Embed Size (px)

Citation preview

MELIOR RESOURCES INC.

FILING STATEMENT

IN RESPECT OF

THE CHANGE OF BUSINESS BYMELIOR RESOURCES INC.

May 15, 2014

Neither the TSX Venture Exchange Inc. nor any securities regulatoryauthority has in any way passed upon the merits of theChange of Business described in this Filing Statement.

TABLE OF CONTENTS

Page

-i-

GLOSSARY OF TERMS............................................................................................................................1

SUMMARY OF FILING STATEMENT....................................................................................................5

CAUTION REGARDING FORWARD LOOKING STATEMENTS........................................................8

OTHER INFORMATION .........................................................................................................................10

RISK FACTORS .......................................................................................................................................11

Acquisition and Integration Risks.................................................................................................18Trading in the Company’s Common Shares may be Volatile.......................................................19

INFORMATION CONCERNING THE COMPANY...............................................................................19

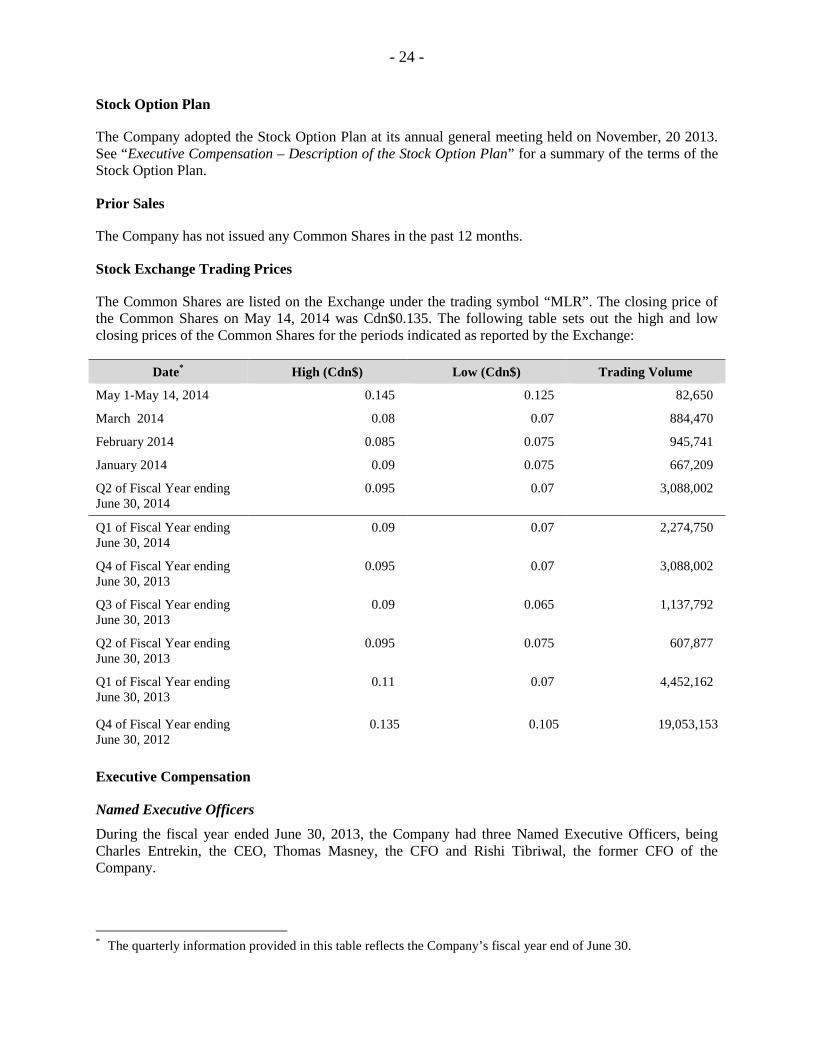

Corporate Structure.......................................................................................................................19General Development of the Business ..........................................................................................19Selected Consolidated Financial Information and Management’s Discussion and Analysis .......23Description of the Securities.........................................................................................................23Stock Option Plan .........................................................................................................................24Prior Sales .....................................................................................................................................24Stock Exchange Trading Prices ....................................................................................................24Executive Compensation ..............................................................................................................24Description of the Stock Option Plan ...........................................................................................27Pension Benefits ...........................................................................................................................29Termination and Change of Control Benefits ...............................................................................29Director Compensation .................................................................................................................30Securities Authorized for Issuance Under Equity Compensation Plans .......................................30Management Contracts .................................................................................................................31Arm’s Length Transaction. ...........................................................................................................31Legal Proceedings.........................................................................................................................31Auditor, Transfer Agent and Registrar .........................................................................................31Material Contracts.........................................................................................................................31

INFORMATION CONCERNING BELRIDGE........................................................................................31

Corporate Structure.......................................................................................................................31General Development of the Business ..........................................................................................32Significant Acquisitions and Dispositions ....................................................................................32Description of the Business ..........................................................................................................32Selected Consolidated Financial Information and Management’s Discussion and Analysis .......95Description of the Securities.........................................................................................................96Consolidated Capitalization ..........................................................................................................96Prior Sales .....................................................................................................................................96Executive Compensation ..............................................................................................................97Arm’s Length Transaction ............................................................................................................97Legal Proceedings.........................................................................................................................97Material Contracts.........................................................................................................................97

-ii-

INFORMATION CONCERNING THE RESULTING ISSUER..............................................................98

Corporate Structure.......................................................................................................................98Intercorporate Relationships .........................................................................................................98Description of the Business ..........................................................................................................98Description of Securities...............................................................................................................99Pro forma Consolidated Capitalization.........................................................................................99Fully Diluted Share Capital ..........................................................................................................99Available Funds and Principal Purposes.....................................................................................100Risk Factors ................................................................................................................................101Principal Securityholders ............................................................................................................101Directors and Officers.................................................................................................................101Anticipated Executive Compensation.........................................................................................106Indebtedness of Directors and Officers.......................................................................................109Investor Relations Arrangements................................................................................................109Options to Purchase Securities....................................................................................................109Escrowed Securities ....................................................................................................................109Auditors, Transfer Agent and Registrar......................................................................................110

GENERAL MATTERS ...........................................................................................................................110

Sponsorship.................................................................................................................................110Experts ........................................................................................................................................110Other Material Facts ...................................................................................................................111Board Approval...........................................................................................................................111

CERTIFICATE OF THE ISSUER ..........................................................................................................112

CERTIFICATE OF BELRIDGE .............................................................................................................113

SCHEDULE “A” - FINANCIAL STATEMENTS.................................................................................115

SCHEDULE “B” - MANAGEMENT DISCUSSION & ANALYSIS ...................................................116

SCHEDULE “C” - PRO-FORMA FINANCIAL STATEMENTS ........................................................117

- 1 -

GLOSSARY OF TERMS

In this Filing Statement, unless otherwise defined or expressly stated herein or something in the subjectmatter or the context is clearly inconsistent therewith:

“Affiliate” means a company that is affiliated with another company as described below. A company isan “Affiliate” of another company if:

(a) one of them is the subsidiary of the other, or

(b) each of them is controlled by the same Person.

A company is “controlled” by a Person if:

(c) voting securities of the company are held, other than by way of security only, by or forthe benefit of that Person, and

(d) the voting securities, if voted, entitle the Person to elect a majority of the directors of thecompany;

A Person beneficially owns securities that are beneficially owned by:

(e) a company controlled by that Person, or

(f) an Affiliate of that Person or an Affiliate of any Company controlled by that Person;

A “subsidiary” is a company that is controlled by a Person.

