Embed Size (px)

Citation preview

Master BudgetingChapter 8

ACTG 202 – Principles of Managerial Accounting“Good plans shape good decisions. That’s why good planning helps make elusive dreams come true.”-Geoffrey Fische

8-2

Learning Objective 1

Understand why organizations budget

and the processes they use to create budgets.

8-3

The Basic Framework of Budgeting

A budget is a detailed quantitative plan for acquiring and using financial and other resources over a specified forthcoming time period.

1. The act of preparing a budget is called budgeting.

2. The use of budgets to control an organization’s activities is known as budgetary control.

8-4

Difference Between Planning and Control

PlanningPlanning – – involves developing involves developing objectives and objectives and preparing various preparing various budgets to achieve budgets to achieve those objectives.those objectives.

PlanningPlanning – – involves developing involves developing objectives and objectives and preparing various preparing various budgets to achieve budgets to achieve those objectives.those objectives.

ControlControl – – involves the steps taken involves the steps taken by management to by management to increase the likelihood that increase the likelihood that the objectives set down the objectives set down while planning are attained while planning are attained and that all parts of the and that all parts of the organization are working organization are working together toward that goal.together toward that goal.

ControlControl – – involves the steps taken involves the steps taken by management to by management to increase the likelihood that increase the likelihood that the objectives set down the objectives set down while planning are attained while planning are attained and that all parts of the and that all parts of the organization are working organization are working together toward that goal.together toward that goal.

8-5

Responsibility Accounting

Managers should be held Managers should be held responsible for those items - responsible for those items - and and onlyonly those items - that those items - that they can actually control they can actually control to a significant extent. to a significant extent. Responsibility accounting Responsibility accounting enables organizations to enables organizations to react react quicklyquickly to deviations from their to deviations from their plans and to plans and to learnlearn from from feedback.feedback.

8-6

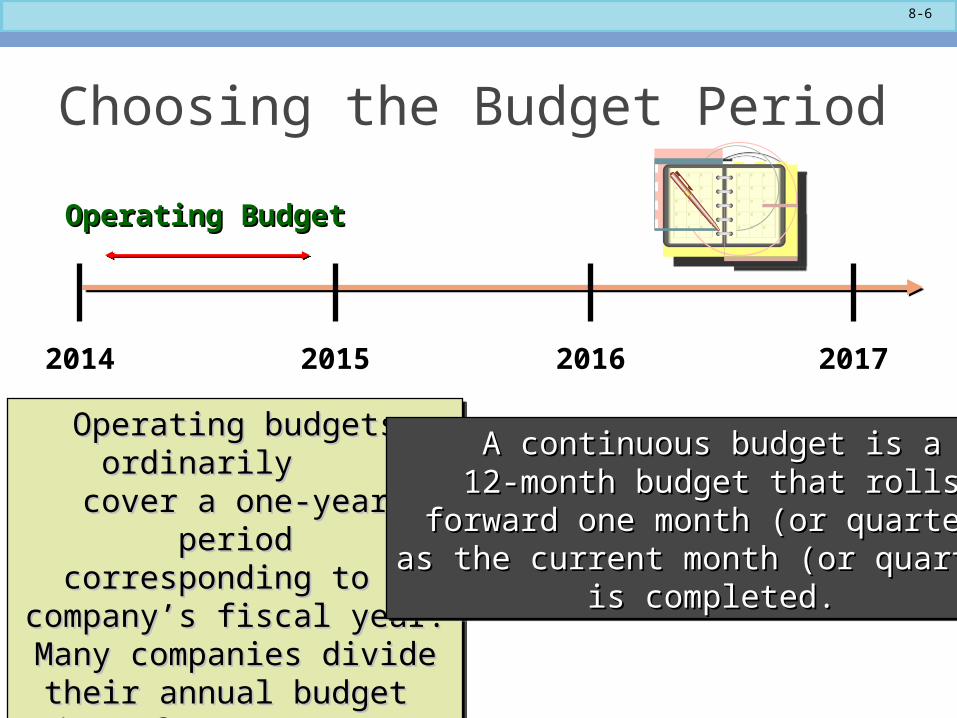

Choosing the Budget Period

Operating BudgetOperating Budget

2014 2015 2016 2017

Operating budgets ordinarily Operating budgets ordinarily cover a one-year periodcover a one-year period

corresponding to a company’s corresponding to a company’s fiscal year. Many companies fiscal year. Many companies divide their annual budget divide their annual budget

into four quarters.into four quarters.

Operating budgets ordinarily Operating budgets ordinarily cover a one-year periodcover a one-year period

corresponding to a company’s corresponding to a company’s fiscal year. Many companies fiscal year. Many companies divide their annual budget divide their annual budget

into four quarters.into four quarters.

A continuous budget is aA continuous budget is a12-month budget that rolls12-month budget that rolls

forward one month (or quarter)forward one month (or quarter)as the current month (or quarter)as the current month (or quarter)

is completed.is completed.

A continuous budget is aA continuous budget is a12-month budget that rolls12-month budget that rolls

forward one month (or quarter)forward one month (or quarter)as the current month (or quarter)as the current month (or quarter)

is completed.is completed.

