Embed Size (px)

Citation preview

March 16, 2017

Initiating Coverage

ICICI Securities Ltd | Retail Equity Research

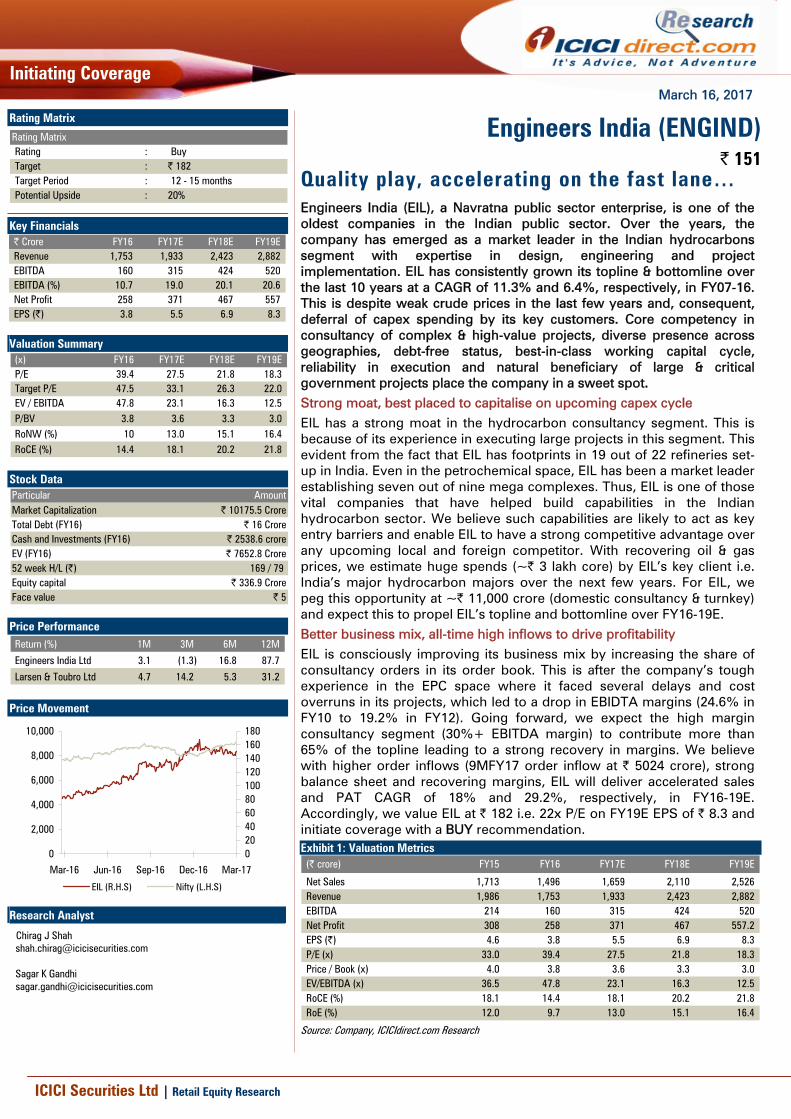

Quality play, accelerating on the fast lane… Engineers India (EIL), a Navratna public sector enterprise, is one of the oldest companies in the Indian public sector. Over the years, the company has emerged as a market leader in the Indian hydrocarbons segment with expertise in design, engineering and project implementation. EIL has consistently grown its topline & bottomline over the last 10 years at a CAGR of 11.3% and 6.4%, respectively, in FY07-16. This is despite weak crude prices in the last few years and, consequent, deferral of capex spending by its key customers. Core competency in consultancy of complex & high-value projects, diverse presence across geographies, debt-free status, best-in-class working capital cycle, reliability in execution and natural beneficiary of large & critical government projects place the company in a sweet spot. Strong moat, best placed to capitalise on upcoming capex cycle EIL has a strong moat in the hydrocarbon consultancy segment. This is because of its experience in executing large projects in this segment. This evident from the fact that EIL has footprints in 19 out of 22 refineries set-up in India. Even in the petrochemical space, EIL has been a market leader establishing seven out of nine mega complexes. Thus, EIL is one of those vital companies that have helped build capabilities in the Indian hydrocarbon sector. We believe such capabilities are likely to act as key entry barriers and enable EIL to have a strong competitive advantage over any upcoming local and foreign competitor. With recovering oil & gas prices, we estimate huge spends (~| 3 lakh core) by EIL’s key client i.e. India’s major hydrocarbon majors over the next few years. For EIL, we peg this opportunity at ~| 11,000 crore (domestic consultancy & turnkey) and expect this to propel EIL’s topline and bottomline over FY16-19E. Better business mix, all-time high inflows to drive profitability EIL is consciously improving its business mix by increasing the share of consultancy orders in its order book. This is after the company’s tough experience in the EPC space where it faced several delays and cost overruns in its projects, which led to a drop in EBIDTA margins (24.6% in FY10 to 19.2% in FY12). Going forward, we expect the high margin consultancy segment (30%+ EBITDA margin) to contribute more than 65% of the topline leading to a strong recovery in margins. We believe with higher order inflows (9MFY17 order inflow at | 5024 crore), strong balance sheet and recovering margins, EIL will deliver accelerated sales and PAT CAGR of 18% and 29.2%, respectively, in FY16-19E. Accordingly, we value EIL at | 182 i.e. 22x P/E on FY19E EPS of | 8.3 and initiate coverage with a BUY recommendation.

Exhibit 1: Valuation Metrics (| crore) FY15 FY16 FY17E FY18E FY19E

Net Sales 1,713 1,496 1,659 2,110 2,526 Revenue 1,986 1,753 1,933 2,423 2,882 EBITDA 214 160 315 424 520 Net Profit 308 258 371 467 557.2 EPS (|) 4.6 3.8 5.5 6.9 8.3 P/E (x) 33.0 39.4 27.5 21.8 18.3 Price / Book (x) 4.0 3.8 3.6 3.3 3.0 EV/EBITDA (x) 36.5 47.8 23.1 16.3 12.5 RoCE (%) 18.1 14.4 18.1 20.2 21.8 RoE (%) 12.0 9.7 13.0 15.1 16.4

Source: Company, ICICIdirect.com Research

Engineers India (ENGIND)| 151

Rating Matrix

Rating MatrixRating : BuyTarget : | 182Target Period : 12 - 15 monthsPotential Upside : 20%

Key Financials | Crore FY16 FY17E FY18E FY19ERevenue 1,753 1,933 2,423 2,882 EBITDA 160 315 424 520 EBITDA (%) 10.7 19.0 20.1 20.6 Net Profit 258 371 467 557 EPS (|) 3.8 5.5 6.9 8.3

Valuation Summary

(x) FY16 FY17E FY18E FY19EP/E 39.4 27.5 21.8 18.3 Target P/E 47.5 33.1 26.3 22.0 EV / EBITDA 47.8 23.1 16.3 12.5 P/BV 3.8 3.6 3.3 3.0 RoNW (%) 10 13.0 15.1 16.4 RoCE (%) 14.4 18.1 20.2 21.8

Stock Data Particular AmountMarket Capitalization | 10175.5 CroreTotal Debt (FY16) | 16 CroreCash and Investments (FY16) | 2538.6 croreEV (FY16) | 7652.8 Crore52 week H/L (|) 169 / 79 Equity capital | 336.9 CroreFace value | 5

Price Performance Return (%) 1M 3M 6M 12M

Engineers India Ltd 3.1 (1.3) 16.8 87.7

Larsen & Toubro Ltd 4.7 14.2 5.3 31.2

Price Movement

020406080100120140160180

Mar-17Dec-16Sep-16Jun-16Mar-16

0

2,000

4,000

6,000

8,000

10,000

EIL (R.H.S) Nifty (L.H.S)

Research Analyst

Chirag J Shah [email protected] Sagar K Gandhi [email protected]

Page 2ICICI Securities Ltd | Retail Equity Research

Company background Engineers India (EIL) is an engineering consultancy and EPC company. It offers complete solutions to the hydrocarbon sector with expertise in design, engineering and project implementation. EIL has a strong track record in the oil & gas value chain – offshore platforms, oil & gas processing, oil refining, petrochemicals and pipeline projects. EIL is the preferred partner of all major oil & gas PSUs like IOC, ONGC, HPCL, BPCL, CPCL and MRPL. EIL has a leadership position in project implementation in almost all major oil & gas verticals. The company has a workforce of ~3200 employees with ~2800 as multi-disciplinary engineers.

In the consultancy segment, EIL has to its credit more than 5000 assignments including over 400 major projects successfully completed and operating smoothly, in many cases at more than rated capacity, creating an array of satisfied clients. Even in the turnkey segment, the company has made major headway having executed 17 EPC projects across the oil & gas spectrum. EIL has also established international footprints by executing projects in the Middle East, North Africa and South East Asia. Most major oil & gas companies in these regions like Sonatrach, Gasco, Adco, Zadco, KNPC, Bapco, Banagas, etc, have utilised EIL’s services for their prestigious projects.

Exhibit 2: Engineers India – Key milestones of company

•EIL founded• EIL became a wholly

owned government company

1965-67

•Diversification into petrochemicals, metallurgy & fertiliser projects, commenced overseas operations

1969-74

• First oil & gas processing project

• Started process plant services

1977- 80

•Set up its R&D centre at Gurgaon

• Subsidiary, certification Engineers International was set up

1989-94

• Company listed on BSE & NSE

•Miniratna status accorded to the company

1997

•Foray into infrastructure sector

•Commenced services related to sub-surface crude storages

2001-06 •JVC with Tata Projects•OFS for 10% equity•Commenced work in

nuclear & solar energy •JVC with Jabal Dhahran Co

IOT Infrastructure & Energy Co Ltd

2008-11

•PSC with GoI for exploration blocks, foray into overseas fertiliser sector, OFS for 10% equity, Navratna status accorded in 2014

•JVC with NFL and FCIL

2012-15

Source: Company, ICICIdirect.com Research

Shareholding pattern (Q3FY17)

Shareholder Holding (%)

Promoters 58.9

Institutional investors 25.5

General public 15.6

FII & DII holding trend (%)

8.0 7.5 8.76.6

19.2 20.0 19.6 18.9

0

5

10

15

20

25

Q4FY16 Q1FY17 Q2FY17 Q3FY17

(%)

FPI DII

Page 3ICICI Securities Ltd | Retail Equity Research

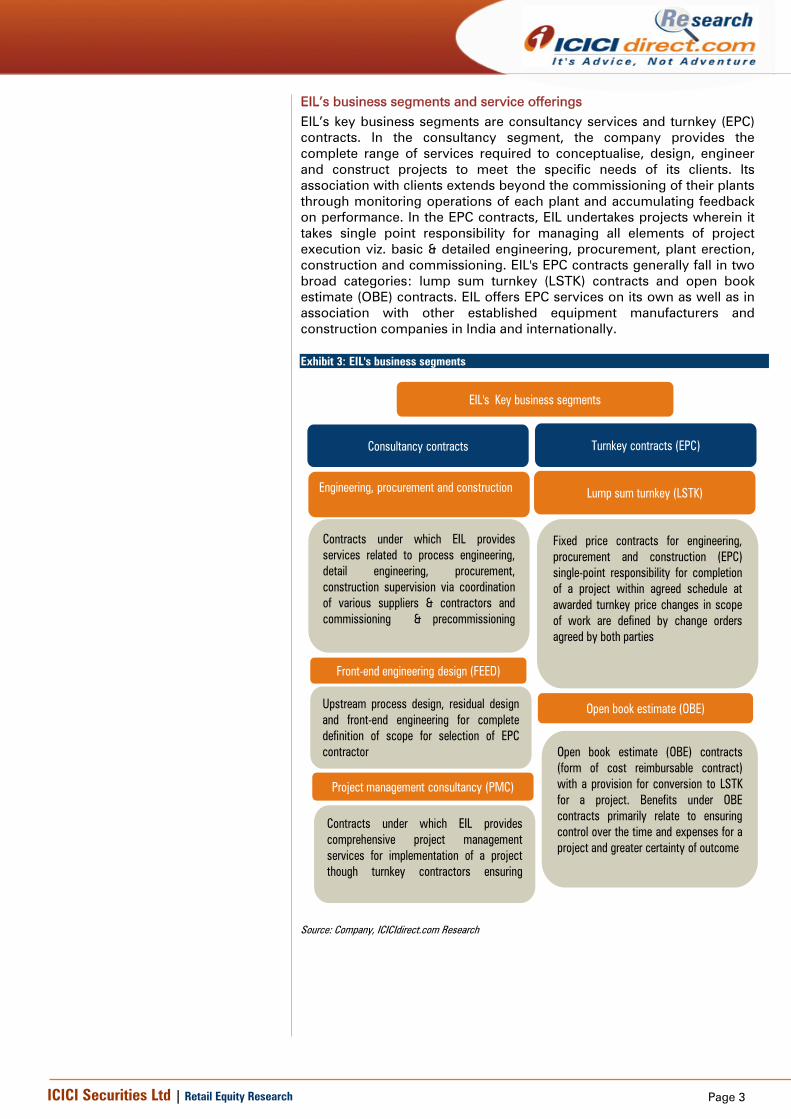

EIL’s business segments and service offerings EIL’s key business segments are consultancy services and turnkey (EPC) contracts. In the consultancy segment, the company provides the complete range of services required to conceptualise, design, engineer and construct projects to meet the specific needs of its clients. Its association with clients extends beyond the commissioning of their plants through monitoring operations of each plant and accumulating feedback on performance. In the EPC contracts, EIL undertakes projects wherein it takes single point responsibility for managing all elements of project execution viz. basic & detailed engineering, procurement, plant erection, construction and commissioning. EIL's EPC contracts generally fall in two broad categories: lump sum turnkey (LSTK) contracts and open book estimate (OBE) contracts. EIL offers EPC services on its own as well as in association with other established equipment manufacturers and construction companies in India and internationally. Exhibit 3: EIL's business segments

Fixed price contracts for engineering,procurement and construction (EPC)single-point responsibility for completionof a project within agreed schedule atawarded turnkey price changes in scopeof work are defined by change ordersagreed by both parties

Lump sum turnkey (LSTK)

Turnkey contracts (EPC)

Open book estimate (OBE)

Open book estimate (OBE) contracts(form of cost reimbursable contract)with a provision for conversion to LSTKfor a project. Benefits under OBEcontracts primarily relate to ensuringcontrol over the time and expenses for aproject and greater certainty of outcome

Contracts under which EIL providesservices related to process engineering,detail engineering, procurement,construction supervision via coordinationof various suppliers & contractors andcommissioning & precommissioning

Engineering, procurement and construction

Consultancy contracts

Upstream process design, residual designand front-end engineering for completedefinition of scope for selection of EPCcontractor

Front-end engineering design (FEED)

Contracts under which EIL providescomprehensive project managementservices for implementation of a projectthough turnkey contractors ensuring

Project management consultancy (PMC)

EIL's Key business segments

Source: Company, ICICIdirect.com Research

Page 4ICICI Securities Ltd | Retail Equity Research

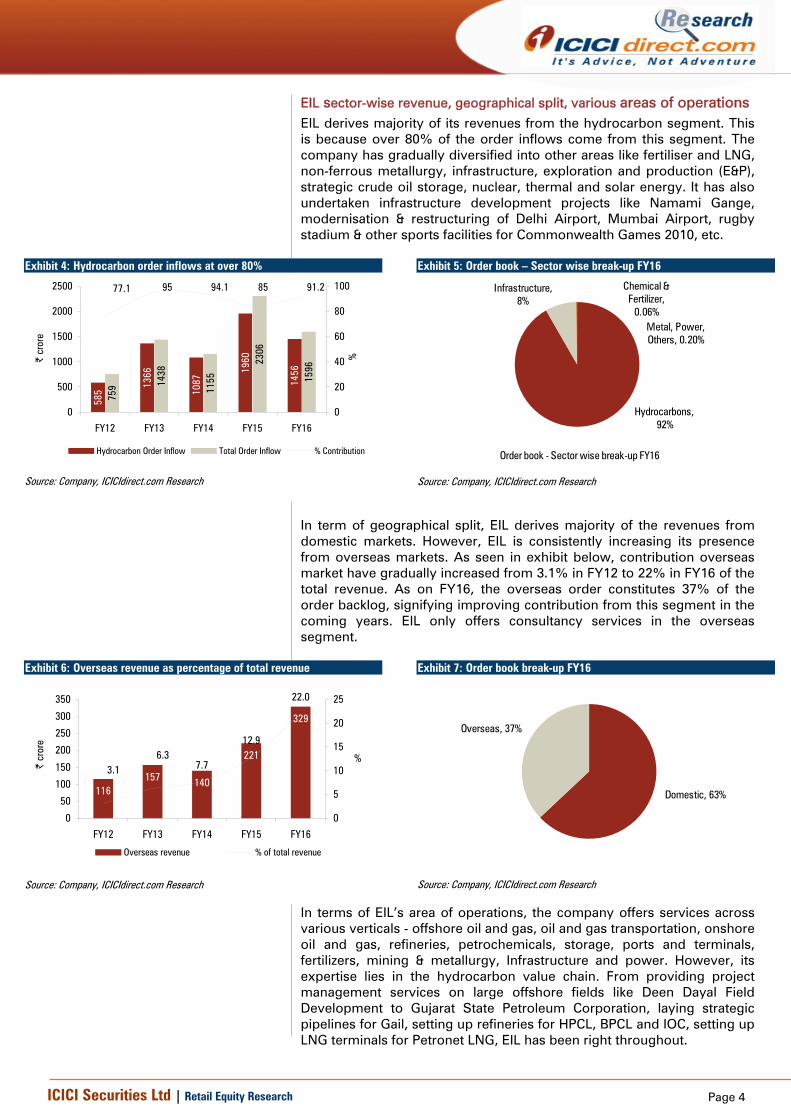

EIL sector-wise revenue, geographical split, various areas of operations

EIL derives majority of its revenues from the hydrocarbon segment. This is because over 80% of the order inflows come from this segment. The company has gradually diversified into other areas like fertiliser and LNG, non-ferrous metallurgy, infrastructure, exploration and production (E&P), strategic crude oil storage, nuclear, thermal and solar energy. It has also undertaken infrastructure development projects like Namami Gange, modernisation & restructuring of Delhi Airport, Mumbai Airport, rugby stadium & other sports facilities for Commonwealth Games 2010, etc.