“Associate” when used to indicate a relationship with a Person, means:

(a) an issuer of which the Person beneficially owns or controls, directly or indirectly, votingsecurities entitling him to more than 10% of the voting rights attached to outstandingsecurities of the issuer,

(b) any partner of the Person,

(c) any trust or estate in which the Person has a substantial beneficial interest or in respect ofwhich the Person serves as trustee or in a similar capacity, and

(d) in the case of a Person that is an individual,

(i) that Person’s spouse or child, or

(ii) any relative of the Person or of his spouse who has the same residence as thatPerson.

“Audit Committee” means the audit committee of the Board;

“BCA” means the Business Corporations Act (British Columbia), as amended from time to time;

“Belridge” means Belridge Enterprises Pty Ltd, a company formed under the laws of Australia;

- 2 -

“Belridge Shareholders” means Belmont Park – Monto Pty Ltd, Panorama Ridge – Monto Pty Ltd andSashimi Investments Pty Ltd, in each case in their capacity as trustees;

“Board” means the board of directors of the Company;

“CEO” means the Chief Executive Officer of the Company;

“CFO” means the Chief Financial Officer of the Company;

“Change of Business” means a transaction or series of transactions which will redirect an issuer’sresources and which changes the nature of its business, for example, through the acquisition of an interestin another business which represents a material amount of the issuer’s market value, assets or operations,or which becomes the principal enterprise of the issuer;

“Closing Date” means the date on which the closing of the Proposed Acquisition occurs;

“Common Shares” means the common shares in the capital of the Company and will also be thecommon shares in the capital of the Resulting Issuer;

“company” unless specifically indicated otherwise, means a corporation, incorporated association ororganization, body corporate, partnership, trust, association or other entity other than an individual;

“Company” means Melior Resources Inc., a company formed under the laws of British Columbia;

“Control Person” means any Person that holds or is one of a combination of Persons that holds asufficient number of any of the securities of an issuer so as to affect materially the control of that issuer,or that holds more than 20% of the outstanding voting securities of an issuer except where there isevidence showing that the holder of those securities does not materially affect the control of the issuer;

“Corporate Governance Committee” means the corporate governance committee of the Board;

“Exchange” means TSX Venture Exchange Inc.;

“Filing Statement” means this filing statement;

“Final Exchange Bulletin” means the bulletin issued by the Exchange following completion of theProposed Acquisition and the submission of all required documentation and that evidences the finalExchange acceptance of the Proposed Acquisition;

“Indicated Mineral Resource” means that part of a Mineral Resource for which quantity, grade orquality, densities, shape and physical characteristics, can be estimated with a level of confidencesufficient to allow the appropriate application of technical and economic parameters, to support mineplanning and evaluation of the economic viability of the deposit. The estimate is based on detailed andreliable exploration and testing information gathered through appropriate techniques from locations suchas outcrops, trenches, pits, workings and drill holes that are spaced closely enough for geological andgrade continuity to be reasonably assumed;

“Inferred Mineral Resource” means that part of a Mineral Resource for which quantity and grade orquality can be estimated on the basis of geological evidence and limited sampling and reasonablyassumed, but not verified, geological and grade continuity. The estimate is based on limited information

- 3 -

and sampling gathered through appropriate techniques from locations such as outcrops, trenches, pits,workings and drill holes;

“Insider” when used in relation to the Company, means:

(a) a director or senior officer of the Company;

(b) a director or senior officer of a company that is an Insider or subsidiary of the Company;

(c) a Person that beneficially owns or controls, directly or indirectly, voting shares carryingmore than 10% of the voting rights attached to all outstanding voting shares of theCompany; or

(d) the Company itself if it holds any of its own securities;

“Goondicum Project” means the ilmenite extraction operations currently owned by Belridge, includingthe mine site, processing plant and supporting infrastructure located 30km due east of Monto, CentralQueensland, Australia, as more particularly described in the Technical Report;

“H&S Consultants” means H&S Consultants Pty. Ltd;

“Measured Mineral Resource” means that part of a Mineral Resource for which quantity, grade orquality, densities, shape and physical characteristics are so well established that they can be estimatedwith confidence sufficient to allow the appropriate application of technical and economic parameters tosupport production planning and evaluation of the economic viability of the deposit. The estimate isbased on detailed and reliable exploration, sampling and testing information gathered through appropriatetechniques from locations such as outcrops, trenches, pits, workings and drill holes that are spaced closelyenough to confirm both geological and grade continuity;

“Mineral Reserve” means the economically mineable part of a Measured or Indicated Mineral Reservedemonstrated by at least a pre-feasibility study. This study must include adequate information on mining,processing, metallurgical, economic and other relevant factors that demonstrate, at the time of reporting,that economic extraction can be justified. A Mineral Reserve includes diluting materials and allowancesfor losses that may occur when the material is mined;

“Mineral Resource” means a concentration or occurrence of diamonds, natural solid inorganic material,or natural solid fossilized organic material, including base and precious metals, coal, and industrialminerals in or on the earth’s crust in such form and quantity and of such grade or quality that it hasreasonable prospects for economic extraction. The location, quantity, grade, geological characteristicsand continuity of a Mineral Resource are known, estimated or interpreted from specific geologicalevidence and knowledge;

“Melior Australia” means Melior Australia Pty Ltd, a company formed under the laws of Australia;

“NEO” has the meaning ascribed to such term on page 25 of this Filing Statement;

“NI 43-101” means National Instrument 43-101 “Standards of Disclosure for Mineral Projects”;

“NI 58-101” means National Instrument 58-101 “Disclosure of Corporate Governance Practices”;

- 4 -

“Nomination and Compensation Committee” means the nomination and compensation committee ofthe Board;

“Non-Arm’s Length Party” means in relation to a company, a promoter, officer, director, other Insideror Control Person of that company (including an issuer) and any Associates or Affiliates of such Persons.In relation to an individual, means any Associate of the individual or any company of which theindividual is a promoter, officer, director, Insider or Control Person;

“Pala” means Pala Investments Limited, a company formed under the laws of Jersey;

“Person” means a company or individual;

“Proposed Acquisition” means, subject to the approval of the Exchange, the proposed acquisition by theCompany of 100% of the issued and outstanding shares of Belridge from the Belridge Shareholders andall matters relating thereto, as described in this Filing Statement;

“Resulting Issuer” means the Company following the completion of the Proposed Acquisition;

“Share Purchase Agreement” means the share sale and purchase agreement between the Company,Melior Australia and the Belridge Shareholders dated March 31, 2014 in respect of the ProposedAcquisition;

“Sojitz” means Sojitz Corporation;

“Stock Option Plan” means the stock option plan of the Company dated October 17, 2006, as amendedand restated September 28, 2007 and November 15, 2010 and as approved by the Company’sshareholders on November 20, 2013; and

“Technical Report” means the independent technical report with the effective date of February 25, 2014entitled “Resource Estimations of the Goondicum Ilmenite Deposit, SE Queensland, Australia” preparedby Simon Tear, PGeo, Eur Geol of H&S Consultants Pty. Ltd, Graham Lee, FAusImm, CP(Geo) ofGraham Lee and Associates Pty Ltd and Chris Desoe, FAusImm, RPEQ, MMICA of Australian MineDesign and Development Pty Ltd, regarding the Goondicum Project.

- 5 -

MELIOR RESOURCES INC.

SUMMARY OF FILING STATEMENT

(as at May 15, 2014 except as otherwise indicated)

The following is a summary of information relating to the Company and the Resulting Issuer (assumingcompletion of the Proposed Acquisition) and should be read together with the more detailed informationand financial data and statements contained elsewhere in this Filing Statement.

Melior Resources Inc.

The Company is incorporated under the laws of British Columbia with its Common Shares listed fortrading on the Exchange as a Tier 1 Investment Issuer. See “Information Concerning the Company”.

