Embed Size (px)

Citation preview

Measuring the EconomicImportance ofthe Meetings Industry

Developing aTourism Satellite Account Extension

Copyright © 2006 World Tourism Organization Calle Capitán Haya, 4228020 Madrid, Spain

Measuring the Economic Importance of the Meetings Industry – Developing a Tourism Satellite Account Extension

ISBN-13: 978-92-844-1195-5ISBN-10: 92-844-1195-5

Published and printed by the World Tourism Organization, Madrid, SpainFirst printing 2006All rights reserved

The designations employed and the presentation of material in this publication do not imply the expression of anyopinions whatsoever on the part of the Secretariat of the World Tourism Organization concerning the legal statusof any country, territory, city or area, or of its authorities or concerning the delimitation of its frontiers orboundaries.

World Tourism OrganizationCalle Capitán Haya, 4228020 Madrid, SpainTel.: (+34) 915 678 100Fax: (+34) 915 713 733Website: www.unwto.org Email: [email protected]

All UNWTO publications are protected by copyright. Therefore and unless otherwise specified, no part of anUNWTO publication may be reproduced, stored in a retrieval system or utilized in any form or by any means,electronic or mechanical, including photocopying, microfilm, scanning, without prior permission in writing.UNWTO encourages dissemination of its work and is pleased to consider permissions, licensing, and translationrequests related to UNWTO publications.

Permission to photocopy UNWTO material in Spain must be obtained through:

CEDRO, Centro Español de Derechos ReprográficosCalle Monte Esquinza, 1428010 Madrid, SpainTel.: (+34) 91 308 63 30, Fax: (+34) 91 308 63 [email protected]; www.cedro.org

For authorization of the reproduction of UNWTO works outside of Spain, please contact one of CEDRO’s partnerorganizations, with which bilateral agreements are in place(see: http://www.cedro.org/ingles_funcion_internacional.asp)

For all remaining countries as well as for other permissions, requests should be addressed directly to the WorldTourism Organization. For applications see: http://www.unwto.org/pub/rights.htm

© 2006 World Tourism Organization - ISBN 978-92-844-1195-5

Table of Contents

Achnowledgements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . v

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . viiAims of the Study . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . viiWhat is a Tourism Satellite Account? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . viiiMethod . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ixKey Finding . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ix

Trends in the Meetings Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ixKey Measures of the Meetings Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xRecommendations on Meetings Industry Data Collection . . . . . . . . . . . . . . . xiRecommendations on Meetings Industry Definitions . . . . . . . . . . . . . . . . . . . . xiiCurrent Problems in Measurement of the Meetings Industry . . . . . . . . . . . . . . xiiLimitations in Use of Existing TSA for Estimating the Economic Contribution of the Meetings Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xiiiAdapting the TSA to Measure the Meetings Industry . . . . . . . . . . . . . . . . . . . xivStatistical Issues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xv

Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xviiProposed Broad Methodological Steps . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xviiFurther Issues to be Considered . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xvii

Main Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31.1 Aims of the Study . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31.2 Background to the Study . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31.3 Scope . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41.4 Structure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41.5 Method . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

2 Global Overview of the Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52.1 Trends in the Global Meetings Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

2.1.1 Trends in Meetings and Conferences. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52.1.2 Trends in Exhibitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92.1.3 Trends in Incentives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

2.2 Current Data Collection Practices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112.2.1 Data Collection by Global Agencies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 122.2.2 Data Collection by National Tourism Organisations . . . . . . . . . . . . . . . . . . . . . 132.2.3 Convention Bureaux and City Reports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

2.2.4 Summary of Previous Studies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142.2.5 Gaps in Meeting Industry Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

2.3 Definitional Issues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 182.3.1 Nomenclature for the Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 182.3.2 Definition of Meetings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

3 Using the TSA to Evaluate the Economic Contribution of the Meetings Industry. . . 213.1 The Economic Contribution of the Meetings Industry has Two Components. . . . . . . . 253.2 Use of an Existing TSA to Provide an Indicative Estimate

of the Economic Contribution of the Meetings Industry . . . . . . . . . . . . . . . . . . . . . . . 253.3 Limitations of the Use of the TSA in Measuring Meetings’ Activity . . . . . . . . . . . . . . . 263.4 The new International Standard Industrial Classification 823,

‘Convention and Trade Show Organisers’ . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 273.5 Implications of ISIC 823 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 283.6 Presentation of Results: A Meetings ‘Satellite Account’ . . . . . . . . . . . . . . . . . . . . . . . 293.7 Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

4 Framework for an Evaluation of the Meetings Industry . . . . . . . . . . . . . . . . . . . . . . . . 334.1 Measurement Problems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 334.2 Data to be Collected . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 344.3 Collection of Expenditure Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 354.4 Lessons from Previous Research in the Meetings Industry . . . . . . . . . . . . . . . . . . . . . 354.5 Surveying Participants in Meetings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 364.6 Expenditure on Travel to Meetings in Other Countries . . . . . . . . . . . . . . . . . . . . . . . . . 374.7 The Use of Survey Data to Measure the Economic Contribution

of the Meetings Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 384.8 Quarterly Measures of Meetings Industry Performance . . . . . . . . . . . . . . . . . . . . . . . . 39

5 Proposed Broad Methodological Steps and Further Issues to be Considered . . . . . 435.1 Proposed Broad Methodological Steps . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 435.2 Further Issues to be Considered . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

Appendices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47A: Summary of Supply of the Meetings Industry Facilities by Country . . . . . . . . . . . . . . . 47B: Congress and Convention Centres in the Americas Region . . . . . . . . . . . . . . . . . . . . 59C: Case Study . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61D: Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63E: Example of Venue Identification from the National Business Events Study (NBES) . . . 67F: ICCA Categories . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69G: Examples of Questionnaires to Collect Relevant Data . . . . . . . . . . . . . . . . . . . . . . . . 71

Bibliography. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

List of Abbreviations. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

iv Measuring the Economic Importance of the Meetings Industry

The publication of this study on Meetings Tourism is the result of a fruitful collaborative effort carriedout by the World Tourism Organization (UNWTO) and Affiliate Members Reed Travel Exhibitions, theInternational Congress & Convention Association (ICCA) and Meeting Professional International (MPI).

Given the common interest in gaining better knowledge of the tourism industry and of all the elementsthat contribute to the development of tourism in general, the UNWTO Department of Statistics andEconomic Measurement of Tourism and the Business Council of the Affiliate Members addressed theconcerns raised by these Members regarding how to measure the meetings industry’s linkage to tourismand the extent to which the conceptual framework of the Tourism Satellite Account is capable ofelucidating this linkage from a macroeconomic perspective consistent with the measurement andanalysis framework of the National Accounts of countries in which this industry is a prominent activity.

Thus the groundwork was laid for an intensive effort carried out with great professionalism by the teamof experts - Margaret Deery, Leo Jago, Larry Dwyer, Ray Spurr and Liz Fredline - of the SustainableTourism Cooperative Research Centre (STCRC) of Australia, which was able to rely on the support ofthe collaborating entities at all times. In fact, the “National Business Events Study: An Evaluation of theAustralian Business Events Industry”, conducted by the STCRC and published in 2005 served as animportant reference source for this new study.

From that perspective, the study constitutes the starting point of a longer-term task that, with the effortsof the parties involved, will contribute to broadening and strengthening the public’s recognition of thisindustry, which has taken off so spectacularly over the past several years and has consolidated itself asa tourism segment of the first order.

We also wish to underline the importance of the coordination efforts carried out by Jens Jensen, initiallyfrom his post within the Business Council, and in the latter stages, as an expert on the subject, whichmade it possible to achieve the necessary coherence of the study within the framework of the objectivesof the programme of the Business Council of the UNWTO Affiliate Members.

Lastly, we would like to acknowledge the editing work carried out by UNWTO consultant StanFleetwood (Australia), who drew on his comprehensive knowledge of the Tourism Satellite Account forthe final revision of this study.

Madrid, November 2006

Victoria MarcosExecutive Director Affiliate Members

Antonio MassieuChief, Statistics and Economic Measurement of Tourism

© 2006 World Tourism Organization - ISBN 978-92-844-1195-5

Acknowledgements

© 2006 World Tourism Organization - ISBN 978-92-844-1195-5

The Meetings Industry has emerged over recent decades as an important contributor to nationaleconomies. It is perceived as a significant and growing component of tourism and other industries andyet little reliable and consistent data exist to support this perception. With the lack of consistentconcepts and definitions, as well as data, it is impossible to measure the industry accurately. Thereforethe industry is unable to credibly demonstrate its value.

