Embed Size (px)

Citation preview

BUFFALO FISCAL STABILITY AUTHORITY

BOARD OF DIRECTORS MEETING

March 18, 2020

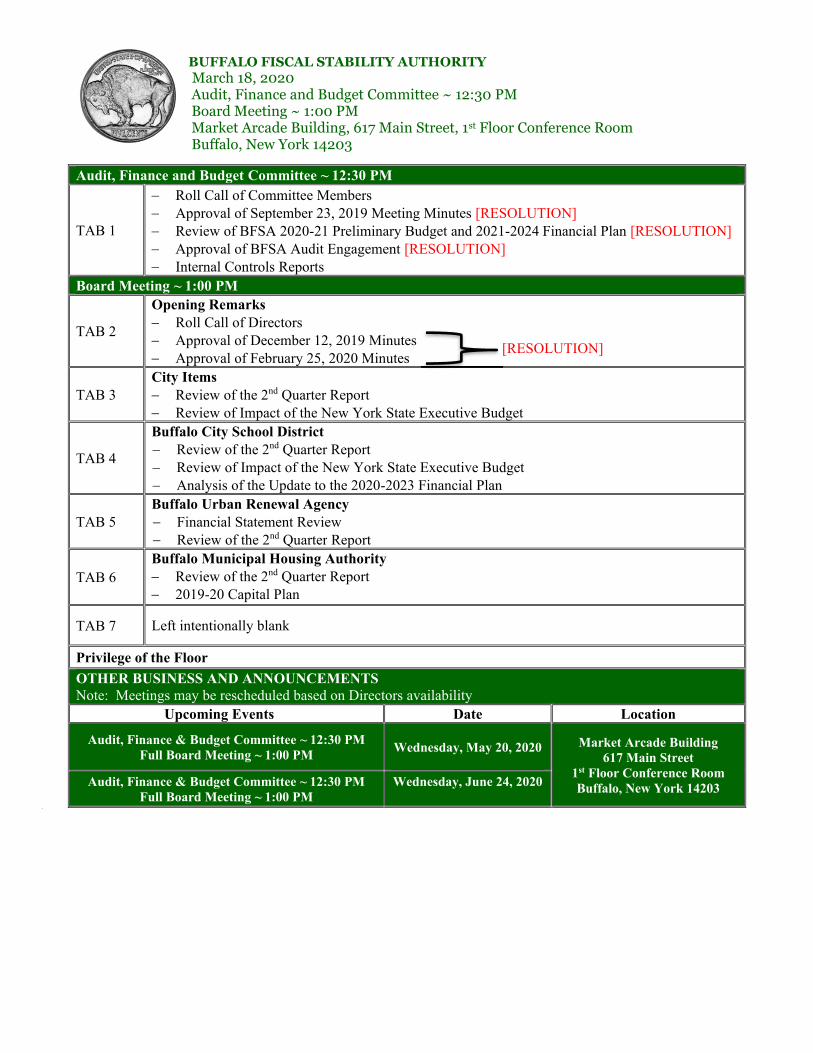

BUFFALO FISCAL STABILITY AUTHORITY March 18, 2020 Audit, Finance and Budget Committee ~ 12:30 PM Board Meeting ~ 1:00 PM Market Arcade Building, 617 Main Street, 1st Floor Conference Room Buffalo, New York 14203

Audit, Finance and Budget Committee ~ 12:30 PM

TAB 1

Roll Call of Committee Members Approval of September 23, 2019 Meeting Minutes [RESOLUTION] Review of BFSA 2020-21 Preliminary Budget and 2021-2024 Financial Plan [RESOLUTION] Approval of BFSA Audit Engagement [RESOLUTION] Internal Controls Reports

Board Meeting ~ 1:00 PM

TAB 2

Opening Remarks Roll Call of Directors Approval of December 12, 2019 Minutes Approval of February 25, 2020 Minutes

TAB 3 City Items Review of the 2nd Quarter Report Review of Impact of the New York State Executive Budget

TAB 4

Buffalo City School District Review of the 2nd Quarter Report Review of Impact of the New York State Executive Budget Analysis of the Update to the 2020-2023 Financial Plan

TAB 5 Buffalo Urban Renewal Agency Financial Statement Review Review of the 2nd Quarter Report

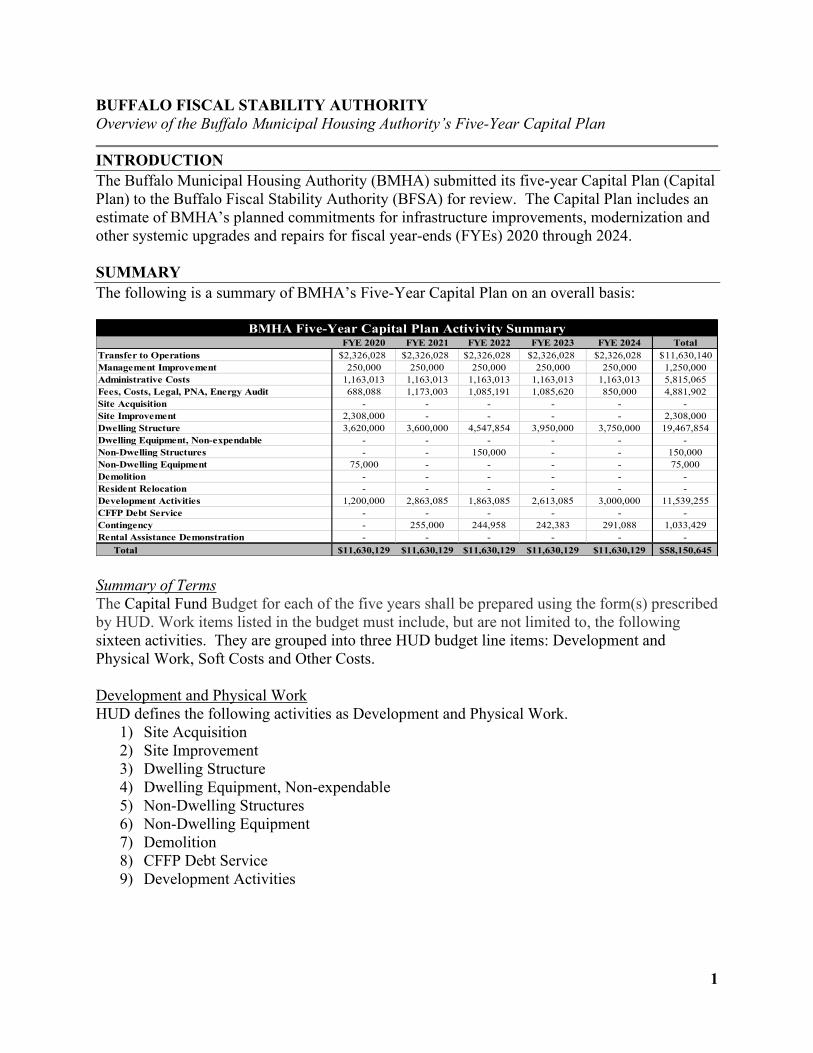

TAB 6 Buffalo Municipal Housing Authority Review of the 2nd Quarter Report 2019-20 Capital Plan

TAB 7

Left intentionally blank

Privilege of the Floor OTHER BUSINESS AND ANNOUNCEMENTS Note: Meetings may be rescheduled based on Directors availability

Upcoming Events Date Location

Audit, Finance & Budget Committee ~ 12:30 PM Full Board Meeting ~ 1:00 PM

Wednesday, May 20, 2020

Market Arcade Building

617 Main Street 1st Floor Conference Room Buffalo, New York 14203 Audit, Finance & Budget Committee ~ 12:30 PM

Full Board Meeting ~ 1:00 PM Wednesday, June 24, 2020

0

[RESOLUTION]

1

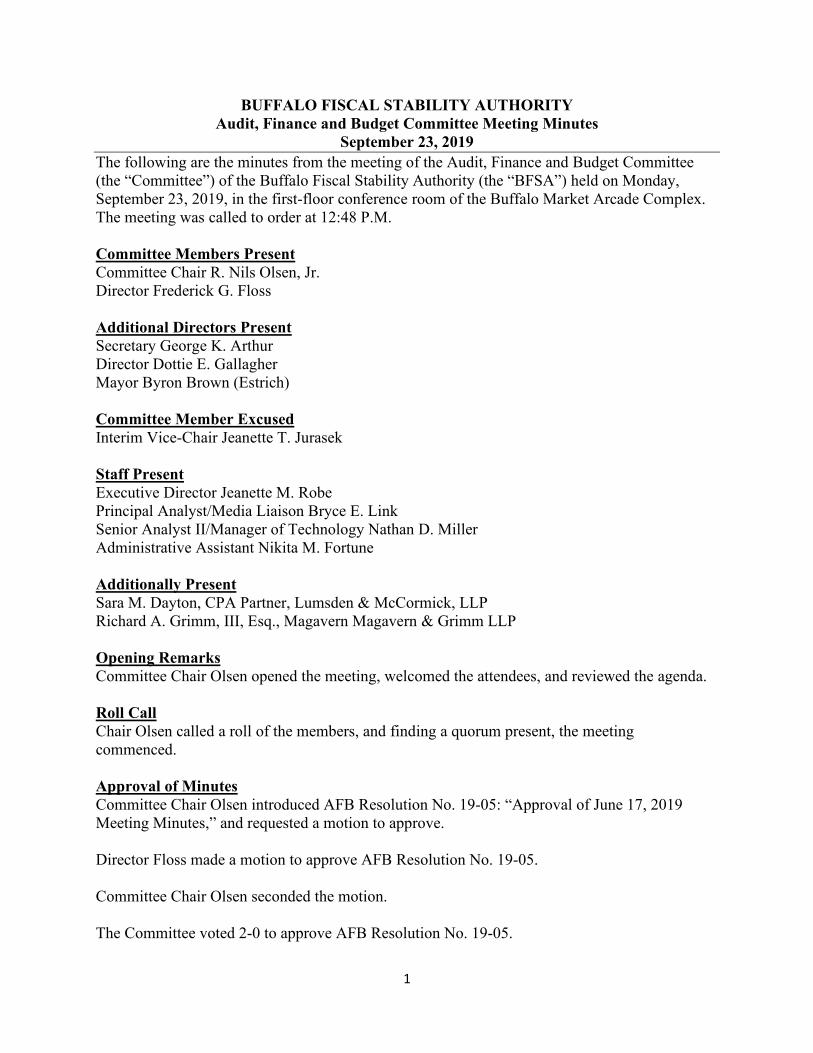

BUFFALO FISCAL STABILITY AUTHORITY

Audit, Finance and Budget Committee Meeting Minutes

September 23, 2019

The following are the minutes from the meeting of the Audit, Finance and Budget Committee (the “Committee”) of the Buffalo Fiscal Stability Authority (the “BFSA”) held on Monday, September 23, 2019, in the first-floor conference room of the Buffalo Market Arcade Complex. The meeting was called to order at 12:48 P.M. Committee Members Present

Committee Chair R. Nils Olsen, Jr. Director Frederick G. Floss Additional Directors Present

Secretary George K. Arthur Director Dottie E. Gallagher Mayor Byron Brown (Estrich) Committee Member Excused

Interim Vice-Chair Jeanette T. Jurasek Staff Present

Executive Director Jeanette M. Robe Principal Analyst/Media Liaison Bryce E. Link Senior Analyst II/Manager of Technology Nathan D. Miller Administrative Assistant Nikita M. Fortune Additionally Present

Sara M. Dayton, CPA Partner, Lumsden & McCormick, LLP Richard A. Grimm, III, Esq., Magavern Magavern & Grimm LLP Opening Remarks

Committee Chair Olsen opened the meeting, welcomed the attendees, and reviewed the agenda.

Roll Call

Chair Olsen called a roll of the members, and finding a quorum present, the meeting commenced. Approval of Minutes Committee Chair Olsen introduced AFB Resolution No. 19-05: “Approval of June 17, 2019 Meeting Minutes,” and requested a motion to approve. Director Floss made a motion to approve AFB Resolution No. 19-05. Committee Chair Olsen seconded the motion.

The Committee voted 2-0 to approve AFB Resolution No. 19-05.

