Embed Size (px)

Citation preview

MONTHLY INVESTMENT STRATEGY

August 2011

2

As the summer holidays approach [according to convention “nothing happens” in August whereas, in fact, it is just as likely to see an inflection point as any other month] the “big three” occupy the foreground, middle distance and the area just below the horizon.

In the foreground the Europiig debacle moves relentlessly forward. The authorities insistence on treating solvency as an issue of short term liquidity more or less guarantees that they will always be running to catch up. As it is, no sooner is Greece “solved” for the second time than the problem has moved on to Italy which is on a quite different scale - the third largest government bond market in the world. Ironically [not that irony is lacking in the Europiig saga] the official attempt to give Spain a clean bill of health by emphasising its low debt/gdp ratio backfired by drawing attention to Italy [and Belgium] both of which look very bad on this measure. Disorder rules; the day following Trichet’s insistence that the ECB would not accept defaulted bonds as collateral and urged “verbal discipline” on Europe’s politicians his fellow council member Nowotny suggested just the opposite.

Each lurch brings Euroland closer to the fork in the road where the explicit choice must be made between a debt union and some countries leaving the Eurozone. Neither seems likely yet, increasingly, the choice is between one or the other. After so much political capital has been invested a breakup seems far fetched but the advocates of a debt union underestimate the political hurdles. The supranational entity issuing the “Eurobond” will need extensive tax raising powers to service its loans. This spells the end of national control over tax policy. Even the main actors don’t know what is going to happen but the ability to obfuscate the underlying issues ebbs away with each new twist.

In the middle distance looms the broader crisis of government debt and public provision. For more than two generations governments in the developed world have made extravagant promises and funded the cash flow shortfall by borrowing. At the same time, the monopoly services they provide have become progressively more expensive - and worse. It is no coincidence, for example, that a list of the top educational institutions in the world is dominated by private universities – a tiny fraction of the whole. Current deficits, however, are dwarfed by the scale of future promises. An attempt to put the UK’s government accounts on the same basis as a private institution estimated the present value of unfunded public pension promises to be some 80% of GDP.

On an accruals basis the US has a deficit this year of about $7 trillion rather than the $1.3 trillion reported. All these numbers make nonsense of the debt/gdp ratios that exercise the ringmasters of the Europiigs circus. As it happens, Greece fares quite well [relatively]on this comparison – providing one uses Greek government bond rates as the “risk free” discount rate. Along with the accumulating evidence of how fiscal stringency affects economic growth the next stage is to see how the US, the only major economy not yet to have tightened fiscal policy, chooses to respond. The conclusion to the debt ceiling impasse [I’m assuming that it will pass the House] means that the US will be cutting government spending even as revised figures show that the recession was deeper and the recovery weaker than had been imagined.

Just below the horizon lies the revelation of the true nature of the Chinese economic miracle. Notwithstanding the weak PMI survey for July, for the moment, a slowdown is a good slowdown. It will be several months before it is clear whether this is a refreshing pause or something more sinister. The political cycle [a change of leadership at the end of 2011] argues for tolerating high inflation rather than risking an immediate hard landing. Best to leave the tough decisions to the new administration. Nick Carn August 2011

Introduction

GLOBAL MONETARY CONDITIONS

4

5

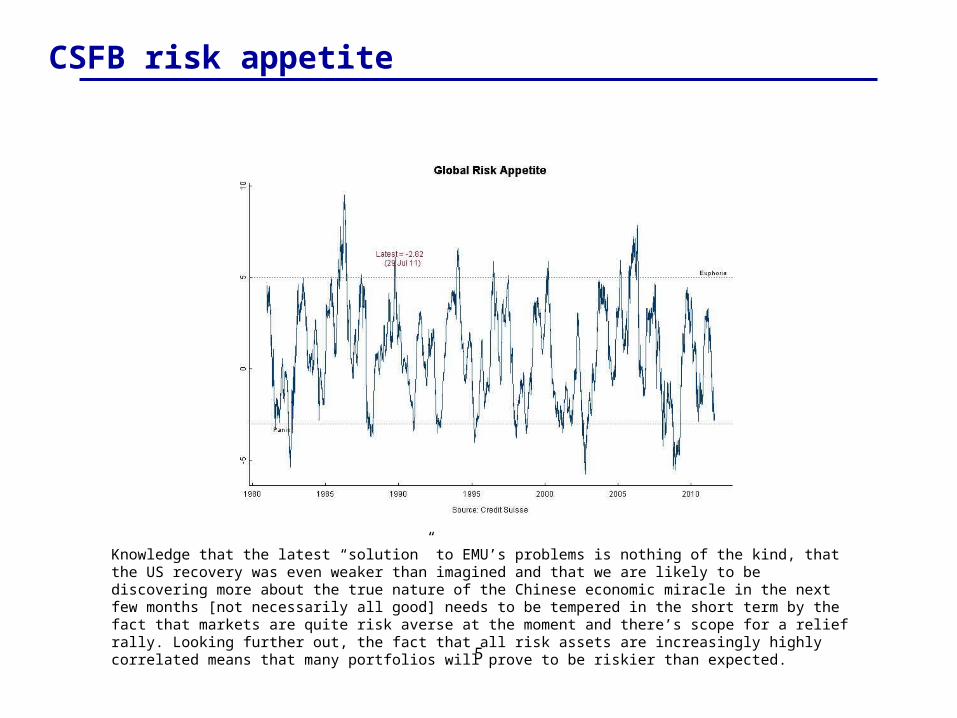

CSFB risk appetite

Knowledge that the latest “solution” to EMU’s problems is nothing of the kind, that the US recovery was even weaker than imagined and that we are likely to be discovering more about the true nature of the Chinese economic miracle in the next few months [not necessarily all good] needs to be tempered in the short term by the fact that markets are quite risk averse at the moment and there’s scope for a relief rally. Looking further out, the fact that all risk assets are increasingly highly correlated means that many portfolios will prove to be riskier than expected.

6

ECONOMIC SNAPSHOTS

8

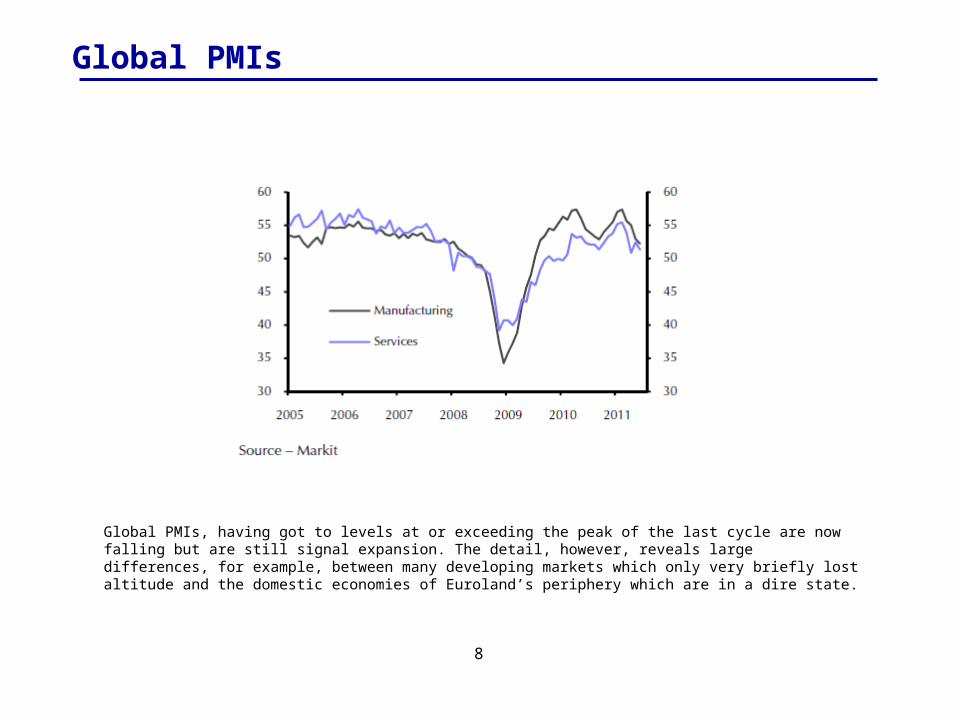

Global PMIs

Global PMIs, having got to levels at or exceeding the peak of the last cycle are now falling but are still signal expansion. The detail, however, reveals large differences, for example, between many developing markets which only very briefly lost altitude and the domestic economies of Euroland’s periphery which are in a dire state.