8-7

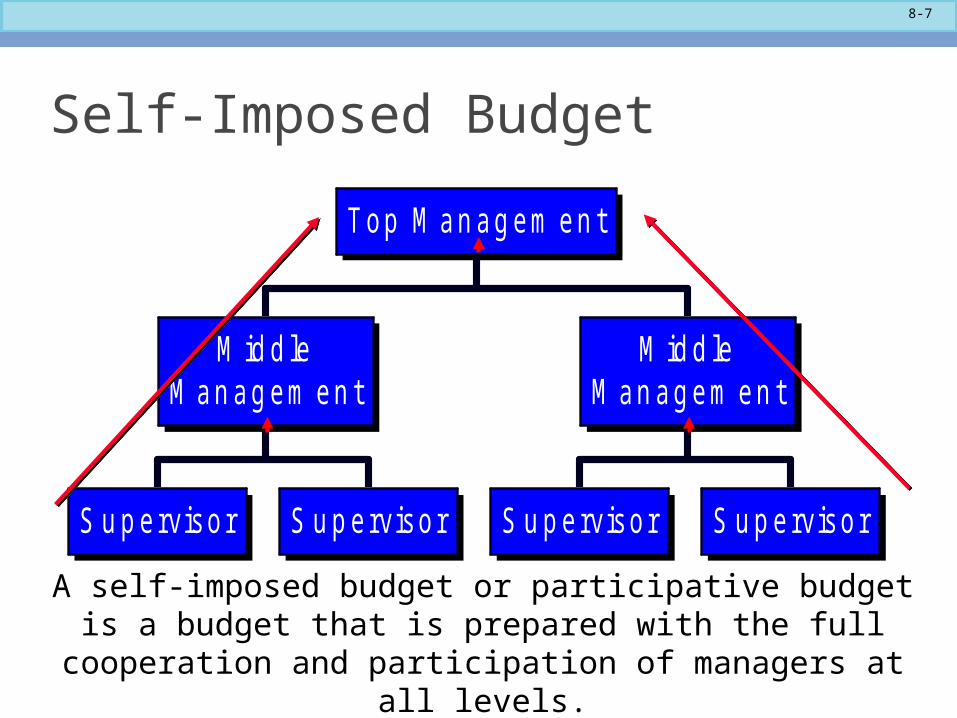

Self-Imposed Budget

A self-imposed budget or participative budget is a budget that is prepared with the full cooperation and participation of managers

at all levels.

S u p erviso r S u p erviso r

M id d leM an ag em en t

S u p erviso r S u p erviso r

M id d leM an ag em en t

Top M an ag em en t

8-8

Advantages of Self-Imposed Budgets1. Individuals at all levels of the organization are viewed as

members of the team whose judgments are valued by top management.

2. Budget estimates prepared by front-line managers are often more accurate than estimates prepared by top managers.

3. Motivation is generally higher when individuals participate in setting their own goals than when the goals are imposed from above.

4. A manager who is not able to meet a budget imposed from above can claim that it was unrealistic. Self-imposed budgets eliminate this excuse.

1. Individuals at all levels of the organization are viewed as members of the team whose judgments are valued by top management.

2. Budget estimates prepared by front-line managers are often more accurate than estimates prepared by top managers.

3. Motivation is generally higher when individuals participate in setting their own goals than when the goals are imposed from above.

4. A manager who is not able to meet a budget imposed from above can claim that it was unrealistic. Self-imposed budgets eliminate this excuse.

8-9

Self-Imposed Budgets

Self-imposed budgets should be reviewed by higher levels of management to

prevent “budgetary slack.”

Most companies issue broad guidelines in terms of overall profits or sales. Lower level managers are directed to prepare

budgets that meet those targets.

Self-imposed budgets should be reviewed by higher levels of management to

prevent “budgetary slack.”

Most companies issue broad guidelines in terms of overall profits or sales. Lower level managers are directed to prepare

budgets that meet those targets.

8-10

Human Factors in BudgetingThe success of a budget program depends on three important factors:1.Top management must be enthusiastic and committed to the budget process.2.Top management must not use the budget to pressure employees or blame them when something goes wrong. 3.Highly achievable budget targets are usually preferred when managers are rewarded based on meeting budget targets.

