Embed Size (px)

Citation preview

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 1/37

1

Title of the Paper

Monetary Policy making: Challenges in an open economy

The Indian Experience

Author

Ms. Radhika PandeyLecturer (Economics)National Law University, JodhpurNH – 65, Nagaur Road, Mandore, Jodhpur (Rajasthan)

PIN – 342304Tel: 0291-5121595; 2013999; 9828122466

Fax: 0291-2577540

Email: [email protected]

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 2/37

2

Abstract

Monetary Policy Making: Challenges in an Open Economy

The Indian Experience

Radhika Malhotra

Whether Central Bank should habitually intervene or should not intervene at all with theexchange rate movements is a burgeoning question. If we accept intervention, thequestion arises as to what should be the extent of Reserve Bank of India’s interventionto contain the expansionary impact of global capital inflows? The ramifications of ‘RBI’sintervention’ has given rise to many complexities which need exploration. This will helpto delineate the possible mechanisms to overcome the trade-off between the variousobjectives of monetary policy.

Indian experience reveals that the large inflows of foreign capital put upward pressure onexchange rate; monetary expansion resulting from intervention tends to exert upwardpressure on domestic price level. This raises the issue of an appropriate exchange ratepolicy and price policy. There is, thus, an imperative to study the various monetary policyinstruments, goals and policy variables in the wake of the changed scenario. The researchpaper inter alia would focus on the following:

• Reasons involved towards changing character of ‘reserve money’;

• Emerging challenges in terms of ‘exchange rate management’ and ‘domestic pricestability’;

• An analysis of the efficacy of the existing instruments used to tackle thechallenges;

•

To suggest alternative policy options for tackling challenges.

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 3/37

3

Monetary Policy making: Challenges in an open economy

The Indian Experience

Introduction

The conduct of monetary policy has become increasingly complex in a globalized

environment. Globalization has considerably expanded the level of economic

interterdepence and interaction among countries. At the same time the evolution of a

globalized economy has brought to the forefront new challenges faced by the monetary

authority. Monetary policy decisions have to be made in an environment characterised by

increased risk and uncertainity. Globalization, as understood in the present context refers

to integration of the financial markets.Financial markets ,driven by massive capital flows

immediately transfer the valuation of risks thus having considerable implications for

exchange rate stability. Thus the formulation of monetary policy has to take into account

not only the domestic macroeconomic policy environment but also impact of cross-

border capital flows and their implication for the macroeconmic variables.

The present paper is divided into five sections. Section I deals with an overview of the

monetary policy during the 1980’s and changes in the institutional environment affecting

the conduct of monetary policy in the post reform period. Section II deals with capital

flows; one of the most important component of external sector reforms, their components,

nature, determinants and their impact on monetary management. Section III elaborates

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 4/37

4

the challenges faced by the monetary policy in its attempt to avoid a trade-off between

price stability and exchange rate stability; their implications and possible alternative

strategies to manage the trade-off. Section IV decsribes the current state of the economy

characterised by acute inflation and the pressure faced by the monetary authority to bring

about an interest hike. Section V concludes the paper.

Section I

Monetary Policy during 1980s:

The conduct of any macroeconomic policy is greatly influenced by the prevailing

institutional environment. The institutional setting during the 1980s was governed by a

strong monetary-fiscal policy interface. The strong monetary-fiscal policy nexus is

measured by the amount of net RBI credit to the Government. The net RBI credit to the

Government constituted 96% of the reserve money growth during the 1980s. The Central

monetary authority financed an increasing portion of the governmnet’s budget deficit.

The fiscal pressure on monetary tergetting had its roots in the practice of automatic

monetisation of Central Government fiscal deficit. An agreement was made between the

officials of the RBI and the Finance Ministry in early 1955 by which the fall in the

balances of the Central Government with the RBI below Rs 50 crore must be replenished

by accepting adhoc treasury bills1. Thus the issue of adhoc treasury bills became a

1 M.Ramachandran, Fiscal Deficit, RBI Autonomy and Monetary Management, Economic and PoliticalWeekly, August 26 – September 2, 2000 PP. 3266-72, available at,<http://www.epw.org.in/showArticles.php?root=2000&leaf=08&filename=1701&filetype=pdf> visited on12.09.2004

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 5/37

5

convenient means of meeting any temporary mismatch between the receipts and

expenditure of the Central Government budget. In course of time it became a regular

practice to finance the deficit through the issue of adhoc Treasury Bills and consequently

an overwhelmingly large portion of government’s fiscal deficit was automatically

monetised.

The 80s decade was characterised by high rates of economic growth. The economy was

able to cross the barrier of the Hindu Rate of Growth of 3.5% and consequently the

economy grew at an annual average rate of growth of 5.6 percent. On the flip side it was

also a period characterised by high fiscal deficits; a significant amount of which was

being financed through the issue of adhoc treasury bills. The monetisation of budgetary

deficit is an important source of inflation. This raised important issues related to the fiscal

impact of monetary expansion. Recognising the dangerous implications of automatic

monetisation on the flexibility and efficacy of monetary policy as an instrument of

economic growth; the RBI appointed a committee under the Chairmanship of Professor

Sukhamoy Chakravarty to suggest measures to improve the effectiveness of monetary

policy. The Chakravarty Committee recommended attaining price stability as the core

objective of monetary policy. Emphasizing monetary policy target, the Committee

suggested that the monetary target must be linked with the rate of growth of output and

prices. In order to achieve the desired monetary expansion, the growth of reserve money

has to be regulated in line with the targeted monetary expansion2. Recognising the fact

that the government borrowing from the Reserve bank has been an important

2 Alok Kumar Mishra (March 2004), Revisiting Monetary Policy Perspectives in India during 1990s’, Vol.III No. 2 Journal of Applied Economics, March 2004, ICFAI University, PP.66-67

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 6/37

6

contributory factor in reserve money growth and hence in money supply, the committee

wanted an agreement between the Central Government and the RBI on the level of

monetary expansion and the extent of monetisation of fiscal deficit3

.

