Embed Size (px)

DESCRIPTION

A dissertation

Citation preview

INILAK (INDEPENDENT INSTITUTE OF LAY ADVENTISTS OF KIGALI)

P.O. Box. 6392 Kigali

Faculty of Economic Sciences

Department of Management

Option of Finance

IMPACT OF FINANCIAL ANALYSIS IN A

COMMERCIAL BANK’ HEALTH CHECK-UP IN

FRAMEWORK OF CAMELS Case study of Banque Commerciale du Rwanda (BCR Ltd)

Period: 2005-2010

A dissertation submitted to the Faculty of Economic Sciences and Management

as a partial fulfillment of the requirements for the award of a Bachelors’

degree in Business Administration (Finance)

By:

HABIYAREMYE Hyacinthe

Reg. No. 02573/03

Supervised by: Dr BIDERI ISHUHELI

Kigali, September 2012

DECLARATION

I, HABIYAREMYE Hyacinthe hereby declare that the work presented in this dissertation

entitled “Impact of financial analysis in a commercial bank’ health check up in framework

of CAMELS, Case study of BCR Ltd (2005-2010)” is my original work and has not been

presented elsewhere for any academic qualification. Any reference in terms of books or any

other written and electronic materials made concerning other people’s work are indicated in

the bibliography.

HABIYAREMYE Hyacinthe

……………………….………………………………

ii

CERTIFICATION

This is to certify that this research project entitled “Impact of financial analysis in a

commercial bank’ health check up in framework of CAMELS, Case study of BCR Ltd

(2005-2010)” was prepared by HABIYAREMYE Hyacinthe under my supervision.

Dr. BIDERI ISHUHERI

……………………..…………………..

iii

DEDICATION

To my beloved wife MUSABYEMARIYA Aline,

To my beloved daughter AMAREBE Mary Benitha,

To my parents HABIYAREMYE Anastase and Uzamukunda Odette,

To my brother and sister, Anicet and Marie Thérèse,

To my late brothers HABIYAREMYE Innocent and Vincent,

To all my family members,

To all my friends.

iv

ACKNOWLEDGEMENTS

I’m so thankful for the excellent support and help of different people without whom I would

not have a successful work.

I recognize that if God had not given me the ability and good health and had not arranged

circumstances I could not accomplish such a success.

I am thankful to my supervisor Dr. BIDERI ISHUHERI, for his advise during the course of

this work although he had a lot to do.

I appreciate the INILAK administration for what they have done for this historic

achievement of completion of my studies and their commitment to facilitate students by

providing the necessary support that has contributed to the success of this work.

I express the gratitude to the authorities of BCR Ltd., for having hosted me to carry out the

research and for their cooperation during data collection exercise.

I’m out of words to express the gratitude I feel towards my Dear wife MUSABYEMARIYA

Aline and my daughter AMAREBE Mary Benitha. I’m also thankful to my dear parents, my

late brothers and the rest of my family who supported both morally and materially in the

completion of this dissertation.

Special thanks go to my classmates who made life at the university so friendly.

HABIYAREMYE Hyacinthe

v

ABSTRACT

This study entitled “Impact of financial analysis in a commercial bank’s health check up in

framework of CAMELS, Case study of BCR Ltd (2005-2010)” is based on the

documentation technique. The analysis is entirely based on the CAMELS framework and as

stated in theoretical prescription, health check up of any Financial Institution in this

framework is centered in the six components: capital adequacy, asset quality, management

quality, earning, liquidity and sensitivity to market.

The importance of findings of this research was to address the specific objectives of the

study and the results prove that the indicators: TCR, CCR and SCR of capital adequacy are

in conformity with the implication of leverage ratio that BCR have met the capital adequacy

ratio as directed by BNR. In such case both NPAR and LLRR indicate that the sound

financial health of the bank is in good conditions. In addition to that, the performance

management of BCR tested using the Management quality component was found

satisfactory due to the fact that OER for the period under study is greater than 50%.

For the earning component, earning performance of BCR, as indicated by ROA, is good.

BCR’s LDR as a whole is high and the two indicators—CETAR and CETDR— proved the

high level of liquidity position of BCR.

For component of the sensitivity to Market, the BCR market price of financial instruments

and credit ratings for the period from 2005 to 2010, the researcher did not find any data

required to exploit them, and for that reason the second objective of the present study, was

not achieved.

vi

SOMMAIRE

Cette étude intitulée «Impact de l'analyse financière en matière de santé d'une banque

commercial dans le cadre de CAMELS, cas d'étude de la BRC Ltd (2005-2010) » est basé sur la

technique de la documentation. L'analyse est entièrement basé sur le cadre CAMELS et comme

indiqué dans la prescription théorique, le bilan de santé de toutes les institutions financières

dans ce cadre est concentrée dans les six composantes: adéquation des fonds propres, la qualité

des actifs, gestion de la qualité, les avoirs, la liquidité et la sensibilité au marché.

L'importance des résultats de cette recherche était d'aborder les objectifs spécifiques de l'étude

et les résultats montrent que les indicateurs: TCR, CCR et SCR, de la suffisance du capital

confirmé avec l'implication de ratio d'endettement que la BCR a rencontré le ratio de solvabilité

tel que prescrit par BNR; deux indicateurs NPAR et LLRR laissé entendre que la bonne santé

financière de la banque est dans de bonnes conditions ainsi que la qualité de la gestion, il a été

constaté que la gestion de la performance de la BCR est satisfaisante en raison du fait que les

OER pour la période de l'étude est supérieure à 50% . Pour le benefice de la capacité BCR, en

moyenne, gagnent les performances de la BCR, comme indiqué par ROA, c'est bien. BCR 'LDR

dans son ensemble est élevé et les deux indicateurs-CÉTAR et CETDR-montrent le niveau

élevé de la position de liquidité de la BCR. Pour le prix du marché BCR des instruments

financiers et des notes de crédit pour la période de 2005-2010, le chercheur n’a pas trouvé les

données nécessaires pour les calculer, et comme ça, le deuxième objectif de la présente étude,

n'a pas été atteint.

Les recommandations à la BNR et BCR ont été formulées où pour la banque centrale

rwandaise, il a été recommandé de proposer des systèmes uniformes pour les banques du pays

tout entier » et toutes les institutions financières comme CAMELS, pour vérifier leur vie

quotidienne. Et fixer le taux du ratio de chaque indicateur de CAMELS. Et pour BCR Ltd, afin

de faciliter l'accès aux données et de fournir des données détaillées pour les étudiants finalistes

en effectuant des recherches à la banque demandant analyse approfondie.

Pour des recherches plus poussées, il a été suggéré de mener leur recherche sur: la vérification

de la santé des institutions financière dans le cadre de CAMELS, au Rwanda. Cas de la BNR. /

La performance et la contribution de CAMELS dans l’atteinte des objectifs de l'institution

financière.

vii

TABLE OF CONTENTS

DECLARATION ..................................................................................................................... ii

CERTIFICATION .................................................................................................................... iii

DEDICATION .................................................................................................................... iv

ACKNOWLEDGEMENTS ....................................................................................................... v

ABSTRACT .................................................................................................................... vi

SOMMAIRE ................................................................................................................... vii

TABLE OF CONTENTS ........................................................................................................ viii

LIST OF ABBREVIATIONS .................................................................................................... x

LIST OF CHARTS ................................................................................................................... xii

LIST OF TABLES .................................................................................................................. xiii Chapter one: GENERAL INTRODUCTION ......................................................................... 1

1.1. Background of the study .................................................................................................... 1

1.2. Problem statement ............................................................................................................. 2

1.3. Objectives of the study ...................................................................................................... 3

1.3.1. General objective ........................................................................................................ 3

1.3.2. Specific objectives ...................................................................................................... 3

1.4. Research questions ............................................................................................................ 3

1.5. Scope of the study .............................................................................................................. 4

1.6. Significance of the study ................................................................................................... 4

1.6.1. To the researcher ......................................................................................................... 4

1.6.2. To BCR Ltd................................................................................................................. 4

1.6.3 To others researchers ................................................................................................... 5

1.7. Company profile ................................................................................................................ 5

1.7.1. Historical background ................................................................................................. 5

1.7.2. Vision .......................................................................................................................... 6

1.7.3. Mission statement ....................................................................................................... 6

1.8. Organization of the study .................................................................................................. 6

viii

Chapter two: LITERATURE REVIEW .................................................................................. 8

THEORIES ON FINANCIAL ANALYSIS ............................................................................. 8

Financial analysis versus situation development .................................................................. 9

Objectives of the Financial Analysis .................................................................................. 10

Basic State for Financial Analysis ...................................................................................... 11

THEORIES ON PERFORMANCE ....................................................................................... 11

Performance management ................................................................................................... 11

The purpose of performance management .......................................................................... 12

Performance measurement .................................................................................................. 12

How to measure performance ............................................................................................. 12

Aspects of the performance ................................................................................................ 14

CAMELS RATING SYSTEM TOWARDS BANK’S PERFORMANCE ............................ 15 Chapter three: RESEARCH METHODOLOGY ................................................................. 22 Chapter four: ANALYSIS OF THE DATA AND INTERPRETATION OF FINDINGS 23

4.1. BCR Ltd. Capital Adequacy ............................................................................................ 23

4.2. BCR Ltd. Asset quality .................................................................................................... 25

4.3. BCR Ltd. Management quality ........................................................................................ 26

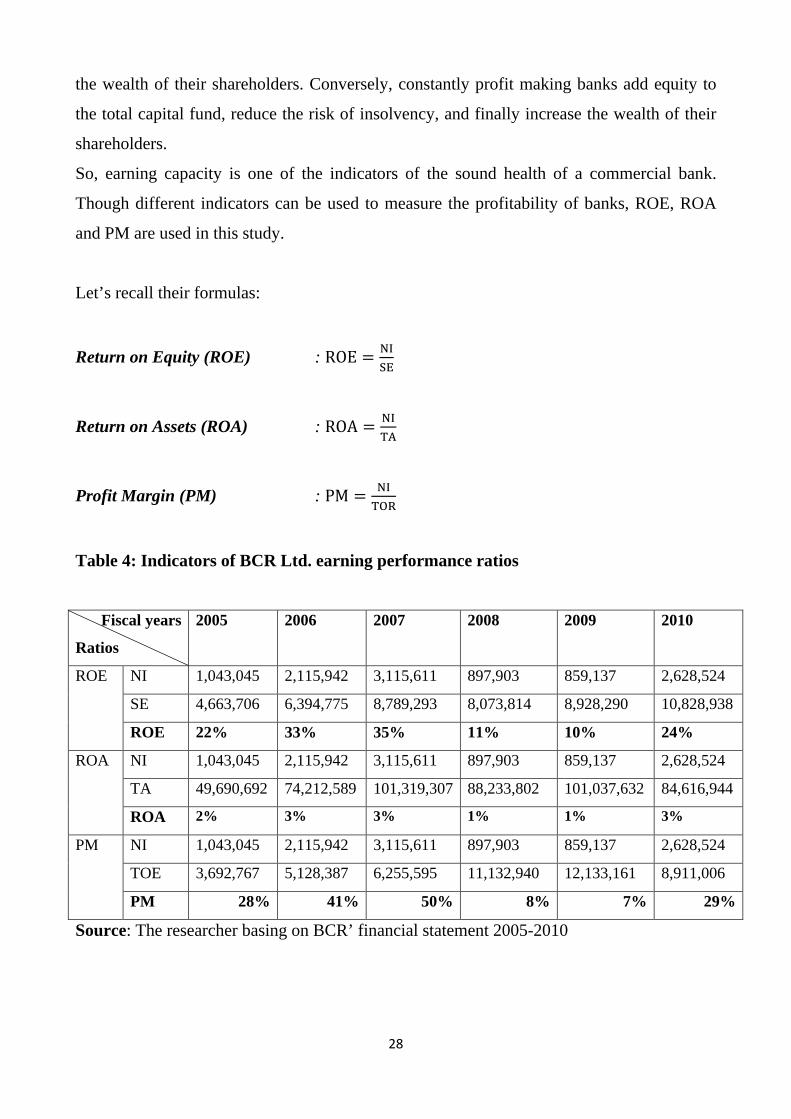

4.4. BCR Ltd. earning performance ratios ............................................................................. 27

