Embed Size (px)

Citation preview

Revamping the Regional Railway Systems in Eastern and Southern AfricaMark Pearson and Bo GiersingRegional Integration Research Network Discussion Paper (RIRN/DP/12/01)

Mineral Resource Based Growth Pole Industrialisation - Phosphate Report

Regional Integration Research NetworkOpen Dialogues for Regional Innovation

C.C. Callaghan

Mineral Resource Based Growth Pole Industrialisation - Phosphates Report

Page i

Preface

Since its establishment in 2009, Trade Mark Southern Africa (TMSA) has supported the

Tripartite of the Common Market of Eastern and Southern Africa (COMESA), the Southern

African Development Community (SADC) and the East African Community (EAC), in

developing and implementing its regional integration agenda. This involves supporting the

design and planned implementation of the Tripartite Free Trade Area (FTA), improving the

economic competitiveness of the region and reducing costs of cross-border transactions

through a transport corridor approach addressing both trade facilitation issues and

infrastructure constraints.

Focused industrial development is essential in the COMESA-EAC-SADC Tripartite region to

fundamentally change the economy and to promote high yield sectors. Such development

brings not only an improvement in the GDP and job provision, but promotes knowledge

accumulation and technological sophistication that have far reaching benefits for the

economy.

This research was conducted under the topic “Tripartite ‘Growth Pole’ Diagnostic

Reports: Analysis of Potentials and Prospects for Minerals-Based Industrialisation.”

The research is packaged in four (4) Sub-Sector Reports on hydrocarbons, ferrous metals,

base metals and phosphates and a Consolidated ‘Growth Poles’ Report. The reports profile

and prioritise a number of potential regional ‘growth poles’ throughout eastern and southern

Africa. In the ‘first sort’ each known minerals deposit was analysed through three (3) filters

as follows:

1. By size of deposit (size of known indicated resource);

2. By status of deposit (levels of investment in developing the deposit); and,

3. By ‘expert group’ assessment (market conditions and supporting infrastructure).

The research reviewed available information on mineral deposits and the status of their

development and analysed the extent to which realisable mining and mineral development

opportunities can contribute to and enhance regional development. Data constraints limited

the research to the Eastern and Southern Africa region and defined a limited number of

plausible ‘growth poles’, which could provide a platform to accelerate industrialisation in the

region.

The results from these three filters were then combined through a ‘second sort’, which

enhanced the analysis by clustering minerals within a defined locality into potential ‘growth-

pole’ value chains. In line with ‘growth pole’ theory the basis for any prioritisation was

whether the initial ‘critical mass’ of investment had been achieved. The minimum critical level

Page ii

of investment is considered to be achieved when five key pre-conditions have been met,

namely:

1. A recognised global multi-national corporation (MNC) has made a significant investment in developing a mineral deposit or a cluster of mineral deposits;

2. Such an investment commitment reflects that the regulatory environment for trade and investment in sufficiently robust to support large-scale projects;

3. Similarly, this size of investment in developing a world-class resource confirms that the long term global market outlook for the target commodity is equally robust;

4. It also acknowledges that any supply-side infrastructure constraints can be overcome by the projects cash-flows and that infrastructure development itself represents an opportunity for the lead developer, in the transport and energy sectors for example; and,

5. Finally, the participation of a strong ‘anchor’ investor substantially strengthens the prospects for developing upstream linkages to local suppliers and new downstream industries as a result of the presence of and initial investment by the global mining company.

In addition to these pre-conditions the research also considers two additional criteria to

prioritize ‘growth-pole’ potential. The first was the extent to which the value-chain could be

developed given prevailing market conditions, and the second was whether value-chain

linkages straddle national borders to assume a regional posture.

Based on these considerations the following seven (7) regional growth poles were prioritised

in order of potential:

1. Tete, Mozambique – Southern Malawi (Hydrocarbons, Ferrous Metals and Phosphates);

2. Copperbelt, Zambia – Copperbelt, DRC (Base Metals);

3. Cabinda, Angola – Bas Congo, DRC – Soyo, Angola (Hydrocarbons and Phosphates);

4. Rovuma Basin, Mozambique – Ruvuma and Songo-Songo Basins, Tanzania (Hydrocarbons);

5. Lephalale, South Africa – Morepule, Botswana (Hydrocarbons);

6. Kabanga, Tanzania – Musongati, Burundi (Base Metals); and,

7. Central Zimbabwe – Central Mozambique (Hydrocarbons and Ferrous Metals).

Page iii

An initial scoping study is currently being conducted to develop a fuller picture of the Tete,

Mozambique – Southern Malawi ‘Growth Pole’, which has been expanded to include

Eastern, Zambia, in collaboration with the World Bank and the governments of Malawi,

Mozambique and Zambia.

TMSA, under its Regional Integration Research Network initiative, commissioned Chris

Callaghan to conduct the research. Chris Callaghan is an independent consultant whose

career includes stints as a Mining Sector Specialist at the Development Bank of Southern

Africa (DBSA) and a Senior Manager at MINTEK South Africa, the state-run Mining

Technology Research Institute. The TMSA lead was Graham Smith, TMSA Programme

Manager - Corridors. The study benefited particularly from guidance and inputs by Dr.

Judith Fessehaie, TMSA Industrial Development Expert and Mr. Bo Giersing, TMSA Ports

and Railway Specialist, Mr. Jurgens Van Zyl, an independent Mining and Development

Finance Specialist, currently under contact to Business Leadership South Africa (BLSA) and

Dr. Paulo Fernandes, a Logistics Specialist at Mott MacDonald/PDNA South Africa. These

individuals ‘peer reviewed’ the prioritisation methodology, which underpinned the selection of

the Growth-Poles. Other TMSA colleagues provided some early inputs into the terms of

reference for the study.

More Information

The reports can be downloaded on the TMSA website at

www.trademarksa.org/publications/mineral-resource-based-growth-pole-industrialisation

Reports include the Consolidated Growth Poles and Value-Chains Report and four (4) Sub-

Sector Minerals Reports on Hydrocarbons (Coal, Oil and Gas), Ferrous Metals (Iron and

Steel), Base Metals (Chrome, Manganese, Nickel, Vanadium, Copper, Zinc and Lead) and

Phosphates report.

Page iv

Table of abbreviations Companhiá de Fosfatos de Angola COFAN

Di-ammonium phosphate DAP

Direct application phosphate rock DAPR

Deoxyribonucleic acid DNA

Democratic Republic of the Congo DRC

El Nasr Phosphate Company ENMC

Life of mine LOM

Mono-ammonium phosphate MAP

Mono-ammonium phosphate with zinc MAPZN

Millions of tonnes Mt

Millions of tonnes per annum Mtpa

Nitrogen-Phosphate-potassium NPK

Phosphorous pentoxide P2O5

Per annum pa

Phosphate rock PR

Run of mine ROM

Single Superphosphate SSP

Tonnes t, ton

Tonnes per annum tpa

Triple superphosphate TSP

Table of Definitions

Single Superphosphate

A relatively simple fertiliser developed from rock phosphate dissolved in sulphuric acid to produce monocalcium phosphate and gypsum. SSP contains 7-9% P (16-20% P2O5)

Triple Superphosphate

TSP is produced by reacting finely ground phosphate rock with liquid phosphoric acid to produce monocalcium phosphate (no gypsum). TSP contains 17-23% P (44-52% P2O5).

Page v

Table of Contents

1 Introduction .......................................................................................................... 1

2 Phosphates .......................................................................................................... 2

2.1 Introduction ............................................................................................................... 2 2.2 Fundamental concepts ............................................................................................. 2

2.2.1 Sedimentary phosphate rocks ............................................................................... 3 2.2.2 Igneous (intrusive) Phosphate rocks ..................................................................... 3

2.3 Market ......................................................................................................................... 4 2.3.1 Uses ...................................................................................................................... 4 2.3.2 Production ............................................................................................................. 4 2.3.3 Demand ................................................................................................................. 6 2.3.4 Supply ................................................................................................................... 6 2.3.5 Trade ..................................................................................................................... 8 2.3.6 Price .................................................................................................................... 11 2.3.7 Value added products and substitution ............................................................... 12 2.3.8 Substitutes .......................................................................................................... 13 2.3.9 Challenges .......................................................................................................... 13

3 Angola ................................................................................................................. 14

3.1 Cabinda Phosphates ............................................................................................... 14 3.1.1 Cacata ................................................................................................................. 14 3.1.2 Chibuete .............................................................................................................. 14 3.1.3 Mongo Tando ...................................................................................................... 16 3.1.4 The Lucunga River phosphates .......................................................................... 16 3.1.5 Carbonatites ........................................................................................................ 16

4 Botswana ............................................................................................................ 18

5 Burundi ............................................................................................................... 19 5.1 Matongo ................................................................................................................... 19

6 Comores ............................................................................................................. 20

7 DRC ..................................................................................................................... 21 7.1 Sedimentary Phosphates ....................................................................................... 21

Page vi

7.1.1 Kanzi Project ....................................................................................................... 21 7.1.2 Igneous phosphates ............................................................................................ 21 7.1.3 Lueshe carbonatite .............................................................................................. 21

8 Djibouti ............................................................................................................... 23

9 Egypt ................................................................................................................... 24 9.1 Introduction ............................................................................................................. 24 9.2 Red Sea Coastal Area ............................................................................................. 24 9.3 Nile Valley deposits ................................................................................................ 25 9.4 Abu Tartur ................................................................................................................ 25 9.5 Resource .................................................................................................................. 26 9.6 Beneficiation ............................................................................................................ 26

10 Eritrea ............................................................................................................... 27

11 Ethiopia ............................................................................................................ 28 11.1 Bikilal ...................................................................................................................... 28 11.2 Other deposits ....................................................................................................... 28

12 Kenya ................................................................................................................ 29

12.1 Mrima Hill Carbonatite .......................................................................................... 29 12.2 Rangwe Area Intrusives ....................................................................................... 29 12.3 Fertiliser plant ....................................................................................................... 29

13 Lesotho ............................................................................................................. 30

14 Libya ................................................................................................................. 31

