Embed Size (px)

Citation preview

RETAILHAMPTON ROADS

R E A L E S TAT E M A R K E T R E V I E W2014

2014 RE

TAIL

13

Author David Machupa Cushman & Wakefi eld | THALHIMER

Survey Collection Kyllie Bullion E.V. Williams Center for Real Estate and Economic Development Old Dominion University

Data Analysis/ David Chapman, Ph.D.Layout Old Dominion University

Financial The E. V. Williams Center for Real Estate and EconomicSupport Development (CREED) functions and reports are funded by donations from the CREED membership, organizations, and individuals.

Disclosure The data used for this report are deemed reliable; however, neither Old Dominion University, the E. V. Williams Center for Real Estate and Economic Development, nor sponsoring companies and/or individuals make any representation or warranty as to its accuracy.

14 2014 Hampton Roads Real Estate Market Review

2 0 1 4 R E TA I L

General Overview

his report analyzes the 2013 retail real estate conditions within the Virginia Beach-Norfolk-New-port News, Virginia Metropolitan Statistical Area (MSA) which is commonly referred to as

Hampton Roads. The report examines supply, vacancy, construction, absorption, and rent data to provide a comparison of data for the specifi c submarkets and product types located within the Southside and Peninsula regions of the Hampton Roads MSA. Southside properties surveyed for the purpose of this report included those located in the cities of Chesapeake, Norfolk, Portsmouth, Smithfi eld, Suffolk and Virginia Beach. Peninsula properties surveyed are located in the cities of Gloucester, Hampton, Newport News, Poquoson, Williamsburg, and York County.

This survey is recognized as the most comprehensive analysis of retail real estate trends in the HamptonRoads MSA. The report includes information on all retail property types including regional malls,freestanding buildings and strip centers of various classifi cations. The scope of the report also includesa summary of new retail construction activity, an analysis of absorption, and a review of selected retailinvestment sales that have occurred in the region in 2013.

This survey gathered information about strip shopping centers and regional malls located in the Hampton Roads MSA that were generally 30,000 square feet in size or larger. Additionally, information on retail-oriented freestanding buildings at least 23,000 square feet and freestanding buildings that contained furniture stores, discounters, grocery stores or category killer retailers that met the established size criteria were included in the survey.

Automotive uses and buildings containing “downtown storefronts” were not included. Although available retail space in many submarkets (e.g. Ghent) is best described as a collection of small specialty shops, storefronts or freestanding buildings, practical limitations dictated that the focus of the survey be on larger product types.

The survey data was collected between October 2013 and January 2014. Questionnaires were mailed to owners, leasing agents and property managers responsible for retail properties meeting the selection criteria. Direct contact was utilized as a follow-up to the mailing to encourage participation. Information on square footage for freestanding buildings was obtained from building owners, tax records, store managers and retail real estate representatives. Sales information was obtained from property owners, real estate agents, appraisers and real estate assessors.

General Overview

METHODOLOGY

2014 RE

TAIL

15

Regional Mall Node: Submarket anchored by regional mall.

Small Shop: In-line retail space usually less than 10,000 square feet located in a multi-tenanted shopping center.

Submarkets: Hampton Roads is divided into 35 retail submarkets (25 Southside submarkets and 10 Peninsula submarkets) which refl ected general concentrations, pockets or corridors of retail product type. Geographical boundaries of the retail submarkets were infl uenced by density of existing retail product, physical or geographical obstacles, existing transportation networks, municipal boundaries, population concentrations and retailers’ per-ceptions of the MSA. Final determination of specifi c boundaries of each submarket was made by a subcommittee of retail real estate professionals who are actively involved in the MSA. Also highlighted were specifi c submarkets that are anchored by regional malls. A map which identifi es the general location of each submarket is included in the centerfold of this report.

Triple Net Lease: Type of lease under which a tenant pays its pro-rata share of real estate taxes, insurance and common area maintenance.

Neighborhood Center 30,000 to 150,000 square feet; supermarket anchored

Community Center 100,000 to 350,000 square feet; discount department store, supermarket or drug store anchored

Fashion/Specialty Center 80,000 to 250,000 square feet; fashion anchored

Power Center 250,000 to 600,000 square feet; category killer, home improvement and discount department store anchored

Theme Festival Center 80,000 to 250,000 square feet; restaurants, entertainment anchored

Outlet Center 50,000 to 400,000 square feet; manufacturer’s outlet store anchored

Freestanding Individual building not considered a shopping center

Mall Shopping center with area designed for pedestrian use only

Other Any center that does not fi t into a typical category

Asking Rates: The market rate per square foot of a retail property (excluding freestanding buildings and malls), exclusive of additional rents that may be paid under a triple net lease. Interpretation of average retail rates in different product types and submarkets should be viewed cautiously given the tremendous variability in rates for like products and for properties located within the same submarket. Factors such as visibility, co-tenancy, and accessibility, are some of the many sources of variation in market rates which should be considered.

Big Boxes: Contiguous retail space that is at least 23,000 square feet and located in any one of the identifi ed product types. Retailers occupying big boxes include, but are not limited to, the following: category killers, specialty stores, discounters, furniture stores, grocery stores and theaters. Bowling alleys, automotive uses, roller rinks and ice-skating rinks were not included.

CAM: Common Area Maintenance.

Product Types: Properties were classifi ed according to one of the following nine retail product types. The International Council of Shopping Centers defi ned the fi rst six categories. Three additional categories were included to accurately categorize the remaining properties.

D E F I N I T I O N S O F T E R M S

16 2014 Hampton Roads Real Estate Market Review

2 0 1 4 R E TA I L

The Hampton Roads market appears to have stabilized. 2013 saw the re-emergence of grocery stores to the market as Walmart and Kroger continued to expand their presence. On a national level, the retail market remained stable and, as such, remained stable here in Hampton Roads. 2013 did not bring a mass exodus of retailers;however, a few large box brands did limp into 2014 and we expect a thinning of the herd as these retailers attempt to remain viable. The fi nancing market is stable with lenders actively seeking opportunities. A disconnect remains on product valuation between buyers, sellers and lenders of retail centers and, as such, we did not see a great deal of investment sales in Hampton Roads this past year.