2

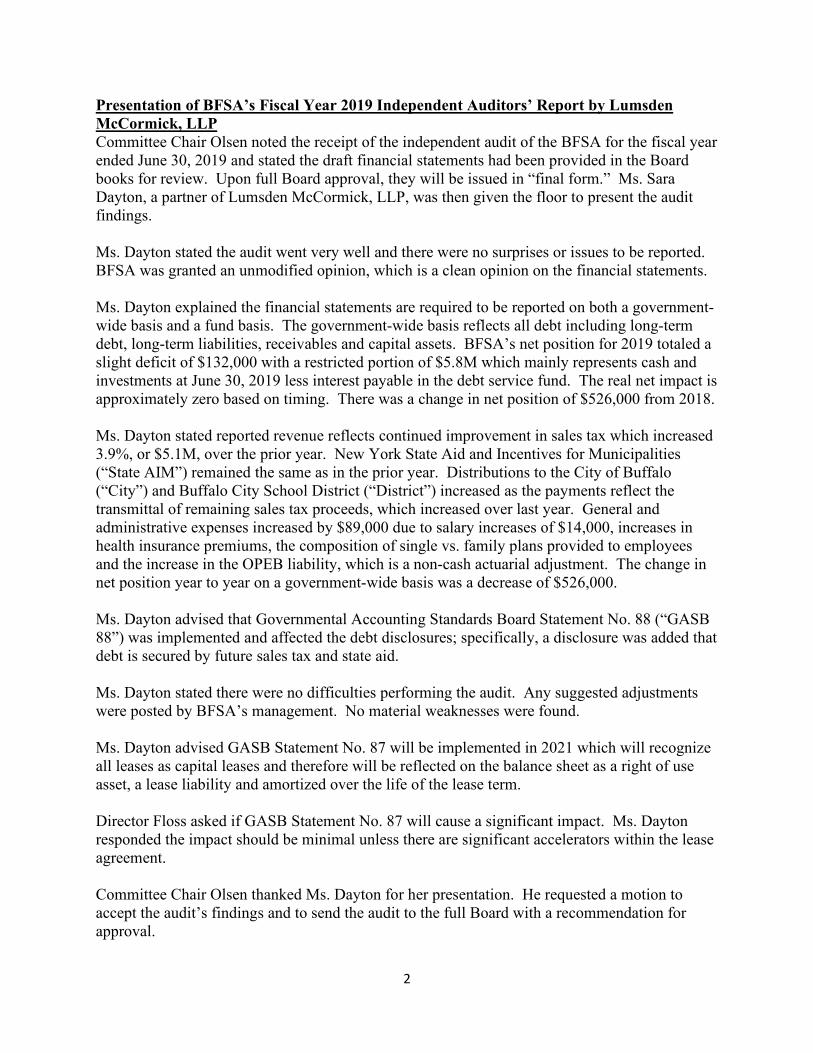

Presentation of BFSA’s Fiscal Year 2019 Independent Auditors’ Report by Lumsden

McCormick, LLP

Committee Chair Olsen noted the receipt of the independent audit of the BFSA for the fiscal year ended June 30, 2019 and stated the draft financial statements had been provided in the Board books for review. Upon full Board approval, they will be issued in “final form.” Ms. Sara Dayton, a partner of Lumsden McCormick, LLP, was then given the floor to present the audit findings. Ms. Dayton stated the audit went very well and there were no surprises or issues to be reported. BFSA was granted an unmodified opinion, which is a clean opinion on the financial statements. Ms. Dayton explained the financial statements are required to be reported on both a government-wide basis and a fund basis. The government-wide basis reflects all debt including long-term debt, long-term liabilities, receivables and capital assets. BFSA’s net position for 2019 totaled a slight deficit of $132,000 with a restricted portion of $5.8M which mainly represents cash and investments at June 30, 2019 less interest payable in the debt service fund. The real net impact is approximately zero based on timing. There was a change in net position of $526,000 from 2018. Ms. Dayton stated reported revenue reflects continued improvement in sales tax which increased 3.9%, or $5.1M, over the prior year. New York State Aid and Incentives for Municipalities (“State AIM”) remained the same as in the prior year. Distributions to the City of Buffalo (“City”) and Buffalo City School District (“District”) increased as the payments reflect the transmittal of remaining sales tax proceeds, which increased over last year. General and administrative expenses increased by $89,000 due to salary increases of $14,000, increases in health insurance premiums, the composition of single vs. family plans provided to employees and the increase in the OPEB liability, which is a non-cash actuarial adjustment. The change in net position year to year on a government-wide basis was a decrease of $526,000. Ms. Dayton advised that Governmental Accounting Standards Board Statement No. 88 (“GASB 88”) was implemented and affected the debt disclosures; specifically, a disclosure was added that debt is secured by future sales tax and state aid. Ms. Dayton stated there were no difficulties performing the audit. Any suggested adjustments were posted by BFSA’s management. No material weaknesses were found. Ms. Dayton advised GASB Statement No. 87 will be implemented in 2021 which will recognize all leases as capital leases and therefore will be reflected on the balance sheet as a right of use asset, a lease liability and amortized over the life of the lease term. Director Floss asked if GASB Statement No. 87 will cause a significant impact. Ms. Dayton responded the impact should be minimal unless there are significant accelerators within the lease agreement. Committee Chair Olsen thanked Ms. Dayton for her presentation. He requested a motion to accept the audit’s findings and to send the audit to the full Board with a recommendation for approval.

3

Director Floss made the requested motion. Committee Chair Olsen seconded the motion. The Committee voted 2-0 to accept the audit’s findings and to send the audit to the full Board with a recommendation for approval. BFSA Annual Report

Committee Chair Olsen advanced the agenda to the review of the BFSA Annual Report to be presented by BFSA Executive Director Ms. Jeanette M. Robe. Director Gallagher entered the meeting at 1:02 P.M. Ms. Robe gave an overview of the components of the BFSA Annual Report which aligns with the requirements of New York State Public Authorities Law and summarizes the accomplishments of the most recent fiscal year ended June 30, 2019. The three main sections of the report are: I. Organizational:

• Information on Board members and staff

• Background information on BFSA

• Mission Statement, general governance and administration information II. Accomplishments:

• Discussion on progress towards fiscal stability by the City of Buffalo and the covered organizations:

o the Buffalo City School District (the “BCSD”) o the Buffalo Municipal Housing Authority (the “BMHA”) o the Buffalo Urban Renewal Agency (“BURA”)

• Discussion on the significance of the multi-year financial planning process as representing the core of BFSA’s financial oversight by the City of Buffalo (the “City”) and the covered organizations.

• A description of each report issued by BFSA over the last year is provided along with recommendations and comments

• Other areas of fiscal monitoring conducted by BFSA, such as the monitoring of workforce trends, are included

• Cumulative financial impact schedule which indicates the total impact of the BFSA as of June 30, 2019 of $458.5M. The City and District’s estimated cumulative financial impact from the wage freeze is $240.4M

III. The four individual reports on the review and analysis of the final budgets and four-year

financial plans for each entity.

4

Ms. Robe stated the annual report will be filed with the New York State (“NYS”) Comptroller, other NYS officials as required by law, as well as posted on the BFSA website. Ms. Robe thanked Mr. Bryce Link for his extensive work on compiling the annual report.

Committee Chair Olsen highlighted BFSA’s continuing impact as an advisory board on the City’s improved bond rating. Director Floss stated the advisory status of the Board has also had a positive impact on the covered organizations and asked if the covered organization will receive copies of the BFSA annual report. Ms. Robe stated she would ensure each entity receives a copy.

BFSA Investment Report

Ms. Robe stated there have been no changes to the investment guidelines which were last reviewed at the July 29, 2019 board meeting. The summary of the investment activity has also been reported in the audited financial statements. Total cash and investments were $6.4M at cost and $6.5M at fair market value at June 30, 2019. All investments mature no later than August 30, 2019 with the exception of one investment in State and Local Government treasury securities of $135,000 which matures September 1, 2021. This investment was structured to avoid any yield restrictions associated with the BFSA 2015A refunding bond. Total investment earnings for the year were $199,555; interest earnings are remitted to the City periodically. The majority was earned on forward delivery agreements, providing guaranteed interest rates ranging between 4.48% and 5.13%, which continues to exceed the market and assists in reducing overall debt costs. The funds are remitted biannually to the City. There were no investment fees or commission paid with respect to the investment portfolio for 2018-19. Trustee fees were reported as $8,790. No fees were paid on operating accounts as the fees were covered by the compensating balances. Hearing no questions or comments, Committee Chair Olsen requested a motion to approve both the BFSA Annual Report and the BFSA Annual Investment Report. Director Floss made a motion to approve both the 2019 BFSA Annual Report and Annual Investment Report. Committee Chair Olsen seconded the motion. The Committee voted 2-0 to accept both the annual report and the investment report.

5

PFM Financial Advisors

Committee Chair Olsen introduced AFB Resolution No. 19-06: “Approve Engagement of Public Financial Management as Financial Advisors.” Public Financial Management (“PFM”) served as the financial advisor for the BFSA’s period of issuing debt on behalf of the City and retains the historical knowledge related to these complex transactions. The engagement serves for October 1, 2019 through September 30, 2020 and would extend the terms of the original contract from 2018. Director Floss made a motion to approve AFB Resolution No. 19-06. Committee Chair Olsen seconded the motion. The Committee voted 2-0 to approve AFB Resolution No. 19-06.

Adjournment

Committee Chair Olsen asked if there was additional business to be considered by the Committee. Director Floss offered a motion to adjourn. Committee Chair Olsen seconded the motion. The Committee voted 2-0 to adjourn the meeting. The Committee adjourned 1:10 P.M.

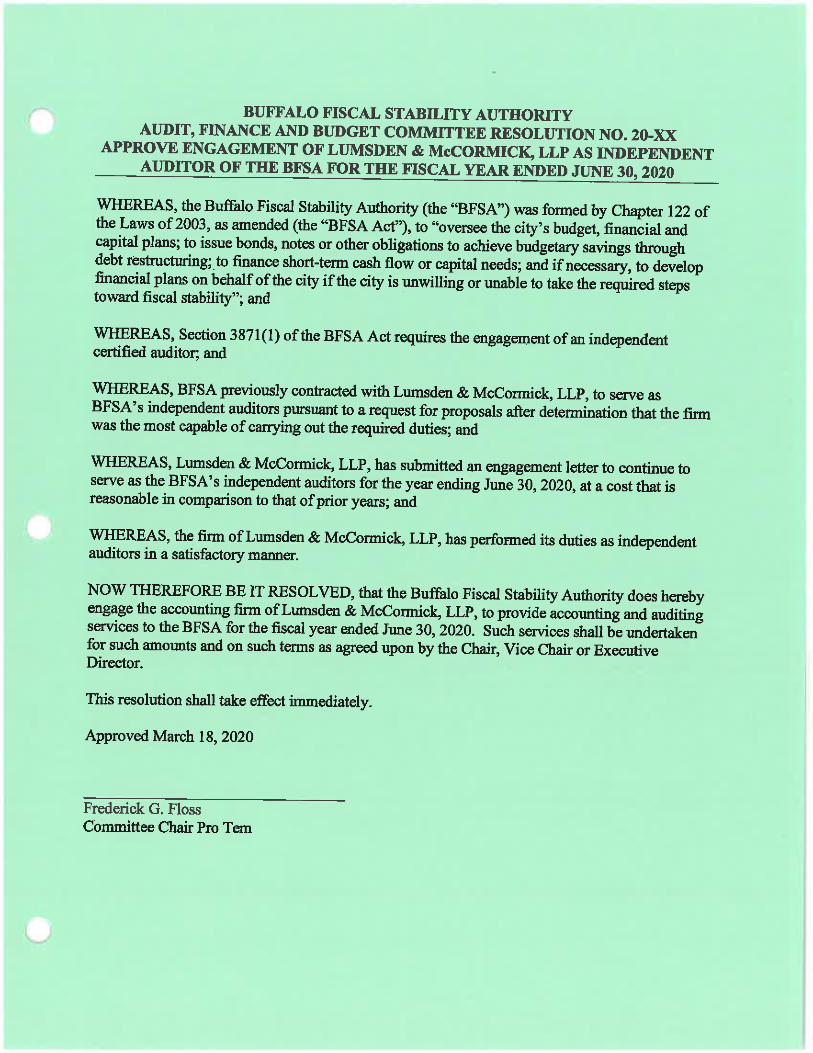

BUFFALO FISCAL STABILITY AUTHORITY AUDIT, FINANCE & BUDGET COMMITTEE RESOLUTION NO. 20-01

APPROVING MINUTES AND RESOLUTIONS FROM

SEPTEMBER 23, 2019

BE IT RESOLVED that the Buffalo Fiscal Stability Authority’s Audit, Finance and

Budget Committee approves the minutes of its meeting on September 23, 2019.

BE IT FURTHUR RESOLVED that the Buffalo Fiscal Stability Authority’s Audit, Finance and

Budget Committee ratifies and affirms Resolution Nos. 19-05 and 19-06 which were

approved as of said date.

This resolution shall take effect immediately.

