Embed Size (px)

Citation preview

RESEARCH

METRO MANILA REAL ESTATE SECTOR REVIEW

METRO MANILAMARKET UPDATE Q1 2017

METRO MANILA AND THE THREAT OF EMERGING CITIESThe attractiveness of Metro Manila for real estate developers and investors continues to exist. Althoughhighly congested and vacancy rates are constantly dwindling, it is still the best location for business andinvestment activities. Considering that the seat of government, head offices of key companies, and the mostreputable universities and institutions are located in Metro Manila, demand is perceived to always be buoyantand pervasive. The real challenge is innovation and the creation of new stock to cater to the limitlessdemand.

1

Source: Wikipedia

The Philippine National Economicand Development Authority definesPhilippine Emerging Cities as cities,relative to Manila, that are rapidlycatching up in terms of businessactivities, innovation and ability toattract people. A few of the notableemerging cities in the Philippinesare Angeles (Clark), Cebu, Davao,Iloilo and Zamboanga. Cebu, Davaoand Iloilo are top 5, 6 and 8,respectively, among the PhilippineHighly Urbanized Cities (HUC) of thecountry. Angeles City’s makings issupplemented by the much-awaited Clark Green City.Zamboanga City was identified asone of the emerging cities when itcomes to information technologyoperations. The city has thepropensity to flourish being the thirdlargest city in the Philippines interms of land area. Furthermore,Bacolod, Bohol, Leyte, Naga,Batangas City, Subic, Baguio,Laoag and Puerto Princesa areother cities displaying high potentialand increasing economicdynamism.

Metro Manila, Metro Cebu andMetro Davao are known centers ofcommercial, financial andadministrative activities. Completingthe list of Metropolitan centers inthe Philippines is Metro Cagayan DeOro. It is labeled as the “Melting Potof Mindanao” due to itsaccessibility, business growth andlocal attractions. Metro Cagayan DeOro is one of the emerging areas towatch out for. Other than being a

major gateway and transshipmenthub in Northern Mindanao, it willcontinue to be a key educationalcenter in the region.

All the same, Metro Manila isexpected to remain as the mostdominant metropolitan in thePhilippines. This is despite thepresent administration’sundertaking to further enrichemerging cities with the end goal ofdecongesting Metro Manila. Severalinfrastructure projects are ongoingand in the pipeline to increaseconnectivity and accessibility ofemerging cities and rural areas. Themain objectives of this effort are toimprove linkages amongsettlements and key areas, directgrowth in areas with greatest

important transportation networks,increase access to jobs andservices by people in smallersettlements, and connect ruralareas to growth centers.

Further to this, majority of the citiesthat made it to the top 10 of thecountry’s HUC are from MetroManila. These are Quezon City,Makati, Manila, Pasig, Muntinlupaand Caloocan. Pasay, Mandaluyongand Taguig, on the other hand,were included in the top 20 HUC.

Makati remains to be number 1 interms of economic dynamism,being the country’s premier financialcenter. Closely following it is PasigCity, which is mainly due to thecontinuously booming OrtigasCenter. Nevertheless, BonifacioGlobal City (BGC) has overtaken

SNAPSHOTS

Economic Indicators

6.4%

3.4%

7.7%

5.8%

2.37%

49.99

2

Ortigas Center in terms of office,residential and retail supply. Thepresent office stock in BGC isdouble the size of Ortigas.

Metro Manila cities haverevolutionized by developing anddemonstrating trends such as saleof office spaces and introduction ofnew products such as Condormitel.

Ayala Land subsidiaries, Alveo Landand Avida Land, are knowndevelopers for selling office spaces.Avida’s One Park Drive and CapitalHouse, and Alveo’s High StreetSouth Corporate Tower and AlveoFinancial Tower are few of therecorded sold out office projects.Alveo’s Gentry Corporate Plaza andThe Stiles Enterprise Plaza, on theother hand, are upcomingdevelopments that will introduceadditional for sale inventory to theoffice market.

A condormitel is a fusion ofcondominium, dormitory and hotel.It is similar to a condotel except thatit is normally furnished with three tosix beds per unit targeting studentsand Business Process Outsourcing(BPO) employees. Major Homes isone of the distinguished developers

of condormitels in Metro Manila.Space U-Belt, Space SanMarcelino, Space Romualdez andSpace Taft are a few of the MajorHomes projects. Other examples ofcondormitels are Harvard Suites ofAscott and Apartment 20 byArkiland.

In addition, an anticipateddevelopment trend in the market isthe retrofitting of old buildings in toBoutique Hotels. The Luneta Hotelhas been restored and reopened in2014. A number of heritagebuildings in Manila are beingtargeted for this special project,such as the Old GSIS Building andMetropolitan Theater in Ermita,Times Theater in Quiapo, CapitolTheater in Escolta, El Hogar Filipinoin Binondo, Monte De PiedadSavings Bank in Sta. Cruz andAduana in Intramuros.