Exhibit 4: Hydrocarbon order inflows at over 80%

585

1366

1087

1960

1456

759 14

38

1155

2306

1596

77.1 95 94.1 85 91.2

0

500

1000

1500

2000

2500

FY12 FY13 FY14 FY15 FY16

| cr

ore

0

20

40

60

80

100

%

Hydrocarbon Order Inflow Total Order Inflow % Contribution

Source: Company, ICICIdirect.com Research

Exhibit 5: Order book – Sector wise break-up FY16

Hydrocarbons, 92%

Infrastructure, 8%

Metal, Power, Others, 0.20%

Chemical & Fertilizer,

0.06%

Order book - Sector wise break-up FY16

Source: Company, ICICIdirect.com Research

In term of geographical split, EIL derives majority of the revenues from domestic markets. However, EIL is consistently increasing its presence from overseas markets. As seen in exhibit below, contribution overseas market have gradually increased from 3.1% in FY12 to 22% in FY16 of the total revenue. As on FY16, the overseas order constitutes 37% of the order backlog, signifying improving contribution from this segment in the coming years. EIL only offers consultancy services in the overseas segment.

Exhibit 6: Overseas revenue as percentage of total revenue

116157 140

221

329

7.7

12.9

22.0

3.16.3

0

50

100

150

200

250

300

350

FY12 FY13 FY14 FY15 FY16

| cr

ore

0

5

10

15

20

25

%

Overseas revenue % of total revenue

Source: Company, ICICIdirect.com Research

Exhibit 7: Order book break-up FY16

Domestic, 63%

Overseas, 37%

Source: Company, ICICIdirect.com Research

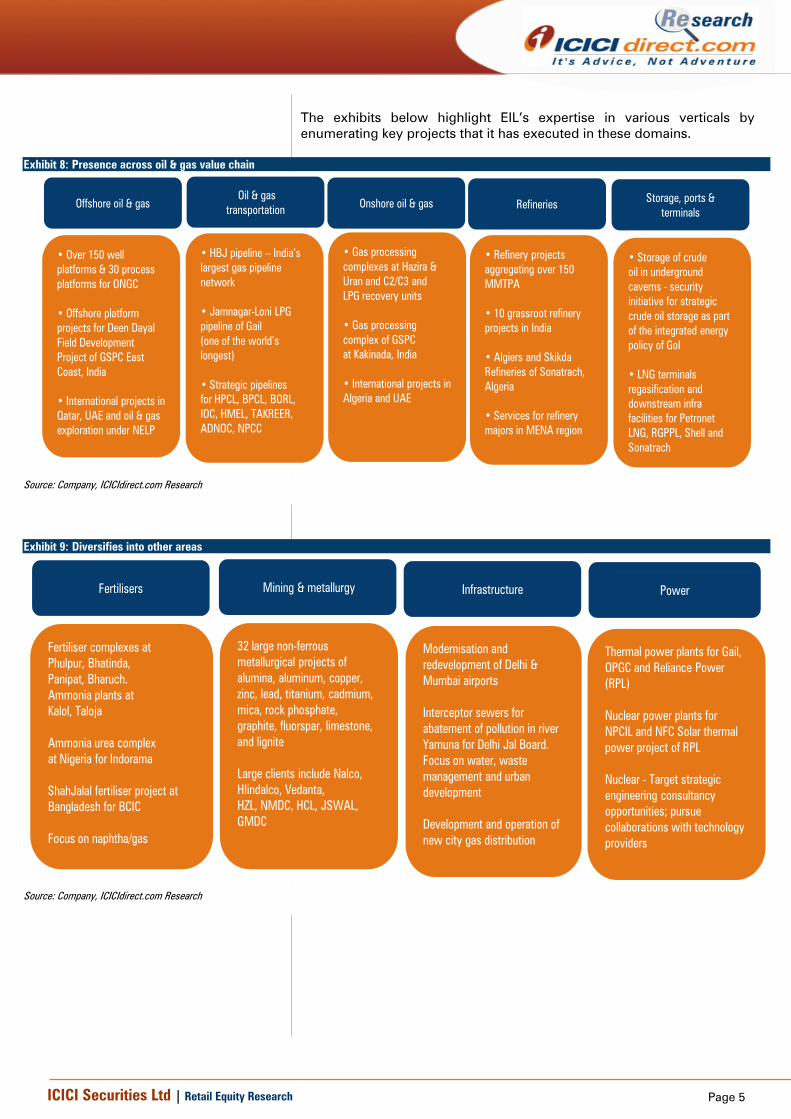

In terms of EIL’s area of operations, the company offers services across various verticals - offshore oil and gas, oil and gas transportation, onshore oil and gas, refineries, petrochemicals, storage, ports and terminals, fertilizers, mining & metallurgy, Infrastructure and power. However, its expertise lies in the hydrocarbon value chain. From providing project management services on large offshore fields like Deen Dayal Field Development to Gujarat State Petroleum Corporation, laying strategic pipelines for Gail, setting up refineries for HPCL, BPCL and IOC, setting up LNG terminals for Petronet LNG, EIL has been right throughout.

Page 5ICICI Securities Ltd | Retail Equity Research

The exhibits below highlight EIL’s expertise in various verticals by enumerating key projects that it has executed in these domains.

Exhibit 8: Presence across oil & gas value chain

Offshore oil & gas

• Over 150 well platforms & 30 process platforms for ONGC

• Offshore platform projects for Deen Dayal Field Development Project of GSPC East Coast, India

• International projects in Qatar, UAE and oil & gas exploration under NELP

Storage, ports &terminals

• Storage of crudeoil in undergroundcaverns - securityinitiative for strategic crude oil storage as part of the integrated energy policy of GoI

• LNG terminalsregasification anddownstream infrafacilities for Petronet LNG, RGPPL, Shell andSonatrach

Oil & gastransportation

• HBJ pipeline – India’s largest gas pipeline network

• Jamnagar-Loni LPGpipeline of Gail(one of the world’slongest)

• Strategic pipelinesfor HPCL, BPCL, BORL, IOC, HMEL, TAKREER,ADNOC, NPCC

Onshore oil & gas

• Gas processingcomplexes at Hazira & Uran and C2/C3 andLPG recovery units

• Gas processingcomplex of GSPCat Kakinada, India

• International projects in Algeria and UAE

Refineries

• Refinery projects aggregating over 150 MMTPA

• 10 grassroot refinery projects in India

• Algiers and SkikdaRefineries of Sonatrach, Algeria

• Services for refinerymajors in MENA region

Source: Company, ICICIdirect.com Research

Exhibit 9: Diversifies into other areas

Fertilisers

Fertiliser complexes atPhulpur, Bhatinda,Panipat, Bharuch.Ammonia plants atKalol, Taloja

Ammonia urea complexat Nigeria for Indorama

ShahJalal fertiliser project at Bangladesh for BCIC

Focus on naphtha/gas

Mining & metallurgy

32 large non-ferrousmetallurgical projects ofalumina, aluminum, copper, zinc, lead, titanium, cadmium, mica, rock phosphate, graphite, fluorspar, limestone, and lignite

Large clients include Nalco, HIindalco, Vedanta,HZL, NMDC, HCL, JSWAL, GMDC

Infrastructure

Modernisation and redevelopment of Delhi & Mumbai airports

Interceptor sewers forabatement of pollution in river Yamuna for Delhi Jal Board. Focus on water, waste management and urban development

Development and operation of new city gas distribution

Power

Thermal power plants for Gail, OPGC and Reliance Power (RPL)

Nuclear power plants for NPCIL and NFC Solar thermal power project of RPL

Nuclear - Target strategic engineering consultancy opportunities; pursue collaborations with technology providers

Source: Company, ICICIdirect.com Research

Page 6ICICI Securities Ltd | Retail Equity Research

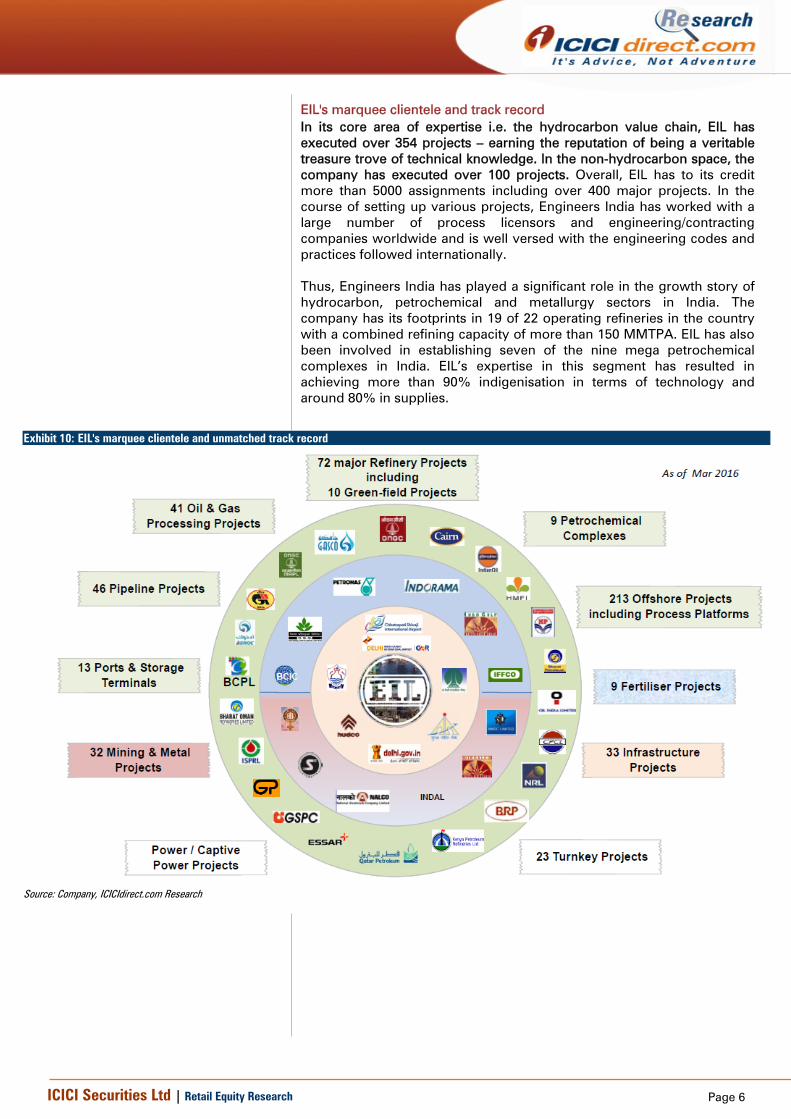

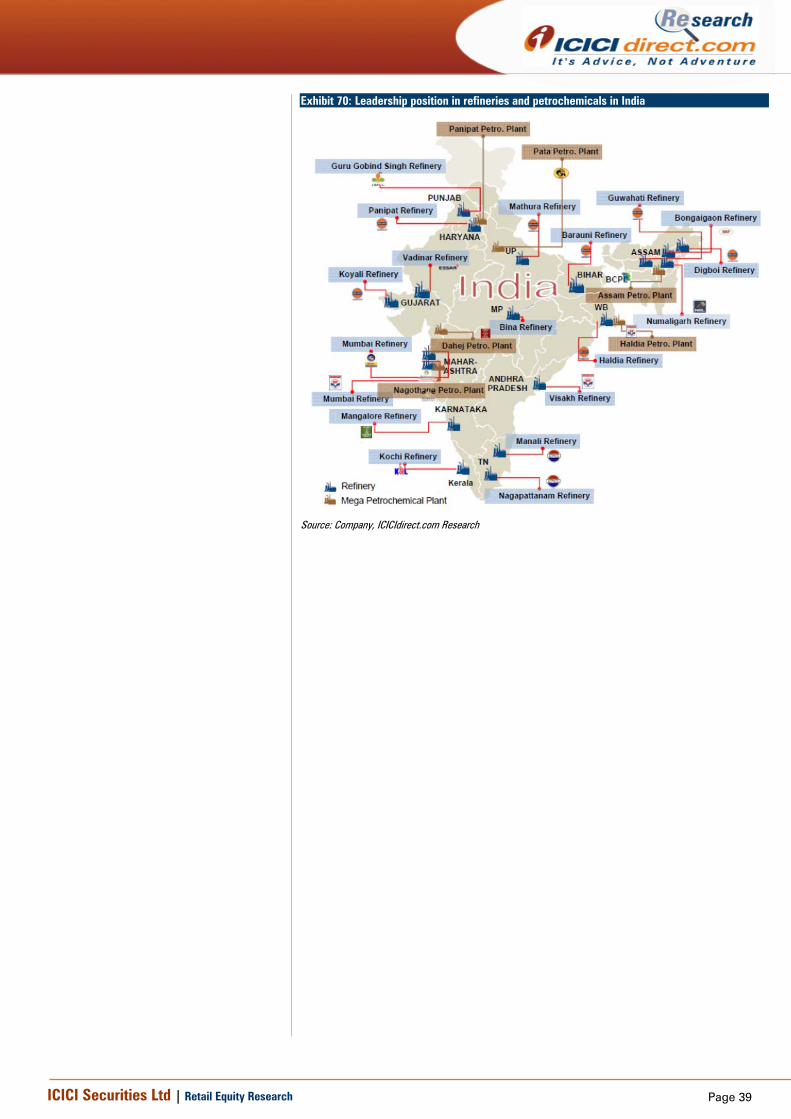

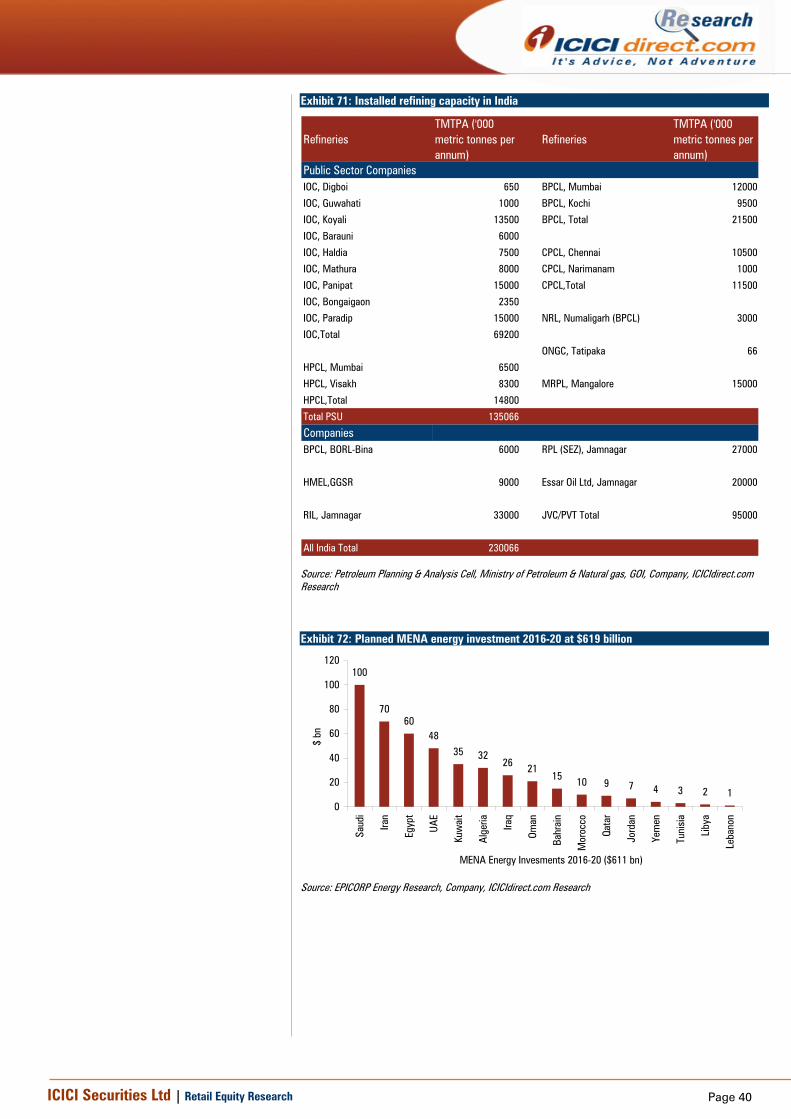

EIL's marquee clientele and track record In its core area of expertise i.e. the hydrocarbon value chain, EIL has executed over 354 projects – earning the reputation of being a veritable treasure trove of technical knowledge. In the non-hydrocarbon space, the company has executed over 100 projects. Overall, EIL has to its credit more than 5000 assignments including over 400 major projects. In the course of setting up various projects, Engineers India has worked with a large number of process licensors and engineering/contracting companies worldwide and is well versed with the engineering codes and practices followed internationally. Thus, Engineers India has played a significant role in the growth story of hydrocarbon, petrochemical and metallurgy sectors in India. The company has its footprints in 19 of 22 operating refineries in the country with a combined refining capacity of more than 150 MMTPA. EIL has also been involved in establishing seven of the nine mega petrochemical complexes in India. EIL’s expertise in this segment has resulted in achieving more than 90% indigenisation in terms of technology and around 80% in supplies.