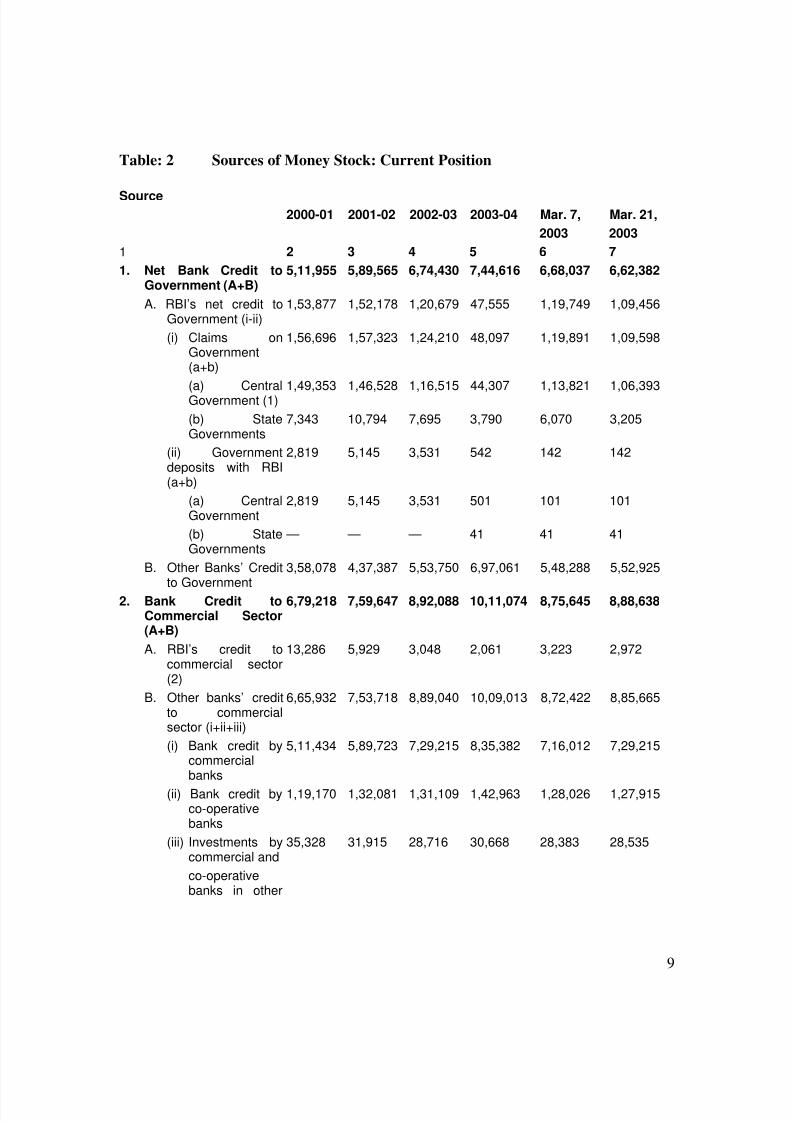

Money Supply Determination

The determination of money supply is a process of determination of the sources of

variation in reserve money and money multiplier. The Reserve Bank of India shows that

there are five sources which contribute to the growth of money supply in India. They are:

a) Net Bank Credit to the Government

b) Bank credit to the commercial sector

c) Net foreign exchange assets of the banking sector

d) Government’s currency liabilities to the public

e) Non-monetary liabilities of the banking sector.

These factors affect money supply by causing variations in the growth of reserve money.

Till the early 90s, the most important component affecting reserve money was the

Reserve Bank credit to the Government. The supply of broad money is related to reserve

money through the following equation:

M3 = mRM

Where m is money multiplier and RM is reserve money. Money Multiplier is related to

behavioural factors, such as currency to deposits ratio, and a policy variable i.e, the cash

reserve ratio.

3 C. Rangarajan, Some critical Issues in Monetary Policy, EPW Special Aricle, June 16 2001, Availableat<http://www.epw.org.in/showArticles.php?root=2001&leaf=06&filename=3129&filetype=html> visitedon 20th September 2004

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 7/37

7

Table: 1 Sources of Money Supply

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 8/37

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 9/37

9

Table: 2 Sources of Money Stock: Current Position

Source2000-01 2001-02 2002-03 2003-04 Mar. 7, Mar. 21,

2003 2003

1 2 3 4 5 6 7

1. Net Bank Credit toGovernment (A+B)

5,11,955 5,89,565 6,74,430 7,44,616 6,68,037 6,62,382

A. RBI’s net credit toGovernment (i-ii)

1,53,877 1,52,178 1,20,679 47,555 1,19,749 1,09,456

(i) Claims onGovernment(a+b)

1,56,696 1,57,323 1,24,210 48,097 1,19,891 1,09,598

(a) CentralGovernment (1)

1,49,353 1,46,528 1,16,515 44,307 1,13,821 1,06,393

(b) StateGovernments

7,343 10,794 7,695 3,790 6,070 3,205

(ii) Governmentdeposits with RBI(a+b)

2,819 5,145 3,531 542 142 142

(a) CentralGovernment

2,819 5,145 3,531 501 101 101

(b) StateGovernments

— — — 41 41 41

B. Other Banks’ Credit

to Government

3,58,078 4,37,387 5,53,750 6,97,061 5,48,288 5,52,925

2. Bank Credit toCommercial Sector(A+B)

6,79,218 7,59,647 8,92,088 10,11,074 8,75,645 8,88,638

A. RBI’s credit tocommercial sector(2)

13,286 5,929 3,048 2,061 3,223 2,972

B. Other banks’ creditto commercialsector (i+ii+iii)

6,65,932 7,53,718 8,89,040 10,09,013 8,72,422 8,85,665

(i) Bank credit bycommercialbanks

5,11,434 5,89,723 7,29,215 8,35,382 7,16,012 7,29,215

(ii) Bank credit byco-operativebanks

1,19,170 1,32,081 1,31,109 1,42,963 1,28,026 1,27,915

(iii) Investments bycommercial and

35,328 31,915 28,716 30,668 28,383 28,535

co-operativebanks in other

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 10/37

10

securities

3. Net Foreign ExchangeAssets of BankingSector (A+B)

2,49,819 3,11,035 3,93,715 5,15,304 3,92,475 3,87,550

A. RBI’s net foreignexchange assets (i-ii) (3)

1,97,175 2,63,969 3,58,244 4,84,413 3,51,484 3,52,079

(i) Gross foreignassets

1,97,192 2,63,986 3,58,261 4,84,431 3,51,501 3,52,097

(ii) Foreignliabilities

17 17 17 17 17 17

B. Other banks’ netforeign exchangeassets

52,644 47,066 35,471 30,891 40,991 35,471

4. Government’sCurrency Liabilities tothe Public

5,354 6,366 7,071 7,291 7,036 7,071

5. Banking Sector’s netNon-monetary

Liabilities Other thanTime Deposits (A+B)

1,33,126 1,68,258 2,48,101 2,77,936 2,26,644 2,26,899

A. Net non-monetaryliabilities of RBI (3)

79,345 1,01,220 1,27,141 1,10,310 1,29,056 1,24,372

B. Net non-monetaryliabilities of otherbanks (residual)

53,781 67,038 1,20,960 1,67,626 97,588 1,02,527

(1+2+3+4-5) 13,13,220 14,98,355 17,19,203 20,00,349 17,16,550 17,18,742M3

16,89,532 (19,83,088) (16,86,605) (16,89,071)

Source: RBI Bulletin No.11 Sources of Money Stock M3.

