Embed Size (px)

Citation preview

COUNCIL of MORTGAGELENDERS

1

UK housing and mortgage market outlook

Jim Cunningham

Senior Economist

COUNCIL of MORTGAGELENDERS

2

Structure

• International background

• UK economy and interest rates

• UK housing and mortgage markets

• Product, segment and channel

• Looking forward – issues and prospects

COUNCIL of MORTGAGELENDERS

3

• International background• UK economy and interest rates

• UK housing and mortgage markets

• Product, segment and channel

• Looking forward – issues and prospects

COUNCIL of MORTGAGELENDERS

4

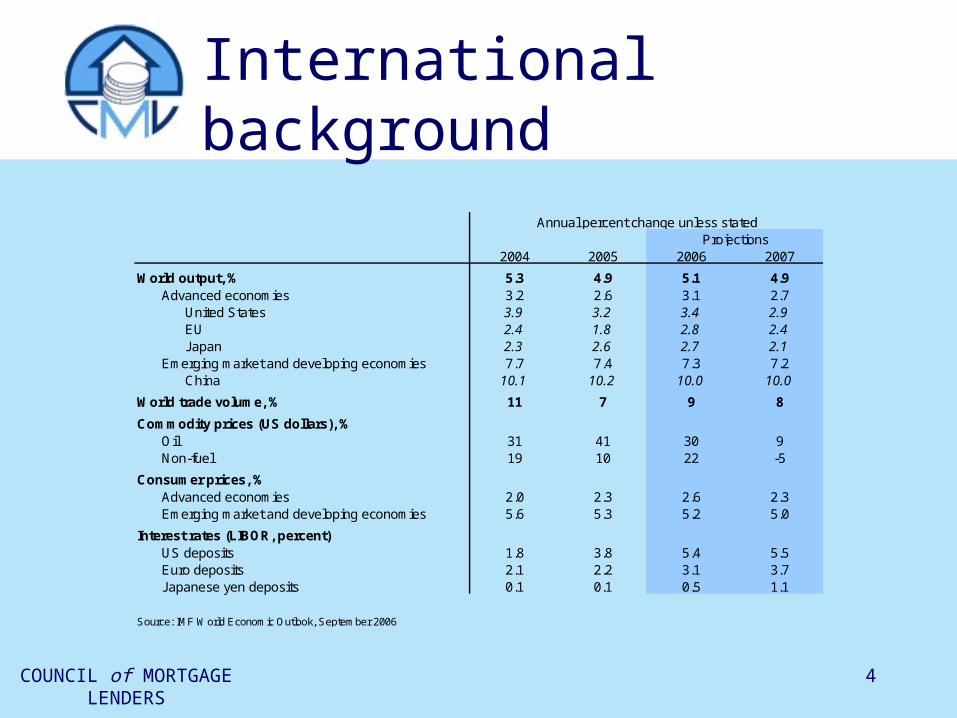

International background

2004 2005 2006 2007

World output, % 5.3 4.9 5.1 4.9Advanced economies 3.2 2.6 3.1 2.7

United States 3.9 3.2 3.4 2.9EU 2.4 1.8 2.8 2.4Japan 2.3 2.6 2.7 2.1

Emerging market and developing economies 7.7 7.4 7.3 7.2China 10.1 10.2 10.0 10.0

World trade volume, % 11 7 9 8

Commodity prices (US dollars), %Oil 31 41 30 9Non-fuel 19 10 22 -5

Consumer prices, %Advanced economies 2.0 2.3 2.6 2.3Emerging market and developing economies 5.6 5.3 5.2 5.0

Interest rates (LIBOR, percent)US deposits 1.8 3.8 5.4 5.5Euro deposits 2.1 2.2 3.1 3.7Japanese yen deposits 0.1 0.1 0.5 1.1

