Embed Size (px)

Citation preview

R E A L K R E D I T R Å D E T

MMORTGAGE FINANCINGIN DENMARK

Introduction 1

The mortgage credit system 2

History of the mortgage credit system 2

Mortgage banks 4

Legislation and supervision 7

Solvency regulations 7

Placement regulations 7

Lending by mortgage banks 8

Raising of loans 8

Types of loan 9

Forward price contracts 10

Redemption and remortgaging 10

Loan costs 12

Lendig limits and maturities 12

Valuation and size of loan 13

The Danish title registation system

(land registration system) 14

Lending distributed by property category 15

Mortgage bonds 16

Funding of the mortgage banks 16

Bond types 16

Callability 17

Yields 18

A high degree of security 18

Rating 19

Characteristics of the Danish bond market 19

Publications of the Association of Danish Mortgage Banks 22

Glossary 23

Addresses of mortgage banks cover 3

Table of contents

In Denmark the financing of real pro-perty and other long-term fixed invest-ments primarily takes place via mort-gage banks. The Danish mortgage-credit market is based on the efficientand inexpensive extension of creditbased on the following characteristics:

• the borrower’s real property is mort-gaged as collateral for the loan;

• the loan is long-term;

• loans are granted within the frame-work of the Mortgage Credit Act;

• effective interest rates are market-determined and transparent;

• the loans are financed by the issueof bonds;

• bond investors are fully aware ofthe security for the bonds, which isbased on mortgages on real proper-ty, the legislative framework and thesolvency of the mortgage bank,

• in the 200-year history of mortgagecredit in Denmark no bond holdershave suffered losses due to thedefault of a mortgage bank.

This publication describes all importantelements of the Danish mortgage creditsystem. It is also available in Danish.Also available in English is “DanishMortgage Bonds” with more detailedinformation on Danish mortgagebonds. These publications and furtherinformation can be found at the Website of the Association of Danish Mortgage Banks at www.realkredit-raadet.dk or can be ordered from theAssociation of Danish Mortgage Banks,which is the trade organisation of themortgage-credit sector.

Torben Gjede

Director General

The Association of Danish Mortgage BanksNovember, 1999

1

Introduction

The mortgage banks have gained acentral position in the Danish eco-nomy thanks to their long-standingactivity as financial enterprises special-ising in the granting of long-term loansagainst mortgages on real property.

As a result of the mortgage bonds’important dual role as effective fundinginstrument and an attractive placementfor investors the bonds play a key rolein the Danish and international capitalmarkets. This position is based on thedevelopment and adjustment of themortgage credit system during its evolution over more than 200 years.

History of the mortgage credit system

The first mortgage bank in Denmarkwas established in 1797 under thename of Husejernes Kreditkasse iKøbenhavn. This was a result of theGreat Fire in Copenhagen in 1795when 900 properties were razed to theground and many others were damaged.The fire damage was assessed at 4.5million rix dollars of which only halfcould be covered by KøbenhavnsBrandforsikring, the only fire insurancecompany in Copenhagen. The Danishstate had to step in and participate inthe reconstruction of Copenhagen.

Husejernes Kreditkasse was the out-come of the investors’ initiative. Thebackground was the existence of aninterest rate regulation stipulating aninterest rate of 4 per cent as the maxi-mum. The investors considered securityto be the most important element inview of this interest ceiling and thesubstantial demand for loans. Securitywas excellent for loans granted byKreditkassen, since the borrowers weresubject to joint and several liability.

The first Mortgage Credit Act wasadopted in 1850 in order to enhanceaccess to private borrowing. In contrastto Husejernes Kreditkasse, mortgageassociations were associations of borrowers subject to joint and several

liability. These associations could grantloans for up to 60 per cent of the valueof a property.

However, the mortgage associationswere unable to meet the full demandfor loans, which led to the establish-ment of second mortgage institutionstowards the end of the 19th century.These institutions granted supplemen-tary loans, to bring total lending up to 75 per cent of the property value (second mortgages). However, super-vision of the second mortgage institu-tions was not established until 1936when an Act on Second Mortgage Institutions was adopted.

After World War II the mortgage associ-ations and second mortgage institutionspursued very restrictive lending policies.Demand arose for further organisedlending to finance the housing market.Against this background special mort-gage funds (granting third mortgages)were established in 1959. In contrast tomortgage associations and secondmortgage institutions the new funds didnot impose joint and several liability onthe borrowers.

The implementation of the MortgageCredit Act of June 1970 entailed somemajor adjustments. Lending ceilingswere lowered, repayment periods werereduced and restrictions were intro-duced on access to mortgage creditfinancing. The most important elementwas the introduction in Denmark of acomprehensive mortgage system, sothat borrowers did not have to raiseloans from several mortgage institu-tions. Moreover, the number of mort-gage associations and second mortgageinstitutions were reduced in order toprovide for nationwide mortgage institutions. The result was a wave of mergers. In 1972 only four mortgageassociations granted loans for residen-tial properties, of which Kreditforenin-gen Danmark (now Realkredit DanmarkA/S) and Byggeriets Realkreditfond(now BRFkredit a/s) were nationwide,while Jyllands Kreditforening and

2

The mortgage credit system

Forenede Kreditforeninger were regional (they merged in 1985 underthe name of Nykredit). There were alsospecial mortgage institutions for agri-culture and industry.

The following years saw frequentamendments to the Mortgage CreditAct. The next major comprehensiveamendment took place in 1989, among other things to comply with a number of obligations regarding the implementation of EC directives,including the 2nd Banking Harmoni-sation Directive of 1989 on the takingup and pursuit of the business of credit institutions. The Act provided for the establishment of new mortgagebanks as limited liability companies,while existing mortgage institutionscould be restructured as limited liabilitycompanies. As a consequence of this Act all mortgage institutions irrespective of organisation form arenamed mortgage banks. Today, mostmortgage banks are limited liabilitycompanies.

The most recent extensive amendmentof the Mortgage Credit Act took placein 1998. Among other things it simpli-fied lending provisions, while the previous special privilege for DanskLandbrugs Realkreditfond to mortgageagricultural properties within the rangeof 45-70 per cent of the property valuelapsed. The current regulatory require-ments of mortgage banks are describedin further detail in “Mortgage banks”and “Lending by mortgage banks”.

3

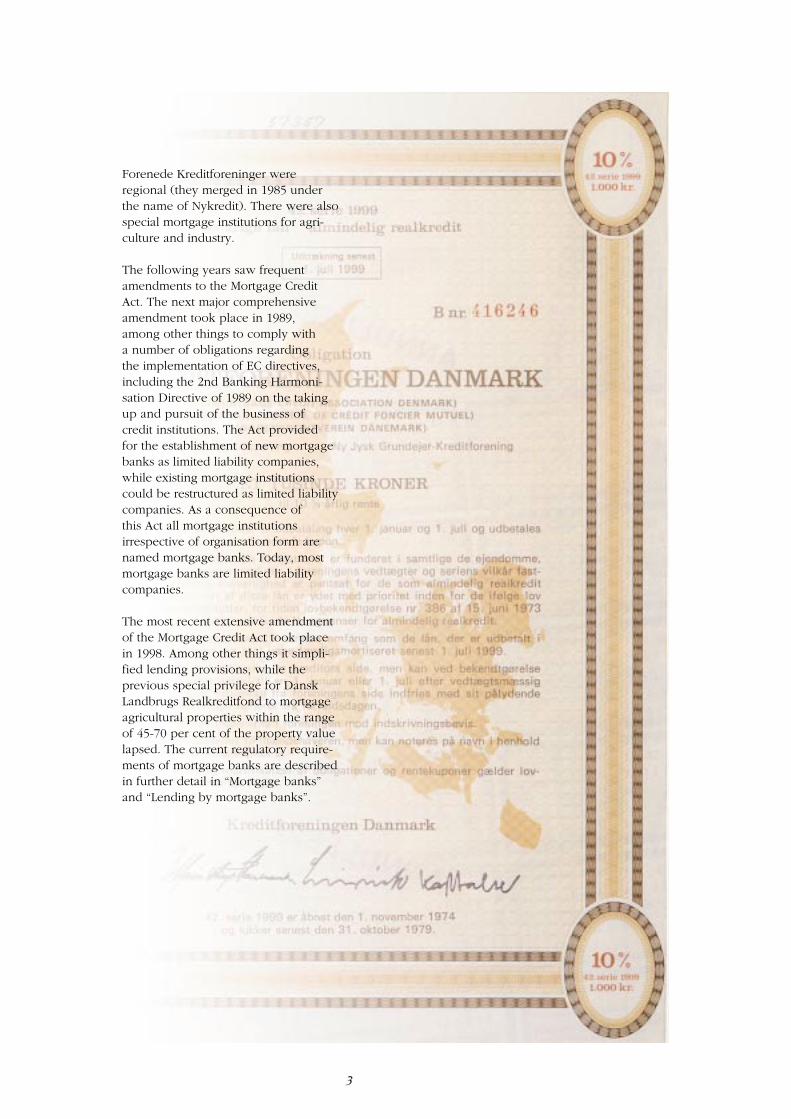

There are currently 10 mortgage banks in Denmark:

BG Kredit A/SBRFkredit a/sDansk Landbrugs Realkreditfond (DLR)Danske Kredit RealkreditaktieselskabFIH Realkredit A/SLandsbankernes Reallånefond (LRF)Nykredit A/SRealkredit Danmark A/STOTALKREDIT RealkreditfondUnikredit Realkreditaktieselskab

BG Kredit was established in 1998 bythe mortgage bank Realkredit Danmarkand the commercial bank BG Bank A/S.As an independent mortgage bank BGKredit grants loans for owneroccupiedhomes, including weekend cottages.The loans are based on bonds issued byRealkredit Danmark.

