Embed Size (px)

DESCRIPTION

Media Market Overview - Cormac O’Shea, Clear Blue Water

Citation preview

Welcome!

Housekeeping

Thank yous

Cormac O’Shea

Media Market Overview

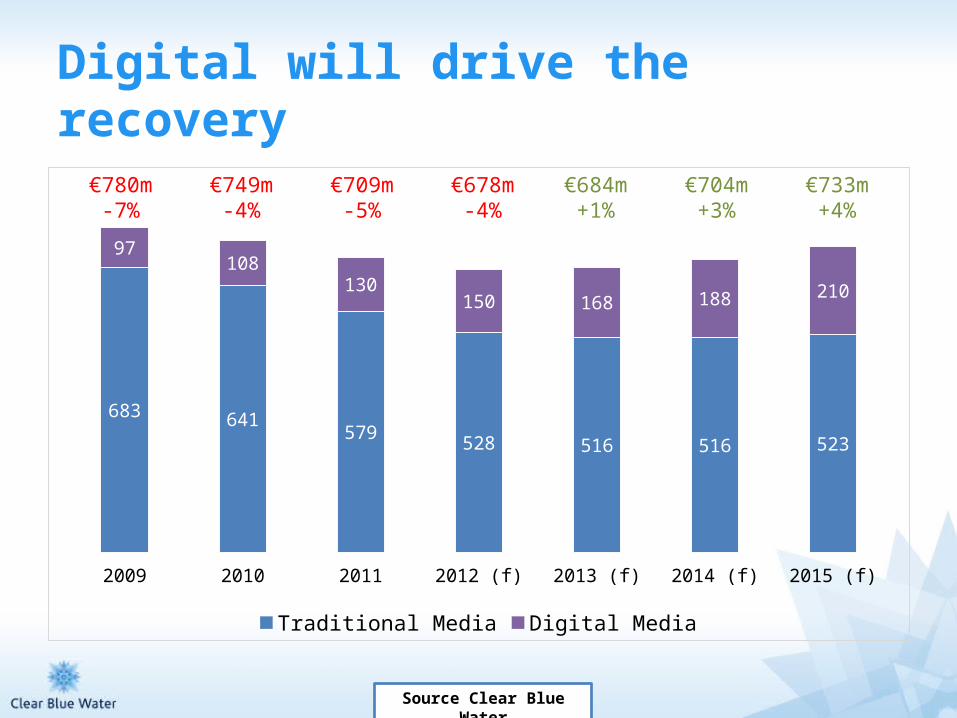

Digital will drive the recovery

2009 2010 2011 2012 (f) 2013 (f) 2014 (f) 2015 (f)

683 641579 528 516 516 523

97108

130150 168 188 210

Traditional Media Digital Media

€709m-5%

€678m-4%

€684m+1%

€704m+3%

€780m-7%

€749m-4%

€733m+4%

Source Clear Blue Water

Value

+2 to 5%

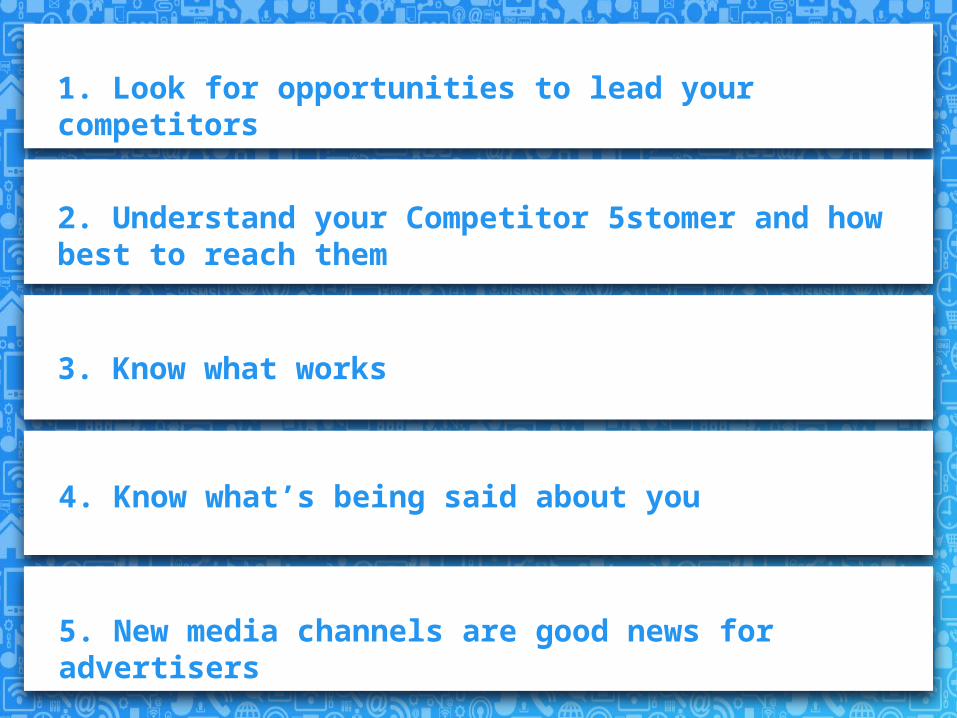

1. Look for opportunities to lead your competitors

2. Understand your Competitor 5stomer and how best to reach them

3. Know what works

4. Know what’s being said about you

5. New media channels are good news for advertisers

1

Look for opportunities to lead your competitors

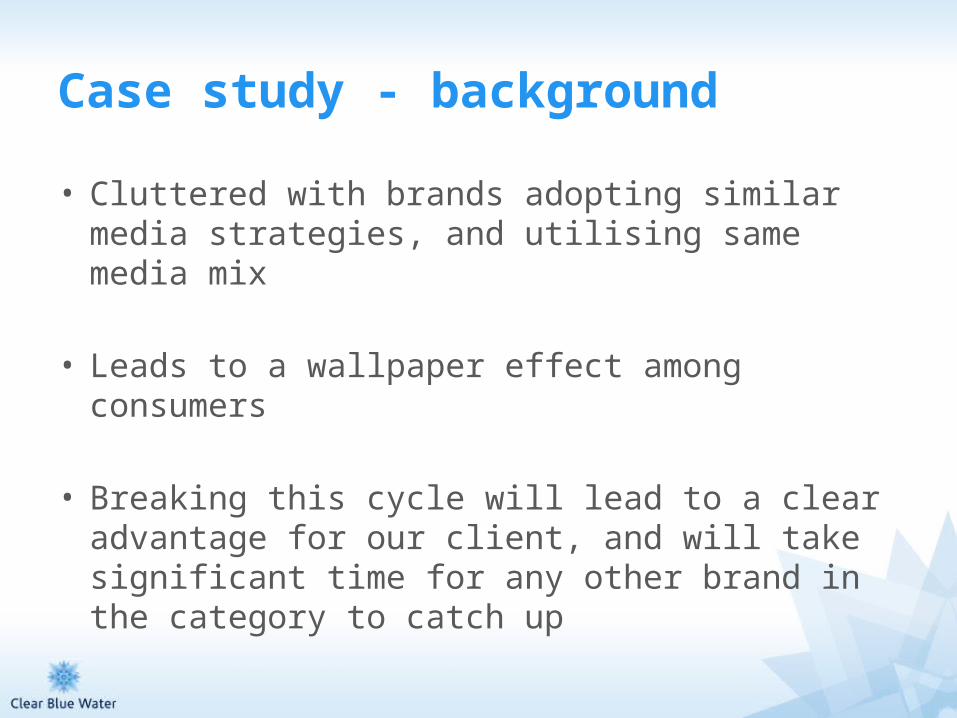

Case study - background

• Cluttered with brands adopting similar media strategies, and utilising same media mix

