Embed Size (px)

Citation preview

MARKETING COSTSMARKETING COSTSIN ALTERNATIVE MARKETING IN ALTERNATIVE MARKETING

CHANNELSCHANNELS

Shermain Hardesty & Penny Shermain Hardesty & Penny LeffLeff

University of CaliforniaUniversity of CaliforniaSmall Farm ProgramSmall Farm Program

OVERVIEWOVERVIEW

Growth in Direct MarketingGrowth in Direct Marketing Objective & ApproachObjective & Approach

detailed review of marketing related detailed review of marketing related expensesexpenses

Application to YOUR farmApplication to YOUR farm Comparing Profitability in Alternative Comparing Profitability in Alternative

ChannelsChannels

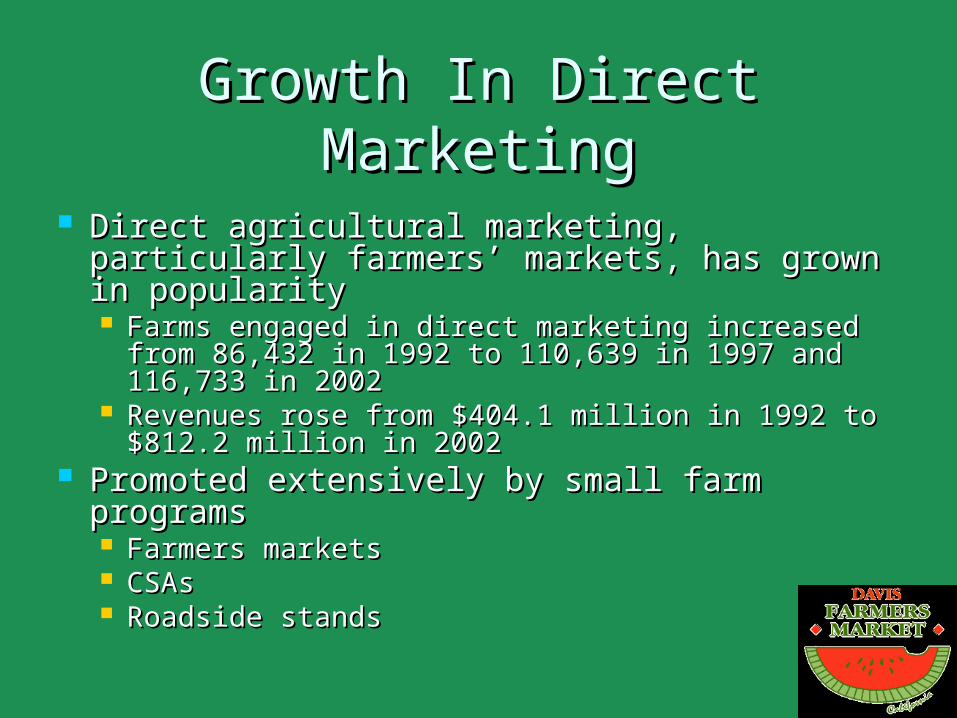

Growth In Direct MarketingGrowth In Direct Marketing

Direct agricultural marketing, particularly Direct agricultural marketing, particularly farmers’ markets, has grown in popularityfarmers’ markets, has grown in popularity Farms engaged in direct marketing increased Farms engaged in direct marketing increased

from 86,432 in 1992 to 110,639 in 1997 and from 86,432 in 1992 to 110,639 in 1997 and 116,733 in 2002116,733 in 2002

Revenues rose from Revenues rose from $404.1 million in 1992 to $404.1 million in 1992 to $812.2 million in 2002 $812.2 million in 2002

Promoted extensively by small farm programsPromoted extensively by small farm programs Farmers marketsFarmers markets CSAsCSAs Roadside standsRoadside stands

Objective & ApproachObjective & Approach

Compare the relative marketing costs and Compare the relative marketing costs and profitability of different marketing channels—profitability of different marketing channels—farmers’ markets, CSAs and wholesale farmers’ markets, CSAs and wholesale markets markets

Based on case studies of 3 organic fruit and Based on case studies of 3 organic fruit and vegetable producersvegetable producers Well establishedWell established Small, medium & largeSmall, medium & large Northern CaliforniaNorthern California Sell through farmers markets, CSA and wholesaleSell through farmers markets, CSA and wholesale

ApproachApproach

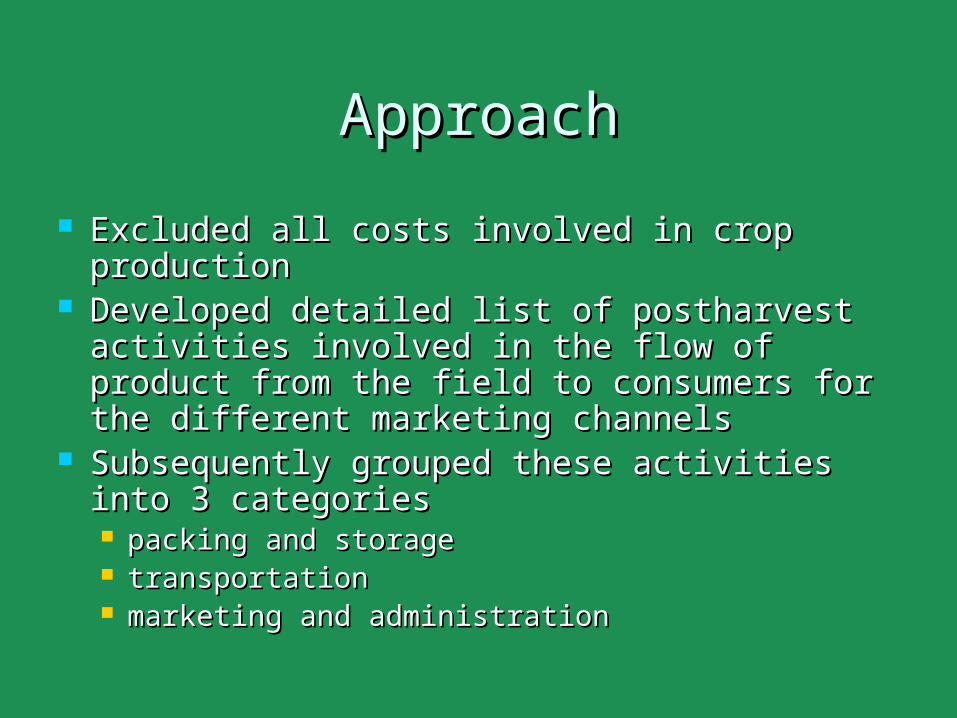

Excluded all costs involved in crop production Excluded all costs involved in crop production Developed detailed list of postharvest Developed detailed list of postharvest

activities involved in the flow of product from activities involved in the flow of product from the field to consumers for the different the field to consumers for the different marketing channelsmarketing channels