BRFkredit was previously a self-gov-erning institution whose original capitalbase was provided by financial institu-tions, business organisations and Dan-marks Nationalbank. Nykredit andRealkredit Danmark were originallyassociations of borrowers whereby thecapital base comprised contributionsfrom the borrowers. Both mortgagebanks are the result of mergers withother institutions over the years.

Today, these three mortgage banks arelimited liability companies. As part of the restructuring the original institutionsbecame foundations or associationswhose capital consists of shares in alimited liability company conductingmortgage credit activities.

Nykredit and Realkredit Danmark grantloans for all categories of property,whereas BRFkredit’s lending is primarilyfor owner-occupied homes, residentialrental properties and office and com-mercial properties.

Dansk Landbrugs Realkredit-fondis an independent institution (founda-tion) established in 1960. In addition toits own funds the capital base consists

4

Mortgage banks

of guarantees from commercial banks.Dansk Landbrugs Realkreditfond is a specialised mortgage bank which exclusively grants loans to finance agri-cultural, horticultural, forestry and otherproperties.

FIH Realkredit, established in 1995, is a limited liability company owned byFinansieringsinstituttet for Industri ogHåndværk (FIH). FIH Realkredit specia-lises in mortgage loans for trade andindustrial properties.

TOTALKREDIT Realkreditfond andLandsbankernes Reallånefond areindependent institutions (foundations).Both were founded in 1959. TOTAL-KREDIT was established under thename of Provinsbankernes Realkredit-fond. In 1971 the institutions stoppednew lending activities and in 1990Provinsbankernes Realkreditfond wasreopened under the name of TOTAL-KREDIT. This mortgage bank grantsloans for owner-occupied homes, week-end cottages and undeveloped sites. Atthe beginning of 1994 Landsbankernes

Reallånefond was reopened. It grantsloans primarily for major constructionprojects, mainly subsidised public construction. The capital base of bothmortgage banks besides own fundscomprises guarantees provided by commercial banks.

The mortgage banks founded as limitedliability companies, Danske Kredit andUnikredit, were both established in1993. They are wholly-owned byrespectively Den Danske Bank and Uni-bank - Denmark’s two largest commer-cial banks. Unikredit’s lending is primarily for owner-occupied homesand agricultural properties, whileDanske Kredit focuses on owner-occu-pied homes and commercial properties.

All 10 mortgage banks are members of the Association of Danish MortgageBanks, which is the trade organisationestablished for the mortgage credit sector.

Table 1 shows key figures for the lend-ing activities of the mortgage banks.

5

DKK. billion BG BRF- DLR Danske FIH LRF Nykredit Realkredit Total Uni- TotalKredit Kredit Kredit Realkredit Danmark Kredit kredit

1)

Gross lending

1998 5.2 35.6 12.4 31.7 1.7 0.5 119.7 81.9 31.2 41.1 359.01997 - 22.7 7.1 18.1 1.1 0.2 81.9 65.4 17.1 26.3 239.8

Bonds incirculation,end of period

1998 - 124.5 42.2 64.7 3.0 1.2 389.8 338.5 59.5 74.5 1,098.01997 - 120.4 40.7 51.0 1.9 0.9 380.6 321.5 44.5 55.2 1,016.9

Liable capital,

end of period 2)

1998 1.5 7.7 4.8 3.3 0.3 2.9 30.3 19.6 2.6 4.4 77.41997 - 7.3 4.4 2.6 0.3 2.8 29.0 21.5 2.2 3.3 73.4

Solvency ratio

3) 4) 5)

1998 56.6 12.9 12.8 10.6 14.6 263.6 13.5 11.5 10.8 11.8 13.11997 - 12.4 12.4 10.8 24.9 311.1 13.4 13.2 11.0 12.2 13.5

Source: The Association of Danish Mortgage of Banks.1) BG Kredit commenced its lending activities in 1998, financed via bonds issued by Realkredit

Danmark.2) Including guarantee capital.3) The solvency ratio is compiled as liable capital as a proportion of risk-weighted assets. 4) Proportion of capital base for issued bonds and other commitments of DLR. The statutory

requirement is at least 10 per cent.5) Average solvency ratio, excluding DLR.

Table 1. Key figures for mortgage banks

6

Legislation and supervision

Mortgage credit activities are governedby the Mortgage Credit Act. The Actdefines mortgage credit activities as thegranting of loans against registeredmortgages on real property from capitalobtained by issuing bonds equivalentto the loans.

The current Mortgage Credit Act andthe executive orders issued pursuant tothe Act provide a detailed regulatoryframework for the activities of themortgage banks. The principal concernbehind these regulations is the securityof the bonds.

Under the Mortgage Credit Act themortgage banks are subject to super-vision by the Danish Financial Super-visory Authority which is an indepen-dent agency under the Ministry of Economic Affairs. The Financial Supervisory Authority also supervisese.g. commercial banks and insurancecompanies. Dansk Landbrugs Real-kreditfond is subject to special legisla-tion and thereby separate supervisionby the Development Directorate underthe Ministry of Food, Agriculture andFisheries.

The principal activity of the FinancialSupervisory Authority vis-à-vis themortgage banks is to safeguard the prudent pursuit of mortgage creditactivities, thereby ensuring that themortgage banks do not put their finan-cial soundness at jeopardy.

It is therefore the task of the FinancialSupervisory Authority to monitor com-pliance with the provisions of the Mortgage Credit Act and the appurte-nant executive orders. This applies inparticular to the provisions concerningvaluation and the size of loans, capitalrequirements and the balance principle,as well as the placement of own funds.The balance principle is described infurther detail in “Mortgage bonds”.

The Financial Supervisory Authoritymay order the rectification of any cir-

cumstances which are in conflict withthe provisions of the Act and executiveorders drawn up pursuant to the Act.Moreover, the infringement of a num-ber of provisions is a criminal offence.

Solvency regulations

All Danish mortgage banks except DLRare subject to the EU directives on sol-vency ratio, capital adequacy and ownfunds. These directives are implemen-ted in the Mortgage Credit Act.

Under the Mortgage Credit Act theliable capital of a mortgage bank mustbe at least 8 per cent of the mortgagebank’s risk-weighted assets, etc. Variouscapital elements are applied to com-pliance with the capital requirement,basically core capital and supplemen-tary capital.

The capital requirement for a mortgagebank is calculated on the basis of aweighting of the bank’s assets and off-balance-sheet items, based on the credit risk associated with each asset.

Loans against mortgages on owner-occupied homes are weighted at 50 per cent since such loans are assumedto be twice as safe as other loans.Loans for trade and industrial proper-ties and for agricultural properties areweighted at 100 per cent, while untilJanuary 1, 2006 the weighting of loansfor office and commercial properties is50 per cent, subject to certain assump-tions.

Placement regulations

The Mortgage Credit Act sets out rulesfor the mortgage banks’ placement oftheir own funds. The capital must as aminimum be invested in stockexchange listed bonds at a marketvalue equivalent to 60 per cent of themortgage bank’s liable capital.

No rules apply to the investment of theremaining 40 per cent. These funds arenormally invested in own bonds, govern-ment bonds, real property and shares.

7

Raising of loans

Mortgage loans are raised in variousways according to type, i.e. loans fornew construction, loans for purchase of an existing property, loans for otherpurposes, or loans for remortgaging(refinancing).

The ongoing costs of new constructionof real property during the constructionphase will as a general rule be financedby a building loan from a commercialbank. The final financing after comple-tion and inauguration of the buildingwill be arranged via a mortgage bank.

Loans raised in connection with pur-chase of an existing property are oftenarranged via the real estate agent whohandles the sale. Borrowers can ap-proach the mortgage bank or an inter-mediary typically a commercial bank,directly with regard to loans for otherpurposes. Concerning mortgage bankswhich are subsidiaries of commercialbanks or commercial bank affiliates theborrower must always contact a com-mercial bank to apply for a mortgageloan.