In an attempt to rectify this gap, the World Tourism Organisation (UNWTO), and Affiliate Members,Reed Travel Exhibitions and International Congress & Convention Association (ICCA) – in cooperationwith Meeting Professional International (MPI) commissioned the Sustainable Tourism CooperativeResearch Centre (STCRC) from Australia “to encourage the UNWTO to focus more on the MeetingsIndustry and in partnership to undertake a study that would lead to proposals for the adaptation of theTourism Satellite Account (TSA) to reflect the real importance of the Meetings Industry and itscontribution to tourism” (Meetings Industry Terms of Reference, p 1).

Tourism, in fact, was confronted with this same problem of being unable to demonstrate its value andhence the TSA was developed. This study is a first important contribution on how the TSA could be usedas an analytical tool to measure the tourism connection of the Meetings Industry. In order to obtaincomparable figures, however, additional efforts by the Meetings Industry will be required to:

1. define the appropriate concepts and definitions to be measured,

2. identify a list of appropriate commodities (services) for inclusion, and

3. promote and cooperate in the collection of data, both from the demand and supply sides.

Aims of the Study

The aim of this study is to analyse whether and how the TSA conceptual framework can be adapted tothe measurement of the Meetings Industry. This approach can provide an analytical framework thatallows the measurement in macroeconomic terms of different sub-sectors of Tourism in the overallframework of tourism’s economic contribution in the economy.

Specific aims of the study are to provide an understanding of the global Meetings Industry withparticular attention to the measurement of the economic importance of the industry. The three keycomponents of the report are:

a) to present an overview of the current measurement of the global Meetings Industry and theinherent gaps in this, including the issue of definitions for meetings;

b) to provide a summary of the demand and supply data that should be collected to evaluate theMeetings Industry using the Tourism Satellite Account (TSA) conceptual and measurementframework;

c) to examine the use of these data in developing a model for evaluating the economic contributionof the Meetings Industry in macroeconomic terms.

Executive Summary

viii Measuring the Economic Importance of the Meetings Industry

What is a Tourism Satellite Account?

The Tourism Satellite Account (TSA) is a measurement framework, based on the concepts, definitionsand classifications of the System of National Accounts (SNA) developed to provide a credible measureof the economic contribution of the tourism sector.

The National Accounts measure the economic contribution of industries that are specified in acountry’s official classification of industries. These classifications are usually based on the InternationalStandard Industrial Classification (ISIC) code (although some countries have their own classificationsystems). Industries are usually defined as groups of businesses producing a similar product.

As tourism is a demand side activity (dependent on the status of the consumer rather than on the typeof supplier), and hence is not identified in ISIC or in countries’ National Accounts. The TSA extracts alltourism-related economic activity which is included in the National Accounts but not identified astourism. Tourism activity is “hidden” in the relevant industry activities, e.g. the Accommodation,Transport, and Travel Agency industries. This activity will be identified and brought together in aseparate but related account, i.e. an account that is a satellite of the core national accounts. Animportant aspect of this approach is that the TSA is an official part of the national accounts, usingsimilar concepts, definitions, valuations and classification systems. This means that for the first time, itis possible to have available an official, objective and credible measure of the tourism sector,comparable with other industries.

Basically, the TSA identifies tourism characteristic industries, i.e. those which would disappear or besubstantially reduced if tourism did not exist. The TSA identifies the total output, costs, value added(GVA) and employment of those industries, (the production account) similar to what is provided for allindustries in the core SNA. Surveys of visitors identify product purchases which can be related to theproduction of characteristic (and other) industries. A tourism-ratio for each industry is calculatedcorresponding to the share of each tourism characteristic industry’s output that is attributable topurchases by visitors. These tourism ratios are applied to the production accounts for tourismcharacteristic industries to calculate the value of these variables that are attributable to tourismdemand.

The results are often split to show the contribution of Domestic and International tourism and of Leisureand Business (including Government) tourism.

The TSA measures only those transactions undertaken directly between the visitor and the provider ofthe goods and services. That is, only measures of the “direct” economic contribution of the tourismsector are included. However, there are other contributions resulting from tourism demand (such asindirect and induced effects). These “up-stream” effects result from the demand by businesses directlysupplying the visitors, for inputs produced by other businesses. For example, a hotel needs to buy food,electricity, possibly cleaning services, etc. Industries producing these products also benefit fromtourism demand.

This indirect contribution from tourism can legitimately be claimed by the tourism sector as part of itsoverall contribution to the economy. Indirect effects can be calculated by the use of modellingtechniques.

It is important when quoting the contribution of an industry, or a sector such as tourism, to an economy,to be clear whether the contribution includes only the direct effects or also includes indirect andinduced effects. This point is also relevant in discussing the measurement of the contribution of theMeetings Industry. If such a measure is based on the TSA, then the result will show only the directcontribution, and further analysis is needed to calculate the other types of effects.

ixExecutive Summary

Method

The consultants collated the data necessary to inform the findings of the study by means of acomprehensive literature search followed by extensive communications with industry experts.

The comprehensive literature search investigated industry reports, national statistical data includingTSA, and academic articles focussing on conferences, meetings, exhibitions and incentives. Inparticular, the search concentrated on the type of statistics collected, how these were collected, andthe use made of the information.

Extensive discussions with industry experts and widespread consultation with organisations such as theUNWTO and ICCA then complemented the literature search.

Industry experts still require a list of identified products provided by the Meetings Industry, so thatmethods can be developed to classify and measure them in terms of revenues received.

A provisional list has been drawn up by industry, represented by the International Association ofProfessional Congress Organizers (IAPCO)1, from which a list could possibly be drawn formeasurement purposes, including items such as:

• assistance with congress bids

• finance consultancy

• secretariat and office facilities

• abstract handling

• delegate transfers and on-site transportation

• accommodation bookings

and many more.

Key Findings

Trends in the Meetings Industry

The Meetings Industry has difficulty in obtaining consistent and credible trend data due to the plethoraof definitions for the various components of the industry. The industry needs to define consistentdefinitions and concepts that can be widely used by its members.

When examining the International Meetings Industry, however, some trends do emerge. The Industryappears to have gone through a period of decline beginning in 2000, but showed improvement in2005. This fits with the notion that the Meetings Industry is cyclical with five-year cycles. Other ‘trends’that appear in the data are:

• while there has been a decrease in the number of events over the 2000-2004 period, thereappears to have been an increase in the number of participants at these events;

• the duration of all events including exhibitions, conventions and incentive travel have becomeshorter;

• the number of exhibitors at exhibitions is increasing;

• the number of new competitors in the Meetings Industry, such as those in China and Dubai, isincreasing; and

• the incentive travel area remains the most lucrative but the most volatile component of theMeetings Industry.

1 Extract from Appendix A, How to Choose the right PCO, copyright, IAPCO, 4th edition, March 2005

x Measuring the Economic Importance of the Meetings Industry

Key Measures of the Meetings Industry

There are two types of measures relating to the economic contribution of activities relating to meetingsfor which information is required:

• Supply side measures of the industry include such variables as income (represented by fees, andcommissions) costs, value added and employment. Businesses may be identified by using therecently developed class of ISIC (International Standard Industrial Classification) 823, forexample. In addition to those businesses which provide meetings services as their primary activity,it is important to include other relevant businesses that provide such services as a secondaryactivity, e.g. government agencies producing these services, hotels, etc.. These variables are thebuilding blocks to measure the contribution of this industry to GDP.

• Demand side measures include such variables as expenditure by participants at meetings onspecific identified services supplied by the meetings industry or other industries. Non-monetaryvariables to be related to the expenditure data include: numbers of participants, lengths ofmeetings, number of nights in hotels, or other accommodation, distance travelled to get to themeeting, and number in the travelling party.

A complete picture of the industry requires measurement of both dimensions. A demand side onlyapproach does not identify the contribution of industry to the economy (e.g. Production account), whilea supply side approach does not identify expenditure by participants on products purchased from otherindustries (e.g. the accommodation industry, transport industry, etc.) while participating in the meeting.

So far this report has not mentioned the possibility of adding a regional dimension to the analysis. Insome countries this aspect is very important, as the type of meetings may be quite different betweenregions of a country. The contribution of the industry to regional GDP and employment may vary.

Data are collected through four main types of agencies:

• Global agencies that collect meetings industry data are the specific industry groups such as ICCA,MPI, SITE, UIA and Reed Exhibitions e.g. FutureWatch (MPI); Five Year Trends Report (EIBTM)

• National Statistics Offices, e.g. Business surveys for hotels, businesses renting out meetingfacilities and other relevant industries

• Other government agencies, such as US Business Traveller to Canada Study Summary 2002(Canadian Tourism Commission)

• Convention Bureau and Regional or City Reports such as those by the Finland Convention Bureauand the Sri Lankan Convention Bureau.

