Embed Size (px)

Citation preview

Rajendra K. Srivastava, Tasadduq A. Shervani, & Liam Fahey

Market-Based Assets andShareholder Value:

A Framework for AnalysisThe authors develop a conceptua] framework of the marketing-finance interface and discuss its implications for thetheory and practice of marketing. The framework proposes that marketing is concerned with the task of developingand managing market-based assets, or assets that arise from the commingling of the firm with entities in its exter-nal environment. Examples of market-based assets include customer relationships, channel relationships, and part-ner relationships. Market-based assets, in turn, increase shareholder value by accelerating and enhancing cashflows, lowering the volatility and vulnerability of cash flows, and increasing the residual value of cash flows.

Too often marketing tends to focus on sales growth andmarket share, and it fails to recognize the impact of mar-keting decisions on such variables as inventory levels,working capital needs, financing costs, debt-to-equityratios, and stock prices. To assume such factors are purelythe responsibility of finance is to be guilty of a kind ofmarketing myopia not less damaging than that originallyenvisioned by Levitt (1960).

—Paul Anderson, "The Marketing Management/Finance Interface"

There is a quiet revolution in the positive way thatmarketing activities are being viewed by some mar-keting professionals, enlightened senior managers,

and innovative managers in other functions, particularlyfinance. Old inviolable assumptions about the purpose,content, and execution of marketing slowly are giving wayto assumptions that more accurately reflect how it is prac-ticed in leading organizations. In this article, we identifythe new assumptions pertaining to the marketing-financeinterface and discuss their consequences for the theory andpractice of marketing.

Although they often are unstated, assumptions underlie,shape, and constrain both theory and practice (Hunt 1983;Senge 1990). Therefore, it is imperative that marketers con-tinually identify and articulate changes in the underlyingassumptions regarding the field of marketing. In particular,as the movement to adopt shareholder value-based measuresof firm performance continues, marketing's traditionalassumptions must be extended to address the marketing-finance interface. These new assumptions about the rela-tionship between marketing and finance do not replace thetraditional assumptions; rather, they add to and incorporatethem. Marketing's traditional assumptions and the addi-

Rajendra K. Srivastava is Senior Associate Dean and Jack R. CrosbyRegent's Chair in Business, Graduate School of Business; and TasadduqA. Shervani is an assistant professor, Department of Marketing, Universityof Texas at Austin. Liam Fahey is an adjunct professor, Babson Collegeand Cranfield University (UK). The authors are grateful to three anony-mous reviewers for their helpful comments.

tional assumptions regarding the marketing-finance inter-face are summarized in Table I.

Traditionally, marketing activities focus on success inthe product marketplace. Increasingly, however, top man-agement requires that marketing view its ultimate purposeas contributing to the enhancement of shareholder retums(Day and Fahey 1988). This change has led to the recog-nition that the relationship between marketing and finaticemust be managed systematically; no longer can marketersafford to rely on the traditional assumption that positiveproduct-market results will translate automatically into thebest financial results. As a result, marketers are adoptingthe perspective that customers and channels are not sitnplythe objects of marketing's actions; they are assets thatmust be cultivated and leveraged (cf. Hunt and Morgan1995). These assets can be conceptualized as market-based assets, or assets that arise from the commingling ofthe firm witb entities in its external environment. Lever-aging such assets requires marketers to go beyond the tra-ditional inputs to marketing analysis, such as marketplaceand organizational knowledge, and to include an under-standing of the financial consequences of marketing deci-sions. Indeed, it also expands the external stakeholders ofmarketing to include explicitly the shareholders andpotential shareholders of the firm and requires broaderinput into marketing decision making by other functionalmanagers.

Another shift in the mind-set of marketers is occurringin the direction of expanding the set of measures of the suc-cess or failure of marketing activities. Marketers are movingbeyond traditional financial measures—such as sales vol-ume, market share, and gross margin—to include additionalfinancial measures, such as the net present value of cashflows and hence shareholder value (Anderson 1979; Dayand Fahey 1988; Pessemier and Root 1973). Indeed, it isinteresting to note that as marketers are moving to assess theimpact of marketing activities on shareholder value, accoun-tants and finance professionals are broadening their thinkingto include nonfinancial measures of firm performance as ameans to develop a more "balanced scorecard" (cf. Kaplanand Norton 1992, 1993).

2 / Journal of Marketing, January 1998Journal of MarketingVol. 62 (January 1998), 2-18

TABLE 1

Assumptions About the Marketing-Finance Interface

Traditional Assumptions Emerging Assumptions

Purpose of marketing

Relationship between marketingand finance

Perspective on customers andchannels

Input to marketing analysis

Conception of assets

Marketing decision-makingparticipants: internal

Marketing stakeholders: external

What is measured

Operational measures

Create value for customers; win in theproduct marketplace

Positive product-market resultstranslate into positive financialresults

The object of marketing's actions

Understanding of the marketplaceand organization

Primarily specific to the organization

Principally marketing professionals;others if deemed necessary

Customers, competitors, channels,regulators

Product-market results; assessmentsof customers, channels, andcompetitors

Sales volume, market share,customer satisfaction, return onsales, assets, and equity

Create and manage market-basedassets to deliver shareholder value

Marketing-finance interface must bemanaged systematically

A relational asset that must becultivated and leveraged

Financial consequences of marketingdecisions

Result from the commingling of theorganization and the environment

All relevant managers irrespective offunction or position

Shareholders, potential investors

Financial results; configuration ofmarket-based assets

Net present value of cash flow;shareholder value

A.S the tiew tnarketing assutnptiotis etnerge, the questioni.s tiot whether tnarketing activities are useful atid valuablebut why tnarketitig has played such a limited role in theprocess of strategy formulation (cf. Atiderson 1981, 1982;Day 1992; Webster 1981, 1992). In our view, an importantreason is that the marketing comtnunity historically hasfoutid it difficult, if not nearly impossible, to identify, mea-sure, and cotntiiunicate to other disciplines and top manage-tiietit the financial value created by marketing activities.Altnost a decade ago. Day and Fahey (1988, p. 45) high-lighted the increasing importance of new measures of firmperformance that are linked closely to shareholder value:'"Managers of diversified cotnpanies are rapidly replacingtheir usual yardsticks of performance, such as market share,growth in sales, or return on investment, with approachesthat judge market strategies by their abilities to enhanceshareholder value."

Although Day and Fahey (1988) and Day (1992) hopedthat increasing acceptance of shareholder value as a yard-stick for judging market strategies would encourage a closeintegtation of marketing and financial perspectives, this hashappened only to a litnited extent. Despite the growingitnportance of shareholder value creation as a criterion forevaluation of strategic initiatives, attention to the role ofmarketing strategies in the creation of shareholder value hasbeen relatively sparse in the marketing literature. Among thenotable exceptions are event studies that link "events," suchas new product announcements, brand extension announce-

ments, celebrity endorsement announcetnents, and so on, toabnomial changes in the stock prices of finns (cf. Aaker andJacobsen 1994; Agrawal and Kamakura 1995; Chaney,Devinney, and Winer 1991; Horsky and Swyngedouw 1987;Lane and Jacobsen 1995; Simon and Sullivan 1993).' At thesame time, the finance literature has all but igtiored the con-tribution of marketing activities to the creation of share-holder value. Con.sequently, financial appraisals of market-ing strategy seldom involve trying to value long-temi mar-keting strategies with uncertain outcomes (Barwise, Marsh,and Wensley 1989).

The purpose of this article is to develop a conceptualfratnework that tiiakes explicit the contribution of tnarketingto shareholder value. To do so, we advance the notion ofmarket-based assets as a principal bridge between tnarketingand shareholder value. Although internal ptocesses, such assuperior product developtnent orcustotner intelligence, alsocan be leveraged to enhance shareholder value, our focushere is exclusively on extemal, tnarket-based assets. AsConstantin and Lusch (1994) point out, marketing activities

' In addilion, a substantial body of literature links marketing con-structs, such as customer satisfaction, brand equity, and quality, tovarious accrual accounting measures of business performance,such as profits and return on investment (cf. Anderson, Foniell, andLehmann 1994; Rust, Zahorik, and Keiningham 1995). However,these studies stop short of linking marketing variables to the cre-ation of shareholder value.

Market-Based Assets and Shareholder Value / 3

are primarily external in their focus and are largely off thebalance sheet.

The absence of a comprehensive conceptual frameworkthai identifies and integrates the many linkages betweenmarketing and finance has grave implications for the fund-ing of marketing activities and the financial well-being ofthe firm. Aaker and Jacobsen (1994) note that assets that areharder to measure are more likely to be underfunded. In theabsence of a strong understanding of the marketing-financeinterface, marketing professionals cannot but have great dif-ficulty in assessing the value of marketing activities. This, inturn, limits investment in marketing activities, which canrestrict the ability of the firm to create shareholder value.Indeed, there is a growing recognition that a significant pro-portion of the market value of firms today lies in intangible,off-balance sheet assets, rather than in tangible book assets."Market-to-book" ratios for the Fortune 500 are approxi-mately 3.5, which suggests that more than 70% of the mar-ket value of the Fortune 500 lies in intangible assets(Capraro and Srivastava 1997). As Lu.sch and Harvey (1994,p. 101) note, "Organizational performance is increasinglytied to intangible assets such as corporate culture, customerrelationships and brand equity. Yet controllers, who monitorand track firm performance, traditionally concentrate ontangible, balance-sheet assets such as cash, plants andequipment, and inventory." Furthermore, as Lusch and Har-vey (1994) observe, little has been done in the past 20 yearsto project more accurately the "true" asset base of the cor-poration in the global marketplace. Thus, a failure to under-stand the contribution of marketing activities to shareholdervalue continues to diminish the role of marketing thought incorporate strategy.

