Embed Size (px)

Citation preview

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 1/37

EQ UITY DERIVATIVE

GLO BA

Un d e r s ta n d in g Min o r ity

S q u e e z e - O u t s

We review different minority squeeze-out transaction structures and the legal

sta nda rds ap plica ble in Delawa re la w to these situa tions. W e then present nine

case studies of minority squeeze-outs, review their general characteristics, and

discuss some de scriptive statistics ba sed o n these ca ses. Finally, we de scribe a

methodology for calculating the probability of a bump in deal terms for minority

sque ez e-outs. W e app ly this methodology to a number of pa st dea ls to discuss its

implications.

n The a cquirer may cond uct a tende r offer ra ther tha n ta ke its offer directly to the

target board so as to exert some timing and pricing discipline on the evaluation

process.

n It a pp ea rs tha t a cquirers were a ble to a fford large r premiums in recent transa ctions

partly because of the large decline in target prices over the three-month period

preceding deal announcements.

n As long as the expected upside from a bump in the terms more than compensates

investors for the opp ortunity cost of their ca pital, lowe r (or more ne ga tive) a rbitrag e

spreads imply higher probabilities of a bump, with all else being equal.

n In a typica l minority squee ze -out situation in which the initia l sprea d is nega tive (or

positive, but narrow) a nd risk a rbitrag eurs sta nd to incur losses upon dea l

termination, a lower expected bump implies a higher probability of a bump, all

else being equal.

n As long as the expected upside from a bump in the terms more than compensates

investors for the op portunity cost of their ca pital, the g rea ter the e xpected loss upon

deal termination, the more positive (or less negative) the spread needs to be for

investors to be willing to put on a risk arbitrage position, with all else being equal.

Evren Ergin, Ph.D.

1.201.524.4212

Christian Correa

1.201.524. 4212

U.S. Risk Arbitrage Research

Andrew T. W hittaker

Evren Ergin, Ph.D.

Sugun V. Kapoor

Christian Correa

1.201.524.4212

January 3, 20 02

http:/ / www.lehman.com

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 2/37

Understa nding Minority Squeeze -O uts

2 January 3 , 2 0 0 2

Ta b l e o f Co n t e n t s

Introduction..................................................... .............................................. 3

Transaction Structures and Lega l Issues. ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... .. 5

Transaction Structures and Dea l Outcomes.... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... ... . 5

Legal Standards in Delawa re Law for Minority Squeeze -Outs.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. 5

Cha racteristics of Nine Minority Squeeze -Outs and Their Descriptive Statistics.. .. .. .. .. .. . 8

Deal Background and Summaries ..... ...... ...... ..... ...... ..... ...... ...... ..... ...... ..... ...... 8

Q ualitative Characteristics..... ...... ..... ..... ...... ..... ...... ..... ...... ...... ..... ...... ..... .... 13

Descriptive Statistics..... ...... ...... ..... ...... ..... ...... ...... ..... ...... ..... ..... ...... ..... ...... 15

Future Minority Squeeze-O uts?.. ..... ...... ..... ...... ..... ..... ...... ..... ...... ..... ...... ...... . 19

W hat is the Proba bility of a Bump? Probability Analysis in Minority Squeeze -Outs.. .. .. 20

Synopsis of Framework and Main Assumptions.... ... ... ... ... ... ... ... ... ... ... ... ... ... ... .. 20

Results......................................................... ............................................ 21

Conclusion..................................................... ............................................ 30

Appendix.................................................................................. ................. 33 Probab ility Framework........ ...... ..... ...... ..... ...... ...... ..... ...... ..... ..... ...... ..... ...... 33

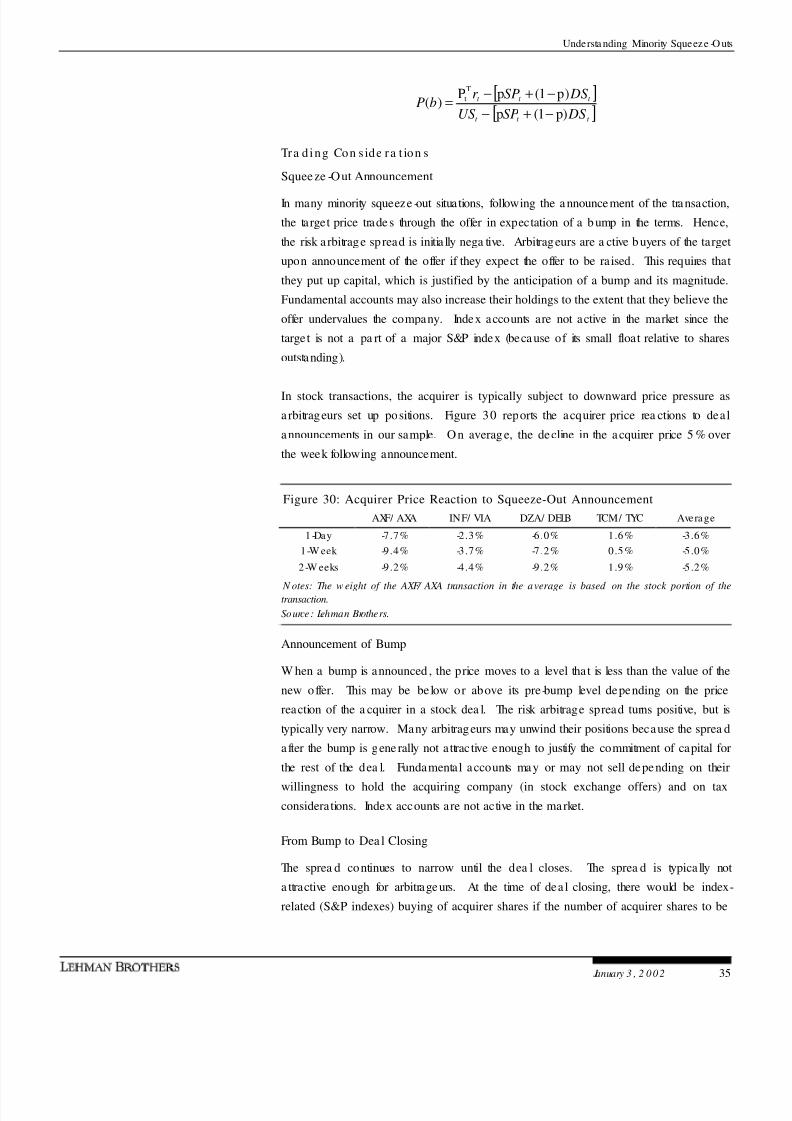

Trading Considerations...... ..... ..... ...... ..... ...... ..... ...... ...... ..... ...... ..... ...... ...... . 35

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 3/37

Understa nding Minority Squeeze -O uts

January 3 , 2 0 02 3

In t roduc t i on

In a minority squeeze -out, a shareholder (acquirer) who owns a majority or a substantial

portion of a target’s outstanding shares offers to purchase the target shares it does not

already own. The acquirer may be the parent of previously carved-out subsidiary or an

affiliate that has previously bought a substantial stake in the target. In either ca se, the

acquirer’s objective is to consolidate its ownership in the target by purchasing the

publicly held minority shares. The acquirer’s offer may be structured as a tender offer, a

merger, or a tender offer followed by a second-step merger.

The interaction between the acquirer and the target board in transactions involving

merge rs may be subject to conflicts of interest. By virtue of holding a significa nt stake in

the target, the acquirer typically has representation on the target’s board of directors.

Several of the target directors are usually officers of the a cquiring company. These

directors have fiduciary duties to both the target and the acquirer and may thus face

conflicts of interest in minority squee ze -out transactions. In order to avoid lawsuits

a lleg ing brea ch of fiduciary duty or unfair dealing, the target board typically establishesa specia l committee of independent directors shortly after the receipt of an a cquisition

proposa l. The special committee evalua tes the offer, neg otiates with the a cquirer, and

makes a recommendation to the board of directors. The board has the final decision-

making a uthority and typica lly follows the recommendation of the special committee .

Even if a transaction is structured as a tender offer, the acquirer may deal with a special

committee o f the targe t’s board of directors to fend off a lleg ations of unfa ir price or unfair

de a ling, to reduce the risk of fa ilure, and to give itself flexibility.

In most minority squeeze -outs, negotiations be tween the a cquirer and the special

committee result in a higher offer and a recommendation of the transaction by the targetboard to the company’s shareholders. The initial offer is typically perceived to be a

lowball figure, as pa rt of the negotia ting strategy of the a cquirer. This perception is

reflected in the target’s share price, as it tends to trade very close to or above the offer

price. The final offer received by the target shareholders depends on a number of

factors including the value of the target compa ny as a go ing-concern, motivation of the

acquirer, concentra tion of control among minority shareholders, existence of other

potential buyers, negotiating power of the acquirer, and premiums offered in comparable

transactions.

An offer higher than the initial one is not a gua ranteed outcome. Negotiations with the

target board may not lead to any agreement, and the acquirer might terminate the offer.

In a tender offer, the acquirer may not be able to obtain sufficient shares to complete the

transaction. It is also possible that the dea l is completed without a “bump” in the terms,

following an endorsement by the target board or acceptance by target shareholders.

This report contains three main sections. In the first section, we review d ifferent minority

squeeze -out transa ction structures and the lega l standa rds applica ble in Delaware law in

these situations. In the second section, we present nine ca se studies of minority squeeze -

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 4/37

Understa nding Minority Squeeze -O uts

4 January 3 , 2 0 0 2

outs, review their general characteristics, and discuss some descriptive statistics based on

these ca ses. At the end of the second section, we also list a number of potential minority

squeeze -out situations ba sed on the implica tions of our ana lysis. In the last section, we

describe a methodology for calculating the probability of a bump in dea l terms for

minority squee ze -outs. W e a pply this methodology to a number of pa st dea ls to discuss

its implica tions. In the a ppendix, we present the deriva tion of our methodology and a lsodiscuss trading considerations.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 5/37

Understa nding Minority Squeeze -O uts

January 3 , 2 0 02 5

Tr a n s a ct io n S tr u c tu r e s a n d Le g a l Is s u e s

Tra nsa c tion S t ructures a nd Dea l Outcom es

The timing a nd value of the final offer in a minority squeeze -out may depend on the

transaction structure. The minority squeeze -out may be in the form of proposed merger or

a tender offer made to target shareholders. A structure that involves a me rger may

require the approva l of the targe t board of directors. A tender offer by itself does not

require target board approval, and the acquirer may take the offer directly to target

shareholders.1 In situa tions involving proposed mergers, the actions of target directors

a re subject to the “entire fa irness” standa rd in Delaware courts. In contrast, this standa rd

is not app lica ble to tender offers made directly to target shareholders by controlling

shareholders. The target directors do not have a duty to de monstrate entire fairness in

these tender situations.2 The ina pplica bility of the “entire fa irness” standa rd is likely to

limit the extent of shareholder litiga tion.

Taking the offer directly to sha reholders may also facilita te negotiations with the special

committee, since the acquirer’s decision to initially bypa ss the boa rd could g ive the

board an incentive to become involved in the process. Moreover, in direct tender offers,

the special committee may have less bargaining leverage than it would in a proposed

merger because the target’s decision-making authority is delegated to the target

shareholders ra ther than to the directors.

The acquirer is not obliged to interact with a special committee in direct tender offers.

Completely circumventing the target board, however, is likely to incite greater

shareholder opposition. In addition, the acquirer would have to rely on obtaining

sufficient ta rget shares (90 %) to be able to conduct a short-form merger.3 Rea ching a

compromise with the target’s special committee may serve the a cquirer’s interests byreducing the proba bility of fa ilure in the tender offer.

Leg a l St an da rds i n De l aw a re La w fo r Mino r i ty Sque eze -Ou t s

Squeeze -outs have built-in conflicts of duties a nd high risk of litiga tion. The boa rd of the

target is usually made up of a majority of appointees from the controlling corporation.

These directors have conflicting duties: a duty to the shareholders of the ta rget to

maximize the price pa id and a duty to the sha reholders of the controlling corporation to

minimize the price pa id. In light of this conflict, the decisions of directors a re not

1 Note that the acquirer typically has a control position, and therefore poison pills and change of control

statutes are generally not applicable.

2In Re Siliconix Incorporated Shareholders Litiga tion, Delawa re Cha ncery Court, Consolida ted C. A. No.

18 70 0, John W. N oble, V.C. , Memorandum Opinion (June 1 9, 20 01 ).

3The short-form merger does not require target board or shareholder votes.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 6/37

Understa nding Minority Squeeze -O uts

6 January 3 , 2 0 0 2

reviewed by Delaware courts under the “business judgment rule.”4 Instead, a Delaware

court will app ly the “entire fairness” test.

Entire Fa irness. The “entire fairness” test req uires that the proponents of the transa ction—

not the p la intiffs—b e a ble to show that the transaction was arrived at through “fair

dea ling” and is a t a “fa ir price. ” This standa rd is broad in scope and very demanding.

Fair dealing is a broad standard which looks at the deal timing, the process by which it

was initiated, negotiated, and structured, and how the approval of directors and

shareholde rs wa s obta ined. Full disclosure of materia l information, p articularly to outside

directors, is crucial. This includes information which would ordinarily never be disclosed,

like interna l financial analysis of the de al va luation.

Fair price standards have been set by appraisal cases, even though appraisal rights are

not technica lly invoked. The appraisal laws look a t all relevant factors, including asset

values, market values, comparable transactions, historical earnings, discounted cash

flows, and future prospects. Expert advice and a n opinion from an investment ba nker

that the value is fair are often used to establish a fair price. Fa ir value may exclude

“specula tive elements” and merger synergies or cost savings. Fa ir value does not include

a minority discount reflecting the lack of control.

A fa ir price does not necessa rily imply fair dea ling and vice versa. Broadly speaking,

both elements of the test must be satisfied a nd court precedents exist where a fair price

was found yet plaintiffs won the case on fair dealing grounds as well as the converse.

Howe ver, in a squeeze -out the dominant concern is fair price, followe d by disclosure of

materia l information. Broader indica tions of fa ir dea ling beyond d isclosure are not

weighed as hea vily.

