Embed Size (px)

Citation preview

1

TO:

HENLEY MANAGEMENT COLLEGE

FROM:

CHEUNG TSE KIN, MICHAEL MASTER OF BUSINESS ADMINISTRATION

PROGRAMME STAGE THREE HONG KONG

SUBJECT:

ASSESSED ASSIGNMENT: BUSINESS FINANCE

March 2000

TOPIC:

1. Prepare a report to be presented to the Chief Executive of Ragus Corporation, recommending whether or not to accept the project proposal. (40%)

2. Identify and discuss the circumstances in which it may be rational to accept

negative net present value projects. (30%) 3. Describe the mechanism whereby shareholders’ wealth is maximised using the

dividend valuation model, raising any difficulties you perceive in this analysis (30%).

2

CONTENTS

Preface

Executive Summary

Part I Purys Project Report

1.1 The Executive Report 5

1.2 Corporate Strategy 5

1.3 Market Information 5

1.4 Resources 6

1.5 Financial Analysis 6

1.6 Financial Evaluation 11

1.7 Recommendations 12

1.8 Comments 14

Summary

Part II Projects with Negative Net Present Value 2.1 Financial Standpoint 15

2.2 Operational Standpoint 16

2.3 Strategic Standpoint 18

2.4 Macro-environmental Standpoint 20

2.5 Stakeholders’ Standpoint 20

Summary

Part III Dividend Valuation Model: Mechanism & Limitations

3.1 Mechanism of the Dividend Valuation Model 22

3.2 Constant Dividend Growth Model 23

3.3 Regular Dividend Payment Intervals 24

3.4 Perpetuity 24

3.5 Constant Required Rate of Return 24

3.6 Market Efficiency 24

3.7 Transaction Costs & Taxation 25

3.8 Information Requirement 25

Summary

BIBLIOGRAPHY

3

PREFACE TOPIC This assignment of Business Finance is the selected elective course in Stage III of

the MBA Programme. It is based on the Ragus Corporation Ltd. case study.

STRUCTURE

This report has 3 parts, divided in accordance to the 3 assignment questions.

Part I presents the Purys project proposal. The report was prepared as if the time

were January 1987 according to the data given from the case. The Tables and

Appendices related to this proposal are inserted here (instead of placing them at the

end), to provide a continuous flow of readability. Some comments are followed after

the proposal.

Part II identifies and discusses a wide range of circumstances whereby it is rational

to accept projects with negative net present value. The analysis starts by taking a

micro-view from the financial standpoint, and expands to a much broader perspective

in the later part. In section 2.3, under the Strategic Standpoint analysis, the writer

uses 3 different examples, from actual work experiences, to validate the discussion.

Part III begins with a simple illustration of the Dividend Valuation Model, followed by

the descriptions on its limitations.

With each Part ends with a section summary, this report has 5,017 words.

As part of the assignment contains confidential information related to the writer’s

employer, please do not disclose this report to those outside of the Henley

Management College. Thank you.

CHEUNG Tse-Kin Michael

March 2000 Hong Kong

4

Executive Summary

Internal information generated from Ragus Corporation indicated that there was a

positive market potential on the Purys product in the U.K. The main resource

requirements for Ragus to implement this new project included production site,

production plant, new manager/workers, raw materials, plus additional power and

maintenance. A projected profit and loss statement revealed that this venture has

a positive net present value in its estimated product life. The Chief Financial

Officer thereby gave a positive recommendation on this project. Apart from the

favourable financial return, it would also improve the overall competitive position

of Ragus Corporation, by means of diversifying business risks, reducing threat

from direct competitors, increasing bargaining power to suppliers, and, reducing

threat from new entrants.

There are situations whereby a firm will undertake a project with negative net

present value. First, if the quantitative information in the projected financial

statement is not entirely accurate, a negative bottom line does not mean that the

project should be discarded. Second, projects arising from the marketing, human

resources and information system departments may be a loss by itself, but could

bring many benefits at the corporate level. Third, projects with strategic

implications will often override the financial results. Fourth, firms are sometimes

forced to undertake ventures when the macro-environment drives them to do so.

Last, major stakeholders of an organization can overrule decision derived from

financial analysis.

The basic concept of the Dividend Valuation Model is to maximise shareholders’

wealth. It does so by finding the sum of the: 1) share price at the time of purchase,

2) present value of the share price at the time of sale, and 3) present values of all

the dividends expected to receive in the investment period. Its limitations are that

it assumes that the dividend growth rate, the dividend payment intervals, and the

required rate of return by investors, are all constants. Other drawbacks of the

theory include: it assumes the firm exist indefinitely, it fails to take transaction

costs and taxation effect into consideration, and, the amount of information

required to conduct this analysis is immense.

5

PART I Pury Project Report

1.1 The Executive Report

The Executive Report, consist of editorial and tabular contents, is presented as follow.

*********************************************************************************************

Purys Project

Submitted to: Mr. Tom Ragus; Chief Executive Office

Prepared by: Chief Financial Officer

Date: January 1987

Objective

To provide recommendation on the new Purys Project based on financial and

strategic analysis.

1.2 Corporate Strategy

The long-term corporate objective of Ragus Corporation is to maximise

shareholders’ value. To achieve this goal, the management team has decided,

through utilising technical expertise, to employ the strategy of Product Development.

1.3 Market Information

The Marketing Department has identified a potential in the Purys market. The

Research & Development team has developed the technology to produce Purys

product. A comprehensive market research, conducted in the last quarter of 1986,

reveals the following facts:

The market potential in the U.K. is 500,000 cases annually.

Setat currently has 75% market share in this product category. Another 5

regional firms hold the remaining 25%.

The market size has remained stable for 5 years.

The demand for Purys, if launch in this year, is estimated to be 100,000 cases,

at selling price of $30 per case.

The demand will double by the end of the 2nd year. Thereafter, the annual

demand will remain steady at 200,000 cases during its product-life.

Product life of Purys is estimated to be 5 years. Beyond that, the environment

would be too difficult and unrealistic to forecast.

6

1.4 Resources

Essential resources include:

A production line at the idle Peterborough factory site.

A production plant (including storage facilities), requiring an investment of

$4,200,000. Its estimated useful life is 8 years.

A new Production Manager (annual salary = $14,000).

A work-team of 16 (annual compensation = $10,000 per worker).

Raw material of 40 kg of Ragus to produce one case of Purys.

Power cost of $10 per case of Purys.

Annual maintenance fees of $550,000.

An allocation of $150,000 of general overheads from the operations of Ragus.

