Embed Size (px)

Citation preview

VOL. I NO. : 08 April 2019 Pages 48

Finance

Export - Import

SkillDevelopment& Training

Branding

Digitalisation

Schemes

MSMELending

MEDC Economic DigestApril 2019�2

MEDC Economic Digest April 2019

MEDC Governing Board

Printed, Published & Edited by

From the President’s Desk

MEDC President:

Mr. Ravindra BoratkarManaging Director, MM ActivSci - Tech Communications Pvt. Ltd.

MEDC Vice Presidents :

Mrs. Meenal MohadikarCEO, Anand Trade DevelopmentService

Mr. Chandrakant SadadekarChairman,Sadadekar Global GroupExport-Import

Mr. Mukund KulkarniDirector, Expert Global SolutionsPvt. Ltd.

MEDC Immediate Past-Presidents:

Cdr. Dipak NaikPresident & CEO,Naik EnvironmentResearch Institute Ltd. (NERIL)

Mr. Nandkishor KagliwalChairman, Nath Group

Ms. Ananya Prem Nath on behalf of

Maharashtra Economic

Development Council (MEDC) and

Printed at Onlooker Press, 16,

Sassoon Dock, Colaba,

Mumbai - 400 005 and Published

from Maharashtra Economic

Developement Council, Y. B. Chavan

Centre, 3rd Floor, Gen. J. Bhosale

M a r g , N a r i m a n P o i n t ,

Mumbai - 400 021.

�3

Dear Members,

e are living in an age of awesomeWtransition wherein change is the onlyconstant. This implies a holistic look atthe concerns of industry, with thefocus remaining on strengthening itscompetitive advantage. In this context,

the country's Micro, Small and Medium Enterprises (MSME)sector has emerged as a vibrant and dynamic sector of theeconomy. Today, the sector produces a wide range of products,from simple consumer goods to high-precision andsophisticated finished products. It also plays a key role in creatinga huge amount of employment at minimum cost of capital incomparison to large industries. This characteristic of the MSMEsector aids in the establishment of industry in socioeconomicallybackward and politically disturbed regions of the country,leading to a justifiable redistribution of national income andwealth. This makes possible an inclusive and balanced growth.

To date, the government has introduced many policies andprogrammes to provide a better enabling environment for thegrowth of the MSME sector. To that end, the importance of thesupportinginfrastructure can never be underestimated. It isnecessary to address infrastructural bottlenecks and streamlinethe forward and backward linkages in the economy to sustain thelong-term growth of MSMEs. There is vast scope for individualMSMEs to benefit from regulatory facilitation, economies ofscale, synergy, and collective bargaining if some strategic issuespertaining to infrastructure development are adequatelyaddressed. The overall state of infrastructure in most areaswhere MSMEs operate continues to be challenging, thus leadingto high transaction costs, and a diminishing of economiccompetitiveness. If the Indian economy is to truly take off,it isimperative to boost the growth of the MSME sector throughsustained infrastructure development.

The current market conditions do not provide enoughopportunities for MSMEs to raise funds at a low cost. Theinterest rate structure of the economy remains too high to

MEDC Economic DigestApril 2019�4

accommodate the smaller players. Credit flow needs to befurther improved, and low cost finance provided to the MSMEsector. As expected, banks remain a dominant source of financefor MSMEs, with over two-third of MSMEs accessing financefrom banks. However, our banking system is today facing acrisis, and the MSME sector seems to be bearing the brunt of it.Some other issues faced by MSMEs include a lack of skilldevelopment, technology, marketing, and ofteninadequatejustification for the denial of finance.

We should not forget that the MSMEsectorcontinues to play avital role in the country's development strategy. It accounts for45% of manufacturing output, over 90% of the industrial units,and 40% of exports. The sector also provides employment toalmost 60 million people, mostly in the rural parts of thecountry, making it the largest source of employment afteragriculture. The proactive development of MSMEs will go along way in poverty alleviation and productivity enhancement.Thus, the successful expansion of this sector holds the key toinclusive growth and distributive justice.

Keeping all these factors in mind, the current issue of the Digestis devoted to analysing the various issues pertaining to thegrowth and development of the MSME sector.

CN

ON

TE

TV

ol.

I N

o.8

Apri

l 2019 F T P ’ D 03ROM HE RESIDENT S ESK

MEDC Economic Digest April 2019 �5

� �C SOVER TORY

The National Small Industries

Corporation Limited

- Mr. P. Krishna Mohan 24

Branding For SMEs

- Mr. Suil Gaitonde 27

MSMES : Performance, Emerging

issues and Policy Initiatives

- Dr. R. K. Pattanik

- Mr. Chinmay Joshi 32

� �& FFACTS IGURES

8

17

Ventspils - port and industiral

centre in Latvia - a natural gateway

between EU and Asia 44

MEDC Economic DigestApril 2019�6

Interim ChairmanMr. Ravindra Boratkar

EditorMs. Ananya Prem NathSenior Manager - Research& Training

Editorial Advisers:

Cdr. Dipak Naik,Immediate Past President,MEDC

Dr. Prakash Hebalkar,President, ProfiTech

Dr. Dhananjay Samant,Chief Economic Adviser,MEDC

Address:MEDC Research Centre,3rd Floor, Y.B. Chavan Centre,Nariman Point,Mumbai - 400 021.Tel.: +91 22 2284 2206/09Fax : 22846394Email: [email protected]: www.medcindia.com

MEDC Economic DigestEditorial Board

VOL. I NO. : 08 April 2019 Pages 48

Finance

Export - Import

SkillDevelopment& Training

Branding

Digitalisation

Schemes

MSMELending

� �C SOVER TORY

�

What Ails the MSME Sector ?

- 36Tulsi Jayakumar

MSMEs in India -

Growth Catalyst

- Mr. R. Kannan 40

� �S FPECIAL EATURE

MEDC Economic Digest April 2019 �7

Maha Facts & Figures

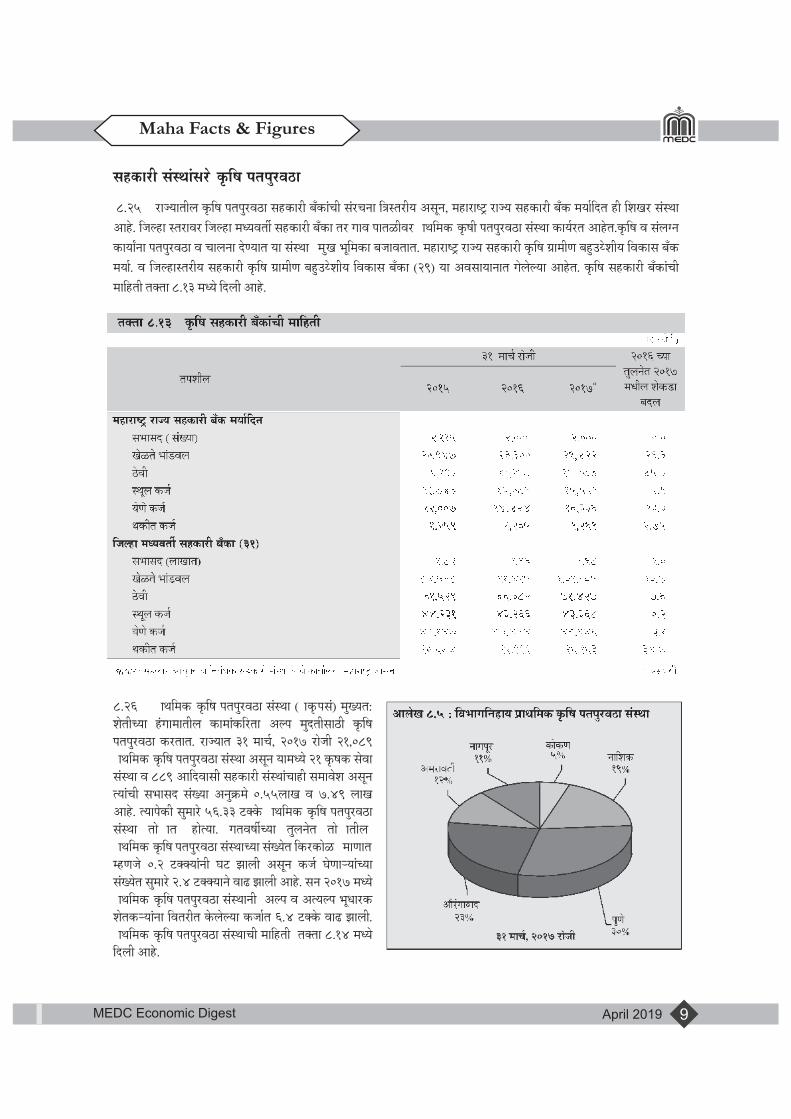

MEDC Economic DigestApril 2019�8

MEDC Economic Digest April 2019 �9

Maha Facts & Figures

Maha Facts & Figures

MEDC Economic DigestApril 2019�10

MEDC Economic Digest April 2019 �11

Maha Facts & Figures

Maha Facts & Figures

MEDC Economic DigestApril 2019�12

MEDC Economic Digest April 2019 �13

Maha Facts & Figures

Maha Facts & Figures

MEDC Economic DigestApril 2019�14

MEDC Economic Digest April 2019 �15

Maha Facts & Figures

Maha Facts & Figures

MEDC Economic DigestApril 2019�16

MEDC Economic Digest April 2019 �17

Cover Story

Cover Story

MEDC Economic DigestApril 2019�18

MEDC Economic Digest April 2019 �19

Cover Story

Cover Story

MEDC Economic DigestApril 2019�20

MEDC Economic Digest April 2019 �21

Cover Story

Cover Story

MEDC Economic DigestApril 2019�22

MEDC Economic Digest April 2019 �23

Cover Story

The National Small Industries Corporation Limited(a Government Of India Enterprise)

Micro, Small and MediumEnterprises are the backboneof the economy of the countryand the Gove r nmen t i sextending support to make thissector strong through variousschemes.

