Embed Size (px)

Citation preview

1

Cambiar Insights1Q 2016

Market Commentary

Brian M. Barish, CFA

2

The first quarter of 2016 saw the continuation of a steep market correction in larger cap U.S. equities and an outright bear market in global equities and small cap stocks. The S&P 500 fell by 12% from the end of the December to the low in mid-February, before rebounding all the way back to flat by the end of the quarter. Small cap stocks and international stocks fell more (17% and 14%, respectively) before recovering about the same amount (12%), leading to net losses of 3-4% for these asset classes. It is worth noting that small cap stocks have been sliding for over a year now in parallel to rising high yield credit spreads, leading to a small cap stock decline of 26% by February from prior highs. International stocks have similarly been churning in a southerly direction, and reached a 25% loss from 2014 highs in February. We expressed concern in our 2015 year-end letter that stocks of all types were unlikely to stabilize until high yield credit stabilized. High yield dislocations have been dominated by energy and other commodities, and these too bottomed around mid-February. Consequently, oil prices, high yield bond prices, and global equities all bottomed within hours of each other. Cross-asset class correlations have seldom been so high aside from major and more newsworthy market events.

Global Equity Indexes & Crude Oil – Notice Any Correlation?

*Source: Bloomberg. Data has been normalized

High Yield Bond Spreads - Peaked But Still Elevated

*Source: Bloomberg.

Market Commentary1Q 2016

-56%-52%-48%-44%-40%-36%-32%-28%-24%-20%-16%-12%-8%-4%0%4%

Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16

S&P 500 Russell 2000 MSCI EAFE Crude Oil

2%

3%

4%

5%

6%

7%

8%

9%

Sep-12 Mar-13 Sep-13 Mar-14 Sep-14 Mar-15 Sep-15 Mar-16

3

Outside the world of equities, sovereign bond yields fell in most developed nations, with the U.S. 10-year yield declining from 2.3% at year-end to the 1.8% range. German bunds fell by a similar 50 bps (from a yield of 0.6% to 0.1%), while in Japan, the ten-year yield went into negative territory as Japan’s Central Bank implemented negative interest rates on the short end of its financing curve. Negative interest rates were employed by smaller countries such as Switzerland and Denmark starting in 2014 to try to discourage investors from parking money in their financial systems and thus inflating their local currency. Negate rates were then adopted by the ECB to stimulate growth and bring down funding costs for peripheral/Mediterranean nations such as Spain and Italy. There still isn’t much growth in Europe, but the funding-cost goals have been highly successful – Spain and Italy currently fund their debt for less than the United States. Japan hardly has a funding cost problem, but has yet to see its anti-deflation growth and price level goals attained. In a move that was likely to the surprise of the Japanese, the Yen promptly rallied from Y120 to Y105 (per dollar), and interbank funding activity dried up. Based on the initial reaction, markets appear skeptical that the negative rate policy will succeed in the intended (stimulative) goal; in contrast, negative rates seem poised to discourage lending and therefore liquidity (i.e., who would pay money to lend?). Technically, negative interest regimes have tried to incentivize lending by charging a negative rate on un-lent reserves. However, with very little credit demand when rates were at 0%, it’s hard to see precisely how taxing excess savings more heavily would stir quality credit growth.

For most of the post-2008 time period, sharp declines in sovereign yields have been associated with poor equity conditions and general market declines. Perhaps owing to the dislocations already in place at the end of 2015 in high yield credit and equities, most markets were able to shrug off the decline in global yields, though defensive utility-like businesses outperformed more cyclical sectors. The yo-yo decline and recovery marked the first instance since the Great Depression of an intra-quarter loss in large cap stocks in excess of 10% and subsequent complete recovery - although I was not able to find a similar move during the 1930s. At one point in early March, the U.S. equity markets had experienced intraday moves of more than 1.0% on over 75% of trading days going back to early December, conjuring up other 1930s parallels. But it isn’t the 1930s, and financial conditions are far from stressed in terms of liquidity and economic activity. Plenty of anecdotal evidence suggests that much of the volatility and price dislocations were triggered by market-neutral hedge funds shorting equities, credit, and whole market sectors, and then getting whipsawed as conviction longs went south and short-cover rallies went north, leading to somewhat forced position long/short position whipsawing and unintended correlations. This is to say that today’s market structure, led by 2-sided equity balance sheets and a variety of passive investment flows, appears to have fostered higher volatility.

