Embed Size (px)

Citation preview

Manufacturing Accounts

Why Prepare this account

• Manufacturers make goods rather than buy them from suppliers

• A manufacturing account is required to provide a value for the Cost of such production

• A Manufacturing account is made up of ALL of the relevant costs of the finished goods sold and can be split into DIRECT and INDIRECT costs

Manufacturing costs

• Direct costs (can be traced to the manufacture of specific products)• Material• Labour• Expenses (carriage in,

royalties)

• Indirect Costs (must be paid but are of a general benefit to production and so are NOT specifically related to any particular product • Supervisors wages• Factory rent• Factory rates• Factory heat/light• Depreciation of factory

machinery

Basic structure

• COST OF RAW MATERIALS CONSUMED• These are direct costs of raw

materials AND relevant expenses• It is calculated as follows

• Opening stock of raw materialsADD• Purchase of raw materials• Carriage in of raw materialsLESS• Closing stock of raw materials

• PRIME COST OF PRODUCTION• This is the total of ALL DIRECT

COSTS incurred in manufacture of the product

• It is calculated by adding the following

• Cost of raw materials consumed• Direct Labour• Royalties

Basic structure

• FACTORY COST OF PRODUCTION• This is the total of ALL DIRECT AND

ALL INDIRECT COSTS incurred in manufacture of the product

• It is calculated by adding the following

•Prime Cost•Indirect Expenses

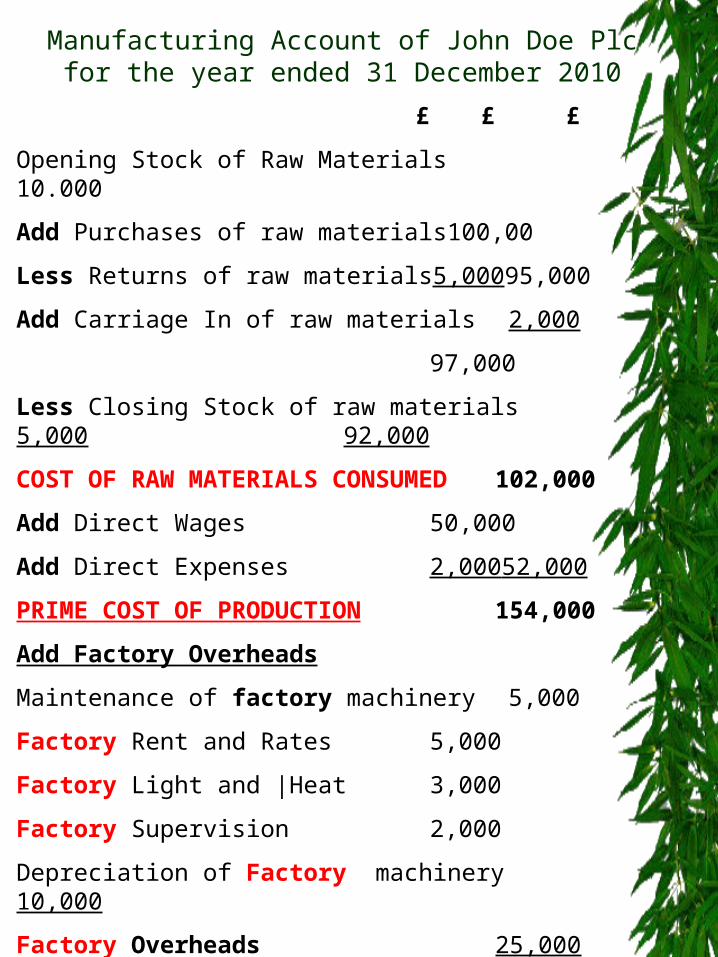

Manufacturing Account of John Doe Plc for the year ended 31 December 2010

£ £ £

Opening Stock of Raw Materials 10.000

Add Purchases of raw materials 100,00

Less Returns of raw materials 5,00095,000

Add Carriage In of raw materials 2,000

97,000

Less Closing Stock of raw materials 5,000 92,000

COST OF RAW MATERIALS CONSUMED 102,000

Add Direct Wages 50,000

Add Direct Expenses 2,000 52,000

PRIME COST OF PRODUCTION 154,000

Add Factory Overheads

Maintenance of factory machinery 5,000

Factory Rent and Rates 5,000

Factory Light and |Heat 3,000

Factory Supervision 2,000

Depreciation of Factory machinery 10,000

Factory Overheads 25,000

FACTORY COST OF PRODUCTION 179,000

Exercise 2Manufacturing Account of Woodcraft Plc

£ £ £

Opening Stock of Raw Materials 2.000

Add Purchases of raw materials 60,000

Less Returns of raw materials 060,000

Add Carriage In of raw materials 0

60,000

Less Closing Stock of raw materials 3,000 57,000

COST OF RAW MATERIALS CONSUMED 59,000