GDP Q1 2017

Inflation Rate March 2017

OFW RemittancesQ1 2017

Avg. Bank LendingMarch 2017

91-Day T-BillMarch 2017

Avg. PHP-USDQ1 2017

Source: Major Homes

Space Romualdez

Source: Luneta Hotel

Luneta Hotel

FLOURISHING MARKET FOR COWORKING SPACE PARTNERED BY ROSY OFFICE SPACE SELLING

3

Office | Industry resiliency powered by innovation

The office market is showing nosigns of slowing down as the sectorcontinues to display resiliencyamidst different issues revolvingaround the business market. In thefirst quarter of the year, the realestate sector further expanded andoutlook remained positivecomplementing the optimistic viewthat the Philippine economy,although growth is slowing down,will stay on as one of the fastestgrowing economies in the Asia-Pacific Region.

With the government’s propagandaof ‘Build, Build, Build’, investorsconveyed an enthusiasticperspective that the country willperform beyond what is expectedof it. Overall vacancy and rental rateare stable despite additional officestock coming from newlycompleted developments.Moreover, new concepts andinnovations emerged in the market.A concept dubbed as ‘CoworkingSpace’ is growing in response tothe demand of young entrepreneursand other professionals that arelooking for a new way of doingbusiness. Office unit sale likewisedisplayed vigor after office projectsbecame fully sold.

Issues concerning PresidentTrump’s protectionism and threat tothe BPO industry were silenced bythe director-general of thePhilippine Economic Zone Authority(PEZA). After the forum held inWashington D.C., uncertaintieswere finally cleared that the serviceindustry in the Philippines would notbe affected by US policies ratherthe concern would fall on themanufacturing sector. The IT-BPOindustry was in a good financialposition after the local currencyfluctuated between the PhP48 –PhP51 level due to the interest rateadjustments made by the Federalsystem of the United States

Adjustments made by the U.S. hadalso affected other nationscurrency. The outcome, however,was a lucrative office sector acrossMetro Manila.

According to the 2017 ASEANBusiness Outlook, The Philippinesregistered the highest satisfactionsentiment with 77%, followed byVietnam with 72% and Myanmarwith 70%. Furthermore, 70% of therespondents plan to expand theiroperations in the country, 55%project an increase in number ofemployees and 79% forecast anincrease in company profit. Suchsurveys help in the decision makingof potential investors seekingopportunities to expand coverage inthe countries included in the survey.For nations with poor ratings, itcould be detrimental to the localbusiness industry. Nevertheless, thecountry could respond throughimprovements and innovation.

In addition to the good news for theoffice sector, more foreign firms areeyeing to invest in the IT-BPOindustry in the Philippines, asreported in the first three months ofthe year. Investments are expectedto come from countries like Qatar,Mexico, Israel, United Kingdom,Canada, and China. Multinationalcompanies (MNC) and offshoringand outsourcing (O&O) firms takeadvantage of the country’s skilledmanpower and cheap labor cost.Some firms from the said countriesare also exploring new opportunitiesoutside Manila, specifically in Iloilo,wherein 14 Chinese delegates weresent to study the local businessclimate in the area.

Looking at the market movement ofthe CBDs in Metro Manila, MakatiCBD presently has more than 3Million Gross Leasable Area and no

new building was added to theoffice supply during the first quarterof the year. However, over 510,000square meters of GLA is scheduledto be turned over until 2022. TheCBD is still the center of businessactivities. The Weighted AverageLease Rate of the CBD grew by11.23% to PhP 1,250.86.Moreover, Makati experienced thelargest growth in rental rates in spiteof having the need to refurbish oldbuildings in order to compete withthe new designs of buildings inother CBDs. Grade A Buildings ledthe occupancy rating with 99.25%,followed by Prime Buildings at98.63%.

FIGURE 1 Weighted Average Lease Rates vs. Rental Growth Rate

Source: Santos Knight Frank Research

Weighted Average Lease Rate

(PHP/sqm/mo.)

Vacancy Rate

Makati CBD 1,250.86 1.00%

Fort Bonifacio 949.19 0.43%

Alabang 669.70 6.59%

Quezon City 760.63 10.08%

Ortigas 635.46 1.34%

Bay City 720.56 0.14%

TABLE 1Q1 2017 Office Data

Source: Santos Knight Frank Research

-12%

-8%

-4%

0%

4%

8%

300400500600700800900

1,000

Q1

2008

Q1

2009

Q1

2010

Q1

2011

Q1

2012

Q1

2013

Q1

2014

Q1

2015

Q1

2016

Q1

2017

PhP

/sqm

/mon

th

Weighted Average Lease Rate

Growth Rate

4

at a remarkable record of38,151.25, the second highestsince 2007.