The trading price of the Common Shares of the Company on March 28, 2014, the last trading day beforeannouncement of the Proposed Acquisition, was Cdn$0.075.

Principal Terms of the Proposed Acquisition

The following summary is subject to the detailed provisions of the Share Purchase Agreement and isqualified in its entirety by reference to the Share Purchase Agreement which is available under theCompany’s profile on SEDAR at www.sedar.com.

The Share Purchase Agreement provides that Melior Australia (a direct wholly-owned subsidiary of theCompany) will acquire 100% of the issued share capital of Belridge in exchange for the issuance by theCompany of 38,087,971 Common Shares (the “Consideration Shares”) to the Belridge Shareholders.Each Belridge Shareholder is a company formed under the laws of Australia. The Consideration Shareswould represent 18.0% of the Company’s issued and outstanding shares immediately after the closing ofthe Proposed Acquisition. Closing of the Proposed Acquisition is subject to Exchange approval and othercustomary conditions. The Company expects closing of the Proposed Acquisition to occur shortlyfollowing the date of this Filing Statement.

The Company has committed to invest following the Closing Date up to US$15 million in the GoondicumProject, subject to the satisfaction of all applicable legal and regulatory requirements and fulfillment of allpermitting, approval and licensing requirements necessary to successfully achieve a full re-start of theGoondicum Project. The Board will direct and have ultimate approval over the total amount invested andthe schedule of drawdowns and conditions for the expenditure of these funds.

Following closing of the Proposed Acquisition, the Belridge Shareholders would be entitled to receive anearn-out payment, payable in Common Shares (or, at the Company’s election, in cash) based on theperformance of the Company by reference to the price of the Common Shares (“Earn-outConsideration”). The parties have agreed to predetermined earn-out payment amounts should the price ofthe Common Shares reach predetermined levels with such predetermined levels being well in excess ofthe price of the Common Shares as of the effective date of the Share Purchase Agreement. The maximumnumber of Common Shares that could be issued as payment for the Earn-out Consideration is 38,087,971.The Earn-out Consideration will be available for a period of up to four years from the date of closing ofthe Proposed Acquisition (“Validity Period”) and may be triggered by either of the following:

Change of control during the Validity Period: If a change of control event (as defined below)occurs during the Validity Period and the price at which the Common Shares are trading exceeds

- 6 -

specified levels above the current market price, the Belridge Shareholders would have a right toreceive the Earn-out Consideration on a pro-rata basis.

No change of control during the Validity Period: In the event that no change of control eventoccurs during the Validity Period, the Belridge Shareholders would, at the end of the ValidityPeriod, be entitled to receive the Earn-out Consideration, on a pro-rata basis, if the trading priceof the Common Shares exceeds specified levels above the current market price.

A change of control event is defined as any party or parties acting in concert, other than Pala (theCompany’s current majority shareholder), acquiring more than 50% of the Common Shares on a fullydiluted basis. The payment of the Earn-out Consideration will be subject to the satisfaction of customaryeligibility and performance conditions including the continuation of operations of the Goondicum Projectand the Belridge Shareholders continuing to hold all the Consideration Shares. For example, assumingthat no change of control occurs during the Validity Period, the Earn-out Consideration payable at the endof the Validity Period will range from zero (if the price of the Common Shares is less than Cdn$0.41 pershare) to 38,087,971 shares if the price of the Common Shares exceeds Cdn$1.11 per share.

The Consideration Shares will be placed in escrow for a period beginning on the Closing Date and endingtwo years after the Closing Date. Should the Company have a successful claim against the BelridgeShareholders during the escrow period, such claim may be satisfied by cash or by a return of theConsideration Shares with equivalent value to such claim. Consideration Shares returned to the Companyare to be valued based on the price of the Common Shares on the Closing Date.

Following closing of the Proposed Acquisition, the Belridge Shareholders will be entitled to nominate onedirector to the Board for so long as they together hold at least 10% of the issued and outstanding CommonShares.

As the Proposed Acquisition is a “Change of Business” transaction, pursuant to Exchange Policy 5.2Melior shareholder approval is required. Melior’s majority shareholder, Pala, has provided writtenconsent approving the Proposed Acquisition which constitutes the requisite shareholder approval. TheProposed Acquisition will be at arm’s length, and accordingly, will not require shareholder approvalbeyond that described above.

Upon completion of the Proposed Acquisition, it is expected that the Company's listing status will changefrom that of a Tier 1 Investment Issuer to a Tier 1 Mining Issuer.

Element Settlement Deed

In connection with the Proposed Acquisition, the Company entered into a settlement deed (the“Settlement Deed”) among the Company, Belridge and Element Capital Management Pty Ltd(“Element”), pursuant to which the Company will following the Closing Date pay Element the sum ofA$250,000 in full and final settlement of all claims (as such term is defined in the Settlement Deed) thatElement has or may have against the Company, Belridge and their respective employees agents andassociates arising under or in connection with an agreement dated July 25, 2013 (the “ElementAgreement”), pursuant to which Element agreed to provide Belridge with certain advisory services withrespect to the sale of Belridge.

Loan Arrangement

Pursuant to a loan agreement, the Company has provided Belridge with short term financing in anaggregate amount of up to Cdn$1,400,000 for ongoing operational costs and to satisfy Belridge’s

- 7 -

obligations with respect to an agreement between Belridge, Goody Investments Pty Ltd and Mr. JohnLeslie Goody, pursuant to which Belridge will purchase back from Goody Investments Pty Ltd, GoodyInvestments Pty Ltd’s royalty rights to a percentage of Belridge’s gross income from ilmenite and apatitesales from tenements including, among others, EPM 9100. It is intended that any amounts outstandingafter the Closing Date will be refinanced in a tax efficient manner for the Company.

See “Information Concerning the Company – General Development of Business”.

Escrow of Securities

See “Principal Terms of the Proposed Acquisition”.

Arm’s Length Transaction

The Proposed Acquisition is not a Change of Business involving Non-Arm’s Length Parties and istherefore not subject to Exchange Manual Policy 5.9.

Available Funds and Principal Purposes

The estimated funds available to the Resulting Issuer after giving effect to the Proposed Acquisition areapproximately US$20,000,000, based on the Company’s estimated consolidated working capital as atApril 15, 2014.

The Resulting Issuer intends to use the funds available to it upon completion of the Proposed Acquisitionto further the Resulting Issuer’s stated business objectives, being principally the restart, development andexpansion of the Goondicum Project. There may be circumstances where, for sound business reasons, areallocation of funds may be necessary or desirable as determined by the Board. See “InformationConcerning the Resulting Issuer – Available Funds and Principal Purposes”.

Selected Pro forma Financial Information

The following table shows selected pro forma balance sheet data for the Resulting Issuer, as at December31, 2013, after giving effect to the Proposed Acquisition:

Current Assets Cdn$21,628,472

Total Assets Cdn$29,662,424

Current Liabilities Cdn$1,388,667

Total Liabilities Cdn$4,036,194

Share Capital and Contributed Surplus Cdn$538,560,891

Deficit (Cdn$512,934,661)

See “Schedule “C” - Pro-Forma Financial Statements”

Directors and Officers

- 8 -

Following completion of the Proposed Acquisition, the directors and officers of the Resulting Issuer willbe:

Name Title

Charles Entrekin Chairman of the Board

Mark McCauley CEO and Director

Thomas Masney CFO and Corporate Secretary

Glenn Black Director

Martyn Buttenshaw Director

Joe Connolly Director

Conflicts of Interest

Certain of the proposed directors and officers of the Resulting Issuer are also directors, officers orshareholders of other companies. Such associations may give rise to conflicts of interest from time totime. See “Risk Factors”.

