Embed Size (px)

Citation preview

Markets in Financial Instruments Directive (MiFID)

What does it mean to the operations practitioner ?

Update

February 1st 2007

2 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Introduction

Simon Bennett

Partner

Capco is .. a business consultant helping our

clients to architect, engineer and implement transformational change

a provider of processing services that transform operational effectiveness

a provider of technology and data products

Capco is .. an industry specialist focused

exclusively on transforming the future of the financial services industry

a global firm of 500+ professionals operating in all the major financial markets of the world.

3 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Objectives and agenda

Objectives Reminder of the wider context for MiFID and why it is more than a regulatory

issue Identify the most important articles overall and the key issues for operations

professionals to consider An update on the UK timetable

MiFID: background and bigger picture

The timetable and process for implementation

Tips on formulating a response

Introduction, objectives for today

The main operational considerations

Key articles of the directive

4 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Contents

MiFID: background and bigger picture

The timetable and process for implementation

Tips on formulating a response

Introduction, objectives for today

The main operational considerations

Key articles of the directive

5 - MiFID - presentation - 1st Feb 2007 - Capco confidential

The wider objectives

MiFID is an important part of the Financial Services Action Plan which has a goal to ……

“Create the most effective and integrated financial services market in the world”

MiFID is one of a number of active and planned regulatory issues (see

next slide) – it replaces the existing ISD (Investment Services Directive)

The intention of MiFID…. and the other FSAP regulations are: Allow European investors wider access to the best available products

within a common framework of protection Give firms access to markets in other member states without

unnecessary additional regulatory burdens Reduce the costs of European cross border trading Improve access to capital and capital allocation

There is significant political will behind MiFID and market changing intent within both MiFID and and the other regulatory initiatives

Known - DirectivesKnown - Directives

Probable/ Possible – White papers

Probable/ Possible – White papers

2006 2007 2008 2009 2010

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Capital Requirements Directive (Basel II; Recasts directives: 200/12/EC & 93/6/EEC)

Markets in Financial Instruments Directive (2004/39/EC)

Reinsurance Directive (2005/68/EC)

3rd Anti-Money Laundering Directive (2005/60/EC)

Transparency Directive (2004/109/EC)

Unfair Commercial Practices Directive (2005/29/EC)

EU Directive on wire transfers (2005 0138)

Payments Services Directive (‘new legal framework’; SEC (2005) 1535)

Solvency 2 Directive (SEC (2005) 1574)

Credit for Consumers Directive (SEC (2005) 1574)

Clearing & Settlement Directive (SEC (2005) 1574)

SEPA (payments white paper; SEC (2005) 1575)

Single regulatory report for EU (SEC (2005) 1574)

Improved access and portability of accounts in EU (SEC (2005) 1574)

Treating customer fairly (retail and pensions focus) (SEC (2005) 1574)

Hedge fund access for retail (categorise risk by product not by asset class; DP05/3)

Single market for mortgage credit (SEC (2005) 1574)

Single VAT level for Europe (SEC (2005) 1574)

AreaArea

AM, B, RI

AM, B, C, I, RI

I

AM, B, C, I, RI

AM, C

AM, B, I, RI

AM, B, C, I, RI

B

I

B, RI

B, C

B

AM, B, C

B, RI

AM, B, I, RI

AM, C, RI

B

AM, B, C, I, RI

1

AM – Asset Management

B – Banking

C – Capital Markets

I – Insurance

RI – Retail intermediaries

1 Recommendations

Consultation

EU Law

Implemented in UK

Takes effect

2

3

4

5

Recommendations

Consultation

Implemented for firms

2

3

Firms reviewing, planning and implementing

EU Process FSA Process

2

Key

4

2 4

2

2

42

2 3 42 2

1 2 3 2 2

42

1 2 3 2 42

1 2 3 2 4

1 2 2

1 2 3 2

2 3

1 2

Other Other

Single EU Corporate Action rules (CESAME group – could be rolled into C&S Dir.)

Standardise OTC matching agreements (CESAME group – could be rolled into C&S Dir.)

