Embed Size (px)

Citation preview

The Value of Co-Creation J.L. van de Mortel

0

Master Thesis

The Value of Co-Creation

Maastricht University

School of Business and Economics

Maastricht, August 31, 2010

Mortel, Jelmer L. van de, i345709

Study: International Business

Concentration: Finance

Master Thesis:

“The Value of Co-Creation”

Supervisor: Dr. T. Post

The Value of Co-Creation

J.L. van de Mortel 1

Abstract

This thesis examines the relation between the use of co-creation as way of doing business and

financial performance measurements of firms listed in the S&P 500. Co-creation is defined as

an active and creative process, based on collaboration between organizations and consumers,

and initiated by the firm to generate value for both, the company and the customer. Based on

balance sheet and income statement driven measures (i.e. Profit Margin, ROE, ROA, Tobin’s

Q) the effect of co-creation on the firm’s financial ratios and financial position is assessed.

The findings indicate that co-creation contributes to the success of a firm as measured by the

financial indicators, Return on Assets, Return on Invested Capital, Cost of Goods Sold, Cash

flow to Sales, Operating and Gross Profit Margin and Tobin’s Q. The results have clear

economic significance and suggest the inclusion of co-creation principles in current business

models to improve firm performance.

Keywords: Co-creation • Financial Performance • Value creation

In memoriam of C.K. Prahalad († April 16, 2010)

The Value of Co-Creation

J.L. van de Mortel 2

Table of Contents

1. Introduction p. 3

2. Literature Review p. 5

2.1. The Changing Business Environment

2.2. The Concept of Co-creation

2.3. Co-creation from the Company Perspective

2.4. Co-creation from a Customer Perspective

3. Research Design p. 22

3.1. Research Agenda

3.2. Sample

3.3. Variables

4. Results p. 29

4.1. Descriptive Statistics

4.2. Regression Analysis

5. Discussion & Conclusion p. 35

5.1. Theoretical Contributions

5.2. Managerial Implications

5.3. Limitations

5.4. Further Research

6. References p. 38

7. Appendices p. 48

The Value of Co-Creation

J.L. van de Mortel 3

1. Introduction

Due to globalization, higher customer demands and an increased level of information-sharing,

many organizations organize their business models in a different way than before.

Information technologies enabled a shift from old established corporations to new, innovative

dot-com firms in the end of the 20th century. Meanwhile, another, new class of firms has

emerged with exclusive business practices. Distinct from other firms, those organizations use

a joint process by the organization and consumer to create value that is unique to the

consumer and sustainable to the firm (Prahalad, 2004a). Everyone and anyone can be part of

this process. This joint process, called co-creation of value, can be of value for the consumer,

stakeholders, the organization and shareholders.

For many years, the debate on the changing dynamics of business has been focused on

alliances, networks, and collaboration (Ramaswamy, 2009b), and it is true that business-to-

business relationships have intensified, but in the interim researchers and managers have

largely ignored the consumer, the agent that is most dramatically transforming the industrial

system as we know it (Prahalad & Ramaswamy, 2000). The customer has recently changed

from a passive recipient of goods and services to an active, valuable partner and resource in

achieving organizational objectives. As such, co-creation is the process that enables firms to

benefit from consumer interaction and is a valuable resource to the firm.

A stream of strategy research posits that organizational resources and capabilities that are

rare, idiosyncratic, valuable and non-substitutable create a competitive advantage for an

organization (Barney, 1991; Conner, 1991; Wernerfelt, 1984). In recent times, studies about

organizational resources, like human resources, copyrights, goodwill, brand equity and

customer life (Hogan et al., 2002; Srivastava et al, 2001; Srinivasan & Hanssens, 2009), have

already illustrated the importance of intangible assets for businesses. Subsequently, it is

expected that co-creation also creates a competitive advantage for an organization.

Remarkable in studies about intangible assets is the great resemblance in chronological

advancement. A number of studies start describing a priori the opportunities of the relevant

concept. Subsequently, some studies, describe a posteriori the impact of an intangible from a

managerial perspective and, ultimately, the concept is evaluated from a financial perspective.

In contrast to the understanding of co-creation from the financial perspective, there has

already been a considerable interest from a managerial perspective in the potential of co-

The Value of Co-Creation

J.L. van de Mortel 4

creation. So far, research investigated the impact of co-creation from a strategic point of view

as a way to, inter alia, enhance innovation (Thomke & von Hippel, 2002), product quality

(Lengnick-Hall, 1996), product development (Gruner & Homberg, 2000) and consumer

satisfaction (Rowley, 2005; Gibbert et al, 2002).

However, hitherto, no research studied co-creation from a financial perspective. Despite the

intuitive, positive impact of co-creation, no study has investigated the relation between firm’s

financial performance and the implementation of co-creation. Subsequently, is hard to

motivate involved stakeholders to implement co-creation initiatives (Pedrosa, 2009) and will

co-creation remain, in the world of corporate finance, a peripheral issue.

Given the rhetoric used by top managers and boards, that the main role of management is to

maximize shareholder value (Black, 2001); it is ipso facto important to incorporate current

financial valuation techniques to properly demonstrate the contribution of co-creation to

shareholder value. If research reveals that co-creation ameliorates shareholder value, the

interest in the concept of co-creation itself (Lukas et al., 2003) will be more intense.

Therefore, given the pivotal importance of creating shareholder value and the probable

positive impact of co-creation, one might expect that co-creation will affect business models

and future strategic policies.

This thesis assesses the main findings of academic contributions about the concept of co-

creation and, most importantly, illustrates the economic impact of co-creation. Subsequently,

an assessment of the specific organizational financial indicators shows the positive

contribution of co-creation to firm performance. As such this thesis contributes to a better

understanding of the concept of co-creation from a financial perspective. As a result, the

central research question throughout this thesis is:

What is the added value of co-creation from a financial perspective?

The remainder of this paper is organized as follows. Chapter 2 will highlight the dynamics in

current business practices, review the concept of co-creation, assess the characteristics of co-

creation and place the concept in perspective. Chapter 3 elaborates on the research design and

outlines the variables and models used. Subsequently, chapter 4 presents the main findings.

The implications of this research are discussed from a managerial and theoretical perspective

in Chapter 5.

The Value of Co-Creation

J.L. van de Mortel 5

2. Literature Review

In light of the worst economic crisis in almost 80 years, many are predicting the end of

capitalism as we know it (Posner, 2010, Vargo and Lusch, 2004). According to their theory,

an era of a new, kinder and gentler way of doing business is dawning (Rifkin, 2010). Yet

could a warm and fuzzy society really be on the horizon? Is this wishful thinking or is a grand

new beginning going to happen?

This literature review will focus on the dynamics in current business practices and the shift

occurring in the respective business models. To create a good understanding of co-creation,

firstly the broader picture will be thrown light on. The concept of “new economy” stresses the

importance of knowledge and in a broader view the shift from tangible asset-driven firms to

intangible assets-driven organizations, highlighting the importance of co-creation. Thereupon,

the characteristics, consequences and possibilities of co-creation will be revealed in detail.

2.1 The Changing Business Environment

To unravel the changing nature of doing business, we must see into, through and beyond the

extant literature on co-creation. Only when the concept of co-creation is elucidated from a

strategic perspective its potential and prospective impact can be fully understood. Many

researchers have considered co-creation from a strategic perspective (Kamp, 2009; Johnson et

al. 2008; Kirah, 2009) or the broader shift occurring in the business environment (Prahalad

and Ramaswamy, 2000; Conner, 1991). However, the two trends discussed below, namely the

shift in resources and the increased importance of customer awareness, are to date not

explicitly mentioned as the crucial elements that gave rise to the concept of co-creation.

Subsequently, the trends are linked to a firm’s strategic mindset.

The early theories in economics, classified as the classical and neoclassical schools, supported

a rather goods-centered view (Smith, 1776; Marshall, 1890). The key objective of a company

was to add value with the help of manufacturing. Classical and neoclassical economists

considered only natural resources as resources. Those resources were static and could

contribute to a competitive advantage. Subsequently, competition was focusing on the

possession of those resources and wealth was created through the acquisition or possession of

natural resources or tangible assets (Vargo and Lusch, 2004). Those traditional schools argued

that the primary reason of economic activity was to produce things that could be sold at the

consumer at a profit. However, the product or output was often standardized in order to

maximize the profit and efficiency (Conner, 1991).

The Value of Co-Creation

J.L. van de Mortel 6

Zimmerman (1951) was one of the first that described the change in resources. A shift

occurred from the main, operand resources, “on which an operation or act is performed to

produce an effect” (Vargo and Lusch 2004, p. 2), i.e. natural resources or tangible assets, to

operant resources (Constantin and Lusch, 1994). The latter concerns resources that produce

an effect, i.e. intangible assets, technology or human capital. The trend described by

Zimmerman persevered in the last century and manifested itself with the rise of energetic dot-

com firms in the nineties and took shape in a new economy.

The shift in resources resulted in business models consistent with the resource advantage

theory (Conner and Prahalad, 1996; Srivastava, Fahey and Christensen, 2001). Instead of

selling standardized products or focusing on delivering superior value to customers in relation

to its competitors, companies should identify, develop and strengthen core competences that

create a competitive advantage. Those core competences are intangible processes and operant

instead of operand (Hamel and Prahalad, 1989).

Simultaneously, in the twentieth century the company focus shifted from a product-centric

model to a consumer-centric model (Vargo and Lusch 2004). The importance of customer-

orientation (Drucker, 1993), the fact that the value was determined in the marketplace (Day,

1999) and consciousness of customer satisfaction, resulted in business models that endorsed

the importance of marketing and the awareness that marketing could contribute to output

maximization (McCarthy, 1960). The customer was no longer just the recipient of goods, but

became the centre of interest.

The reasons for the transformation from product-centric to consumer-centric are diverse.

Intensifying pressures to improve marketing productivity are because of inter alia the increase

in market diversity and intensification of competition. Moreover consumers demand more and

are better informed, mainly due to accelerating advances in technology. Additionally, research

has shown that organizational processes and results improve, if a business model is more

relationship-oriented then transaction-oriented; the organizational focus is externally instead

of internally (Mizik and Jacobson, 2007); management criteria is based on a portfolio of

customers instead on a portfolio of products; and customer knowledge is used as a valuable

asset and not as a control mechanism (Gupta and Zeithaml, 2006).

The transitions in resources and company focus have resulted in different roles for the

consumer. The change in resources shifted the role from consumers from operand to operant

resource and as such made them partners in creating a competitive advantage. The change to

customer-orientation shifted the role of the consumer from simply being seen as buyer to a

The Value of Co-Creation

J.L. van de Mortel 7

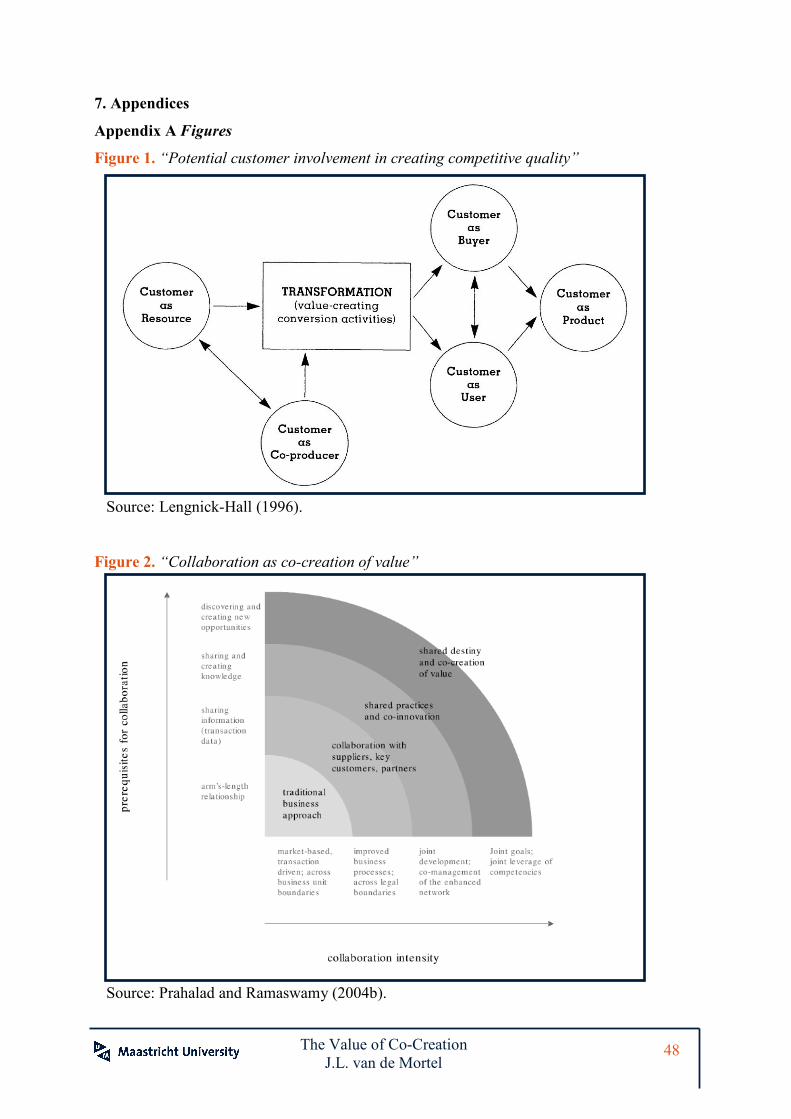

more intense role: the customer as an active user. The different roles for consumers, two

input-focused three output-focused consumer roles, are illustrated by Lengnick-Hall (1996)

and can be seen in figure 1.