Source: IMF World Economic Outlook, September 2006

Annual percent change unless statedProjections

COUNCIL of MORTGAGELENDERS

5

Global economic risks

• Slanted to downside: 1. Inflationary pressure and tighter monetary policy

2. Even higher oil prices

3. Weakening US housing market

• Concern over disorderly unwinding of global imbalances

• US current account deficit 7% of GDP

COUNCIL of MORTGAGELENDERS

6

• International background

• UK economy and interest rates• UK housing and mortgage markets

• Product, segment and channel

• Looking forward – issues and prospects

COUNCIL of MORTGAGELENDERS

7

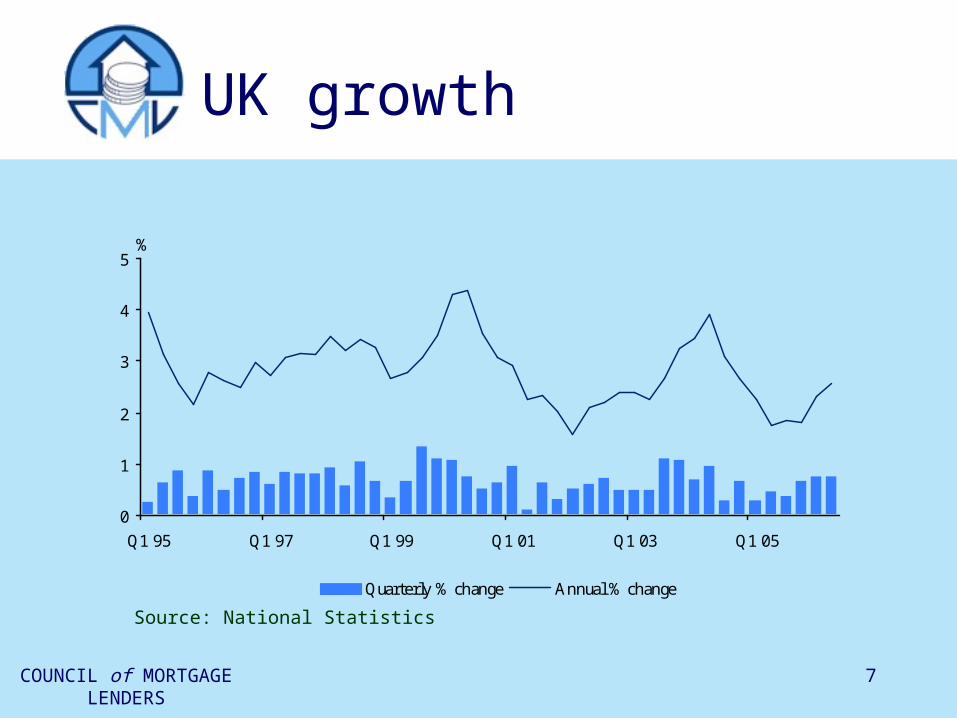

UK growth

0

1

2

3

4

5

Q1 95 Q1 97 Q1 99 Q1 01 Q1 03 Q1 05

%

Quarterly % change Annual % change

Source: National Statistics

COUNCIL of MORTGAGELENDERS

8

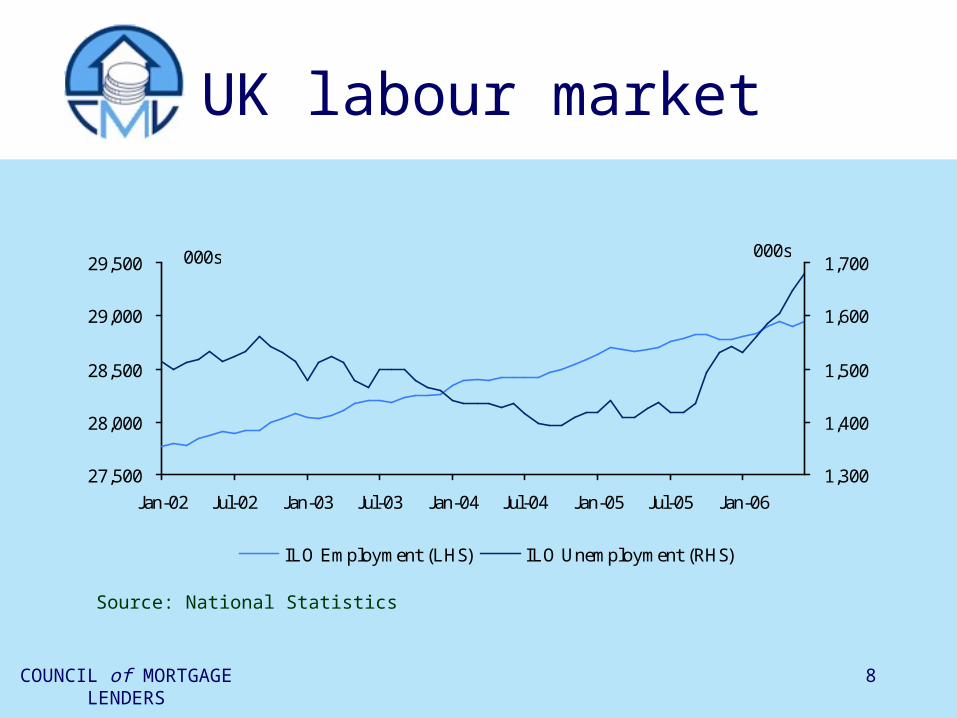

UK labour market

27,500

28,000

28,500

29,000

29,500

Jan-02 Jul-02 Jan-03 Jul-03 Jan-04 Jul-04 Jan-05 Jul-05 Jan-06

000s

1,300

1,400

1,500

1,600

1,700000s

ILO Employment (LHS) ILO Unemployment (RHS)

Source: National Statistics

COUNCIL of MORTGAGELENDERS

9

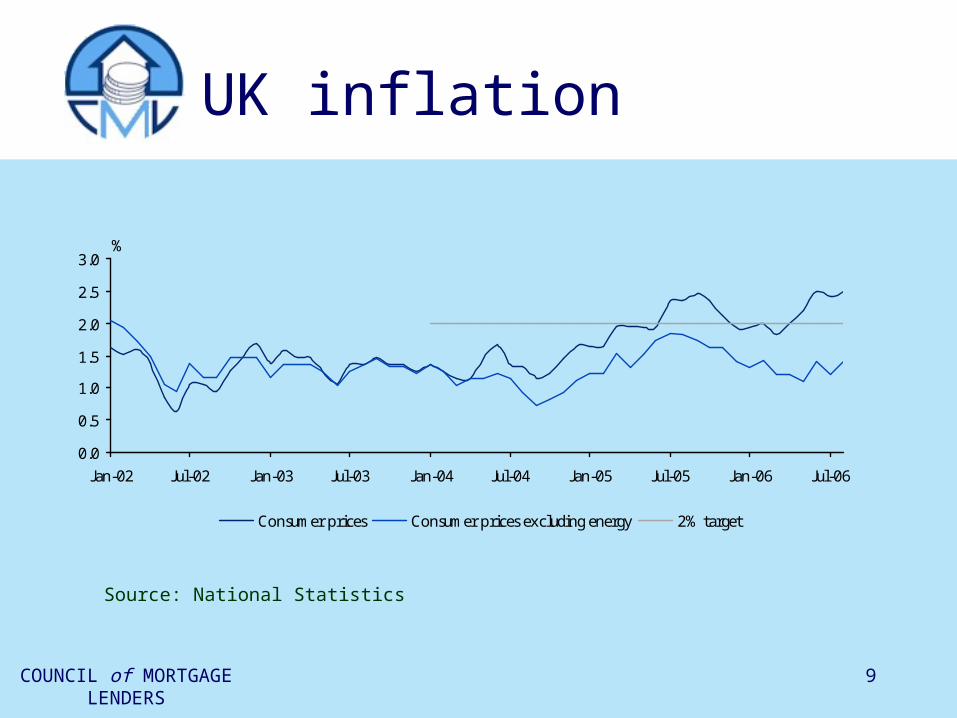

UK inflation

Source: National Statistics

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jan-02 Jul-02 Jan-03 Jul-03 Jan-04 Jul-04 Jan-05 Jul-05 Jan-06 Jul-06

