Embed Size (px)

Citation preview

Mobilephones,Internet,informa3on,andknowledge:Myanmar2016

PresentedbyHelaniGalpayaResearchTeam:HelaniGalpaya,Ayesha

Zainudeen,SuthaharanPerumpalam,GayaniHurulle,HtaikeHtaikeAung,PhyuPhyuThi

ThisworkwascarriedoutwiththeaidofagrantfromtheInternaAonalDevelopmentResearchCentre,CanadaandtheDepartmentforInternaAonalDevelopmentUK..

1

AboutLIRNEasia

• Ourmission:– “Catalyzingpolicychangethroughresearchtoimprovepeople’slivesintheemergingAsiaPacificbyfacilita<ngtheiruseofhardandso>infrastructuresthroughtheuseofknowledge,informa<onandtechnology.“

2

Countriesthatweengagewith

3

MIDO

• www.myanmarido.org• Myanmar-basednon-governmentalorganizaAon,focusingonInformaAonandCommunicaAonTechnologyforDevelopment(ICT4D)andInternetPolicy.

• Vision:tonarrowthedigitaldividebetweenruralandurbanMyanmar,withtheapplicaAonofICTinsocioeconomicsectorswiththeaimofreducingpovertyandpromoAnginclusiveness.

• Headedbyaboardofdirectors,MIDOhasfull-Ameandpart-Amestaff,aswellasvolunteers.

• ConductsnaAonwidecapacitybuildinginICTsandengagesinresearchwiththeaimofstrengtheningthecoredevelopmentgoalsofMyanmar.

4

ThirdEye–contractedforfieldresearch

• Myanmarbasedmarketresearchfirm(selectedthroughacompeAAveprocurementprocess)– Carriedoutfieldwork(includingpilottesAngofquesAonnaire)

• CreatedinOctober2013asajointventurebetweenDecisionSupportService(DSS)andaninternaAonalinvestorgroupwithextensivemarkeAngandresearchbackground.

• Withitsrootsinsocialresearch,ThirdEyehasnowexpandedintotheconsumerarena.

• Experiencedinawiderangeofservicesincludingmarketresearch,social,economic,andpovertystudies.

• AlsoprovideanalyAcalsupportforthedatathattheycollect.

5

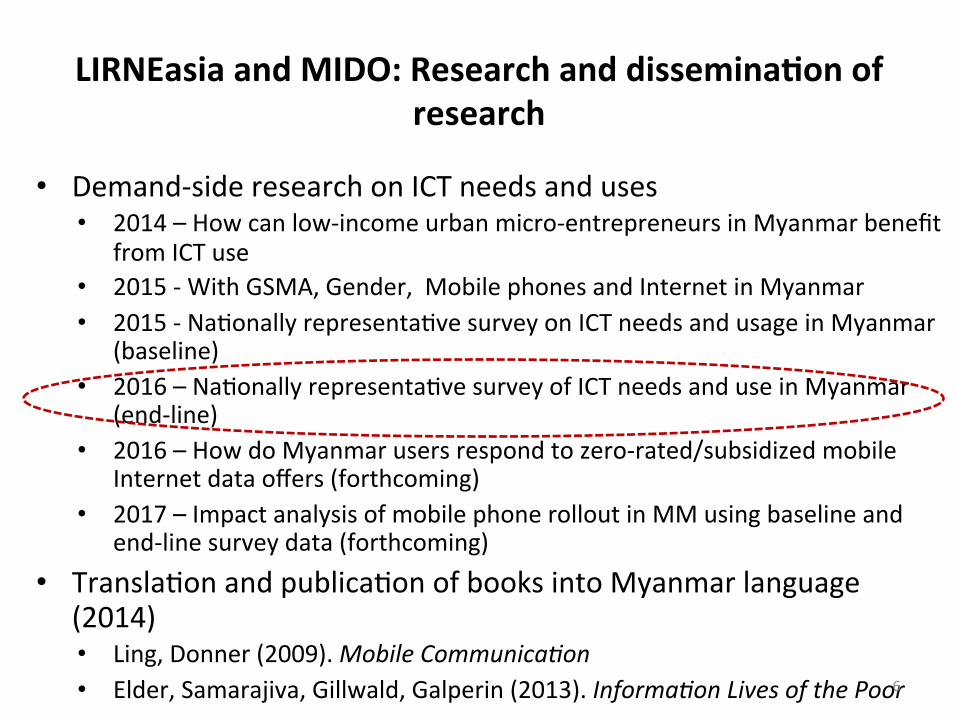

LIRNEasiaandMIDO:Researchanddissemina3onofresearch

• Demand-sideresearchonICTneedsanduses• 2014–Howcanlow-incomeurbanmicro-entrepreneursinMyanmarbenefit

fromICTuse• 2015-WithGSMA,Gender,MobilephonesandInternetinMyanmar• 2015-NaAonallyrepresentaAvesurveyonICTneedsandusageinMyanmar

(baseline)• 2016–NaAonallyrepresentaAvesurveyofICTneedsanduseinMyanmar

(end-line)• 2016–HowdoMyanmarusersrespondtozero-rated/subsidizedmobile

Internetdataoffers(forthcoming)• 2017–ImpactanalysisofmobilephonerolloutinMMusingbaselineand

end-linesurveydata(forthcoming)• TranslaAonandpublicaAonofbooksintoMyanmarlanguage

(2014)• Ling,Donner(2009).MobileCommunica<on• Elder,Samarajiva,Gillwald,Galperin(2013).Informa<onLivesofthePoor6

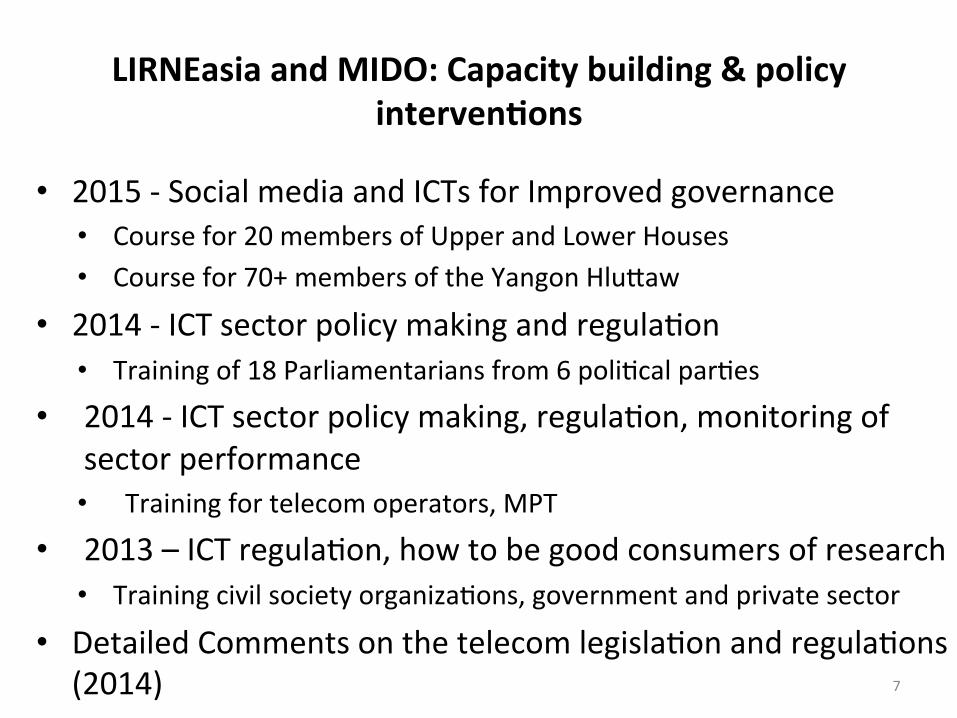

LIRNEasiaandMIDO:Capacitybuilding&policyinterven3ons

• 2015-SocialmediaandICTsforImprovedgovernance• Coursefor20membersofUpperandLowerHouses• Coursefor70+membersoftheYangonHlufaw

• 2014-ICTsectorpolicymakingandregulaAon• Trainingof18Parliamentariansfrom6poliAcalparAes

• 2014-ICTsectorpolicymaking,regulaAon,monitoringofsectorperformance• Trainingfortelecomoperators,MPT

• 2013–ICTregulaAon,howtobegoodconsumersofresearch• TrainingcivilsocietyorganizaAons,governmentandprivatesector

• DetailedCommentsonthetelecomlegislaAonandregulaAons(2014)

7

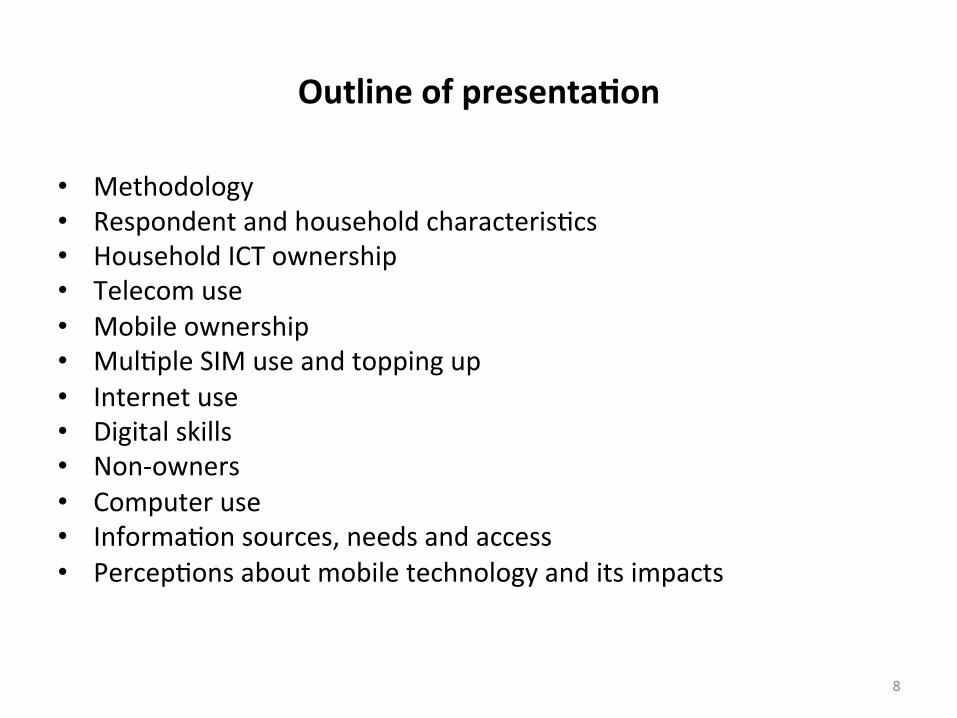

Outlineofpresenta3on

• Methodology• RespondentandhouseholdcharacterisAcs• HouseholdICTownership• Telecomuse• Mobileownership• MulApleSIMuseandtoppingup• Internetuse• Digitalskills• Non-owners• Computeruse• InformaAonsources,needsandaccess• PercepAonsaboutmobiletechnologyanditsimpacts

8

METHODOLOGY

9

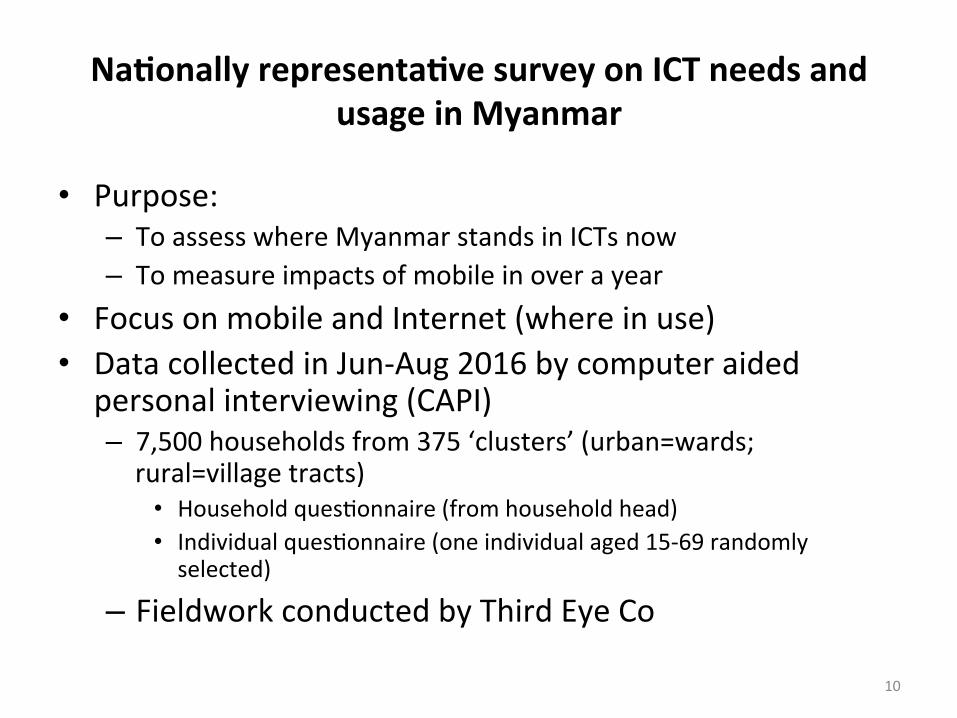

Na3onallyrepresenta3vesurveyonICTneedsandusageinMyanmar

• Purpose:– ToassesswhereMyanmarstandsinICTsnow– Tomeasureimpactsofmobileinoverayear

• FocusonmobileandInternet(whereinuse)• DatacollectedinJun-Aug2016bycomputeraided

personalinterviewing(CAPI)– 7,500householdsfrom375‘clusters’(urban=wards;rural=villagetracts)

• HouseholdquesAonnaire(fromhouseholdhead)• IndividualquesAonnaire(oneindividualaged15-69randomlyselected)

– FieldworkconductedbyThirdEyeCo

10

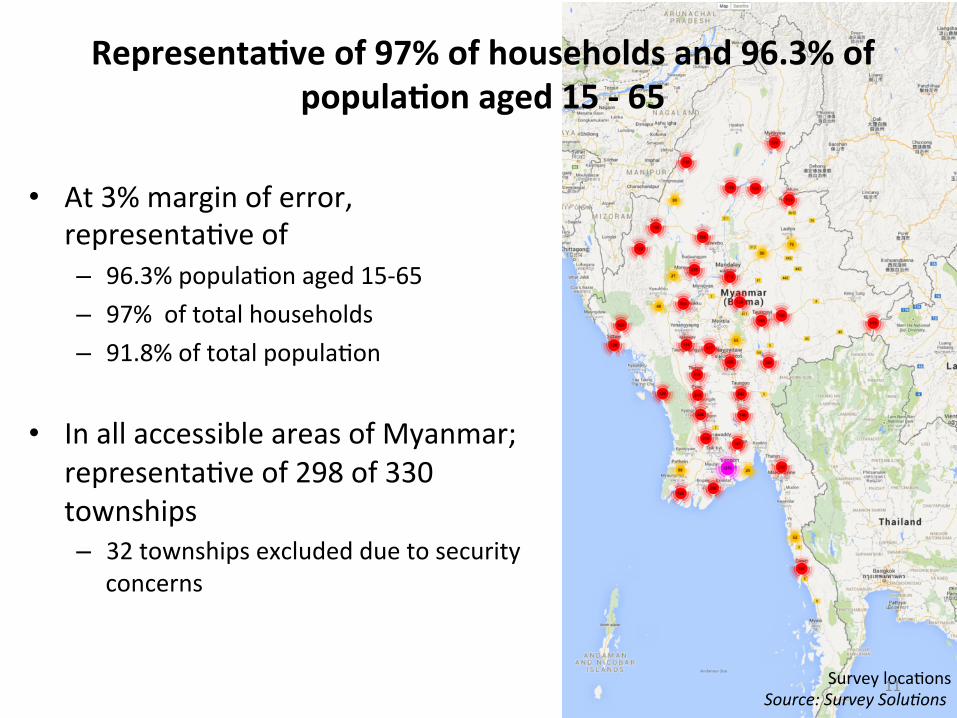

Representa3veof97%ofhouseholdsand96.3%ofpopula3onaged15-65

• At3%marginoferror,representaAveof– 96.3%populaAonaged15-65– 97%oftotalhouseholds– 91.8%oftotalpopulaAon

• InallaccessibleareasofMyanmar;representaAveof298of330townships– 32townshipsexcludedduetosecurity

concerns

SurveylocaAonsSource:SurveySolu<ons

11

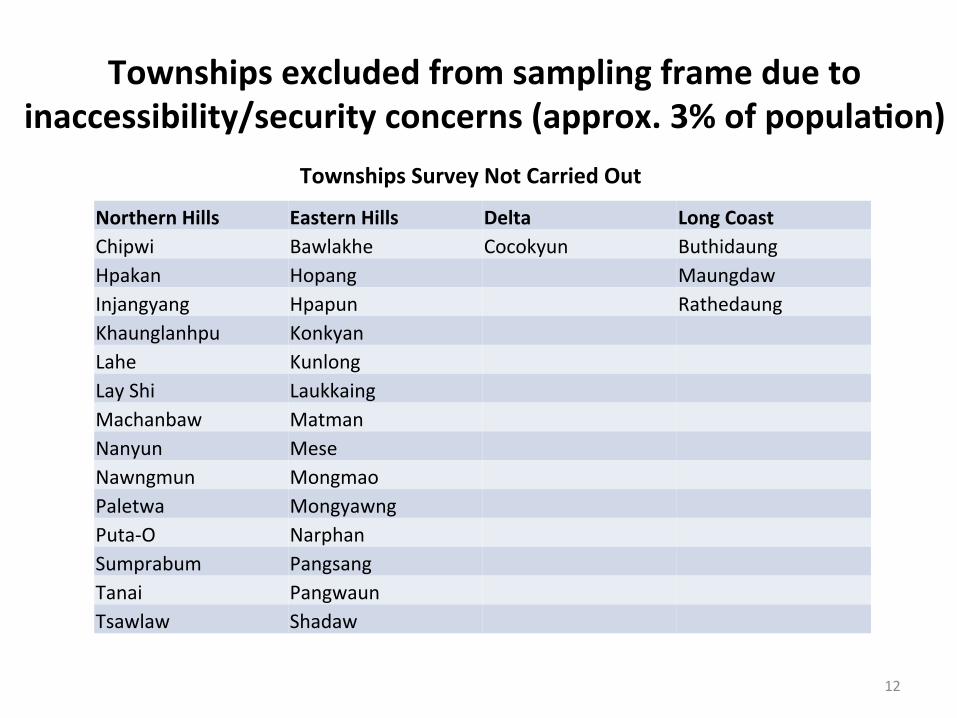

Townshipsexcludedfromsamplingframeduetoinaccessibility/securityconcerns(approx.3%ofpopula3on)

12

NorthernHills EasternHills Delta LongCoastChipwi Bawlakhe Cocokyun ButhidaungHpakan Hopang MaungdawInjangyang Hpapun RathedaungKhaunglanhpu KonkyanLahe KunlongLayShi LaukkaingMachanbaw MatmanNanyun MeseNawngmun MongmaoPaletwa MongyawngPuta-O NarphanSumprabum PangsangTanai PangwaunTsawlaw Shadaw

TownshipsSurveyNotCarriedOut

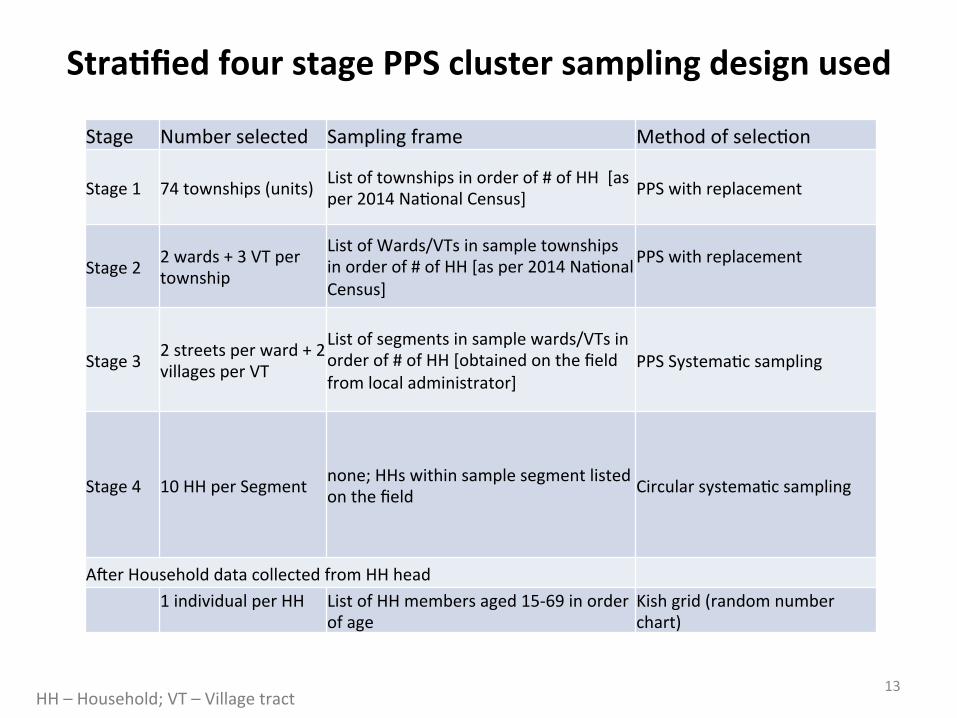

Stra3fiedfourstagePPSclustersamplingdesignused

Stage Numberselected Samplingframe MethodofselecAon

Stage1 74townships(units) Listoftownshipsinorderof#ofHH[asper2014NaAonalCensus] PPSwithreplacement

Stage2 2wards+3VTpertownship

ListofWards/VTsinsampletownshipsinorderof#ofHH[asper2014NaAonalCensus]

PPSwithreplacement

Stage3 2streetsperward+2villagesperVT

Listofsegmentsinsamplewards/VTsinorderof#ofHH[obtainedonthefieldfromlocaladministrator]

PPSSystemaAcsampling

Stage4 10HHperSegment none;HHswithinsamplesegmentlistedonthefield CircularsystemaAcsampling

AserHouseholddatacollectedfromHHhead1individualperHH

ListofHHmembersaged15-69inorderofage

Kishgrid(randomnumberchart)

13HH–Household;VT–Villagetract

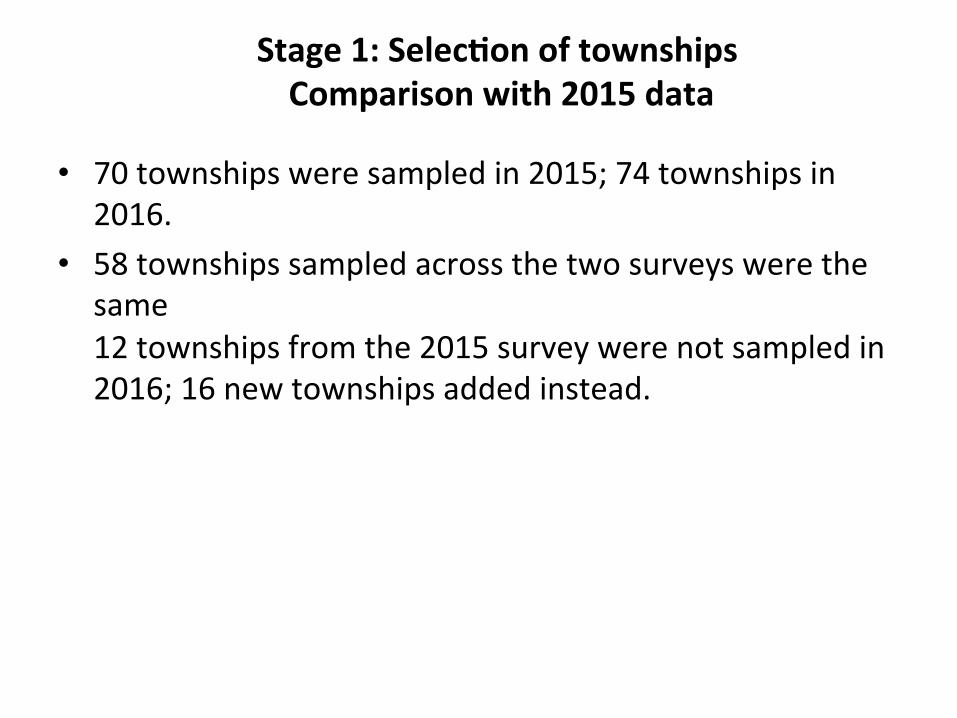

Stage1:Selec3onoftownshipsComparisonwith2015data

• 70townshipsweresampledin2015;74townshipsin2016.

• 58townshipssampledacrossthetwosurveyswerethesame12townshipsfromthe2015surveywerenotsampledin2016;16newtownshipsaddedinstead.

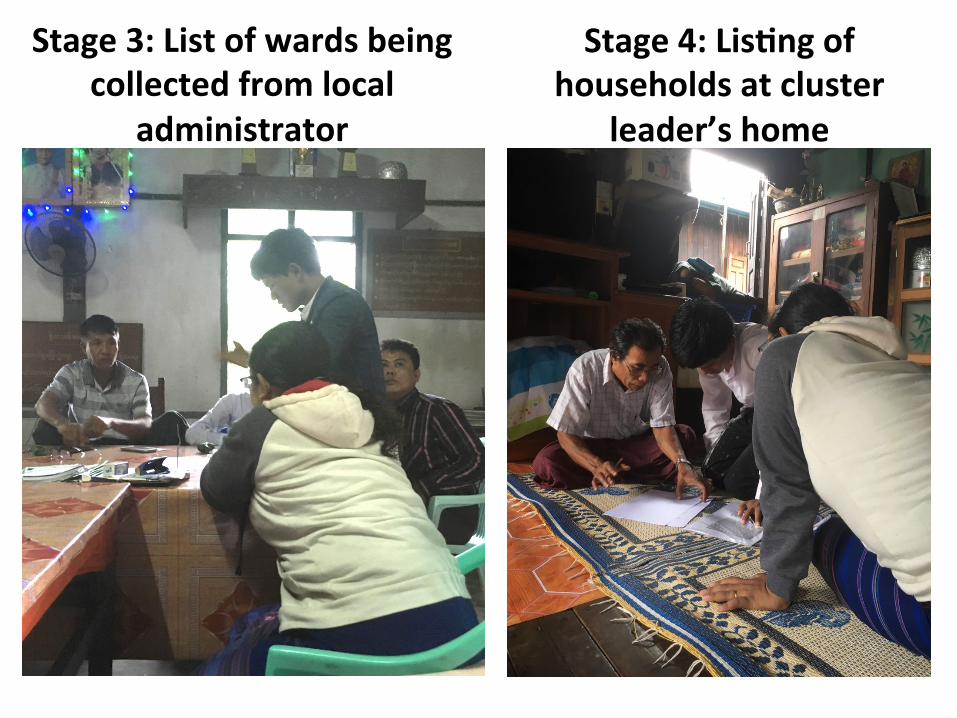

Stage3:Listofwardsbeingcollectedfromlocal

administrator

Stage4:Lis3ngofhouseholdsatcluster

leader’shome

Getngtotherespondent’shouseholds InterviewsbeingconductedbyCAPI

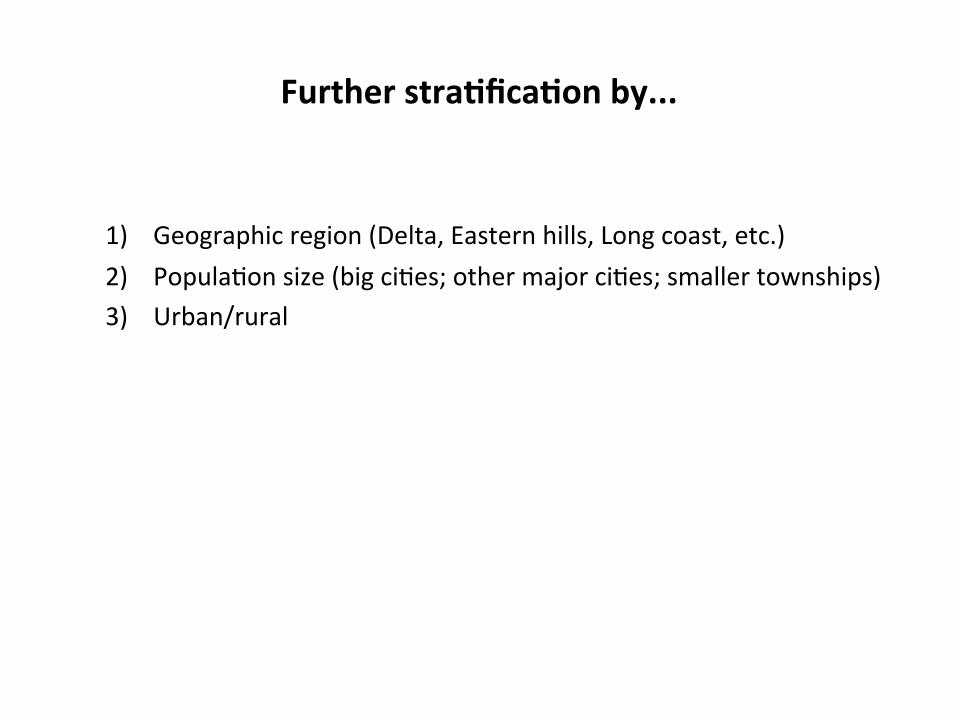

Furtherstra3fica3onby...

1) Geographicregion(Delta,Easternhills,Longcoast,etc.)2) PopulaAonsize(bigciAes;othermajorciAes;smallertownships)3) Urban/rural

NorthernHills(8.9%)

EasternHills(14.4%)

MiddleDryZone(26.3%)incl.

MDY&NPT5.7%

LongCoast(13.7%)

LowerValley(23.8%)

incl.YGN10%Delta(12.9%)

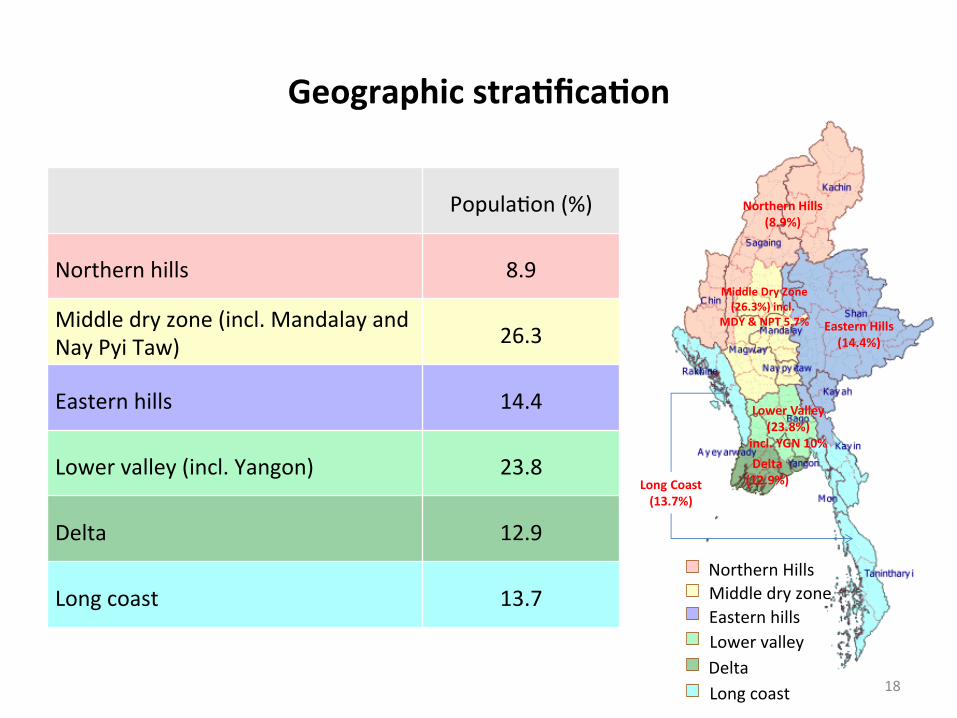

Geographicstra3fica3on

PopulaAon(%)

Northernhills 8.9

Middledryzone(incl.MandalayandNayPyiTaw) 26.3

Easternhills 14.4

Lowervalley(incl.Yangon) 23.8

Delta 12.9

Longcoast 13.7

18

NorthernHillsMiddledryzoneEasternhillsLowervalleyDeltaLongcoast

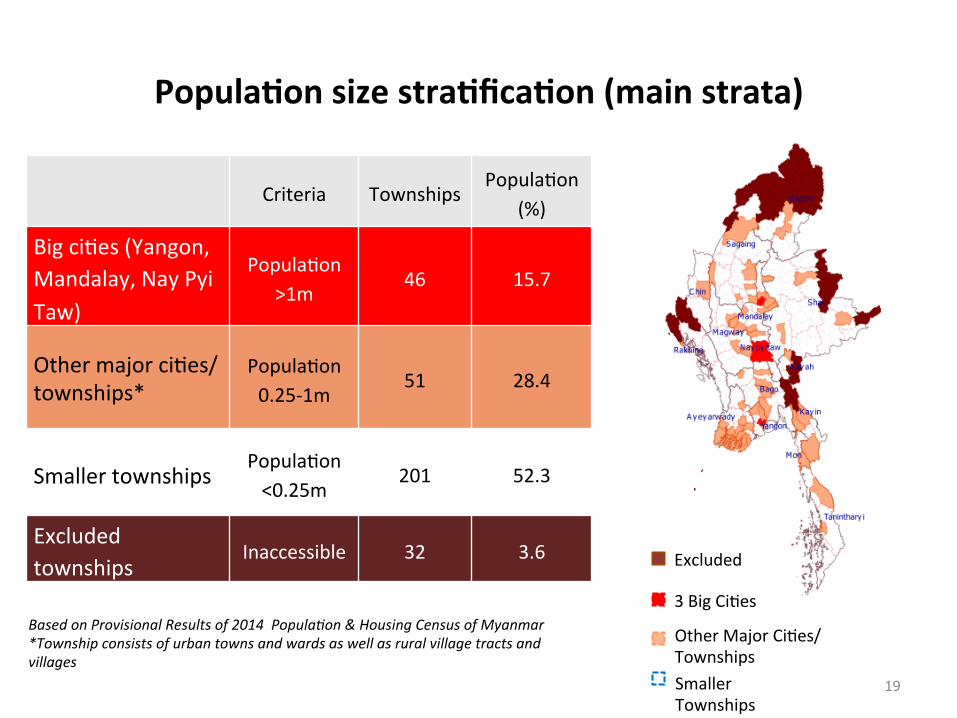

Popula3onsizestra3fica3on(mainstrata)

19

Excluded

3BigCiAesOtherMajorCiAes/TownshipsSmallerTownships

Criteria Townships

PopulaAon(%)

BigciAes(Yangon,Mandalay,NayPyiTaw)

PopulaAon>1m

46 15.7

OthermajorciAes/townships*

PopulaAon0.25-1m

51 28.4

SmallertownshipsPopulaAon<0.25m

201 52.3

Excludedtownships

Inaccessible 32 3.6

BasedonProvisionalResultsof2014Popula<on&HousingCensusofMyanmar*Townshipconsistsofurbantownsandwardsaswellasruralvillagetractsandvillages

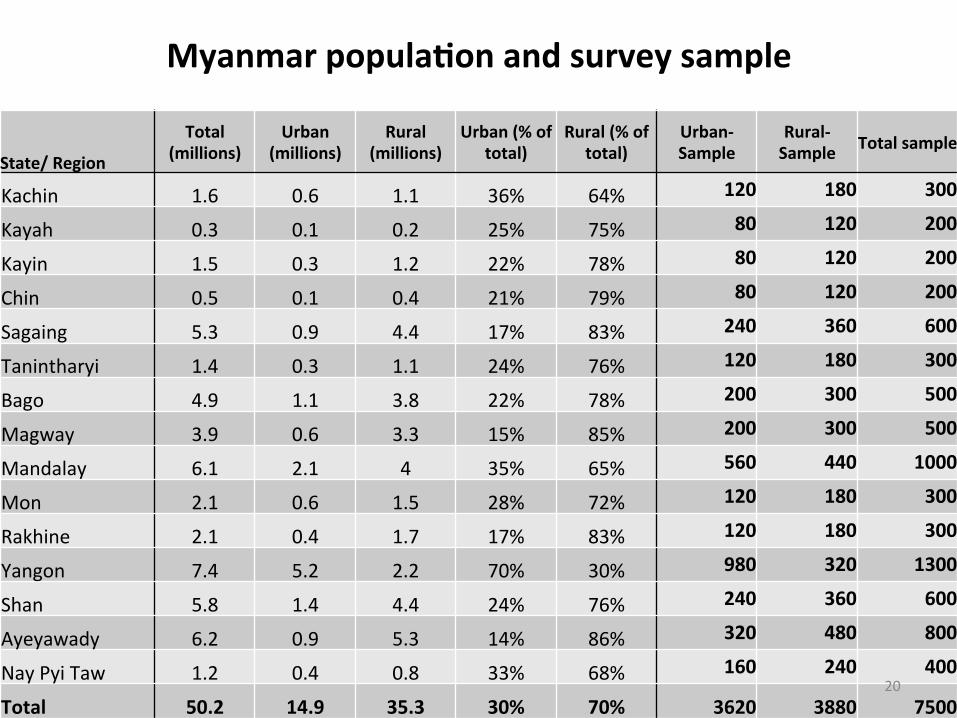

State/Region

Total(millions)

Urban(millions)

Rural(millions)

Urban(%oftotal)

Rural(%oftotal)