National Small IndustriesC o r p o r a t i o n ( N S I C ) ,established in 1955, is an ISO9 0 0 1 - 2 0 1 5 c e r t i fi e dGovernment of IndiaEnterprise under Ministry ofMicro, Small and MediumEnterprises (MSME). Since itsinception, NSIC has beenworking to promote, aid andfoster the growth of micro,small and medium enterprisesin the country. NSIC operatesthrough countrywide networkof offices, with its Head Officeat New Delhi..

Mission: “To promote andsuppor t Micro, Smal l &Medium Enterprises (MSMEs)Sector” by providing integratedsupport services encompassingMarketing, Technology,Finance and other services.

Vision: “To be a premierOrganization fostering thegrowth of Micro, Small andMedium Enterprises (MSMEs)Sector”

1. Single Point RegistrationScheme

The Micro and Small(Manufacturing and ServiceIndustries) units registeredunder Single Point RegistrationSchemes (SPRS) with NSICget following benefits as perpublic procurement policy2012

a) Issue of the Tender Setsfree of Cost.

b) Exemption from Paymentof earnest Money Deposit(EMD).

c) In Participating Micro &Small Enterprises quotingprice within Price band ofL1+15 percent shall also beallowed to supply a portionof requirement by bringingdown their price to L1 Pricein a situation where L1Price is from someoneother than a Micro & SmallEnterprises and such Micro& Small Enterprises shallbe allowed to supply up to20 Percent of the totaltendered value.

d) Every Central Ministries /Departments / PSUs shallset an annual goal ofminimum 20percent of the

total annual purchases ofthe products or servicesproduced or tendered byMSEs. Out of annualr e q u i r e m e n t o f 2 5 %procurement from MSEs,4% is earmarked for unitsowned by Schedule Caste/Schedule Tribes and 3% toWomen Entrepreneurs. Inaddition of the above, 358items are also reserved forexclusive purchase fromMSEs.

Maharashtra State Governmenthas notified the purchase ruledated 01.12.2016 to avail thefollowing benefit by MSEsregistered with NSIC.

I. Tender sets free of cost andEMD exempted.

II. 241 items are reservedexclusively for MSEs.Against 241 items, 20%purchase is to be madecompulsorily from MSEunits belonging to SC/STentrepreneurs.

III. To purchase non reserveditems, 20% are reserved tobe procured from MSEsand out of 20%, 4% goodsto be procured exclusivelyfrom the SC ST MSEs./

Mr. P. Krishna MohanDy. General [email protected]/[email protected]

Cover Story

MEDC Economic DigestApril 2019�24

2. Raw Material AssistanceScheme

NSIC facilitates credit toMSMEs for their Raw Materialrequirement for procurementof raw materials.

MSMEs stand to benefitadditional fund leverage underthe Raw Material AssistanceScheme of NSIC against BankGuarantee along with assuredsupply of raw material fromleading raw material producers.

Rate of Interest P.A. @ 10.50 % P.A. Micro Industries.

@11.00 % P.A Small Industries.

@11.00% P.A. Medium Industries

Processing fee @ 1% P.A.

� 95% of payment to RawMaterial Supplier againstBank Guarantee.

� Concession in rate ofinterest from 0.5 to 1%depending on Credit Ratingsubject to SME-1 or SME-2Rating.

3 . R aw M a t e r i a lDistribution Scheme:

NSIC has signed agreements /MoUs with the major bulkproducers (Aluminium, IronSteel, Paraffin Wax, Coal andPolymer products etc.) Thesearrangements facilitateMSMEs in getting material atthe manufacturer 's price,leading to reduction in the costof raw materials and makingthe end products of MSMEs

competi t ive. The creditsupport is also available forprocurement of raw material(s)at competitive rates.

4. Consortia and TenderMarketing

Small Enterprises in theiri nd iv idua l c apac i t y f a ceproblems to procure & executelarge orders, which deny them alevel playing field vis-a'-vis largeenterpr ises. NSIC for msconsortia of Micro and Small

units manufacturing the sameproduct, thereby pooling intheir capacity.

NSIC applies the tenders onb e h a l f o f s i n g l eMSE/Consortia of MSEs forsecuring orders for them.T h e s e o r d e r s a r e t h e ndistributed amongst MSEs intune with their productioncapacity.

5 . Credi t Faci l i ta t ionThrough Bank

To meet the creditrequirements of MSME unitsNSIC has entered into aM e m o r a n d u m o fUnderstanding with variousNationalized and Private SectorBanks. Through syndicationwi th these banks, NSIC

facilitates MSME in accessingcredit support (fund based ornon-fund based limits) fromthe banks. NSIC ass i s t sMSMEs in completion of thedocumentation for submittingthe proposals to the banks andalso does the follow up with thebanks. These handholdingsupport are provided by NSICwithout any cost to the MSMEs

6 SME B. M Global Mart B2Web Portal For M s (freeSMEFor S S Entrepreneurs)C/ R

With increase in competitiona n d m e l t i n g a w a y o finternational boundaries, thedemand for information isreaching new heights. NSIC,realizing the needs of MSMEs,is offering InfomediaryServices which is a one-stop,one-window bouquet of aidsthat will provide informationon business & technology andalso exhibit the corecompetence of IndianMSMEs. B2B Webportal isoffering following benefits tothe members of InfomediaryServices.

� Interactive database ofMSMEs

� Self web development tool

� National Tenders on email

� Centralized mail system

� Popular Products Section

� Unlimited global TradeLeads

� Trust Seal of NSIC

� MSME Web Store

MEDC Economic Digest April 2019 �25

Cover Story

� Multiple Language Support

� Discussion Board

� Call Centre Support & LiveChat

� Other Value added Services

� Payment Gateway formembership subscription

7. Exhibitions andTechnology Fairs

To showcase the competenciesof Indian SSIs and to capturemarket opportunities, NSICp a r t i c i p a t e s i n s e l e c tInternational and NationalExhibitions and Trade Fairsevery year. NSIC facilitates theparticipation of the smallenterpr ises by providingconcessions in rental etc.Participation in these eventsexposes SSI units tointernational practices andenhances the i r bus ines sprowess.

For more details please go to:http://www.nsic.co.in/Schemes/Ex h i b i t i o n - C o m p l e x - E v e n t -Management.aspx

8. Buyer-Seller meets

Bulk and departmental buyerssuch as the Railways, Defence,Communication departmentsand large companies are invitedto participate in buyer-sellermeets to enrich smallenterpr ises knowledge

r e g a r d i n g t e r m s a n dconditions, quality standards,etc required by the buyer. Theseprogrammes are aimed atvendor development fromMSMEs for the bulkmanufacturers.

9. National Scheduled Caste-Scheduled Tribe Hub

Scheme Implemented by theMinistry of MSME throughNational Small IndustriesCorporation (NSIC)

� ObjectivesFacilitate SC/STentr epr eneur s ina c h i e v i n g 4 %procurement mandate ofC P S E s / C e n t r a lGovernment Depts. asper Public ProcurementPolicy 2012.

Impar t appl icableindustry best practices

Leverage the Stand- upIndia initiative forencouraging new SC/STentrepreneurs

Special Subsidy to the SC-STEntrepreneurs underfollowing three schemes

Single Point RegistrationScheme (SPRS) :

100% Subsidy SC-STApplicant unit has to payonly Rs.100 plus ST

1 0 0 % s u b s i d y o nmember sh ip of B2BPortal (www.msme.com)

Special MarketingAssistance Scheme (SMAS) :

100% subsidy (subject toMax. cap) for participation /visit in 2International Fairs and 4Domestic fairs in a financialyear

Reimbursement of bankcharges for PerformanceBank Guaran tee f o rparticipation in Govt.Tenders upto maximum ofRs.1,00,000/-.

Reimbursement ofMembership fee of variousExport Promotion Councilsu p t o m a x i m u m o fRs.20,000/-.

Reimbursement of BankLoan Processing Chargesu p t o m a x i m u m o fRs.1,00,000/-

Reimbursement of fees fortwo short term managementcourses from top institutesup to maximum ofRs.1,00,000/-.

Reimbursement of 50%Testing Charges from NABLaccredited laboratories andlicense or certificate fee fromBIS with a ceiling limit ofRs.1,00,000/- whichever islower in a given financialyear.

Cover Story

MEDC Economic DigestApril 2019�26

Branding For SMEs

At a couple of seminars where Ihappened to be a speaker, someof the prospec t ivee n t r e p r e n e u r s r a i s e d apertinent question. It was akinto the chicken or egg puzzlethat is always talked aboutwhen deciding what comesfirst. How does a prospectiveentrepreneur raise the initialf unds ? T he prospec t iveentrepreneur may have ideasbut may not have money tosupport the ideas. He has nomoney to buy place, buymachinery, hire people, doresearch…. In short, no moneyto set up his business.

Having seen new businessesbeing set up, having helpedsome start-ups, and above all,having set up my personalprofessional practice morethan 35 years back, I have aword of adv i c e fo r theprospective entrepreneurs aswell as the small and mediumenterprises (SMEs).