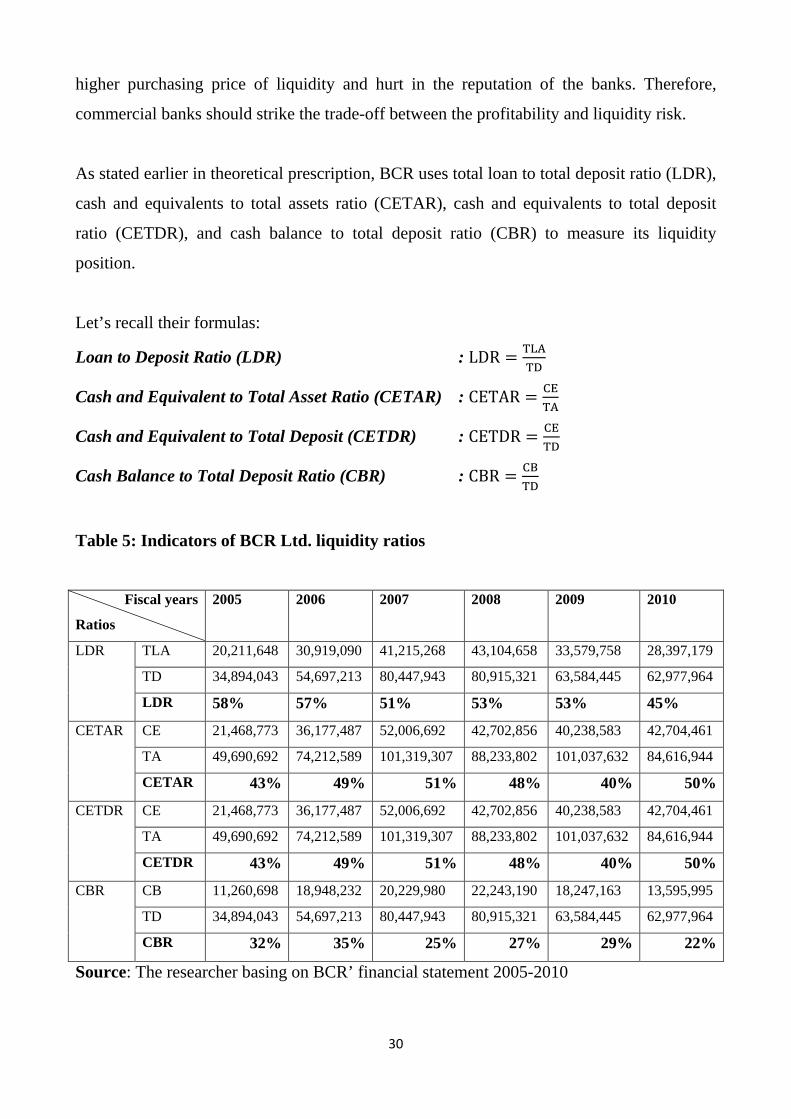

4.5. BCR Ltd. Liquidity .......................................................................................................... 29 Chapter five: SUMMARY OF FINDINGS, CONCLUSION AND SUGGESTIONS ....... 32

5.1. Summary of the major findings ....................................................................................... 32

5.2. Conclusion ....................................................................................................................... 33

5.3. Recommendations ........................................................................................................... 34

5.4. Suggestions for further studies ........................................................................................ 35 BIBLIOGRAPHY ................................................................................................................... 36

APPENDICES ................................................................................................................... 38

ix

LIST OF ABBREVIATIONS

BCR : Banque Commerciale du Rwanda

BNR : Banque Nationale du Rwanda

CB : Cash Balance

CBR : Cash Balance to Total Deposit Ratio

CC : Core Capital

CCR : Core Capital Ratio

CETAR : Cash and Equivalent to Total Asset Ratio

CETDR : Cash and Equivalent to Total Deposit

EPE : Earning per Employee

EU : European Union

FDICIA : Federal Deposit Insurance Corporation Improvement Act

FIs : Financial Institutions

FSC : Financial Stability Committee

http : Hyper Text Transfer Protocol

INILAK : Independent institute of Lay Adventists of Kigali

LDR : Loan to Deposit Ratio

LLR : Loan Loss Reserve

LLRR : Loan Loss Reserve Ratio

LR : Leverage Ratio

Ltd. : Limited

NI : Net Income

NOE : number of employees

NOI : net operating income

NPA : Non-Performing Assets

NPAR : Nonperforming Loan Ratio

OER : Operating Expenses Ratio

PM : Profit Margin

RDB : Rwanda Development board

ROA : Return On Assets

ROE : Return on Equity

x

RWA : Risk Weighted Assets

Rwf : Rwandan francs

SC : Supplementary Capital

SCP : Structure Conduct Performance

SCR : Supplementary Capital Ratio

SE : Shareholder Equity

TA : Total Assets

TA : Total Assets

TC : Total Capital

TCR : Total Capital Ratio

TD : Total Deposit

TLA : Total Loan and Advance

TLA : Total Loan and Advance

TOE : Total Operating Expenses

TOR : Total Operating Revenue

U.S.A. : United State of America

UNDP : United Nation Development Program

www : World Wide Web

xi

LIST OF CHARTS

Chart 1: BCR Capital Adequacy ratios evolution .................................................................. 24

Chart 2: Asset quality ratios evolution ................................................................................... 26

Chart 3: BCR profitability evolution ...................................................................................... 29

Chart 4: BCR Ltd. liquidity ratios evolution .......................................................................... 31

xii

LIST OF TABLES

Table 1: indicators of BCR’ Capital adequacy ratios ........................................................ 24

Table 2: Indicators of BCR Asset quality ratios ............................................................... 25

Table 3: Indicators of BCR Ltd. Management quality ratios ............................................ 27

Table 4: Indicators of BCR Ltd. earning performance ratios ............................................ 28

Table 5: Indicators of BCR Ltd. liquidity ratios ............................................................... 30

xiii

CHAPTER ONE: GENERAL INTRODUCTION

GENERAL INTRODUCTION

1.1. Background of the study

In Rwanda, in the period under review, the BNR continued to employ important reforms to

ensure that the financial system mainly composed of the banking system, microfinance and

non-banking financial institutions is robust and continue to show good financial health.

These reforms included the establishment of appropriate market infrastructure (efficient

legal and regulatory framework, supervisory tools, modern payment systems and the private

credit reference bureau). In addition, the BNR established the Financial Stability Committee

(FSC) in May 2012 with the mission to promote the stability of the Rwandan financial

system by analyzing the system in its environment on a permanent basis, and by identifying,

monitoring and publishing associated risks. The outcome of the 2011 financial stability

reports and first meeting of FSC substantiate that Rwanda’s financial system is sound and

stable and able to mitigate systemic risks. (BNR, 2012: 29)

The financial services sector in Europe has altered fundamentally in recent years. The

change has been caused by the increasing weight of the capital markets in mediating offer

and demand for capital (disintermediation), the enforced diffusion of IT in sales,

development and processing of financial services, fierce competition in national markets as

well as the rising globalization of the entire industry. The transformation of the banking

sector will be accelerated by the current financial market crisis. Additionally, the regulatory

environment has changed dramatically. This holds especially true for Europe. Economic and

political target of the process of deregulation and harmonization is to intensify competition

in a single and homogeneous European market for financial services (EU Commission

2005).

Bank’s overall performance or rather solvency or insolvency has been given much attention

both at the local and international level. Financial ratios are often used to measure the

overall financial soundness of a bank and the quality of its management.

1

Although, empirical research into explanatory factors of banks’ financial performance as

much as efficiency measurement in banking was and still is predominated by an economic

point of view. Numerous studies were performed to decide between the efficient structure

hypothesis and the Structure Conduct Performance (SCP) paradigm. While the first suggests

that high profitability, high market share, and high market concentration are results of high

efficiency, the latter attributes high profitability to anticompetitive collusion among market

participants (traditional SCP) or to the abuse of market power of large individual players

(relative market power hypothesis). Traditionally, theses hypotheses were tested without

any direct efficiency measure (Molyneux and Forbes 1995).

Not only the commercial banks but also any Financial Institutions (FIs) require regular self

health check up to maintain the confidence of private sector in financial system of the

country and protect the interest of depositors, lenders, shareholders and other stakeholders.

The gravity of the importance of sound financial sector has increased tremendously after the

international financial turmoil of the second half of the 1990s. International monetary

authorities such as International Monetary Fund and international FI like the World Bank

have underpinned the need of healthy financial sector to build up the confidence of private

sector in the liberalized financial system. Therefore, they have directed their member

countries to reform the financial sector and conduct the regular health checkup of Financial

Institutions through onsite and offsite supervision. (Keshar J. Baral, 2005: 42)

1.2. Problem statement

Health checkup of the banking and finance industry plays a significant role in determining

financial stability of any country. Furthermore, globalization and technological

advancement has created a highly competitive market. This affects all organizations

regardless of business emphasis. Banks are of no exception.

During the first half of 2012, the sector demonstrated good performance as a result of

strengthened legal and supervisory framework as well as good macroeconomic

environment. (BNR, 2012: 30)

2

Furthermore, total loans increased by 20% from RWF 631.2 billion in December 2011 to

RWF 757.1 billion in June 2012, while deposits have grown by 12.8% from RWF 716.5

billion in December 2011 to RWF 808.4 billion end June 2012. (BNR, 2012: 30)

While reviewing this situation, it points toward that there is a remarkable field of research

and therefore this has attracted the researcher’s attention to find out what impact can have a

financial analysis in BCR health check up in framework of CAMELS.

1.3. Objectives of the study

1.3.1. General objective

The general objective of the study is to assess the financial analysis based on CAMELS

framework in BCR health check up.

1.3.2. Specific objectives

The following specific objectives must be achieved.

• To assess BCR bank’ capital adequacy, asset quality, management soundness,

earning and profitability, liquidity, sensitivity to market risk for the period from

2005-2010.

• To assess BCR bank’ market based indicators like market price of financial

instruments and credit ratings for the period from 2005-2010.

1.4. Research questions

The following questions guide this research to achieve the above objectives:

• What is the situation of BCR bank’ health, in CAMELS’ framework, for the period

from 2005-2010?