1.5 Financial Analysis

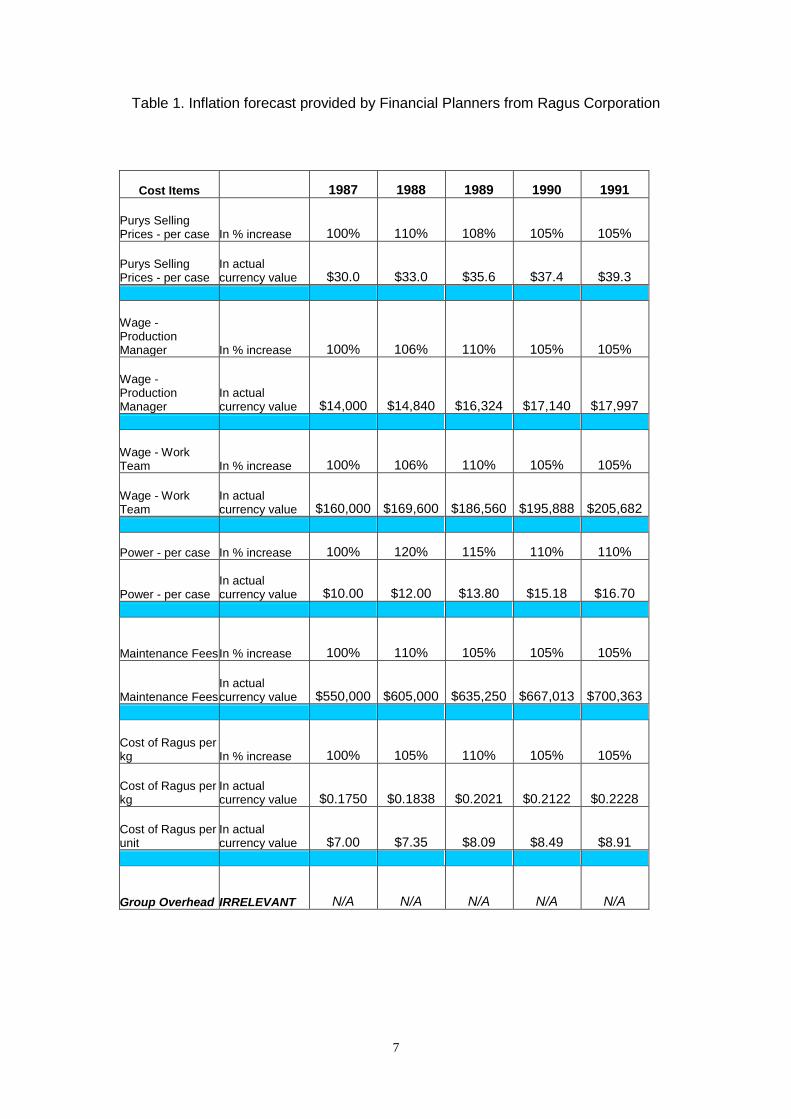

Table 1 is the Inflationary forecast provided by the Financial Planners.

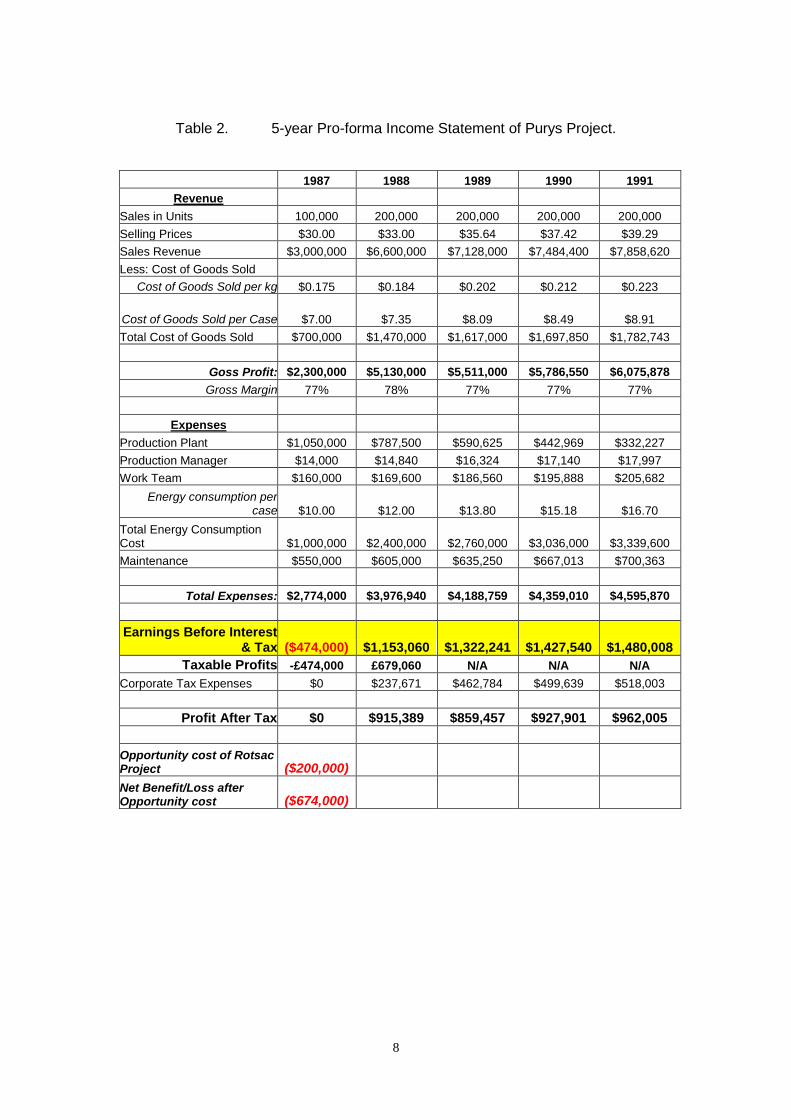

Table 2 is a 5-year Pro-forma Income Statement of the Purys project.

Appendix A computes the weight average cost of capital being used in this

analysis, which is 23.42%.

Appendix B lists the itemised explanations in the Pro-forma Income Statement.

Summary of the Pro-forma Income Statement Analysis

The gross profit is $2.3 million in 1987. Then grew over double to $5.13 million

in 1988. Thereafter, GP increases by 7%, 5% & 5% respectively in the following

3 years.

Gross margin remains steady at 77% throughout the product life.

A negative EBIT results only in 1987 due to premature sales performance and

high initial investments in production plant.

In 1987, the net benefit of the Purys Project is EBIT less the opportunity loss

from the Rotsac project. The Purys & Rotsac Projects are mutually exclusive.

Thus, $200,000 would have been gained if Purys Project were discarded.