EMV (spread of chip + pin through Europe due to change in liability rules)

SOX

SWIFT (single protocol for all products)

- Market infrastructure

- Cross border participants

TARGET 2

C

AM, C

B

AM, B, C, I, RI

AM, B, C

B

Notes:1. Incorporates expected changes to published dates2. Where dates are known they are correct as at Jan 073. Incorporates Capco views and predictions on timings and potential areas of regulation

Sources: Capco research, EU Directives, FSA International Regulatory Outlook 11/05 and 12/06, KPMG working to rules (Autumn 05), EU white papers (SEPA, FS Policy), E&Y FS brief, CESAME Group update (10/05), ECB

53

3 5

3 5

53

3

3

3

32 54

32 2

53

54

4 5

5

53 4

53

1 2 3 2 42

3 5

53

4 53

1 2 3 2 4 53

4

2

7 - MiFID - presentation - 1st Feb 2007 - Capco confidential

MiFID is more than a compliance/regulatory exercise

EU objectives for MiFID Increased transparency across all trading venues Enhanced protection for the retail investor Greater competition between markets Opportunity for cross border competition Increased levels of disclosure, in particular to the retail investor

Commisioner McCreevy’s view* “MiFID will be the catalyst for significant market changes. It will dramatically

increase levels of competition” “(Europe) has nearly 40 equity exchanges ..the US has two ..economic logic

indicates rationalization in the EU is both necessary and inevitable” “.. the ‘single passport’ .. allows provision of investment services in 25

Member States on the basis of a single authorisation.. investor protection rules will be harmonised.. there will be important impacts on investment service providers. There will be a first-mover advantage”

“.. firms that try to ignore MiFID may well find themselves fatally weakened” * Speech to LSE Christmas lunch 16/12/2005

8 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Contents

MiFID: background and bigger picture

The timetable and process for implementation

Tips on formulating a response

Introduction, objectives for today

The main operational considerations

Key articles of the directive

9 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Investment Firms

Clients

Retail

Professional

Execution VenuesExecution Venues

Authorised Markets

MTFs

Regulators

Investment advicePortfolio management

Order execution

Overview – scope is wider than ISD

EligibleCounterparty

• Investment Banks• Asset Managers• Broker Dealers• Corporate Banks• Retail Banks• Futures & Options

Firms• Commodities Traders

1. Transferable Securities2. Money Market

Instruments3. Units in Collective

Investments4. Securities Derivatives5. Commodity Derivatives

6. Credit Derivatives7. Contracts for

Difference8. Derivatives in

Freight, Climatic Variables, Emissions, Inflation

Products

10 - MiFID - presentation - 1st Feb 2007 - Capco confidential

The main articles (in brief)

Operating Conditions – more extensive requirements around compliance, risk management and avoidance of conflict of interest …. these also extend to firms providing BPO services

Client Classification – 3 client categories that do not match the current FSA definitions. Clients may fall into different categories for specific products or services. Obligations to clients are different to today

Suitability and Appropriateness – KYC requirements around advice similar to today but they also apply to some professionals. Appropriateness rules limit execution only service to non-complex instruments

Best Execution – firms must maintain and apply a best execution policy that achieves the best possible results for the client – firms will need to monitor their policy and prove that it is followed

Order Management – the regulation has specific guidelines around the prioritisation of orders, management of aggregated orders and allocation of client assets

Pre-Trade Transparency – new categorisation of Systematic Internaliser, a firm that crosses client trades internally across its own book. These firms must make public firm quotes for the “liquid” shares in which it deals. In addition all firms that deal with client orders must make limit orders that cannot be executed public “immediately”

Post-Trade Transparency – all trades to be made public in near to real time. All trades made outside of a market must be reported. Transaction reporting increases in scope to cover all instruments traded in EU regulated markets, the competent authority for reporting becomes the home state regulator of the firm

Passporting – the range of services and products that can benefit from a passport is expanded allowing firms to offer services cross border more readily and consider structural rationalisation

11 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Indirect impacts

Fragmentation of liquidity

Why? - Concentration Rules repealed; authorisation regimes simplified between MTFs and national exchanges; barriers to remote membership removed; the role of the Systematic Internaliser (SI) as an execution venue