• How is BCR Ltd. Sensitive to market risk for the period under study (2005-2010)?

3

1.5. Scope of the study

The study encompassed ideas concerning the financial management field, especially the

impact of a financial analysis utilized in BCR Ltd. to its overall performance in framework

of CAMELS; for a period of 5 years (2005-2010) and the study is carried out in BCR Ltd.

main branch, located in Kigali City. The area was chosen due to its accessibility to the

researcher.

1.6. Significance of the study

The study will benefit different groups of people and aims to get means and ways on how a

strong financial analysis can improve the performance of a commercial bank. The study

benefited the following groups of people in this order respectively.

1.6.1. To the researcher

• The study enabled the researcher to know the impact of a financial analysis to the

performance of BCR Ltd. and how that performance is calculated in framework of

CAMELS.

• The study benefited the researcher to gain more experience of coordinating other studies

and to add a pool of knowledge, especially when making other more research.

1.6.2. To BCR Ltd.

• The study aim at giving the recommendations on how BCR Ltd. can assist his financial

analysts to do their work well.

• The study will help the finance managers and others who are responsible in increasing

the performance of the company.

• The study will help the financial analysis department to know their weaknesses and

strength in increasing the performance of the bank.

4

1.6.3 To others researchers

• The report of this study will serve as basis and guide for future reference by other

researchers and other academic references;

• This research will also help other people especially on how they could improve their

methods of calculating the performance or profit by the use of CAMELS ratings system,

without forgetting, the way they will benefit explanations on the impact of a financial

analysis to the overall performance of BCR Ltd.

1.7. Company profile

1.7.1. Historical background

Banque Commerciale du Rwanda Limited (BCR) was incorporated on 25th May 1963 as

the first commercial bank in Rwanda. In December 2004, BCR marked another milestone

when it was privatized and acquired by Actis after recapitalization of the Company’s equity.

Actis (at that time Common Development Corporation) is owned 40% by the Government

of United Kingdom and 60 % privately owned by the partners of Actis. Since Actis’

acquisition of an 80% share in BCR, the Bank has grown rapidly over the last few years and

is now one of the foremost banking institutions in Rwanda. BCR has a strong reputation of

reliability, solidity and innovation with a passion to serve and satisfy its customers.

The bank has won several local and international awards, which include:

• Winner of the prestigious awards by The Banker magazine - awarded “Banker of the

year’’

• Winner of Best bank of the year in Rwanda by Global Finance 2008, 2009, 2010 &

2010

• Winner of the Best customer Service Bank by Rwanda Development board (RDB)

2009

5

BCR is the first bank to:

• To list a 10 year corporate bond on the Rwandan capital market,

• Introduce Mortgages to the Rwandan Market,

• Introduce Leasing to the Rwandan Market,

• Introduce and successfully conclude the largest size loan syndication in Rwanda,

• Introduce Online banking, SMS banking and Phone banking services,

• Launch mobile money transfer in partnership with a major mobile phone operator,

• Introduce forward Treasury products,

• Issue a Treasury Newsletter to customers,

• Offer dedicated counters to Institutional & VIP clients

1.7.2. Vision

“To be the most respected and leading provider of innovative financial services solutions in

the region”

1.7.3. Mission statement

BCR seeks to grow shareholder value while playing a key role in transforming the economy

and enhancing the well being of Rwandans.

• To support the development of the banking sector

• To support the drive for private sector investment for the development of the

economy

• To be the leading bank in Rwanda

• To offer our shareholders the best returns

1.8. Organization of the study

This research work is divided into five chapters.

Chapter one consists of the general introduction which comprises the background of the

study, statement of the problem, objectives of the study, research questions, scope of the

study, significance of the study, Company profile and organization of the study. Chapter

6

two presents a review of existing literature on financial analysis; overall performance

(health) and commercial banks as far as the financial analysis have an impact on the

performance of a commercial bank. Chapter three presents the methodology used for data

collection. Chapter four is the analysis of the data and interpretation of findings. And finally

chapter five is about the summary of research findings, conclusion and suggestions for

future research.

7

CHAPTER TWO: LITERATURE REVIEW LITERATURE REVIEW

The literature review provides a theoretical framework of the research topic related

literature. It is important for a researcher to show how his/ her research fits into the body of

knowledge generated over the ages.

This chapter provides explanation of the key concepts related to the impact of financial

analysis in a commercial bank’ health check up (overall performance) in framework of

CAMELS rating system and it portrays the views of different authors and researchers in the

discipline of financial analysis and performance in order to arrive at conceptual framework

of the study. It sets to find out their findings, arguments, ideas, and observation that are

available to this study.

THEORIES ON FINANCIAL ANALYSIS

According to Investopedia, financial analysis means the process of evaluating businesses,

projects, budgets and other finance-related entities to determine their suitability for

investment. Typically, financial analysis is used to analyze whether an entity is stable,

solvent, liquid, or profitable enough to be invested in. When looking at a specific company,

the financial analyst will often focus on the income statement, balance sheet, and cash flow

statement. In addition, one key area of financial analysis involves extrapolating the

company's past performance into an estimate of the company's future performance.

Investopedia continues explaining 'Financial Analysis' as one of the most common ways of

analyzing financial data is to calculate ratios from the data to compare against those of other

companies or against the company's own historical performance. For example, return on

assets is a common ratio used to determine how efficient a company is at using its assets

and as a measure of profitability. This ratio could be calculated for several similar

companies and compared as part of a larger analysis. (Investopedia, 2012)

According to the businessdictionary, Assessment of the (1) effectiveness with which funds

(investment and debt) are employed in a firm, (2) efficiency and profitability of its

8

operations, and (3) value and safety of debtors' claims against the firm's assets. It employs

techniques such as 'funds flow analysis' and financial ratios to understand the problems and

opportunities inherent in an investment or financing decision. (Business dictionary, 2012)

Financial analysis versus situation development

Users of this information are many and varied, from business managers interested in

evaluating it, financial managers about the viability of new investments, new projects and

what is the best way of financing to foreign banks on whether to grant credit or not to

undertake such investments.

From an external perspective, are very useful for anyone interested in knowing the situation

and expected development of the company, such as those listed below:

• Entities credit.

• Actions.

• Store of purchase.

• Customers.

• Employees, works councils and trade unions.

• Auditor of Accounts.

• Advice.

• Analyst Financial.

• Administration public.

• Competitors.

• Inverter and prospective buyers of the company.

Through the Financial Analysis can be diagnosed with the company, which is the result of

analysis of all relevant data and report the same weaknesses and strengths.

For diagnosis have been useful to give the following circumstances:

• Must be based on the analysis of all relevant data.

• Must be on time.

9

• It has to be right.

• Must be immediately accompanied by appropriate remedial measures to address

weaknesses and build on the strengths.

This diagnosis day to day business is a key tool for proper management. This helps to

achieve those objectives could be considered the majority of businesses

• Surviving: Continue running along the years, covering all the commitments.

• Be profitable, generate profits to reward shareholders adequately and properly fund

the necessary investments.

• Grow: Increase sales, market share, profits and company value.

Objectives of the Financial Analysis

Among the objectives to be taken into account in the Financial Analysis are:

• Assessing the results of the activity.

• To reveal the internal reserves in the enterprise.

• Achieve the increase in activity, while raising the quality of it.

• Increase the productivity of labor.

• Work efficiently represents means of fixed assets and inventories.

• Reduce the cost of services and achieve the planned efficiency.

Other important objectives of the analysis of economic activity fall below

• The search for internal reserves for further improvement work.

• The study of errors that occurred, in order to eliminate them in the future.

• The review of all information about the management aims of the work in the

company.

• The impact of social organizations in improving the financial activity of the

company.

To complement the goals is an analysis of all financial and economic process, starting from

the basic states for this analysis.

10

Basic State for Financial Analysis

The Financial Analysis is based on the use of information sources that provide data on past

and present of a company, allowing making predictions about the future of it, this source of

information are the Financial Statements. (Object guild, 2012)

THEORIES ON PERFORMANCE

According to Armstrong and Baron (1998:150), performance management is the strategic

and integrated approach to delivering sustained success to organizations by improving the

productivity and performance of people who work in them and by developing the

capabilities to teams and individual contributors.

In other words, performance can be referred to as the extent to which behavior results in the

attainment of work or organizational goals.

Decenzo and Robbins (1999:200) defined performance as a function of skill, abilities,

motivation and opportunity to perform.

According to Roger Moore (1993:159), performance management is therefore, a method of

connecting organizational objectives to people who are there to carry them out.

In this regard therefore, the managers’ responsibility is to coordinate resources in the most

effective and efficient manner to accomplish the institution’s goals and the analysis of

investment decision making in this context can be one of the criterions to evaluate the social

security performance as good or bad.

Performance management

Roger Mores (1993:5), defined performance management as a method of connecting an

organizations objective to the people who are there to carry them out. It makes the use of

procedures and communication drills the organization already has, it takes into account the 11

organizations culture, and establishes the key link between individual staff development and

corporate goals.

The purpose of performance management

It is the means of getting better results from the organization team and individuals trough

managing performance within an agreed framework of planned goals, standards, and

competence requirements. It is also a process, which establishes shares understanding about

what is to be achieved.

Performance management is also an approach to managing and developing people in a way

that increases the probability that it will be achieved in the short and longer term. It is

therefore concerned with performance improvement and individual effectiveness,

employee’s development by use of effective progress of continuous development and

satisfying their needs and expectations of all the organizations stakeholders whereby it

should recognize that these stakeholders’ needs and those of the organization will not

coincide.

Performance measurement

Performance measures will always be agreed upon when setting objectives since there is no

single measuring that can provide clear performance target or focuses attention on the

critical areas of business or work as commended by Kaplan and Orton (1992).

Therefore, a performance measure gives evidence or not intended results have been

achieved and show the extent to which the job holder has produced that result.

How to measure performance

Performance can be measured against four dimensions such as financial results, customer

services and internal process (how well things are done) and people management. The tools

12

that can be used when measuring performance are: finance, output or productivity, impact,

reaction and time.

Financial standard:

Some income of financial is invested in government enterprises and then managers should

compare the attained returns and costs incurred to measure the performance. The managers

here will be able to determine the performance after knowing the organizations costs benefit

during his operations.

Productivity (output):

This can be defined in different terms for example: the technical efficiency, which

maximizes output relation to input. The output attained is compare to the input and when

high and quality output was realized, and then the organizations performance is considered

good.

However Dalton (1988), argued that, as human factors are important in examining how

inputs are used to achieve results, output may likewise be interpreted as organizations

effectiveness and how both can be maximized is through employee or staff motivations, the

degree of staff development, participation ad consensus process

Impact on attainment of performance standards:

Managers will base on their motivation packages, staff development, and change of

behavior and level of innovation to measure performance. He will evaluate whether those

incentives have any positive impact on the attainment of standards like good quality

production, level of services, competition of work and ability to capture the customers.

13

Aspects of the performance

Economic performance:

It gets along like the profitability of the company. It resides in the service of the company is

its capacity to achieve the laid down goals. Some criteria of economic performance

evaluation.

• The productivity

• The quality of the products and services

• Economy of the resources

• Competitiveness

• Profitability

• The sales turnover

• Profit

• The respect of the deadlines

Organizational performance:

Marmuse (1997: 36) defines the organizational performance as being "the way in which it

manages to reach them its objectives and the way in which it arrives has to reach them".

