Embed Size (px)

Citation preview

ANCORD | Sao Paulo, Brazil | March 2015

Market Structure TrendsBrazil and Abroad

Presented by

Larry Tabb (Founder & CEO)

2

Agenda

Trading trends US/Europe Competition Electronification HFT Institutional trading

Brazil Local challenges New competition What to expect How to prepare How Brazil will be different

Conclusion 2

3

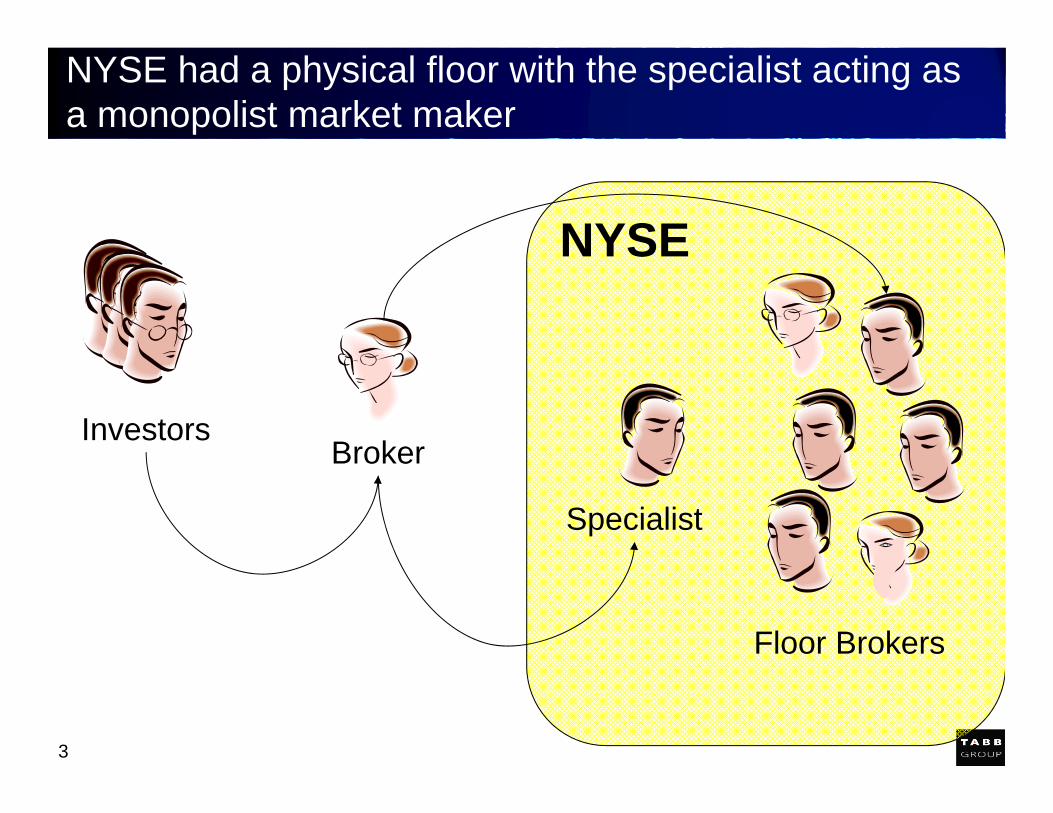

NYSE

NYSE had a physical floor with the specialist acting as a monopolist market maker

InvestorsBroker

Specialist

Floor Brokers

4

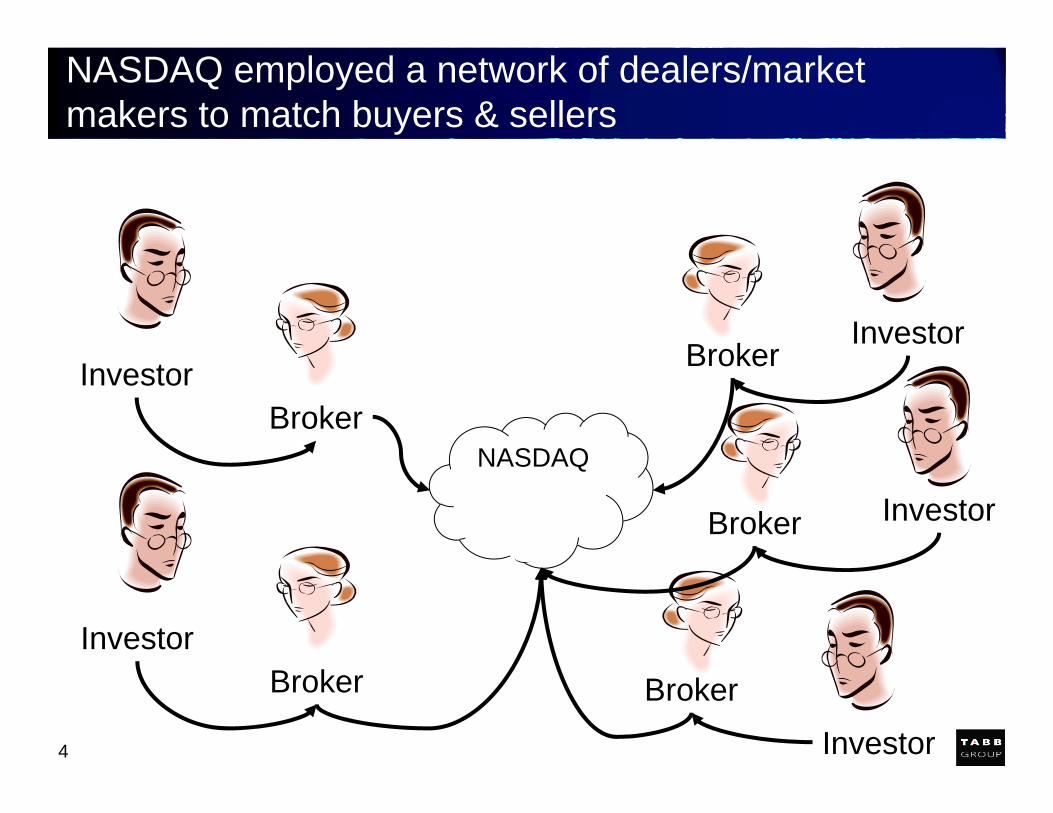

NASDAQ employed a network of dealers/market makers to match buyers & sellers

InvestorBroker

InvestorBroker

Investor

Investor

Investor

Broker

Broker

Broker

NASDAQ

5

SEC Order Handling Rules and Reg ATS Changed Equity Trading Life

SEC found NASDAQ market makers colluding on pricing

In 1997 developed order handing rules mandating the development of electronic execution

First execution platform was called SOES Small Order Execution System

Enabled small investors to electronically interact with posted quotes Turned indicative quotes into actionable

Island soon followed as first upstart ECN

Soon there were 9 or 10 significant ECNs Consolidation has followed

6

Decimals is the second major market structure change that has radically changed equity trading