*** Insert Appendix A, figure 1 here ***

Moreover, the shift in resources and the increase of customer-orientation had a huge impact

on the strategic mindset of a firm (Prahalad and Ramaswamy, 2000). In a deterministic

worldview, those changes in the environment of a company would result in “structuralist

strategies”, i.e. strategies that assume that the environment is given (Kim and Mauborgne,

2009). This “structure-conduct-performance paradigm” has resulted for instance in the

theories of Porter, like his five forces analysis (1979), generic strategies (1980) and the value

chain (1985) either focusing on the environment, the product or the production process.

Strategic frameworks that recognize the importance of the consumer, and that differ

substantially from conventional strategic positioning are, for instance, the Balanced

Scorecard, developed by Kaplan and Norton (1996), that provided metrics to better measure

strategic impact on organizational learning and growth, internal business processes and

customer satisfaction; and the Delta Model of Hax and Wilde (1999). Hax and Wilde argue

that the generic strategies by Porter do not provide the necessary guidance and support for

decision making in a world of change, complexity, and uncertainty. In stead of best-product

solutions, like cost leadership or a differentiation strategy, the Delta model is based on

customer economics and customer bonding. “Customer bonding, obtained trough close

proximity to the client, allows a company to anticipate needs and work jointly to develop new

products” (Hax and Wilde, 1999, p. 13).

In contrast to Porter (1979; 1980 & 1985), who argued the importance to adapt a company’s

strategy to the environmental and industry conditions, Kim and Mauborgne (2009) illustrate

that a company’s performance is not necessarily determined by an industry’s competitive

environment. Kim and Mauborgne (2009) argue that the structuralist strategies are suitable to

gain a competitive advantage if the structural conditions for a company are attractive or the

company has the right resources and capabilities. Otherwise, if a company does not posses the

right set of resources or when structural conditions are unattractive, then they should opt for a

“reconstructionist strategy”, i.e. strategies that shape the environment. However, “when

structural conditions and resources and capabilities do not distinctively indicate one approach

or the other, the right choice will turn on the organization’s strategic mind-set” (Kim and

Mauborgne, 2009, p. 75).

The Value of Co-Creation

J.L. van de Mortel 8

Co-creation fits in the Delta Model and seeks to build on the reconstructionist strategy by

examining company-customer interactions in detail and redesigning experience environments

at the individual level, in effect getting customers and their communities to do more of the

work that the firm used to do, while allowing them to create a better experience. In this sense,

co-creation is not about adapting to or anticipating on the environment, but about “changing

the very nature of engagement and relationship between the institution of management and its

employees, and between them and co-creators of value: customers” (Ramaswamy, 2009b, p.

33). As such it can be seen that several conversations at the strategic level converge in de

direction of co-creation and argue the validity of a new business model (Johnson et al., 2008).

2.2 The Concept of Co-creation

Co-creation is not entirely new and a number of companies have been using the rudiments of

co-creation for many years (Pedrosa, 2009). Currently co-creation is happening in various

settings (Sanders and Simons, 2009; Prahalad and Ramaswamy, 2004b). Except for

companies that use firm production, Meuter and Bitner (1998) argue that co-creation can take

place at companies that use joint production or customer production. The latter is a situation

where self-service is key and customers themselves perform tasks that were once done for

them by others, examples are Automatic Teller Machines (ATMs), Internet transactions, self-

scanning supermarket check-outs and information services available via cell phones (Liu,

2009). Joint production is a more intense form of co-creation, in which both the customer and

the firm's contact employees interact and participate in the process.

The difference in locus of production can be seen in the examples of co-creation as well.

Firstly, co-creation is happening among consumer themselves or social groups that work

together, for instances, within communities, like the Harley Davidson club, or within online

communities, like SecondLife. Secondly, a more visual phenomenon is co-creation between

companies and their business partners (Roser et al., 2009). A good example of collaboration

that strengthens the competitive advantage of both companies is Senseo, a coffee-maker

produced by Philips, but which for a long time span used solely the coffee pads of Douwe

Egberts. Besides the locus of production, the intensity of co-creation practices can vary as

well, as can be seen in figure 2, indicating the different forms of engagement and the different

set of outcomes.

*** Insert Appendix A, figure 2 here ***

The Value of Co-Creation

J.L. van de Mortel 9

Given the different settings in which co-creation takes place and the different interpretations

of the concept of co-creation, this thesis will adhere to the definition of Roser (2009) to deal

with an unambiguous and clear understanding of co-creation. The definition elucidates the

two main features of all co-creation approaches, namely the expansion of product or

organizational boundaries due the interaction with the consumer, and the joint creation of

value, and provides a clear-cut and well-delineated understanding of the matter.

“Co-creation is an active, creative and social process, based on collaboration between

producers and users, that is initiated by the firm to generate value for customers.”

As such co-creation is pro-active process that brings companies and consumers together to

share knowledge, and improves relations, product or service quality. As an adaptive

framework that facilitates innovation and as a development tool that facilitate change by

intertwining organizational knowledge with relationship building, co-creation has the

potential to become a concept that will change traditional ways of doing business and a

crucial element of companies’ competitive advantage.

Co-creation can be seen as a coming together of aspects of marketing and management

theory, psychology and techniques derived from group decision making, innovation and

knowledge processes. First of all, co-creation can bee seen as a tool that serves as a decision-

making support system in which the consumer has a say, is able to make decisions and co-

creation finally results in a process that defines how perceptions are formed. Furthermore, the

eliminated boundary between firm and consumer results in the possibility for consumers to

express desires, identities and wishes and as such this psychological play “acknowledges

consumer’s subjectivity, which is inherently idiosyncratic, contextual and experience-based”

(Roser et al, 2009, p. 10). Accordingly, central to the concept of co-creation is the belief that

each individual is creative and seeks outlets for creativity in their lives (Sanders and Simons,

2009). Thirdly, co-creation is a concept that represents a trend in marketing innovations to

capture knowledge residing in consumers and improves customer relationships (Maklan et al.,

2008). Finally, the consumer contributes to the success of a firm by enabling the company to

adapt earlier to marketing trends, reducing the cost in various elements of the value chain and

as such the consumer becomes a co-creator to generate value.

The Value of Co-Creation

J.L. van de Mortel 10

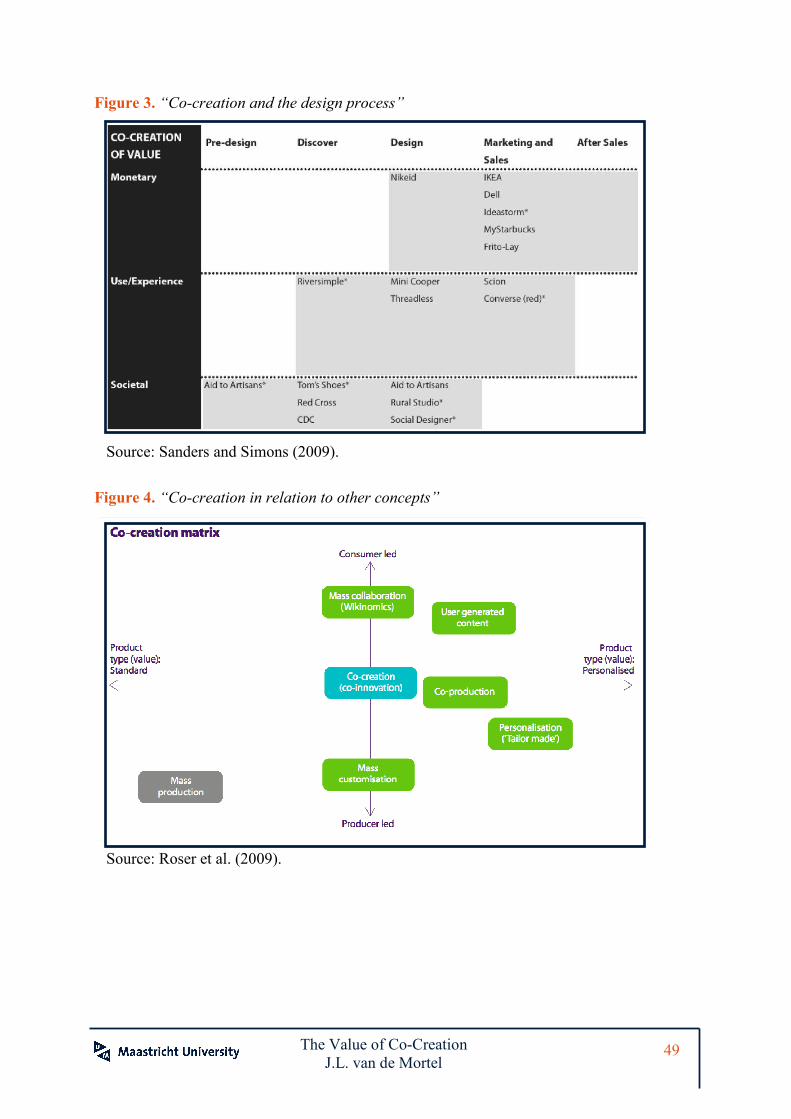

2.2.1 Three Types of Co-creation

As argued before, there are many different definitions and interpretations of co-creation.

However, within the definition of Roser et al. (2009) a distinction can be made between three

different types of co-creation, namely the monetary, the use/experience and societal value of

co-creation (Sanders and Simons, 2009). Each type has idiosyncratic objectives, particular

mindsets and occurs at specific levels in the value chain (see figure 3).

*** Insert Appendix A, figure 3 here ***

The type of co-creation that usually receives the most attention in business settings is the

co-creation of monetary value (Sanders and Simons, 2009). The monetary type of co-creation

occurs generally at the final stages of the value chain, e.g. the marketing, distribution and

sales stage. From a commercial and economic mindset the objective is to maximize

shareholder wealth, increase revenues and production number. From this perspective

individuals are still seen as customers or consumers. Since the time frame is short term, the

deliverables are limited to “products that sell” and business improvements. Furthermore,

physic contact between the company and customer is not necessarily required since the

conversation can take place by tools like web-based surveys.

The use/experience value of co-creation is driven by companies’ desires to transform

consumers into users so that the products and services they design, produce and sell will

better meet people’s wants and needs as such the value offered extends monetary gain. The

shift in meaning of value is rapidly changing from product-centric to personalized consumer

experiences (Prahalad and Ramaswamy, 2004a). Therefore, an experience-driven and

customer-orientated mindset is required at the company level to indeed create positive

experiences and customization. In this case the individuals are seen as end-users of the value

proposition (Johnson, 2008) and as empowered consumers.

Given its potential impact, the value of co-creation can be seen on a societal basis. Inspired by

the idea of systems thinking (Senge, 2010) the impact of co-creation can be considered by “its

next larger context” (Sanders and Simons, 2009, p. 30). From a human-centered and

ecological way of thinking, the objective is to create sustainable ways of living and improve

quality of life. As such the social value of co-creation is the most intense and extreme type of

co-creation. In this setting the individuals are considered as participants and over many

generations or in a long-term perspective the deliverables are transformation, learning,

behavioral change, happiness and survival (Sanders and Simons, 2009). Prahalad (2004b)

The Value of Co-Creation

J.L. van de Mortel 11

argues that when the consumers get involved in company processes this will have a positive

effect on democracy, since more people do have a say, and equality, since more knowledge is

becoming publicly available. As such co-creation empowers consumers and enriches, in

utopia, society and humankind.

All three types of value in co-creation are important to create customer satisfaction and to

enable consumers to participate in a creative process. To further increase customer

satisfaction the three types of co-creation can be bundled and as such there is a focus on the

whole of an experience and not on just an episode or single touch point. Besides, the different

types are often inextricably linked, i.e. social value can provide use/experience value and

financial reward as well.

2.2.2 Co-creation in Perspective

Hitherto, the concept of co-creation is explained. However, in recent decennia other concepts

became existent that are closely linked to co-creation. All concepts contain elements of

purpose-driven innovation, consumer involvement or organizational cross-boundary

collaboration. For a clear understanding of co-creation, co-creation and its related concepts

can be discussed on two dimensions, the role of the company and the type of value created, as

can be seen in figure 4. The latter makes a distinction between standardized value, customized

value and personalized value; and between consumer-led and producer-led concepts.

*** Insert Appendix A, figure 4 here ***

To improve the understanding of co-creation, seven related models are distinguished. The first

is mass collaboration (Ghazawneh, 2008). Based on joint actions, mass collaboration is a

collaboration model which involves large numbers of participants and or contributors. The

rationale behind mass collaboration is to involve the customers to do some of the work that

firms historically did themselves. A shining example is Wikipedia.