15 Madagascar ...................................................................................................... 32

16 Malawi ............................................................................................................... 33

16.1 Tundulu .................................................................................................................. 33

17 Mauritius ........................................................................................................... 34

18 Mozambique ..................................................................................................... 35 18.1 Sedimentary deposits ........................................................................................... 35 18.2 Igneous deposits ................................................................................................... 35

18.2.1 Cone Negose .................................................................................................... 35 18.2.2 Evate ................................................................................................................. 35

Page vii

18.2.3 Lucuisse ............................................................................................................ 37 18.2.4 Mont Muande .................................................................................................... 37

19 Namibia ............................................................................................................. 38 19.1 Igneous deposits ................................................................................................... 38 19.2 Sedimentary offshore deposits ........................................................................... 38

19.2.1 The Sandpiper project ....................................................................................... 38 19.2.2 Phosphate in Tailings ........................................................................................ 39

20 Rwanda ............................................................................................................. 40

21 Seychelles ........................................................................................................ 41

22 South Africa ..................................................................................................... 42 22.1 Foskor Mine (Palaborwa) ...................................................................................... 42 22.2 Glenover ................................................................................................................. 42 22.3 Schiel ...................................................................................................................... 43 22.4 Spitskop ................................................................................................................. 43 22.5 Sedimentary phosphates ..................................................................................... 43

22.5.1 Agulhas Bank deposits ...................................................................................... 43 22.5.2 Other deposits ................................................................................................... 44

23 South Sudan .................................................................................................... 45

24 Sudan ................................................................................................................ 46 24.1 Jebel Abyad and Abu Hasem .............................................................................. 46 24.2 Halaib District ........................................................................................................ 46 24.3 Nuba Mountains .................................................................................................... 46 24.4 Other Phosphates ................................................................................................. 47

25 Swaziland ......................................................................................................... 49

26 Tanzania ........................................................................................................... 50

26.1 Igneous (carbonatite) Phosphates ...................................................................... 50 26.1.1 The Sangu-Ikola carbonatite ............................................................................. 50 26.1.2 The Ngualla carbonatite .................................................................................... 50 26.1.3 Mbalizi, Songwe and Sengeri Hill ...................................................................... 50 26.1.4 Panda Hill .......................................................................................................... 50 26.1.5 Metamorphic Apatite limestones ....................................................................... 51

Page viii

26.1.6 Lacustrine Phosphates ...................................................................................... 51

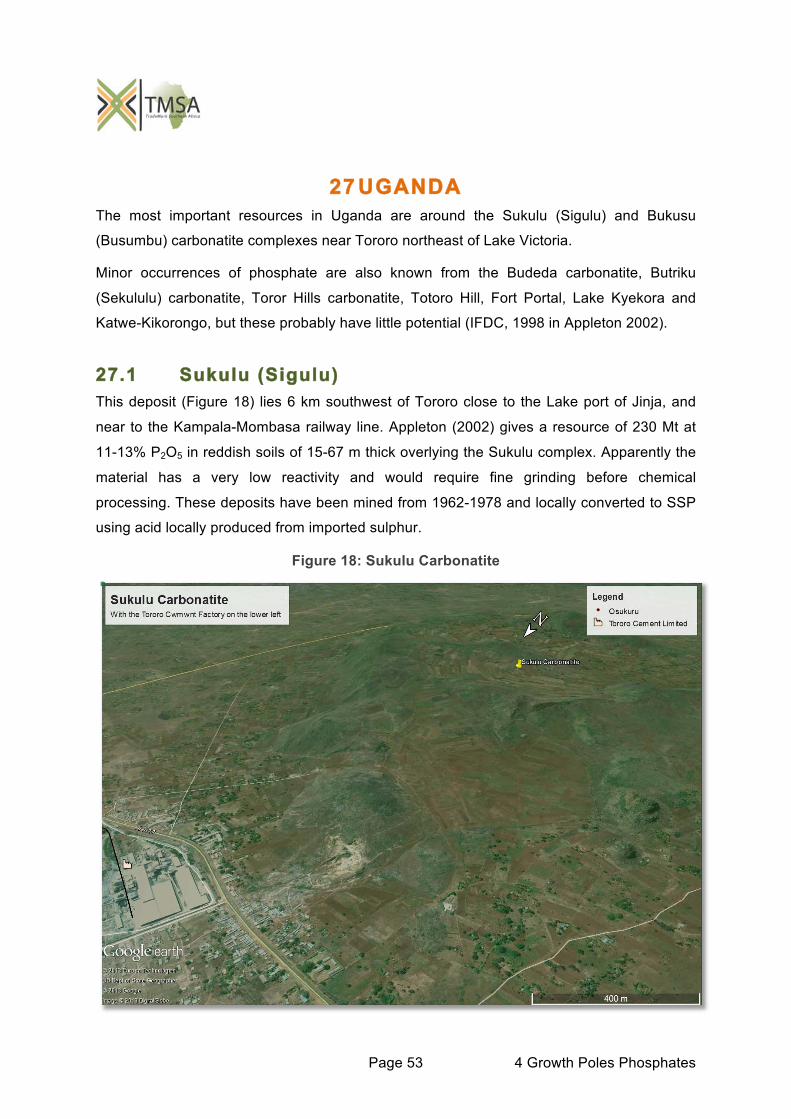

27 Uganda ............................................................................................................. 53 27.1 Sukulu (Sigulu) ...................................................................................................... 53 27.2 Bukusu (Busumbu) ............................................................................................... 54

28 Zambia .............................................................................................................. 55 28.1 Nkombwa Hill carbonatite .................................................................................... 55 28.2 Kaluwe carbonatite. .............................................................................................. 55 28.3 Chilembwe phosphate deposit ............................................................................ 55 28.4 Mumbwa North phosphate deposit ..................................................................... 56

29 Zimbabwe ......................................................................................................... 57 29.1 Dorowa carbonatite ............................................................................................... 57 29.2 Shawa ..................................................................................................................... 57 29.3 Chishanya .............................................................................................................. 57 29.4 Katete ..................................................................................................................... 58

Appendix I. Deposit size categories (kt) .............................................................. 62

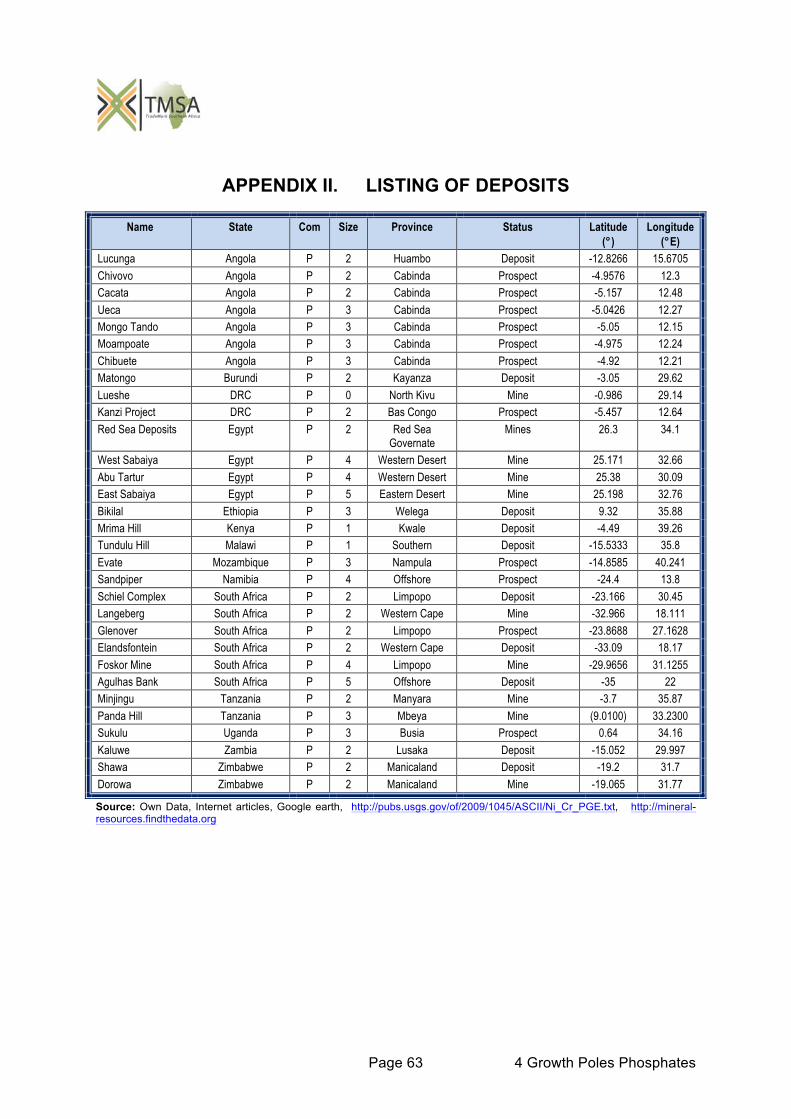

Appendix II. Listing of deposits ........................................................................... 63

Appendix III. Rock phosphate minerals .............................................................. 64

List of Figures

Figure 1: World Phosphate deposits ........................................................................................ 3

Figure 2: Phosphate surplus and deficit in arable soils ........................................................... 5

Figure 3: World Phosphate Mine Production 2011 .................................................................. 5

Figure 4: World fertiliser use 2010 (45 Mt nutrients) ................................................................ 7

Figure 5: World fertiliser use estimate 2020 (60 Mt Nutrients) ................................................ 7

Figure 6: World Phosphate reserves ....................................................................................... 8

Figure 7: Phosphate fertiliser production 2010 (46 Mt nutrients) ............................................. 9

Figure 8: Phosphate Rock exports 2010 ................................................................................. 9

Figure 9: Phosphate fertiliser Exports 2010 ........................................................................... 10

Figure 10: Phosphate Rock imports 2010 ............................................................................. 10

Figure 11: Phosphate fertiliser Imports 2010 ......................................................................... 11

Page ix

Figure 12: Phosphate Rock price 2011-2013 ........................................................................ 11

Figure 13: Phosphate fertiliser products ................................................................................ 12

Figure 14: Cabinda and DRC phosphate field ....................................................................... 15

Figure 15: The Tundulu Carbonatite Complex, Malawi ......................................................... 33

Figure 16: Phosphate occurrences in Mozambique .............................................................. 36

Figure 17: Phosphate prospect at Jebel Abyad ..................................................................... 47

Figure 18: Sukulu Carbonatite ............................................................................................... 53

Figure 19: Dorowa Phosphate Mine ...................................................................................... 58

List of Tables

Table 1: Tripartite Countries with a Phosphate resource ......................................................... 6

Page 1 4 Growth Poles Phosphates

1 INTRODUCTION TradeMark Southern Africa has awarded the first stage of a study to set out a pragmatic

approach for industrial development, based on mineral resources in southern and eastern

Africa to Letlapa Consulting. This report is the fourth in a series of reports for this project.