• Leads to a wallpaper effect among consumers

• Breaking this cycle will lead to a clear advantage for our client, and will take significant time for any other brand in the category to catch up

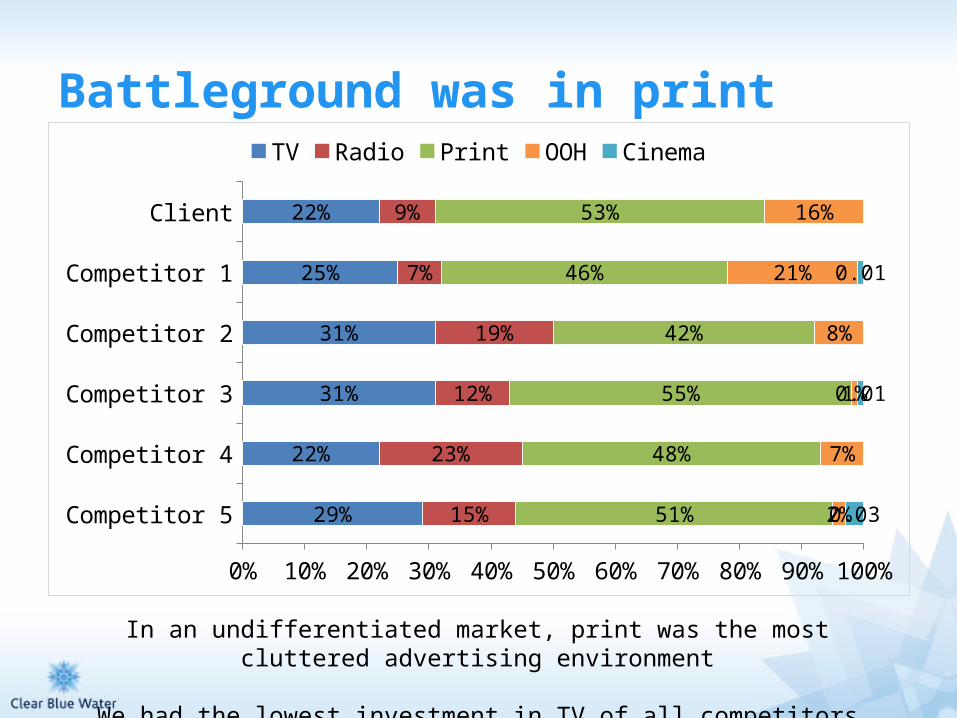

Battleground was in print

Competitor 5

Competitor 4

Competitor 3

Competitor 2

Competitor 1

Client

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

29%

22%

31%

31%

25%

22%

15%

23%

12%

19%

7%

9%

51%

48%

55%

42%

46%

53%

2%

7%

1%

8%

21%

16%

0.03

0.01

0.01

TV Radio Print OOH Cinema

In an undifferentiated market, print was the most cluttered advertising environment

We had the lowest investment in TV of all competitors

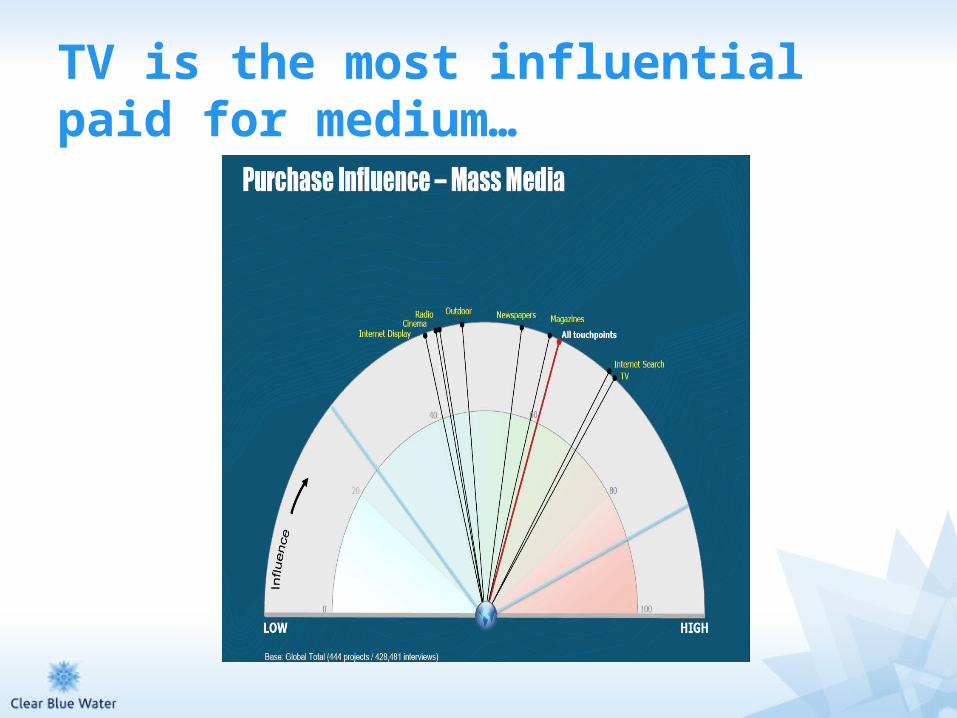

TV is the most influential paid for medium…

…and has strongest return on investment

Source: Thinkbox, IPA, Neilsen

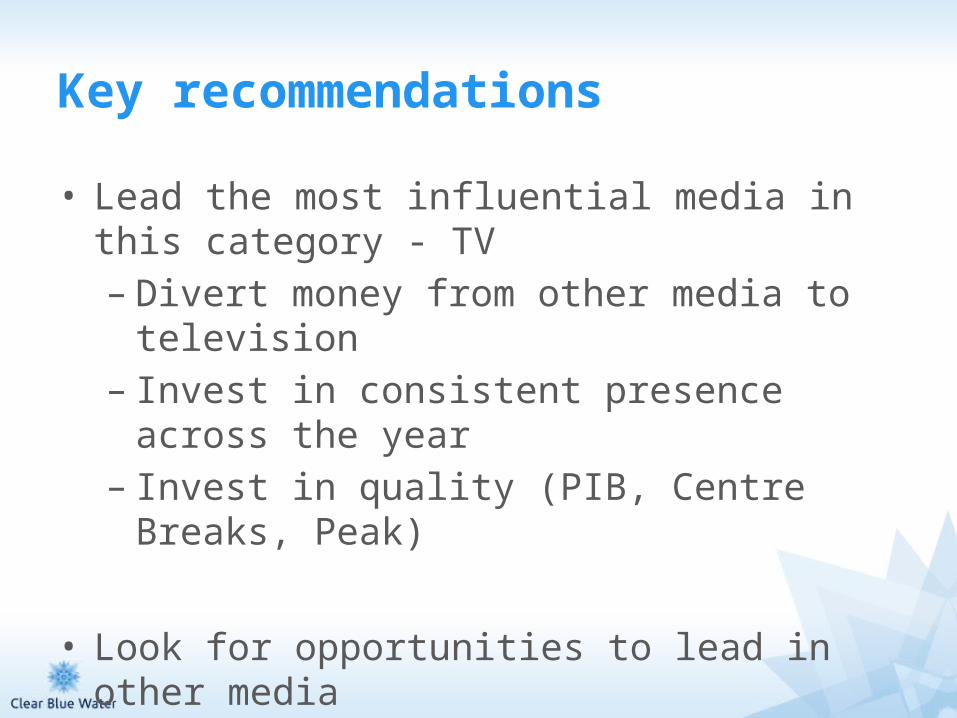

Key recommendations

• Lead the most influential media in this category - TV– Divert money from other media to television– Invest in consistent presence across the year– Invest in quality (PIB, Centre Breaks, Peak)