Some criteria of organizational performance evaluation:

• The quality of the information flow

• Relations between the services

• Coordination

• The degree of control

• The communication

• Decentralization

• Flexibility

The human performance:

Martory and Crozet (1988: 45) affirm that the human performance is analyzed through the

resulting one obtained by the employees on the working stations in a group, a service or a

whole entity.

14

This result is expressed by the richness creates, the produced added value, the supplement of

value given to the unit and the improvement of the establishment in the environment. some

criteria of human performance evaluation.

• The productivity of the personnel,

• The engagement of the personnel,

• Job satisfaction,

• The initiative,

• Speed of decision-making

• Formation.

Let us recall that the performance is thus regarded as being the sum of satisfactions

(resulting financial and non-financial create for the whole of the parts fascinating is the

aptitude of the organization to produce these satisfactions in a durable way).

CAMELS RATING SYSTEM TOWARDS BANK’S PERFORMANCE

In 1979, the Uniform Financial Institutions Rating System was adopted to provide federal

bank regulatory agencies with a framework for rating financial condition and performance

of individual banks (Siems and Barr; 1998). Since then, the use of the CAMEL factors in

evaluating a bank’s financial health has become widespread among regulators.

Piyu (1992) notes “currently, financial ratios are often used to measure the overall financial

soundness of a bank and the quality of it management. Bank regulators, for example, use

financial ratios to help evaluate a bank’s performance as part of the CAMEL system”. The

evaluation factors are as follows;

C : Capital adequacy

A : Asset quality

M : Management quality

E : Earnings ability

L : Liquidity.

Each of the five factors is scored from one to five, with one being the strongest rating. An

overall composite CAMEL rating, also ranging from one to five, is then developed from this 15

evaluation. As a whole, the CAMEL rating, which is determined after an on-site

examination, provides a means to categorize banks based on their overall health, financial

status, and management.

The Basle Committee on Banking Supervision of the Bank of International Settlements

(BIS) has recommended using capital adequacy, assets quality, management quality, earnings

and liquidity (CAMEL) as criteria for assessing a FI in 1988 (ADB 2002). The sixth

component, market risk (S) was added to CAMEL in 1997 (Gilbert, Meyer and Vaughan 2000).

However, most of the developing countries are using CAMEL instead of CAMELS in the

performance evaluation of the FIs.

CAMELS’ framework is a common method for evaluating the soundness of Financial

Institutions. This system was developed by regulatory authorities of the U.S banks. The

Federal Reserve Bank, the Comptroller of the Currency and the Federal Deposit Insurance

Corporation all use this system (McNally 1996).

Monetary authorities in the most of the countries are using this system to check up the health

of an individual FI. In addition, International Monetary Fund also is using the aggregated

indicators of individual FIs to assess the financial system soundness of its member countries

as part of its surveillance work (Hilbers, Krueger and Moretti 2000).

Capital Adequacy

CAMELS’ framework system looks at six major aspects of any Financial Institution: capital

adequacy, asset quality, management soundness, earnings, liquidity, and sensitivity to

market risk (Hilbers, Krueger and Moretti 2000).

The first component, capital adequacy ultimately determines how well FIs can manage with

shocks to their balance sheets. Thus, it tracks capital adequacy ratios that take into account

the most important financial risks—foreign exchange, credit, and interest rate risks—by

assigning risk weightings to the institution's assets. For the purpose of capital adequacy

measurement, bank capital is divided into Tier I and Tier II. Tier I capital is primary capital

and Tier II capital is supplementary capital.

16

Leverage ratio can be used to measure the capital adequacy of a bank. This is the ratio of

bank's book value of core capital to the book value of its assets. The higher ratio shows the

higher level of capital adequacy. The U.S.A. Federal Deposit Insurance Corporation

Improvement Act (FDICIA) of 1991 has fixed the five target zones:

i. 5 percent and above

ii. 4 percent and above

iii. under 4 percent,

iv. under 3 percent,

v. 2 percent and less, of leverage ratio.

The leverage ratio falling in the first zone implies that bank is well capitalized. Similarly, the

leverage falling in the second zone shows that bank is adequately capitalized. The leverage

falling in the last three zones indicates that bank is inadequately capitalized and regulators

should take prompt corrective action to bring the capital to the desirable level (Saunders and

Cornett 2004).

The leverage ratio stated in the foregoing discussion is simple capital to assets ratio. In other

words, assets are not risk adjusted. The 1993 Basel Accord enforced the capital ratio to risk

adjusted assets of commercial banks. According to this accord, core capital must equal to or

exceed 4 percent of the risk weighted assets of the commercial banks. Similarly, the amount

of the supplementary capital should not exceed the amount of the core capital and the total

capital must equal or exceed 8 percent of risk weighted assets (Saunders and Cornett 2004).

The Following are the Capital Adequacy ratios formulas:

Leverage Ratio (LR)

𝐿𝑅 = 𝐶𝐶𝑇𝐴

…………………….……. (1.1)

Where : CC = core capital

: TA = total assets

17

Core Capital Ratio (CCR)

𝐶𝐶𝑅 = 𝐶𝐶𝑅𝑊𝐴

………………………… (1.2)

Where : RWA =risk weighted assets

Total Capital Ratio (TCR)

𝑇𝐶𝑅 = 𝑇𝐶𝑅𝑊𝐴

………………………… (1.3)

Where : TC = total capital (core capital plus supplementary capital)

Supplementary Capital Ratio (SCR)

𝑆𝐶𝑅 = 𝑆𝐶𝑅𝑊𝐴

…………………..…… (1.4)

Where : SC = supplementary capital

Asset Quality

Credit risk is one of the factors that affect the health of an individual FI. The extent of the

credit risk depends on the quality of assets held by an individual FI. The quality of assets held

by an FI depends on exposure to specific risks, trends in non-performing loans, and the health

and profitability of bank borrowers—especially the corporate sector. We can use a number of

measures to indicate the quality of assets held by FIs.

The following are Assets Quality ratios formulas:

Nonperforming Loan Ratio (NPAR)

NPAR = NPATLA

………………………. (2.1)

Where : NPA = nonperforming assets (loan and advance)

: TLA = total loan and advance

Loan Loss Reserve Ratio (LLRR)

LLRR = LLRTLA

……………………… (2.2)

Where : LLR = loan loss reserve

18

Management Quality

Sound management is key to bank performance but is difficult to measure. It is primarily a

qualitative factor applicable to individual institutions. Several indicators, however, can

jointly serve as an indicator of management soundness. Expenses ratio, earning per

employee, cost per loan, average loan size and cost per unit of money lent can be used as a proxy

of the management quality.

The following are Management Efficiency ratios formulas:

Operating Expenses Ratio (OER)

OER = TOETOR

………………………… (3.1)

Where : TOE = total operating expenses, and it includes interest expenses, employees

expenses, office operating expenses, currency exchange loss, bad

loan advance written off and loan loss provision.

: TOR = total operating revenue, and it includes interest income and non-

interest income.

Earning per Employee (EPE)

EPE = NOINOE

…………………………. (3.2)

Where : NOI = net operating income

: NOE = number of employees

Earning Performance

Earning capacity or profitability keeps up the sound health of an FI. Chronically unprofitable FI

risks insolvency on one hand and on the others, unusually high profitability can reflect

excessive risk taking of an FI. There are different indicators of profitability. Return on

assets, return on equity, interest-spread ratio, earning-spread ratio, gross margin, operating

profit margin and net profit margin are commonly used profitability indicators.

The following are Earning Performance ratios formulas:

19

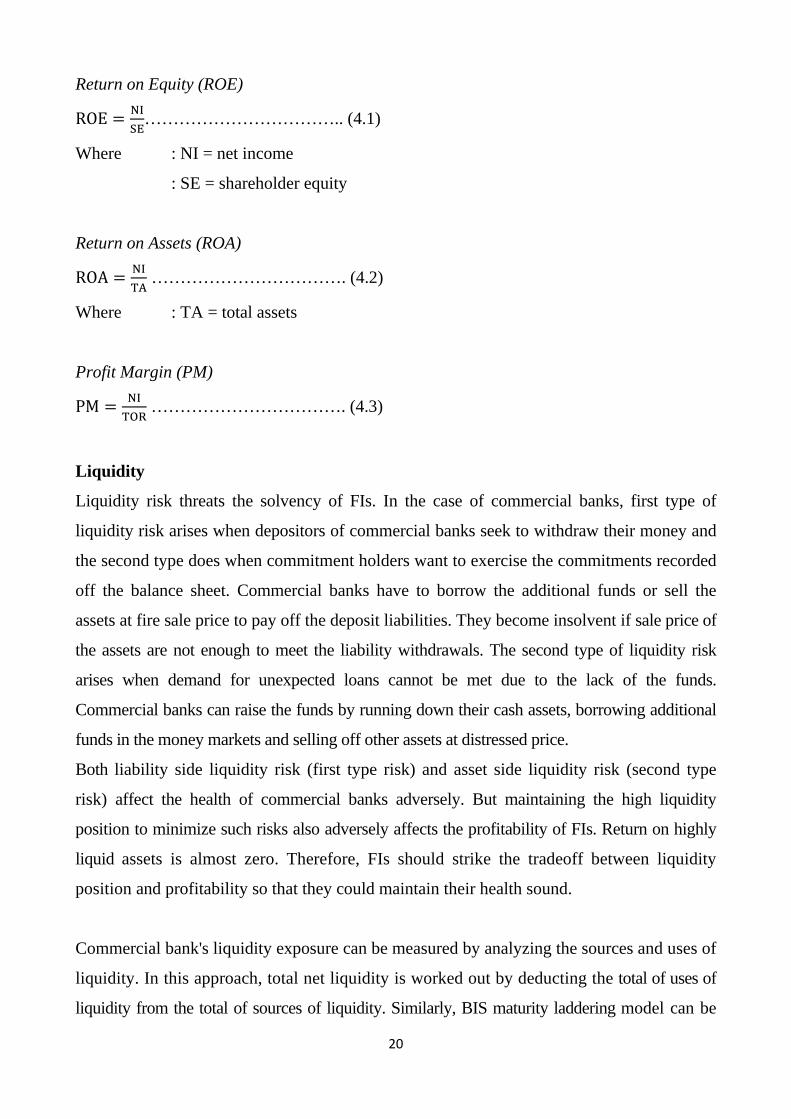

Return on Equity (ROE)

ROE = NISE

…………………………….. (4.1)

Where : NI = net income

: SE = shareholder equity

Return on Assets (ROA)

ROA = NITA

……………………………. (4.2)

Where : TA = total assets

Profit Margin (PM)

PM = NITOR

……………………………. (4.3)

Liquidity

Liquidity risk threats the solvency of FIs. In the case of commercial banks, first type of

liquidity risk arises when depositors of commercial banks seek to withdraw their money and

the second type does when commitment holders want to exercise the commitments recorded

off the balance sheet. Commercial banks have to borrow the additional funds or sell the

assets at fire sale price to pay off the deposit liabilities. They become insolvent if sale price of

the assets are not enough to meet the liability withdrawals. The second type of liquidity risk

arises when demand for unexpected loans cannot be met due to the lack of the funds.