Role o f the Specia l Co mmittee . The most common technique for sa tisfying the court’s

entire fairness standa rd is the appointment of a special committee. A committee of

outside directors who are disinterested may be appointed by the target’s board of

directors to a pprove the transaction. This committee negotia tes on be half of the e ntire

board, representing the interests of minority shareholders and protecting the controlling

compa ny from leg al liability.

A special committee must be disinterested a nd ca pa ble of performing its task. This

involves being informed, having appropriate incentives and having access to good,

independent lega l and financial advice. W ith this support a special committee should

see k the best possible price without rejecting a transaction that is in the interest of

minority shareholders. A concomitant of this is tha t the controlling corporation is limited

4 The business judgment rule shields directors from being second-guessed by courts. A court app lying the

rule will de fer to the business judgment of the direc tors. A director ca n still be liable for gross negligence

under the business judgment rule.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 7/37

Understa nding Minority Squeeze -O uts

January 3 , 2 0 02 7

in its ability to withhold information from the specia l committee or use certa in tactics,

including “take-it-or-lea ve-it” offers. Note that the specia l committee does not necessarily

have the power to “shop” the company to other buyers, and the controlling company is

not obliged to follow through on its offer. A controlling company can withdraw in light

of unfavorable negotiations before a definitive agreement is signed.

A squeeze -out may proceed over the op position of the spe cial committee . Techniques

which may be used to a void viola ting entire fairness include granting appraisal rights to

a ll minority shareholders, a llowing the minority shareholders to receive sha res in the

controlling corporation as consideration, thus participating in merger synergies, or

conditioning the transaction on a vote of the minority shareholders.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 8/37

Understa nding Minority Squeeze -O uts

8 January 3 , 2 0 0 2

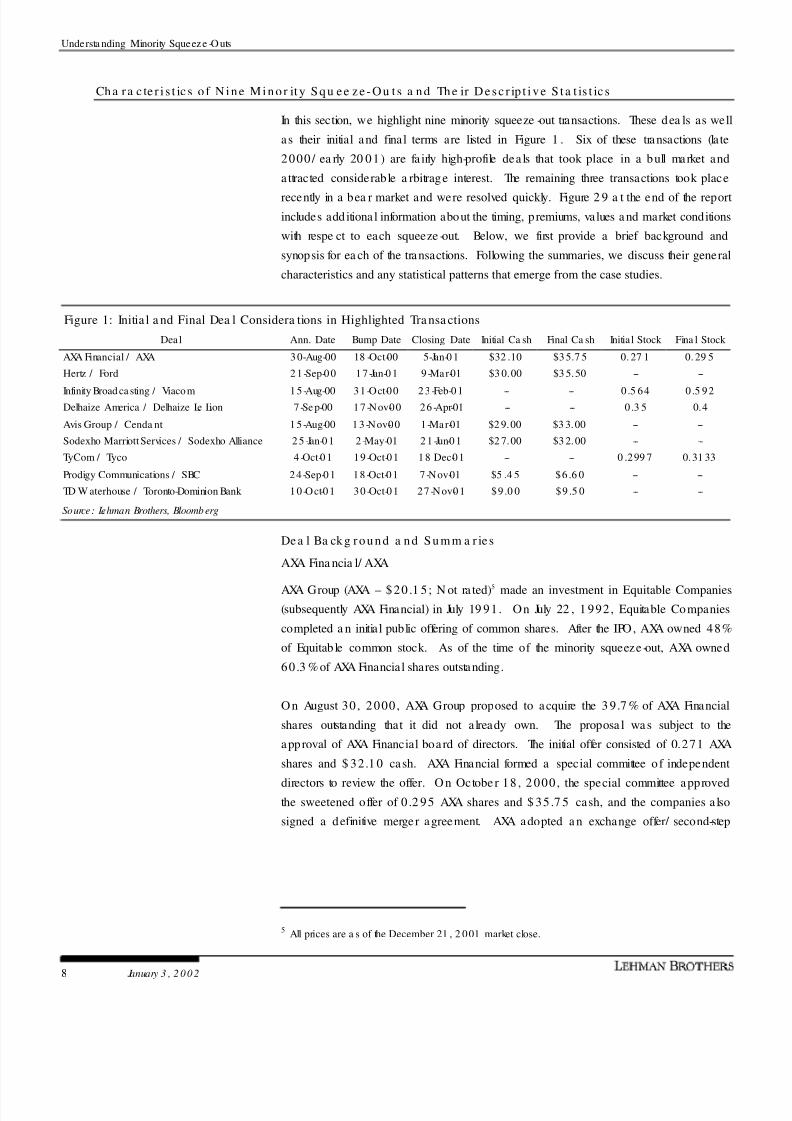

Cha ra c te r i s t ic s o f N ine Mino r it y Squ ee ze -Ou t s a nd The ir Desc r ip t i ve S t a t is t ic s

In this section, we highlight nine minority squeeze -out transactions. These dea ls as well

as their initial and final terms are listed in Figure 1 . Six of these transactions (la te

2000/ ea rly 20 01) are fa irly high-profile dea ls that took place in a bull market and

a ttracted considerable a rbitrage interest. The remaining three transactions took place

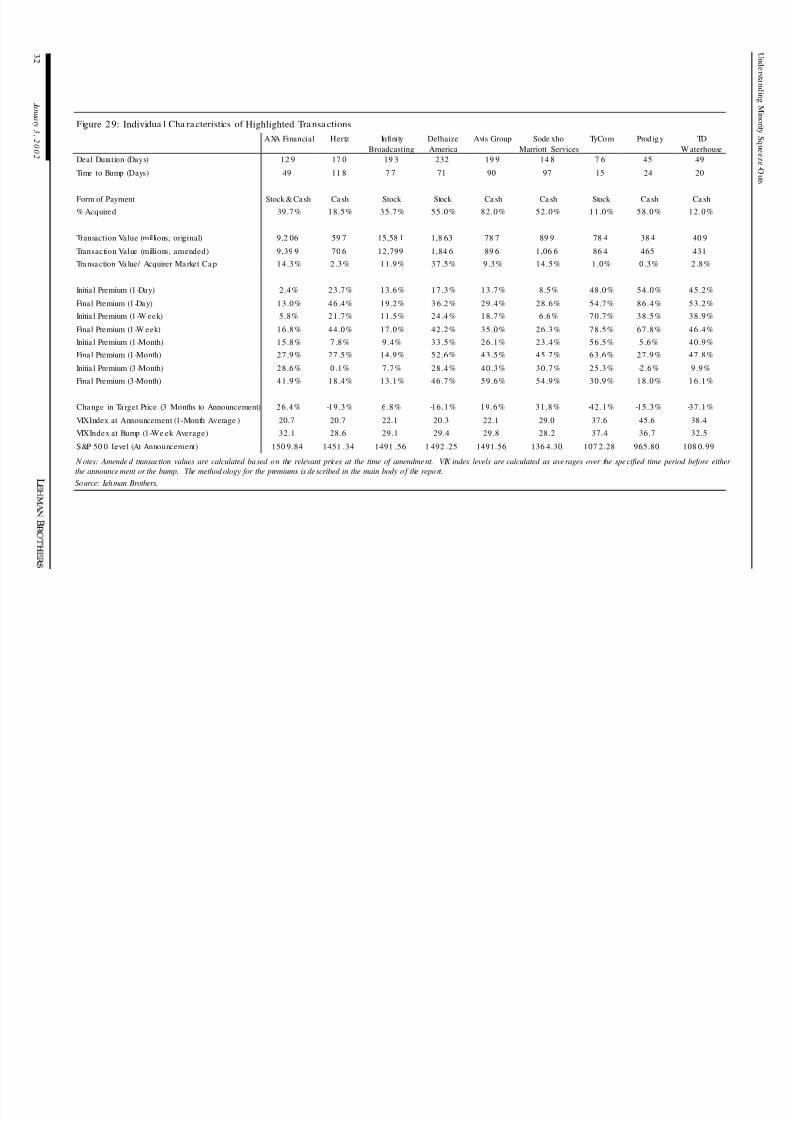

recently in a bea r market and were resolved quickly. Figure 2 9 a t the end of the report

includes additiona l information about the timing, p remiums, values a nd market conditions

with respe ct to each squeeze -out. Below, we first provide a brief background and

synopsis for ea ch of the transactions. Following the summaries, we discuss their general

characteristics and any statistical patterns that emerge from the case studies.

Figure 1: Initia l a nd Final Dea l Considera tions in Highlighted Transa ctions

Deal Ann. Date Bump Date Closing Date Initial Ca sh Final Ca sh Initial Stock Fina l Stock

AXA Financial / AXA 3 0-Aug-00 18 -Oct-00 5-Jan-0 1 $32 .10 $3 5.7 5 0. 27 1 0. 29 5

Hertz / Ford 2 1 -Sep-0 0 1 7 -Jan-0 1 9 -Mar-01 $3 0.00 $3 5.50 -- --

Infinity Broad ca sting / Viacom 1 5-Aug-00 31 -Oct-00 2 3 -Feb-0 1 -- -- 0 .5 64 0 .5 92Delhaize America / Delhaize Le Lion 7 -Se p-00 1 7 -Nov-00 26 -Apr-01 -- -- 0 .3 5 0.4

Avis Group / Cenda nt 1 5 -Aug-00 1 3 -Nov-00 1 -Mar-01 $2 9.00 $3 3.00 -- --

Sodexho Marriott Services / Sodexho Alliance 2 5 -Jan-0 1 2 -May-01 2 1 -Jun-0 1 $2 7.00 $3 2.00 -- --

TyCom / Tyco 4 -Oct-0 1 19 -Oct-01 1 8 -Dec-01 -- -- 0 .299 7 0.31 33

Prodigy Communications / SBC 2 4-Sep-0 1 18 -Oct-01 7 -Nov-01 $5 .4 5 $6 .6 0 -- --

TD W aterhouse / Toronto-Dominion Bank 1 0-Oct-0 1 30 -Oct-01 27 -Nov-0 1 $9 .0 0 $9 .5 0 -- --

Source: Lehman Brothers, Bloomb erg

Dea l Ba ckg round a nd Summ a r ie s

AXA Fina ncia l/ AXA

AXA Group (AXA – $ 20 .1 5 ; N ot ra ted)5 made an investment in Equitable Companies(subsequently AXA Financial) in July 19 91 . On July 22 , 1 992 , Equitable Companies

completed a n initia l public offering of common shares. After the IPO, AXA owned 48%

of Equitab le common stock. As of the time of the minority squeeze -out, AXA owned

60.3 % of AXA Financial shares outstanding.

O n August 30 , 2 000 , AXA Group proposed to acquire the 3 9.7 % of AXA Financial

shares outstanding that it did not a lready own. The proposa l wa s subject to the

approval of AXA Financial board of directors. The initial offer consisted of 0.271 AXA

shares and $ 32.1 0 cash. AXA Financial formed a special committee o f independent

directors to review the offer. O n Octobe r 18 , 2 000 , the special committee approvedthe sweetened offer of 0 .2 95 AXA shares and $ 35 .7 5 cash, and the companies a lso

signed a definitive merger agreement. AXA adopted a n exchange offer/ second-step

5 All prices are a s of the December 21 , 2 001 market close.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 9/37

Understa nding Minority Squeeze -O uts

January 3 , 2 0 02 9

merge r structure, with the possibility of conducting a short-form merger.6 The transaction

closed on January 5, 2001 .

Hertz/ Ford

Ford Motor Company (F – $ 15 .4 5 ; 2 Buy) first acquired an ownership interest in Hertz

in 19 87 . Hertz be ca me a wholly-owned subsidiary of Ford as a result of a series of transactions in 1993 a nd 19 94. On April 30, 1997, Hertz issued and sold shares of

its Class A common stock in an initia l public offering. After the IPO , Ford bene ficia lly

owned 49.4% of the outstanding Hertz Class A common stock (with one vote per share)

and 1 00% of the outstanding Hertz Class B common stock (with five votes per share). As

of Dece mber 31 , 1 999 , Ford had 9 4 .6 % voting powe r and 81.2 % economic interest in

Hertz.

O n September 21 , 2000 , Ford Motor Compa ny proposed to acquire the 18 .5 % of

Hertz outstanding stock that it did not alrea dy own through a merger transaction. The

initia l offer was $3 0 ca sh. The proposed merger wa s subject to Hertz boa rd approvaland the negotiation, execution, and performance of a de finitive merger agreement. On

January 17, 2001, Ford reached an agreement with the Hertz special committee and

boa rd of directors and increased its offer to $3 5.5 0 ca sh. Ford adop ted a cash

offer/ second-step merger structure, with the possibility of conducting a short-form merger.

The merger was completed on March 9, 2001.

Infinity/ Viacom

Infinity Broadcasting Corp. was incorporated in September 1998 to own and operate

the radio and outdoor advertising business of CBS Corp. (la ter acq uired by Viacom). In

December 1 998, Infinity completed an initial public offering of its Class A commonstock. O n May 4 , 2 000 , CBS merged with Viacom (VIA/ B – $41 .7 0 ; 1 Strong Buy),

and consequently, Infinity beca me a majority-owned subsidiary of Viacom. As of

September 30, 2000, Viacom held 100% of the Infinity’s Class B common stock, which

represented approximately 64.2% of the equity and 90.0% of the voting power.

O n August 15 , 2 000 , Viacom offered to purchase the remaining sha res of Infinity tha t it

did not alrea dy own in a merger transa ction. The initial offer was 0. 564 VIA/ B shares.

The merger proposal was subject to the approval of the independent directors of Infinity.

A numbe r of lawsuits were filed by shareholders seeking a higher consideration following

the initial announcement. O n October 31 , 2 000 , the compa nies rea ched a definitive

merger agreement after Viacom raised its offer to 0 .5 92 VIA/ B shares. Viacom

adop ted a merger structure for the exchange of shares. On January 5 , 2001 , the

6 Delaware law allows an acquirer that holds more than 90%of target shares outstanding to conduct a

short-form merger without the requirement of holding a targe t shareholder meeting.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 10/37

Understa nding Minority Squeeze -O uts

10 January 3 , 2 0 0 2

companies announced that Infinity would hold a shareholder meeting to seek approval

on the merger.7 The transaction closed on February 23, 2001.