Recognising the dangers of strong monetary –fiscal policy nexus, there was a conscious

effort to devise a mechanism by which budget deficit and monetisation could be delinked.

This had been formalised by an agreement between the Government of India and the RBI

signed on September 9 1994, by which automatic monetisation of treasury bills could be

phased out over a period of three years and from 1997-98 this instrument could be

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 11/37

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 12/37

12

• Modulation of import demand on the basis of the availability of current receipts to

ensure a level of current account deficit consistent with normal capital flows.

• Enhancement of non-debt creating flows to limit the debt service burden

• Adoption of market-determined exchange rate

• Adequate build up of foreign exchange reserves to avoid liquidity crisis and to

eliminate the dependence on short term debt.

The external sector reforms paid rich dividends in terms of sustainability of the current

account deficit and resilience to a series of external and domestic shocks.

These external sector reforms played their part in further global economic integration in

terms of reduced barriers on the inflows and ouflows of capital in response to interest

differentials. This emphasises the need for a closer coordination between monetary and

exchange rate policy to maintain monetary and exchange rate stability.

Section II

The Changing nature of capital flows and their determinants

One of the most significant developments in the global economy has been the spectacular

surge in international capital flows. These flows emanate from a greater financial

liberalisation, emergence and proliferation of institutional investors such as mutual and

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 13/37

13

pension funds and a spate of financial innovations.5. It is widely recognised that financial

liberalization can contribute significantly to growth in developing economies through

augmenting domstic savings, enhancing competitive pressures,reducing cost of capital

and transferring technology. In the endogeneous growth framework, the contributions to

growth attributed to capital flows comprise the spillovers associated with foreign capital

in the form of technology, skills and introduction of new products as well as positive

externalities in terms of higher efficiency of domestic financial market resulting in

improved resource allocation. At the same time it is also recognised that surges in capital

flows cause several concerns. Large capital flows create inflationary tendencies,

destabilise the exchange rates. Moreover there is a risk of domestic macroeconomic

instability arising from volatility of short-term capital flows and from the export of

domestic savings. In extereme cases premature capital account liberalization can lead to

currency substituion, capital flight and balance of payments crisis.

Before analysing the implications of capital flows on domestic monetary management it

is important to trace the changes in the composition of capital flows. An important

feature of the enhanced capital flows to developing economies in the nineties decade is

that private (debt and equity) as opposed to official flows have become an important

source of financing large current account imbalances. Another change has been a shift

away from debt flows towards equity flows especially foreign direct investment and

foreign portfolio investment. If we analyse the trends of capital flows to developing

countries as a whole we find that foreign direct investment flows to developing countries

5 Reserve Bank of India, Report: Report on Currency and Finance, Management of Capital Flows, (Government of India, 2003)

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 14/37

14

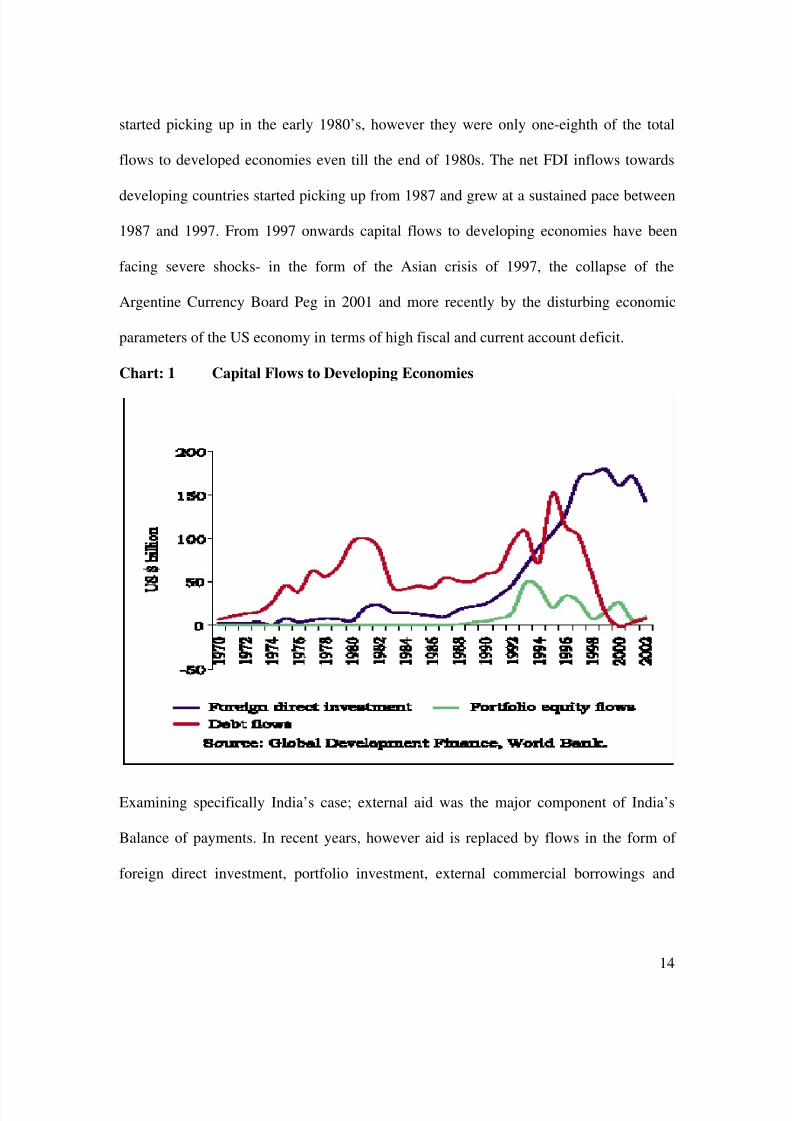

started picking up in the early 1980’s, however they were only one-eighth of the total

flows to developed economies even till the end of 1980s. The net FDI inflows towards

developing countries started picking up from 1987 and grew at a sustained pace between

1987 and 1997. From 1997 onwards capital flows to developing economies have been

facing severe shocks- in the form of the Asian crisis of 1997, the collapse of the

Argentine Currency Board Peg in 2001 and more recently by the disturbing economic

parameters of the US economy in terms of high fiscal and current account deficit.