Interests of Experts

The Company’s auditors, MNP LLP, Chartered Accountants, of 701 Evans Avenue 8th Floor, Toronto,Ontario, M9C 1A3, have audited the financial statements for the years ended June 30, 2013 and 2012included in this Filing Statement. MNP LLP report that they are independent from the Company.

Information regarding the Goondicum Project has been reproduced from the Technical Report entitled“Resource Estimations of the Goondicum Ilmenite Deposit, SE Queensland, Australia”, which wasprepared in compliance with NI 43-101 by Simon Tear, PGeo, Eur Geol of H&S Consultants Pty. Ltd,Graham Lee, FAusImm, CP(Geo) of Graham Lee and Associates Pty Ltd and Chris Desoe, FAusImm,RPEQ, MMICA of Australian Mine Design and Development Pty Ltd, regarding the Goondicum Project.The authors of the Technical Report and H&S Consultants Pty. Ltd, have no direct or indirect interest inthe Goondicum Project, Belridge, the Company or the Resulting Issuer. It is anticipated that the TechnicalReport will be filed on SEDAR at www.sedar.com prior to the completion of the Proposed Acquisition.

Conditional Approval

The Exchange has conditionally accepted the Proposed Acquisition, subject to the Company completingall of the requirements of the Exchange.

Sponsorship

The Exchange provided the Company with an exemption from the requirement to obtain a sponsor inconnection with the Proposed Acquisition.

CAUTION REGARDING FORWARD LOOKING STATEMENTS

Certain statements in this Filing Statement are forward-looking statements or information (collectively“forward-looking statements”) within the meaning of applicable securities legislation. The Company ishereby providing cautionary statements identifying important factors that could cause actual results oroutcomes to differ materially from those projected in the forward-looking statements. Any statements thatexpress, or involve discussions as to, expectations, beliefs, plans, objectives, assumptions or future events

- 9 -

or performance are not historical facts and may be forward-looking and may involve estimates,assumptions and uncertainties and are subject to risks which could cause actual results or outcomes todiffer materially from those expressed in the forward-looking statements.

Often, but not always, forward-looking information can be identified by the use of words such as “plans”,“expects”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”,“projects”, “potential” or “believes” or the negatives thereof or variations of such words and phrases orstatements that certain actions, events or results “may”, “could”, “would”, “should”, “might” or “will” betaken, occur or be achieved.

Forward-looking information in this Filing Statement includes, but is not limited to:

statements related to the completion of the Proposed Acquisition and the events related theretoand contingent thereon;

information with respect to the Company’s future financial and operating performance;

the skill and knowledge of the Company’s management with respect to the exploration anddevelopment of mineral properties, and the relevance of that skill and knowledge to theGoondicum Project;

the Company’s plan to re-start, develop, operate and expand the Goondicum Project;

the estimated Mineral Resources at the Goondicum Project and the benefits of the ProposedAcquisition;

the Company’s ability to successfully obtain any necessary environmental, mining and otherlicenses and permits;

future exploration, development operating and expansion activities, and the costs and timing ofthose activities;

timing and receipt of approvals, consents and permits under applicable legislation;

the Company’s assessment of potential environmental liabilities;

results of future exploration, drilling and operations;

adequacy of financial resources;

forward-looking information attributed to third party industry sources; and

statements related to the Company’s expected executive compensation.

Forward-looking information is based on the assumptions, estimates, analysis and opinions ofmanagement made in light of its experience and its perception of trends, current conditions and expecteddevelopments, as well as other factors that management believes to be relevant and reasonable in thecircumstances at the date that such statements are made, but which may prove to be incorrect.Management believes that the assumptions and expectations reflected in such forward-lookinginformation are reasonable. Assumptions have been made regarding, among other things: the Company’sability to carry on exploration and development activities and to restart, operate and expand the

- 10 -

Goondicum Project, the timely receipt of required approvals, the price of minerals, the Company’s abilityto operate in a safe, efficient and effective manner and the Company’s ability to obtain financing as andwhen required and on reasonable terms. Readers are cautioned that the foregoing list is not exhaustive ofall factors and assumptions which may have been used.

By their nature, forward-looking statements involve numerous assumptions, inherent risks anduncertainties, both general and specific, which contribute to the possibility that the predicted outcomesmay not occur or may be delayed. The risks, uncertainties and other factors, many of which are beyondthe control of the Company or the Resulting Issuer, that could influence actual results include, but are notlimited to: risks relating to exploration, development and operating matters; dependence on theGoondicum project; delay and interruptions to re-start program; increase in capital costs for theGoondicum project; the Goondicum project may not meet its production targets or its cost estimates;mineral titles; history of losses; commodity prices; no off-take agreements; commodity hedging; fundingneeds; financing risks and dilution; limited operating history; reliability of resource estimates;uninsurable risks; environmental and safety regulations and risks; land reclamation; competition;personnel; litigation risk; government regulations, licenses and permits; conflicts of interest; currencyfluctuations; acquisition and integration risks; absence of dividend history or policy; and independentcontractors. See “Risk Factors”.

Readers are cautioned that the material assumptions used in the preparation of such information, althoughconsidered reasonable at the time of preparation, may prove to be imprecise. Actual results, performanceor outcomes could differ materially from those expressed in, or implied by, this forward-lookinginformation and, accordingly, no assurance can be given that any of the events anticipated by the forward-looking information will transpire or occur, or if any of them do, when that might happen or what benefitsthe Company will derive therefrom. The Company disclaims any intention or obligation to update orrevise any forward-looking information, whether as a result of new information, future events orotherwise, except as required by applicable securities laws.

This Filing Statement contains references to estimates of Mineral Resources. The estimation of MineralResources is inherently uncertain and involves subjective judgments about many relevant factors. MineralResources that are not Mineral Reserves do not have demonstrated economic viability. The accuracy ofany such estimates is a function of the quantity and quality of available data, and of the assumptions madeand judgments used in engineering and geological interpretation (including estimated future production,the anticipated tonnages and grades that will be mined and the estimated level of recovery that will berealized), which may prove to be unreliable and depend, to a certain extent, upon the analysis of drillingresults and statistical inferences that may ultimately prove to be inaccurate. Mineral Resource estimatesmay have to be re-estimated based on: (i) fluctuations in mineral prices; (ii) results of drilling; (iii)metallurgical testing and other studies; (iv) proposed mining operations, including dilution; (v) theevaluation of mine plans subsequent to the date of any estimates; and (vi) the possible failure to receiverequired permits, approvals and licences.

OTHER INFORMATION

Currency

All references to “$”, “US$” or “dollars” in this Filing Statement mean U.S. dollars, unless otherwiseindicated. References to “Cdn$” mean Canadian dollars and references to “A$” mean Australian dollars.

Scientific and Technical Information

- 11 -

The scientific and technical information with respect to the Goondicum Project contained in this FilingStatement is reproduced from the Technical Report. The full text of the Technical Report has been filedwith Canadian securities regulatory authorities pursuant to NI 43-101 and is available for review underthe Company’s SEDAR profile at www.sedar.com.

Simon Tear, PGeo, Eur Geol of H&S Consultants Pty. Ltd, Graham Lee, FAusImm, CP(Geo) of GrahamLee and Associates Pty Ltd and Chris Desoe, FAusImm, RPEQ, MMICA of Australian Mine Design andDevelopment Pty Ltd have reviewed and approved the scientific and technical information in respect ofthe Goondicum Project contained in this Filing Statement. Each of Mr. Tear, Mr. Lee and Mr. Desoe areconsidered, by virtue of their education, experience and professional association, to be a qualified personfor the purposes of NI 43-101. Mr. Tear, Mr. Lee and Mr. Desoe are independent within the meaning ofNI 43-101.