%

Consumer prices Consumer prices excluding energy 2% target

COUNCIL of MORTGAGELENDERS

10

Market interest rates

3.0

3.5

4.0

4.5

5.0

5.5

6.0

Jan-03 Jul-03 Jan-04 Jul-04 Jan-05 Jul-05 Jan-06 Jul-06

%

Bank of England repo rate 2 year rate 3 year rate 5 year rate

Source: Bank of England

COUNCIL of MORTGAGELENDERS

11

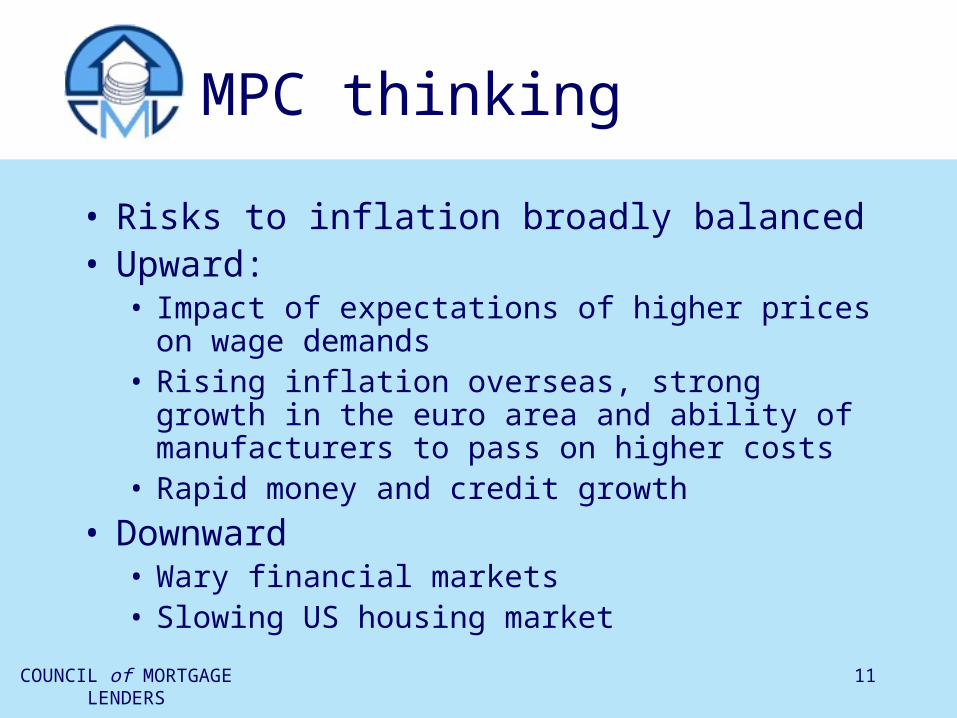

MPC thinking

• Risks to inflation broadly balanced• Upward:

• Impact of expectations of higher prices on wage demands

• Rising inflation overseas, strong growth in the euro area and ability of manufacturers to pass on higher costs

• Rapid money and credit growth

• Downward• Wary financial markets• Slowing US housing market

COUNCIL of MORTGAGELENDERS

12

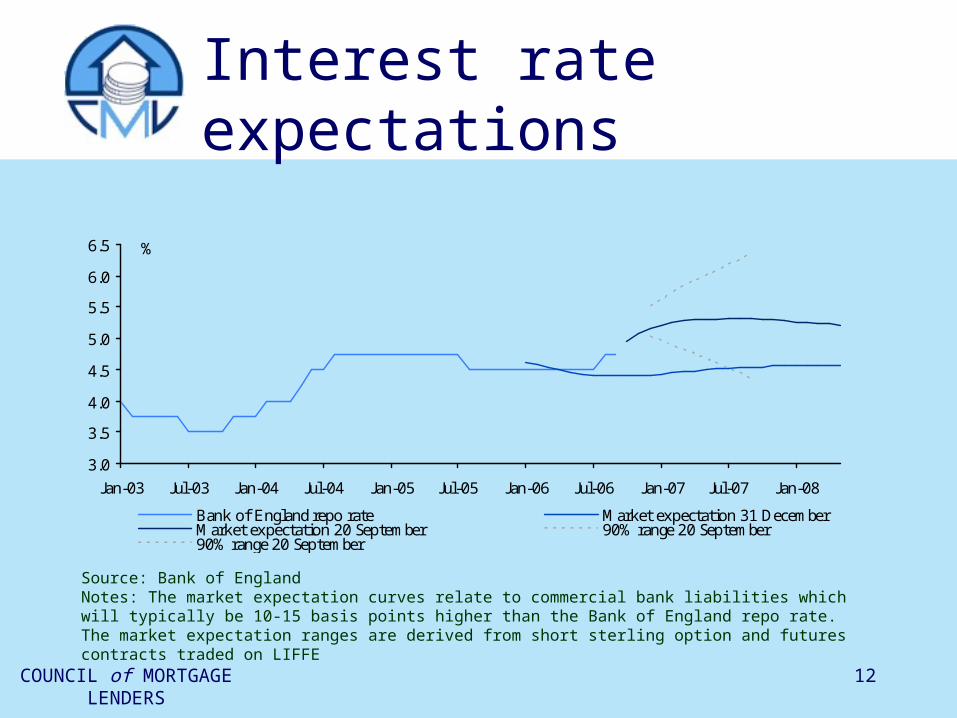

Interest rate expectations

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

Jan-03 Jul-03 Jan-04 Jul-04 Jan-05 Jul-05 Jan-06 Jul-06 Jan-07 Jul-07 Jan-08

%

Bank of England repo rate Market expectation 31 DecemberMarket expectation 20 September 90% range 20 September90% range 20 September

Source: Bank of EnglandNotes: The market expectation curves relate to commercial bank liabilities which will typically be 10-15 basis points higher than the Bank of England repo rate. The market expectation ranges are derived from short sterling option and futures contracts traded on LIFFE