8-11

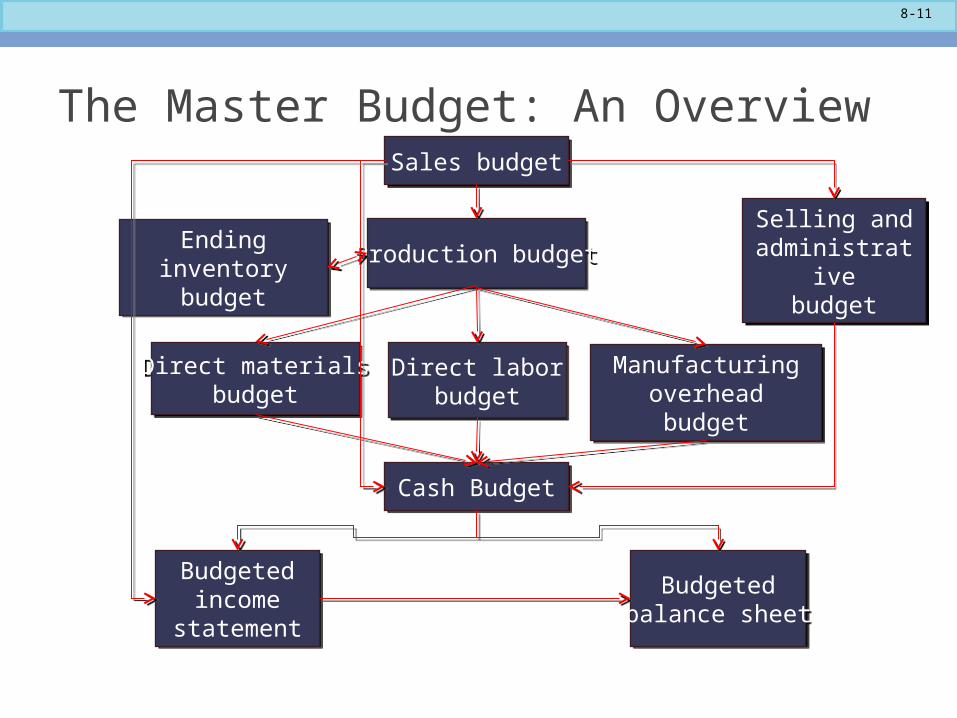

The Master Budget: An Overview

Production budgetProduction budgetSelling and

administrativebudget

Selling andadministrative

budget

Direct materialsbudget

Direct materialsbudget

Manufacturingoverhead budgetManufacturing

overhead budgetDirect labor

budgetDirect labor

budget

Cash BudgetCash Budget

Sales budgetSales budget

Ending inventorybudget

Ending inventorybudget

Budgetedbalance sheet

Budgetedbalance sheet

Budgetedincome

statement

Budgetedincome

statement

8-12

Learning Objective 2

Prepare a sales budget, including a schedule of

expected cash collections.

8-13

The Sales Budget

•The sales budget is the starting point in preparing a master budget

•All other steps in the budgeting process depend on the sales budget

•Most big budgeting problems result from a poor sales budget

8-14

The Sales Budget

•A sales budget is constructed by multiplying budgeted unit sales by the selling price

•Revenue and cash receipts may happen in different time periods▫Both are important

8-15

Learning Objective 3

Prepare a production budget.

8-16

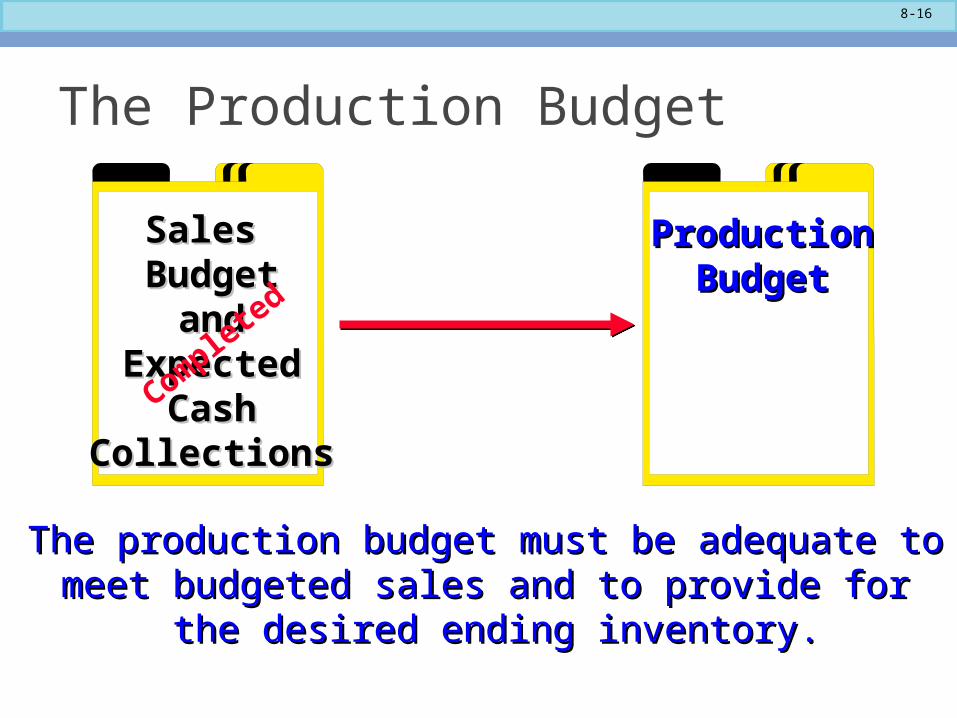

The Production Budget

ProductionProductionBudgetBudget

Sales Sales BudgetBudget

andandExpectedExpected

CashCashCollectionsCollections

Complete

d

The production budget must be adequate to The production budget must be adequate to meet budgeted sales and to provide for meet budgeted sales and to provide for

the desired ending inventory.the desired ending inventory.