Delhaize America/ Delhaize Le Lion

Delha ize America , Inc. was incorpora ted in North Carolina in 195 7 . As of 200 0 , it

wa s the la rgest operating compa ny in the globa l supermarkets group of Delhaize Le Lion(Brusse ls: DELB – e58.7 0 ; 2 Buy). Before the minority squeeze -out transaction, the

Delhaize Group owned approximately 37% of Delhaize America's Class A (non-voting)

common stock and a pp roximately 56% of its Class B (voting) common stock, or

approximately 45% of Delhaize America 's total shares outstanding.

O n September 9 , 2 000 , Delhaize Le Lion proposed to acquire, contingent on the

approval of Delhaize America’s boa rd and independent directors, 55 % of Delhaize

America ’s tota l shares outstanding that it did not a lrea dy own. The initial offer was 0.35

DELB shares for every share of Delhaize America. The companies rea ched an

agreement for a statutory share exchange under North Ca rolina Corporation Law onNovember 1 7 , 2 000 a t a fina l offer of 0 .4 0 DELB shares. The share exchange was

completed on April 26, 2001.

Avis Group/ Cendant

On October 17, 1996, Cendant (CD – $19.60; 1 Strong Buy) purchased Avis, Inc.

and its subsidiaries (subsequently Avis Group Holdings). O n September 24 , 1 997 , Avis

completed an initia l public offering of its common stock. Before the minority squeeze -out

transaction, Cendant owned approximately 18% of Avis' outstanding common shares

and also owned preferred stock of an Avis subsidiary that was convertible into Avis

shares. These p referred shares were convertible into a combination of non-voting a ndvoting Avis Group common shares that would have resulted in Cendant having up to a

20% voting interest in Avis Group and a pproximately a 3 3% economic interest.

O n August 15 , 2000 , C enda nt Corporation made a preliminary and non-binding

proposal to acquire all of the outstanding shares of Avis Group that it did not already

own for $2 9 per share in cash. Avis appointed a special committee of independent

directors to evaluate the proposal. Some Avis shareholders filed class action complaints

at the Delaware Chancery Court, cla iming that the Cenda nt offer was inadequa te. The

companies reached a definitive merger agreement on November 13, 2000, after

Cendant increased the offer to $3 3 pe r share. Cendant adopted a ca sh merger

structure for the transa ction. The merger was conditioned upon a pproval of a majority of

the votes ca st by Avis Group stockholders who were unaffiliated with Cendant. The

merger closed on March 1, 2001.

7 The decision to hold a shareholder meeting came after a Delaware Chancery court decision regarding

Digex created uncertainty ab out whether such a vote might be required for Delawa re corporations.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 11/37

Understa nding Minority Squeeze -O uts

January 3 , 2 0 02 11

Sodexho Marriott Services/ Sodexho Alliance

O n March 27 , 1998 , Sodexho Ma rriott Services (Marriott a t the time) consummated a

series of transa ctions that, among o thers, resulted in the acquisition of the North

America n operations of Sodexho Alliance, S.A. (Paris: SW – -e46.76; 3 Market

Perform). Concurrent to this transaction, a ll busine sses of Marriott other than food

services and the facilities mana ge ment business were spun off to Marriott’s shareholdersthrough a special dividend of stock in a ne w company—Marriott Internationa l, Inc.

Following the transactions, the former Ma rriott wa s rena med Sodexho Marriott Services,

Inc. As part of the transactions, Sodexho Marriott Services and Sodexho entered into

arrangements under which Sodexho provided Sodexho Marriott Services with a variety

of consulting and advisory services and guaranteed a portion of its indebtedness.

Sodexho Alliance has owned an approximate 48% stake in Sodexho Marriott Services

ever since the formation of the company.

O n January 25, 2 001, Sode xho Alliance proposed to acquire a ll the Sodexho Marriott

Services shares tha t it did not alrea dy own for $2 7 in ca sh per share. This offer wasconditional on due diligence and negotiation and execution of a definitive merger

agreement. Following the a nnouncement, a number of class action compla ints were filed

in the Dela wa re Chancery Court a lleg ing tha t the Sodexho Alliance offer did not provide

adequate value to Sodexho Marriott shareholders and that the defendants were

breaching their fiducia ry duties.

On May 2, 2001, the companies reached a definitive merger agreement after Sodexho

Alliance increa sed its offer to $ 3 2 and the Sodexho Ma rriott Services board of directors

received the recommendation of its specia l committee . Sodexho Alliance adopted a

ca sh offer/ second-step merger structure, with the possibility of conducting a short-form

merger. The transaction was completed on June 2 1 , 2 001 .

TyCom/ Tyco

TyCom was incorporated on March 8, 2000 as a wholly-owned subsidiary of Tyco

(TYC – $ 58 .2 0 ; 1 Strong Buy) to serve a s the holding company for its undersea fiber

optic cable communica tions business. On July 27 , 2 000, TyCom sold approximately

14% of its common shares in an initial public offering. Before the minority squeeze -out,

Tyco he ld 8 9% of TyCom common shares.

O n October 4 , 2 001 , Tyco International offered to a cquire the outstanding 11 %minority

interest in TyCom to bring TyCom back into the Tyco corporate structure as a wholly-

owned subsidia ry. The initial offer was 0.2 997 Tyco shares. The offer was conditional

on the negotia tion a nd execution of a definitive merge r agreement. The transaction was

cha lleng ed in an investor lawsuit a lleg ing that Tyco was using its majority control of

TyCom to reach an agreement that did not give TyCom's minority shareholders an

ade qua te or fa ir price for their stock. The companies rea ched a de finitive a greement on

O ctober 19 , 200 1 , after Tyco increa sed its offer to 0.3 133 TYC shares. The

transaction closed on December 18, 2001.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 12/37

Understa nding Minority Squeeze -O uts

12 January 3 , 2 0 0 2

Prodigy/ SBC

O n February 11 , 1 999 , Prodigy completed an initial public offering of its stock. In May

2000, Prodigy and SBC (SBC – $39.30; 1 Strong Buy) established a strategic

operating partnership in which SBC acquired an initial indirect interest in Prodigy of

approximately 43%. Per the terms of the partnership, SBC ha d the right to exchange its

units in the ope rating partnership for shares of Class A common stock. Direct ownershipof Class A shares was concentrated among Carlos Slim Helu, Carso Global Telecom

and Telmex, whose collective ownership of Prodigy Class A common stock represented

approximately 34 .3 % of the voting power of a ll outstanding securities of Prodigy.

O n September 24 , 2 001 , SBC announced a tender offer for the shares of Prodigy that it

did not a lready own for $5 .4 5 p er share. SBC indicated that it would commence the

offer a s soon a s practica ble. A number of class action compla ints were filed in the

Delaware Chancery Court, alleging that the SBC offer did not provide sufficient value to

Prodigy shareholders, Prodigy directors faced conflicts of interest, a nd that certain

directors were acting to better SBC interests at the expense of Prodigy publicshareholders.

Prodigy formed a special committee of independent directors to review the offer and

advised its shareholders not to take any action until the board had a chance to complete

its review. In ea rly October, SBC representatives a nd a special committee of Prodigy

independent directors enga ged in discussions regarding the offer. O n October 1 5 ,

20 01 , the companies informed the p ublic that the special committee informally

suggested a tender offer price of $6.55, whereas SBC indicated the possibility of

increa sing the offer price to the $6 .0 0 to $6 .2 5 range. O n O ctober 18 , 2001 , the

companies reached a definitive agreement on a revised tender offer according to which

SBC would pa y $6 .6 0 per share. The transaction was structured a s a ca sh

tender/ second-step merge r, with the possibility of a short-form merger. The transa ction

closed on November 7 , 2 0 01 .

TD Wa terhouse Group/ Toronto-Dominion Bank

W aterhouse Investor Services, Inc. (now TD Waterhouse) was acquired in 1996 by

Toronto-Dominion Bank (TD – $ 25 .5 2 ; Not rated). O n June 23 , 1999 , TD Bank

conducted a n initia l public offering of TD W aterhouse stock.

O n October 10 , 2 001 , Toronto-Dominion Bank announced a ca sh tender offer for all of

the approximately 12% of the outstanding shares of TD Waterhouse tha t it (and its

subsidiaries) did not alrea dy own for $9 .0 0 per share. The offer was conditioned upon

the a cquisition of sufficient shares such that Toronto-Dominion Bank would own a t lea st

9 0 % of the outstanding TD W aterhouse Group common stock (so as to be a ble to do a

short-form merger). TD indica ted initia lly that the commencement and completion of the

tende r offer or the consummation of the merger did not require a ny approva l by the TD

W aterhouse boa rd of directors.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 13/37

Understa nding Minority Squeeze -O uts

January 3 , 2 0 02 13

Following announcement, severa l investors filed class a ction complaints in the Delawa re

Chancery Court po inting to existing conflicts of interest and a lleg ing that Toronto-

Dominion was acting in its self interest a t the expense of TD Waterhouse public

shareholders. O n October 30 , 2001 , Toronto-Dominion Bank increased the offer to

$9.50 per share in cash and revised the completion condition of the tender to require a

majority of the p ublicly-held sha res. The revision resulted from discussions be tweenToronto Dominion and the special committee of independent TD W aterhouse d irectors.

The non-tendered shares were a cquired through a short-form merger. The tender expired

on November 14, 2001 and the transaction closed on November 27, 2001.

Qu a lita t ive Cha ra cter is t ics

Minority Squeeze-Out Process and Structure

The target board appointed a special committee to evaluate the acquirer’s offer in all the

transactions we highlight (Figure 2 ). Seven of the nine offers were conditional on target

board approva l and the signing of a definitive merger agree ment. Following ta rget

board approval and the signing of a definitive agreement, the acquirers either initiatedtender offers or mergers.

Figure 2: Transa ction Process a nd Structure

Deal % Ta rget Shares

Sought

Conditional

on BoardApproval?

Special

CommitteeAppointed?

Merger

AgreementRea ched?

Structure of

Transaction

Time to Bump

AXA Fina ncia l 3 9 .7 % Ye s Ye s Ye s Excha ng e O ffe r 4 9Hertz 18 .5% Yes Ye s Yes Cash O ffer 1 1 8

Infinity Broa dca sting 3 5 .7 % Ye s Ye s Ye s Me rg er 7 7De lha ize Ame rica 5 5 .0 % Ye s Ye s Ye s Sha re Excha ng e 7 1

Avis Group 82 .0% Yes Ye s Yes Merger 9 0Sodexho Marrio tt Services 52 .0% Yes Yes Yes Cash Offer 97

TyCom 1 1.0 % Ye s Ye s Ye s Ama lga ma tion 1 5

Prodig y C ommunica tions 5 8 .0 % N o Ye s Ye s C ash O ffe r 2 4TD W aterhouse 1 2.0 % N o Ye s Ye s Ca sh O ffer 2 0

Source: Lehman Brothers, Bloomb erg

In the remaining two situations, Prod igy/ SBC a nd TD W aterhouse/ Toronto-Dominion,

the acquirer initia ted a tender offer following a nnouncement and did not seek the

approval of the ta rget board. Nevertheless, the target appointed a special committee .

In these two deals, the acquirer and the target eventually reached an agreement on a

final offer, a nd the target recommended the dea l to its shareholders. The time from

announcement to the final offer in these two transactions wa s considerably less than that

in six of the other seven dea ls that were conditional on board approva l. Even though theTyCom/ Tyco deal required boa rd a pproval, the bump came after only 15 da ys, most

likely beca use the minority holdings represented a mere 11% of outstanding shares and

the target board did not have much leverage.

Shareholding Structure

Investors who hold a disprop ortiona tely la rge number of target shares will have more

incentive to oppose a transaction that they believe does not provide fair value.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 14/37

Understa nding Minority Squeeze -O uts

14 January 3 , 2 0 0 2

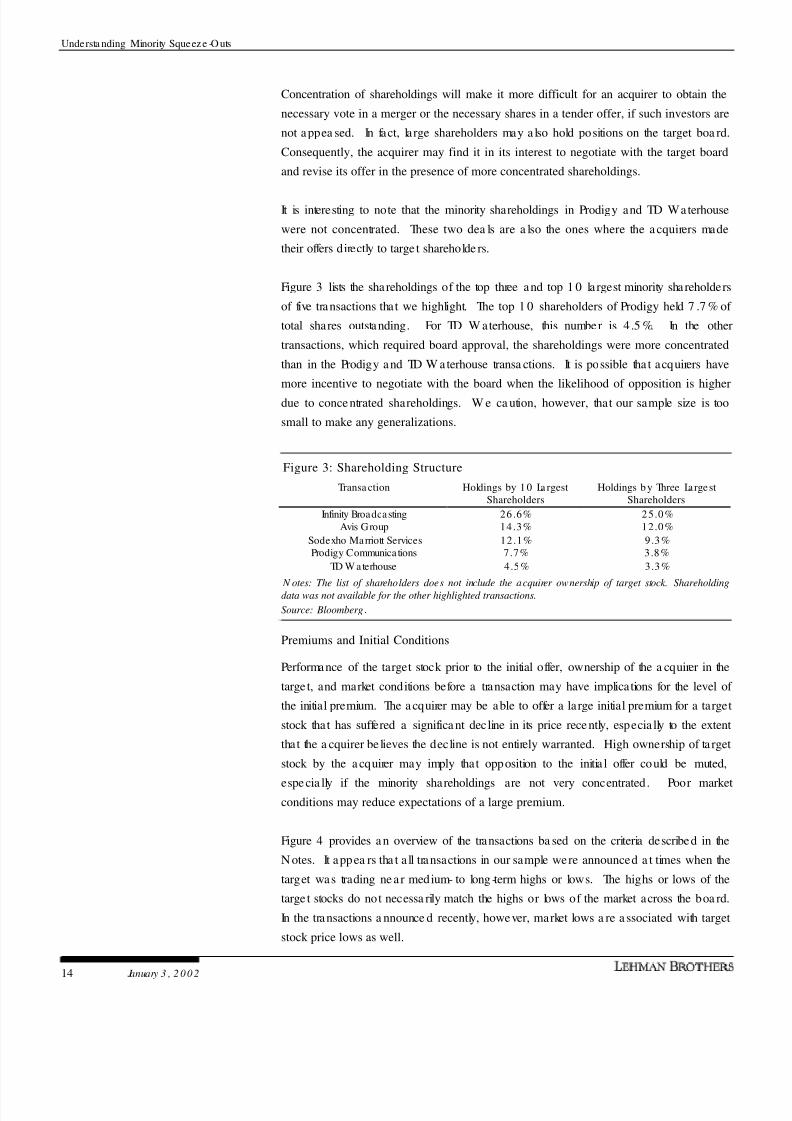

Concentration of shareholdings will make it more difficult for an acquirer to obtain the

necessary vote in a merger or the necessary shares in a tender offer, if such investors are

not appea sed. In fact, large shareholders may a lso hold positions on the target boa rd.