Other surveys are conducted – either specifically designed or by adding questions to existing surveys– of members of industry associations (such as IAPCO), to obtain their views, or to explore possibilitiesof the types of data that could be collected.

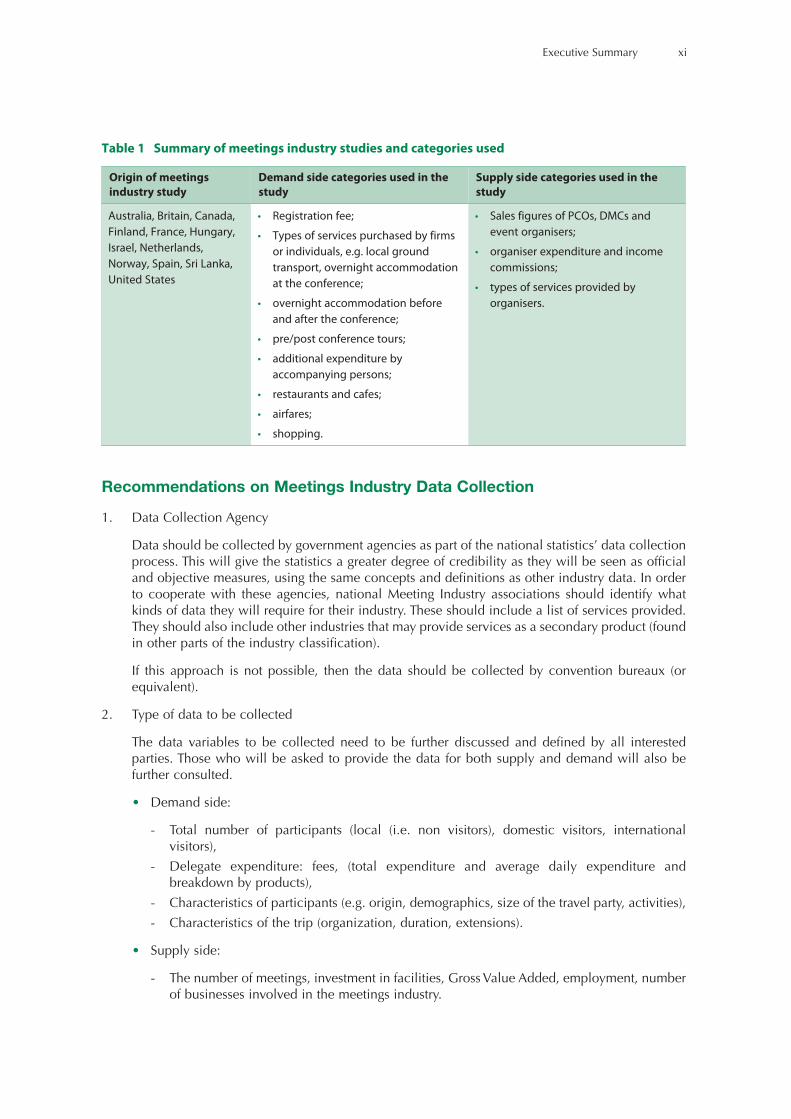

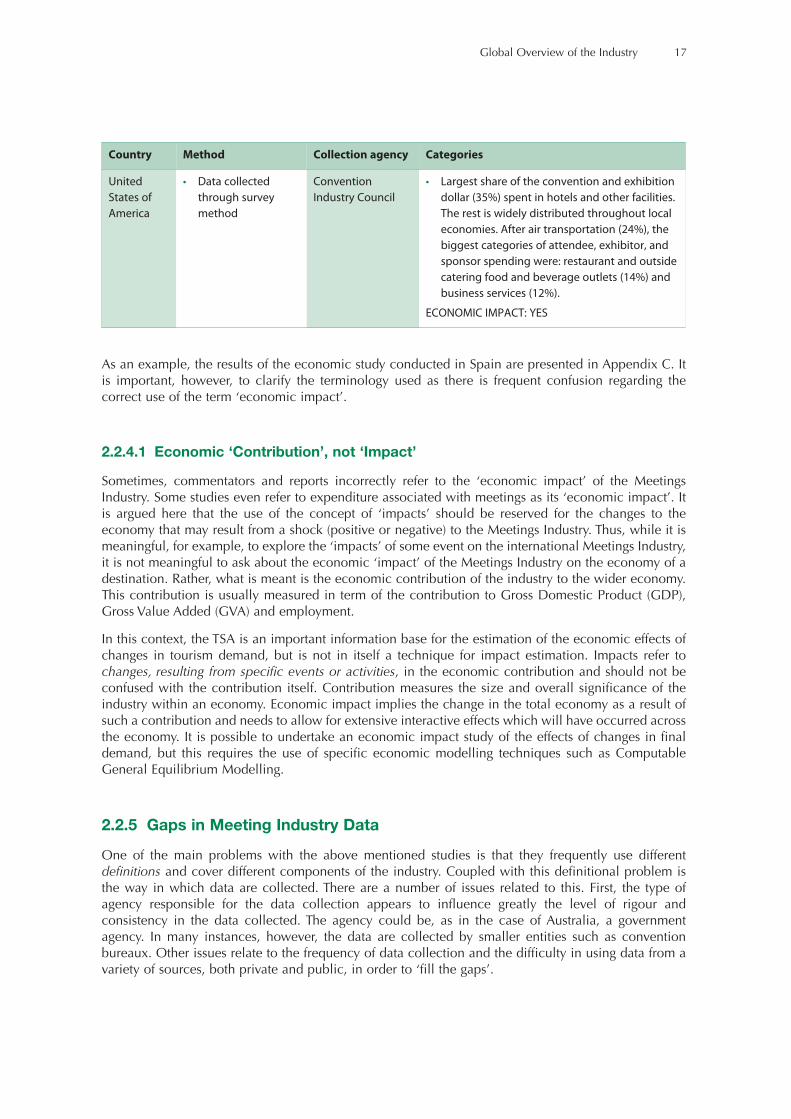

A number of countries and regions have undertaken economic studies on the Meetings Industry. Someof these are mis-named as ‘economic impact’ studies, although it is likely that they are either economiccontribution studies or expenditure estimates. This study examined twelve detailed studies of theMeetings Industry over the last three years. A summary of the studies and the categories used isprovided in Table 1.

xiExecutive Summary

Table 1 Summary of meetings industry studies and categories used

Recommendations on Meetings Industry Data Collection

1. Data Collection Agency

Data should be collected by government agencies as part of the national statistics’ data collectionprocess. This will give the statistics a greater degree of credibility as they will be seen as officialand objective measures, using the same concepts and definitions as other industry data. In orderto cooperate with these agencies, national Meeting Industry associations should identify whatkinds of data they will require for their industry. These should include a list of services provided.They should also include other industries that may provide services as a secondary product (foundin other parts of the industry classification).

If this approach is not possible, then the data should be collected by convention bureaux (orequivalent).

2. Type of data to be collected

The data variables to be collected need to be further discussed and defined by all interestedparties. Those who will be asked to provide the data for both supply and demand will also befurther consulted.

• Demand side:

- Total number of participants (local (i.e. non visitors), domestic visitors, internationalvisitors),

- Delegate expenditure: fees, (total expenditure and average daily expenditure andbreakdown by products),

- Characteristics of participants (e.g. origin, demographics, size of the travel party, activities),

- Characteristics of the trip (organization, duration, extensions).

• Supply side:

- The number of meetings, investment in facilities, Gross Value Added, employment, numberof businesses involved in the meetings industry.

Origin of meetings

industry study

Demand side categories used in the

study

Supply side categories used in the

study

Australia, Britain, Canada,

Finland, France, Hungary,

Israel, Netherlands,

Norway, Spain, Sri Lanka,

United States

• Registration fee;

• Types of services purchased by firms

or individuals, e.g. local ground

transport, overnight accommodation

at the conference;

• overnight accommodation before

and after the conference;

• pre/post conference tours;

• additional expenditure by

accompanying persons;

• restaurants and cafes;

• airfares;

• shopping.

• Sales figures of PCOs, DMCs and

event organisers;

• organiser expenditure and income

commissions;

• types of services provided by

organisers.

xii Measuring the Economic Importance of the Meetings Industry

Recommendations on Meetings Industry Definitions

A major problem with the previously-mentioned studies is that they frequently use different definitionsand include different components of the industry. In examining the many definitions adopted byvarious organisations, the following definitions are recommended for adoption by the MeetingsIndustry.

Table 2 Recommended meetings industry definitions and rationale for definitions

As noted in Table 2, some definitions, such as the size of a meeting, are not really necessary for the taskof evaluating the economic contribution of the Meetings Industry. The minimum essential criteria arethe meeting aims and the meeting venue.