8-17

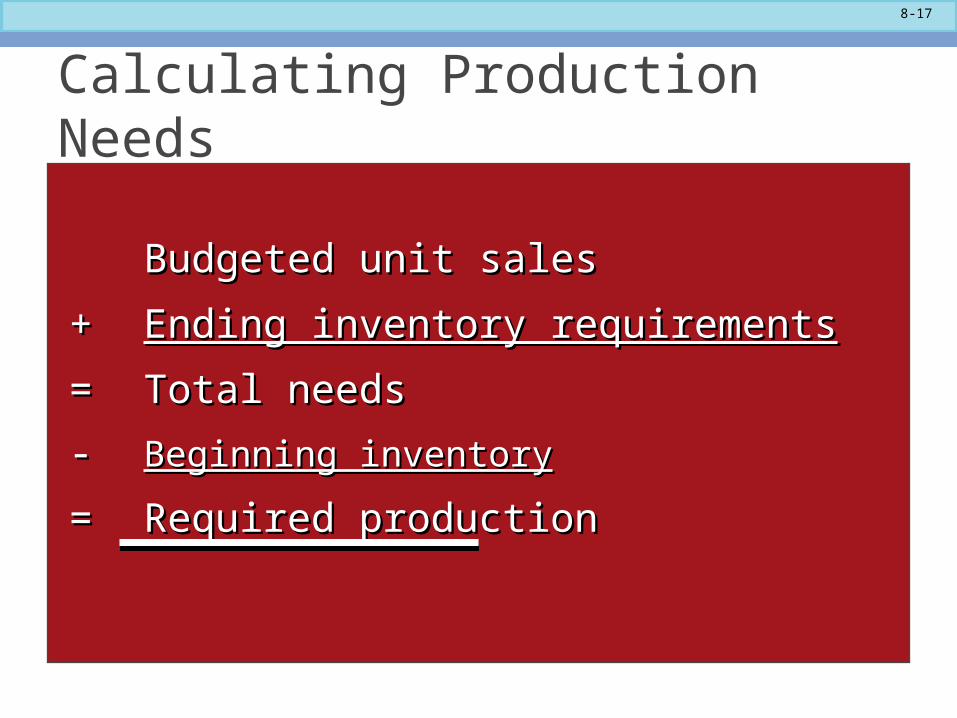

Calculating Production Needs

Budgeted unit salesBudgeted unit sales

++ Ending inventory requirementsEnding inventory requirements

== Total needs Total needs

-- Beginning inventoryBeginning inventory

== Required production Required production

8-18

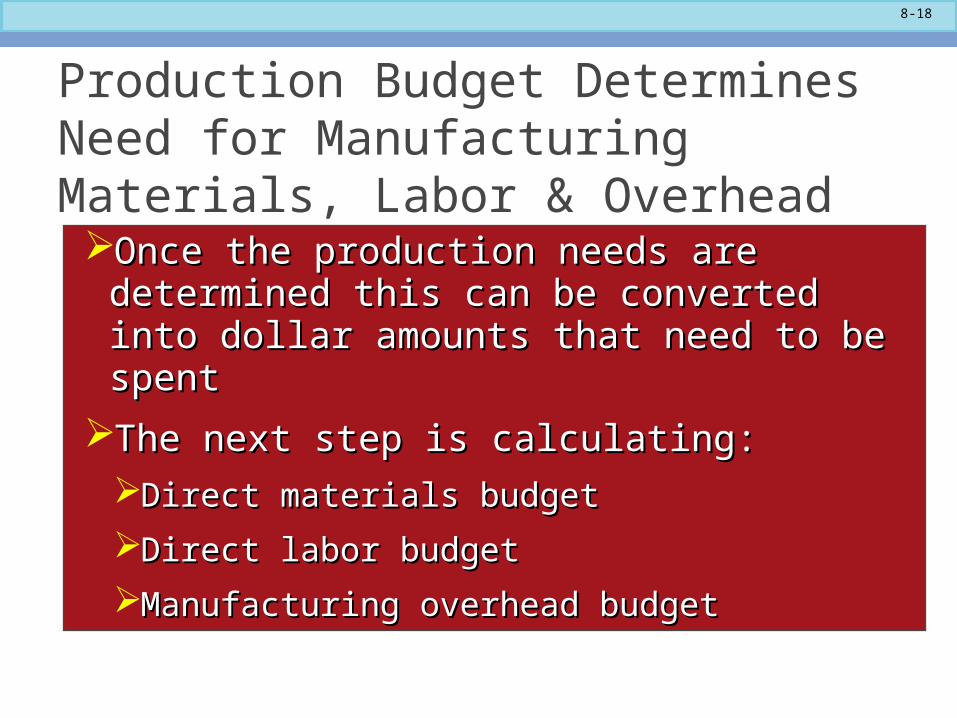

Production Budget Determines Need for Manufacturing Materials, Labor & OverheadOnce the production needs are determined Once the production needs are determined

this can be converted into dollar amounts that this can be converted into dollar amounts that need to be spentneed to be spent

The next step is calculating:The next step is calculating:

Direct materials budgetDirect materials budget

Direct labor budgetDirect labor budget

Manufacturing overhead budgetManufacturing overhead budget

8-19

Learning Objectives 4, 5, and 6

Prepare a direct materials budget, labor

budget, and manufacturing overhead

budget

8-20

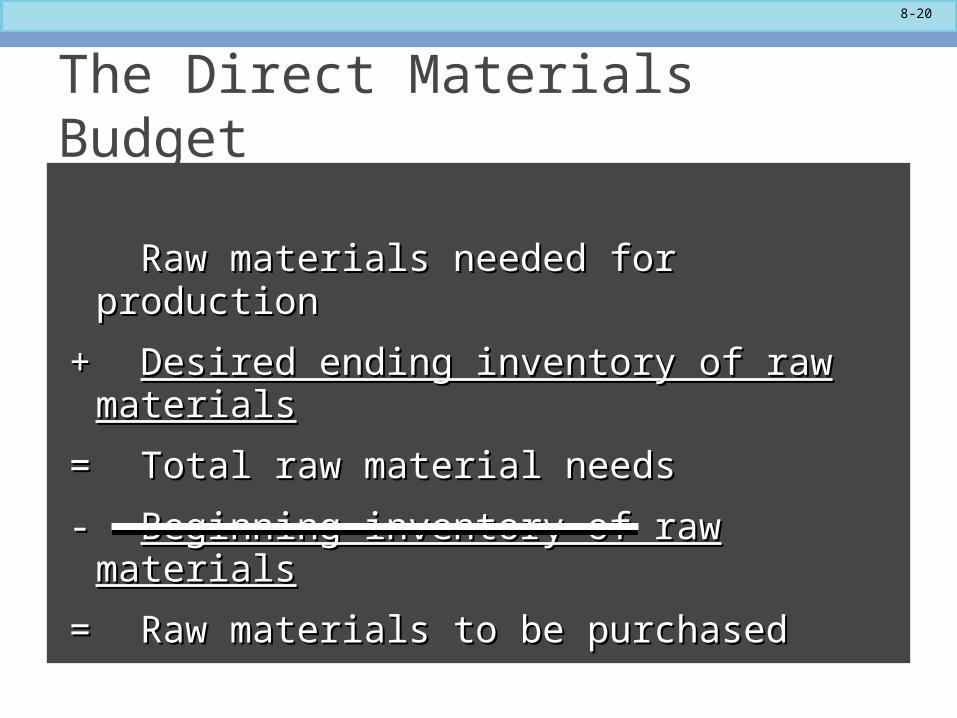

The Direct Materials Budget

Raw materials needed for productionRaw materials needed for production

++ Desired ending inventory of raw materialsDesired ending inventory of raw materials

== Total raw material needs Total raw material needs

-- Beginning inventory of raw materialsBeginning inventory of raw materials

== Raw materials to be purchased Raw materials to be purchased

8-21

The Direct Labor Budget

•To create a direct labor budget we need

▫Required production (from Production Budget)

▫Number of labor hours required per unit

▫The direct labor rate per hour

Note: if production labor amounts are fixed than there may be a minimum total labor cost

8-22

Manufacturing Overhead Budget

•A manufacturing overhead budget should A manufacturing overhead budget should be divided into:be divided into:

▫Variable costs, andVariable costs, and

▫Fixed costsFixed costs

•Which costs are fixed and which are Which costs are fixed and which are variable should be reviewed and adjusted variable should be reviewed and adjusted during the budgeting processduring the budgeting process

•A manufacturing overhead budget should A manufacturing overhead budget should be divided into:be divided into:

▫Variable costs, andVariable costs, and

▫Fixed costsFixed costs

•Which costs are fixed and which are Which costs are fixed and which are variable should be reviewed and adjusted variable should be reviewed and adjusted during the budgeting processduring the budgeting process

8-23

Manufacturing Overhead Budget

•The manufacturing overhead budget is The manufacturing overhead budget is used to calculate the predetermined used to calculate the predetermined overhead rateoverhead rate

▫As illustrated in Chapter 3, the As illustrated in Chapter 3, the predetermined overhead rate is used to predetermined overhead rate is used to allocate overhead to productsallocate overhead to products

•Often, some of the fixed overhead costs, Often, some of the fixed overhead costs, such as depreciation, are noncash itemssuch as depreciation, are noncash items

•The manufacturing overhead budget is The manufacturing overhead budget is used to calculate the predetermined used to calculate the predetermined overhead rateoverhead rate

▫As illustrated in Chapter 3, the As illustrated in Chapter 3, the predetermined overhead rate is used to predetermined overhead rate is used to allocate overhead to productsallocate overhead to products

•Often, some of the fixed overhead costs, Often, some of the fixed overhead costs, such as depreciation, are noncash itemssuch as depreciation, are noncash items

8-24

Learning Objective 7

Prepare a selling and administrative expense

budget.

8-25

Selling and Administrative Expense Budget•The selling and administrative expense budget lists The selling and administrative expense budget lists

the budgeted expenses for areas other than the budgeted expenses for areas other than manufacturingmanufacturing

• In large organizations, this budget would be a In large organizations, this budget would be a compilation of many smaller, individual budgets compilation of many smaller, individual budgets submitted by different departmentssubmitted by different departments

•To complete the selling and administrative expense To complete the selling and administrative expense budget, costs should be divided into variable and budget, costs should be divided into variable and fixed costsfixed costs

•There may be noncash selling and administrative There may be noncash selling and administrative expenses such as depreciationexpenses such as depreciation

8-26

Learning Objective 8

Prepare a cash budget.