2013 brought increased activity from grocery stores. Kroger, Walmart Neighborhood Market, and Harris Teeter were very active. Harris Teeter was purchased by Kroger and we will pause to see how this will curtail expansion by both retailers. Walmart opened on Jefferson Avenue and is under construction in the Pembroke area of Virginia Beach with a Super Center. Five of the smaller Neighborhood Market concepts are under construction in Hampton Roads. Harris Teeter will open in the Red Mill area of Virginia Beach and in the Wards Corner area of Norfolk. Kroger opened its 124,000 square foot Marketplace concept on Holland Road in Virginia Beach and is under construction with two more in Portsmouth and Northern Suffolk respectively. Additionally, Whole Foods has an-nounced they will anchor Tech Center at Oyster Point in Newport News and The Fresh Market will open in the Ghent section of Norfolk. Dave and Buster’s opened at Lynnhaven Mall and West Marine opened in Loehman’s Plaza in Virginia Beach. Starbucks opened a drive thru only location in Virginia Beach; this was the fi rst in Virginia and only the seventh in the country. CVS and 7-11 both continued aggressive expansion within the market. Simon Properties has Lake Wright under contract and is working to bring an outlet mall to the Norfolk site. We saw two small redevelopment projects along Lynnhaven Parkway near the mall with Noodles, Five Guys and Mattress Firm anchoring those developments. Lynnhaven Convenience, a mostly vacant property along Virginia Beach Boulevard anchored by Farm Fresh, is being redeveloped. Farm Fresh closed and has been replaced by Walmart Neighborhood Market, One Life Fitness, and Hobby Lobby. Bahama Breeze and Old Navy opened at the entrance of Pembroke Mall. Settler’s Market in Williamsburg came full circle. After starting off slowly, going through foreclosure, and sitting partially constructed, the new ownership was able to re-energize the project and Home Goods, Stein Mart, Michaels, Ulta, Shoe Carnival and 5 Below opened in March occupying roughly 200,000 sf of a 250,000 sf project.

There is concern for certain retailers as they continue to struggle on a national level. K-Mart and Sears are closing stores on both a local and national level. K-mart closed the Chesapeake Square and Tidewater Drive locations with many more being offered for lease with or without K-Mart. J.C. Penney’s announced the closing of the Military Highway location, while Ruby Tuesday shuttered thirty stores across the country and one here in Virginia Beach. Blockbuster fi nally threw in the towel and closed the last of its stores across the country, Radio Shack is closing 500 stores, Best Buy tried to go private, but could not obtain fi nancing and Barnes and Noble placed themselves for sale, but did not fi nd any suitors. The retail landscape is constantly changing and those tenants that do not change with it will be closing their doors.

Hampton Roads is stable, new tenants are looking for locations within the market, and we are seeing new development. We do expect the vacancy rate to increase because of the amount of big box space that will come to the market, but we also expect rental rates to increases as quality retail product is limited at this time.

YEAR IN REVIEW 2013

2014 RE

TAIL

17

HAMPTON ROADS MARKET SURVEY

The Hampton Roads retail market contained approximately 54,222,598 square feet of gross leasable area (“GLA”) in 422 properties with anaverage asking rental rate of $15.97 with triple net charges (Common Area Maintenance, Real Estate Taxes and Insurance) running $2.87 per square foot. The US Census Bureau indicates the population of Hampton Roads is approximately 1.7 Million resulting in a 31.90 square feet of retail supply per person. Certain methodological differences (e.g., the inclusion of freestanding buildings and malls in this survey) make it diffi cult to compare per capita supply in the MSA to a national average statistic.

Hampton Roads consist of two markets, the Southside and Peninsula. The Southside market has approximately 35,835,277 square feet, roughly 66% of the total square footage in the market, in 288 properties. The average asking rent for small shop space increased $.20 over 2012 numbers to $16.56 triple net. The increase in rental rates can be attributed to consistent demand as vacancy rates remained low at 6.74% in 2013. While 89,200 square feet of new construction came on line in 2013, Hampton Roads has signifi cant amounts of new construction in the pipeline for 2014.

The Peninsula also experienced some mixed change this past year. The 134 properties on the Peninsula that were surveyed combined for 18,387,321 square feet of product. The average asking price of small shop space was $14.61 per square foot with $2.69 in triple net charges. The vacancy rate for the greater Peninsula was 11.55%; however, activity and interest in the Peninsula market is strong in the fi rst quarter of 2014. The Williamsburg submarket rebounded as new ownerships were able to reposition previously faltering projects.

In 2013, the Hampton Roads market did see a slight increase in the vacancy rate as 2012’s overall 7.85% vacancy rate gave way to 2013’s 8.37%. This increase is largely due to more Big Box space coming onto the market. While landlords and tenants continue to get creative in the deal making process and retailers are repositioning themselves within the market creating new developments, as well as second generation opportunities, local tenants are not as abundant as in years past. Landlords are approaching these second generation spaces with both traditional and non-traditional retailers to back fi ll the space. Unlike years past, the market was not saturated with retail product due to mass store closings; however, we expect a fair amount of big box retail space to enter in 2014. Specifi cally, K-mart and Sears present large blocks that may enter the market.

We move forward acknowledging 2014 is off to a strong start. We will see the size of the overall market increase due to grocery store expansion as multiple new centers are currently under construction and will be opening this year. We will approach the older second generation space for re-use and redevelopment. It should be noted some of the larger vacant space highest and best use may no longer be retail. These spaces will continue to negatively impact the overall Hampton Roads numbers until such time as they are redeveloped.