Mass customization (Kotha, 1995) illustrates the economies of scope that result in a broader

product range and reduced cost for the firm, due to the fact that customers can alter the

products themselves (Dell Computers). Pine (1997) makes a distinction between four types of

mass customization, i.e. adaptive, cosmetic, transparent and collaborative customization, each

with a different customer approach and product characteristics.

A third model is User-Generated-Content or User-Created Content, of which YouTube and

SecondLife are probably the most alluring examples. This model is financially attractive due

to the possibility to monetize content, the advertisement possibilities and the lower costs and

The Value of Co-Creation

J.L. van de Mortel 12

entry barriers (Wunsch and Vickery, 2007) and is made possible due to technological

advancements in global broadband density, simpler tools for creating and editing content and

the increased quality of technological devices for audio and video purposes.

User-involvement deals with participative decision-making, in either a consultative,

representative or consensus setting (Mumford, 1979), and should result in improved quality of

the system and increased acceptance of the system (Ives and Olsen, 1985). The quality of the

system is improved due to a more accurate assessment of user requirements, the expertise

provided about the organization, the avoidance of unacceptable or unimportant features and

the improvements in user understanding of the system (Robey and Farrow, 1982). On the

other hand the acceptance of the system may be increased by the development of realistic

expectations, commitment of users to the system, decreasing user resistance to change and the

possibility to bargain and solve conflict situation in the design phase (Lucas, 1974).

Probably the most appealing concept related to co-creation is co-production. Bendapudi and

Leone (2003) call the recognition to encourage customers to be co-producers “the next

frontier in competitive effectiveness” and define co-production as a process where a consumer

is an active participant in the production or delivery of a service, whereby the participant has

the possibility to customize the product or service.

The last two models are based on innovation, namely collaborative innovation and open

innovation. The former is more focused on business-to-business relations (Roger et al., 2009)

and open innovation is based on internal R&D, but complemented with external R&D. Where

in the past, internal R&D was a valuable strategic asset and a formidable barrier to entry by

competitors in many markets, nowadays external R&D can create significant value

(Chesbrough, 2003).

Above mentioned concepts contribute to the competitive advantage of a firm and will increase

customer satisfaction. Where some overlap exists between the concepts and co-creation; it

also enables one to distinct co-creation from those concepts. The uniqueness of co-creation is

based on the consumer interaction, the consumer orientation and the added value created for

both parties. As such co-creation does not solely focus on the role of R&D, the adaption of

customer needs or simply facilitating a method for customer to express their needs, but is a

broadly oriented concept.

The Value of Co-Creation

J.L. van de Mortel 13

2.3 Co-creation from the Company Perspective

Previous section elaborated on the concept of co-creation. As explained the concept of co-

creation is based on the interaction between organizational structures and consumers. While

both are of paramount importance, the review will continue with an assessment of the

importance of co-creation for the company, strategic methods for implementation and the

possible implications. However, first of all the ingredients of a consumer-oriented firm will be

discussed.

2.3.1 A Pathway towards Successful Integration of Co-creation

If an organization will shift from product-centric to consumer-oriented practices the execution

of concepts, like co-production, mass-customization, becomes relevant. To extent and enrich

the consumer-oriented organizations with the concept of co-creation, it should be

implemented in the right format and have the right set of preconditions to create a customer-

centric model firm-wide. Such a customer-centric model entails more then solely improving

customer satisfaction. A customer-centric model means “collaborating with and learning from

customers and being adaptive to their individual and dynamic needs. A customer-centered

dominant logic implies that value is defined by and co-created with the consumer rather than

embedded in output” (Vargo and Lusch, 2004, p. 6).

While the concept of consumer-centricity is discussed for more then fifty years, many firms

are still struggling to align themselves to the customer-centric paradigm (Shah et al., 2006).

Often, the elements as organizational culture, organizational structure or financial-driven

structures deter a firm to align themselves. However, Shah et al. (2006) argue that if a

company focuses on leadership commitment, organizational realignment and financial

structures that better cover the non-monetary benefits, a firm will be able to adopt a

consumer-oriented business model.

2.3.1.1 The Organizational Structure as Basis for Co-creation Implementation

An ideal customer-centric organizational structure should have all functional activities

integrated and aligned in order to deliver superior customer value. In contrast to a structure

were products are dominant and with sales managers for specific products or product

categories, an integrated and aligned structure will be better able to identify customer needs

and able to provide a single point of contact for consumers (Day, 2003). Shah et al. (2006)

argue that such a single point of contact can be strengthened by segment marketers or

customer-based front-end units, with product providing back-end units to assemble solutions.

The Value of Co-Creation

J.L. van de Mortel 14

Another essential element for organizational realignment is based on the marketing function,

“whose role is critical in transforming the firm to customer centricity” (Shah et al., 2006, p.

120). The marketing department is of paramount importance to gather information, to develop

knowledge and skills and to connect the customer to the product. The best organizational

environment for the marketing department is based on a horizontal structure, which is less

hierarchical, based on natural work flows and enables rapid sharing of knowledge among all

team members. However, if a company for decennia is based on product-led growth, a hybrid

structure may be more feasible, combining horizontal and vertical structures (Day, 1999)

To overcome current challenges to transform organizational structures, like deeply rooted

functional differences in incentives, backgrounds, task priorities and time scales (Day, 1999),

Webster (1992) argues that customer-oriented values and beliefs should be the responsibility

of top management. A signal that acknowledges the importance of this consumer focus is the

designation of a Chief Customer Officer, which signals to stakeholders the intent to align the

organizational structure to the customer-centric paradigm on a boardroom level (Shah et al.,

2006).

2.3.1.2 Inclusion of Customer Knowledge and Relationship Management

The concept of co-creation has evolved over the past decennia. Market-driven or consumer-

oriented firms use for a while concepts to manage their knowledge about their consumers and

the knowledge that is residing in their consumers. Two concepts that preceded co-creation,

and are essential elements of co-creation, are Customer Knowledge and Customer

Relationship Management.

The objective of Customer Knowledge Management is to, in collaboration with customers,

create joint value and enhance organizational learning (Gibbert et al., 2002). However, often

Customer Knowledge Management is only based on employee’s knowledge about customers,

and has only the objective to reduce costs and improve efficiency at the company level. Both,

Customer Knowledge Management and co-creation enable a firm to gain information residing

in your customer based on interactive sessions. The main difference, however, is the final

outcome and implications of the process. While for Customer Knowledge Management the

outcome is not a criteria but a logical consequence, co-creation takes a broader view and

integrates the concept of Customer Knowledge Management with the final value that will be

generated.

The Value of Co-Creation

J.L. van de Mortel 15

In addition to Customer Knowledge Management, of equal importance in the process of co-

creation is Customer Relationship Management. Payne and Frow (2005, p. 168) define

Customer Relationship Management as “a strategic approach that is concerned with creating

improved shareholder value through the development of appropriate relationships with key

customers and customer segments” and “provides enhanced opportunities to use data and

information to both understand customers and co-create value with them”. Companies that

implement Customer Knowledge Management systems, will sense emerging market

opportunities before their competitors and more rapidly create economic value for the

corporation and its stakeholders, especially its consumers (Gibbert et al., 2002). Customer

Relationship Management will retain consumers, but the role of the consumer is often

passive, whereas in Customer Knowledge Management the role of the consumer is more

active and the consumer becomes a valuable partner in the value-creation process.

2.3.1.3 The Relevance of Intangible Assets and Financial Metrics

In recent years intangible assets have become more important, from a company and

shareholder point of view, in contrast to tangible assets (Abeysekera and Guthrie, 2004). The

role intangibles often play, is the creation of a sustainable competitive advantage (Villalonga,

2004) and as such contribute to future generation of cash flows (OECD, 2008). Nowadays

companies spend more economic resources on intangibles than on tangible assets and are,

consequently, the main cause of economic growth (Lev, 2001; Lev and Zambon, 2003).

Characterizing intangibles as assets that create future benefits can ran radically change the

way managers and investors see a business and make key decisions about it. However, many

have argued that the traditional accounting methods are inadequate in capturing intangible

assets in financial reporting (Edvisson, 1997; Lev & Zarowin, 1999; Garcia-Ayuso, 2003; Lev

& Zambon, 2003, Burgman & Roos, 2007). “The GAAP-based accounting systems that all

companies use today were designed for stable business environments in which the most

important assets were psychical” (Prahalad and Ramaswamy, 2000, p. 87). So far, GAAP

requires companies to report intangible assets acquired form other entities, but does not

consider in-house developed identifiable intangible assets (IASB, 2008). However, the

accounting for intangible assets is relevant since extensive research shows that intangible-

intensive organizations are systematically underpriced (Lev, 2004) and that “comprehendible

data on a company intangible investments give investors a more complete picture of the

company’s capital than the one GAAP provides” (Lev, 2004, p. 115)

The Value of Co-Creation

J.L. van de Mortel 16

Despite the potential of intangible assets, they are often considered to be risky from a

shareholder perspective, since their value is hard to estimate. Due to the fact that intangibles

are rarely traded, the information asymmetry between organizations and shareholders, and the

related lack of transparency, a misallocation of funds in intangible-intensive organizations is

often the result (OECD, 2008). Consequently companies with an overabundance of intangible

assets may find it hard to attract capital.

Internal financial metrics play a crucial role in motivating individual employees, but, most

important, are also relevant to measure the financial implications of decision-making by the

marketing department and to think of intangible assets as investments (Srivastava et al., 1998;

Srinivasan and Hanssens, 2009). The latter is important because the transformation to a

customer-centric organization is often costly.

The challenge lies in the quantification of marketing assets, like brand equity, customer

satisfaction and customer life time value, to determine the optimal level of investments in

those assets. Johnson and Schultz (2004) argue that a firm should measure the impact of at

least two or three relevant intangible assets, like co-creation, and report those results regularly

to the senior management. Additionally, the results should be used to allocate incentives, e.g.

a sales manager is rewarded for increasing the equity and a relationship manager is rewarded

for extending the customer lifetime value.

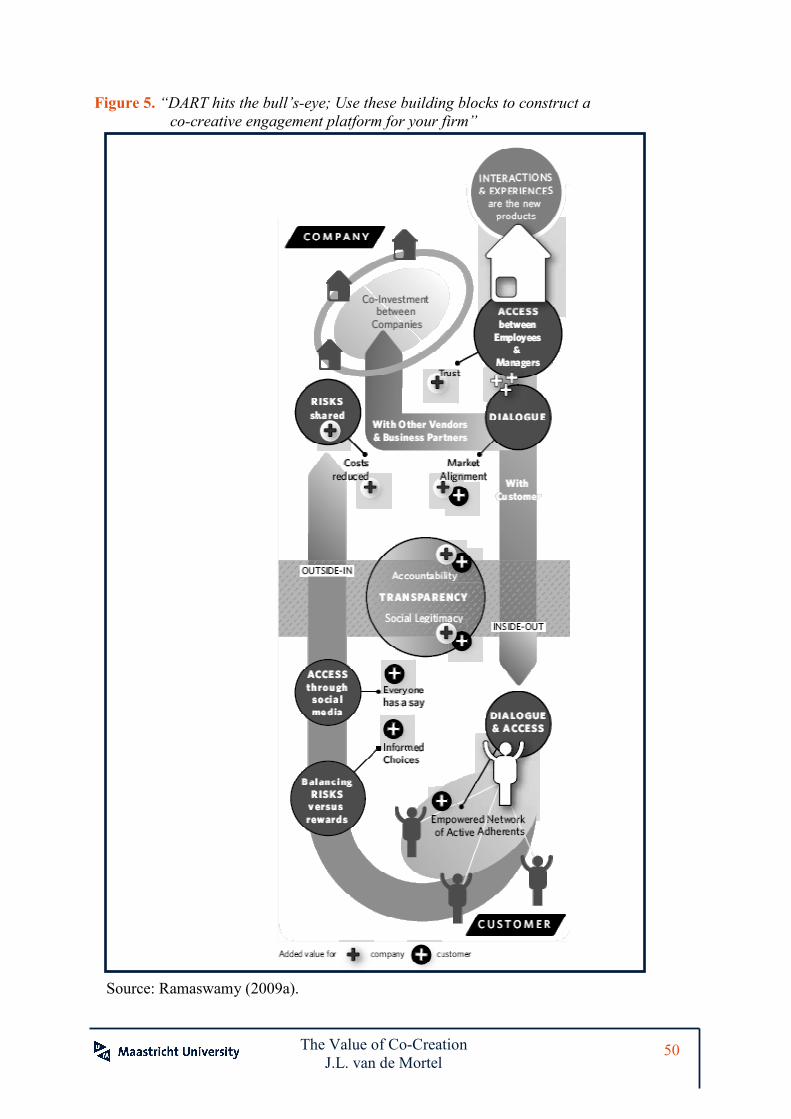

2.3.2 A Framework for Co-creation

So far, two models for a proper inclusion of co-creation practices are proposed, a model by

Prahalad (2004b), based on four building blocks and, secondly, a model by Payne et al.

