Embed Size (px)

Citation preview

MERRILL LYNCH SUN CITY CONFERENCE

March 2017

Darryll Castle - CEO

Tryphosa Ramano – CFO

2MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

AGENDA

IntroductionCorporate

Update

Operational Update

Going Forward Questions

CORPORATE UPDATE

4MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

PROGRESS ON KEY DELIVERABLES

Delivering on our short term strategy

A. DIVERSIFIED PORTFOLIO

• Increasingly diversified portfolio with multiple operating sites in South Africa, embedding of the materials division and expansion into the rest of the African continent

• Operations in the rest of the African continent contributing >30% of group EBITDA

• Delivery of Harare Msasa mill on-time and below budget

• Commissioning of cement plants underway in the DRC and Ethiopia

• Materials division contributing ~20% of group revenue

• The business remains highly cash generative with cash earnings per share consistently exceeding headline earnings per share

B. CAPITAL STRUCTURE MANAGEMENT

• Successful rights issue has led to a significantly improved capital structure

• Net debt reduced from R9billion to R5,3 billion after the rights issue in September 2016

• Equity attributable to shareholders of PPC has risen from R3 billion to almost R7 billion as at September 2016

• In December 2016, net debt reduced further to R4,4 billion following inflows from the B-BBEE I transaction

C. SIGNIFICANTLY ENHANCING

EFFICIENCIES

• Profit Improvement Programme target of R400 million exceeded in less than 18 months – programme continues to be driven and measured internally

• Commissioning of Slurry SK9 upgrade project will yield material cost savings due to lower energy and maintenance costs

• PPC’s inland kilns will be as cost competitive as other modern players in the industry

• 3 mega-plant strategy is bearing fruit with variable and fixed costs reducing over time; while productivity levels rose 12% since 2012

• New Harare mill will ensure reduced costs, improving Zimbabwe’s EBITDA margin by 3% -5%

5MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

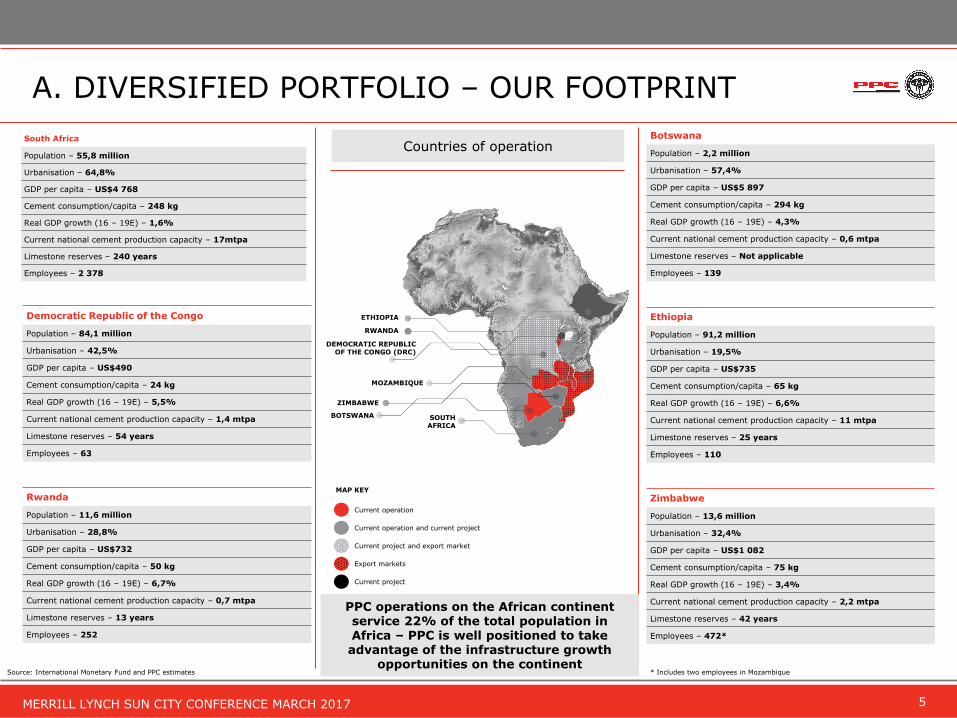

Botswana

Population – 2,2 million

Urbanisation – 57,4%

GDP per capita – US$5 897

Cement consumption/capita – 294 kg

Real GDP growth (16 – 19E) – 4,3%

Current national cement production capacity – 0,6 mtpa

Limestone reserves – Not applicable

Employees – 139

Ethiopia

Population – 91,2 million

Urbanisation – 19,5%

GDP per capita – US$735

Cement consumption/capita – 65 kg

Real GDP growth (16 – 19E) – 6,6%

Current national cement production capacity – 11 mtpa

Limestone reserves – 25 years

Employees – 110

Zimbabwe

Population – 13,6 million

Urbanisation – 32,4%

GDP per capita – US$1 082

Cement consumption/capita – 75 kg

Real GDP growth (16 – 19E) – 3,4%

Current national cement production capacity – 2,2 mtpa

Limestone reserves – 42 years

Employees – 472*

A. DIVERSIFIED PORTFOLIO – OUR FOOTPRINT

Democratic Republic of the Congo

Population – 84,1 million

Urbanisation – 42,5%

GDP per capita – US$490

Cement consumption/capita – 24 kg

Real GDP growth (16 – 19E) – 5,5%

Current national cement production capacity – 1,4 mtpa

Limestone reserves – 54 years

Employees – 63

Rwanda

Population – 11,6 million

Urbanisation – 28,8%

GDP per capita – US$732

Cement consumption/capita – 50 kg

Real GDP growth (16 – 19E) – 6,7%

Current national cement production capacity – 0,7 mtpa

Limestone reserves – 13 years

Employees – 252

* Includes two employees in Mozambique

Countries of operation

Source: International Monetary Fund and PPC estimates

ETHIOPIA

RWANDA

DEMOCRATIC REPUBLIC OF THE CONGO (DRC)

MOZAMBIQUE

ZIMBABWE

BOTSWANA SOUTH AFRICA

MAP KEY

Current operation

Current operation and current project

Current project and export market

Export markets

Current project

South Africa

Population – 55,8 million

Urbanisation – 64,8%

GDP per capita – US$4 768

Cement consumption/capita – 248 kg

Real GDP growth (16 – 19E) – 1,6%

Current national cement production capacity – 17mtpa

Limestone reserves – 240 years

Employees – 2 378

PPC operations on the African continent service 22% of the total population in Africa – PPC is well positioned to take advantage of the infrastructure growth