The inspection and valuation of theproperty prior to the submission of theloan offer are the basis for calculationof the lending value. The mortgagebanks may undertake inspection andvaluation themselves or commissionexternal parties (usually real estateagents or commercial banks) to do thisaccording to the mortgage bank’sguidelines. However, this applies onlyif the lending value is less than DKK2.5 million. Valuation of real property isdescribed in further detail below in“Valuation and size of loan”.

The mortgage bank will prepare a loanoffer on the basis of the valuation ofthe property and the borrower’s needsand requirements and financial situa-tion. The offer is then submitted to theborrower or the intermediary (normallythe real estate agent or a commercialbank). The offer sets out certain condi-

8

Lending by mortgage banks

tions to be fulfilled before the loan canbe disbursed. For example, onerequirement is documentation of a fireinsurance policy for the property.

If the borrower decides to accept theoffer the mortgage bank’s mortgage onthe borrower’s property must be registered. The Danish title registrationsystem is described in further detailbelow. The borrower may enter into a registration agreement with the mort-gage bank to handle the registration.

Once a mortgage deed has been regis-tered without endorsements in connec-tion with the registration and otherconditions of the offer have been ful-filled, the loan may be disbursed.

If the loan is required to be disbursedbefore the conclusion of the registra-tion procedure the borrower must pro-vide a commercial bank guarantee thatthe mortgage deed will be registeredwithout endorsements in connectionwith the registration and that any con-ditions set out in the offer can be ful-filled.

Types of loan

Mortgage loans can be either bondloans or cash loans, including variationsof cash loans on variable interest termsand index-linked loans.

With regard to bond loans the principalcorresponds to the volume of bondswhich the mortgage bank sells in orderto finance its lending. The repaymentprofile of the bond loan is thus fixedwhen the loan offer is made, whereasthe borrower does not know the priceof the bonds or the loan proceeds untilthe time of disbursement of the loan.

On the other hand, a characteristic feature of cash loans is that the prin-cipal matches the market value of theissued bonds. The loan proceeds arethus known to the borrower. On theother hand, the rate of interest on theloan, and thus the instalments, are notknown until the bonds are sold. The

capital loss arising on the sale of thebonds is converted into tax-deductibleinterest, giving the borrower a highertax deduction than if a bond loan hadbeen raised. On the other hand, in certain cases private individuals areliable to tax on any capital gains inconnection with extraordinary redemp-tion of the loan, cf. “Redemption andremortgaging” below. Business enter-prises are generally subject to capitalgains tax.

The uncertainty concerning the pro-ceeds from bond loans and the instal-ments on cash loans can be avoidedvia forward price contracts, cf. below.

Bond loans and cash loans can begranted as annuity loans, serial loansor bullet loans, i.e. with varying repay-ment profiles.

Annuity loans are the most frequentlyused. Repayments are identicalthroughout the lifetime of the loan. The interest element of the repaymentdecreases while the instalment elementincreases. For a serial loan the borrow-er makes equal instalments during thelifetime of the loan, so that in contrastto annuity loans the repayments de-crease. No repayments are made on abullet loan during its lifetime, i.e. onlyinterest and administration fee are paidon the principal and the principal fallsdue for full repayment on expiry of theloan. Bullet loans are granted primarilyin connection with mortgaging of com-mercial properties and are not appli-cable to owner-occupied homes.

By tradition, mortgage credit has beenprovided at a fixed interest rate for thelifetime of the loan, but the mortgagebanks also offer loans subject to regularinterest-rate adjustment. The rate ofinterest for this type of loan is adjustedto the market rate after a predeter-mined number of years as chosen bythe borrower. The borrower’s optionsare variable-interest loans with a fixedor variable maturity, or loans with partial interest-rate adjustment of theprincipal.

9

Several mortgage banks also offer eurodenominated loans at lower interestrates than for krone-denominatedloans, although a loan raised in eurowill entail a limited element of risk dueto exchange-rate fluctuation.

Another type of loan is index-linkedloans which are subject to ongoingprice-index adjustment of the outstand-ing principal and the repayments forthe duration of the loan. These loansare on the other hand characterized bya relatively low rate of interest. Up toJanuary 1, 1999 issue of these loanswas subject to a number of restrictionsin that index-linked loans were to agreat extent mandatory for new construction and subsidised public construction, for which they were pri-marily used. The restrictions were associated with the tax benefit relatedto pension savings placed in index-linked bonds, which had a positiveeffect on the bond prices. This tax benefit was eliminated for bonds issuedafter January 1, 1999 when the previousmandatory financing of subsidised public construction with index-linkedloans was discontinued. After January1, 1999 issuance of index-linked loanshas been very moderate.

Forward price contracts

The proceeds from a bond loan andthe repayments/interest payments on acash loan depend on the price of thebonds as on the date of disbursement.As a result the borrower will be uncer-tain of the financial consequences during the period from the mortgagebank’s loan offer until the date of disbursement.

The borrower can eliminate this uncer-tainty by entering into a forward pricecontract as a fixed-price contract withthe mortgage bank or a price contractwith a commercial bank. The period of financial uncertainty can also bereduced if the loan is disbursed againsta commercial bank guarantee before amortgage deed without endorsementsin connection with the registration hasbeen registered.

In a forward price contract the settle-ment price of the loan is fixed at thecurrent stock exchange price less asmall discount. This discount is deter-mined by the current bond market conditions and the length of the perioduntil the loan is disbursed.

If the borrower does not enter into aforward price contract or have the loanpaid out against a commercial bankguarantee the borrower may realise acapital gain on the bond market or riskmaking a capital loss if the price of thebonds drops during the period fromacceptance by the borrower until theissue of the bonds. A forward pricecontract may be entered into at anytime up to the disbursement of the loan.

Fixed-price contracts/price contractsmay be concluded for loans to beraised as well as for bonds to be usedto redeem an existing loan, e.g. onremortgaging to a new mortgage loan.

Redemption and remort-gaging (refinancing)

If the borrower fulfils all obligations tothe mortgage bank a mortgage loanmay not be terminated by the mortgagebank during the lifetime of the loan.

The borrower, on the other hand, hasthe option to redeem the loan at anytime, i.e. full or partial redemption ofthe loan before it matures. This may beoutright redemption or redemption inconnection with remortgaging of theloan whereby the borrower redeemsthe existing loan and at the same timeraises a new loan to replace it.

Mortgage banks usually offer severalredemption methods, depending onwhether the loans to be redeemed arebased on callable or non-callable.

Non-callable loans may be redeemedsolely with bonds of the same kind(series, section and nominal interest) asthe bonds which were the basis for disbursement of the original loan. Variable-interest loans and index-linkedloans are non-callable.

10

Callable loans - i.e. most of the existingmortgage loans - may be redeemedwith bonds, but the borrower also hasthe right to redeem the loan for anamount equivalent to the outstandingbond debt at par value. The callable

loans may be redeemed at par eitherby terminating the loan as of an ordi-nary settlement date or as immediateredemption.

The period of notice for termination as of an ordinary settlement date is typically two or five months before the following settlement date (creditor settlement dates are normally January1, April 1, July 1 and October 1),depending on whether the loan hasquarterly or binannual settlement dates. The factor determining thechoice of redemption as of an ordinarysettlement date or redemption withbonds is whether the price of thebonds associated with the loan to beredeemed is above or below par. In the latter case redemption with bondsmay be most advantageous.

Immediate redemption is used primarilyin connection with remortgaging of amortgage loan. The existing loan isredeemed at par and the new loan isdisbursed immediately. However, theborrower must provide a commercialbank guarantee to the mortgage bankto the effect that the new loan can beregistered, which is the condition setby the mortgage bank. In the case ofimmediate redemption the borrowerthus does not have to wait to redeemthe loan until the next settlement date.On the other hand, the borrower must

pay the mortgage bank interest for theperiod from the date of redemption until the date (ordinary settlement date) as of which the loan could have beenredeemed. The interest is calculated asthe difference between the interest

payable by the mortgage bank to thebond holders and the rate of compen-sation interest the mortage bank canoffer on the redemption amount duringthe period from the redemption dateup to the settlement date for termina-tion.

Cash loans are subject to special rulesfor early redemption of existing loanssince private individuals are liable totax on certain capital gains (if theredemption amount is lower than theoutstanding cash debt on the date ofredemption). Cash loans can thus beremortgaged to a lower bond interestwithout tax consequences, whileremortgaging to a higher bond interestwill in principle entail a tax on theresulting capital gain. In the event ofchange of ownership, divorce or deathcash loans can usually be redeemedwithout tax liability on any capital gain.This special rule applying to cash loansshould be viewed against the back-ground that the capital loss when theloan is raised is remortgaged to tax-deductible interest expenditure.

Private individuals are not liable to taxon capital gains on bond loans raisedin connection with early redemption.

Business enterprises are subject to ageneral capital gains tax on both loancategories.