(2008) that is build around the centrality of processes.

To set up a system for co-creation, Prahalad (2004b) introduces four building blocks as the

basis for interaction between the consumer and the organization. Dialog, Access, Risk-Benefit

and Transparency (DART) are needed to create a solid basis for the interaction (see figure 5).

Key ingredient is the dialogue between the organization and consumer. The dialogues, often

based on platforms, online communities and forums, but still often on a face-to-face basis,

create a social community and allow consumers to satisfy their social needs (Etgar, 2009).

The dialogue implies a deep level of engagement, interactivity and the ability and willingness

to act on both sides. Results are best when both participants, consumer and organization, are

equal and joint problem solvers.

To improve the quality of the dialogue consumers should have easy access and transparent

information. Traditionally, organizations benefitted from the information asymmetry between

The Value of Co-Creation

J.L. van de Mortel 17

the organization and the consumer, but nowadays have to reduce these barriers for effective

communication. Therefore an organization has to invest in infrastructure capabilities, enable

experiences and facilitate self-expression.

A final issue in the interaction between organization and consumer is the Risk-Benefit

building block. Both parties will be able to manage risk and evaluate the co-creation practices

on the trade-off between risk and rewards. Organization will no longer be competent to solely

manage those risks in a co-creation setting, and consequently a new level of trust between the

company and the consumer has to be established (Prahalad, 2004b).

*** Insert Appendix A, figure 5 & 6 here ***

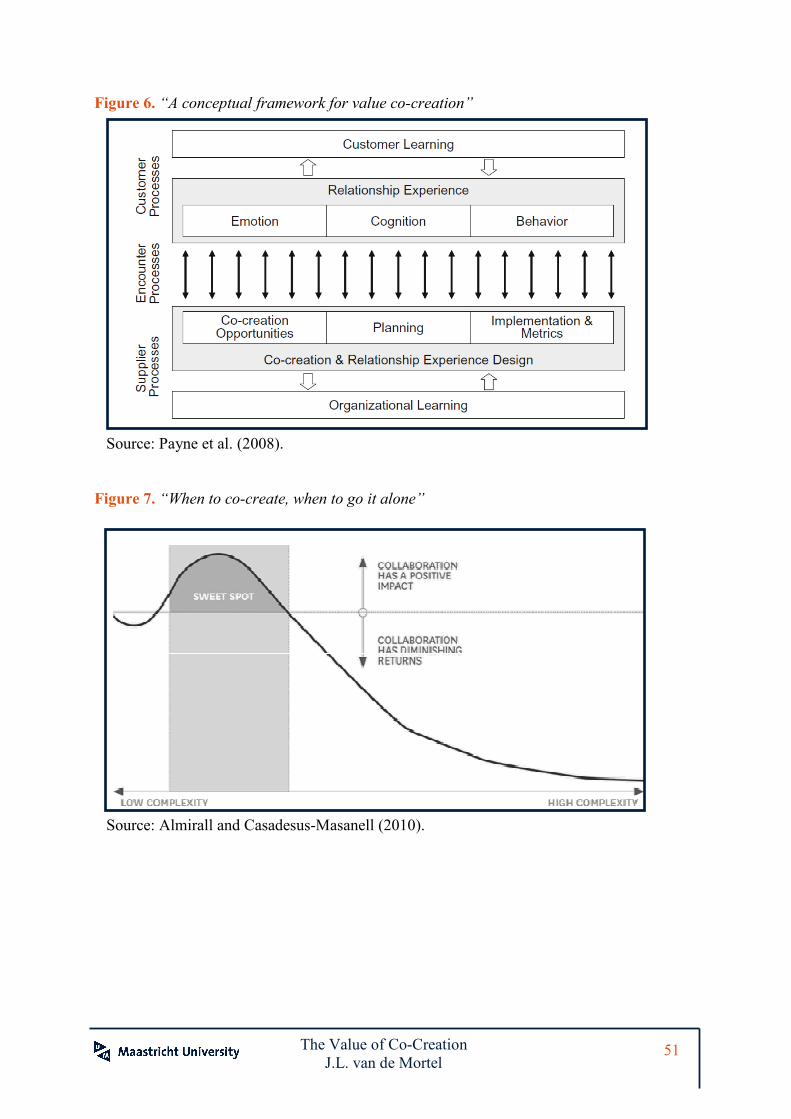

Next to the building blocks of Prahalad, Payne et al. (2008) developed a framework (see

figure 6) based on the centrality of processes. Those “processes include the procedures, tasks,

mechanisms, activities and interactions which support the co-creation of value” (Payne et al.,

2008, p. 85). Three key processes are, respectively, the Customer and Supplier (Organization)

Value Creating Processes and the Encounter processes.

The customer value-creating processes, built around the fact that meaning is created by

experiences, recognizes the consumer’s ability to create value based on the consumers amount

of information, knowledge and other operant resources. The link (figure 6) between customer

processes and customer learning indicates the positive learning processes a consumer goes

through based on experiences, improving future co-creation practices. The supplier value-

creating processes, assists co-creation through the design and delivery of relevant consumer

experiences and, additionally, facilitates organizational learning. To conclude, the encounter

process describes the interaction between the organization and the consumer, initiated by

either the organization or the consumer.

Additional to the theories of Payne (2008) and Prahalad (2004b), Almirral and Casadesus-

Masanell (2010) argue that the level of product complexity is of vital importance for the

success of co-creation as can be seen in figure 7. For very simple products, like a calculator or

a basic phone, a company can probably find the best innovation solutions on its own and does

not need to expose itself to potential conflicts over the product’s development and marketing.

However, if products become more complex they should outperform simple products.

Therefore a company stands to benefit greatly from ideas that may emerge from a partner

with a different set of priorities, and the benefits of those ideas outweigh any negatives from

differences over development and marketing. Finally, Almirral and Casadesus-Masanell

The Value of Co-Creation

J.L. van de Mortel 18

(2010) argue that the most complex products, based on “rocket-science”, and technologies

that push the design envelope, should be innovated within the company.

*** Insert Appendix A, figure 7 here ***

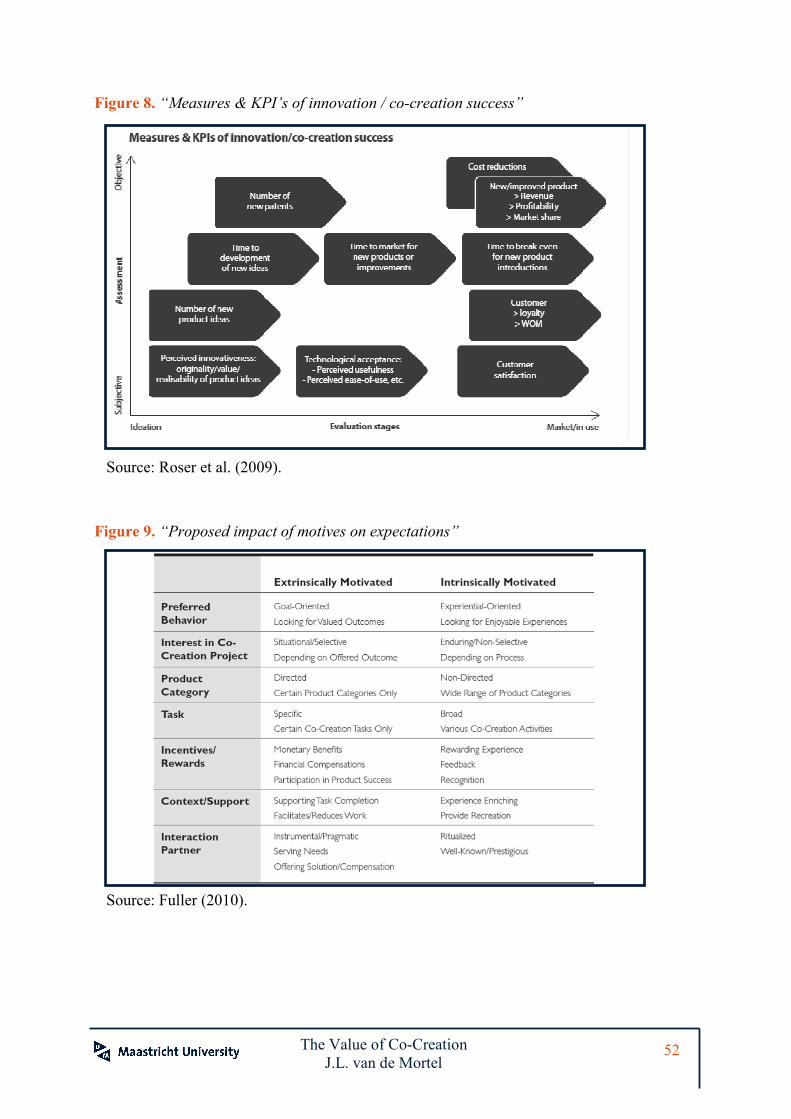

2.3.3 Key Performance Indicators of Co-creation

A major drive to engage in co-creation is economic. The best illustration hereof is given by

the illustration of the related concept of co-production. Through co-production, consumers

reduce production cost for manufacturers and retailers due to their participation in activities

along the value creation chain. These costs reductions will result in price reductions for

consumers, but imposes other costs upon the co-producing consumers. These reflect the fact

that such cost reduction is achieved by transferring the work previously done by the firm to

the co-producing consumer. To perform these activities, consumers need to use various

resources, e.g. time, and the impact of these costs must be considered by consumers before

they decide whether their contribution in the co-production is worthwhile (Bendapudi &

Leone, 2003).

Besides lower production costs, several other benefits of co-creation include the impact on

traditional innovation practices and processes, the affect on the quality and speed at which

decisions are made in relation to the development and filtering of ideas, the creativity enabled

at individual and group level and the impact on organizational learning. However, to express

the impact and success of co-creation figure 8 illustrates an overview of several performance

indicators (also used in Appendix B, Framework 1). The figure shows that for the different

stages different measurements can be used. In the phase of ideation, the level of perceived

innovativeness and, better observable, the number of new products ideas and new patents can

be measured to quantify the benefits of co-creation. Once the results of co-creation practices

reach the in-use stage, success can be measured through customer satisfaction and loyalty

(including word of mouth) as well as through financial indicators such as increased market

share. The latter can be assessed more objectively then for instance the perceived

innovativeness and will consequently be preferred by organizations.

*** Insert Appendix A, figure 8 here *** 2.3.4 Problems Associated with Co-creation

Besides the multifaceted benefits, the collaboration with players outside the organization has

also some potential problems. A first problem that may arise is the fact that company

The Value of Co-Creation

J.L. van de Mortel 19

processes will have an increased dependency on the consumer which in extreme case may

result in delayed outcomes or to the disruption of business processes. Secondly, there are

costs associated to the coordination of co-creation activities. The facilitation structures have

to be managed and organizational structures have to be rearranged in a way that will

maximize co-creation benefits. Additionally new management skills, like negotiation,

collaboration and cross-boundary knowledge transfer skills (Roser et al., 2009) are required.

A final issue is the access given to customers to confidential information and proprietary

skills. The latter could be a reason for companies to limit the information provided to

consumers. However, this can have serious consequences for the benefits of co-creation.

The disadvantages may serve as a threshold for companies to implement co-creation

initiatives and brings new challenges that have to be dealt with throughout the organization.

Nonetheless, none of the problems will have a devastating impact on the potential benefits of

co-creation. Consequently, organizations should use their technological, organizational and

marketing competences to better deal with a changing environment and increased complexity.

In the new economy the generation, combination, dissemination and application of knowledge

and ideas are key to achieve sustainable success. To access their collaborative capacities,

firms must critically evaluate their experiences with different modes of collaboration and

identify necessary improvements, for instance, with the help of in-depth case studies

(Prahalad, 2004b).

2.4 Co-creation from a customer perspective

Nowadays, organizations in highly competitive and innovative markets must build market

share quickly and deliver fast, high-quality and innovative solutions. As discussed in the

previous section, a key competence is to create organizational learning and knowledge

management (Drucker, 1993; Prusak 1997). A high quality customer knowledge management

can be seen as a process that generates knowledge about specific customers and seeks

opportunities for partnering with their customers as equal co-creators of organizational value

(Day, 1999).

Essential for successful co-creation is to understand why customers are willing to participate

in co-creation. Consumers are only willing to share their creative ideas, honestly state their

product preferences, and spend significant amounts of time modifying existing product

concepts if their expectations are met. Therefore, consumer expectations and motivations

should be considered to utilize the full potential of co-creation. The best way to understand

The Value of Co-Creation

J.L. van de Mortel 20

those expectations is with the help of segmentation (Gruner, 2000). The more a company can

break down its customers into different groups with different needs and expectations, the

better it can serve them (Day, 2003).

Fuller (2010) identifies ten different categories of motives that motivate consumers in co-

creation. Two motives are categorized as intrinsic motivation. The first, intrinsic playful task

argues that individuals contribute to new product development because they may consider it

as a playful and enjoyable activity (Deci & Ryan, 2002). The other, curiosity, argues that

consumers may engage in co-creation projects just because they are curious and have a desire

of knowledge because of intrinsic reasons.