Approved March 18, 2020

Frederick G. Floss

Committee Chair Pro Tem

BUFFALO FISCAL STABILITY AUTHORITY

2021-2024

PRELIMINARY BUDGET AND FINANCIAL PLAN

BUFFALO FISCAL STABILITY AUTHORITY

ii

Buffalo Fiscal Stability Authority

Authority Directors and Staff as of March 18, 2020

Directors

R. Nils Olsen, Jr., Chair

Jeanette T. Jurasek, Interim Vice-Chair

George K. Arthur, Secretary

Frederick G. Floss

Byron W. Brown (ex officio)

Mark C. Poloncarz (ex officio)

Staff

Jeanette M. Robe, CPA

Executive Director

Nikita M. Fortune, BA

Administrative Assistant

Bryce E. Link, MPA

Principal Analyst/Media Contact/Treasurer

Nathan D. Miller, BS

Senior Analyst/Manager of Technology

Claire A. Waldron, CPA

Comptroller

Contact

Market Arcade Building

617 Main Street, Suite 400

Buffalo, New York 14203

Phone: 716.853.0907

Media: 716.359.1443

Fax: 716.853.9052

Email: [email protected]

Web: www.bfsa.state.ny.us

iii

Table of Contents ORGANIZATION ............................................................................................................ 1

BUDGET PROCESS ........................................................................................................ 3

PRINCIPAL BUDGETARY ASSUMPTIONS AND ASSESSMENT

OF BUDGETARY RISKS ............................................................................................... 4

2021 PRELIMINARY BUDGET & RELATED FOUR-YEAR FINANCIAL PLAN 6

FORECASTED 2020 REVENUES AND EXPENDITURES ....................................... 8

NUMBER OF EMPLOYEES .......................................................................................... 9

STATEMENT OF BORROWED DEBT ........................................................................ 9

SCHEDULE OF LONG-TERM DEBT ........................................................................ 11

LONG-TERM DEBT-DEBT SERVICE REQUIREMENTS: ................................... 11

1

ORGANIZATION

The Buffalo Fiscal Stability Authority (“BFSA” or “Authority”) is a corporate governmental

agency and instrumentality of the State of New York constituting a public benefit corporation

created by the BFSA Act (the “Act”), Chapter 122 of the Laws of 2003, as amended from time to

time, and signed by the Governor on July 3, 2003. BFSA has a broad range of financial control

and oversight powers over the City of Buffalo (the “City”) and its non-exempted Covered

Organizations including the Buffalo Public School District (the “School District”), the Buffalo

Municipal Housing Authority, the Buffalo Urban Renewal Agency, the Joint Schools

Construction Board and other covered organizations as defined by the Act.

According to its enabling statute, BFSA will continue in existence until its oversight, control or

other responsibilities and its liabilities, which include the payment of BFSA bonds and notes,

have been met or discharged, which in no event may be later than June 30, 2037. In addition,

BFSA has certain powers under the Act to control, oversee and monitor the City’s finances,

including Covered Organizations, particularly during a “control period”, which began on the

effective date of the BFSA Act of July 3, 2003.

BFSA is governed by a board of nine directors, seven of which are to be appointed by the

Governor of the State. Of the seven directors appointed by the Governor, one must be a resident

of the City, one is to be appointed following the recommendation of the State Comptroller, and

one is to be appointed on the joint recommendation of the Speaker of the Assembly and the

Temporary President of the Senate. The Mayor of the City and the County Executive serve as ex

officio directors. The Governor designates the Chairperson and Vice Chair from among the

directors. Five directors constitute a quorum. All directors of BFSA serve without salary.

The Act provides for BFSA to have different financial control and oversight powers depending

upon whether the City’s financial condition causes it to be in a “control period” or an “advisory

period.”

Under the Act, BFSA began its existence during a City control period, which means that BFSA

commenced operation with its maximum authorized complement of financial control and

oversight powers. Under an advisory period, the BFSA operates with a reduced set of financial

oversight powers and responsibilities.

On May 29, 2012, BFSA made a determination that all provisions of the Act with respect to

transitioning into an advisory period had been met and resolved to enter into an advisory period

effective July 1, 2012. An advisory period shall continue through June 30, 2037, unless a control

period is reimposed.

2

After an advisory period has been established, a control period could be reimposed on the City

upon a determination by BFSA that a fiscal crisis is imminent or that any of the following events

has occurred or that there is a substantial likelihood and imminence of its occurrence: (a) the City

shall have failed to adopt a balanced budget, financial plan or budget modification as required by

Sections 3856 and 3857 of the Act; (b) the City shall have failed to pay the principal of or

interest on any of its bonds or notes when due; (c) the City shall have incurred an operating

deficit of one percent or more in the aggregate results of operations of any major fund of the City

or a Covered Organization during its fiscal year assuming all revenues and expenditures are

reported in accordance with generally accepted accounting principles, subject to the provisions

of the Act; (d) the chief fiscal officer’s certification at any time, at the request of BFSA or on the

chief fiscal officer’s initiative, which certification shall be made from time to time as promptly as

circumstances warrant and reported to BFSA, that on the basis of facts existing at such time such

officer could not make the certification described in subdivision one of Section 3851 of the Act;

or (e) the City shall have violated any provision of the Act.

During a control period, BFSA is empowered, among other things, (i) to approve or disapprove

contracts, including collective bargaining agreements to be entered into by the City or any

Covered Organization, binding or purporting to bind the City or any Covered Organization; (ii)

to approve or disapprove the terms of borrowings by the City and Covered Organizations; (iii) to

approve, disapprove or modify the City’s financial plans and take any action necessary in order

to implement the financial plan should the City or any Covered Organization fail to comply with

any material action necessary to fulfill the plan, including issuing binding orders to the

appropriate local officials; (iv) to set a maximum level of spending for any proposed budget of

any Covered Organization; (v) to impose a wage or hiring freeze, or both, with respect to

employees of the City or any Covered Organization; (vi) to review the operation, management,

efficiency and productivity of the City and any Covered Organization; and (vii) to terminate the

control period upon finding that no condition exists which would permit imposition of a control

period, provided that budgetary operations for the prior three years were balanced without

Authority assistance.

During an advisory period, as defined in the Act, BFSA is empowered, among other things, (i) to

review the operation, management, efficiency and productivity of City operations and of any

Covered Organization’s operations, and to make reports and recommendations thereon; (ii) to

review and comment on the budget, financial plan and financial plan modifications of the City

and any of the Covered Organization’s; (iii) to audit compliance with the City and any of the

Covered Organization’s financial plans; (iv) to review and comment on the terms of any

proposed borrowing, including the prudence of each proposed issuance of bonds or notes by the

City; (v) to assess and comment on the impact of any collective bargaining agreement to be

entered by the City; and (vi) to impose a control period upon making one of the statutory

findings.

3

Revenues of BFSA consist of state aid, sales tax revenue and investment earnings on funds

deposited in BFSA bank accounts and on set-aside funds deposited with the bond trustee to pay

bond interest and principal payments. Revenues of BFSA that are not required to pay operating

expenses and other costs of BFSA are payable to the City and the School District as frequently as

practicable.

BUDGET PROCESS

Adopted Budget and Financial Plan

BFSA’s adopted budget and financial plan are prepared in accordance with accounting principles

generally accepted in the United States of America on a full accrual basis, but also include

information for cash basis accounting as necessary. Comparative amounts for the fiscal year

ended June 30, 2019 were derived from BFSA’s audited financial statements, copies of which

were previously delivered to the BFSA’s Board of Directors and approved by Resolution No. 19-

24 on September 23, 2019. Amounts budgeted for fiscal year ending June 30, 2021 and forecasts

included in the financial plan have been developed using assumptions and methods of estimation

disclosed in budget and financial plan notes and sections herein. Working papers that document

the reasonable assumptions and methods of estimation, consistent with prudent budgetary

practices, have been prepared contemporaneously with the plan and will be maintained by

BFSA.

The proposed budget and financial plan is submitted to BFSA’s Audit, Finance and Budget

Committee and also to the Board of Directors for review no later than 60 days prior to the

commencement of its next fiscal year along with a certification by BFSA’s Executive Director

attesting to the reasonableness of the assumptions and methods of estimation used to prepare the

budget and financial plan. The proposed budget and financial plan is posted on BFSA’s website

and made available to the public for a period of not less than 45 days, at least 30 of which must

be prior to approval by the Board.

The budget and financial plan, and all amendments or modifications to the budget and financial

plan, are approved by the BFSA’s Board of Directors. Additionally, the final approved budget

and financial plan is posted to the BFSA website not less than 7 days before commencement of

the next fiscal year and is submitted to the State Comptroller within 7 days of approval.

Approved Budget and Financial Plan

BFSA staff provides the BFSA’s Board of Directors with quarterly updates on actual revenues

and expenses compared to annual budget targets. No later than 90 days after the close of each

fiscal year, BFSA staff report publicly on the prior year’s actual versus budgeted results. Should

any situation arise that has the potential to have a material, adverse effect on the approved budget

and financial plan, BFSA staff are required to notify the State Comptroller in writing of the

situation.

4

PRINCIPAL BUDGETARY ASSUMPTIONS AND ASSESSMENT OF BUDGETARY

RISKS

The budget and financial plan includes estimates developed using assumptions as disclosed in

notes to the plan. Estimates are subject to risk due to assumptions made about future scenarios.

State aid and sales tax receipt estimates constitute the majority of BFSA’s budgeted and

forecasted revenue. State aid is forecasted at amounts consistent with the Governor’s Executive

Budget. Sales tax revenue is conservatively projected at levels consistent with the 2020

forecasted sales tax revenue amount and held flat over the out-years of the financial plan. Sales

tax receipts are sensitive to the fluctuations in economic activity in the City, which has gone

through numerous cycles of expansion and contraction over the years.

Investment income is earned by BFSA primarily from set-aside funds deposited with financial

services firms to pay the semi-annual interest payment and annual principal payment. These

funds are invested in accordance with forward delivery agreements and earn a guaranteed rate of

return on the investments. Investment income also includes investment earnings on funds

deposited in BFSA trustee accounts and bank accounts; these earnings are subject to fluctuation

due to the balances held by BFSA as well as changes in interest rates.

BFSA has a perfected interest in the state aid and sales tax collections for the City and the School

District and receives remittances from the NYS Department of Taxation and Finance for the

purpose of withholding debt service set-aside monies and expenses, prior to remittance to the

City and the School District. BFSA’s costs are closely monitored by BFSA staff. As a result,

there is little budget risk to BFSA or its bond holders.

No material non-recurring resources or transactions that shift material resources from one year to

another or from reserves are included in this preliminary budget or financial plan.

Approximately 64% of total budgeted operating expenses represents staff related costs. The

budget includes five budgeted positions, all of which are filled. There is a 2% salary increase

budgeted for each position annually. Staff related costs also include employee benefits such as

health insurance, pension expense and payroll taxes. Employee health insurance is budgeted at

current rates and is projected to increase by 5.5% annually over the course of the financial plan;

this projected increase is based on recent historical experience as well as available market data.

Pension expense is determined based on the projected contribution rates as provided by the New

York State Comptroller.

Professional fees are the second largest category of operating expenses, representing

approximately 27% of the total budget. This category includes amounts budgeted for litigation,

general legal counsel services, the independent audit, trustee fees and bank charges, and other

professional fees. This category is estimated based on past historical experience and

conservatively includes amounts so that in the event such services are necessary, there are

adequate amounts budgeted.

5

All other operating expenses represent approximately 9% of the total budget for operating

expenses. The BFSA operates as leanly as possible, understanding that fiscal constraint is

extraordinarily important.

Salaries expense is budgeted to decrease 1.6% as compared to prior year. The BFSA was able to

replace the full-time budgeted position for Comptroller with a part-time position, resulting in the

year-to-year decrease. There were no other significant fluctuations noted from last year’s final

budget.

After amounts are retained for debt service, operating expenses, and for any other purpose as

provided for in New York State law, sales taxes are remitted as soon as practical to the City of

Buffalo and the Buffalo City School District. Those amounts are represented as Distributions

within the Adopted Budget.