11

Loan costs

Apart from interest to the bond holdersthe borrowers must also pay a risk andadministration fee to the mortgagebank. The fee covers administrationcosts, losses, tax payments and a contribution to reserves. The fee ischarged on every settlement date forthe full term of the loan and is relati-vely low compared to the loan amount,often between 0.5 and 1 per cent ofthe outstanding debt. The fee dependson the category of property, the secu-rity ranking of the loan and its size andmaturity.

In addition, a one-off establishment feeis charged for the loan, typically 1 percent of the principal. However, thisdoes not apply to loans for owner-occupied homes. The mortgage banksalso charge loan fees and fees for spe-cific services, e.g. a title registration service, debt transfer, early redemptionand property valuation. Mortgage loansare also subject to title registration duty.

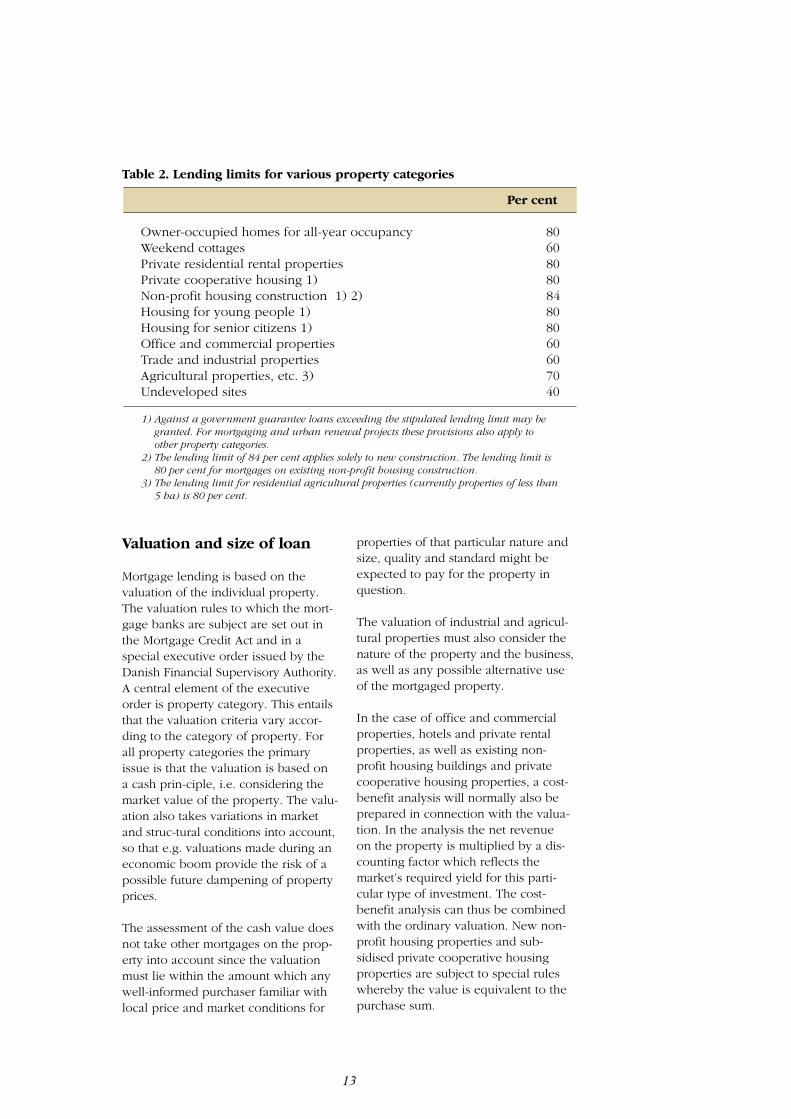

Lending limits and maturities

The following is an overview of thelending limits for various property categories. For each category the maximum lending limit is stated as apercentage of the property value.

In principle, there are no rules gover-ning which categories of loan may beused to finance the various propertycategories. However, loans for owner-occupied homes, including weekendcottages, may not be amortized moreslowly than a 30-year annuity loan.Subsidised public construction is sub-ject to special rules. The loan categoryto be used to finance the subsidisedconstruction is thus determined by theMinister for Building and Housing forone year at a time, but with the optionof rapid adjustment in the event of ashift in market conditions. The Mini-ster’s decision is published in the Dan-ish Statstidende.

The maximum term of mortgage loansis 30 years, except loans to establishnon-profit housing construction forwhich the maximum term laid down inthe Mortgage Credit Act is 35 years.However, the Ministry of Building andHousing has proposed a type of loanfor financing of subsidised constructionwith a term of 30 years.

12

Valuation and size of loan

Mortgage lending is based on the valuation of the individual property.The valuation rules to which the mort-gage banks are subject are set out inthe Mortgage Credit Act and in a special executive order issued by theDanish Financial Supervisory Authority.A central element of the executiveorder is property category. This entailsthat the valuation criteria vary accor-ding to the category of property. For all property categories the primaryissue is that the valuation is based on a cash prin-ciple, i.e. considering themarket value of the property. The valu-ation also takes variations in marketand struc-tural conditions into account,so that e.g. valuations made during aneconomic boom provide the risk of a possible future dampening of propertyprices.

The assessment of the cash value doesnot take other mortgages on the prop-erty into account since the valuationmust lie within the amount which anywell-informed purchaser familiar withlocal price and market conditions for

properties of that particular nature andsize, quality and standard might be expected to pay for the property inquestion.

The valuation of industrial and agricul-tural properties must also consider thenature of the property and the business,as well as any possible alternative useof the mortgaged property.

In the case of office and commercialproperties, hotels and private rentalproperties, as well as existing non-profit housing buildings and privatecooperative housing properties, a cost-benefit analysis will normally also beprepared in connection with the valua-tion. In the analysis the net revenue on the property is multiplied by a dis-counting factor which reflects the market’s required yield for this parti-cular type of investment. The cost-benefit analysis can thus be combinedwith the ordinary valuation. New non-profit housing properties and sub-sidised private cooperative housingproperties are subject to special ruleswhereby the value is equivalent to thepurchase sum.

13

Per cent

Owner-occupied homes for all-year occupancy 80Weekend cottages 60Private residential rental properties 80Private cooperative housing 1) 80Non-profit housing construction 1) 2) 84 Housing for young people 1) 80Housing for senior citizens 1) 80Office and commercial properties 60Trade and industrial properties 60Agricultural properties, etc. 3) 70Undeveloped sites 40

1) Against a government guarantee loans exceeding the stipulated lending limit may begranted. For mortgaging and urban renewal projects these provisions also apply toother property categories.

2) The lending limit of 84 per cent applies solely to new construction. The lending limit is80 per cent for mortgages on existing non-profit housing construction.

3) The lending limit for residential agricultural properties (currently properties of less than5 ha) is 80 per cent.

Table 2. Lending limits for various property categories

Where in the mortgage bank’s organi-zation the valuation function is placedvaries. In respect of owner-occupiedhomes some mortgage banks undertakeall valuations themselves via local andregional offices and only resort to exter-nal assistance from e.g. real estateagents in the event of peak loads. Othermortgage banks almost exclusively usereal estate agents or partner banks forthe valuation of private homes. Randomtests and valuations for properties witha lending value exceeding DKK 2.5 million are always undertaken by themortgage banks’ own officers. The valuation of other properties thanowner-occupied homes is also alwaysperformed by the mortgage banks’ ownstaff, either from district or regionaloffices or from the head office.

The Danish title registration system (land registration system)

A prerequisite for the effectiveness ofthe Danish mortgage credit system isthe protection of the mortgage banks’mortgage right on the borrower’s realproperty, which is the basis for thesecurity provided for the bonds. Themortgage right must thus be protectedagainst other parties with whom theborrower contracts to mortgage the realproperty, and against the borrower’screditors under legal proceedings. Thisprotection, which safeguards the rank-ing of the mortgage bank’s mortgage on the borrower’s real property, ensuresoptimum cover for the mortgage bankin the event of enforced sale of the borrower’s real property. Enforced salewill take place only in the event ofdefault by the borrower. Protection ofthe mortgage right is achieved via regi-stration which is the secure noting ofthe security vis-à-vis a public authority.

The title registration system is thereforedesigned to protect both bond holdersand the mortgage bank itself, so theregistration requirement is a central element of Danish mortgage credit.

Any plot of land in Denmark can beidentified by a title number. The title

number system is administered by anagency (the National Survey andCadaster) under the Danish Ministry ofBuilding and Housing. The title numbersystem is of vital significance to the reg-istration system since the informationconcerning the real property statedwhen rights concerning the propertyare filed for registration is limited tobuilding number, street and title num-ber. This means that the title number iscited instead of a lengthy description ofthe property.

