Embed Size (px)

Citation preview

2006

1234L

AT

VIJA

SB

AN

KA

MONETĀRAIS APSKATS MONETARY REVIEW

MO

NE

TÂ

RA

ISA

PS

KA

TS

MO

NE

TA

RY

RE

VIE

W�

42

00

6�

MONETÂRAIS APSKATS • MONETARY REVIEW 4• 2006

ISSN 1407–2815

© Latvijas Banka, 2007

Pârpublicçjot obligâta avota norâde.The source is to be indicated when reproduced.

Latvijas BankaK. Valdemâra ielâ 2A, Rîgâ, LV-1050Tâlrunis: 6702 2300 Fakss: 6702 2420http://[email protected]ìistrâcijas apliecîba Nr. 1450Iespiests "Premo"

Latvijas Banka (Bank of Latvia)K. Valdemâra ielâ 2A, Riga, LV-1050, LatviaTel.: +371 6702 2300 Fax: +371 6702 2420http://[email protected] of Registration No. 1450Printed by Premo

SATURS

Saîsinâjumi 4Ievads 5Ârçjâ ekonomiskâ vide 6Ârçjâ sektora attîstîba 8

Ârçjâ tirdzniecîba un konkurçtspçja 8Maksâjumu bilance 10

Iekðzemes ekonomiskâ aktivitâte 11Kopçjais pieprasîjums 11Kopçjais piedâvâjums 12Nodarbinâtîba un darba samaksa 13

Cenu dinamika 14Fiskâlais sektors 15Monetârâ un finanðu attîstîba 17

Banku likviditâte un Latvijas Bankas operâcijas 17Naudas râdîtâju dinamika 18

Procentu likmes 22Valûtas un vçrtspapîru tirgus attîstîba 24MFI darbîba 27Naudas râdîtâju sezonâlâ izlîdzinâðana 27Latvijas Bankas starpbanku maksâjumu sistçmu statistika 30Kredîtiestâþu maksâjumu statistika 31

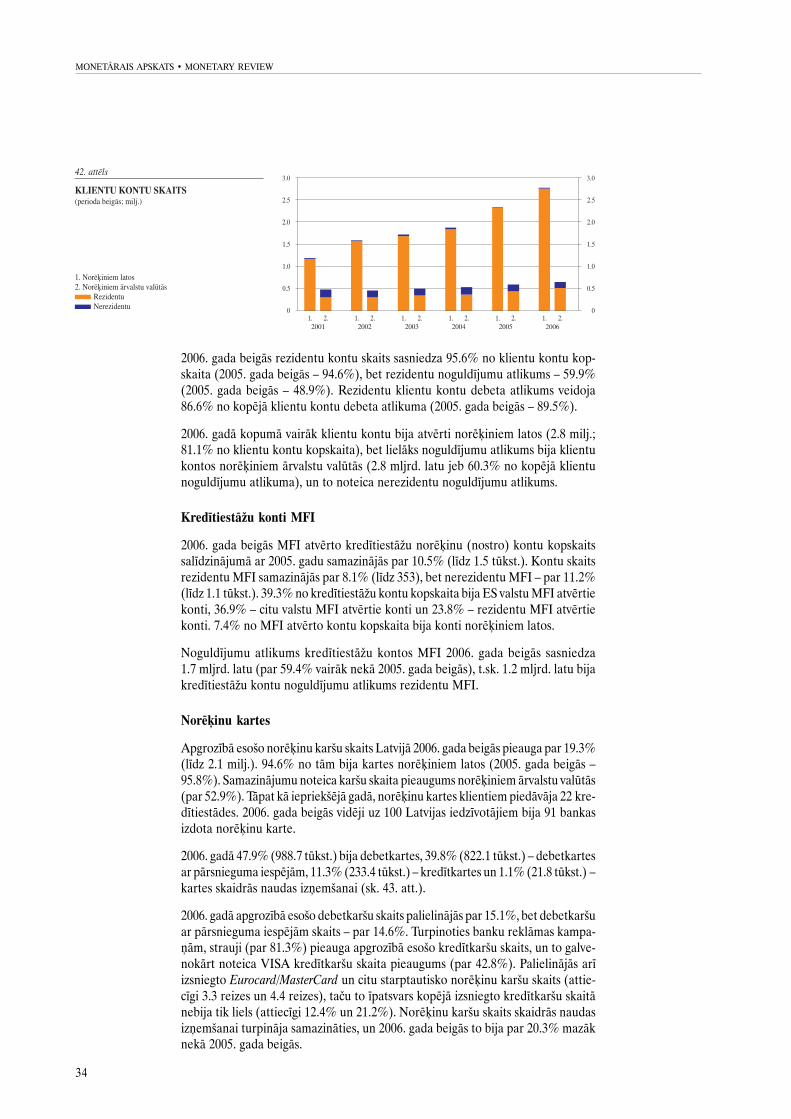

Maksâðanas lîdzekïi 31Konti 33Kredîtiestâþu konti MFI 34Norçíinu kartes 34Bankomâti un norçíinu karðu pieòemðanas vietas 35

Latvijas Bankas pamatuzdevumu izpildes normatîvâs aktualitâtes 36Statistiskâ informâcija 69Papildinformâcija 135

CONTENTS

Abbreviations 4Introduction 36External Economic Environment 37External Sector Developments 39

Foreign Trade and Competitiveness 39Balance of Payments 41

Domestic Economic Activity 42Aggregate Demand 42Aggregate Supply 43Employment, Wages and Salaries 44

Price Dynamics 45Fiscal Sector 46Monetary and Financial Developments 48

Bank Liquidity and the Bank of Latvia's Operations 48Dynamics of Monetary Aggregates 50

Interest Rates 54Foreign Exchange and Securities Market Developments 56MFI Developments 58Seasonal Adjustment of Monetary Aggregates 59Statistics Relating to the Bank of Latvia Interbank Payment Systems 62Credit Institution Payment Statistics 63

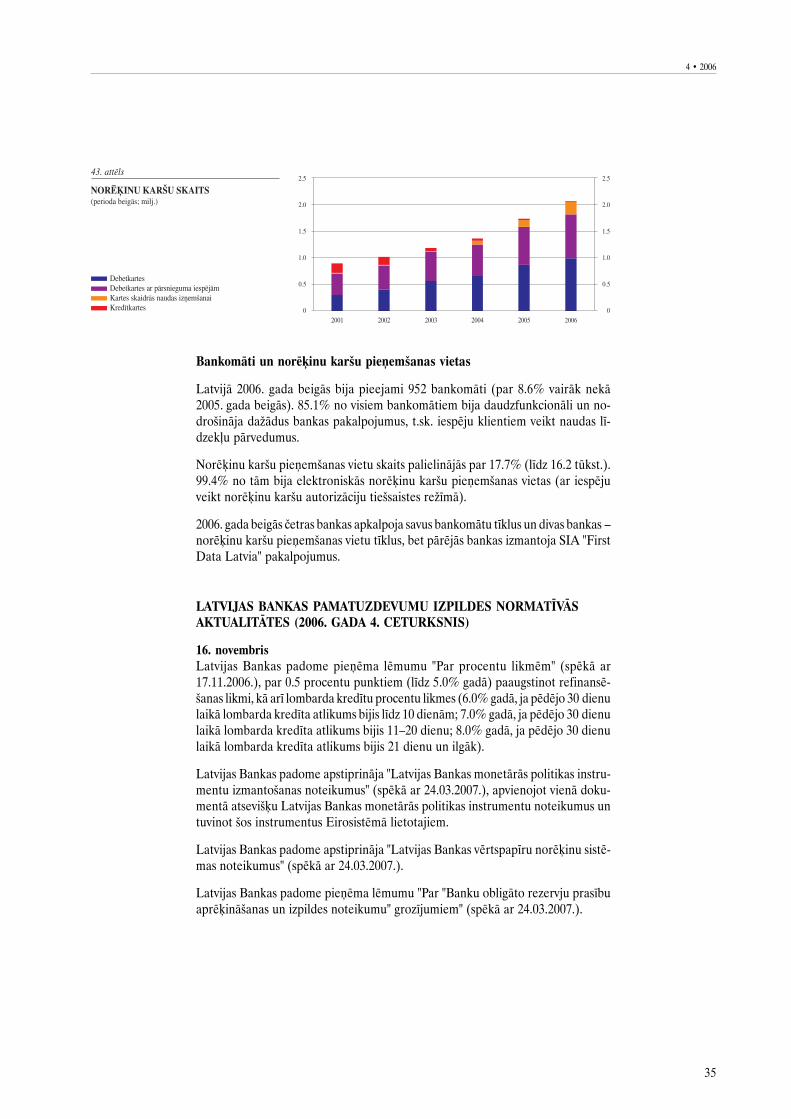

Payment Instruments 63Accounts 65Credit Institution Accounts with MFIs 66Payment Cards 66Automated Teller Machines and Points of Sale 66

Highlights of Resolutions and Regulations Adopted in Pursuitof the Bank of Latvia's Main Tasks 67Statistics 69Additional Information 138

3

4

MONETÂRAIS APSKATS · MONETARY REVIEW

SAÎSINÂJUMI

AS – akciju sabiedrîbaASV – Amerikas Savienotâs ValstisBALTIX – vienotais Baltijas valstu birþu kapitalizâcijas indekssCSP – Latvijas Republikas Centrâlâ statistikas pârvaldeECB – Eiropas Centrâlâ bankaEKS – Latvijas Bankas elektroniskâ klîringa sistçmaEMS – Ekonomikas un monetârâ savienîbaES – Eiropas SavienîbaES8 valstis – Èehija, Igaunija, Latvija, Lietuva, Polija, Slovâkija,Slovçnija, UngârijaES10 valstis – valstis, kuras pievienojâs ES 2004. gada 1. maijâES15 valstis – valstis, kuras ietilpa ES pirms 2004. gada 1. maijaFRS – Federâlo rezervju sistçmaIKP – iekðzemes kopproduktsLCD – Latvijas Centrâlais depozitârijsMFI – monetârâ finanðu iestâdeNVS – Neatkarîgo Valstu SavienîbaPVN – pievienotâs vçrtîbas nodoklisRFB – Rîgas Fondu birþaRIGIBOR – Riga Interbank Offered Rate; Latvijas starpbankukredîtu procentu likmju indekssRIGSE (ar 2005. gada 3. oktobri – OMX Riga) – kapitalizâcijasindekss, kas tiek attiecinâts pret iepriekðçjo vçrtîbu un raksturokopçjo ieguldîjuma atdevi un kurâ ietvertas visas RFB Oficiâlâun Otrâ saraksta uzòçmumu akcijasROA – aktîvu atdeveROE – kapitâla atdeveSAMS – Latvijas Bankas starpbanku automatizçtâ maksâjumusistçmaSIA – sabiedrîba ar ierobeþotu atbildîbuSPCI – saskaòotais patçriòa cenu indekssVAS – valsts akciju sabiedrîbaVKM II – Valûtas kursa mehânisms II

ABBREVIATIONS

BALTIX – Pan-Baltic capitalisation-weighted chain-linked totalreturn indexCIS – Commonwealth of Independent StatesCPI – Consumer Price IndexCSB – Central Statistical Bureau of LatviaECB – European Central BankEKS – Bank of Latvia's Electronic Clearing SystemEMU – Economic and Monetary UnionERM II – Exchange Rate Mechanism IIEU – European UnionEU8 – Czech Republic, Estonia, Hungary, Latvia, Lithuania,Poland, Slovakia, SloveniaEU10 – countries which joined the EU on May 1, 2004EU15 – EU countries before May 1, 2004FRS – Federal Reserve SystemGDP – gross domestic productHICP – Harmonised Index of Consumer PricesJSC – joint stock companyLCD – Latvian Central DepositoryMFI – monetary financial institutionRIGIBOR – Riga Interbank Offered RateRIGSE (as of October 3, 2005 – OMX Riga) – capitalisation-based total return index including all company shares quoted onthe RSE Official List and the RSE Second ListROA – return on assetsROE – return on equityRSE – Riga Stock ExchangeSAMS – Bank of Latvia's Interbank Automated Payment SystemSJSC – state joint stock companyUK – United KingdomUS – United States of America

5

4 · 2006

IEVADS

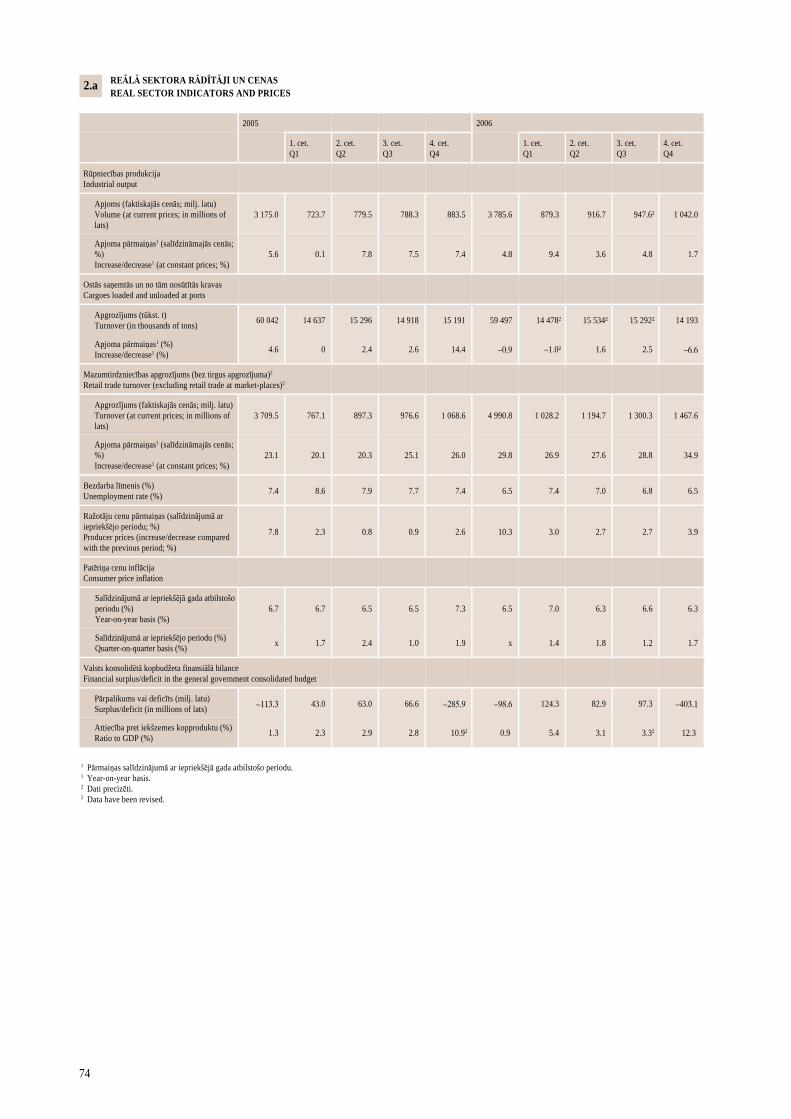

Strauja, bet nesabalansçta Latvijas tautsaimniecîbas izaugsme turpinâjâs arî2006. gada 4. ceturksnî. Tâs virzîtâji joprojâm bija iekðzemes pieprasîjuma kompo-nenti – rekordlielais privâtais patçriòð un stabili augstais investîciju pieaugums.Ârçjais pieprasîjums bija samçrâ augsts, bet ar lejupvçrstu pârmaiòu tendenci.Eksporta pieauguma temps samazinâjâs, un spçcîgâ iekðzemes pieprasîjumanoteiktais importa kâpums palielinâja tekoðâ konta deficîtu. Pieprasîjuma spiedienaietekmç paaugstinâjâs inflâcijas (galvenokârt – pamatinflâcijas) lîmenis. Lai ganturpinâja palielinâties noguldîjumu atlikums bankâs, kreditçðanas pieaugumugalvenokârt nodroðinâja ârvalstu MFI finansçjums, tâdçjâdi palielinot Latvijasârçjo parâdu. Gandrîz nemainîjâs naudas piedâvâjuma kâpums: decembrî plaðâsnaudas M3 un iekðzemes noguldîjumu atlikuma gada pieauguma temps sasniedzaattiecîgi 40.3% un 41.0%. Saglabâjoties lielam pieprasîjumam pçc mâjokïiem,kredîtu atlikuma, îpaði mâjsaimniecîbâm mâjokïa iegâdei izsniegto kredîtuatlikuma, pieauguma temps bija straujð, lai gan augstâs bâzes ietekmç nedaudzsamazinâjâs (no 59.5% septembrî lîdz 58.4% decembrî). Kredîtu procentu likmjupieaugumam pagaidâm nozîmîgas ietekmes nebija, un stabili palielinâjâs arî finanðuiestâdçm un nefinanðu sabiedrîbâm izsniegto kredîtu atlikums. 2006. gadâ valstskonsolidçtâ kopbudþeta finansiâlais deficîts bija 0.9% no IKP, 2006. gada divospçdçjos mçneðos budþeta izdevumiem ievçrojami pârsniedzot ieòçmumus unpalielinot jau tâ augsto iekðzemes pieprasîjumu. Ðâda budþeta izdevumu eskalâcijanav adekvâta situâcijâ, kad tautsaimniecîbai raksturîga strauja izaugsme.

2006. gada 4. ceturksnî IKP gada pieaugums sasniedza 11.7% (2006. gadâ kopumâ –11.9%). Arî 4. ceturksnî saglabâjâs lîdzðinçjâs tendences – ïoti liels privâtâ patçriòaun importa pieaugums, lçnâks eksporta pieauguma temps un straujâka to nozaruattîstîba, kas piedâvâ preces un pakalpojumus iekðzemes tirgum, nevis eksportam.Mazumtirdzniecîbas apgrozîjuma tâlâku strauju izaugsmi noteica ilglietojuma pre-èu dinamiskais pieprasîjums. Pasliktinâjâs dzelzceïa un ostu darbîbas râdîtâji, betpalielinâjâs automobiïu kravu pârvadâjumu apjoms un pa cauruïvadu transportçtonaftas produktu apjoms, uzlabojâs arî Rîgas lidostas darbîbas un sakaru nozaresrâdîtâji. Saglabâjâs mçrens apstrâdes rûpniecîbas pieauguma temps. Vienlaikusturpinâja palçninâties eksporta kâpuma temps. Latvijas Bankas prognozes liecina,ka 2007. gadâ nedaudz samazinâsies kopçjâs pievienotâs vçrtîbas kâpums. Tas sais-tîts ar iekðzemes pieprasîjuma pieauguma palçninâðanos tâ augstâs bâzes dçï, kâarî reâlo kredîtu procentu likmju kâpuma, darbaspçka trûkuma un augstâs inflâcijasietekmç. Gaidâma arî mçrenâka ârçjâ pieprasîjuma palielinâðanâs.

Darbaspçka tirgû turpinâjâs iepriekðçjos mçneðos vçrojamâs tendences – nodar-binâtîbas pieaugums, augoðs darbaspçka trûkums un darba algu kâpums. Bezdarbalîmenis decembrî saruka lîdz 6.5%.

Arvien lielâks kïûst importa pârsvars pâr eksportu, lîdz ïoti augstam lîmenim pa-lielinot maksâjumu bilances tekoðâ konta deficîtu, kas 2006. gadâ sasniedza 21.1%no IKP (2005. gadâ – 12.6%), bet 4. ceturksnî – 26.3% no IKP. Deficîta kâpumuvisvairâk ietekmçja preèu bilances negatîvâ saldo pieaugums, jo importa kâpumsgada laikâ (29.3%) bija vairâk nekâ divreiz straujâks par eksporta pieaugumu(11.6%). Nepiecieðamo finansçjumu nodroðinâja ârvalstu tieðâs investîcijas (35.1%no tekoðâ konta deficîta) un aizòçmumi (galvenokârt banku ilgtermiòa aizòçmumino mâtesbankâm). Tekoðâ konta deficîtu sedza ilgtermiòa kapitâls. Neto ârvalstutieðo investîciju apjoms pieauga 2.5 reizes.

Latvijas Banka turpinâja îstenot ierobeþojoðu monetâro politiku, jo noturîgais inflâ-cijas lîmenis, tekoðâ konta negatîvais saldo un kreditçðanas veicinâtâ tautsaimnie-cîbas izaugsme pârsniedza ilgtermiòâ uzturamu lîmeni. Òemot vçrâ makroekono-miskâs attîstîbas tendences Latvijâ un procentu likmju kâpumu eiro zonâ, Latvijas

6

MONETÂRAIS APSKATS · MONETARY REVIEW

Banka ar 2006. gada 17. novembri par 0.5 procentu punktiem (lîdz 5.0%) paaug-stinâja refinansçðanas likmi. Par 0.5 procentu punktiem (attiecîgi lîdz 6.0%, 7.0%un 8.0%) tika paaugstinâtas arî lombarda kredîtu procentu likmes aizdevumiemar izmantoðanas termiòu pçdçjo 30 dienu laikâ lîdz 10 dienâm, no 11 lîdz 20 dienâmun 21 dienu un ilgâk.

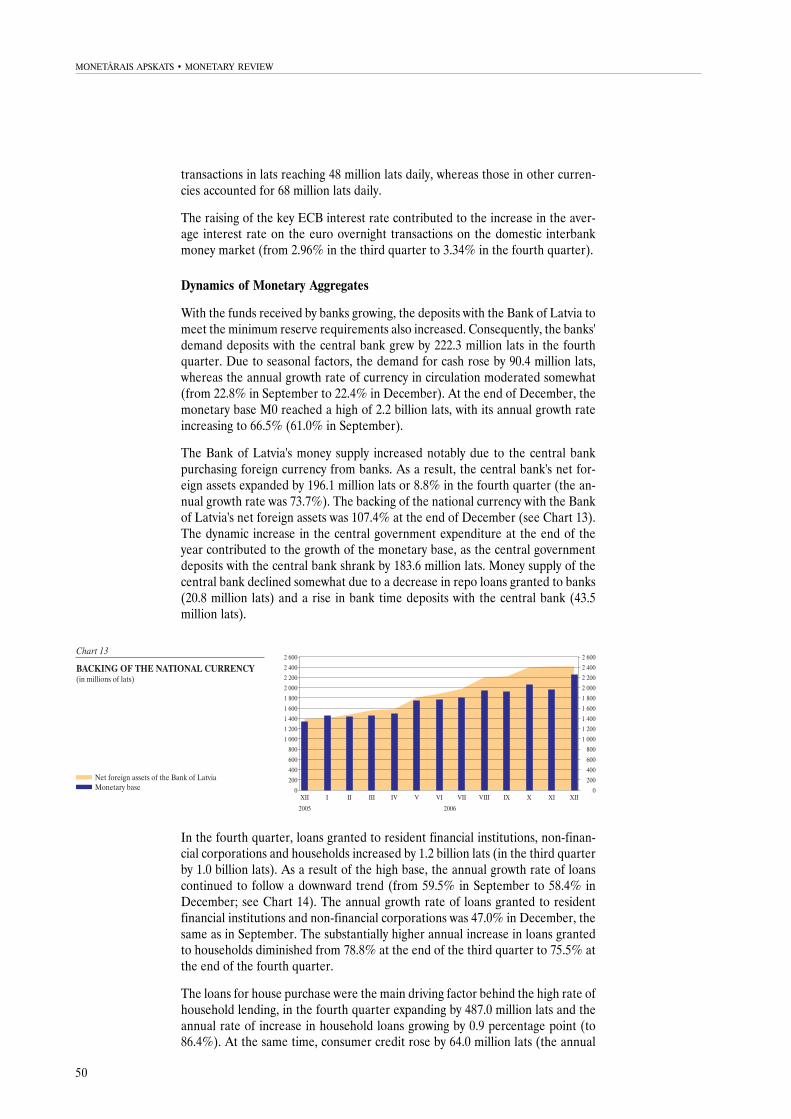

Centrâlâs bankas naudas piedâvâjuma apjomu oktobrî bûtiski ietekmçja ârvalstuvalûtas pirkðana no bankâm, un 4. ceturksnî Latvijas Bankas tîrie ârçjie aktîvipalielinâjâs par 196.1 milj. latu, gadâ pieaugot par 73.7%. Emitçtâs nacionâlâsvalûtas segums ar Latvijas Bankas tîrajiem ârçjiem aktîviem decembra beigâs bija107.4%.

ÂRÇJÂ EKONOMISKÂ VIDE

Pasaules tautsaimniecîba kopumâ 4. ceturksnî turpinâja veiksmîgi attîstîties. Eirozonas un Âzijas reìiona valstîs bija vçrojams tautsaimniecîbas izaugsmes tempapaâtrinâjums. Strauja ekonomiskâ attîstîba turpinâjâs arî ES8 valstîs. Pasaules eko-nomisko attîstîbu 4. ceturksnî nozîmîgi ietekmçja naftas cenu kritums salîdzinâ-jumâ ar vasaras vidu, vienlaikus mazinot inflâcijas draudus nâkotnç. Naftas cenasoktobrî sasniedza 2006. gada minimumu – 55 ASV dolârus par barelu (gada beigâs –59 ASV dolâri par barelu).

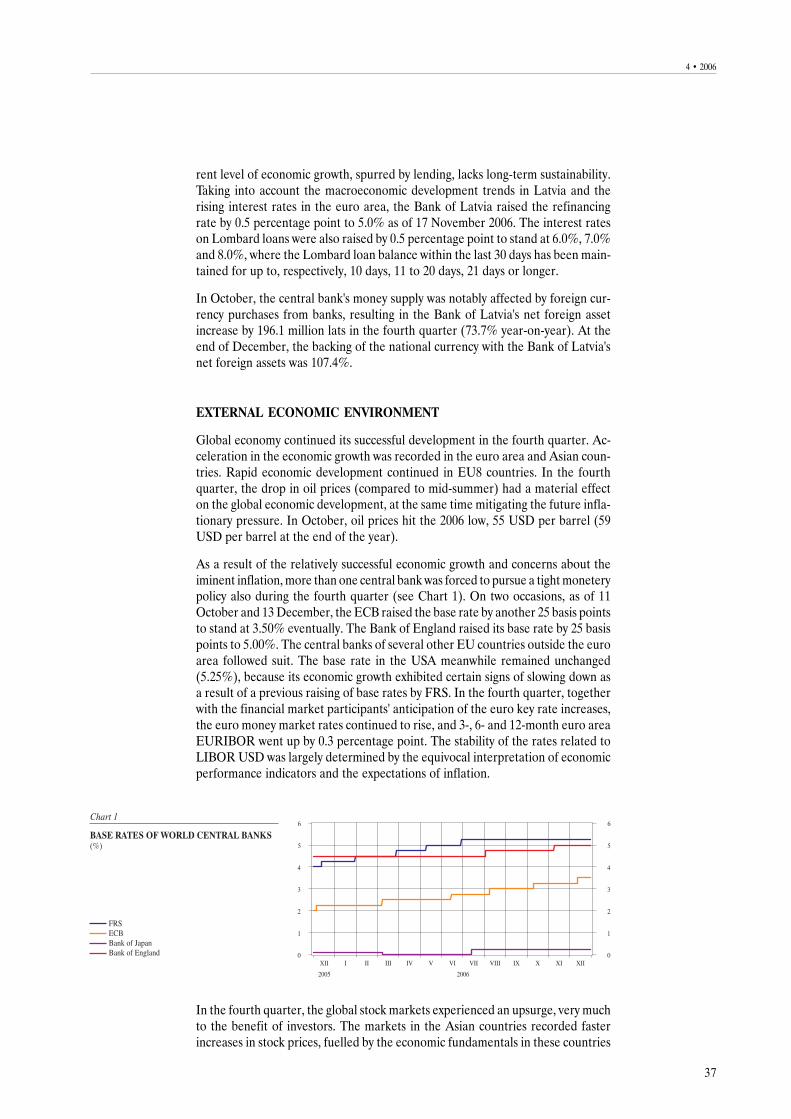

Samçrâ veiksmîgâ tautsaimniecîbas izaugsme un baþas par inflâcijas draudiemvairâkâm centrâlajâm bankâm 4. ceturksnî lika turpinât ierobeþojoðas monetârâspolitikas îstenoðanu (sk. 1. att.). ECB divas reizes paaugstinâja bâzes likmi vçl par25 bâzes punktiem (ar 11. oktobri un 13. decembri; lîdz 3.50%). Anglijas Bankapaaugstinâja bâzes likmi par 25 bâzes punktiem (lîdz 5.00%). Bâzes likmes pa-augstinâja arî vairâku citu ES valstu, kuras nav eiro zonas valstis, centrâlâs bankas.Savukârt FRS iepriekð veikto bâzes likmju paaugstinâjumu ietekmç bija vçrojamastautsaimniecîbas attîstîbas tempa palçninâðanâs pazîmes, un bâzes likme ASV ne-tika mainîta (5.25%). Lîdz ar finanðu tirgus dalîbnieku gaidâm par galveno ECBprocentu likmju iespçjamo paaugstinâðanu 4. ceturksnî turpinâja celties eiro naudastirgus procentu likmes, eiro zonas 3, 6 un 12 mçneðu EURIBOR pieaugot par0.3 procentu punktiem. Savukârt daþâdi vçrtçjamie tautsaimniecîbas attîstîbas râ-dîtâji un inflâcijas gaidas noteica LIBOR USD procentu likmju nemainîgumu.

Pasaules akciju tirgum 4. ceturksnî bija raksturîgs ieguldîtâjiem labvçlîgs akcijucenu pieaugums. Cenas straujâk cçlâs Âzijas reìiona akciju tirgos, un kâpumuveicinâja ðo valstu tautsaimniecîbas pamatrâdîtâji un samçrâ zemâs procentu lik-mes. Eiropas akciju tirgus indekss Dow Jones EURO STOXX 50 4. ceturksnî pieaugapar 4.1%, ASV akciju tirgus indekss S&P 500 – par 6.5%, NASDAQ Composite –par 7.9% un Japânas akciju tirgus indekss Nikkei 225 – par 6.0%. Akciju cenu

7

4 · 2006

kâpums turpinâjâs arî ES8 valstîs – Dow Jones STOXX EU Enlarged 15 4. ceturksnîpieauga par 19.6%. Krievijas akciju tirgus indekss RTS palielinâjâs par 23.4% unÍînas akciju tirgus indekss SSE A Share – pat par 50.1%. ECB lçmumi par galvenoprocentu likmju celðanu, tirgus dalîbniekiem gaidot arî tâlâku procentu likmjukâpumu, mazinâja ienesîguma lîknes slîpumu, Vâcijas valdîbas 10 gadu obligâcijupeïòas likmei palielinoties par 0.25 procentu punktiem. Ienesîguma lîknes slîpumsASV, valdîbas 10 gadu obligâciju peïòas likmei pieaugot par 0.07 procentu pun-ktiem, 4. ceturksnî saglabâjâs negatîvs.

ASV IKP 4. ceturksnî palielinâjâs straujâk nekâ iepriekðçjos divos ceturkðòos –par 2.2%. Tas varçtu liecinât par gada vidû mâjokïu tirgus stagnâcijas izraisîtoASV tautsaimniecîbas lejupslîdes pârvarçðanu. Strauji pieauga privâtais un valdîbaspatçriòð, kâ arî eksports, bet mâjokïu iegâdei un uzòçmçjdarbîbâ ieguldîto in-vestîciju apjoms saruka. Rûpnieciskâs raþoðanas apjoms pçc trîs mçneðus ilguðâkrituma decembrî atkal pieauga (salîdzinâjumâ ar iepriekðçjo mçnesi – par 0.5%).Inflâcija ASV 4. ceturksnî nedaudz pazeminâjâs.

