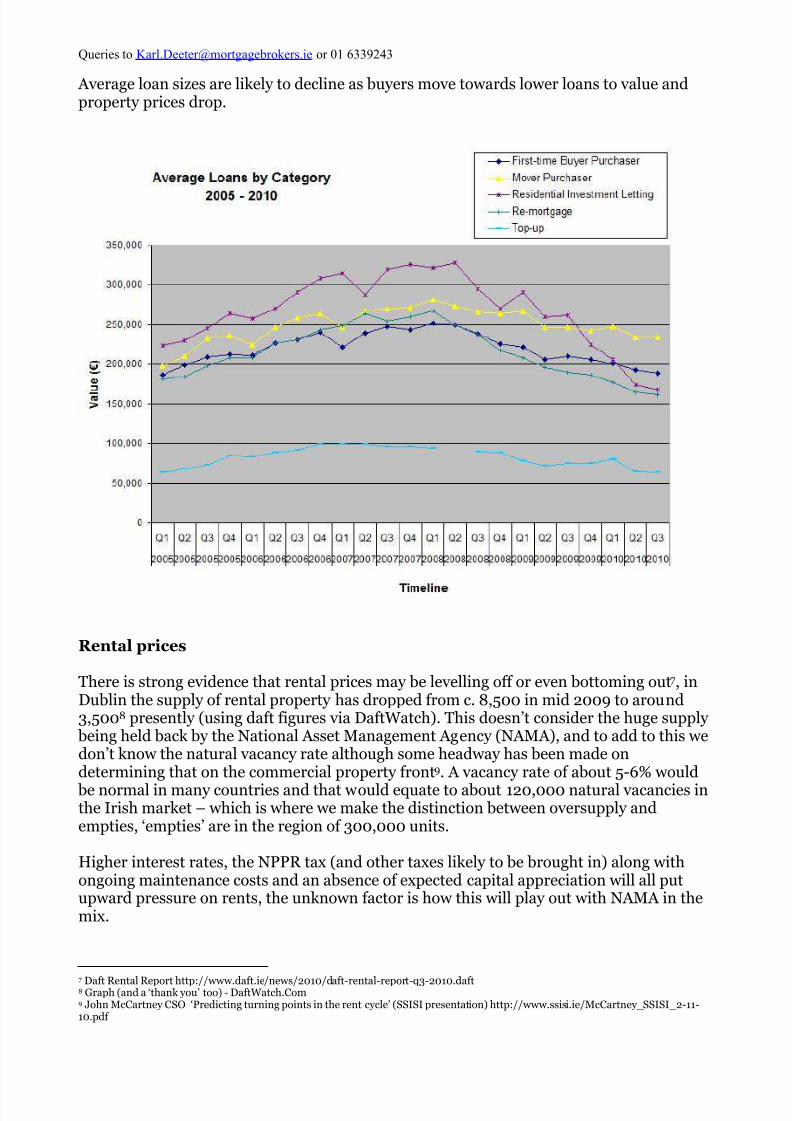

Average loan sizes are likely to decline as buyers move towards lower loans to value andproperty prices drop.

Rental prices

There is strong evidence that rental prices may be levelling off or even bottoming out7, inDublin the supply of rental property has dropped from c. 8,500 in mid 2009 to around3,5008 presently (using daft figures via DaftWatch). This doesn’t consider the huge supply

being held back by the National Asset Management Agency (NAMA), and to add to this wedon’t know the natural vacancy rate although some headway has been made ondetermining that on the commercial property front9. A vacancy rate of about 5-6% would

be normal in many countries and that would equate to about 120,000 natural vacancies inthe Irish market – which is where we make the distinction between oversupply andempties, ‘empties’ are in the region of 300,000 units.

Higher interest rates, the NPPR tax (and other taxes likely to be brought in) along withongoing maintenance costs and an absence of expected capital appreciation will all putupward pressure on rents, the unknown factor is how this will play out with NAMA in themix.

7 Daft Rental Report http://www.daft.ie/news/2010/daft-rental-report-q3-2010.daft8 Graph (and a ‘thank you’ too) - DaftWatch.Com9 John McCartney CSO ‘Predicting turning points in the rent cycle’ (SSISI presentation) http://www.ssisi.ie/McCartney_SSISI_2-11-10.pdf

8/8/2019 Mortgage Market Trend Outlook 2011

http://slidepdf.com/reader/full/mortgage-market-trend-outlook-2011 8/13

Queries to [email protected] or 01 6339243

Repossessions

They will be far higher this year than in 2010, at least a 300% or more increase –proceedings may take the bulk of cases through to 2012 because there is a lengthy processand our judiciary are pro-borrower, but now that there is a text book definition of ‘unsustainable mortgage10’, the banks at least have grounds to present their case, the

ongoing forced forbearance will also start to run out for many households.