6

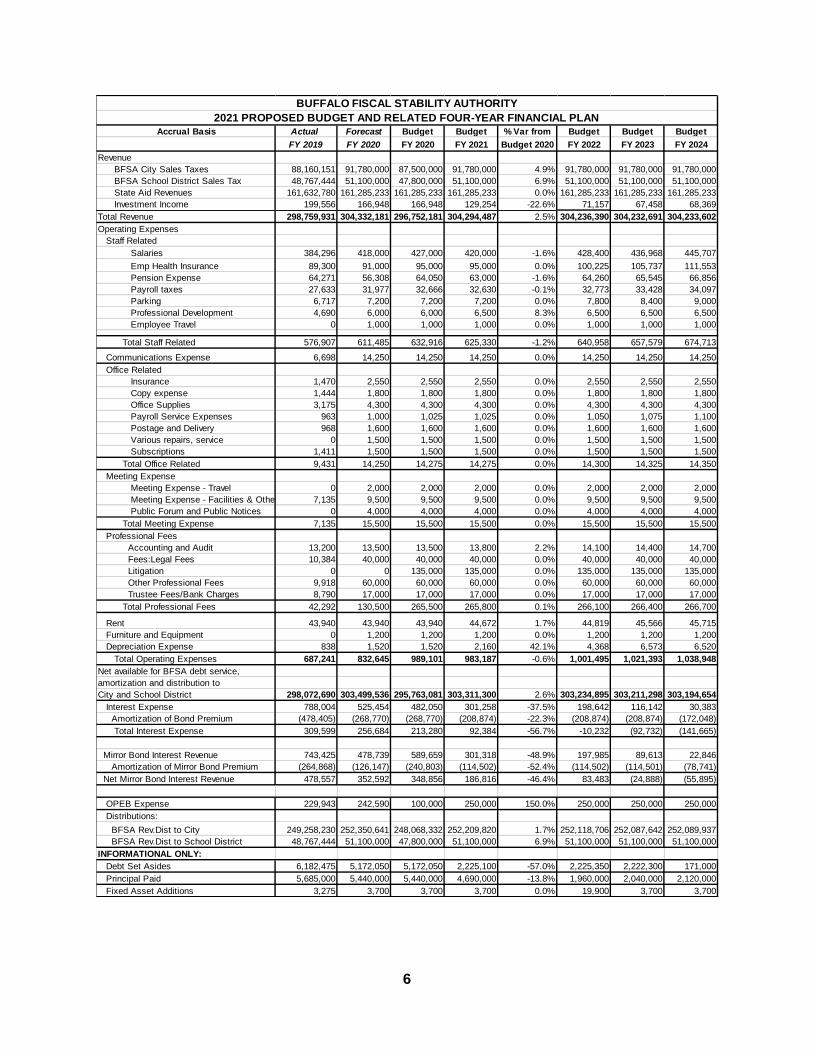

Accrual Basis Actual Forecast Budget Budget % Var from Budget Budget Budget

FY 2019 FY 2020 FY 2020 FY 2021 Budget 2020 FY 2022 FY 2023 FY 2024

Revenue

BFSA City Sales Taxes 88,160,151 91,780,000 87,500,000 91,780,000 4.9% 91,780,000 91,780,000 91,780,000

BFSA School District Sales Tax 48,767,444 51,100,000 47,800,000 51,100,000 6.9% 51,100,000 51,100,000 51,100,000

State Aid Revenues 161,632,780 161,285,233 161,285,233 161,285,233 0.0% 161,285,233 161,285,233 161,285,233

Investment Income 199,556 166,948 166,948 129,254 -22.6% 71,157 67,458 68,369

Total Revenue 298,759,931 304,332,181 296,752,181 304,294,487 2.5% 304,236,390 304,232,691 304,233,602

Operating Expenses

Staff Related

Salaries 384,296 418,000 427,000 420,000 -1.6% 428,400 436,968 445,707

Emp Health Insurance 89,300 91,000 95,000 95,000 0.0% 100,225 105,737 111,553

Pension Expense 64,271 56,308 64,050 63,000 -1.6% 64,260 65,545 66,856

Payroll taxes 27,633 31,977 32,666 32,630 -0.1% 32,773 33,428 34,097

Parking 6,717 7,200 7,200 7,200 0.0% 7,800 8,400 9,000

Professional Development 4,690 6,000 6,000 6,500 8.3% 6,500 6,500 6,500

Employee Travel 0 1,000 1,000 1,000 0.0% 1,000 1,000 1,000

Total Staff Related 576,907 611,485 632,916 625,330 -1.2% 640,958 657,579 674,713

Communications Expense 6,698 14,250 14,250 14,250 0.0% 14,250 14,250 14,250

Office Related

Insurance 1,470 2,550 2,550 2,550 0.0% 2,550 2,550 2,550

Copy expense 1,444 1,800 1,800 1,800 0.0% 1,800 1,800 1,800

Office Supplies 3,175 4,300 4,300 4,300 0.0% 4,300 4,300 4,300

Payroll Service Expenses 963 1,000 1,025 1,025 0.0% 1,050 1,075 1,100

Postage and Delivery 968 1,600 1,600 1,600 0.0% 1,600 1,600 1,600

Various repairs, service 0 1,500 1,500 1,500 0.0% 1,500 1,500 1,500

Subscriptions 1,411 1,500 1,500 1,500 0.0% 1,500 1,500 1,500

Total Office Related 9,431 14,250 14,275 14,275 0.0% 14,300 14,325 14,350

Meeting Expense

Meeting Expense - Travel 0 2,000 2,000 2,000 0.0% 2,000 2,000 2,000

Meeting Expense - Facilities & Other 7,135 9,500 9,500 9,500 0.0% 9,500 9,500 9,500

Public Forum and Public Notices 0 4,000 4,000 4,000 0.0% 4,000 4,000 4,000

Total Meeting Expense 7,135 15,500 15,500 15,500 0.0% 15,500 15,500 15,500

Professional Fees

Accounting and Audit 13,200 13,500 13,500 13,800 2.2% 14,100 14,400 14,700

Fees:Legal Fees 10,384 40,000 40,000 40,000 0.0% 40,000 40,000 40,000

Litigation 0 0 135,000 135,000 0.0% 135,000 135,000 135,000

Other Professional Fees 9,918 60,000 60,000 60,000 0.0% 60,000 60,000 60,000

Trustee Fees/Bank Charges 8,790 17,000 17,000 17,000 0.0% 17,000 17,000 17,000

Total Professional Fees 42,292 130,500 265,500 265,800 0.1% 266,100 266,400 266,700

Rent 43,940 43,940 43,940 44,672 1.7% 44,819 45,566 45,715

Furniture and Equipment 0 1,200 1,200 1,200 0.0% 1,200 1,200 1,200

Depreciation Expense 838 1,520 1,520 2,160 42.1% 4,368 6,573 6,520

Total Operating Expenses 687,241 832,645 989,101 983,187 -0.6% 1,001,495 1,021,393 1,038,948

Net available for BFSA debt service,

amortization and distribution to

City and School District 298,072,690 303,499,536 295,763,081 303,311,300 2.6% 303,234,895 303,211,298 303,194,654

Interest Expense 788,004 525,454 482,050 301,258 -37.5% 198,642 116,142 30,383

Amortization of Bond Premium (478,405) (268,770) (268,770) (208,874) -22.3% (208,874) (208,874) (172,048)

Total Interest Expense 309,599 256,684 213,280 92,384 -56.7% -10,232 (92,732) (141,665)

Mirror Bond Interest Revenue 743,425 478,739 589,659 301,318 -48.9% 197,985 89,613 22,846

Amortization of Mirror Bond Premium (264,868) (126,147) (240,803) (114,502) -52.4% (114,502) (114,501) (78,741)

Net Mirror Bond Interest Revenue 478,557 352,592 348,856 186,816 -46.4% 83,483 (24,888) (55,895)

OPEB Expense 229,943 242,590 100,000 250,000 150.0% 250,000 250,000 250,000

Distributions:

BFSA Rev.Dist to City 249,258,230 252,350,641 248,068,332 252,209,820 1.7% 252,118,706 252,087,642 252,089,937

BFSA Rev.Dist to School District 48,767,444 51,100,000 47,800,000 51,100,000 6.9% 51,100,000 51,100,000 51,100,000

INFORMATIONAL ONLY:

Debt Set Asides 6,182,475 5,172,050 5,172,050 2,225,100 -57.0% 2,225,350 2,222,300 171,000

Principal Paid 5,685,000 5,440,000 5,440,000 4,690,000 -13.8% 1,960,000 2,040,000 2,120,000

Fixed Asset Additions 3,275 3,700 3,700 3,700 0.0% 19,900 3,700 3,700

BUFFALO FISCAL STABILITY AUTHORITY

2021 PROPOSED BUDGET AND RELATED FOUR-YEAR FINANCIAL PLAN

7

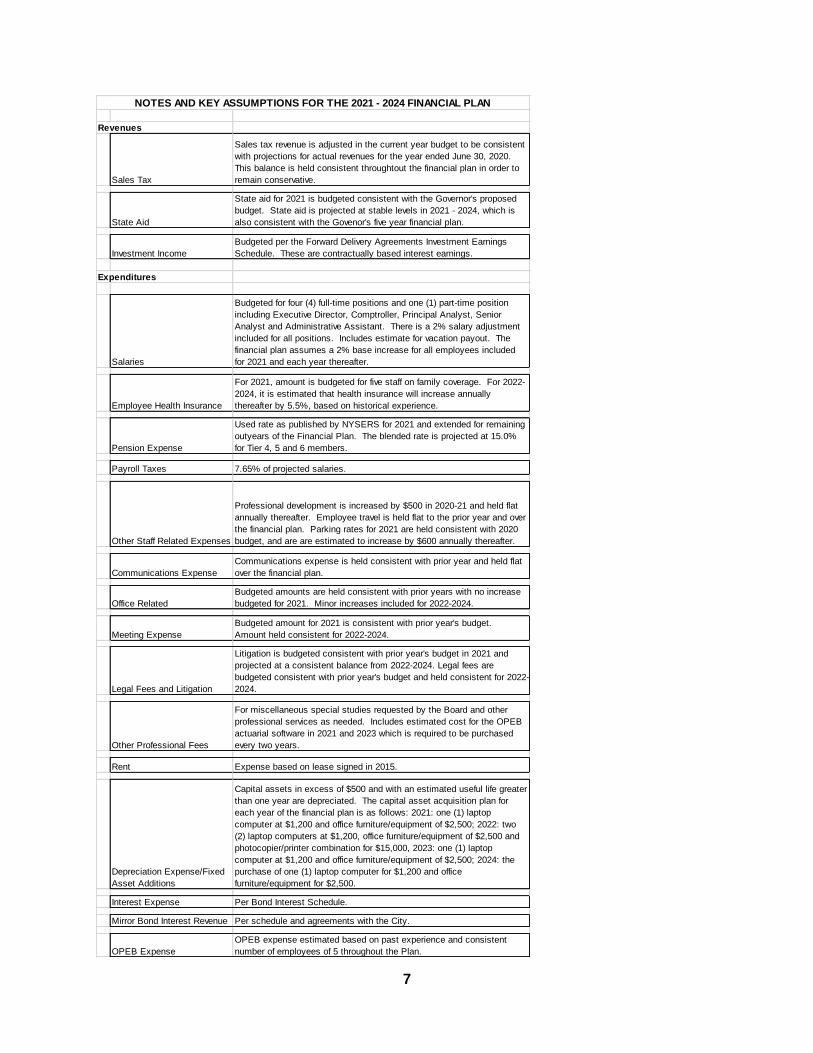

Revenues

Sales Tax

Sales tax revenue is adjusted in the current year budget to be consistent

with projections for actual revenues for the year ended June 30, 2020.

This balance is held consistent throughtout the financial plan in order to

remain conservative.

State Aid

State aid for 2021 is budgeted consistent with the Governor's proposed

budget. State aid is projected at stable levels in 2021 - 2024, which is

also consistent with the Govenor's five year financial plan.

Investment Income

Budgeted per the Forward Delivery Agreements Investment Earnings

Schedule. These are contractually based interest earnings.

Expenditures

Salaries

Budgeted for four (4) full-time positions and one (1) part-time position

including Executive Director, Comptroller, Principal Analyst, Senior

Analyst and Administrative Assistant. There is a 2% salary adjustment

included for all positions. Includes estimate for vacation payout. The

financial plan assumes a 2% base increase for all employees included

for 2021 and each year thereafter.

Employee Health Insurance

For 2021, amount is budgeted for five staff on family coverage. For 2022-

2024, it is estimated that health insurance will increase annually

thereafter by 5.5%, based on historical experience.

Pension Expense

Used rate as published by NYSERS for 2021 and extended for remaining

outyears of the Financial Plan. The blended rate is projected at 15.0%

for Tier 4, 5 and 6 members.

Payroll Taxes 7.65% of projected salaries.

Other Staff Related Expenses

Professional development is increased by $500 in 2020-21 and held flat

annually thereafter. Employee travel is held flat to the prior year and over

the financial plan. Parking rates for 2021 are held consistent with 2020

budget, and are are estimated to increase by $600 annually thereafter.

Communications Expense

Communications expense is held consistent with prior year and held flat

over the financial plan.

Office Related

Budgeted amounts are held consistent with prior years with no increase

budgeted for 2021. Minor increases included for 2022-2024.

Meeting Expense

Budgeted amount for 2021 is consistent with prior year's budget.

Amount held consistent for 2022-2024.

Legal Fees and Litigation

Litigation is budgeted consistent with prior year's budget in 2021 and

projected at a consistent balance from 2022-2024. Legal fees are

budgeted consistent with prior year's budget and held consistent for 2022-

2024.