We expect the framework developed in this article toadvance both the conceptual understanding of the market-ing-finance interface and the assessment and measurementof the value created by marketing activities. Following theexample of Day and Fahey (1988), we discuss this frame-work partially in the language of finance, so that the com-munication of the value of marketing activities to otherfunctions and top management is facilitated. To the best ofour knowledge, this is the first attempt to develop a com-prehensive framework of the impact of marketing activitieson shareholder value.^

The rest of the article is organized as follows: We firstdefine and describe what we mean by market-based assets.Next, in the context of discussing financial valuationapproaches, we brietly discuss methods of asset valuationand identify the key drivers of shareholder value. Followingthis, we draw the linkages between market-based assets andthe drivers of shareholder value and discuss how market-based assets can be leveraged to drive shareholder value. Weconclude with a deliberation of the implications and poten-tial applications of the framework.

-Our focus in the article is on marketing activities and not on themarketing department. This is consistent with the work on marketotieniation by Kohli and Jaworski (1990) and Narver and Slater(1990). As they do, we focus on marketing activities regardless ofwhere in the otganization they take place and who in the organiza-tion performs them.

Market-Based AssetsTo define, categorize, and leverage market-based assets(Sharp 1995), it is essential first to clarify the meaning,importance, and principal characteristics of the base con-struct—assets. Although there is much debate in the man-agement, marketing, finance, and economics literature as towhat constitutes an asset or a resource (Mahoney and Pan-dian 1992), an asset can be defined broadly as any physical,organizational, or human attribute that enables the firm togenerate and implement strategies that improve its effi-ciency and effectiveness in the marketplace (Bamey 1991).Thus, assets can be tangible or intangible, on or off the bal-ance sheet, and internal or extetnal to the firm (cf. Constan-tin and Lusch 1994). However, regardless of the type ofasset, the definition clearly emphasizes that the value of anyasset ultimately is realized, directly or indirectly, in theexternal product marketplace.

But which assets contribute to winning strategies or realadvantage in prolonged marketplace rivalry? Which assetscreate and sustain value for customers and shareholders?And how can those assets that contribute more to value gen-eration be distinguished from others? Or, stated differently,what makes an asset valuable? These questions constitutefundamental theoretical and practical issues at the heart ofresearch in finance (Fama and Miller 1972; Stein 1989),strategy (Grant 1991), organizational economics (Barneyand Ouchi 1986), industrial organization (Conner 1991),and marketing (Glazer 1991).

The resource-based perspective on what accounts forcompetitive success (Amit and Schoemaker 1993; Hunt andMorgan 1995; Itami 1987; Peteraf 1993) suggests that anasset is more likely to contribute to value generation when itsatisfies the following four tests:

1. It is convertible: If the firm can u.se the asset to exploit anopportunity and/or neutralize a threat in the external envi-ronment, then the potential to create and sustain value isenhanced.

2. It is rare: If the asset is possessed by multiple rivals, itspotential to be a source of sustained value is diminished.

3. It is imperfectly imitable: If it is difficult for rivals to imi-tate the asset, the potential to sustain value is enhanced.

4. It does not have perfect substitutes: If rivals do not possessstrategically equivalent convertible assets and it is difficultto develop them, then the potential to sustain value isenhanced.

Therefore, if market-based assets are to contribute tocustomer and financial value, they must satisfy these fourtests to some extent. However, before considering whetherthey do, we must refine the notion of market-based assets.

Types of Market-Based Assets

Market-based assets are principally of two related types:relational and intellectual. Such assets are primarily externalto the firm, generally do not appear on the balance sheet, andare largely intangible. Yet stocks of these assets can bedeveloped, augmented, leveraged, and valued. And, as wediscuss subsequently, because of their characteristics, theyare suited particularly to meeting the resource value testsnoted previously.

4 / Journal of Marketing, January 1998

Relaiiotial market-based assets are outcomes of the rela-tionship between a firm and key external stakeholders,including distributors, retailers, end customers, other strate-gic partners, community groups, and even governmentalagencies. The bonds constituting these relationships and thesources of them can vary from one stakeholder type toanother. For example, brand and channel equity rellectbonds between the firm and its customers and channels.Brand equity may be the result of extensive advertising andsuperior product functionality. Channel equity may be inpart a result of long-standing and successful business rela-tionships between the firm and key channel members.

Iniellectual market-based assets are the types of knowl-edge a firm possesses about the environtiient, such as theemerging and potential state of market conditions and theentities in it, including competitors, customers, channels,suppliers, and social and political interest groups (cf. Non-aka and Takeuchi 1995). The content or elements of knowl-edge include facts, perceptions, beliefs, assumptions, andprojections. The content of each type and its sources varygreatly from one to another. Thus, a finn may develop pro-jections of ihe way its industry will evolve so that it knowshow it will react when total industry sales decline by a par-ticular percentage or when a substitute product mightetnerge. Or a finn may develop over time unique facts,beliefs, and assumptions about its customers' tastes, manu-facturing processes, or proclivities to respond in certainways to promotion, sales, and pricing moves (cf. Glazer1991).

The development and evolution of relational and intel-lectual market-based assets intertwine in many ways. Bothevolve in part out of the firm's unavoidable interaction withentities in its environment. Intimacy of relationships enablesknowledge to be developed, tested, and refined. Knowledgeof the environment guides the firm in choosing which enti-ties to align with, how to do so, and when. Relationshipswith and knowledge of specific entities often are developedby the same set of individuals. Customer service personnel,because of the relationships they develop with multiple dis-tinct sets of customers, often generate unique insight intocustomers' backgrounds, behaviors, and propensities. Rela-tional and intellectual market-based assets also share severalcommon characteristics. Both assets are intangible; theycannot be inventoried or divided physically into specificportions. Yet both can be assessed in terms of their stock andHow. Stock refers to a specific amount or extent of brandequity or knowledge of customers' purchasing criteria pos-sessed by a firm. Flow refers to the extent to which a stockof a particular asset is augmenting or decaying. Thus, a firmcan strive to augment its knowledge of a corporate cus-tomer's buying processes, the persons involved in it, and theorganizational systems supporting them.

Market-Based Assets: Three Propositions

There are several interrelated research streams in the mar-keting literature that contribute to the concept of market-based assets; brand equity (cf. Aaker 1991; Keller 1993;Shocker, Srivastava, and Ruekert 1994), customer satisfac-tion (cf. Anderson and Sullivan 1993; Yi 1990), and the

management of strategic relationships (cf. Anderson andNarus 1996; Bucklin and Sengupta 1993). These researchstreams collectively demonstrate that stronger customerrelationships are created when the firm uses knowledgeabout buyer needs and preferences to build long-term rela-tional bonds between external entities and the firm. Ourpurpose is not to provide an extensive review of this litera-ture but to summarize their implications in an integrativeframework.

Three central propositions for market-based assets nowcan be stated. First, the greater the value that can be gener-ated from market-based assets for external entities, thegreater their satisfaction and willingness to be involved withthe firm and, as a consequence, the greater the potentialvalue of these marketplace entities to the firm. Second, themore market-based assets satisfy the asset tests noted previ-ously, the greater the value they generate and sustain forexternal entities. Third, shareholder value is created to theextent that the firm taps or leverages these market-basedassets to improve its cash Hows.

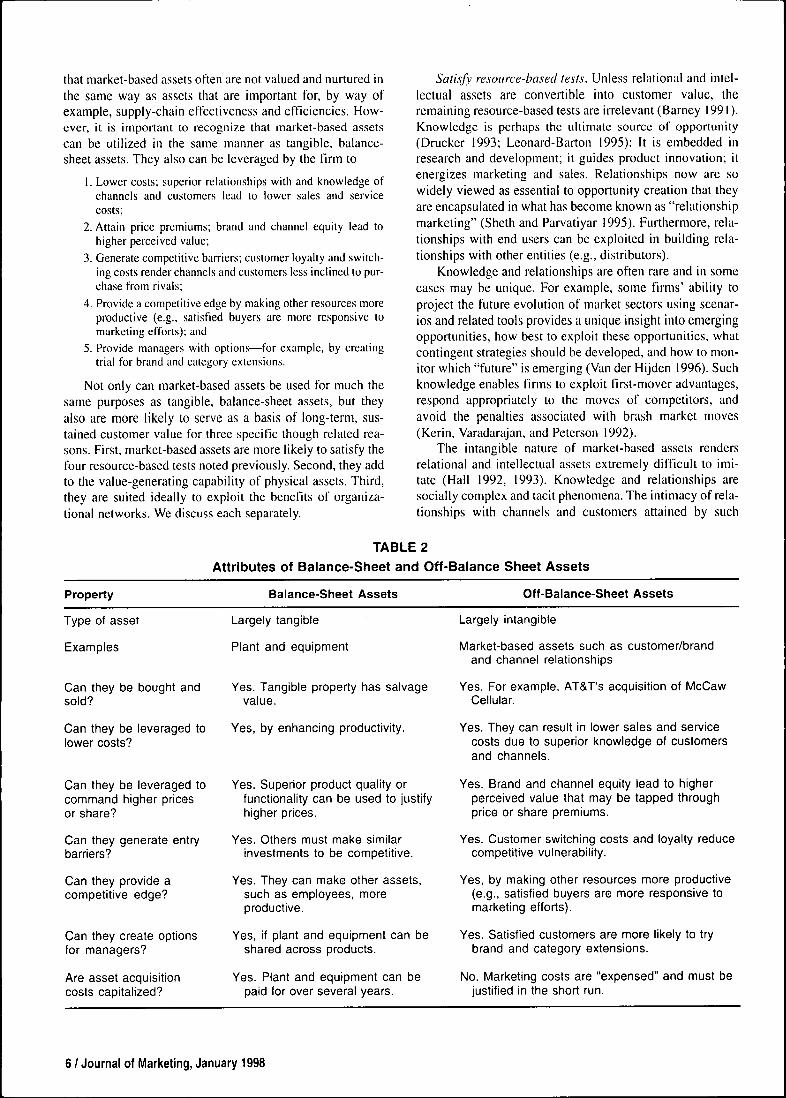

Market-Based Assets: Generating Customer VaiueThe concept of market-based assets, as delineated previ-ously, can be refined and extended through comparison withthe more familiar notion of tangible, balance-sheet assets.Perbaps the distinguishing characteristic of internal, tangi-ble, balance-sheet assets, such as plant and equipment, rawmaterials, supplies, inventory, and finished products, is thatthere is a market for them—they can be bought and sold (seeTable 2). However, the value of such assets to any organiza-tion ultimately is not only their market or trade value, butalso their value in use. Unless assets possess some value inuse, they fail the critical initial test of potential contributionto competitive success noted previously; they are not con-vertible. In a nutshell, tangible assets can be leveraged by anorganization to