COUNCIL of MORTGAGELENDERS

13

• International background

• UK economy and interest rates

• UK housing and mortgage markets

• Product, segment and channel

• Looking forward – issues and prospects

COUNCIL of MORTGAGELENDERS

14

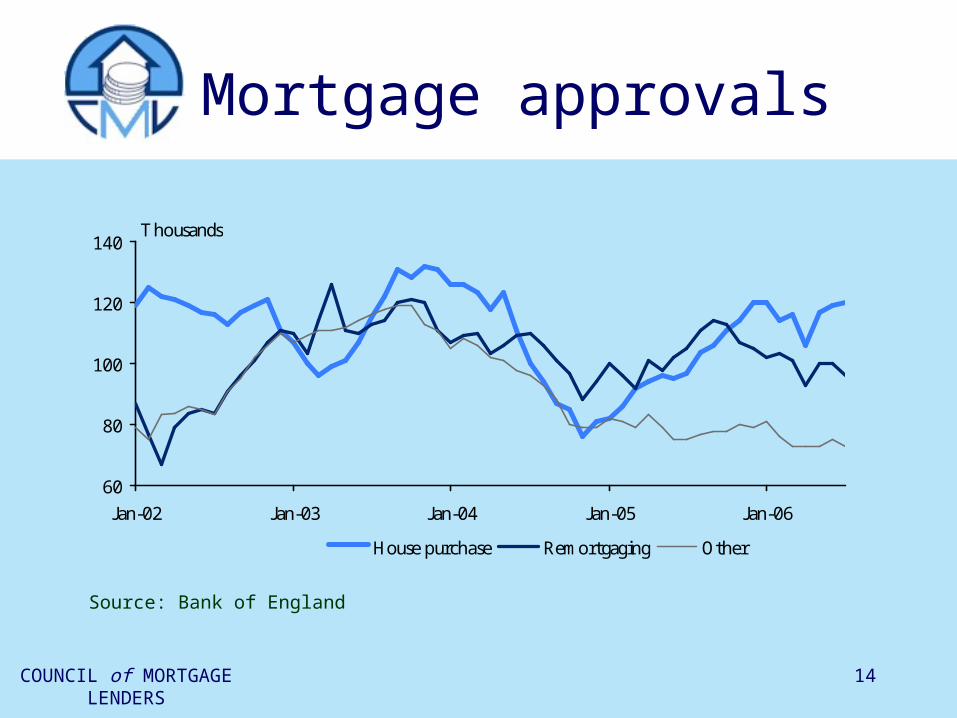

Mortgage approvals

Source: Bank of England

60

80

100

120

140

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06

Thousands

House purchase Remortgaging Other

COUNCIL of MORTGAGELENDERS

15

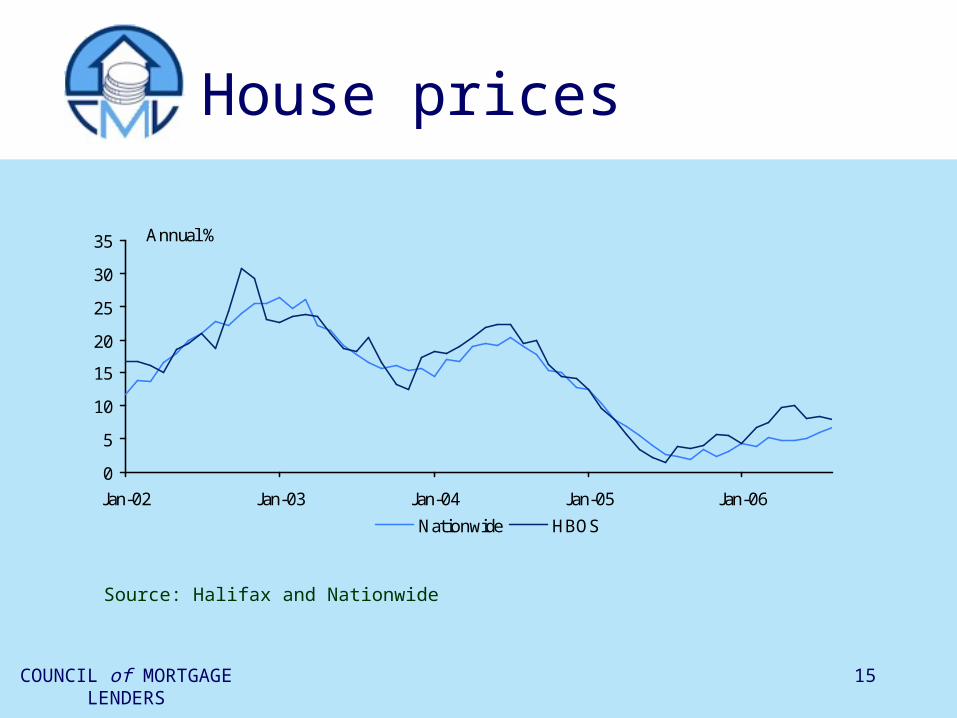

House prices

Source: Halifax and Nationwide

0

5

10

15

20

25

30

35

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06

Annual %

Nationwide HBOS

COUNCIL of MORTGAGELENDERS

16

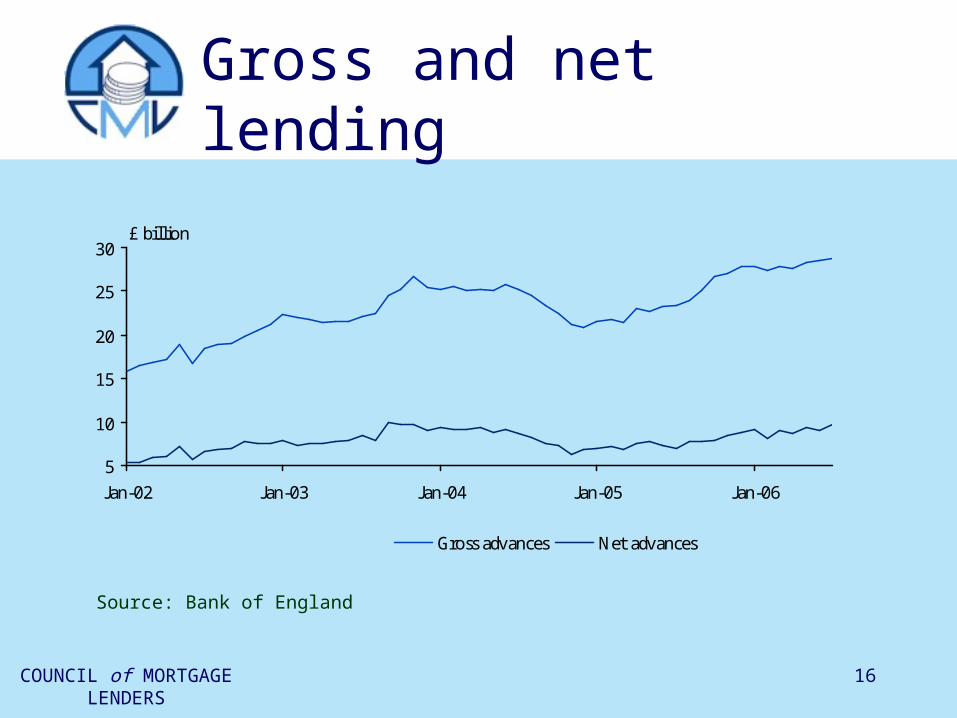

Gross and net lending

5

10

15

20

25

30