The title registration system is admini-stered by the title registration officeswhich are specialised, judicial depart-ments under the courts (the city courts).There are 83 title registration offices inDenmark, equivalent to the number ofjurisdictions. All real property in Den-mark is registered in the title register,duly identified by title number. All judi-cial transactions concerning a propertyare registered to the individual proper-ty’s page of the title register. In virtuallyall jurisdictions registration is performedelectronically.

The ranking of the holders of rights oneach property is also established via thetitle registration system, which is basedon the principle of “first in time, first inright”. The mortgage ranking mustalways be stated clearly on any docu-ment concerning a right which is to beregistered. In this way the ranking atwhich an execution order should bedirected in the event of default by thedebtor is also determined.

The ranking of the mortgages on agiven property must be set out in thetitle register in which registration ismade subject to a judicial examination.The decisions of the registration judgemay therefore be appealed to a highercourt (the Danish High Court).

Any person who suffers a loss as a consequence of errors committed withinthe title registration system may claimcompensation from the Danish Treasury.This provision emphasises the impor-tance to Danish society of the title registration system.

14

Lending distributed by property category

The mortgage banks grant loans for allcategories of property against mortgageson real property. Table 3 presents thedistribution of Danish mortgage lending.

The mortgage banks are the preferredsource of financing for private homeowners, but they are also a significantplayer in the commercial financing market. This is related to the fact that corporate bonds are not widely used inDenmark, and mortgage bonds areused extensively instead. The mortgagebanks are also one of the most impor-tant financing sources for agricultureand for subsidised public residentialconstruction as well as private residen-tial construction. As the table shows forvirtually all loan categories lending bymortgage banks increased in the period1997-1998.

15

1997 1998

DKK billion Gross- Net Outstanding Gross Net Outstanding

lending lending bond debt lending lending bond debt

Residential properties

Subsidised construction 7.0 0.7 146.5 9.4 2.1 149.9

Private rental 14.9 4.4 54.6 22.6 5.3 59.8

Owner-occupiedhomes 145.7 42.4 519.4 220.4 47.5 570.9

Commercial properties

Agriculture 30.0 3.7 117.2 47.3 6.3 123.5

Industry and trade 13.2 0.5 35.7 15.9 -0.2 35.0

Offices andcommercialproperties 25.0 0.9 69.9 36.8 2.5 72.5

Other properties 4.0 0.8 15.3 6.7 1.4 16.8

Total 239.8 53.4 958.8 359.0 65.0 1028.4

Note: Gross lending is the mortgage principal converted to a cash value. Net lending is theprincipal less ordinary repayments as well as transfers and redemptions. The outstandingbond debt is the nominal amount of bonds required to redeem the nominal outstanding debtof the mortgage loan.Source: The Association of Danish Mortgage Banks.

Table 3. The Danish mortgage banks’ lending by property category

Funding of the mortgage banks

The funds lent by the mortgage banksare obtained via the current issues ofbonds, i.e. as tap issues.

This means when a mortgage bankgrants a loan with a given repaymentprofile and maturity, the mortgage bankat the same time issues an equivalentnumber of bonds with the same repay-ment profile and maturity. However,variable-interest loans are funded on acurrent basis by bonds with a shortertime to maturity than the loan.

Issue of bonds is subject to a globalbalance principle which implies thatthe total repayments from the borrowersand the total payments by the mortgagebanks to the bond holders must be inbalance. This requirement is set out inthe Mortgage Credit Act. It ensures thatno interest risk is imposed on the mort-gage banks. In principle, the risk of themortgage bank is thus limited to theactual credit risk, i.e. the risk of defaulton interest and instalments on the partof the borrower.

However, the Mortgage Credit Act doesallow for a small deviation from thebalance principle. The mortgage banksmay also make e.g. wholesale issues.The Act furthermore stipulates that amortgage bank may at no time be subject to a risk of loss resulting fromdifferences between the redemptionterms or currency compositions ofissued mortgage bonds on the onehand, and the loan terms on the other.

Bond types

The bond holders receive the currentrepayments by the borrowers to themortgage banks. The repayments andproceeds from loans drawn for earlyredemption are pooled for each bondseries, after which mortgage bonds forredemption at par are drawn by lot.

16

Mortgage bonds

The drawing and payment of interestare handled via the Danish SecuritiesCentre (Værdipapircentralen).

The mortgage banks primarily issuethree types of bonds: annuity bonds,serial bonds and bullet bonds.

A characteristic of annuity bonds is thatthe volume of drawn bonds equivalentto the borrower’s repayments is smallin the first stage of the maturity term,but then rises towards the end of thematurity of the bonds.

A characteristic of serial bonds is thatthe volume of drawn bonds equivalentto the repayments on the serial loansremains constant on each settlementdate.

A characteristic of bullet bonds is thatthe entire principal of the bond isdrawn on maturity, i.e. no repaymentsare made as drawing forredemption during thematurity period.

Most mortgage bondsare fixed-interest bonds,and primarily annuitybonds are issued. Themortgage banks alsoissue index-linkedbonds to a minorextent. Besides a fixed nominal interest,the return on index-linked bonds is thecurrent index adjustment of the bonds.Mortgage bonds are generally charac-terized by a long maturity, often 20 or30 years.

As a consequence of the introductionof a number of new loan products,including variable-interest loans, themortgage banks also issue a number ofnon-callable fixed-interest bonds with ashort maturity (typically between 1 and11 years).

Callability

A callable bond can be drawn forextraordinary redemption at par in theevent of early termination of the under-lying loans. This applies to the majorityof mortgage bonds.

For the bond holder - the investor -early redemption of the bonds entails arisk of having to reinvest the proceedsat a lower interest. The investor willnormally require compensation for thisrisk (refinancing risk) as a higher yieldon callable bonds than on non-callablebonds. The size of the higher yield willdepend on the investor’s assessment ofthe risk of the borrower’s right ofremortgaging being exercised.

Several factors can play a role in theinvestor’s evaluation of the borrowers’propensity for remortgaging. The current interest level in relation to

the nominal interest on the loan is naturally a decisive factor for any decision to remortgage to a new loan.Other factors often emphasised are thesize of the loans and the borrower’sstatus (private/commercial). All mort-gage banks publish this data on theunderlying loans on a monthly basis.

17

Yields

By tradition yields on Danish mortgagebonds have always been very high. Figure 1 shows yields on mortgagebonds and Danish government bonds.As the figure shows, the mortgage bond

index increased from 100 to 193 in theperiod 1993-1999. During the sameperiod the index for government bondsrose to 186. Evaluation of these yieldsmust also take into account the addi-tional interest in relation to e.g. interestlevels in Germany.

A high degree of security

The only risk associated with invest-ment in mortgage bonds is the risk of a

drop in market price. Mortgage bondsare therefore regarded as “gilt-edged”securities in line with government bonds with regard to statutory place-ment rules for insurance companies andinstitutional investors. Mortgage bondsalso enjoy special legislative advantages

as a consequence of EU regulations.They include that insurance companiesmay place up to 40 per cent of theirassets in bonds issued by one singlemortgage bank, and that mortgagebonds are recognised as securities ofhigh quality (Tier 1) when loans areraised from the European Central Bank.This implies official acknowledgementof the soundness of the mortgage banksand the mortgage bonds.

18

100

Jan.

1993 Jul.

Jan.

1994 Jul.

Jan.

1995 Jul.

Jan.

1996 Jul.

Jan.

1997 Jul.

Jan.

1998 Jul.

Jan.

1999 Jul.

120

140

160

180

200

Index

Mortgage bonds Government bonds

Figure 1. Yields on mortgage bonds and government bonds

Note: The figure shows yields on a portfolio of selected mortgage bonds (the Nykredit MortgageBond Index consisting of the ten largest groups of fixed-interest bonds in relation to the volume ofbonds in circulation) in the period 1993 to 1999 compared to the yield on a benchmark govern-ment bond index (J.P. Morgan Government Bond Index).Source: Nykredit.