Chart: 1 Capital Flows to Developing Economies

Examining specifically India’s case; external aid was the major component of India’s

Balance of payments. In recent years, however aid is replaced by flows in the form of

foreign direct investment, portfolio investment, external commercial borrowings and

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 15/37

15

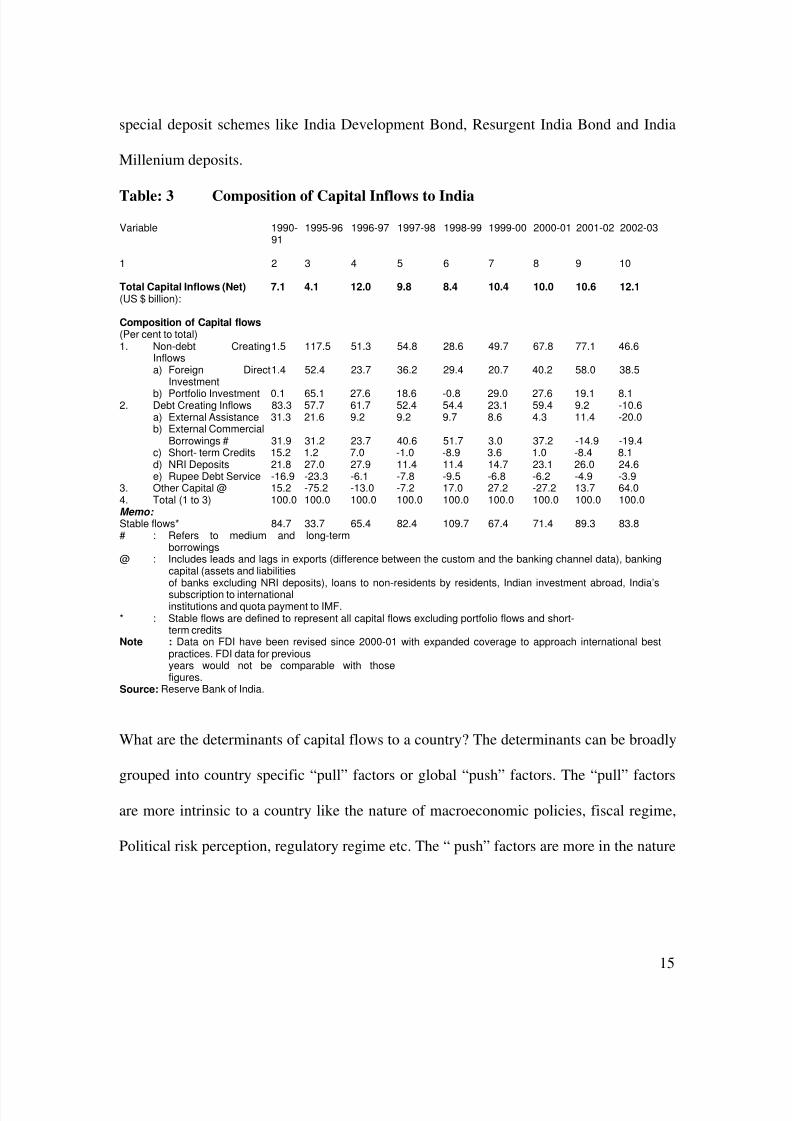

special deposit schemes like India Development Bond, Resurgent India Bond and India

Millenium deposits.

Table: 3 Composition of Capital Inflows to India

Variable 1990-91

1995-96 1996-97 1997-98 1998-99 1999-00 2000-01 2001-02 2002-03

1 2 3 4 5 6 7 8 9 10

Total Capital Inflows (Net) 7.1 4.1 12.0 9.8 8.4 10.4 10.0 10.6 12.1(US $ billion):

Composition of Capital flows(Per cent to total)1. Non-debt Creating

Inflows1.5 117.5 51.3 54.8 28.6 49.7 67.8 77.1 46.6

a) Foreign DirectInvestment

1.4 52.4 23.7 36.2 29.4 20.7 40.2 58.0 38.5

b) Portfolio Investment 0.1 65.1 27.6 18.6 -0.8 29.0 27.6 19.1 8.12. Debt Creating Inflows 83.3 57.7 61.7 52.4 54.4 23.1 59.4 9.2 -10.6

a) External Assistance 31.3 21.6 9.2 9.2 9.7 8.6 4.3 11.4 -20.0b) External Commercial

Borrowings # 31.9 31.2 23.7 40.6 51.7 3.0 37.2 -14.9 -19.4c) Short- term Credits 15.2 1.2 7.0 -1.0 -8.9 3.6 1.0 -8.4 8.1d) NRI Deposits 21.8 27.0 27.9 11.4 11.4 14.7 23.1 26.0 24.6e) Rupee Debt Service -16.9 -23.3 -6.1 -7.8 -9.5 -6.8 -6.2 -4.9 -3.9

3. Other Capital @ 15.2 -75.2 -13.0 -7.2 17.0 27.2 -27.2 13.7 64.04. Total (1 to 3) 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0Memo:

Stable flows* 84.7 33.7 65.4 82.4 109.7 67.4 71.4 89.3 83.8# : Refers to medium and long-term

borrowings@ : Includes leads and lags in exports (difference between the custom and the banking channel data), banking

capital (assets and liabilitiesof banks excluding NRI deposits), loans to non-residents by residents, Indian investment abroad, India’ssubscription to internationalinstitutions and quota payment to IMF.

* : Stable flows are defined to represent all capital flows excluding portfolio flows and short-term credits

Note : Data on FDI have been revised since 2000-01 with expanded coverage to approach international bestpractices. FDI data for previousyears would not be comparable with thosefigures.

Source: Reserve Bank of India.

What are the determinants of capital flows to a country? The determinants can be broadly

grouped into country specific “pull” factors or global “push” factors. The “pull” factors

are more intrinsic to a country like the nature of macroeconomic policies, fiscal regime,

Political risk perception, regulatory regime etc. The “ push” factors are more in the nature

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 16/37

16

of a stimulus provided by some external factor. For example a decline in US interest rates

or recessionary trends in the US economy may push capital flows out of US to India.

The jump in the foreign inward capital that India experienced after liberalisation as well

as the composition of these inflows upholds the role of ‘internal’ or ‘pull’ factors such as

credible economic reforms, improved macroeconomic performance and domestic policies

that encouraged investor confidence and attracted foreign investors. The ‘push’ factors

are equally important as the relatively high rates of return on Indian assets also attract

capital inflows.

Capital Flows and their Macroeconomic Impact:

An inflow of foreign capital exerts an upward pressure on the real exchange rate. The

transmission channel of the real exchange rate depends upon the exchange rate regime

being followed in the recipient country. If a country follows a freely floating exchange

rate with no Central Bank intervention, the appreciation will take place through a nominal

appreciation6 leading to a current account deficit with profound implications for external

competitiveness.Alternatively if the exchange rate regime is fixed and the Central Bank

intervenes to counter appreciation pressures, then capital inflows would be visible in

increases in foreign exchange reserves.