For Quezon City, vacancy remainedwithin the 10% mark due to thelarge number of available rentablespaces in CyberPark Tower One.Conversely, vacancy of Bay Areadecreased to 0.14% in the firstquarter. Further to this, Ortigasdisplayed a modest uptick invacancy, growing to 1.34% fromthe recorded 1.14% in the lastquarter of 2016. Weighted AverageLease Rates of Quezon City, BayArea, and Ortigas are now peggedat PhP760.63, PhP720.56, andPhP635.46, respectively.

Quick Background on Coworking

Due to scarcity of space and rentsgetting more expensive, users aretrying to find more efficient ways ofutilizing spaces. Office rental ratesin CBDs are now at a price range ofPhP635 to PhP1,250 per squaremeter and are increasing gradually.Moreover, lease terms are for long-term periods and a minimum size ofrented space is imposed.

To address these limitations intraditional offices, a global term‘Coworking Space’ was born and iscurrently positioning itself in theoffice industry. The first coworkingspace in the Philippines, Co Lab,pioneered during the year 2011.After its success, other flexibleoffice spaces started to spur in the

market providing a leeway for start-up businesses in the centralbusiness districts of Metro Manila.Ayala Land Inc. recently offeredcoworking spaces through ‘Clock-in’ which targets sales people,freelancers and other workingprofessionals in search for adifferent work environment.

In today’s world and present timewhere people are always on the go,the need to access your e-mail,print proposals and surf the nethappens anytime and anywhere.Business transactions andnegotiations are now done outsidethe office. High-level executives,young professionals and start-upentrepreneurs used to work incoffee shops and hotel lobbies.With coworking spaces, they nowhave an alternative venue toconduct business activities.

According to the 2017 GlobalCoworking Survey, worldwidecoworking spaces are now ataround 11,300 and can grow to14,000 by the end of the year.Growth rate of coworking spaceusers is projected at 41% in 2017,reaching almost 1.2 million people,an increase of 345,000 from itspreviously estimated total of835,000. At present, there are 14recorded buildings in Makati, 8 inBGC, 1 in Alabang, 2 in QuezonCity, 2 in Pasay and 3 in Ortigasthat offer flexible spaces and sharedspaces.

On the other end of Makati is thenew favorite destination ofinvestors, Bonifacio Global City(BGC). More tenants aretransferring to BGC due to threenotable reasons. First is toconsolidate all their business lines inone building. Next, buildings in BGCare newer and are LEED certified.Lastly, the rental rate is cheaper inBGC compared to Makati. Thismovement lead to cannibalization ofmarkets, particularly in Makati andOrtigas. BGC’s Weighted AverageLease Rate was PhP949.19 in thefirst quarter of 2017 fromPhP908.78 same time last year.Vacancy rate was likewise at animpressive rate of 0.43% amidstnew building turn overs. Six WestCampus, Eight West Campus, OreCentral, and World Plaza were thenewly completed buildings whichhad little effect on the CBD’svacancy as most spaces in thesebuildings are already pre-leased orpre-committed before the start ofoperations.

While vacancy in BGC lowered inthe first quarter, vacancy in Alabangincreased to 6.59% from sameperiod last year’s 2.94%. This wasdue to the additional inventorycoming from newly developedbuildings, such as Vector 3 andCapella Building. Additional officestock amounted to 54,445.48square meters of Gross LeasableArea. Net absorption likewise grew

Source: Santos Knight Frank Research

Capella Building

1,130 2,070 3,600

5,800 8,700

11,300 13,800

530 940

1,530

2,200

2,900

2,600

2,500

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2011 2012 2013 2014 2015F 2016F 2017F

Total Stock New Stock

FIGURE 2Number of Coworking Spaces Worldwide as of October 31, 2016

Source: Deskmag and Social Workplace

5

concept as 35% of the 2015Philippine population are comprisedof people aged 15 to 34. Theirpresence in the market would soonbe dictating activities in the officefield, its concepts, and the growthof new and innovative businesses.

Brisk Office Sale

Pre-selling of office spaces hasbeen a trend since 2012 asdevelopers see selling anddeveloping office buildings as agood source of recurring income. A

year after the last market report onoffice pre-selling, the market forselling office spaces is still upbeat.Currently, Ayala Land’s subsidiaryunit, Alveo Land, has marketed ninedevelopments with for sale officespaces. High Street SouthCorporate Tower 1 was Alveo’s firstoffice project under this concept. Atpresent, five of the mentioned Alveoprojects are fully sold. Park TriangleCorporate Plaza North Tower andThe Stiles Enterprise Plaza WestTower are now at 99% and 95%sold, respectively. The remainingtwo, Gentry Corporate Plaza andThe Stiles Enterprise Plaza EastTower, are currently selling atPhP250,000 per square meter andPhP175,000 per square meter,respectively.