9

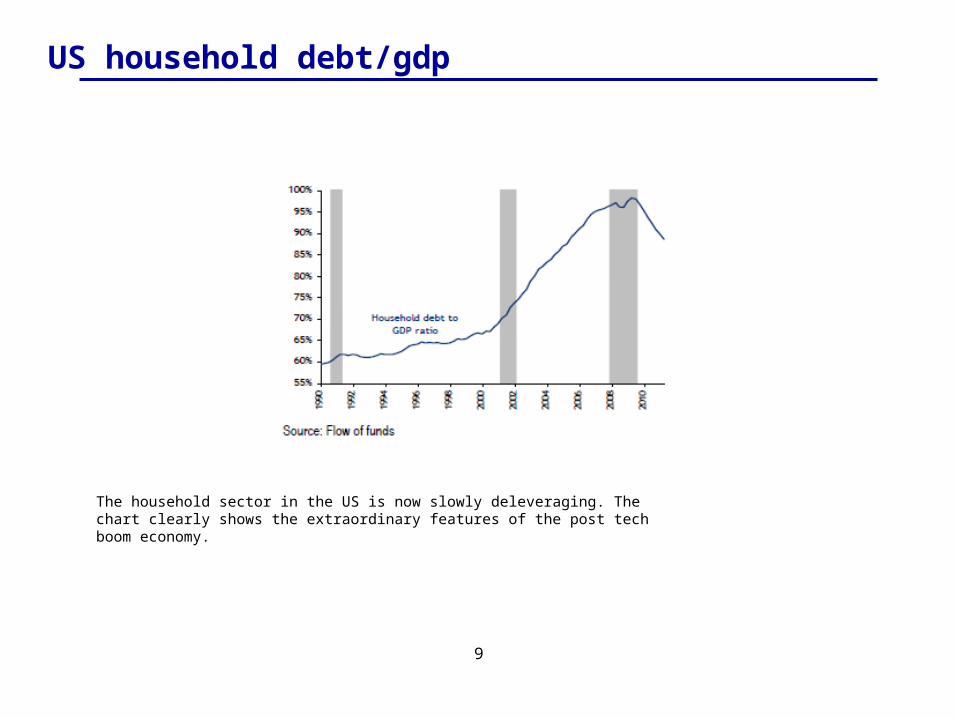

US household debt/gdp

The household sector in the US is now slowly deleveraging. The chart clearly shows the extraordinary features of the post tech boom economy.

10

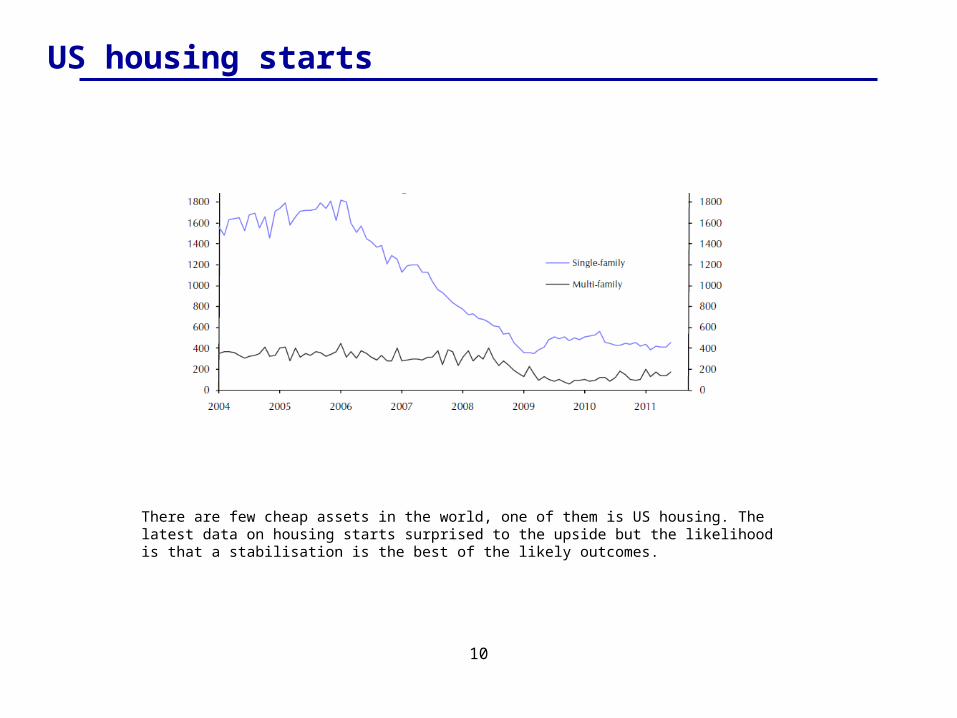

US housing starts

There are few cheap assets in the world, one of them is US housing. The latest data on housing starts surprised to the upside but the likelihood is that a stabilisation is the best of the likely outcomes.

11

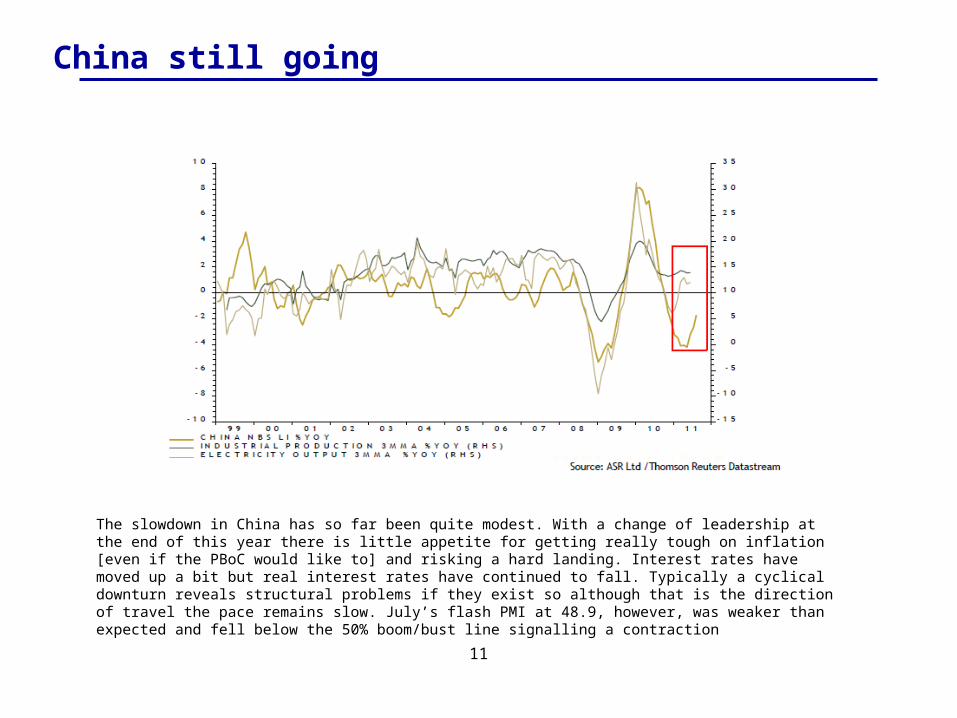

China still going

The slowdown in China has so far been quite modest. With a change of leadership at the end of this year there is little appetite for getting really tough on inflation [even if the PBoC would like to] and risking a hard landing. Interest rates have moved up a bit but real interest rates have continued to fall. Typically a cyclical downturn reveals structural problems if they exist so although that is the direction of travel the pace remains slow. July’s flash PMI at 48.9, however, was weaker than expected and fell below the 50% boom/bust line signalling a contraction