The Laws of Unintended ConsequencesWhen negative interest rates cause one’s currency to rise sharply, and market neutral investment strategies layered on top of each other inflate volatility rather than curb it, it’s safe to say that there are unintended forces at play. We observe aspects of these phenomena on a daily basis:

Trading costs down, liquidity down? - Despite trading costs being as low as they have ever been historically, volatility is higher and equity trading volumes have fallen steadily. The decline in trading volumes for stocks (large and small) is neither good nor bad in and of itself; yet given the large number of investment vehicles (e.g. ETFs, mutual funds, hedge funds) dwarfing the number of publicly traded stocks, a serial decline in liquidity seems an awfully strange outcome.

Predictable unpredictability? – Every quarter, our research analysts are bombarded by earnings releases, guidance revisions and a lot of expected volatility around such disclosures. Stocks historically would tend to react in one direction to earnings misses or beats and keep going in that direction. Increasingly, we see price action “the day of” earnings releases to be in one direction, only to witness stock prices doing something very different in the following weeks. This trend suggests many stocks’ fundamentals are better digested by people that are not in the business of publishing professional revenue and eps estimates, or wagering on near term trading reactions.

Market-neutral, or just more exposed? – It’s become an accepted financial dogma that a market-neutral long/short fund that is short $1.00 of stocks for every $1.00 it is long should have less market-specific risk (or Beta) than $1.00 invested in the markets “unhedged”. That may be true on paper, but with less liquidity and less predictable stock behavior to information and investment

Market Commentary1Q 2016

The yo-yo decline and recovery marked the first instance since

the Great Depression of an intra-quarter loss in large cap stocks

in excess of 10% and subsequent complete recovery...

4

Market Commentary1Q 2016

flows, the $2.00 invested long/short is 100% more exposed than the $1.00, and perhaps even riskier yet than that $1.00 if it is invested in something that the holder plans on owning for a long while.

The explosion of the alternatives business rests in no small part on a desire by institutional investors to minimize market-based volatility, or alternatively to absorb market Beta at de-minimus costs in the form of indexes. The core-satellite portfolio allocation model has merit, but if investor cash flows are wish-boned between pure Beta indexes and heavily leveraged yet market-neutral exposures, who exactly is supposed to facilitate liquidity as market-neutral strategies recalibrate their holdings? It may very well have been other market-neutral strategies in the first quarter, leading to some rather extreme price movements. There is probably a good financial drama to be written in the future on this topic. I can give you a one-sentence version of the current story: long/short strategies can only get so large relative to the rest of the actively managed market before they begin to concentrate (versus dampen) risks. There are a lot fewer dollars as a percentage of the stock market being actively managed than ever before.

These ecosystems do need to balance, and appear to be tipping towards a riskier and more volatile imbalance – ironically through institution investor efforts to achieve the opposite.

Stimulation through negation? - With Japan’s move to negative interest rates, a majority of reserve currencies apart from the U.S. dollar now have negative short-term interest rates. In theory, low borrowing costs should incentivize banks to lend reserves, rather than parking them in negatively yielding reserve accounts. This increase in loan growth should then (again, in theory) help to staunch deflation. In practice, Japanese banks promptly reduced interbank lending lines for fear of monies being trapped in negatively yielding accounts, and the Yen (historically a funding currency) became more scarce and appreciated sharply. There is some evidence to suggest similar conclusions for customers to exit the financial system entirely and hold cash in other negative yield currencies. Japan is unique because its savings to loans ratio is very high – the Japanese are now better off saving money outside their financial system. Sales of safes (to hold cash) are on the rise globally, and some insurance companies have reportedly begun holding stores of physical cash rather than risking it in a reserve account in the financial system. The negative rate experiment probably plays on for a bit longer, but just as the equity markets can only be de-risked so far, the credit markets can only be de-yielded so far before they start functioning oddly.