Urban-Sample

Rural-Sample Totalsample

Kachin 1.6 0.6 1.1 36% 64% 120 180 300

Kayah 0.3 0.1 0.2 25% 75% 80 120 200

Kayin 1.5 0.3 1.2 22% 78% 80 120 200

Chin 0.5 0.1 0.4 21% 79% 80 120 200

Sagaing 5.3 0.9 4.4 17% 83% 240 360 600

Tanintharyi 1.4 0.3 1.1 24% 76% 120 180 300

Bago 4.9 1.1 3.8 22% 78% 200 300 500

Magway 3.9 0.6 3.3 15% 85% 200 300 500

Mandalay 6.1 2.1 4 35% 65% 560 440 1000

Mon 2.1 0.6 1.5 28% 72% 120 180 300

Rakhine 2.1 0.4 1.7 17% 83% 120 180 300

Yangon 7.4 5.2 2.2 70% 30% 980 320 1300

Shan 5.8 1.4 4.4 24% 76% 240 360 600

Ayeyawady 6.2 0.9 5.3 14% 86% 320 480 800

NayPyiTaw 1.2 0.4 0.8 33% 68% 160 240 400

Total 50.2 14.9 35.3 30% 70% 3620 3880 7500

Myanmarpopula3onandsurveysample

20

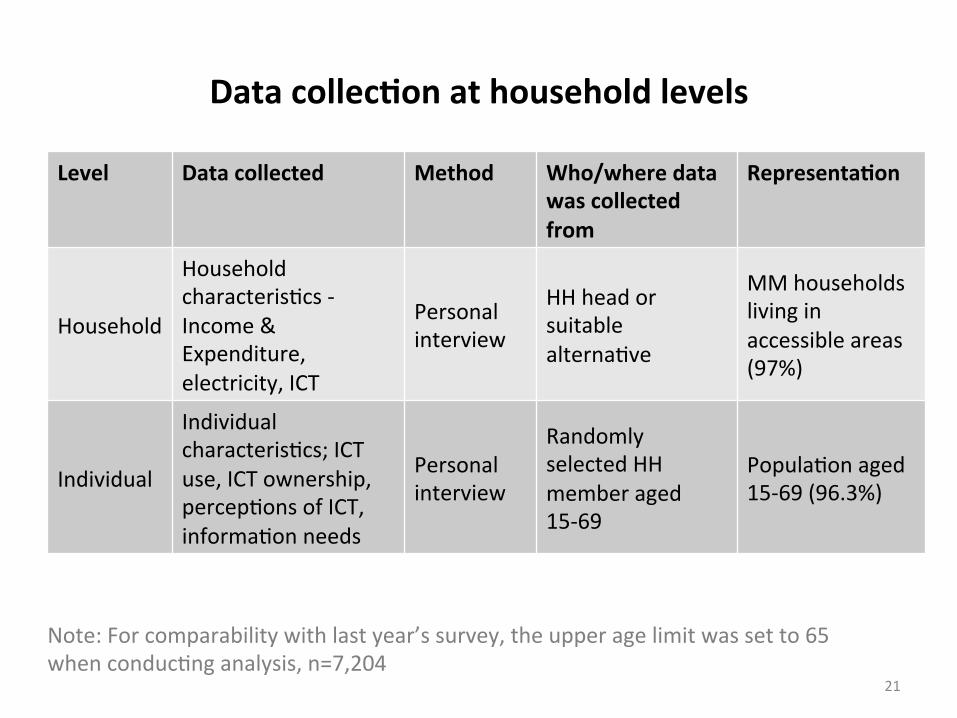

Datacollec3onathouseholdlevels

Level Datacollected Method Who/wheredatawascollectedfrom

Representa3on

Household

HouseholdcharacterisAcs-Income&Expenditure,electricity,ICT

Personalinterview

HHheadorsuitablealternaAve

MMhouseholdslivinginaccessibleareas(97%)

Individual

IndividualcharacterisAcs;ICTuse,ICTownership,percepAonsofICT,informaAonneeds

Personalinterview

RandomlyselectedHHmemberaged15-69

PopulaAonaged15-69(96.3%)

21

Note:Forcomparabilitywithlastyear’ssurvey,theupperagelimitwassetto65whenconducAnganalysis,n=7,204

RESPONDENT&HOUSEHOLDCHARACTERISTICS

22

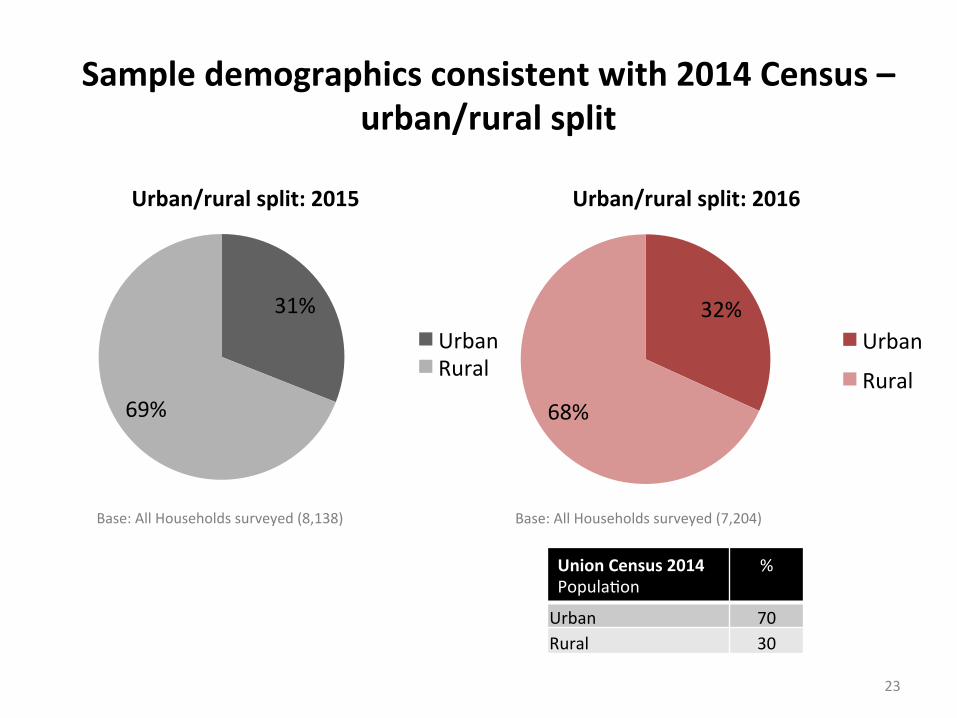

Sampledemographicsconsistentwith2014Census–urban/ruralsplit

31%

69%

UrbanRural

Urban/ruralsplit:2015

32%

68%

Urban

Rural

Urban/ruralsplit:2016

Base:AllHouseholdssurveyed(8,138) Base:AllHouseholdssurveyed(7,204)

23

UnionCensus2014PopulaAon

%

Urban 70Rural 30

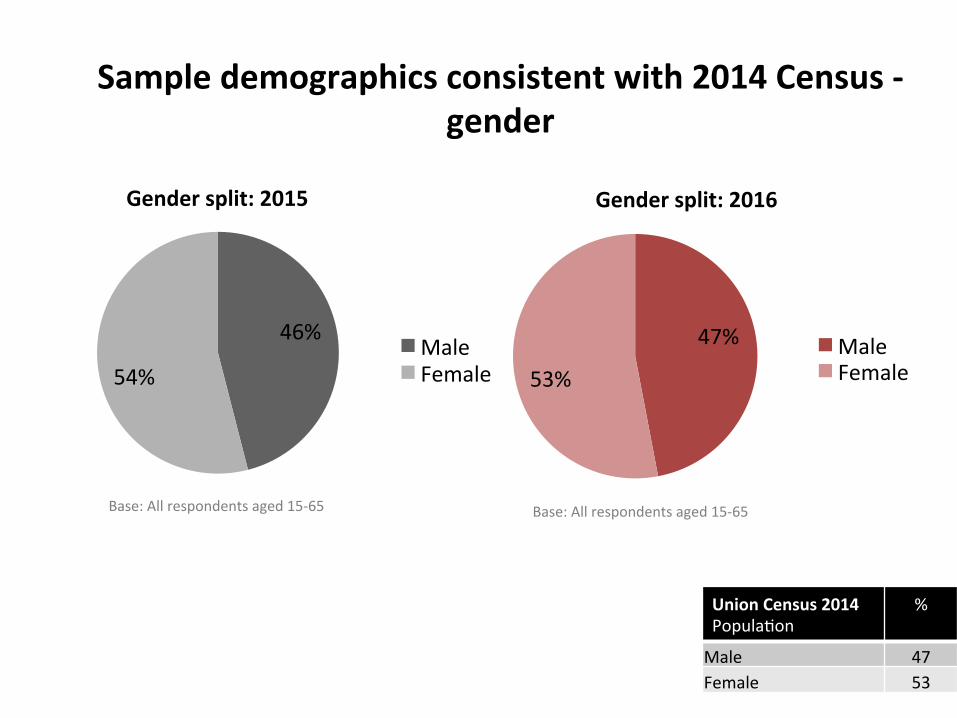

Sampledemographicsconsistentwith2014Census-gender

46%

54%MaleFemale

Gendersplit:2015

47%

53%MaleFemale

Gendersplit:2016

Base:Allrespondentsaged15-65 Base:Allrespondentsaged15-65

24

UnionCensus2014PopulaAon

%

Male 47Female 53

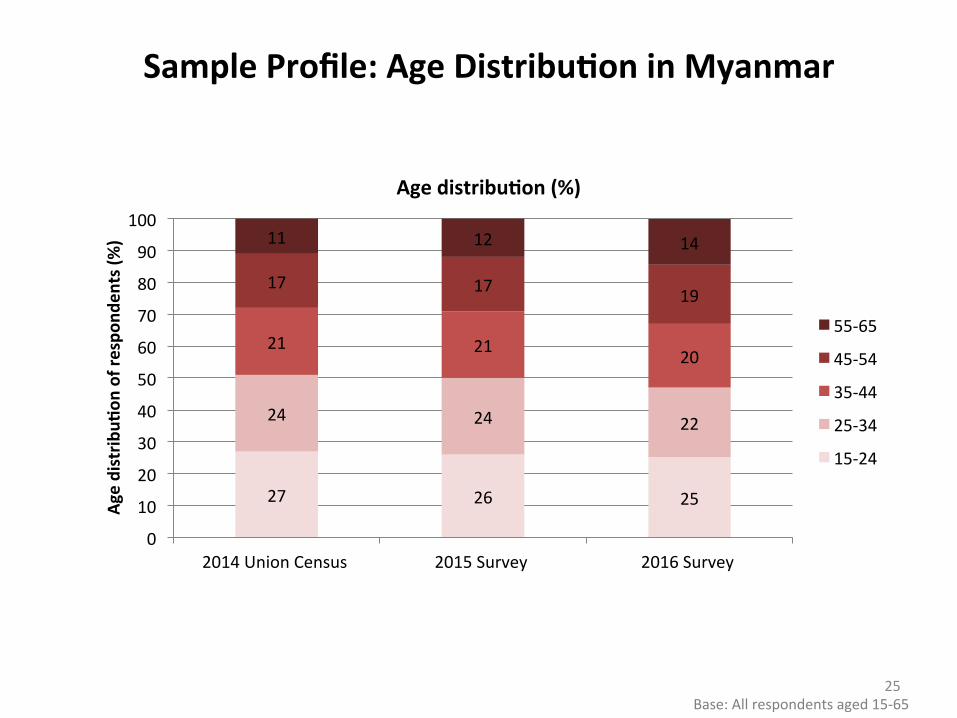

SampleProfile:AgeDistribu3oninMyanmar

27 26 25

24 24 22

21 21 20

17 17 19

11 12 14

0

10

20

30

40

50

60

70

80

90

100

2014UnionCensus 2015Survey 2016Survey

Agedistrib

u3on

ofrespo

nden

ts(%

)

Agedistribu3on(%)

55-65

45-54

35-44

25-34

15-24

25Base:Allrespondentsaged15-65

0

0

1

1

1

2

8

15

15

15

41

-

0

-

-

0

4

0

8

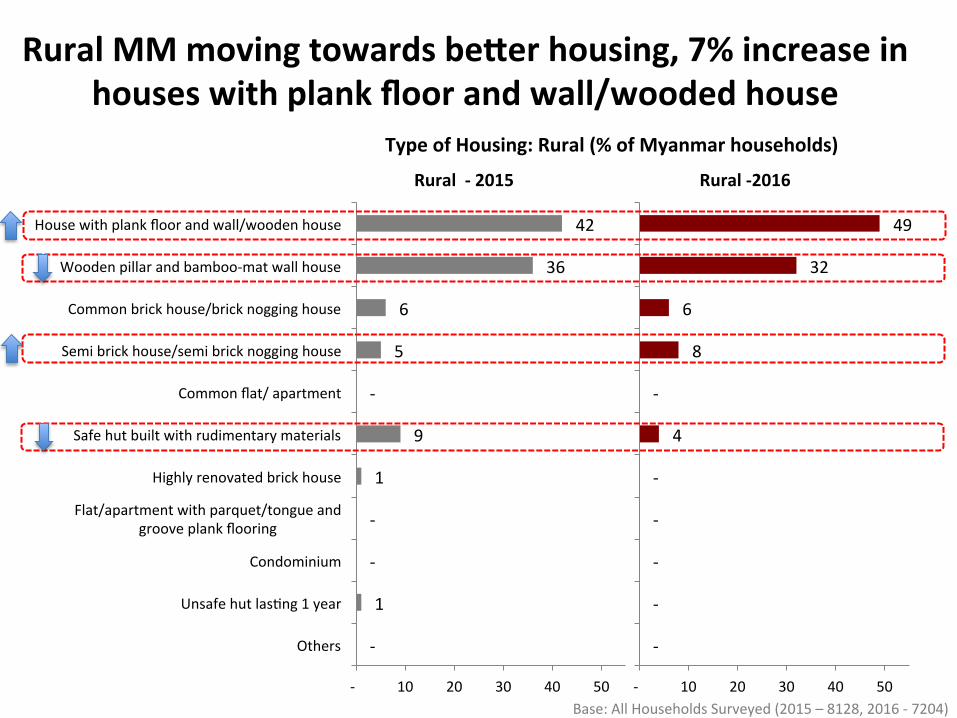

6

32

49

- 10 20 30 40 50 60

Others

UnsafehutlasAng1year

Condominium

Flat/apartmentwithparquet/tongueandgrooveplankflooring

Highlyrenovatedbrickhouse

Safehutbuiltwithrudimentarymaterials

Commonflat/apartment

Semibrickhouse/semibricknogginghouse

Commonbrickhouse/bricknogginghouse

Woodenpillarandbamboo-matwallhouse

Housewithplankfloorandwall/woodenhouse

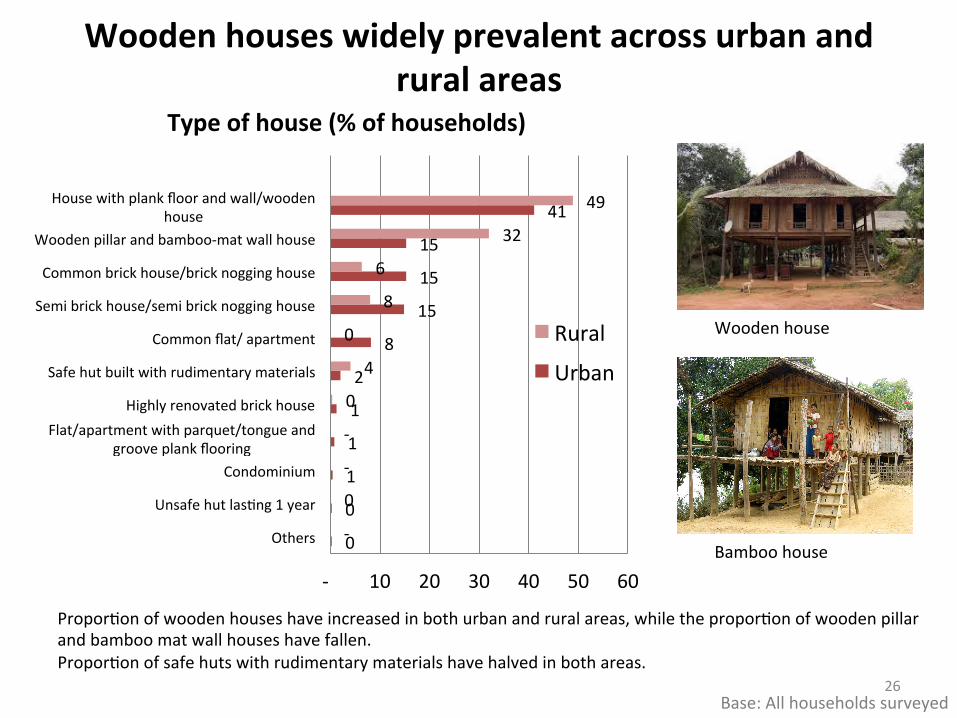

Typeofhouse(%ofhouseholds)

Rural

Urban

Woodenhouseswidelyprevalentacrossurbanandruralareas

Base:Allhouseholdssurveyed

ProporAonofwoodenhouseshaveincreasedinbothurbanandruralareas,whiletheproporAonofwoodenpillarandbamboomatwallhouseshavefallen.ProporAonofsafehutswithrudimentarymaterialshavehalvedinbothareas.

Woodenhouse

26

Bamboohouse

0

1

1

1

2

4

11

12

15

18

36

- 10 20 30 40 50

Others

UnsafehutlasAng1year

Condominium

Flat/apartmentwithparquet/tongueandgrooveplankflooring

Highlyrenovatedbrickhouse

Safehutbuiltwithrudimentarymaterials

Commonflat/apartment

Semibrickhouse/semibricknogginghouse

Commonbrickhouse/bricknogginghouse

Woodenpillarandbamboo-matwallhouse

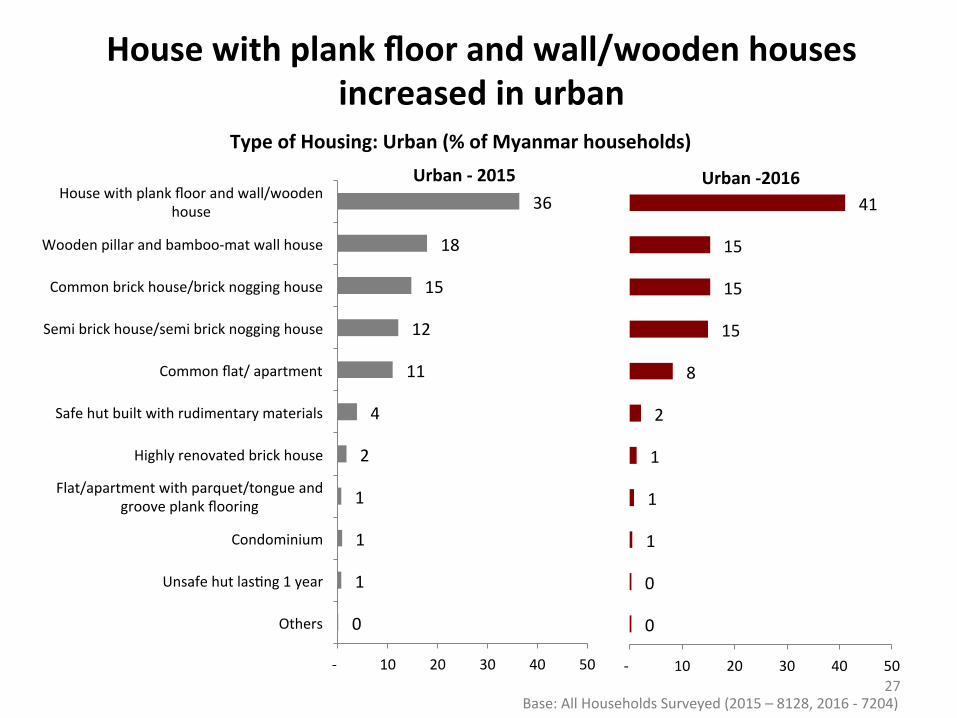

Housewithplankfloorandwall/woodenhouse

Urban-2015

0

0

1

1

1

2

8

15

15

15

41

- 10 20 30 40 50

Urban-2016

Base:AllHouseholdsSurveyed(2015–8128,2016-7204)

TypeofHousing:Urban(%ofMyanmarhouseholds)

Housewithplankfloorandwall/woodenhousesincreasedinurban

27

-

-

-

-

-

4

-

8

6

32

49

- 10 20 30 40 50

Others

UnsafehutlasAng1year

Condominium

Flat/apartmentwithparquet/tongueandgrooveplankflooring

Highlyrenovatedbrickhouse

Safehutbuiltwithrudimentarymaterials

Commonflat/apartment

Semibrickhouse/semibricknogginghouse

Commonbrickhouse/bricknogginghouse

Woodenpillarandbamboo-matwallhouse

Housewithplankfloorandwall/woodenhouse

Rural-2016

-

1

-

-

1

9

-

5

6

36

42

- 10 20 30 40 50

Others

UnsafehutlasAng1year

Condominium

Flat/apartmentwithparquet/tongueandgrooveplankflooring

Highlyrenovatedbrickhouse

Safehutbuiltwithrudimentarymaterials

Commonflat/apartment

Semibrickhouse/semibricknogginghouse

Commonbrickhouse/bricknogginghouse

Woodenpillarandbamboo-matwallhouse

Housewithplankfloorandwall/woodenhouse

Rural-2015

Base:AllHouseholdsSurveyed(2015–8128,2016-7204)

TypeofHousing:Rural(%ofMyanmarhouseholds)

RuralMMmovingtowardsbeeerhousing,7%increaseinhouseswithplankfloorandwall/woodedhouse

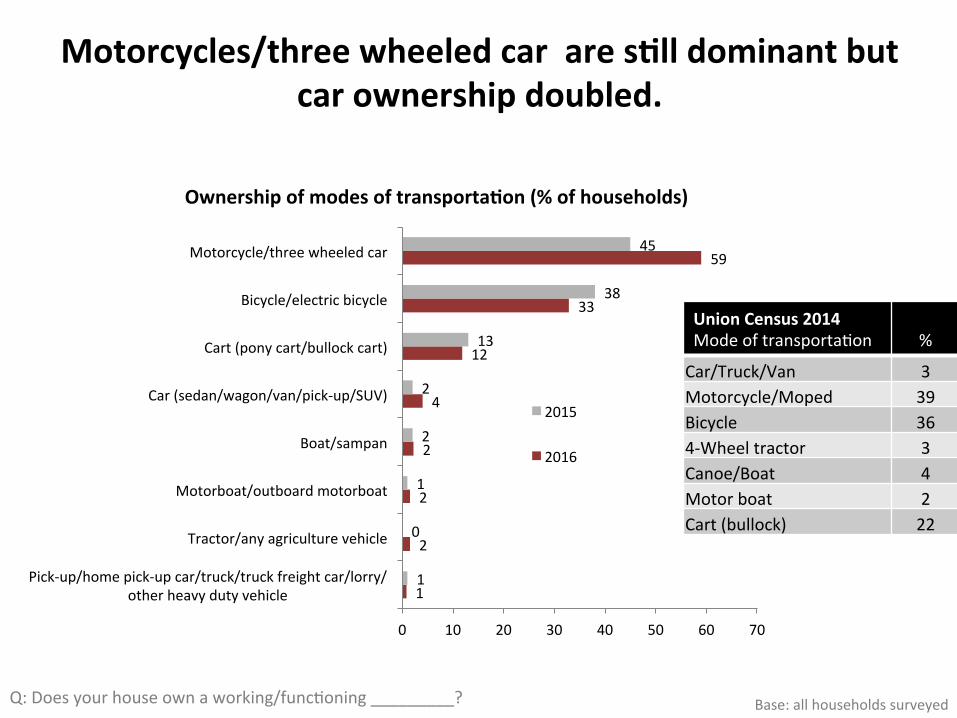

Motorcycles/threewheeledcarares3lldominantbutcarownershipdoubled.

UnionCensus2014ModeoftransportaAon

%

Car/Truck/Van 3Motorcycle/Moped 39Bicycle 364-Wheeltractor 3Canoe/Boat 4Motorboat 2Cart(bullock) 22

Q:Doesyourhouseownaworking/funcAoning_________?

1

2

2

2

4

12

33

59

1

0

1

2

2

13

38

45

0 10 20 30 40 50 60 70

Pick-up/homepick-upcar/truck/truckfreightcar/lorry/otherheavydutyvehicle

Tractor/anyagriculturevehicle

Motorboat/outboardmotorboat

Boat/sampan

Car(sedan/wagon/van/pick-up/SUV)

Cart(ponycart/bullockcart)

Bicycle/electricbicycle

Motorcycle/threewheeledcar

Ownershipofmodesoftransporta3on(%ofhouseholds)

2015

2016

Base:allhouseholdssurveyed

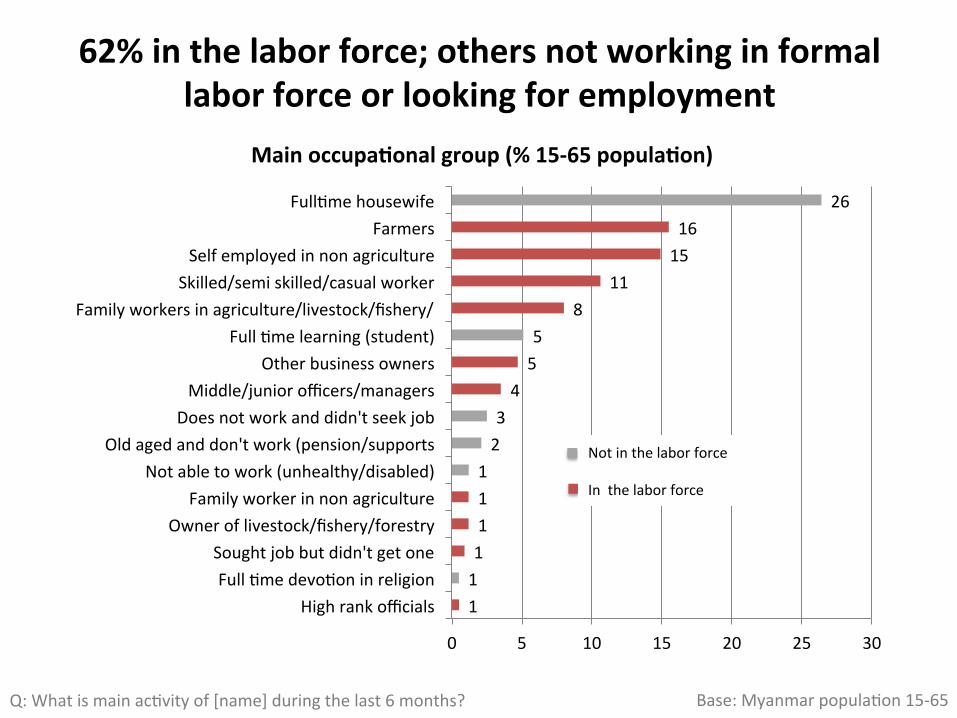

Q:WhatismainacAvityof[name]duringthelast6months? Base:MyanmarpopulaAon15-65

11111123455

811

1516

26

0 5 10 15 20 25 30

HighrankofficialsFullAmedevoAoninreligionSoughtjobbutdidn'tgetone

Owneroflivestock/fishery/forestryFamilyworkerinnonagriculture

Notabletowork(unhealthy/disabled)Oldagedanddon'twork(pension/supports

Doesnotworkanddidn'tseekjobMiddle/juniorofficers/managers

OtherbusinessownersFullAmelearning(student)

Familyworkersinagriculture/livestock/fishery/Skilled/semiskilled/casualworkerSelfemployedinnonagriculture

FarmersFullAmehousewife

Mainoccupa3onalgroup(%15-65popula3on)

Notinthelaborforce Inthelaborforce

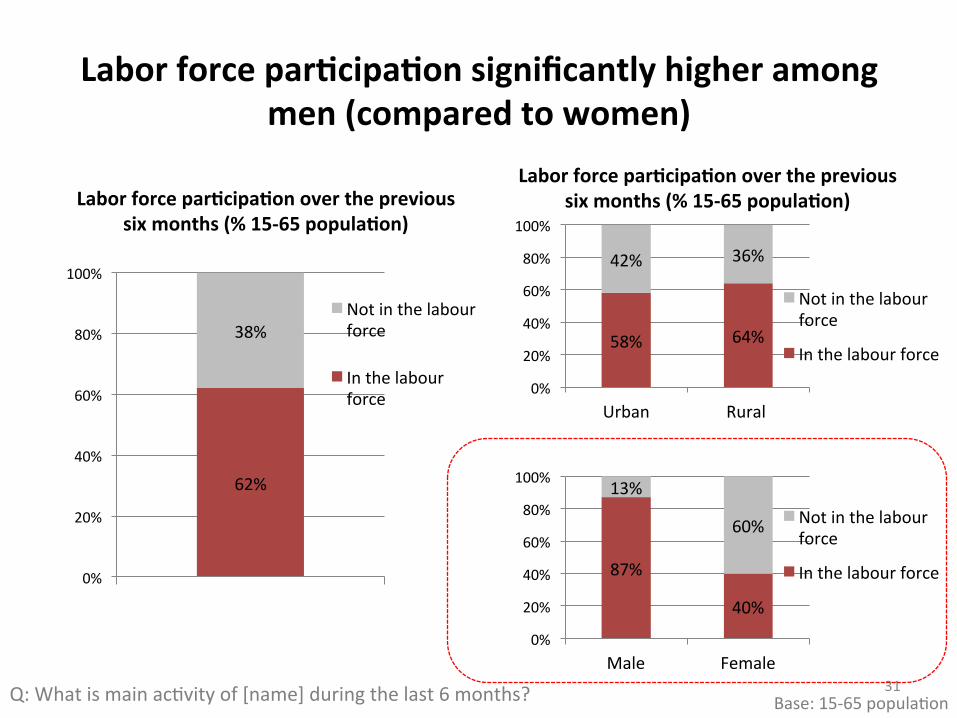

62%inthelaborforce;othersnotworkinginformallaborforceorlookingforemployment

87%

40%

13%

60%

0%

20%

40%

60%

80%

100%

Male Female

Notinthelabourforce

Inthelabourforce

58% 64%

42% 36%

0%

20%

40%

60%

80%

100%

Urban Rural

Laborforcepar3cipa3onovertheprevioussixmonths(%15-65popula3on)

Notinthelabourforce

Inthelabourforce

Laborforcepar3cipa3onsignificantlyhigheramongmen(comparedtowomen)

Base:15-65populaAon31Q:WhatismainacAvityof[name]duringthelast6months?

62%

38%

0%

20%

40%

60%

80%

100%

Laborforcepar3cipa3onovertheprevioussixmonths(%15-65popula3on)

Notinthelabourforce

Inthelabourforce

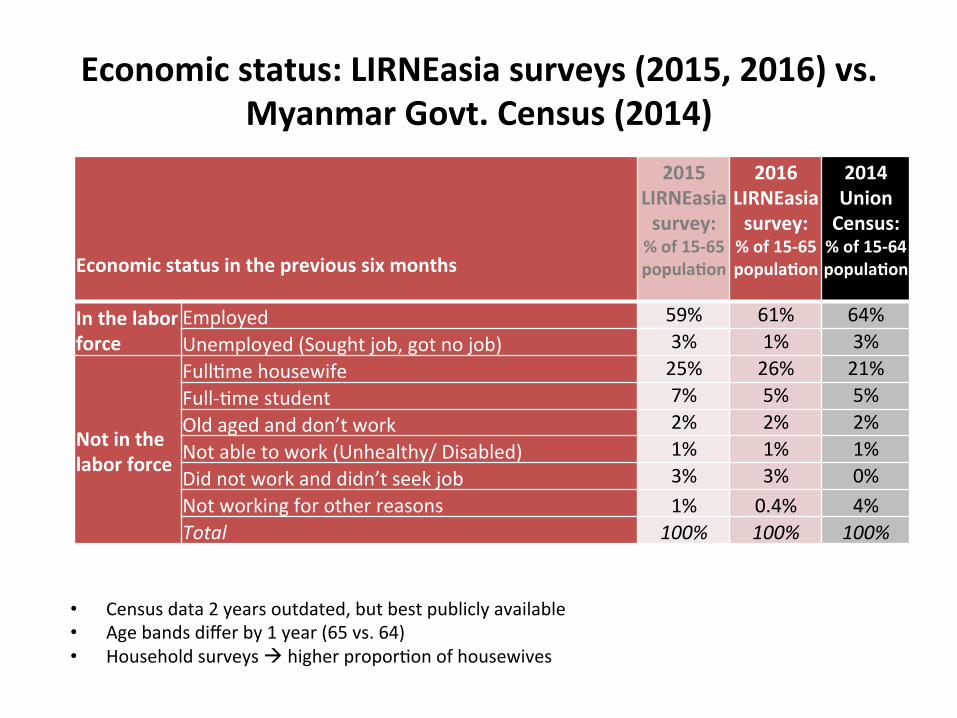

Economicstatus:LIRNEasiasurveys(2015,2016)vs.MyanmarGovt.Census(2014)

• Censusdata2yearsoutdated,butbestpubliclyavailable• Agebandsdifferby1year(65vs.64)• HouseholdsurveysàhigherproporAonofhousewives

Economicstatusintheprevioussixmonths

2015LIRNEasiasurvey:%of15-65popula3on

2016LIRNEasiasurvey:%of15-65popula3on

2014UnionCensus:%of15-64popula3on

Inthelaborforce

Employed 59% 61% 64%Unemployed(Soughtjob,gotnojob) 3% 1% 3%

Notinthelaborforce

FullAmehousewife 25% 26% 21%Full-Amestudent 7% 5% 5%Oldagedanddon’twork 2% 2% 2%Notabletowork(Unhealthy/Disabled) 1% 1% 1%Didnotworkanddidn’tseekjob 3% 3% 0%Notworkingforotherreasons 1% 0.4% 4%Total 100% 100% 100%

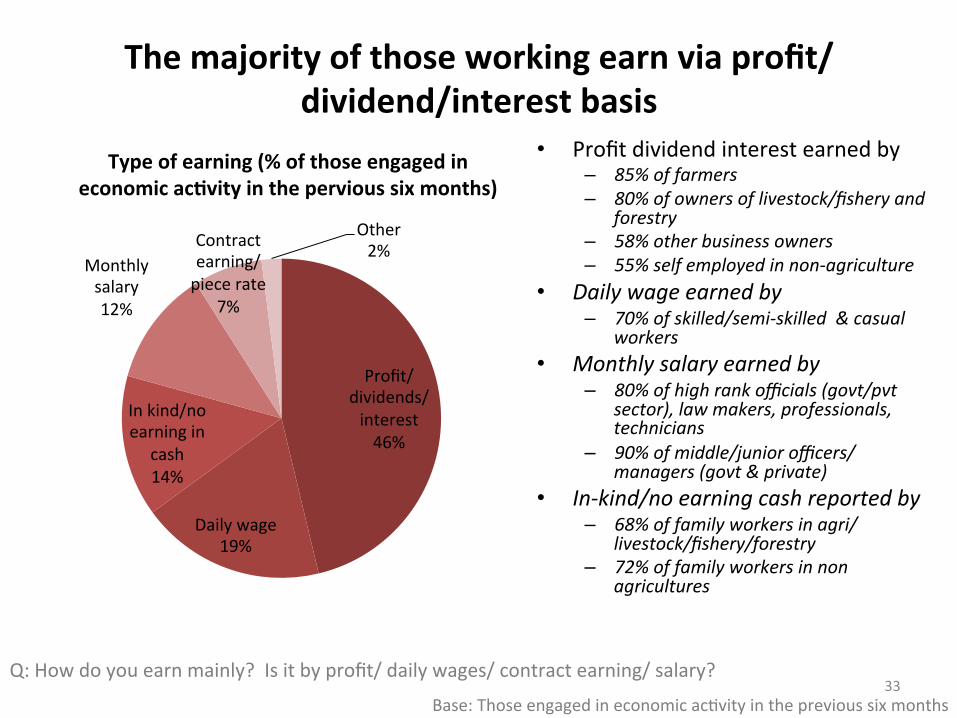

Themajorityofthoseworkingearnviaprofit/dividend/interestbasis

Q:Howdoyouearnmainly?Isitbyprofit/dailywages/contractearning/salary?33

Base:ThoseengagedineconomicacAvityintheprevioussixmonths

Profit/dividends/interest46%

Dailywage19%

Inkind/noearningin

cash14%

Monthlysalary12%

Contractearning/piecerate

7%

Other2%

Typeofearning(%ofthoseengagedineconomicac3vityinthepervioussixmonths)

• Profitdividendinterestearnedby– 85%offarmers– 80%ofownersoflivestock/fisheryand

forestry– 58%otherbusinessowners– 55%selfemployedinnon-agriculture

• Dailywageearnedby– 70%ofskilled/semi-skilled&casual

workers• Monthlysalaryearnedby

– 80%ofhighrankofficials(govt/pvtsector),lawmakers,professionals,technicians

– 90%ofmiddle/juniorofficers/managers(govt&private)

• In-kind/noearningcashreportedby– 68%offamilyworkersinagri/

livestock/fishery/forestry– 72%offamilyworkersinnon

agricultures

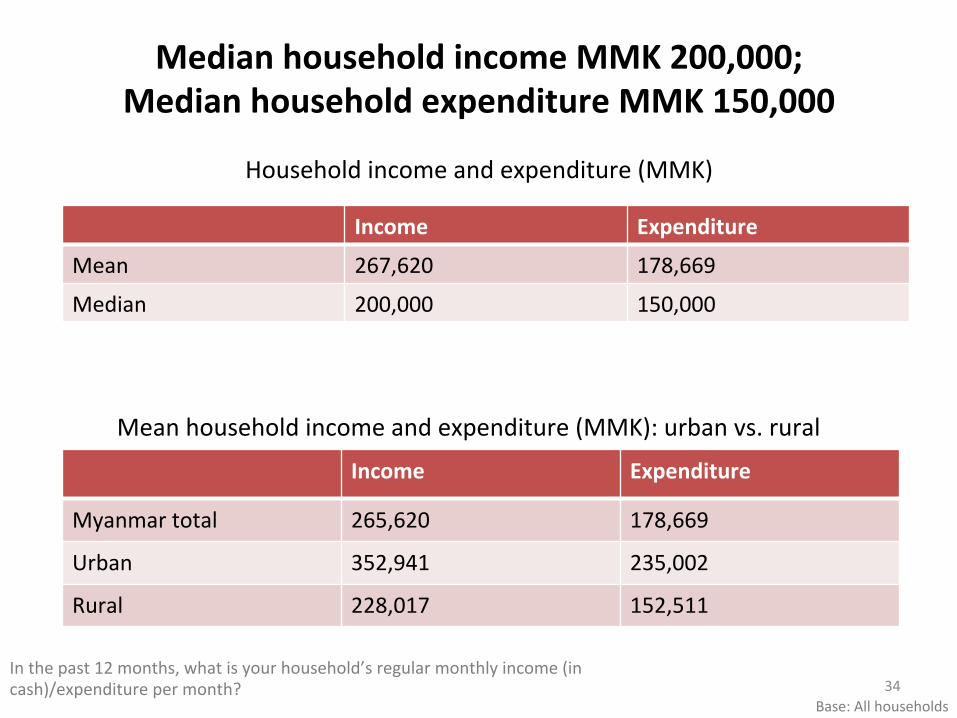

Householdincomeandexpenditure(MMK)

Income Expenditure

Myanmartotal 265,620 178,669

Urban 352,941 235,002

Rural 228,017 152,511

Income Expenditure

Mean 267,620 178,669

Median 200,000 150,000

Inthepast12months,whatisyourhousehold’sregularmonthlyincome(incash)/expenditurepermonth?