Besides the intrinsic motives, Fuller identifies six internalized extrinsic motives. Firstly,

consumers may participate in co-creation to get in touch with like-minded people (Making

friends). Beyond the interest in the topic, the social aspect and the possibility to get in contact

with like-minded people can motivate them (Community support) (Hennig-Thurau et al.,

2004). Additionally, consumers may derive a sense of accomplishment due to their

contributions, which is known as self-efficacy. Moreover, motives as Information-Seeking and

Recognition Visibility may be a reason because consumers seeking innovation or product-

related information pertinent to their hobby, upcoming product purchase, or just through

novelty seeking behavior (Manning et al., 1995) and are motivated “to share their know-how

and participate in activities for ego gratification or the desire for peer recognition” (Franke

and Shah, 2003, p. 162). Finally, skill-development can be a possible driver, since consumers

want to improve their skills, gain new knowledge and want to find solutions to hitherto

unanswered questions.

The final two motives are entirely extrinsically motivated. Fuller (2010) argues that

consumers “start to modify or develop their own products because they are dissatisfied with

existing products and because they derive benefit from using their innovation” (Fuller, 2010,

p. 105), labeled as Personal Need-Dissatisfaction. Ultimately, immediate or delayed rewards

or compensation may be a motive for consumers to engage in co-creation.

If a customer knowledge management system can identify to which extent a consumer is

motivated, i.e. intrinsic or extrinsic, a company can better understand the behavior of a

customer. As can be seen in figure 9, intrinsically motivated consumers exhibit more often

experiential-oriented behaviors and, on the contrary, extrinsically motivated consumers tend

to prefer goal-oriented behaviors (Hoffman & Novak, 1996). The latter is characterized by

situational participation, selective engagement and utilitarian benefits (Hoffman & Novak,

The Value of Co-Creation

J.L. van de Mortel 21

2009), while experiential-oriented behavior is “characterized by enduring involvement,

ritualized orientation, interest in the medium and the content, non-directed engagement, fun,

affect, less intentional and selective orientation, time-filling and recreation activity, and

hedonic benefits” (Fuller, 2003, p. 103).

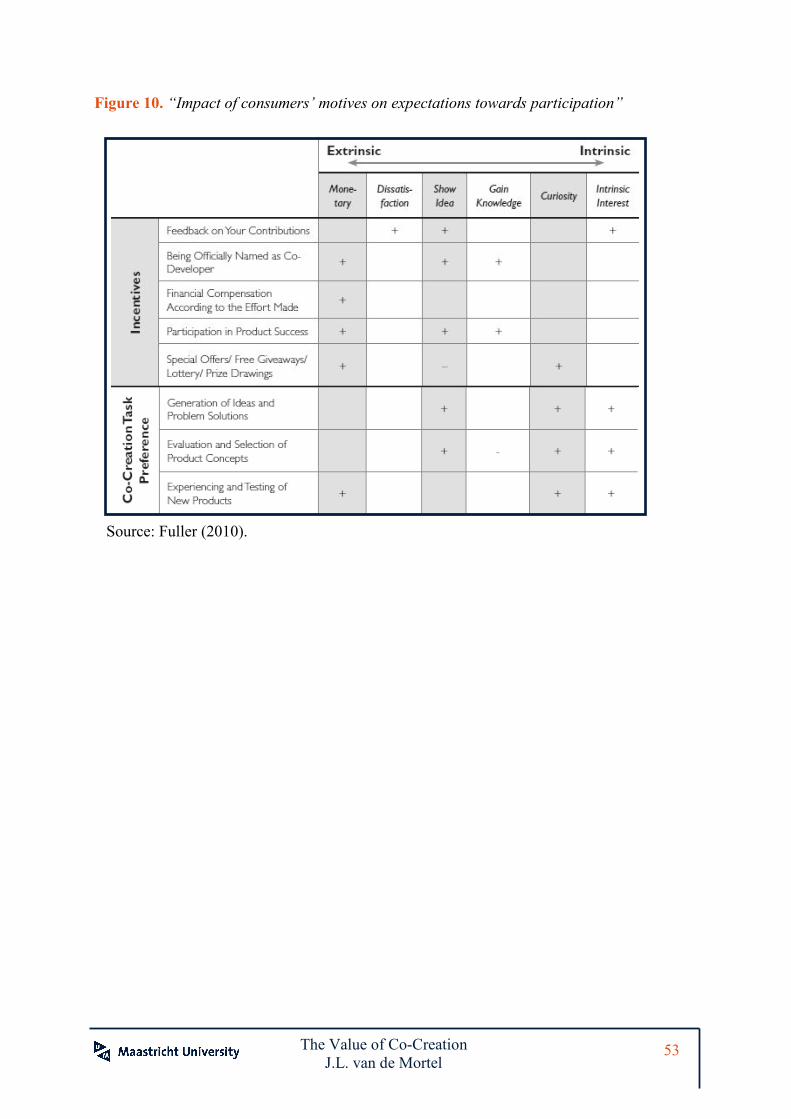

Moreover, extrinsically motivated consumers highly value incentives, like financial

compensation or being named as co-developer (figure 10). Intrinsically motivated consumers,

on the other hand, may be animated by incentives to make more and even better contributions.

However, those incentives may crowd out intrinsically motivated consumers as well.

Consumers may realize that they can gain economic benefits with their ideas and

consequently perceive the compensation by the organizations as unfair. Consequently, in

general incentives will attract consumers that otherwise would not participate, but do

sometimes results in “conceptualized minimax” (Kruglanski et al., 1977), i.e. consumers will

reduce their input and amount of effort to a minimum for the maximum possible amount of

reward. Therefore, the consequences of the incentives have to be evaluated, to analyze the

impact on co-creation success.

*** Insert Appendix A, figure 9 & 10 here ***

Based on cluster analysis on the different kind of motives, Fuller (2010) distinguishes four

kinds of customers that engage in co-creation, i.e. reward-oriented consumers, need-driven

consumers, curiosity-driven consumers and intrinsically-interested consumers. Fuller (2010,

p. 113) states, that “intrinsically-oriented and reward-oriented consumers show high and

enduring interest in virtual co-creation projects”, while curiosity-driven and need-driven

consumers participate because of a singular reason, i.e. curiosity or dissatisfaction with

existing product solutions. Subsequently, intrinsically-interested and reward-oriented

consumers are most appropriate for co-creation engagement.

Besides consumer specific incentive schemes, task design or partners, the allocation of

consumers’ idiosyncratic input should be considered, because consumers’ personal drivers are

related to specific stages in the value chain (Fuller, 2010; Kamp, 2009). If the major motive of

a consumer is monetary, the consumer should be involved in the testing of new products,

whereas consumers with the drivers curiosity and intrinsic interest are suitable for idea

generation (figure 10).

The Value of Co-Creation

J.L. van de Mortel 22

3. Research Design

The remainder of this thesis elaborates on the empirical investigation on performance

indicators of firms that employ co-creation. At first, a framework is developed to illustrate the

impact of co-creation on a business chain. Thereafter, the right set of variables and the

operationalization of the co-creation concept will be described. Chapter four will portray the

reliable and valid models, which with the help of statistical programs prove the economic

significance of co-creation.

3.1 Research Agenda

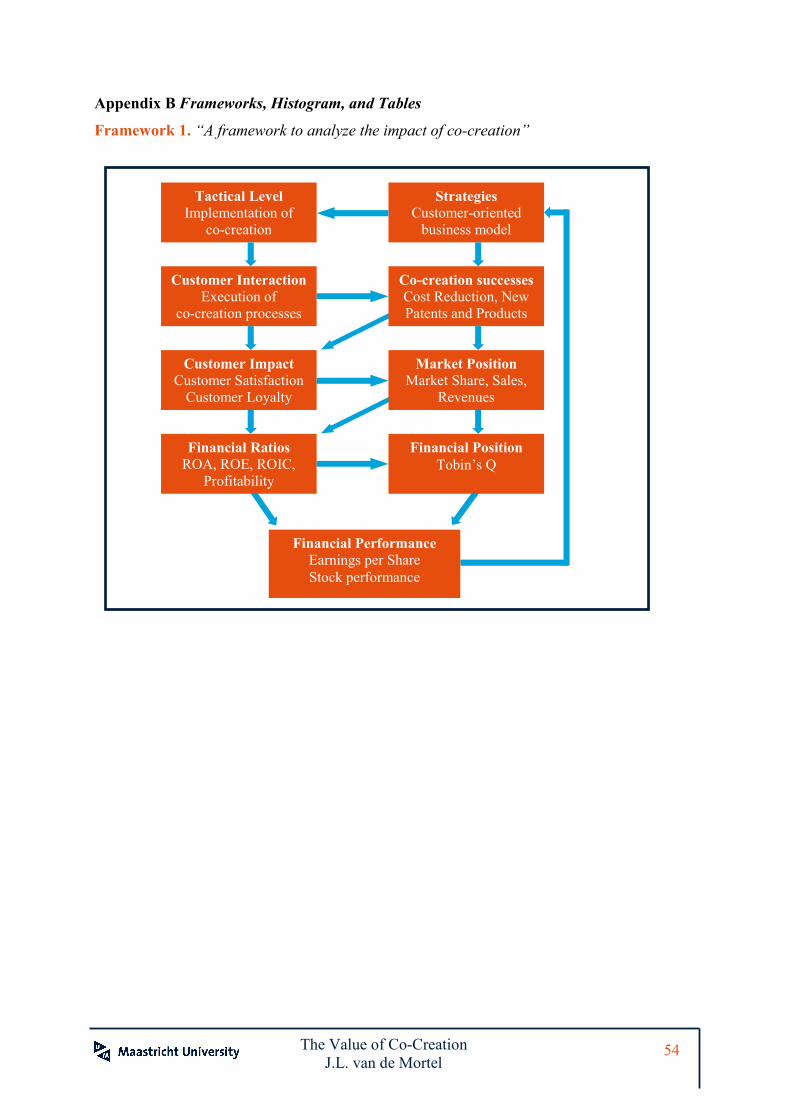

Based on the models developed by Rust et al. (2004) and Srivastava et al. (2001) a framework

is constructed to illustrate the impact of co-creation. The framework of Srivastava et al.

(2001) represents the relation between investments in market-based assets and value

extraction, which is an improvement on the model written by Srivastava et al. (1998) that

described the link between market-based assets, market performance and shareholder value.

The framework of Rust et al. (2004) links firm actions to marketing outcomes and the

combined impact on firm value.

Framework 1 illustrates the impact of co-creation. The data analysis will focus on the impact

of co-creation on parameters in the categories financial ratios and financial position.

Financial performance is deliberately not analyzed in this thesis. Assessing the relation

between stock performance and the implementation of market-based assets would require a

meticulous time-series analysis to extract meaningful statistics.

*** Insert Appendix B, Framework 1 here ***

Based on the framework three hypotheses are derived. Firstly, given the potential that co-

creation creates sales, results in innovations and improves business processes it is expected

that co-creation positively contributes to indicators that measure business performance as