12

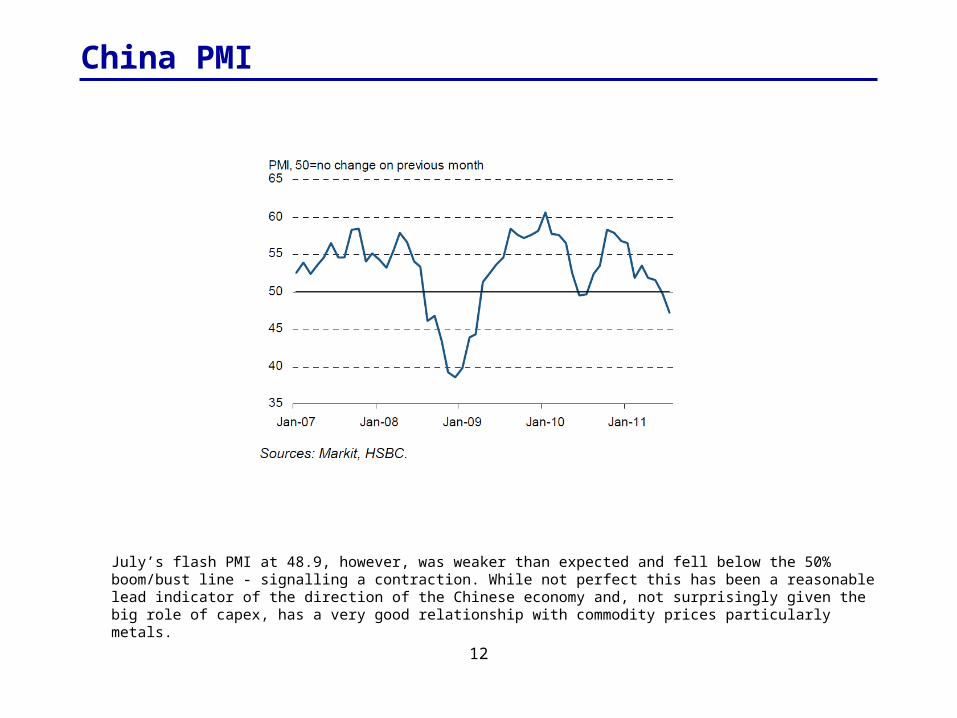

China PMI

July’s flash PMI at 48.9, however, was weaker than expected and fell below the 50% boom/bust line - signalling a contraction. While not perfect this has been a reasonable lead indicator of the direction of the Chinese economy and, not surprisingly given the big role of capex, has a very good relationship with commodity prices particularly metals.

13

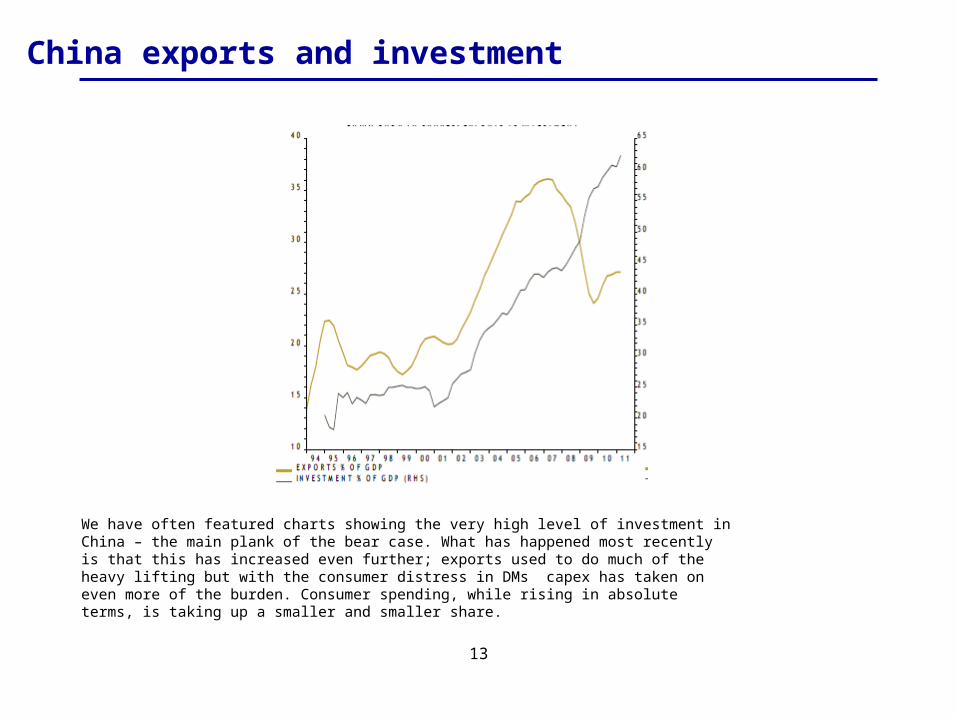

China exports and investment

We have often featured charts showing the very high level of investment in China – the main plank of the bear case. What has happened most recently is that this has increased even further; exports used to do much of the heavy lifting but with the consumer distress in DMs capex has taken on even more of the burden. Consumer spending, while rising in absolute terms, is taking up a smaller and smaller share.

14

China; local and central government finances

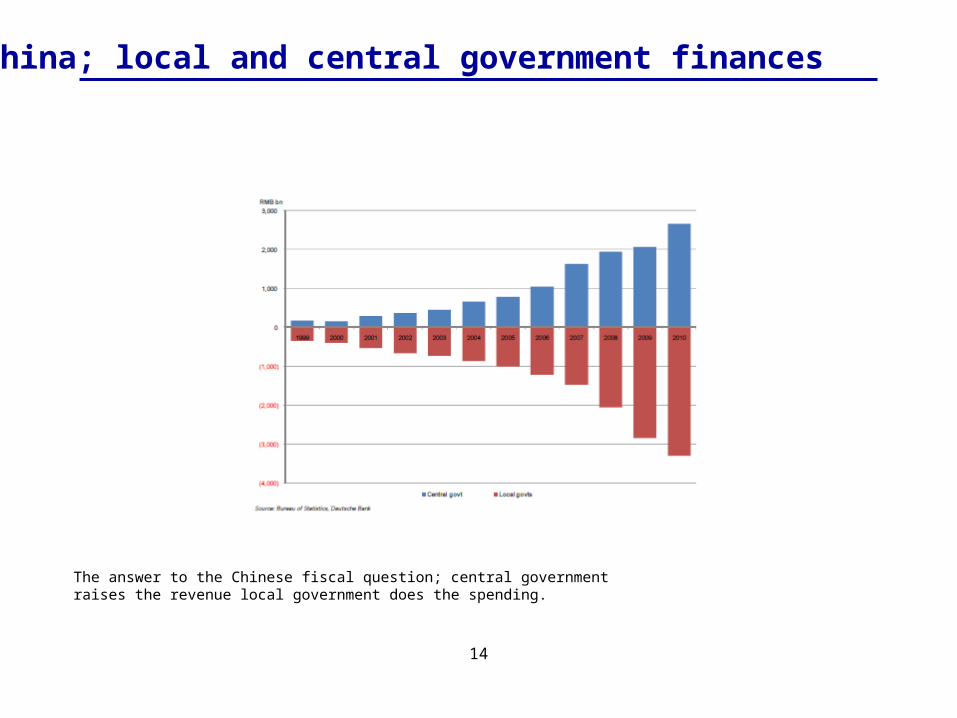

The answer to the Chinese fiscal question; central government raises the revenue local government does the spending.

15

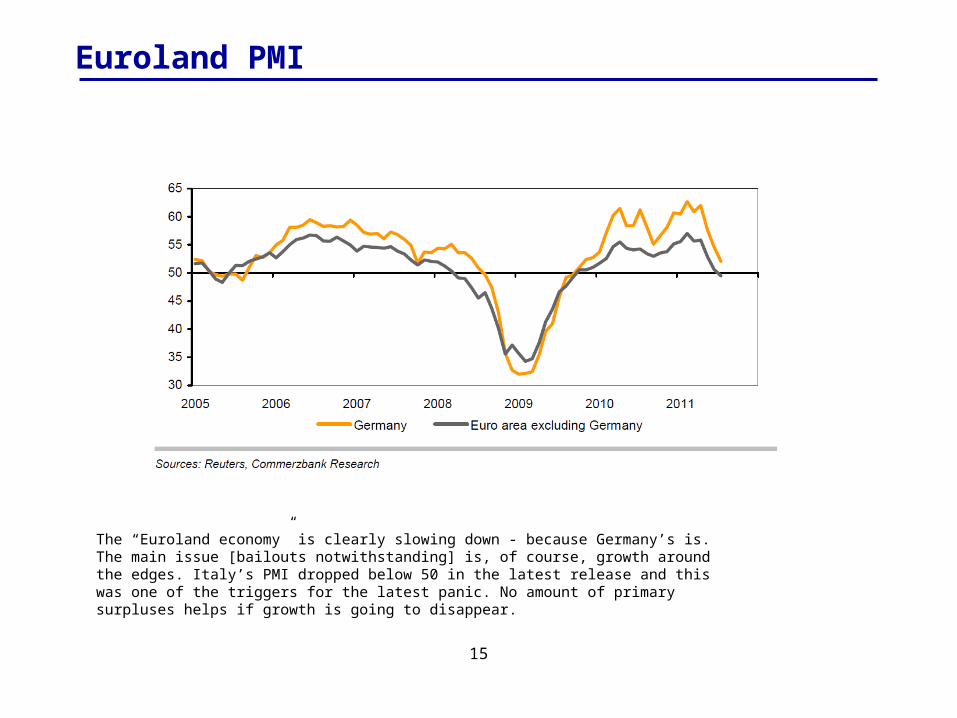

Euroland PMI

The “Euroland economy” is clearly slowing down - because Germany’s is. The main issue [bailouts notwithstanding] is, of course, growth around the edges. Italy’s PMI dropped below 50 in the latest release and this was one of the triggers for the latest panic. No amount of primary surpluses helps if growth is going to disappear.