18 2014 Hampton Roads Real Estate Market Review

2 0 1 4 R E TA I L

Market Overview Table

Southside 288 35,835,277 2,416,346 6.74% 89,200 33,418,931 701,392 Peninsula 134 18,387,321 2,123,718 11.55% 21,411 16,263,603 (280,018)Total 422 54,222,598 4,540,064 8.37% 110,611 49,682,534 421,374 Southside 286 34,924,153 2,206,614 6.32% 57,442 32,717,539 1,896,773 Peninsula 138 18,532,649 1,989,028 10.73% 6,576 16,543,621 775,368 Total 424 53,456,802 4,195,642 7.85% 64,018 49,261,160 2,672,141 Southside 279 34,150,108 2,534,765 7.42% 103,380 31,615,343 794,577Peninsula 138 18,494,461 1,944,109 10.51% 999,389 16,550,352 782,099Total 417 52,644,569 4,478,874 8.51% 1,102,769 48,165,695 1,576,676Southside 274 34,019,555 2,523,754 7.42% 18,880 31,495,801 675,035Peninsula 138 18,548,407 2,175,793 11.73% - 16,372,614 604,361Total 412 52,567,962 4,699,547 8.94% 18,880 47,868,415 1,279,396Southside 273 33,535,280 2,714,514 8.09% 302,352 30,820,766 (288,440)Peninsula 136 18,160,963 2,392,710 13.18% 981,463 15,768,253 362,777Total 409 51,696,243 5,107,224 9.88% 1,283,815 46,589,019 74,337Southside 265 33,265,028 2,155,822 6.48% 275,252 31,109,206 238,525Peninsula 133 17,112,012 1,706,536 9.97% - 15,405,476 (109,898)Total 398 50,377,040 3,862,358 7.67% 275,252 46,514,682 128,627Southside 263 33,086,160 2,215,479 6.70% 1,038,291 30,870,681 339,596Peninsula 133 17,133,079 1,617,705 9.44% 1,009,000 15,515,374 100,485Total 396 50,219,239 3,833,184 7.63% 2,047,291 46,386,055 440,081Southside 259 32,407,761 1,876,676 5.79% 1,552,392 30,531,085 1,741,962Peninsula 131 16,895,155 1,480,266 8.76% 1,042,451 15,414,889 576,788Total 390 49,302,916 3,356,942 6.81% 2,594,843 45,945,974 2,318,750Southside 246 30,852,210 2,063,087 6.69% 593,520 28,789,123 1,280,869Peninsula 129 16,337,458 1,499,357 9.18% 618,179 14,838,101 687,097Total 375 47,189,668 3,562,444 7.55% 1,211,699 43,627,224 1,967,966Southside 243 30,184,395 2,676,141 8.87% 271,610 27,508,254 341,736Peninsula 125 15,799,778 1,648,774 10.44% 185,000 14,151,004 496,338Total 368 45,984,173 4,324,915 9.41% 456,610 41,659,258 838,074Southside 243 30,336,266 3,169,748 10.45% 419,458 27,166,518 419,138Peninsula 127 16,094,161 2,027,477 12.60% 330,000 14,066,684 412,018Total 370 46,430,427 5,197,225 11.19% 749,458 41,233,202 831,156Southside 245 30,180,691 3,433,311 11.38% 574,400 26,747,380 535,167Peninsula 126 15,546,085 1,891,419 12.17% 676,000 13,654,666 932,008Total 371 45,726,776 5,324,730 11.64% 1,250,400 40,402,046 1,467,175Southside 239 29,760,443 3,548,230 11.92% 828,800 26,212,213 1,185,818Peninsula 123 14,906,530 2,183,872 14.65% 202,750 12,722,658 242,563Total 362 44,666,973 5,732,102 12.83% 1,031,550 38,934,871 1,428,381Southside 230 29,436,515 3,760,087 12.77% 918,100 25,676,428 (158,181)Peninsula 121 14,477,970 1,997,875 13.80% 212,229 12,480,095 147,115Total 351 43,914,485 5,757,962 13.11% 1,130,329 38,156,523 (11,066)Southside 220 28,816,383 2,933,294 10.18% 2,064,727 25,883,089 1,344,209Peninsula 118 15,249,617 2,012,637 13.20% 758,370 13,236,980 292,785Total 338 44,066,000 4,945,931 11.22% 2,823,097 39,120,069 1,636,994Southside 208 27,089,939 2,551,059 9.42% 1,414,805 24,538,880 1,961,927Peninsula 112 14,548,482 1,604,287 11.03% 1,253,342 12,944,195 1,592,805Total 320 41,638,421 4,155,346 9.98% 2,668,147 37,483,075 3,554,732