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06

£ billion

Gross advances Net advances

Source: Bank of England

COUNCIL of MORTGAGELENDERS

17

• International background

• UK economy and interest rates

• UK housing and mortgage markets

• Product, segment and channel• Looking forward – issues and prospects

COUNCIL of MORTGAGELENDERS

18

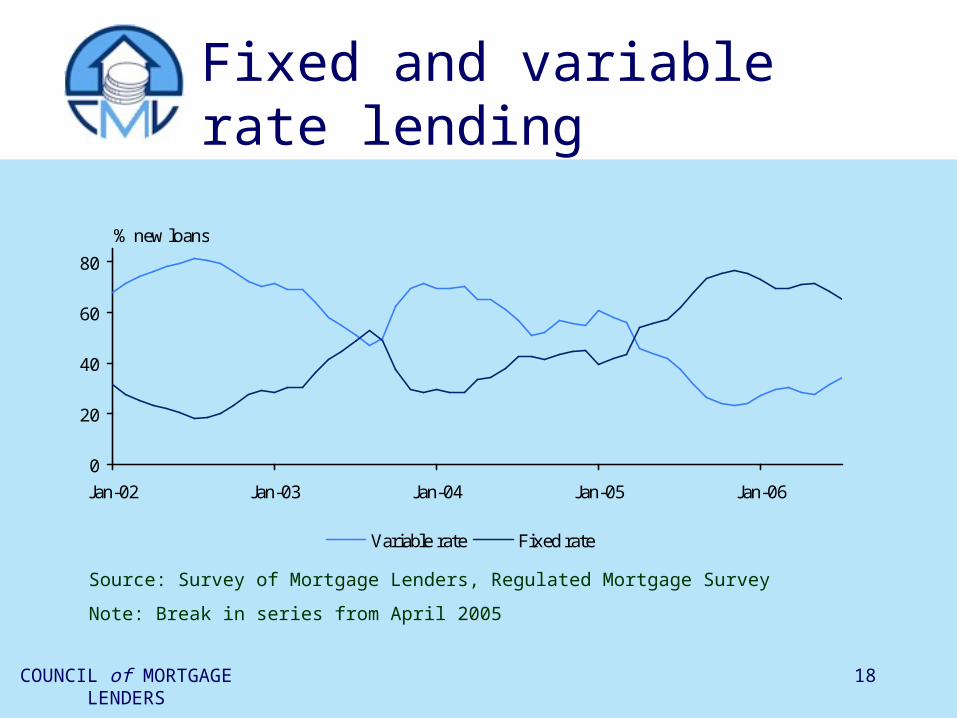

Fixed and variable rate lending

0

20

40

60

80

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06

% new loans

Variable rate Fixed rate

Source: Survey of Mortgage Lenders, Regulated Mortgage Survey

Note: Break in series from April 2005

COUNCIL of MORTGAGELENDERS

19

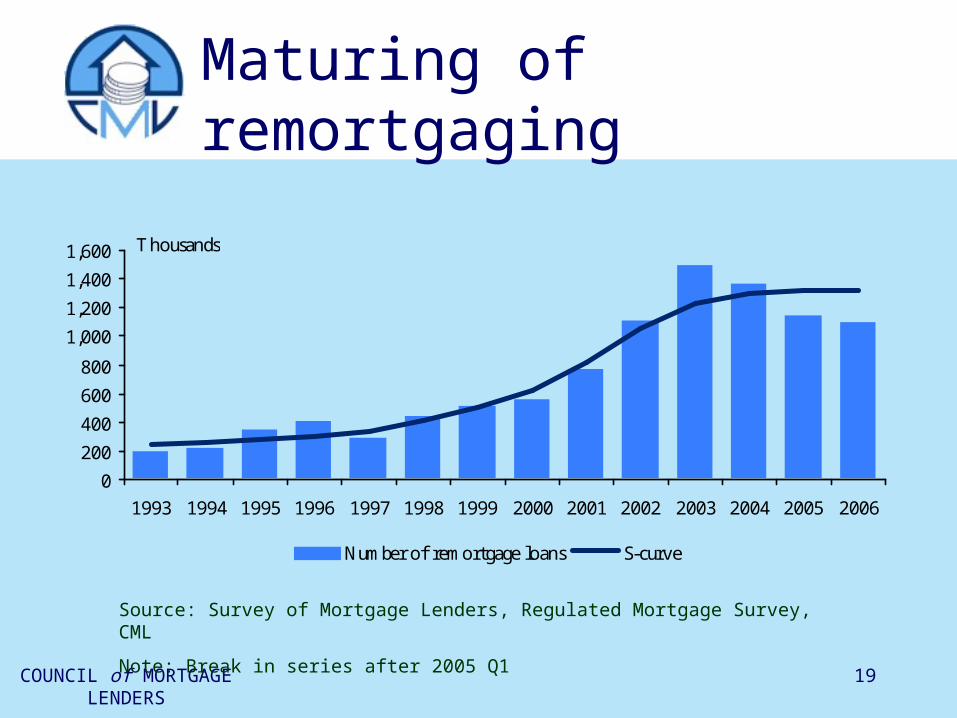

Maturing of remortgaging

0

200

400

600

800

1,000

1,200

1,400

1,600

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Thousands