Base:Allhouseholds34

Meanhouseholdincomeandexpenditure(MMK):urbanvs.rural

MedianhouseholdincomeMMK200,000;MedianhouseholdexpenditureMMK150,000

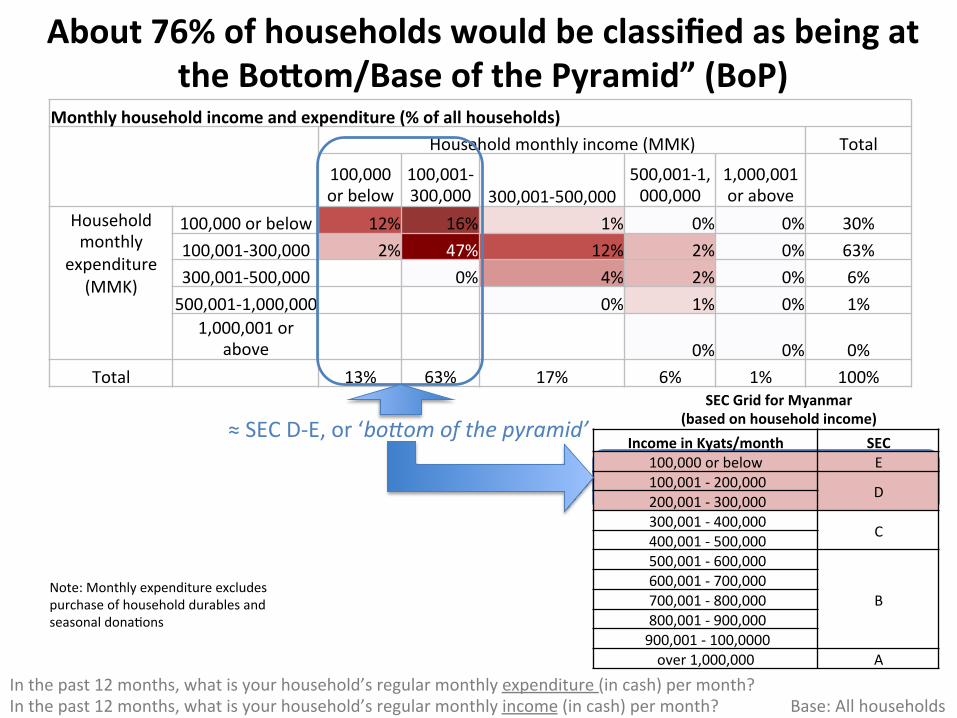

Monthlyhouseholdincomeandexpenditure(%ofallhouseholds)Householdmonthlyincome(MMK) Total

100,000orbelow

100,001-300,000 300,001-500,000

500,001-1,000,000

1,000,001orabove

Householdmonthly

expenditure(MMK)

100,000orbelow 12% 16% 1% 0% 0% 30%100,001-300,000 2% 47% 12% 2% 0% 63%300,001-500,000 0% 4% 2% 0% 6%500,001-1,000,000 0% 1% 0% 1%

1,000,001orabove 0% 0% 0%

Total 13% 63% 17% 6% 1% 100%

Inthepast12months,whatisyourhousehold’sregularmonthlyexpenditure(incash)permonth?Inthepast12months,whatisyourhousehold’sregularmonthlyincome(incash)permonth?Base:Allhouseholds

Note:MonthlyexpenditureexcludespurchaseofhouseholddurablesandseasonaldonaAons

≈SECD-E,or‘bo_omofthepyramid’

IncomeinKyats/month SEC100,000orbelow E100,001-200,000 D200,001-300,000300,001-400,000 C400,001-500,000500,001-600,000

B600,001-700,000700,001-800,000800,001-900,000900,001-100,0000over1,000,000 A

SECGridforMyanmar(basedonhouseholdincome)

NEWSLIDE

About76%ofhouseholdswouldbeclassifiedasbeingattheBoeom/BaseofthePyramid”(BoP)

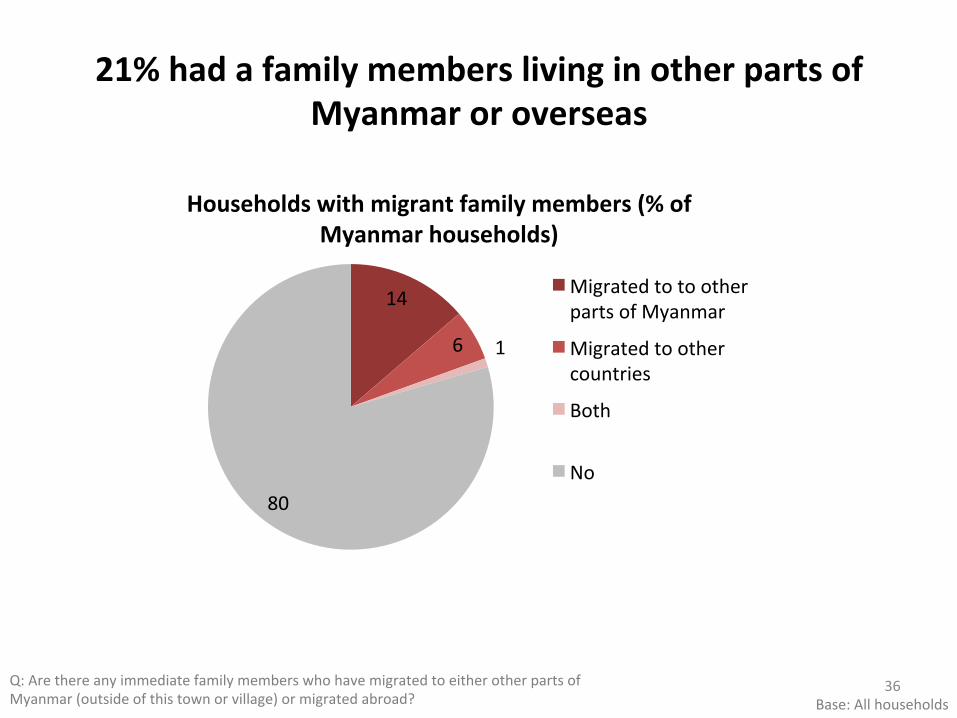

21%hadafamilymemberslivinginotherpartsofMyanmaroroverseas

14

6 1

80

Householdswithmigrantfamilymembers(%ofMyanmarhouseholds)

MigratedtotootherpartsofMyanmar

Migratedtoothercountries

Both

No

Q:ArethereanyimmediatefamilymemberswhohavemigratedtoeitherotherpartsofMyanmar(outsideofthistownorvillage)ormigratedabroad? Base:Allhouseholds

36

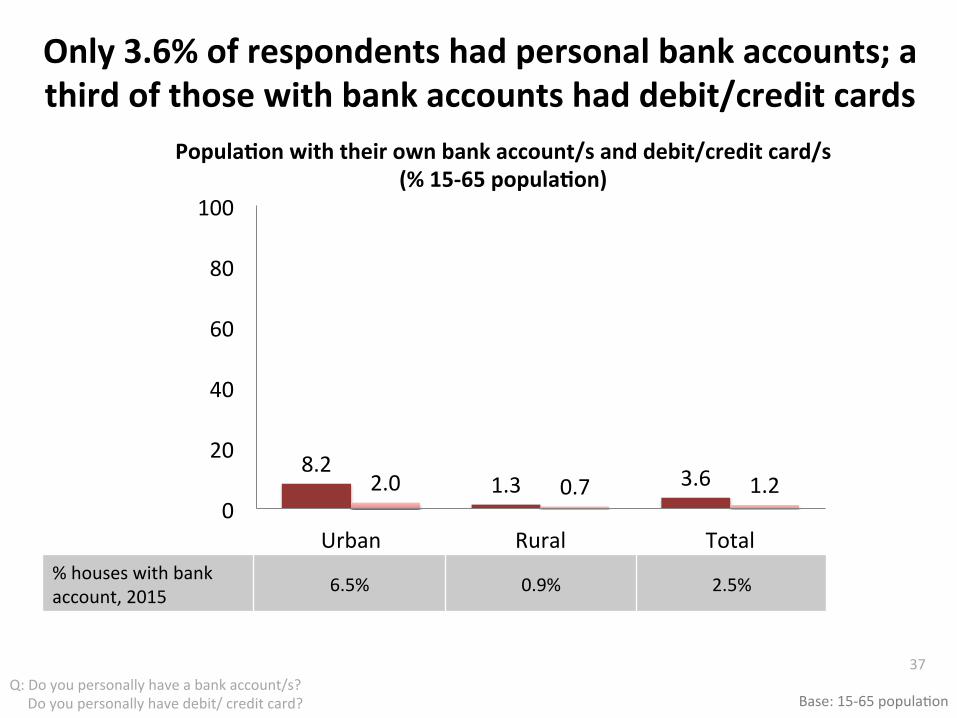

Only3.6%ofrespondentshadpersonalbankaccounts;athirdofthosewithbankaccountshaddebit/creditcards

Q:Doyoupersonallyhaveabankaccount/s?Doyoupersonallyhavedebit/creditcard?

37

Base:15-65populaAon

8.21.3 3.62.0 0.7 1.2

0

20

40

60

80

100

Urban Rural Total

Havetheirownbankaccount Havetheirowndebit/creditcard

Popula3onwiththeirownbankaccount/sanddebit/creditcard/s(%15-65popula3on)

%houseswithbankaccount,2015 6.5% 0.9% 2.5%

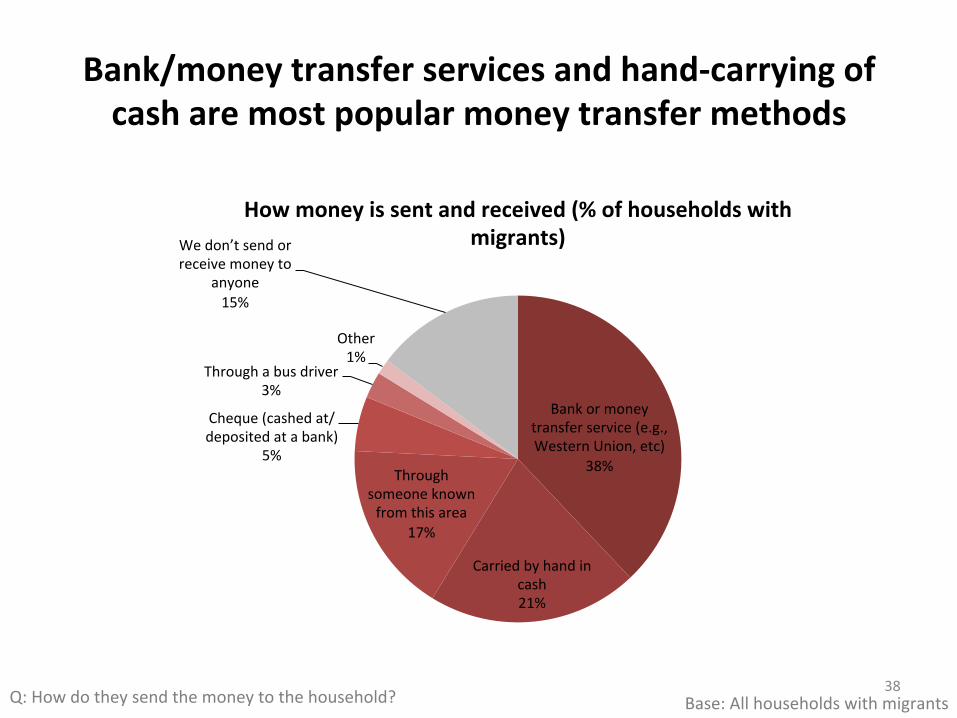

Bank/moneytransferservicesandhand-carryingofcasharemostpopularmoneytransfermethods

Base:AllhouseholdswithmigrantsQ:Howdotheysendthemoneytothehousehold? 38

Bankormoneytransferservice(e.g.,WesternUnion,etc)

38%

Carriedbyhandincash21%

Throughsomeoneknownfromthisarea

17%

Cheque(cashedat/depositedatabank)

5%

Throughabusdriver3%

Other1%

Wedon’tsendorreceivemoneyto

anyone15%

Howmoneyissentandreceived(%ofhouseholdswithmigrants)

45%

9%

46%

2016

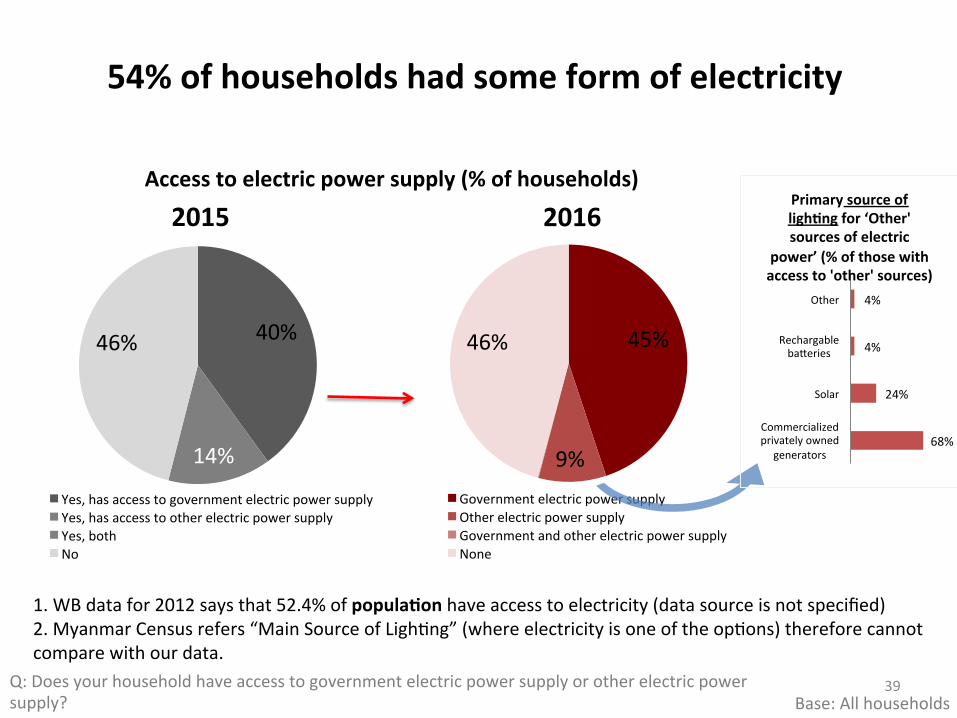

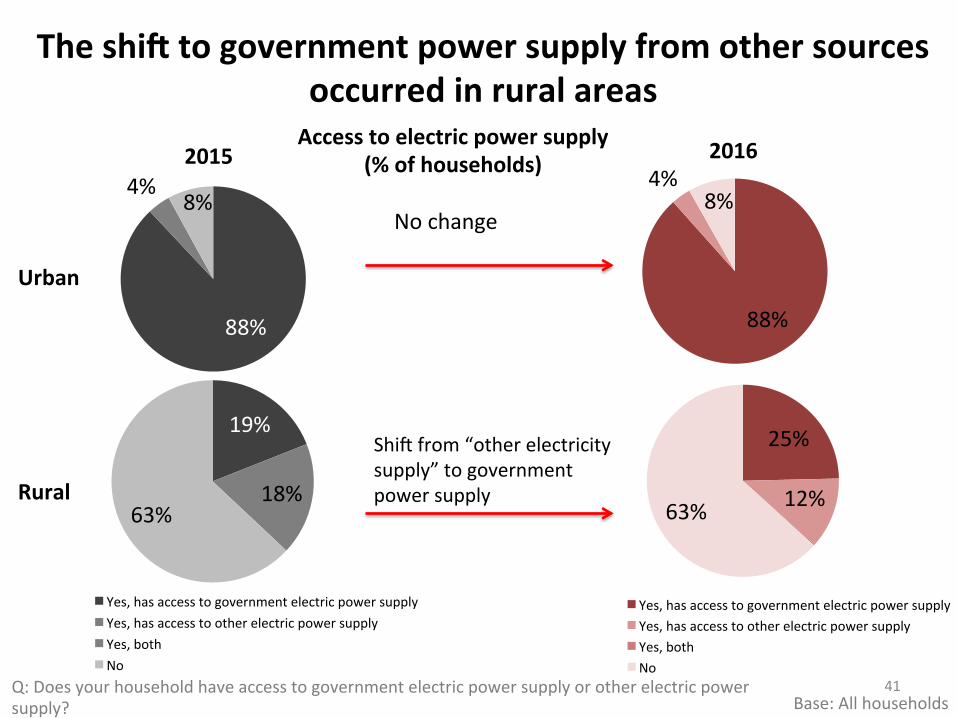

GovernmentelectricpowersupplyOtherelectricpowersupplyGovernmentandotherelectricpowersupplyNone

Q:Doesyourhouseholdhaveaccesstogovernmentelectricpowersupplyorotherelectricpowersupply?

54%ofhouseholdshadsomeformofelectricity

Base:Allhouseholds39

Accesstoelectricpowersupply(%ofhouseholds)

68%

24%

4%

4%

Commercializedprivatelyowned

generators

Solar

Rechargablebaferies

Other

Primarysourceofligh3ngfor‘Other'sourcesofelectric

power’(%ofthosewithaccessto'other'sources)

40%

14%

46%

2015

Yes,hasaccesstogovernmentelectricpowersupplyYes,hasaccesstootherelectricpowersupplyYes,bothNo

1.WBdatafor2012saysthat52.4%ofpopula3onhaveaccesstoelectricity(datasourceisnotspecified)2.MyanmarCensusrefers“MainSourceofLighAng”(whereelectricityisoneoftheopAons)thereforecannotcomparewithourdata.

Governmentownedpower

supply,88

Commercialized

privatelyownedpower

supply,3

Owngenerator

Solarpower,2

Carbafery

Rechargeable

bafery,4

Kerosene,diesel Candle,1

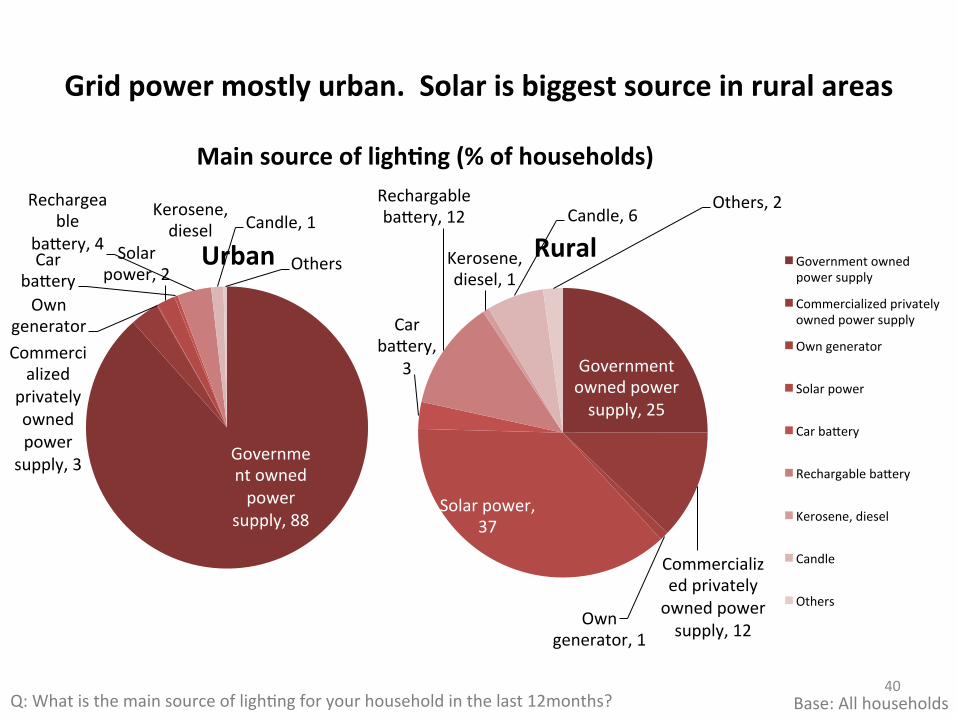

OthersUrban

Gridpowermostlyurban.Solarisbiggestsourceinruralareas

40

Mainsourceofligh3ng(%ofhouseholds)

Q:WhatisthemainsourceoflighAngforyourhouseholdinthelast12months? Base:Allhouseholds

Governmentownedpowersupply,25

Commercializedprivatelyownedpowersupply,12

Owngenerator,1

Solarpower,37

Carbafery,

3

Rechargablebafery,12

Kerosene,diesel,1

Candle,6Others,2

RuralGovernmentownedpowersupply

Commercializedprivatelyownedpowersupply

Owngenerator

Solarpower

Carbafery

Rechargablebafery

Kerosene,diesel

Candle

Others

19%

18%63%

Yes,hasaccesstogovernmentelectricpowersupplyYes,hasaccesstootherelectricpowersupplyYes,bothNo

88%

4%8%

88%

4%8%

25%

12%63%

Yes,hasaccesstogovernmentelectricpowersupplyYes,hasaccesstootherelectricpowersupplyYes,bothNo

Theshimtogovernmentpowersupplyfromothersourcesoccurredinruralareas

20162015

Nochange

Shisfrom“otherelectricitysupply”togovernmentpowersupply

Urban

Rural

41Base:Allhouseholds

Q:Doesyourhouseholdhaveaccesstogovernmentelectricpowersupplyorotherelectricpowersupply?

Accesstoelectricpowersupply(%ofhouseholds)

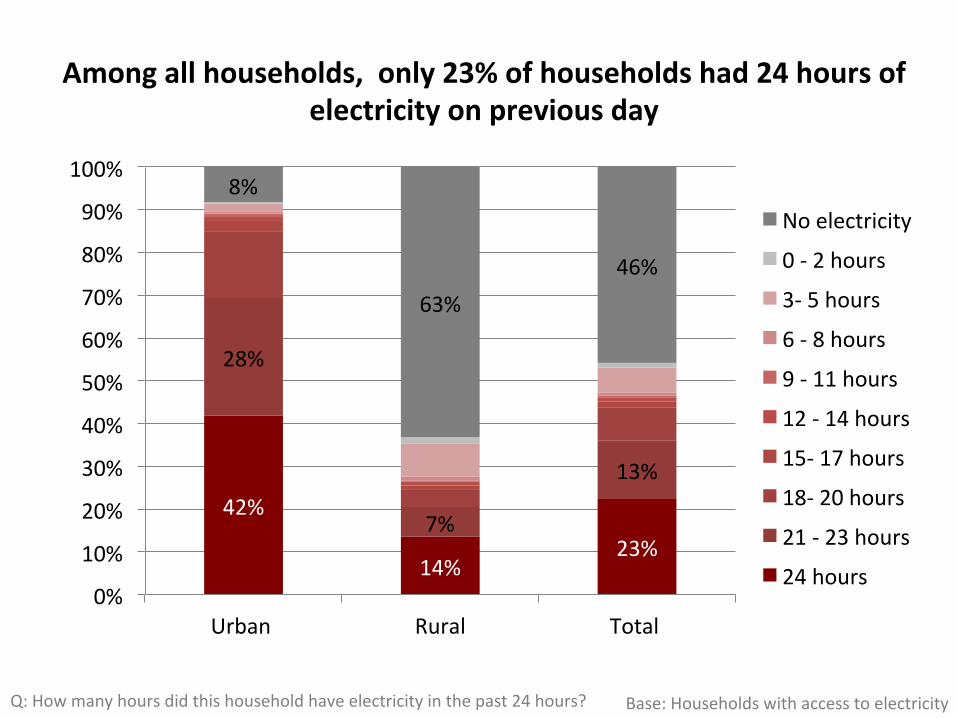

Amongallhouseholds,only23%ofhouseholdshad24hoursofelectricityonpreviousday

Q:Howmanyhoursdidthishouseholdhaveelectricityinthepast24hours? Base:Householdswithaccesstoelectricity

42%

14%23%

28%

7%

13%

8%

63%46%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Urban Rural Total

Noelectricity

0-2hours

3-5hours

6-8hours

9-11hours

12-14hours

15-17hours

18-20hours

21-23hours

24hours

HOUSEHOLDICTOWNERSHIP

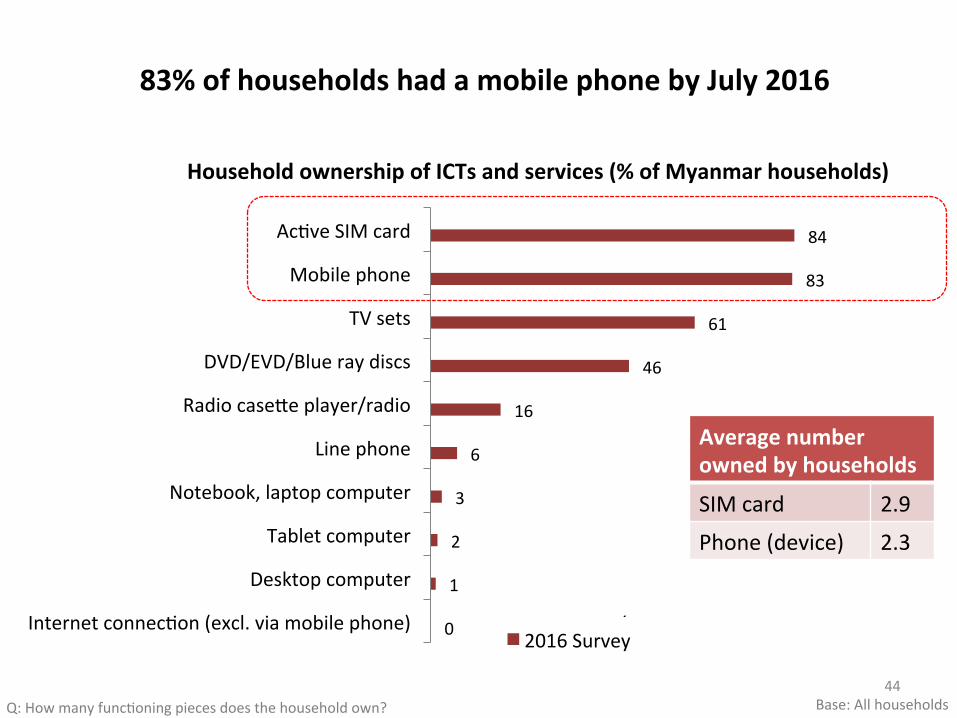

43

84

83

61

46

16

6

3

2

1

0

AcAveSIMcard

Mobilephone

TVsets

DVD/EVD/Blueraydiscs

Radiocasefeplayer/radio

Linephone

Notebook,laptopcomputer

Tabletcomputer

Desktopcomputer

InternetconnecAon(excl.viamobilephone)

HouseholdownershipofICTsandservices(%ofMyanmarhouseholds)

2015Survey

2016Survey

83%ofhouseholdshadamobilephonebyJuly2016

Averagenumberownedbyhouseholds

SIMcard 2.9

Phone(device) 2.3

Base:AllhouseholdsQ:HowmanyfuncAoningpiecesdoesthehouseholdown?44

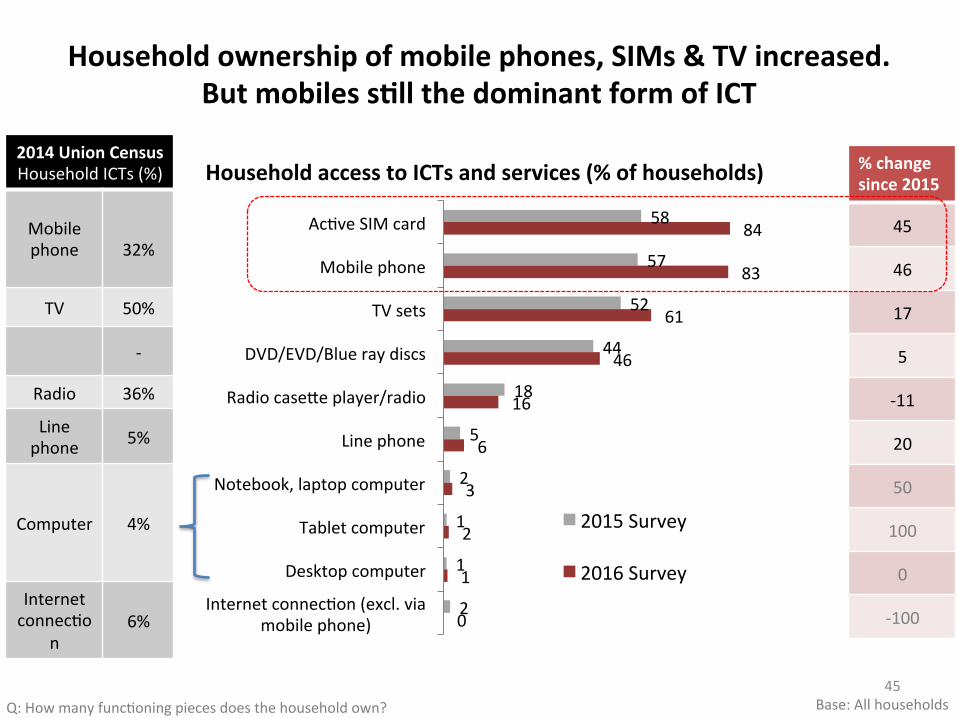

58

57

52

44

18

5

2

1

1

2

84

83

61

46

16

6

3

2

1

0

AcAveSIMcard

Mobilephone

TVsets

DVD/EVD/Blueraydiscs

Radiocasefeplayer/radio

Linephone

Notebook,laptopcomputer

Tabletcomputer

Desktopcomputer

InternetconnecAon(excl.viamobilephone)

HouseholdaccesstoICTsandservices(%ofhouseholds)

2015Survey

2016Survey

Householdownershipofmobilephones,SIMs&TVincreased.Butmobiless3llthedominantformofICT

Base:AllhouseholdsQ:HowmanyfuncAoningpiecesdoesthehouseholdown?45

2014UnionCensusHouseholdICTs(%)

Mobilephone

32%

TV 50%

-

Radio 36%

Linephone 5%

Computer 4%

InternetconnecAo

n6%

%changesince2015

45

46

17

5

-11

20

50

100

0

-100

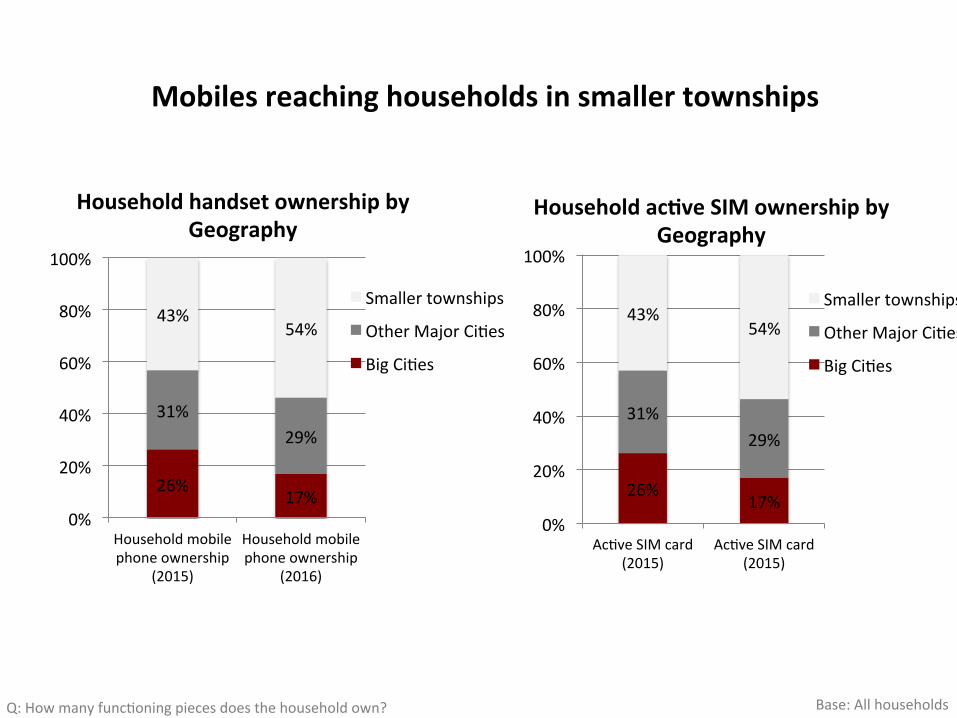

26%17%

31%29%

43%54%

0%

20%

40%

60%

80%

100%

Householdmobilephoneownership

(2015)

Householdmobilephoneownership

(2016)

HouseholdhandsetownershipbyGeography

Smallertownships

OtherMajorCiAes

BigCiAes

26%17%

31%29%

43%54%

0%

20%

40%

60%

80%

100%

AcAveSIMcard(2015)

AcAveSIMcard(2015)

Householdac3veSIMownershipbyGeography

Smallertownships

OtherMajorCiAes

BigCiAes

Mobilesreachinghouseholdsinsmallertownships

Base:AllhouseholdsQ:HowmanyfuncAoningpiecesdoesthehouseholdown?

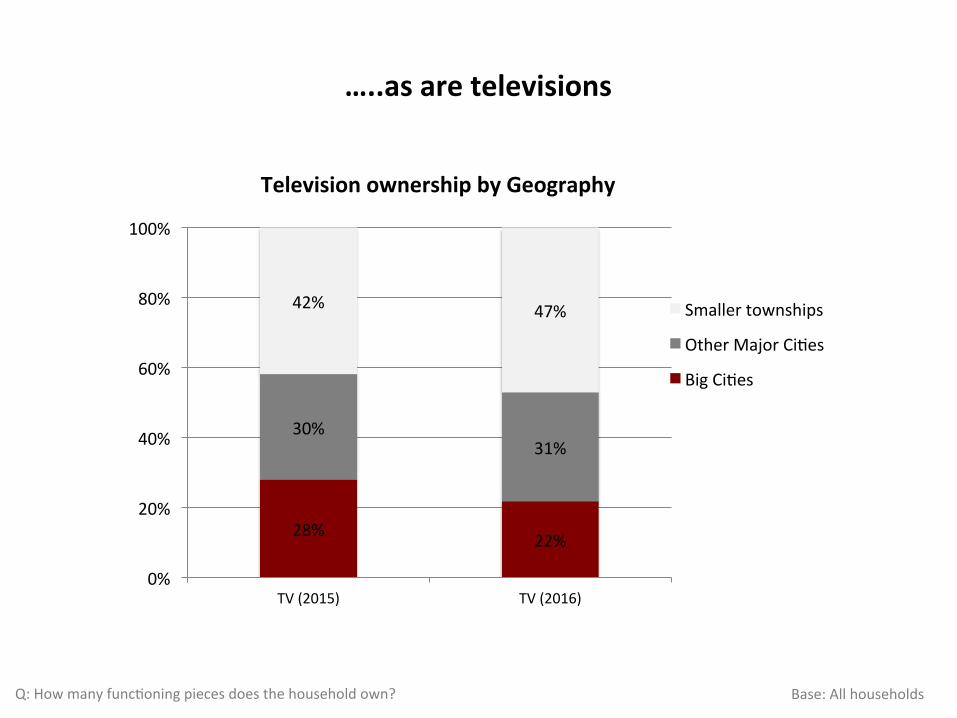

28% 22%

30%31%

42% 47%

0%

20%

40%

60%

80%

100%

TV(2015) TV(2016)

TelevisionownershipbyGeography

Smallertownships

OtherMajorCiAes

BigCiAes

…..asaretelevisions

Base:AllhouseholdsQ:HowmanyfuncAoningpiecesdoesthehouseholdown?