A recent proposal from the UNWTO for a new International Standard Industrial Classification (ISIC)code 8230 “Convention and trade show organisers” represents an important new step towardagreement on the scope of the ‘Meetings Industry’.

• This class includes the organisation, promotion and/or management of events, such as businessand trade shows, conventions, conferences and meetings, whether or not including themanagement and provision of the staff to operate the facilities in which these events take place.

As a result of the inclusion of activity 8230 in ISIC, there is now the capacity to identify allestablishments who undertake trade show organization activities (as their primary activity). We nowhave the possibility to have a picture of all establishments that produce convention and trade showorganization, with more comprehensive coverage than has been possible previously. These activitieswere all included before in macro economic measurement, but could not easily be separatelyidentified.

Current Problems in Measurement of the Meetings Industry

The economic contribution of the Meetings Industry internationally appears to be significant but thereare several major problems with its measurement and, hence, comparability. These measurementproblems, affecting both supply side and demand side measures, arise because of the following:

• The standard industrial classifications (e.g. ISIC) do not currently identify a separate ‘Meetings’industry.

Issue Recommendation Rationale

Nomenclature for

the industry

Meetings industry This name represents the supply side. It has

support from key industry participants.

Meeting aims To motivate participants, to conduct

business, share ideas, to learn, socialise and

hold discussions.

These aims, or similar aims, were the most

common in the industry and academic

literature .

Meeting size Minimum number of ten (10) participants Many meetings organisations use this

number.

Meeting venue Venues where there is payment for the use

of the venue for meetings

Where there is payment for the use of a

contracted venue, there will be an economic

contribution to the economy.

Meeting duration A half-day (four hours) or more Although a minimum duration may not be

needed, the limit of four hours will provide a

practical and sensible in-scope boundary for

data collection.

xiiiExecutive Summary

• The data collected show enormous diversity and inconsistency.

• The statistics are based on different measures of both supply side and demand side data.

• The data are created for different purposes using different methodologies and thus cannot becompared.

• The quality of the data collection is often not up to strict statistical standards and thus results areof questionable reliability.

Some work can be done in the future by the meetings industry to ensure greater consistency todefinitions and methods.

Limitations in Use of Existing TSA for Estimating the Economic Contributionof the Meetings Industry

In the TSA, products are those which are purchased by or for visitors. Products – which comprise goodsand services – are what are purchased by consumers.

Activities (industries) produce products.

The TSA splits products into two categories, specific tourism products, (comprising tourismcharacteristic and tourism connected products) and non-specific products (all those which areconsidered of no major direct tourism interest). Broadly, “Tourism characteristic products” are thoseproducts which represent an important part of tourism consumption, or for which a significantproportion of the sales are to visitors.

Productive units include tourism-specific activities/industries (comprising tourism characteristic andtourism connected activities/industries) and non-specific activities/industries (which includes all otherproductive activities). “Tourism characteristic activities” are those industries that would either cease toexist in their present form or would be significantly affected if tourism were to cease.

Table 3 provides these characteristic industries and characteristic products (UNWTO).

Table 3 List of tourism characteristic industries and products2

Industries: Products:

1. Hotels and similar 1. Accommodation Services

2. Second home ownership (imputed) 2. Food and Beverage Serving Industries

3. Restaurants and similar 3. Passenger Transport Services

4. Railway passenger transport services 4. Travel Agency, tour operator and tourist guide services

5. Road passenger transport services 5. Cultural Services

6. Water passenger transport services 6. Recreation and Other Equipment Services

7. Air passenger transport services 7. Miscellaneous tourism services (e.g. insurance, travel

card services

8. Transport supporting services

9. Transport equipment rental

10. Travel agencies and similar

11. Cultural Services

12. Sporting and other recreational services

2 Tourism Satellite Account (TSA): Recommended Methodological Framework,UNWTO/UNSD/OECD/Eurostat

xiv Measuring the Economic Importance of the Meetings Industry

In applying these lists to the Meetings Industry, however, there are limitations to the use of these lists,including:

• The lack of clear definition of the Meetings Industry

• The lists of tourism characteristic industries and products do not reflect meetings’ activity (i.e.meetings’ characteristic industries and products)

The underlying issue is that meetings activity cannot be explicitly identified as a sub-set of tourismactivity. Because of this the TSA cannot be used, in its existing form, to provide a complete measure ofthe Meetings Industry. Modifications are required to the presentation and to the data collectioncurrently used in production of the TSA (see page 16). This is clearly technically possible, but it wouldinvolve extra expense, particularly for data collection, than would be required if the current TSA resultscould be used to provide a measure of Meetings Industry activity.

One way to partially address this would be to add the Meetings Industry to the TSA as a tourismcharacteristic industry. This would work if it can be determined approximately what share of theMeetings Industry output goes to visitors, rather than local residents. The criterion could be set atsomething like 25-30% of the output going to visitors. If this criterion is not met, the Meeting Industrycould be separately identified in the TSA as a ‘special’ case.

Adapting the TSA to Measure the Meetings Industry

The recommended new ISIC code ‘8230 – Convention and trade show organisers’ represents animportant development regarding adaptation of the TSA to measure the Meetings Industry. Countries’classifications of industries and products to be used for measuring meetings’ activity can in future betaken from the international standards, ISIC and CPC (Central Product Classification). Two products willbe identified at present in the CPC: Services of convention organisers, and services of trade showorganisers.

The new ISIC categories are:

• 823 Convention and trade show organisers

See class 8230

• 8230 Convention and trade show organisers

This class includes the organisation, promotion and/or management of events, such as business and trade shows,conventions, conferences and meetings, whether or not including the management and provision of the staff to operatethe facilities in which these events take place.

The TSA approach enables the supply side (industry) contribution to be measured through the activityof the Meetings Industry and all other relevant ISIC industries (e.g. Accommodation industry), and alsoenables the full contribution of meetings’ participants to be measured through their total consumptionof goods and services associated with their participation in meetings. The separate identification of theMeetings Industry means that, once implemented, statistical agencies will be able to survey thisindustry in the same way as other industries in the economy are surveyed.

Several issues need to be highlighted:

1. The new ISIC category excludes some supplier types that one may wish to count as part of theMeetings Industry.

- Types of businesses that possibly may not be represented in the 8230 ISIC code includeIncentive Houses, as well as a range of other organisations.

- The great majority of meetings take place without using the services of businesses whoseprimary activity is organising meetings, conferences, conventions and trade shows. Thus, use

xvExecutive Summary

of the code to define the Meetings Industry from the supply side will capture only a smallpercentage of the production of meetings’ goods and services. The identification of industriesfor which meetings’ organization is a secondary activity can be measured as well.

2. Different and unique bundles of services related to meetings can be packaged. This characteristiccan complicate the measurement issues. Normally, consumption of accommodation, transport,food, etc. by meetings’ participants would be an activity of the relevant industries providing theseservices to the participants, and not of the Meetings Industry. However, a complication ariseswhen, for example, the meeting organiser includes in the meeting/conference registration fee, thecost of accommodation, entertainment, and possibly some transport – services which will beprovided directly to the meeting participant by the business rather than the meeting organiser. Thesame issues arise when an exhibition organiser pays for various goods and services from exhibitorfees which are provided directly to participants.

The question is: should the Gross Value Added in providing these services be attributed to themeetings’ organiser, treating the package as a single product (known as the “gross” approach), orshould the Gross Value Added be attributed to the direct providers of each of the packages’components, i.e. to the Accommodation industry, the Transport industry, the Tourist Attractionsindustry, etc. (known as the “net” approach).

In compiling the TSA, the UNWTO recommends that the “net” approach is taken. Consistencywith UNWTO guidelines would suggest that this approach should be taken in measuring theMeetings Industry. The potential ‘downside’ of this is that the apparent economic contribution ofthe Meetings Industry will be lower compared to what the gross approach would indicate. Theoverall total Gross Value Added will not be affected as the GVA associated with the supply ofthese products will be attributed to the supplying industry (rather than to the Meetings Industry).It is important that the approach taken be consistent with existing official standards to ensure thatthe method is accepted as providing an objective and credible measure of the industry.

3. The listing of the new ISIC code for the Meetings Industry does not, in itself, ensure that centralstatistical agencies will implement the new code, or that they will automatically collect thisinformation as they would for other industries. In most cases industry information is collected ata higher level than the 3 (or 4)-digit level. The agencies would have to be persuaded to collectdata on this industry at this lower level. This would involve more costs for the agency in datacollection and might be resisted for this reason.

