Embed Size (px)

Citation preview

Merrill Lynch Affluent Insights Survey

February 22, 2012

For Internal Use Only

About Bank of America

Bank of America is one of the world's largest financial institutions, serving individual consumers, small- and middle-market businesses and large

corporations with a full range of banking, investing, asset management and other financial and risk management products and services. The

company provides unmatched convenience in the United States, serving approximately 57 million consumer and small business relationships

with approximately 5,700 retail banking offices and approximately 17,750 ATMs and award-winning online banking with 30 million active users.

Bank of America is among the world's leading wealth management companies and is a global leader in corporate and investment banking and

trading across a broad range of asset classes, serving corporations, governments, institutions and individuals around the world. Bank of America

offers industry-leading support to approximately 4 million small business owners through a suite of innovative, easy-to-use online products and

services. The company serves clients through operations in more than 40 countries. Bank of America Corporation stock (NYSE: BAC) is a

component of the Dow Jones Industrial Average and is listed on the New York Stock Exchange.

Merrill Lynch Global Wealth Management

Merrill Lynch Global Wealth Management is a leading provider of comprehensive wealth management and investment services for individuals

and businesses globally. With more than 17,300 Financial Advisors and more than $1.5 trillion in client balances as of December 31, 2011, it is

among the largest businesses of its kind in the world. More than two-thirds of Merrill Lynch Global Wealth Management relationships are with

clients who have a net worth of $1 million or more. Within Merrill Lynch Global Wealth Management, the Private Banking & Investment Group

provides tailored solutions to ultra affluent clients, offering both the intimacy of a boutique and the resources of a premier global financial

services company. These clients are served by more than 160 Private Wealth Advisor teams, along with experts in areas such as investment

management, concentrated stock management and intergenerational wealth transfer strategies. Merrill Lynch Global Wealth Management is

part of Bank of America Corporation

Merrill Lynch Wealth Management makes available products and services offered by Merrill Lynch, Pierce, Fenner & Smith Incorporated

(MLPF&S) and other subsidiaries of Bank of America Corporation.

Banking products are provided by Bank of America, N.A. and affiliated banks, Members FDIC and wholly owned subsidiaries of Bank of America

Corporation.

Investment products:

MLPF&S is a registered broker-dealer, Member SIPC and a wholly owned subsidiary of Bank of America Corporation.

© 2012 Bank of America Corporation. All rights reserved.

Are Not FDIC Insured Are Not Bank Guaranteed May Lose Value

About Bank of America and Merrill Lynch Wealth Management

2

For Internal Use Only

What We Set Out to Accomplish How We Did It

• Phone survey conducted by Braun Research in December 2011 on behalf of Merrill Lynch Wealth Management

• National sample of 1,000 affluent individuals with investable assets of $250,000 or more

• Oversample of 300 affluent respondents in five target markets, including Atlanta, Chicago, Dallas, Detroit and San Francisco

• Margin of Error:

National: +/- 3.1%

Oversampled Markets: +/- 5.7%

• Since 2009, this survey has examined the

goals, values and financial concerns of

affluent Americans. This latest survey reveals

how new retirement realities and longer life

expectancy are causing many to rethink their

approach to planning for later years. Key

areas of focus include:

• Managing money differently in light of

longevity

• Considering lifestyle tradeoffs to ensure

retirement assets last

• Making health care costs part of a more

holistic planning process

• Evolving role of financial advisors in

helping clients prepare for retirement

Merrill Lynch Affluent Insights Survey ™

3

For Internal Use Only

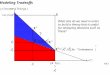

Age of Opportunity: Average Life Expectancy Has Risen Dramatically

Over the Last Century

4

The U.S. Census Bureau estimates that the number of people who live to be 100

rose from 2,300 in 1950 to nearly 80,000 in 2010, and will exceed 600,000 by 2050.

According to the Society of Actuaries a 65-year-old couple now has a 31% chance

of at least one spouse living past the age of 95.

40.0

50.0

60.0

70.0

80.0

90.0

1800 1900 1940 1980 2010 2030 2050

Ag

e

Year

Life Expectancy at Birth

2050: 83 years

Today : 78 years

1950: 68 years

1900: 47 years

For Internal Use Only

Longer Life Expectancy Causes Many to Rethink Their Approach to

Planning for Later Years

5

This Merrill Lynch survey finds that many affluent Americans (58%) have a positive view of

the prospect of living to be 100. However, three out of four (75%) would approach their

money management differently if they knew today that they were going to live that long. To

financially accommodate a longer life, they would:

29%

32%

32%

37%

39%

Purchase long-term care insurance

Invest in a lifetime income product, such as an annuity

Contribute more to a 401(k), IRA or other retirement savings vehicle

Work with their financial advisor to re-evaluate their savings and investment strategies

Continue to work at least part-time during retirement

In light of longer life expectancies, the majority of respondents (59%) also believe that the age

at which Americans are eligible to collect Social Security should be raised.