Commercial banks can raise the funds by running down their cash assets, borrowing additional

funds in the money markets and selling off other assets at distressed price.

Both liability side liquidity risk (first type risk) and asset side liquidity risk (second type

risk) affect the health of commercial banks adversely. But maintaining the high liquidity

position to minimize such risks also adversely affects the profitability of FIs. Return on highly

liquid assets is almost zero. Therefore, FIs should strike the tradeoff between liquidity

position and profitability so that they could maintain their health sound.

Commercial bank's liquidity exposure can be measured by analyzing the sources and uses of

liquidity. In this approach, total net liquidity is worked out by deducting the total of uses of

liquidity from the total of sources of liquidity. Similarly, BIS maturity laddering model can be

20

used to measure the liquidity of a commercial banks. In addition, different liquidity exposure

ratios such as borrowed funds to total assets, core deposit to total assets, loans to deposits, and

commitments to lend to total assets are used to measure the liquidity position of a commercial

bank (Saunders and Cornett 2004).

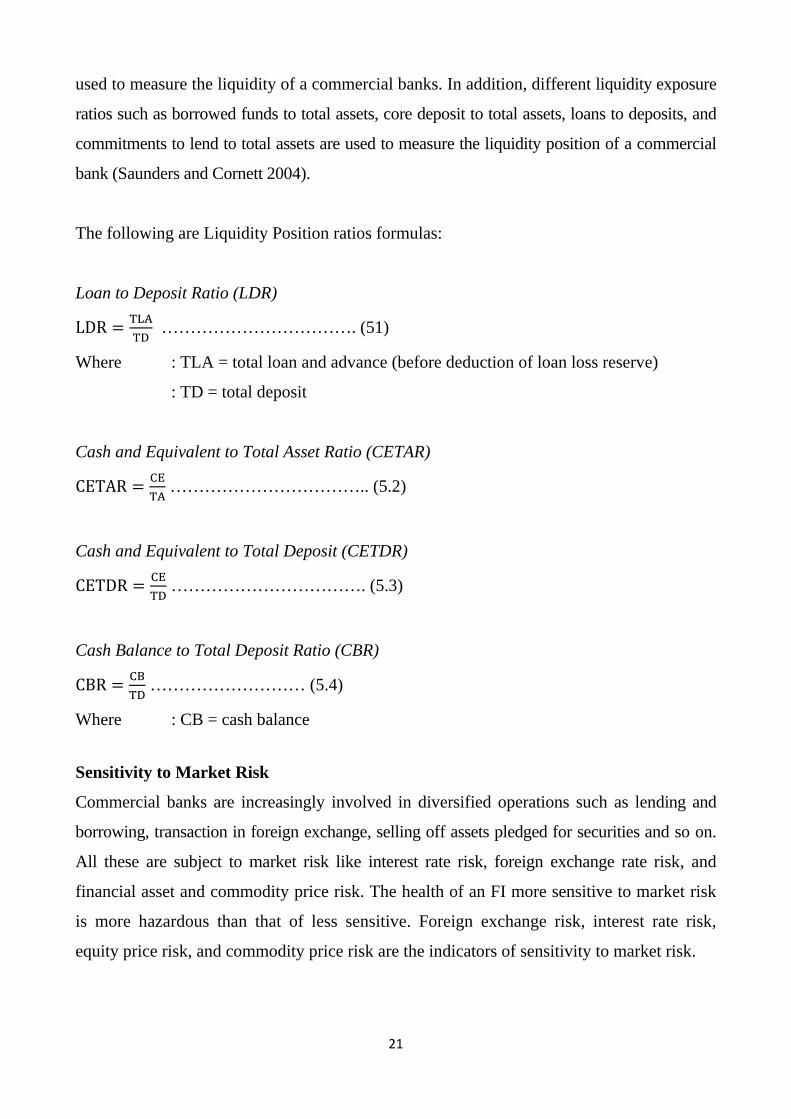

The following are Liquidity Position ratios formulas:

Loan to Deposit Ratio (LDR)

LDR = TLATD

……………………………. (51)

Where : TLA = total loan and advance (before deduction of loan loss reserve)

: TD = total deposit

Cash and Equivalent to Total Asset Ratio (CETAR)

CETAR = CETA

…………………………….. (5.2)

Cash and Equivalent to Total Deposit (CETDR)

CETDR = CETD

……………………………. (5.3)

Cash Balance to Total Deposit Ratio (CBR)

CBR = CBTD

……………………… (5.4)

Where : CB = cash balance

Sensitivity to Market Risk

Commercial banks are increasingly involved in diversified operations such as lending and

borrowing, transaction in foreign exchange, selling off assets pledged for securities and so on.

All these are subject to market risk like interest rate risk, foreign exchange rate risk, and

financial asset and commodity price risk. The health of an FI more sensitive to market risk

is more hazardous than that of less sensitive. Foreign exchange risk, interest rate risk,

equity price risk, and commodity price risk are the indicators of sensitivity to market risk.

21

CHAPTER THREE: RESEARCH METHODOLOGY RESEARCH METHODOLOGY

This chapter presents the methodological approach of data collection techniques for the

purpose of the study. According to the book of social research methods by Richard M.

HESSLER [1989:80] Research methodology is a science of how to make research decisions

and it includes the practice of evaluating the goodness or badness of decisions made in

course of research.

This study is based on the documentation technique where, the documents that have been

consulted include book, Internet websites, related to the topic under the study, and the report

published by BCR Ltd.

Carl and Roger (1991:41) defined data analysis as the next step after data have been

collected in the research process whose purpose is to interpret and draw conclusions from

the mass of collected data. Data collected were analyzed and edited using EXCEL software.

The process of data analysis will have to begin and this involves the following steps.

This study is based on the historical data disclosed by annual reports of BCR Ltd. BCR has

dictated its financial statements to disclose the financial information in the prescribed

format since the Fiscal Year 2005/2010.

The analysis of this study is entirely based on the CAMELS framework. As stated in

theoretical prescription, health check up of any Financial Institutions in this framework is

concentrated in the six components: capital adequacy, asset quality, management quality,

earning, liquidity and sensitivity to market.

But in this study, the last component has been dropped due to the presence of much more

complication.

So, analysis of financial health of BCR Ltd. bank is carried out in the framework of

CAMEL. Indicators of each component also have been used according to the financial data

disclosed in annual reports.

22

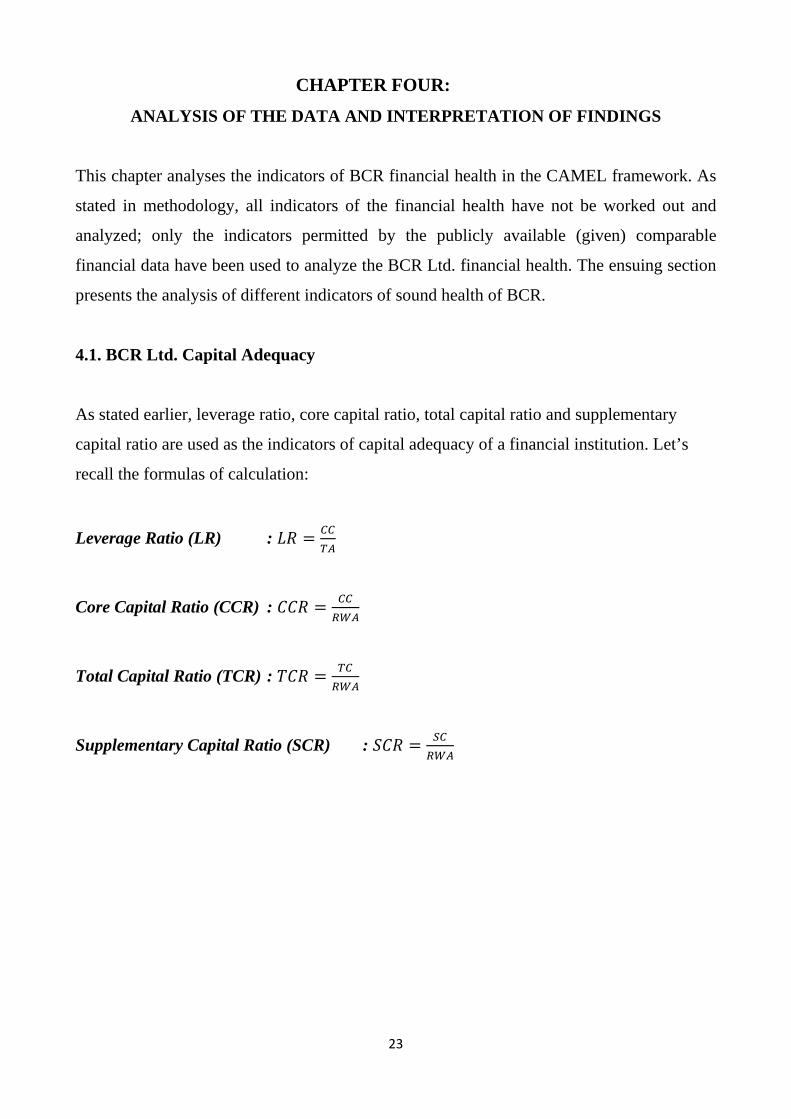

CHAPTER FOUR: ANALYSIS OF THE DATA AND INTERPRETATION OF FINDINGS

ANALYSIS OF THE DATA AND INTERPRETATION OF FINDINGS

This chapter analyses the indicators of BCR financial health in the CAMEL framework. As

stated in methodology, all indicators of the financial health have not be worked out and

analyzed; only the indicators permitted by the publicly available (given) comparable

financial data have been used to analyze the BCR Ltd. financial health. The ensuing section

presents the analysis of different indicators of sound health of BCR.

