Embed Size (px)

Citation preview

Fundamental

Resources & ScarcityMini Lesson 1

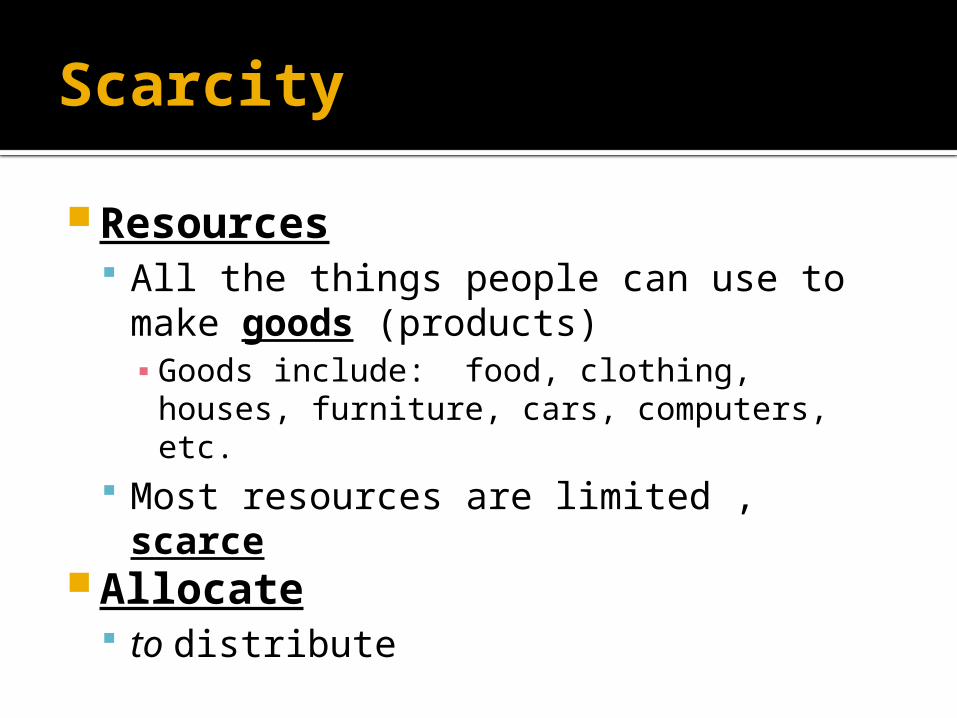

Scarcity

Resources All the things people can use to make

goods (products)▪ Goods include: food, clothing, houses,

furniture, cars, computers, etc. Most resources are limited , scarce

Allocate to distribute

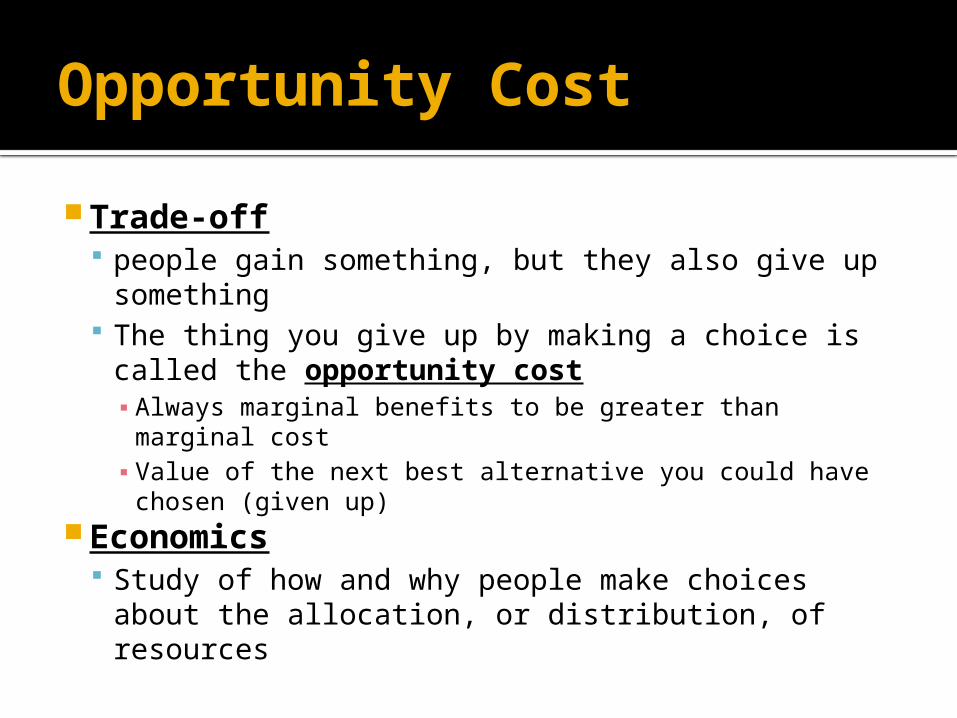

Opportunity Cost

Trade-off people gain something, but they also give up

something The thing you give up by making a choice is

called the opportunity cost▪ Always marginal benefits to be greater than marginal

cost▪ Value of the next best alternative you could have

chosen (given up) Economics

Study of how and why people make choices about the allocation, or distribution, of resources