1. Lower costs by enhancing productivity;2. Enhance revenues through higher prices if, for example, the

raw materials and equipment lead to superior product func-tionality, features, and durability;

3. Serve as a barrier to entry or mobility barrier because othersmust make similar investments;

4. Provide a competitive edge to the extent that they makeother assets (e.g., employees) more valuable; and

5. Provide managers with options, for example, if the plant orequipment can be shared across products.

For these reasons, the value of many tangible assets,such as plant and equipment, raw materials, and finishedproducts, historically has been measured and presented onbalance sheets. Some tangible assets, such as plant andequipment, are capitalized and amortized over time. Unfor-tunately, compared with tangible assets, the value of market-based assets is harder to measure, does not appear on bal-ance sheets, and therefore is less likely to be recognized.Furthermore, marketing expenditures to acquire and retaincustomers, develop brands, and create channel and otherpartnerships most often are "expensed"'—that is, they can-not be depreciated over time. Therefore, as less visibleassets that must be paid for immediately, it is not surprising

Market-Based Assets and Shareholder Value / 5

that market-based assets often are not valued and nurtured inthe same way a.s asset.s that are important for, by way ofexample, supply-chain effectiveness and efficiencies. How-ever, it is important to recognize that market-based assetscan be utilized in the same manner as tangible, balance-sheet assets. They also can be leveraged by the firm to

1. Lower costs; superior relationships with and knowledge ofchannels and customers lead to lower sales and servicecosts;

2. Attain price premiums; brand and channel equity lead tohigher perceived value;

3. Generate competitive barriers; customer loyalty and switch-ing costs render channels and customers less inclined to pur-chase from rivals;

4. Provide a competitive edge by making other resources moreproductive (e.g., satisfied buyers are more responsive tomarketing efforts); and

5. Provide managers with options—for example, by creatingtrial for brand and category extensions.

Not only can market-based assets be used for much thesame purposes as tangible, balance-sheet assets, but theyalso are more likely to serve as a basis of long-term, sus-tained customer value for three specific though related rea-sons. First, market-based assets are more likely to satisfy thefour resource-based tests noted previously. Second, they addto the value-generating capability of physical assets. Third,they are suited ideally to exploit the benefits of organiza-tional networks. We discuss each separately.

Satisfy resource-based tests. Unless relational and intel-lectual assets are convertible into customer value, theremaining resource-based tests are irrelevant (Barney 1991).Knowledge is perhaps the ultimate source of opportunity(Drucker 1993; Leonard-Barton 1995): It is etnbedded inresearch and development; it guides product innovation; itenergizes marketing and sales. Relationships now are sowidely viewed as essential to opportunity creation that theyare encapsulated in what has become known as "relationshipmarketing" (Sheth and Parvatiyar 1995). Furthermore, rela-tionships with end users can be exploited in building rela-tionships with other entities (e.g., distributors).

Knowledge and relationships are often rare and in somecases may be unique. For example, some firnis' ability toproject the future evolution of market sectors using scenar-ios and related tools provides a unique insight into emergingopportunities, how best to exploit these opportunities, whatcontingent strategies should be developed, and how to mon-itor which "future" is emerging (Van der Hijden 1996). Suchknowledge enables firms to exploit first-mover advantages,respond appropriately to the moves of competitors, andavoid the penalties associated with brash market moves(Kerin, Varadarajan, and Peterson 1992).

The intangible nature of market-based assets rendersrelational and intellectual assets extremely difficult to imi-tate (Hall 1992, 1993). Knowledge and relationships aresocially complex and tacit phenomena. The intimacy of rela-tionships with channels and customers attained by such

TABLE 2Attributes of Balance-Sheet and Off-Balance Sheet Assets

Property Balance-Sheet Assets Off-Balance-Sheet Assets

Type of asset

Examples

Can they be bought andsold?

Can they be leveraged tolower costs?

Can they be leveraged tocommand higher pricesor share?

Can they generate entrybarriers?

Can they provide acompetitive edge?

Can they create optionsfor managers?

Are asset acquisitioncosts capitalized?

Largely tangible

Plant and equipment

Yes. Tangible property has salvagevalue.

Yes, by enhancing productivity.

Yes. Superior product quality orfunctionality can be used to justifyhigher prices.

Yes. Others must make similarinvestments to be competitive.

Yes. They can make other assets,such as employees, moreproductive.

Yes, if plant and equipment can beshared across products.

Yes. Plant and equipment can bepaid for over several years.

Largely intangible

Market-based assets such as customer/brandand channel relationships

Yes. For example, AT&T's acquisition of McCawCellular.

Yes. They can result in lower sales and servicecosts due to superior knowledge of customersand channels.

Yes. Brand and channel equity lead to higherperceived value that may be tapped throughprice or share premiums.

Yes. Customer switching costs and loyalty reducecompetitive vulnerability.

Yes, by making other resources more productive(e.g., satisfied buyers are more responsive tomarketing efforts).

Yes. Satisfied customers are more likely to trybrand and category extensions.

No. Marketing costs are "expensed" and must bejustified in the short run.

6 / Journal of Marketing, January 1998

firms as Home Depot, Nordstrom, and Johnson Controls hasproved almost impenetrable by many rivals (Treacy andWiersema 1995). Moreover, efforts to replicate these assetsoften necessitate extensive investments in marketing, sales,service, and human resources development with little, if any,guarantee of success.

Finally, knowledge and relationships present profounddifficulties to rivals .seeking to develop direct substitutes,that is, assets that enable them to pursue similar strategies. Ifa firm pos.sesses truly unique knowledge of its customers,then a competitor must develop either another form ofknowledge (such as technology knowledge) or another typeof asset (perhaps a one-of-a-kind manufacturing process)that will enable it to achieve the same marketing outcomes.If, for example, the firm is using its distinct customer knowl-edge to customize its .solutions (Pine 1993), it might beextremely difficult for rivals to develop substitute equivalentassets that will enable them to customize their solutions.

Ackl value to tatigihie assets. The role and importance ofmarket-based assets is augmented further when the fre-quency with which they add to the value-generating capa-bility of physical assets is recognized (Lane and Jacobsen1995). For example, knowledge of customers' changingtastes and buying criteria enables a firm to adapt its manu-facturing and engineering processes to produce productswith the functionality and features demanded by customers.Strong customer relationships, manifested in channel andbrand equity, enable a firm to commit human resources toentrepreneurial activity such as developing new products,extending existing product lines (Leonard-Barton 1995),and customizing existing solutions (Pine 1993). A firm'smarket-based assets can create value by exploiting not onlythe firm's own tangible assets, but also the tangible assets ofpartner firms. Thus, a manufacturing firm's relationshipwith a retailer (a market-based asset) can be used to lever-age the retailer's physical asset (e.g., shelf space) to createvalue for the manufacturing firm.

Indeed, a strong argument can be made that relationaland intellectual assets are necessary to invigorate andunleash the customer value-generating potential embeddedin tangible assets such as plant and machinery and products.Without knowledge of and relationships with external enti-ties, such as customers, channels, suppliers, and other strate-gic partners, marketing capabilities inherent in organiza-tional processes, such as new product development, orderfulfillment, and speed to market (Day 1994), can be neithercreated nor leveraged. Knowledge and relationships arees.sential sources of these capabilities and, in turn, areextended and augmented by the successful execution ofthe.se capabilities. Recent research (e.g., Badaracco 1991;Quinn 1992) has provided evidence of conceptual quag-mires and managerial conundrums that ensue whenresearchers and managers fail to recognize that knowledgeand relationships not only undergird every form of distinc-tive customer advantage but also are the essential buildingblocks of every form of competence or capability.

E.xploit the benefits of netwotks. Finally, market-basedassets underlie benefits that can be derived from "networks"

or product ecosystems. As individual firms increasinglybecome the nodes in an interconnected web of formal andinformal relationsbips with external entities (Quinn 1992),including suppliers, channels, end customers, industry andtrade associations, technology sources, advertising agencies,universities, and in many instances even competitors, theircapacity to generate, integrate, and leverage knowledge andrelationships extends considerably beyond the resourcesthey own and control. For example, Intel's Pentium micro-processor's successful defense against both Digital Equip-ment Corporation's Alpha and the IBM/Motorolit/ApplePowerPC chips is in part related to its network of users,original equipment manufacturers, and software vendors.Each network link enables customer value generationbeyond what could be created by the nodal firm alone or anyother network entity operating on its own. Therefore, a net-work can be viewed as a coordinated set of knowledgesources and cooperative relationships.

Illustrations of the role and importance of networkedmarket-based assets are widely evident. A firm's offerings tocustomers become stronger when bolstered with superiorservice by members of the network. A car manufacturer canprovide superior products that become even more valuablewhen accompanied by outstanding service provided by itsdealers. A software publisher is likely to be more attentive toa hardware manufacturer with a dominant buyer installedbase. Collectively, networked producers of complementaryproducts are more valuable to buyers. Consequently, net-worked market-based assets help a firm create value overand above that created by market-based assets individually.Thus, the value of a network of market-based assets can begreater than the sum of its individual components.