16

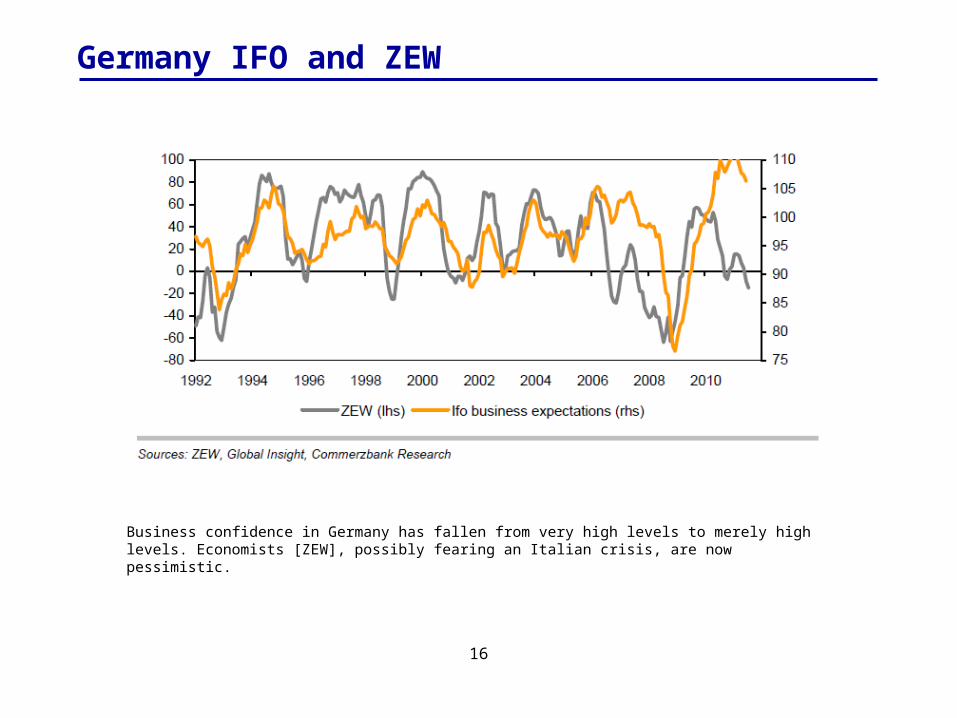

Germany IFO and ZEW

Business confidence in Germany has fallen from very high levels to merely high levels. Economists [ZEW], possibly fearing an Italian crisis, are now pessimistic.

17

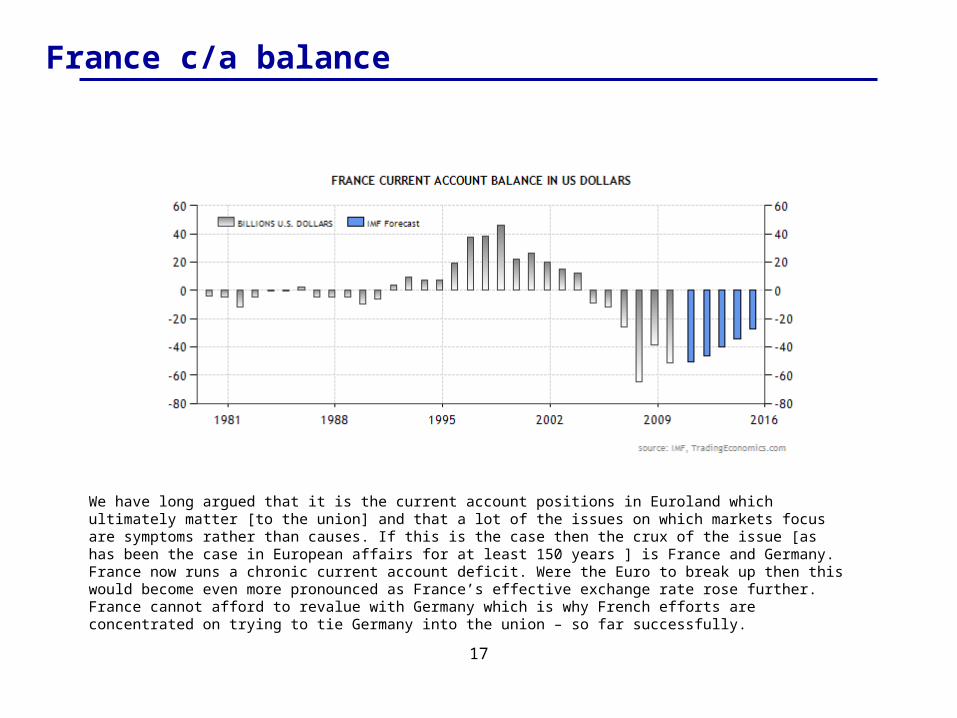

France c/a balance

We have long argued that it is the current account positions in Euroland which ultimately matter [to the union] and that a lot of the issues on which markets focus are symptoms rather than causes. If this is the case then the crux of the issue [as has been the case in European affairs for at least 150 years ] is France and Germany. France now runs a chronic current account deficit. Were the Euro to break up then this would become even more pronounced as France’s effective exchange rate rose further. France cannot afford to revalue with Germany which is why French efforts are concentrated on trying to tie Germany into the union – so far successfully.

18

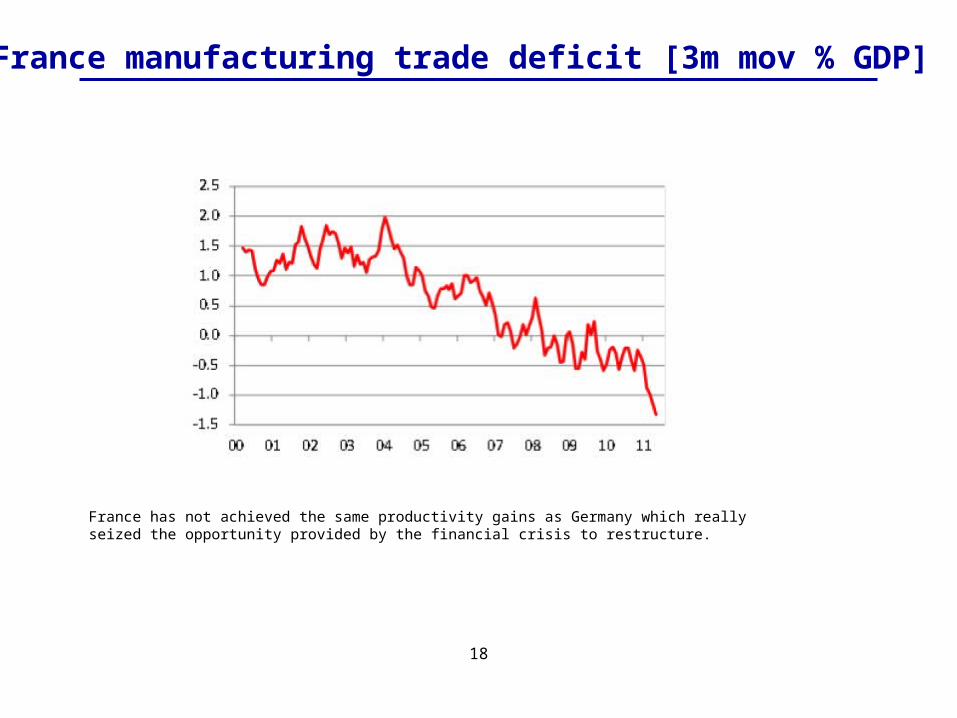

France manufacturing trade deficit [3m mov % GDP]

France has not achieved the same productivity gains as Germany which really seized the opportunity provided by the financial crisis to restructure.