Subsequently grouped these activities into 3 Subsequently grouped these activities into 3 categoriescategories packing and storagepacking and storage transportationtransportation marketing and administration marketing and administration

Sorting & Packing CostsSorting & Packing Costs

Sort & pack product – facilities & Sort & pack product – facilities & equipmentequipment

Sort & pack product – labor & Sort & pack product – labor & materialsmaterials

Load, unload truck – laborLoad, unload truck – labor Maintain market supplies & equipment Maintain market supplies & equipment

– labor– labor Training & supervision - labor Training & supervision - labor

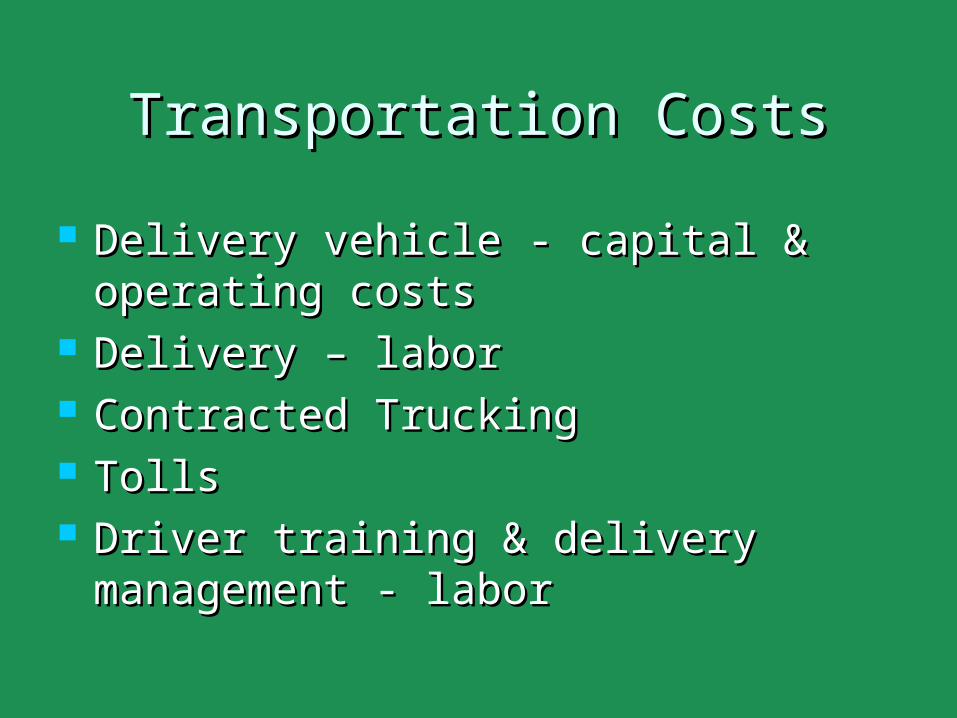

Transportation CostsTransportation Costs

Delivery vehicle - capital & operating Delivery vehicle - capital & operating costscosts

Delivery – laborDelivery – labor Contracted TruckingContracted Trucking TollsTolls Driver training & delivery Driver training & delivery

management - labormanagement - labor

Selling & Administrative Selling & Administrative CostsCosts

Market Market communications – laborcommunications – labor

Wholesale sales – laborWholesale sales – labor Retail sales – laborRetail sales – labor Marketing materials Marketing materials

costs – labor and costs – labor and materialsmaterials

Sales staff Sales staff administration – laboradministration – labor

Office facilities, Office facilities, equipment, supplies, equipment, supplies, services useservices use

Record keeping systemsRecord keeping systems Account maintenance, Account maintenance,

banking, bookkeeping – banking, bookkeeping – laborlabor

Other office staff – laborOther office staff – labor Business planning – Business planning –

labor labor

Measuring CostsMeasuring Costs

Chronological sequence of events involved Chronological sequence of events involved from harvest through salesfrom harvest through sales examined separately for each day of the week examined separately for each day of the week

for the seasons (winter, summer) and for each for the seasons (winter, summer) and for each market channelmarket channel

elicited estimates of staffing and hours of labor elicited estimates of staffing and hours of labor involved for each marketing activity in each involved for each marketing activity in each market channel typemarket channel type

determined what purchased goods and determined what purchased goods and services and capital assets were utilizedservices and capital assets were utilized

Measuring CostsMeasuring Costs Used original purchase values and Used original purchase values and

straight line method to calculate straight line method to calculate depreciationdepreciation

Valued operator labor at same rates Valued operator labor at same rates paid to hired labor for same activitypaid to hired labor for same activity

MEASURING MARKETING MEASURING MARKETING COSTS FOR YOUR OPERATIONCOSTS FOR YOUR OPERATION

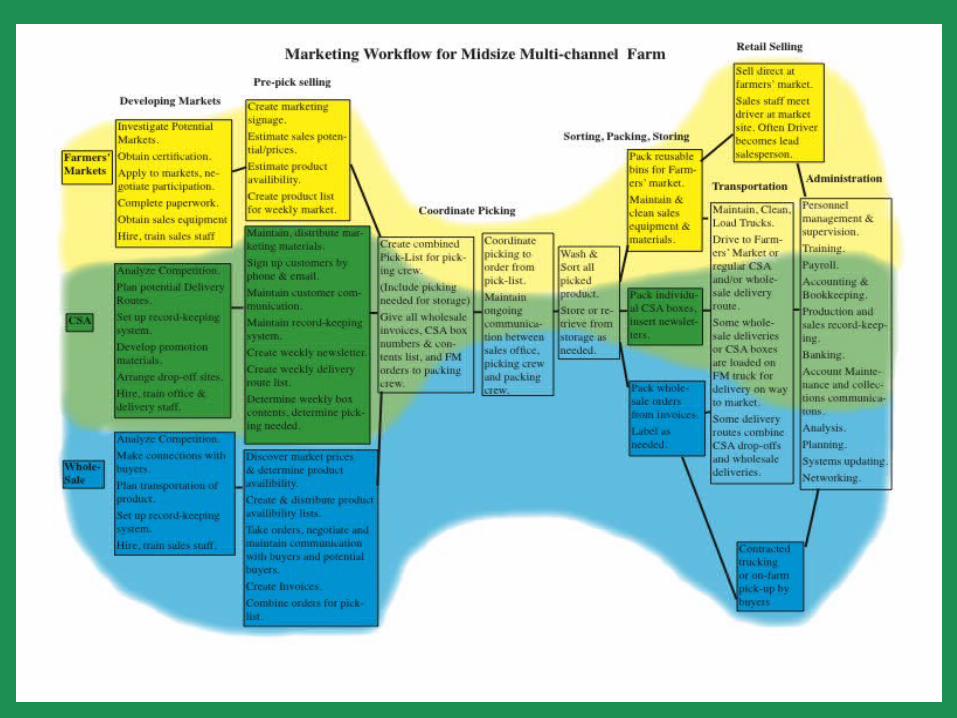

Combining direct marketing and Combining direct marketing and wholesale selling as a small or mid-wholesale selling as a small or mid-size grower usually involves a size grower usually involves a complicated pattern of shared use of complicated pattern of shared use of labor, vehicles and facilities by the labor, vehicles and facilities by the different marketing channels.different marketing channels.