Other Professional Fees

For miscellaneous special studies requested by the Board and other

professional services as needed. Includes estimated cost for the OPEB

actuarial software in 2021 and 2023 which is required to be purchased

every two years.

Rent Expense based on lease signed in 2015.

Depreciation Expense/Fixed

Asset Additions

Capital assets in excess of $500 and with an estimated useful life greater

than one year are depreciated. The capital asset acquisition plan for

each year of the financial plan is as follows: 2021: one (1) laptop

computer at $1,200 and office furniture/equipment of $2,500; 2022: two

(2) laptop computers at $1,200, office furniture/equipment of $2,500 and

photocopier/printer combination for $15,000, 2023: one (1) laptop

computer at $1,200 and office furniture/equipment of $2,500; 2024: the

purchase of one (1) laptop computer for $1,200 and office

furniture/equipment for $2,500.

Interest Expense Per Bond Interest Schedule.

Mirror Bond Interest Revenue Per schedule and agreements with the City.

OPEB Expense

OPEB expense estimated based on past experience and consistent

number of employees of 5 throughout the Plan.

NOTES AND KEY ASSUMPTIONS FOR THE 2021 - 2024 FINANCIAL PLAN

8

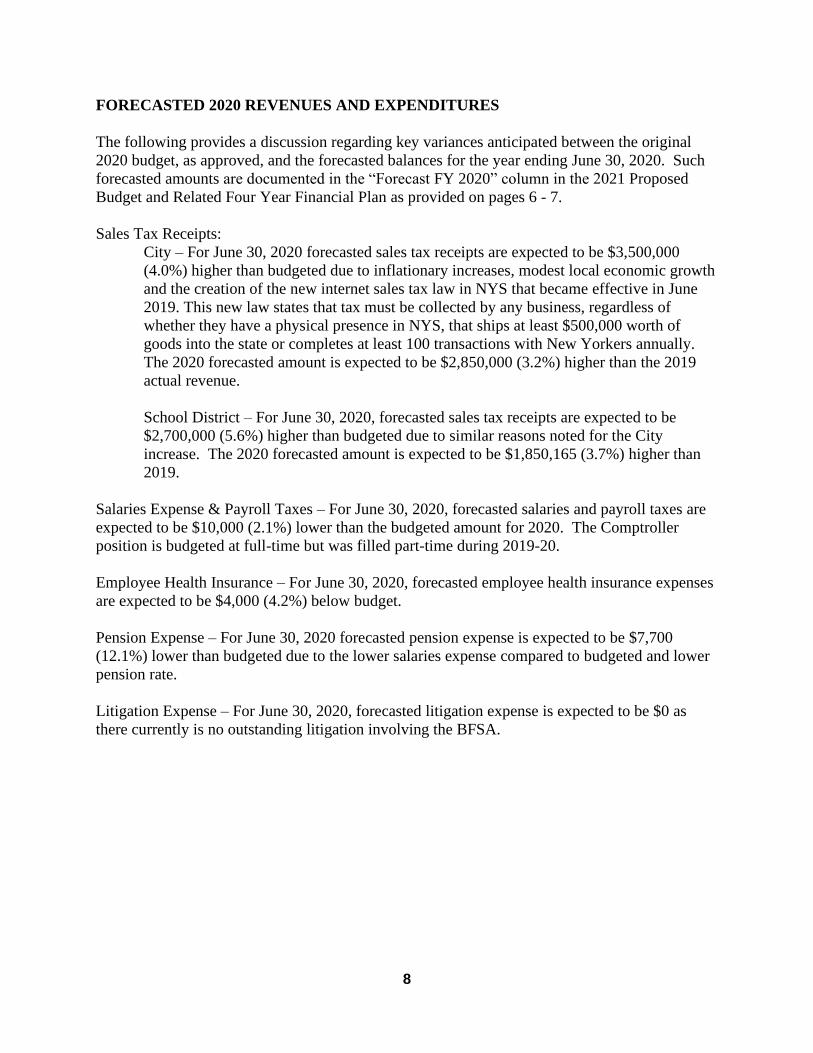

FORECASTED 2020 REVENUES AND EXPENDITURES

The following provides a discussion regarding key variances anticipated between the original

2020 budget, as approved, and the forecasted balances for the year ending June 30, 2020. Such

forecasted amounts are documented in the “Forecast FY 2020” column in the 2021 Proposed

Budget and Related Four Year Financial Plan as provided on pages 6 - 7.

Sales Tax Receipts:

City – For June 30, 2020 forecasted sales tax receipts are expected to be $3,500,000

(4.0%) higher than budgeted due to inflationary increases, modest local economic growth

and the creation of the new internet sales tax law in NYS that became effective in June

2019. This new law states that tax must be collected by any business, regardless of

whether they have a physical presence in NYS, that ships at least $500,000 worth of

goods into the state or completes at least 100 transactions with New Yorkers annually.

The 2020 forecasted amount is expected to be $2,850,000 (3.2%) higher than the 2019

actual revenue.

School District – For June 30, 2020, forecasted sales tax receipts are expected to be

$2,700,000 (5.6%) higher than budgeted due to similar reasons noted for the City

increase. The 2020 forecasted amount is expected to be $1,850,165 (3.7%) higher than

2019.

Salaries Expense & Payroll Taxes – For June 30, 2020, forecasted salaries and payroll taxes are

expected to be $10,000 (2.1%) lower than the budgeted amount for 2020. The Comptroller

position is budgeted at full-time but was filled part-time during 2019-20.

Employee Health Insurance – For June 30, 2020, forecasted employee health insurance expenses

are expected to be $4,000 (4.2%) below budget.

Pension Expense – For June 30, 2020 forecasted pension expense is expected to be $7,700

(12.1%) lower than budgeted due to the lower salaries expense compared to budgeted and lower

pension rate.

Litigation Expense – For June 30, 2020, forecasted litigation expense is expected to be $0 as

there currently is no outstanding litigation involving the BFSA.

9

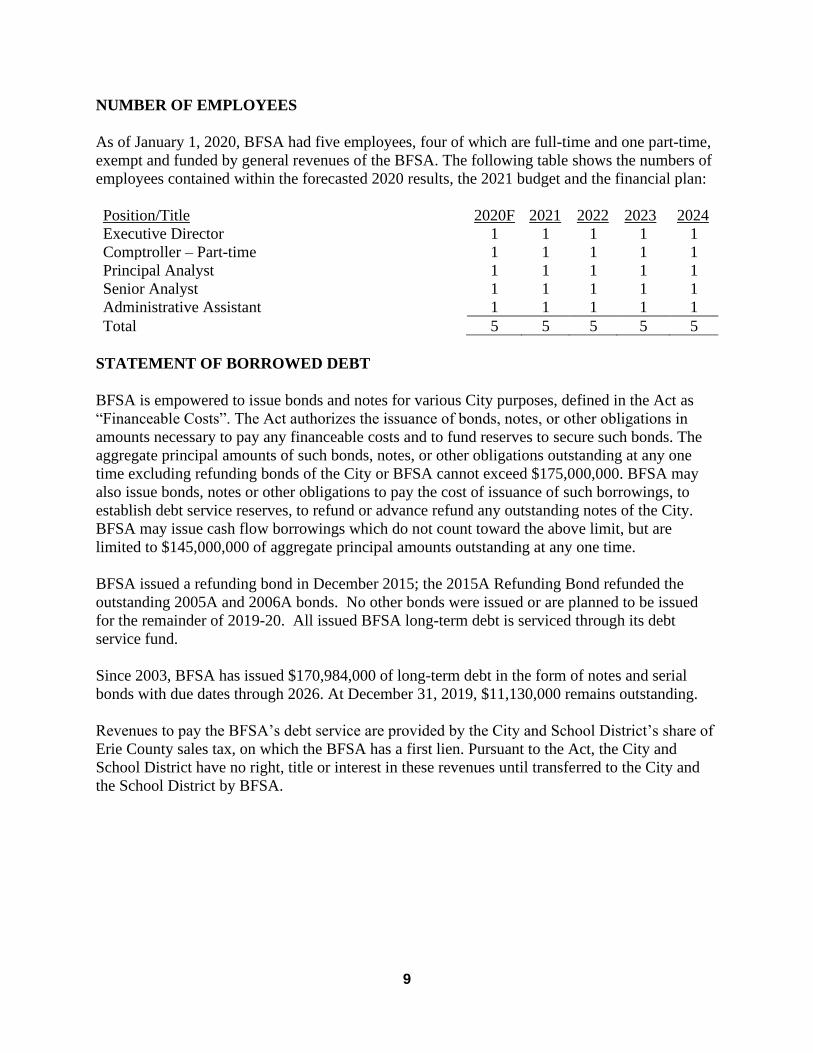

NUMBER OF EMPLOYEES

As of January 1, 2020, BFSA had five employees, four of which are full-time and one part-time,

exempt and funded by general revenues of the BFSA. The following table shows the numbers of

employees contained within the forecasted 2020 results, the 2021 budget and the financial plan:

Position/Title 2020F 2021 2022 2023 2024

Executive Director 1 1 1 1 1

Comptroller – Part-time 1 1 1 1 1

Principal Analyst 1 1 1 1 1

Senior Analyst 1 1 1 1 1

Administrative Assistant 1 1 1 1 1

Total 5 5 5 5 5

STATEMENT OF BORROWED DEBT

BFSA is empowered to issue bonds and notes for various City purposes, defined in the Act as

“Financeable Costs”. The Act authorizes the issuance of bonds, notes, or other obligations in

amounts necessary to pay any financeable costs and to fund reserves to secure such bonds. The

aggregate principal amounts of such bonds, notes, or other obligations outstanding at any one

time excluding refunding bonds of the City or BFSA cannot exceed $175,000,000. BFSA may

also issue bonds, notes or other obligations to pay the cost of issuance of such borrowings, to

establish debt service reserves, to refund or advance refund any outstanding notes of the City.

BFSA may issue cash flow borrowings which do not count toward the above limit, but are

limited to $145,000,000 of aggregate principal amounts outstanding at any one time.

BFSA issued a refunding bond in December 2015; the 2015A Refunding Bond refunded the

outstanding 2005A and 2006A bonds. No other bonds were issued or are planned to be issued

for the remainder of 2019-20. All issued BFSA long-term debt is serviced through its debt

service fund.

Since 2003, BFSA has issued $170,984,000 of long-term debt in the form of notes and serial

bonds with due dates through 2026. At December 31, 2019, $11,130,000 remains outstanding.

Revenues to pay the BFSA’s debt service are provided by the City and School District’s share of

Erie County sales tax, on which the BFSA has a first lien. Pursuant to the Act, the City and

School District have no right, title or interest in these revenues until transferred to the City and

the School District by BFSA.

10

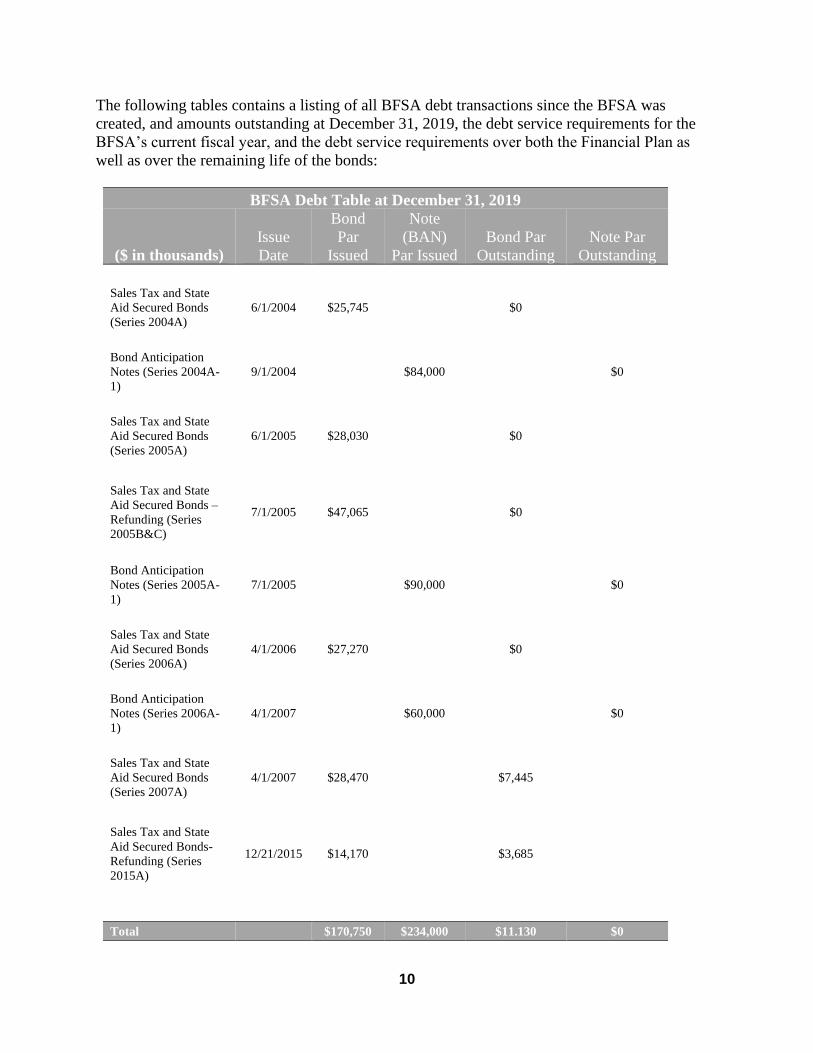

The following tables contains a listing of all BFSA debt transactions since the BFSA was

created, and amounts outstanding at December 31, 2019, the debt service requirements for the