Consequently, the acquirer may find it in its interest to negotiate with the target board

and revise its offer in the presence of more concentrated shareholdings.

It is interesting to note that the minority shareholdings in Prodigy and TD Waterhouse

were not concentrated. These two dea ls are a lso the ones where the a cquirers made

their offers directly to targe t shareholde rs.

Figure 3 lists the shareholdings of the top three and top 1 0 la rgest minority shareholders

of five transactions that we highlight. The top 1 0 shareholders of Prodigy held 7 .7 % of

total shares outstanding. For TD W aterhouse, this number is 4 .5 %. In the other

transactions, which required board approval, the shareholdings were more concentrated

than in the Prodigy and TD W aterhouse transa ctions. It is possible tha t acquirers have

more incentive to negotiate with the board when the likelihood of opposition is higher

due to conce ntrated shareholdings. W e ca ution, however, that our sample size is too

small to make any generalizations.

Figure 3: Shareholding Structure

Transa ction Holdings by 1 0 La rgestShareholders

Holdings b y Three LargestShareholders

Infinity Broadcasting 26 .6% 25.0%Avis Group 14 .3% 12.0%

Sodexho Marriott Services 12 .1% 9.3%Prodigy Communica tions 7 .7% 3.8%

TD W aterhouse 4 .5% 3.3%

N otes: The list of shareholders does not include the acquirer ownership of target stock. Shareholding

data was not available for the other highlighted transactions.

Source: Bloomberg.

Premiums and Initial Conditions

Performance of the target stock prior to the initial offer, ownership of the a cquirer in the

targe t, and market conditions before a transaction may have implications for the level of

the initial premium. The a cquirer may be able to offer a large initial premium for a target

stock that has suffered a significa nt decline in its price rece ntly, especia lly to the extent

that the a cquirer be lieves the decline is not entirely warranted. High ownership of ta rget

stock by the a cquirer may imply that opposition to the initia l offer could be muted,

espe cia lly if the minority shareholdings are not very concentrated. Poor marketconditions may reduce expectations of a large premium.

Figure 4 provides a n overview of the transactions ba sed on the criteria described in the

N otes. It appea rs tha t a ll transactions in our sample were announced a t times when the

target was trading ne ar medium- to long -term highs or lows. The highs or lows of the

targe t stocks do not necessa rily match the highs or lows of the market across the boa rd.

In the transactions a nnounce d recently, however, market lows a re a ssociated with target

stock price lows as well.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 15/37

Understa nding Minority Squeeze -O uts

January 3 , 2 0 02 15

The initial premiums in transa ctions where the targets were trading near their lows can be

classified a s modera te to high. Conversely, the initial premiums for ta rgets with pre -

announcement prices nea r their high appea r to be low to moderate -low. There doe s not

appear to be a close relationship between the size of the bump and the initial premium.

A low premium may be followed by a small bump, and a high premium may be

followed by a large bump. W e a lso do not detect a relationship between the pre-dea lownership of the ta rget stock by the a cquirer a nd the initial premium (or the size of the

bump).

Figure 4: Qualitative Overview of Highlighted Transactions

Deal Pre-Dea l Ta rge tPrice is Near

Pre-Dea lO wnership

Pre-Dea l Ma rket Co nditions Initial Premium Bump

Level (SPX) Vola tility (VIX) O ne -da y O ne -we ek

AXA Financia l High (all-time) Moderate -high High Low Low Low Small

Hertz Low (2-year) High High Low Moderate Moderate Large

Infinity Broadcasting High (2-yea r) Moderate -high High Low Moderate -low Moderate -low Small

Delhaize America Low (2-year) Moderate High Low Moderate -low Moderate ModerateAvis Group High (6-month) Low High Low Moderate -low Moderate -low Moderate

Sodexho Ma rriott Services High (2-yea r) Moderate Mod.-high Moderate Low Low Large

TyCom Low (2-year) High Low High High High Small

Prodigy Communications Low (2-year) Moderate Low High High Moderate -high Large

TD W aterhouse Low (2-year) High Low High High Moderate -high Small

N otes: For pre-deal ownership, “high” means ownership in excess of 70 %, “moderate -high” 60-70%, “moderate” 40-60%, “low” less than 30 %. For the

S&P 500 level, “high” means higher than 14 00, “mode rate-high”means 1300 to 14 00, and “low” means less than 1100 . For the VIX index, “low”

means up to 25, “mode rate” means 25 to 35 , “high”means 35 and higher. For the initial premium, “low” means 0 -10%, “moderate -low” means 10 -20 %,

“mode rate” means 20 -30 %, “moderate high” means 3 0-40%, and “high” means 40 %+. For the bump, “small” means an absolute percentage point

increase of 10 or less, “mode rate” means an increase of 10 to 20 , “large”means an increase of 20 or more.

Source: Lehman Brothers.

Des criptive Sta tistics

Market Conditions

O f the nine dea ls we highlight, three were transa cted in volatile markets and six took

place in ca lm markets with market indexes trad ing at or nea r their highs. There is a

noticeable difference between the initial market conditions of transactions announced in

the latter half of 2000 and the initial conditions of those announced in September and

O ctober 2001 . The AXA Financial, Hertz, Infinity, Delhaize a nd Avis offers were a ll

announced when the S&P 500 index was trading nea r its a ll-time high levels and market

volatility wa s low.8 The TyCom, Prodigy, and TD W aterhouse offers, on the other hand,

were announced following the terrorist attacks of September 11 in a period of high

market vola tility. Based on previous obse rva tions, it a lso appea rs that depressed market

conditions g ive opportunity for a higher initia l premium.

8 W e use the C BOE S&P 100 Volatility Index (VIX) as a measure of market volatility. The VIXindex

reflects a market estimate of future volatility, based on the "at the money" quotes o f S&P 10 0 index

options.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 16/37

Understa nding Minority Squeeze -O uts

16 January 3 , 2 0 0 2

Figure 5: Ma rket Vola tility (CBO E S&P 100 Vola tility Index -- VIX) a nd S&P 500

Levels

Late 200 0/ Early 20 01

Transa ctions (6 )

Rece nt Transa ctions (3 )

VIXa t Announcement (One-Month Average) 22. 5 40 .5

VIXa t Bump (One-We ek Average ) 29. 5 35 .5

S&P 500 Index Level 1466 .81 1039.69Source: Lehman Brothers.

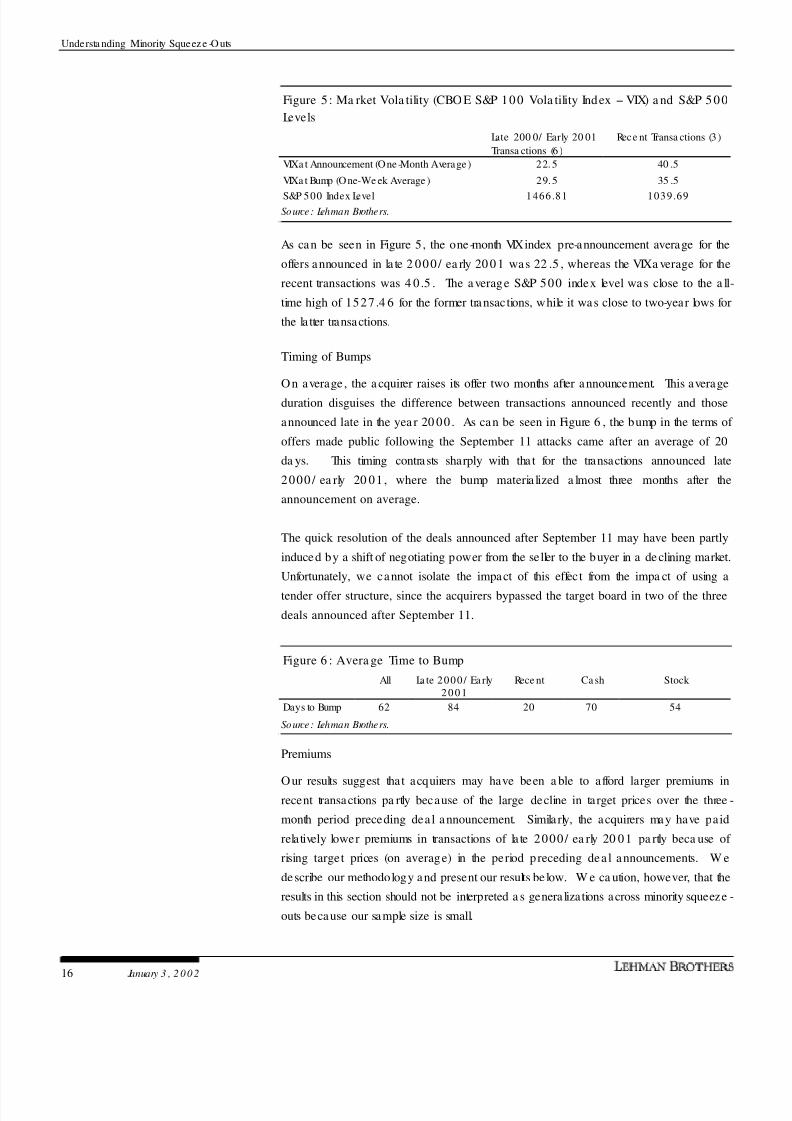

As can be seen in Figure 5, the one-month VIXindex pre-announcement average for the

offers announced in la te 2 00 0/ ea rly 20 0 1 was 22 .5 , whereas the VIXa verage for the

recent transactions was 4 0 .5 . The a verage S&P 500 index level was close to the a ll-

time high of 1527 .4 6 for the former transactions, while it was close to two-year lows for

the la tter transactions.

Timing of Bumps

O n average , the a cquirer raises its offer two months after announcement. This average

duration disguises the difference between transactions announced recently and those

announced late in the yea r 20 00 . As can be seen in Figure 6 , the bump in the terms of

offers made public following the September 11 attacks came after an average of 20

da ys. This timing contrasts sharply with tha t for the transactions announced late

2000 / ea rly 20 01 , where the bump materia lized a lmost three months after the

announcement on average.

The quick resolution of the deals announced after September 11 may have been partly

induced by a shift of negotiating power from the seller to the buyer in a de clining market.

Unfortunately, we cannot isolate the impact of this effect from the impa ct of using a

tender offer structure, since the acquirers bypassed the target board in two of the three

deals announced after September 11.

Figure 6 : Avera ge Time to Bump

All La te 2000 / Ea rly2 0 0 1

Rece nt Ca sh Stock

Days to Bump 62 84 20 70 54

Source: Lehman Brothers.

Premiums

O ur results suggest that acquirers may have been a ble to afford larger premiums inrecent transactions pa rtly because of the large decline in target prices over the three -

month period preceding dea l announcement. Simila rly, the acquirers may have paid

relatively lower premiums in transactions of la te 2000/ ea rly 20 01 pa rtly beca use of

rising target prices (on average) in the period preceding dea l announcements. W e

describe our methodology and present our results be low. W e ca ution, however, that the

results in this section should not be interpreted a s genera lizations across minority squeeze -

outs because our sample size is small.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 17/37

Understa nding Minority Squeeze -O uts

January 3 , 2 0 02 17

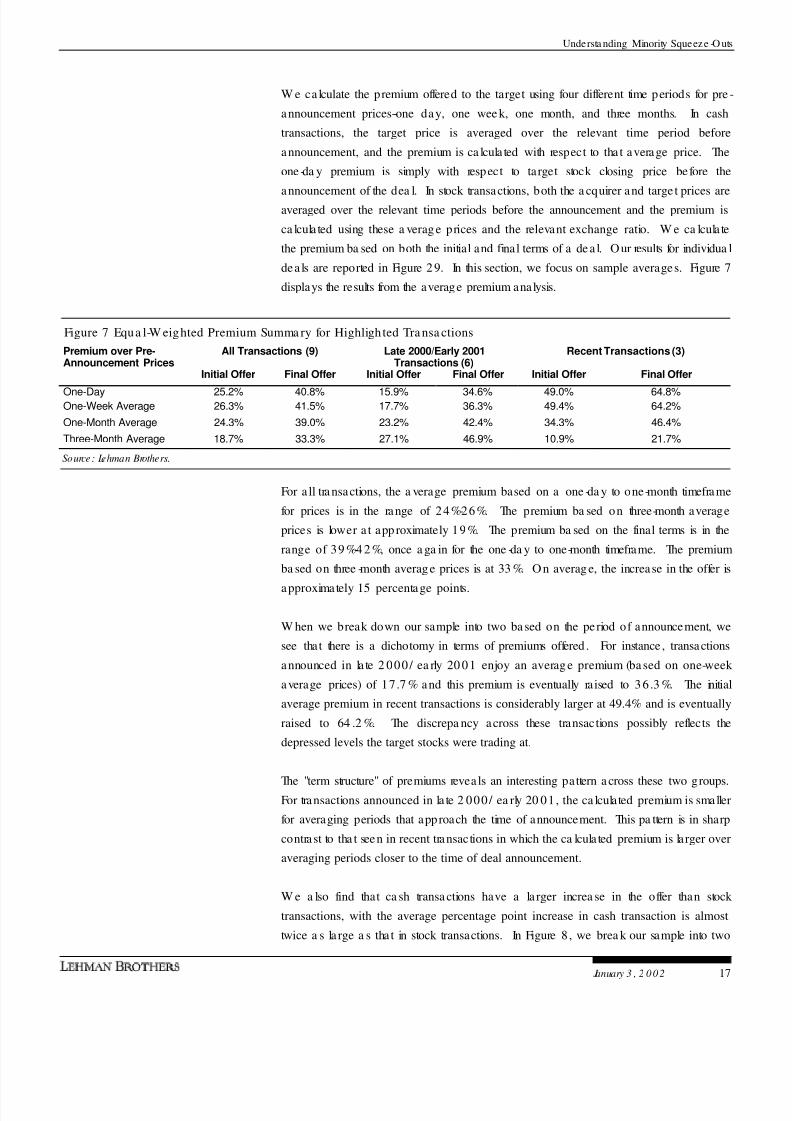

W e ca lculate the premium offered to the target using four different time periods for pre -

announcement prices--one day, one wee k, one month, and three months. In cash

transactions, the target price is averaged over the relevant time period before

announcement, and the premium is ca lcula ted with respect to tha t average price. The

one -da y premium is simply with respect to target stock closing price before the

announcement of the dea l. In stock transactions, both the a cquirer and targe t prices areaveraged over the relevant time periods before the announcement and the premium is

ca lcula ted using these a verag e prices and the relevant exchange ratio. W e ca lcula te

the premium ba sed on both the initial and final terms of a de a l. O ur results for individua l

dea ls are reported in Figure 2 9. In this section, we focus on sample averages. Figure 7

displays the results from the average premium analysis.