Thinking About REITs In a low nominal growth world, yield is indeed poised to be a scarce commodity, and yield-driven equity asset classes have multiplied to satisfy demand. In some cases, there is dubious financial engineering afoot. We would caution that well-covered dividend paying stocks and REITs are proven equity-plus-yield instruments. Publicly traded LPs and MLPs are much less proven and have not evidenced consistent durability thus far.

The REIT universe is poised to enjoy a unique catalyst in the form of an industry re-classification to its own market sector. The historical market cap of all publically traded REITs in the U.S. has expanded from $1.5 billion in December 1971 to $939 billion in December 2015; as a result, MSCI will separate all non-mortgage REITs into its own sector on August 31st (REITs were previously part of the Financials Services sector). The stand-alone REIT sector is expected to be the 2nd-largest sector (after Financials) in the small cap and mid cap value indices (the Russell 2000 Value and Russell Mid Cap Value benchmarks). Historically, many investors did not look at REITs as being compatible with a stock portfolio. Legally speaking, REITs are not stocks, and were instituted as a liquid way for investors to hold real estate assets in a tax-friendly manner. The tax-friendly treatment came at a cost (namely, fewer degrees of freedom to disburse income), but some of these limitations have been engineered-around financially. With this pending re-classification and the market’s thirst for yield, a further discussion is warranted.