0

.10

.15

.20

.25

1/4

1/8

1/16

3/16

0 From 16 price points to 100

Less liquidity at any one point

Less expensive to jump bids

More need for specialist to bridge liquidity

Less profitability for dealers

Market structure change to agency model

More expensive for large investors

Fractions

Decimals

1

2

3

4

5

10

15

20

25

.05

7

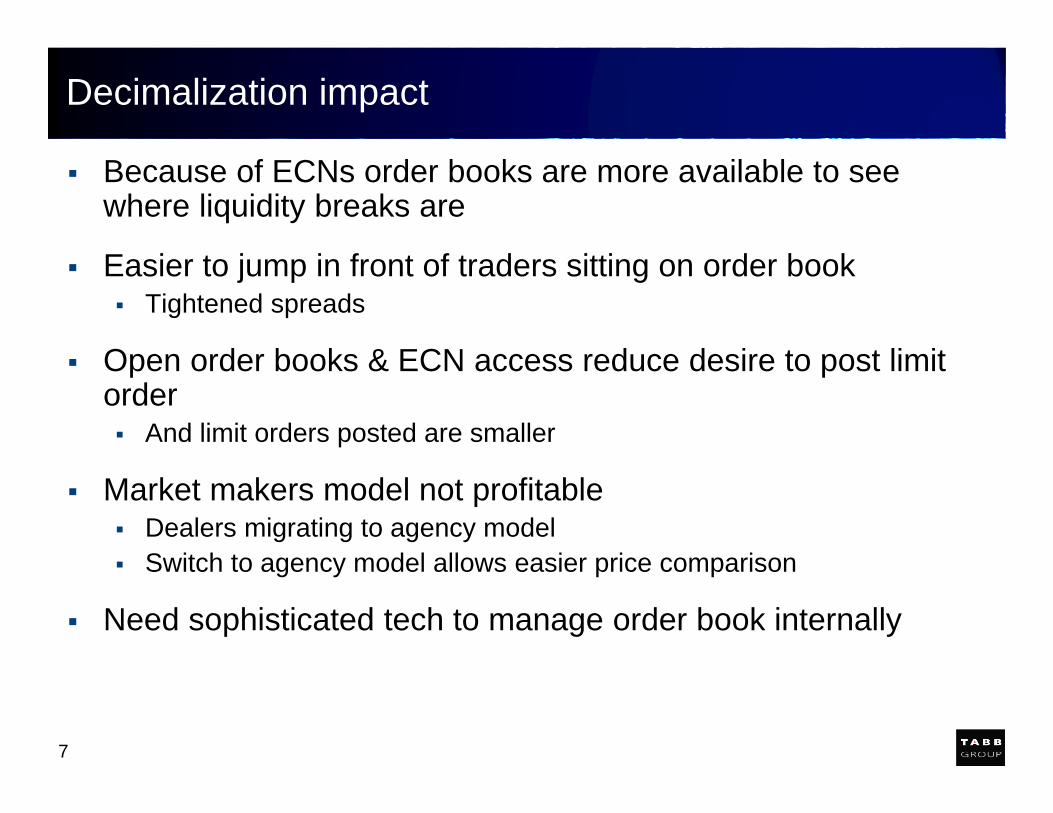

Decimalization impact

Because of ECNs order books are more available to see where liquidity breaks are

Easier to jump in front of traders sitting on order book Tightened spreads

Open order books & ECN access reduce desire to post limit order And limit orders posted are smaller

Market makers model not profitable Dealers migrating to agency model Switch to agency model allows easier price comparison

Need sophisticated tech to manage order book internally

8

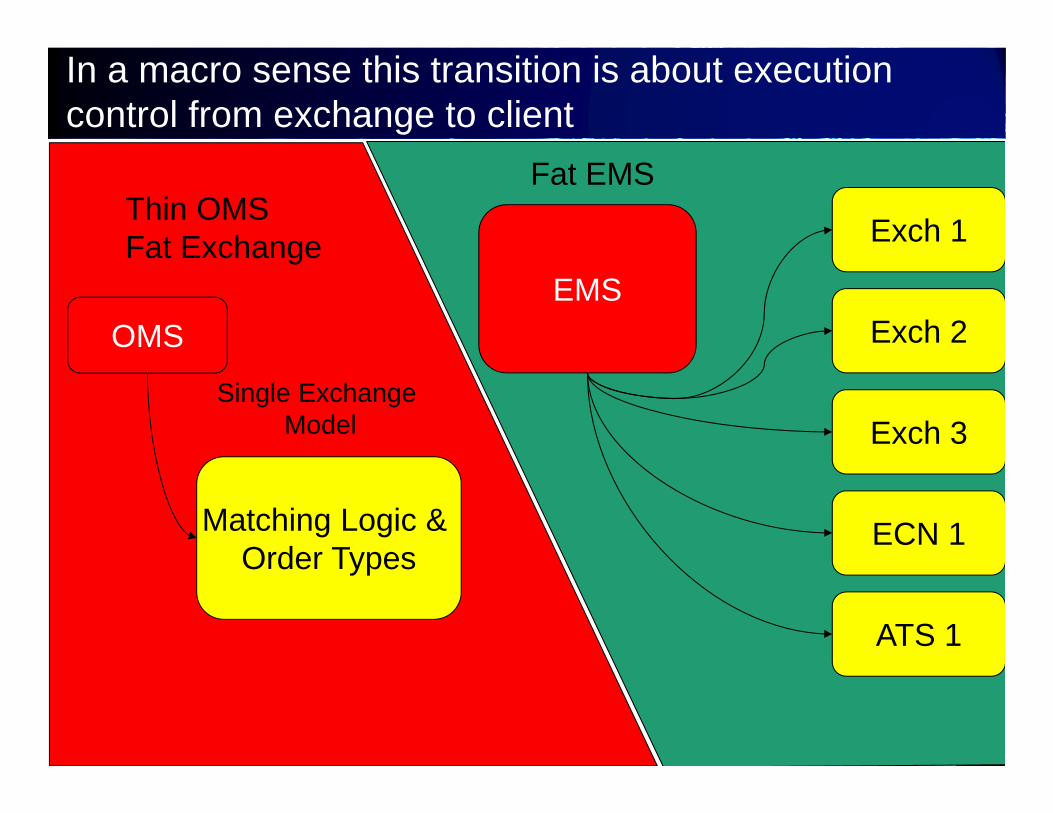

In a macro sense this transition is about execution control from exchange to client