2014

2013

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

2000

1999

New Construction in

SFNumber of Properties GLA in SF Vacant SF % Vacant

Occupiedin SF

Absorption in SF

2014 RE

TAIL

19

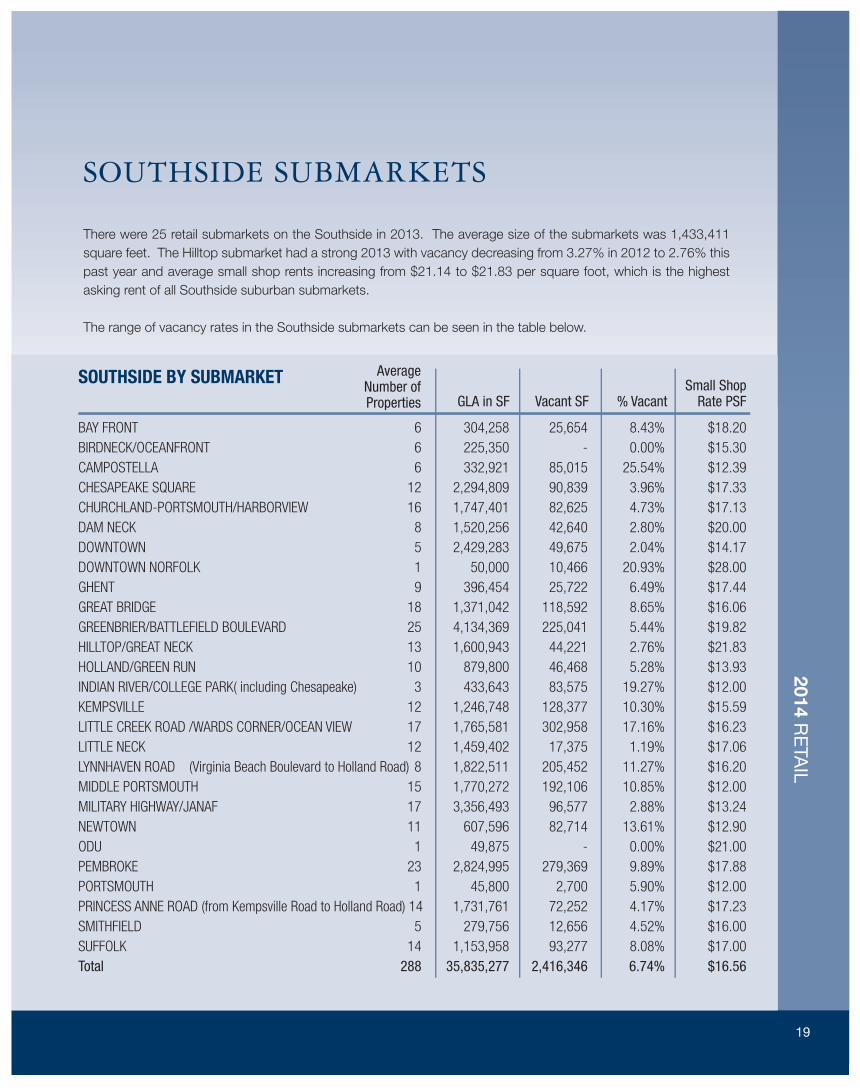

SOUTHSIDE SUBMARKETS

There were 25 retail submarkets on the Southside in 2013. The average size of the submarkets was 1,433,411 square feet. The Hilltop submarket had a strong 2013 with vacancy decreasing from 3.27% in 2012 to 2.76% this past year and average small shop rents increasing from $21.14 to $21.83 per square foot, which is the highest asking rent of all Southside suburban submarkets.

The range of vacancy rates in the Southside submarkets can be seen in the table below.

SOUTHSIDE BY SUBMARKET

BAY FRONT 6 304,258 25,654 8.43% $18.20 BIRDNECK/OCEANFRONT 6 225,350 - 0.00% $15.30 CAMPOSTELLA 6 332,921 85,015 25.54% $12.39 CHESAPEAKE SQUARE 12 2,294,809 90,839 3.96% $17.33 CHURCHLAND-PORTSMOUTH/HARBORVIEW 16 1,747,401 82,625 4.73% $17.13 DAM NECK 8 1,520,256 42,640 2.80% $20.00 DOWNTOWN 5 2,429,283 49,675 2.04% $14.17 DOWNTOWN NORFOLK 1 50,000 10,466 20.93% $28.00 GHENT 9 396,454 25,722 6.49% $17.44 GREAT BRIDGE 18 1,371,042 118,592 8.65% $16.06 GREENBRIER/BATTLEFIELD BOULEVARD 25 4,134,369 225,041 5.44% $19.82 HILLTOP/GREAT NECK 13 1,600,943 44,221 2.76% $21.83 HOLLAND/GREEN RUN 10 879,800 46,468 5.28% $13.93 INDIAN RIVER/COLLEGE PARK( including Chesapeake) 3 433,643 83,575 19.27% $12.00 KEMPSVILLE 12 1,246,748 128,377 10.30% $15.59 LITTLE CREEK ROAD /WARDS CORNER/OCEAN VIEW 17 1,765,581 302,958 17.16% $16.23 LITTLE NECK 12 1,459,402 17,375 1.19% $17.06 LYNNHAVEN ROAD (Virginia Beach Boulevard to Holland Road) 8 1,822,511 205,452 11.27% $16.20 MIDDLE PORTSMOUTH 15 1,770,272 192,106 10.85% $12.00 MILITARY HIGHWAY/JANAF 17 3,356,493 96,577 2.88% $13.24 NEWTOWN 11 607,596 82,714 13.61% $12.90 ODU 1 49,875 - 0.00% $21.00 PEMBROKE 23 2,824,995 279,369 9.89% $17.88 PORTSMOUTH 1 45,800 2,700 5.90% $12.00 PRINCESS ANNE ROAD (from Kempsville Road to Holland Road) 14 1,731,761 72,252 4.17% $17.23 SMITHFIELD 5 279,756 12,656 4.52% $16.00 SUFFOLK 14 1,153,958 93,277 8.08% $17.00 Total 288 35,835,277 2,416,346 6.74% $16.56

Small Shop Rate PSF% VacantVacant SFGLA in SF

Average Number of Properties

20 2014 Hampton Roads Real Estate Market Review

2 0 1 4 R E TA I L

COLISEUM CENTRAL 16 4,051,110 496,819 12.26% $15.40

DENBIGH 15 1,785,033 451,642 25.30% $11.25

FOXHILL/BUCKROE/EAST MERCURY 7 708,425 91,796 12.96% $13.17

GLOUCESTER 8 894,676 68,664 7.67% $14.38

HAMPTON MISC 1 64,327 10,910 16.96% $10.00

NEWMARKET/MAIN (TO INCLUDE HAMPTON) 12 974,957 198,407 20.35% $9.48

NEWPORT NEWS 1 21,240 1,400 6.59% $14.00

PATRICK HENRY/OYSTER POINT/KILN CREEK 30 4,200,077 157,415 3.75% $16.31

POQUOSON 2 108,521 5,250 4.84% $13.50

WILLIAMSBURG 30 4,745,579 570,487 12.02% $18.64

YORK COUNTY 12 833,376 70,928 8.51% $14.41

Total 134 18,387,321 2,123,718 11.55% $14.61

PENINSULA BY SUBMARKET Average Small Shop

Rate PSF% VacantVacant SFGLA in SFNumber of properties

PENINSULA SUBMARKETS

RETAIL PRODUCT TYPE

There were 10 retail submarkets on the Peninsula with an average size of 1,671,574 square feet. The two largest Peninsula submarkets are now Patrick Henry and Williamsburg. The Patrick Henry submarket is anchored by a regional mall and has the lowest vacancy rate on the Peninsula.