Number of remortgage loans S-curve

Source: Survey of Mortgage Lenders, Regulated Mortgage Survey, CML

Note: Break in series after 2005 Q1

COUNCIL of MORTGAGELENDERS

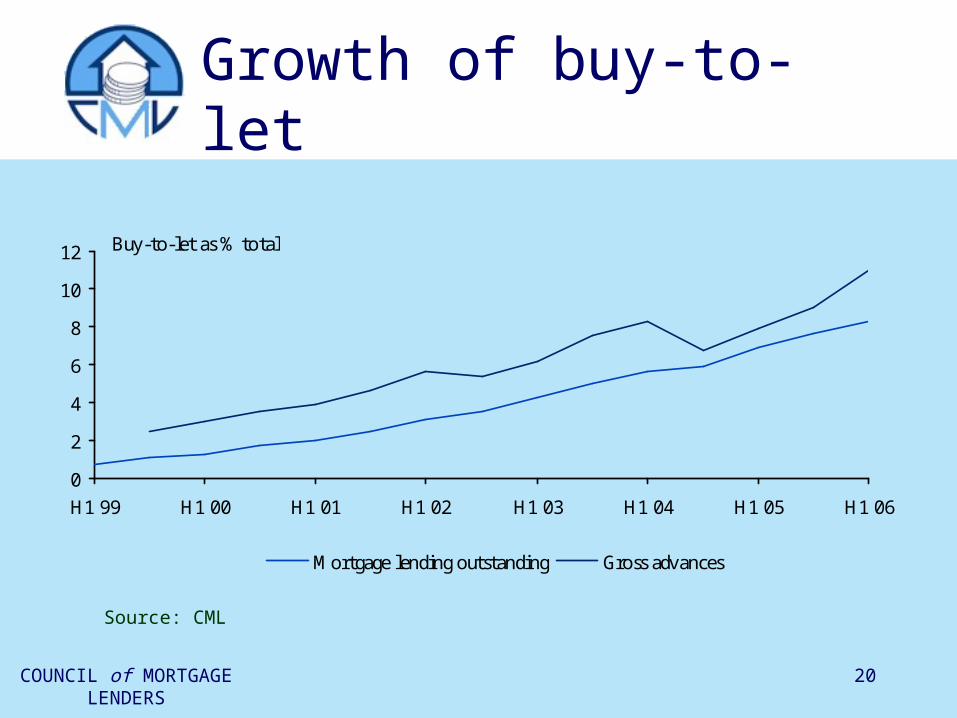

20

Growth of buy-to-let

0

2

4

6

8

10

12

H1 99 H1 00 H1 01 H1 02 H1 03 H1 04 H1 05 H1 06

Buy-to-let as % total

Mortgage lending outstanding Gross advances

Source: CML

COUNCIL of MORTGAGELENDERS

21

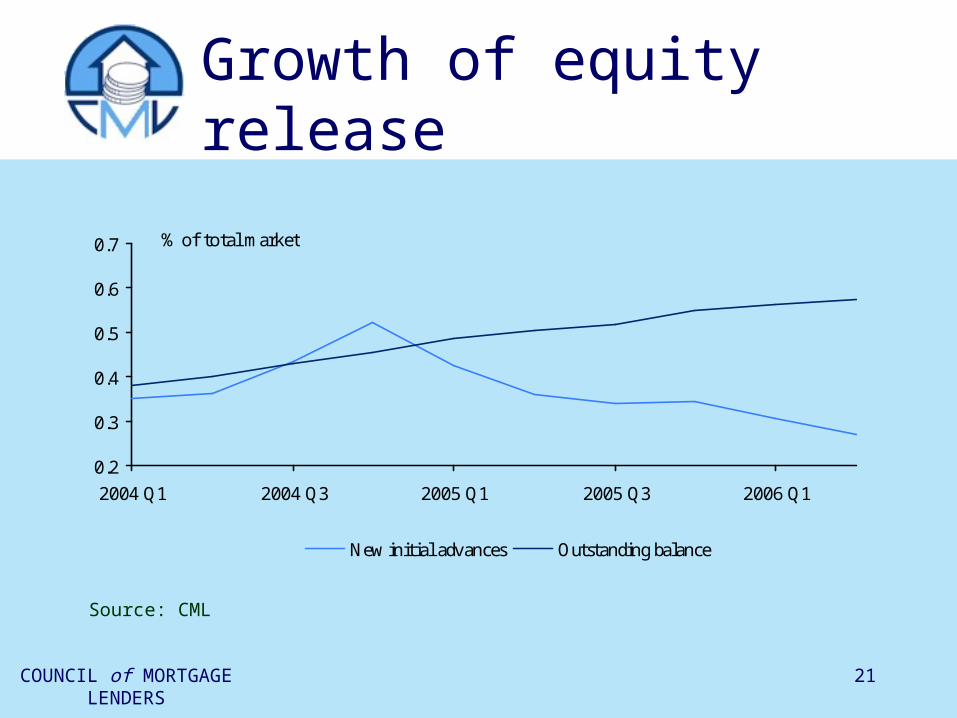

Growth of equity release

Source: CML

0.2

0.3

0.4

0.5

0.6

0.7

2004 Q1 2004 Q3 2005 Q1 2005 Q3 2006 Q1

% of total market

New initial advances Outstanding balance

COUNCIL of MORTGAGELENDERS

22

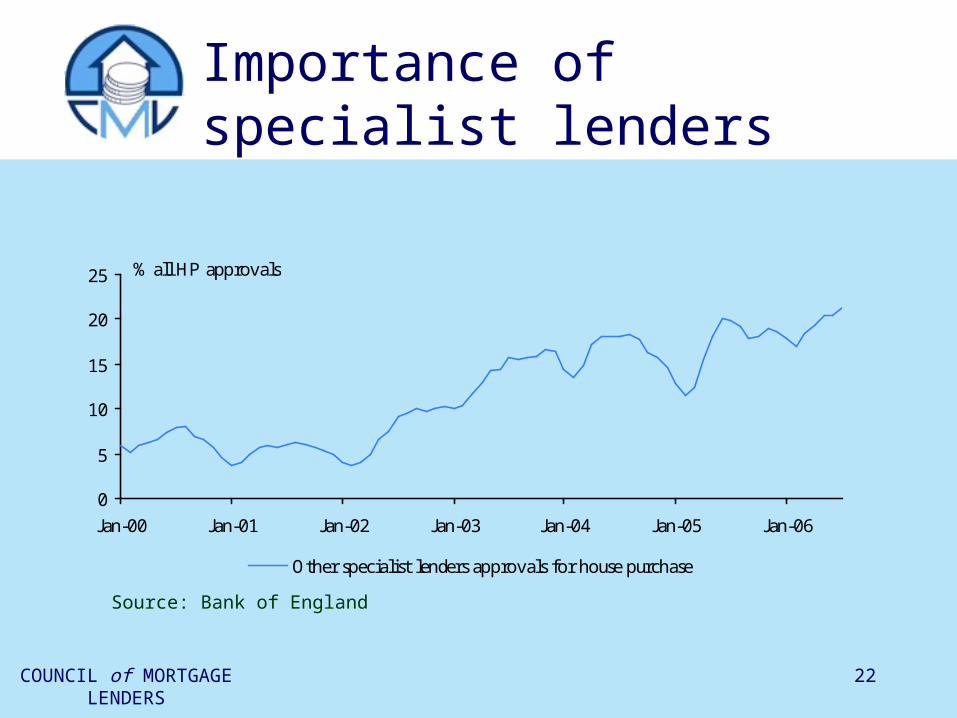

Importance of specialist lenders

0

5

10

15

20

25

Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06