5

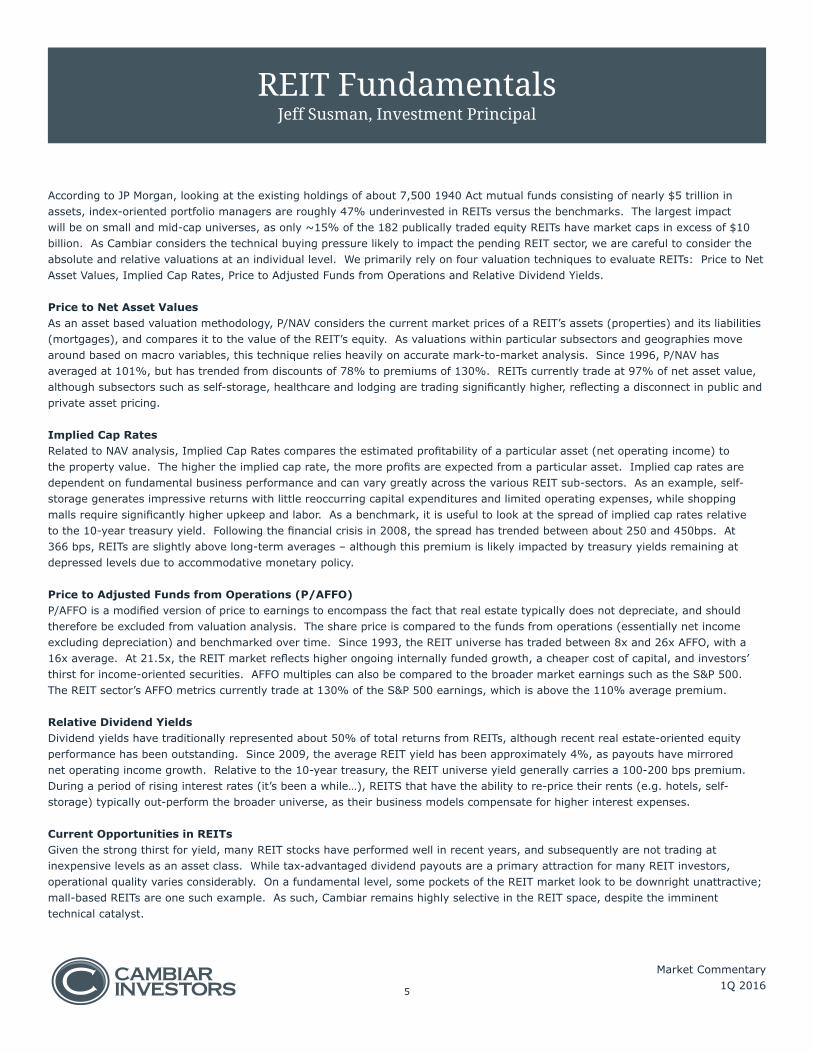

According to JP Morgan, looking at the existing holdings of about 7,500 1940 Act mutual funds consisting of nearly $5 trillion in assets, index-oriented portfolio managers are roughly 47% underinvested in REITs versus the benchmarks. The largest impact will be on small and mid-cap universes, as only ~15% of the 182 publically traded equity REITs have market caps in excess of $10 billion. As Cambiar considers the technical buying pressure likely to impact the pending REIT sector, we are careful to consider the absolute and relative valuations at an individual level. We primarily rely on four valuation techniques to evaluate REITs: Price to Net Asset Values, Implied Cap Rates, Price to Adjusted Funds from Operations and Relative Dividend Yields.

Price to Net Asset ValuesAs an asset based valuation methodology, P/NAV considers the current market prices of a REIT’s assets (properties) and its liabilities (mortgages), and compares it to the value of the REIT’s equity. As valuations within particular subsectors and geographies move around based on macro variables, this technique relies heavily on accurate mark-to-market analysis. Since 1996, P/NAV has averaged at 101%, but has trended from discounts of 78% to premiums of 130%. REITs currently trade at 97% of net asset value, although subsectors such as self-storage, healthcare and lodging are trading significantly higher, reflecting a disconnect in public and private asset pricing.

Implied Cap RatesRelated to NAV analysis, Implied Cap Rates compares the estimated profitability of a particular asset (net operating income) to the property value. The higher the implied cap rate, the more profits are expected from a particular asset. Implied cap rates are dependent on fundamental business performance and can vary greatly across the various REIT sub-sectors. As an example, self-storage generates impressive returns with little reoccurring capital expenditures and limited operating expenses, while shopping malls require significantly higher upkeep and labor. As a benchmark, it is useful to look at the spread of implied cap rates relative to the 10-year treasury yield. Following the financial crisis in 2008, the spread has trended between about 250 and 450bps. At 366 bps, REITs are slightly above long-term averages – although this premium is likely impacted by treasury yields remaining at depressed levels due to accommodative monetary policy.

Price to Adjusted Funds from Operations (P/AFFO) P/AFFO is a modified version of price to earnings to encompass the fact that real estate typically does not depreciate, and should therefore be excluded from valuation analysis. The share price is compared to the funds from operations (essentially net income excluding depreciation) and benchmarked over time. Since 1993, the REIT universe has traded between 8x and 26x AFFO, with a 16x average. At 21.5x, the REIT market reflects higher ongoing internally funded growth, a cheaper cost of capital, and investors’ thirst for income-oriented securities. AFFO multiples can also be compared to the broader market earnings such as the S&P 500. The REIT sector’s AFFO metrics currently trade at 130% of the S&P 500 earnings, which is above the 110% average premium.

Relative Dividend YieldsDividend yields have traditionally represented about 50% of total returns from REITs, although recent real estate-oriented equity performance has been outstanding. Since 2009, the average REIT yield has been approximately 4%, as payouts have mirrored net operating income growth. Relative to the 10-year treasury, the REIT universe yield generally carries a 100-200 bps premium. During a period of rising interest rates (it’s been a while…), REITS that have the ability to re-price their rents (e.g. hotels, self-storage) typically out-perform the broader universe, as their business models compensate for higher interest expenses.