The reports are:

1. Inception report, in which the project is formulated

2. Ferrous metals report outlining ferrous metals opportunities in the tripartite area.

3. Non Ferrous metals report summarising the principle deposits of copper, lead and zinc in the tripartite area.

4. Phosphate report (this report). This report will summarise the principle deposits of phosphates in the tripartite area.

5. Energy commodities report. This report will outline the major deposits of coal oil and gas in the tripartite area.

6. Growth poles and value chains. This report will be the culmination of the first stage of the greater study on growth poles based on mineral resources and will outline high level value chains for a set of mineral clusters that may develop into growth poles.

Page 2 4 Growth Poles Phosphates

2 PHOSPHATES

2.1 Introduction Sedimentary marine phosphorites make up the majority of phosphate rock resources, with

the largest sedimentary deposits to be found in northern Africa, China, the Middle East, and

the United States. Intrusive deposits (carbonatite) are found in Brazil, Canada, Finland,

Russia, as well as southern and eastern Africa. Phosphate resources have also been

identified on the continental shelves and on seamounts in the Atlantic Ocean and Pacific

Ocean (Jasinski, 2013).

Phosphate mines vary in grade from as low as 5% to more than 40 % P2O5. Since

phosphoric acid plants generally require a feedstock of 26-34% P2O5, lower grade mines

must upgrade their product to a suitable level

2.2 Fundamental concepts Phosphorous is an essential primary nutrient in the growth of crops and is an important

constituent of DNA. Because the world has a very large population, food to support the

population can no longer be grown on available land without the support of fertiliser.

Phosphates are therefore required in increasing quantities for food security. Most farmland

soils are phosphorus deficient and in addition, phosphorous readily combines with iron and

aluminium in the soil to produce insoluble phosphates that are not available for plant uptake,

which may mean that more phosphate needs to be added to get the desired growth

stimulation.

Consumption of phosphate rock is mainly by the fertiliser sector (85% of all phosphate rock).

Although phosphate rock can be used directly as fertilizer, the release of the phosphate from

most sources is too slow and phosphate rock is usually converted to chemical fertilizer

before use in the agricultural industry. Deposits that are suitable for direct use have a high

reactivity (the phosphate is relatively soluble in acid soils with low Ca and P concentrations)

and these include “Langfos” from Langebaan in the Western Cape Province of South Africa,

phosphates from Minjingu in Tanzania, and possibly those from Cabinda and Bas Congo

(van Straaten, 2002).

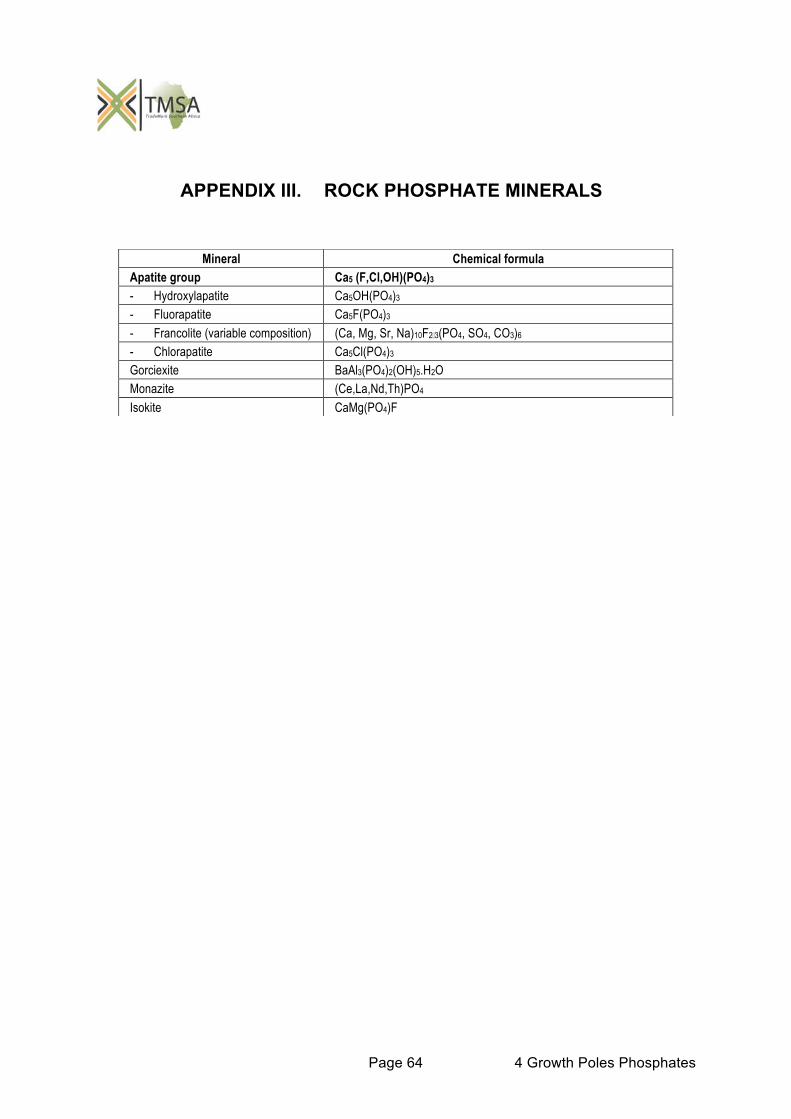

Rock phosphate consists most often of minerals in the apatite group. Pure apatite is rare

since it allows substitution of various other molecules within its lattice and a number of

Page 3 4 Growth Poles Phosphates

varieties are found in deposits. A list of the major mineral species can be found in Appendix

III. Depending on the accessory minerals present and the amount of apatite or related

minerals in the phosphate rock, it may have a wide range of solubility. The most soluble

varieties can be applied directly and are referred to as direct application phosphate rock

(DAPR).

There are broadly two types of phosphate deposit, sedimentary and igneous (island deposits

– not dealt with here – are recent deposits and technically a subset of sedimentary deposits).

The deposits in the tripartite area are largely igneous in nature (see Figure 1).

Figure 1: World Phosphate deposits

Source: Van Kauwenbergh, 2011

2.2.1 Sedimentary phosphate rocks Sedimentary phosphate deposits range in age from Precambrian to Recent and occur

throughout the world. About 80% of phosphate rock used commercially is obtained from

marine sedimentary deposits containing an apatite variety called francolite which typically

contains about 30-35% P2O5. Most sedimentary deposits were probably formed in offshore

marine conditions on continental shelves. Sedimentary phosphate rocks range from

unconsolidated to weakly cemented and to highly indurated rocks (Van Kauwenbergh,

2010).

2.2.2 Igneous (intrusive) Phosphate rocks Igneous phosphate rocks commonly contain one of the apatite varieties (fluorapatite,

hydroxyapatite or chlorapatite) with some 35-42% P2O5. Igneous phosphate rock is exploited

Page 4 4 Growth Poles Phosphates

chiefly in Russia, South Africa, Brazil, Finland and Zimbabwe. Igneous phosphate ores are

often low in grade (less than 5% P205), but can often be easily upgraded to high-grade

products (Van Kauwenbergh, 2010).

2.3 Market

2.3.1 Uses Phosphate rock is used primarily to produce phosphate fertilisers (~85%) but also in animal

feed supplements (~7%), detergents, food preservatives, safety matches, fire extinguishers,

anti-corrosion agents, cosmetics, fungicides, ceramics, water treatment and in the chemical,

dental and pharmaceutical industries. Phosphorous is also used in metallurgy especially in

the steel and copper industry. For use in the fertiliser industry the phosphate rock needs to

contain at least 26% P2O5 and about 5% CaCO3. Furthermore it should have less than 4%

combined iron and aluminium oxides and have a very low chlorine content of less than

0.02%.

Overuse, especially of poor quality phosphatic fertilisers can lead to severe soil pollution.

De Ridder and others (2012) point out that cadmium concentration in EU soils is already a

concern. Furthermore Moroccan phosphates are high in cadmium and unless the cadmium

is removed from the final product the situation can be expected to become more severe.

Even though Africa has by far the greatest phosphate resources much of African arable land

is highly deficient in phosphate (see Figure 2) and enhanced crop production is to be

expected once more fertilisers are applied to African cropland.

2.3.2 Production The USGS expected world phosphate rock production to increase from 220 Mtpa in 2012 to

256 Mtpa by 2018, with most of the growth from Morocco. Phosphate rock mines are also

being developed or expanded within Africa in Angola, Congo (Brazzaville), Egypt, Ethiopia,

Guinea-Bissau, Namibia, Mali, Mauritania, Mozambique, Senegal, South Africa, Togo,

Tunisia, Uganda, and Zambia (Jasinski, 2013). In the rest of the world there is development

in Australia, Brazil, Canada, China, Kazakhstan, and New Zealand.

China, the USA and Morocco (including Western Sahara) accounted for over 60% of global

production in 2011 (See Figure 3), whilst Morocco is by far the world’s largest exporter (De

Ridder, et al, 2012).

Page 5 4 Growth Poles Phosphates

Figure 2: Phosphate surplus and deficit in arable soils

Due to the threat posed by lack of access to phosphates for the EU, steps for recovery and

recycling of phosphate from human sewage sludge are underway in Europe, but

infrastructure and governance mechanisms remain obstacles (De Ridder, et al, 2012).