TELECOMUSE

48

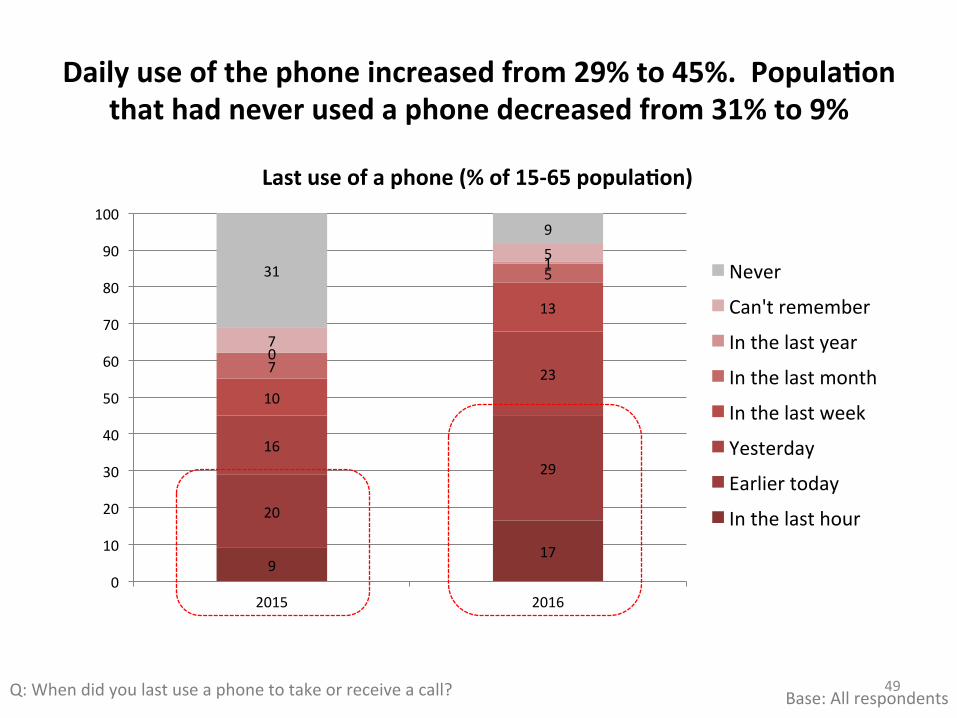

Dailyuseofthephoneincreasedfrom29%to45%.Popula3onthathadneverusedaphonedecreasedfrom31%to9%

Q:Whendidyoulastuseaphonetotakeorreceiveacall? Base:Allrespondents49

917

20

2916

2310

13

7

5

0

1

7

531

9

0

10

20

30

40

50

60

70

80

90

100

2015 2016

Lastuseofaphone(%of15-65popula3on)

Never

Can'tremember

Inthelastyear

Inthelastmonth

Inthelastweek

Yesterday

Earliertoday

Inthelasthour

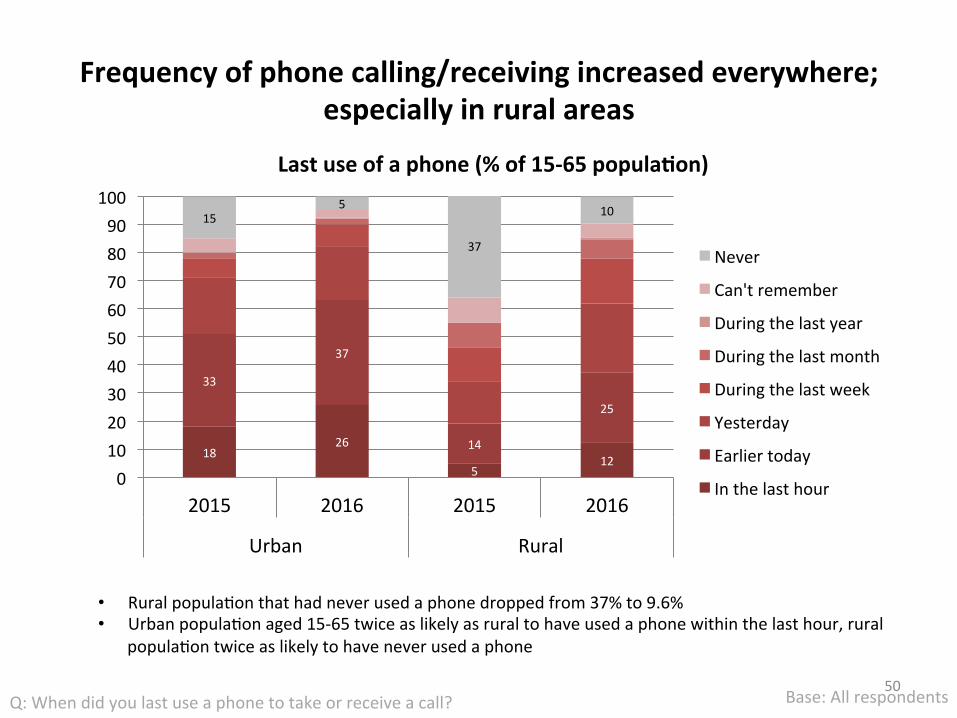

Frequencyofphonecalling/receivingincreasedeverywhere;especiallyinruralareas

50Q:Whendidyoulastuseaphonetotakeorreceiveacall? Base:Allrespondents

• RuralpopulaAonthathadneverusedaphonedroppedfrom37%to9.6%• UrbanpopulaAonaged15-65twiceaslikelyasruraltohaveusedaphonewithinthelasthour,rural

populaAontwiceaslikelytohaveneverusedaphone

1826

512

33

37

14

25

155

37

10

0102030405060708090

100

2015 2016 2015 2016

Urban Rural

Lastuseofaphone(%of15-65popula3on)

Never

Can'tremember

Duringthelastyear

Duringthelastmonth

Duringthelastweek

Yesterday

Earliertoday

Inthelasthour

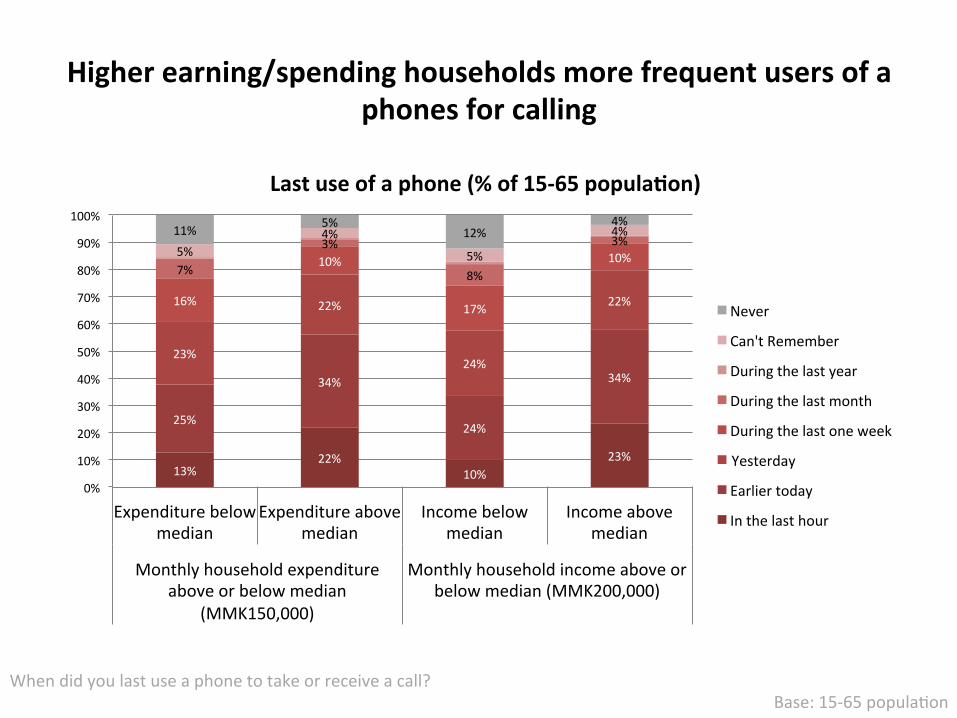

Higherearning/spendinghouseholdsmorefrequentusersofaphonesforcalling

Whendidyoulastuseaphonetotakeorreceiveacall?Base:15-65populaAon

13%22%

10%23%

25%

34%

24%

34%

23%

22%

24%

22%16%

10%

17%

10%7%

3%

8%

3%5%

4%

5%

4%11% 5%12%

4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Expenditurebelowmedian

Expenditureabovemedian

Incomebelowmedian

Incomeabovemedian

Monthlyhouseholdexpenditureaboveorbelowmedian

(MMK150,000)

Monthlyhouseholdincomeaboveorbelowmedian(MMK200,000)

Lastuseofaphone(%of15-65popula3on)

Never

Can'tRemember

Duringthelastyear

Duringthelastmonth

Duringthelastoneweek

Yesterday

Earliertoday

Inthelasthour

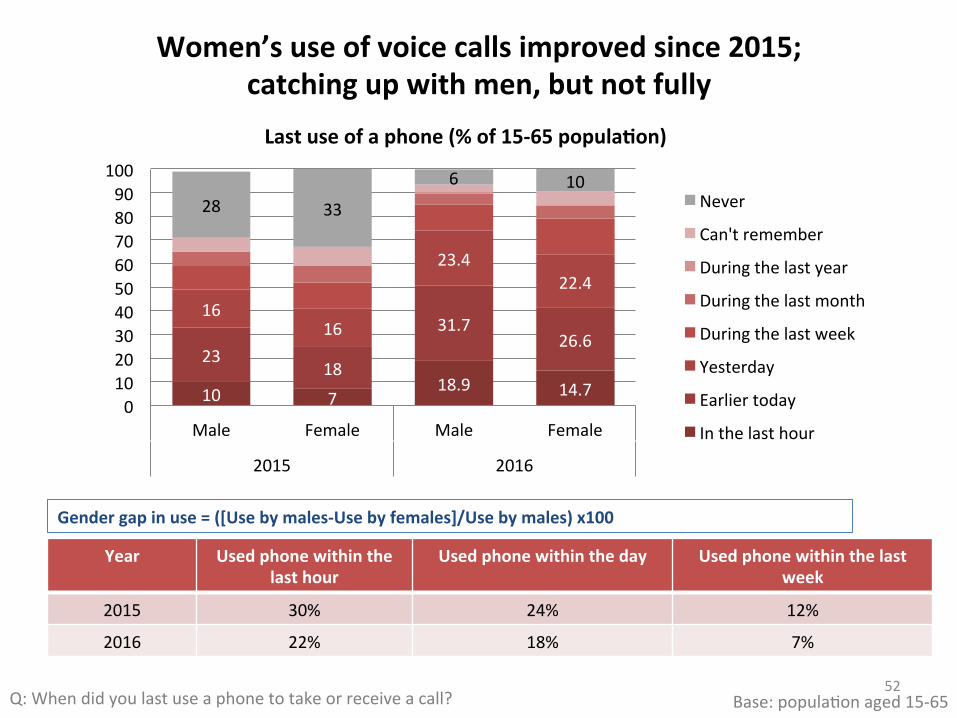

Women’suseofvoicecallsimprovedsince2015;catchingupwithmen,butnotfully

Year Usedphonewithinthelasthour

Usedphonewithintheday

Usedphonewithinthelastweek

2015 30% 24% 12%

2016 22% 18% 7%

Q:Whendidyoulastuseaphonetotakeorreceiveacall? Base:populaAonaged15-65

10 718.9 14.7

2318

31.726.6

1616

23.422.4

28 33

6 10

0102030405060708090

100

Male Female Male Female

2015 2016

Lastuseofaphone(%of15-65popula3on)

Never

Can'tremember

Duringthelastyear

Duringthelastmonth

Duringthelastweek

Yesterday

Earliertoday

Inthelasthour

Gendergapinuse=([Usebymales-Usebyfemales]/Usebymales)x100

52

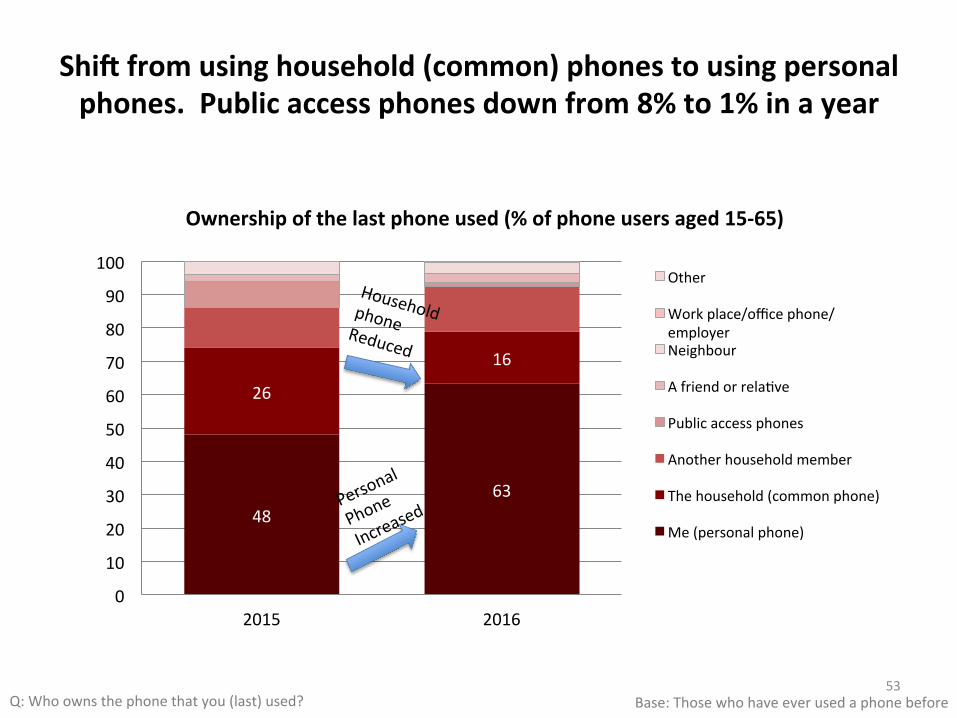

Shimfromusinghousehold(common)phonestousingpersonalphones.Publicaccessphonesdownfrom8%to1%inayear

Q:Whoownsthephonethatyou(last)used?

53

4863

26

16

0

10

20

30

40

50

60

70

80

90

100

2015 2016

Ownershipofthelastphoneused(%ofphoneusersaged15-65)

Other

Workplace/officephone/employerNeighbour

AfriendorrelaAve

Publicaccessphones

Anotherhouseholdmember

Thehousehold(commonphone)

Me(personalphone)

Base:Thosewhohaveeverusedaphonebefore

HouseholdphoneReduced

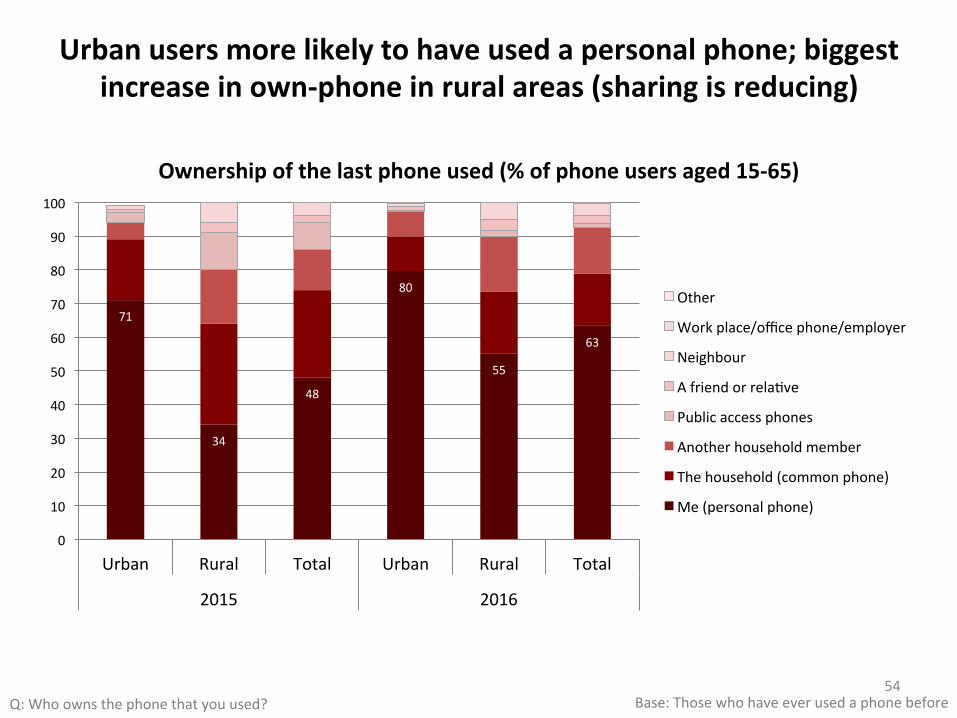

Urbanusersmorelikelytohaveusedapersonalphone;biggestincreaseinown-phoneinruralareas(sharingisreducing)

Q:Whoownsthephonethatyouused?54

Base:Thosewhohaveeverusedaphonebefore

71

34

48

80

55

63

0

10

20

30

40

50

60

70

80

90

100

Urban Rural Total Urban Rural Total

2015 2016

Ownershipofthelastphoneused(%ofphoneusersaged15-65)

Other

Workplace/officephone/employer

Neighbour

AfriendorrelaAve

Publicaccessphones

Anotherhouseholdmember

Thehousehold(commonphone)

Me(personalphone)

Q:Whoownsthephonethatyouused?

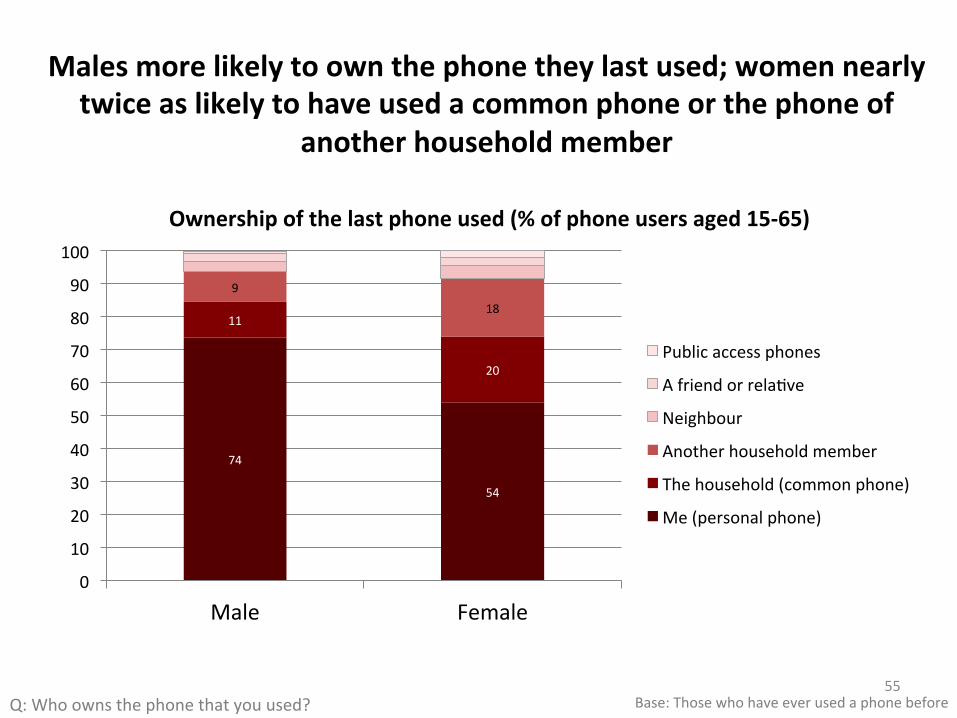

Malesmorelikelytoownthephonetheylastused;womennearlytwiceaslikelytohaveusedacommonphoneorthephoneof

anotherhouseholdmember

55

74

54

11

20

918

0

10

20

30

40

50

60

70

80

90

100

Male Female

Ownershipofthelastphoneused(%ofphoneusersaged15-65)

Publicaccessphones

AfriendorrelaAve

Neighbour

Anotherhouseholdmember

Thehousehold(commonphone)

Me(personalphone)

Base:Thosewhohaveeverusedaphonebefore

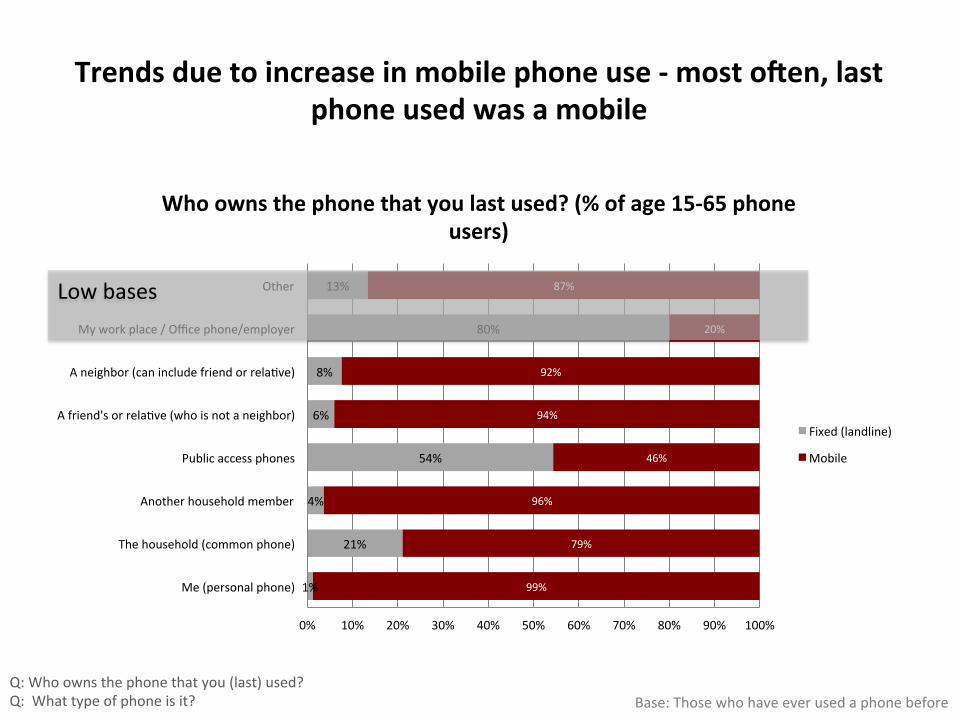

Trendsduetoincreaseinmobilephoneuse-mostomen,lastphoneusedwasamobile

Q:Whoownsthephonethatyou(last)used?Q:Whattypeofphoneisit?

Base:Thosewhohaveeverusedaphonebefore

1%

21%

4%

54%

6%

8%

80%

13%

99%

79%

96%

46%

94%

92%

20%

87%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Me(personalphone)

Thehousehold(commonphone)

Anotherhouseholdmember

Publicaccessphones

Afriend'sorrelaAve(whoisnotaneighbor)

Aneighbor(canincludefriendorrelaAve)

Myworkplace/Officephone/employer

Other

Whoownsthephonethatyoulastused?(%ofage15-65phoneusers)

Fixed(landline)

Mobile

Lowbases

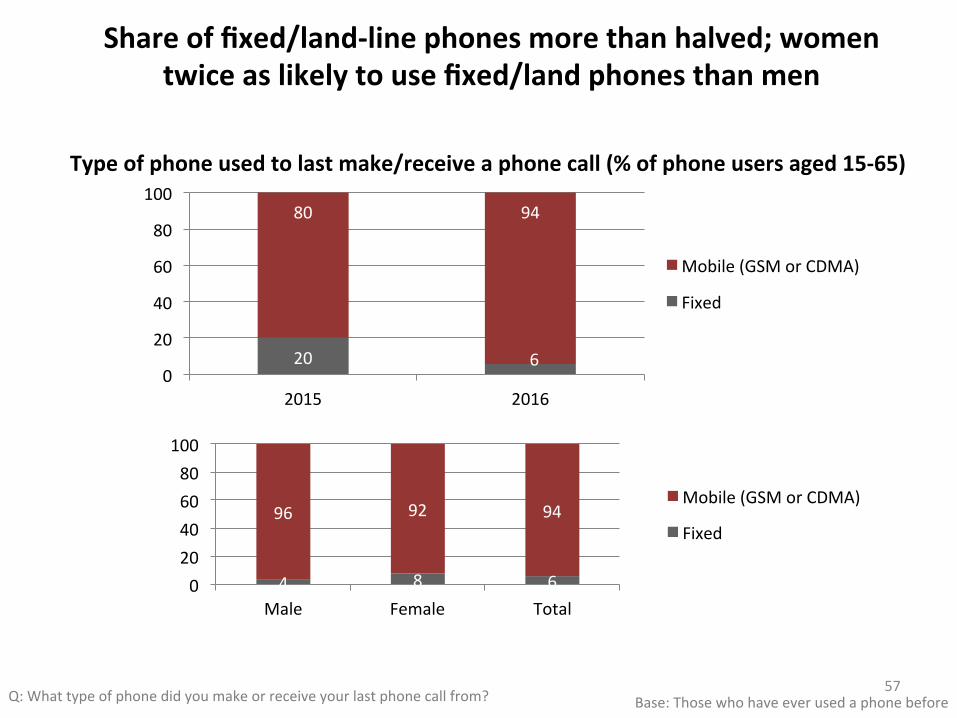

Shareoffixed/land-linephonesmorethanhalved;womentwiceaslikelytousefixed/landphonesthanmen

Base:Thosewhohaveeverusedaphonebefore

4 8 6

96 92 94

020406080

100

Male Female Total

Mobile(GSMorCDMA)

Fixed

Q:Whattypeofphonedidyoumakeorreceiveyourlastphonecallfrom?

57

20 6

80 94

0

20

40

60

80

100

2015 2016

Mobile(GSMorCDMA)

Fixed

Typeofphoneusedtolastmake/receiveaphonecall(%ofphoneusersaged15-65)

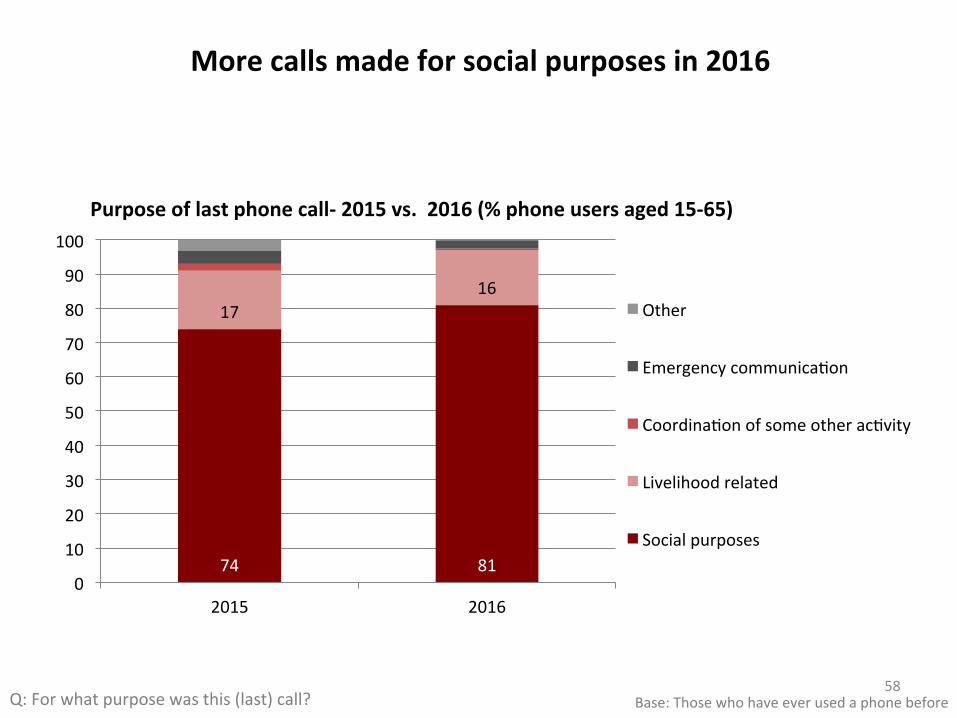

Q:Forwhatpurposewasthis(last)call?

Morecallsmadeforsocialpurposesin2016

58

74 81

1716

0

10

20

30

40

50

60

70

80

90

100

2015 2016

Purposeoflastphonecall-2015vs.2016(%phoneusersaged15-65)

Other

EmergencycommunicaAon

CoordinaAonofsomeotheracAvity

Livelihoodrelated

Socialpurposes

Base:Thosewhohaveeverusedaphonebefore

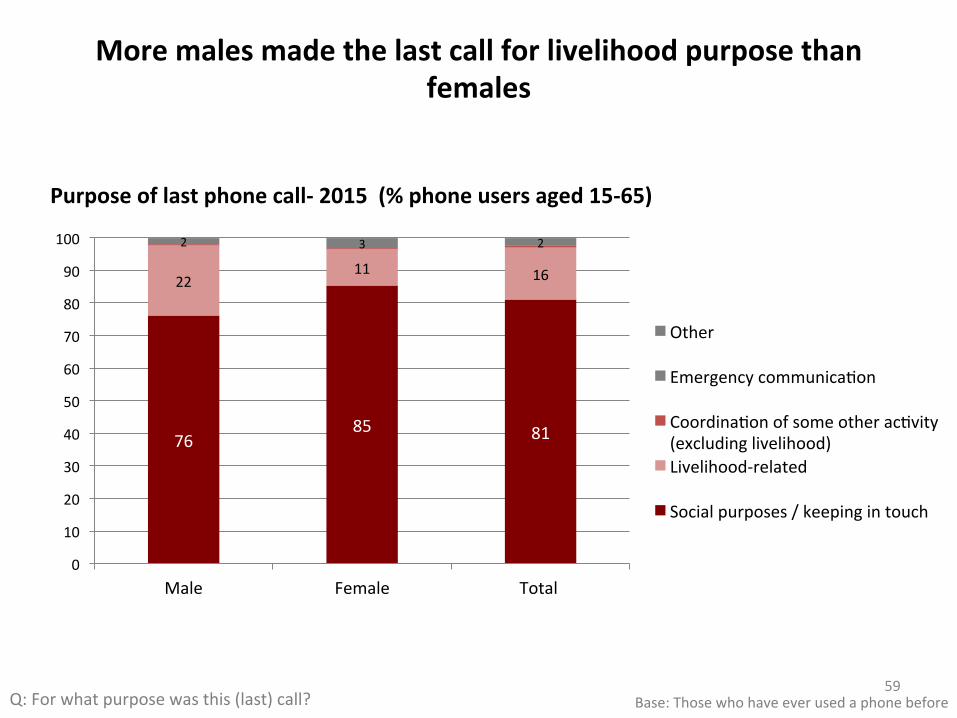

7685 81

2211 16

2 3 2

0

10

20

30

40

50

60

70

80

90

100

Male Female Total

Purposeoflastphonecall-2015(%phoneusersaged15-65)

Other

EmergencycommunicaAon

CoordinaAonofsomeotheracAvity(excludinglivelihood)Livelihood-related

Socialpurposes/keepingintouch

Moremalesmadethelastcallforlivelihoodpurposethanfemales

Q:Forwhatpurposewasthis(last)call?59

Base:Thosewhohaveeverusedaphonebefore

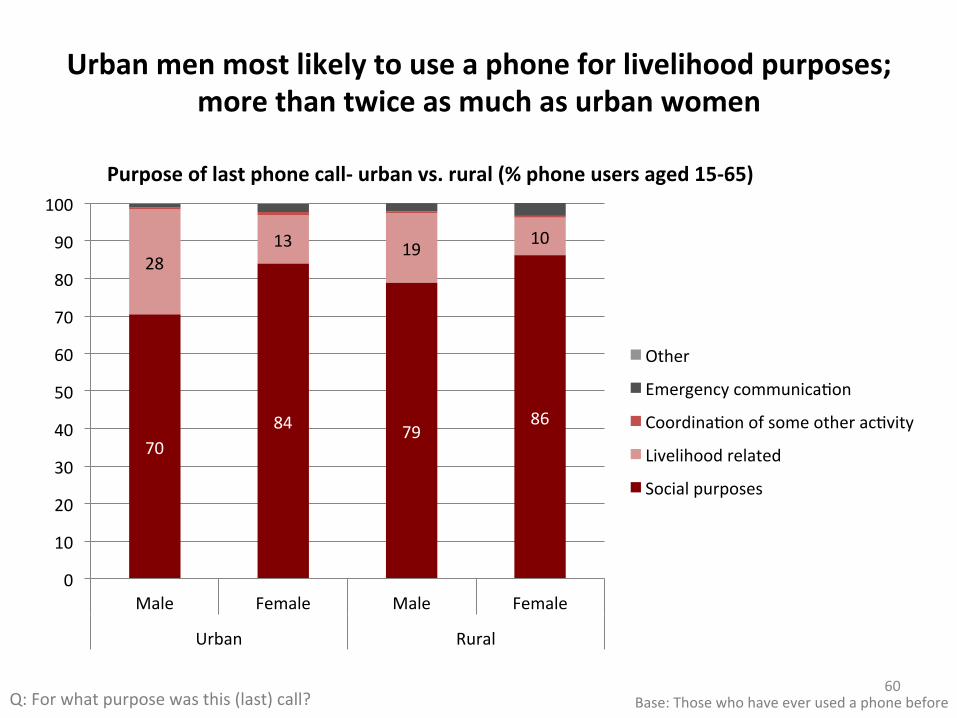

Urbanmenmostlikelytouseaphoneforlivelihoodpurposes;morethantwiceasmuchasurbanwomen

7084 79

86

2813 19 10

0

10

20

30

40

50

60

70

80

90

100

Male Female Male Female

Urban Rural

Purposeoflastphonecall-urbanvs.rural(%phoneusersaged15-65)

Other

EmergencycommunicaAon

CoordinaAonofsomeotheracAvity

Livelihoodrelated

Socialpurposes

60Base:ThosewhohaveeverusedaphonebeforeQ:Forwhatpurposewasthis(last)call?

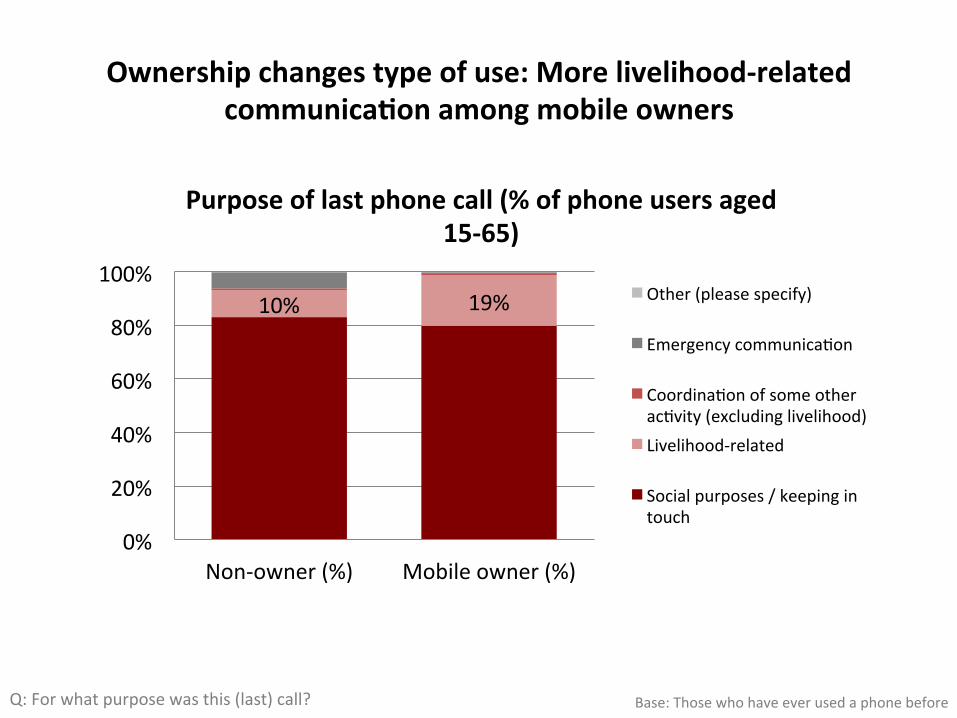

Ownershipchangestypeofuse:Morelivelihood-relatedcommunica3onamongmobileowners

10% 19%

0%

20%

40%

60%

80%

100%

Non-owner(%) Mobileowner(%)

Purposeoflastphonecall(%ofphoneusersaged15-65)

Other(pleasespecify)

EmergencycommunicaAon

CoordinaAonofsomeotheracAvity(excludinglivelihood)Livelihood-related

Socialpurposes/keepingintouch

Q:Forwhatpurposewasthis(last)call? Base:Thosewhohaveeverusedaphonebefore

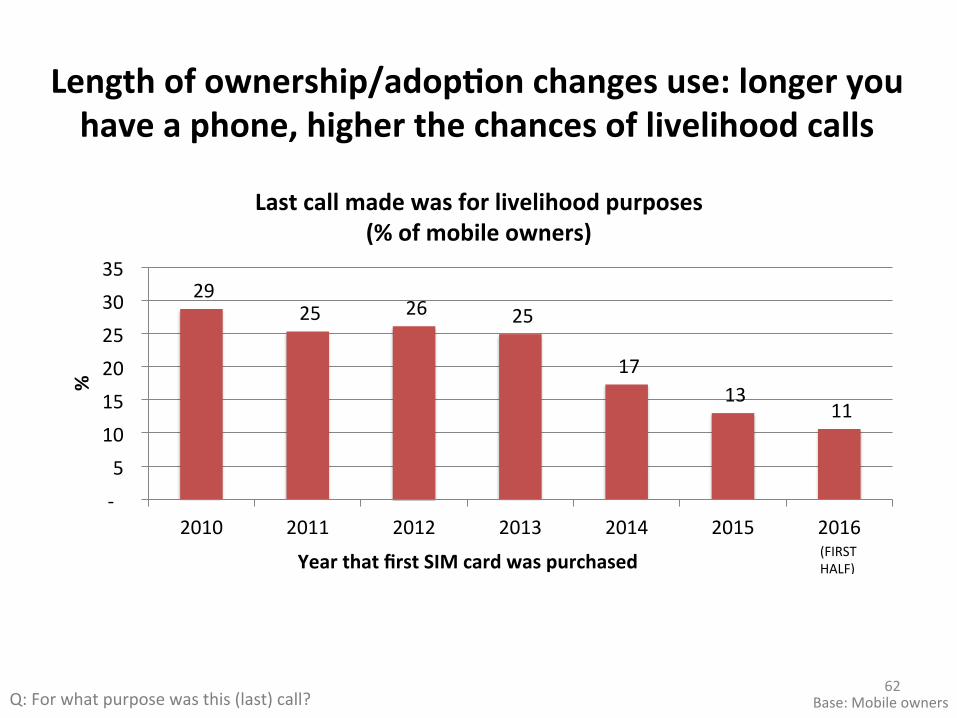

Lengthofownership/adop3onchangesuse:longeryouhaveaphone,higherthechancesoflivelihoodcalls

2925 26 25

1713

11

-5101520253035

2010 2011 2012 2013 2014 2015 2016

%

YearthatfirstSIMcardwaspurchased

Lastcallmadewasforlivelihoodpurposes(%ofmobileowners)

(FIRSTHALF)

62Base:MobileownersQ:Forwhatpurposewasthis(last)call?

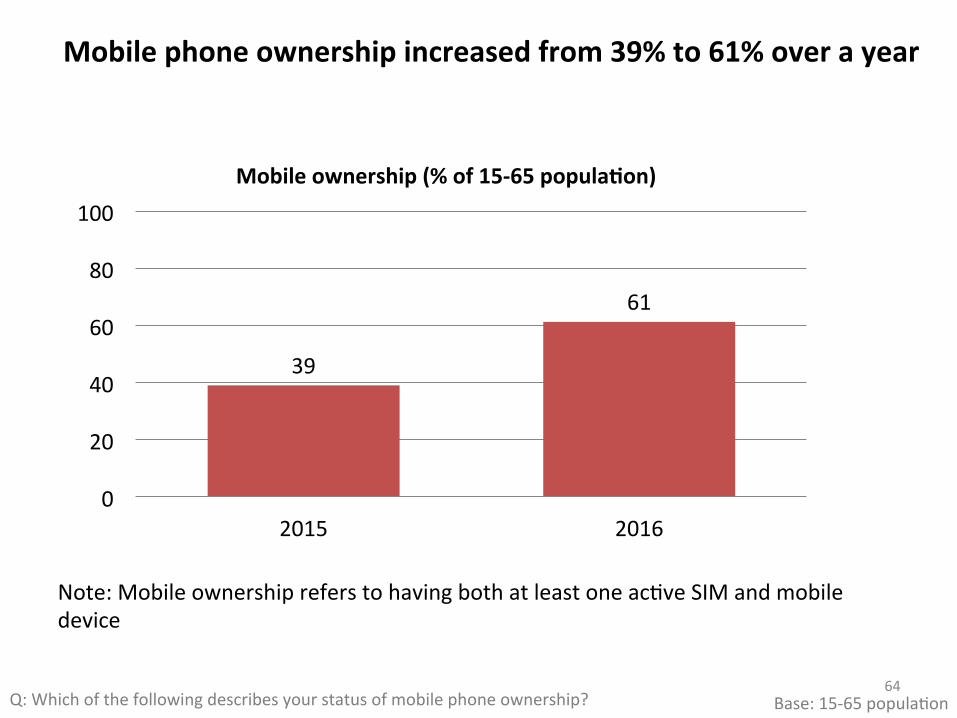

MOBILEOWNERSHIP

Q:Whichofthefollowingdescribesyourstatusofmobilephoneownership?

Mobilephoneownershipincreasedfrom39%to61%overayear

64

39

61

0

20

40

60

80

100

2015 2016

Mobileownership(%of15-65popula3on)

Note:MobileownershipreferstohavingbothatleastoneacAveSIMandmobiledevice

Base:15-65populaAon

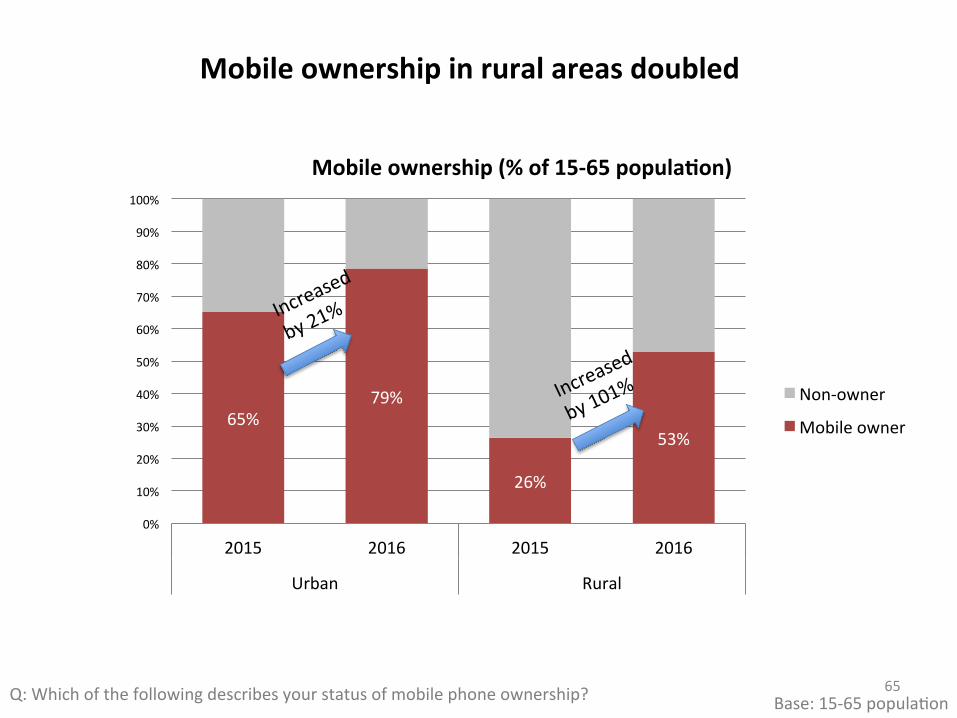

65%79%

26%

53%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2016 2015 2016

Urban Rural

Mobileownership(%of15-65popula3on)

Non-owner

Mobileowner

Mobileownershipinruralareasdoubled

Q:Whichofthefollowingdescribesyourstatusofmobilephoneownership?