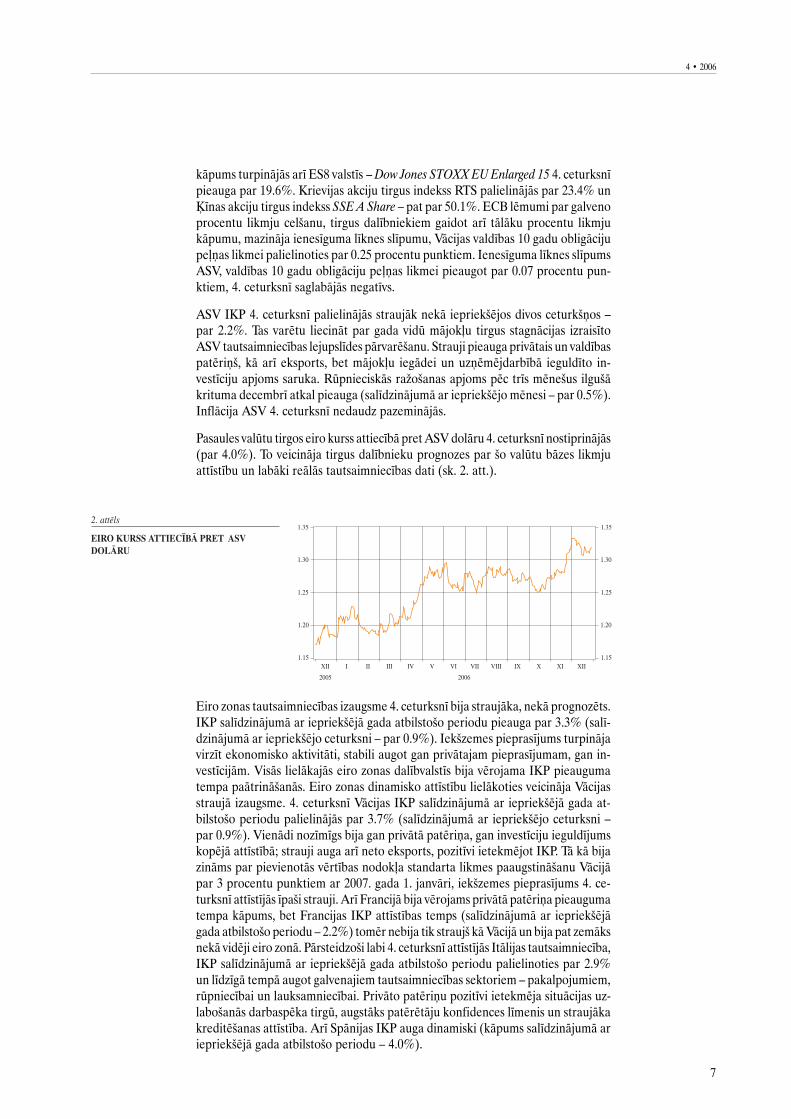

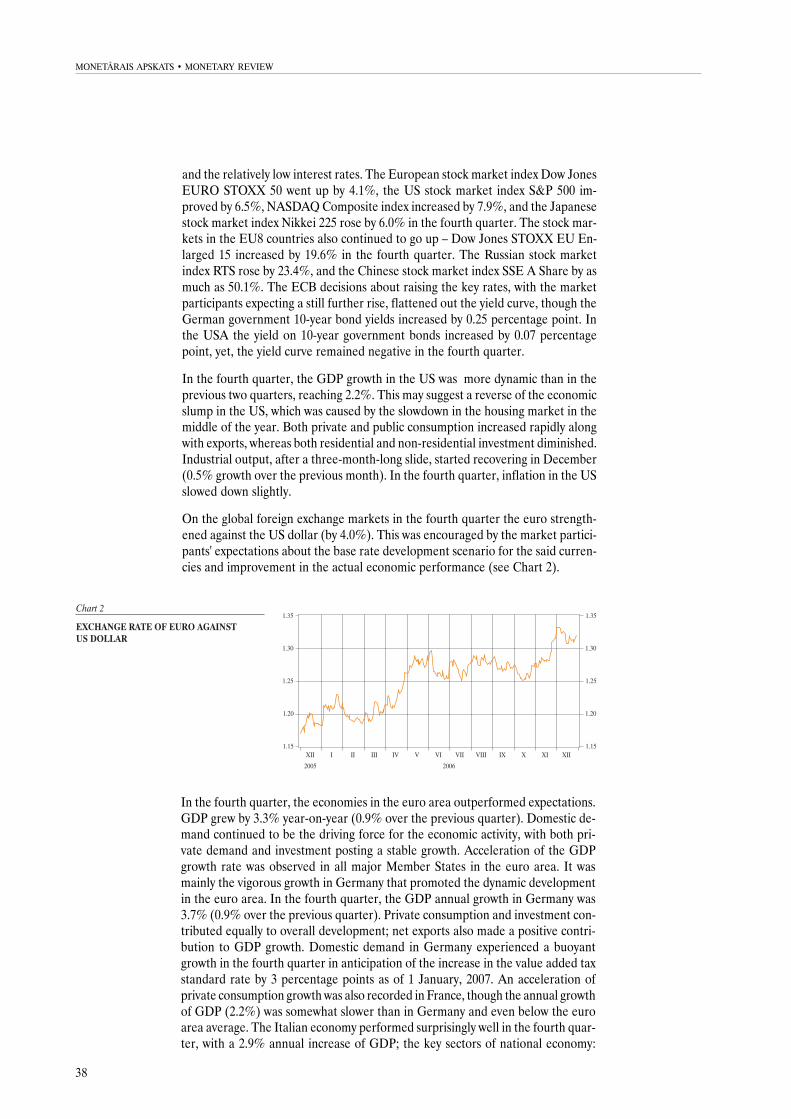

Pasaules valûtu tirgos eiro kurss attiecîbâ pret ASV dolâru 4. ceturksnî nostiprinâjâs(par 4.0%). To veicinâja tirgus dalîbnieku prognozes par ðo valûtu bâzes likmjuattîstîbu un labâki reâlâs tautsaimniecîbas dati (sk. 2. att.).

Eiro zonas tautsaimniecîbas izaugsme 4. ceturksnî bija straujâka, nekâ prognozçts.IKP salîdzinâjumâ ar iepriekðçjâ gada atbilstoðo periodu pieauga par 3.3% (salî-dzinâjumâ ar iepriekðçjo ceturksni – par 0.9%). Iekðzemes pieprasîjums turpinâjavirzît ekonomisko aktivitâti, stabili augot gan privâtajam pieprasîjumam, gan in-vestîcijâm. Visâs lielâkajâs eiro zonas dalîbvalstîs bija vçrojama IKP pieaugumatempa paâtrinâðanâs. Eiro zonas dinamisko attîstîbu lielâkoties veicinâja Vâcijasstraujâ izaugsme. 4. ceturksnî Vâcijas IKP salîdzinâjumâ ar iepriekðçjâ gada at-bilstoðo periodu palielinâjâs par 3.7% (salîdzinâjumâ ar iepriekðçjo ceturksni –par 0.9%). Vienâdi nozîmîgs bija gan privâtâ patçriòa, gan investîciju ieguldîjumskopçjâ attîstîbâ; strauji auga arî neto eksports, pozitîvi ietekmçjot IKP. Tâ kâ bijazinâms par pievienotâs vçrtîbas nodokïa standarta likmes paaugstinâðanu Vâcijâpar 3 procentu punktiem ar 2007. gada 1. janvâri, iekðzemes pieprasîjums 4. ce-turksnî attîstîjâs îpaði strauji. Arî Francijâ bija vçrojams privâtâ patçriòa pieaugumatempa kâpums, bet Francijas IKP attîstîbas temps (salîdzinâjumâ ar iepriekðçjâgada atbilstoðo periodu – 2.2%) tomçr nebija tik straujð kâ Vâcijâ un bija pat zemâksnekâ vidçji eiro zonâ. Pârsteidzoði labi 4. ceturksnî attîstîjâs Itâlijas tautsaimniecîba,IKP salîdzinâjumâ ar iepriekðçjâ gada atbilstoðo periodu palielinoties par 2.9%un lîdzîgâ tempâ augot galvenajiem tautsaimniecîbas sektoriem – pakalpojumiem,rûpniecîbai un lauksamniecîbai. Privâto patçriòu pozitîvi ietekmçja situâcijas uz-laboðanâs darbaspçka tirgû, augstâks patçrçtâju konfidences lîmenis un straujâkakreditçðanas attîstîba. Arî Spânijas IKP auga dinamiski (kâpums salîdzinâjumâ ariepriekðçjâ gada atbilstoðo periodu – 4.0%).

8

MONETÂRAIS APSKATS · MONETARY REVIEW

Lielbritânijas IKP 4. ceturksnî salîdzinâjumâ ar iepriekðçjo ceturksni pieauga par0.8%. Izaugsmes virzîtâjspçks bija pakalpojumu sektora attîstîba, îpaði viesnîcuun restorânu nozare, bet rûpnieciskâ raþoðana stagnçja ârçjâ pieprasîjuma svârstî-guma un Lielbritânijas sterliòu mârciòas kursa kâpuma dçï. Tomçr inflâcija Liel-britânijâ bija virs mçría inflâcijas lîmeòa, tâpçc, lai gan tautsaimniecîbas attîstîbasperspektîvas bija labas, Anglijas Banka novembrî paaugstinâja bâzes likmi.

Zviedrijâ 4. ceturksnî IKP salîdzinâjumâ ar iepriekðçjo ceturksni pieauga par 1.2%.Tautsaimniecîbai attîstoties, palielinâjâs kreditçðanas apjoms un nekustamâ îpa-ðuma cenas, lai gan inflâcija saglabâjâs samçrâ zema. Tas skaidrojams ar augstoproduktivitâtes lîmeni: firmas spçja saraþot vairâk produkcijas, nepiesaistot papildudarbaspçku, tâpçc nebija ievçrojama darba algu spiediena uz inflâciju. Tomçr,òemot vçrâ nâkotnes prognozes un cenu stabilitâtes riskus, Sveriges Riksbank arî4. ceturksnî turpinâja palielinât bâzes likmi.

4. ceturksnî saglabâjâs samçrâ dinamisks ES8 valstu tautsaimniecîbas izaugsmestemps. Igaunijas IKP salîdzinâjumâ ar iepriekðçjâ gada atbilstoðo periodu pieaugapar 11.2%, un kâpumu noteica rûpniecîbas un tirdzniecîbas izaugsme un transportapakalpojumu un finanðu nozares attîstîba. Ïoti strauji auga arî Slovâkijas IKP –4. ceturksnî tas salîdzinâjumâ ar iepriekðçjâ gada atbilstoðo periodu pieauga par9.5%. Izlietojumâ bija nozîmîga gan ârçjâ, gan iekðçjâ pieprasîjuma loma; izaugsminoteica rûpniecîbas, vairumtirdzniecîbas un finanðu pakalpojumu attîstîba. LietuvasIKP palielinâjâs lçnâk (par 7.0%), izaugsmi veicinot galvenokârt bûvniecîbas unfinanðu pakalpojumu attîstîbai. Polijas IKP pieaugums sasniedza 6.6%, jo iekðzemespieprasîjuma ietekmç auga investîcijas pamatkapitâlâ un privâtais patçriòð. Un-gârijas IKP pieauga lçnâk – par 3.4%. Inflâcija daudzâs ES8 valstîs arî 4. ceturksnîsaglabâjâs samçrâ augsta. Decembrî augstâkâ inflâcija bija Latvijâ (6.8%), Ungârijâ(6.6%) un Igaunijâ (5.1%), bet Polijâ un Èehijâ tâ bija zemâka nekâ vidçji ES(attiecîgi 1.4% un 1.6%).

Krievijas tautsaimniecîba 2006. gada pirmajos deviòos mçneðos attîstîjâs veiksmîgi,un arî 4. ceturksnî turpinâjâs strauja izaugsme. Decembrî ievçrojami palielinâjâsmazumtirdzniecîbas apgrozîjuma apjoms (salîdzinâjumâ ar iepriekðçjâ gada at-bilstoðo periodu – par 14.8%), jo iedzîvotâju ienâkumi pieauga. Vienlaikus rûp-nieciskâs raþoðanas kâpuma temps pçc straujâ pieauguma oktobrî un novembrîdecembrî bija lçnâks. Lai gan 2006. gada pçdçjos mçneðos bija vçrojams nozîmîgsimporta kâpums, Krievijas ârçjâs tirdzniecîbas bilance tomçr saglabâjâs pozitîva,jo dinamiski attîstîjâs eksports.

ÂRÇJÂ SEKTORA ATTÎSTÎBA

Ârçjâ tirdzniecîba un konkurçtspçja

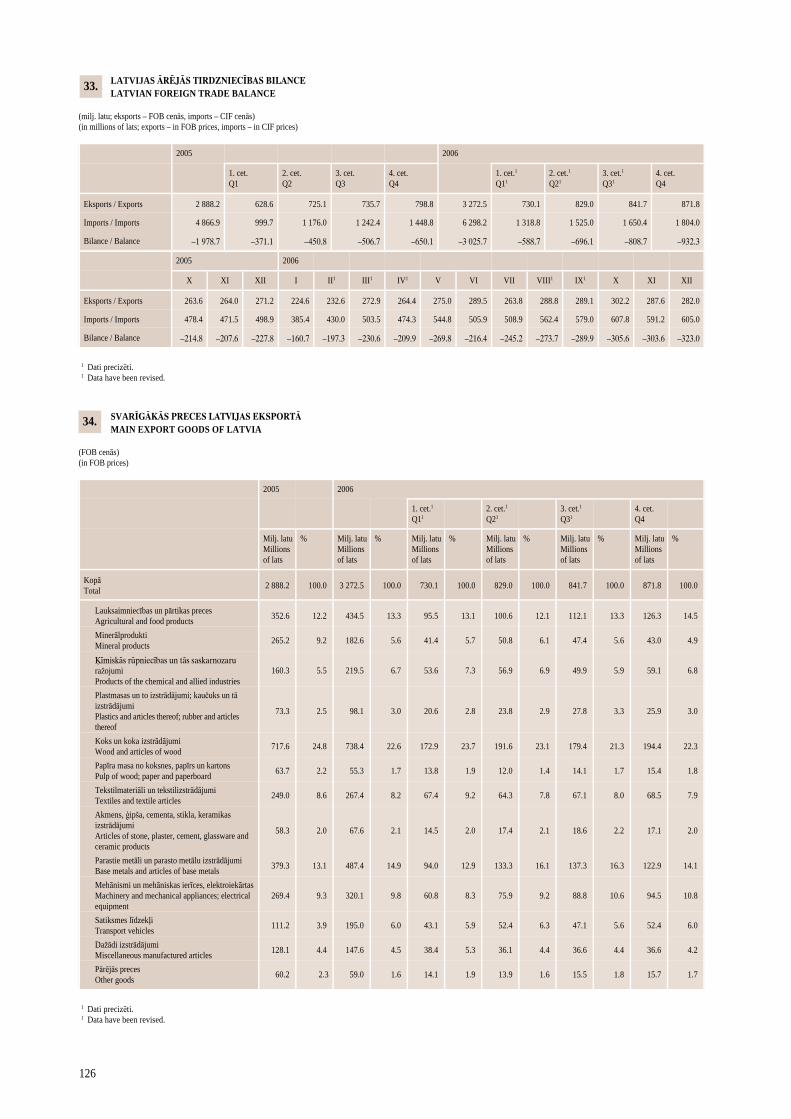

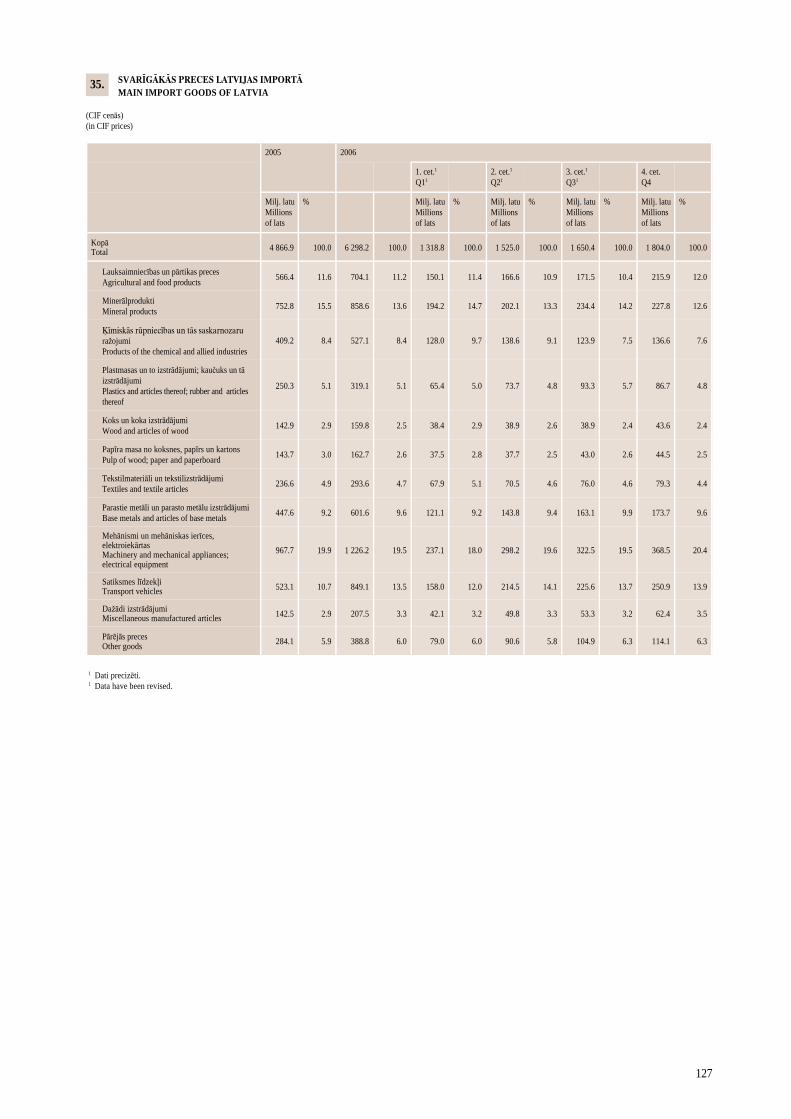

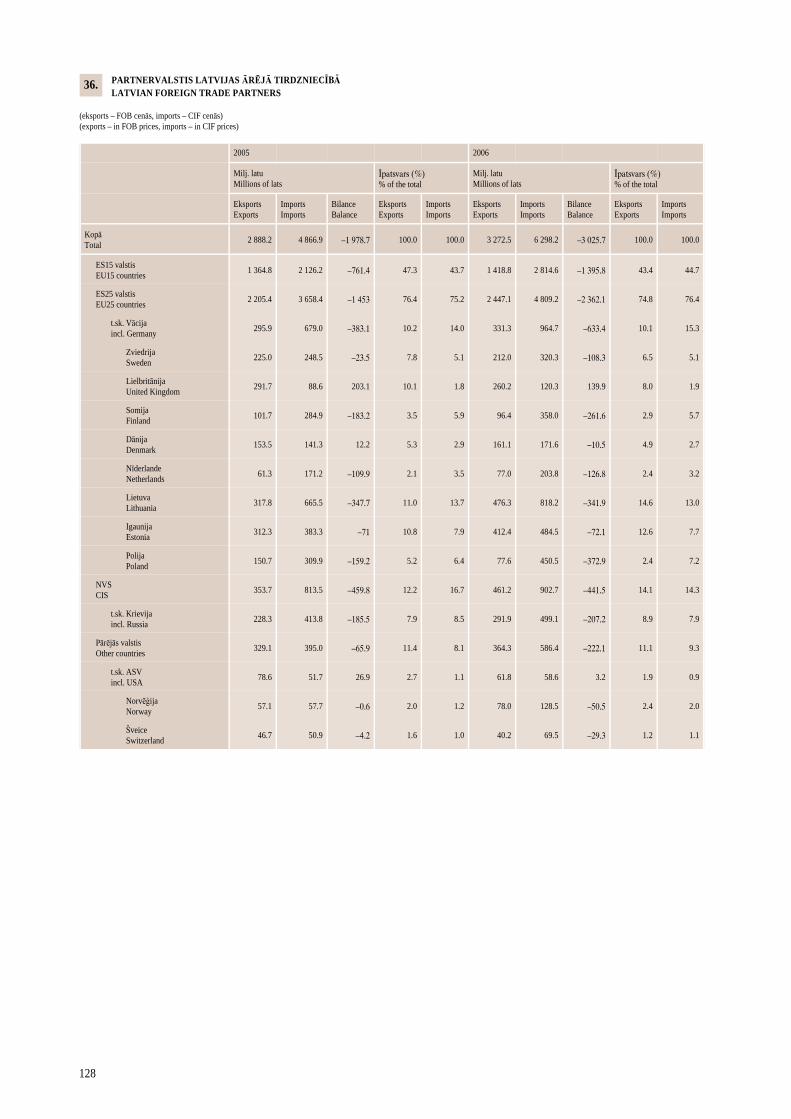

Latvijas ârçjâs tirdzniecîbas izaugsme 4. ceturksnî salîdzinâjumâ ar iepriekðçjâgada atbilstoðo periodu kïuva mçrenâka. Tirdzniecîbas apgrozîjums sasniedza2.7 mljrd. latu, eksportam palielinoties par 9.1%, bet importam – par 24.5%. Jo-projâm augoðâ iekðzemes pieprasîjuma ietekmç importa apjoms divas reizes pâr-sniedza eksporta apjomu. Eksporta pieauguma palçninâðanos noteica augstais iekð-zemes pieprasîjums un konkurçtspçjas samazinâðanâs.

Latvijas preèu eksportâ 4. ceturksnî salîdzinâjumâ ar iepriekðçjâ gada atbilstoðoperiodu vislielâkais bija koka un koka izstrâdâjumu, parasto metâlu un parastometâlu izstrâdâjumu un satiksmes lîdzekïu eksporta pieaugums, savukârt bûtiskikritâs minerâlproduktu izvedums. Preèu eksportâ joprojâm dominçja koks un kokaizstrâdâjumi, lauksaimniecîbas un pârtikas preces, parastie metâli un parasto metâ-

9

4 · 2006

lu izstrâdâjumi, mehânismi un mehâniskas ierîces, elektroiekârtas un tekstilmate-riâli un tekstilizstrâdâjumi. Eksporta pieaugumu kopumâ noteica cenu kâpums,jo eksporta fiziskais apjoms samazinâjâs. Preèu grupu dalîjumâ vienîgi lauksaim-niecîbas un pârtikas preèu izveduma pieaugumu ietekmçja fiziskâ apjoma palieli-nâðanâs. Gan fiziskâ apjoma, gan cenu kâpums noteica íîmiskâs rûpniecîbas untâs saskarnozaru raþojumu, satiksmes lîdzekïu, tekstilmateriâlu un tekstilizstrâ-dâjumu un mehânismu un mehânisku ierîèu, elektroiekârtu eksporta pieaugumu.Kritâs minerâlproduktu, koka un koka izstrâdâjumu, parasto metâlu un parastometâlu izstrâdâjumu un daþâdu izstrâdâjumu (mçbeïu) fiziskais apjoms. To izve-duma pieaugumu noteica vienîgi cenu kâpums.

Preèu eksporta vienîbas vçrtîba auga katru ceturksni, un 4. ceturksnî kâpums salî-dzinâjumâ ar iepriekðçjâ gada atbilstoðo periodu sasniedza 14.2%. Vislielâkaisbija parasto metâlu un parasto metâlu izstrâdâjumu (28.7%), koka un koka izstrâ-dâjumu (19.6%), satiksmes lîdzekïu (13.2%), daþâdu izstrâdâjumu (mçbeïu; 11.3%)un íîmiskâs rûpniecîbas un tâs saskarnozaru raþojumu (8.7%) cenu pieaugums.Lîdz ar straujâku eksporta cenu kâpumu gada beigâs uzlabojâs tirdzniecîbas no-sacîjumi.

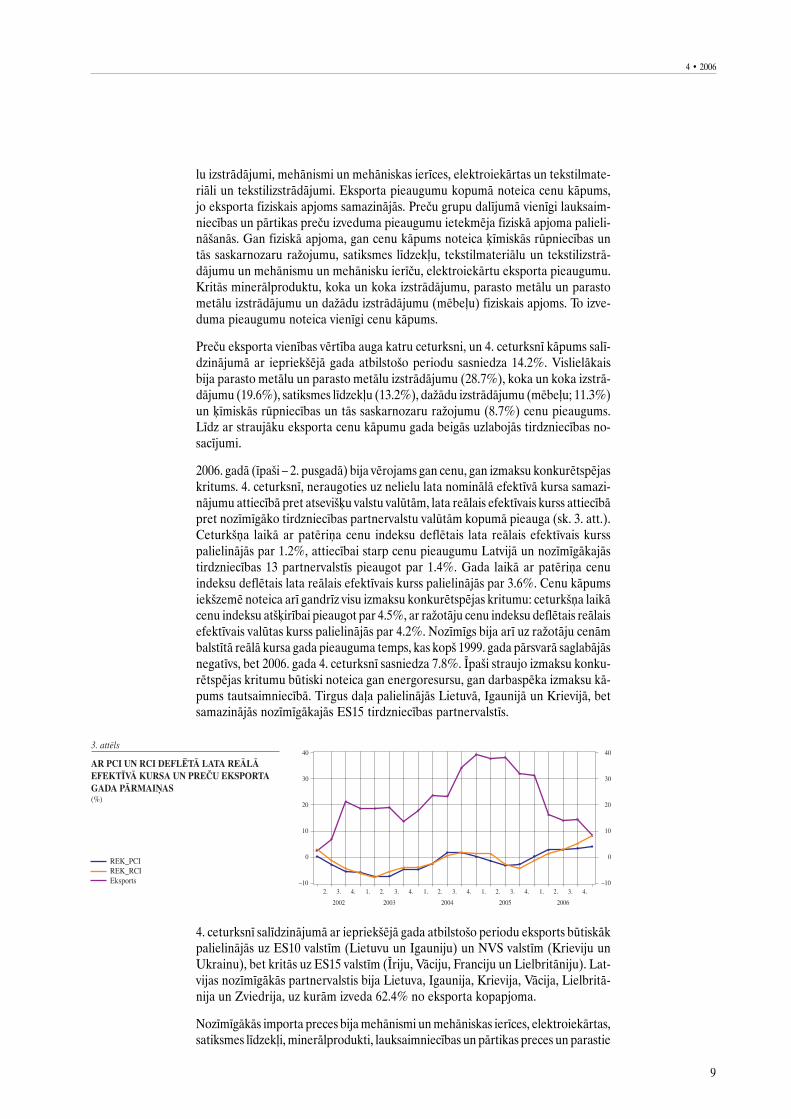

2006. gadâ (îpaði – 2. pusgadâ) bija vçrojams gan cenu, gan izmaksu konkurçtspçjaskritums. 4. ceturksnî, neraugoties uz nelielu lata nominâlâ efektîvâ kursa samazi-nâjumu attiecîbâ pret atseviðíu valstu valûtâm, lata reâlais efektîvais kurss attiecîbâpret nozîmîgâko tirdzniecîbas partnervalstu valûtâm kopumâ pieauga (sk. 3. att.).Ceturkðòa laikâ ar patçriòa cenu indeksu deflçtais lata reâlais efektîvais kursspalielinâjâs par 1.2%, attiecîbai starp cenu pieaugumu Latvijâ un nozîmîgâkajâstirdzniecîbas 13 partnervalstîs pieaugot par 1.4%. Gada laikâ ar patçriòa cenuindeksu deflçtais lata reâlais efektîvais kurss palielinâjâs par 3.6%. Cenu kâpumsiekðzemç noteica arî gandrîz visu izmaksu konkurçtspçjas kritumu: ceturkðòa laikâcenu indeksu atðíirîbai pieaugot par 4.5%, ar raþotâju cenu indeksu deflçtais reâlaisefektîvais valûtas kurss palielinâjâs par 4.2%. Nozîmîgs bija arî uz raþotâju cenâmbalstîtâ reâlâ kursa gada pieauguma temps, kas kopð 1999. gada pârsvarâ saglabâjâsnegatîvs, bet 2006. gada 4. ceturksnî sasniedza 7.8%. Îpaði straujo izmaksu konku-rçtspçjas kritumu bûtiski noteica gan energoresursu, gan darbaspçka izmaksu kâ-pums tautsaimniecîbâ. Tirgus daïa palielinâjâs Lietuvâ, Igaunijâ un Krievijâ, betsamazinâjâs nozîmîgâkajâs ES15 tirdzniecîbas partnervalstîs.

4. ceturksnî salîdzinâjumâ ar iepriekðçjâ gada atbilstoðo periodu eksports bûtiskâkpalielinâjâs uz ES10 valstîm (Lietuvu un Igauniju) un NVS valstîm (Krieviju unUkrainu), bet kritâs uz ES15 valstîm (Îriju, Vâciju, Franciju un Lielbritâniju). Lat-vijas nozîmîgâkâs partnervalstis bija Lietuva, Igaunija, Krievija, Vâcija, Lielbritâ-nija un Zviedrija, uz kurâm izveda 62.4% no eksporta kopapjoma.

Nozîmîgâkâs importa preces bija mehânismi un mehâniskas ierîces, elektroiekârtas,satiksmes lîdzekïi, minerâlprodukti, lauksaimniecîbas un pârtikas preces un parastie

10

MONETÂRAIS APSKATS · MONETARY REVIEW

metâli un parasto metâlu izstrâdâjumi. Preèu ieveduma pieaugumâ 4. ceturksnîsalîdzinâjumâ ar iepriekðçjâ gada atbilstoðo periodu dominçja satiksmes lîdzekïi,mehânismi un mehâniskas ierîces, elektroiekârtas, lauksaimniecîbas un pârtikaspreces un parastie metâli un parasto metâlu izstrâdâjumi. Importa pieaugumunoteica fiziskâ apjoma palielinâðanâs, mazâk – cenu kâpums. Fiziskâ apjoma palie-linâðanâs dominçja pârtikas rûpniecîbas raþojumu un satiksmes lîdzekïu importapieaugumâ. Mehânismu un mehânisku ierîèu, elektroiekârtu un parasto metâluun parasto metâlu izstrâdâjumu ieveduma kâpumu ietekmçja gan fiziskâ apjoma,gan cenu celðanâs. No importâ dominçjoðâm precçm cenas visvairâk auga paras-tajiem metâliem un parasto metâlu izstrâdâjumiem (par 16.7%), mehânismiemun mehâniskâm ierîcçm, elektroiekârtâm (par 7.9%), satiksmes lîdzekïiem (par7.1%) un zemâs bâzes ietekmç – tekstilmateriâliem un tekstilizstrâdâjumiem (par13.4%). Kopumâ preèu importa vienîbas vçrtîba 4. ceturksnî salîdzinâjumâ ar ie-priekðçjâ gada atbilstoðo periodu palielinâjâs par 8.1%, joprojâm sarûkot cenukâpumam.

Importa preèu ievedums palielinâjâs no visâm valstu grupâm (visvairâk – no ESvalstîm). Pusi no importa kopapjoma 4. ceturksnî ieveda no piecâm nozîmîgâkajâmpartnervalstîm – Vâcijas, Lietuvas, Krievijas, Igaunijas un Polijas. Salîdzinâjumâar iepriekðçjâ gada atbilstoðo periodu bûtiski palielinâjâs imports no Vâcijas, Igau-nijas, Polijas, Zviedrijas, Krievijas un Somijas.

Maksâjumu bilance

Latvijas maksâjumu bilances tekoðâ konta negatîvais saldo 4. ceturksnî bija864.1 milj. latu jeb 26.3% no IKP (iepriekðçjâ gada atbilstoðajâ periodâ – 15.2%).Salîdzinâjumâ ar iepriekðçjâ gada atbilstoðo periodu preèu un ienâkumu negatîvâsaldo attiecîba pret IKP bûtiski palielinâjâs, bet pakalpojumu un kârtçjo pârvedumupozitîvâ saldo attiecîba pret IKP samazinâjâs.

Pakalpojumu pozitîvais saldo 4. ceturksnî salîdzinâjumâ ar iepriekðçjâ gadaatbilstoðo periodu samazinâjâs par 31.3 milj. latu, jo saòemto pakalpojumu apjomakâpums bija lielâks nekâ sniegto pakalpojumu apjoma pieaugums visâs pakalpo-jumu grupâs. Pakalpojumu eksportâ joprojâm dominçja pârvadâjumu pakalpojumi(50.8% no pakalpojumu eksporta kopapjoma), tomçr palielinâjâs braucienu pa-kalpojumu îpatsvars (17.6%). Saòemto pakalpojumu apjomâ nedaudz saruka pâr-vadâjumu pakalpojumu (lîdz 29.3% no pakalpojumu importa kopapjoma) un brau-cienu pakalpojumu (35.2%) îpatsvars.

Pârvadâjumu pakalpojumu pozitîvais saldo 4. ceturksnî saruka, galvenokârt sa-mazinoties sniegto un palielinoties saòemto citu ar pârvadâjumiem saistîto pakal-pojumu apjomam jûras transportâ. Braucienu pakalpojumu negatîvais saldo pie-auga nedaudz. Lai gan saskaòâ ar CSP datiem 4. ceturksnî salîdzinâjumâ ar ie-priekðçjâ gada atbilstoðo periodu Latviju apmeklçjuðo ârvalstu ceïotâju skaits palie-linâjâs par 13.5%, bet uz ârvalstîm devuðos Latvijas ceïotâju skaits bûtiski nemai-nîjâs, tomçr Latvijas ceïotâju tçriòi ârvalstîs joprojâm bija lielâki nekâ ârvalstuceïotâju tçriòi Latvijâ. Vidçjais Latvijas ceïotâju uzturçðanâs laiks ârvalstîs turpinâjaaugt, bet ârvalstu ceïotâju uzturçðanâs laiks Latvijâ – samazinâties. Citu pakalpo-jumu pozitîvâ saldo bûtisku sarukumu noteica saòemto citu saimnieciskâs darbîbaspakalpojumu, apdroðinâðanas un bûvniecîbas pakalpojumu apjoma kâpums. Vien-laikus palielinâjâs sniegto finanðu pakalpojumu apjoms.

Ienâkumu negatîvais saldo salîdzinâjumâ ar iepriekðçjâ gada atbilstoðo periodupieauga par 86.2 milj. latu, jo nerezidentu Latvijâ gûto ienâkumu apjoma kâpumslîdz ar nozîmîgo tieðo investîciju apjoma palielinâðanos Latvijâ èetras reizes pâr-sniedza rezidentu ieguldîjumu ienâkumu pieaugumu. Visvairâk palielinâjâs nere-

11

4 · 2006

zidentu tieðo investîciju (galvenokârt reinvestçtâs peïòas veidâ) un citu ieguldîjumuienâkumu apjoms.

Kârtçjo pârvedumu pozitîvais saldo 4. ceturksnî salîdzinâjumâ ar iepriekðçjâ gadaatbilstoðo periodu samazinâjâs par 51.4 milj. latu, un to noteica bûtiska debetadarîjumu apjoma palielinâðanâs citos sektoros. Saòemto kârtçjo pârvedumu apjomapieaugums bija daudz mazâks.

Kapitâla un finanðu konta pozitîvais saldo bija 872.2 milj. latu, un lielâko daïu notâ veidoja ilgtermiòa finansçjums.

Tieðâs investîcijas Latvijâ (293.4 milj. latu; 8.9% no IKP) bija 4.1 reizi lielâkasnekâ iepriekðçjâ gada atbilstoðajâ periodâ un sedza 34.0% no tekoðâ konta negatîvâsaldo. Ârvalstu tieðâs investîcijas Latvijâ ieplûda galvenokârt reinvestçtâs peïòas(45.0% no ârvalstu tieðajâm investîcijâm Latvijâ) un paðu kapitâla (18.2%) veidâ.Investîcijas Latvijâ visvairâk pieauga no Kipras, Maltas un Zviedrijas (finanðu starp-niecîbâ, operâcijâs ar nekustamo îpaðumu, nomâ un citâ komercdarbîbâ un vairum-tirdzniecîbâ un mazumtirdzniecîbâ).

Portfeïieguldîjumu saldo 4. ceturksnî bija pozitîvs (84.1 milj. latu), jo bankas ievç-rojami samazinâja aktîvus, pârdodot parâda vçrtspapîrus.

Citu ieguldîjumu pozitîvais saldo bija 700.1 milj. latu (21.3% no IKP). Pasîvu kâ-pums jau otro ceturksni pçc kârtas pârsniedza miljarda latu robeþu, 4. ceturksnîpalielinoties par 1 058.0 milj. latu. 91.2% no pasîvu pieauguma veidoja bankusektora aizòçmumi (galvenokârt no mâtesbankâm). Ilgtermiòa saistîbu kâpumsveidoja lielâko daïu (83.7%) no citu ieguldîjumu pozitîvâ saldo.