4.1. BCR Ltd. Capital Adequacy

As stated earlier, leverage ratio, core capital ratio, total capital ratio and supplementary

capital ratio are used as the indicators of capital adequacy of a financial institution. Let’s

recall the formulas of calculation:

Leverage Ratio (LR) : 𝐿𝑅 = 𝐶𝐶𝑇𝐴

Core Capital Ratio (CCR) : 𝐶𝐶𝑅 = 𝐶𝐶𝑅𝑊𝐴

Total Capital Ratio (TCR) : 𝑇𝐶𝑅 = 𝑇𝐶𝑅𝑊𝐴

Supplementary Capital Ratio (SCR) : 𝑆𝐶𝑅 = 𝑆𝐶𝑅𝑊𝐴

23

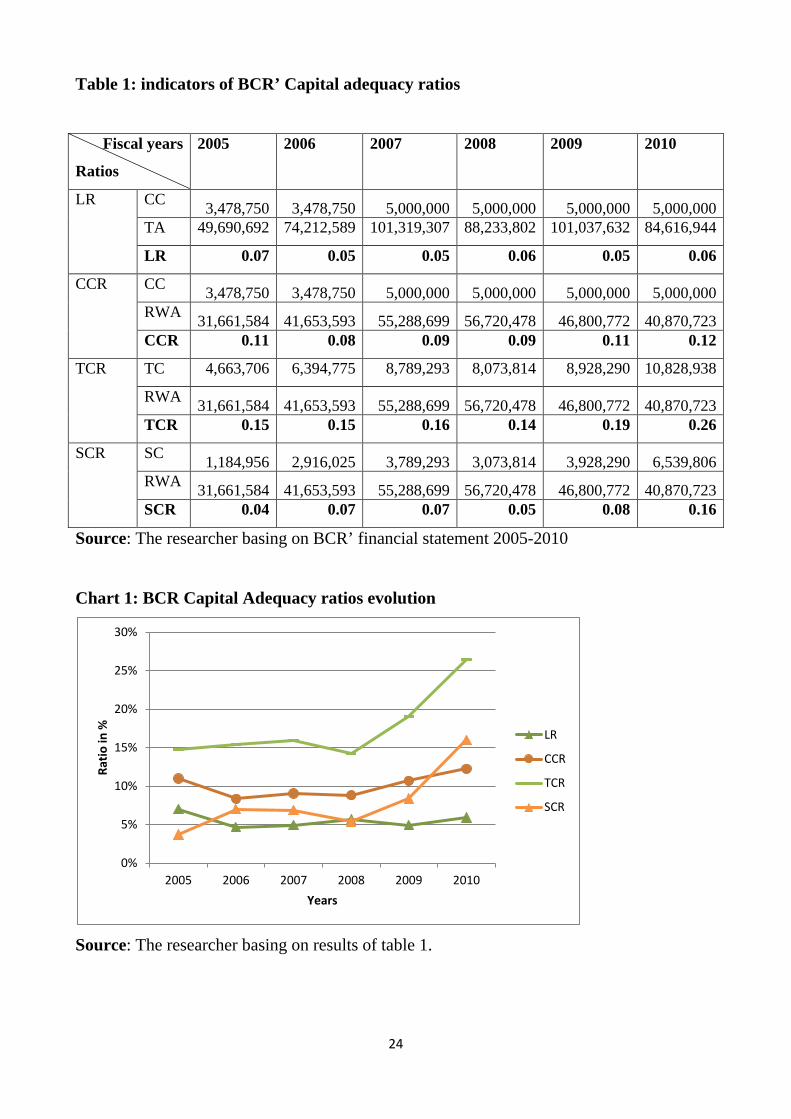

Table 1: indicators of BCR’ Capital adequacy ratios

Fiscal years

Ratios

2005 2006 2007 2008 2009 2010

LR CC 3,478,750 3,478,750 5,000,000 5,000,000 5,000,000 5,000,000 TA 49,690,692 74,212,589 101,319,307 88,233,802 101,037,632 84,616,944

LR 0.07 0.05 0.05 0.06 0.05 0.06

CCR CC 3,478,750 3,478,750 5,000,000 5,000,000 5,000,000 5,000,000 RWA 31,661,584 41,653,593 55,288,699 56,720,478 46,800,772 40,870,723 CCR 0.11 0.08 0.09 0.09 0.11 0.12

TCR TC 4,663,706 6,394,775 8,789,293 8,073,814 8,928,290 10,828,938

RWA 31,661,584 41,653,593 55,288,699 56,720,478 46,800,772 40,870,723 TCR 0.15 0.15 0.16 0.14 0.19 0.26

SCR SC 1,184,956 2,916,025 3,789,293 3,073,814 3,928,290 6,539,806 RWA 31,661,584 41,653,593 55,288,699 56,720,478 46,800,772 40,870,723 SCR 0.04 0.07 0.07 0.05 0.08 0.16

Source: The researcher basing on BCR’ financial statement 2005-2010

Chart 1: BCR Capital Adequacy ratios evolution

Source: The researcher basing on results of table 1.

0%

5%

10%

15%

20%

25%

30%

2005 2006 2007 2008 2009 2010

Ratio

in %

Years

LR

CCR

TCR

SCR

24

As it is shown by results from the table above and chart 1, BCR leverage ratios, in general,

show that the bank is well capitalized and it is strong enough to manage the shock to

balance sheet. Since the leverage ratios during the study periods are greater than 5 percent

(5%). Conventionally, leverage ratio of 5 percent or greater than 5 percent indicates that

commercial banks are well capitalized.

The indicators: TCR, CCR and SCR, of capital adequacy also confirm with the implication

of leverage ratio. In general, BCR have met the capital adequacy ratio as directed by BNR.

4.2. BCR Ltd. Asset quality

It is obvious from the theoretical prescription that the health of commercial banks largely

depends on the quality of assets held by them, and quality of the assets relies on the

financial health of their borrowers. As stated earlier, many indicators can be used to

measure the quality of assets held by BCR bank. But, here, only two simple indicators—

non-performing asset ratio and loan loss reserve ratio—are used to measure the quality of

assets being held by BCR Ltd. bank. Let’s recall the formulas of calculation:

Nonperforming Loan Ratio (NPAR) : NPAR = NPATLA

Loan Loss Reserve Ratio (LLRR) : LLRR = LLRTLA

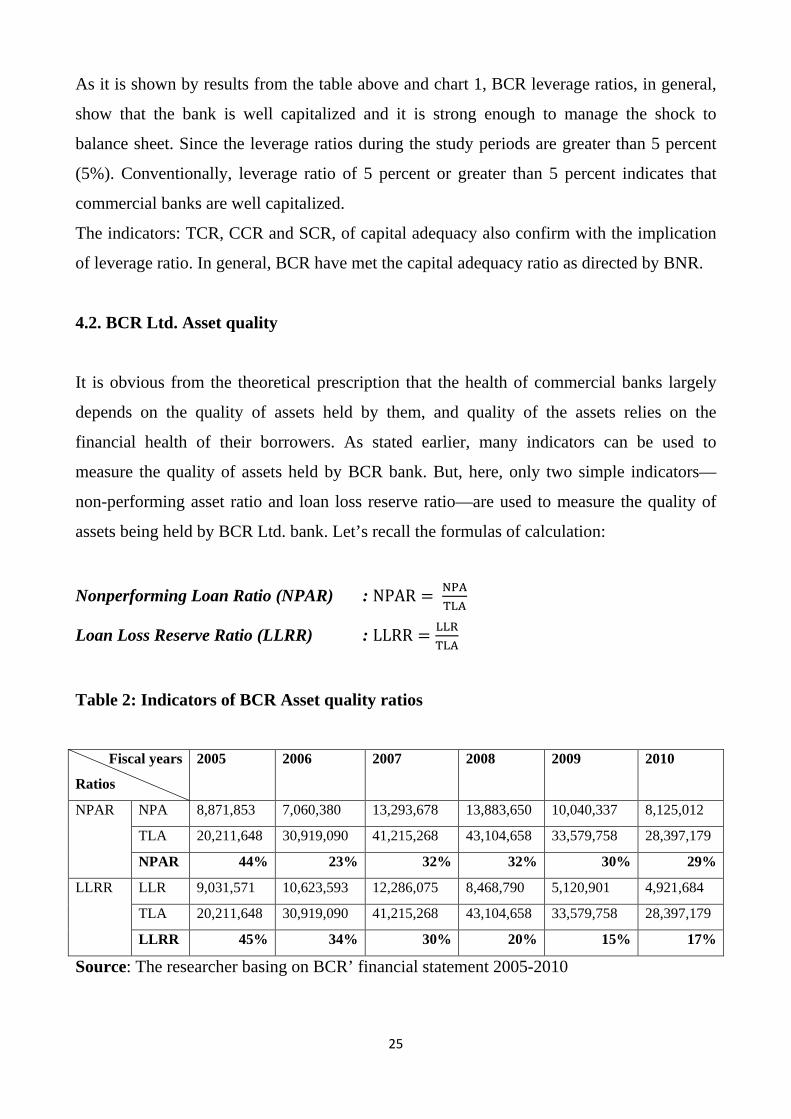

Table 2: Indicators of BCR Asset quality ratios

Fiscal years

Ratios

2005 2006 2007 2008 2009 2010

NPAR NPA 8,871,853 7,060,380 13,293,678 13,883,650 10,040,337 8,125,012

TLA 20,211,648 30,919,090 41,215,268 43,104,658 33,579,758 28,397,179

NPAR 44% 23% 32% 32% 30% 29%

LLRR LLR 9,031,571 10,623,593 12,286,075 8,468,790 5,120,901 4,921,684

TLA 20,211,648 30,919,090 41,215,268 43,104,658 33,579,758 28,397,179

LLRR 45% 34% 30% 20% 15% 17%

Source: The researcher basing on BCR’ financial statement 2005-2010

25

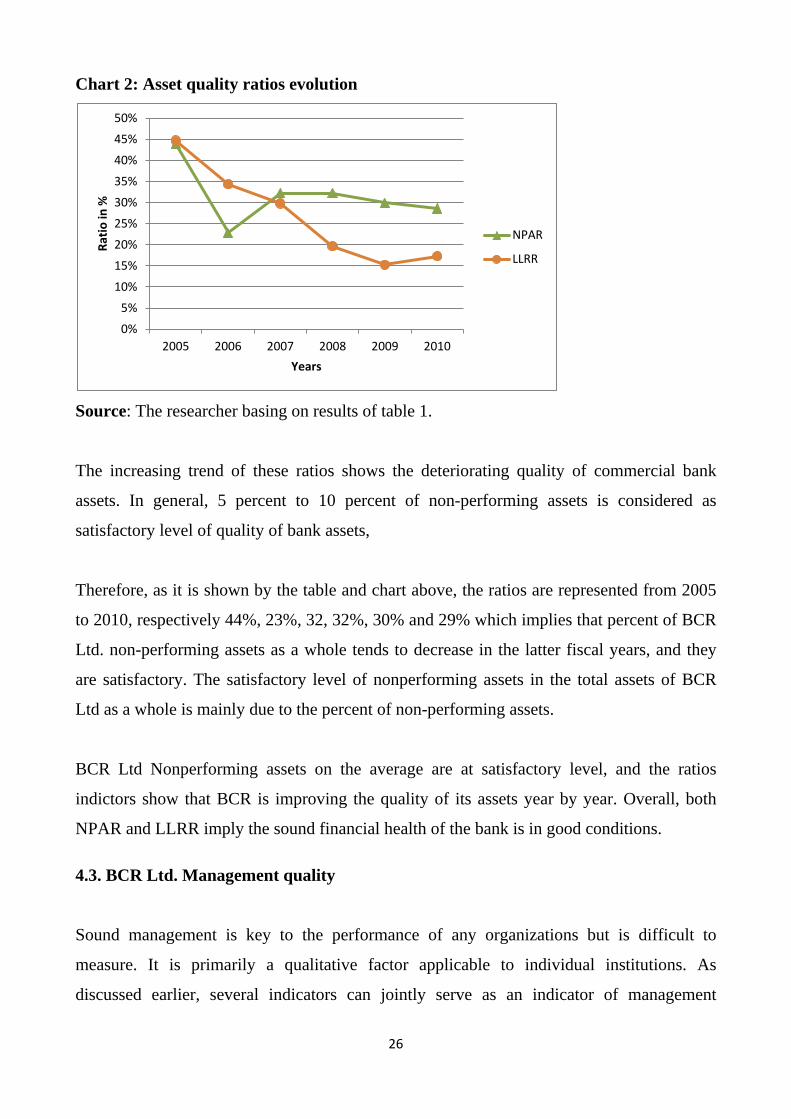

Chart 2: Asset quality ratios evolution

Source: The researcher basing on results of table 1.