For Internal Use Only

Redefining Retirement

6

Age is far less of a factor when it comes

to retirement. Only 14% of respondents

over the age of 50 cite “hitting a certain

age” as the factor that would most lead

them to retire. Others include:

7%

14%

18%

19%

25%

Feeling they've achieved a certain level of success in

their career

Hitting a certain age

A health condition (their own or that of a family member)

Don't plan to retire

Believing they have enough assets to live the lifestyle they

want in retirement

Non-Retired, 51+

7%

14%

22%

30%

Starting their own business

Working part-time in their current job

Working in a job they enjoy more (part or full-

time)

Cycling between work and leisure

Longevity and the desire to work later in life,

because they have to or want to, is also

redefining the meaning of retirement. Three out

of four (73%) respondents not yet retired view

this life stage as a second act during which

they intend to work part or full-time:

Only one out of four (24%) define

retirement as never working again

For Internal Use Only

7

Making Lifestyle Tradeoffs to Ensure Their Assets Last

24%

25%

27%

31%

32%

35%

38%

Downsizing their home

Leaving less of an inheritance

Keeping the same car longer

Cutting back on entertainment

Limiting budgets for vacations

Purchasing fewer personal luxuries

Trimming day-to-day expenses

If given the choice, half (51%) of affluent Americans not yet retired would rather retire later

than make tradeoffs to their current lifestyle. However, when push comes to shove, and

tradeoffs are needed to help ensure their assets sustain them throughout retirement, 81%

would make them, including a combination of:

For Internal Use Only

8

Preparing to Retire

15%

19%

20%

36%

39%

39%

Providing less financial support to their adult-age children

Clipping more coupons

Consolidating assets with fewer financial institutions

Developing a plan for monthly expenses and other financial needs once retired

Tracking expenses more closely

Saving more

Among affluent Americans preparing to retire in the next 5 years, many are taking additional

steps to help ensure their assets last throughout their lifetime, including:

For Internal Use Only

9

27%

41% Over 50

Under 50

While many baby boomers are struggling to save for and fund their retirement, most respondents

(79%) believe that Americans under the age of 35 today won’t have it any easier. Likely to live longer

and to depend less on government entitlements and pensions as lifetime income sources, younger

generations may well have an increasingly difficult time saving for retirement.

Evaluating Current Lifetime Income Sources

38%

57% No Yes

Affluent Americans who currently or expect to rely in part on a

pension as a source of lifetime income:

Affluent Americans who expect to receive lifetime income from a

source other than Social Security:

43% of respondents expect to or already receive lifetime income from a source other than

Social Security, such as a pension or annuity

For Internal Use Only

For the third year in a row, survey respondents cite rising health care costs as their top

financial concern (79%). One-third (34%) went so far as to say that they are more concerned

about the financial strain associated with a significant health situation, such as a chronic

illness or disability, than they are about how it may compromise their quality of life.

Rising Cost of Health Care Tops List of Financial Concerns

10

41%

47%

54%

55%

60%

61%

64%

65%

73%

76%

79%

Preserving an inheritance for their children or grandchildren

Current state of the real estate market

Impact of the economy on ability to meet financial goals

Being able to afford the lifestyle they want in retirement

Ensuring retirement assets will last throughout their lifetime

European financial crisis

Nation’s political standing with the world

Potential for rising tax rates

U.S. unemployment rate

Nation's budget deficit

Rising health care costs

Other Top Concerns of Affluent Americans in 2012

For Internal Use Only

Despite Being Their Top Concern, Few Have Factored Health Care

Costs into Retirement Planning

11

Two-thirds (67%) have not estimated what their health care costs may amount to in

retirement. While less surprising that those under the age of 50 have not thought this

through, it is surprising that those over the age of 50 have yet to consider what these

costs may be during their later years.

Survey respondents believe future health care costs (26%) and life expectancy (25%) to

be the most difficult unknowns when planning for future financial needs.

62%

78% Under 50

Over 50

For Internal Use Only

Women More Concerned About Retirement and Financial Security

12

On average, women today live more than five years longer than men1. This may be one of the

reasons affluent women are more concerned than men about their retirement assets lasting

throughout their lifetime. Additionally, women are more concerned about:

25%

44%

59%

54%

37%

56%

76%

66%

Prospect of what caring for an aging parent could do to their

own financial security

Rising cost of their children's college education

Future of Social Security benefits

Ensuring retirement assets last throughout their lifetime

Women

Men

1Health, United States, 2010; U.S. Department of Health and Human Services, Centers for

Disease Control and Prevention, and the National Center for Health Statistics

For Internal Use Only

Client to Financial Advisor: How do I live well longer?

13

When it comes to helping clients prepare for retirement, the role of a financial advisor has evolved

beyond asset accumulation strategies and portfolio structuring. Nearly half (47%) of affluent

Americans cite that conversations with their advisor regularly go much further than general investing

to focus on broader aspects of retirement. Financial advisors today are a source of insight and advice

around how tradeoffs, health care costs and longevity may impact retirement outcomes.

21%

25%

25%

26%

29%

30%

Making lifestyle choices today that will improve long-term financial security

The impact of rising health care costs on retirement income

How they hope to live their life during their retirement years

Balancing competing near- and long-term financial demands

Managing cash flow and liquidity in retirement

How to financially plan for the possibility of living to be 100

When asked what retirement-focused topics they would like to discuss

more with their financial advisor, affluent Americans cited:

For Internal Use Only

14

Qualities that Keep Clients Loyal

44%

46%

48%

51%

58%

Provides relevant research and market insights to help them feel informed and in control

Has specific expertise advising their unique financial circumstances

Understands and respects their preferred methods of communication, e.g. face-to-face,

email, phone, social media, etc.

Understands their goals, dreams and personal values

Understands their current financial situation

When asked what core qualities their financial advisor possesses that keep them loyal to

their relationship, affluent Americans cited:

Merrill Lynch Affluent Insights Survey

February 22, 2012