Some of the existing buildings thatare also strata titled include, theEnterprise Center, Philam LifeTower, Ayala Tower One, PBComTower, LKG Tower, Citibank Tower,BDO Plaza, One World Plaza, OneGlobal Place, and Bonifacio HighStreet -Central and East. Indicativeprice range in Makati and BGC is atPhP150,000 to PhP250,000 persquare meter.

Additionally, some of the morepopular coworking spaces includeRegus, vOffice, A Space Manila andBoardroom Ph. Websites withAirBnB-like concept are likewisepresent in the market adding easyaccess to coworking spaces.Typical coworking space rates inMakati range from PhP400 toPhP1,200 per person per day.

Trends similar to shared workspaces and coworking spaces areseen to grow further, creating asignificant impact to the officebusiness in the future. Millennialswould also be a valuable contributorto the expansion of this concept

FIGURE 3 Number of Members Worldwide as of October 31, 2016 (in thousands)

21

5

32

5

34

5

51

0

83

5

1,1

80

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2011 2012 2013 2014 2015F 2016F 2017F

Total Members New Members

Source: Deskmag and Social Workplace

Source: Santos Knight Frank Research

Filinvest Cyberzone Bay City

GROWING INVESTOR BASE SPURS NEW SUPPLY ACROSS SEGMENTSResidential | Robust head start for PH residential market

6

Source: HLURB

The local condominium salesmarket opened the year on apositive note as investment buyingactivities became more prominentduring the first quarter of 2017.Immense investor activity propelledthe performance of the marketfollowing the sustained momentumof the Philippine economy in the lastquarter of 2016. Majority of thebuyers purchased large number ofunits, some an entire floor, andhave the units rented out to end-users. Moreover, a huge demandfor residential projects that areproximate to offices was noticeableas local and foreign companieslooked to acquire units to housetheir respective employees,particularly studio units.

A number of investors purchasedproperties with the intention ofoperating the units as condotels forshort term-staying guests. Theseguests are given full access tobuilding facilities and amenities,much like the Airbnb concept. Thecondotel model is more evident inthe middle to high-enddevelopments that offer anexpansive range of higher classamenities compared to affordableprojects. Presently, condominiumsin the Bay Area enjoy brisk salesdue to such demand combinedwith commercial and entertainmentestablishments proliferating in thevicinity.

End-user demand, on the otherhand, was fairly robust as it is stillbuoyed by the prevailing lowinterest rates and flexible paymentschemes. These enticed moreaffluent locals such as retirees andprofessionals to acquire residentialproperties. Similarly, the weakerpeso provided a relatively highpurchasing power to foreigncurrency earners, i.e. overseas

Filipino workers (OFWs) andexpatriates.