I believe, the SMEs initiallystruggle for issues like, amongothers:

� How to raise the initialfunds – here, your initialcontribution is a must andthere is no running awayfrom this. This ini t ia l

contribution is meant toshow your commitmenttowards your new businessventure – and ins t i l l sconfidence in the minds ofthe prospective lender aboutyour intentions;

� How to sell the product –for any new entrant in eithera crowded market place, orf o r s o m e o n e w h o i sintroducing an altogethernew product in the market,acceptance in the market is abig hurdle. Will you be ableto create a nitch for yourproduct in the crowdedmarket by introducing auniquely different productor service with a robustquality?

At this juncture the chicken andthe egg story starts. Should Iinvest in a product or a servicenot knowing whether I willsucceed in marketing them? Onthe other hand, though I amconvinced about being able tomarket a product or a service,how to raise the initial capital /funds to produce it?

As regards funding, I am sureyou will all agree that you needt o d e m o n s t r a t e y o u rearnestness and seriousness bybringing in your own money to

start with. You cannot play withpeople's money while keepingyour own intact. Even in thelarger version of enterprises,the percentage of promotersholding is one of the decisiveelements for the investors.

Coming to marketing, oneneeds to keep in mind certainprinciples of economics. If youare a monopoly, your profitmargins are expected to be highbecause you can afford tocharge higher prices due to lackof competition. However,attracted by your profitmargins, new and newer playersstart entering the market andnow, in the crowded market, theprices see a downwardmovement eating up yourprofits. Here, the rule survivalof the fittest comes into play.

Today, we live in ane n v i r o n m e n t w h e r ecompetition is immense andthe market is crowded. Youstart with a new idea today andwithin days, many others willfollow. Whether you get thebenefit of being the first in themarket or the person enteringthe market later gets the benefitof being aware about thecustomer reactions andexpectations, and thus, has thebenefit of being an enlightened

Mr. Sunil GaitondeVice chairman

NKGSB

MEDC Economic Digest April 2019 �27

Cover Story

entrepreneur is a debatableissue.

In my humble v iew, thes o l u t i o n t o b o t h t h e s eproblems lies in systematicbranding i.e., creating anidentity or an image – for youren te r pr i s e and for yourproducts. This is the universaltruth and there is no escapingfrom it. Infosys wasn't built bypeople who were flush withfunds having loads of money toinvest. It was started as SME bypeople like you and me. Theyhad to borrow their initialmoney from a cooperativebank as no PSU bank waswilling to lend. Look at thescenario today, I am sure,bankers may be lining upoutside Infosys gate to get theiraccount. This is the value of thebrand.

Adidas and Puma, brandleaders in their own right, werestarted by Adolf and RudolfDassler, who were cobblers,f r o m a s m a l l v i l l a g e i nGermany. Look at where thebrands are today. Like this,t h e r e a r e i n n u m e r a b l eexamples. What really makesthese brands stand out is theconviction of their creators tobe the front-runners forever.Zero tolerance as regardsquality and an ear constantlynear the ground have helpedthese organizations to sustainand grow in a crowded marketplace.

That brand is universal is anaccepted truth. Products and

services are associated with thecountries, regions, cities as wellas with individuals. SwissWatches, Belgian Diamonds,G e r m a n C a r s , Ja p a n e s eElectronic Products, FrenchWine etc. are examples ofcertain products associatedwith certain countries. Similarly,there is a regional identity forproducts like Assamese Tea,Paithani Saree, Banarasi Paan,Shimla Apples etc. Next comesthe identity associated with theorganizations and the familiesbehind them like the House ofTatas, Birlas, Ambanis and thelike. At the individual level,people like Mr. JRD Tata,Mr. Nani Palkhiwala,Mr. Dhirubhai Ambani etc. areregarded not only as ikons butas brands.

When one thinks about theseC o u n t r i e s , Re g i o n s ,Organizations or Individuals,certain products, services cometo one's mind and with thatenters the perception that onehas about those products orservices. Like for instance,Swiss Watches, Paithani Sarees,Shimla Apples etc. have to begood. Similarly, any productfrom the house of Tatas oradvise / opinion given by Mr.Nani Palkhiwala has to be theultimate and beyond questions.

Branding.

Branding plays a verysignificant role throughout thelifecycle of any business. Whypeople prefer product X toproduct Y, depends on their

perception of X comparedwith Y. In the long run, qualityac t s a s a d i f f e ren t i a to r.However, in the short run,being associated with a productor a service, that is, brandingplays an important role. In mypersonal view, branding plays akey role because as they say ineconomics, “other things beinge q u a l ” , o n e p r o d u c t i spreferred over the other basedon its perception or image inthe minds of the buyers. Thisperception or image is nothingbut branding.

Wikipedia defines a Brand as aname, term, design, symbol, orother feature that distinguishesan organization or productfrom its rivals in the eyes of thecustomer.

In other words, Brands areinherently striking and play therole of creating an indelibleimpression.

This explains why commonerslike me buy Camel ink, Fevicoladhesive, Lijjat Papad and so onand the people from the higherstrata of the society aspire tohave a Mercedese car, Rolexwatch etc. Certain attributes getattributed to these brands andcreate a permanent impressionin the minds of the buyers – beit quality, price, delivery, taste,comfort, robustness or acombination of all of these.

Standout from the crowd.

Major advantage of a Brand isundoubtedly, that it helps anorganization or a product tostand out from the crowd.

Cover Story

MEDC Economic DigestApril 2019�28

The most powerful marketingtool for any organization intoday's crowded market spaceis a standout organizationidentity. With a standouti d e n t i t y i n p l a c e , a norganization can earn trustfaster, benefit from positiveword of mouth, enjoy frequentreferrals, attract larger numbero f c u s t o m e r s , c r e a t e aprofessional image, growawareness faster, and motivatec u s t o m e r s t o t a ke p r e -determined actions and bea c c e p t a b l e . A p r o d u c tintroduced by Tata may needl e s s e r m a r ke t i n g e f f o r tcompared to the s imi larproduct introduced by anunknown competitor. Whenyou go to the market, you go tobuy XYZ toothpaste or ABCfan depending on either yourown past experience, or, mostlyon the image the brand hassucceeded in imbibing in yourmind.

Every organization, big orsmall, needs to be professionalto the core be it the quality ofthe product or service since wea l l a r e l i v i n g i n ahypercompetitive world,. Asthe competitors are sitting atour doorsteps, any lapse inprofess iona l i sm and thecustomer may be lost forever.And, this can happen within afew seconds even before werealize it.

Every organization, whether ithas been in the business for anumber of years or is a startup,

has to be prepared to facecompetition. This competitionkeeps getting intense every day.Under the circumstances, theonly survival strategy could be astrong brand loyalty thatdifferentiates us from thecompetition. If we fail to dothis, we will be marginalizedsooner or later and will becomeredundant.

Importance of brandbuilding.

Brand is, beyond doubt, themost important and sustainableasset of any organization. Howmany of us still relate cameraswith Kodak and mobile phoneswith Nokia as these were greatbrands a few years ago.

In fact, the good organizationsare so conscious about theirbrand, that the brand becomesthe main theme around whichall their decisions and actionsare woven.

All the great companies strivehard to protect the reputationof their brand. In fact, for thesecompanies, the importance ofbrand reputation provides thestrongest incentive to protectthe reputation of its brand atany cost. I remember, as ayoung man, ever eager to graspthe words of wisdom of ourikons, a question that was askedto late Mr. Abasaheb Garware.The question related taggingthe name Garware to clubs,bridges, university etc. Thequestioner implied that this wasbeing done for publicity. The

answer given by Abasaheb wassimple and logical. Accordingto him, by associating his familyname with these structures, hehoped that his futuregenerations would look afterand maintain them well.

If a brand delivers what itpromises, behaves in aresponsib le manner, andcontinues to innovate and addvalue, people will continue tofollow it with respect andaffection. How many of ushave been using Fevicol forag e s now? Desp i t ecompetition, the brand Fevicolhas become so strong that is hasbecome synonym withadhesives in India just as Xeroxhas become synonym withphoto-copying the world over.

The biggest advantage of abrand is that it allows thec o n s u m e r t o s h o p w i t hconfidence. If the choice isbetween a branded Atta andloose Atta at your grocer, youare, most likely to go for abranded Atta unless yourexperience with the Atta soldby your local grocer has beencons i s t en t l y g ood . T h i sphenomena is also referred toas the “known devil” approach.But in the first place, how doesthat devil become “known”?When you are buying a Zodiac42” shirt, you know exactlywhat size it will fit. Can you saythe same about ABC 42” shirt?In shor t , b r and imp l i e sstandardization – quality,service, comfort, pricing and soon.

MEDC Economic Digest April 2019 �29

Cover Story

Obviously, the real power ofany successful brand is that itmeets the expectations of itsbuyers. These brands areconstantly aware about thepromises to be kept and thequality to be maintained.

Branding in service industry.

Why does one prefer HospitalA over Hospital B? Why does apatient prefer Dr. C? Why dowe approach a lawyer D?

In the service industry, thereputation travels fast and widemainly through the word ofmouth. At the same time, anydamaging news or opiniontravels faster and wider.

Reputation is paramount andthe organizations that areknown for the quality of theirproducts and services and theirintegrity are the ones bestplaced to enjoy a competitiveadvantage.

In the brand savvy world,people have become more and

more discr iminat ing anddifficult to please. I remember,during my childhood, my (aswell as those of my cousins)school uniforms and otherclothes were stitched by a tailorat a small village near Goawhere we all would gather tospend our summer vacations.None of us ever complained aswe did not know any brandsthen. In fact, we would all behappy at getting new clothes towear. How many of us wouldbe willing to get our clothesstitched there today? This isbecause, all of us have becomeconscious of brands. In fact,the brands have succeeded increating that feeling of comfortand assurance in our minds.