To determine the profitability of To determine the profitability of each channel, we need to look each channel, we need to look closely at this pattern and closely at this pattern and allocate the costs as accurately allocate the costs as accurately as possible. We have prepared a as possible. We have prepared a series of worksheets to help put series of worksheets to help put all this information into a useful all this information into a useful order.order.

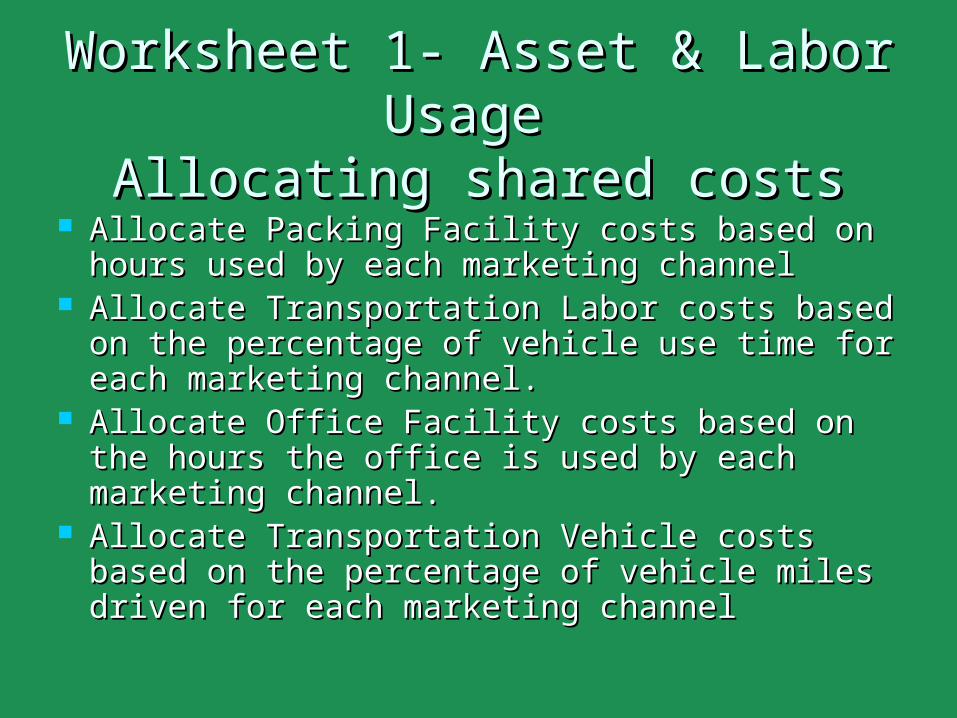

Worksheet 1- Asset & Labor Worksheet 1- Asset & Labor Usage Usage

Allocating shared costsAllocating shared costs Allocate Packing Facility costs based on hours Allocate Packing Facility costs based on hours

used by each marketing channelused by each marketing channel Allocate Transportation Labor costs based on Allocate Transportation Labor costs based on

the percentage of vehicle use time for each the percentage of vehicle use time for each marketing channel. marketing channel.

Allocate Office Facility costs based on the Allocate Office Facility costs based on the hours the office is used by each marketing hours the office is used by each marketing channel.channel.

Allocate Transportation Vehicle costs based on Allocate Transportation Vehicle costs based on the percentage of vehicle miles driven for the percentage of vehicle miles driven for each marketing channeleach marketing channel

Very Important note:Very Important note: Because owners and family members Because owners and family members usually do many marketing tasks on a usually do many marketing tasks on a small farm, payroll records are not small farm, payroll records are not sufficient for allocating costs. When sufficient for allocating costs. When computing the hours and miles for the computing the hours and miles for the different marketing activities, be sure different marketing activities, be sure to include time spent by the farm to include time spent by the farm owners and family members, even if owners and family members, even if they are not paid a wage, in order to they are not paid a wage, in order to get an accurate picture of the labor get an accurate picture of the labor cost of each channel.cost of each channel.

Worksheet 1 -Worksheet 1 - Allocating Allocating Packing Facility CostsPacking Facility Costs

Start with a normal workweek in SummerStart with a normal workweek in Summer List each task in packing facility, starting with List each task in packing facility, starting with

washing or cleaning produce and ending with washing or cleaning produce and ending with loading delivery vehiclesloading delivery vehicles Determine how many people-hours each task takes Determine how many people-hours each task takes

for product destined for each marketing channel, for product destined for each marketing channel, estimating where neededestimating where needed

Include owner & family labor hoursInclude owner & family labor hours Add up usual weekly labor hours for each Add up usual weekly labor hours for each

channel for Summer work patternchannel for Summer work pattern Total should equal 100% of weekly Summer packing Total should equal 100% of weekly Summer packing

facility labor hours, including cleaning & facility labor hours, including cleaning & maintenancemaintenance

Worksheet 1 -Worksheet 1 - Allocating Allocating Packing Facility CostsPacking Facility Costs

Repeat the process for Winter or other Repeat the process for Winter or other seasonal weekly work patternseasonal weekly work pattern

Multiply by number of weeks for each patternMultiply by number of weeks for each pattern Add seasonal totals to determine total annual Add seasonal totals to determine total annual

packing facility hours for each marketing packing facility hours for each marketing channelchannel

Divide annual hours for each channel by total Divide annual hours for each channel by total annual hours for all channels to determine annual hours for all channels to determine percentage use of packing facility by each percentage use of packing facility by each channel. This is the basis for allocating costs.channel. This is the basis for allocating costs.

Worksheet 1 - Allocating Worksheet 1 - Allocating Transportation Labor CostsTransportation Labor Costs

Using first a normal Summer weekly work pattern, then Using first a normal Summer weekly work pattern, then a normal Winter weekly work pattern, list all delivery a normal Winter weekly work pattern, list all delivery vehicle usage hours, broken down by marketing channelvehicle usage hours, broken down by marketing channel Assign hours that vehicle is parked at a farmers’ market as Assign hours that vehicle is parked at a farmers’ market as

farmers’ market hours for this purposefarmers’ market hours for this purpose For combined loads, assign hours based on the percent value of For combined loads, assign hours based on the percent value of

product going to each marketing channelproduct going to each marketing channel Determine total annual delivery vehicle hours for each Determine total annual delivery vehicle hours for each

marketing channel, making sure that combined total marketing channel, making sure that combined total equals 100% of delivery hoursequals 100% of delivery hours

Divide total hours for each channel by combined total to Divide total hours for each channel by combined total to determine percentage use for each channel. This is the determine percentage use for each channel. This is the basis for allocating transportation labor costs.basis for allocating transportation labor costs.