Matching Logic & Order Types

OMS

Single Exchange Model

Thin OMS Fat Exchange

EMS

Exch 1

Exch 2

Exch 3

ECN 1

ATS 1

Fat EMS

9

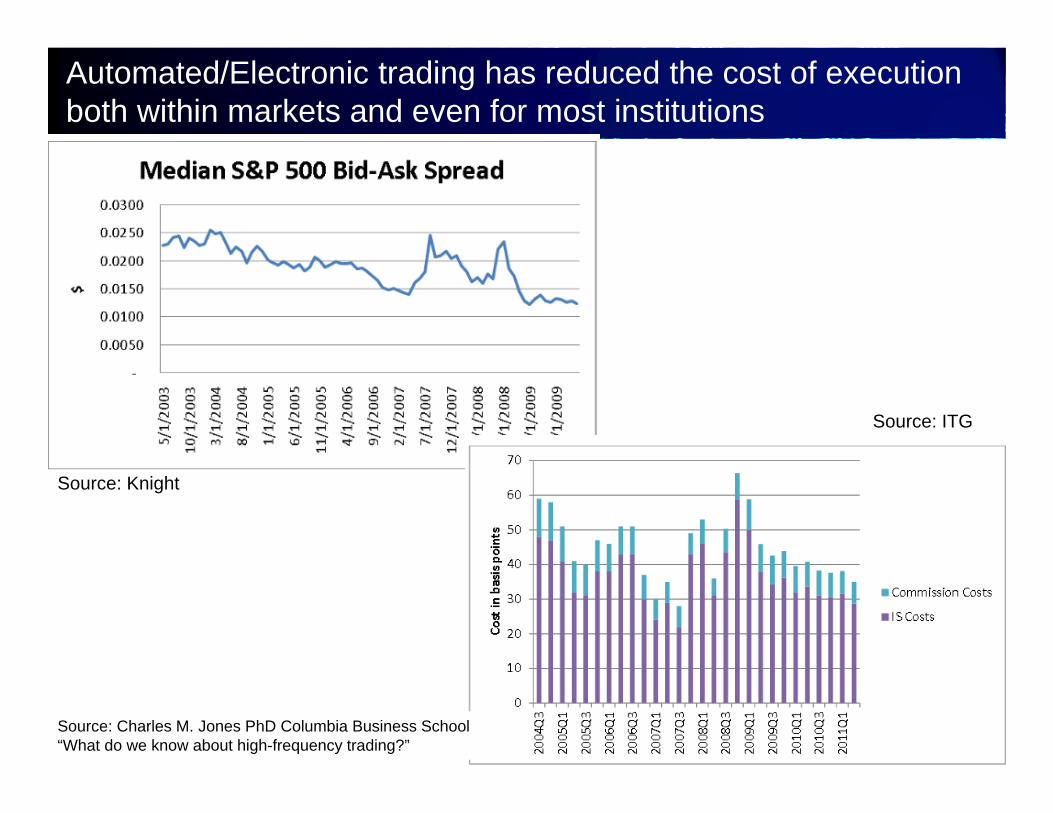

Automated/Electronic trading has reduced the cost of execution both within markets and even for most institutions

Source: Charles M. Jones PhD Columbia Business School “What do we know about high-frequency trading?”

Source: Knight

Source: ITG

10

Most academic studies say that competition / HFT overall reduces spreads & lowers transaction costs

Foresight Report: The Future of Computer Trading in Financial Markets (2012) Improved liquidity, lower transaction cost, and more efficient pricing

Hagströmer, Björn and Norden (2012) - The Diversity of High Frequency Traders Market making and opportunistic HFT strategies mitigate intraday price volatility

Hasbrouck, Saar "Low--‐Latency Trading", May 2011 Low latency automated trading was associated with lower quoted and effective spreads, lower

volatility and greater liquidity

Angel,Harris &Spatt: "Equity trading in the 21st century", February 2010 Trading costs have declined, bid‐ask spreads narrowed and available liquidity has increased

Chaboud, Hjalmarsson, Vega and Chiquoine “Rise of the Machines: Algorithmic Trading in the Foreign Exchange Market”, October 2009 Automated trades increased liquidity and may have lowered volatility

Hendershott, Riordan “Algorithmic Trading and Information”, August 2009 Automated trades made prices more efficient and did not contribute to higher volatility

10

1111

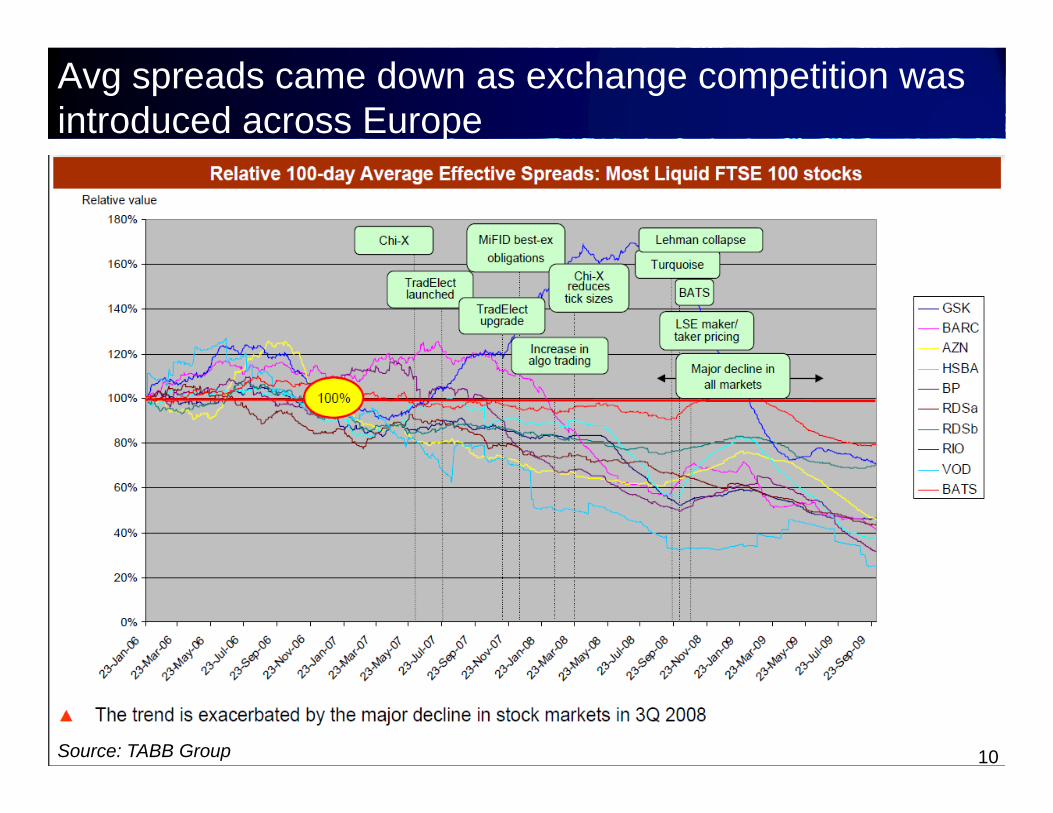

Across Europe effective spread has declined in 92% of 60 most liquid stocks (20 each in FTSE, DAX & CAC)

Source: TABB Group 9

1212

Avg spreads came down as exchange competition was introduced across Europe

Source: TABB Group 10

1313

Despite drop in volume, competition has kept pressure on effective spreads even during height of crisis