Figure 7 Equa l-W eighted Premium Summa ry for Highlighted Transa ctions

Premium over Pre-Announcement Prices

All Transactions (9) Late 2000/Early 2001Transactions (6)

Recent Transactions (3)

Initial Offer Final Offer Initial Offer Final Offer Initial Offer Final Offer

One-Day 25.2% 40.8% 15.9% 34.6% 49.0% 64.8%One-Week Average 26.3% 41.5% 17.7% 36.3% 49.4% 64.2%

One-Month Average 24.3% 39.0% 23.2% 42.4% 34.3% 46.4%

Three-Month Average 18.7% 33.3% 27.1% 46.9% 10.9% 21.7%

Source: Lehman Brothers.

For a ll tra nsactions, the a verage premium based on a one -da y to one-month timeframe

for prices is in the range of 24%-26%. The premium ba sed on three-month average

prices is lower a t app roximately 19%. The premium ba sed on the final terms is in the

range of 39 %-4 2 %, once a ga in for the one -da y to one-month timeframe. The premium

ba sed on three -month averag e prices is at 33 %. O n averag e, the increase in the offer is

approximately 15 percentage points.

W hen we break down our sample into two ba sed on the period of announcement, we

see that there is a dichotomy in terms of premiums offered . For instance , transactions

announced in la te 2 000/ ea rly 20 01 enjoy an averag e premium (ba sed on one-week

average prices) of 17.7 % and this premium is eventually raised to 3 6 .3 %. The initial

average premium in recent transactions is considerably larger at 49.4% and is eventually

raised to 64 .2 %. The discrepa ncy across these transactions possibly reflects the

depressed levels the target stocks were trading at.

The "term structure" of premiums revea ls an interesting pattern a cross these two groups.For transactions announced in la te 2 000/ ea rly 20 01 , the ca lculated premium is smaller

for averaging periods that approach the time of announcement. This pa ttern is in sharp

contrast to tha t seen in recent transactions in which the ca lcula ted premium is larger over

averaging periods closer to the time of deal announcement.

W e a lso find that ca sh transa ctions have a la rger increa se in the offer than stock

transactions, with the average percentage point increase in cash transaction is almost

twice a s la rge a s tha t in stock transactions. In Figure 8 , we brea k our sample into two

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 18/37

Understa nding Minority Squeeze -O uts

18 January 3 , 2 0 0 2

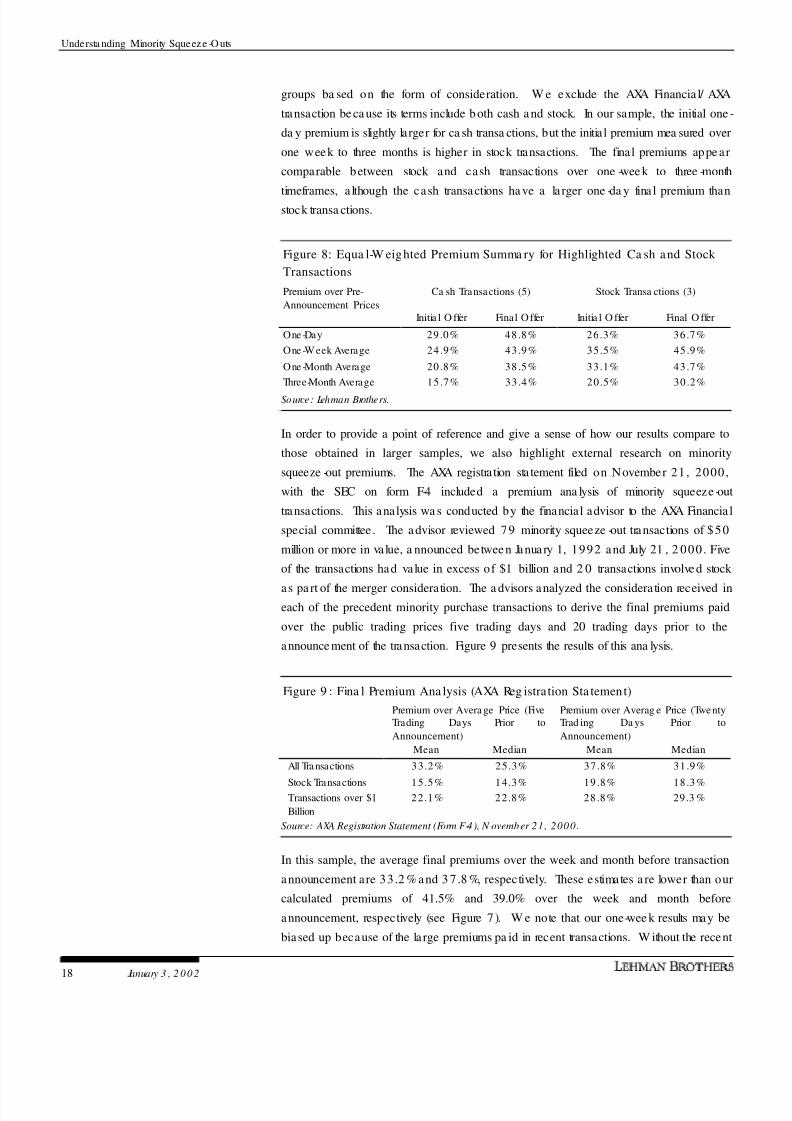

groups ba sed on the form of consideration. W e exclude the AXA Financia l/ AXA

transaction be ca use its terms include b oth cash a nd stock. In our sample, the initial one -

da y premium is slightly larger for ca sh transa ctions, but the initia l premium mea sured over

one week to three months is higher in stock transactions. The final premiums appe ar

comparable between stock and cash transactions over one -wee k to three -month

timeframes, a lthough the cash transactions ha ve a la rger one -da y fina l premium thanstock transa ctions.

Figure 8: Equa l-W eighted Premium Summa ry for Highlighted Ca sh and Stock

Transactions

Premium over Pre-

Announcement Prices

Ca sh Transactions (5) Stock Transa ctions (3)

Initia l O ffer Final O ffer Initia l O ffer Final O ffer

One-Day 29 .0% 48 .8% 26.3% 36 .7%

One-W eek Average 24 .9% 43 .9% 35.5% 45 .9%

One-Month Average 20 .8% 38 .5% 33.1% 43 .7%

Three-Month Average 15 .7% 33 .4% 20.5% 30 .2%

Source: Lehman Brothers.

In order to provide a point of reference and give a sense of how our results compare to

those obtained in larger samples, we also highlight external research on minority

squeeze -out premiums. The AXA registration sta tement filed on November 21 , 2000 ,

with the SEC on form F-4 included a premium ana lysis of minority squeeze -out

transactions. This analysis wa s conducted by the financial advisor to the AXA Financia l

special committee . The a dvisor reviewed 79 minority squeeze -out transactions of $ 50

million or more in value, a nnounced between January 1, 1992 and July 21 , 2 000 . Five

of the transactions had value in excess of $1 billion and 2 0 transactions involve d stock

as pa rt of the merger consideration. The a dvisors analyzed the considera tion received ineach of the precedent minority purchase transactions to derive the final premiums paid

over the public trading prices five trading days and 20 trading days prior to the

announce ment of the transaction. Figure 9 presents the results of this ana lysis.

Figure 9 : Fina l Premium Ana lysis (AXA Reg istration Sta tement)

Premium over Avera ge Price (FiveTrading Days Prior to

Announcement)

Premium over Averag e Price (TwentyTrad ing Da ys Prior to

Announcement)

Mean Median Mean Median

All Transactions 33.2% 25.3% 37 .8% 31 .9%

Stock Transactions 15.5% 14.3% 19 .8% 18 .3%Transactions over $1

Billion

22.1% 22.8% 28 .8% 29.3 %

Source: AXA Registration Statement (Form F-4), N ovember 21, 2000.

In this sample, the average final premiums over the week and month before transaction

announcement are 33 .2 % and 3 7 .8 %, respectively. These estimates a re lower than our

calculated premiums of 41.5% and 39.0% over the week and month before

announcement, respectively (see Figure 7). W e note that our one-wee k results may be

biased up because of the la rge premiums pa id in recent transactions. W ithout the recent

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 19/37

Understa nding Minority Squeeze -O uts

January 3 , 2 0 02 19

transactions, our average final premium decrea ses to 36 .3 % using one-week average

prices. For stock transactions, we believe that our sample is too small to make a

mea ningful compa rison. Overall, our findings do not diverge significantly from these

larger-sample results.

Future Mino r ity Sque eze -Ou ts?

Based on our ana lysis of minority squeeze -outs, we have observed that recent

transactions were initiated following significant decline in the price of a subsidiary that

wa s previously carved out of the a cquirer. In Figure 1 0 , we list seven potential minority

squeeze -out situations ba sed on how recently the ca rve -out took place and whether the

subsidia ry is trading nea r its lows since the IPO .

Figure 10 : Potentia l Minority Squeez e-Outs

Pa rent N a me Subsidia ry N a me Economic %

Owned

IPO da te Value of

Minority Shares($ mill)

Change in

Subsidia ry Pricesince IPO

Change in SPX

since IPO

SPXCorp Inra nge Technologies 8 9.5 % 2 1-Sep-0 0 1 21 -2 0.0 % -2 0.5 %

Sea Conta iners O rient Express Hotels 6 3.0 % 9 -Aug-0 0 1 7 5 -2 1.6 % -2 1.7 %

DTE Energy Plug Power 3 1.8 % 2 8-Oct-9 9 2 82 -44 .0 % -1 4.1 %

Ba rnes & N oble Ba rnesa ndnoble.com 3 6.2 % 2 4 -Ma y-9 9 1 5 0 -9 2.2 % -1 1.8 %

Unite dG loba lC om United Pa n-Europe Comm 5 2 .4 % 1 1 -Fe b-9 9 1 0 6 -9 5 .6 % -8 .1 %

N exte l Communica tions N exte l Pa rtne rs 3 3 .0 % 2 2 -Fe b-0 0 1 ,6 9 1 -4 9 .3 % -1 4 .8 %

AO LTime W a rne r America O nline La tin America 3 8 .0 % 7 -Aug-0 0 1 9 2 -4 2 .0 % -2 2 .1 %

Source: Lehman Brothers.

The risk in using this criterion is tha t tha t the pa rent may just as well decide to complete

the divestiture of a p reviously ca rved-out subsidiary, ra ther than purcha sing the minority

shares, e ven following a significant price decline since the IPO . For example, onNovember 29, 2001, FMC Corporation announced plans to complete the spin-off of

FMC Technologies, which was carved out on June 13 , 2 001 . This situation would have

been on our list of potential squeeze -out ca ndida tes ba sed on our selection criteria. The

spin-off of a subsidiary may serve to put further downward pressure on its price, lea ding

investors to incur losses from trading strategies ba sed on the expectation of a squeeze -

out.9

A significant de cline in a subsidiary stock price ma y not necessa rily imply an increa sed

likelihood of a squeeze -out if the market conditions also deteriorate. The acquirer may

not view such a decline as an opportunity to consolida te ownership in its subsidia ry.W hile Inrange stock price has declined by 20% since the IPO , the S&P 500 index has

a lso de clined by 2 0 .5 %. Simila rly, the d ecline in the price o f O rient Express Hotels

stock is in line with the de cline in the S&P 50 0 since the time of the IPO .

9 See our “Spin-Off Study: Performance Post Spin” for the e ffec ts of a spin-off on the ne ar-term

performance of the pa rent and the subsidiary. W e find that spinning off a major subsidiary is a positive

catalyst for the parent company and a negative catalyst for the subsidiary.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 20/37

Understa nding Minority Sque eze -O uts

20 January 3 , 2 0 0 2

W h a t is t h e P r o b a b i lit y o f a B u m p ? P r o b a b i lit y An a ly s i s in M in o r it y S q u e e z e - O u t s

Synops is o f Fr a me w ork a nd Ma in Assum pt ions

W e use a simple risk-rewa rd framework to estimate the proba bility of a bump using the

risk arbitrage sprea d in minority squeeze -outs. O ur framework is described in technical

de tail in the Append ix. The following formula forms the basis of our ca lculations:

[ ][ ] [ ]

t t t t

t t t

DSSP DSUS

DSSPr bP

)p1(p)p1(p

)p1(pP)(

22

T

t

−+−−+

−+−=

This formula implies that the p robability of a bump (P(b)) de pe nds primarily on the

following factors:

1 . Current risk a rbitrage sprea d (t

SP )

2 . Downside if dea l brea ks (t

DS )

3 . Expected ca sh or stock consideration following the bump (this variable factors in

throught

US , the upside if there is a bump)

4 . Current target stock price ( T

t P )

5 . Alterna tive ra te of return on investment (t r ) until the expected time of bump.