19

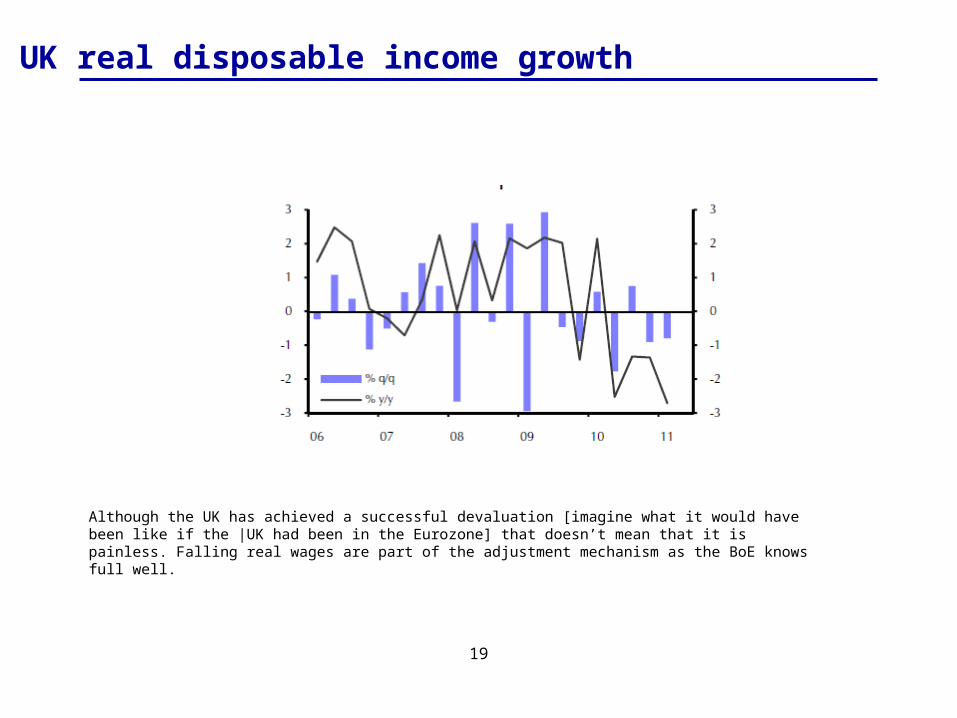

UK real disposable income growth

Although the UK has achieved a successful devaluation [imagine what it would have been like if the |UK had been in the Eurozone] that doesn’t mean that it is painless. Falling real wages are part of the adjustment mechanism as the BoE knows full well.

20

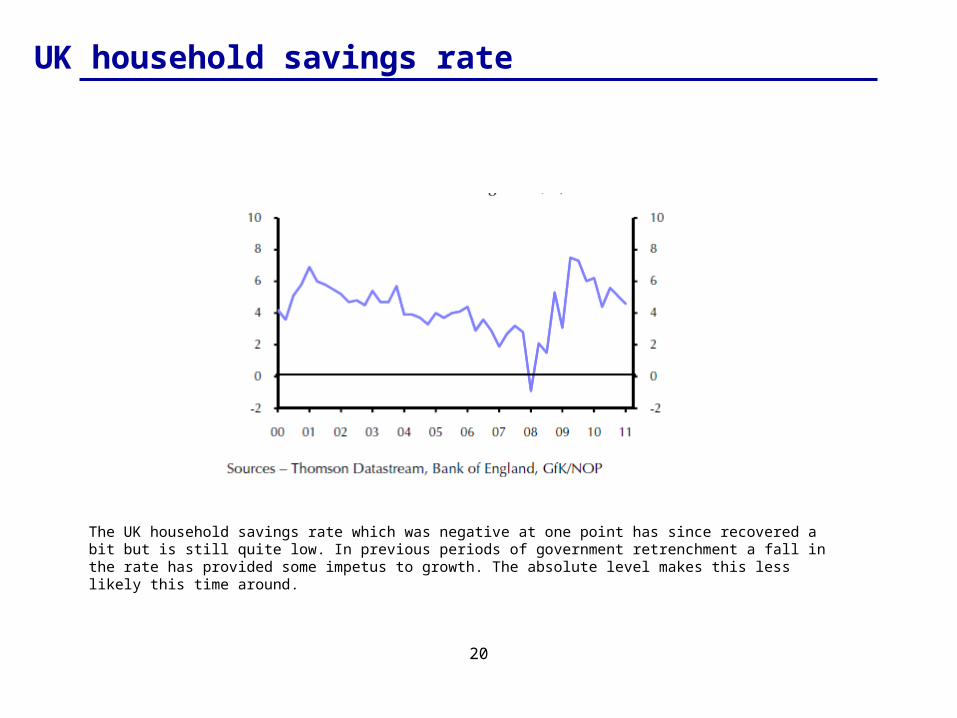

UK household savings rate

The UK household savings rate which was negative at one point has since recovered a bit but is still quite low. In previous periods of government retrenchment a fall in the rate has provided some impetus to growth. The absolute level makes this less likely this time around.

21

MARKETS

22

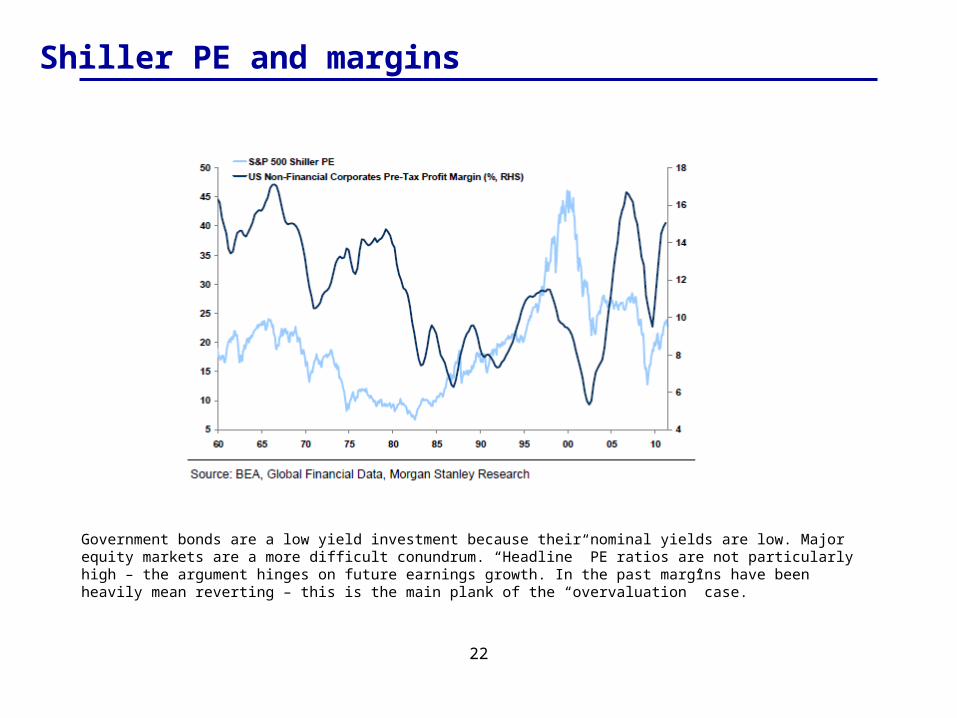

Shiller PE and margins

Government bonds are a low yield investment because their nominal yields are low. Major equity markets are a more difficult conundrum. “Headline” PE ratios are not particularly high – the argument hinges on future earnings growth. In the past margins have been heavily mean reverting – this is the main plank of the “overvaluation” case.

23

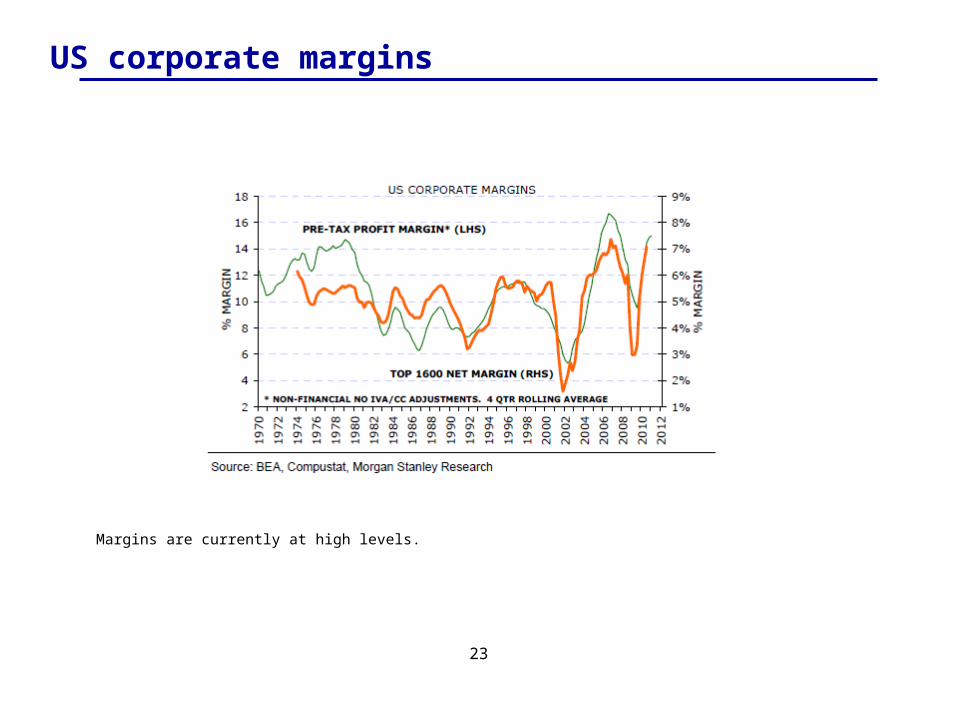

US corporate margins

Margins are currently at high levels.

