Embed Size (px)

Citation preview

1 Quitter suite Lex < <| >

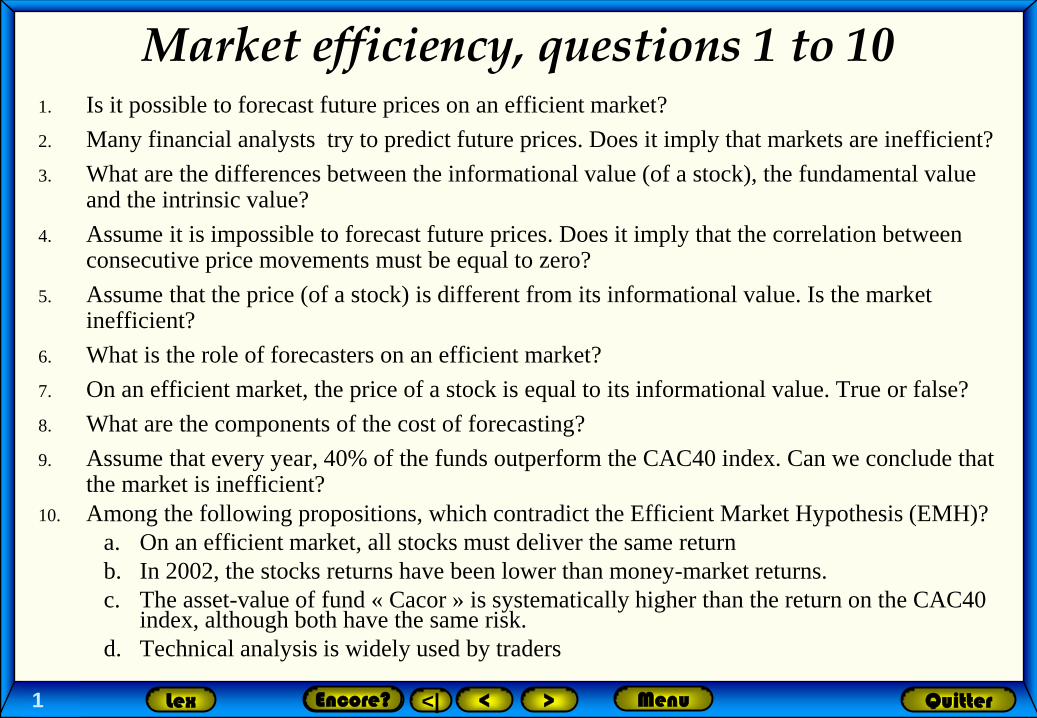

Market efficiency, questions 1 to 10 1. Is it possible to forecast future prices on an efficient market?

2. Many financial analysts try to predict future prices. Does it imply that markets are inefficient?

3. What are the differences between the informational value (of a stock), the fundamental value and the intrinsic value?

4. Assume it is impossible to forecast future prices. Does it imply that the correlation between consecutive price movements must be equal to zero?

5. Assume that the price (of a stock) is different from its informational value. Is the market inefficient?

6. What is the role of forecasters on an efficient market?

7. On an efficient market, the price of a stock is equal to its informational value. True or false?

8. What are the components of the cost of forecasting?

9. Assume that every year, 40% of the funds outperform the CAC40 index. Can we conclude that the market is inefficient?

10. Among the following propositions, which contradict the Efficient Market Hypothesis (EMH)?

a. On an efficient market, all stocks must deliver the same return

b. In 2002, the stocks returns have been lower than money-market returns.

c. The asset-value of fund « Cacor » is systematically higher than the return on the CAC40 index, although both have the same risk.