This puts the onus on the brandowners who have to ensure thatthey del iver high-qual i tyservices that are focused on ag enu ine commi tment tocustomer satisfaction. Take thecase of Virgin Atlantic. Theimage that pops up is of their

commitment and genuineenthusiasm to strive to offer adifferent experience for theirc o n s u m e r s . S u c h acommitment towards brandresults in a well-managedcus tomer expe r i ence -distinctive and memorable. Thecustomers would want to flywith them again and again.That's the success of the brand.

In the case of institutions likebanks and other ser v iceoriented institutions, it isextremely difficult for them todifferentiate. Most of theseh a v e b r o a d l y t h e s a m eproducts, similar premises andfacilities and offer similarservices.

However, in their case, theire m p l o y e e s a c t a sdifferentiators. They can makea huge difference and as is said,c a n m a k e o r b r e a k i ninstitution. Employees canmake or mar a long-standingrelationship forgetting the factthat institutions like banks,have, traditionally been thebusiness of “relationships”.

Hence, a properly trained staffis clearly one of the mostimportant commitments tobrand management that suchservice oriented organizationscan make. This training couldencompass business and socialskills that may excite theemployees.This enthusiasmand commitment of theemployees, is contagious to thecustomers.

Cover Story

MEDC Economic DigestApril 2019�30

What makes brands great?

As suggested by Mr. ChuckBrymer, brands are aboutchoice, and these brands haveto compete in a crowded andnoisy market place. Some ofthe distinctive traits that makebrands great according to Mr.Brymer are:

� Consistency in delivering ontheir promise. Leadingbrands communicate theirpromise to the market,encouraging customers topurchase the product orservice. They must doeverything in their power todeliver on the promise;

� Superior products andprocesses. To attractcustomers and maintaintheir loyalty, organizationsmust offer those products orservices that are superior toothers, thereby reducing therisk that the customer willnot be satisfied.

� Distinctive positioning andcustomer experience. Brandleaders capture what isspecial about their offering,convey it to the desiredaud ience and a l lowcustomers to experience it.Customers prefer anenvironment that iscustomer centric andpersona l as ag a ins tenvironments that arec o n f u s i n g , n o i s y a n dimpersonal;

� Alignment of internal andexternal commitment to the

brand. Leading brandsunderstand that an internalculture supportive of thebrand strategy has a farbetter chance of delivering aconsistent yet differentiatedexperience. The internalvalues are aligned with brandv a l u e s t o s h a p e t h eorganization's culture andembed the core purpose.The true test of a leadingbrand is whether employeescommitment to the brand ishigh, as that will help keepcustomer commitment high.In other words, those wholive the brand will deliver thebrand.

� An ability to stay relevant.Leading brands constantlymaintain their relevance tothe targeted set ofc u s t o m e r s , e n s u r i n gownership of clear points ofdifference compared withthe compet i t ion. Theysustain their credibility byincreasing customers' trustand loyalty to them.

Once a brand loses touch withi t s cus tomer or i gnore spotential new audience, it haslost relevance. Differentiationis a critical component of thebranding process

As Jim Collins writes in hisbook Good to be Great, tobuild a great company, you haveto have a strong set of corevalues, that you nevercompromise.

Brand-building skills.

We must represent our brand.We must embody the brand. Allour communicat ions andactions must align with the corepurpose and values reflectingthe brand. Every person in theorganization needs to act as arole model portraying anappropriate behavior and act inthe bes t in teres t of theorganization.

We must also continuously tryto keep identifying the factorsthat may give our brand aunique identity. We need to behands on as regards, customerpreferences, competition, andmarket conditions as these areincredibly dynamic. We need tobe constantly in the know ofthem.

Conclusion.

To sum up, if you succeed inbuilding a brand, half yourworries are taken care of. It maybe easy to arrange for finance,easy to sell your product, easy toconvince the customers to tryout a new product, easy to geta n d r e t a i n h i g h c a l i b e remployees and easy to managethe supply chain.

So the advice to the SMEs is totry and create a strong brandwith a focus on delivering whatyou promise and a policy ofzero tolerance towardsdeviations.

MEDC Economic Digest April 2019 �31

Cover Story

MSMES: Performance, Emerging issuesand Policy Initiatives

1. Introduction

Over the last five decades, theMicro, Small and MediumEnterprises (MSME) sector hasemerged as a highly vibrant anddynamic sector of the Indianeconomy. This sector hascontributed significantly toIndia's growth, employmentgeneration and export. Besides,the contribution to economicdevelopment this sector hasmade significant contributionto social development byfostering entrepreneurship. Inthe current scenario, MSMEsare playing a complementaryrole to large industries asancillary units. It is pertinent tonote that the MSMEs arewidening their domain acrosssectors of the economy,producing diverse range ofproducts and services to meetdemands of domestic as well asglobal markets. Recognising theimportance of MSMEs, Mao-Tse-Tung once said, “Let abillion MSMEs bloom!” Thusempowering MSMEs is key tosustainable growth of India.The present article makes anattempt to analyse ways andm e a n s f o r e m p o w e r i n g

MSMEs. The organisation ofthis article is as follows. Section2 presents an overview of theperformance of the MSMEsector. Section 3 outlinesemerging issues. Policy optionsare discussed in section 4 andsection 5 concludes.

2. Overview of theperformance

2.1 Structure of MSMEs

The Government of India hasenacted the micro, small andmedium enterprisesdevelopment (MSMED) Act,2006 in which the definitions ofmicro, small and mediumenterprises have been set out. Amicro enterprise is havinginves tment in p lant andmachinery not exceeding Rs. 25Lakhs. A small enterprise inhaving investment in plant andmachinery not exceeding Rs. 5Crores. A medium enterprise ishaving investment in plant andmachinery more than Rs. 5Crores but not exceeding Rs.10Crores

As per the national samplesurvey, there were 633.88 lakhunincorporated non -agriculture MSMEs in the

country engaged in differenteconomic activities (196.64lakh in Manufacturing, 230.35lakh in Trade and 206.84 lakh inOther services). Thus around31 per cent MSMEs wereengaged in manufacturingactivities, 36 per cent are intrade and 33 per cent are inservices. As per the categorywise distribution of enterprises,micro sector comprises 99 percent of the total MSMEs. Theper cent share of rural andurban MSMS's reveal that 51per cent are rural and 49percent are urban. There hasbeen a strong predominance ofmale entrepreneurs at around80 per cent of the total.

2.2 Contribution to outputand employment

According to the annual report2017-18 of the MSMEs thecontribution of this sector, andtotal output if the economy hasremained at 42 percent for thelast 5 years. As per the NSS,73rd round, MSME sector hascreated 11.10 crores jobs ofwhich 32 per cent are inmanufacturing sector, 35 percent are in trade sector and 33per cent are in services sector.

Mr. Chinmay JoshiResearch Assistant (RA)

SPJIMR

Dr. R. K. PattnaikProfessor, SPJIMR

Cover Story

MEDC Economic DigestApril 2019�32

Micro sector with 630.52 lakhsenterprises providesemployment to 1076.19 lakhspersons are 97 per cents oftotal employment in the sector.T h e d i s t r i b u t i o n o femployment in its urban andrural category, showed that theshare of urban employmentwas 55 per cent. State of UttarPradesh and West Bengalaccount for 28 per cent of theMSMEs.

2.3 Major schemes forMSMEs

Recognising the potential thatMSME sector holds, thegovernment of India has beenlaying a focused attention toenergise the sector this includeUdyog AADHAR, start- upIndia, make in India andstrengthening the ease of doingbusiness. These initiatives haveresulted in praiseworthyimprovement of India'sposition in the world bankreport of Ease Doing Business.India's rank improved to 77 asagainst 130 two years back.A p a r t f r o m t h i s , p r i m eminister's employmentgeneration program is aimed atgenerating self-employmentopportunities by establishingmacro enterprises. Creditguarantee scheme for microand small enterprises coverscollateral free credit facilityextended by eligible lendinginstitutions including NBFCs,to new and existing enterprises.Credit linked capital subsidyscheme (CLCSS) aims atf ac i l i t a t ing t echno log y

upgradation of the MSMEsector. The RBI, has revised itspriority sector lendingguidelines to facilitate credit tothis sector.

3. Emerging issues3.1 Credit �ow to MSMEs

Bank's lending to MSMEs, iseligible to be reckoned forpriority sector advances. Thepriority sector lending includesthose sectors that impact largesection of the populationparticularly the weaker sectionsand sections which areemployment incentive. Thebanks have been advised toachieve a 20 per cent year onyear basis. As on March 2017,there were, 2998 specializedMSME branches of theschedule commercial banks forlending to MSMEs.

According to economic survey2017-18, Government of India(GoI), in the total outstandingcredit given to both, largebusiness and MSMEs, the shareof MSMEs is only 17 per cent.This is because MSMEs isperceived to be risky andcostlier, timely availability ofcredit is a very critical issuewhich the small entrepreneursface. There are evidences ofcumbersome processesinvolved and thus concomitantdelays in getting finances of thebanks. Some of the banks haveimplemented a credit proposaland tracking system. However,a potential borrower continuesto face uncertainties in terms ofthe magnitude of credit and

timeliness of delivery of credit.In this regard, there was arecommendation to explore asystem of professional creditadvisors for MSMEs. Since,MSMEs are typicallyenterprises with weak credithistory and inadequateexpertise.