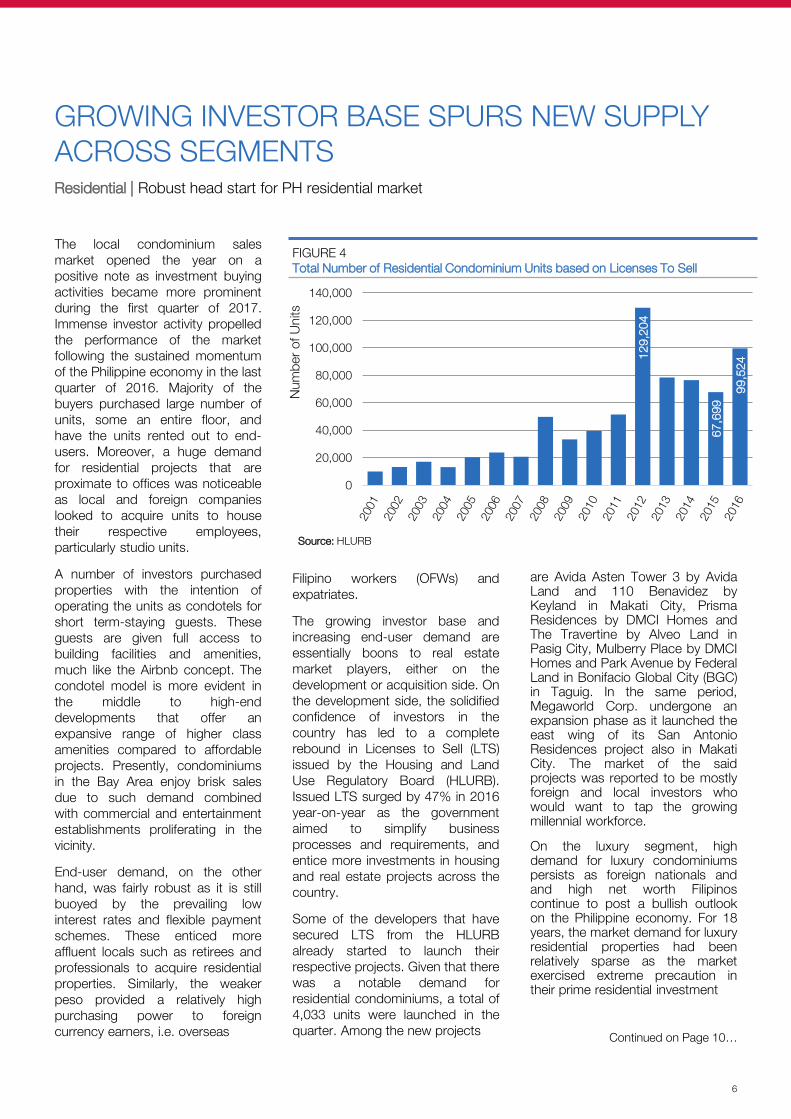

The growing investor base andincreasing end-user demand areessentially boons to real estatemarket players, either on thedevelopment or acquisition side. Onthe development side, the solidifiedconfidence of investors in thecountry has led to a completerebound in Licenses to Sell (LTS)issued by the Housing and LandUse Regulatory Board (HLURB).Issued LTS surged by 47% in 2016year-on-year as the governmentaimed to simplify businessprocesses and requirements, andentice more investments in housingand real estate projects across thecountry.

Some of the developers that havesecured LTS from the HLURBalready started to launch theirrespective projects. Given that therewas a notable demand forresidential condominiums, a total of4,033 units were launched in thequarter. Among the new projects

are Avida Asten Tower 3 by AvidaLand and 110 Benavidez byKeyland in Makati City, PrismaResidences by DMCI Homes andThe Travertine by Alveo Land inPasig City, Mulberry Place by DMCIHomes and Park Avenue by FederalLand in Bonifacio Global City (BGC)in Taguig. In the same period,Megaworld Corp. undergone anexpansion phase as it launched theeast wing of its San AntonioResidences project also in MakatiCity. The market of the saidprojects was reported to be mostlyforeign and local investors whowould want to tap the growingmillennial workforce.

On the luxury segment, highdemand for luxury condominiumspersists as foreign nationals andand high net worth Filipinoscontinue to post a bullish outlookon the Philippine economy. For 18years, the market demand for luxuryresidential properties had beenrelatively sparse as the marketexercised extreme precaution intheir prime residential investment

Continued on Page 10…

FIGURE 4Total Number of Residential Condominium Units based on Licenses To Sell

129,

204

67,6

99

99,5

24

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000N

umbe

r of

Uni

ts

BRISK RETAIL TAKE-UP DRIVEN BY NEW ENTRANTS AND BRAND EXPANSIONS Retail | Consumer demand seen sustained until end of summer season

7

With the conclusion of the holidayseason, consumer spending sloweddown but only at a minimal level. Anupturn of spending is anticipateddue to the approaching summerseason. Moreover, consumerdemographics and expenditurelevels remain constant asevidenced by the improvingemployment opportunities andstable macroeconomicfundamentals. Positive businessoutlook was sustained in the firstquarter of 2017 with new andinnovative business strategiesformulated, backed by continuedbusiness expansions and brandlaunches carrying transformedportfolios of both retailers and malldevelopers.

Vacancy rate in Metro Manila hasbeen stable at 5% with local andforeign brands unveiling stores inrecently-opened shopping malls.Brands such as Mumuso and Petrolalready set foot in South Park Mallin Alabang. Tim Hortons, the largestcoffee shop in Canada and knownfor its unique tasting brewed coffeeand freshly baked goods, openedtheir first branch in Uptown MallBGC. The said coffee brand islikewise planning to open 8 morebranches in the country. Targetlocations are retail components ofoffice buildings.

S Maison, the retail component ofthe 25,000-square meter ConradHotel in the Bay Area, hassuccessfully leased out vacantspaces since its soft opening acouple of quarters ago. Some of thenew stores are Zero Halliburton,Pandora, Moressi and Cole Haan.

Brands such as Tokyo Milk CheeseFactory, The French Baker, RayBan, Swarovski, Lacoste and Marks& Spencer have already opened in

Okada Manila, the biggest gamingand entertainment integrated resortin Parañaque City. The resorts’upscale retail area spans more than8,000 square meter with a numberof retail brands scheduled to beopened in the coming months.

The Ayala Malls group unveiledAyala the 30th along MeralcoAvenue in Pasig early this year.Ayala the 30th , with a gross leasablearea of approximately 28,000square meter, is the first Ayala Mallto be built and operated withinOrtigas Center. Brands like GenkiSushi, Wang Fu, Mumuso, BaseLondon, Florsheim and S&R NewYork Style Pizza have already beenlaunched and are frequently visitedby mall-goers.