The Patrick Henry submarket continues to be one of the most highly desired submarkets in Hampton Roads having 4,374,256 square feet and a vacancy rate of just 3.75%. The Williamsburg market continues to have good retail activity along the Monticello corridor.

The Neighborhood Center remains the predominant product type with 173 properties with over 12 million square feet of GLA. The Community Centers comprised almost 10 million square feet with both product types showing a decrease in vacancy rate and an increase in rental rate. We do anticipate new Neighborhood Centers in 2014 and expect they will contain less small shop space than traditionally developed.

2014 RE

TAIL

21

Total Retail Product By Type

Neighborhood Center 173 12,448,491 36,000 1,473,678 11.84% $14.95 $2.71 Community Center 56 9,442,322 26,800 1,097,952 11.63% $15.62 $2.41 Fashion/Specialty Center 10 1,551,243 26,400 134,993 8.70% $24.89 $4.03 Power Center 31 10,851,642 - 786,746 7.25% $19.67 $3.58 Theme Festival Center 1 100,000 - - No data No data No data Outlet Center 1 349,927 - - No data No data No data Other 57 2,177,439 - 235,642 10.82% $16.19 $3.02 Freestanding 82 8,482,893 21,411 358,318 4.22% $14.87 $3.31 Mall 11 8,818,641 - 452,735 5.13% $20.50 $17.75 Total 422 54,222,598 110,611 4,540,064 8.37% $15.97 $2.87

Average Small Shop

Rate PSFAverage

CAM PSF% VacantVacant SF

NewConstruction

in SFGLA in SFNumber of Properties

Southside By Type

Neighborhood Center 125 9,150,514 36,000 1,084,314 11.85% $15.50 $2.73 Community Center 36 5,721,904 26,800 491,022 8.58% $16.17 $2.41 Fashion/Specialty Center 8 1,068,243 26,400 80,026 7.49% $24.75 $4.03 Power Center 21 6,616,525 - 271,371 4.10% $19.53 $3.58 Theme Festival Center 1 100,000 - - No data No data No dataOutlet Center - - - - No data No data No dataOther 40 1,433,737 - 121,324 8.46% $16.59 $3.03 Freestanding 49 4,994,709 - 35,225 0.71% $17.12 $3.31 Mall 8 6,749,645 - 333,064 4.93% $20.50 $18.86Total 288 35,835,277 89,200 2,416,346 6.74% $16.56 $2.95

Average Small Shop

Rate PSFAverage

CAM PSF% VacantVacant SF

NewConstruction

in SFGLA in SFNumber of Properties

Peninsula By Type

Neighborhood Center 48 3,297,977 - 389,364 11.81% $13.54 $2.33 Community Center 20 3,720,418 - 606,930 16.31% $14.68 $2.54 Fashion/Specialty Center 2 483,000 - 54,967 11.38% $26.00 $5.40 Power Center 10 4,235,117 - 515,375 12.17% $19.95 $3.00 Theme Festival Center - - - - No data No data No data Outlet Center 1 349,927 - - No data No data No data Other 17 743,702 - 114,318 15.37% $15.32 $2.53 Freestanding 33 3,488,184 21,411 323,093 9.26% $10.00 $2.50 Mall 3 2,068,996 - 119,671 5.78% #DIV/0! $17.75 Total 134 18,387,321 21,411 2,123,718 11.55% $14.61 $2.69

Average Small Shop

Rate PSFAverage

CAM PSF% VacantVacant SF

NewConstruction

in SFGLA in SFNumber of Properties

22 2014 Hampton Roads Real Estate Market Review

2 0 1 4 R E TA I L

BIG BOX VACANCYBig box vacancy increased in 2013 and is expected to climb again in 2014. The thought being several big box retailers limped into 2014. Additionally, a few small shop retailers are struggling as well. We will see tenants right size their units as they modify their footprints to stay current to what the market dictates. The boxes that we believe will bring the most product to market are K-Mart, Sears, and J.C. Penney. The 1,825,202 square feet of vacant space represents 40% of the total retail vacancy in the market. It is important to note some of the vacant boxes are now functionally or practically obsolete for today’s retailer. They will remain on the report as retail product until such time as they are demolished, converted to a non-retail use, or redeveloped.

Big Box Vacancy

Big Box Vacancy

Southside2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20132,073,115 2,207,416 2,220,935 1,906,391 1,513,523 1,142,319 957,887 948,288 907,688 1,102,093 880,568 855,979 821,993 929,713

Peninsula2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1,328,841 1,435,489 1,407,021 1,556,029 1,141,207 982,263 819,163 827,360 880,805 989,305 837,025 794,484 767,637 895,489

TOTAL2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 3,401,956 3,642,905 3,627,956 3,462,420 2,654,730 2,124,582 1,777,050 1,775,648 1,788,493 2,091,398 1,717,593 1,650,463 1,589,630 1,825,202

4,000,000

3,500,000

3,000,000

2,500,000

2,000,000

1,500,000

1,000,000

500,000

01999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Vaca

nt S

quar

e Fe

et

SouthsidePeninsulaTOTAL

1 Bayfront2 Birdneck/Oceanfront3 Campostella4 Chesapeake Square5 Churchland/Harbourview6 Dam Neck7 Downtown Norfolk8 Ghent9 Great Bridge10 Greenbrier/Battlefi eld Boulevard

11 Hilltop/Great Neck12 Holland/Green Run13 Indian River/College Park14 Kempsville15 Little Creek Road/ Wards Corner16 Little Neck17 Lynnhaven18 Middle Portsmouth19 Military Highway/Janaf20 Newtown