Add Direct Wages 36,000

Add Direct Expenses 0 36,000

PRIME COST OF PRODUCTION 95,000

Add Factory Overheads

Insurance of factory building 900

Depreciation of FactoryEquipment 2,500

Factory Light and |Heat 800

Factory Rates 520

FACTORY OVERHEADS 4,720

FACTORY COST OF PRODUCTION 99,720

Accruals / Prepayments• Accruals occur when a debt is

outstanding/ still owing when drawing up the final accounts

• Prepayments occur when a debt has been paid in advance/overpaid at the time of creating the final accounts

• The Manufacturing and Trading profit & Loss account must show what SHOULD HAVE been paid for the year therefore

• If an amount is underpaid/accrued – the amount due is added to the figure in the trial balance and the adjusted figure taken to the P&L account.

• The amount due is transferred to the Balance sheet as a Current Liabiity

Accruals / Prepayments

• If an amount is prepaid – the amount due is deducted from the figure in the trial balance and the adjusted figure taken to the P&L account.

• The amount prepaid is then transferred to the balance sheet as a current asset

Depreciation

• This is the amount by which an asset drops in value over a period of time (usually a year), due to wear and tear

• The amount of depreciation for the year is taken to the Manufacturing/Profit & Loss account

• The accumulated depreciation is posted in the company’s balance sheet

Exercise 3Manufacturing Account of Acorn Plc for the year

ended 31 July£ £ £

Opening Stock of Raw Materials 2,300

Add Purchases of raw materials 87,600

Less Closing Stock of raw materials 3,250 84,350

Cost of Raw Materials consumed 86,650

Add Direct Wages 48,000

Add Direct Expenses 0 48,000

PRIME COST 134,650

Add Factory Overheads

General Expenses 3,450

Lighting & Heating 4,320

Insurance 980

Rent & Rates 1,430

Factory Overheads 10,180

144,830

ADD WIP at beginning 4,500

149,330

Less WIP at end 4,200

FACTORY COST OF PRODUCTION 145,130

Exercise 3Trading Account of Acorn Plc for the

year ended 31 July

£ £ £

Sales 200,000

LESS Cost of Sales

Opening stock of finished goods 6,200

ADD Factory cost of Production 145,130

151,330

Less Closing stock of finished goods 7,500

Cost of Sales 143,830

GROSS PROFIT 56,170

Exercise 4The Vineyard

Notes for the Manufacturing Account

ACCRUALS

Lighting and Heating

Amount paid 3,400

Add Accrual 720 Liability (Balance Sheet)

4,120 Manufacturing Acc

PREPAYMENTS

Insurance

Amount paid 2,400

Less Prepayment 600 Asset (Balance Sheet)