3.2 Tiding over the

�uctuations in business

MSME entrepreneurs do nothave sufficient technicalknowledge to tide overbusiness fluctuations and at thesame time they don't havesizable resources like bigindustries. Therefore, they areunable to respond in time to theuncertainties of associated withbusiness fluctuations. It isimportant to recognise thatmicro entrepreneurs l ikeweavers, artisans in remoteareas do not have skills to meettheir working capital needs.Therefore, they fall prey to localmoney lenders. Deepening ofbanking services is critical toaddress this issue. Banks shouldproactively have their bankingoutlets in this areas.

3.3 Non-performing assets(NPAs)

One of the critical issues isstressed assets of the MSMEs.MSMEs had 11.8 per cent(Rs.650 billion) share in totalNPAs by public sector bank inthe priority sector. The NPAguidelines suggest that banksand NBFCs generally classify aloan account as NPA based on

MEDC Economic Digest April 2019 �33

Cover Story

90 day and 120 day delinquencynorms, respectively. In order tofac i l i t a te meaningfu lrestructuring of MSMEaccounts that have becomestressed. RBI has decided topermit a one-time restructuringof existing loans to MSMEsthat are in default but 'standard'as on January 1, 2019, withoutan asset c lass ificat iondowngrade. To be eligible forthe scheme, the aggregateexposure, including non-fundbased facilities of banks andNBFCs, to a borrower shouldnot exceed 250 million as on�

Janua r y 1 , 2019 . T herestructuring has to beimplemented by March 31,2020. A provision of 5% inaddition to the provisionsalready held, shall be made inrespect of accountsrestructured under this scheme.Each bank/NBFC shouldformulate a policy for thisscheme with Board approvalwhich shall, inter alia, includef r amework fo r v i ab i l i t y

assessment of the stresseda c c o u n t s a n d r e g u l a rmonitoring of the restructuredaccounts.

3.4 Enhancing businesssense and awareness

The potential and buddingentrepreneur requires technicaland financial guidance tounderstand intricacies of theglobal and domestic markets,banking and financial sectordevelopments, marketing skills,available technology. In thiscontext, it is important to trainthe self-employed individualsfor an entrepreneurial venture.One of the major initiatives int h e d i r e c t i o n i s t h eestablishment of Rural SelfEmployment. It is reported that(R-SETI) R-SETI is sufferingfrom lack of well definedobjectives, robust process forselection of trainees, absenceof upgradation of trainingmethodology. To overcomethis, the approach towardsoperations and management ofR-SETIs needs to be lookedinto.

3.5 Revival and rehabilitationof MSMEs

As alluded to earlier, the MSMEentrepreneurs lack skill toaddress business fluctuations.As a result, even though theyare potentially viable they areprone to temporary duress. Onaccount of this, the time periodbetween operationalization ofthe enterprise and enterprisebecoming sick is very limited.Therefore, revival andrehabilitation of MSMEs hasbeen announced to provide aframework which needs to betriggered either by the bankeror by the entrepreneur whenfirst sign of the stress appear.

3.6 One size �ts all

Currently, from the angle ofproviding finance to theM S M E s, t h e b a n k s a n dNBFCs, follow the approachof one size fits all . Thisapproach has limitations asmicro sector consist of diverseset of enterprises. It is thereforeimportant to adopt adifferentiate approach. In thisc o n t e x t , t h e b a n k s a n dborrowers should share asynergetic and interdependentrelationship so that bothborrower and lender clearlyunderstand their respectiveresponsibilities and therebyenhance mutual cooperation.

4. Policy initiatives4.1 12 Initiatives

Government of India launchessupport and outreach initiativefor greater synergy to MSMEsector. 12 historic initiativestaken by Government of Indiafor MSME sector.

Cover Story

MEDC Economic DigestApril 2019�34

i) Loans up to 1 crore within59 minutes through onlineportal

ii) Interest subvention of 2 percent for all GST registeredMSMEs on fresh orincremental loans

i i i )Al l companies with aturnover of more than Rs.500 crores to be mandatorilyon TReDS platform toenable entrepreneurs toaccess credit from banks,based on their upcomingreceivables, thus, solving theproblems of cash cycles.

iv)All PSUs to compulsorilyprocure 25 per cent fromMSMEs instead of 20 percent of their total purchases.

v) Out of these 25 per cent, 3per cent is reserved forwomen entrepreneurs.

v i ) A l l c e n t r a l P S U s t ocompu l so r i l y p rocu r ethrough Government-e-Market (GeM) portal

vii) 100 technology centres areto be established with a costof Rs. 6000 crores

viii) Govt. of India to bear 70per cent of the cost for

establishing pharma clustersix) Returns under 8 labours laws

and 10 union regulations tobe filled once in a year.

x) Visit to the establishment byan inspector through acompute r i s ed r andomallotment.

xi) Single consent under air andwater pollution laws.Returns will be acceptedthrough self certificationand only 10 per cent MSMEunits to be inspected.

xii) For minor violations underthe Companies Act ,entrepreneurs no longerhave to approach court butcan correct them throughsimple procedures.

The above 12 initiatives willhelp MSMEs to access tocredit , access to market ,technology upgradation, easeof doing business, and a senseof security for employees.4.2 Announcement in UnionBudget 2019-20

The finance minister in thebudget speech highlighted theabove 12 initiatives by the

g over nment . He fur thermentioned that MSMEs havean opportunity to sell theirp roduc t s th rough GeM.Transactions of over Rs. 17,500crores have taken place,resulting in average savings of25-28%. The GeM platform isnow being extended to allCPSEs. The finance ministera l so ment ioned that thegovernment has focussed onsupporting domestic trade andservices. Our Government hasrecently assigned the subject of“promotion of internal tradeincluding retail trading andwelfare of traders, and theiremployees” to the Departmentof Industr ia l Pol icy andPromotion, which will now berenamed as the Department forPromotion of Industries andInternal Trade.

5. Conclusion

MSMEs form an importantcomponent of Ind ianeconomy. Over the years, it hascontributed largely to India'seconomic growth, exports,indus t r i a l ou tpu t andemployment generation. It istherefore, important thatempowering MSMEs is criticalfor India 's inclus ive andsustainable growth.Recognising this, theauthorities have taken numberof policy initiatives which arepath breaking and will go in along way in empoweringMSMEs. However, a betterunderstanding of MSMEs bythe banking and financial sectoris important as timely financialsupport to distressed MSMEsassumes critical importance.

MEDC Economic Digest April 2019 �35

Cover Story

What Ails The Msme Sector?

The Indian Micro, Small andMedium Enterprises (MSME)sector has been the subject ofmuch government attention in2019, with the pre-electionbudget aimed at amelioratingthis key electoral segment,which has borne the brunt ofthe three major disruptionsover the tenure of the recentgovernment: demonetization,the introduction of the Goodsand Services Tax (GST) and thecrisis in the non-bankingfinancial sector.

The budget has recognised thetwin burden of lack of financeas also that of coping with thecomplexities introduced by thenew GST regime upon thissector. As such, it hasaddressed the needs of theSME sector through thefollowing key proposals:

� Loans up to Rs 1 crore to besanctioned in 59 minutes

� GST-registered SME unitsto get 2% interest rebate onan incremental loan of Rs 1crore.

� Government enterprises tomandatorily source fromSMEs up to 25 per cent viat h e G o v e r n m e n t e -Marketplace (GeM). Ofthis, material to the extent

of at least 3 per cent to besourced from women-owned SMEs.

� Businesses having an annualturnover less than Rs 5 crorecomprising over 90% ofGST payers to be allowedto file quarterly return

� GST exemptions for smalltraders, manufacturers andservice providers doubledfrom Rs 20 lakh to Rs 40lakh

� Small businesses havingturnover up to Rs 1.5 crorehave been given anattract ive composit ionscheme wherein they payonly 1% flat rate and have tofile one annual return only.Similarly, small serviceproviders with turnover upto Rs 50 lakhs can now optfor composition schemeand pay GST at 6% insteadof 18%.

� To promote the “Make inIndia” initiative, thegovernment has abolishedduties on 36 capital goods.

� A r e v i s e d s y s t e m o fimporting duty-free capitalg oods and inputs formanufacture and export hasbeen introduced, along withintroduction of single point

of approval under section65 of the Customs Act.

� Threshold l imit forpresumptive taxation ofbusiness was raised fromRs 1 crore to Rs 2 crore. Thebenefit of presumptivetaxation was extended forthe first time to smallprofess ionals fixingthreshold limit at Rs 50 lakh.

� The tax rate for companieswith turnover of up to Rs250 crore, covering almost99% of the companies, wasreduced to 25% which wasalso applicable to newmanufacturing companieswithout any turnover limits.

Without doubt, some of theseproposals would provide acertain relief to the SME sector.However, notwithstanding theFinance Minister, PiyushGoyal. playing late Santa andshowering the SME sector withsops, there are key issues withregard to the SME sector whichwill need to be addressed by thenew government which will beassume office in May 2019.

Lack Of Institutional Credit:Problems On The SupplySide

A survey by the OmidyarNetwork and the Boston

Dr. Tulsi JayakumarProfessor, Economics & Program Head, PGP- Family Managed Business

S.P. Jain Institute of Management & [email protected]

Cover Story

MEDC Economic DigestApril 2019�36

C o n s u l t i n g G r o u p i nNovember 2018 found that

1

one of the greatest constraintsin the growth of the IndianMSME sector, comprising of55-60 million enterprises, wasthe lack of access to formalcredit. The survey pointed outto the fact that roughly 40percent of India's MSMElending was done through theinformal sector, where interestrates were at least twice as highas the formal market.