7

Table 1. Inflation forecast provided by Financial Planners from Ragus Corporation

Cost Items 1987 1988 1989 1990 1991

Purys Selling Prices - per case In % increase 100% 110% 108% 105% 105%

Purys Selling Prices - per case

In actual currency value $30.0 $33.0 $35.6 $37.4 $39.3

Wage - Production Manager In % increase 100% 106% 110% 105% 105%

Wage - Production Manager

In actual currency value $14,000 $14,840 $16,324 $17,140 $17,997

Wage - Work Team In % increase 100% 106% 110% 105% 105%

Wage - Work Team

In actual currency value $160,000 $169,600 $186,560 $195,888 $205,682

Power - per case In % increase 100% 120% 115% 110% 110%

Power - per case In actual currency value $10.00 $12.00 $13.80 $15.18 $16.70

Maintenance Fees In % increase 100% 110% 105% 105% 105%

Maintenance Fees In actual currency value $550,000 $605,000 $635,250 $667,013 $700,363

Cost of Ragus per kg In % increase 100% 105% 110% 105% 105%

Cost of Ragus per kg

In actual currency value $0.1750 $0.1838 $0.2021 $0.2122 $0.2228

Cost of Ragus per unit

In actual currency value $7.00 $7.35 $8.09 $8.49 $8.91

Group Overhead IRRELEVANT N/A N/A N/A N/A N/A

8

Table 2. 5-year Pro-forma Income Statement of Purys Project.

1987 1988 1989 1990 1991

Revenue

Sales in Units 100,000 200,000 200,000 200,000 200,000

Selling Prices $30.00 $33.00 $35.64 $37.42 $39.29

Sales Revenue $3,000,000 $6,600,000 $7,128,000 $7,484,400 $7,858,620

Less: Cost of Goods Sold

Cost of Goods Sold per kg $0.175 $0.184 $0.202 $0.212 $0.223

Cost of Goods Sold per Case $7.00 $7.35 $8.09 $8.49 $8.91

Total Cost of Goods Sold $700,000 $1,470,000 $1,617,000 $1,697,850 $1,782,743

Goss Profit: $2,300,000 $5,130,000 $5,511,000 $5,786,550 $6,075,878

Gross Margin 77% 78% 77% 77% 77%

Expenses

Production Plant $1,050,000 $787,500 $590,625 $442,969 $332,227

Production Manager $14,000 $14,840 $16,324 $17,140 $17,997

Work Team $160,000 $169,600 $186,560 $195,888 $205,682

Energy consumption per case $10.00 $12.00 $13.80 $15.18 $16.70

Total Energy Consumption Cost $1,000,000 $2,400,000 $2,760,000 $3,036,000 $3,339,600

Maintenance $550,000 $605,000 $635,250 $667,013 $700,363

Total Expenses: $2,774,000 $3,976,940 $4,188,759 $4,359,010 $4,595,870

Earnings Before Interest & Tax ($474,000) $1,153,060 $1,322,241 $1,427,540 $1,480,008

Taxable Profits -£474,000 £679,060 N/A N/A N/A

Corporate Tax Expenses $0 $237,671 $462,784 $499,639 $518,003

Profit After Tax $0 $915,389 $859,457 $927,901 $962,005

Opportunity cost of Rotsac Project ($200,000)

Net Benefit/Loss after Opportunity cost ($674,000)

9

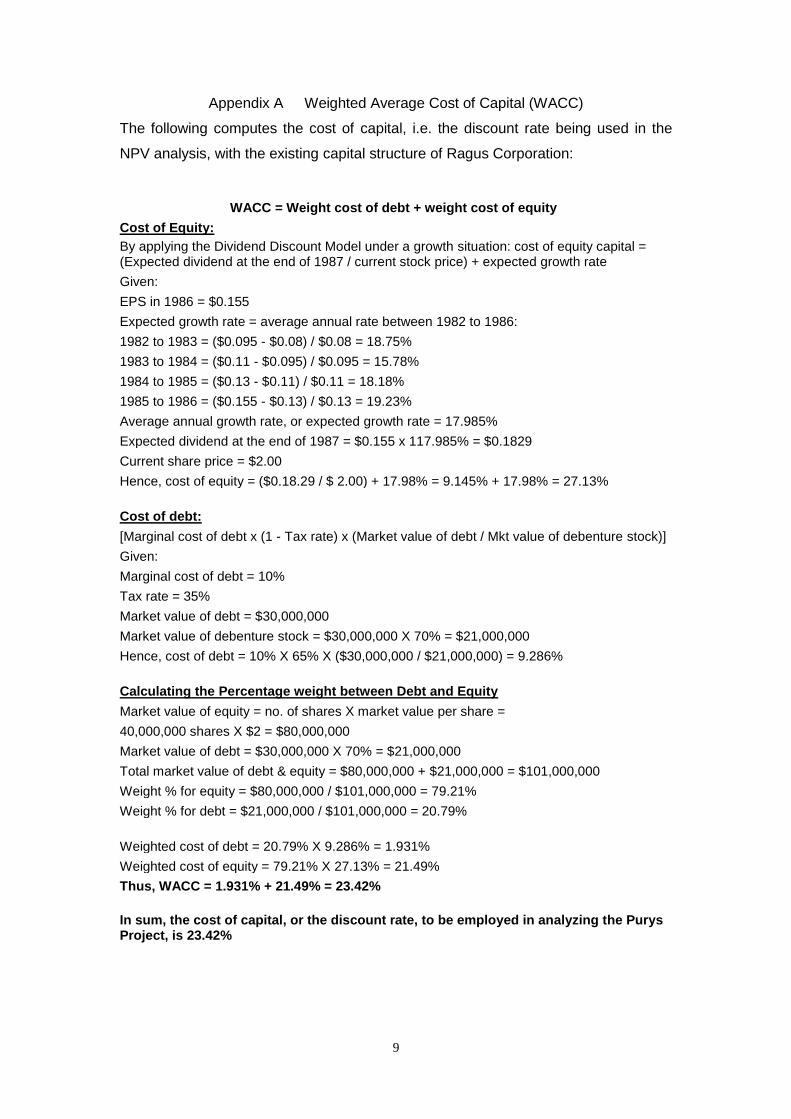

Appendix A Weighted Average Cost of Capital (WACC)

The following computes the cost of capital, i.e. the discount rate being used in the

NPV analysis, with the existing capital structure of Ragus Corporation:

WACC = Weight cost of debt + weight cost of equity

Cost of Equity:

By applying the Dividend Discount Model under a growth situation: cost of equity capital = (Expected dividend at the end of 1987 / current stock price) + expected growth rate

Given:

EPS in 1986 = $0.155

Expected growth rate = average annual rate between 1982 to 1986:

1982 to 1983 = ($0.095 - $0.08) / $0.08 = 18.75%

1983 to 1984 = ($0.11 - $0.095) / $0.095 = 15.78%

1984 to 1985 = ($0.13 - $0.11) / $0.11 = 18.18%

1985 to 1986 = ($0.155 - $0.13) / $0.13 = 19.23%

Average annual growth rate, or expected growth rate = 17.985%

Expected dividend at the end of 1987 = $0.155 x 117.985% = $0.1829

Current share price = $2.00

Hence, cost of equity = ($0.18.29 / $ 2.00) + 17.98% = 9.145% + 17.98% = 27.13%

Cost of debt:

[Marginal cost of debt x (1 - Tax rate) x (Market value of debt / Mkt value of debenture stock)]

Given:

Marginal cost of debt = 10%

Tax rate = 35%

Market value of debt = $30,000,000

Market value of debenture stock = $30,000,000 X 70% = $21,000,000

Hence, cost of debt = 10% X 65% X ($30,000,000 / $21,000,000) = 9.286%

Calculating the Percentage weight between Debt and Equity

Market value of equity = no. of shares X market value per share =

40,000,000 shares X $2 = $80,000,000

Market value of debt = $30,000,000 X 70% = $21,000,000

Total market value of debt & equity = $80,000,000 + $21,000,000 = $101,000,000

Weight % for equity = $80,000,000 / $101,000,000 = 79.21%

Weight % for debt = $21,000,000 / $101,000,000 = 20.79%

Weighted cost of debt = 20.79% X 9.286% = 1.931%

Weighted cost of equity = 79.21% X 27.13% = 21.49%

Thus, WACC = 1.931% + 21.49% = 23.42%

In sum, the cost of capital, or the discount rate, to be employed in analyzing the Purys Project, is 23.42%

10

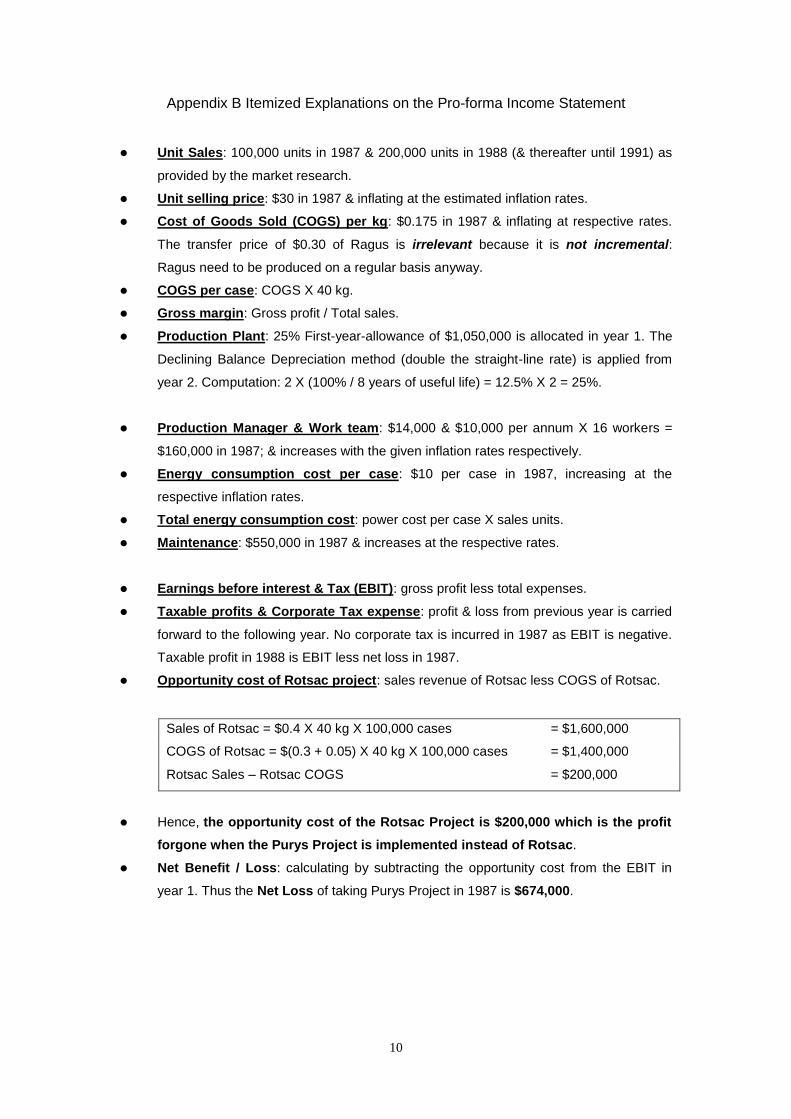

Appendix B Itemized Explanations on the Pro-forma Income Statement

Unit Sales: 100,000 units in 1987 & 200,000 units in 1988 (& thereafter until 1991) as

provided by the market research.

Unit selling price: $30 in 1987 & inflating at the estimated inflation rates.

Cost of Goods Sold (COGS) per kg: $0.175 in 1987 & inflating at respective rates.

The transfer price of $0.30 of Ragus is irrelevant because it is not incremental:

Ragus need to be produced on a regular basis anyway.

COGS per case: COGS X 40 kg.

Gross margin: Gross profit / Total sales.

Production Plant: 25% First-year-allowance of $1,050,000 is allocated in year 1. The

Declining Balance Depreciation method (double the straight-line rate) is applied from

year 2. Computation: 2 X (100% / 8 years of useful life) = 12.5% X 2 = 25%.

Production Manager & Work team: $14,000 & $10,000 per annum X 16 workers =

$160,000 in 1987; & increases with the given inflation rates respectively.

Energy consumption cost per case: $10 per case in 1987, increasing at the

respective inflation rates.

Total energy consumption cost: power cost per case X sales units.

Maintenance: $550,000 in 1987 & increases at the respective rates.

Earnings before interest & Tax (EBIT): gross profit less total expenses.

Taxable profits & Corporate Tax expense: profit & loss from previous year is carried

forward to the following year. No corporate tax is incurred in 1987 as EBIT is negative.

Taxable profit in 1988 is EBIT less net loss in 1987.

Opportunity cost of Rotsac project: sales revenue of Rotsac less COGS of Rotsac.

Sales of Rotsac = $0.4 X 40 kg X 100,000 cases = $1,600,000

COGS of Rotsac = $(0.3 + 0.05) X 40 kg X 100,000 cases = $1,400,000

Rotsac Sales – Rotsac COGS = $200,000

Hence, the opportunity cost of the Rotsac Project is $200,000 which is the profit

forgone when the Purys Project is implemented instead of Rotsac.

Net Benefit / Loss: calculating by subtracting the opportunity cost from the EBIT in

year 1. Thus the Net Loss of taking Purys Project in 1987 is $674,000.