RISK FACTORS

Following the Proposed Acquisition, the primary business of the Resulting Issuer will be the exploration,development, restart, operation and expansion of the Goondicum Project. Common Shares of theResulting Issuer will be a risky and speculative investment. The Resulting Issuer will be exposed to anumber of risks and uncertainties. Such risks could materially affect the Resulting Issuer’s future resultsand could cause actual events to differ materially from those described in forward-looking statementsrelating to the Resulting Issuer. The risks described herein will apply to the Resulting Issuer followingthe closing of the Proposed Acquisition and may not be the only risks facing the Resulting Issuer.Additional risks not currently known or not currently considered to be material may also have an adverseimpact on the Resulting Issuer’s business.

Overview of Exploration, Development and Operating Risk

The Company is a development stage company engaged in mineral exploration and development. Mineralexploration and development is highly speculative in nature, involves many risks and is frequently noteconomically successful. Increasing mineral resources or reserves depends on a number of factorsincluding, among others, the quality of a company’s management and their geological and technicalexpertise and the quality of land available for exploration. Once mineralization is discovered it may takeseveral years of additional exploration and development until production is possible, during which timethe economic feasibility of production may change. Substantial expenditures are required to establishproven and probable reserves through drilling or drifting to determine the optimal metallurgical processand to finance and construct mining and processing facilities. At each stage of exploration, development,construction and mine operation, various permits and authorizations are required. Applications for manypermits require significant amounts of management time and the expenditure of substantial capital forengineering, legal, environmental, social and other activities. At each stage of a project’s life, delays maybe encountered because of permitting difficulties. Such delays add to the overall cost of a project and mayreduce its economic feasibility. As a result of these uncertainties, there can be no assurance that a mineralexploration and development company’s programs will result in profitable commercial production. As ofthe date of this Filing Statement, the Goondicum Project has no established reserves and is not inoperation. There is no assurance that the project can be mined profitably. Accordingly, it is not assuredthat the Company will realize any profits in the short to medium term, if at all. Any profitability in thefuture from the business of the Company will be dependent upon developing and commercially mining aneconomic deposit of minerals.

The operations of companies engaged in mining activities are vulnerable to supply chain disruptionsincluding shortages of, as well as lead times to deliver, strategic spares, critical consumables and miningequipment. In the past, other mining companies have experienced shortages in critical consumables,

- 12 -

particularly as production capacity in the global mining industry has expanded in response to increaseddemand for commodities, and have experienced increased delivery times for these items. Shortages ofstrategic spares, critical consumables or mining equipment, could in the future, result in production delaysand productions shortfalls, and increases in prices could result in an increase in both operating costs andthe capital expenditure to maintain and develop mining operations. In certain cases, there may be onlylimited suppliers for certain strategic spares, critical consumables or mining equipment who commandsuperior bargaining power relative to the Company. The Company could at times face increased costs,limited supply and/or increased lead time in the delivery of such items.

Companies engaged in mining activities are subject to all of the hazards and risks inherent in exploringfor, developing and operating natural resource projects. These risks and uncertainties include, but are notlimited to, environmental hazards, industrial accidents, labour disputes, social unrest, encounteringunusual or unexpected geological formations or other geological or grade problems, unanticipatedmetallurgical characteristics or less than expected mineral recovery, encountering unanticipated ground orwater conditions, cave-ins, pit wall failures, flooding, rock bursts, periodic interruptions due to inclementor hazardous weather conditions and other acts of God or unfavourable operating conditions and losses.Should any of these risks or hazards affect the Company’s exploration, development or mining activitiesit may: cause the cost of exploration, development or production to increase to a point where it would nolonger be economic to operate the Company’s mineral projects; result in a write down or write-off of thecarrying value of one or more mineral projects; cause delays or stoppage of exploration, development,mining or processing activities; result in damage to or the destruction of mineral properties, processingfacilities or third party facilities necessary to the Company’s operations; cause personal injury or deathand related legal liability; or result in the loss of insurance coverage — any or all of which could have amaterial adverse effect on the financial condition, results of operations or cash flows of the Company.

Dependence on the Goondicum Project

The Company is primarily focused on the development of the Goondicum Project. Other than its equityinterest in Asian Mineral Resources Limited (“AMR”), the Company does not own any significant assetsother than the Goondicum Project, which would be the Company’s only mineral property and representsthe Company’s only immediate potential for future generation of operating revenues. Unless theCompany acquires additional property interests, any adverse developments affecting the GoondicumProject such as, but not limited to, delays in or failure to successfully restart production, obtaining projectfinancing beyond the Company’s initial investment on commercially suitable terms, hiring suitablepersonnel and mining contractors, or securing supply agreements on commercially suitable terms, couldhave a material adverse effect upon the Company and would materially and adversely affect the potentialmineral resource production, profitability, financial performance and results of operations of theCompany.

Delay and Interruptions to Re-Start Program

There are significant risks that the re-start of the Goondicum Project could be delayed due tocircumstances beyond the Company’s control. There can be no assurance that the Goondicum Project willbe re-started on time, on budget or according to specifications. The Company depends on the third partieswith whom it works, including the management and labour force of its supply chain, for the supply ofconstruction materials and equipment. There can be no assurance that the required construction supplieswill be readily available and delivered on time to the construction site. Such supplies may be sourcedfrom additional third parties, which may be affected by factors beyond the Company’s control.Additionally, changes to government regulations, contractual and/or union disputes, labour stoppages,workplace accidents, availability of supplies, materials, tools and equipment, delay in shipment ofmaterials and unseasonable weather patterns and conditions may hinder the re-start timeline and progress.

- 13 -

It is possible that issues with the design, specifications and/or physical location of the facilities of theGoondicum Project may arise during the re-start process due to unforeseen engineering, physical,geological and/or economic circumstances.

Government and building code regulations may change requiring substantial revision to the design planand specifications for the Goondicum Project. The resolution of these issues may require the additionalassistance and cost of experts, additional financing, a change to the construction plan, design,specifications, layouts and/or locations. Any such changes will delay the overall re-start of theGoondicum Project and will increase (possibly significantly) the costs associated therewith. Since theGoondicum Project will not earn income before re-start, longer construction times translate directly intohigher overall project costs. Further, the delay, cost and alterations required may potentially adverselyaffect the timeline and the expected output.

Increase in Capital Costs for the Goondicum Project

The Company plans to invest, subject to Board approval, up to US$15,000,000 in the re-start of theGoondicum Project operation. There can be no assurance that capital costs for the restart of theGoondicum Project will not exceed such amount. A significant increase in the capital costs of the restartof the Goondicum Project would have a material adverse effect on the Company’s ability to complete theGoondicum Project as well as on its financial condition.

The Goondicum Project may not meet its production targets or its cost estimates

The re-start of the Goondicum Project is premised on projected production, capital and operating costestimates. The Company’s ability to meet ilmenite production targets is dependent on the successful re-start of the mine and expansion of mining operations in the future. Meeting these targets will also dependon the accuracy of predicted factors including capital and operating costs, metallurgical recoveries,resource estimates future commodity prices, accuracy of applicable technical studies and reports,acquisition of land and surface rights and issuance of necessary permits/approvals. There is no assurancethat the mining operations will be expanded or that mining operations will be profitable if expanded.Actual production and costs may vary from the estimates for a variety of reasons such as grade, tonnage,dilution and metallurgical and other characteristics of the ore mined varying from estimates, revisions tomine plans, risks and hazards associated with mining, adverse weather conditions, unexpected laborshortages or strikes, equipment failures and other interruptions in production capabilities. Productioncosts may also be affected by increased stripping costs, increases in level of ore impurities, labor costs,raw material costs, inflation and fluctuations in currency exchange rates. Failure to achieve productiontargets or cost estimates could have a material adverse impact on the Company’s sales, profitability, cashflow and overall financial condition and performance.