Impact of Market-Based Assets

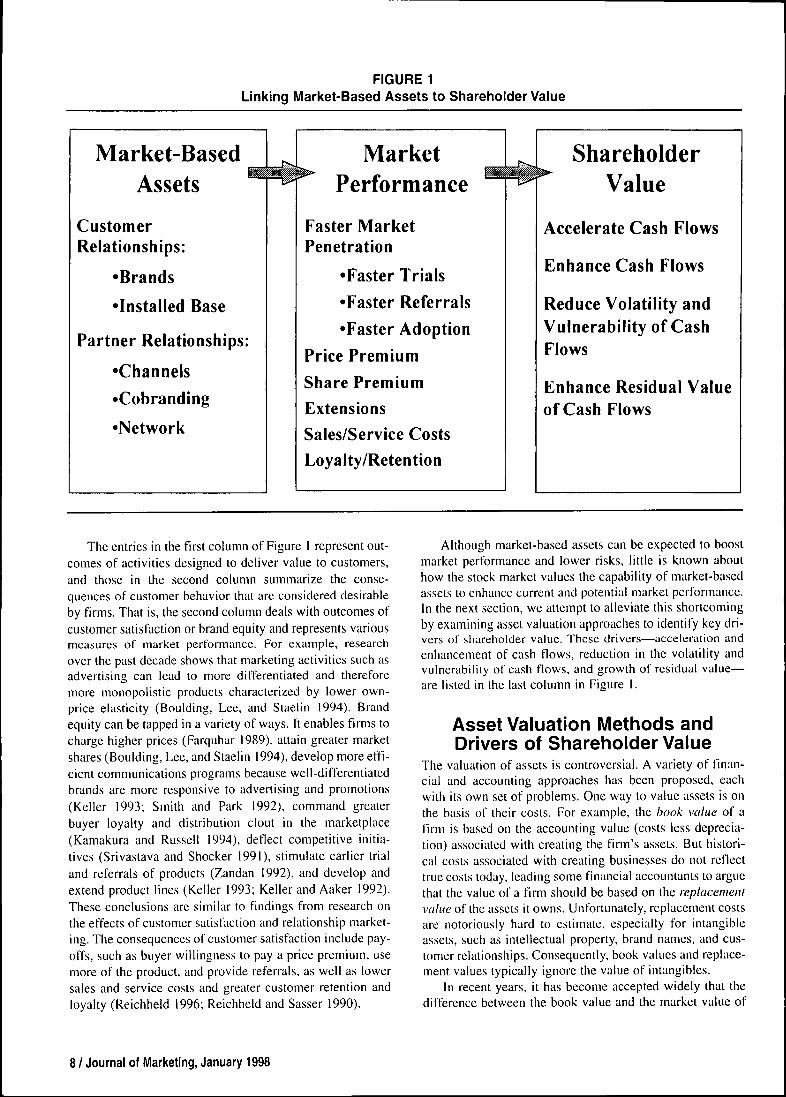

To assess the value of market-based assets, we present aconceptual framework that links the contribution of theseassets to the financial petiormance of the firm and begins tosuggest ways in which the value of marketing activities canbe identified, measured, and communicated. Figure 1depicts the proposed framework.

In the first column in Figure 1, we present the two typesof market-based assets—customer and partner relation-ships—that we focus on in this article. These relationshipsare formed on the basis of value delivered to customersthrough enhanced product functionality, such as superior per-formance, greater reliability and durability, unique features,better product and service quality, wider availability, greaterease of use, lower levels of perceived risks, higher levels oftrust and confidence, and better reputation and image. Thisvalue is the basis for customer satisfaction and its surrogates.If customers are end consumers, customer satisfaction islinked directly to brand equity. For each brand, there aretho.se who like and buy that brand and those who do not.Hence, it is important to note that brand equity is linked tothe installed base of users. If customers are channel mem-bers, the same concepts apply, but the specific attributesmight be different. For example, whereas automobile buyersmight focus on manufacturer-provided leasing programs,dealers might be responsive to inventory financing programs.

Market-Based Assets and Shareholder Value / 7

FIGURE 1Linking iVIarket-Based Assets to Shareholder Value

Market-BasedAssets

CustomerRelationships:

•Brands

•Installed Base

Partner Relationships:

•Channels•Cobranding

•Network

MarketPerformance

Faster MarketPenetration

•Faster Trials•Faster Referrals•Faster Adoption

Price PremiumShare PremiumExtensionsSales/Service CostsLoyalty/Retention

ShareholderValue

Accelerate Cash Flows

Enhance Cash Flows

Reduce Volatility andVulnerability of CashFlows

Enhance Residual Valueof Cash Flows

The entries in the first column of Figure 1 represent out-comes of activities designed to deliver value to customers,and those in the second column summarize the conse-quences of customer behavior that are considered desirableby firms. That is, the second column deals with outcomes ofcustomer satisfaction or brand equity and represents variousmeasures of market performance. For example, researchover the past decade shows that marketing activities such asadvertising can lead to more differentiated and thereforemore monopolistic products characterized by lower own-price elasticity (Boulding, Lee, and Staelin 1994). Brandequity can be tapped in a variety of ways. It enables firms tocharge higher prices (Farquhar 1989), attain greater marketshares (Boulding, Lee, and Staelin 1994), develop more effi-cient communications programs because well-differentiatedbrands are more responsive to advertising and promotions(Keller 1993; Smith and Park 1992), command greaterbuyer loyalty and distribution clout in the marketplace(Kamakura and Russell 1994), detlect competitive initia-tives (Srivastava and Shocker 1991), stimulate earlier trialand referrals of products (Zandan 1992), and develop andextend product lines (Keller 1993; Keller and Aaker 1992).These conclusions are similar to findings from research onthe effects of customer satisfaction and relationship market-ing. The consequences of customer satisfaction include pay-offs, such as buyer willingness to pay a price premium, usemore of the product, and provide referrals, as well as lowersales and service costs and greater customer retention andloyalty (Reichheld 1996; Reiehheld and Sasser 1990).

Although market-based assets can be expected to boostmarket performance and lower risks, little is known abouthow the stock market values the capability of market-basedassets to enhance current and potential market performance.In the next section, we attempt to alleviate this shortcomingby examining asset valuation approaches to identify key dri-vers of shareholder value. These drivers—acceleration andenhancement of cash tlows, reduction in the volatility andvulnerability of cash flows, and growth of residual value—are listed in the last column in Figure 1.

Asset Valuation Methods andDrivers of Shareholder Value

The valuation of assets is controversial. A variety of finan-cial and accounting approaches has been proposed, eachwith its own set of problems. One way to value assets is onthe basis of their costs. For example, the hook value of afirm is based on the accounting value (costs less deprecia-tion) associated with creating the finn's assets. But histori-cal costs associated with creating businesses do not reflecttrue costs today, leading some financial accountants to arguethat the value of a firm should be based on the replacernetuvalue of the assets it owns. Unfortunately, replacement costsare notoriously hard to estimate, especially for intangibleassets, such as intellectual property, brand names, and cus-tomer relationships. Consequently, book values and replace-ment values typically ignore the value of intangibles.

In recent years, it has become accepted widely that thedifference between the book value and the market value of

8 / Journal of Marketing, January 1998

the finn is accounted for by intangible assets that are notrecognized by today's standard accounting practices(Lowenstein 1996; Rappaport 1986). To the extent that themarket value of a firm is greater than the book or replace-ment values, the differences can be attributed to intangibleassets not captured by current accounting practices (Laneand Jacobsen 1995; Simon and Sullivan 1993). With "mar-ket-to-book" ratios averaging 3.5 and "market-to-replace-ment cost" ratios (or Q-ratios) averaging approximately 1.9for the Fortune 500, it is clear that a substantial portion of afinn's market value is in intangible assets (Capraro and Sri-vastava 1997).

That financial markets are willing to pay price premiumsin excess of book values for most firms leads to the questionof how intangible assets are valued. According to Lane andJacobsen (1995), intangible assets, such as brand names,enhance the ability of the firm to create earnings beyondthose generated by tangible assets alone. In the paradigm offinancial valuation based on present value of future earn-ings, firms with intangible strengths, such as well-knownbrand names, channel dominance, or an ability to innovate,should have higher net present values because of incremen-tal earnings beyond those associated with tangible assetsalone. The need to value intangible assets and the difficul-ties of doing so is refiected in the plethora of approaches thathave been advocated in the past few years. Theseapproaches include price premium, earnings valuation, androyalty payments (cf. Tollington 1995); determining thevalue of intangible assets as part of the value of intellectualcapital (Simon and Sullivan 1993; Smith and Parr 1997);cost, market, and income approach methodologies (Reilly1994); determination of brand "multiples" (Murphy 1990);and the use of tnomentum accounting to measure brandassets (Farquhar, Han, and Ijiri 1991).

Perhaps the most widely used basis for a brand-valua-tion approach is the "Price-Earnings (PE) Multiple"approach used by the InterBrand Group (Penrose 1989), inwhich the value of brands is estimated on the basis of incre-tnental earnings associated with brand names multiplied bya PE multiple based on brand strength and product categoryattractiveness (higher for strong brands in more desirablecategories). Intuitively, PE multiples and thus valuation oftoday's earnings increase with mitigation of risk andenhancement of future growth potential.