11

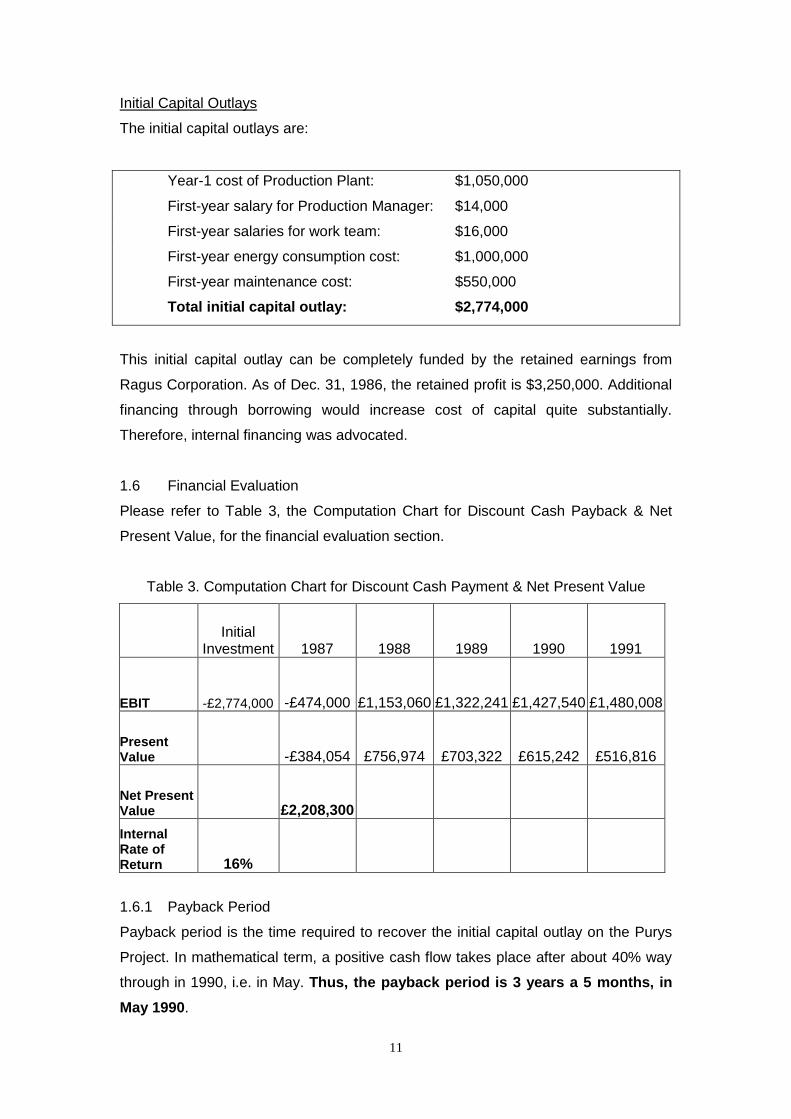

Initial Capital Outlays

The initial capital outlays are:

Year-1 cost of Production Plant: $1,050,000

First-year salary for Production Manager: $14,000

First-year salaries for work team: $16,000

First-year energy consumption cost: $1,000,000

First-year maintenance cost: $550,000

Total initial capital outlay: $2,774,000

This initial capital outlay can be completely funded by the retained earnings from

Ragus Corporation. As of Dec. 31, 1986, the retained profit is $3,250,000. Additional

financing through borrowing would increase cost of capital quite substantially.

Therefore, internal financing was advocated.

1.6 Financial Evaluation

Please refer to Table 3, the Computation Chart for Discount Cash Payback & Net

Present Value, for the financial evaluation section.

Table 3. Computation Chart for Discount Cash Payment & Net Present Value

Initial Investment 1987 1988 1989 1990 1991

EBIT -£2,774,000 -£474,000 £1,153,060 £1,322,241 £1,427,540 £1,480,008

Present Value -£384,054 £756,974 £703,322 £615,242 £516,816

Net Present Value £2,208,300

Internal Rate of Return 16%

1.6.1 Payback Period

Payback period is the time required to recover the initial capital outlay on the Purys

Project. In mathematical term, a positive cash flow takes place after about 40% way

through in 1990, i.e. in May. Thus, the payback period is 3 years a 5 months, in

May 1990.

12

1.6.2 Discount Cash Payback

Discount cash payback is the time required to recover the initial capital outlays

discounting at the cost of capital. The cumulative present value of the Purys Project,

at the end of the estimated project life in 1991, is $2,208,300. Hence, it is unable to

recover the initial capital outlays in the first 5 years of operations.

1.6.3 Net Present Value (NPV)

The NPV is the present value of the expected cash flows of the Purys Project,

discount at the cost of capital, and subtract from it the initial capital outlay. The NPV

from the first 5 years of operations, is +$2,208,300.

1.6.4 Internal Rate of Return (IRR)

The IRR is the interest rate that equates the present value of the expected future

cash flows, to the initial capital outlay. The IRR is 16%.

1.7 Recommendation

The Purys Project is recommended, for 3 valid reasons:

1 From a financial perspective, an NPV of + $2,208,300 is profitable.

2 From an operational perspective, the idle building at the Peterborough site can

now be fully utilised – making best use of fixed asset. As Group overhead can be

allocated to the project, much economies of scale can be gained.

3 From a strategic perspective, the project can strengthen the company’s

competitive position in 4 dimensions.

I. Increase product image to diversify business risks. The project nature is

highly consistent with the product-development strategy of Ragus. It

capitalizes on the strength of technical expertise to launch new product in

markets identified by the Marketing Department. More importantly, by adding a

new product, the overall business risk is diversified. As the market size of

Ragus has not been growing since 1970, it is critical to explore and

establish new markets and new customer base. Otherwise, the company

is vulnerable to changes in the environment that will negatively affect the

demand of Ragus. Such change could well be outside of the company control.

13

II. Reduce threat from direct competitor. Setat is the biggest competitor in the

Purys market. It is a major company and is also strong in marketing, in

addition to research and development. It poses constant threat to Ragus. By

establishing a committed and well-planned attack on the existing Purys

market, Ragus can generate a solid market signal that it is determined to

maintain and strengthen its leadership status in the UK. Striving to gain

substantial market share from Setat’s existing terrain will certainly create

a competitive reaction from Setat. In doing so, Setat must assign

additional resources to defend its territory. Then, it will have less

resource to develop new product(s) to threaten Ragus. Thus, the Purys

project can strengthen Ragus’ competitive position by reducing the threat from

this direct competitor.

III. Increase bargaining power to suppliers. Adding the Purys product into the

marketplace requires additional resource input. Ragus can ask for lower

price and / or more favourable terms from vendors. Such as: fight for a

price reduction on raw materials as volume grows; ask for discount from the

freight forwarder as distribution expands; request for a lower rate from media

companies as more advertising space is committed; etc. In short, whenever

applicable, Ragus’ competitive position is enhanced through reducing the

bargaining power of suppliers.

IV. Reduce threat of new entrants / competitor(s). Setat currently holds 75% of

the existing Purys market share, while other 5 regional firms hold the rest.