opportunities on the continent

6MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

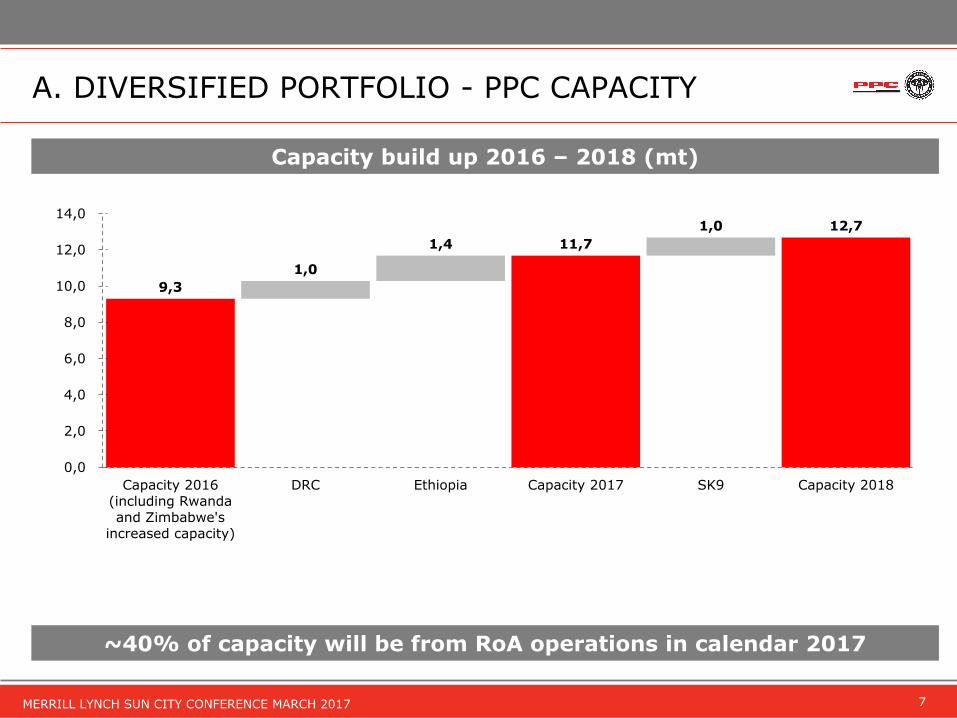

A. DIVERSIFIED PORTFOLIO – PPC CAPACITY

0

100 000

200 000

300 000

400 000

500 000

600 000

700 000

2013 2015

Rwanda Capacity (tpa)

0

500 000

1 000 000

1 500 000

2001 2016

Zimbabwe Capacity (tpa)

PPC invested in CIMERWA in 2013 aspart of its expansion strategy into therest of Africa

CIMERWA had a 100 000 tpa wet feedkiln system

In 2015, CIMERWA commissioned the600 000 tpa state-of-the-art five stagepreheater calciner

CIMERWA is now a regional player withEBITDA margins >30% and share of theRwandan market of ~50%

Now contributes over one tenth ofgroup EBITDA

PPC invested in Zimbabwe in 2001 as oneof the first movers into the rest of Africa

PPC Zimbabwe cement capacity has nowincreased from 1mtpa to 1.4mtpa

The Harare Msasa mill was commissionedat the end of 2016 on-time and belowbudget

PPC Zimbabwe contributes in excess of20% to group EBITDA

PPC is well positioned to take advantage of growth in these key

markets

7MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

Capacity build up 2016 – 2018 (mt)

A. DIVERSIFIED PORTFOLIO - PPC CAPACITY

9,3

1,0

1,4 11,7

1,0 12,7

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

Capacity 2016(including Rwandaand Zimbabwe's

increased capacity)

DRC Ethiopia Capacity 2017 SK9 Capacity 2018

~40% of capacity will be from RoA operations in calendar 2017

8MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

A. DIVERSIFIED PORTFOLIO – MATERIALS DIVISION

Rm 6m Mar2016 (A)

6m Sept 2016 (B)

12m(A+B)

Revenue Revenue Revenue

Lime 383 406 789

Aggregates & Readymix

503 713 1 216

Total 886 1 119 2 005

Rm 6m Mar2016 (A)

6m Sept2016 (B)

12m(A+B)

EBITDA EBITDA EBITDA

Lime 96 96 192

Aggregates& Readymix

76 103 282

Total 172 199 371

PPC has a diverse offering with the Lime division and the Aggregates and Readymix division

Acquisitions of Pronto Readymix and 3Q Mahuma Concrete have given further impetus to the materials division strategy

The materials division contributes ~20% of group revenue

• Reviewed interim results used for figures relating to 6m to Sept 2016

• Twelve month figure has been aggregated and not annually adjusted

9MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

Highly cash-generative business

Business continues to generate superior cash earnings despite capital expenditure requirements

Cash conversion target of 1x continues to be actively monitored

Good working capital management critical for enhanced cash generation

A. DIVERSIFIED PORTFOLIO – CASH MGMT.

0

50

100

150

200

250

300

350

400

450

Sep-0

8

Sep-0

9

Sep-1

0

Sep-1

1

Sep-1

2

Sep-1

3

Sep-1

4

Sep-1

5

Mar-

16*

Cash Earnings Per Share (cents) LHS

Headline Earnings Per Share (cents) LHS

*Restated per pro-forma information 31 March 2016

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

Sep-0

8

Sep-0

9

Sep-1

0

Sep-1

1

Sep-1

2

Sep-1

3

Sep-1

4

Sep-1

5

**Sep-1

6

Capex Additions (Rm) Debt (Rm)

** CAPEX figure is a twelve month figure and has been aggregated and not annually adjusted

10MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

B. CAPITAL STRUCTURE MGMT. – DEBT PROFILE

-

500

1 000

1 500

2 000

2 500

2017 2018 2019 2020 2021 2022 2023 2024

Financial Years

RoA

RSA

Group Debt (Rm)

Maturity Profile (Rm)

Significant de-gearing post a successful rights issue coupled with inflows relating to the B-BBEE I transaction

Net debt reduced from R9 billion to R5,3 billion after the rights issue in September 2016

In December 2016, net debt reduced further to R4,4 billion following inflows from the B-BBEE I transaction

Included in net debt is ~R1 billion in cash, with ~45% of this relating to Zimbabwe and Rwanda

Maturity profile reflects R1,6 billion of SA debt maturing in September 2017 – much progress has been made in lengthening the maturity profile

The improved balance sheet will mitigate the adverse impact of the cyclical nature of the business

2000

3000

4000

5000

6000

7000

8000

9000

10000

Mar-16 June-16 Sep-16 Dec-16

Gross Debt Net debt

11MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

Country Project Cost Project Debt PTA Portion IFC Portion

Rwanda US$165 million ~US$88 million ~US$25 million

Zimbabwe US$82 million ~US$55 million** ~US$55 million**

DRC US$280 million ~US$168 million ~US$84 million ~US$84 million

Ethiopia* ~US$175 million ~US$86 million ~US$56 million

Total US$702 million ~US$397 million ~US$220 million ~US$84 million

Preferential Trade Area (PTA) Bank and International Financial Corporation (IFC) are development funding institutions (DFIs) with significant exposure and appetite for investments in the African continent

PPC has deliberately partnered with DFIs as they have a long term commitment to the development of the African continent through economic and infrastructure development

~70% of PPC’s debt relates to the rest of Africa projects; of which PTA Bank’s portion alone exceeds US$200 million (>R2,8 billion)

The IFC is a member of the World Bank Group; it is owned by 184 member countries and has six decades of experience in providing loans, equity and advisory services to private sector companies in emerging markets – its annual funding programme for its FY17 is US$17 billion

B. CAPITAL STRUCTURE MGMT. – FUNDING PARTNERS

*PPC does not consolidate debt relating to Ethiopia **US$5 million was paid in December 2016

12MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

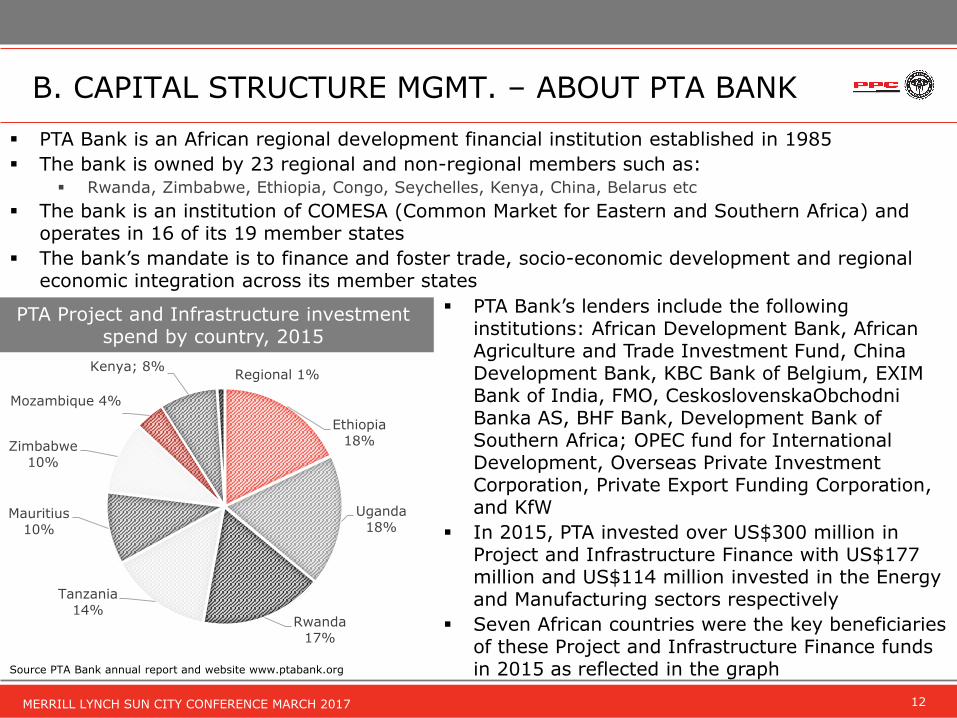

PTA Bank is an African regional development financial institution established in 1985

The bank is owned by 23 regional and non-regional members such as: Rwanda, Zimbabwe, Ethiopia, Congo, Seychelles, Kenya, China, Belarus etc

The bank is an institution of COMESA (Common Market for Eastern and Southern Africa) and operates in 16 of its 19 member states

The bank’s mandate is to finance and foster trade, socio-economic development and regional economic integration across its member states

Source PTA Bank annual report and website www.ptabank.org

B. CAPITAL STRUCTURE MGMT. – ABOUT PTA BANK

PTA Project and Infrastructure investment spend by country, 2015

Ethiopia 18%

Uganda18%

Rwanda17%

Tanzania14%

Mauritius 10%

Zimbabwe 10%

Mozambique 4%

Kenya; 8%Regional 1%

PTA Bank’s lenders include the following institutions: African Development Bank, African Agriculture and Trade Investment Fund, China Development Bank, KBC Bank of Belgium, EXIM Bank of India, FMO, CeskoslovenskaObchodniBanka AS, BHF Bank, Development Bank of Southern Africa; OPEC fund for International Development, Overseas Private Investment Corporation, Private Export Funding Corporation, and KfW

In 2015, PTA invested over US$300 million in Project and Infrastructure Finance with US$177 million and US$114 million invested in the Energy and Manufacturing sectors respectively

Seven African countries were the key beneficiaries of these Project and Infrastructure Finance funds in 2015 as reflected in the graph

13MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

C. SIGNIFICANTLY ENHANCING EFFICIENCY

Profit Improvement Programme

Aimed to achieve sustainable improvement of R400 million over three years

Target was exceeded in less than 18 months

Internal drive and measurement of PIP continues

Slurry kiln 9 cost savings and efficiencies to be realised

The R1,7 billion Slurry kiln 9 project includes the construction of a new 3000tpd production line using the latest energy efficient technology - a kiln system with six cyclone preheater stages and a precalciner

SK9’s guaranteed specific thermal energy consumption is 3.1 MJ/kg clinker which compares well with modern cement plants globally and is more than 25% and 50% more energy efficient than SK8 and SK7 respectively

Once SK9 is commissioned, PPC’s inland kilns will collectively perform at an average of 3.4 MJ/kg, which is equivalent to the performance of a new 5 stage preheater kiln system

The state-of-the-art system will also lead to reduced maintenance costs; SK9 offers an expected maintenance cost reduction from R22/ton to R12/ton clinker

Post commissioning of SK9, Slurry’s variable costs will decline by ~10% - 15%

14MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

C. SIGNIFICANTLY ENHANCING EFFICIENCY

SA Cement Costs of production (Real Rm based to 100) SA Cement Costs of production per ton (based to 100)

20

40

60

80

100

120

Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 Sep-15 Sep-16

Variable cost of production (Rm)

Variable delivered cost of production (Rm)

20

40

60

80

100

120

Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 Sep-15 Sep-16

Rand per ton VCOP Rand per ton VDCOP

20

40

60

80

100

120

Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 Sep-15 Sep-16

Fixed costs of production (Rm) Rand per ton

SA Cement Fixed costs of production (Real Rm based to 100)

Volumes sold in the SA Cement business declined significantly post the global financial crisis and World Cup 2010, however since 2012, volumes have shown some improvement to 2016

Since the focus on our 3 mega plant strategy, variable and fixed costs have shown an improvement since 2013

The use of our most efficient plants, restructuring our operations and optimising our logistics have all contributed

15MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

C. SIGNIFICANTLY ENHANCING EFFICIENCY

SA Cement delivered cost of coal (based to 100)

Over this period the real delivered cost of coal has reduced markedly due to:

Procuring from various key coal suppliers and maintaining sustainable relationships with them

Operating the most efficient kilns which negates higher energy consumption costs

Lower volumes produced over the period

Since 2009, electricity costs have risen significantly but PPC has managed to achieve cost increases below the prevailing inflation rate due to effectively managing time of use and operating our most efficient units

Richards Bay Coal Price & Exchange Rate

6,00

8,00

10,00

12,00

14,00

16,00

18,00

20

40

60

80

100

120

140

2009-0

1-0

1

2009-0

6-0

1

2009-1

1-0

1

2010-0

4-0

1

2010-0

9-0

1

2011-0

2-0

1

2011-0

7-0

1

2011-1

2-0

1

2012-0

5-0

1

2012-1

0-0

1

2013-0

3-0

1

2013-0

8-0

1

2014-0

1-0

1

2014-0

6-0

1

2014-1

1-0

1

2015-0

4-0

1

2015-0

9-0

1

2016-0

2-0

1

2016-0

7-0

1

2016-1

2-0

1

Richard's Bay Coal Price ($/tonne) LHS USDZAR (RHS)

40

50

60

70

80

90

100

110

40

50

60

70

80

90

100

110

Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 Sep-15 Sep-16

Delivered cost of coal (Rm) LHS Rand per ton (RHS)

SA Cement Electricity costs (based to 100)

50

100

150

200

250

Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 Sep-15 Sep-16

Total power Real Rm (consumed & maximum demand)

Rand per ton

Eskom Megaflex price increase (Real)

16MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

C. SIGNIFICANTLY ENHANCING EFFICIENCY

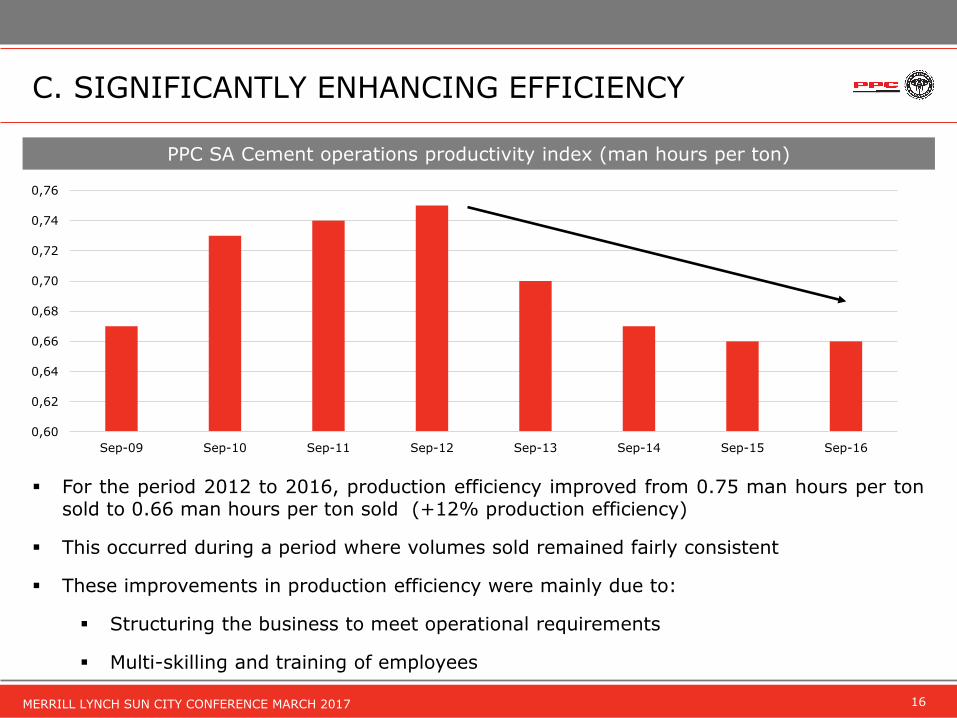

PPC SA Cement operations productivity index (man hours per ton)

For the period 2012 to 2016, production efficiency improved from 0.75 man hours per tonsold to 0.66 man hours per ton sold (+12% production efficiency)

This occurred during a period where volumes sold remained fairly consistent

These improvements in production efficiency were mainly due to:

Structuring the business to meet operational requirements

Multi-skilling and training of employees

0,60

0,62

0,64

0,66

0,68

0,70

0,72

0,74

0,76

Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 Sep-15 Sep-16

OPERATIONAL UPDATE

18MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

SOUTH AFRICAN OPERATING ENVIROMENT

Real % growth 2014-2016

Average2017F 2018F 2019F

Household consumption

1.1 1.3 2.0 2.3

Gross domestic expenditure

0.6 1.3 1.8 2.2

Gross fixed capital formation

0.1 1.5 1.6 2.8

Real GDP growth 1.1 1.3 2.0 2.2

Consumer Price Index 5.7 6.4 5.7 5.6

Producer Price Index 6.0 5.0 4.8 5.3

Source National Treasury 2017 Budget Speech and Bureau of Economic Research

Real GDP growth has disappointed, averaging only 1% over the past three years; with a slight improvement to 2% forecast only in 2018

Over the past three years, growth in Gross Fixed Capital Formation (GFCF) has been very weak, averaging about 0% - this is forecast to see some improvement in the medium term

Consumer confidence has also been muted mainly due to consumers being downbeat on the economic outlook and their personal finances

Over the past few years, public sectorexpenditure on infrastructure in theprovinces has consistently exceededthe allocated budget, while this hasbeen the opposite in local governmentand with state owned companies

86% of public sector infrastructurespend is executed by provincialgovernment, local government andstate owned enterprises

Public Sector Infrastructure Expenditure Budgeted vs. Spend (Rm)

20

40

60

80

100

120

140

Provincial governments Local government State Owned Companies

2013F 2013A 2014F 2014A 2015F 2015A 2016F 2016A

19MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

CARBON TAX UPDATE

The 2017 budget speech confirmed there will be a revised carbon tax bill which will bepublished for public consultation and tabled to parliament in mid-2017

CO2 emission in the cement industry is as a result of the thermal and chemical processesrequired in the manufacturing of cement

According to the proposed draft bill dated November 2015, the carbon tax for PPC Group isexpected to be ~R90 million

Currently the tax structure proposes R120 per ton of CO2e emitted for the first phase

Carbon tax will be treated as an environmental levy as contemplated in section 54A of theCustoms and Excise Act

There are allowances that PPC qualifies for in the first phase (up to 2020) whichsubstantially reduces the effective tax rate to less than 30% of the proposed value

PPC is currently looking at a number of initiatives to reduce the carbon tax burden, includingthe replacement of coal with other carbon neutral energy sources and improving theopportunity to increase cement extension

The carbon tax regime does not apply to imports into South Africa and these have not beenmeaningfully implemented elsewhere; they were scrapped in Australia due to the impact onindustry

PPC is ready for the implementation of the carbon tax regime in January 2018 however, we willcontinue to engage government on this matter

20MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

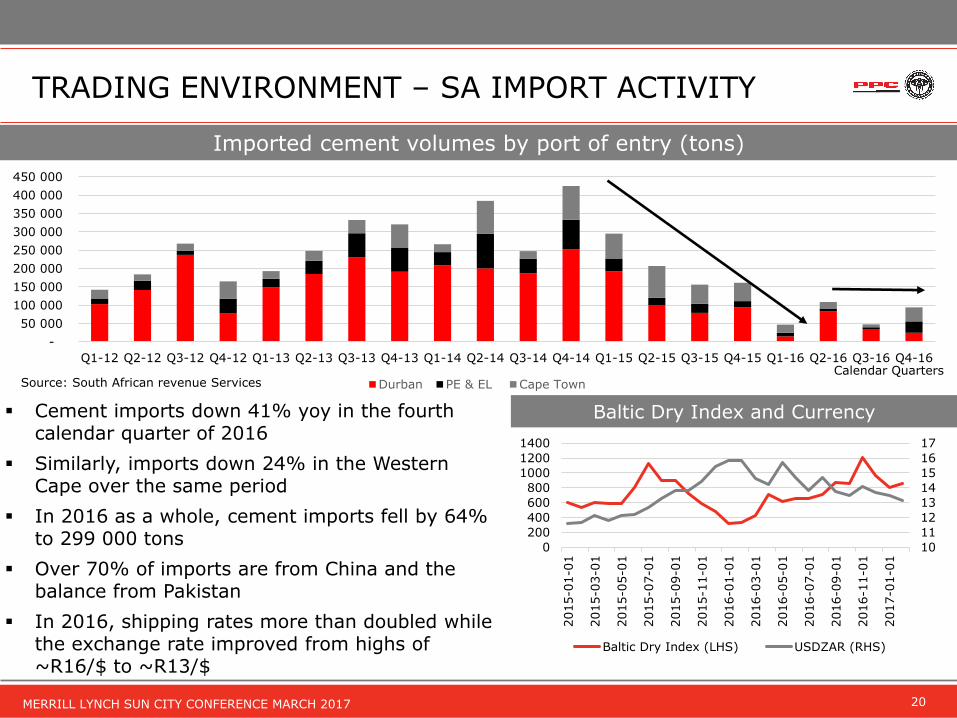

TRADING ENVIRONMENT – SA IMPORT ACTIVITY

-

50 000

100 000

150 000

200 000

250 000

300 000

350 000

400 000

450 000

Q1-12 Q2-12 Q3-12 Q4-12 Q1-13 Q2-13 Q3-13 Q4-13 Q1-14 Q2-14 Q3-14 Q4-14 Q1-15 Q2-15 Q3-15 Q4-15 Q1-16 Q2-16 Q3-16 Q4-16

Durban PE & EL Cape Town

Imported cement volumes by port of entry (tons)