Uzòçmumu sektora citu ieguldîjumu saldo 4. ceturksnî bija negatîvs (1.5% noIKP). Turpinâjâs uzòçmumu no nerezidentiem saòemto ilgtermiòa aizòçmumupieauguma tendence, taèu bûtiski tika samazinâtas îstermiòa ârçjâs saistîbas (tirdz-niecîbas kredîti) un palielinâts noguldîjumu apjoms.

Rezerves aktîvi 4. ceturksnî pieauga par 237.3 milj. latu, bankâm konvertçjot âr-valstu valûtu latu pieprasîjuma apmierinâðanai.

IEKÐZEMES EKONOMISKÂ AKTIVITÂTE

Kopçjais pieprasîjums

2006. gada 3. ceturksnî tautsaimniecîbas izaugsmi noteica privâtais patçriòð, sagla-bâjoties augstam kopçjâs pamatkapitâla veidoðanas pieauguma tempam. Ârçjâpieprasîjuma pieauguma temps bûtiski samazinâjâs, palielinot negatîvo neto eks-porta devumu IKP pieaugumâ. Privâtais patçriòð palielinâjâs par 16.8%, nosakotpusi no iekðzemes pieprasîjuma kâpuma. Mâjsaimniecîbu tçriòu pieaugumu vei-cinâja joprojâm dinamiskâ kreditçðanas attîstîba un rîcîbâ esoðo ienâkumu nozîmîgspalielinâjums, ko noteica nodarbinâtîbas, reâlâs vidçjâs darba algas, kâ arî sociâlopabalstu un pensiju apjoma pieaugums. Papildus ðiem tieðas ietekmes faktoriempatçriòa kâpumu veicinâja cenu pieauguma gaidas, kâ arî iedzîvotâju aktîvu vçrtîbaspalielinâjuma un straujâs tautsaimniecîbas izaugsmes radîtais optimistiskaisnoskaòojums.

Kopçjâ pamatkapitâla veidoðana 3. ceturksnî pieauga par 10.0%, ko veicinâja labiuzòçmumu iepriekðçjo periodu finanðu rezultâti (reinvestçtâ peïòa), dinamiskakreditçðanas attîstîba un straujas tautsaimniecîbas izaugsmes gaidas, kuras galve-nokârt veicinâjuðas ieguldîjumus visstraujâk augoðajâs nozarçs – tirdzniecîbâ unoperâcijâs ar nekustamo îpaðumu.

12

MONETÂRAIS APSKATS · MONETARY REVIEW

Preèu un pakalpojumu eksporta reâlais kâpums 3. ceturksnî bija 7.5%, savukârtimports palielinâjâs trîs reizes straujâk (par 24.0%), un to noteica iekðzemes pie-prasîjuma ekspansija, t.sk. liela apjoma atseviðíu investîciju projektu îstenoðana.Eksporta pieauguma tempa samazinâjums bija saistîts ar atseviðíu produktu grupueksporta apjomu samazinâjumu vai pieauguma tempa kritumu (minerâlprodukti,papîra un kartona izstrâdâjumi, koks un koka izstrâdâjumi u.c.). Izmaksu un cenupalielinâjums samazinâja konkurçtspçju ârçjos tirgos, kas papildus mudinâjauzòçmçjus par prioritâti izvçlçties iekðzemes pieprasîjuma apmierinâðanu.

Vienlaikus arvien spçcîgâk iezîmçjâs tautsaimniecîbas turpmâko attîstîbu ierobe-þojoði faktori – augoða spriedze darba tirgû, cenu kâpums, nesamçrîga iekðzemespieprasîjuma izaugsme, kas noteica negatîvu neto eksporta devumu, bûtisks mâj-saimniecîbu parâda palielinâjums, strauji augoðas investîcijas mâjokïos, automo-biïos un nozarçs ar samçrâ zemu pievienoto vçrtîbu.

Kopçjais piedâvâjums

4. ceturksnî turpinâjâs strauja Latvijas tautsaimniecîbas attîstîba. IKP salîdzinâ-majâs cenâs salîdzinâjumâ ar iepriekðçjâ gada atbilstoðo periodu palielinâjâs par11.7%, 2006. gadâ faktiskajâs cenâs sasniedzot 11 264.7 milj. latu. Kopçjo tautsaim-niecîbas izaugsmi visvairâk ietekmçja straujais pievienotâs vçrtîbas kâpums tirdz-niecîbâ (15.3%).

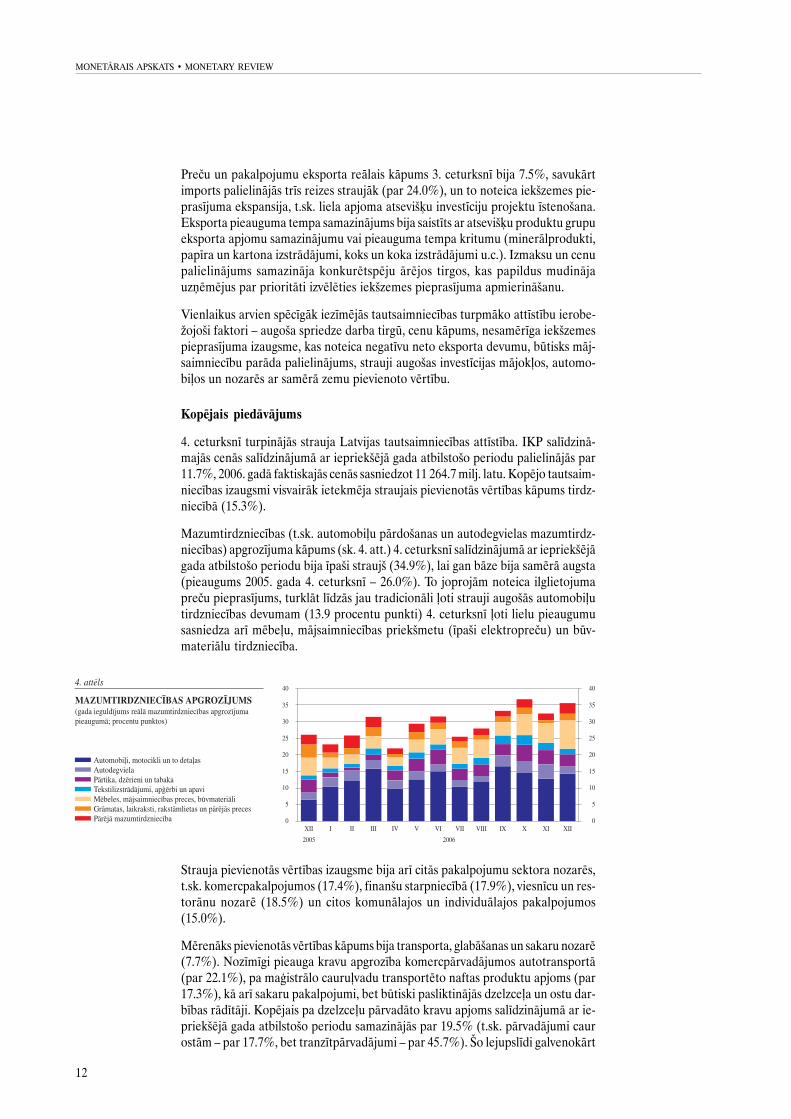

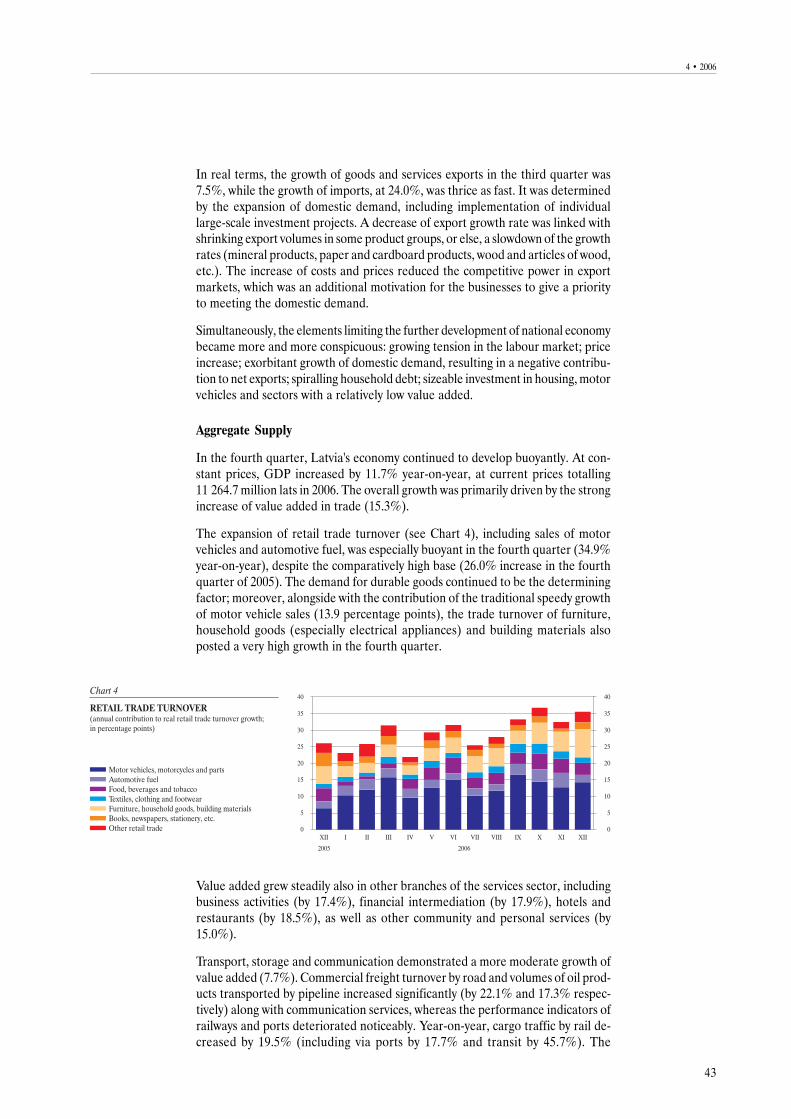

Mazumtirdzniecîbas (t.sk. automobiïu pârdoðanas un autodegvielas mazumtirdz-niecîbas) apgrozîjuma kâpums (sk. 4. att.) 4. ceturksnî salîdzinâjumâ ar iepriekðçjâgada atbilstoðo periodu bija îpaði straujð (34.9%), lai gan bâze bija samçrâ augsta(pieaugums 2005. gada 4. ceturksnî – 26.0%). To joprojâm noteica ilglietojumapreèu pieprasîjums, turklât lîdzâs jau tradicionâli ïoti strauji augoðâs automobiïutirdzniecîbas devumam (13.9 procentu punkti) 4. ceturksnî ïoti lielu pieaugumusasniedza arî mçbeïu, mâjsaimniecîbas priekðmetu (îpaði elektropreèu) un bûv-materiâlu tirdzniecîba.

Strauja pievienotâs vçrtîbas izaugsme bija arî citâs pakalpojumu sektora nozarçs,t.sk. komercpakalpojumos (17.4%), finanðu starpniecîbâ (17.9%), viesnîcu un res-torânu nozarç (18.5%) un citos komunâlajos un individuâlajos pakalpojumos(15.0%).

Mçrenâks pievienotâs vçrtîbas kâpums bija transporta, glabâðanas un sakaru nozarç(7.7%). Nozîmîgi pieauga kravu apgrozîba komercpârvadâjumos autotransportâ(par 22.1%), pa maìistrâlo cauruïvadu transportçto naftas produktu apjoms (par17.3%), kâ arî sakaru pakalpojumi, bet bûtiski pasliktinâjâs dzelzceïa un ostu dar-bîbas râdîtâji. Kopçjais pa dzelzceïu pârvadâto kravu apjoms salîdzinâjumâ ar ie-priekðçjâ gada atbilstoðo periodu samazinâjâs par 19.5% (t.sk. pârvadâjumi caurostâm – par 17.7%, bet tranzîtpârvadâjumi – par 45.7%). Ðo lejupslîdi galvenokârt

13

4 · 2006

noteica naftas produktu un akmeòogïu pârvadâjumu kritums. Latvijas ostâs ko-pçjais saòemto un nosûtîto kravu apjoms samazinâjâs par 6.6%, sarûkot visâs ostâs,t.sk. Ventspils ostâ (par 6.5%) un Rîgas ostâ (par 4.6%).

Preèu sektorâ joprojâm spçcîga bija bûvniecîbas izaugsme (10.3%), bet samçrâneliels bija pievienotâs vçrtîbas kâpums apstrâdes rûpniecîbâ. 4. ceturksnî salîdzi-nâmajâs cenâs samazinâjâs koksnes, koka un koría izstrâdâjumu (izòemot mçbeles)un metâlu raþoðanas produkcijas eksports, kas noteica raþoðanas apjoma reâlo kri-tumu salîdzinâjumâ ar iepriekðçjâ gada atbilstoðo periodu. Tas bija galvenais fak-tors, kas kavçja apstrâdes rûpniecîbas izaugsmes tempu. Vienlaikus augoðs pie-prasîjums iekðçjâ tirgû un eksporta pieaugums veicinâja izaugsmi vairâkâs citâsnozarçs, no kurâm vislielâko ieguldîjumu deva tekstilizstrâdâjumu raþoðana, íî-misko vielu, to izstrâdâjumu un íîmisko ðíiedru raþoðana, gatavo metâlizstrâdâ-jumu (izòemot maðînas un iekârtas) raþoðana un citu transportlîdzekïu raþoðana.Tâdçjâdi sezonâli izlîdzinâtais fiziskais apstrâdes rûpniecîbas produkcijas apjomaindekss salîdzinâjumâ ar iepriekðçjâ gada atbilstoðo periodu palielinâjâs par 3.9%un pievienotâ vçrtîba – par 4.5%.

Nefinanðu investîcijas tautsaimniecîbâ 4. ceturksnî sasniedza 719.8 milj. latu (par25.7% vairâk nekâ iepriekðçjâ gada atbilstoðajâ periodâ). Lielâkie ieguldîjumi veiktiapstrâdes rûpniecîbâ (128.7 milj. latu), valsts pârvaldç un aizsardzîbâ un obligâtajâsociâlajâ apdroðinâðanâ (107.4 milj. latu), transportâ, glabâðanâ un sakaros(84.5 milj. latu), enerìçtikâ (84.3 milj. latu), tirdzniecîbâ (83.8 milj. latu), kâ arîoperâcijâs ar nekustamo îpaðumu, nomâ un citâ komercdarbîbâ (76.5 milj. latu),kur bija vçrojams visstraujâkais investçto lîdzekïu gada pieaugums. Apstrâdes rûp-niecîbâ lielâkâs investîcijas veiktas pârtikas produktu un dzçrienu raþoðanâ(39.0 milj. latu), koksnes, koka un koría izstrâdâjumu raþoðanâ (izòemot mçbeles;24.4 milj. latu), kâ arî nemetâlisko minerâlu izstrâdâjumu raþoðanâ (21.0 milj.latu).

Nodarbinâtîba un darba samaksa

Reìistrçtâ bezdarba lîmenis 4. ceturksnî turpinâja samazinâties gan salîdzinâjumâar iepriekðçjo ceturksni (par 0.3 procentu punktiem), gan salîdzinâjumâ ar iepriek-ðçjâ gada atbilstoðo periodu (par 0.9 procentu punktiem) un gada beigâs bija 6.5%no ekonomiski aktîvo iedzîvotâju skaita.

Sarûkot bezdarbnieku skaitam un augot reìistrçto vakanèu skaitam (par 91.2%vairâk nekâ 2005. gada 4. ceturksnî), darba tirgus noslodzes koeficients samazinâjâslîdz 3.8. Salîdzinâjumâ ar iepriekðçjâ gada atbilstoðo periodu bezdarbnieku skaitsuz vienu reìistrçto brîvo darba vietu bija vairâk nekâ divas reizes mazâks.

Darba meklçtâju îpatsvars 4. ceturksnî saglabâjâs nemainîgs (6.2% no ekonomiskiaktîvo iedzîvotâju skaita). Darba meklçtâju skaits joprojâm bija ievçrojami mazâksnekâ iepriekðçjâ gada atbilstoðajâ periodâ, taèu ceturkðòa laikâ tas îpaði nemainîjâs.

Tautsaimniecîbâ nodarbinâto skaita palielinâðanos (salîdzinâjumâ ar iepriekðçjâgada atbilstoðo periodu – par 5.0%) noteica straujâ ekonomiskâ izaugsme, kasizraisîja darbaspçka pieprasîjuma kâpumu un jaunu darba vietu izveidi. Preèu sek-torâ nodarbinâto skaits palielinâjâs par 9.4%, visstraujâk augot bûvniecîbâ, betapstrâdes rûpniecîbâ nodarbinâto skaits salîdzinâjumâ ar iepriekðçjâ gada atbilstoðoperiodu pieauga nedaudz. Savukârt pakalpojumu sektora nodarbinâto skaita mç-renajâ pieaugumâ (2.9%) lielâkais devums, kâ arî straujâkâ izaugsme bija operâcijâsar nekustamo îpaðumu, nomâ un citâ komercdarbîbâ. Ievçrojami pieauga arî tirdz-niecîbâ nodarbinâto skaits, savukârt lielâkais nodarbinâto skaita samazinâjumsbija sabiedriskajos, sociâlajos un individuâlajos pakalpojumos, veselîbas un sociâlâsaprûpes un izglîtîbas nozarç.

14

MONETÂRAIS APSKATS · MONETARY REVIEW

Tradicionâlie faktori – augoðais darbaspçka pieprasîjums, produktivitâtes un pa-tçriòa cenu kâpums, darbaspçka migrâcija un çnu ekonomikas mazinâðanâs noteicastrauju darba samaksas pieaugumu arî 4. ceturksnî. Tautsaimniecîbâ strâdâjoðomçneða vidçjâ bruto darba samaksa 4. ceturksnî bija Ls 343.75 (par 27.9% vairâknekâ iepriekðçjâ gada atbilstoðajâ periodâ). Straujâk (par 29.9%) auga sabiedriskajâsektorâ strâdâjoðo darba samaksa. To ietekmçja izglîtîbas darbinieku darba samak-sas pieaugums par 43.3%. Privâtajâ sektorâ darba samaksa palielinâjâs par 27.4%.Straujâkais darba samaksas pieaugums bija bûvniecîbâ (37.0%), finanðustarpniecîbâ (30.7%) un tirdzniecîbâ (29.8%). Reâlâ bruto darba samaksa tautsaim-niecîbâ palielinâjâs par 20.4%.

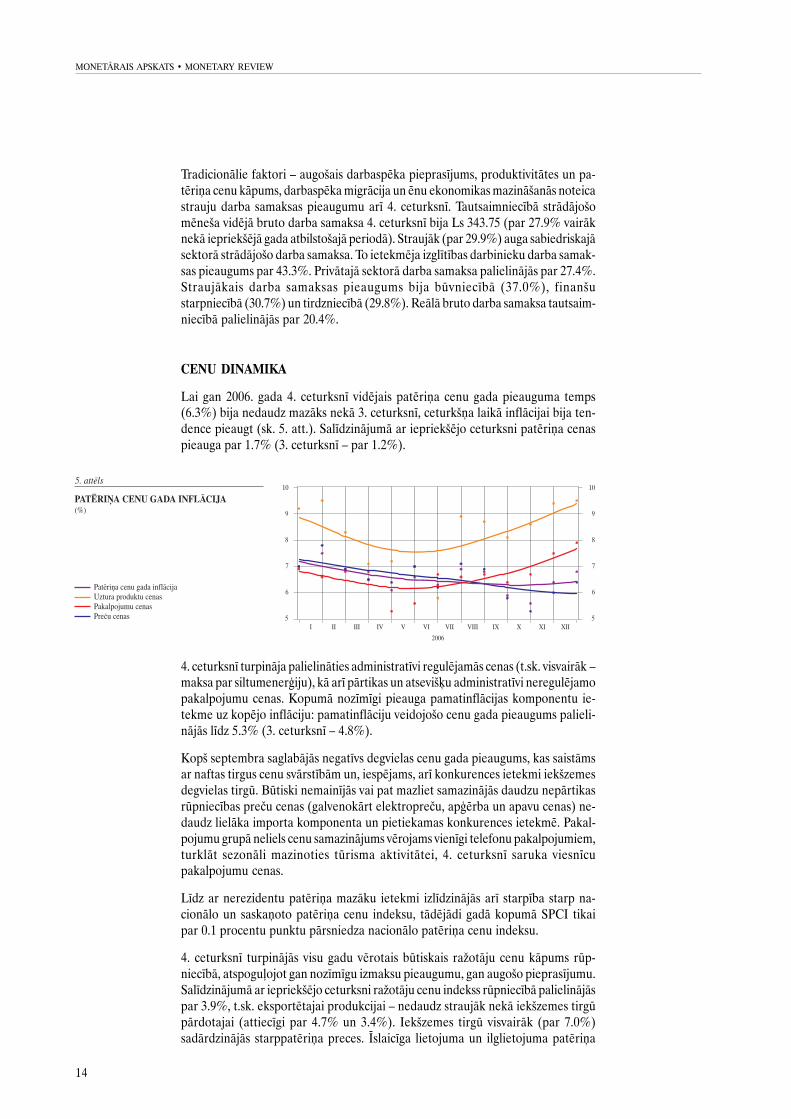

CENU DINAMIKA

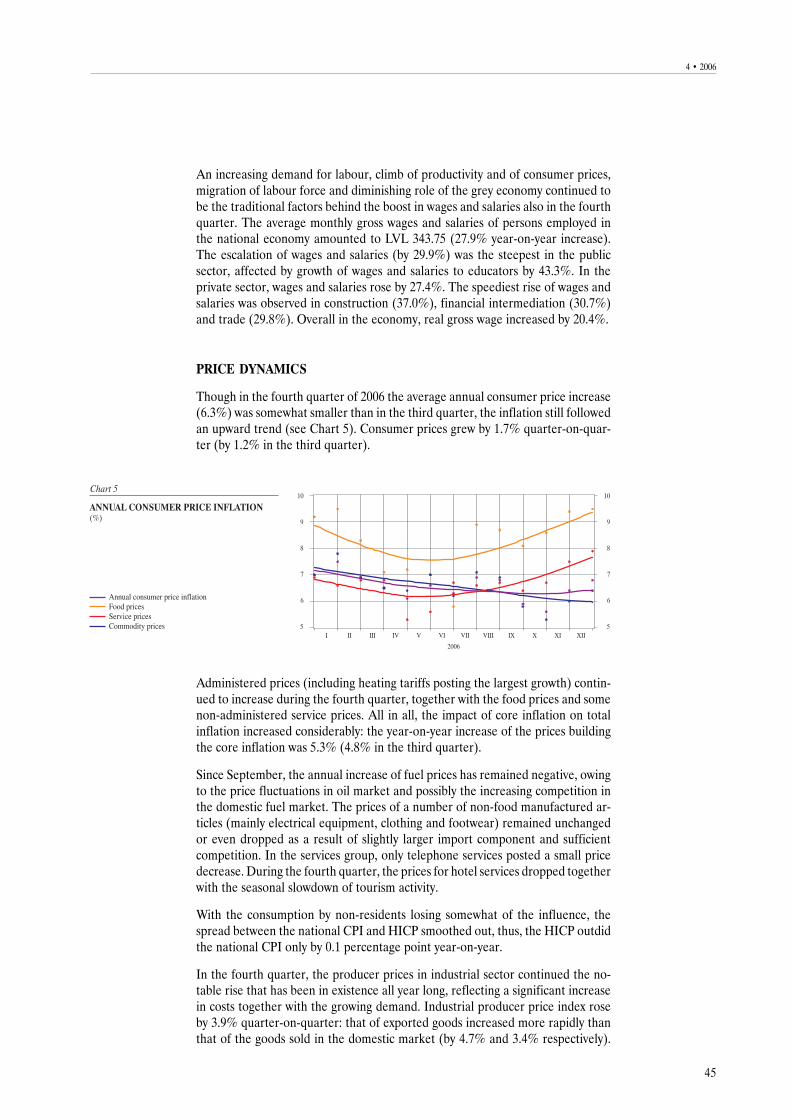

Lai gan 2006. gada 4. ceturksnî vidçjais patçriòa cenu gada pieauguma temps(6.3%) bija nedaudz mazâks nekâ 3. ceturksnî, ceturkðòa laikâ inflâcijai bija ten-dence pieaugt (sk. 5. att.). Salîdzinâjumâ ar iepriekðçjo ceturksni patçriòa cenaspieauga par 1.7% (3. ceturksnî – par 1.2%).

4. ceturksnî turpinâja palielinâties administratîvi regulçjamâs cenas (t.sk. visvairâk –maksa par siltumenerìiju), kâ arî pârtikas un atseviðíu administratîvi neregulçjamopakalpojumu cenas. Kopumâ nozîmîgi pieauga pamatinflâcijas komponentu ie-tekme uz kopçjo inflâciju: pamatinflâciju veidojoðo cenu gada pieaugums palieli-nâjâs lîdz 5.3% (3. ceturksnî – 4.8%).

Kopð septembra saglabâjâs negatîvs degvielas cenu gada pieaugums, kas saistâmsar naftas tirgus cenu svârstîbâm un, iespçjams, arî konkurences ietekmi iekðzemesdegvielas tirgû. Bûtiski nemainîjâs vai pat mazliet samazinâjâs daudzu nepârtikasrûpniecîbas preèu cenas (galvenokârt elektropreèu, apìçrba un apavu cenas) ne-daudz lielâka importa komponenta un pietiekamas konkurences ietekmç. Pakal-pojumu grupâ neliels cenu samazinâjums vçrojams vienîgi telefonu pakalpojumiem,turklât sezonâli mazinoties tûrisma aktivitâtei, 4. ceturksnî saruka viesnîcupakalpojumu cenas.

Lîdz ar nerezidentu patçriòa mazâku ietekmi izlîdzinâjâs arî starpîba starp na-cionâlo un saskaòoto patçriòa cenu indeksu, tâdçjâdi gadâ kopumâ SPCI tikaipar 0.1 procentu punktu pârsniedza nacionâlo patçriòa cenu indeksu.

4. ceturksnî turpinâjâs visu gadu vçrotais bûtiskais raþotâju cenu kâpums rûp-niecîbâ, atspoguïojot gan nozîmîgu izmaksu pieaugumu, gan augoðo pieprasîjumu.Salîdzinâjumâ ar iepriekðçjo ceturksni raþotâju cenu indekss rûpniecîbâ palielinâjâspar 3.9%, t.sk. eksportçtajai produkcijai – nedaudz straujâk nekâ iekðzemes tirgûpârdotajai (attiecîgi par 4.7% un 3.4%). Iekðzemes tirgû visvairâk (par 7.0%)sadârdzinâjâs starppatçriòa preces. Îslaicîga lietojuma un ilglietojuma patçriòa

15

4 · 2006

preèu un enerìijas cenas pieauga daudz mazâk: attiecîgi par 1.9%, 1.7% un 1.6%.Salîdzinâjumâ ar iepriekðçjâ gada atbilstoðo periodu raþotâju cenas rûpniecîbâpalielinâjâs par 12.8%, t.sk. eksportçtajai produkcijai – par 14.0%, bet iekðzemestirgû pârdotajai – par 12.0%. Gada laikâ iekðzemes tirgû pârdotajai produkcijaivislielâkais raþotâju cenu indeksa rûpniecîbâ kâpums bija starppatçriòa precçm(17.3%), enerìijai (16.6%) un raþoðanas lîdzekïiem (11.4%). Lçnâks cenu kâpumsbija îslaicîga lietojuma patçriòa precçm (5.6%) un nenozîmîgs – ilglietojumapatçriòa precçm (0.6%).

Kopçjâs bûvniecîbas izmaksas 4. ceturksnî sadârdzinâjâs par 4.1%, visvairâk (par7.6%) augot maðînu un mehânismu uzturçðanas izmaksâm. Savukârt strâdniekudarba samaksa pieauga par 4.1% un bûvmateriâlu izmaksas – par 3.3%. Salîdzinâ-jumâ ar iepriekðçjâ gada atbilstoðo periodu bûvniecîbas izmaksas palielinâjâs par25.0% (t.sk. darba samaksa – par 41.1%, maðînu un mehânismu uzturçðanas iz-maksas – par 30.3% un bûvmateriâlu izmaksas – par 15.2%).

FISKÂLAIS SEKTORS

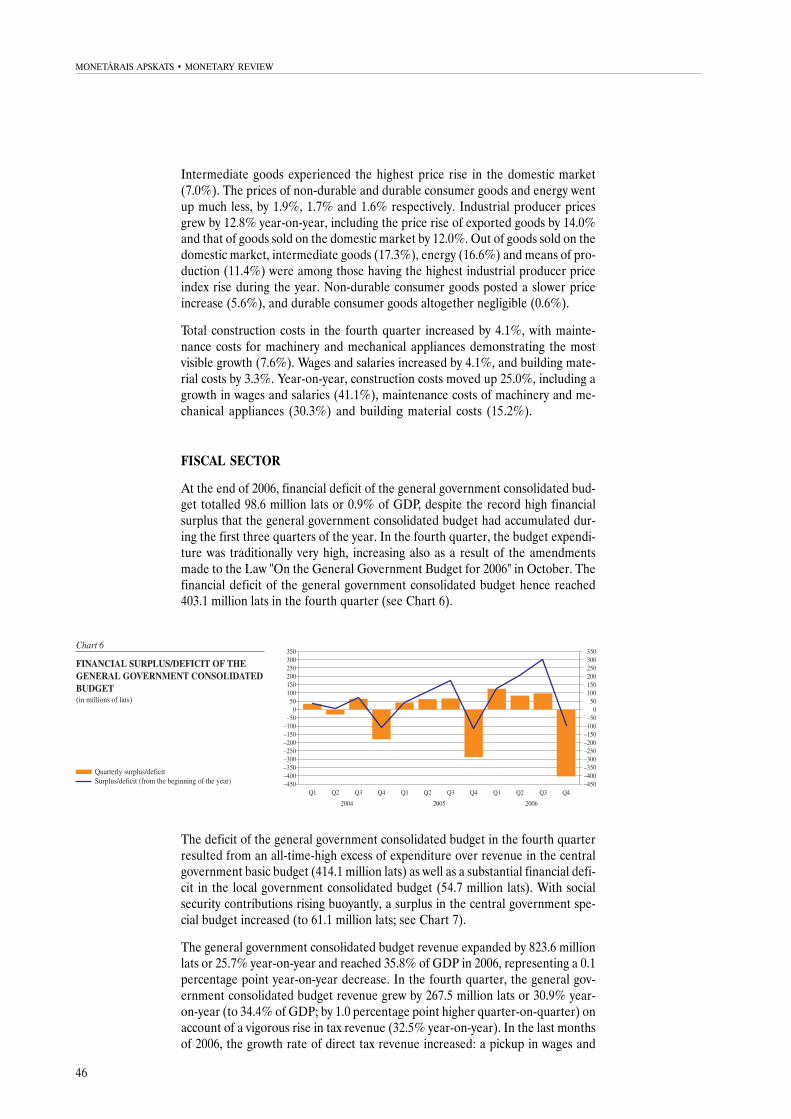

Valsts konsolidçtâ kopbudþeta finansiâlais deficîts 2006. gada beigâs bija 98.6 milj.latu jeb 0.9% no IKP, lai gan 2006. gada pirmajos trijos ceturkðòos valsts konsoli-dçtajâ kopbudþetâ bija uzkrâjies rekordliels finansiâlais pârpalikums. Budþeta iz-devumi 4. ceturksnî tradicionâli bija ïoti lieli, turklât izdevumus palielinâja arîoktobrî veiktie grozîjumi likumâ "Par valsts budþetu 2006. gadam". Tâdçjâdi valstskonsolidçtâ kopbudþeta finansiâlais deficîts 4. ceturksnî sasniedza 403.1 milj. latu(sk. 6. att.).

Valsts konsolidçtâ kopbudþeta deficîtu 4. ceturksnî noteica gan rekordaugsts iz-devumu pârsniegums pâr ieòçmumiem valsts pamatbudþetâ (414.1 milj. latu), ganarî nozîmîgais finansiâlais deficîts paðvaldîbu konsolidçtajâ budþetâ (54.7 milj.latu). Savukârt, strauji pieaugot sociâlâs apdroðinâðanas iemaksâm, palielinâjâsvalsts speciâlâ budþeta pârpalikums (lîdz 61.1 milj. latu; sk. 7. att.).