Source: TABB Group 11

14

Too much of a good thing

14

15

LavaFlow

DirectEdge

Instinet

Brut

These regulations opened up a floodgate of competition. This is just the early stage competitors

Island

Attain

Strike

TradeBook

Redi

NextTrade

Arca

BATS

Brut

NASDAQ Knight

Citi

Instinet

NASDAQ Arca

NYSE

Track

16

US Market structure has spun out of control. Trading venues have proliferated. The US has 11 exchanges & 41 ATSs, but starting to consolidate

16

ExchangesNYSENYSE ArcaNYSE AmexNASDAQNASDAQ BXNASDAQ PSXBATS BZXBATS BYXDirectEdge EdgeADirectEdge EdgeXCBSXCBSX / NSXCSX

ATSs

AQUA Credit Suisse CrossFinder ITG POSITMorgan Stanley (MS Pool)

Barclays (3) Credit Suisse Light PoolJ.P. MORGAN SECURITIES LLC

Morgan Stanley (Trajectory Cross)

Barclays DirectEx Cross StreamJEFFERIES EXECUTION SERVICES, INC. PDQ

Barclays LX Dealer Web Knight Link by KCG RiverCross

BIDS Deutsche Bank SuperX LavaFlow ECNPro Securities SpeedRoute

BLOOMBERG TRADEBOOK LLC

FOLIOFN INVESTMENTS, INC. LeveL State Street (Block Cross)

Citadel Apogee Goldman Sachs Sigma X Liquidnet H2O UBS

Citi Cross IEX Liquidnet Negotiated Weeden XE

Citi LIQUIFI Instinet CBX Merrill Lynch (2)

ConvergEx Group Millennium Instinet Crossing Merrill Lynch (MLXN)

17

But Brazil isn’t the US

17

18

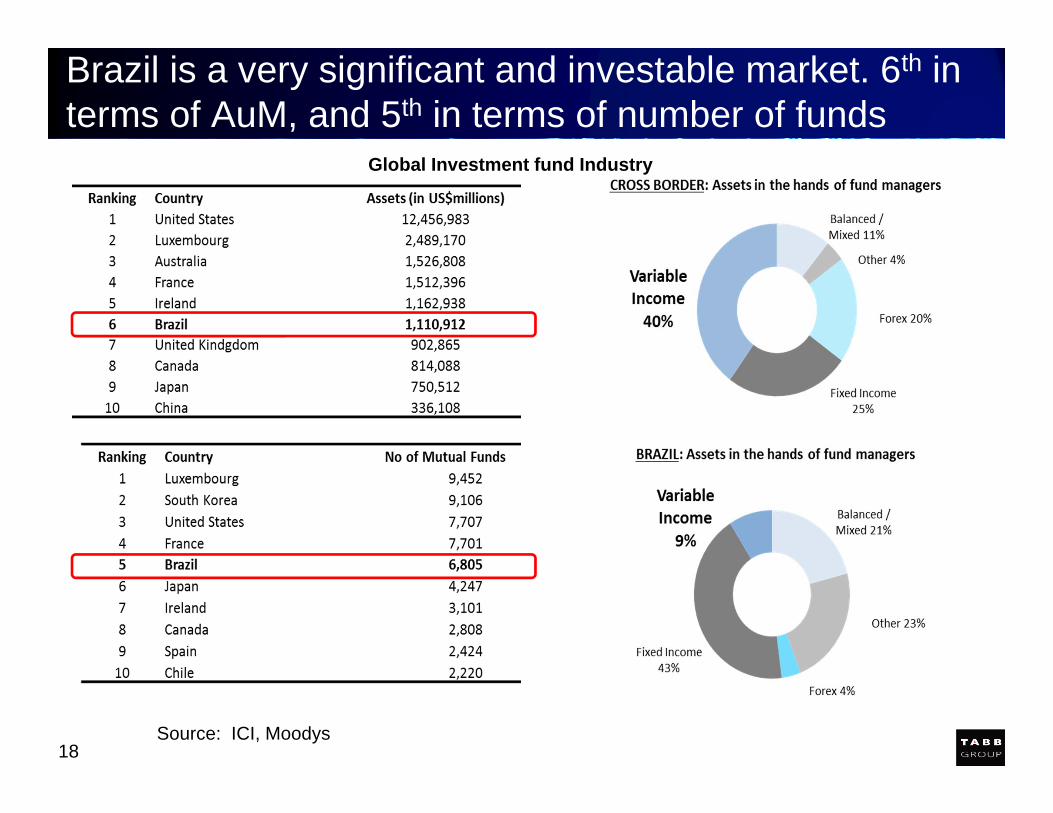

Brazil is a very significant and investable market. 6th in terms of AuM, and 5th in terms of number of funds

Source: ICI, Moodys

Global Investment fund Industry

19

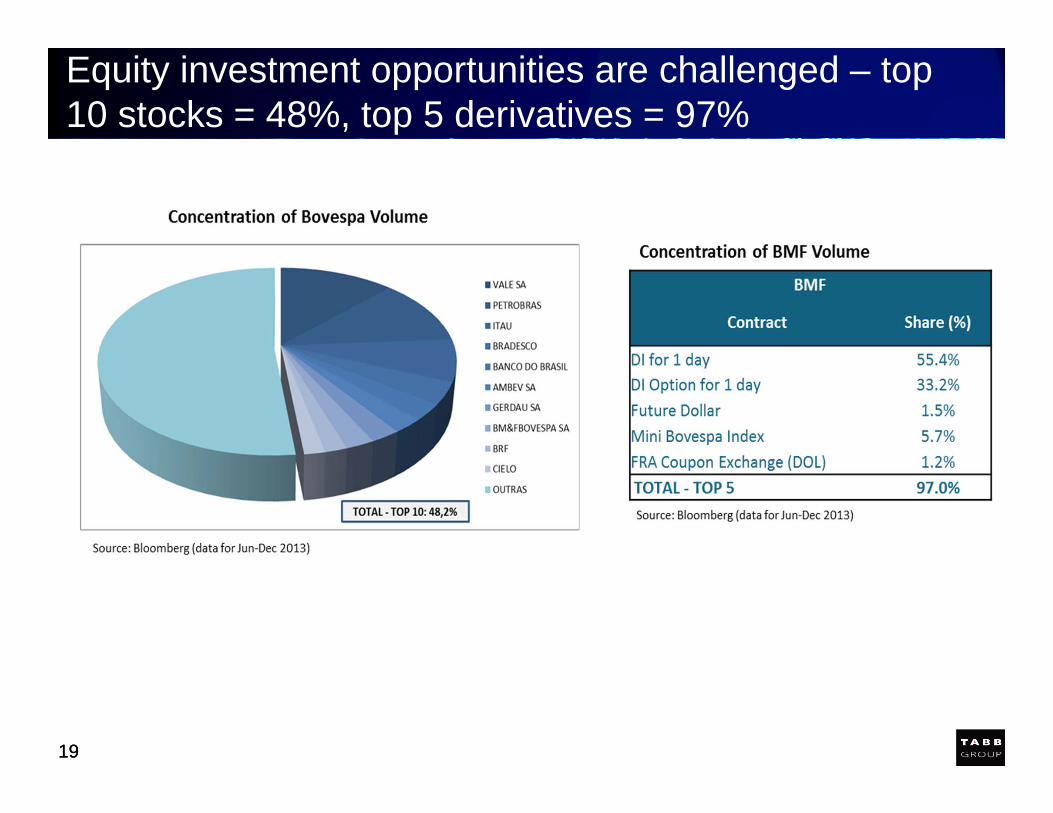

Equity investment opportunities are challenged – top 10 stocks = 48%, top 5 derivatives = 97%