• Look for opportunities to lead in other media

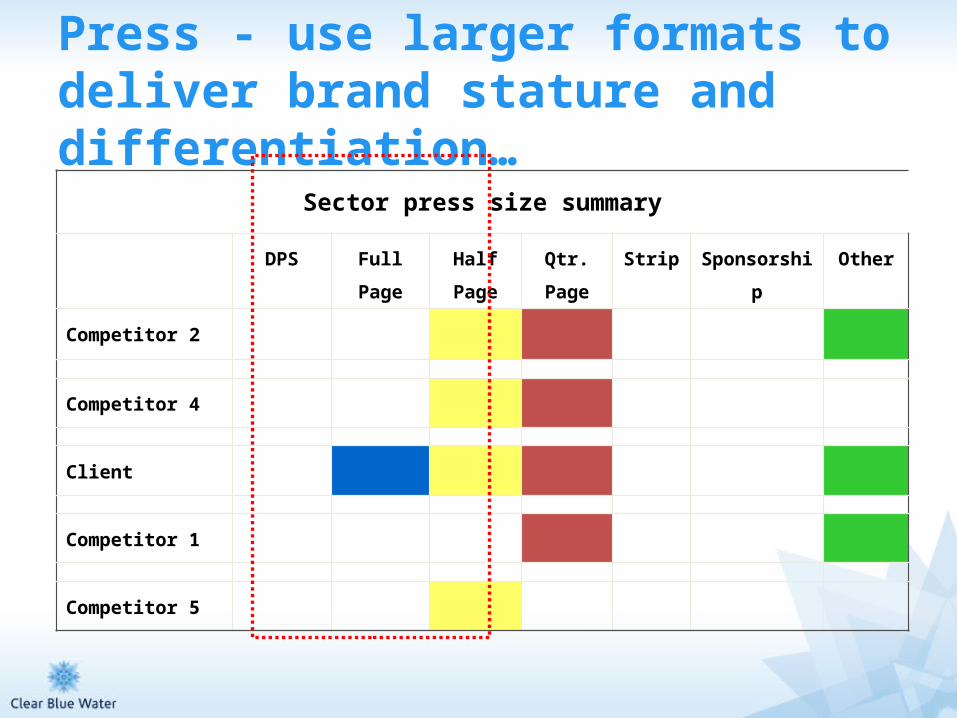

Press - use larger formats to deliver brand stature and differentiation…

Sector press size summary

DPS Full Page Half Page Qtr. Page Strip Sponsorship Other

Competitor 2

Competitor 4

Client

Competitor 1

Competitor 5

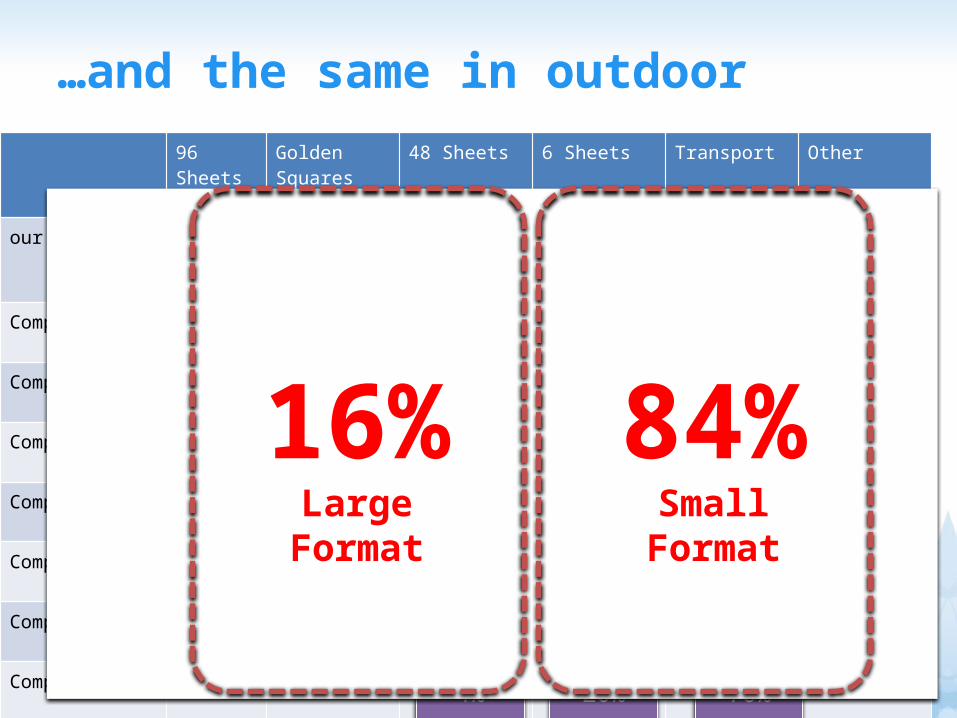

…and the same in outdoor96 Sheets Golden

Squares48 Sheets 6 Sheets Transport Other

our client

Competitor 1

Competitor 2

Competitor 4

Competitor 5

Competitor 6

Competitor 3

Competitor 7

1% 35% 34% 11% 18%

17% 2% 80%

10% 67% 19% 4%

45% 23% 32%

1% 42% 2%55%

46% 54%

4% 20% 76%

5% 3% 4% 89%

1% 35% 34% 11% 18%

17% 2% 80%

10% 67% 19% 4%

45% 23% 32%

1% 42% 2%55%

46% 54%

4% 20% 76%

5% 3% 4% 89%

16%Large

Format

84%Small

Format

What happened?

Consideration increased by 12% over the yearShare of market increased by 1.4% over the year

2

Understand your customer and how best to reach them

TGI media and marketing survey

• Annual

• c.5,000 per annum

• TV, radio, newspapers, magazines, outdoor, internet, direct mail

• 18 sectors, 500 categories, 4,000 brands

• 270+ lifestyle statements, socio-demographic classifications, geo-demographics

Example of how we use this research

The brief:

“We want to reach heavy shoppers who would use their mobile phones to accumulate loyalty points while shopping”