Impact – Makes best execution policy more complex to manage. Firms need to demonstrate that their best execution policy “takes all reasonable steps” to achieve best execution. If a new venue can consistently demonstrate liquidity and good prices then this will need to be taken into account in developing the policy

Changes in Market Data

Why? – Trade reporting will be a more complex environment than today with Investment Firms, SIs, Exchanges and MTFs having roles to play – the role of current data aggregators may change as they offer new services and respond to competitive threats

Impact – understand changes proposed and planned by suppliers and utilise services that reduce the burden on firms

12 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Contents

MiFID: background and bigger picture

The timetable and process for implementation

Tips on formulating a response

Introduction, objectives for today

The main operational considerations

Key articles of the directive

13 - MiFID - presentation - 1st Feb 2007 - Capco confidential

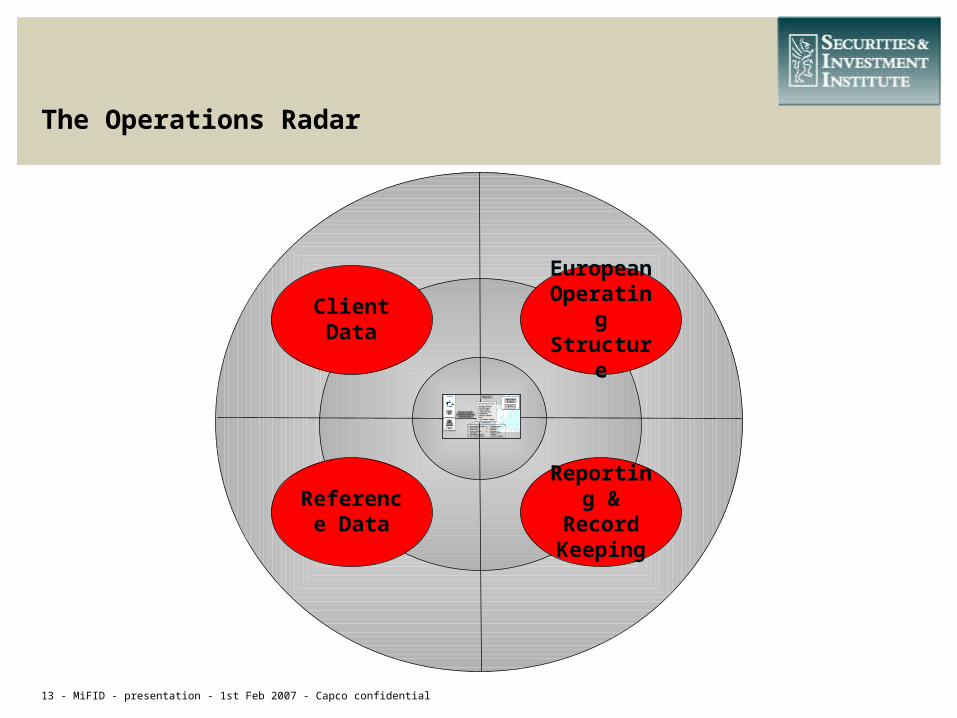

The Operations Radar

Reference Data

Investment Firms

Clients

Retail

Professional

Execution VenuesExecution Venues

Authorised Markets

MTFs

Regulators

Investment advicePortfolio management

Order execution

EligibleCounterparty

• Investment Banks• Asset Managers• Broker Dealers• Corporate Banks• Retail Banks• Futures & Options

Firms• Commodities Traders

1. Transferable Securities2. Money Market

Instruments3. Units in Collective

Investments4. Securities Derivatives5. Commodity Derivatives

6. Credit Derivatives7. Contracts for

Difference8. Derivatives in

Freight, Climatic Variables, Emissions, Inflation

Products

Client Data

Reporting & Record Keeping

European Operating Structure

14 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Client data: ‘Investor Classification’

Classification: There are 3 client classifications (different to current FSA classifications)