65Base:15-65populaAon

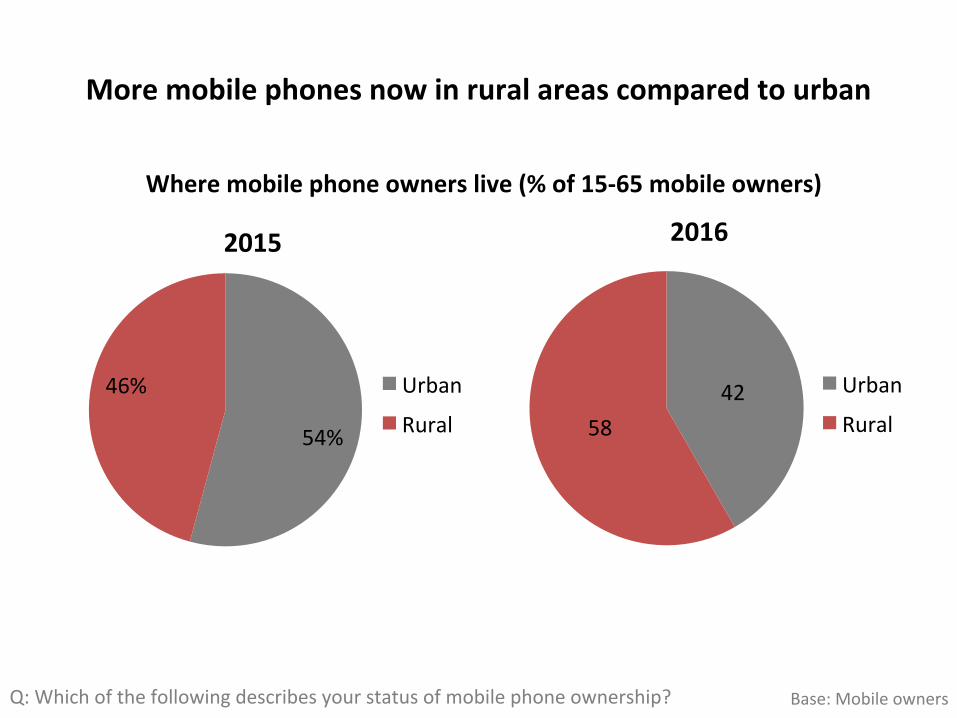

4258

2016

Urban

Rural

Wheremobilephoneownerslive(%of15-65mobileowners)

Moremobilephonesnowinruralareascomparedtourban

Q:Whichofthefollowingdescribesyourstatusofmobilephoneownership?

Base:Mobileowners

54%

46%

2015

Urban

Rural

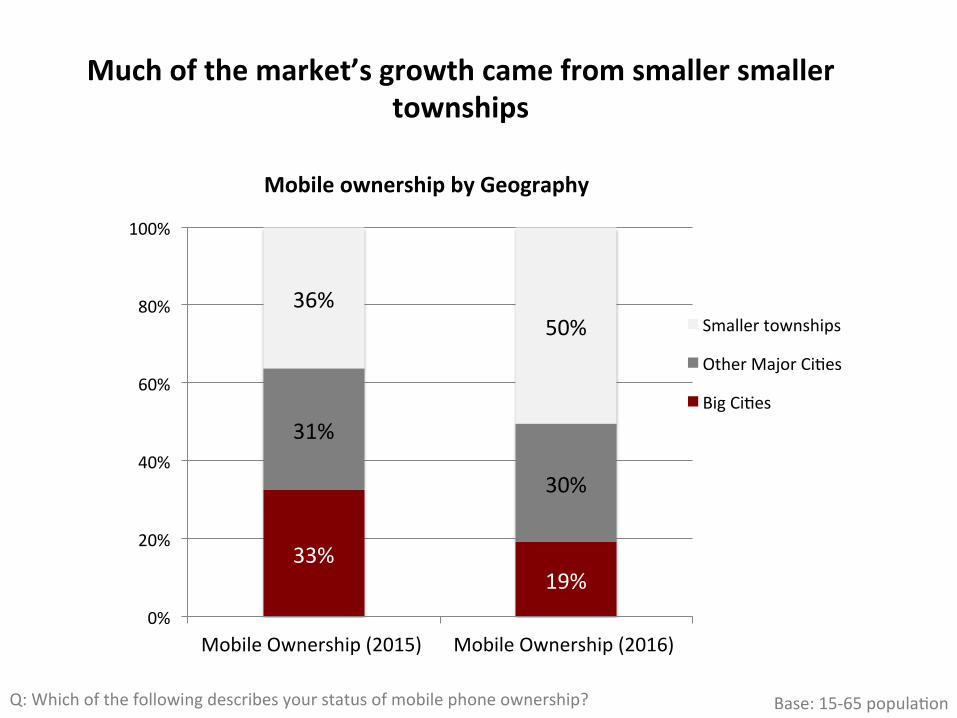

33%19%

31%

30%

36%50%

0%

20%

40%

60%

80%

100%

MobileOwnership(2015) MobileOwnership(2016)

MobileownershipbyGeography

Smallertownships

OtherMajorCiAes

BigCiAes

Muchofthemarket’sgrowthcamefromsmallersmallertownships

Q:Whichofthefollowingdescribesyourstatusofmobilephoneownership?

Base:15-65populaAon

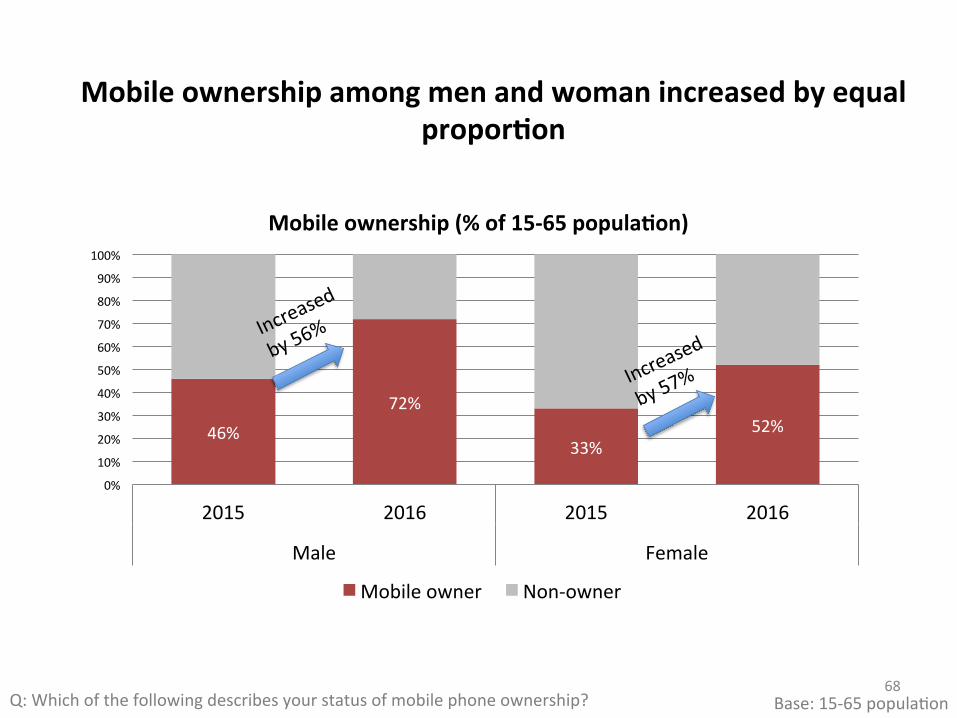

Mobileownershipamongmenandwomanincreasedbyequalpropor3on

Q:Whichofthefollowingdescribesyourstatusofmobilephoneownership?68

46%

72%

33%52%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2016 2015 2016

Male Female

Mobileownership(%of15-65popula3on)

Mobileowner Non-owner

Base:15-65populaAon

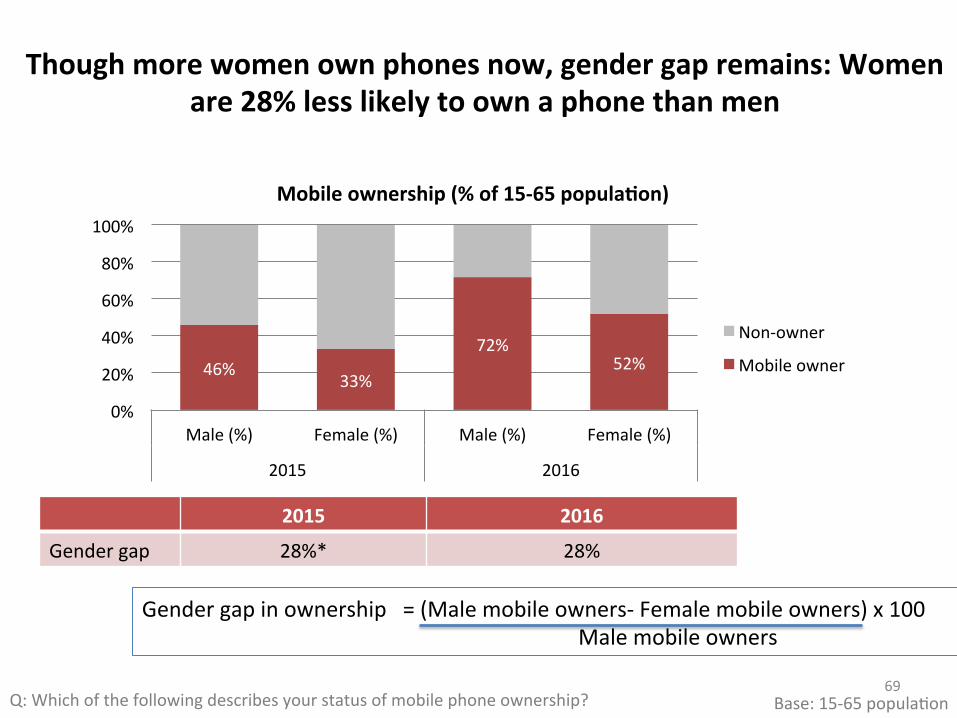

Thoughmorewomenownphonesnow,gendergapremains:Womenare28%lesslikelytoownaphonethanmen

2015 2016

Gendergap 28%* 28%

Q:Whichofthefollowingdescribesyourstatusofmobilephoneownership?69

Gendergapinownership=(Malemobileowners-Femalemobileowners)x100 Malemobileowners

Base:15-65populaAon

46%33%

72%52%

0%

20%

40%

60%

80%

100%

Male(%) Female(%) Male(%) Female(%)

2015 2016

Mobileownership(%of15-65popula3on)

Non-owner

Mobileowner

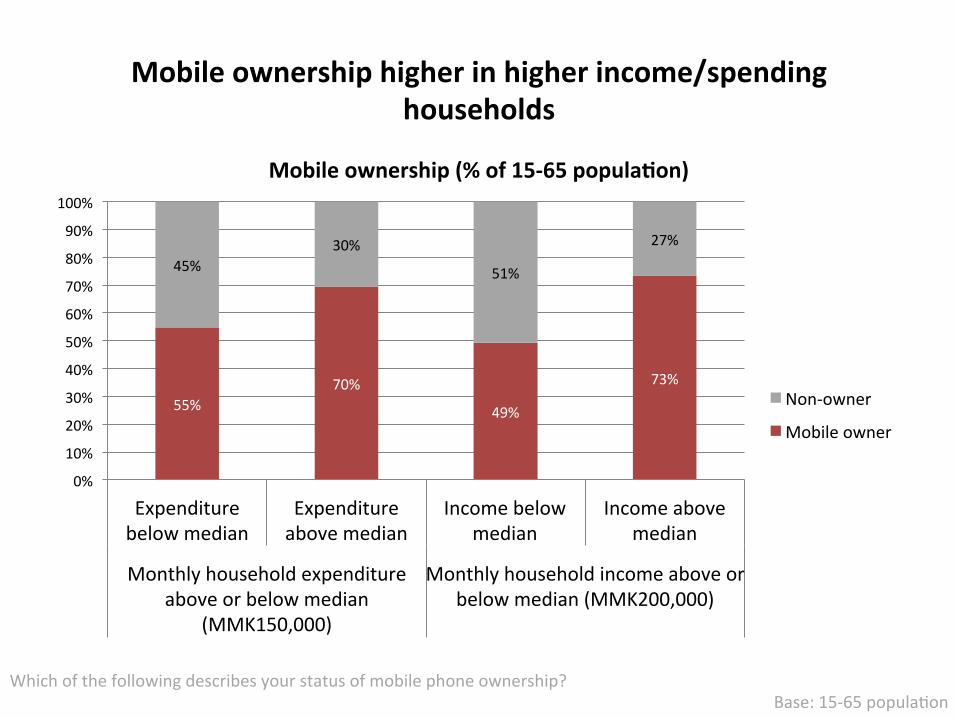

Mobileownershiphigherinhigherincome/spendinghouseholds

55%70%

49%

73%

45%30%

51%

27%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Expenditurebelowmedian

Expenditureabovemedian

Incomebelowmedian

Incomeabovemedian

Monthlyhouseholdexpenditureaboveorbelowmedian

(MMK150,000)

Monthlyhouseholdincomeaboveorbelowmedian(MMK200,000)

Mobileownership(%of15-65popula3on)

Non-owner

Mobileowner

Whichofthefollowingdescribesyourstatusofmobilephoneownership?Base:15-65populaAon

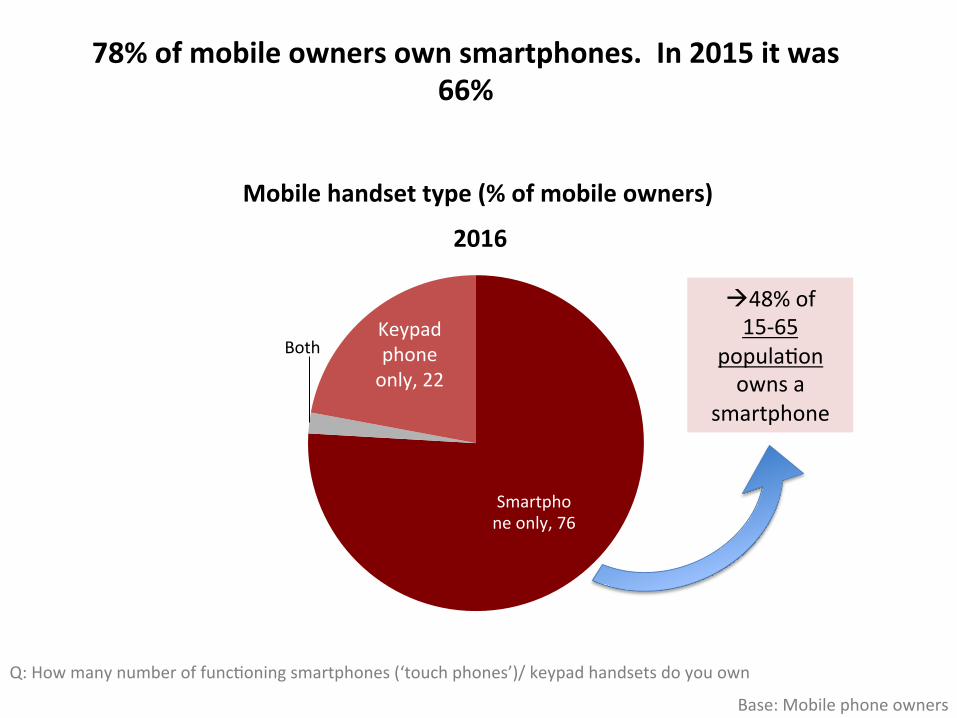

Smartphoneonly,76

Smartphoneandkeypadphone,2

Keypadphoneonly,22

2016

Both

78%ofmobileownersownsmartphones.In2015itwas66%

Q:HowmanynumberoffuncAoningsmartphones(‘touchphones’)/keypadhandsetsdoyouown

Base:Mobilephoneowners

Mobilehandsettype(%ofmobileowners)

à48%of15-65

populaAonownsa

smartphone

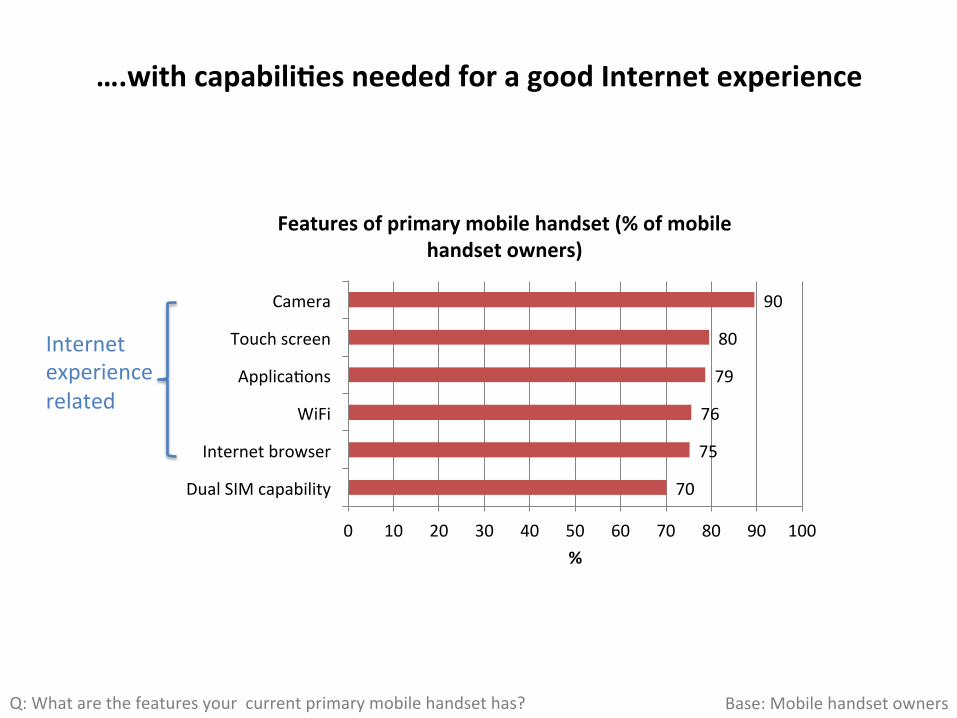

….withcapabili3esneededforagoodInternetexperience

70

75

76

79

80

90

0 10 20 30 40 50 60 70 80 90 100

DualSIMcapability

Internetbrowser

WiFi

ApplicaAons

Touchscreen

Camera

%

Featuresofprimarymobilehandset(%ofmobilehandsetowners)

Q:Whatarethefeaturesyourcurrentprimarymobilehandsethas?

Internetexperiencerelated

Base:Mobilehandsetowners

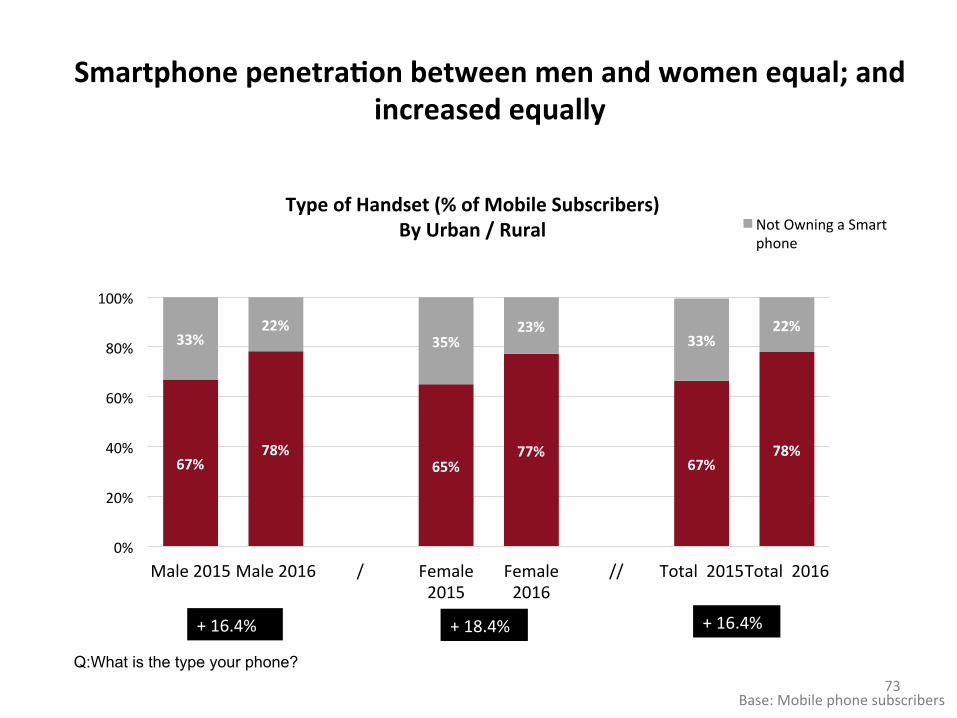

Smartphonepenetra3onbetweenmenandwomenequal;andincreasedequally

Base:Mobilephonesubscribers73

67%78%

65%77%

67%78%

33%22%

35%23%

33%22%

0%

20%

40%

60%

80%

100%

Male2015Male2016 / Female2015

Female2016

// Total2015Total2016

TypeofHandset(%ofMobileSubscribers)ByUrban/Rural NotOwningaSmart

phone

Q:What is the type your phone?

+16.4% +18.4% +16.4%

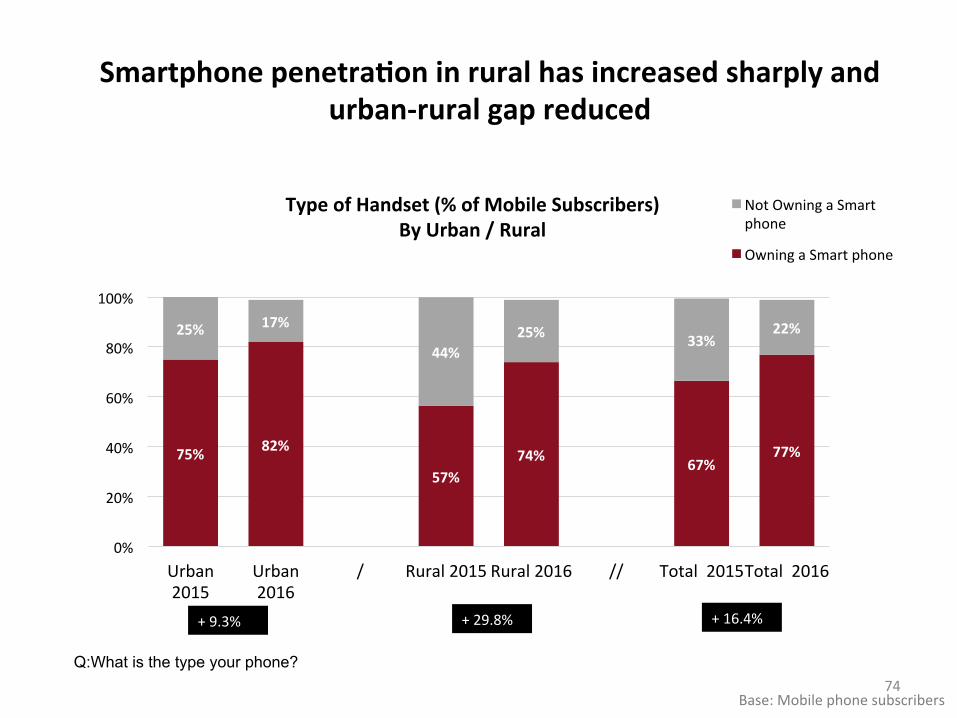

Smartphonepenetra3oninruralhasincreasedsharplyandurban-ruralgapreduced

Base:Mobilephonesubscribers74

75% 82%

57%74% 67%

77%

25% 17%

44%25% 33%

22%

0%

20%

40%

60%

80%

100%

Urban2015

Urban2016

/ Rural2015Rural2016 // Total2015Total2016

TypeofHandset(%ofMobileSubscribers)ByUrban/Rural

NotOwningaSmartphone

OwningaSmartphone

Q:What is the type your phone?

+16.4%+29.8%+9.3%

84%

73%

57%51%

44%

67%

93%84%

76%

62%55%

78%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

15-24years 25-34years 35-44years 45-54years 55-64years OverallMyanmar

SmartPhonePenetra3on(%ofMobileOwners)

2015Survey

Base:AllMobileOwners

Smartphoneownerships3llhighestamongyoungeragegroups;buttheolderarecatchingup

75

+10.7% +15.0% +33.3% +21.5% +24.0% +16.4%

75Q:What is the type your phone?

%increasesince2015

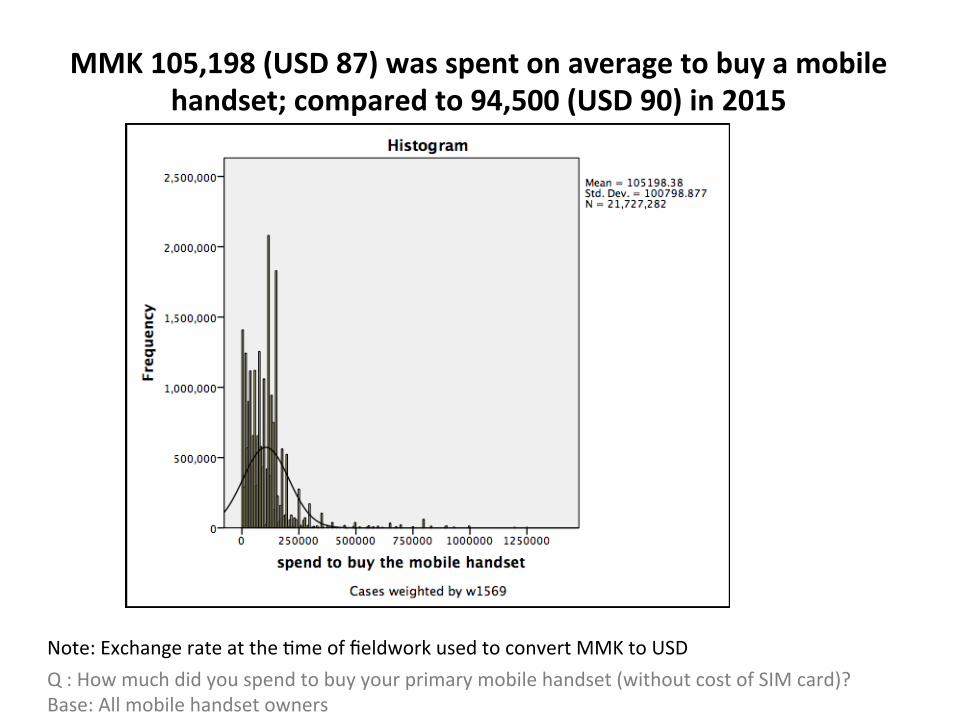

Q:Howmuchdidyouspendtobuyyourprimarymobilehandset(withoutcostofSIMcard)?Base:Allmobilehandsetowners

MMK105,198(USD87)wasspentonaveragetobuyamobilehandset;comparedto94,500(USD90)in2015

Note:ExchangerateattheAmeoffieldworkusedtoconvertMMKtoUSD

MULTIPLESIMUSEANDTOPPING-UP

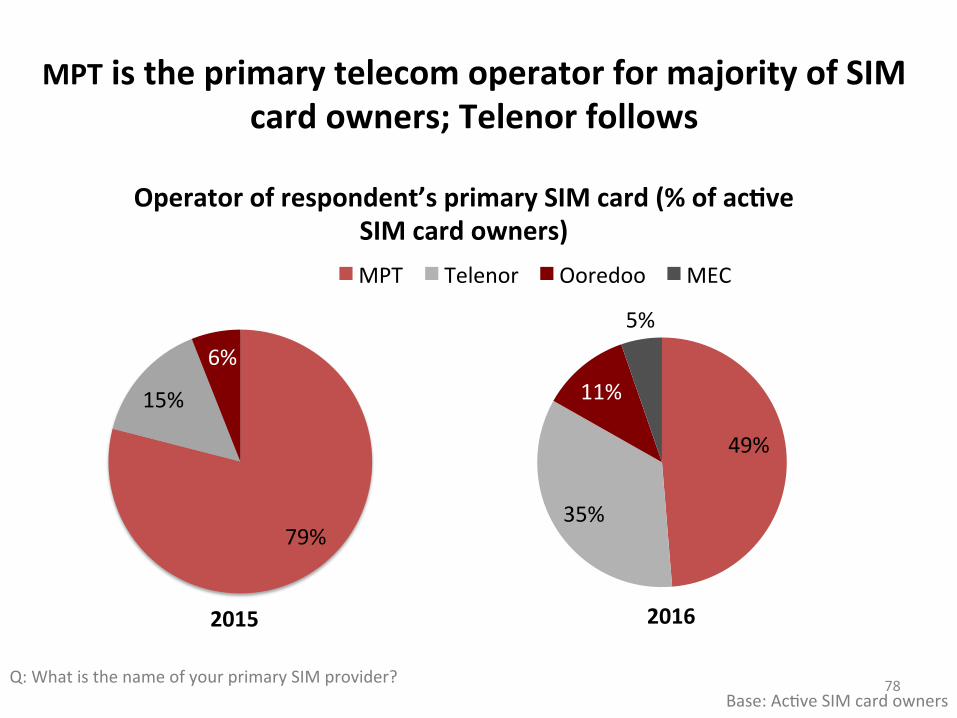

MPTistheprimarytelecomoperatorformajorityofSIMcardowners;Telenorfollows

49%

35%

11%

5%

MPT Telenor Ooredoo MEC

Q:WhatisthenameofyourprimarySIMprovider? 78Base:AcAveSIMcardowners

Operatorofrespondent’sprimarySIMcard(%ofac3veSIMcardowners)

79%

15%

6%

2015 2016

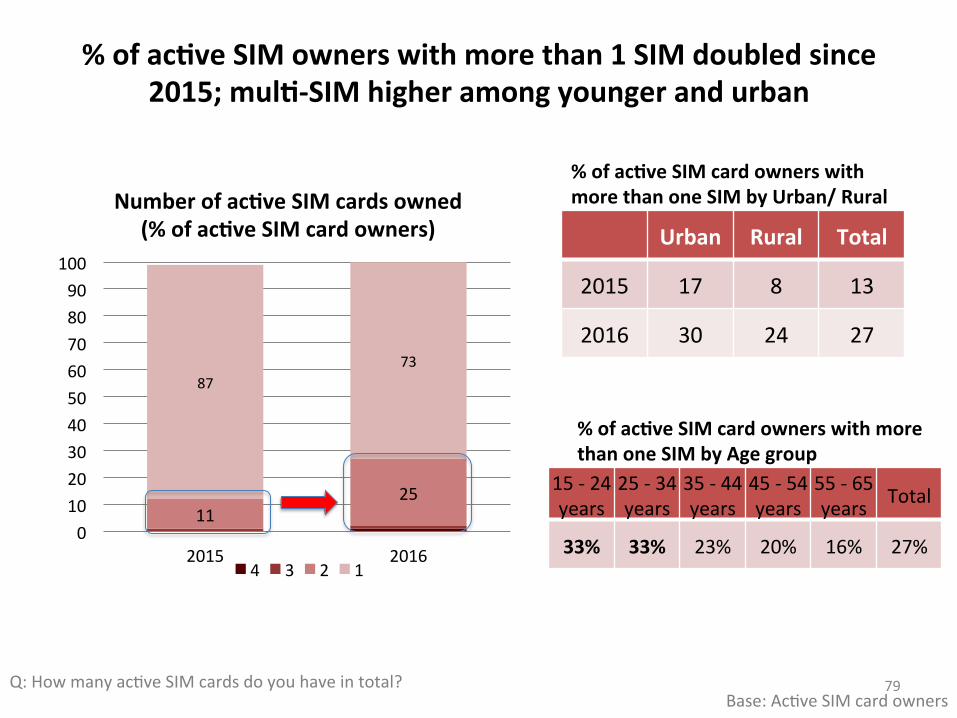

%ofac3veSIMownerswithmorethan1SIMdoubledsince2015;mul3-SIMhigheramongyoungerandurban

79Q:HowmanyacAveSIMcardsdoyouhaveintotal?

Urban Rural Total

2015 17 8 13

2016 30 24 27

%ofac3veSIMcardownerswithmorethanoneSIMbyUrban/Rural

1125

8773

0102030405060708090

100

2015 2016

Numberofac3veSIMcardsowned(%ofac3veSIMcardowners)

4 3 2 1

Base:AcAveSIMcardowners

15-24years

25-34years

35-44years

45-54years

55-65years Total

33% 33% 23% 20% 16% 27%

%ofac3veSIMcardownerswithmorethanoneSIMbyAgegroup

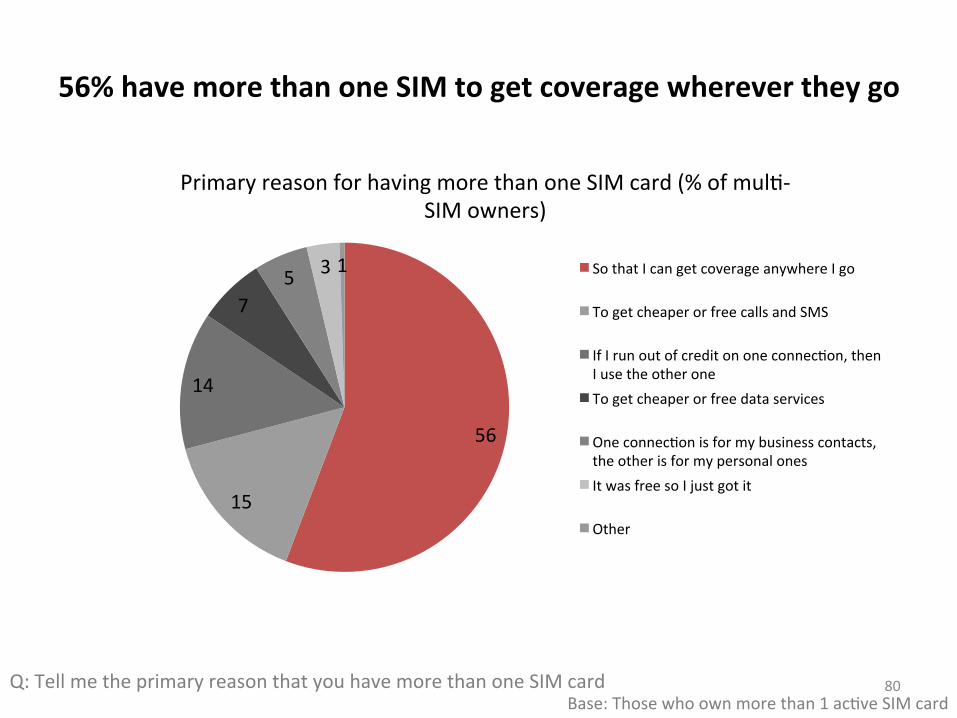

56%havemorethanoneSIMtogetcoveragewherevertheygo

Q:TellmetheprimaryreasonthatyouhavemorethanoneSIMcard

80

56

15

14

75 31

PrimaryreasonforhavingmorethanoneSIMcard(%ofmulA-SIMowners)

SothatIcangetcoverageanywhereIgo

TogetcheaperorfreecallsandSMS

IfIrunoutofcreditononeconnecAon,thenIusetheotheroneTogetcheaperorfreedataservices

OneconnecAonisformybusinesscontacts,theotherisformypersonalonesItwasfreesoIjustgotit

Other

Base:Thosewhoownmorethan1acAveSIMcard

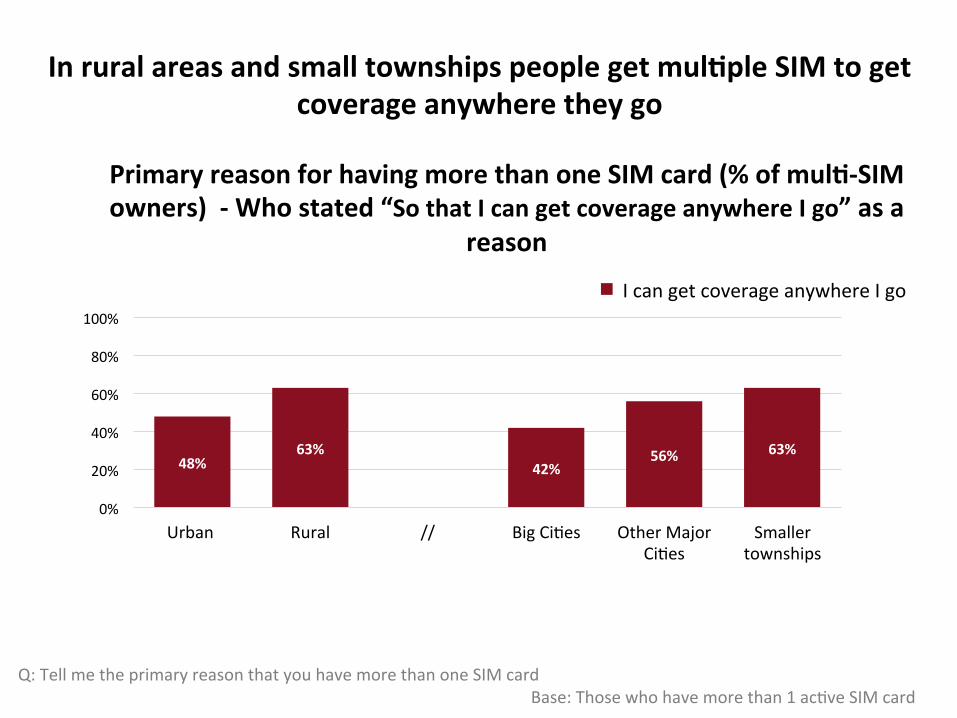

Inruralareasandsmalltownshipspeoplegetmul3pleSIMtogetcoverageanywheretheygo

48%63%

42%56% 63%

0%

20%

40%

60%

80%

100%

Urban Rural // BigCiAes OtherMajorCiAes

Smallertownships

IcangetcoverageanywhereIgo

PrimaryreasonforhavingmorethanoneSIMcard(%ofmul3-SIMowners)-Whostated“SothatIcangetcoverageanywhereIgo”asa

reason

Q:TellmetheprimaryreasonthatyouhavemorethanoneSIMcard Base:Thosewhohavemorethan1acAveSIMcard