Exhibit 10: EIL's marquee clientele and unmatched track record

Source: Company, ICICIdirect.com Research

Page 7ICICI Securities Ltd | Retail Equity Research

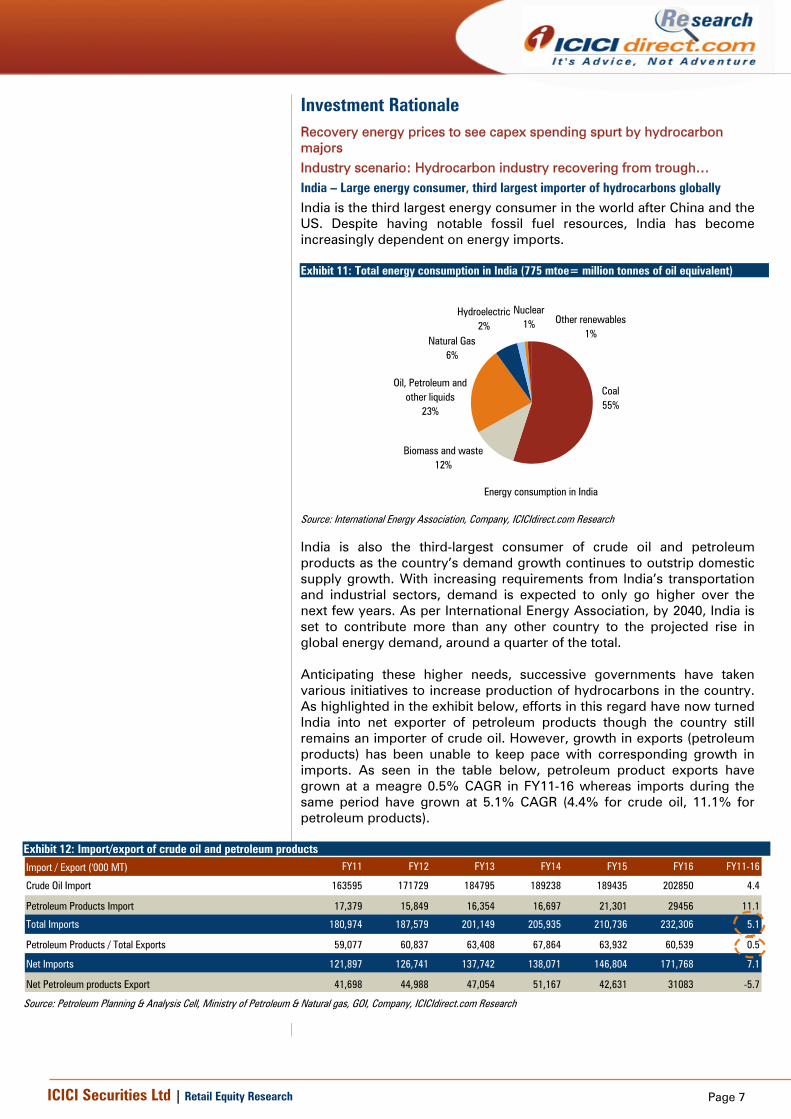

Investment Rationale Recovery energy prices to see capex spending spurt by hydrocarbon majors Industry scenario: Hydrocarbon industry recovering from trough… India – Large energy consumer, third largest importer of hydrocarbons globally India is the third largest energy consumer in the world after China and the US. Despite having notable fossil fuel resources, India has become increasingly dependent on energy imports. Exhibit 11: Total energy consumption in India (775 mtoe= million tonnes of oil equivalent)

Energy consumption in India

Coal55%

Biomass and waste12%

Oil, Petroleum and other liquids

23%

Natural Gas6%

Hydroelectric2%

Nuclear1% Other renewables

1%

Source: International Energy Association, Company, ICICIdirect.com Research

India is also the third-largest consumer of crude oil and petroleum products as the country’s demand growth continues to outstrip domestic supply growth. With increasing requirements from India’s transportation and industrial sectors, demand is expected to only go higher over the next few years. As per International Energy Association, by 2040, India is set to contribute more than any other country to the projected rise in global energy demand, around a quarter of the total. Anticipating these higher needs, successive governments have taken various initiatives to increase production of hydrocarbons in the country. As highlighted in the exhibit below, efforts in this regard have now turned India into net exporter of petroleum products though the country still remains an importer of crude oil. However, growth in exports (petroleum products) has been unable to keep pace with corresponding growth in imports. As seen in the table below, petroleum product exports have grown at a meagre 0.5% CAGR in FY11-16 whereas imports during the same period have grown at 5.1% CAGR (4.4% for crude oil, 11.1% for petroleum products).

Exhibit 12: Import/export of crude oil and petroleum products

Import / Export ('000 MT) FY11 FY12 FY13 FY14 FY15 FY16 FY11-16

Crude Oil Import 163595 171729 184795 189238 189435 202850 4.4

Petroleum Products Import 17,379 15,849 16,354 16,697 21,301 29456 11.1

Total Imports 180,974 187,579 201,149 205,935 210,736 232,306 5.1

Petroleum Products / Total Exports 59,077 60,837 63,408 67,864 63,932 60,539 0.5

Net Imports 121,897 126,741 137,742 138,071 146,804 171,768 7.1

Net Petroleum products Export 41,698 44,988 47,054 51,167 42,631 31083 -5.7

Source: Petroleum Planning & Analysis Cell, Ministry of Petroleum & Natural gas, GOI, Company, ICICIdirect.com Research

Page 8ICICI Securities Ltd | Retail Equity Research

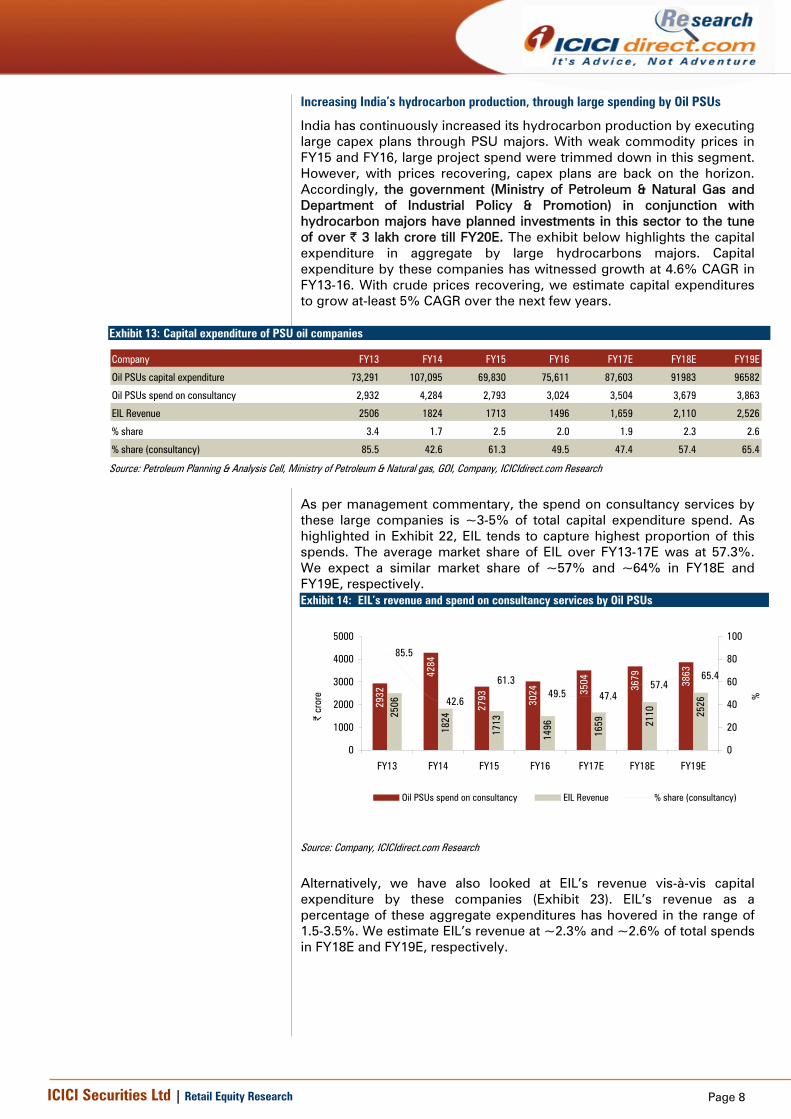

Increasing India’s hydrocarbon production, through large spending by Oil PSUs

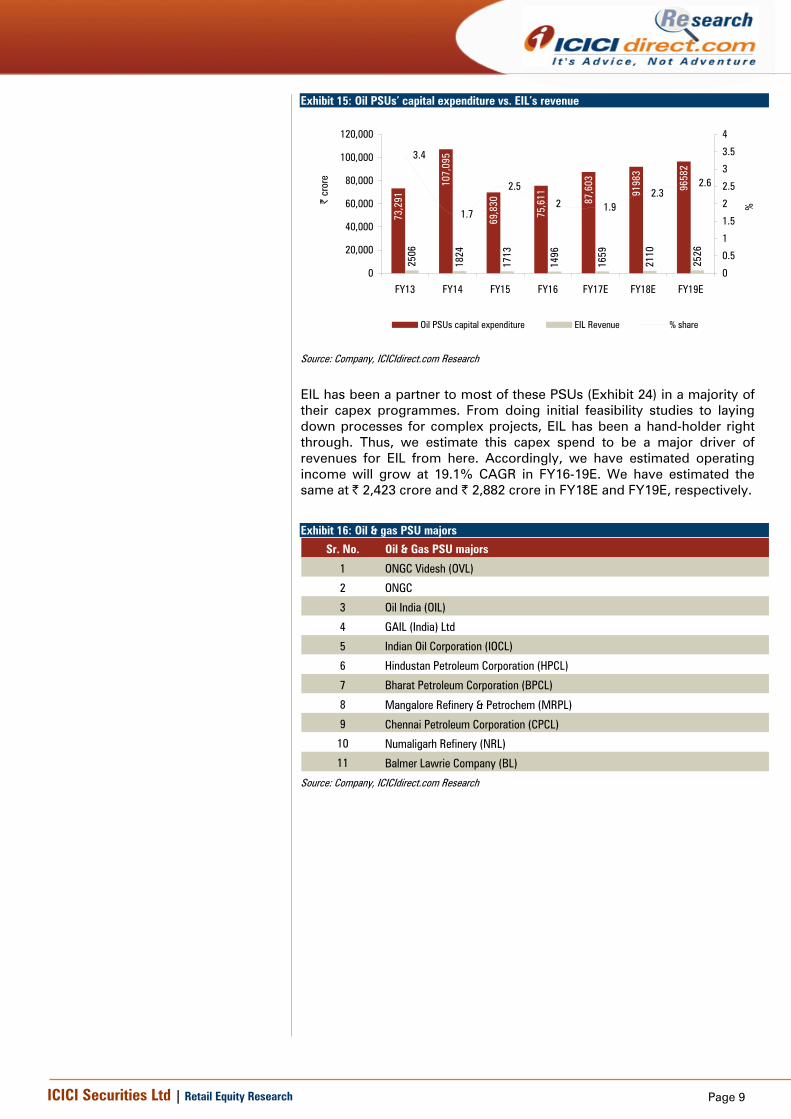

India has continuously increased its hydrocarbon production by executing large capex plans through PSU majors. With weak commodity prices in FY15 and FY16, large project spend were trimmed down in this segment. However, with prices recovering, capex plans are back on the horizon. Accordingly, the government (Ministry of Petroleum & Natural Gas and Department of Industrial Policy & Promotion) in conjunction with hydrocarbon majors have planned investments in this sector to the tune of over | 3 lakh crore till FY20E. The exhibit below highlights the capital expenditure in aggregate by large hydrocarbons majors. Capital expenditure by these companies has witnessed growth at 4.6% CAGR in FY13-16. With crude prices recovering, we estimate capital expenditures to grow at-least 5% CAGR over the next few years.

Exhibit 13: Capital expenditure of PSU oil companies

Company FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Oil PSUs capital expenditure 73,291 107,095 69,830 75,611 87,603 91983 96582

Oil PSUs spend on consultancy 2,932 4,284 2,793 3,024 3,504 3,679 3,863

EIL Revenue 2506 1824 1713 1496 1,659 2,110 2,526

% share 3.4 1.7 2.5 2.0 1.9 2.3 2.6

% share (consultancy) 85.5 42.6 61.3 49.5 47.4 57.4 65.4

Source: Petroleum Planning & Analysis Cell, Ministry of Petroleum & Natural gas, GOI, Company, ICICIdirect.com Research

As per management commentary, the spend on consultancy services by these large companies is ~3-5% of total capital expenditure spend. As highlighted in Exhibit 22, EIL tends to capture highest proportion of this spends. The average market share of EIL over FY13-17E was at 57.3%. We expect a similar market share of ~57% and ~64% in FY18E and FY19E, respectively. Exhibit 14: EIL’s revenue and spend on consultancy services by Oil PSUs

2932

4284

2793 30

24 3504 3679 3863

2506

1824

1713

1496

1659 21

10 2526

85.5

42.6

61.349.5 47.4

57.465.4

0

1000

2000

3000

4000

5000

FY13 FY14 FY15 FY16 FY17E FY18E FY19E

| cr

ore

0

20

40

60

80

100

%

Oil PSUs spend on consultancy EIL Revenue % share (consultancy)

Source: Company, ICICIdirect.com Research

Alternatively, we have also looked at EIL’s revenue vis-à-vis capital expenditure by these companies (Exhibit 23). EIL’s revenue as a percentage of these aggregate expenditures has hovered in the range of 1.5-3.5%. We estimate EIL’s revenue at ~2.3% and ~2.6% of total spends in FY18E and FY19E, respectively.

Page 9ICICI Securities Ltd | Retail Equity Research

Exhibit 15: Oil PSUs’ capital expenditure vs. EIL’s revenue

73,2

91

107,

095

69,8

30

75,6

11 87,6

03

9198

3

9658

2

2506

1824

1713

1496

1659

2110

2526

3.4

1.7

2.5

2 1.92.3

2.6

0

20,000

40,000

60,000

80,000

100,000

120,000

FY13 FY14 FY15 FY16 FY17E FY18E FY19E

| cr

ore

0

0.5

1

1.5

2

2.5

3

3.5

4

%

Oil PSUs capital expenditure EIL Revenue % share

Source: Company, ICICIdirect.com Research

EIL has been a partner to most of these PSUs (Exhibit 24) in a majority of their capex programmes. From doing initial feasibility studies to laying down processes for complex projects, EIL has been a hand-holder right through. Thus, we estimate this capex spend to be a major driver of revenues for EIL from here. Accordingly, we have estimated operating income will grow at 19.1% CAGR in FY16-19E. We have estimated the same at | 2,423 crore and | 2,882 crore in FY18E and FY19E, respectively.