Figure 3: World Phosphate Mine Production 2011

Source: Mineral commodity Survey, Jasinski (2013)

Page 6 4 Growth Poles Phosphates

Table 1: Tripartite Countries with a Phosphate resource

Angola

DRC

Egypt

Ethiopia

Kenya

Malawi

Mozambique

Namibia

South Africa

Sudan

Uganda

United Republic of Tanzania

Zambia

Zimbabwe

2.3.3 Demand After many years of oversupply, the phosphate market moved into undersupply in 2007 and

2008. Jasinski (2013) projected world consumption of P2O5 in fertilizer to increase from

41.9 Mtpa in 2012 to 45.3 Mtpa in 2016. Global demand in phosphate is expected to

continue to grow by 2-3% pa in line with growth in the fertiliser industry. Since there is no

substitute for phosphate and as long as populations grow so will the phosphate industry to

allow those populations to be fed. It is notable that there is an increasing trend towards

conversion of phosphate rock into phosphoric acid before export; this is most likely due to

the cost of transport.

China was the major user of fertiliser phosphates in 2010 (see Figure 4) and is likely to

remain the highest consumer due to its population. Although African consumption is

currently low, if one looks at continued strong growth in Africa, and because of the

population pressure exerted, and the need for food security, Africa could grow to be the third

major consumer by 2020 (see Figure 5).

2.3.4 Supply There are many arguments for and against the concept of “peak phosphorous”, but

regardless of individual opinion on the theory there is no doubt that land based phosphates

outside of Morocco and Western Sahara are in relatively short supply and that inhabitants of

many countries may feel that their food security is under threat.

Page 7 4 Growth Poles Phosphates

Figure 4: World fertiliser use 2010 (45 Mt nutrients)

Source: NPK101, FAO, 2011

Figure 5: World fertiliser use estimate 2020 (60 Mt Nutrients)

Note: Own Estimate

Although phosphate rock may be relatively plentiful it is important note that to manufacture

fertilizers profitably the rock must contain at least 26% P2O5, and preferably be free of

deleterious elements (and especially of heavy metals).

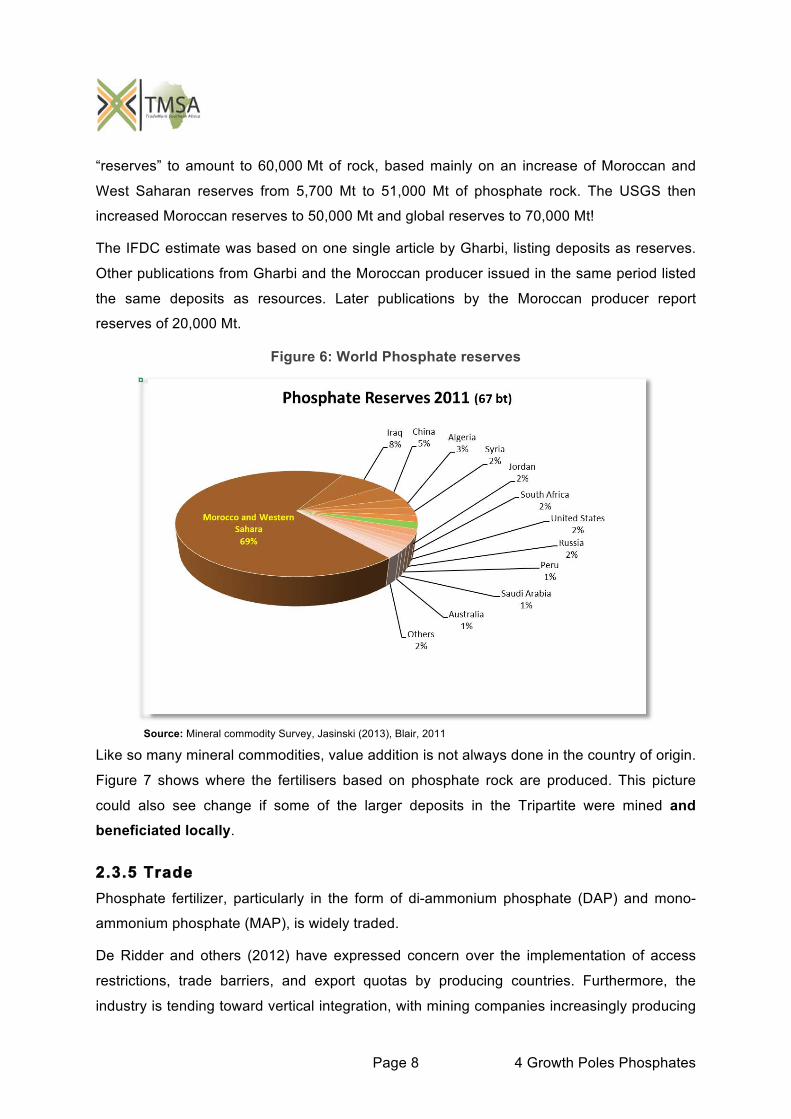

Up to 2009 the USGS estimated world “reserves” to be in the range of 16,000 Mt of

phosphate rock (5,600 Mt in Morocco) and a global “reserve base” to be 47,000 Mt of

phosphate rock (20,000 Mt in Morocco). In 2010 in the face of strong peak phosphate

projections, the International Fertilizer Development Centre (IFDC) reported world global

Page 8 4 Growth Poles Phosphates

“reserves” to amount to 60,000 Mt of rock, based mainly on an increase of Moroccan and

West Saharan reserves from 5,700 Mt to 51,000 Mt of phosphate rock. The USGS then

increased Moroccan reserves to 50,000 Mt and global reserves to 70,000 Mt!

The IFDC estimate was based on one single article by Gharbi, listing deposits as reserves.

Other publications from Gharbi and the Moroccan producer issued in the same period listed

the same deposits as resources. Later publications by the Moroccan producer report

reserves of 20,000 Mt.

Figure 6: World Phosphate reserves

Source: Mineral commodity Survey, Jasinski (2013), Blair, 2011

Like so many mineral commodities, value addition is not always done in the country of origin.

Figure 7 shows where the fertilisers based on phosphate rock are produced. This picture

could also see change if some of the larger deposits in the Tripartite were mined and beneficiated locally.

2.3.5 Trade Phosphate fertilizer, particularly in the form of di-ammonium phosphate (DAP) and mono-

ammonium phosphate (MAP), is widely traded.

De Ridder and others (2012) have expressed concern over the implementation of access

restrictions, trade barriers, and export quotas by producing countries. Furthermore, the

industry is tending toward vertical integration, with mining companies increasingly producing

Page 9 4 Growth Poles Phosphates

fertilizers, phosphoric acid and other products, especially where there is local demand. As a

result the picture for phosphate rock export is very different from the production (see Figure

8) and because of the location of beneficiation centres; it is also different to exports of

phosphate fertilisers (Figure 9).

Figure 7: Phosphate fertiliser production 2010 (46 Mt nutrients)

Source: NPK101

Figure 8: Phosphate Rock exports 2010

Source: IFA, 2013.

Page 10 4 Growth Poles Phosphates

Figure 9: Phosphate fertiliser exports 2010

Source: NPK101

If the importing areas are considered then it becomes very clear which regions have a

phosphate deficit and these are mainly Europe and India. Africa is also in deficit but

fertilizers are still underused in Africa at this point in time and as a result there is not much

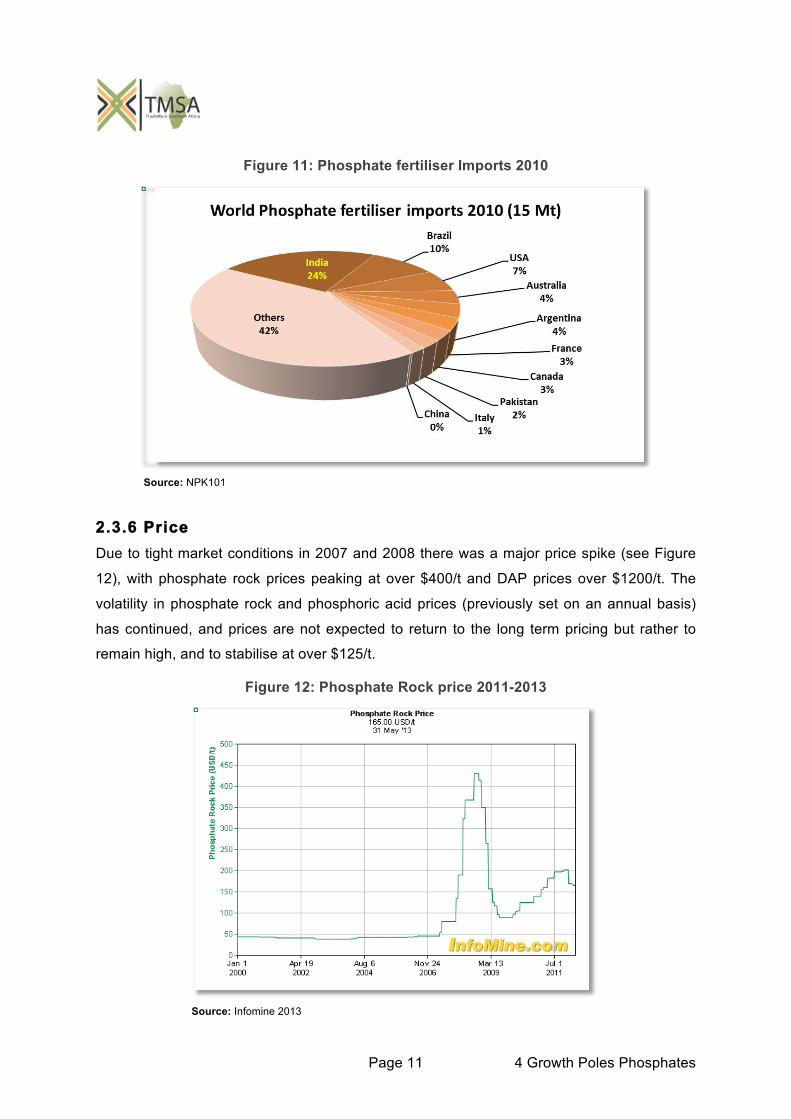

import into Africa (see Figure 10). In Figure 11 the fertiliser imports are shown. This shows

‘other’ is the major importer because most countries have neither mines nor factories to

beneficiate phosphate rock.