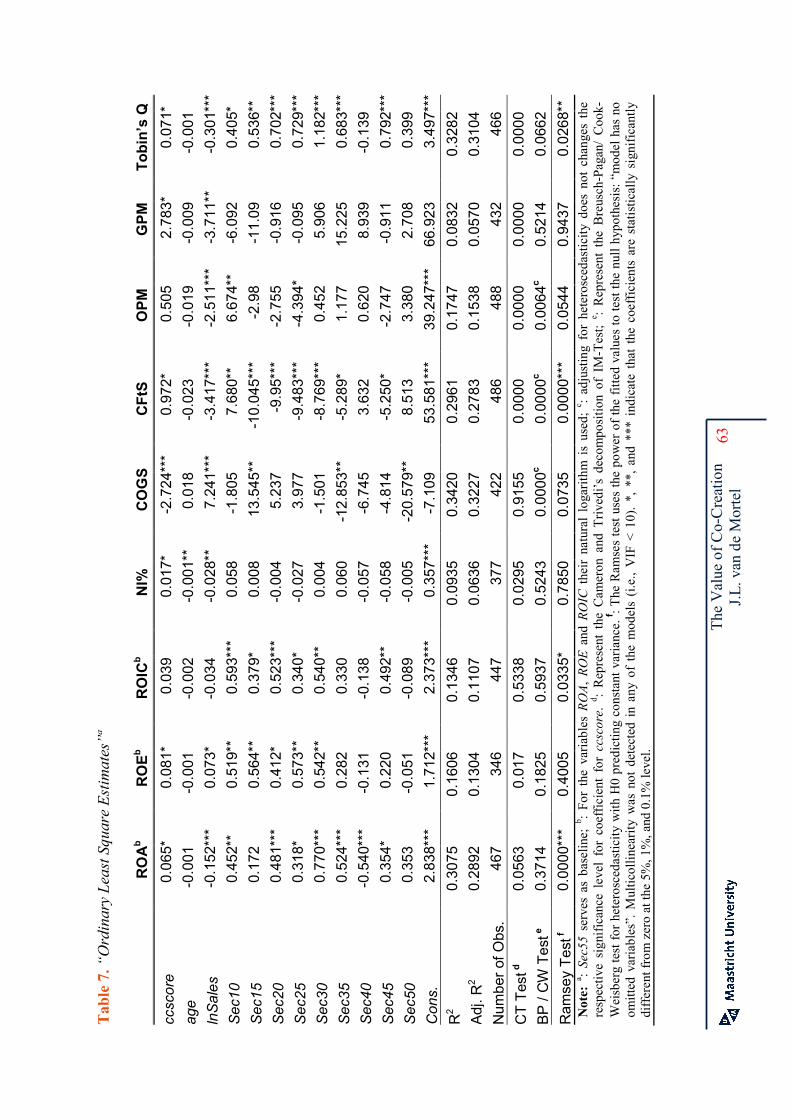

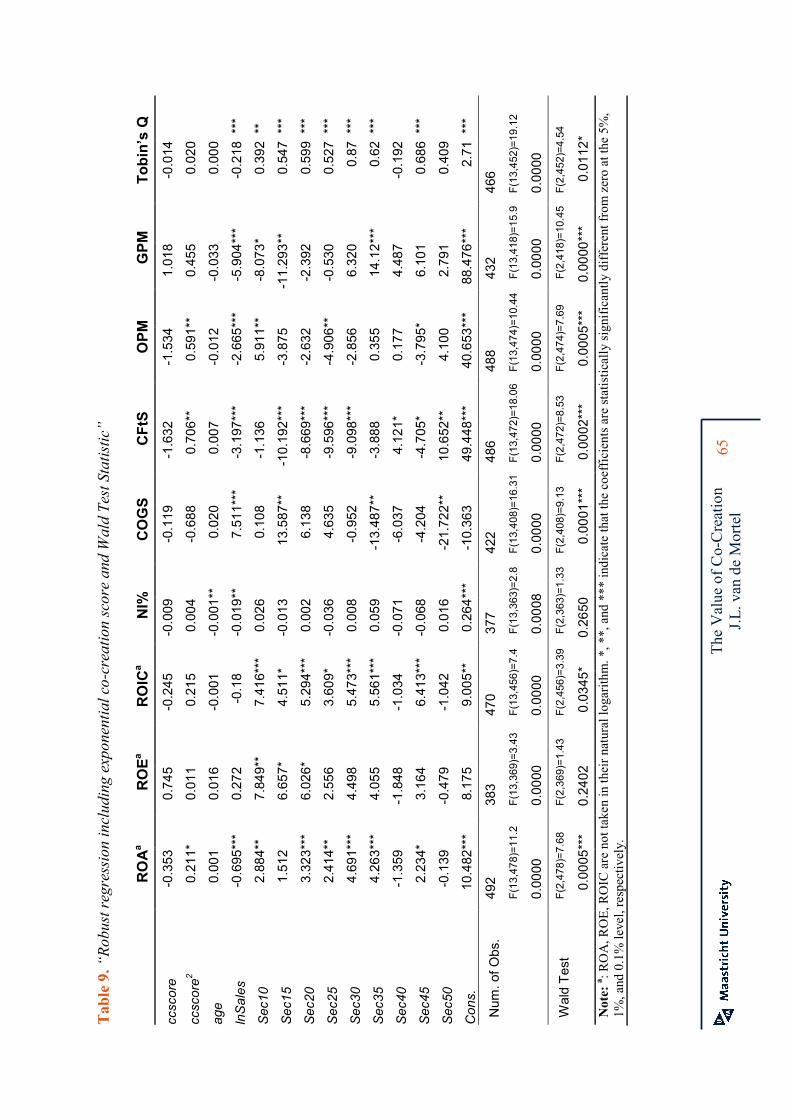

formulated in the first hypothesis (the variables are discussed extensively in section 3.3.2.)

Secondly, given the literature on co-creation (e.g. Sanders and Simons, 2009; Prahalad and

Ramaswamy, 2004b) co-creation can reduce direct labor and overhead costs resulting in a

lower Cost of Goods Sold to Sales. Finally, the fact that shareholders recognize the positive

impact of co-creation on firm performance results in a higher Tobin’s Q for firms that employ

co-creation and is stated in hypothesis 3.

The Value of Co-Creation

J.L. van de Mortel 23

H1 Co-creation is positively associated with the firms’ Return on Assets, Return on Equity,

Return on Invested Capital, Net Income Growth, Cash Flow to Sales, Operating Profit

Margin and Gross Profit Margin.

H2 Co-creation is negatively associated with firms’ Cost-of-Goods-Sold-to-Sales.

H3 Co-creation is positively associated with the firms’ Tobin’s Q.

3.2 Sample

The companies under investigation in this thesis are all the firms listed on the S&P 500 on

January 12, 2010. This is an appropriate sample because of three main reasons. First of all,

the data on these firms is present in the databases of CompuStat and Thomson ONE banker,

enabling a sound data analysis on financial performance indicators. Secondly, during the

literature study already several companies, listed on the S&P500 were identified that exploit

co-creation, indicating that within the sample, a certain number of companies use co-creation.

Finally, the S&P 500 provides a broadly defined sample, with a diversified set of companies,

each with a different focus on innovation and marketing, specific business practices and

various levels of customer-orientation.

3.3 Variables

Although that some studies analyzed the impact of co-creation on consumer variables, like

number of customers, the retention levels (Gupta et al., 2004), detailed customer satisfaction

rates (Ittner and Larcker, 1998), number of complaints by customers and the brand awareness

(Barth et al., 1998; Fuller, 2010), this research focuses on idiosyncratic financial performance

measures. Detailed descriptions of the variables used are given.

3.3.1. Independent variables

3.3.1.1 Operationalization of co-creation

A structured content analysis is applied to translate the results of a keyword search tool for

each firm, into scores for co-creation (Ferrier, 2001; Allen et al., 2009). A keyword search

tool from Google.com was used to ransack corporate information on the use of co-creation.

The corporate website from the company was the unit of analysis and included at least the

corporate information for investors and the news articles published by the company itself. If

The Value of Co-Creation

J.L. van de Mortel 24

an additional server or domain was used, next to the primary company website, the additional

server was ransacked as well. The use of corporate website for the operationalization of co-

creation was a convenient method, since many companies use their website as their primary

communication channel for corporate information.

An iterative process was used to investigate the right sets of keywords to maximize the

available, relevant content to analyze. Keyword sets that were to narrow, like “Customer-

Involvement” or “Customer Engagement”, gave too few results. Therefore, a specific

keyword set was solely focusing on co-creation and two others were broadly defined,

increasing the number of results given by the keyword search tool. Finally three searches

were performed with different sets of keywords. The first keyword set was constructed as

follows: “co creation” OR “cocreation” OR “co create” OR “cocreate”; the second as:

“consumer” OR “consumers”; and the third set as: “customer” OR “customers”.

The keyword search tool returned in total 9,612 results (4,752 disregarding Yahoo, Google

and Amazon.com) for the first set of keywords. Of the 500 companies in the sample, 63 firms

had a positive integer on the first set of keywords with an average of 152 (µ=79, if the results

of Yahoo, Google and Amazon.com are not taken into consideration). Since the websites of

Amazon.com, Yahoo and Google include many references to other websites or irrelevant

products, the results are not representative if those results are taken into consideration. The

second and third set of keywords gave respectively 1,861,534 and 8,570,988 results

(66,744,534 and 135,042,988 results if the results of Amazon.com, Google and Yahoo are

taken into consideration). So the average amount of results per firm was 3,746 and 17,245

(without Google, Yahoo and Amazon.com), with a respective standard deviation of 6,117 and

28,361 illustrating the large deviations in the amount of results in the sample.

The results were screened for co-creation and quotes were recorded in the case of relevant

signs of co-creation. If more then 2,000 result were given by the keyword search tool for the

second and third set of keywords, an additional keyword was added (like “involvement”,

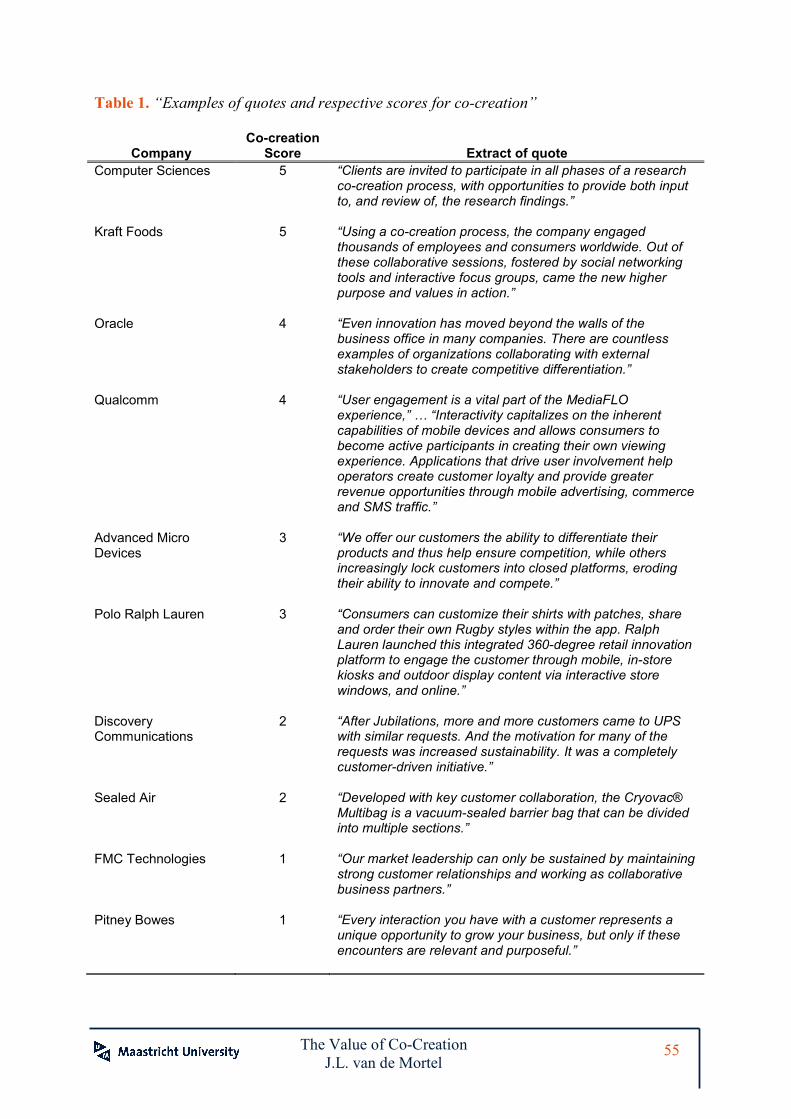

“engagement” or “input”) to speed up the search for relevant quotes. A snapshot of the quotes

can be seen in Appendix B, Table 1.

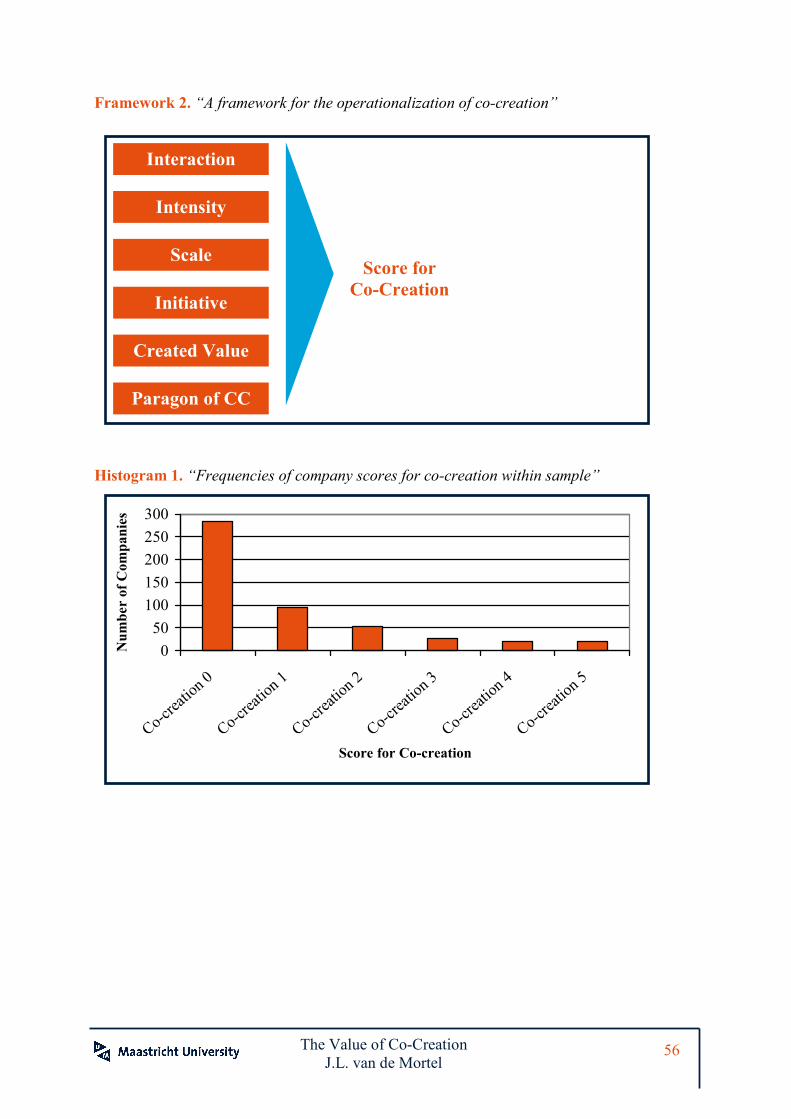

To quantify the eminence of co-creation the quotes were analyzed based on a framework

specifically developed for this thesis, since no proper scaling method was available in existing

literature. However, inspiration was drawn from the quantification of brand value (Barth et

al., 1998) and an intensive literature review on co-creation. The framework (see Framework

2) illustrates the elements that together composed the score for co-creation for each specific

The Value of Co-Creation

J.L. van de Mortel 25

firm in the sample. The different elements are Interaction, Intensity, Scale, Initiative, Created

Value, and Paragon of Co-creation.