The implications of the two alternative exchange rate regimes can be plotted against time

to find out what strategy India had been adopting to counter the expansionary impact of

6 Renu Kohli, Capital Account Liberalisation Empirical Evidence and Policy Issues – I, EPW, SpecialArticle, April 14, 2001 P. 1199 available at<http://www.epw.org.in/showArticles.php?root=2001&leaf=04&filename=2377&filetype=pdf > visited on12. 09.2004

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 17/37

17

capital flows. The two implications being the current account deficit as a percent of GDP

( resulting from freely floating exchange rate regime) and the accumulation of foreign

exchange reserves (resulting from fixed exchange rate regime). The following two graphs

trace the trend of foreign exchange reserves and current account balance from 1970 to

1998. The graphs can give us an idea of the behaviour of these two variables in the pre

and post reform period.

Chart: 2A Foreign Exchange Reserves (excluding Gold and SDR)

Source: see bibliography (Renu Kohli, 2001)

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 18/37

18

Chart: 2B Current Account Balance

Source: see bibliography (Renu Kohli,2001)

The current account deficit has shown a narrowing trend after touching the peak of 3.2

percent of GDP in 1991, the crisis year. The steep increase in foreign exchange reserves

is synchronous with this trend, suggesting absorption of foreign currency inflows by the

central bank. In 1993, almost entire increase in foreign exchange inflows were absorbed

as foreign exchange reserves. Since then a substantial portion of capital inflows has been

absorbed by the Reserve Bank thus resulting in adequate build-up of foreign exchange

reserves. The accumulation of international reserves with the RBI represents an increase

in the net foreign exchange assets of the central bank and directly affects the monetary

base. What has been the impact of capital inflows on money supply and how monetary

poliy has responded to these inflows?

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 19/37

19

Though India has had a market-determined exchange rate since 1993; flexibility in the

true sense has never been adopted by the central monetary authority. The degree of

intervention by the central bank has substantially increased and the foreign exchange

reserve build-up has been substantial. Before examining the monetary implications of

reserve build-up it would be worthwhile to examine the major sources of reserve

accretion since 1991.

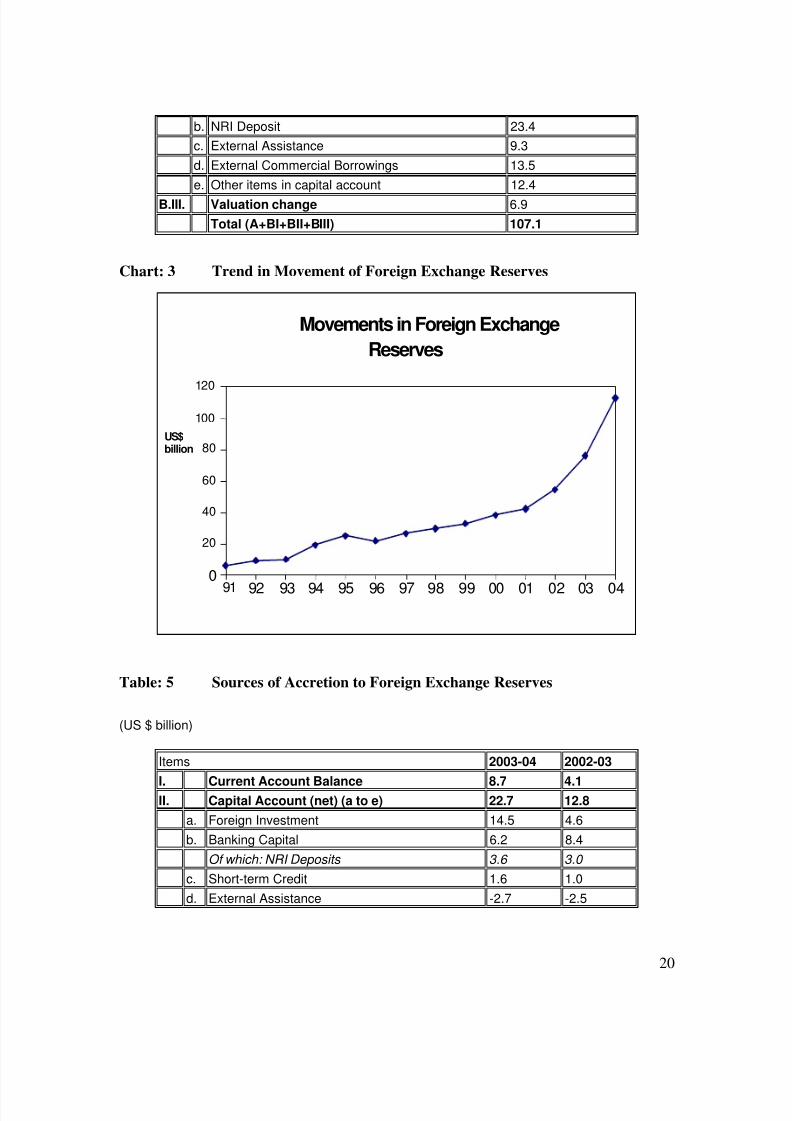

Movement of reserves with the RBI- a disaggregative analysis

The level of reserves with the RBI has substantially increased from US$ 5.8 billion as at

end March 1991 to US$ 113 billion by end- March 2004. The increase in foreign

exchange reserves has been on account of capital and other flows. In the recent period the

major sources of accretion to foreign exchange reserves has been the items both under the

current account and the capital account of the Balance of payments. The current account

account has been witnessing a surplus due to increase in invisble earnings. Current

account posted a surplus of 1.4% of GDP in the fiscal year 2003-04. Under the capital

account the major components responsible for reserve accretion are a) foreign investment

b) banking capital c) short term capital d) valuation changes in reserves 7.