6 . Acquirer and targe t share prices at the time of the bump (these variables factor in

throught

US )

7 . Expected divide nds until the time of bump

8 . Proba bility of deal completion conditional on a bump in terms (2

p )

9 . Probability of dea l completion conditional on no bump in terms (p )

O nly the current risk arbitrag e spread a nd the current ta rget stock price a re known

variables at the time of estimation. W e need to either estimate the remaining variables

or make assumptions about their values. Therefore, the estimation of the probability of a

bump is a subjective exercise that depends on how closely our assumptions approximaterea lity.

In most of our calculations, deal break-up values for the target and acquirer stocks are

ba sed on spe cified pre-announcement trading levels adjusted by the change in the S&P

500 index according to the relevant be tas. In a few ca ses in which this method does

not produce meaningful results, we use alternative methods based on initial arbitrage

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 21/37

Understa nding Minority Squeeze -O uts

January 3 , 2 0 02 21

impa ct. Given that the time to bump is relatively short in many transactions, we believe

that these methods a re sufficiently reliable.

W e a lso make the simplifying a ssumptions tha t the market’s expectation of the value of

the bump and its timing are in fact accurate ex post : the acquirer eventually raises its

offer to reflect the market’s expected va lue of a bump a t the time p redicted by themarket. Consequently, the probability tha t we e stimate should be interpreted a s the

probability of a bump of a given size.

W e assume that there is minimal regulatory risk such that the arbitrage sprea d essentially

collapses to zero at the time of the bump announcement. This assumption is quite

reasonable. In many ca ses, the ta rget and the a cquirer a re in different lines of business.

In other cases, the investment of the acquirer in the target has been in place for a long

period of time a nd likely has pa ssed regula tory muster. In rea lity, arbitrage sprea ds

narrow to unattractive levels following a bump, a nd we presume that arbitrageurs unwind

their positions to pursue investment opportunities elsewhere. The a cquirer prices at the

time of a bump are assumed to be equal to current levels adjusted for any dividend

payments.

Finally, we assume that the probability of deal completion conditional on a bump is one:

the dea l is certa in to go through following a b ump in the terms. This assumption is

consistent with the a ssumption of minimal regula tory risk and is predica ted on similar

reasoning. W e do not make assumptions about the proba bility of deal completion

conditiona l on the terms remaining the same, but rather display results for varying values

of this probability.1 0 If there is no bump in the terms, the boa rd of directors of the target

may find it in its shareholde rs’ be st interest to reject the offer. The boa rd’s proclivity to

reject the offer may depend on a number of factors such as the target’s business outlook

on a standalone basis, availability of alternative bidders, and the board’s negotiating

position.

Results

Nine of the following 18 figures (Figures 11-28) trace out the risk arbitrage spread

according to both the initial and final terms of dea ls. The sprea d using the fina l terms is

ca lcula ted from one month before the announcement until the a nnouncement of a bump.

At the time of the bump, the two spreads converge as we apply the final terms to both.

1 0 W e ha ve some preliminary information on conditional probabilities of dea l outcomes a nd bumps. W e

looked a t 34 a ll-cash all-U.S. minority squeeze -outs announced between 19 89 and 20 00. Of these, 21

(61.8%) were completed with a bump, six (17.6%) were completed without a bump, and seven (20.6%)were terminated without a bump. Two of the seven dea ls terminated without a bump had initial acquirer

ownership of ta rget shares of 80% or more. Two of the six deals completed with a bump had initial

acquirer ownership of target shares of 80 % or more. Based on this information: (i) conditional on nobump, sample probability of deal termination is 54%; (ii) conditional on a bump, sample probability of

deal completion is 10 0%; (iii) conditional on no bump and initia l ownership exceeding 8 0%, the sampleprobability of dea l termination is 50 %. These results suggest that dea l completion is a coin flip without a

bump and practica lly a certainty with a bump. But since our sample is not very large, we would not

generalize these results.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 22/37

Understa nding Minority Squeeze -O uts

22 January 3 , 2 0 0 2

The remaining nine figures display our ca lcula tions of the probability of a bump from the

time of dea l announcement until the time of the bump a s a function of the proba bility of

dea l completion conditional on the terms rema ining the same. Juxtaposing the behavior

of the spread and the probability is useful for highlighting the relationship between the

two variables.

W e make several observations from these figures. Below, we note these observa tions

and a lso indica te generaliza tions we derive using the formula for the proba bility of a

bump:1 1

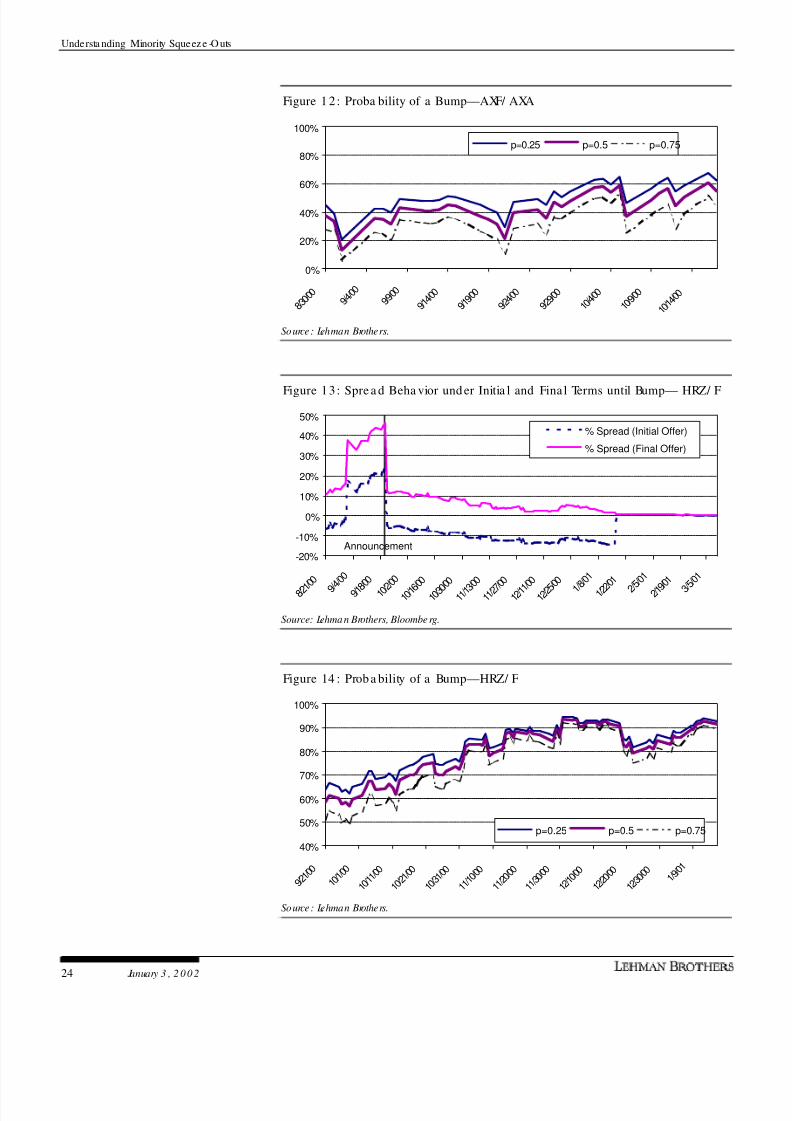

1 . More nega tive a rbitrage sprea ds tend to be associated with higher estimated

proba bilities of a bump in de a l terms. The behavior of the spread a nd the

proba bility in the Hertz/ Ford transaction (see Figure 13 a nd Figure 14 ) display this

result very clea rly (also visible in Prodigy/ SBC, TD Waterhouse/ Toronto-Dominion

Bank figures). The initia lly nega tive spread in Hertz/ Ford beca me increasingly

nega tive over time. At the same time, the probability of a bump increa sed from

around 60% initially (for a p of 0.5) to approximately 90% at the time of the final

offer.

Generally, as long as the expected upside from a bump in the terms more than

compensates investors for the opportunity cost of their capital, lower (or more

negative) arbitrage spreads imply higher probabilities of a bump, with all else the

same. A negative sprea d implies that investors incur an immedia te loss by entering

into a risk arbitrag e position. In order to be willing to invest, a rbitrag eurs need to

be ever more confident of a bump in the terms, the more initial loss they incur.

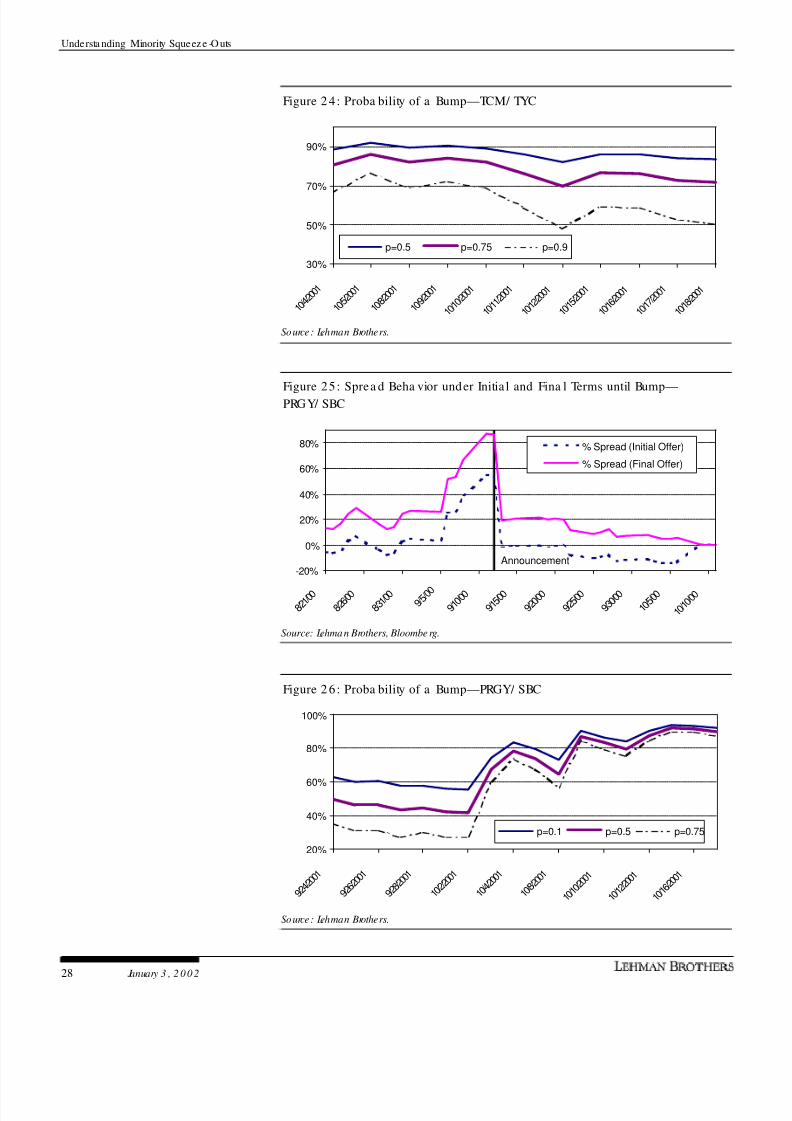

2 . The e stima ted proba bility of a b ump is ge nera lly highe r, the smaller the

expected b ump built into our ca lcula tions. This type of result may be seen in the

TyCom/ Tyco transa ction in which the final offer wa s not significantly higher than the

initia l offer. In this situation, the spread, while nega tive, wa s not wide in absolute

terms. Despite such sprea d beha vior, there wa s still a fairly high expectation of a

small bump. If we a ssume that the dea l completion proba bility in the a bsence of a

bump was fairly high, for example 75%, Figure 24 indicates that the probability of a

bump (exchange ratio rising from 0.2997 TYC shares to 0.3133 TYC shares)

ranged be tween 7 0% and 8 0%.

In a typica l minority squeeze -out situation in which the initial sprea d is nega tive (or

positive, but narrow) and risk arbitrageurs stand to incur losses upon deal

termination, a lower expected bump implies a higher probability of a bump, all else

equal. In other words, if investors expect a small bump, they need to be highly

confident that such a bump will materialize in order to invest in the transa ction.