Additionally, a well-known footwearbrand which offers products fromflip flops and sandals down toregular shoes and boots designedfor comfort and style has recentlyentered the Philippine market.Vionic recently revealed its first evershop in Ayala the 30th. The brand’sunique natural alignment andelevated support technologyrendered the product as a “musthave” in the retail scene. Otheranticipated upcoming brandsinclude Mango, Yamato Bakery,UCC Coffee, Terranova, MitsuyadoSei-Men and Gold’s Gym.

Retail openings under food andbeverages, ranging from fast foodand restaurants to coffee shops,accounted for about 63% of thetotal retail openings in the firstquarter of 2017. This was followedby clothing and apparel with 26%.The remaining percentage wasdistributed among homeware,

consumer electronics, departmentstores and other consumerservices.

In addition, slight increases in retailrental rates were recorded in thefirst quarter of 2017 following thelaunch of new shopping mallsduring the previous quarters.Average rental rate in the MakatiCBD was pegged at PhP1,212 persquare meter. In Bonifacio GlobalCity (BGC), retail space rents wereat PhP1,536 per square meter onan average. Ortigas Centercommanded a PhP1,390 persquare meter average rental rate.

Continued on Page 10…

Source: Ayala Land

Ayala Malls The 30th

FIGURE 5Retail Openings by Sector Q1 2017

Food & Beverage

63%

Clothing & Apparel

26%

Others11%

Source: Santos Knight Frank Research

POSITIVE INVESTOR OUTLOOK BOLSTERS INVESTMENT INFLOWSIndustrial | The Philippines solidifies economic footing

8

The Philippine economy posted a6.4% growth rate in the first quarterof 2016. The economy continues togrow but at a slower pace, which istypical of a post-election year whereelection spending alreadydissipated. Moreover, growth isexpected to pick-up in the comingquarters as investor confidenceremains positive backed by soundmacroeconomic fundamentals.

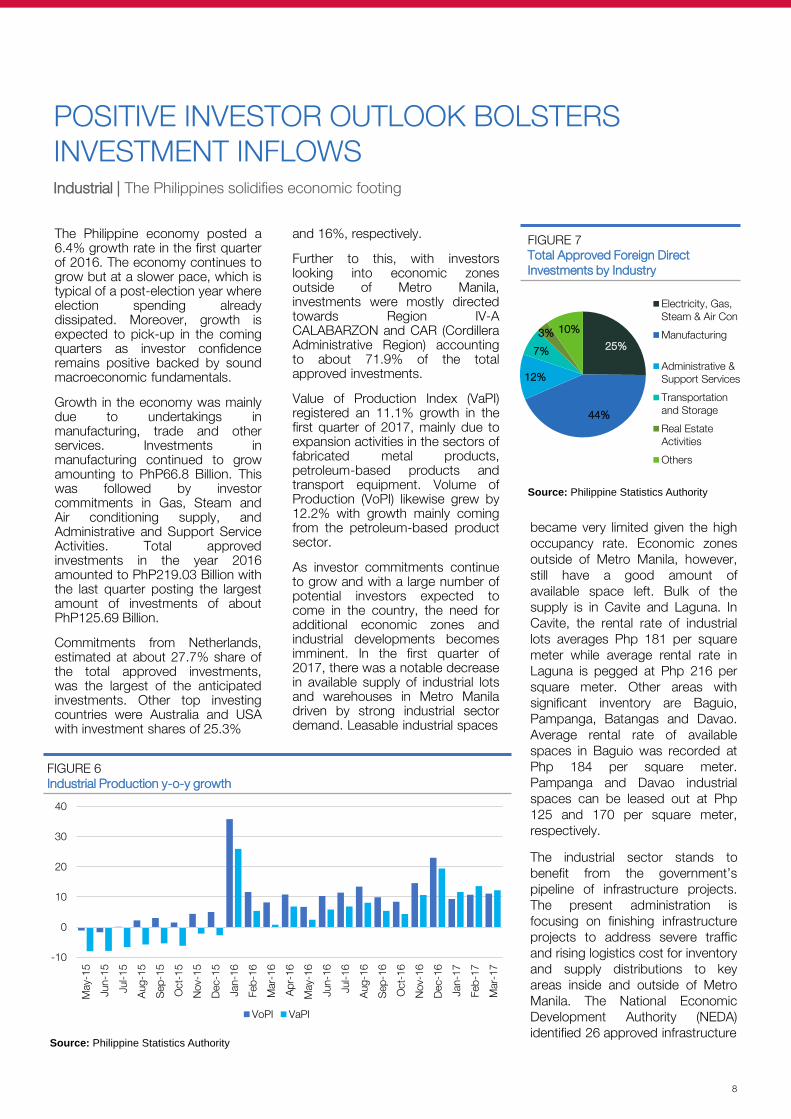

Growth in the economy was mainlydue to undertakings inmanufacturing, trade and otherservices. Investments inmanufacturing continued to growamounting to PhP66.8 Billion. Thiswas followed by investorcommitments in Gas, Steam andAir conditioning supply, andAdministrative and Support ServiceActivities. Total approvedinvestments in the year 2016amounted to PhP219.03 Billion withthe last quarter posting the largestamount of investments of aboutPhP125.69 Billion.

