Embed Size (px)

Citation preview

Market Recommendation: Buy

September 26, 2013

Analysis by: William Carver

9x 7x Mul$ple Expansion Capital Advisors, L.L.C

Presenta6on Road Map

Market Backdrop

Company Overview

Valua6on

Fkldas;Ekdsaf;adEsn;sadfndsaflkadn

Market Backdrop

9x 7x Mul$ple Expansion Capital Advisors, L.L.C

§ Vola6le year-‐to-‐year revenue growth § Divergent energy prices

§ Mature life cycle stage § Stable demand for industry services

§ Heavy regula6on level § Regulatory concerns may constrain future

produc6on § Compe66ve environment

§ Major players well established § Barriers to entry

§ Vary depending on services provided § High capital intensity and High globaliza6on

Market Segment Revenue 2013

Products and Services Segmenta6on 2013 Industry Structure Nonmetalic ore mining support

1%

Metallic ore mining support

2%

Coal mining support

3%Natural gas drilling

services8%

Natural gas well support services

17%

Oil drilling services22%

Oilfield support services47%

Oil and Gas Field Service Overview

9x 7x Mul$ple Expansion Capital Advisors, L.L.C

Well Count

Service Intensity

Input Costs Star6ng to Ease

Pricing Pressure

Observa6ons

Key External Drivers

• Con6nued high levels of drilling in the companies core basins, driven by aYrac6ve economics • Improved midstream infrastructure • AYrac6ve commodity profiles

• Significant por6on of RES business levered to well count, not rig count • Drilling efficiencies expected to con6nue

• Operators are drilling longer laterals and increasing the number of stages • Trend not relegated to select basins

• RES maintains significant market share • Pricing pressure within pressure pumping business

• Ability to control costs has allowed RES to con6nue genera6ng significant cash flow • Pricing pressure star6ng to be felt in the coiled tubing business

• Guar costs down significantly • Frac sand availability has increased

Fkldas;Ekdsaf;adEsn;sadfndsaflkadn

9x 7x Mul$ple Expansion Capital Advisors, L.L.C

Industry Revenue

2006 2007 2008 2009 2010 2011 2012 201320

40

60

80

100

120

140

160

107.33

2006 2007 2008 2009 2010 2011 2012 2013

2

4

6

8

10

12

14

16

3.42

North America Rotary Rig Count

WTI Crude Oil Spot Price ($/barrel) Henry Hub Natural Gas($/MMbtu)

Industry Trends

9x 7x Mul$ple Expansion Capital Advisors, L.L.C

(40%)

(30%)

(20%)

(10%)

0%

10%

20%

30%

40%

50%

2001 2003 2005 2007 2009 2011 2013

Growth %

§ Improving worldwide financial condi6ons

§ Projected posi6ve demand for support

services

§ Expanding global energy demand and increasing

crude oil prices

§ Expected to underpin growth in domes6c

oil drilling

§ Industry revenue expected to increase

§ Regulatory concerns

§ Compe66ve environment

§ Stable long-‐term demand for industry operators

Pressure Pumping Services Revenue

Industry Revenue Growth Key Observa6ons

Industry Outlook

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

2005 2006 2007 2008 2009 2010 2011 2012 2013

Millions

Company Overview

9x 7x Mul$ple Expansion Capital Advisors, L.L.C

9x 7x Mul$ple Expansion Capital Advisors, L.L.C

Execu6ve Summary

§ Headquarters in Atlanta, GA

§ Large Inside Ownership

§ Strong Balance Sheet

§ Generates Healthy Cash Flows

§ High ROIC

§ Recent Share Price $15.76

§ Annual Dividend 2.7%

Fkldas;Ekdsaf;adEsn;sadfndsaflkadn

9x 7x Mul$ple Expansion Capital Advisors, L.L.C

53%

14%

11%

5%

4%4%

9%

Service Line RevenuePressure Pumping

Thru Tubing Solutions

Coiled Tubing

Rental Tools

Snubbing -‐ HydraulicWorkover

Nitrogen

§ Services primarily provided in the Permian, Eagle Ford and Marcellus, three of the most ac6ve basins in NAM

§ Pressure pumping business levered to well count

q ~8,800 wells were drilled in 2Q13, up 3% from 1Q13

q An average of 5.2 wells were drilled per rig versus 5.0 the prior quarter

q Wall Street research es6mates the well count to improve moderately and frac intensity to rise sufficiently

§ Top of the line margins rela6ve to peers, resul6ng in an aYrac6ve free cash flow profile

q Cash flow profile has allowed management to return capital to shareholders through dividends