Exhibit 16: Oil & gas PSU majors

Sr. No. Oil & Gas PSU majors

1 ONGC Videsh (OVL)

2 ONGC

3 Oil India (OIL)

4 GAIL (India) Ltd

5 Indian Oil Corporation (IOCL)

6 Hindustan Petroleum Corporation (HPCL)

7 Bharat Petroleum Corporation (BPCL)

8 Mangalore Refinery & Petrochem (MRPL)

9 Chennai Petroleum Corporation (CPCL)

10 Numaligarh Refinery (NRL)

11 Balmer Lawrie Company (BL)

Source: Company, ICICIdirect.com Research

Page 10ICICI Securities Ltd | Retail Equity Research

Overseas hydrocarbon capex: Storehouse of opportunity

EIL’s overseas presence

Engineers India has a significant overseas presence with offices in the UK, UAE, Malaysia, China & Italy. EIL is continuously expanding its international operations to establish a global execution platform. The company is seeking to identify markets where it can provide cost and operational advantages to clients and distinguish itself from other competitors. EIL is particularly focused on regions where it has previously implemented projects like in the Middle East, North Africa and South East Asia to capitalise on its local experience, established contacts with local clients & suppliers and familiarity of the local working conditions. It has executed some major projects that led EIL to emerge as a global player. Exhibit 17: Major projects executed in overseas markets

Sr. No. Major projects executed in overseas markets

1

Dangote Refinery and Petrochemical Project comprising a 460,000 bpsd grassroot petroleum refinery & 690,000 TPA petrochemical complex at Lekki Free Trade Zone, Nigeria for Dangote oil refining company

2Liwa Plastics Project in Sohar, Oman for Oman Refineries and Petroleum Industries Company (Orpic)

3 Qusahwira Field Development of ADCO, Abu Dhabi

4 Pipeline Projects (five) of Abu Dhabi Gas Industries (Gasco), Abu Dhabi

5 Rehabilitation & Adaptation of Algiers & Skikda Refineries of Sonatrach, Algeria

6Olefins conversion unit and Polypropylene Unit of Abu Dhabi Polymer Company (Borouge) at Ruwais, Abu Dhabi

7 Replacement of NGL Pipeline Network of Gasco, Abu Dhabi

8 Development of engineering capabilities for Sonatrach, Algeria

9Integrity enhancement of fire protection system for Abu Dhabi Refinery Ph-II & Ph-III of Abu Dhabi Oil Refining Company (Takreer), Abu Dhabi

10Ethylbenzene and styrene monomer plant at Bandar Assaluyeh Petrochemical Industries Development Company (PIDMCO), Iran

11 ABBR modification project of Gasco, Abu Dhabi

12 Aromatics complex in Kuwait for Technimont, Italy13 Mumbasa refinery upgrade project of Kenya Petroleum Refineries (KPRL), Kenya14 Engineering Services to Qatar Petrochemical Company (QAPCO), Qatar

15Design & engineering of water injection plant and cathodic protection system for pipelines of Petro Venezolana SA, Venezuela

Source: Company, ICICIdirect.com Research

Targeting regions with high spending power – Middle East & North Africa According to the International Energy Agency (IEA), global investments in the oil & gas space witnessed cuts for three consecutive years of 2014, 2015 and 2016, the first time since the mid-1980s. Against this trend, the Middle East & North Africa (MENA) region saw heavy investments as major energy-exporting countries in this region wanted to expand their size and, consequently, strengthen their positions in global markets. The Gulf Cooperation Council (GCC), an alliance of six Middle Eastern countries (Saudi Arabia, Kuwait, the United Arab Emirates, Qatar, Bahrain and Oman) as well as Iran and Iraq, made regular investments so as to be well positioned when prices take an upturn.

Planned investments in the hydrocarbon sector in the MENA region are estimated at $417 billion for the five-year period 2016-20. Within the hydrocarbon space, the oil & gas sector’s planned spend is at $190 billion and $149 billion, respectively, whereas the same is at $78 billion in the petrochemical sector in 2016-20.

Page 11ICICI Securities Ltd | Retail Equity Research

Exhibit 18: Planned MENA investments in hydrocarbon sector in FY16-20

Planned expendiutre in hydrocarbon sector $ bn In | crore

Oil & Gas 339 2271300

Petroleum chemicals 78 522600

Total spend 417 2793900

Source: EPICORP Energy Research, Company, ICICIdirect.com Research

Committed investments This includes investments in projects currently being executed, that is, contracts for these projects have been signed. Total committed investment is the sum of the estimated cost over the five-year period based on the contract value. Of the planned investments of $417 billion, investments in projects under execution are at $208 billion. The oil sector accounts for the largest share of investments at $110 billion, with the majority in upstream projects. Total committed gas investments are at $76 billion, followed by petrochemicals at $22 billion. In rupee terms, this number is at | 13, 93,600 crore. Exhibit 19: Committed MENA investments in hydrocarbon sector

Committed investments in hydrocarbon sector $ bn In | crore

Oil & gas 186 1246200

Petroleum chemicals 22 147400

Total spend 208 1393600 Source: EPICORP Energy Research, Company, ICICIdirect.com Research

EIL’s continuous effort to build higher business on this side coupled with a huge opportunity in the MENA region (committed investments of | 13,93,600 crore) is likely to improve contribution of overseas revenues to the total topline. As seen in exhibit below, contribution overseas market have already increased from 3.1% in FY12 to 22% in FY16. We expect this contribution to increase further to 25% of the topline by FY19E. As on FY16, the overseas order constitutes 37% of the order backlog. Accordingly, we expect EIL’s overseas business to grow at 24.3% CAGR in FY16-19E. We expect revenues of | 631 crore from this segment by FY19E. Exhibit 20: Growth in overseas revenue and as percentage of total topline

116 157 140221

329 356

485

631

3.16.3 7.7

12.9

22.0 2325

21.5

0

100

200

300

400

500

600

700

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

| cr

ore

0

5

10

15

20

25

30

%

Overseas revenue % of total revenue

29.8%

24.3%

Source: Company, ICICIdirect.com Research

Page 12ICICI Securities Ltd | Retail Equity Research

Brownfield refinery expansions/greenfield projects to support growth

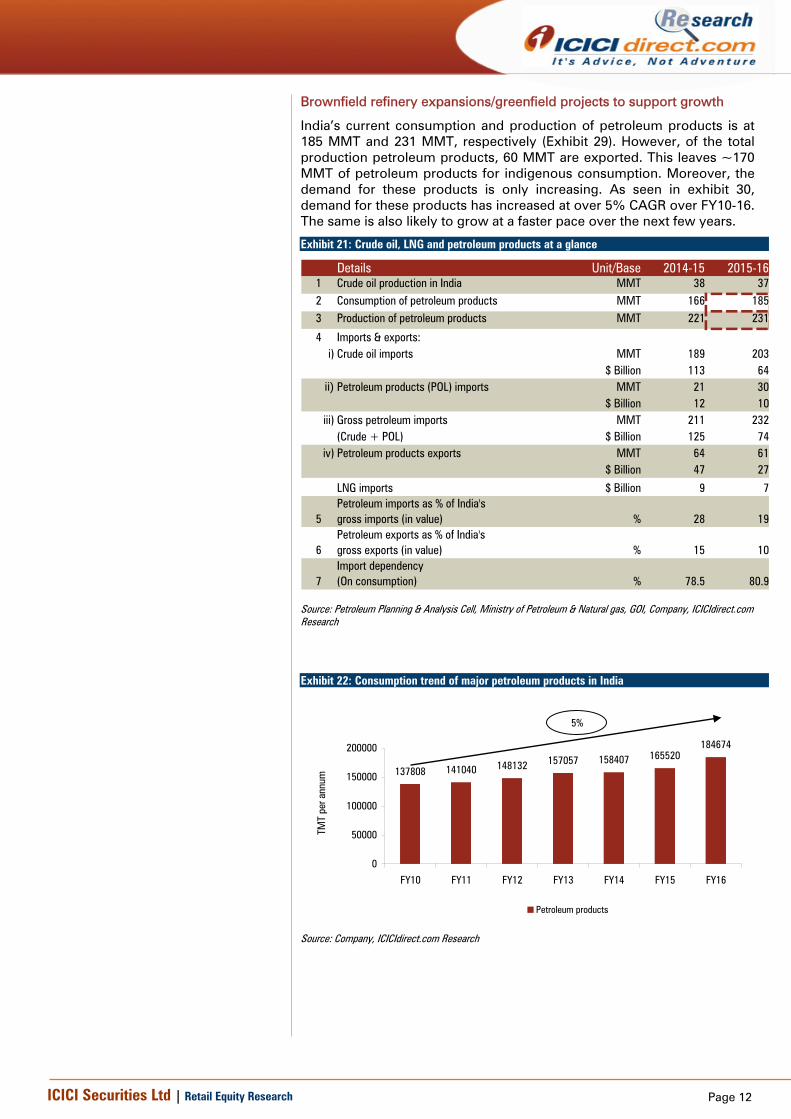

India’s current consumption and production of petroleum products is at 185 MMT and 231 MMT, respectively (Exhibit 29). However, of the total production petroleum products, 60 MMT are exported. This leaves ~170 MMT of petroleum products for indigenous consumption. Moreover, the demand for these products is only increasing. As seen in exhibit 30, demand for these products has increased at over 5% CAGR over FY10-16. The same is also likely to grow at a faster pace over the next few years.

Exhibit 21: Crude oil, LNG and petroleum products at a glance

Details Unit/Base 2014-15 2015-161 Crude oil production in India MMT 38 372 Consumption of petroleum products MMT 166 1853 Production of petroleum products MMT 221 231

4 Imports & exports:i) Crude oil imports MMT 189 203

$ Billion 113 64ii) Petroleum products (POL) imports MMT 21 30

$ Billion 12 10iii) Gross petroleum imports MMT 211 232

(Crude + POL) $ Billion 125 74iv) Petroleum products exports MMT 64 61

$ Billion 47 27

LNG imports $ Billion 9 7

5Petroleum imports as % of India'sgross imports (in value) % 28 19

6Petroleum exports as % of India'sgross exports (in value) % 15 10

7Import dependency(On consumption) % 78.5 80.9

Source: Petroleum Planning & Analysis Cell, Ministry of Petroleum & Natural gas, GOI, Company, ICICIdirect.com Research

Exhibit 22: Consumption trend of major petroleum products in India

137808 141040 148132 157057 158407 165520184674

0

50000

100000

150000

200000

FY10 FY11 FY12 FY13 FY14 FY15 FY16

TMT

per a

nnum

Petroleum products

5%

Source: Company, ICICIdirect.com Research

Page 13ICICI Securities Ltd | Retail Equity Research

Anticipating this higher demand, some brownfield programmes that have been announced/in progress are;

Exhibit 23: Brownfield expansions announced/proposed by PSU majors

Company Name Refinery

Current Capacity (TMTPA)

Proposed Capacity (TMTPA)

Incremental Capacity (TMTPA)

Hindustan Petroleum Corporation Visakh 8300 15000 6700

Indian Oil Corporation Koyali 13500 18500 5000

Mathura 8000 11000 3000

Panipat 15000 20000 5000

BPCL-Bharat Oman Refineries Bina 6000 7800 1800

Mangalore Refinery and Petrochemicals Mangalore 15000 25000 10000

Total 31500

Source: Company, ICICIdirect.com Research

Estimated spends for the above brownfield expansion programmes are part of total capex spends estimated in Exhibit 21. Thus, the opportunity arising for EIL from these brownfield expansions is considered part of the total capex spends and, hence, not highlighted separately.

Greenfield mega project – West Coast Refinery

The Government of Maharashtra along with OMC majors - Bharat Petroleum Corporation (BPCL), Hindustan Petroleum Corporation (HPCL) and Indian Oil Corporation (IOC) - have proposed India’s biggest refinery with a capacity of ~60,000 MT at a cost of ~| 2,00,000 crore. This refinery has been planned with the aim of meet the country’s projected requirement of petroleum products of 5,50,000 MT by 2040. A mega petrochemical complex is also likely to come up along with the refinery. The entire project is likely to be built in two phases. Phase-1 will be ~40,000 MT together with an aromatic complex, naphtha cracker and a polymer complex. This phase is likely to cost | 1.2-1.5 lakh crore and will take about five to six years for construction & development. The second phase is likely to cost | 50,000-60,000 crore. This mega refinery is likely to produce petrol, diesel, LPG, ATF and feedstock for petrochemical plants in plastic, chemical and textile industries in Maharashtra. An MoU to this effect was also signed in December 2016. In addition to the MoU signed for the west coast refinery, state run oil marketing companies and refineries also entered into 10 other MoUs for ethanol refinery projects.

Such mega-projects, in addition to other smaller projects, are likely to provide substantial order inflow and revenue visibility to knowledge based consultancy players like EIL in the coming five to seven years. From the west coast refinery, we envisage an opportunity of estimated ~4% of | 2 lakh crore over the next six years. Thus, the opportunity for FY17E-20E is estimated at ~2% of total opportunity at ~| 4000 crore.

Page 14ICICI Securities Ltd | Retail Equity Research

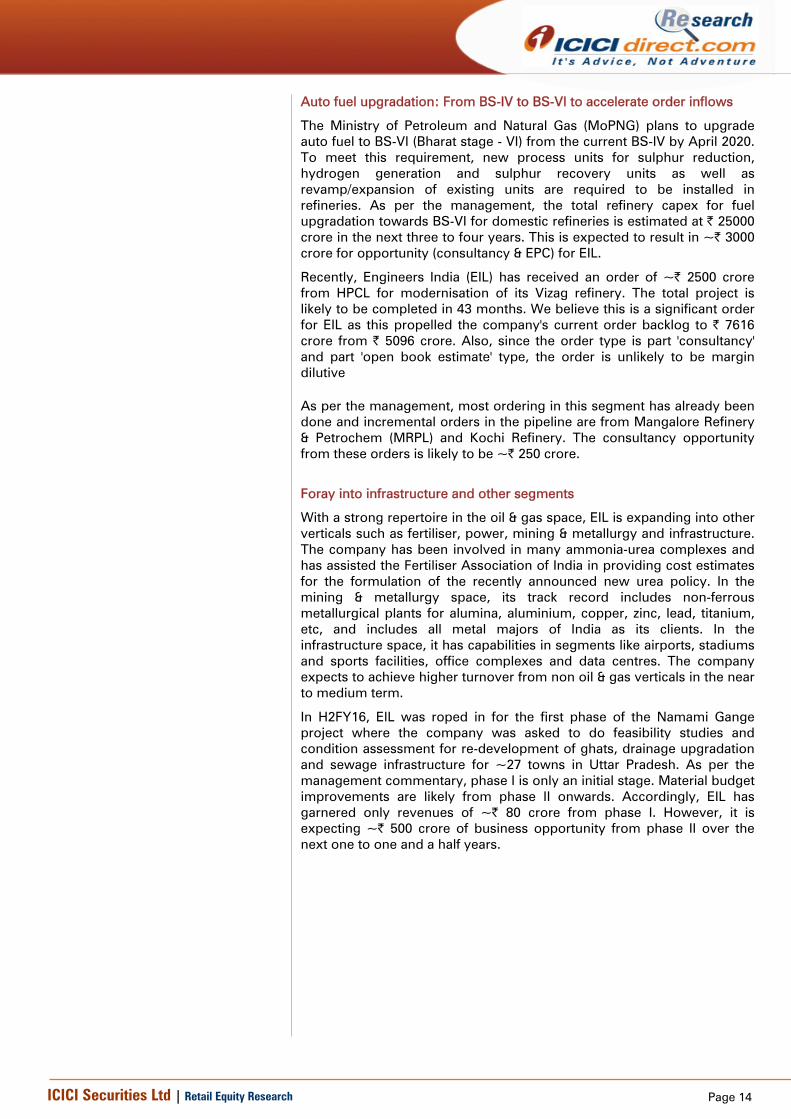

Auto fuel upgradation: From BS-IV to BS-VI to accelerate order inflows

The Ministry of Petroleum and Natural Gas (MoPNG) plans to upgrade auto fuel to BS-VI (Bharat stage - VI) from the current BS-IV by April 2020. To meet this requirement, new process units for sulphur reduction, hydrogen generation and sulphur recovery units as well as revamp/expansion of existing units are required to be installed in refineries. As per the management, the total refinery capex for fuel upgradation towards BS-VI for domestic refineries is estimated at | 25000 crore in the next three to four years. This is expected to result in ~| 3000 crore for opportunity (consultancy & EPC) for EIL.

Recently, Engineers India (EIL) has received an order of ~| 2500 crore from HPCL for modernisation of its Vizag refinery. The total project is likely to be completed in 43 months. We believe this is a significant order for EIL as this propelled the company's current order backlog to | 7616 crore from | 5096 crore. Also, since the order type is part 'consultancy' and part 'open book estimate' type, the order is unlikely to be margin dilutive As per the management, most ordering in this segment has already been done and incremental orders in the pipeline are from Mangalore Refinery & Petrochem (MRPL) and Kochi Refinery. The consultancy opportunity from these orders is likely to be ~| 250 crore.