Mineral Titles

Although the Company has obtained a title opinion for the tenements underlying the Goondicum Project,there is no guarantee that title to such mineral property interests will not be challenged or impugned andno assurances can be given that there are no title defects affecting its mineral properties. The Company’smineral property interests may be subject to prior unregistered agreements or transfers and title may beaffected by undetected defects.

History of Losses

Prior owners have experienced significant losses historically in connection with the Goondicum Project.There can be no assurance that significant additional losses will not occur in the future, or that the

- 14 -

Company will be profitable in the future. The Company’s operating expenses and capital expendituresmay increase in the coming years as the costs for consultants, personnel and equipment associated withadvancing exploration, development and re-start of commercial production of the Goondicum Project areincurred.

Commodity Prices

The Company’s operations will be affected by commodity prices which are subject to significantfluctuation and are affected by a number of factors which are beyond the control of the Company. Suchfactors include, but are not limited to, interest rates, exchange rates, inflation or deflation, fluctuation inthe value of the United States dollar and other foreign currencies, global and regional supply and demand,and political and economic conditions. The prices of ilmenite and other minerals have fluctuated widelyin recent years, and future price declines could cause any future development and commercial productionto be impracticable. Depending on the price of ilmenite and other minerals, projected cash flow fromplanned mining operations may not be sufficient and the Company could be forced to discontinuedevelopment and/or operational activities.

No Off-Take Agreements

While Belridge has entered into an agreement with Sojitz, whereby Belridge grants Sojitz the exclusiveright to promote and sell ilmenite mined from ML 80044 into Japan and Korea and a non-exclusive rightto promote and sell ilmenite into other countries, the Resulting Issuer has not entered into any off-takeagreements for the sale of ilmenite and there can be no assurance that the Resulting Issuer will enter intoany off-take agreement or other binding sales commitment for the sale of ilmenite produced from theResulting Issuer’s operations.

Commodity Hedging

The Company does not currently have a policy in place to hedge future commodity sales. There is noassurance that a hedging program can be put in place. If put into place, there is no assurance that acommodity hedging program designed to reduce the risk associated with fluctuations in commodity priceswill be successful. Hedging may not protect adequately against declines in commodity prices. Althoughhedging may protect the Company from a decline in commodity prices, it may also prevent the Companyfrom benefiting fully from price increases.

Funding Needs, Financing Risks and Dilution

The Company has no history of significant earnings and, due to the nature of its business and theGoondicum Project, there can be no assurance that the Company will be profitable. Future exploration,development, mining, and processing of minerals from the Company’s properties will require substantialfinancing. The Company has paid no dividends on the Common Shares since incorporation and does notanticipate doing so in the foreseeable future. The only current sources of funds available to the Companyare current owned assets and cash reserves, the sale of additional equity capital and/or the borrowing offunds. There is no assurance that external funding will be available to the Company, that it will beobtained on terms favorable to the Company or that it will provide the Company with sufficient funds tomeet its objectives, which may adversely affect the Company’s business and financial position. TheCompany may not have sufficient funds to complete the re-start or expansion of the Goondicum Projector to pursue other exploration, development or acquisition activities. If available, future equity financingmay result in substantial dilution to existing shareholders of the Company and reduce the value of theirinvestment.

- 15 -

Limited Operating History

The Resulting Issuer will be a development stage company with no recent history of profitability, and alimited recent operating history in the mineral exploration, development and production business. TheCompany has no history of producing minerals from the Goondicum Project and Belridge has limitedhistory in doing so. The Company is subject to all of the risks associated with the re-start, development,operation and expansion of mining operations and business enterprises including:

the timing and cost, which can be considerable, of the preparation and construction of mining andprocessing facilities;

the availability and costs of skilled labour and mining equipment; and

the need to obtain necessary environmental and other governmental approvals and permits, andthe timing of those approvals and permits.

It is common in mining operations to experience unexpected problems and delays during construction,development and mine start-up. In addition, delays in the commencement of mineral production oftenoccur. Accordingly, there are no assurances that the Company’s activities will result in profitable miningoperations or that the Company will successfully establish mining operations or profitably produceminerals at any of its current or future properties, or at all.

Reliability of Resource Estimates

There is no certainty that any of the mineral resource estimates described in the Technical Report areaccurate or will be realized. Until a deposit is actually mined and processed, the quantity of mineralresources and grades must be considered as estimates only. In addition, the quantity of mineral resourcesmay vary depending on, among other things, mineral prices. Any material change in quantity of mineralresources, grade or stripping ratio may affect the economic viability of any project undertaken by theCompany. In addition, there can be no assurance that ilmenite recoveries or other mineral recoveries insmall scale laboratory tests will be duplicated in a larger scale test under on-site conditions or duringproduction.

Fluctuations in ilmenite and other mineral prices, results of drilling, metallurgical testing and productionand the evaluation of studies, reports and plans subsequent to the date of any estimate may requirerevision of such estimate. Any material reductions in estimates of mineral resources could have a materialadverse effect on the Company’s results of operations and financial condition.

Uninsurable Risks

In the course of exploration, development and production of mineral properties, certain risks, and inparticular, unexpected or unusual geological operating conditions including rock bursts, cave-ins, fires,flooding and earthquakes may occur. It may not be possible to insure fully or at all against such risks andthe Company may decide not to take out insurance against such risks as a result of high premiums orother reasons. Should such risks arise, they could reduce or eliminate the funds available to the Companyto fund its operations or investments, increase costs to the Company, reduce future profitability and/ormaterially adversely affect the Company’s financial condition.

Environmental and Safety Regulations and Risks

- 16 -

Environmental and safety laws and regulations will significantly affect the operations of the Company.These laws and regulations set various standards regulating environmental, health and safety matters,including air and water quality, mine reclamation, solid and hazardous waste handling and disposal andthe promotion of occupational health and safety. These laws provide for penalties and other liabilities forthe violation of such standards and establish, in certain circumstances, obligations to rehabilitate currentand former facilities and locations where operations are or were conducted. The permission to operate canbe withdrawn temporarily where there is evidence of serious breaches of health and safety standards, oreven permanently in the case of extreme breaches. Significant liabilities could be imposed on theCompany for damages, clean-up costs or penalties in the event of certain discharges into the environment,environmental damage caused by previous owners of acquired properties or noncompliance withenvironmental laws or regulations. To the extent that the Company becomes subject to environmentalliabilities, the satisfaction of any such liabilities would reduce funds otherwise available to the Companyand could have a material adverse effect on the Company. The Company intends to minimize risks bytaking steps to ensure compliance with environmental, health and safety laws and regulations andoperating to applicable environmental standards. There is a risk that environmental laws and regulationsmay become more onerous, making the Company’s operations more expensive or materially restrictingthose operations.

Land Reclamation

Although they vary, depending on location and the governing authority, land reclamation requirementsare generally imposed on mineral exploration companies, as well as companies with mining operations, inorder to minimize long term effects of land disturbance. Reclamation obligations may includerequirements to control dispersion of potentially deleterious effluents and to reasonably re-establish pre-disturbance land forms and vegetation. In order to carry out reclamation obligations imposed on theCompany in connection with its mining operations and mineral exploration, the Company may berequired to allocate significant financial resources and/or secure bonding or other financial assurancesrelating to such obligations.

Competition

The mining industry is intensely competitive in all its phases. There is a high degree of competition forthe discovery and acquisition of properties considered to have commercial potential. The Companycompetes for the acquisition of mineral properties, claims, leases and other mineral interests as well as forthe recruitment and retention of qualified employees with many companies possessing greater financialresources and technical facilities than the Company. Competition in the mining industry could have amaterial adverse effect on the Company’s ability to acquire suitable properties in the future and to attractand retain qualified employees.