It is not as though the problemof access to credit has not beenaddressed by the governmentearlier. The Prime MinisterM u d r a Yo j a n a ( P M M Y )announced in Budget 2015 andthe MUDRA loans disbursedunder the scheme since 2015-16 were aimed at addressingthis challenge of 'Funding theunfunded' micro and smallenterprises and integratingthem with the formal financialsystem. Government dataseems to suggest a successfulredressal of the sector 'sfinancial needs, with actuald i sbursements a lmostachieving targets in the threeyears since its inception .

2

However, the budgetar yapproach to spurring thisimportant and polit ical lysensitive sector, which holdsthe key to India's larger growthstory, will need to be more thanmere incremental.

The problem of creditdisbursal under the Mudrascheme hardly addresses thecrux of the MSMEs' financingproblem. One: Such loans areonly available to microenterprises engaged inmanufacturing, processing,trading and service sectoractivities, for small loans up toRs 10 lakh. Such credit has beenprovided largely by PublicSector Banks in the form ofmicro and small loans, whichconstitute part of theirmandatory priority sectorlending. Such credit by PSBsenjoy government guaranteesof up to Rs. 3000 crores. Suchguarantees, as also the goal-oriented nature of prioritysector lending point to thepossibility of creation of Non-Performing Assets for PSBs,exacerbating the government'sfiscal deficit as well. Again, suchbank credit cannot be expectedto truly foster such micro andsmall enterprises.

Two, the credit disbursals underthe Mudra scheme have beenhighly skewed. Such skewnessis seen both in the dispersion of

https://www.omidyar.com/sites/default/files/18-11-29_Report_Credit_Disrupted_Digital_FINAL.pdf1

Annual Report of Mudra, 2017-18,2

https://www.mudra.org.in

Ibid., p.253

the loan accounts, as also in theloans sanctioned. A majority ofthe loan accounts - 88.65 percent, were of the Shishucategory, and comprised ofextremely small loans up toRs. 50,000. Loans under theKishor category (i.e. between50,001 and Rs. 5 lakhs)accounted for 9.67 per cent ofthe loan accounts, while Taruncategory loans, i .e. loansbetween Rs. 5 lakhs and Rs. 10lakhs, contributed to 1.68 percent of the total loan accounts.Further, 41.78 per cent of suchMudra loans sanctioned anddisbursed in FY 2017-18 wereextremely small loans under theShishu category, while 34.19percent were under the Kishorcategory. 24.02 per cent of theoverall loans disbursed andsanctioned in FY 2017-18 werein the category .Tarun

3

The disturbing trend witnessedis also the decline in the averageloan size under the Kishor andTarun category, despite anincrease, albeit marginal, in theloan size under the Shishucategory, as also total loan size(Figure 1).

Source: Annual Report of Mudra, 2017-18, p. 28, https://mudra.org.in

MEDC Economic Digest April 2019 �37

Cover Story

4https://rbi.org.in/Scripts/PublicationsView.aspx?id=18511

http://www.indiabudget.gov.in/budget2016-2017/ub2016-17/eb/sbe58.pdf, http://www.indiabudget.gov.in/ub2017-18/eb/sbe64.pdf5

Moreover, the potential forcredit risks is accentuated bythe fact that the top ten states:Tamil Nadu, Karnataka,Maharashtra, West Bengal,Uttar Pradesh, Bihar, MadhyaPradesh, Rajasthan, Gujaratand Odisha, accounted forabout 71 per cent of theamount sanctioned anddisbursed under the MudraLoan scheme.

Three, the government has notcarried out the impactassessment of the PMMYprogram, especially onemployment generation.Anecdotal evidence suggeststhat Indian SMEs, especiallyGen-Next, would increasinglyprefer to use capital-intensivetechnologies due to theirpositive impact on profitability,as also the problems associatedwith employing labour.MSMEs have the power ofscaling up, and being enginesof substantial employmentgeneration creation. The truetest of the Modi governmentwill be in the employmentgenerating nature of this andvarious other schemes.

Four, the larger financingproblem of the micro, smalland medium enterpr i sescontinues to persist. The shareof such enterprises in theoverall non-food credit frombanks has declined since 2010-11, with the share of micro and

small enterprises in overall non-food bank credit declining from5.73 per cent to 4.85 per centbetween 2010-11 to 2017-18,w h i l e t h a t o f m e d i u menterprises in overall non-foodbank credit has declined from3.18 per cent in 2009-10 to 1.35per cent in 2017-18 (Figure 2) .

4

Source: Calculated from: RBI, Table 46, Sectoral Deployment of Non-Food Gross Bank Credit,Handbook of Statistics on the Indian Economy,

https://rbi.org.in/Scripts/PublicationsView.aspx?id=18511

The problem of financingMSMEs will need to thenaddress all such anomalies.

Again, interestingly, while thegovernment had announced anincrease in the budgetaryallocation for the Ministry ofMSME to Rs. 6481.96 croresfrom the budgeted 3464.77crores in FY 2016-17, thereappear to be two problems withthis approach. A perusal of pastbudget data reveals that thebudgets of the Ministry ofMSME have been actuallylapsing, with a discrepancy

b e t we e n t h e a c t u a l a n dbudgeted spends. For instance,actual spends in 2015-16 ofRs. 2828.74 crores were lesserthan the budgeted values ofRs.3007.42 crores . The

5

government will need to ensurethat the budgeted amounts arespent productively. More

importantly, even the higherbudgeted spends lookminiscule when considering asector with a significantcontribution to output,employment and exports of a$2 trillion economy.

Finally, governments will needto redress the problem of non-availability of credible datapertaining to this crucial sectorfor research and policypurposes. Much of the currentdebate around the MSMEsector, especially itsproductivity, contribution to

Cover Story

MEDC Economic DigestApril 2019�38

the Gross Domestic Productand employment, has beentaking place in the absence ofaccurate data and analysis. Suchdata collection may befacilitated by a nodal agencysuch as the National SmallIndustries Corporation (NSIC)through a budgetary allocationfor the same. Appropriateincentives may be provided forSMEs which register with theNSIC, and demonstrate a goodrepayment record in terms ofcheaper credit facilities.

Institutional credit and thedemand side

However, the problems ailingthe institutional creditmechanism pertaining to theMSME sector need to be seenfrom a holistic perspective,especially from the demandside as well. On the demandside, the MSME sector isplagued by several problems,which prevents them frombecoming the 'preferredplayers' for the organised sectorfor disbursement ofinstitutional credit.

The MSME sector has hardlyinvested seriously in Research& Development, productdesign and quality beyondstatutory requirements. This isdue to the myth going thatIndian customers are only“cost conscious”, leading to theMSME sector producingproduc t s and de l ive r ingservices purely with a low costfocus. The focus is on Sales,rather than Marketing and

Business Development. Thishas led to inadequate market-making on the part of SMEs.

SMEs are also characterised byabysmally low standards ofgovernance. There are nosystems and processes inherentin decision making. Risk is notclearly understood. Thereforerisk mitigation mechanisms areat best knee jerk reactions andat worst those that lead to longterm damage to employees ands u p p l i e r s , a n d m o r eimportantly to creditors. Thereis very little depth at themanagerial level and most aremerely performing a clericalrole with little empowerment indecision making.

The metric that matters forSME largely pertain to the topline. The MSME sector givesundue importance to top lineover bottom line. Perhaps thisis a cultural issue where weglorify revenue overprofitability and long termgrowth. Such an att itudesmacks of a “poverty mindset”that is yet to shake off our longhistory of famine andshortages. Business ownersfrom MSMEs who speak ofprofitability and return oncapital employed – metrics thatreally matter- as measures ofsuccess, are few.

The inability to distinguishbetween 'Capita l for thebusiness' vs 'capital for theowner' is a critical lacuna thatsignificantly impacts the abilityof the sector to attract low cost

capital. Capital is available, butthere are not enough meatybusiness plans that can befunded with institutionalmoney. Bankers are averse tolending to MSMEs when thereis a lurking fear that money willbe deployed in non-businessactivities.

Prof. Hermann Simon, founderand chairman of theinternational strategy andmarketing consulting firm,S i m o n & K u t c h e r , h a dpopularized the term 'HiddenChampions ' in 1996. Heattributed Germany's exportstrength to German SMEs('Mittelstand' referred to as the'Hidden Champions) with aturnover of less than US $4billion and having a low level ofrecognition with the generalpublic. It is time we recogniseour own 'hidden' growthchampions.

The lacunae that prevents theMSME sector from growingstem from both the demandand supply side. It is high timethat the MSME sector stopsexpecting sops and subsidiesfrom the government andmoves to a space whereinnovat ion and bus inessleadership is demonstrated. Atthe same time, the budgetaryapproach to spurring thisimportant and polit ical lysensitive sector, which holdsthe key to India's larger growthstory, will need to be moreholistic, rather than merelyincremental. The path ofpopulism, while tempting, isbest avoided.

MEDC Economic Digest April 2019 �39

Cover Story

MSMEs in India Growth Catalyst-

India has the largest number ofentrepreneurs in the world andit produces the largest numberof entrepreneurs in a year.According to the latest surveyby Dun and Bradstreet, thereare 81 mn economic entities inthe country (excluding entitiesinvolved in crop, publ icadministration and defense).Many of them are single-person units operating fromhuts in villages, non-permanentstructures. Excluding theseentities, there are over 27 mnentities which we could beter med as 'commerc ia l lyvisible'. MSMEs account foraround 99.9% of these 27 mnentities, they contribute to 35%of India's GDP and employ25% of India's non-farmworkforce.