19

20

And IPO market is pretty much nonexistent with only one IPO in 2014

IPOs US, UK, & EU vs. Brazil 2014

BR

L in

Bill

ions

BRL 0.00

BRL 50.00

BRL 100.00

BRL 150.00

BRL 200.00

BRL 250.00

BRL 300.00

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Brazil US UK Euro Australia

21

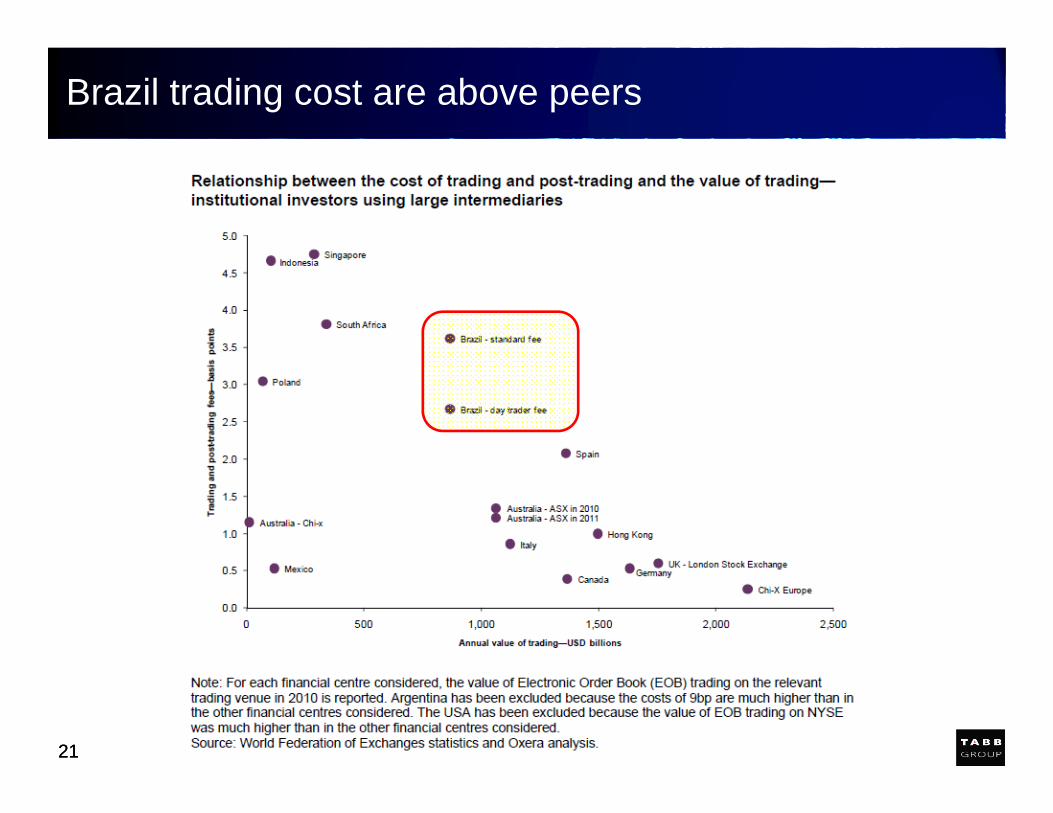

Brazil trading cost are above peers

21

22

0

1

2

3

4

5

6

7

8

User 1 - Intermediary 1 User 2- Intermediary 2User 3 - Intermediary 3 User 4-Intermediary 4

4X Expense vs USA

The cost of trading in Brazil is significantly higher than that of many smaller markets

Source: CVM Brazil

Cost of Trading (bps) & Distribution of Costs in each Financial Center

23

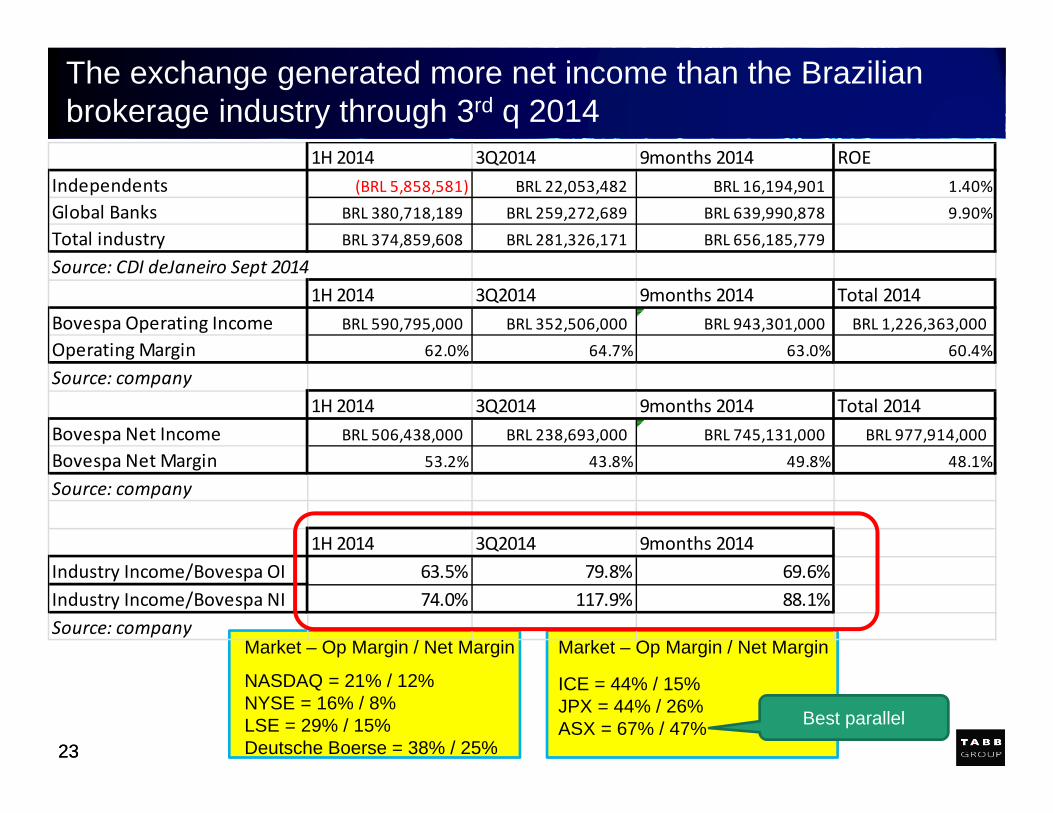

The exchange generated more net income than the Brazilian brokerage industry through 3rd q 2014