Table: 4 Sources of Accretion to Foreign Exchange Reserves since 1991

(US$ million)

Items 1991-92 to 2003-04A Reserve Outstanding as on end-March 1991 5.8

B.I. Current Account Balance -23.9

B.II. Capital Account (net) (a to e) 124.1

a. Foreign Investment 65.5

7 Report on Foreign Exchange Reserves, Reserve Bank of India, (Government of India, 2003-04)

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 20/37

20

b. NRI Deposit 23.4

c. External Assistance 9.3

d. External Commercial Borrowings 13.5

e. Other items in capital account 12.4

B.III. Valuation change 6.9

Total (A+BI+BII+BIII) 107.1

Chart: 3 Trend in Movement of Foreign Exchange Reserves

Movements in Foreign Exchange

Reserves

0

20

40

60

80

100

120

91 92 93 94 95 96 97 98 99 00 01 02 03 04

US$billion

Table: 5 Sources of Accretion to Foreign Exchange Reserves

(US $ billion)

Items 2003-04 2002-03

I. Current Account Balance 8.7 4.1 II. Capital Account (net) (a to e) 22.7 12.8

a. Foreign Investment 14.5 4.6

b. Banking Capital 6.2 8.4

Of which: NRI Deposits 3.6 3.0

c. Short-term Credit 1.6 1.0

d. External Assistance -2.7 -2.5

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 21/37

21

e. External Commercial Borrowings -1.9* -2.3

f. Other items in Capital Account 5.0 3.6

III. Valuation Change 5.4 4.4

Total (I+II+III) 36.8 21.3

The changing monetary policy paradigm

In the changed scenario, with a massive reserve build-up of reserves with the RBI; the

central bank has the added responsibility of countering the expansionary impact of capital

flows and maintaining a stable exchange rate apart from pursuing an independent

monetary policy. The question is whether the central bank can manage all these

responsibilities with the existing monetary instruments?

The theoretical understanding of the interrelationship amonst the various macroeconomic

aggregates as well as the working of the the Reserve bank reveals that the trinity of

desirable objectives, viz., a fixed/managed exchange rate, an independent monetary

policy and an open capital account cannot be achieved simultaneously. For example if the

domestic macroeconomic conditions necessitate that the domestic interest rates should

be higher than the international rates, this would attract capital flows from the rest of the

world. Persistent capital flows would exert an upward appreciation pressure on the

exchange rate with implications for external competitiveness. Alternatively, the monetary

authorities may attempt to moderate the appreciation pressure through absorption of these

flows; this would, however, have an expansionary impact on money supply, (as has been

happening in India’s case) which over time, could create inflationary tendencies. Thus

only two of the three objectives are mutually consistent With an open capital account the

policy makers can either pursue an independent monetary authority or a fixed /managed

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 22/37

22

exchange rate. If the policy makers follow a fixed/managed exchange rate it has to forego

its objcetive of price stability. These inherent trade-offs among the policy objectives have

been described as Macroeconomic Policy Trilemma

Section III

Challenges to monetary policy- What needs to be done

A reflection on the monetary and exchange rate dynamics reveals that the possibility of

having a fixed rate mechanism is no longer feasible and the dominant view is that, for

most countries floating or flexible rates is the most sustainable way of having a less

crisis- prone exchange rate regime. Opinions also vary on the extent and degree of

flexibility in exchange rates. But a completely “ free” float without intervention is clearly

out of favour. Studies by the IMF and other experts have showed that most countries have

adopted intermediate regimes of various types, such as, managed floats with no pre-

announced path, and independent floats with foreign exchange intervention moderating

the rate of change and preventing undue fluctuations.

Another argument put forth against free float is that a freely floating regime does not

attach any importance to maintaining an adequate level of foreign exchange reserves. If

demand for foreign exchange is higher than supply, domestic currency will depreciate

and if supply exceeded demand, domestic currency will appreciate thus equilibrating

demand and supply over time. However in the light of volatility induced by capital flows,

there is now a growing consensus that emerging market economies, as a policy must

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 23/37

23

maintain adequate level of reserves.8 Earlier the adequacy of reserves was defined in

terms of months of imports; now an additional indicator of the adequacy is that reserves

should be atleast sufficient to cover likely variations in capital flows or “liquidity at risk”

Thus the above discussion can be converged into the following three points

• Exchange rate should be flexible and not fixed or pegged

• Countries should be able to manage or intervene or manage exchange rate to

atleast some degree if the movements are believed to be destabilising in the short

run

• Reserves should be adequate to take care of variations in capital flows and

“liquidity at risk”

With a massive build-up of foreign exchange reserves with the RBI; it is imperative to

devise mechanisms to check the inflationary pressures arising from increased intervention

in the face of a surge in capital flows. The basic relationship is:

Change in M3 =m( change in NFA + change in RCG)

Where M3 is broad money, ‘m’ is the money multiplier, NFA is the net foreign assets and

RCG is the reserve bank credit to the Government. When RBI purchases foreign currency

to stabilise the value of rupee, NFA goes up. This relationship suggests two ways of

mounting a response:

8 Dr. Bimal Jalan, Governor, Reserve Bank of India, speech delivered on August 14 2003 at the 14 th National Assembly of Forex Association of India in Mumbai on Exchange Rate Management: AnEmerging Consensus?

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 24/37

24

Impact on reserve money: The rise in NFA can be sterilized by reducing the central

bank’s credit to the Government. If the rise in NFA is completely offset by a reduction in

Reserve Bank credit to the Government; there is no change in money supply (M3).

Another channel for sterilization is the repo operations conducted by the RBI wherein the

Government bonds are pledged to banks when borrowing from them.

Another channel is the outright sale of government securities through open market

operations.

Impact on money multiplier: The second strategy which the Central bank can adopt is to

follow monetary tightening mechanisms which would reduce the value of money

multiplier ‘m’. This would involve policy initiatives such as raising CRR, forcing public

sector entities to directly hold accounts with the RBI etc.9

• Two major episodes of surges in capital flows can be identified to examine RBI’s

policy response towards them and their implications for monetary and exchange

rate parameters. Episode I can be identified as running from March 1993 to April

1995. As Virmani observes, in dealing with the surge in capital flows a three-

pronged startegy was suggested:

a) to partially sterilize the reserve build-up and to watch the situation on the inflation

front carefully.

9 Ila Patnaiak (2003), The Consequences of Currency Intervention in India, ICRIER Working . Paper. No.114

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 25/37

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 26/37

26

This led to attempts by RBI to control the growth in money supply through containing

the money multiplier by raising the reserve requirements. Thus we find that there

were consistent increase in the Cash Reserve ratio from June 1994 to July 1995

Table: 6 Monetary Tightening in episode I

We identify Episode II as having commenced from April 2002 and is still continuing. In

sharp contrst to Episode I, the intervention by the RBI in Episode II was motivated by a

current account surplus rather than by a capial surge. The capital surge only took place

from 2002-03 onwards whereas foreign exchange reserves with the RBI grew sharply in

2001-02, that is before the increase in capital flows in the following year. The figure on

currency intervention in episode II shows that the policy response of RBI was governed

by sterilized intervention. Sterilization was conducted through open market operations i.e

sale of government securities. In the figure we see a striking relation where months with

high purchases of USD were months where substantial sale of GOI securities took place.

Since sterilization was adopted as a monetary tightening mechanism; the need to reduce

money supply throgh reserve requirements was not required. On the contrary, cash

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 27/37

27

reserve ratio was reduced as apart of the broader monetary policy objective of avoiding

burden on the banking sector to maintain reserves.