d. Technical analysis is widely used by traders

Encore? Menu

2 Quitter suite Lex < <| >

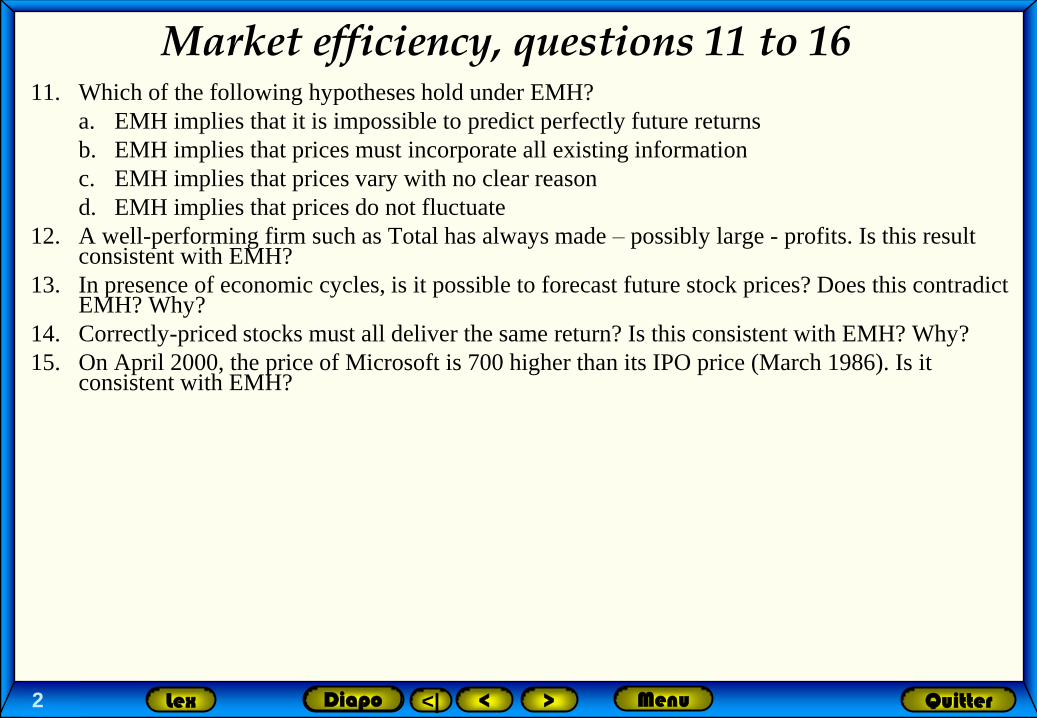

Market efficiency, questions 11 to 16 11. Which of the following hypotheses hold under EMH?