Commitments from Netherlands,estimated at about 27.7% share ofthe total approved investments,was the largest of the anticipatedinvestments. Other top investingcountries were Australia and USAwith investment shares of 25.3%

and 16%, respectively.

Further to this, with investorslooking into economic zonesoutside of Metro Manila,investments were mostly directedtowards Region IV-ACALABARZON and CAR (CordilleraAdministrative Region) accountingto about 71.9% of the totalapproved investments.

Value of Production Index (VaPI)registered an 11.1% growth in thefirst quarter of 2017, mainly due toexpansion activities in the sectors offabricated metal products,petroleum-based products andtransport equipment. Volume ofProduction (VoPI) likewise grew by12.2% with growth mainly comingfrom the petroleum-based productsector.

As investor commitments continueto grow and with a large number ofpotential investors expected tocome in the country, the need foradditional economic zones andindustrial developments becomesimminent. In the first quarter of2017, there was a notable decreasein available supply of industrial lotsand warehouses in Metro Maniladriven by strong industrial sectordemand. Leasable industrial spaces

became very limited given the highoccupancy rate. Economic zonesoutside of Metro Manila, however,still have a good amount ofavailable space left. Bulk of thesupply is in Cavite and Laguna. InCavite, the rental rate of industriallots averages Php 181 per squaremeter while average rental rate inLaguna is pegged at Php 216 persquare meter. Other areas withsignificant inventory are Baguio,Pampanga, Batangas and Davao.Average rental rate of availablespaces in Baguio was recorded atPhp 184 per square meter.Pampanga and Davao industrialspaces can be leased out at Php125 and 170 per square meter,respectively.

The industrial sector stands tobenefit from the government’spipeline of infrastructure projects.The present administration isfocusing on finishing infrastructureprojects to address severe trafficand rising logistics cost for inventoryand supply distributions to keyareas inside and outside of MetroManila. The National EconomicDevelopment Authority (NEDA)identified 26 approved infrastructure

FIGURE 7Total Approved Foreign Direct Investments by Industry

FIGURE 6Industrial Production y-o-y growth

25%

44%

12%

7%

3% 10%

Electricity, Gas,Steam & Air Con

Manufacturing

Administrative &Support Services

Transportationand Storage

Real EstateActivities

Others

Source: Philippine Statistics Authority

-10

0

10

20

30

40

May

-15

Jun-

15

Jul-1

5

Aug

-15

Sep

-15

Oct

-15

Nov

-15

Dec

-15

Jan-

16

Feb-

16

Mar

-16

Apr

-16

May

-16

Jun-

16

Jul-1

6

Aug

-16

Sep

-16

Oct

-16

Nov

-16

Dec

-16

Jan-

17

Feb-

17

Mar

-17

VoPI VaPI

Source: Philippine Statistics Authority

Continued from Page 7 Retail

Alabang, Quezon City NorthTriangle and Araneta Center rateswere averaging PhP839 per squaremeter, PhP1,165 per square meterand PhP1,279 per square meter,respectively.

With the significant number ofupcoming retail spaces and thecontinuous entry of retail brands,the retail industry is projected totake a sustainable track backed byincreased consumer spending inthe coming season. The retailcomponent of Double Dragon’sMeridian Plaza mixed-usedevelopment and other Ayala Mallsnamely Vertis North Mall, ParkTriangle Mall and Cloverleaf Mall aresome of the upcoming retaildevelopments to watch out for.Together with expansions ofRobinsons Galleria, Festival Malland SM Mall of Asia, upcomingretail spaces sum up toapproximately 835,000 squaremeters in 2017 alone.

Continued from Page 8 Industrial

projects under implementingagencies such as the Departmentof Transportation (DOTr),Department of Tourism (DOT) andDepartment of Public Works andHighways (DPWH). Approvedprojects include refurbishment ofkey tourism locations in MetroManila, airport rehabilitation,construction of tollways andhighways and railway extensionsand improvement.

With the country’s promisingindustrial market, local and foreigninvestors are drawn to invest in thePhilippines, as evidenced by theinflux of capitals from othercountries. The robustmanufacturing sector iscomplemented by the progressiveindustrial sector. Consequently, thecountry remains one of the mostattractive investment hubs inSoutheast Asia assertive of itseconomic resiliency anddevelopment.