Current Opportunities in REITsGiven the strong thirst for yield, many REIT stocks have performed well in recent years, and subsequently are not trading at inexpensive levels as an asset class. While tax-advantaged dividend payouts are a primary attraction for many REIT investors, operational quality varies considerably. On a fundamental level, some pockets of the REIT market look to be downright unattractive; mall-based REITs are one such example. As such, Cambiar remains highly selective in the REIT space, despite the imminent technical catalyst.

REIT FundamentalsJeff Susman, Investment Principal

Market Commentary1Q 2016

6

Market Commentary1Q 2016

Host Hotels & Resorts (HST) The largest lodging REIT in the world, with more than 100 properties and 56,000 rooms. Host is heavily focused on the U.S. market, and the company has a strong track record of recycling capital by purchasing inferior assets on the cheap, upgrading the properties, and then selling the hotels at significant premiums to other investors. As an example, Host bought the Phoenician Resort in Scottsdale; the company will spend the next two years upgrading and expanding the property before potentially looking to redeploy the invested capital into other projects. Unlike most other lodging REITs, Host maintains a very conservative balance sheet; net debt/EBITDA is only 2.7x. This capital structure should be a significant benefit to expenses as interest rates increase. Host is trading at approximately 9.8x P/AFFO, or 80% of NAV; the company pays regular cash dividend and is currently yielding 5.1%. With additional asset sales likely in the coming quarters, a large stock buyback and the potential for a special dividend are possible. Cambiar holds Host in the Large Cap Value portfolio.

Colony Starwood (SFR) The third-largest owner of Single Family Rentals (“SFRs”), with 31,000 properties. The available bulk pools of single family homes came about in the aftermath of the financial crisis. Cambiar views Colony Starwood’s business model to be attractive, as the company benefits from the increased tendency of households to rent. This trend is evidenced by the low home ownership rate relative to historical levels. Colony and other SFR providers also benefit from a lack of supply, as single family construction levels remain below the level of replacement. The lack of inventory is particularly skewed at the low end (i.e., $200k price point, where most rental homes are owned), as homebuilders have been more focused on providing supply higher up on the price spectrum. The convergence of increased demand for rental units and limited supply conditions should offer continued firmness for both occupancy levels and pricing. Trading at 70-80% of NAV (which should appreciate over time in tandem with underlying home prices), Colony represent an attractive risk/reward opportunity for capital appreciation, while also offering a 3.5% dividend yield. Cambiar holds Colony Starwood in the Small-Mid Value portfolio.

Final Comments Financial markets and monetary systems have changed a great deal since the 2008 Global Financial Crisis. It is reasonably clear that global growth (especially in the developed world) is slow and poised to stay this way, with demographics and technology representing leading obstacles to higher nominal growth. It is less clear what the changes in market structure, regulations, and unconventional monetary policy have wrought. We would argue that conventional financial wisdoms appear less applicable given these changes, and that there are clear limits to financial “de-risking” through complex artifices.

With that said, Cambiar’s in-house playbook is to remain patient, and try to not overthink a generally overanalyzed financial system. I personally suspect the first quarter volatility may repeat later in the year, with little net effect unless one is foolish enough to over-react to it. As a follow-up to our value investing discussion in Q4, a key internal goal at Cambiar is to sustain a value temperament to our stocks – don’t chase on the upside, don’t over-react to negative news flow on the downside, and try to stick with more transparent operating businesses versus opaque financial engineering. If the financial weather does not change much between now and a year from now, that ought to be the correct path.

Thanks for your continued confidence in Cambiar.

Brian M. Barish, CFAPresident, Cambiar Investors LLC

Certain information contained in this communication constitutes “forward-looking statements”. Due to market risk and uncertainties, actual events or results, or the actual performance of any of the Cambiar strategies, may differ materially from that reflected or contemplated in such forward-looking statements. All information is provided for informational purposes only. The information provided is not intended to be, and should not be construed as, investment, legal or tax advice. Nothing contained herein should be construed as a recommendation or advice to purchase or sell any security, investment, or portfolio allocation.