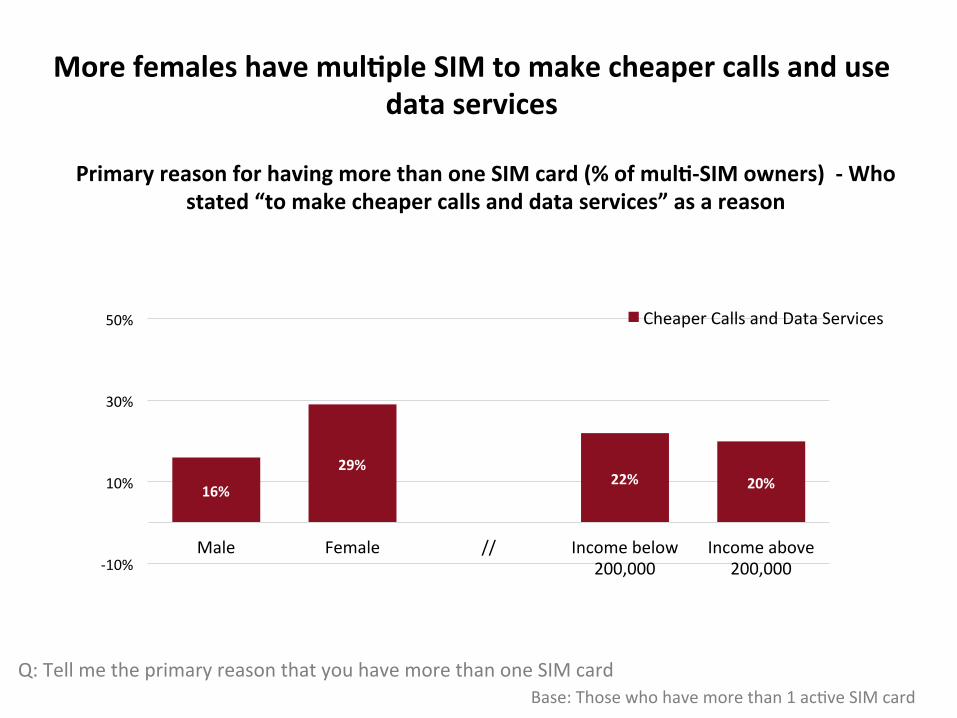

Morefemaleshavemul3pleSIMtomakecheapercallsandusedataservices

16%

29%22% 20%

-10%

10%

30%

50%

Male Female // Incomebelow200,000

Incomeabove200,000

CheaperCallsandDataServices

PrimaryreasonforhavingmorethanoneSIMcard(%ofmul3-SIMowners)-Whostated“tomakecheapercallsanddataservices”asareason

Q:TellmetheprimaryreasonthatyouhavemorethanoneSIMcard Base:Thosewhohavemorethan1acAveSIMcard

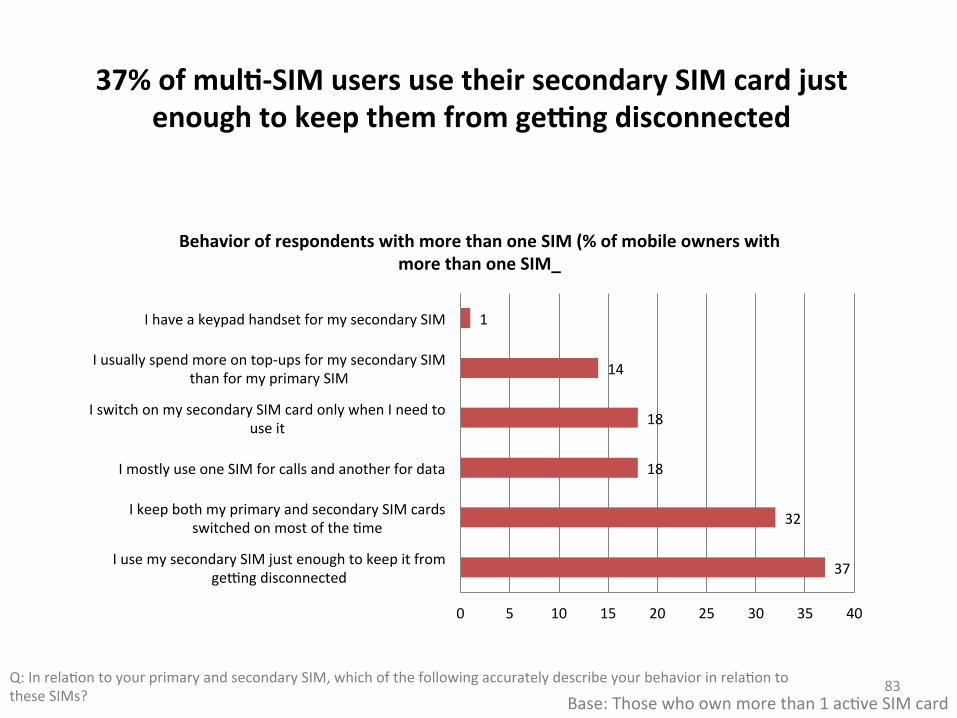

Q:InrelaAontoyourprimaryandsecondarySIM,whichofthefollowingaccuratelydescribeyourbehaviorinrelaAontotheseSIMs? 83

37%ofmul3-SIMusersusetheirsecondarySIMcardjustenoughtokeepthemfromgewngdisconnected

Base:Thosewhoownmorethan1acAveSIMcard

37

32

18

18

14

1

0 5 10 15 20 25 30 35 40

IusemysecondarySIMjustenoughtokeepitfromgetngdisconnected

IkeepbothmyprimaryandsecondarySIMcardsswitchedonmostoftheAme

ImostlyuseoneSIMforcallsandanotherfordata

IswitchonmysecondarySIMcardonlywhenIneedtouseit

Iusuallyspendmoreontop-upsformysecondarySIMthanformyprimarySIM

IhaveakeypadhandsetformysecondarySIM

BehaviorofrespondentswithmorethanoneSIM(%ofmobileownerswithmorethanoneSIM_

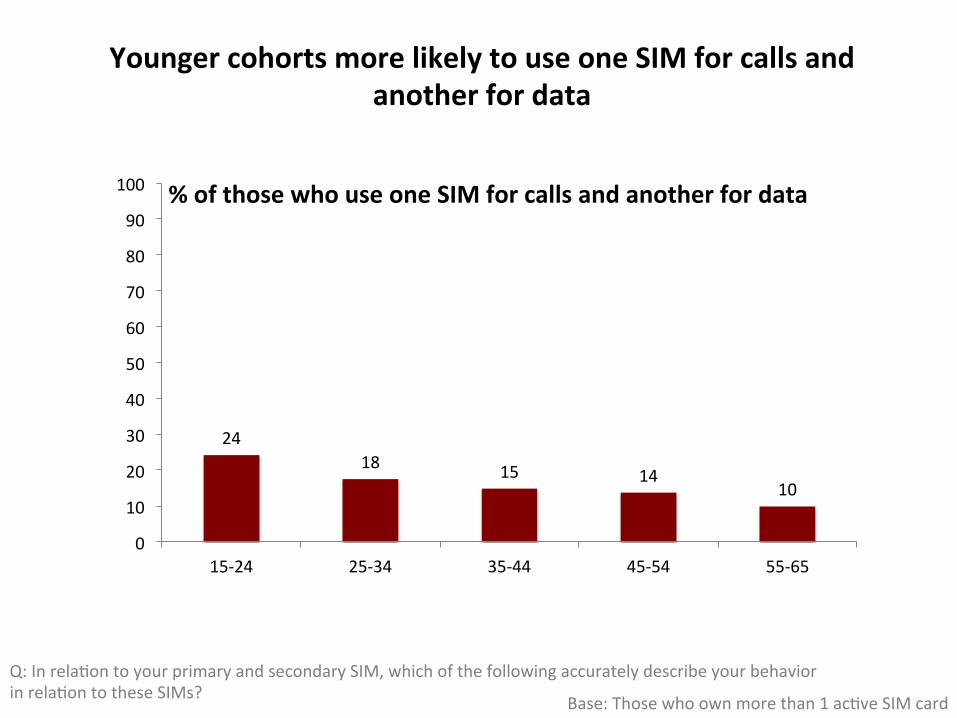

2418 15 14

10

0

10

20

30

40

50

60

70

80

90

100

15-24 25-34 35-44 45-54 55-65

Q:InrelaAontoyourprimaryandsecondarySIM,whichofthefollowingaccuratelydescribeyourbehaviorinrelaAontotheseSIMs?

%ofthosewhouseoneSIMforcallsandanotherfordata

YoungercohortsmorelikelytouseoneSIMforcallsandanotherfordata

Base:Thosewhoownmorethan1acAveSIMcard

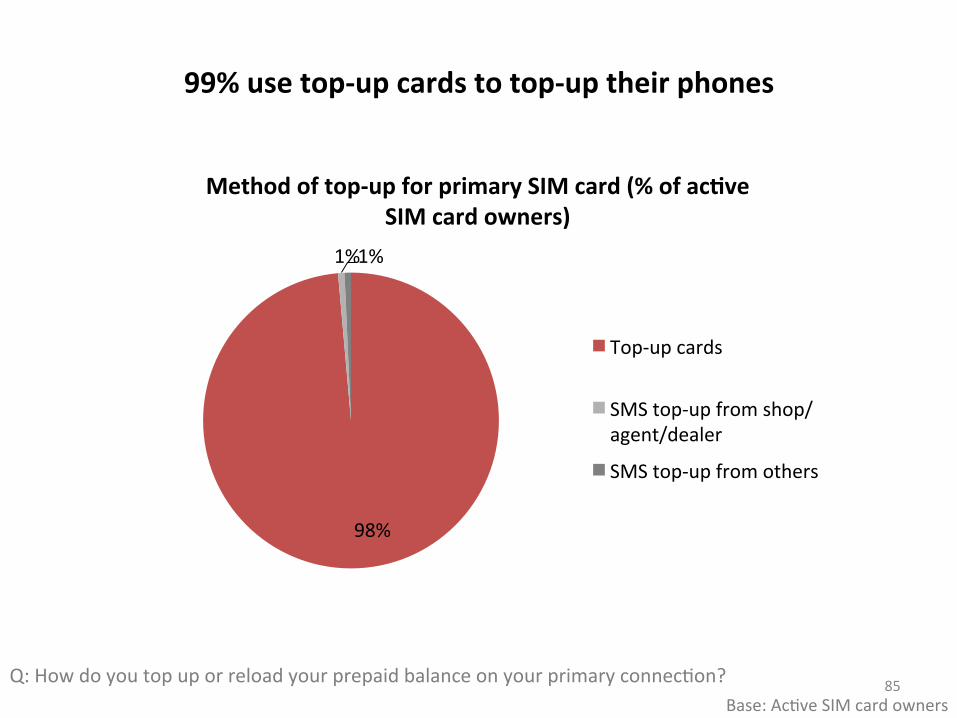

99%usetop-upcardstotop-uptheirphones

Q:HowdoyoutopuporreloadyourprepaidbalanceonyourprimaryconnecAon?

85

98%

1%1%

Methodoftop-upforprimarySIMcard(%ofac3veSIMcardowners)

Top-upcards

SMStop-upfromshop/agent/dealer

SMStop-upfromothers

Base:AcAveSIMcardowners

86

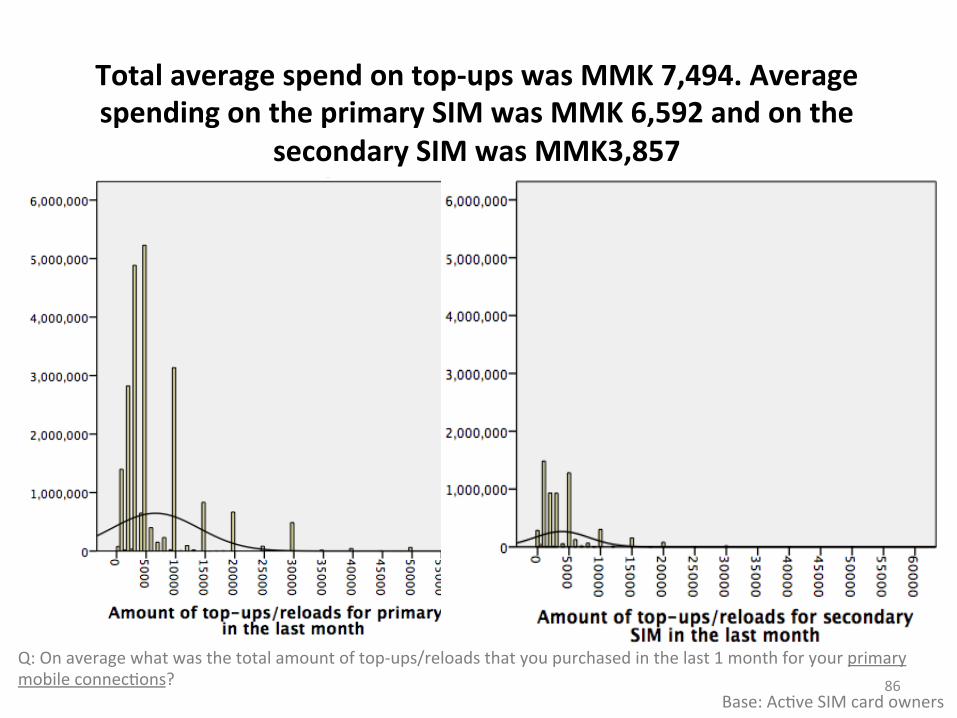

Q:Onaveragewhatwasthetotalamountoftop-ups/reloadsthatyoupurchasedinthelast1monthforyourprimarymobileconnecAons? Base:AcAveSIMcardowners

Totalaveragespendontop-upswasMMK7,494.AveragespendingontheprimarySIMwasMMK6,592andonthe

secondarySIMwasMMK3,857

9331

6182

79966890

7494

0100020003000400050006000700080009000

10000

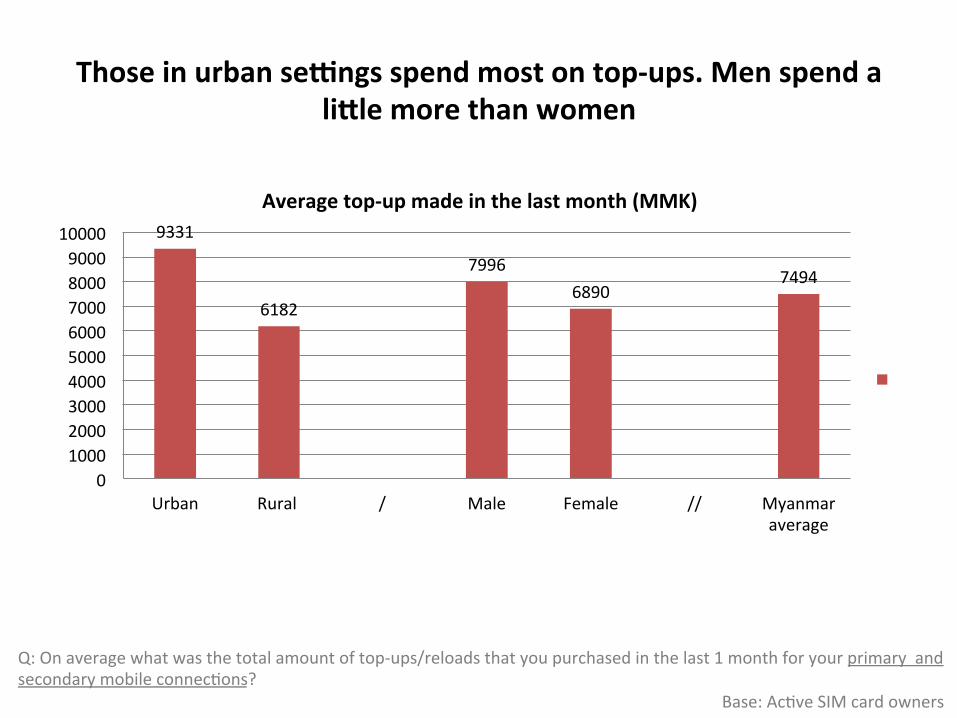

Urban Rural / Male Female // Myanmaraverage

Averagetop-upmadeinthelastmonth(MMK)

Thoseinurbansewngsspendmostontop-ups.Menspendalielemorethanwomen

Q:Onaveragewhatwasthetotalamountoftop-ups/reloadsthatyoupurchasedinthelast1monthforyourprimaryandsecondarymobileconnecAons? Base:AcAveSIMcardowners

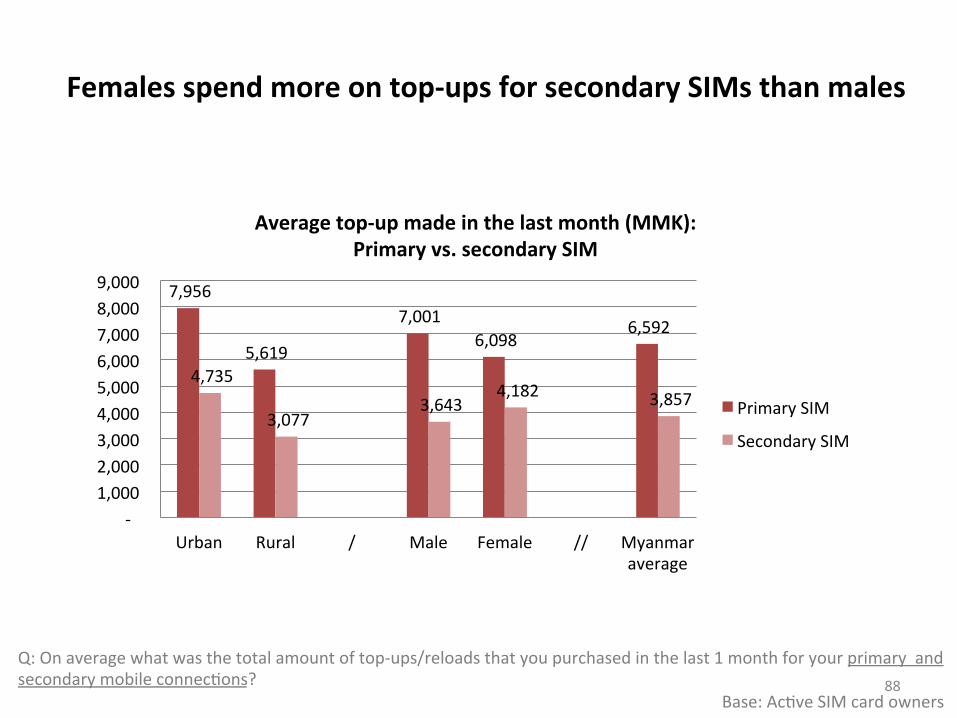

Q:Onaveragewhatwasthetotalamountoftop-ups/reloadsthatyoupurchasedinthelast1monthforyourprimaryandsecondarymobileconnecAons? Base:AcAveSIMcardowners

88

Femalesspendmoreontop-upsforsecondarySIMsthanmales

7,956

5,619

7,0016,098

6,592

4,735

3,0773,643

4,182 3,857

-1,0002,0003,0004,0005,0006,0007,0008,0009,000

Urban Rural / Male Female // Myanmaraverage

Averagetop-upmadeinthelastmonth(MMK):Primaryvs.secondarySIM

PrimarySIM

SecondarySIM

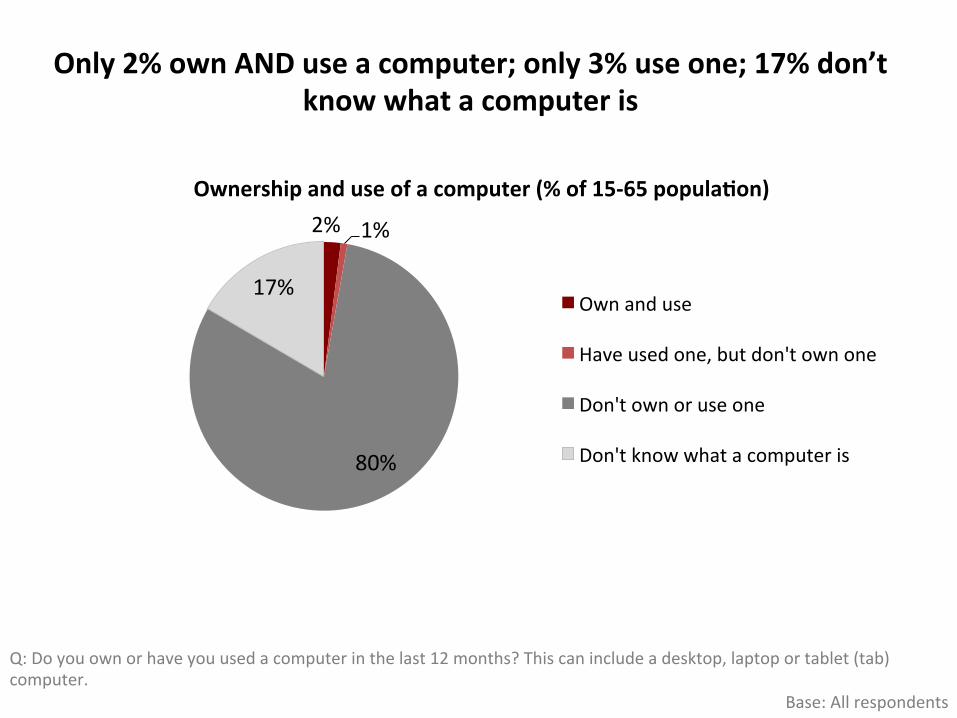

COMPUTEROWNERSHIPANDUSE

89

Only2%ownANDuseacomputer;only3%useone;17%don’tknowwhatacomputeris

2% 1%

80%

17%

Ownershipanduseofacomputer(%of15-65popula3on)

Ownanduse

Haveusedone,butdon'townone

Don'townoruseone

Don'tknowwhatacomputeris

Q:Doyouownorhaveyouusedacomputerinthelast12months?Thiscanincludeadesktop,laptoportablet(tab)computer.

Base:Allrespondents

Nearlyallthosewhoown/usecomputersliveinurbanareas

2

5

83

10

Urban

80

20

Rural Ownanduse

Haveusedone,butdon'townone

Don'townoruseone

Don'tknowwhatacomputeris

Ownershipanduseofacomputer(%of15-65popula3on)

Q:Doyouownorhaveyouusedacomputerinthelast12months?Thiscanincludeadesktop,laptoportablet(tab)computer.

Base:Allrespondents

INTERNETUSE

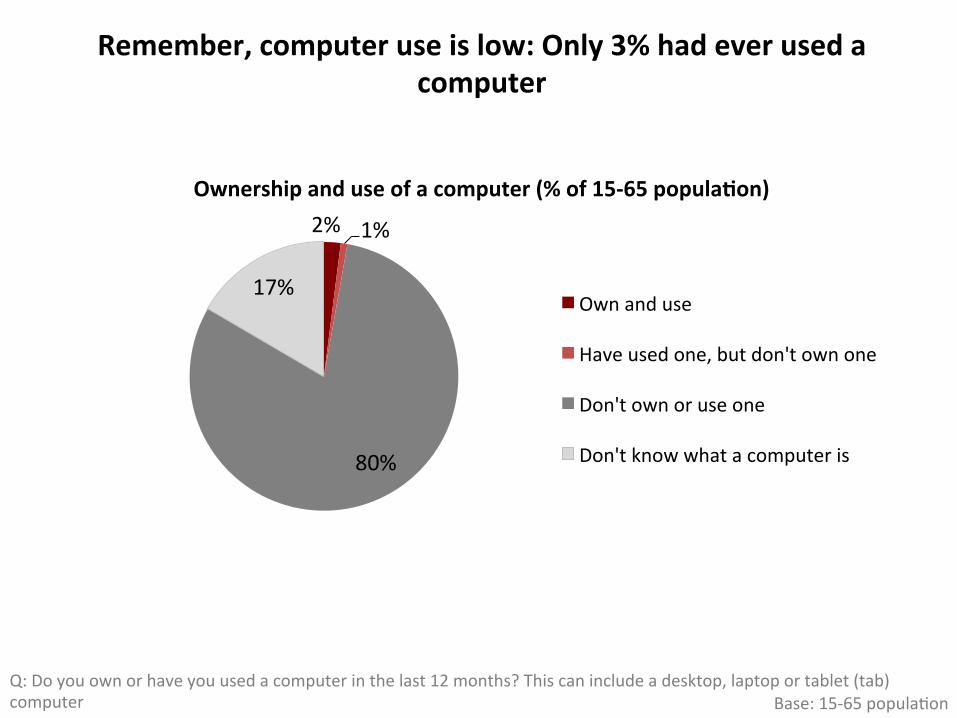

Remember,computeruseislow:Only3%hadeverusedacomputer

2% 1%

80%

17%

Ownershipanduseofacomputer(%of15-65popula3on)

Ownanduse

Haveusedone,butdon'townone

Don'townoruseone

Don'tknowwhatacomputeris

Q:Doyouownorhaveyouusedacomputerinthelast12months?Thiscanincludeadesktop,laptoportablet(tab)computer Base:15-65populaAon

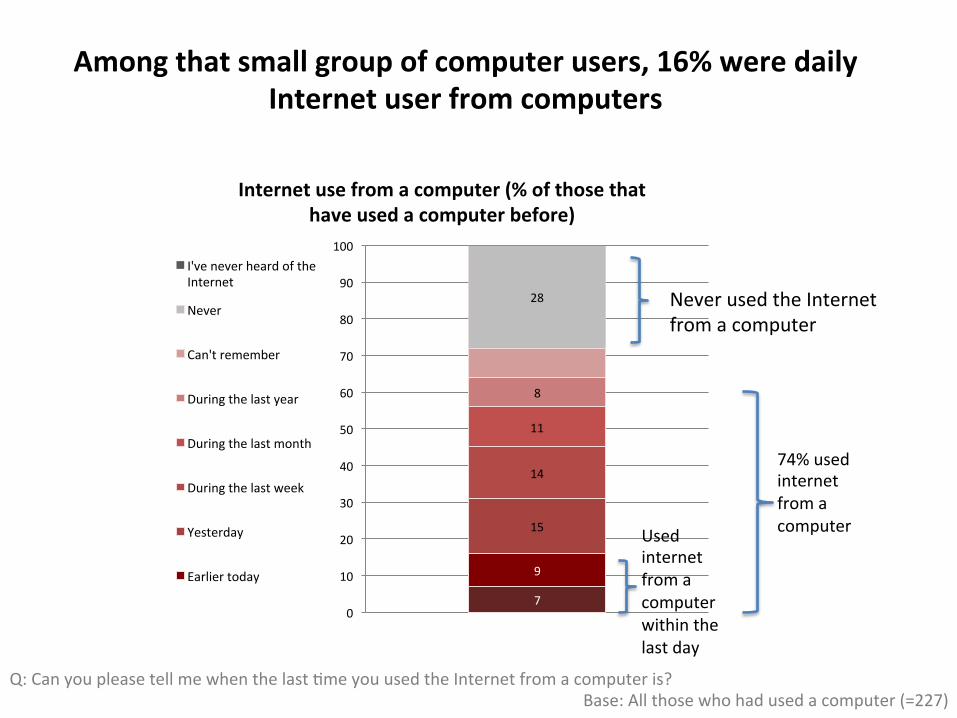

Amongthatsmallgroupofcomputerusers,16%weredailyInternetuserfromcomputers

Q:CanyoupleasetellmewhenthelastAmeyouusedtheInternetfromacomputeris?Base:Allthosewhohadusedacomputer(=227)

7

9

15

14

11

8

28

0

10

20

30

40

50

60

70

80

90

100

Internetusefromacomputer(%ofthosethathaveusedacomputerbefore)

I'veneverheardoftheInternet

Never

Can'tremember

Duringthelastyear

Duringthelastmonth

Duringthelastweek

Yesterday

Earliertoday

Usedinternetfromacomputerwithinthelastday

NeverusedtheInternetfromacomputer

74%usedinternetfromacomputer

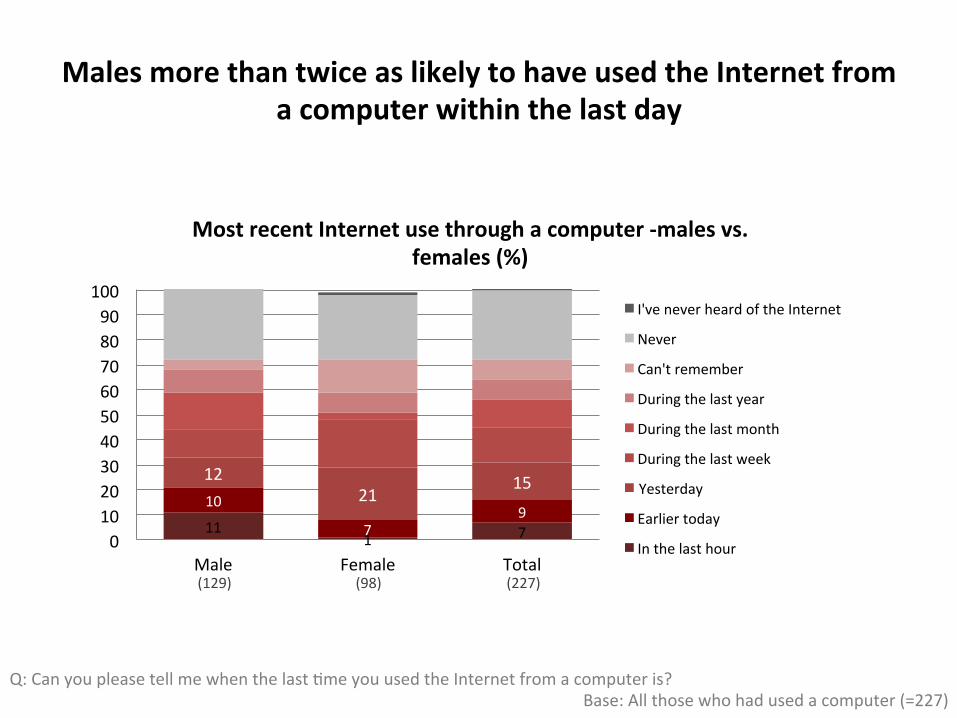

MalesmorethantwiceaslikelytohaveusedtheInternetfromacomputerwithinthelastday

111 7

10

79

1221

15

0102030405060708090

100

Male Female Total

MostrecentInternetusethroughacomputer-malesvs.females(%)

I'veneverheardoftheInternet

Never

Can'tremember

Duringthelastyear

Duringthelastmonth

Duringthelastweek

Yesterday

Earliertoday

Inthelasthour

Q:CanyoupleasetellmewhenthelastAmeyouusedtheInternetfromacomputeris?Base:Allthosewhohadusedacomputer(=227)

(129) (98) (227)

Q:Whichofthefollowingdescribesyourstatusofmobilephoneownership?

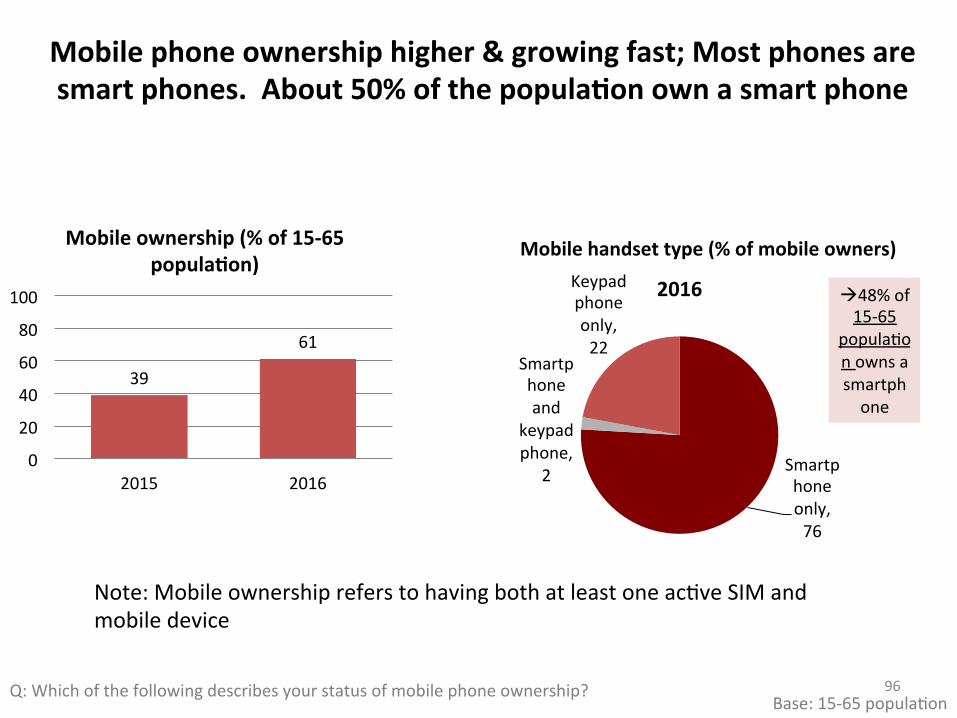

Mobilephoneownershiphigher&growingfast;Mostphonesaresmartphones.About50%ofthepopula3onownasmartphone

96

39

61

0

20

40

60

80

100

2015 2016

Mobileownership(%of15-65popula3on)

Note:MobileownershipreferstohavingbothatleastoneacAveSIMandmobiledevice

Base:15-65populaAon

Smartphoneonly,76

Smartphoneand

keypadphone,

2

Keypadphoneonly,22

2016

Mobilehandsettype(%ofmobileowners)

à48%of15-65

populaAonownsasmartphone

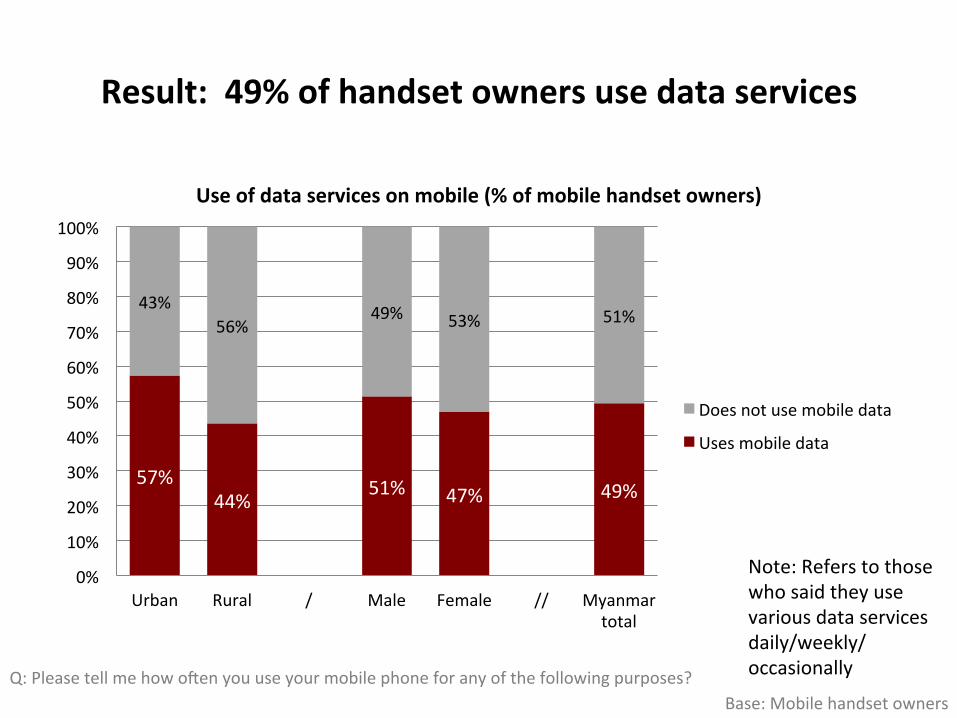

Result:49%ofhandsetownersusedataservices

Q:Pleasetellmehowosenyouuseyourmobilephoneforanyofthefollowingpurposes?Base:Mobilehandsetowners

57%44%

51% 47% 49%

43%56%

49% 53% 51%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Urban Rural / Male Female // Myanmartotal

Useofdataservicesonmobile(%ofmobilehandsetowners)

Doesnotusemobiledata

Usesmobiledata

Note:Referstothosewhosaidtheyusevariousdataservicesdaily/weekly/occasionally

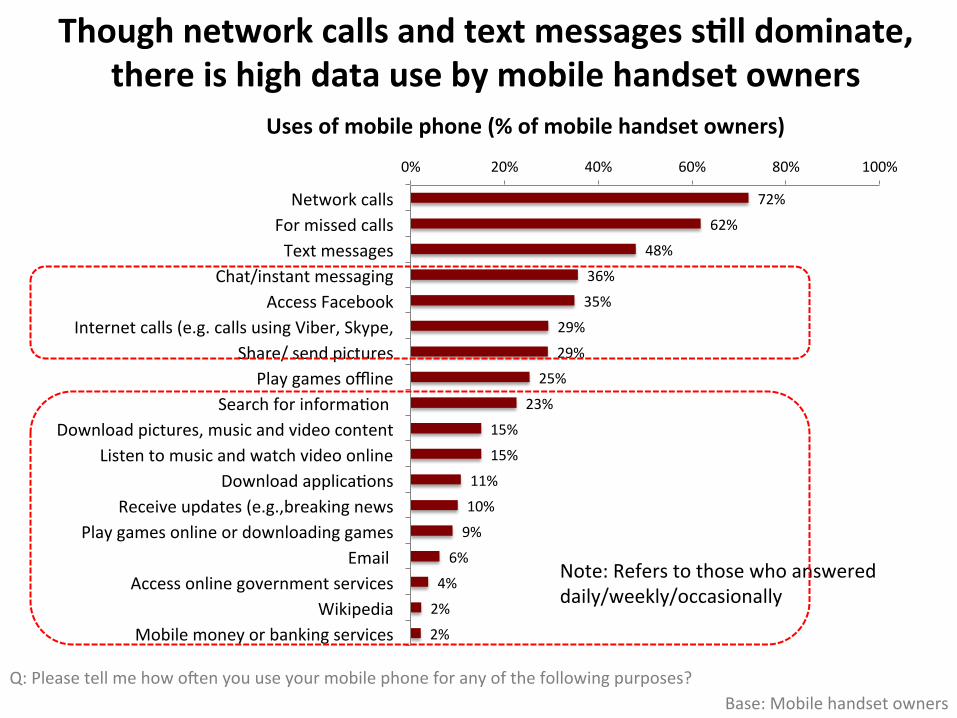

72%

62%

48%

36%

35%

29%

29%

25%

23%

15%

15%

11%

10%

9%

6%

4%

2%

2%

0% 20% 40% 60% 80% 100%

NetworkcallsFormissedcallsTextmessages

Chat/instantmessagingAccessFacebook

Internetcalls(e.g.callsusingViber,Skype,Share/sendpicturesPlaygamesoffline

SearchforinformaAonDownloadpictures,musicandvideocontent

ListentomusicandwatchvideoonlineDownloadapplicaAons

Receiveupdates(e.g.,breakingnewsPlaygamesonlineordownloadinggames

EmailAccessonlinegovernmentservices

WikipediaMobilemoneyorbankingservices

Usesofmobilephone(%ofmobilehandsetowners)

Q:Pleasetellmehowosenyouuseyourmobilephoneforanyofthefollowingpurposes?Base:Mobilehandsetowners

Thoughnetworkcallsandtextmessagess3lldominate,thereishighdatausebymobilehandsetowners

Note:Referstothosewhoanswereddaily/weekly/occasionally

21%

15%

8%

6%

3%

3%

2%

1%

1%

1%

1%

0%

0%

4%

4%

4%

2%

2%

1%

1%

1%

0%

0%

1%

0%

0%

10%

17%

18%

15%

25%

6%

12%

13%

10%

3%

5%

2%

2%

0% 20% 40% 60% 80% 100%

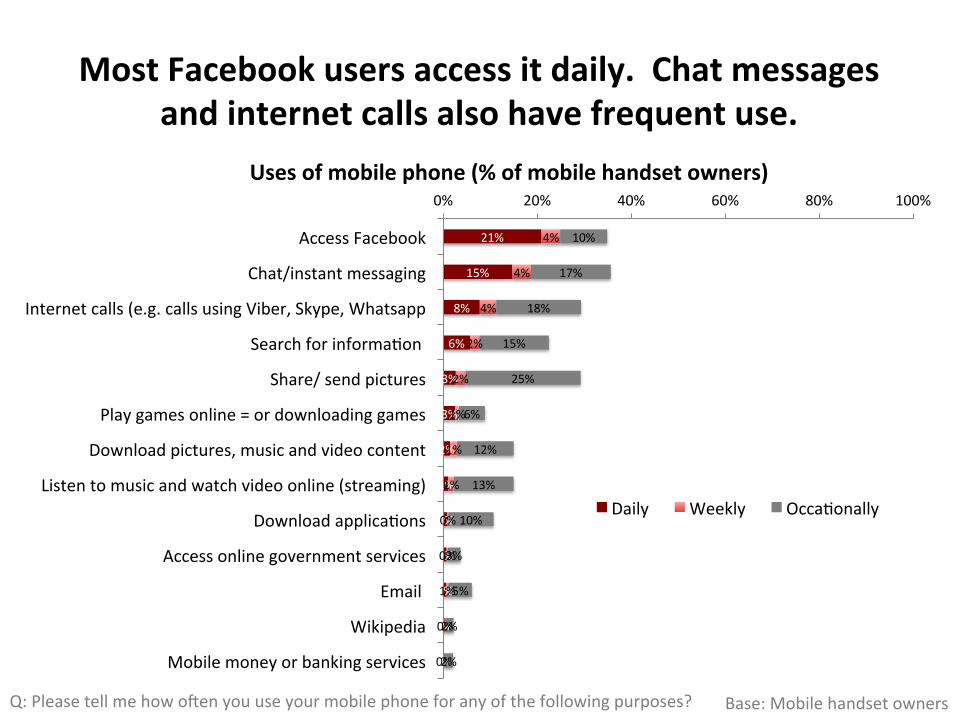

AccessFacebook

Chat/instantmessaging

Internetcalls(e.g.callsusingViber,Skype,Whatsapp

SearchforinformaAon

Share/sendpictures

Playgamesonline=ordownloadinggames

Downloadpictures,musicandvideocontent

Listentomusicandwatchvideoonline(streaming)

DownloadapplicaAons

Accessonlinegovernmentservices

Wikipedia

Mobilemoneyorbankingservices

Daily Weekly OccaAonally

Usesofmobilephone(%ofmobilehandsetowners)

MostFacebookusersaccessitdaily.Chatmessagesandinternetcallsalsohavefrequentuse.