Other potential new entrants might consider attacking one or more of these

players. By implementing the Purys project, other potential competitors

that might be interested in entering into this market, will probably not do

so. Ragus will intensify the industry competition by entering the playing

field as a new major player, and will likely eliminate some of the weaker

contestants. Hence, this project reduces the threat of new entrants in the

Purys market.

Therefore, the Corporate Finance Department recommends the Chief Executive to

approve the Purys project to take place this year.

********************** End of Report to C.E.O. Tom Ragus *********************

14

1.8 Comment

The technology process development cost of $75,000, the market research

cost of $50,000, the general overhead of $150,000, and the original building

cost of $10,000 (in 1976) are all excluded from the analysis: ‘Only the increment

in costs and benefits as a result of the decision are relevant; benefits we would receive

irrespective, and costs which we would have had to incur are irrelevant. It follows from

this that past, historic data can never be relevant for decisions. Sunk costs which have

been committed to a project in the past, and are therefore irretrievable.’ (Higson 1995)

The opportunity cost of $200,000 of Rotsac project is probably an

overstated amount in reflecting the profit forgone. This figure has NOT

taken the associated costs into consideration, such as the incremental

expenditures in plant and equipment, manpower or marketing. The actual

opportunity cost is likely to be less than $200,000. Nevertheless, as these data

are unavailable, the $200,000 amount is used in this analytical context.

Summary of Part I

Internal information generated from Ragus Corporation indicated that there is a

positive market potential on the Purys product in the U.K.

The main resource requirements for Ragus to implement this new project

include production site, production plant, new manager and workers, raw

materials, and additional power maintenance.

A detailed projected profit and loss statement revealed that this new venture

has a positive net present value in its product life cycle. The Chief Financial

Officer thereby gave a positive recommendation on this project.

Apart from the favourable financial return, it also improves the overall

competitive position of Ragus Corporation, by means of diversifying business

risks, reducing threat from direct competitor, increasing bargaining power to

supplier, and, reducing threat from new entrants.

15

PART II Projects with Negative Net Present Value

‘People began to search for methods of evaluating projects which recognise that a dollar

received immediately is preferable to a dollar received at some future date. This recognition

led to the development of discount cash flow techniques to take account of the time value of

money. One such technique is called the net present value method. To implement this

approach, find the PV of the expected net cash flows of an investment, discount at the cost of

capital, and subtract from it the initial outlay of the project. If two projects are mutually

exclusive, the one with higher NPV should be chosen.’ (Weston & Copeland 1992)

There are numerous reasons whereby it is rational for a company to undertake a

project with negative NPV. The rationales are divided into different categories from 5

different standpoints.

2.1 Financial Standpoint

Mathematically, referring to Table 2 in Part I, all the items in the pro-forma income

statement affect the NPV. An expected change, which has not been taken into

account when doing the projection, will also affect the NPV.

From the financial standpoint, it may be rational to accept a negative NPV project if

and when one or more of the following occurs:

1. The sales revenue in the forecast is extremely conservative, or even

pessimistic, that it is very likely that the actual sales revenue is much

greater. From an accounting perspective, sales forecast may be understated for

various reasons. In this case, the bottle-line figures – profit after tax, are under-

estimated too. An expected revenue increase in the forthcoming periods

eventually will increase the NPV, and may bring a whole new picture to the

project.

2. An expected decrease in 1) cost of goods sold, or 2) any of the listed

expense items, which has not been factor-in into the forecast. Unofficial or

informal market information may not indicate that a new technology is under

development and it likely to reduce the raw material cost or production process

substantially. But by conventional accounting standard, such information is not

permitted to apply in the forecast, and thus, the gross profit is understated.

Hence, the profit after tax figure can also change positively which makes the

project more attractive than in pure financial terms.

16

3. A tax rate reduction is likely to take place. This may sound unusual but there

may be ways to reduce taxable profits, or, decrease tax expenses, so that the

bottom line becomes larger. This ultimately increases the NPV. The trade

industry may be negotiating with the government on new tax regulations; or, the

government may amend tax laws due to political or social pressures. These are

qualitative factors, which are often not reflected in the financial forecast.

Consequently, tax effects can change the NPV figures and turn management

decision from rejection to approval.

4. A change in the company’s capital structure is expected, which causes a

drop in cost of capital. The costs of capital for debt financing and equity

financial vary in accordance to market conditions. Cost of capital is the discount

rate being used in computing the present value of the future earnings from a

project. An expected reduction of cost of capital, caused by whatever reasons,

can apparently increase the overall NPV of the project, and thus turning the

decision around.

In short, a pro-forma profit-and-loss statement is computed with the facts and

information given at one point in time. Expectations in the future, especially

qualitative information, are not factor-in into the analysis, for accounting reasons.

Therefore, from a financial standpoint, it may be rational to accept a negative NPV

project, when any item in the pro-forma income statement is likely to change in

favour to the bottom-line figures.

2.2 Operational Standpoint

The next level is taken from the operational standpoint. 3 common areas are relevant

here.

1. Marketing Strategy. A company may decide to extend a product category with

its brand to gain market share or increase the overall brand equity. It may also

employ a product development strategy to achieve the same goal. Not all of

these products/projects are profit-driven: it may be a strategic move to

divert competitors’ attention. A new product may well be aiming purely to

increase brand awareness for future products. The firm could have a

series of projects as its marketing strategy. The 1st and 2nd projects could

knowingly be non-profitable, while the 3rd and 4th one are the true revenue

drivers. For instance, the 1st project might aim at dominating a new

17

distribution channel for the 3rd project. The 2nd project might aim at

misleading a competitor to the wrong action that is advantageous to the

firm. As stated: ‘Marketing strategy deals with the interplay of 3 forces:

customer, competition and corporation. Marketing strategy is defined as an

endeavour by a corporation to differentiate itself positively from its competitors,

using its relative corporate strengths to better satisfy customer needs. Strategic

marketing starts from the premise that different businesses have varying roles.

Each position in the life cycle requires a different strategy and affords different

expectation.’ (Jain 1990) Hence, negative NPV projects may exist in a firm’s

marketing plan.

2. Human Resources Development. Often, a firm will carry internal personnel-

related projects that are non-profitable. E.g. a new training and development

program (which includes facility, course materials and new staff) is required to

boost employee morale in the long run. It is extremely difficult to quantify the

benefits and a negative NPV could result. But the firm will gain positive public

image, enhance staff relation, and increase company goodwill from such

programs. This is particularly true for corporation that are about to, or have just

become, a publicly listed company. Such kind of project may be a ‘loss’ by itself,

but produces long-term benefits in a broader environmental context.

3. Management Information System. Rapid development in the e-commerce and

internet arenas might prompt many firms to undertake corporate-wide IT project.