19

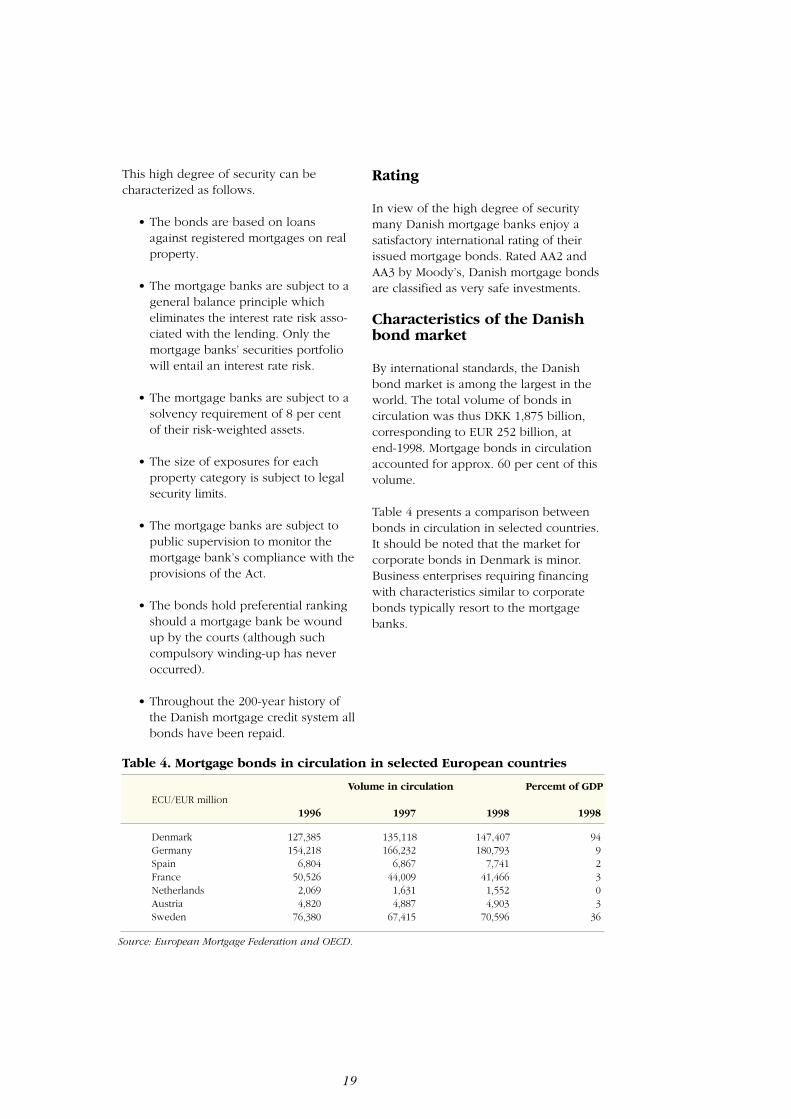

Table 4. Mortgage bonds in circulation in selected European countries

Source: European Mortgage Federation and OECD.

This high degree of security can be characterized as follows.

• The bonds are based on loansagainst registered mortgages on realproperty.

• The mortgage banks are subject to ageneral balance principle which eliminates the interest rate risk asso-ciated with the lending. Only themortgage banks’ securities portfoliowill entail an interest rate risk.

• The mortgage banks are subject to asolvency requirement of 8 per centof their risk-weighted assets.

• The size of exposures for each property category is subject to legalsecurity limits.

• The mortgage banks are subject topublic supervision to monitor themortgage bank’s compliance with theprovisions of the Act.

• The bonds hold preferential rankingshould a mortgage bank be woundup by the courts (although suchcompulsory winding-up has neveroccurred).

• Throughout the 200-year history ofthe Danish mortgage credit system allbonds have been repaid.

Rating

In view of the high degree of securitymany Danish mortgage banks enjoy a satisfactory international rating of theirissued mortgage bonds. Rated AA2 andAA3 by Moody’s, Danish mortgage bondsare classified as very safe investments.

Characteristics of the Danish bond market

By international standards, the Danishbond market is among the largest in theworld. The total volume of bonds in circulation was thus DKK 1,875 billion, corresponding to EUR 252 billion, at end-1998. Mortgage bonds in circulationaccounted for approx. 60 per cent of thisvolume.

Table 4 presents a comparison betweenbonds in circulation in selected countries.It should be noted that the market for corporate bonds in Denmark is minor.Business enterprises requiring financingwith characteristics similar to corporatebonds typically resort to the mortgagebanks.

Volume in circulation Percemt of GDPECU/EUR million

1996 1997 1998 1998

Denmark 127,385 135,118 147,407 94Germany 154,218 166,232 180,793 9Spain 6,804 6,867 7,741 2France 50,526 44,009 41,466 3Netherlands 2,069 1,631 1,552 0Austria 4,820 4,887 4,903 3Sweden 76,380 67,415 70,596 36

Apart from its considerable size theDanish bond market is also varied andliquid. In 1998 just below 2,500 bondseries were listed on the CopenhagenStock Exchange, of which mortgagebonds accounted for around 2,000.Total turnover on the Danish bondmarket amounted to EUR 1,096 billionin 1998, corresponding to average dailyturnover of EUR 4.4 billion. This turn-over is concentrated in particular on asmall number of large series. The 10largest mortgage bond series thusaccount for more than one quarter ofthe total volume of mortgage bonds incirculation. The benchmark mortgagebonds were bonds with a nominalinterest of respectively 6 per cent and 7 per cent, both maturing in 2029.

Other characteristic features of the Danish bond market are efficiency andtransparency. The extensive informationavailable to the market participantshelps to ensure this efficiency and highdegree of transparency. The Copen-hagen Stock Exchange provides infor-mation such as the following to thebond market: daily prices, yields beforeand after tax, and the volume of bondsin circulation. Average interests forrespectively uniform bonds and bondsin circulation are also published.

The mortgage banks provide currentsupplementary information on theloans underlying the mortgage bonds.This includes details of the compositionof the debtor group, instalment profiles,extraordinary redemptions and drawingnotifications. This data is distributed viathe electronic information system of theCopenhagen Stock Exchange.

20

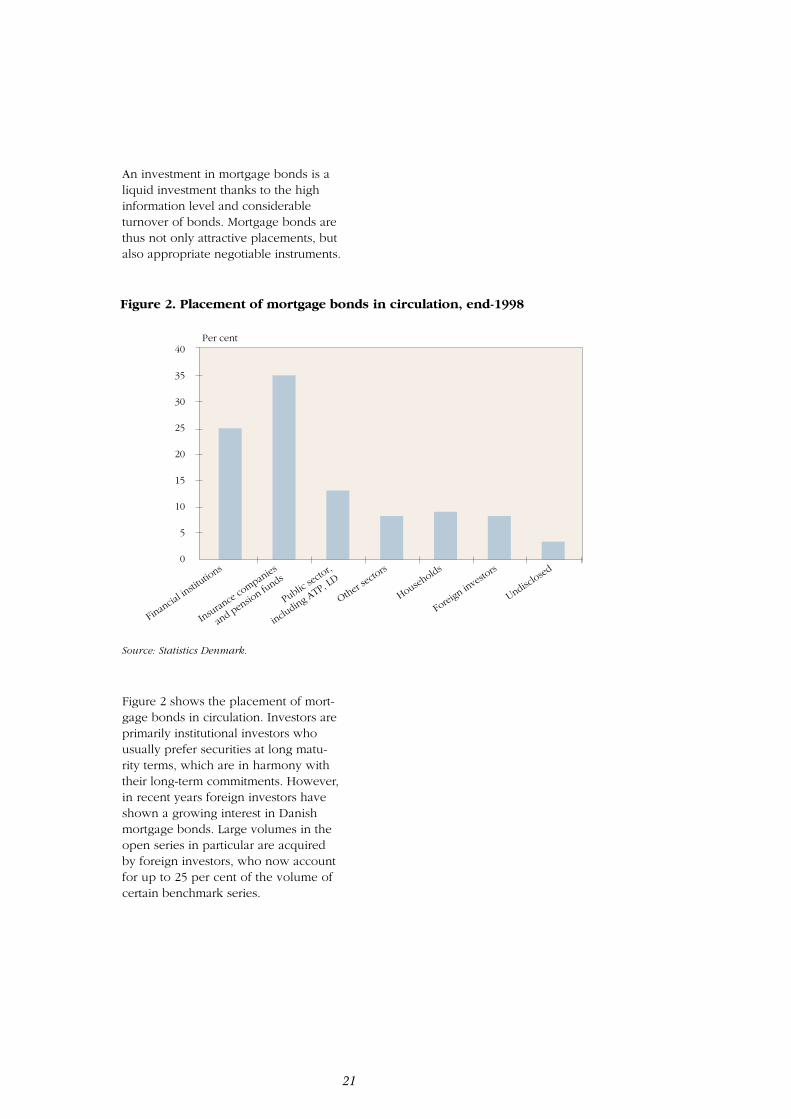

An investment in mortgage bonds is aliquid investment thanks to the highinformation level and considerableturnover of bonds. Mortgage bonds arethus not only attractive placements, butalso appropriate negotiable instruments.

Figure 2 shows the placement of mort-gage bonds in circulation. Investors areprimarily institutional investors whousually prefer securities at long matu-rity terms, which are in harmony withtheir long-term commitments. However,in recent years foreign investors haveshown a growing interest in Danishmortgage bonds. Large volumes in theopen series in particular are acquiredby foreign investors, who now accountfor up to 25 per cent of the volume ofcertain benchmark series.

21

Figure 2. Placement of mortgage bonds in circulation, end-1998

0

5

10

15

20

25

30

35

40

Financial in

stitutio

ns

Insurance companies

and pension fu

nds

Public se

ctor,

including ATP, L

D

Other secto

rs

Households

Foreign investo

rs

Undisclosed

Per cent

Source: Statistics Denmark.