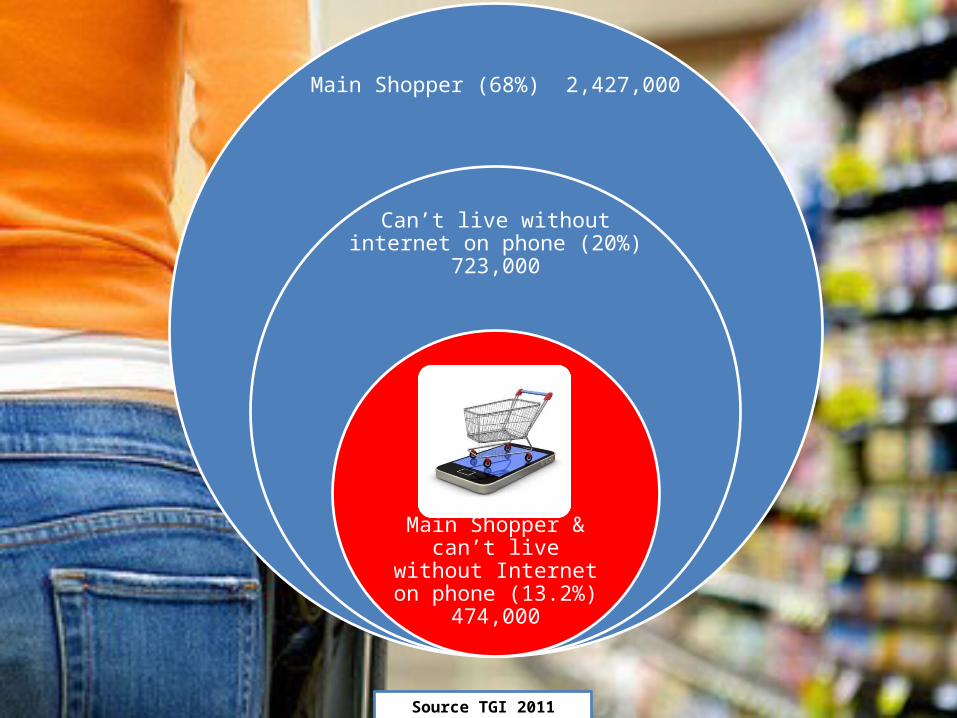

Main Shopper (68%) 2,427,000

Can’t live without internet on phone

(20%) 723,000

Main Shopper & can’t live without Internet on phone (13.2%) 474,000

Source TGI 2011

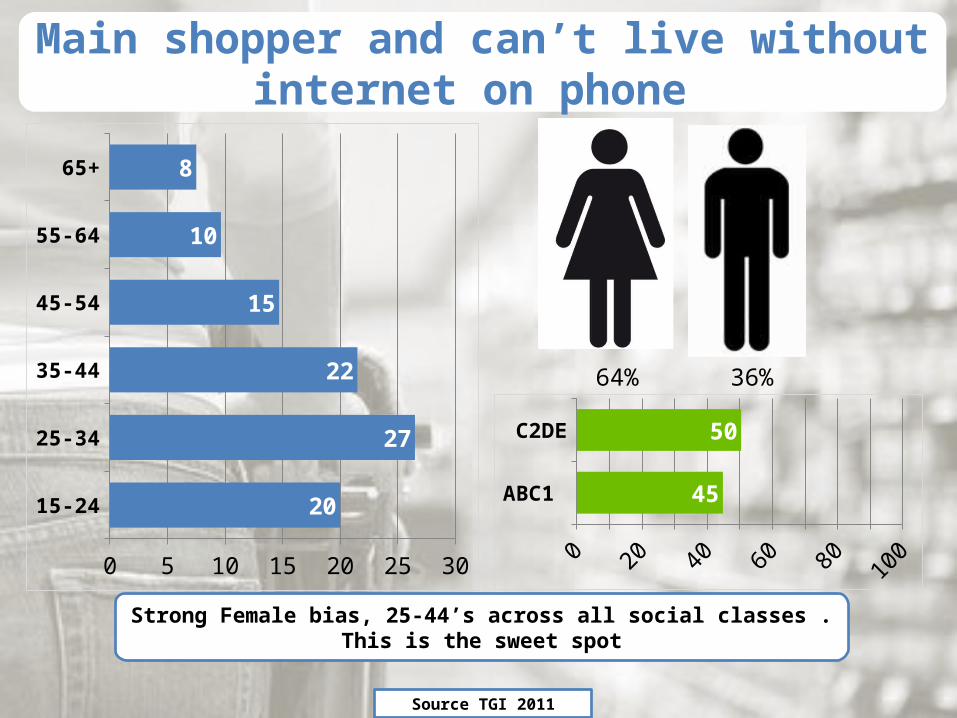

15-24

25-34

35-44

45-54

55-64

65+

0 5 10 15 20 25 30

20

27

22

15

10

8

ABC1

C2DE

0 10 20 30 40 50 60 70 80 90 100

45

50

64% 36%

Strong Female bias, 25-44’s across all social classes . This is the sweet spot

Main shopper and can’t live without internet on phone

Source TGI 2011

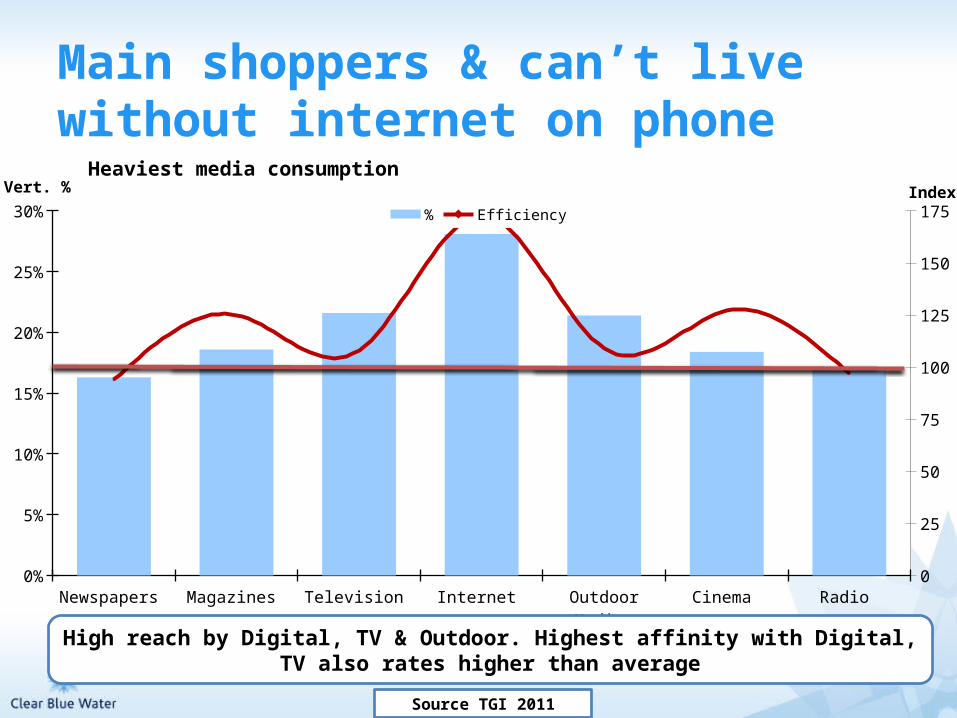

Newspapers Magazines Television Internet Outdoor Media Cinema Radio 0%

5%

10%

15%

20%

25%

30%

0

25

50

75

100

125

150

175

Heaviest media consumption

% EfficiencyVert. % Index

High reach by Digital, TV & Outdoor. Highest affinity with Digital, TV also rates higher than average