Foray into infrastructure and other segments

With a strong repertoire in the oil & gas space, EIL is expanding into other verticals such as fertiliser, power, mining & metallurgy and infrastructure. The company has been involved in many ammonia-urea complexes and has assisted the Fertiliser Association of India in providing cost estimates for the formulation of the recently announced new urea policy. In the mining & metallurgy space, its track record includes non-ferrous metallurgical plants for alumina, aluminium, copper, zinc, lead, titanium, etc, and includes all metal majors of India as its clients. In the infrastructure space, it has capabilities in segments like airports, stadiums and sports facilities, office complexes and data centres. The company expects to achieve higher turnover from non oil & gas verticals in the near to medium term.

In H2FY16, EIL was roped in for the first phase of the Namami Gange project where the company was asked to do feasibility studies and condition assessment for re-development of ghats, drainage upgradation and sewage infrastructure for ~27 towns in Uttar Pradesh. As per the management commentary, phase I is only an initial stage. Material budget improvements are likely from phase II onwards. Accordingly, EIL has garnered only revenues of ~| 80 crore from phase I. However, it is expecting ~| 500 crore of business opportunity from phase II over the next one to one and a half years.

Page 15ICICI Securities Ltd | Retail Equity Research

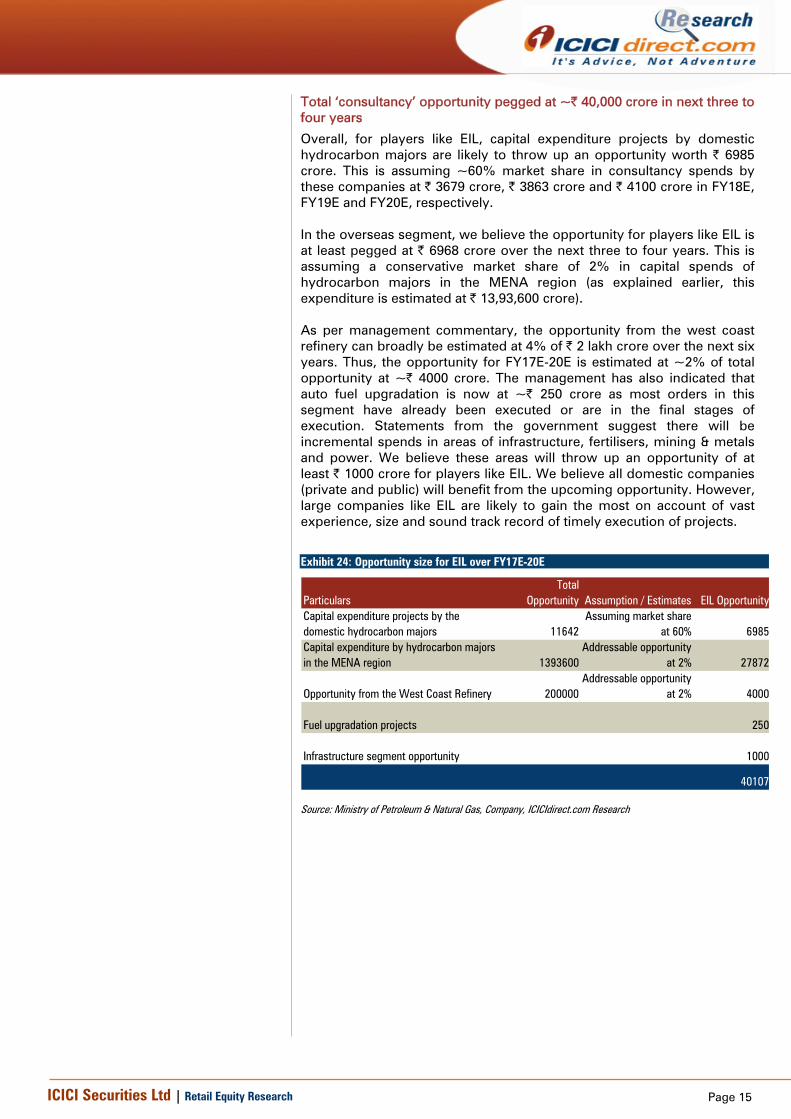

Total ‘consultancy’ opportunity pegged at ~| 40,000 crore in next three to four years

Overall, for players like EIL, capital expenditure projects by domestic hydrocarbon majors are likely to throw up an opportunity worth | 6985 crore. This is assuming ~60% market share in consultancy spends by these companies at | 3679 crore, | 3863 crore and | 4100 crore in FY18E, FY19E and FY20E, respectively. In the overseas segment, we believe the opportunity for players like EIL is at least pegged at | 6968 crore over the next three to four years. This is assuming a conservative market share of 2% in capital spends of hydrocarbon majors in the MENA region (as explained earlier, this expenditure is estimated at | 13,93,600 crore). As per management commentary, the opportunity from the west coast refinery can broadly be estimated at 4% of | 2 lakh crore over the next six years. Thus, the opportunity for FY17E-20E is estimated at ~2% of total opportunity at ~| 4000 crore. The management has also indicated that auto fuel upgradation is now at ~| 250 crore as most orders in this segment have already been executed or are in the final stages of execution. Statements from the government suggest there will be incremental spends in areas of infrastructure, fertilisers, mining & metals and power. We believe these areas will throw up an opportunity of at least | 1000 crore for players like EIL. We believe all domestic companies (private and public) will benefit from the upcoming opportunity. However, large companies like EIL are likely to gain the most on account of vast experience, size and sound track record of timely execution of projects.

Exhibit 24: Opportunity size for EIL over FY17E-20E

ParticularsTotal

Opportunity Assumption / Estimates EIL OpportunityCapital expenditure projects by the domestic hydrocarbon majors 11642

Assuming market share at 60% 6985

Capital expenditure by hydrocarbon majors in the MENA region 1393600

Addressable opportunity at 2% 27872

Opportunity from the West Coast Refinery 200000Addressable opportunity

at 2% 4000

Fuel upgradation projects 250

Infrastructure segment opportunity 1000

40107

Source: Ministry of Petroleum & Natural Gas, Company, ICICIdirect.com Research

Page 16ICICI Securities Ltd | Retail Equity Research

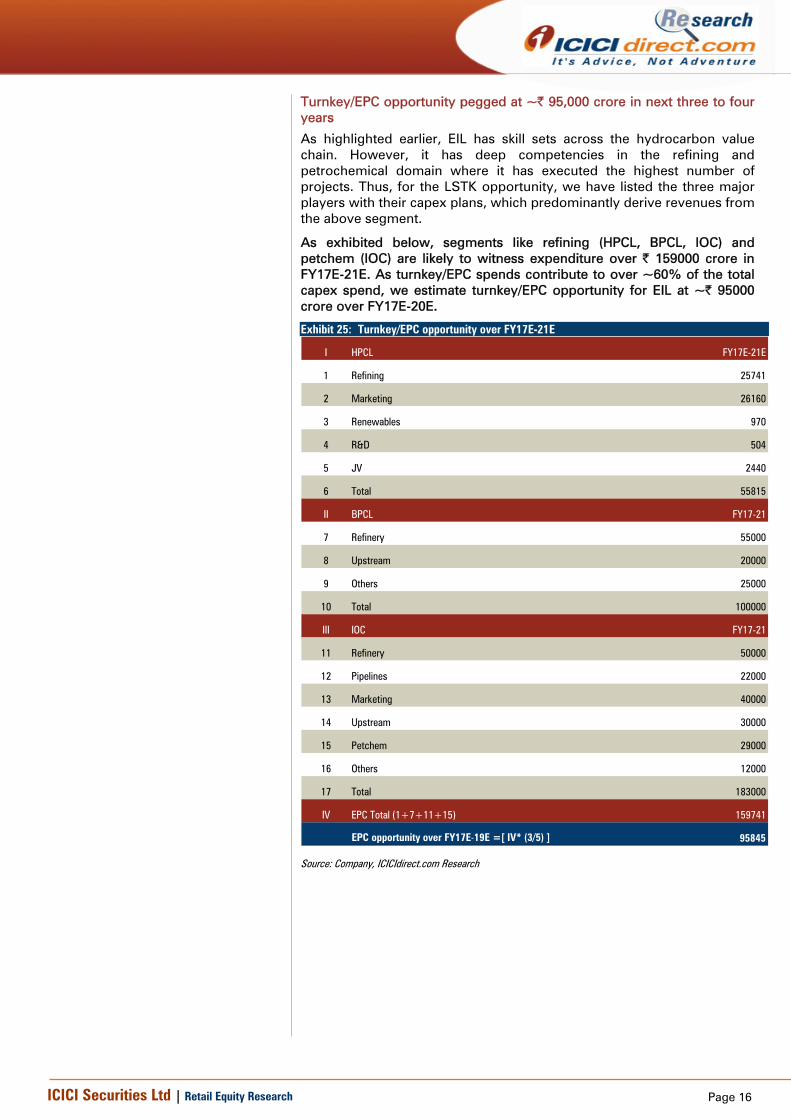

Turnkey/EPC opportunity pegged at ~| 95,000 crore in next three to four years

As highlighted earlier, EIL has skill sets across the hydrocarbon value chain. However, it has deep competencies in the refining and petrochemical domain where it has executed the highest number of projects. Thus, for the LSTK opportunity, we have listed the three major players with their capex plans, which predominantly derive revenues from the above segment.

As exhibited below, segments like refining (HPCL, BPCL, IOC) and petchem (IOC) are likely to witness expenditure over | 159000 crore in FY17E-21E. As turnkey/EPC spends contribute to over ~60% of the total capex spend, we estimate turnkey/EPC opportunity for EIL at ~| 95000 crore over FY17E-20E.

Exhibit 25: Turnkey/EPC opportunity over FY17E-21E

I HPCL FY17E-21E

1 Refining 25741

2 Marketing 26160

3 Renewables 970

4 R&D 504

5 JV 2440

6 Total 55815

II BPCL FY17-21

7 Refinery 55000

8 Upstream 20000

9 Others 25000

10 Total 100000

III IOC FY17-21

11 Refinery 50000

12 Pipelines 22000

13 Marketing 40000

14 Upstream 30000

15 Petchem 29000

16 Others 12000

17 Total 183000

IV EPC Total (1+7+11+15) 159741

EPC opportunity over FY17E-19E =[ IV* (3/5) ] 95845

Source: Company, ICICIdirect.com Research

Page 17ICICI Securities Ltd | Retail Equity Research

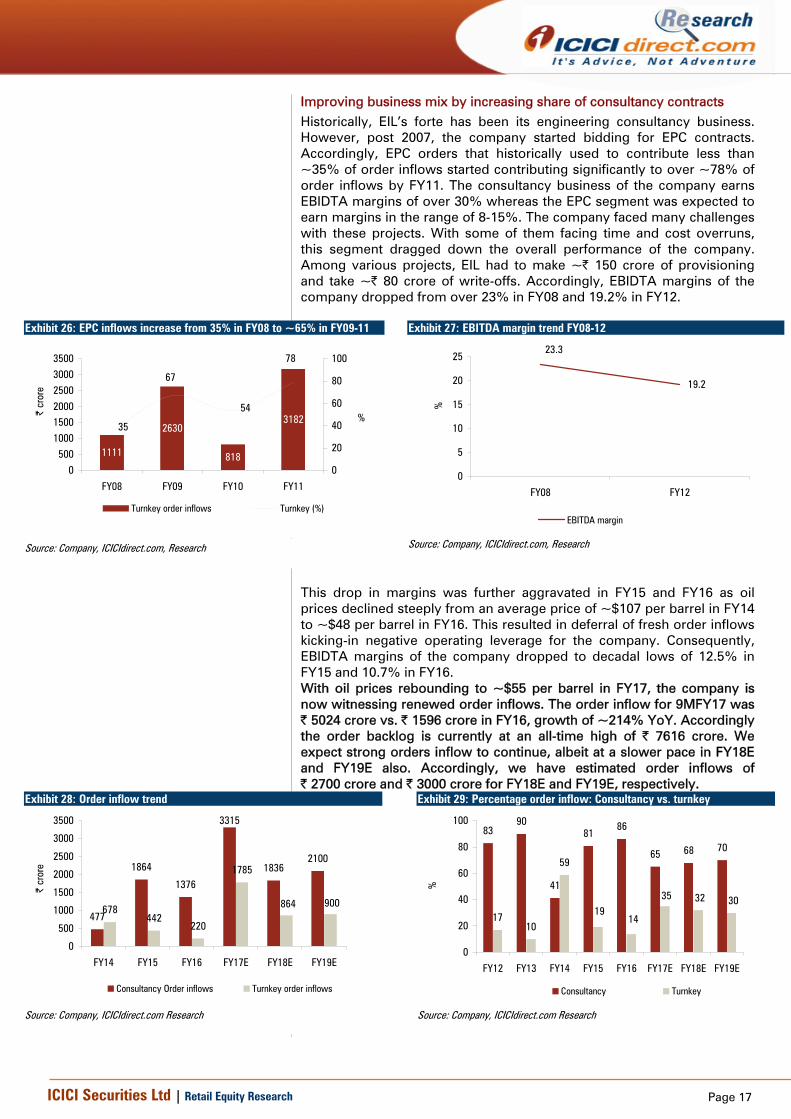

Improving business mix by increasing share of consultancy contracts Historically, EIL’s forte has been its engineering consultancy business. However, post 2007, the company started bidding for EPC contracts. Accordingly, EPC orders that historically used to contribute less than ~35% of order inflows started contributing significantly to over ~78% of order inflows by FY11. The consultancy business of the company earns EBIDTA margins of over 30% whereas the EPC segment was expected to earn margins in the range of 8-15%. The company faced many challenges with these projects. With some of them facing time and cost overruns, this segment dragged down the overall performance of the company. Among various projects, EIL had to make ~| 150 crore of provisioning and take ~| 80 crore of write-offs. Accordingly, EBIDTA margins of the company dropped from over 23% in FY08 and 19.2% in FY12.

Exhibit 26: EPC inflows increase from 35% in FY08 to ~65% in FY09-11

1111

2630

818

318235

67

54

78

0500

100015002000

250030003500

FY08 FY09 FY10 FY11

| cr

ore

0

20

40

60

80

100

%

Turnkey order inflows Turnkey (%)

Source: Company, ICICIdirect.com, Research

Exhibit 27: EBITDA margin trend FY08-12

19.2

23.3

0

5

10

15

20

25

FY08 FY12

%

EBITDA margin

Source: Company, ICICIdirect.com, Research

This drop in margins was further aggravated in FY15 and FY16 as oil prices declined steeply from an average price of ~$107 per barrel in FY14 to ~$48 per barrel in FY16. This resulted in deferral of fresh order inflows kicking-in negative operating leverage for the company. Consequently, EBIDTA margins of the company dropped to decadal lows of 12.5% in FY15 and 10.7% in FY16. With oil prices rebounding to ~$55 per barrel in FY17, the company is now witnessing renewed order inflows. The order inflow for 9MFY17 was | 5024 crore vs. | 1596 crore in FY16, growth of ~214% YoY. Accordingly the order backlog is currently at an all-time high of | 7616 crore. We expect strong orders inflow to continue, albeit at a slower pace in FY18E and FY19E also. Accordingly, we have estimated order inflows of | 2700 crore and | 3000 crore for FY18E and FY19E, respectively.