Q:Pleasetellmehowosenyouuseyourmobilephoneforanyofthefollowingpurposes? Base:Mobilehandsetowners

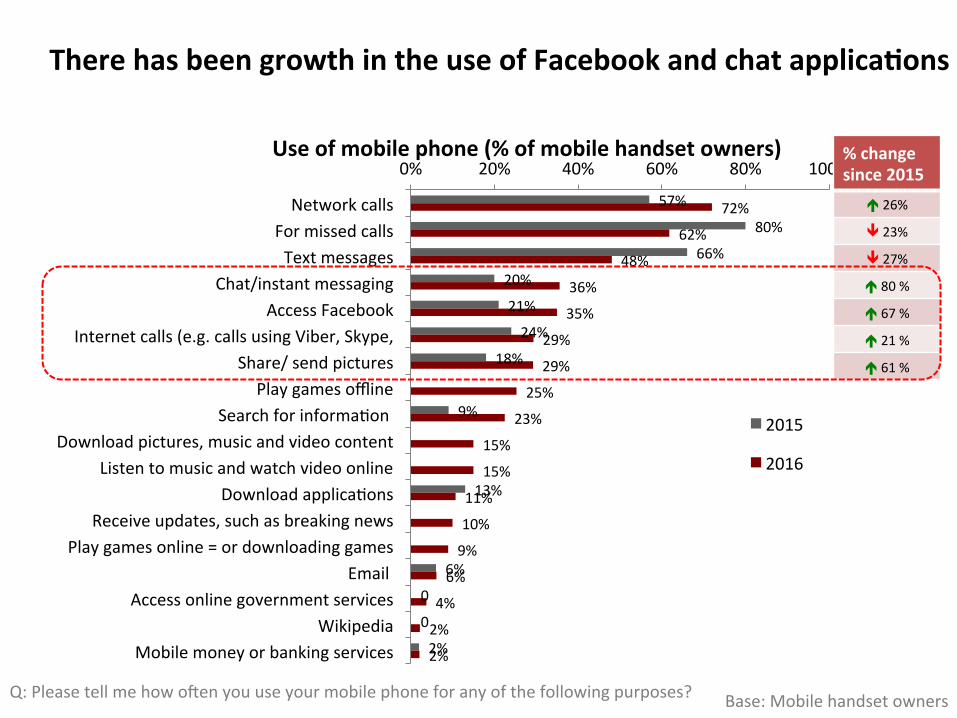

57%

80%

66%

20%

21%

24%

18%

9%

13%

6%

0

0

2%

72%

62%

48%

36%

35%

29%

29%

25%

23%

15%

15%

11%

10%

9%

6%

4%

2%

2%

0% 20% 40% 60% 80% 100%

NetworkcallsFormissedcallsTextmessages

Chat/instantmessagingAccessFacebook

Internetcalls(e.g.callsusingViber,Skype,Share/sendpicturesPlaygamesoffline

SearchforinformaAonDownloadpictures,musicandvideocontent

ListentomusicandwatchvideoonlineDownloadapplicaAons

Receiveupdates,suchasbreakingnewsPlaygamesonline=ordownloadinggames

EmailAccessonlinegovernmentservices

WikipediaMobilemoneyorbankingservices

2015

2016

Useofmobilephone(%ofmobilehandsetowners)

Q:Pleasetellmehowosenyouuseyourmobilephoneforanyofthefollowingpurposes? Base:Mobilehandsetowners

TherehasbeengrowthintheuseofFacebookandchatapplica3ons

%changesince2015

é26%

ê23%

ê27%

é80%

é67%

é21%

é61%

Base:Mobilehandsetowners

Note:Referstothosewhoansweredbothdaily,weeklyandoccasionally

Usesofmobilephone(%ofmobilehandsetowners)

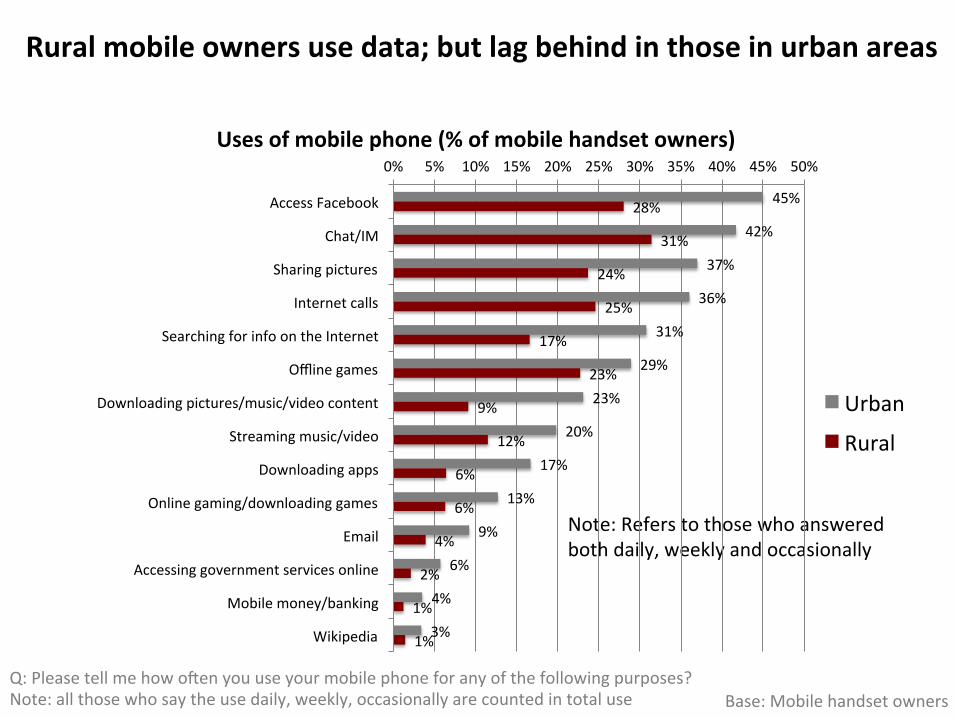

45%

42%

37%

36%

31%

29%

23%

20%

17%

13%

9%

6%

4%

3%

28%

31%

24%

25%

17%

23%

9%

12%

6%

6%

4%

2%

1%

1%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

AccessFacebook

Chat/IM

Sharingpictures

Internetcalls

SearchingforinfoontheInternet

Offlinegames

Downloadingpictures/music/videocontent

Streamingmusic/video

Downloadingapps

Onlinegaming/downloadinggames

Accessinggovernmentservicesonline

Mobilemoney/banking

Wikipedia

Urban

Rural

Q:Pleasetellmehowosenyouuseyourmobilephoneforanyofthefollowingpurposes?Note:allthosewhosaytheusedaily,weekly,occasionallyarecountedintotaluse

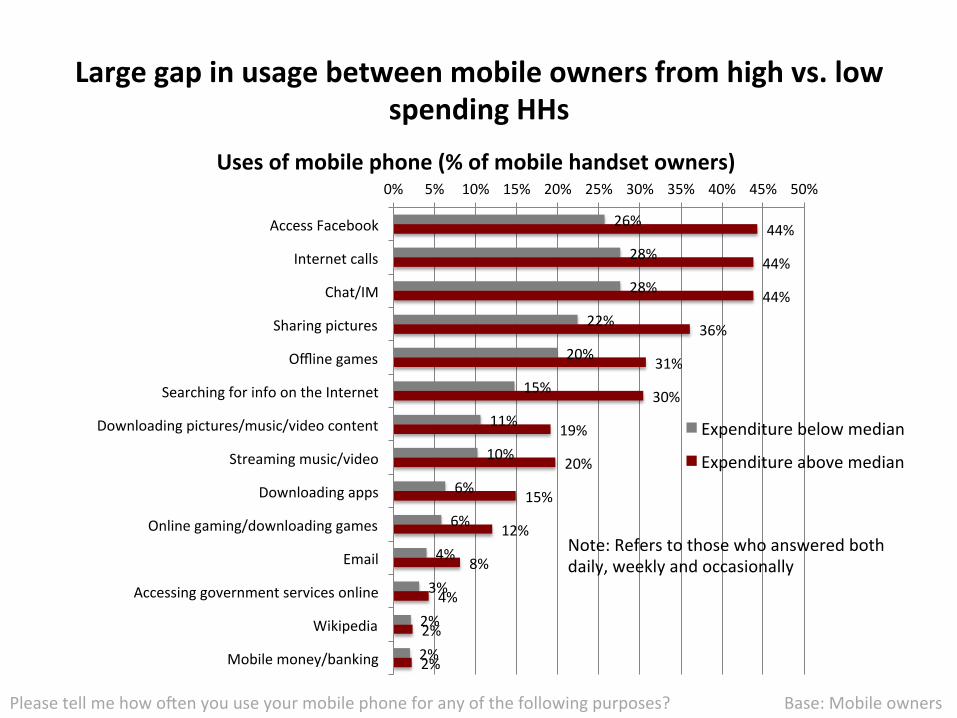

Ruralmobileownersusedata;butlagbehindinthoseinurbanareas

Largegapinusagebetweenmobileownersfromhighvs.lowspendingHHs

Pleasetellmehowosenyouuseyourmobilephoneforanyofthefollowingpurposes?Base:Mobileowners

Base:Mobilehandsetowners

26%

28%

28%

22%

20%

15%

11%

10%

6%

6%

4%

3%

2%

2%

44%

44%

44%

36%

31%

30%

19%

20%

15%

12%

8%

4%

2%

2%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

AccessFacebook

Internetcalls

Chat/IM

Sharingpictures

Offlinegames

SearchingforinfoontheInternet

Downloadingpictures/music/videocontent

Streamingmusic/video

Downloadingapps

Onlinegaming/downloadinggames

Accessinggovernmentservicesonline

Wikipedia

Mobilemoney/banking

Expenditurebelowmedian

Expenditureabovemedian

Note:Referstothosewhoansweredbothdaily,weeklyandoccasionally

Usesofmobilephone(%ofmobilehandsetowners)

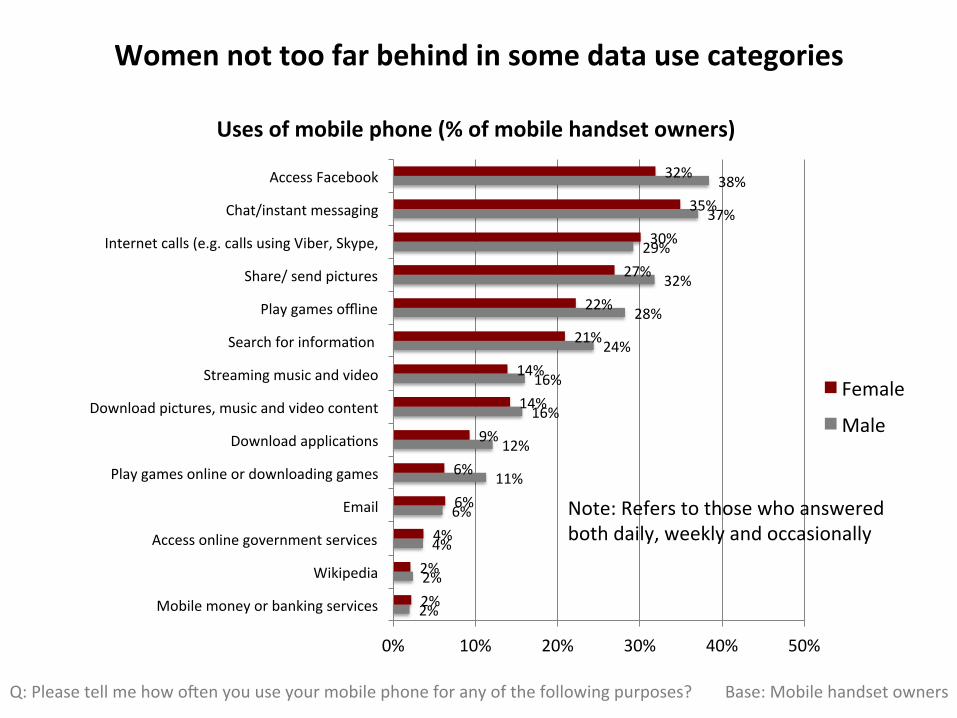

2%

2%

4%

6%

11%

12%

16%

16%

24%

28%

32%

29%

37%

38%

2%

2%

4%

6%

6%

9%

14%

14%

21%

22%

27%

30%

35%

32%

0% 10% 20% 30% 40% 50%

Mobilemoneyorbankingservices

Wikipedia

Accessonlinegovernmentservices

Playgamesonlineordownloadinggames

DownloadapplicaAons

Downloadpictures,musicandvideocontent

Streamingmusicandvideo

SearchforinformaAon

Playgamesoffline

Share/sendpictures

Internetcalls(e.g.callsusingViber,Skype,

Chat/instantmessaging

AccessFacebook

Female

Male

Note:Referstothosewhoansweredbothdaily,weeklyandoccasionally

Usesofmobilephone(%ofmobilehandsetowners)

Womennottoofarbehindinsomedatausecategories

Q:Pleasetellmehowosenyouuseyourmobilephoneforanyofthefollowingpurposes? Base:Mobilehandsetowners

DIGITALSKILLS

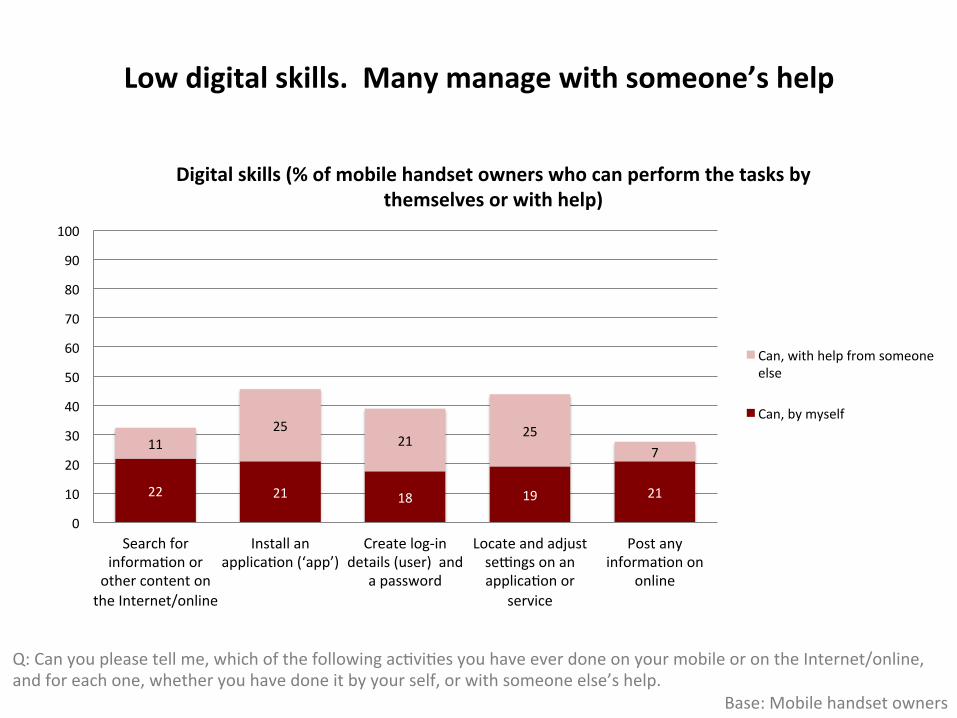

Lowdigitalskills.Manymanagewithsomeone’shelp

Q:Canyoupleasetellme,whichofthefollowingacAviAesyouhaveeverdoneonyourmobileorontheInternet/online,andforeachone,whetheryouhavedoneitbyyourself,orwithsomeoneelse’shelp.

Base:Mobilehandsetowners

22 21 18 19 21

1125

2125

7

0

10

20

30

40

50

60

70

80

90

100

SearchforinformaAonorothercontentontheInternet/online

InstallanapplicaAon(‘app’)

Createlog-indetails(user)and

apassword

LocateandadjustsetngsonanapplicaAonor

service

PostanyinformaAonon

online

Digitalskills(%ofmobilehandsetownerswhocanperformthetasksbythemselvesorwithhelp)

Can,withhelpfromsomeoneelse

Can,bymyself

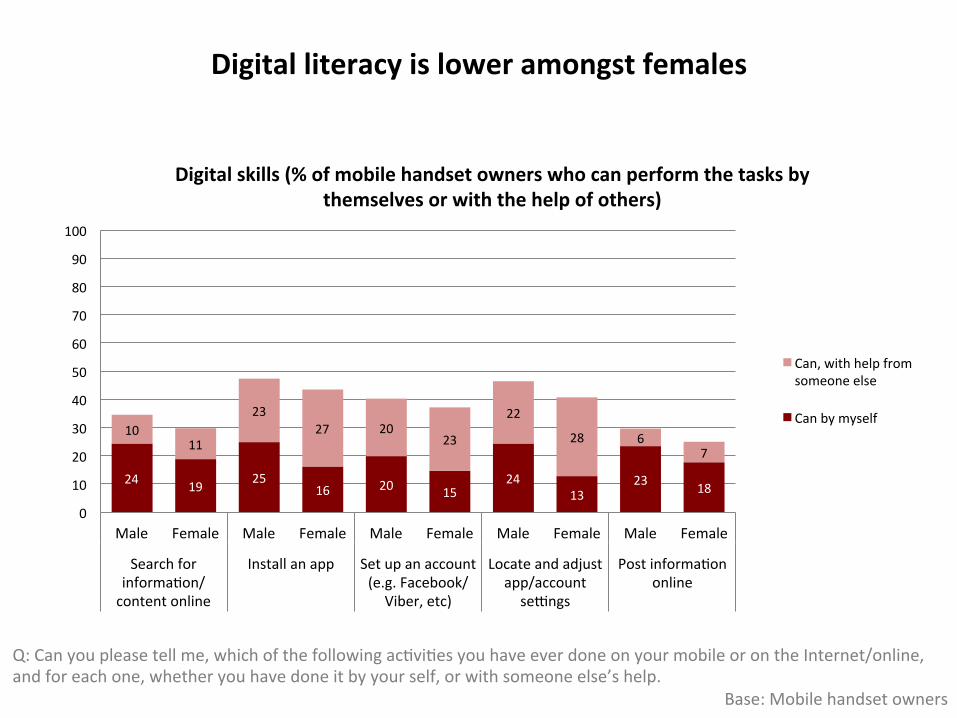

Digitalliteracyisloweramongstfemales

24 19 2516 20 15

2413

23 18

1011

2327 20

23

22

28 67

0

10

20

30

40

50

60

70

80

90

100

Male Female Male Female Male Female Male Female Male Female

SearchforinformaAon/contentonline

Installanapp Setupanaccount(e.g.Facebook/

Viber,etc)

Locateandadjustapp/accountsetngs

PostinformaAononline

Digitalskills(%ofmobilehandsetownerswhocanperformthetasksbythemselvesorwiththehelpofothers)

Can,withhelpfromsomeoneelse

Canbymyself

Q:Canyoupleasetellme,whichofthefollowingacAviAesyouhaveeverdoneonyourmobileorontheInternet/online,andforeachone,whetheryouhavedoneitbyyourself,orwithsomeoneelse’shelp.

Base:Mobilehandsetowners

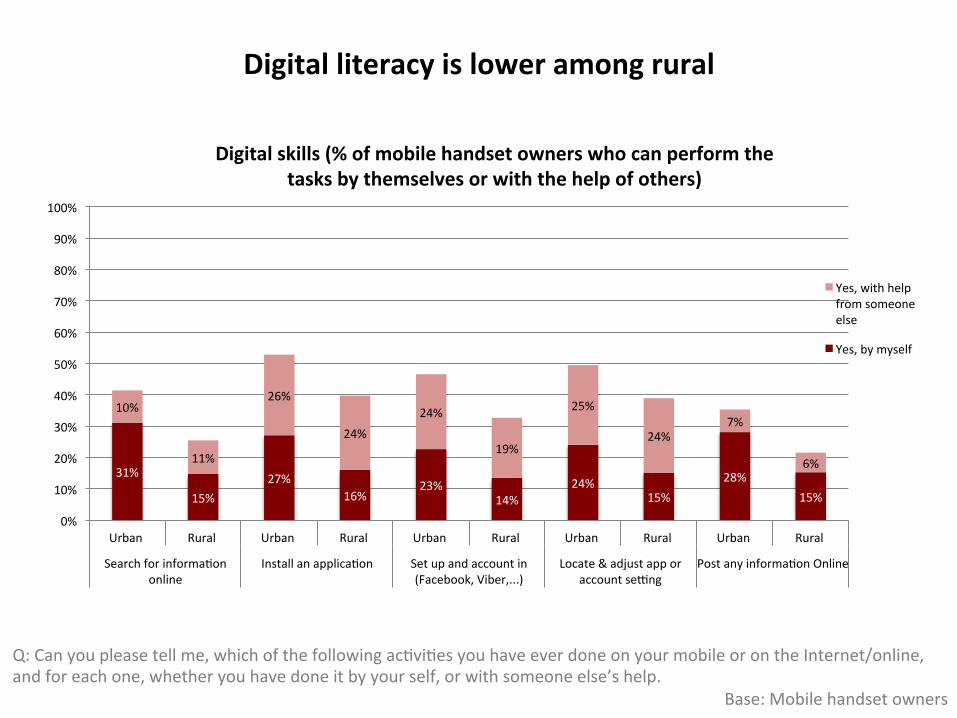

Digitalliteracyisloweramongrural

Q:Canyoupleasetellme,whichofthefollowingacAviAesyouhaveeverdoneonyourmobileorontheInternet/online,andforeachone,whetheryouhavedoneitbyyourself,orwithsomeoneelse’shelp.

Base:Mobilehandsetowners

31%

15%27%

16%23%

14%24%

15%28%

15%

10%

11%

26%

24%24%

19%

25%

24%7%

6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Urban Rural Urban Rural Urban Rural Urban Rural Urban Rural

SearchforinformaAononline

InstallanapplicaAon Setupandaccountin(Facebook,Viber,...)

Locate&adjustapporaccountsetng

PostanyinformaAonOnline

Yes,withhelpfromsomeoneelse

Yes,bymyself

Digitalskills(%ofmobilehandsetownerswhocanperformthetasksbythemselvesorwiththehelpofothers)

NON-OWNERSOFMOBILEPHONES

108

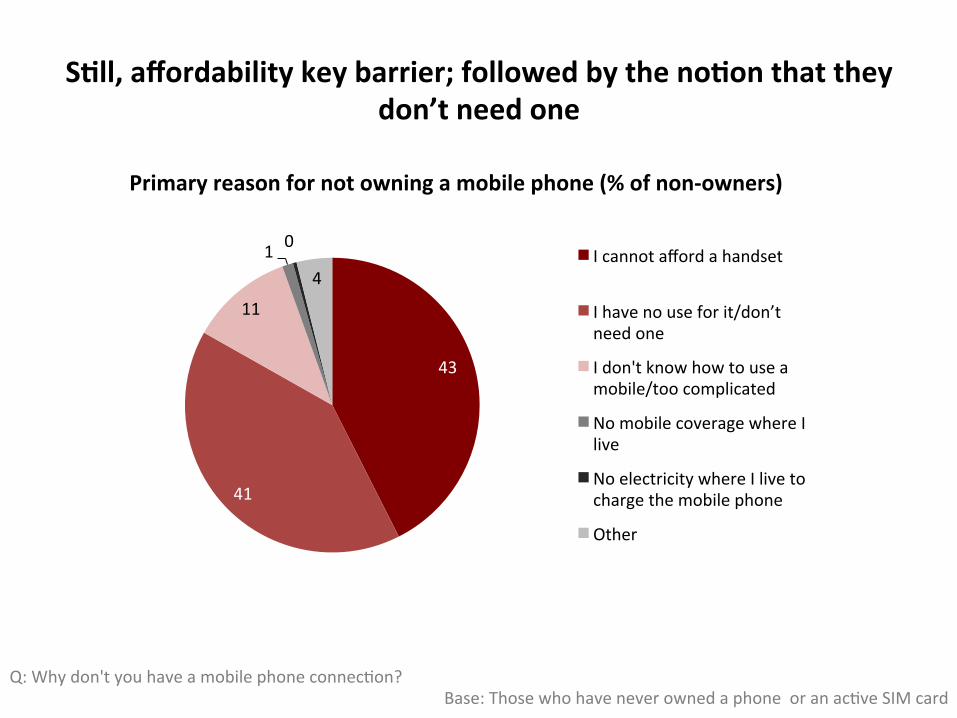

S3ll,affordabilitykeybarrier;followedbytheno3onthattheydon’tneedone

43

41

11

1 0

4Icannotaffordahandset

Ihavenouseforit/don’tneedone

Idon'tknowhowtouseamobile/toocomplicated

NomobilecoveragewhereIlive

NoelectricitywhereIlivetochargethemobilephone

Other

Primaryreasonfornotowningamobilephone(%ofnon-owners)

Q:Whydon'tyouhaveamobilephoneconnecAon?Base:ThosewhohaveneverownedaphoneoranacAveSIMcard

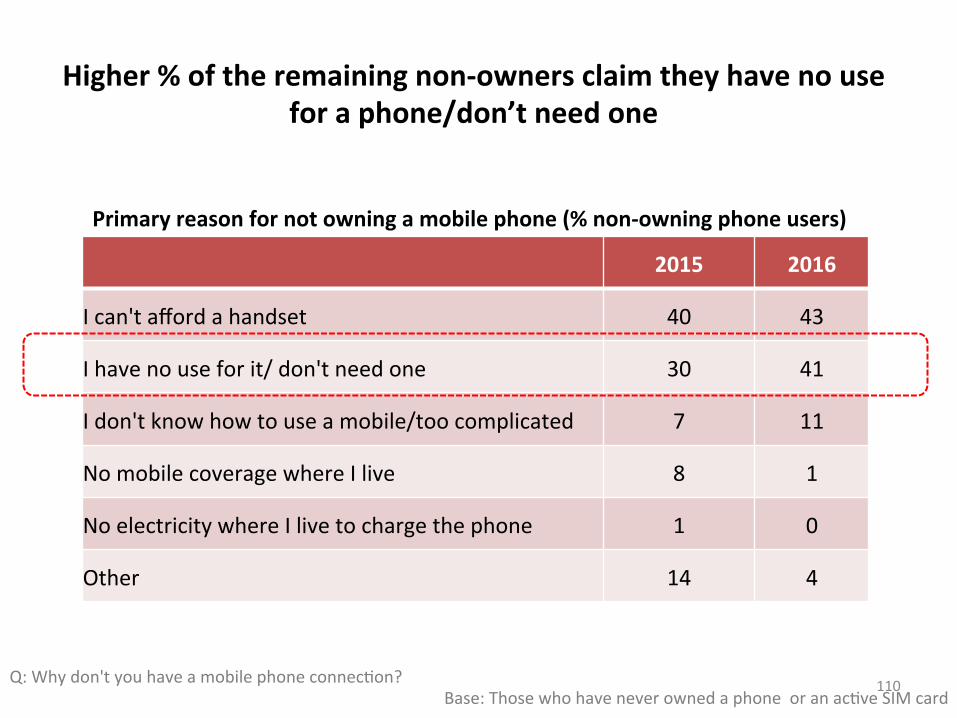

Higher%oftheremainingnon-ownersclaimtheyhavenouseforaphone/don’tneedone

110

Primaryreasonfornotowningamobilephone(%non-owningphoneusers)

2015 2016

Ican'taffordahandset 40 43

Ihavenouseforit/don'tneedone 30 41

Idon'tknowhowtouseamobile/toocomplicated 7 11

NomobilecoveragewhereIlive 8 1

NoelectricitywhereIlivetochargethephone 1 0

Other 14 4

Q:Whydon'tyouhaveamobilephoneconnecAon?Base:ThosewhohaveneverownedaphoneoranacAveSIMcard

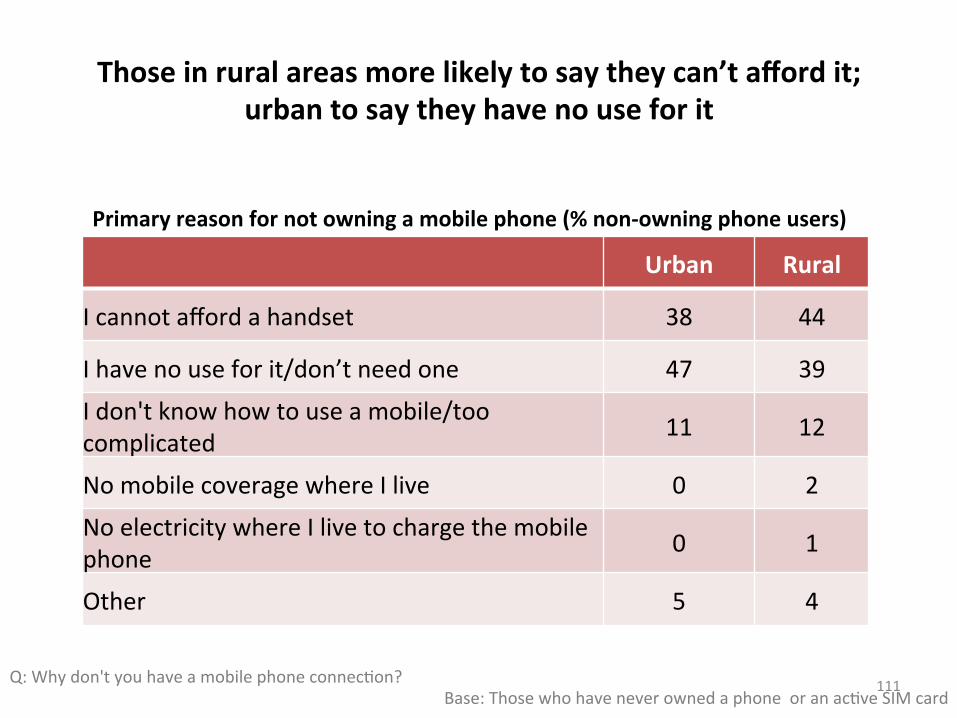

Thoseinruralareasmorelikelytosaytheycan’taffordit;urbantosaytheyhavenouseforit

111

Primaryreasonfornotowningamobilephone(%non-owningphoneusers)

Urban Rural

Icannotaffordahandset 38 44

Ihavenouseforit/don’tneedone 47 39

Idon'tknowhowtouseamobile/toocomplicated 11 12

NomobilecoveragewhereIlive 0 2

NoelectricitywhereIlivetochargethemobilephone 0 1

Other 5 4

Q:Whydon'tyouhaveamobilephoneconnecAon?Base:ThosewhohaveneverownedaphoneoranacAveSIMcard

INFORMATIONSOURCES,NEEDSANDACCESS

112

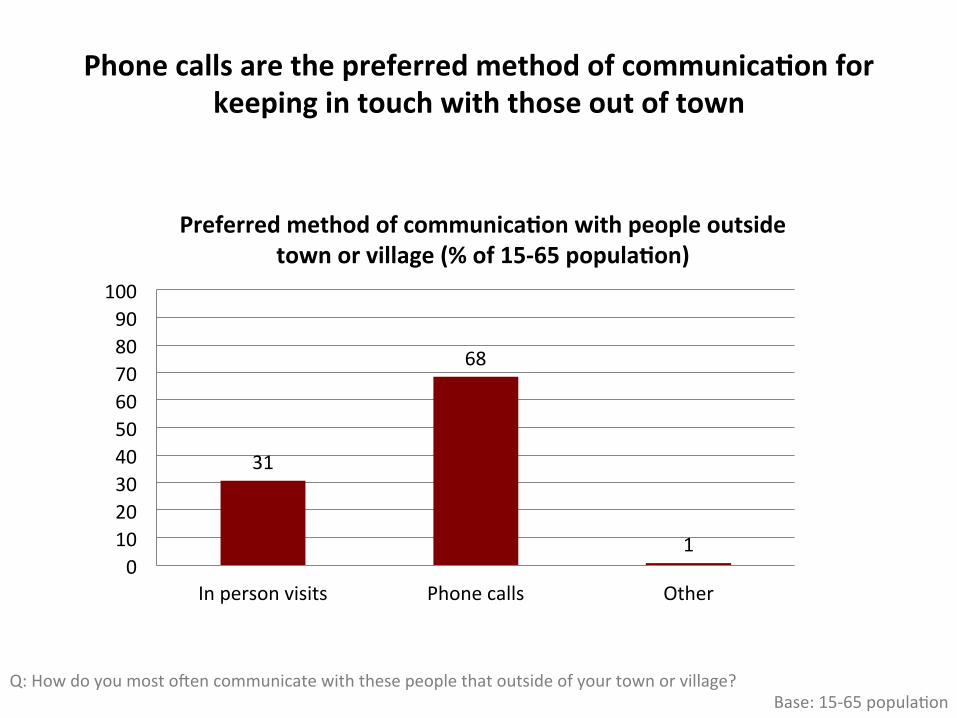

Phonecallsarethepreferredmethodofcommunica3onforkeepingintouchwiththoseoutoftown

31

68

10102030405060708090100

Inpersonvisits Phonecalls Other

Preferredmethodofcommunica3onwithpeopleoutsidetownorvillage(%of15-65popula3on)

Q:Howdoyoumostosencommunicatewiththesepeoplethatoutsideofyourtownorvillage?Base:15-65populaAon

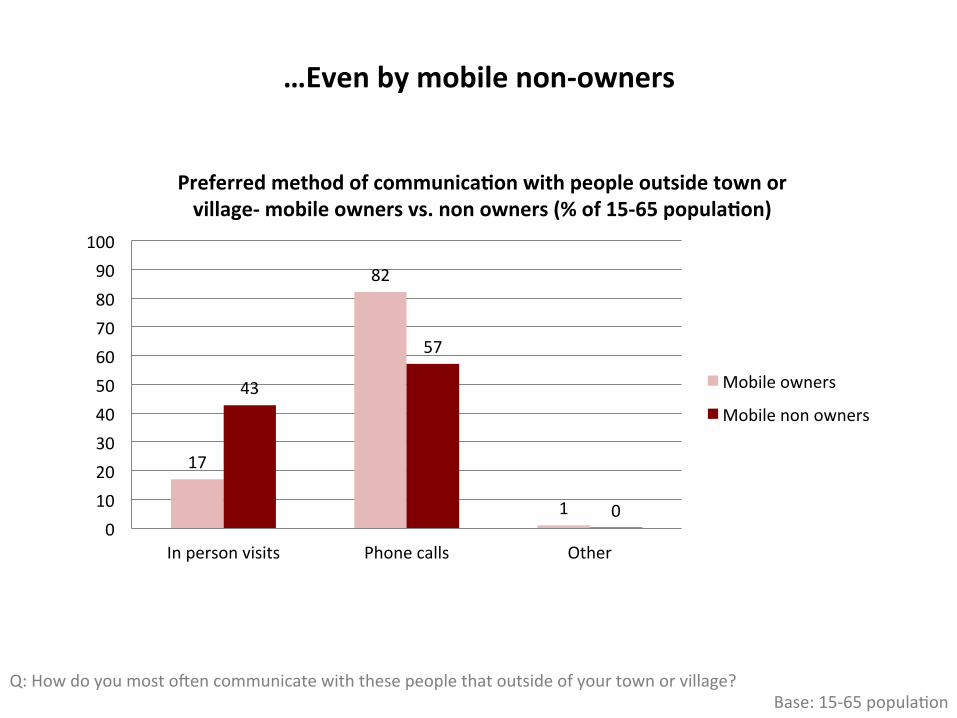

…Evenbymobilenon-owners

17

82

1

43

57

00102030405060708090

100

Inpersonvisits Phonecalls Other

Preferredmethodofcommunica3onwithpeopleoutsidetownorvillage-mobileownersvs.nonowners(%of15-65popula3on)

Mobileowners

Mobilenonowners

Q:Howdoyoumostosencommunicatewiththesepeoplethatoutsideofyourtownorvillage?Base:15-65populaAon

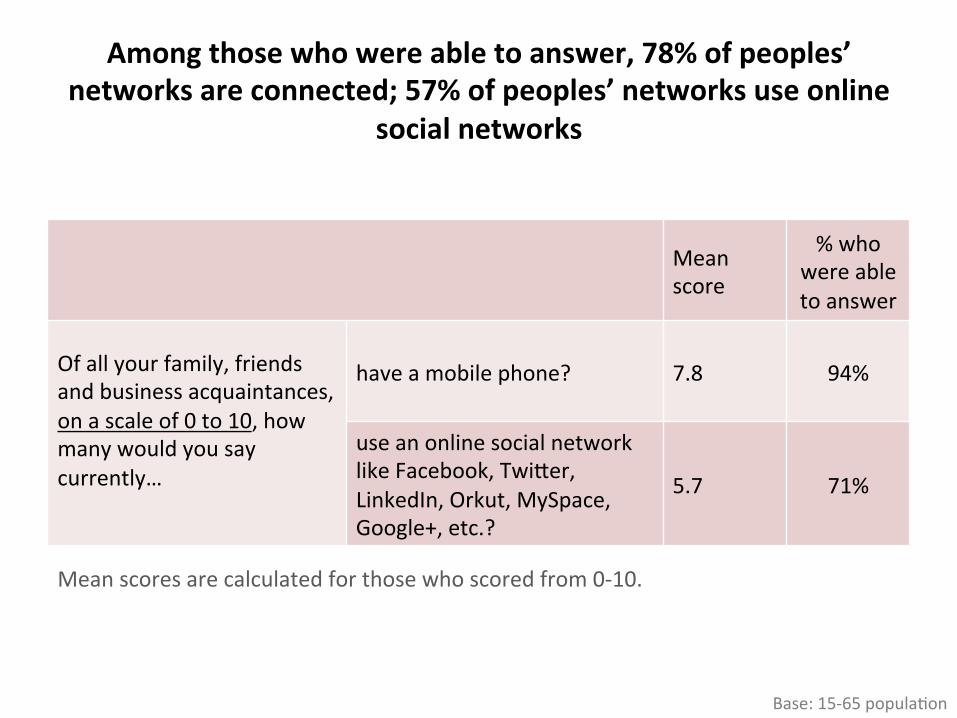

Amongthosewhowereabletoanswer,78%ofpeoples’networksareconnected;57%ofpeoples’networksuseonline

socialnetworks

Meanscore

%whowereabletoanswer

Ofallyourfamily,friendsandbusinessacquaintances,onascaleof0to10,howmanywouldyousaycurrently…

haveamobilephone? 7.8 94%

useanonlinesocialnetworklikeFacebook,Twifer,LinkedIn,Orkut,MySpace,Google+,etc.?