Worksheet 1 - Allocating Worksheet 1 - Allocating Facility Costs, Sales & Facility Costs, Sales &

Admin OfficeAdmin Office List the people who work in the office, including List the people who work in the office, including

owners & family membersowners & family members List total hours in office for each personList total hours in office for each person Break total hours down for each person, listing Break total hours down for each person, listing

hours spent on tasks for each marketing hours spent on tasks for each marketing channel, and also hours for non-marketing office channel, and also hours for non-marketing office tasks such as production payroll & planningtasks such as production payroll & planning

Determine percent of office labor hours used for Determine percent of office labor hours used for each marketing channel. Total will be less than each marketing channel. Total will be less than 100% of all office labor hours if office is used 100% of all office labor hours if office is used also for production administration. also for production administration.

Worksheet 1 - Allocating Worksheet 1 - Allocating Transportation Asset & Operations Transportation Asset & Operations

CostsCosts Starting with weekly delivery vehicle use Starting with weekly delivery vehicle use

patterns, compute annual miles delivery vehicles patterns, compute annual miles delivery vehicles are used for each marketing channel, and then are used for each marketing channel, and then percent of total combined mileage for each percent of total combined mileage for each channel, using methods used above.channel, using methods used above. Mileage for each portion of a mixed load delivery route Mileage for each portion of a mixed load delivery route

can be estimated by allocation to each segment the can be estimated by allocation to each segment the proportion of the total miles for the route that is the proportion of the total miles for the route that is the same as the proportion of value of product delivered, or same as the proportion of value of product delivered, or the proportion of space used in the vehicle.the proportion of space used in the vehicle.

If delivery vehicles are also used for personal use or If delivery vehicles are also used for personal use or production, note the percent of use for delivery.production, note the percent of use for delivery.

If different vehicles have significantly different If different vehicles have significantly different operating costs, use Worksheet 2 as a guide.operating costs, use Worksheet 2 as a guide.

Worksheet 3 - Labor CostWorksheet 3 - Labor Cost

List the wage rate for each worker in a List the wage rate for each worker in a category, such as “driver” or “packer” or category, such as “driver” or “packer” or “market sales”“market sales”

Look up or estimate the number of Look up or estimate the number of overtime hours in the year.overtime hours in the year.

Use this information to figure out the actual Use this information to figure out the actual average hourly wage for each categoryaverage hourly wage for each category

Add employer tax, workers’ comp, health & Add employer tax, workers’ comp, health & other benefit costs per hour to determine other benefit costs per hour to determine average hourly cost for each labor categoryaverage hourly cost for each labor category

Worksheet 3 - Labor CostWorksheet 3 - Labor Cost

Figure average legal wage rate for all Figure average legal wage rate for all categories of work, including any work categories of work, including any work customarily paid in cash and work often customarily paid in cash and work often done by owners & family members.done by owners & family members.

Note that the owner’s work is valued at Note that the owner’s work is valued at the rate per hour that is the same as the rate per hour that is the same as the average legal labor cost of a worker the average legal labor cost of a worker doing the same work. doing the same work.

Worksheet 4 - Allocations of Worksheet 4 - Allocations of Asset & Operations CostsAsset & Operations Costs

Now we will add up the actual costs to be Now we will add up the actual costs to be allocated to each channelallocated to each channel

First, the transportation operations costsFirst, the transportation operations costs List all delivery vehicle operating costsList all delivery vehicle operating costs If vehicles are used for both business and If vehicles are used for both business and

personal use, or for production activities, list personal use, or for production activities, list only the portion of costs that approximate the only the portion of costs that approximate the portion of marketing use of the vehicles.portion of marketing use of the vehicles.

Add all the costs listed. Add all the costs listed.

Worksheet 4 - Allocations of Worksheet 4 - Allocations of Asset & Operations CostsAsset & Operations Costs

When computing packing and delivery labor When computing packing and delivery labor cost, use the total numbers of hours cost, use the total numbers of hours computed in worksheet 1computed in worksheet 1 Multiply the total number of hours by the average Multiply the total number of hours by the average

labor cost for each category of workerlabor cost for each category of worker Be sure to include owner and family labor hoursBe sure to include owner and family labor hours

Selling labor costs will be added later for Selling labor costs will be added later for each marketing channeleach marketing channel

Sum listed costs and other costs as needed, Sum listed costs and other costs as needed, to determine total shared costs to be to determine total shared costs to be allocatedallocated

Worksheet 5 - Channel Worksheet 5 - Channel Specific CostsSpecific Costs

Costs that can be clearly connected to a specific Costs that can be clearly connected to a specific marketing channelmarketing channel

Selling labor costs are all directly charged to the Selling labor costs are all directly charged to the channel where the sales occurchannel where the sales occur

For selling labor costs for the farmers’ market For selling labor costs for the farmers’ market channel, add the total number of hours of selling channel, add the total number of hours of selling labor and multiply by the average hourly labor cost labor and multiply by the average hourly labor cost of a farmers’ market salesperson from Worksheet 3of a farmers’ market salesperson from Worksheet 3 Include owner and family members’ hoursInclude owner and family members’ hours Do not count the driver/lead salespersons’ time at market Do not count the driver/lead salespersons’ time at market

twicetwice

Worksheet 6 - Marketing Worksheet 6 - Marketing Cost SummaryCost Summary

This worksheet puts all our computations This worksheet puts all our computations together. together.

Find percentage rates for allocations from Find percentage rates for allocations from Worksheet 1Worksheet 1

Find costs to be allocated from Worksheet 4Find costs to be allocated from Worksheet 4 Multiply the appropriate percentage by the Multiply the appropriate percentage by the

cost to be allocated, and enter the results cost to be allocated, and enter the results for each channel.for each channel.

Enter channel specific costs from Worksheet Enter channel specific costs from Worksheet 5 as needed.5 as needed.

Worksheet 6 - Marketing Worksheet 6 - Marketing Cost SummaryCost Summary

Total each category of costs (packing, Total each category of costs (packing, transportation, selling & admin.) for each transportation, selling & admin.) for each marketing channelmarketing channel

Divide each total by the total revenue for that Divide each total by the total revenue for that channel to get cost as a percent of revenue.channel to get cost as a percent of revenue.

Add category totals to get total marketing Add category totals to get total marketing cost for each channel.cost for each channel.

Divide total marketing cost by total revenue Divide total marketing cost by total revenue for each channel to get marketing cost as a for each channel to get marketing cost as a percent of revenue for each marketing percent of revenue for each marketing channel.channel.