4. The presentation of statistical results needs close consideration. Adoption of the new ISIC 8230code will be a useful step towards higher credibility if implemented by central statistical agenciesbecause it will provide central statistical agency imprimatur to the measurement of the MeetingsIndustry.

Statistical Issues

A number of statistical issues need to be addressed, including:

• Creation of a list of services provided by meeting organisers. Some such lists exist already, whichcould be utilized.

• Central statistical agencies should be encouraged to collect the data in their annual businesssurveys. This will involve additional costs and the need for ‘political’ will/support. The appropriatebusiness surveys, which would cover where primary and secondary products are produced for themeetings industry, need to be identified.

• Meeting Industry associations could complement this information with business intention surveys(also called business opinion or expectation surveys, condition or climate surveys) which collectqualitative type information from business managers on a monthly and/or quarterly basis.

xvi Measuring the Economic Importance of the Meetings Industry

• The new ISIC code 8230 does not necessarily resolve all of the supply side data issues. Industryshould identify what is missing.

• Many meetings do not make use of a professional meetings’ organiser. ISIC code 8230 may notinclude:

- Incentive Houses,

- Exhibition organisers (perhaps),

- Exhibition contractors,

- Speaker bureaux,

- Corporate entertainment,

- Catering companies,

- Hotels which host meetings but would not regard themselves as meetings specialists.

A further issue relates to how the results of any measurement of the Meetings Industry would bepresented. In practice options are limited to the following typology:

1. incorporated in the TSA, with the “Meetings Industry” identified as another tourism industry;

2. incorporated in the TSA framework as a complementary set of tables specifically identifyingmeetings’ activity; or

3. as a separate satellite account.

Therefore there are three options:

The first option implies that the Meeting Industry is a tourism characteristic activity such asAccommodation, Passenger Transportation, Travel Agencies, etc. There is no clear evidence that this isthe case at least on a national level The Meetings Industry is not a clear subset of the Tourism sector –indeed the new ISIC 8230 code will cover activity by conference organisers on behalf of residentconference and meeting participants as well as those for visitor participants (whether domestic orinternational visitors). Some organisers which fall under the code may do very little of their businesswith ‘visitors’ as defined under the TSA

The second option (to consider the development of a separate industry extension relevant for theMeetings Industry) seems the proper way to proceed. Such an extension could involve, for example,the usual supply and demand information for the industry plus other information and characteristicsnot normally found in the TSA. The TSA could be a supporting instrument and framework, but moreinformation about the industry could be incorporated. Although such specific industry extensionscannot be referenced, analogies of this approach appear, for example, in the Balance of Payments asmemoranda items, where information is provided outside the specific BOP guidelines, but which is stillof interest to users. In one specific case, (in Canada), a memorandum item has been used to provide aprovincial breakdown for travel. This is not actually a component of the BOP. It elaborates the usualBOP compilation, but provides additional useful information. (Such an analysis could be assembled forany industry in the SNA, where some descriptive characteristics are available and important, but lieoutside the specific SNA requirements). In this context, the Meetings Industry could use the synergy ofthe TSA framework, but add supplementary information of particular interest as a memorandum item.The industry itself could elaborate such characteristics as they wish.

The tables to be produced as supplements to the main TSA tables could be set up along the lines of theTSA-RMF (consumption by products and categories of visitors, and production accounts for theindustry). Below are examples of such tables, using the Tourism Satellite Account: RecommendedMethodological Framework (TSA-RMF) as an example and some hypothetical detail.

The Meetings Industry would make a valuable contribution to the discussion by reviewing theseproposals before identifying the optimal alternative for their specific situation.

Finally, the third option while perhaps ideal from the industry viewpoint, is most unlikely to beaccepted by statistical agencies, at least until they have some sense of the importance of the industry.

xviiExecutive Summary

Summary

Proposed Broad Methodological Steps

This proposed method relates to measuring the economic contribution at the national level. It is basedon, and an extension of the Tourism Satellite Account.

As previously indicated, a regional perspective may be important, as diversity of Meetings Industryactivity among regions in a country may exist. Some regions may have a Meetings Industry that issufficiently important to be considered part of a tourism industry, while others may not.

Steps required are:

1. Decide scope of industry and meetings participants

2. Identify data requirements on the supply side and demand side

3. Develop data collection methods

4. Surveying organisation should, where possible, be the National Statistical Office

5. Incorporation of the data into the Tourism Satellite Account (TSA)

6. The results should at a minimum, show (1) the demand side value of consumption resulting frommeetings’ activity, and (2) how much meetings’ activity contributes to a country’s Gross ValueAdded (and/or GDP).

See sub-chapter 5.1 for more details of proposed method.

Further Issues to be Considered

Throughout this report, we have noted many issues that need further consideration, mainly by theMeetings Industry in conjunction with the relevant technical experts.

The following is an outline of the main issues that need to be considered by the Steering Committee toprogress this exercise:

1. Discuss with technical experts and any other relevant international agencies, how an internationalstandard method can be adopted, by building on the findings of this report.

2. Agree on the scope of the industry.

3. How will national industry associations be “brought on board” to actively support themeasurement of the industry in their country?

4. How will national industry associations be encouraged to educate their members and otherindustry participants to actively support the implementation of the measurement?

5. How will industry participants be persuaded to fully co-operate with and contribute to theimplementation of the adopted measurement of their industry?

Further information on these issues is provided in sub-chapter 5.2.

Main Report

1.1 Aims of the Study

This report outlines some steps that could be taken to overview the characteristics of the MeetingsIndustry, using the analytical model of the Tourism Satellite Account (TSA) that would show theimportance of this industry and identify how it could be defined and measured. The benefits of usingthe TSA are that it establishes an analytical framework that would provide credible results for theMeetings Industry. This would be of value in the context of the industry’s wish to draw the attention ofgovernments to the economic importance of the sector.

More specifically, the report aims to provide an understanding of the global Meetings Industry, withparticular attention to the measurement of its economic importance.

The three key objectives of the report are to:

a. present an overview of the current measurement of the global Meetings Industry and the gapsinherent in this, including the issue of definitions for meetings;

b. provide a summary of the demand and supply side data that should be collected to evaluate theMeetings Industry using a TSA; and

c. use these data in developing a model for evaluating the economic contribution of the MeetingsIndustry.

1.2 Background to the Study

Competition for the tourist dollar is becoming more intense and countries around the world are seekingto gain a competitive edge through niche tourism activity. Meetings and business events are one suchniche tourism activity that contributes significantly to Gross Domestic and Regional Product as well asto the branding and awareness of tourist destinations. While the benefits of meetings and businessevents are becoming recognised by the industry, the size and importance of this sector is not reflectedsystematically in official statistics. National Statistical Offices generally do not produce data on theactivities of business event segments such as meetings, conferences, exhibitions and incentives in thestructural and economic statistics.

In response to this lack of systematic data collection and the growth of business event activity, theWorld Tourism Organisation (UNWTO) Affiliate Members Reed Travel Exhibitions and the InternationalCongress & Convention Association (ICCA) – in cooperation with Meeting Professionals International(MPI) encouraged the UNWTO to undertake a study that would lead to proposals for the modificationof the TSA to reflect the real importance of the Meetings Industry and its contribution to tourism. TheUNWTO thus commissioned the Australian based Sustainable Tourism Co-operative Research Centre(STCRC) to undertake this study.

Chapter 1

Introduction

© 2006 World Tourism Organization - ISBN 978-92-844-1195-5

4 Measuring the Economic Importance of the Meetings Industry

1.3 Scope

The UNWTO, MPI and ICCA have developed a definition for the International Standard IndustrialClassification (ISIC) revision process, recently undertaken. (The ISIC is the official internationalstatistical classification system for identifying industries. Many countries base their own industrialclassification system on this international standard).

Based on this definition, we have defined a Meetings sector (sometimes referred to as the Meetings,Incentives, Conferences and Exhibitions – or ‘MICE’ Sector) to include: activities based on theorganisation, promotion, sales and delivery of meetings and events; products and services that includecorporate, association and government meetings, corporate incentives, seminars, congresses,conferences, conventions events, exhibitions and fairs.

Although this definition provides substantial detail in terms of defining the various components of theMeetings Industry, further refinement of this definition will ultimately be required. Issues that will needto be considered include:

• whether this definition applies only to purpose built conference facilities,

• the minimum number of participants and duration for a meeting, and

• the criteria to distinguish international meetings.

These issues and others will be considered in a later section.

1.4 Structure

There are five chapters making up the remainder of this report. The method chapter appears next,followed by a chapter relating to each part of the project as identified in the project brief, and a finalchapter on further actions needed.