Chart: 5 Currency Intervention in episode II

Source: Ila Patnaik (Oct 2003)

Chart: 6 Drop in CRR in Recent Years

Source: Ila Patnaik (Oct 2003)

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 28/37

28

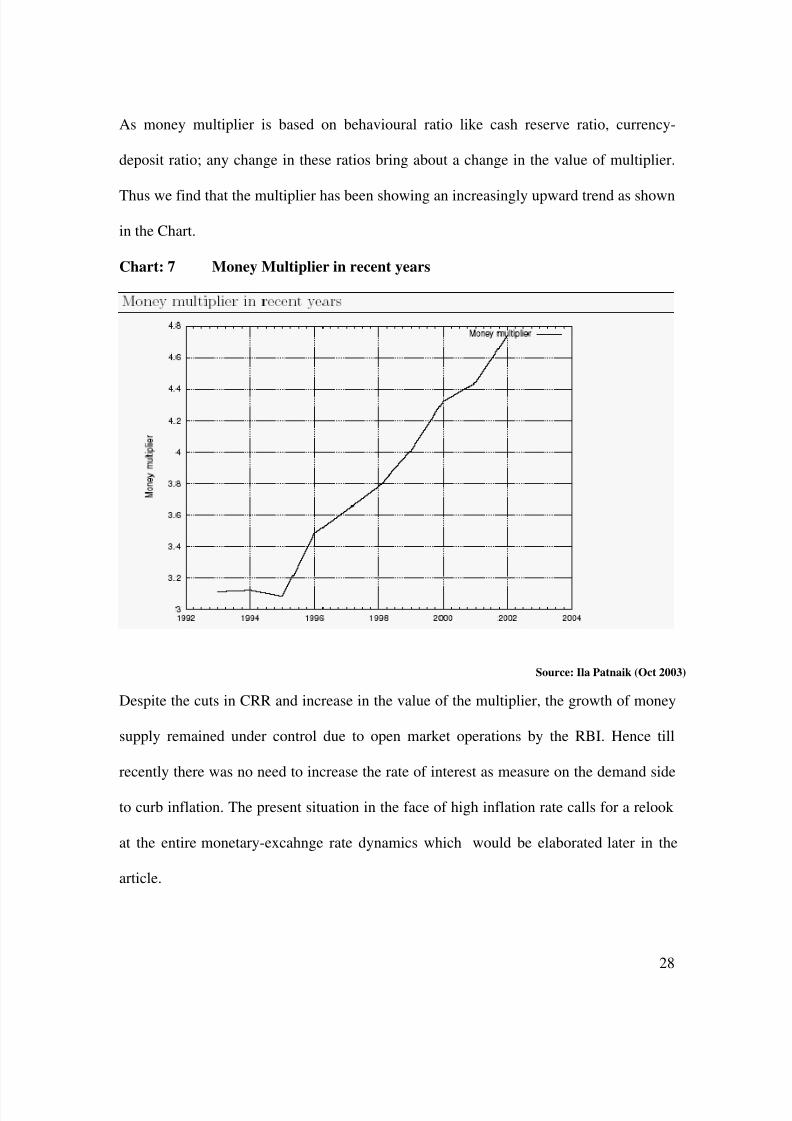

As money multiplier is based on behavioural ratio like cash reserve ratio, currency-

deposit ratio; any change in these ratios bring about a change in the value of multiplier.

Thus we find that the multiplier has been showing an increasingly upward trend as shown

in the Chart.

Chart: 7 Money Multiplier in recent years

Source: Ila Patnaik (Oct 2003)

Despite the cuts in CRR and increase in the value of the multiplier, the growth of money

supply remained under control due to open market operations by the RBI. Hence till

recently there was no need to increase the rate of interest as measure on the demand side

to curb inflation. The present situation in the face of high inflation rate calls for a relook

at the entire monetary-excahnge rate dynamics which would be elaborated later in the

article.

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 29/37

29

Chart: 8 Money Supply and inflation in Episode II

Source: Ila Patnaik (Oct 2003)

Consequences of Sterilised Intervention:

The consequences of sterilised intervention can be analysed in terms of its quasi-fiscal

cost and interest implications. Quasi-fiscal cost arises from the substitution of domestic

assets by foreign assets on the Central Bank’s balance sheet. In order to assess the impact

of quasi-fiscal cost of sterilisd intervention we compare the interest differential between

the returns on domestic government bonds and foreign interest rate times the amount of

foreign exchange reserves held by the Central bank. According to RBI estimates the

sterilized intervention by the RBI between April 2001 and March 2002 cost an estimated

Rs 2813.3 crores as QFC. This was about 0.56% of GDP in both 2001-02 and 2002-03.

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 30/37

30

Another implication of sterilized intervention is that when RBI sells bonds, this tends to

drive up the domestic interest rate and invite further capital inflows.

Moreover the availability of sufficient government marketable government securities

with the RBI could also constrain the extent of sterilization operations. There has been a

consistent decline in the share of domestic assets in the Reserve Money through out the

1990’s. In particular the stock of the Government of India securities- the main instrument

of sterilization- declined from 1,46,534 crore at end March 2001 to rs 36,919 crore by

January 16, 200410

.

Suggestions of the RBI Working Group

The depleting stock of government securities with the RBI has brought into a sharp focus

the limitations on the RBI to sterilise capital flows in future. Keeping this in mind RBI

constituted an Internal working Group on the Instruments of Sterilization to review the

working of various instuments with their associated costs and benefits and their

applicability. The Group suggests a two pronged approach a) strengthening the existing

instruments b) exploring new instruments applicable in the Indian context.

The Group examined the option of sterilisation of inflows by using/refining the existing

instrument without changing the legal framework. These instruments included: (i)

Liquidity Adjustment Facility (LAF); (ii) Open Market Operations (OMO); (iii) Balances

of the Government of India with the Reserve Bank; (iv) Forex Swaps; and, (v) Cash

Reserve Requirements. The Group also considered the introduction of cer tain new

instruments which would involve amendments to the RBI Act: (i) Interest Bearing

Deposits by Commercial Banks; and (ii) Issuance of Central Bank Securities. Moreover,

10 Report on Currency and Finance, Chapter VI, Reserve Bank of India, 2003

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 31/37

31

the Group explored the possibility whether the Government could issue Market

Stabilisation Bills / Bonds for sterilisation purposes if the existing instruments are found

to be inadequate to meet the size of operations in future.11

In pursuance of the

recommendation of the working group, a Market Stabilisation Scheme was introduced on

April 1,2004 under a Memorandum of Understanding between the Government of India

and the Reserve Bank. Under the MSS, treasury bills and dated securities of the Central

Government are issued for conducting sterilisation operations.