Retail clients – afforded the greatest protection

Professional clients – greater protection than “intermediate clients” today

Eligible counterparty – similar to market counterparty and explicitly excluded from some articles, notably Articles 19 (disclosure and appropriateness), 21(best execution) and 22(1) (order prioritisation)

Classification effort

Clients may need to be reclassified based upon the new definitions

Clients will need to be informed of their classification (except in cases of grandfathering, as provided by the FSA) and the impact that this has on their treatment, client agreements will need to be reviewed and may need amendment

Clients may ask/need to be treated differently dependent upon product and service

15 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Client data: ‘Investor Classification’

KYC - Suitability and Appropriateness

Firms providing advice and discretionary portfolio management need to understand the customers profile, objectives and risk appetite – data captured and procedures must support procedures to ensure advice is suitable

Firms providing execution services for “complex” instruments need to understand the experience and knowledge level of the customer

In the UK firms will need to keep records of: the client information it obtains to assess suitability; and

each suitability report it provides

16 - MiFID - presentation - 1st Feb 2007 - Capco confidential

European Operating Structure

Instrument and country scope The expansion of scope in respect to instruments and countries will require firms to

review their branch structures and booking names to ensure that all MiFID regulated products are traded within correctly authorised entities

Passporting The ability to passport a wider range of services and products cross border may result

in opportunity to rationalise how business is conducted within Europe Hub operating models and rationalisation of booking structures that have become

common practice in securities may be extended to include the wider range of MiFID products

17 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Record Keeping and Reporting

Trade reporting Investment firms have the obligation to make trade information public (as near to real

time as possible) on a reasonable commercial basis – they can choose to use Exchanges, MTFs or other third party suppliers to do so

Information will have to be published as close to instantaneously as technically possible (with 3 min cap)

Systematic Internalisers will be able to report anonymously but if so they must publish aggregate quarterly data (no later than 1 month after end of each calendar quarter) as to the transactions they executed as SIs

Exchanges will be allowed to provide Block Trade Facilities and will be able to adopt higher thresholds and/or shorter delays if they wish to do so

The FSA indicates that responsibility for publication will be dictated by agreement between parties and in absence of an agreement by the default MiFID list in Art. 27.4 of the Implementing Regulation

Only the transaction interacting with an Exchange, MTF or SI should trigger a post-trade publication (this leaves out any intermediation chains)

18 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Record Keeping and Reporting

Trade reporting The FSA has produced guidance for making information public. The minimum standards

will be: verification mechanism; use of industry standards to publish information; make information accessible by automated electronic means; accompany with instructions on how to access information

To avoid duplication of information the FSA will implement a Trade Data Monitor Framework (TDM) to ensure each trade is published to one primary publication channel and to avoid deterioration in the quality of market data. Information will be published in a standard data format to ease consolidation (use of ISO formats and open protocols)

The TDM model will be implemented on a voluntary market driven basis. Firms who choose not to use an approved TDM will be monitored closely

19 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Record Keeping and Reporting

Transaction reporting Scope of transaction reporting increases to cover any instrument traded on an EU

regulated market – this will impact in particular trades on commodities and commodity derivatives and on trades on non EU exchanges for instruments also traded on EU regulated exchanges

The FSA has established that firms will continue to transaction report OTC equity and debt derivatives, but only those:

… priced or valued by reference to debt or equity instruments admitted to trading on a prescribed market or exchange and

… priced or valued by references to indices constituted by instruments admitted to trading on a prescribed market or exchange

The FSA will require that firms provide seconds in the trade time of their transactions report where systems permit (adopt HHMMSS format and use ’00’ as default for seconds where true value is not available - e.g. OTC)

The host country reporting offers the opportunity for firms that trade in multiple markets to report once in one format to their home country regulator

20 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Record Keeping and Reporting

Client reporting MiFID has specific requirements relating to reporting to clients on the details of

transactions and on their portfolios. This is likely to reduce the flexibility of the current UK environment and impact on content and frequency of reports:

Retail clients must receive a notice confirming execution no later than T + 1 Unit price must be included in the notice. For orders executed in tranches, the firm may supply information

about the price of each tranche or the average price (but in this case it will have to provide tranche prices upon client request)