The need to be electronically compatible with customers, suppliers and business

partners is increasingly critical to a firm’s viability. By itself, it is hard to quantify

the dollar benefits from IT project because its effects are far-reaching and

abstract. Nevertheless, corporate decision-makers would still proceed despite

seeing an unfavourable financial figure.

2.3 Strategic Standpoint

It may also be sensible to accept negative NPV project if it supports the overall long-

term corporate strategy of the firm.

Cost leadership strategy means ‘a firm sets out to become the low-cost producer in

its industry. A low cost producer must find and exploit all sources of cost advantage.

If a firm can achieve and sustain overall cost leadership, then it will be an above

18

average performer in its industry, provided it can command prices at or near the

industry average.’ (Porter 1985)

The writer works at the Hong Kong office of a multinational notebook computer-case

manufacturer, Tulip Asia Pacific (TAP). In mid-1998, TAP competed at multi-million

dollar bidding against a local rival. TAP supplies high quality, internationally

recognisable products, with above-average pricing. The rival is a low-cost, local

producer with factory pricing. Reliable source indicated that the rival was actually

losing money on this particular product bidding by submitting an extremely low price.

The rival won the business in July; and subsequently won other businesses from

TAP in the following 2 years.

The rival was willing to undertake a negative NPV project to develop new

markets. In doing so, it successfully reduced the threat from direct

competitor(s), and reduced the bargaining power of customer(s): gaining

competitive advantage in its marketplace. Although one product segment is

non-profitable, winning the bid gained access to new channels, which lead to

profits in subsequent businesses.

Differentiation strategy is ‘to be unique in the industry along some dimensions that

are valued by buyers. It is rewarded with its uniqueness with a premium price. The

logic of it requires a firm to choose attributes in which to differentiate itself from it

rivals’ (Porter 1985).

When the new Hong Kong International Airport opened in July 1998, several

business luggage suppliers, including TAP, were attempting to gain shelf-space at

the prestigious Duty-free shops. As Duty-free was (and still is) the dominant retailer,

its profit margin requirement was outrageous: over double of the market rate. Most

vendors eventually decided to stay away because it was simply not profitable to sell

in this channel. However, TAP still went ahead with the program, which was part of

the overall marketing plan:

‘Brand awareness is the ability of potential buyer to recognise or recall that a brand is

a member of a certain product category. Brand recognition is the basic first step in

the communication task. A name is like a special file folder in the mind which can be

filled with names-related facts and feelings. Without such a file readily accessible in

19

the memory, the facts and feelings become misfiled, and cannot be readily accessed

when needed.’ (Aaker 1991)

The move had several strategic implications. First, it increased brand

awareness and raise international image to enhance the differentiation strategy.

Second, it built entry barrier for new comers to enter this retail channel. Third,

it enlarges TAP’s bargaining power to other customers in opening new

distribution channels. The launch program at the Duty-free shop by itself was non-

profitable in pure financial term, but the qualitative benefits received, in the overall

territorial distribution, were far reaching.

Focus strategy is ‘based on the choice of a narrow competitive scope within an

industry. The focuser selects a segment or group of segments in the industry and

tailors its strategy to serving them to the exclusion of others’. (Johnson & Scholes

1993)

TAP has a parent company called Tulip International Inc. (TI) based in Seattle, USA.

TI has offices in 5 continents and distributes computer-cases in over 140 countries.

Its target market is sharply defined as: notebook computer users with medium to high

income, managers, executives and professionals.

TI’s mission is to become an international corporation with worldwide brand presence.

In 1999, the author received direction from TI to expand distribution in China

aggressively, As China marketing plan was prepared and showed a loss in the first 3

years, plus no definite promise on profit afterwards either.

Nevertheless, TAP was instructed to proceed. The rationale was that, first, focus-

differentiation was, and still is, the global long-term corporate strategy of TI:

focus on mobile professionals with quality and functionality as product-

differentiation attributes. The China expansion project supports the global

direction. Second, TI intended to expand business scope through mergers and

acquisitions. An established distribution network in China will substantially

increase TI’s competitive position by raising its bargaining power to potential

partners. TI’s global corporate profile would increase tremendously, when its

business covers difficult markets such as China, South Korea and Russia. In

sum, TI lost the battle but won the war.

20

2.4 Macro-environment Standpoint

There are situations whereby a firm is forced to implement negative NPV projects

due to macro-environmental pressures.

Political: A manufacturer may be forced to switch its production facility from one

country to another because the former is experiencing political upheavals. War,

sanction, embargo, and riots are some typical reasons. Under these

circumstances, the firm often has no choice but to proceed to relocation.

Legal: a firm might have to fulfil a legal requirement before having a chance to

achieve a goal. A petroleum company may first need to conduct scientific

project to prove that it is environmentally safe to perform oil-drilling in a location.

A properly developer may need to complete a pre-construction reclamation as

land law requires.

By the same token, other economic, social and technological conditions can also

exert pressures on an organization to undertake projects with negative NPV.

2.5 Stakeholders’ Standpoint

Stakeholders are those who have a strong interest and influence on the direction or

operations of the firm. Common stakeholders include shareholders, board of

directors and senior managers. In a practical business environment, stakeholders’

influence on decision-making is no less then the elements above.

A business owner will accept negative NPV project, which he/she believes is worth

pursuing beyond financial evaluation. Similar situations may occur at different levels

of an organization, whereby the stakeholders take a personal interest in the

circumstances.

Summary of Part II

There are situations whereby a firm will undertake a project with negative net

present value.

First, if the quantitative information in the projected financial statement is not

entirely accurate, a negative bottom line may not mean that the project should

be discarded.

Second, projects arising from the marketing, human resource and information

system department may be a loss by itself, but could bring many benefits at a

corporate level.

21

Third, projects with strategic implications will often override the financial results.

Fourth, firms are sometimes forced to undertake ventures when the macro-

environment drives them to do so.

Last, major stakeholders of an organization can over-rule decision derived from

financial analysis.

22

PART III Dividend Valuation Model: Mechanism and

Limitation

3.1 Mechanism of the Dividend Valuation Model

Maximising shareholders’ wealth has long been the long-term corporate objective for

organizations. There are essentially 2 ways to increase the share value. First,

investors purchase shares with the expectation of an increase in share value

sometime in the future. The share being bought in year 1 at $10 is expected to grow

and worth more than $10 in year 2. This is termed as capital gain on share prices.

But this occurs in a somewhat long-term timeframe. Second, then, to reward

investors in the short-term, dividends are declared intermittently. These dividends, in

the eyes of the investors, are their investment profits.