The Reserve Bank notifies the amount, tenure and timing of issuances under the MSS

under a calendar of issuances. The ceiling on the outstanding obligations of the

Government for the year 2004-05 under the MSS was fixed at Rs.60,000 crore, which is

now revised to Rs 80,000 crore. Through the Market Stabilisation Scheme, any increase

in the Reserve Bank’s net foreign assets would be matched by an accretion in

Government balances under the MSS driving down the net Reserve Bank credit to the

Government. The decline in Reserve Money nullifies the monetary impact of the increase

in Reserve Bank’s NFA.12

. In August, 2004 the Central Government raised Rs 5000 crore

from MSS.

11 Ibid12 Annual Report 2003-04, Reserve Bank of India

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 32/37

32

Section IV

Monetary Policy in the Current Inflationary Scenario

The rise in the annual inflation rate from 5.5 percent on June5 to 7.87% for the week

ended Setember 11 has raised serious concerns about the conduct of monetary policy.

The Reserve Bank is under pressure to curb inflation which is showing no signs of

abating. Government started its inflation control programme on the fiscal front through a

reduction in customs and excise duties on petroleum products. It was followed by RBI’s

decision to increase the cash reserve ratio by 50 basis points to 5 % in stages. So far RBI

has refrained from raising any of the interest rate under its control-the bank rate or the

repo rate as a part of its preference for soft interest policy stance which yielded

favourable results for the economy; industrial investment and output have begun to look

up. But there are apprehensions that the prevailing macroeconomic situation may place

pressure on the RBI to raise the rate of interest. The mid term review of the Annual

Policy Statement to be announced on October 26 also signals a hike in the interest rate.

Notwithstanding these pressures, the balance of considerations suggest that the RBI

should resist them so that the incipient recovery that is now discernable after a long

period of recession, particularly in the manufacturing sector is not throttled.

Monetary Policy also faces the challenge of managing the rupee-dollar exchange rate

which is continually oscillating between appreciation and depreciation in response to

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 33/37

33

factors like rising inflation rate, surges in oil prices, slow down in foreign exchange

inflows etc13.

Section V

Conclusion

Monetary policy through plethora of its instruments both direct and indirect attempts to

manage the inherent conflicts between exchange rate stability and price stability.

Monetary policy has been responsive to the developments in the external sector and has

been able to fine tune itself in the changed operational environment. The major challenge

is in the form of high order of capital inflows and the swelling foreign exchange reserves

which has raised doubts about the sustainability of sterilization operations which are

currently underway to curb the expansionary impact of capital inflows. The thrust of the

monetary policy is therefore to explore new and more effective instruments of

sterilization. A positive step in this direction is the introduction of the Market

Stabilization Scheme introduced since April 1 2004 to absorb the excess liquidity in the

market. Besides Sterilization operations are also conducted through repos under the

Liquidity Adjustment Facility (LAF).

Another aspect which is a cause of serious concern and requires serious thinking is the

conduct of monetary policy in a situation characterised by rising inflation triggered by

external developments in the form of oil price hike. A serious consideration is thus

13 EPW Research Foundation, Interest Rates: Case against a Hike, Economic and Political Weekly, Vol.XXXIX No. 38 September 18, 2004. PP. 4202-4204

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 34/37

34

required into the effectiveness of various direct and indirect instruments of monetary

control because their implication is not limited to price control but affects the overall

prospects of investment growth in the country.

Thus in short the monetary policy transmission mechanism has to be carefully examined

to minimise the negative externalities arising from its conduct to make it more

meaningful for the attainment of our broad objective of economic growth.

****

Bibliography

Alok Kumar Mishra, Revisiting Monetary Policy Perspectives in India during 1990s’,

Vol. III No. 2 Journal of Applied Economics, March 2004, ICFAI University, PP.66-67,

March 2004

Annual Report 2003-04, Reserve Bank of India

C. Rangarajan, Select Essays on Indian Economy, Vol. I, edited by R. Kannan, Academic

Foundation, New Delhi, 2004.

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 35/37

35

C. Rangarajan, Some critical Issues in Monetary Policy, EPW Special Aricle, June 16

2001,

Dr. Bimal Jalan, Governor, Reserve Bank of India, speech delivered on August 14 2003

at the 14th

National Assembly of Forex Association of India in Mumbai on Exchange

Rate Management: An Emerging Consensus?

EPW Research Foundation, Interest Rates: Case against a Hike, Economic and Political

Weekly, Vol. XXXIX No. 38 September 18, 2004. PP. 4202-4204

Ila Patnaiak, The Consequences of Currency Intervention in India, ICRIER Working .

Paper. No. 114, 2003

M. S. Ahluwalia, et al, (eds), Macroeconomics and Monetary Policy: Issues for a

Reforming Economy, Oxford University Press, New Delhi, 2002

M.Ramachandran, Fiscal Deficit, RBI Autonomy and Monetary Management , Economic

and Political Weekly, August 26 – September 2, 2000 PP. 3266-72,

Renu Kohli, Capital Account Liberalisation Empirical Evidence and Policy Issues – I,

EPW, Special Article, April 14, 2001 P. 1199

Report on Currency and Finance, Chapter VI, Reserve Bank of India, 2003

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 36/37

36

Report on Foreign Exchange Reserves, Reserve Bank of India, (Government of India,

2003-04)

Reserve Bank of India, Report: Report on Currency and Finance, Management of Capital

Flows, (Government of India, 2003)

Y. V. Reddy, Lectures on Economic and Financial Sectors Reforms in India, Oxford

University Press, New Delhi, 2002

Tables and Charts

Table: 1 Sources of Money Supply

Table: 2 Sources of Money Stock: Current Position

Table: 3 Composition of Capital Inflows to India

Table: 4 Sources of Accretion to Foreign Exchange Reserves since 1991

Table: 5 Sources of Accretion to Foreign Exchange Reserves

Table: 6 Monetary Tightening in episode I

Chart: 1 Capital Flows to Developing Economies

Chart: 2A Foreign Exchange Reserves (excluding Gold and SDR)

Chart: 2B Current Account Balance

8/10/2019 Monitory Policy Making in Open Economy

http://slidepdf.com/reader/full/monitory-policy-making-in-open-economy 37/37

Chart: 3 Trend in Movement of Foreign Exchange Reserves

Chart: 4 Money Supply & Inflation in episode I

Chart: 5 Currency Intervention in episode II

Chart: 6 Drop in CRR in Recent Years

Chart: 7 Money Multiplier in recent years

Chart: 8 Money Supply and inflation in Episode II