Personnel

The Company’s prospects depend significantly on the ability of its executive officers and seniormanagement to operate effectively, both independently and as a group. The success of the Companydepends to a large extent upon its ability to retain the services of its senior management and key personneland to attract additional key personnel. The loss of the services of any of these persons could have amaterial adverse effect on the Company’s business and prospects. There is no assurance the Company canmaintain the services of its directors, officers or other qualified personnel required to operate or overseeits business or attract additional or replacement qualified personnel.

Litigation Risk

- 17 -

All industries, including the mining industry, are subject to legal claims, with and without merit. TheCompany may be involved from time to time in various legal proceedings, which may include labourmatters such as unfair termination claims, supplier matters and property issues incidental to its business.Defence and settlement costs can be substantial, even with respect to claims that have no merit. Due to theinherent uncertainty of the litigation process, the resolution of any particular legal proceeding could havea material adverse effect on the Company’s financial position and results of operations.

Government Regulations, Licenses and Permits

Exploration and development activities and mining operations are subject to laws and regulationsgoverning health and worker safety, employment standards, environmental matters, mine development,prospecting, mineral production, exports, taxes, labour standards, reclamation obligations and othermatters. It is possible that future changes in applicable laws and regulations, or changes in theirenforcement or regulatory interpretation could result in changes in legal requirements or in the terms ofpermits applicable to the Company or its properties which could have a material adverse impact on theCompany’s business. Obtaining necessary permits and licences can be a complex, time consumingprocess and there can be no assurance that required permits will be obtainable on acceptable terms, in atimely manner, or at all. The costs and delays associated with obtaining permits and licenses andcomplying with these permits and licenses and applicable laws and regulations could stop, materiallydelay or restrict the Company from proceeding with the exploration and development activities or theoperation or further development of a mine.

Any failure to comply with applicable laws and regulations or permits, even if inadvertent, could result inenforcement actions, including orders issued by regulatory or judicial authorities causing interruption orclosure of exploration, development or mining operations or material fines and penalties, including, butnot limited to, corrective measures requiring capital expenditures, installation of additional equipment,remedial actions or other liabilities. Parties engaged in mining operations or in the exploration ordevelopment of mineral properties may be required to compensate those suffering loss or damage byreason of these activities and may have civil or criminal fines or penalties imposed for violations ofapplicable laws or regulations.

In addition, amendments to current laws and regulations governing the Company’s activities or morestringent implementation thereof could have a substantial adverse impact on the Company and causeincreases in exploration expenses, capital expenditures or production costs or reduction in levels ofproduction at producing properties or require abandonment or delays in development of new miningproperties.

Conflicts of Interest

Certain of the directors and officers of the Company may also serve as directors and/or officers of othercompanies involved in natural resource exploration and development and consequently there exists thepossibility for such directors and officers to be in a position of conflict. See “Directors and Officers –Other Reporting Issuer Experience”.

Currency Fluctuations;

The operations of the Company will be subject to currency exchange rate fluctuations and suchfluctuations may materially affect the financial position and results of the Company. The Company issubject to the risks associated with the fluctuation of the rate of exchange of the U.S. dollar, the Canadiandollar, the Australian dollar and other currencies. The majority of the Company’s operating costs areexpected to be incurred in Australian dollars, while the prices for its products are expected to be based in

- 18 -

U.S. dollars or other currencies. The Company does not currently take any steps to hedge against currencyfluctuations. Although it may elect to hedge against the risk of currency fluctuations in the future, therecan be no assurance that steps taken by the Company to address such currency fluctuations will eliminateall adverse effects of currency fluctuations. Accordingly, the Company may suffer losses due to adverseforeign currency fluctuations.

Acquisition and Integration Risks

There are several risks relating to the Proposed Acquisition, including that the parties may be unable tocomplete the Proposed Acquisition, problems may arise with the ability to successfully integrate thebusiness of Belridge and the Company, the Company may not be able to achieve the benefits of theProposed Acquisition or it may take longer than expected to achieve those benefits and the ProposedAcquisition may involve unexpected costs and/or liabilities.

In addition, the Company may acquire additional mining properties and operations. However, there canbe no assurance that the Company will identify attractive acquisition candidates in the future or that it willsucceed in effectively managing the integration of any acquired operations.

If the expected synergies from such transactions do not materialize or if the Company fails to successfullyintegrate such acquired operations into its existing operations, the Company’s results could be adverselyaffected. To the extent that prior owners of businesses acquired by the Company failed to comply with orotherwise violated applicable laws or contractual requirements or otherwise incurred liabilities, theCompany, as a successor owner, may be financially responsible for these violations and other liabilities.The discovery of any material liabilities could have a material adverse effect on the Company’s business,financial condition and future prospects.

Absence of Dividend History or Policy

No dividends on the Common Shares have been paid by the Company to date. The Company anticipatesthat for the foreseeable future it will retain future earnings and other cash resources for the operation anddevelopment of its business. Payment of any future dividends will be at the discretion of the Board aftertaking into account many factors, including the Company’s operating results, financial condition andcurrent and anticipated cash needs.

Independent Contractors

The Company’s success depends, to a significant extent, on the performance and continued service ofindependent contractors. The Company will contract the services of professional drillers and others forexploration, environmental, construction and engineering services. Poor performance by such contractorsor the loss of such services could have a material and adverse effect on the Company and its business andresults of operations and could result in failure to meet business objectives.

Political Risk/Foreign Operations

The Goondicum Project is located in Australia. The Company believes that the government of Australiasupports the development of its natural resources by foreign operators. There is no assurance that futurepolitical and economic conditions in Australia will not result in the government adopting differentpolicies respecting foreign development and ownership of mineral resources. Any such changes in policymay result in changes in laws affecting ownership of assets, taxation, rates of exchange, sales of mineralproducts, environmental protection, labour relations, repatriation of income and return of capital, whichmay affect both the ability of the Company to undertake exploration and development activities in respect

- 19 -

of future properties, as well as its ability to continue to explore, develop and operate the GoondicumProject. The possibility that a future government of Australia may adopt substantially different policies,which might extend to expropriation of assets, cannot be ruled out.

Trading in the Company’s Common Shares may be Volatile

The securities of publicly traded companies, particularly mineral exploration and developmentcompanies, can experience a high level of price and volume volatility and the value and trading price ofthe Company’s securities can be expected to fluctuate depending on various factors, not all of which aredirectly related to the success of the Company and its operating performance, underlying asset values orprospects. These include the risks described elsewhere in this “Risk Factors” section as well as thefollowing: worldwide economic conditions, changes in government policies, investor perceptions,movements in global interest rates and global stock markets, variations in operating costs and the cost ofcapital that the Company may require in the future and market conditions that are specific to the miningindustry.

INFORMATION CONCERNING THE COMPANY

Corporate Structure

The Company was incorporated under the laws of the Province of British Columbia on June 1, 1995 asMadoc Mining Company Ltd. The Company changed its name to Adobe Ventures Inc., on January 28,1999, to Coalcorp Mining Inc., on October 27, 2005, and subsequently to Melior Resources Inc., onSeptember 29, 2011. The Company is incorporated under the BCA.

The Company’s head office is located at 120 Adelaide Street West, Suite 2500, Toronto, Ontario M5H1T1. The Company’s registered office is located at 355 Burrard Street, Suite 1900, Vancouver, BritishColumbia V6C 2G8.

General Development of the Business

The following describes the general development of the business of the Company over the last threecompleted financial years.