23

1H 2014 3Q2014 9months 2014 ROEIndependents (BRL 5,858,581) BRL 22,053,482 BRL 16,194,901 1.40%Global Banks BRL 380,718,189 BRL 259,272,689 BRL 639,990,878 9.90%Total industry BRL 374,859,608 BRL 281,326,171 BRL 656,185,779

Source: CDI deJaneiro Sept 20141H 2014 3Q2014 9months 2014 Total 2014

Bovespa Operating Income BRL 590,795,000 BRL 352,506,000 BRL 943,301,000 BRL 1,226,363,000Operating Margin 62.0% 64.7% 63.0% 60.4%

Source: company1H 2014 3Q2014 9months 2014 Total 2014

Bovespa Net Income BRL 506,438,000 BRL 238,693,000 BRL 745,131,000 BRL 977,914,000Bovespa Net Margin 53.2% 43.8% 49.8% 48.1%

Source: company

1H 2014 3Q2014 9months 2014Industry Income/Bovespa OI 63.5% 79.8% 69.6%Industry Income/Bovespa NI 74.0% 117.9% 88.1%Source: company

Market – Op Margin / Net Margin

NASDAQ = 21% / 12%NYSE = 16% / 8%LSE = 29% / 15%Deutsche Boerse = 38% / 25%

Market – Op Margin / Net Margin

ICE = 44% / 15%JPX = 44% / 26%ASX = 67% / 47% Best parallel

24

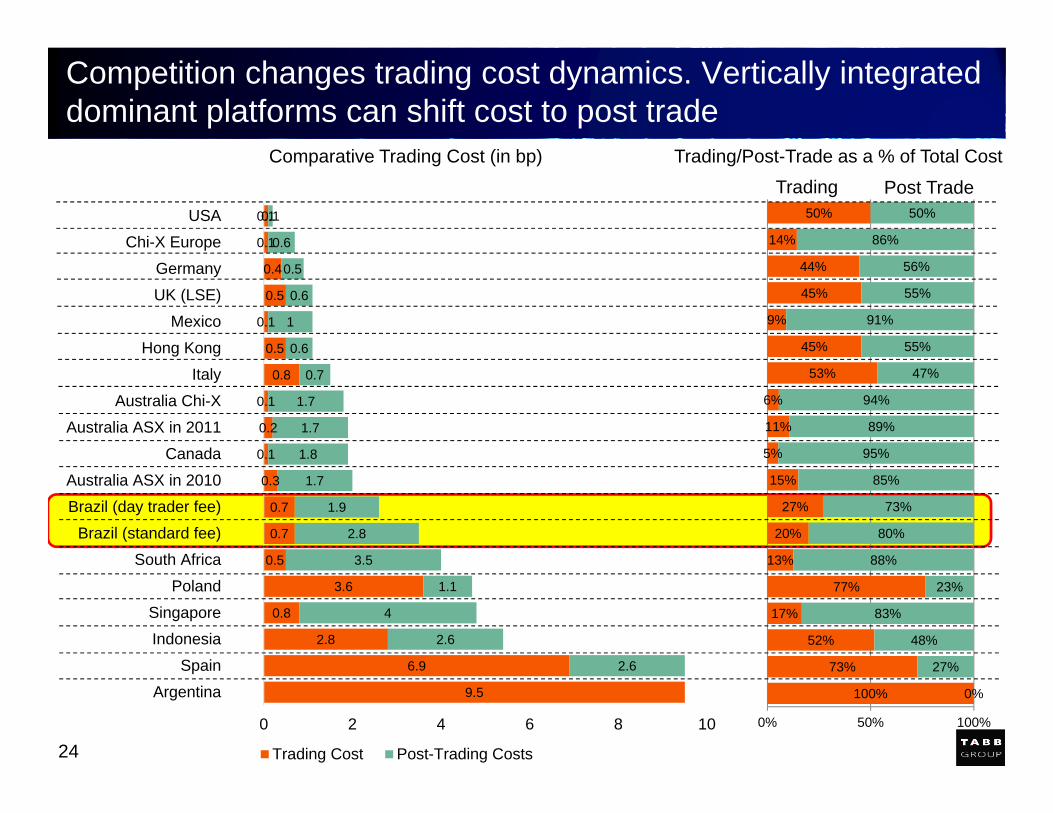

Competition changes trading cost dynamics. Vertically integrated dominant platforms can shift cost to post trade