10 http://www.merrionstreet.ie/wp-content/uploads/2010/11/Mortgage-Arrears-and-Personal-Debt-Group-Report-17th-November-

2010.pdf

8/8/2019 Mortgage Market Trend Outlook 2011

http://slidepdf.com/reader/full/mortgage-market-trend-outlook-2011 9/13

Queries to [email protected] or 01 6339243

Currently there are 12,000 households who have paid nothing in over a year 11, to now they have been afforded protection from the Regulator via moratoria on repossessions and pro-

borrower legislation in the annually updated Codes of Conduct for Mortgage Arrears12, butmany can expect to start receiving civil bills in 2011. The trend in arrears is going one way only 13 and the subdued level of repossessions (a mere 311 in 2010)14 in light of this is

unlikely to last.

Unemployment is expected to remain high for some time, that will also be an issue thatplays into arrears and ultimately repossessions for some time, people don’t pay theirmortgage with macro economic announcements of growth, they pay with their pay check and as long as this figure remains high so too will the levels of arrears, that doesn’t factorin the rate hikes we spoke of earlier, reduced take home pay due to changes in taxation andany further wage cuts that people may experience15.

Distressed property sales

This will start in 2011 but it will be residential investors who are first in line for losing thehomes they bought. Several things will hit them at once

1. Lenders are demanding repayment mortgages and not offering ongoing interestonly facilities, or in some cases they will do so but take back the current rate (e.g.tracker mortgages on investment properties).

2. Tax treatment of mortgage interest changed, now only 75% of the cost can be offsetagainst the income.

3. S23 Changes16 in the 2011 Budget (if brought in) will literally break thousands of households or cause landlords on the edge to go right over it.

Banks will increasingly rely upon a ‘receiver of rent’ clause being enforced, so that they canobtain rights to receive any rent that is being paid, in 2011 banks will have to get heavy handed with residential investment property owners who are in arrears, ‘pay or possess’

will become the order of the day. Of the €334bn in private sector credit €143bn of that ismortgages17, and about €30bn is non-principle private residence.

When you consider the drop in rent prices, along with the rise in unemployment andincreased rates and removal of interest only facilities it makes sense that we’ll seeliquidations.

Bank Branch Closures

Many banks have stated that they are closing branches already (but these are primarily satellite branches), Ireland is already over banked, and it doesn’t make any sense forseveral state owned banks to compete against each other in regional towns.In effect we have had a ‘bonus bonanza’ in Irish banks whereby thousands of people have

jobs that shouldn’t even exist any more, it makes the AIB bonus scandal look like peanutsin comparison.

11 http://www.independent.ie/business/irish/12000-mortgages-unpaid-for-year-or-more-2471633.html12 http://www.financialregulator.ie/press-area/press-releases/Pages/NewMeasurestoProtectMortgageHoldersFacingArrears.aspx13 http://www.mortgagebrokers.ie/blog/index.php/2010/09/02/mortgage-arrears-for-the-first-half-of-2010/14 http://www.irishtimes.com/newspaper/ireland/2011/0104/1224286702036.html15 http://www.independent.ie/national-news/grim-choices-are-being-made-as-households-struggle-to-survive-2437256.html16 Section B7 http://www.budget.gov.ie/budgets/2011/Documents/Summary%20of%20Measures%20Combined.pdf 17 http://www.centralbank.ie/data/site/cmbs/Developments%20in%20PSC%20by%20Economic%20Sector%20Q32010.pdf

8/8/2019 Mortgage Market Trend Outlook 2011

http://slidepdf.com/reader/full/mortgage-market-trend-outlook-2011 10/13

Queries to [email protected] or 01 6339243

This will need to end and 2011 is likely to be the year when it does, you have to getoperational efficiency and loss making branches are abundant in Ireland, the taxpayerowns about half of them now and the only fair thing to do is shut down 20-25% of AIB

branches, BoI and EBS will likely need to reduce numbers by about 10-15%.

In Finland during their crisis of the 90’s one third of bank staff were let go18

, unfortunately we must replicate this (although we have been avoiding doing so for some time), thoselosing jobs will also be the least culpable for the crisis and in that respect it will be quiteunfair but it won’t stop the job losses from coming (eventually).