1,800 Manufacturing Acc

Exercise 4Manufacturing Account of The Vineyard for the y/e

30 Nov£ £ £

Opening Stock of Raw Materials 12,400

Add Purchases of raw materials 230,820

Less Closing Stock of raw materials 10,660 220,160

Cost of Raw Materials consumed 232,560

Add Direct Wages 124,000

Add Direct Expenses 0 124,000

PRIME COST 356,560

Add Factory Overheads

General Expenses 14,500

Lighting & Heating 4,120

Insurance 1,800

Rent & Rates 6,000

Depreciation of factory equipment 20,000

Factory Overheads 46,420

402,980

ADD WIP at beginning 32,460

435,440

Less WIP at end 46,500

FACTORY COST OF PRODUCTION 388,940

Exercise 4Trading Account of The Vineyard for the year

ended 31 JulyE £ £

Sales 480,000

LESS Cost of Sales

Opening stock of finished goods 60,800

ADD Factory cost of Production 388,940

449,740

Less Closing stock of finished goods 85,340

Cost of Sales 364,400

GROSS PROFIT 115,600

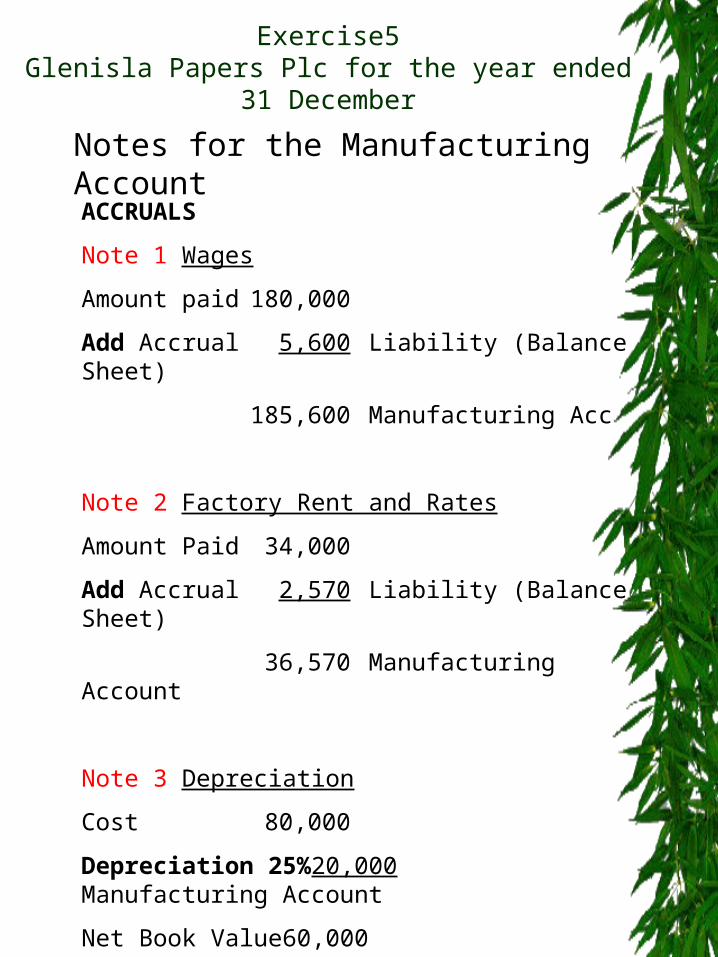

Exercise5Glenisla Papers Plc for the year ended 31

December

Notes for the Manufacturing Account

ACCRUALS

Note 1 Wages

Amount paid 180,000

Add Accrual 5,600 Liability (Balance Sheet)

185,600 Manufacturing Acc

Note 2 Factory Rent and Rates

Amount Paid 34,000

Add Accrual 2,570 Liability (Balance Sheet)

36,570 Manufacturing Account

Note 3 Depreciation

Cost 80,000

Depreciation 25% 20,000 Manufacturing Account

Net Book Value 60,000

Exercise 5Manufacturing Account of Glenisla Papers Plc

for the year ended 31 December£ £

Opening Stock of Raw Materials 15,000

Add Purchases of raw materials 220,000

Less Returns of raw materials 6,500 213,500

Less Closing Stock of raw materials 12,500 201,000

Cost of Raw Materials consumed 216,000

Add Direct Wages * Note 1 185,600

Add Direct Expenses 0 185,600

PRIME COST 401,600

Add Factory Overheads

Maintenance of factory machinery 18,000

Factory Rent and Rates *Note 2 36,570

Factory Light and |Heat 2,600

Factory Supervision 25,000

Depreciation of factory machinery *Note3 20,000

Factory Overheads 102,170

FACTORY COST OF PRODUCTION 503,770

Exercise 6Northern Lights

Notes for the Manufacturing Account

PREPAYMENTS

Rent

Amount paid 16,500

Less Prepayment 3,400 C Asset (Balance Sheet)

13,100 Manufacturing Acc

Insurance

Amount Paid 4,500

Less Prepayment 1,200 C Asset (Balance Sheet)

3,300 Manufacturing Account

ACCRUAL

Lighting and Heating

Amount paid 4,200

Add Accrual 840 Asset (Balance Sheet)