Exhibit 28: Order inflow trend

477

1864

1376

3315

18362100

678442

220

1785

864 900

0

500

1000

1500

2000

2500

3000

3500

FY14 FY15 FY16 FY17E FY18E FY19E

| cr

ore

Consultancy Order inflows Turnkey order inflows

Source: Company, ICICIdirect.com Research

Exhibit 29: Percentage order inflow: Consultancy vs. turnkey

8390

41

8186

65 68 70

1710

59

1914

35 32 30

0

20

40

60

80

100

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

%

Consultancy Turnkey

Source: Company, ICICIdirect.com Research

Page 18ICICI Securities Ltd | Retail Equity Research

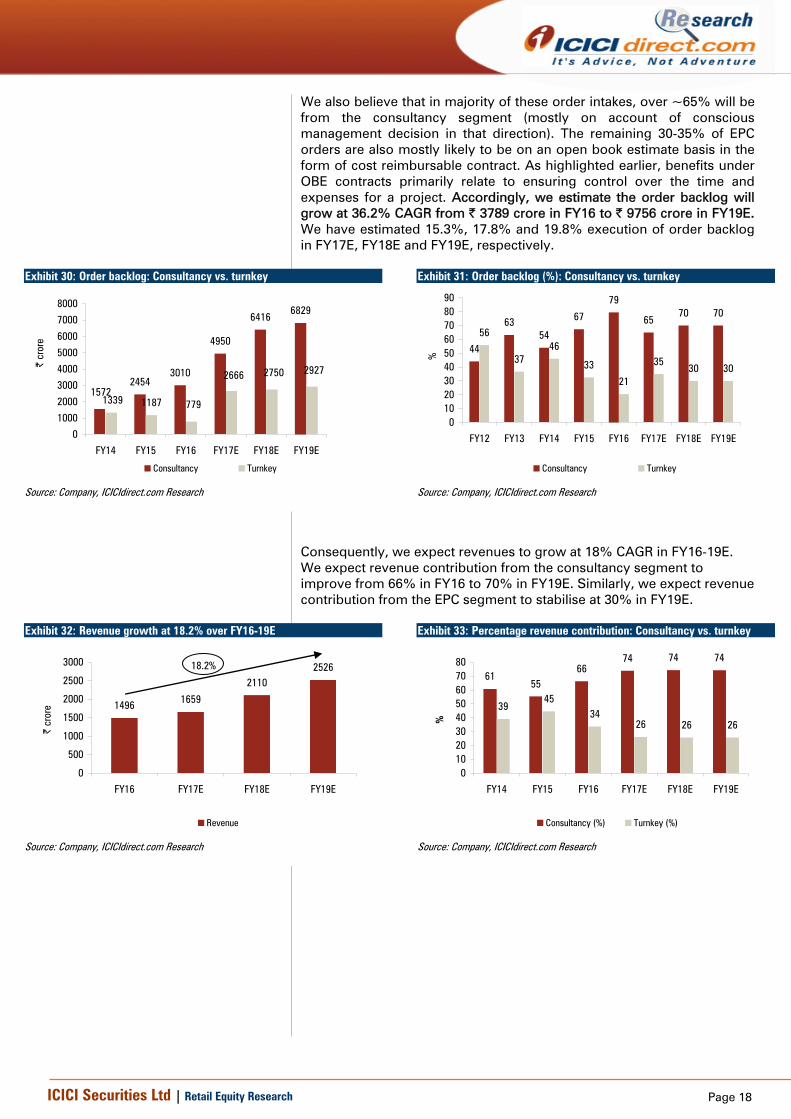

We also believe that in majority of these order intakes, over ~65% will be from the consultancy segment (mostly on account of conscious management decision in that direction). The remaining 30-35% of EPC orders are also mostly likely to be on an open book estimate basis in the form of cost reimbursable contract. As highlighted earlier, benefits under OBE contracts primarily relate to ensuring control over the time and expenses for a project. Accordingly, we estimate the order backlog will grow at 36.2% CAGR from | 3789 crore in FY16 to | 9756 crore in FY19E. We have estimated 15.3%, 17.8% and 19.8% execution of order backlog in FY17E, FY18E and FY19E, respectively.

Exhibit 30: Order backlog: Consultancy vs. turnkey

24543010

4950

64166829

11871572

1339 779

2666 2750 2927

0

1000

2000

3000

4000

5000

6000

7000

8000

FY14 FY15 FY16 FY17E FY18E FY19E

| cr

ore

Consultancy Turnkey

Source: Company, ICICIdirect.com Research

Exhibit 31: Order backlog (%): Consultancy vs. turnkey

44

6354

67

79

6570 70

56

3746

33

21

3530 30

0102030405060708090

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E%

Consultancy Turnkey

Source: Company, ICICIdirect.com Research

Consequently, we expect revenues to grow at 18% CAGR in FY16-19E. We expect revenue contribution from the consultancy segment to improve from 66% in FY16 to 70% in FY19E. Similarly, we expect revenue contribution from the EPC segment to stabilise at 30% in FY19E.

Exhibit 32: Revenue growth at 18.2% over FY16-19E

1496 1659

21102526

0

500

1000

1500

2000

2500

3000

FY16 FY17E FY18E FY19E

| cr

ore

Revenue

18.2%

Source: Company, ICICIdirect.com Research

Exhibit 33: Percentage revenue contribution: Consultancy vs. turnkey

6155

6674 74 74

3945

3426 26 26

01020304050607080

FY14 FY15 FY16 FY17E FY18E FY19E

%

Consultancy (%) Turnkey (%)

Source: Company, ICICIdirect.com Research

Page 19ICICI Securities Ltd | Retail Equity Research

Research & innovation: Aiding EIL’s growth

EIL is a technology driven organisation, which believes that continuous innovation and investment in technology is imperative for maintaining its leadership position in the hydrocarbon sector. The company has to its credit more than 30 process technologies that include Visbreaker Technology for petroleum residual fractions, delayed coking technology, diesel hydro treating, food grade hexane, light naphtha isomerisation and wax deoiling technology, among others. EIL currently holds 16 patents and has 14 pending patent applications related to various process technologies and hardware developed by the company. The exhibit below shows various process technologies in the refining space that EIL has either developed or leased to large corporations present in the hydrocarbons space. Exhibit 34: Technologies in refining segment

Source: Company, ICICIdirect.com Research

Technology at the forefront of consultancy services In addition to technologies developed in the refining space, EIL has also done a commendable job in developing in-house technologies in the oil & gas and aromatics space. EIL has developed a state-of-the-art R&D centre at Gurgaon that pursues technology developments both in-house and in collaboration with oil & gas PSUs and premier research institutions. As part of technology development programmes, EIL also has separate pilot facilities to perform experimental activities for hydrodynamics and other complex processes in the plant.

Page 20ICICI Securities Ltd | Retail Equity Research

Exhibit 35: Technologies in oil & gas segment

Source: Company, ICICIdirect.com Research

Exhibit 36: Technologies in aromatics segment

Source: Company, ICICIdirect.com Research

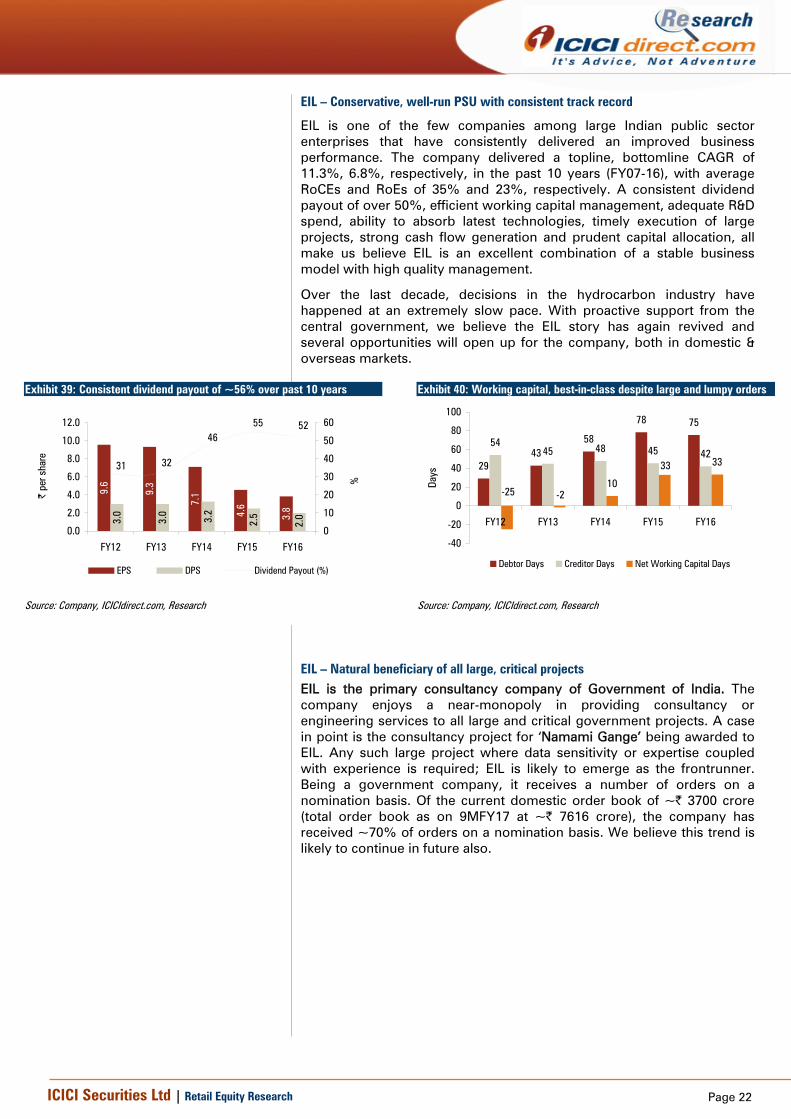

EIL has consistently increased/maintained its R&D spend over the past few years. This was despite a weak business outlook over the past few years. The company’s R&D spends as a percentage of revenues have continuously improved from 0.4% in FY12 to ~1% in FY16. Higher R&D spends are likely to continue, as the push to newer technologies and processes demands higher allocation towards the same. Exhibit 37: EIL’s R&D spend

15.5 16.1 20.9 16.9 17.7 16.6 21.1 25.3

3723

2506

1824 17131496 1659

21102526

0.4

0.6

1.1

1.0

1.2

1.0 1.0 1.0

0

500

1000

1500

2000

2500

3000

3500

4000

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

R&D expenditure Revenue % R&D spend

Source: Company, ICICIdirect.com Research

Page 21ICICI Securities Ltd | Retail Equity Research

Joint ventures & subsidiary companies

Exhibit 38: Summary of EIL's subsidiary and joint venture

Joint Venture / Subsidary Partner Area of Co-operation

Equity investment

by EIL

Equity Holding by EIL and partners

Joint VentureRamagundam Fertilizers and Chemicals Limited (RFCL)

National Fertilizers Limited

(NFL) and Fertilizer

Corporation of India (FCIL),

This JVC is responsible for setting up a Urea and an Ammonia plant at

Ramagundam in Karimnagar district of Telengana. The JV will be responsible for setting up a gas based urea plant with a

capacity of 3850 TPD.

| 2.6 crore EIL - 26%, NFL - 26 %, FCIL -

48%

SubsidiaryCertification Engineers International Limited (CEIL)

CEIL provides certification as well as Third Party Inspection (TPI) services to various

clients

| 7.1 crore 100%

Source: Company, ICICIdirect.com Research

Ramagundam Fertilizers and Chemicals (RFCL)

In order to augment domestic urea capacity, Engineers India along with National Fertilizers (NFL) and Fertilizer Corporation of India (FCIL) signed an agreement to form a joint venture company (JVC) to set up new ammonia and urea plants at the existing site of Ramagundam Fertilizer plant in Karimnagar district of Telangana. The joint venture agreement for the new company was signed on January 2015.

The JV is primarily responsible for setting up gas based ammonia-urea plants. NFL and EIL each hold 26% equity in the JV. EIL would take up the project construction under the EPC model. Pre-project activities have started from FY16. NFL’s expertise would be utilised for the operation and maintenance of the plant. FCIL’s equity stake of 11% in the JV is in consideration of FCIL granting concession rights in the land, opportunity cost and value of usable assets and other items on the land at Ramagundam to the company. The remaining 37% equity stake is untied and will be used to raise funds as the project progresses.

The project comprises 2200 metric tonne per day (MTPD) ammonia plant and 3850 MTPD urea plant. FCIL will hold a stake in the JV, being the provider of existing infrastructure of Ramagundam Project. It is estimated that the commissioning of new plant would be completed by 2018-19.

Certification Engineers International (CEIL)

CEIL, a wholly-owned subsidiary of EIL, provides certification and third party inspection (TPI) services to various clients like ONGC, VMSS, RINL, GSPL, BPCL, Reliance Industries and various state governments like TEDA, VMSS, Rajasthan Housing Board and others.

Notable clients’ for which CEIL is executing services include, • ONGC- Certification services for Mumbai High Daman Development Project & C-26 Pipeline and TPI services for Sagar Samrat Conversion Project, Additional Development of Vasai East and Additional Pipeline Project • TEDA, VMSS, Rajasthan Housing Board - TPI for various infrastructure Projects. • GSPL - TPI for various Pipeline Projects • RIL for marketing terminals at Chennai, Kanpur and Haldia Apart from these, CEIL secured many third party Inspection assignments from clients like IOC, MDL, DRDO, Afcon Infrastructure, Jindal Saw ERDMP & statutory audit assignments from Gail, IOC, Cairn India, etc.

Page 22ICICI Securities Ltd | Retail Equity Research

EIL – Conservative, well-run PSU with consistent track record

EIL is one of the few companies among large Indian public sector enterprises that have consistently delivered an improved business performance. The company delivered a topline, bottomline CAGR of 11.3%, 6.8%, respectively, in the past 10 years (FY07-16), with average RoCEs and RoEs of 35% and 23%, respectively. A consistent dividend payout of over 50%, efficient working capital management, adequate R&D spend, ability to absorb latest technologies, timely execution of large projects, strong cash flow generation and prudent capital allocation, all make us believe EIL is an excellent combination of a stable business model with high quality management.

Over the last decade, decisions in the hydrocarbon industry have happened at an extremely slow pace. With proactive support from the central government, we believe the EIL story has again revived and several opportunities will open up for the company, both in domestic & overseas markets.

Exhibit 39: Consistent dividend payout of ~56% over past 10 years

9.6

9.3

7.1

3.0

3.0

3.2

2.5

2.04.

6

3.8

31 32

4655 52

0.0

2.0

4.0

6.0

8.0

10.0

12.0

FY12 FY13 FY14 FY15 FY16

| pe

r sha

re

0

10

20

30

40

50

60

%

EPS DPS Dividend Payout (%)

Source: Company, ICICIdirect.com, Research

Exhibit 40: Working capital, best-in-class despite large and lumpy orders

2943

58

78 75

5445 48 45 42

10

33

-25 -2

33

-40

-20

0

20

40

60

80

100

FY12 FY13 FY14 FY15 FY16

Days

Debtor Days Creditor Days Net Working Capital Days

Source: Company, ICICIdirect.com, Research

EIL – Natural beneficiary of all large, critical projects EIL is the primary consultancy company of Government of India. The company enjoys a near-monopoly in providing consultancy or engineering services to all large and critical government projects. A case in point is the consultancy project for ‘Namami Gange’ being awarded to EIL. Any such large project where data sensitivity or expertise coupled with experience is required; EIL is likely to emerge as the frontrunner. Being a government company, it receives a number of orders on a nomination basis. Of the current domestic order book of ~| 3700 crore (total order book as on 9MFY17 at ~| 7616 crore), the company has received ~70% of orders on a nomination basis. We believe this trend is likely to continue in future also.

Page 23ICICI Securities Ltd | Retail Equity Research

Financials Revenues to grow at 18% CAGR in FY16-19E, to be driven by 23.6% growth in the consultancy segment

We expect revenues to increase from | 1596 crore in FY16 to | 2881.8 crore in FY19E at a CAGR of 23.4%, mainly on the back of accelerated growth of 23.6% in FY16-19E in the consulting segment. Over FY12-16, revenues of EIL declined at a CAGR of 20.4%. As highlighted earlier, this was primarily on account of steep decline in prices of oil from an average price of ~$107 per barrel in FY14 to ~$48 per barrel in FY16, which resulted in deferral of fresh order inflows, kicking-in negative operating leverage for the company. However, with prices of oil rebounding to ~$50 per barrel in FY17, the company is now witnessing renewed order inflows. The order inflow for 9MFY17 has been | 5024 crore vs. | 1596 crore in FY16, a growth of ~214% YoY. We expected strong orders inflow to continue, albeit at a slower pace in FY18E and FY19E too. Accordingly, we have estimated order inflows of | 2700 crore and | 3000 crore for FY18E and FY19E respectively. We also believe that the majority of these order intakes, over ~65% will be from the consultancy segment (mostly on account of conscious management decision in that direction). The rest 30-35% of the EPC orders are also mostly likely to be on open book estimate basis - form of cost reimbursable contract. As highlighted earlier, benefits under OBE contracts primarily relate to ensuring control over the time and expenses for a project. Accordingly, we estimate order backlog will grow at a 36.2% CAGR from | 3789 crore in FY16 to | 9756 crore in FY19E. We expect the book to bill to remain healthy at over 3.5x. We expect order backlog execution of 43.8%, 36.9% & 27.6% in FY17E, FY18E and FY19E, respectively. Consequently, we expect revenues to grow at 18% CAGR over FY16-19E. We expect revenue contribution from the consultancy segment to improve from 66% in FY16 to 70% in FY19E. Similarly, we expect revenue contribution from the EPC segment to stabilize at 30% in FY19E.