Cement imports down 41% yoy in the fourth calendar quarter of 2016

Similarly, imports down 24% in the Western Cape over the same period

In 2016 as a whole, cement imports fell by 64% to 299 000 tons

Over 70% of imports are from China and the balance from Pakistan

In 2016, shipping rates more than doubled while the exchange rate improved from highs of ~R16/$ to ~R13/$

Calendar Quarters Source: South African revenue Services

Baltic Dry Index and Currency

10

11

12

13

14

15

16

17

0

200

400

600

800

1000

1200

1400

2015-0

1-0

1

2015-0

3-0

1

2015-0

5-0

1

2015-0

7-0

1

2015-0

9-0

1

2015-1

1-0

1

2016-0

1-0

1

2016-0

3-0

1

2016-0

5-0

1

2016-0

7-0

1

2016-0

9-0

1

2016-1

1-0

1

2017-0

1-0

1

Baltic Dry Index (LHS) USDZAR (RHS)

21MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

OPERATING UPDATE

As at December 2016, group cement sales volumes were up 4% when compared to the previous nine month period ending December 2015

Selling price increases were implemented in Gauteng and the inland regions in October 2016 – however this led to high single digit declines in cement sales volumes for the quarter ended December 2016

For the nine month period to December 2016, PPC’s overall cement volumes in South Africa increased by 4% and the average selling prices decreased by 4%

PPC has implemented further price increases in selected regions effective 1 February 2017 and the impact of this will begin to reflect on the average selling price in the next few months

22MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

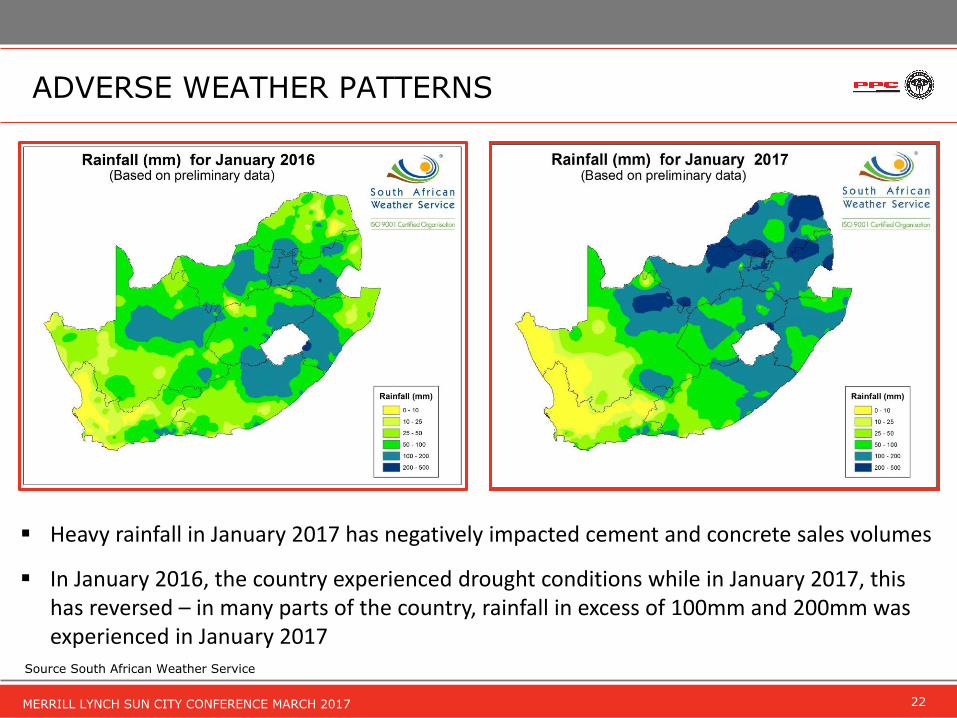

ADVERSE WEATHER PATTERNS

Source South African Weather Service

Heavy rainfall in January 2017 has negatively impacted cement and concrete sales volumes

In January 2016, the country experienced drought conditions while in January 2017, this has reversed – in many parts of the country, rainfall in excess of 100mm and 200mm was experienced in January 2017

23MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

Source South African Weather Service

ADVERSE WEATHER PATTERNS

Heavy rainfall in February 2017 has negatively impacted cement and concrete sales volumes

In February 2016, the country experienced drought conditions while in February 2017, this has reversed – in many parts of the country, rainfall in excess of 100mm and 200mm was experienced in February 2017

24MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

REST OF AFRICA & MATERIALS DIVISION

Zimbabwe

The rest of Africa operations collectively recorded cement sales volume increases of 9% for the nine month period to December 2016

Performance in the lime division continues to be negatively impacted by the local steel and alloys industries

Volumes in the aggregates and readymix division continued to show growth on the back of the recent acquisition of 3Q Mahuma Concrete

With the commissioning of the Harare mill, the cement sales volume performance has shown an improvement when compared to previous quarter ending December 2016

There are however liquidity challenges in Zimbabwe which makes it difficult to import key inputs and management is exploring various solutions to overcome these challenges

Botswana

Rwanda

The steady ramp-up in Rwanda continues with 81 000 tonnes of cement sales recorded in the quarter ending December 2016 and 230 000 tonnes of cement sales recorded for the nine month period to December 2016

Since March 2016, debt is being repaid monthly (over a 10 year period)

~60% of debt is USD denominated however progress is being made to convert this to local currency

Cement sales volumes in Botswana showed a 12% growth for the quarter ending December 2016 on the back of increased sales promotions

25MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

ZIMBABWE PROJECT

The US$82 million Msasa mill in Harare wascompleted on time and US$3 million below budgetwithout a single lost time injury

The project debt was initially anticipated to be US$75million however, the use of own-cash resourcesreduced debt drawdowns by US$20 million

The first bi-annual debt and interest repayment wasmade in December 2016 and outstanding debt is now~US50 million

Debt is being repaid over five years

All the performance tests have now been successfullyconcluded with final handover achieved late inJanuary 2017

A dividend of US$7 million is due to PPC Ltd

New 700 000 tpa Harare plant

26MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

ETHIOPIA PROJECT

As at January 2017, project construction was at an advanced stage

Electrical installation work from the limestone crusher to the cement proportioning station, including the general substation had been completed

Once the national utility company has concluded the requisite tests and energising of the substation, the kiln will be fired and hot commissioning will commence