21 ODU 22 Pembroke23 Princess Anne24 Smithfi eld25 Suffolk

Retail SubmarketsSouthside

26 Coliseum Central27 Denbigh28 Foxhill/Buckroe29 Gloucester30 Hampton Miscellaneous31 Patrick Henry32 Poquoson33 Newmarket/Main34 Williamsburg35 York County

Peninsula

2014 RE

TAIL

23

24

The following is a list of theproperties included in this year’s surveylisted by submarket with a coderepresenting the type of property The GLA of the property is also listed

A Neighborhood CenterB Community CenterC Fashion/Specialty CenterD Power CenterE Theme Festival

F Outlet CenterG OtherH FreestandingI Mall

southside

BAY FRoNt CapeHenryPlaza A 58,424

Chic’sBeachShoppingCenter A 79,397

Kroger H 47,000

KrogerShops A 13,540

LakeShoresPlazaShoppingCenter A 58,230

MarinaShores G 47,667

BiRdNeCK/oCeANFRoNt

BirdneckSC A 65,460

BirdneckShoppes B 24,000

FarmFresh H 29,296

HarrisTeeter H 48,000

LinkhornShops A 48,899

PacificPlaza H 9,695

CAMPosteLLA

AtlanticCommons A 63,393

BainbridgeMarketplace A 46,444

CampostellaCorner A 43,375

GeorgeWashingtonCommons A 44,942

HollyPointSC A 65,338

SouthgatePlaza A 69,429

ChesAPeAKe sQuARe

BJ’s H 115,660

CastleShops H 37,464

ChesapeakeCenter B 270,602

ChesapeakeSquareMall I 800,000

ChesapeakeSquareShops H 13,559

CrossroadsCenteratChesapeakeSquare D 332,464

[email protected]. H 45,000

HomeDepot H 130,060

Lowes H 115,000

ShopsatChesapeakeSquare H 25,000

TaylorRoadPlaza A 60,000

Wal-MartSupercenter/Sam’sClub H 350,000

ChuRChLANd-PoRtsMouth/hARBoRVieW

ChurchlandPlaceShoppes G 21,000

ChurchlandSC A 149,741

ChurchlandSquare A 72,189

CollegePkwyCrossingatHarbourView A 86,130

Grand H 30,000

HarborViewShoppes A 17,000

HarbourViewEast D 172,000

HarbourViewMarketplace H 96,624

HarbourviewStationEast D 217,308

HarbourviewStationWest D 83,007

MarketplaceSquare A 12,461

PlanetFitnessPlaza A 52,966

PoplarHillPlaza B 102,326

SterlingCreek A 75,660

TownPointSquare A 58,989

VictoryCrossing H 500,000

dAM NeCK

2236GeneralBoothBlvd.A 11,500

DamNeckCrossing B 138,571

DamNeckSquare A 67,917

GeneralBoothPlaza A 71,639

RedMillCommons D 750,000

RedMillWalk D 240,000

SandbridgeSC A 66,800

StrawbridgeMarketplace A 173,829

doWNtoWN

BerkleyCenter A 47,945

ChurchStreetCrossing A 51,000

MacArthurCenterMall I 2,200,000

WatersideFestivalMarketplaceI 130,338

doWNtoWN NoRFoLK

WellsFargoRetail G 50,000

GheNt

201TwentyOne A 15,616

21stStreetPavilion G 21,000

CenterShops A 139,081

ColleyVillage A 44,585

GhentPlace G 13,000

HarrisTeeter H 27,000

PalaceShopsI,II C 78,669

PalaceStation G 37,503

TheCornerShops G 20,000

GReAt BRidGe

CahoonCommons D 278,023

CedarLakesCenter A 35,659

CentervilleCrossing A 46,000

CountryClubShoppes H 17,700

CrossingsatDeepCreek A 68,970

DominionMarketplace A 73,103

DominionPlazaSC A 63,733

GlenwoodSquare A 73,859

GreatBridgeSC A 156,937

HanburyVillage A 100,560

HarborWatchShoppes G 21,505

LasGaviotas A 82,000

MillwoodPlaza G 16,930

Mt.PleasantShoppingCenterA 100,000

Mt.PleasantVillage A 34,180

WilsonVillage A 52,500

WoodfordShoppes B 9,760

WoodfordSquare B 139,623

GReeNBRieR/BAttLeFieLd BouLeVARd

BattlefieldMarketplace G 30,000

ChesapeakeCrossing B 287,679

CountryClubSquare H 12,600

CrosswaysCntr I

&EdenWayShops D 438,725

EdinburghCommons D 184,232

EdinburghEast D 133,000

GainsboroughSquare A 88,862

GreenbrierMall I 899,665

GreenbrierMarketCenter D 487,580

GreenbrierShops A 37,500

GreenbrierSouthSC A 97,500

HomeDepot H 130,060

K-Mart/OfficeMax H 165,000

Knell’sRidgeSquare G 40,000

Lowes H 114,000

OrchardSquare A 88,728

Parkview@Greenbrier A 83,711

PlantationWoods A 16,800

RegalCinemas H 60,763

TheShoppesatGreenbrierG 40,000

Thn G 80,160

TownePlaceatGreenbrierC 127,109

VillageSquare G 15,000

VolvoParkwaySC G 41,874

Wal-Mart/Sam’sClub/Kohl’sD 433,821

hiLLtoP/GReAt NeCK

GreatNeckSquare A 94,587

GreatNeckVillage A 73,736

HilltopEast C 144,100

HilltopNorth A 202,346

HilltopPlaza B 152,025

HilltopSquare B 270,093

HilltopWest G 55,784

LaPromenade C 63,280

MarketplaceatHilltop C 113,000

MillDamCrossing A 25,776

RegencyHilltop B 236,549

RenaissancePlace G 47,667

Target H 122,000

hoLLANd/GReeN RuN

AuburnPlace A 42,709

ChimneyHill B 207,175

GreenRunSquare A 75,000

HollandPlazaSC A 155,000

HollandWindsorCrossing B 74,200

Lowes H 125,323

LynnhavenGreen A 50,838

RosemontCenter A 12,700

ShippsCorner A 63,355

TimberlakeSC A 73,500

iNdiAN RiVeR/CoLLeGe PARK(includingChesapeake)