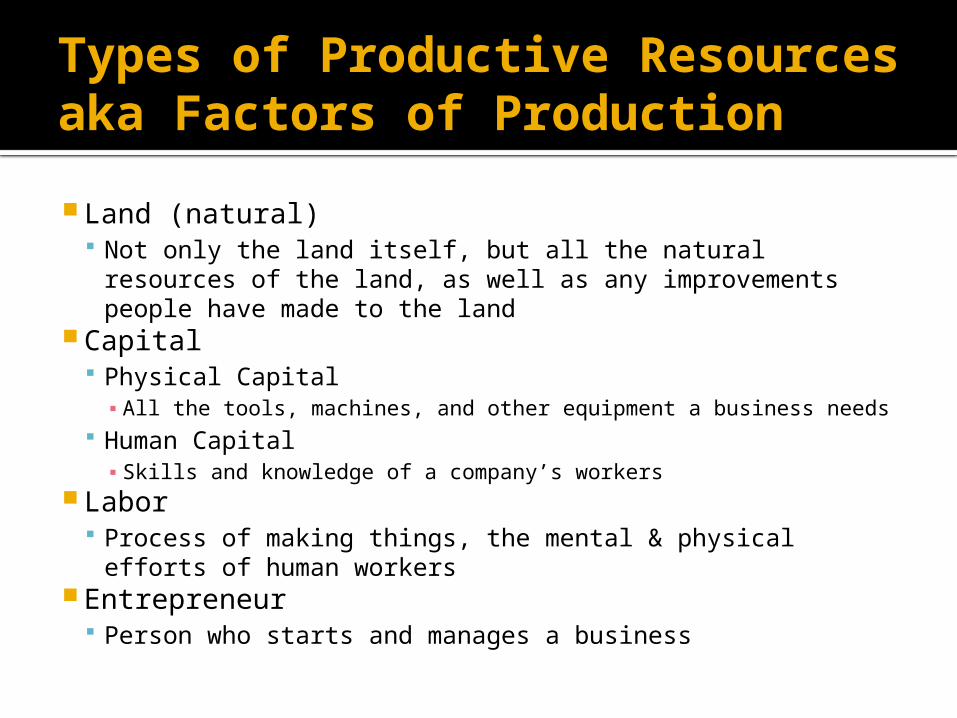

Types of Productive Resourcesaka Factors of Production

Land (natural) Not only the land itself, but all the natural resources of the

land, as well as any improvements people have made to the land

Capital Physical Capital▪ All the tools, machines, and other equipment a business needs

Human Capital▪ Skills and knowledge of a company’s workers

Labor Process of making things, the mental & physical efforts of

human workers Entrepreneur

Person who starts and manages a business

Cost Benefit, Specialization, & Voluntary Exchange

Mini Lesson 2

Rational Decisions

Rational Decisions Cost-benefit analysis▪ Marginal benefit▪ What you gain from decision

▪ Marginal Cost▪ What you give up from the decision

MB > MC = you have made a rational decision

Specialization & Voluntary Exchange

Voluntary exchange Mutual agreement between different parties

Specialization Doing just 1 thing (1 job, producing 1 item,

selling 1 product) Productivity

Efficient use of resources Division of Labor

Different workers do different parts of the job making

Economic SystemsMini Lesson 3

The 3 Basic Questions

What should we produce? How should we produce it? For whom should we produce it?

Economic Systems #1

Command Economies The government makes all basic

decisions Doomed to fail because▪ Can 1 committee do it all? NO▪ Inefficient▪ Shortages & resources were wasted

Economic Systems #2

Market Economies Based on private ownership▪ Private individuals & companies control the resources▪ Supply & Demand▪ Shows the distribution of goods & services determined by prices

Competition is driving force▪ Consumers—people who buy things & compete to buy

scarce products▪ Producers—people who sell things & compete to sell the

products people want most, driving down prices. AKA Capitalist or Laissez-faire▪ French word that means “to leave alone”▪ Government does not interfere with free markets

Economic Systems #3

Mixed Economies Most economies are based on various

combinations of market forces & government interventions

The Role of the Government

Mini Lesson 4

The Role of the Government

1) Protecting Property Rights & Contracts Legal rights of producers & consumers must

be protected Exchange of goods & services depends on

contracts, legal documents, between buyers & sellers

Government protects▪ Ideas, intellectual property▪ Patents for new inventions and medicines▪ Copyrights for books, songs, and creative works

The Role of the Government

2) Providing Public Goods & Services Private Goods▪ When you pay the entire cost of a

good/service and you receive all the benefits Public Good▪ When you pay taxes on a good/service and

the benefits are shared by everyone in society

The Role of the Government

3) Redistributing Income Transfer payments▪ money payments made by governments for

which no services are required in return▪ Done by collecting taxes from wealthy citizens to

make transfer payments to poor, disabled, and elderly citizens

▪ Examples:▪ Welfare benefits in cash, food stamps, low-income

housing, Medicaid benefits, unemployment benefits, Social Security retirement benefits, Medicare

The Role of the Government

4) Promoting Competition Free competition between producers

keep prices low and quality high Congress has passed antitrust laws

(laws that prevent the formation of monopolies) ▪ Monopoly market structure in which one

company has control over production and prices▪ Trust is a group of companies that combine

their resources in order to control production & prices. ▪ Been illegal in the US since 1890

The Role of the Government

5) Resolving Market Failures Market failure occurs when a private

company benefits from production for which other people end up paying some of the costs

6) Effects of Regulation & Deregulation Regulation—using laws to control what

businesses can do▪ Purpose: to increase public benefit & decrease

negative consequences of market system Deregulation—when government stop

regulating a particular industry

Productivity & GrowthMini Lesson 5

Economic Growth

Occurs when a society is able to produce more things that people want & improve its members’ standard of living

In order for an economy to grow, it must increase its productivity by producing more output (products) per each unit of resources they use, or their input

Productivity = output of products

input of resources

Capital Investment

Key to economic growth is capital investment Using some of an economy’s profits to: ▪ buy new machines and equipment ▪ to research and implement new technologies▪ Improve education of the workplace

Making Capital Investments

To increase productivity and profits in the future Invest in capital goods (new equipment)

or human capital (more training)

Using the PPC to Show Economic Growth

PPC on board