% all HP approvals

Other specialist lenders approvals for house purchase

Source: Bank of England

COUNCIL of MORTGAGELENDERS

23

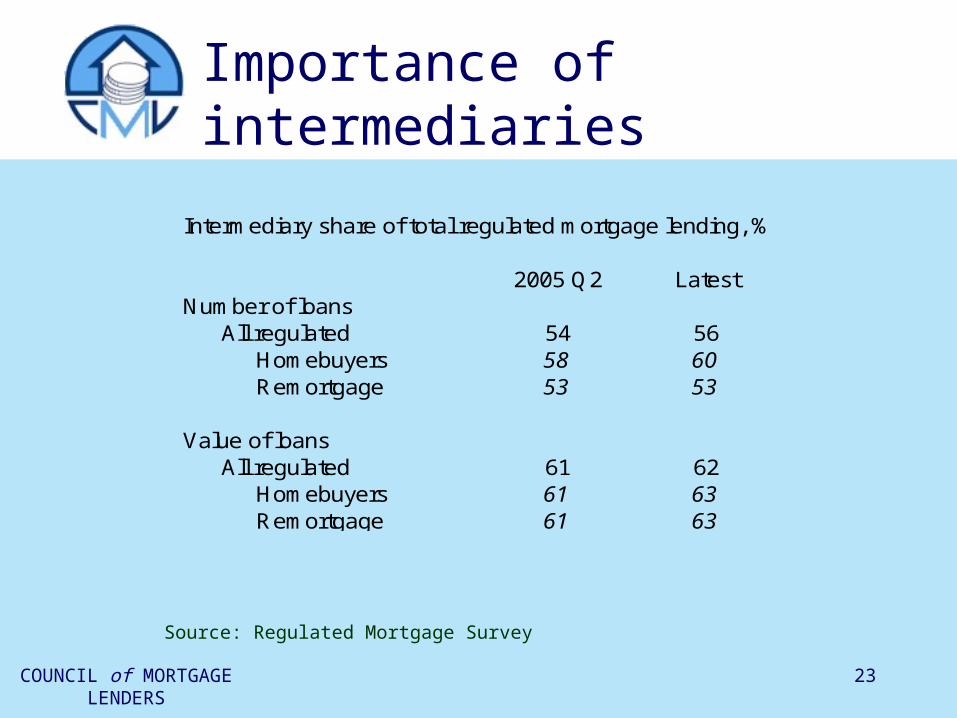

Importance of intermediaries

Source: Regulated Mortgage Survey

Intermediary share of total regulated mortgage lending, %

2005 Q2 LatestNumber of loans

All regulated 54 56Homebuyers 58 60Remortgage 53 53

Value of loansAll regulated 61 62

Homebuyers 61 63Remortgage 61 63

COUNCIL of MORTGAGELENDERS

24

• International background

• UK economy and interest rates

• UK housing and mortgage markets

• Product, segment and channel

• Looking forward – issues and prospects

COUNCIL of MORTGAGELENDERS

25

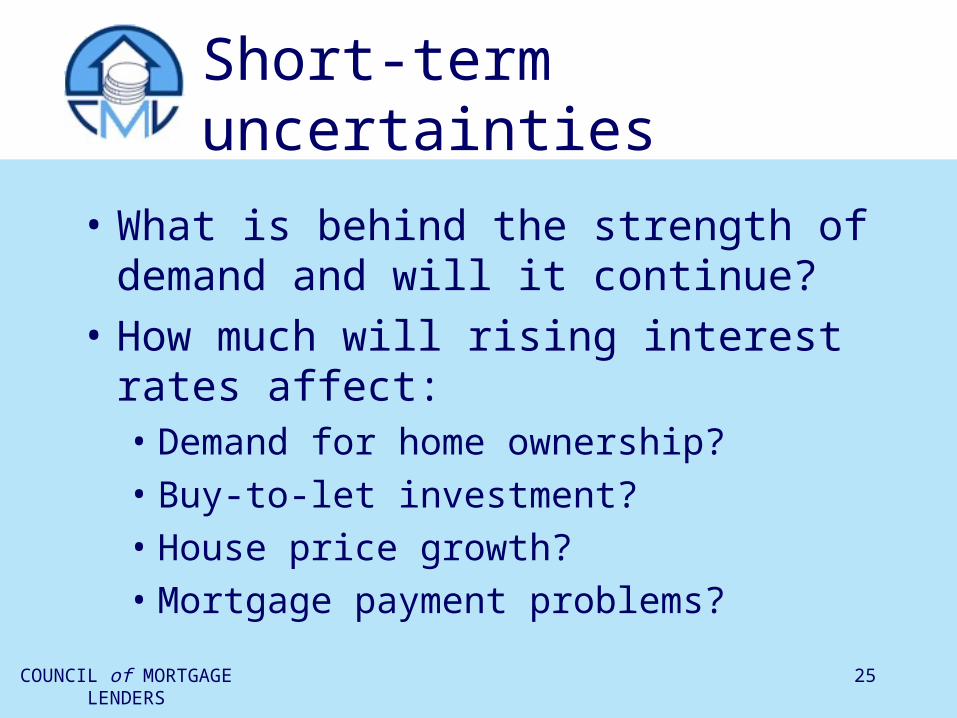

Short-term uncertainties

• What is behind the strength of demand and will it continue?