§ AYrac6ve balance sheet rela6ve to peers

q Minimal debt and desire to run business debt free

q Lack of leverage offers poten6al to materially accelerate growth if opportunity presents itself (organic or M&A)

RPC Company Highlights

Valua6on

9x 7x Mul$ple Expansion Capital Advisors, L.L.C

9x 7x Mul$ple Expansion Capital Advisors, L.L.C

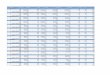

A B C D E F G H I J K L M N O

Stock Diluted Price Revenue Debt/

Price @ Equity Enterprise EPS CFPS EV/EBITDA EBITDA Margin Growth EBITDA EBITDA

Company 8/13/13 Value Value 2013E 2014E 2013E 2014E 2013E 2014E 2013E 2014E 2013E - 2014E 2013E 2013E

C&J Energy Services 20.93 1,138 1,269 13.4x 11.6x 6.6x 6.2x 5.9x 5.3x 20% 20% 9% 0.7x $213

Calfrac Well Services 32.28 1,485 1,934 26.7x 11.9x 8.7x 5.6x 9.1x 6.1x 14% 18% 14% 2.3x $220

Superior Well Services 25.64 4,091 5,853 13.9x 10.4x 4.5x 4.0x 4.9x 4.2x 25% 27% 10% 1.5x $1,197

Trican Well Service 13.90 2,070 2,643 NA 15.0x 9.8x 6.2x 10.6x 6.4x 12% 16% 17% 2.5x $257

Median $1,778 $2,289 13.9x 11.8x 7.6x 5.9x 7.5x 5.7x 17% 19% 12% 1.9x $238

Mean $2,196 $2,925 18.0x 12.2x 7.4x 5.5x 7.6x 5.5x 18% 20% 12% 1.8x $472

Low $1,138 $1,269 13.4x 10.4x 4.5x 4.0x 4.9x 4.2x 12% 16% 9% 0.7x $213

High $4,091 $5,853 26.7x 15.0x 9.8x 6.2x 10.6x 6.4x 25% 27% 17% 2.5x $1,197

RPC Inc. 14.52 3,203 3,280 18.6x 14.5x 8.2x 6.9x 6.6x 5.7x 27% 30% 8% 0.2x $495

Aug-11 Oct-11 Dec-11 Feb-12 Apr-12 Jun-12 Aug-12 Oct-12 Dec-12 Feb-13 Apr-13 Jun-13

50%

60%

70%

80%

90%

100%

110%

(30%)

(23%)

(22%)

0%

(13%)

Equity Performance

Trading Comparables

RPC

CFW

CJES

SPN

TCW

9x 7x Mul$ple Expansion Capital Advisors, L.L.C

0x

2x

4x

6x

8x

10x

12x

14x

16x

Jan

-08

Mar

-08

May

-08

Jul-

08

Sep-

08

Nov

-08

Jan

-09

Mar

-09

May

-09

Jul-

09

Sep-

09

Nov

-09

Jan

-10

Mar

-10

May

-10

Jul-

10

Sep-

10

Nov

-10

Jan

-11

Mar

-11

May

-11

Jul-

11

Sep-

11

Nov

-11

Jan

-12

Mar

-12

May

-12

Jul-

12

Sep-

12

Nov

-12

Jan

-13

Mar

-13

May

-13

Jul-

13

TCW-CA CFW-CA CJES SPN RES Peer Median Multiple

Rolling EV / NTM EBITDA Mul6ple

RES trades in-‐line with its peers despite best-‐in-‐class EBITDA margins, high single digit top line growth and the ability to accelerate

Current 5-yr Median % Premium / (Discount) to 5-yr

Trican 9.0x 7.0x 27.6%

Calfrac 7.4x 6.3x 17.4%

CJES 5.7x 3.6x 58.1%

SPN 4.6x 4.6x (0.4%)

RPC 6.1x 5.2x 16.3%

Current Mul6ple Not Indica6ve of Fundamentals

9x 7x Mul$ple Expansion Capital Advisors, L.L.C

A B C D E F G H I J K L M N O

Stock Diluted Price Revenue Debt/

Price @ Equity Enterprise EPS CFPS EV/EBITDA EBITDA Margin Growth EBITDA EBITDA

Company 8/13/13 Value Value 2013E 2014E 2013E 2014E 2013E 2014E 2013E 2014E 2013E - 2014E 2013E 2013E

C&J Energy Services 20.93 1,138 1,269 13.4x 11.6x 6.6x 6.2x 5.9x 5.3x 20% 20% 9% 0.7x $213