Press releases:

The Association of Danish MortgageBanks issues regular press releases onthe development in the mortgage creditmarket, as well as press releases asrequired on the economic and politicalconditions of relevance to mortgagecredit.

Quarterly press releases are issued onthe development in respectively property prices and mortgage lending.The details of property price trends inthe press releases are based on datareported by the mortgage banks forloans granted to finance house pur-chases. The statistics are published forthe individual local authority. The pressrelease on mortgage lending includesinformation on the development in themarket shares of individual mortgagebanks.

Remortgaging tables:

The Association of Danish MortgageBanks issues monthly remortgagingtables to intermediary lenders, etc.

The Annual Report of the Association of Danish Mortgage Banks

The report on the current year, inclu-ding the Chairman’s report, summary

and special sections on e.g. amend-ments to mortgage credit legislation,EU-related issues, the property market,lending by mortgage banks, creditextension and the bond market. AnEnglish summary is also published.

Mortgage credit statistics:

The annual report also includes a special statistical publication with dataon lending by mortgage banks, etc.

The mortgage credit system:

Collection of articles published to markthe 25th anniversary of the Associationof Danish Mortgage Banks in 1997.

Mortgage financing in Denmark:

The Association of Danish MortgageBanks publishes brochures on mort-gage financing in Denmark in Danishand English. These publications presentan overview of mortgage lending andcurrent regulations.

Danish Mortgage Bonds:

A publication designed to informinvestors about Danish mortgage bondsand the underlying security.

Mortgage credit calendar

Calendar of legislative amendments,etc. of relevance to the mortgage creditsystem. The calendar is available in aprinted version for the period 1980-89and has been reprinted as updated insubsequent annual accounts.

Most of the publications stated aboveare available on the Web site of theAssociation of Danish Mortgage Banksat www.realkreditraadet.dk. The Website also includes the Mortgage CreditAct and a list of executive orders issuedpursuant to the Act.

22

Publications of the Association of Danish Mortgage Banks

AcknowledgementAcknowledgement of receipt of a notifi-cation, e.g. of assignment.

Administration feeCovers the interest margin of the mort-gage bank. The administration fee covers e.g. the mortgage bank’s costsof working, allocations to reserves,losses and surplus. The fee is usuallycalculated as a percentage of the outstanding debt. For old loans the feemay be calculated as a percentage ofthe instalment or the principal, and thefee is tax deductible.

Advance loanLoan related to properties to be deve-loped. The loan is granted on the basisof the expected lending value andagainst an appropriate commercialbank guarantee or other secure guaran-tee that the loan will be redeemed orreduced if it cannot be granted at theallocated amount after the expiry of thedeadline for final development of thesite.

AmortizeTo repay a loan.

Annuity loanA characteristic of an annuity loan isthat the repayments to cover interestand instalments remain constantthroughout the term of the loan. As theloan is repaid the proportion of therepayment which is interest declinesand the instalment share increases.Since interest is tax-deductible theinstalment payment after tax increases.

BondWritten instrument of debt issued bye.g. a mortgage bank, most frequentlysubject to interest payments.

Bond loanA loan of which the principal corre-sponds to the volume of bonds to beissued, the interest on the loan and onthe bond is the same.

Bond principalThe principal stated on the mortgagedeed as regards bond loans, and forcash loans the underlying bonds ondisbursement of the loan.

Bond interest percentageSee “Face interest”.

Brokerage commissionThe fee charged by the mortgage bank,commercial bank or stockbroker whichcarries out the bond transaction. Thecommission is calculated in points perthousand of the bonds’ market value.

Bullet loanLoans which are not repaid until ma-turity, i.e. the entire principal falls dueon the maturity of the loan.

Callable bondsSee “remortgaging/refinancing”.

Capital lossFor example the loss arising on sale ofa bond at a price below the nominalvalue of the bonds.

Cash interest rateThe rate of interest on a cash loan. Thecash interest rate includes the capitalloss on sale of the bonds. The capitalloss/gain is repaid throughout the termof the loan. The size of the cash interest rate depends on the price atwhich the loan is paid out. The higherthe price, the lower the rate of interest,and vice versa.

Cash loanThe principal of a cash loan is equi-valent to the market value of the bondssold on the granting of the loan. Thecapital loss (at prices below par) isrepaid over the term of the loan as partof the interest on the loan. The capitalloss is tax-deductible since it is inclu-ded in the interest payments on theloan.

23

Glossary

Cash valuationValuation of the market price of a property in a cash sale. Can be regardedas the opposite of the financed price.

Commercial bank guaranteeGuarantee given by a commercial bankor a savings bank as security that a per-son will meet all commitments vis-à-visa third party.

Copenhagen Stock ExchangeThe Copenhagen Stock Exchange is thevenue for official trading in and listingof securities. Trading takes place byelectronic means among the stock-brokers.

Coupon ratePayment by the buyer to the seller ofthe first interest amount falling due.The payment comprises the nominalinterest from the last due date until thedate on which the buyer pays for thebonds.

Credit associationSee “Mortgage bank”.

CreditorClaimant, e.g. a bond holder.

Creditor settlement dateInterest and drawn bonds fall due tothe bond holders on the creditor settle-ment dates. There are two or four suchdates per year.

DebtorA person who owes money, for example a borrower in relation to amortgage bank.

Debtor settlement dateThe debtor settlement dates are thedates on which the repayments on theloan fall due. There are two or fourdebtor settlement dates per year. However, one mortgage bank offers amonthly payment scheme.

Differential interest rateThe difference between the interest onthe redeemed loan from the redemptiondate until the subsequent ordinary settle-ment date on which the loan couldhave been terminated according to theloan terms, and the interest offered bythe mortgage bank to the customer ascompensation for access to the redemp-tion amount during that period.

DrawingDrawing by lot of the bonds to beredeemed at par on the relevant ordi-nary settlement date.

Drawing gainThe difference between the drawingprice (=100) and the current marketprice (a loss if the market price isbelow par).

Effective interest rateThe effective interest rate is the totalprice for the loan. Other factors besidesthe ordinary interest rate are taken intoaccount, i.e. capital loss, administrationfee, brokerage commission, initial com-mission, stamp duty and registrationduty, as well as the repayment date.See also “Percentage annual costs”.

Endorsement in connection withthe registrationEndorsement by the court registry on aregistered document to the effect thatits contents deviate from the record inthe title register and as a consequencethe creditor cannot accept the endorse-ment. The endorsement may concerne.g. a mortgage deed if more mort-gages or restrictive covenants are statedin the title register than on the mort-gage deed.

Executive orderSupplements an Act. Executive ordersare issued by a minister or an agencywith appropriate authorization underan Act. An executive order is binding,i.e. it can only be amended by a newexecutive order, or by amendment ofthe underlying Act.

24

Face valueThe amount stated on a bond. Thesame as the nominal value.

Face interestThe interest stated on a bond. Thesame as the nominal interest.

FeePayment for a service, e.g. valuationand case handling, in connection withthe raising of mortgage loans.

Fixed-price contractA contract concluded with a mortgagebank. The debtor may obtain forwardcover of price fluctuations by conclu-ding a contract on the disbursement ofa new loan at a fixed price on a futuredate. A fixed-price contract can thus beconcluded for a loan to be raised, orfor a loan to be redeemed. See also“Price contract”.

FlexLoanA FlexLoan is a variable-interest loanwhich is taxed as a cash loan. Since the rate of interest is adjusted on eachaddition of interest, the instalmentamount or the maturity of the loan willchange, depending on the type ofFlexLoan chosen. See also “Variableinterest loans”.

Forward price contractForward price contracts by which it isagreed on the date of the contractwhen a bond holding will be sold andat which price.

FundingProcurement of funds for lending viaissue of bonds, etc. on the capital market.

Index-linked bondsBonds with a low nominal interestwhose value is written up in step withthe development in an agreed index,typically the ordinary price level (theindex of net retail prices), so that thevalue of the bonds has the same pur-chasing power.

Index-linked loanA loan category with ongoing adjust-ment of principal and outstanding debt,and thus of interest and repayments,according to the development in anagreed price index.

InstalmentIs the part of the repayment whichreduces the outstanding debt of theloan.

Interest rateSee “Face interest”.

IssueIssue of e.g. bonds, shares, etc. Thiscan either be tap issue, whereby eachbond is divested in step with the len-ding, or wholesale issue whereby abond amount is issued as a totalamount which is independent of theamount lent, with a view to subsequentapplication of the proceeds for lendingpurposes.

Joint and several liabilityThe liability of each debtor in the eventof joint and several liability for a shareddebt (one for all, all for one). A distinction is made between primaryjoint and several liability whereby acreditor may file an immediate claimfor the entire amount vis-à-vis anydebtor and subsidiary joint and severalliability whereby the other debtors arenot charged until the individual debtoris unable to repay all or part of thedebt. Joint and several liability hasnever been invoked in connection withmortgage credit loans.