Source TGI 2011

Main shoppers & can’t live without internet on phone

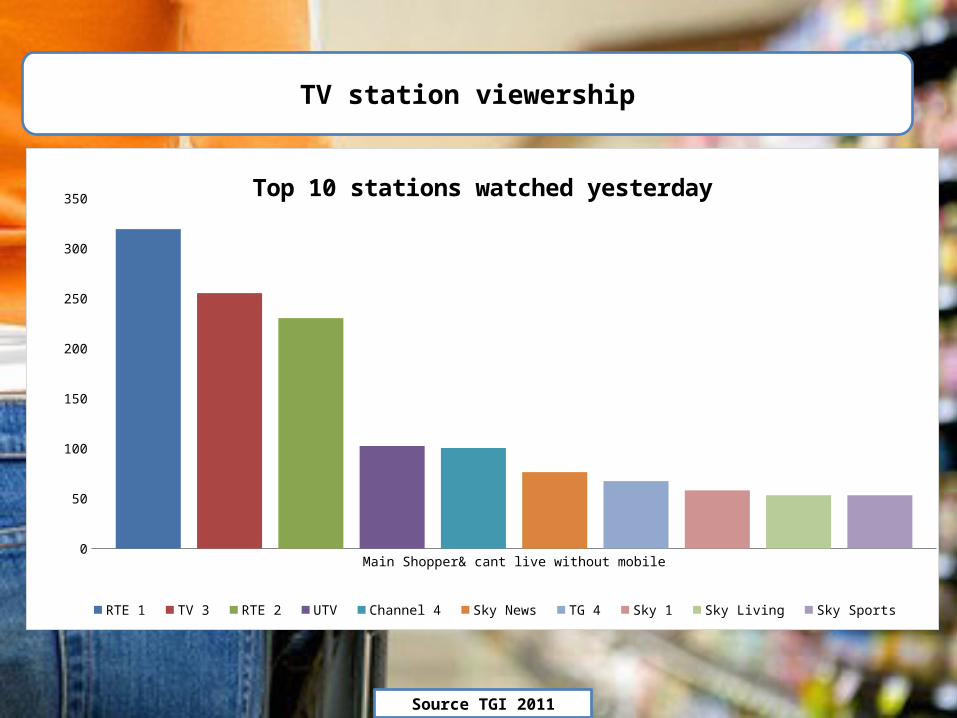

Main Shopper& cant live without mobile0

50

100

150

200

250

300

350Top 10 stations watched yesterday

RTE 1 TV 3 RTE 2 UTV Channel 4 Sky News TG 4 Sky 1 Sky Living Sky Sports

TV station viewership

Source TGI 2011

Daytime is key to delivering this audience efficiently

Main Shopper& cant live without mobile0

20

40

60

80

100

120

140

Viewership of RTE 1 by Index

9.30 - 11.59 am 8.00 - 10.59 pm 5.30 - 7.59 pm 12.00 - 3.59 pm 11.00 - 12.59 am 4.00 - 5.29 pm 6.00 - 9.29 am 1.00 - 5.59 am

Source TGI 2011

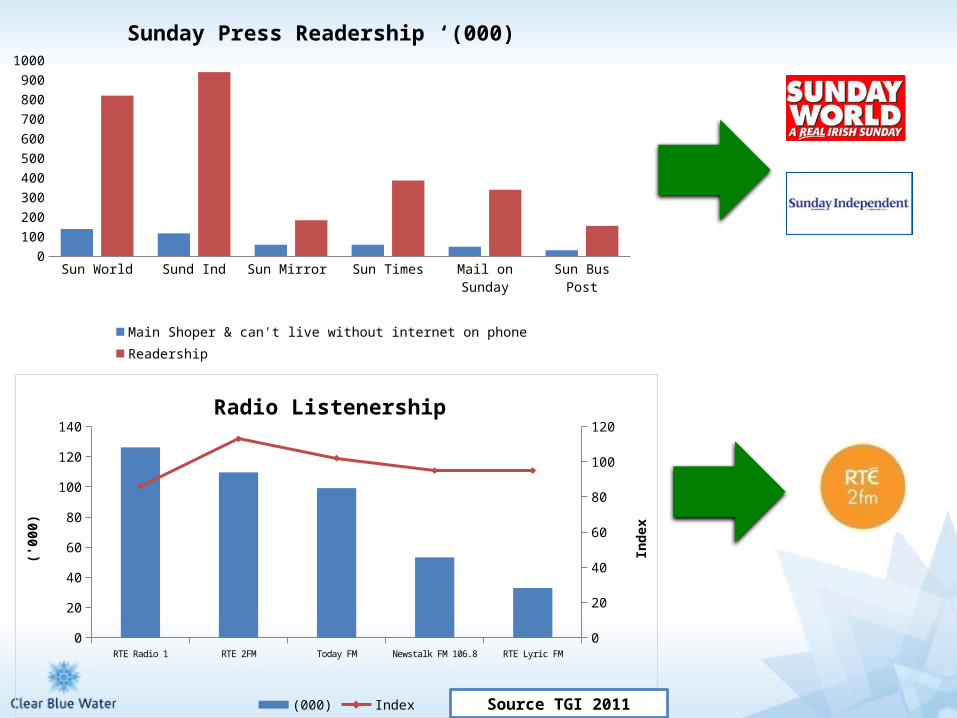

Sun World Sund Ind Sun Mirror Sun Times Mail on Sunday Sun Bus Post0

100

200

300

400

500

600

700

800

900

1000

Sunday Press Readership ‘(000)

Main Shoper & can't live without internet on phone Readership

RTE Radio 1 RTE 2FM Today FM Newstalk FM 106.8 RTE Lyric FM0

20

40

60

80

100

120

140

0

20

40

60

80

100

120

Radio Listenership

(000) Index

('000

)

Inde

x

Source TGI 2011

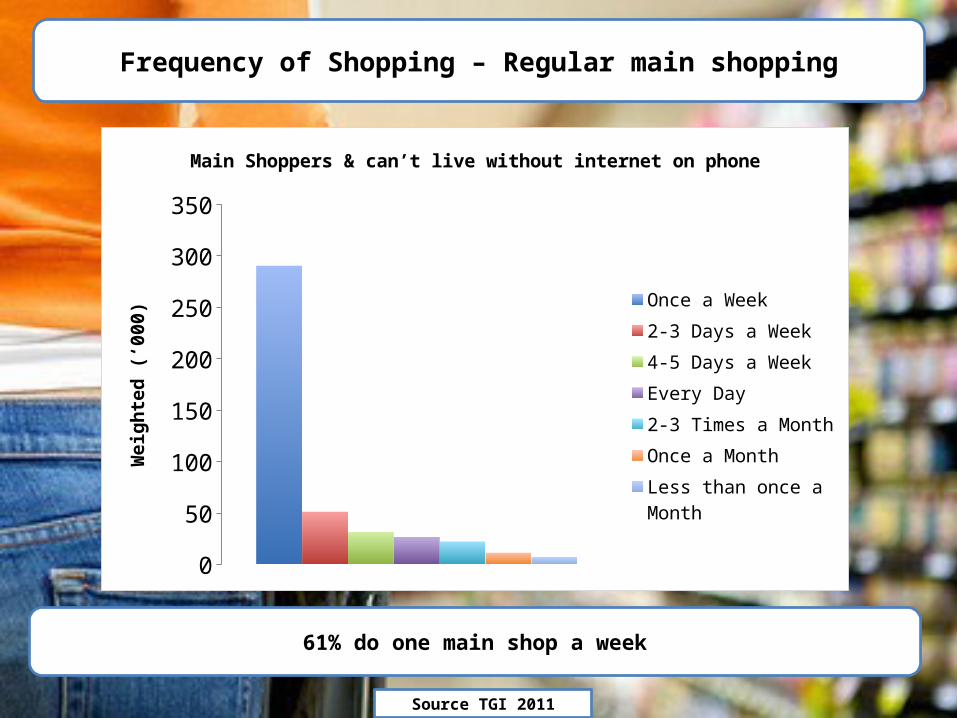

Frequency of Shopping – Regular main shopping

61% do one main shop a week

0

50

100

150

200

250

300

350

Main Shoppers & can’t live without internet on phone

Once a Week

2-3 Days a Week

4-5 Days a Week

Every Day

2-3 Times a Month

Once a Month

Less than once a Month

Wei

ghte

d (‘0

00)

Source TGI 2011

Main Shopping Day

69% of main regular shopping done Thursday, Friday & Saturday

0

20

40

60

80

100

120

140

MondayTuesdayWednesdayThursdayFridaySaturdaySundayNo particular dayW

eigh

ted

(‘000

)

Source TGI 2011

3

Know what works

Which elements of your marketing mix work?