2.0 Method

3.0 Global Overview of the Industry

4.0 The Role and Use of the TSA in an evaluation

5.0 Framework for an Evaluation of the Meetings Industry

6.0 Roadmap for Further Action for Shareholders

1.5 Method

The consultants used two methods to collate the data necessary to inform the findings.

First, a comprehensive literature search investigated industry reports, national statistical data includingTSA, and academic articles focussing on conferences, meetings, exhibitions and incentives. Inparticular, the search concentrated on the type of statistics collected, how these were collected and theuse made of the information.

The second phase of the project entailed extensive interviews and discussions with industry experts andwidespread consultation with organisations such as the UNWTO and ICCA. These interviews providedinvaluable material and industry insights that confirmed and expanded the information obtained fromthe reports and other literature.

© 2006 World Tourism Organization - ISBN 978-92-844-1195-5

In undertaking the search for information, reports were obtained from a number of sources within theMeetings Industry such as ICCA, MPI and the Convention Industry Council (CIC), as well as fromtourism bodies such as the UNWTO. Although some of this information comes from tourism, there isthe recognition that meetings are broader than tourism in that some participants are local residents andnot tourists.

In addition, a search was conducted of the academic literature, which added to the findings. The keyaim of this part of the report is to document trends within the industry and the current data collectionpractices. This leads to identification of gaps in the statistics on the Meetings Industry that inhibit aconsistent and reliable evaluation of its economic importance.

2.1 Trends in the Global Meetings Industry

The Meetings Industry has three main components that will be examined here:

• meetings and conferences,

• exhibitions, and

• incentives.

Of these three key segments, the meetings and conference component has been examined more often,while the exhibitions and incentives components have been relatively under-researched. That said,there are many inconsistencies in the ways meetings and conferences are measured and reported, andthe trends presented here illustrate these inconsistencies.

2.1.1 Trends in Meetings and Conferences

Weber and Ladkin (2004), in their study on trends affecting the convention industry in the 21st century,argue that the growth of the knowledge economy has enhanced the growth of the conventions industry.The continual need for information and updating of knowledge provides a strong platform forconventions as a key medium for the dissemination of such knowledge. A number of countries andconvention associations have recognised the importance of meetings and conventions in this growth ofthe knowledge economy and have attempted to evaluate the size and scope of the industry. Thesestudies have been undertaken at varying levels of complexity.

Unfortunately, however, these evaluations have been undertaken in isolation and so comparing theresults and making global estimations is difficult. To illustrate the difficulties, Table 1 provides asummary of some of the most recent evaluations of the industry.

Chapter 2

Global Overview of the Industry

6 Measuring the Economic Importance of the Meetings Industry

Table 1 Some recent meetings industry evaluations

The majority of these reports indicate an upturn in the Meetings Industry for 2005 after some years ofdecline. The exception to this is the report by The Union of International Associations (UIA). (TheBrookings Institute evaluation also predicts a decline, but this was written from the perspective of theinvestment climate in relation to convention centres.) The UIA report highlights the definitionalproblems that exist in the industry. The UIA criteria for an international meeting are:

• a minimum of 300 participants,

• lasting a minimum of three days, and

• with representatives from at least five different countries.

A definition such as this only allows data to be collected from a select group of meetings and does notprovide a more general overview of the industry. In many ways, such a definition disadvantages theMeetings Industry, since it narrows the scope of industry activity.

One report, however, conducted annually by the ICCA, International Association and CorporateMeetings Market: Statistics Report, does attempt to bring some consistency into the reporting of theMeetings Industry, and the definition of international meetings1 used by ICCA has been adopted by theUNWTO when collecting Meetings Industry data for its Tourism Market Trends. This definesinternational meetings as having a minimum of 50 participants, be held regularly and rotate among atleast three different countries. The data collected in the ICCA annual reports have been collated andsummarised here to provide some trend data for the industry.

Meetings industry

evaluation report Source and frequency of report Snapshots from the evaluation

State of the Industry

2005

Successful Meetings

Bi annual

“For the last few years, the Meetings Industry as a

whole seemed like a seriously ill patient.” (p. 1) 2005

looks promising: The majority of planners expect

meeting size and frequency to increase (p. 2)

Future Watch 2004 Meeting Professionals

International 2004 (MPI)

Annual

“In a positive indicator for international business travel,

USA planners expect an 11% growth in international

meetings in 2004, twice that of 2003. Overall predicted

international meetings by European planners are

about the same in 2004 as in 2003. The difference is the

significant increase in projected travel to the United

States with European planners indicating a 50% rise in

travel to USA destinations, up to 9% vs. 6% of all

meetings last year.

International

Meetings Statistics

for the Year 2004

Union of International

Associations (UIA)

Annual

“While two year projections suggest a levelling out, the

number of meetings already scheduled for 2005 is

–22% lower than the same time last year; this suggests

a downturn for 2005” (p. 2)

The Realities of

Convention Centres

as Economic

Development

Strategy 2005

Brookings Institute

Annual

“The overall convention marketplace is declining in a

manner that suggests that a recovery or turnaround is

unlikely to yield much increased business for any

given community, contrary to repeated industry

projections.” (p. 1)

1 International meetings are defined by ICCA as having a minimum of 50 participants, be held regularly and rotate among atleast 3 different countries.

2000 2001 2002 2003 20040

500

1.000

1.500

2.000

2.500

7Global Overview of the Industry

2.1.1.1 Trends in the international Meetings Industry

2.1.1.1.1 Demand

The research by ICCA on the trends in the international Meetings Industry provides consistentlongitudinal data on this component of the industry. The data are important in that they use a consistentdefinition and are collected from the six global UNWTO tourism regions. In using these data, it ispossible to examine the trends over time and location as well as aligning the Meetings Industry withinthe tourism industry. This enables comparisons of, for example, meetings visitors to leisure visitors. Thenumber of international meetings held globally over the 2000-2004 period is presented in Figure 1.

Figure 1 The number of international meetings by region (ICCA statistics adapted from UNWTO)2000-2004

Source: ICCA statistics adapted from UNWTO, 2005, Basic Introductory Report: The Meeting Conventions Market in the Americas’,

International Seminar on MICE Tourism and Business Tourism, World Tourism Organisation, Chile, 25-26 May 2005.

As illustrated in Figure 1, there appears to have been a decrease in the number of internationalmeetings over the last five-year period. The decrease in the number of international meetings isparticularly marked in Europe, although each region shows a drop in numbers.

It is argued, however, that the Meetings Industry is cyclical in nature (Weber and Ladkin, 2004;UNWTO, 2005) and in arguing this, the UNWTO report suggests that the year 2000 is the peak of afive year cycle. The report further argues that the ICCA 2005 results show a significant improvement innumbers and it states that “2005 […] looks as if it will be an excellent year – the best since the previousworld peak figure in 2000” (p. 3).

In providing reasons for the variation in the industry, the report suggests that there was a general declinein the world economy; the impact of events such as September 11, SARS and the Iraq war curtailedtravel; and, there were budgetary restrictions within some important industries, such aspharmaceuticals.

Although there appears to have been a decrease in the number of events during the 2000 to 2004period, the numbers of attendees appear to have increased. Figure 2 illustrates the trend in the numberof attendees to international meetings.

Europe

Asia

North America

Latin America

Australia/Pacific

Africa

2000 2001 2002 2003 20040

200

400

600

800

1.000

1.200

1.400

1.600

8 Measuring the Economic Importance of the Meetings Industry

Figure 2 Average numbers of participants in meetings by region (ICCA statistics adapted fromUNWTO) 2000-2004

Source: ICCA statistics adapted from UNWTO, 2005, Basic Introductory Report: The Meeting Conventions Market in the Americas’,International Seminar on MICE Tourism and Business Tourism, World Tourism Organisation, Chile, 25-26 May 2005.

The numbers of attendees to international meetings in North America rose substantially in 2004,following the continuous decline from 2000. Industry sources suggest that visa difficulties for thoseentering the USA, for example, may have contributed to this fall in numbers, with these restrictionsbeing eased in 2004. By 2004, the number of participants in international meetings had increased inall but the Latin America region. It is also interesting to note that the growth in the size of meetings wasin the smaller meetings category (50-249 participants), which grew by 37% (ICCA, 2004).

Another important variable for examining trends in the industry is the duration of the meeting. The trendhas been for shorter meetings and in 2004, the average duration for international meetings was 4.2days, the lowest average for the past 10 years (ICCA, 2004). These statistics are confirmed in otherstudies such as the Australian study by Deery et al (2005), the research on Israel conference tourism(Sultan, Ditzan and Darsa, 2002) and the Korean Meetings Industry study by Kim et al (2003).