Congratulations!Congratulations!

You have just determined a You have just determined a close estimate of the close estimate of the

marketing costs of each of marketing costs of each of your marketing channels, your marketing channels,

including the cost of the farm including the cost of the farm owners’ and family members’ owners’ and family members’

time.time.

Return to MarketingReturn to Marketing

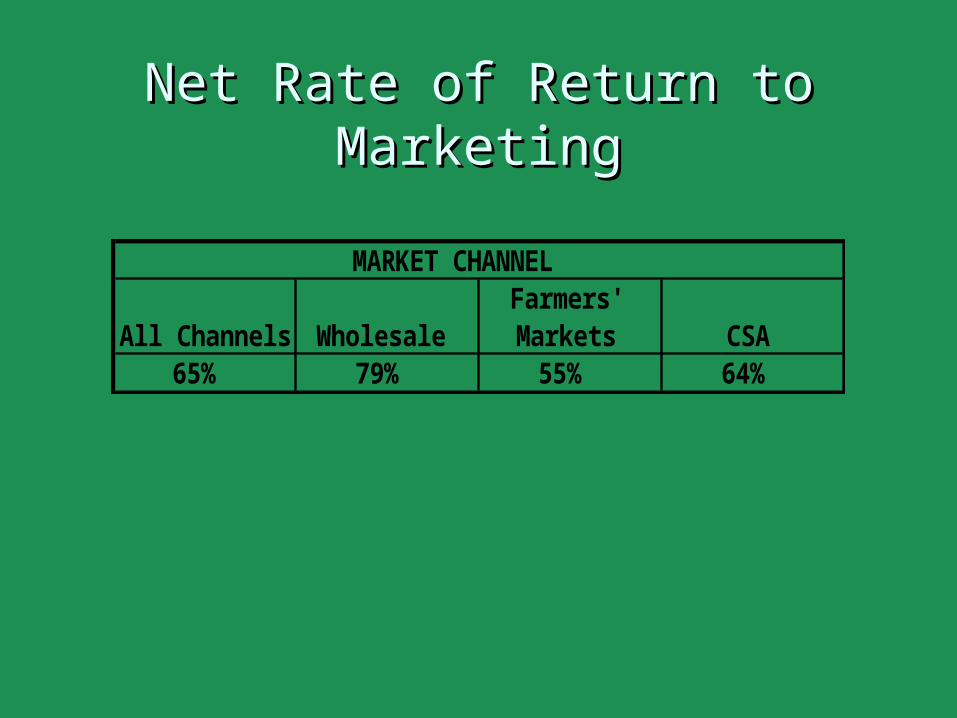

Subtract the final line in Worksheet Subtract the final line in Worksheet 6, the marketing costs as a percent 6, the marketing costs as a percent of total revenue, from 1 to get a of total revenue, from 1 to get a percentage called “Return to percentage called “Return to Marketing”Marketing”

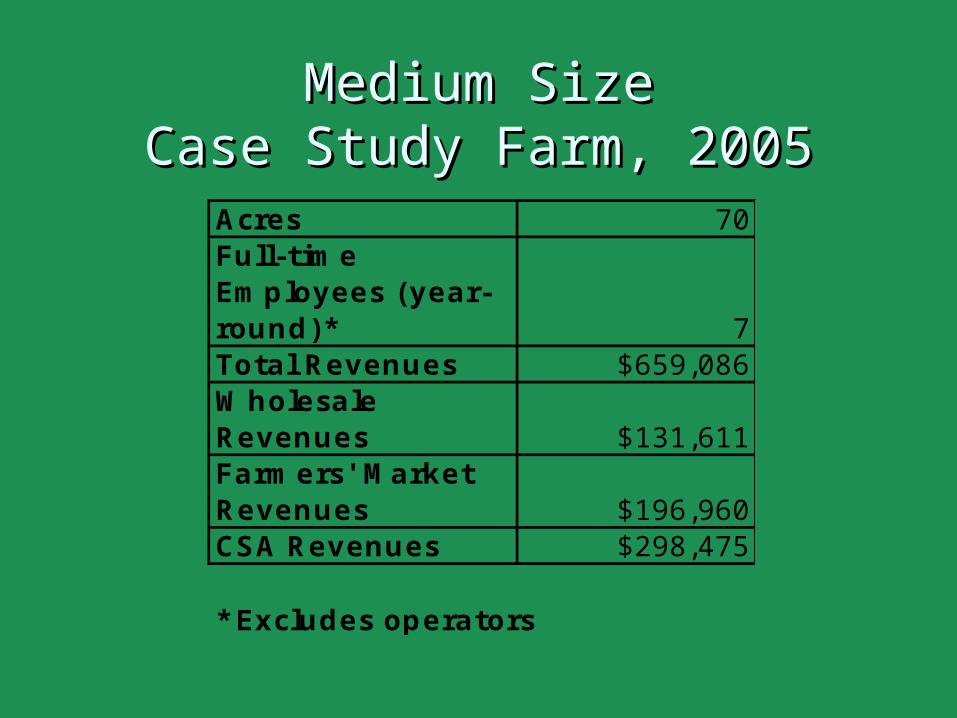

Medium SizeMedium SizeCase Study Farm, 2005Case Study Farm, 2005

Acres 70Full-time Employees (year-round)* 7Total Revenues $659,086Wholesale Revenues $131,611Farmers' Market Revenues $196,960CSA Revenues $298,475

* Excludes operators

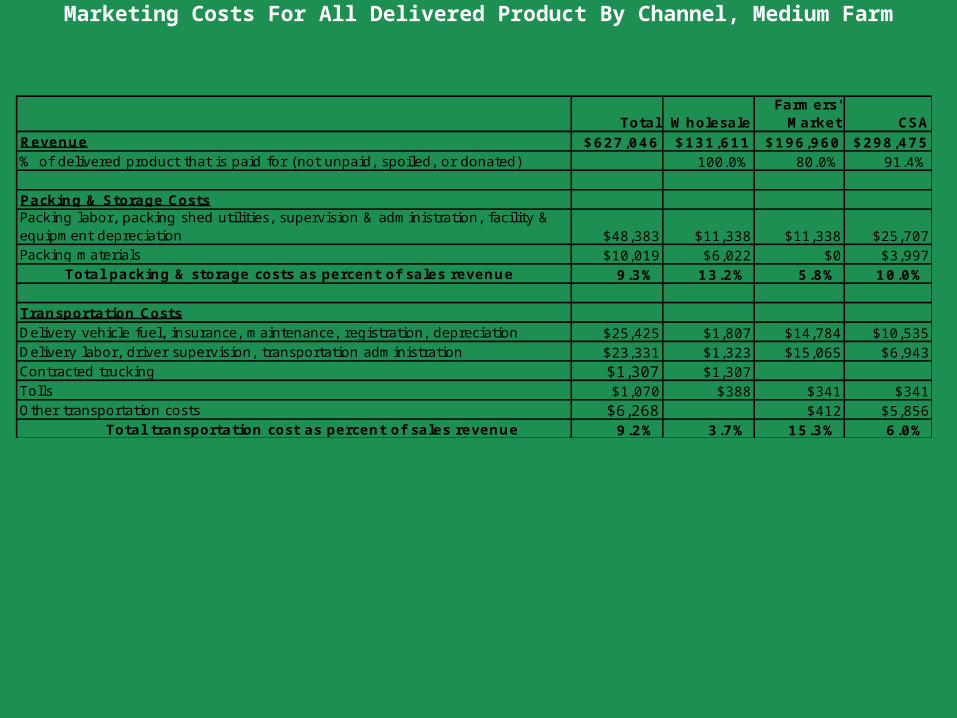

Marketing Costs For All Delivered Product By Channel, Medium Farm Total Wholesale