The increasing trend of these ratios shows the deteriorating quality of commercial bank

assets. In general, 5 percent to 10 percent of non-performing assets is considered as

satisfactory level of quality of bank assets,

Therefore, as it is shown by the table and chart above, the ratios are represented from 2005

to 2010, respectively 44%, 23%, 32, 32%, 30% and 29% which implies that percent of BCR

Ltd. non-performing assets as a whole tends to decrease in the latter fiscal years, and they

are satisfactory. The satisfactory level of nonperforming assets in the total assets of BCR

Ltd as a whole is mainly due to the percent of non-performing assets.

BCR Ltd Nonperforming assets on the average are at satisfactory level, and the ratios

indictors show that BCR is improving the quality of its assets year by year. Overall, both

NPAR and LLRR imply the sound financial health of the bank is in good conditions. 4.3. BCR Ltd. Management quality

Sound management is key to the performance of any organizations but is difficult to

measure. It is primarily a qualitative factor applicable to individual institutions. As

discussed earlier, several indicators can jointly serve as an indicator of management

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2005 2006 2007 2008 2009 2010

Ratio

in %

Years

NPAR

LLRR

26

soundness. However, only operating expenses ratio (OER) and earning per employee (EPE)

are used to indicate the quality of management here.

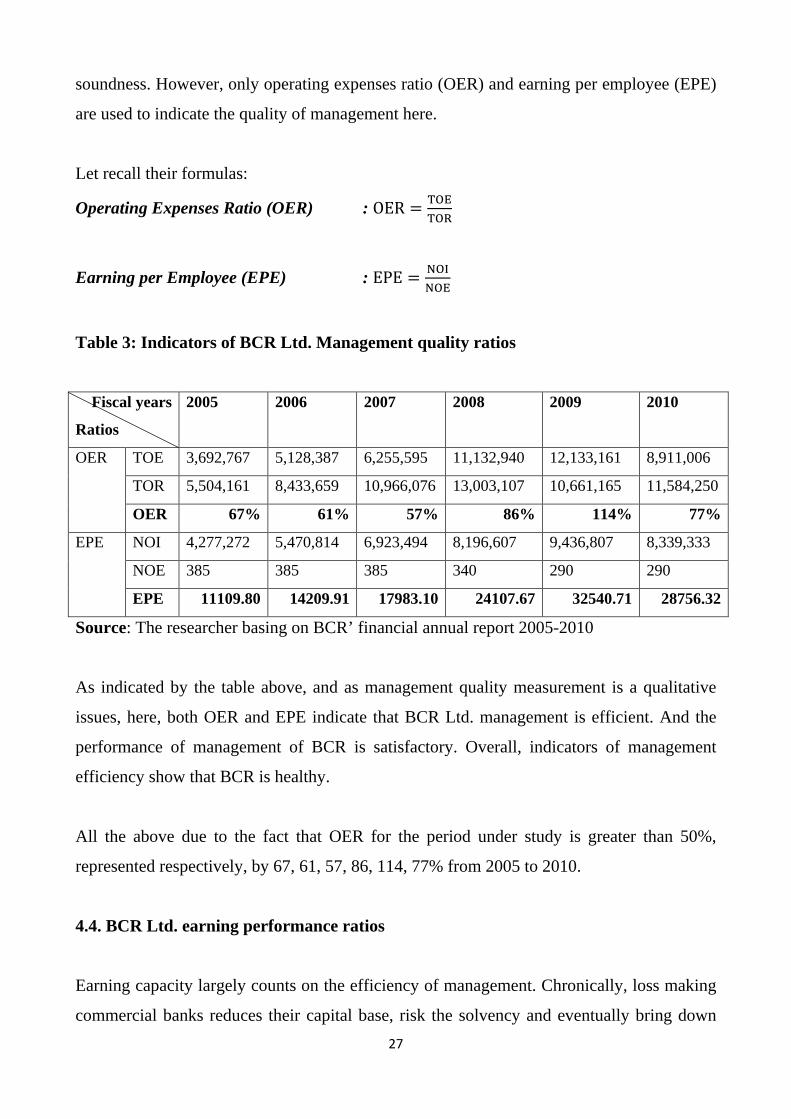

Let recall their formulas:

Operating Expenses Ratio (OER) : OER = TOETOR

Earning per Employee (EPE) : EPE = NOINOE

Table 3: Indicators of BCR Ltd. Management quality ratios

Fiscal years

Ratios

2005 2006 2007 2008 2009 2010

OER TOE 3,692,767 5,128,387 6,255,595 11,132,940 12,133,161 8,911,006

TOR 5,504,161 8,433,659 10,966,076 13,003,107 10,661,165 11,584,250

OER 67% 61% 57% 86% 114% 77%

EPE NOI 4,277,272 5,470,814 6,923,494 8,196,607 9,436,807 8,339,333

NOE 385 385 385 340 290 290

EPE 11109.80 14209.91 17983.10 24107.67 32540.71 28756.32

Source: The researcher basing on BCR’ financial annual report 2005-2010

As indicated by the table above, and as management quality measurement is a qualitative

issues, here, both OER and EPE indicate that BCR Ltd. management is efficient. And the

performance of management of BCR is satisfactory. Overall, indicators of management

efficiency show that BCR is healthy.

All the above due to the fact that OER for the period under study is greater than 50%,

represented respectively, by 67, 61, 57, 86, 114, 77% from 2005 to 2010.

4.4. BCR Ltd. earning performance ratios

Earning capacity largely counts on the efficiency of management. Chronically, loss making

commercial banks reduces their capital base, risk the solvency and eventually bring down 27

the wealth of their shareholders. Conversely, constantly profit making banks add equity to

the total capital fund, reduce the risk of insolvency, and finally increase the wealth of their

shareholders.

So, earning capacity is one of the indicators of the sound health of a commercial bank.

Though different indicators can be used to measure the profitability of banks, ROE, ROA

and PM are used in this study.

Let’s recall their formulas:

Return on Equity (ROE) : ROE = NISE

Return on Assets (ROA) : ROA = NITA

Profit Margin (PM) : PM = NITOR

Table 4: Indicators of BCR Ltd. earning performance ratios

Fiscal years

Ratios

2005 2006 2007 2008 2009 2010

ROE NI 1,043,045 2,115,942 3,115,611 897,903 859,137 2,628,524

SE 4,663,706 6,394,775 8,789,293 8,073,814 8,928,290 10,828,938

ROE 22% 33% 35% 11% 10% 24%

ROA NI 1,043,045 2,115,942 3,115,611 897,903 859,137 2,628,524

TA 49,690,692 74,212,589 101,319,307 88,233,802 101,037,632 84,616,944

ROA 2% 3% 3% 1% 1% 3%

PM NI 1,043,045 2,115,942 3,115,611 897,903 859,137 2,628,524

TOE 3,692,767 5,128,387 6,255,595 11,132,940 12,133,161 8,911,006

PM 28% 41% 50% 8% 7% 29%

Source: The researcher basing on BCR’ financial statement 2005-2010

28

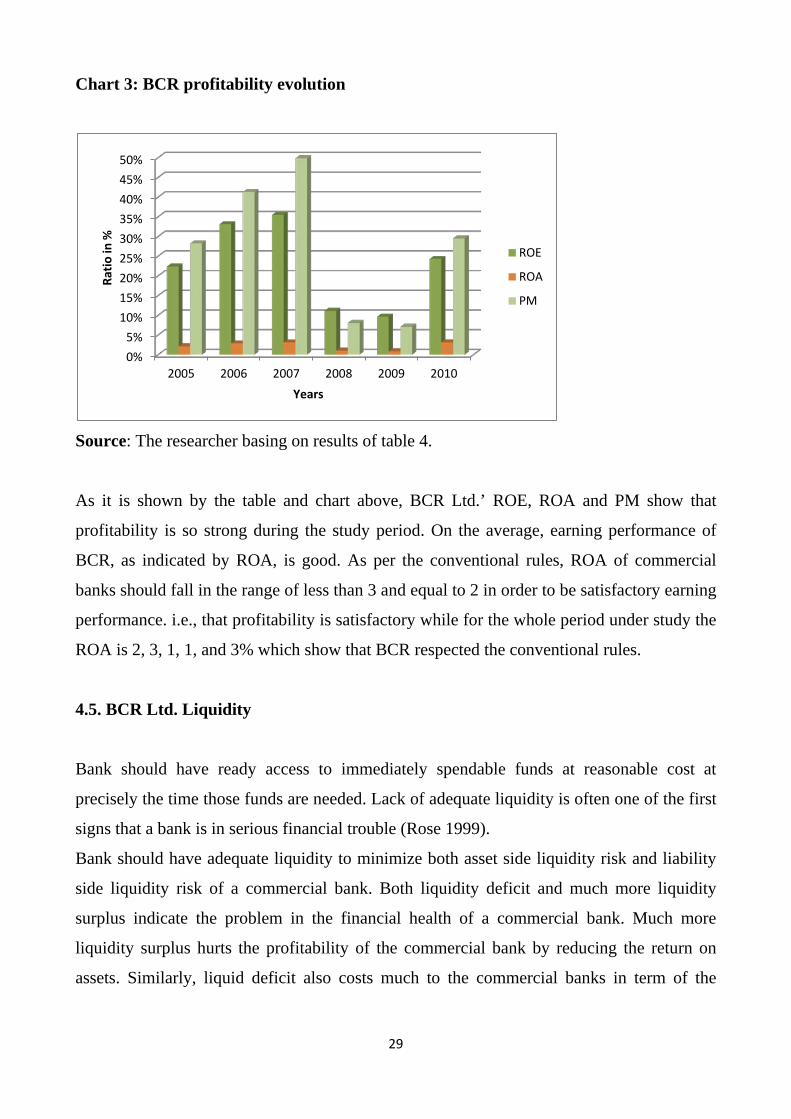

Chart 3: BCR profitability evolution

Source: The researcher basing on results of table 4.

As it is shown by the table and chart above, BCR Ltd.’ ROE, ROA and PM show that

profitability is so strong during the study period. On the average, earning performance of

BCR, as indicated by ROA, is good. As per the conventional rules, ROA of commercial

banks should fall in the range of less than 3 and equal to 2 in order to be satisfactory earning

performance. i.e., that profitability is satisfactory while for the whole period under study the

ROA is 2, 3, 1, 1, and 3% which show that BCR respected the conventional rules.

4.5. BCR Ltd. Liquidity

Bank should have ready access to immediately spendable funds at reasonable cost at

precisely the time those funds are needed. Lack of adequate liquidity is often one of the first

signs that a bank is in serious financial trouble (Rose 1999).

Bank should have adequate liquidity to minimize both asset side liquidity risk and liability

side liquidity risk of a commercial bank. Both liquidity deficit and much more liquidity

surplus indicate the problem in the financial health of a commercial bank. Much more

liquidity surplus hurts the profitability of the commercial bank by reducing the return on

assets. Similarly, liquid deficit also costs much to the commercial banks in term of the

0%5%

10%15%20%25%30%35%40%45%50%

2005 2006 2007 2008 2009 2010

Ratio

in %

Years

ROE

ROA

PM

29

higher purchasing price of liquidity and hurt in the reputation of the banks. Therefore,

commercial banks should strike the trade-off between the profitability and liquidity risk.