9.5

6.9

2.8

0.8

3.6

0.5

0.7

0.7

0.3

0.1

0.2

0.1

0.8

0.5

0.1

0.5

0.4

0.1

0.1

2.6

2.6

4

1.1

3.5

2.8

1.9

1.7

1.8

1.7

1.7

0.7

0.6

1

0.6

0.5

0.6

0.1

0 2 4 6 8 10

ArgentinaSpain

IndonesiaSingapore

PolandSouth Africa

Brazil (standard fee)Brazil (day trader fee)Australia ASX in 2010

CanadaAustralia ASX in 2011

Australia Chi-XItaly

Hong KongMexico

UK (LSE)Germany

Chi-X EuropeUSA

Trading Cost Post-Trading Costs

100%

73%

52%

17%

77%

13%

20%

27%

15%

5%

11%

6%

53%

45%

9%

45%

44%

14%

50%

0%

27%

48%

83%

23%

88%

80%

73%

85%

95%

89%

94%

47%

55%

91%

55%

56%

86%

50%

0% 50% 100%

Trading Post Trade

Comparative Trading Cost (in bp) Trading/Post-Trade as a % of Total Cost

25

In a vertical model the Exchange, CCP and possibly the depository are affiliated

BrokersExchange CCP Depository

AlternativePlatforms

BarriersOperational,Technological,and/or Cost

26

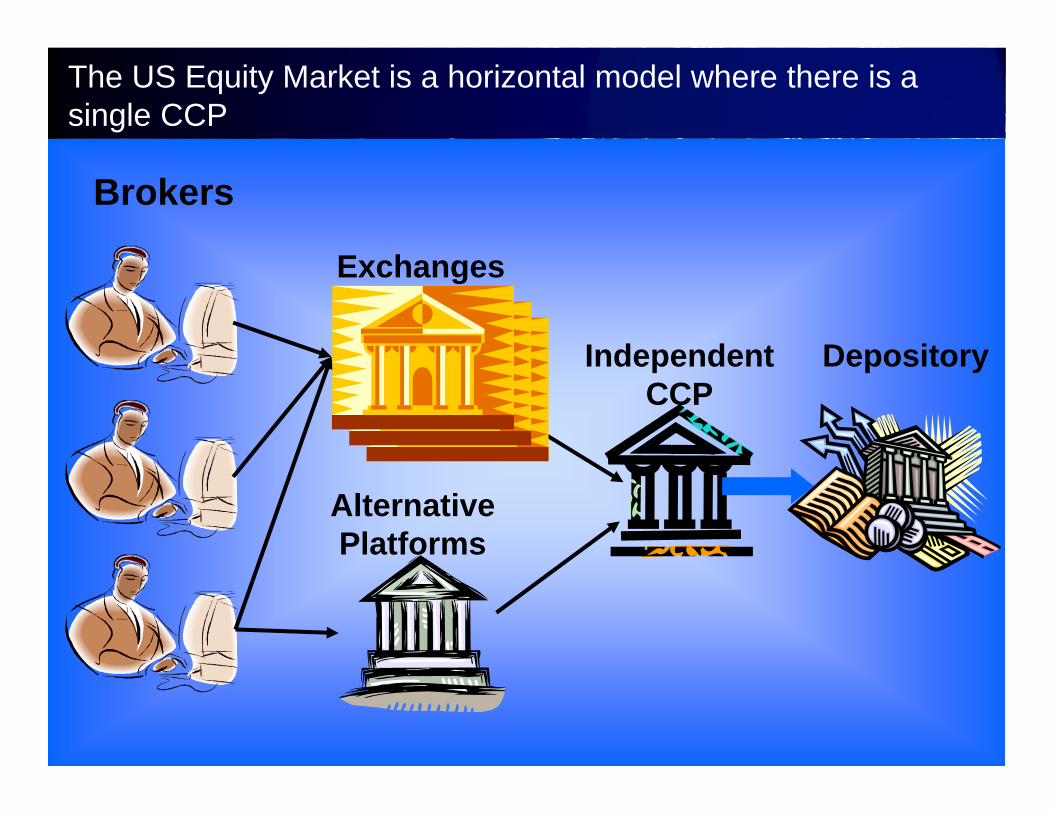

The US Equity Market is a horizontal model where there is a single CCP

Brokers

Exchanges

IndependentCCP

Depository

AlternativePlatforms

27

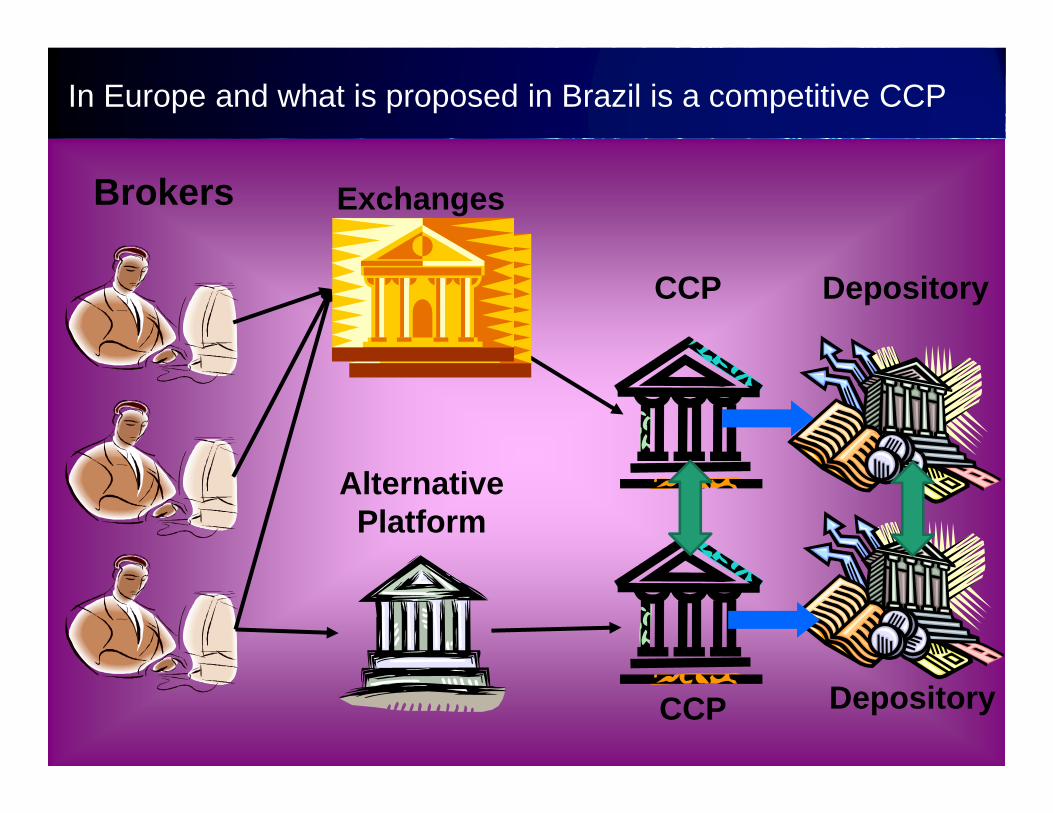

In Europe and what is proposed in Brazil is a competitive CCP

Brokers Exchanges

CCP Depository

AlternativePlatform

CCP Depository

28

DMA volume on Bovespa is gradually increasing – from 39% to 46% in Sept 2014

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

DMA Non-DMASource ATB Brazil, TABB Group

DMA vs. Non-DMA Volumes (Bovespa)Monthly BM&F BOVESPA DMA percentage

46%4242394242444145374543413943384038423739%

29

Increasing DMA will increase buy-side algo usage to implement strategies, capture spreads, and provide liquidity