Farmers' Market CSA

Revenue $627,046 $131,611 $196,960 $298,475% of delivered product that is paid for (not unpaid, spoiled, or donated) 100.0% 80.0% 91.4%

Packing & Storage CostsPacking labor, packing shed utilities, supervision & administration, facility & equipment depreciation $48,383 $11,338 $11,338 $25,707Packing materials $10,019 $6,022 $0 $3,997 Total packing & storage costs as percent of sales revenue 9.3% 13.2% 5.8% 10.0%

Transportation CostsDelivery vehicle fuel, insurance, maintenance, registration, depreciation $25,425 $1,807 $14,784 $10,535Delivery labor, driver supervision, transportation administration $23,331 $1,323 $15,065 $6,943Contracted trucking $1,307 $1,307Tolls $1,070 $388 $341 $341Other transportation costs $6,268 $412 $5,856 Total transportation cost as percent of sales revenue 9.2% 3.7% 15.3% 6.0%

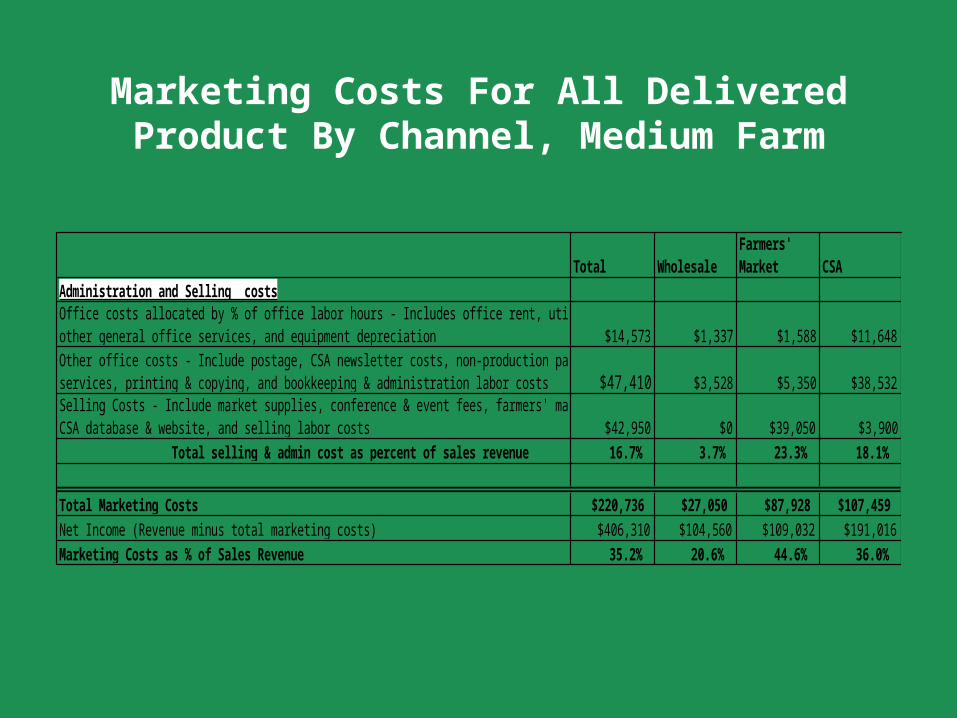

Marketing Costs For All Delivered Product By Channel, Medium Farm

Total WholesaleFarmers' Market CSA

Administration and Selling costsOffice costs allocated by % of office labor hours - Includes office rent, utilities, phone, other general office services, and equipment depreciation $14,573 $1,337 $1,588 $11,648Other office costs - Include postage, CSA newsletter costs, non-production payroll services, printing & copying, and bookkeeping & administration labor costs $47,410 $3,528 $5,350 $38,532Selling Costs - Include market supplies, conference & event fees, farmers' market fees, CSA database & website, and selling labor costs $42,950 $0 $39,050 $3,900 Total selling & admin cost as percent of sales revenue 16.7% 3.7% 23.3% 18.1%

Total Marketing Costs $220,736 $27,050 $87,928 $107,459Net Income (Revenue minus total marketing costs) $406,310 $104,560 $109,032 $191,016Marketing Costs as % of Sales Revenue 35.2% 20.6% 44.6% 36.0%