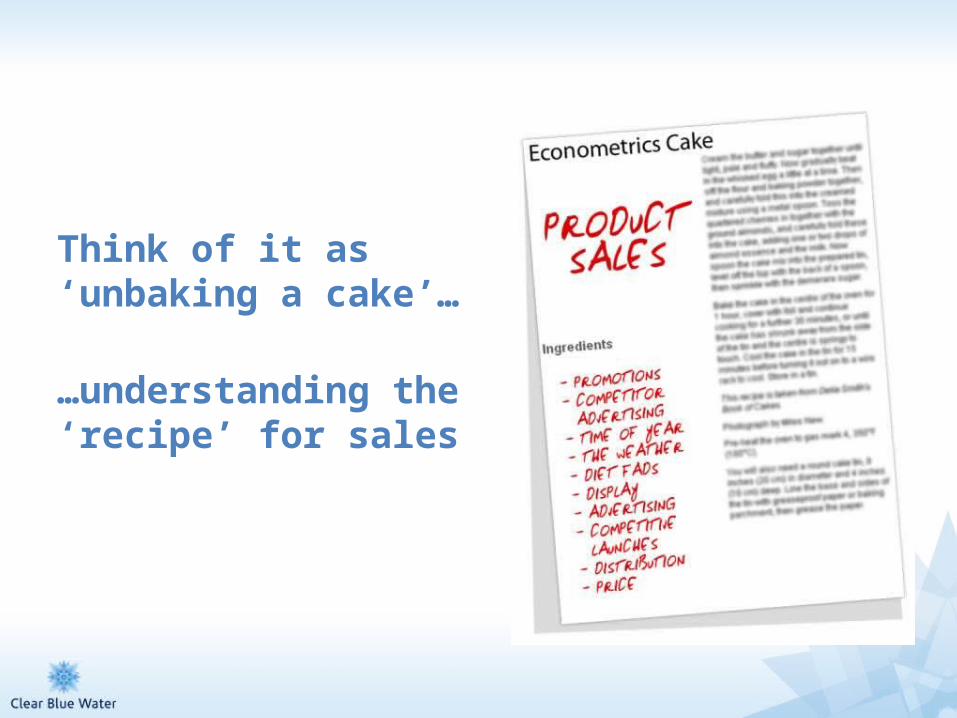

Econometric modelling - relates the size and timings of different marketing mix activity to movements in sales

Think of it as ‘unbaking a cake’…

…understanding the ‘recipe’ for sales

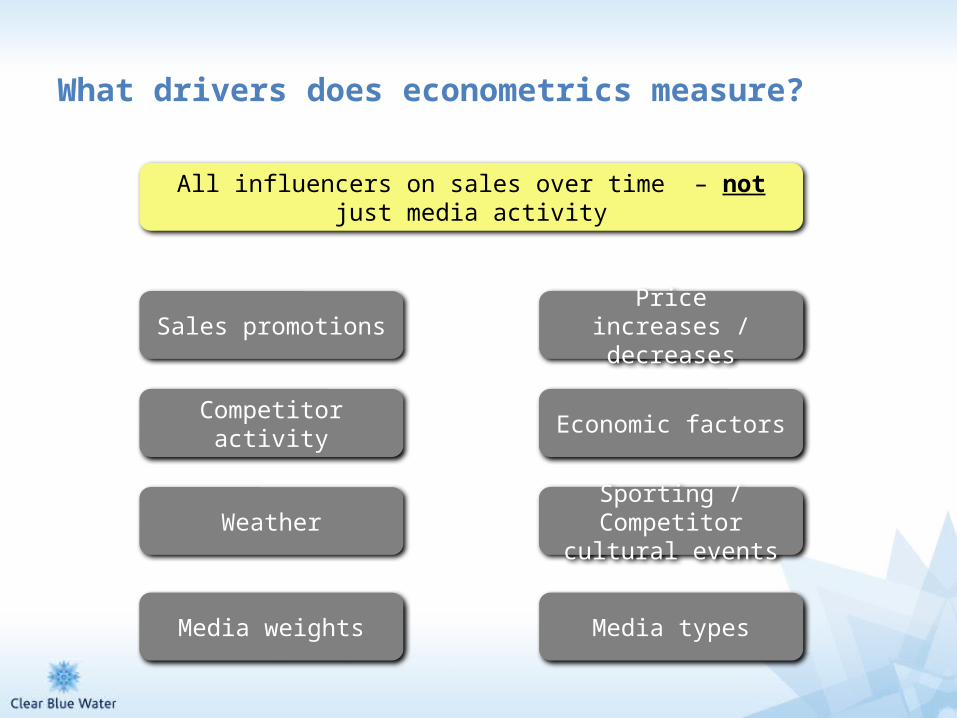

What drivers does econometrics measure?