1 1Note that not a ll of our results may be directly observable from the figures.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 23/37

Understa nding Minority Squeeze -O uts

January 3 , 2 0 02 23

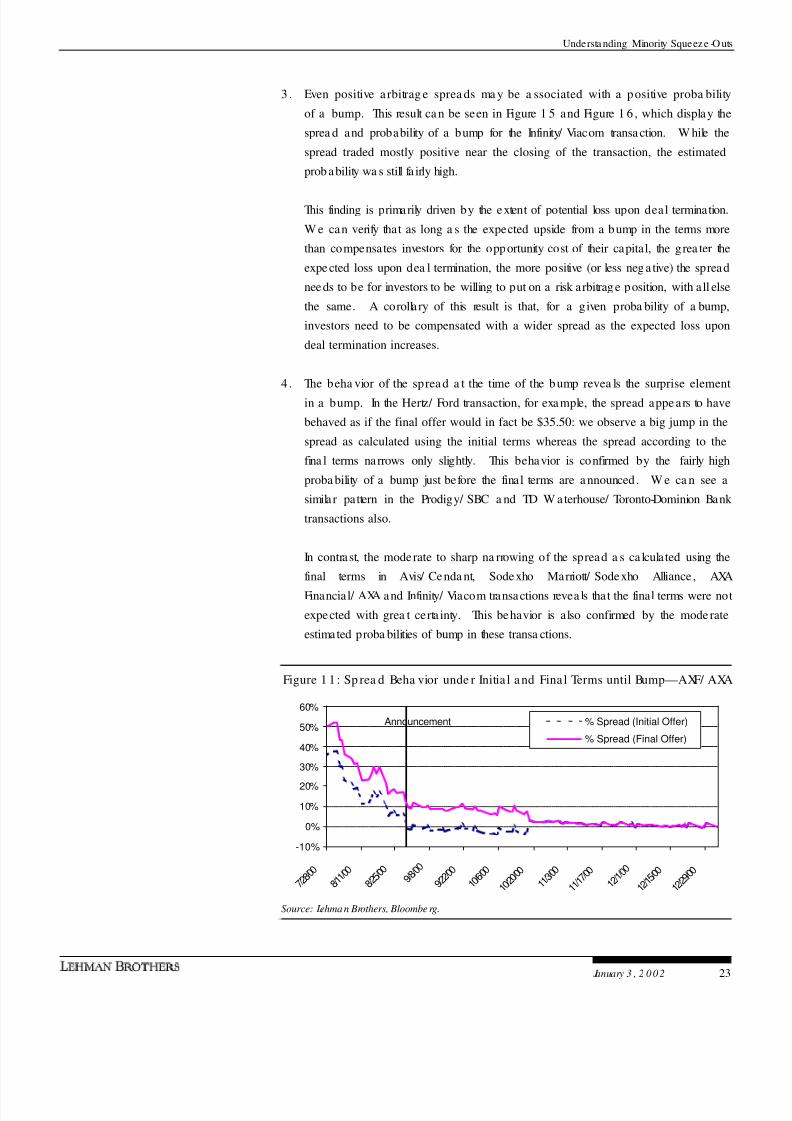

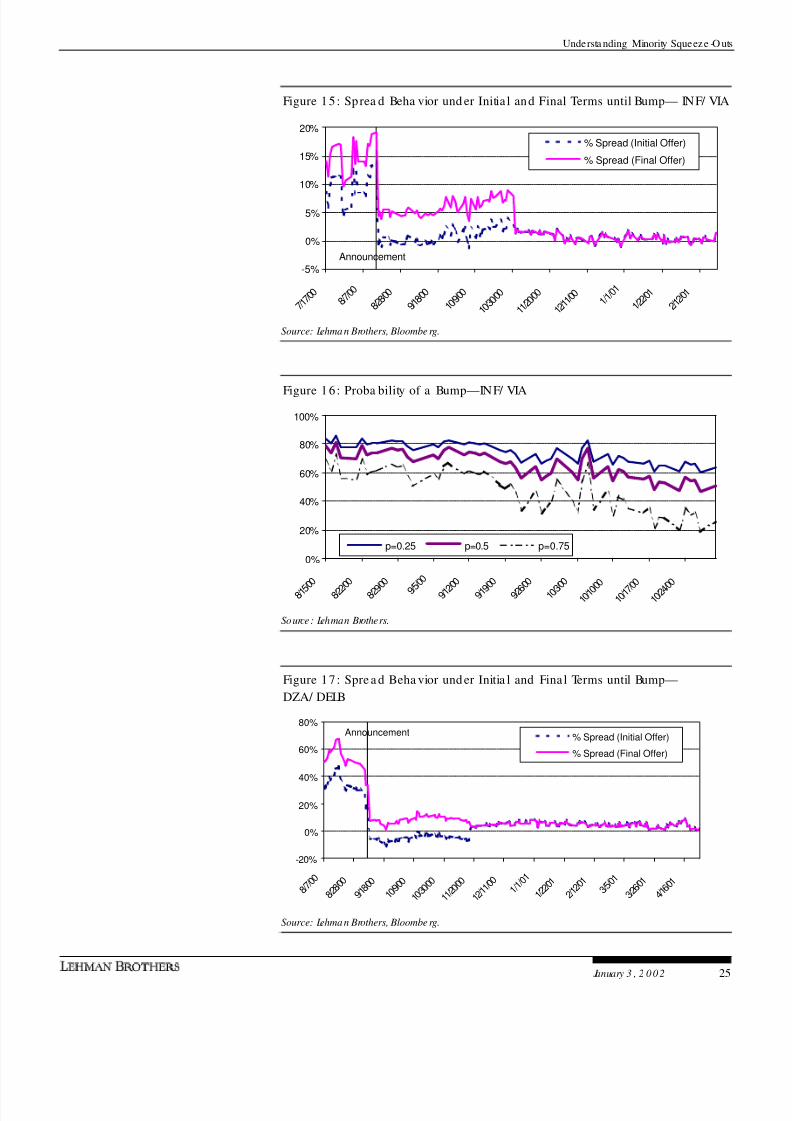

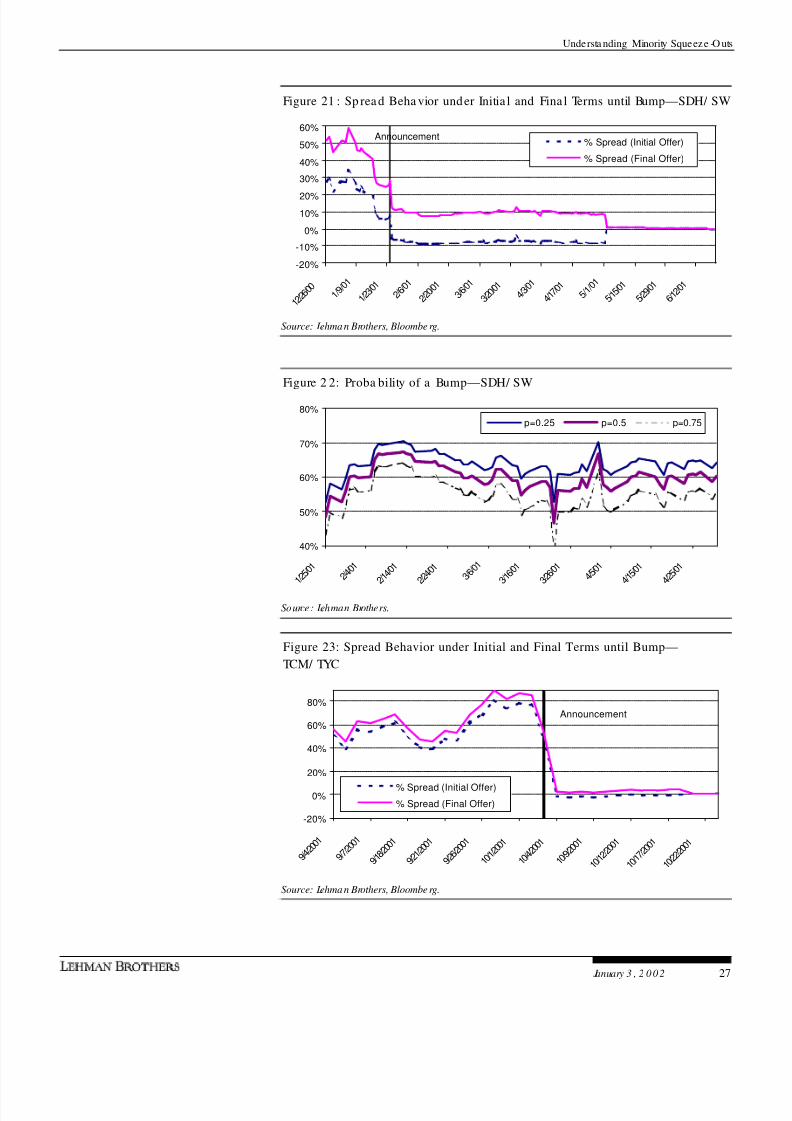

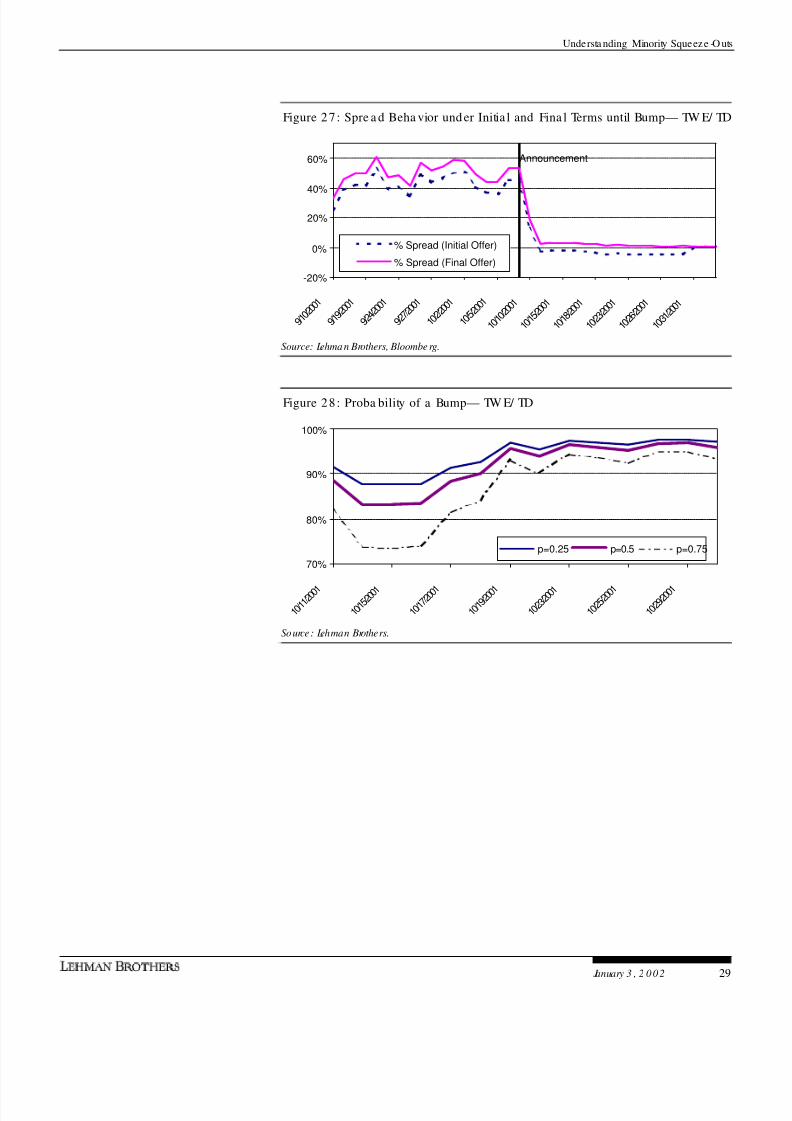

3 . Even positive a rbitrag e sprea ds ma y be a ssociated with a positive proba bility

of a bump. This result ca n be seen in Figure 1 5 and Figure 1 6 , which display the

sprea d and probability of a bump for the Infinity/ Viacom transa ction. W hile the

spread traded mostly positive near the closing of the transaction, the estimated

prob ability wa s still fa irly high.

This finding is primarily driven by the extent of potential loss upon deal termination.

W e can verify that as long a s the expected upside from a bump in the terms more

than compensates investors for the opportunity cost of their capital, the grea ter the

expe cted loss upon dea l termination, the more positive (or less neg a tive) the spread

needs to be for investors to be willing to put on a risk arbitrag e position, with all else

the same. A corolla ry of this result is that, for a given proba bility of a bump,

investors need to be compensated with a wider spread as the expected loss upon

deal termination increases.

4 . The beha vior of the sprea d a t the time of the bump revea ls the surprise element

in a bump. In the Hertz/ Ford transaction, for example, the spread appe ars to have

behaved as if the final offer would in fact be $35.50: we observe a big jump in the

spread as calculated using the initial terms whereas the spread according to the

fina l terms narrows only slightly. This behavior is confirmed by the fairly high

proba bility of a bump just before the final terms are a nnounced . W e ca n see a

simila r pattern in the Prodigy/ SBC a nd TD W aterhouse/ Toronto-Dominion Bank

transactions also.

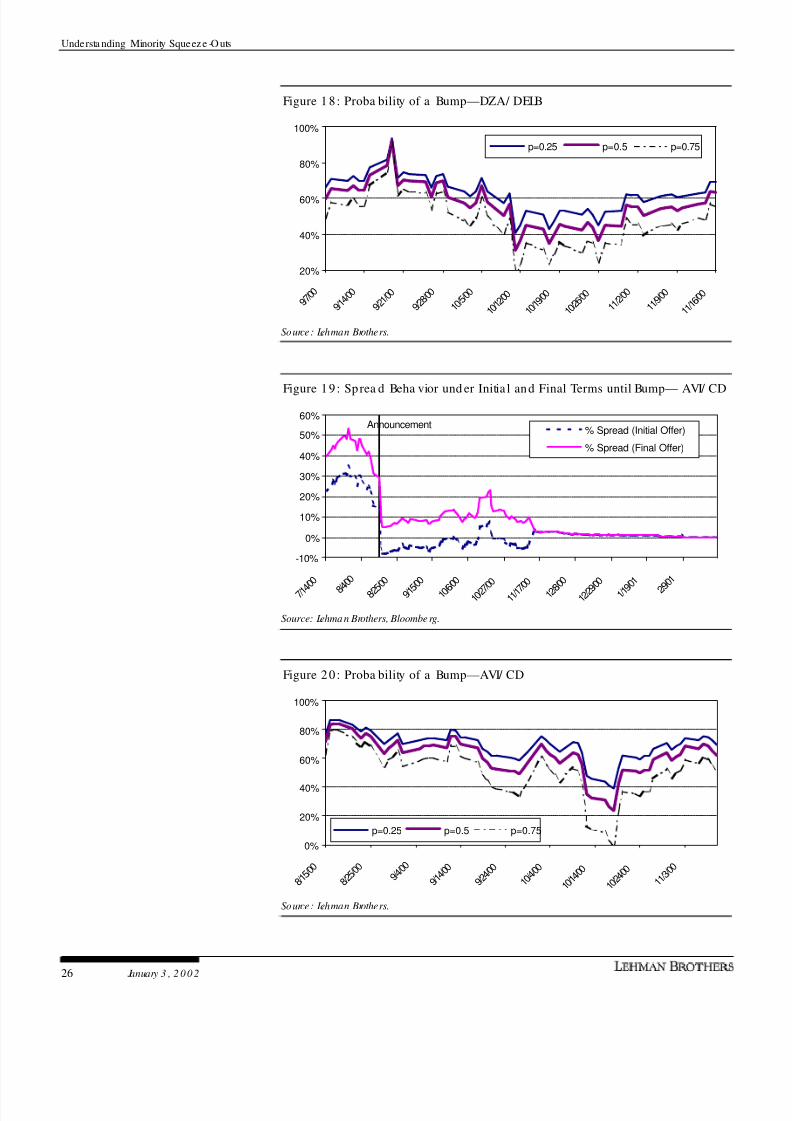

In contrast, the moderate to sharp na rrowing of the spread a s ca lculated using the

final terms in Avis/ Cenda nt, Sodexho Marriott/ Sodexho Alliance , AXA

Financial/ AXA and Infinity/ Viacom transactions revea ls that the final terms were not

expected with grea t certa inty. This behavior is also confirmed by the mode rate

estimated proba bilities of bump in these transa ctions.