Exhibit 41: Revenue trend

1,9861,753

1,933

2,423

2,882

-

500

1,000

1,500

2,000

2,500

3,000

3,500

FY15 FY16 FY17E FY18E FY19E

| cr

ore

Revenue

18% CAGR

Source: Company, ICICIdirect.com Research

Page 24ICICI Securities Ltd | Retail Equity Research

Exhibit 42: Execution of order book (%)

3641

3789

7616 91

66 9756

1713

1496

1659

2110

2526

58.8

41.1 43.8

27.7 27.6

0

2000

4000

6000

8000

10000

12000

FY15 FY16 FY17E FY18E FY19E

| cr

ore

0

10

20

30

40

50

60

70

%

Total Order Book Revenue % Execution

Source: Company, ICICIdirect.com Research

Exhibit 43: Order book to bill

3641

3789

7616 91

66 9756

1713

1496

1659

2110

2526

2.12.5

4.64.3 3.9

0

2000

4000

6000

8000

10000

12000

FY15 FY16 FY17E FY18E FY19E

| cr

ore

0

1

2

3

4

5

(x)

Total Order Book Revenue Order book to bill

Source: Company, ICICIdirect.com Research

Exhibit 44: Revenue segmentation

948 992 1225 1568 1875765 504 434

542651

273257 273

313356

0500

100015002000250030003500

FY15 FY16 FY17E FY18E FY19E

| cr

ore

Consultancy Turnkey Other Income

Source: Company, ICICIdirect.com, Research

Exhibit 45: Revenues: Domestic vs. Overseas

1986 1753 19332423 2882

221 329 356485

631

0500

1000150020002500300035004000

FY15 FY16 FY17E FY18E FY19E

| cr

ore

Domestic Overseas

Source: Company, ICICIdirect.com, Research

Page 25ICICI Securities Ltd | Retail Equity Research

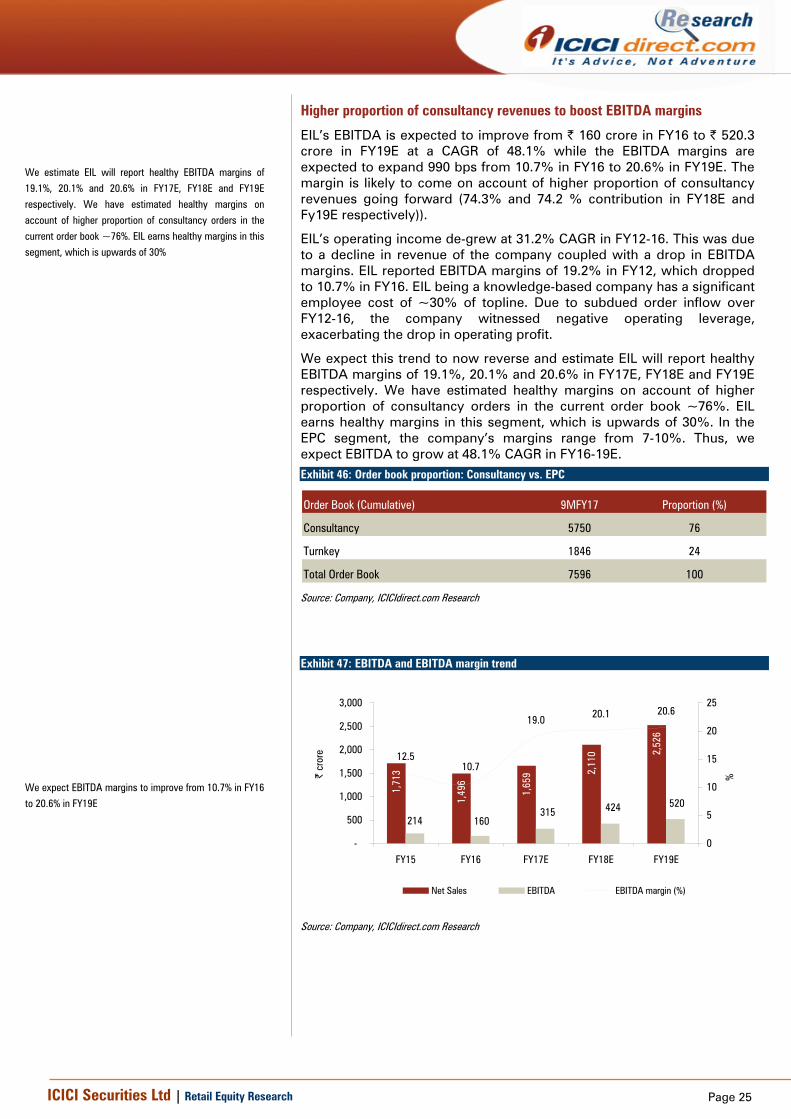

Higher proportion of consultancy revenues to boost EBITDA margins

EIL’s EBITDA is expected to improve from | 160 crore in FY16 to | 520.3 crore in FY19E at a CAGR of 48.1% while the EBITDA margins are expected to expand 990 bps from 10.7% in FY16 to 20.6% in FY19E. The margin is likely to come on account of higher proportion of consultancy revenues going forward (74.3% and 74.2 % contribution in FY18E and Fy19E respectively)).

EIL’s operating income de-grew at 31.2% CAGR in FY12-16. This was due to a decline in revenue of the company coupled with a drop in EBITDA margins. EIL reported EBITDA margins of 19.2% in FY12, which dropped to 10.7% in FY16. EIL being a knowledge-based company has a significant employee cost of ~30% of topline. Due to subdued order inflow over FY12-16, the company witnessed negative operating leverage, exacerbating the drop in operating profit.

We expect this trend to now reverse and estimate EIL will report healthy EBITDA margins of 19.1%, 20.1% and 20.6% in FY17E, FY18E and FY19E respectively. We have estimated healthy margins on account of higher proportion of consultancy orders in the current order book ~76%. EIL earns healthy margins in this segment, which is upwards of 30%. In the EPC segment, the company’s margins range from 7-10%. Thus, we expect EBITDA to grow at 48.1% CAGR in FY16-19E. Exhibit 46: Order book proportion: Consultancy vs. EPC

Order Book (Cumulative) 9MFY17 Proportion (%)

Consultancy 5750 76

Turnkey 1846 24

Total Order Book 7596 100 Source: Company, ICICIdirect.com Research

Exhibit 47: EBITDA and EBITDA margin trend

1,71

3

1,49

6

1,65

9 2,11

0 2,52

6

214 160315 424 520

12.510.7

19.0 20.1 20.6

-

500

1,000

1,500

2,000

2,500

3,000

FY15 FY16 FY17E FY18E FY19E

| cr

ore

0

5

10

15

20

25

%

Net Sales EBITDA EBITDA margin (%)

Source: Company, ICICIdirect.com Research

We estimate EIL will report healthy EBITDA margins of

19.1%, 20.1% and 20.6% in FY17E, FY18E and FY19E

respectively. We have estimated healthy margins on

account of higher proportion of consultancy orders in the

current order book ~76%. EIL earns healthy margins in this

segment, which is upwards of 30%

We expect EBITDA margins to improve from 10.7% in FY16

to 20.6% in FY19E

Page 26ICICI Securities Ltd | Retail Equity Research

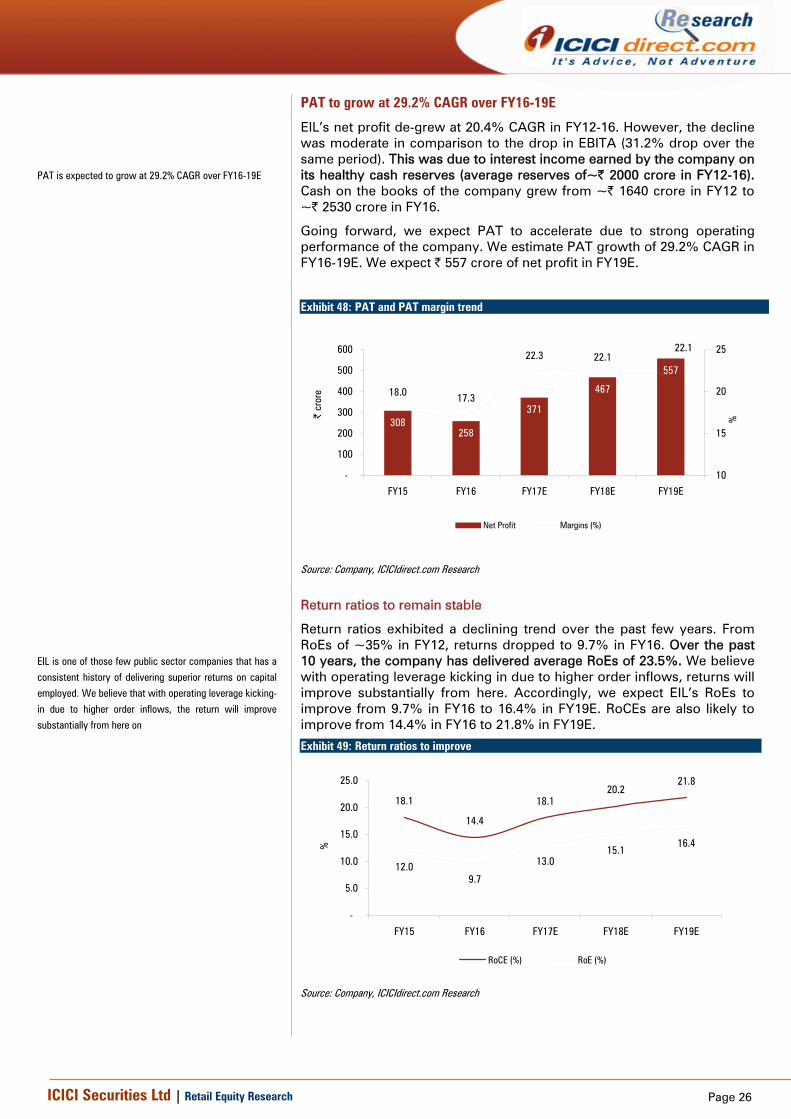

PAT to grow at 29.2% CAGR over FY16-19E

EIL’s net profit de-grew at 20.4% CAGR in FY12-16. However, the decline was moderate in comparison to the drop in EBITA (31.2% drop over the same period). This was due to interest income earned by the company on its healthy cash reserves (average reserves of~| 2000 crore in FY12-16). Cash on the books of the company grew from ~| 1640 crore in FY12 to ~| 2530 crore in FY16.

Going forward, we expect PAT to accelerate due to strong operating performance of the company. We estimate PAT growth of 29.2% CAGR in FY16-19E. We expect | 557 crore of net profit in FY19E.

Exhibit 48: PAT and PAT margin trend

308258

371

467

557

18.0 17.3

22.3 22.122.1

-

100

200

300

400

500

600

FY15 FY16 FY17E FY18E FY19E

| cr

ore

10

15

20

25

%

Net Profit Margins (%)

Source: Company, ICICIdirect.com Research

Return ratios to remain stable

Return ratios exhibited a declining trend over the past few years. From RoEs of ~35% in FY12, returns dropped to 9.7% in FY16. Over the past 10 years, the company has delivered average RoEs of 23.5%. We believe with operating leverage kicking in due to higher order inflows, returns will improve substantially from here. Accordingly, we expect EIL’s RoEs to improve from 9.7% in FY16 to 16.4% in FY19E. RoCEs are also likely to improve from 14.4% in FY16 to 21.8% in FY19E.

Exhibit 49: Return ratios to improve

18.1

14.4

18.120.2

21.8

12.09.7

13.015.1

16.4

-

5.0

10.0

15.0

20.0

25.0

FY15 FY16 FY17E FY18E FY19E

%

RoCE (%) RoE (%)

Source: Company, ICICIdirect.com Research

PAT is expected to grow at 29.2% CAGR over FY16-19E

EIL is one of those few public sector companies that has a

consistent history of delivering superior returns on capital

employed. We believe that with operating leverage kicking-

in due to higher order inflows, the return will improve

substantially from here on

Page 27ICICI Securities Ltd | Retail Equity Research

Cash flows set to improve; CFO/EBITDA healthy at 1.4x

The company is expected to generate healthy cash flows with cash flow from operations (CFO) increasing from | 457 crore in FY16 to | 746 crore in FY19E. The FCF is also likely to remain healthy on the back of strong CFO. We expect EIL to deliver FCF of | 604 crore and | 636 crore in FY18E and FY19E respectively. Net cash as a percentage of net worth is also likely to remain over 100% in both FY18E as well as FY19E.

Exhibit 50: CFO/EBITDA to remain strong

161

865

457

620 661746

377

214160

315424

520

0.4

4.0

2.9

1.6 1.4

2.0

0100200300400500600700800900

1000

FY14 FY15 FY16 FY17E FY18E FY19E

| cr

ore

0.00.51.01.52.02.53.03.54.04.5

(x)

CFO EBITDA CFO:EBITDA

Source: Company, ICICIdirect.com Research

Exhibit 51: Strong FCF generation, FCF yield

807

417

575686

606

7.9

4.15.6 6.0 6.7

0100200300400500600700800900

FY15 FY16 FY17E FY18E FY19E

| cr

ore

-6

-3

0

3

6

9

12

%

FCF FCF Yield

Source: Company, ICICIdirect.com Research

Exhibit 52: Net cash as percentage of net worth (95% in FY16)

1768 23

56

2539 2928 33

38 3785

72

92 95103 108 111

0500

1000150020002500300035004000

FY14 FY15 FY16 FY17E FY18E FY19E

| cr

ore

0

20

40

60

80

100

120

%Net Cash As %age of Networth

Source: Company, ICICIdirect.com Research

Page 28ICICI Securities Ltd | Retail Equity Research

Risks & concerns Subdued oil & gas prices/increase in alternative sources of energy

Oil & gas prices are subject to significant fluctuations in response to relatively minor changes in their supply or demand. EIL witnessed a significant slowdown in order inflows when oil prices started trending downwards. This is primarily on account of deferral of capital expenditure plans by its major customers that derive revenues from the hydrocarbons sector. Thus, subdued oil & gas prices for long periods of time may result in weak operations and financial condition for the company. Similarly, increase in use of alternative sources of energy can push large hydrocarbon companies to defer or even cancel their capex plans. This may severely dent the business outlook of the company.

Heavy dependence on hydrocarbon revenues

Currently, EIL derives ~92% of revenue from the hydrocarbon sector. Hydrocarbon exploration is a capital intensive and high risk-high reward business subject to the risk that even after a considerable investment, the discovered hydrocarbon reserve may not be commercially viable for production. Thus, EIL’s success in this sector depends, to a great extent, on its ability to maintain and/or establish relationship with key clients and other partners and also its ability to deploy additional management, financial and operational resources. Additionally, if the hydrocarbon sector ceases to be a growth driver for EIL’s business, the company’s financial condition may be adversely affected.

Failure to effectively manage diversification/stake acquisitions may derail growth, profitability

EIL continuously identifies and targets specific project segments and industries where it believes there is high potential for growth. These include projects in the power-solar and nuclear, oil & gas exploration, gas based fertiliser projects, coal to liquid, water and waste management, liquefied natural gas and city gas distribution. These additional business activities may require additional management, financial and operational resources, which may weigh heavily on the current margin profile of the company. EIL’s stake acquisition in Ramagundam fertiliser plant (along with NFL, EIL investment of | 1250 crore, investment in 125 MW solar thermal project, office investments of | 560 crore in various cities, investment in BOT assets and nuclear plant BOP are moves that can dilute the return profile of the company.

EPC business may lead to reduced profit

EIL engages in EPC contracts under various types of contractual arrangements where costs are estimated in advance. A majority of its engineering consultancy and EPC projects (by value) are cost-reimbursable contracts that allocate the risk of cost overruns to its clients. However, some engineering consultancy and EPC contracts are fixed-price or lumpsum contracts, where EIL bears a portion of the risk for cost overruns. Under these types of contracts, contract prices are established in part on cost and scheduling estimates, which are based on a number of assumptions. For EPC contracts, these assumptions include assumptions relating to future economic conditions, prices and availability of labour, equipment and materials. If these estimates prove inaccurate, or circumstances change such as unanticipated technical problems, difficulties in obtaining permits or approvals, changes in local laws or labour conditions, weather delays, cost of raw materials, or its suppliers' or subcontractors' inability to perform, cost overruns may occur. In that case, the company could experience reduced profits.