BFSA’s current fiscal year, and the debt service requirements over both the Financial Plan as

well as over the remaining life of the bonds:

BFSA Debt Table at December 31, 2019

($ in thousands)

Issue

Date

Bond

Par

Issued

Note

(BAN)

Par Issued

Bond Par

Outstanding

Note Par

Outstanding

Sales Tax and State

Aid Secured Bonds

(Series 2004A)

6/1/2004 $25,745 $0

Bond Anticipation

Notes (Series 2004A-

1)

9/1/2004 $84,000 $0

Sales Tax and State

Aid Secured Bonds

(Series 2005A)

6/1/2005 $28,030 $0

Sales Tax and State

Aid Secured Bonds –

Refunding (Series

2005B&C)

7/1/2005 $47,065 $0

Bond Anticipation

Notes (Series 2005A-

1)

7/1/2005 $90,000 $0

Sales Tax and State

Aid Secured Bonds

(Series 2006A)

4/1/2006 $27,270 $0

Bond Anticipation

Notes (Series 2006A-

1)

4/1/2007 $60,000 $0

Sales Tax and State

Aid Secured Bonds

(Series 2007A)

4/1/2007 $28,470 $7,445

Sales Tax and State

Aid Secured Bonds-

Refunding (Series

2015A)

12/21/2015 $14,170 $3,685

Total $170,750 $234,000 $11.130 $0

11

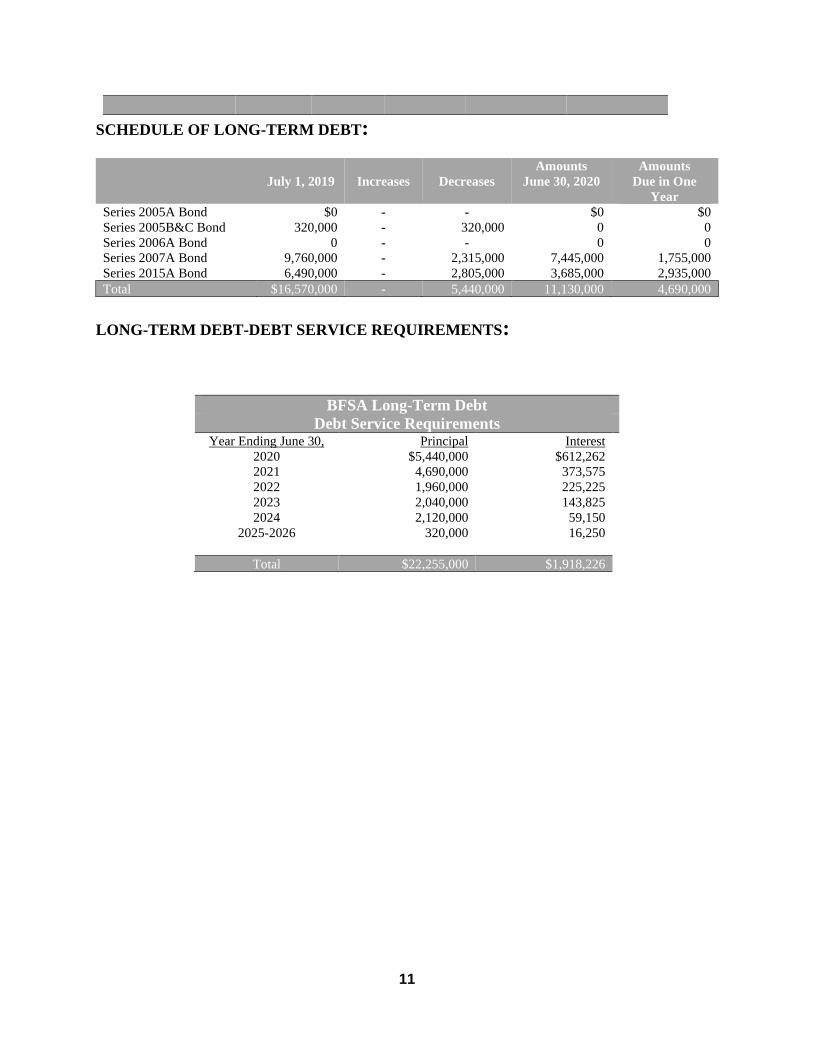

SCHEDULE OF LONG-TERM DEBT:

July 1, 2019

Increases

Decreases

Amounts

June 30, 2020

Amounts

Due in One

Year

Series 2005A Bond $0 - - $0 $0

Series 2005B&C Bond 320,000 - 320,000 0 0

Series 2006A Bond 0 - - 0 0

Series 2007A Bond 9,760,000 - 2,315,000 7,445,000 1,755,000

Series 2015A Bond 6,490,000 - 2,805,000 3,685,000 2,935,000

Total $16,570,000 - 5,440,000 11,130,000 4,690,000

LONG-TERM DEBT-DEBT SERVICE REQUIREMENTS:

BFSA Long-Term Debt

Debt Service Requirements Year Ending June 30, Principal Interest

2020 $5,440,000 $612,262

2021 4,690,000 373,575

2022 1,960,000 225,225

2023 2,040,000 143,825

2024 2,120,000 59,150

2025-2026 320,000 16,250

Total $22,255,000 $1,918,226

BUFFALO FISCAL STABILITY AUTHORITY

AUDIT, FINANCE AND BUDGET COMMITTEE

RESOLUTION NO. 20-XX

AUTHORIZE THE BFSA TO POST THE PRELIMINARY 2021 BUDGET AND RELATED

FOUR-YEAR FINANCIAL PLAN

WHEREAS, the Buffalo Fiscal Stability Authority (the “BFSA”) was created by Chapter 122 of the

Laws of 2003, as amended from time to time (“the BFSA Act”), to be a corporate governmental agency

and instrumentality of the State of New York constituting a public benefit corporation with a broad

range of financial control and oversight powers over the City of Buffalo; and

WHEREAS, the BFSA will have costs and expenses to operate and carry out its functions including, but

not limited to, paying the costs and expenses of its agents, employees, and facilities hereof,

reimbursement of costs incurred by Directors for actual and necessary expenses incurred in the

performance of such Director’s official duties, and otherwise to carry on and effectively carry out the

obligations required by the BFSA Act; and

WHEREAS, the staff of the BFSA has carefully reviewed the revenues to be received and expenses and

costs anticipated to be incurred in carrying out the duties and functions of the BFSA and has prepared a

budget (attached) based upon its reasonable assumptions of such revenues, costs and expenses; and

WHEREAS, the staff of the BFSA has forecasted revenues to be received and expenses and costs

anticipated in carrying out the duties and functions of the BFSA over the period for fiscal years 2021

through 2024; and

WHEREAS, consistent with the regulations of the Office of the State Comptroller, the BFSA will make

available proposed budgets and financial plans for public inspection at least 30 days before approval by

the Board, and not less than 60 days before the commencement of the next fiscal year, and for a period

of not less than 45 days.

NOW THEREFORE BE IT RESOLVED, that the Buffalo Fiscal Stability Authority’s Audit, Finance

and Budget Committee does hereby authorize the posting of the preliminary 2021 budget and related

four-year financial plan in a minimum of five separate locations of the Buffalo and Erie County Public

Library system for the next 45 days.

BE IT FURTHER RESOLVED, that the Buffalo Fiscal Stability Authority’s Audit, Finance and Budget

Committee does hereby authorize the posting of its preliminary 2021 budget and related four-year

financial plan on its website for the next 45 days.

This resolution shall take effect immediately.

Approved March 18, 2020

____________________________

Frederick G. Floss,

Committee Chair Pro Tem

1

BUFFALO FISCAL STABILITY AUTHORITY

Meeting Minutes

December 12, 2019

The following are the minutes from the meeting of the Buffalo Fiscal Stability Authority (the

“BFSA” or the “Authority”) held on Thursday, December 12, 2019 in the first-floor conference

room of the Buffalo Market Arcade Complex. The meeting was called to order at 1:04 PM.

Board Members Present

Chair R. Nils Olsen, Jr. (via video)

Interim Vice-Chair Jeanette Jurasek

Secretary George K. Arthur

Director Frederick G. Floss

Mayor Byron W. Brown (proxy Estrich)

County Executive Mark C. Poloncarz (proxy Cornell)

Staff Present

Executive Director Jeanette M. Robe

Principal Analyst/Media Liaison Bryce E. Link

Senior Analyst II/Manager of Technology Nathan D. Miller

Administrative Assistant Nikita M. Fortune

Comptroller Claire Waldron

Additionally Present

Mr. James L. Magavern, Esq., Magavern Magavern & Grimm LLP

Mr. Jason Shell, Commissioner of Assessment and Taxation, City of Buffalo

Opening Remarks

Interim Vice Chair Jurasek served as Chair Pro Tem, welcomed everyone to the December

Board meeting, thanked all who were in attendance, reviewed the logistics and agenda of the

meeting and advised that the Governance Committee met earlier, and recommended that the full

Board approve several items.

Roll Call of the Directors

Secretary Arthur called the roll, a quorum being present, the meeting commenced.

Erie County Budget Analyst, Mr. Mark Cornell, represented County Executive Mark C.

Poloncarz, while City of Buffalo Commissioner of Finance, Administration, Policy, and Urban

Affairs, Ms. Donna Estrich, represented Mayor Byron W. Brown, in accordance with

Subdivision 1 of §3853 of the BFSA Act.

Subdivision 1 of §3853 of the BFSA Act reads: “…The Mayor and the County Executive shall

serve as ex officio members. Every director, who is otherwise an elected official of the City or

County, shall be entitled to designate a single representative to attend, in his or her place,

meetings of the Authority and to vote or otherwise act in his or her behalf. Such designees shall

be residents of the City of Buffalo. Written notice of such designation shall be furnished prior to

any participation by the signal designee….”

2

Chair Pro Tem Jurasek introduced Resolution No. 19-25, “Approving Minutes and Resolutions

from September 23, 2019 and October 29, 2019.”

Director Floss made a motion to approve.

Chair Olsen seconded the motion.

The Board voted 6-0 to approve Resolution No. 19-25.

BFSA Items

Chair Pro Tem Jurasek advanced the agenda and stated that the Governance Committee met

earlier in the day and recommended the approval of the following items:

1. 2020 BFSA Board Meeting Calendar

2. 2020-21 Minority and Women-Owned Business Enterprise (“MWBE”) Goal Plan

3. 2020-21 Service-Disabled Veteran-Owned Business Development (“SDVOB”) Goal

Plan

Secretary Arthur made a motion to approve Resolution No. 19-26, “Adoption of a BFSA Board

of Director Regular Meeting Schedule for Calendar Year 2020.”

Chair Olsen seconded the motion.

The Board voted 6 to 0 to approve.

Chair Pro Tem Jurasek requested a motion to approve Resolution No. 19-27, “Approval of 2020-

21 MWBE Master Goal Plan.”

Director Floss made the motion as requested.

Secretary Arthur seconded the motion.

The Board voted 6 to 0 to approve.

Chair Pro Tem Jurasek requested a motion to approve Resolution No. 19-28, “Approval of the

2020-1 SDVOB Enterprise Master Goal Plan.”

Director Floss made the motion as requested.

Secretary Arthur seconded the motion.

The Board voted 6 to 0 to approve.

Director Floss asked Executive Director Robe to provide an overview of the MWBE and

SDVOB plans and achievements from the last fiscal year. Ms. Robe stated the goals of both

programs remain consistent with prior years. The SDVOB goal is 6% of qualified expenditures,

while the MWBE goal is 30% (Minority-owned Business Enterprises 15% and Woman-owned

Business Enterprises 15%). The majority of the BFSA budget is not subject to the goals,

therefore the total available budget for goals is $9,200 and the MWBE goal is $2,760 and

3

SDVOB goal is $522. Ms. Robe stated the goals were exceeded for both programs for fiscal

year (“FY”) 2018-19 as follows:

• MBE expenditure 23.6%

• WBE expenditures 20.2%

• SDVOB expenditures 6.24%

Director Floss expressed his appreciation for staff exceeding the established goals.