5.7 71%

Meanscoresarecalculatedforthosewhoscoredfrom0-10.

Base:15-65populaAon

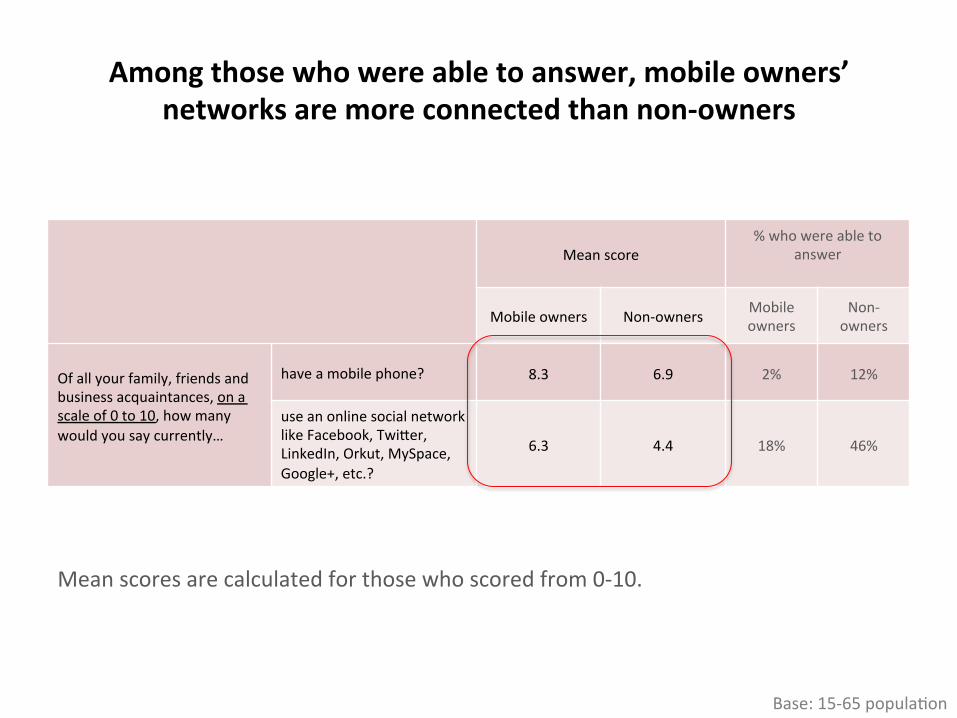

Amongthosewhowereabletoanswer,mobileowners’networksaremoreconnectedthannon-owners

Meanscore%whowereableto

answer

Mobileowners Non-owners Mobileowners

Non-owners

Ofallyourfamily,friendsandbusinessacquaintances,onascaleof0to10,howmanywouldyousaycurrently…

haveamobilephone? 8.3 6.9 2% 12%

useanonlinesocialnetworklikeFacebook,Twifer,LinkedIn,Orkut,MySpace,Google+,etc.?

6.3 4.4 18% 46%

Meanscoresarecalculatedforthosewhoscoredfrom0-10.

Base:15-65populaAon

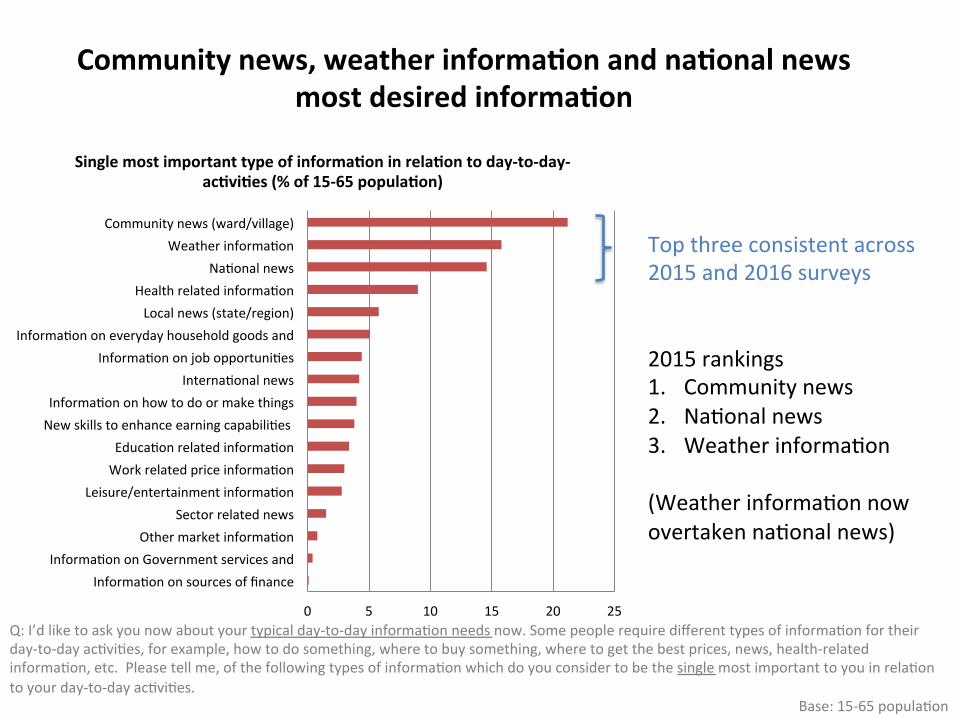

Communitynews,weatherinforma3onandna3onalnewsmostdesiredinforma3on

0 5 10 15 20 25

InformaAononsourcesoffinanceInformaAononGovernmentservicesand

OthermarketinformaAonSectorrelatednews

Leisure/entertainmentinformaAonWorkrelatedpriceinformaAonEducaAonrelatedinformaAon

NewskillstoenhanceearningcapabiliAesInformaAononhowtodoormakethings

InternaAonalnewsInformaAononjobopportuniAes

InformaAononeverydayhouseholdgoodsandLocalnews(state/region)

HealthrelatedinformaAonNaAonalnews

WeatherinformaAonCommunitynews(ward/village)

Singlemostimportanttypeofinforma3oninrela3ontoday-to-day-ac3vi3es(%of15-65popula3on)

Topthreeconsistentacross2015and2016surveys2015rankings1. Communitynews2. NaAonalnews3. WeatherinformaAon

(WeatherinformaAonnowovertakennaAonalnews)

Q:I’dliketoaskyounowaboutyourtypicalday-to-dayinformaAonneedsnow.SomepeoplerequiredifferenttypesofinformaAonfortheirday-to-dayacAviAes,forexample,howtodosomething,wheretobuysomething,wheretogetthebestprices,news,health-relatedinformaAon,etc.Pleasetellme,ofthefollowingtypesofinformaAonwhichdoyouconsidertobethesinglemostimportanttoyouinrelaAontoyourday-to-dayacAviAes.

Base:15-65populaAon

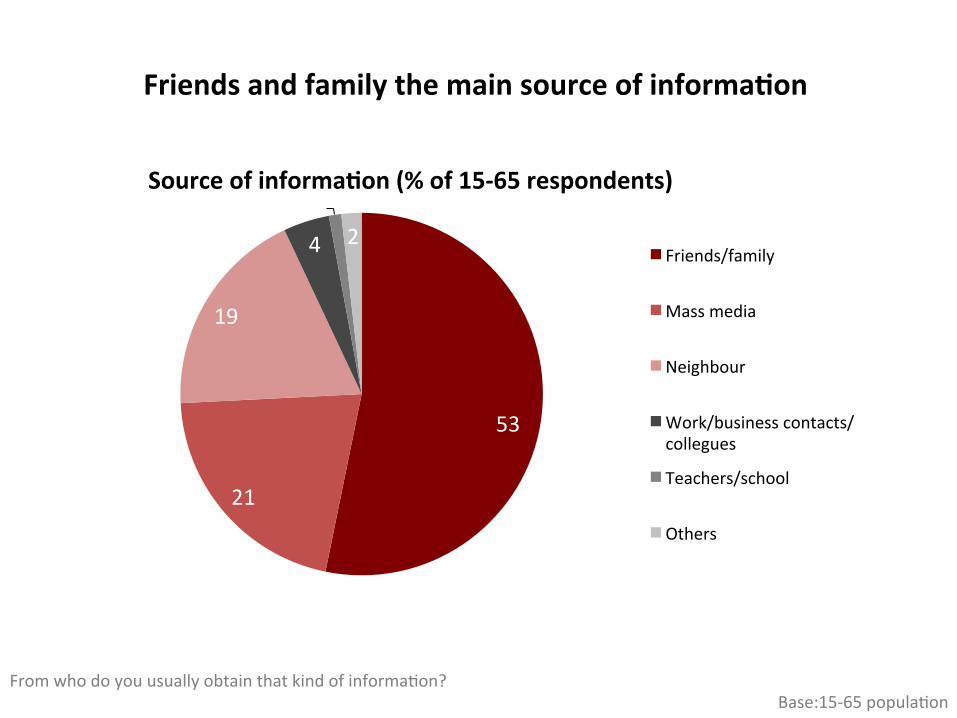

Friendsandfamilythemainsourceofinforma3on

FromwhodoyouusuallyobtainthatkindofinformaAon?Base:15-65populaAon

53

21

19

4

12

Friends/family

Massmedia

Neighbour

Work/businesscontacts/collegues

Teachers/school

Others

Sourceofinforma3on(%of15-65respondents)

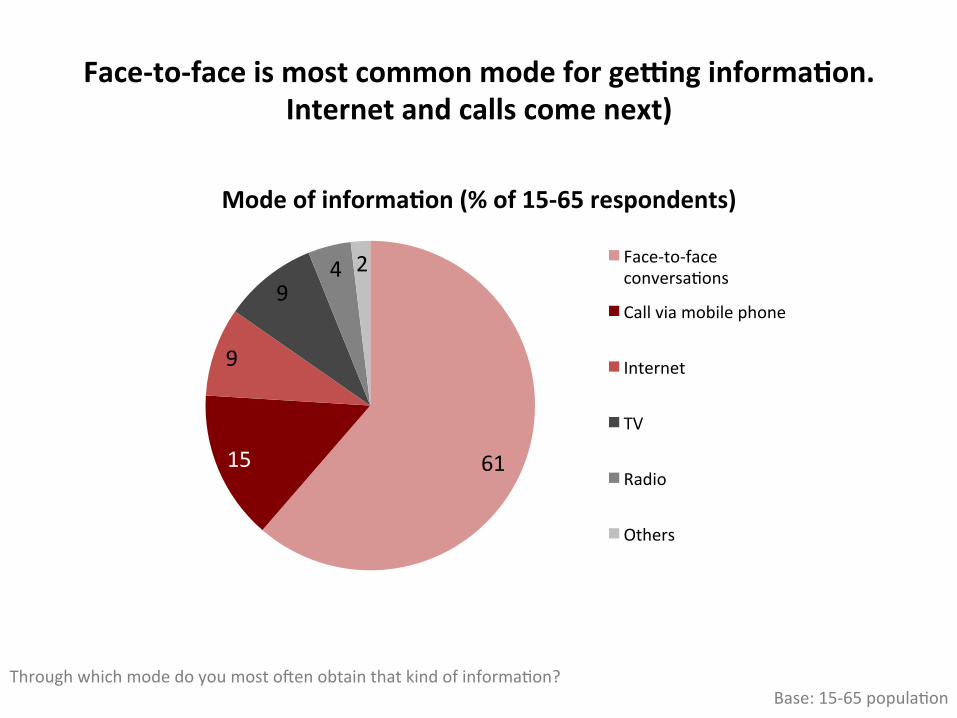

Face-to-faceismostcommonmodeforgewnginforma3on.Internetandcallscomenext)

ThroughwhichmodedoyoumostosenobtainthatkindofinformaAon?Base:15-65populaAon

6115

9

94 2 Face-to-face

conversaAons

Callviamobilephone

Internet

TV

Radio

Others

Modeofinforma3on(%of15-65respondents)

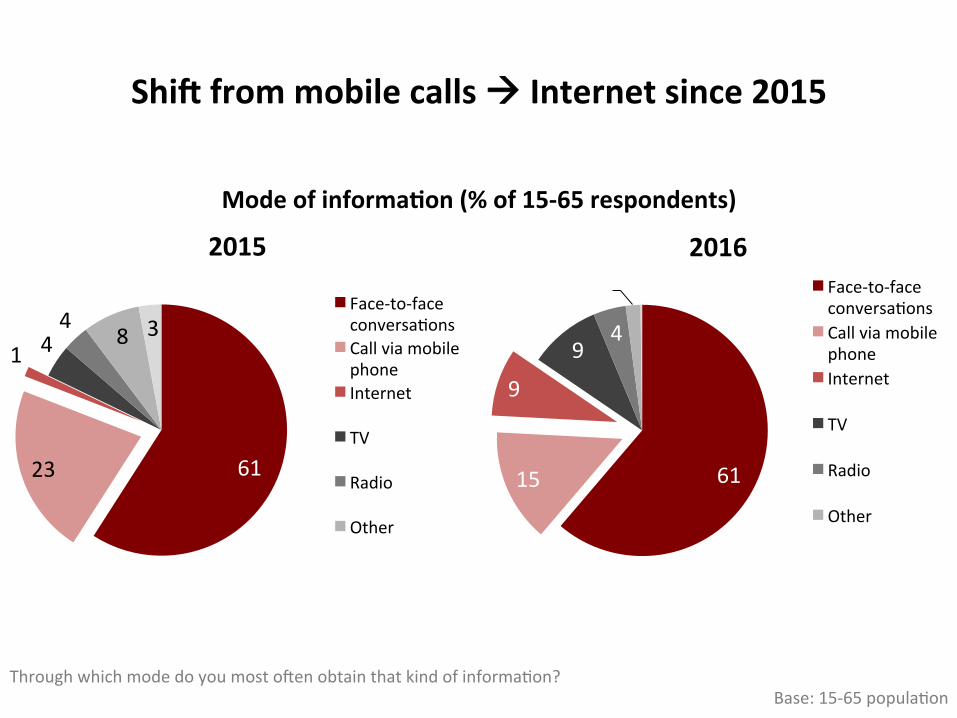

ShimfrommobilecallsàInternetsince2015

6123

1 44

8 3

2015

Face-to-faceconversaAonsCallviamobilephoneInternet

TV

Radio

Other

6115

9

94

2 02016

Face-to-faceconversaAonsCallviamobilephoneInternet

TV

Radio

Other

ThroughwhichmodedoyoumostosenobtainthatkindofinformaAon?Base:15-65populaAon

Modeofinforma3on(%of15-65respondents)

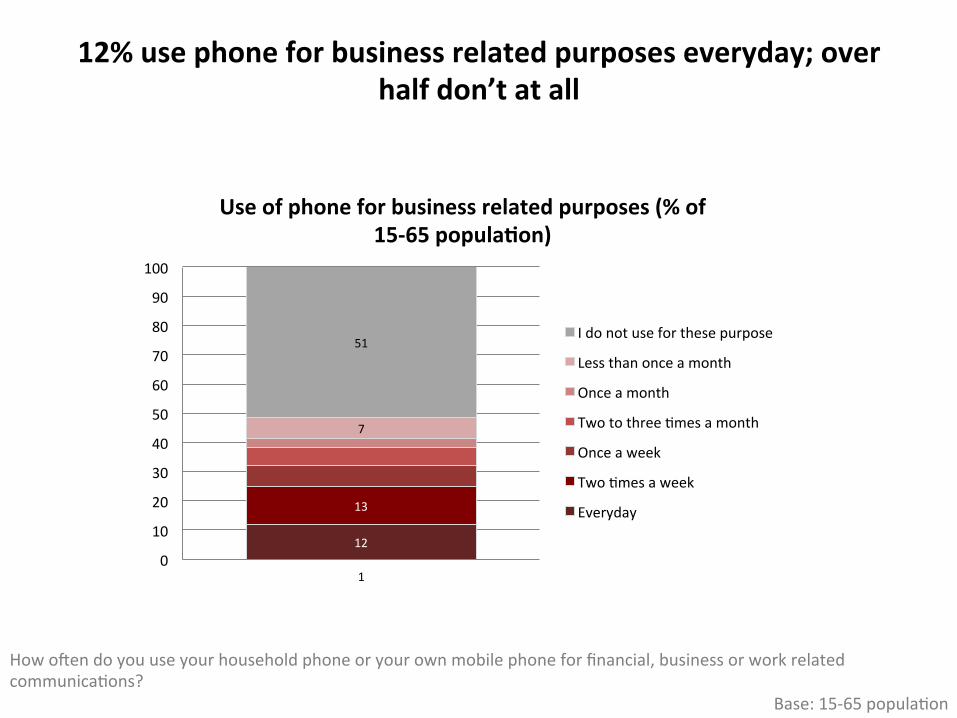

12%usephoneforbusinessrelatedpurposeseveryday;overhalfdon’tatall

Howosendoyouuseyourhouseholdphoneoryourownmobilephoneforfinancial,businessorworkrelatedcommunicaAons?

Base:15-65populaAon

12

13

7

51

0

10

20

30

40

50

60

70

80

90

100

1

Useofphoneforbusinessrelatedpurposes(%of15-65popula3on)

Idonotuseforthesepurpose

Lessthanonceamonth

Onceamonth

TwotothreeAmesamonth

Onceaweek

TwoAmesaweek

Everyday

PERCEPTIONSABOUTMOBILETECHNOLOGYANDITSIMPACTS

122

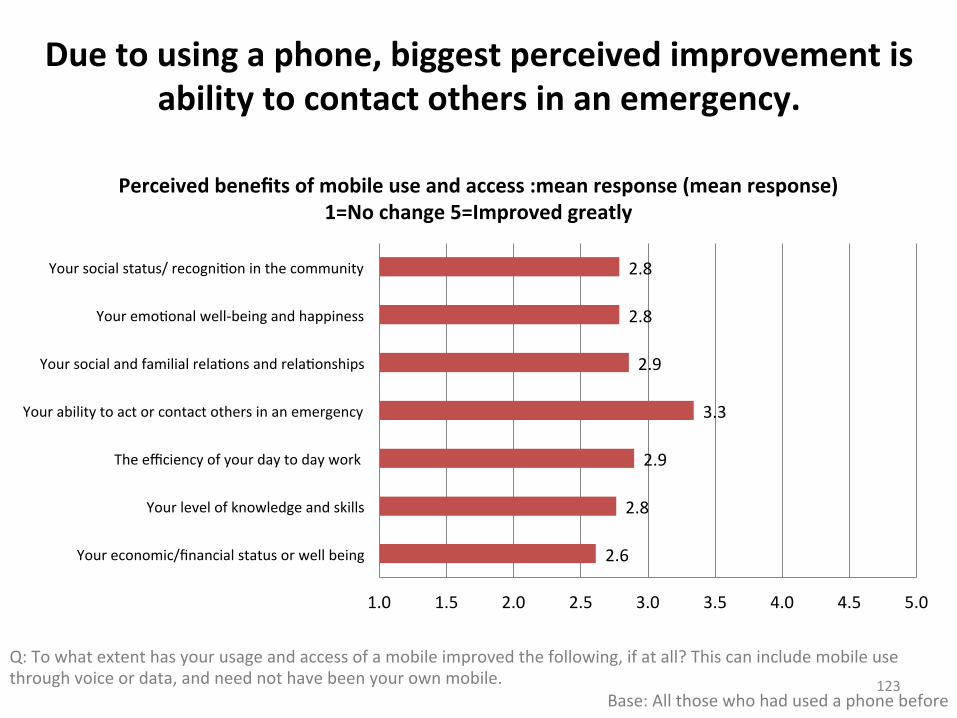

Q:Towhatextenthasyourusageandaccessofamobileimprovedthefollowing,ifatall?Thiscanincludemobileusethroughvoiceordata,andneednothavebeenyourownmobile.

Base:Allthosewhohadusedaphonebefore

2.6

2.8

2.9

3.3

2.9

2.8

2.8

1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

Youreconomic/financialstatusorwellbeing

Yourlevelofknowledgeandskills

Theefficiencyofyourdaytodaywork

Yourabilitytoactorcontactothersinanemergency

YoursocialandfamilialrelaAonsandrelaAonships

YouremoAonalwell-beingandhappiness

Yoursocialstatus/recogniAoninthecommunity

Perceivedbenefitsofmobileuseandaccess:meanresponse(meanresponse)1=Nochange5=Improvedgreatly

123

Duetousingaphone,biggestperceivedimprovementisabilitytocontactothersinanemergency.

2.6

2.8

2.9

2.8

2.5

2.4

2.8

2.5

1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

Youreconomic/financialstatusorwellbeing

Yourlevelofknowledgeandskills

YoursocialandfamilialrelaAonsandrelaAonships

YouremoAonalwell-beingandhappiness

Perceivedbenefitsofmobileuseandaccess:meanresponse(meanresponse)1=Nochange5=Improvedgreatly

2015

2016

124

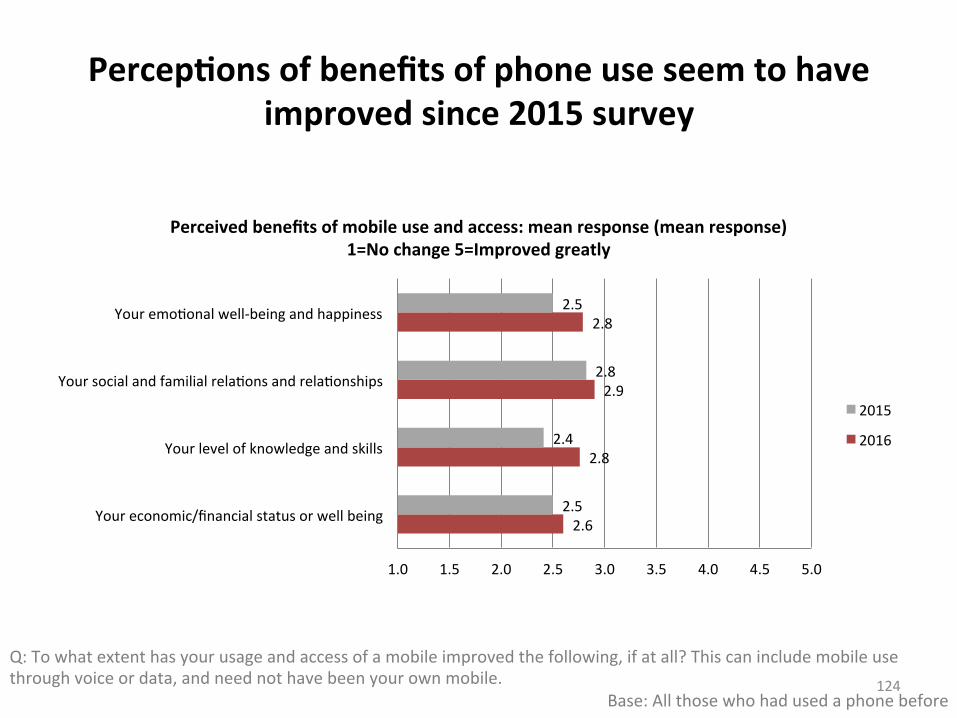

Percep3onsofbenefitsofphoneuseseemtohaveimprovedsince2015survey

Q:Towhatextenthasyourusageandaccessofamobileimprovedthefollowing,ifatall?Thiscanincludemobileusethroughvoiceordata,andneednothavebeenyourownmobile.

Base:Allthosewhohadusedaphonebefore

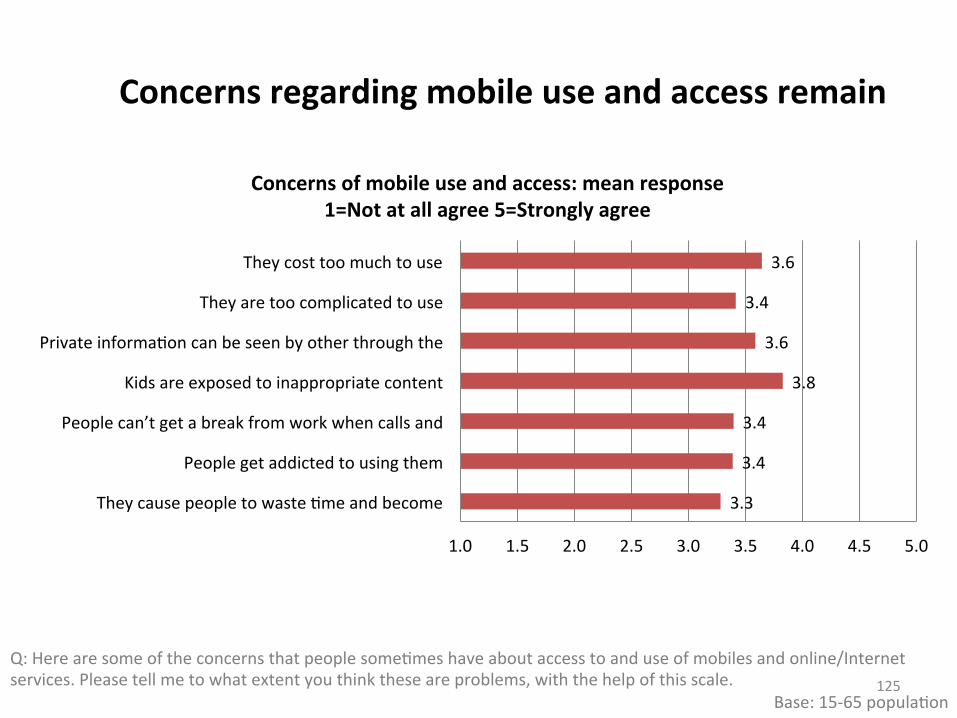

Concernsregardingmobileuseandaccessremain

Q:HerearesomeoftheconcernsthatpeoplesomeAmeshaveaboutaccesstoanduseofmobilesandonline/Internetservices.Pleasetellmetowhatextentyouthinktheseareproblems,withthehelpofthisscale.

Base:15-65populaAon

3.3

3.4

3.4

3.8

3.6

3.4

3.6

1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

TheycausepeopletowasteAmeandbecome

Peoplegetaddictedtousingthem

Peoplecan’tgetabreakfromworkwhencallsand

Kidsareexposedtoinappropriatecontent

PrivateinformaAoncanbeseenbyotherthroughthe

Theyaretoocomplicatedtouse

Theycosttoomuchtouse

Concernsofmobileuseandaccess:meanresponse1=Notatallagree5=Stronglyagree

125

Q:HerearesomeoftheconcernsthatpeoplesomeAmeshaveaboutaccesstoanduseofmobilesandonline/Internetservices.Pleasetellmetowhatextentyouthinktheseareproblems,withthehelpofthisscale.

Base:15-65populaAon126

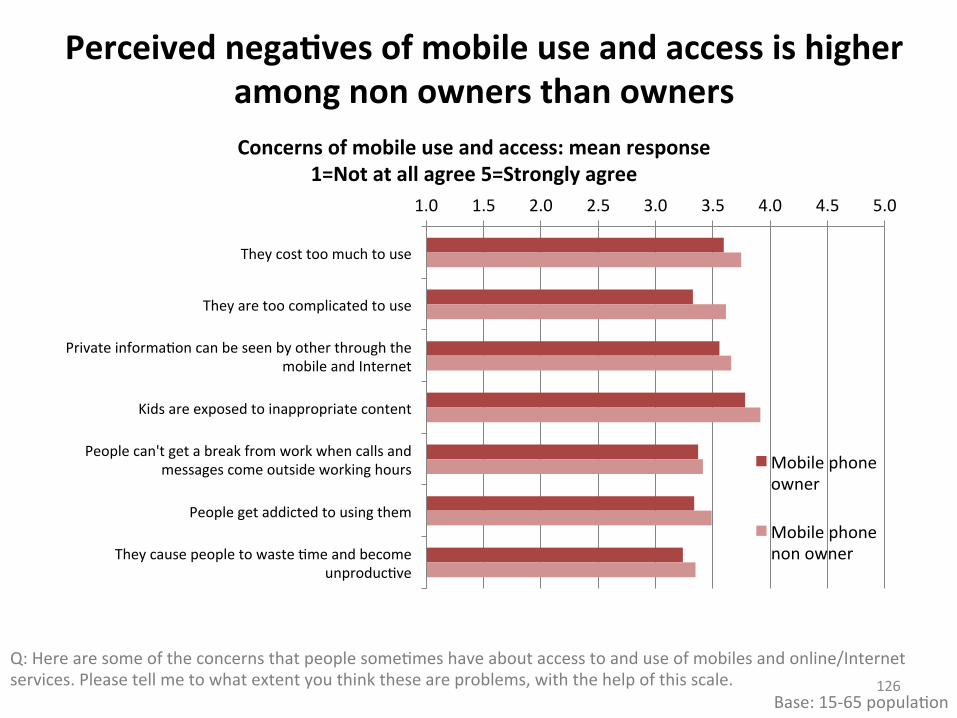

1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

Theycosttoomuchtouse

Theyaretoocomplicatedtouse

PrivateinformaAoncanbeseenbyotherthroughthemobileandInternet

Kidsareexposedtoinappropriatecontent

Peoplecan'tgetabreakfromworkwhencallsandmessagescomeoutsideworkinghours

Peoplegetaddictedtousingthem

TheycausepeopletowasteAmeandbecomeunproducAve

Mobilephoneowner

Mobilephonenonowner

Perceivednega3vesofmobileuseandaccessishigheramongnonownersthanownersConcernsofmobileuseandaccess:meanresponse

1=Notatallagree5=Stronglyagree

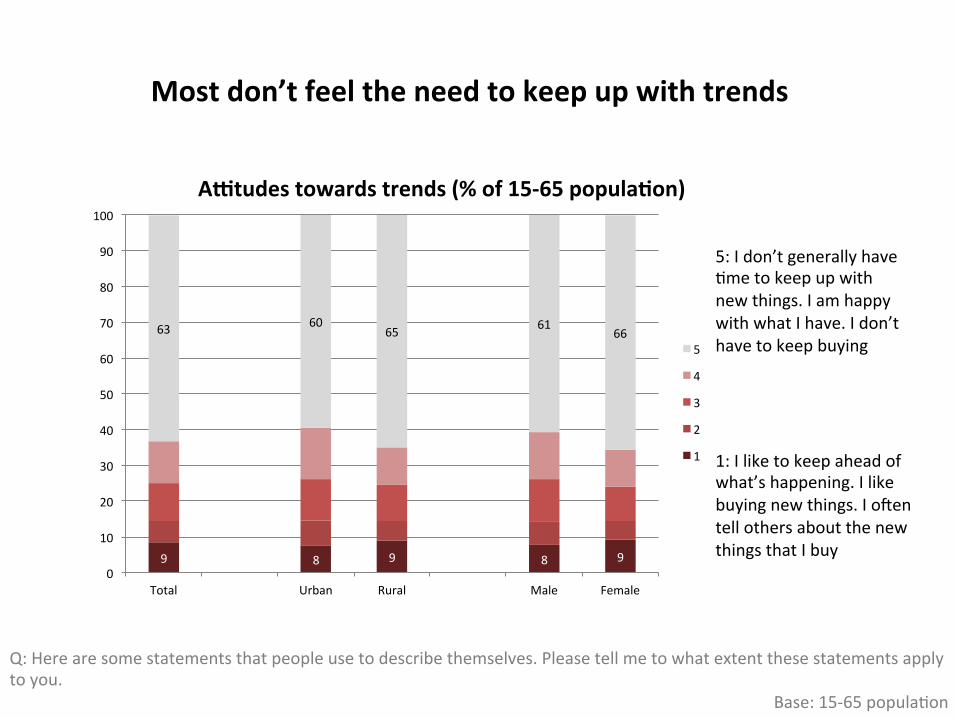

Mostdon’tfeeltheneedtokeepupwithtrends

9 8 9 8 9

63 6065 61

66

0

10

20

30

40

50

60

70

80

90

100

Total Urban Rural Male Female

5

4

3

2

1 1:Iliketokeepaheadofwhat’shappening.Ilikebuyingnewthings.IosentellothersaboutthenewthingsthatIbuy

5:Idon’tgenerallyhaveAmetokeepupwithnewthings.IamhappywithwhatIhave.Idon’thavetokeepbuying

Awtudestowardstrends(%of15-65popula3on)

Q:Herearesomestatementsthatpeopleusetodescribethemselves.Pleasetellmetowhatextentthesestatementsapplytoyou.

Base:15-65populaAon

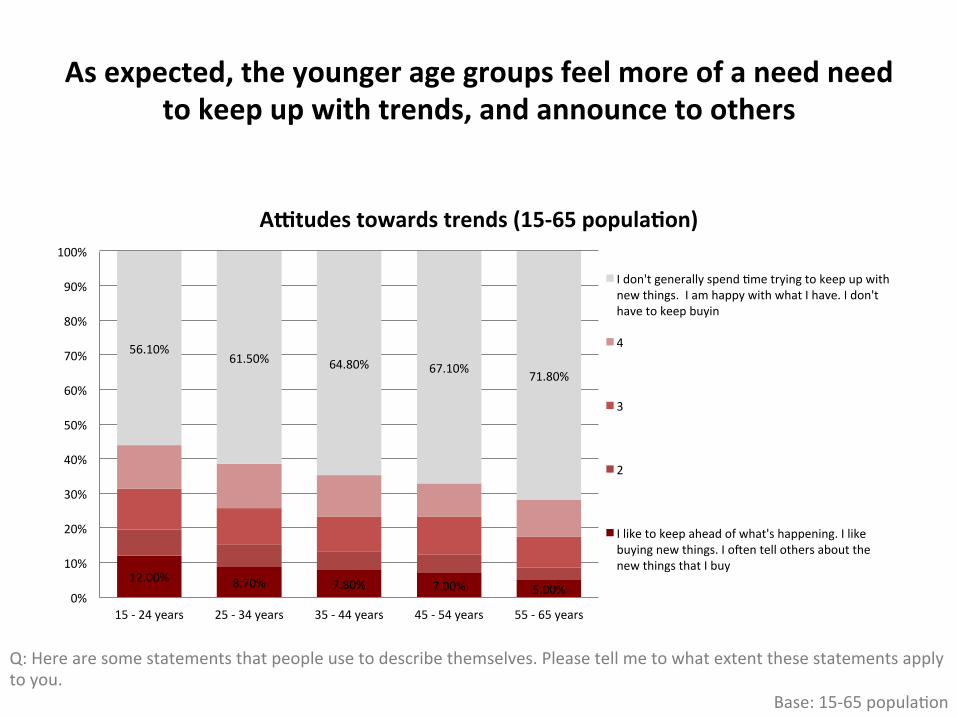

Asexpected,theyoungeragegroupsfeelmoreofaneedneedtokeepupwithtrends,andannouncetoothers

12.00% 8.70% 7.80% 7.00% 5.00%

56.10%61.50% 64.80% 67.10% 71.80%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

15-24years 25-34years 35-44years 45-54years 55-65years

Awtudestowardstrends(15-65popula3on)

Idon'tgenerallyspendAmetryingtokeepupwithnewthings.IamhappywithwhatIhave.Idon'thavetokeepbuyin

4

3

2

Iliketokeepaheadofwhat'shappening.Ilikebuyingnewthings.IosentellothersaboutthenewthingsthatIbuy

Q:Herearesomestatementsthatpeopleusetodescribethemselves.Pleasetellmetowhatextentthesestatementsapplytoyou.

Base:15-65populaAon

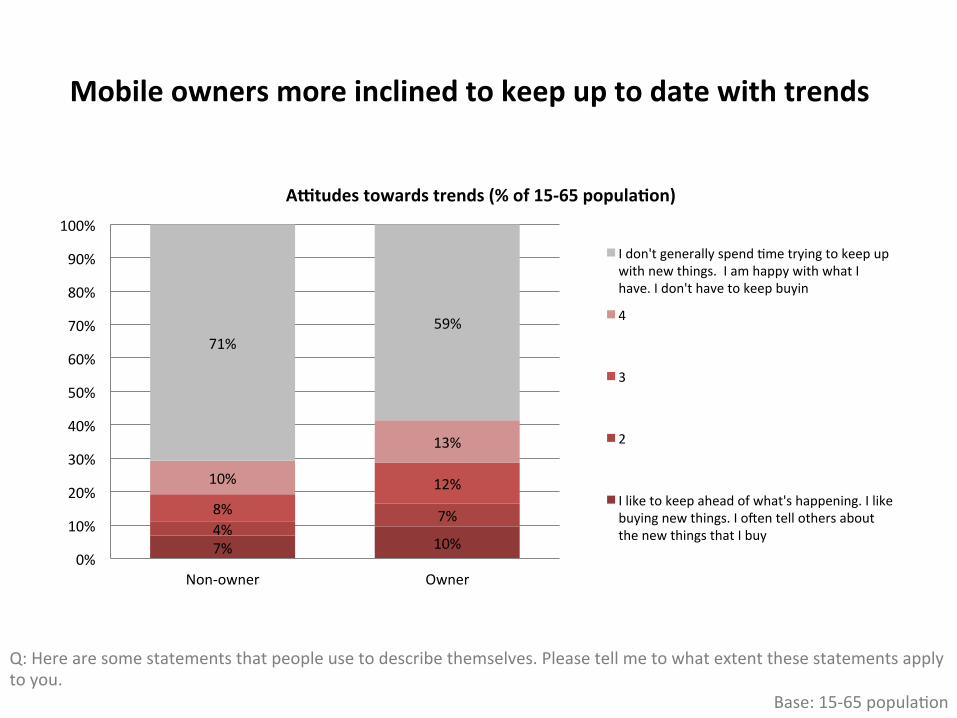

Mobileownersmoreinclinedtokeepuptodatewithtrends

Q:Herearesomestatementsthatpeopleusetodescribethemselves.Pleasetellmetowhatextentthesestatementsapplytoyou.

Base:15-65populaAon

7% 10%4%

7%8%12%10%

13%

71%59%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Non-owner Owner

Awtudestowardstrends(%of15-65popula3on)

Idon'tgenerallyspendAmetryingtokeepupwithnewthings.IamhappywithwhatIhave.Idon'thavetokeepbuyin

4

3

2

Iliketokeepaheadofwhat'shappening.Ilikebuyingnewthings.IosentellothersaboutthenewthingsthatIbuy

Thankyou

• Analysisatmoregranularlevel(e.g.byregion)ispossible.

• Ifneeded,pleasecontact:– helani[at]lirneasia.net