Embed Size (px)

Citation preview

Manufacturing and Distribution SummitOlympia & Lynnwood, WashingtonSeptember 14 & 15, 2010

National & Washington Survey Results

Survey demographics

Fifth annual national survey

Survey in field March 2 – April 5

1,061 individual company respondents - 69 Washington

68% Mfg / 32% Dist – 85%/15% Washington

84% C level executives – 78% Washington

62% $25 million and above - both

Tax policy results issued April 20th

Official release of results June 7th

3

Current condition of business

4

“Thriving and growing” by industry segment

5

Anticipated recovery timeframe

6

Credit availability

Overall 19% of respondents report difficulty securing credit

29% of companies <$25M in revenue report the same

Southwest U.S. has tightest credit

Those reporting lack of available financing also report delayed recovery into 2011 or beyond

Companies with $100 – $250 million in revenue have the highest level of worry about future credit availability

7

Top Growth Strategies

8

Export sales

9

Change in export sales

10

Projected health care cost increases

11

Challenges of new product development

12

Survey data indicates those companies introducingnew products have higher gross margins

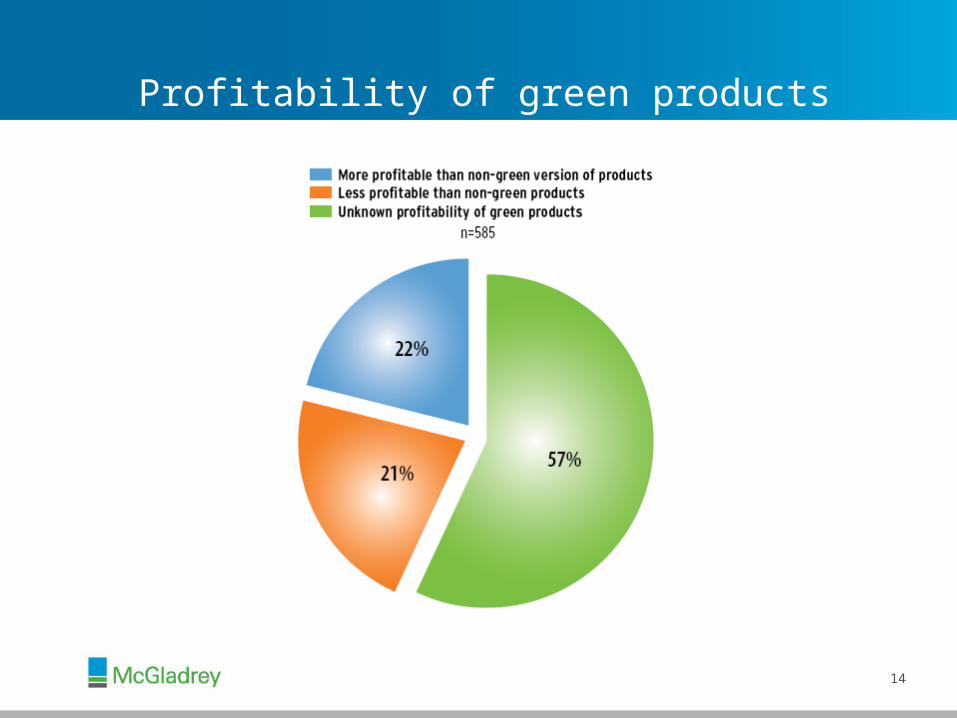

Industry segments offering green products

13

Profitability of green products

14

Projected Employment Levels

15

Skilled labor recruiting needs (manufacturing)

16

Concern about pending legislation

17

Concerns about tax increases for pass-through entities

18

Current Manufacturing Situation and Outlook

Source: U.S. Department of Commerce

Growth in Real Output: U.S. Manufacturing vs. Overall GDP

0

100

200

300

400

500

1958 1968 1978 1988 1998 2008

Qantity Index of GDP (1947=100)

GDP Manufacturing

Source: National Association of Manufacturers

Source: U.S. Bureau of Labor StatisticsCompiled by The Manufacturing Institute for the 8th Edition of Facts About Modern Manufacturing

Manufacturing Drives Productivity Growth

Source: U.S. Patent and Trademark OfficeCompiled by The Manufacturing Institute for the 8th Edition of Facts About Modern Manufacturing