For portfolio management, statements must be provided to retail clients once every semester and for leveraged portfolios once every month

The reporting requirements for detailed cost breakdowns for trading and transactions will require firms to be more detailed in reporting to retail clients and to understand and make transparent the cost of trading (includes fees, commissions, charges and expenses, all taxes payable and currency conversion rates and costs)

21 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Reference Data

Key transaction reporting proposals adopted by the FSA Investment management firms will not need to transaction report if the other

party - the sell side broker will do so. However, the report from the latter will have to identify the investment management firm with the FSA reference number or BIC or, in absence of these a internal unique code

For on-exchange instruments the transaction report must contain a valid ISIN to identify the instrument (from this, the FSA will auto populate all data fields relating to the characteristics of the instrument)

The FSA has been working with Swift to ensure that MTFs have a Market Identifier Code (MIC) for the market identifier field where firms will report whether the transaction was conducted on an MTF and if so, which one

The FSA will require firms to identify the client in each transaction by using BIC codes (full 11 character code or 8 character code or codes with ‘XXX’ at the end) or where these are not available a unique internal code

This will result in costly consolidation of codes for EEA passported branches. To mitigate this, the FSA will grant temporary waivers

22 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Reference Data

Key transaction reporting proposals adopted by the FSA The ISIN will be the unique code used for transferring reports between

competent authorities (ISINs will be created for all reportable on-exchange products that do not currently have one)

The FSA will introduce a separate classification for Credit Default Swaps (CDS). The underlying ISIN for a CDS can identify any of the instruments issued by the entity that the CDS relates to, or simply identify the reference obligation

The FSA will publish a Transaction Reporting Users Pack (TRUP) with technical details on how to provide the reports and what to include (e.g. new fields)

23 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Contents

MiFID: background and bigger picture

The timetable and process for implementation

Tips on formulating a response

Introduction, objectives for today

The main operational considerations

Key articles of the directive

24 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Introduction process and timetable

MiFID is being implemented following the 4 level Lamfalussy process

It has both regulatory and directive elements and these dictate different paths as to how the legislation is enacted

The Lamfalussy procedure

• Legislation and directives – EC

• Technical implementation advice – CESR & ESC

• Local conduct of business rules – CESR and local regulators

• Enforcement of rules – member states

Level 1

Level 2

Level 3

Level 4

CESR = Committee of European Securities Regulators

ESC = The European Securities Committee

Regulation comes into effect directly as European Legislation

Transaction Reporting – (Article 25, 56,58, 28, 30, 45) : transaction reporting and information to be shared between regulators

Systematic Internalisers - (Article 4, 25, 27): criteria for defining a Systematic Internaliser, the obligations of a Systematic Internalisers and the definition of liquid shares

Directive measures are transcribed into local law by the FSA and Parliament in the UK)

Organisational Requirements – (Article 13, 18, 19) : conduct of business including conflict of interest

Best Execution - (Article 21)

Eligible Counterparty Definition – (Article 24)

Order Management (Article 22): obligations around prioritisation of orders and amalgamation and allocation of orders