Source ATB Brazil, TABB Group

Estimated Buy Side Algorithm Usage in Brazil

30

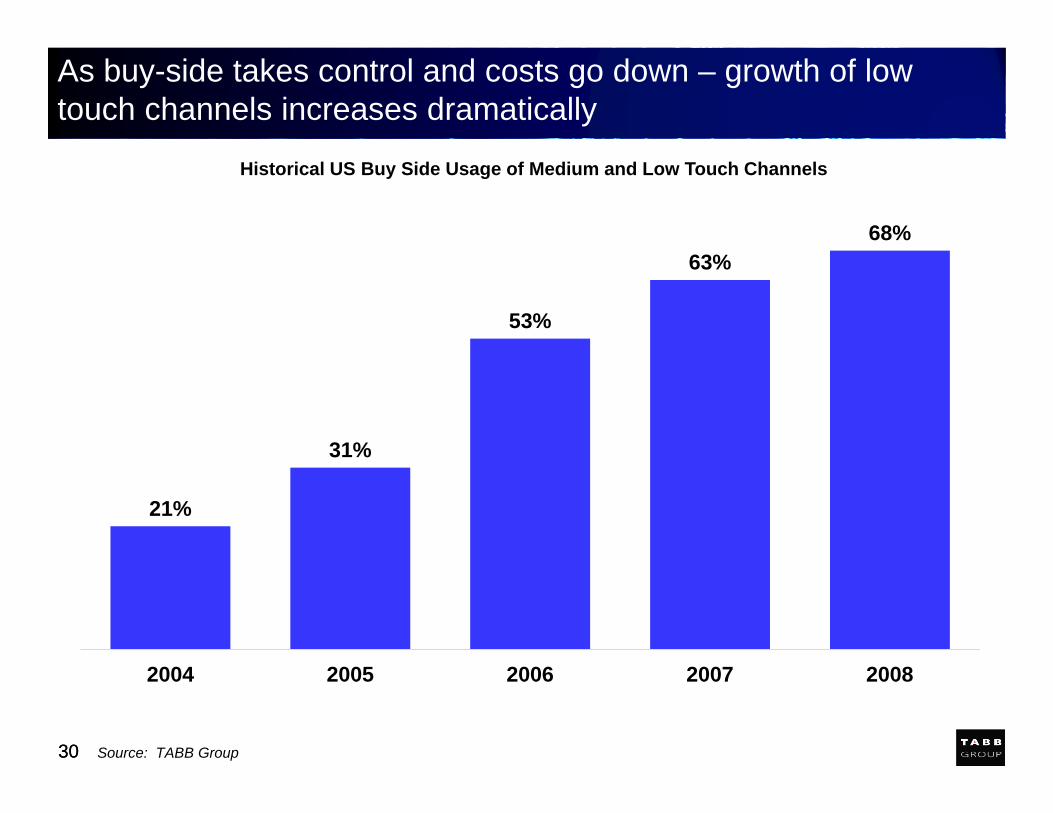

As buy-side takes control and costs go down – growth of low touch channels increases dramatically

30

21%

31%

53%

63%68%

2004 2005 2006 2007 2008

Source: TABB Group

Historical US Buy Side Usage of Medium and Low Touch Channels

31

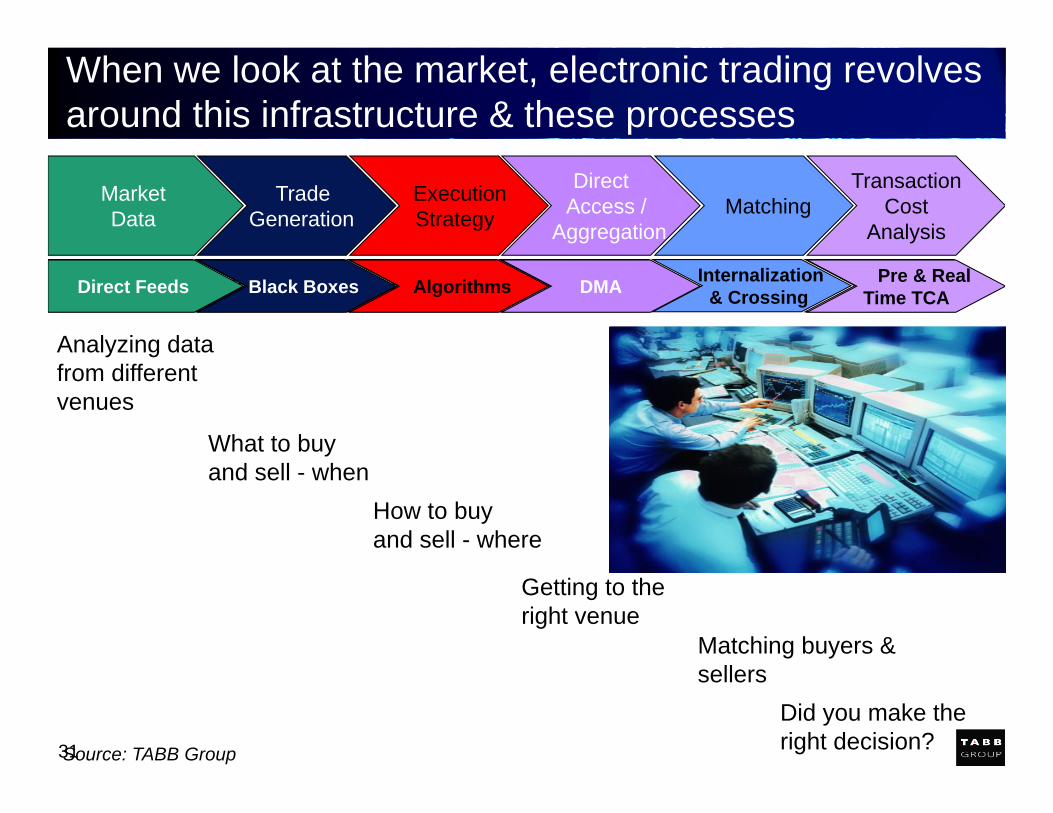

Direct Feeds Black Boxes Algorithms DMA Internalization& Crossing

Pre & RealTime TCA

When we look at the market, electronic trading revolves around this infrastructure & these processes

Source: TABB Group

MarketData

Analyzing data from different venues

Direct Feeds

Trade Generation

What to buy and sell - when

Black Boxes

ExecutionStrategy

How to buy and sell - where

Algorithms

DirectAccess /

Aggregation

Getting to theright venue

DMA

Matching

Matching buyers & sellers

TransactionCost

Analysis

Did you make the right decision?

Pre & RealTime TCA

32

What does this mean for Brazilian brokers?

Opportunities Cost of execution & clearing will decline with added competition

Exchange Op margins should fall from 60% to 40% & Net Margin from 50% to 25% Ability to offer differentiated services

Today all orders go to one place: future – routing becomes factor in best execution A second market will increase resiliency Liquidity will increase as cost declines & new players come into the market

Both market makers & investors (cost decline & greater market resiliency) Balance of power will begin to tip away from exchange

Impacts Need to increase connectivity expense More technology (SOR, CEP, market data, TCA…) Different skills (more technical and analytical) will be needed

However Brazil will never be as fragmented or complex as US or Europe

Regulators do not want this type of market Market structure won’t cure all market ills. But relief is needed & a new competitor will help32

33

Conclusions

Market competition is good Lower’s cost, creates new opportunities, crates a more efficient market, spurs innovation Competition needs either open clearing or independent clearing to be successful

Market competition does create complexities With multiple markets, more technology is needed Speed does become more important But increasingly technology is needed even in a unified market structure as technology is

faster, cheaper, and more accurate than humans As markets become more electronic strategies change

Blocks become fewer, algos become more prevalent But this lowers cost Also transfer’s risk from sell-side to buy-side

Now Brazil won’t be like US 2 markets instead of 50, No dark pools Depth of book trade through

Need to think about electronic trading as a series of technologies Data, market maker algos, buy-side algos, routers/access, electronic matching, and TCA

ANCORD | Sao Paulo, Brazil | March 2015

Market Structure TrendsBrazil and Abroad

Presented by

Larry Tabb (Founder & CEO)