Net Rate of Return to Net Rate of Return to MarketingMarketing

All Channels WholesaleFarmers' Markets CSA

65% 79% 55% 64%

MARKET CHANNEL

COMPARING COMPARING PROFITABILITY ACROSS PROFITABILITY ACROSS

CHANNELSCHANNELS

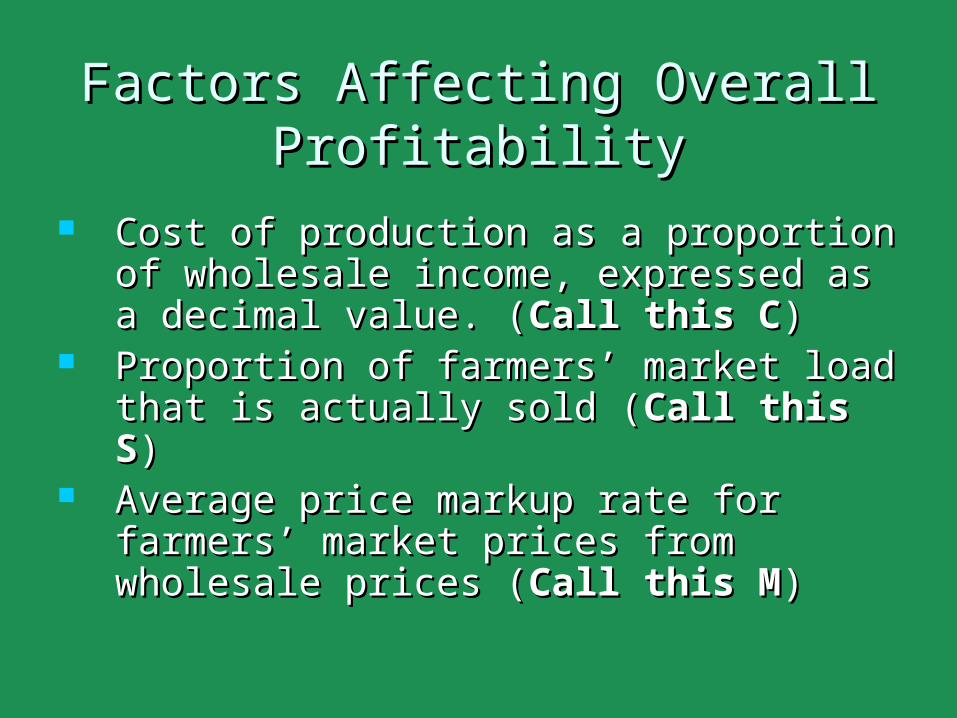

Factors Affecting Overall Factors Affecting Overall ProfitabilityProfitability

Cost of production as a proportion Cost of production as a proportion of wholesale income, expressed as of wholesale income, expressed as a decimal value. (a decimal value. (Call this CCall this C))

Proportion of farmers’ market load Proportion of farmers’ market load that is actually sold (that is actually sold (Call this SCall this S))

Average price markup rate for Average price markup rate for farmers’ market prices from farmers’ market prices from wholesale prices (wholesale prices (Call this MCall this M) )

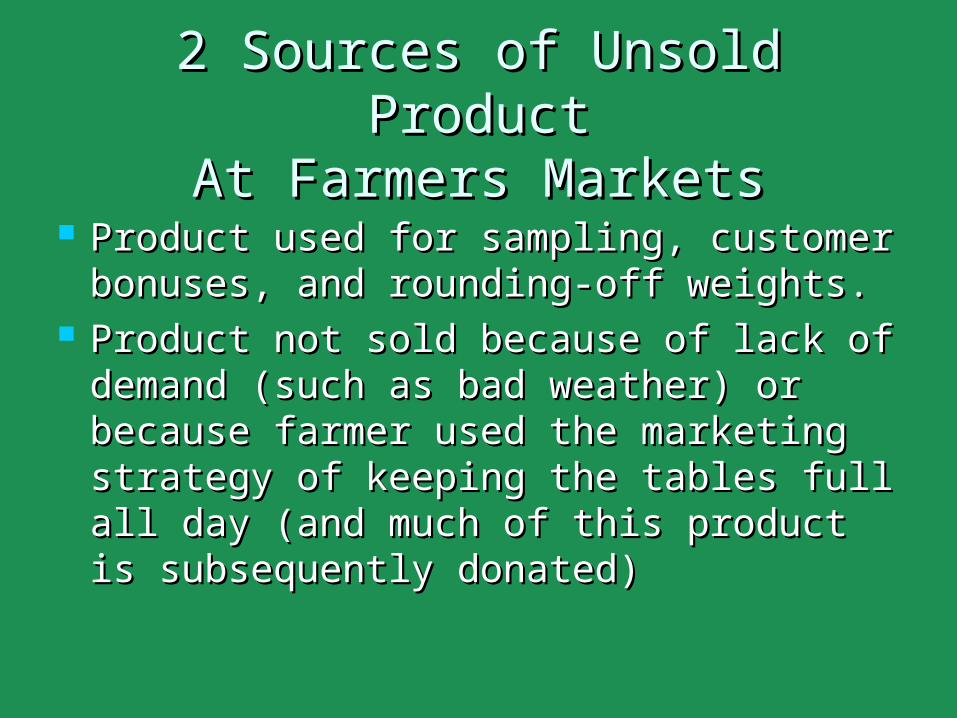

2 Sources of Unsold Product2 Sources of Unsold ProductAt Farmers MarketsAt Farmers Markets

Product used for sampling, customer Product used for sampling, customer bonuses, and rounding-off weights.bonuses, and rounding-off weights.

Product not sold because of lack of Product not sold because of lack of demand (such as bad weather) or demand (such as bad weather) or because farmer used the marketing because farmer used the marketing strategy of keeping the tables full all strategy of keeping the tables full all day (and much of this product is day (and much of this product is subsequently donated)subsequently donated)

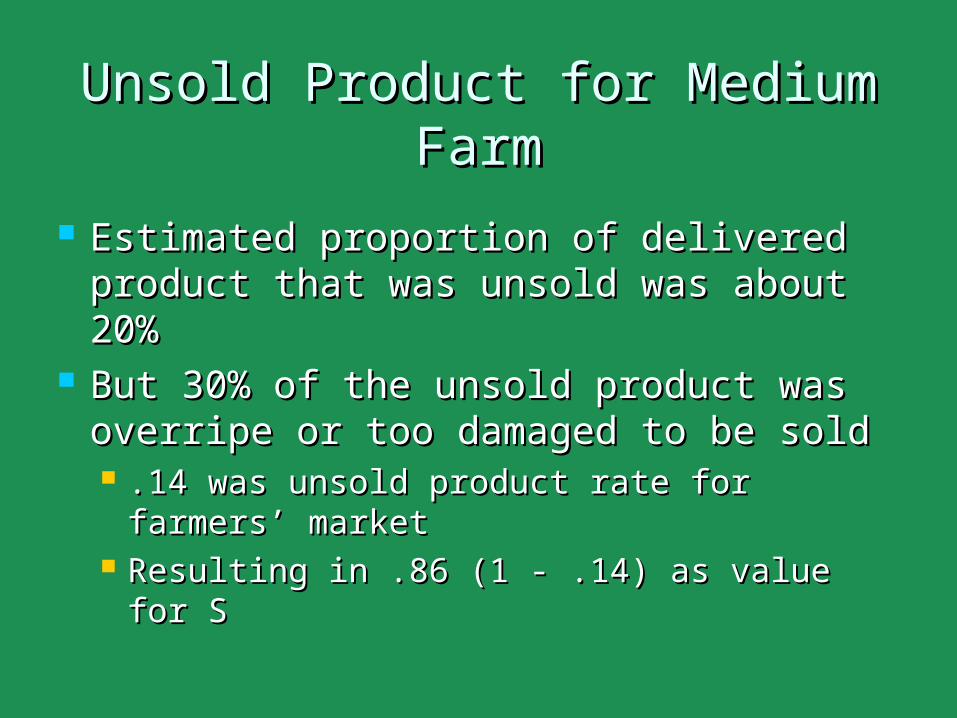

Unsold Product for Medium Unsold Product for Medium FarmFarm

Estimated proportion of delivered Estimated proportion of delivered product that was unsold was about product that was unsold was about 20%20%