The element Interaction indicates the necessity of the involvement of both parties, consumers

and companies, and one extra point was given if the Initiative was taken by the company.

Intensity represents the strength of engagement; while Scale corresponds to the extent co-

creation is applied within the firm. Created Value measures whether the outcome of the co-

creation process resulted in joint value creation. Paragon of Co-creation was used to allocate

an additional point to those firms who mentioned, for instance, co-creation in their mission

statement or to those that are a shining example of co-creation, like for instance Nike with

Nike ID.

*** Insert Appendix B, Table 1 and Framework 2 here ***

Each of the six elements is rewarded with a maximum of one point, making it possible to

score in total a maximum of six, albeit the maximum score given was five. Although the fact

that the quotes are evaluated on the six elements (see Framework 2), only a singular overall

score per firm is given. Since only a maximum of two quotes was recorded, while

components of co-creation were present in other quotes, and sometimes the overall

impression of the quotes was taken into consideration, it was not practical to score the

specific components. Finally, the scoring model resulted in a scale standing midway between

a Likert scale and an ordinal scale.

To check the reliability and validity of the scores for co-creation two peer-students were

asked to score each the quotes for a sample of hundred firms. However, the scores were

almost identical and no significant deviations in scoring, between the scores of the author and

the scores of the peer students, were present. Therefore, the scores for co-creation given by

the author were used for further analysis.

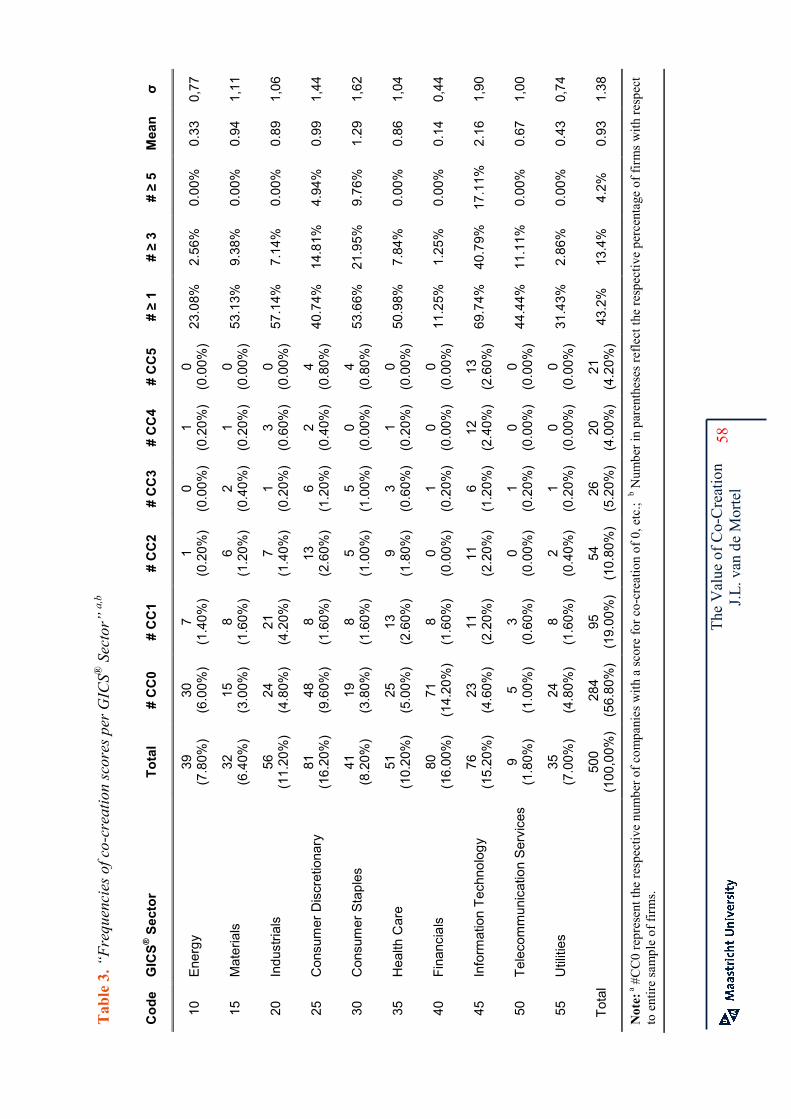

The dispersion of the 500 companies among the scores for co-creation can be seen in

Histogram 1. 284 companies had a score for co-creation of zero, after the evaluation of all the

results of the keyword search tool, indicating that those companies did not use the concept of

co-creation or did not explicitly communicate the use of co-creation practices via their

corporate website. The remaining 216 companies were disproportionately allocated among

the categories, with 95 companies in category 1, 54 in category 2, 26 in category 3, 20 in

category 4 and 21 in category 5.

*** Insert Appendix B, Histogram 1 here ***

The Value of Co-Creation

J.L. van de Mortel 26

The first keyword set resulted in a selective amount of results (4,572 results), but of the 63

companies that had at least one result for the first search performance, 53 had a positive score

for co-creation (averaging 3.50). Of the twenty companies in the highest category for co-

creation (ccscore = 5), 19 companies had at least one result for the first keyword set,

indicating a strong relation between the results for the first keyword set and the score for co-

creation (Correlation = 0.3316).

The relation between the score for co-creation and the second and third keyword set was less

obvious, the more so since many companies indicated their awareness of customer

satisfaction, resulting in more hits. However, a customer focus is not necessarily linked to co-

creation. The correlation between the co-creation score and the results for the second keyword

set is only 0.1214 and 0.1957 for the third keyword set.

This was clearly visible at the sectors Customer Discretionary (GICS® Sector code 25) and

Telecommunication Services (GICS® Sector 50). Companies in the Customer Discretionary

and Telecommunication Services sector had on average 6,839 and 13,847 results for the

second keyword set (sample average is 3,746) and 29,095 and 32,135 for the third keyword

set (sample average is 17,245), while their respective average co-creation score was only 0.86

for Customer Discretionary and 0.67 for companies in the sector Telecommunication Services

(sample mean is 0.94).

3.3.1.2 The control variables

The validity of the models used should be proven to make sure that the difference in the

values observed represent equal changes in the true underlying measure and not the impact of

other factors (Pedhazur & Pedhazur-Schmelkin, 1991). Jegadeesh and Titman (1993) argue

that it is necessary to control for the effect of company size, industry and age in a comparable

study. The necessity to control for size is shown, for instance, by Bommer and Jalajas (2004),

who illustrate that small and medium-sized enterprises valued customers and marketing more

highly, whereas large organizations valued the importance of relationships with other

businesses and suppliers in particular. The explanations on the variables Sales and Age are

described in Appendix B, Table 2. A short elaboration is given on the control variable

Industry.

The Value of Co-Creation

J.L. van de Mortel 27

Industry

Because industry is a categorical variable, the ten GICS® sectors of interest in this study are

converted into a set of dichotomous independent variables (Tabachnick & Fidell, 2001).

Consequently, the 10 dichotomous variables are entered into the regressions as dummy

variables, controlling for the relevant sector. In the regressions described in section 4.2 the

GICS® sector Utility (GICS® Sector code 55) is used as baseline and therefore not visible in

the relevant statistic summaries in Appendix B.

3.3.2 Dependent variables

To test the impact of co-creation on financial ratios and financial position specific variables

are identified to test the impact of co-creation (ccscore). Those variables are technically

described in Table 2 and theoretically explained below.

*** Insert Appendix B, Table 2 here ***

Return on Assets / Return on Equity / Return on Invested Capital - It is assumed that Return

on Assets, Return on Equity and Return on Invested Capital is higher for companies that use

co-creation, because of two reasons. First of all, because of the higher return on business

processes due to an increase in sales and side effects of customer satisfaction. Secondly,

because companies that use co-creation have business processes with relatively lower costs.

Specifically, the Return on Assets is assumed to be higher since companies that use co-

creation have relatively more assets than stated in their balance sheet, since the intangible

processes are not recognized in current accounting methods (Lev, 2004).

Net Income Growth - The Net Income Growth illustrates the firms’ ability to improve their

profitability. It is expected that co-creation will contribute to an increase in Net Income

Growth because of improved business processes and an increase in sales volume due to e.g.

high customer retention and satisfaction rates and new product developments.

Cost of Goods Sold to Sales - The literature study suggest that co-creation will decrease the

Cost of Goods Sold to Sales. Cost of Goods Sold does not include advertising expenditures

and expenditures on Research on Development, which are assumed to be lower when co-

creation is present, but do include direct labour and overhead costs. However, Corbett (1998)

argues that GAAP and the International Accountings Standards (IAS) do not correclty reflect

on Cost of Goods Sold. Corbett argues that direct labour and overhead costs should not be

incorporated in the Cost of Goods Sold, thereby diminishing the impact of co-creation on the

Cost of Goods Sold.

The Value of Co-Creation

J.L. van de Mortel 28

Cash Flow to Sales - Srivastava et al. (1998) point out that market based assets, on the one

hand, can result in an acceleration of cash flows due to a faster response to marketing needs,

earlier brand trials, strategic alliances and cross promotions. On the other hand, market based

assets can results in an enhancement of cash flows due to the development of new uses, a

reduction of working capital and lower sales and service costs. With co-creation it can work

both ways and consequently a higher Cash Flow to Sales ratio is expected for firms that have

co-creation aspirations. Moreover, Srivastava et al. (1997) argue that processes similar to that

of co-creation can reduce the vulnerability and volatility of the cash flows, but that is beyond

the scope of this thesis.

Operating Profit Margin – Disregarding the fact that it is often hard to compare idiosyncratic

Profit Margins, due to firms’ specific operating and financing arrangement, it is a good

overall measure because of two reasons. First of all, a low Operating Profit Margin increases

risk and results in a low margin of financial safety, while co-creation is expected to increase

stability and financial performance. Additionally, the Operating Profit Margin illustrates the

firm’s ability to control cost and quality of profitability.

Gross Profit Margin - Given the potential of co-creation to reduce the Cost of Goods Sold,

ipso facto the Gross Profit Margin (Net Sales minus Cost of Goods Sold divided by Net

Sales) will be higher. If a model is applied with Gross Profit Margin as dependent variable, it

is especially important to control for industry related factors since for some industries, like

Customer Discretionary, Gross Profit Margins are expected to be around 40%. However, for

companies in the GICS® Sector Information Technology, the gross profit margin can be more

than 80%.

Tobin’s Q - Tobin’s Q is a good parameter to measure the impact of co-creation since it takes

into consideration the assets employed by the firm, the market sentiment and the intellectual

capital (Tobin, 1969). The value of intangible assets lies in their contribution to generate

future cash flows. The discrepancy between market and book value suggests that investors

recognize this (Fama, 1970).

The Value of Co-Creation

J.L. van de Mortel 29

4. Results

4.1 Descriptive statistics

It is useful to discover the differences between companies that do use the principles of co-

creation and those that do not use the principles of co-creation. Therefore an initial analysis

will detail the characteristics of companies that implement co-creation. A start is made with

an analysis of the differences in co-creation scores among sectors. Thereafter the firm

characteristics Age, Beta and Free Cash Flow to Sales will be examined.