16

MONETÂRAIS APSKATS · MONETARY REVIEW

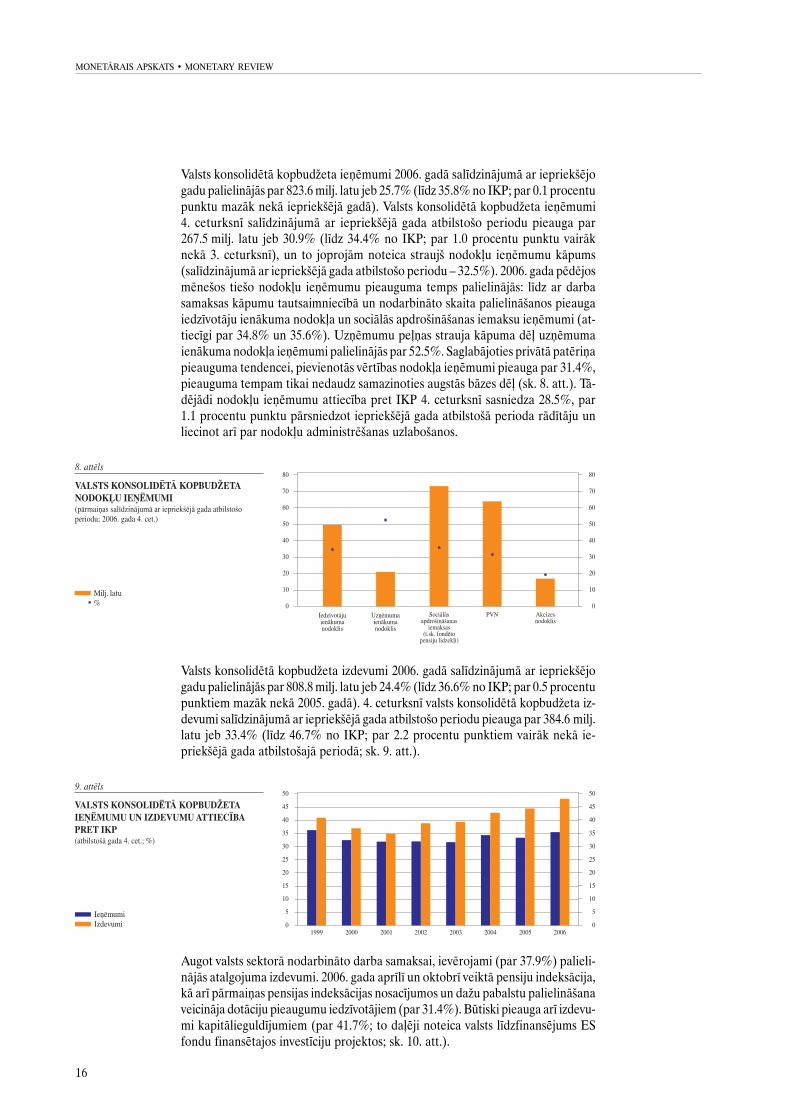

Valsts konsolidçtâ kopbudþeta ieòçmumi 2006. gadâ salîdzinâjumâ ar iepriekðçjogadu palielinâjâs par 823.6 milj. latu jeb 25.7% (lîdz 35.8% no IKP; par 0.1 procentupunktu mazâk nekâ iepriekðçjâ gadâ). Valsts konsolidçtâ kopbudþeta ieòçmumi4. ceturksnî salîdzinâjumâ ar iepriekðçjâ gada atbilstoðo periodu pieauga par267.5 milj. latu jeb 30.9% (lîdz 34.4% no IKP; par 1.0 procentu punktu vairâknekâ 3. ceturksnî), un to joprojâm noteica straujð nodokïu ieòçmumu kâpums(salîdzinâjumâ ar iepriekðçjâ gada atbilstoðo periodu – 32.5%). 2006. gada pçdçjosmçneðos tieðo nodokïu ieòçmumu pieauguma temps palielinâjâs: lîdz ar darbasamaksas kâpumu tautsaimniecîbâ un nodarbinâto skaita palielinâðanos pieaugaiedzîvotâju ienâkuma nodokïa un sociâlâs apdroðinâðanas iemaksu ieòçmumi (at-tiecîgi par 34.8% un 35.6%). Uzòçmumu peïòas strauja kâpuma dçï uzòçmumaienâkuma nodokïa ieòçmumi palielinâjâs par 52.5%. Saglabâjoties privâtâ patçriòapieauguma tendencei, pievienotâs vçrtîbas nodokïa ieòçmumi pieauga par 31.4%,pieauguma tempam tikai nedaudz samazinoties augstâs bâzes dçï (sk. 8. att.). Tâ-dçjâdi nodokïu ieòçmumu attiecîba pret IKP 4. ceturksnî sasniedza 28.5%, par1.1 procentu punktu pârsniedzot iepriekðçjâ gada atbilstoðâ perioda râdîtâju unliecinot arî par nodokïu administrçðanas uzlaboðanos.

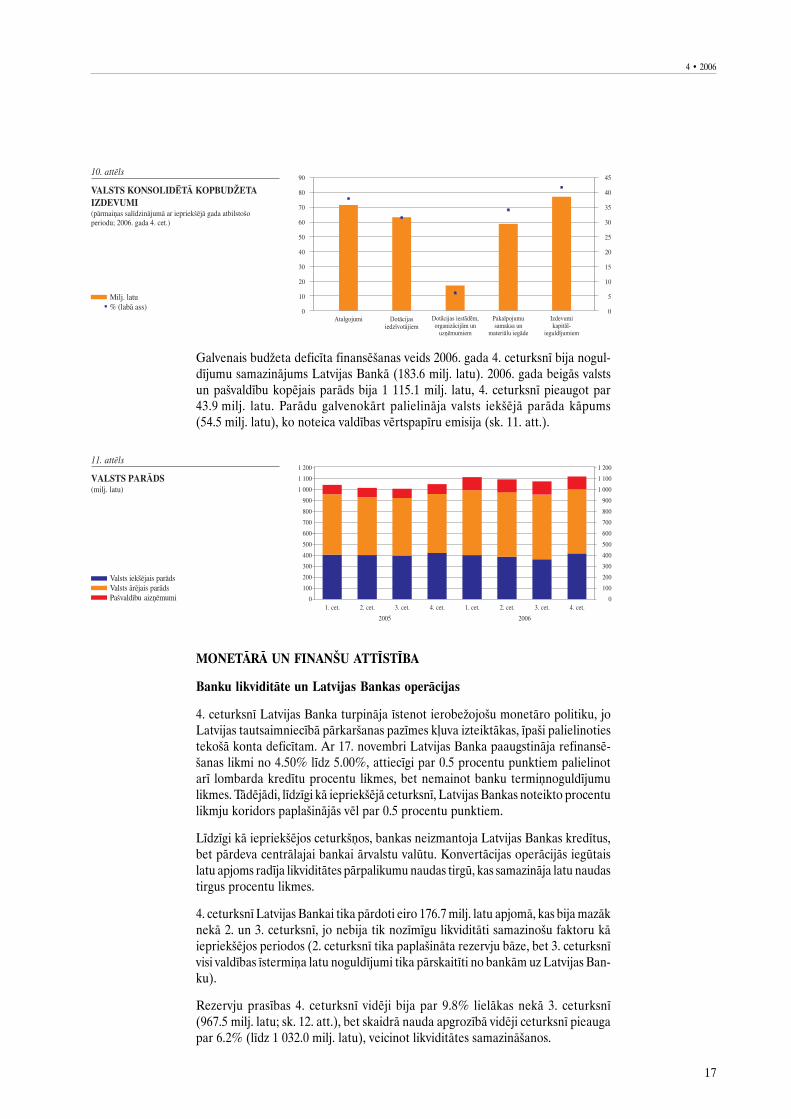

Valsts konsolidçtâ kopbudþeta izdevumi 2006. gadâ salîdzinâjumâ ar iepriekðçjogadu palielinâjâs par 808.8 milj. latu jeb 24.4% (lîdz 36.6% no IKP; par 0.5 procentupunktiem mazâk nekâ 2005. gadâ). 4. ceturksnî valsts konsolidçtâ kopbudþeta iz-devumi salîdzinâjumâ ar iepriekðçjâ gada atbilstoðo periodu pieauga par 384.6 milj.latu jeb 33.4% (lîdz 46.7% no IKP; par 2.2 procentu punktiem vairâk nekâ ie-priekðçjâ gada atbilstoðajâ periodâ; sk. 9. att.).

Augot valsts sektorâ nodarbinâto darba samaksai, ievçrojami (par 37.9%) palieli-nâjâs atalgojuma izdevumi. 2006. gada aprîlî un oktobrî veiktâ pensiju indeksâcija,kâ arî pârmaiòas pensijas indeksâcijas nosacîjumos un daþu pabalstu palielinâðanaveicinâja dotâciju pieaugumu iedzîvotâjiem (par 31.4%). Bûtiski pieauga arî izdevu-mi kapitâlieguldîjumiem (par 41.7%; to daïçji noteica valsts lîdzfinansçjums ESfondu finansçtajos investîciju projektos; sk. 10. att.).

17

4 · 2006

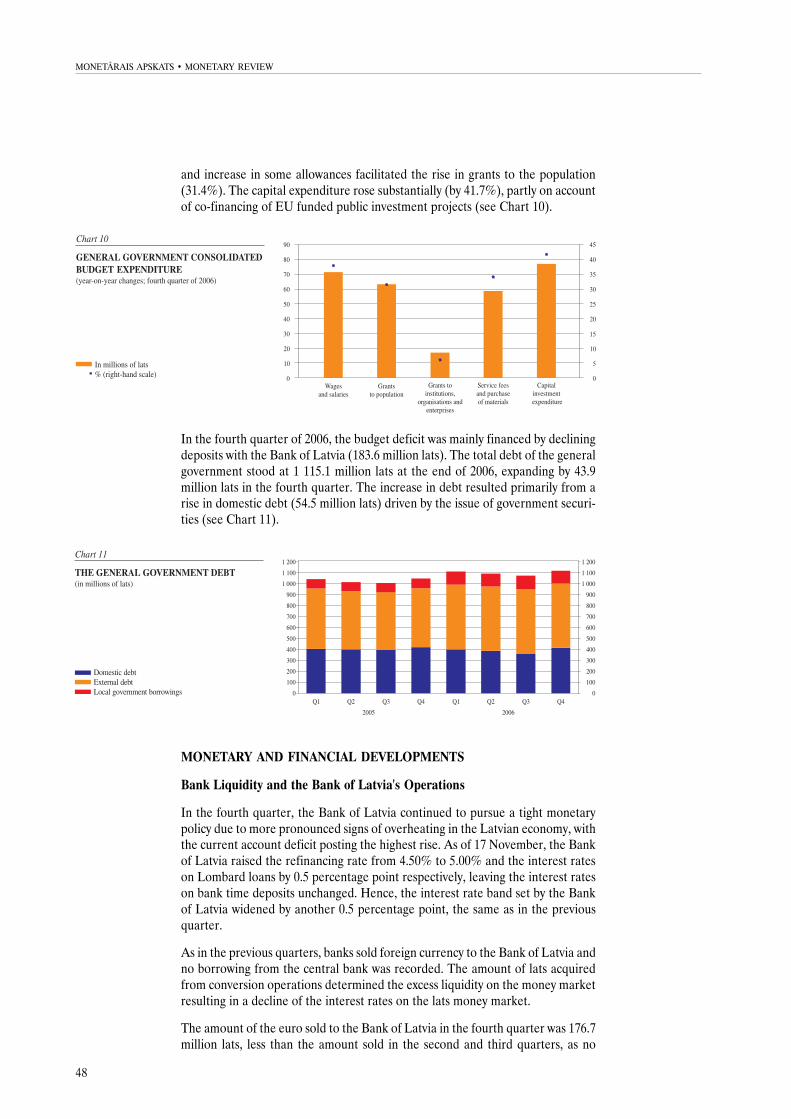

Galvenais budþeta deficîta finansçðanas veids 2006. gada 4. ceturksnî bija nogul-dîjumu samazinâjums Latvijas Bankâ (183.6 milj. latu). 2006. gada beigâs valstsun paðvaldîbu kopçjais parâds bija 1 115.1 milj. latu, 4. ceturksnî pieaugot par43.9 milj. latu. Parâdu galvenokârt palielinâja valsts iekðçjâ parâda kâpums(54.5 milj. latu), ko noteica valdîbas vçrtspapîru emisija (sk. 11. att.).

MONETÂRÂ UN FINANÐU ATTÎSTÎBA

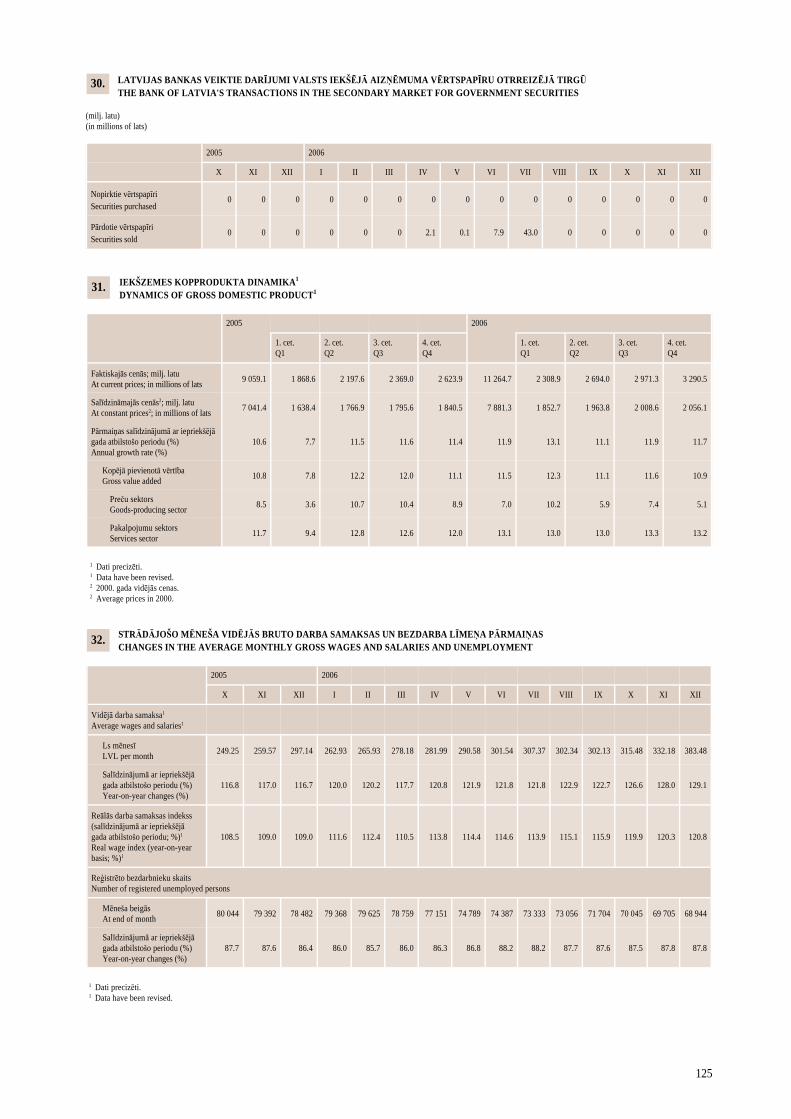

Banku likviditâte un Latvijas Bankas operâcijas

4. ceturksnî Latvijas Banka turpinâja îstenot ierobeþojoðu monetâro politiku, joLatvijas tautsaimniecîbâ pârkarðanas pazîmes kïuva izteiktâkas, îpaði palielinotiestekoðâ konta deficîtam. Ar 17. novembri Latvijas Banka paaugstinâja refinansç-ðanas likmi no 4.50% lîdz 5.00%, attiecîgi par 0.5 procentu punktiem palielinotarî lombarda kredîtu procentu likmes, bet nemainot banku termiònoguldîjumulikmes. Tâdçjâdi, lîdzîgi kâ iepriekðçjâ ceturksnî, Latvijas Bankas noteikto procentulikmju koridors paplaðinâjâs vçl par 0.5 procentu punktiem.

Lîdzîgi kâ iepriekðçjos ceturkðòos, bankas neizmantoja Latvijas Bankas kredîtus,bet pârdeva centrâlajai bankai ârvalstu valûtu. Konvertâcijas operâcijâs iegûtaislatu apjoms radîja likviditâtes pârpalikumu naudas tirgû, kas samazinâja latu naudastirgus procentu likmes.

4. ceturksnî Latvijas Bankai tika pârdoti eiro 176.7 milj. latu apjomâ, kas bija mazâknekâ 2. un 3. ceturksnî, jo nebija tik nozîmîgu likviditâti samazinoðu faktoru kâiepriekðçjos periodos (2. ceturksnî tika paplaðinâta rezervju bâze, bet 3. ceturksnîvisi valdîbas îstermiòa latu noguldîjumi tika pârskaitîti no bankâm uz Latvijas Ban-ku).

Rezervju prasîbas 4. ceturksnî vidçji bija par 9.8% lielâkas nekâ 3. ceturksnî(967.5 milj. latu; sk. 12. att.), bet skaidrâ nauda apgrozîbâ vidçji ceturksnî pieaugapar 6.2% (lîdz 1 032.0 milj. latu), veicinot likviditâtes samazinâðanos.

18

MONETÂRAIS APSKATS · MONETARY REVIEW

4. ceturksnî Latvijas Bankas piedâvâjums repo izsolçs nemainîjâs, bet banku pie-prasîjums un tâm izsniegtais apjoms bija 35.0 milj. latu – attiecîgi 8.9 un 6.3 reizesmazâks nekâ iepriekðçjâ ceturksnî. Visi izsniegtie repo kredîti bija ar 7 dienu ter-miòu, to vidçjâ svçrtâ procentu likme, atspoguïojot Latvijas Bankas refinansçðanaslikmes kâpumu, palielinâjâs no 4.73% 3. ceturksnî lîdz 5.00% 4. ceturksnî. Repo

kredîtu vidçjais atlikums samazinâjâs 4.4 reizes (lîdz 3.6 milj. latu). Lombardakredîti netika izmantoti, netika veikti arî valûtas mijmaiòas darîjumi.

Banku termiònoguldîjumu vidçjais atlikums palielinâjâs 7.0 reizes (lîdz 69.0 milj.latu), un 4. ceturksnî bankas katru darbadienu veica termiònoguldîjumus LatvijasBankâ. Vidçjâ svçrtâ banku termiònoguldîjumu procentu likme palielinâjâs no2.13% lîdz 2.15%, jo bankas nedaudz vairâk izvçlçjâs iespçju veikt 14 dienu termiò-noguldîjumus. Arî banku termiònoguldîjumu lîmenis liecinâja par augstu bankulikviditâti.

Gada beigâs pieaugot valdîbas izdevumiem, ievçrojama valdîbas latos Latvijas Ban-kâ veiktâ noguldîjuma daïa nonâca banku rîcîbâ. Tâdçjâdi bankâm izveidojâs laturesursu pârpalikums un bûtiski kritâs latu naudas tirgus procentu likmes. Novembrîvidçjâs svçrtâs Latvijas starpbanku latu naudas tirgus darîjumu uz nakti procentulikmes bija pat 1.76%, bet gada beigâs tâs nedaudz pieauga (lîdz 2.40%).

4. ceturksnî vidçjâs svçrtâs Latvijas starpbanku latu naudas tirgus darîjumu uznakti procentu likmes samazinâjâs par 79 bâzes punktiem (lîdz 2.83%). Prognozespar zemu latu îstermiòa procentu likmju saglabâðanos 2007. gada janvârî veicinâjamâjsaimniecîbu kreditçðanâ bieþâk lietotâ 3 mçneðu RIGIBOR samazinâjumupar 26 bâzes punktiem (lîdz 4.53%). Savukârt eiro naudas tirgus procentu likmjukâpums veicinâja 1 gada RIGIBOR kâpumu par 18 bâzes punktiem (lîdz 5.19%),bet 6 mçneðu RIGIBOR pieauga tikai par 3 bâzes punktiem (lîdz 4.92%). Tâdçjâdilatu ienesîguma lîkne kïuva stâvâka un 1 gada RIGIBOR pârsniegums pârRIGIBOR darîjumiem uz nakti pieauga no 94 lîdz 213 bâzes punktiem. Lai arîîstermiòa latu procentu likmes samazinâjâs, RIGIBOR ietvertâs 3 mçneðuRIGIBOR darîjumiem pçc 3 mçneðiem turpinâja augt. Latvijas starpbanku kredîtudarîjumu dienas vidçjais apgrozîjums pieauga par 32%, latos veiktajiem darîjumiemsasniedzot 48 milj. latu dienâ, bet darîjumiem pârçjâs valûtâs – 68 milj. latu dienâ.

Galvenâs ECB procentu likmes palielinâðana ietekmçja arî eiro veikto darîjumuuz nakti vidçjâs procentu likmes kâpumu Latvijas starpbanku tirgû (no 2.96%3. ceturksnî lîdz 3.34% 4. ceturksnî).

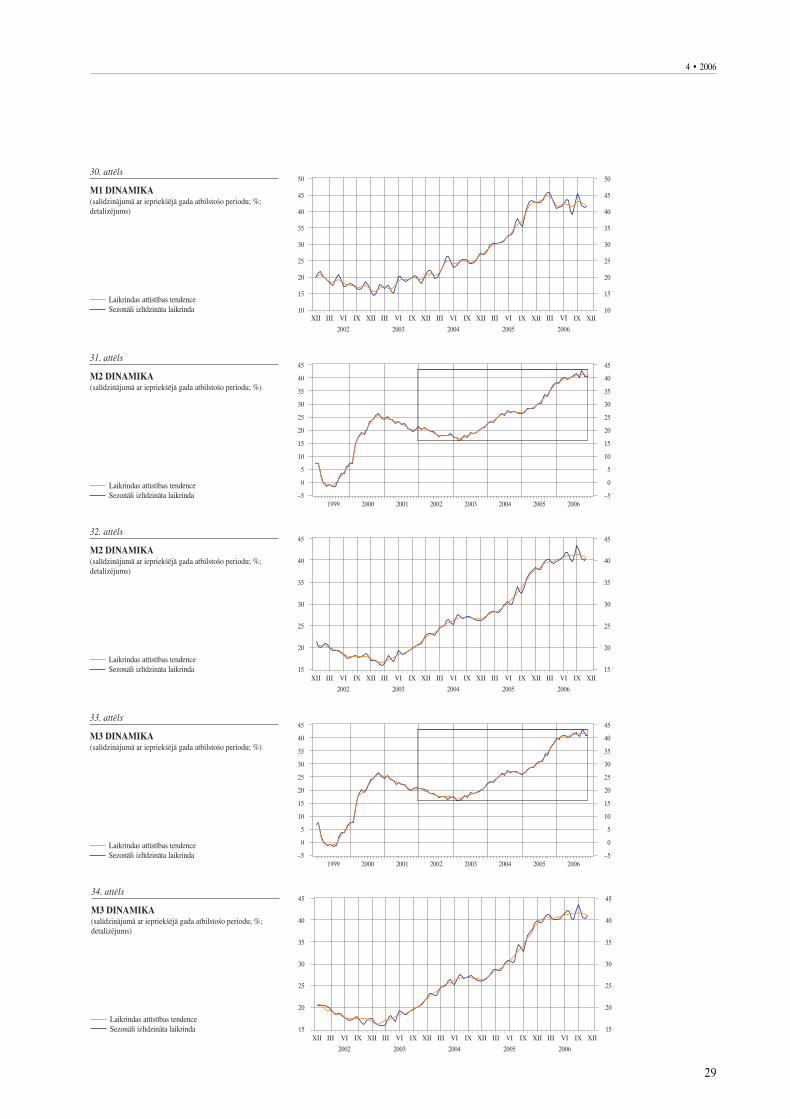

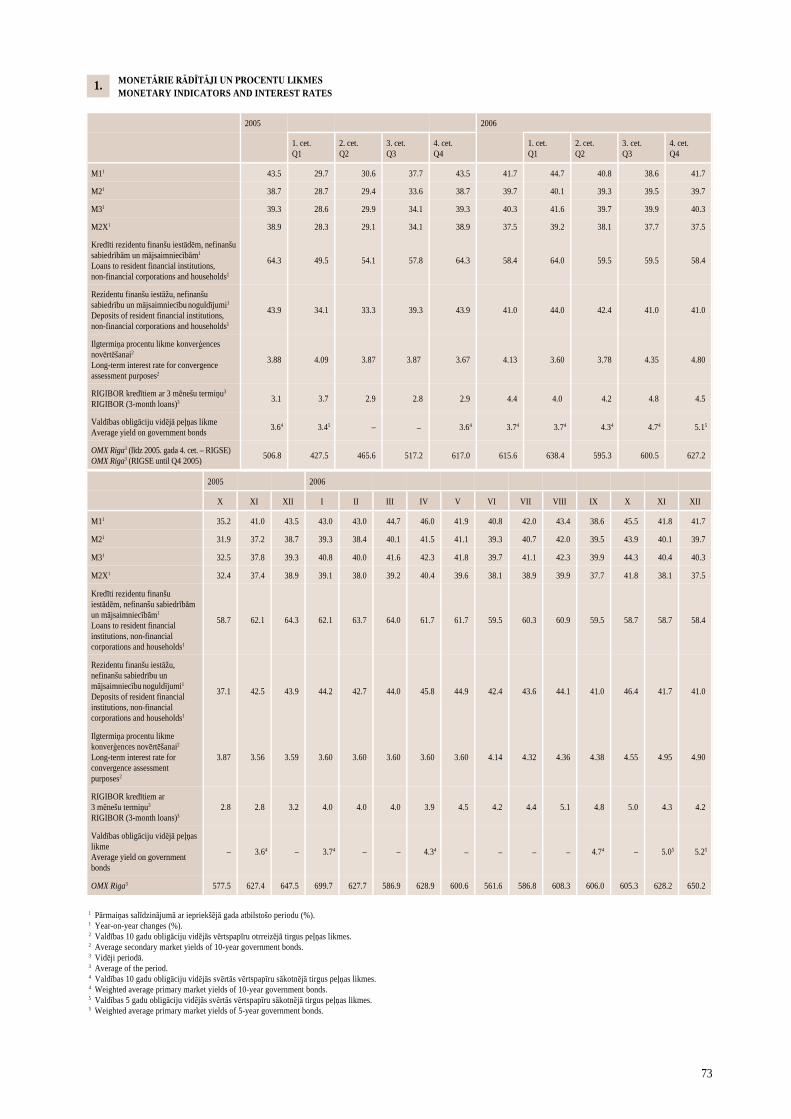

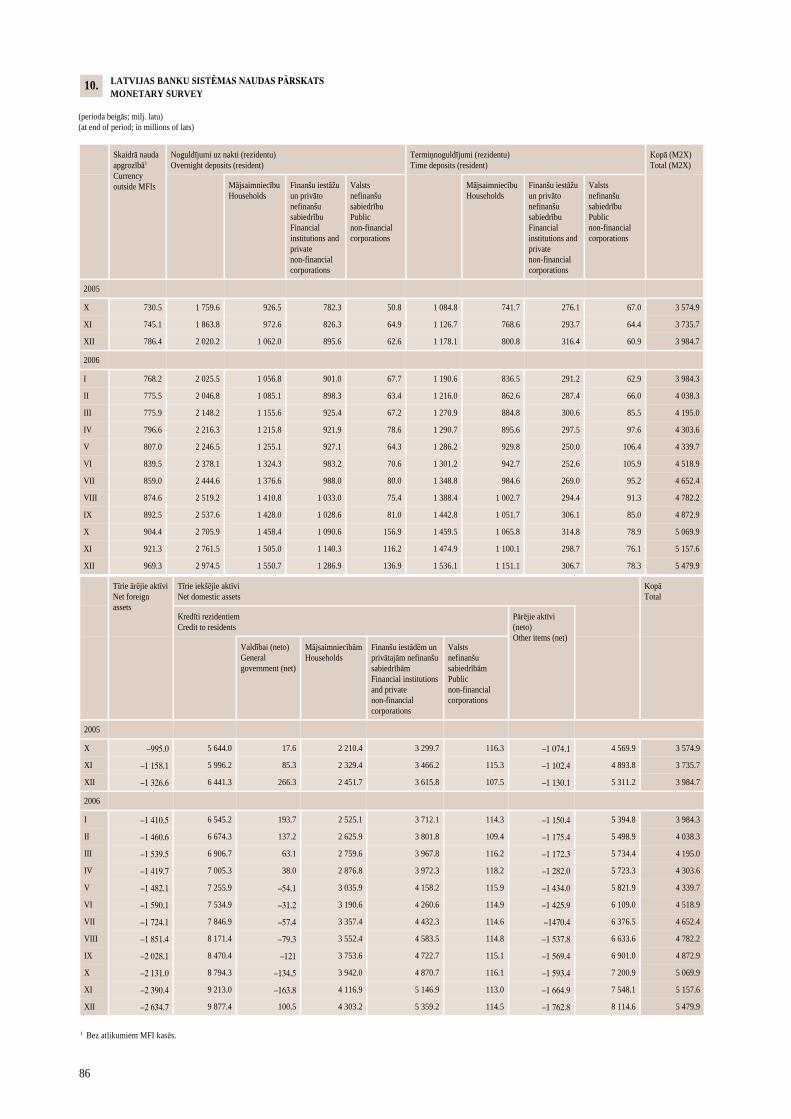

Naudas râdîtâju dinamika

Turpinot augt banku piesaistîto lîdzekïu apjomam, palielinâjâs arî obligâto rezervjuprasîbu izpildei nepiecieðamo lîdzekïu apjoms kontos Latvijas Bankâ. Tâdçjâdibanku pieprasîjuma noguldîjumu atlikums centrâlajâ bankâ 4. ceturksnî palielinâjâspar 222.3 milj. latu. Sezonâlu faktoru dçï par 90.4 milj. latu pieauga skaidrâs naudas

19

4 · 2006

pieprasîjums, tomçr skaidrâs naudas apgrozîbâ gada kâpuma temps nedaudzsamazinâjâs (no 22.8% septembrî lîdz 22.4% decembrî). Naudas bâze M0 decembrabeigâs sasniedza augstu lîmeni – 2.2 mljrd. latu, lîdz 66.5% palielinoties arî tâsgada kâpuma tempam (septembrî – 61.0%).

Latvijas Bankas naudas piedâvâjumu bûtiski palielinâja centrâlâs bankas veiktâârvalstu valûtas pirkðana no bankâm, tâpçc centrâlâs bankas tîrie ârçjie aktîvi 4. ce-turksnî pieauga par 196.1 milj. latu jeb 8.8% (gada kâpuma temps – 73.7%). Emi-tçtâs nacionâlâs valûtas segums ar centrâlâs bankas tîrajiem ârçjiem aktîviem de-cembra beigâs bija 107.4% (sk. 13. att.). Palielinoða ietekme uz naudas bâzi bijaarî straujajam centrâlâs valdîbas izdevumu pieaugumam gada nogalç (centrâlâsvaldîbas noguldîjumu atlikums centrâlajâ bankâ saruka par 183.6 milj. latu). Savu-kârt centrâlâs bankas naudas piedâvâjumu nedaudz mazinâja bankâm izsniegtorepo kredîtu atlikuma sarukums (par 20.8 milj. latu) un banku termiònoguldîjumucentrâlajâ bankâ atlikuma palielinâðanâs (par 43.5 milj. latu).

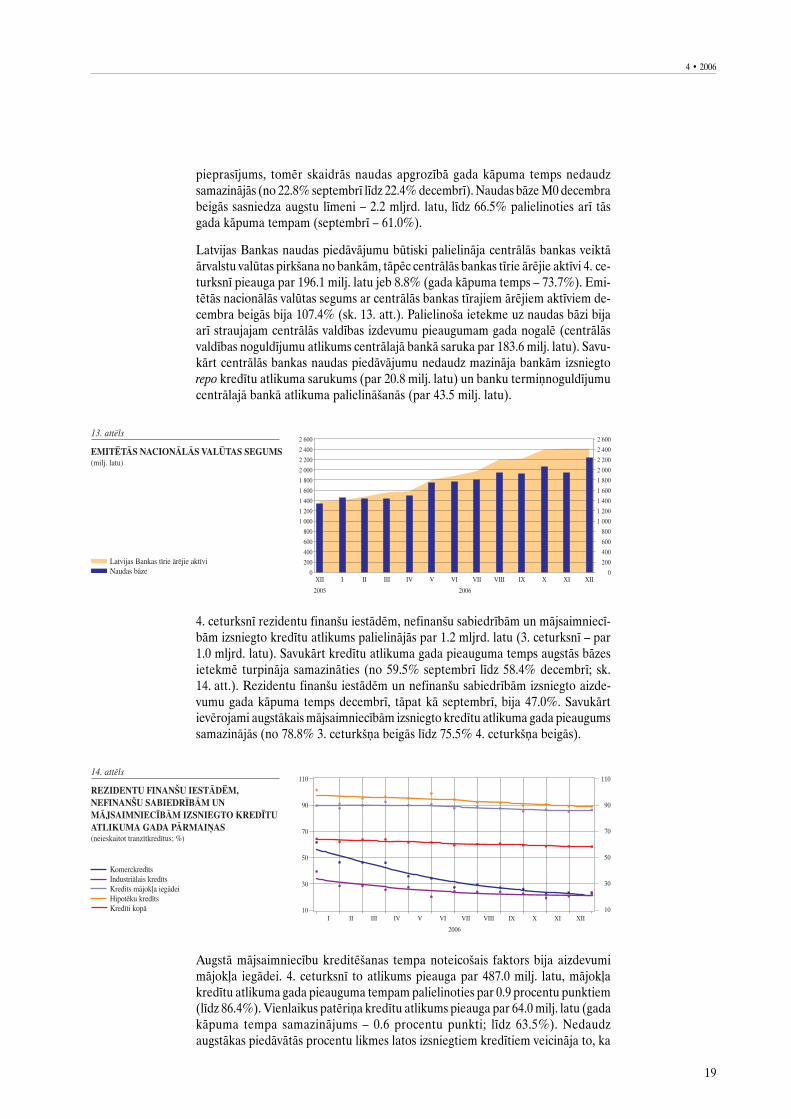

4. ceturksnî rezidentu finanðu iestâdçm, nefinanðu sabiedrîbâm un mâjsaimniecî-bâm izsniegto kredîtu atlikums palielinâjâs par 1.2 mljrd. latu (3. ceturksnî – par1.0 mljrd. latu). Savukârt kredîtu atlikuma gada pieauguma temps augstâs bâzesietekmç turpinâja samazinâties (no 59.5% septembrî lîdz 58.4% decembrî; sk.14. att.). Rezidentu finanðu iestâdçm un nefinanðu sabiedrîbâm izsniegto aizde-vumu gada kâpuma temps decembrî, tâpat kâ septembrî, bija 47.0%. Savukârtievçrojami augstâkais mâjsaimniecîbâm izsniegto kredîtu atlikuma gada pieaugumssamazinâjâs (no 78.8% 3. ceturkðòa beigâs lîdz 75.5% 4. ceturkðòa beigâs).