Calfrac Well Services 32.28 1,485 1,934 26.7x 11.9x 8.7x 5.6x 9.1x 6.1x 14% 18% 14% 2.3x $220

Superior Well Services 25.64 4,091 5,853 13.9x 10.4x 4.5x 4.0x 4.9x 4.2x 25% 27% 10% 1.5x $1,197

Trican Well Service 13.90 2,070 2,643 NA 15.0x 9.8x 6.2x 10.6x 6.4x 12% 16% 17% 2.5x $257

Median $1,778 $2,289 13.9x 11.8x 7.6x 5.9x 7.5x 5.7x 17% 19% 12% 1.9x $238

Mean $2,196 $2,925 18.0x 12.2x 7.4x 5.5x 7.6x 5.5x 18% 20% 12% 1.8x $472

Low $1,138 $1,269 13.4x 10.4x 4.5x 4.0x 4.9x 4.2x 12% 16% 9% 0.7x $213

High $4,091 $5,853 26.7x 15.0x 9.8x 6.2x 10.6x 6.4x 25% 27% 17% 2.5x $1,197

RPC Inc. 14.52 3,203 3,280 18.6x 14.5x 8.2x 6.9x 6.6x 5.7x 27% 30% 8% 0.2x $495

9%

14%

10%

17%

8%

C&J EnergyServices

Calfrac WellServices

Superior WellServices

Trican WellService

RPC Inc.

13-'14 E Median: 9.8%

20%

14%

25%

12%

27%

20% 18%

27%

16%

30%

C&J EnergyServices

Calfrac WellServices

Superior WellServices

Trican WellService

RPC Inc.

2013E 2014E 2013E Median 2014E Median

Growth EBITDA Margin

Stable Growth and Unmatched Margins

9x 7x Mul$ple Expansion Capital Advisors, L.L.C

§ 7/1/2013 valua6on date § Mid-‐year conven6on for discoun6ng § Value includes

§ 5 years of discounted cash flows § Terminal value based upon 2018E

EV / EBITDA mul6ple § Financial projec6ons used based upon

assump6ons previously presented § Marginal tax rate of 35%

§ No NOLs / company assumed to pay cash taxes

§ Net debt of $77 MM § 217 MM shares outstanding (adj. for

dilu6on)

Exit EV / EBITDA

$17.42 5.0x 6.0x 7.0x

9.0% $14.56 $16.89 $19.21

10.0% $14.06 $16.30 $18.53

11.0% $13.59 $15.74 $17.89

12.0% $13.13 $15.20 $17.27Disc

ount

Rat

e (%

)

Assump6ons Valua6on

$661

$495

$580 $543

$693 $713

$175 $127 $152 $125

$215 $222

2012A 2013A 2014A 2015A 2016A 2017A

EBITDA Unlevered Free Cash Flow

Cash Flow Profile

Discounted Cash Flow Analysis

9x 7x Mul$ple Expansion Capital Advisors, L.L.C

Oilfield Services Investment Risks § Demand for services dependent upon vola6le oil and natural gas prices § Strength of global economy and its impact on global demand for oil and natural gas § Regulatory changes § Upstream budget fluctua6ons that directly impact demand for services

Risk Factors

Company Specific Risks § Maintaining compe66ve posi6on

amongst larger OFS peers § Lack of diversifica6on in revenue

genera6ng services § High cost of comple6ng wells in

unconven6onal shale plays

9x 7x Mul$ple Expansion Capital Advisors, L.L.C

Market Recommendation: Buy

September 19, 2013

Ques6ons?

Analysis by: William Carver

9x 7x Mul$ple Expansion Capital Advisors, L.L.C

§ We expect to have revenue of $320 MM and EBITDA of $137 MM in 2013E

§ Expect 3% revenue growth from 2014E onward

q Revenue growth assumed to equal well count growth

§ EBITDA margins based on 2013E with 10bps annual escala6on to reflect increased market share / pricing power

§ D&A assumed at 25% of sales

§ Maintenance cap ex was $50 MM in 2012 and we expect it to grow in-‐line with infla6on

§ For Every $10 increase in sales, we use $1 in Working Capital

Overview of Assump6ons

$1,945 $1,815

$1,954 $1,978 $2,037 $2,160

$2,289

2012A 2013E 2014E 2015E 2016E 2017E 2018E

$329

$264

$300 $304 $313 $322

2012A 2013E 2014E 2015E 2016E 2017E

Revenue Projec6ons

Capex Projec6ons