A bank workers strike or serious curtailment of services could come about during thisprocess; we had several of them in the past 1967, 1970, 1976 and 1992. The laggingcorrelation of these strikes with recessions may yet come to fruition.

EBS is 50/50 to PTsb or Cardiff/Ross, but there will be an extension on the new final biddate (which was already extended to c.14th Jan 2011). EBS will either have new owners or

get brought into an existing bank in 2011 and in that transition jobs will go.

Anglo/Nationwide deposit books will be auctioned; this may seem like an attractive optionfor the desperately deposit hungry Irish banks but TUPE19 (Transfer of Undertakings andProtection of Employment) will likely apply meaning the buyer will have a large headacheon their hands of having to employ all of the origination staff with the service. The only

way to fix that problem is for the banks to rapidly shed staff but they have been unwillingto do this in large numbers to date.

Banks are going to push clients toward automated transactions (online/phone/atm based)and use charges to punish branch users as a means to funnel more people away from the

branches in conjunction with the closures.

Failure of the mortgage scheme.

As surely as it has been announced we believe it is likely to fail20. This is assuming thatIrish policy makers do not somehow outsmart policy makers in the UK and the USA whohave tried similar schemes (the UK one actually being superior to our own as an offering).Of the 70-100,000 borrowers in trouble we doubt that even 5% of them will get into thescheme and those that do may likely continue to default anyway. The UK scheme which

was originally designed to help 42,000 borrowers21 had, more than a year after its

inception, helped a paltry 34 borrowers22, not even 1/1000th of the intended result.

Further funding issues in Irish Banks

The original PCAR (Prudential Capital Assessment Review) which was seen as a successhas been recalled and new targets set which mean banks must be able to take losses ontheir loan books of 12%. This will leave a funding gap for many banks; the only way to fill

18 Jaakko Kiander (Labour Institute for Economic Research) THE GREAT DEPRESSIO OF FILAD 1990-1993: causes and consequences http://www.esri.ie/news_events/latest_press_releases/esri_policy_conference_th/index.xml

19 http://www.irishstatutebook.ie/2003/en/si/0131.html and also 1981/2006 legislation. As well as Acquired Rights Directives (77/187/EC),(98/50/EC), Acquired Rights Amendment Directive (2001/23/EC)20 Charlie Weston (Independent) http://www.independent.ie/national-news/deferredinterest-plan-for-homeloans-is-doomed-to-fail-2441119.html21 BSA ‘Understanding Mortgage Arrears’ pg 25 of report http://www.bsa.org.uk/docs/publications/understanding_mortgage_arrears.pdf 22 BBC http://www.bbc.co.uk/news/business-10686369

8/8/2019 Mortgage Market Trend Outlook 2011

http://slidepdf.com/reader/full/mortgage-market-trend-outlook-2011 11/13

Queries to [email protected] or 01 6339243

this at present is via the state, but that won’t stop shocks from occurring, we may seeseveral serious credit events before 2011 is out.

In 2010 €70 billion in deposits left our banks23, foreign deposit takers are reportingmassive increases in business, NationwideUK (Ireland) have seen their daily business gofrom about 30 accounts and just under €1m a day in new business to over 160 accounts

and €10m per day in new business, this is indicative of the deposit flight showing up inretail deposits – to now it has primarily been in corporate and institutional deposits. A full banking or lending freeze in Q2 is a genuine risk.

Loan to Value trends

LTV’s may start to come back down. Last year we believed that more stringentunderwriting and lower LTV’s would be a hallmark of the year, and for much of it that wasthe case, however the percentage a bank was willing to lend on a property did creep back up with several lenders, this may reverse in 2011 and return to a point where biggerdeposits are required. It would also not be surprising to see the return of MIG’s (Mortgage

Indemnity Guarantees) with the bill being footed by the borrower [average cost is just over€1,000]. Already several borrowers are only willing to go beyond 80% with a MIG.

On that note, it is worth mentioning that many banks are likely to move to a position whereby a solicitor can no longer work for two parties at once (dual undertaking for the borrower and bank) and this will embed a cost into property transactions for all buyers andsellers, equally, stamp duty may help ‘start the market’ but it will not be kick startinganything for first time buyers who are currently the majority in the market at 38%. In fact,the only group likely to really benefit are commercial buyers (which may help NAMA dotheir job) and to a lesser extent second home/mover-purchasers because almost every other group is either already exempt from stamp duty (remortgage, top up mortgage) or

they pay it anyway (investors).