Reorganization

In December 2010, Compañía Carbones del Cesar S.A., a former subsidiary of the Company domiciled inColombia, entered into voluntary liquidation. GC Coal Limited, a former subsidiary of the Companydomiciled in Ireland, was dissolved in the 2010-2011 fiscal year.

On March 16, 2012, the Company completed the sale of all of the common stock of its wholly-ownedsubsidiary, Coalcorp International A.V.V. (“Coalcorp AVV”), which was the holding company fornumerous off-shore subsidiaries. As a result of the sale, assets of discontinued operations ofapproximately Cdn$3.6 million, liabilities of discontinued operations of approximately Cdn$0.4 millionand other associated liabilities of approximately Cdn$3.0 million, as reported on the unaudited statementof financial position as at December 31, 2011, were removed from the Company’s balance sheet as of theclosing. Under the share purchase and wind-down agreement, the Company is entitled to receive, subjectto certain terms and conditions, a share of net recoveries of cash, if any, that the purchaser receives as aresult of winding up or reorganizing any of the Coalcorp AVV subsidiaries.

- 20 -

Investment in Formation Metals Inc.

Pursuant to a subscription agreement dated May 6, 2010, the Company purchased a Cdn$8,000,000unsecured convertible debenture (the “Debenture”) from Formation Metals Inc. (“Formation”). TheDebenture had an initial term of 18 months with an interest rate of 12%, payable in common shares in thecapital of Formation (“Formation Shares”). The Debenture was convertible into Formation Shares atCdn$1.50 per Formation Share during the initial term.

On March 14, 2011, the Company announced that it had completed an agreement with Formation for theprepayment by Formation of the Debenture. Pursuant to such agreement, the Company surrendered theDebenture to Formation against payment of US$9,333,333 in cash and 400,000 Formation Shares. As atthe date hereof, the Company no longer holds any Formation Shares.

Investment in Oracle Mining Corp.

The Company entered into a subscription agreement dated October 25, 2010 with Gold Hawk ResourcesInc., which subsequently changed its name to Oracle Mining Corp. (“Oracle”). Pursuant to thesubscription agreement, the Company purchased 6,000,000 common shares in the capital of Oracle(“Oracle Shares”) at a price of US$1.25 per Oracle Share for an aggregate purchase price of US$7.5million. As at the date hereof, the Company no longer holds any Oracle Shares.

Settlement of Litigation

The Company, Xira Investment Inc. (“Xira”) and certain former members of the Company’s managementand other parties to various claims amongst them entered into a settlement agreement dated January 31,2010 (the “Settlement Agreement”). Under the terms of the Settlement Agreement, Xira agreed to payUS$34 million to the Company payable as follows: (i) US$7 million on February 8, 2010; (ii) US$17million on March 15, 2010; (iii) US$8 million on September 15, 2010; and (iv) US$2 million on January31, 2011. The Company received all such payments.

The Settlement Agreement also provided that: (i) on March 15, 2010, the 40% shareholding in CarbonesColombianos del Cessejon S.A. (“CCC”) (the owner of the Caypa Mine) held in escrow would bereleased to Xira and the remaining 60% shareholding in CCC held by certain of the Company’ssubsidiaries would be assigned to Xira; (ii) Andean Coal Corporation B.V.I. agreed to waive its salescommission on production from the Caypa Mine and cancel any outstanding payments; (iii) Blue PacificAssets Corp. agreed to terminate its royalty on production from the La Francia I Mine and cancel anyoutstanding royalty payments; (iv) all litigation and regulatory proceedings among the parties would beterminated; (v) all parties would release the others as part of the settlement; and (vi) the releases in favourof Xira and the former management group would be held in escrow until receipt of the final payment fromXira due on January 31, 2011.

On March 21, 2011 the Company announced that it had entered into a settlement and mutual release (the“GS Settlement Agreement”) with certain affiliates of the Goldman Sachs Group, Inc., includingColombian Natural Resources I SAS (“CNRI”). Pursuant to the GS Settlement Agreement, the partiesirrevocably released and discharged each other from any and all claims, including those raised by CNRIin the Notices of Claim announced on November 3, 2010 and December 3, 2010, arising out of or relatingto the sale by certain of the Company’s subsidiaries of the La Francia I Mine and related infrastructureassets and all of the issued and outstanding shares of Adromi Capital Corp., the holder of the La FranciaII Mine, to a subsidiary of the Goldman Sachs Group, Inc., which transaction was completed on March19, 2010 (the “La Francia Transaction”).

In accordance with the terms of an escrow agreement dated March 19, 2010 among Computershare TrustCompany of Canada (“Computershare”), the Company, and CNRI and Colombian Natural Resources II

- 21 -

SAS (collectively, the “CNR Parties”), Computershare was holding US$8,000,000 in escrow inconnection with the La Francia Transaction. Pursuant to the GS Settlement Agreement, US$6,230,576was released to the CNR Parties and US$1,769,423 was released to the Company.

Changes in the Board of Directors and Management.

On March 24, 2011, the Company announced the appointment of Robert Dietrich to Board. In addition,Richard Lister, then Chairman of the Company, assumed the added responsibilities of CEO and StevenCresswell stepped down as Interim CEO and assumed the responsibility of CFO.

On August 17, 2011, the Company announced the appointment of Charles Entrekin to the positions ofCEO and Chairman of the Board. Charles Entrekin replaced Richard Lister following his resignation forpersonal reasons; however, the Company retained Richard Lister as a consultant for four months to assistin a smooth transition. On September 9, 2011, the Company announced the appointment of Daniel Dumasto the Board.

On December 1, 2011, the Company announced the appointment of Rishi Tibriwal, CA, as the CFOfollowing the resignation of Steven Cresswell.

On October 1, 2012, the Company announced the appointment of Thomas Masney, CA, as the CFO onthe resignation of Rishi Tibriwal.

On February 14, 2013, Charles Entrekin, Evgenij Iorich, Remo Mancini and Muneeb Yusuf were electedas directors of the Company at the annual and special meeting of the shareholders.

On March 30, 2014, Remo Mancini, Muneeb Yusuf and Evgenij Iorich resigned as directors of theCompany and Martyn Buttenshaw, Glenn Black and Joseph Connolly were appointed as directors of theCompany by the Board.

Graduation from NEX and Recategorization as an Investment Issuer

Effective April 1, 2011, the Company commenced trading on Tier 1 of the Exchange as an “InvestmentIssuer”. The Company received the consent of shareholders holding greater than 50% of the issued andoutstanding shares in the capital of the Company to the change of business from a mineral resourcecompany to an investment issuer. Shareholder approval was obtained by written consent.

In conjunction with its recategorization, the Company adopted an Investment Policy which providesguidelines and criteria for all of the Company’s investment activities. The Investment Policy is attachedas Schedule “A” to the Company’s news release issued and filed under the Company’s profile onSEDAR on March 31, 2011. In connection with the completion of the Proposed Acquisition, theCompany’s Investment Policy will be terminated.

Senior Notes

On August 31, 2011, the Company’s outstanding 12% senior secured guaranteed notes due August 31,2011 (Series A) matured and the Company made a final payment of US$8.4 million in respect of theaggregate principle amount of US$8.27 million, plus accrued interest.

2012 Strategic Alternatives Review

On May 16, 2012, the Company announced that the Board had commenced a review of strategicalternatives with the objective of enhancing shareholder value. A special committee of the Board wasestablished to oversee the review. The Company evaluated its options including, but not limited to,

- 22 -

continuing to explore investment opportunities, a corporate reorganization, reverse takeovers and a returnof capital to shareholders. It was concluded that the Company should continue to pursue its businessstrategy of investing and aiding growth in projects in the mining, metallurgical and mineral industries,with the objective of growing the Company and increasing shareholder value.

Investment in Asian Mineral Resources Limited