City of Buffalo (“City”)

Real Property Tax Assessment Review and Discussion

Chair Pro Tem Jurasek advanced the agenda to review the City’s recent property tax

reassessment and welcomed Mr. Jason Shell, Commissioner of Assessment and Taxation, to

present the findings to the Board.

Mr. Shell stated a total reassessment had not been completed in over twenty years. He stated

New York State Real Property Tax Law requires every property be assessed uniformly, fairly

and accurately which was the primary goal of the project for the City’s 94,000 properties that

were valued for reassessment. Outreach was conducted across the City for interested parties in a

myriad of community spaces via hand outs and power point presentations. On average, all of the

93 tax districts in the City increased in value. Mr. Shell stated all property owners were assessed

and paying taxes at a uniform level of assessment. Prior to the reassessment project properties

were assessed at 64% of full market value; it is expected the equalization rate will be at 90%

value of the full market value after the reassessment goes into effect on July 1, 2020. Since

2014, the City saw dramatic increases in real estate transactions. Mr. Shell stated an inequity

was created within the tax roll when assessments weren’t conducted regularly, which resulted in

some properties being subsidized by others. Reassessment redistributed the tax base in a more

equitable manner. Reassessment itself does not raise the tax levy, as that is based on the tax rates

that result from the budget. Mr. Shell explained the difference between budget and levy in that a

budget is determined by City Administration and Common Council, and the levy amount is

determined as the funds needed to fully cover the expenses after all other revenues and fees have

been accounted for and that the levy is then distributed amongst the taxpayers. The tax cap

prevents the amount of the levy from going up more than 2% annually without certain override

procedures. The tax cap has been in place since 2011.

There was an increase of 63% in total assessed value for the City of Buffalo and an increase of

84% in the value of the taxable properties of the City. The formal review process, which was the

first phase to challenge new assessments, has been completed. The second opportunity to

challenge assessments is the board of assessment review process. The third process is small

claims assessment reviews (“SCARs”) for residential and commercial challenges. There is an

expectation that some projects will decrease in value once all challenge processes have been

completed.

Secretary Arthur asked Mr. Shell what stage of the challenge process his office participates in.

Mr. Shell responded that while the second phase of challenge is taking place, the board of

assessment review, and his office offers support by providing information from tax rolls, real

property services database and any supporting documentation that may be requested, in addition

4

to scheduling the appointments.

Mr. Shell stated the large increase in taxable assessed value would cause a large decrease in the

tax rate and property owners were notified by disclosure notices of their assessment change

based on the market value of their home.

Director Floss asked what steps are in place to assist seniors on fixed incomes regarding a higher

reassessment. Mr. Shell replied four or five of the twelve available exemptions are specifically

for seniors, including Enhanced Star, Low-Income Seniors and Long-Time Resident exemptions.

There are also payment plans available to assist homeowners

Secretary Arthur expressed his concern that Fruit Belt residents, specifically senior property

owners, may not be aware of their options to challenge their assessments in a timely manner.

Mr. Shell stated specific exemptions were made available for the Fruit Belt and other census

tracks which were passed by local law in early November 2019 and several meetings were held

across the City, as established by individual council offices, to disseminate information regarding

reassessment and exemptions. Mr. Shell stated Assemblymember Crystal Peoples-Stokes and

Council President Darius Pridgen worked for the past year on distributing information

throughout the Fruit Belt Community. Secretary Arthur stated the timing of the passing of the

law was inadequate as grievances are only able to be filed December 1st thru December 31st and

hearings begin in January.

Director Floss asked how the Board can assist the City with disseminating information regarding

the reassessment and grievance process. Mr. Shell stated standard media notifications were sent

out, and public information sessions were held. Additionally, notifications were included in the

property tax bill were sent to each property owner within the targeted census tracks. Secretary

Arthur emphasized there are less than 14 business days remaining for grievances to be filed.

Chair Olsen asked what percentage of Fruit Belt property owners took advantage of the

assistance navigating the process as the renaissance is geographic and there are neighborhoods

being left behind. Secretary Arthur highlighted the fact that absentee landlords with tax

increases will then pass the increase on to their renters.

Chair Pro Tem Jurasek asked if there is a way BFSA could assist to maximize the Assessment

Department’s efforts for educational outreach and if Ms. Robe would work with Mr. Shell to

identify such ways to ensure there are no residents negatively impacted by the reassessments and

penalized due to the timing of the grievance process. Mr. James Magavern stated that the

Partnership for the Public Good has a coalition that focuses on educational efforts and

encouraged contacting them for possible collaboration.

Secretary Arthur requested statistics in the Fruit Belt regarding absentee ownership and

residential ownership. Mr. Shell replied he will work to provide that information.

Mr. Cornell expressed his personal experience and dissatisfaction with the reassessment

grievance process as he found it difficult and confusing. Mr. Shell acknowledged there were a

few errors with the process and advised problems would be rectified if they haven’t been already.

Mr. Shell also stated over 3300 people took advantage of the informal review process and

5

approximately 1900 obtained changes.

Ms. Estrich, Commissioner of Audit of Finance, stated the City made multiple attempts through

Councilmembers and other agencies to distribute information in as timely a manner as possible.

Chair Olsen emphasized the concern to monitor the effective use of exemptions especially in

neighborhoods that might be adversely affected in terms of long-term residents, so people are not

being taken advantage of. Chair Pro Tem Jurasek agreed and directed Ms. Robe to work with

Mr. Shell to capture data required to ensure equity and fairness are not encumbered.

Chair Pro Tem asked for clarification on Assemblymember Crystal Peoples-Stokes’ and Council

President Darius Pridgen’s involvement in the reassessment process, specifically the new

exemption for long-term residents residing in certain census tracks. Mr. Shell stated the two of

them were the driving force behind legislation to include the new long-term resident exemption

passed at the New York State legislature. Secretary Arthur explained the Common Council had

to pass a Home Rule message before the New York State Legislature could pass the exemption;

therefore, the two worked together to get the process finalized.

Director Floss offered his services to assist with any needed analysis as it is something he is

familiar with.

Chair Pro Tem Jurasek thanked Mr. Shell for his presentation and advanced the agenda.

Audited City of Buffalo Financial Statements FY ended June 30, 2019

Ms. Robe reviewed the City’s audited financial statements as submitted by the Comptroller’s

Office in early November.

Ms. Robe gave the following overview:

• Total revenues reported were $491.6M, or 96.5% of the total budget of $509.6M

• Total expenditures were $490.7M, or 95.4% of the adopted budget. In addition there are

$7.3M of encumbrances reported at year-end

• The result is a surplus of $0.9M and total fund balance of $92.9M

• The difference between the adopted budget and the final budget of $8.4M is for

encumbrances which were carried over from the previous year

• On a year-to-year basis, total revenues increased 5.4% or $24.3M. Other financing

sources declined by $4.0M for a total increase of $20.3M, or 4.3% due to the following:

o Intergovernmental revenue increase of $8.9M

▪ $7.5M in Tribal State Compact revenue advance by NYS, which leaves $9.5M

outstanding. The outstanding receivable is not included as a revenue in the

2019-20 budget.

▪ $2.6M in increased sales tax collections year-to-year

▪ All other net decrease of $1.2M

o Property taxes, assessments, and other taxes increased $6.3M due to the increase

in the property tax levy which was offset by a decrease in STAR by $1.0M

o Miscellaneous increased $4.7M, due mainly to real estate sales and $0.8M in

donations

o Licenses, permits, fines and service charges increased $1.6M; street metered

parking increased $0.5M

6

o All other revenue sources provided a net increase of $2.8M

o Transfers in decreased $4.0M

▪ $4.3M decrease from Parking Enterprise Fund

▪ $0.3M increase from Water Enterprise Fund

▪ Transfers had increased by $4.4M in the prior year

Ms. Robe stated final real property tax revenue totaled $137.5M which represents 29% of total

revenue; 82% of the City’s total revenue is comprised of three buckets:

o Property tax levy (increased $5.7M year-to-year)

o Sales tax (increased $2.6M, or 3.1% year-to-year)

o State AIM (held flat since FY 2012)

• General Fund expenditures were overall consistent year-to-year and decreased by $3.5M,

which was less than 1% of the budget

o Departmental expenditures increased year-to-year by $2.2M; no significant

fluctuations

o General Charges decreased $4.7M primarily due to judgements and claims

• Interfund transfers out decreased $1.0M

o $3.6M decrease to Solid Waste & Recycling Enterprise Fund

o $0.5M decrease to Capital Projects Fund

o $3.1M increase for debt service

Historically, over the last four years, the City has recognized 96-97% of total budgeted revenues.

There was an unfavorable budgeted revenue variance of $18.0M compared to the Adopted

Budget:

• $7.0M unfavorable variance in miscellaneous revenue:

o $4.0M due to real property sales and capital assets sales

o $2.0M due to City-owned venue surcharge

o $1.2M lower in gifts & donations - $0.8M was received

Secretary Arthur asked for clarification on the City’s venue surcharge. Ms. Estrich stated

negotiations are ongoing to capture monies with a method other than through a ticket surcharge.

• $7.0M unfavorable variance in intergovernmental revenue:

o Casino revenue under budget by $9.5M

o Sales tax positive variance of $2.8M

• $4.1M unfavorable variance in fines

o $3.1M unfavorable variance for traffic violation fines

o $0.7M unfavorable variance for parking fines

o $0.3M net unfavorable variance for all other fines

• $1.5M unfavorable variance from transfers in from the parking enterprise fund

Ms. Robe explained the City’s total expenditures, including encumbrances, has been between

95% -99% of budget over the past four fiscal years.

7

There was a FY 2018-19 favorable variance for budgeted appropriations of $24.0M:

• $14.2M favorable variance in fringe benefits

o Health insurance – active = $(0.4M)

o Health insurance – retiree = $2.8M

o NYSERS = $4.2M

o NYSPFRS = $4.5M

o Salary Adjustment Line = $2.4M

• Combined $0.4M unfavorable variance in the fire and police departments due to

overtime. While this category usually has a significant impact on the budget it was

noted that expenses were well maintained for both fire and police.

• $9.7M favorable variance in all other departments due to vacancies and decrease in

expenditures for supplies and services.

The fund balance summary demonstrated a $22.9M decrease in fund balance from FYE 2017 to

FYE 2019. The individual fund balance categorizes were discussed.

It was noted fund balance was $36.0M when BFSA oversight began in FY 2002-03 whereas at

the end of FY 2018-19 the City had a fund balance of $92.9M.

Ms. Robe shared the present value of the Other Postemployment Benefits (“OPEB”) liability was

$1.128B as of June 30, 2019 on an all funds basis, $54.0M represented the liability of the

Enterprise Funds. The year-to-year reduction from $1.255B 1was largely due to the change in

the assumed increase in the healthcare costs from 7.6% to 5.3%. It was noted this category is

expensed on a pay-as-you go basis and therefore is not captured on the general fund financial

statements except as a payment for retiree health insurance.

Solid Waste and Recycling Fund

Charges for services were enhanced this last year for refuse fees which resulted in operating

income of $6.0M being reported after many years of operating at a loss. There was a $2.9M

reduction in fringe benefits related to a decrease in the OPEB liability. For the first time in a

number of years there was a reduction to the cash advances made to the solid waste and

recycling fund from the general fund. While there isn’t a formal repayment policy in place, there

is an informal one in which the liability will be repaid from surpluses.

Mr. Cornell asked for clarification on the State’s advance of casino monies and the potential of

the State re-capturing the advance. Ms. Estrich responded the State is confident the funds will be

received since the arbitration has been finalized.

Director Floss exited the meeting at 2:17pm.

Chair Olsen commended the City on presenting a balanced budget with ample constitutional

taxing authority and noted the BFSA is appropriately in an advisory status.