a. EMH implies that it is impossible to predict perfectly future returns

b. EMH implies that prices must incorporate all existing information

c. EMH implies that prices vary with no clear reason

d. EMH implies that prices do not fluctuate

12. A well-performing firm such as Total has always made – possibly large - profits. Is this result consistent with EMH?

13. In presence of economic cycles, is it possible to forecast future stock prices? Does this contradict EMH? Why?

14. Correctly-priced stocks must all deliver the same return? Is this consistent with EMH? Why?

15. On April 2000, the price of Microsoft is 700 higher than its IPO price (March 1986). Is it consistent with EMH?

Diapo Menu

3 Quitter suite Lex < <| >

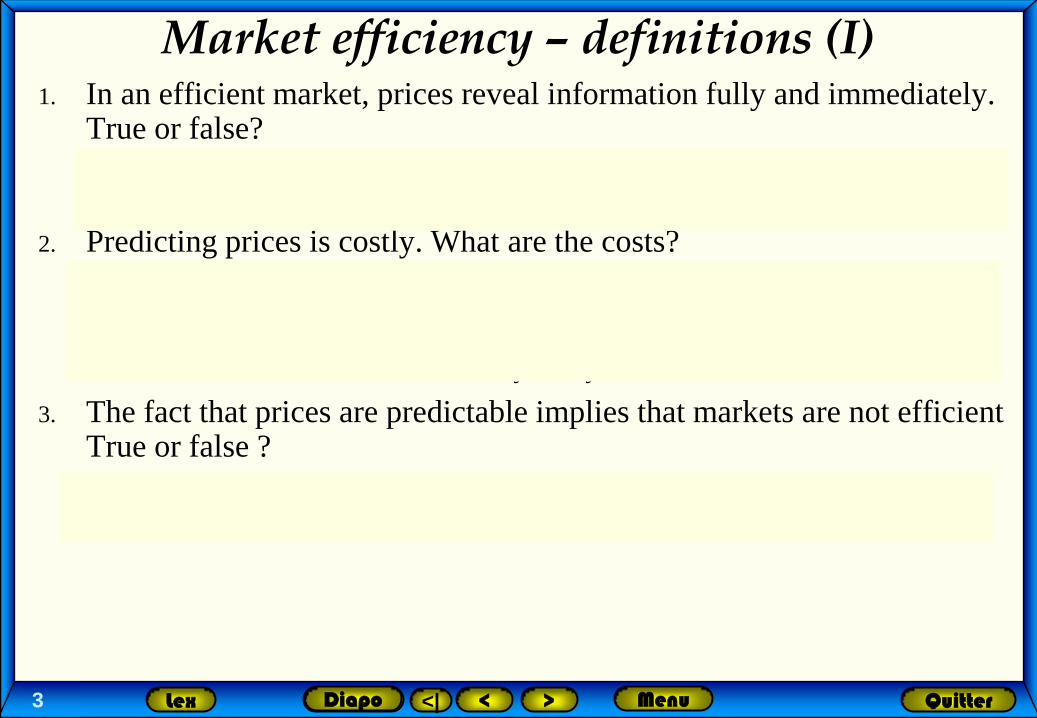

Market efficiency – definitions (I) 1. In an efficient market, prices reveal information fully and immediately.

True or false?

No, due to information processing costs and frictions, we can not observe a fully revealing equilibrium, neither prices can react instantaneously.

2. Predicting prices is costly. What are the costs?

Information is not accessible by everyone and is not free. Either you have to pay for it or produce it (which is again costly due to salaires, rents, and cost of other means to access information). Furthermore, to execute a strategy based on information you have to bear transaction costs each time you buy/sell assets.

3. The fact that prices are predictable implies that markets are not efficient True or false ?

No, actually this is not the right question to ask. The more important question is: Are the profits related with forecasts enough to cover costs associated with the forecast?

Diapo Menu

4 Quitter suite Lex < <| >

Market efficiency – definitions (II)

4. An informationally efficient market is necessarily an allocationally efficient market. True or false?

No. The observed prices and informational (fundamental) value of the asset can be considerably different in an efficient market. Informational efficiency is about non-predictability of this difference not how big the difference is.

5. Who first established the existence of a linkage between prices and information ?

Hayek (1945, The Use of Knowledge in Society). “We must look at the price system as such a mechanism for communicating information” .

6. Suppose there exist significant statistical dependencies between successive prices. Does the existence of such dependencies imply that markets are inefficient?

No. You have to test whether this statistical dependency is practically exploitable. One needs to take into account frictions such as transaction costs or costs associated with running an actively managed portfolio.

Diapo Menu

5 Quitter suite Lex < <| >

Market efficiency and the October 1987 market crash (20-1)

On October 19, 1987, the NYSE went down 22% in a day although no particular information was likely to justify such a large drop. Does it prove that markets are inefficient?

1. Efficient market theory (EMT) was « the most remarkable error in the history of economic theory », Wall Street Journal

2. EMT is « a failure », Business Week.

3. « the stock in the efficient market hypothesis (…) crashed along with the rest of the market on October 19, 1987 », L. Summers

4. Tanous (question to Fama in Investment Gurus, 97) : Another question that comes up frequently is if markets are correctly priced, how do you explain crashes when they go down twenty percent in one day?

Solution: Fama (1965), Fama in Investment Gurus

Diapo Menu

6 Quitter suite Lex < <| >

"Investment Gurus", 1997 Tanous (20-1)

Fama: Take your example of growth stocks. If their prospects don’t go as well as expected, then there will be a big decline. The same thing can happen for the market as a whole. It can also be a mistake. I think the crash in ’87 was a mistake.

Tanous: But if ’87 was a mistake, doesn’t that suggest that there are moments in time when markets are not efficiently priced?

Fama: Well, no. Take the previous crash in 1929. That one wasn’t big enough. So you have two crashes. One was too big [1987] and one was too small [1929]!

Tanous: But in an efficient market context, how are these crashes accounted for in terms of “correct pricing”? I mean, if the market was correctly priced on Friday,why did we need a crash on Monday?

Fama: That’s why I gave the example of two crashes. Half the time, the crashes should be too little, and half the time they should be too big.

Tanous: That’s not doing it for me. What am I missing?