MSMEs provide largeemployment opportunities atlower capital cost than largeindustries. At present, morethan 15 crore are be ingemployed in the MSME sector.The MSMEs in India aredefined as follows :

The enterprises go through anevolution, they evolve frommicro to small to medium andt h e n l a r g e e n t i t i e s . I ndeveloped markets, around50% of the entities are micro

Manufacturing Sector

Enterprises Investment in plant & machinery

Micro Enterprises Does not exceed twenty five lakh rupees

Small Enterprises

More than twenty five lakh rupees but does not exceed five crore

rupees

Medium

Enterprises More than five crore rupees but does not exceed ten crore rupees

Service Sector

Enterprises Investment in equipments

Micro Enterprises Does not exceed ten lakh rupees:

Small Enterprises More than ten lakh rupees but does not exceed two crore rupees

Medium

Enterprises More than two crore rupees but does not exceed five crore rupees

and 40% are small/medium. InIndia, over 95% of total entitiesare micro and 4% aresmall/medium. Indian microenterprises are finding itdifficult to scale up and growinto small and medium sizes.The challenges they face inIndia are, access to finance,availability of adequateinfrastructure, availability ofskilled labour and inadequatepower supply. Considering thecontribution of MSMEs to theEconomy, lot of newgovernment initiatives weretaken by the government toaccelerate the growth of theMSMEs. To support the

MSME, RBI has constituted acommittee in the month ofMarch 2019 to enable higherlevel of funding to the MSMEsin India.

Realising the contribution, theMSMEs can make it to theIndian Economy , severalinitiatives by Government. Theministry of MSME plays a keyrole in accelerating the growthof the MSMEs. A special cadreof officers have been created inthe Ministry to focus only onMSME sector and those whojoin this cadre will mainly workin MSME department in theircareer.

Mr. R. KannanHead of Corporate Performance Monitoring and Research

Hinduja [email protected]

Cover Story

MEDC Economic DigestApril 2019�40

One of the issues, relating toMSMEs is the access to thecredit. As per the survey ofDun and Bradstreet, only 4%of micro enterprises haveaccess to the format credit.This is one of the majorchallenges for the growth. Tomake this process simple, thegovernment had introducedthe Mudra Scheme. Thisscheme is operated underSIDBI and it refinances theloans given by Banks andNBFCs to the enterprises ,which avail the loans under theMudra scheme. In the year ,2017 – 2018, Mudra loansd i s b u r s e d a m o u n t e d t oRs.2,46,437 cr and in 2018 – 19 ,so far, the loans disbursedamounted to Rs.2,02,668 cr.The total loans disbursed underthis scheme stood at Rs.7.23Lakh crore and more than15.56 crore people benefitedfrom this scheme. This schemehas benefited many in the neweconomy sector includingthose who are focussed onselling their products throughCe ommerce and those who

wanted to run ride hailingservices. Many enterprises werecreated in Food and servicesector and small scalemanufacturing and they areus ing the e ommerceCplatforms.

Star t up India Scheme.Startup India Scheme is anin i t i a t ive o f the Ind i angovernment, the primaryobjective of which is thep r o m o t i o n o f s t a r t u p s ,

generation of employment, andwealth creation. It was launchedon the 16th of January, 2016.Under the scheme, New-entrants are granted a tax-holiday for three years. Thegovernment has provided afund of Rs.2500 crore forstartups, as well as a creditguarantee fund of Rs.500 crorerupees. The Eligibility ForStartup Registration is asfollows and many have availedthis scheme.

� The company to be formedmust be a private limitedcompany or a l imi tedliability partnership.

� It should be a new firm ornot older than five years,and the total turnover of thecompany should be notexceeding 25 crores.

� The firms should haveobtained the approval fromt h e D e p a r t m e n t o fIndus t r i a l Po l i c y andPromotion (DIPP).

� To get approval from DIPP,the firm should be fundedby an Incubation fund,Angel Fund or PrivateEquity Fund.

� The fir m should haveobtained a patron guaranteefrom the Indian patent andTrademark Office.

� It must have arecommendation letter byan incubation.

� Capital gain is exemptedfrom income tax under thestartup India campaign.

� The firm must provide

innovative schemes orproducts.

� Angel fund, Incubationfund, Accelerators, PrivateE q u i t y F u n d , A n g e lnetwork must be registeredwith SEBI ( Securities andExchange Board of India).

Skill India Scheme. One ofthe challenges, MSMEs is facetoday is availability of talent. Toovercome this, ski l ldevelopment initiatives weretaken at both Centre and statelevels and there is an objectiveto train more than 50 cr peoplein the coming years. The modelwill be focussing on Vocationaltraining similar to thevocational training system inGermany. Under this scheme,Pradhan Mantri Kaushal VikasYo j a n a ( P M K V Y ) w a sintroduced and it is the flagshipscheme of the Ministry of SkillD e v e l o p m e n t &Entrepreneurship (MSDE).The objective of this SkillCertification Scheme is toenable a large number ofIndian youth to take upindustry-relevant skill trainingthat will help them in securing abetter livelihood. Individualswith prior learning experienceor skills will also be assessedand certified under Recognitionof Prior Learning (RPL).Under this Scheme, Trainingand Assessment fees arec o m p l e t e l y p a i d by t h eGovernment. In four years,this scheme is likely to benefitmore than 10 million youth.

Cluster development Scheme.

MEDC Economic Digest April 2019 �41

Cover Story

Indus t r i e s in a countr y.Government of India hasadopted the ClusterDevelopment approach as akey strategy for enhancing theproduct iv i t y andcompetitiveness as well ascapacity building of Micro andSmall Enterprises (MSEs) andtheir collectives in the country.A c lus ter i s a g roup ofenterprises located within anidentifiable and as far aspracticable, contiguous areaand producing same / similarproducts / services. Theessential characteristics ofenterprises in a cluster are (a)Similarity or complementarityin the methods of production,quality control & testing,energy consumption, pollutioncontrol, etc., (b) Similar level oftechnolog y & market ingstrategies / practices, (c)S imi la r channe ls forcommunication among themembers of the cluster, and (d)Common challenges &opportunities. By part of beinga cluster, MSMEs will be easyto source raw material andbuyers for the products.Further, the common costs arebe ing shared among theenterprises operating in thecluster. There are varioussubsidy schemes operated byCentre and States and in manyclusters, the participatingcompanies have to incur only10% of the total cost of clusterdevelopment.

PSU procurement. One ofthe challenges for MSMEs is to

find buyers for their produce.To faci l i tate the demandcreation for MSMEs,government has created ascheme , whereby , Now it ismandatory for all Central PSUsto take membership of theGovernment e-Marketplace(GeM) and they will put theirpurchase requirements in themarket place, which MSMEsc a n i d e n t i f y e a s i l y a n dparticipate in the process. Now,PSUs have to procure, at least aquarter of their requirement(25%) from MSMEs. With aview to encourage, morew o m e n t o p u r s u eentrepreneurship, out of the25% procurement mandatedfrom MSMEs from PSUs, 3%has been reserved for womenentrepreneurs. A website hasbeen created under the brandof MSME Sambandh and allthe procurement notices ofPSUs have to be placed on thewebsi te. In the previousfinancial year, more thanRs.25,000 cr was procured fromMSMEs and this is likely tocross Rs.30,000 cr, this year.

Digitisation. To make thep r o c e d u r e s s i m p l e , t h egovernment has embarked ons e ve r a l i n i t i a t i v e s . T h eMyMSME is portal for webbased application module tosubmit and track onl ineapplication under the variousschemes of the ministry.Under the Udyog AadhhaarMemorandum, mobile friendlyapplication could be used forregistration of MSMEs on self– certification basis. MSME

Samadhaan scheme has beencreated to resolve the issues ofdelayed payments to MSMEs.Further, the digitisation andIntroduction of GST hasbrought many MSMEs into theformal economy and this ishelping MSMEs to build acredit profile and enable creditr a t ings by Cred i t r a t ingagencies. This enables MSMEsto avail the formal channels offinance.

Some of the recent initiativesof the government include,approval of Rs.1 crore loan in59 minutes, rebates in interestto be paid by them, TradeReceivables e- DiscountingSystem (TReDS) , e marketplace for MSMEs, Clusterdevelopment subsidy forpharma companies, singleannual return to be filed forcomp l i ance ma t t e r s ,simplifying the factoryinspection procedures andcer ta in exemptions frompunishment for minorviolations.

In conclusion, a good,supportive and growthoriented, eco system has beencreated for the MSMEdevelopment in India andvarious initiatives are beingtaken to create effect iveimplementation policies andprocedures. By creating anawareness among al l theMSMEs about the variousschemes and ensuring inter –departmental coordination inthe government, the potentialo f MSMEs can be fu l l ycap i t a l i s ed fo r a h ighe reconomic growth.

Cover Story

MEDC Economic DigestApril 2019�42

MEDC Economic Digest April 2019 �43

Ventspils port and industrial centre in Latvia- -a natural gateway between EU and Asia

Basic Facts About Latvia

Name of country Republic of LatviaCountry code LVSize of area 64,573 km2Population (at the beginningof 2017)

1.93 million

Capital city RigaLanguage Latvian (official); Russian,

English and German are alsowidely spoken

Political system Republic, parliamentarydemocracy

Membership in internationalorganizations

Member of OECD since2016,Member of NATO since2004;Member of WTO since 1998Memebr of EU since 2004

Latvia, one of the countrieslocated by the Baltic Sea,member of the EuropeanU n i o n , h a s a u n i q u egeographical and culturalposition, providing a strategicl o c a t i o n f o r b u s i n e s soperations targeting developedeconomies of the EU andemerging markets of easternneighbours. Latvia is a naturalgateway between the US, EUand Asia (especiallyRussia/CIS). One of therapidly growing industrial andlogistic centres of Latvia isVentspils, providing not onlyexperience-based expertise in

both logistic and industrialsectors, but also a wide range ofpossibilities for internationalbusiness.