8

City of Buffalo (“City”)

First Quarter Report

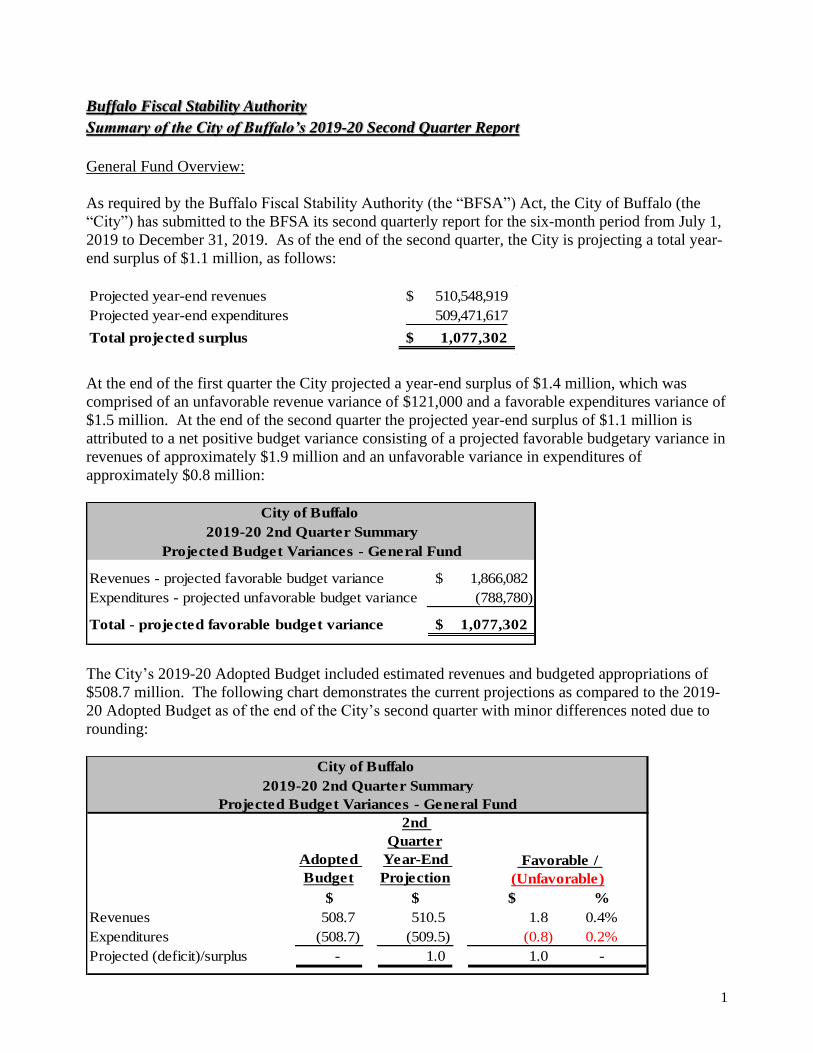

Chair Pro Tem Jurasek advanced the agenda to the review of the City’s first quarter. Ms. Robe

began the presentation stating adopted budget revenues were $508.7M; the City is projecting

year-end revenues of $508.6M which is consistent with the budget. The City is also projecting

$507.2M for actual year-end expenditures resulting in a total projected surplus of $1.4M. Ms.

Robe gave the following overview of FYE total revenue projection:

o $121,000 total unfavorable variance consisting of:

• $0.6M projected to be under budget in Service Charges

▪ $0.4M due to easement fees with National Fuel Gas

▪ $0.2M in relation to the mortgage default fee

• $0.5M over budget in Miscellaneous revenue

▪ $0.6M variance is attributed to an awarded SAFR Grant

▪ $0.2M variance is attributed to estimated parking fees from parking

surcharge at public City facilities

Ms. Robe noted miscellaneous revenue for sale of property and assets for the first quarter has

already exceeded the total year-end budget largely due to the sale of the former police

headquarters.

The total expenditure projection for FYE 2020 is $1.5M below the adopted budget and explained

as follows:

o $1.2M total favorable budgetary variance projected for Departmental expenditures

• Fire Department expected to exceed the budget by $1.0M

• Police Department expected to be favorable by $1.2M

• Remaining departments projected to be favorable by $1.0M

o $0.3M total projected favorable budgetary variance in General Charges for debt service

• The City does not expect to issue a RAN during the current fiscal year

As of September 30, 2019, the vacancy rate for positions funded through the General Fund was

9.4%. The police department had an 8.3% vacancy rate and the fire department had a vacancy

rate of 5.4%. Ms. Estrich confirmed the vacancy rate usually trends about 10%.

Recommendations and Considerations

Ms. Robe noted casino revenue was included as a projection for year-end and does not include

the past due amount of $9.5M which would increase the surplus at year-end if received before

June 30. BFSA continues to recommend the monitoring of revenues and expenditures,

especially overtime in the fire department, in order determine how the collective bargaining

agreements have changed overtime.

Three unions are out of contract which are expected to be settled during the current fiscal year:

o Police Benevolent Association

o Local 264 – Blue Collar

o Crossing Guards

Ms. Robe stated the City’s finances are trending well and Chair Pro Tem Jurasek advanced the

agenda.

9

Capital Budget

Review of 2020 Capital Budget and related 2020-2024 Capital Improvement Program

Mr. Bryce Link began his presentation stating the Common Council passed the Capital Budget

on December 10, 2019 with minor amendments. The proposed capital budget is in the amount of

$37.2M, of which $19.9M is requested for financing and $17.3M will be for projects that are

authorized but unissued. The Comptroller’s debt limit for the current year is $25.3M.

Requested financing of $25.3M is categorized as follows:

• City buildings $7.1M, or 28%;

• Infrastructure $9.4M, or 37%;

• Vehicles $3.3M, or 13%;

• Economic development and culturals $2.4M, or 9%;

• Demolition and tree management $1.7M, or 7%;

• Parks $1.4M, or 6%.

Additionally, the requested financing of $25.3M consists of the following:

o $19.9M – from the Capital Plan

o $4.0M – previously authorized but unissued

o $1.4M – previously budgeted but unauthorized

Secretary Arthur asked if the Hurd decision is still in effect regarding the sale of bonds. Mr.

Magavern responded that the Hurd decision was an attempt to capitalize on an investment in

vocational education and human services, and that the Hurd decision is no longer in effect.

Mr. Link stated the City has not borrowed on behalf of the Buffalo City School District

(“BCSD”) since 2012. Since then the District has been utilizing refunding savings from the Joint

School Construction Board (“JSCB”) debt and has approximately $8.2M available for projects.

As of June 30, 2019, the City has $23.3M of unspent capital bond proceeds outstanding.

Conclusion

Mr. Link provided the following summary:

o No projects again included for the District

• District is currently using savings from refundings of JSCB debt; $8.2M is

remaining for capital projects

o BFSA has recommended to minimize long-term financing for ongoing general operating

expenses (i.e., demolitions and tree removal)

• Uses limit bonding capacity

▪ $1.7 M included in proposed 2020 borrowing, or 7% of total

▪ $8.4 M over the five-year Capital Improvements Program (6.2% of total)

• Recognition of fiscal pressure if such projects were funded on a pay-as-you-go

basis

o There is $24.0M in total authorized and unissued projects

• Approximately $15.6M are provided for in the out-years of the Capital

Improvements Program

10

▪ Remaining balance of $8.4M to be provided for beyond the current plan

o There remains $6.3M in budgeted and unauthorized projects

Once the minor amendments that were approved by Common Council on December 10, 2019 are

submitted to the BFSA the analysis will be updated. Ms. Estrich commented that the

amendments do not change the dollar amount of the budget, only the allocation of funds within

their respective council districts.

Chair Pro Tem Jurasek thanked staff for the presentation and advanced the agenda to the next

item.

Buffalo City School District (“BCSD” or “District”)

Hearing no additional comments Chair Pro Tem Jurasek advanced the agenda to review several

District items as presented by Mr. Nathan Miller.

Audited Financial Statement FY ended June 30, 2019

Mr. Miller provided the following overview of the 2018-19 final budget as compared to the fiscal

year-end (“FYE”) actual:

• The 2018-19 original budget included $897.4M in revenue and expenditures of $916.4M.

There was a planned deficit of $19.0M. The actual revenue totaled $911.5M with

expenditures of $882.6M resulting in a surplus of $28.9M.

• Actual revenues exceeded budgeted revenues by $14.1M, or 101.6% of final budget, due

to a one-time $15.0M reimbursement for the overpayment of healthcare premium-

equivalent payments. Other contributing factors were:

o Erie County sales tax receipts were favorable by $1.9M

o NYS Aid was favorable by $4.1M

Chair Pro Tem Jurasek asked if there were other revenue enhancements which were being

monitored as gap closing measures. Mr. Miller replied that health insurance savings was an

indentified gap closing measure. The District is focusing on efficiencies and enhancements in

order to provide health insurance more effectively and at at reduced rate of increase.

• Total actual expenditures were $36.3M under the final budget, or 96.6% of final budget.

Significant variances included employee benefits of $17.2M due to the District

converting to a traditional method of self-insurance for employee and retiree healthcare

costs effective July 1, 2018. In addition, New York State Employee Retirement

System/Teachers’ Retirement System pension payments were favorable by $1.1M.

Positive variances were also noted for the following expenditures:

o Regular school instruction $9.1M

o General support $5.0M

o Pupil transportation $3.9M

Mr. Miller provided the following fund balance summary:

• FYE 2019 had total fund balance of $223.7M:

o Nonspendable/restricted $25.7M

o Assigned $111.9M

o Unassigned $86.1M

11

• FYE 2018 had total fund balance of $194.8M

o Nonspendable/restricted $25.6M

o Assigned $91.4M

o Unassigned $77.8M

• The net change to total fund balance was a favorable $28.9M

The total assigned fund balance increased by $20.5M from year-to-year. Two new categories

were added for FY 2019:

o Designated for health insurance: this funding helps to support the new self-

insured model, and equal to $15.1M

o Designated for school budget equity: this funding is provided as a resource to

address issues identified with respect to inequitable individual school funding

and is equal to $5.0M

Mr. Miller reviewed significant fluctuations in general fund revenue over the prior fiscal year of

$32.7M, or 3.7%:

• NYS Aid increased $13.9M, or 1.9%

• City contribution increased $0.0M, or 0%

• Erie County sales tax increased $2.3M, or 5.3%

• Miscellaneous increased $16.0M or 151.0% (one-timed recognition for reimbursement of

prior year overpayments for health insurance)

Significant fluctuations in general fund expenditures over the prior year of $15.9M, or 1.8%

were:

• Operating expenditures decreased $1.7M, or 0.2%

o Instruction regular schools increased $18.9M, or 5.9%

o Instruction charter schools increased $7.0M, or 5.9%

o General support decreased $4.6M, or 6.4%

o Employee benefits decreased $11.1M, or 6.0%

Mr. Miller stated the actuarial accrued liability of other postemployment benefits (“OPEB”)

increased to almost $2.4B as compared to almost $2.3B in FY 2018 in part due to changed

assumptions as well as from District efforts to curtail retiree health insurance expenditures.

Mr. Magavern noted that the Annual Required Contribution (“ARC”) includes both the cost of

OPEB benefits attributable to the current year of services as well as an amortization of past

service costs to fund the Actuarial Accrued Liability. The ARC is significantly greater than the

actual retiree benefits paid in any given year in that it includes the accrued liability. Mr.

Magavern noted that there have been efforts to establish a formal process for governmental

entities to set funds aside for the full ARC. Mr. Miller responded that there was no current,

formal legal mechanism for entities such as the District to set aside funds for the full ARC. The

District is on a pay-as-you-go system for actual post-employment benefits. District management

had designated $52.1 million for OPEB at July1, 2019 to address this accrued liability.

12

BCSD First Quarter

Mr. Miller stated the 2019-20 budget was adopted with a $10.0M deficit; however, a favorable

variance of $0.6M is currently projected for FYE. District management has every intention to

fill vacancies, if they are not filled, additional savings can be recognized at mid-year within all

employee compensation benefit categories. Two revenue items expected to have a positive

variance are Erie County sales tax of $0.4M and Federal Medicaid reimbursement of $0.2M.

Expenditures are not anticipated to differ from revenues as of September 30, 2019.

As of September 30, 2019, there were 237.5 vacancies on an All Funds basis and 162.1

vacancies on a General Funds basis. The majority of which were teachers and white-collar

employees. The vacancy rate of 4.1% is substantial.

Summary

The District’s FY 2019-20 budget is currently balanced with the appropriation of $10.0M in

Fund Balance with a minor $0.6 M favorable budgetary surplus currently projected.

BFSA notes that the District had a substantial vacancy rate of 4.1% at September 30, 2019 and

recognizes if a significant vacancy level continues, various Employee Compensation and

Employee Benefit lines will be less-than-budget. The District has conveyed its intent to fill the

vacant positions and that the FY 2019-20 Second Quarter Report will provide adjustments to

various Employee Compensation and Employee Benefit expenditure lines as appropriate.

Chair Pro Tem Jurasek thanked Mr. Miller for his presentation and asked for the student numbers

for the District as compared to Charter schools. Mr. Miller replied that staff would provide the

requested materials.

Hearing no additional comments or questions Chair Pro Tem Jurasek asked for a motion that

BMHA reports scheduled to be reviewed today be tabled until the next Board meeting.

Secretary Arthur made the motion as requested.

Ms. Estrich seconded the motion.

The Board voted 5 to 0 to approve.

Chair Pro Tem Jurasek asked that BURA reports scheduled to be presented today be tabled until

the next Board meeting.