Sales promotions

Competitor activity

Media weights

Economic factors

Weather Sporting / Competitor cultural events

All influencers on sales over time – not just media activity

Media types

Price increases / decreases

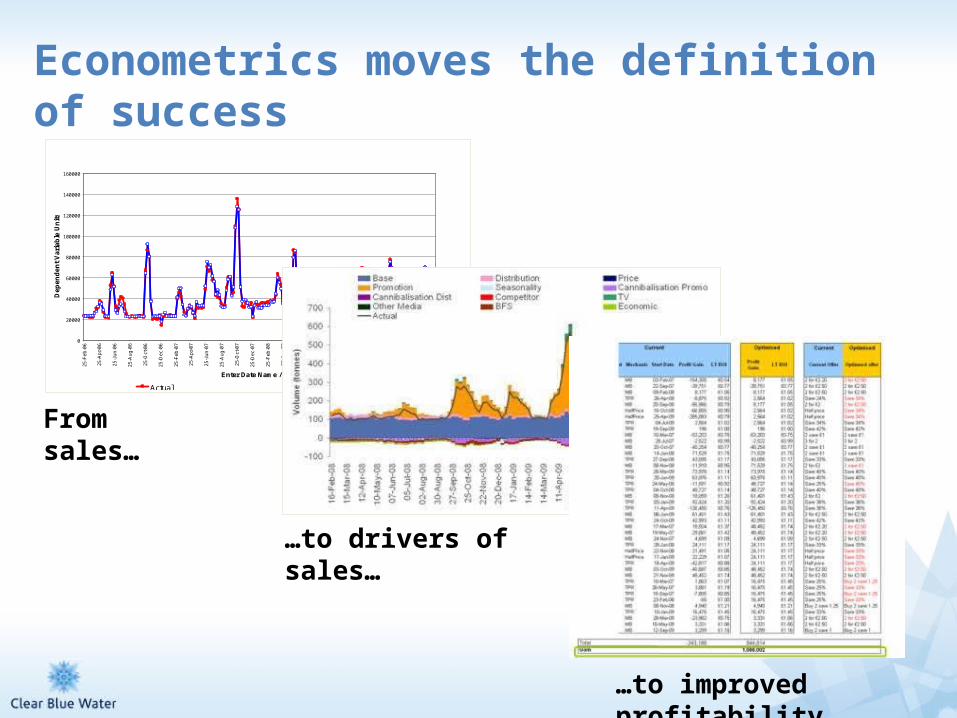

Econometrics moves the definition of success

0

20000

40000

60000

80000

100000

120000

140000

160000

25

-Fe

b-0

6

25

-Ap

r-0

6

25

-Ju

n-0

6

25

-Au

g-0

6

25

-Oct

-06

25

-De

c-0

6

25

-Fe

b-0

7

25

-Ap

r-0

7

25

-Ju

n-0

7

25

-Au

g-0

7

25

-Oct

-07

25

-De

c-0

7

25

-Fe

b-0

8

25

-Ap

r-0

8

25

-Ju

n-0

8

25

-Au

g-0

8

25

-Oct

-08

25

-De

c-0

8

25

-Fe

b-0

9

25

-Ap

r-0

9

25

-Ju

n-0

9

25

-Au

g-0

9

25

-Oct

-09

25

-De

c-0

9

Enter Date Name / Type

Dep

en

den

t V

ari

ab

le U

nit

s

Actual Model

Sum of Fitted Regions

Real

From sales…

…to drivers of sales…

…to improved profitability

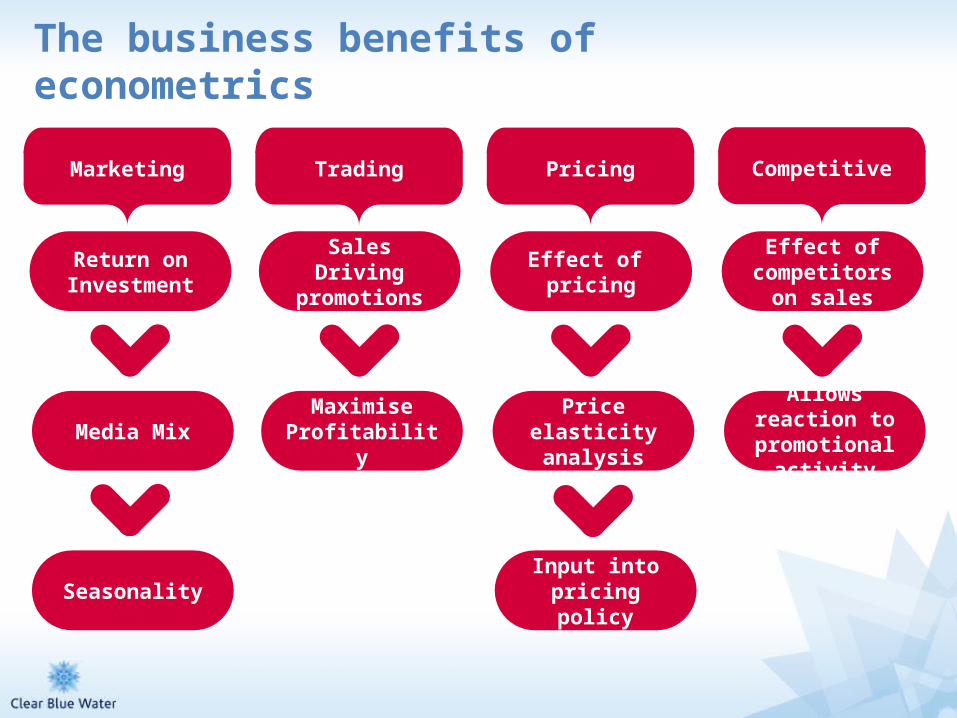

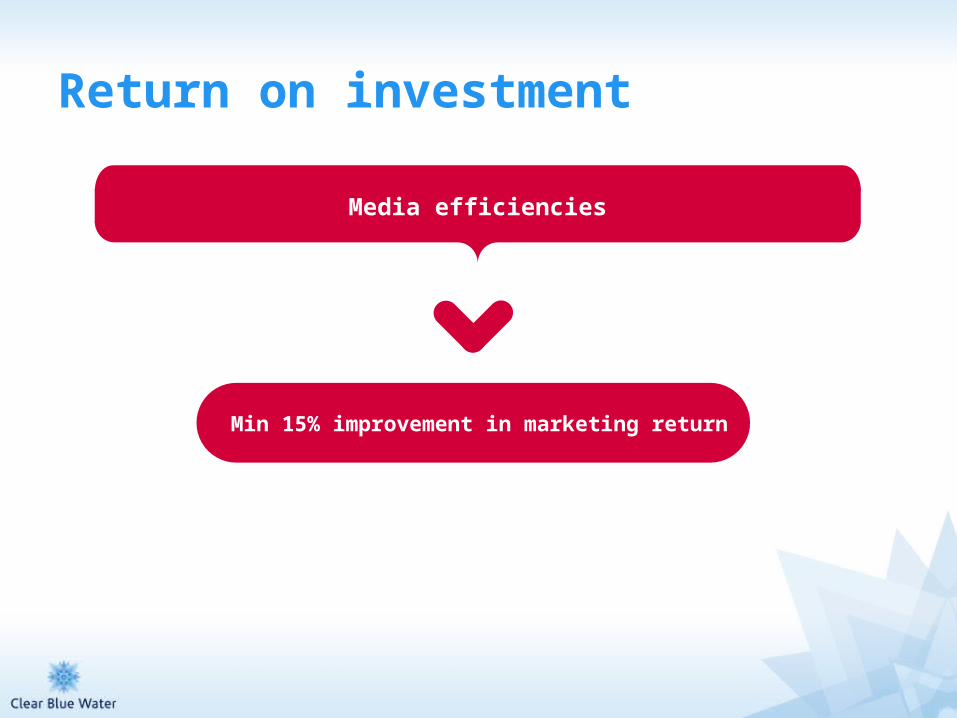

The business benefits of econometrics

Marketing Trading Pricing Competitive

Return on Investment

Media Mix

Seasonality

Sales Driving promotions

Maximise Profitability

Effect of pricing

Price elasticity analysis

Input into pricing policy

Effect of competitors

on sales

Allows reaction to promotional

activity

Return on investment

Media efficiencies

Min 15% improvement in marketing return

4

Know what’s being said about you