The ‘Maybe’ trends of 2011:

Mortgage strike

This may come about due to rate hikes or by owners of investment property who simply give up. It would be no surprise to see a mobilization of the indebted into a more singular

voice there are already groups speaking of doing this (or representing those indifficulties24); to date they have not gained traction; that could always change.

New Lender

With rates going north of 5% a well capitalized bank with strict underwriting may see anopportunity to enter the Irish market with a new offering on a limited basis. Anything onthis front in 2011 is perhaps likely an announcement of entry to the market in 2012. Thismay not be via a new entrant (as BOSI entered in the past) but via a buyout of a stateowned institution by a bank with money to lend.

23 Irish Independent http://www.independent.ie/business/irish/over-euro70bn-in-deposits-fled-irish-banks-in-2010-2482304.html 24

www.newbeginning.ie

8/8/2019 Mortgage Market Trend Outlook 2011

http://slidepdf.com/reader/full/mortgage-market-trend-outlook-2011 12/13

Queries to [email protected] or 01 6339243

Last years forecast and how it stacks up to what actually happened.

Now we can take a look at what we expected in 2010, below are the predictions we madefor the Irish market.

1. An increase of 100bps or 1% in variable rate mortgages with rate increasesas early as March on existing loans and new business

This was entirely accurate; the idea that it would start in Q1 was largely discounted butproved accurate with AIB making their move in late March followed closely by BOI andEBS on the same day. The pattern has tended to be that banks are making the move withindays of each other.

2. Banks seeking lower LTV's with more stringent underwriting

Entirely accurate, banks in general held lower LTV's for most of 2010 while they may have been ‘open to business’ at 90%+ it was nigh impossible to place deals and some reports were suggesting that 80% of applications were being turned away 25.

3. A virtual end to Standard Variable rates and a move towards Tiered Variables

Entirely accurate, variable rates are almost universally contingent upon LTV heading into2011; TVR's have effectively taken over.

4. ECB rate changes that would be lip service

From last years report ‘We believe that one surprise in 2010 may be that the ECB doesnothing other than talk up their devotion to controlling any potential inflation’ accurate,they did talk up the fact that rates can't stay low forever and the minor move never came.

5. Specific as opposed to widespread recovery in certain neighbourhoods atcertain price levels.

Mildly accurate, yields at some price levels (sub €200k) in certain neighbourhoods (cities)are pointing towards there being sensible, where yields make sense from an investmentperspective and also where massive price drops are no longer happening.

6. Lending not to pass €15bn with overall credit being stagnant or negative

On the lending call this was entirely inaccurate and our worst call in a long time, onmortgage credit being stagnant or negative we were on the ball, 2010 was a year whererepayment and prepayment outstripped lending, central bank figures showing that massdeleveraging to the tune of €7 billion occurred.

25http://www.irishtimes.com/newspaper/breaking/2010/1109/breaking44.html

8/8/2019 Mortgage Market Trend Outlook 2011

http://slidepdf.com/reader/full/mortgage-market-trend-outlook-2011 13/13

Queries to [email protected] or 01 6339243

How did we get the first part so wrong? We though that low base rates and cash injectionsto banks along with falling prices would encourage buyer activity that missed the fact thatthe nation went over a cliff edge and Regulation /political will stopped the market from

adjusting more rapidly due to extended forbearance which means that about 35,000properties that should be for sale at a discount are not on the market.

7. Fixed rates of early 2010 to represent historic lows

This has held true, fixed rates are not likely to hit the prices seen in late 09' early 2010 for along time, anybody who locked in during Q1 of 2010 made a very good choice.

8. A mortgage rescue scheme to be announced in H1 of 2010 as pressuremounts

This call was made before the Green Party Minister Eamon Ryan called for a MortgageExpert Group. The call was only partially accurate, there was a scheme announced but it was in H2. The expert group that was set up to consider this were only formed in themiddle of H1, so it was a decent call but we got the timing wrong.

In short, our forecasts for developments in 2010 were broadly accurate with the exceptionof the credit figures which we are still beating ourselves up over having gotten themembarrassingly wrong. That's the danger of forecasts. It is important to remember that atthe time these forecasts were made most of them were considered equally unlikely andmuch of what we spoke about was not in the public domain to any meaningful degree.

The same can be said of this years forecast, like all forecasts read this with a healthy pinchof salt.