Due to possible future phosphate shortages some countries remain very protective of their

phosphate resources. For example Business week (2013) indicated that China had imposed

a 135% tariff on phosphate rock exports.

Figure 10: Phosphate Rock imports 2010

Source: IFA, 2013.

Page 11 4 Growth Poles Phosphates

Figure 11: Phosphate fertiliser Imports 2010

Source: NPK101

2.3.6 Price Due to tight market conditions in 2007 and 2008 there was a major price spike (see Figure

12), with phosphate rock prices peaking at over $400/t and DAP prices over $1200/t. The

volatility in phosphate rock and phosphoric acid prices (previously set on an annual basis)

has continued, and prices are not expected to return to the long term pricing but rather to

remain high, and to stabilise at over $125/t.

Figure 12: Phosphate Rock price 2011-2013

Source: Infomine 2013

Page 12 4 Growth Poles Phosphates

2.3.7 Value added products and substitution Although phosphate rock used for soil fertilisation may be used directly if the activity of the

phosphate is high, most often it is formed into a fertiliser product (Figure 13), to make

transporting of the products easier, and to ensure that final application rates can be better

controlled.

Figure 13: Phosphate fertiliser products

Source: NPK101

2.3.7.1 Phosphoric Acid

Phosphoric acid is obtained by combining phosphate rock with sulphuric acid, to produce

3H3PO4. The main environmental problem presented from this process is the disposal of the

great quantity of gypsum produced as a by-product. Since there is a distinct lack of

phosphate resources in South Asia this region is a captive market. Note that gypsum finds

use in many industries dependent on its specific quality. It is also an important soil

ameliorant especially where clayey soils are found.

2.3.7.2 MAP & DAP Phosphoric acid can be combined with ammonia to form mono-ammonium phosphate (MAP)

and di-ammonium phosphate (DAP). The advantages of these ammonium phosphates are:

Both nitrogen and phosphorus are available in the fertiliser

They can be produced in granular form

Page 13 4 Growth Poles Phosphates

2.3.7.3 NPK Nitrogen-Phosphate-potassium (NPK) fertilizers are compound fertilizers consisting of the

three major plant nutrients (often also with micronutrients). NPK is usually available in

granule form to make distribution easy. NPK is produced by neutralizing phosphoric and

sulphuric acid with ammonia and adding potassium chloride and UAN (a solution of urea and

ammonium nitrate), followed by drying and granulation.

2.3.7.4 Single Superphosphate (SSP) Single superphosphate (SSP) is produced made by acidifying phosphate rock. The P2O5

content of SSP is 16-20% (8-9% P). A sulphuric acid plant is usually a prerequisite.

Hydrofluoric acid (HF), which escapes from the process as a gas may be captured to

represent a significant by-product.

2.3.7.5 Triple Superphosphate (TSP)

Triple Superphosphate (TSP) is formed by treating phosphate rock with phosphoric acid. It

has 40-49% P2O5 (about 20% P). The major advantage of TSP is the high concentration of

phosphorous which leads to lower transport costs per tonne of phosphorous. However, the

majority of the phosphorous in the product comes from the phosphoric acid, which is

expensive; furthermore it does require rock with a high P2O5 content.

2.3.8 Substitutes There are no substitutes for phosphorous, and there would not be enough supply from

organic sources to meet the world demand.

2.3.9 Challenges The availability of water is critical in the phosphate rock beneficiation process. Without water,

deposits may be left untouched, or only partially utilised. Dry screening may be used to

produce concentrates if ore characteristics are suitable. Seawater or brack water may be

used for washing and size classification and for flotation. However a final rinse will be

required to remove the impurities introduced (eg NaCl).

Page 14 4 Growth Poles Phosphates

3 ANGOLA Van Straaten (2002) reports phosphates in the Cabinda area, at Lucunga River, northeast of

Luande and in 8 carbonatite complexes

3.1 Cabinda Phosphates Extensive sedimentary phosphate deposits occur in Cabinda and stretch into the DRC

(Figure 14). The phosphate beds are Upper Cretaceous to Lower Eocene in age and are

concentrated in two zones. A lower phosphate zone with three beds, 3 m, 12 m and 9 m

thick, and the upper phosphate zone with a single bed of 13-23 m thick. The phosphates are

made up of pellets, oolites and organic fragments. The lower beds grade at 10-20% P2O5

and of the upper beds at 15-20% P2O5. Weathering and leaching extend to depths of 100 m

or more and in some places have increased the grade of the phosphate beds to 32-38%

P2O5 (Hodge and Partners 1978 in van Straaten, 2002). Minbos Resources is currently busy

with exploration in Angola and the DRC and has an exploration target of 333 – 538 Mt

grading 10% - 20% P2O5 in its Cabinda licence area (Minbos, 2012). Currently there is an

inferred resource of 304.8 Mt at 11.5% P2O5. Van Kauwenbergh (2006) gives data on costs

and some engineering data of a proposed Companhiá de Fosfatos de Angola (COFAN)

mine and beneficiation facility.

3.1.1 Cacata The Cacata deposit is in the Nhenha river valley, some 60 km east of Cabinda City. The

Cacata area has an indicated resource (included in the overall Cabinda licence resource) of

30.4 Mt at 17.2% P2O5. The Cacata area would be mined first and it is expected that it would

be able to support a large scale phosphate rock complex producing about 1.25 Mtpa over 10

years LOM. It will be an open-pit operation with a conventional beneficiation process to

produce a 35% P2O5 product (Minbos, 2012).

3.1.2 Chibuete The deposit occurs north-northeast of Lake Massabi near the Congo Border, COFAN

estimated a “probable reserve” of 93.66 Mt at 15.55% P2O5 was estimated. Chibuete is

included in the overall Minbos Cabinda licence estimate, it has a 150 Mt inferred resource at

8.3% P2O5 (Minbos, 2013).

Page 15 4 Growth Poles Phosphates

3.1.2.1 Ueca

Also included in the Minbos licence area, this deposit is about 8.25 km long and 460-550 m

wide. COFAN planned to mine this deposit which they estimated at 147.08 Mt at 11.91%

P2O5, under 9.8 m of overburden (Van Kauwenbergh, 2006).

Figure 14: Cabinda and DRC phosphate field

Source: Minbos, 2012

3.1.2.2 Moampoate

A small deposit included in the Minbos licence, COFAN estimated that it had 37.83 Mt at

33% P2O5 divided into several localised sections (Van Kauwenbergh, 2006).

3.1.2.3 Chivovo

Also included in the Minbos licence area and reserve estimate is the Chivovo deposit which

occurs some 10 km north of Dinge. It consists of lenticular phosphatic sandstones which

Page 16 4 Growth Poles Phosphates

contain 29% P2O5 (van Straaten, 2002). Minbos has an inferred resource of 6.7 Mt at 20.3%

P2O5 at this deposit (Minbos, 2013).

3.1.3 Mongo Tando This deposit was studied by COFAN and is included in the Minbos licence area. COFAN

estimated a resource of 37.2 Mt under 38.2 m of overburden. Average P2O5 content is not

given (Van Kauwenbergh, 2006). Minbos has an inferred resource of 117.7 Mt at 13.6%

P2O5 at this locality (Minbos, 2013).

3.1.4 The Lucunga River phosphates The second largest potential for Tertiary phosphate development in Angola exists in the

Lucunga River area some 40 km north of the port of Ambrizete. The phosphate beds are of

the unconsolidated nodular type. There are deposits at Coluge, Lendiacolo and

Quindonacaxa. The phosphate reserves at Quindonacaxa, based on data of Antonio Martins

(1963) are 20,255,903 tonnes at 18.54% P2O5 (van Straaten, 2002). Agronomic work by

Melo (1984) indicated good agronomic effectiveness of Quindonacaxa PR applied directly on

acid soils (pH< 5.5). This deposit was mined intermittently between 1981 and 1984 by the

state owned company Fosfatos de Angola (FOSFANG) under a joint venture with Bulgaria

(Premoli 1994 in van Straaten, 2002).

Total resources for the Lucunga river phosphates have been estimated at 28 Mt at 18-26%

P2O5. The phosphate beds are commonly 0.2-2.0 m thick with localized areas having a

thickness of over 5 m. Overburden varies from 0.1 m in the Lendiacola area to 2.4 m in the

Quindonacaxa area (van Straaten, 2002).

3.1.5 Carbonatites Igneous phosphates are known from several Cretaceous carbonatite complexes. They are:

Canata, Capuia, Bailundo, Longonjo, Bonga, Capunda, Lupongola and Virulundo

carbonatites. More work needs to be done to establish resources and grades on these

deposits.

3.1.5.1 Longonjo

Black Fire Minerals has a rare-earth project license at Longonjo, about 600 km southeast of

Luanda, which covers an area of 3,670 km2. Previous explorations at Longonjo have

returned up to 18.9% total rare earth oxides, and up to 9% copper and 6 g/t of gold from the

Page 17 4 Growth Poles Phosphates

Cassenha Hill prospect (Finlayson, 2012). Exploration is currently being undertaken by

Dromana Estate for rare earths.

Page 18 4 Growth Poles Phosphates

4 BOTSWANA There are no significant phosphate deposits known in Botswana.

Page 19 4 Growth Poles Phosphates

5 BURUNDI The economy of Burundi is largely based on agriculture and therefore it is of particular

importance to understand the relevant mineral resources in the area for the better production

of crops.