Continued from Page 6 Residential

activities following the aftermaths ofthe Asian Financial Crisis in 1998and Global Financial Crisis in 2008.But when the Philippines was nolonger considered as the “sick manof Asia”, demand-supply dynamicsbegan to work again. Somedevelopers created an exclusiveclientele comprised of tycoons,wealthy businessmen, anddiplomats to name a few.Foreigners and expatriates alsocontinued to keep the demandafloat by purchasing units either forwealth accumulation or as place ofresidence.

Currently, AyalaLand Premier’s ParkCentral Towers (South Tower)project in Makati CBD commandsthe highest monthly take-up of 47units, followed by RobinsonsLuxuria’s newest project in Ortigas–The Residences at The WestinManila Sonata Place–with a take-upof 30 units per month. Both projectshave been selling for five (5) monthssince their respective launch dates.In terms of selling prices, the latteroffers 1-bedroom to penthouseunits ranging from PhP186,000 toPhP196,000 per square meter.

Despite the limited supply ofdevelopable land for luxurydevelopments, four (4) new projectsare expected to be unveiled thisyear. In Taguig City, Federal Land isset to continue the success of itsGrand Hyatt Residences project,which is already 97% sold, throughGrand Hyatt Gold. Selling priceswere reported to range fromPhP350,000 to PhP400,000 persquare meter. Megaworld alsoenvisioned its most luxuriousdevelopment in McKinley West withits medium-rise project, The Albany.Selling prices per square meterwere disclosed to start atPhP300,000. Other projects in thepipeline include the North Tower ofPark Central Towers, and the3,500-square meter lot owned bySMDC and Federal Land in MakatiCity. The latter is a PhP5-billiondevelopment and is envisioned tobe the most beautiful skyscraper inthe country.

*Cumulative value since Q1 2017Source: Santos Knight Frank Research

FIGURE 8Upcoming Retail Supply*

0

200,000

400,000

600,000

800,000

1,000,000

2017 2018 2019F

Estimated GFA Upcoming Supply

Source: BCDA

Subic-Clark Cargo Railway

Santos Knight Frank Research provides strategic advice, consultancy services and forecasting to awide range of clients worldwide including developers, investors, funding organizations, corporateinstitutions and the public sector. All our clients recognize the need for expert independent advicecustomized to their specific needs.

© Santos Knight Frank 2017This report is published for general information only and not to be relied upon in any way. Although high standardshave been used in the preparation of the information, analysis, views and projections presented in this report, noresponsibility or liability whatsoever can be accepted by Santos Knight Frank for any loss or damage resultant fromany use of, reliance on or reference to the contents of this document. As a general report, this material does notnecessarily represent the view of Santos Knight Frank in relation to particular properties or projects. Reproductionof this report in whole or in part is not allowed without prior written approval of Santos Knight Frank to the form andcontent within which it appears. Santos Knight Frank is a long-term franchise partnership registered in thePhilippines with registered number A199818549. Our registered office is 10/F Ayala Tower One, Ayala Ave., MakatiCity where you may look at a list of members’ names.

MANAGEMENT

Rick SantosChairman and CEO+63 917 528 [email protected]

TENANT REPRESENTATION &OFFICE AGENCY

Joey RadovanVice Chairman+63 920 906 [email protected]

INVESTMENTS AND CAPITAL MARKETS

Calvin JaviniarSenior Director+63 917 574 [email protected]

VALUATIONS

Mabel LunaDirector+63 917 865 [email protected]

RESIDENTIAL SERVICES

Yvette AcebedoDirector+63 917 574 [email protected]

ASSET SERVICES GROUP

Nelson Del MundoVice President+63 917 574 [email protected]

PROJECT MANAGEMENT

Allan NapolesExecutive Director+63 917 [email protected]

RESEARCH & CONSULTANCY

Jan CustodioSenior Director+63 917 574 [email protected]

Emlin JavillonarResearch Manager+63 917 888 [email protected]

Von SalazarResearch [email protected]

Christian OcampoResearch [email protected]

Aira PalomarResearch [email protected]

RECENT MARKET-LEADING RESEARCH PUBLICATIONS

Santos Knight Frank Research Reports are available at santos.knightfrank.ph/research

Manila Office10th Floor, Ayala Tower One & Exchange PlazaAyala Avenue, Makati City, 1226t: (632) 752-2580 / 848-7388f: (632) 752-2571w: www.santos.knightfrank.ph

Cebu OfficeUnit 30 11F AppleOne Equicom Tower Mindanao Avenue & Biliran Rd.Cebu Business Park, Cebu City 6000t: (6332) 318-0070

Metro Cebu Market Update 2H 2016

The Wealth Report 2017

Global Cities: The 2017 Report

Asia Pacific Prime Office Rental Index Q1 2017