8-27

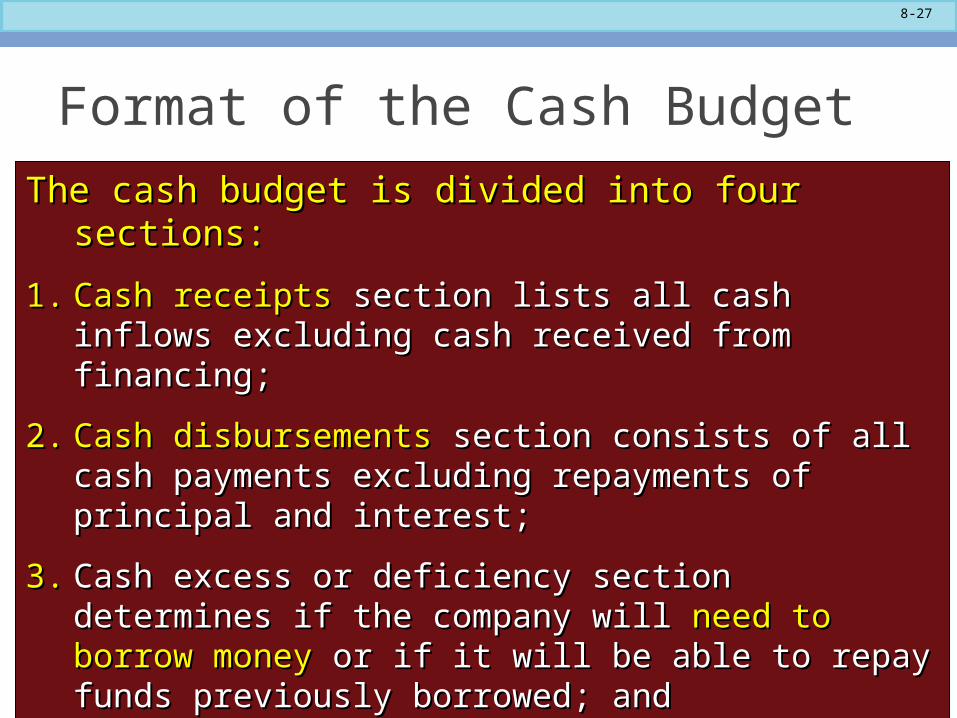

Format of the Cash Budget

The cash budget is divided into four sections:The cash budget is divided into four sections:

1.1. Cash receipts Cash receipts section lists all cash inflows excluding cash section lists all cash inflows excluding cash received from financing;received from financing;

2.2. Cash disbursementsCash disbursements section consists of all cash payments section consists of all cash payments excluding repayments of principal and interest;excluding repayments of principal and interest;

3.3. Cash excess or deficiency section determines if the Cash excess or deficiency section determines if the company will company will need to borrow money need to borrow money or if it will be able to or if it will be able to repay funds previously borrowed; andrepay funds previously borrowed; and

4.4. Financing sectionFinancing section details the borrowings and repayments details the borrowings and repayments projected to take place during the budget period.projected to take place during the budget period.

The cash budget is divided into four sections:The cash budget is divided into four sections:

1.1. Cash receipts Cash receipts section lists all cash inflows excluding cash section lists all cash inflows excluding cash received from financing;received from financing;

2.2. Cash disbursementsCash disbursements section consists of all cash payments section consists of all cash payments excluding repayments of principal and interest;excluding repayments of principal and interest;

3.3. Cash excess or deficiency section determines if the Cash excess or deficiency section determines if the company will company will need to borrow money need to borrow money or if it will be able to or if it will be able to repay funds previously borrowed; andrepay funds previously borrowed; and

4.4. Financing sectionFinancing section details the borrowings and repayments details the borrowings and repayments projected to take place during the budget period.projected to take place during the budget period.