Saleable cement production is expected in the second calendar quarter of 2017

New 1.4 mtpa Habesha plant

27MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

DEMOCRATIC REPUBLIC OF THE CONGO PROJECT

As at January 2017 the overall project construction was at 95% and the construction of the cement factory complete and ready for commissioning

The village construction was 80% complete and handover of houses was underway

Construction of the 13km overhead transmission line to the plant, line testing and commissioning with SNEL* was completed in January

Full power to the factory and village was available from the end of January 2017 allowing for the commencement of hot commissioning

Saleable cement production will commence at the end of March 2017

First limestone stockpile * Société Nationale d’Electricité

28MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

Project financed on a limited recourse basis to PPC Ltd

Therefore, any funding shortfalls incurred prior to Project Financial Completion will be for the account of PPC Ltd (as First Sponsor)

Project Financial Completion occurs when certain working capital and debt ratios have been met for four consecutive quarters (then project becomes fully ring-fenced)

Maintaining the debt and interest repayment schedule is key, however the full debt accelerates and becomes due only if the project is expropriated or nationalised before Project Financial Completion

Repayment of funding obligations commences July 2017 however negotiations are underway with funders to lengthen the repayment period

Other strategic options to reduce PPC risk exposure to the DRC are also being explored

Project Costs

US$280 million project likely

to rise by 4%-6%

Start up Funding

Likely to be between US$20

million and US$30 million –

relates to VAT repayment &

settling of bank facilities for

trading losses

Ops Cash Flows

Project likely to generate

positive free cash flows before

funding repayments

DEMOCRATIC REPUBLIC OF THE CONGO

29MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

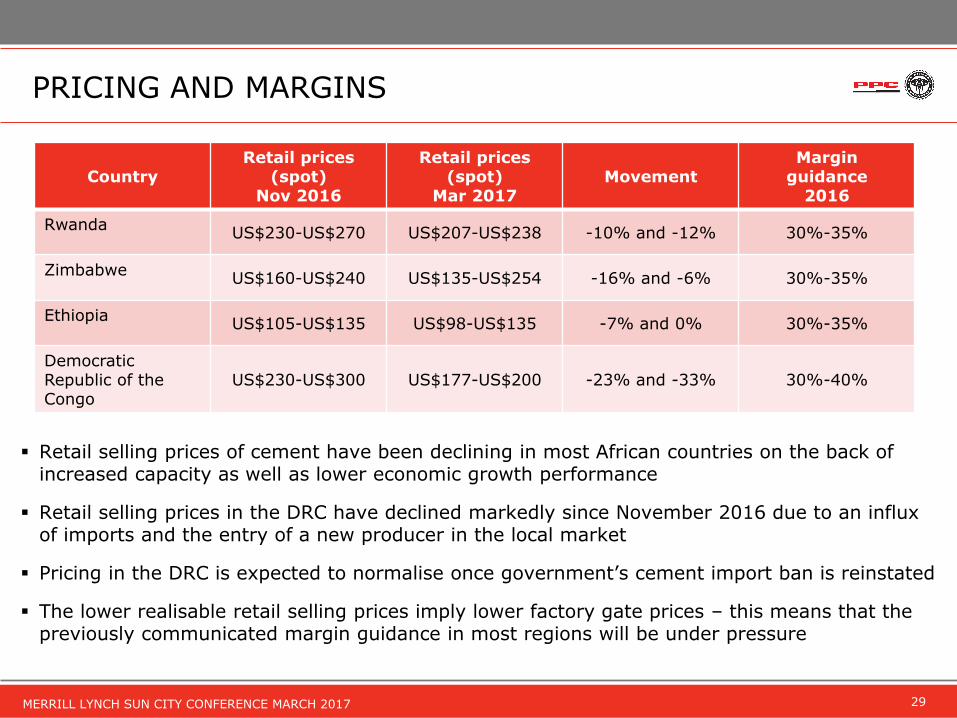

PRICING AND MARGINS

CountryRetail prices

(spot) Nov 2016

Retail prices (spot)

Mar 2017 Movement

Marginguidance

2016

Rwanda US$230-US$270 US$207-US$238 -10% and -12% 30%-35%

ZimbabweUS$160-US$240 US$135-US$254 -16% and -6% 30%-35%

Ethiopia US$105-US$135 US$98-US$135 -7% and 0% 30%-35%

DemocraticRepublic of the Congo

US$230-US$300 US$177-US$200 -23% and -33% 30%-40%

Retail selling prices of cement have been declining in most African countries on the back of increased capacity as well as lower economic growth performance

Retail selling prices in the DRC have declined markedly since November 2016 due to an influx of imports and the entry of a new producer in the local market

Pricing in the DRC is expected to normalise once government’s cement import ban is reinstated

The lower realisable retail selling prices imply lower factory gate prices – this means that the previously communicated margin guidance in most regions will be under pressure

30MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

SLURRY SK9 PROJECT

The Slurry SK9 project is progressing as well and with overall progress at 54% in January 2017

Commissioning remains scheduled for the first half of 2018

The R1.7 billion Slurry kiln 9 project includes:

construction of a new 3000tpd production line (SK9) using the latest energy efficient technology

replacement of SK8’s electrostatic precipitator (ESP) with a bag filter in order to ensure compliance with environmental legislation in 2020

New 1 mtpa Slurry kiln line

GOING FORWARD

32MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

Key focus areas going forward

The company remains focused on delivering its expansion projects timeously and cost effectively

As the international projects are at advanced stages, the focus has largely shifted to operational performance and achieving maximum ramp-up without disrupting the market

Management also continues to give special attention to the cash generating units; specifically managing costs within management’s control while maximising efficiencies

Work is also underway to further optimise the company´s capital structure while also exploring ways to de-risk the project in the DRC

Details relating to the proposed new B-BBEE III transaction will be communicated to shareholders during the first half of the 2017 calendar year

MANAGEMENT FOCUS

33MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

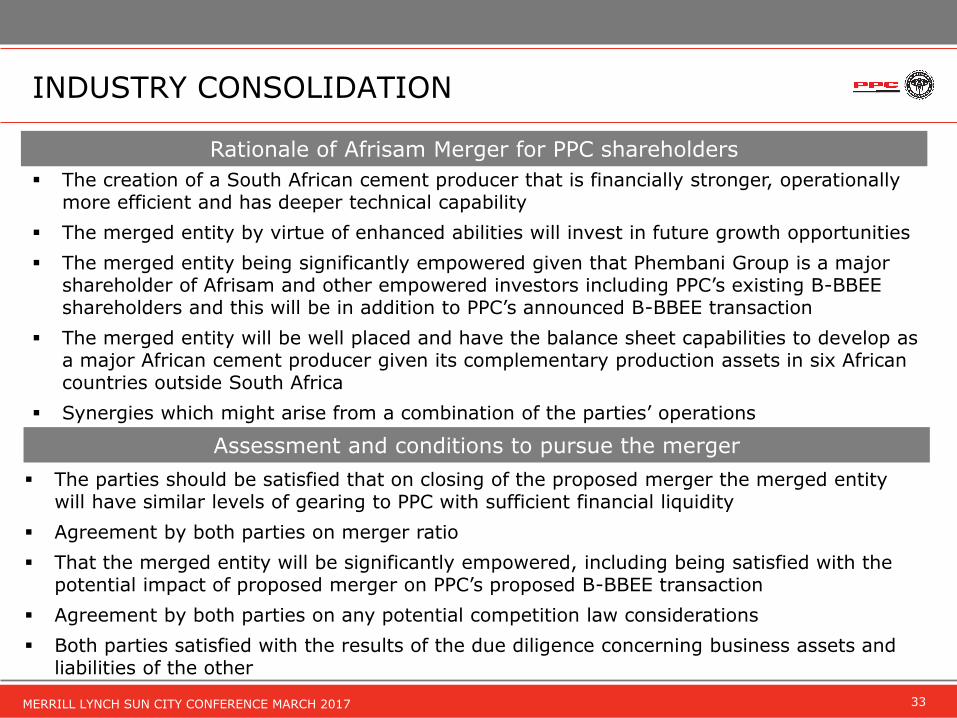

INDUSTRY CONSOLIDATION

Rationale of Afrisam Merger for PPC shareholders

The creation of a South African cement producer that is financially stronger, operationally more efficient and has deeper technical capability