Lending limitThe maximum permitted mortgaging of the value of the property. The Mortgage Credit Act stipulates a maxi-mum lending limit for various propertycategories.

25

Lending valueThe value of the property calculated bythe mortgage bank according to currentrules. The lending value may corre-spond to the reasonable cash marketvalue of the property, but in principlemay not exceed this value.

LifetimeNumber of years from the disbursementof the loan until it falls due.

ListingFixing of prices on the Stock Exchange.

Market valueIs the nominal value multiplied by theprice of the bond.

Market value of index-linked bondsIs the nominal value, the current indexfactor (index of net retail prices) multi-plied by the price.

Mortgage bankAn institution which grants loansagainst registered mortgages on realproperty by issuing bonds.

Net repaymentThe repayment, after tax deduction ofinterest and administration fee.

Nominal loanNominal loan is a joint term for otherloans than index-linked loans.

Nominal valueFace value. The face value of a bond.

Nominal interestFace interest, i.e. the interest on thenominal value of a bond disregardingthe discounted value of the principal.

Non-callable bondsLoans based on non-callable bonds canbe redeemed solely by purchasing thebonds at market price. See also“Remortgaging”.

Non-profit public housingProperties constructed and operated on a non-profit basis according to theDanish Non-Profit Housing Act.

Official listingValuation by the Copenhagen StockExchange of e.g. securities.

Ordinary settlement dateLast due payment date for e.g. therepayment on a mortgage loan.

Outstanding bond debtThe outstanding debt on a bond loan.For cash loans the outstanding debt onthe underlying bonds.

Outstanding debtThe amount owed at any time.

Outstanding debt on cash loansThe outstanding debt on a cash loan,i.e. the outstanding debt for the under-lying bonds.

ParPrice 100.

Percentage annual costsStated in the credit information sectionof the loan offer. Includes bond interest,capital loss, administration fee, brokeragecommission, initial commission, regis-tration duty and case processing fee.Often abbreviated PAC.

PointsAn increase or decrease in the price isstated in points. The differencebetween price 90 and price 91 is thusone point.

Price contractPrice contracts can be applied to allloan categories. The purpose of thescheme is to arrange forward cover forthe mortgage loan at the time that it israised. The price contract is concludedwith a commercial bank, which meansthat the loan can be disbursed at afixed price on the required date. Pricecontracts may be concluded for loans

26

to be raised, as well as loans to beredeemed. See also “Fixed-price contract”.

PrincipalThe original amount of the loan. Themortgage bank undertakes registrationof this amount as a mortgage on theproperty.

Private mortgageMortgage deed issued to a “creditorother than a mortgage bank”, often amortgage secured to the vendor.

ProceedsIncome, dividend, gain. For example,the proceeds from a mortgage loan arethe amount disbursed, equivalent to theloan (for bond loans the product of theprincipal and the price) less brokeragecommission, initial commission andother fees.

Property categoriesA division of properties into variousgroups such as owner-occupied homesfor all-year occupancy, agriculturalproperties, etc. The property categoryaffects the lending scope of the mort-gage banks.

Property valueThe official valuation of a propertywhich provides the basis for taxation.The value is divided into the value ofrespectively site and buildings.

RealkreditrådetRealkreditrådet (the Association of Dan-ish Mortgage Banks) is the trade organ-isation of the Danish mortgage banks.

Real propertyConstitutes land and the buildingsregarded as a single entity with regardto allotment and registration laws.

RedemptionRepayment of a loan on maturity, or asextraordinary redemption before matu-rity. Extraordinary redemption may beof the whole amount or a part of it.

Refinancing riskThe bond investor’s risk with regard tothe debtor’s access to remortgage loansto a lower interest rate, which entailsthe drawing of the bonds.

Registration1. Official registration of rights, particu-larly those pertaining to real property.

2. Registration in the title register.

RemortgagingRaising of a new loan in connectionwith extraordinary redemption of anold loan.

Remortgaging/refinancingRemortgaging of loans in connectionwith shifts in interest rates.

Remortgaging in the event of a drop ininterest rates (downward remortgaging)is to a new loan at a lower interest rateand thereby reduced repayment.

Remortgaging in the event of a rise ininterest rates (upward remortgaging) isto a new loan at a higher rate of interest and thereby higher repayments,while the outstanding bond debt isreduced. The purpose is usually tomake new downward remortgagingpossible in the event of a subsequentdrop in interest rates.

Repayment Is the amount, including interest, anyinterest on overdue payments, instal-ment and administration fee, pertainingto a mortgage loan which is payable oneach ordinary settlement date.

Reserve fundFund to offset e.g. losses. In certaincases there are statutory requirementsconcerning minimum reserve funds.Such requirements apply to e.g. mort-gage banks whose reserve funds mustbe calculated on the basis of the vol-ume of lending.

27

SectionA subdivision of bonds. Bonds issuedunder the same section normally haveidentical characteristics, apart from theinterest. Several securities IDs (see thisitem) can be issued in the various sections.

Securities IDA unique code for each paper listed onCopenhagen Stock Exchange.

Serial loanLoans with equal repayments on eachsettlement date, i.e. declining instal-ments throughout the term of the loan.

Settlement amountThe amount to be repaid on a loan oneach ordinary settlement date. It com-prises instalments, interest and admini-stration fee.

Stamp dutyDuty payable to the Danish state, e.g.for title registration of mortgages andconveyances. See also “Title registrationduty”.

Supplementary loanA loan against real property outside aspecific purpose category. Such loansare raised after e.g. redemption of anumber of old loans, thereby creating afree lending value on the property.

Term of noticeThe last possible date on which theloan or the refinancing amount may beterminated as of the following bondsettlement date.

The Danish Securities CentreSelf-governing institution which e.g.registers bond issues and bond trading.

Title numberUnique identification of real property,including number and plotowner association.

Title registerRegisters of real property held by thecourt registries. Rights pertaining to realproperty such as conveyances, mort-gages and easements are registered. Alltitle registers are expected to be avail-able electronically by the year 2000.

Title registration dutyAs of January 1, 2000 the stamp dutyand the fixed title registration duty arereplaced by a registration duty, i.e. afixed amount as well as a certain per-centage.

Variable-interest loansCash loans whereby interest and instal-ments are adjusted after an agreednumber of years. These loans are mar-keted as e.g. FlexLoans and AdjustmentLoans with varying characteristics. Themost recent type of variable-interestloan is a euro loan whereby the rate ofinterest depends on the development inEuroland.

Wholesale issuesSee “Issues”.

28

BG Kredit A/S

Stamholmen 153, 1.

DK-2650 Hvidovre

tlf. +45 3688 4330 · fax +45 3688 4399

www.bgbank.dk

BRFkredit a/s

Klampenborgvej 205

DK-2800 Lyngby

tlf. +45 4593 4593 · fax +45 4593 4522

www.brfkredit.dk

Dansk Landbrugs Realkreditfond

Nyropsgade 21

DK-1780 Copenhagen V

tlf. +45 7010 0090 · fax +45 3393 9500

www.dlr.dk

Danske Kredit Realkreditaktieselskab

Holmens Kanal 2-12

DK-1092 Copenhagen K

tlf. +45 4324 0024 · fax +45 4325 1566

www.danskekredit.dk

FIH Realkredit A/S

La Cours Vej 7

DK-2000 Frederiksberg

tlf. +45 3816 6800 · fax +45 3816 6860

www.fih.dk

Landsbankernes Reallånefond

Nyropsgade 21

DK-1780 Copenhagen V

tlf. +45 3312 7500 · fax +45 3312 7502

www.lrf.dk

Nykredit A/S

Otto Mønsteds Plads 9

DK-1780 Copenhagen V

tlf. +45 3377 2000 · fax +45 3377 2020

www.nykredit.dk

Realkredit Danmark A/S

Jarmers Plads 2

DK-1590 Copenhagen V

tlf. +45 3312 5300 · fax +45 3688 2400

www.rd.dk

TOTALKREDIT Realkreditfond

Helgeshøj Allé 53

DK-2630 Taastrup

tlf. +45 4332 6700 · fax +45 4332 6767

www.totalkredit.dk

Unikredit Realkreditaktieselskab

Trommesalen 4, Postboks 850

DK-0900 Copenhagen C

tlf. +45 3333 3636 · fax +45 3333 3637

www.unikredit.dk

er di

DANSKE KREDIT

LRF

R E A L K R E D I T R Å D E T

Z i e g l e r s G a a r d · N y b r o g a d e 1 2 · D K - 1 2 0 3 C o p e n h a g e n KT e l e p h o n e : + 4 5 3 3 1 2 4 8 1 1 · T e l e f a x : + 4 5 3 3 3 2 9 0 1 7

Hel

ge P

rahl

Gra

fik ·

Prin

ted

in D

enm

ark