8-28

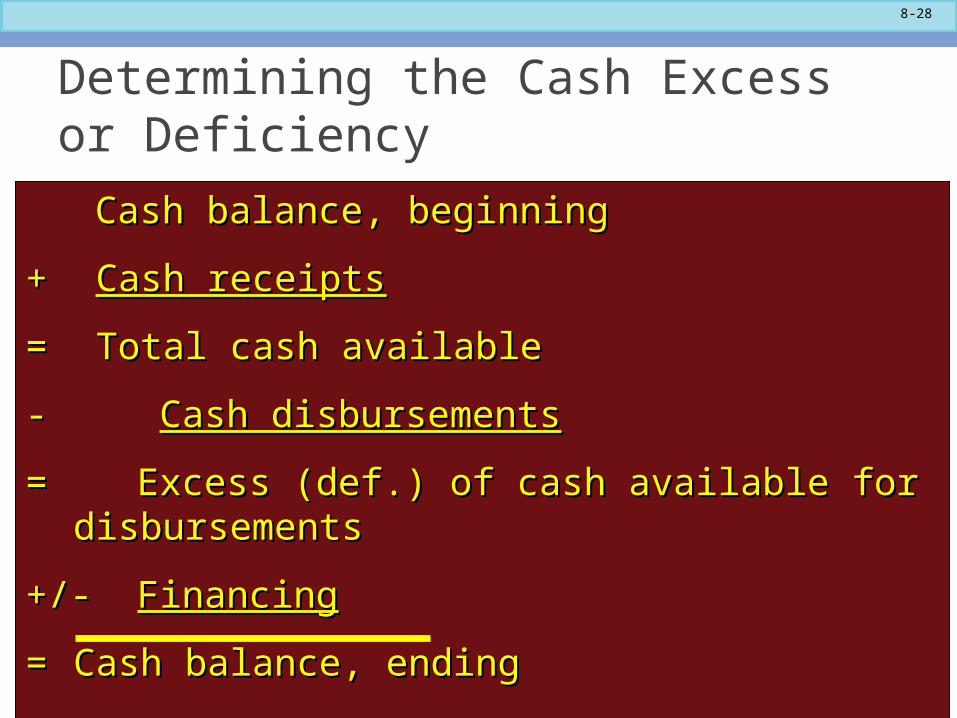

Cash balance, beginningCash balance, beginning

++ Cash receiptsCash receipts

== Total cash available Total cash available

- - Cash disbursementsCash disbursements

= Excess (def.) of cash available for disbursements= Excess (def.) of cash available for disbursements

+/- +/- FinancingFinancing

== Cash balance, endingCash balance, ending

Cash balance, beginningCash balance, beginning

++ Cash receiptsCash receipts

== Total cash available Total cash available

- - Cash disbursementsCash disbursements

= Excess (def.) of cash available for disbursements= Excess (def.) of cash available for disbursements

+/- +/- FinancingFinancing

== Cash balance, endingCash balance, ending

Determining the Cash Excess or Deficiency

8-29

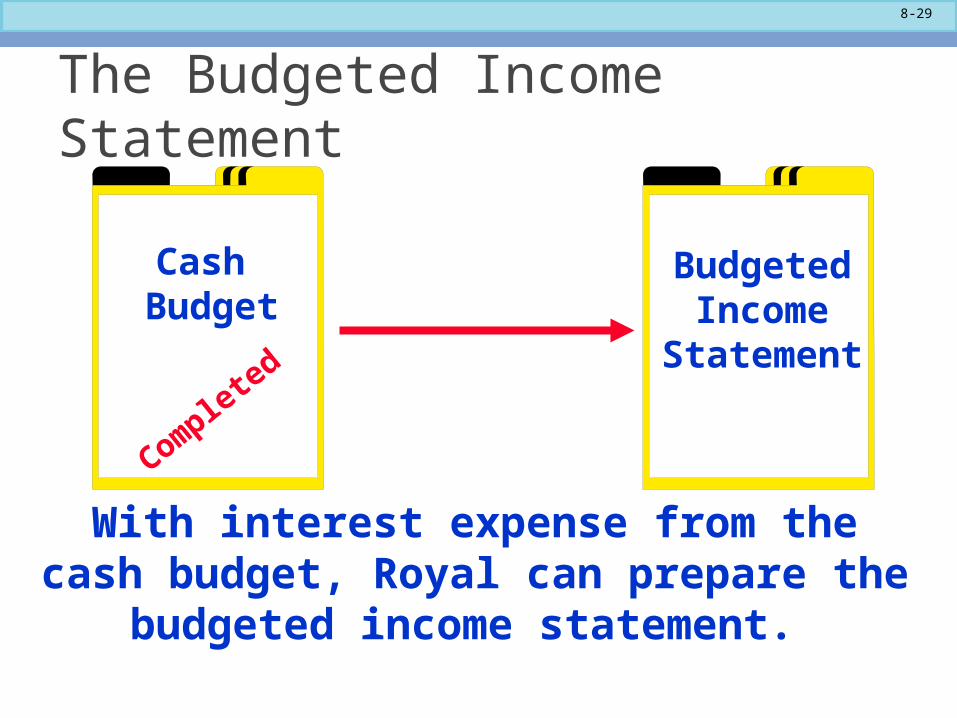

The Budgeted Income Statement

Cash Budget

BudgetedIncome

Statement

Complete

d

With interest expense from the cash budget, Royal can prepare the budgeted

income statement.

8-30

Learning Objective 9

Prepare a budgeted income statement.