Figure 1 1: Sp rea d Beha vior unde r Initia l and Final Terms until Bump—AXF/ AXA

-10%

0%

10%

20%

30%

40%

50%

60%

7 / 2 8 / 0 0

8 / 1 1 / 0 0

8 / 2 5 / 0 0

9 / 8 / 0 0

9 / 2 2 / 0 0

1 0 / 6 / 0 0

1 0 / 2 0 / 0 0

1 1 / 3 / 0 0

1 1 / 1 7 / 0 0

1 2 / 1 / 0 0

1 2 / 1 5 / 0 0

1 2 / 2 9 / 0 0

% Spread (Initial Offer)

% Spread (Final Offer)

Announcement

Source: Lehman Brothers, Bloombe rg.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 24/37

Understa nding Minority Squeeze -O uts

24 January 3 , 2 0 0 2

Figure 1 2: Proba bility of a Bump—AXF/ AXA

0%

20%

40%

60%

80%

100%

8 / 3 0 / 0 0

9 / 4 / 0 0

9 / 9 / 0 0

9 / 1 4 / 0 0

9 / 1 9 / 0 0

9 / 2 4 / 0 0

9 / 2 9 / 0 0

1 0 / 4 / 0 0

1 0 / 9 / 0 0

1 0 / 1 4 / 0 0

p=0.25 p=0.5 p=0.75

Source: Lehman Brothers.

Figure 13: Spre a d Beha vior under Initia l and Final Terms until Bump— HRZ/ F

-20%

-10%

0%

10%

20%

30%

40%

50%

8 / 2 1 / 0 0

9 / 4 / 0 0

9 / 1 8 / 0 0

1 0 / 2 / 0 0

1 0 / 1 6 / 0 0

1 0 / 3 0 / 0 0

1 1 / 1 3 / 0 0

1 1 / 2 7 / 0 0

1 2 / 1 1 / 0 0

1 2 / 2 5 / 0 0

1 / 8 / 0 1

1 / 2 2 / 0 1

2 / 5 / 0 1

2 / 1 9 / 0 1

3 / 5 / 0 1

% Spread (Initial Offer)

% Spread (Final Offer)

Announcement

Source: Lehman Brothers, Bloombe rg.

Figure 14 : Proba bility of a Bump—HRZ/ F

40%

50%

60%

70%

80%

90%

100%

9 / 2 1 / 0 0

1 0 / 1 / 0 0

1 0 / 1 1

/ 0 0

1 0 / 2 1

/ 0 0

1 0 / 3 1 / 0 0

1 1 / 1 0 / 0 0

1 1 / 2 0 / 0 0

1 1 / 3 0 / 0 0

1 2 / 1 0 / 0 0

1 2 / 2 0 / 0 0

1 2 / 3 0 / 0 0 1 / 9

/ 0 1

p=0.25 p=0.5 p=0.75

Source: Lehman Brothers.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 25/37

Understa nding Minority Squeeze -O uts

January 3 , 2 0 02 25

Figure 15: Sprea d Beha vior und er Initia l and Final Terms until Bump— INF/ VIA

-5%

0%

5%

10%

15%

20%

7 / 1 7 / 0 0

8 / 7 / 0 0

8 / 2 8 / 0 0

9 / 1 8 / 0 0

1 0 / 9 / 0 0

1 0 / 3 0 / 0 0

1 1 / 2 0 / 0 0

1 2 / 1 1 / 0 0 1 /

1 / 0 1

1 / 2 2 / 0

1

2 / 1 2 / 0

1

% Spread (Initial Offer)

% Spread (Final Offer)

Announcement

Source: Lehman Brothers, Bloombe rg.

Figure 16: Proba bility of a Bump—INF/ VIA

0%

20%

40%

60%

80%

100%

8 / 1 5 / 0 0

8 / 2 2 / 0 0

8 / 2 9 / 0 0

9 / 5 / 0 0

9 / 1 2 / 0 0

9 / 1 9 / 0 0

9 / 2 6 / 0 0

1 0 / 3 / 0 0

1 0 / 1 0 / 0

0

1 0 / 1 7 / 0 0

1 0 / 2 4 / 0 0

p=0.25 p=0.5 p=0.75

Source: Lehman Brothers.

Figure 17: Spre a d Beha vior under Initia l and Final Terms until Bump—

DZA/ DELB

-20%

0%

20%

40%

60%

80%

8 / 7 / 0 0

8 / 2 8 / 0 0

9 / 1 8 / 0 0

1 0 / 9 / 0 0

1 0 / 3 0 / 0 0

1 1 / 2 0 / 0 0

1 2 / 1 1

/ 0 0 1 / 1 / 0 1

1 / 2 2 / 0

1

2 / 1 2 / 0

1 3 / 5 / 0 1

3 / 2 6 / 0

1

4 / 1 6 / 0

1

% Spread (Initial Offer)

% Spread (Final Offer)

Announcement

Source: Lehman Brothers, Bloombe rg.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 26/37

Understa nding Minority Squeeze -O uts

26 January 3 , 2 0 0 2

Figure 1 8: Proba bility of a Bump—DZA/ DELB

20%

40%

60%

80%

100%

9 / 7 / 0 0

9 / 1 4 / 0 0

9 / 2 1 / 0 0

9 / 2 8 / 0

0

1 0 / 5 / 0 0

1 0 / 1 2 / 0 0

1 0 / 1 9 / 0 0

1 0 / 2 6 / 0 0

1 1 / 2 / 0 0

1 1 / 9 / 0 0

1 1 / 1 6 / 0 0

p=0.25 p=0.5 p=0.75

Source: Lehman Brothers.

Figure 19: Sprea d Beha vior und er Initia l and Final Terms until Bump— AVI/ CD

-10%

0%

10%

20%

30%

40%

50%

60%

7 / 1 4 / 0 0

8 / 4 / 0 0

8 / 2 5 / 0 0

9 / 1 5 / 0 0

1 0 / 6 / 0 0

1 0 / 2 7 / 0 0

1 1 / 1 7 / 0 0

1 2 / 8 / 0 0

1 2 / 2 9 / 0 0

1 / 1 9 / 0 1

2 / 9 / 0 1

% Spread (Initial Offer)

% Spread (Final Offer)

Announcement

Source: Lehman Brothers, Bloombe rg.

Figure 20: Proba bility of a Bump—AVI/ CD

0%

20%

40%

60%

80%

100%

8 / 1 5 / 0 0

8 / 2 5 / 0 0

9 / 4 / 0 0

9 / 1 4 / 0 0

9 / 2 4 / 0 0

1 0 / 4 / 0 0

1 0 / 1 4 / 0 0

1 0 / 2 4 / 0 0

1 1 / 3 / 0 0

p=0.25 p=0.5 p=0.75

Source: Lehman Brothers.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 27/37

Understa nding Minority Squeeze -O uts

January 3 , 2 0 02 27

Figure 21 : Sp read Beha vior under Initia l and Final Terms until Bump—SDH/ SW

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

1 2 / 2 6 / 0 0

1 / 9 / 0 1

1 / 2 3 / 0

1 2 / 6 / 0 1

2 / 2 0 / 0

1 3 / 6 / 0 1

3 / 2 0 / 0

1 4 / 3 / 0 1

4 / 1 7 / 0

1 5 / 1 / 0 1

5 / 1 5 / 0

1

5 / 2 9 / 0

1

6 / 1 2 / 0

1

% Spread (Initial Offer)

% Spread (Final Offer)

Announcement

Source: Lehman Brothers, Bloombe rg.

Figure 2 2: Proba bility of a Bump—SDH/ SW

40%

50%

60%

70%

80%

1 / 2 5 / 0

1 2 / 4

/ 0 1

2 / 1 4 / 0

1

2 / 2 4 / 0 1

3 / 6 / 0 1

3 / 1 6 / 0

1

3 / 2 6 / 0

1 4 / 5 / 0 1

4 / 1 5 / 0

1

4 / 2 5 / 0

1

p=0.25 p=0.5 p=0.75

Source: Lehman Brothers.

Figure 23: Spread Behavior under Initial and Final Terms until Bump—

TCM/ TYC

-20%

0%

20%

40%

60%

80%

9 / 4 / 2 0 0 1

9 / 7 / 2 0 0 1

9 / 1 8 / 2

0 0 1

9 / 2 1 / 2 0 0

1

9 / 2 6 / 2

0 0 1

1 0 / 1 / 2 0 0 1

1 0 / 4 / 2 0 0 1

1 0 / 9 / 2 0 0 1

1 0 / 1 2

/ 2 0 0 1

1 0 / 1 7

/ 2 0 0 1

1 0 / 2 2 / 2 0 0 1

% Spread (Initial Offer)

% Spread (Final Offer)

Announcement

Source: Lehman Brothers, Bloombe rg.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 28/37

Understa nding Minority Squeeze -O uts

28 January 3 , 2 0 0 2

Figure 2 4: Proba bility of a Bump—TCM/ TYC

30%

50%

70%

90%

1 0 / 4 / 2 0 0 1

1 0 / 5 / 2 0 0 1

1 0 / 8 / 2 0 0 1

1 0 / 9 / 2 0 0 1

1 0 / 1 0 / 2 0 0 1

1 0 / 1 1 / 2 0 0 1

1 0 / 1 2 / 2 0 0 1

1 0 / 1 5 / 2 0 0 1

1 0 / 1 6 / 2 0 0 1

1 0 / 1 7 / 2 0 0 1

1 0 / 1 8 / 2 0 0 1

p=0.5 p=0.75 p=0.9

Source: Lehman Brothers.

Figure 25: Sprea d Beha vior under Initia l and Fina l Terms until Bump—PRGY/ SBC

-20%

0%

20%

40%

60%

80%

8 / 2 1 / 0 0

8 / 2 6 / 0 0

8 / 3 1 / 0 0

9 / 5 / 0 0

9 / 1 0 / 0 0

9 / 1 5 / 0 0

9 / 2 0 / 0 0

9 / 2 5 / 0 0

9 / 3 0 / 0 0

1 0 / 5 / 0 0

1 0 / 1 0 / 0 0

% Spread (Initial Offer)

% Spread (Final Offer)

Announcement

Source: Lehman Brothers, Bloombe rg.

Figure 2 6: Proba bility of a Bump—PRGY/ SBC

20%

40%

60%

80%

100%

9 / 2 4 / 2 0 0

1

9 / 2 6 / 2 0 0

1

9 / 2 8 / 2 0 0

1

1 0 / 2 / 2 0 0 1

1 0 / 4 / 2 0 0 1

1 0 / 8 / 2 0 0 1

1 0 / 1 0 / 2 0 0 1

1 0 / 1 2 / 2 0 0 1

1 0 / 1 6 / 2 0 0 1

p=0.1 p=0.5 p=0.75

Source: Lehman Brothers.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 29/37

Understa nding Minority Squeeze -O uts

January 3 , 2 0 02 29

Figure 27: Spre a d Beha vior under Initia l and Fina l Terms until Bump— TW E/ TD

-20%

0%

20%

40%

60%

9 / 1 0 / 2 0 0

1

9 / 1 9 / 2 0 0

1

9 / 2 4 / 2 0 0

1

9 / 2 7 / 2 0 0

1

1 0 / 2 / 2 0 0 1

1 0 / 5 / 2 0 0 1

1 0 / 1 0 / 2 0 0 1

1 0 / 1 5 / 2 0 0 1

1 0 / 1 8 / 2 0 0 1

1 0 / 2 3 / 2 0 0 1

1 0 / 2 6 / 2 0 0 1

1 0 / 3 1 / 2 0 0 1

% Spread (Initial Offer)

% Spread (Final Offer)

Announcement

Source: Lehman Brothers, Bloombe rg.

Figure 28: Proba bility of a Bump— TW E/ TD

70%

80%

90%

100%

1 0 / 1 1 / 2 0 0 1

1 0 / 1 5 / 2 0 0 1

1 0 / 1 7 / 2 0 0 1

1 0 / 1 9 / 2 0 0 1

1 0 / 2 3 / 2 0 0 1

1 0 / 2 5 / 2 0 0 1

1 0 / 2 9 / 2 0 0 1

p=0.25 p=0.5 p=0.75

Source: Lehman Brothers.

8/3/2019 Minority Squeeze Final

http://slidepdf.com/reader/full/minority-squeeze-final 30/37

Understa nding Minority Squeeze -O uts

30 January 3 , 2 0 0 2

Conclus ion

Delaware courts app ly the entire fairness test in reviewing de cisions of directors in

minority squeeze -outs. The target boa rd typically hires a special committee of

independent directors to evaluate the acquirer’s offer in a manner that satisfies the legal

criteria a ssocia ted with the entire fairness test. The a cquirer may conduct a tender offer

rather than take its offer directly to the target board so as to exert some timing and

pricing d iscipline on the e va luation process. W e witness this structure in two of the dea ls

we highlight, Prodigy/ SBC and TD Waterhouse/ Toronto Dominion.