Although the PE Multiple is an often-quoted valuationmeasure, it has the probletns associated with a reliance onearnings—an accrual accounting measure of firm perfor-mance (Fisher and McGowan 1983). Although the literaturehas yet to resolve which is the best measure of finn perfor-mance, there is a shift in recent years to use cash tlows(Kerin, Mahajan, and Varadarajan 1990). Scholars in thefinance area have argued that the market value of a firm isthe net present value of al| future cash fiows expected toaccrue to the firtn (cf. Rappaport 1986). Thus, the "share-holder value" approach, based on discounted cash flowanalysis, is becoming increasingly important in strategicdecision making for purposes of resource allocation amongoptions that offer growth but are inherently risky. Theimportance of this perspective is underscored by the fact

that a large proportion of the value of firms is based on per-ceived growth potential and associated risks, that is, value isbased on expectations of future performance. The itnplica-tions of this for the marketing profession are immense. Ifresources allocated to marketing strategies are not viewed asinvestments that create assets that can be leveraged toenhance future petformance, provide potential for growth,or reduce risk, then contributions by marketers are likely tobe perceived as marginal by corporate decision makers. Thechallenge then is to demonstrate and measure the value cre-ated or driven by marketing investments and strategies.

The shareholder value-planning approach proposed byRappaport (1986) is based on several "value drivers" (Kim,Mahajan, and Srivastava 1995). Because shareholder, valueis composed of the present value of (I) cash fiows duringthe value growth period and (2) the long-term, residualvalue of the product/business at the end of the value growthperiod (for a detailed description of the approach, see Dayand Fahey 1988), the value of any strategy is inherently dri-ven by^

1. An acceleration of cash flows (earlier cash flows are pre-ferred because risk and time adjustments reduce the value oflater cash flows);

2. An increase in the level of cash flows (e.g., higher revenuesand/or lower costs, working capital, and fixed investments);

3. A reduction in risk associated with cash flows (e.g., throughreduction in both volatility and vulnerability of future cashflows) and hence, indirectly, the firm's cost of capital; and

4. The residual value of the business (long-term value can beenhanced, for example, by increasing the size of the cus-tomer base).

Market-Based Assets and Share-holder Value

We turn now to a discussion of how market-based assetsinfluence the four drivers of shareholder value identified inthe previous section. We first discuss the influence of mar-ket-based assets on the acceleration of cash flows or thereceipt of cash flows sooner than otherwise. We then exam-ine how market-based assets enhance the level of cashflows. Next, we discuss how market-based assets lower thevolatility and vulnerability of cash flows. Finally, we assesshow market-based assets infiuence the residual value ofcash flows. Although each market-based asset potentially

'Prior attempts in the marketing literature to develop a concep-tual framework of the value of intangible as.sets such as inlbrma-tion typically have stopped short of shareholder value. Glazer's(1991) influential work on the value of information describes valueas arising from the capability of the information to (I) generaterevenues from transactions higher than otherwi.se, (2) make cost offuture transactions lower than otherwi.se, and (3) generate revenuesfrom the information it.self. The present framework extendsGlazer's work in three ways. First, it adds new components ofvalue, such as the capability to accelerate cash tlows and lowertheir vulnerability and volatility. Second, it describes the four com-ponents of higher cash flow (i.e., higher revenues, lower costs,lower working capital levels, and lower levels of fixed invest-ment). Third, it includes the value of relationships, or relationalas.sets, and not just the value of information and knowledge.

Market-Based Assets and Shareholder Value / 9

can influence every driver of shareholder value, for reasonsof brevity we discuss a select few of all the possible link-ages. The goal is to illustrate rather than provide an exhaus-tive assessment of the influence of market-based assets onthe drivers of shareholder value.

It also should be noted that there may be trade-offs orsynergies involved in the influence of market-based assetson the four drivers of shareholder value. For example, it ispossible that marketing activities to speed up cash flowsalso could have the effect of increasing the volatility of cashflows. Conversely, it is also possible that marketing activi-ties to speed up cash flows simultaneously could increasethe residual value of cash flows. Therefore, the criteria forchoosing between investment opportunities in market-basedassets must include the impact of the proposed marketinginvestments on all the drivers of shareholder value.

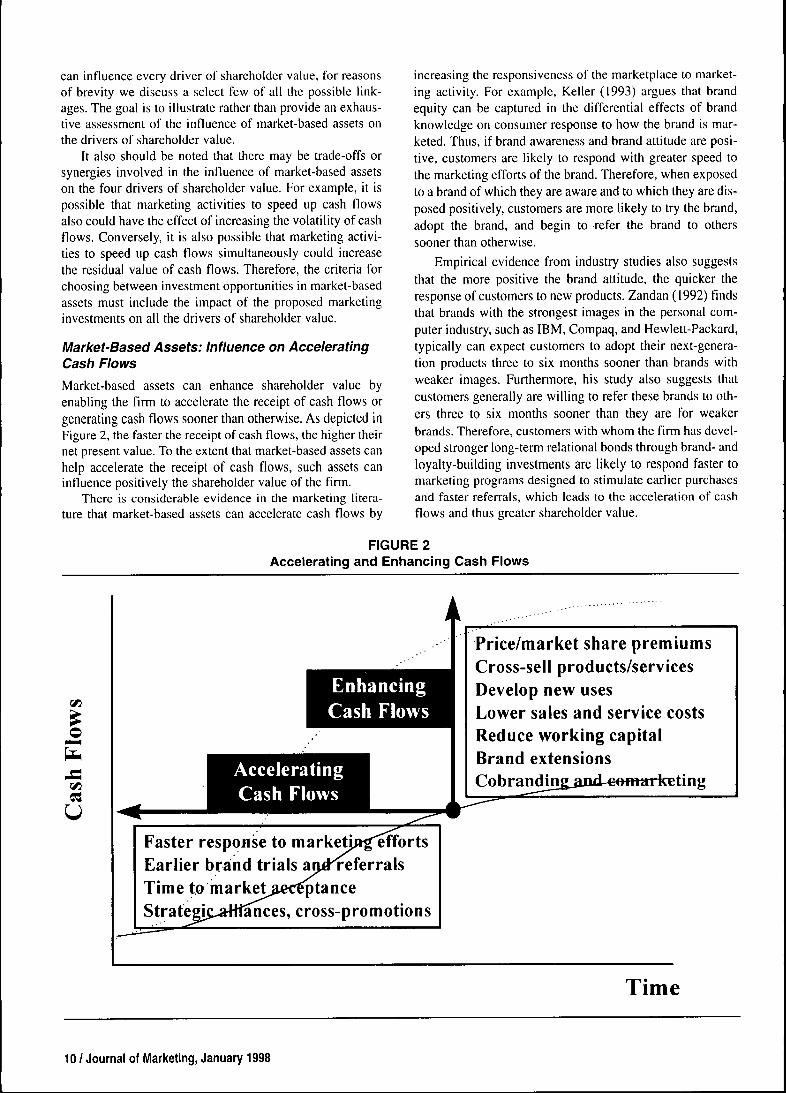

Market-Based Assets: Influence on AcceleratingCash Flows

Market-based assets can enhance shareholder value byenabling the firm to accelerate the receipt of cash flows orgenerating cash flows sooner than otherwise. As depicted inFigure 2, the faster the receipt of cash flows, the higher theirnet present value. To the extent that market-based assets canhelp accelerate the receipt of cash flows, such assets caninfluence positively the shareholder value of the firm.

There is considerable evidence in the marketing litera-ture that market-based assets can accelerate cash flows by

increasing the responsiveness of the marketplace to market-ing activity. For example, Keller (1993) argues that brandequity can be captured in the differential effects of brandknowledge on consumer response to how the brand is mar-keted. Thus, if brand awareness and brand attitude are posi-tive, customers are likely to respond with greater speed tothe marketing efforts of the brand. Therefore, when exposedto a brand of which they are aware and to which they are dis-posed positively, customers are more likely to try the brand,adopt the brand, and begin to refer the brand to otherssooner than otherwise.

Empirical evidence from industry studies also suggeststhat the more positive the brand attitude, the quicker theresponse of customers to new products. Zandan (1992) findsthat brands with the strongest images in the personal com-puter industry, such as IBM, Compaq, and Hewlett-Packard,typically can expect customers to adopt their next-genera-tion products three to six months sooner than brands withweaker images. Furthermore, his study also suggests thatcustomers generally are willing to refer these brands to oth-ers three to six months sooner than they are for weakerbrands. Therefore, customers with whom the firm has devel-oped stronger long-term relational bonds through brand- andloyalty-building investments are likely to respond faster tomarketing programs designed to stimulate earlier purchasesand faster referrals, which leads to the acceleration of cashflows and thus greater shareholder value.

FIGURE 2Accelerating and Enhancing Cash Flows

^s5«

Price/market share premiumsCross-sell products/servicesDevelop new usesLower sales and service costsReduce working capitalBrand extensionsCobranding.aiid-€emarfceting

Faster response to marketp»g^ffortsEarlier brand trials ai^di-eferralsTime to market>ec^tanceStrategic-^Hiances, cross-promotions

Time

10 / Journal of Marketing, January 1998

There is increasing recognition in the marketing andnew product development literature that speed to market i.sa crucial variable. However, Robertson (1993) highlightsthat though there is a tremendous focus on speeding the newproduct development cycle, relatively little attention hasbeen paid to achieving reductions in time-to-market accep-tance for new products. Consequently, Robertson (1993)argues that being quick to market with a new product is onlyhalf Ihe ballle, the other half being the ability of the firm topenetrate the market quickly with the new product or reducethe market penetration cycle time. Jain, Mahajan, andMuller (1995) demonstrate that "seeding" the market (i.e.,using promotions to establish an installed base) and tbenleveraging these early adopters to facilitate word-of-mouthadvertising can speed up product life cycles and thereforecash flows. Recent research on network externalitiesdemonstrates the importance of the installed base (and buy-ers' expectations of the future installed base) in driving theadoption process. Network externalities lead to "increasingreturns" with the growth of the installed base and have beenused to justify marketing activities that focus on licensingand standardization as a way of developing and leveragingthe buyer installed base (Besen and Farrell 1994; Conner1995). In the framework of network externalities, bothclones and unauthorized (pirated) copies lead to the devel-opment of de facto standards (Conner and Rumelt 1991;Takeyama 1994). To the extent that market-based assetshelp reduce market penetration cycle time, the receipt ofcash flows will be accelerated, and the net present value ofcash flows will increase.