8-31

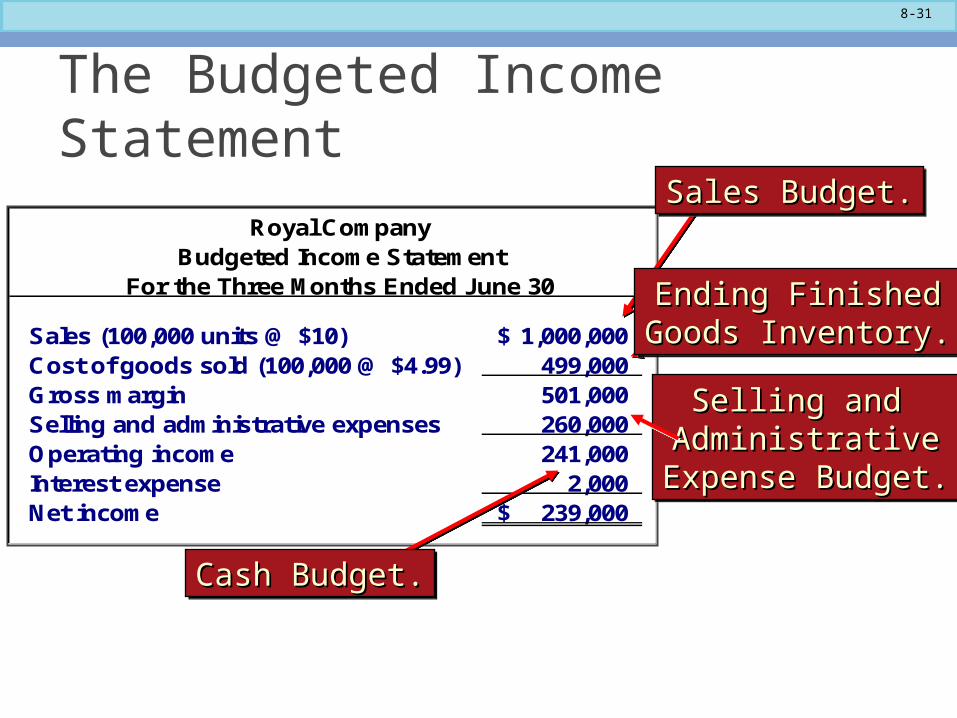

The Budgeted Income Statement

Royal CompanyBudgeted Income Statement

For the Three Months Ended June 30

Sales (100,000 units @ $10) 1,000,000$ Cost of goods sold (100,000 @ $4.99) 499,000 Gross margin 501,000 Selling and administrative expenses 260,000 Operating income 241,000 Interest expense 2,000 Net income 239,000$

Sales Budget.Sales Budget.Sales Budget.Sales Budget.

Ending FinishedEnding FinishedGoods Inventory.Goods Inventory.Ending FinishedEnding FinishedGoods Inventory.Goods Inventory.

Selling and Selling and AdministrativeAdministrative

Expense Budget.Expense Budget.

Selling and Selling and AdministrativeAdministrative

Expense Budget.Expense Budget.

Cash Budget.Cash Budget.Cash Budget.Cash Budget.

8-32

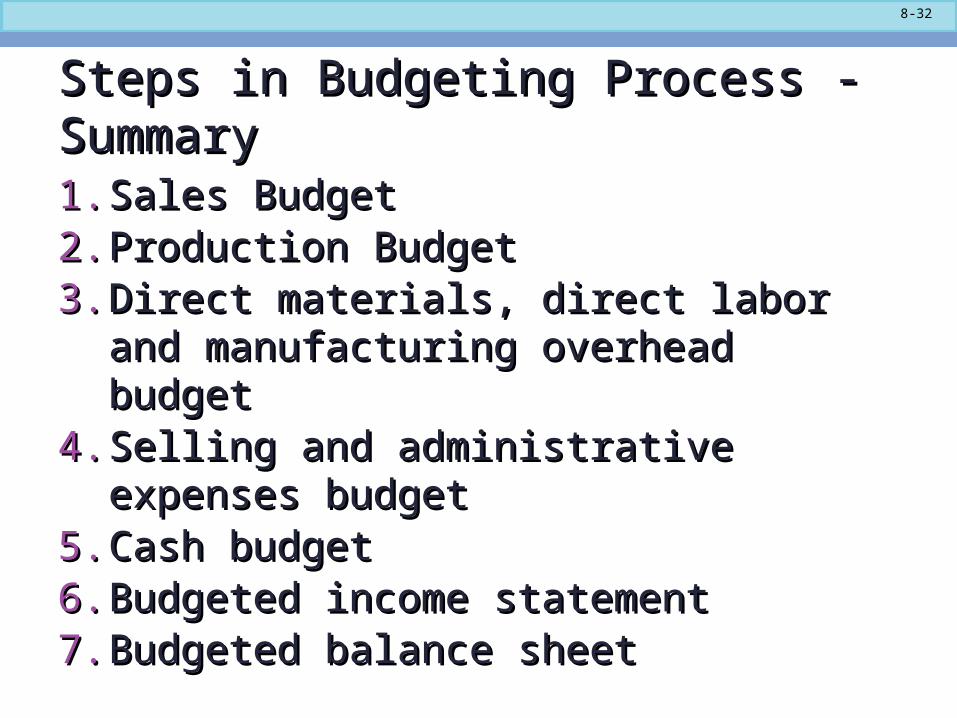

Steps in Budgeting Process - SummarySteps in Budgeting Process - Summary

1.1. Sales BudgetSales Budget2.2. Production BudgetProduction Budget3.3. Direct materials, direct labor and Direct materials, direct labor and

manufacturing overhead budgetmanufacturing overhead budget4.4. Selling and administrative expenses Selling and administrative expenses

budgetbudget5.5. Cash budgetCash budget6.6. Budgeted income statementBudgeted income statement7.7. Budgeted balance sheetBudgeted balance sheet