24

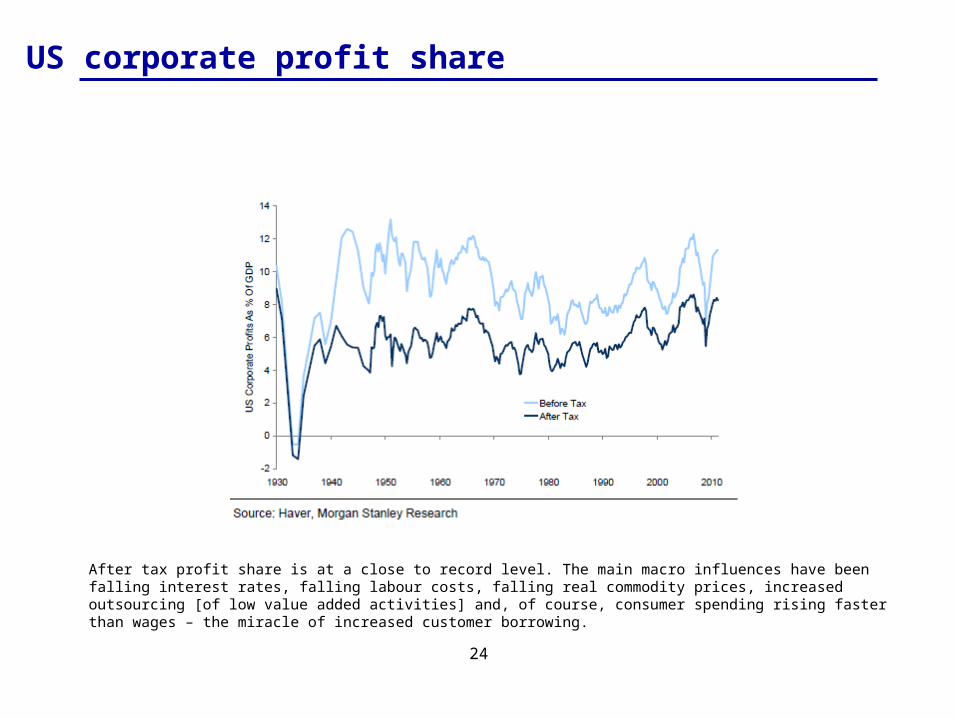

US corporate profit share

After tax profit share is at a close to record level. The main macro influences have been falling interest rates, falling labour costs, falling real commodity prices, increased outsourcing [of low value added activities] and, of course, consumer spending rising faster than wages – the miracle of increased customer borrowing.

25

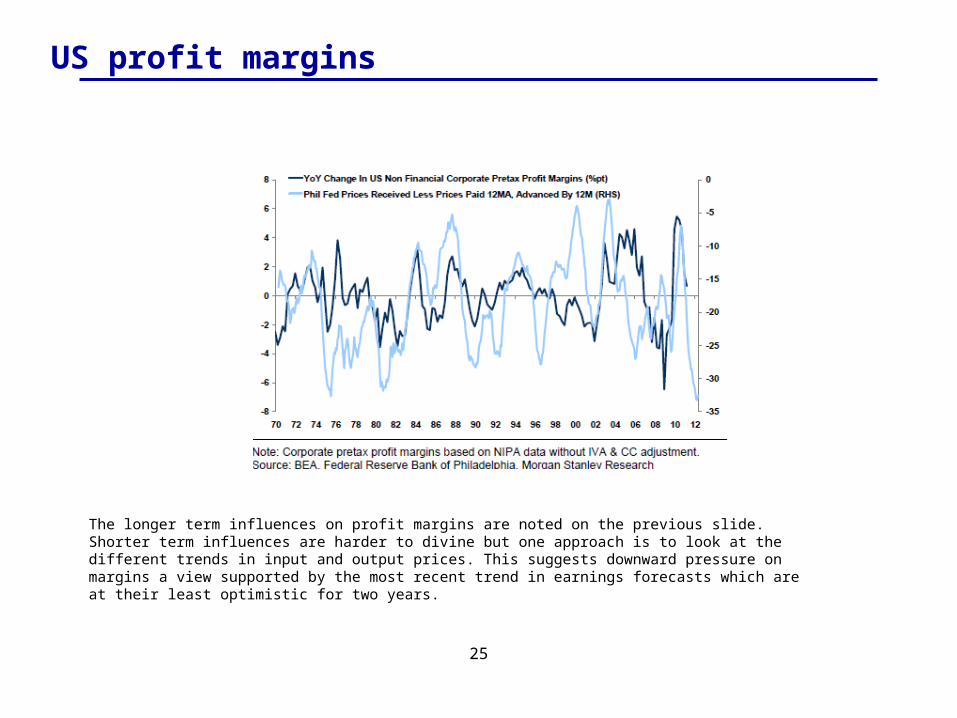

US profit margins

The longer term influences on profit margins are noted on the previous slide. Shorter term influences are harder to divine but one approach is to look at the different trends in input and output prices. This suggests downward pressure on margins a view supported by the most recent trend in earnings forecasts which are at their least optimistic for two years.

26

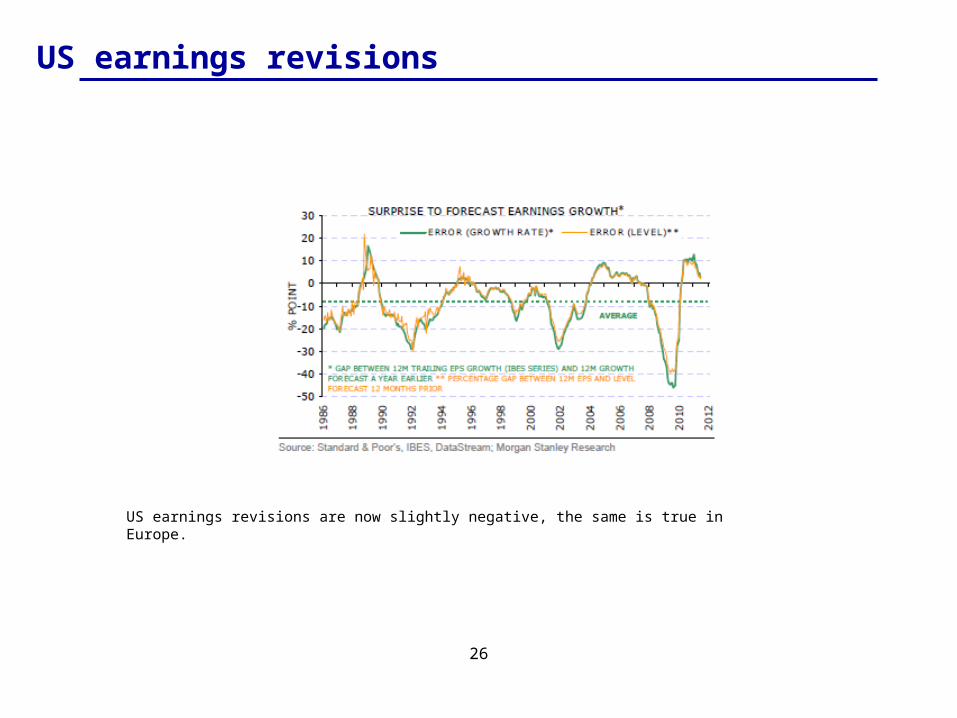

US earnings revisions

US earnings revisions are now slightly negative, the same is true in Europe.