Ice-free Deep-water Port

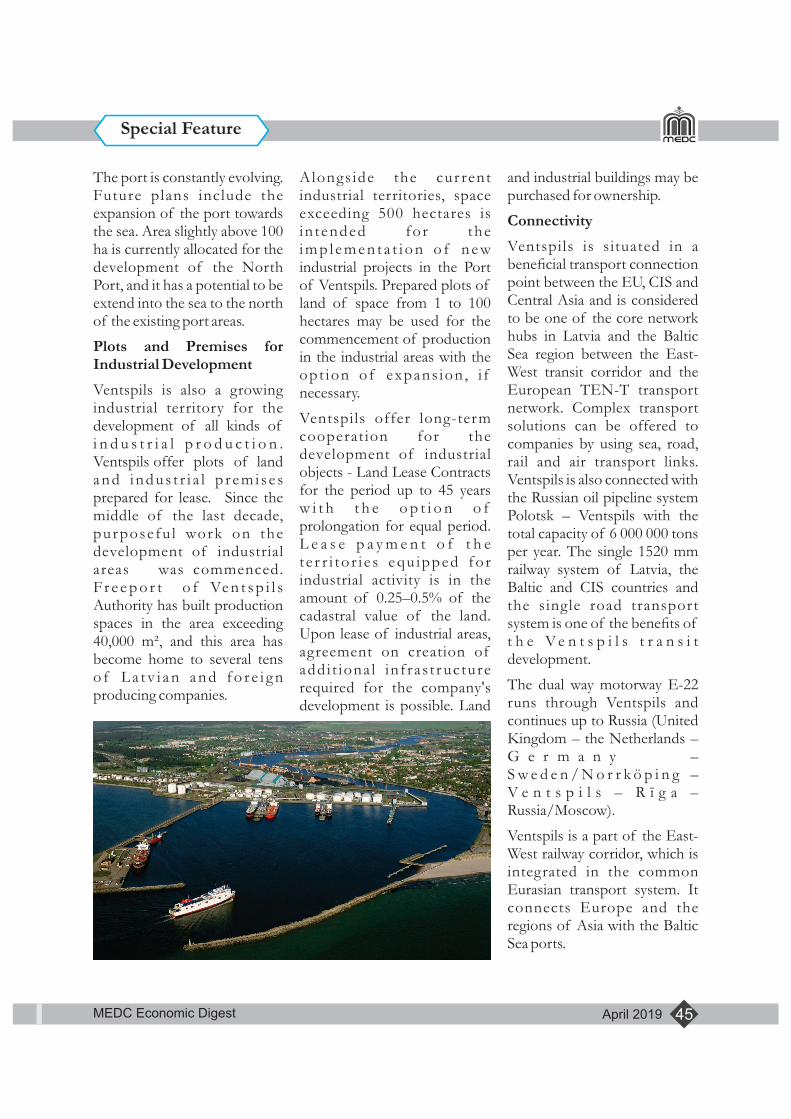

The ice-free port of Ventspils isone of the leading deep-waterports of the EU on the Eastcoast of the Baltic Sea. Sinceancient times Ventspils hasbeen a strategic transitconnection of export goods forRussia and the CIS countries infreight of chemicals, potassiumsalt, coal, grain, general cargo,ro-ro and others. TodayVentspils port is multi-modalfor any freight. The annualturnover of the port is around20-30 million tons and the portcharges are one of the mostattractive in the Baltic States.The technical indicators of theice-free port allow serving thelargest vessels entering theBaltic Sea throughout thewhole year.

Special Feature

MEDC Economic DigestApril 2019�44

The port is constantly evolving.Future plans include theexpansion of the port towardsthe sea. Area slightly above 100ha is currently allocated for thedevelopment of the NorthPort, and it has a potential to beextend into the sea to the northof the existing port areas.

Plots and Premises forIndustrial Development

Ventspils is also a growingindustrial territory for thedevelopment of all kinds ofi n d u s t r i a l p r o d u c t i o n .Ventspils offer plots of landand indus t r i a l p r em i s e sprepared for lease. Since themiddle of the last decade,purposefu l work on thedevelopment of industrialareas was commenced.Fr e e p o r t o f Ve n t s p i l sAuthority has built productionspaces in the area exceeding40,000 m², and this area hasbecome home to several tenso f L a t v i a n a n d f o r e i g nproducing companies.

Alongs ide the cur rentindustrial territories, spaceexceeding 500 hectares isin tended for thei m p l e m e n t a t i o n o f n e windustrial projects in the Portof Ventspils. Prepared plots ofland of space from 1 to 100hectares may be used for thecommencement of productionin the industrial areas with theopt ion of expans ion , i fnecessary.

Ventspils offer long-termcooperat ion for thedevelopment of industrialobjects Land Lease Contracts-for the period up to 45 yearsw i t h t h e o p t i o n o fprolongation for equal period.L e a s e p a y m e n t o f t h ete r r i to r i e s equ ipped forindustrial activity is in theamount of 0.25–0.5% of thecadastral value of the land.Upon lease of industrial areas,agreement on creation ofaddi t iona l inf ras t r ucturerequired for the company'sdevelopment is possible. Land

and industrial buildings may bepurchased for ownership.

Connectivity

Ventspils is situated in abeneficial transport connectionpoint between the EU, CIS andCentral Asia and is consideredto be one of the core networkhubs in Latvia and the BalticSea region between the East-West transit corridor and theEuropean TEN-T transportnetwork. Complex transportsolutions can be offered tocompanies by using sea, road,rail and air transport links.Ventspils is also connected withthe Russian oil pipeline systemPolotsk – Ventspils with thetotal capacity of 6 000 000 tonsper year. The single 1520 mmrailway system of Latvia, theBaltic and CIS countries andthe single road transportsystem is one of the benefits oft h e V e n t s p i l s t r a n s i tdevelopment.

The dual way motorway E-22runs through Ventspils andcontinues up to Russia (UnitedKingdom – the Netherlands –G e r m a n y –S w e d e n / N o r r k ö p i n g –V e n t s p i l s – R ī g a –Russia/Moscow).

Ventspils is a part of the East-West railway corridor, which isintegrated in the commonEurasian transport system. Itconnects Europe and theregions of Asia with the BalticSea ports.

Special Feature

MEDC Economic Digest April 2019 �45

One of the world's largest ferryoperators with the broadestnetwork in Europe – Stena Line– provides regular ferry linesfrom Ventspils to Sweden.

Ven t sp i l s – Nynäshamn( S w e d e n , 5 8 k m f r o mStockholm, 545 km from Oslo)runs 12 times a week. Thefastest sea route connectsStockholm, the central part ofSweden and also the economicactivity centers of Norway withLatvia, from where it is possibleto reach Russia, other CIScountries and further regionswith the help of land transport.

Ventspi ls is locatedapproximately 175 km or 2hours away from the biggest airtraffic center in Latvia - the RigaInternational Airport (RIX).

Tax Incentives

Ventspils freeport is a specialeconomic zone (SEZ) withconsiderable tax incentives thatpromote export and industrialactivities as well as strengthenthe global competition of EUcompanies. L icensedcompanies are entitled to applyconsiderable direct and indirecttax breaks. In the specialeconomic zone the CorporateIncome Tax and Real EstateTax are reduced by 80% untilthe company compensates upt o 3 5 % ( 5 5 % f o r s m a l lcompan ies and 45% formedium-size companies) ofthe investments. It means thatduring the compensation timethe Corporate Income Tax rate

is 4% and the Real Estate Taxrate is 0.3%. If, in turn,dividends are distributed to acompany in SEZ, the profit taxis 4% instead of the usual 20%.Reliefs are also available onindirect taxes: Value AddedTax, Excise and CustomsDuties.

Support for Business Start-Ups – Business Incubation

Anyone who starts productionin Ventspils receives maximumsupport from the municipality.The support instruments in thestart-up period are various –from suitable premises andspecialist consultations to thedevelopment of a large-scaleinfrastructure. The long-termmunicipal aid is attributed toboth large already existing andstart-up businesses.

Ventspils – the Center ofIntelligent Technologies

Ventspils has all the conditionsfor ICT, including the onesnecessary for the developmentof powerful data centers. Amodern communicat ioninfrastructure providesopportunities to store andprocess large volumes of datathat require the power of high-speed connections.

The concentration of ICT inVentspils has increasedsignificantly and thedevelopment continues. Theincreasing number of local andinternationally recognizedbusinesses serves as evidence.

A Multilingual Environment– for the Cooperationbetween the East and West

Special advantage for startinginternationally based businessin Ventspils is the ability tocooperate equally well with thecountries to the East (Russia,CIS countries) and West (EUpartners). 57% of thepopulation are Latvians, but fordaily communication purposesthe Russian language is alsoused – around 28% of thepopulation are ethnic Russians.Due to the geographicallocation and the open labormarket Scandinavian languageskills increase; also English andGerman are used freely.

Comfortable and tidy urbanenvironment

Ventspils is also one of themost attractive coastal cities ofthe Baltic Sea. Ventspils is notonly a port and an industrialpark, but also a gorgeousenvironment for everyday lifeand tourism offering first-classinfrastructure, a wide range ofcultural, sports and leisureactivities, all forms ofeducation and a unique beach.

Contact Freeport ofVentspils Authority, if youwant to find the best solutionof land and premises foryour company in any of theseven industrial areas ofVentspils.www.portofventspils.lvwww.investinventspils.lv

Special Feature

MEDC Economic DigestApril 2019�46

MEDC Economic Digest April 2019 �47