5,040 Manufacturing Acc

Exercise 6Manufacturing Account of Northern Lights for

the y/e 28 February

£ £ £

Opening Stock of Raw Materials 18,300

Add Purchases of raw materials 126,900

Less Closing Stock of raw materials15,630111,270

Cost of Raw Materials consumed 129,570

Add Direct Wages 143,560

Add Direct Expenses 0 143,560

PRIME COST 273,130

Add Factory Overheads

General Expenses 21,500

Lighting & Heating 5,040

Insurance 3,300

Rent 13,100

Depreciation of Machinery 40,000

Factory Overheads 82,940

356,070

ADD WIP at beginning 24,600

380,670

Less WIP at end 32,500

FACTORY COST OF PRODUCTION 348,170

Exercise 6Trading Account of Northern Lights for

the year ended 28 February

£ £ £

Sales 600,000

LESS Cost of Sales

Opening stock of finished goods 38,000

ADD Factory cost of Production 348,170

386,170

Less Closing stock of finished goods 36,210

Cost of Sales 349,960

GROSS PROFIT 250,040

Exercise 7Sunseekers Products Plc

Notes for the Manufacturing /Trading Acc ACCRUAL

Direct Wages

Amount paid 210,800

Add Accrual 41,400 C Liability (Balance Sheet)

252,200 Manufacturing Acc

PREPAYMENTS

Factory Insurance

Amount paid 12,250

Less Prepayment 3,220 Asset (Balance Sheet)

9,030 Manufacturing Acc

Office Insurance

Amount Paid 14,520

Less Prepayment 1,050 Asset (Balance Sheet)

13,470 Profit & Loss Acc

Exercise 7Sunseekers Products Plc

Notes for the Manufacturing /TPL Acc DEPRECIATION

Factory Machinery

Cost 140,000

Depreciation 20% 28,000 Manufacturing Acc

Net Book Value 112,000

Office Equipment

Cost 60,000

Depreciation 15% 9,000 Profit & Loss Acc

Net Book Value 51,000

Exercise 7Manufacturing Account of Sunseekers Products

Plc for the y/e 30 April£ £ £

Opening Stock of Raw Materials 26,000

Add Purchases of Raw Materials 320,000

Less Closing Stock of Raw Materials 32,500 287500

COST OF RAW MATERIALS CONSUMED 313,500

Add Direct Wages 252,200

Add Direct Expenses 0 252,200

PRIME COST 565,700

ADD FACTORY OVERHEADS

Maintenance and Machinery 48,000

Insurance of Buildings (12250-3220) 9,030

Rent and Rates 43,600

General Expenses 22,430

Depreciation of Machinery 28,000

FACTORY OVERHEADS 151,060

716,760

Add WIP at Beginning 12,500

729,260

Less WIP at End 16,780

FACTORY COST OF PRODUCTION 712,480

Exercise 7Trading Profit & Loss Acc of Sunset Products

Plc for the y/e 30 April £ £ £ Sales

900,000

LESS COST OF GOODS SOLD

Opening stock of finished goods 84,000

Add Factory Cost of Production 712,480

796,480

Less Closing stock of finished goods 98,420 698,060

GROSS PROFIT 201,940

LESS EXPENSES

Insurance 3,320

Rent and Rates 14,520

Advertising 80,000

Provision for Doubtful Debts 5,000

Provision for Dep Office Equipment 9,000 111,840

NET PROFIT 90,100

BAD DEBTS Bad debts are amounts of money

owed to a business by DEBTORS who WILL NOT pay their debt due to bankruptcy etc

Bad Debts listed as an entry in the trial balance should ONLY be entered as an EXPENSE in the PROFIT AND LOSS Account

PROVISION FOR BAD DEBTS

If you are asked to create this account in the notes:

Profit and Loss Account Calculate the TOTAL value (eg

5% of Debtors, etc). Enter the total value of Provision

as an EXPENSE in the Profit and Loss Account

2. Balance Sheet SUBTRACT the TOTAL value

of provision from the Debtors Figure in the Balance Sheet

INCREASE IN PROVISION FOR BAD DEBT

If after calculating the new Provision for Bad Debts figure it shows an increase - eg from £3,000 to £5,000 then:

Add the difference (ie £2000) as an expense in the Profit and Loss Account

2. Subtract the new amount (ie £5,000) from the Debtors figure in the balance sheet

A DECREASE IN PROVISION FOR BAD DEBT

If after calculating the new Provision for Bad Debts figure it shows a decrease - eg from £6,000 to £4,000 then:

Add the difference (ie £2000) to the Gross Profit figure

2. Subtract the new amount (ie £4,000) from the Debtors figure in the balance sheet

Exercise 8Beachwear Plc

Notes for the Manufacturing /TPL Acc PREPAYMENTS

Factory Rent & Rates

Amount paid 26,700

Less Prepayment 4,200 Asset (Balance Sheet)

22,500 Manufacturing Acc

Office Rent & Rates

Amount paid 4,500

Less Prepayment 750 Asset (Balance Sheet)

3,750 Profit & Loss Acc

ACCRUALS

Office Salaries

Amount Paid 43,200

Add Accrual 4,380 Liability (Balance Sheet)

47,580 Profit & Loss Acc

Exercise 8Beachwear plc

Notes for the Manufacturing /Trading Acc PROVISION FOR DOUBTFUL DEBTS

Provision so far 2,000

Adjusted to 6,000 Deducted from Debtors B/S

Difference +£4,000 Increase to Man Acc

DEPRECIATION

Factory Machinery

Cost 220,000

Depreciation 25% 55,000 Manufacturing Acc

Net Book Value 165,000

Office Equipment

Cost 30,000

Depreciation 10% 3,000 Profit & Loss Acc

Net Book Value 27,000

Exercise 8Manufacturing Account of Beachwear plc for

the y/e 30 June£ £ £

Opening Stock of Raw Materials 14,500

Add Purchases of Raw Materials 235,600

Less Closing Stock of Raw Materials 12,500 223,100

COST OF RAW MATERIALS CONSUMED 237,600

Add Direct Wages 167,830

Add Direct Expenses (royalties) 8,000 175,830

PRIME COST 413,430

ADD FACTORY OVERHEADS

Maintenance and Machinery 12,000

Electricity 4,355

Insurance of Buildings 3,500

Rent and Rates (26700-4200) 22,500

Depreciation of Machinery 55,000

FACTORY OVERHEADS 97,355

510,785

Add WIP at Beginning 23,480

534,265

Less WIP at End 23,560

FACTORY COST OF PRODUCTION 510,705

Exercise 8Manufacturing Account of Beachwear plc for

the y/e 30 June

£ £ £ Sales

620,000

Less Cost of Goods Sold

Opening stock of finished goods 64,595

Add Factory Cost of Production 510,705

575,300

Less Closing stock of finished goods 82,300 493,000

GROSS PROFIT 127,000

Less Expenses

Electricity 1,420

Insurance of Buildings 985

Rent and Rates (4500-750) 3,750

Office Salaries(43200+4380) 47,580

Provision for Doubtful Debts 4,000

Prov for Depreciation of Equipment 3,000 60,735

NET PROFIT 66,265

Exercise 11Harvey & Nicholl

Notes for the Manufacturing /TPL Acc DEPRECIATION

Factory Machinery

Cost 180

Depreciation 25% 45 Manufacturing Acc

135

Office Equipment

Cost 40

Depreciation 15% 6 Profit & Loss Acc

34

Delivery Van

Cost 76

Depreciation 25% 19 Profit & Loss Acc

57

Exercise 11Harvey & Nicholl

Notes for the Manufacturing /Trading Acc ACCRUALS

Indirect Wages

Amount Paid 97

Add Accrual 4 Liability (Balance Sheet)

101 Profit & Loss Acc

Office Salaries

Amount Paid 54

Add Accrual 6 Liability (Balance Sheet)

60 Profit & Loss Acc

PREPAYMENT

Rent and Rates

Amount Paid 30

Less Prepayment 5 Asset (Balance Sheet)

25

Exercise 11Harvey & Nicholl

Notes for the Manufacturing /Trading Acc ALLOCATION OF EXPENSES

Rent and Rates

Amended Figure 25

Factory 60% 15 Manufacturing Account

Admin 40% 10 Profit & Loss Account

Insurance of Buildings

Amount Paid 12

Factory 75% 9 Manufacturing Account

Admin 25% 3 Profit & Loss Account

PROVISION FOR DOUBTFUL DEBTS

Debtors 80

Provision 10% 8 Profit & Loss Account

Net Debtors 72 Asset (Balance Sheet)