Fama: Think of a distribution of errors. Unpredictable economic outcomes generate price changes. The distribution is around a mean—the expected return that people require to hold stocks. Now that distribution, in fact, has fat tails. That means that big pluses and big minuses are much more frequent than they are under a normal distribution. So we observe crashes way too frequently, but as long as they are half the time under-reactions and half the time overreactions,there is nothing inefficient about it.

Diapo Menu

7 Quitter suite Lex < <| >

o Chicago school of “rational expectations,” of which Eugene Fama is one of the biggest followers has dominated mainstream economics for the last twenty-five years.

– With economic agents supposedly possessing perfect information about all possible contingencies, systemic crises could never happen except as a result of accidents and surprises beyond the reach of economic theory.

8 Quitter suite Lex < <| >

Speed of adjustment (20-2)

1. How long does it take for prices to adjust on an efficient market?

The delay should be such that one should not be able to make a profit from the information disseminated.

2. Assuming fully-revealing equilibrium, how long does it take for prices to adjust to new information?

With no delay.

Diapo Menu

9 Quitter suite Lex < <| >

Expectations and market efficiency (20-3)

1. Assume an investor has rational expectations. For him, today’s price is the best predictor of tomorrow’s price. True or false?

No. Only under naive expectations.

2. Do rational expectations allow to account for other agents’ expected behavior ? If yes, how?

Yes. This is actually captured by the information set It. Taking a conditional expectation impicitly accounts for other agents’ expectations.

Menu Diapo

10 Quitter suite Lex < <| >

Consensus (20-5)

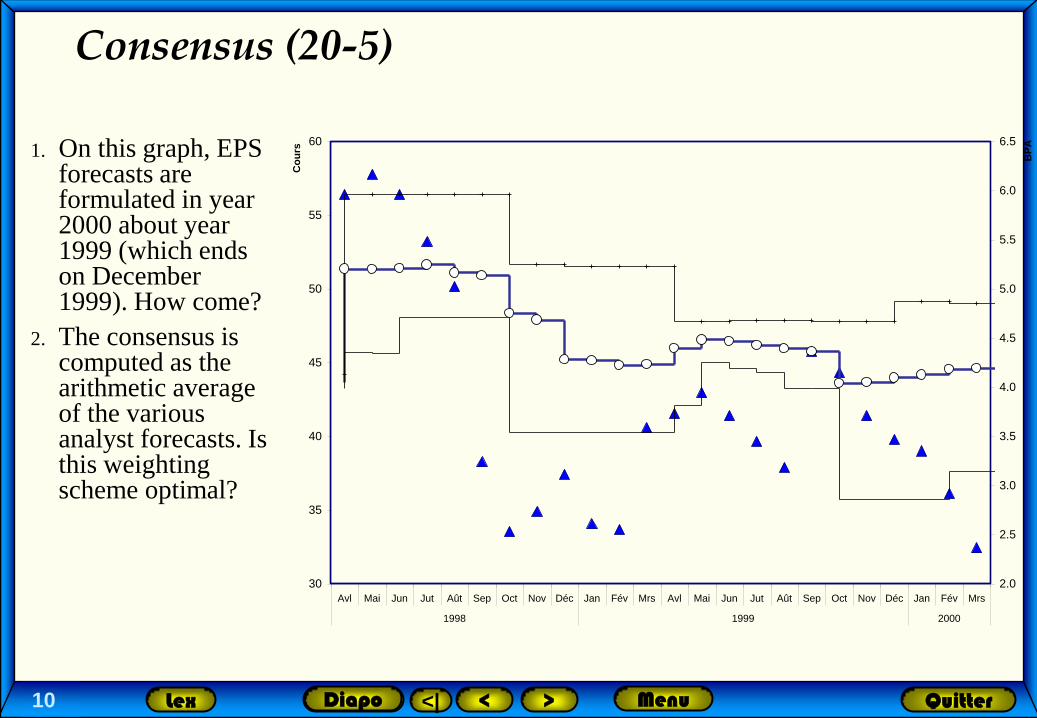

1. On this graph, EPS forecasts are formulated in year 2000 about year 1999 (which ends on December 1999). How come?

2. The consensus is computed as the arithmetic average of the various analyst forecasts. Is this weighting scheme optimal?