The merged entity by virtue of enhanced abilities will invest in future growth opportunities

The merged entity being significantly empowered given that Phembani Group is a major shareholder of Afrisam and other empowered investors including PPC’s existing B-BBEE shareholders and this will be in addition to PPC’s announced B-BBEE transaction

The merged entity will be well placed and have the balance sheet capabilities to develop as a major African cement producer given its complementary production assets in six African countries outside South Africa

Synergies which might arise from a combination of the parties’ operations

Assessment and conditions to pursue the merger

The parties should be satisfied that on closing of the proposed merger the merged entity will have similar levels of gearing to PPC with sufficient financial liquidity

Agreement by both parties on merger ratio

That the merged entity will be significantly empowered, including being satisfied with the potential impact of proposed merger on PPC’s proposed B-BBEE transaction

Agreement by both parties on any potential competition law considerations

Both parties satisfied with the results of the due diligence concerning business assets and liabilities of the other

APPENDIX

35MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

PRO-FORMA CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME: 12 MONTHS ENDED 31 MARCH 2016

Revenue 9 187

Cost of sales 6 492

Gross profit 2 695

Administration and other operating expenditure 1 065

Operating profit before item listed below: 1 630

Empowerment transactions IFRS 2 charges 36

Operating profit 1 594

Fair value adjustments on financial instruments 5 3

Finance costs 5 572

Investment income 29

1 054

Loss from equity accounted investments (13)

Impairments (42)

Other exceptional adjustments and profit on disposal of non-core assets 116

Profit before taxation 1 115

Taxation 384

Profit for the period 731

Attributable to:

Shareholders of PPC Ltd 793

Non-controlling interests (62)

Other comprehensive income, net of taxation

Items that will be reclassified to profit or loss 6 952

Cash flow hedges 48

Taxation on cash flow hedges (14)

Reclassification of profit on sale of available-for-sale financial asset to profit and loss (82)

Taxation impact on reclassification of profit on sale of available-for-sale financial asset to profit and loss 15

Revaluation of available-for-sale financial asset (7)

Taxation impact on the revaluation of available-for-sale financial asset 3

Translation of foreign operations 7 743

Total comprehensive income 1 437

Attributable to:

Shareholders of PPC Ltd 1 377

Non-controlling interests 60

Earnings per share (cents) 8

Basic 151

Diluted 149

Profit before equity accounted earnings and exceptional items

36MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

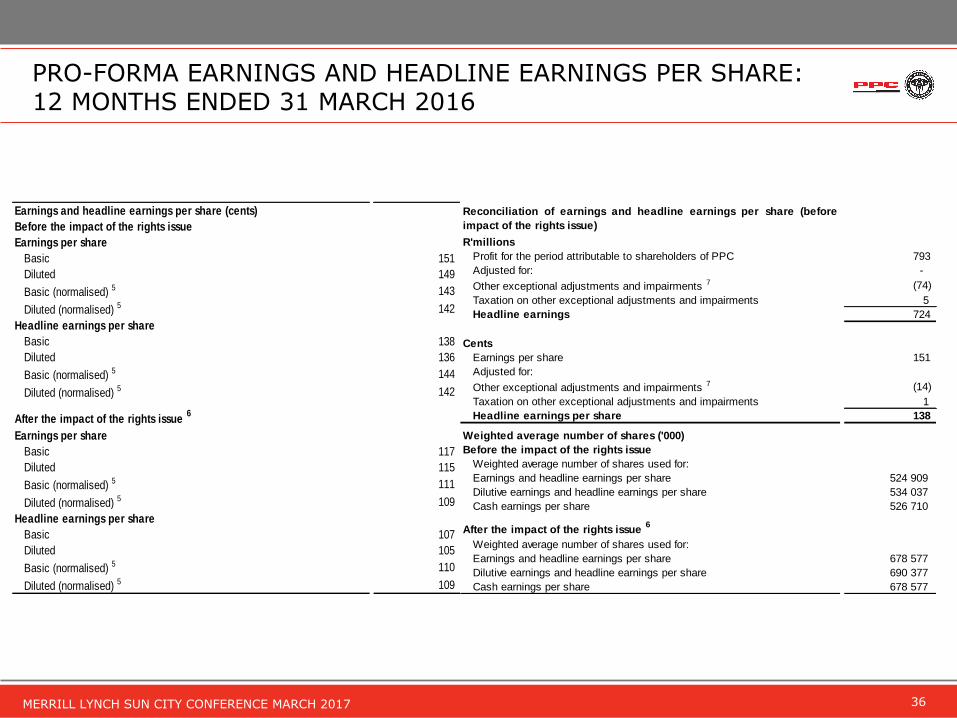

PRO-FORMA EARNINGS AND HEADLINE EARNINGS PER SHARE: 12 MONTHS ENDED 31 MARCH 2016

Earnings and headline earnings per share (cents)

Before the impact of the rights issue

Earnings per share

Basic 151

Diluted 149

Basic (normalised) 5 143

Diluted (normalised) 5 142

Headline earnings per share

Basic 138

Diluted 136

Basic (normalised) 5 144

Diluted (normalised) 5 142

After the impact of the rights issue 6

Earnings per share

Basic 117

Diluted 115

Basic (normalised) 5 111

Diluted (normalised) 5 109

Headline earnings per share

Basic 107

Diluted 105

Basic (normalised) 5 110

Diluted (normalised) 5 109

R'millions

Profit for the period attributable to shareholders of PPC 793

Adjusted for: -

Other exceptional adjustments and impairments 7 (74)

Taxation on other exceptional adjustments and impairments 5

Headline earnings 724

Cents

Earnings per share 151

Adjusted for:

Other exceptional adjustments and impairments 7 (14)

Taxation on other exceptional adjustments and impairments 1

Headline earnings per share 138

Weighted average number of shares ('000)

Before the impact of the rights issue

Weighted average number of shares used for:

Earnings and headline earnings per share 524 909

Dilutive earnings and headline earnings per share 534 037

Cash earnings per share 526 710

After the impact of the rights issue 6

Weighted average number of shares used for:

Earnings and headline earnings per share 678 577

Dilutive earnings and headline earnings per share 690 377

Cash earnings per share 678 577

Reconciliation of earnings and headline earnings per share (before

impact of the rights issue)

37MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

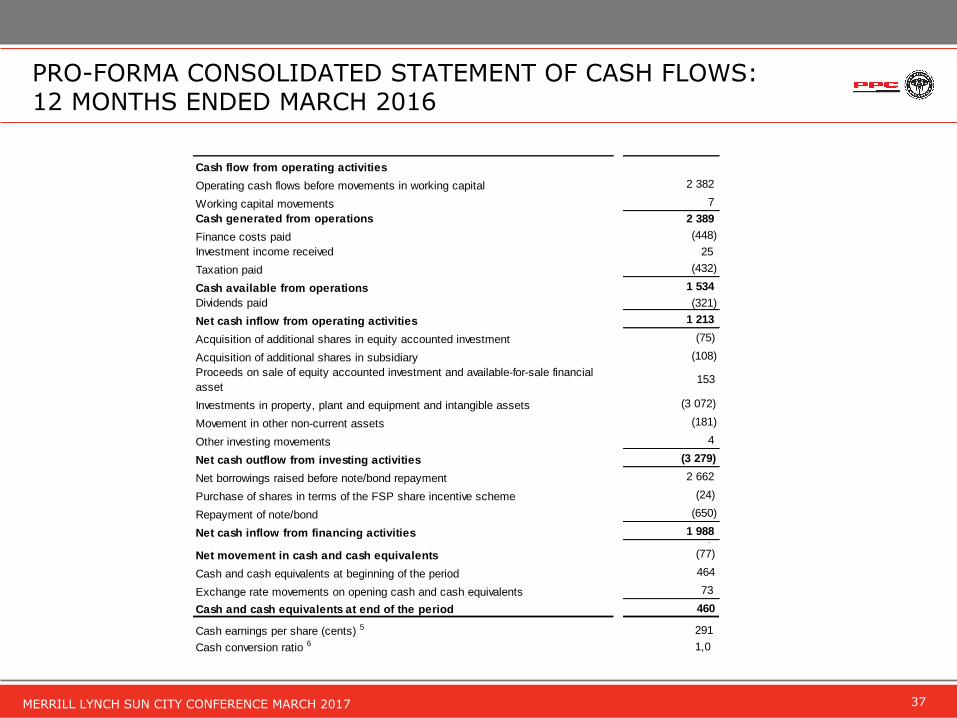

PRO-FORMA CONSOLIDATED STATEMENT OF CASH FLOWS: 12 MONTHS ENDED MARCH 2016

Cash flow from operating activities

Operating cash flows before movements in working capital 2 382

Working capital movements 7

Cash generated from operations 2 389

Finance costs paid (448)

Investment income received 25

Taxation paid (432)

Cash available from operations 1 534

Dividends paid (321)

Net cash inflow from operating activities 1 213

Acquisition of additional shares in equity accounted investment (75)

Acquisition of additional shares in subsidiary (108)

Proceeds on sale of equity accounted investment and available-for-sale financial

asset 153

Investments in property, plant and equipment and intangible assets (3 072)

Movement in other non-current assets (181)

Other investing movements 4

Net cash outflow from investing activities (3 279)

Net borrowings raised before note/bond repayment 2 662

Purchase of shares in terms of the FSP share incentive scheme (24)

Repayment of note/bond (650)

Net cash inflow from financing activities 1 988 -

Net movement in cash and cash equivalents (77)

Cash and cash equivalents at beginning of the period 464

Exchange rate movements on opening cash and cash equivalents 73

Cash and cash equivalents at end of the period 460

Cash earnings per share (cents) 5 291

Cash conversion ratio 6 1,0

38MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

PPC’S FOOTPRINT IN SOUTHERN AFRICA

39MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

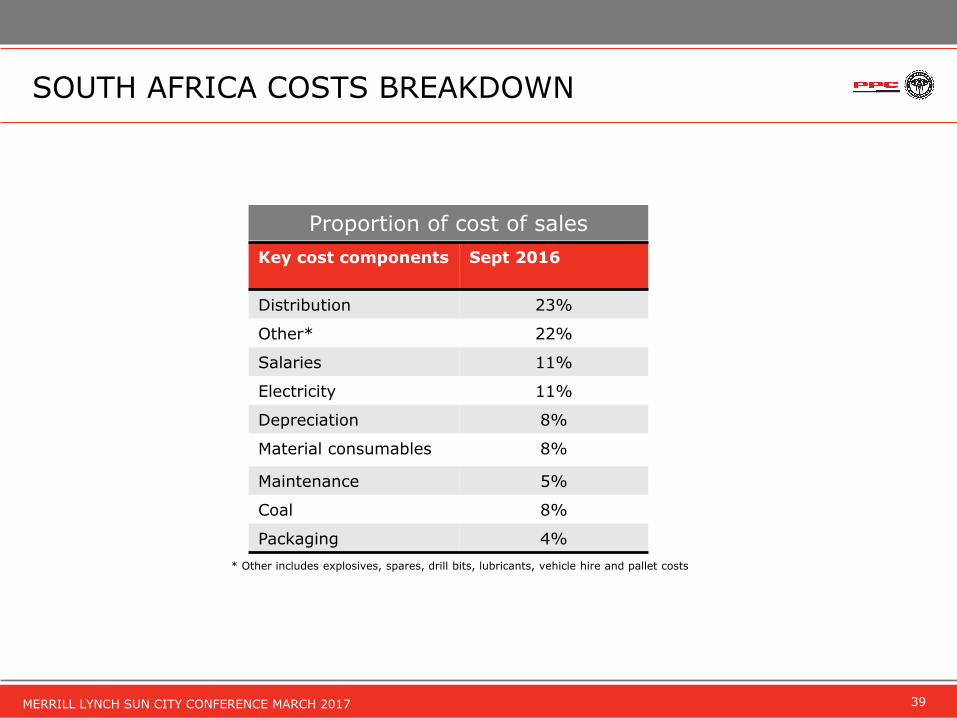

Key cost components Sept 2016

Distribution 23%

Other* 22%

Salaries 11%

Electricity 11%

Depreciation 8%

Material consumables 8%

Maintenance 5%

Coal 8%

Packaging 4%

Proportion of cost of sales

* Other includes explosives, spares, drill bits, lubricants, vehicle hire and pallet costs

SOUTH AFRICA COSTS BREAKDOWN

40MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

This document including, without limitation, those statements concerning the demandoutlook, PPC’s expansion projects and its capital resources and expenditure, contain certainforward-looking statements and views. By their nature, forward-looking statements involverisk and uncertainty and although PPC believes that the expectations reflected in suchforward-looking statements are reasonable, no assurance can be given that such expectationswill prove to be correct. Accordingly, results could differ materially from those set out in theforward-looking statements as a result of, among other factors, changes in economic andmarket conditions, success of business and operating initiatives, changes in the regulatoryenvironment, other government action and business and operational risk management.

Whilst PPC takes reasonable care to ensure the accuracy of the information presented, PPCaccepts no responsibility for any damages, be they consequential, indirect, special orincidental, whether foreseeable or unforeseeable, based on claims arising out ofmisrepresentation or negligence arising in connection with a forward-looking statement. Thisdocument is not intended to contain any profit forecasts or profit estimates, and theinformation published in this document is unaudited.

DISCLAIMER

41MERRILL LYNCH SUN CITY CONFERENCE MARCH 2017

INVESTOR CONTACTS

Azola Lowan Investor Relations

Vuyo Nombila Investor Relations

Tel. +27 11 386 9000www.ppc.co.za