5.1 Matongo A phosphate deposit occurs at Matongo (70 km north of Bujumbura (3o 4' S; 29o 37' E)). The

deposit is a residual phosphate overlying a strongly weathered carbonatite, which is part of

the Neoproterozoic Upper Ruvubu alkaline complex. The phosphate deposit is up to 55 m

thick. The composition of the ore varies considerably but contains approximately 30%

fluorapatite and 17% “caxonite” (an iron-phosphate mineral), as well as minor clay, feldspar

and limonite. A feasibility study showed reserves of 17.3 Mt of ore at 11.0% P2O5 (cutoff 5%

P2O5) or 40 Mt at 5.6% P2O5 (Kurtanjek and Tandy 1989 in Van Straaten 2002). The

engineering company MacKay and Schnellmann showed that there was insufficient high-

grade material to support a superphosphate plant (Songore 1996 in Van Straaten 2002).

Page 20 4 Growth Poles Phosphates

6 COMORES The Comoros has no significant phosphate deposits.

Page 21 4 Growth Poles Phosphates

7 DRC

7.1 Sedimentary Phosphates Sedimentary phosphates occur in the Bas Congo region, at the border with the Cabinda

enclave. These are a continuation of the Cabinda deposits.

UNDP exploration in the late 1970’s focused on the Fundu Nzobe, Vuangu, and Kanzi areas.

Fundu Nzobe in the north has five phosphate bearing layers. The thickness and grade of

these sedimentary phosphate beds are: Bed I: 11.5 m, 11.5-18.5% P2O5; Bed II: 5.5 m, 18-

19.4% P2O5; Bed III: 20 m, 18-19.7% P2O5; Bed IV: 5.1 m, 20.6% P2O5; Bed V: 10.7 m, 31%

P2O5. However mining would be complicated as a result of structural deformation (open

folding and faulting) and overburden. Superficial sand overburden reaches 20 m and more in

some places. The resources in the Fundu Nzobe area are substantial but have not been

assessed with certainty due their complex structural setting (Barry 1981 in van Straaten,

2002).

7.1.1 Kanzi Project Kanzi in Bas Congo, has a single, relatively uniform layer of phosphorite which is 8-10 m

thick with 14% P2O5. It is covered by a thick sandy giving a 'waste-to-ore' ratio of 2:1-10:1.

The Kanzi project was drilled in 1974 and 1978-1980 and metallurgical test work done then

produced a concentrate of 34% P2O5 with recoveries of 60%-70%.

The project is now a part of the Minbos licence area and Minbos has declared a maiden

inferred resource of 46 Mt at 17.2% P2O5 including a high grade zone of 31 Mt at 21.4%

P2O5. More land adjacent to this is currently under application for licencing.

7.1.2 Igneous phosphates Other phosphate resources available in the DRC include igneous phosphate resources,

mainly associated with carbonatites.

7.1.3 Lueshe carbonatite The Lueshe carbonatite (1°0'S; 29°8'E) is mainly made up of a syenite and carbonatite, with

little apatite as an accessory mineral (Maravic and Morteani 1980 in van Straaten, 2002). An

average chemical analysis of the lateritic residual soils is 5-9% P2O5 (Maravic et al. 1983 in

van Straaten 2002). Lueshe pyrochlore mine has operated on and off since 2000 (Yager,

2013), and it is uncertain what its current status is.

Page 22 4 Growth Poles Phosphates

7.1.3.1 Bingu (Bingo) The Bingu carbonatite (0°5'N; 29°31'E) is a carbonatite with possible phosphate reserves,

however like Lueshe it really is more a niobium deposit that could produce phosphate as a

byproduct (Appleton, 2002).

Page 23 4 Growth Poles Phosphates

8 DJIBOUTI There are no known phosphate deposits in Djibouti.

Page 24 4 Growth Poles Phosphates

9 EGYPT

9.1 Introduction Egyptian producer El Nasr has recently secured a long term offtake agreement for 600 ktpa

of rock phosphate, valued at $90 M from Malaysian Phosphate Additives. Malaysian

Phosphate Additives may also assist local companies to set up a plant to serve the local

demand in Egypt for about 200 ktpa, for food, industrial and feed phosphates (Business

Times, 2013).

Jasinski (2013) indicates Egyptian reserves are 100 Mt, this is the same figure given by the

USGS 2 years ago.

Egyptian sedimentary phosphates occur in the upper Cretaceous to lower Tertiary sediments

of the Duwi Formation. There are three main groups of deposits, all lying between the

latitudes 26.67°N and 29.5°N (Notholt et al).

Deposits along the Red Sea coast: the deposits occur primarily some 20-30 km south and southwest of the Port City of Safaga, and inland from the Port of Quseir to the south.

Along the Nile Valley: Deposits occur mainly between Idfu and Qena, especially near Sebaiya

On the Abu Tartur Plateau

The phosphates all occur in one of three phosphate members of the Duwi Formation

9.2 Red Sea Coastal Area Most of the Red Sea deposits have been structurally deformed and the phosphates are

preserved in basin-like structures surrounded by Precambrian rocks, however at Wadi

Gasus the sedimentary sequence extends all the way to the coast (van Kauwenbergh,

2010). Phosphate beds were mined in the Safaga area from 1911, with P2O5 content ranging

from 20-28%. The mines were underground room and pillar operations, and the product was

shipped to Safaga. The final product contained 29.3% P2O5.

There were also seven underground mines operating inland of the port of Quseir (Kosseir),

on preserved potash deposits in synclinal or monoclonal structures. Here the P2O5 content

was 20-30% but could be as high as 37% in places (Savage, 1987 in van Kauwenbergh,

2010). The Quseir deposits were worked since 1912; the final product had about 30% P2O5.

Interestingly in some cases the material was washed with seawater (van Kauwenbergh,

2010).

Page 25 4 Growth Poles Phosphates

There was originally a “reserve” of some 40 Mt at the Hamrawein underground mine some

40 km south of Safaga, the P2O5 content was 12.5-20% when the mine stared in 1978. The

planned capacity of 600 ktpa concentrate was never achieved (Van Kauwenbergh, 2010).

In 2000 the red sea phosphate company merged together with the Hamrawein mine into the

El Nasr Phosphate Company (ENMC). The ENMC indicated in 2006 that there were still

1.6 Mt of reserves in the Red sea area, with a minimum of 27% P2O5 and 5.0 Mt of (ENMC,

2006 in van Kauwenbergh, 2010). The state owned EI Nasr Mining Company (NMC) now

controls all the reserves and resources of the Sebaiya area, the eastern desert and the Red

Sea coastal area (Van Kauwenbergh, 2010). Reserves are very limited in the Red Sea area

and several deposits have been worked out many years ago (Notholt, et al 2005)

9.3 Nile Valley deposits ENMC had 10 working mines in the area in 2010. A total estimated resource of phosphate

in the eastern desert is 1,878 Mt (Abdel Malik Farah, 2005 in Van Kauwenbergh, 2010).

West Sebaiya proven reserves were as 24 Mt of ore, whilst East Sebaiya reserves were

indicated as 34 Mt at about 29-30% P205. The concentrate reserves of the West Sebaiya

area are 15 Mt at about 27% P205.

Notholt et al (2005), indicate that the most promising deposits here are those of Abu Had

and Wadi Batur with a probable resource of 395 Mt at 20-24% P2O5.

9.4 Abu Tartur At Abu Tartur phosphate beds occur in the lower member of the Duwi formation and are

some 3.9 m thick. They were discovered in 1961, and in 1979 the World Bank financed an

$11m feasibility study. The bed averages ~25% P2O5 and tests showed that it could be

upgraded to 31.31% P2O5 (van Kauwenbergh, 2010). In 1980, an underground mine was

developed using the fully mechanised longwall mining technique with an average panel

length of 1,100 m. The ore is beneficiated and loaded onto trains. In 2006 the production

was 500-600 ktpa of concentrate at 28-30% P2O5. The concentrate was produced into single

superphosphate (SSP), triple superphosphate (TSP) by Abu Zaabal Chemical and Fertiliser

Company and to SSP by the Egyptian Financial and Industrial Company (EFIC).

“Indicated reserves” were 715 Mt, although within the mine area the reserve was 65 Mt of

unoxidised ore and 20 Mt of oxidised ore.

Page 26 4 Growth Poles Phosphates

9.5 Resource There are several widely differing figures for reserves and resources in Egypt and

unfortunately none of these appear to conform to any internationally accepted standard.

There are also many more deposits than discussed here, but again few references appear to

be consistent and a much more detailed study of the literature would be required to

understand the full ambit of Egyptian phosphate deposits. Van Kauwenbergh (2010) gives

the IFDC reserve estimate for Egypt as 52 Mt and the resource as 3,400 Mt.

9.6 Beneficiation Output from the West Sebaiya mines is used to manufacture phosphoric acid and phosphate

fertilisers at Abu Zaabal near Cairo.

Page 27 4 Growth Poles Phosphates

10 ERITREA

There are no known phosphate deposits in Eritrea.

Page 28 4 Growth Poles Phosphates

11 ETHIOPIA Ethiopia occupies the northern end of the Eastern Rift valley, and as a result thick

sequences of Tertiary volcanic rocks occupy much of the country along the rift valley. Older

(Proterozoic) rocks occur in western and to some extent in eastern Ethiopia. The Rift Valley

has relatively young lacustrine sediments and volcanics, but although several alkaline plugs

are known from Ethiopia, no carbonatite has been found (van Straaten, 2002).

11.1 Bikilal The phosphate mineralization in the Bikilal deposit, 17 km north-northeast of Ghimbi, in the

Welega region, is unusual, in that it is associated with a Proterozoic layered gabbro-

anorthosite intrusion. Low-grade phosphates (mean of 4.56% P2O5) occur as apatite-

magnetite-ilmenite mineralization in hornblendites (Abera 1988; Assefa 1991 in van Straaten

2002). The mineralised zone is about 15 km long and 0.7 to 1.2 km wide. The apatite is a

relatively unreactive fluorapatite and “reserve” estimates to a depth of 200 m, are 127 Mt at

3.5% P2O5, 23.8% Fe203, 7.3% Ti02 (Yohannes 1994, in van Straaten 2002). Gebre-Selassie

(2000) reported that the Ethiopian Geological Survey had verified more than 200 Mt at Bikilal

(Van Kauwenbergh, 2010). Ghebre (2010) set the minable reserve of the deposit to be

181 Mt at 3.5% P2O5. He gives an indicated resource of 435 Mt at 3% and an inferred

resource of 145 Mt at 3.1% P2O5.