27

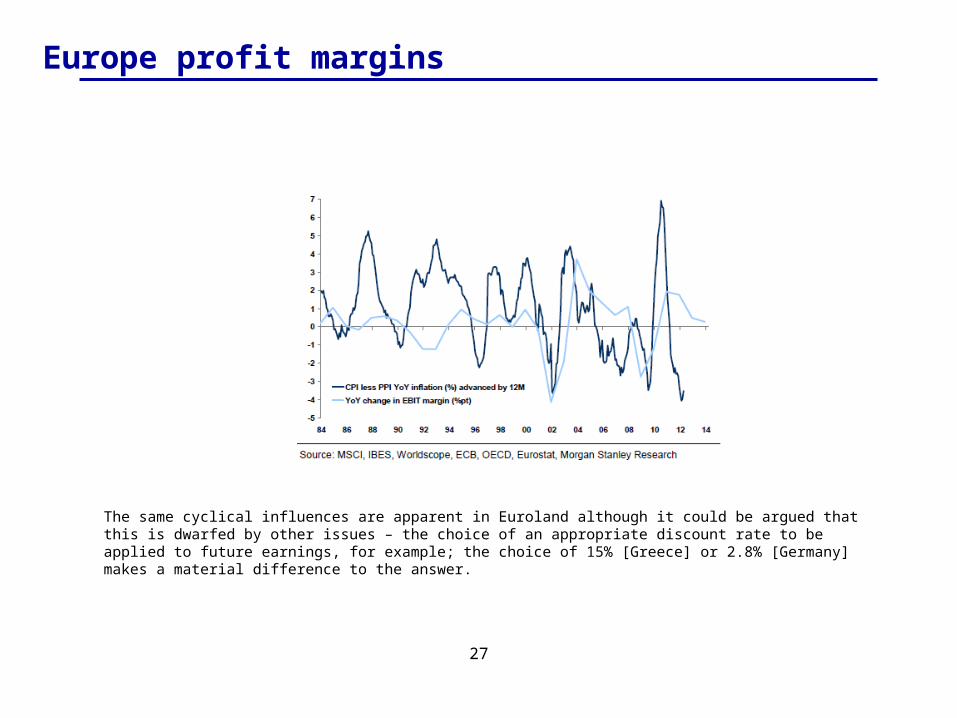

Europe profit margins

The same cyclical influences are apparent in Euroland although it could be argued that this is dwarfed by other issues – the choice of an appropriate discount rate to be applied to future earnings, for example; the choice of 15% [Greece] or 2.8% [Germany] makes a material difference to the answer.

BONDS

29

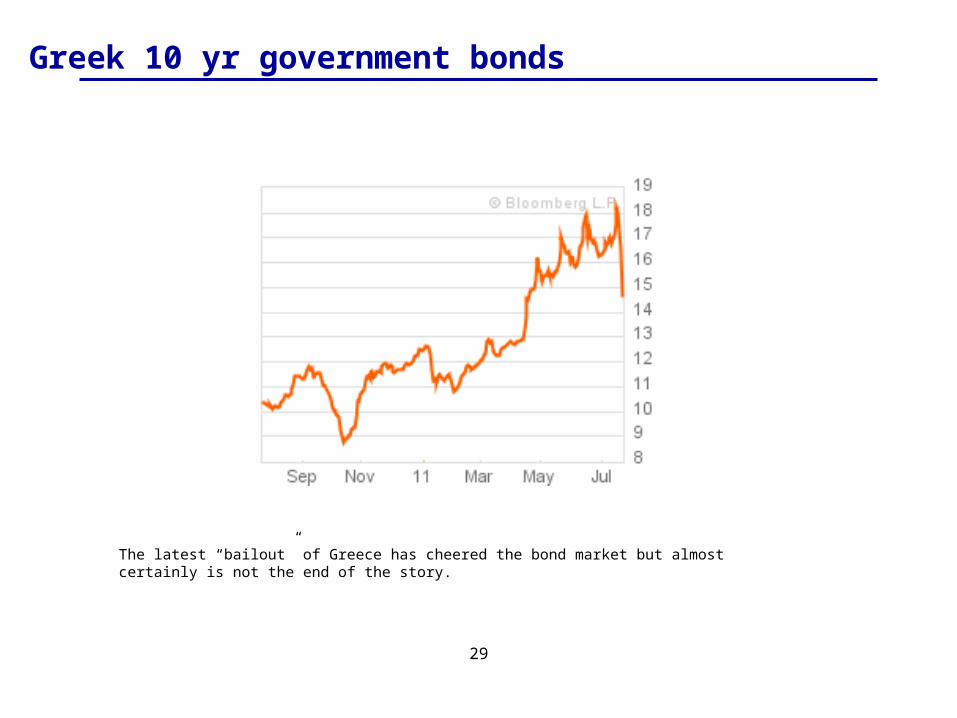

Greek 10 yr government bonds

The latest “bailout” of Greece has cheered the bond market but almost certainly is not the end of the story.

30

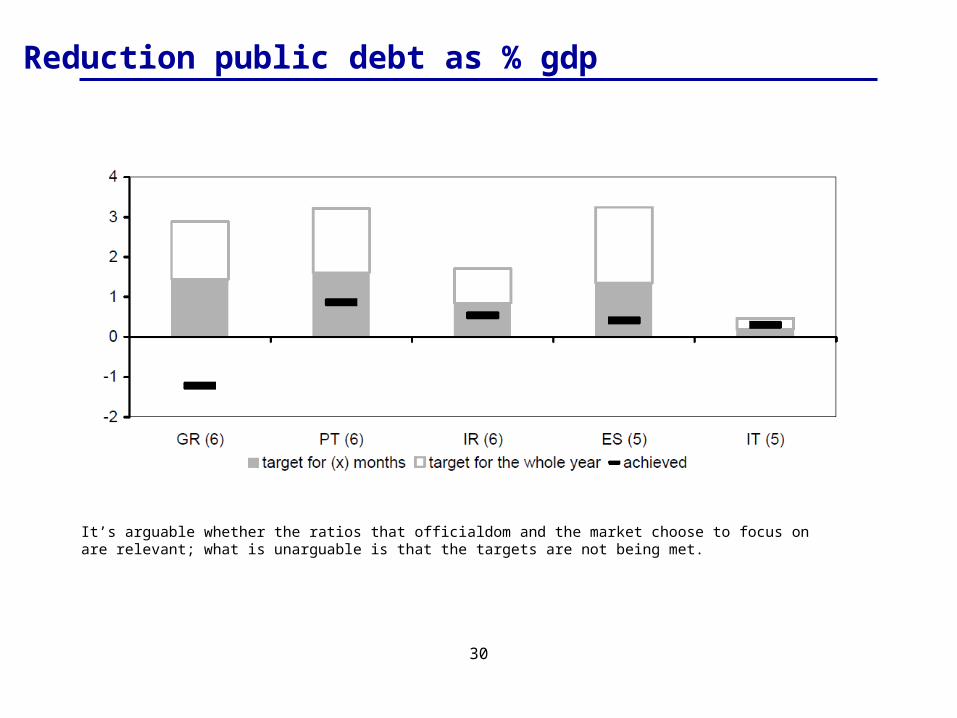

Reduction public debt as % gdp

It’s arguable whether the ratios that officialdom and the market choose to focus on are relevant; what is unarguable is that the targets are not being met.

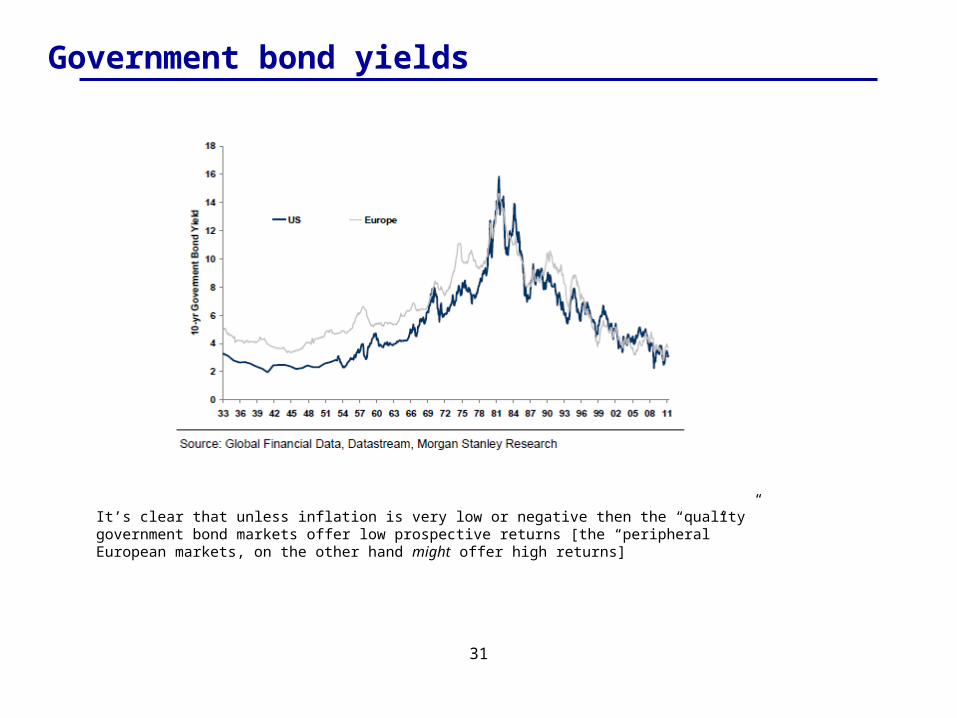

31

Government bond yields

It’s clear that unless inflation is very low or negative then the “quality” government bond markets offer low prospective returns [the “peripheral” European markets, on the other hand might offer high returns]