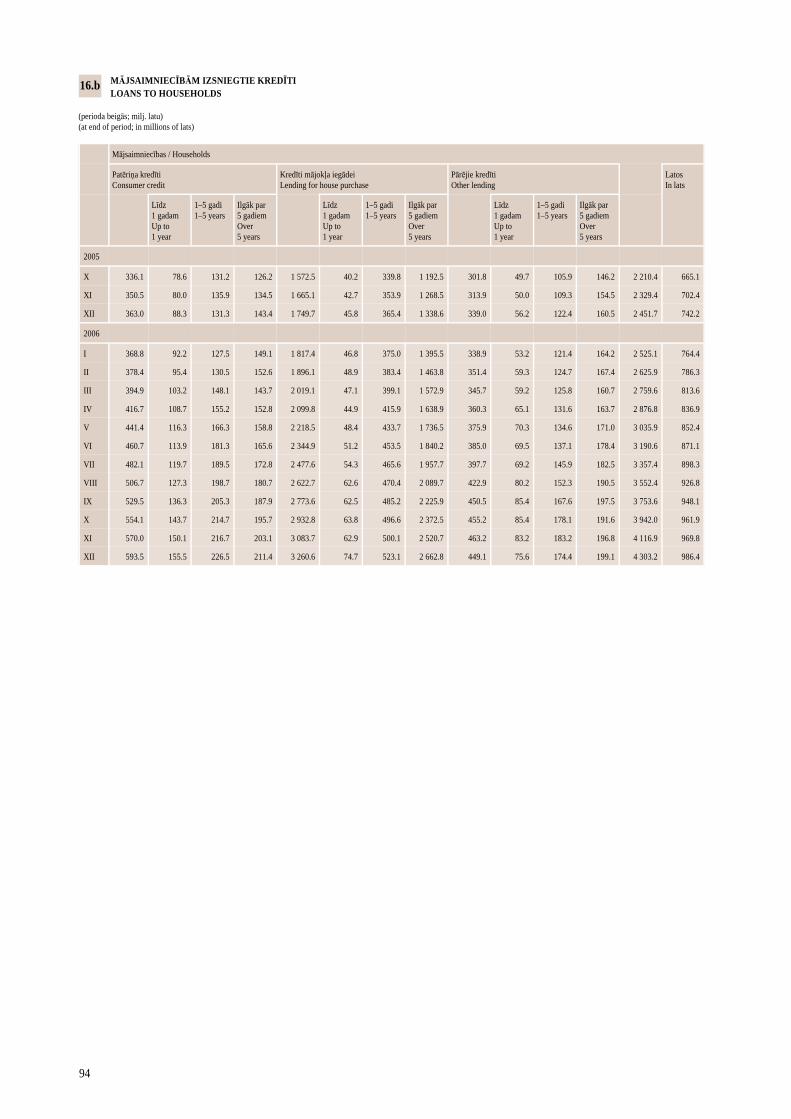

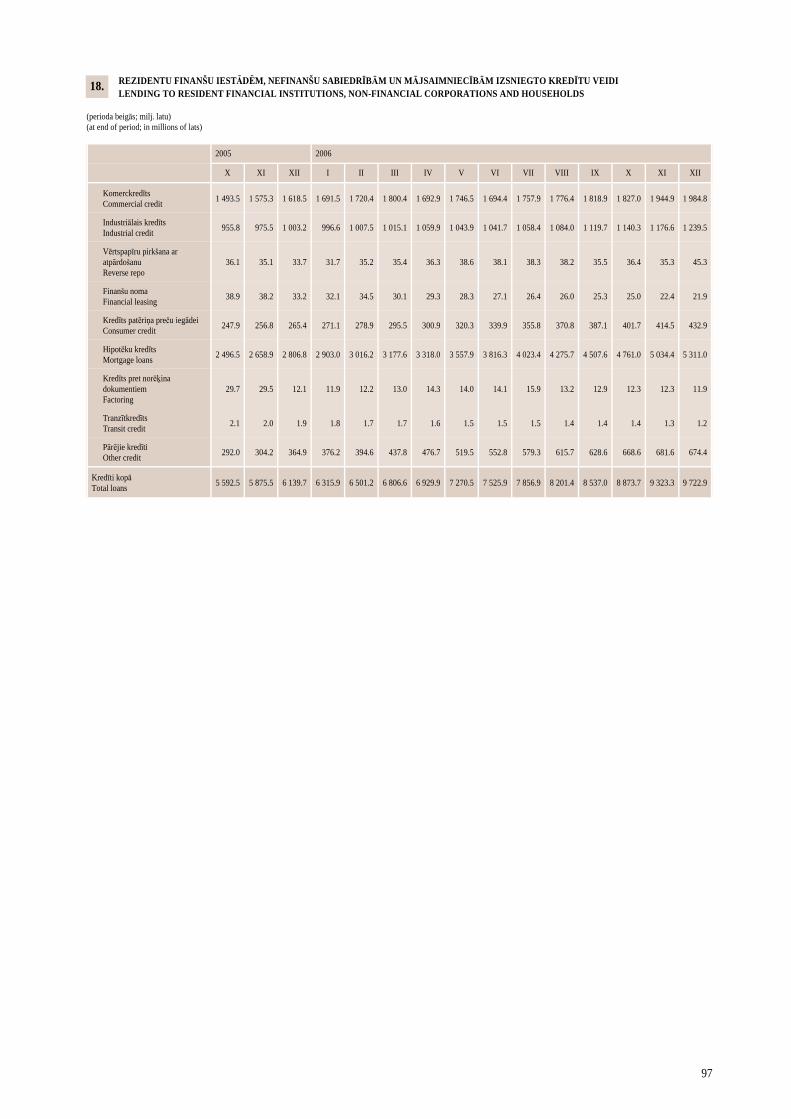

Augstâ mâjsaimniecîbu kreditçðanas tempa noteicoðais faktors bija aizdevumimâjokïa iegâdei. 4. ceturksnî to atlikums pieauga par 487.0 milj. latu, mâjokïakredîtu atlikuma gada pieauguma tempam palielinoties par 0.9 procentu punktiem(lîdz 86.4%). Vienlaikus patçriòa kredîtu atlikums pieauga par 64.0 milj. latu (gadakâpuma tempa samazinâjums – 0.6 procentu punkti; lîdz 63.5%). Nedaudzaugstâkas piedâvâtâs procentu likmes latos izsniegtiem kredîtiem veicinâja to, ka

20

MONETÂRAIS APSKATS · MONETARY REVIEW

mâjsaimniecîbas pieprasîja aizdevumus gandrîz tikai eiro. Ðâdu kredîtu atlikums4. ceturksnî pieauga par 520.4 milj. latu (latos izsniegto – tikai par 38.3 milj. latu),un to atlikuma gada kâpuma temps bija 123.5% (latos izsniegtajiem kredîtiem –32.9%). Latos izsniegto kredîtu mâjokïa iegâdei atlikuma îpatsvars 4. ceturkðòabeigâs samazinâjâs lîdz 18.8% (3. ceturkðòa beigâs – 21.5%), bet eiro izsniegtokredîtu mâjokïa iegâdei – pieauga lîdz 78.0% (3. ceturkðòa beigâs – 74.5%). Savu-kârt patçriòa kredîtu valûtu struktûrâ latos izsniegto kredîtu îpatsvars samazinâjâslîdz 53.7% (3. ceturkðòa beigâs – 55.2%), bet eiro izsniegto kredîtu îpatsvars pa-lielinâjâs lîdz 43.1% (3. ceturkðòa beigâs – 41.6%).

Eiro izsniegto kredîtu dominçðana bija vçrojama arî uzòçmçjdarbîbai izsniegtajoskredîtos – to atlikums pieauga par 625.3 milj. latu (latos izsniegto – par 29.4 milj.latu; gada pieauguma temps decembrî – attiecîgi 80.6% un 13.9%). Tâdçjâdi eiroizsniegto kredîtu atlikuma îpatsvars visos izsniegtajos kredîtos 4. ceturkðòa beigâssasniedza 72.9%, bet latos izsniegto – samazinâjâs lîdz 23.2%.

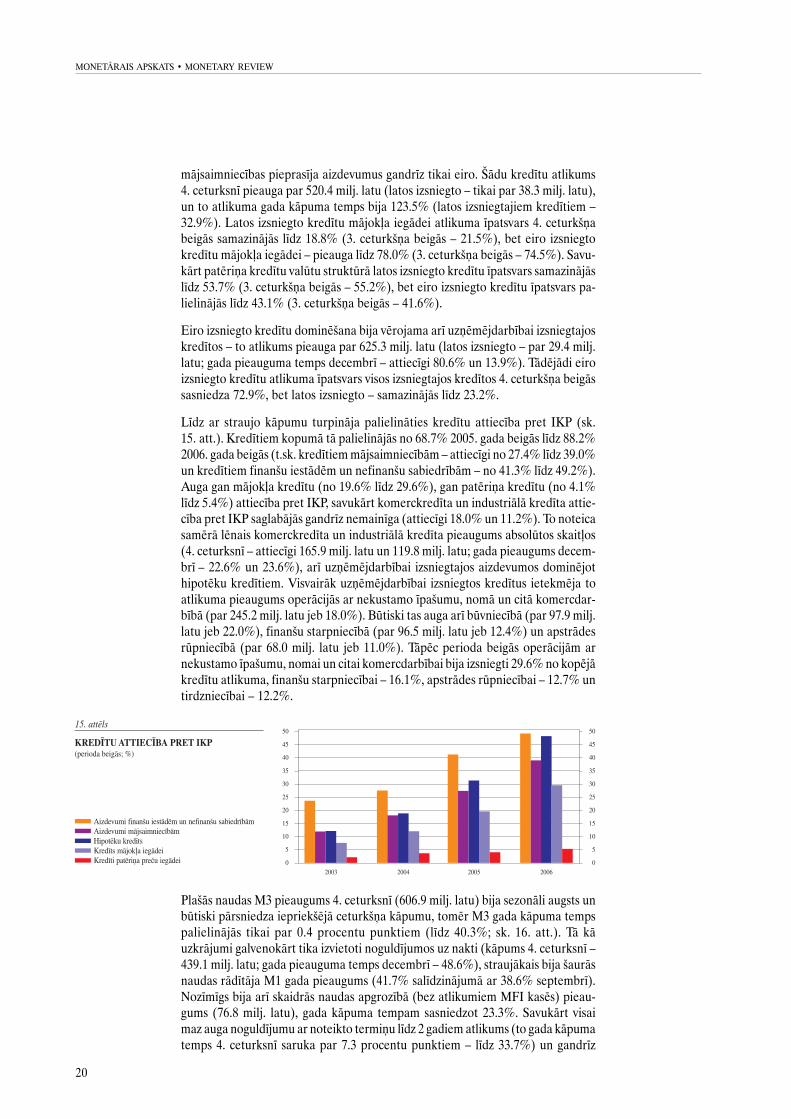

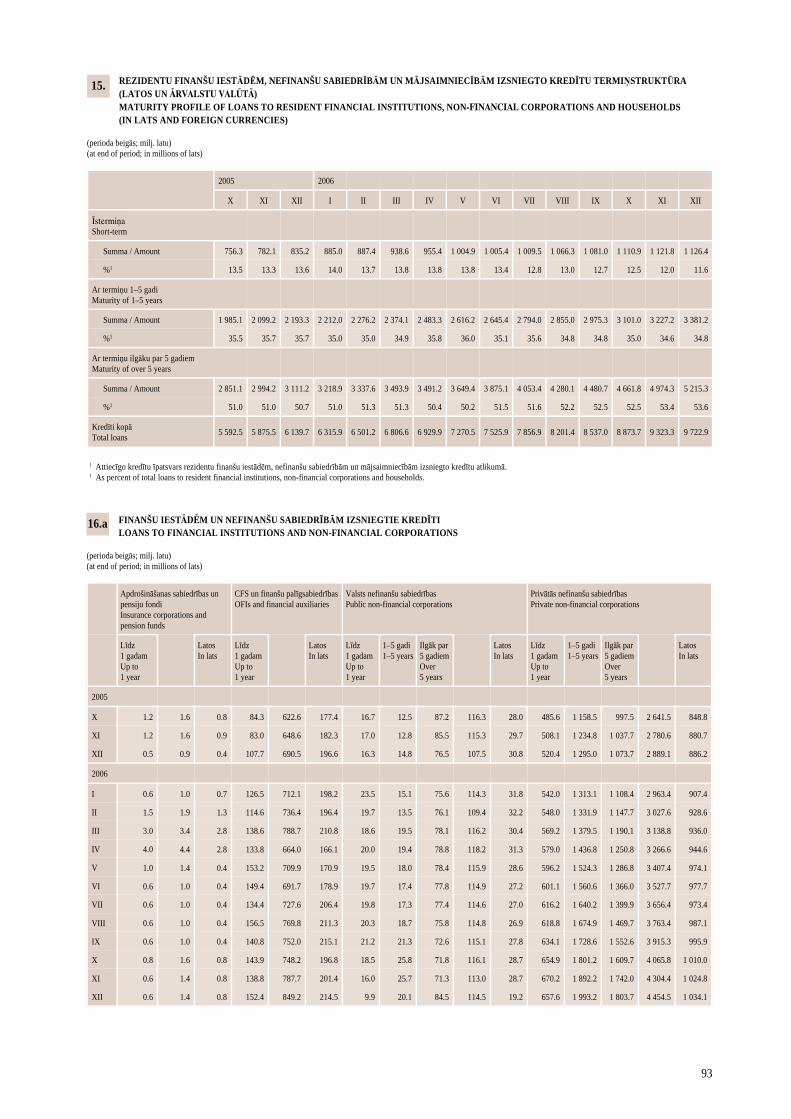

Lîdz ar straujo kâpumu turpinâja palielinâties kredîtu attiecîba pret IKP (sk.15. att.). Kredîtiem kopumâ tâ palielinâjâs no 68.7% 2005. gada beigâs lîdz 88.2%2006. gada beigâs (t.sk. kredîtiem mâjsaimniecîbâm – attiecîgi no 27.4% lîdz 39.0%un kredîtiem finanðu iestâdçm un nefinanðu sabiedrîbâm – no 41.3% lîdz 49.2%).Auga gan mâjokïa kredîtu (no 19.6% lîdz 29.6%), gan patçriòa kredîtu (no 4.1%lîdz 5.4%) attiecîba pret IKP, savukârt komerckredîta un industriâlâ kredîta attie-cîba pret IKP saglabâjâs gandrîz nemainîga (attiecîgi 18.0% un 11.2%). To noteicasamçrâ lçnais komerckredîta un industriâlâ kredîta pieaugums absolûtos skaitïos(4. ceturksnî – attiecîgi 165.9 milj. latu un 119.8 milj. latu; gada pieaugums decem-brî – 22.6% un 23.6%), arî uzòçmçjdarbîbai izsniegtajos aizdevumos dominçjothipotçku kredîtiem. Visvairâk uzòçmçjdarbîbai izsniegtos kredîtus ietekmçja toatlikuma pieaugums operâcijâs ar nekustamo îpaðumu, nomâ un citâ komercdar-bîbâ (par 245.2 milj. latu jeb 18.0%). Bûtiski tas auga arî bûvniecîbâ (par 97.9 milj.latu jeb 22.0%), finanðu starpniecîbâ (par 96.5 milj. latu jeb 12.4%) un apstrâdesrûpniecîbâ (par 68.0 milj. latu jeb 11.0%). Tâpçc perioda beigâs operâcijâm arnekustamo îpaðumu, nomai un citai komercdarbîbai bija izsniegti 29.6% no kopçjâkredîtu atlikuma, finanðu starpniecîbai – 16.1%, apstrâdes rûpniecîbai – 12.7% untirdzniecîbai – 12.2%.

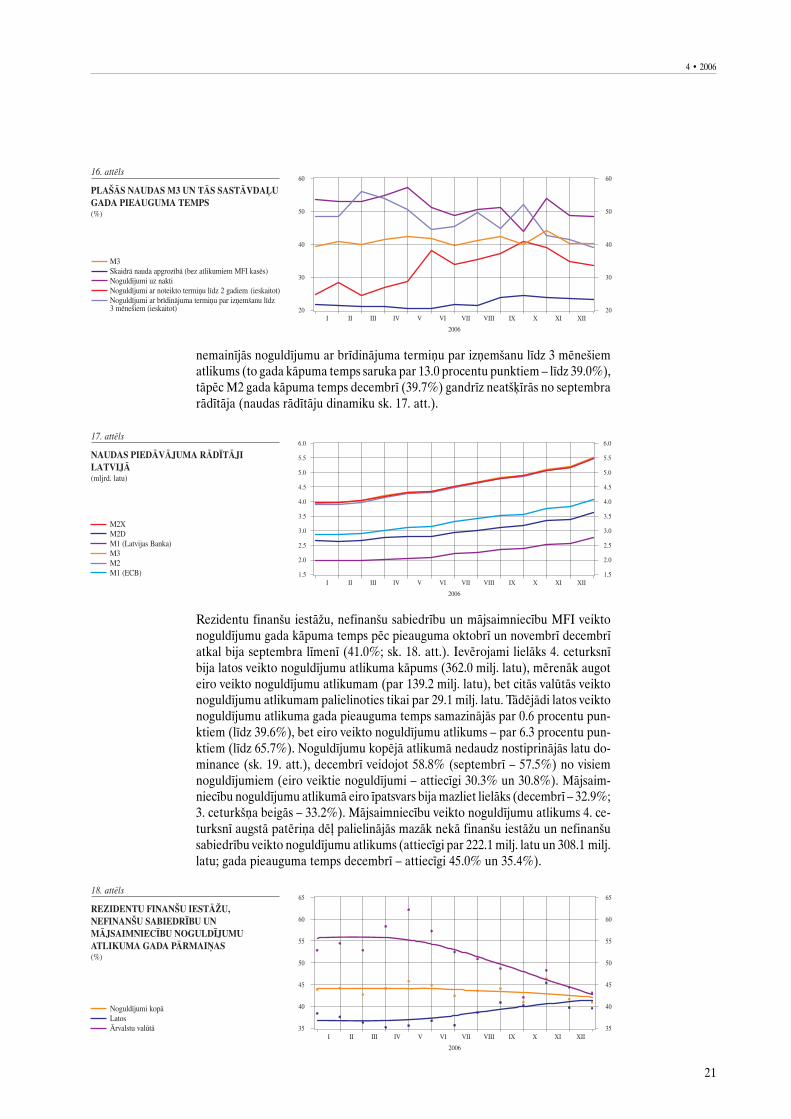

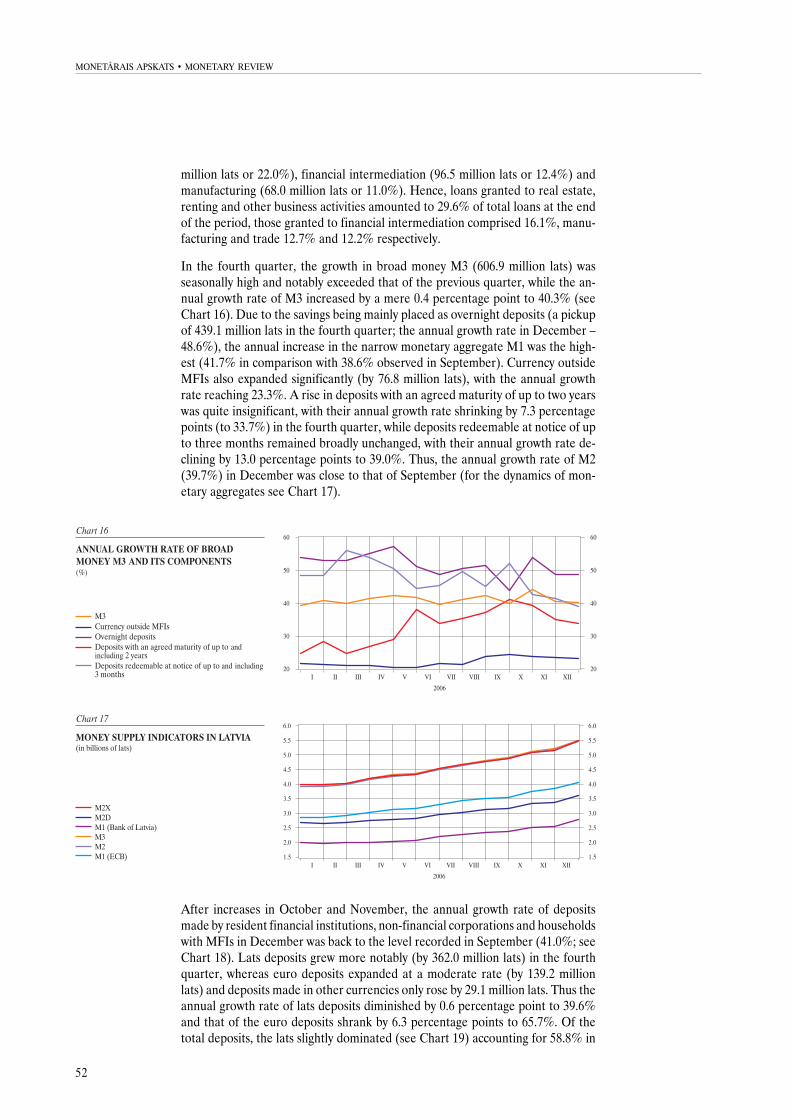

Plaðâs naudas M3 pieaugums 4. ceturksnî (606.9 milj. latu) bija sezonâli augsts unbûtiski pârsniedza iepriekðçjâ ceturkðòa kâpumu, tomçr M3 gada kâpuma tempspalielinâjâs tikai par 0.4 procentu punktiem (lîdz 40.3%; sk. 16. att.). Tâ kâuzkrâjumi galvenokârt tika izvietoti noguldîjumos uz nakti (kâpums 4. ceturksnî –439.1 milj. latu; gada pieauguma temps decembrî – 48.6%), straujâkais bija ðaurâsnaudas râdîtâja M1 gada pieaugums (41.7% salîdzinâjumâ ar 38.6% septembrî).Nozîmîgs bija arî skaidrâs naudas apgrozîbâ (bez atlikumiem MFI kasçs) pieau-gums (76.8 milj. latu), gada kâpuma tempam sasniedzot 23.3%. Savukârt visaimaz auga noguldîjumu ar noteikto termiòu lîdz 2 gadiem atlikums (to gada kâpumatemps 4. ceturksnî saruka par 7.3 procentu punktiem – lîdz 33.7%) un gandrîz

21

4 · 2006

nemainîjâs noguldîjumu ar brîdinâjuma termiòu par izòemðanu lîdz 3 mçneðiematlikums (to gada kâpuma temps saruka par 13.0 procentu punktiem – lîdz 39.0%),tâpçc M2 gada kâpuma temps decembrî (39.7%) gandrîz neatðíîrâs no septembrarâdîtâja (naudas râdîtâju dinamiku sk. 17. att.).

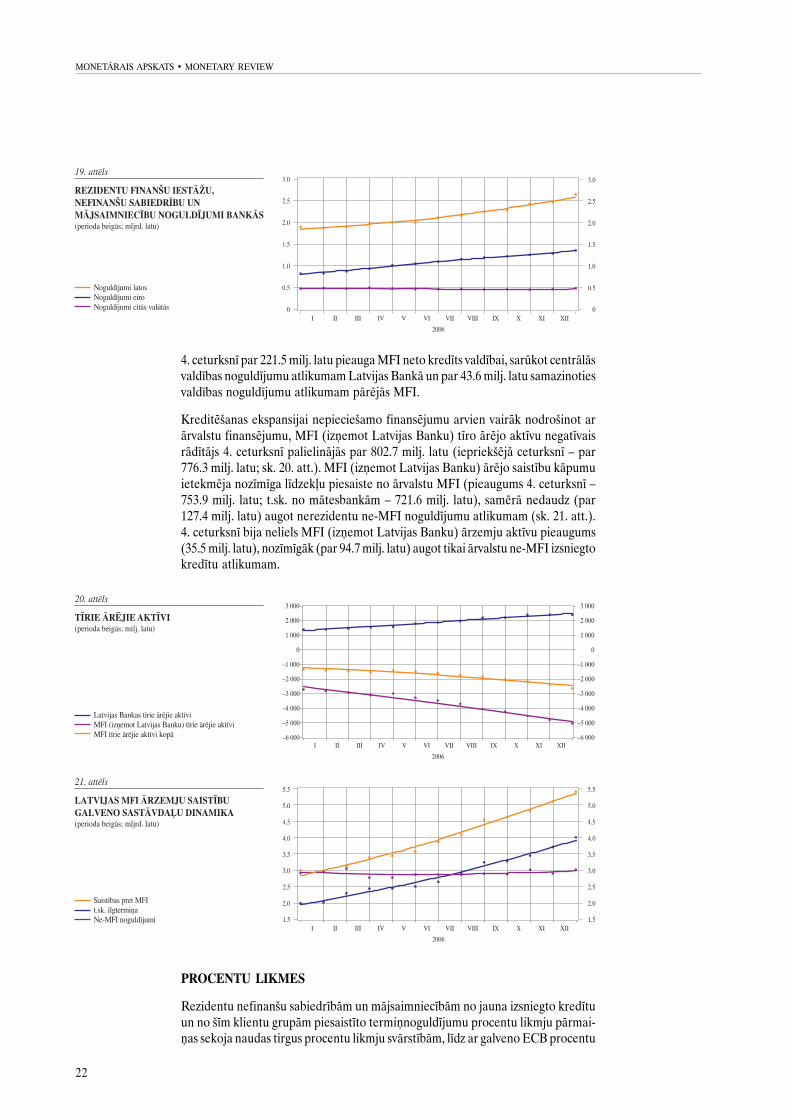

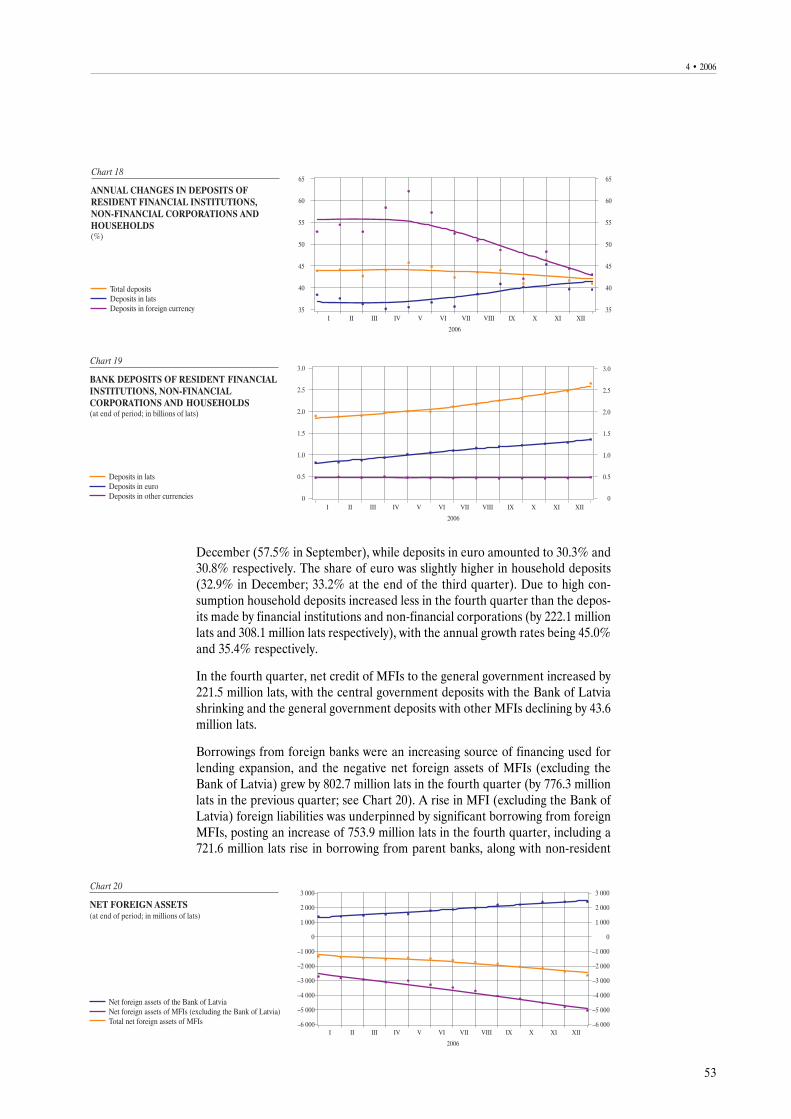

Rezidentu finanðu iestâþu, nefinanðu sabiedrîbu un mâjsaimniecîbu MFI veiktonoguldîjumu gada kâpuma temps pçc pieauguma oktobrî un novembrî decembrîatkal bija septembra lîmenî (41.0%; sk. 18. att.). Ievçrojami lielâks 4. ceturksnîbija latos veikto noguldîjumu atlikuma kâpums (362.0 milj. latu), mçrenâk augoteiro veikto noguldîjumu atlikumam (par 139.2 milj. latu), bet citâs valûtâs veiktonoguldîjumu atlikumam palielinoties tikai par 29.1 milj. latu. Tâdçjâdi latos veiktonoguldîjumu atlikuma gada pieauguma temps samazinâjâs par 0.6 procentu pun-ktiem (lîdz 39.6%), bet eiro veikto noguldîjumu atlikums – par 6.3 procentu pun-ktiem (lîdz 65.7%). Noguldîjumu kopçjâ atlikumâ nedaudz nostiprinâjâs latu do-minance (sk. 19. att.), decembrî veidojot 58.8% (septembrî – 57.5%) no visiemnoguldîjumiem (eiro veiktie noguldîjumi – attiecîgi 30.3% un 30.8%). Mâjsaim-niecîbu noguldîjumu atlikumâ eiro îpatsvars bija mazliet lielâks (decembrî – 32.9%;3. ceturkðòa beigâs – 33.2%). Mâjsaimniecîbu veikto noguldîjumu atlikums 4. ce-turksnî augstâ patçriòa dçï palielinâjâs mazâk nekâ finanðu iestâþu un nefinanðusabiedrîbu veikto noguldîjumu atlikums (attiecîgi par 222.1 milj. latu un 308.1 milj.latu; gada pieauguma temps decembrî – attiecîgi 45.0% un 35.4%).

22

MONETÂRAIS APSKATS · MONETARY REVIEW

4. ceturksnî par 221.5 milj. latu pieauga MFI neto kredîts valdîbai, sarûkot centrâlâsvaldîbas noguldîjumu atlikumam Latvijas Bankâ un par 43.6 milj. latu samazinotiesvaldîbas noguldîjumu atlikumam pârçjâs MFI.

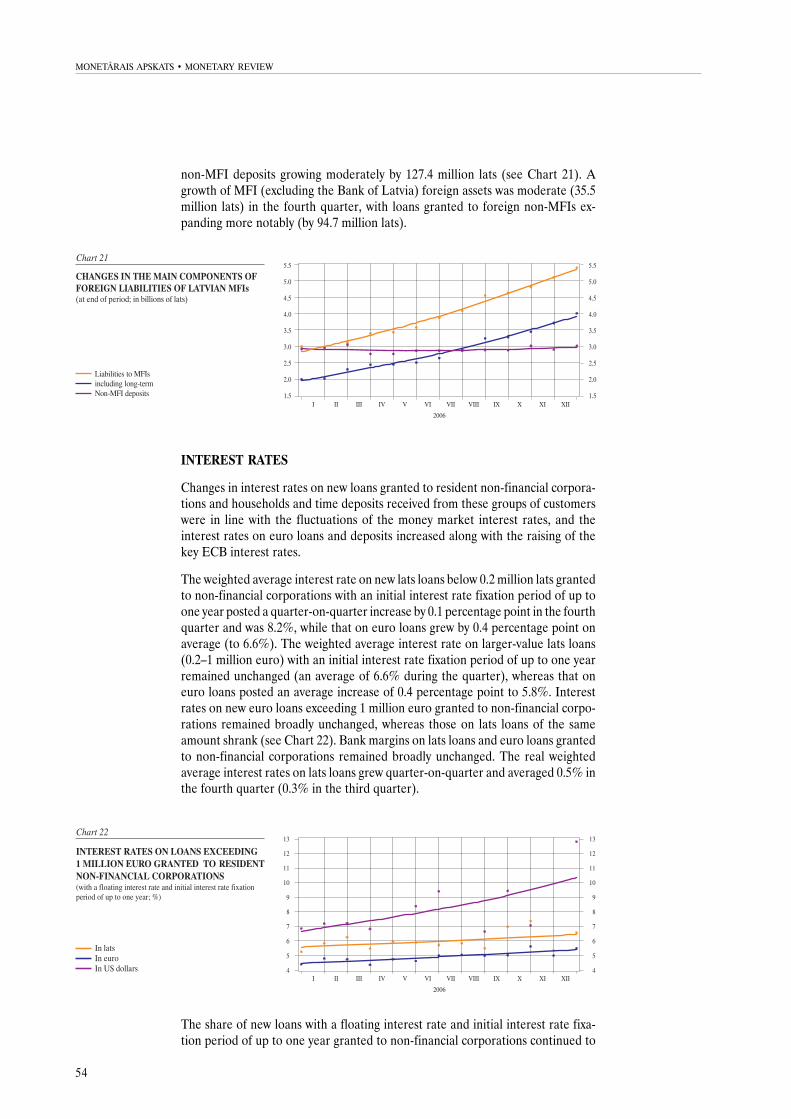

Kreditçðanas ekspansijai nepiecieðamo finansçjumu arvien vairâk nodroðinot arârvalstu finansçjumu, MFI (izòemot Latvijas Banku) tîro ârçjo aktîvu negatîvaisrâdîtâjs 4. ceturksnî palielinâjâs par 802.7 milj. latu (iepriekðçjâ ceturksnî – par776.3 milj. latu; sk. 20. att.). MFI (izòemot Latvijas Banku) ârçjo saistîbu kâpumuietekmçja nozîmîga lîdzekïu piesaiste no ârvalstu MFI (pieaugums 4. ceturksnî –753.9 milj. latu; t.sk. no mâtesbankâm – 721.6 milj. latu), samçrâ nedaudz (par127.4 milj. latu) augot nerezidentu ne-MFI noguldîjumu atlikumam (sk. 21. att.).4. ceturksnî bija neliels MFI (izòemot Latvijas Banku) ârzemju aktîvu pieaugums(35.5 milj. latu), nozîmîgâk (par 94.7 milj. latu) augot tikai ârvalstu ne-MFI izsniegtokredîtu atlikumam.