The United States leads the way in innovation

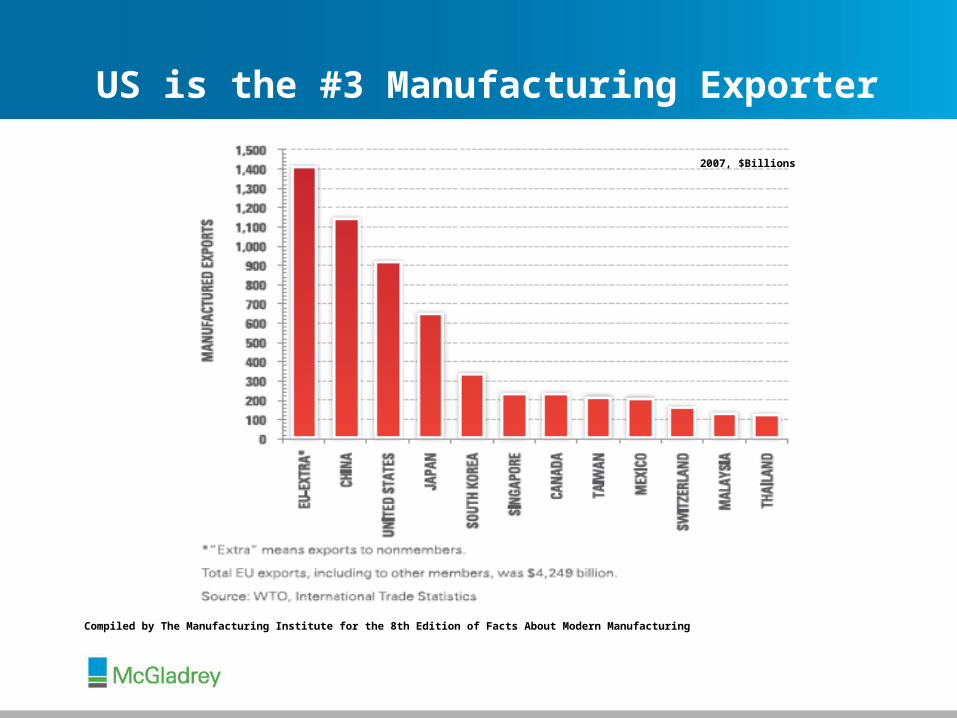

US is the #3 Manufacturing Exporter

2007, $Billions

Compiled by The Manufacturing Institute for the 8th Edition of Facts About Modern Manufacturing

Source: National Association of Manufacturers

Jobs Supported by Manufacturing Exports

The Employment Situation

Source: Department of Labor

Deeper Recession, Slower Recovery

27

Consumer Confidence

Source: Conference Board

0

20

40

60

80

100

120

140

160

180 2001.10 = 100

July 07 (131.2)

August 10 (62.7)

Source: Commerce Department

1

1.1

1.2

1.3

1.4

1.5

2006.09 2007.06 2008.03 2008.12 2009.09 2010.06

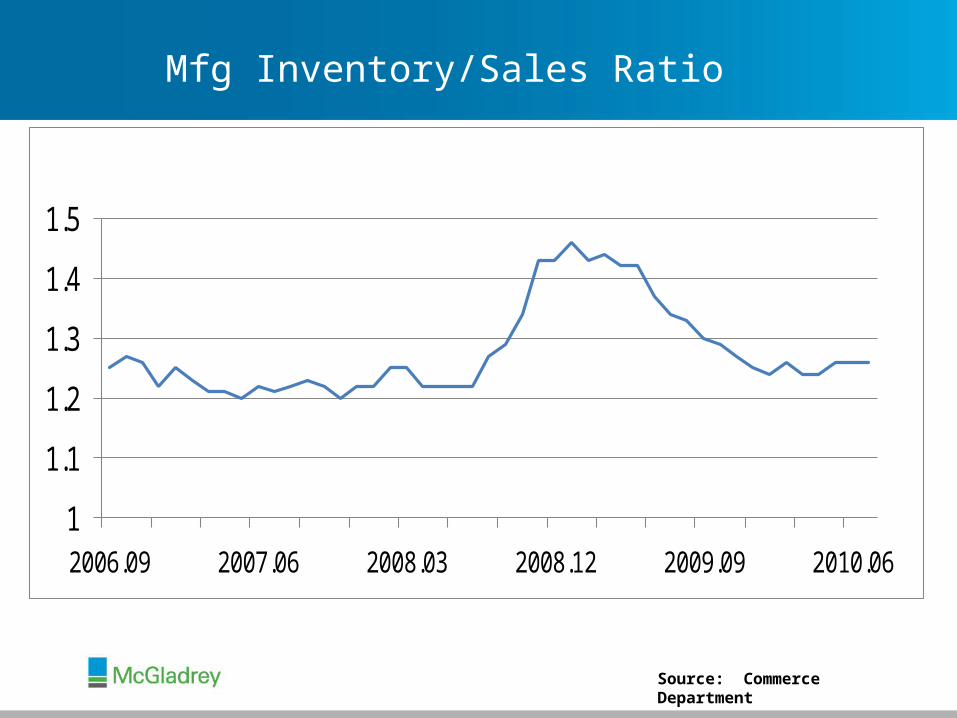

Mfg Inventory/Sales Ratio

Housing Market

0

20

40

60

80

100

1995.10 1997.08 1999.06 2001.04 2003.02 2004.12 2006.10 2008.08 2010.06

*SAAR (seasonally-adjusted annual rate)Source: U.S. Department of Commerce, OECD

US Trade and the Global Economy

92

94

96

98

100

102

104

106

108

-50

-40

-30

-20

-10

0

10

20

30

40

50

2007.12 2008.04 2008.08 2008.12 2009.04 2009.08 2009.12 2010.04

OECD Leading Indicators

(100=long-term average)

U.S. Trade3 Month Percent Change (SAAR*)

Exports Imports OECD Leading Indicators

Manufacturing Production

Source: Federal Reserve

Source: Federal Reserve, and NAM Forecast

The Manufacturing Outlook

Source: Department of Commerce, and NAM Forecast

The Outlook for GDP

Summary

• Business conditions improved• Some limited credit availability especially for smalls• New export markets driving international sales growth• Capacity increasing • Less inventory reduction planned• Potential for inflation• New product development increases gross margins• Go green but understand the cost• Workforce skills shortages will only increase• Unprecedented concern exist over policy issues

35

36

Experience the power of being understood.SM

Note our new web address: www.mcgladrey.com

Continue the conversation

37

http//mfgblog.mcgladrey.com