CollegeParkI&II B 183,874

IndianRiverPlaza B 126,017

IndianRiverSC A 123,752

25

KEMPSVILLE

Arrowhead Plaza A 97,006

Fairfi eld SC B 239,763

Kemps Corner Shoppes G 25,929

Kemps River Center A 62,507

Kemps River Crossing B 245,268

Kempsville Crossing A 94,477

Kempsville Plaza A 60,778

Parkway Marketplace A 26,602

Providence Square SC A 144,904

University Shoppes A 47,200

Witchduck Exchange A 50,000

Woods Corner A 152,314

LITTLE CREEK ROAD/

WARDS CORNER/OCEAN VIEW

Ames/Kroger B 140,568

Dollar Tree Shopping Center A 51,415

East Beach Marketplace B 202,000

East Beach Shoppes A 63,000

Farm Fresh - Little Creek H 66,120

Glenwood Shoppes A 53,255

Little Creek and Tidewater Shops B 119,820

Little Creek Square A 82,300

Meadowbrook S C G 27,260

Mid-Town A 75,768

Mid-Way SC G 31,000

Ocean View SC A 73,658

Roosevelt Gardens SC A 109,175

Southern Shopping Center B 245,868

Super Wal-Mart H 225,000

Wards Corner Strip A 61,540

Wedgewood SC A 137,834

LITTLE NECK

Birchwood SC A 358,635

Colony Building A 23,625

Home Depot H 130,060

Kroger H 45,000

London Bridge Plaza B 114,584

Lowes H 160,000

Lynnhaven 2600 H 13,300

Lynnhaven Convenience G 36,900

Lynnhaven Shopping Center B 191,136

Princess Anne Plaza West C 77,558

Regatta Bay Shops G 60,000

Sam’s Club Plaza D 248,604

LYNNHAVEN ROAD

(Virginia Beach Boulevard to Holland Road)

Lynnhaven Crossing G 55,550

Lynnhaven East B 97,303

Lynnhaven Mall I 1,293,100

Lynnhaven North B 176,254

Lynnshores Shopping Center G 12,692

Lynnway Place G 30,213

Parkway Plaza A 44,287

Wal-Mart H 113,112

MIDDLE PORTSMOUTH

Afton SC A 106,500

Airline Marketplace A 69,000

Airline Plaza A 99,549

Alexander’s Corner Shopping Center A 50,826

Elmhurst Square A 66,250

Gilmerton Square A 43,236

Manor Commerce Center G 67,060

Manor Shops G 14,573

Old Towne Marketplace A 42,000

Rodman SC A 45,000

Super Wal-Mart H 200,000

Triangle SC A 84,437

Victory Crossing D 500,000

Victory West Shopping Center A 167,102

Williams Court B 214,739

MILITARY HIGHWAY/JANAF

3455 Azalea Garden Road A 1,024

Best Square B 140,030

Broad Creek Crossing Phase 1 and Phase 2 D 100,000

Broad Creek SC D 205,417

Bromley SC A 67,790

CostCo H 110,000

Dump/Mega Offi ce G 115,854

Farm Fresh H 60,000

Food Lion #170 H 41,000

Grand Outlet H 35,000

Janaf D 882,262

Lowes H 115,000

Military Crossing D 192,000

Military Triangle G 10,061

Super K-Mart & Shoppes B 200,000

Super Wal-Mart H 224,513

The Gallery @ Military Circle I 856,542

NEWTOWN

Cypress Point A 117,958

Diamond Springs North (Shopping Center) A 23,880

Diamond Springs Shoppes H 18,840

Mattress Discounters Plaza A 59,892

Newpointe SC A 92,978

Newtown Baker Crossing A 91,687

Newtown Center H 19,800

Newtown Convenience Center G 19,800

Northampton Business Center G 85,000

Thomas Corner SC G 23,557

Wesleyan Commons Shopping Center A 54,204

ODU

First Floor Retail Shops at

University Village Apartments G 49,875

PEMBROKE

Aragona SC A 69,700

Best Buy H 45,000

Collins Square A 123,870

Columbus Village East A 63,000

Columbus Village Entertainment Center E 100,000

Dean Plaza (Former HQ) D 140,000

Former Bloom Brothers H 165,000

Giant Square B 150,000

Goodwill H 34,000

Haverty’s H 55,000

Haygood SC B 165,000

Haynes H 228,000

Hunter’s Mill Shoppes G 22,827

Loehmann’s Plaza C 139,380

Northern Super Center G 36,588

Pembroke East B 24,806

Pembroke Mall I 570,000

Pembroke Meadows SC A 81,592

Pembroke Place B 165,000

Pembroke Plaza G 34,900

Roomstore H 50,000

The Town Center

of Virginia Beach C 325,147

Town Center Station B 36,185

PORTSMOUTH

Academy Crossing A 45,800

PRINCESS ANNE ROAD

(from Kempsville Road to Holland Road)