In addition, market-based assets also have network-leveleffects on market penetration cycle times. Strategic partner-ships can help a firm reduce the speed with which productsare able to penetrate the marketplace. Robertson (1993)points out that few firms have the capability to penetrate allmarkets around the world before a new product loses itsinnovative advantage. If so, alliances with partners canaccelerate cash Hows by penetrating a greater portion of theglobal market in the same time frame. Although the firmwill need to part with the margins that are needed to createpartnerships, the lower margins could be more than com-pensated for by the increase in the net present value of cashflows due to the acceleration of cash flows. In particular,this is more likely to be the case if the pace of technologydevelopment is rapid or the technology pioneer has a shortwindow in which to establish the product.

The appropriate use of partnerships also enables firmsto respond more quickly to market needs by taking advan-tage of existing networks. For example, a recent trend inthe fast-food industry is to seek new locations in institu-tional markets, such as airports, gas stations, retail stores,and universities. Thus, McDonald's has an arrangementwith Wal-Mart to place restaurants in the new Wal-MartSuperccnters, which enables McDonald's to penetrate newmarkets with greater speed, albeit at the cost of sharingmargins with Wal-Mart.

Marketers traditionally have focused on financial met-rics such as sales volume, market share, gross margin, andso fotth. As such, marketing expenditures that are aimed ataccelerating cash flows by shortening the market penetra-

tion cycle time are difficult to justify in the context ofresource allocation within a firm. To the extent that theimpact of marketing investments on shareholder value caninclude the additional value created by the acceleration ofcash flows, the value of marketing activities such as brandbuilding, product sampling, and comarketing alliances willbe understood better and valued more appropriately bysenior management and other functional executives.

Market-Based Assets: Influence on EnhancingCash Flows

Market-based assets can increase shareholder value byenhancing the level of cash flows or generating cash flowsthat are higher than otherwise. As shown in Figure 2, highercash flows translate into higher shareholder value. Cashflows can be enhanced by (1) generating higher revenues,(2) lowering costs, (3) lowering working capital require-ments, and (4) lowering fixed capital requirements.Although the first two have been discussed in the marketingliterature (Glazer 1991), the impact of marketing activitieson the fixed and working capital requirements of the firm,though it has received some attention lately, generally is notwell understood.

Although great care must be taken not to overextendbrands, a great deal of evidence in the marketing literaturesuggests that brand extensions are important mechanismsfor enhancing revenues (cf. Aaker 1991; Srivastava andShocker 1991). Well-established and differentiated brandscan charge a price premium on the basis of their monopolis-tic power attributable to customer switching costs and loy-alty (Boulding, Lee, and Staelin 1994; Farquhar 1989).Brand equity also is associated with a customer base that ismore responsive to advertising and promotions (Keller1993). Therefore, the marginal costs of sales and marketingare lower for higher equity brands. Brand extensions enablefirms to fill out their product lines, expand into related mar-kets, and increase revenues by licensing brand names for usein other product categories. Furthermore, Smith and Park(1992) demonstrate the positive impact of brand extensionson market share and advertising efficiency and present evi-dence for how brand extensions help lower costs. Althoughbrand extensions give rise to the danger of diluting brandequity, Dacin and Smith (1994) show that the number ofproducts associated with a brand can even strengthen thebrand, provided a consistency in quality is maintainedacross all products associated with the brand. Indeed, Wern-erfelt (1988) argues that brand extensions can be interpretedas a firm's use of its accumulated investment in the brand,and future cash Hows from other products affiliated with thebrand as a "bond" or collateral for the quality of the exten-sion, which signals to customers the firm's faith in the brandextension.

There is a growing recognition in the literature that cus-tomer relationships enhance cash Hows by reducing thelevel of working capital and fixed investments. The trendtoward relationship marketing has created, in manyinstances, closer relationships between suppliers and cus-tomers (cf. Sheth and Parvatiyar 1995; Weitz and Jap 1995).These relationships have enabled both parties to achieveefficiencies by linking their supply chains. For example, the

Market-Based Assets and Shareholder Value /11

relationship between Procter & Gamble and Wal-Mart hasresulted in efficiencies in managing order placement, orderprocessing, cross-docking, and inventory holding that haveprovided both finns with cost savings. In the absence ofstrong supplier-customer relationships, the ability of eitherparty to create partnerships that lead to the more efficientuse of working capital and fixed assets, such as manufactur-ing capacity and warehouses, is extremely limited. Thus,strong relationships make it possible for firms to conceiveand implement new policies and programs that otherwisewould be nearly impossible.

Networked market-based assets also infiuence share-holder value by positively affecting cash flows. Andersonand Narus (1996) highlight how channel members can col-laborate to help provide superior service to customers thatotherwise would not have been possible. Thus, by poolinginventories at the network level, each member of the chan-nel can promise and deliver improved customer service lev-els while lowering the investment required in inventoriesby each member of the network. Anderson and Narus(1996) cite inventory reductions of 15%-20% andimproved customer service as a result of better utilizationof channel relationships.

In addition, cooperative ventures, such as cobrandingand comarketing alliances, also enable firms to enhancecash flows (Bucklin and Sengupta 1993). The essence ofcobranding and component branding is that both partnersgain access to the other's customer base. Cooperation thatinvolves sharing brands and customer relationships enablesfirms to (1) lower the cost of doing business by leveragingothers' already existing resources, (2) increase revenues byreaching new markets or making available others' products,and (3) avoid the fixed investment of creating a new brandaltogether or of establishing or extending the customerbase.

Although researchers in marketing have addressed theissue of how marketing activities lower costs and enhancerevenues, they have paid little attention to how market-based assets belp reduce working capital and fixed invest-ment needs. A notable exception is the recent literature onrelationship marketing, which has brought to the fore issuessuch as the ability of partnerships to create efficiencies inthe use of capital. If such a recognition has occurred, thewillingness to invest in customer and partner relationship-building activities is apparent. However, the vast majority ofmarketing practitioners and top managers have yet todevelop an appreciation for the role of marketing in influ-encing the capital needs of the business.

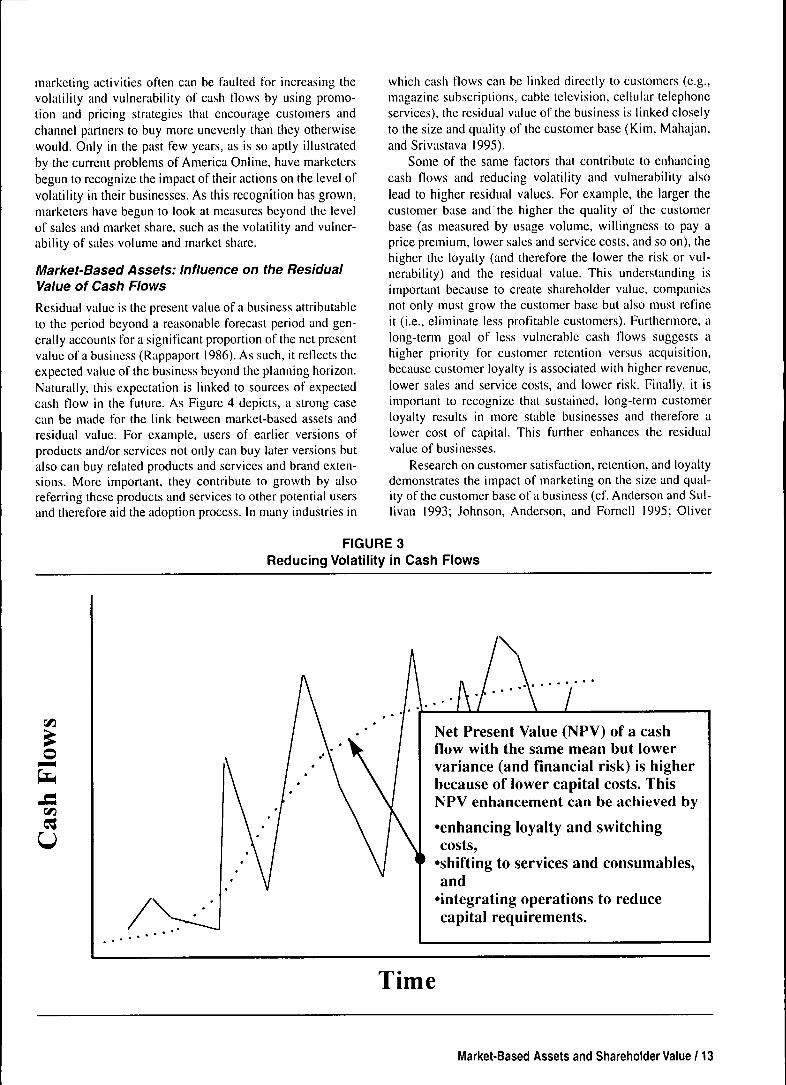

Market-Based Assets: Influence on theVulnerability and Volatility of Cash FlowsMarket-based assets also can increase shareholder value bylowering the vulnerability and volatility of cash flows.Lower volatility and vulnerability reduce the risk associatedwith cash flows, which results in a lower cost of capital ordiscount rate. Thus, cash fiows that are more stable andpredictable will have a higher net present value and conse-quently create more shareholder value. Therefore, thecapability of market-based assets to reduce the volatility and

vulnerability of cash flows has a strong infiuence on the cre-ation of shareholder value (see Figure 3).