2.1.1.1.2 Supply

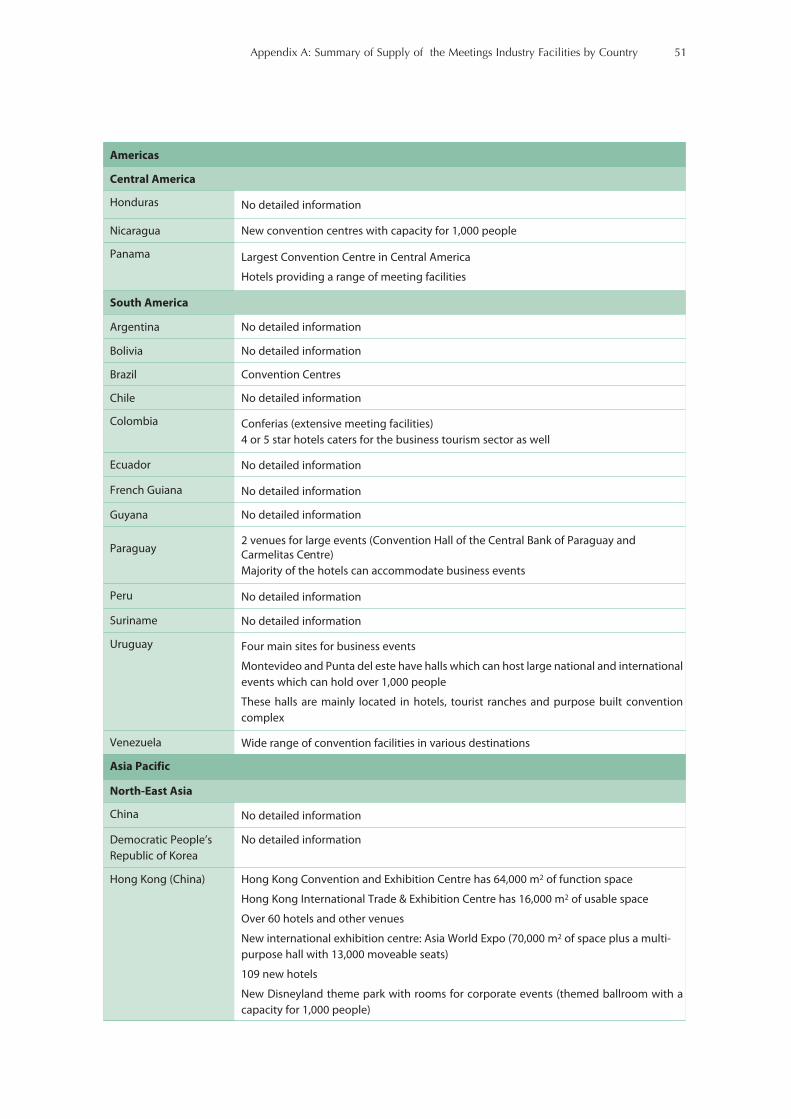

The growth of the international Meetings Industry can be illustrated through a discussion of the supplyside of the industry. With regard to the supply of convention facilities and convention capacity, thefollowing discussion is structured according to the five regions identified by the UNWTO. The data aretaken from the Tourism Market Trends, 2005 Edition (UNWTO). Appendix A of this report provides asummary for each country within these regions.

Africa

The report on the supply of convention facilities is divided into North and South Africa. In North Africa,countries such as Morocco and Algeria have substantial facilities for the Meetings Industry. Many of thecountries have conference facilities that could host between 400 and 3,000 conference delegates andmost have high quality accommodation nearby the convention centre. In the South Africa region, therewould appear to be stronger development of the industry – Botswana, Kenya and Mozambique haveall acquired new conference centres. In some areas, however, such as Eritrea, there are constraints onthe growth of the industry due to the frequency, capacity and cost of flights into the country. Littleinformation is provided on the impact of political unrest in these areas on the Meetings Industry.

Latin America

North America

Australia

Africa

Asia

Europe

9Global Overview of the Industry

Americas

Some regions, such as the Americas, have collected data on the main congress and convention centresin the key areas of the region. These data are presented in Appendix B and although it provides asnapshot of the size and location of key centres, it unfortunately does not provide a full picture of thesupply side in this region. The UNWTO report, The Meeting Conventions Market in the Americas(2005b, p. 45), suggests that “while the more mature parts of the region have seen little growth insupply, there has been a considerable amount of activity in the Caribbean, Central America and SouthAmerica.”

Asia and the Pacific

One of the main Asian convention destinations is Hong Kong, with its Hong Kong Convention &Exhibition Centre of 64,000 m2. In addition, Macao, China and India have increased their capacity forholding large conventions, with major destinations being Beijing, Shanghai, New Delhi, Agra,Bangalore, Chennai and Mumbai. In Oceania, some of the Pacific Islands such as New Caledonia andFiji are expanding their convention facilities while Australia and New Zealand both provide acomprehensive range of convention properties.

Europe

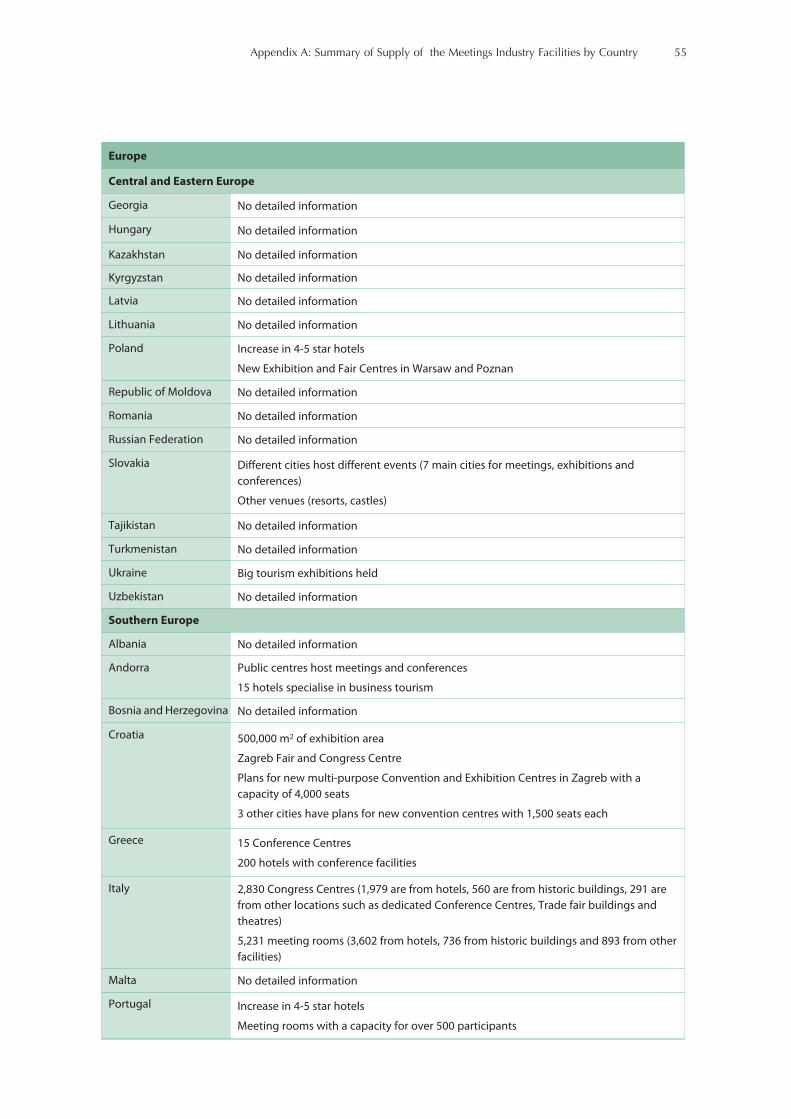

Europe is traditionally one of the key locations for the Meetings Industry. Many European countrieshave state-of-the-art facilities and the easy access to these countries make them favoured MeetingsIndustry destinations. It is a highly competitive environment. France, for example, currently has 120convention centres, making it the top European country in terms of facilities. Those countries thatprovide value-added conference facilities, such as the Netherlands and Spain, have excellentinfrastructure with a wide range of product. In addition, countries which are new to themeetings/conference industry, such as Estonia and Andorra, are developing their Meetings Industryfacilities and offering different types of facilities.

Middle East

According to the UNWTO (2005b), Dubai offers the most comprehensive Meetings Industry supply inthe Middle East. Other countries in this region, however, such as Saudi Arabia, Bahrain and Syria, alsohave excellent facilities that compete strongly with other destinations.

2.1.2 Trends in Exhibitions

2.1.2.1 Demand

A global overview of the exhibition industry is even more difficult to provide. While there is generalagreement on the definition of exhibitions2, and the Convention Industry Council’s (CIC) definitionpresents an example of this, there is little global information on the trends in this sector. The industrytends to assess its performance on the size of the space used for exhibitions, but there is no consistencyin the boundaries of these measures.