But 30% of the unsold product was But 30% of the unsold product was overripe or too damaged to be soldoverripe or too damaged to be sold .14 was unsold product rate for farmers’ .14 was unsold product rate for farmers’

marketmarket Resulting in .86 (1 - .14) as value for SResulting in .86 (1 - .14) as value for S

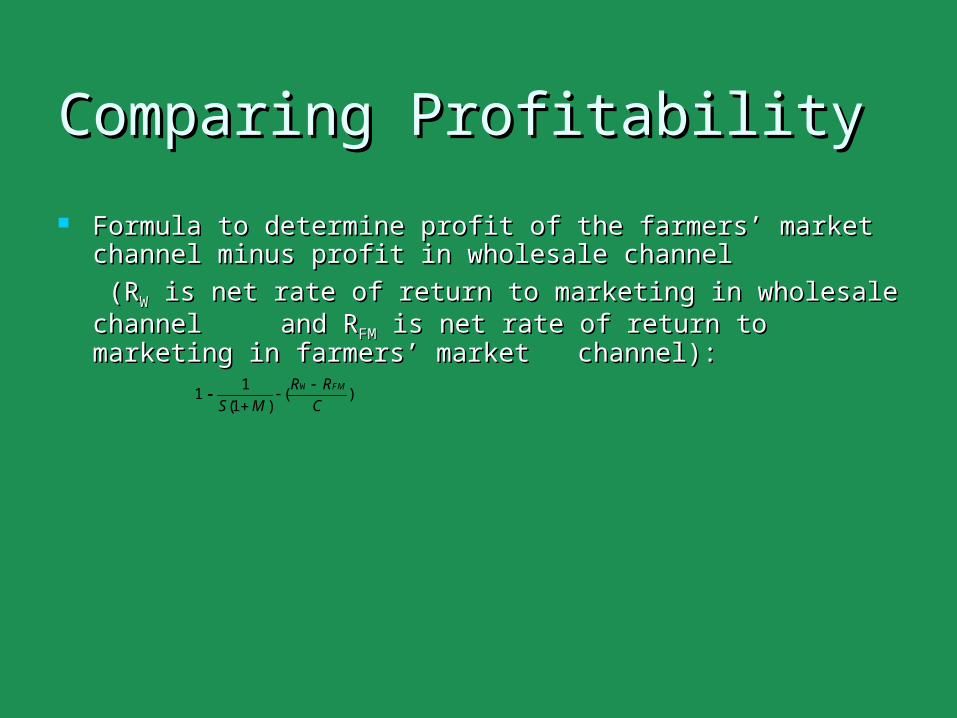

Comparing Profitability Comparing Profitability

Formula to determine profit of the farmers’ market channel Formula to determine profit of the farmers’ market channel minus profit in wholesale channel minus profit in wholesale channel

(R(RWW is net rate of return to marketing in wholesale is net rate of return to marketing in wholesale channel channel and Rand RFMFM is net rate of return to marketing in is net rate of return to marketing in farmers’ marketfarmers’ market channel): channel):

1 - W1

( )(1 )

FMR R

S M C

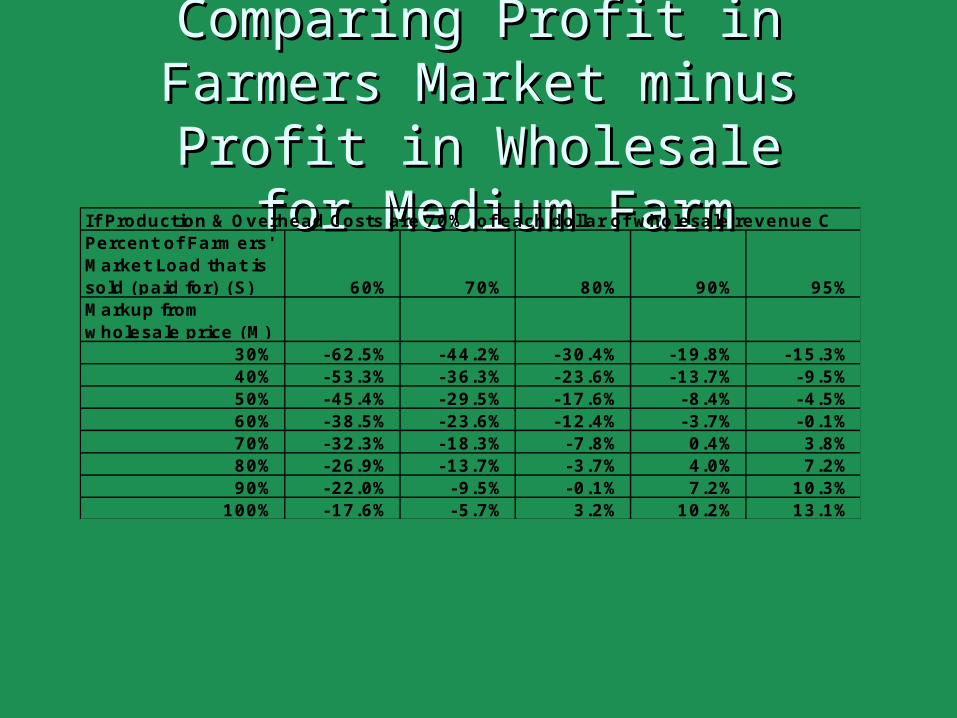

Comparing Profit in Farmers Comparing Profit in Farmers Market minus Profit in Market minus Profit in

WholesaleWholesale for Medium Farm for Medium FarmIf Production & Overhead Costs are 70% of each dollar of wholesale revenue C

Percent of Farmers' Market Load that is sold (paid for) (S) 60% 70% 80% 90% 95%Markup from wholesale price (M)

30% -62.5% -44.2% -30.4% -19.8% -15.3%40% -53.3% -36.3% -23.6% -13.7% -9.5%50% -45.4% -29.5% -17.6% -8.4% -4.5%60% -38.5% -23.6% -12.4% -3.7% -0.1%70% -32.3% -18.3% -7.8% 0.4% 3.8%80% -26.9% -13.7% -3.7% 4.0% 7.2%90% -22.0% -9.5% -0.1% 7.2% 10.3%

100% -17.6% -5.7% 3.2% 10.2% 13.1%

ConclusionsConclusions

Higher prices charged when direct marketing Higher prices charged when direct marketing are necessary to cover higher marketing costsare necessary to cover higher marketing costs

Differences in profitability across market Differences in profitability across market channels are affected by:channels are affected by: Net rate of return to marketing in each channel (R)Net rate of return to marketing in each channel (R) Proportion of product actually sold (S)Proportion of product actually sold (S) Markup rate (M)Markup rate (M) Cost of production (C)Cost of production (C)

Direct marketing can provide a market for Direct marketing can provide a market for produce that is not sellable in wholesale produce that is not sellable in wholesale channel channel