32

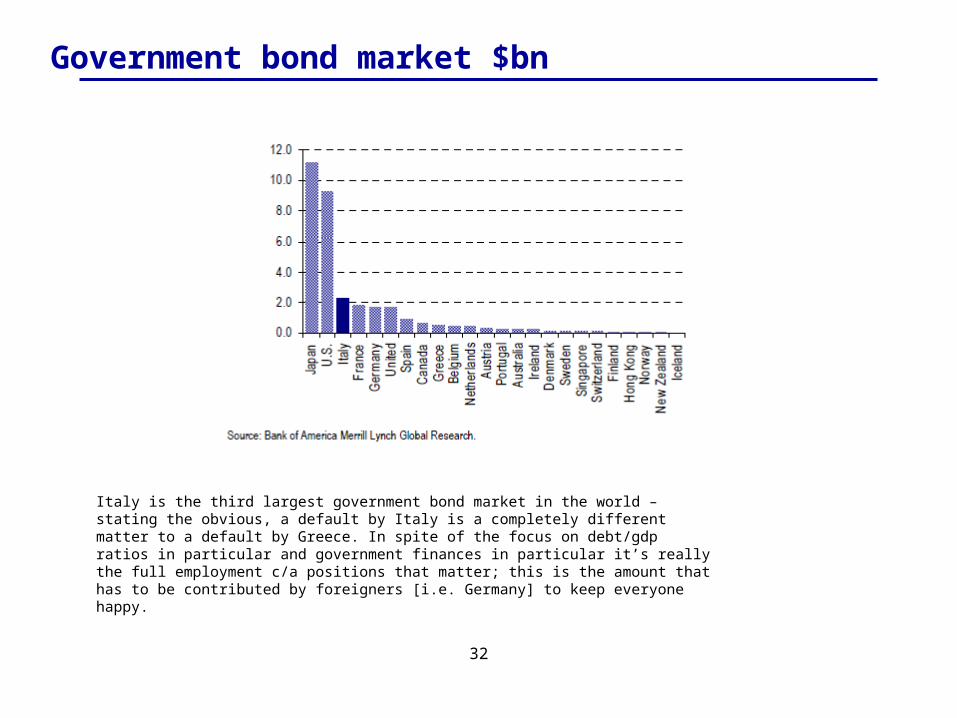

Government bond market $bn

Italy is the third largest government bond market in the world – stating the obvious, a default by Italy is a completely different matter to a default by Greece. In spite of the focus on debt/gdp ratios in particular and government finances in particular it’s really the full employment c/a positions that matter; this is the amount that has to be contributed by foreigners [i.e. Germany] to keep everyone happy.

33

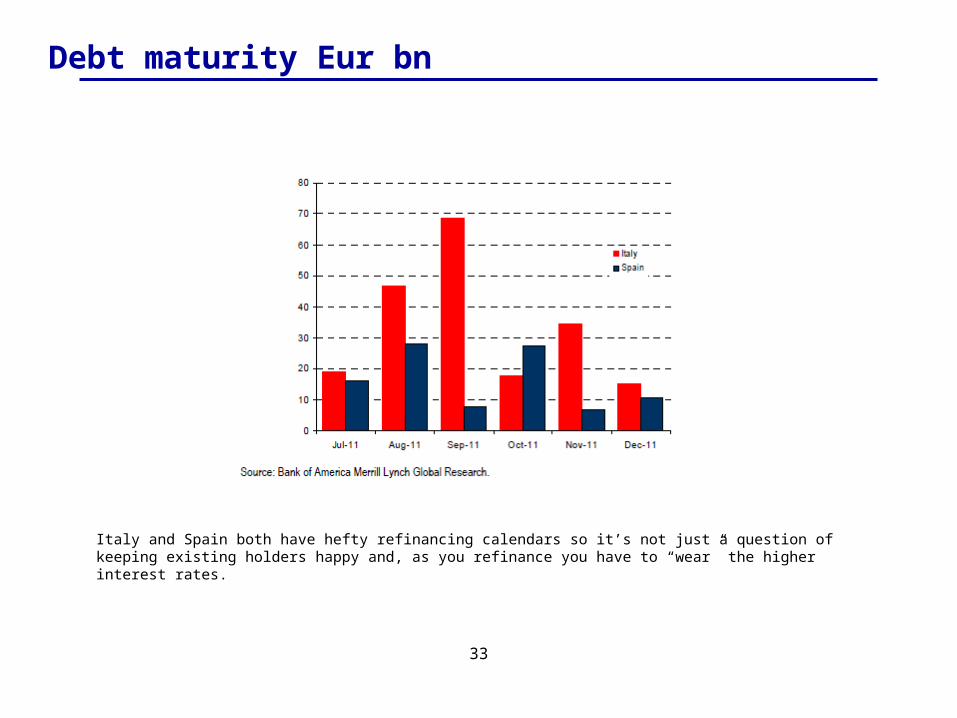

Debt maturity Eur bn

Italy and Spain both have hefty refinancing calendars so it’s not just a question of keeping existing holders happy and, as you refinance you have to “wear” the higher interest rates.

34

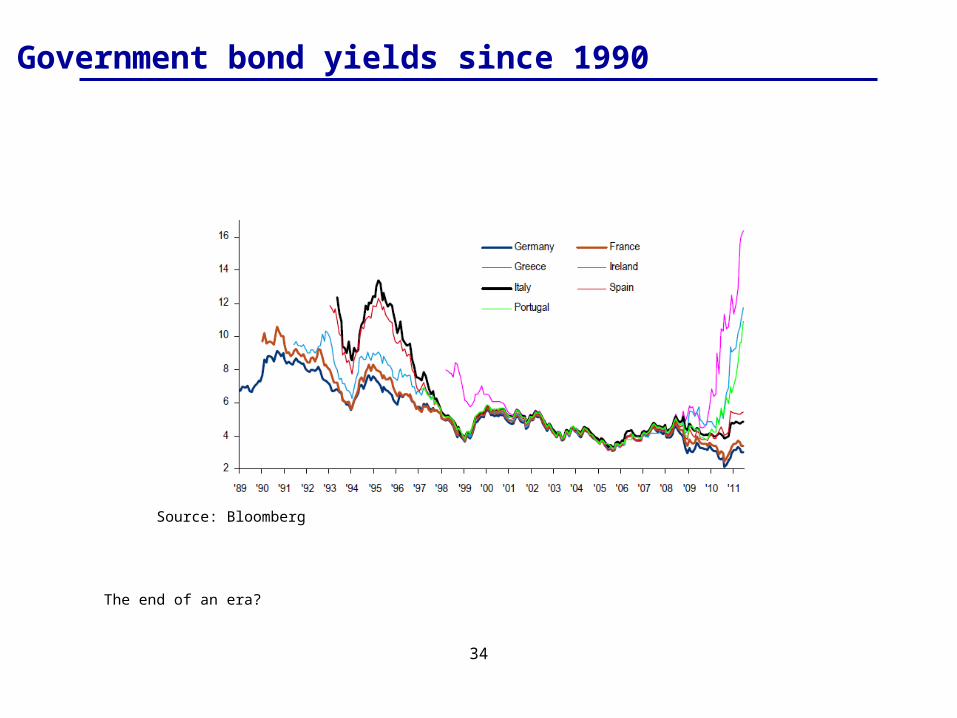

Government bond yields since 1990

Source: Bloomberg

The end of an era?