2 Convention Industry Council definition of exhibition: 1) An event at which products and services are displayed. The primaryactivity of attendees is visiting exhibits on the show floor. These events focus primarily on business-to-business (B2B) rela-tionships. 2) Display of products or promotional material for the purposes of public relations, sales and/or marketing.

10 Measuring the Economic Importance of the Meetings Industry

A study undertaken on the South African Exhibition sector (Heath et al, 2005) and that undertaken inAustralia (Deery et al, 2005) show some trends that could be extrapolated to the global situation. InSouth Africa, for example, the average number of exhibitions per exhibition organiser increased from1.97 in 2001 to 2.2 exhibitions per organiser in 2004. The majority of exhibitions (77%) take placeannually, which is consistent with the Australian situation (73% in 2003).

Paralleling trends in the international Meetings Industry, the actual number of show days declined from4.86 days in 2002 to 4 days in 2004. This 4-day average was also in line with international trends inthe exhibition sector with a 3.7 days average duration in the United States in 2004 and 3 days durationin Australia in 2003 (Heath et al, 2005).

In an attempt to obtain consistent data from the USA and Canadian exhibition sectors, the Centre forExhibition Industry Research (CEIR) has developed an Exhibition Industry Index which measures arange of indicators of the industry’s development. This provides data for the North American scene butdoes not provide any global overview.

2.1.2.2 Supply

The information provided on the supply side of the exhibition sector is somewhat limited andinconsistent in the way it is reported. In Africa, for example, the UNWTO reports that while places suchas Tunisia, Zimbabwe and Ghana have dedicated facilities for exhibitions and fairs, other countrieswithin the region appear to use convention centres and other spaces such as cultural and sportingcentres for the purposes of exhibiting.

Within the Americas region, there appears to have been considerable growth in the exhibition sectorwith countries such as Mexico, Cuba, Curacao, Brazil, Chile, Barbados and Bermuda all expandingtheir facilities. The more mature markets, such as North America, do not appear to have grown theexhibition component substantially.

The Asia and Pacific region possesses significant exhibition facilities with countries such as Hong Kong,China and India being among the largest providers of exhibition space. Although there was a decreasein the number of exhibitions in Hong Kong due to the SARS outbreak, the sector appears to haverecovered and a new exhibition centre has been completed.

Europe has traditionally held some of the largest and most comprehensive exhibitions in the world. Inparticular, Germany has six very large exhibition locations while countries such as the UnitedKingdom, Luxembourg and Monaco have increased their exhibitions’ capacity.

Finally, it is the Middle East that has increased its profile within the exhibition arena. In particular, thehigh-tech, purpose-built Dubai Airport Exhibition Centre and the Bahrain International ExhibitionCentre have increased the Middle East exhibition capacity.

In summary, the exhibition sector appears to be following similar trends to the international MeetingsIndustry, with predicted growth in exhibition events, but a decrease in the duration of the exhibitions.

One of the greatest challenges for the exhibition industry is the increase in competition globally withthe emergence of countries such as China, where there are 57 new convention and exhibition centrescurrently under construction, Dubai, which is planning a dedicated city for exhibitions spread over 74acres, and India, which has five new convention and exhibition centres planned (Tourism Australia,2005). For the smaller exhibition countries, such as South Africa and Australia, there is an opportunityfor strategic regional alliances to combat such competition.

11Global Overview of the Industry

2.1.3 Trends in Incentives

Of the three key components of the Meetings Industry, the incentives sector is the least researched.Corporations implement incentive programs to drive sales, increase profits, improve service, enhancemorale, retain staff or provide high-profile recognition.

The level of secrecy surrounding this component largely explains the lack of research and, as stated inthe Sri Lankan Convention Bureau Report 2004 (p.3), “The Incentive Travel figures had been left outonce again in view of the reluctance of producing such data with the perception that informationprovided will be detrimental to their business and/or inability to separate incentive travel figures byhotels from general tourism data“. Incentive Travel is regarded, within the Meetings Industry, as thehighest yielding sector of the industry. The world wide incentive market is a ‘multi-billion dollar globalindustry’. (The Society of Incentive & Travel Executives (SITE)), 2004.

While it is difficult to provide world-wide trends, there are common elements in the changes occurringin the industry around the world. For example, the shortening of the duration of incentive programsfrom seven days to an average of four days is recorded in the USA (SITE, 2005) and 5.1 days in Australia(Deery et al, 2005). In a comprehensive study undertaken by the Malta Tourism Authority on theincentive sector in 2000-2001, incentive program duration had already decreased to four days duringthis period.

The incentive travel sector is probably the most vulnerable to volatility in world events. According tothe Incentive Federation’s Incentive Study 2003, of the respondents who did not use incentives in thepast 2 years, a concern about cost was the main reason for their companies not using incentives. Otherconcerns included difficulties in making the program fair, uncertainty of program outcomes,uncertainty about the kind of incentives to offer, not knowing enough about incentive programs or howto measure results, administration, legal/liabilities and management resistance.

The Australian study (Deery et al, 2005) found that a number of those organizations involved in theincentive travel industry had lost business for a variety of reasons. These included that companies werechoosing cheaper options, the impact of world events such as SARS, September 11, and the Balibombing, additional competition, the non availability of flights, the destination’s inability to meet needsof participants, the distance barrier and visa problems.

In summary, the incentive travel area is a lucrative, yet volatile, component of the Meetings Industry.While this component is an extremely competitive one as new destinations replace older, less attractiveand potentially less safe destinations, new markets such as China and India are emerging. Thechallenge for those involved in the incentive travel component is to attract these new markets – whichtend to be presently lower yield markets- into longer stay programs.

2.2 Current Data Collection Practices

Data are collected on the Meetings Industry in a myriad of ways, and this section summarises thetechniques used in existing studies.

However, there is value in considering the components of the Meetings Industry to provide a contextfor the discussion. A simple model of the meetings industry is presented in Figure 3.

12 Measuring the Economic Importance of the Meetings Industry

Figure 3 The Meetings Industry

The Meetings Industry can be regarded as having two broad dimensions: the demand side and thesupply side. For the purposes of this study, the demand side is defined as the delegates (the consumers)– or participants, as they will be referred to in this report – and the supply side is defined as comprisingthe organiser, the venue and the host organisation. While the activities of suppliers of other goods andservices, e.g. accommodation, transport, etc., that delegates use in conjunction with their attendanceat the meeting will be measured in assessing the economic contribution of meetings’ participants, thesesuppliers are not components of the Meetings Industry. The overlapping hashed lines above indicatethat in some cases the host organisation acts as the organiser, and in some cases, the venue will act asthe organiser. This has implications for data collection.

Demand side research collects data about the delegates in terms of their total numbers, their origin andexpenditure on registration and other goods and services. Supply side research collects data about themeetings, the organisers, the numbers of participants, and the costs and revenues associated withhosting/organising the meeting.

A complete picture of the industry requires data from both the demand and supply sides. A demandonly approach does not identify the full economic contribution of the industry, while the supply sideapproach does not identify additional expenditure by participants incurred in the host region.

2.2.1 Data Collection by Global Agencies

The UNWTO, in its Tourism Market Trends 2004 survey, collates data by asking each country whetherstatistics are collected on international meetings in their country. No definition of the Meetings Industryis provided as none existed at the time of the data collection. If the answer is ‘yes’, there is a smalldescription of the importance and size of the industry and another on the evolution of the MeetingsIndustry.

Typically, these are demand estimates, with countries providing an estimate of the size of theirinternational meetings tourism as a percentage of total inbound tourism. The difficulties with thismethod are:

Demand Supply

DelegatesOrganiser Host Organisation

Venue

Other Goods and

Services e.g. transport,

accommodation,

restaurants, retail

Pay other suppliers for

various goods and services

Pay registration

fee to organisers

Exhibitors

13Global Overview of the Industry

a) there is no consistent definition used for the meetings industry and so the estimates of the size ofmeetings activity vary widely from country to country, and

b) these figures do not include the domestic meetings market which can be a sizeable market.

Other global agencies that collect meetings industry data are the specific industry groups such as ICCA,MPI, SITE, UIA and Reed Exhibitions. These organisations issue regular reports including:

• FutureWatch (MPI)

• The State of the Industry (Successful Meetings)

• International Association Meetings Market: Statistics Report (ICCA)

• Five Year Trends Report (EIBTM)

• Economic Impact Study (CIC)

• International Meetings Statistics (UIA)

• The SITE Foundation Industry Reports (SITE)