30

35

40

45

50

55

60

Avl Mai Jun Jut Aût Sep Oct Nov Déc Jan Fév Mrs Avl Mai Jun Jut Aût Sep Oct Nov Déc Jan Fév Mrs

1998 1999 2000

Co

urs

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

BP

A

Menu Diapo

11 Quitter suite Lex < <| >

1. At the end of accounting year, accounting data is still not public. Accounting figures are published with a lag. Furthermore, there are still several accounting adjustments made even after the data are published (for example on the way earnings were calculated, depreciation methods used, tax carryforwards, backwards, etc.).

2. Arithmetic average gives the same weight to every analyst. However, certain analysts can be more credible than the others. For example, if an analyst revises his forecast systematically after the others by copying them, his forecast will appear with a gap affecting the average consensus. Value-weighted averages (where analyst are weighted with respect to their creditworthiness) can prove to be more effective in such cases.

Consensus (20-5)

12 Quitter suite Lex < <| >

Super-Bowl (20-7)

When the team that wins the Super Bowl (around the end of January) belongs to the “Old American” (East Coast) stock prices go down over the corresponding year!

On the Monday that immediately follows the Super Bowl, market prices react.

In their 1990 paper, Krueger and Kennedy only document 2 classification errors, in 1970 and 1978. On both years, the DJIA index only exhibits weak variations.

On January 26, 1998, CNN markets writes « Despite AFC’s Super Bowl win, S&P futures recover losses on mega deal » while the Agéfi (February 1, 1993), notices that « although the Dallas Cow-Boys defeated the Bills from Buffalo, the market goes up ».

1. Update Krueger and Kennedy’s analysis by incorporating recent data.

2. What are your findings?

Krueger TM et WF Kennedy, 1990, An examination of the super bowl stock market predictor, Journal of

Finance, Vol 45, n° 2, p. 691-697.

Morel C., 2004, L’anomalie du Super-Bowl, Banque et Marchés,

Kester G.W., 2010, What happened to the super bowl stock market predictor?, Journal of Investing, spring,

p. 82-87 Menu Diapo

13 Quitter suite Lex < <| >

Sell in may and go away (20-8)

There are various sayings expressing the same idea. One is about coming back to the market on Halloween (US version – see references), or « come back to the Derby day » (UK version).

o Using daily data on the DowJones index since 1896, compare the returns of the following 2 strategies : 1/ passive strategy ; 2/ active strategy where stocks are sold at the beginning of May and are bought back at the beginning of next year's November

o Make comments about this quick and simple test.

References

Bouman et Jacobsen, 2002, The halloween indicator, « sell in may and go away »,

American Economic Review, Vol 92, n° 5, p. 1617-1635.

Jacobsen et Zhang, 2010, Are monthly seasonals real? A three century perspective,

SSRN

14 Quitter suite Lex < <| >

Fundamental indexing (20-12)

o Suppose that some investors can forecast stock prices (in a profitable way), but not you. You thus follow a passive portfolio management strategy. Does the fact that markets are not informationally efficient have to change your investment strategy? Reading Treynor (2005, Financial Analysts Journal), can help you to answer the following questions:

1. Are market capitalization (value) weighted indices better benchmarks in informationally inefficient markets? Why?

2. How can you define appropriate benchmarks in informationally inefficient markets?

3. Give examples of investment funds and indices which use this reasoning.

15 Quitter suite Lex < <| >

Fundamental indexing (20-12)

1. No. In an informationally inefficient market there will be a gap between (unobservable) value and (observable) market capitalization and this gap will be more for large firms. Thus putting more weight on large caps will further bias the performance of the benchmark. Eventually, you would be investing more money to overpriced stocks than underpriced stocks.

2. Benchmark should be with respect to operational size, i.e. firm’s capacity to generate free cash flows, revenues, cash dividends, etc.

3. RAFI (Research Affiliates Fundamental Index) indices provide a good benchmark. Many ETFs track their performances.

![[heaven] #Unchained : comment quitter Facebook ?](https://img.pdfslide.us/doc/110x75/5586e3bbd8b42abd5a8b46c6/heaven-unchained-comment-quitter-facebook-.jpg)