Brenneman Farm SC A 254,197

Courthouse Marketplace A 103,263

Home Depot H 130,000

Kempsville Marketplace A 71,460

Landstown Commons D 505,766

Lynnhaven Square S C G 22,933

Parkway SC A 64,820

Pleasant Valley Marketplace A 88,107

Princess Anne Marketplace B 209,500

Princess One SC A 84,725

Salem Crossing D 92,316

Salem Lakes Marketplace A 42,087

Salem Lakes SC A 37,087

Woodtide SC A 25,500

SMITHFIELD

Cypress Run SC G 25,000

Eagle Harbor A 77,049

Shoppes at Eagle Harbor A 23,343

Smithfi eld Plaza B 89,120

Smithfi eld Square A 65,244

SUFFOLK

Bennetts Creek Crossing A 119,812

Bennetts Creek Food Lion A 64,544

Centerbrooke Village A 12,600

Creekside Village A 18,835

Holland Plaza A 69,345

Kensington Square A 66,421

Lowes H 150,000

Oak Ridge Plaza A 38,700

Suffolk Plaza B 176,733

Suffolk Plaza West A 60,000

Suffolk Shopping Center B 155,733

Suffolk Specialty Shops G 15,200

Suffolk Village SC G 11,875

Wal-Mart Super Center H 194,160

26

PENINSULA

COLISEUM CENTRAL Coliseum Corner A 49,267

Coliseum Crossing B 221,004

Coliseum Marketplace A 105,998

Coliseum Specialty Shops G 15,026

Coliseum Square G 43,307

Hampton Towne Centre D 376,100

Hampton Woods A 89,092

Home Depot H 130,060

Newmarket South D 368,085

Peninsula Towncenter I 1,174,389

Riverdale Plaza D 260,316

Sports Authority H 40,000

Target H 122,000

The Power Plant D 621,150

Todd Center & Todd Lane Shops B 242,000

Wal-Mart Super Center H 193,316

DENBIGH

Beaconsdale SC A 28,000

Denbigh Speciality Shops G 24,504

Denbigh Village Centre B 334,299

Denbigh Village Shopping Center H 327,322

Ferguson Center G 118,000

Former Hills Denbigh H 86,589

Jefferson Crossing

(formerly Denbigh Crossing) A 145,000

Kmart H 115,854

Lee Hall Plaza A 36,000

Newport Crossing B 200,000

Richneck Shopping Center A 63,425

Stoneybrook Shopping Center A 74,340

Turnberry Crossing A 53,775

Village Square A 40,000

Warwick Denbigh SC B 137,925

FOXHILL/BUCKROE/EAST MERCURY

Buckroe SC A 76,000

Farm Fresh Phoebus H 60,411

Kmart H 94,500

Langley Square A 120,646

Marketplace @ Nickerson A 75,850

Nickerson Plaza A 83,849

Willow Oaks Village Square S.C. B 197,169

GLOUCESTER

Food Lion H 40,000

Hayes Plaza SC A 52,651

Hayes SC A 100,000

Home Depot H 100,000

Lowe’s H 125,000

Shoppes at Gloucester B 82,025

Wal-Mart Super Center H 220,000

York River Crossing B 175,000

HAMPTON MISC

Kecoughtan SC A 64,327

NEWMARKET/MAIN (TO INCLUDE HAMPTON)

4113 W Mercury Blvd. H 49,770

4205 W. Mercury Blvd. H 28,080

Brentwood SC A 53,600

Dresden SC G 35,000

Forest Park Square B 150,000

Fransisco Village A 55,865

Hampton Plaza B 173,199

Hilton SC A 74,000

Midway Shopping Center G 58,780

Plaza @ Newmarket B 117,377

Warwick Center A 103,886

Warwick Village A 75,400

NEWPORT NEWS

Jefferson Shoppes A 21,240

PATRICK HENRY/OYSTER POINT/KILN CREEK

Bayberry Village A 72,883

Best Buy Building H 135,000

City Center C 230,000

Commonweatlh Center G 30,279

Fairway Plaza G 37,950

Glendale SC G 30,000

Grand Furniture H 35,000

Harris Teeter H 52,334

Haverty’s H 45,000

Haynes H 85,000

Hidenwood SC A 100,000

Jefferson Commons D 400,000

Jefferson Greene G 57,430

Kroger H 55,000

Lowes H 120,000

Market Place @ Oyster Point A 69,660

Newport Marketplace D 450,000

Newport Square B 184,126

Offi ce Depot H 30,122

Oyster Point Plaza A 73,197

Oyster Point Square A 83,089

Patrick Henry Mall I 714,607

Patrick Henry Place A 17,000

Sam’s Club H 133,880

The Shoppes at Oyster Point G 30,000

Victory Center @ Kiln Creek A 78,000

Village Square @ Kiln Creek B 267,021

Villages of Kiln Creek G 45,300

Wal-Mart Super Center H 201,146

Yoder Plaza SC D 337,053

POQUOSON

Poquoson SC A 57,458

Wythe Creek Plaza SC A 51,063

WILLIAMSBURG

Colony Square A 66,806

Governor’s Green SC A 100,000

Home Depot H 130,000

James York Plaza B 137,708

Kingsgate Green B 138,348

Lowes H 163,000

Marketplace Shoppes G 32,026

Marketplace Shopping Center A 36,000

Monticello Marketplace B 299,792

Monticello SC A 82,000

New Town Shops on Main C 253,000

Norge Crossing H 52,000

Olde Towne SC G 30,000

Prime Outlets F 349,927

Quarterpath Crossing A 85,600

Settlers Market at New Town D 232,808

Staples H 37,400

The Marquis (Phase I) D 1,000,000

The Shops at High Street B 114,449

Village Shops at Kingsmill G 82,200

Wal-Mart SuperCenter H 210,000

Williamsburg Crossing A 150,000

Williamsburg Farm Fresh A 79,188

Williamsburg Marketcenter B 120,920

Williamsburg Outlet Mall I 180,000

Williamsburg Pavillion Shops G 50,000

Williamsburg SC I & II B 251,000

Williamsburg Towne and Cnty A 49,802

WindsorMeade Marketplace D 189,605

Yankee Candle H 42,000

YORK COUNTY

Grafton SC A 32,000

Heritage Square A 73,865

Kiln Creek Center A 45,700

Lakeside 17 H 8,400

Marketplace @ Yorktown A 73,050

Patriots Square A 47,231

Pavilion at Kiln Creek A 26,820

Shady Banks SC A 56,634

Wal-Mart SuperCenter H 220,000

Washington Square

Shopping Center B 177,056

York Square A 48,720

Yorkshire Downs G 23,900