As stated earlier in theoretical prescription, BCR uses total loan to total deposit ratio (LDR),

cash and equivalents to total assets ratio (CETAR), cash and equivalents to total deposit

ratio (CETDR), and cash balance to total deposit ratio (CBR) to measure its liquidity

position.

Let’s recall their formulas:

Loan to Deposit Ratio (LDR) : LDR = TLATD

Cash and Equivalent to Total Asset Ratio (CETAR) : CETAR = CETA

Cash and Equivalent to Total Deposit (CETDR) : CETDR = CETD

Cash Balance to Total Deposit Ratio (CBR) : CBR = CBTD

Table 5: Indicators of BCR Ltd. liquidity ratios

Fiscal years

Ratios

2005 2006 2007 2008 2009 2010

LDR TLA 20,211,648 30,919,090 41,215,268 43,104,658 33,579,758 28,397,179

TD 34,894,043 54,697,213 80,447,943 80,915,321 63,584,445 62,977,964

LDR 58% 57% 51% 53% 53% 45%

CETAR CE 21,468,773 36,177,487 52,006,692 42,702,856 40,238,583 42,704,461

TA 49,690,692 74,212,589 101,319,307 88,233,802 101,037,632 84,616,944

CETAR 43% 49% 51% 48% 40% 50%

CETDR CE 21,468,773 36,177,487 52,006,692 42,702,856 40,238,583 42,704,461

TA 49,690,692 74,212,589 101,319,307 88,233,802 101,037,632 84,616,944

CETDR 43% 49% 51% 48% 40% 50%

CBR CB 11,260,698 18,948,232 20,229,980 22,243,190 18,247,163 13,595,995

TD 34,894,043 54,697,213 80,447,943 80,915,321 63,584,445 62,977,964

CBR 32% 35% 25% 27% 29% 22%

Source: The researcher basing on BCR’ financial statement 2005-2010

30

Chart 4: BCR Ltd. liquidity ratios evolution

Source: The researcher basing on results of table 5.

According to results from the table above, BCR’ LDR as whole is high. It hovers in the

range of 50 percent to 64.59 percent of the total deposit except the last year 2010. This

implies it is heavily relying on the short-term money market and they will not face the

liquidity problems in future. Other two indicators—CETAR and CETDR—also show the

high liquidity position of BCR. On the whole liquidity position is higher.

As directed by BNR, commercial banks had to maintain 30 percent cash of the total deposits

in their vault in 2005-2008, and 20 percent in 2008-2010 (BNR 2010).

In spite of the withdrawal of the provision, level of liquid assets, on the average, is higher

during the study period. On the whole, CBR is higher during the study period but CETDR is

greater.

All the above results permitted the research to achieve his first objective of the research

where he indicated the capital adequacy, asset quality, management soundness, earning,

profitability and liquidity of BCR Ltd.

The second objective was not achieved due to lack of required data.

0%

10%

20%

30%

40%

50%

60%

2005 2006 2007 2008 2009 2010

Ratio

in %

Years

LDR

CETAR

CETDR

CBR

31

CHAPTER FIVE: SUMMARY OF FINDINGS, CONCLUSION AND SUGGESTIONS

SUMMARY OF FINDINGS, CONCLUSION AND SUGGESTIONS

5.1. Summary of the major findings

Carrying out the study entitled “Impact of financial analysis in a commercial bank’ health

check up in framework of CAMELS, Case study of BCR Ltd (2005-2010)” the following

findings qualified as ‘major’ acquired the researchers’ attention:

While Health check up of the banking and finance industry plays a significant role in

determining financial stability of any country, analysis of financial health of BCR Ltd. bank

was carried out in the framework of CAMEL. And indicators of each component of

CAMEL have been used according to the financial data disclosed in annual reports.

Leverage ratio, core capital ratio, total capital ratio and supplementary capital ratio are used

as the indicators of capital adequacy of a financial institution, Case of BCR Ltd. And it has

been found that leverage ratios, in general, show that the bank is well capitalized and it is

strong enough to manage the shock to balance sheet.

The health of commercial banks largely depends on the quality of assets held by them, and

quality of the assets relies on the financial health of their borrowers. As stated earlier, many

indicators can be used to measure the quality of assets held by BCR bank. But, in this study

only two simple indicators: non-performing asset ratio and loan loss reserve ratio.

Sound management is a key to the performance of any organizations but is difficult to

measure. It is primarily a qualitative factor applicable to individual institutions. However,

only operating expenses ratio (OER) and earning per employee (EPE) were used to indicate

the quality of management in this study.

Earning capacity largely counts on the efficiency of management. Earning capacity as one

of the indicators of the sound health of a commercial bank, though different indicators used

32

to measure the profitability of banks would have been applied but for the case of this study

ROE, ROA and PM were used.

Lack of adequate liquidity is often one of the first signs that a bank is in serious financial

trouble. Both liquidity deficit and much more liquidity surplus indicate the problem in the

financial health of a commercial bank. While for the case of this study, total loan to total

deposit ratio (LDR), cash and equivalents to total assets ratio (CETAR), cash and

equivalents to total deposit ratio (CETDR), and cash balance to total deposit ratio (CBR)

were used to measure BCR Ltd. liquidity position.

Regarding the second objective of this study, while looking for data for BCR’ market price

of financial instruments and credit ratings for the period from 2005-2010 calculation the

researcher did not find them.

5.2. Conclusion

The importance of findings of this research was to address the specific objectives of the

study and results are as follow:

For BCR’ capital adequacy, the leverage ratios during the study periods are greater than 5

percent (5%) whereas conventionally, leverage ratio of 5 percent or greater than 5 percent

indicates that commercial banks are well capitalized. And as the indicators: TCR, CCR and

SCR, of capital adequacy confirmed with the implication of leverage ratio that BCR have

met the capital adequacy ratio as directed by BNR.

For the BCR’ quality assets, the non-performing asset ratio and loan loss reserve ratio, while

in general, 5 percent to 10 percent of non-performing assets is considered as satisfactory

level of quality of bank assets, results showed that BCR Ltd. non-performing assets as a

whole tends to decrease in the latter fiscal years, and the satisfactory level of nonperforming

assets in the total assets of BCR Ltd as a whole is mainly due to the percent of non-

performing assets. So, overall, both NPAR and LLRR implied that the sound financial

health of the bank is in good conditions. 33

While assessing the Management quality it was found that the performance management of

BCR is satisfactory, due to the indicators of management efficiency which show that BCR

is healthy, also due to the fact that OER (operating expenses ratio) for the period under

study is greater than 50%.

For the BCR earnings capacity, on the average, earning performance of BCR, as indicated

by ROA, is good while, as per the conventional rules, ROA of commercial banks should fall

in the range of less than 3 and equal to 2 in order to be satisfactory earning performance,

that profitability is satisfactory for the whole period under study the ROA is 2, 3, 1, 1, and

3% which show that BCR respected the conventional rules.

BCR’ LDR as whole is high. It hovers in the range of 50 percent to 64.59 percent of the

total deposit except the last year 2010. The two indicators—CETAR and CETDR—also

show the high liquidity position of BCR, while as directed by BNR, commercial banks had

to maintain 30 percent cash of the total deposits in their vault in 2005-2008, and 20 percent

in 2008-2010 (BNR 2010). In spite of the withdrawal of the provision, level of liquid assets,

on the average, is higher during the study period.

For BCR’ market price of financial instruments and credit ratings for the period from 2005-

2010 calculations, the researcher did not find the data required to calculate them, and like

that, the second objective of the present study, was not achieved.

5.3. Recommendations

According to the findings of this study and results obtained, the researcher recommends the

following:

To BNR, the Rwandan Central bank, to propose the uniformly systems for the whole

country’ banks and all financial institutions; like CAMELS to check up their daily life. And

Fix the rate of each CAMELS indicator’s ratio.

34

To BCR Ltd., the researcher recommended that, it should facilitate the access more data and

give detailed data to finalists’ students while carrying out research to the bank.

5.4. Suggestions for further studies

For further research, it is recommended that the following topics may be considered:

• Financial institutions health checks up in framework of CAMELS, in Rwanda. Case

of BNR.

• The performance and contribution of CAMEL in financial institution objectives

achievement.

35

BIBLIOGRAPHY

1. Books

1. Decenzo and Stephen p Robbins (1988) personnel/human resource management 3rd

edition prentice –hall inc Englewood.

2. Evan, Owns and others. 2000. "Macroprudential Indicators of Financial System

Soundness."Occasional Paper 192. Washington DC: International Monetary Fund.

3. Hessler Richard M. (1989), Social research methods, USA.

4. Hilbers, Paul, Russell Krueger, and Marina Moretti. 2000. New Tools for Assessing

Financial System Soundness. Finance and Development 37 :8-12

5. McNally, Edward A. 1996. "Basic Topics in Sound Bank Management." EDI Working

Paper, Washington DC: The World Bank.

6. Roger moores (1993) managing for higher performance.

7. Rogers bennette (1997) employee relations 2nd edition, p w s –kent publishing company

USA.

8. Saunders, Anthony and Marcia Millon Cornett. 2004. Financial Markets and

Institutions. New Delhi: Tata McGraw-Hill Publishing Company Limited.

2. Reports

1. BNR (2012), monetary policy and financial stability statement.

2. ADB (2002), Guidelines for the Financial Governance and Management of Investment

Projects Financed by the ADB. Manila: ADB.

3. Electronics references

1. Gilbert, R. Alton, Andrew P. Meyer and Mark D.Vaughan. 2000. "The Role of a CAMEL

Downgrade Model in Bank Surveillance." Working Paper 2000-021A, the Federal

Reserve Bank of St. Louis. Nov. 1, 2005 (http://research.stlouisfed.org/wp/2000/2000-

021.pdf).

2. http://fic.wharton.upenn.edu/fic/papers/95/9511b.pdf, accessed in August 2012.

36

3. http://fsi.imf.org/misc/FSI%20Concepts%20and%20Definitions.pdf, accessed in August

2012.

4. http://objectguild.com/financial-statement-analysis/importance-of-economic-and-

financial-analysis-for-decision-making/, accessed in August 2012.

5. http://pdf.usaid.gov/pdf_docs/PNADQ079.pdf, accessed in August 2012.

6. http://www.bis.org/ifc/publ/ifcb33n.pdf, accessed in August 2012.

7. http://www.businessdictionary.com/definition/financial-analysis.html#ixzz225L9Q8o8,

accessed in August 2012.

8. http://www.fdicoig.gov/reports02/02-033.pdf, accessed in August 2012.

9. http://www.imf.org/external/np/sta/fsi/eng/2003/051403bp.pdf, accessed in August

2012.

10. http://www.investopedia.com/terms/c/camelrating.asp, accessed in August 2012.

11. http://www.investopedia.com/terms/f/financial-analysis.asp#ixzz225GRMo1X, accessed

in August 2012.

12. http://www.kesdee.com/pdf/financialanalysis.pdf, accessed in August 2012.

13. http://www.mixmarket.org/sites/default/files/medialibrary/10011.150/CAMEL.pdf,

accessed in August 2012.

37

APPENDICES

38