Page 29ICICI Securities Ltd | Retail Equity Research

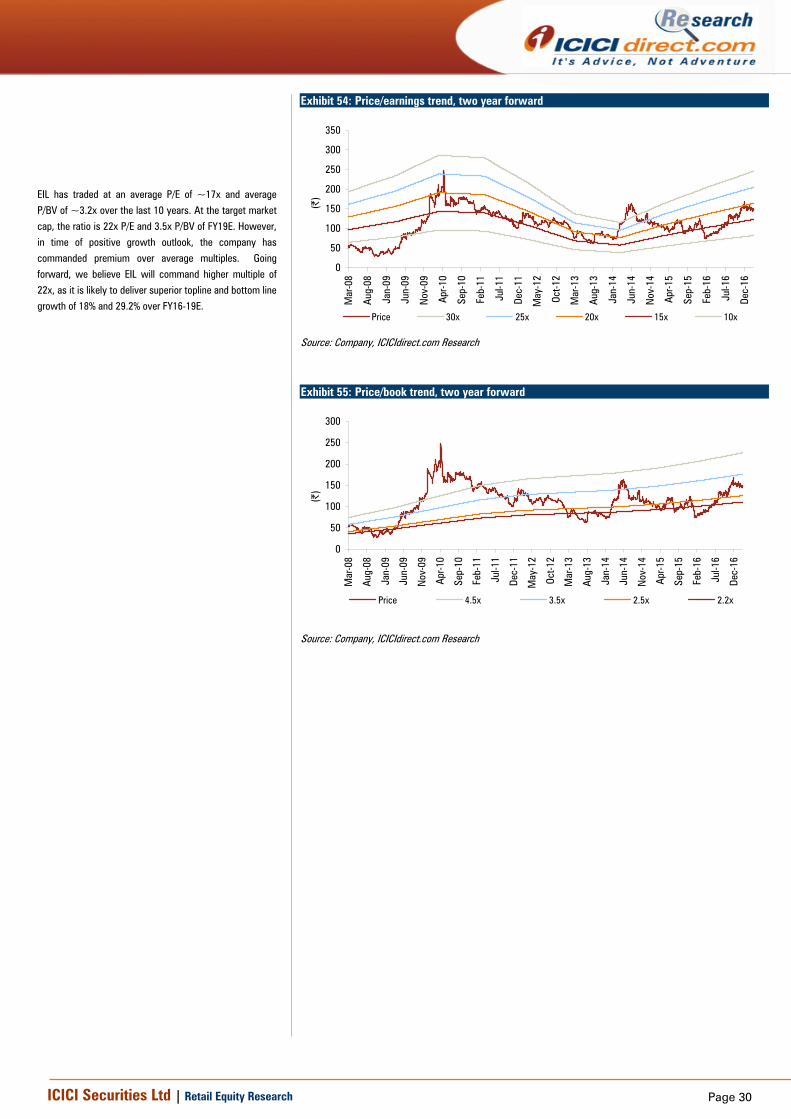

Valuation EIL has a sound track record of delivering topline and bottomline growth despite cyclical nature of the industry due to volatile oil prices. Across business cycles, EIL has managed to keep its P&L and net worth ticking. The same is reflected in the growth of topline, bottomline and net worth of 11.3%, 6.8% and 11% CAGR over FY07-16, respectively. On the valuation front, EIL has commanded ~17x its earnings, which is 10 year average of two year forward earnings. However, in time of positive growth outlook, the company has commanded premium over average multiples. Going forward, we believe EIL will command higher premium (~22x) as it is likely to deliver superior topline and bottom line growth of 18% and 29.2% over FY16-19E. Exhibit 53: EIL’s valuation history: P/E multiple vs. Growth outlook Year EPS P/E Revenue PAT

(|) 2 year Forward 2 year Forward CAGR 2 year Forward CAGR

FY01 1.8 21 1.9 -28.0

FY02 0.4 8 41.1 80.1

FY03 1.0 22 5.8 32.5

FY04 1.2 15 -14.0 31.5

FY05 1.7 12 -21.0 12.7

FY06 2.1 21 -3.4 18.5

FY07 2.1 23 63.8 55.2

FY08 2.9 9 64.4 49.6

FY09 5.1 6 35.7 23.2

FY10 6.5 19 36.2 20.9

FY11 7.8 18 -5.8 9.7

FY12 9.6 16 -29.8 -13.2

FY13 9.3 20 -17.3 -30.0

FY14 7.1 19 -9.4 -26.6

FY15 4.6 27 -1.6 9.6

FY16 3.8 20 18.8 34.5

FY17E 5.5 18 23.3 22.7

FY18E 6.9

FY19E 8.3 22 18 29 Source: Company, ICICIdirect.com Research

The company is also currently sitting on highest ever order backlog of ~| 7616 crore as on 9MFY17. We also believe EIL has a superior business model vis-à-vis its capital goods peers given EIL’s high reliance on non-project related, non-capital intensive consulting business. The upcoming opportunity from the overseas segment has potential to transform this medium-sized company to a bigger and stronger project management consultant. Accordingly, we ascribe EIL a price earning multiple of 22x for improved visibility in the performance of the company over the next few years on account of all time high order backlog of ~| 7616 crore and scarcity premium (no other large listed pure-play consultancy company). We value EIL at | 182 per share (22x FY19E EPS of | 8.3) and have a BUY recommendation on the stock.

EIL has a sound track record of delivering topline and

bottomline growth despite the cyclical nature of the

industry due to volatile oil prices. Across business cycles,

EIL has managed to keep its P&L and net worth ticking.

The same is reflected in the growth of topline, bottomline

and net worth of 11.3%, 6.8% and 11% CAGR over FY07-16

respectively.

Page 30ICICI Securities Ltd | Retail Equity Research

Exhibit 54: Price/earnings trend, two year forward

0

50

100

150

200

250

300

350

Mar

-08

Aug-

08

Jan-

09

Jun-

09

Nov

-09

Apr-1

0

Sep-

10

Feb-

11

Jul-1

1

Dec-

11

May

-12

Oct-1

2

Mar

-13

Aug-

13

Jan-

14

Jun-

14

Nov

-14

Apr-1

5

Sep-

15

Feb-

16

Jul-1

6

Dec-

16

(|)

Price 30x 25x 20x 15x 10x

Source: Company, ICICIdirect.com Research

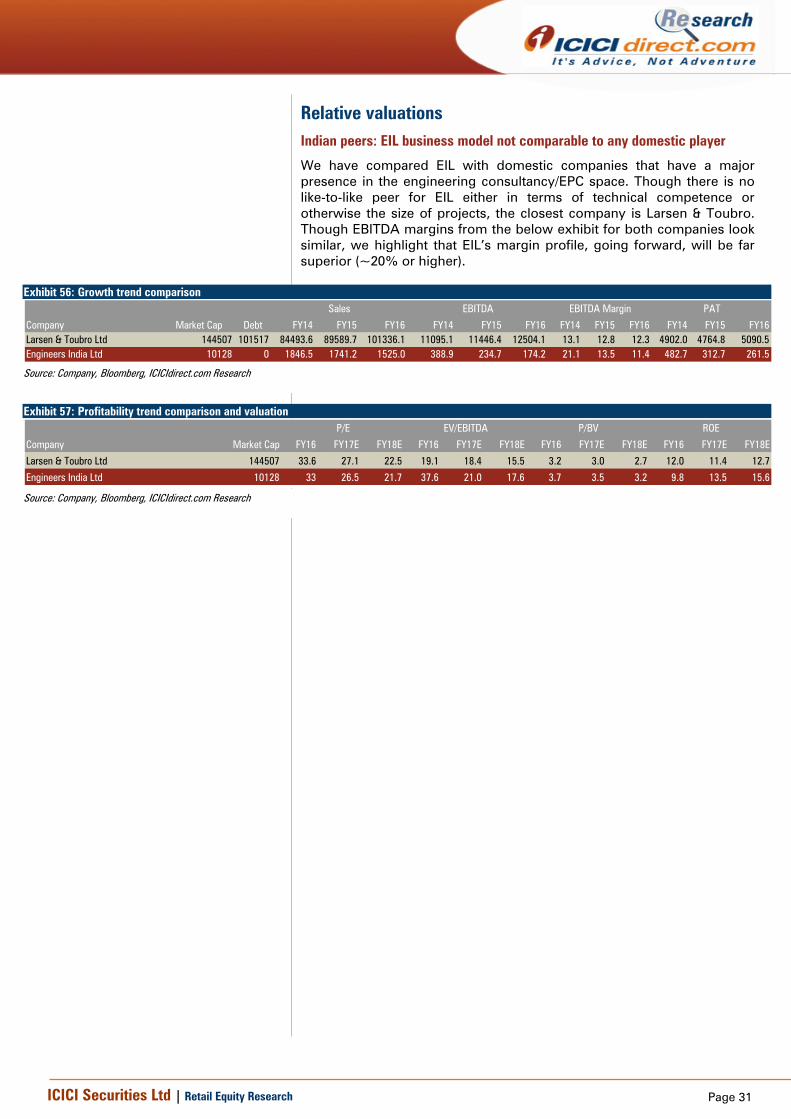

EIL has traded at an average P/E of ~17x and average

P/BV of ~3.2x over the last 10 years. At the target market

cap, the ratio is 22x P/E and 3.5x P/BV of FY19E. However,

in time of positive growth outlook, the company has

commanded premium over average multiples. Going

forward, we believe EIL will command higher multiple of

22x, as it is likely to deliver superior topline and bottom line

growth of 18% and 29.2% over FY16-19E.

Exhibit 55: Price/book trend, two year forward

0

50

100

150

200

250

300

Mar

-08

Aug-

08

Jan-

09

Jun-

09

Nov

-09

Apr-1

0

Sep-

10

Feb-

11

Jul-1

1

Dec-

11

May

-12

Oct-1

2

Mar

-13

Aug-

13

Jan-

14

Jun-

14

Nov

-14

Apr-1

5

Sep-

15

Feb-

16

Jul-1

6

Dec-

16

(|)

Price 4.5x 3.5x 2.5x 2.2x

Source: Company, ICICIdirect.com Research

Page 31ICICI Securities Ltd | Retail Equity Research

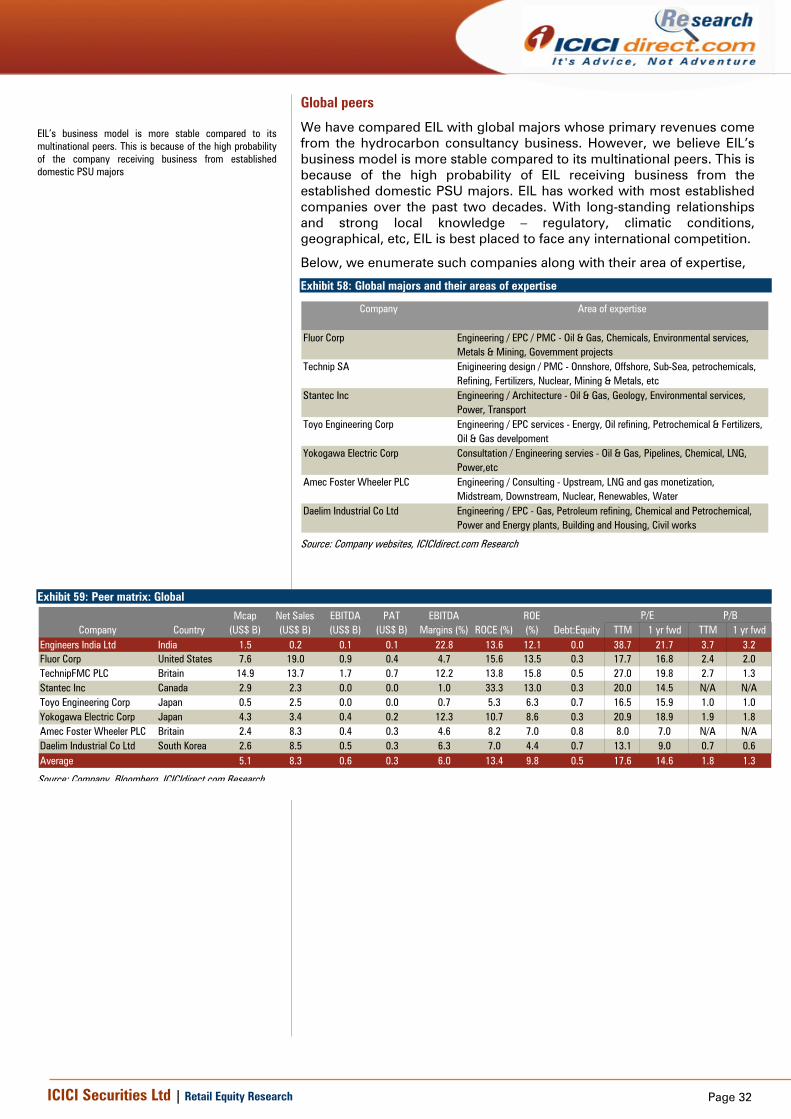

Relative valuations Indian peers: EIL business model not comparable to any domestic player

We have compared EIL with domestic companies that have a major presence in the engineering consultancy/EPC space. Though there is no like-to-like peer for EIL either in terms of technical competence or otherwise the size of projects, the closest company is Larsen & Toubro. Though EBITDA margins from the below exhibit for both companies look similar, we highlight that EIL’s margin profile, going forward, will be far superior (~20% or higher).

Exhibit 56: Growth trend comparison

FY14 FY15 FY16 FY14 FY15 FY16 FY14 FY15 FY16 FY14 FY15 FY16Larsen & Toubro Ltd 144507 101517 84493.6 89589.7 101336.1 11095.1 11446.4 12504.1 13.1 12.8 12.3 4902.0 4764.8 5090.5Engineers India Ltd 10128 0 1846.5 1741.2 1525.0 388.9 234.7 174.2 21.1 13.5 11.4 482.7 312.7 261.5

Company

PAT

Market Cap Debt

Sales EBITDA MarginEBITDA

Source: Company, Bloomberg, ICICIdirect.com Research

Exhibit 57: Profitability trend comparison and valuation

FY16 FY17E FY18E FY16 FY17E FY18E FY16 FY17E FY18E FY16 FY17E FY18E

Larsen & Toubro Ltd 144507 33.6 27.1 22.5 19.1 18.4 15.5 3.2 3.0 2.7 12.0 11.4 12.7

Engineers India Ltd 10128 33 26.5 21.7 37.6 21.0 17.6 3.7 3.5 3.2 9.8 13.5 15.6

Company Market Cap

P/E EV/EBITDA P/BV ROE

Source: Company, Bloomberg, ICICIdirect.com Research

Page 32ICICI Securities Ltd | Retail Equity Research

Global peers

We have compared EIL with global majors whose primary revenues come from the hydrocarbon consultancy business. However, we believe EIL’s business model is more stable compared to its multinational peers. This is because of the high probability of EIL receiving business from the established domestic PSU majors. EIL has worked with most established companies over the past two decades. With long-standing relationships and strong local knowledge – regulatory, climatic conditions, geographical, etc, EIL is best placed to face any international competition.

Below, we enumerate such companies along with their area of expertise,

Exhibit 58: Global majors and their areas of expertise

Fluor Corp Engineering / EPC / PMC - Oil & Gas, Chemicals, Environmental services, Metals & Mining, Government projects

Technip SA Enigineering design / PMC - Onnshore, Offshore, Sub-Sea, petrochemicals, Refining, Fertilizers, Nuclear, Mining & Metals, etc

Stantec Inc Engineering / Architecture - Oil & Gas, Geology, Environmental services, Power, Transport

Toyo Engineering Corp Engineering / EPC services - Energy, Oil refining, Petrochemical & Fertilizers, Oil & Gas develpoment

Yokogawa Electric Corp Consultation / Engineering servies - Oil & Gas, Pipelines, Chemical, LNG, Power,etc

Amec Foster Wheeler PLC Engineering / Consulting - Upstream, LNG and gas monetization, Midstream, Downstream, Nuclear, Renewables, Water

Daelim Industrial Co Ltd Engineering / EPC - Gas, Petroleum refining, Chemical and Petrochemical, Power and Energy plants, Building and Housing, Civil works

Company Area of expertise

Source: Company websites, ICICIdirect.com Research

Exhibit 59: Peer matrix: Global

TTM 1 yr fwd TTM 1 yr fwdEngineers India Ltd India 1.5 0.2 0.1 0.1 22.8 13.6 12.1 0.0 38.7 21.7 3.7 3.2Fluor Corp United States 7.6 19.0 0.9 0.4 4.7 15.6 13.5 0.3 17.7 16.8 2.4 2.0TechnipFMC PLC Britain 14.9 13.7 1.7 0.7 12.2 13.8 15.8 0.5 27.0 19.8 2.7 1.3Stantec Inc Canada 2.9 2.3 0.0 0.0 1.0 33.3 13.0 0.3 20.0 14.5 N/A N/AToyo Engineering Corp Japan 0.5 2.5 0.0 0.0 0.7 5.3 6.3 0.7 16.5 15.9 1.0 1.0Yokogawa Electric Corp Japan 4.3 3.4 0.4 0.2 12.3 10.7 8.6 0.3 20.9 18.9 1.9 1.8Amec Foster Wheeler PLC Britain 2.4 8.3 0.4 0.3 4.6 8.2 7.0 0.8 8.0 7.0 N/A N/ADaelim Industrial Co Ltd South Korea 2.6 8.5 0.5 0.3 6.3 7.0 4.4 0.7 13.1 9.0 0.7 0.6Average 5.1 8.3 0.6 0.3 6.0 13.4 9.8 0.5 17.6 14.6 1.8 1.3

CompanyMcap

(US$ B)PAT

(US$ B)EBITDA

Margins (%)Net Sales (US$ B)

EBITDA (US$ B)Country ROCE (%)

ROE (%) Debt:Equity

P/E P/B

Source: Company, Bloomberg, ICICIdirect.com Research

EIL’s business model is more stable compared to its multinational peers. This is because of the high probability of the company receiving business from established domestic PSU majors

Page 33ICICI Securities Ltd | Retail Equity Research

Tables and ratios: Standalone Exhibit 60: Profit & loss account