• How much will rising interest rates affect:• Demand for home ownership?• Buy-to-let investment?• House price growth?• Mortgage payment problems?

COUNCIL of MORTGAGELENDERS

26

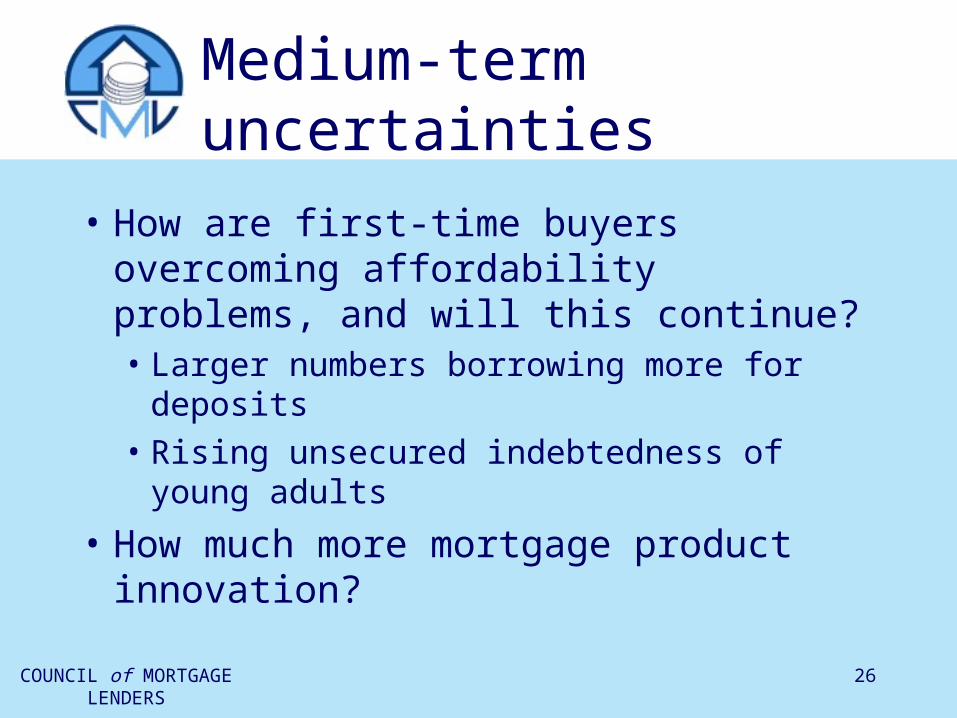

Medium-term uncertainties

• How are first-time buyers overcoming affordability problems, and will this continue?• Larger numbers borrowing more for deposits • Rising unsecured indebtedness of young adults

• How much more mortgage product innovation?

COUNCIL of MORTGAGELENDERS

27

Longer-term uncertainties

• Sustainable house price growth• Household formation and housing supply

• Magnitude and success of government affordable housing and shared equity initiatives

• Split of housing tenure

• Aging population and take up of equity release products

COUNCIL of MORTGAGELENDERS

28

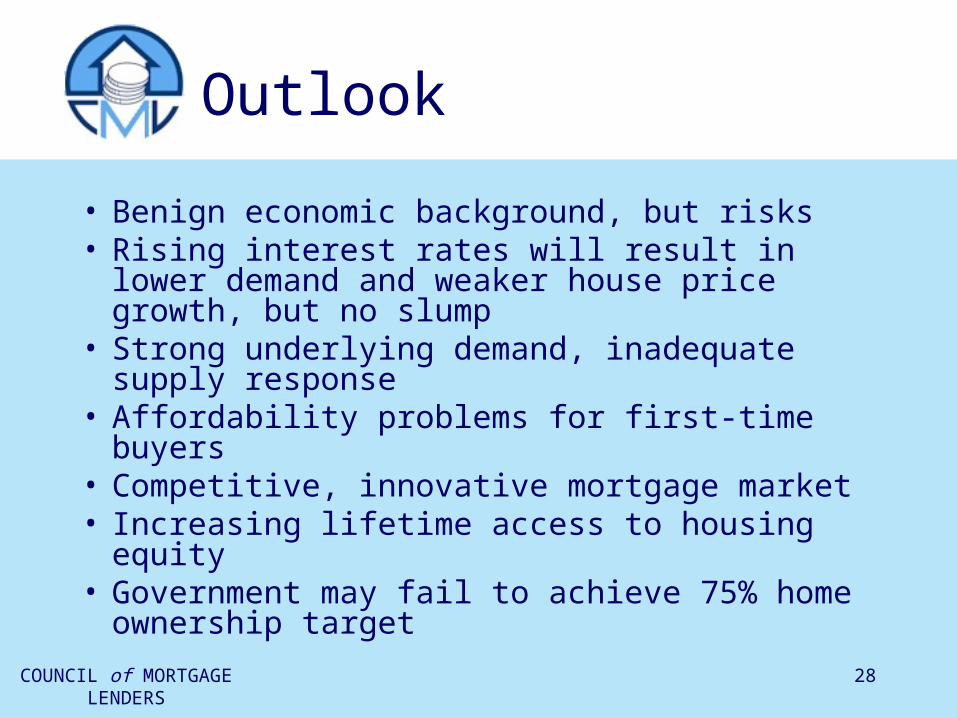

Outlook

• Benign economic background, but risks• Rising interest rates will result in lower demand

and weaker house price growth, but no slump• Strong underlying demand, inadequate supply

response• Affordability problems for first-time buyers• Competitive, innovative mortgage market• Increasing lifetime access to housing equity• Government may fail to achieve 75% home

ownership target