Exercise 11Manufacturing Account of Harvey Nicholl for

the y/e 31 December

Ledger Balances at 31 December 2004 £000Stocks at 1 January:Raw Materials 75Work in Progress 64Finished Goods 72Direct Factory Wages 682Indirect Factory Wages 97Royalties 23Purchases of Raw Materials 820Returns of Raw Materials 28Carriage on Raw Materials 8Purchases of Finished Goods 107Rent and Rates 30Insurance of Building 12Factory Machinery at cost 180Provision for Depreciation on Factory Machinery 64Office Equipment at cost 40Provision for Depreciation on Office Equipment 26Delivery vans at cost 76Provision for Depreciation on Delivery Vans 28Maintenance of Factory Machinery 23Sales 2,000Office Salaries 54Provision for Doubtful Debts 6Debtors 80Creditors 46NotesStocks at 31 December:Raw Materials 67Work in Progress 59Finished Goods 84

Exercise 11Manufacturing Account of Harvey Nicholl for

the y/e 31December £ £

£ Opening Stock of Raw Materials75

Add Purchases of Raw Materials 820Less Returns of Raw Materials 28 792Add Carriage of Raw Materials 8

800Less Closing Stock of Raw Materials 67 733

COST OF RAW MATERIALS CONSUMED 808 Add Direct Wages 682Add Direct Expenses (royalties) 23 705PRIME COST 1,513 ADD FACTORY OVERHEADSIndirect Wages (97+4) 101Rent and Rates(30 - 5)*60% 15Insurance of building (12* 75%) 9 Provision for Dep of Machinery 45Maintenance of Machinery 23FACTORY OVERHEADS 193

1,706Add WIP at Beginning +64

1,770Less WIP at End -59FACTORY COST OF PRODUCTION 1,711

Exercise 11Trading Profit & Loss Acc of Harvey Nicholl for

the y/e 31 December £ £ £Sales 2,000Less Cost of Goods SoldOpening stock of finished goods (1 Jan) 72Add Factory Cost of Production 1,711Add Purchases of Finished Goods 107

1,890Less Closing stock of finished goods 84 1,806GROSS PROFIT 194Less ExpensesRent and Rates (30-5)*40% 10Insurance of Buildings(12*25%) 3

Provision for Depreciation Of Equip 6Provision for Depreciation Del Vans 19Office Salaries(54+6) 60Provision for Doubtful Debts 2 100NET PROFIT 94

MANUFACTURING PROFIT/LOSS ON MARKET VALUE/PRICE

MARKET VALUE/ PRICE This is the price that the finished goods

could have been purchased for – Instead of the company manufacturing them themselves

MANUFACTURING PROFIT/LOSS A Manufacturing profit is made if the

company can make the goods for less than the market value

A manufacturing loss is made if the cost to make the goods is more than the market value

Therefore:

Market price of Prod – Factory Cost of Prod = Manufacturing profit /loss

Transfer to Trading Account

MARKET VALUE If the MARKET VALUE is known, it

is this amount that is transferred to the TRADING ACCOUNT and NOT the MANUFACTURING COST OF PRODUCTION

MANUFACTURING PROFIT / LOSS A manufacturing PROFIT (calculated

at end of manufacturing account) is ADDED TO the Gross Profit in the trading account

A manufacturing LOSS is DEDUCTED FROM the Gross Profit in the Trading account

Depreciation – Reducing Balance A fixed percentage of Depreciation

is calculated on the NET BOOK VALUE or written down value of the Fixed Asset each year

As the Asset decreases in value the provision for depreciation each year will also reduce

The YEARLY AMOUNT of depreciation is charged to the P&L ACCOUNT

The accumulated depreciation is taken off the Asset’s COST in the BALANCE SHEET

Depreciation – Reducing Balance (Continued)

ExampleOn 1 January Year 1, XYZ plc purchased Fixtures for £30,000 by cheque.

Assets are depreciated by 10% per annum using the reducing balance method.