Although concentrates of up to 36% P2O5 were produced using simple processing

techniques, the recovery rate was low at only 40-58% (Abera et al. 1994 in van Straaten,

2002), However, Ghebre (2010) records that bulk samples sent to Bateman Phosphate

technologies in South Africa for processing gave a concentrate of 33% P2O5 with a 38%

recovery. The concentrate had low contaminants and Ghebre considers it to be suitable for

phosphoric acid production.

11.2 Other deposits Phosphates have been reported in several boreholes drilled elsewhere in Ethiopia, but there

is no indication of the possible size of these occurrences.

Page 29 4 Growth Poles Phosphates

12 KENYA The phosphate resources of Kenya include small guano deposits and small igneous

phosphate resources associated with carbonatites with the most significant deposit being at

Mrima Hill carbonatite. Phosphates also occur in the Rangwe area, in the Koru carbonatite

and associated with vein type iron ore at Ikutha.

12.1 Mrima Hill Carbonatite Lying some 65 km southwest of Mombasa the ferruginous soils covering the Mrima Hill

carbonatite represent a niobium and phosphate target. The resource is given by Notholt and

others (2005) as 37 Mt at 0.67% Nb2O5. The phosphate is mainly in the form of the minerals

gorceixite and monazite and although the phosphate content can be as high as 23%, the

average is 3-4% P2O5. The deposit probably has little value for its agricultural phosphate

potential.

12.2 Rangwe Area Intrusives Although individual samples in this area on the eastern shore of Lake Victoria have been

interesting, no appreciable volume of material has been located.

12.3 Fertiliser plant It is understood that a fertiliser plant at Mombasa is being considered, utilising Kenyan and

Tanzanian raw materials.

Page 30 4 Growth Poles Phosphates

13 LESOTHO Small amounts of phosphates have been found in sediments of the Karoo Supergroup. No

significant deposit appears to exist.

Page 31 4 Growth Poles Phosphates

14 LIBYA There are no significant phosphate deposits known in Libya.

Page 32 4 Growth Poles Phosphates

15 MADAGASCAR Madagascar is underlain by Precambrian metamorphic basement rocks in the eastern part of

the country, and Karoo and younger sedimentary formations which overlie the basement in

the west.

Sedimentary phosphates with <20% P2O5 occur in Cretaceous and Tertiary sediments of the

Mahajanga Basin of northwest Madagascar. Phosphates also occur in upper Cretaceous

sediments near Marovoay, and south of Soalara, as well as near Sitampiky. Phosphates

have also been reported from the Antonibe Peninsula where they occur at the base of

Palaeocene sediments. Low-grade phosphatic sediments occur in lacustrine environments

at Lake Alaotra, and in Pliocene marls near Antanifotsy (van Straaten, 2002).

Igneous apatites are reported from phlogopite-bearing pyroxenites, near Betroka and Bekily

(van Straaten, 2002).

None of the occurrences of phosphate appear on current knowledge to be significant.

Page 33 4 Growth Poles Phosphates

16 MALAWI Apatite is found in several igneous bodies in Malawi with the Tundulu Carbonatite in the

Mlanje district being of economic importance. Resources at Tundulu are about 800 kt at

>20% P2O5. At a lower grade of 17% the reserve is 2 Mt (Appleton, 2002). There are also

some 2.4 Mt of phosphate at 7-14% P2O5 in residual soils over a metapyroxenite at Mlindi.

Notholt (2005) referring to a written communication with Appleton (1986) indicates that

eluvial deposits at Chingale contain 8.8 Mt at 3.7% P2O5. There may also be interesting

enrichments at Chilwa island, the Kangankunde carbonatite complex, and at several other

intrusions.

16.1 Tundulu Lying at the southern end of Lake Chilwa this apatite rich rock has 20.80-38.94% P2O5 with a

very low solubility. The phosphate alone does not lead to an economic prospect but Malunga

(1999) quoted in Van Kauwenbergh (2010) suggests that together with the Niobium

(0.017%) and medium weight Rare Earths (0.019%), this may still prove to be profitable.

The deposit at Tundulu in Malawi contains some 1.9 Mt ore to a depth of 50 m with a P2O5

content of 15-20%, which equates to more than 275 kt of P2O5 according to Malunga, 2001.

Figure 15: The Tundulu Carbonatite Complex, Malawi

Page 34 4 Growth Poles Phosphates

17 MAURITIUS The only phosphate known in Mauritius is based on Guano at the islands of Cargados.

Page 35 4 Growth Poles Phosphates

18 MOZAMBIQUE Mozambique has several phosphate deposits (Evate, Cone Negose, Mont Muande Mont

Fema). Several pegmatites also contain phosphate minerals.

18.1 Sedimentary deposits Besides small guano deposits, there are strong indications of sedimentary Tertiary

phosphates in Mozambique (Davidson 1986 in van Straaten 2002). One such deposit occurs

to the west and northwest of Beira, in the glauconite-bearing Eocene Cheringoma

Formation, which contains fossil fish and teeth beds, and is seen as a potential source rock

for phosphorites (see Figure 16, van Straaten, 2002). The Cheringoma Formation appears to

be an extension of the Miocene Uloa beds in South Africa. Van Kauwenbergh (2006)

referring to Manhica (1991) reports that there are sediments containing 0.7-3.1% P2O5 near

Magude, north of Maputo.

18.2 Igneous deposits

18.2.1 Cone Negose Occurring some 80 km southwest of Fingoe, this is a metasomatic enrichment in a Mesozoic

volcanic carbonatite, with vents and dikes cutting Karoo sediments. Phosphate enrichment

occurs in late stage carbonatite rock (Manhica 1991 in van Straaten, 2002). No estimates on

phosphate grade and tonnage are available.

18.2.2 Evate The Evate deposit is located on the SE flank of the Monapo Complex about 100 km east of

Nampula. The Monapo Complex measures 40 x 53 km and is one of the largest alkaline

complexes in the world. The rocks of the complex form steeply dipping, concentric lithologies

suggesting multiple intrusions of cone sheets. Apatite concentrations occur in mineralised

zones about 3 km long, 830 m wide and 600 m thick. The most important mineralization

occurs in lenticular bodies, about 400 m long and 4-20 m wide with P2O5 grades of 4-6%.

Apatite mineralization grades from 6-30% and is associated with magnetite, pyrrhotite,

calcite, olivine and pyrite (Callaghan, 2002 after Goncalves and Deus, 2002).

The Evate deposit is large and contains 155.4 Mt of ore at 9.32% P2O5, (Orris and Chernoff,

2002) 5.76% Fe, 1.21% TiO2, 47.69% CaO. However, the phosphates here have high

chlorine content of 0.18%, clearly in excess of industry standards of 200 ppm (Siegfried,

Page 36 4 Growth Poles Phosphates

2001). This would cause excessive corrosion of vessels within a phosphoric acid plant and is

a major drawback of the deposit since the capital costs of a plant would be greatly increased

due to expensive alloys being required that will better resist the corrosion.

However, it may be possible to remove some of the chlorine as is done by the Jordan

phosphate company.

Vale has a mining right for 30 years on Evate and plans to bring it into production by 2017

with a 3.5 Mtpa capacity (myinvestorguide, 2013). The project includes using the phosphate

in a fertiliser factory to be built in the coastal district of Nacala-a-Velha. The project is still in

its prefeasibility stage.

Figure 16: Phosphate occurrences in Mozambique

Source: van Straaten, 2002 after Cilek, 1989.

Page 37 4 Growth Poles Phosphates

18.2.3 Lucuisse Lucuisse is a carbonatite with possible metasomatic enrichment, which contains monazite,

apatite, pyrochlore, columbite, zircon and magnetite.

18.2.4 Mont Muande The Mont Muande prospect is about 30 km northwest of Tete, on the north bank of the

Zambezi River. On the other side of the river it is known as the Mont Fema deposit

In accordance with a joint venture with North River Resources plc, Baobab can earn up to

90% in the Mont Muande magnetite project. They have completed stage 1 in April 2013 and

have currently earned a 60% shareholding. Baobab commissioned Coffey Mining Pty Ltd to

assess the exploration target based on the previous work. Coffey Mining defined an

exploration target of 200-250 Mt of ore. The estimates were made based on to an average

depth of 42 m (deepest hole # 135 m).

The 10 hole diamond drilling programme completed during 2011 intersected broad packages

of magnetite and phosphate mineralisation. Results from 9 of the holes have shown

magnetite rich intersections. Tests show that these can be concentrated to 69% Fe at a

mass recovery of 26%. Magnetite intercepts generally report an enrichment of phosphate

compared to background values with an average head grade of 4% P2O5. In the non-

magnetic component of the Davis Tube recovery process, phosphate ran at 5.5% on

average. Testwork is still awaited for final phosphate concentration (Baobab, 2013).

Van Straaten, 2002 cites Davidson 1986 as indicating a 200 kt content of P2O5 at Mont

Muande.

Page 38 4 Growth Poles Phosphates

19 NAMIBIA Phosphates on the Namibian shelf were discovered in the late 1960s. The phosphate

deposit off Walvis Bay was called the Sandpiper Deposit by Gencor and has retained that

name. In the 1990s the Sandpiper deposit was considered as sub economic based on the

price for rock phosphate concentrate (1991: $42.50/t). After the 2008 price shock, the price

has settled at a new level of around $150-$200/t.

19.1 Igneous deposits Low-grade phosphates are associated with several of the alkaline and carbonatite

complexes in Namibia. These have an average P2O5 content as follows:

Okorusu complex, in the Otjiwarongo District: 3-4% P2O5,

Ondumakorume complex, 13 km northeast of Kalkfeld: 7% P2O5, - Appleton (2002) suggests that this may be the most promising carbonatite in Namibia

Kalkfeld complex, 11 km northwest of Kalkfeld: 6.7% P2O5,

Osongombe complex, southwest of Kalkfeld: 6.5% P2O5,

Otjisazu complex, southeast of Kalkfeld, in the Okahandja District: 3-9% P2O5. Van Straaten (2002) indicates that, based on the work of Schneider and Schreuder (1992), this deposit has at least 35 Mt of phosphate ore at 3-9% P2O5 to a depth of 30m.