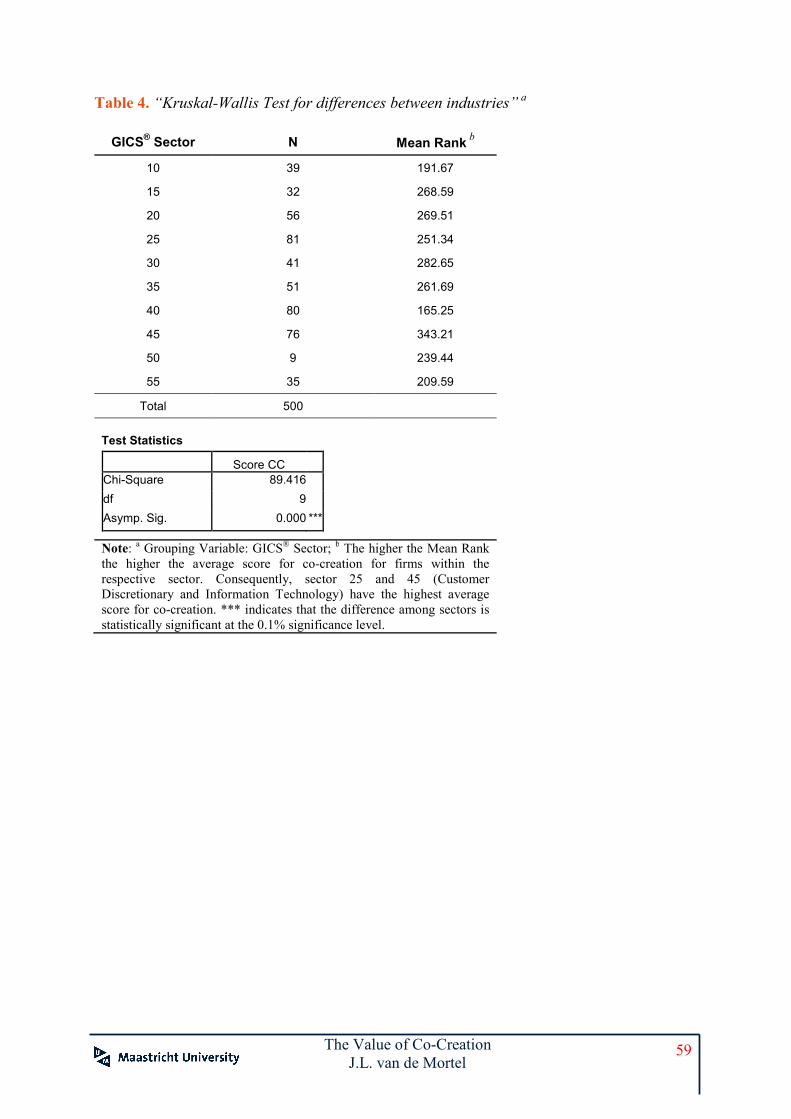

To test for differences among the different GICS® Sectors a KruskalWallis test is applied. The

KruskalWallis test is suitable to test equalities of population medians among the sectors,

comparable to a one-way ANOVA test, with the data being replaced by their ranks and is an

extension of the MannWhitney U test (Kruskal and Wallis, 1952). Given the high Chi Square

value (χ2=89.42) and the significance at 0.000% we can conclude that there is a statistically

significant difference in the score for co-creation across the GICS® Sectors. A closer look on

the Mean Ranks given by the KruskalWallis test suggests that Information Technology,

Consumer Staples and Industrials, have the highest score for co-creation, while the sector

Financials reports the lowest.

*** Insert Appendix B, Table 3 and Table 4 here *** The differences among sectors is in line with the reasoning of Almirall and Casadesus-

Masanell (2010), who argue that co-creation is only beneficial at a certain level of product

complexity (see Appendix A, figure 7). Many companies in the GICS® Sectors Energy and

Utilities have either very complex, like the drilling-technology for oil companies, or very

basal company processes, diminishing the possible positive impact of co-creation.

Additionally, companies in the GICS® Sectors Energy and Utilities have considerably more

Business-to-Business relations, enabling companies in those sectors to establish partnerships

and collaboration possibilities, but limiting the opportunities to jointly create value with the

consumer. Finally, many scholars (e.g. Schneider & Bowen, 1995; Zeithaml et al., 1990) have

highlighted the distinctions between goods and services and have underscored the

implications of these differences for business processes and the related difficulty in

comparing various dimensions of performance indicators.

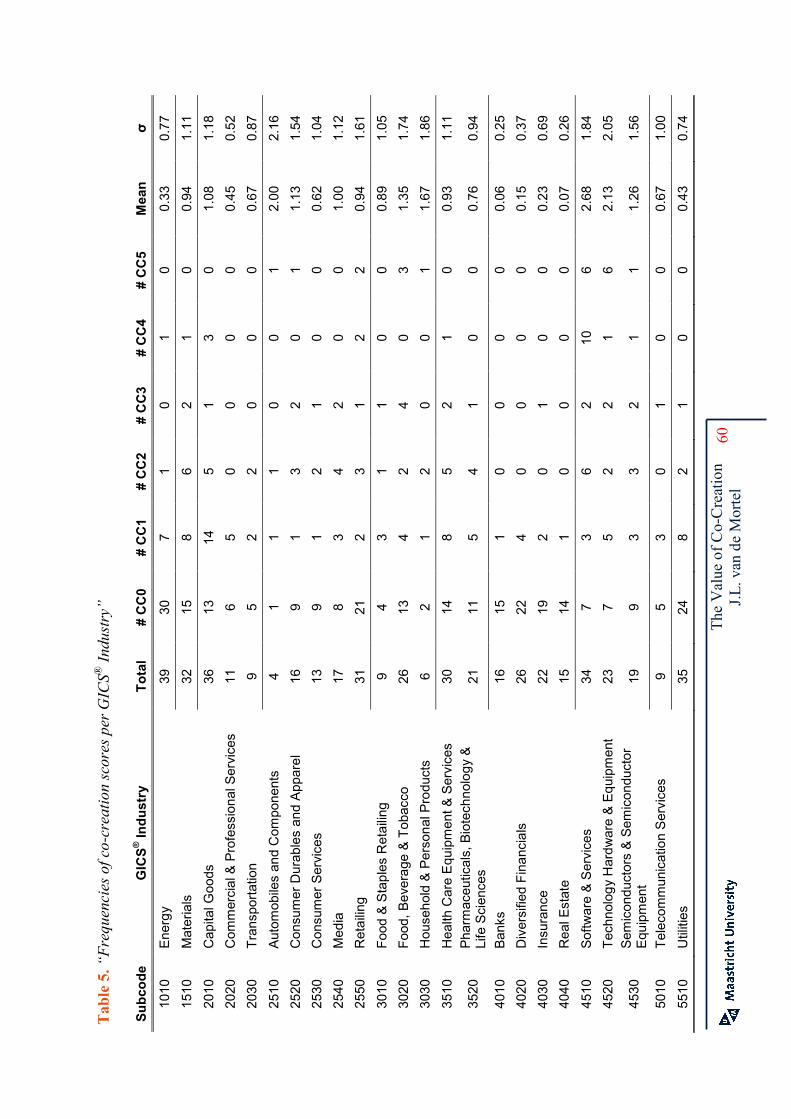

Appendix B, Table 5 details the level of implementation and the mean score for co-creation

considered on an industry level. The mean score is highest for the industries Technology

Hardware, Software and Automobiles, although the latter has actually only one company with

a score for co-creation above 2. While banks often have a focus on customer satisfaction the

The Value of Co-Creation

J.L. van de Mortel 30

respective industry mean is low, just as for the industries Real Estate, Diversified Financials

and Insurance. Additionally, there are respectively 7 and 5 companies in the industries Food,

Beverage and Tobacco; and Retailing with a co-creation score equal or larger then 3,

illustrating the potential for co-creation in those industries.

*** Insert Appendix B, Table 5 here ***

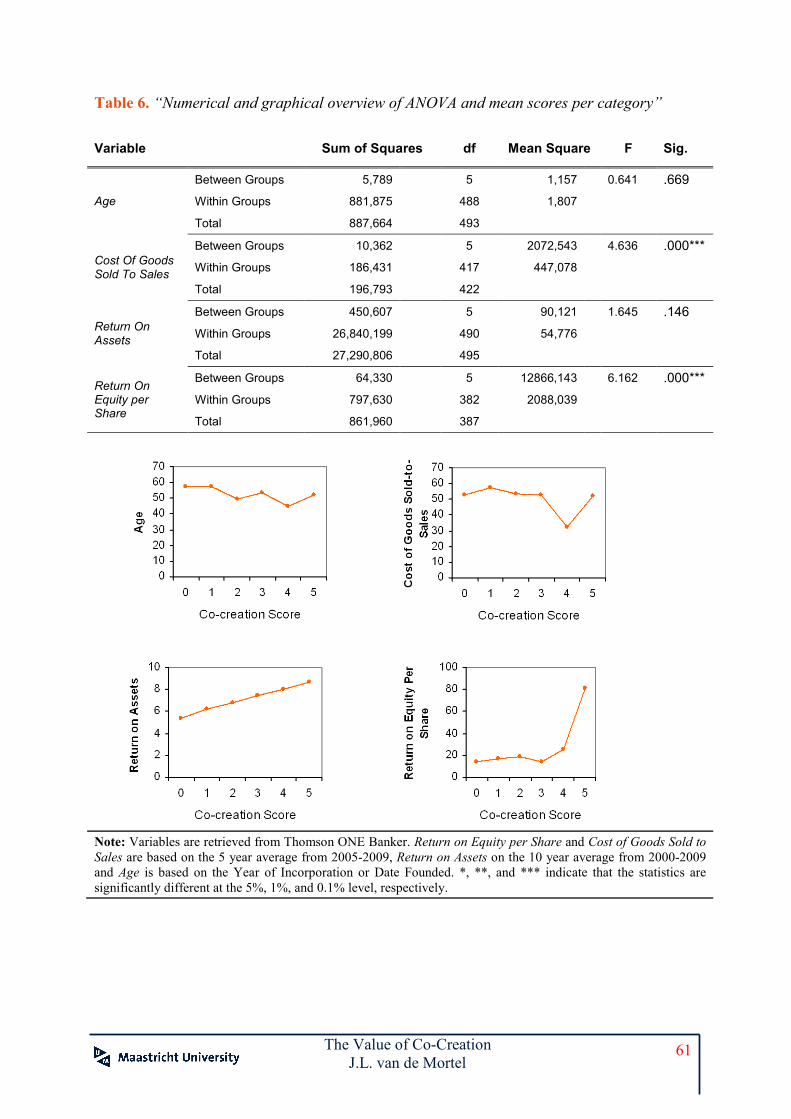

Besides the differences for co-creation scores among GICS® sectors and industries, several

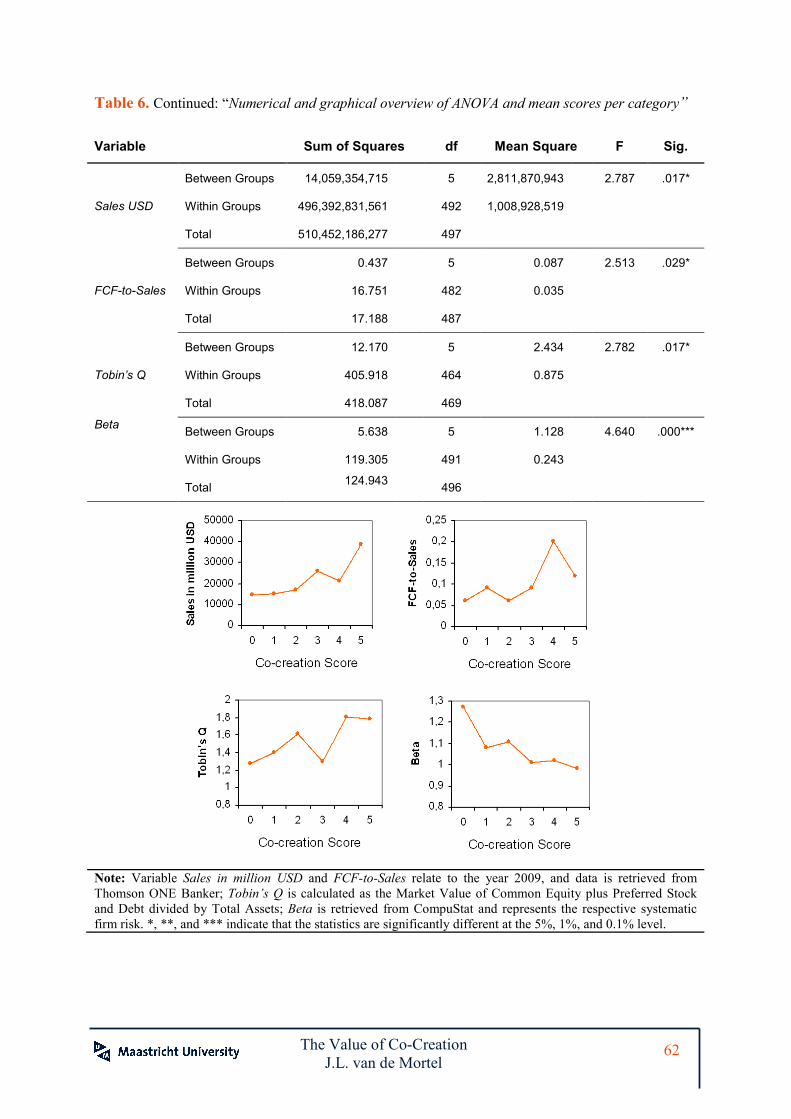

ANOVA tests illustrate the differences for companies with a specific co-creation score. Table

6 shows the statistical significance of the differences among co-creation categories and

graphically illustrates the respective discrepancy on inter alia Return on Assets, Return on

Equity, Tobin’s Q and Free Cash Flow to Sales. Three firm characteristics will be elaborated,

namely a firm’s Beta and the Free Cash Flow to Sales.