Year 1 Asset cost 30,000Depreciation = 10% 3,000 P&L AccNBV year 1 27,000 Bal Sheet Year 2NBV from year 1 27,000Depreciation = 10% 2,700 P&L AccNBV year 2 24,300Bal Sheet

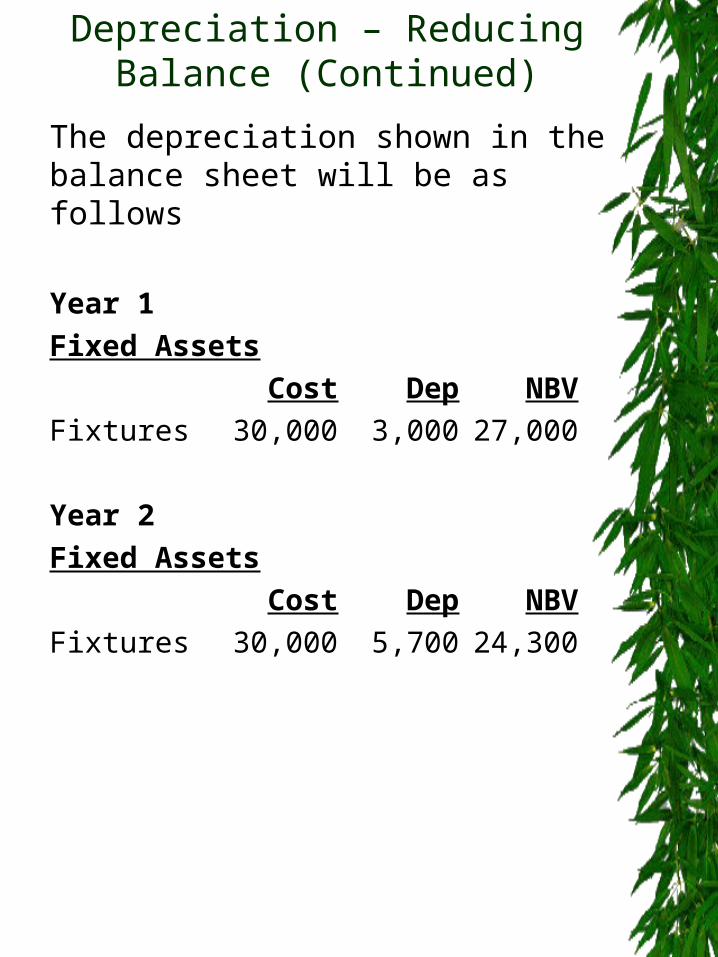

Depreciation – Reducing Balance (Continued)

The depreciation shown in the balance sheet will be as follows Year 1Fixed Assets

Cost Dep NBVFixtures 30,000 3,000 27,000 Year 2Fixed Assets

Cost Dep NBVFixtures 30,000 5,700 24,300

Nethermains

Notes for the Manufacturing/ P&L Account

ACCRUAL

Rates

Amount paid 36

Add Accrual 4 Liab (Balance Sheet)

40 Manufacturing Acc/P&L

APPORTIONMENT

Rates 40

Factory 75% 30 Man O/Head

Admin 25% 10 P&L

Management Salaries 50

Factory 80% 40 Man / O’Head

Admin 20% 10 P&L

Nethermains

DEPRECIATION – REDUCED BALANCE METHOD

Factory Machiney

Cost 60

Depreciation to date 20

Current NBV 40

Yearly Depreciation 20% 8 Man O’Head

New NBV 32

Delivery Vehicles

Cost 20

Depreciation to date 5

Current NBV 15

Yearly Depreciation 20% 3 P&L

New NBV 12

Notes for the Manufacturing/ P&L Account

Manufacturing Account of Nethermains for the y/e 31 May £ £

Opening Stock of Raw Materials 8

Add Purchases of raw materials 250

Add Carriage In of raw materials 5

255

Less Closing Stock of raw materials 6 249

Cost of Raw Materials consumed 257

Add Direct Wages 100

Add Direct Expenses (Royalties) 10

PRIME COST 367

Add Factory Overheads

Management Salaries 40

Factory Labour 13

Factory Power 10

Repairs to Factory Machinery 5

Rates 30

Heat & Light 24

Dep of Factory Machinery 8

Factory Overheads 130

497

Manufacturing Account of Nethermains for the y/e 31 May

£ £

B/F 497

ADD WIP at beginning 4

501

Less WIP at end 5

FACTORY COST OF PRODUCTION 496

Market value of finished goods 520

Less Factory Cost of Production 496

Manufacturing Profit 24

Trading Account of Nethermains for the year ended 31 May

£ £

Sales 960

LESS Cost of Sales

Opening stock of finished goods 12

Add purchases of finished goods 119

131

Less return of finished goods 2

129

ADD Mkt V of finished goods 520

649

Less Closing stock of finished goods 9

Cost of Sales 640

GROSS PROFIT 320

Add Manufacturing Profit 24

344