Epembe Carbonatite southwest of Swartbooisdrift: 3.5% P2O5

19.2 Sedimentary offshore deposits

19.2.1 The Sandpiper project Namibia Marine Phosphate (Pty) Ltd., (NMP) is proceeding with the sandpiper project on the

Namibian continental shelf about 120 km south-southwest of Walvis Bay in water depths of

180-300 m. The eastern boundary of the Mining Licence Area is approximately 40-60 km off

the coast (directly west of Conception Bay). The Mining Licence covers an area of

2,233 km2. NMP plans to dredge marine sediments containing 18% to 20% P2O5. A

feasibility study completed in 2012 showed that a 3 Mtpa facility to produce a concentrate of

28% P2O5 was viable dependent on market conditions.

The deposit is very uniform and continuous and comprises unconsolidated fine sand sized

phosphorite ooliths and pellets, falling in the 100 to 500 micron grain size range. These

pellets are made up mainly of calcium carbonate and phosphate (P2O5). They can also

contain quartz grains, ilmenite and sulphides (UCL, 2013).

Page 39 4 Growth Poles Phosphates

NMP has confirmed a JORC compliant resource of 4,313 Mt at 20.43% P2O5. The company

plans to dredge initially from water depths of up to 225 m and recover 5 Mtpa of ore. This will

be transported to shore and pumped by means of a sinker line pipeline to a buffer pond.

Here oversize will take place and the final slurry pumped to a processing plant near Walvis

Bay for desliming, gravity separation, attrition, washing and drying. It is expected that about

3 Mtpa will be bulk loaded for export from Walvis Bay for a 25 year life of mine.

19.2.2 Phosphate in Tailings The tailings dams at Okuruso Fluorspar mine (situated between Otjiwarongo and Otavi)

contain sufficient phosphates to merit further investigation for using the substance in crop

fertiliser and animal feeds (Waldo, 2013).

The consultant chemist working on the project is confident that the project will be feasible at

full scale production. In the laboratory process Calcium nitrate - also valuable in the

agricultural industry - is also being produced as a byproduct of the phosphate.

Page 40 4 Growth Poles Phosphates

20 RWANDA There are no significant phosphate deposits known in Rwanda.

Page 41 4 Growth Poles Phosphates

21 SEYCHELLES Besides guano, the only phosphates present in the Seychelles are some oolitic phosphorites

that cover some solution eroded limestone surfaces on the island of Esprit.

Page 42 4 Growth Poles Phosphates

22 SOUTH AFRICA

22.1 Foskor Mine (Palaborwa) The Palaborwa Igneous Complex, in the Limpopo Province, has 14 distinct rock types. The

deposit comprises a volcanic plug some 1.5 - 3.5 km in width and 6.5 km in length. There

are three lobes to the intrusion, they are: the North Pyroxenite, Loolekop and South

Pyroxenite. Apatite is the only phosphate mineral present and copper minerals and

magnetite are present in the Loolekop lobe (Foskor, 2012).

There are four mines operating in the Palaborwa Igneous Complex. Palaborwa Mining

Company (PMC) operates a copper mine in the central portion of the complex, as well as a

vermiculite mine in the southern portion of the complex. Foskor operates two phosphate rock

mining operations, one situated in the North Pyroxenite area and another in the South

Pyroxenite area (Foskor, 2012).

The SAMREC compliant ore reserves were calculated taking into account a cut-off that

would provide a feed grade to economically produce a saleable (36.5% P2O5) phosphate

rock concentrate (Foskor, 2012). The mineral reserves at 31 March 2012 are given for the

north and south pyroxenites pits and total 1,553 Mt at 6.9% P2O5 (Proved: 1,391 Mt at

6.93%; Probable: 162 Mt at 6.62%). The measured and indicated mineral resource is given

as 4,856 Mt at 6.7% P2O5.

22.2 Glenover Phosphate mineralization occurs at the Glenover Carbonatite Complex some 88 km north of

Thabazimbi in Limpopo Province. Phosphates occur in all three rock types that make up the

complex, the apatite haematite breccia zone, as well as the carbonatite and pyroxenite

intrusives. The complex is 4.7 km long and 3.5 km wide and intrudes the sedimentary rocks

of the Waterberg Group. The breccia body occurs near the centre of the complex. Between

1962 and 1983 Goldfields mined the high grade (>30% P2O5) central portion of the ore body

to produce 1.45 Mt of 36% P2O5 concentrate (Wilson 1998).

Galileo Resources is currently undertaking a prefeasibility study on the deposit with the aim

of re-opening the mine. Their resource study (Geo-Consult, 2012) gave an indicated

resource of 16.78 Mt at 9.71%. The Galileo annual report gives the resource at 28.928 Mt at

Page 43 4 Growth Poles Phosphates

1.24% total rare earth oxides and 9.52% P2O5 (Galileo, 2013), it appears that the project is

now being seen as a rare earth play.

22.3 Schiel The Schiel Complex is a large syenitic complex with subordinate carbonatite, foskorite, and

syeno-gabbro. Verwoerd (1986) as quoted in ‘Rocks for Crops’ records an ore “reserve” of

36 Mt at 5.1% P2O5 in the weathered zone to a depth of 39.6 m.

22.4 Spitskop The Spitskop Complex is about 14 km across. Three concentric, vertical apatite-rich zones

occur. The inner ring grades 6.5% P2O5 whilst two small lenticular bodies associated with

the outer rings grade 6.5 and 8.5% P2O5. The apatite is finely intergrown with iron oxides,

and producing a phosphate concentrate with more than 20% P2O5 has been difficult (Wilson

1998).

22.5 Sedimentary phosphates The largest known sedimentary phosphate resources in South Africa are the offshore

deposits. On the western coast phosphorite pellets have been found both offshore and on

adjacent coastal terraces extending from Cape Town for about 220 km to the north. Small

occurrences are associated with Upper Tertiary sediments in the coastal area of KwaZulu

and Upper Dwyka Shales and Upper Ecca Shales of the Karoo Supergroup.

22.5.1 Agulhas Bank deposits Large diagenetic replacement phosphate resources occur over limestones on the continental

shelf. The deposits consist of boulders and cobbles of phosphatized limestone, in a matrix of

glauconite, microfossils and quartz sand. Grade in samples ranges from 10-25% P2O5.

The largest concentration occurs between Cape Point and Saldanha Bay with an estimated

resource of 5,500 Mt at 17.8% P2O5. In the area from Cape Agulhas to Cape Recife there is

estimated to be a further 3,500 Mt at 16.2% P2O5 (Wilson 1998).

Although the Agulhas bank deposits are very large, Roux and others (1989) indicate that

they are not amenable to upgrading.

Page 44 4 Growth Poles Phosphates

Jara Exploration has a 26% stake in an offshore mineral exploration licence of the South

African Coast, close to Ports. The licence, applied for in 2011 is for glauconitic sand, potash,

and phosphate. The licence is valid for 5 years. After exploration is finalized Jara Exploration

will apply for a Mining licence. It plans to start mining 2020 or when a mining licence is

granted (Jara, 2013).

22.5.2 Other deposits A mine on the farm Langeberg, near Langebaanweg produced 24 Mt at 10% P2O5 before it

closed in 1992. There remains a proven reserve of 25 Mt at 8.5% P2O5 (Wilson, 1998). In

2010 a new mine (Gecko Fert) was opened at Langebaanweg and is currently in operation.

On the farm Philips Kraal and its surrounds there is a 30.2 Mt deposit at 4-6% P2O5 (Wilson,

1998).

On the farm Elandsfontein, 15 km east of Langebaan there is a deposit of some 50 Mt at

8.5% P2O5. There is an unexploited deposit of 23.6 Mt at 6% P2O5 on the farm Sandheuvel.

There are also several other, smaller deposits in the area.

There is a small bed of nodular phosphate in Miocene beds in the Uloa area along the lower

reaches of the Umfolozi River in northern KwaZulu-Natal. The deposit extends into

Mozambique. There are also numerous other small deposits in South Africa.

.

Page 45 4 Growth Poles Phosphates

23 SOUTH SUDAN There are no phosphate deposits known in South Sudan.

Page 46 4 Growth Poles Phosphates

24 SUDAN

24.1 Jebel Abyad and Abu Hasem Regency Mines plc, is currently conducting an exploration programme in Sudan for

phosphate. Faith Khalil, governor of the Northern State, announced the discovery of big

quantities of phosphate at the Jebel Abyad (White Mountain) in 2011 Sudan news Agency,

2011).

Regency has farm-in rights under an option agreement with International Mineral Resources

(Agrominerals Sudan) Ltd. Regency announced in April 2013 that it had added 26,000 km2

area to north of Jebel Abyad (Figure 17) and dropped some less prospective zones, based

on the results of geological desk-top studies by the Company of publicly available material

and data from the Sudanese Ministry of Minerals.

A 26,000 km2 area to the north of the Abu Hashem licence, known as Jebel Abyad, has

been granted to IMRAS by the Ministry of Minerals. At the same time the IMRAS holdings at

Abu Hashem have been reduced following field trips and sampling by Regency geologists in

2012 and 2013. Regency is currently developing a programme of work, consisting of

geochemical sampling and geological mapping along 350 km of transect lines.

24.2 Halaib District Some 300 km north-northwest of Port Sudan phosphates occur in association with Upper

Cretaceous to Tertiary clastic sediments (Van Straaten, 2002).

24.3 Nuba Mountains There are two occurrences of phosphate breccia (Uro and Kurun) in the northeastern Nuba

Mountains some 250 km southeast of El Obeid. The phosphate mineralization of Uro

(11°40'N; 31°23'E) is associated with a uranium anomaly. Secondary Al-rich phosphates