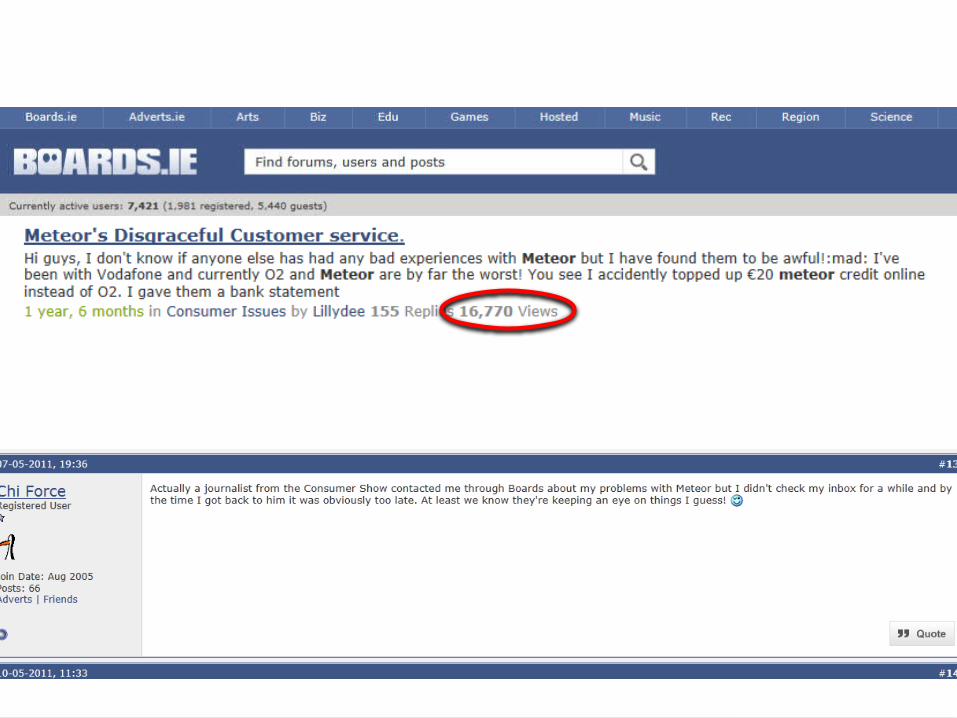

Pre digital age

Family and friendsPotential reach - 10-20

Digital age

Family and friendsPotential reach - 100’s

Digital age

Forums, blogs etc.Potential reach – 1,000’s ++

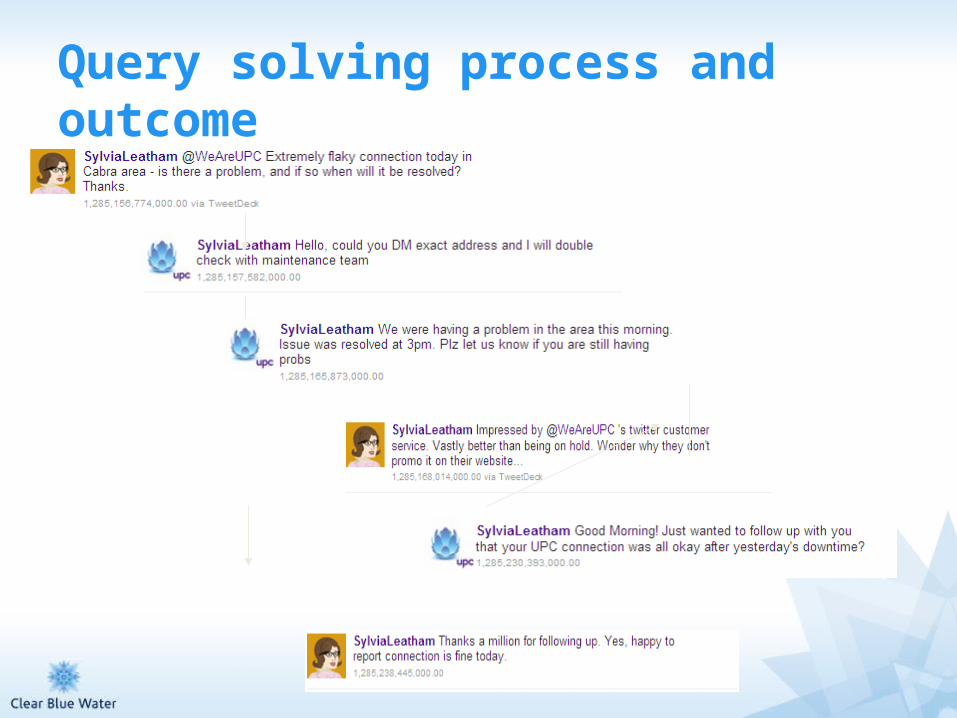

Query solving process and outcome

5

New media channels are good for advertisers

CostTargetin

g

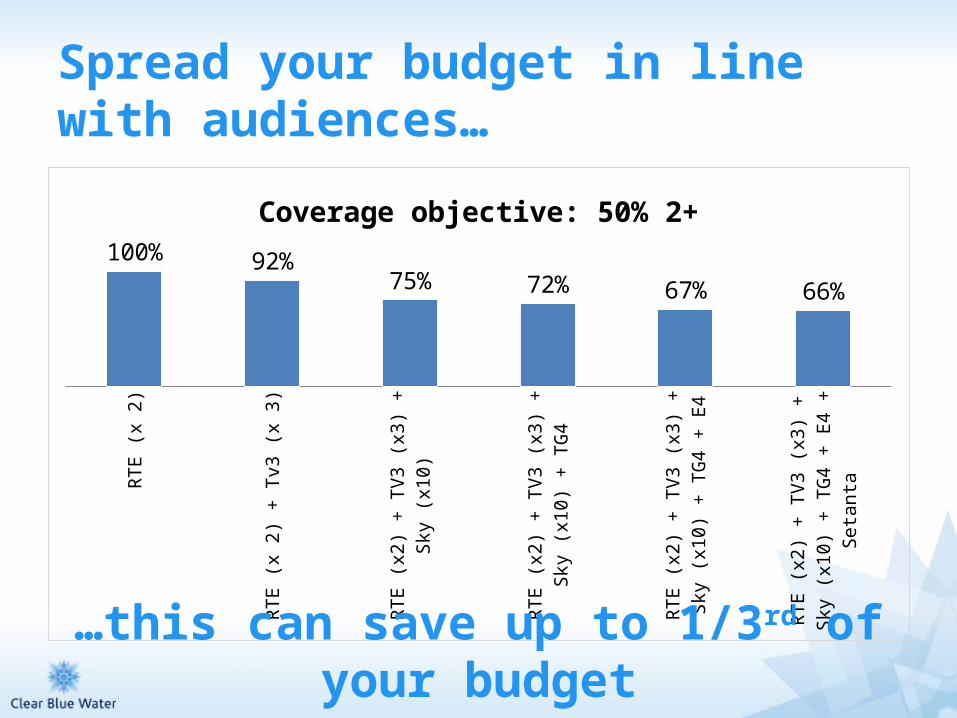

Spread your budget in line with audiences…

RTE

(x 2

)

RTE

(x 2

) + T

v3 (x

3)

RTE

(x2)

+ T

V3 (x

3) +

Sky

(x10

)

RTE

(x2)

+ T

V3 (x

3) +

Sky

(x10

) +

TG4

RTE

(x2)

+ T

V3 (x

3) +

Sky

(x10

) +

TG4

+ E4

RTE

(x2)

+ T

V3 (x

3) +

Sky

(x10

) +

TG4

+ E4

+ S

etan

ta

100% 92%75% 72% 67% 66%

Coverage objective: 50% 2+

…this can save up to 1/3rd of your budget

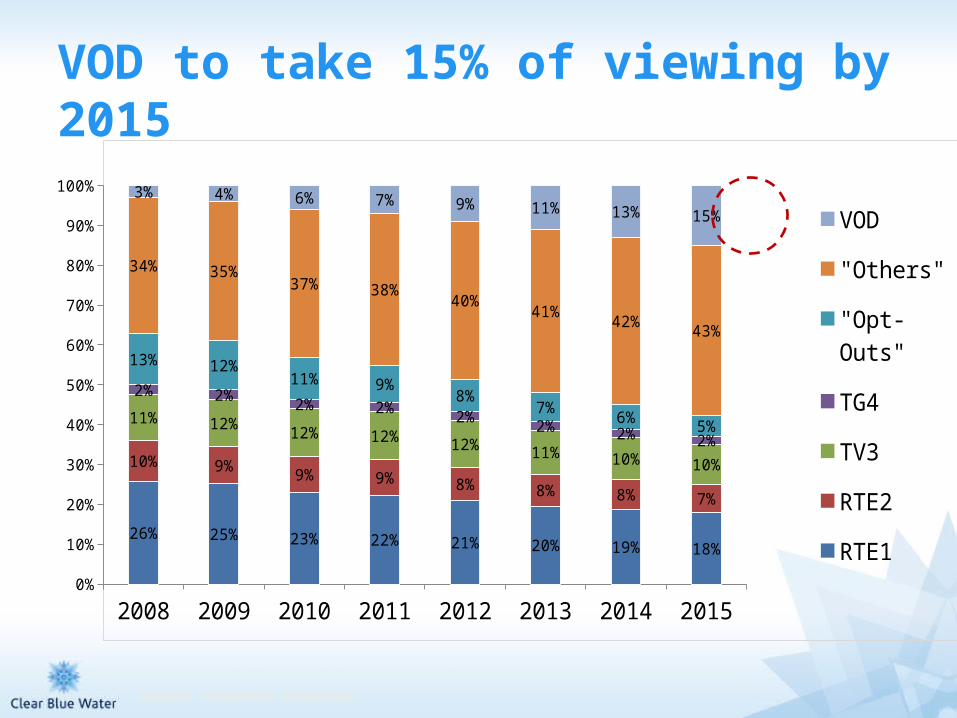

VOD to take 15% of viewing by 2015

2008 2009 2010 2011 2012 2013 2014 20150%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

26% 25% 23% 22% 21% 20% 19% 18%

10% 9% 9% 9% 8% 8% 8% 7%

11% 12% 12% 12% 12% 11% 10% 10%

2% 2% 2% 2% 2% 2% 2% 2%

13% 12%11% 9%

8%7%

6% 5%

34% 35%37% 38%

40%41%

42% 43%

3% 4% 6% 7% 9% 11% 13% 15% VOD

"Others"

"Opt-Outs"

TG4

TV3

RTE2

RTE1

Source: MediaVest estimates

1. Look for opportunities to lead your competitors

2. Understand your customer and how best to reach them

3. Know what works

4. Know what’s being said about you

5. New media channels are good news for advertisers