To compute the present value of a share price, the idea is similar to that of the Net

Present Value concept. If an investor purchases a share and intends to hold for 1

year, the total value of the share is the sum of:

Share price at the time of purchase in year 1, plus

Present value of the share price at the time of sale in year 2, plus

Present values of all the intermittent dividends expect to receive in that year

Mathematically, the Dividend valuation model is expressed as:

D + S2

S1 = -------------------

(1 + R)

Where:

S1 = Current share price

D = Dividend received in time 1

S2 = Share price at time of sale

R = Equity return by investors

Dividend payments are a collection of future profits received at different time intervals.

It can be viewed as the annual EBIT received from a project, such as the Ragus

project described in Part 1. Dividends serve as an incentive to reward investors in

investing in the organization. When historical dividend payment trends are available,

one can somewhat forecast future dividend behaviour. These payments are then

discounted back to reach their present values. Adding these 2 with the original

purchase price of the share, the ‘net present value’ of the share price is found.

23

If the investor intends to hold the share price indefinitely, the formula becomes:

1tt

t

)(1

D S1

R

In this case, the dividend amount after the share is sold simply becomes zero. If one

assumes that the dividend grows at a constant discount rate, G, the formula can be

re-expressed as:

D2

S1 = -------------------

(R - G)

Looking at the Dividend valuation model from both a conceptual and mathematical

standpoints, shareholders’ value can be maximized by:

1. Increasing the future dividend value as much as possible

2. Growing the future share value as much as possible

3. Minimizing the investors’ required rate of return

This is the basic theoretical and mathematical concept of the Dividend valuation

model. In practice, the Dividend valuation model poses numerous drawbacks.

3.2 Constant Dividend Growth Rate

First, the model assumes that the dividend growth rate is constant throughout

the computation period. In reality, it is not. Dividend payments are taken from the

organization’s retained earnings. Dividend policy depends on a large number of

interrelated factors, such as:

Historical corporate performances

Present and future corporate performances

Product demand (tastes, income, etc.)

Competitive environment (substitute products, new entrants, etc.)

Taxation

Future strategic directions (acquisition, merger, strategic alliances, etc.)

Future capital investment

Shareholders’ expected rate of return

Economics (interest rate, cost of capital, inflation, etc.)

Macro-environment (political, legal, technological, etc.)

Consequently, forecasting dividend payment is like forecasting future.

24

3.3 Regular Dividend Payment Intervals

Second, the model also assumes that the dividend payments have regular

interval, this is impractical in the real world. At good times a firm may choose to

pay dividend to reward its shareholders, or, invest the fund in the future projects. At

bad time, a firm may hold back dividend payment simply due to shortage of capital,

or, declare a dividend instead to battle the negative market rumour. Dividend policy I

therefore subject to fluctuations.

3.4 Perpetuity

The model further assumes that dividend payments take place perpetually –

that the firm (and its dividend policy) exists indefinitely. Again, for rationale

given before, perpetuity is seldom a reality. It is not uncommon for a firm to liquidate

willingly or unwillingly. Future is simply unpredictable.

3.5 Constant Required Rate of Return

Moreover, the model assumes the investors’ required rate of return is constant.

Investors set their required rate of return in accordance to several criteria. First, they

compare the return from a risk-free investment. Second, returns provided by similar

companies are examined, in order to generate a picture on the appropriate return

level. Third, the future prospect of the relevant industry is investigated. Fourth, the

management structure and leadership capabilities are explored. Given all these,

investors can establish the desired rate of return in accordance to risk and

uncertainty level. Inevitably, the rate of return fluctuates as one or more of the above-

mentioned factors changes.

3.6 Market Efficiency

In addition, the Market Efficiency assumption is not always true. The Market

Efficiency theory assumes that all investors act rationally and they are able to gather

all relevant information before making a decision. Recalling the Purys project in Part

1, the information is supplied by knowledgeable managers from Ragus Corporation.

These managers can access first-handed information to provide a project appraisal

which is reasonably accurate. The dividend valuation model is performed by analysts

outside of the company. These analysts can only access and gather second-handed

or third-handed information. This fact further dilutes the accuracy of the result.

25

3.7 Transaction Costs and Taxation

Another deficiency in the model is that it failed to take transaction costs and

taxation effects into consideration. Transaction costs include administrative costs

and issue discount during the issue of new shares. Taxation at corporate and

personal levels will also have impact on the final level of earnings.

3.8 Information Requirement

The last limitation of the model is simply the fact that it is extremely difficult, if not

impossible, to research such as immense amount of future information for the

formula. By the time the 3rd piece of information is found at some point in time, it is

likely that the 1st piece is already outdated. The determinants of the demand include

market size, taste, income, expectation, and price of related goods. The economic

growth is the sum of consumption, investment, government purchase and net export.

Predicting all these is indeed a challenging task.

These are the difficulties in implementing the dividend valuation model analysis. And

this concludes the entire assignment.

Summary of Part III

The basic concept of the dividend valuation model is to maximize shareholders’

wealth. It does so by finding the sum of the 1) share price at the time of

purchase, 2) present value of the share price at the time of sale, and 3) values

of all dividends expected to receive in the investment period.

Its limitations are that it assumes the dividend growth rate, the dividend

payment intervals, and, the required rate of return by investors, are all constants.

Other drawbacks of the theory include: it assumes the firm exist indefinitely, it

fails to take transaction costs and taxation effect into considerations, and, the

amount of information required to conduct this analysis is immense.

End

26

Bibliography

Aaker, A. D. (1991). Managing Brand Equity: Capitalising on the Value of a Brand Name. New York: The Free Press. Henley Management College. MBA Module Business Finance: Guide to Economic Appraisal (1996 Edition). Henley Management College. MBA Module Business Finance: Managing a Cash Flow Crisis – A Guide for Businessmen and Managers. (1996 Edition). Henley Management College. MBA Module Business Finance: Readings (1996 Edition). Henley Management College. MBA Module Business Finance: Workbook (1996 Edition).

Higson, C. (1995). Business Finance. London: Butterworths Publishing Ltd.

Jain C. S. (1990). Marketing Planning & Strategy (3

rd Edition). Cincinnati: South-Western

Publishing Co. Johnson, G. & Scholes, K. (1993). Exploring Corporate Strategy (3

rd Edition). London:

Prentice-Hall International (UK) Ltd.

Mills, W. R. & Robertson, J. (1993). Fundamentals of Managerial Accounting and Finance (3

rd Edition). Glos: Mars Business Associates Ltd.

Mills, W. R. (1994). Finance, Strategy and Strategic Value Analysis. Glos: Mars Business Associates.

Porter, E. M. (1980). Competitive Strategy: Techniques for Analysing Industries & Competitors. New York: The Free Press-Macmillan, Inc.

Van Horne, C. J. (1998). Financial Management And Policy (11

th Edition). New Jersey:

Prentice Hall, Inc.

Weston, J. F. & Copeland, E. T. (1992). Managerial Finance (9

th Edition). Fort Worth: The

Dryden Press.