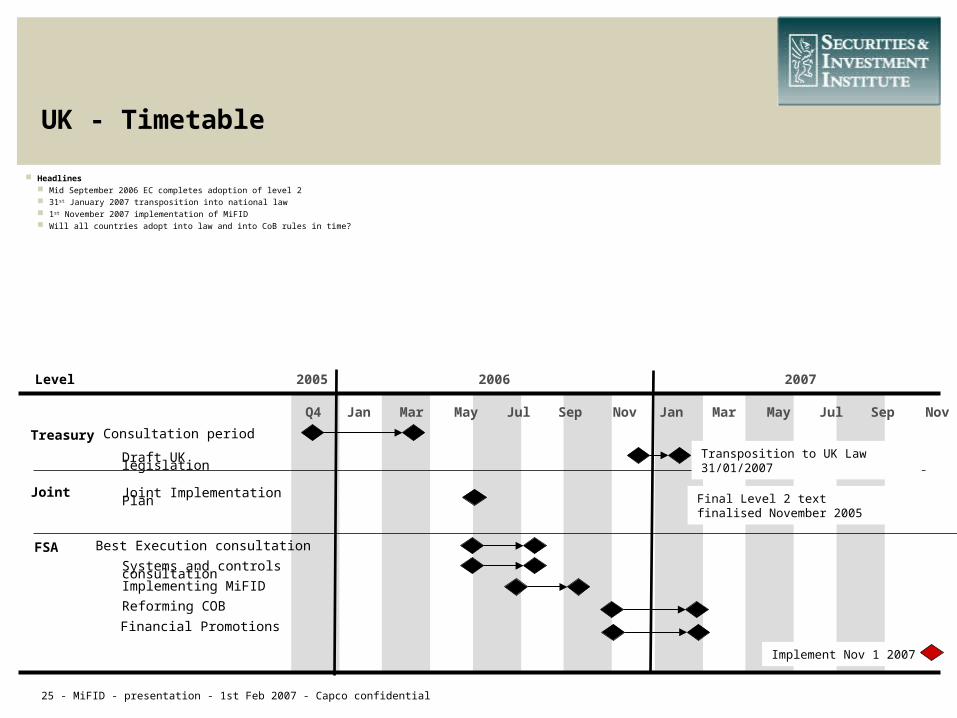

25 - MiFID - presentation - 1st Feb 2007 - Capco confidential

UK - Timetable

20072005 2006

Q4 Jan Mar May Jul Sep Nov

FSA

Systems and controls consultation

Best Execution consultation

Implementing MiFID

Joint Implementation PlanJoint

Treasury Consultation period

Draft UK legislation

Level

Final Level 2 text finalised November 2005

Transposition to UK Law 31/01/2007

Implement Nov 1 2007

Headlines Mid September 2006 EC completes adoption of level 2 31st January 2007 transposition into national law 1st November 2007 implementation of MiFID Will all countries adopt into law and into CoB rules in time?

Jan Mar May Jul Sep Nov

Reforming COB

Financial Promotions

26 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Contents

MiFID: background and bigger picture

The timetable and process for implementation

Tips on formulating a response

Introduction, objectives for today

The main operational considerations

Key articles of the directive

27 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Smart response – key principle: do not respond in isolation

Consider potential “big picture” impacts in formulating a response. Some of the major ramifications may include: fragmentation of liquidity, exchange consolidation, new competition, opportunity to expand cross border…..

Consider the response of suppliers who might help :- Data vendors for consolidated price information Exchanges/MTFs looking to provide new services Connectivity routing providers looking to simplify best execution

obligations Data vendors looking to provide aggregator/publisher services Outsource service providers (..care with possible additional obligations)

Consider common non-competitive issues and consider cooperation with peers (consortia approach e.g. Project Boat; Project Turquoise)

Engage with industry consultation process, e.g. with FSA, JWG, LSE… (consultation process nearly completed)

28 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Smart response – 6 health check points for your firm

1. Broad representation: MiFID requires input from business, operations, IT and legal and regulatory; it cannot be dealt with as a narrow compliance issue

2. “Big Picture” first: the first assessment should look across all of the activity of the firm to identify where the main impacts are before going into detail

3. Proactive approach to suppliers: identify key suppliers and understand their plans, interact to influence them

4. Proactive approach to regulators: be prepared to seek guidance early and to interact with the local regulators to clarify specifics

5. Clearly identified champion: that will ensure the firm keeps up to date with developments and will participate in, or even lead, the market consultation and potential cooperation with peers. An internal single point of contact.

6. Alignment with other programs: leverage existing or planned initiatives that align with MiFID requirements (e.g. AML & KYC, reference data initiatives, workflow implementation and, potential synergies with Reg NMS). Aim to minimise the need for duplicate “regret spend” and maximise the effective use of scarce resource

29 - MiFID - presentation - 1st Feb 2007 - Capco confidential

Further information

www.mifid.com – JWG web site

www.hm-treasury.gov.uk – Treasury

www.fsa.gov.uk – FSA

www.cesr-eu.org – Committee of European Securities Regulators

www.capco.com – White paper on MiFID “A smart response”