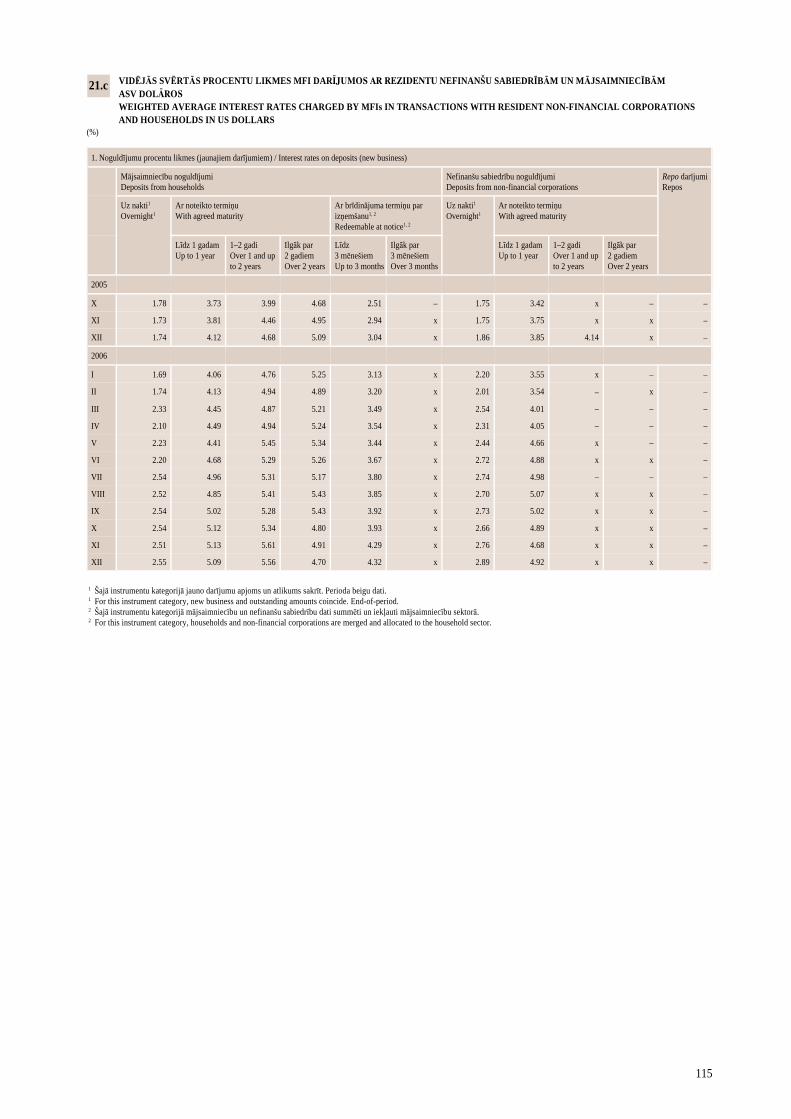

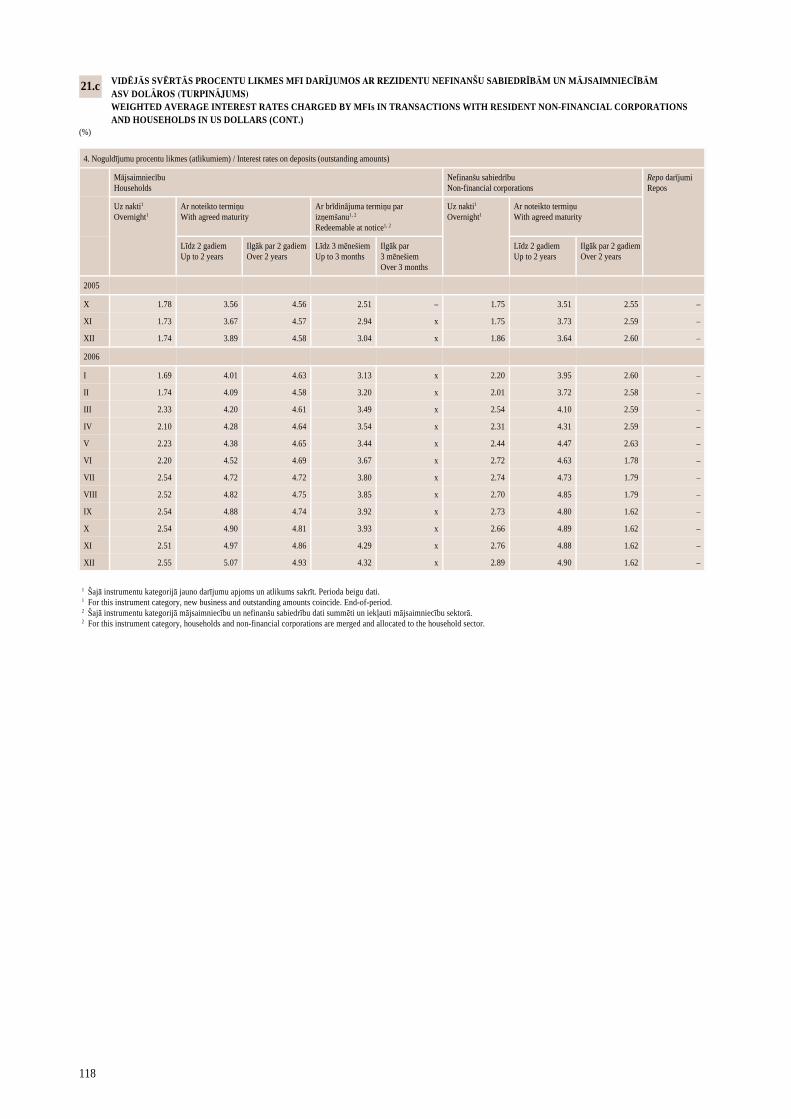

PROCENTU LIKMES

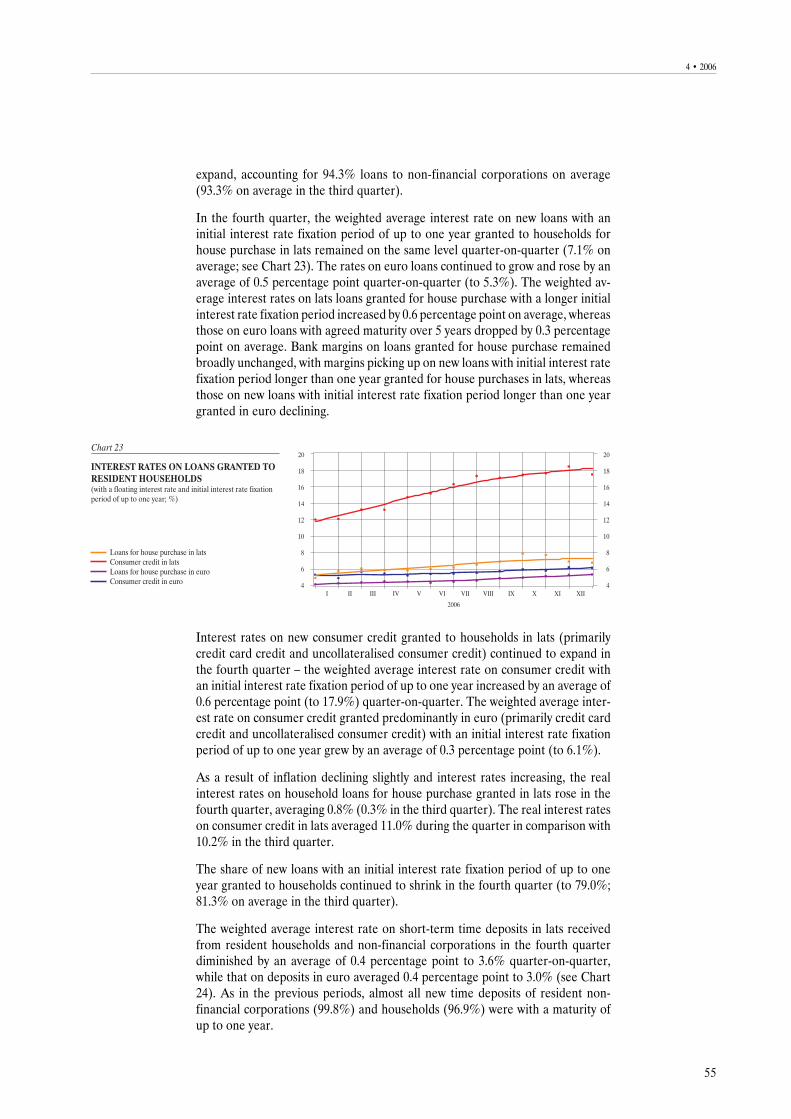

Rezidentu nefinanðu sabiedrîbâm un mâjsaimniecîbâm no jauna izsniegto kredîtuun no ðîm klientu grupâm piesaistîto termiònoguldîjumu procentu likmju pârmai-òas sekoja naudas tirgus procentu likmju svârstîbâm, lîdz ar galveno ECB procentu

23

4 · 2006

likmju paaugstinâðanu pieaugot eiro izsniegto kredîtu un piesaistîto noguldîjumuprocentu likmçm.

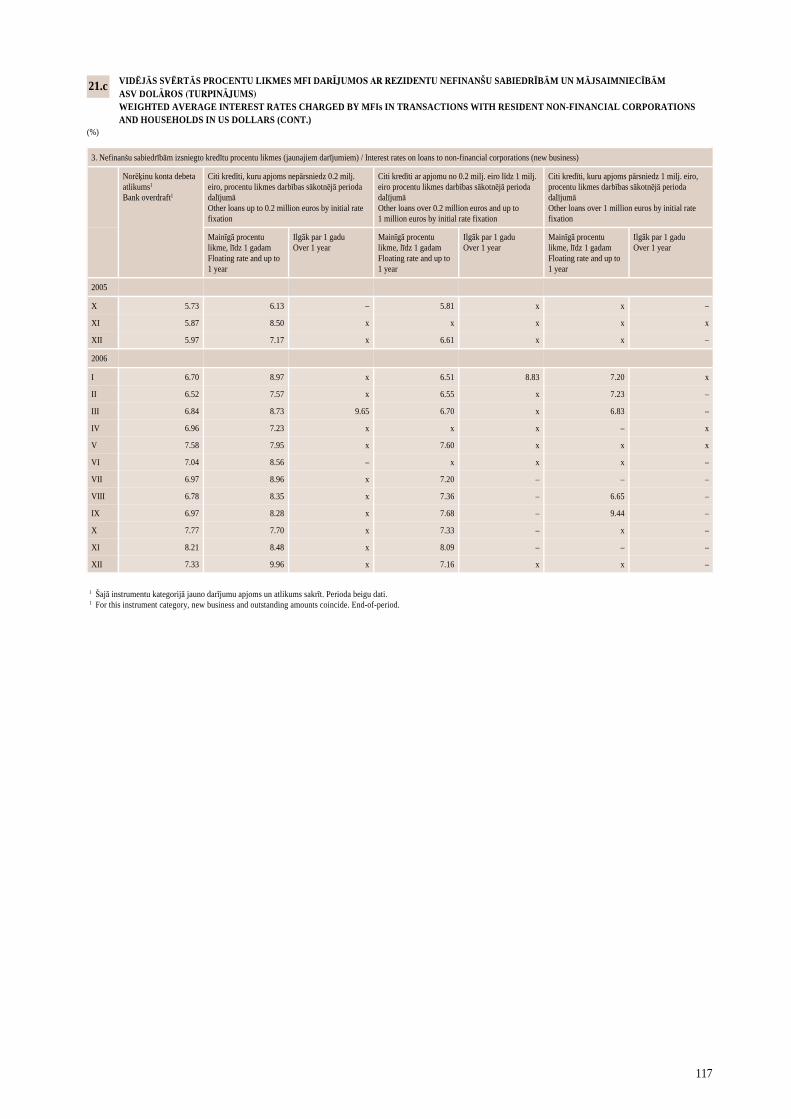

Nefinanðu sabiedrîbâm latos no jauna izsniegtajiem kredîtiem, kuru apjoms mazâkspar 0.2 milj. eiro, ar procentu likmes darbîbas sâkotnçjo periodu lîdz 1 gadamvidçjâ svçrtâ procentu likme 4. ceturksnî salîdzinâjumâ ar attiecîgo râdîtâju ie-priekðçjâ ceturksnî pieauga vidçji par 0.1 procentu punktu (lîdz 8.2%), bet eiroizsniegtajiem kredîtiem – vidçji par 0.4 procentu punktiem (lîdz 6.6%). Savukârtlielâka apjoma (0.2–1 milj. eiro) kredîtu ar procentu likmes darbîbas sâkotnçjoperiodu lîdz 1 gadam vidçjâ svçrtâ procentu likme latos izsniegtajiem kredîtiemnemainîjâs (vidçji ceturksnî – 6.6%), bet eiro izsniegtajiem kredîtiem – pieaugavidçji par 0.4 procentu punktiem (lîdz 5.8%). Bûtiski nemainîjâs arî procentu likmesnefinanðu sabiedrîbâm eiro no jauna izsniegtajiem kredîtiem ar apjomu lielâkupar 1 milj. eiro, savukârt ðâda apjoma latos izsniegtajiem kredîtiem procentu likmessaruka (sk. 22. att.). Pievienotâs procentu likmes nefinanðu sabiedrîbâm latos uneiro izsniegtajiem kredîtiem mainîjâs maz. Savukârt vidçjâs svçrtâs reâlâs procentulikmes latos izsniegtajiem kredîtiem salîdzinâjumâ ar iepriekðçjo ceturksni palie-linâjâs un vidçji ceturksnî bija 0.5% (3. ceturksnî – vidçji 0.3%).

Nefinanðu sabiedrîbâm no jauna izsniegto kredîtu ar mainîgo procentu likmi unar procentu likmes darbîbas sâkotnçjo periodu lîdz 1 gadam îpatsvars turpinâjapalielinâties, vidçji 4. ceturksnî sasniedzot 94.3% no nefinanðu sabiedrîbâm iz-sniegtajiem kredîtiem (3. ceturksnî – vidçji 93.3%).

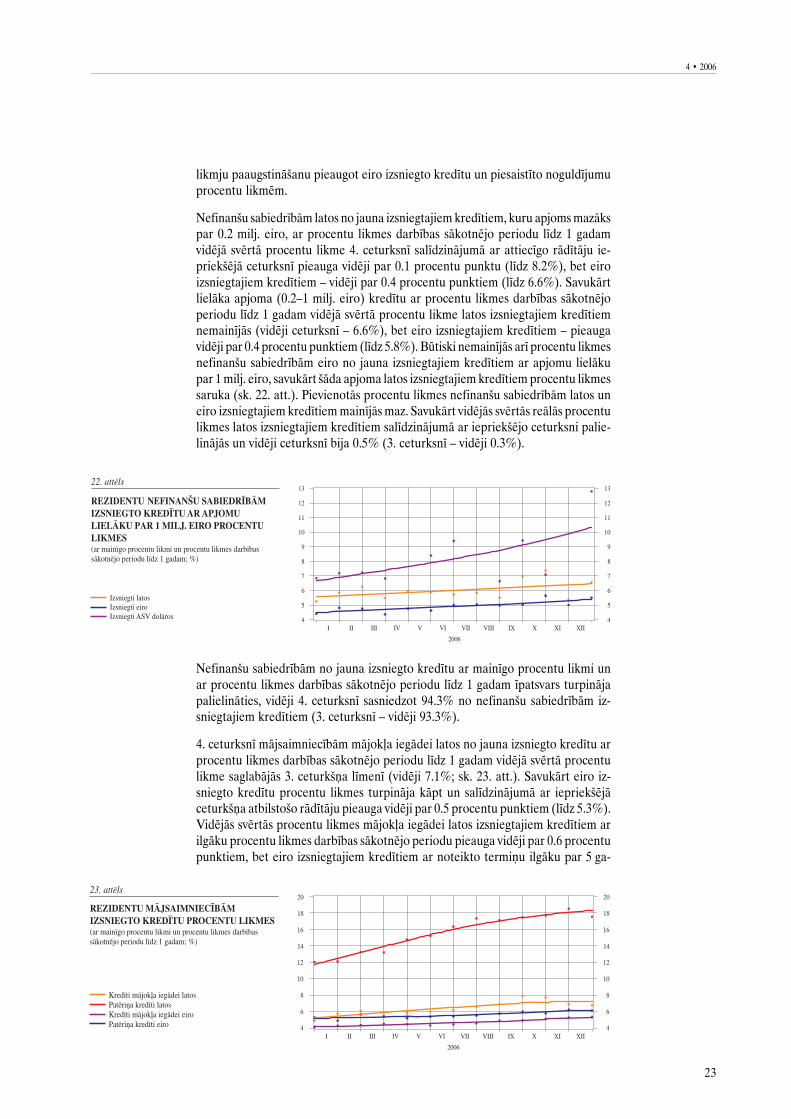

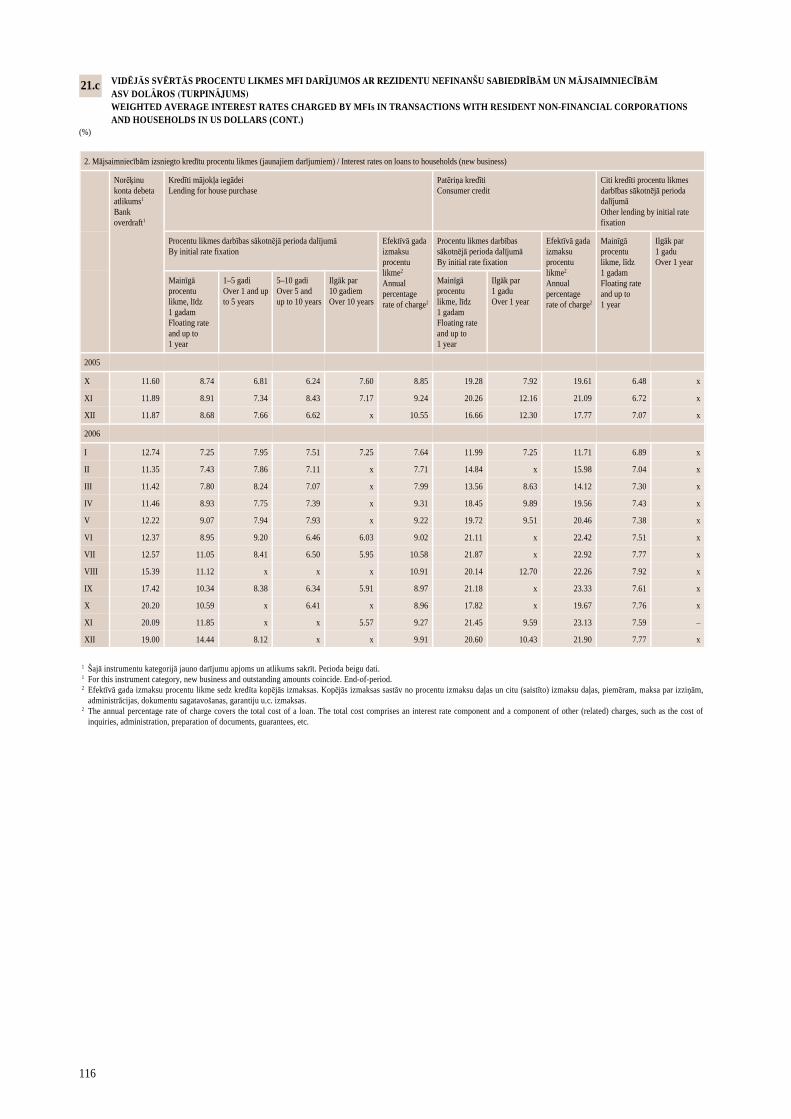

4. ceturksnî mâjsaimniecîbâm mâjokïa iegâdei latos no jauna izsniegto kredîtu arprocentu likmes darbîbas sâkotnçjo periodu lîdz 1 gadam vidçjâ svçrtâ procentulikme saglabâjâs 3. ceturkðòa lîmenî (vidçji 7.1%; sk. 23. att.). Savukârt eiro iz-sniegto kredîtu procentu likmes turpinâja kâpt un salîdzinâjumâ ar iepriekðçjâceturkðòa atbilstoðo râdîtâju pieauga vidçji par 0.5 procentu punktiem (lîdz 5.3%).Vidçjâs svçrtâs procentu likmes mâjokïa iegâdei latos izsniegtajiem kredîtiem arilgâku procentu likmes darbîbas sâkotnçjo periodu pieauga vidçji par 0.6 procentupunktiem, bet eiro izsniegtajiem kredîtiem ar noteikto termiòu ilgâku par 5 ga-

24

MONETÂRAIS APSKATS · MONETARY REVIEW

diem – samazinâjâs vidçji par 0.3 procentu punktiem. Pievienotâs procentu likmesmâjokïa iegâdei izsniegtajiem kredîtiem bûtiski nemainîjâs, uzcenojumam pieaugotmâjokïa iegâdei latos no jauna izsniegtajiem kredîtiem ar procentu likmes dar-bîbas sâkotnçjo periodu ilgâku par 1 gadu, bet samazinoties mâjokïa iegâdei eirono jauna izsniegtajiem kredîtiem ar procentu likmes darbîbas sâkotnçjo perioduilgâku par 1 gadu.

Mâjsaimniecîbâm latos no jauna izsniegto patçriòa kredîtu (galvenokârt norçíinukarðu kredîti un patçriòa kredîti bez nodroðinâjuma) procentu likmes 4. ceturksnîturpinâja palielinâties – patçriòa kredîtiem ar procentu likmes darbîbas sâkotnçjoperiodu lîdz 1 gadam vidçjâ svçrtâ procentu likme 4. ceturksnî salîdzinâjumâ arattiecîgo râdîtâju iepriekðçjâ ceturksnî pieauga vidçji par 0.6 procentu punktiem(lîdz 17.9%). Dominçjoðo eiro izsniegto patçriòa kredîtu (galvenokârt patçriòakredîti ar nodroðinâjumu) ar procentu likmes darbîbas sâkotnçjo periodu lîdz 1 ga-dam vidçjâ svçrtâ procentu likme pieauga vidçji par 0.3 procentu punktiem (lîdz6.1%).

Nedaudz samazinoties inflâcijai un augot procentu likmçm, mâjsaimniecîbâm mâ-jokïa iegâdei latos izsniegto kredîtu reâlâs procentu likmes 4. ceturksnî palielinâjâs,vidçji ceturksnî veidojot 0.8% (3. ceturksnî – 0.3%). Latos izsniegto patçriòa kredîtureâlâs procentu likmes vidçji ceturksnî sasniedza 11.0% (3. ceturksnî – 10.2%).

4. ceturksnî turpina samazinâties mâjsaimniecîbâm no jauna izsniegto kredîtu arprocentu likmes darbîbas sâkotnçjo periodu lîdz 1 gadam îpatsvars (lîdz 79.0%;vidçji 3. ceturksnî – 81.3).

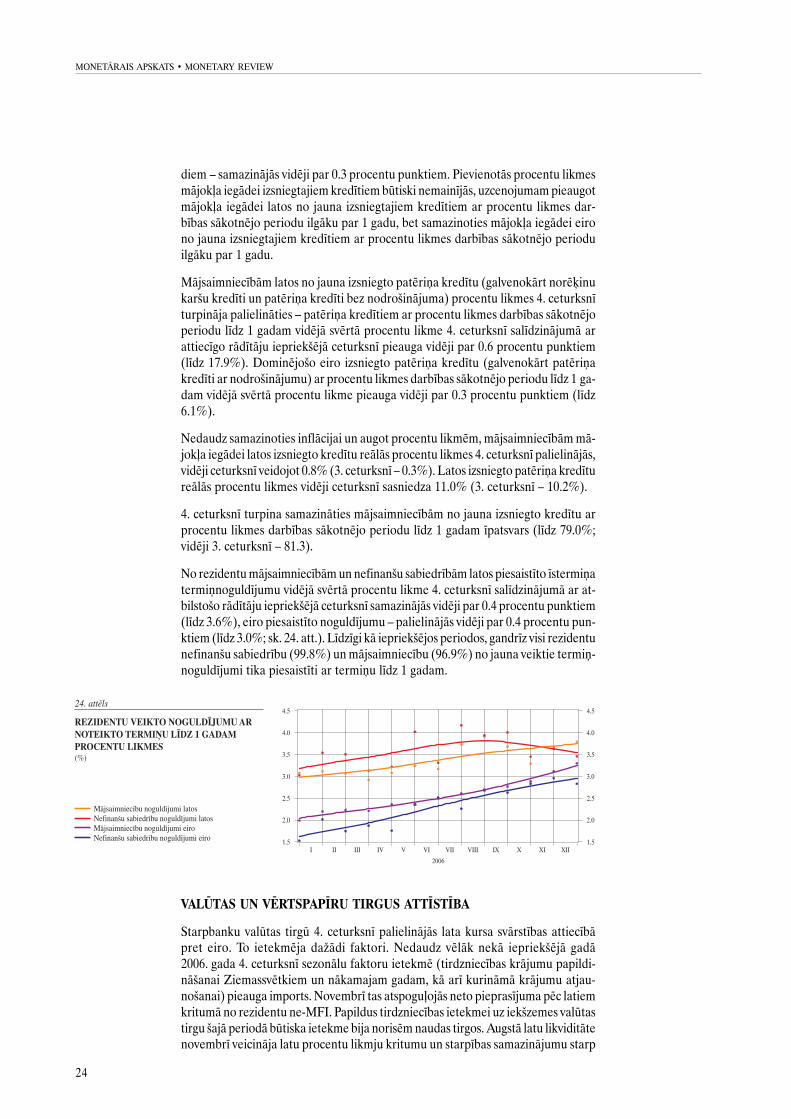

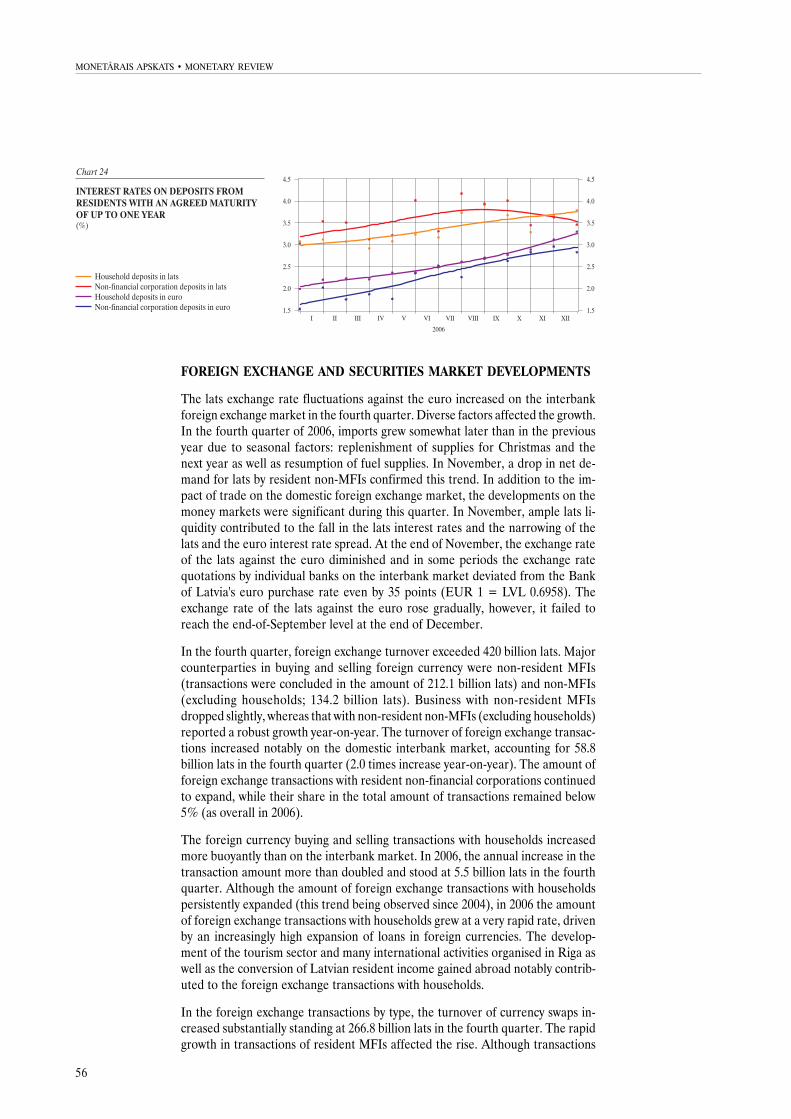

No rezidentu mâjsaimniecîbâm un nefinanðu sabiedrîbâm latos piesaistîto îstermiòatermiònoguldîjumu vidçjâ svçrtâ procentu likme 4. ceturksnî salîdzinâjumâ ar at-bilstoðo râdîtâju iepriekðçjâ ceturksnî samazinâjâs vidçji par 0.4 procentu punktiem(lîdz 3.6%), eiro piesaistîto noguldîjumu – palielinâjâs vidçji par 0.4 procentu pun-ktiem (lîdz 3.0%; sk. 24. att.). Lîdzîgi kâ iepriekðçjos periodos, gandrîz visi rezidentunefinanðu sabiedrîbu (99.8%) un mâjsaimniecîbu (96.9%) no jauna veiktie termiò-noguldîjumi tika piesaistîti ar termiòu lîdz 1 gadam.

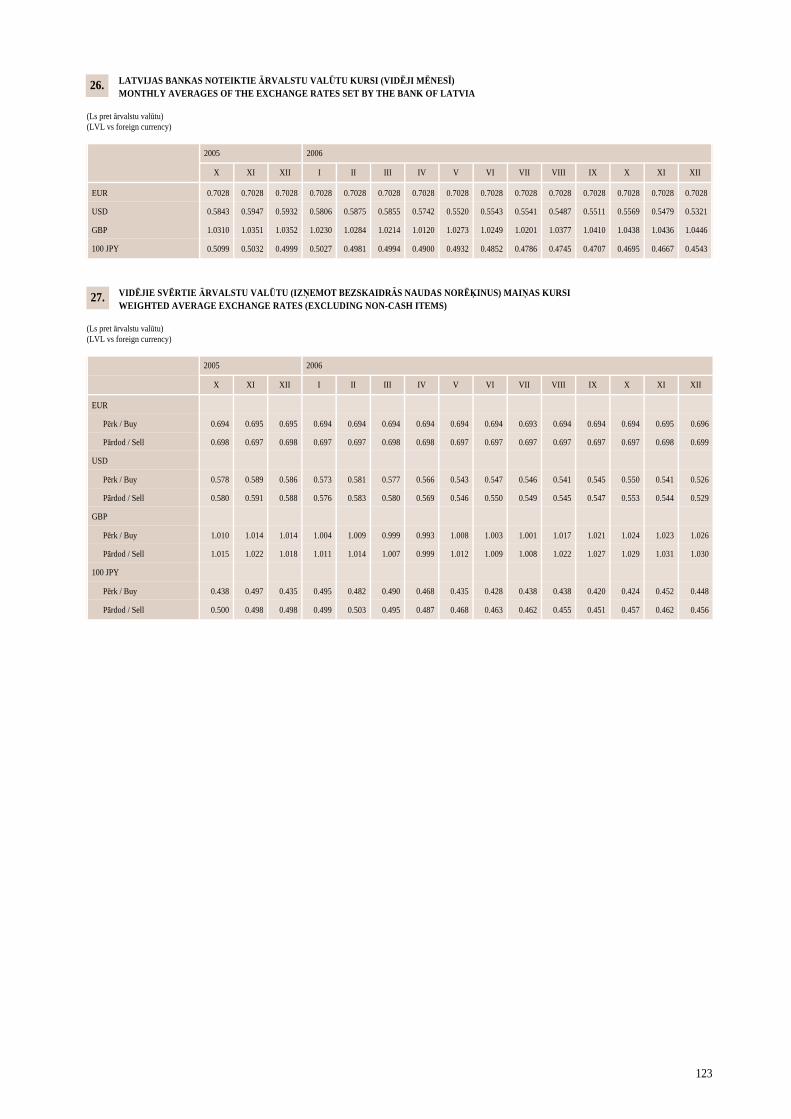

VALÛTAS UN VÇRTSPAPÎRU TIRGUS ATTÎSTÎBA

Starpbanku valûtas tirgû 4. ceturksnî palielinâjâs lata kursa svârstîbas attiecîbâpret eiro. To ietekmçja daþâdi faktori. Nedaudz vçlâk nekâ iepriekðçjâ gadâ2006. gada 4. ceturksnî sezonâlu faktoru ietekmç (tirdzniecîbas krâjumu papildi-nâðanai Ziemassvçtkiem un nâkamajam gadam, kâ arî kurinâmâ krâjumu atjau-noðanai) pieauga imports. Novembrî tas atspoguïojâs neto pieprasîjuma pçc latiemkritumâ no rezidentu ne-MFI. Papildus tirdzniecîbas ietekmei uz iekðzemes valûtastirgu ðajâ periodâ bûtiska ietekme bija norisçm naudas tirgos. Augstâ latu likviditâtenovembrî veicinâja latu procentu likmju kritumu un starpîbas samazinâjumu starp

25

4 · 2006

eiro un latu procentu likmçm. Novembra beigâs lata kurss attiecîbâ pret eiro sa-mazinâjâs, un atseviðíos periodos banku individuâlâs kursa kotâcijas starpbankuvalûtas tirgû attâlinâjâs no Latvijas Bankas noteiktâ eiro pirkðanas kursa (1 EUR =Ls 0.6958) pat par 35 punktiem. Pakâpeniski lata kurss attiecîbâ pret eiro palieli-nâjâs, taèu decembra beigâs tas nebija sasniedzis septembra beigu lîmeni.