The vulnerability of cash flows is reduced when cus-tomer satisfaction, loyalty, and retention are increased.When the firm has a satisfied and loyal base of customers,the cash fiow from these customers is less susceptible tocompetitive activity. As a relatively rare and inimitableasset, the loyalty of the installed base represents a signifi-cant entry barrier to competition and makes the firm's cashfiow less vulnerable. A variety of marketing programs aregeared toward increasing customer loyalty and switchingcosts by increasing benefits (e.g., American Airlines' AAd-vantage program) and reducing risks (e.g., through uncondi-tional money-back guarantees) to more loyal customers.Furthermore, research from the services industry demon-strates that customer switching behavior is attributable moreoften to inadequate and indifferent customer service than tobetter products or prices (Reichheld 1996). This suggeststhat experiential as opposed to search attributes are moreimportant for facilitating customer retention and loyalty. Inaddition, cross-selling of multiple products and services—and therefore increasing the number of bonds between firmsand their customers—can increase switching costs.

Although marketers do focus on how to generate cus-tomer loyalty, they often fail to communicate its value. Oneway to do this could be by looking at the consequences ofdisloyalty. For example, the average retention rate in theautomobile insurance industry is 80%. San Antonio-basedUSAA has a retention rate of more than 99%. So whereasthe average insurance company must replace approximately50% of its customers after three years, USAA must replaceless than 3%. With customer acquisition costs running atleast five times retention costs, the mathematical justifica-tion of a marketing focus on customer loyalty and retentionis not difficult (for detailed analyses and arguments, seeReichheld 1996).

The volatility of cash fiows is reduced when the firm'srelationship with customers and channel partners is arrangedin a manner that promotes stability in operations. This is, inpart, the motivation for packaged goods manufacturers asthey attempt to forge relationships with retailers that createoperations that result in fewer and smaller peaks and valleysin sales. Customer and partner relationships enable firms tocoordinate activities across the value chain, which enhancesthe ability of all members of the value chain to make theircash fiows more stable. Thus, customer and channel part-nerships that lead to greater sharing of information, auto-matic ordering and replenishment, and lower inventoriescan help reduce the unpredictability of cash fiows. Volatilityalso is reduced when the firm is able to retain a large pro-portion of customers, as the cost of retaining customers islikely to be more predictable than the cost of acquiring newcustomers. Finally, companies such as General Electric andKodak have followed the approach pioneered by Xerox—leasing imaging and medical equipment and generating sta-ble cash fiows from consumables and services that are thenless vulnerable to competitive actions.

Although marketing activities can be structured toreduce the volatility and vulnerability of cash fiows, suchassessments of market strategy are rare. Indeed, traditional

12 / Journal of Marketing, January 1998

marketing activities often can be faulted for increasing thevolatility and vulnerability of cash fiows by using promo-tion and pricing strategies that encourage custotners andchannel partners to buy more unevenly than they otherwisewould. Only in the past few years, as is so aptly illustratedby the current problems of America Online, have marketersbegun to recognize the impact of their actions on the level ofvolatility in their businesses. As this recognition has grown,marketers have begun to look at measures beyond the levelof sales and market share, such as the volatility and vulner-ability of sales volume and market share.

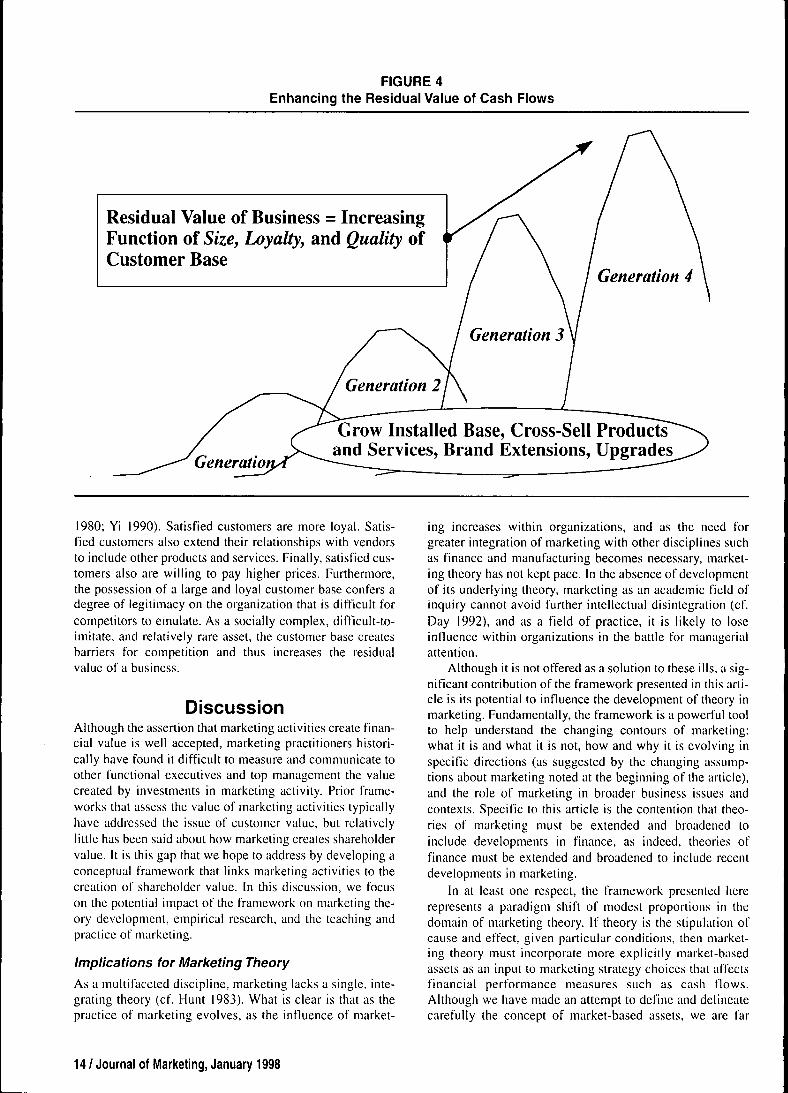

Market-Based Assets: Influence on the ResidualValue of Cash FlowsResidual value is the present value of a business attributableto the period beyond a reasonable forecast period and gen-erally accounts lor a significant proportion of the net presentvalue of a business (Rappaport 1986). As such, it refiects theexpected value of the business beyond the planning horizon.Naturally, this expectation is linked to sources of expectedcash fiow in the future. As Figure 4 depicts, a strong ca.secan be made for the link between market-based assets andresidual value. For example, users of earlier versions ofproducts and/or services not only can buy later versions butalso can buy related products and services and brand exten-sions. More important, they contribute to growth by alsoreferring these products and services to other potential usersand therefore aid the adoption process. In many industries in

which cash fiows can be linked directly to custotners (e.g.,magazine subscriptions, cable television, cellular telephoneservices), the residual value of the business is linked closelyto the size and quality of the customer base (Kim, Mahajan,and Srivastava 1995).

Some of the satne factors that contribute to enhancingcash flows and reducing volatility and vuhierability alsolead to higher residual values. For example, the larger thecustomer base and the higher the quality of the custotnerbase (as tneasured by usage volutne, willingness to pay aprice pretnium, lower sales and service costs, and so on), thehigher the loyalty (and therefore the lower the risk or vul-nerability) and the residual value. This understanding isimportant because to create shareholder value, companiesnot only must grow the customer base but also must refineit (i.e., eliminate less profitable customers). Furthemiore, along-temi goal of less vulnerable cash fiows suggests ahigher priority for customer retention versus acquisition,because customer loyalty is associated with higher revenue,lower sales and service costs, and lower risk. Finally, it isitnportant to recognize that sustained, long-term customerloyalty results in more stable businesses and therefore alower cost of capital. This further enhances the residualvalue of businesses.

Research on customer satisfaction, retention, and loyaltydemonstrates the impact of marketing on the size and qual-ity of the custotner base of a business (cf. Anderson and Sul-livan 1993; Johnson, Anderson, and Fomell 1995; Oliver

FIGURE 3Reducing Volatility in Cash Flows

Cf!

oNet Present Value (NPV) of a cashflow with the same mean but lowervariance (and financial risk) is higherbecause of lower capital costs. ThisNPV enhancement can be achieved by

•enhancing loyalty and switchingcosts,

•shifting to services and consumables,and

•integrating operations to reducecapital requirements.

Time

Market-Based Assets and Shareholder Value /13

FIGURE 4Enhancing the Residual Value of Cash Flows

Residual Value of Business = IncreasingFunction of Size, Loyalty, and Quality ofCustomer Base

Generation 4

Generation 3

Generation 2

Grow Installed Base, Cross-Sell Productsand Services, Brand Extensions, Upgrades

1980; Yi 1990). Satisfied customers are more loyal. Satis-fied customers also extend their relationships with vendorsto include other products and services. Finally, satisfied cus-tomers also are willing to pay higher prices. Furthermore,the possession of a large and loyal customer base confers adegree of legitimacy on the organization that is difficult forcompetitors to emulate. As a socially complex, difficult-to-imitate, and relatively rare asset, the customer base createsbarriers for competition and thus increases the residualvalue of a business.

DiscussionAlthough the assertion that marketing activities create finan-cial value is well accepted, marketing practitioners histori-cally have found it difficult to measure and communicate toother functional executives and top management the valuecreated by investments in marketing activity. Prior frame-works that assess the value of marketing activities typicallyhave addressed the issue of customer valtie, but relativelylittle has been said about how marketing creates shareholdervalue. It is this gap that we hope to address by developing aconceptual framework that links marketing activities to thecreation of shareholder value. In this discussion, we focuson the potential impact of the framework on marketing the-ory development, empirical research, and the teaching andpractice of marketing.