4. ceturksnî valûtas darîjumu apgrozîjums pârsniedza 420 mljrd. latu. Nozîmîgâkiedarîjuma partneri valûtu pirkðanâ un pârdoðanâ bija nerezidentu MFI (noslçgtidarîjumi par 212.1 mljrd. latu) un ne-MFI (izòemot mâjsaimniecîbas; 134.2 mljrd.latu). Darîjumu apjoma pieaugums ar nerezidentu MFI nedaudz samazinâjâs, betdarîjumos ar nerezidentu ne-MFI (izòemot mâjsaimniecîbas) tas salîdzinâjumâar iepriekðçjâ gada atbilstoðo periodu uzrâdîja stabilu kâpumu. Bûtiski un straujipieauga valûtas darîjumu apgrozîjums iekðzemes starpbanku tirgû (4. ceturksnî –58.8 mljrd. latu; 2.0 reizes vairâk nekâ iepriekðçjâ gada atbilstoðajâ periodâ). Valûtasdarîjumu apjoms ar rezidentu nefinanðu sabiedrîbâm turpinâja palielinâties, taèuto îpatsvars kopçjâ valûtas darîjumu apjomâ, tâpat kâ 2006. gadâ kopumâ, joprojâmbija mazâks par 5%.

Vçl straujâk nekâ starpbanku tirgû pieauga valûtas pirkðanas un pârdoðanas apjomsar mâjsaimniecîbâm veiktajos darîjumos. 2006. gadâ ðo darîjumu gada pieaugumspârsniedza divas reizes, un 4. ceturksnî to apjoms bija 5.5 mljrd. latu. Lai arî armâjsaimniecîbâm veikto valûtas maiòas darîjumu apjoms jau ilgstoði palielinâjâs(ðî tendence ir kopð 2004. gada), 2006. gadâ notika ïoti straujð ar mâjsaimniecîbâmveikto valûtas darîjumu apjoma pieaugums, kuru noteica joprojâm straujais ârvalstuvalûtâs izsniegto kredîtu atlikuma kâpums. Ar mâjsaimniecîbâm veiktajos valûtasmaiòas darîjumos nozîmîgs bija arî tûrisma nozares attîstîbas un daudzo Rîgânotikuðo starptautisko pasâkumu ieguldîjums, kâ arî Latvijas iedzîvotâju ârvalstîsgûto darba ienâkumu konvertâcija.

Valûtas darîjumu veidu dalîjumâ bûtiski pieauga valûtas mijmaiòas darîjumu ap-grozîjums (4. ceturksnî – 266.8 mljrd. latu). To ietekmçja tieði rezidentu MFI sav-starpçjo darîjumu apjoma straujais pieaugums. Lai gan mijmaiòas darîjumu kop-apjomâ darîjumi ar rezidentu MFI veido ne vairâk par 25%, to apjoms 4. ceturksnî,tâpat kâ 2006. gadâ kopumâ, katru mçnesi salîdzinâjumâ ar iepriekðçjâ gada at-bilstoðo periodu palielinâjâs vidçji 2.2 reizes. 4. ceturksnî veikto tagadnes darîjumukopapjoms (150.0 mljrd. latu) salîdzinâjumâ ar 2005. gada 4. ceturksni samazinâjâspar 5.9%.

Kopð 2005. gada jûlija valûtas maiòas darîjumos pret latiem dominç eiro. Tomçrpretstatâ 2006. gada 1. pusgadam, kad eiro îpatsvars valûtu darîjumos ar latiemkonsekventi pieauga, bet ASV dolâra îpatsvars – tikpat konsekventi samazinâjâs,2006. gada 2. pusgadâ (t.sk. 4. ceturksnî) abu valûtu relatîvâ nozîme valûtas maiòasdarîjumos pret latiem stabilizçjâs. 4. ceturksnî eiro îpatsvars visos valûtas maiòasdarîjumos pret latiem svârstîjâs ap 60%, savukârt ASV dolâra îpatsvars bija aptu-veni 37%.

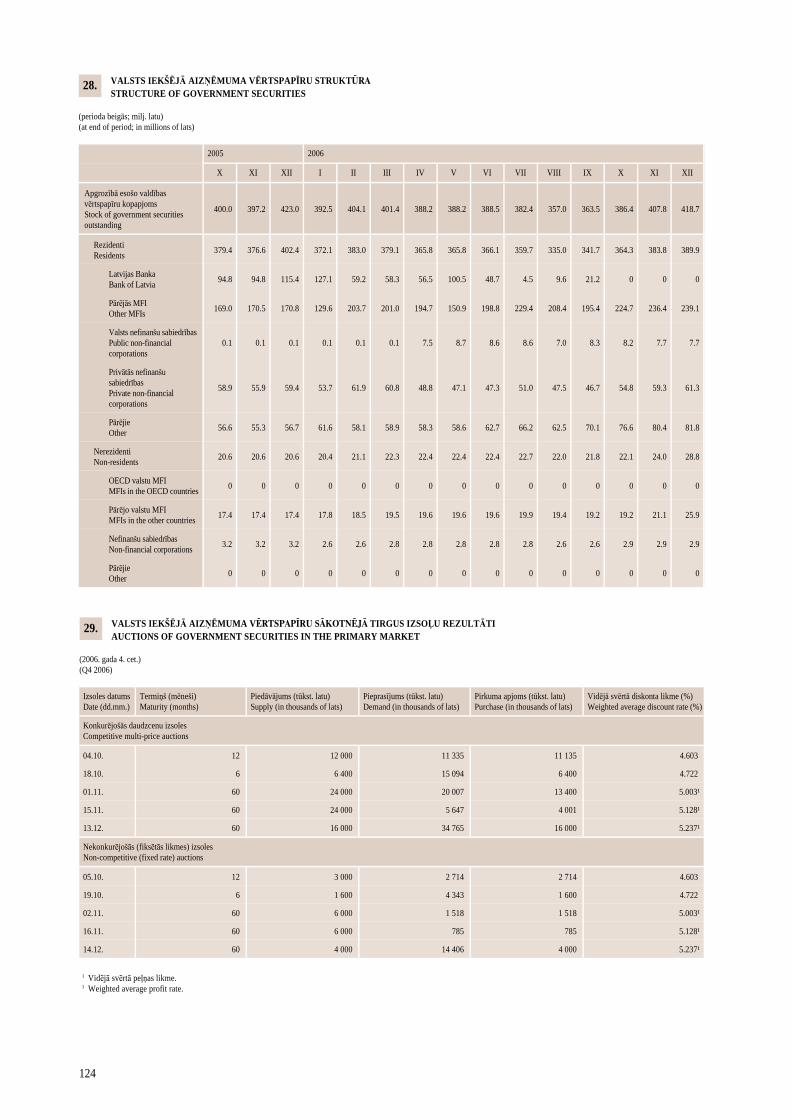

Sâkotnçjâ tirgû 4. ceturksnî notika valsts iekðçjâ aizòçmuma 6 un 12 mçneðu pa-râdzîmju un 5 gadu obligâciju izsole. Tâ kâ Valsts kasei bija lieli lîdzekïu uzkrâjumi,tâ no decembrî plânotajâm divâm valsts iekðçjâ aizòçmuma vçrtspapîru (tâlâk tek-stâ – valdîbas vçrtspapîri) izsolçm rîkoja tikai vienu. Valdîbas vçrtspapîru kopçjaispiedâvâjums bija 103.0 milj. latu (2.9 reizes lielâks nekâ iepriekðçjâ ceturksnî).Piedâvâjuma pieaugumu noteica nepiecieðamîba finansçt valdîbas izdevumu kâ-pumu. Savukârt pieprasîjums bija 110.6 milj. latu, bet pârdotais apjoms – 61.6 milj.latu (attiecîgi 9.8 un 26.3 reizes vairâk nekâ iepriekðçjâ ceturksnî). Arî vçrtspapîrupârdotâ apjoma attiecîba pret piedâvâjumu 4. ceturksnî bija augstâka, jo izsolçspalielinâjâs procentu likmes. Salîdzinâjumâ ar iepriekðçjâm izsolçm 6 mçneðu pa-

26

MONETÂRAIS APSKATS · MONETARY REVIEW

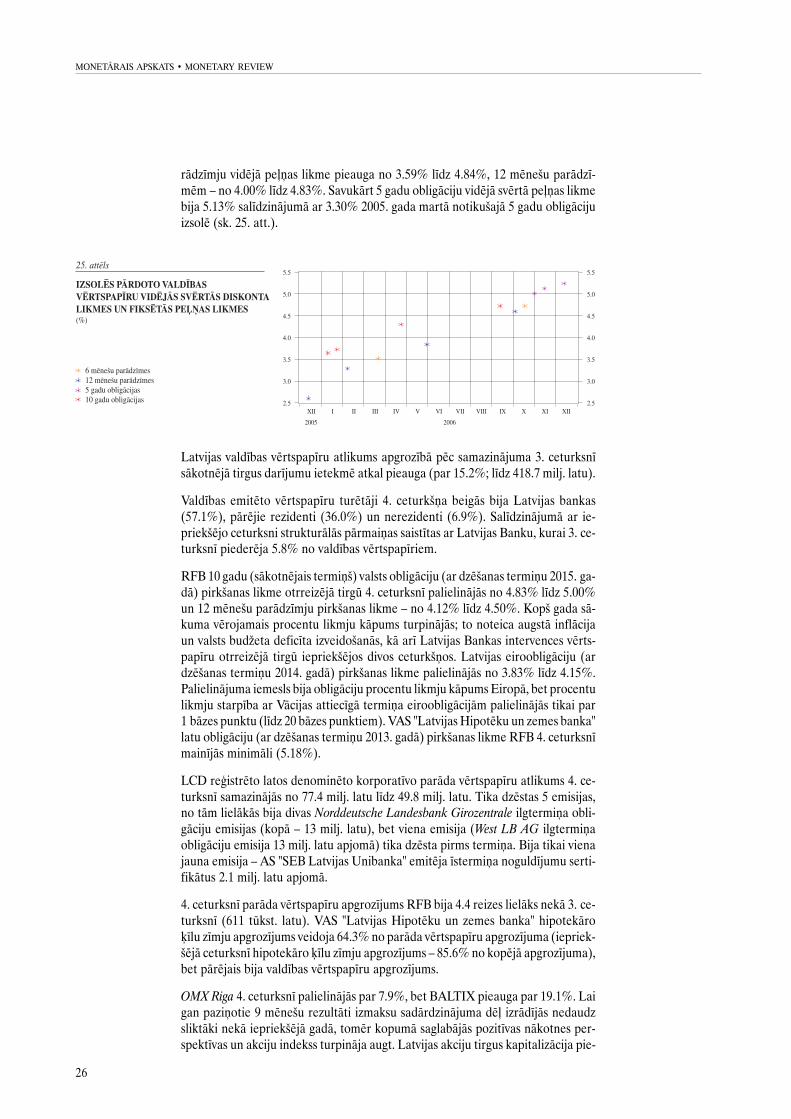

râdzîmju vidçjâ peïòas likme pieauga no 3.59% lîdz 4.84%, 12 mçneðu parâdzî-mçm – no 4.00% lîdz 4.83%. Savukârt 5 gadu obligâciju vidçjâ svçrtâ peïòas likmebija 5.13% salîdzinâjumâ ar 3.30% 2005. gada martâ notikuðajâ 5 gadu obligâcijuizsolç (sk. 25. att.).

Latvijas valdîbas vçrtspapîru atlikums apgrozîbâ pçc samazinâjuma 3. ceturksnîsâkotnçjâ tirgus darîjumu ietekmç atkal pieauga (par 15.2%; lîdz 418.7 milj. latu).

Valdîbas emitçto vçrtspapîru turçtâji 4. ceturkðòa beigâs bija Latvijas bankas(57.1%), pârçjie rezidenti (36.0%) un nerezidenti (6.9%). Salîdzinâjumâ ar ie-priekðçjo ceturksni strukturâlâs pârmaiòas saistîtas ar Latvijas Banku, kurai 3. ce-turksnî piederçja 5.8% no valdîbas vçrtspapîriem.

RFB 10 gadu (sâkotnçjais termiòð) valsts obligâciju (ar dzçðanas termiòu 2015. ga-dâ) pirkðanas likme otrreizçjâ tirgû 4. ceturksnî palielinâjâs no 4.83% lîdz 5.00%un 12 mçneðu parâdzîmju pirkðanas likme – no 4.12% lîdz 4.50%. Kopð gada sâ-kuma vçrojamais procentu likmju kâpums turpinâjâs; to noteica augstâ inflâcijaun valsts budþeta deficîta izveidoðanâs, kâ arî Latvijas Bankas intervences vçrts-papîru otrreizçjâ tirgû iepriekðçjos divos ceturkðòos. Latvijas eiroobligâciju (ardzçðanas termiòu 2014. gadâ) pirkðanas likme palielinâjâs no 3.83% lîdz 4.15%.Palielinâjuma iemesls bija obligâciju procentu likmju kâpums Eiropâ, bet procentulikmju starpîba ar Vâcijas attiecîgâ termiòa eiroobligâcijâm palielinâjâs tikai par1 bâzes punktu (lîdz 20 bâzes punktiem). VAS "Latvijas Hipotçku un zemes banka"latu obligâciju (ar dzçðanas termiòu 2013. gadâ) pirkðanas likme RFB 4. ceturksnîmainîjâs minimâli (5.18%).

LCD reìistrçto latos denominçto korporatîvo parâda vçrtspapîru atlikums 4. ce-turksnî samazinâjâs no 77.4 milj. latu lîdz 49.8 milj. latu. Tika dzçstas 5 emisijas,no tâm lielâkâs bija divas Norddeutsche Landesbank Girozentrale ilgtermiòa obli-gâciju emisijas (kopâ – 13 milj. latu), bet viena emisija (West LB AG ilgtermiòaobligâciju emisija 13 milj. latu apjomâ) tika dzçsta pirms termiòa. Bija tikai vienajauna emisija – AS "SEB Latvijas Unibanka" emitçja îstermiòa noguldîjumu serti-fikâtus 2.1 milj. latu apjomâ.

4. ceturksnî parâda vçrtspapîru apgrozîjums RFB bija 4.4 reizes lielâks nekâ 3. ce-turksnî (611 tûkst. latu). VAS "Latvijas Hipotçku un zemes banka" hipotekâroíîlu zîmju apgrozîjums veidoja 64.3% no parâda vçrtspapîru apgrozîjuma (iepriek-ðçjâ ceturksnî hipotekâro íîlu zîmju apgrozîjums – 85.6% no kopçjâ apgrozîjuma),bet pârçjais bija valdîbas vçrtspapîru apgrozîjums.

OMX Riga 4. ceturksnî palielinâjâs par 7.9%, bet BALTIX pieauga par 19.1%. Laigan paziòotie 9 mçneðu rezultâti izmaksu sadârdzinâjuma dçï izrâdîjâs nedaudzsliktâki nekâ iepriekðçjâ gadâ, tomçr kopumâ saglabâjâs pozitîvas nâkotnes per-spektîvas un akciju indekss turpinâja augt. Latvijas akciju tirgus kapitalizâcija pie-

27

4 · 2006

auga par 13.9% (lîdz 1 430 milj. latu). RFB apgrozîjums 4. ceturksnî bija 16.2 milj.latu (par 62.0% vairâk nekâ 3. ceturksnî). Vislielâkais apgrozîjums bija ar AS "Grin-deks" akcijâm (6.0 milj. latu). AS "Grindeks" izteica akciju atpirkðanas piedâvâjumuAS "Tallinas Farmaceitiskâ rûpnîca" mazajiem akcionâriem, kâ arî palielinâja inves-tîcijas raþoðanas attîstîbai. Bija vçrojama ârvalstu investoru interese par AS "Grin-deks" akcijâm.

5. oktobrî tika pârdotas valstij piederoðâs AS "Ventspils nafta" akcijas, piedâvâjot38.6% no kopapjoma jeb 40.3 milj. akciju un minimâlo cenu nosakot Ls 1.81 parakciju. Izolç pieprasîjums bija mazliet lielâks nekâ piedâvâjums un akcijas tikanopirktas, maksâjot Ls 1.84 par akciju. Nîderlandes naftas kompânija Vitol Group

nopirka 34% no AS "Ventspils nafta" akcijâm, apòemoties palielinât AS "Ventspilsnafta" naftas terminâïu apgrozîjumu.

MFI DARBÎBA

4. ceturkðòa beigâs Latvijas Republikâ bija reìistrçtas 64 MFI (izòemot LatvijasBanku), t.sk. 21 banka, trîs ârvalstu banku filiâles, 35 krâjaizdevu sabiedrîbas, trîselektroniskâs naudas institûcijas un divi naudas tirgus fondi.

Kopçjais apmaksâtais MFI pamatkapitâls 4. ceturkðòa beigâs bija 590.1 milj. latu(par 1.4% vairâk nekâ 3. ceturkðòa beigâs). Ârvalstu kapitâla îpatsvars apmaksâtajâpamatkapitâlâ nedaudz palielinâjâs (lîdz 68.6%).

Visi nozîmîgâkie MFI darbîbas râdîtâji salîdzinâjumâ ar 3. ceturkðòa beigâm tur-pinâja augt, t.sk. aktîvi (neieskaitot aktîvus pârvaldîðanâ) – par 11.0% (lîdz15.9 mljrd. latu), izsniegto kredîtu atlikums (ieskaitot tranzîtkredîtus) – par 13.3%(lîdz 10.8 mljrd. latu) un noguldîjumu atlikums – par 8.7% (lîdz 7.7 mljrd. latu).MFI neauditçtâ 2006. gada peïòa bija 266.9 milj. latu (1.4 reizes vairâk nekâ ie-priekðçjâ gadâ). Kapitâls un rezerves palielinâjâs par 97.6 milj. latu un 4. ceturkðòabeigâs sasniedza 1.2 mljrd. latu.

Banku pelnîtspçjas râdîtâji nedaudz pieauga. Kapitâla atdeve (ROE) 4. ceturkðòabeigâs bija 26.3% un aktîvu atdeve (ROA) – 2.1%. Kapitâla pietiekamîbas râdîtâjssamazinâjâs (lîdz 10.2%).

Galvenie banku ienâkumu avoti 4. ceturksnî joprojâm bija procentu ienâkumi none-MFI izsniegtajiem kredîtiem (50.9% no kopçjiem banku ienâkumiem) un ko-misijas naudas ienâkumi (17.8%), kâ arî procentu ienâkumi par prasîbâm pretMFI (8.8%).

Lai gan kreditçðana joprojâm strauji pieauga, kredîtu kvalitâte arî 4. ceturksnîbija augsta. Ienâkumus nenesoðo kredîtu atlikums 4. ceturkðòa beigâs, tâpat kâ3. ceturksnî, bija 0.4% no ne-MFI izsniegto kredîtu atlikuma.

Speciâlo uzkrâjumu ne-MFI izsniegtajiem kredîtiem attiecîba pret ne-MFI iz-sniegto kredîtu atlikumu salîdzinâjumâ ar iepriekðçjo ceturksni nemainîjâs (0.5%).Speciâlie uzkrâjumi ne-MFI izsniegtajiem kredîtiem 4. ceturkðòa beigâs sedza116.6% ienâkumus nenesoðo kredîtu atlikuma.

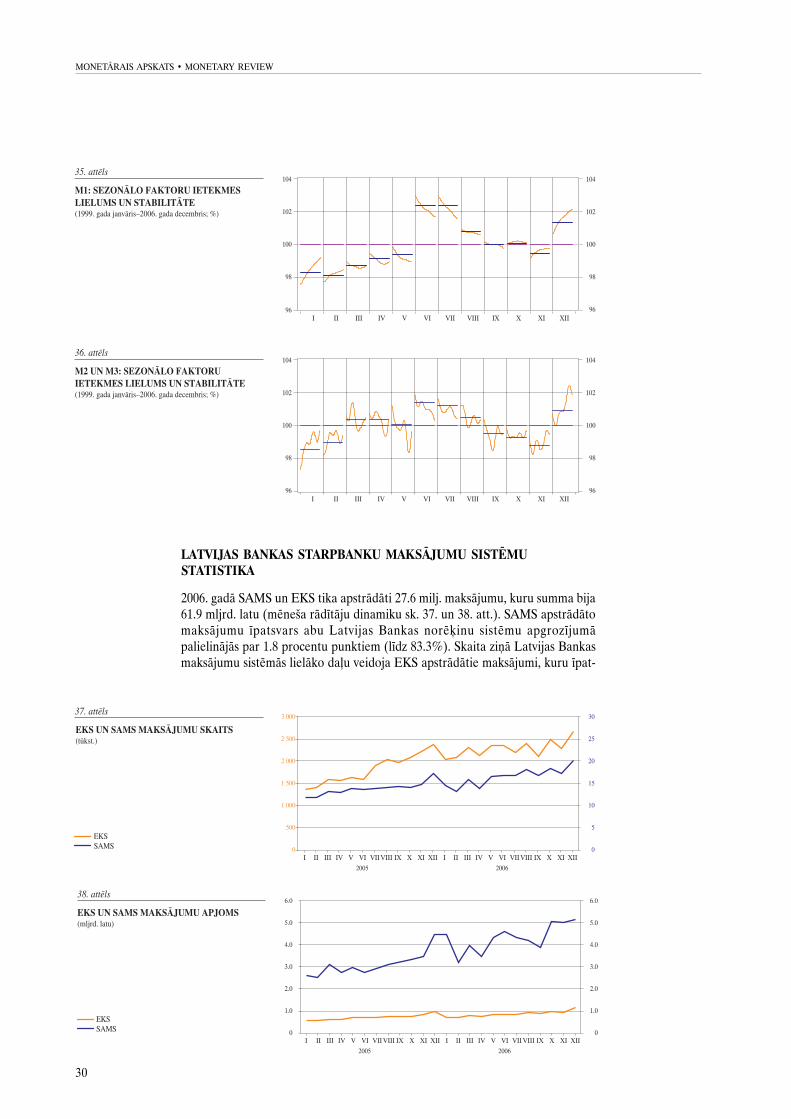

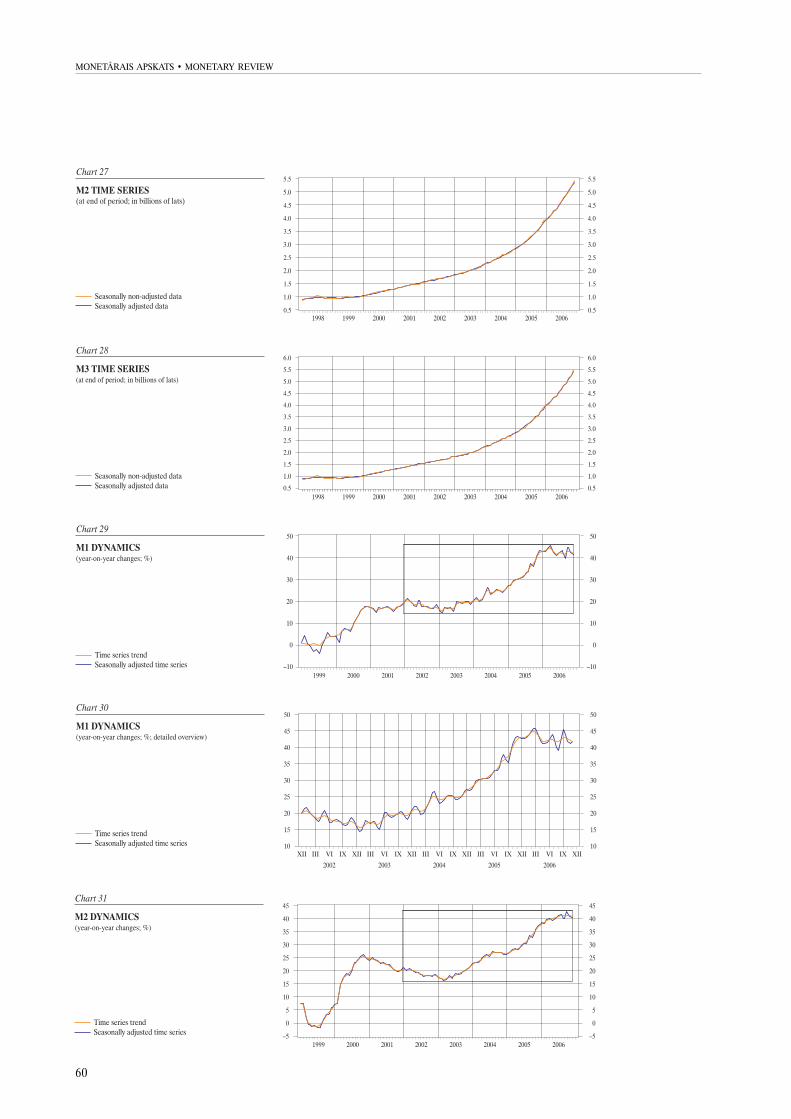

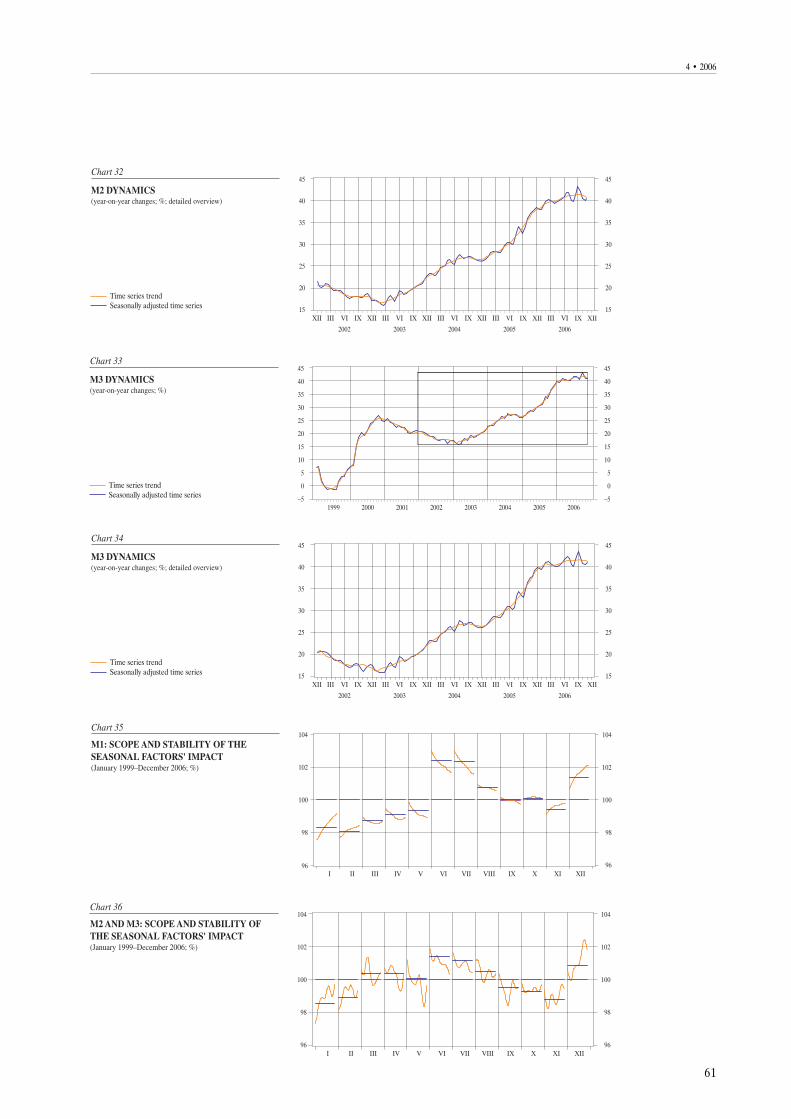

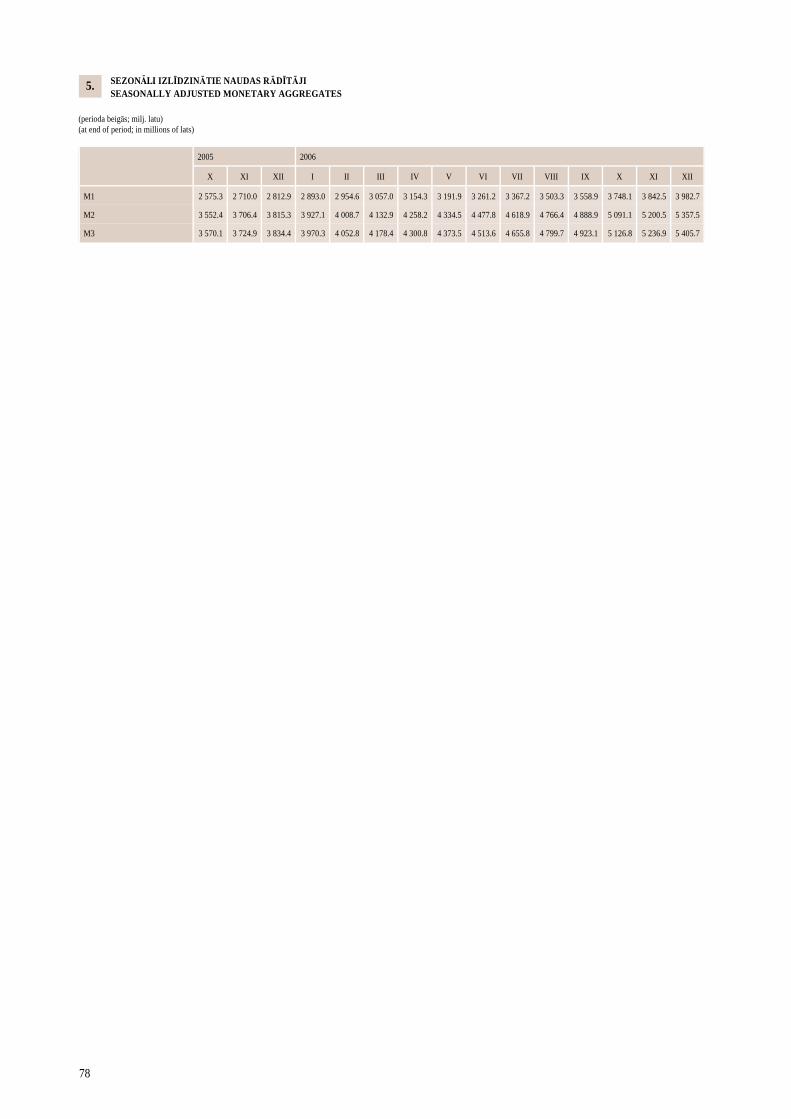

NAUDAS RÂDÎTÂJU SEZONÂLÂ IZLÎDZINÂÐANA

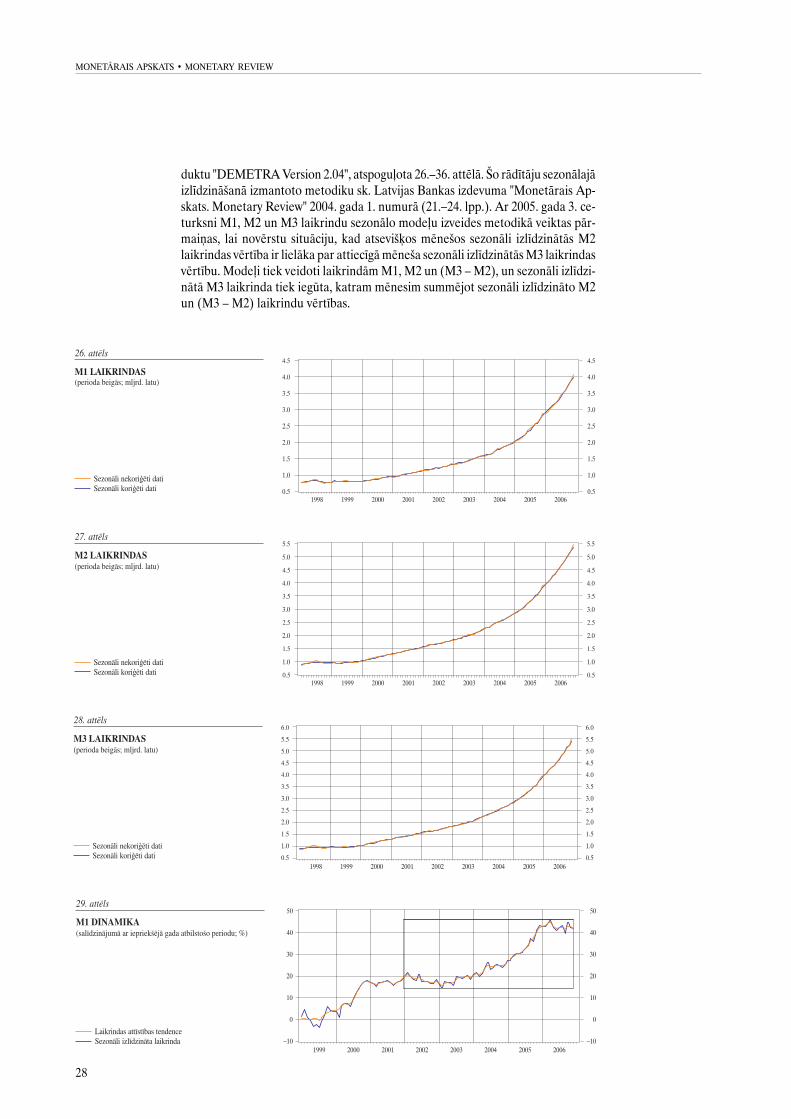

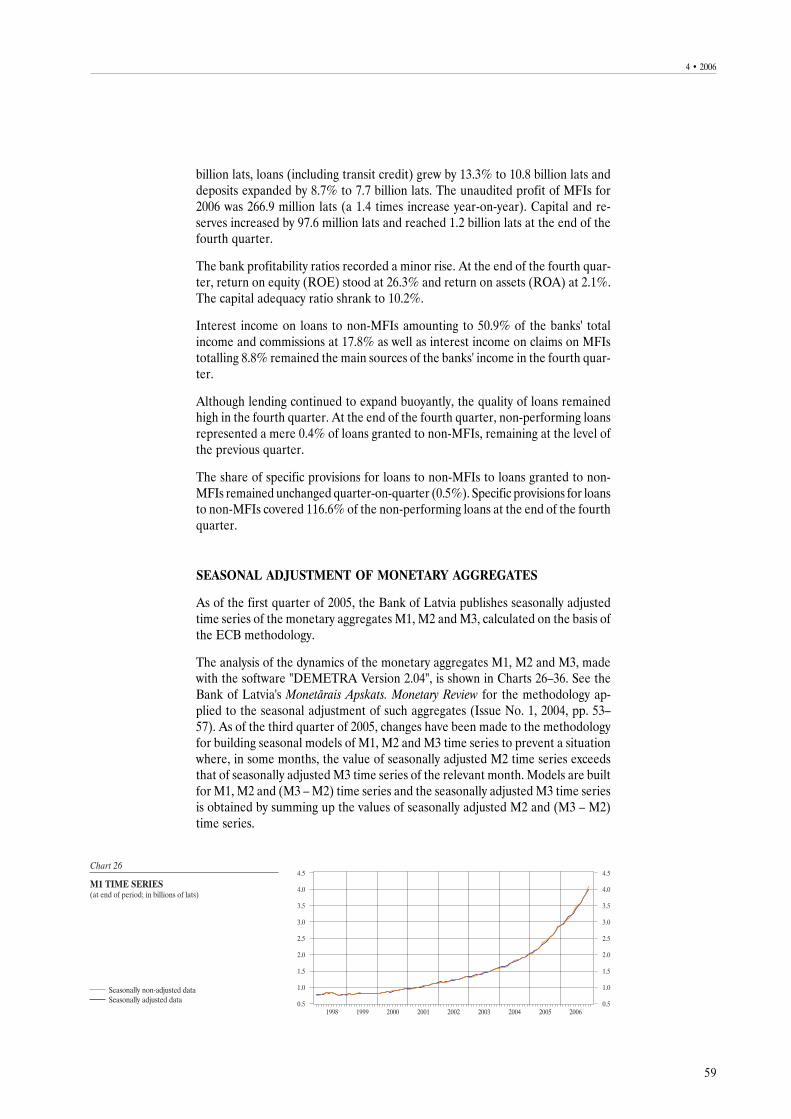

Latvijas Banka ar 2005. gada 1. ceturksni publicç atbilstoði ECB metodoloìijaiaprçíinâto monetâro râdîtâju M1, M2 un M3 sezonâli izlîdzinâtâs laikrindas.

Monetâro râdîtâju M1, M2 un M3 dinamikas analîze, kas veikta ar programmpro-

28

MONETÂRAIS APSKATS · MONETARY REVIEW

duktu "DEMETRA Version 2.04", atspoguïota 26.–36. attçlâ. Ðo râdîtâju sezonâlajâizlîdzinâðanâ izmantoto metodiku sk. Latvijas Bankas izdevuma "Monetârais Ap-skats. Monetary Review" 2004. gada 1. numurâ (21.–24. lpp.). Ar 2005. gada 3. ce-turksni M1, M2 un M3 laikrindu sezonâlo modeïu izveides metodikâ veiktas pâr-maiòas, lai novçrstu situâciju, kad atseviðíos mçneðos sezonâli izlîdzinâtâs M2laikrindas vçrtîba ir lielâka par attiecîgâ mçneða sezonâli izlîdzinâtâs M3 laikrindasvçrtîbu. Modeïi tiek veidoti laikrindâm M1, M2 un (M3 – M2), un sezonâli izlîdzi-nâtâ M3 laikrinda tiek iegûta, katram mçnesim summçjot sezonâli izlîdzinâto M2un (M3 – M2) laikrindu vçrtîbas.

29

4 · 2006

30

MONETÂRAIS APSKATS · MONETARY REVIEW

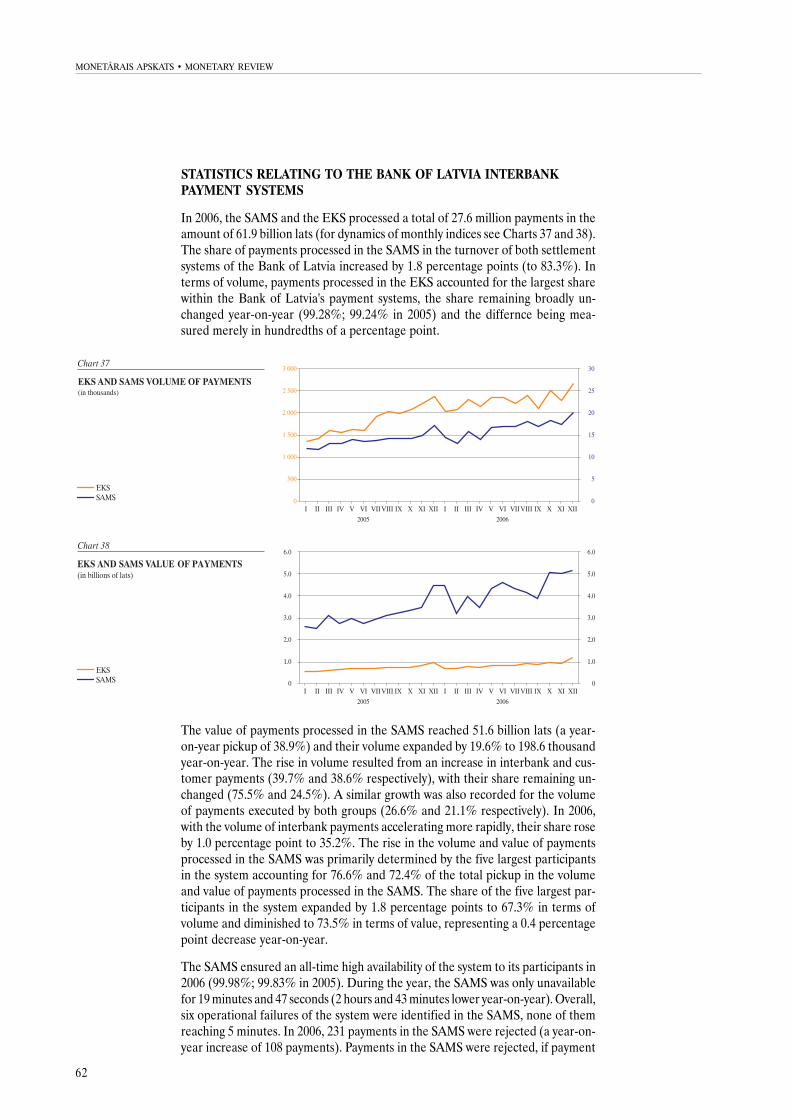

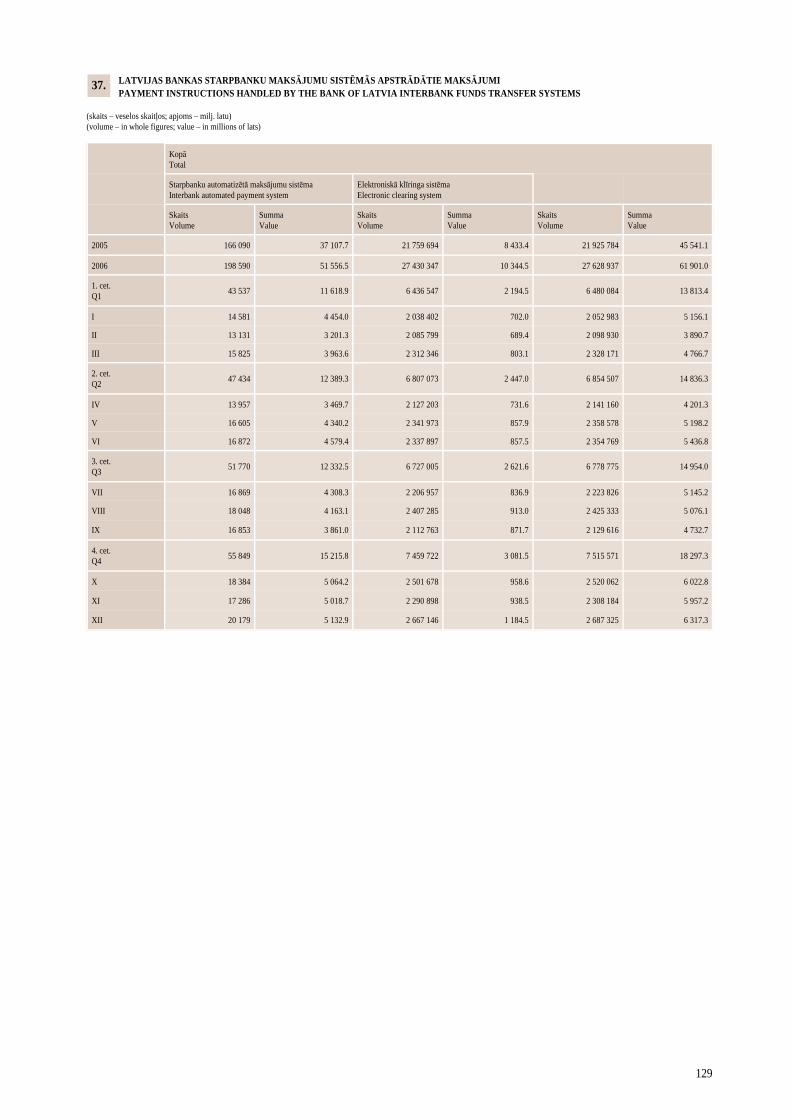

LATVIJAS BANKAS STARPBANKU MAKSÂJUMU SISTÇMUSTATISTIKA

2006. gadâ SAMS un EKS tika apstrâdâti 27.6 milj. maksâjumu, kuru summa bija61.9 mljrd. latu (mçneða râdîtâju dinamiku sk. 37. un 38. att.). SAMS apstrâdâtomaksâjumu îpatsvars abu Latvijas Bankas norçíinu sistçmu apgrozîjumâpalielinâjâs par 1.8 procentu punktiem (lîdz 83.3%). Skaita ziòâ Latvijas Bankasmaksâjumu sistçmâs lielâko daïu veidoja EKS apstrâdâtie maksâjumi, kuru îpat-

31

4 · 2006

svars salîdzinâjumâ ar iepriekðçjo gadu saglabâjâs gandrîz nemainîgs un atðíîrâstikai procentu punktu simtdaïâs (99.28%; 2005. gadâ – 99.24%).

SAMS apstrâdâto maksâjumu apjoms sasniedza 51.6 mljrd. latu (par 38.9% vairâknekâ 2005. gadâ), bet apstrâdâto maksâjumu skaits salîdzinâjumâ ar 2005. gadupieauga par 19.6% (lîdz 198.6 tûkst.). Apjoma kâpumu noteica gan starpbanku,gan klientu maksâjumu pieaugums (attiecîgi 39.7% un 38.6%), tâdçjâdi saglabâjotlîdzðinçjo îpatsvaru – 75.5% un 24.5%. Lîdzîgi pieauga arî ðo abu grupu maksâjumuskaits (attiecîgi par 26.6% un 21.1%). 2006. gadâ, straujâk palielinoties starpbankumaksâjumu skaitam, to îpatsvars pieauga par 1 procentu punktu (lîdz 35.2%).SAMS kâpumu galvenokârt noteica pieci lielâkie sistçmas dalîbnieki, kuri veidojaattiecîgi 76.6% un 72.4% no kopçjâ SAMS apstrâdâto maksâjumu skaita un apjomapieauguma. Ðo piecu lielâko sistçmas dalîbnieku îpatsvars sistçmâ skaita ziòâ pa-lielinâjâs par 1.8 procentu punktiem (lîdz 67.3%), bet apjoma ziòâ samazinâjâslîdz 73.5% (par 0.4 procentu punktiem mazâk nekâ 2005. gadâ).

2006. gadâ SAMS tâs dalîbniekiem nodroðinâja lîdz ðim augstâko sistçmas pieeja-mîbu tâs pastâvçðanas laikâ (99.98%; 2005. gadâ – 99.83%). Gada laikâ SAMSnebija pieejama tikai 19 minûtes un 47 sekundes (par 2 stundâm un 43 minûtçmmazâk nekâ 2005. gadâ). Kopumâ SAMS konstatçti 6 sistçmas darbîbas pârtrau-kumi, bet neviens no tiem nesasniedza 5 minûðu robeþu. 2006. gadâ SAMS tikanoraidîts 231 maksâjums (par 108 maksâjumiem vairâk nekâ 2005. gadâ). Maksâ-jumi SAMS tika noraidîti, ja maksâjuma rîkojumi nebija sagatavoti saskaòâ ar"Latvijas Bankas starpbanku norçíinu veikðanas noteikumiem" un SAMS funk-cionâlajâ aprakstâ noteikto kârtîbu.

2006. gadâ EKS tika apstrâdâti 27.4 milj. maksâjumu 10.3 mljrd. latu apjomâ (at-tiecîgi par 26.1% un 22.7% vairâk nekâ 2005. gadâ). 2006. gadâ bija vçrojamspakâpenisks EKS apstrâdâto maksâjumu skaita pieaugums (gada sâkumâ – 2 milj.mçnesî, decembrî – vairâk nekâ 2.6 milj.). Decembrî tika sasniegts lîdz ðim lielâkaisapstrâdâto maksâjumu apjoms – 1.18 mljrd. latu.

EKS maksâjumu skaita kâpumu galvenokârt noteica pirmajâ klîringa ciklâ ap-strâdâto maksâjumu skaita palielinâðanâs (par 29.5%). Otrajâ klîringa ciklâ ap-strâdâto maksâjumu skaits pieauga mazâk (par 19.5%). Tâdçjâdi otrâ klîringa ciklamaksâjumu skaita îpatsvars samazinâjâs lîdz 32.5% (2005. gadâ – 34.3%). TurpretîEKS otrâ klîringa cikla îpatsvars apjoma ziòâ palielinâjâs lîdz 41.2% (par 2.7 pro-centu punktiem vairâk nekâ 2005. gadâ). To noteica otrâ klîringa cikla maksâjumuapjoma kâpums par 31.3%, pirmâ klîringa cikla maksâjumu apjomam tajâ paðâlaikâ pieaugot par 17.2%.

KREDÎTIESTÂÞU MAKSÂJUMU STATISTIKA

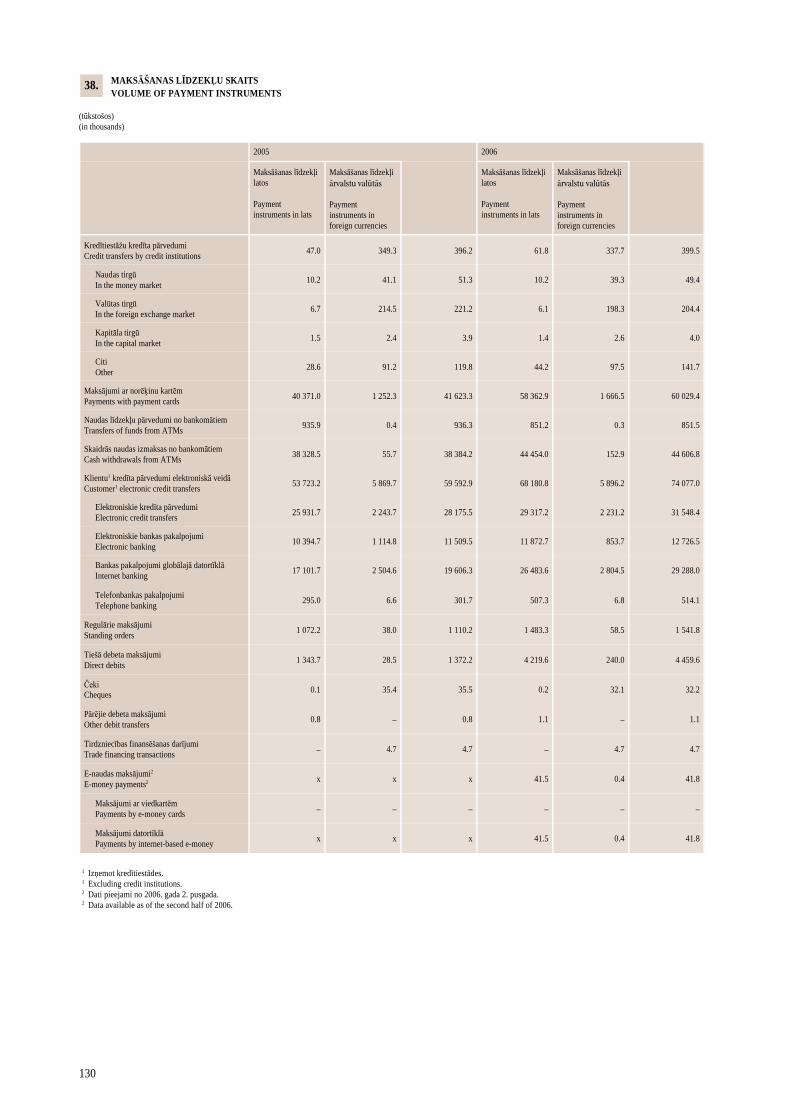

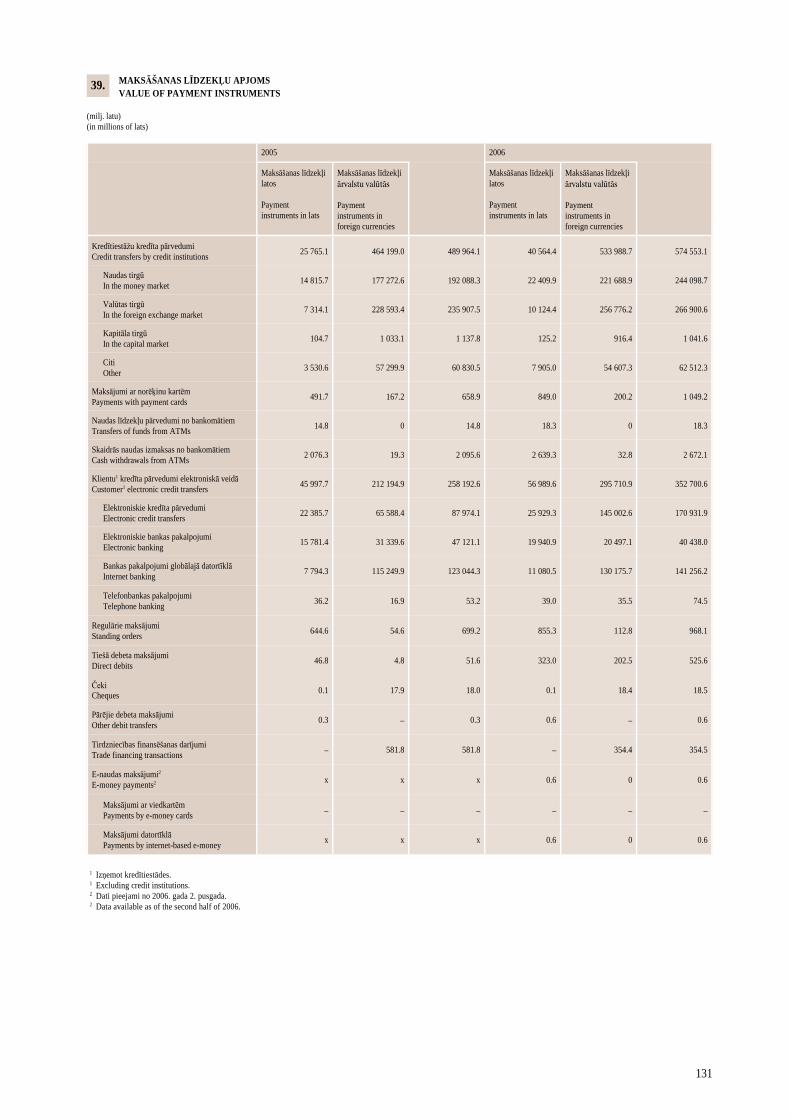

Maksâðanas lîdzekïi

Latvijas kredîtiestâþu kredîta pârvedumu skaits 2006. gadâ salîdzinâjumâ ar ie-priekðçjo gadu pieauga par 0.8% (lîdz 399.5 tûkst.), bet apjoms – par 17.3% (lîdz574.6 mljrd. latu). Pieaugumu veicinâja pârvedumu apjoma kâpums naudas unvalûtas tirgos attiecîgi par 27.1% (52.0 mljrd. latu) un 13.1% (31.0 mljrd. latu).Kredîtiestâþu kredîta pârvedumos skaita ziòâ dominçja pârvedumi valûtas tirgû(51.2%), bet apjoma ziòâ – pârvedumi valûtas un naudas tirgos (attiecîgi 46.5%un 42.5%). Lielâkâ daïa kredîta pârvedumu gan skaita, gan apjoma ziòâ bija âr-valstu valûtâs veiktie kredîtiestâþu kredîta pârvedumi (attiecîgi 84.5% un 92.9%).

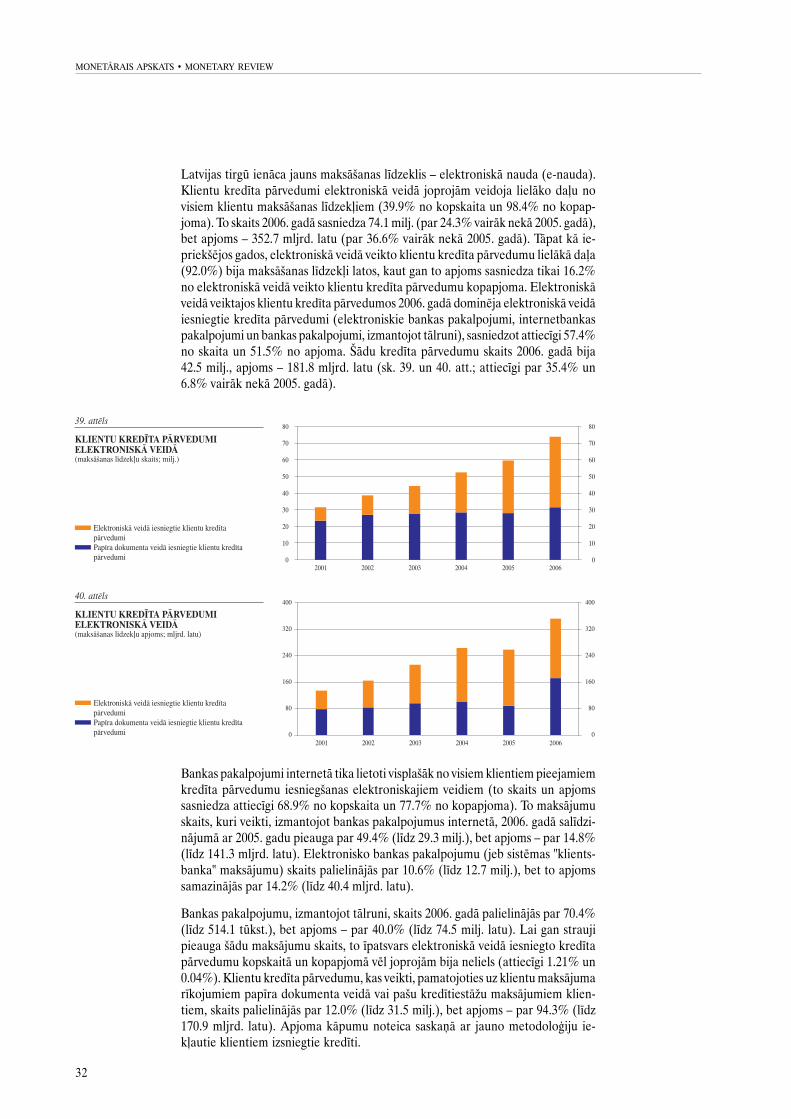

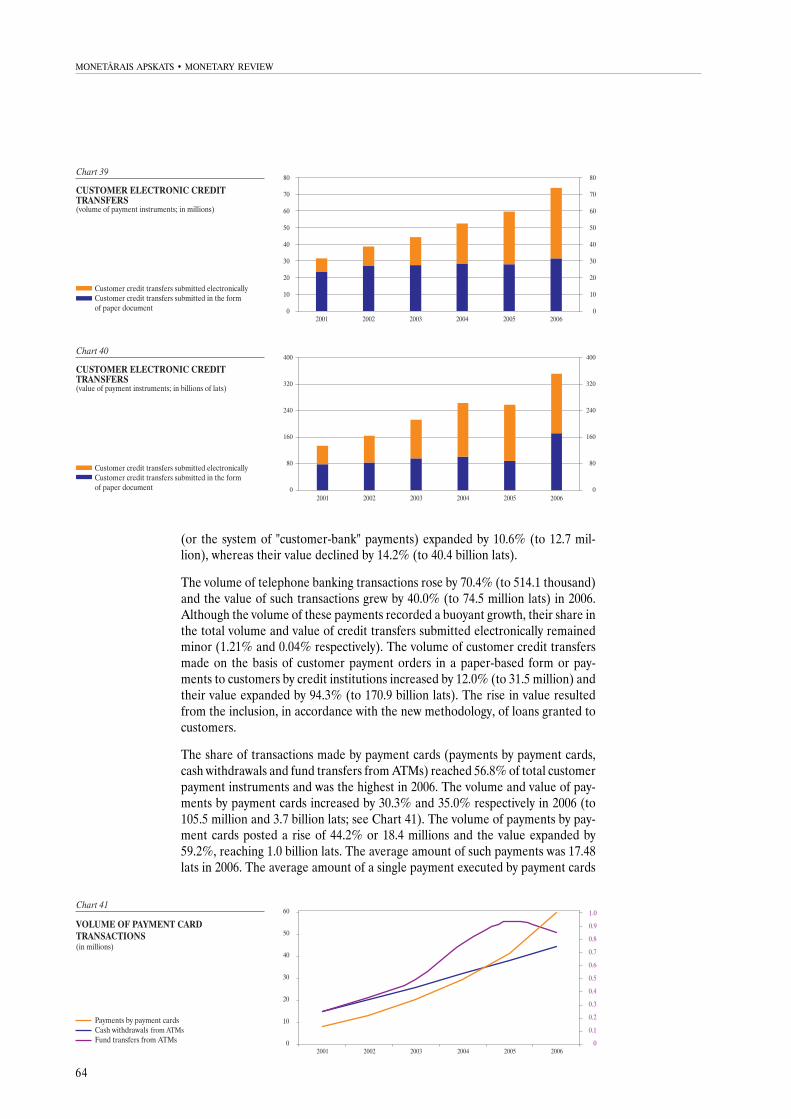

2006. gada 2. pusgadâ papildu ierastajiem klientu maksâðanas lîdzekïiem (kredîtapârvedumiem, maksâjumiem ar norçíinu kartçm, tieðâ debeta maksâjumiem u.c.)

32

MONETÂRAIS APSKATS · MONETARY REVIEW

Latvijas tirgû ienâca jauns maksâðanas lîdzeklis – elektroniskâ nauda (e-nauda).Klientu kredîta pârvedumi elektroniskâ veidâ joprojâm veidoja lielâko daïu novisiem klientu maksâðanas lîdzekïiem (39.9% no kopskaita un 98.4% no kopap-joma). To skaits 2006. gadâ sasniedza 74.1 milj. (par 24.3% vairâk nekâ 2005. gadâ),bet apjoms – 352.7 mljrd. latu (par 36.6% vairâk nekâ 2005. gadâ). Tâpat kâ ie-priekðçjos gados, elektroniskâ veidâ veikto klientu kredîta pârvedumu lielâkâ daïa(92.0%) bija maksâðanas lîdzekïi latos, kaut gan to apjoms sasniedza tikai 16.2%no elektroniskâ veidâ veikto klientu kredîta pârvedumu kopapjoma. Elektroniskâveidâ veiktajos klientu kredîta pârvedumos 2006. gadâ dominçja elektroniskâ veidâiesniegtie kredîta pârvedumi (elektroniskie bankas pakalpojumi, internetbankaspakalpojumi un bankas pakalpojumi, izmantojot tâlruni), sasniedzot attiecîgi 57.4%no skaita un 51.5% no apjoma. Ðâdu kredîta pârvedumu skaits 2006. gadâ bija42.5 milj., apjoms – 181.8 mljrd. latu (sk. 39. un 40. att.; attiecîgi par 35.4% un6.8% vairâk nekâ 2005. gadâ).

Bankas pakalpojumi internetâ tika lietoti visplaðâk no visiem klientiem pieejamiemkredîta pârvedumu iesniegðanas elektroniskajiem veidiem (to skaits un apjomssasniedza attiecîgi 68.9% no kopskaita un 77.7% no kopapjoma). To maksâjumuskaits, kuri veikti, izmantojot bankas pakalpojumus internetâ, 2006. gadâ salîdzi-nâjumâ ar 2005. gadu pieauga par 49.4% (lîdz 29.3 milj.), bet apjoms – par 14.8%(lîdz 141.3 mljrd. latu). Elektronisko bankas pakalpojumu (jeb sistçmas "klients-banka" maksâjumu) skaits palielinâjâs par 10.6% (lîdz 12.7 milj.), bet to apjomssamazinâjâs par 14.2% (lîdz 40.4 mljrd. latu).

Bankas pakalpojumu, izmantojot tâlruni, skaits 2006. gadâ palielinâjâs par 70.4%(lîdz 514.1 tûkst.), bet apjoms – par 40.0% (lîdz 74.5 milj. latu). Lai gan straujipieauga ðâdu maksâjumu skaits, to îpatsvars elektroniskâ veidâ iesniegto kredîtapârvedumu kopskaitâ un kopapjomâ vçl joprojâm bija neliels (attiecîgi 1.21% un0.04%). Klientu kredîta pârvedumu, kas veikti, pamatojoties uz klientu maksâjumarîkojumiem papîra dokumenta veidâ vai paðu kredîtiestâþu maksâjumiem klien-tiem, skaits palielinâjâs par 12.0% (lîdz 31.5 milj.), bet apjoms – par 94.3% (lîdz170.9 mljrd. latu). Apjoma kâpumu noteica saskaòâ ar jauno metodoloìiju ie-kïautie klientiem izsniegtie kredîti.

33

4 · 2006

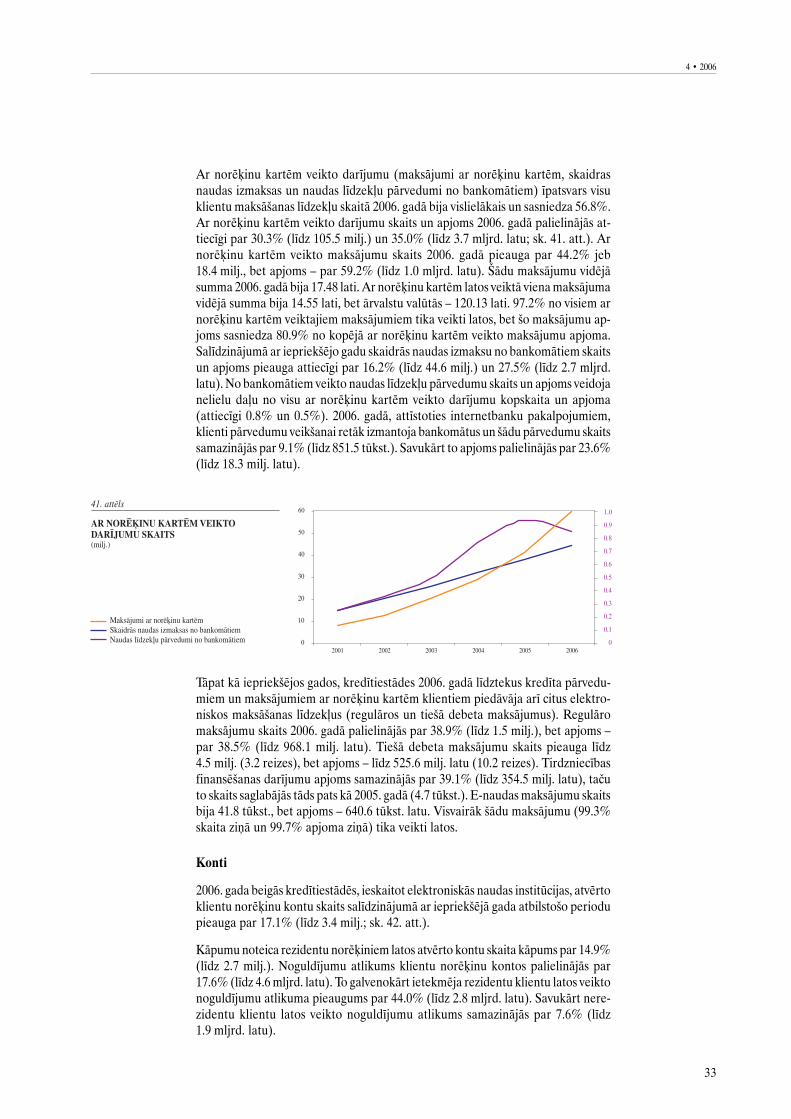

Ar norçíinu kartçm veikto darîjumu (maksâjumi ar norçíinu kartçm, skaidrasnaudas izmaksas un naudas lîdzekïu pârvedumi no bankomâtiem) îpatsvars visuklientu maksâðanas lîdzekïu skaitâ 2006. gadâ bija vislielâkais un sasniedza 56.8%.Ar norçíinu kartçm veikto darîjumu skaits un apjoms 2006. gadâ palielinâjâs at-tiecîgi par 30.3% (lîdz 105.5 milj.) un 35.0% (lîdz 3.7 mljrd. latu; sk. 41. att.). Arnorçíinu kartçm veikto maksâjumu skaits 2006. gadâ pieauga par 44.2% jeb18.4 milj., bet apjoms – par 59.2% (lîdz 1.0 mljrd. latu). Ðâdu maksâjumu vidçjâsumma 2006. gadâ bija 17.48 lati. Ar norçíinu kartçm latos veiktâ viena maksâjumavidçjâ summa bija 14.55 lati, bet ârvalstu valûtâs – 120.13 lati. 97.2% no visiem arnorçíinu kartçm veiktajiem maksâjumiem tika veikti latos, bet ðo maksâjumu ap-joms sasniedza 80.9% no kopçjâ ar norçíinu kartçm veikto maksâjumu apjoma.Salîdzinâjumâ ar iepriekðçjo gadu skaidrâs naudas izmaksu no bankomâtiem skaitsun apjoms pieauga attiecîgi par 16.2% (lîdz 44.6 milj.) un 27.5% (lîdz 2.7 mljrd.latu). No bankomâtiem veikto naudas lîdzekïu pârvedumu skaits un apjoms veidojanelielu daïu no visu ar norçíinu kartçm veikto darîjumu kopskaita un apjoma(attiecîgi 0.8% un 0.5%). 2006. gadâ, attîstoties internetbanku pakalpojumiem,klienti pârvedumu veikðanai retâk izmantoja bankomâtus un ðâdu pârvedumu skaitssamazinâjâs par 9.1% (lîdz 851.5 tûkst.). Savukârt to apjoms palielinâjâs par 23.6%(lîdz 18.3 milj. latu).