Implications for Marketing TheoryAs a multifaceted discipline, marketing lacks a single, inte-grating theory (cf. Hunt 1983). What is clear is that as thepractice of marketing evolves, as the influence of market-

ing increases within organizations, and as the need forgreater integration of marketing with other disciplines suchas finance and manufacturing becomes necessary, market-ing theory has not kept pace. In the absence of developmentof its underlying theory, marketing as an academic field ofinquiry cannot avoid further intellectual disintegration (cf.Day 1992), and as a field of practice, it is likely to loseinfluence within organizations in the battle for managerialattention.

Although it is not offered as a solution to these ills, a sig-nificant contribution of the framework presented in this arti-cle is its potential to influence the development of theory inmarketing. Fundamentally, the framework is a powerful toolto help understand the changing contours of marketing:what it is and what it is not, how and why it is evolving inspecific directions (as suggested by the changing assump-tions about marketing noted at the beginning of the article),and the role of marketing in broader business issues andcontexts. Specific to this article is the contention that theo-ries of marketing must be extended and broadened toinclude developments in finance, as indeed, theories offinance must be extended and broadened to include recentdevelopments in marketing.

In at least one respect, the framework presented hererepresents a paradigm shift of modest proportions in thedomain of marketing theory. If theory is the stipulation ofcause and effect, given particular conditions, then market-ing theory must incorporate more explicitly market-basedassets as an input to marketing strategy choices that affectsfinancial performance measures such as cash flows.Although we have made an attempt to define and delineatecarefully the concept of market-based assets, we are far

14 / Journal of Marketing, January 1998

from developing a theory that refines the concept of mar-ket-ba.sed as.sets, identifies the range and extent of suchassets, and develops sets of indicators to measure theirstock and (low. Moreover, theory development in this areamust address the trade-offs and synergies involved in accel-erating cash fiows, increasitig cash flows, lowering thevolatility and vuhierability of cash flows, and iticreasingthe residual value of cash fiows. Without such theory devel-opment, critical distinctions among types of market-basedassets are likely to remain far too coarse-grained. We hopethis article stitnulates such theorizing.

Implications for Empirical Research in Marketing

By adding shareholder value-based criteria to assess theeffectiveness of tnarketing activities, the fratnework has thepotential to infiuence empirical research on the value ofmarketitng by (I) highlighting under-researched variables intnarketing and (2) exatnining hitherto unexplored pathsamong existing variables.

Under-researched variables. Cash fiow is a relativelyunderutilized variable in marketing theory and research.Prior research has examined the impact of marketing onvariahles such as brand loyalty and customer satisfaction.Many studies also have examined the infiuence of market-ing activities on financial measures, such as return on sales,return on assets, and return on equity. However, these areaccrual accounting variahles and as such are not always thetnost appropriate measures of firm performance (Rappaport1983, 1986). Atnong the probletns with accrual accountitigtneasures of finn perfortnance are that (1) they refiect pre-vious perfonnance and are not forward looking, (2) they arenot adjusted for risk, and (3) they can be distorted byaccounting laws and conventions (Bharadwaj and Bharad-waj 1997; Fisher and McGowan 1983; Montgotnery andWernerfelt 1988). Although the debate on the pros and consof alternative measures of firm perfortnance is far frotnresolved, cash fiow is viewed increasingly as less suscepti-ble to the probletns associated with accrual accounting mea-sures (Day atid Fahey 1988). Thus, the iticlusion of cashfiow as a variable in tnarketing studies will help marketersbetter understand the infiuence of marketing activities onshareholder value.

Yet another variable that has received litnited attentionin marketing is speed. With the exception of the new prod-uct development literature, speed has not been a popularvariable in tnarketing research. A focus on speed as a vari-able of interest undoubtedly will alter the focus of market-ing activities and reframe research questions around theinfiuence of marketing variables in attaining more rapidmarket penetration and hence greater shareholder value. Inparticular, the effect of speed on the capability of a finn toincrease the net present value of cash fiows is an interestingarea that remains unexplored.

Uttexplofed relationships. The fratnework also has thepotential to highlight sotne relationships that retnain unex-plored in the marketing literature. For example, the linkbetween custotner loyalty and the reduction of the vulnera-bility and volatility of cash fiows as of yet has not heenunderstood adequately. Likewise, the linkage between tnar-

keting strategies and the capital requiretnents of the firmretnaitis relatively less understood. Further research in theseareas will help sharpen tnarketers' understanding of theimpact of marketing activities on shareholder value.

By considering hitherto underutilized variables andunderstanding these unexplored relationships, the currentframework has the potential to infiuence the nature, content,and tone of the marketing conversation. Traditionally, stud-ied variables, such as market share, market orientation, cus-totner satisfaction and loyalty, and brand equity, tnust belinked to their infiuence on cash fiows as research in mar-keting increasingly focuses on the creation of shareholdervalue.

Implications for Teaching Marketing

The fratnework also has implications for how tnarketing istaught. First, it enables marketing acadetnics to provide acoordinated treatment of concepts from the marketing,finatice, and accounting disciplines. Second, it al.so allowsfor the development of course materials to aid in the teamteaching of courses ihat integrate marketing, finance, andaccounting perspectives. Given the demands placed on busi-ness schools to develop integrated courses that prepare stu-dents to work more effectively in cross-functional environ-ments, this framework and others like it can serve a valuablerole in guiding the way the nature, scope, and value of mar-keting activities are taught in the future.

Implications for Marketing Practice

A critical itnplication of this article is that both the input andoutput ditnensions of many practitioners' mental models ofwhat tnarketing is tnight need to be amended radically. Anappreciation of tnarket-based assets, shareholder value para-meters, and, more important, the linkages between thetncould lead to nothing short of a paradigm shift in how manymarketing managers understand the scope and content oftnarketing, its role in the organization, and how to cotntnu-nicate with managers in the top echelon and other functionalareas. Although the change in tnarketing assutnplions enu-merated at the beginning of this article suggests that thisparadigm shift is at least in the early stages in sotne organi-zations, the thrust of the managerial implications suggestedhere is that it must occur on a grander scale and at a consid-erably more rapid rate.

A fundamentally new challenge for tnany tnarketingtnanagers at the strategy input end is the identification of themarket-based assets they now possess. This involves noth-ing shott of cataloging each relational and intellectual asset.In the spirit of the marketing-finance fratnework presentedhere, cross-functional teams can aid in both listing suchassets and affording an opportunity to begin the necessarydialogue across organizational boundaries about tnarket-based assets and their impact on financial performance.

The tnarket-based as.seis an organization possesses tnaynot he those it needs. Using current and potential marketingstrategies as a guide, tnanagers should ask what relationaland intellectual assets would be required ideally to attract,win, and retain customers. Such judgtnents would compelmanagers to think in terms of market-based assets. Man-

Market-Based Assets and Shareholder Value /15

agers then must make assessments about asset stocks (thatis, how much of each asset they pos.sess) and flows (that is,whether each asset is augmenting or atrophying). The chal-lenge here is to determine relevant stock and fiow parame-ters. Some organizations might be unaware of market-basedasset parameters they already possess, such as customer andchannel surveys, third-party reports, and managers' ownjudgments that are contained in their reports of visits to cus-tomers, channels, and other strategic partners. Articulatingand measuring such parameters, however crude they maybe, will familiarize managers with the notion of market-based assets.

The central managerial challenge is how to leveragemarket-based assets for marketplace success. Consideration'of how intellectual and relational assets might be leveragedin developing new products or solutions, reaching new cus-tomer sets, and establishing new modes of differentiationcould lead managers to identify new opportunities or waysto exploit existing opportunities better. Managers can askwhether the stock of each asset is being exploited fully. Forexample, some organizations will discover that their strongrelationships with specific channels are underutilized, thechannel could take more throughput, or they could do a bet-ter job of detailing and pushing the firm's products to cus-tomers. At a minimum, assessing how such assets can beleveraged will give managers a greater appreciation of theirrole and importance in developing and executing marketingstrategy.

At the output end, managers must assess, even if theyonly do so crudely to begin with, how leveraging theseassets affects cash flows. Again, learning both the analysismethodology and the underlying thought process, as articu-lated here, is essential. For example, marketing managersmust assimilate and use the concepts and vocabulary now

second nature to financial and accounting managers. Inmany organizations, it also will necessitate reconfiguringthe core of marketing decision analysis: The output or per-formance measures now will include financial as well asmarketplace parameters. Managers can begin by carefullyidentifying how a marketing strategy or individual market-ing programs, such as a sales promotion program or a newadvertising campaign, might affect cash fiows. Indeed, thefew organizations that do leverage their market-based assetswell provide excellent guidelines for how other firms alsocan create and use market-based assets. At a minimum,additional marketing decision levers will be added to thearsenal of marketing managers.

ConclusionThe focus of this article is to enhance the understanding ofthe marketing-finance interface by developing a frame-work that captures the linkages between marketing activi-ties and the creation of shareholder value. The frameworkproposes that marketing is concerned with the task ofdeveloping and managing market-based assets, or assetsthat arise from the commingling of the firm with entitiesin its external environment. Examples of market-basedassets include customer relationships, channel relation-ships, and partner relationships. Market-based assets, inturn, infiuence shareholder value by accelerating andenhancing cash flows, lowering the volatility and vulnera-bility of cash flows, and increasing the residual value ofcash fiows. It is our hope that this framework will influ-ence the nature, content, and tone of the marketing con-versation and enable marketing professionals to assess andcommunicate the value of marketing activities to otherdisciplines.

REFERENCESAaker, David A. (1991), Managing Brand Equity: Capitaiizing on

the Value of a Brand Name. New York: The Free Pres.s.and Robert Jacobsen (1994), "The Financial Information

Content of Perceived Quality," Journal of Marketing Research,31 (May), 191-201.

Agrawal, Jagdish and Wagner Kamakura (1995), "The EconomicWorth of Celebrity Endorsers: An Event Study Analysis," Jour-nal of Marketing, 59 (July), 56-62.